Lecture 1 Historical development of Accounting

30

1 LECTURE 1

Transcript of Lecture 1 Historical development of Accounting

1

LECTURE 1

LEARNING OBJECTIVES

At the end of this lecture, the student should be able to:

Describe the age of record keeping Understand the birth of double entry

accounting Describe the age of stagnation Relate to the age of scientific accounting

and issues of recognition and measurement

2

3

LEARNING OBJECTIVE 1LEARNING OBJECTIVE 1

The age of record keeping

Record keeping

Accounting emerged from an old tradition of stewardship, eg. in ancient society, steward assumed responsibility for estate supervision and act as proxy to the ruler or over-lord.

Stewards were members of the lord’s central council and often occupied by ambitious clergy or law graduates.

Record keeping was just aimed at maintaining integrity and discovering misappropriation.

4

Record keeping – continued.

In most ancient societies, after the annual harvest had been gathered in autumn, a party of auditors would physically check the record against the volume harvested.

Among the most ancient records are on clay tablets dating from 2500BC relating to the Sumerian civilisation showing a series of transaction involving grain.

5

Record keeping – continued.In terms of volume the clay tablets found in Mesopotamia (now Iraq) indicate considerable attachment to written record keeping where each party of the transaction would affix their signatures by impressing their seals into the clay tablet.

Pharoahs in Egypt operated an advanced form of stores accounting recording receipts and disbursements which was regularly audited when papyrus was introduced.

6

Record keeping – continued.

The record keepers could rise to high office in these ancient societies, however irregularities could be punished-Woolf,1986.

Records are important as they reminded owners of the quantities of stores held and enabled owners to control the activities of their stewards.

However many record keepers (stewards) have operated a system of income smoothing as medieval auditors contented themselves with meeting standards yields.

7

Record keeping – continued.They understate the natural increase of livestock, or make good any trading losses from money accumulated, holding back surpluses and report during bad times.

However not all those eligible wanted to be a steward as they were personally liable for errors of omission or commission.

8

Record keeping – continued.Mid fourteenth century, written accounts and knowledge of standard levels of achievement became more widespread and as a consequence, the control of the steward became less direct.

During the 20th century, modern ideas of accountability, performance measurement and managerialism in a way weakened the concept of stewardship which rests on assumptions of independence, indirect control and standard expectations.

9

Record keeping – continued.In 1950s there has been transfer of power from semi-independent stewards to managers who demand full accountability and new performance measurements were determined.

The transition from independent stewardship to full accountability had been very gradual and spread over many centuries.

10

Written accounting records

From the 14th to the late 15th century, written forms of accounting became more common.

Numeric systems were based on English accounts, Roman numerals and Arabic numerals and operated for some 400 years.

Written single entry records were largely that of receipts and payments, and settle differences between partners or of inventories interspersed with chronological narratives and were meant to serve only internal purposes.

Even rendered into a written forms, there were problems. Why?

11

Written accounting records - continued

Use of Roman numerals in the 15th century made calculation and understanding more difficult as Roman numerals have neither zero nor place values, and therefore addition, subtraction, division and multiplication cannot be done.

Records were in narrative form and research (Noke, 1981) found that there was no attempt to have a money or quantity column extended from the narrative.

The use of Arabic numerals was resisted on the grounds that they could be more easily changed for fraudulent purposes by adding, removing or altering a single figure.

12

Written accounting records - continued

Records were quantified in terms of physical volumes rather than currency value, thus without values account could not be inter linked and the concepts of income and performance could not be applied.

Early records were intended to keep a check on workers and to prevent fraud and misappropriation and not as a basis of performance measurement.

13

Learning Objective 2 The birth of double entry accounting

14

The birth of double entry accounting

The earliest double entry records, which have survived are from a bank ledger from Florence of 1211 and books from Genoa of between 1340 – 1466.

Florence was the hub of a European banking network and Genoa was an overseas trading centre (Martinelli, 1983).

Some scholars argue that origins of double entry accounting come from China and was brought to Italy by the explorer, Marco Polo while others claim that double entry originated in India.

It is argued that Indian traders took the double entry system to Italy.

Whatever the case, the origin of double entry are shrouded in mystery.

15

The birth of double entry accounting - continued

The technique of double entry was publicised by Luca Pacioli, in a book published in Venice in 1494.

The technique was well established in Italian banks of the period, who financed maritime operations, in particular, the Christian crusades to re-capture Jerusalem from Arab posession.

The technique was superior to single entry as it enable transactions to be recorded in a more systematic and orderly manner, and trial balance produced provided an arithmetical check on records and a balancing of the books.

The internal control elements inherent in double entry allowed the division of duties between bookkeepers facilitating specialisation, thus reducing errors and making fraud more difficult.

16

The birth of double entry accounting - continuedFollowing the recommendation of Pacioli’s ‘Summa’ of 1494, in order to open a merchant’s books, the values of all assets and liabilities need to be entered.

Operations are then recorded, first in a memorandum, then expressed as debits and credits in a journal before being recorded in the ledger.

Summa however showed little interest in trading performance or the calculation of profit; probably because merchant enterprises of the period were short term ventures terminating in cash distributions.

17

Learning Objective 3The age of stagnation

18

The age of stagnation 1500 - 1800In this period, there were few improvements in accounting techniques and in most societies single entry still dominated record keeping.

The techniques of double entry very slowly gained ground and became more widespread and acceptable.

Prolonged use of single entry are most likely due to the small size of businesses with little distinction between ownership and management and the relatively few transactions involved.

Most merchants were owner managers and familiar with every aspect of their trade.

19

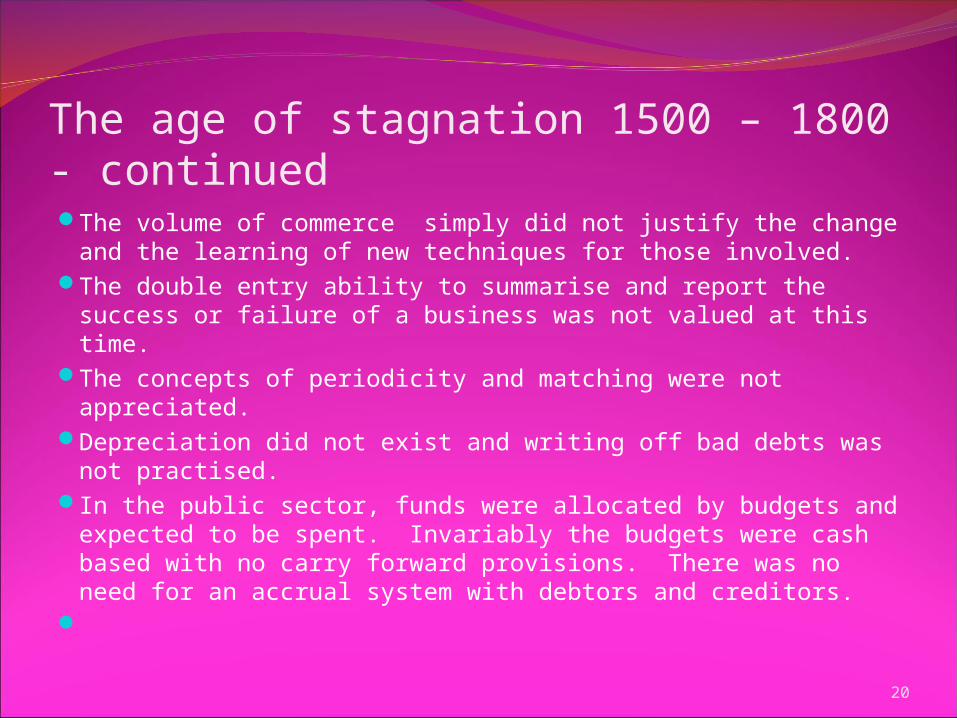

The age of stagnation 1500 – 1800 - continuedThe volume of commerce simply did not justify the change and the learning of new techniques for those involved.

The double entry ability to summarise and report the success or failure of a business was not valued at this time.

The concepts of periodicity and matching were not appreciated.

Depreciation did not exist and writing off bad debts was not practised.

In the public sector, funds were allocated by budgets and expected to be spent. Invariably the budgets were cash based with no carry forward provisions. There was no need for an accrual system with debtors and creditors.

20

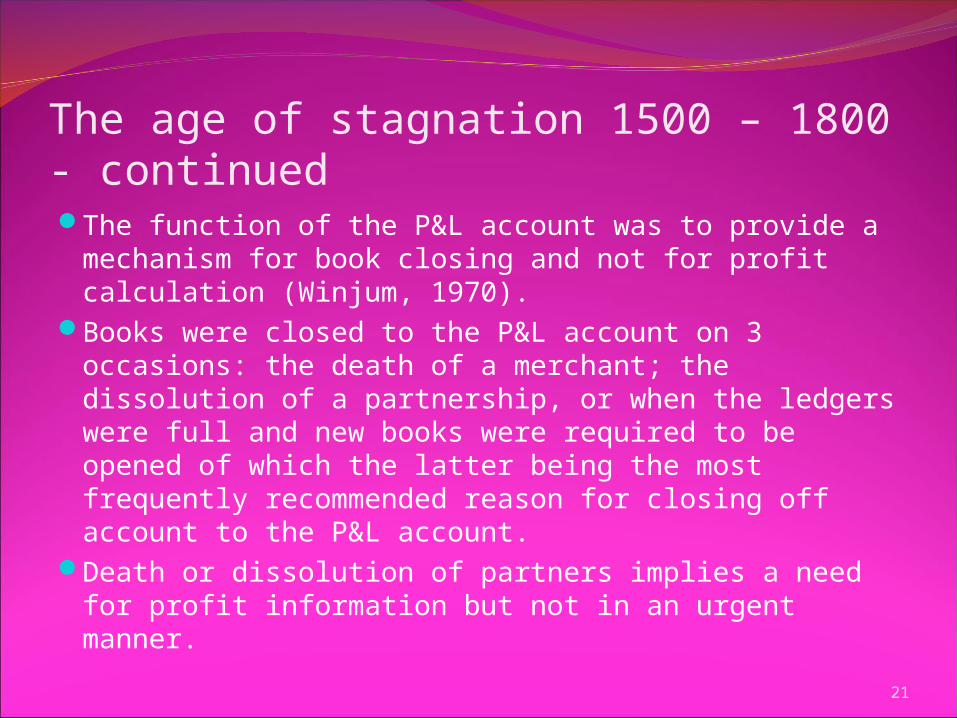

The age of stagnation 1500 – 1800 - continuedThe function of the P&L account was to provide a mechanism for book closing and not for profit calculation (Winjum, 1970).

Books were closed to the P&L account on 3 occasions: the death of a merchant; the dissolution of a partnership, or when the ledgers were full and new books were required to be opened of which the latter being the most frequently recommended reason for closing off account to the P&L account.

Death or dissolution of partners implies a need for profit information but not in an urgent manner.

21

Learning Objective 4The age of scientific accounting

22

The age of scientific accounting

By the 19th century, accounting had become much more discriminating.

Professional specialists were learning how to tailor profits to fulfill owners’ expectations.

The growth of company legislation and professional societies limited and legitimised discretion as to what should be recognised and how assets should be measured.

The Industrial Revolution that occurred in England posed new problems of recognition, measurement and accountability to accountants.

23

The age of scientific accounting - continuedThe problems surfaced due to the separation of ownership and management in large scale industrial enterprises. Industrial operations eg. railways and utility companies require large initial amount of capital which was raised from a scattered group of shareholders.

As such management were expected to regular reports to the shareholders as to what was happening with their money.

Healthy profits and regular dividends were promised, which it was not always possible to deliver.

24

The age of scientific accounting - continuedNew practices of accounting was demanded during this era. Accountants were required to distinguish between capital and revenue items, private and business transactions, measure the value of fixed assets, determine rates and methods of depreciation, provisions, and write-off bad debts.

There was no smooth path of progress in adopting these techniques.

Many of the practices accountants use today was determined in this era as a result of business failure and loss of shareholders confidence.

Creative accounting techniques were adopted during this time to give the illusion of profits and in some cases dividends were paid from borrowings off-balance sheet.

25

The age of scientific accounting - continuedMany of the early 19th century railway companies collapsed after the managers and their employee accountants constructed illusory profits to attract or appease owners.

What and how to report to investors was left up to the managers to decide. Unfortunately sometimes, the managers for reasons of self interest, choose to exaggerate performance and present to shareholders glowing reports of the industry and business acumen while hiding potentially disastrous liabilities.

The share market were then crashed after a brief period of investor frenzy, prompted by claims of vast but illusory profits from the promoters of new railway companies.

26

The age of scientific accounting - continuedThe chief causes of failure centred around the accounting problems of distinguishing between capital and revenue and the allocation of asset depreciation to expenses with both issues were extremely relevant to railways with a high level of capital investment.

UK government stepped in and passed the Railway Act 1867 requiring compulsory audits for railway companies and that dividend to be paid only after audit certification.

Many issues such as valuation of fixed assets were eventually assumed to have been settled by adopting such concepts as prudence, going-concern, matching and historical cost concept less depreciation as a standard method for measurement. The accruals principle was also adopted.

The approaches were eventually cemented by various companies Acts and the conceptual framework and professional standards known as ‘recommendations’ introduced by the UK professional bodies in 1943.

27

Accounting regulationOnly in 20th century, the practice which can be traced back many hundreds of years were subject to regulation

Why increasing level of separation between owners and managers in recent centuries

Previously there was a limited separation between the ownership & management

Increase separation in recent centuries leads to an increased tendency to regulate the accounting practices

28

Accounting regulation-continuedInitially, there was limited work to codify the existing practices.

In 1930, accounting profession within US cooperated with NYSE to develop a list of broadly used accounting principles.

The publication basically set the foundation for the codification & acceptance of Generally Accepted Accounting Principles

Later on, in 1934, within US, specific disclosures of financial information were required for those organisation seeking to trade their securities where it was administered by SEC

In UK, was not until 1970 when the Accounting Standards Steering Committee was established where UK accountants had to conform with professionally developed mandatory accounting standards.

Prior to that, ICAEW released a series of recommendations to members.

29

30

End of Lecture 1