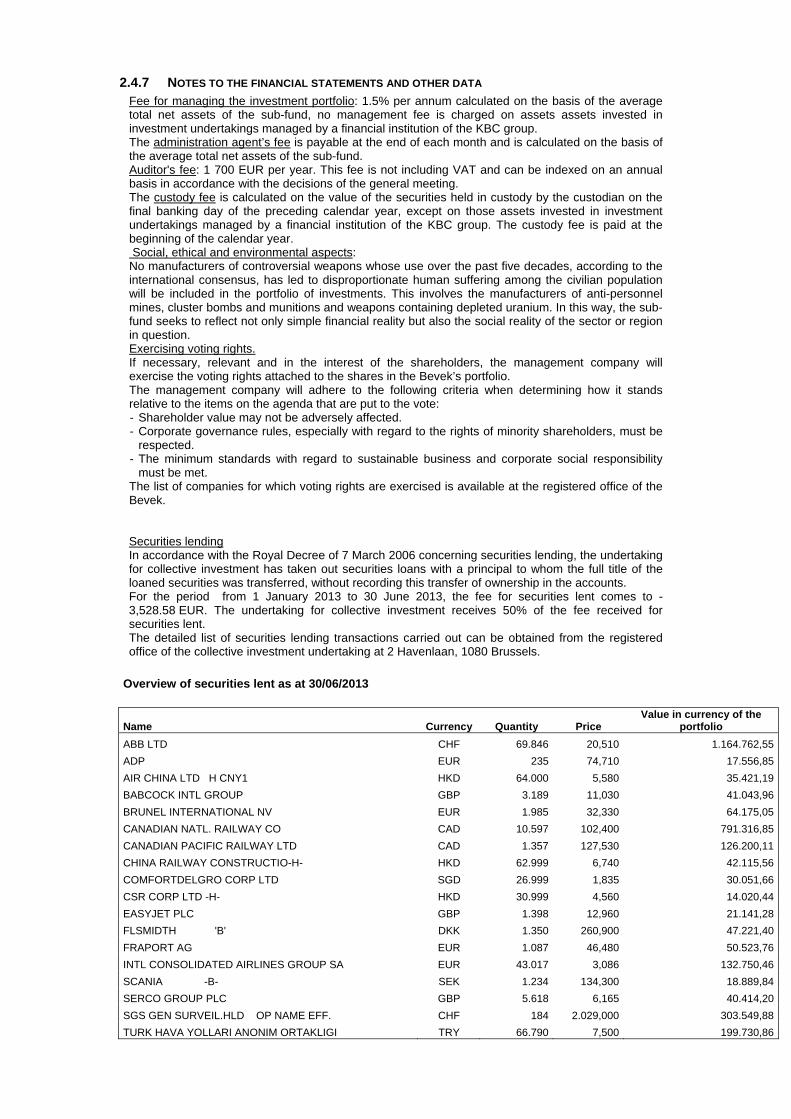

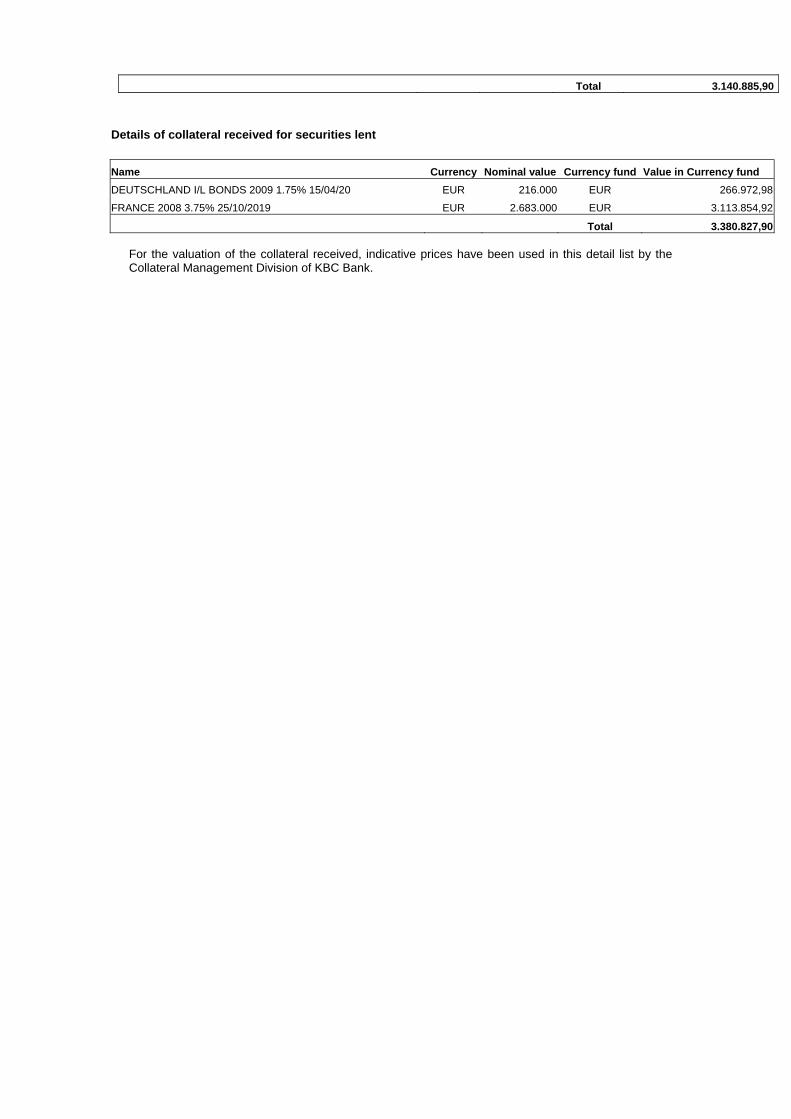

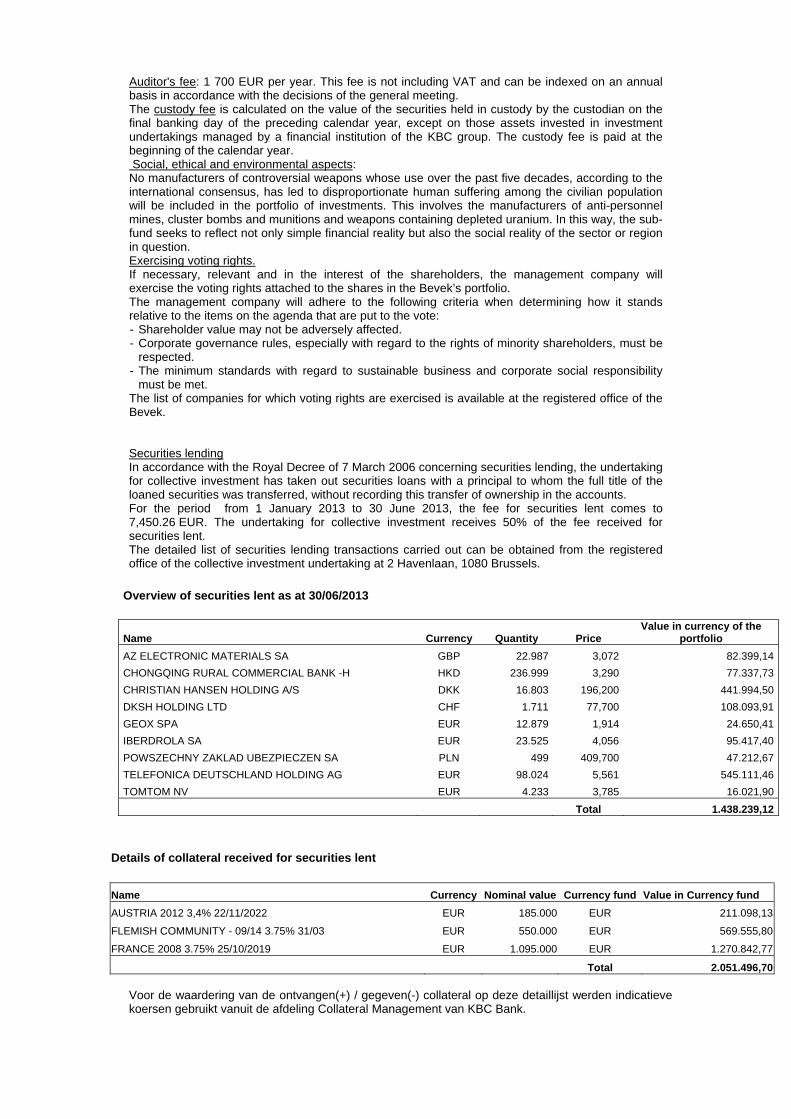

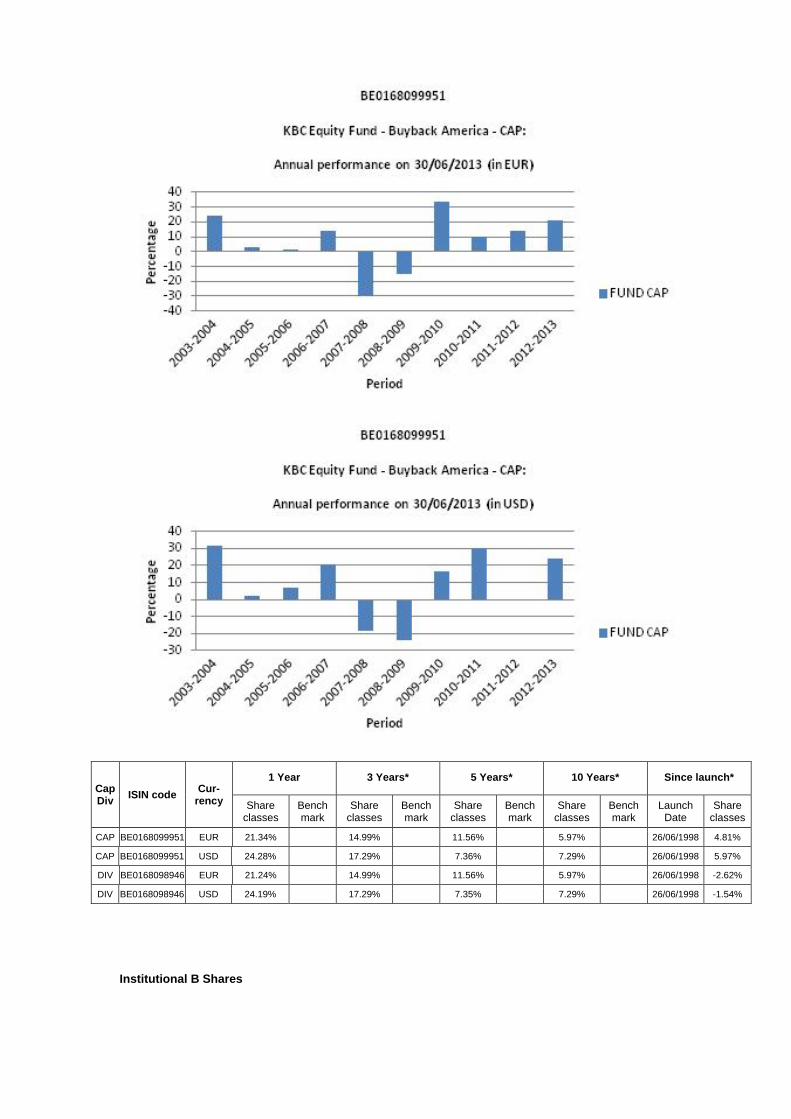

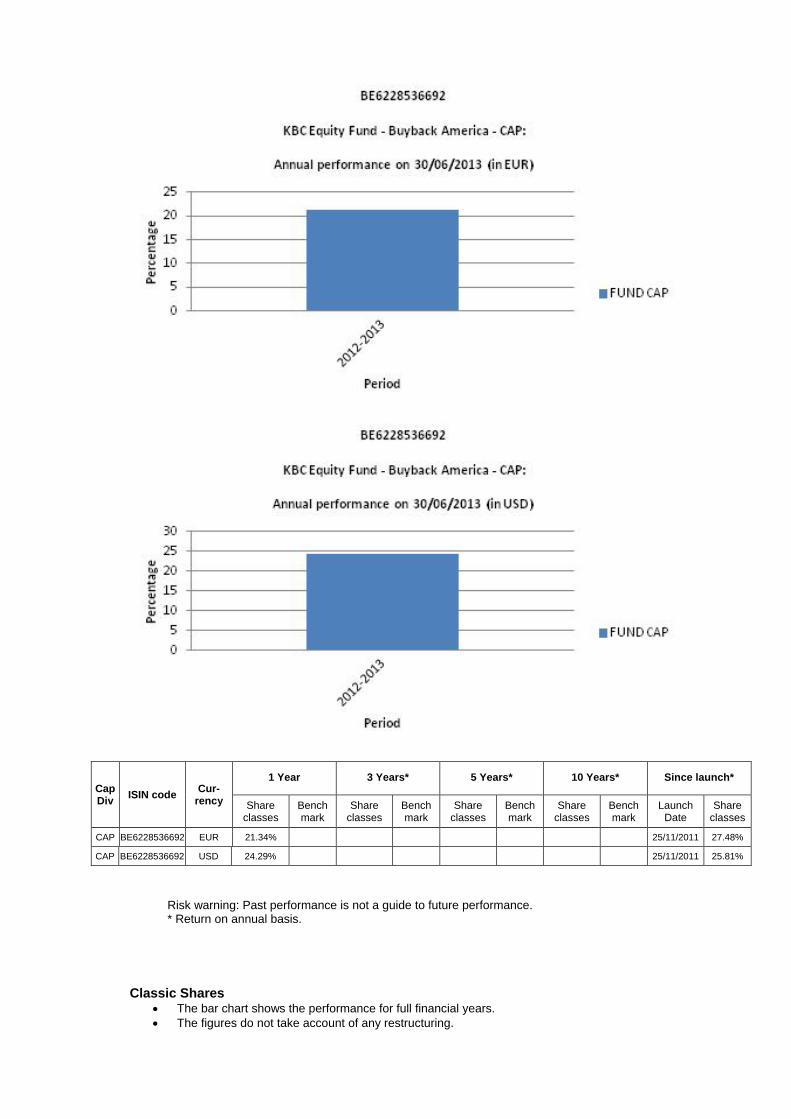

KBC Equity Fund - TeleTrader.com

1252

Semi-Annual report as at 30 th June 2013 KBC Equity Fund Public open-ended investment company under Belgian law (bevek) with a variable number of units/shares opting for Investments complying with the conditions of Directive 2009/65/EC UCITS No subscriptions will be accepted on the basis of this report. Subscriptions will only be valid if effected after a free copy of the key investor information or prospectus has been provided.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of KBC Equity Fund - TeleTrader.com

Semi-Annual report as at 30th June 2013

KBC Equity Fund

Public open-ended investment company under Belgian law (bevek) with a variable number of units/shares opting for Investments

complying with the conditions of Directive 2009/65/EC UCITS

No subscriptions will be accepted on the basis of this report. Subscriptions will only be valid if

effected after a free copy of the key investor information or prospectus has been provided.

TABLE OF CONTENTS

1. General information on the bevek

1.1. Organization of the bevek

1.2. Management report 1.2.1. Information for shareholders 1.2.2. General market overview

1.3. Aggregate balance sheet

1.4. Aggregate profit and loss account

1.5. Summary of recognition and valuation rules

1.5.1. Summary of the rules 1.5.2. Exchange Rates

SWI

Schreibmaschinentext

SWI

Schreibmaschinentext

SWI

Schreibmaschinentext

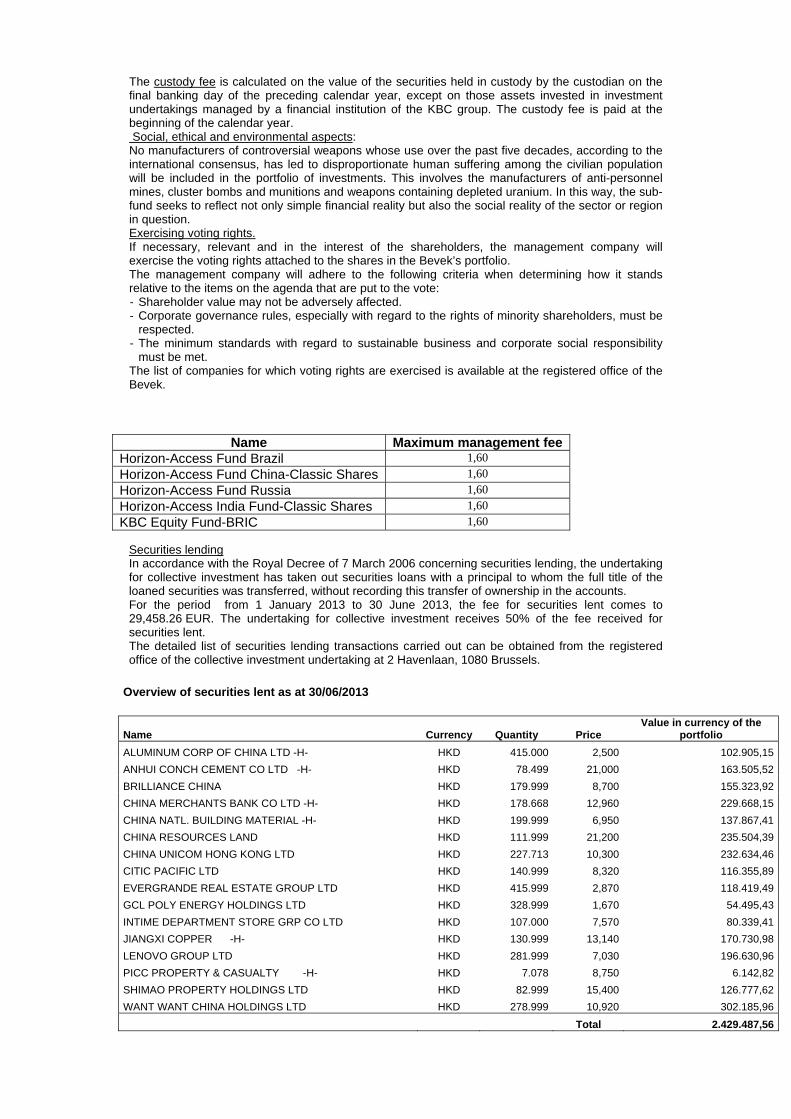

No notification has been submitted for the sub-fund CSOB Akciovy Fond Dividendovych Firem and consequently this sub-fund must not be publicly marketed in Germany.

SWI

Schreibmaschinentext

SWI

Schreibmaschinentext

SWI

Schreibmaschinentext

SWI

Schreibmaschinentext

SWI

Schreibmaschinentext

SWI

Schreibmaschinentext

1. GENERAL INFORMATION ON THE BEVEK

1.1 ORGANIZATION OF THE BEVEK

REGISTERED OFFICE : 2 Havenlaan - B-1080 Brussels, Belgium.

DATE OF INCORPORATION: 21 March 1991

LIFE: Unlimited.

BOARD OF DIRECTORS OF THE BEVEK: Dirk Thiels, Head of Asset Allocation and Strategy Portfolios KBC Asset Management NV Wouter Vanden Eynde, Managing Director KBC Asset Management NV Olivier Morel, Financial Manager CBC Banque SA Theo Peeters, Independent Manager Luc Vanderhaegen, Private Banking & Wealth Management Branch General Manager KBC Bank NV

Chairman: Luc Vanderhaegen, Private Banking & Wealth Management Branch General Manager KBC Bank NV Natural persons to whom the executive management of the bevek has been entrusted: Dirk Thiels, Head of Asset Allocation and Strategy Portfolios KBC Asset Management NV Wouter Vanden Eynde, Managing Director KBC Asset Management NV

MANAGEMENT TYPE: Bevek that has appointed a company for the management of undertakings for collective investments. The appointed management company is KBC Asset Management NV, Havenlaan 2, B-1080 Brussels.

DATE OF INCORPORATION OF THE MANAGEMENT COMPANY: 30 December 1999.

NAMES AND POSITIONS OF THE DIRECTORS OF THE MANAGEMENT COMPANY: Chairman: L. Gijsens Directors: D. Mampaey, President of the Executive Committee J. Peeters, Independent Director P. Buelens, Managing Director J. Daemen, Non-Executive Director P. Konings, Non-Executive Director J. Verschaeve, Managing Director G. Rammeloo, Managing Director O. Morel, Non-Executive Director K. Mattelaer, Non-Executive Director K. Van Eeckhoutte, Non-Executive Director W. Vanden Eynde, Managing Director C. Sterckx, Managing Director D. Cuypers, Managing Director

NAMES AND POSITIONS OF THE NATURAL PERSONS TO WHOM THE EXECUTIVE MANAGEMENT OF

THE MANAGEMENT COMPANY HAS BEEN ENTRUSTED: D. Mampaey, President of the Executive Committee P. Buelens, Managing Director

J. Verschaeve, Managing Director G. Rammeloo, Managing Director W. Vanden Eynde, Managing Director C. Sterckx, Managing Director D. Cuypers, Managing Director These persons may also be directors of various beveks.

AUDITOR OF THE MANAGEMENT COMPANY: Ernst & Young Bedrijfsrevisoren BCVBA, represented by Christel Weymeersch, Company Auditor and auditor recognized by the Belgian Financial Services and Markets Authority, De Kleetlaan 2, 1831 Diegem.

STATUS OF THE BEVEK: Bevek with various sub-funds that has opted for investments complying with the conditions of Directive 2009/65/EC and which, as far as its operations and investments are concerned, is governed by the Act of 3 August 2012 on certain forms of collective management of investment portfolios.

FINANCIAL PORTFOLIO MANAGEMENT: In this regard, please see ‘Information concerning the sub-fund’.

FINANCIAL-SERVICES PROVIDERS: The financial services providers in Belgium are: KBC Bank NV, Havenlaan 2, B-1080 Brussels CBC Banque SA, Grand Place 5, B-1000 Brussels

CUSTODIAN: KBC Bank N.V., 2 Havenlaan - B-1080 Brussels, Belgium.

ADMINISTRATION AND ACCOUNTING MANAGEMENT: KBC Asset Management N.V., 2 Havenlaan - B-1080 Brussels, Belgium.

ACCREDITED AUDITOR OF THE BEVEK: Deloitte Bedrijfsrevisoren BV o.v.v.e. CVBA, in the form of a CVBA (co-operative limited liability company), Berkenlaan 8b, B-1831 Diegem, represented by partner Frank Verhaegen, company auditor and auditor recognised by the Belgian Financial Services and Markets Authority.

DISTRIBUTOR: KBC Asset Management S.A., 5, Place de la Gare, L-1616 Luxembourg.

PROMOTER: KBC

LIST OF SUB-FUNDS OF KBC EQUITY FUND

1. America

2. Belgium

3. BRIC

4. Buyback America

5. Buyback Europe

6. Central Europe

7. Commodities & Materials

8. Consumer Durables

9. CSOB Akciovy Fond Dividendovych Firem

10. CSOB BRIC

11. Eastern Europe

12. Euro Cyclicals

13. Euro Finance

14. Euro Non Cyclicals

15. Euro Telecom & Technology

16. Europe

17. Eurozone

18. Fallen Angels

19. Finance

20. Flanders

21. Food & Personal Products

22. Global Leaders

23. Growth by Innovation

24. High Dividend

25. High Dividend Eurozone

26. High Dividend New Markets

27. High Dividend North America

28. Industrials & Infrastructure

29. Japan

30. Latin America

31. Luxury & Tourism

32. Medical Technologies

33. New Asia

34. New Markets

35. New Shares

36. Oil

37. Pacific

38. Pharma

39. Pharma Growth

40. Quant EMU

41. Quant Europe

42. Quant Global 1

43. Satellites

44. SRI Equity

45. Technology

46. Telecom

47. Trends

48. Turkey

49. US Small Caps

50. Utilities

51. World

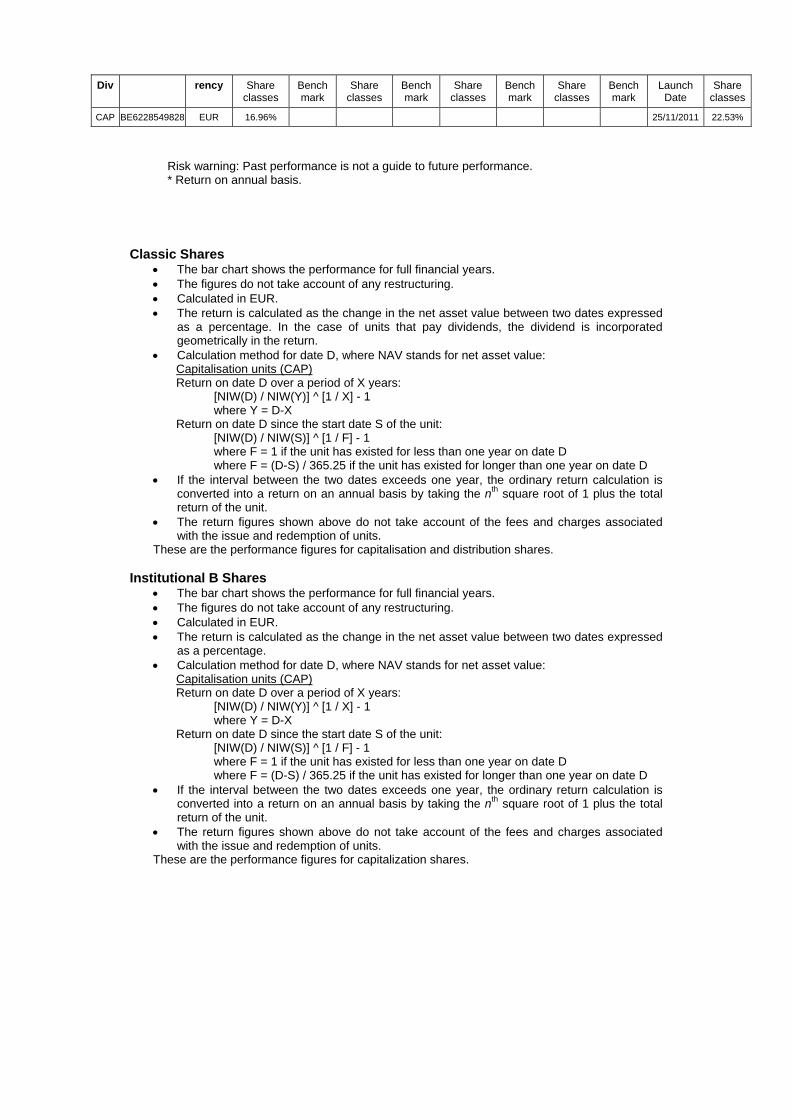

SHARE CLASSES The characteristics of the different share classes are given in the prospectus. The following sub-funds have a share class called ‘Classic Shares’:

America

Buyback America

Buyback Europe

Central Europe

Commodities & Materials

Consumer Durables

Eastern Europe

Euro Cyclicals

Euro Finance

Euro Non Cyclicals

Euro Telecom & Technology

Eurozone

Finance

Food & Personal Products

Global Leaders

Growth by Innovation

High Dividend

High Dividend Eurozone

High Dividend New Markets

High Dividend North America

Industrials & Infrastructure

Japan

Luxury & Tourism

Medical Technologies

Millennium

New Asia

New Markets

Oil

Pacific

Pharma

Pharma Growth

Quant EMU

Quant Europe

Quant Global 1

Satellites

SRI Equity

Technology

Telecom

Turkey

US Small Caps The following sub-funds have a share class called ‘Institutional Shares’:

SRI Equity

The following sub-funds have a share class called ‘Institutional B Shares’:

America

Buyback America

Buyback Europe

Central Europe

Commodities & Materials

Consumer Durables

Eastern Europe

Euro Cyclicals

Euro Finance

Euro Non Cyclicals

Euro Telecom & Technology

Eurozone

Finance

Food & Personal Products

Global Leaders

Growth by Innovation

High Dividend

High Dividend Eurozone

High Dividend New Markets

High Dividend North America

Industrials & Infrastructure

Japan

Luxury & Tourism

Medical Technologies

Millennium

New Asia

New Markets

Oil

Pacific

Pharma

Pharma Growth

Quant EMU

Quant Europe

Quant Global 1

Satellites

SRI Equity

Technology

Telecom

Turkey

US Small Caps

In the event of discrepancies between the Dutch and the other language versions of the (Semi-)Annual report, the Dutch will prevail.

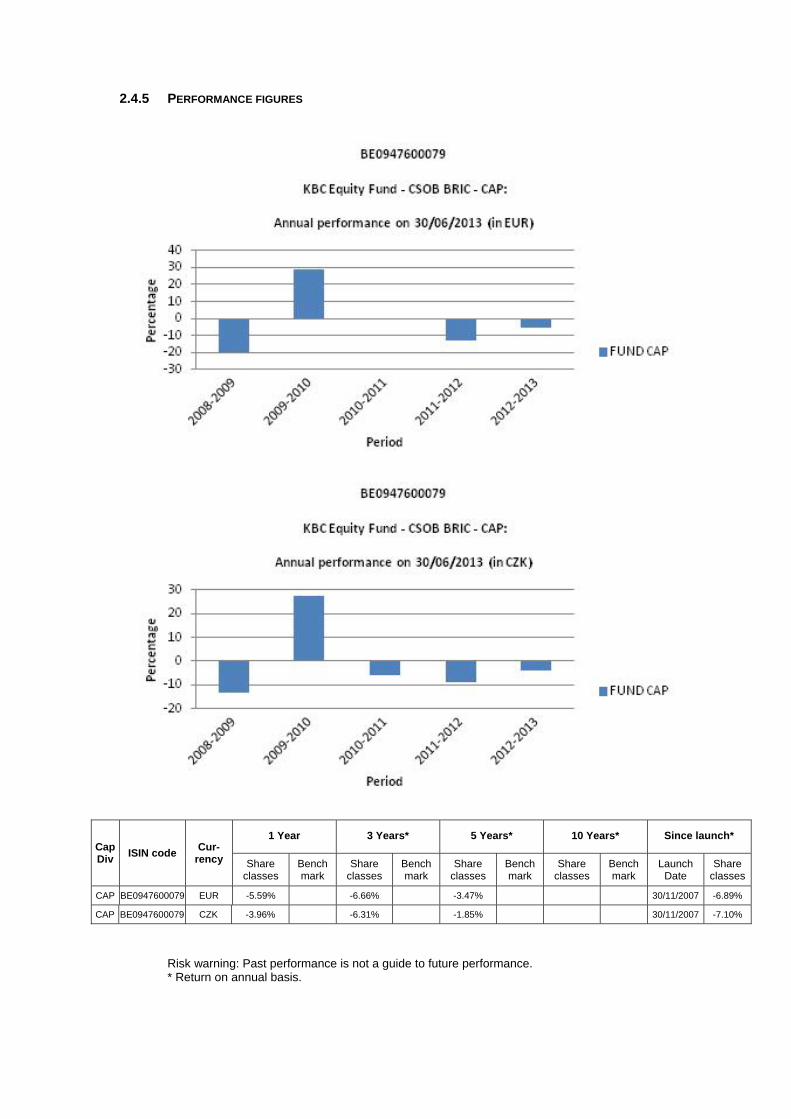

1.2 MANAGEMENT REPORT

1.2.1 INFORMATION FOR THE SHAREHOLDERS

Not applicable.

1.2.2 GENERAL MARKET OVERVIEW

General investment climate 1 January – 30 June 2013 Doubts about the sustainability of the economic recovery continued to shape investor sentiment. The debt crisis in Europe continued unabated, although the European Central Bank (ECB) managed to convince the market that it had the crisis under control. Major steps were taken in the United States to reform the federal budget, seemingly without adversely affecting economic growth too much. Fortunately, strong economic growth in Asia created export opportunities for American and European businesses. The economic tightrope Although more jobs have been created than lost in the US since 2010, the rate of employment growth remained on the thin side for some considerable time. The situation began to improve in the recent reporting period, with the result that the jobless rate has declined more markedly. Pay has remained virtually flat, barely rising ahead of inflation. Taken together, these two factors ensured that household purchasing power only grew to a very limited extent and so contributed very modestly to economic growth. The latter was therefore limited (+1.6% growth year-on-year in the four quarters to the first three months of 2013). Real GDP in the EMU contracted by an annualised 1.1%. The austerity programme and credit restrictions pushed Southern Europe into a deep recession. Germany played its traditional role as the driver for European economic growth to a lesser extent than in the recent past. Greater divergence within Europe resulted primarily in a further decline in unemployment in Germany and an alarmingly rapid rise in unemployment in countries such as Greece, Spain and Portugal. Belgium was closer to the strong core of the euro area. The weak growth in the Western economies was not without its impact on the export performance in emerging countries. In recent years, however, domestic demand (due to a rapidly growing middle class with a high consumption rate) and intra-regional trade within Asia have been playing an increasingly important role. The region is better armed to deal with financial crises than it was in the past. Public finances are healthy, the balance of payments is generally neutral (China actually has an astronomical surplus) and the internal savings buffer is high. Asia’s economic development no longer depends on fickle foreign capital. Thanks to the contribution by the emerging markets the growth of world GDP held up in 2012–13 (estimated at 2–2.5%). Stemming the euro crisis There have been no significant bankruptcies in the business sector in recent years. The solvency and liquidity of non-financial companies have seldom been as strong as they are at present. A new feature of this cycle is that government paper, which had previously been seen as entirely risk-free, also started to be tainted with a degree of credit risk. Greece, Ireland, Portugal and Cyprus were no longer able to finance their sovereign debt through the usual channels and are now under the curatorship of the ECB, EU and IMF troika. Private bondholders were obliged to accept a rescheduling of Greek government debt. In Cyprus deposit holders are being required to help defray the cost of cleaning up the banking sector. Italy and Spain were frequently in the firing line. Spain has already applied for European assistance for the recapitalisation of its banks. During all these storms euro area

leaders have tried to reform the rules of the game of the monetary union, but it takes a lot of time and effort to get 17 parties singing from the same hymn sheet. The ESM became operational after much delay. The new budget treaty, which came into force on 1 January 2013, is already being questioned. The competitiveness pact does not include any solid commitments. The negotiations on the formation of a banking union have been tricky. So it is no wonder that the eurosceptics are having a field day. As inherently loyal investors in government bonds, European banks were highly sensitive to the consequences of the euro crisis and the write-downs on their bond portfolios, as they had already seen their capital base seriously eroded in the 2008–09 credit crisis. The euro crisis could easily have ended up therefore as a systemic crisis, something that the ECB wanted to avoid at all costs. Various programmes were launched to ensure and accelerate the provision of liquidity to the sector. The ECB deployed its bazooka in September 2012: the OMT (Outright Monetary Transactions) programme. The ECB is prepared to buy up (short-dated) bonds of under-fire countries for an unlimited period and in unlimited quantities, provided a number of conditions are met. The most important of these is that the government in question submits a formal request for a bailout under the ESM. That explains why, almost a year later, the OMT programme has yet to launch. The financial markets have not however been disturbed by this. For them the setting up of the European bazooka was enough in itself to regard the euro crisis as having been averted. At least for the time being. Public finances have gone off the rails not only in the EMU, but also in the UK and the US. The budget debate in the US had reached a political impasse. The ideological divisions between Republicans and Democrats long prevented a compromise. Decisions were postponed, and so 31 December 2012 became an important deadline. A whole series of tax cuts and other temporary support measures from the past would then lapse. In total these involved a sum of 550 billion USD. Extending all the measures again was not feasible in budgetary terms, while allowing them all to expire was economic suicide. The fiscal cliff was averted on 1 January 2013 by means of an agreement in Congress: half the stimulus measures were made permanent or were extended for a further twelve months, while the other half lapsed. This has not been the only measure involving tightening of budgetary policy in 2013: on 1 March, automatic spending cuts came into effect under which Federal expenditure will be pruned by 85 billion USD each year for a period of ten years. Since no budget has been approved in the current financial year, the federal administrations have only been assigned budgets equal to the expenditure in the previous financial year. That too is automatically leading to more frugal management. New record for corporate earnings The recovery in corporate earnings as from Q4 2009 was just as impressive as the decline in earnings during the recession. So although the economic recovery in the West may be modest, the same has certainly not been true of corporate earnings. After going from negative to positive in the last quarter of 2009, earnings per share of the S&P 500 companies as a whole rose by an average 48% in 2010, by 14% in 2011 and by 4.8% in 2012. The lacklustre economic situation in the West was not an obstacle to a strong increase in turnover. The emerging economies, which are booming, are becoming an increasingly significant market outlet for Western companies. However, the improved earnings were due more to a sharp reduction in (wage) cost pressure than to increased turnover, at least until the first quarter of 2012. Expensive commodities: more than a gauge of the economic recovery The Arab Spring and the conflict in Libya pushed up the price of Brent crude to 126 USD per barrel at the end of April 2011. In the past two years, the supply and demand situation (weak global demand and high stocks, increasing supply) has depressed oil prices, but this was offset by increased geopolitical tension (embargo on Iranian oil exports). At the end of June 2013 the price of a barrel of crude oil was 102.60 USD. The steep price rises on most other commodity markets had already come to an end. The prices of many industrial metals and agricultural products peaked around mid-February

2011. This was followed by a correction of 20–30%. This too could be interpreted as a sign of increasing doubts about the economy. Inflation cooled as a result. In the US the annual increase in the consumer price index fell from a peak of 3.9% in September 2011 to 1.6% in May 2013. Inflation in the EMU dipped from 3% to 1.4% in the same period. A policy of (almost) free money and other unconventional measures The US central bank (the Fed) had already cut its key rate very early on in the crisis. Since December 2008 the rate has been a symbolic 0.25%. The ECB waited much longer before cutting rates. When Mario Draghi took the helm at the ECB on 1 November 2011, the die was cast in favour of monetary easing. The ECB’s key rate is 0.50% at present. This interest rate policy failed to place the economic recovery on a sustainable basis. The Fed therefore explored the scope for other measures, intervening directly on the bond markets and buying up large amounts of debt paper in an attempt to keep the long-term rate low, as well. The ECB dragged its feet, and only followed the Fed’s example much later. The intensification of the euro crisis in fact left the ECB no other choice. Bond markets volatile Increasing doubts about the economy and the ongoing euro crisis have pushed US and German bond rates down since March 2011. This trend continued in 2012 and well into spring 2013 too. On 1 June 2012, US and German ten-year rates hit lows of 1.45% and 1.15% respectively. Ten-year rates continued to move around these low levels (lower than inflation) for almost an entire year. Yields on government bonds then shot up in June, after Fed Chairman Ben Bernanke floated the idea at the end of May of beginning to scale down quantitative easing. At the end of the period under review, ten-year yields stood at 2.48% in the US and 1.78% in Germany. Bond portfolios were restructured en masse. Debt paper issued by under-fire European governments was dumped, in spite of the international guarantees, and replaced by German paper. In the course of 2012 Spanish government bonds were the most targeted. The Belgian-German rate spread also suffered from the tensions in the euro area at times. The days when Belgium could borrow money at the same terms as Germany are long gone. The Belgian-German rate spread, which peaked on 25 November 2011 at 365 basis points, fell by more than the euro area average during the period under review. On 30 June, bond investors were satisfied with a premium of 90 basis points for their ‘Belgium risk’. The health of the European banks is closely linked to the euro crisis. Pessimism about the intractability of the euro problems and optimism about an ultimate and radical breakthrough produced alternating waves of panic and relief concerning the solvency of European banks. This was in turn reflected in highly erratic movements in the rates at which banks were able to obtain funding in the bond market. Similarly the interest-rate premiums for non-financial debtors suffered from the credit risk fears. The fact that these companies could in most cases boast cast-iron balance sheets was not always taken into account. In brief, even though credit spreads have narrowed substantially in recent months, they are still on the high side. Every reserve currency has its problems In a year marked by problems in keeping the EMU from imploding, the EUR/USD exchange rate was no more volatile than at other times. The euro was trading at USD 1.30 at the end of June 2013, which is roughly the same rate as 2012 year-end. Of course the US dollar also has its problems. The dollar’s image as the global reserve currency suffered as a result of QE2, QE3 and TWIST, acronyms for the purely monetary financing of budget deficits that were increasing to irresponsible levels. The rise of the yen – a notable feature in recent years – was finally halted. The Japanese government’s policy of talking down the currency bore fruit. At the end of June 2013 the yen was already 12.5% lower against the USD than at 2012 year-end, when the Abe

government came to power – a state of affairs regarded by other Asian countries as a looming currency war. The Australian dollar (-10.8%), Norwegian krone (-6.3%), Polish zloty (-5.6%), sterling (-5.1%) and Canadian dollar (-4.3%) all fell substantially against the euro in 2013. Consolidation of the stock-market rally The initial phase of the economic recovery went hand in hand with a fine stock-market rally, leaving the S&P 500 75% higher at the end of April 2010 than its low point on 9 March 2009. Since then, the equity markets have struggled to find fresh impetus. The euro crisis and fear that the European banking sector would collapse naturally continued to cast a dark cloud over the market. On top of this, the stock markets were affected by vacillating sentiment about the economic situation. This was also true in recent months. In the first three months of 2012 the markets were buoyed up by relative economic optimism. In April/May 2012 the markets ran out of steam but from early June 2012 there was a further fine rally that disregarded the deteriorating economic signals. Jitters were sparked at the end of the reporting period by comments from the Fed Chairman (signalling the imminent end of quantitative easing?) and concerns about China (local authority debt problems). Overall, the MSCI All Countries (the broadest global index) was up 7.9% in euro terms on 30 June 2013 compared to year-end 2012. Among the traditional markets, Western Europe (MSCI Europe return index over the same period: +4.1%) was unable to continue the catch-up process begun in 2012. Fear that the EMU’s problems entailed a systemic risk nevertheless faded from the market. Europe’s cheaper valuation (compared to the US) was unable to offer any support either. European corporate earnings fell well short of expectations since the first quarter of 2012. They have displayed a downward trend, in sharp contrast with developments in other regions. Wall Street ended June substantially higher than 2012 year-end (S&P 500: +12.6%, Dow Jones: +13.8%). The BEL 20 (+2.0%) performed more or less in line with the other European markets. Delhaize made a strong comeback, after the supermarket chain’s share had suffered badly in 2011 and 2012 from problems with its US operations. The bank stocks KBC and Delta Lloyd also recorded fine performances. Belgacom, Unicore and the biotech firm Thrombogenics, which had triumphantly joined the BEL 20 in 2012, were the biggest disappointments. The Brussels stock exchange welcomed Bpost in June. Japan was ultimately an outperformer (+10.0% in euros), despite the steep depreciation of the yen. The winds of change have been blowing through Tokyo since the advent of the Abe government in December. The prospect of fresh tax stimuli, a cheaper yen and large-scale money creation have contributed to an atmosphere of optimism about the economy, something very rare in this country, which has been struggling with defeatism for many years. The emerging regions performed downright badly. The Asian emerging markets (-4.3%) were unable to capitalise on their role as the growth engine of the world economy. Confidence indicators began to decline in mid-2012, breaking through barriers that pointed to a serious economic slowdown. That failed to materialise but it was sufficient to perpetuate the doubts concerning the growth narrative in the region. This was further exacerbated by concerns about Chinese local authority debt levels, an overheating Chinese housing market and fear of a credit crisis – especially when the Chinese interbank rate shot up to 30% within the space of a few days in June. Stock-market valuations remain favourable, especially given the high growth forecasts, sound macroeconomic balance and a banking sector that was barely – if at all – affected by the credit crisis. Latin America (-13.4%) was hit by an economic slowdown. The link to the commodity markets is always at the fore in this region. Eastern Europe (-10.5%) was also a disappointment. Russia was likewise not immune to the weakness of European economic growth. Oil prices below 100 USD per barrel mean trouble for Russian state finances. The Turkish stock market suffered from street protests against increasing Islamisation.

There were significant differences in the returns of the various sectors. The best performing sectors included Financials, Pharmaceuticals and Consumer Discretionary. Materials, Technology and Energy lagged behind. The outperformance of Banks may be attributed to the quantitative easing programmes undertaken by the central banks. By this we mean the Fed’s QE3 programme, and especially the announcement by the ECB of its OMT programme, which took the heat out of the euro crisis. Pharmaceuticals had been shunned for a long time due to a lack of product innovation, patent expiry and the reforms to healthcare insurance in the US. In recent months, however, investors began to focus more on the sector’s response to these challenges: restructuring operations and the sell-off of non-strategic divisions. The car industry has risen from the ashes, in the US and the European luxury segment at least. Demand from the emerging markets is also strong, despite the slowdown in Chinese growth, where German luxury marques generate 50% of their profits. In spite of the slow growth, advertising budgets have also held up surprisingly well. The rise of the e-book and ongoing breakthrough of digital television continue undiminished. More and more media companies are successfully exploiting these trends. Mining companies lost ground on excessive expectations concerning commodity prices. A failed stock market flotation by Facebook and the giant leaps made by Apple meant that price trends in the Technology sector differed from what might have been expected on the basis of the fundamentals. The oil companies suffered from the vagaries of the oil market, the political instability in the Middle East and frequent accidents. The Real Estate sector (+3.0%) eased up a little in 2013 compared to its strong performance in 2012. The financial turbulence in 2007–08 forced real estate companies to clean up their balance sheets. This accordingly provided the sector with a sound base to make the most of the recovery. The traditional discount against the intrinsic value at which the sector normally trades consequently disappeared, leaving the sector somewhat overvalued. Outlook The US and European barometers measuring confidence among business leaders peaked in spring 2011 at record levels, but have slipped heavily over the past two years. In the US they are in the twilight zone between recession and expansion. We are expecting US growth to remain positive but modest (around 2% y-o-y in the coming quarters) as pay increases are barely keeping pace with inflation and budgetary policy has now finally (and probably for many years) struck down the path of austerity. The fragile recovery of the housing market and corporate investment could be sustained. How strong the growth proves to be will depend largely on the dynamic of the labour market. In recent months employment in the US has grown by around 200 000 new jobs each month. This will need to continue in order to achieve +2% growth in 2013 and in 2014. Confidence indicators in Europe are well below freezing point. The budgetary plans, tighter lending policy of the banks and major uncertainty among consumers and producers will continue to depress growth. 2013 will see a contraction of GDP in Europe. Recovery is not expected until the first half of 2014. Deflation or depression scenarios, which are currently dominating bond market sentiment, are not however justified. The foundations for more sustainable growth in 2014 and beyond have been laid in recent years. US households have trimmed back their debt level significantly, the savings rate has already increased considerably and loan servicing (instalments and interest payments combined) now accounts for only 8% of household budgets (the lowest level in 15 years – it was still 14% three years ago). Households are gradually moving towards a position where they can spend more of their money on consumption. The explosive growth in earnings between 2009 and 2012 bolstered companies’ already substantial cash positions. During the crisis investments were scaled back heavily, with the foundations being laid for a catch-up process. In the US, Republicans and Democrats may have totally different views about the required budgetary policy, but a common thread throughout the negotiations in recent months has

been that the federal finances need to be reformed step by step and that a tighter budgetary policy than in the recent past will need to be implemented in the years ahead. Tighter also than the average budgetary policy in the EMU. This is being counterbalanced by extremely accommodating monetary policy. The Fed is making unprecedented cash injections with its programme for purchasing government bonds and other debt paper. In doing so, the Fed wants to prevent the banks from being preoccupied with their own solvency and hence imposing unduly strict lending conditions, which would undermine economic growth. These cash injections will either find their way into the real economy or generate inflationary expectations. In any case they will keep long rates low and banish any fears of deflation. Economic growth in Europe will remain below par. Sky-high unemployment and the euro crisis are undermining consumer confidence and the banks’ willingness to provide ready access to credit. The ECB’s monetary policy is also much less aggressive than the Fed’s. In contrast, real wage rises (however limited) will be somewhat higher in Europe than in the US. Today’s world is one of two-speed economies. The mature industrialised economies (US, Europe, Japan) still find themselves in a low-growth environment, with no underlying inflationary pressure, persistently low interest rates and runaway public finances. The picture in the emerging markets is altogether different. The strong economic growth has already created inflationary pressure in Asia. Appropriate monetary policy is therefore required: sometimes restrictive (as in 2011) and at other times stimulatory (as at present). Monetary policy in China and elsewhere in Asia is highly geared to preventing asset-price inflation. Countries are not only deploying the interest-rate weapon to this end, they are also actively intervening in the credit and housing markets. One of the major challenges for this decade will be the further development of consumption in China and the rest of Asia. That could help bring about a more balanced economic world order: it will not only reduce the region’s dependence on exports but, at least as importantly, will have an effect on international capital flows. More consumption in China will mean lower savings and higher imports, including from the US and Europe. That will help the West to ‘grow out’ of its debt problems. Time is of the essence for the euro area. Everyone knows that the EMU is not a perfect monetary union. In its twelve-year history, little has been done to improve its internal operation. National autonomy was sacrosanct. The crisis brought the realisation that ‘economic governance’, as it is now called in Eurospeak, needs to be tackled as a matter of urgency. In concrete terms, this involves measures such as supranational supervision of banks (to be in place by the beginning of 2015), strict monitoring and sanctioning of budgetary policy (a huge challenge given the emergence of austerity fatigue), monitoring of pay policy and harmonising European taxation (a big taboo). The capital base of banks will need to be strengthened further to ensure the stability of the financial system, so that there is a sufficient buffer to offset reserves and unforeseen write-downs. This will remain high on the agenda in the current and following years. A great many measures have already been taken in this context. Examples include the almost 2 000 billion euros that were set aside in the space of two years to ensure the smooth funding of European governments; the introduction of stress tests to establish whether the banks have sufficient capital to cope with a new and serious crisis; the gradual introduction of new and stricter capital requirements under Basel III; and making ESM reserves available for direct loans to ailing European banks. Maintaining a (virtually) zero money market rate also fits with this. There is no urgent macroeconomic reason to adopt a more restrictive policy so long as the economic situation in the West remains weak and there is no sign of any real inflationary pressure. The central banks are conducting a policy of low interest rates and have totally given up their resistance to quantitative easing measures. They are intervening directly on the capital markets on a large scale. By buying bonds and other debt instruments, they are

having a direct influence on the bond yield in certain market segments, ensuring secondary trading (for instance, in paper issued by governments in which the market could lose confidence) and flooding the financial system with cash. The ECB, too, is now firmly set on this path. Concern about inflation has given way to worries about the economic situation and stemming the euro crisis. The ECB is probably still striving for a normal short rate of 3% for the euro area (its official target for inflation in the euro area is 2%), but that has now become a very long-term objective and is totally ruled out in the short term. The ECB is more likely to cut than raise the key rate in the coming months, inasmuch as this is still feasible. The first rate hike is not expected until the second half of 2014 at the soonest. In our opinion, the central banks in the US, the UK and Japan will wait even longer before raising their key rates. The US Federal Reserve has already officially postponed the earliest date for a rate hike to mid-2015. The official stance is that the key rate will not be increased so long as unemployment (currently 7.6% of the working population) remains above 6.5%. Bond yields may well have bottomed out, at least as regards issues of German Bunds or US Treasuries. It would be logical for yields to increase again from the current record lows, on the back of an improved economic environment (or an ongoing reduction in the downside risks to growth). As a result, the market might, in the coming months, start to anticipate tighter monetary policy in 2014 or 2015. A number of unconventional measures will first be withdrawn in the US; only after that can the market begin to anticipate a normalisation of the key rate. This rate increase need not, however, be very big. The measures taken by the central banks are also keeping the short end of the yield curve artificially low. If necessary, they will not hesitate to intervene actively in market segments where yields threaten to head too rapidly in the wrong direction. The default risk premium in the corporate bond market has fallen very steeply in recent years. It remains relatively high, both by historical standards and considering that most companies have a healthy financial structure and only limited funding requirements. There is therefore still some potential for a narrowing of spreads. Rate spreads in the euro area will probably remain volatile for a long time yet due to the many problems that have yet to be solved. Thanks to the continuing strength of the emerging markets, the global economy could post growth of 2.5–3% in 2013 and 2014. This is one of the reasons why corporate earnings could continue to grow in the coming quarters at a rate of 5–10%. It seems paradoxical that companies have emerged as the winners from the 2008–09 crisis. They are now reaping the benefits of the considerable restructuring measures pushed through during the recession. Cost controls go beyond (one-off and in some cases spectacular) restructuring measures and have now become an integral part of business culture. The recession of 2008–09 caused companies to be even more aware of risks (i.e. money, and hence costs). Investment projects are subject to a more thorough profitability study. A combination of debt reduction and low interest rates has resulted in a steep drop in financial charges. Globalisation (pressure of relocation) and ongoing high unemployment have made employees powerless to demand high pay increases. Maintaining purchasing power is now about all that is on offer. There is no question of real wage rises. In brief, every one-cent increase in revenue translates (almost) entirely into an extra cent of profit, rather than into higher pay. Money market rates will not increase rapidly and bond yields are close to their historical lows. Everything seems to point to shares being the most attractive investment option for the months ahead. The lack of alternatives is not, of course, sufficient reason to increase the market valuation. For that to happen, investors will need to be more predisposed to taking risk. The current valuation of equities continues to discount a number of very pessimistic scenarios. Based on forecast earnings for the coming 12 months, the price-earnings ratio is 14.5 for the US S&P 500 index and 11.4 for the MSCI Europe. That is 25–30% lower than the historical average. Equities are certainly dirt-cheap compared with bonds. The earnings yield – the inverse of the price/earnings ratio – is currently 8.8% for

the MSCI Europe, an unprecedented premium of 700 basis points above German bond yields. Edited to 4 July 2013

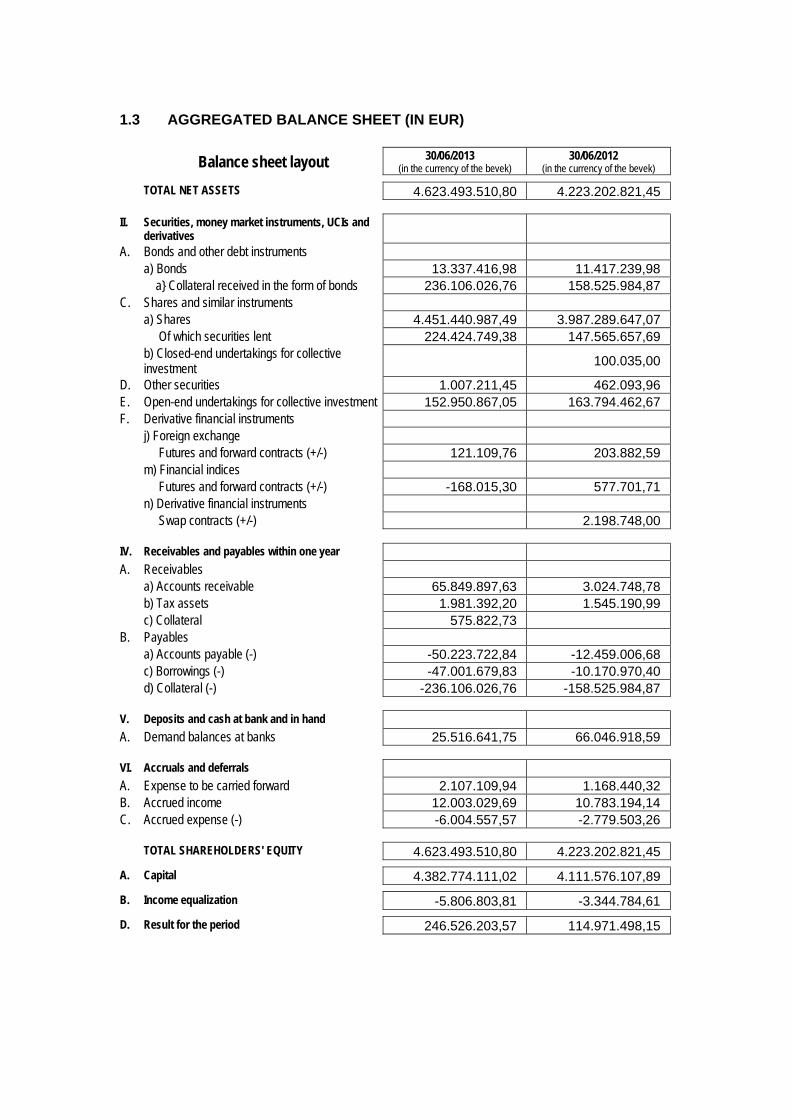

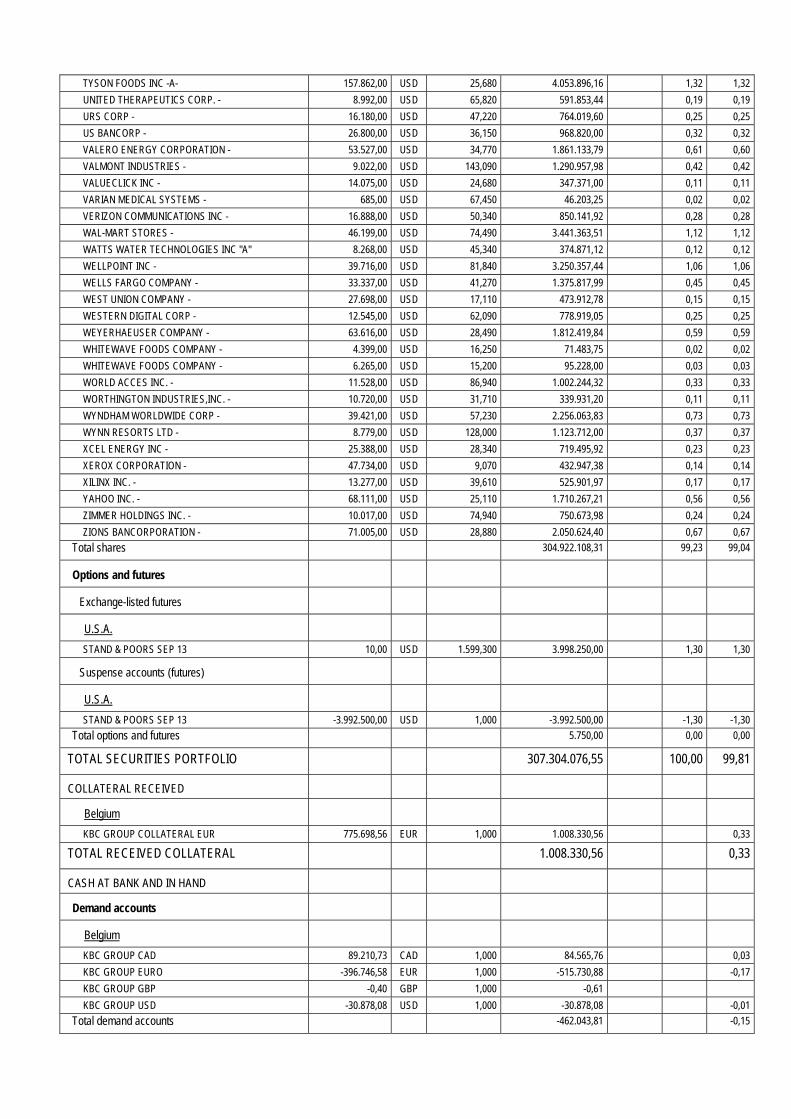

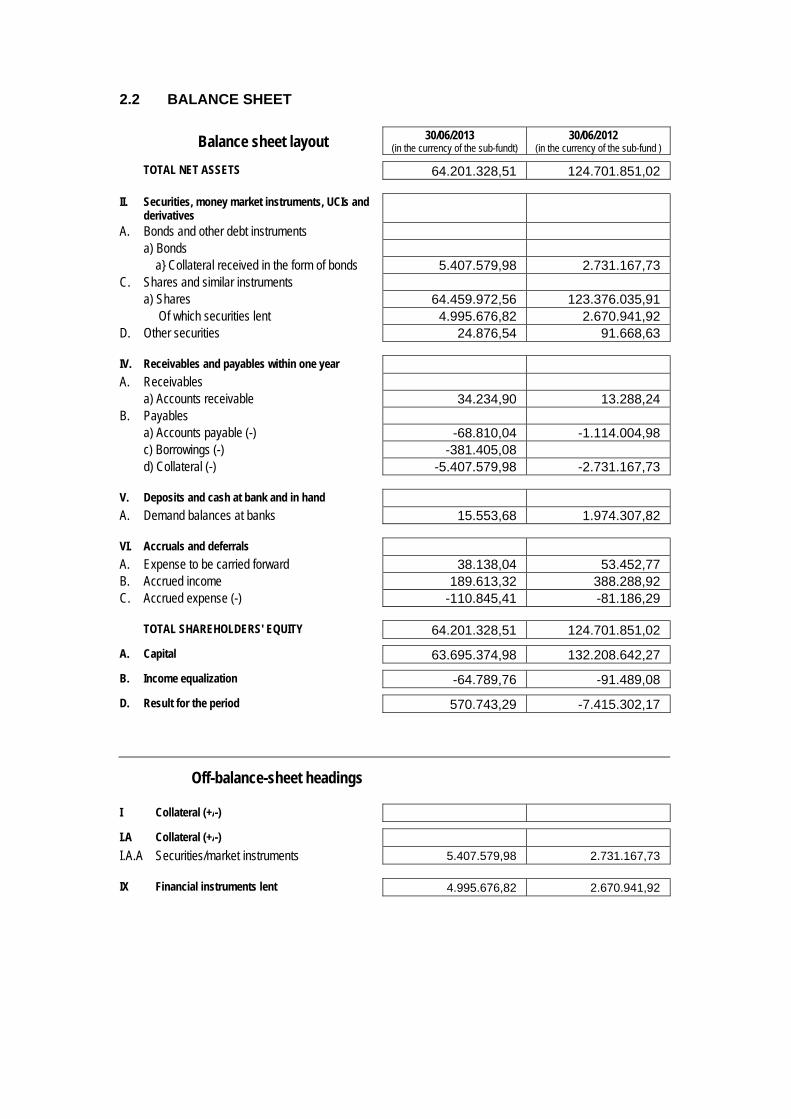

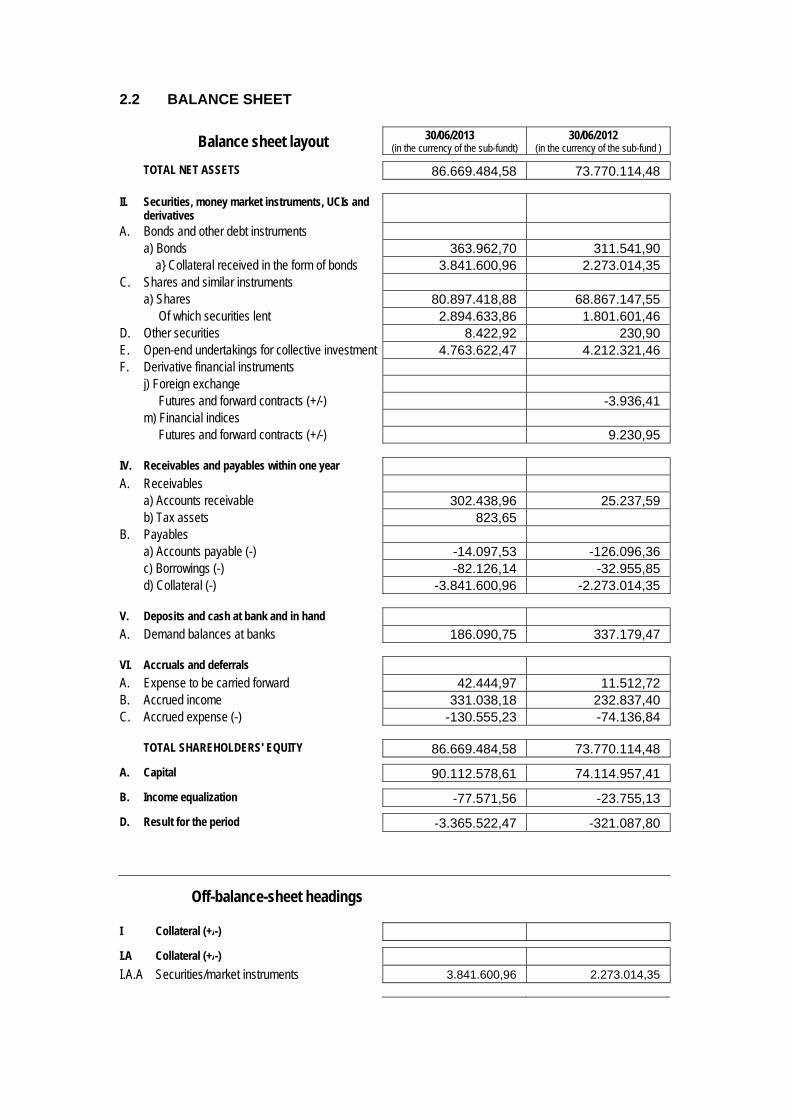

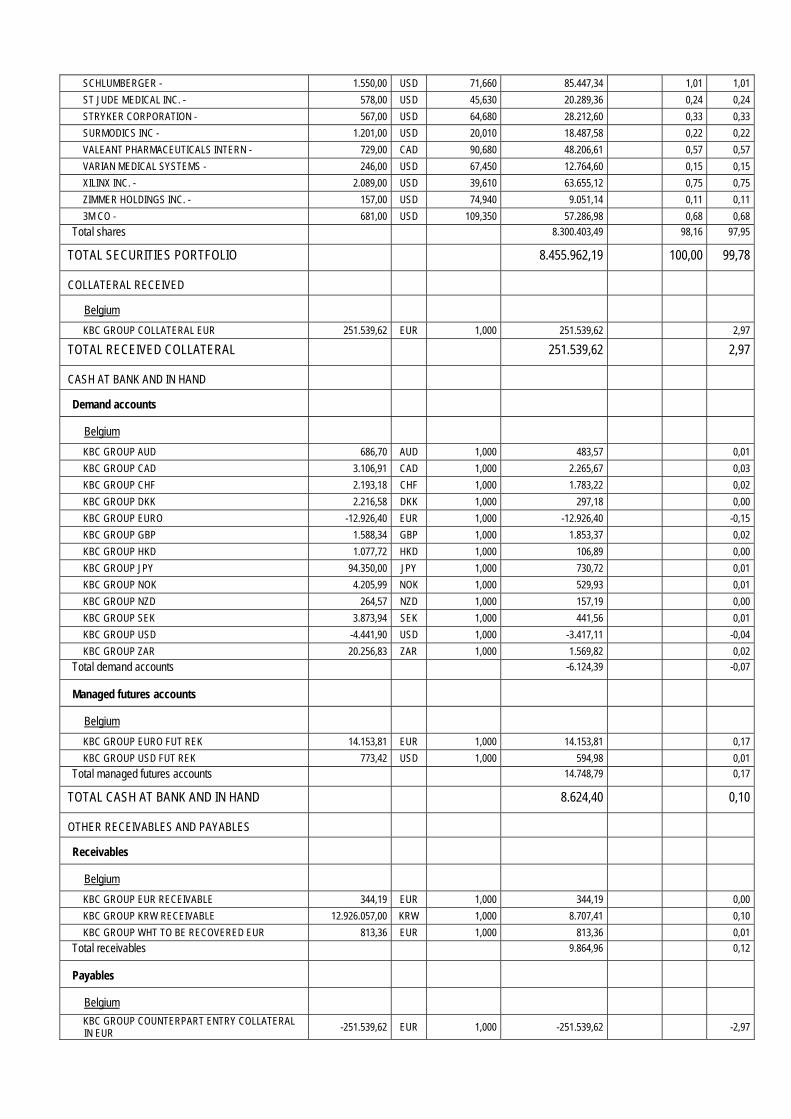

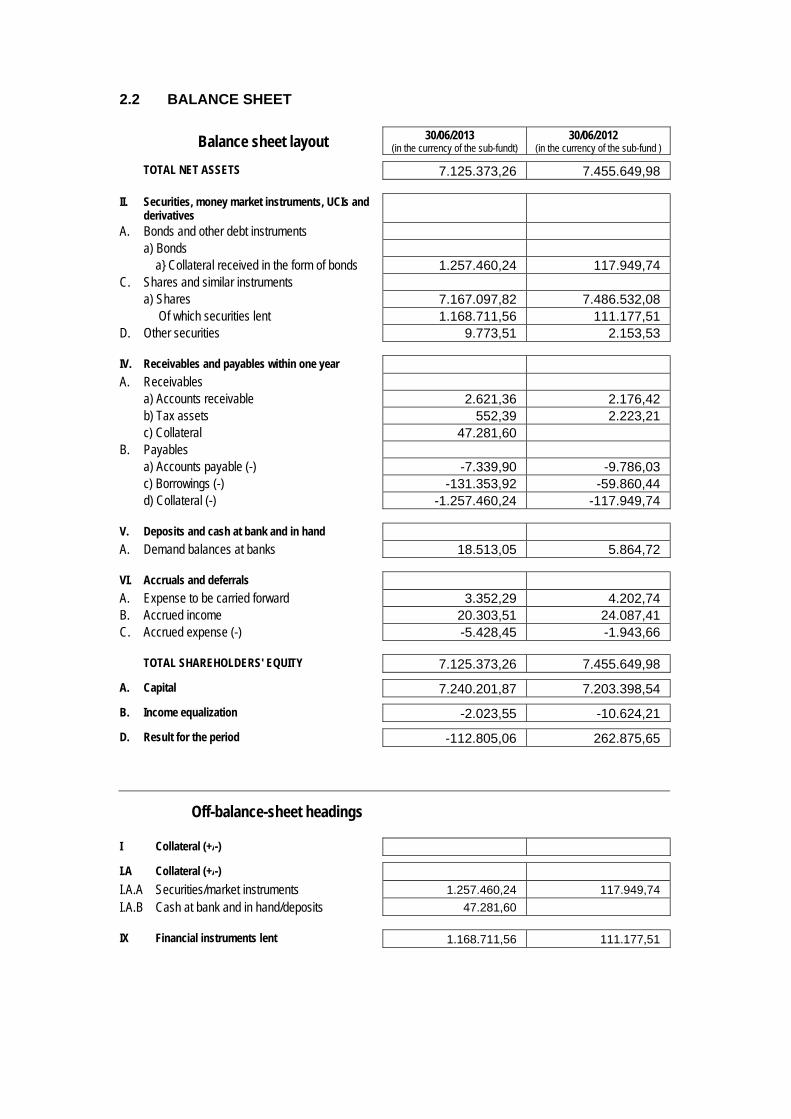

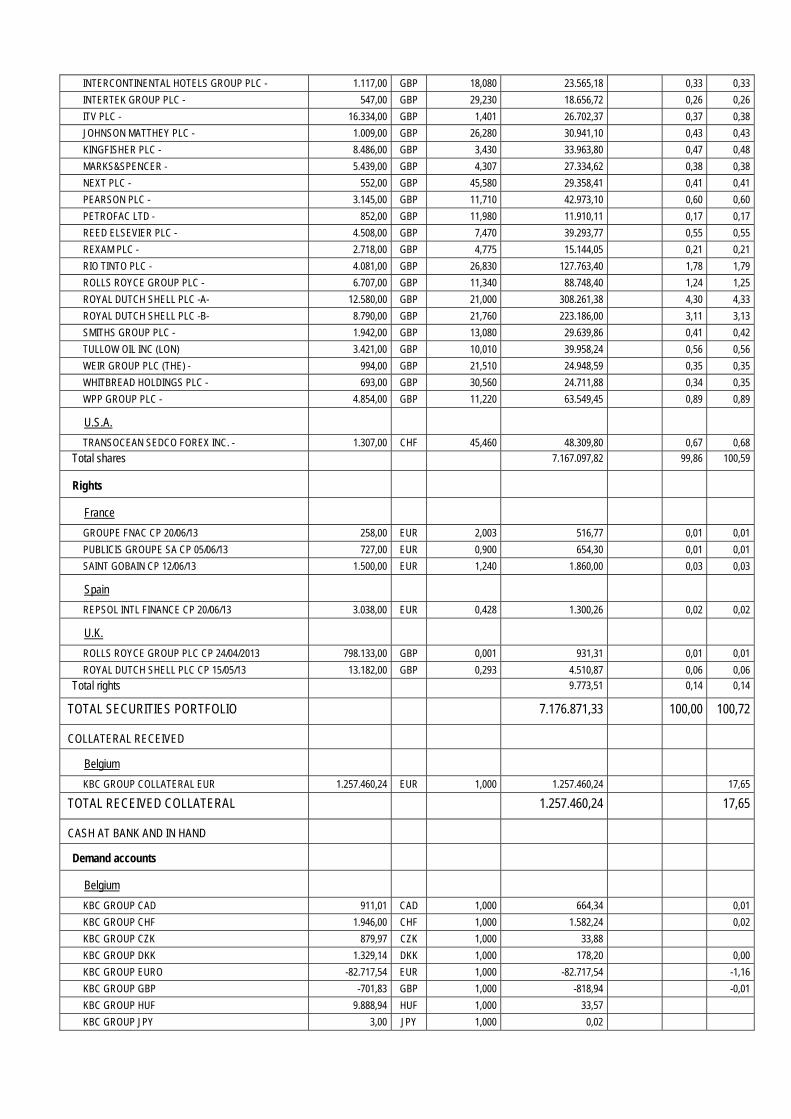

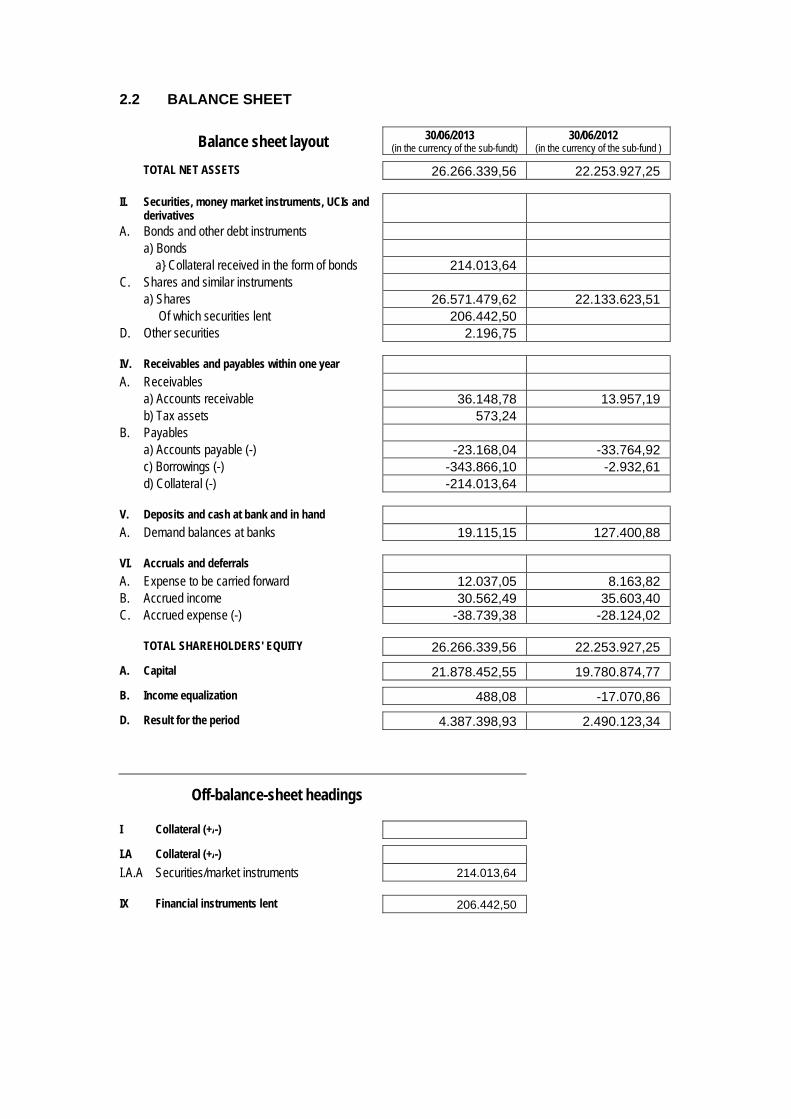

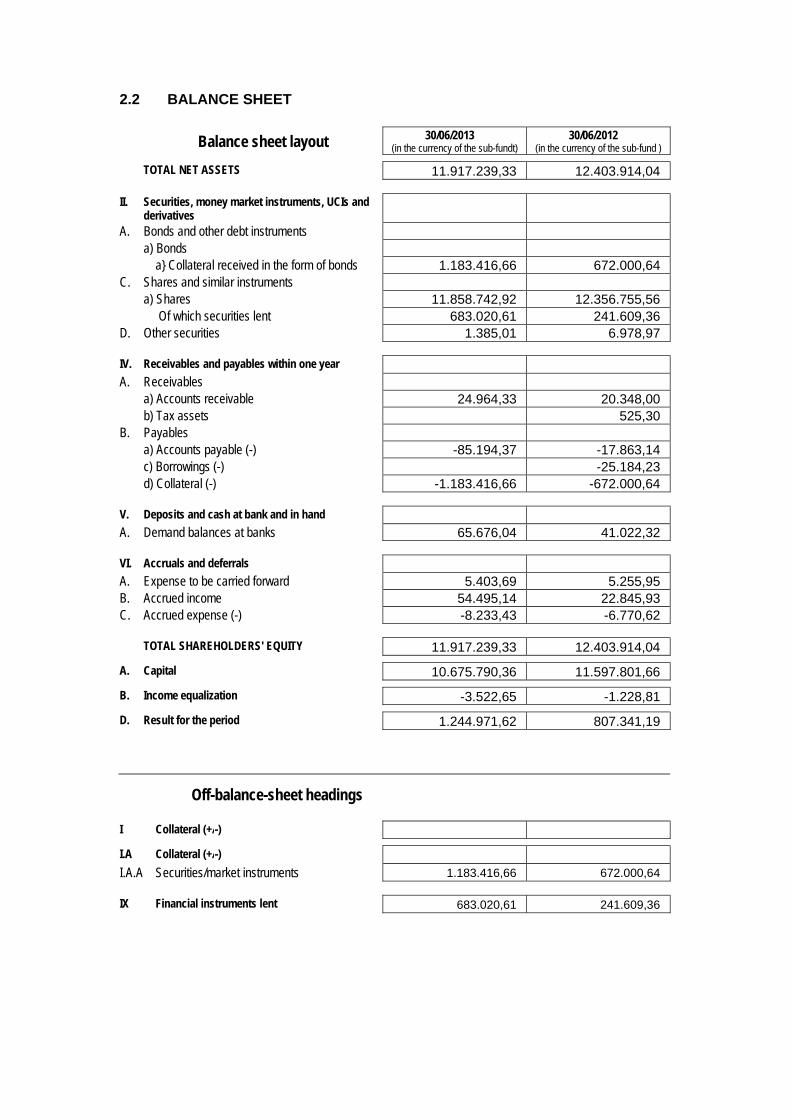

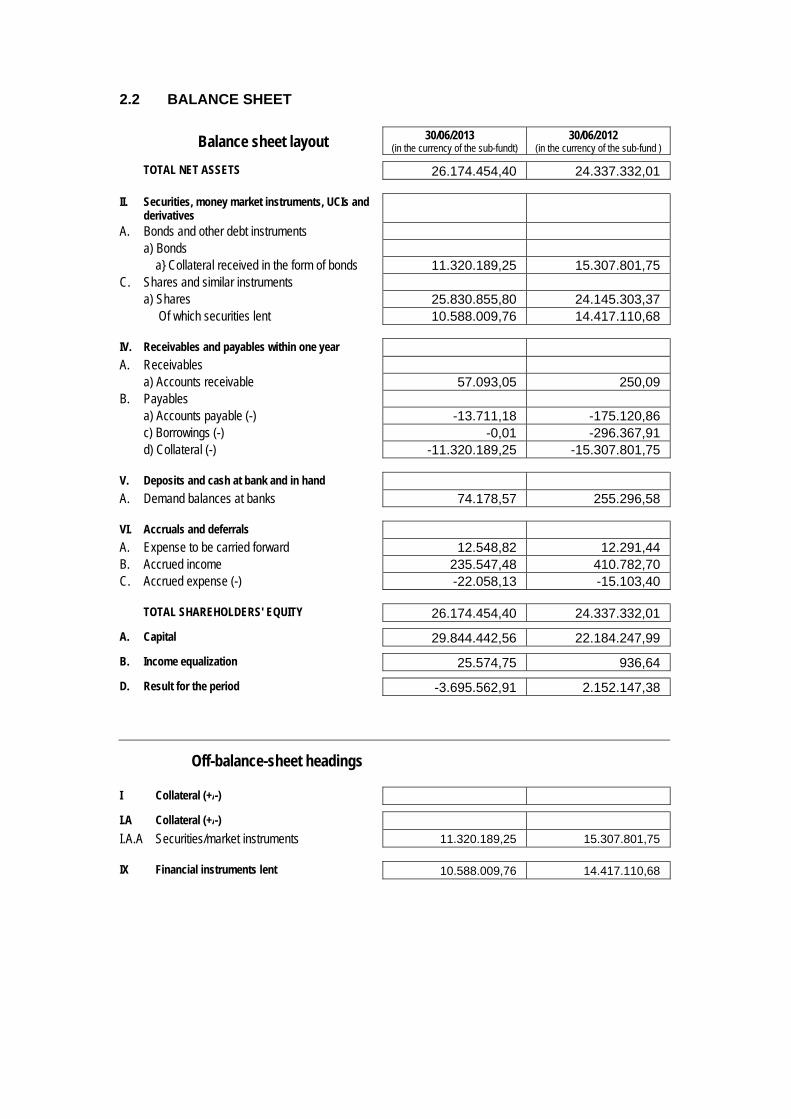

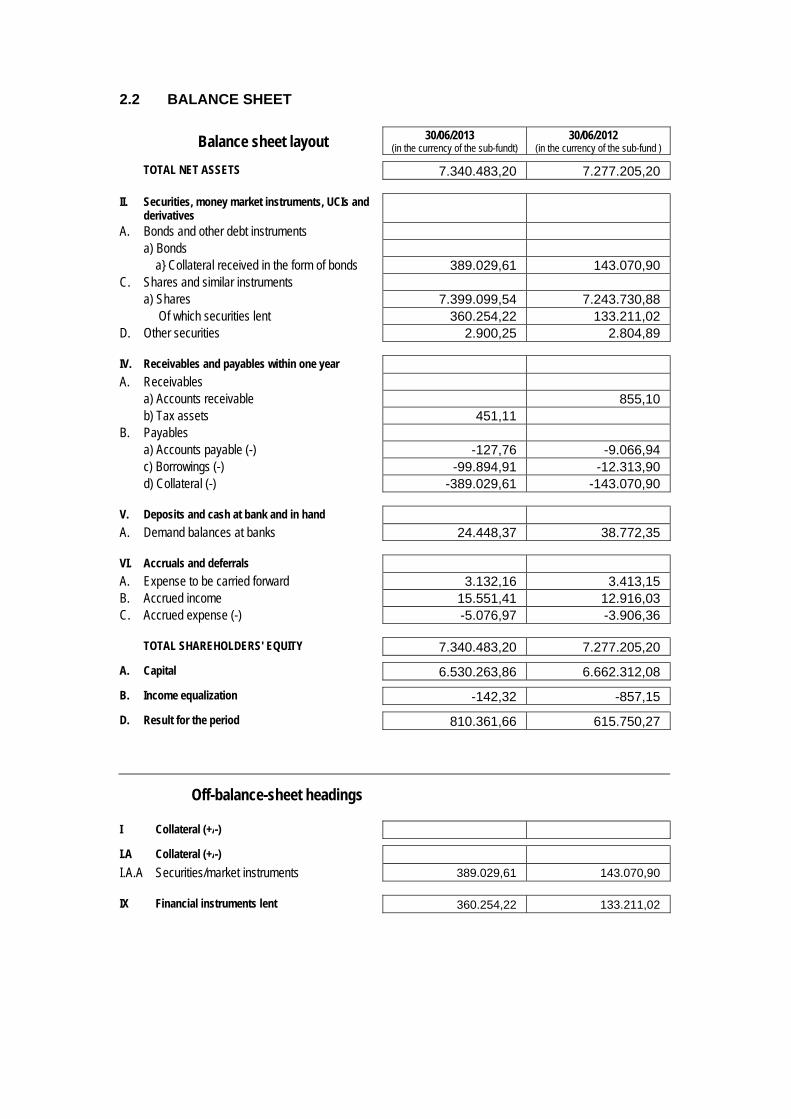

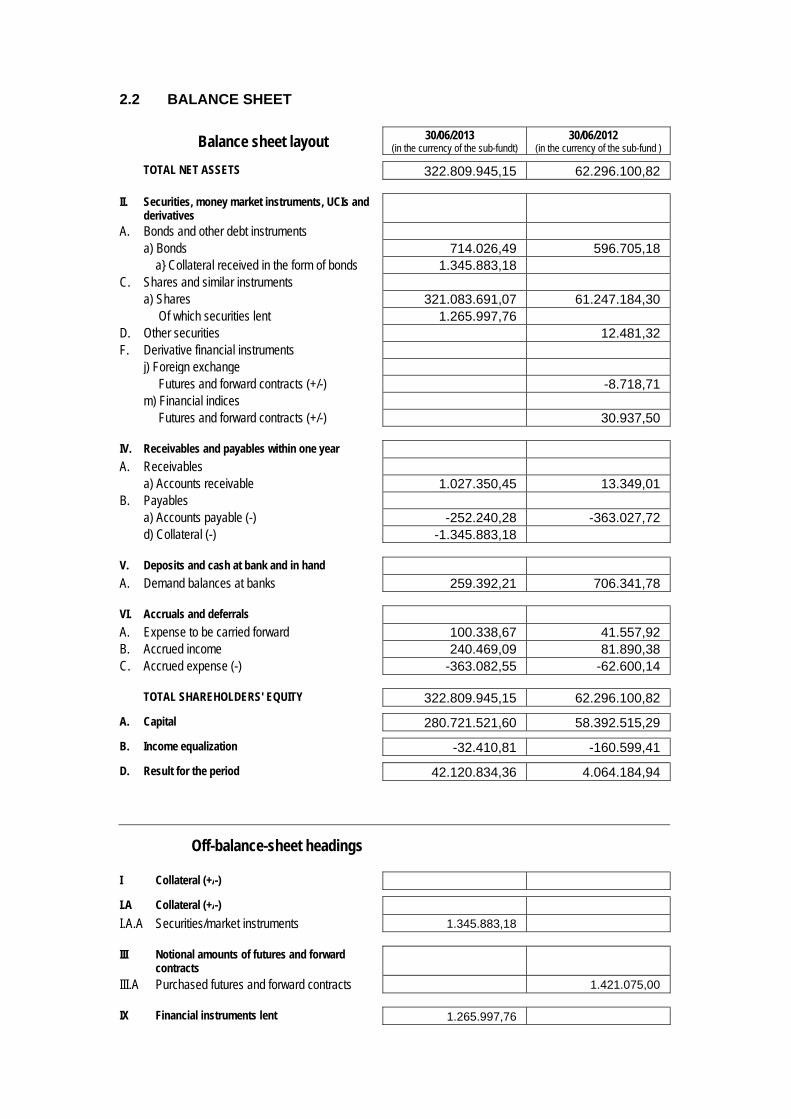

1.3 AGGREGATED BALANCE SHEET (IN EUR)

Balance sheet layout 30/06/2013 (in the currency of the bevek)

30/06/2012 (in the currency of the bevek)

TOTAL NET ASSETS 4.623.493.510,80 4.223.202.821,45

II. Securities, money market instruments, UCIs and derivatives

A. Bonds and other debt instruments a) Bonds 13.337.416,98 11.417.239,98 a} Collateral received in the form of bonds 236.106.026,76 158.525.984,87 C. Shares and similar instruments a) Shares 4.451.440.987,49 3.987.289.647,07 Of which securities lent 224.424.749,38 147.565.657,69 b) Closed-end undertakings for collective

investment 100.035,00

D. Other securities 1.007.211,45 462.093,96 E. Open-end undertakings for collective investment 152.950.867,05 163.794.462,67 F. Derivative financial instruments j) Foreign exchange Futures and forward contracts (+/-) 121.109,76 203.882,59 m) Financial indices Futures and forward contracts (+/-) -168.015,30 577.701,71 n) Derivative financial instruments Swap contracts (+/-) 2.198.748,00

IV. Receivables and payables within one year A. Receivables a) Accounts receivable 65.849.897,63 3.024.748,78 b) Tax assets 1.981.392,20 1.545.190,99 c) Collateral 575.822,73 B. Payables a) Accounts payable (-) -50.223.722,84 -12.459.006,68 c) Borrowings (-) -47.001.679,83 -10.170.970,40 d) Collateral (-) -236.106.026,76 -158.525.984,87

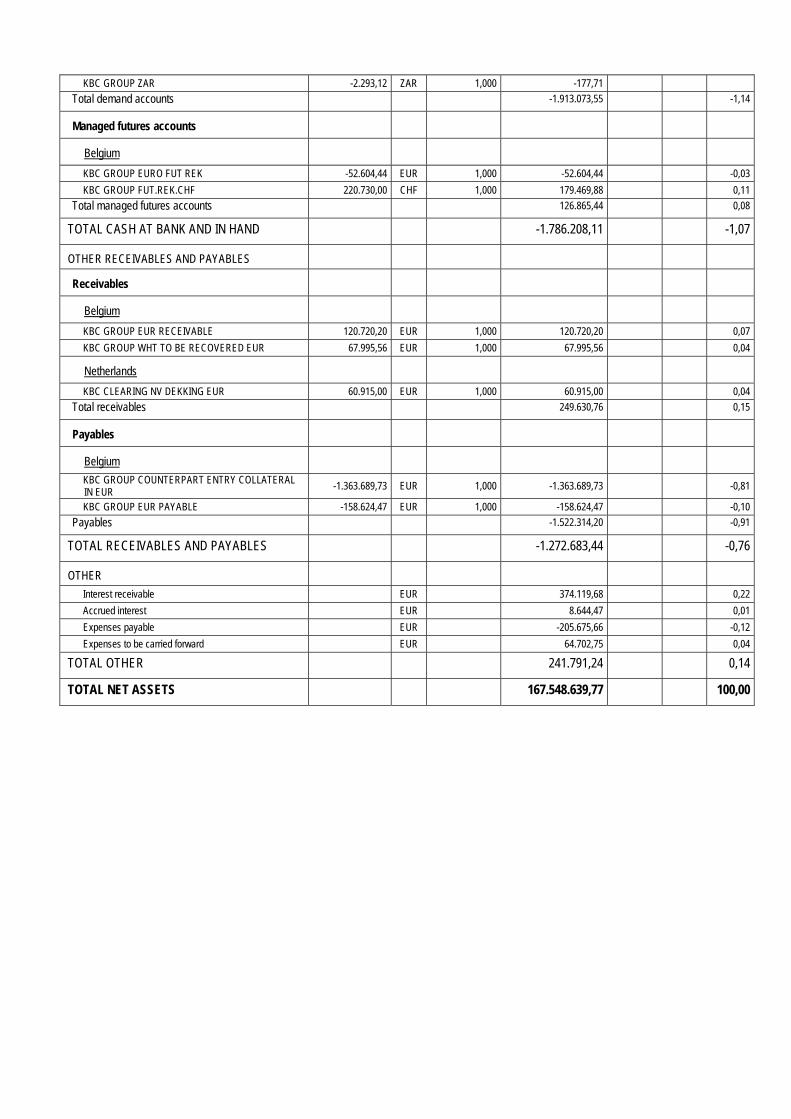

V. Deposits and cash at bank and in hand A. Demand balances at banks 25.516.641,75 66.046.918,59

VI. Accruals and deferrals A. Expense to be carried forward 2.107.109,94 1.168.440,32 B. Accrued income 12.003.029,69 10.783.194,14 C. Accrued expense (-) -6.004.557,57 -2.779.503,26

TOTAL SHAREHOLDERS' EQUITY 4.623.493.510,80 4.223.202.821,45

A. Capital 4.382.774.111,02 4.111.576.107,89

B. Income equalization -5.806.803,81 -3.344.784,61

D. Result for the period 246.526.203,57 114.971.498,15

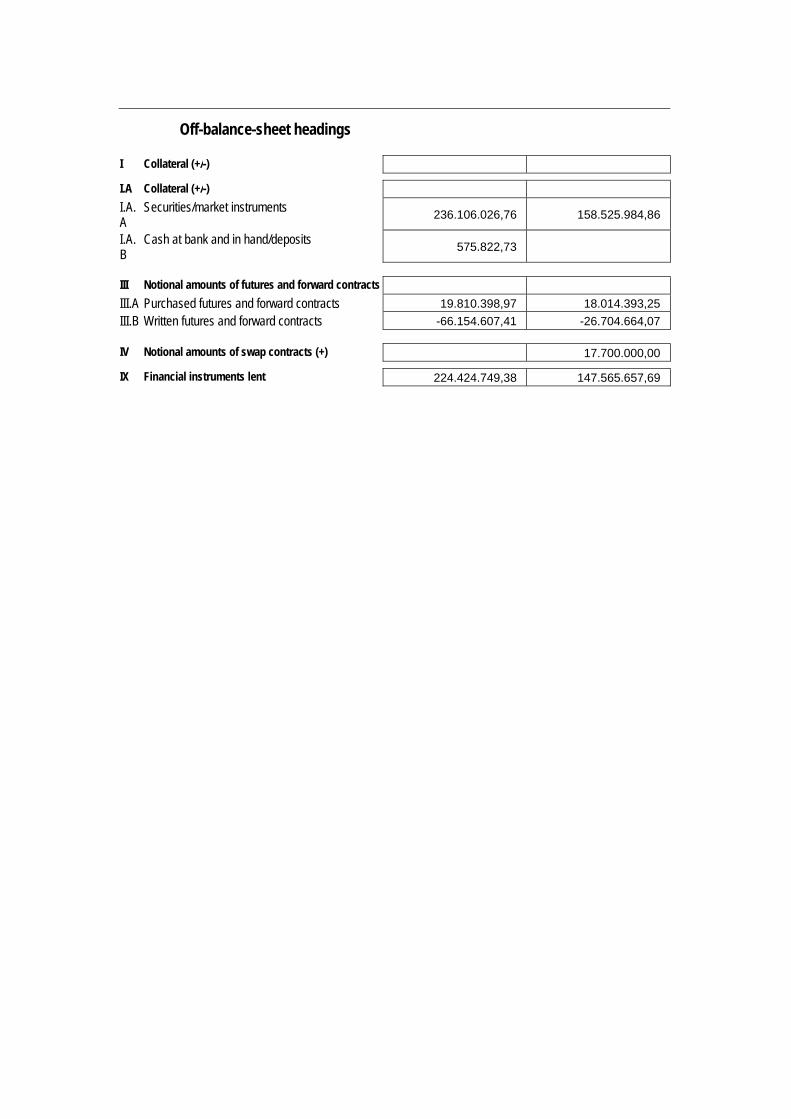

Off-balance-sheet headings

I Collateral (+/-)

I.A Collateral (+/-)

I.A.A

Securities/market instruments 236.106.026,76 158.525.984,86

I.A.B

Cash at bank and in hand/deposits 575.822,73

III Notional amounts of futures and forward contracts

III.A Purchased futures and forward contracts 19.810.398,97 18.014.393,25

III.B Written futures and forward contracts -66.154.607,41 -26.704.664,07

IV Notional amounts of swap contracts (+) 17.700.000,00

IX Financial instruments lent 224.424.749,38 147.565.657,69

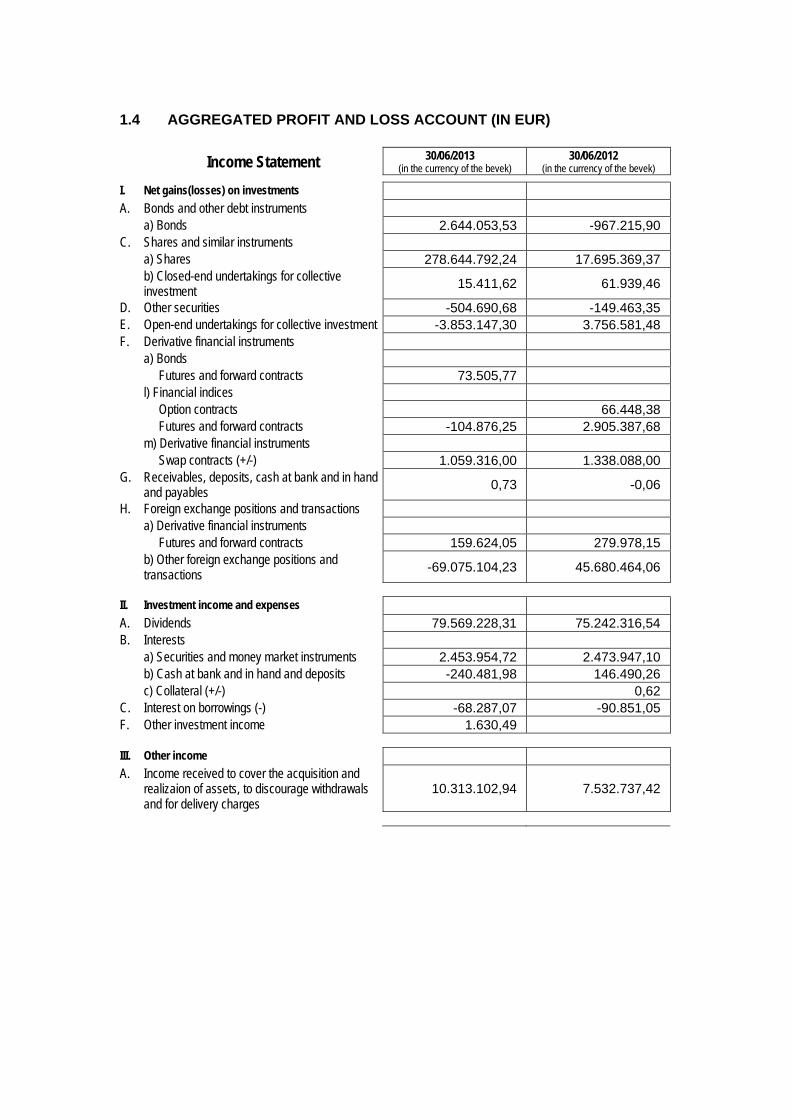

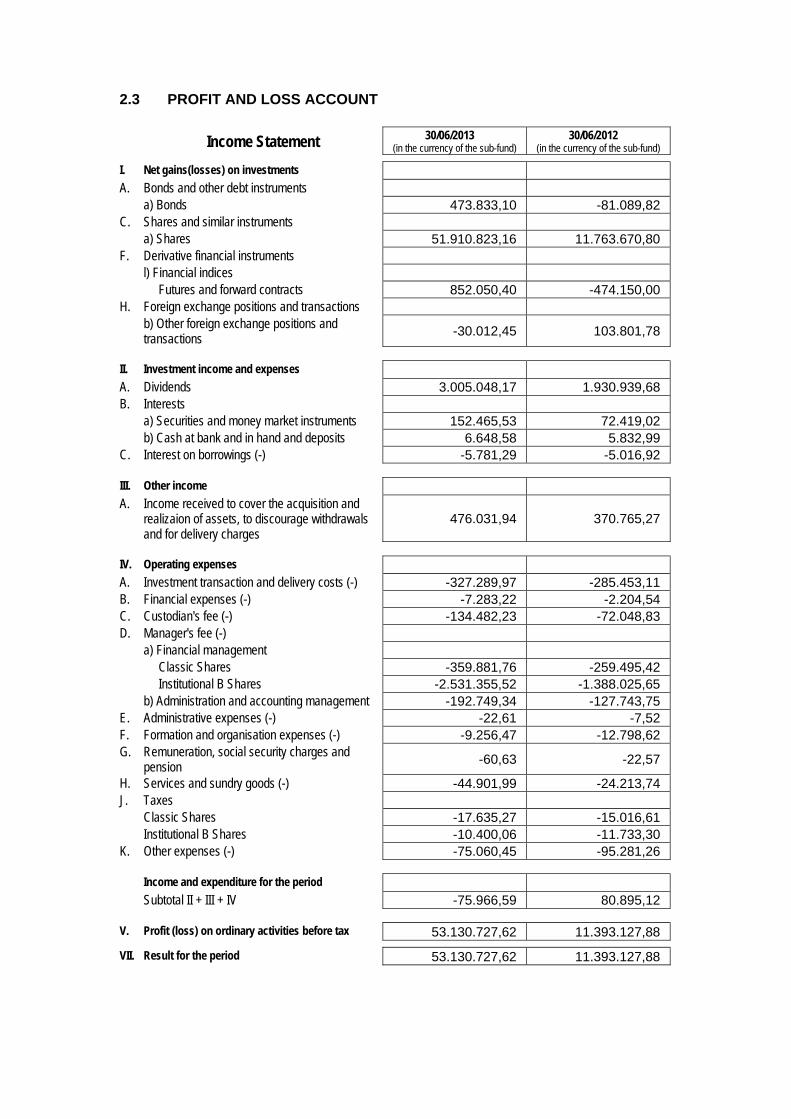

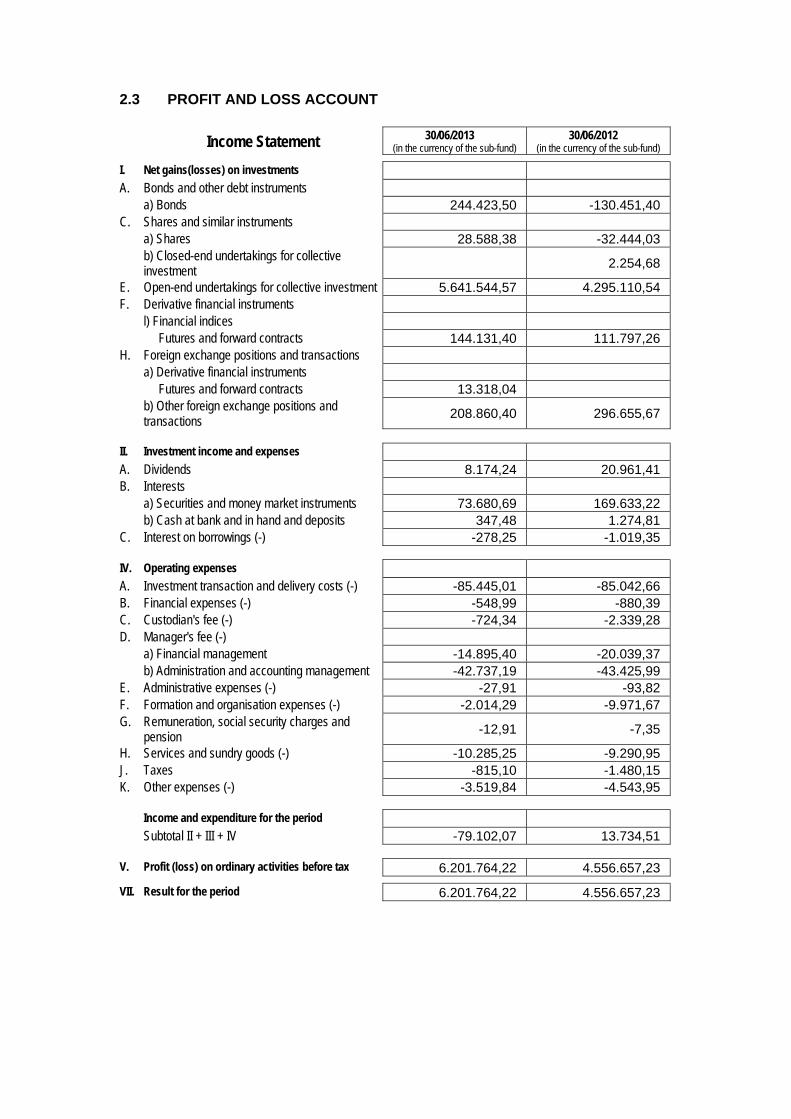

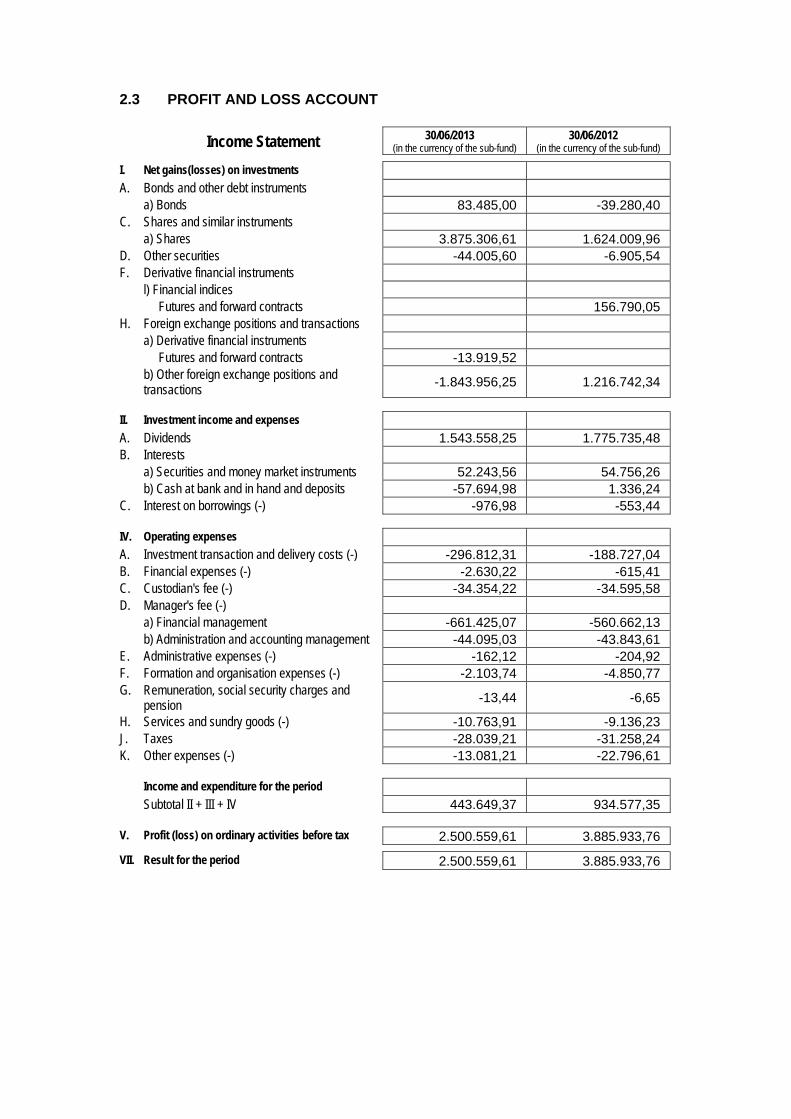

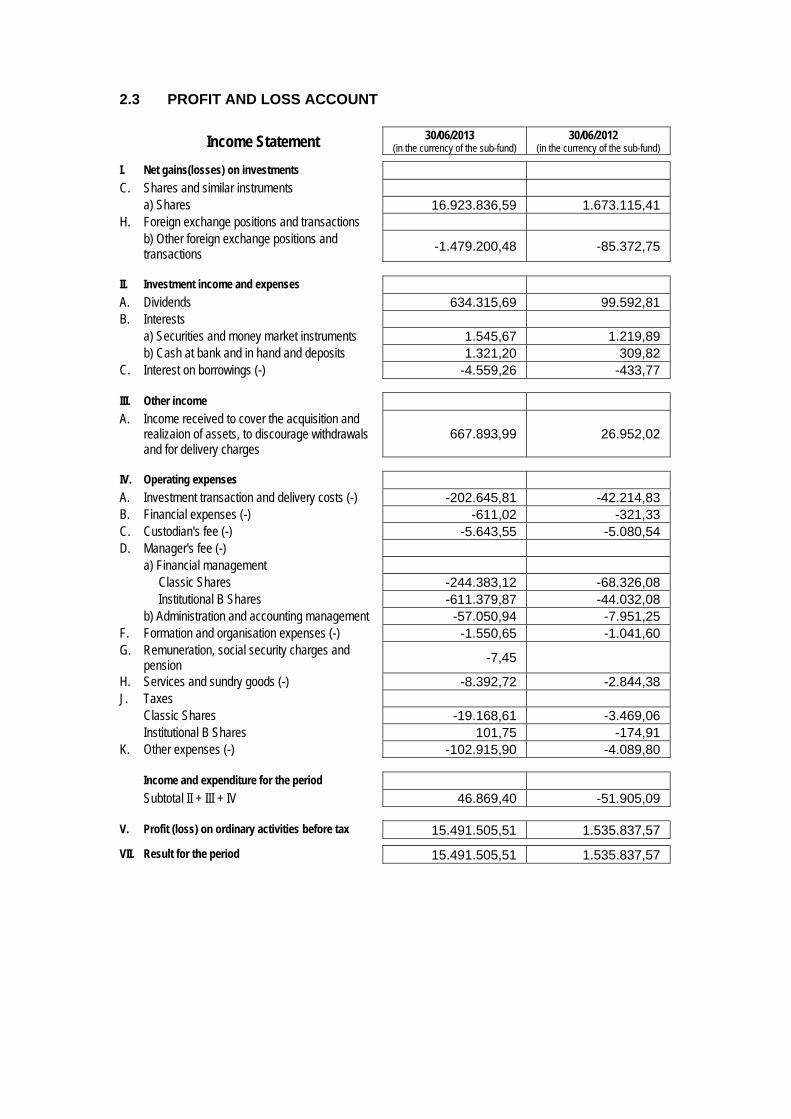

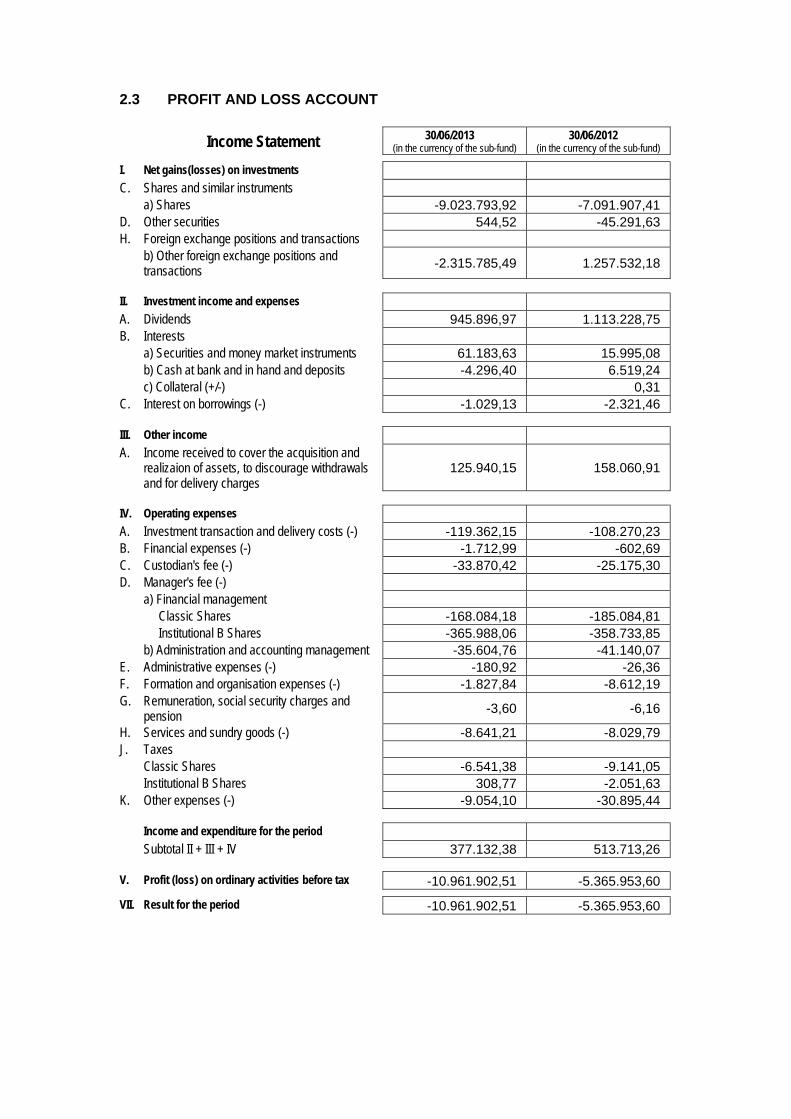

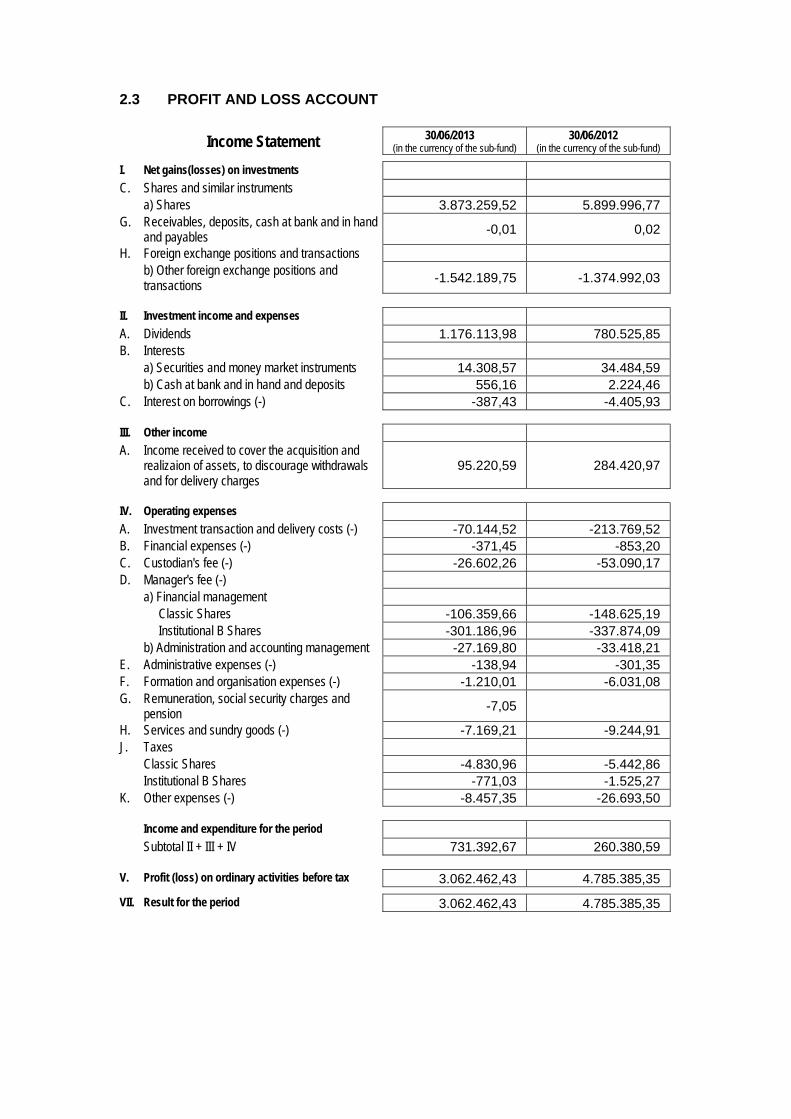

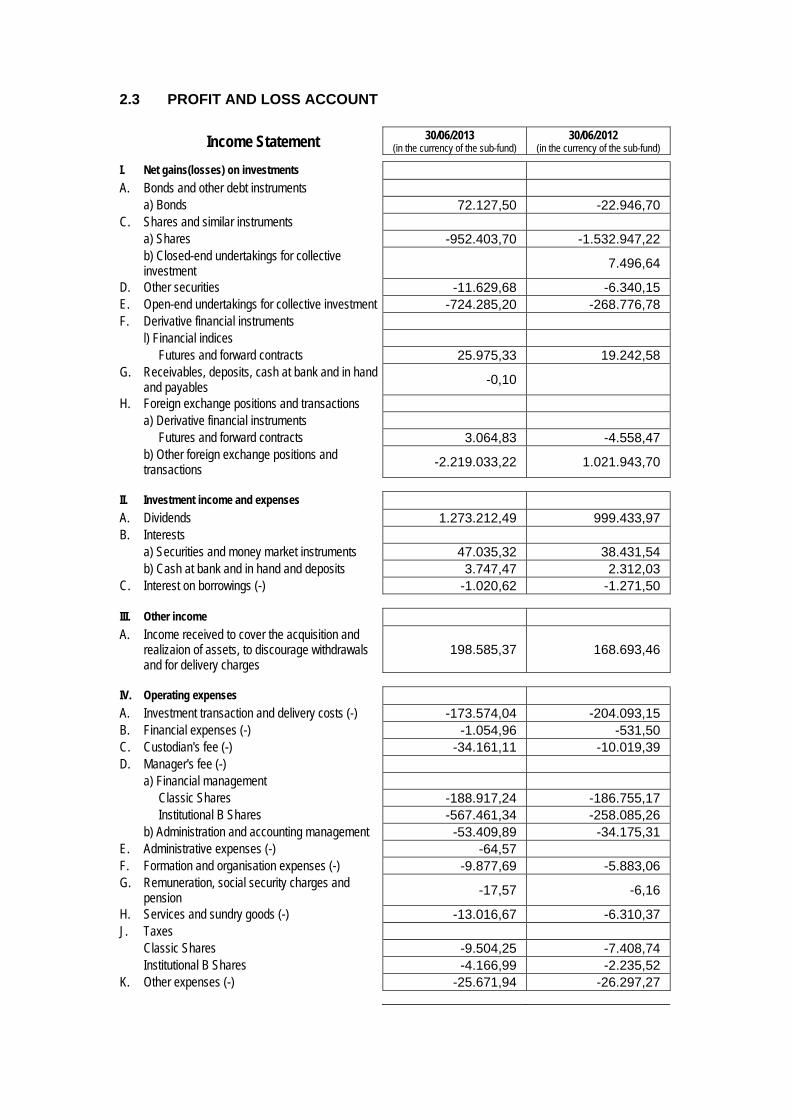

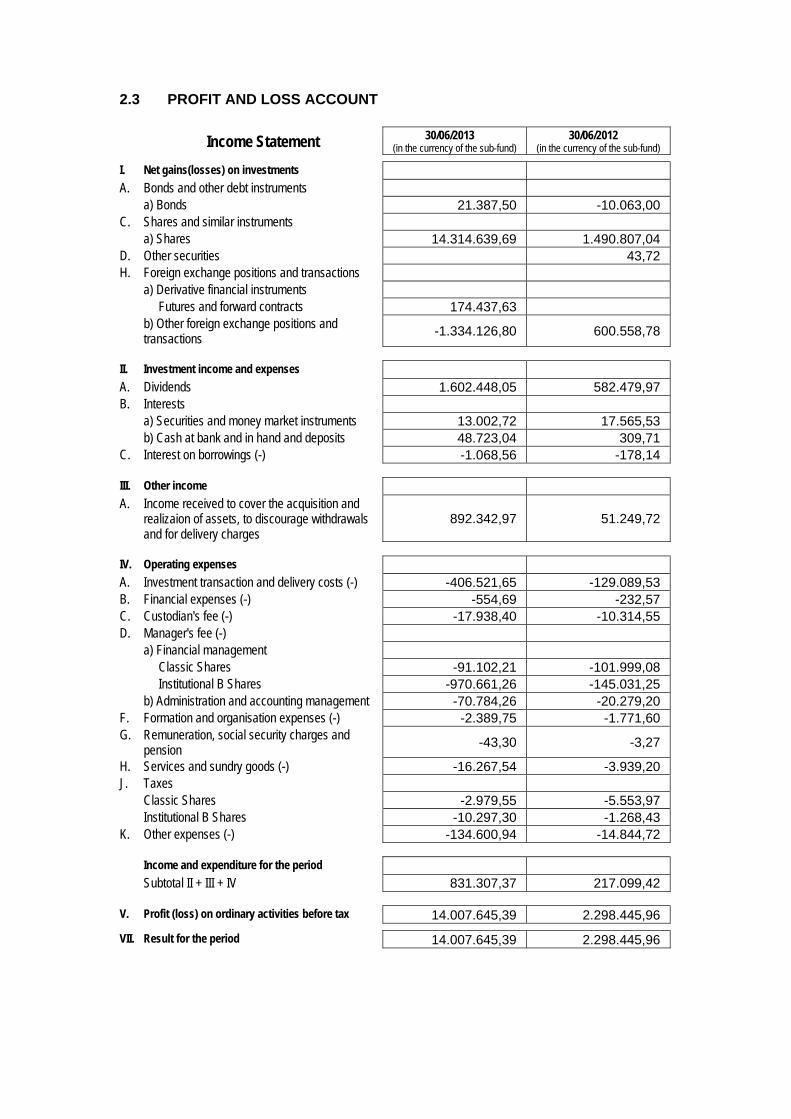

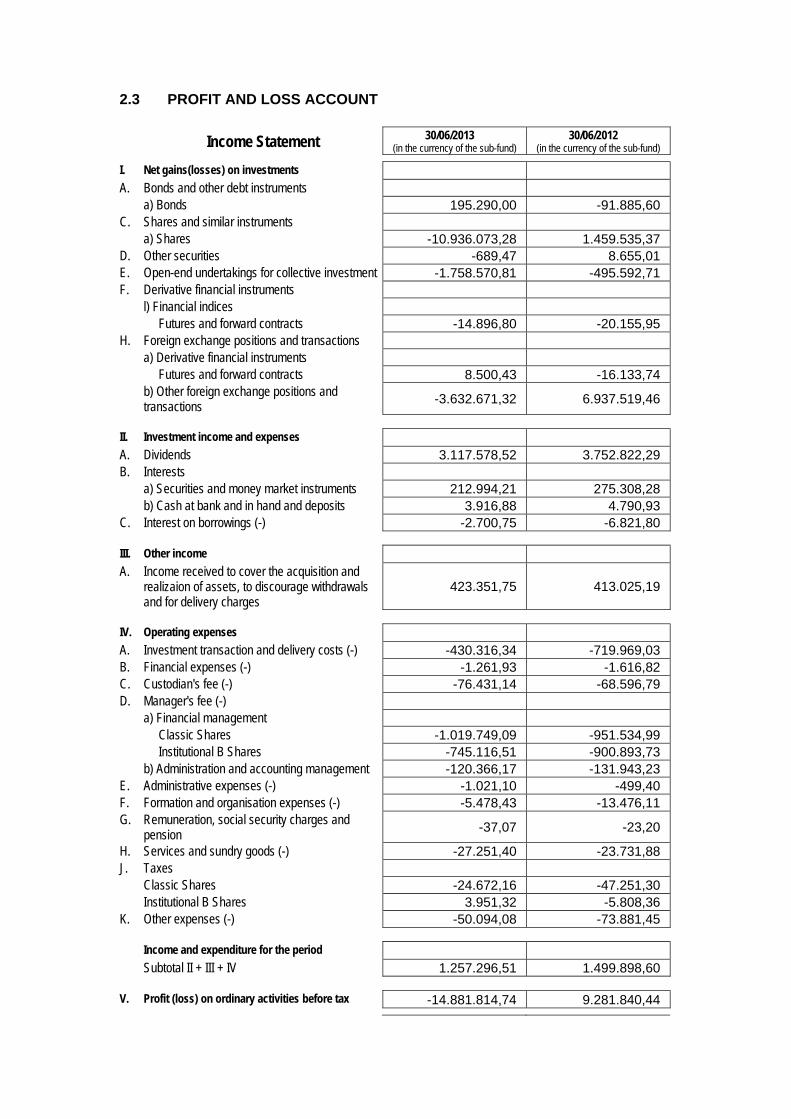

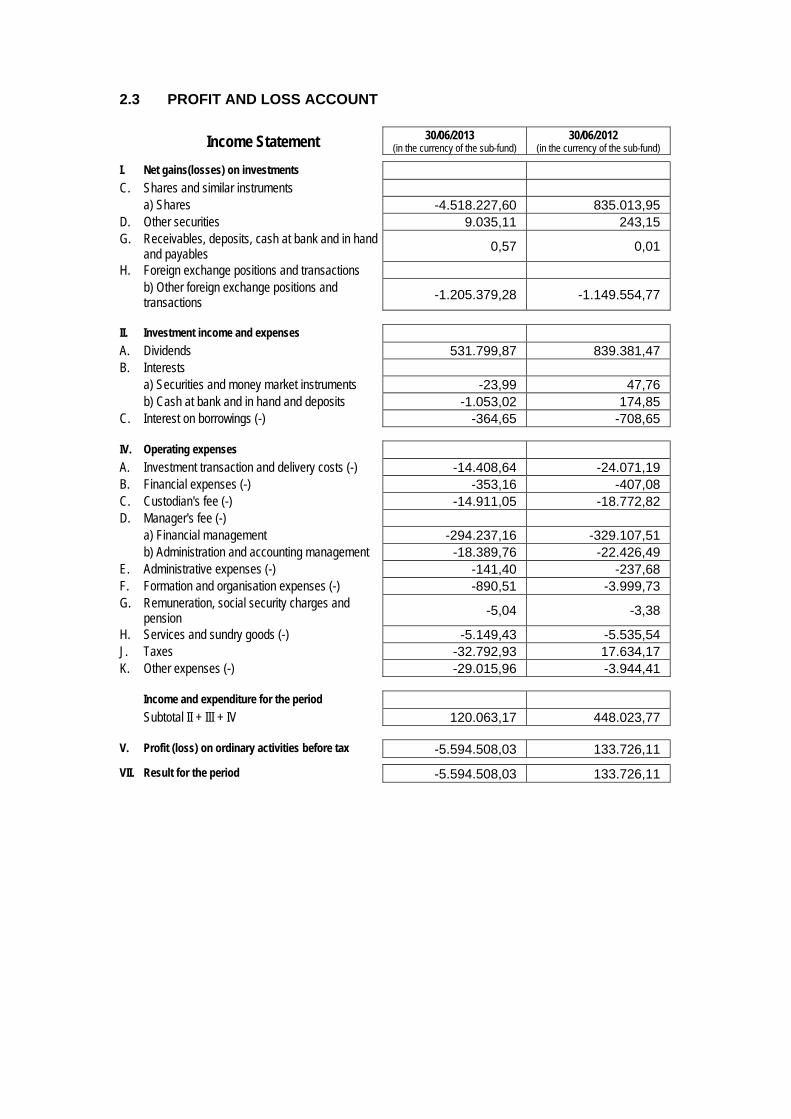

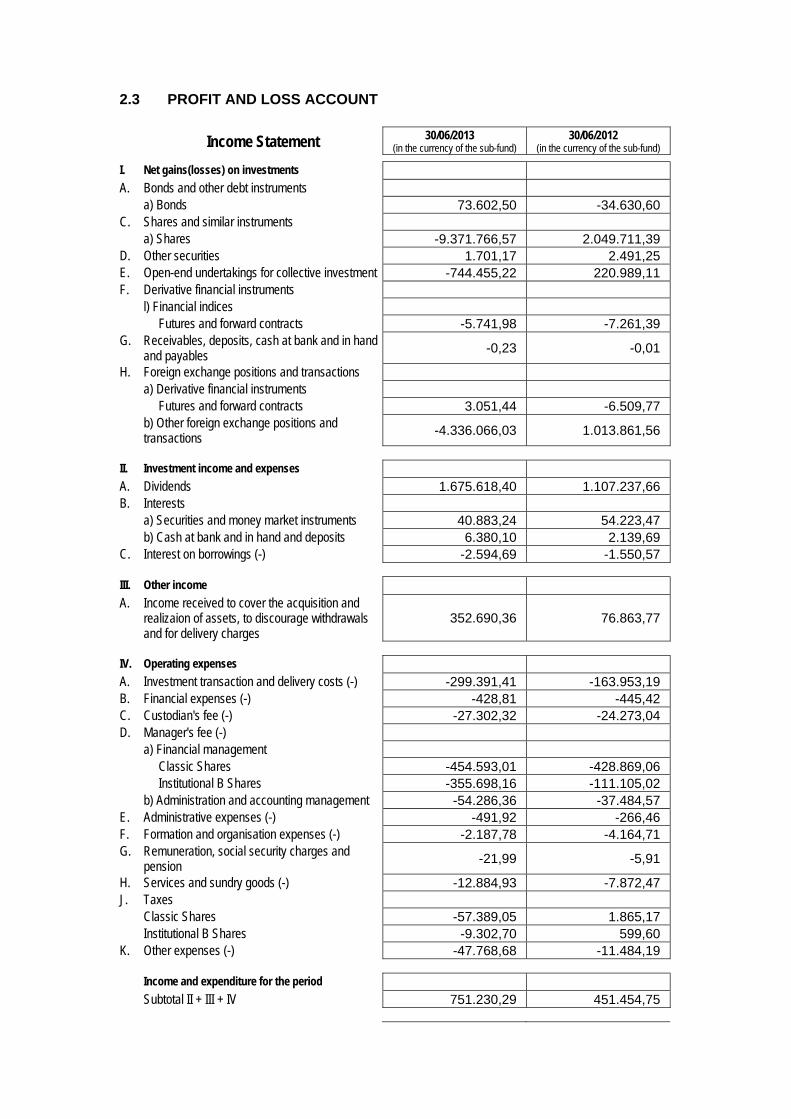

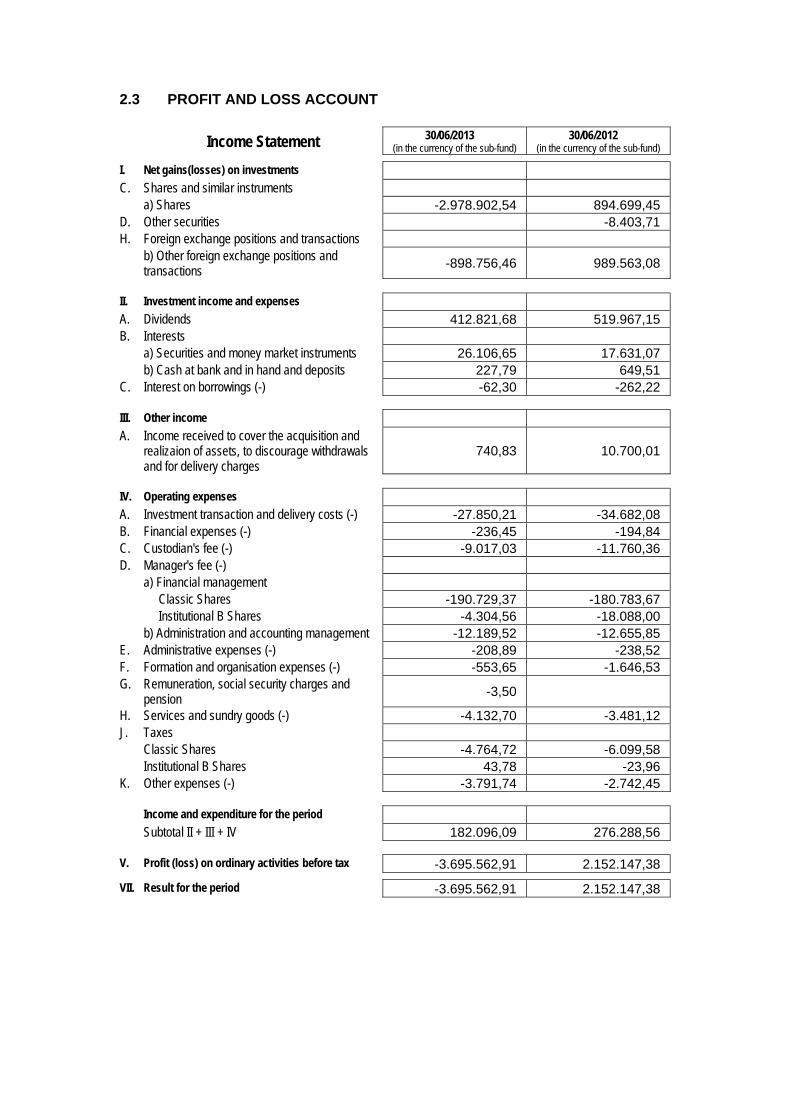

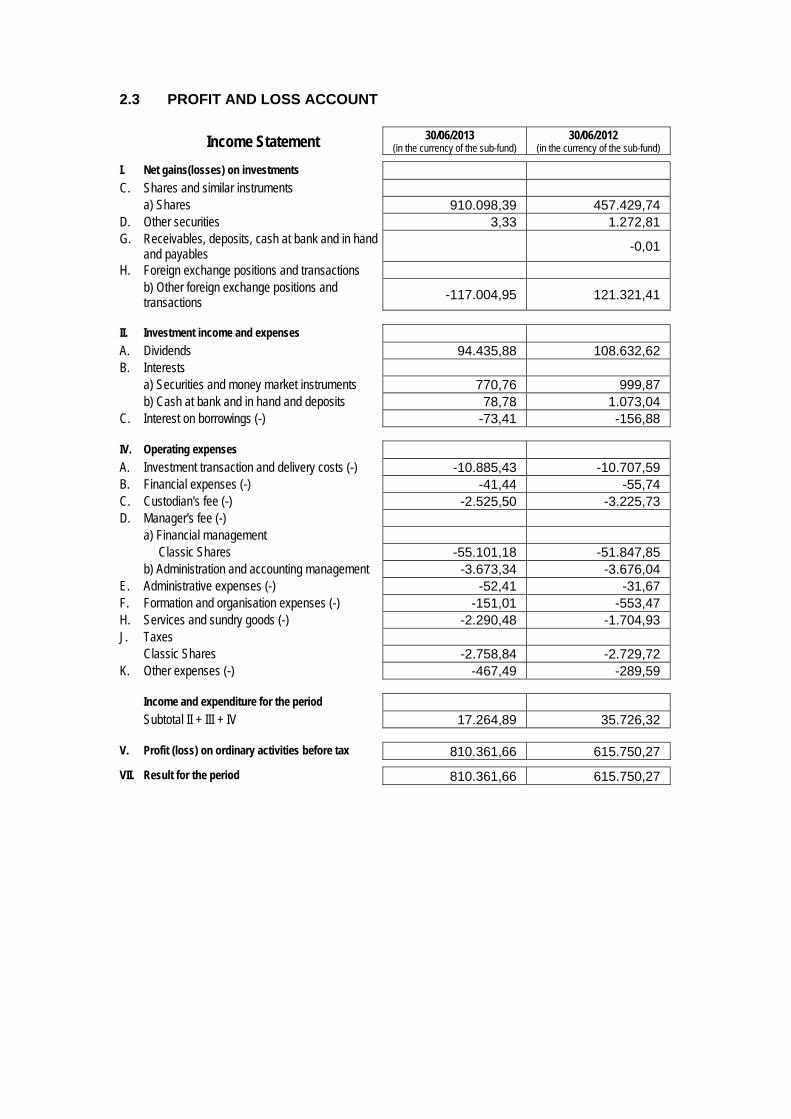

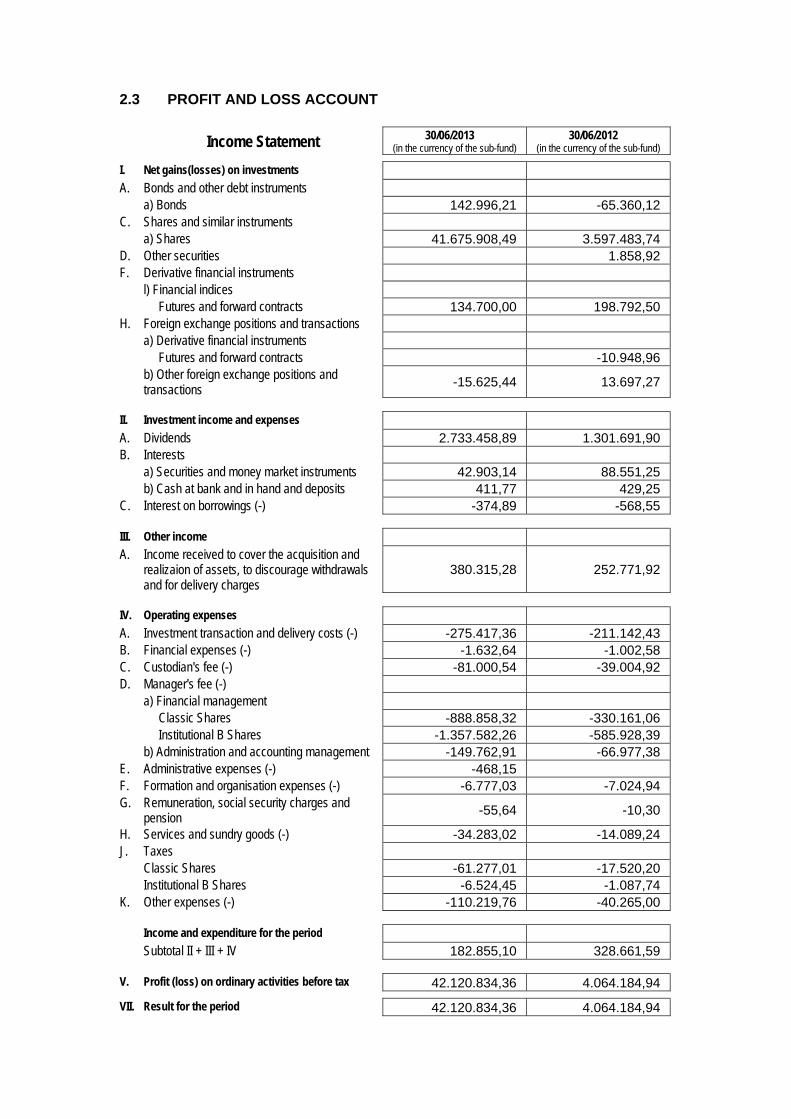

1.4 AGGREGATED PROFIT AND LOSS ACCOUNT (IN EUR)

Income Statement 30/06/2013 (in the currency of the bevek)

30/06/2012 (in the currency of the bevek)

I. Net gains(losses) on investments A. Bonds and other debt instruments a) Bonds 2.644.053,53 -967.215,90 C. Shares and similar instruments a) Shares 278.644.792,24 17.695.369,37 b) Closed-end undertakings for collective

investment 15.411,62 61.939,46

D. Other securities -504.690,68 -149.463,35 E. Open-end undertakings for collective investment -3.853.147,30 3.756.581,48 F. Derivative financial instruments a) Bonds Futures and forward contracts 73.505,77 l) Financial indices Option contracts 66.448,38 Futures and forward contracts -104.876,25 2.905.387,68 m) Derivative financial instruments Swap contracts (+/-) 1.059.316,00 1.338.088,00 G. Receivables, deposits, cash at bank and in hand

and payables 0,73 -0,06

H. Foreign exchange positions and transactions a) Derivative financial instruments Futures and forward contracts 159.624,05 279.978,15 b) Other foreign exchange positions and

transactions -69.075.104,23 45.680.464,06

II. Investment income and expenses A. Dividends 79.569.228,31 75.242.316,54 B. Interests a) Securities and money market instruments 2.453.954,72 2.473.947,10 b) Cash at bank and in hand and deposits -240.481,98 146.490,26 c) Collateral (+/-) 0,62 C. Interest on borrowings (-) -68.287,07 -90.851,05 F. Other investment income 1.630,49

III. Other income A. Income received to cover the acquisition and

realizaion of assets, to discourage withdrawals and for delivery charges

10.313.102,94 7.532.737,42

IV. Operating expenses A. Investment transaction and delivery costs (-) -8.384.559,63 -7.841.333,86 B. Financial expenses (-) -72.952,92 -29.528,62 C. Custodian's fee (-) -1.691.861,96 -1.128.783,80 D. Manager's fee (-) a) Financial management -38.719.696,50 -27.325.123,67 b) Administration and accounting management -2.647.623,05 -2.060.056,23 E. Administrative expenses (-) -10.312,24 -10.177,76 F. Formation and organisation expenses (-) -128.768,80 -252.797,48 G. Remuneration, social security charges and

pension -869,01 -346,71

H. Services and sundry goods (-) -656.438,39 -416.924,35 J. Taxes -724.468,76 -518.766,08 K. Other expenses (-) -1.524.277,97 -1.416.881,46

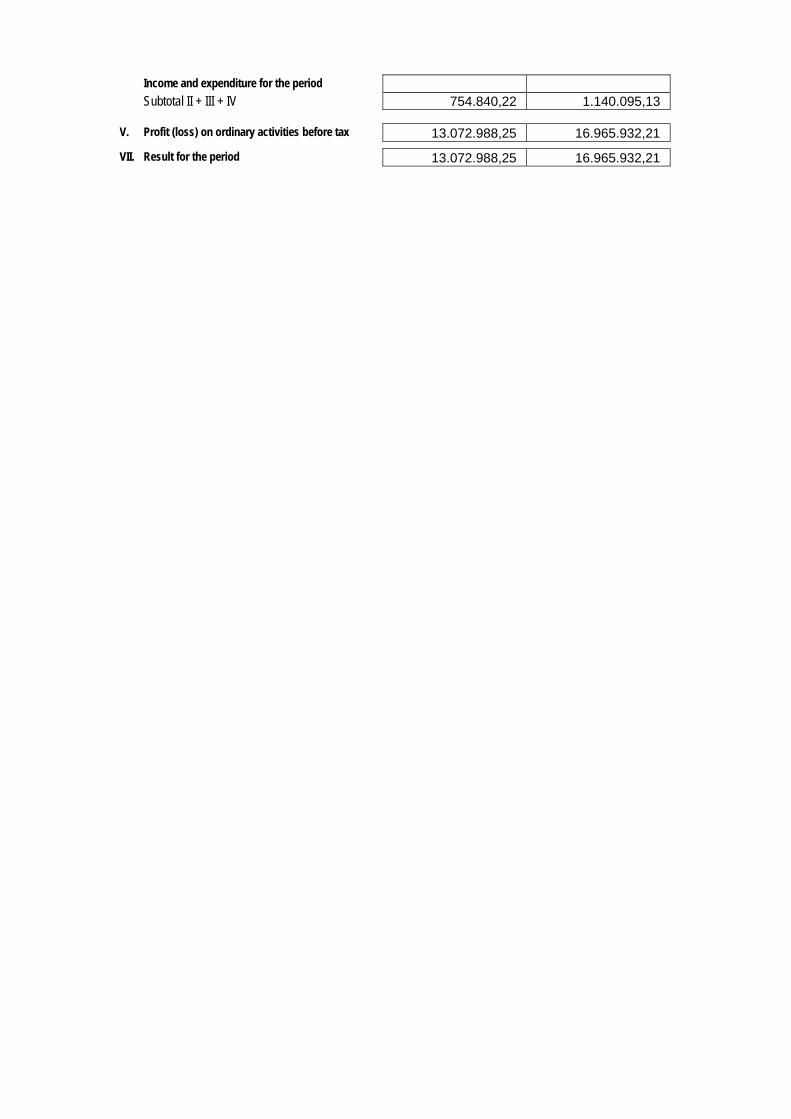

Income and expenditure for the period Subtotal II + III + IV 37.467.318,11 44.303.920,90

V. Profit (loss) on ordinary activities before tax 246.526.203,57 114.971.498,15

VII. Result for the period 246.526.203,57 114.971.498,15

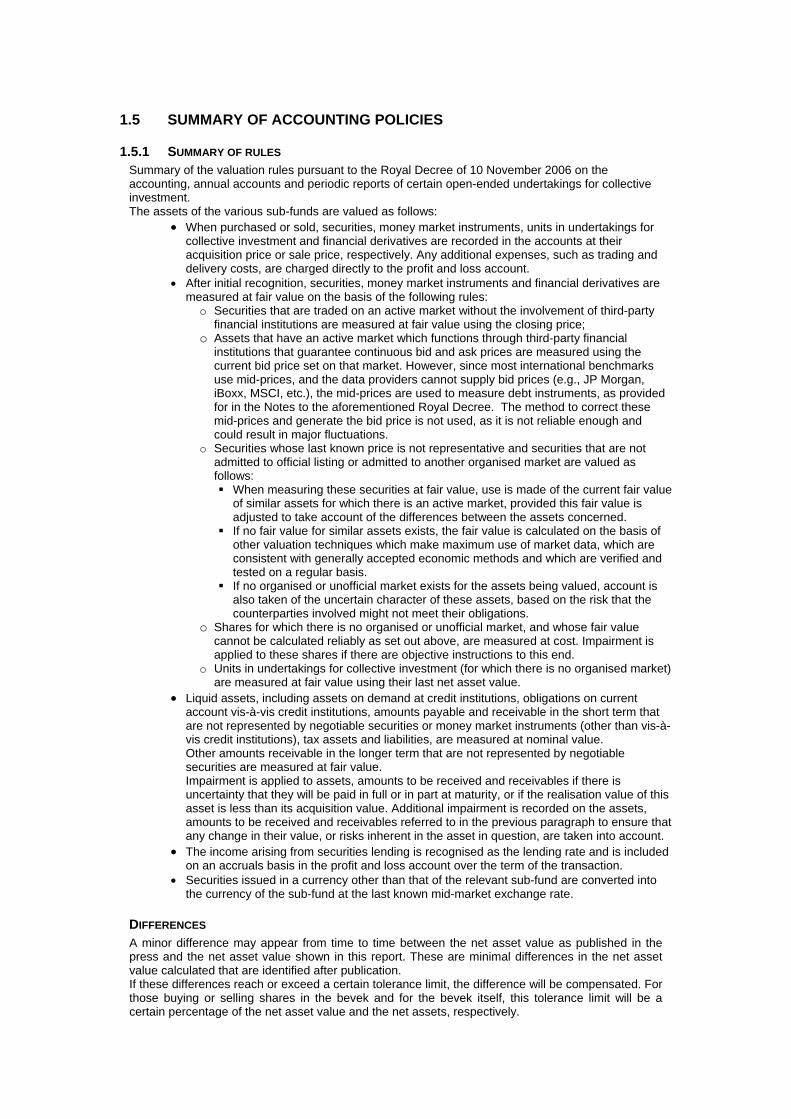

1.5 SUMMARY OF ACCOUNTING POLICIES

1.5.1 SUMMARY OF RULES Summary of the valuation rules pursuant to the Royal Decree of 10 November 2006 on the accounting, annual accounts and periodic reports of certain open-ended undertakings for collective investment. The assets of the various sub-funds are valued as follows:

When purchased or sold, securities, money market instruments, units in undertakings for collective investment and financial derivatives are recorded in the accounts at their acquisition price or sale price, respectively. Any additional expenses, such as trading and delivery costs, are charged directly to the profit and loss account.

After initial recognition, securities, money market instruments and financial derivatives are measured at fair value on the basis of the following rules:

o Securities that are traded on an active market without the involvement of third-party financial institutions are measured at fair value using the closing price;

o Assets that have an active market which functions through third-party financial institutions that guarantee continuous bid and ask prices are measured using the current bid price set on that market. However, since most international benchmarks use mid-prices, and the data providers cannot supply bid prices (e.g., JP Morgan, iBoxx, MSCI, etc.), the mid-prices are used to measure debt instruments, as provided for in the Notes to the aforementioned Royal Decree. The method to correct these mid-prices and generate the bid price is not used, as it is not reliable enough and could result in major fluctuations.

o Securities whose last known price is not representative and securities that are not admitted to official listing or admitted to another organised market are valued as follows: When measuring these securities at fair value, use is made of the current fair value

of similar assets for which there is an active market, provided this fair value is adjusted to take account of the differences between the assets concerned.

If no fair value for similar assets exists, the fair value is calculated on the basis of other valuation techniques which make maximum use of market data, which are consistent with generally accepted economic methods and which are verified and tested on a regular basis.

If no organised or unofficial market exists for the assets being valued, account is also taken of the uncertain character of these assets, based on the risk that the counterparties involved might not meet their obligations.

o Shares for which there is no organised or unofficial market, and whose fair value cannot be calculated reliably as set out above, are measured at cost. Impairment is applied to these shares if there are objective instructions to this end.

o Units in undertakings for collective investment (for which there is no organised market) are measured at fair value using their last net asset value.

Liquid assets, including assets on demand at credit institutions, obligations on current account vis-à-vis credit institutions, amounts payable and receivable in the short term that are not represented by negotiable securities or money market instruments (other than vis-à-vis credit institutions), tax assets and liabilities, are measured at nominal value. Other amounts receivable in the longer term that are not represented by negotiable securities are measured at fair value. Impairment is applied to assets, amounts to be received and receivables if there is uncertainty that they will be paid in full or in part at maturity, or if the realisation value of this asset is less than its acquisition value. Additional impairment is recorded on the assets, amounts to be received and receivables referred to in the previous paragraph to ensure that any change in their value, or risks inherent in the asset in question, are taken into account.

The income arising from securities lending is recognised as the lending rate and is included on an accruals basis in the profit and loss account over the term of the transaction.

Securities issued in a currency other than that of the relevant sub-fund are converted into the currency of the sub-fund at the last known mid-market exchange rate.

DIFFERENCES A minor difference may appear from time to time between the net asset value as published in the press and the net asset value shown in this report. These are minimal differences in the net asset value calculated that are identified after publication. If these differences reach or exceed a certain tolerance limit, the difference will be compensated. For those buying or selling shares in the bevek and for the bevek itself, this tolerance limit will be a certain percentage of the net asset value and the net assets, respectively.

This tolerance limit is: o money market funds: 0.25% o bond funds, balanced funds and funds offering capital guarantee: 0.50% o equity funds: 1% o other funds (real estate funds, etc.): 0.50%

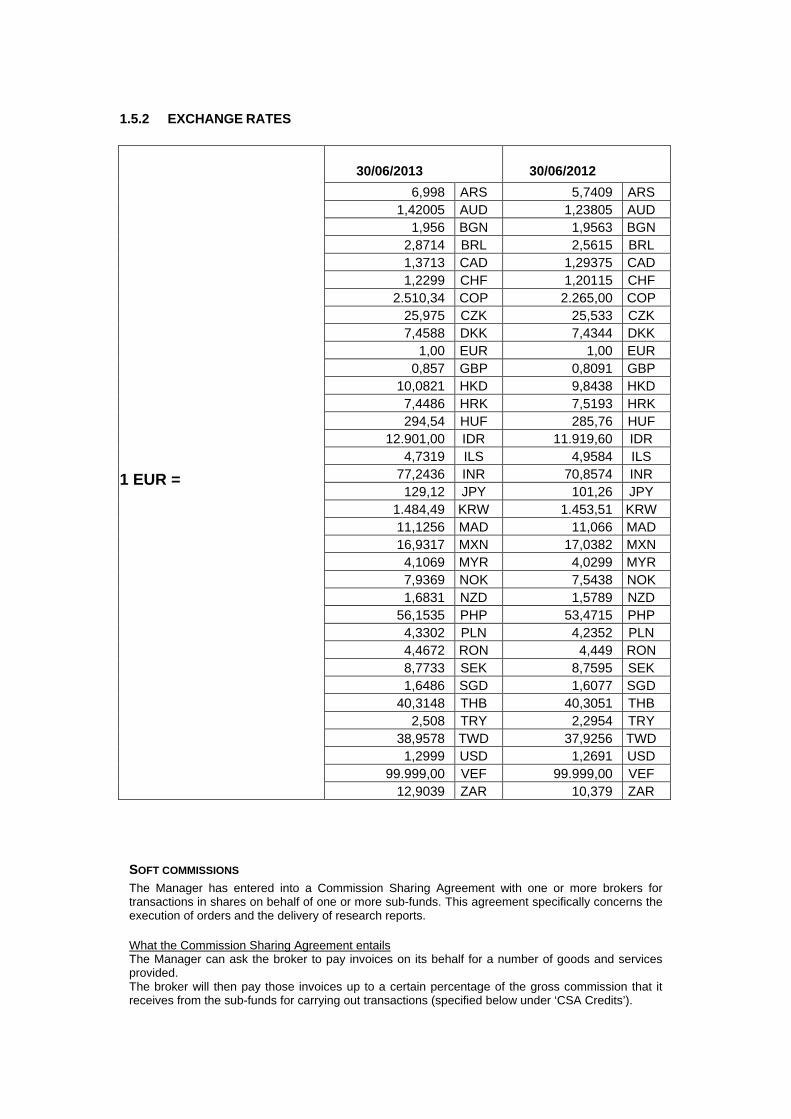

1.5.2 EXCHANGE RATES

1 EUR =

30/06/2013 30/06/2012

6,998 ARS 5,7409 ARS 1,42005 AUD 1,23805 AUD

1,956 BGN 1,9563 BGN 2,8714 BRL 2,5615 BRL 1,3713 CAD 1,29375 CAD 1,2299 CHF 1,20115 CHF

2.510,34 COP 2.265,00 COP 25,975 CZK 25,533 CZK 7,4588 DKK 7,4344 DKK

1,00 EUR 1,00 EUR 0,857 GBP 0,8091 GBP

10,0821 HKD 9,8438 HKD 7,4486 HRK 7,5193 HRK 294,54 HUF 285,76 HUF

12.901,00 IDR 11.919,60 IDR 4,7319 ILS 4,9584 ILS

77,2436 INR 70,8574 INR 129,12 JPY 101,26 JPY

1.484,49 KRW 1.453,51 KRW 11,1256 MAD 11,066 MAD 16,9317 MXN 17,0382 MXN 4,1069 MYR 4,0299 MYR 7,9369 NOK 7,5438 NOK 1,6831 NZD 1,5789 NZD

56,1535 PHP 53,4715 PHP 4,3302 PLN 4,2352 PLN 4,4672 RON 4,449 RON 8,7733 SEK 8,7595 SEK 1,6486 SGD 1,6077 SGD

40,3148 THB 40,3051 THB 2,508 TRY 2,2954 TRY

38,9578 TWD 37,9256 TWD 1,2999 USD 1,2691 USD

99.999,00 VEF 99.999,00 VEF 12,9039 ZAR 10,379 ZAR

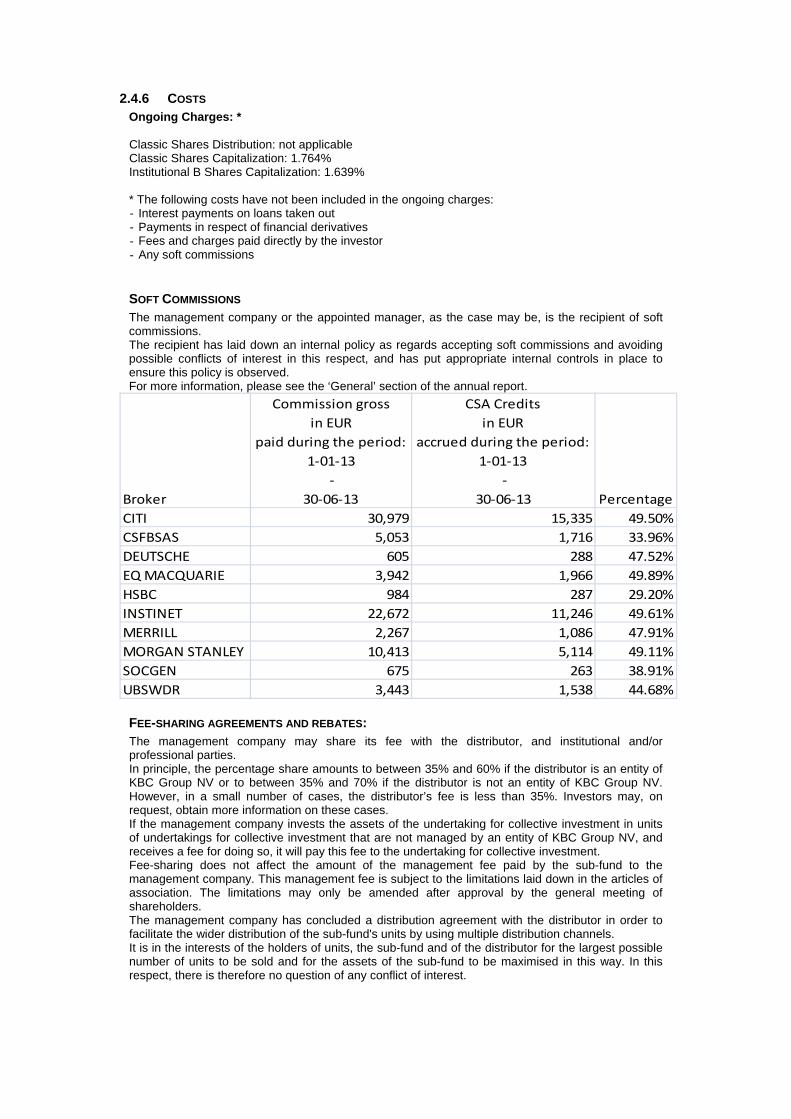

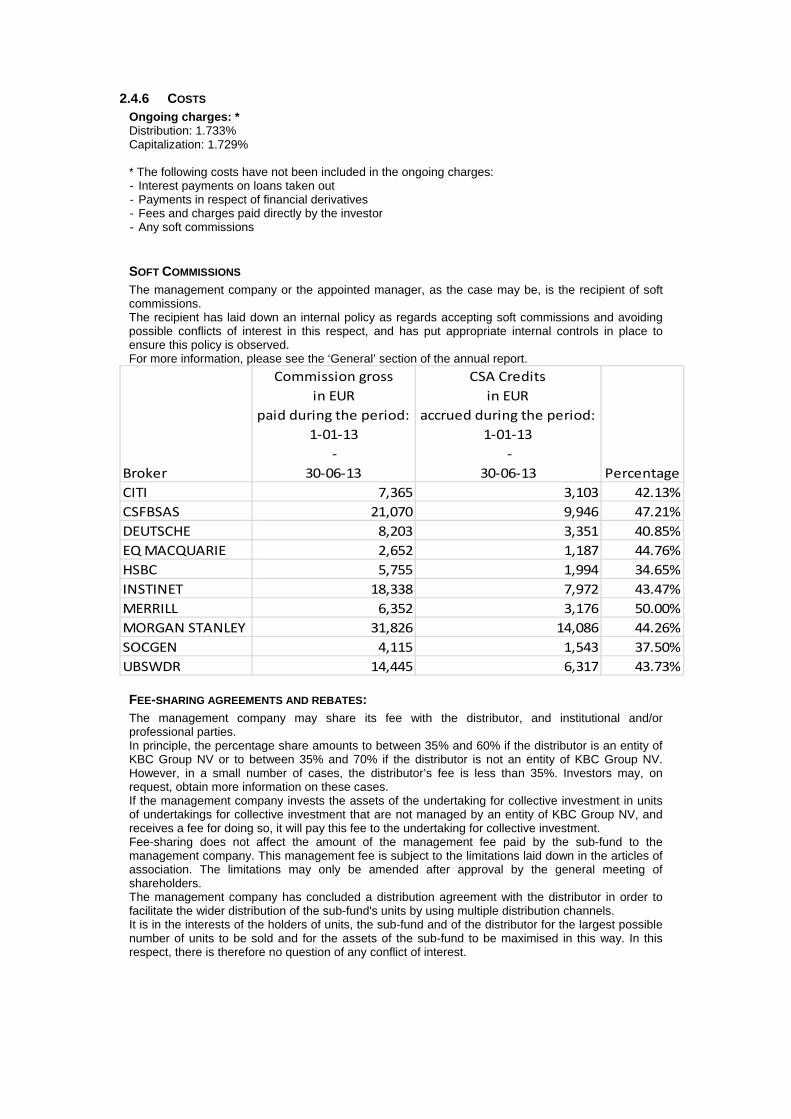

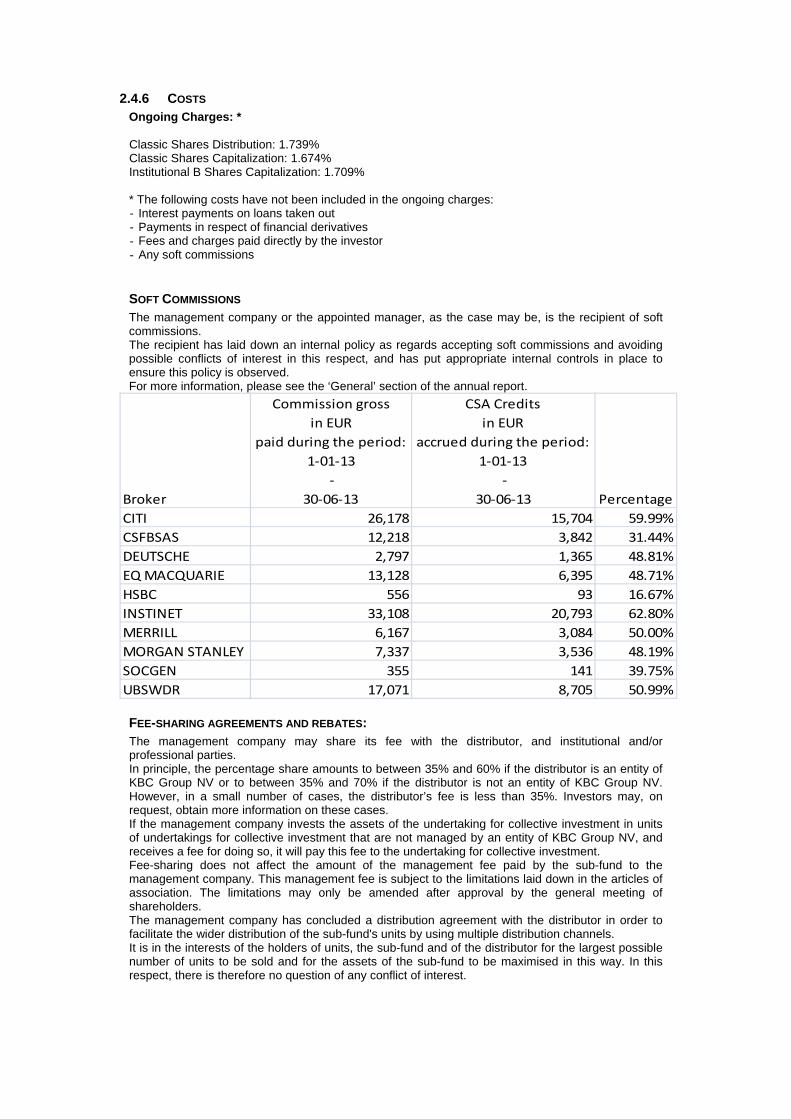

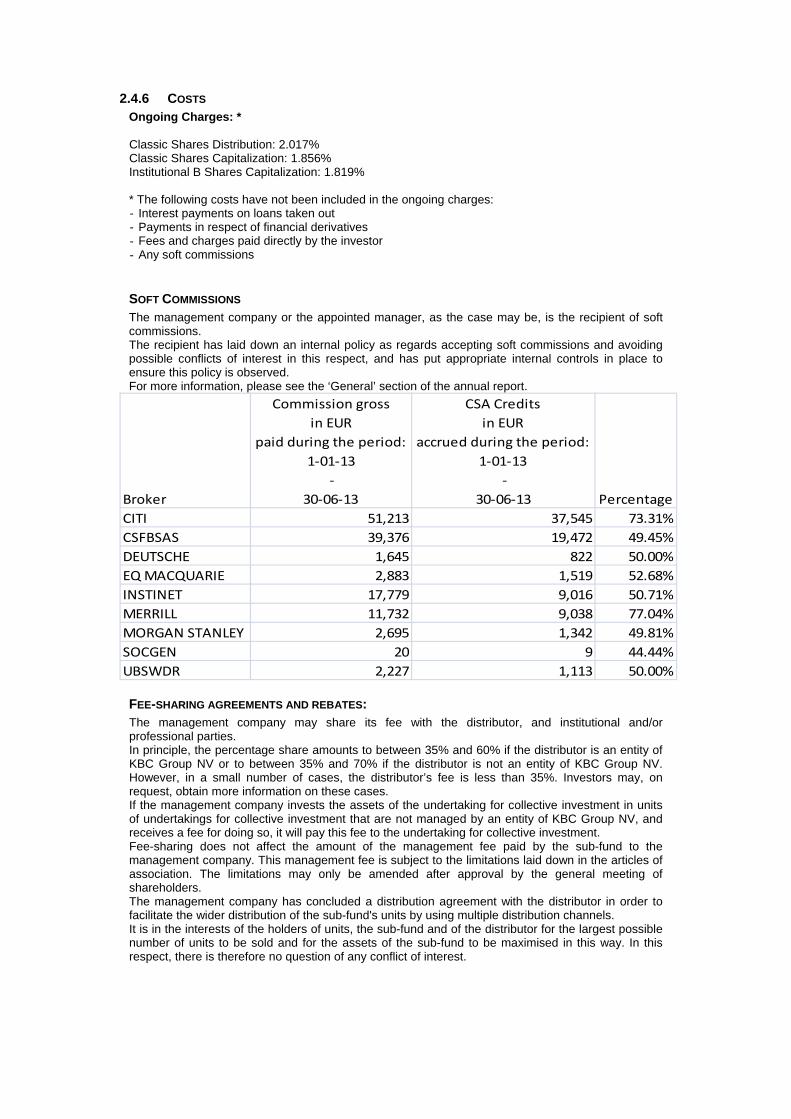

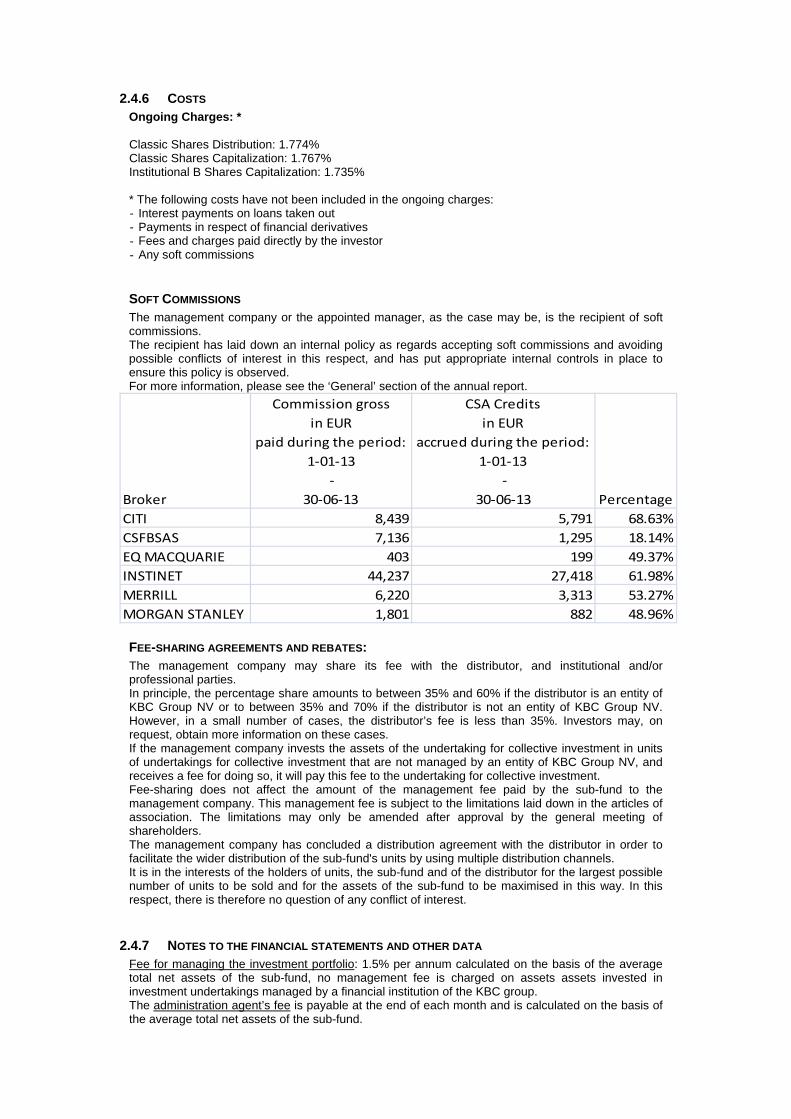

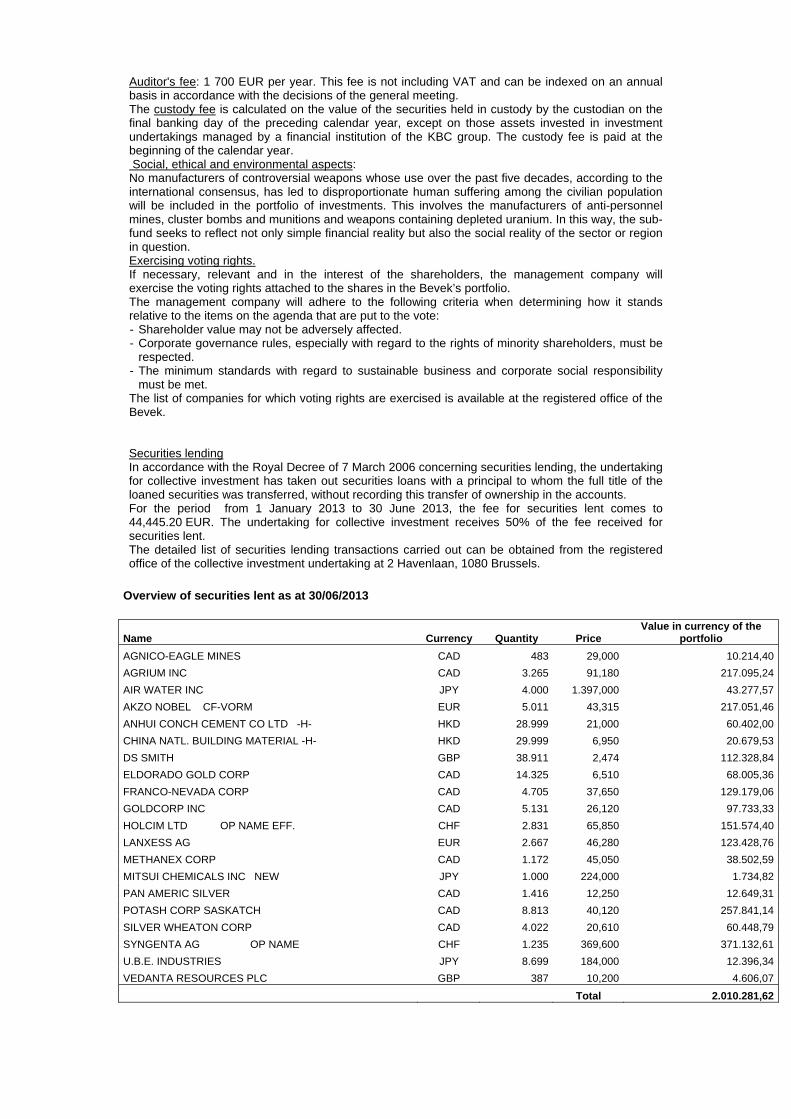

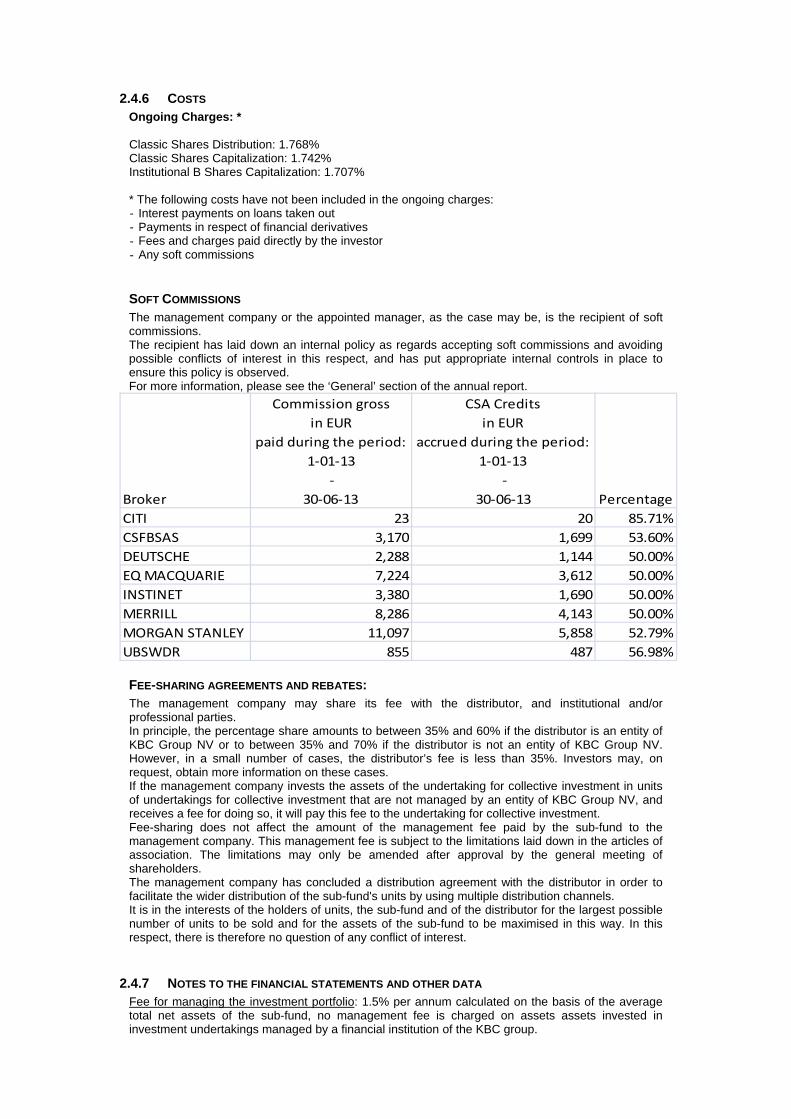

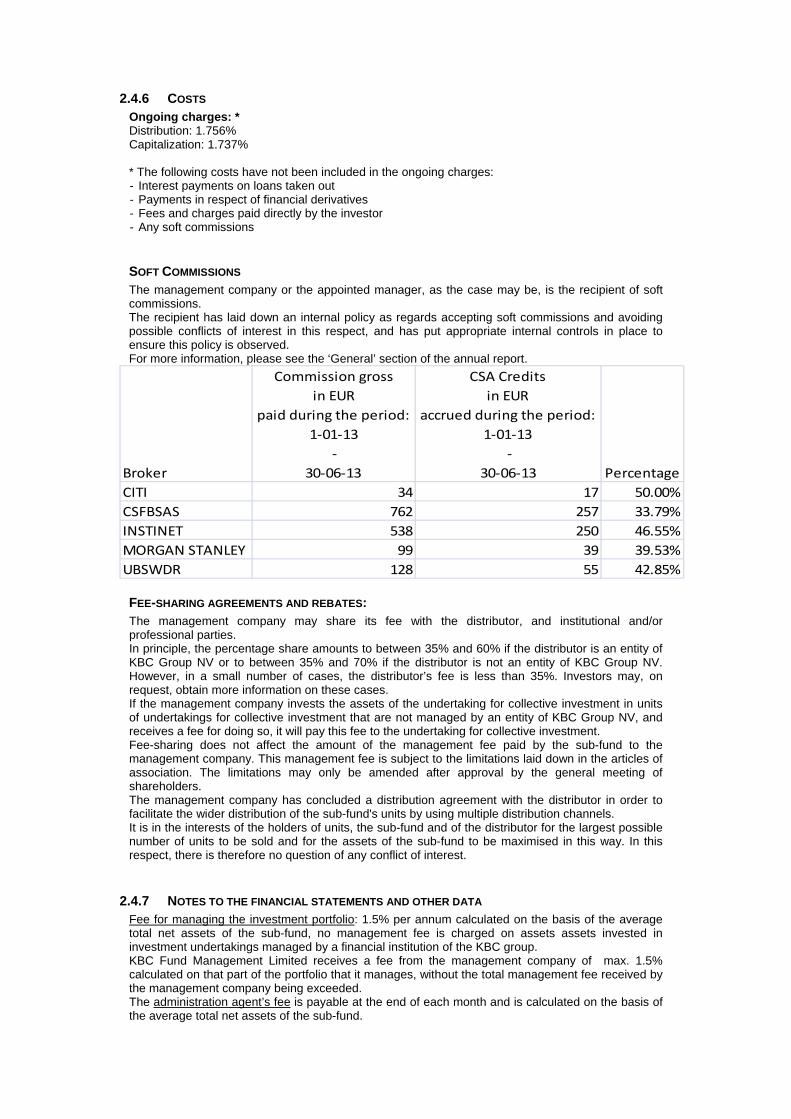

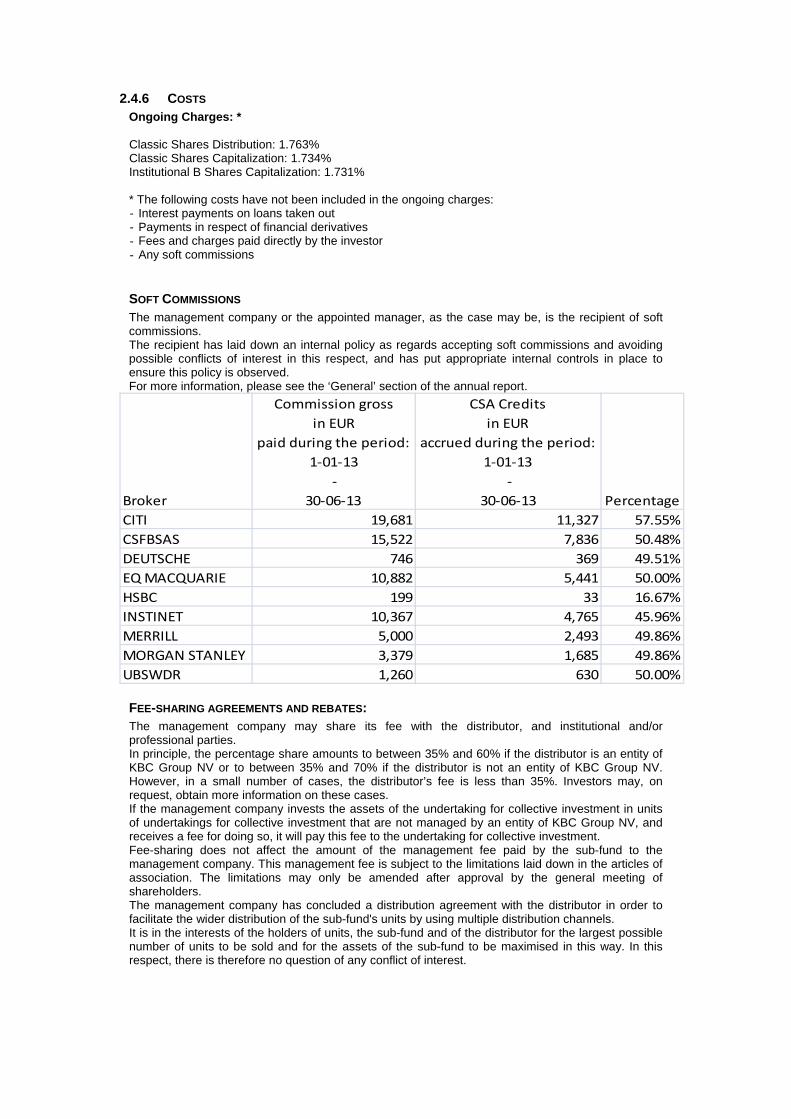

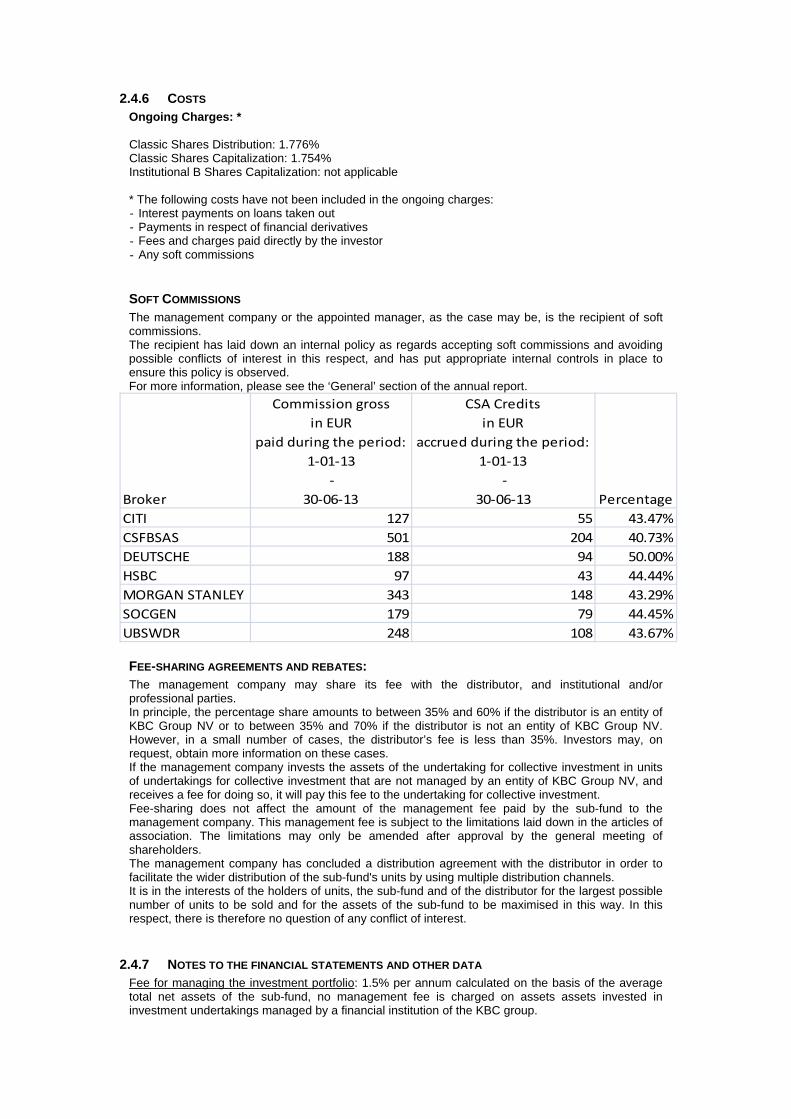

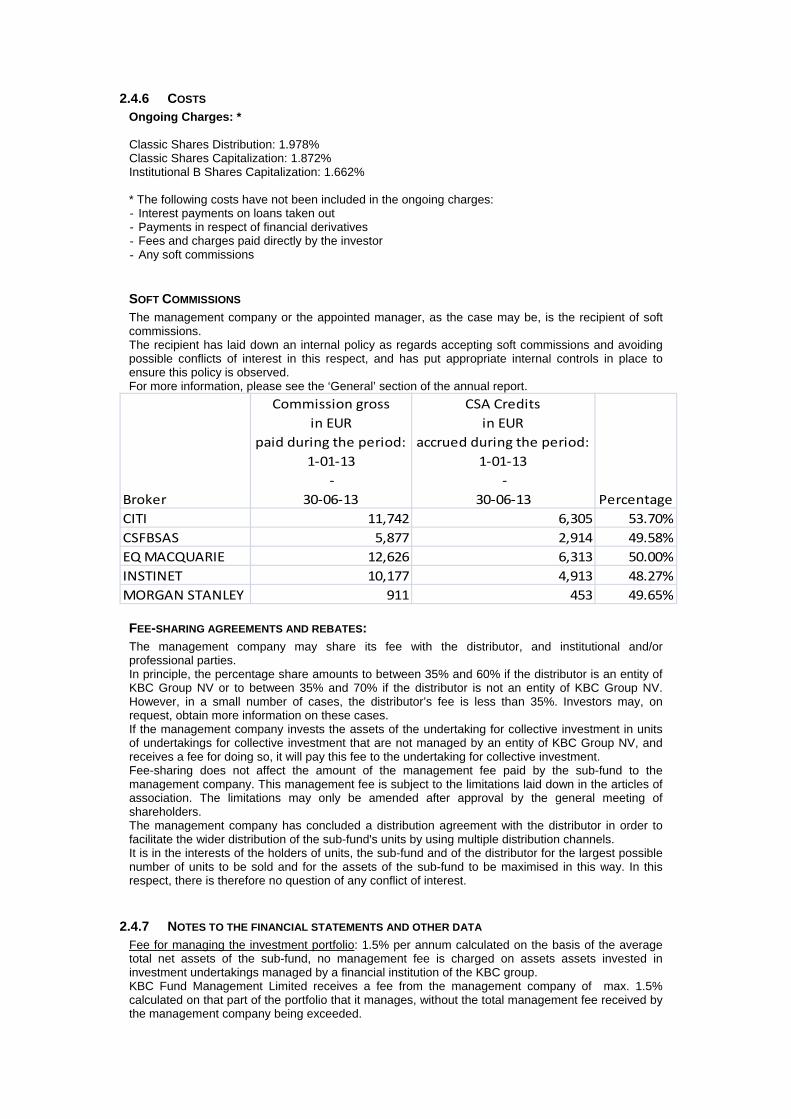

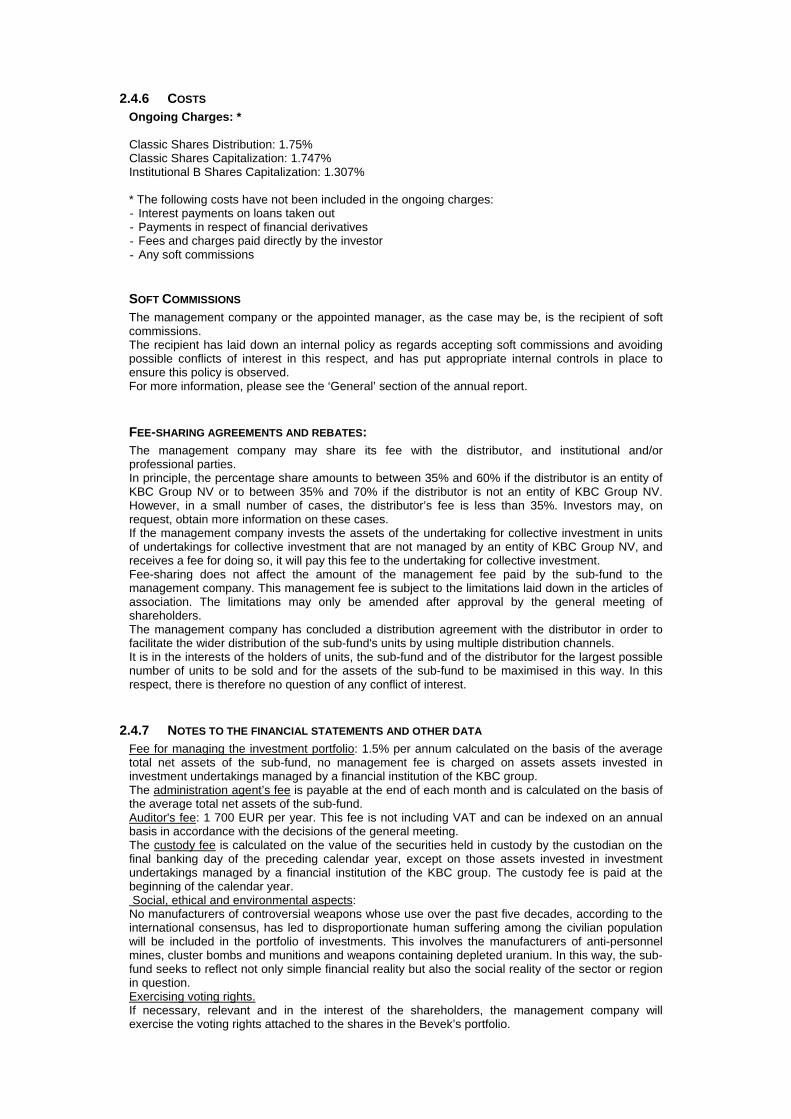

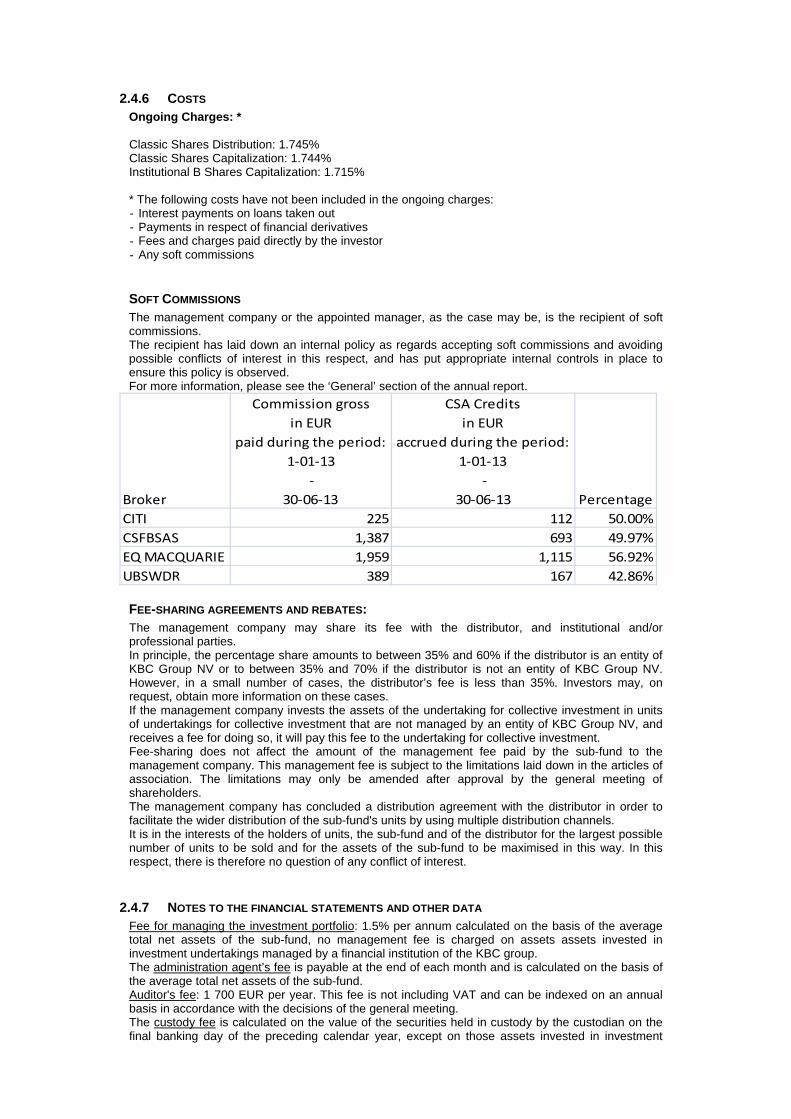

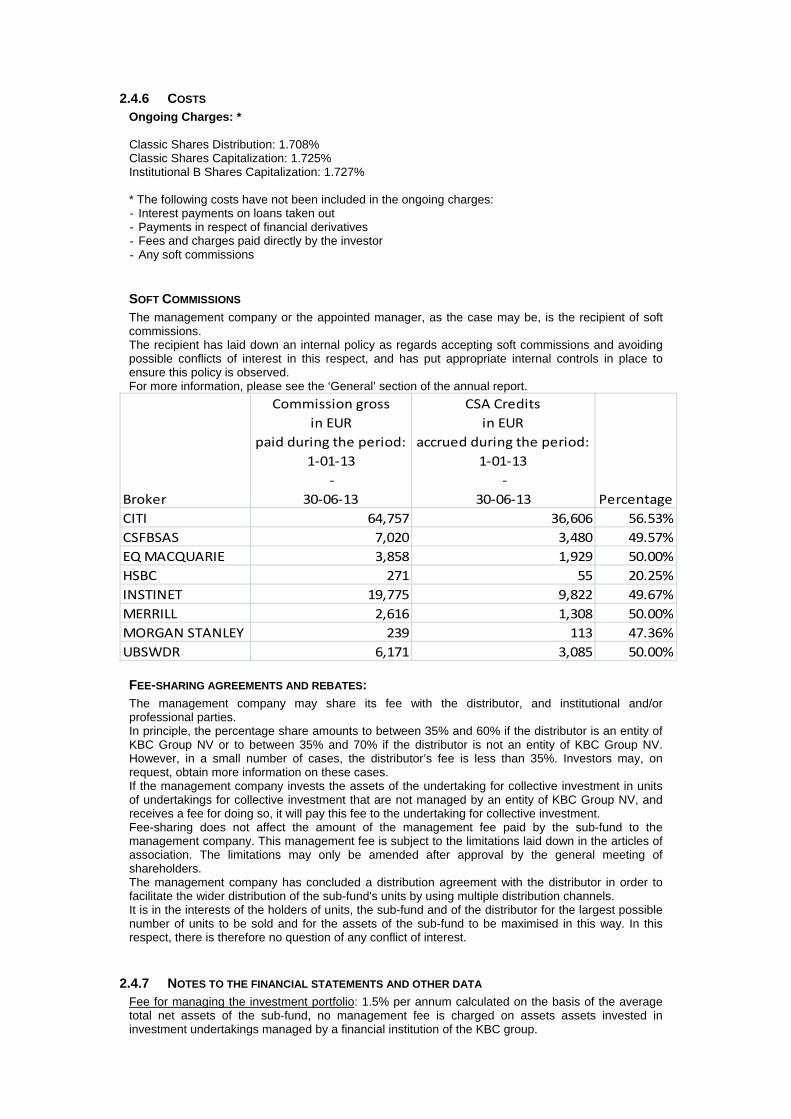

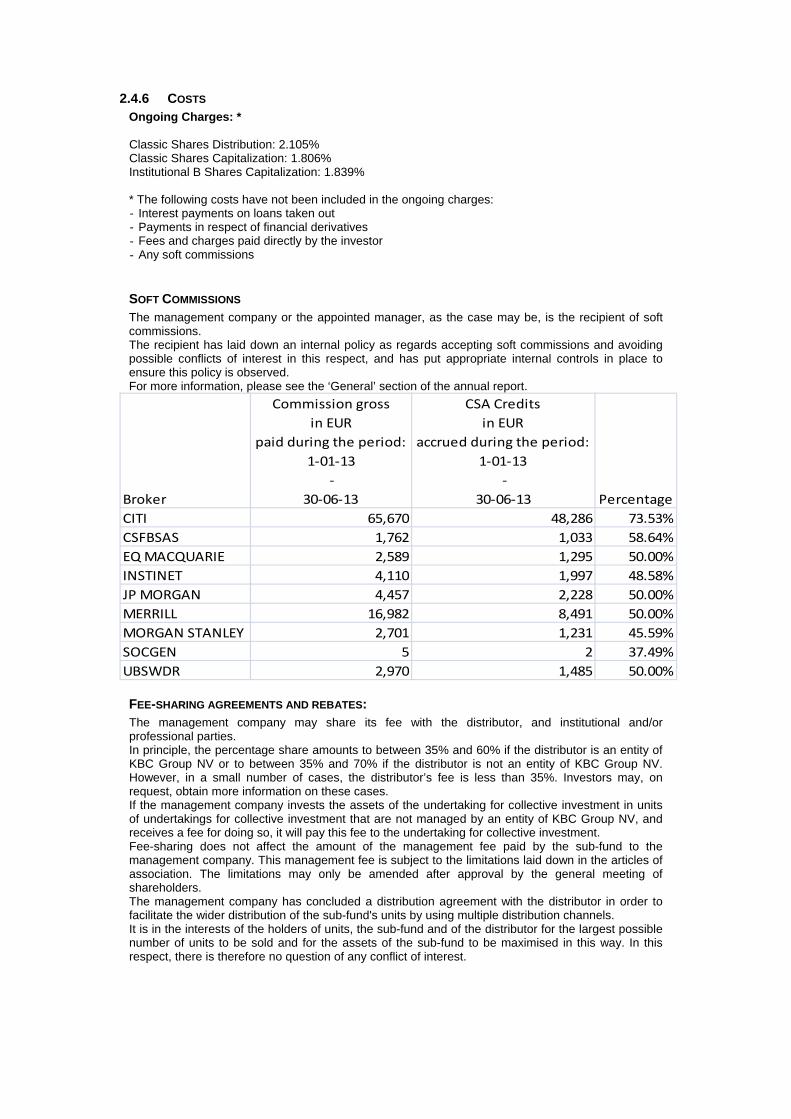

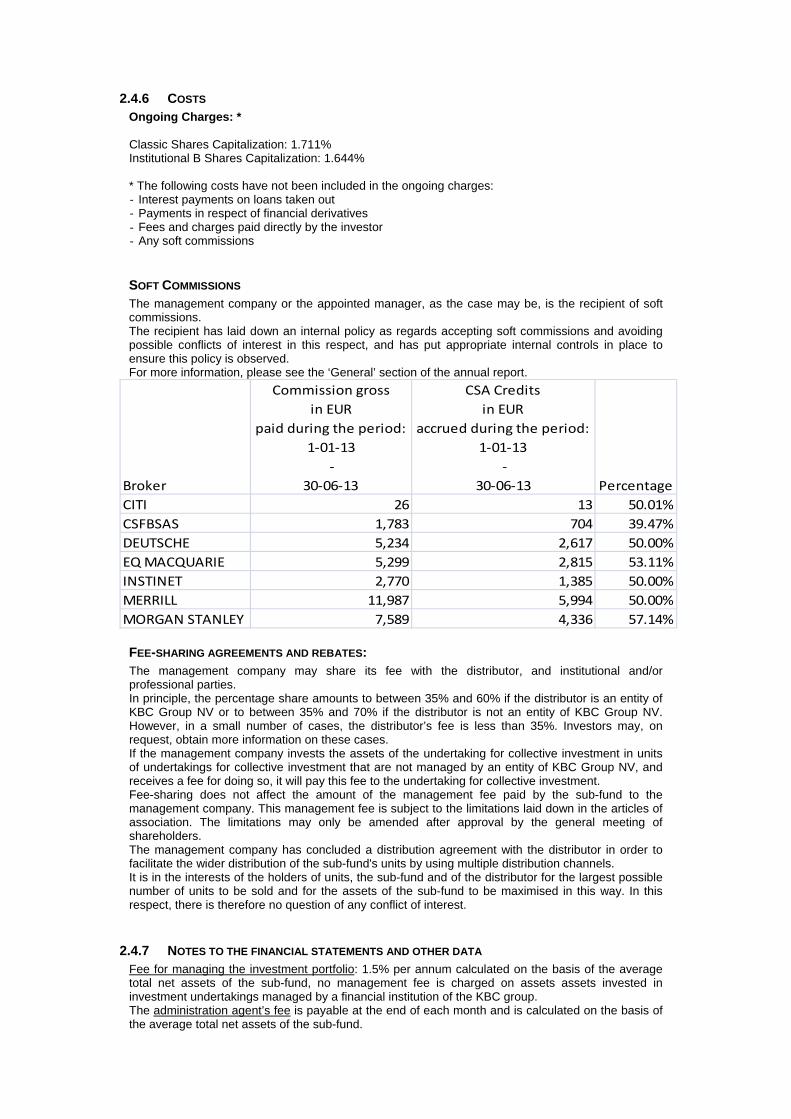

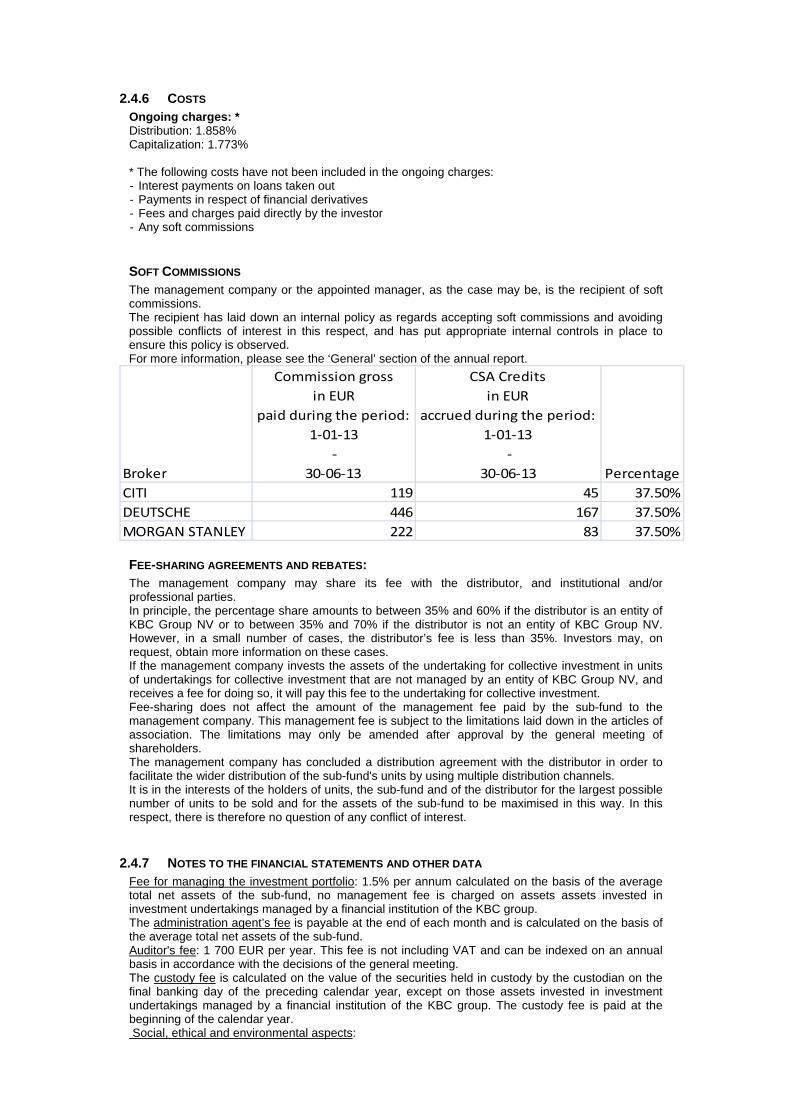

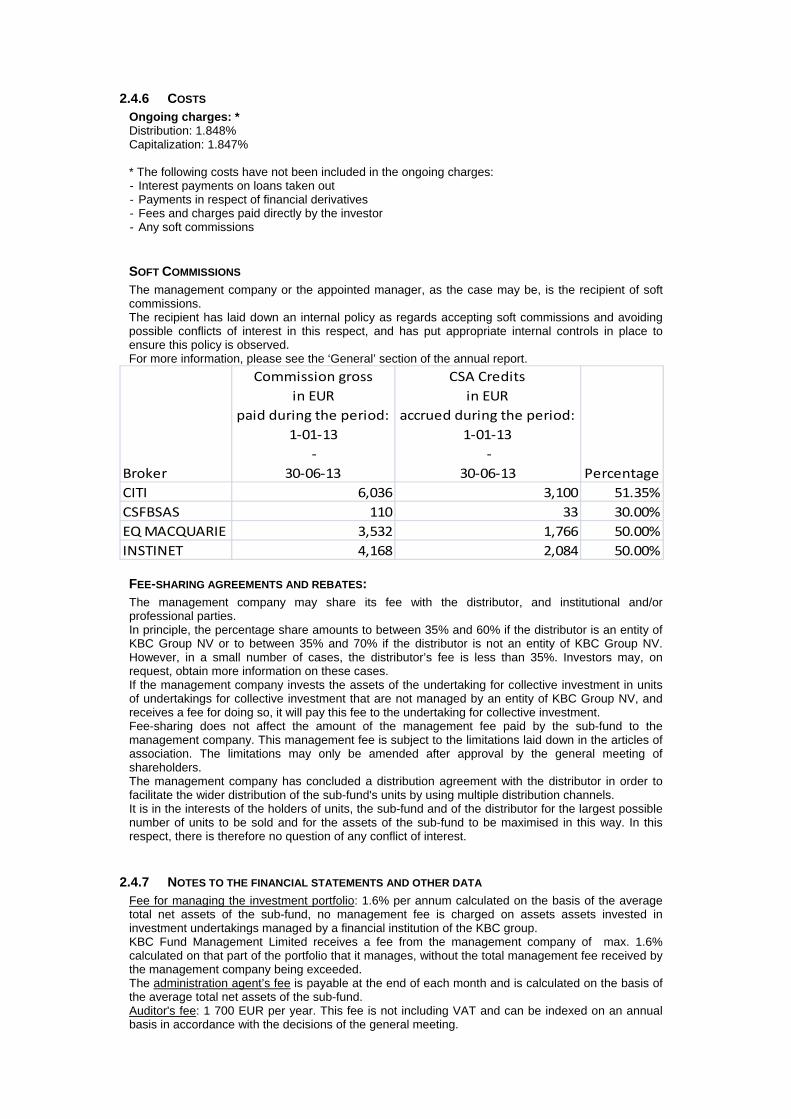

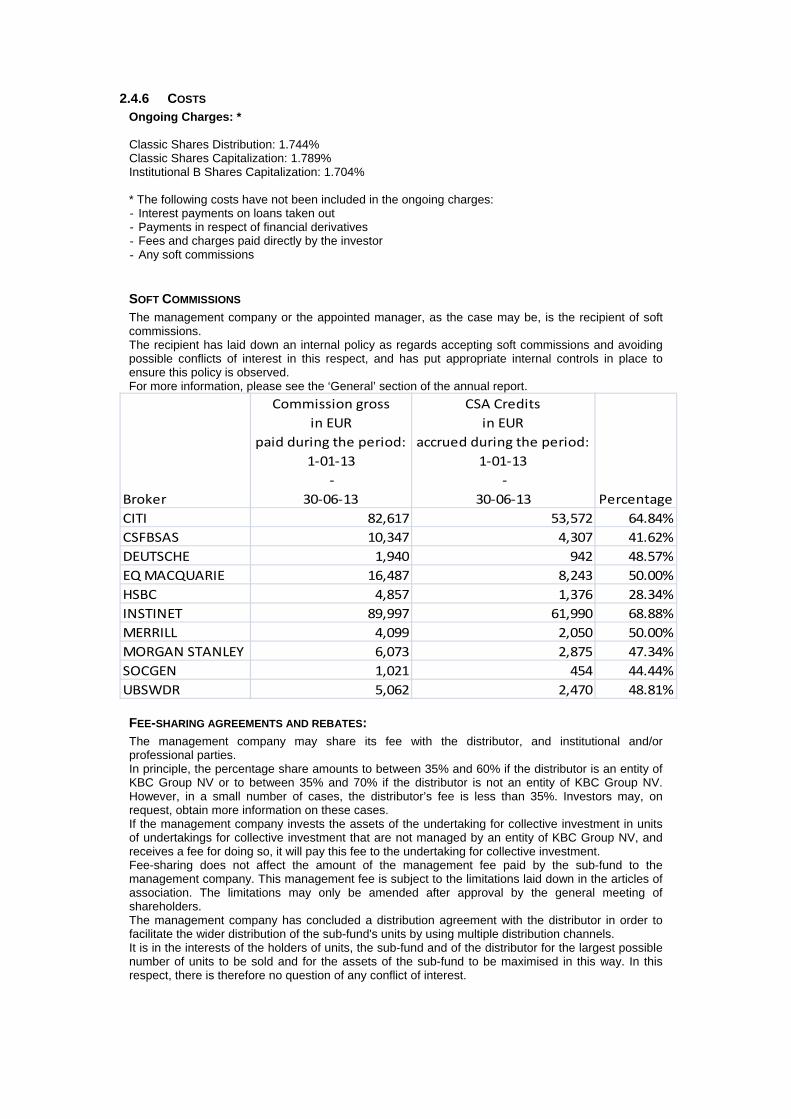

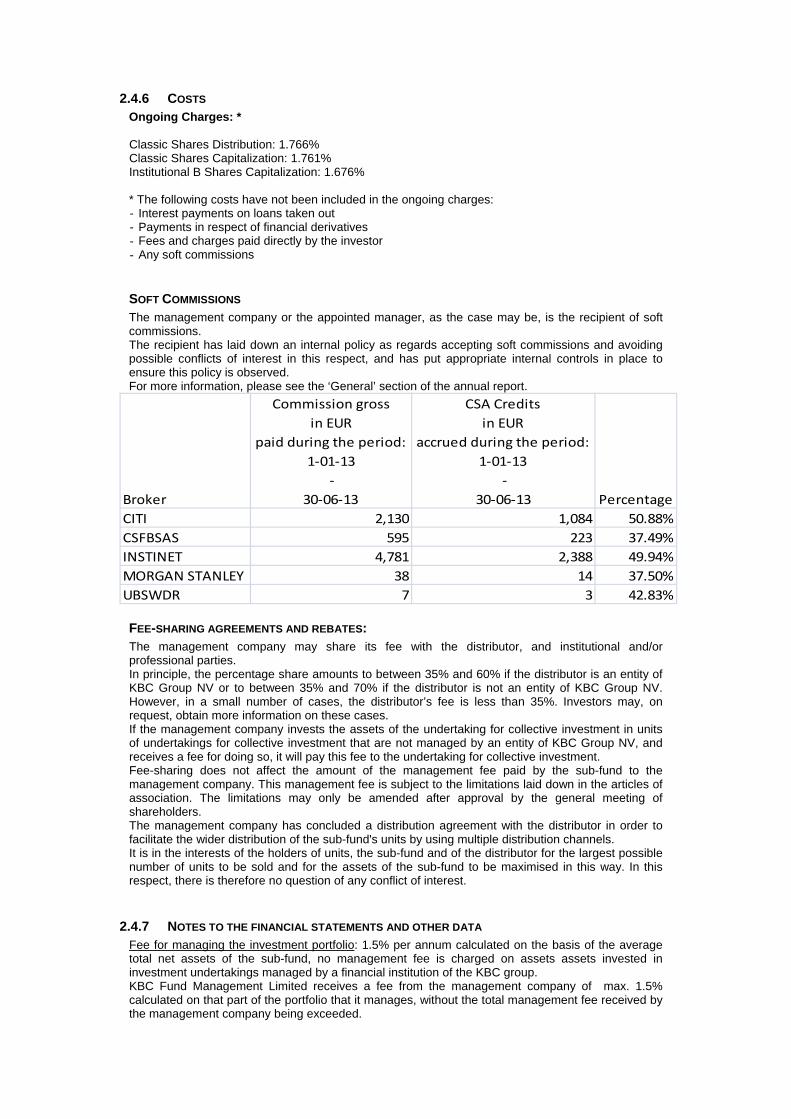

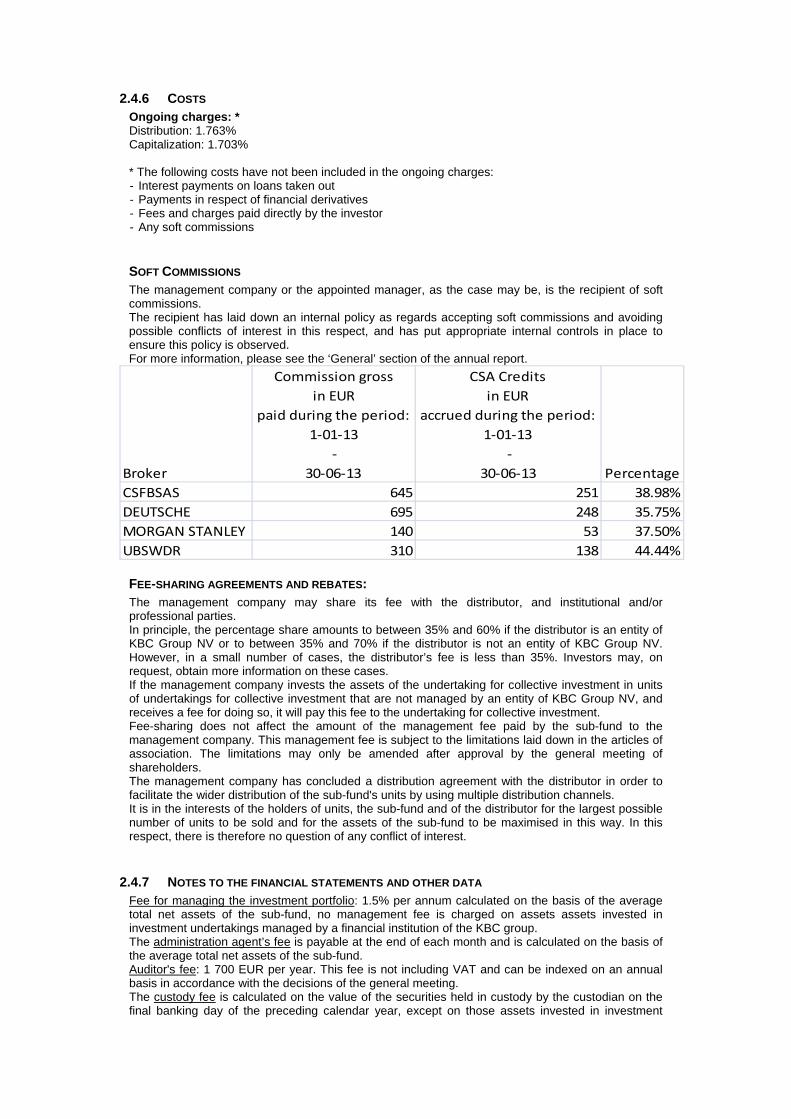

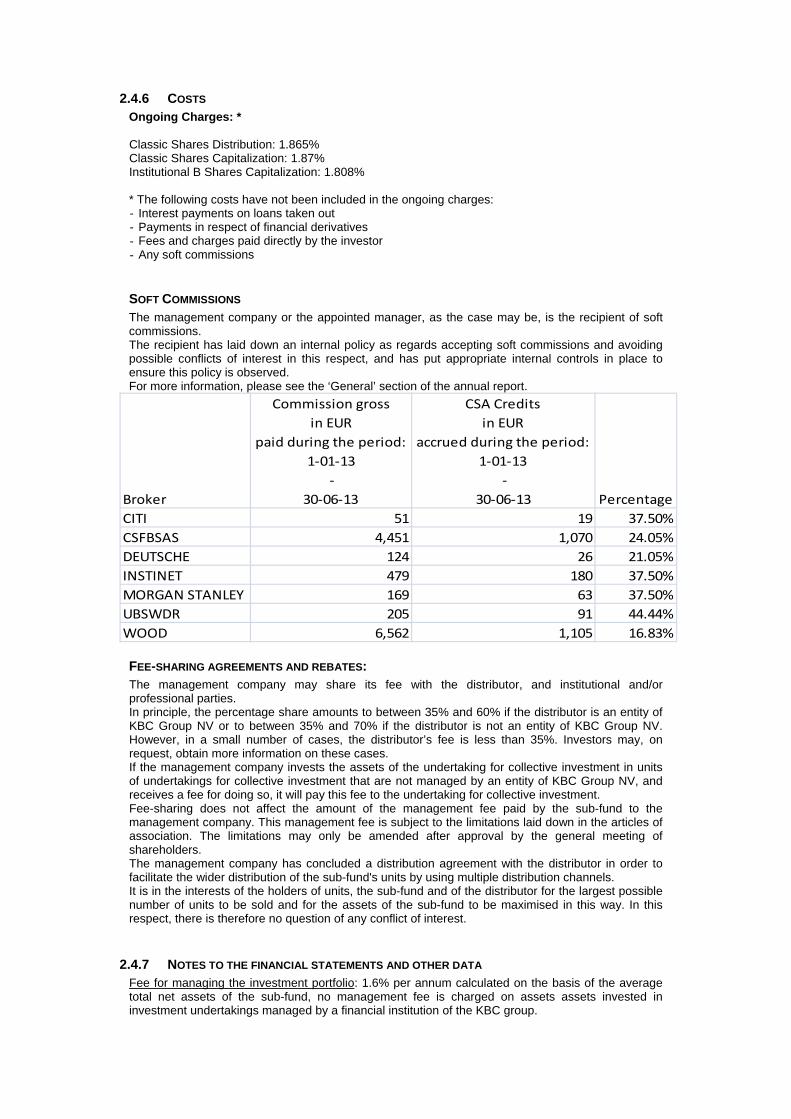

SOFT COMMISSIONS The Manager has entered into a Commission Sharing Agreement with one or more brokers for transactions in shares on behalf of one or more sub-funds. This agreement specifically concerns the execution of orders and the delivery of research reports. What the Commission Sharing Agreement entails The Manager can ask the broker to pay invoices on its behalf for a number of goods and services provided. The broker will then pay those invoices up to a certain percentage of the gross commission that it receives from the sub-funds for carrying out transactions (specified below under ‘CSA Credits’).

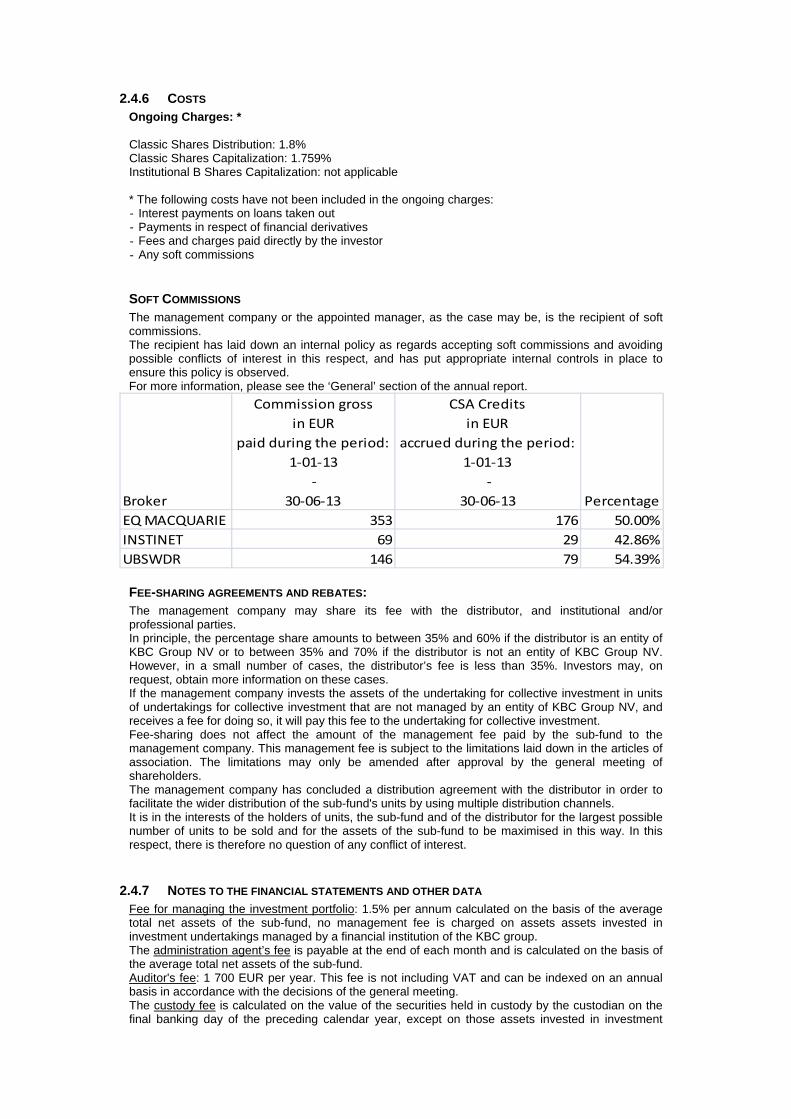

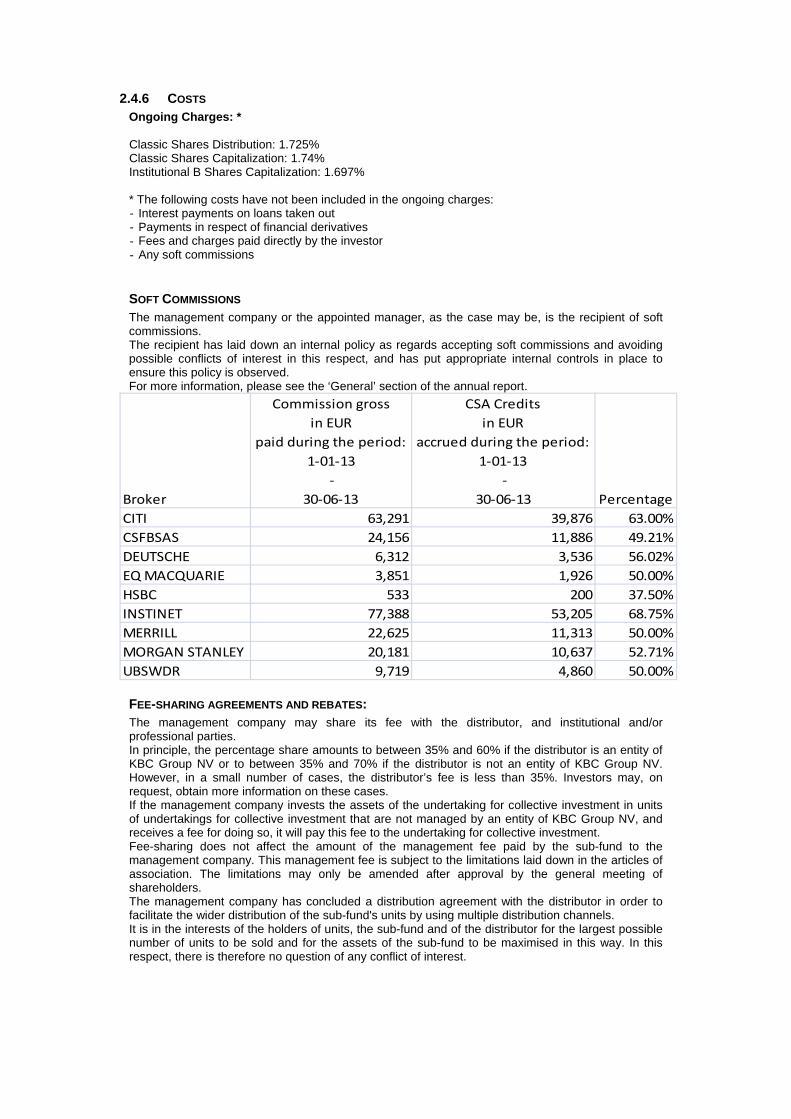

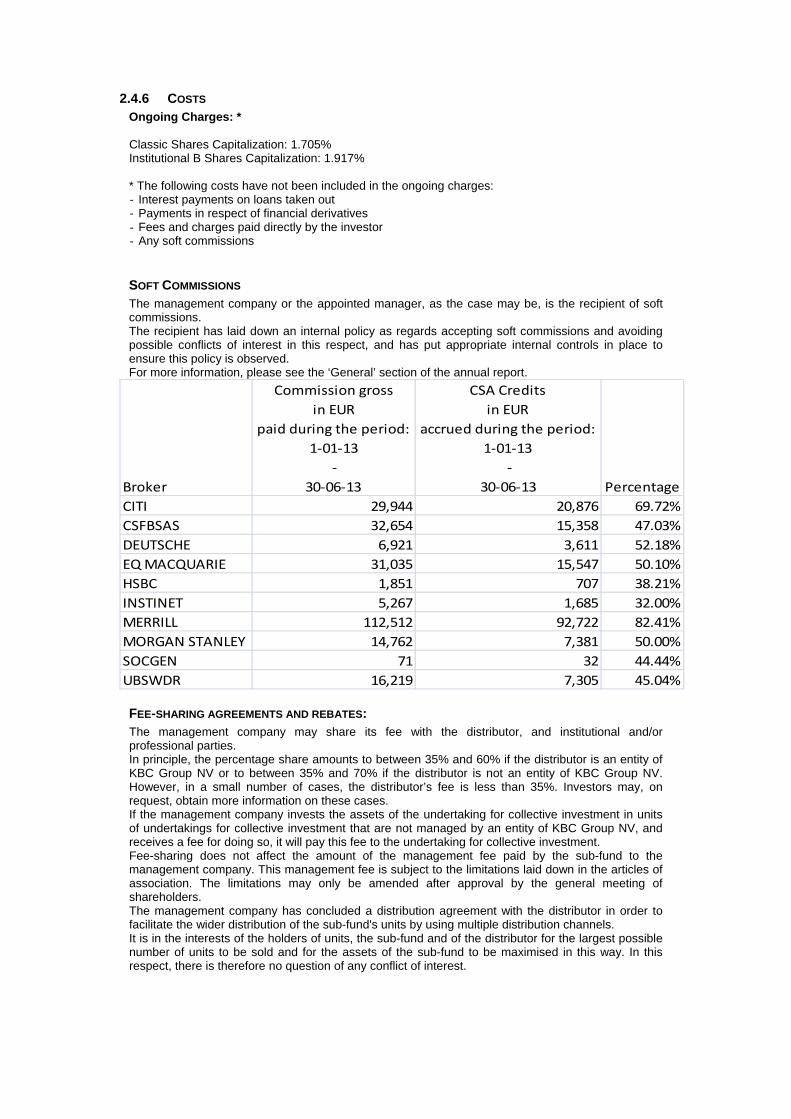

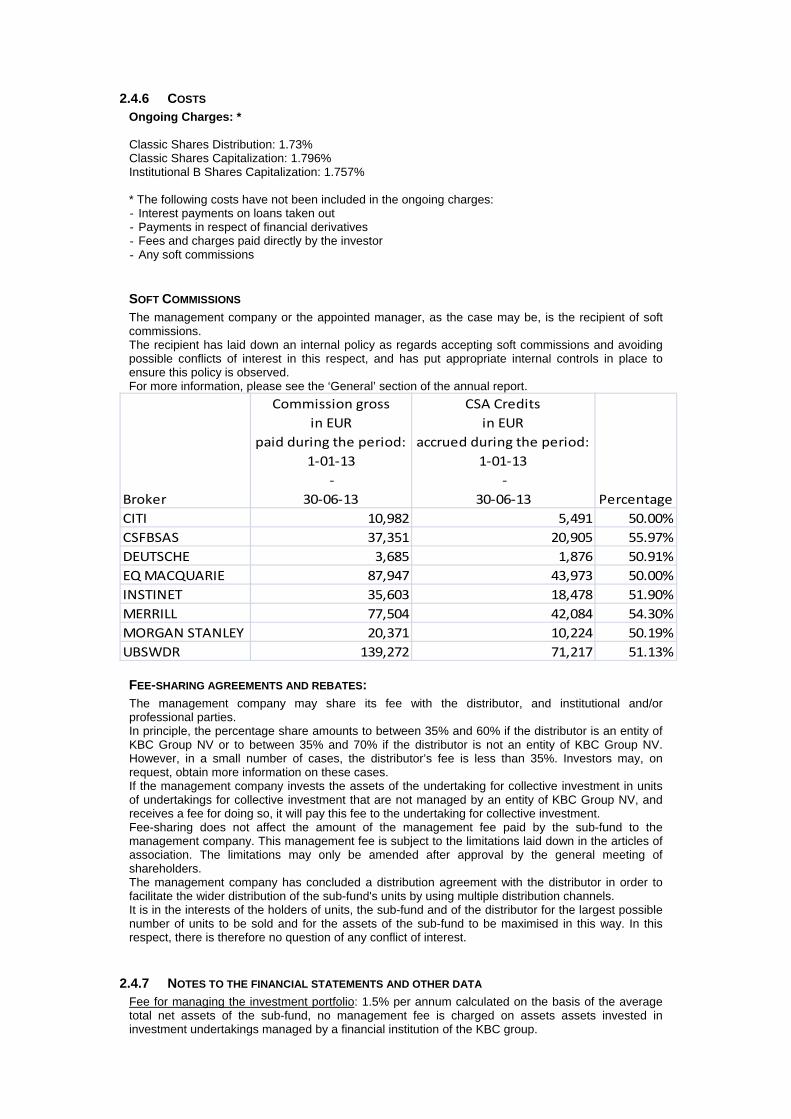

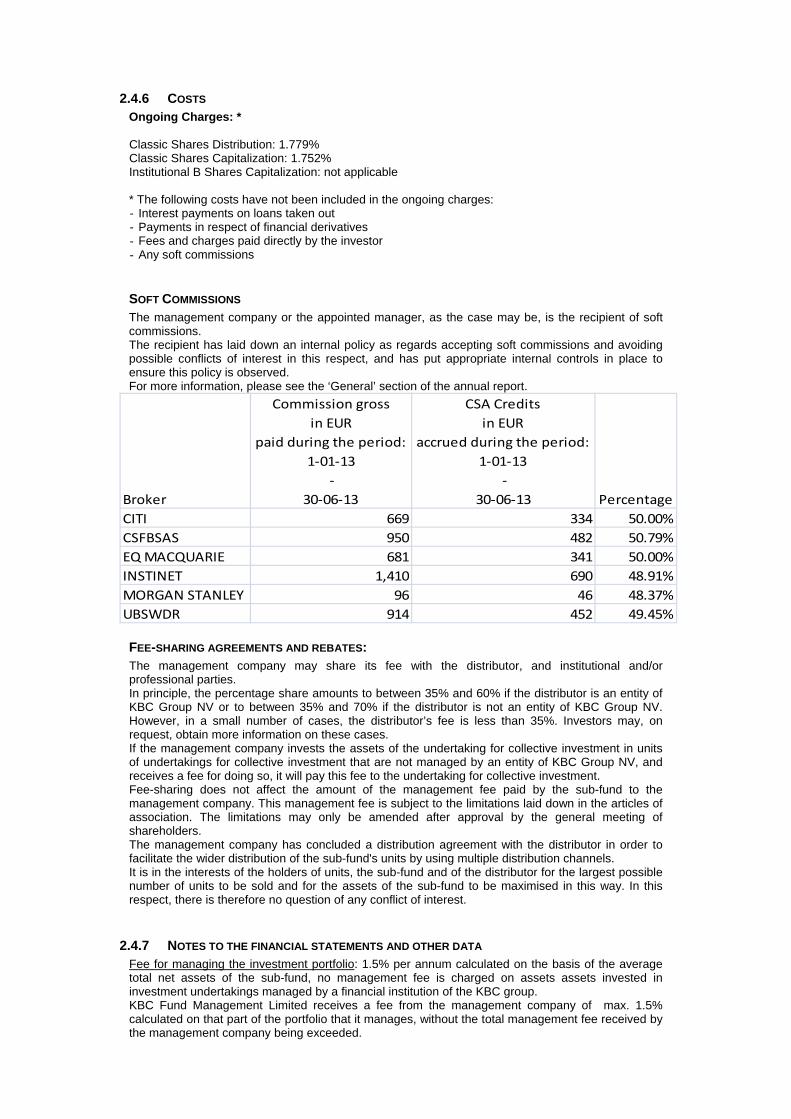

N.B.: Only goods and services that assist the manager in managing the sub-funds in the interest of the bevek can be covered by a Commission Sharing Agreement. Goods and services eligible for a Commission Sharing Agreement: Research and advisory services Portfolio valuation and analysis Performance measurement Market price services Computer hardware associated with specialised computer software or research services Dedicated telephone lines Seminar fees, where the subject matter is of relevance to the provision of investment services Publications, where the subject matter is of relevance to the provision of investment services.

Broker

Commission gross

in EUR

paid during the period:

1‐01‐13

‐

30‐06‐13

CSA Credits

in EUR

accrued during the period:

1‐01‐13

‐

30‐06‐13 Percentage

CITI 902,292 542,386 60.11%

CSFBSAS 584,184 312,984 53.58%

DEUTSCHE 263,068 129,559 49.25%

EQ MACQUARIE 444,982 239,300 53.78%

HSBC 69,789 19,201 27.51%

INSTINET 794,607 430,206 54.14%

JP MORGAN 4,457 2,228 50.00%

MERRILL 489,711 280,379 57.25%

MORGAN STANLEY 345,585 167,695 48.52%

SOCGEN 15,299 6,035 39.44%

UBSWDR 395,519 198,950 50.30%

WOOD 11,064 1,855 16.76%

Semi-Annual report as at 30th June 2013

TABLE OF CONTENTS

2. Information on KBC Equity Fund CSOB Akciovy Fond Dividendovych Firem

2.1. Management report 2.1.1. Launch date and subscription price 2.1.2. Stock exchange listing 2.1.3. Aim and distinctive features of the investment policy 2.1.4. Financial portfolio management 2.1.5. Distributors 2.1.6. Index and benchmark 2.1.7. Policy conducted during the financial year 2.1.8. Future policy 2.1.9. Synthetic risk and reward indicator (SRRI)

2.2. Balance sheet

2.3. Profit and loss account

2.4. Composition of the assets and key figures

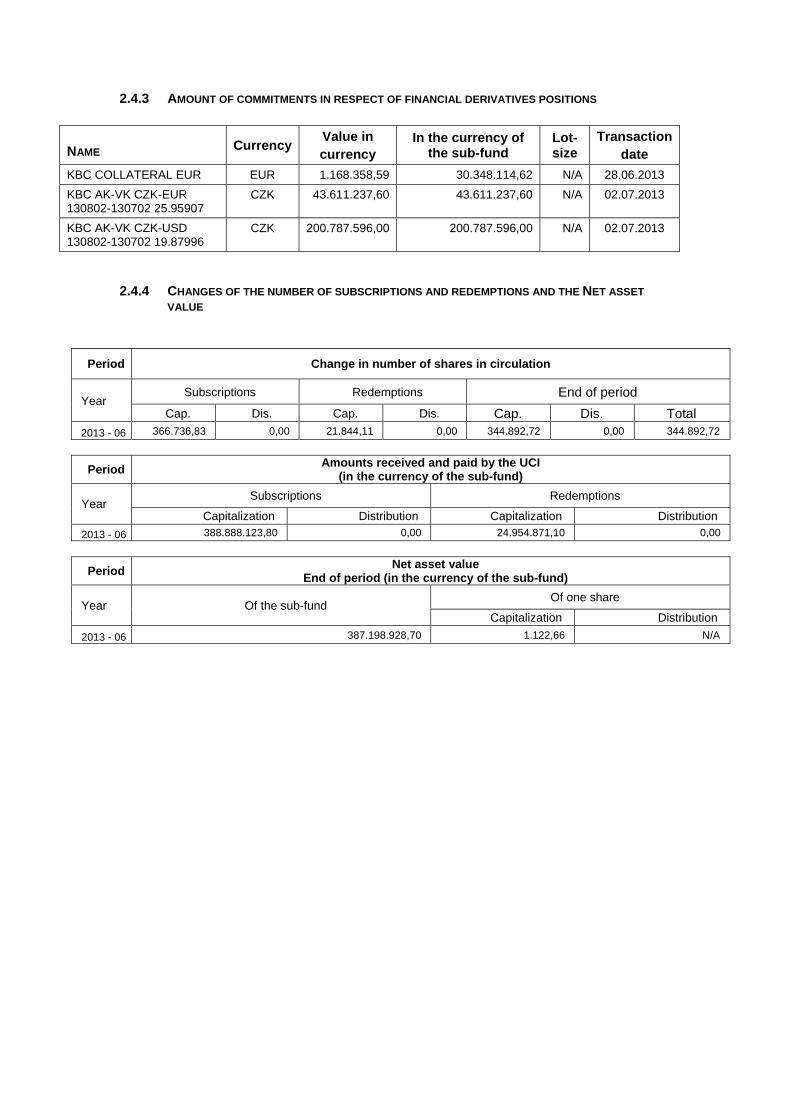

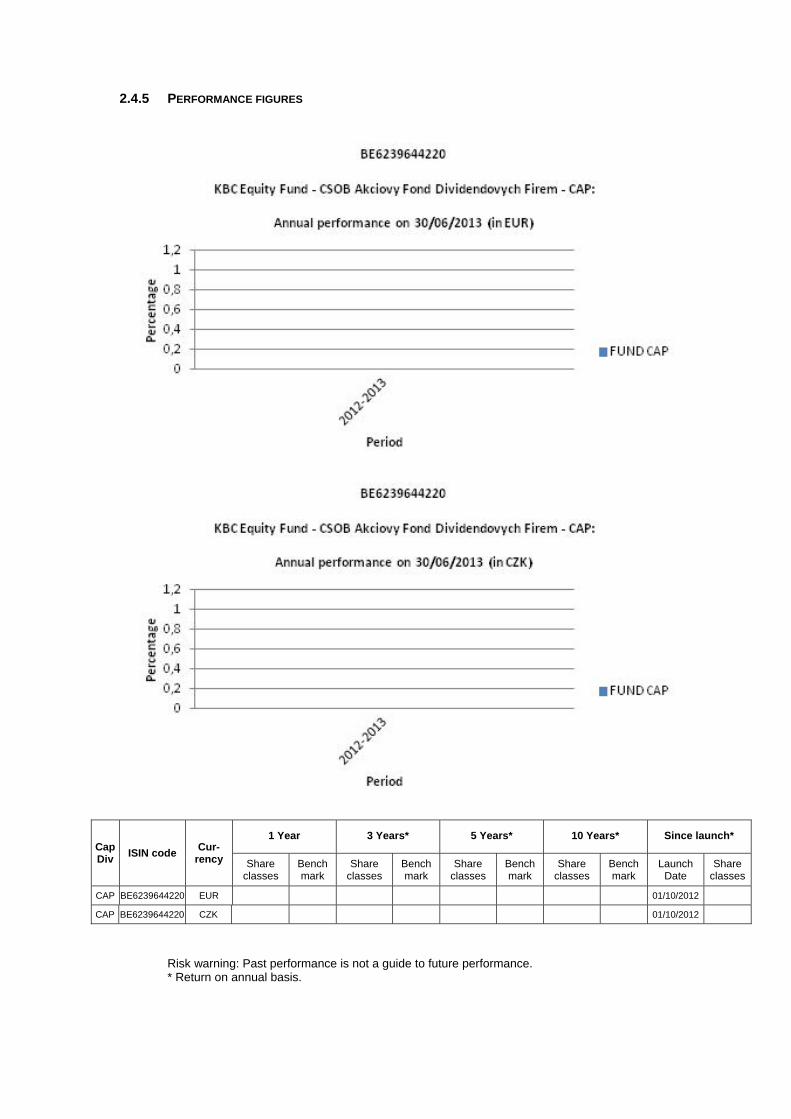

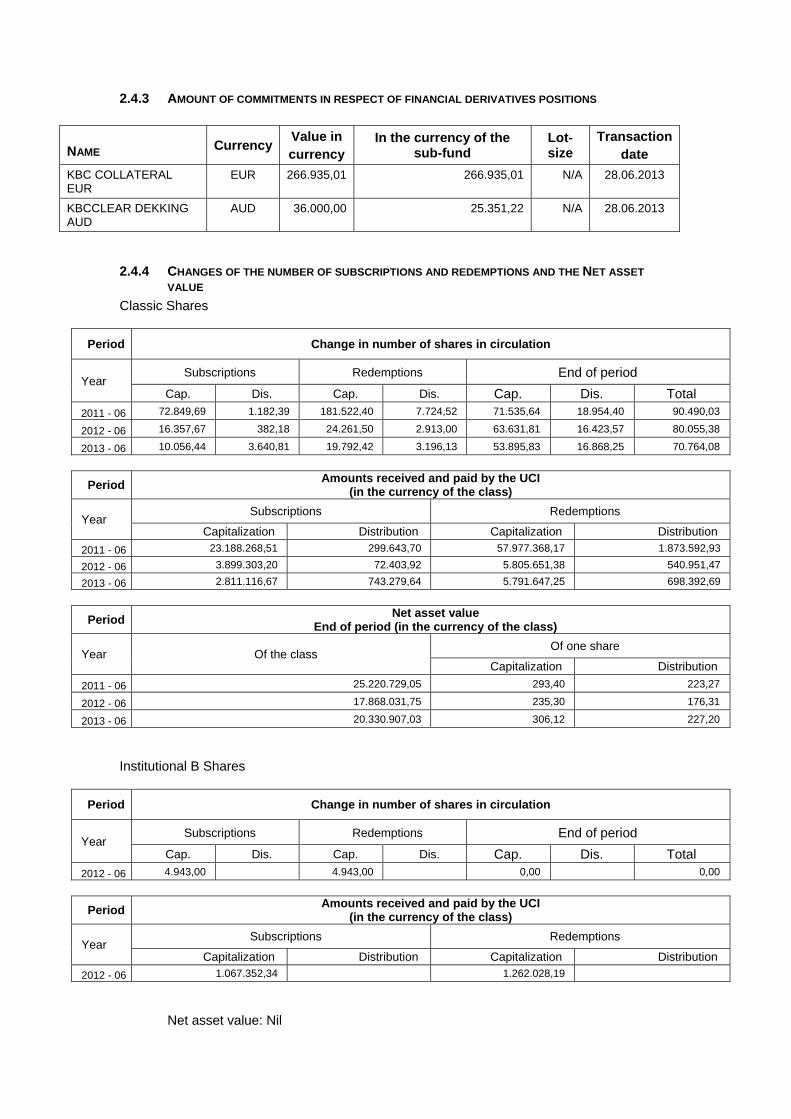

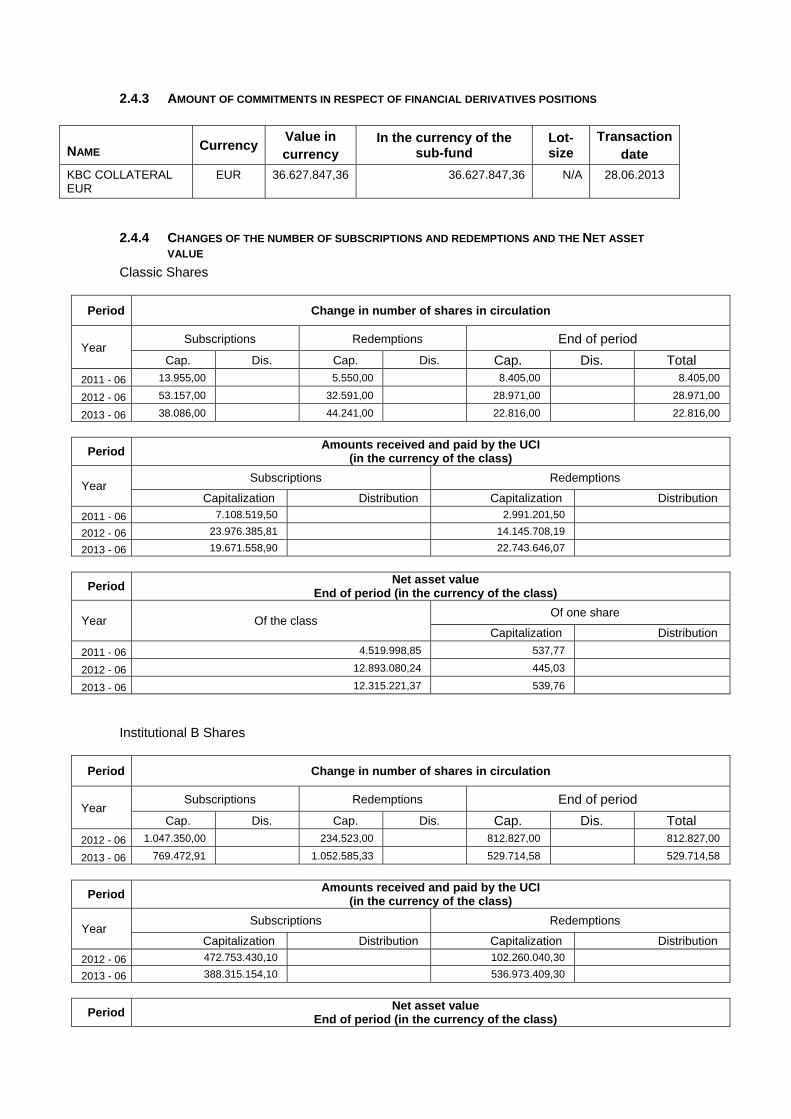

2.4.1. Composition of the assets 2.4.2. Change in the composition of the assets 2.4.3. Value of commitments in respect of financial derivatives positions 2.4.4. Evolution of the number of subscriptions, repayments and the net asset value 2.4.5. Return figures 2.4.6. Expenses 2.4.7. Notes to the financial statements and other data

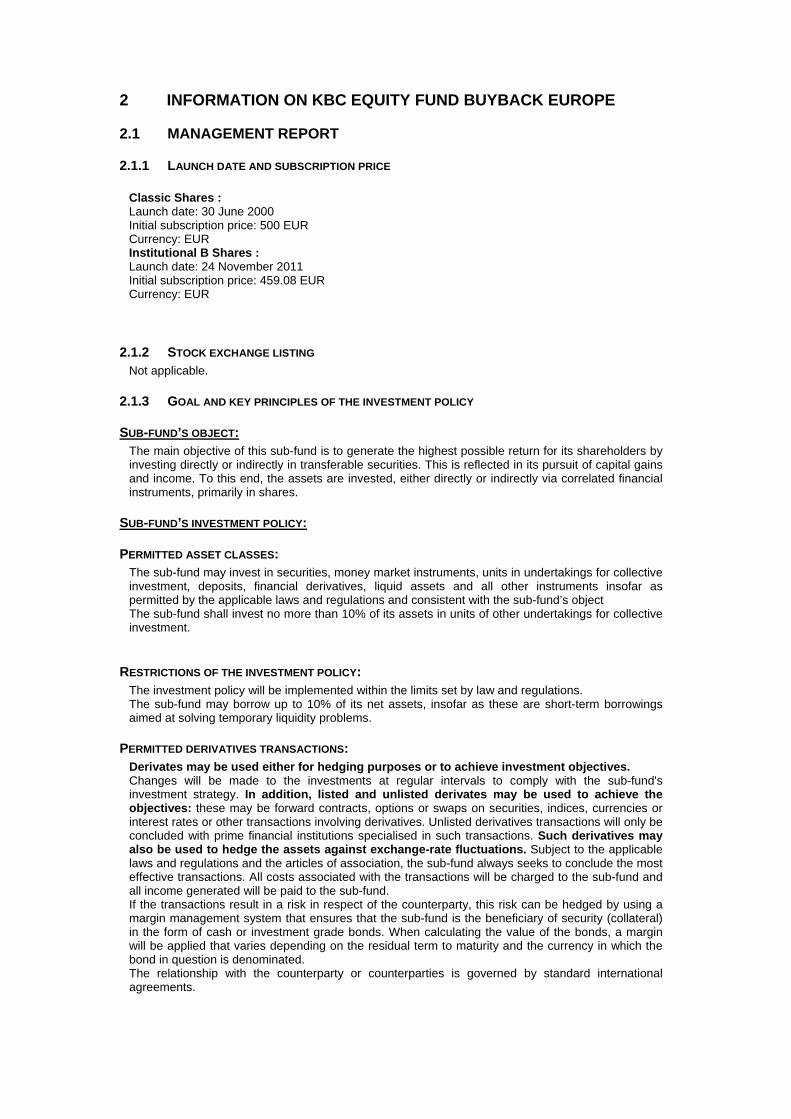

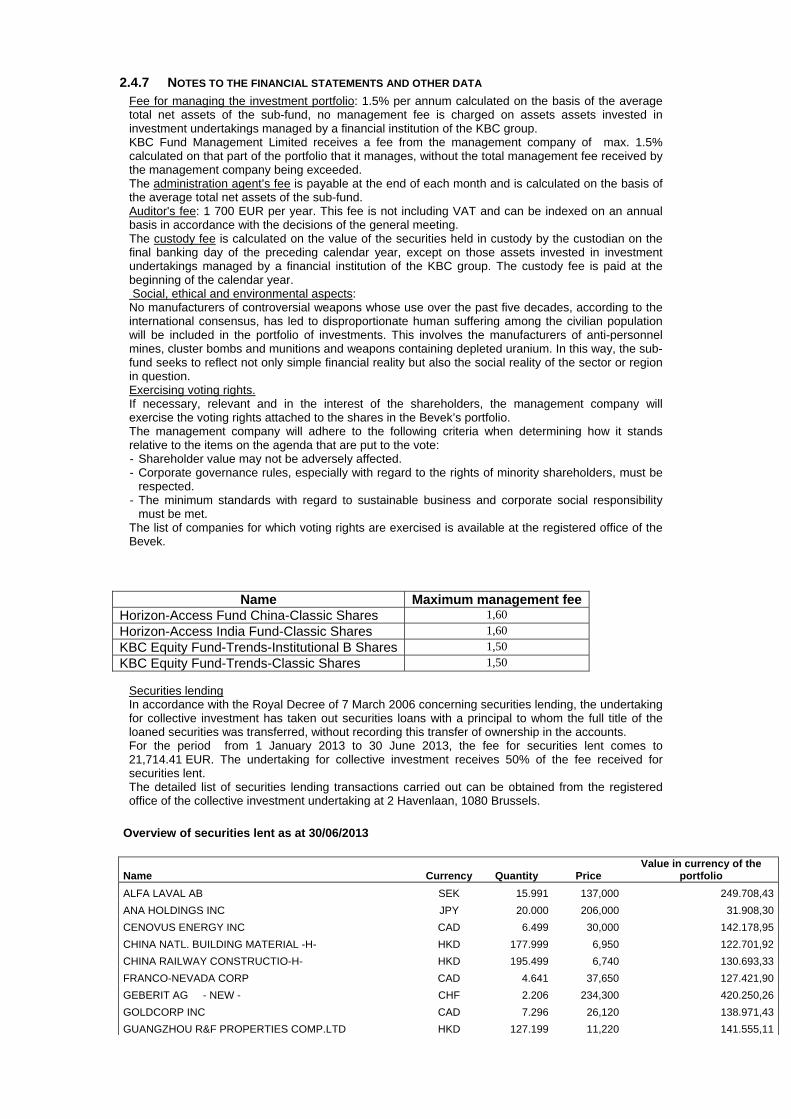

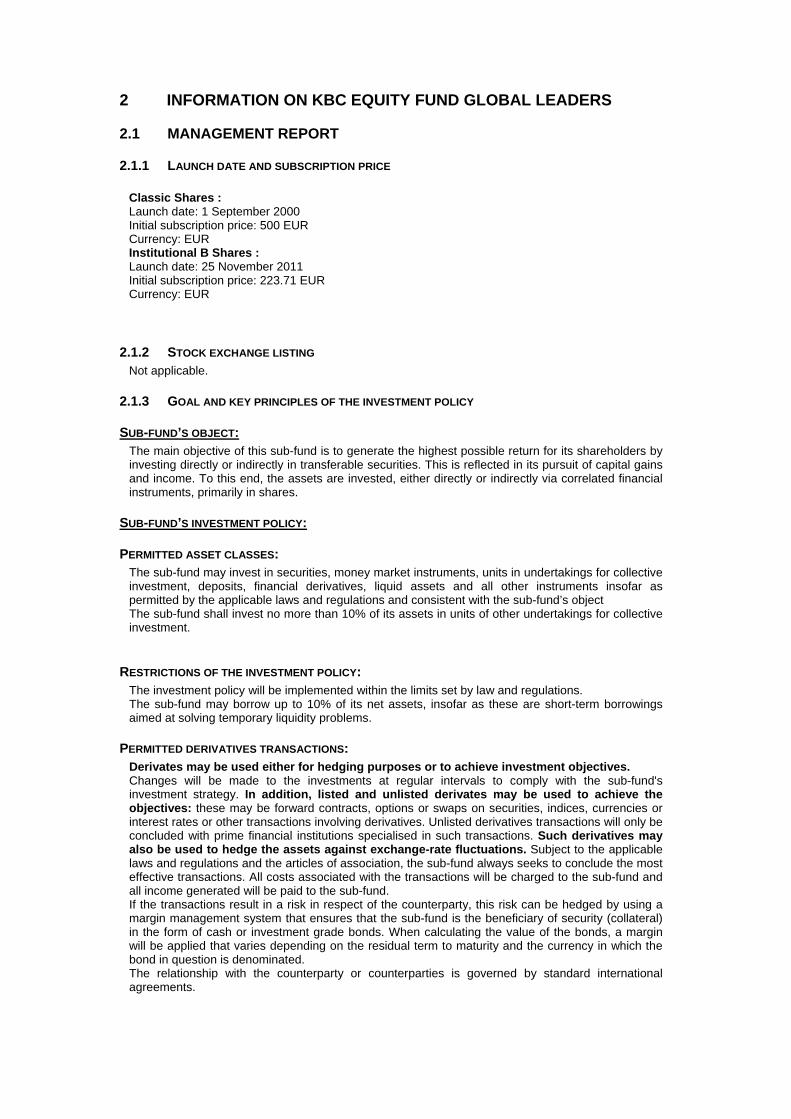

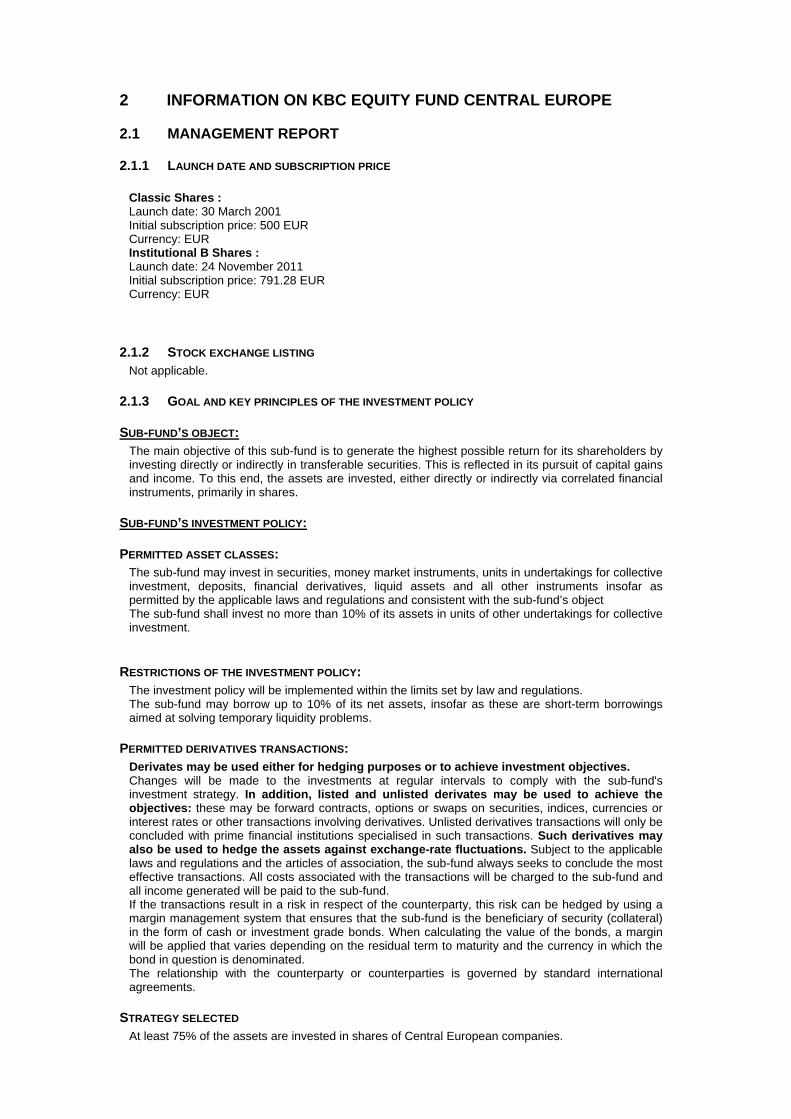

2 INFORMATION ON KBC EQUITY FUND CSOB AKCIOVY FOND DIVIDENDOVYCH FIREM

2.1 MANAGEMENT REPORT

2.1.1 LAUNCH DATE AND SUBSCRIPTION PRICE Launch date: 28 September 2012 Initial subscription price: 1000 CZK Currency: CZK

2.1.2 STOCK EXCHANGE LISTING Not applicable.

2.1.3 GOAL AND KEY PRINCIPLES OF THE INVESTMENT POLICY

SUB-FUND’S OBJECT: The main objective of this sub-fund is to generate the highest possible return for its shareholders by investing directly or indirectly in transferable securities. This is reflected in its pursuit of capital gains and income. To this end, the assets are invested, either directly or indirectly via correlated financial instruments, primarily in shares.

SUB-FUND’S INVESTMENT POLICY:

PERMITTED ASSET CLASSES: The sub-fund may invest in securities, money market instruments, units in undertakings for collective investment, deposits, financial derivatives, liquid assets and all other instruments insofar as permitted by the applicable laws and regulations and consistent with the sub-fund’s object The sub-fund shall invest no more than 10% of its assets in units of other undertakings for collective investment.

RESTRICTIONS OF THE INVESTMENT POLICY: The investment policy will be implemented within the limits set by law and regulations. The sub-fund may borrow up to 10% of its net assets, insofar as these are short-term borrowings aimed at solving temporary liquidity problems.

PERMITTED DERIVATIVES TRANSACTIONS: Derivates may be used either for hedging purposes or to achieve investment objectives. Changes will be made to the investments at regular intervals to comply with the sub-fund's investment strategy. In addition, listed and unlisted derivates may be used to achieve the objectives: these may be forward contracts, options or swaps on securities, indices, currencies or interest rates or other transactions involving derivatives. Unlisted derivatives transactions will only be concluded with prime financial institutions specialised in such transactions. Such derivatives may also be used to hedge the assets against exchange-rate fluctuations. Subject to the applicable laws and regulations and the articles of association, the sub-fund always seeks to conclude the most effective transactions. All costs associated with the transactions will be charged to the sub-fund and all income generated will be paid to the sub-fund. If the transactions result in a risk in respect of the counterparty, this risk can be hedged by using a margin management system that ensures that the sub-fund is the beneficiary of security (collateral) in the form of cash or investment grade bonds. When calculating the value of the bonds, a margin will be applied that varies depending on the residual term to maturity and the currency in which the bond in question is denominated. The relationship with the counterparty or counterparties is governed by standard international agreements.

STRATEGY SELECTED

KBC Equity Fund CSOB Akciovy Fond Dividendovych Firem aims to generate a return by investing at least 75% of its assets in shares with a high dividend yield. All regions, sectors and themes may be taken into consideration. The rest of the assets will be invested in bonds, debt instruments, money market instruments and deposits.

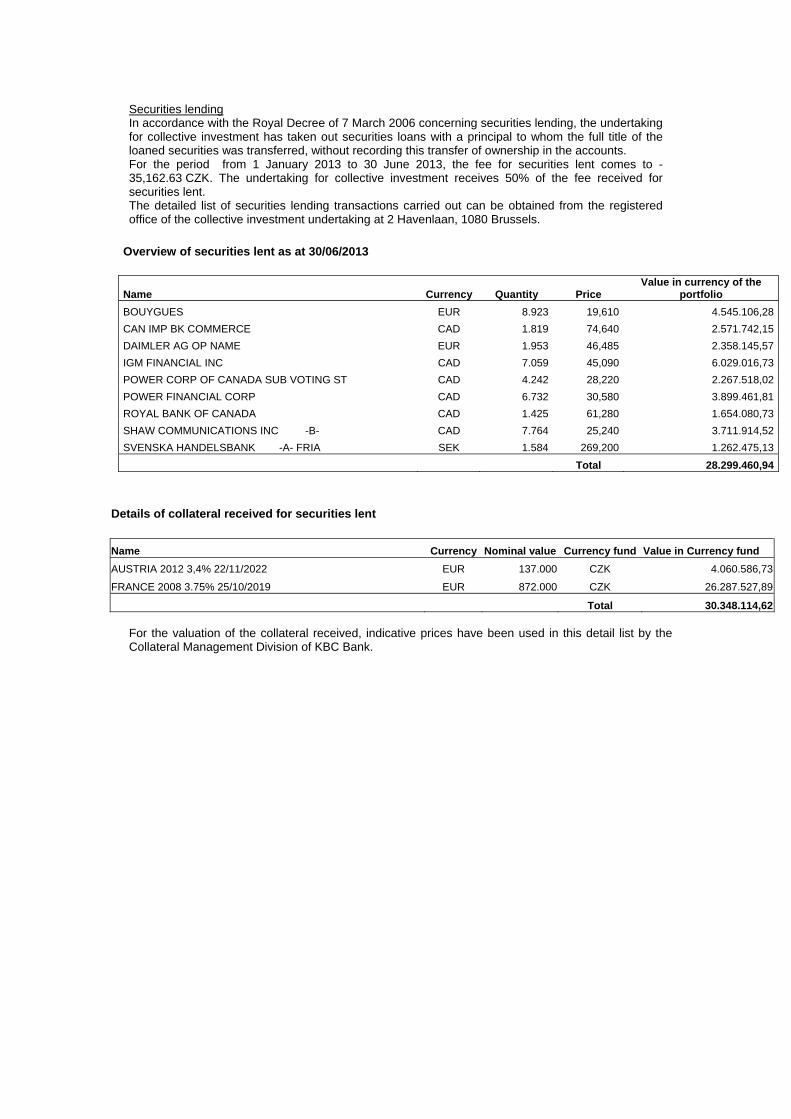

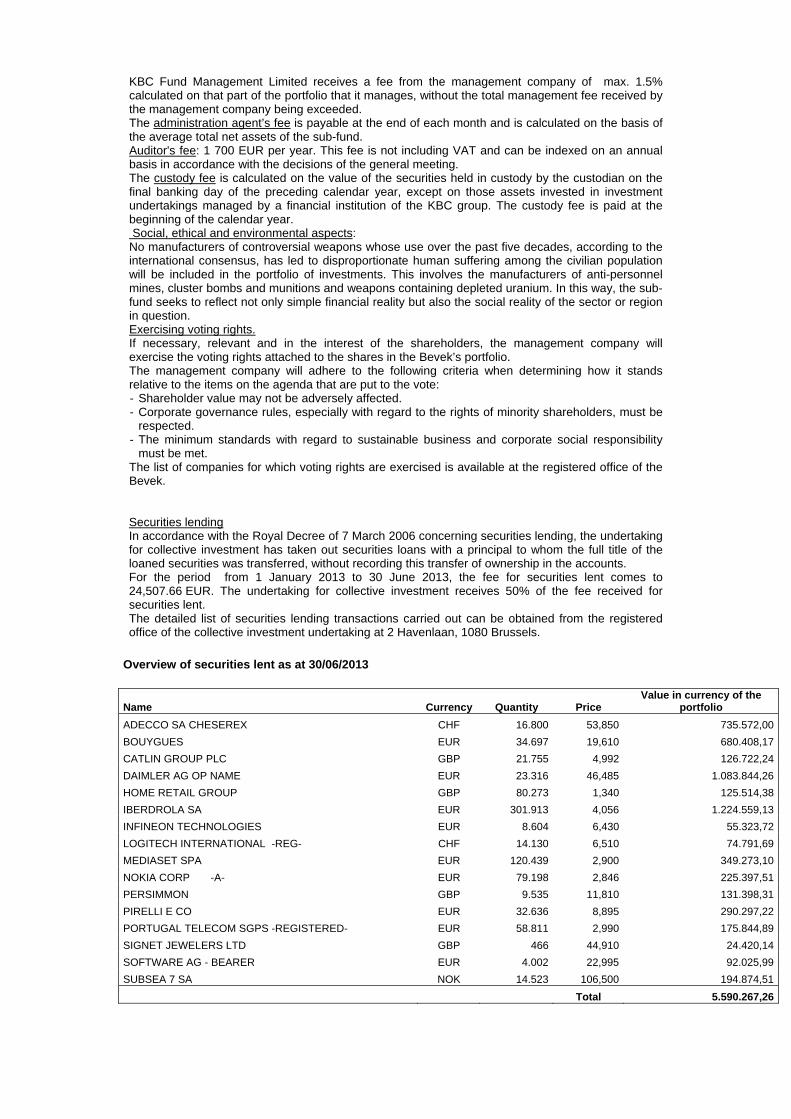

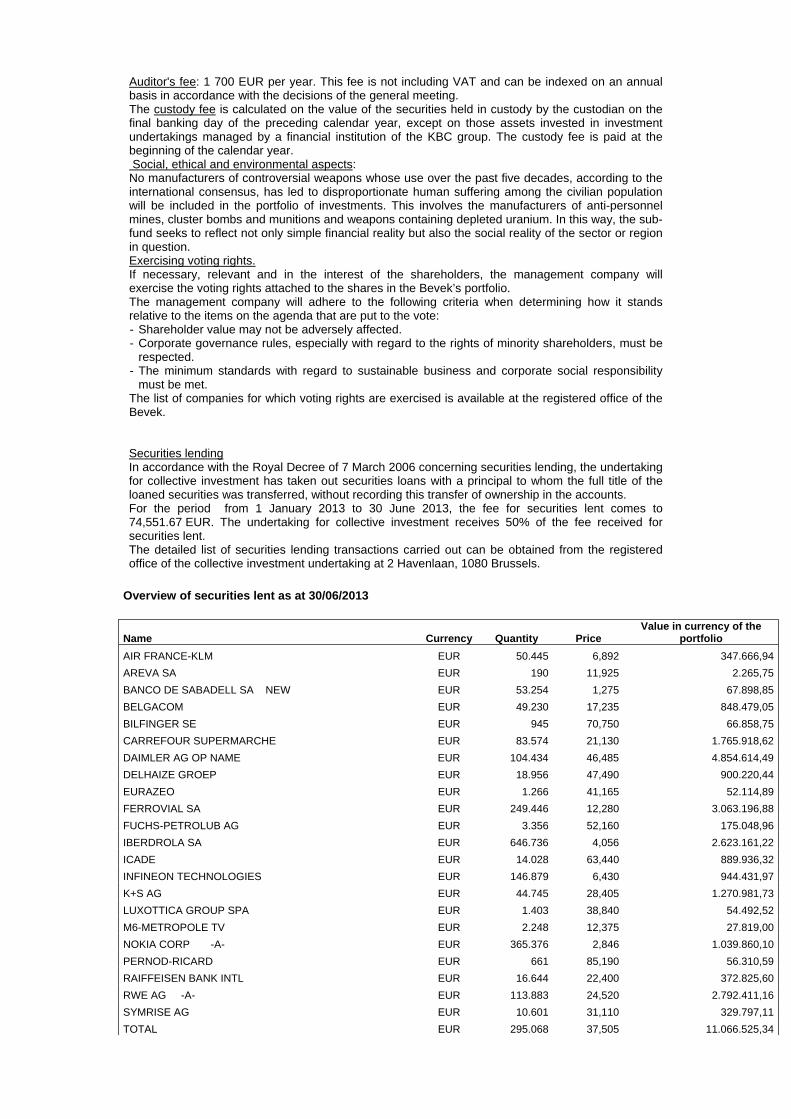

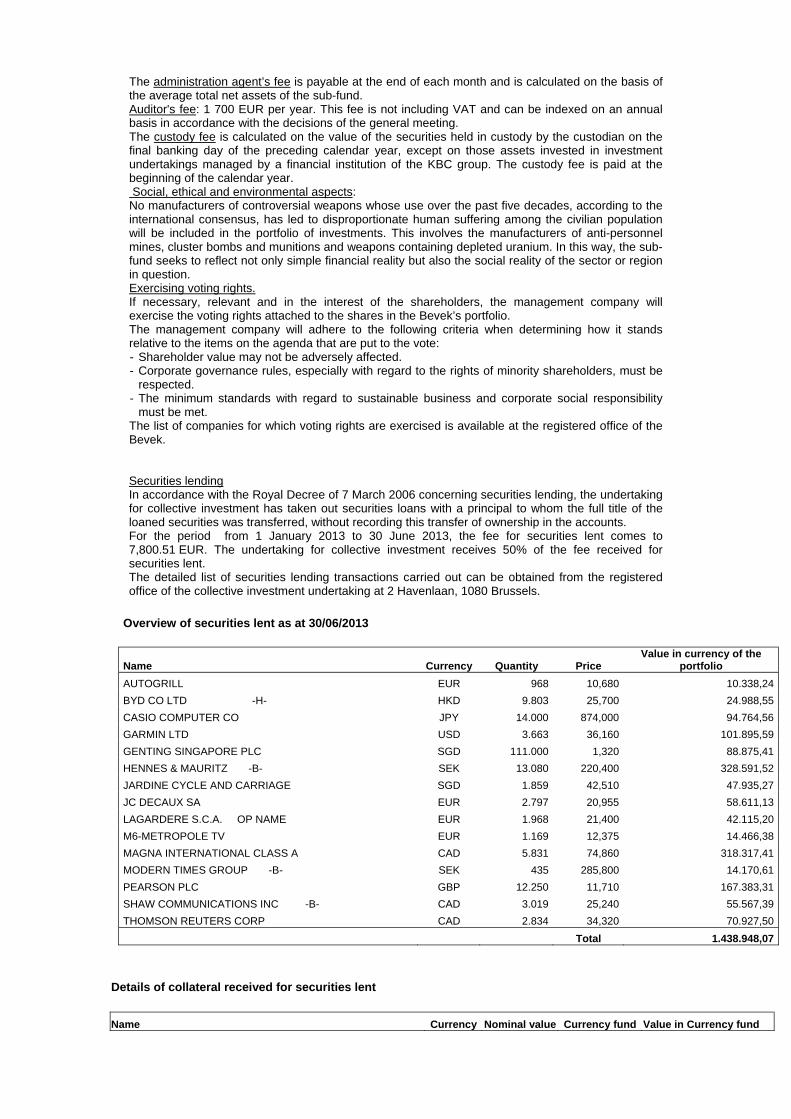

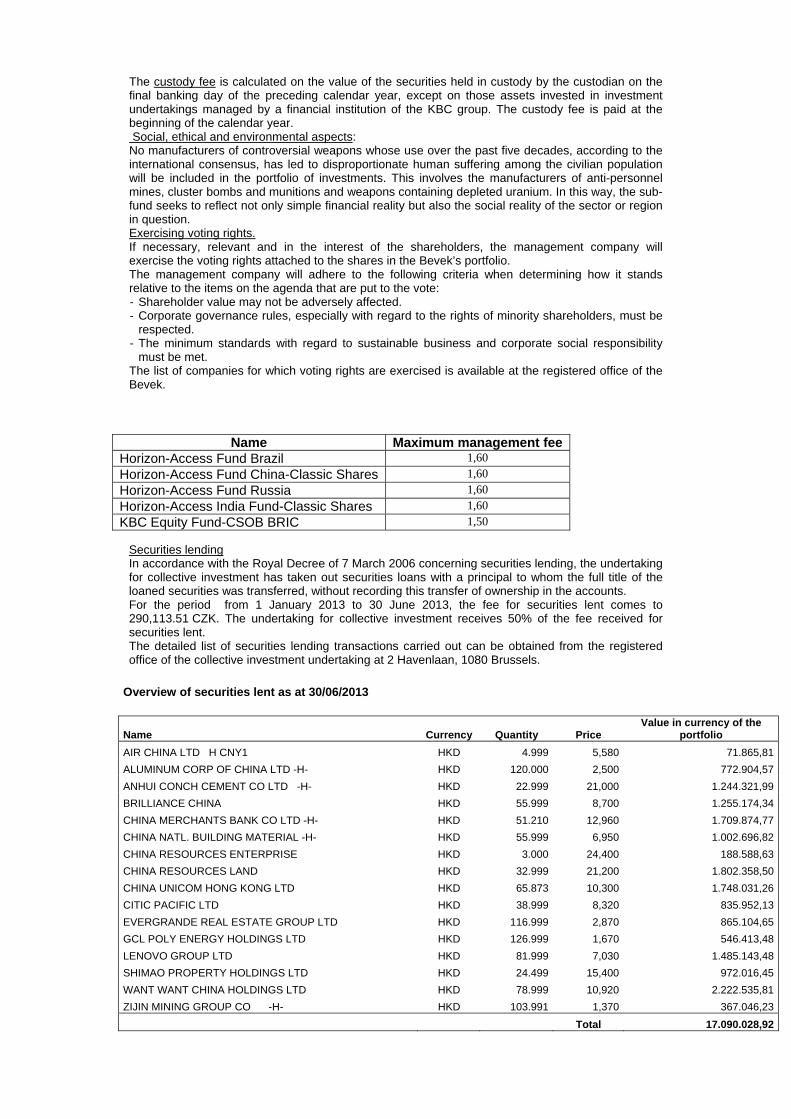

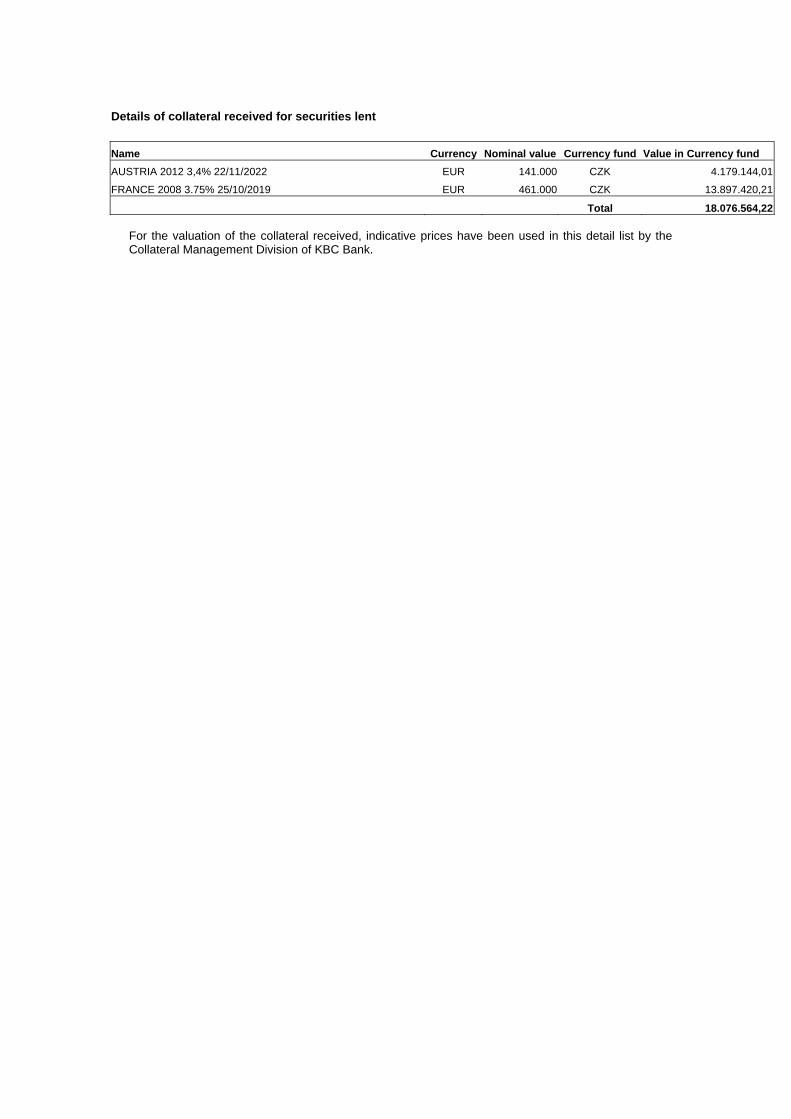

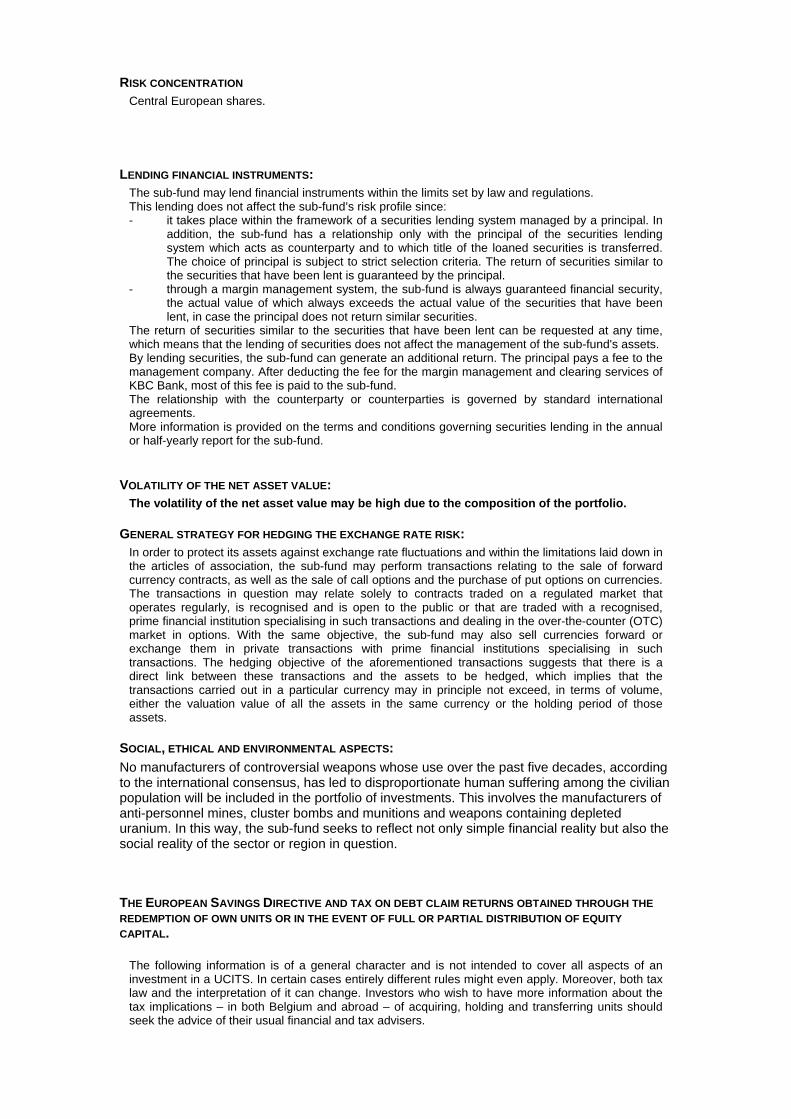

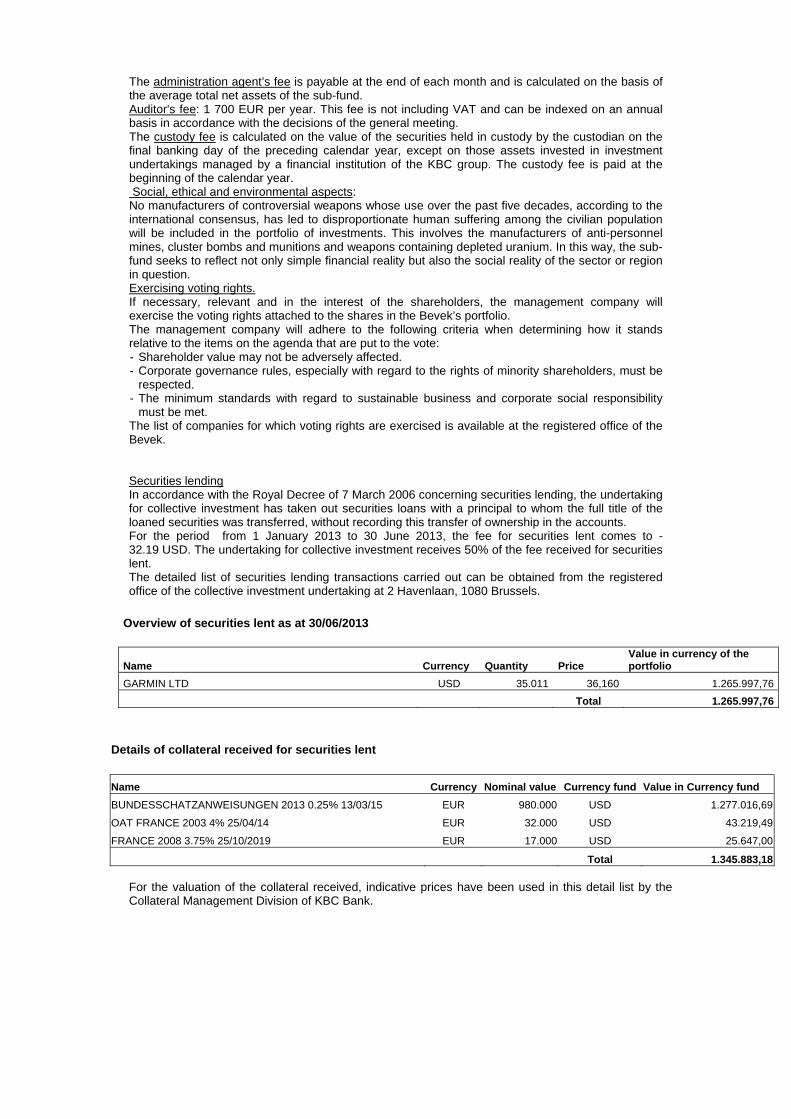

LENDING FINANCIAL INSTRUMENTS: The sub-fund may lend financial instruments within the limits set by law and regulations. This lending does not affect the sub-fund’s risk profile since: - it takes place within the framework of a securities lending system managed by a principal. In

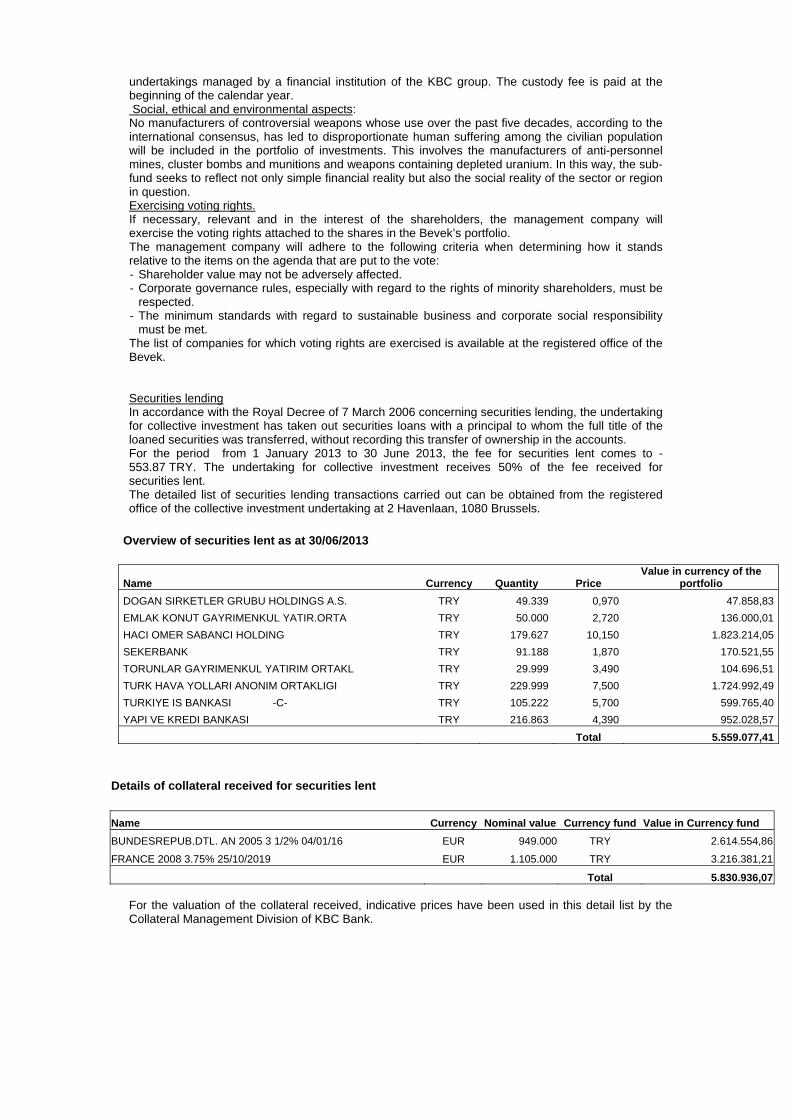

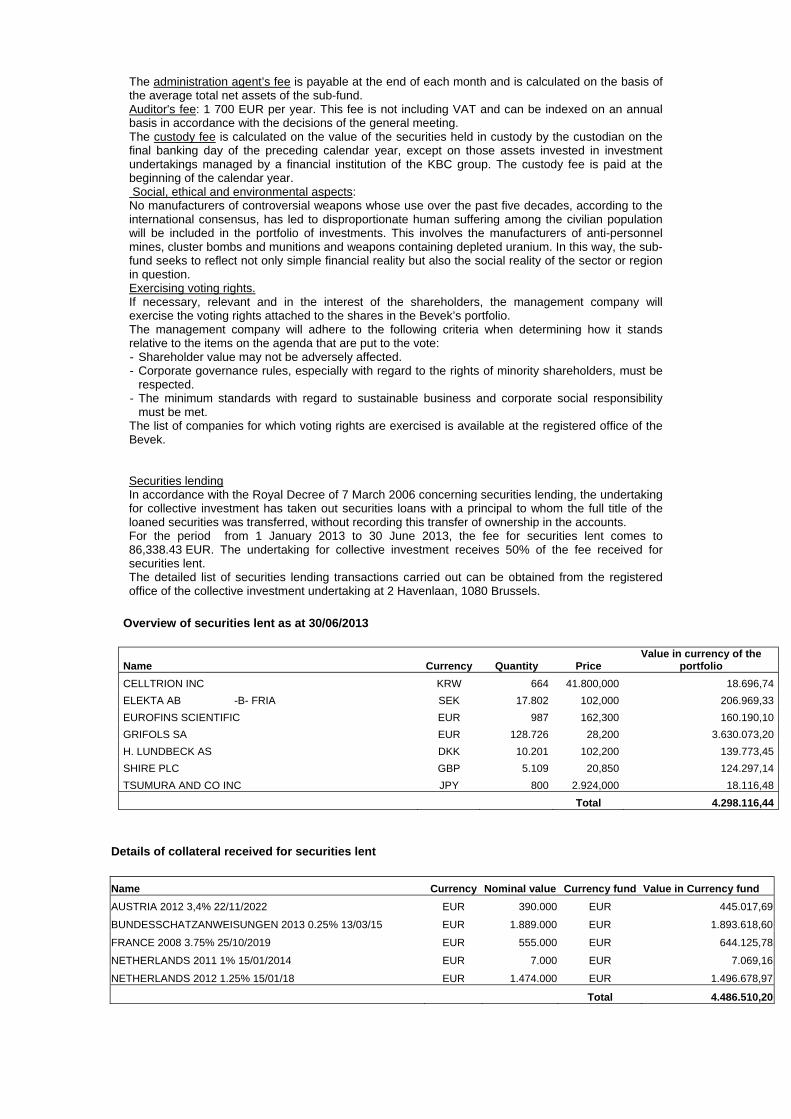

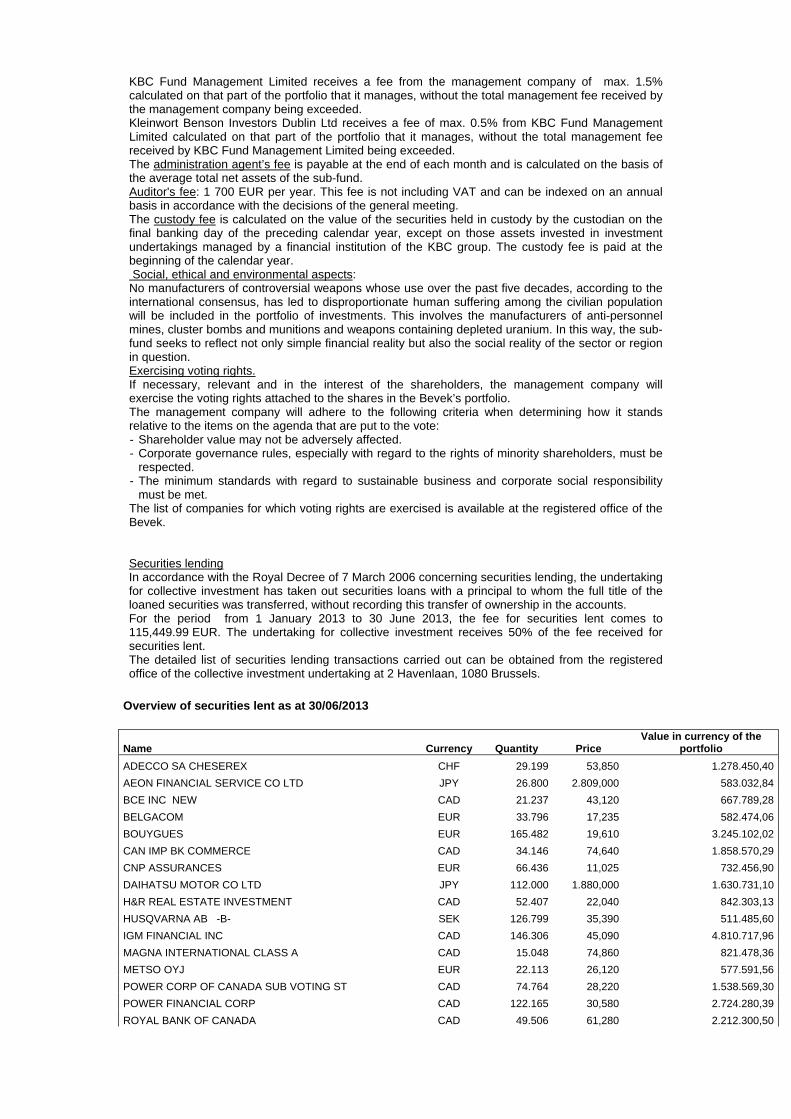

addition, the sub-fund has a relationship only with the principal of the securities lending system which acts as counterparty and to which title of the loaned securities is transferred. The choice of principal is subject to strict selection criteria. The return of securities similar to the securities that have been lent is guaranteed by the principal.

- through a margin management system, the sub-fund is always guaranteed financial security, the actual value of which always exceeds the actual value of the securities that have been lent, in case the principal does not return similar securities.

The return of securities similar to the securities that have been lent can be requested at any time, which means that the lending of securities does not affect the management of the sub-fund's assets. By lending securities, the sub-fund can generate an additional return. The principal pays a fee to the management company. After deducting the fee for the margin management and clearing services of KBC Bank, most of this fee is paid to the sub-fund. The relationship with the counterparty or counterparties is governed by standard international agreements. More information is provided on the terms and conditions governing securities lending in the annual or half-yearly report for the sub-fund.

VOLATILITY OF THE NET ASSET VALUE: The volatility of the net asset value may be high due to the composition of the portfolio.

GENERAL STRATEGY FOR HEDGING THE EXCHANGE RATE RISK: In order to protect its assets against exchange rate fluctuations and within the limitations laid down in the articles of association, the sub-fund may perform transactions relating to the sale of forward currency contracts, as well as the sale of call options and the purchase of put options on currencies. The transactions in question may relate solely to contracts traded on a regulated market that operates regularly, is recognised and is open to the public or that are traded with a recognised, prime financial institution specialising in such transactions and dealing in the over-the-counter (OTC) market in options. With the same objective, the sub-fund may also sell currencies forward or exchange them in private transactions with prime financial institutions specialising in such transactions. The hedging objective of the aforementioned transactions suggests that there is a direct link between these transactions and the assets to be hedged, which implies that the transactions carried out in a particular currency may in principle not exceed, in terms of volume, either the valuation value of all the assets in the same currency or the holding period of those assets.

SOCIAL, ETHICAL AND ENVIRONMENTAL ASPECTS:

No manufacturers of controversial weapons whose use over the past five decades, according to the international consensus, has led to disproportionate human suffering among the civilian population will be included in the portfolio of investments. This involves the manufacturers of anti-personnel mines, cluster bombs and munitions and weapons containing depleted uranium. In this way, the sub-fund seeks to reflect not only simple financial reality but also the social reality of the sector or region in question.

THE EUROPEAN SAVINGS DIRECTIVE AND TAX ON DEBT CLAIM RETURNS OBTAINED THROUGH THE

REDEMPTION OF OWN UNITS OR IN THE EVENT OF FULL OR PARTIAL DISTRIBUTION OF EQUITY

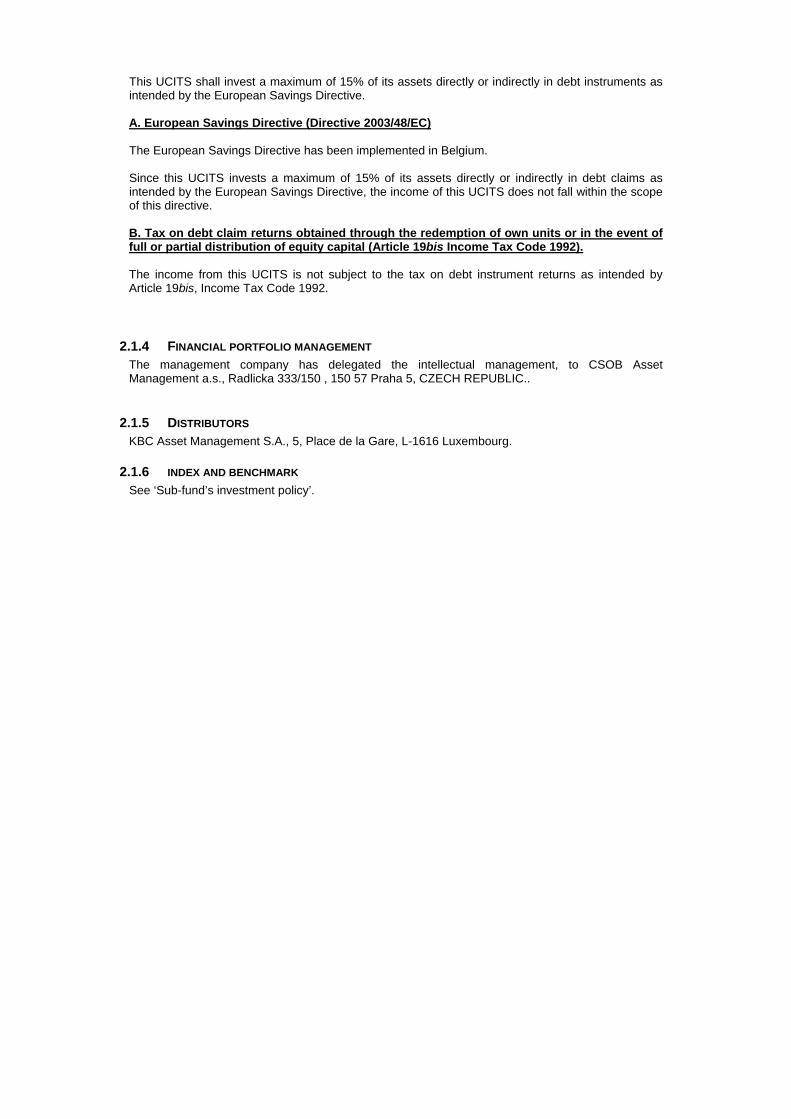

CAPITAL. The following information is of a general character and is not intended to cover all aspects of an investment in a UCITS. In certain cases entirely different rules might even apply. Moreover, both tax law and the interpretation of it can change. Investors who wish to have more information about the tax implications – in both Belgium and abroad – of acquiring, holding and transferring units should seek the advice of their usual financial and tax advisers. This UCITS shall invest a maximum of 15% of its assets directly or indirectly in debt instruments as intended by the European Savings Directive. A. European Savings Directive (Directive 2003/48/EC)

The European Savings Directive has been implemented in Belgium. Since this UCITS invests a maximum of 15% of its assets directly or indirectly in debt claims as intended by the European Savings Directive, the income of this UCITS does not fall within the scope of this directive. B. Tax on debt claim returns obtained through the redemption of own units or in the event of full or partial distribution of equity capital (Article 19bis Income Tax Code 1992). The income from this UCITS is not subject to the tax on debt instrument returns as intended by Article 19bis, Income Tax Code 1992.

2.1.4 FINANCIAL PORTFOLIO MANAGEMENT The management company has delegated the intellectual management, to KBC Fund Management Limited, Joshua Dawson House, Dawson Street , Dublin 2, IRELAND..

2.1.5 DISTRIBUTORS KBC Asset Management S.A., 5, Place de la Gare, L-1616 Luxembourg.

2.1.6 INDEX AND BENCHMARK See ‘Sub-fund’s investment policy’.

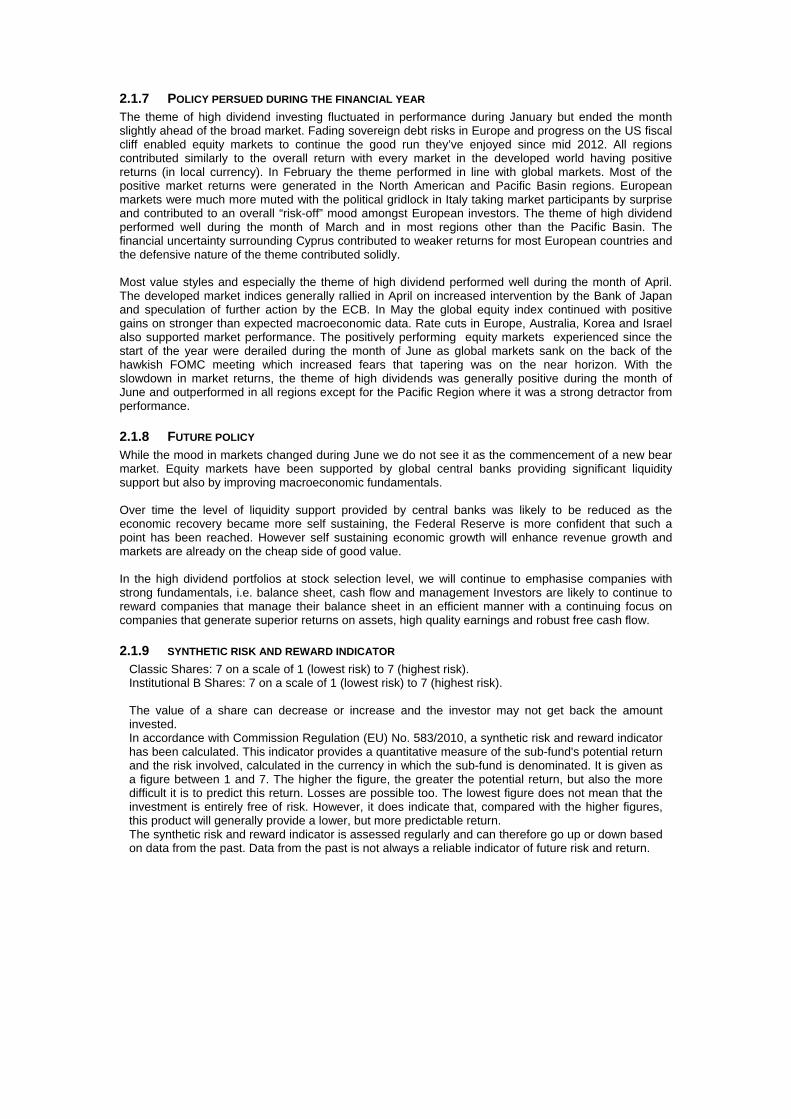

2.1.7 POLICY PERSUED DURING THE FINANCIAL YEAR The theme of high dividend investing fluctuated in performance during January but ended the month slightly ahead of the broad market. Fading sovereign debt risks in Europe and progress on the US fiscal cliff enabled equity markets to continue the good run they’ve enjoyed since mid 2012. All regions contributed similarly to the overall return with every market in the developed world having positive returns (in local currency). In February the theme performed in line with global markets. Most of the positive market returns were generated in the North American and Pacific Basin regions. European markets were much more muted with the political gridlock in Italy taking market participants by surprise and contributed to an overall “risk-off” mood amongst European investors. The theme of high dividend performed well during the month of March and in most regions other than the Pacific Basin. The financial uncertainty surrounding Cyprus contributed to weaker returns for most European countries and the defensive nature of the theme contributed solidly. Most value styles and especially the theme of high dividend performed well during the month of April. The developed market indices generally rallied in April on increased intervention by the Bank of Japan and speculation of further action by the ECB. In May the global equity index continued with positive gains on stronger than expected macroeconomic data. Rate cuts in Europe, Australia, Korea and Israel also supported market performance. The positively performing equity markets experienced since the start of the year were derailed during the month of June as global markets sank on the back of the hawkish FOMC meeting which increased fears that tapering was on the near horizon. With the slowdown in market returns, the theme of high dividends was generally positive during the month of June and outperformed in all regions except for the Pacific Region where it was a strong detractor from performance.

2.1.8 FUTURE POLICY While the mood in markets changed during June we do not see it as the commencement of a new bear market. Equity markets have been supported by global central banks providing significant liquidity support but also by improving macroeconomic fundamentals. Over time the level of liquidity support provided by central banks was likely to be reduced as the economic recovery became more self sustaining, the Federal Reserve is more confident that such a point has been reached. However self sustaining economic growth will enhance revenue growth and markets are already on the cheap side of good value. In the high dividend portfolios at stock selection level, we will continue to emphasise companies with strong fundamentals, i.e. balance sheet, cash flow and management Investors are likely to continue to reward companies that manage their balance sheet in an efficient manner with a continuing focus on companies that generate superior returns on assets, high quality earnings and robust free cash flow.

2.1.9 SYNTHETIC RISK AND REWARD INDICATOR 6 on a scale of 1 (lowest risk) to 7 (highest risk). The value of a share can decrease or increase and the investor may not get back the amount invested. In accordance with Commission Regulation (EU) No. 583/2010, a synthetic risk and reward indicator has been calculated. This indicator provides a quantitative measure of the sub-fund's potential return and the risk involved, calculated in the currency in which the sub-fund is denominated. It is given as a figure between 1 and 7. The higher the figure, the greater the potential return, but also the more difficult it is to predict this return. Losses are possible too. The lowest figure does not mean that the investment is entirely free of risk. However, it does indicate that, compared with the higher figures, this product will generally provide a lower, but more predictable return. The synthetic risk and reward indicator is assessed regularly and can therefore go up or down based on data from the past. Data from the past is not always a reliable indicator of future risk and return.

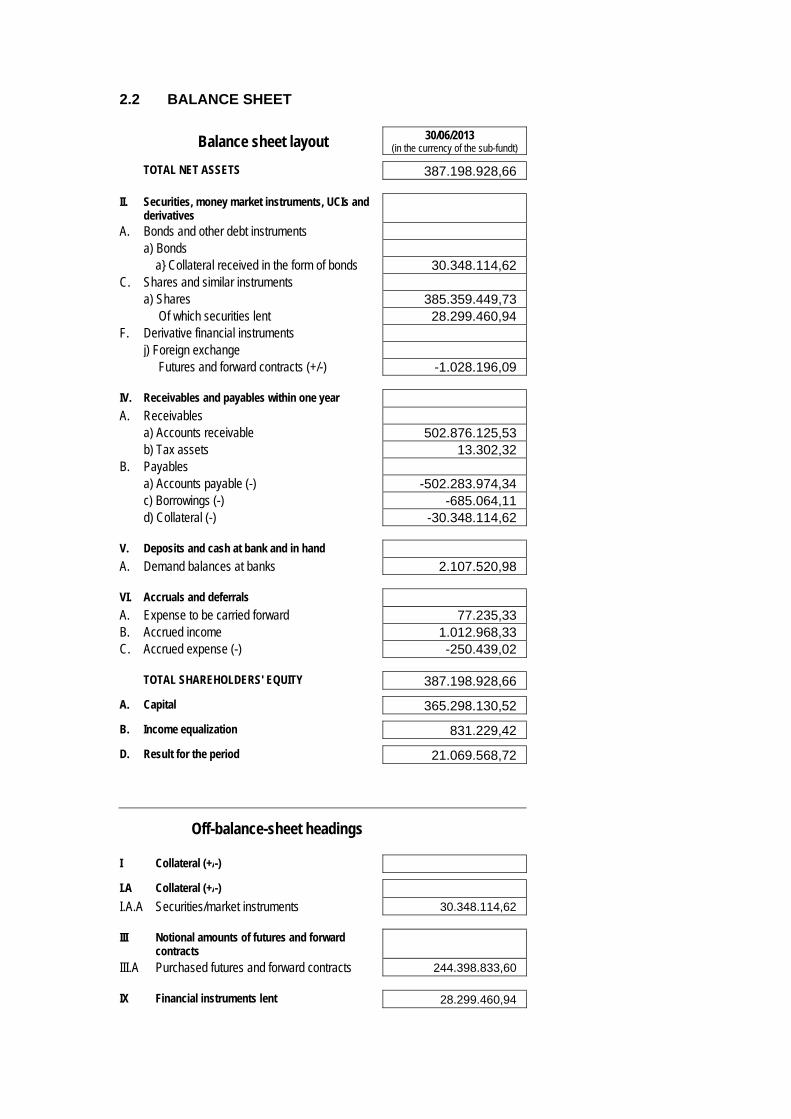

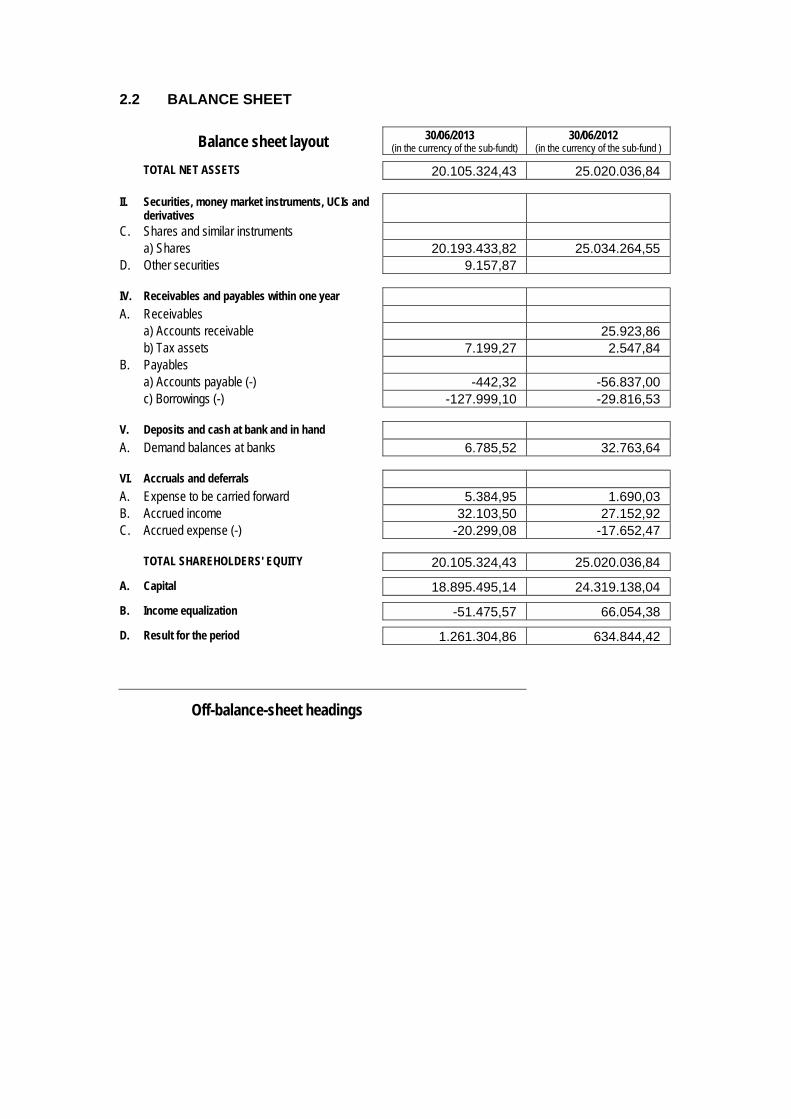

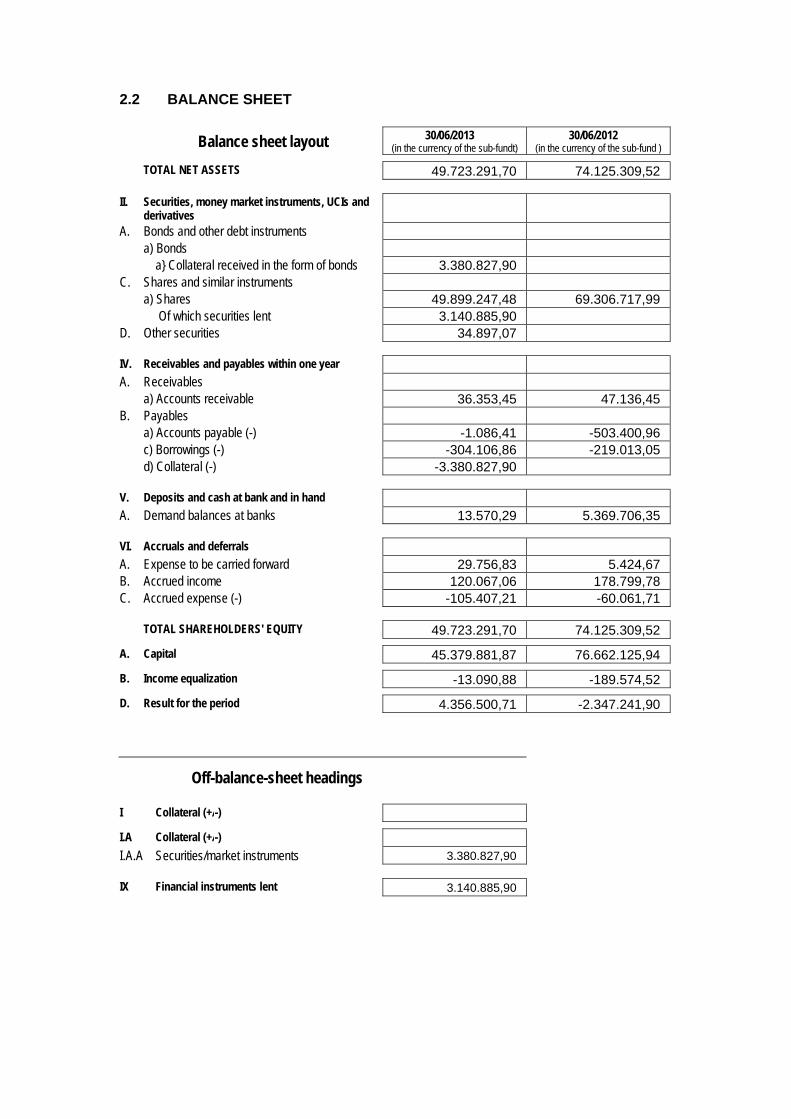

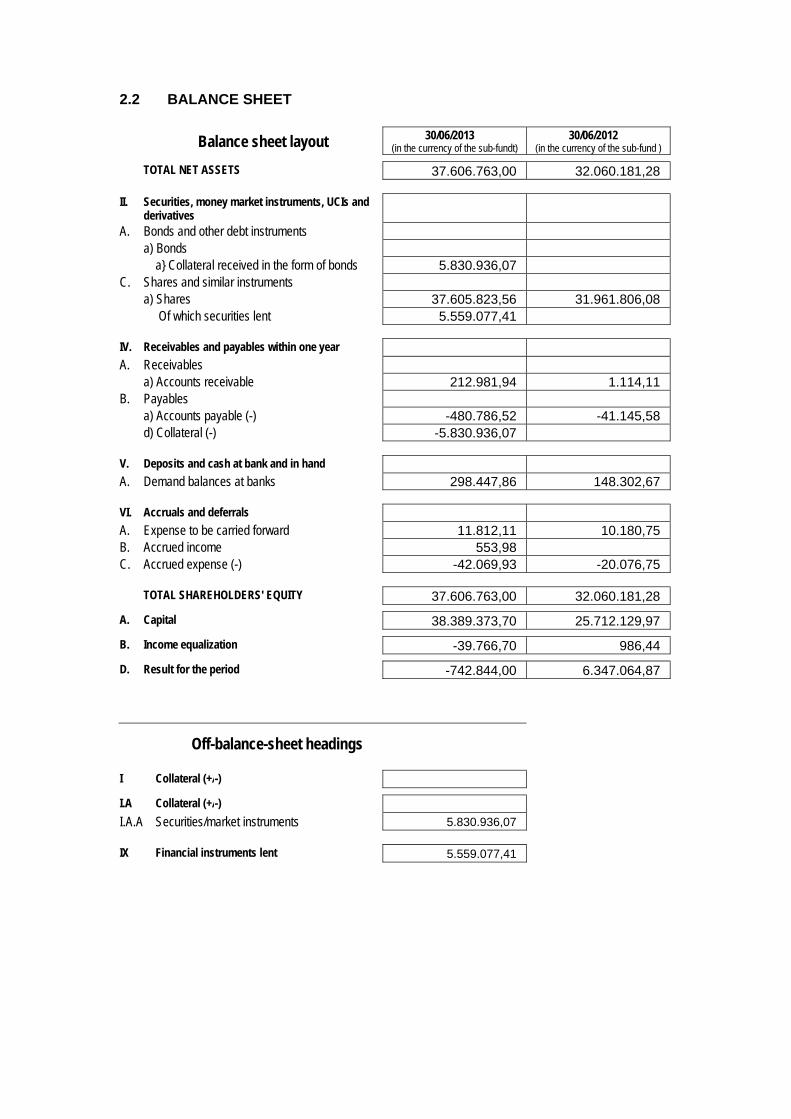

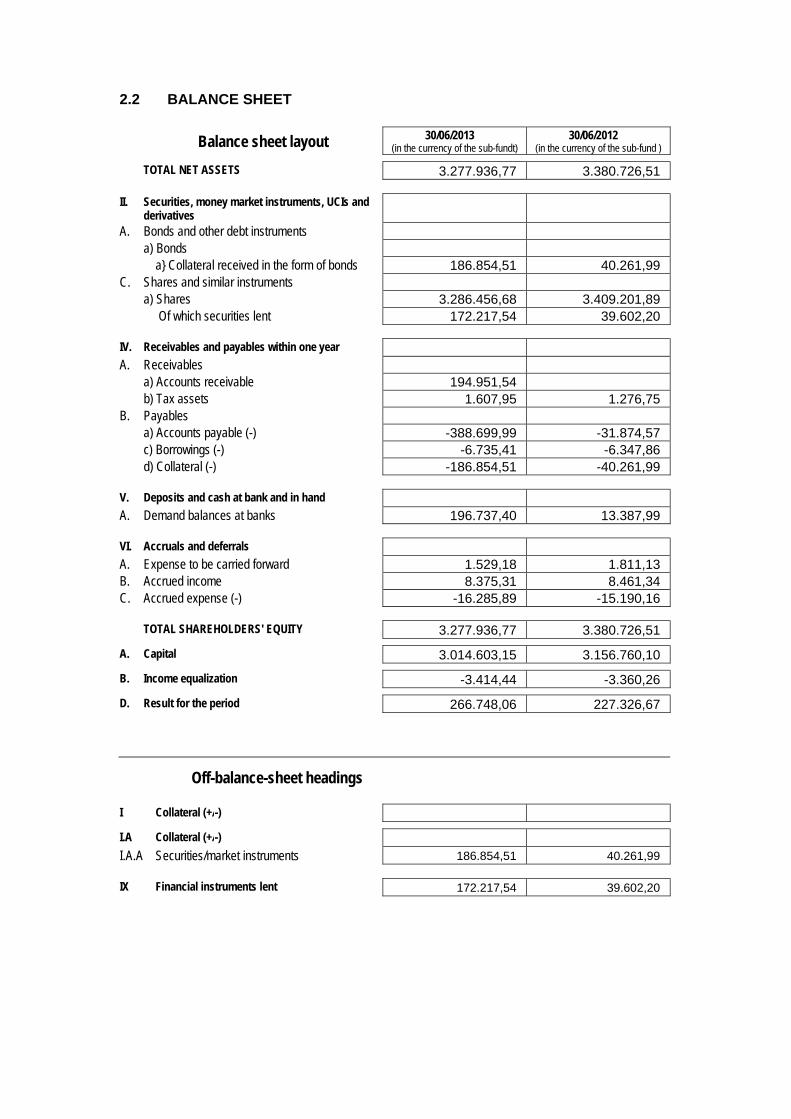

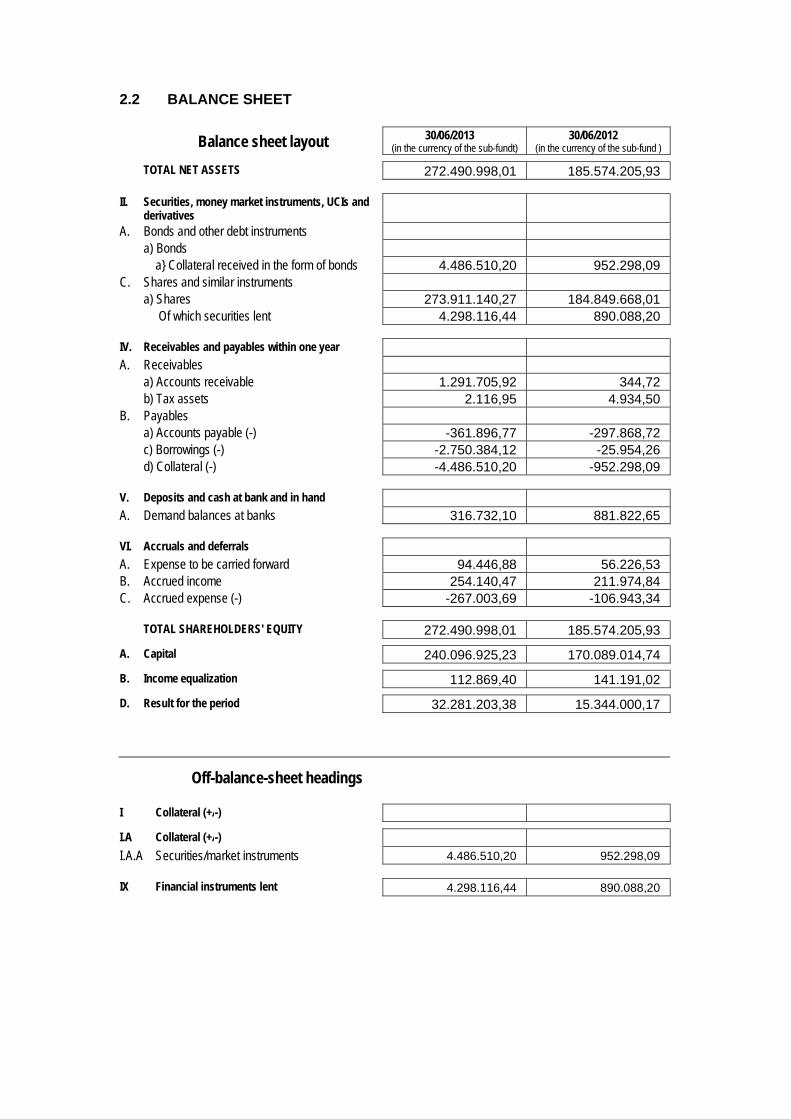

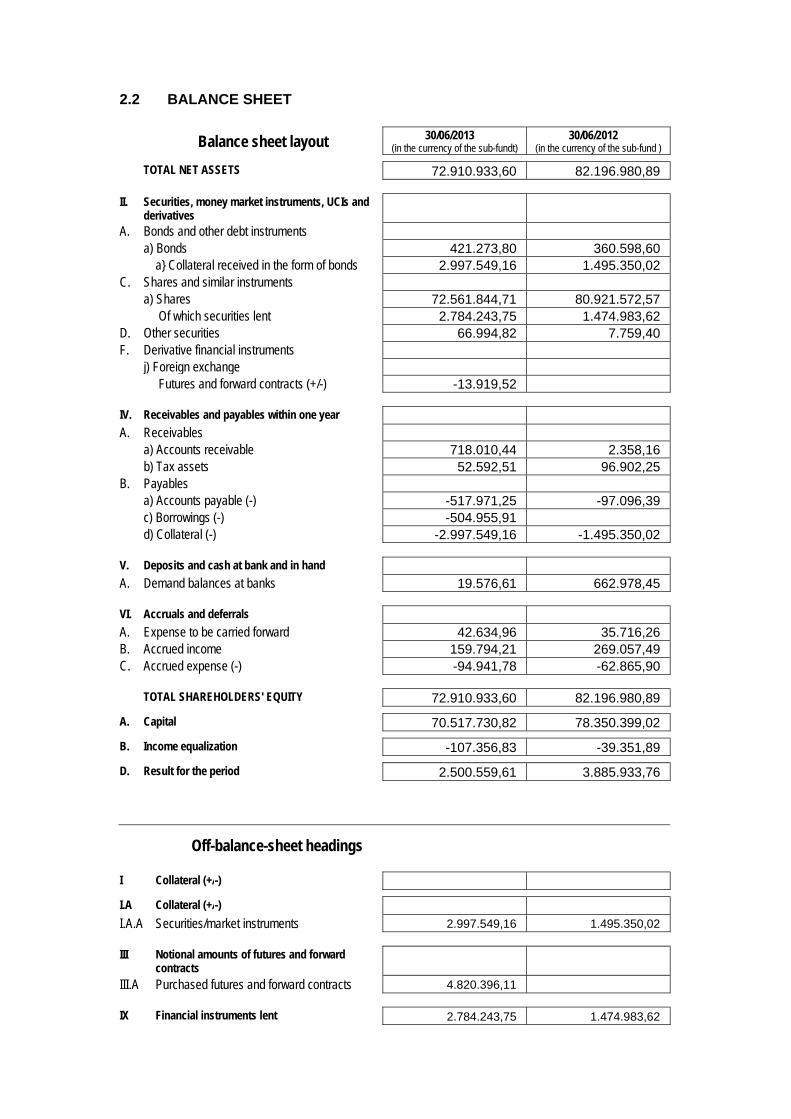

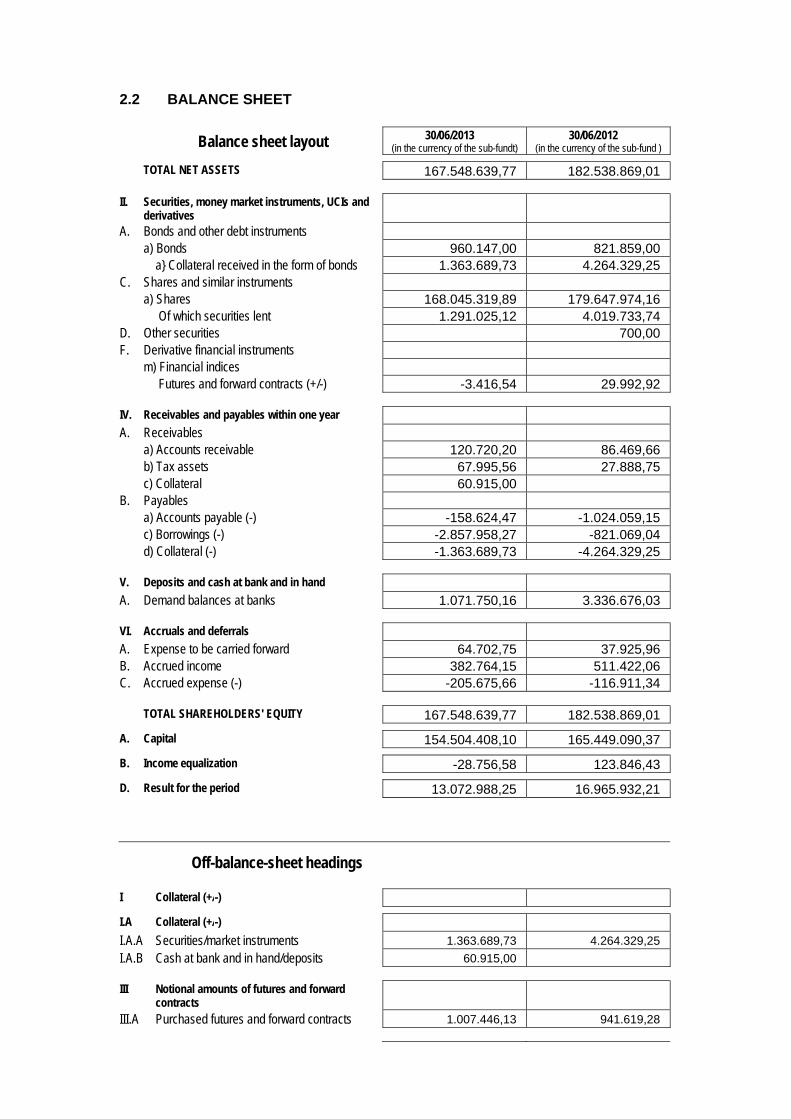

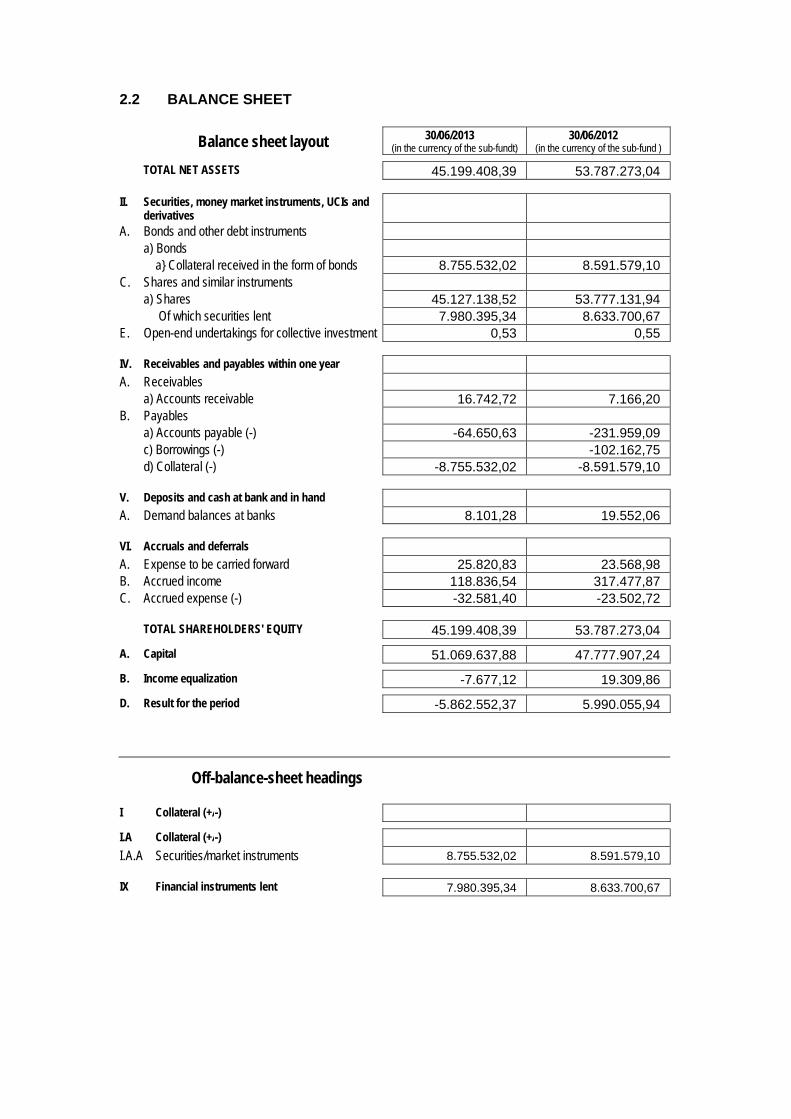

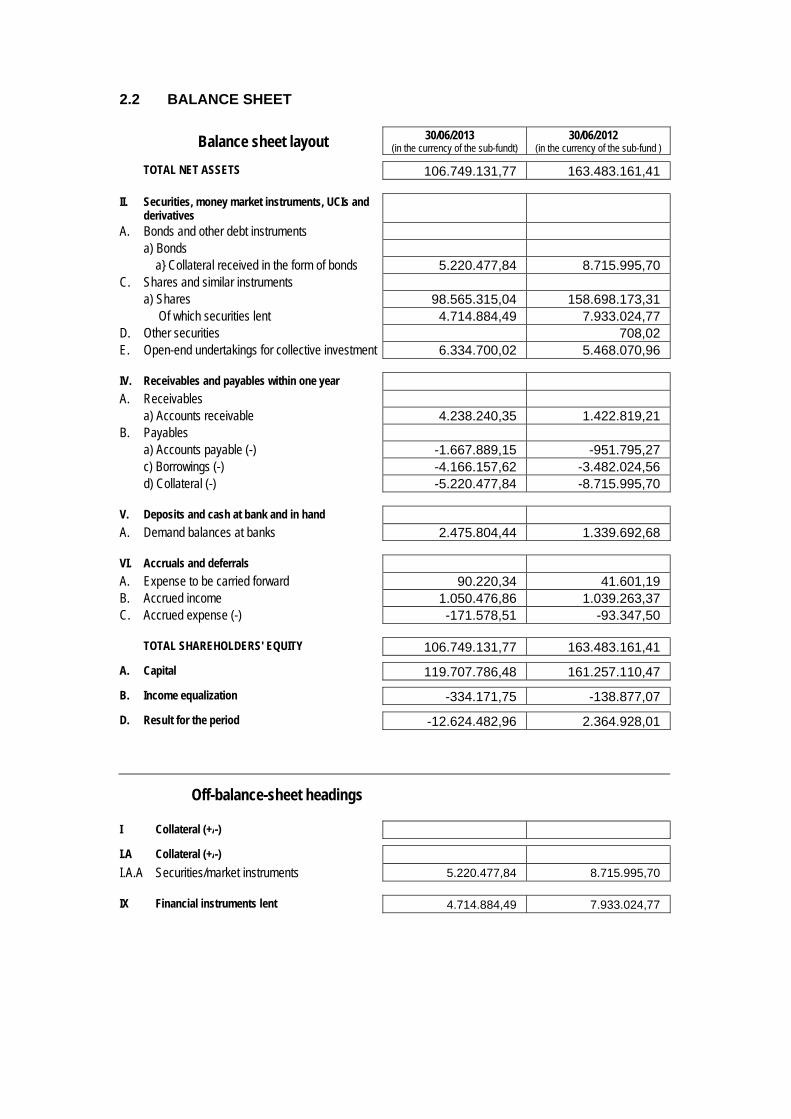

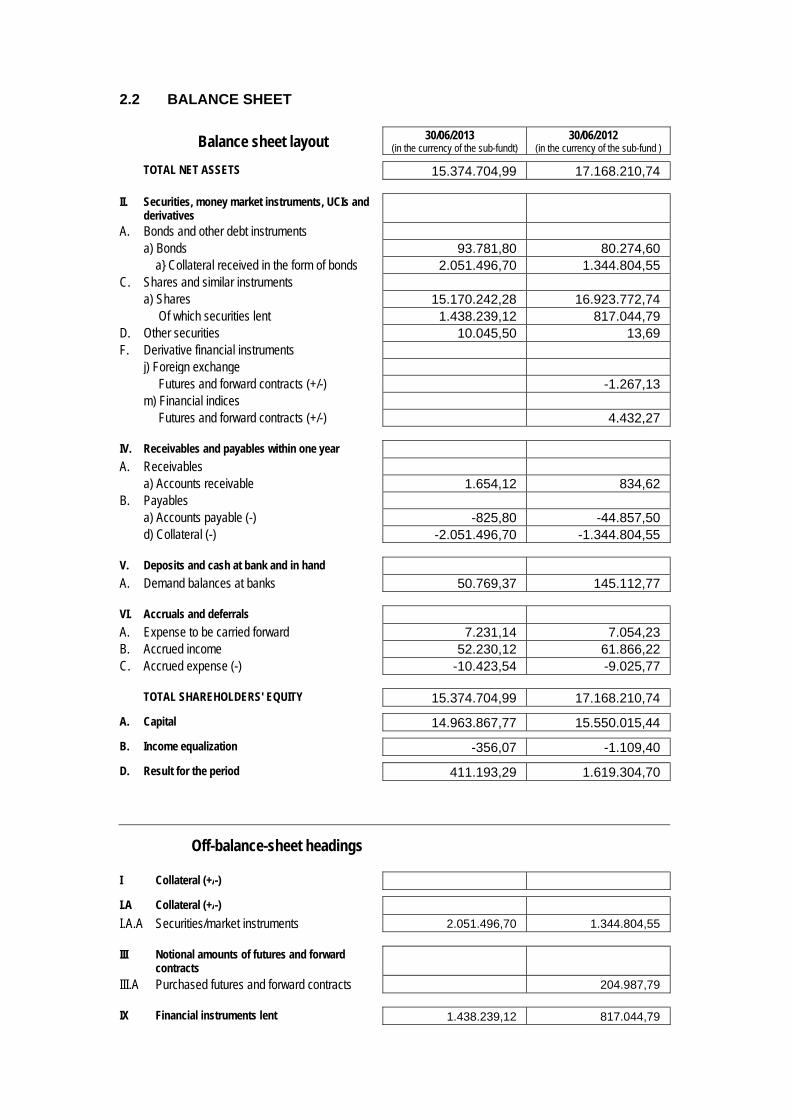

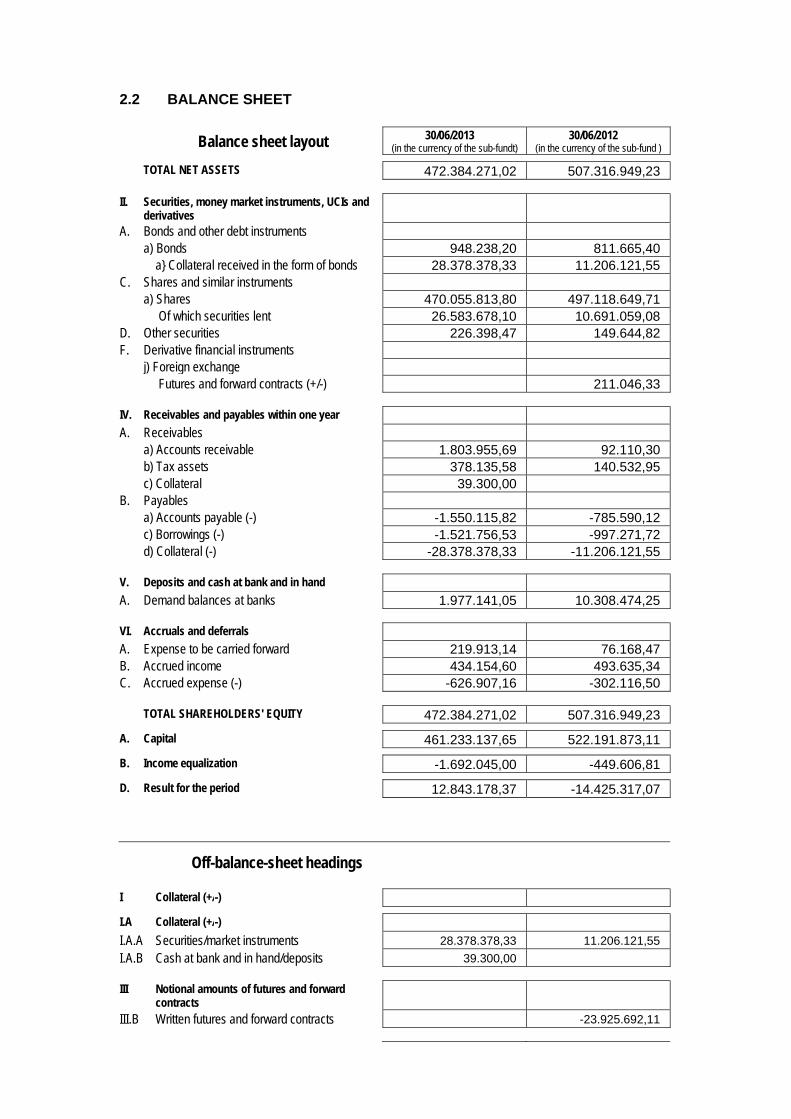

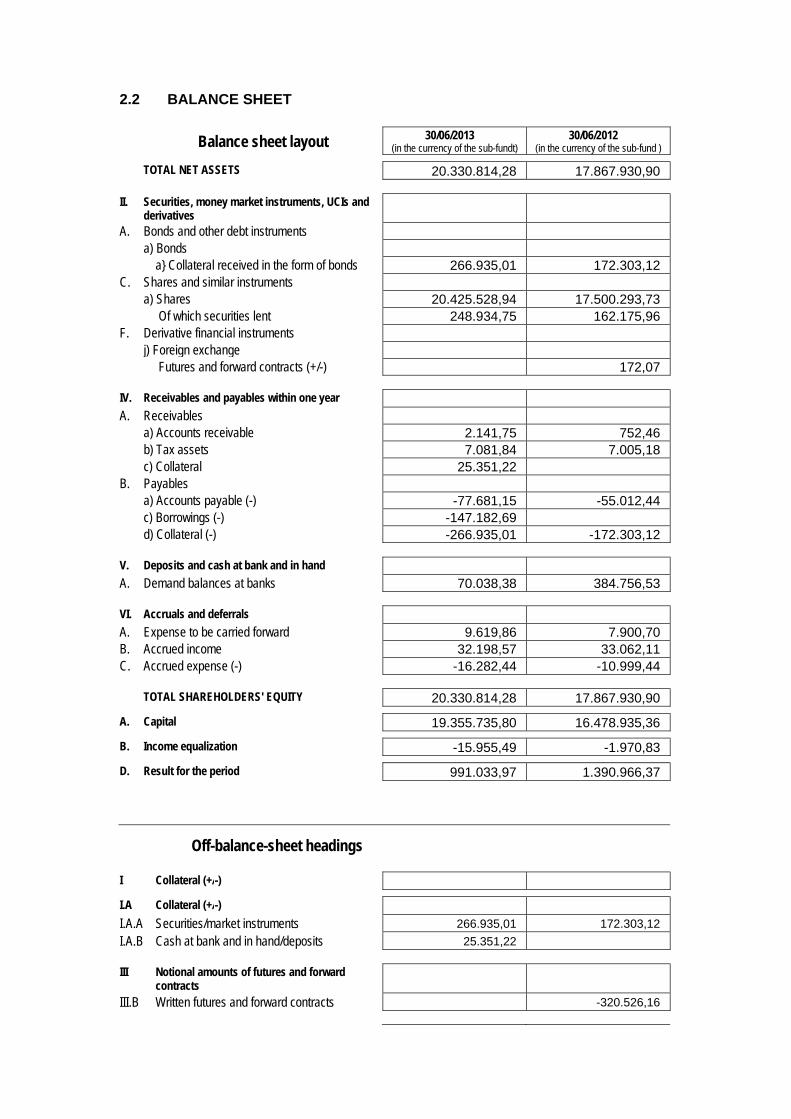

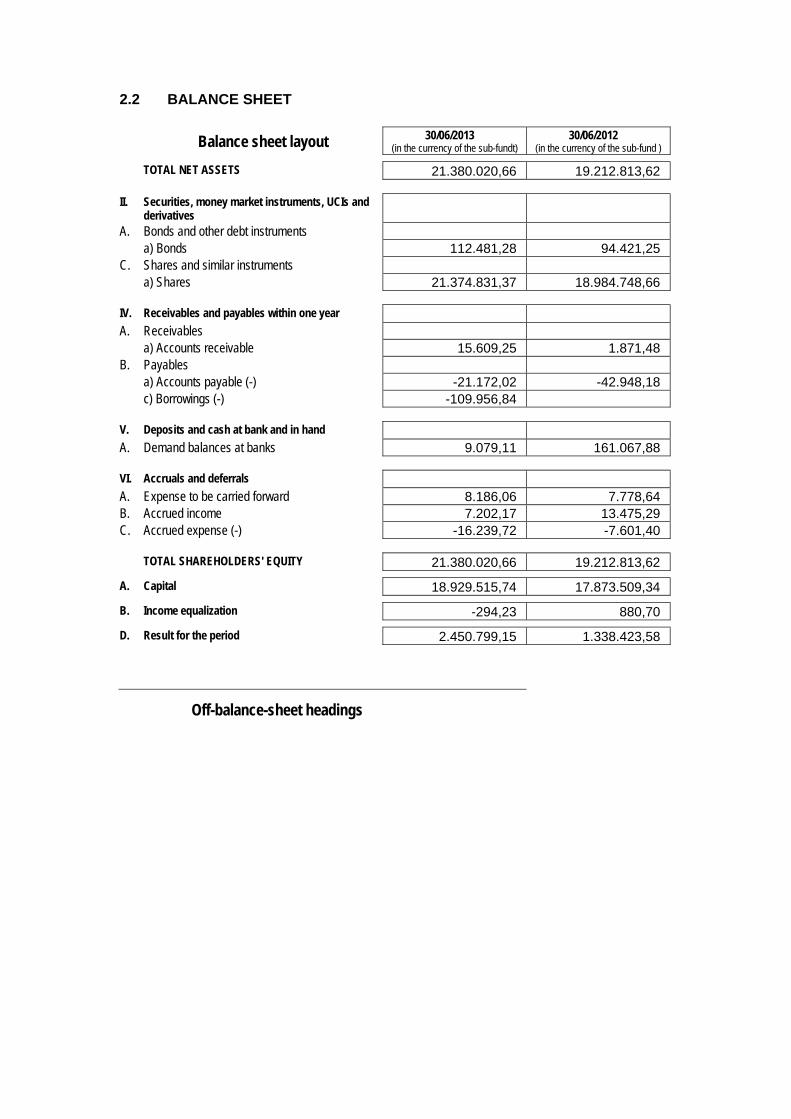

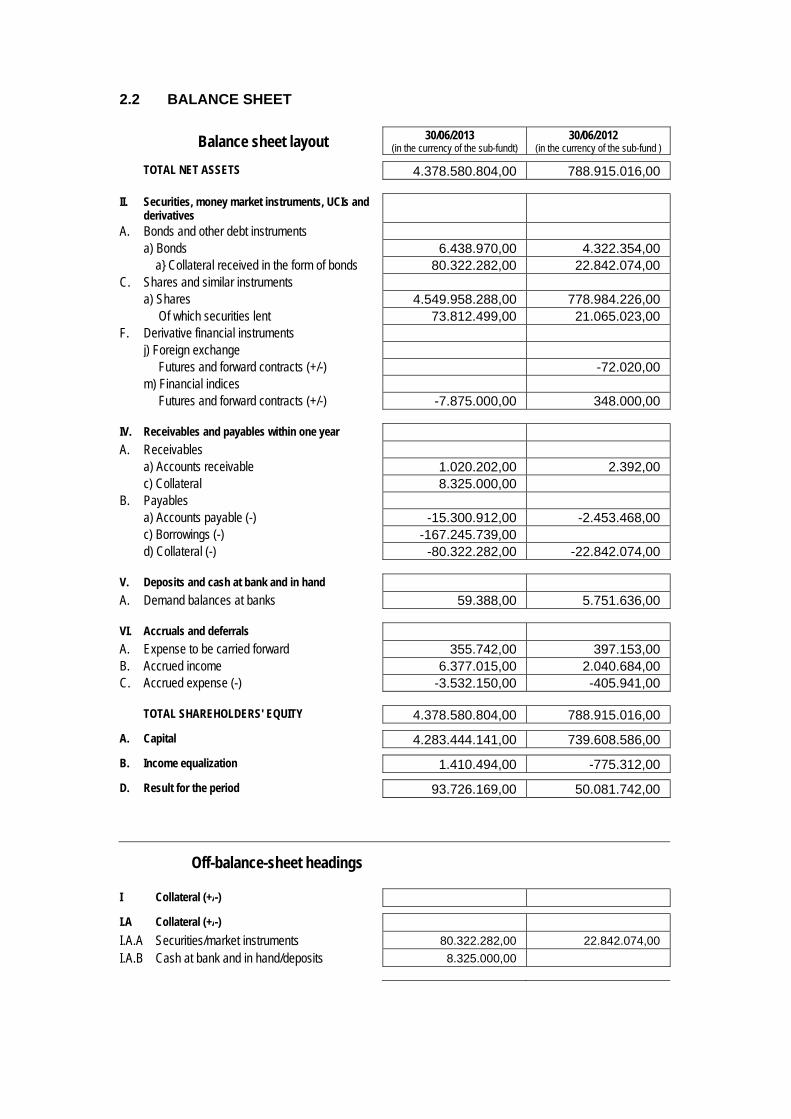

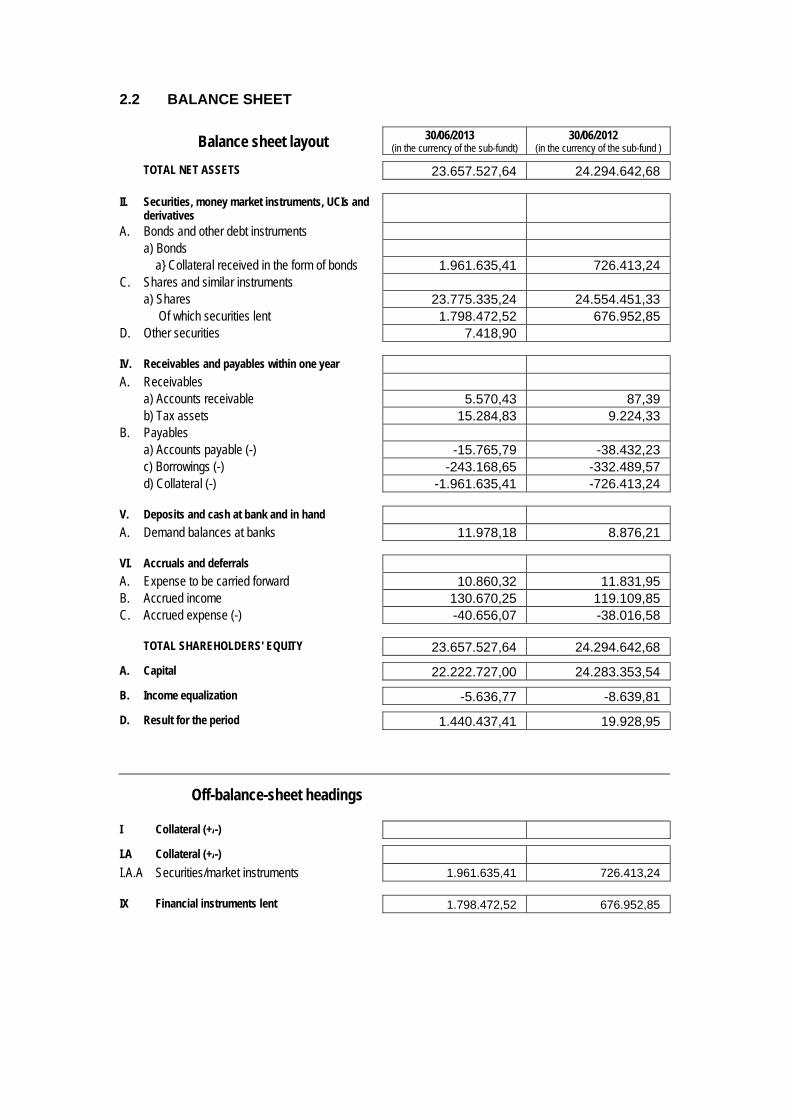

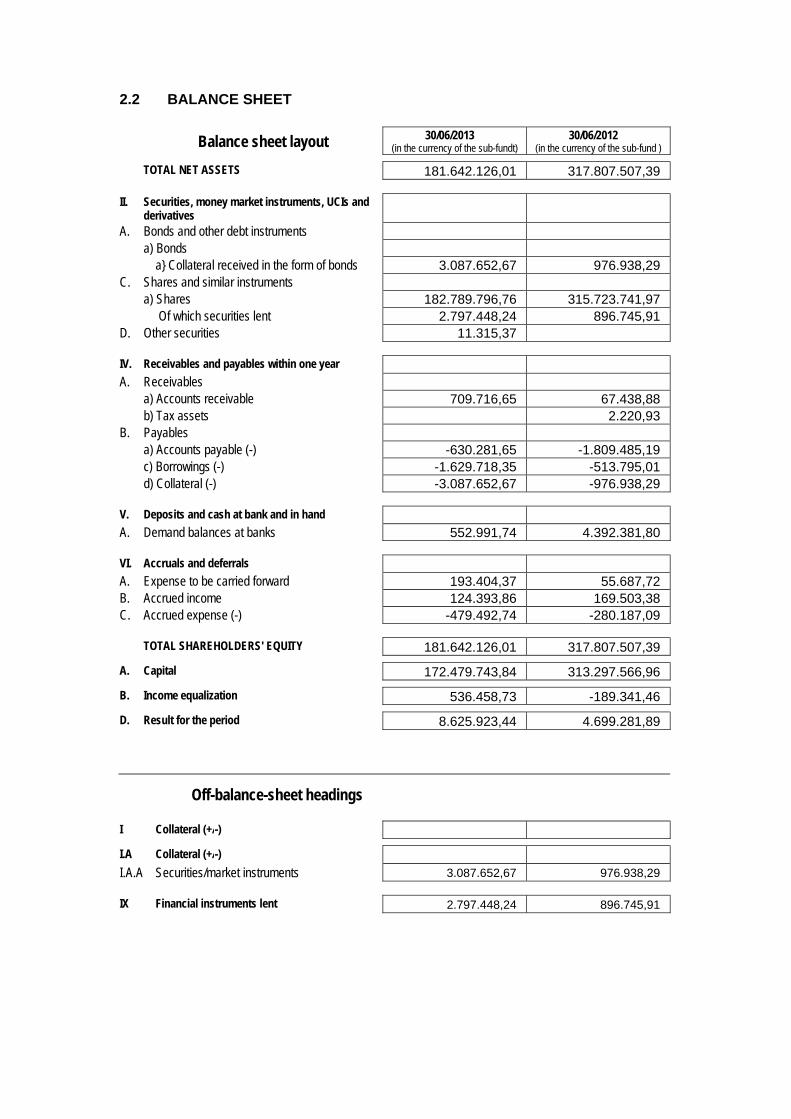

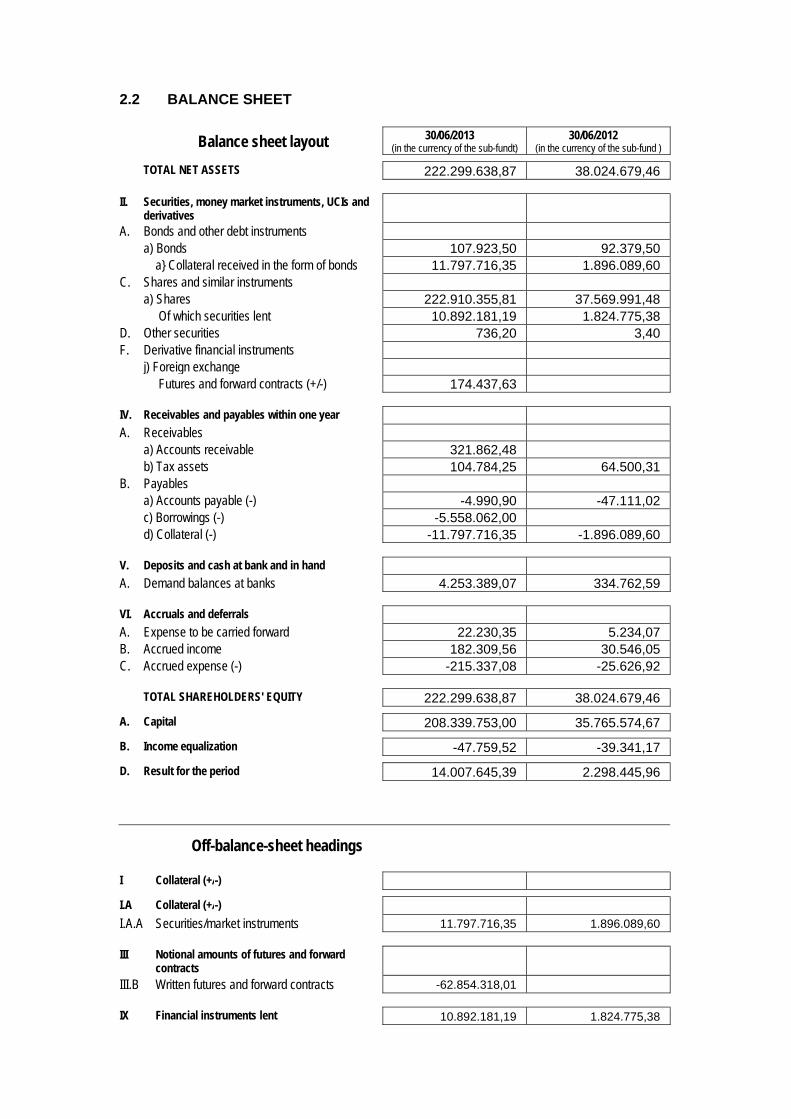

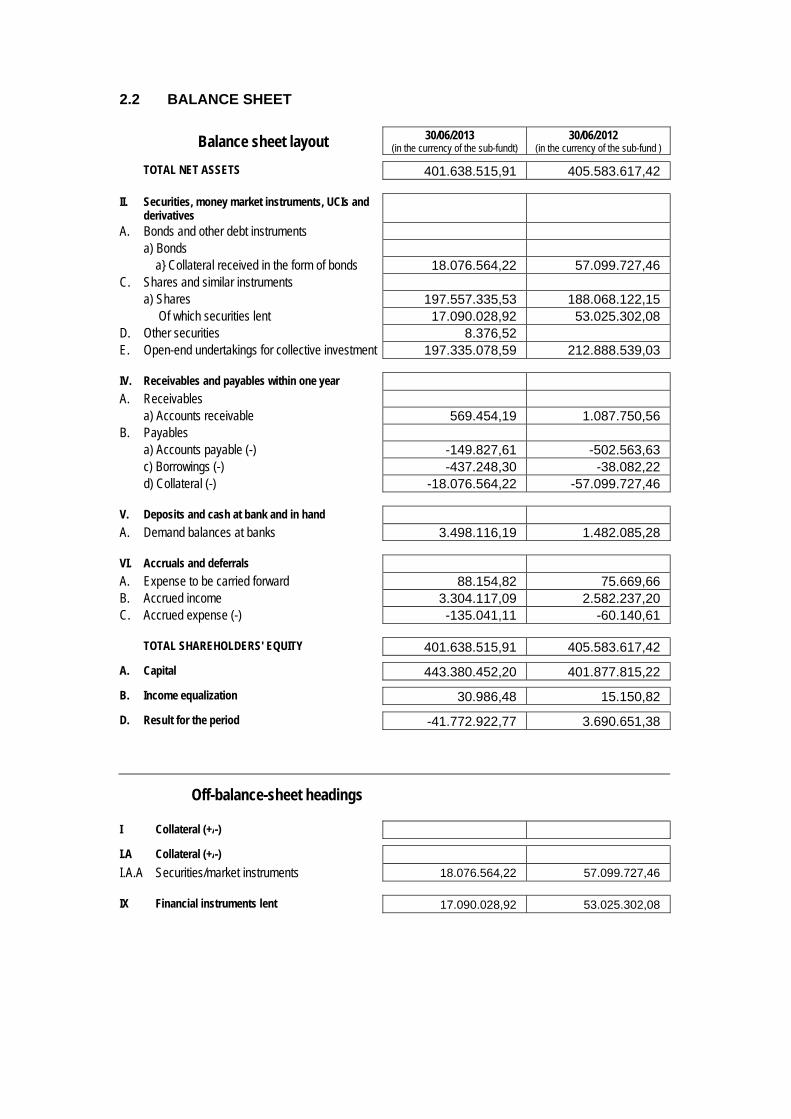

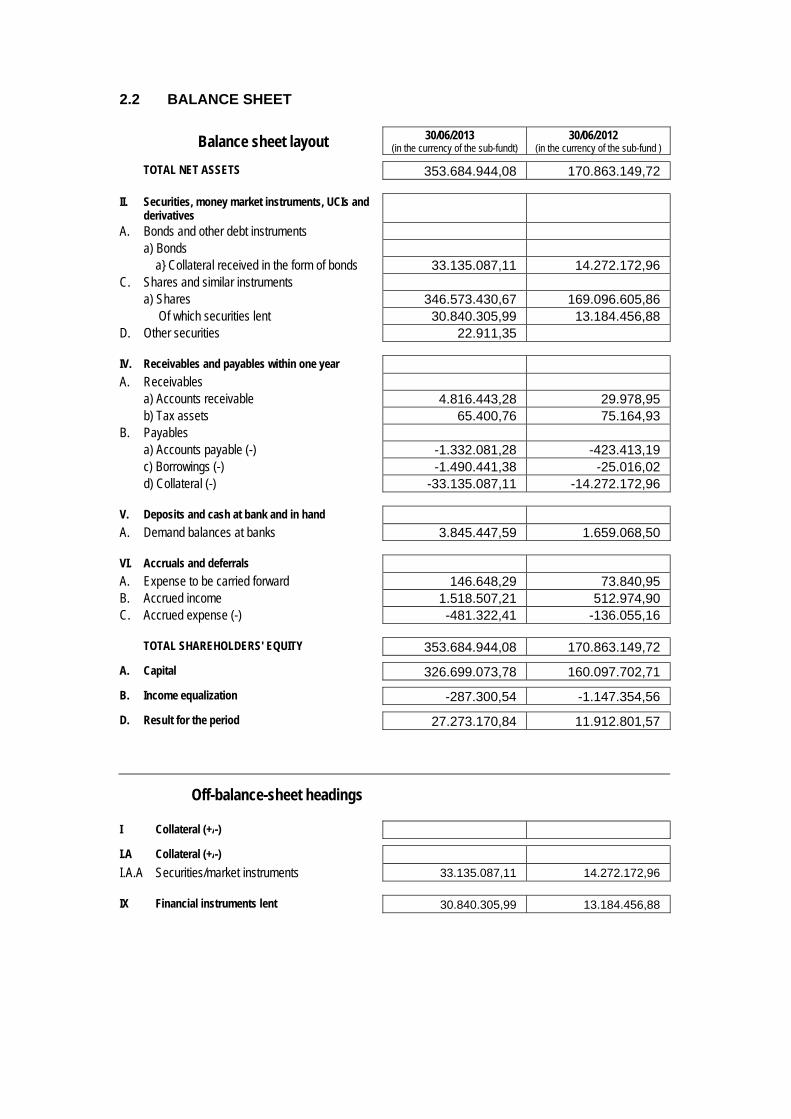

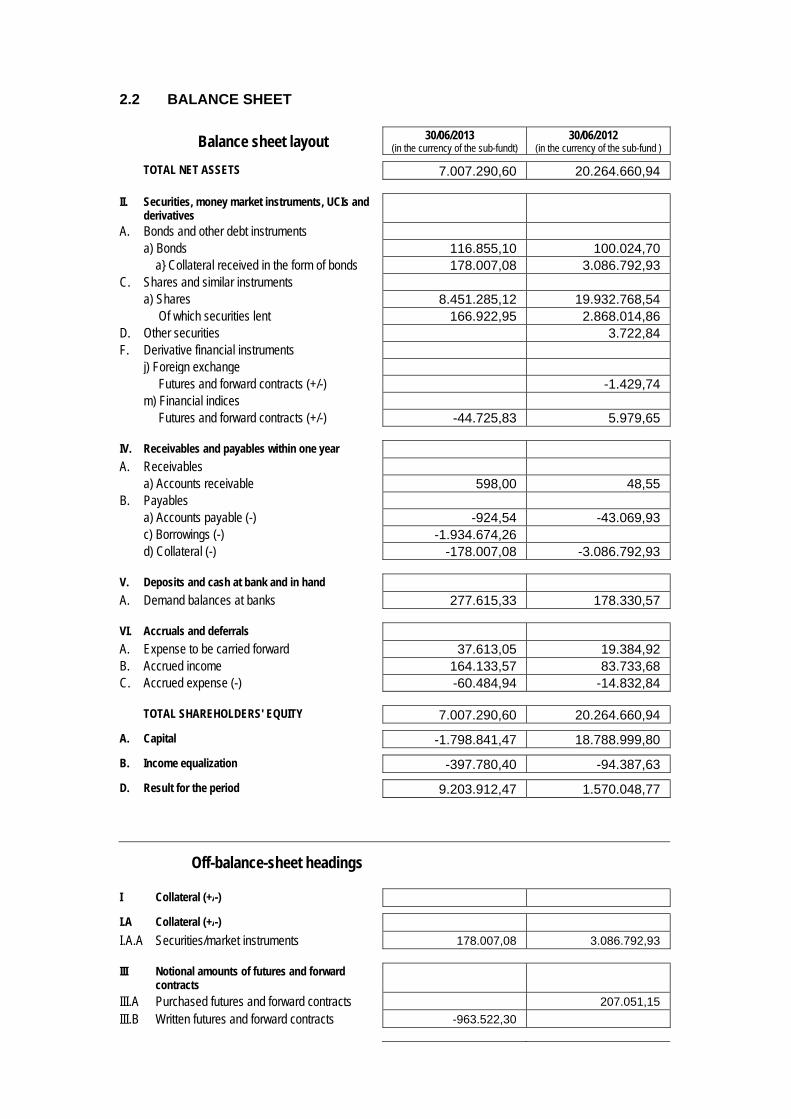

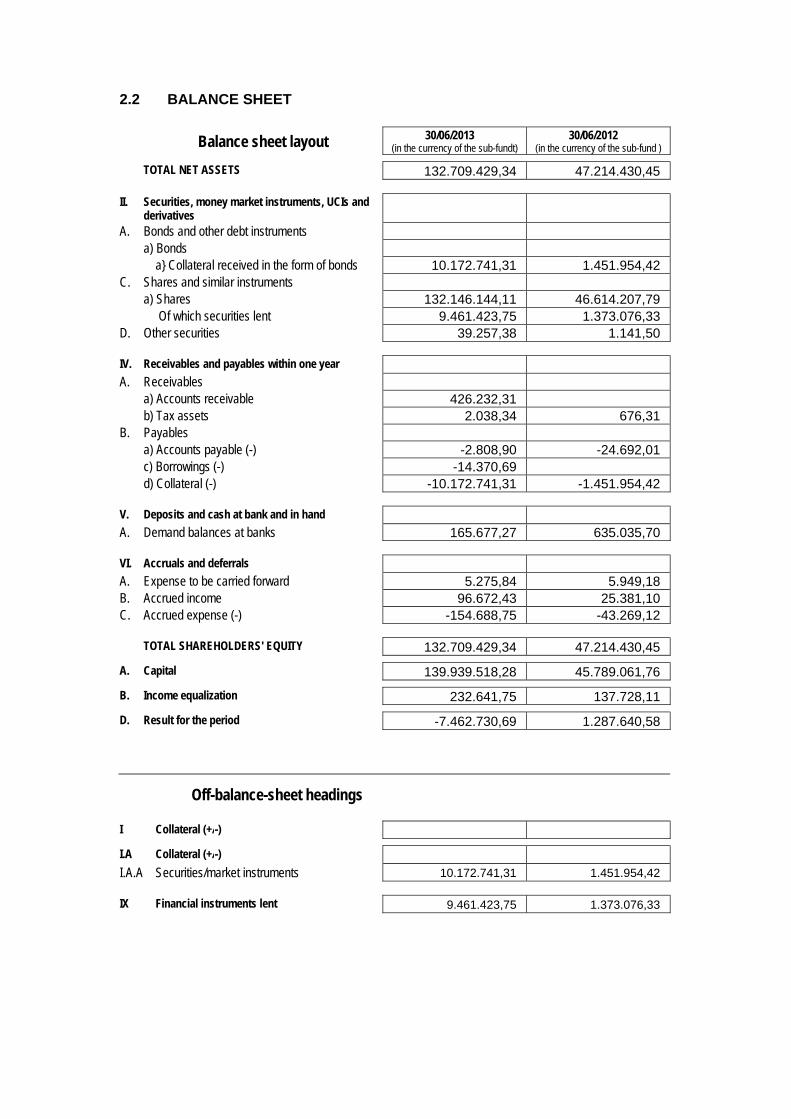

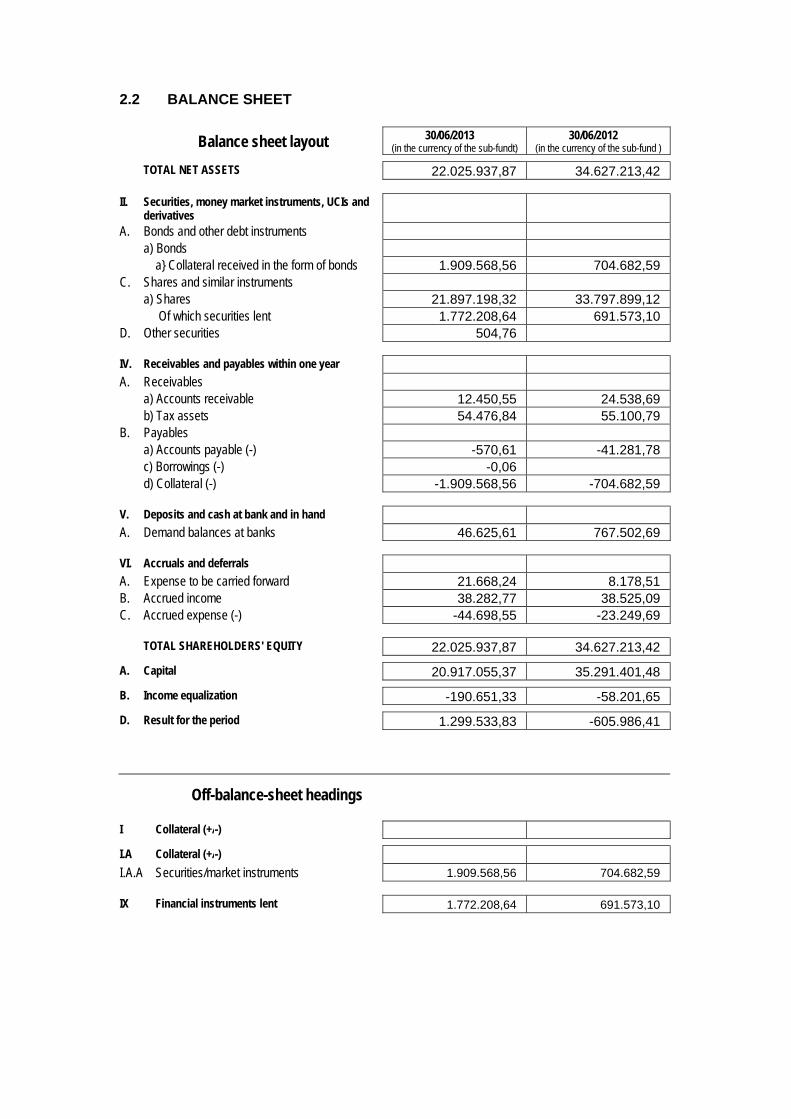

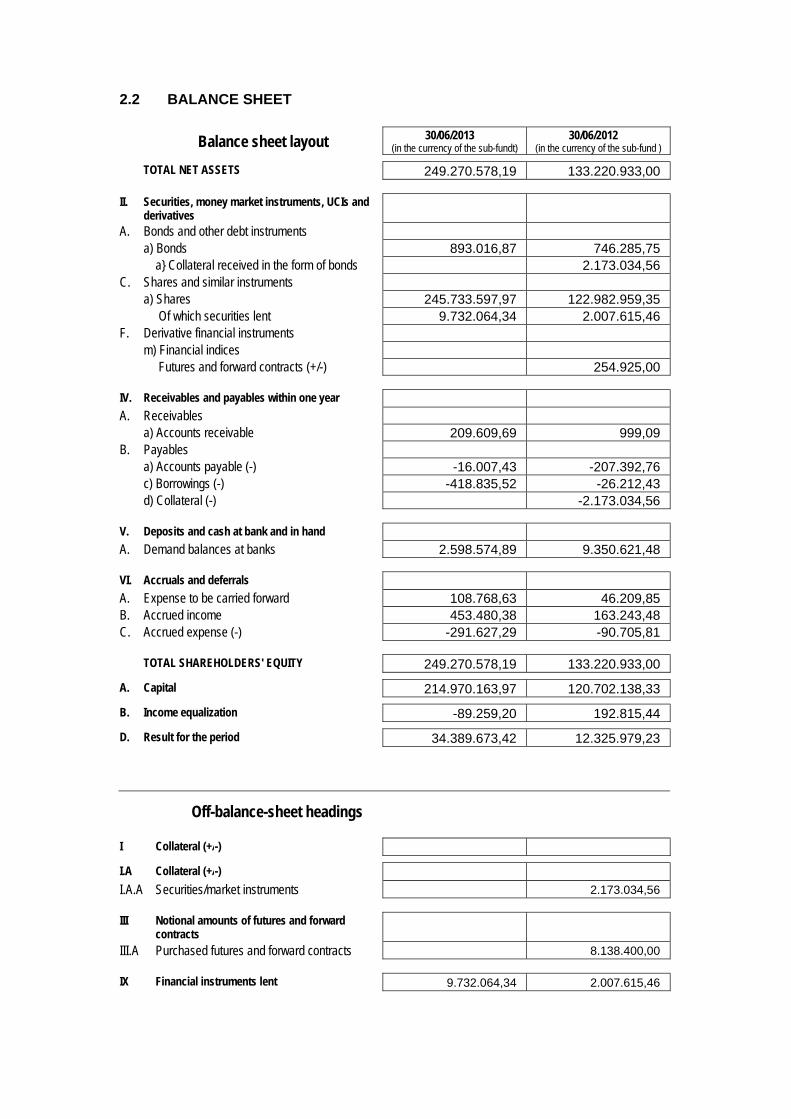

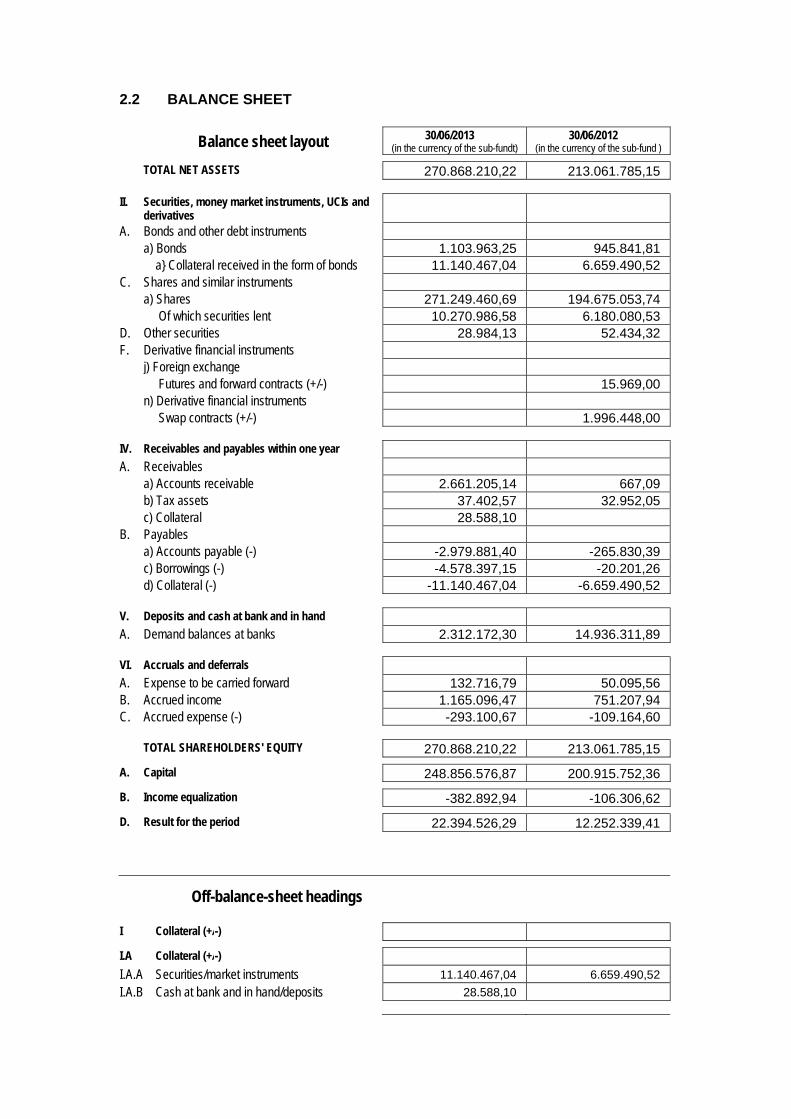

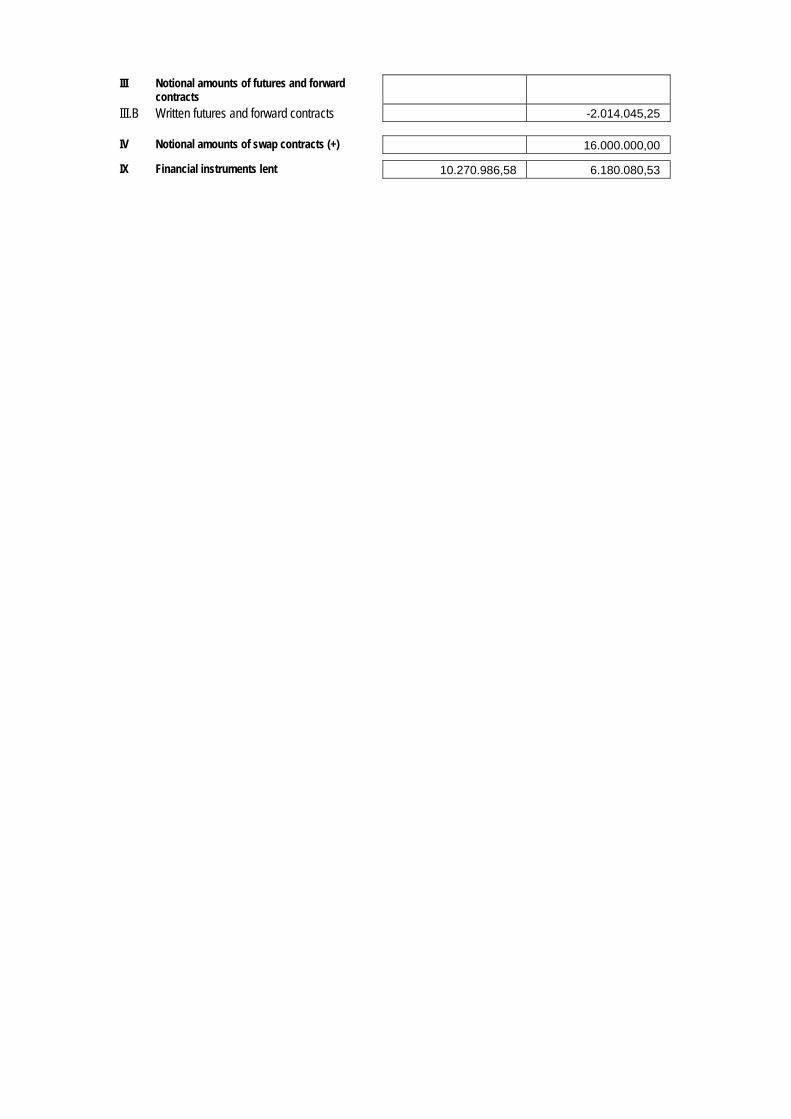

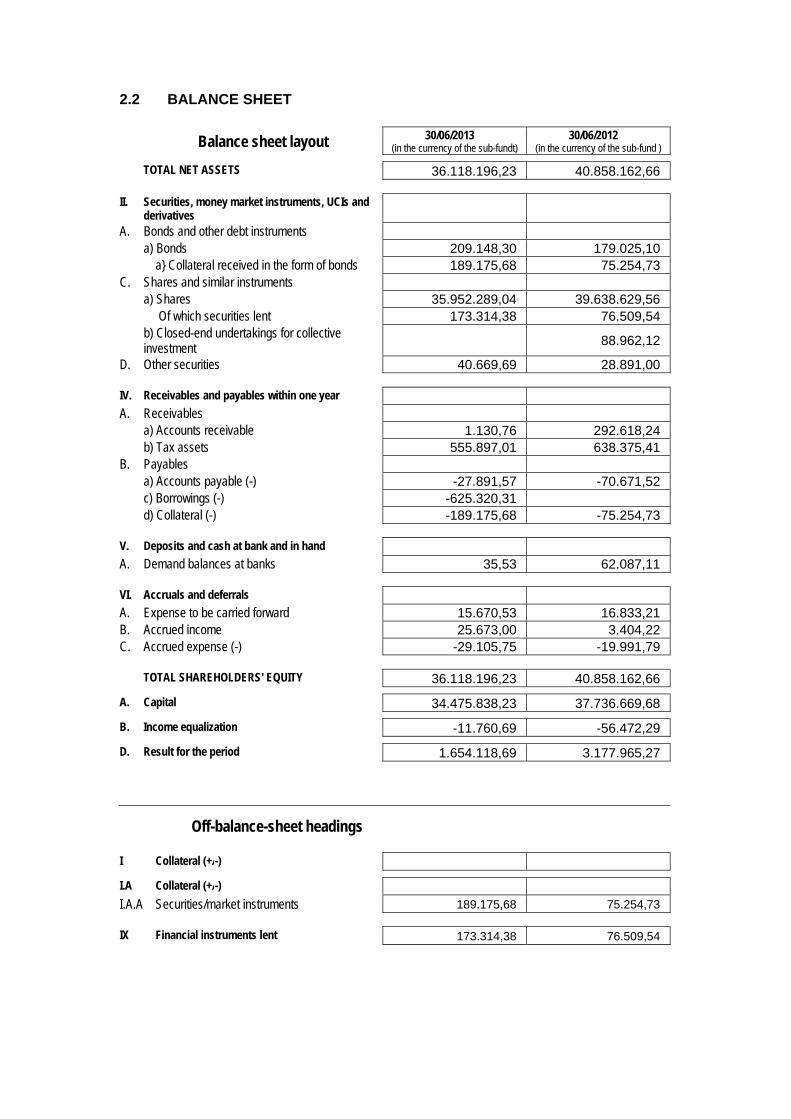

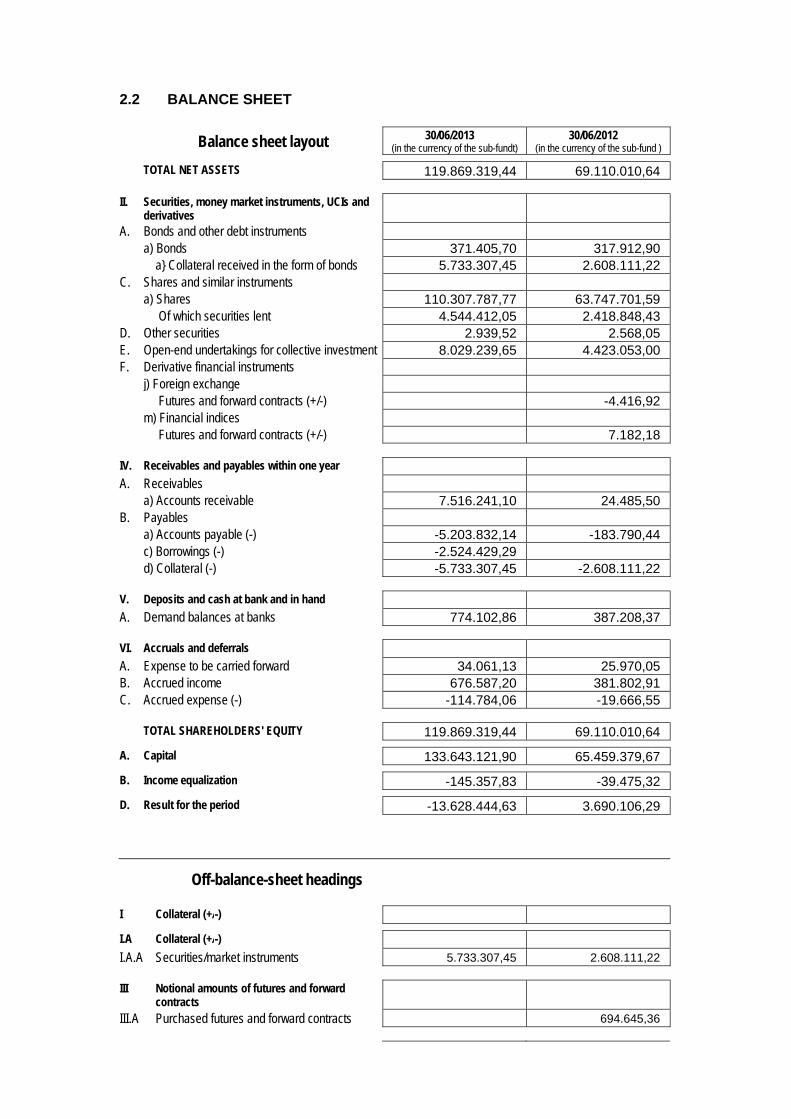

2.2 BALANCE SHEET

Balance sheet layout 30/06/2013 (in the currency of the sub-fundt)

TOTAL NET ASSETS 387.198.928,66

II. Securities, money market instruments, UCIs and derivatives

A. Bonds and other debt instruments a) Bonds a} Collateral received in the form of bonds 30.348.114,62 C. Shares and similar instruments a) Shares 385.359.449,73 Of which securities lent 28.299.460,94 F. Derivative financial instruments j) Foreign exchange Futures and forward contracts (+/-) -1.028.196,09

IV. Receivables and payables within one year A. Receivables a) Accounts receivable 502.876.125,53 b) Tax assets 13.302,32 B. Payables a) Accounts payable (-) -502.283.974,34 c) Borrowings (-) -685.064,11 d) Collateral (-) -30.348.114,62

V. Deposits and cash at bank and in hand A. Demand balances at banks 2.107.520,98

VI. Accruals and deferrals A. Expense to be carried forward 77.235,33 B. Accrued income 1.012.968,33 C. Accrued expense (-) -250.439,02

TOTAL SHAREHOLDERS' EQUITY 387.198.928,66

A. Capital 365.298.130,52

B. Income equalization 831.229,42

D. Result for the period 21.069.568,72

Off-balance-sheet headings

I Collateral (+/-)

I.A Collateral (+/-)

I.A.A Securities/market instruments 30.348.114,62

III Notional amounts of futures and forward contracts

III.A Purchased futures and forward contracts 244.398.833,60

IX Financial instruments lent 28.299.460,94

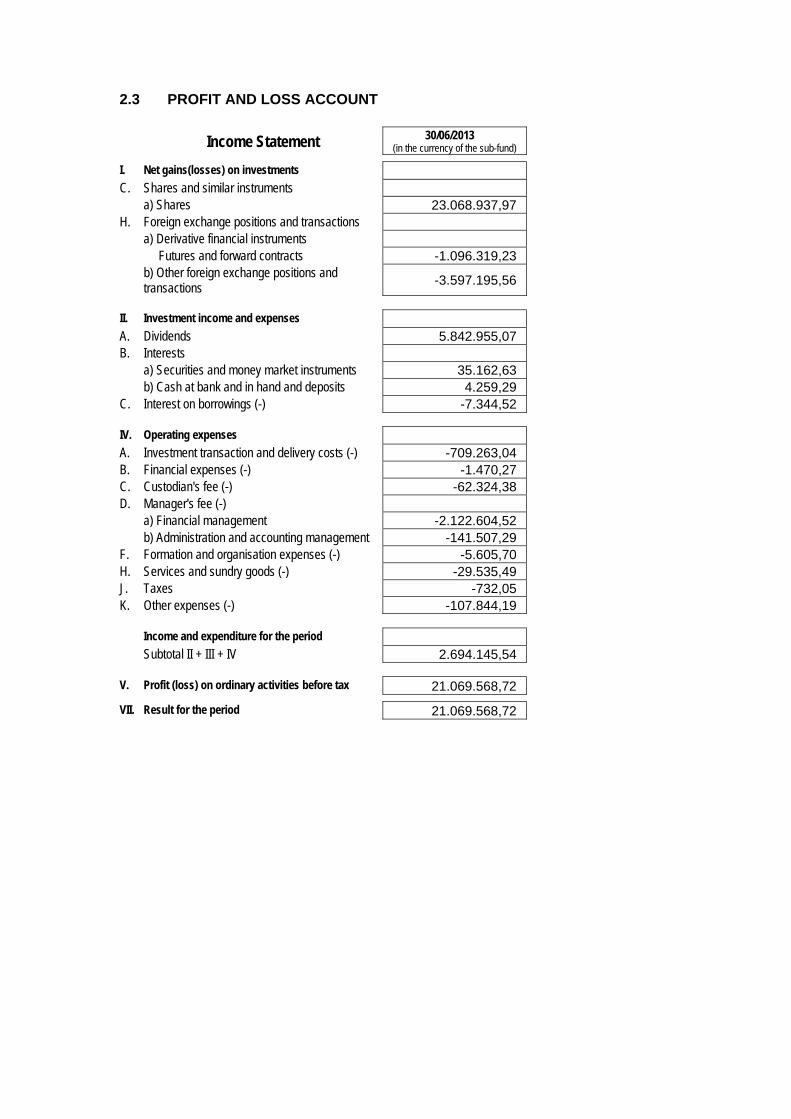

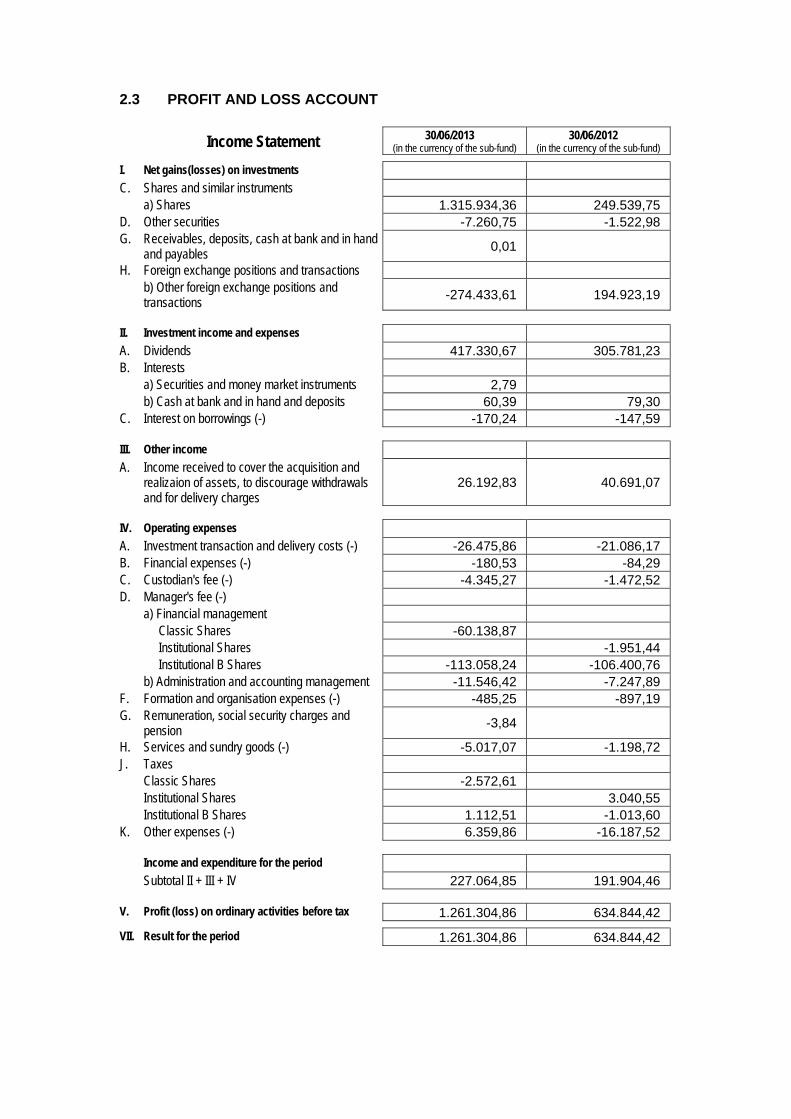

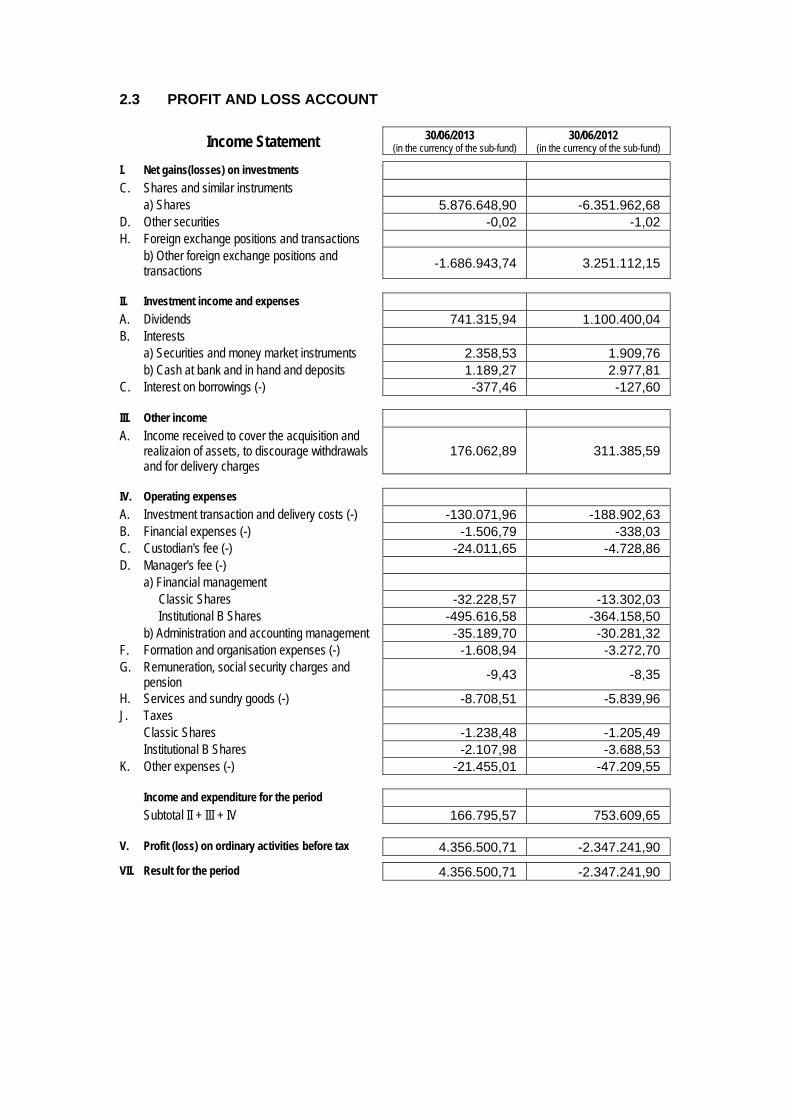

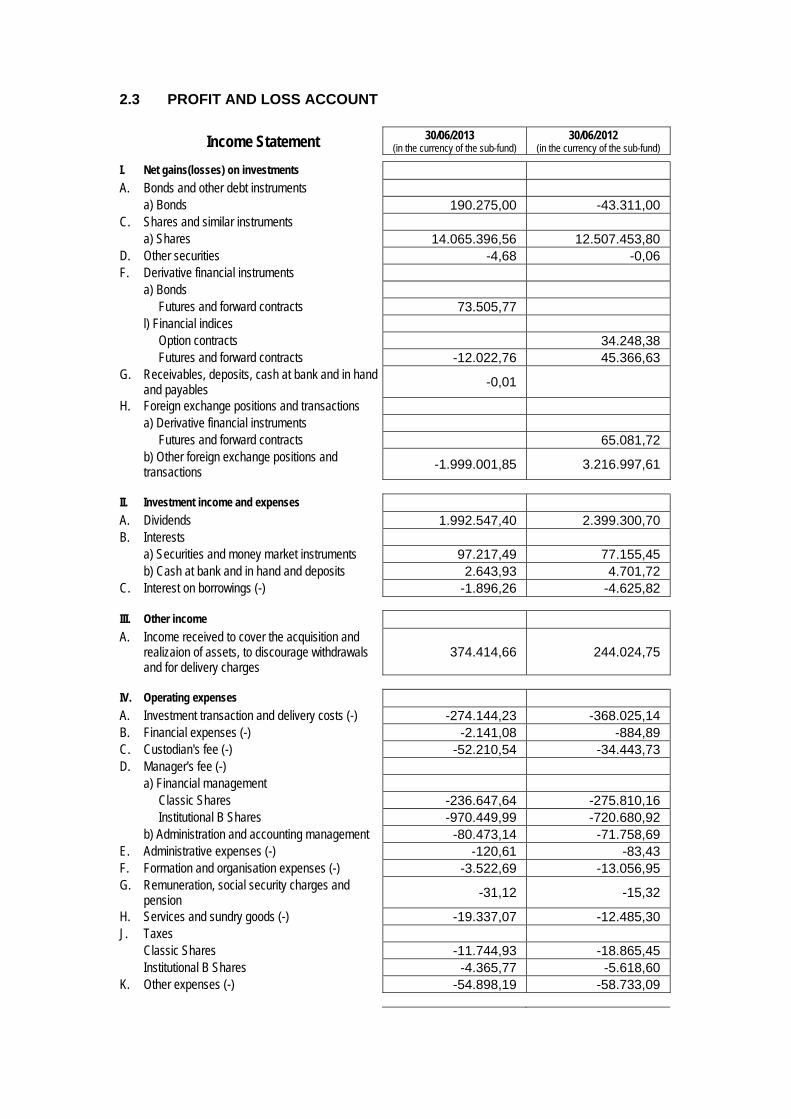

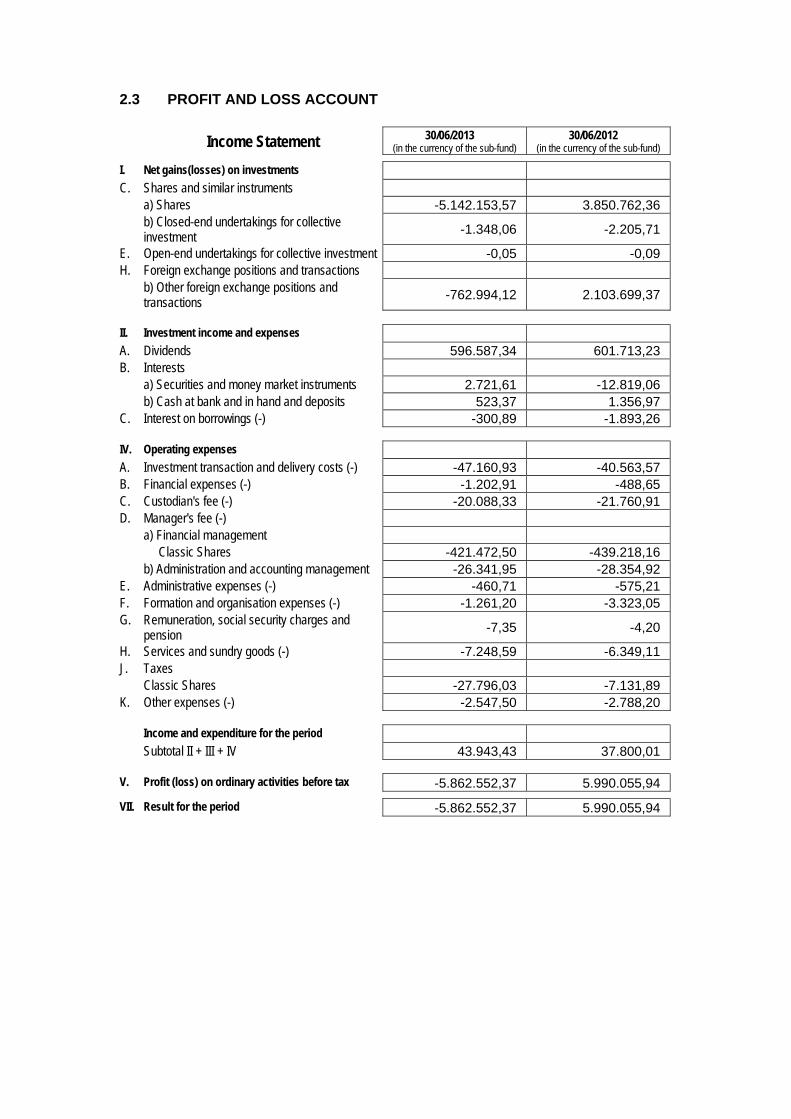

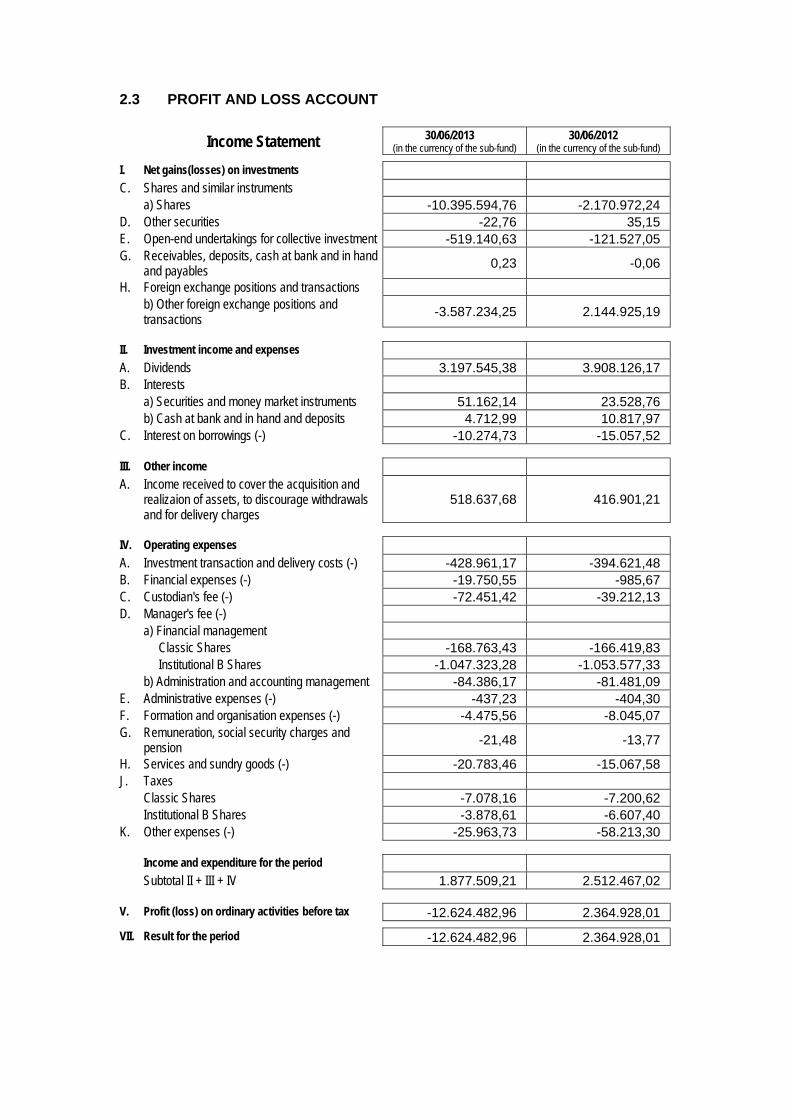

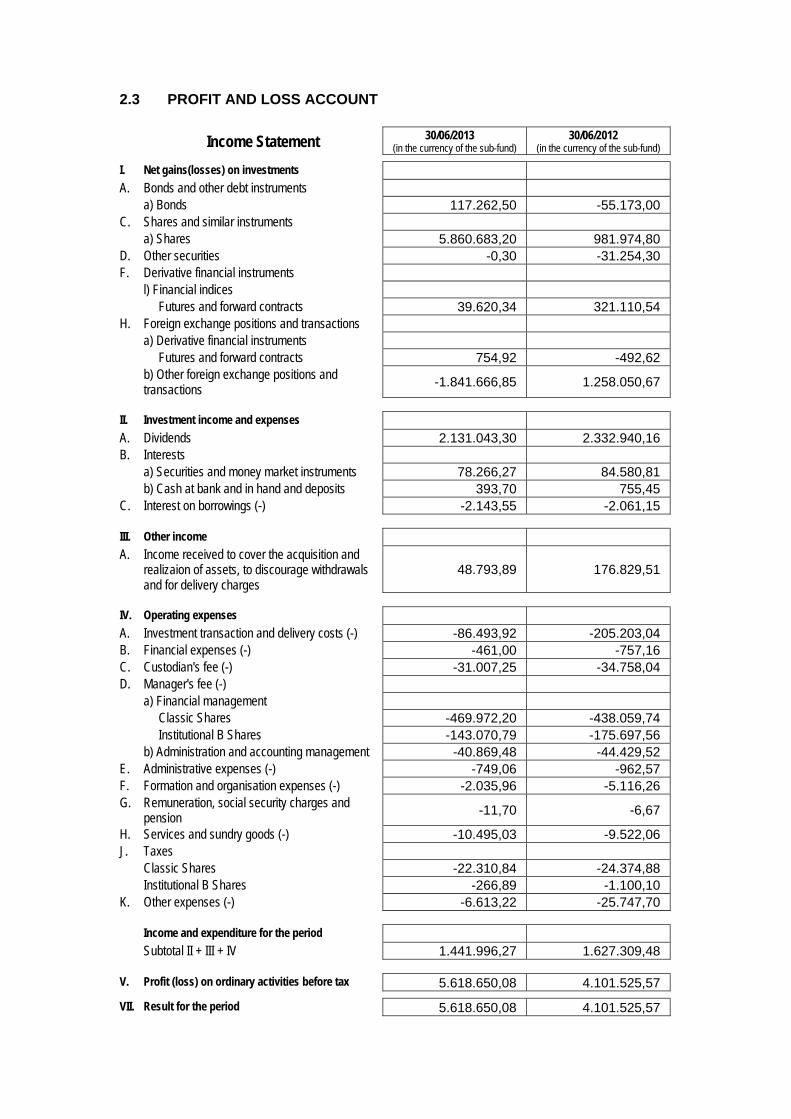

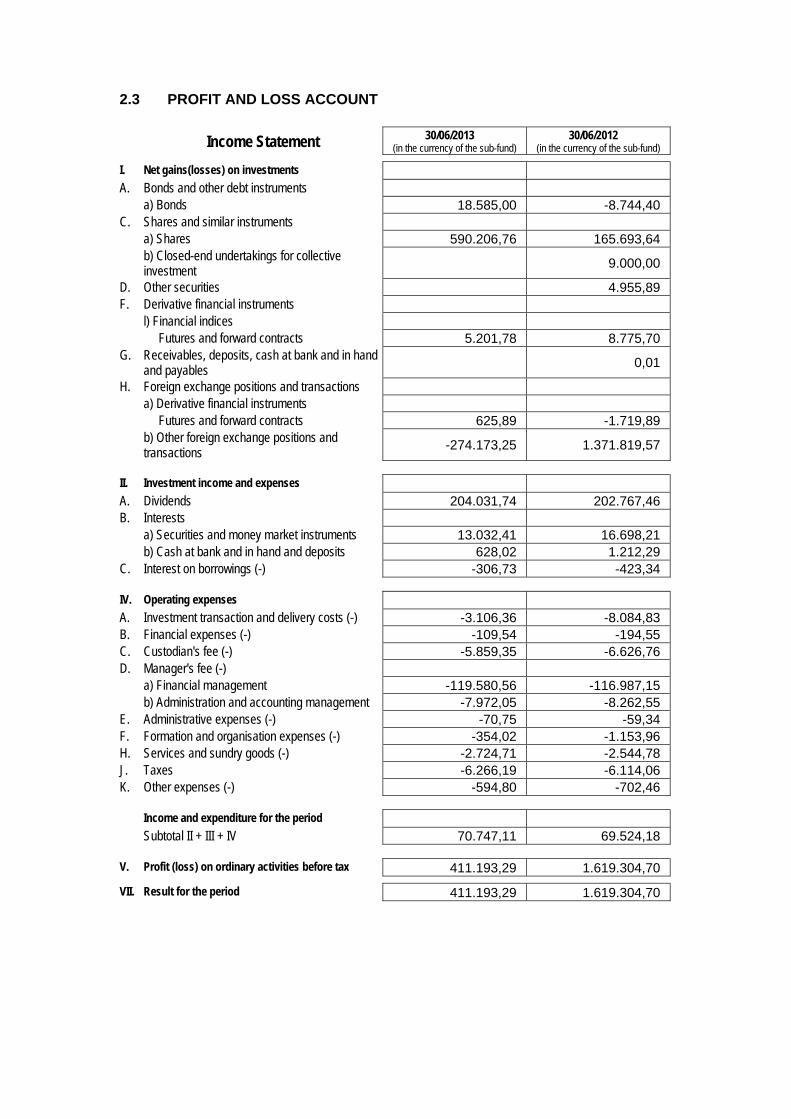

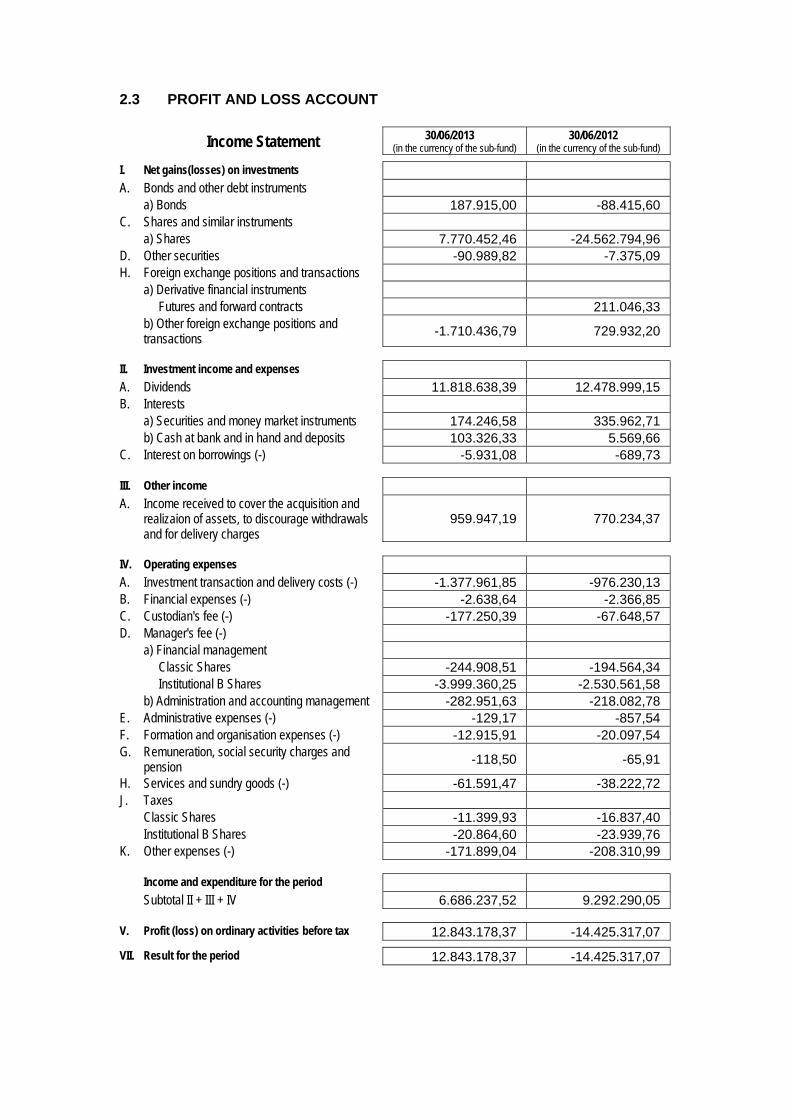

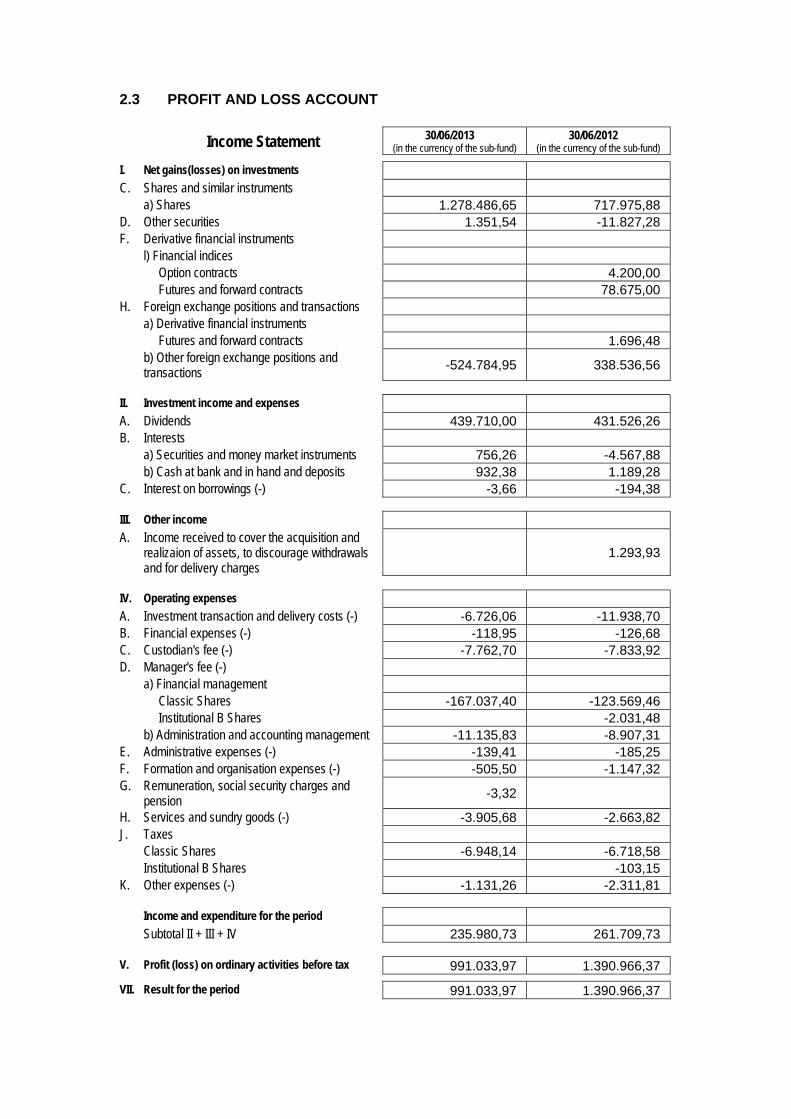

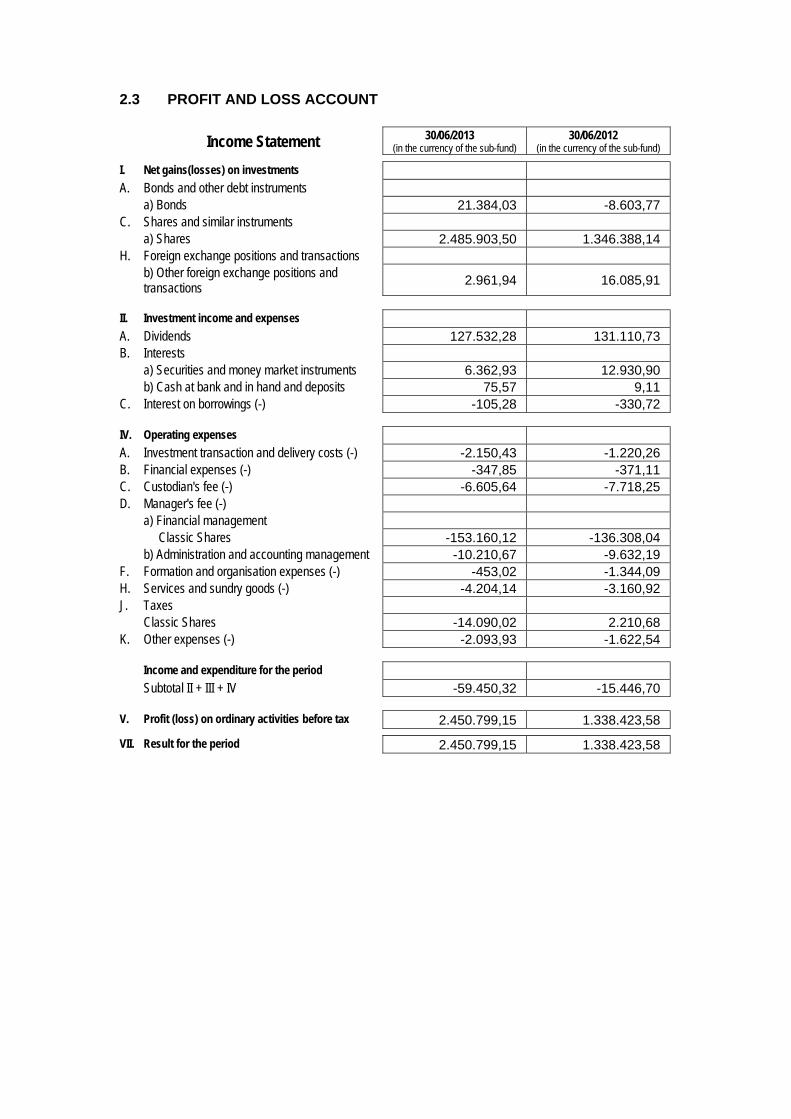

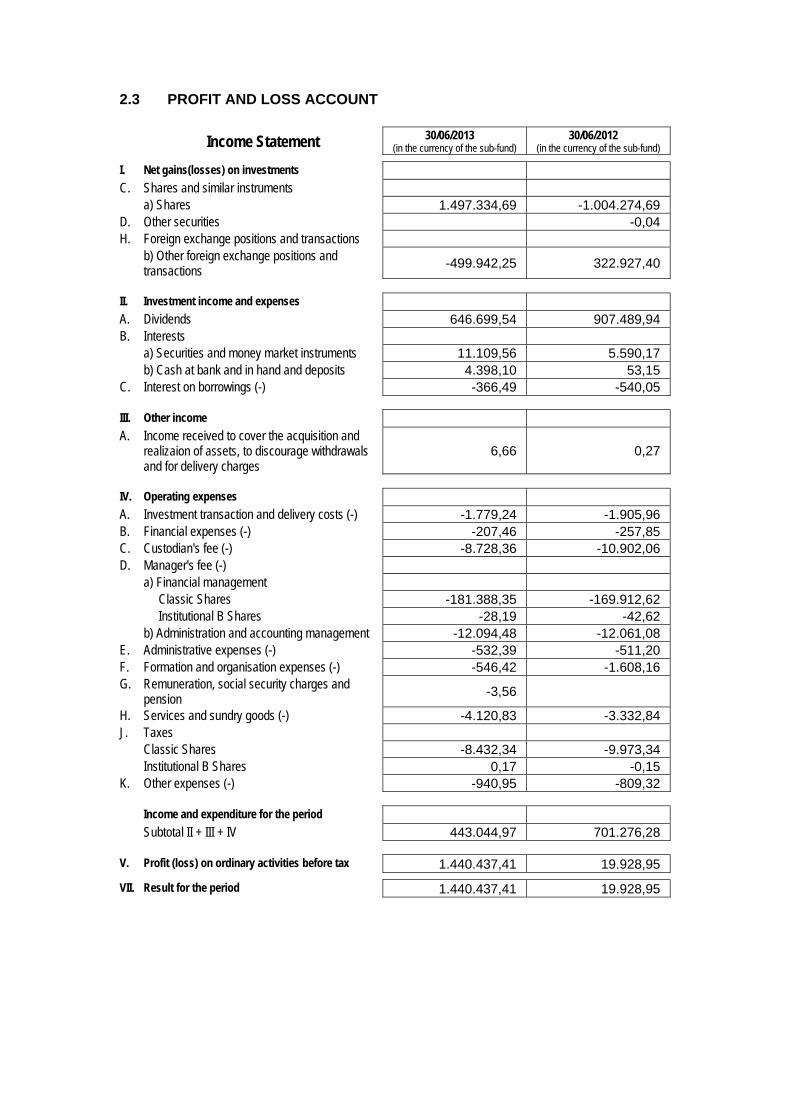

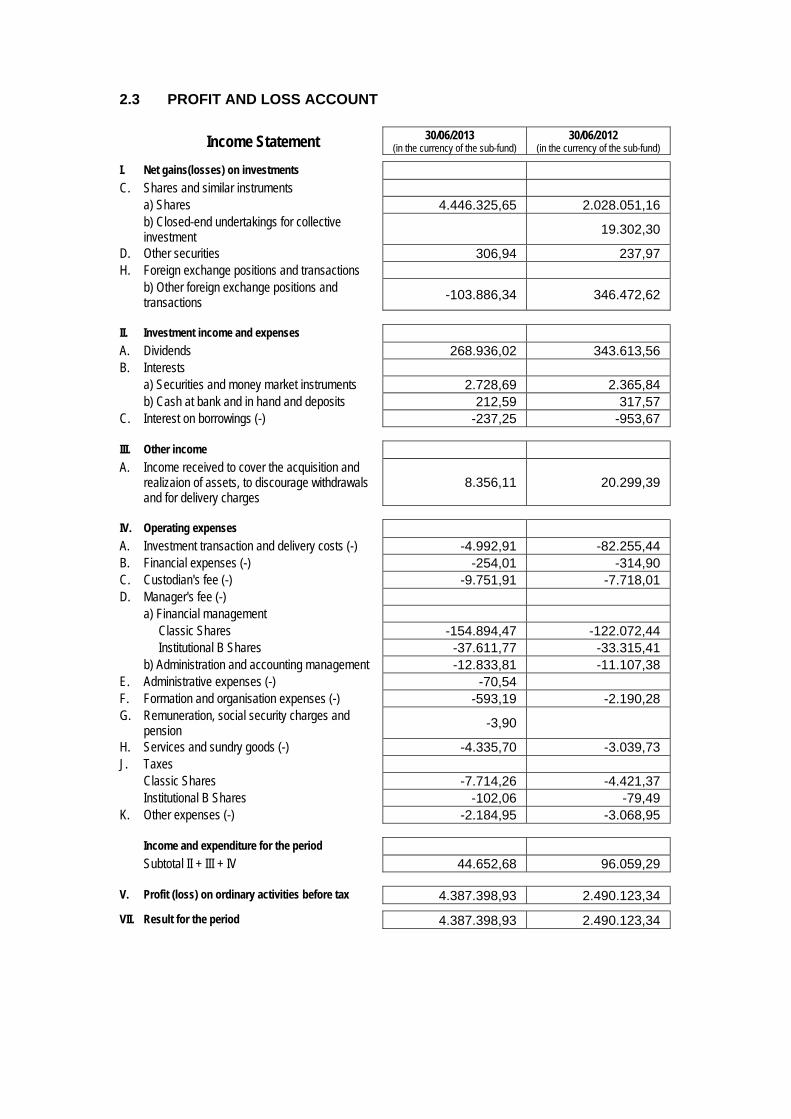

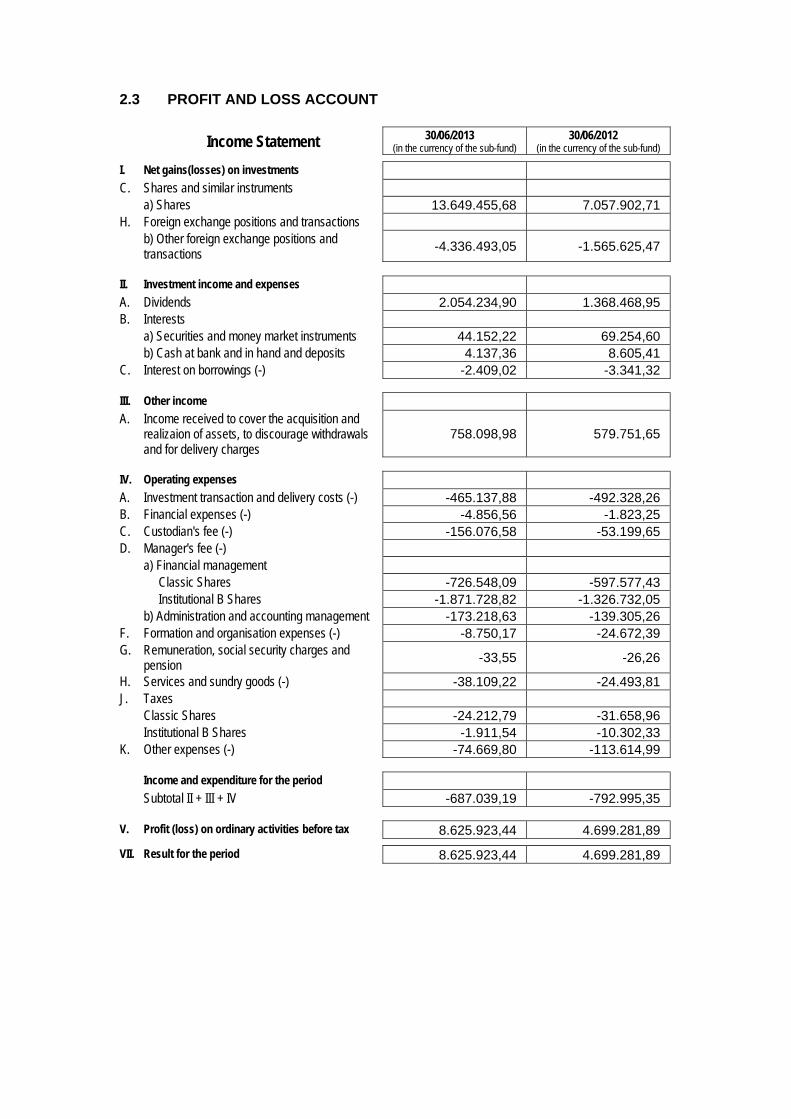

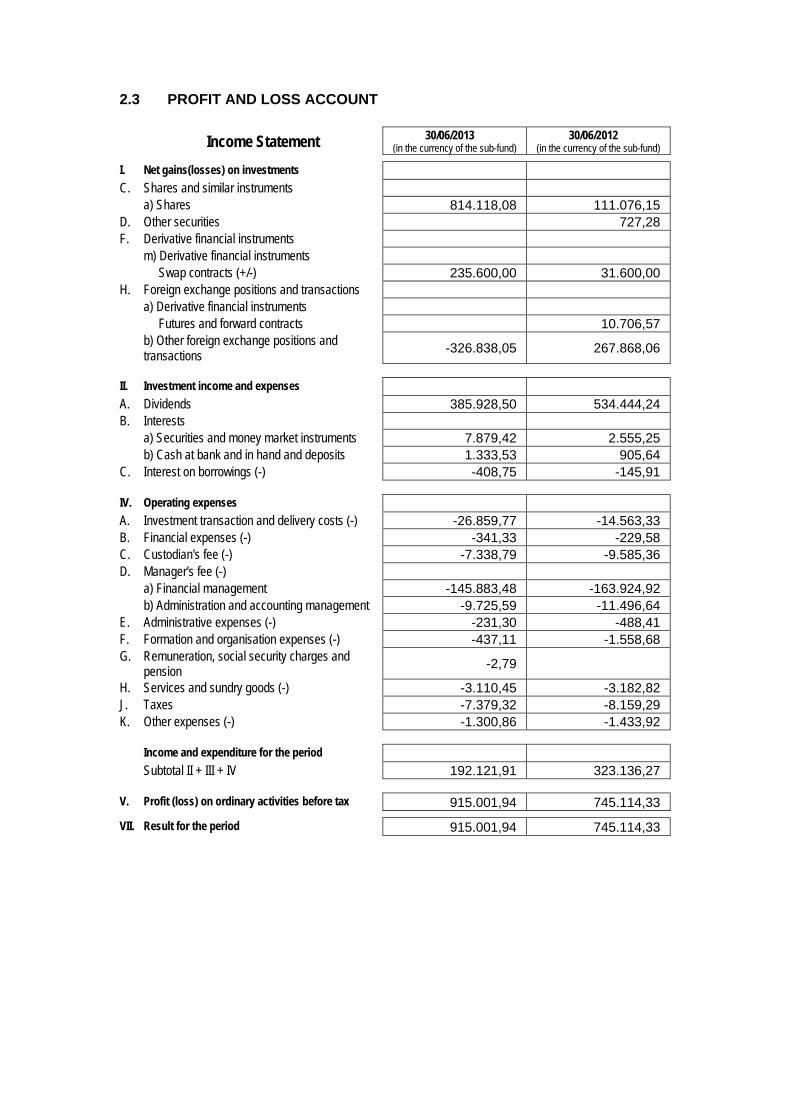

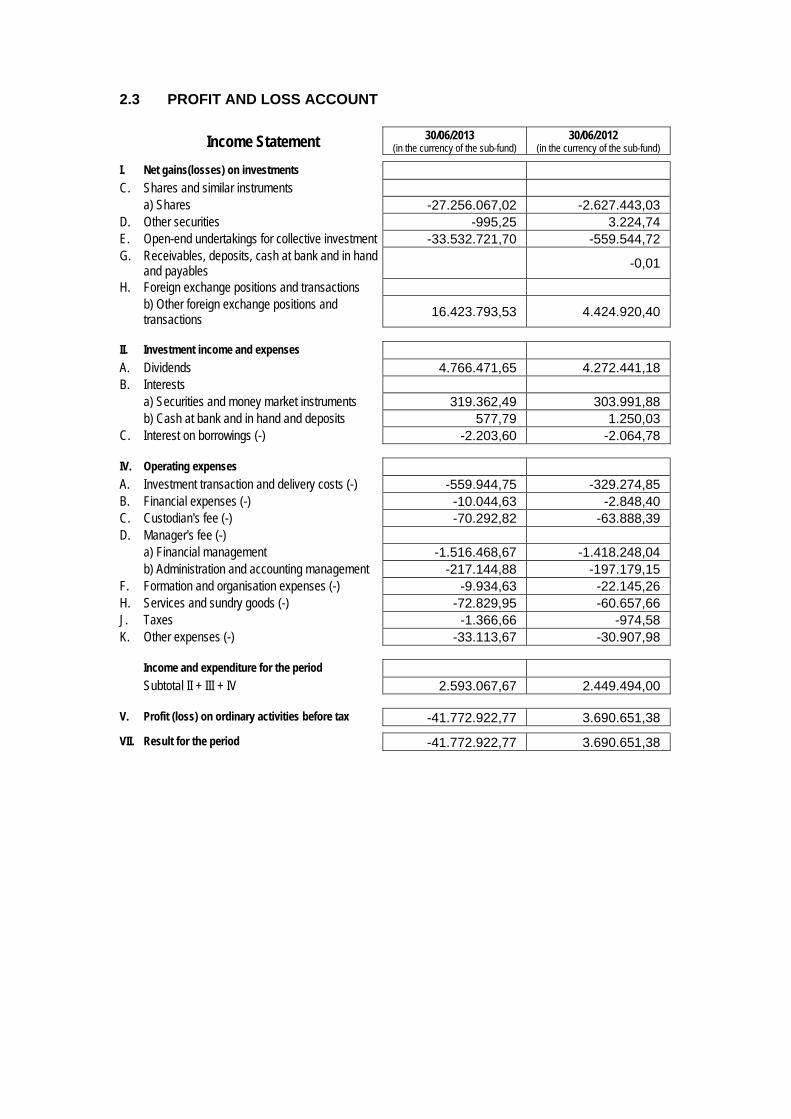

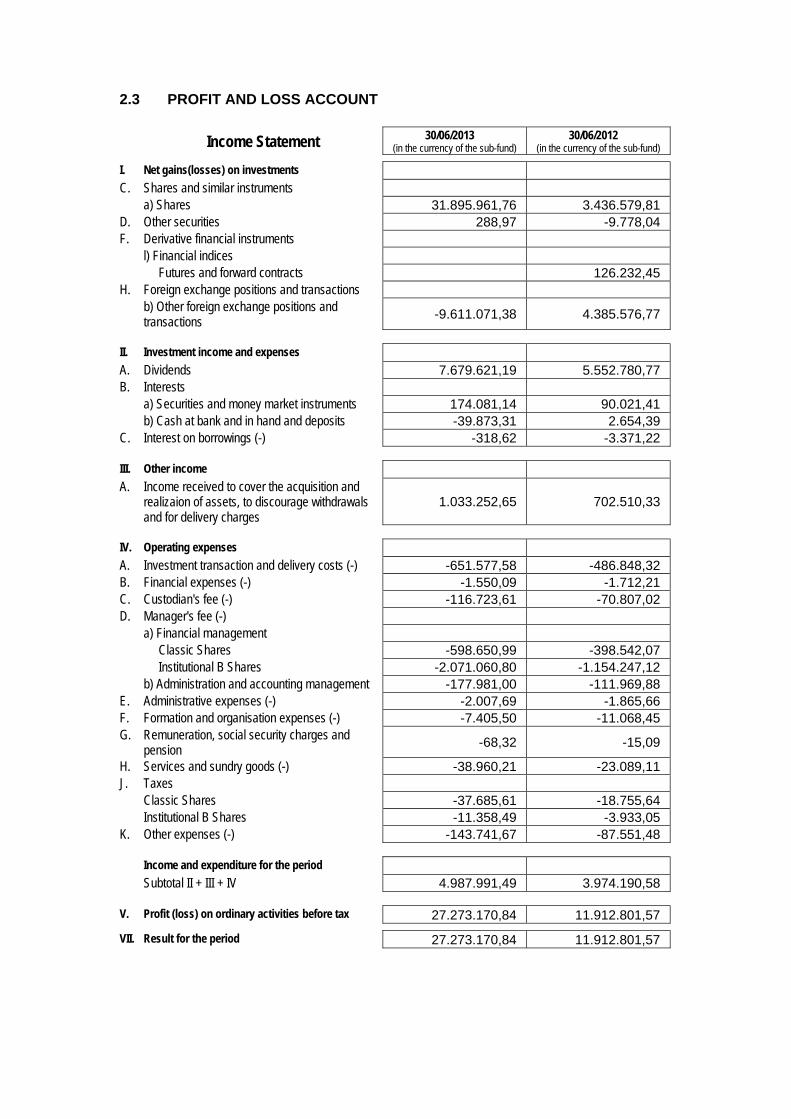

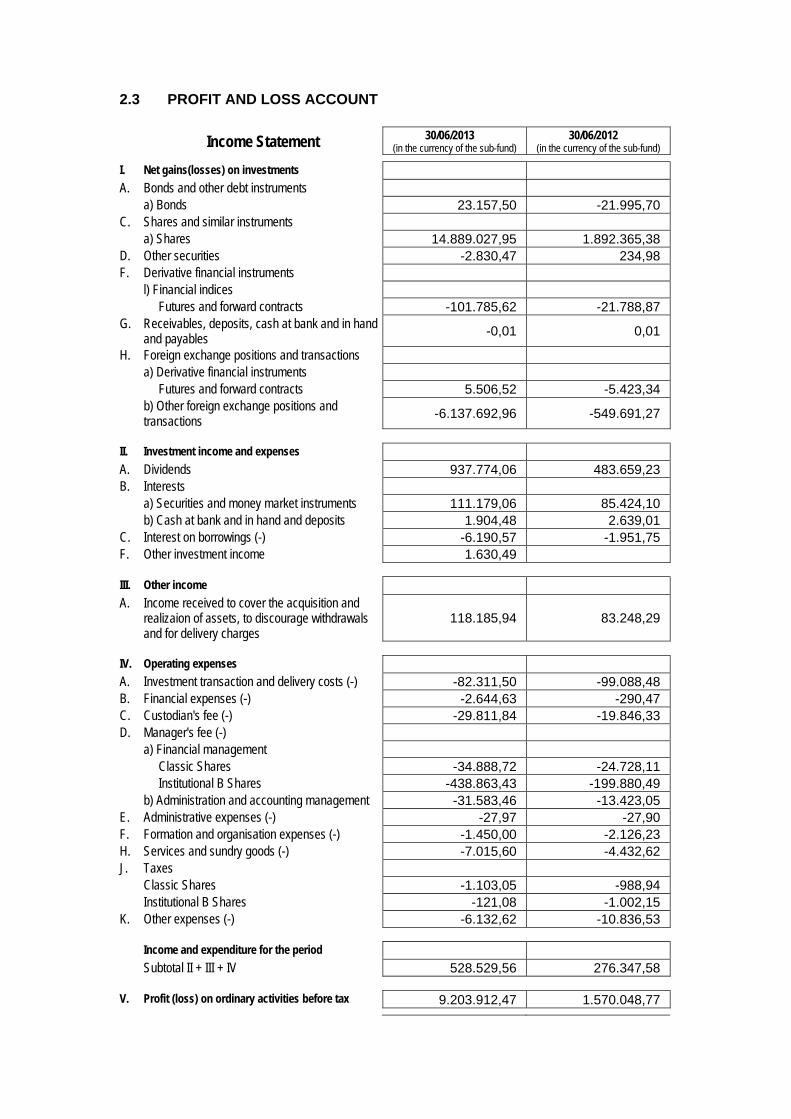

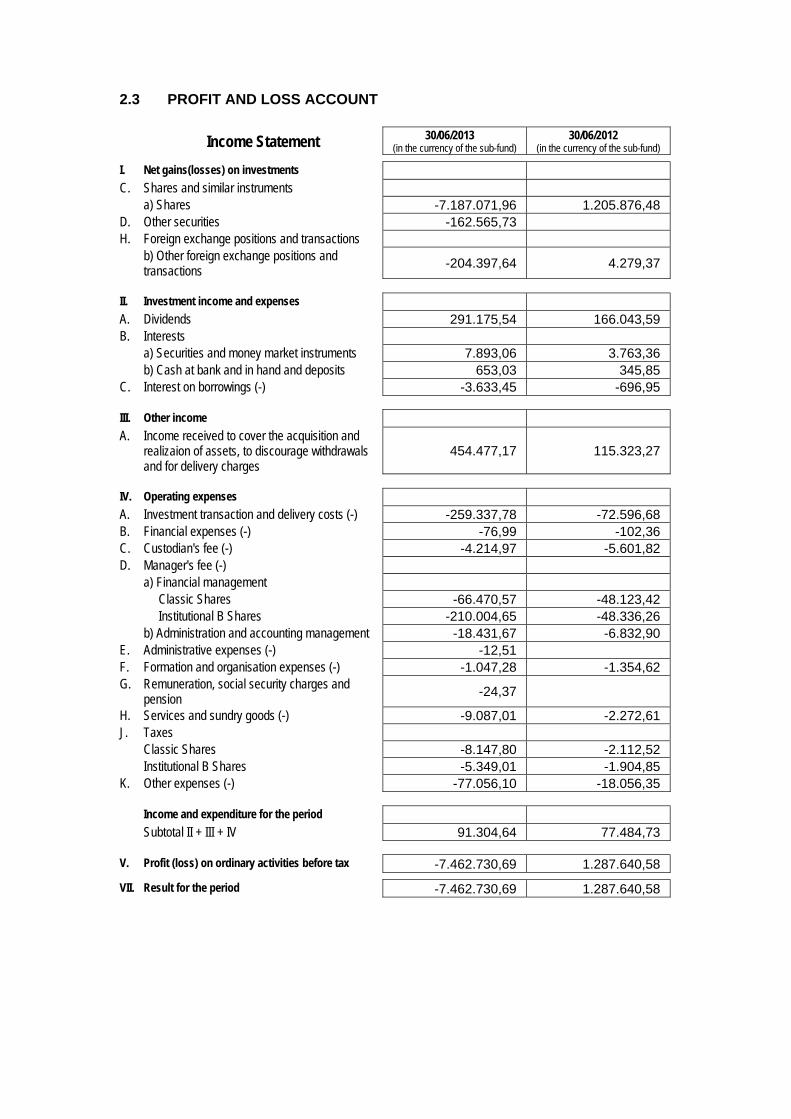

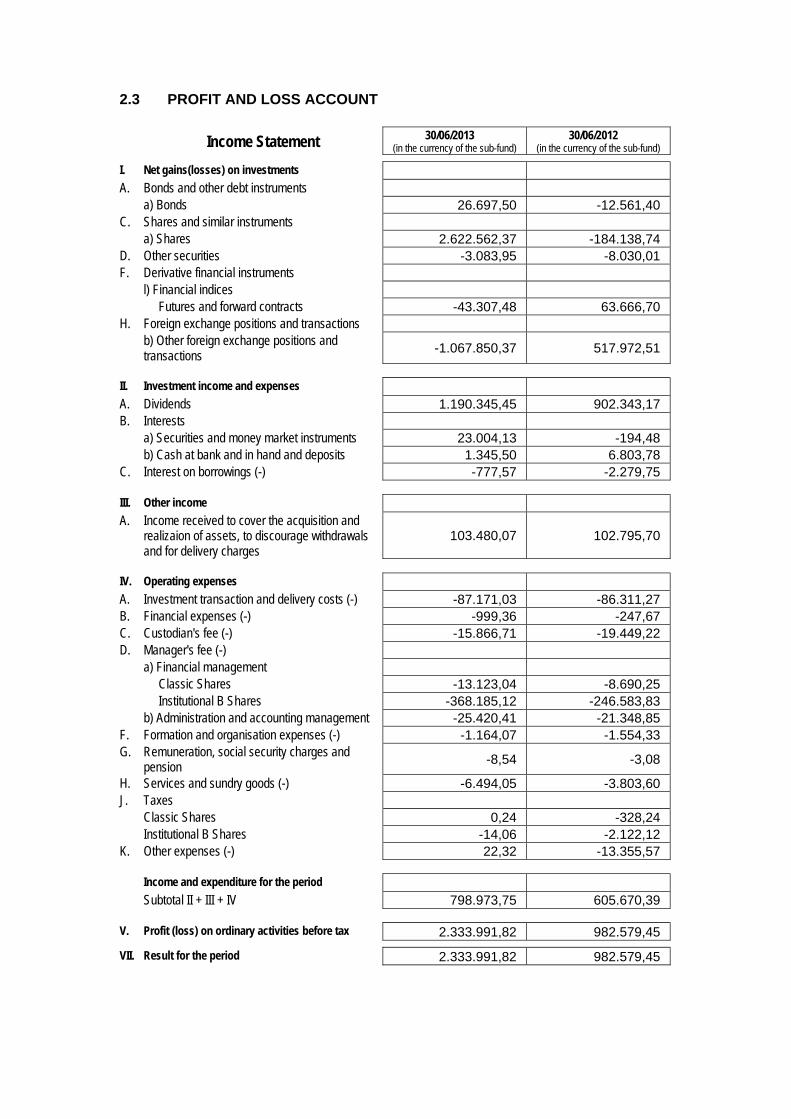

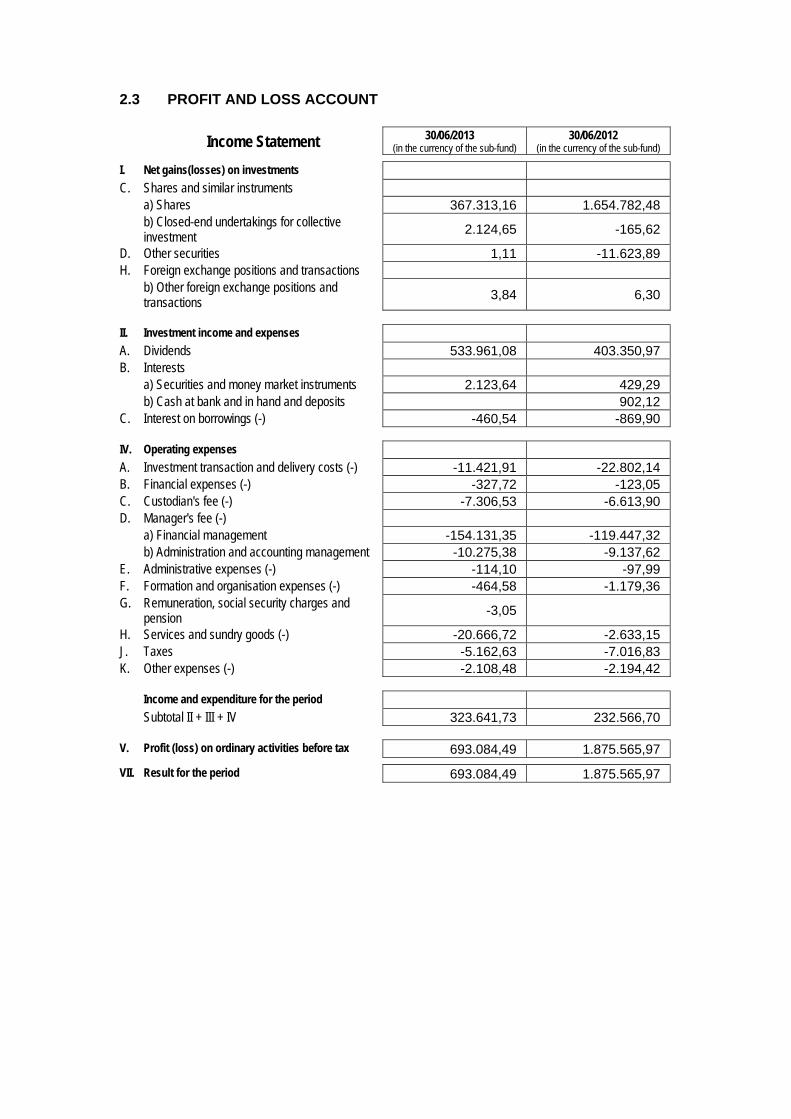

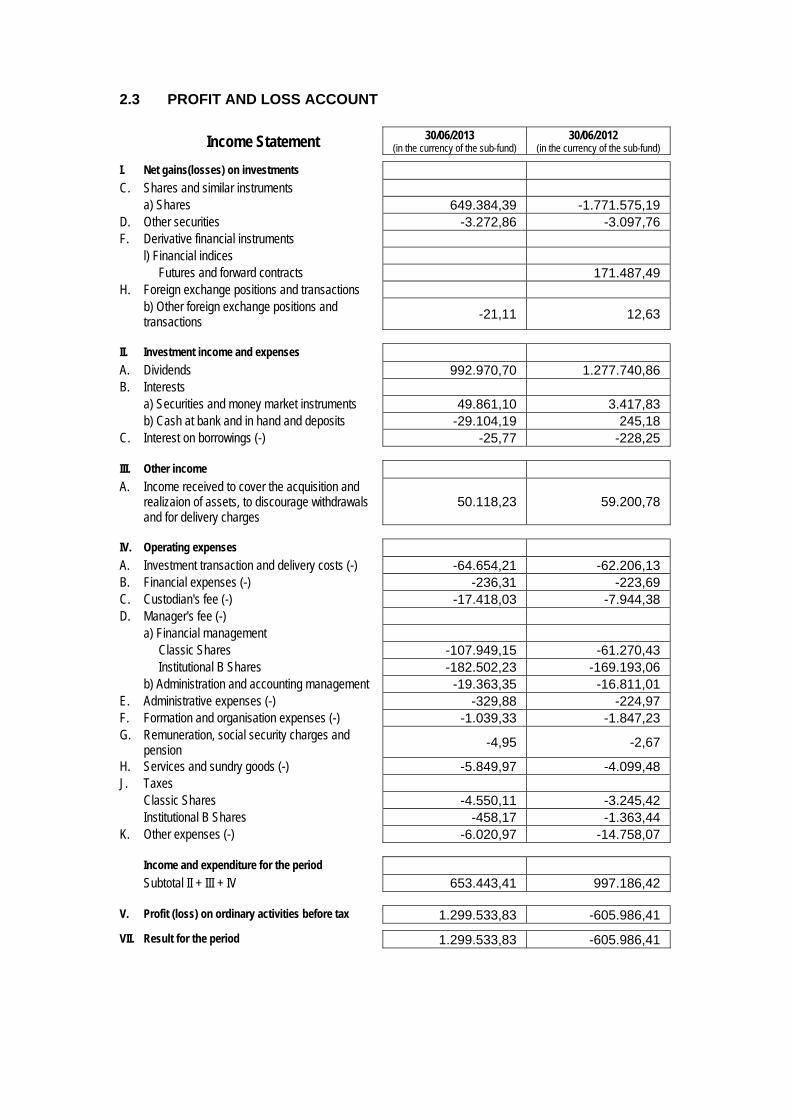

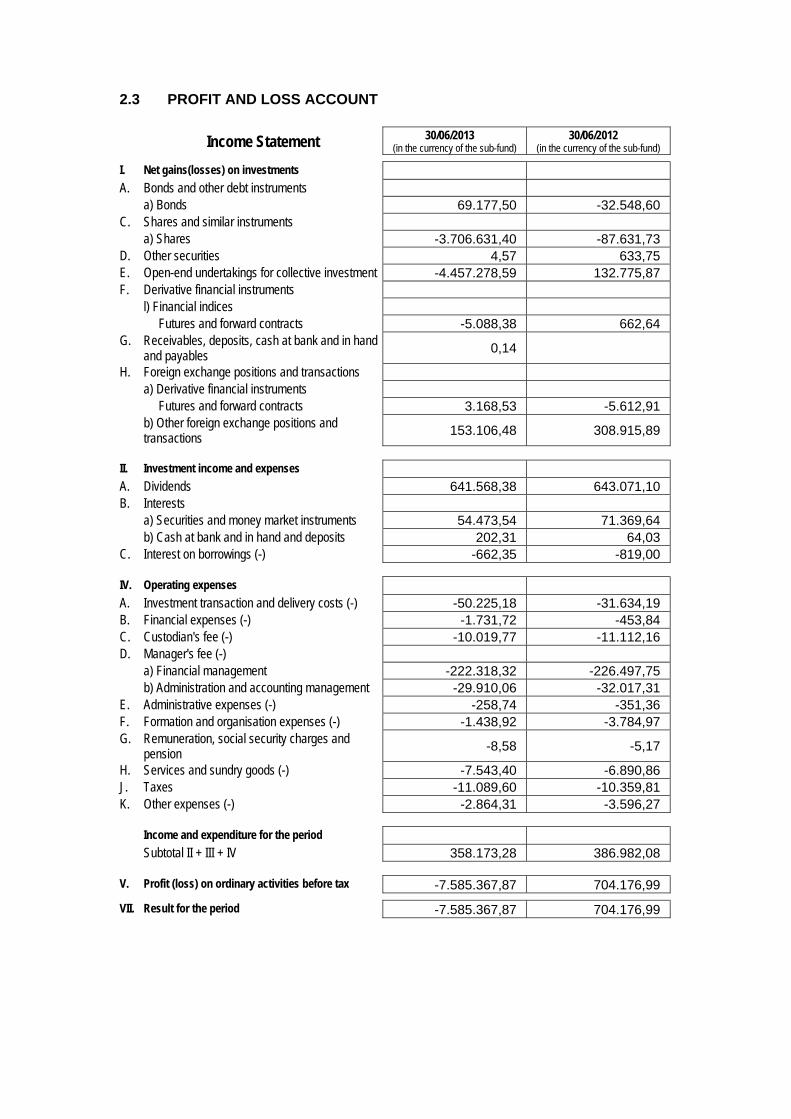

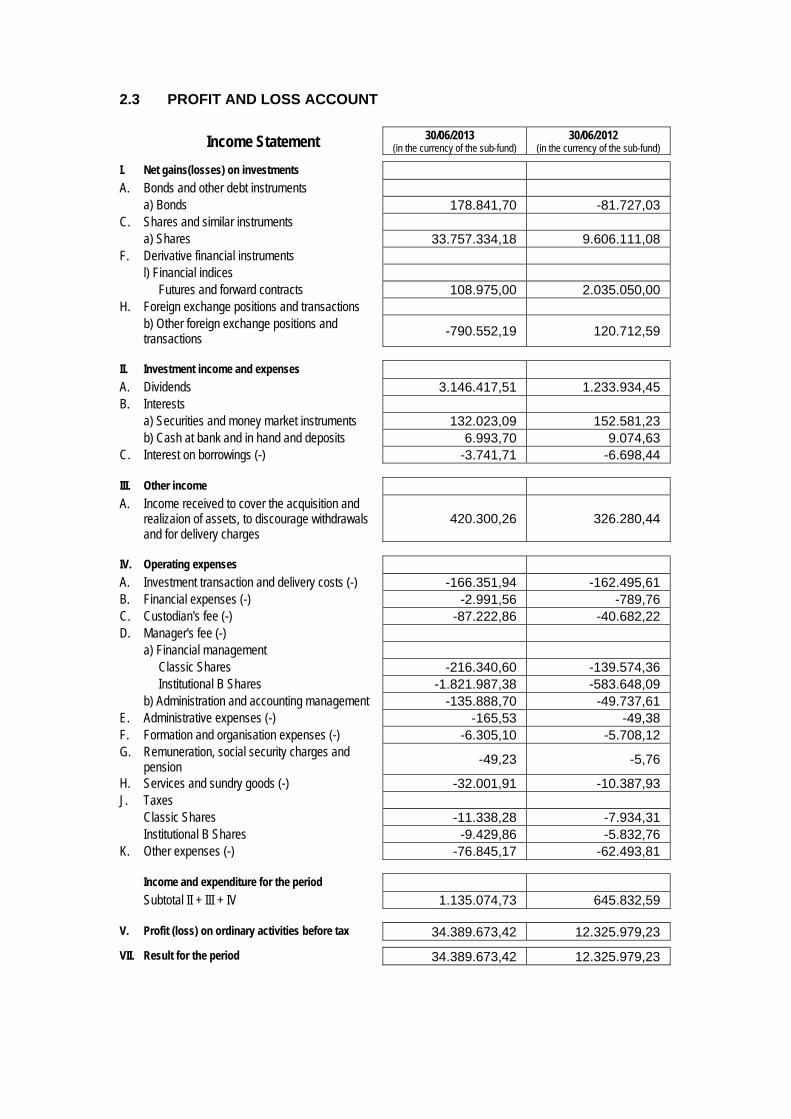

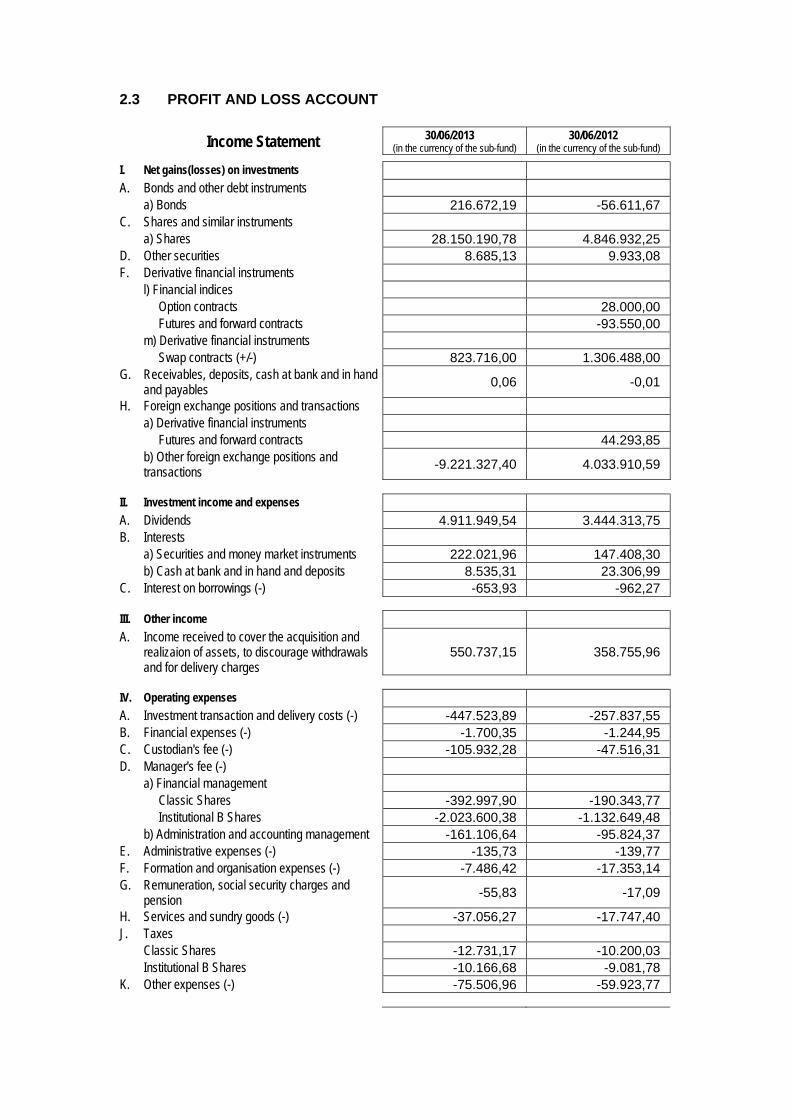

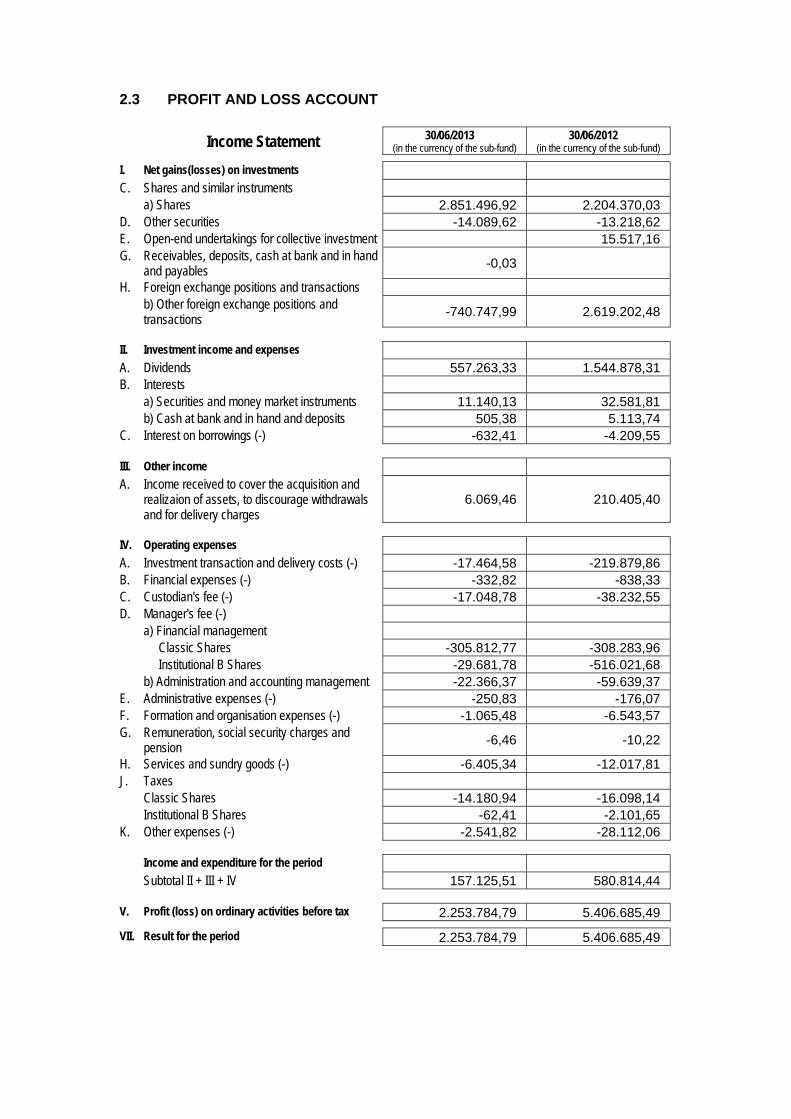

2.3 PROFIT AND LOSS ACCOUNT

Income Statement 30/06/2013 (in the currency of the sub-fund)

I. Net gains(losses) on investments C. Shares and similar instruments a) Shares 23.068.937,97 H. Foreign exchange positions and transactions a) Derivative financial instruments Futures and forward contracts -1.096.319,23 b) Other foreign exchange positions and

transactions -3.597.195,56

II. Investment income and expenses A. Dividends 5.842.955,07 B. Interests a) Securities and money market instruments 35.162,63 b) Cash at bank and in hand and deposits 4.259,29 C. Interest on borrowings (-) -7.344,52

IV. Operating expenses A. Investment transaction and delivery costs (-) -709.263,04 B. Financial expenses (-) -1.470,27 C. Custodian's fee (-) -62.324,38 D. Manager's fee (-) a) Financial management -2.122.604,52 b) Administration and accounting management -141.507,29 F. Formation and organisation expenses (-) -5.605,70 H. Services and sundry goods (-) -29.535,49 J. Taxes -732,05 K. Other expenses (-) -107.844,19

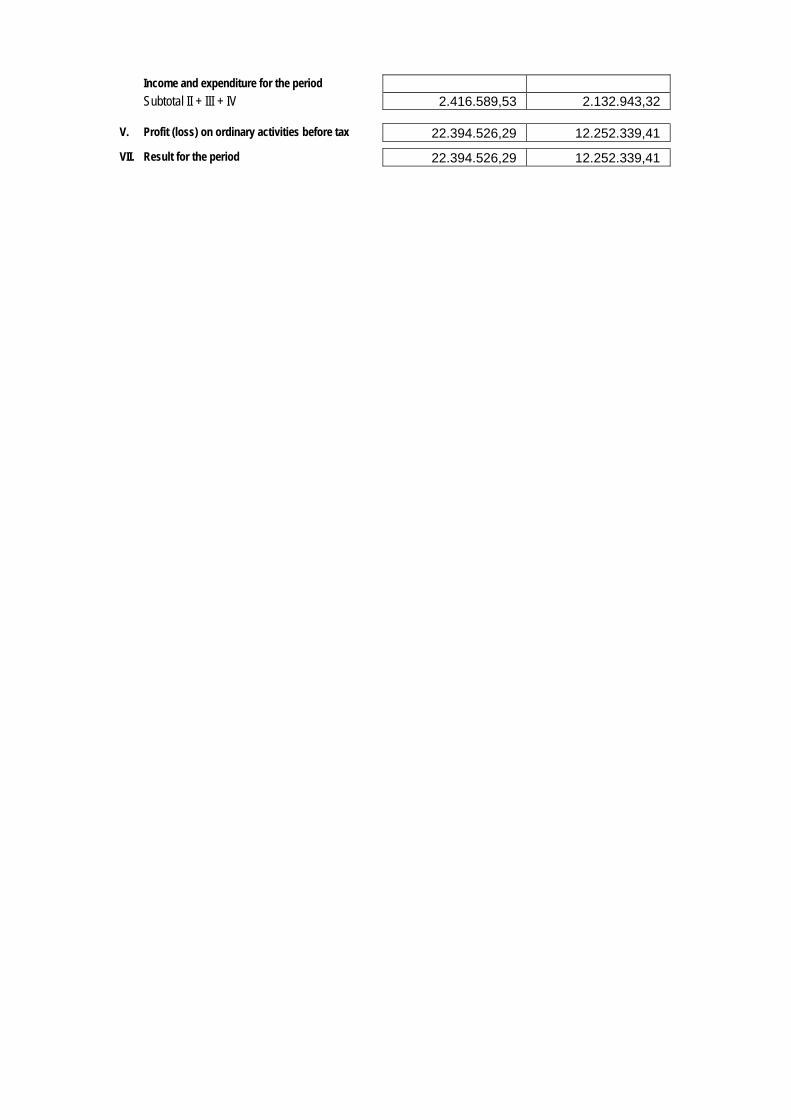

Income and expenditure for the period Subtotal II + III + IV 2.694.145,54

V. Profit (loss) on ordinary activities before tax 21.069.568,72

VII. Result for the period 21.069.568,72

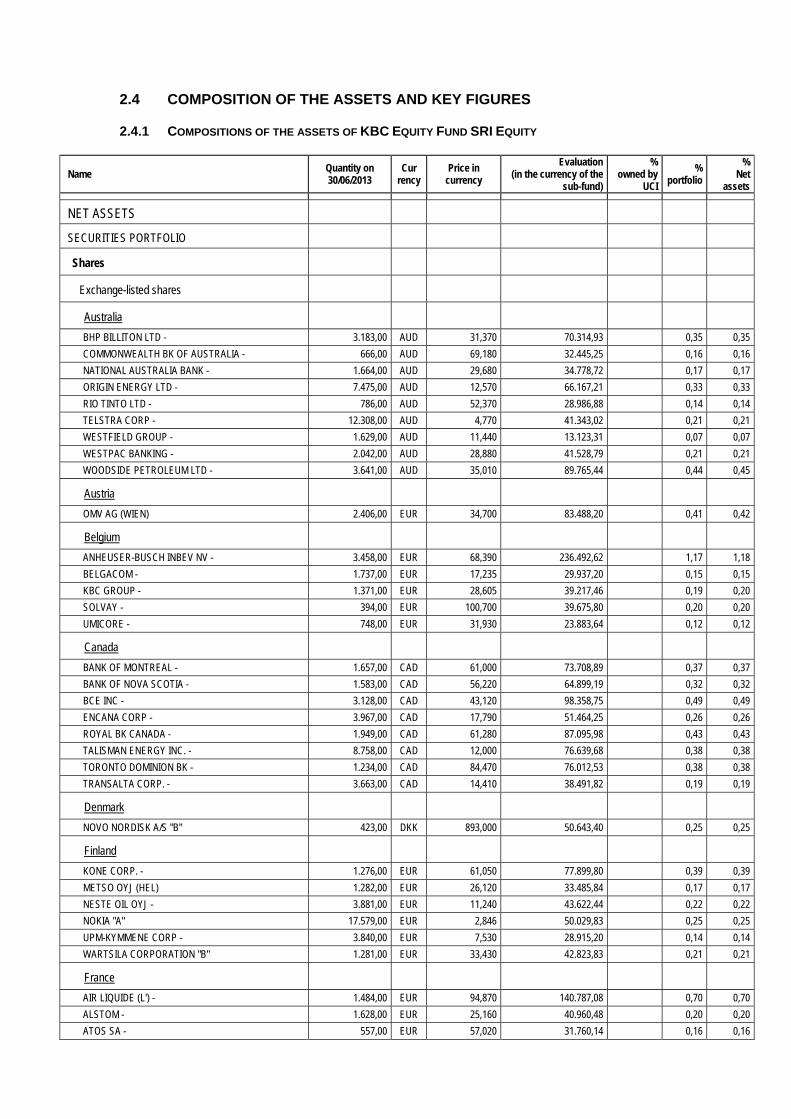

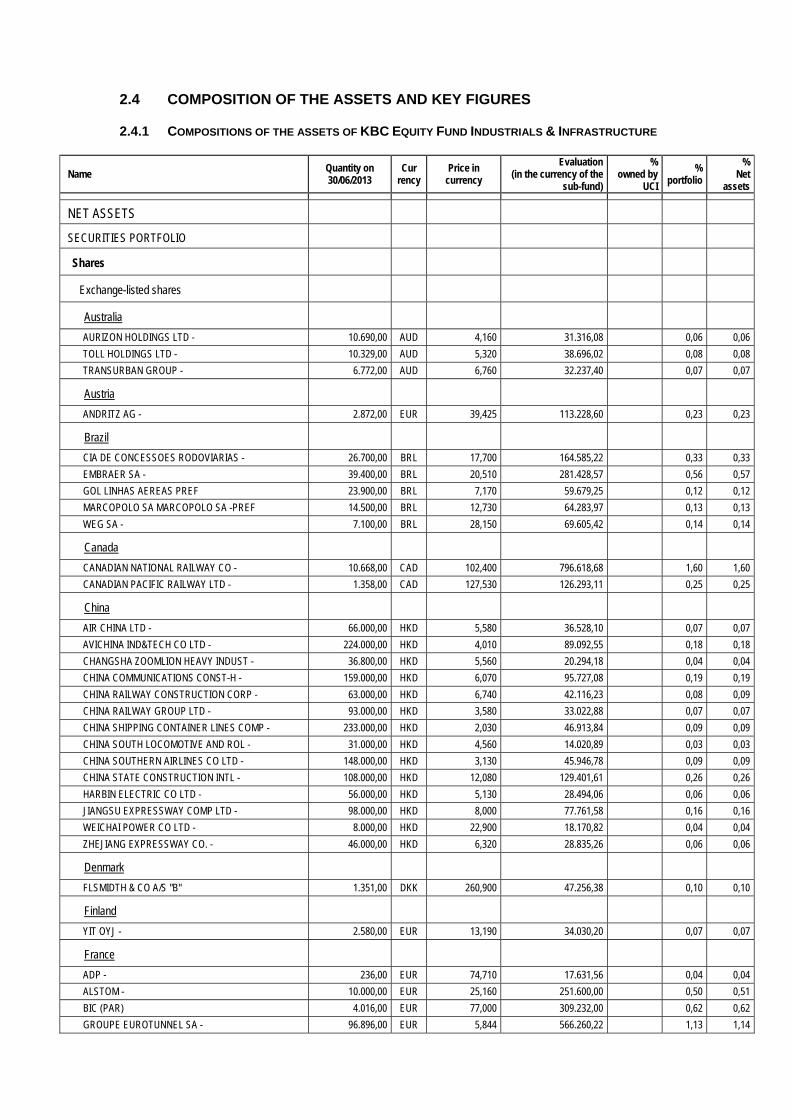

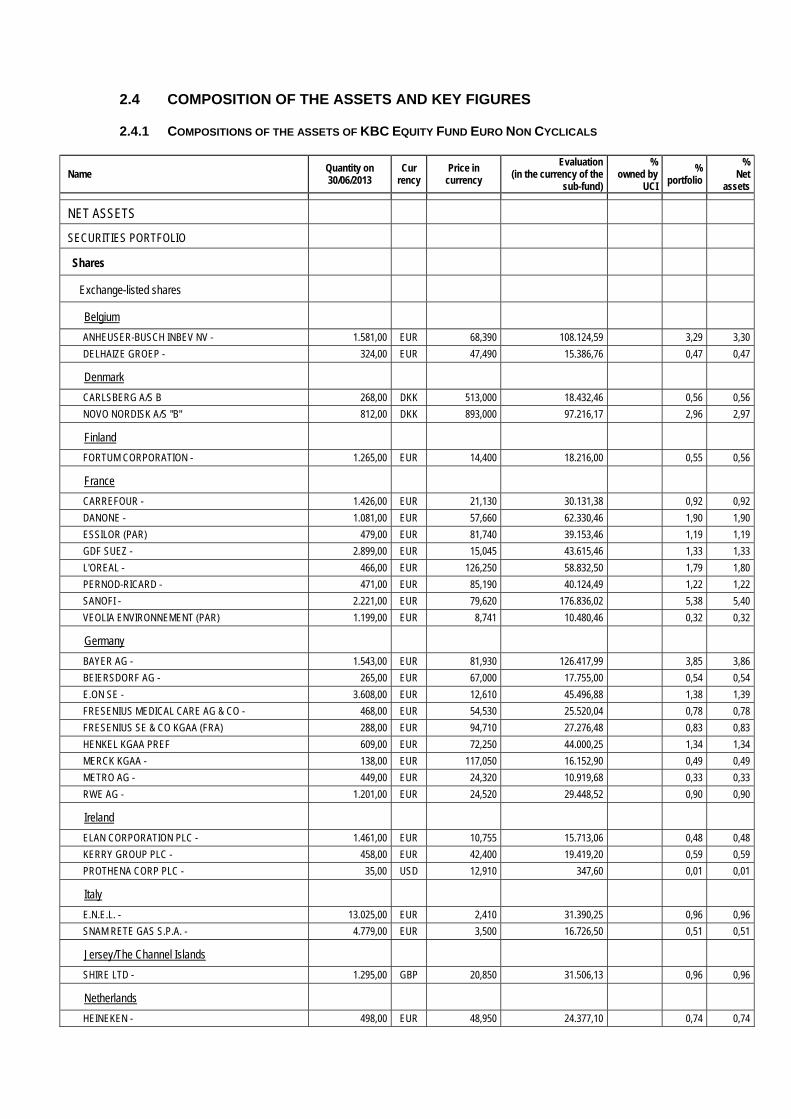

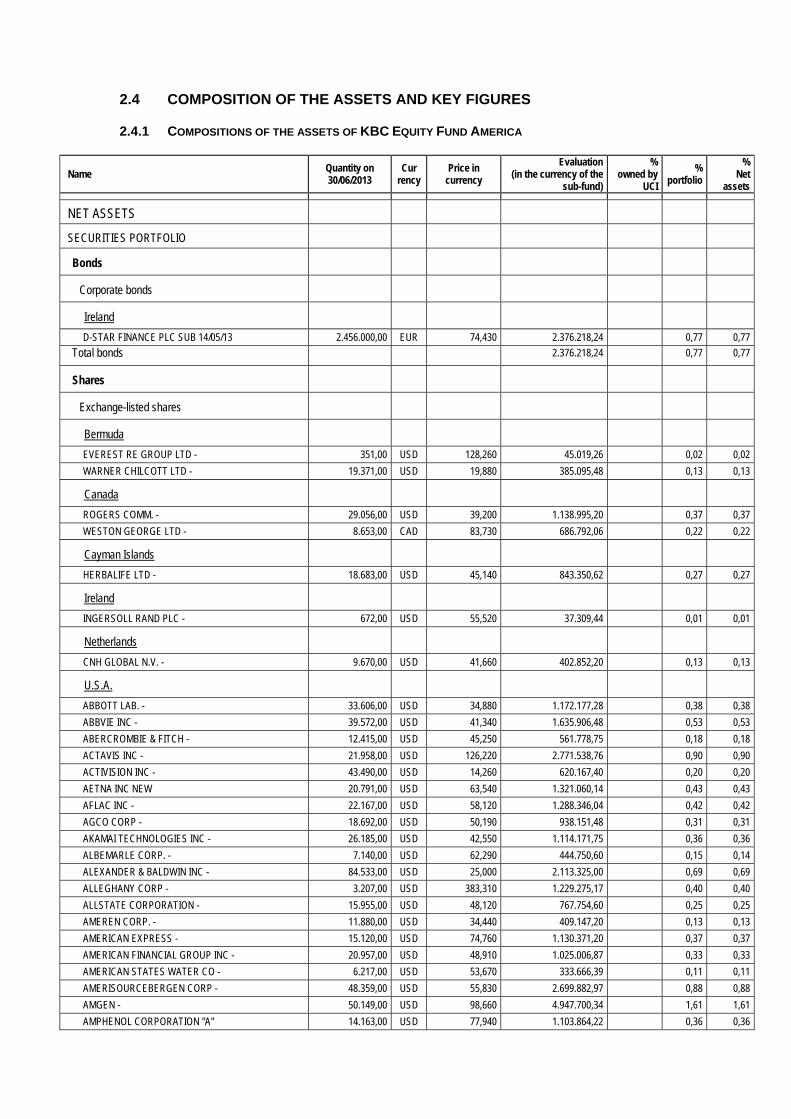

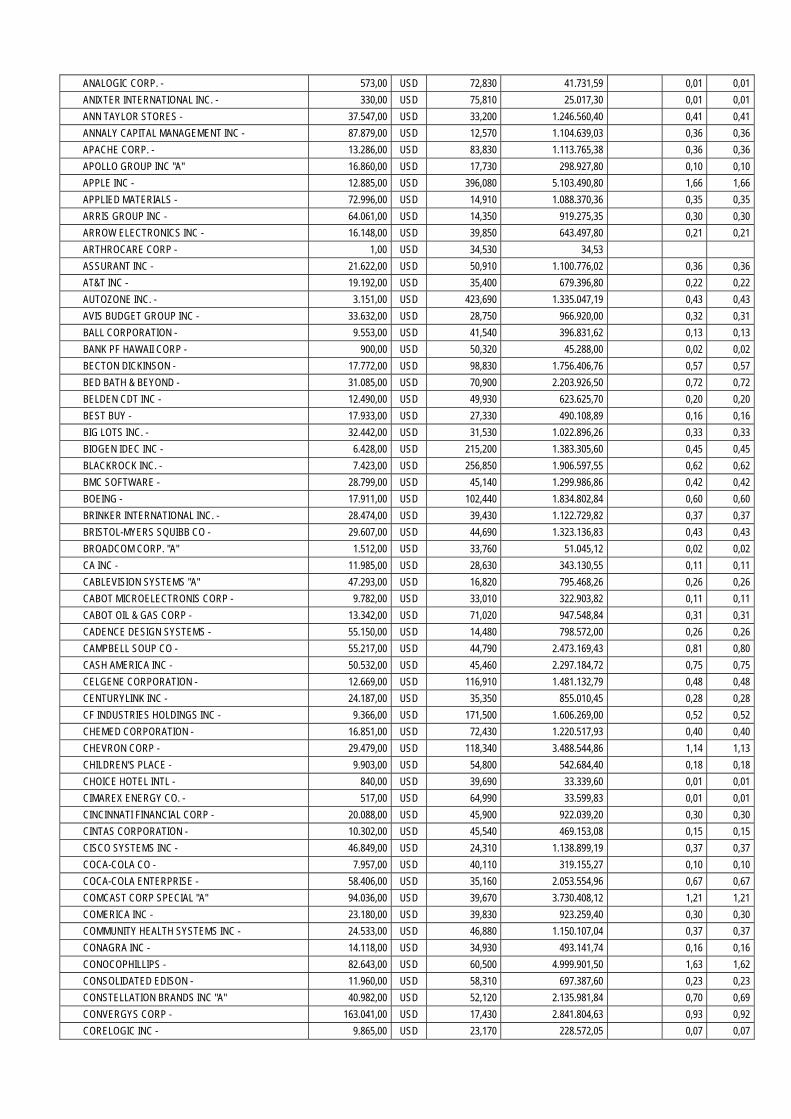

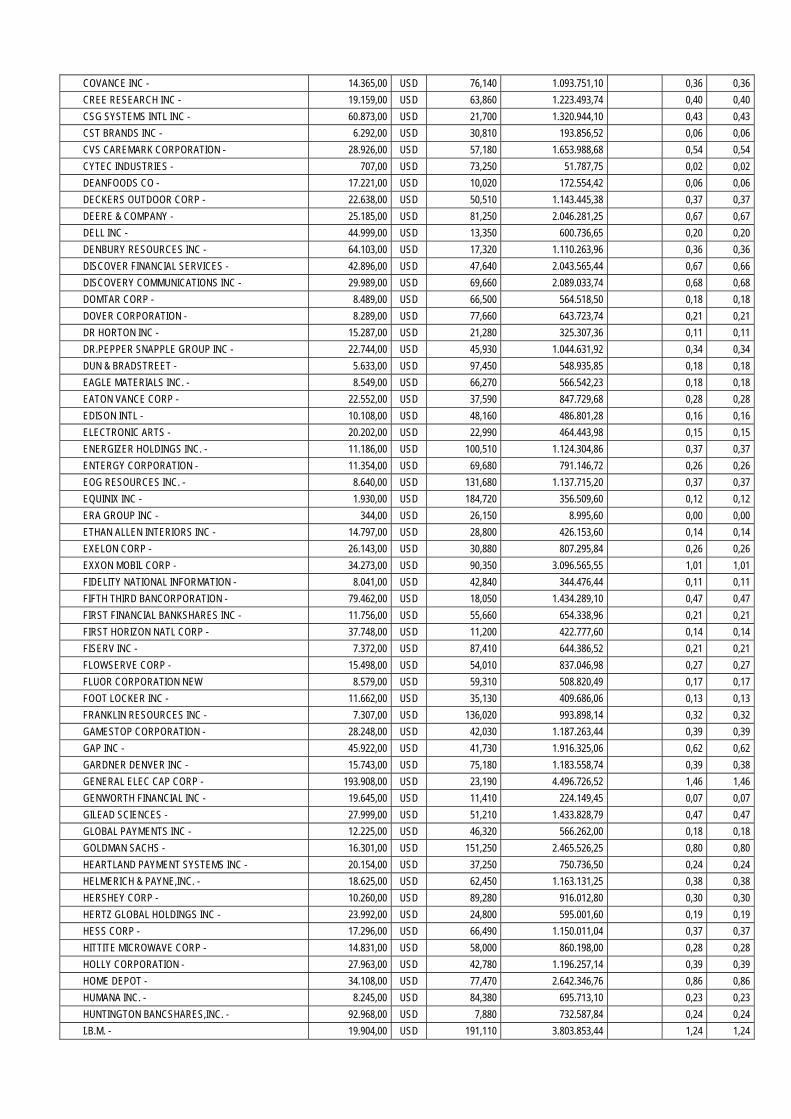

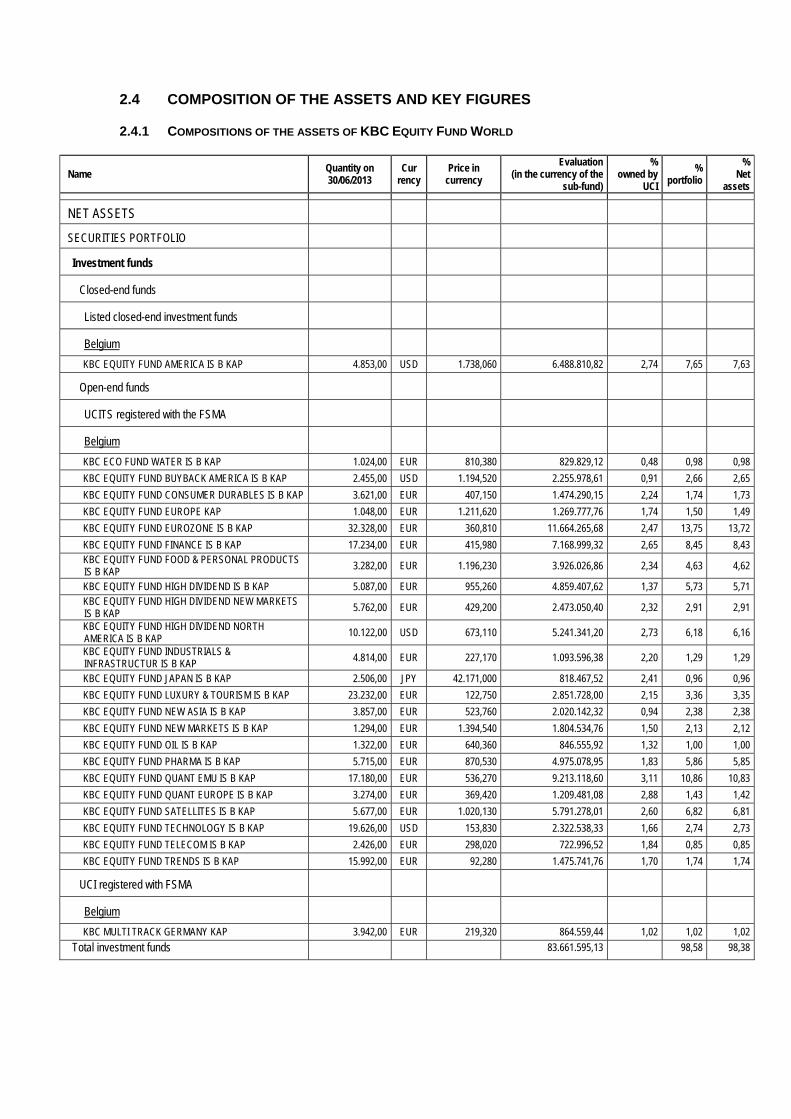

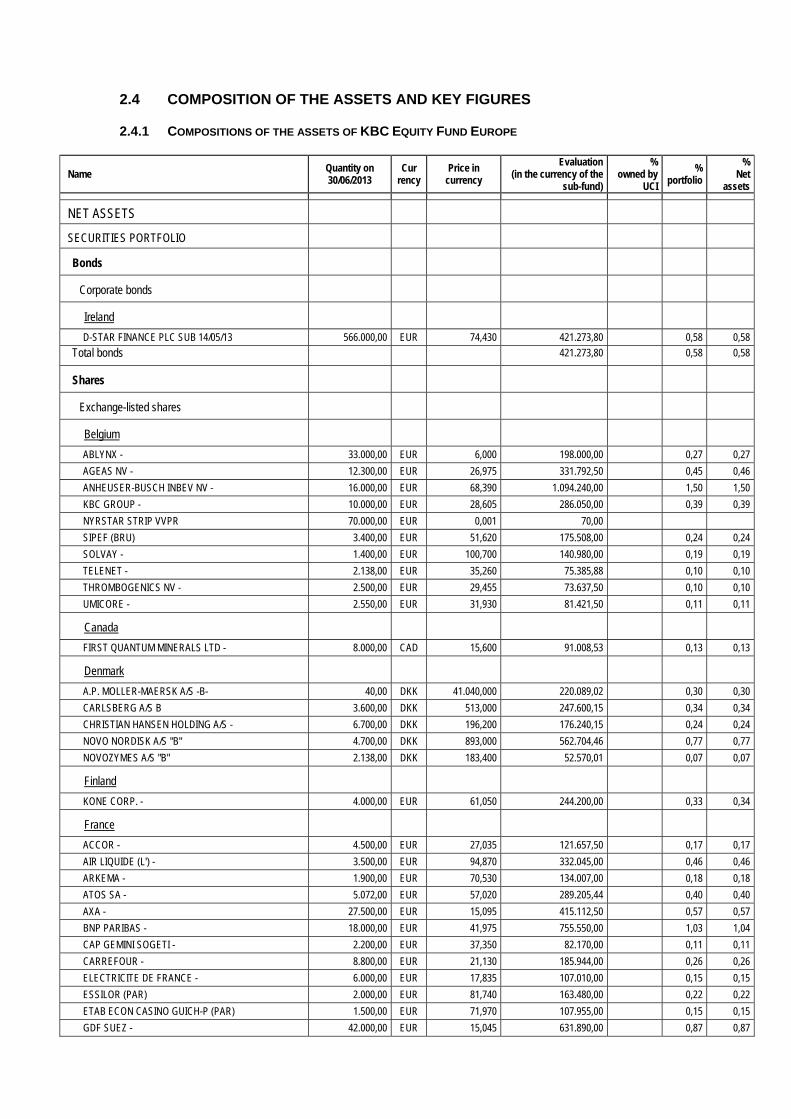

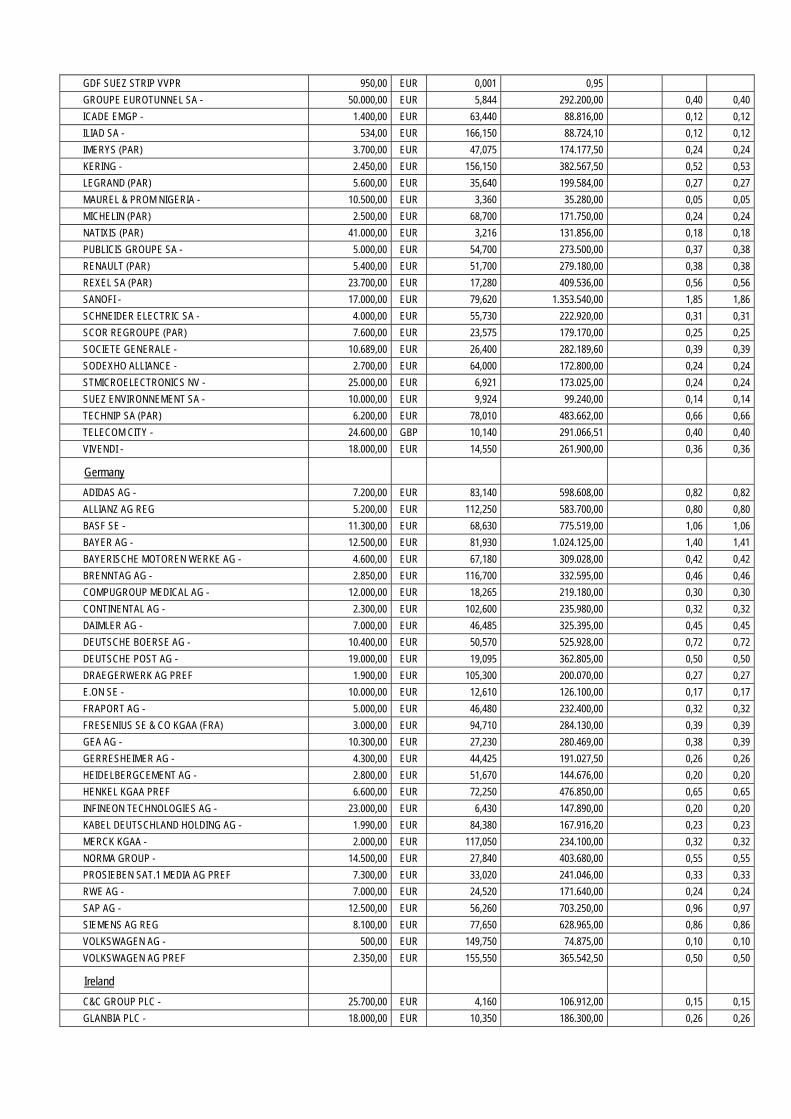

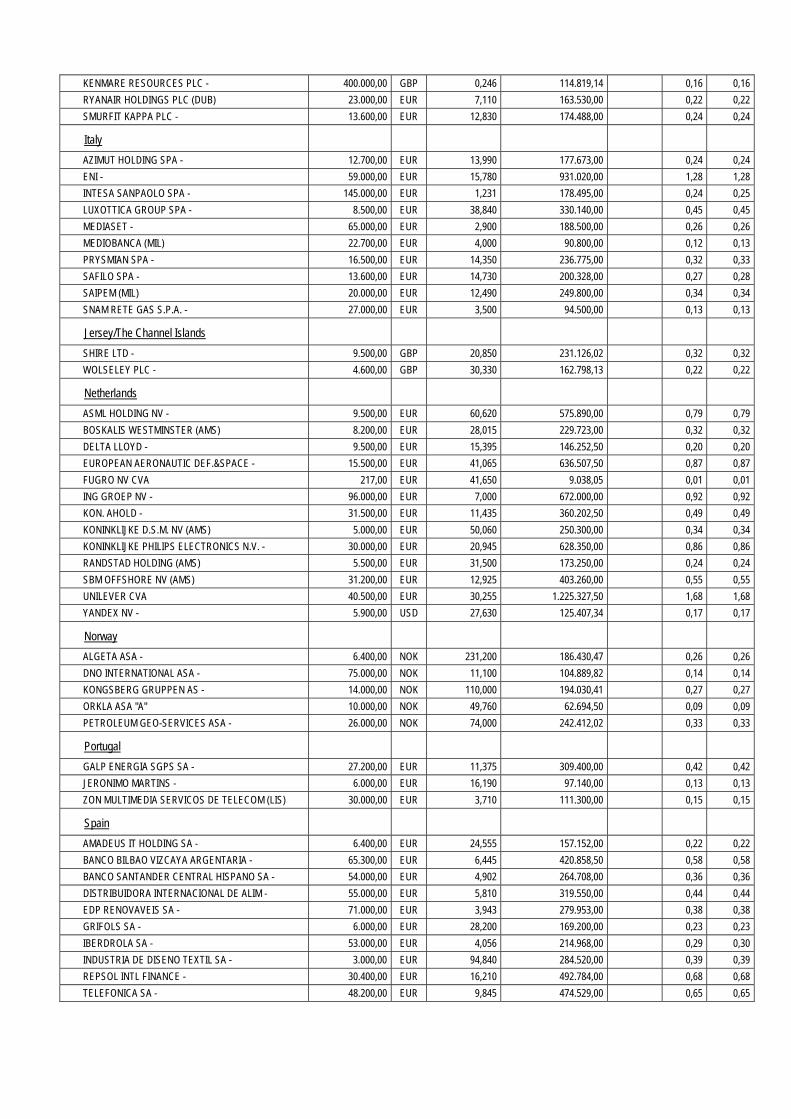

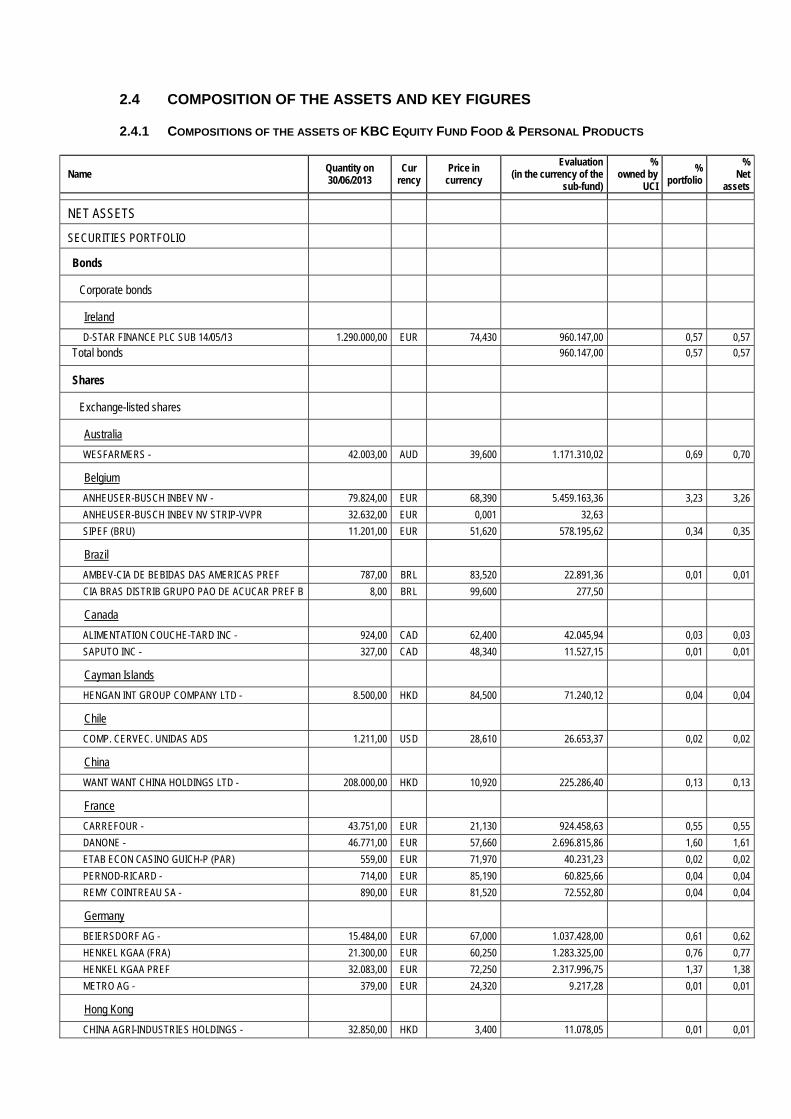

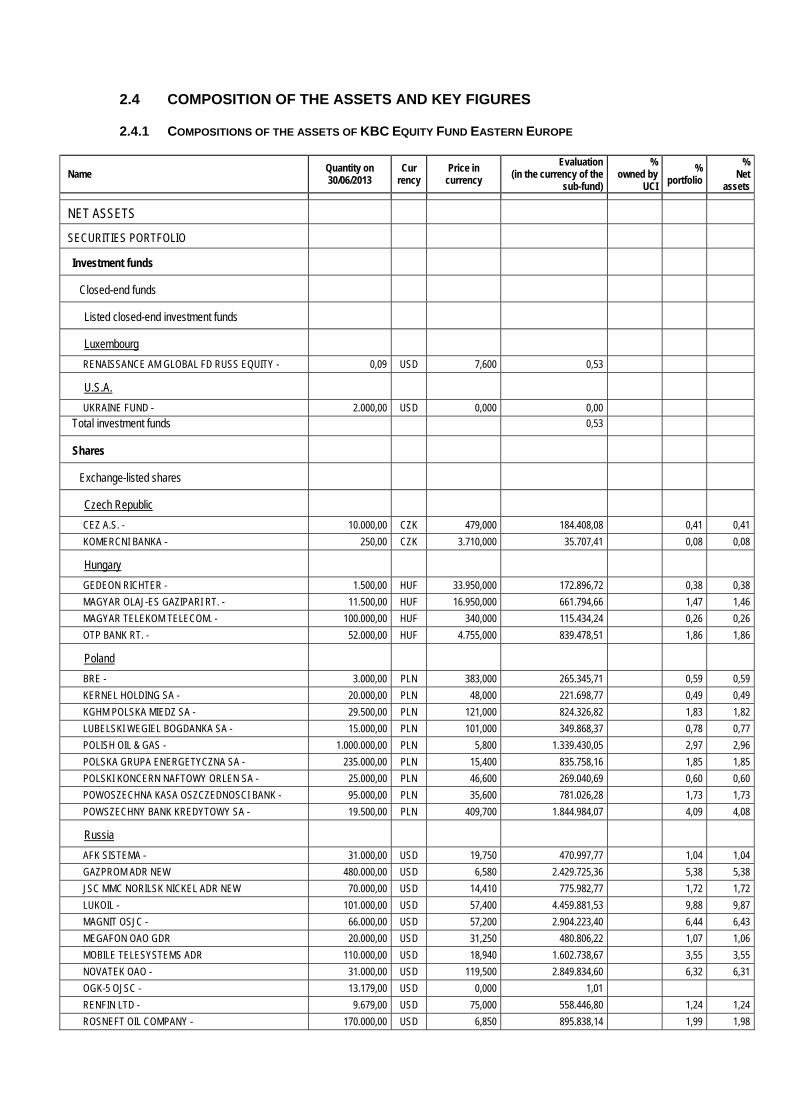

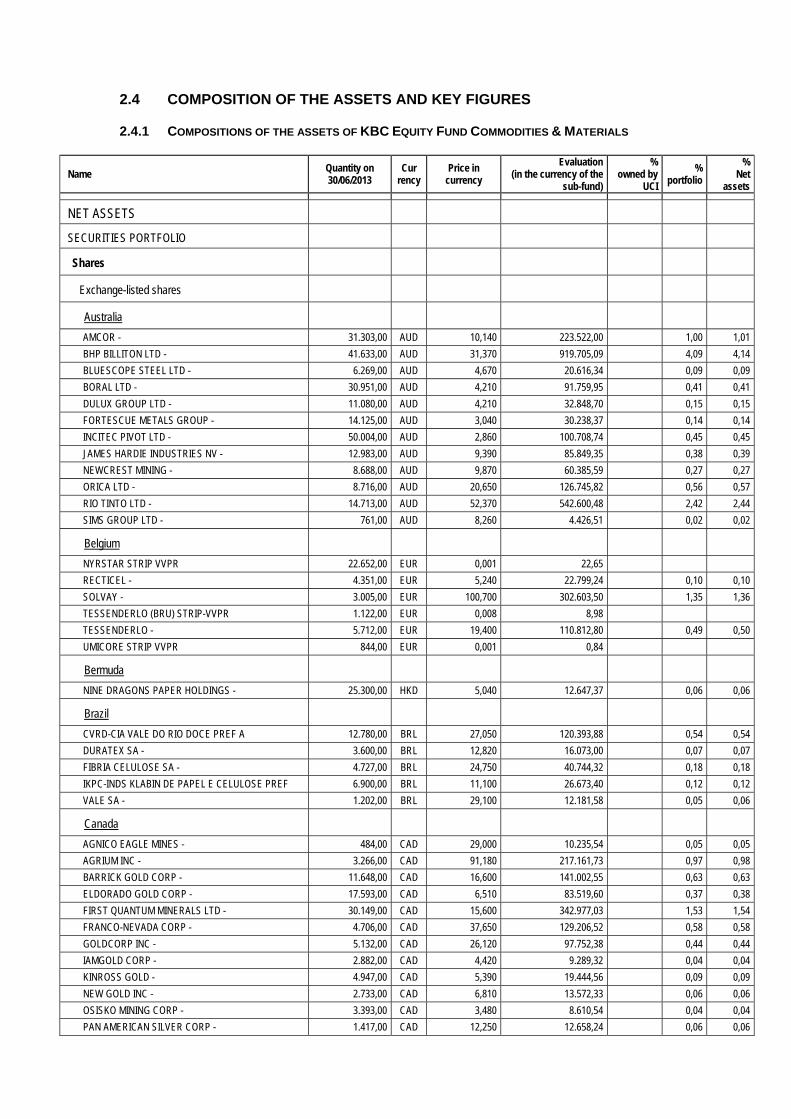

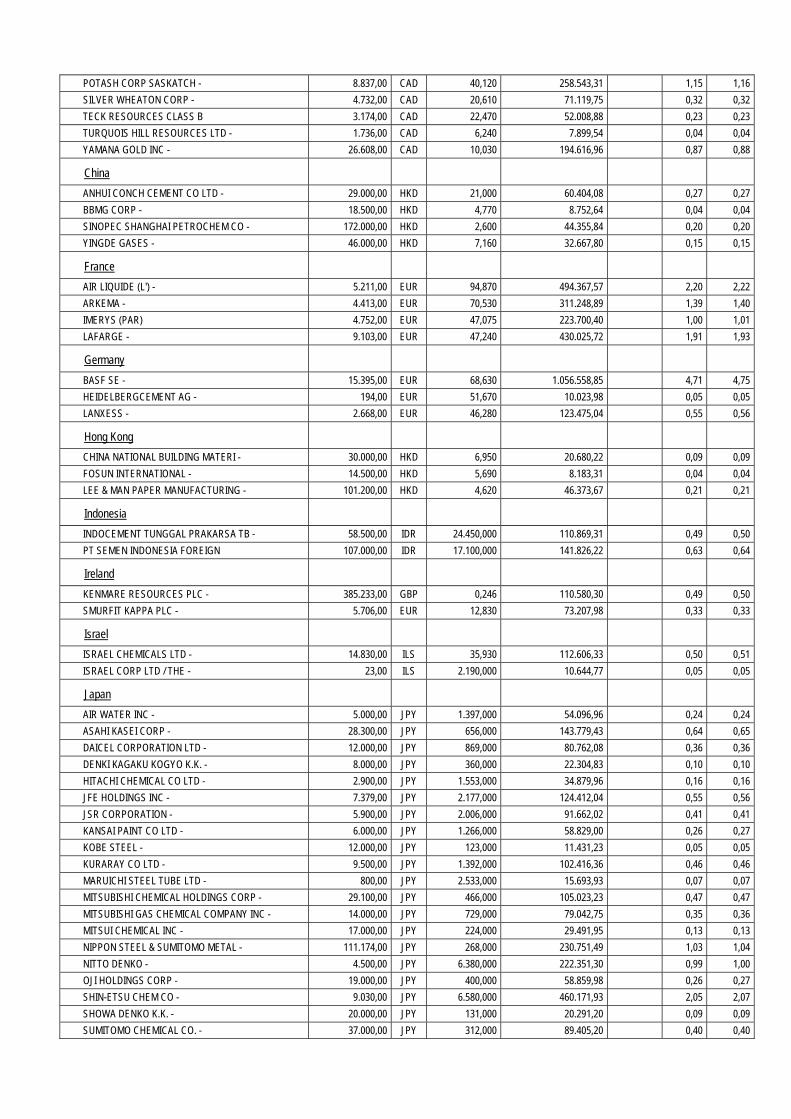

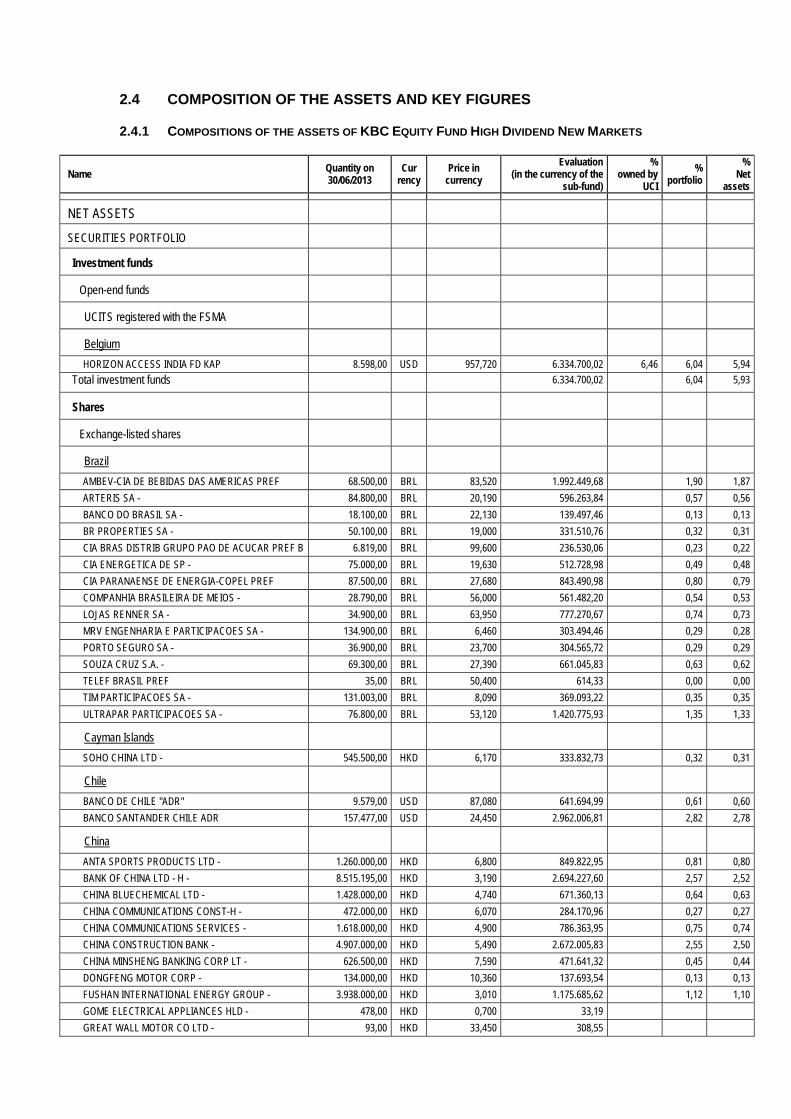

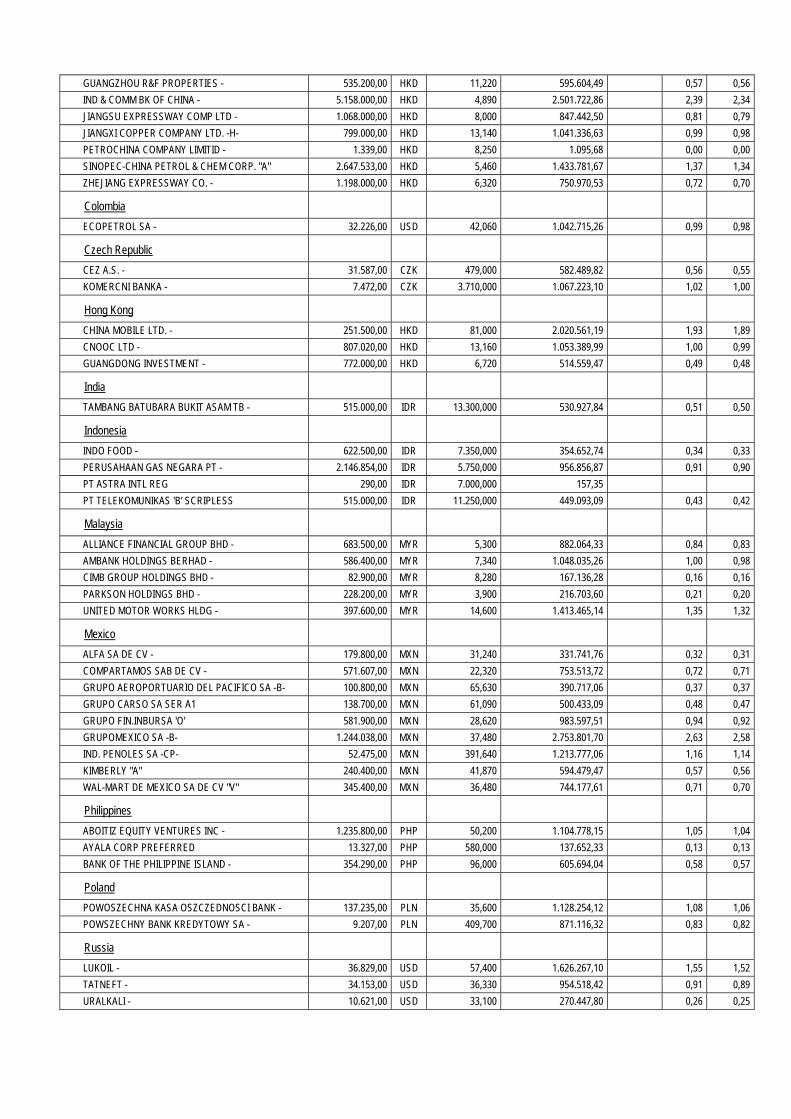

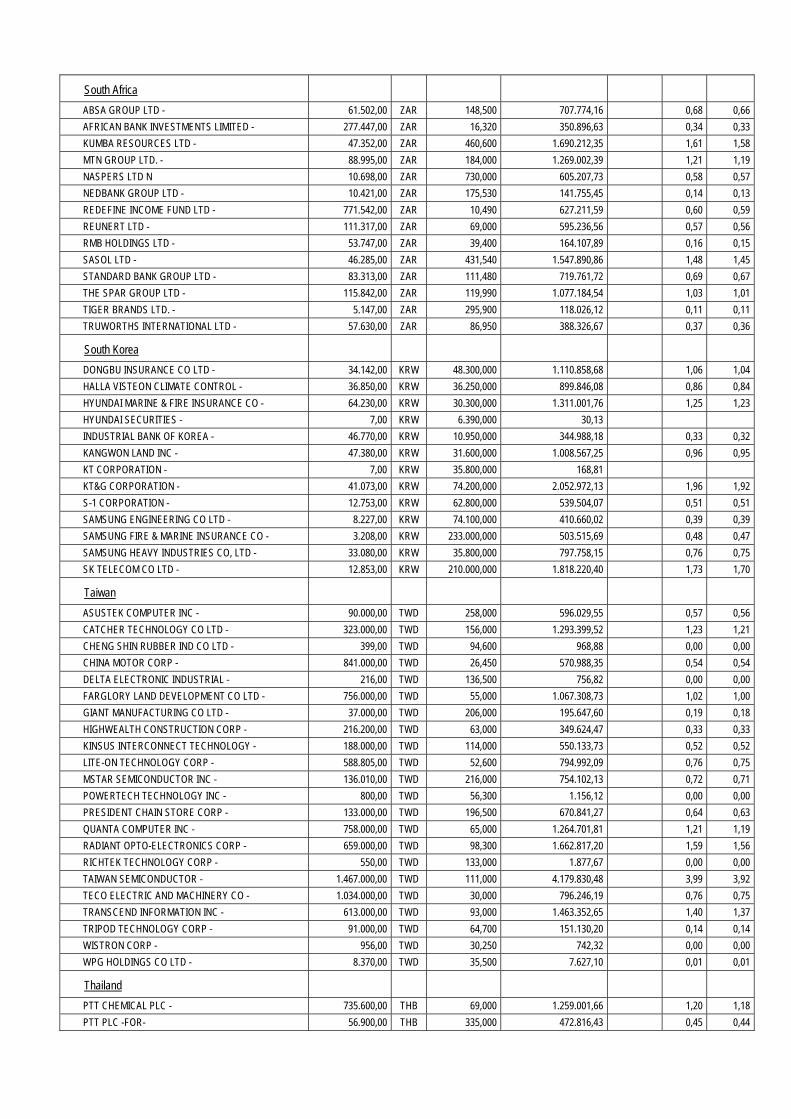

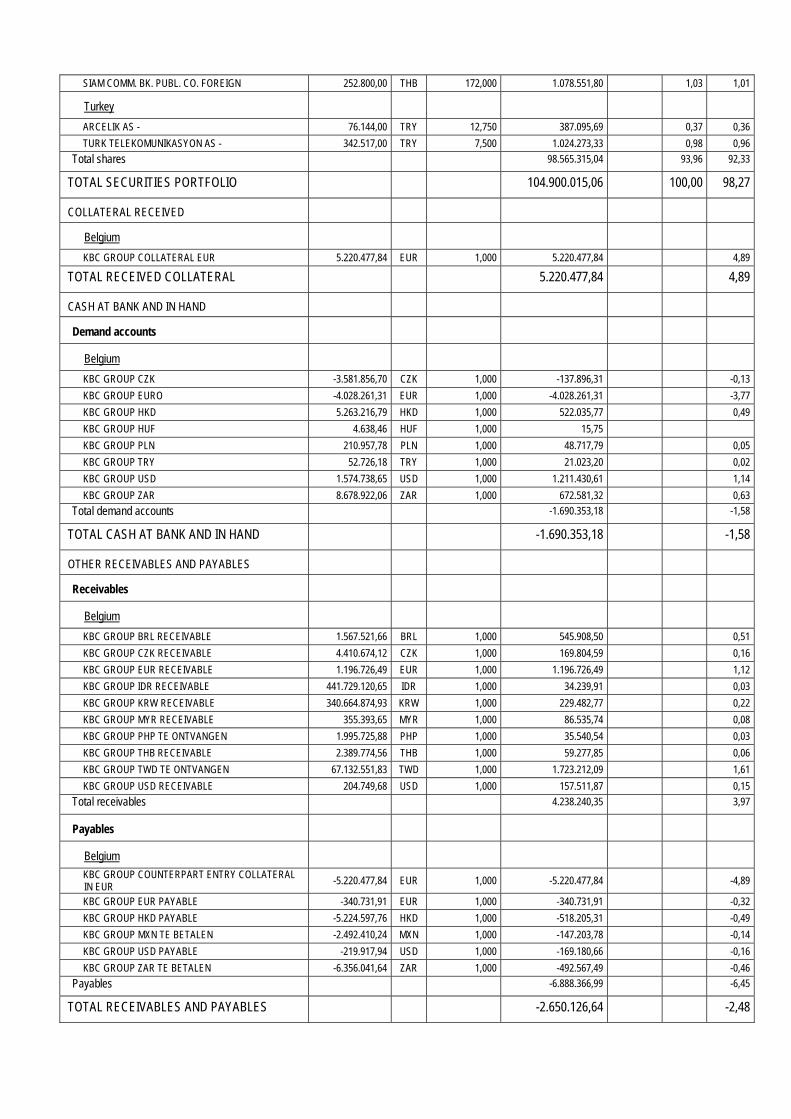

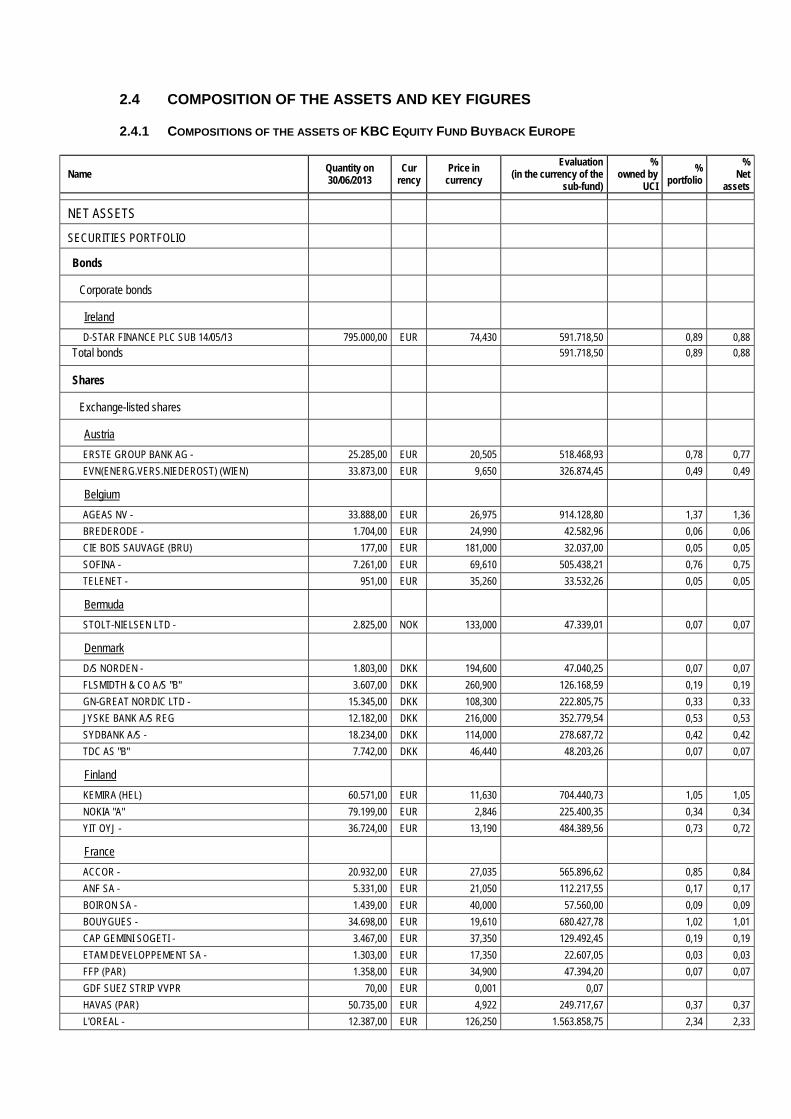

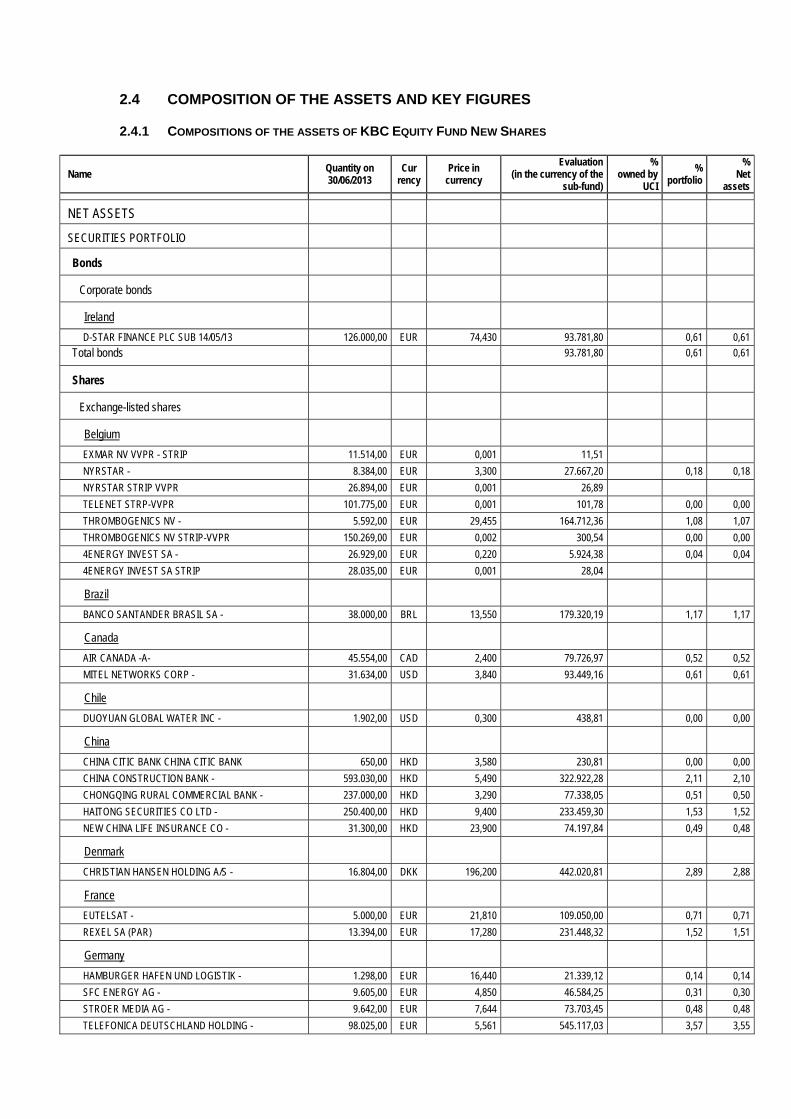

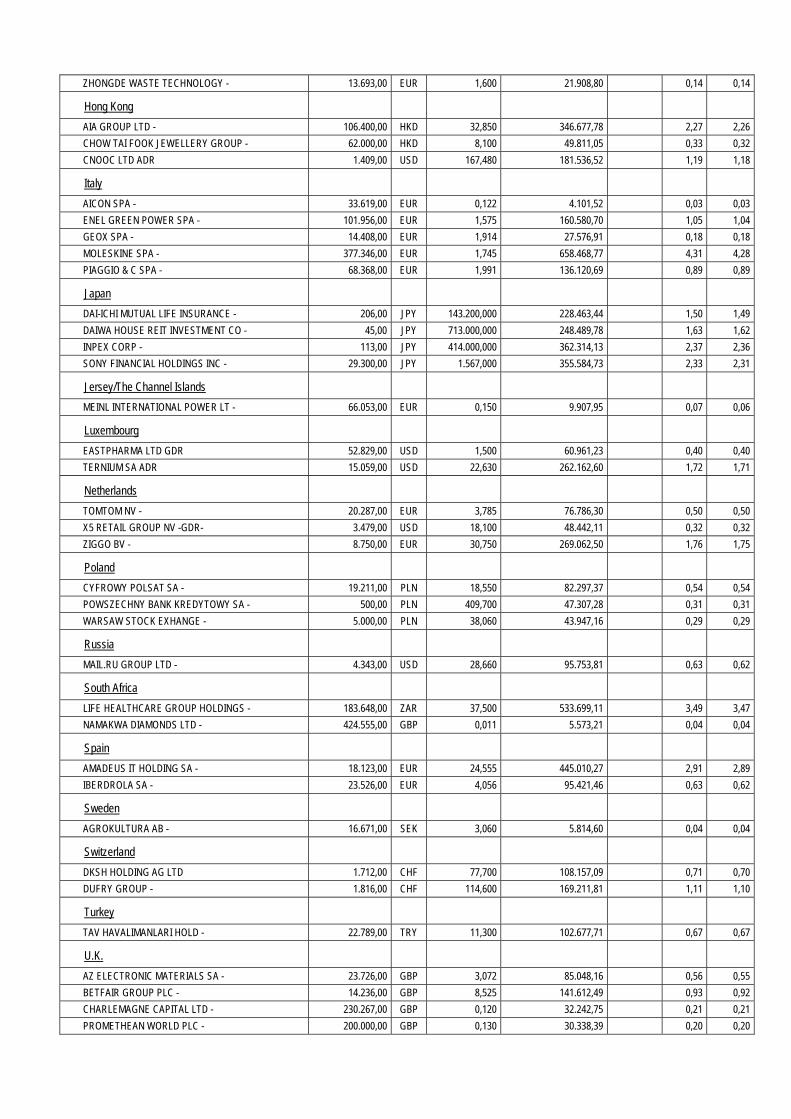

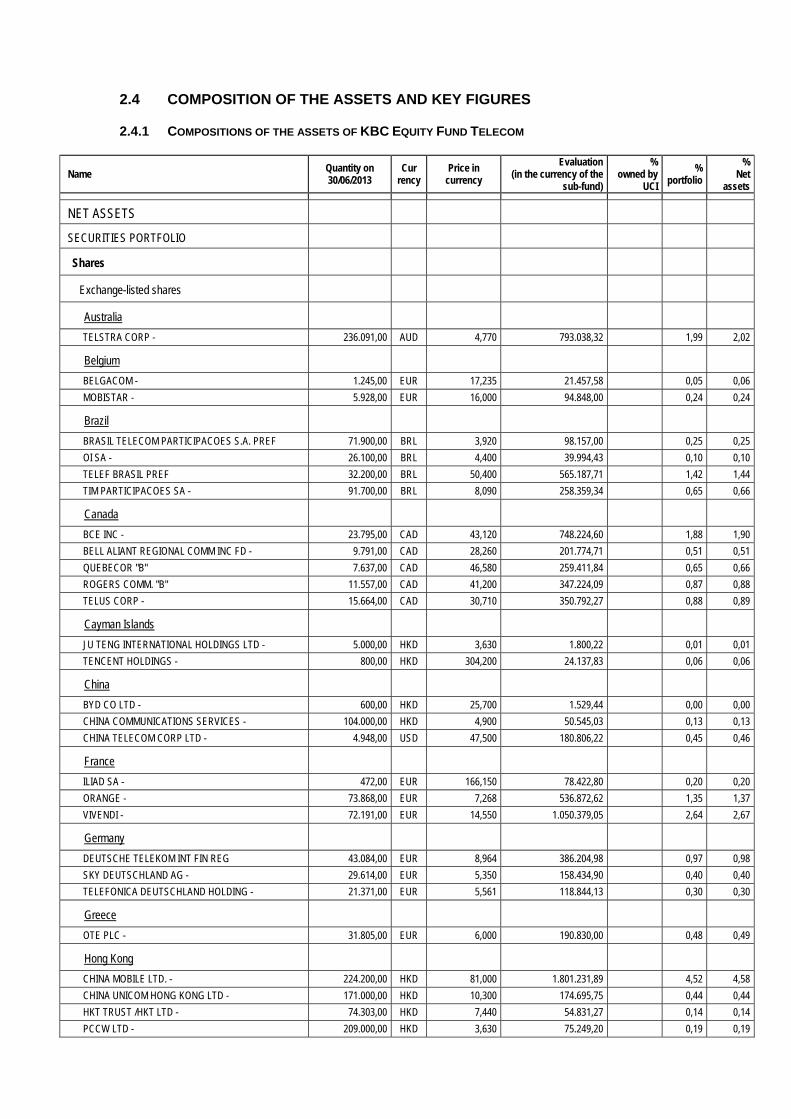

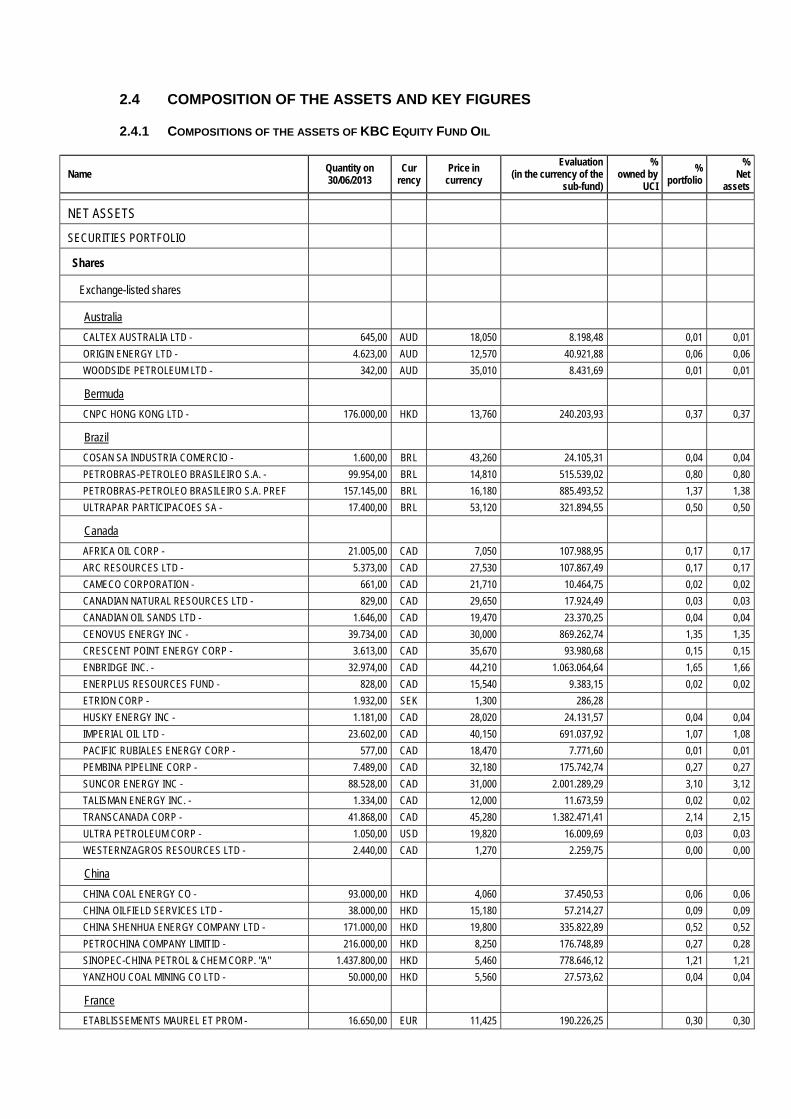

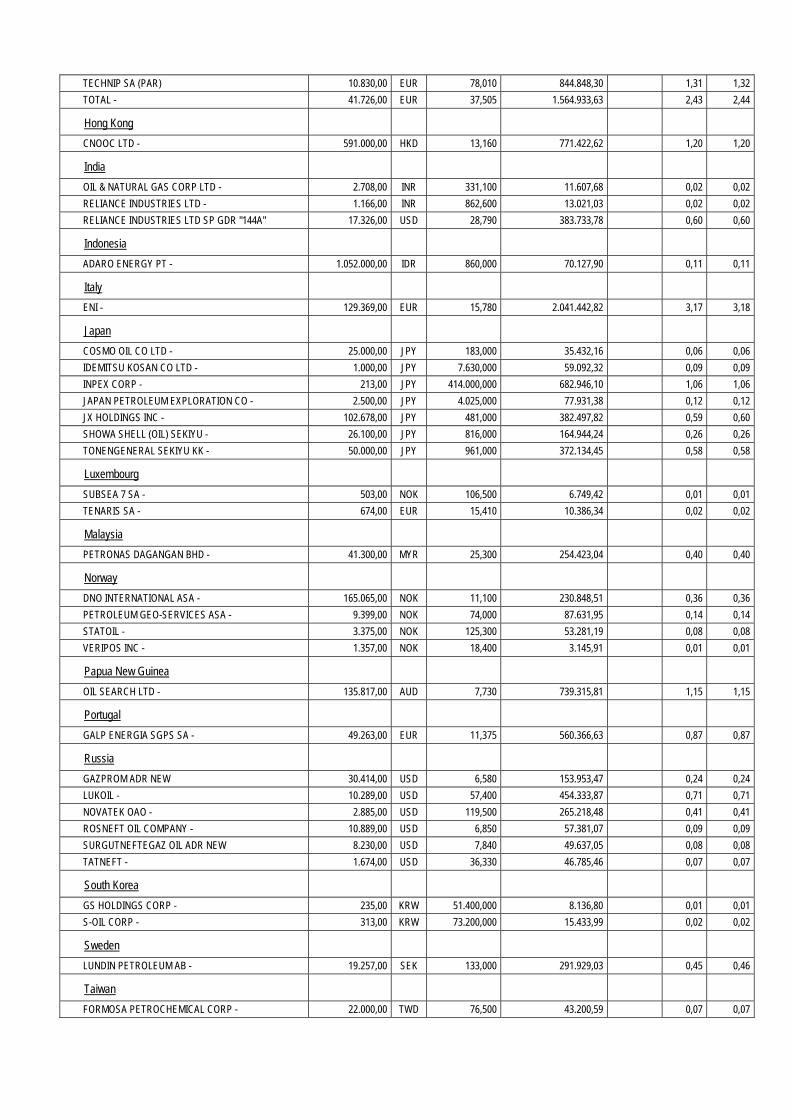

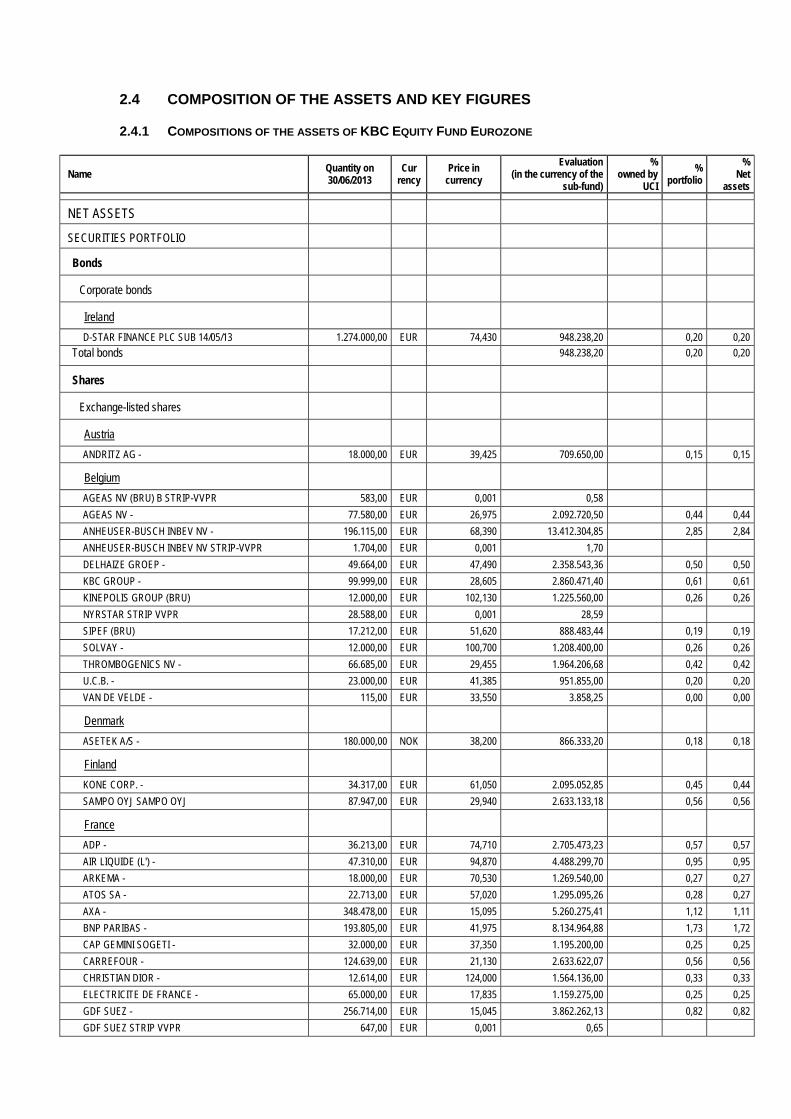

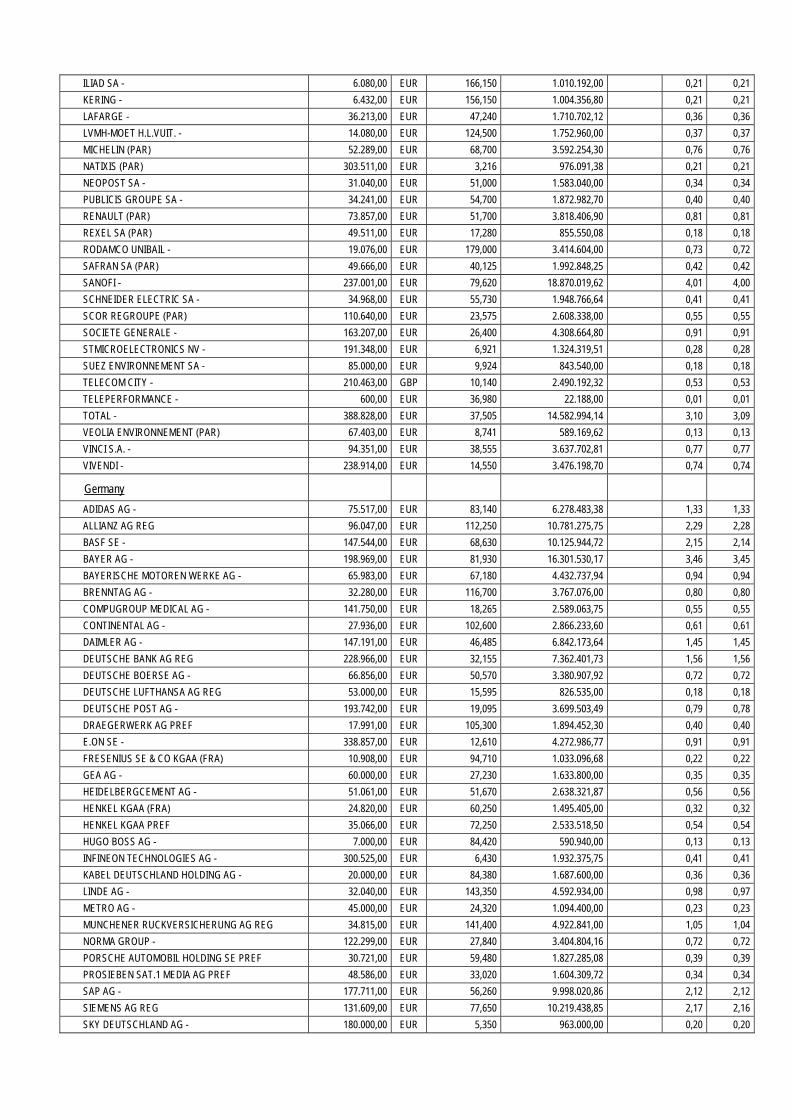

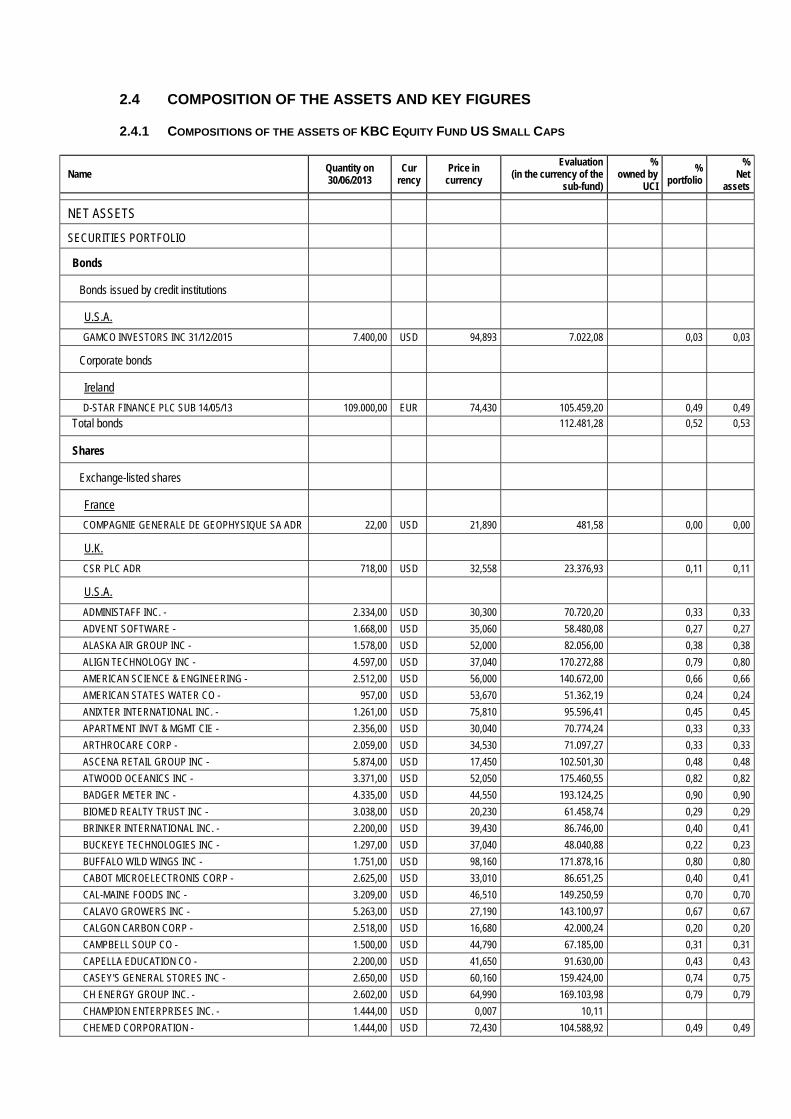

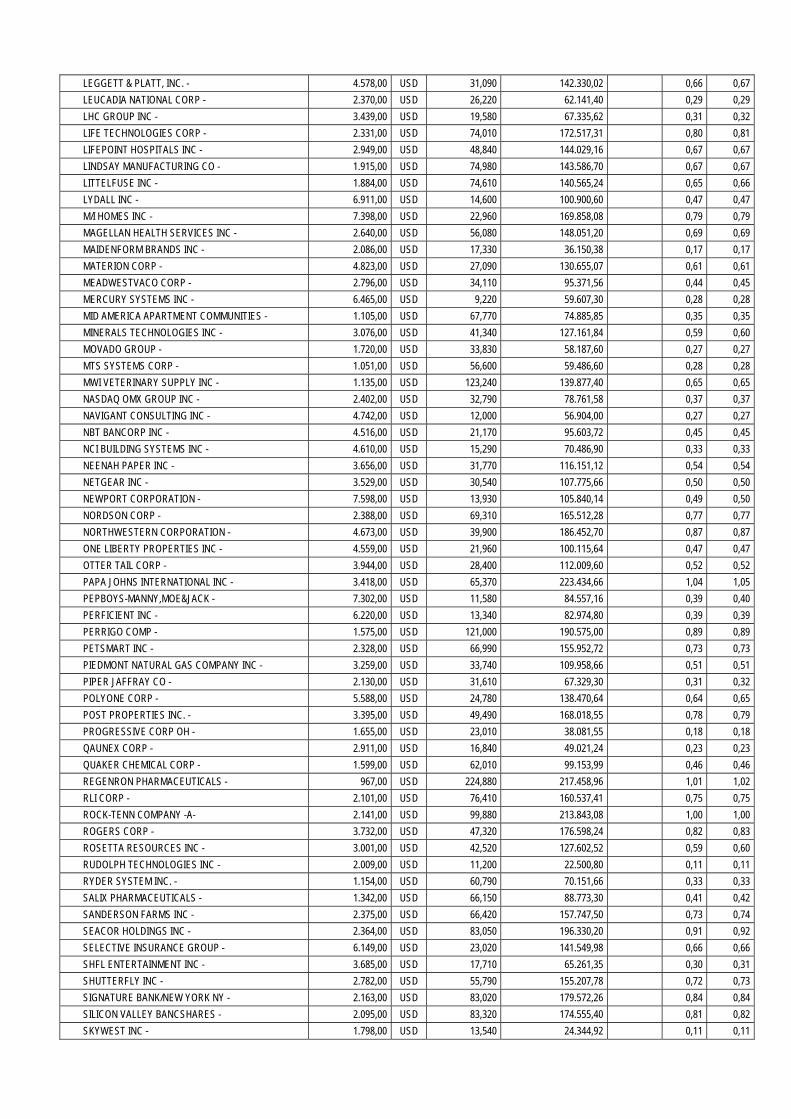

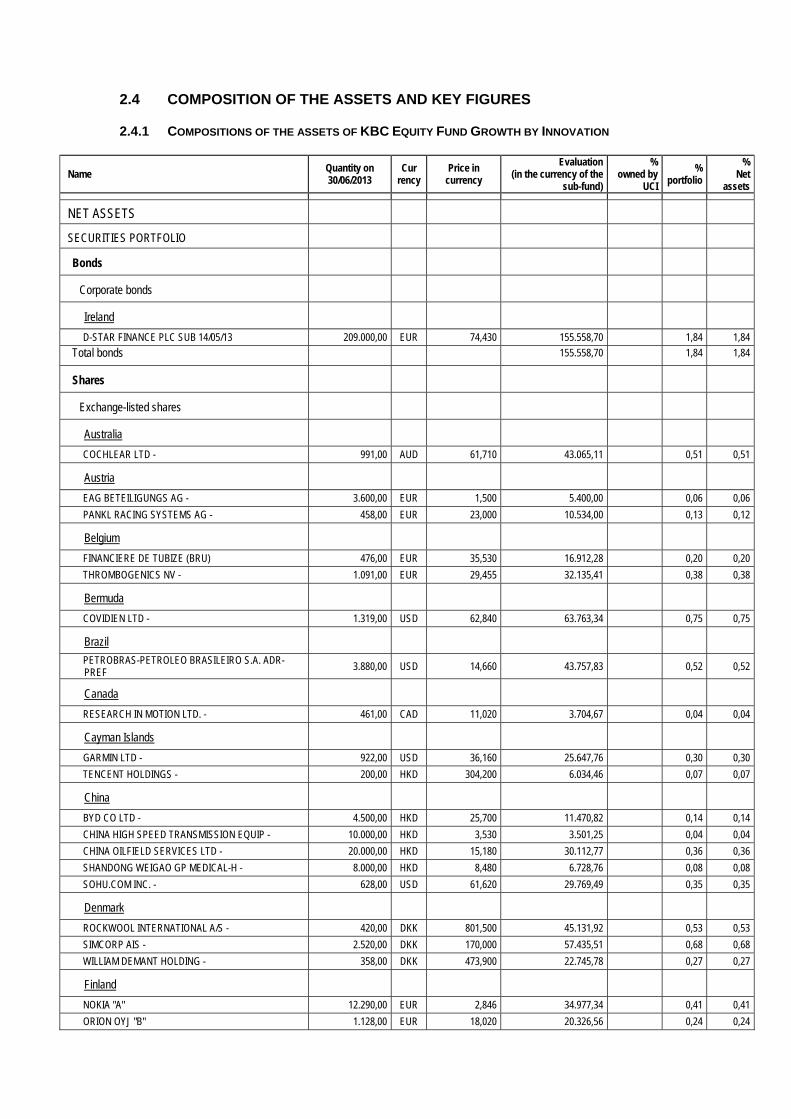

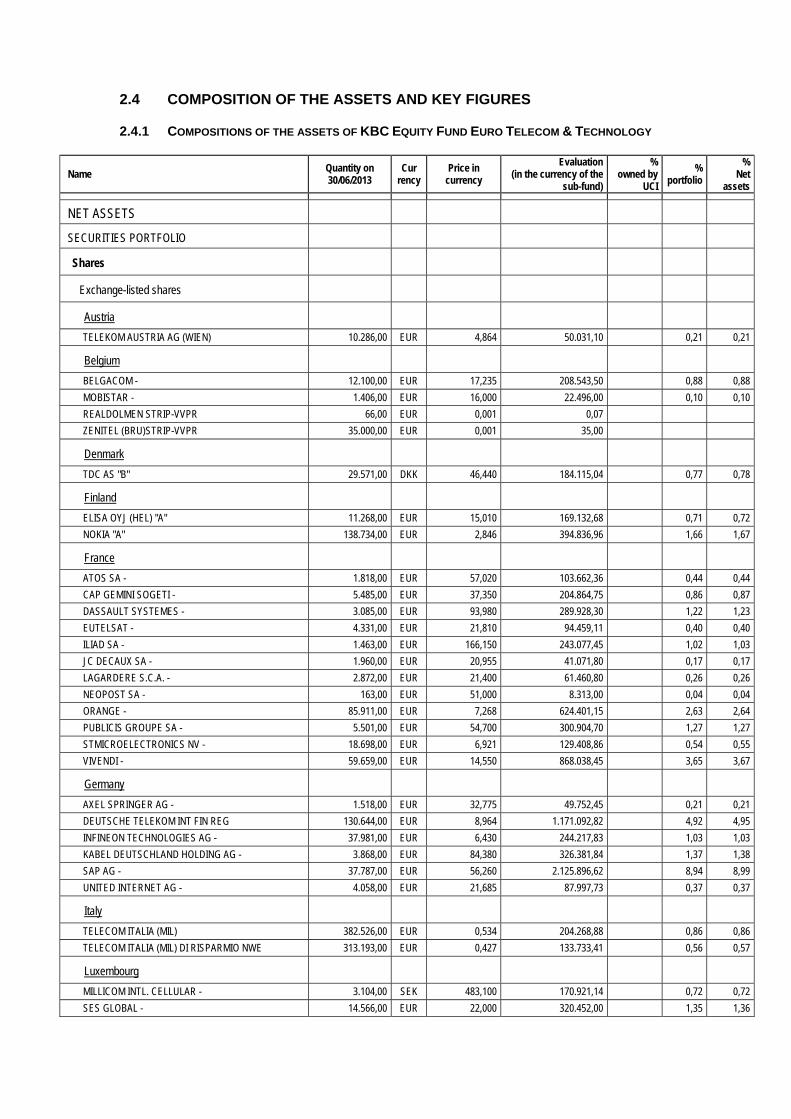

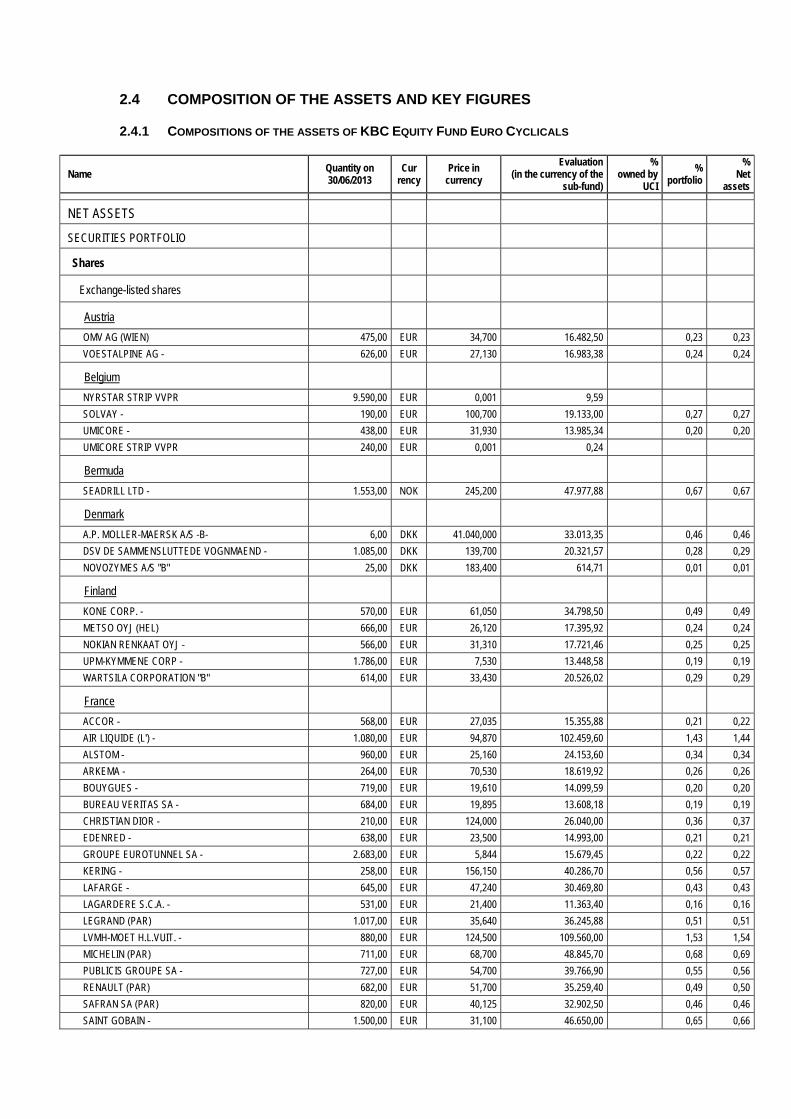

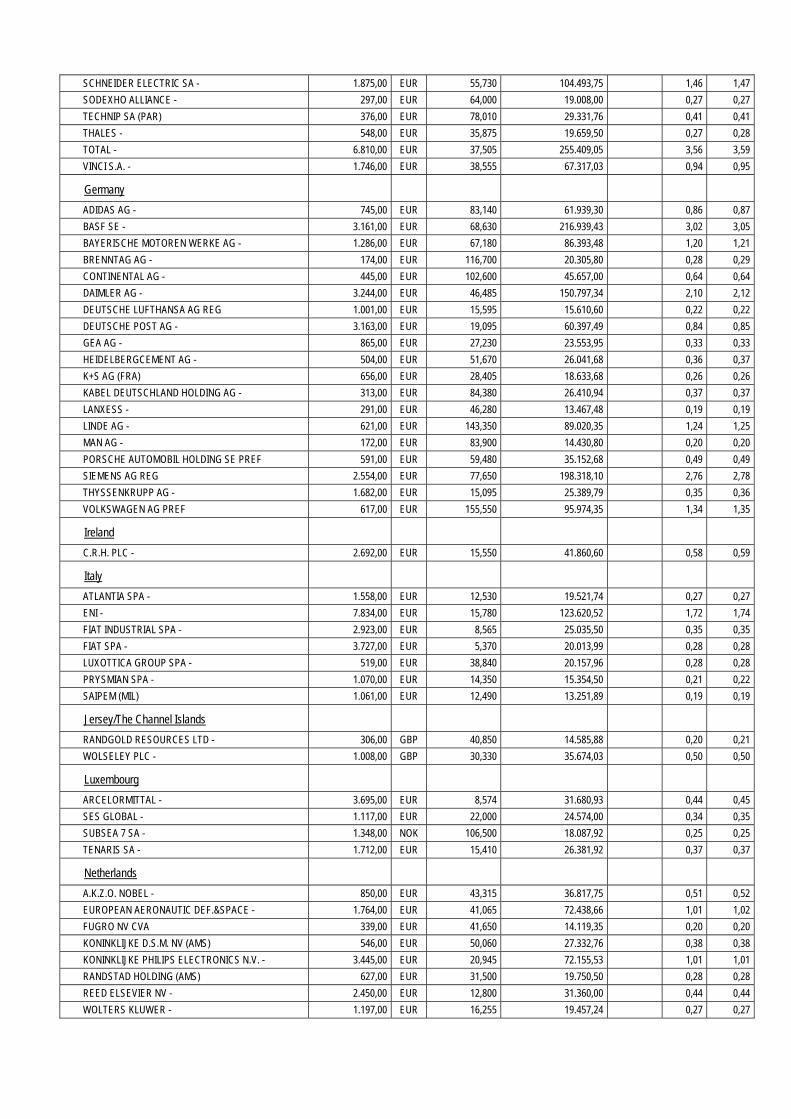

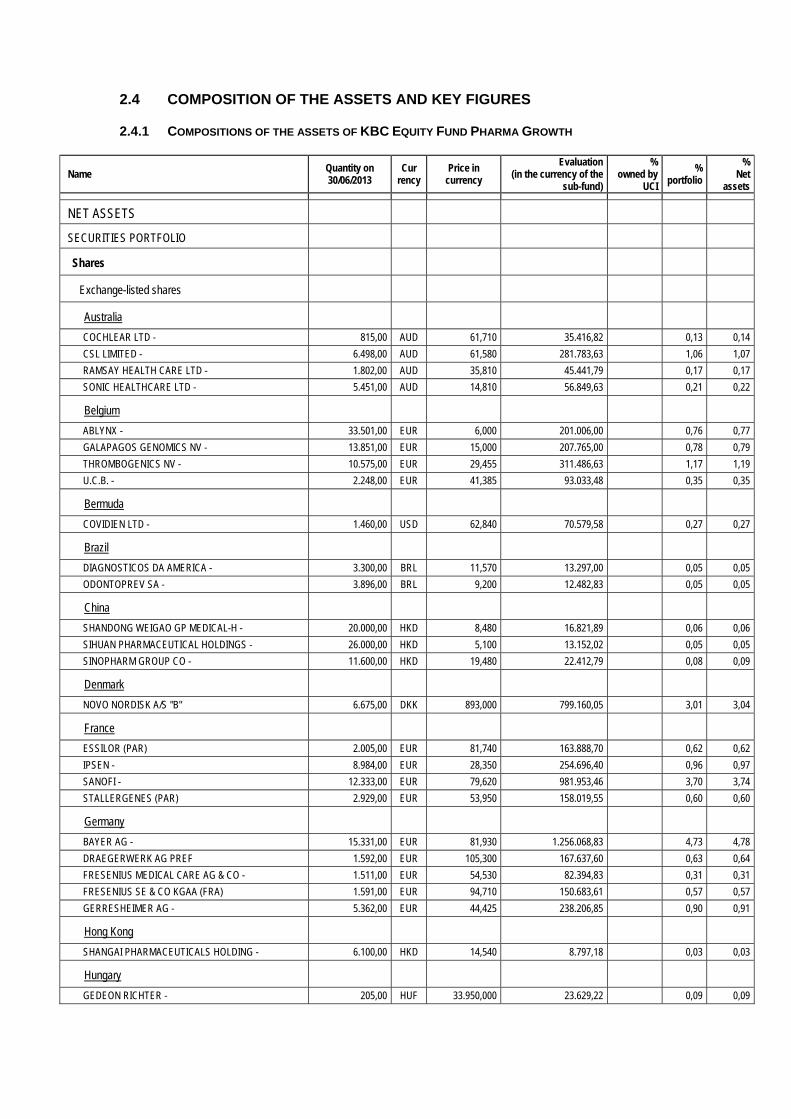

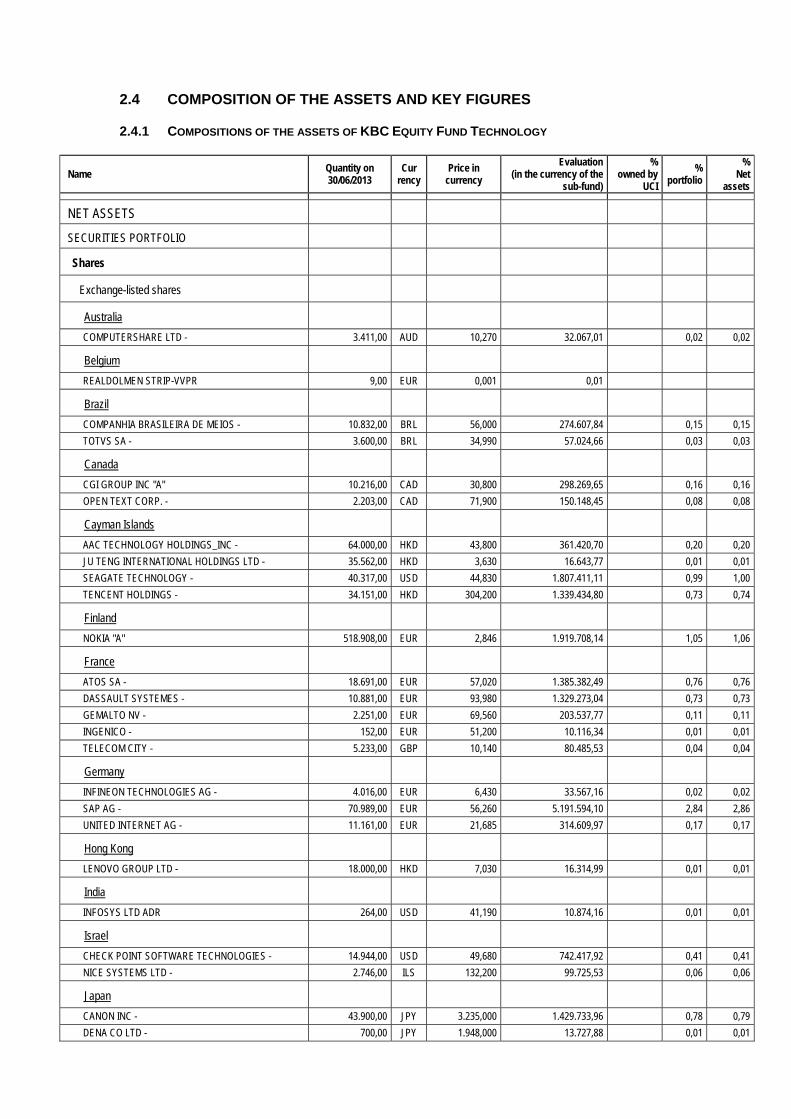

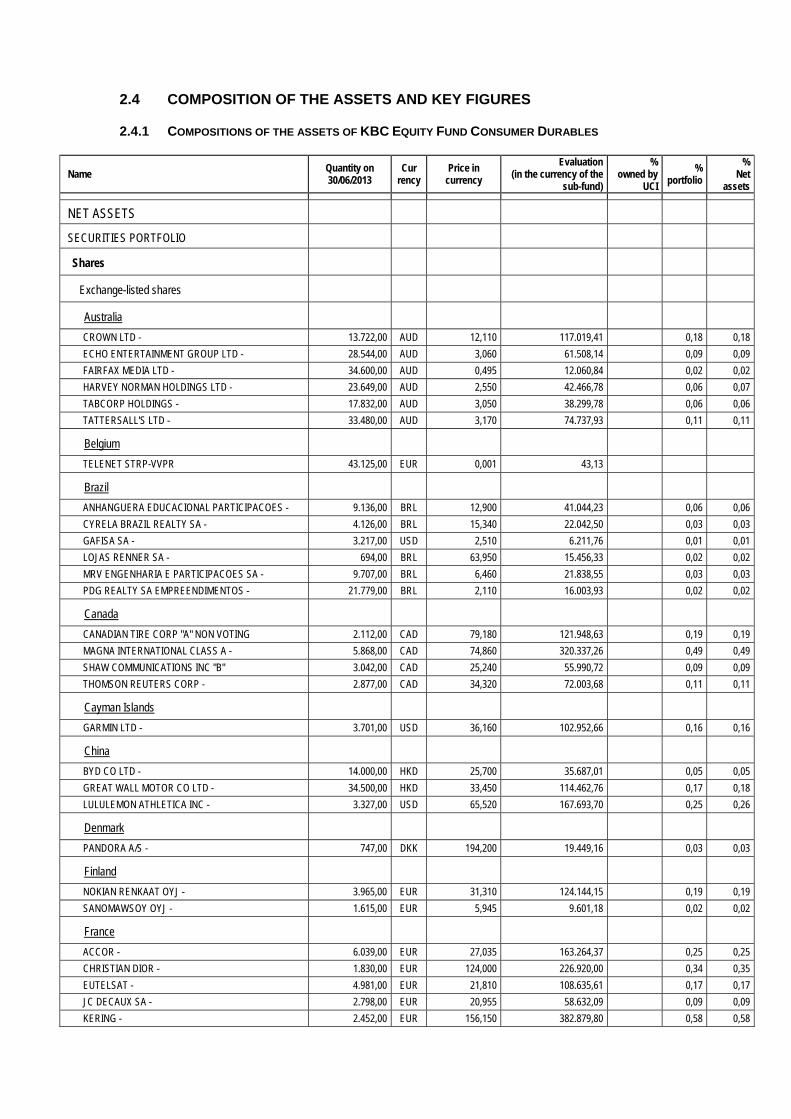

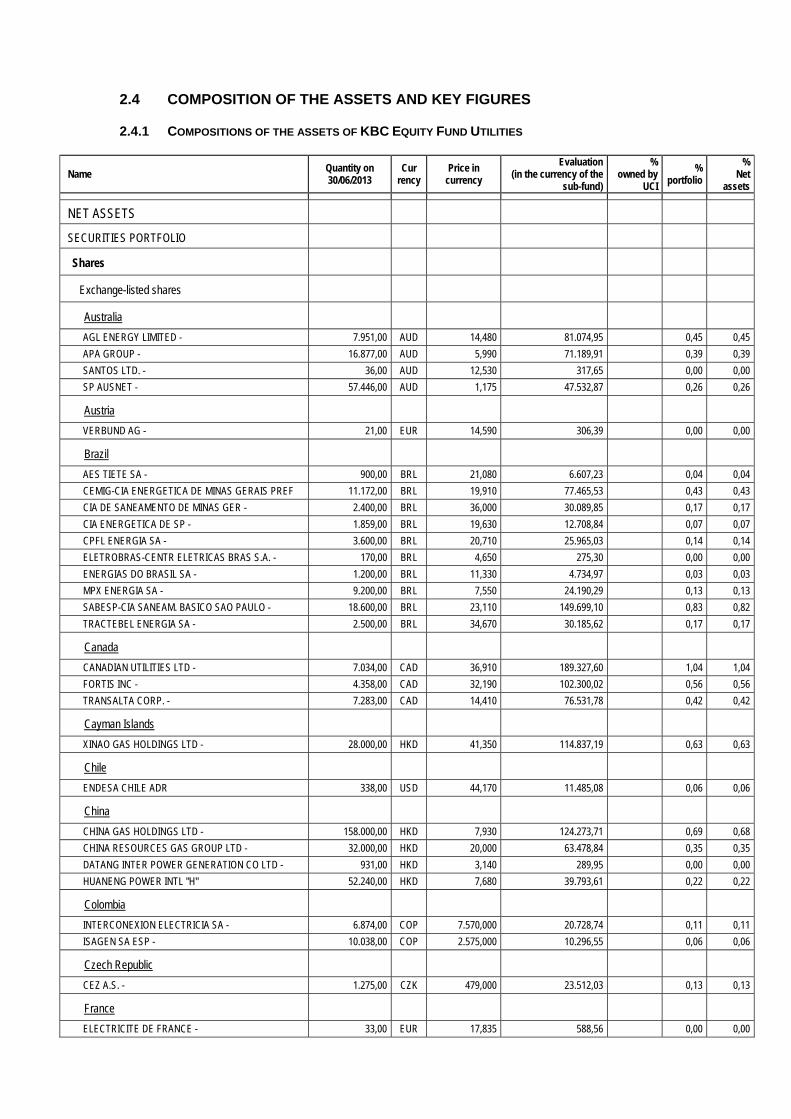

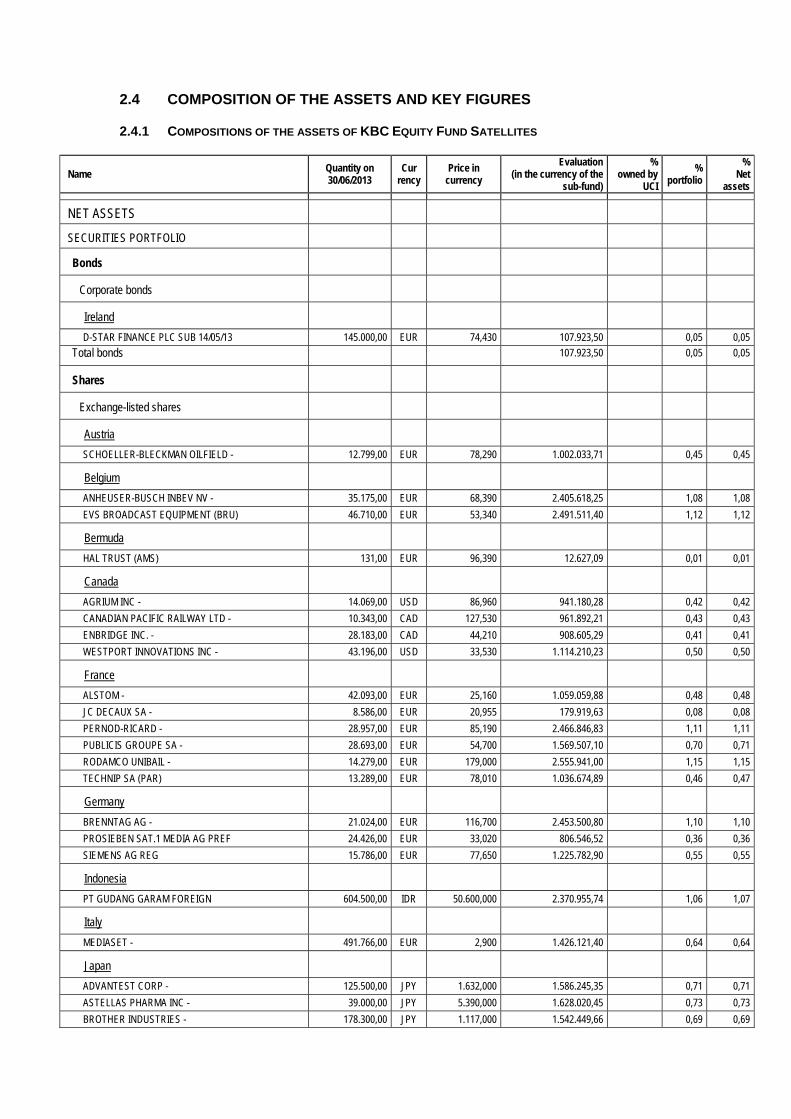

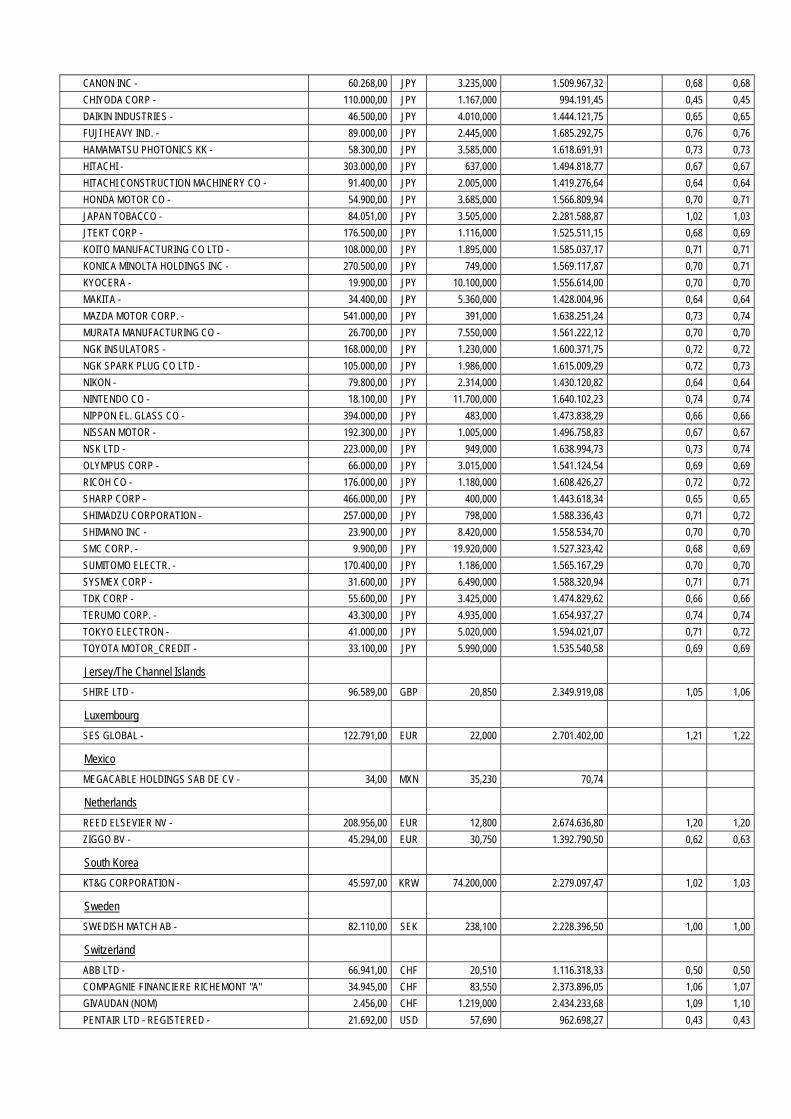

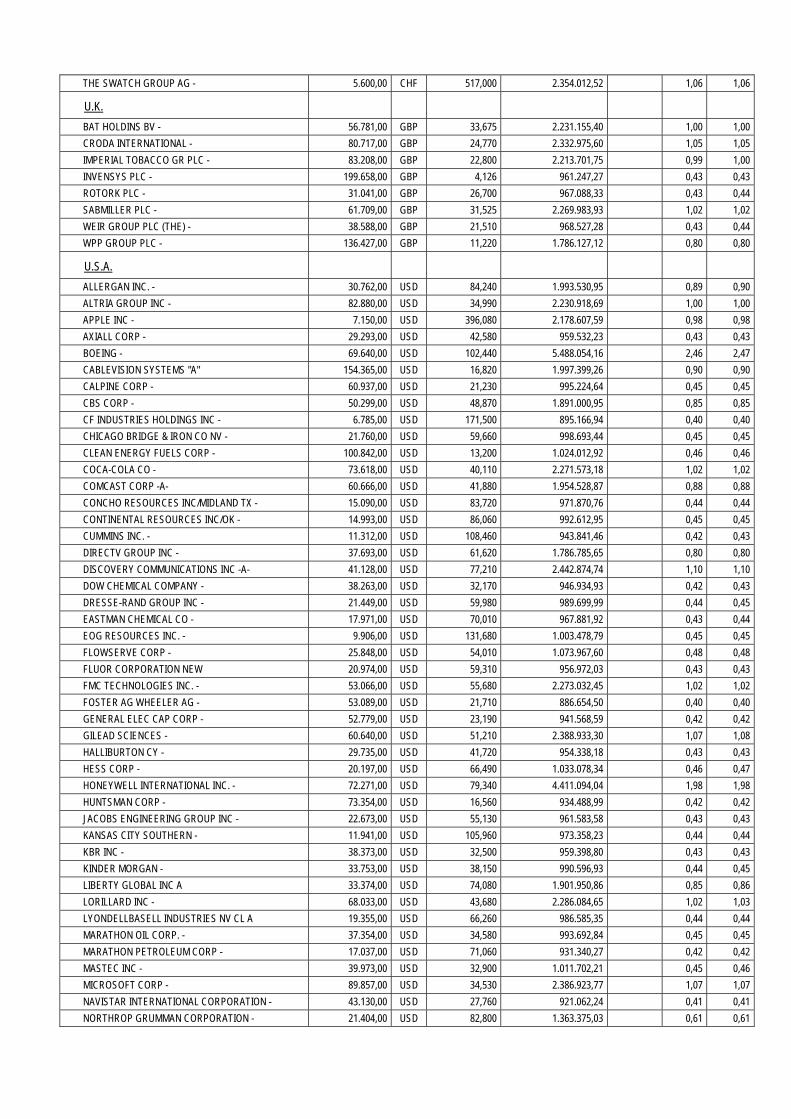

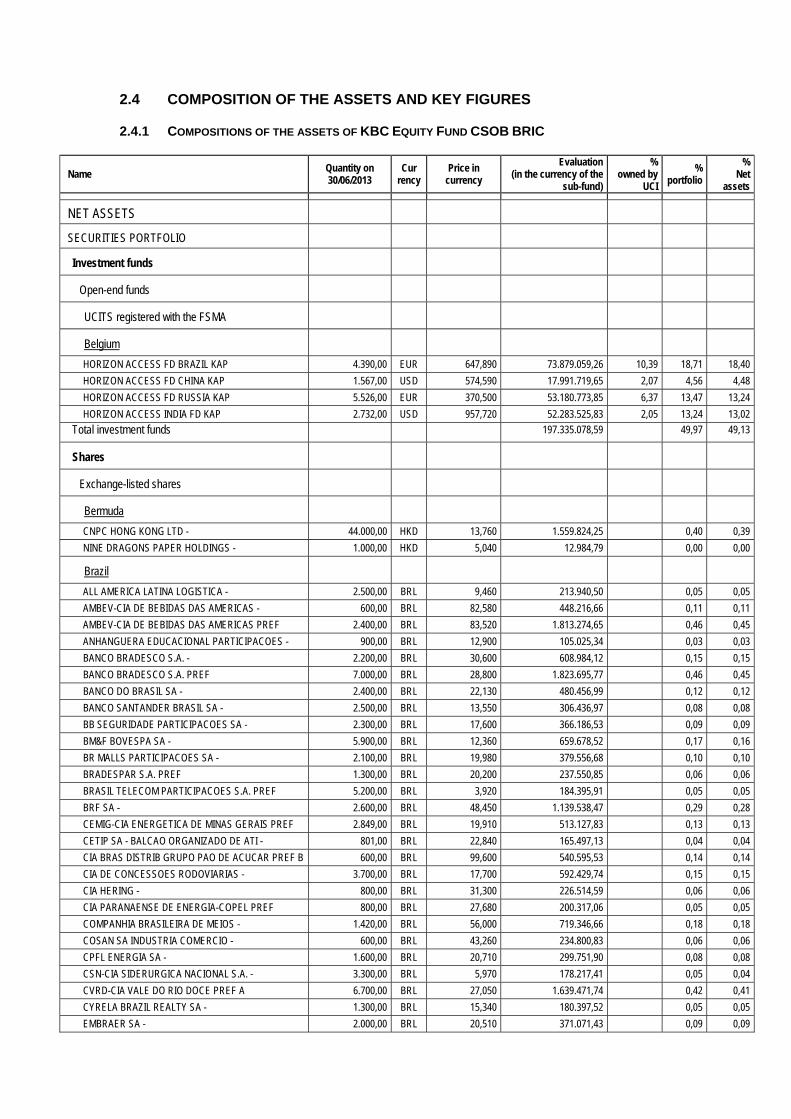

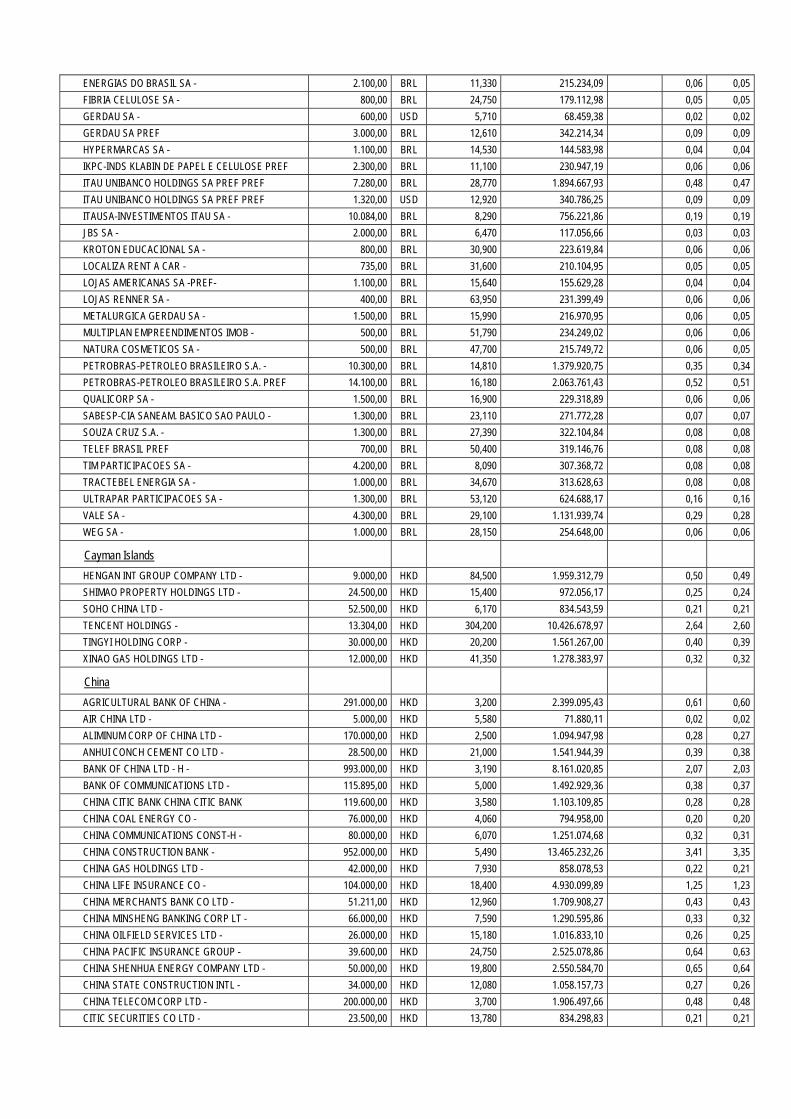

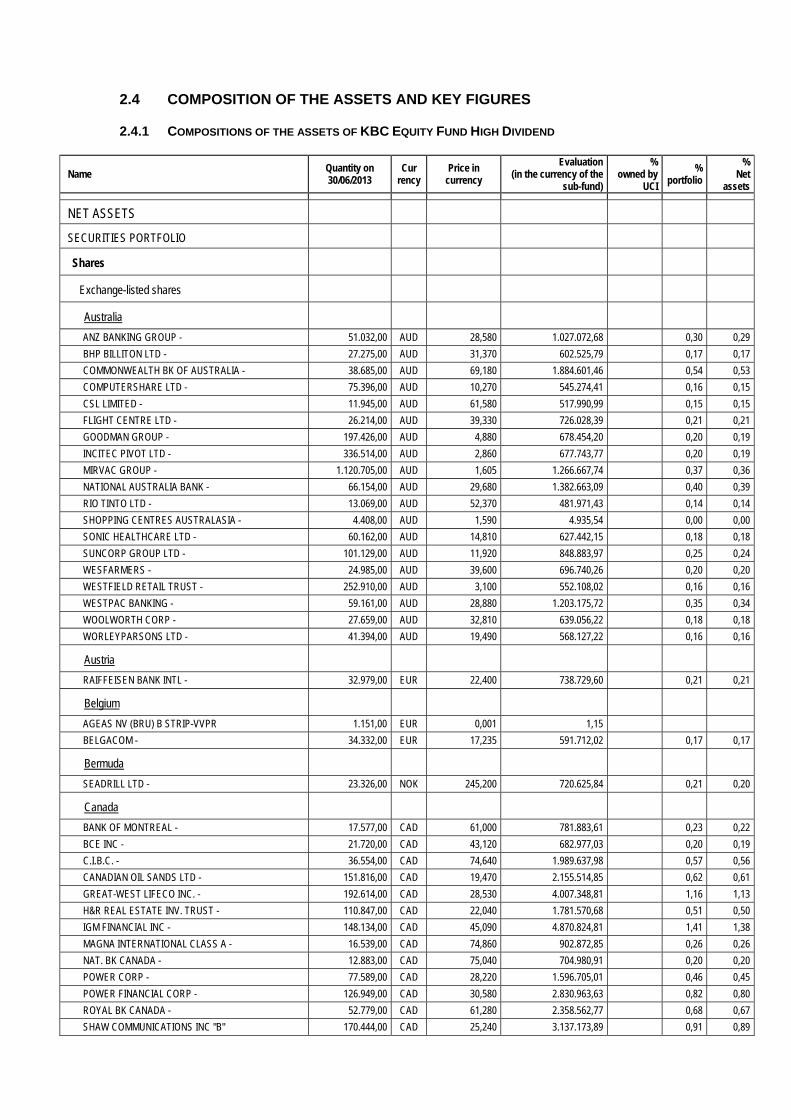

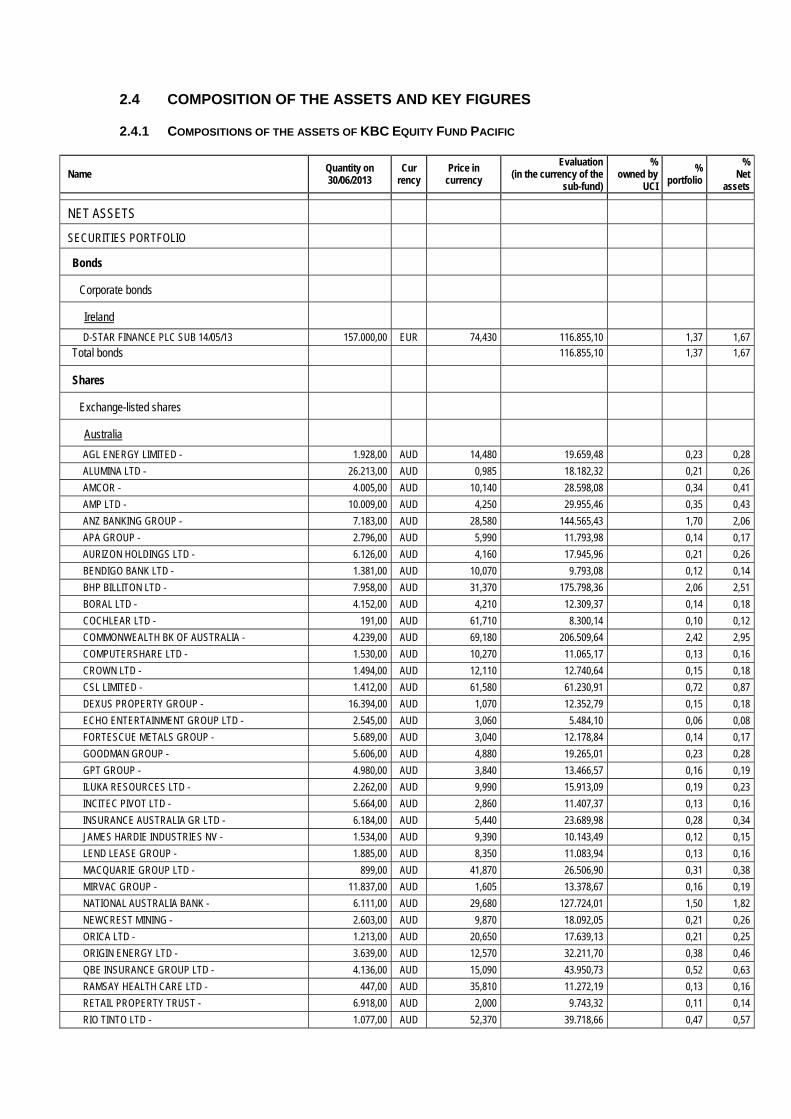

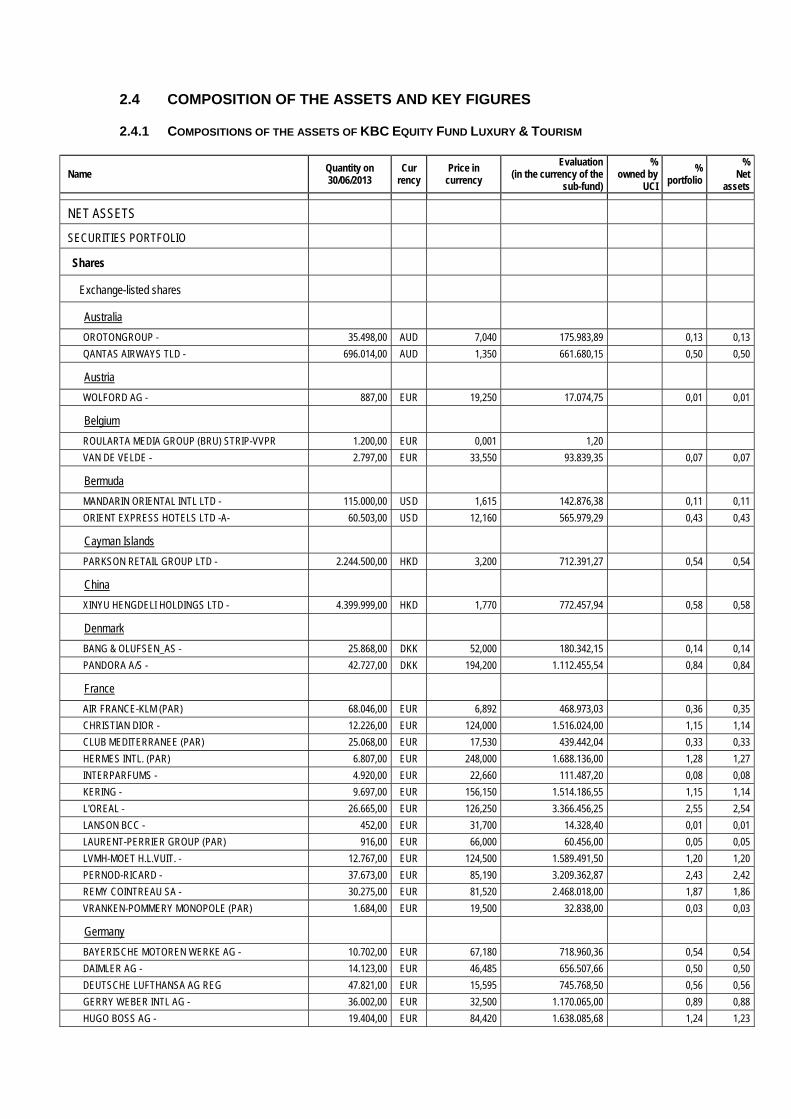

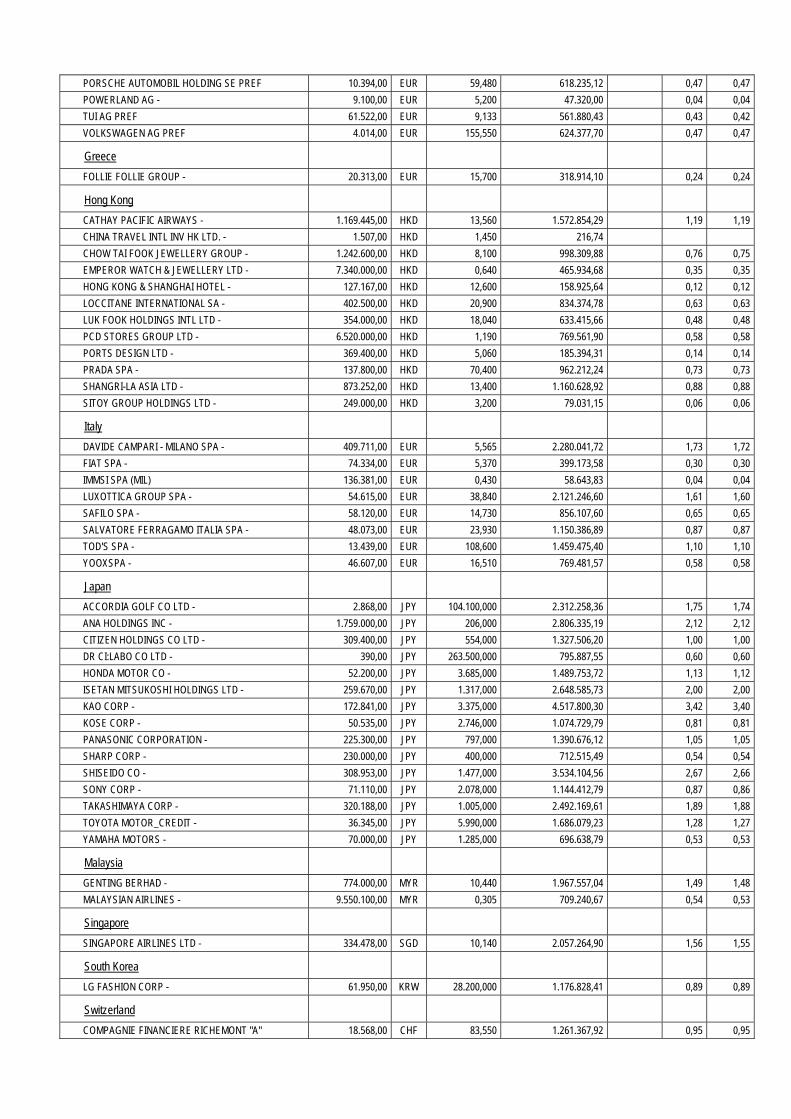

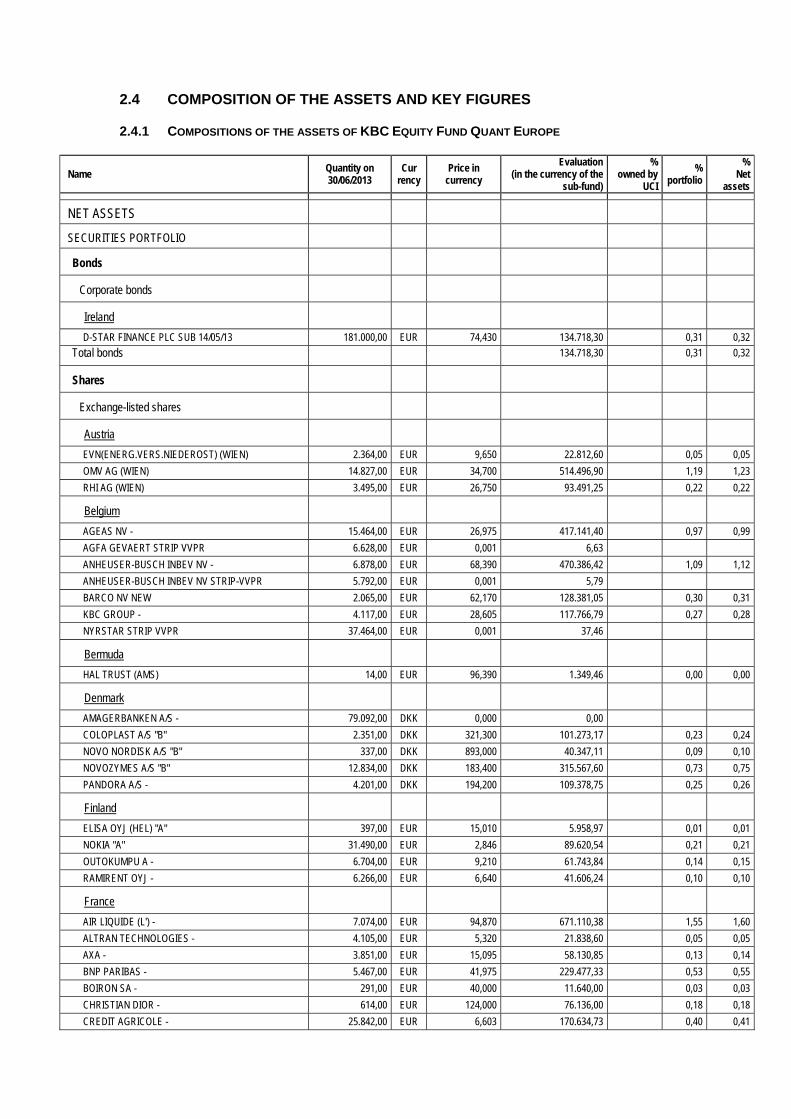

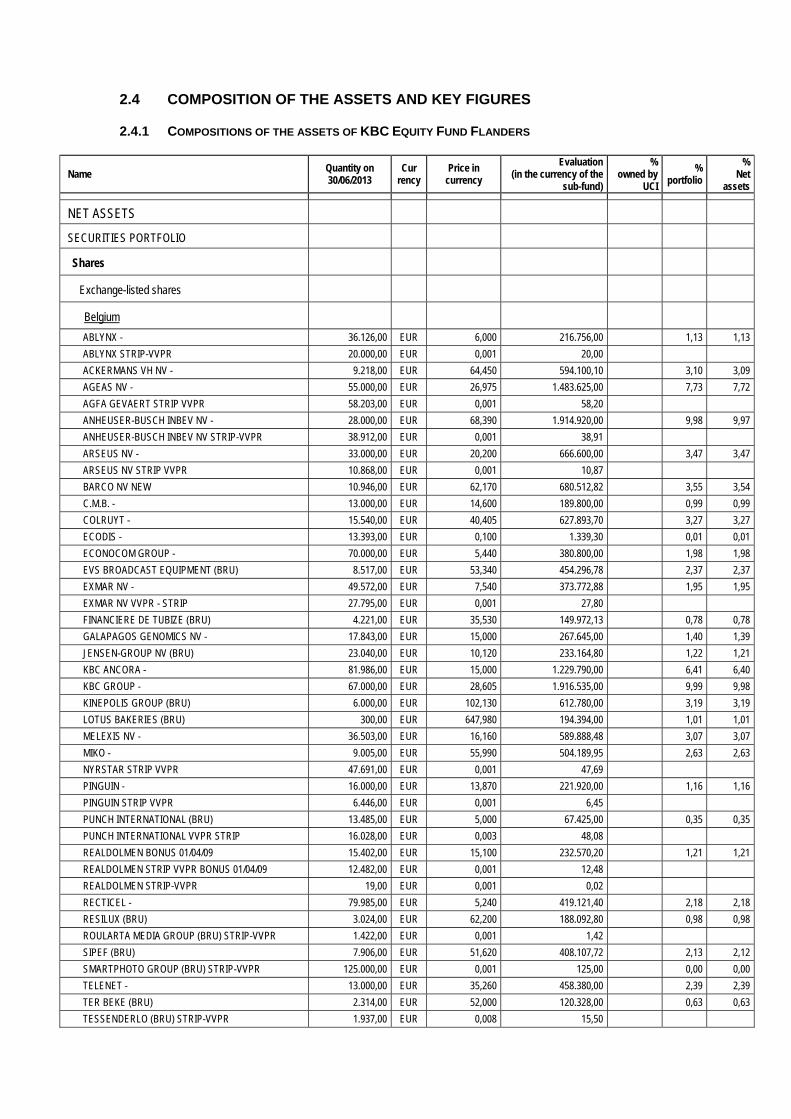

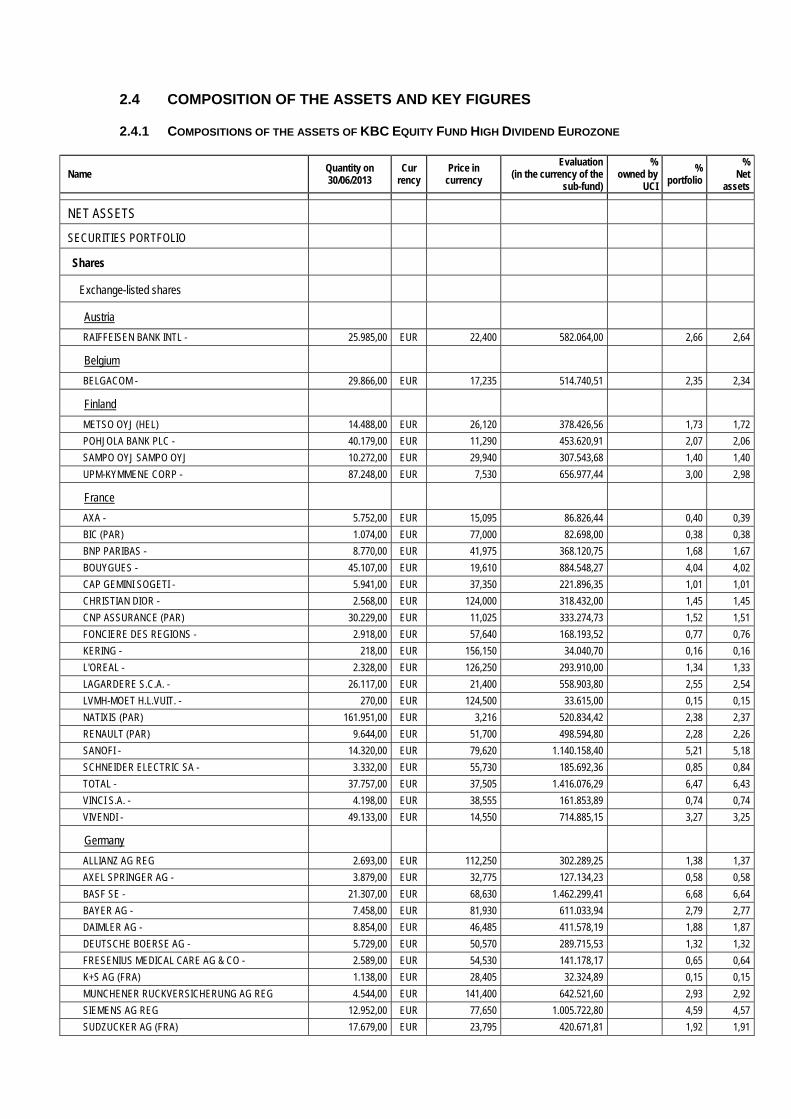

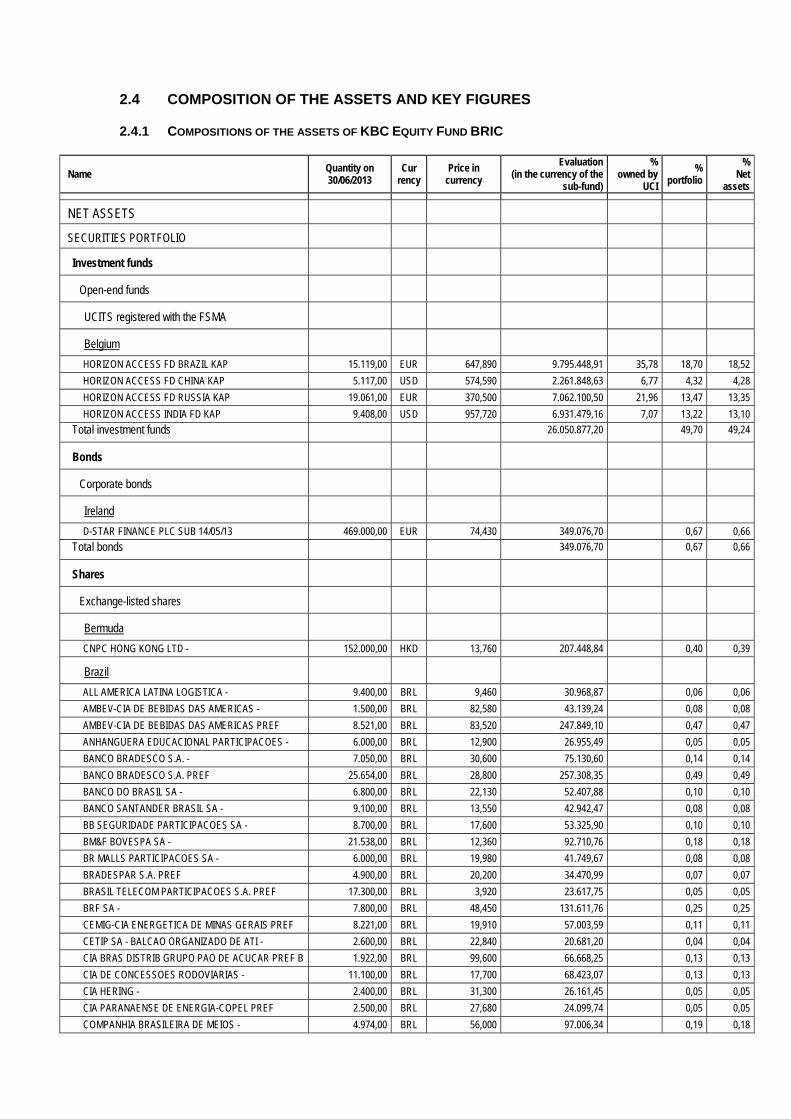

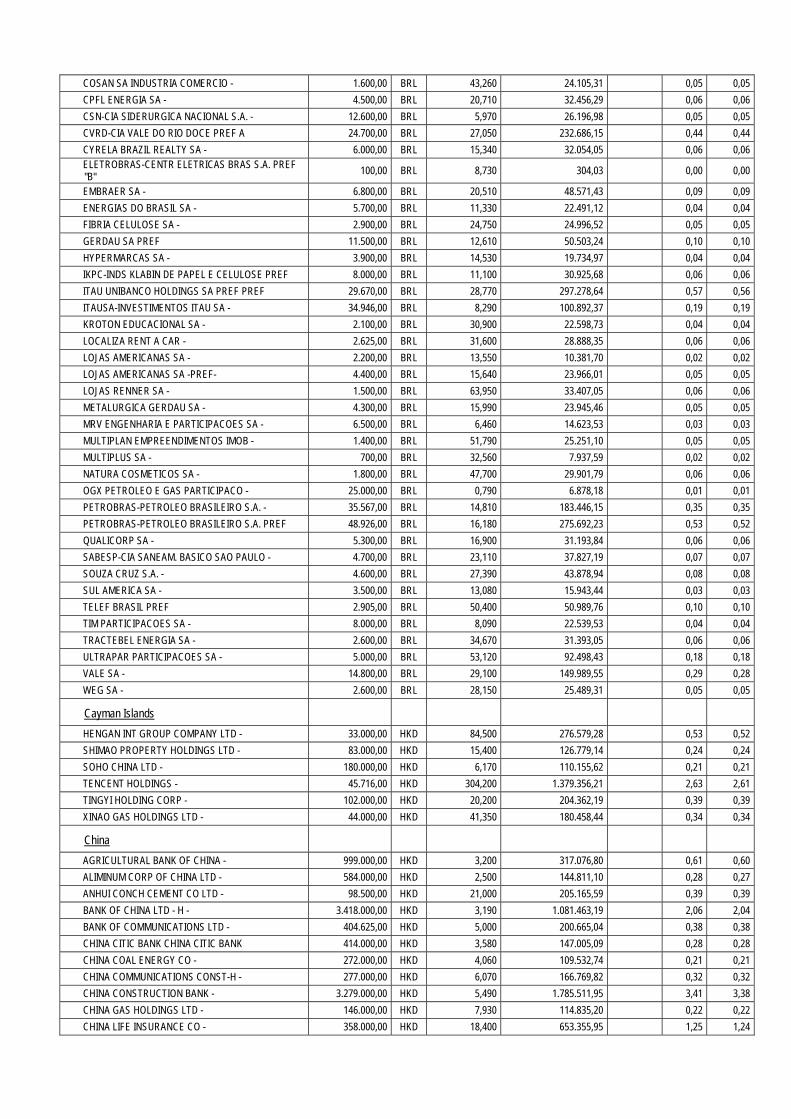

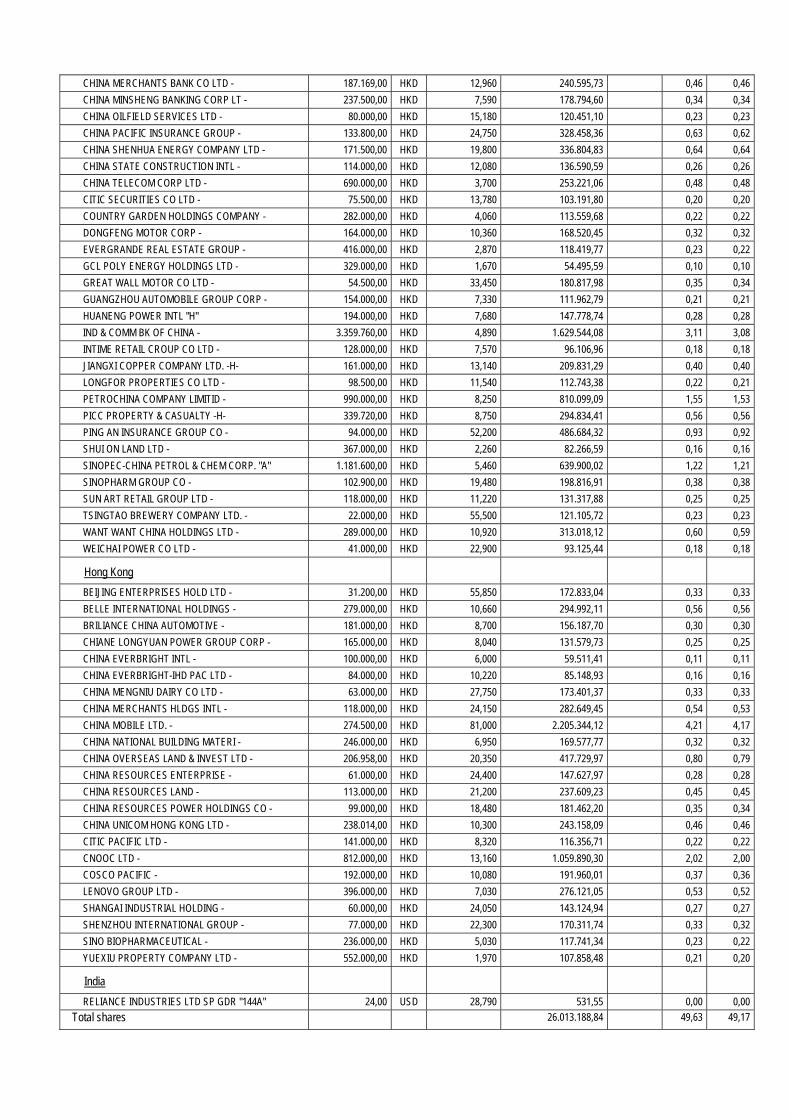

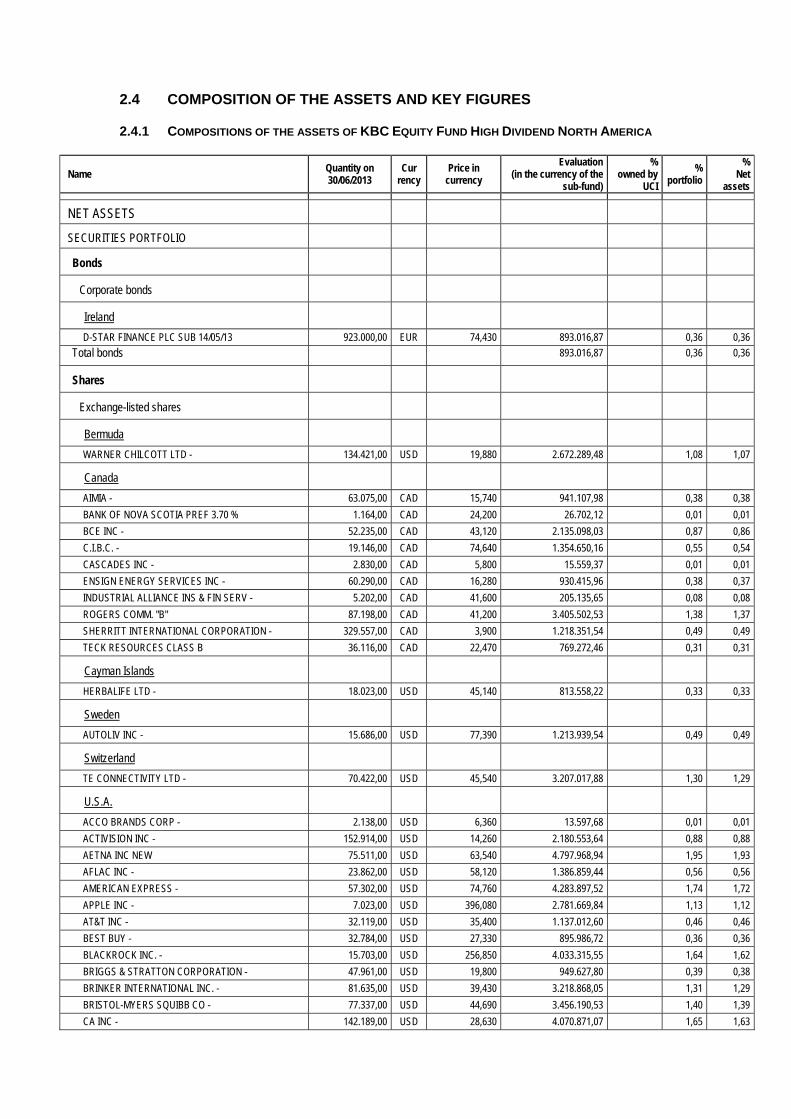

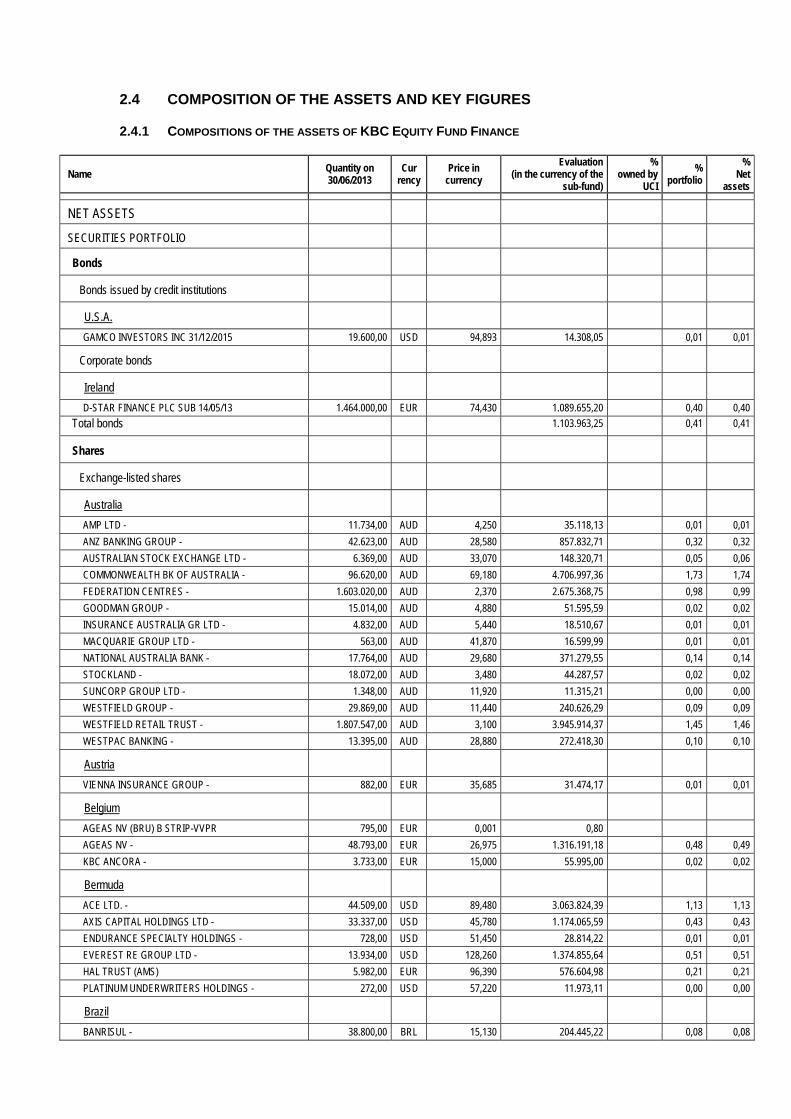

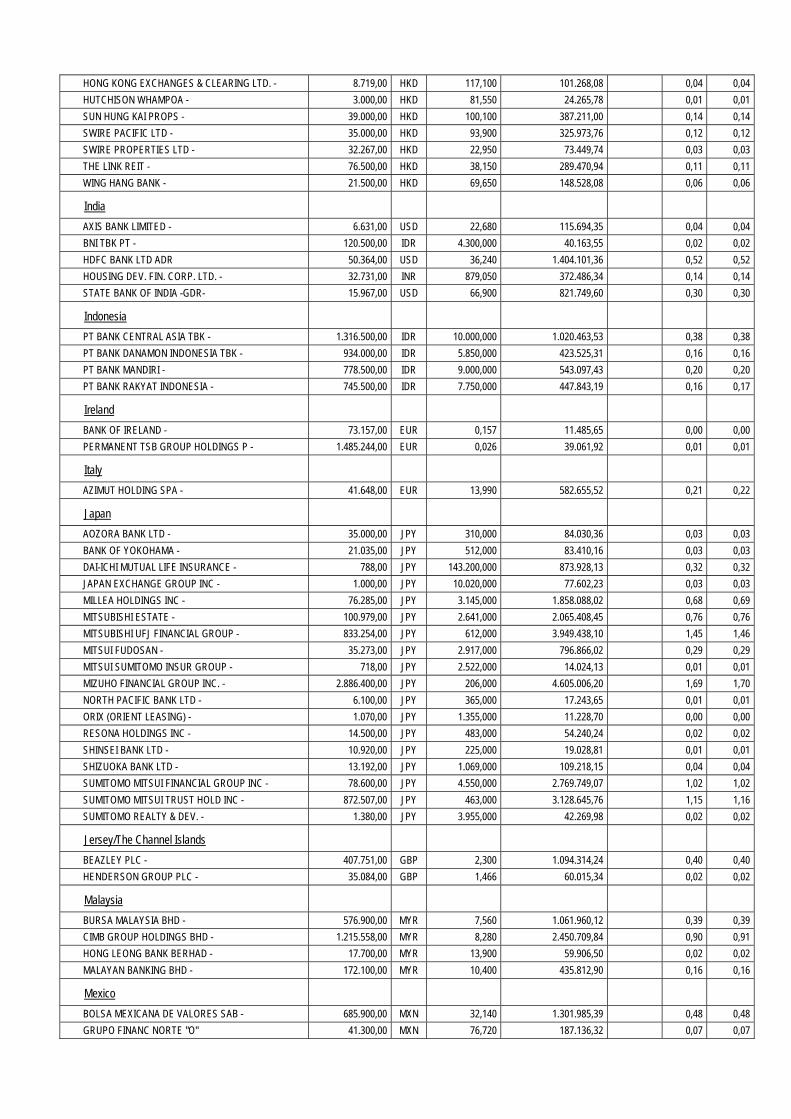

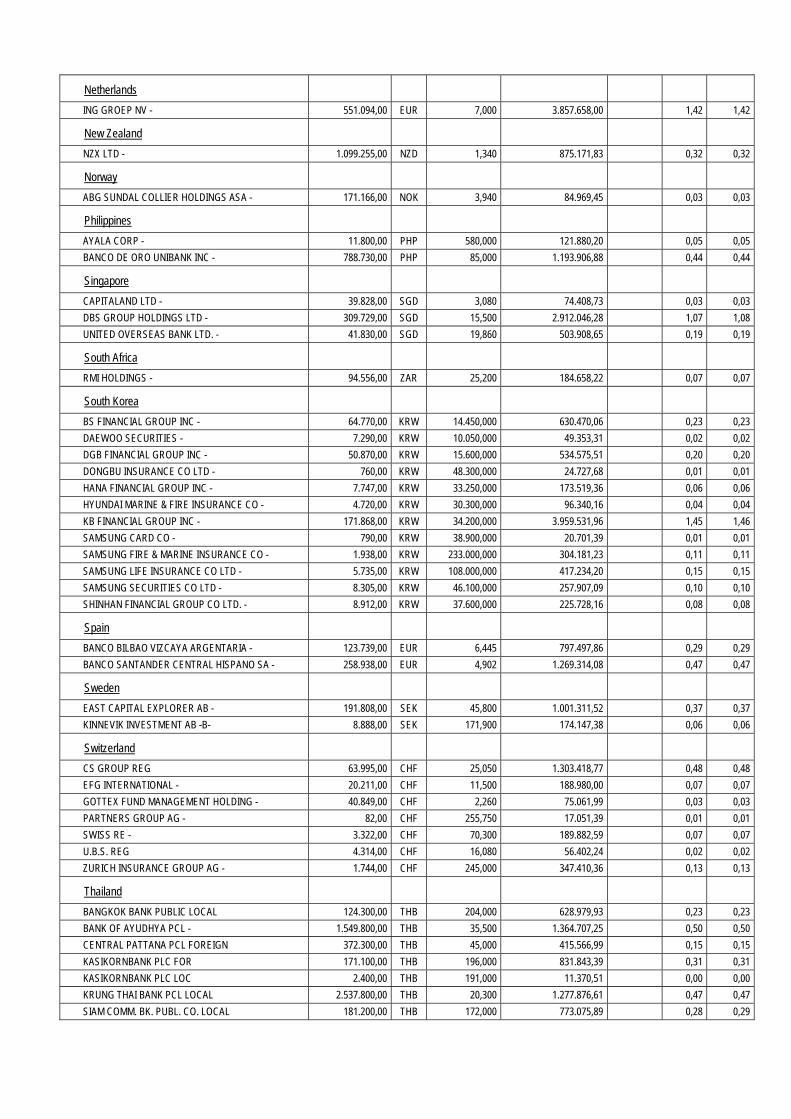

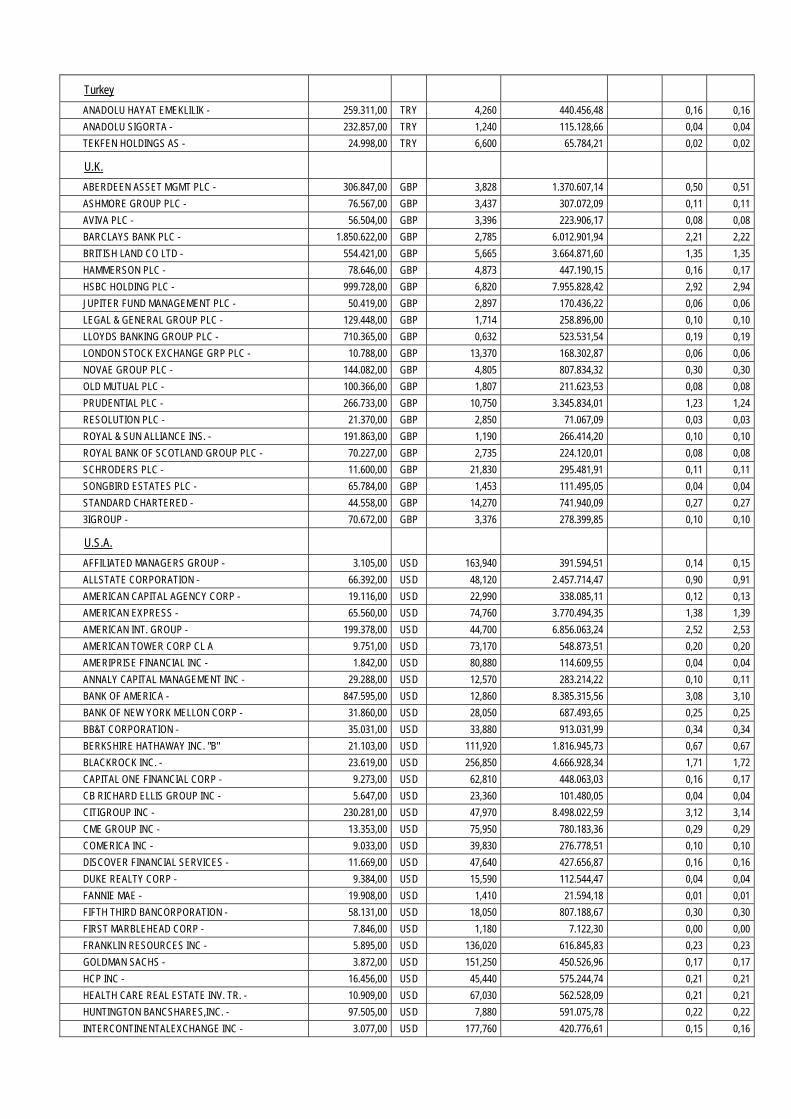

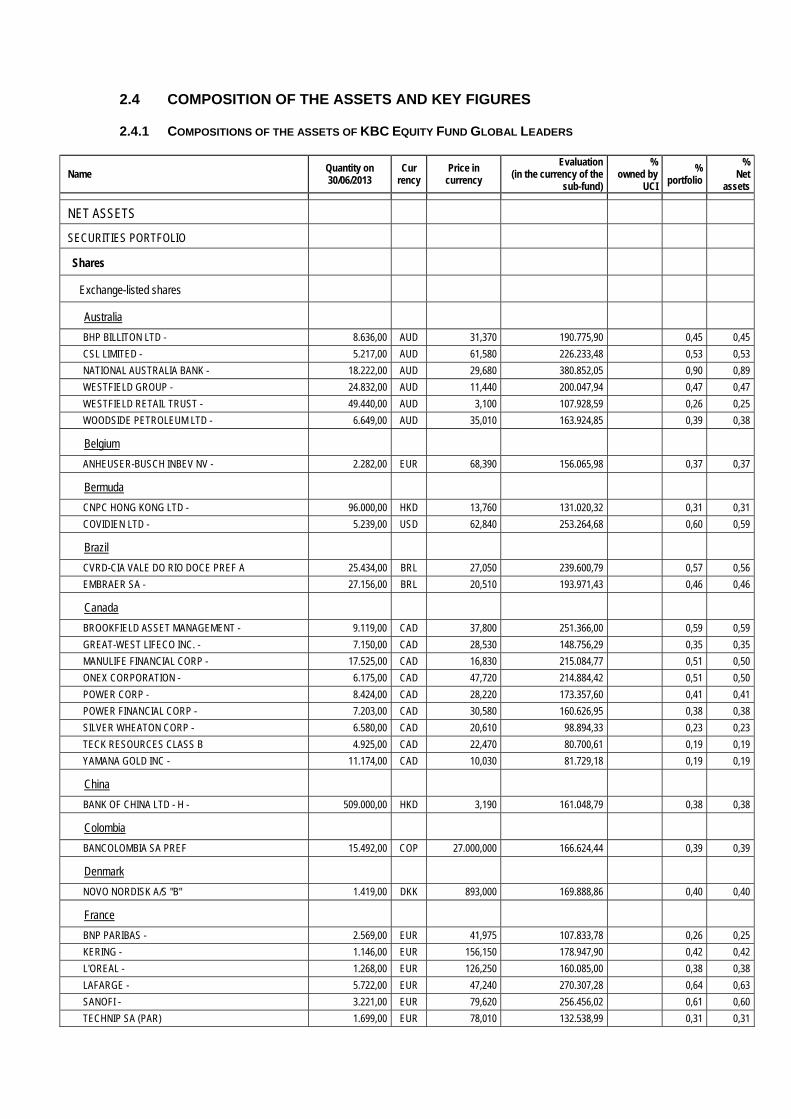

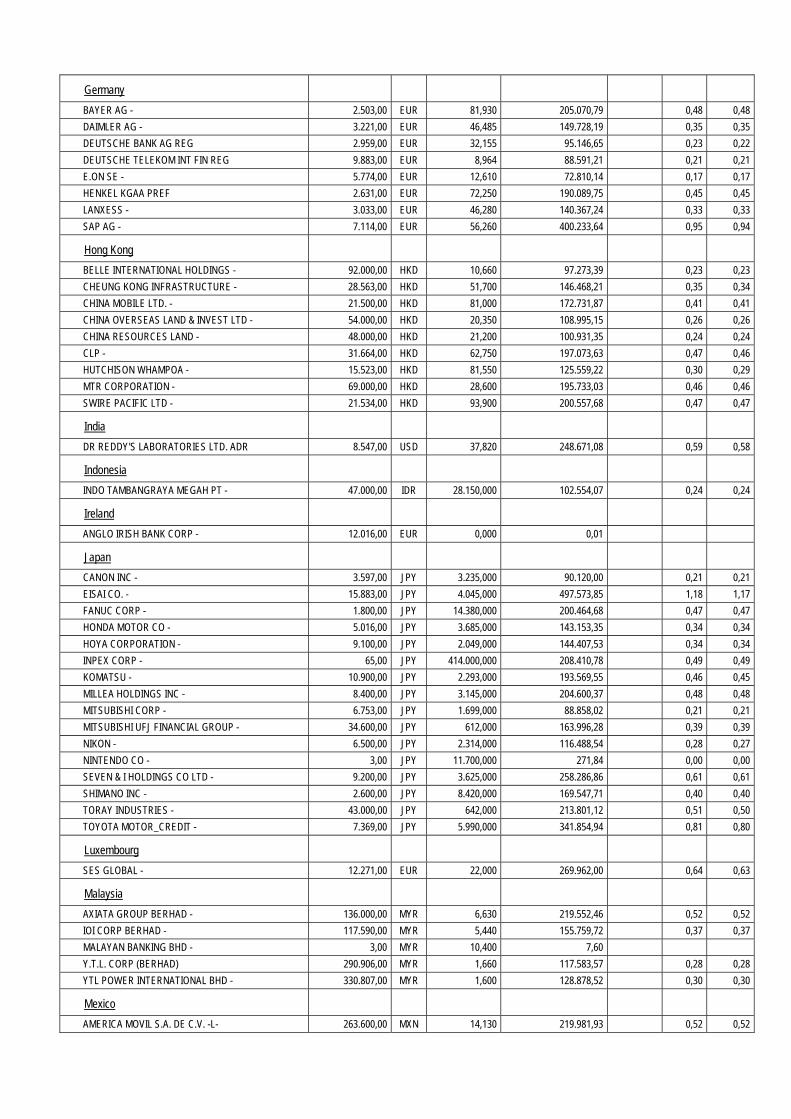

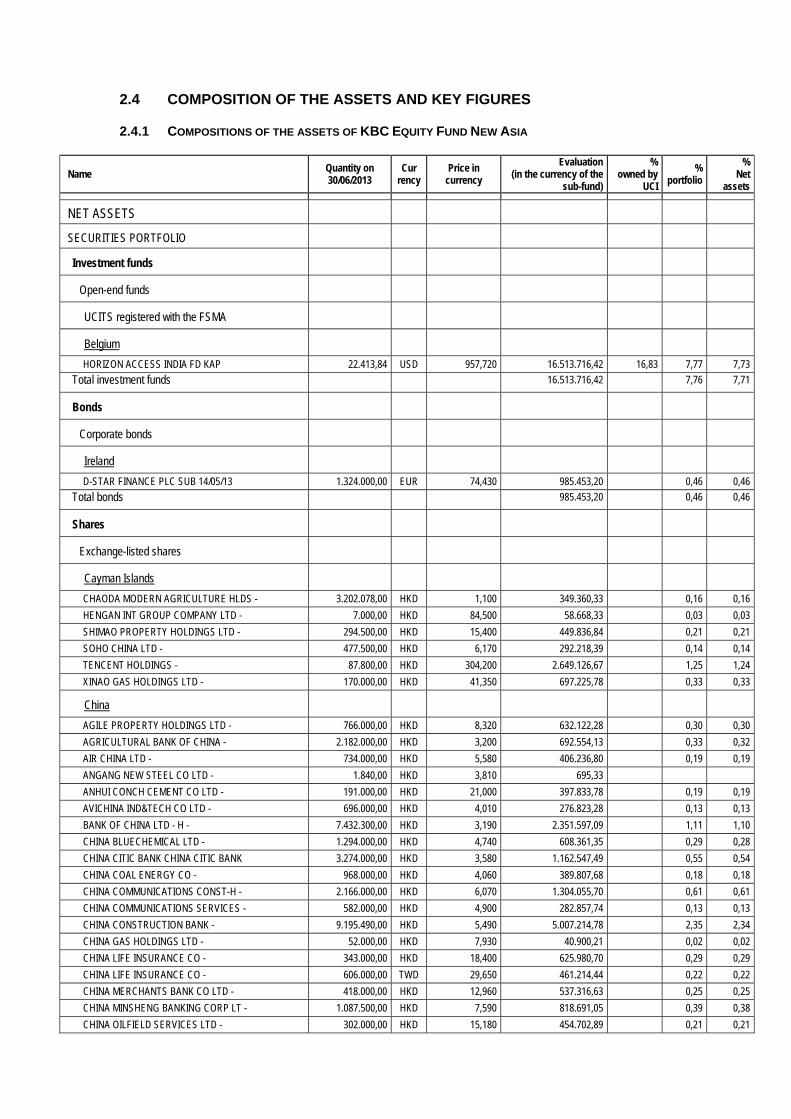

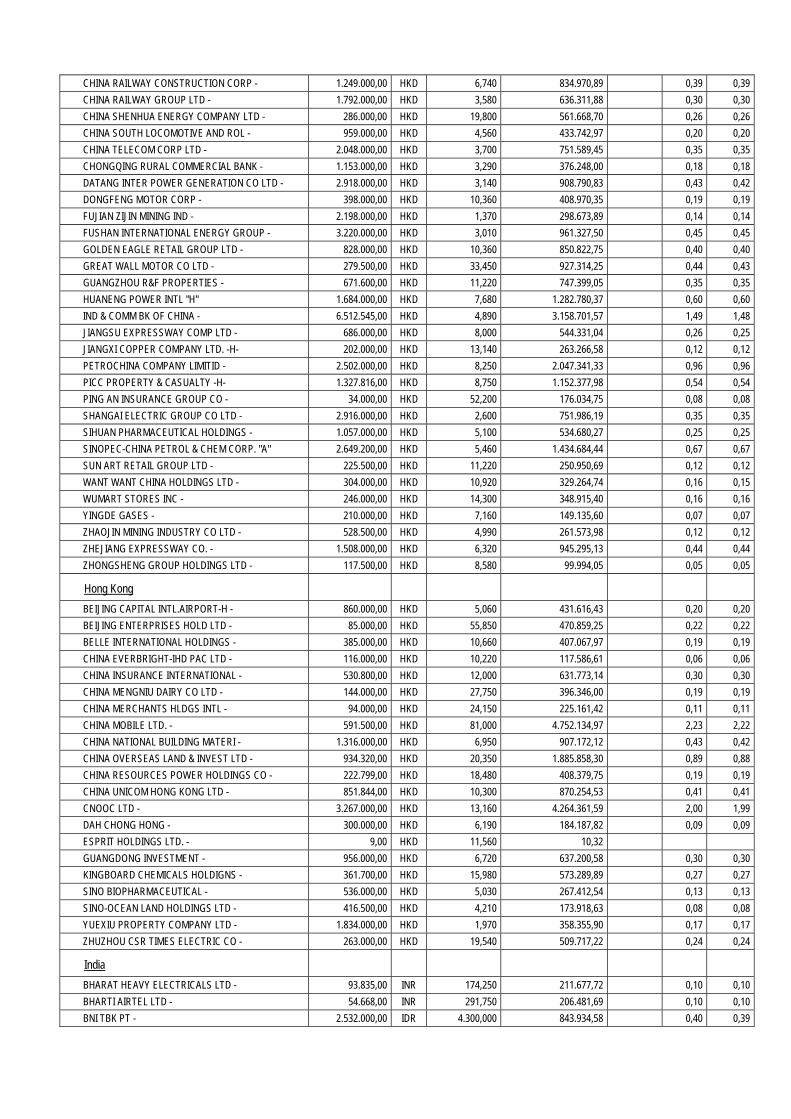

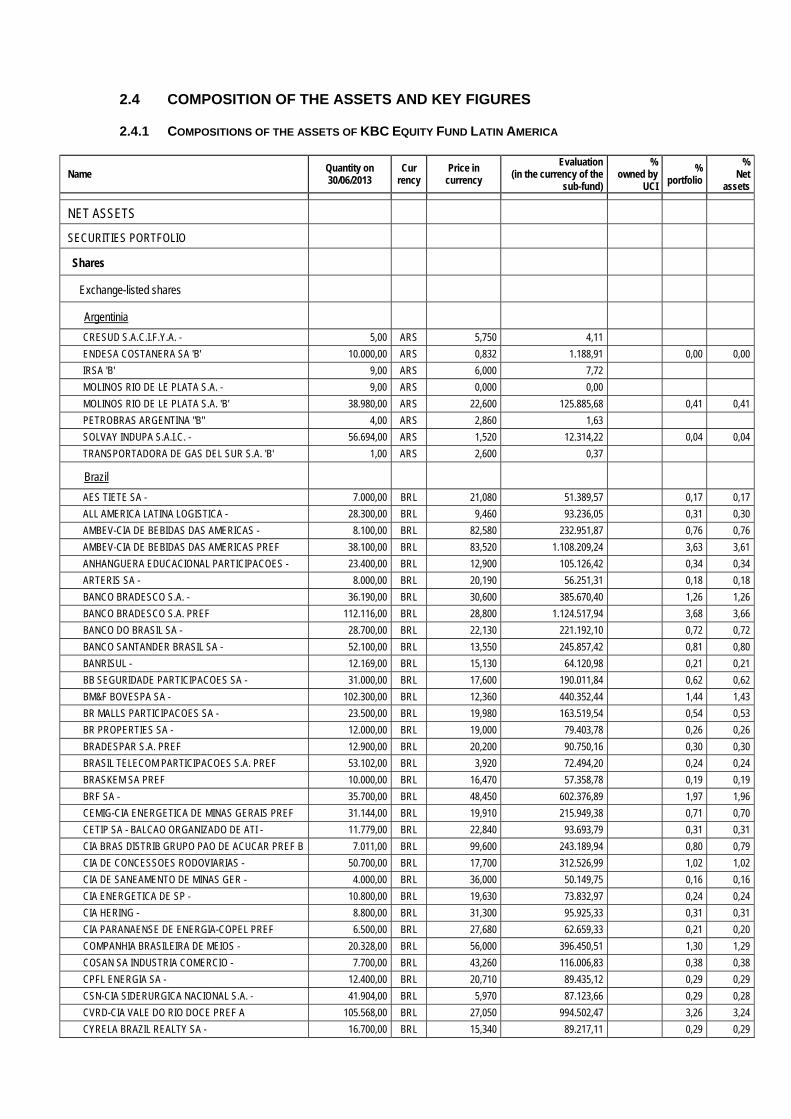

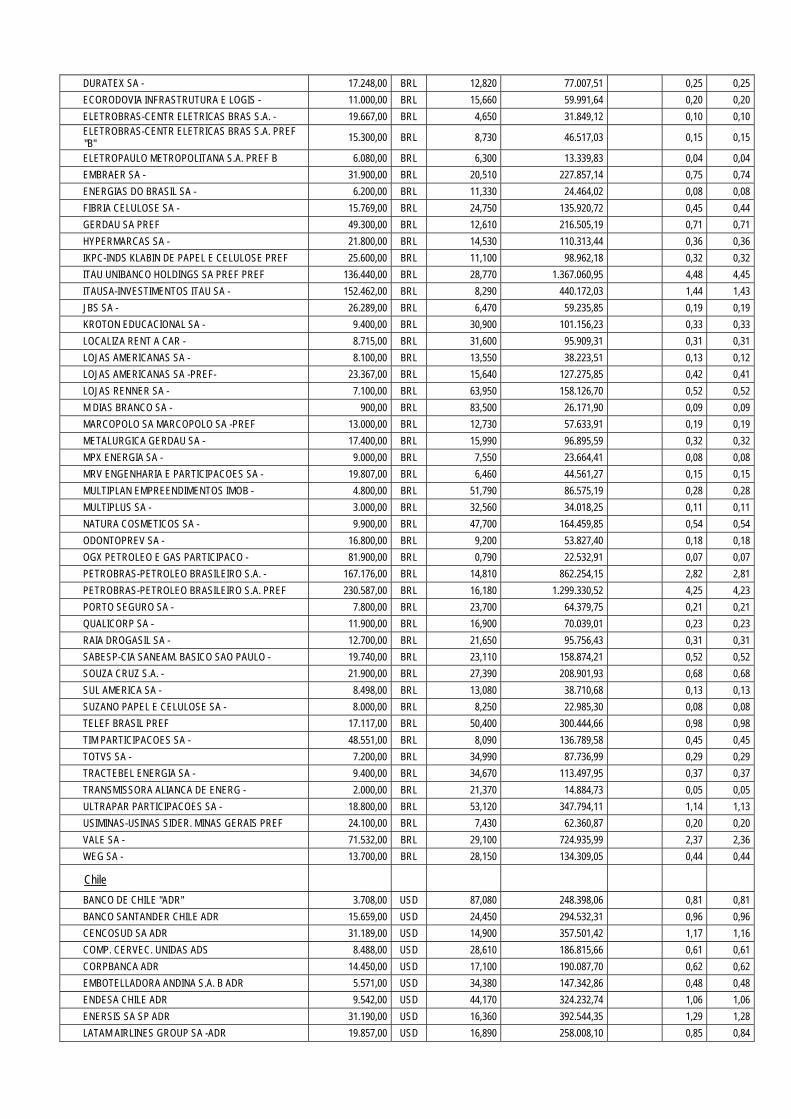

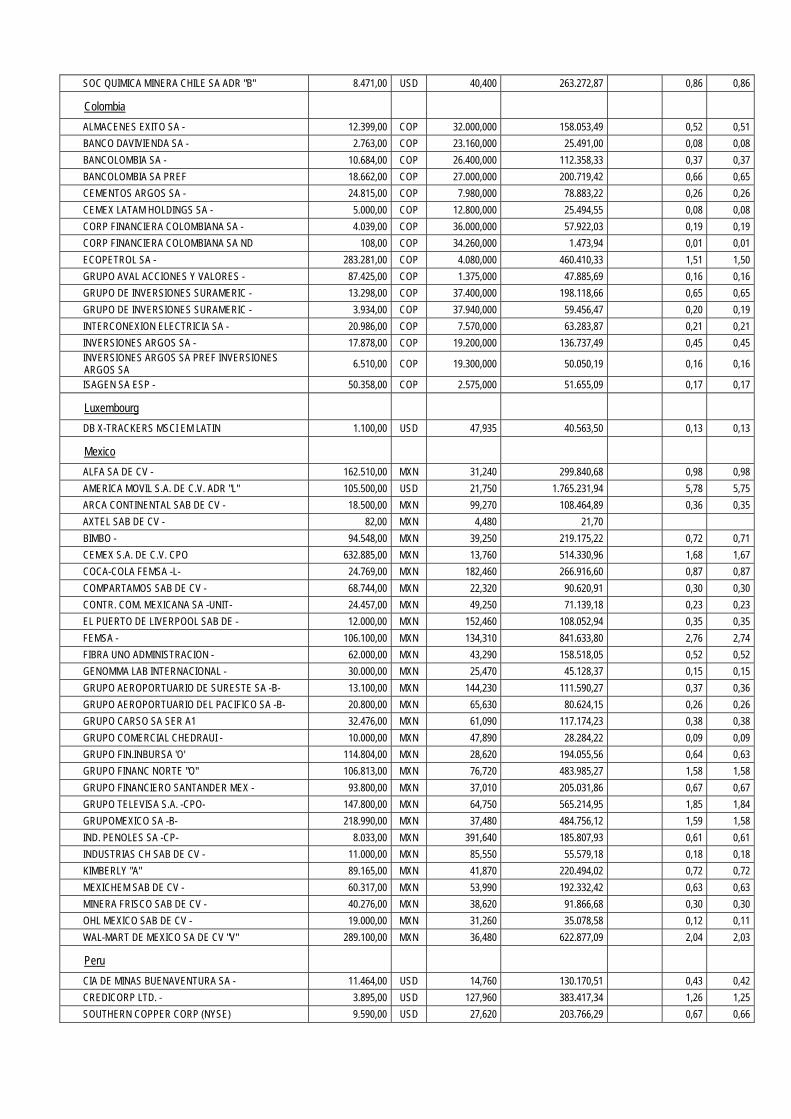

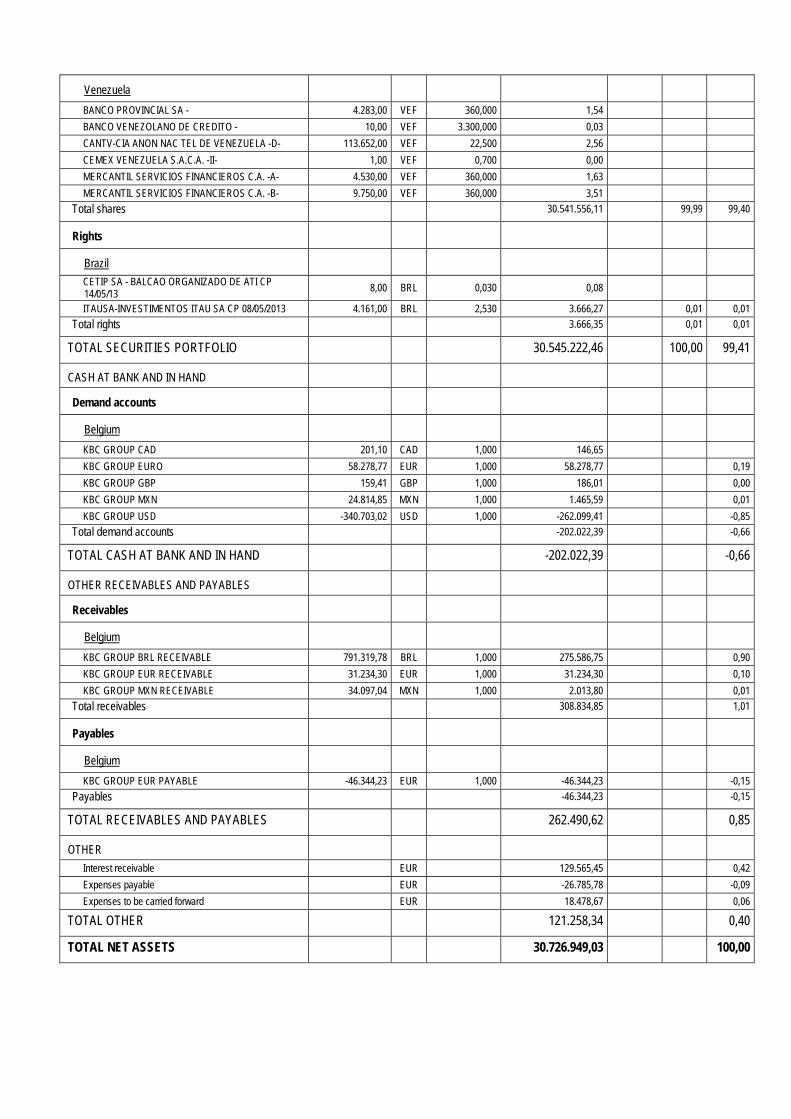

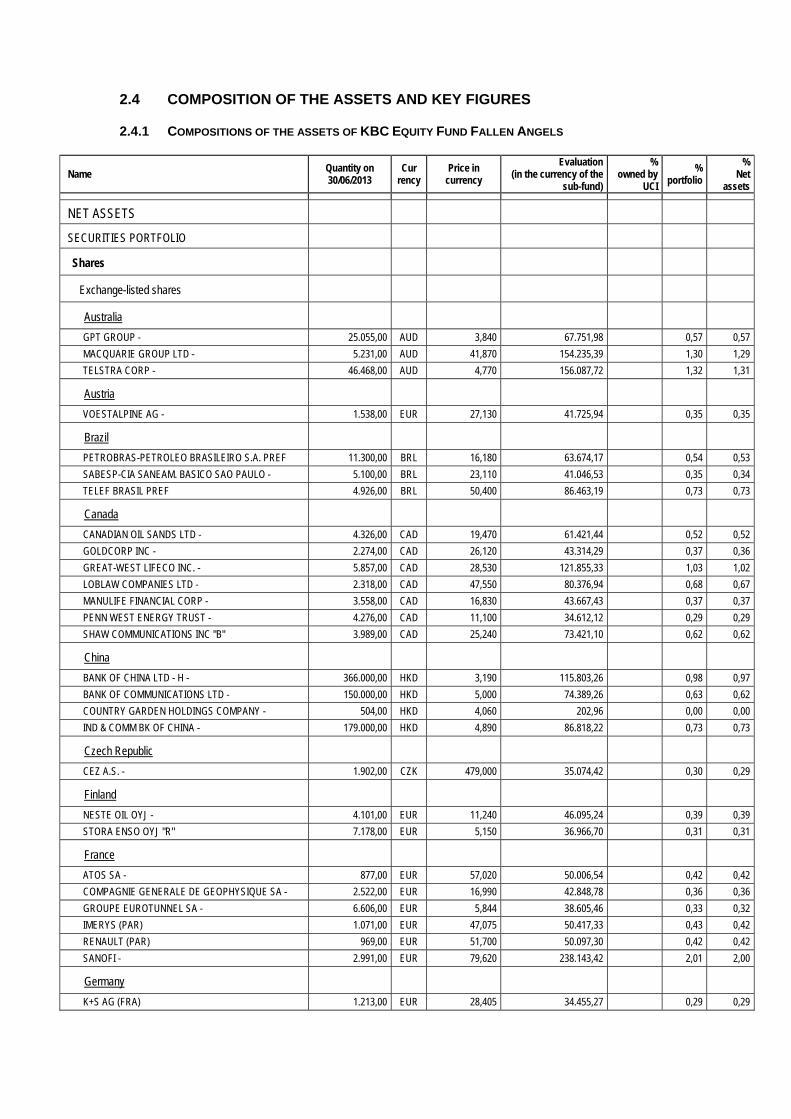

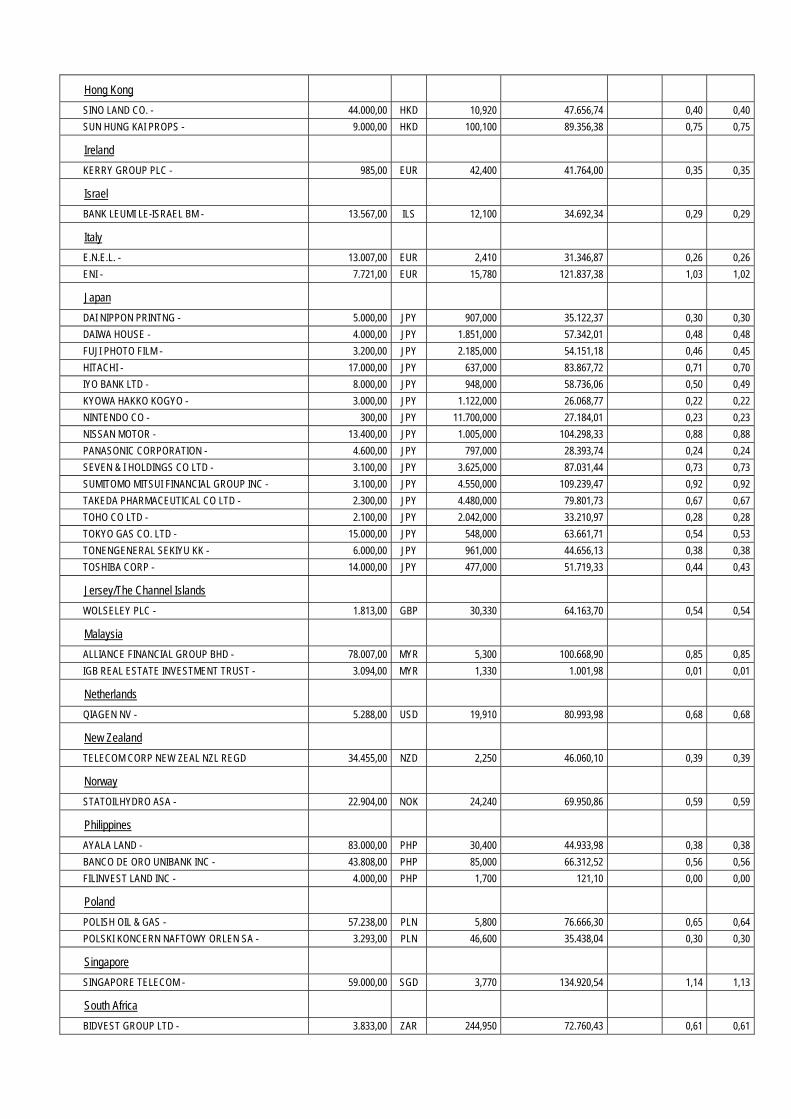

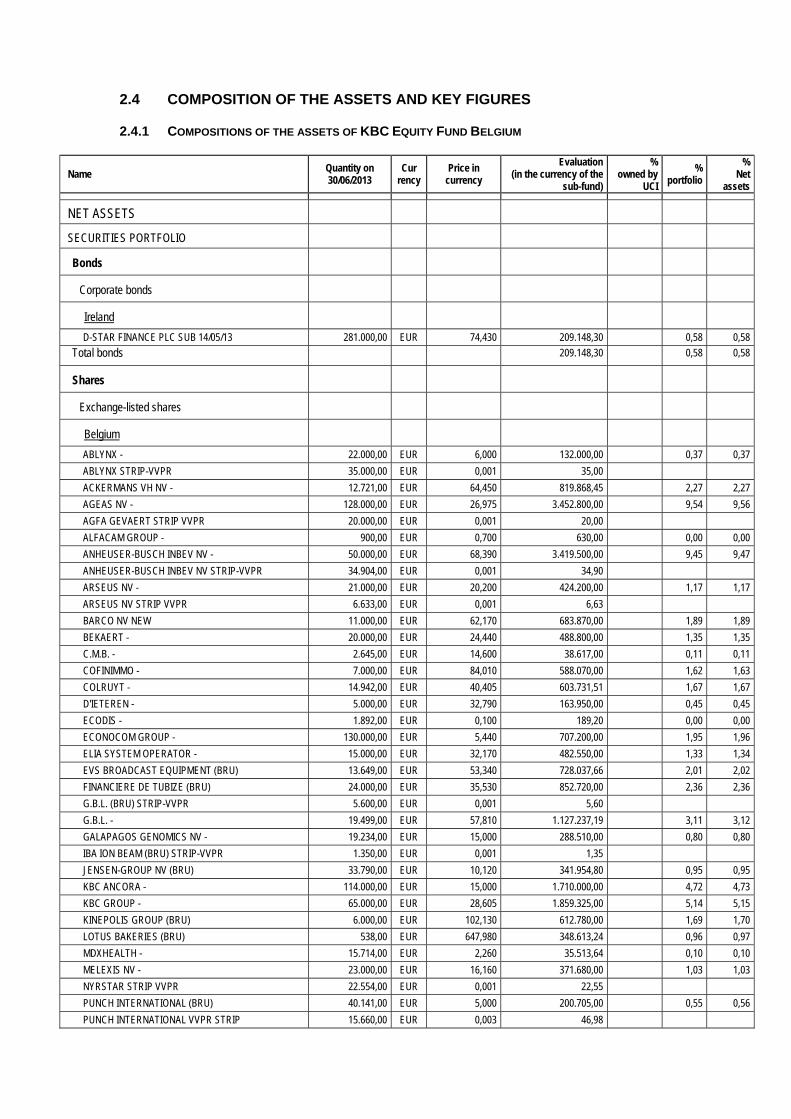

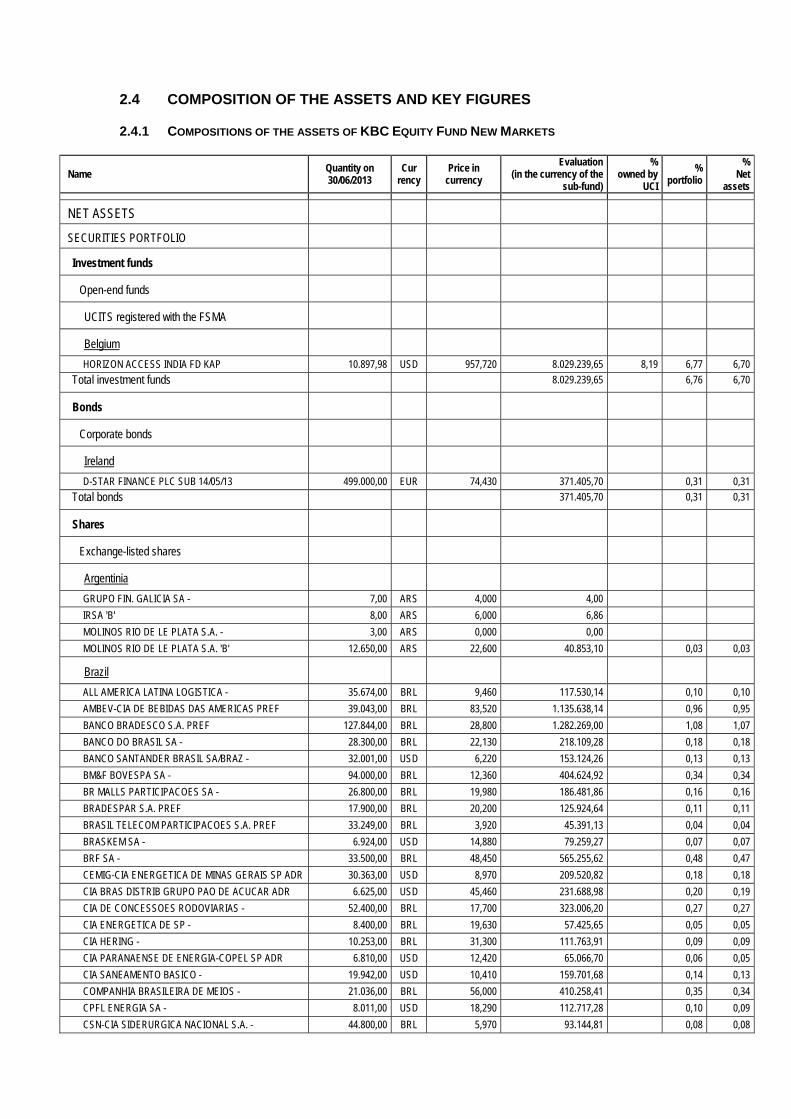

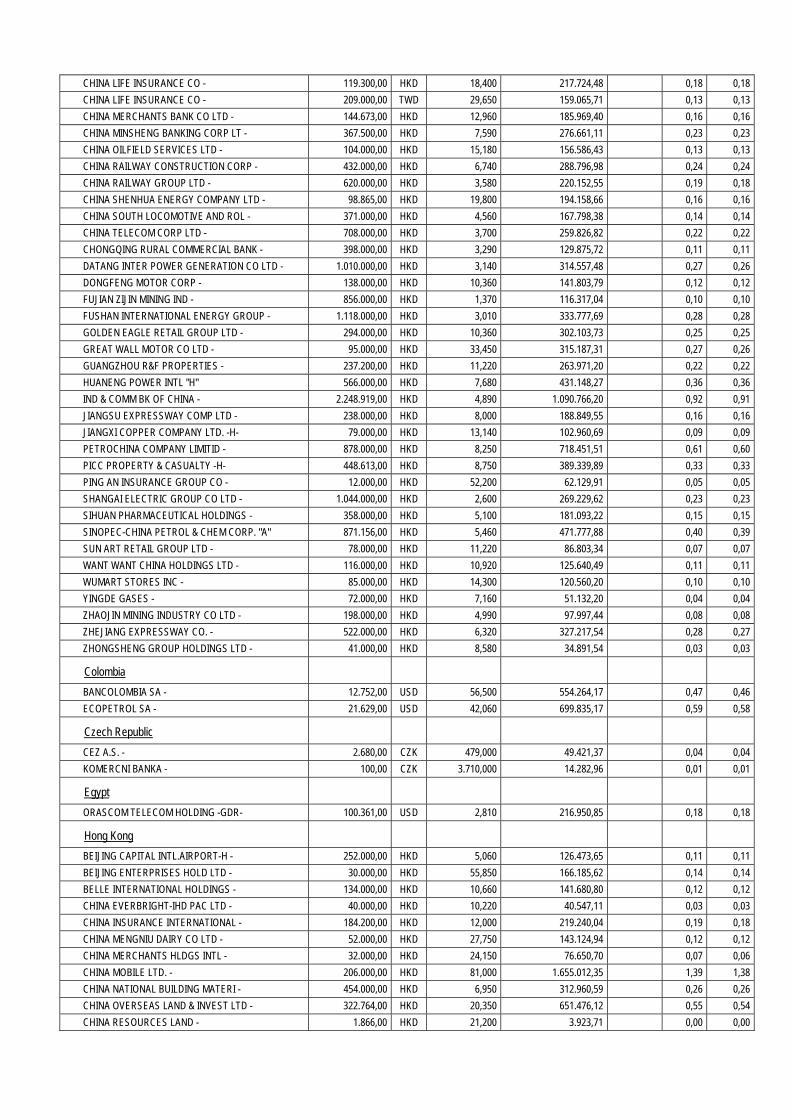

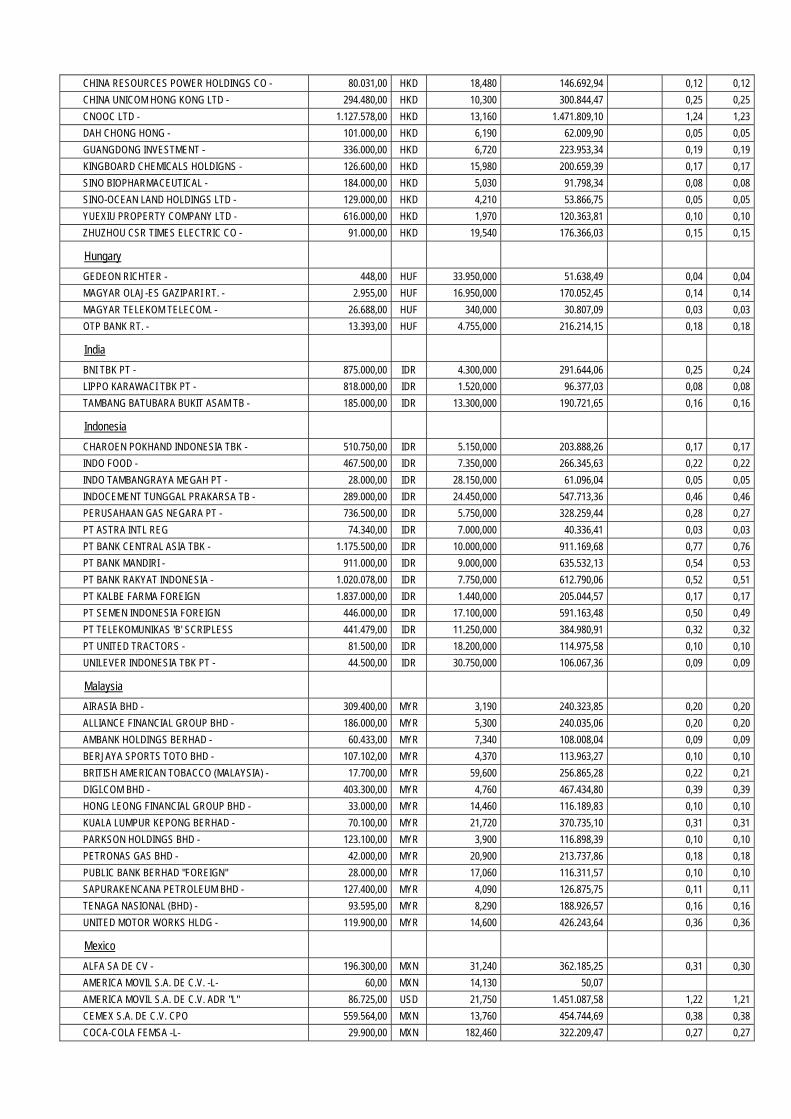

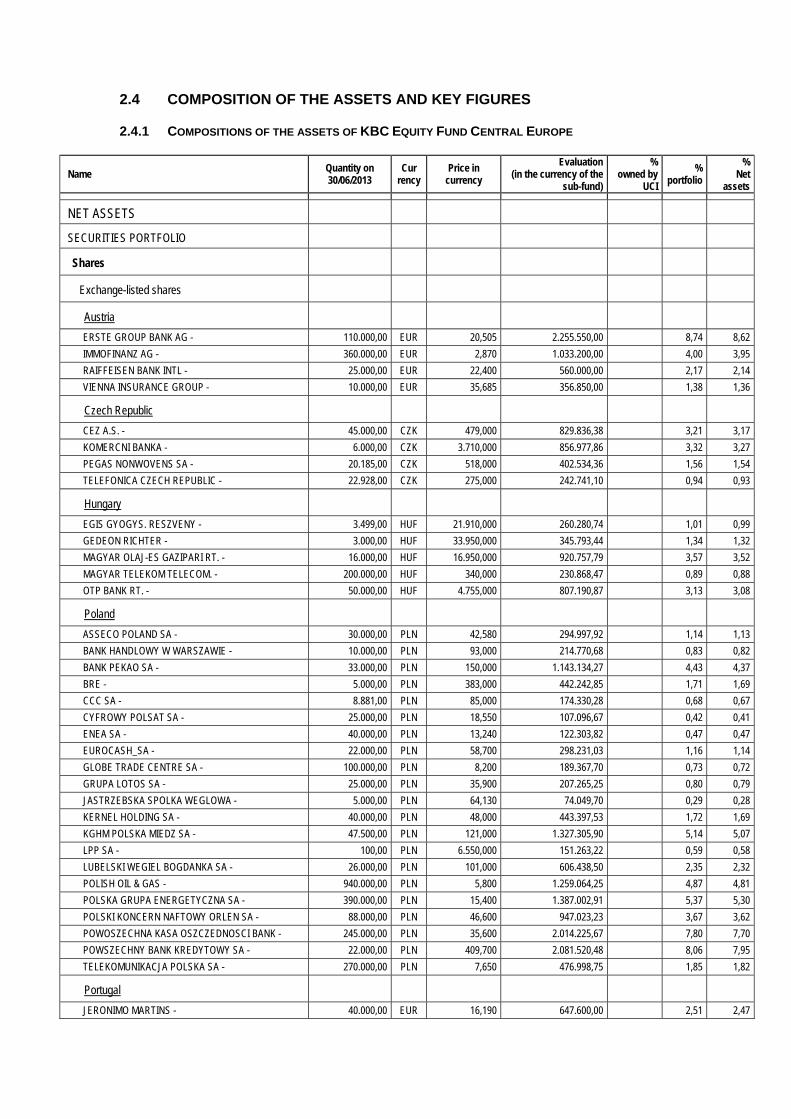

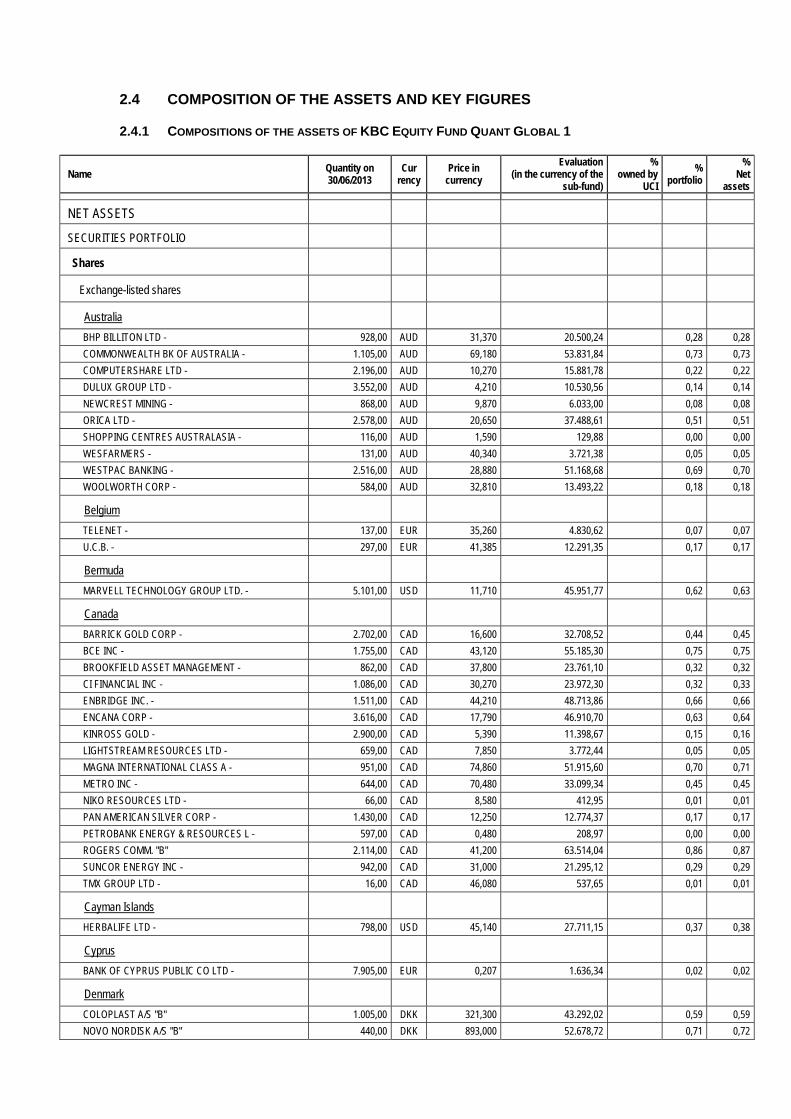

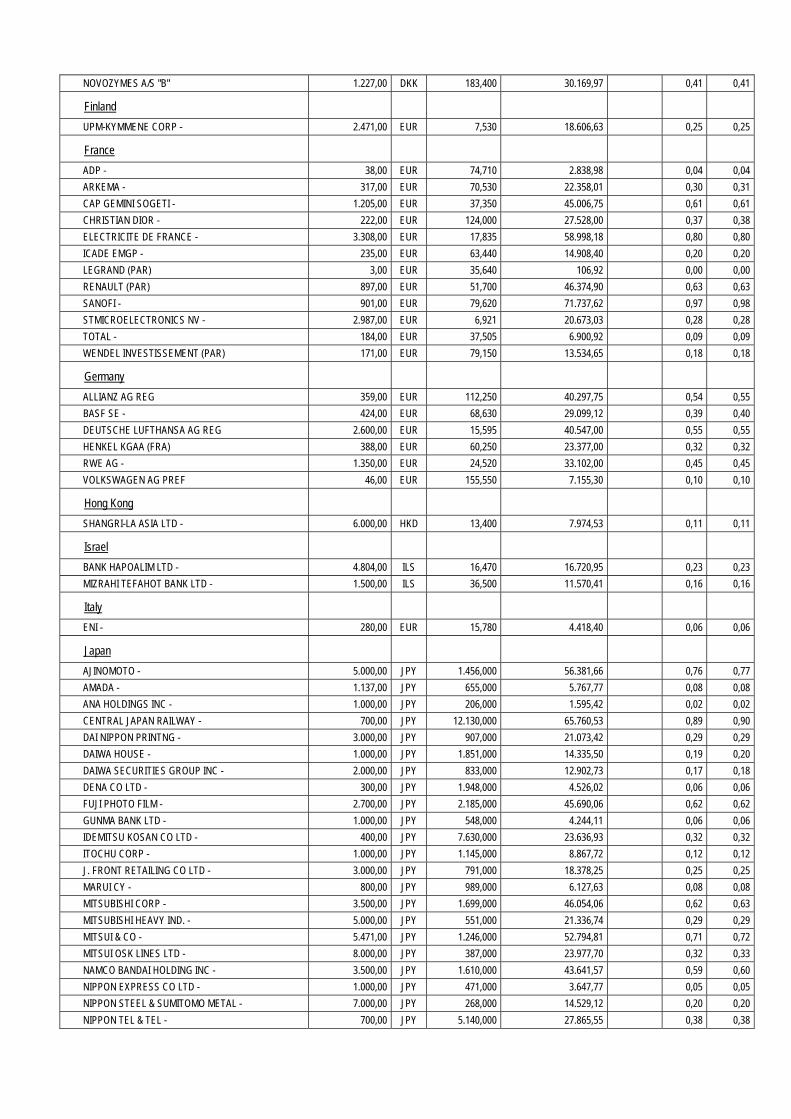

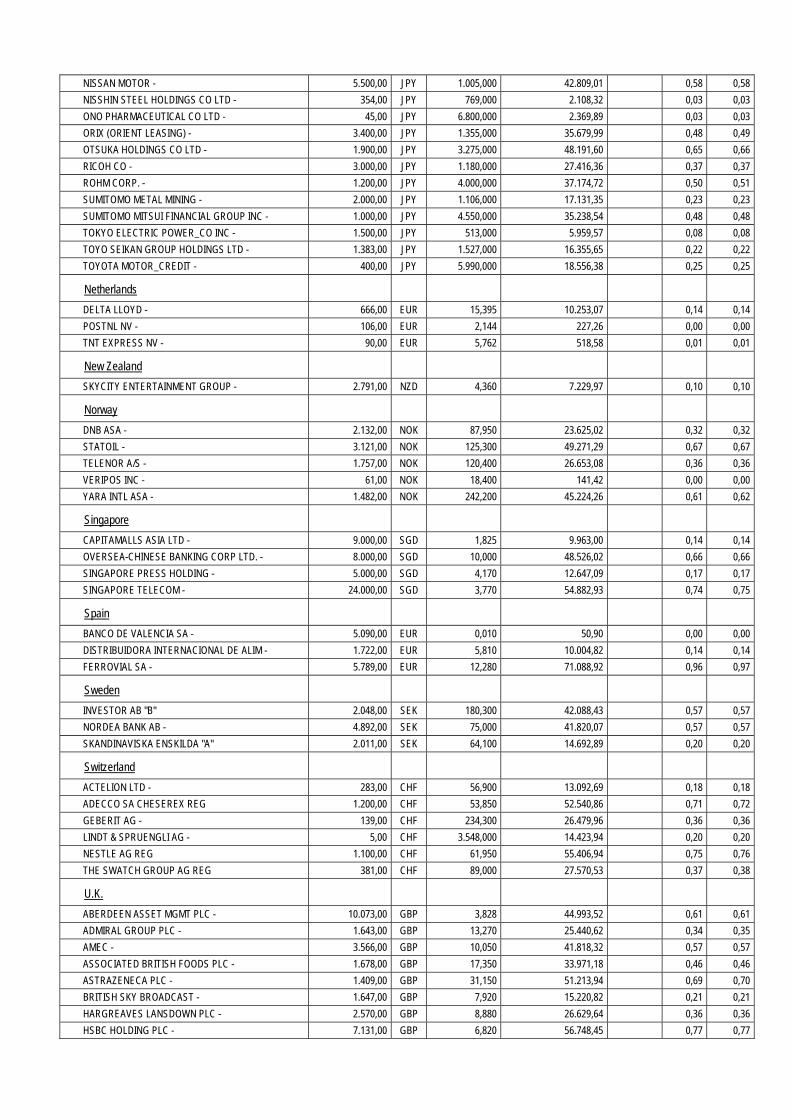

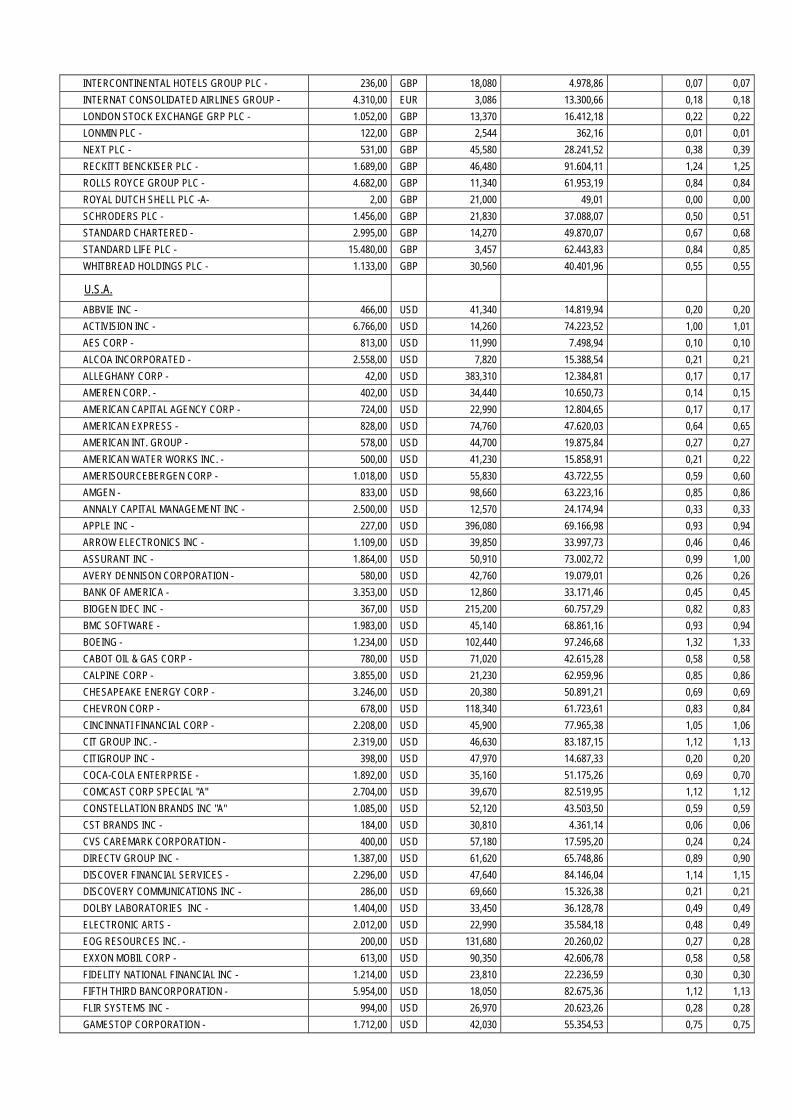

2.4 COMPOSITION OF THE ASSETS AND KEY FIGURES

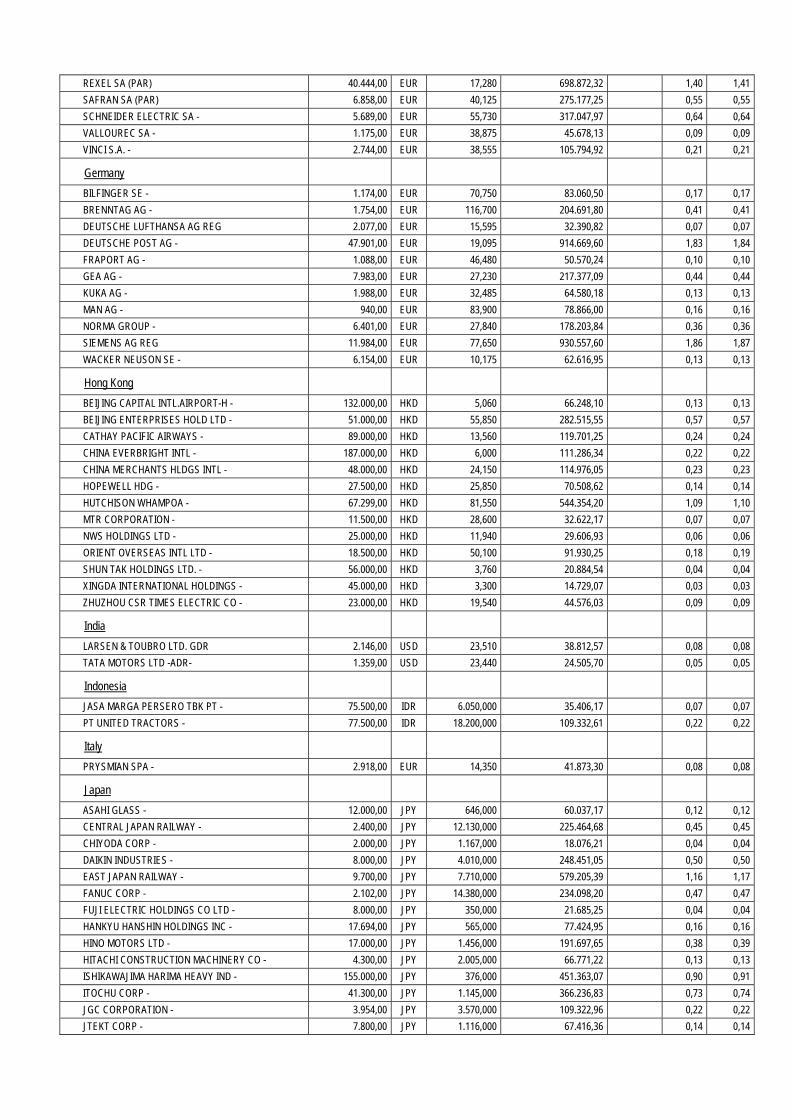

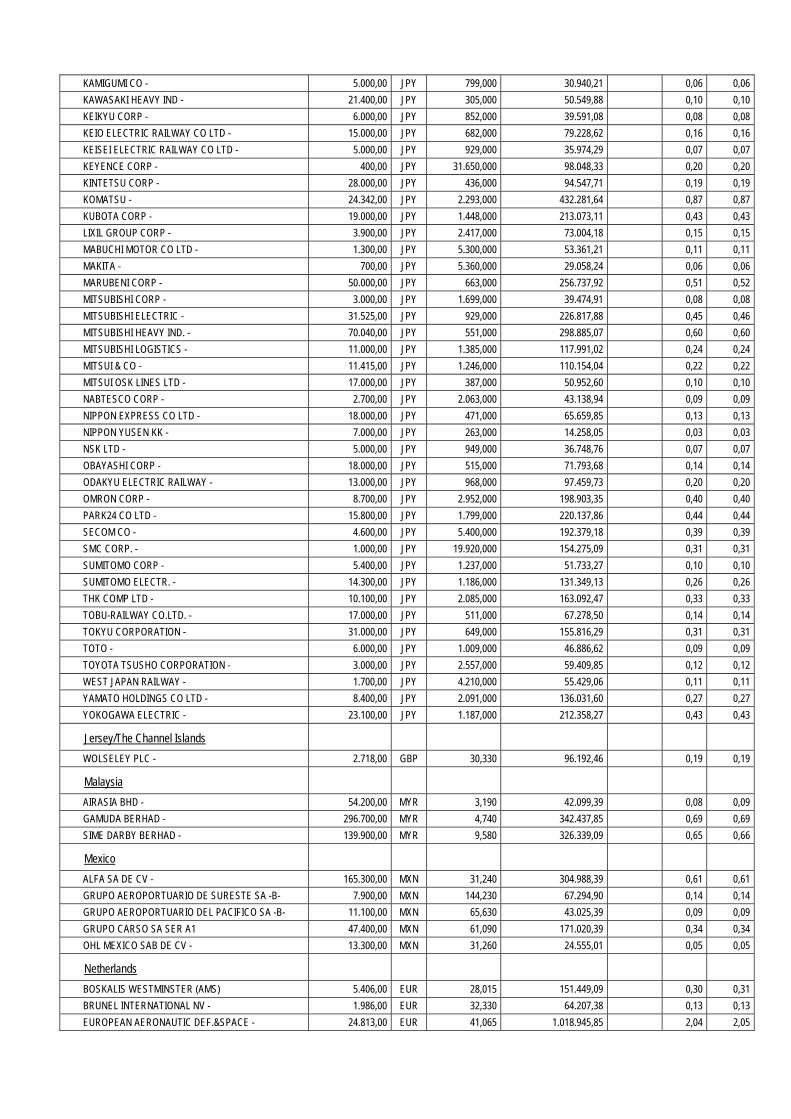

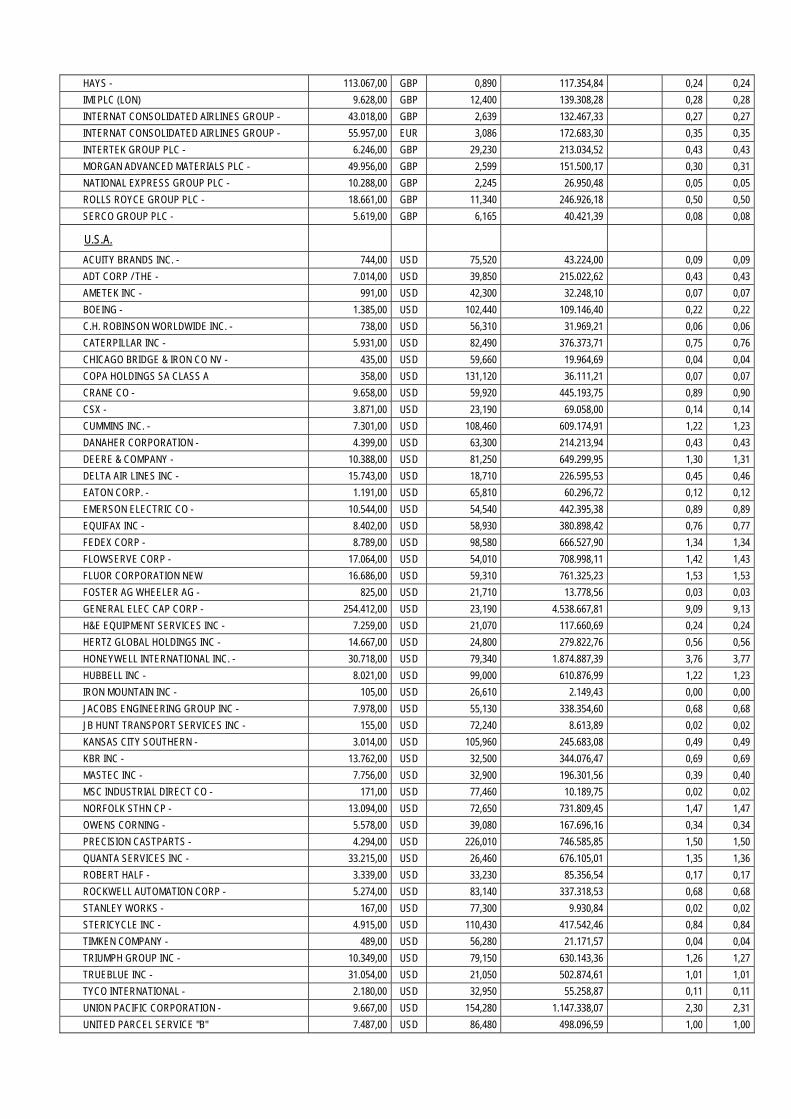

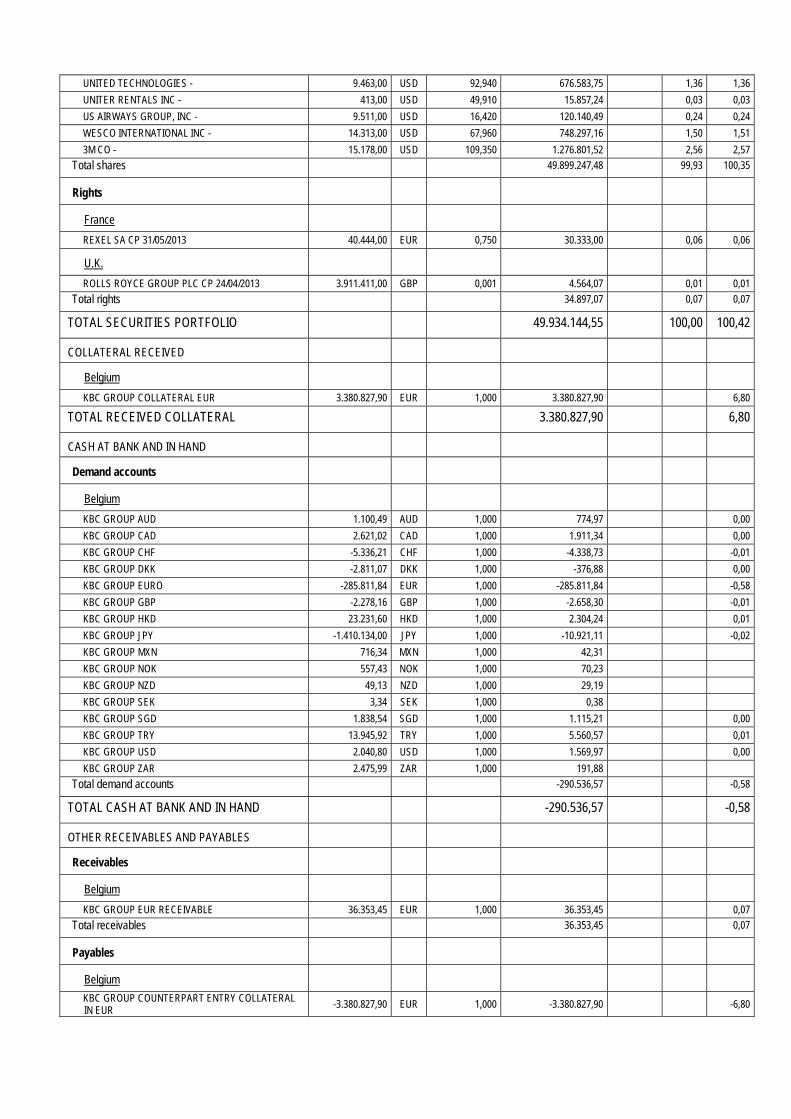

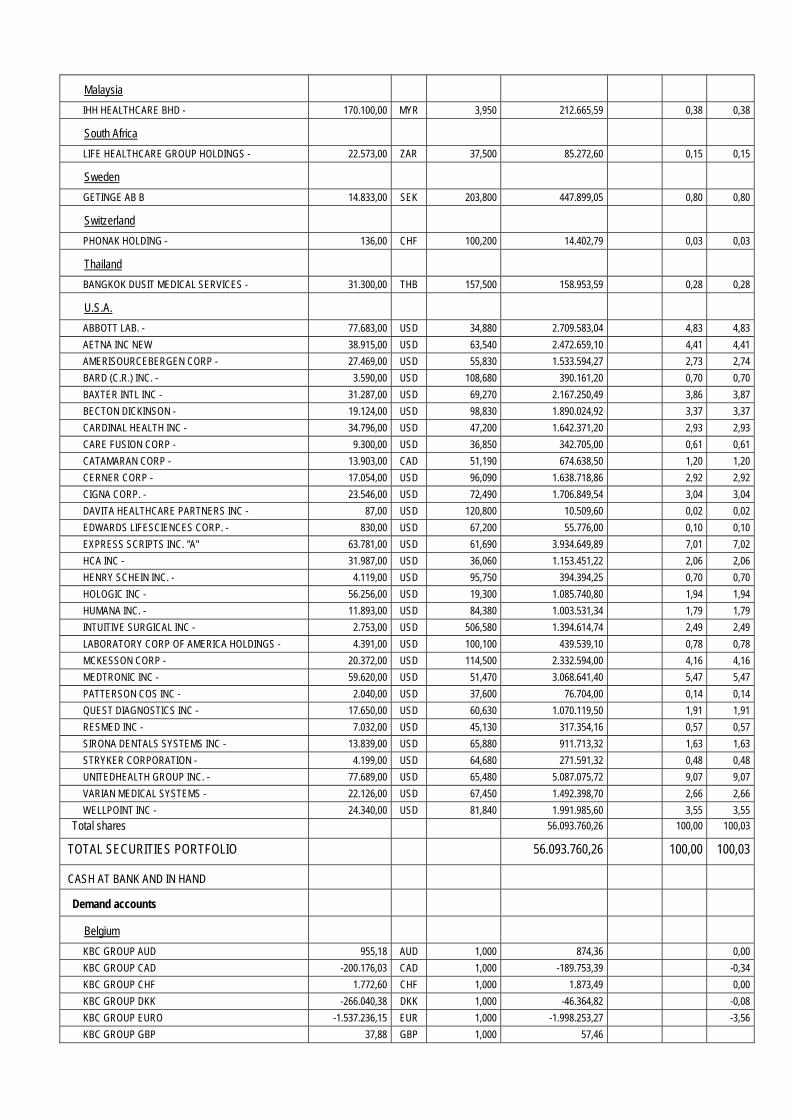

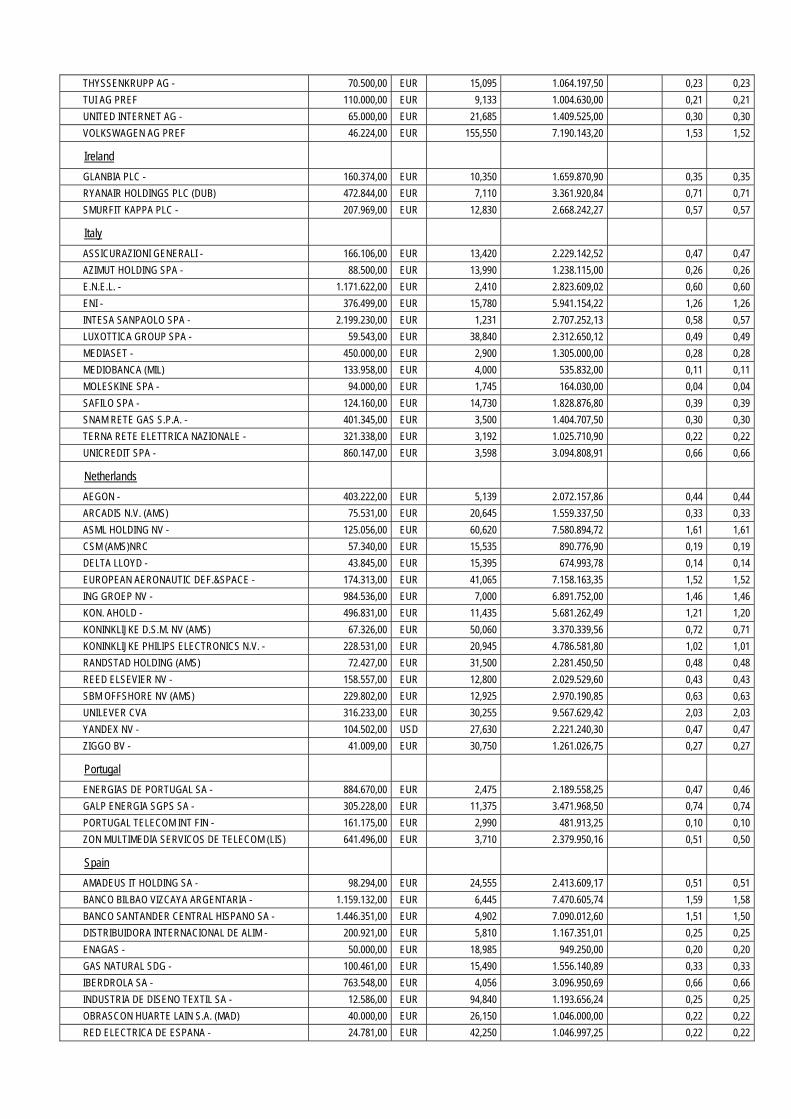

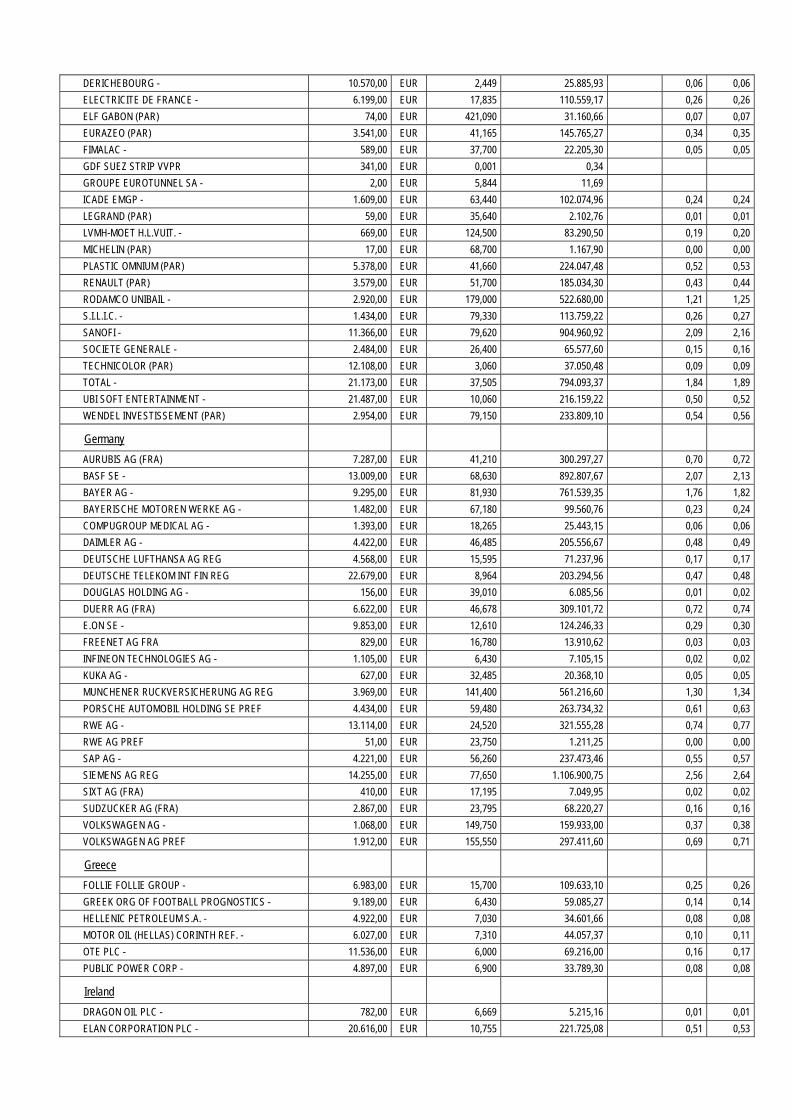

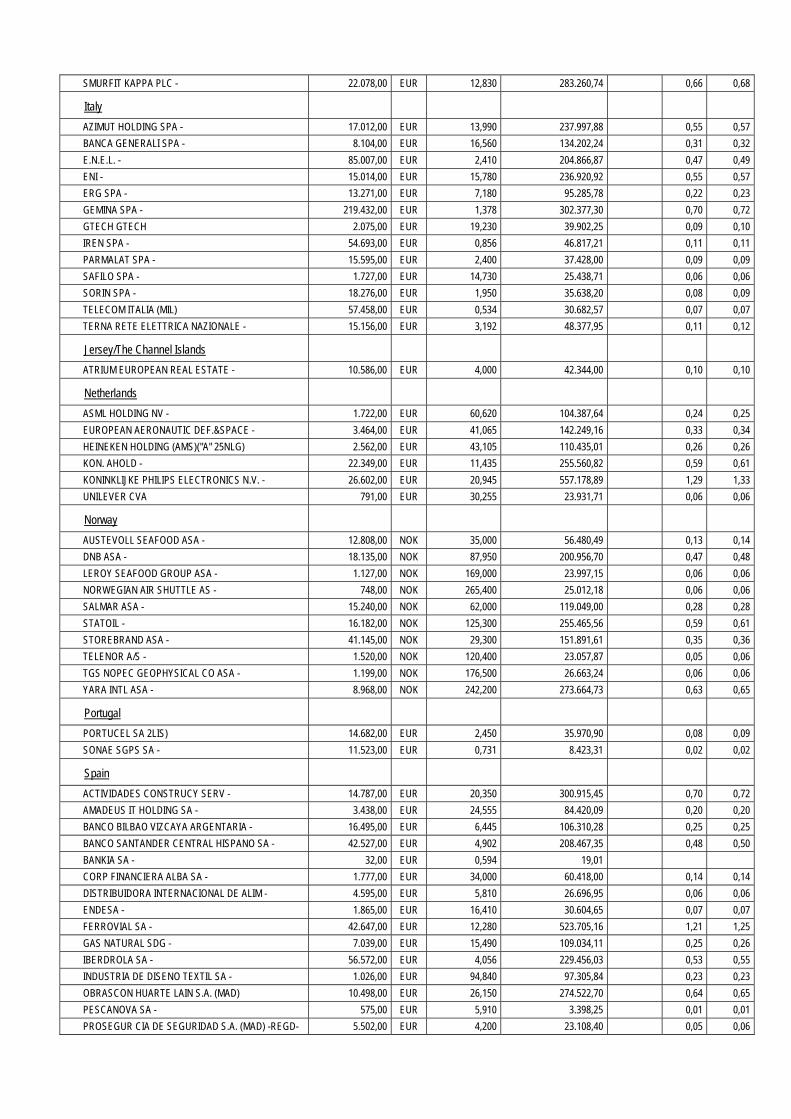

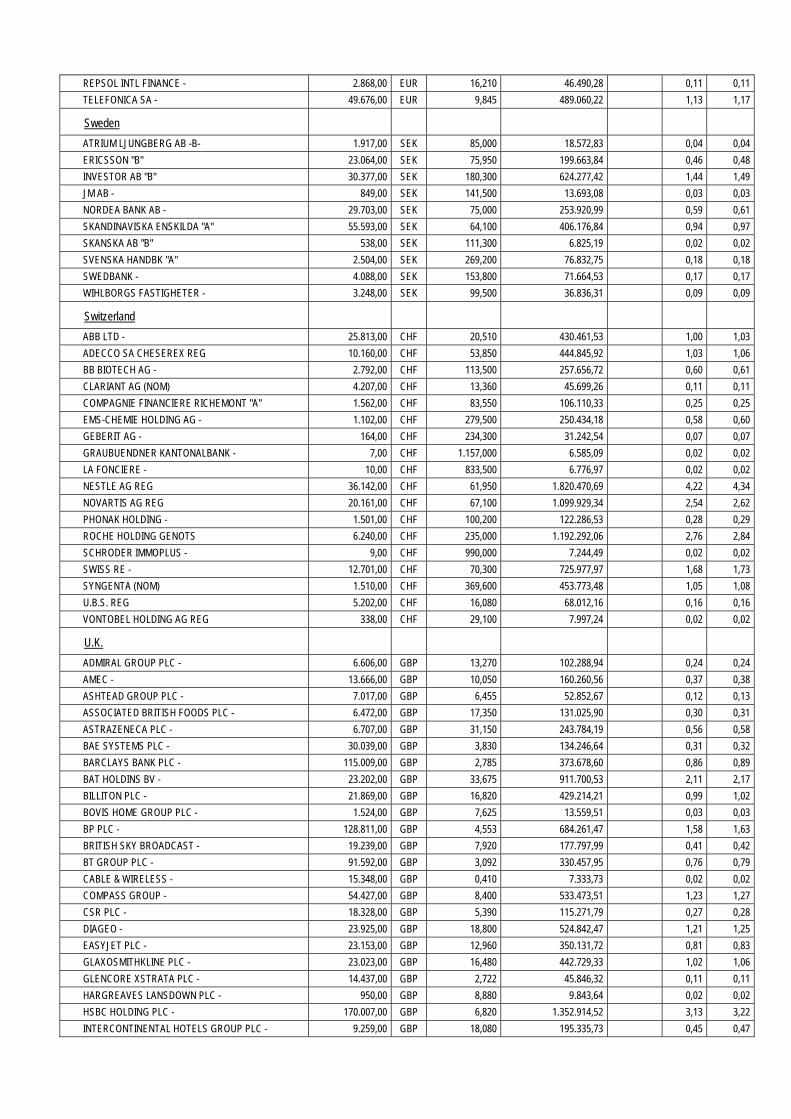

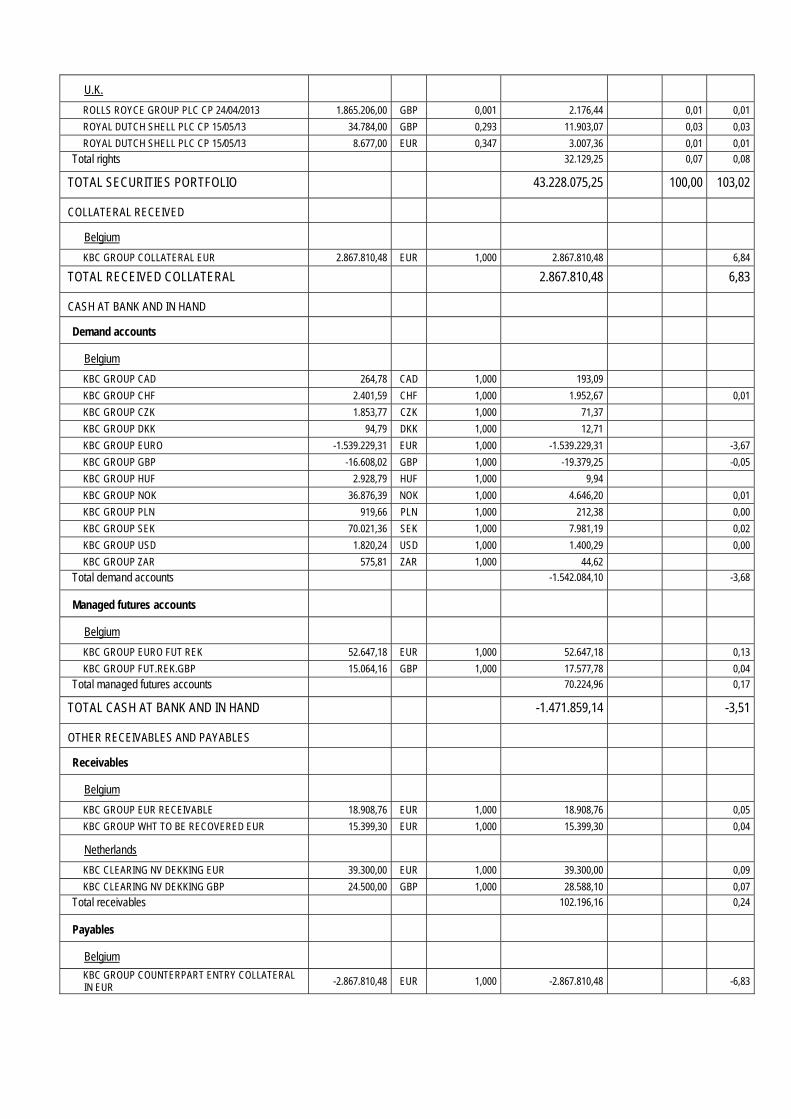

2.4.1 COMPOSITIONS OF THE ASSETS OF KBC EQUITY FUND CSOB AKCIOVY FOND

DIVIDENDOVYCH FIREM

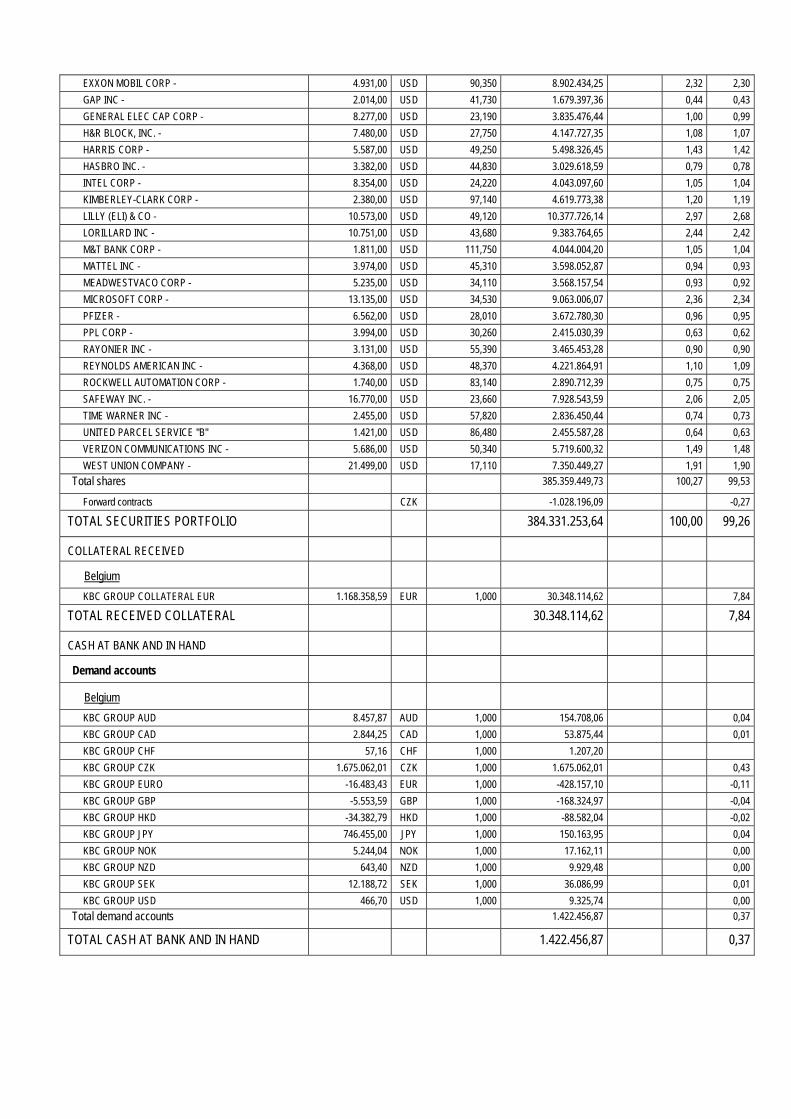

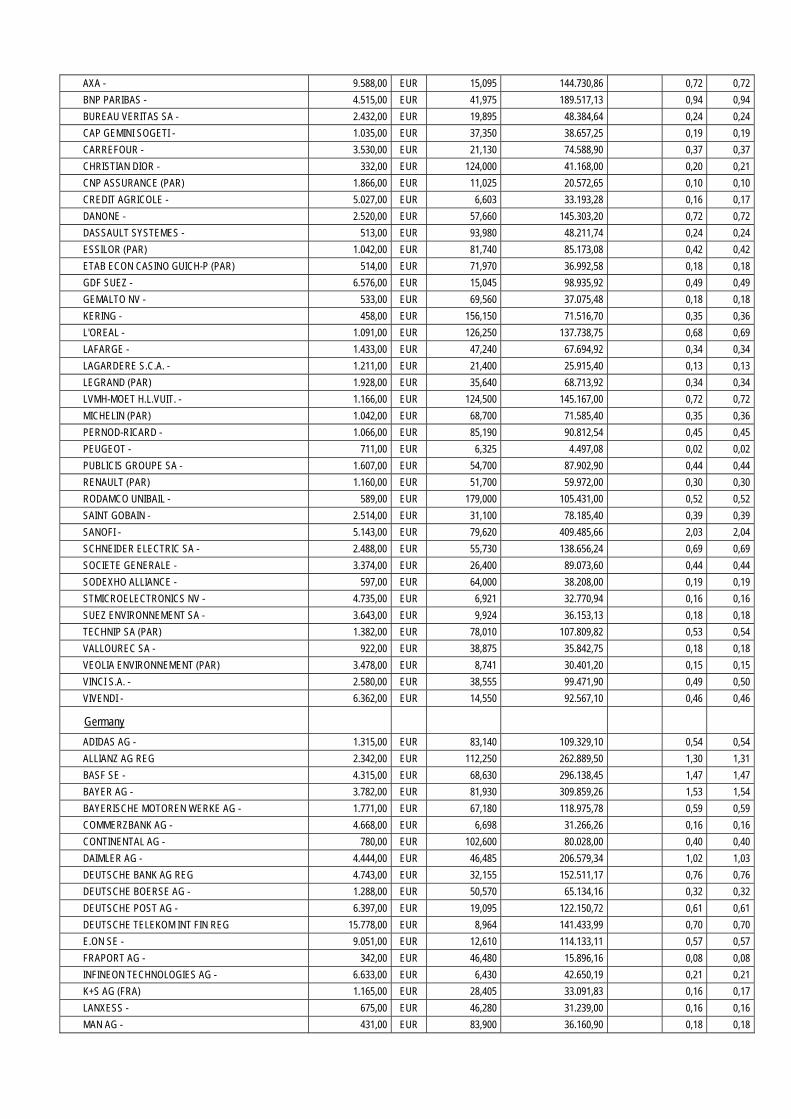

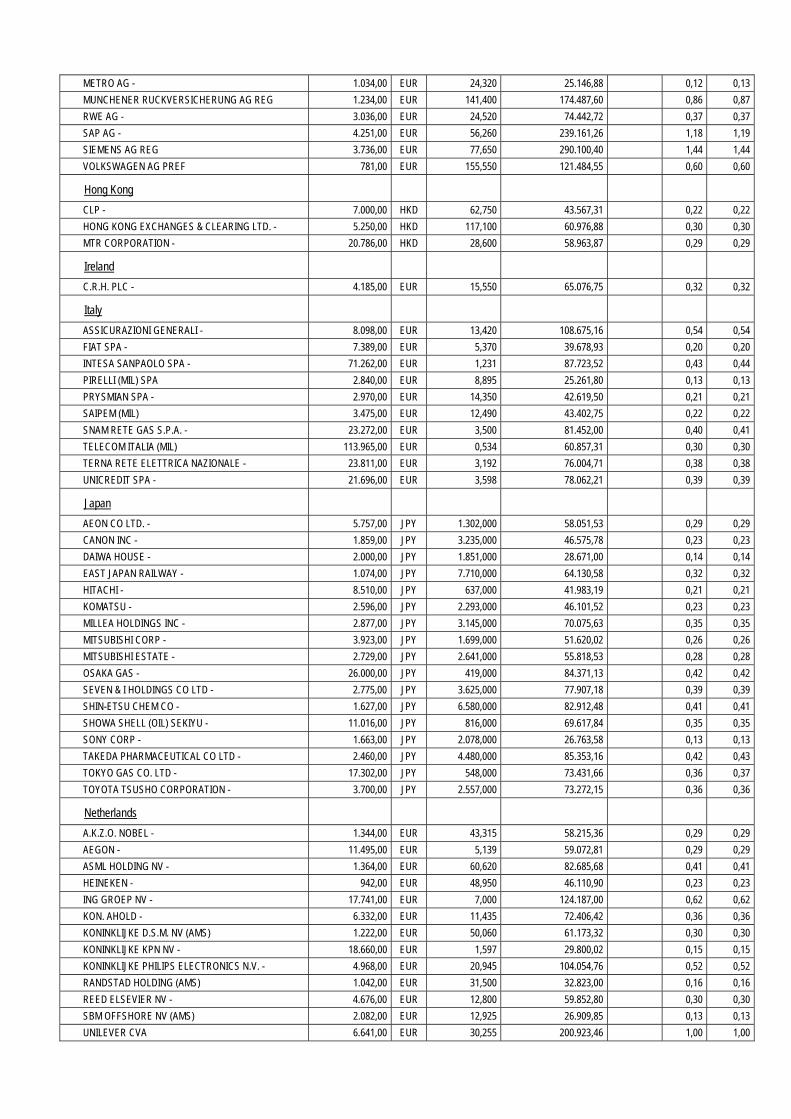

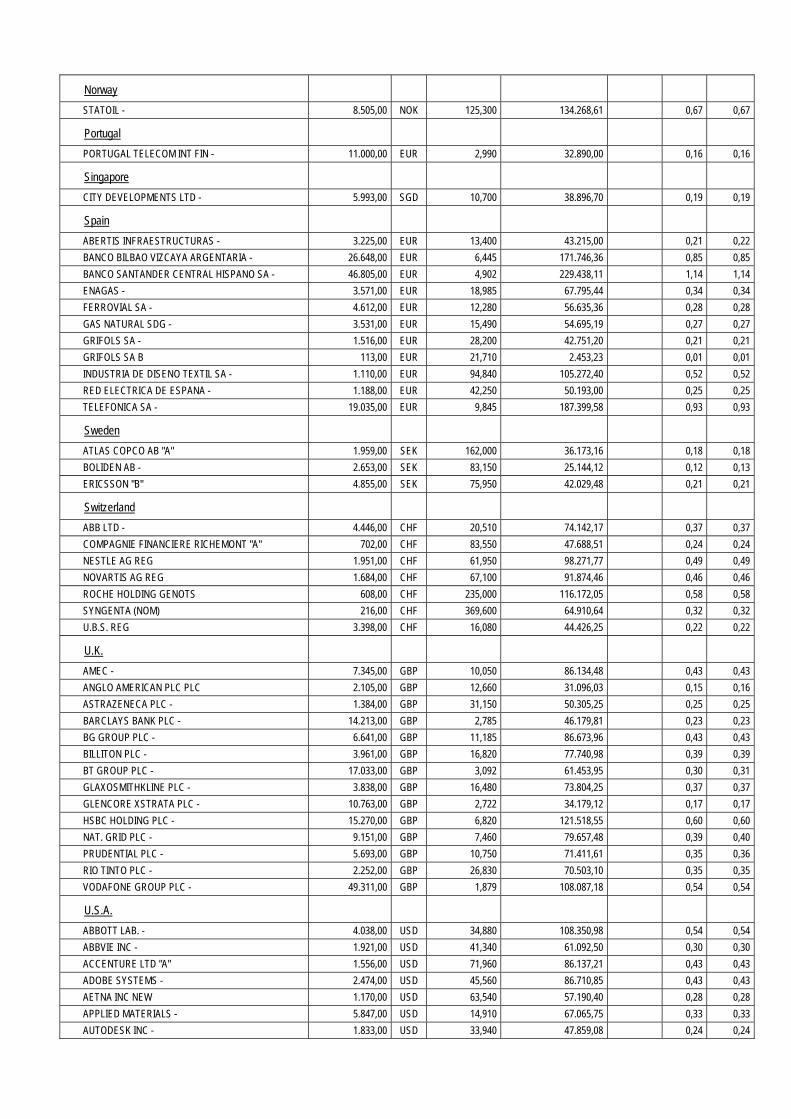

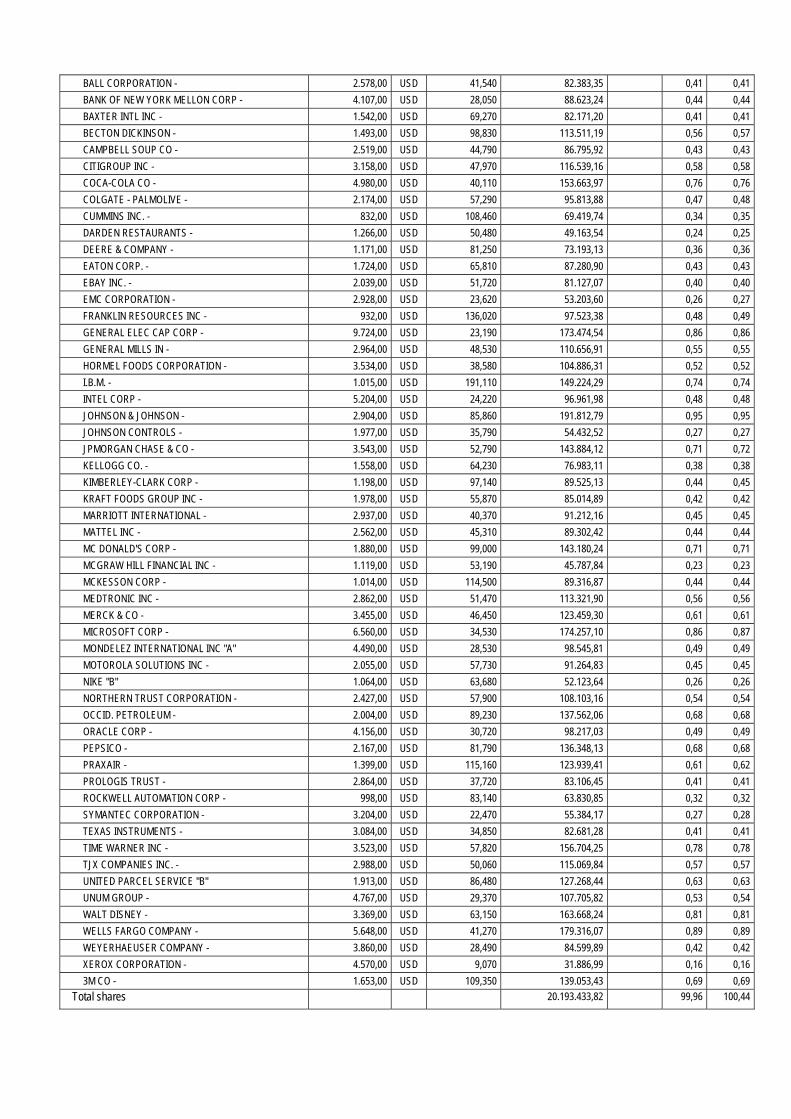

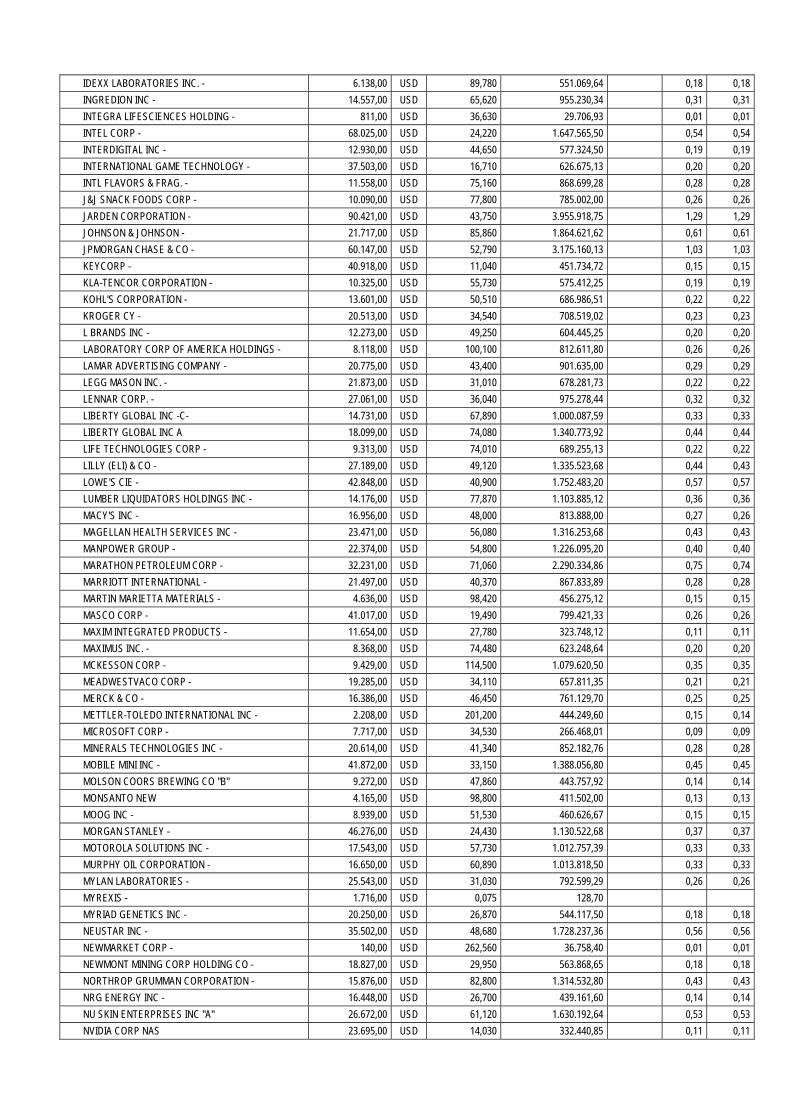

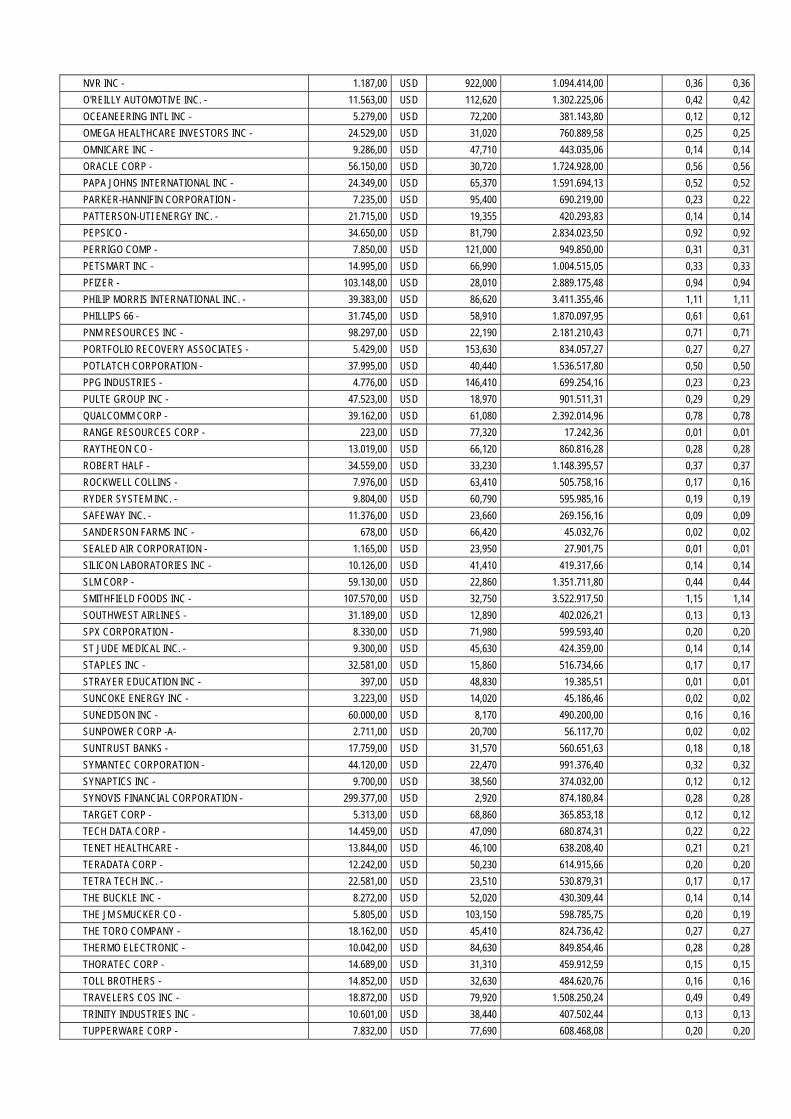

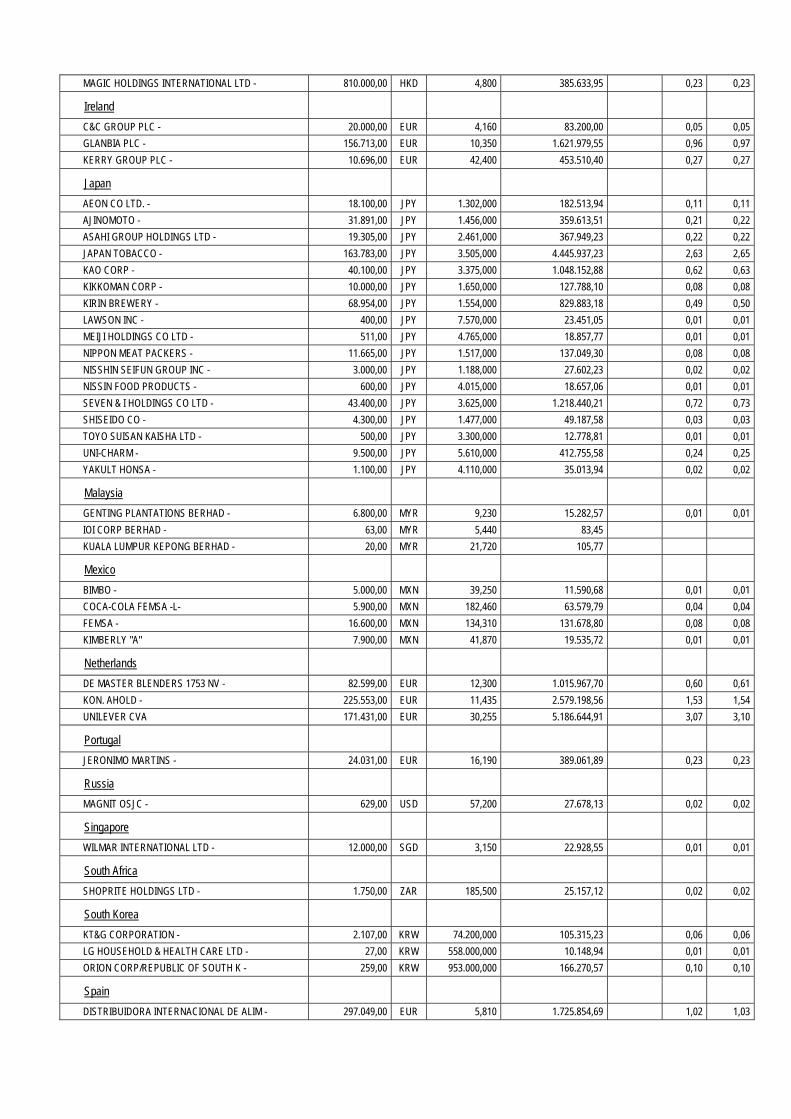

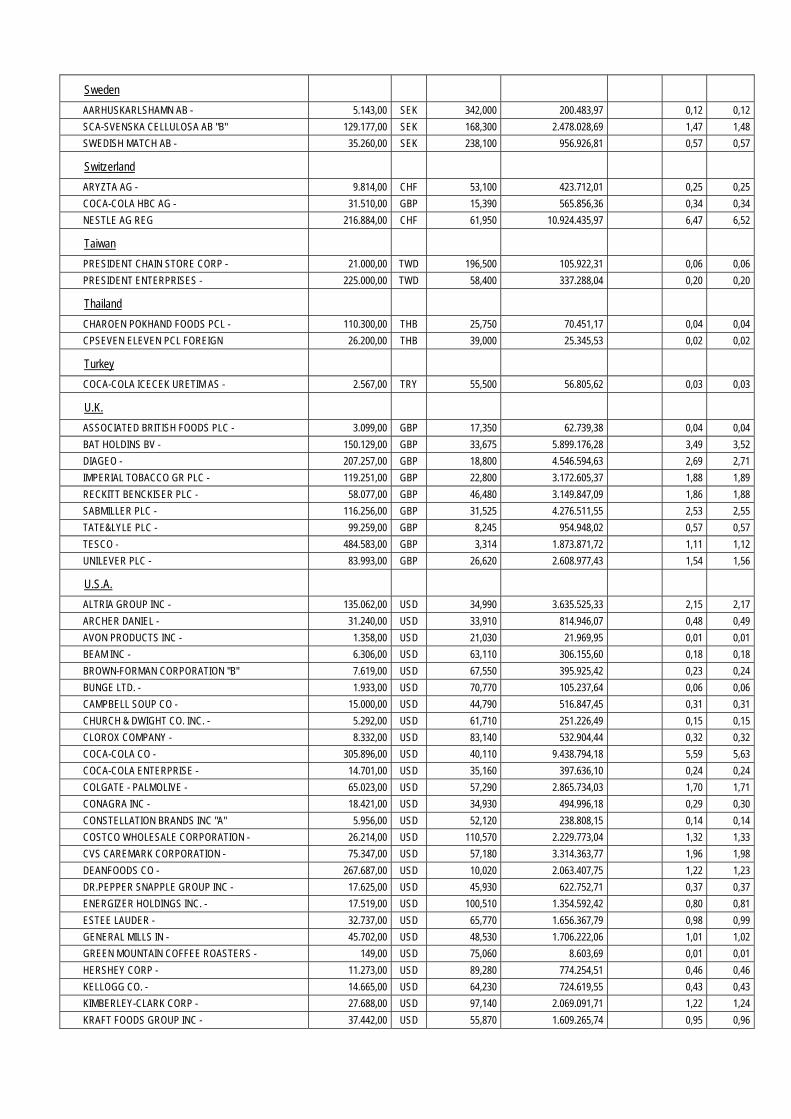

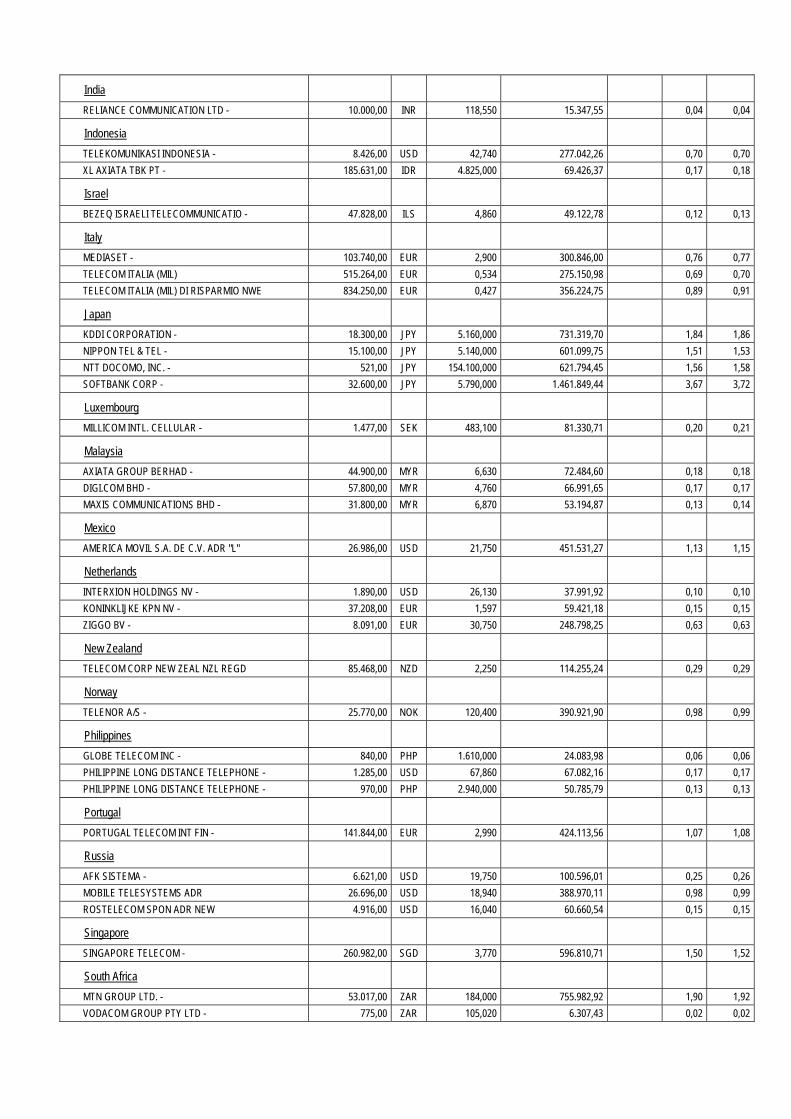

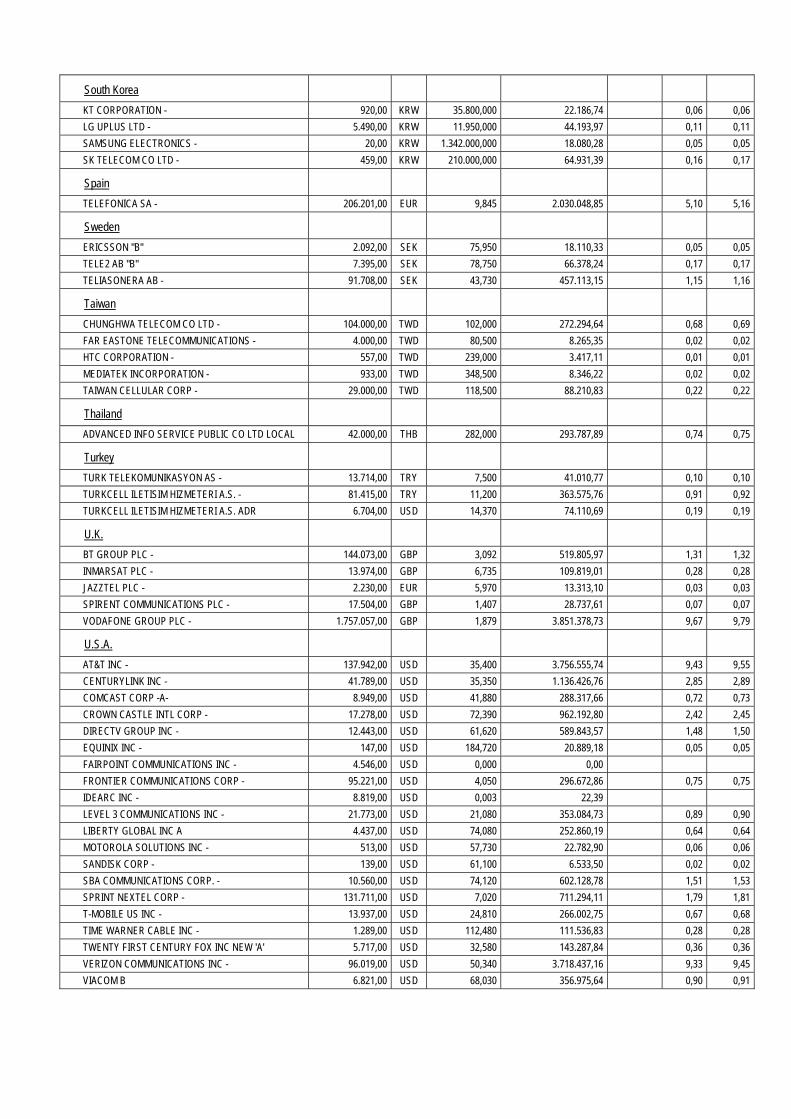

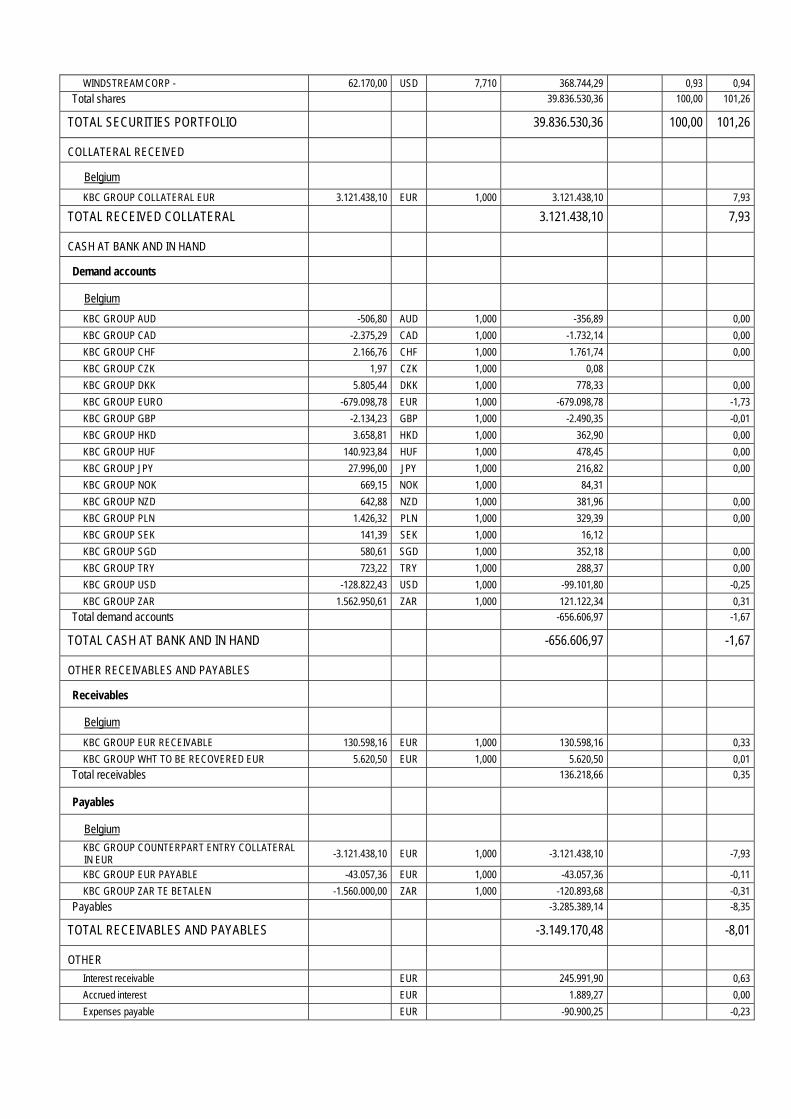

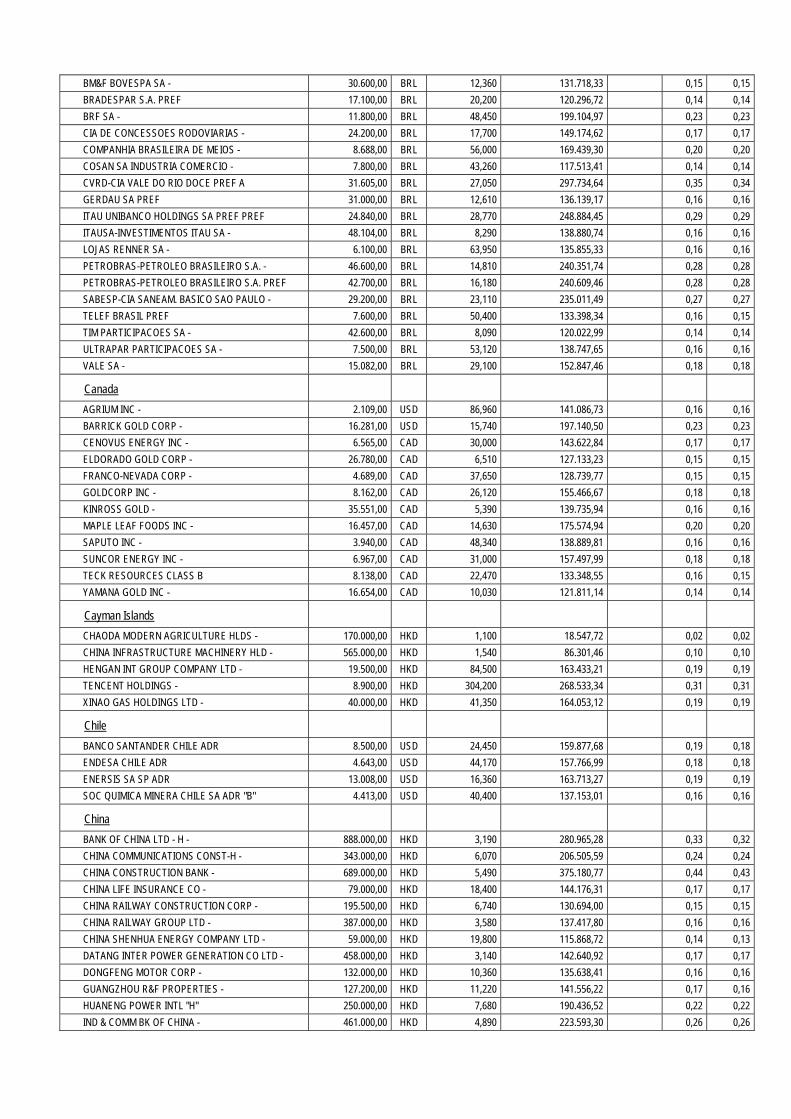

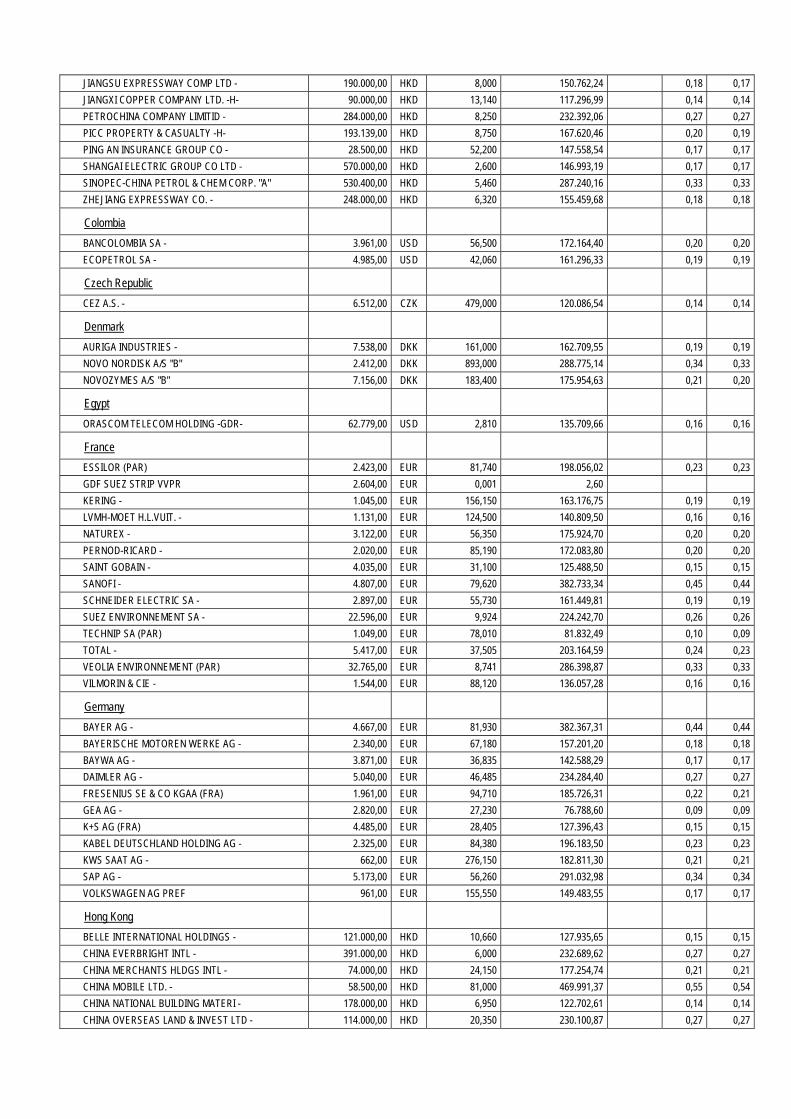

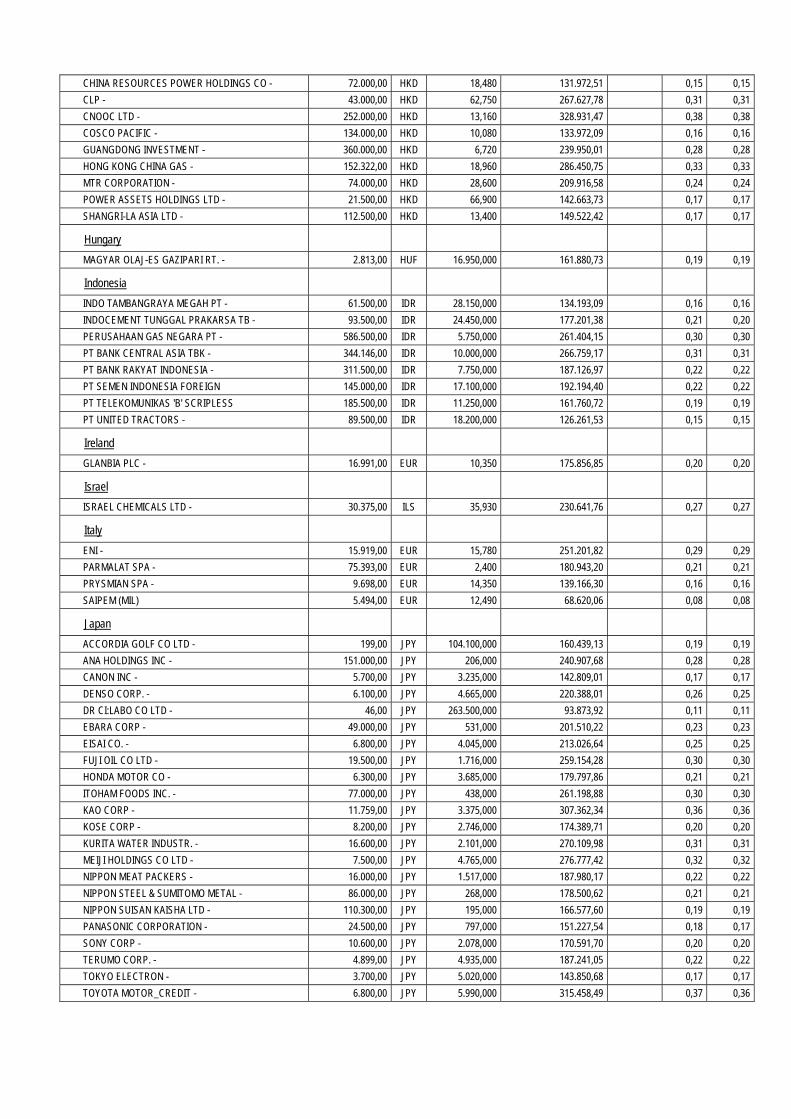

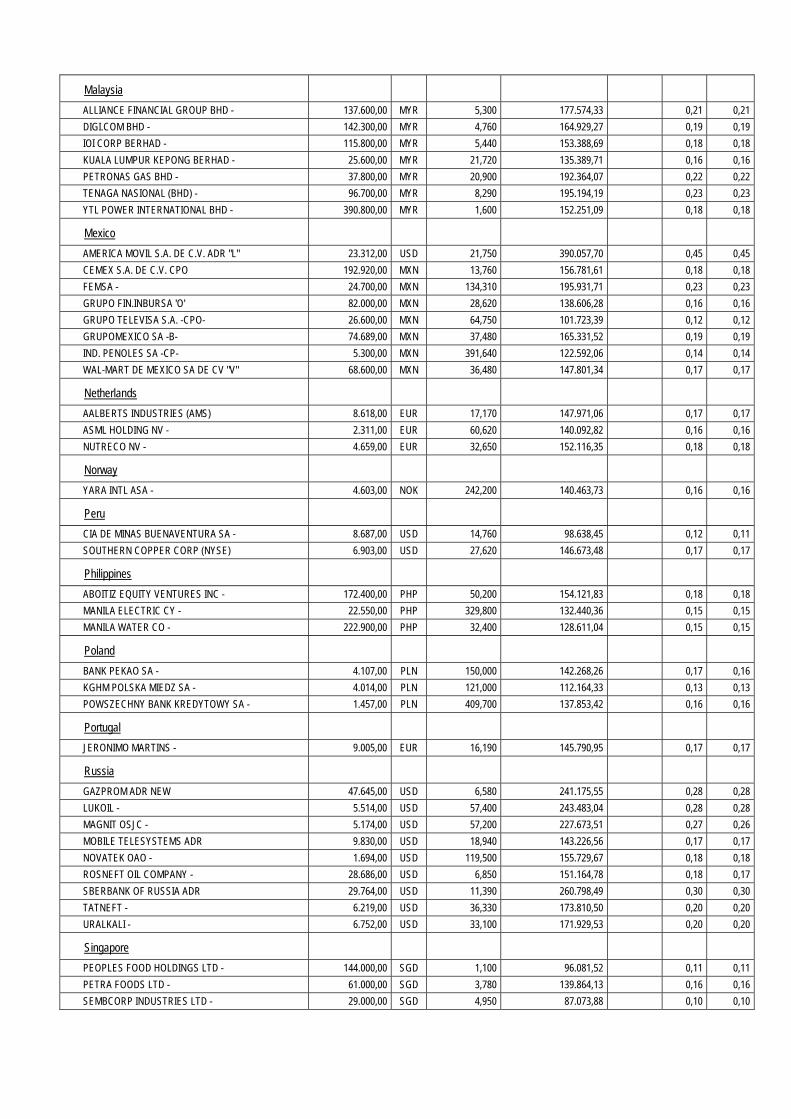

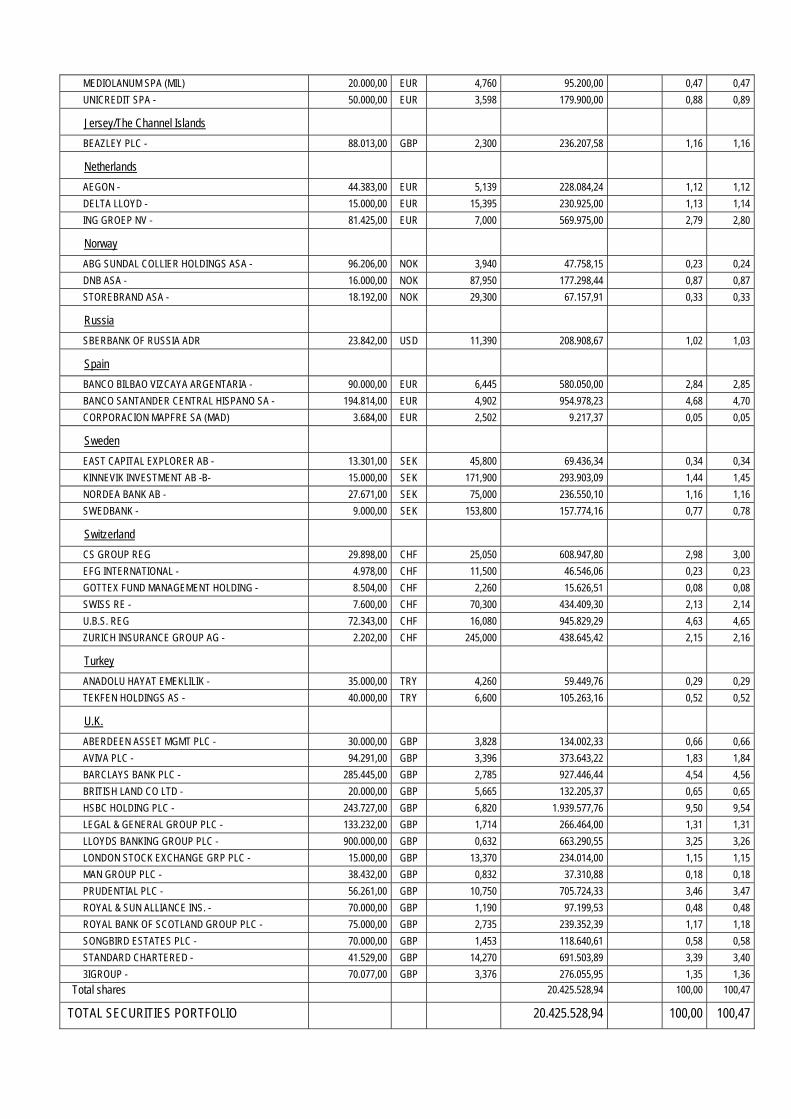

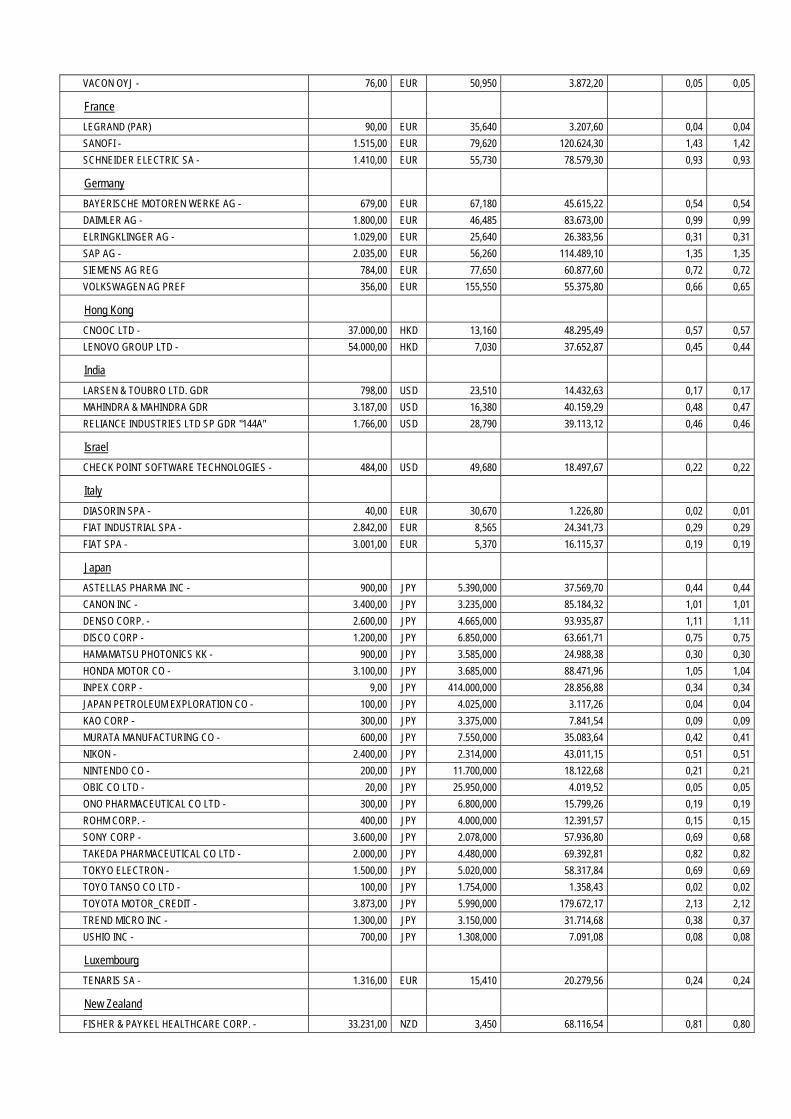

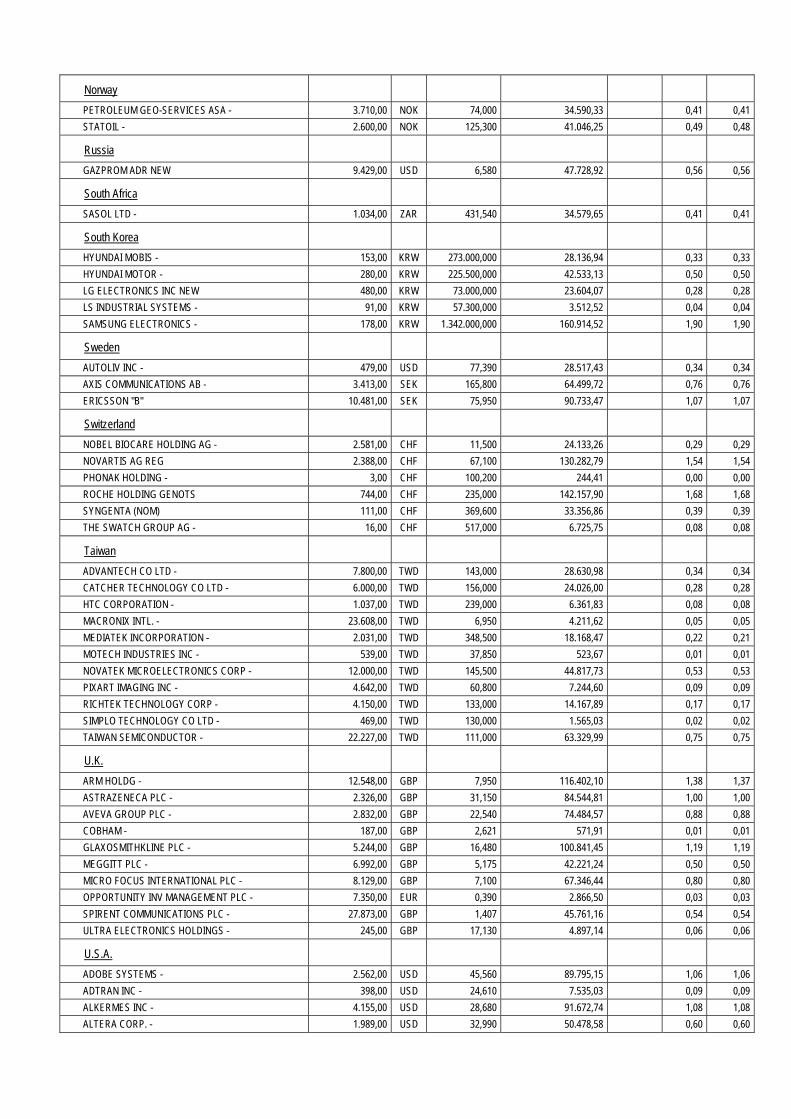

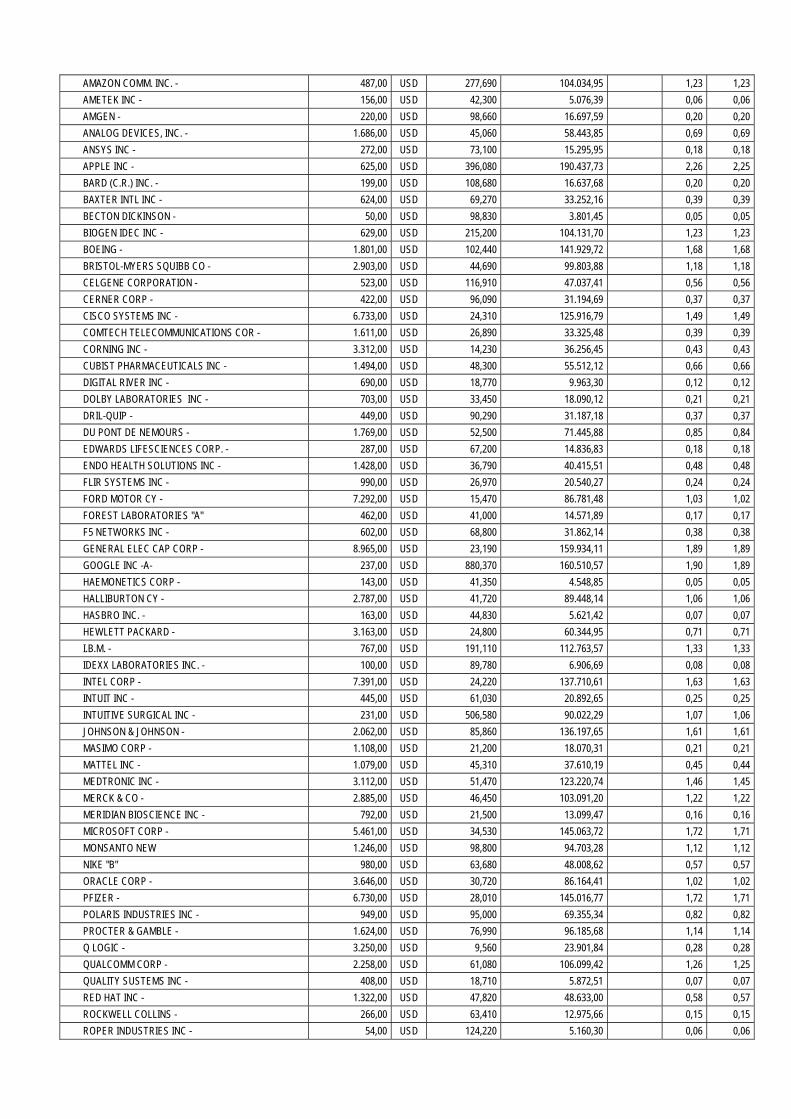

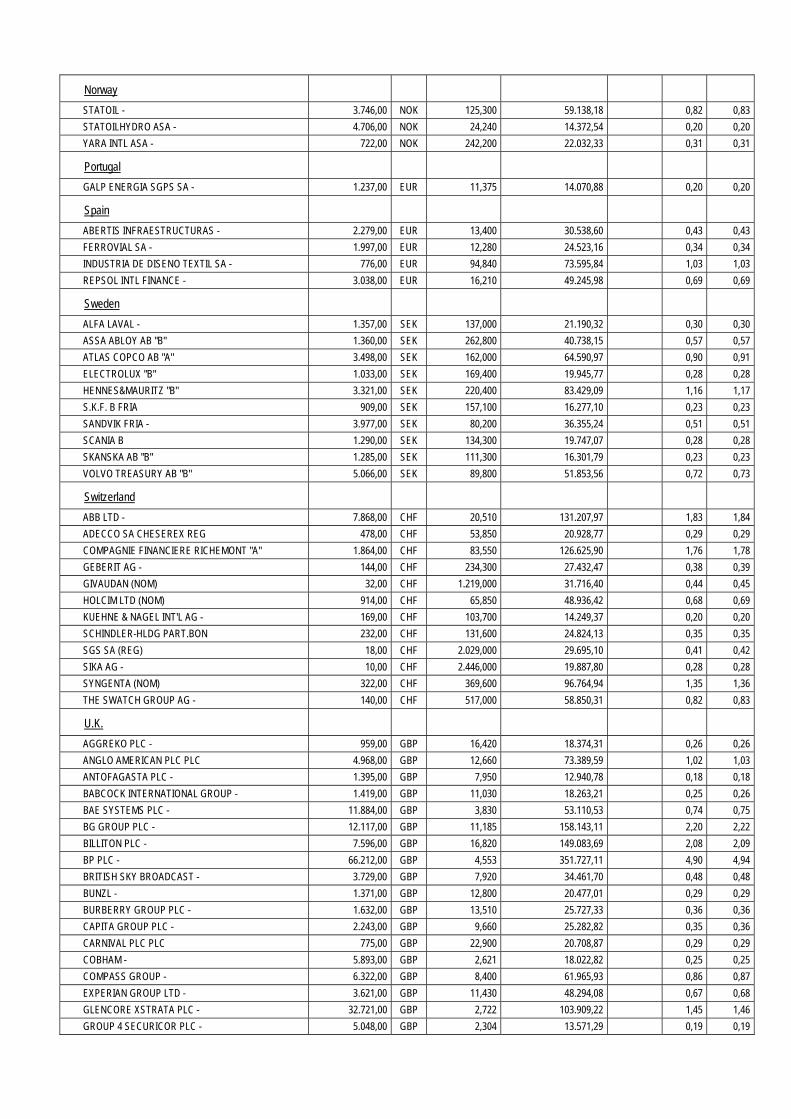

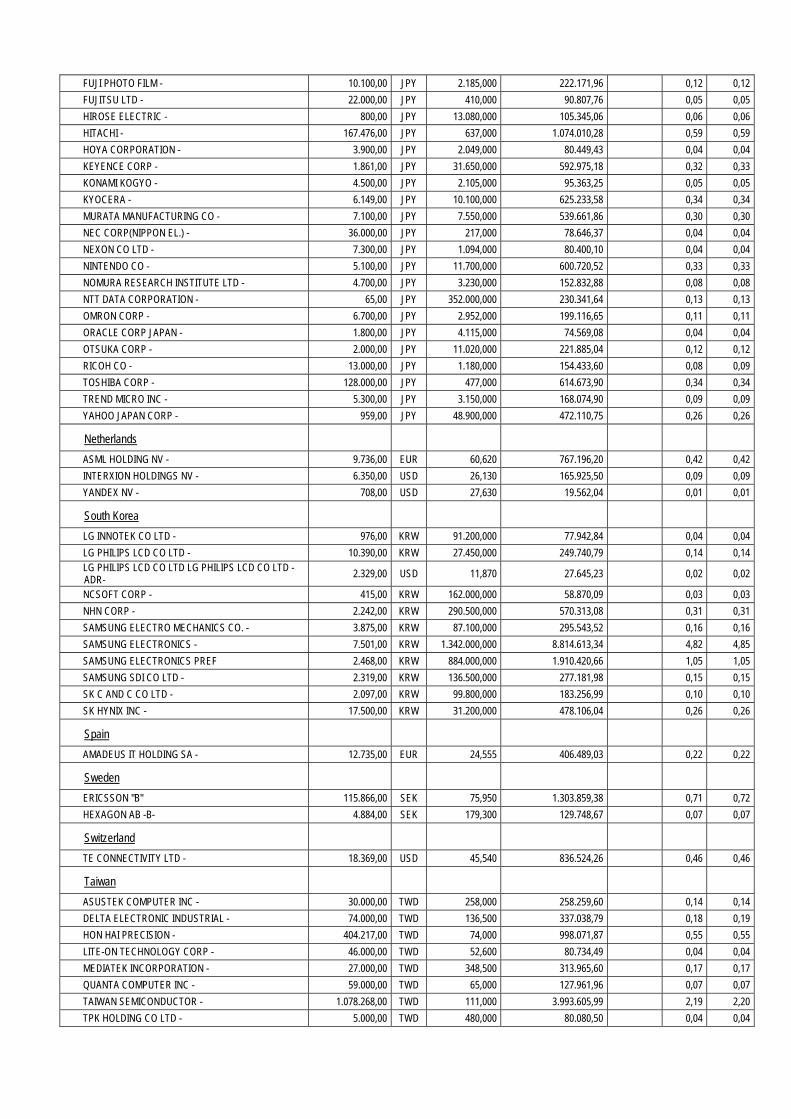

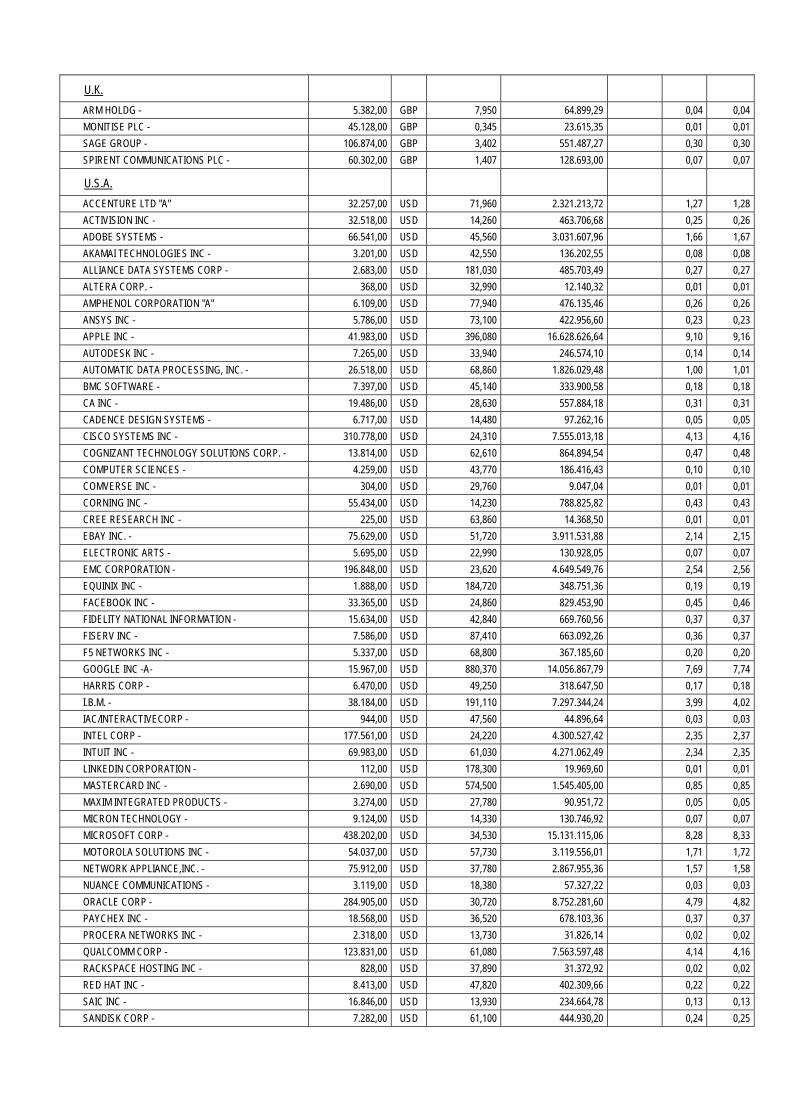

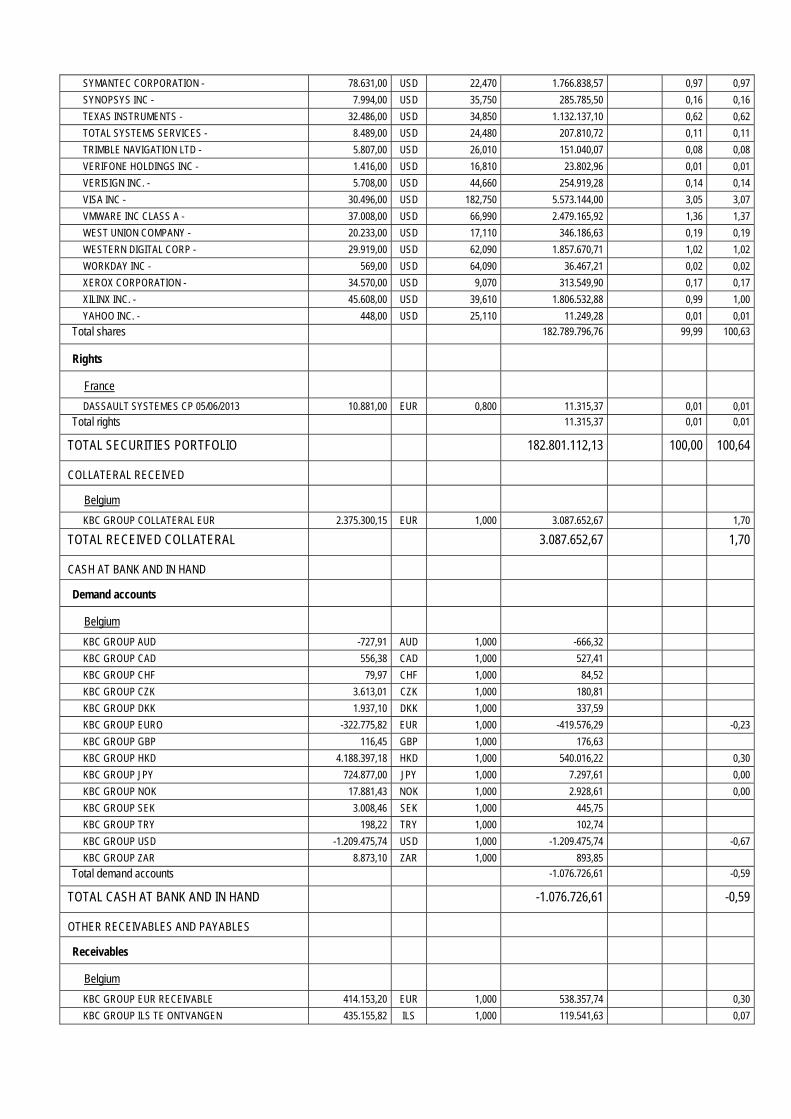

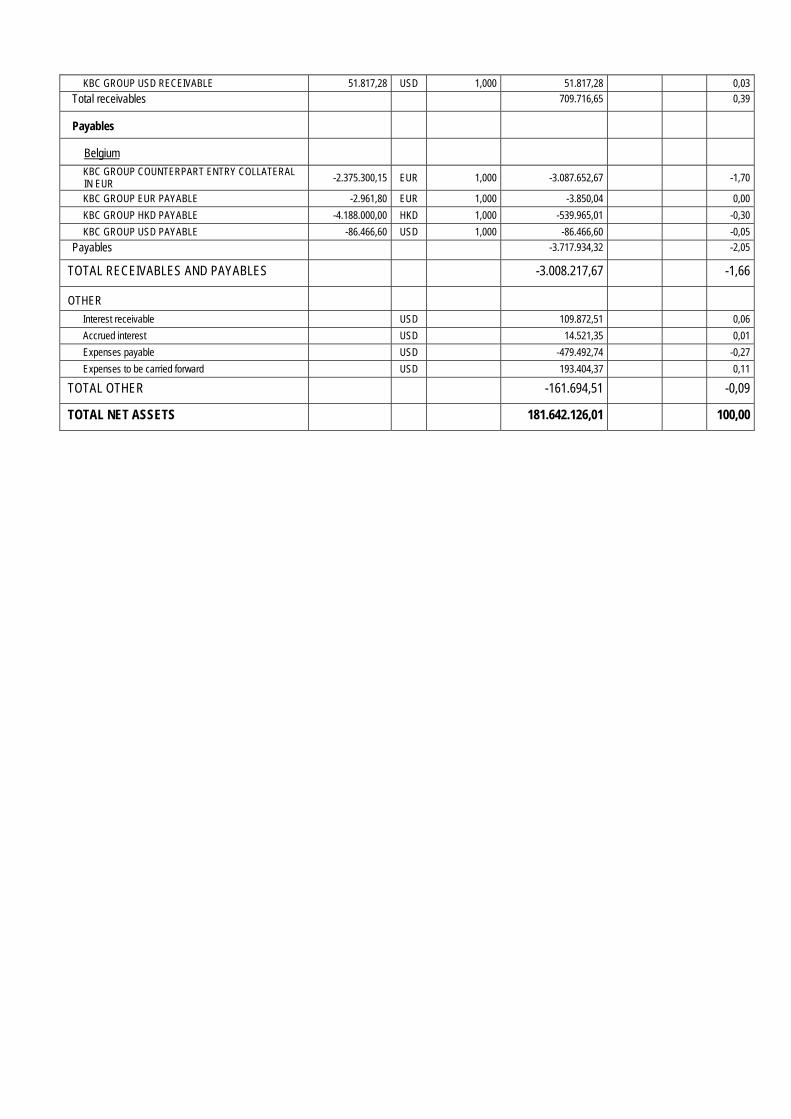

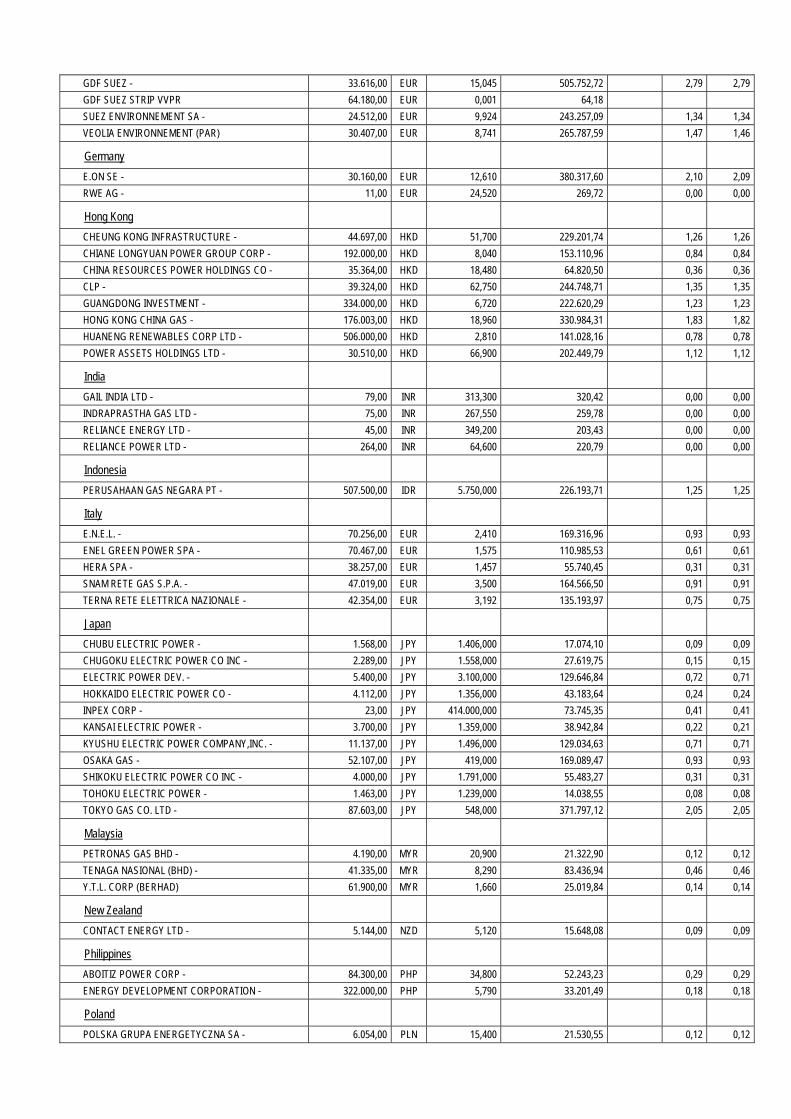

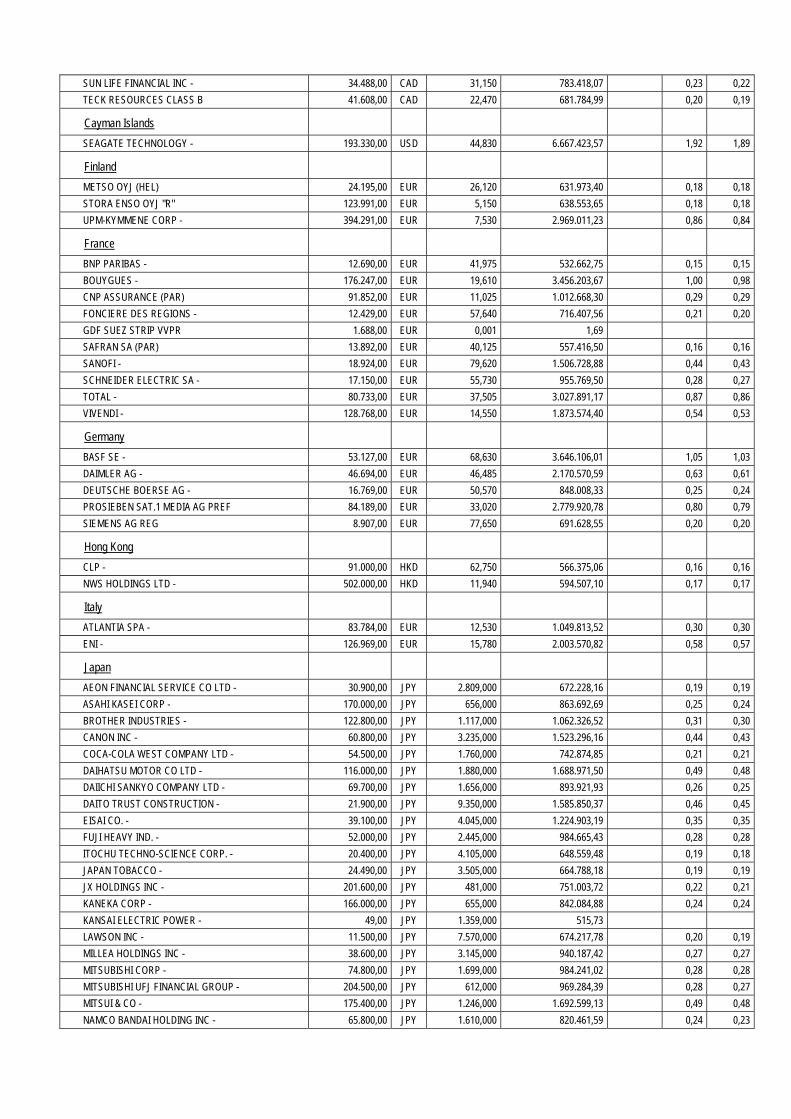

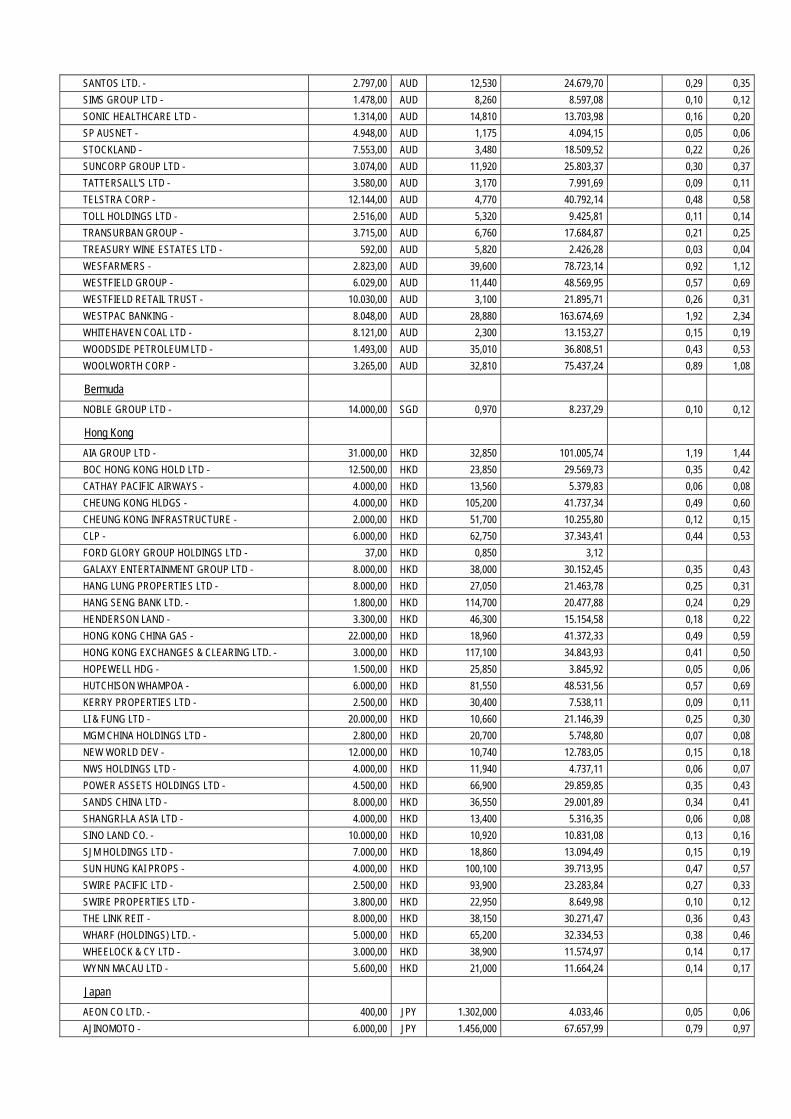

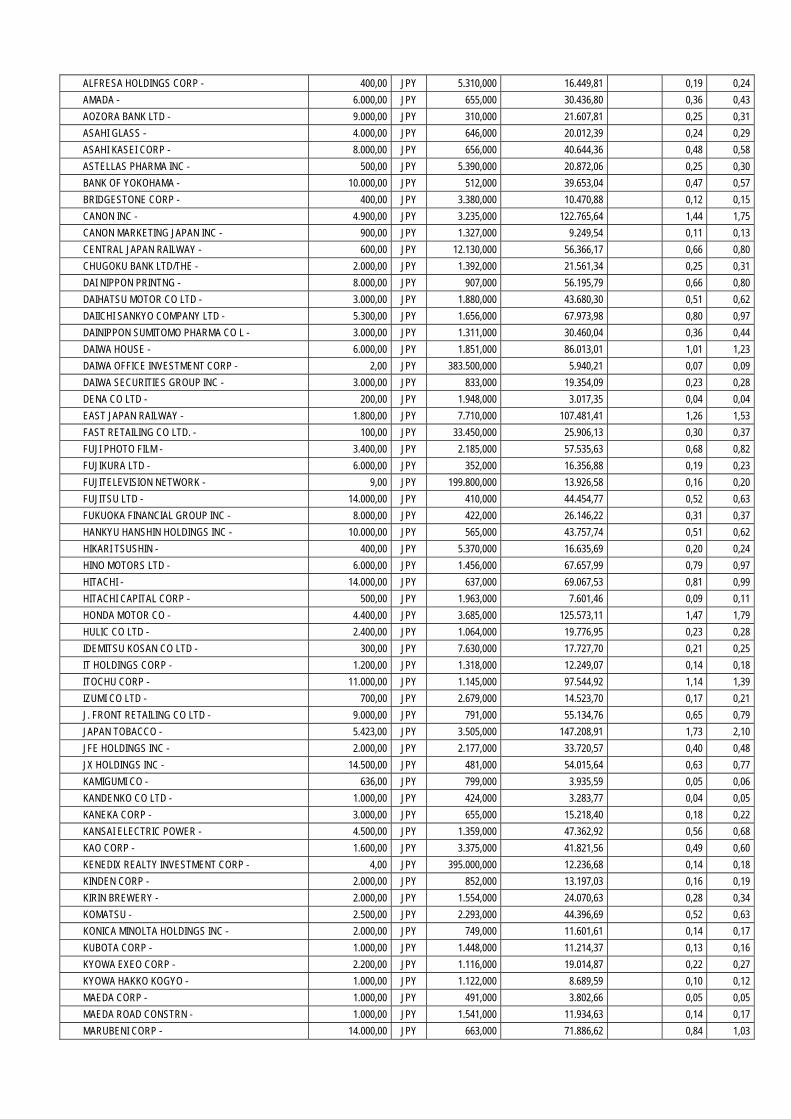

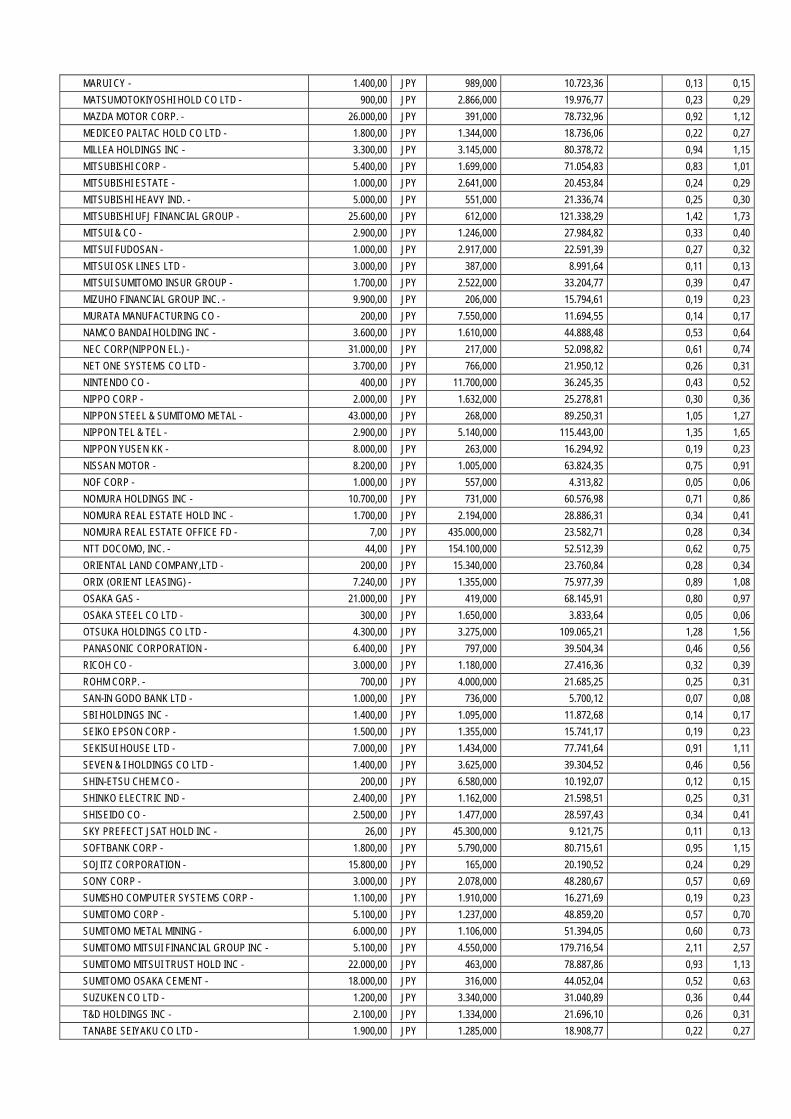

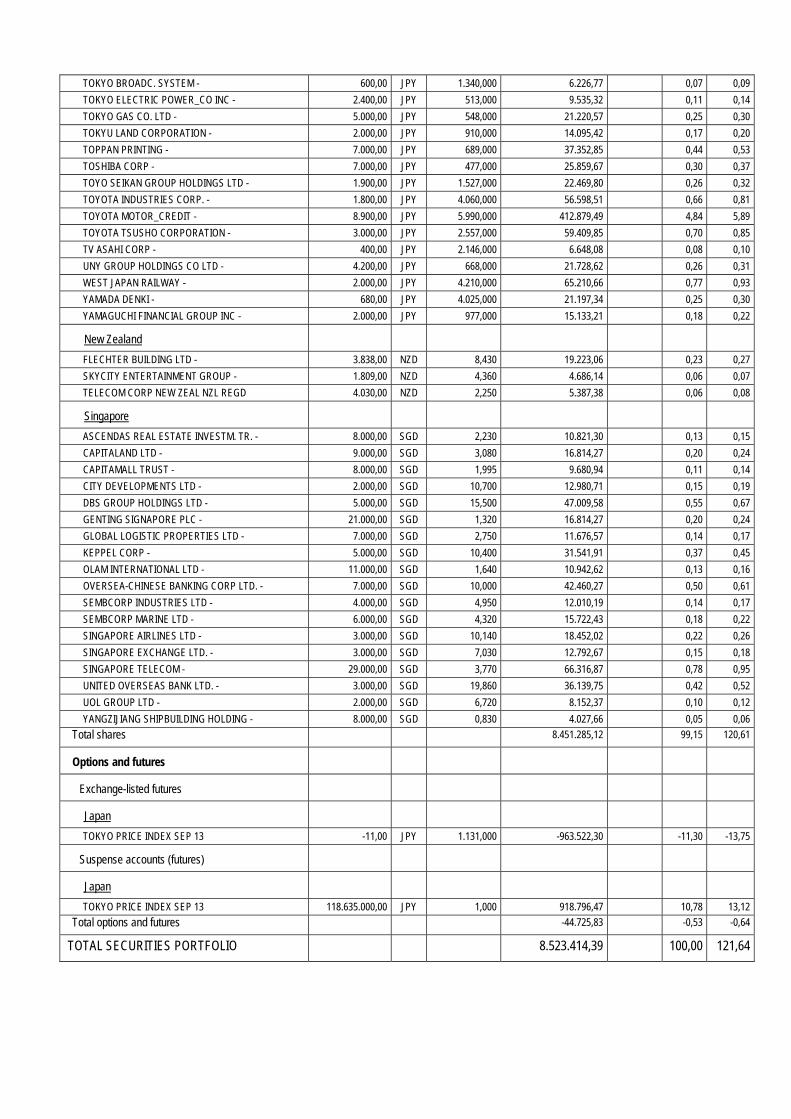

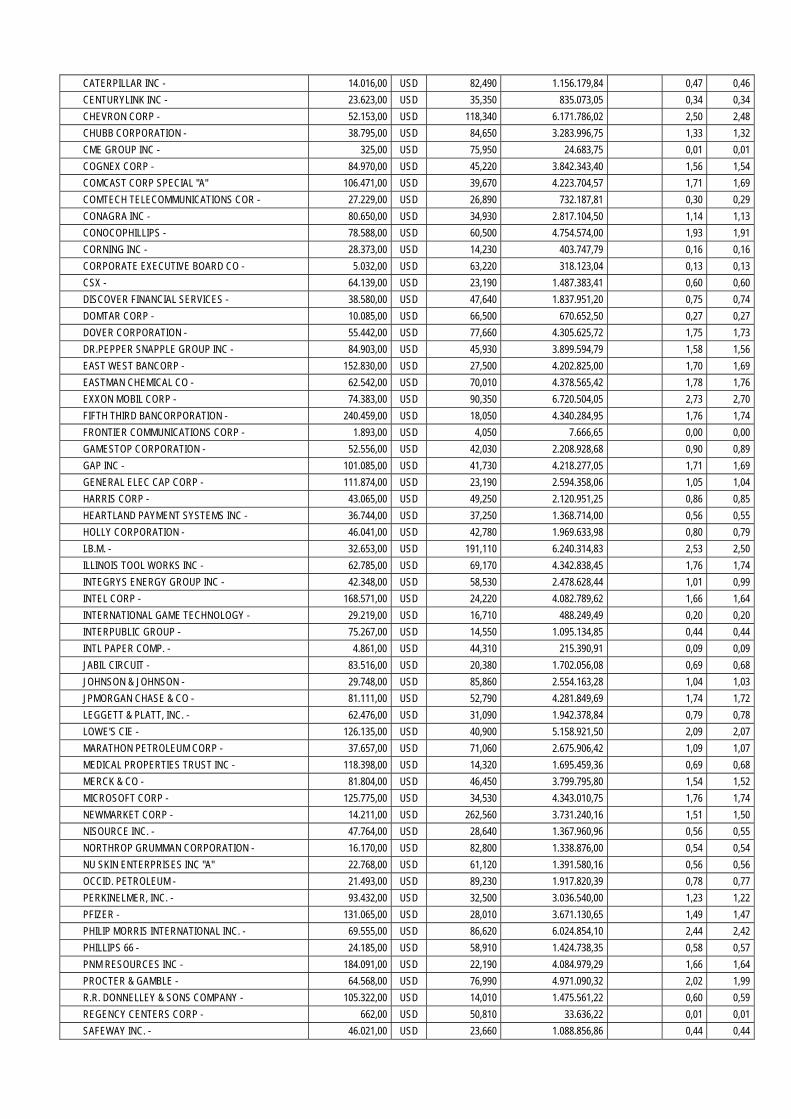

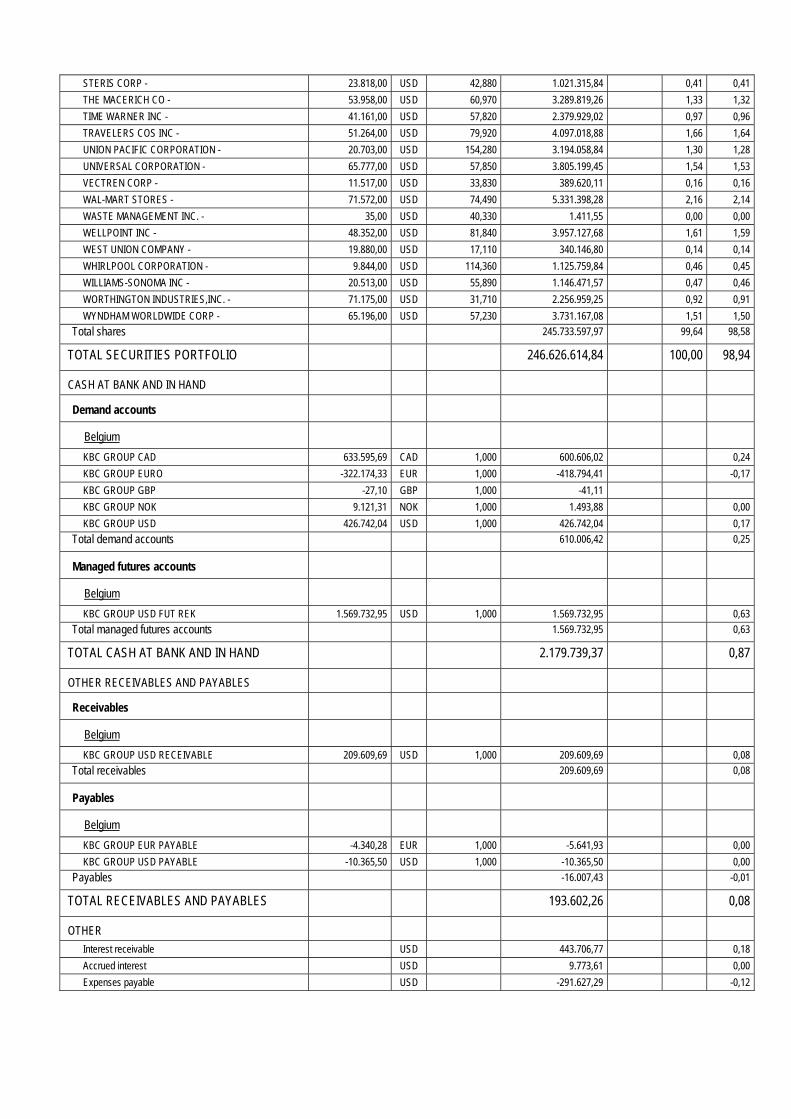

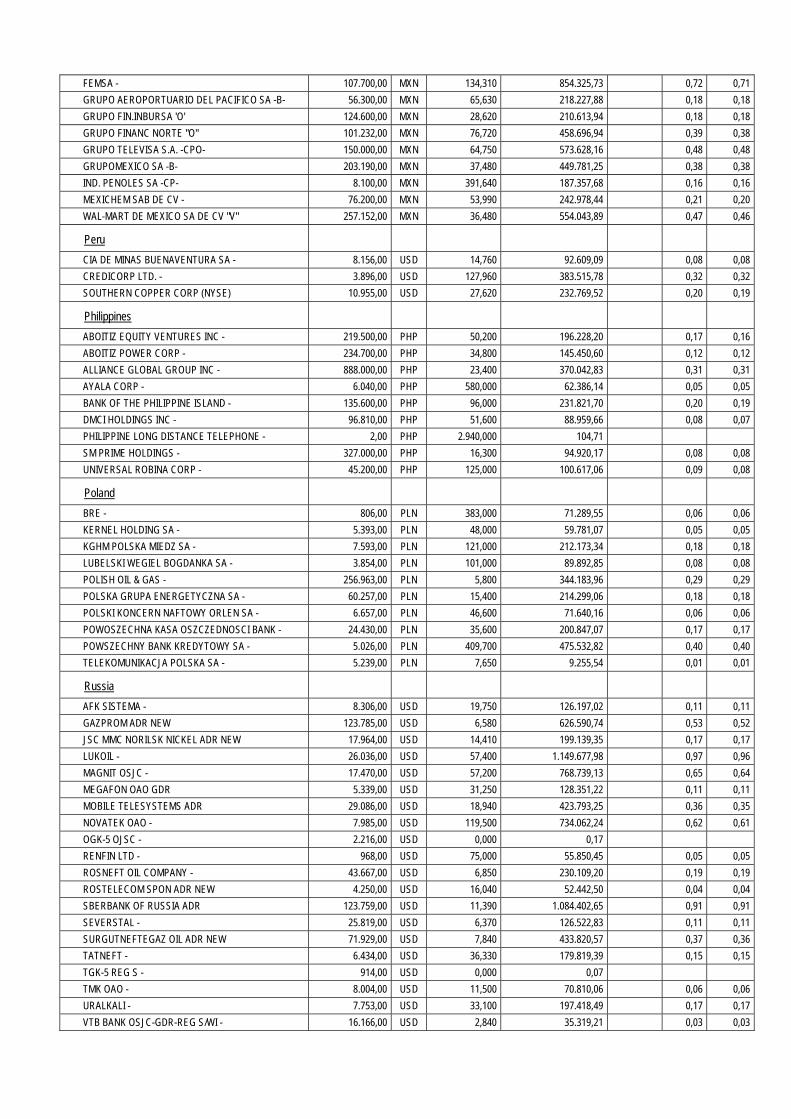

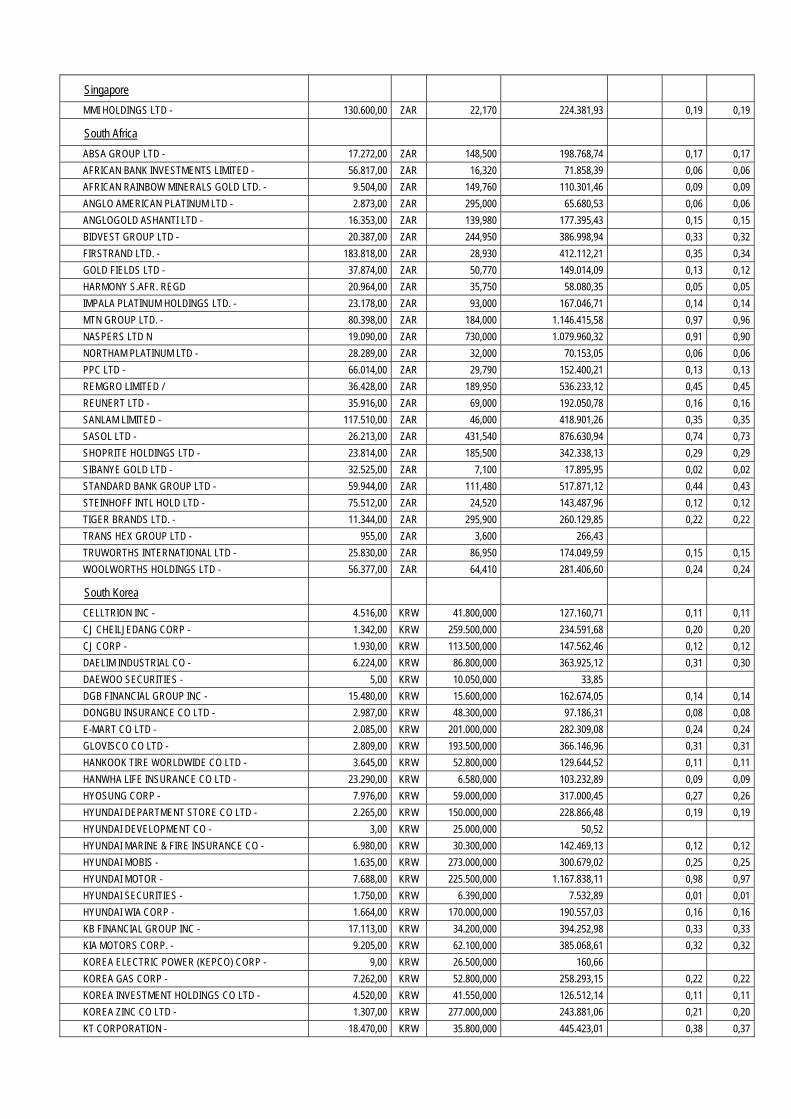

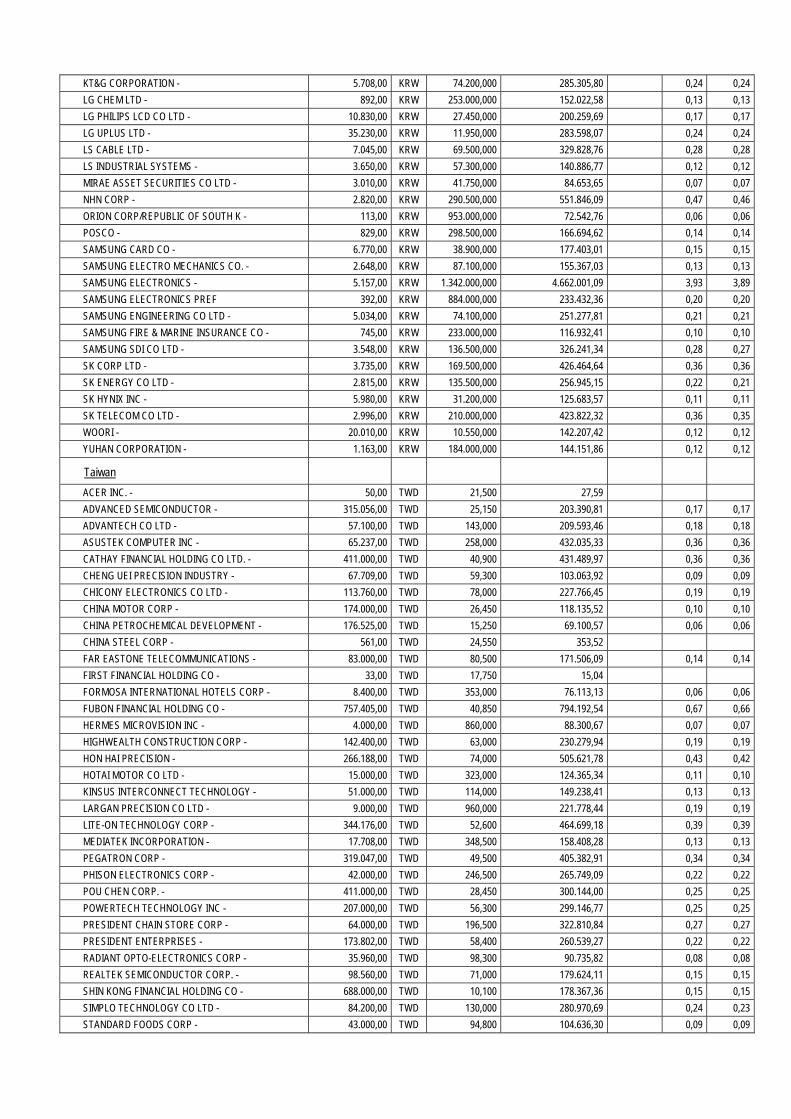

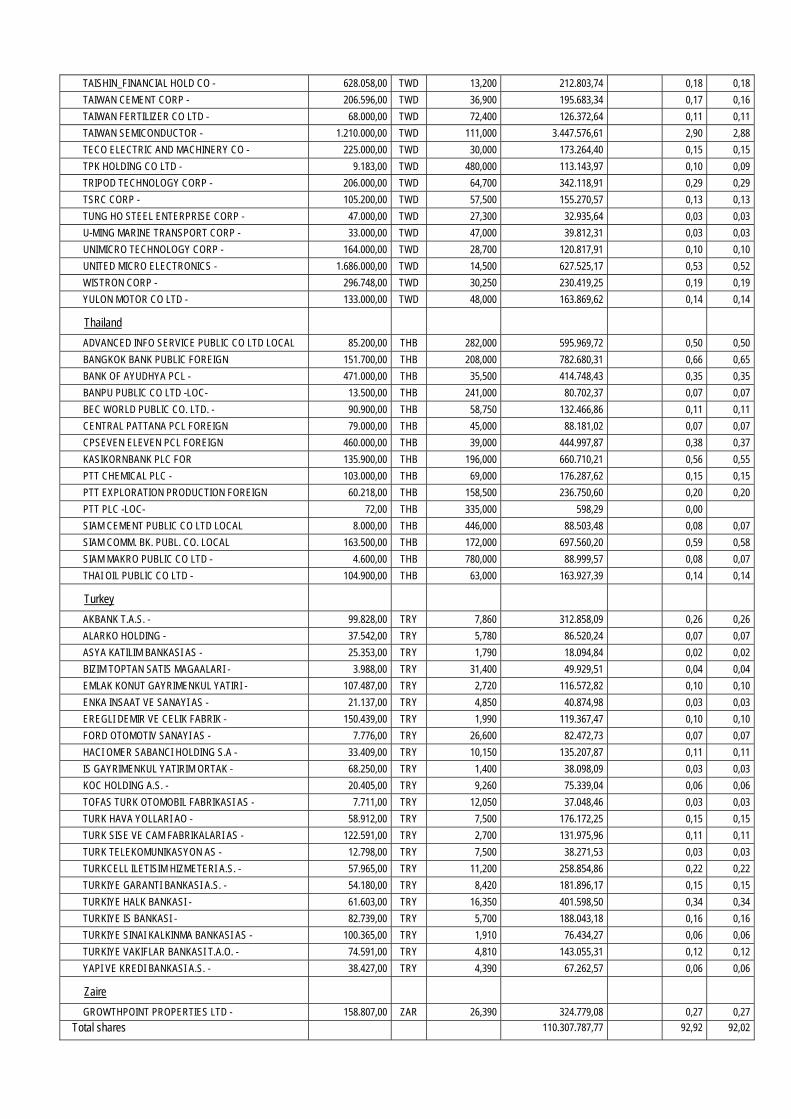

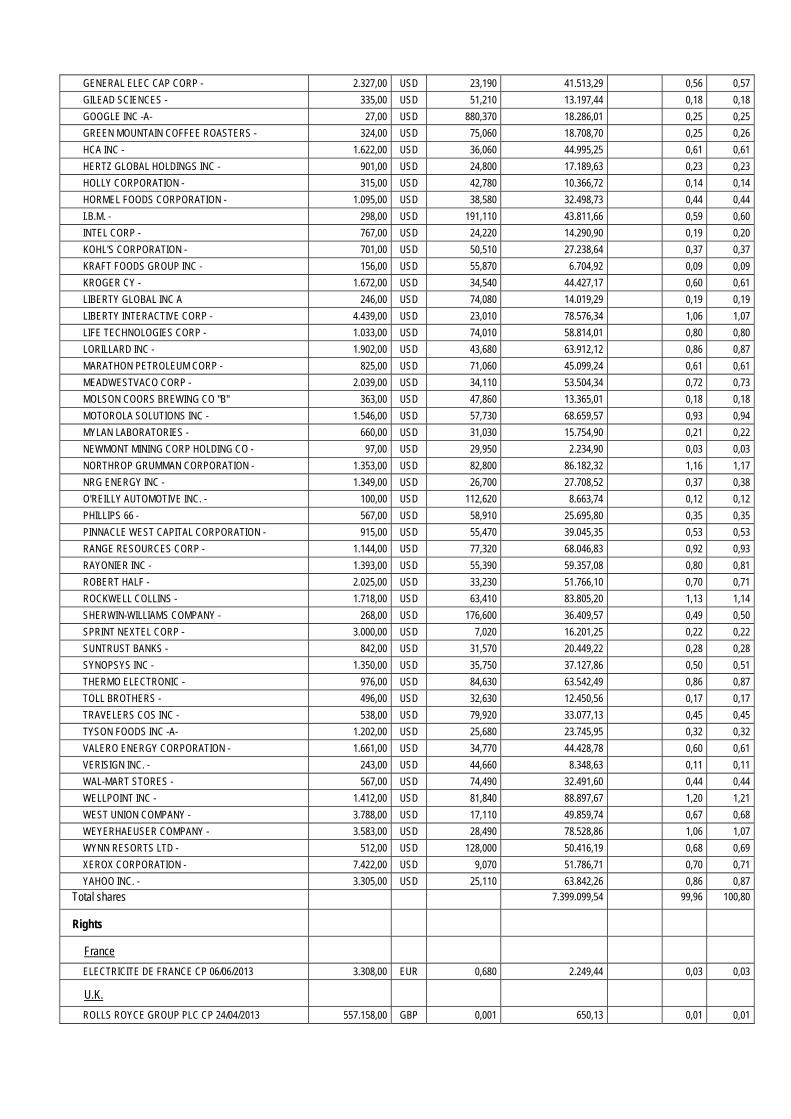

Name Quantity on 30/06/2013

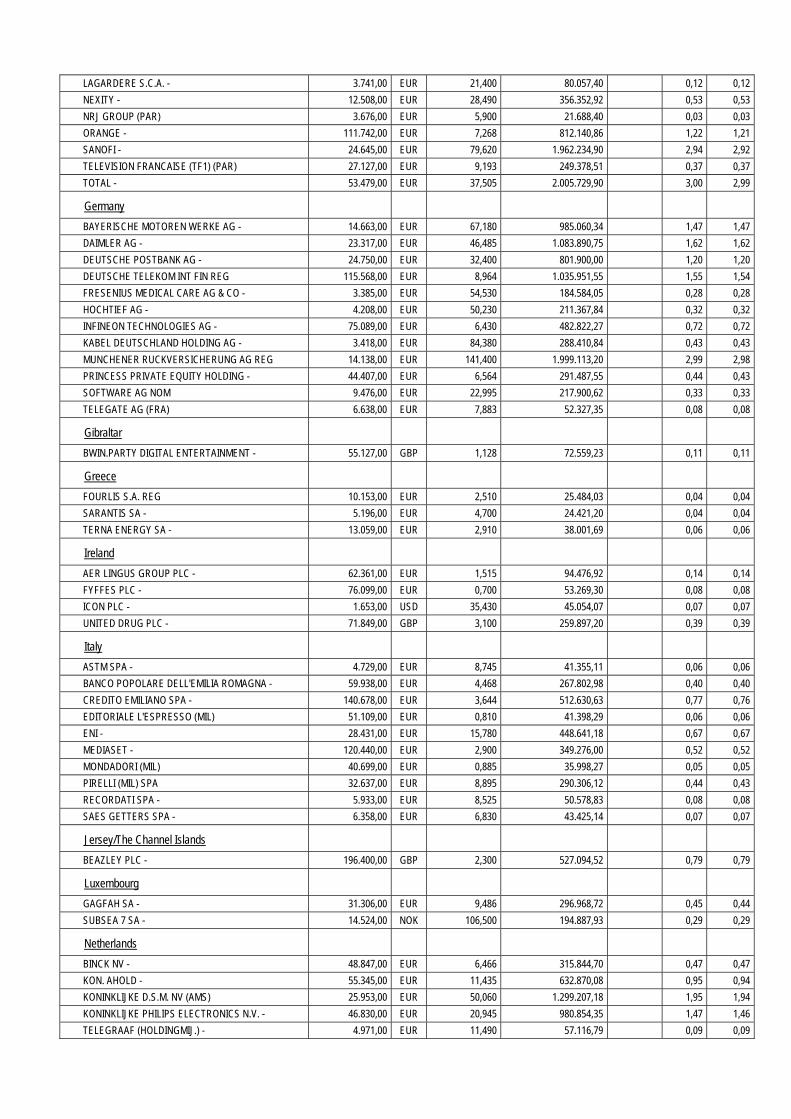

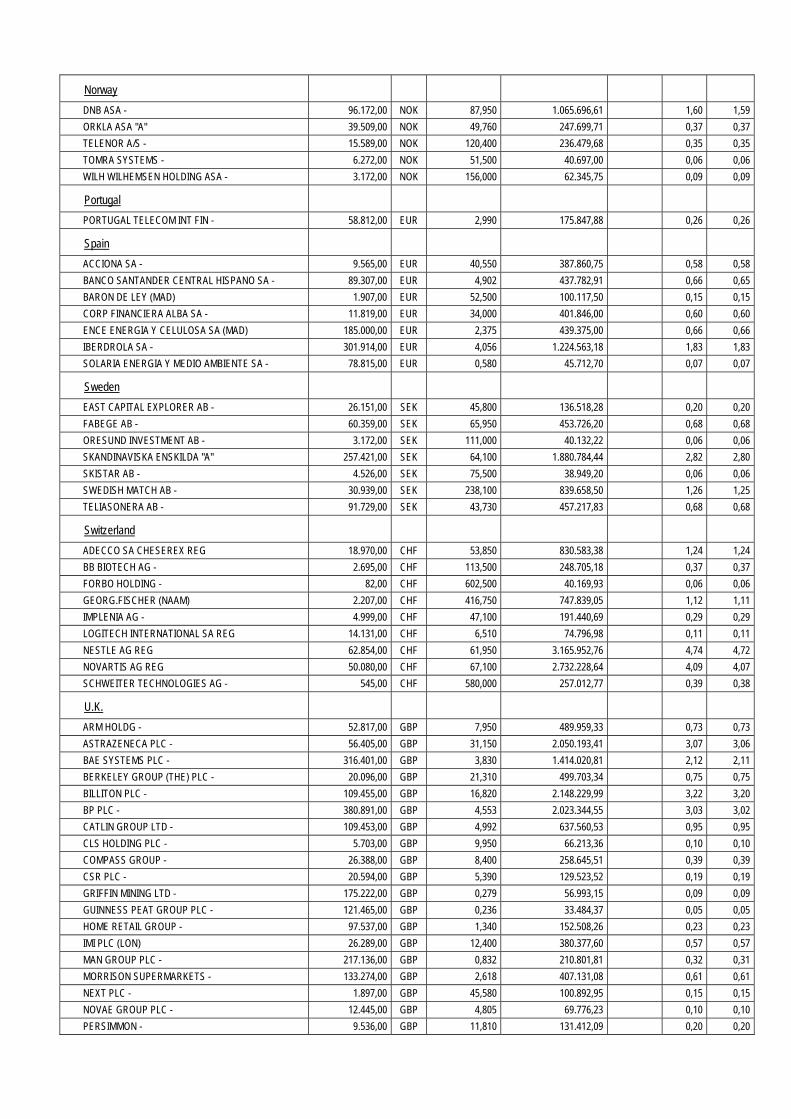

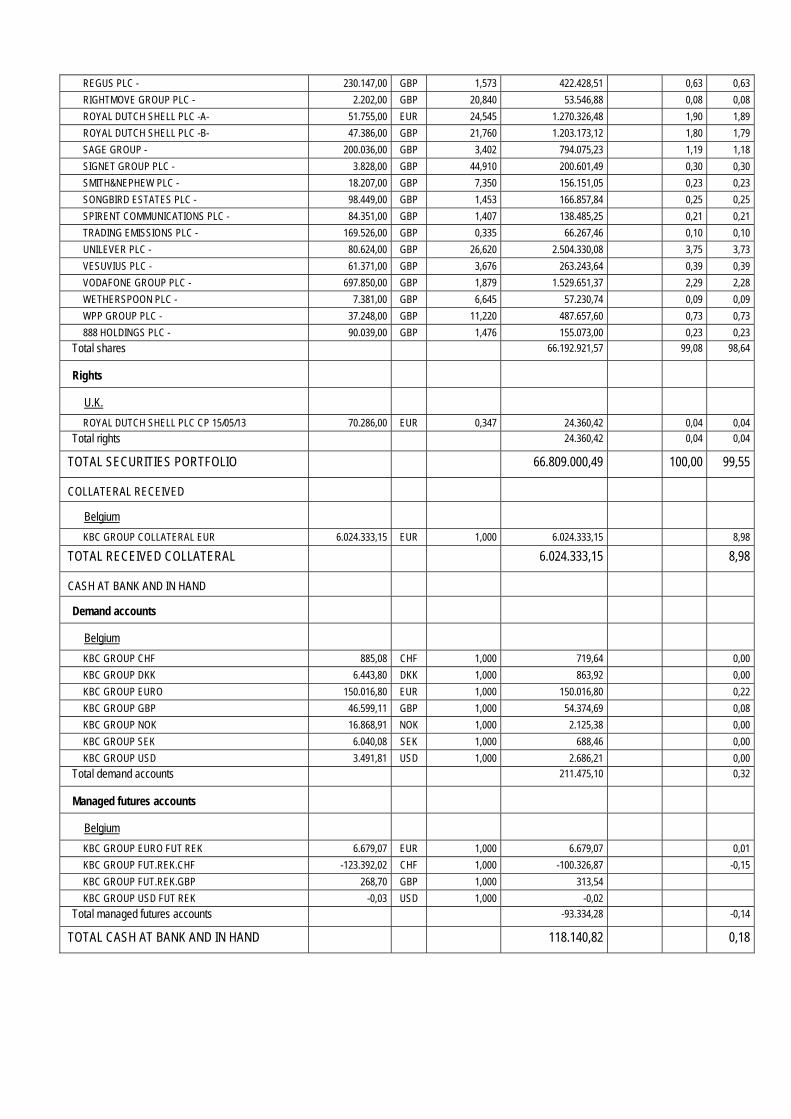

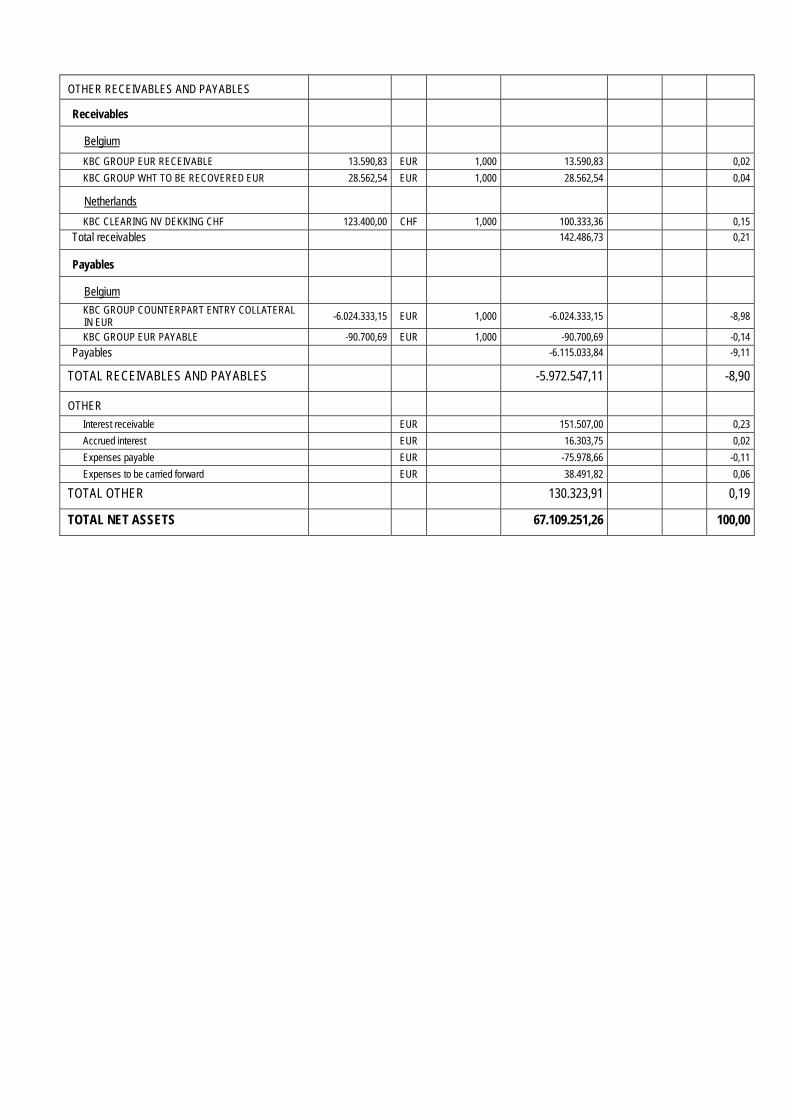

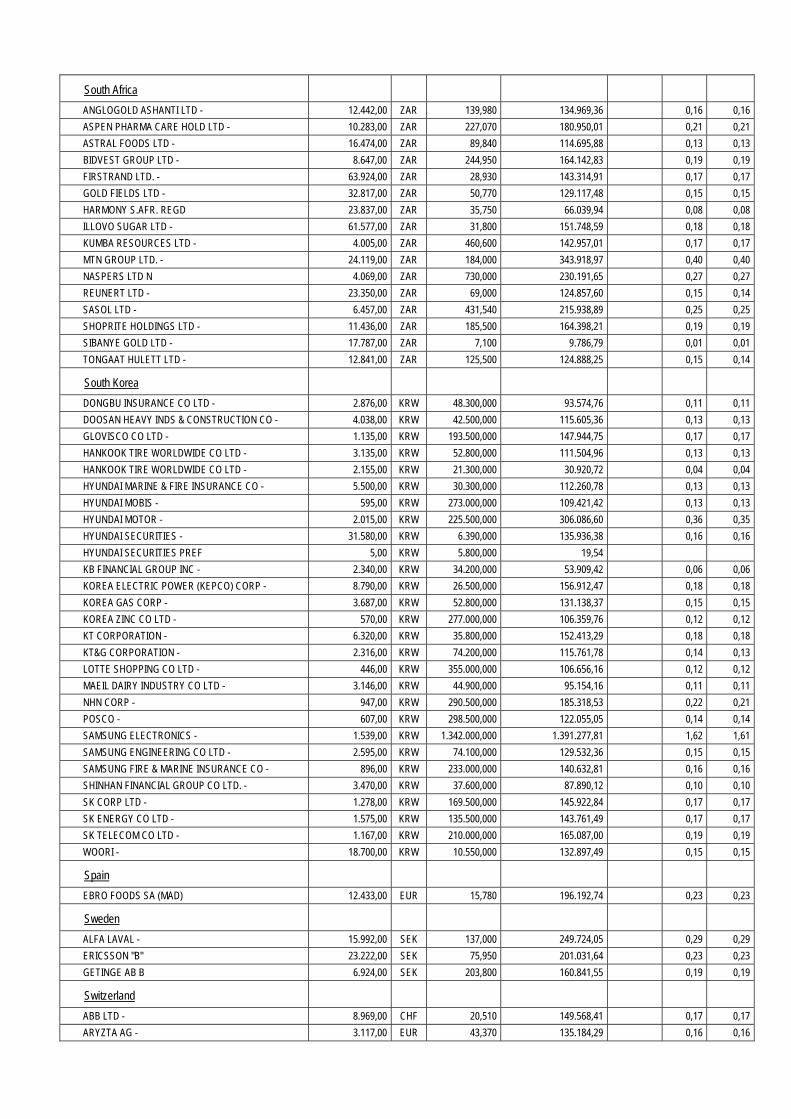

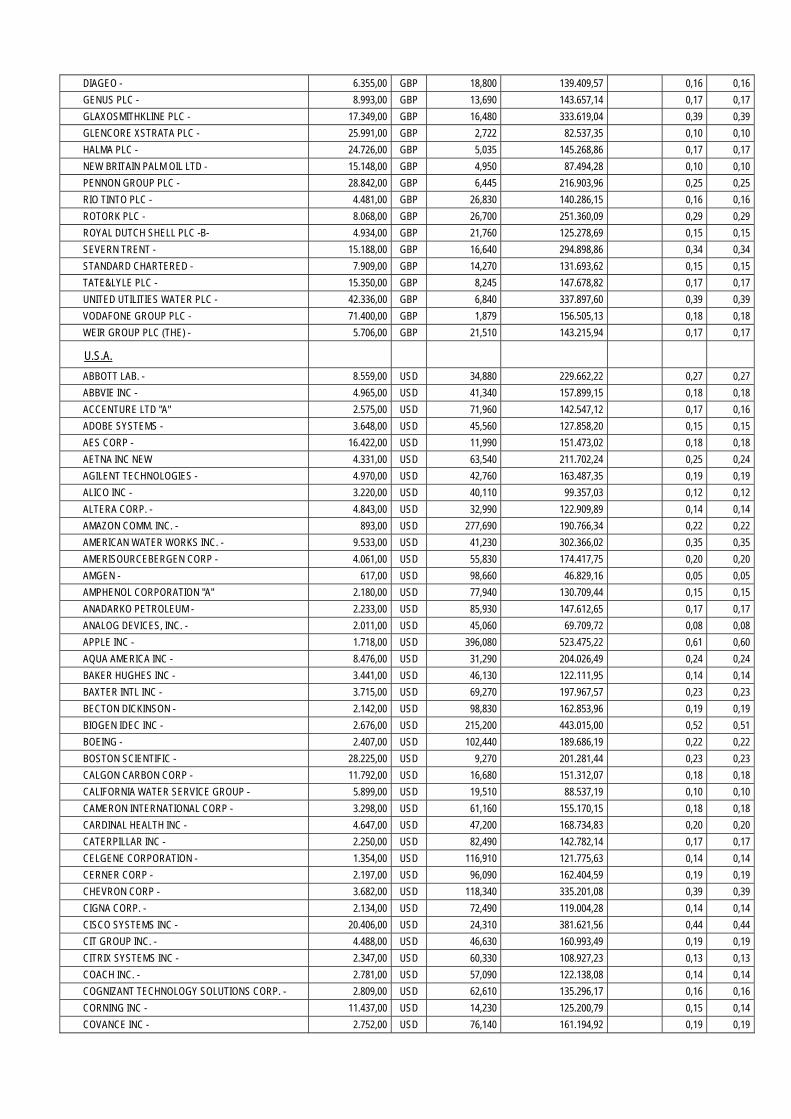

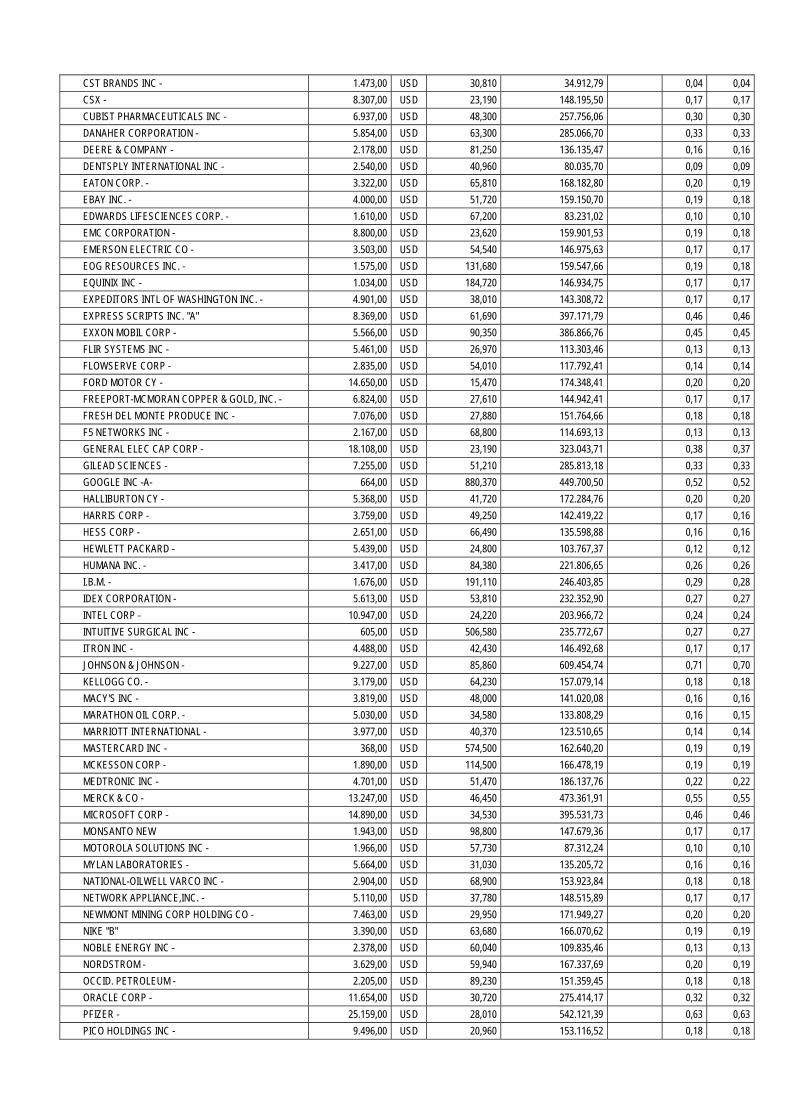

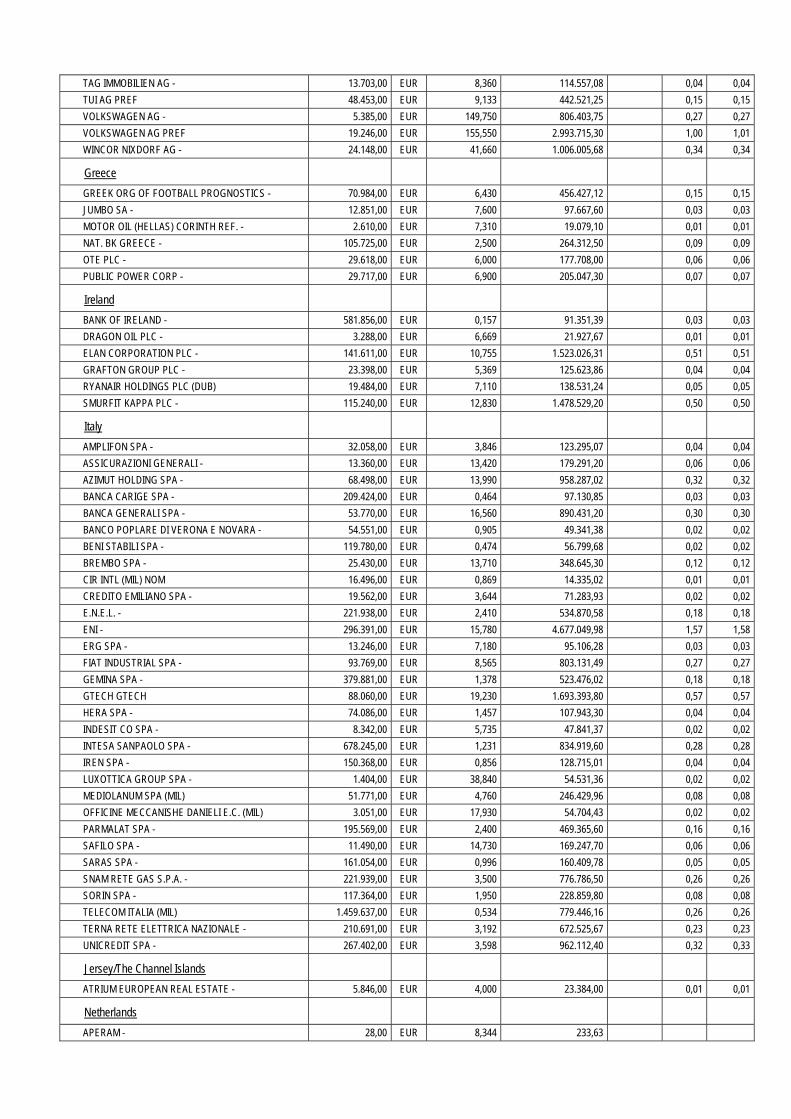

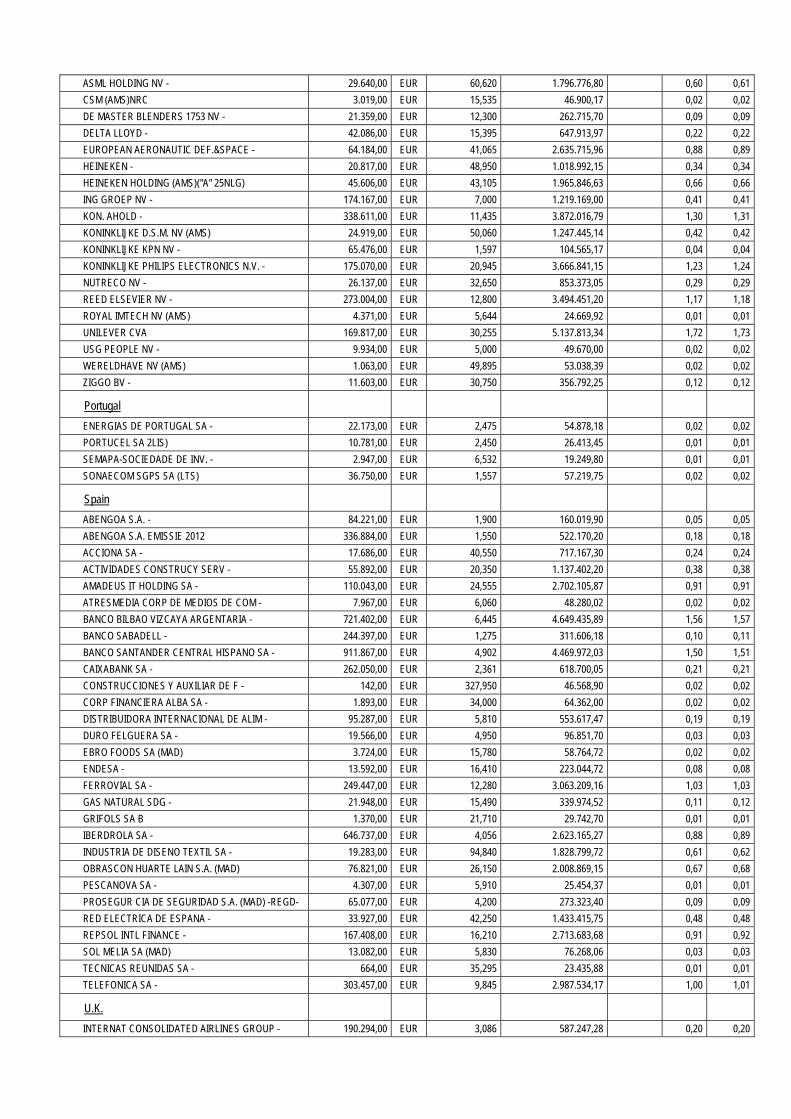

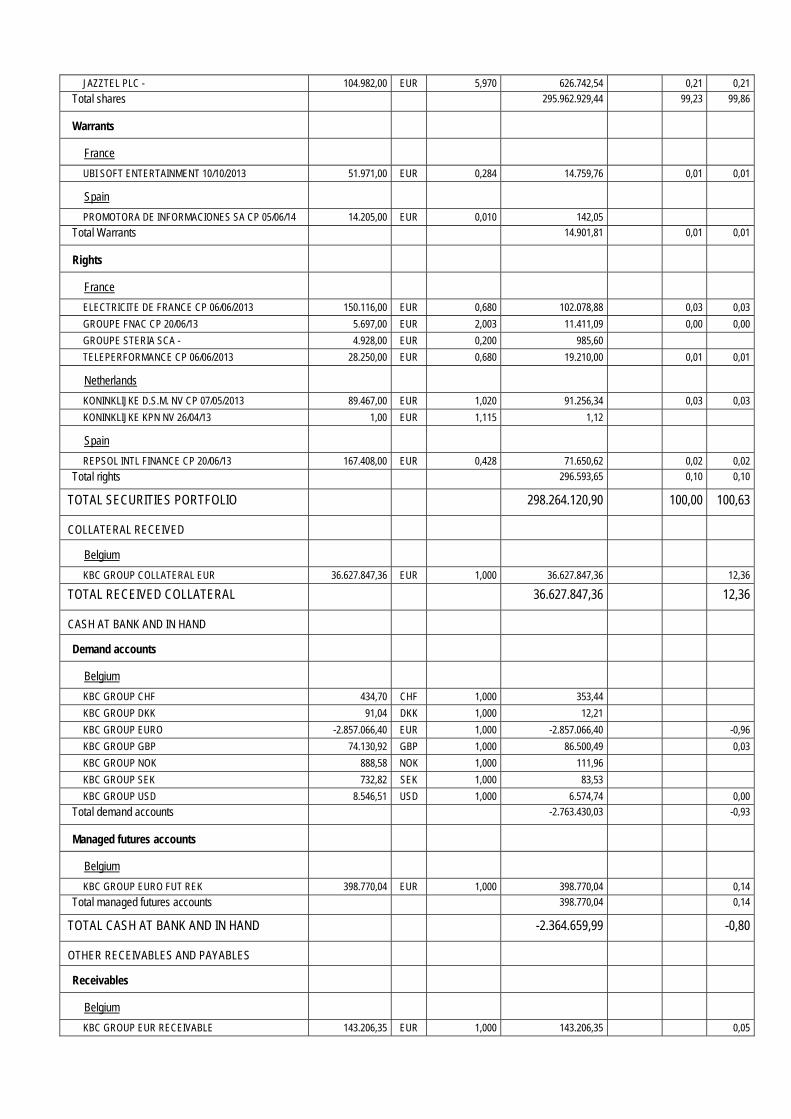

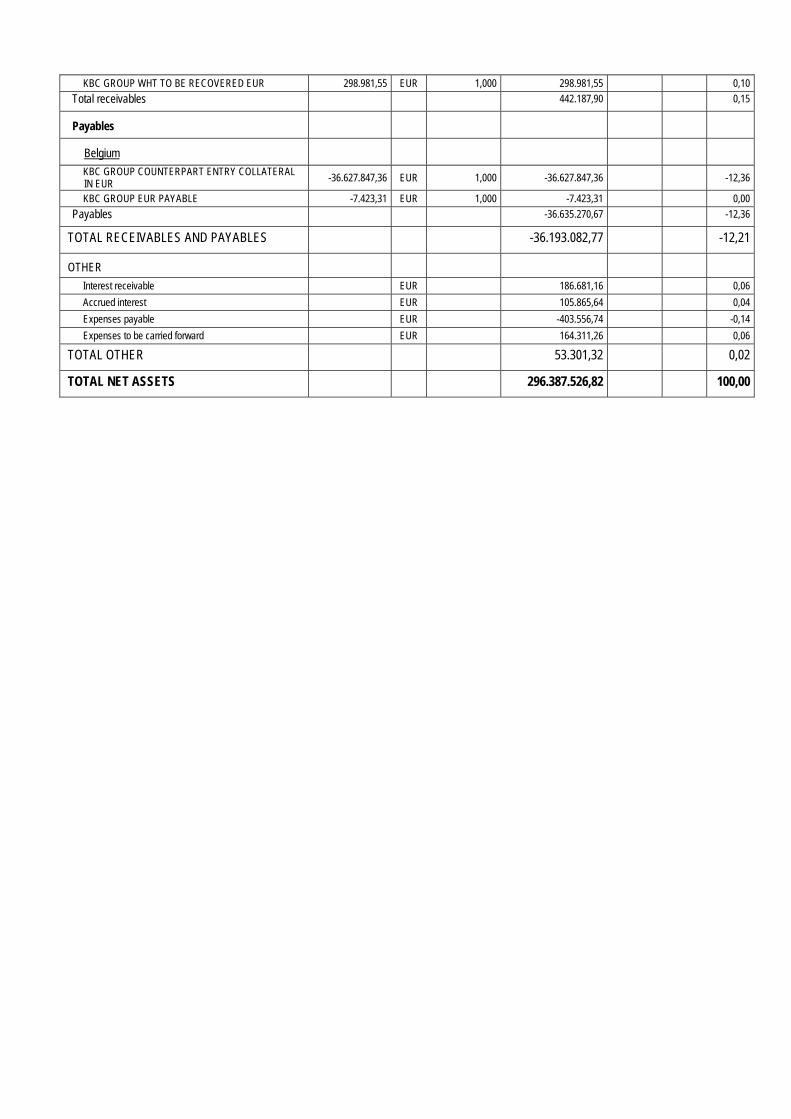

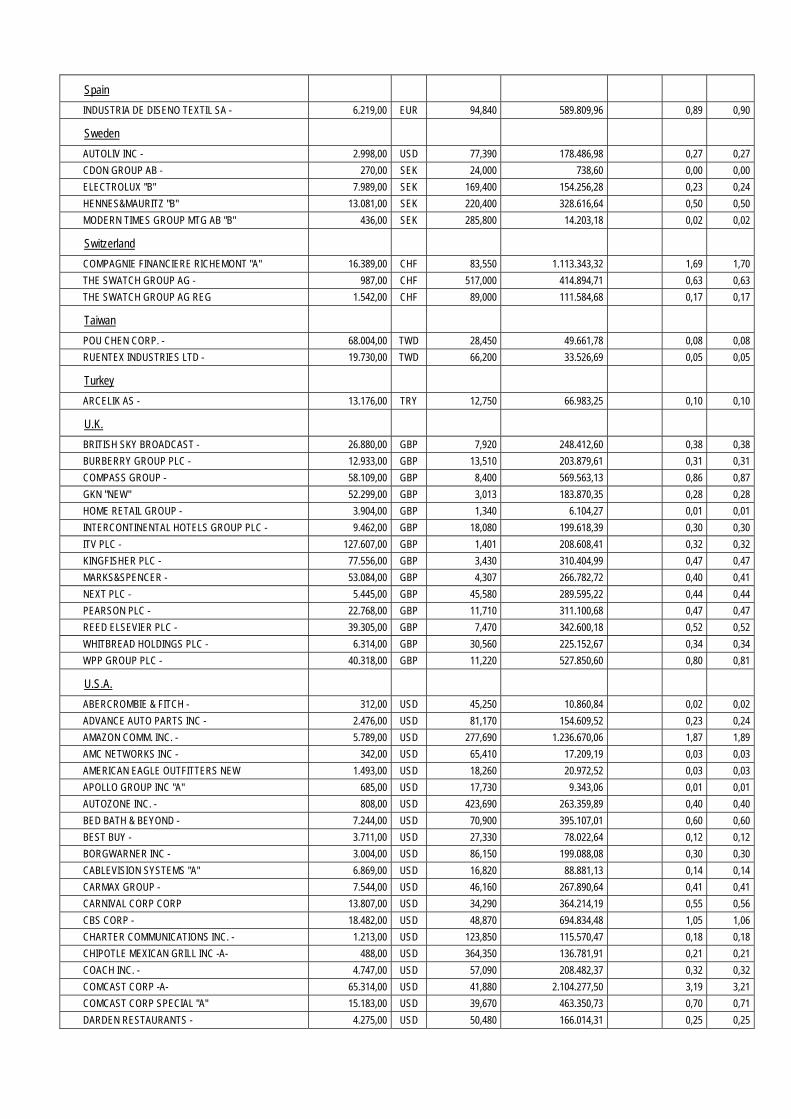

Cur rency

Price in currency

Evaluation (in the currency of the

sub-fund)

% owned by

UCI

% portfolio

% Net

assets

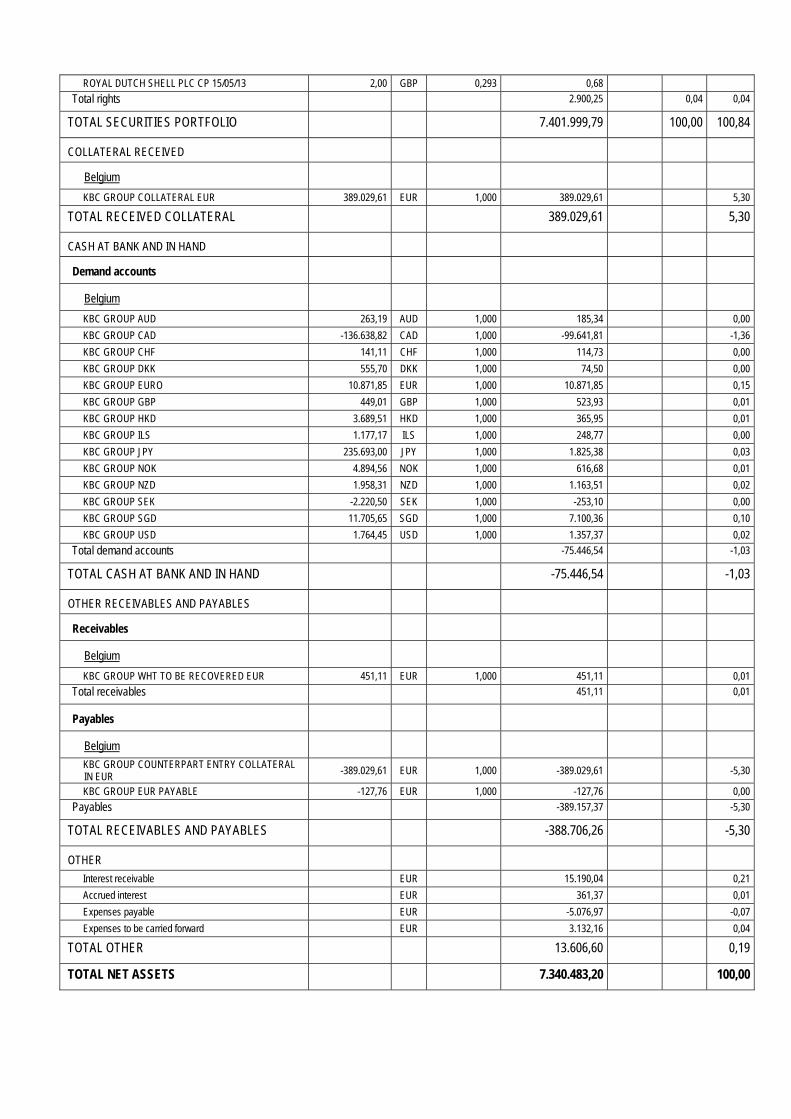

NET ASSETS

SECURITIES PORTFOLIO

Shares

Exchange-listed shares

Australia

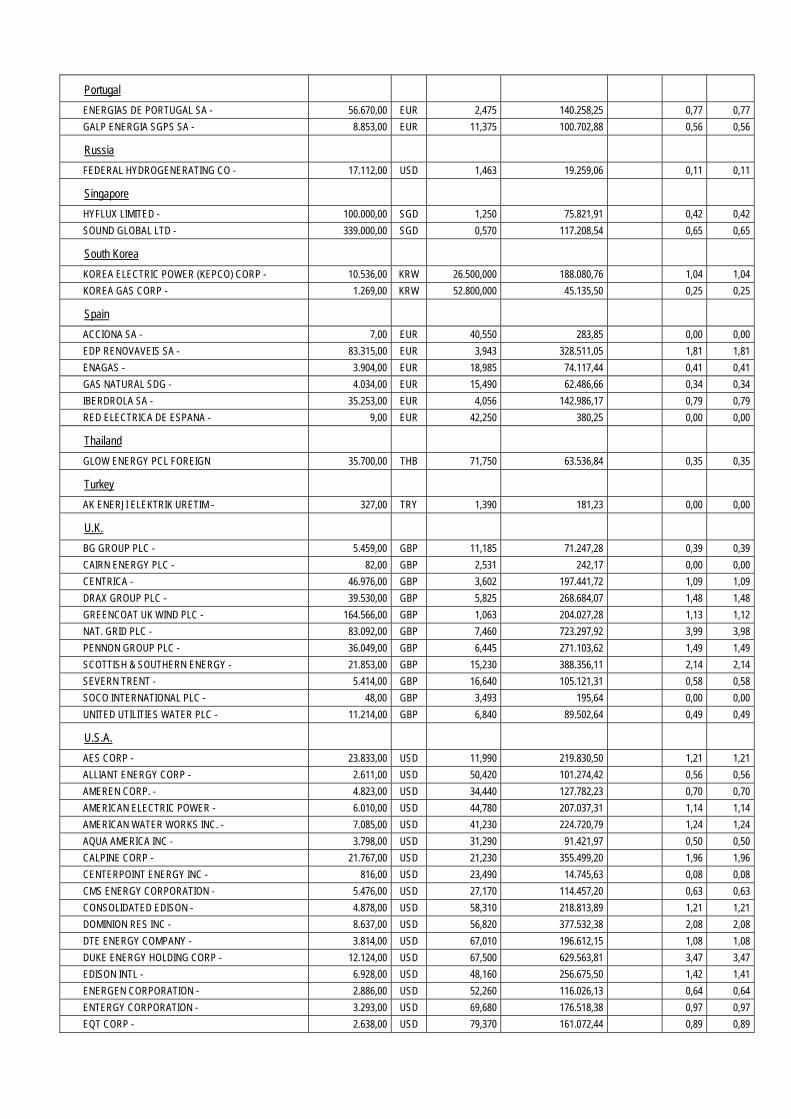

ANZ BANKING GROUP - 4.297,00 AUD 28,580 2.246.360,77 0,58 0,58

BHP BILLITON LTD - 5.578,00 AUD 31,370 3.200.699,90 0,83 0,83

COMMONWEALTH BK OF AUSTRALIA - 2.664,00 AUD 69,180 3.371.061,73 0,88 0,87

MIRVAC GROUP - 85.006,00 AUD 1,605 2.495.609,01 0,65 0,65

NATIONAL AUSTRALIA BANK - 4.788,00 AUD 29,680 2.599.381,15 0,68 0,67

WESTPAC BANKING - 4.602,00 AUD 28,880 2.431.060,29 0,63 0,63

Canada

C.I.B.C. - 1.820,00 CAD 74,640 2.573.155,91 0,67 0,67

CANADIAN OIL SANDS LTD - 8.547,00 CAD 19,470 3.152.119,97 0,82 0,81

GREAT-WEST LIFECO INC. - 9.504,00 CAD 28,530 5.136.074,11 1,34 1,33

H&R REAL ESTATE INV. TRUST - 6.837,00 CAD 22,040 2.854.304,17 0,74 0,74

IGM FINANCIAL INC - 7.867,00 CAD 45,090 6.719.121,09 1,75 1,74

POWER CORP - 5.505,00 CAD 28,220 2.942.641,90 0,77 0,76

POWER FINANCIAL CORP - 6.733,00 CAD 30,580 3.900.041,05 1,02 1,01

ROYAL BK CANADA - 2.639,00 CAD 61,280 3.063.241,44 0,80 0,79

SHAW COMMUNICATIONS INC "B" 9.614,00 CAD 25,240 4.596.386,61 1,20 1,19

Cayman Islands

SEAGATE TECHNOLOGY - 8.626,00 USD 44,830 7.727.229,45 2,01 2,00

Finland

UPM-KYMMENE CORP - 21.948,00 EUR 7,530 4.292.847,76 1,12 1,11

France

BOUYGUES - 8.924,00 EUR 19,610 4.545.615,68 1,18 1,17

SANOFI - 1.212,00 EUR 79,620 2.506.572,97 0,65 0,65

TOTAL - 4.874,00 EUR 37,505 4.748.213,67 1,24 1,23

VIVENDI - 6.938,00 EUR 14,550 2.622.121,72 0,68 0,68

Germany

BASF SE - 2.803,00 EUR 68,630 4.996.807,93 1,30 1,29

DAIMLER AG - 2.509,00 EUR 46,485 3.029.486,74 0,79 0,78

PROSIEBEN SAT.1 MEDIA AG PREF 4.136,00 EUR 33,020 3.547.424,48 0,92 0,92

Italy

ENI - 8.658,00 EUR 15,780 3.548.788,69 0,92 0,92

Japan

ASAHI KASEI CORP - 20.000,00 JPY 656,000 2.639.343,25 0,69 0,68

CANON INC - 3.600,00 JPY 3.235,000 2.342.819,47 0,61 0,61

DAIHATSU MOTOR CO LTD - 7.000,00 JPY 1.880,000 2.647.390,03 0,69 0,68

DAITO TRUST CONSTRUCTION - 1.300,00 JPY 9.350,000 2.445.214,72 0,64 0,63

EISAI CO. - 3.300,00 JPY 4.045,000 2.685.310,47 0,70 0,69

MITSUBISHI CORP - 6.000,00 JPY 1.699,000 2.050.721,42 0,53 0,53

MITSUBISHI UFJ FINANCIAL GROUP - 16.300,00 JPY 612,000 2.006.786,01 0,52 0,52

MITSUI & CO - 11.000,00 JPY 1.246,000 2.757.228,55 0,72 0,71

NIPPON EXPRESS CO LTD - 25.000,00 JPY 471,000 2.368.770,33 0,62 0,61

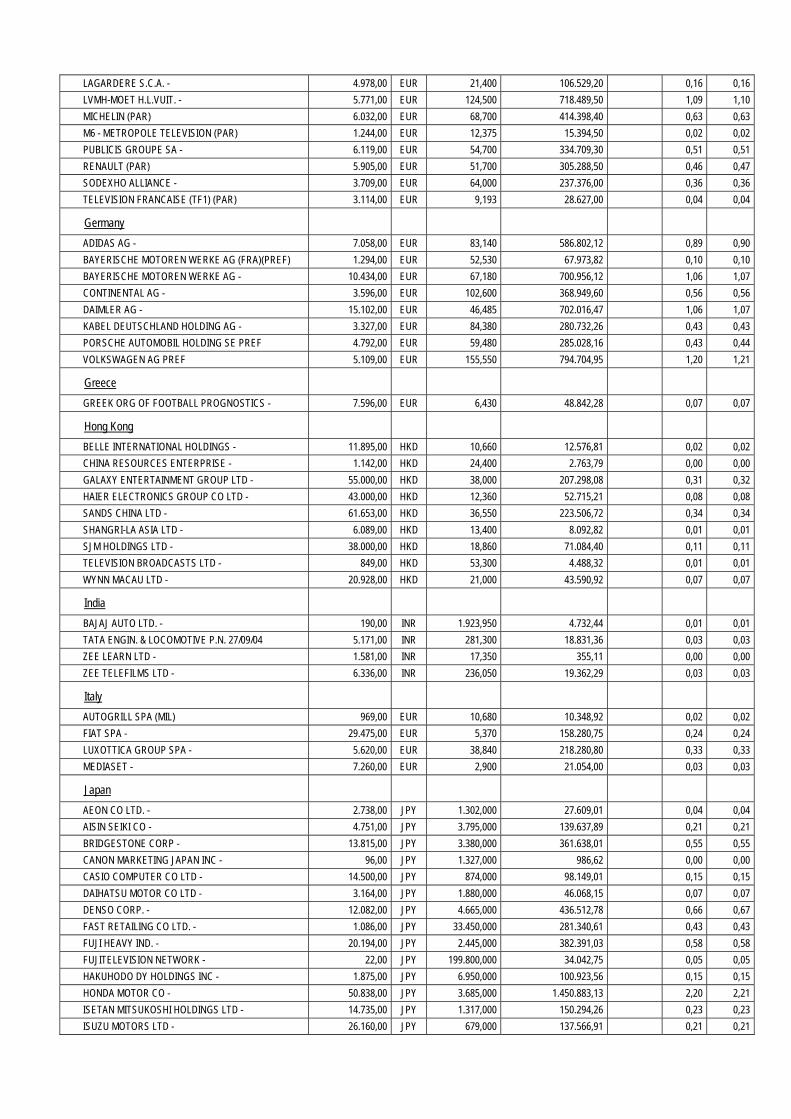

NISSAN MOTOR - 10.100,00 JPY 1.005,000 2.041.970,55 0,53 0,53

SUMITOMO CORP - 12.300,00 JPY 1.237,000 3.060.813,37 0,80 0,79

SUMITOMO MITSUI FINANCIAL GROUP INC - 3.400,00 JPY 4.550,000 3.112.091,47 0,81 0,80

TOYOTA INDUSTRIES CORP. - 3.600,00 JPY 4.060,000 2.940.292,75 0,77 0,76

Netherlands

BOSKALIS WESTMINSTER (AMS) 4.244,00 EUR 28,015 3.088.314,79 0,80 0,80

KON. AHOLD - 10.943,00 EUR 11,435 3.250.335,03 0,85 0,84

Norway

GJENSIDIGE FORSIKRING ASA - 10.272,00 NOK 89,350 3.003.683,83 0,78 0,78

STATOIL - 8.459,00 NOK 125,300 3.468.763,93 0,90 0,90

Spain

ENAGAS - 5.390,00 EUR 18,985 2.657.999,69 0,69 0,69

Sweden

INVESTOR AB "B" 6.930,00 SEK 180,300 3.699.316,91 0,96 0,96

SVENSKA HANDBK "A" 2.089,00 SEK 269,200 1.664.968,69 0,43 0,43

SWEDBANK - 9.144,00 SEK 153,800 4.163.754,63 1,08 1,08

Switzerland

ADECCO SA CHESEREX REG 2.422,00 CHF 53,850 2.754.517,94 0,72 0,71

NESTLE AG REG 3.295,00 CHF 61,950 4.311.044,32 1,12 1,11

ZURICH INSURANCE GROUP AG - 550,00 CHF 245,000 2.845.866,56 0,74 0,74

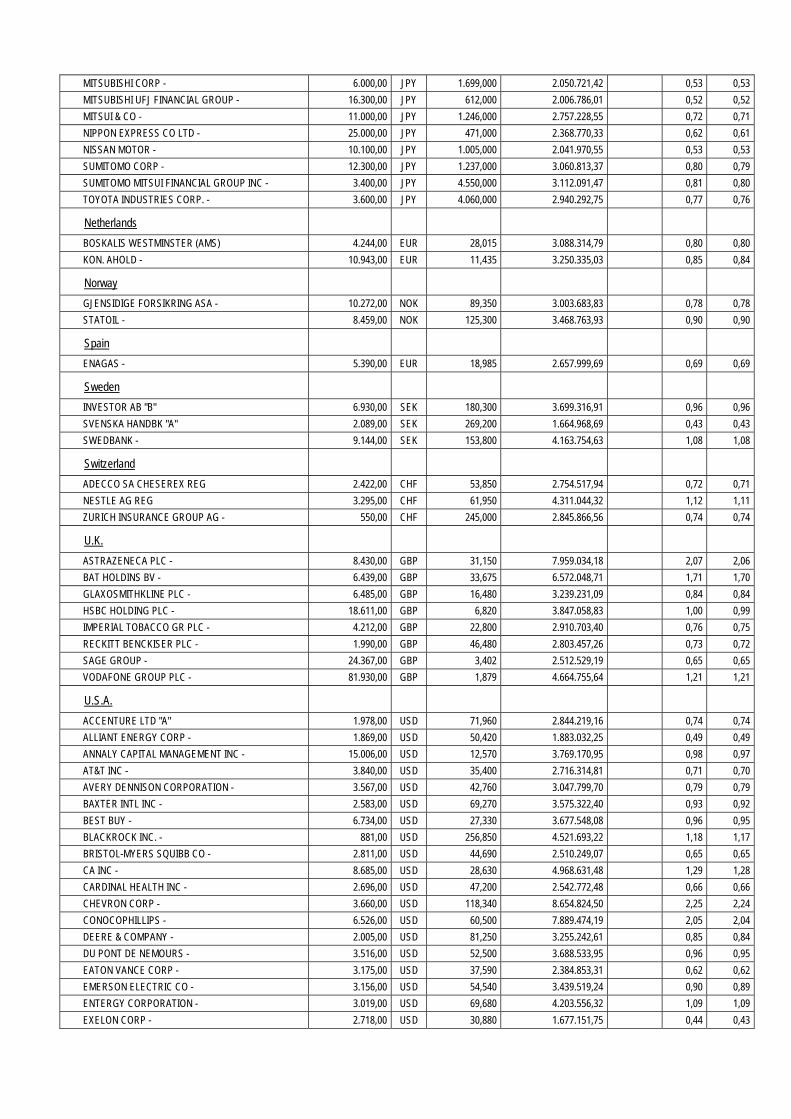

U.K.

ASTRAZENECA PLC - 8.430,00 GBP 31,150 7.959.034,18 2,07 2,06

BAT HOLDINS BV - 6.439,00 GBP 33,675 6.572.048,71 1,71 1,70

GLAXOSMITHKLINE PLC - 6.485,00 GBP 16,480 3.239.231,09 0,84 0,84

HSBC HOLDING PLC - 18.611,00 GBP 6,820 3.847.058,83 1,00 0,99

IMPERIAL TOBACCO GR PLC - 4.212,00 GBP 22,800 2.910.703,40 0,76 0,75

RECKITT BENCKISER PLC - 1.990,00 GBP 46,480 2.803.457,26 0,73 0,72

SAGE GROUP - 24.367,00 GBP 3,402 2.512.529,19 0,65 0,65

VODAFONE GROUP PLC - 81.930,00 GBP 1,879 4.664.755,64 1,21 1,21

U.S.A.

ACCENTURE LTD "A" 1.978,00 USD 71,960 2.844.219,16 0,74 0,74

ALLIANT ENERGY CORP - 1.869,00 USD 50,420 1.883.032,25 0,49 0,49

ANNALY CAPITAL MANAGEMENT INC - 15.006,00 USD 12,570 3.769.170,95 0,98 0,97

AT&T INC - 3.840,00 USD 35,400 2.716.314,81 0,71 0,70

AVERY DENNISON CORPORATION - 3.567,00 USD 42,760 3.047.799,70 0,79 0,79

BAXTER INTL INC - 2.583,00 USD 69,270 3.575.322,40 0,93 0,92

BEST BUY - 6.734,00 USD 27,330 3.677.548,08 0,96 0,95

BLACKROCK INC. - 881,00 USD 256,850 4.521.693,22 1,18 1,17

BRISTOL-MYERS SQUIBB CO - 2.811,00 USD 44,690 2.510.249,07 0,65 0,65

CA INC - 8.685,00 USD 28,630 4.968.631,48 1,29 1,28

CARDINAL HEALTH INC - 2.696,00 USD 47,200 2.542.772,48 0,66 0,66

CHEVRON CORP - 3.660,00 USD 118,340 8.654.824,50 2,25 2,24

CONOCOPHILLIPS - 6.526,00 USD 60,500 7.889.474,19 2,05 2,04

DEERE & COMPANY - 2.005,00 USD 81,250 3.255.242,61 0,85 0,84

DU PONT DE NEMOURS - 3.516,00 USD 52,500 3.688.533,95 0,96 0,95

EATON VANCE CORP - 3.175,00 USD 37,590 2.384.853,31 0,62 0,62

EMERSON ELECTRIC CO - 3.156,00 USD 54,540 3.439.519,24 0,90 0,89

ENTERGY CORPORATION - 3.019,00 USD 69,680 4.203.556,32 1,09 1,09

EXELON CORP - 2.718,00 USD 30,880 1.677.151,75 0,44 0,43

EXXON MOBIL CORP - 4.931,00 USD 90,350 8.902.434,25 2,32 2,30

GAP INC - 2.014,00 USD 41,730 1.679.397,36 0,44 0,43

GENERAL ELEC CAP CORP - 8.277,00 USD 23,190 3.835.476,44 1,00 0,99

H&R BLOCK, INC. - 7.480,00 USD 27,750 4.147.727,35 1,08 1,07

HARRIS CORP - 5.587,00 USD 49,250 5.498.326,45 1,43 1,42

HASBRO INC. - 3.382,00 USD 44,830 3.029.618,59 0,79 0,78

INTEL CORP - 8.354,00 USD 24,220 4.043.097,60 1,05 1,04

KIMBERLEY-CLARK CORP - 2.380,00 USD 97,140 4.619.773,38 1,20 1,19

LILLY (ELI) & CO - 10.573,00 USD 49,120 10.377.726,14 2,97 2,68

LORILLARD INC - 10.751,00 USD 43,680 9.383.764,65 2,44 2,42

M&T BANK CORP - 1.811,00 USD 111,750 4.044.004,20 1,05 1,04

MATTEL INC - 3.974,00 USD 45,310 3.598.052,87 0,94 0,93

MEADWESTVACO CORP - 5.235,00 USD 34,110 3.568.157,54 0,93 0,92

MICROSOFT CORP - 13.135,00 USD 34,530 9.063.006,07 2,36 2,34

PFIZER - 6.562,00 USD 28,010 3.672.780,30 0,96 0,95

PPL CORP - 3.994,00 USD 30,260 2.415.030,39 0,63 0,62

RAYONIER INC - 3.131,00 USD 55,390 3.465.453,28 0,90 0,90

REYNOLDS AMERICAN INC - 4.368,00 USD 48,370 4.221.864,91 1,10 1,09

ROCKWELL AUTOMATION CORP - 1.740,00 USD 83,140 2.890.712,39 0,75 0,75

SAFEWAY INC. - 16.770,00 USD 23,660 7.928.543,59 2,06 2,05

TIME WARNER INC - 2.455,00 USD 57,820 2.836.450,44 0,74 0,73

UNITED PARCEL SERVICE "B" 1.421,00 USD 86,480 2.455.587,28 0,64 0,63

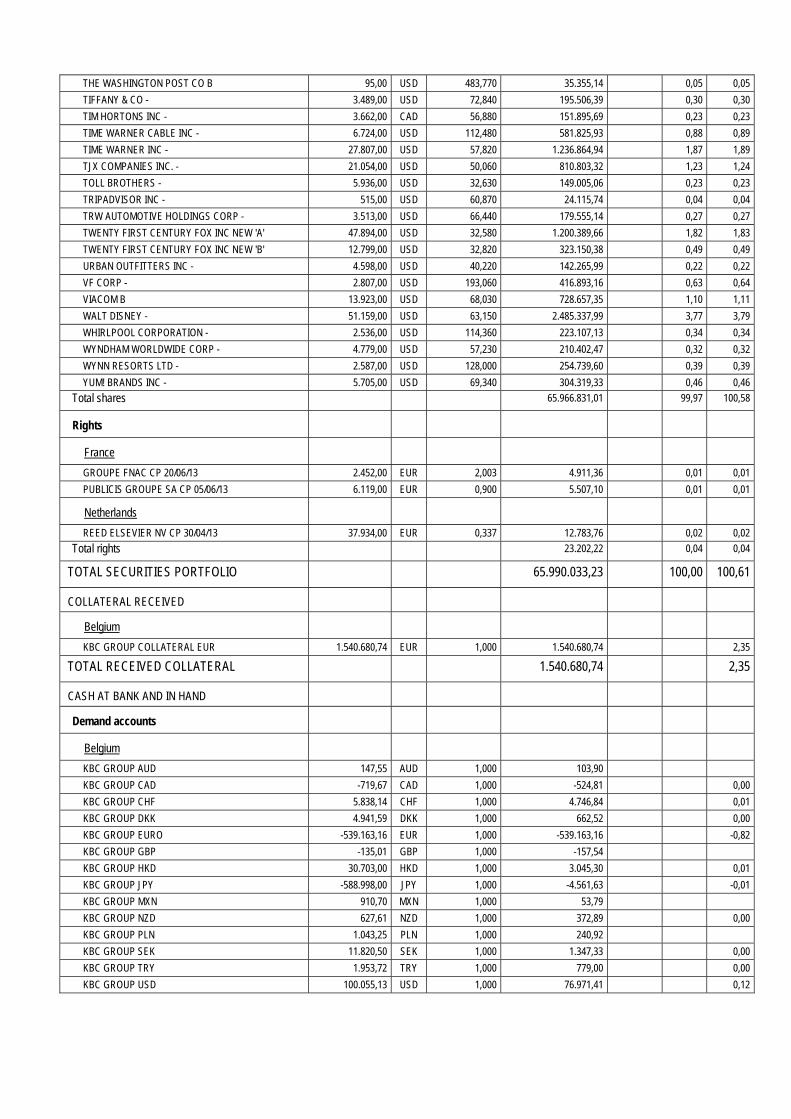

VERIZON COMMUNICATIONS INC - 5.686,00 USD 50,340 5.719.600,32 1,49 1,48

WEST UNION COMPANY - 21.499,00 USD 17,110 7.350.449,27 1,91 1,90

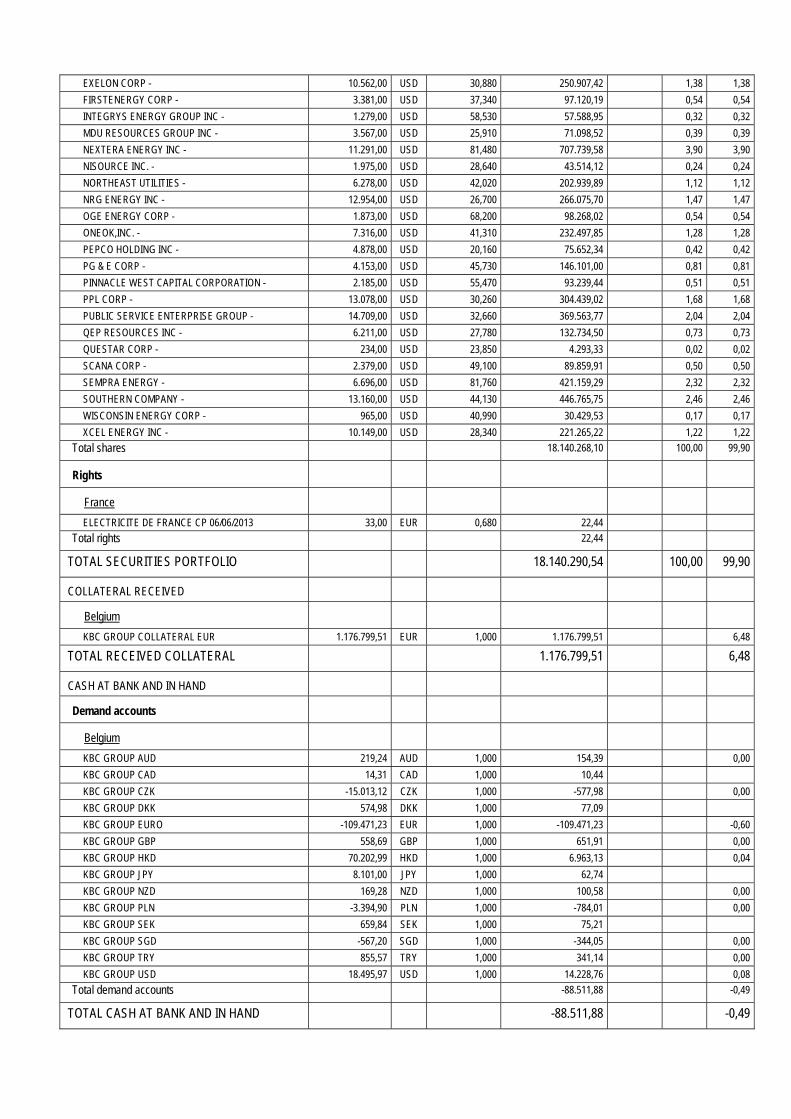

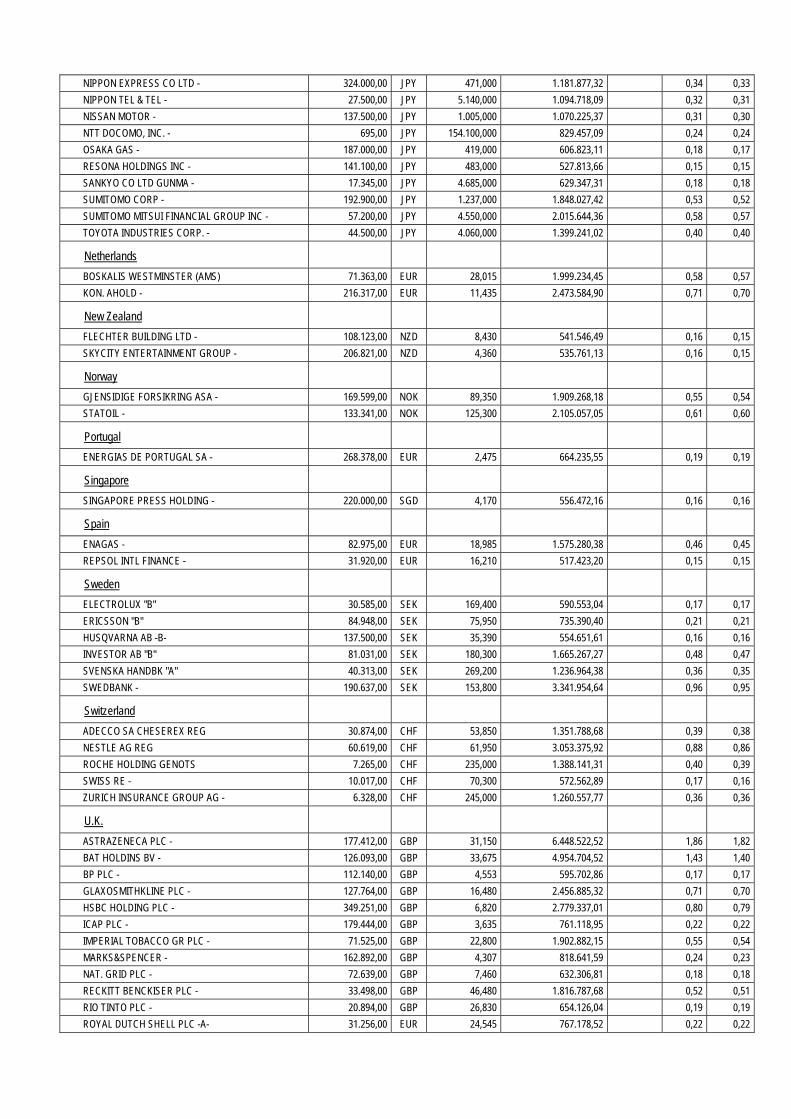

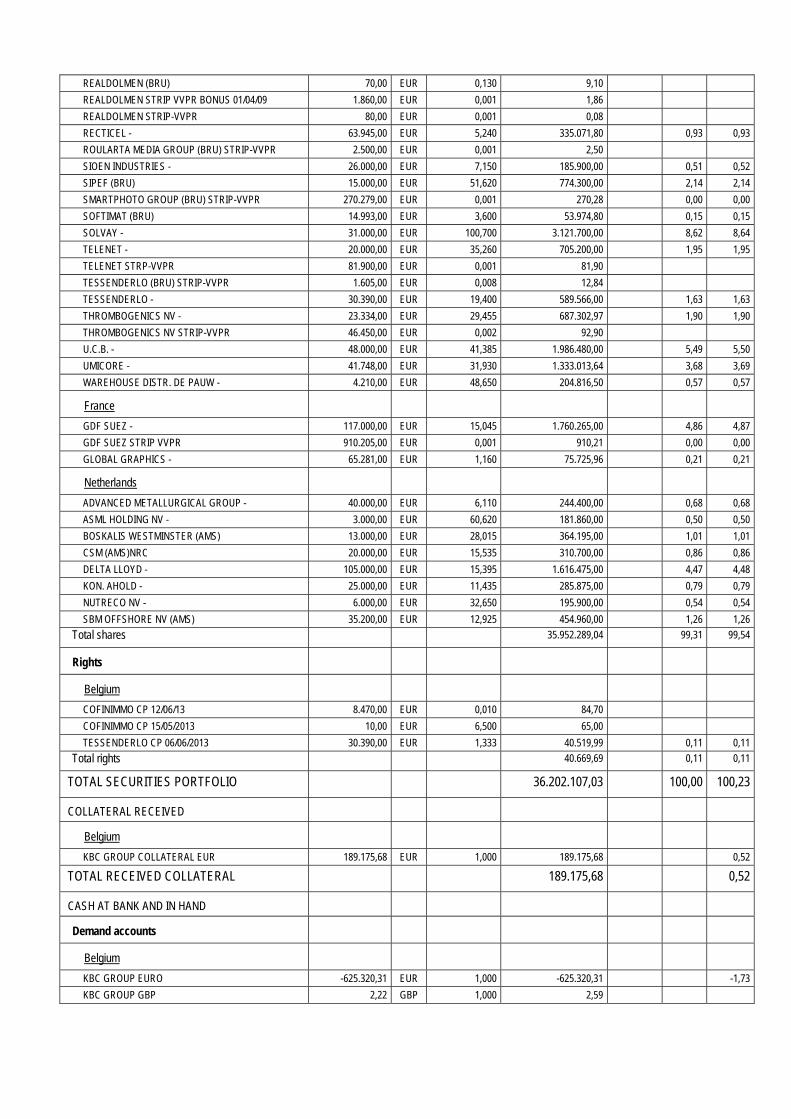

Total shares 385.359.449,73 100,27 99,53

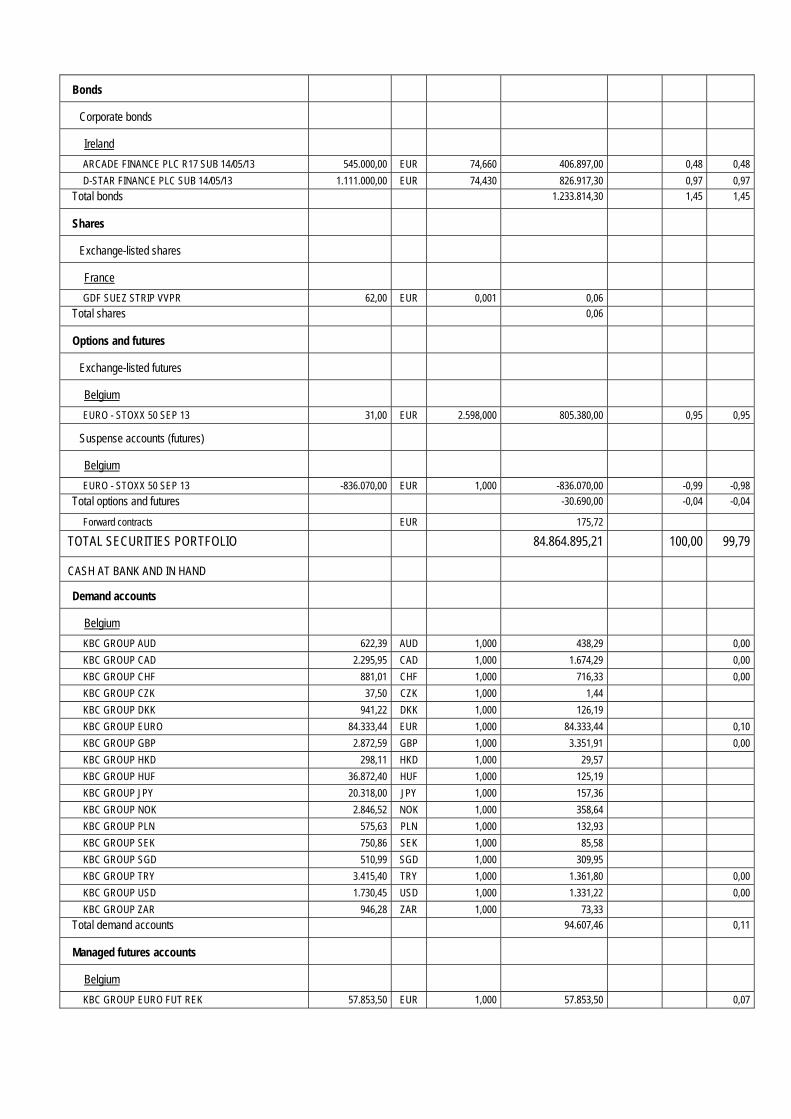

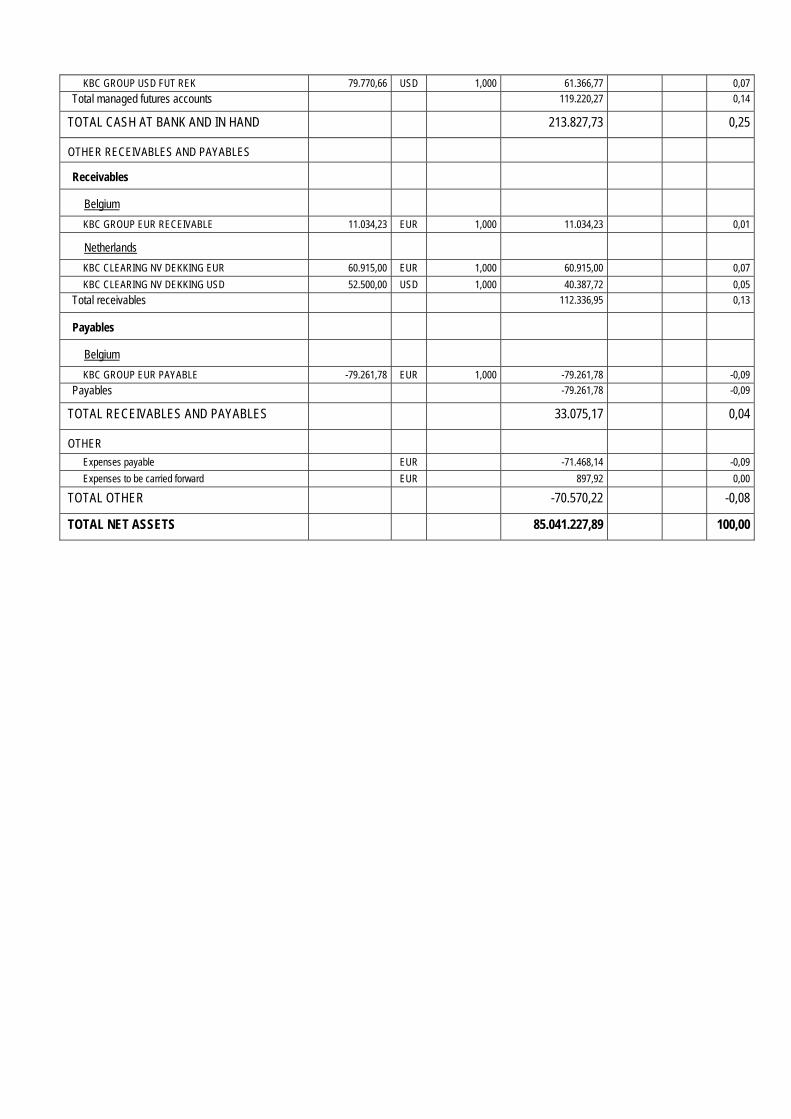

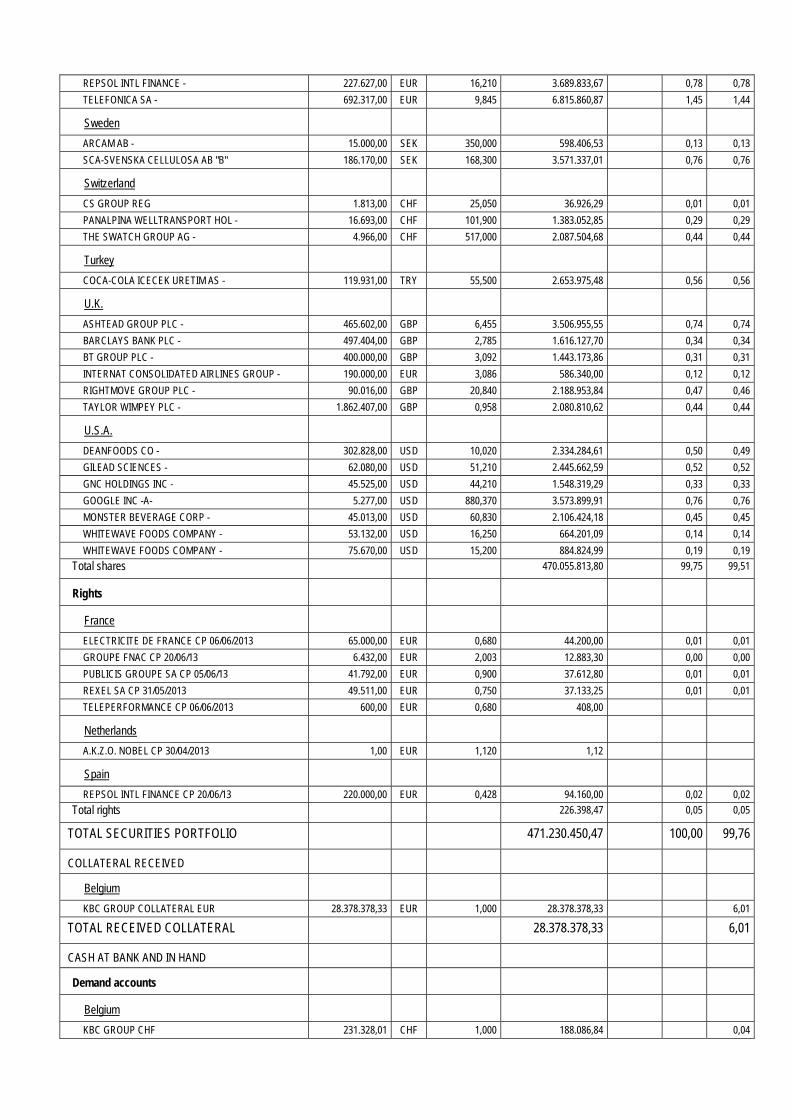

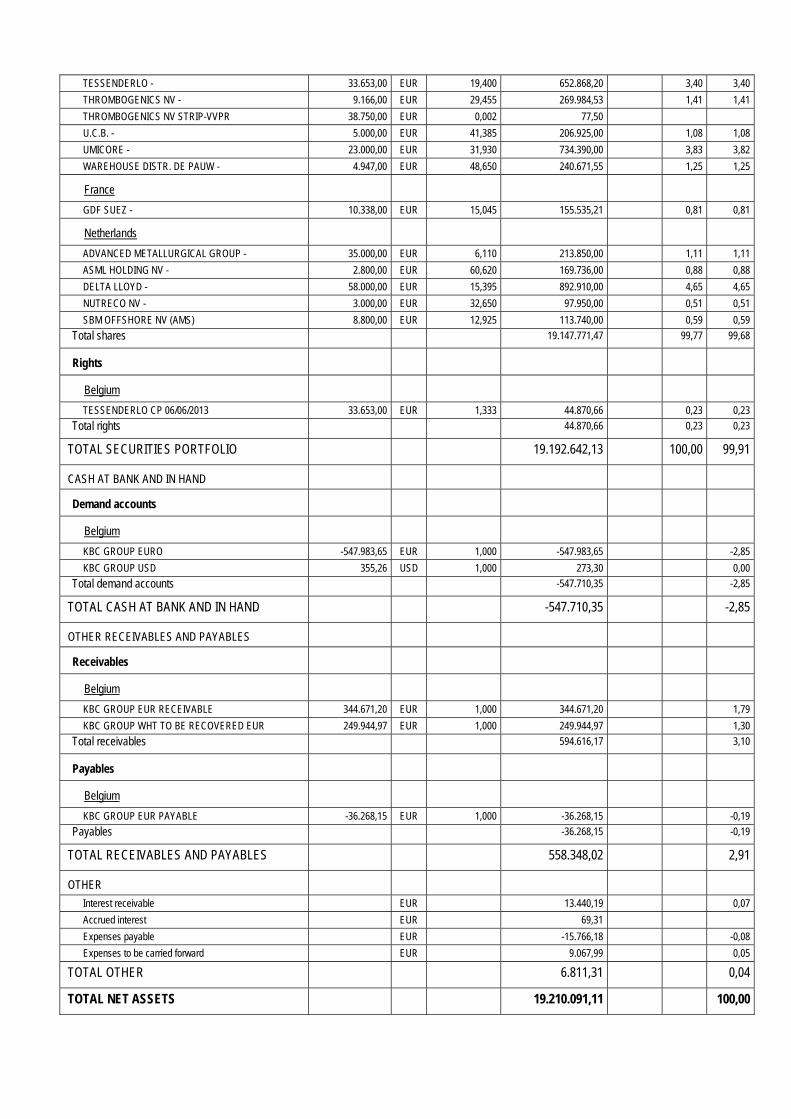

Forward contracts CZK -1.028.196,09 -0,27

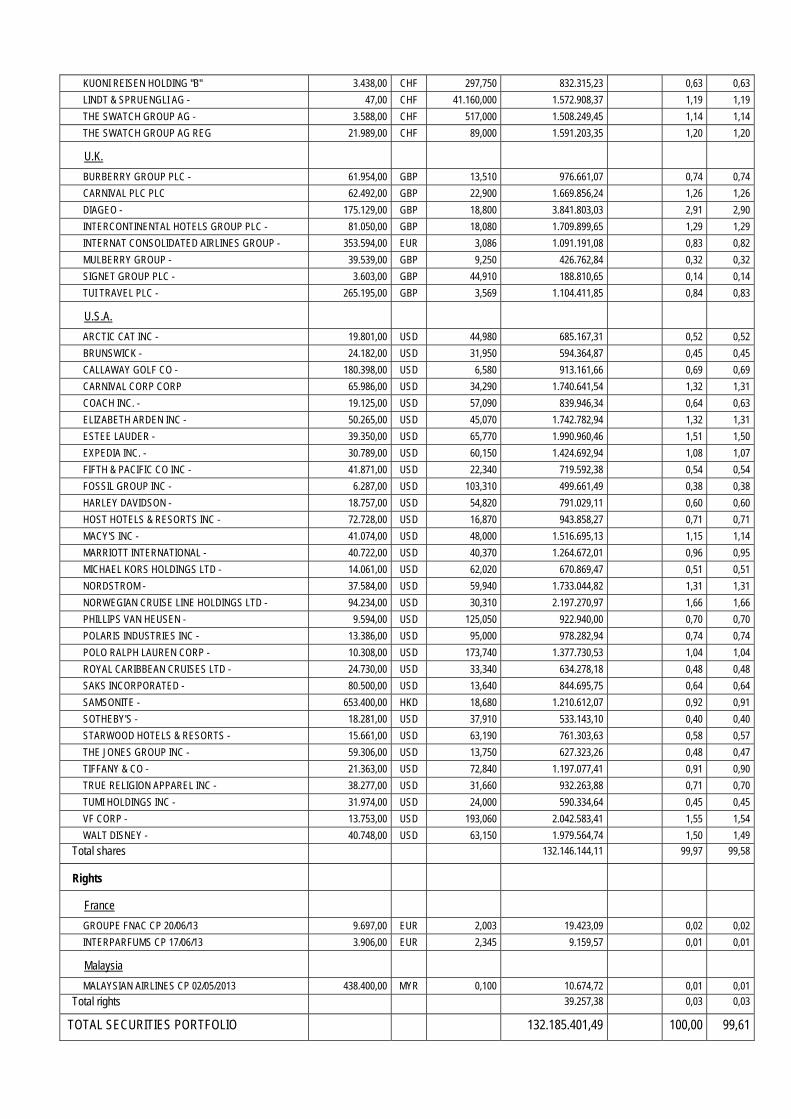

TOTAL SECURITIES PORTFOLIO 384.331.253,64 100,00 99,26

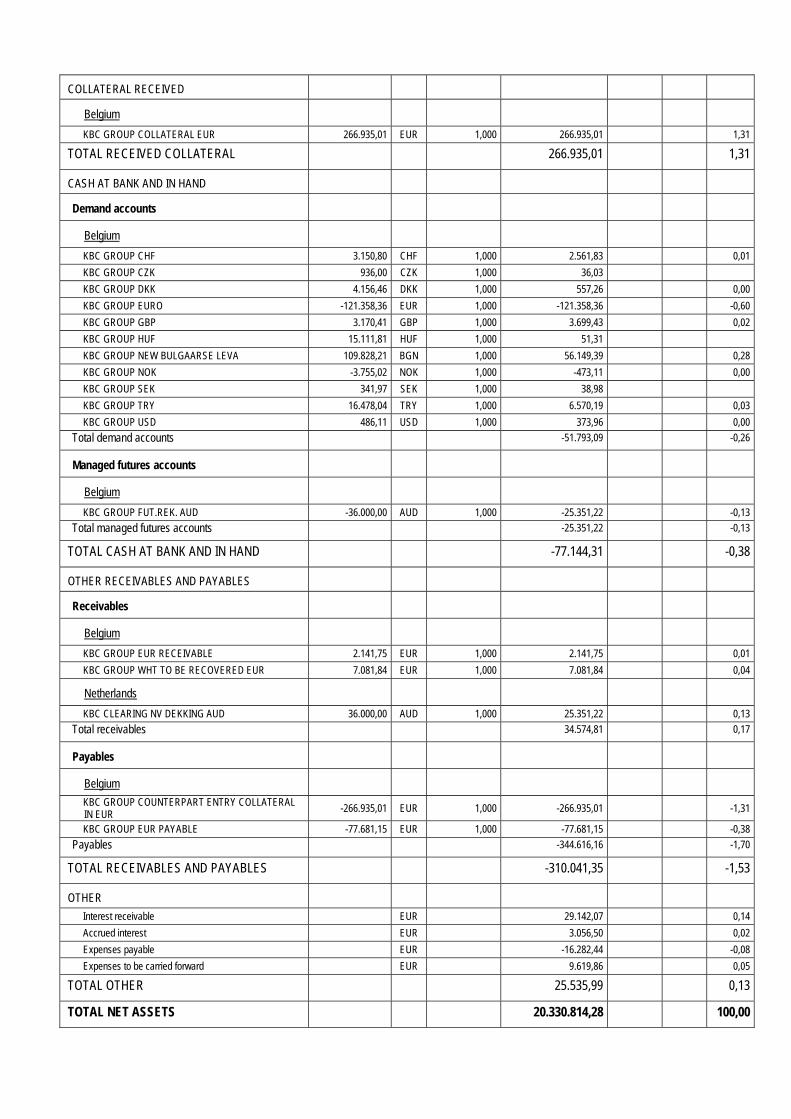

COLLATERAL RECEIVED

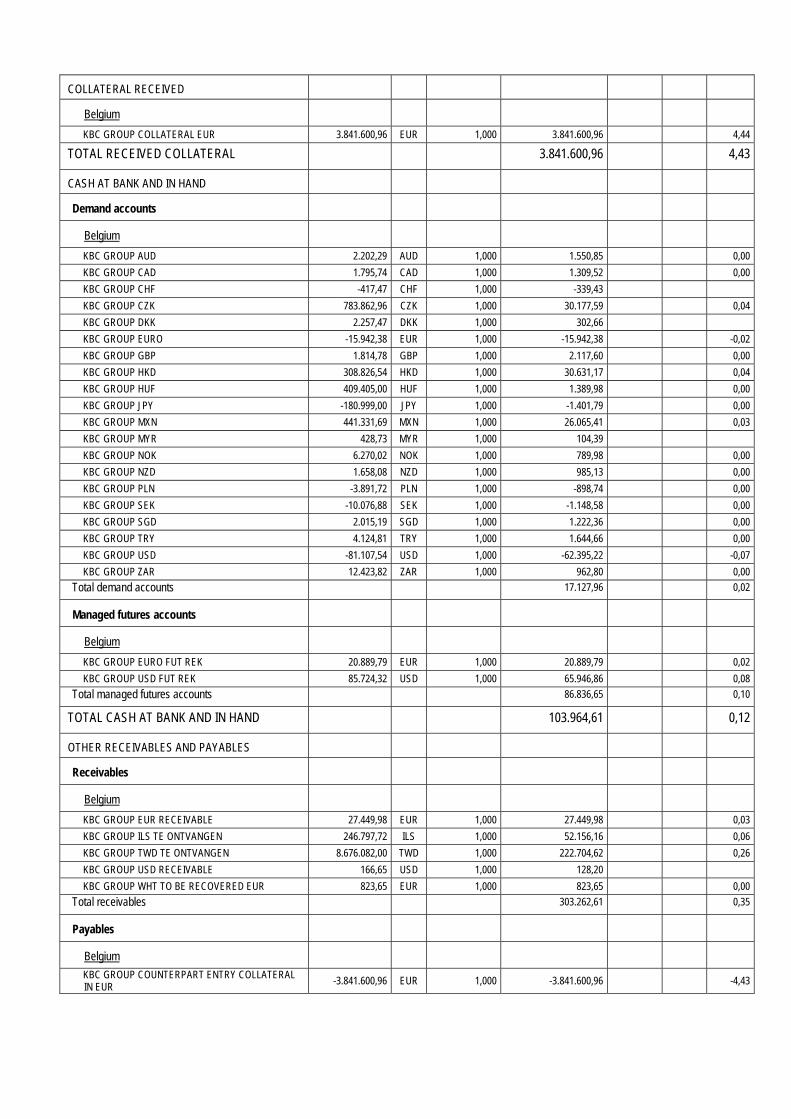

Belgium

KBC GROUP COLLATERAL EUR 1.168.358,59 EUR 1,000 30.348.114,62 7,84

TOTAL RECEIVED COLLATERAL 30.348.114,62 7,84

CASH AT BANK AND IN HAND

Demand accounts

Belgium

KBC GROUP AUD 8.457,87 AUD 1,000 154.708,06 0,04

KBC GROUP CAD 2.844,25 CAD 1,000 53.875,44 0,01

KBC GROUP CHF 57,16 CHF 1,000 1.207,20

KBC GROUP CZK 1.675.062,01 CZK 1,000 1.675.062,01 0,43

KBC GROUP EURO -16.483,43 EUR 1,000 -428.157,10 -0,11

KBC GROUP GBP -5.553,59 GBP 1,000 -168.324,97 -0,04

KBC GROUP HKD -34.382,79 HKD 1,000 -88.582,04 -0,02

KBC GROUP JPY 746.455,00 JPY 1,000 150.163,95 0,04

KBC GROUP NOK 5.244,04 NOK 1,000 17.162,11 0,00

KBC GROUP NZD 643,40 NZD 1,000 9.929,48 0,00

KBC GROUP SEK 12.188,72 SEK 1,000 36.086,99 0,01

KBC GROUP USD 466,70 USD 1,000 9.325,74 0,00

Total demand accounts 1.422.456,87 0,37

TOTAL CASH AT BANK AND IN HAND 1.422.456,87 0,37

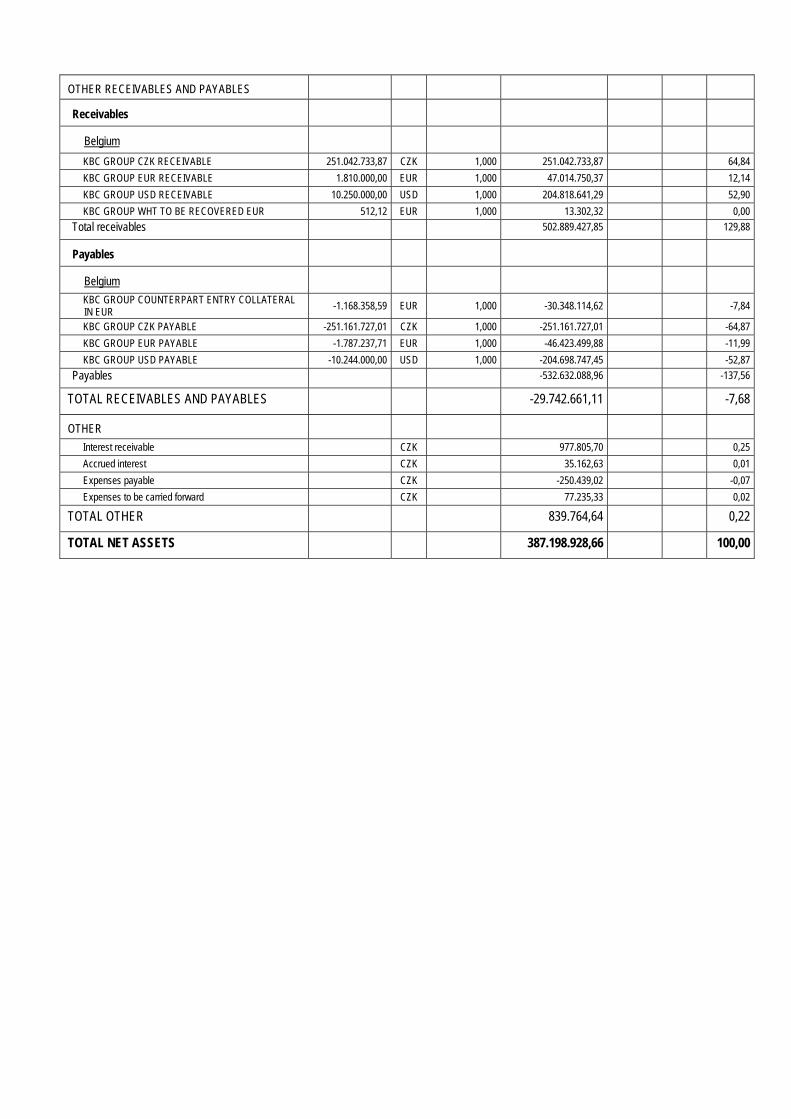

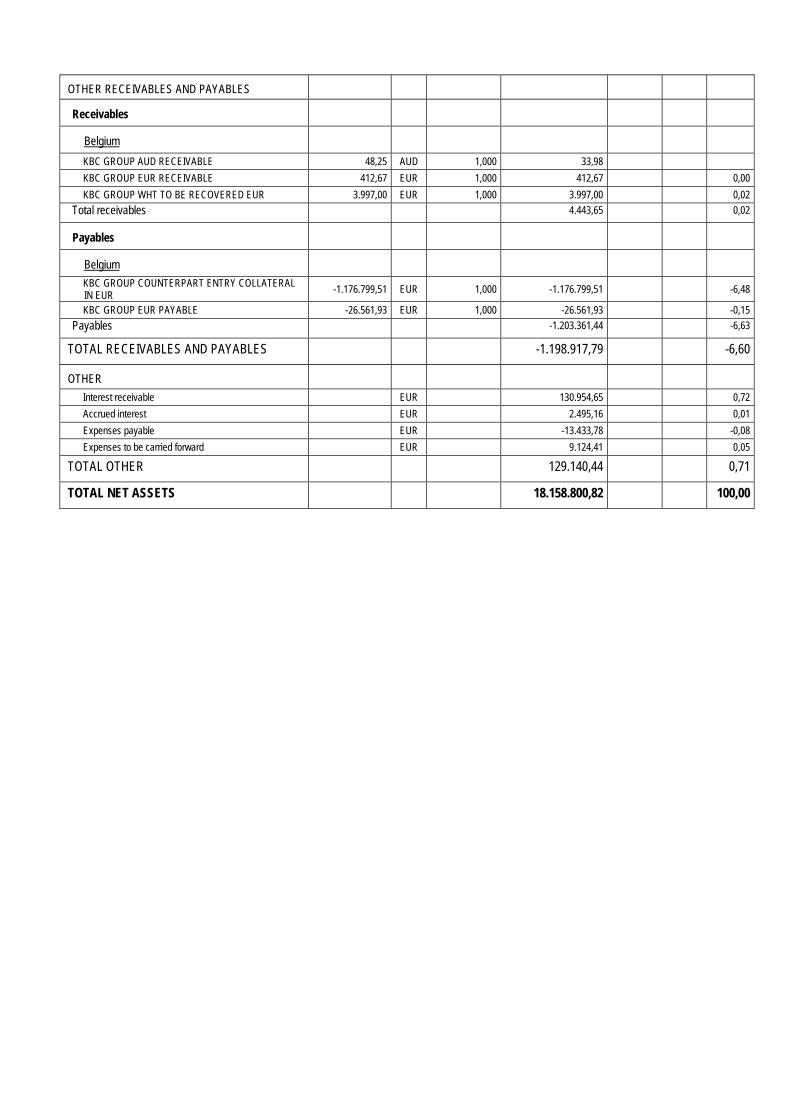

OTHER RECEIVABLES AND PAYABLES

Receivables

Belgium

KBC GROUP CZK RECEIVABLE 251.042.733,87 CZK 1,000 251.042.733,87 64,84

KBC GROUP EUR RECEIVABLE 1.810.000,00 EUR 1,000 47.014.750,37 12,14

KBC GROUP USD RECEIVABLE 10.250.000,00 USD 1,000 204.818.641,29 52,90

KBC GROUP WHT TO BE RECOVERED EUR 512,12 EUR 1,000 13.302,32 0,00

Total receivables 502.889.427,85 129,88

Payables

Belgium

KBC GROUP COUNTERPART ENTRY COLLATERAL IN EUR

-1.168.358,59 EUR 1,000 -30.348.114,62 -7,84

KBC GROUP CZK PAYABLE -251.161.727,01 CZK 1,000 -251.161.727,01 -64,87

KBC GROUP EUR PAYABLE -1.787.237,71 EUR 1,000 -46.423.499,88 -11,99

KBC GROUP USD PAYABLE -10.244.000,00 USD 1,000 -204.698.747,45 -52,87

Payables -532.632.088,96 -137,56

TOTAL RECEIVABLES AND PAYABLES -29.742.661,11 -7,68

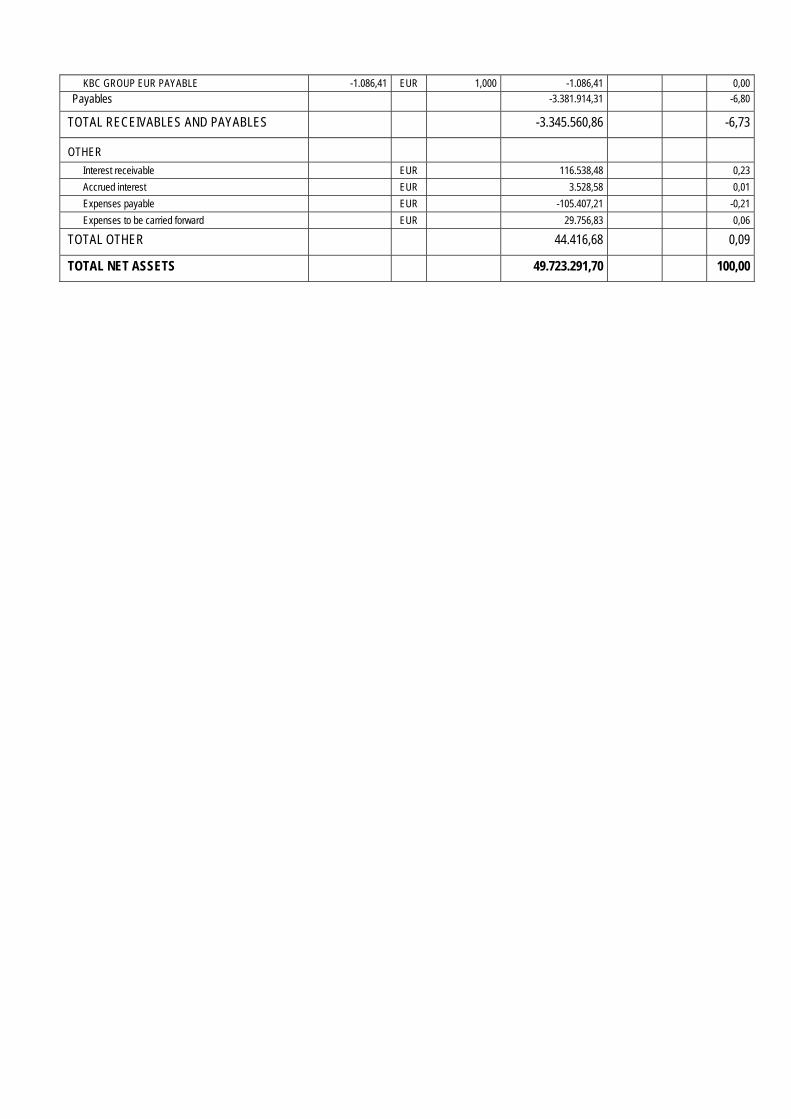

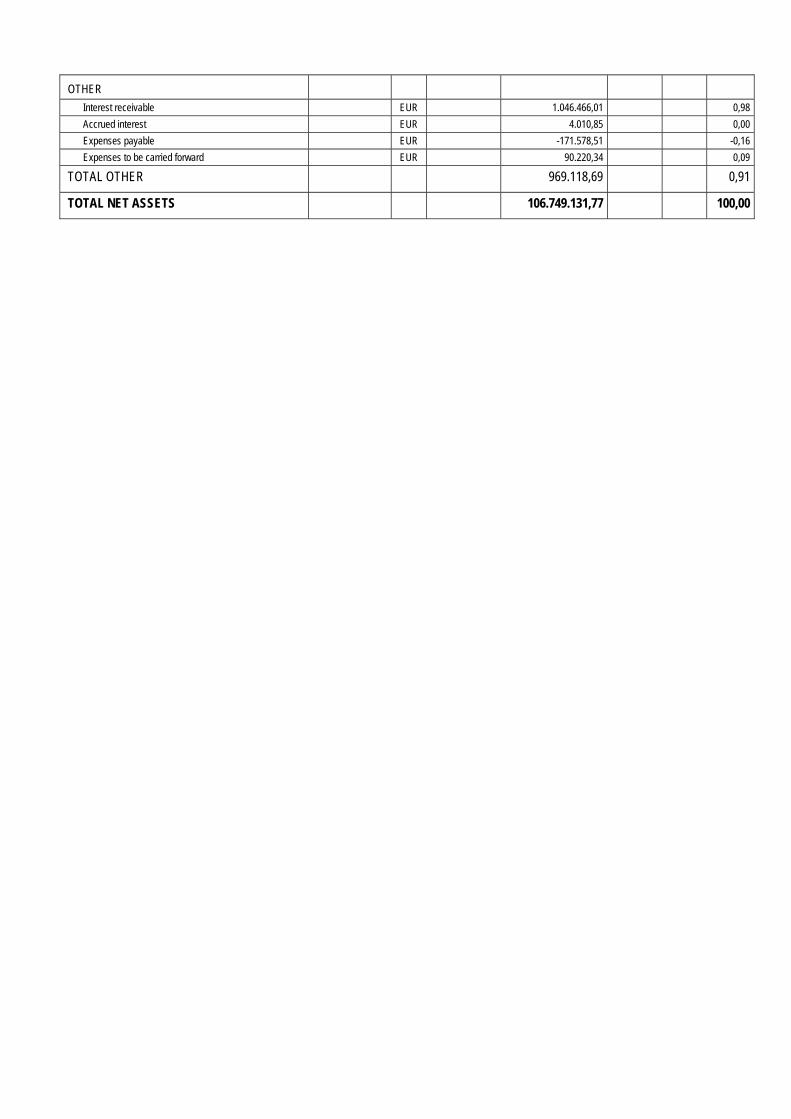

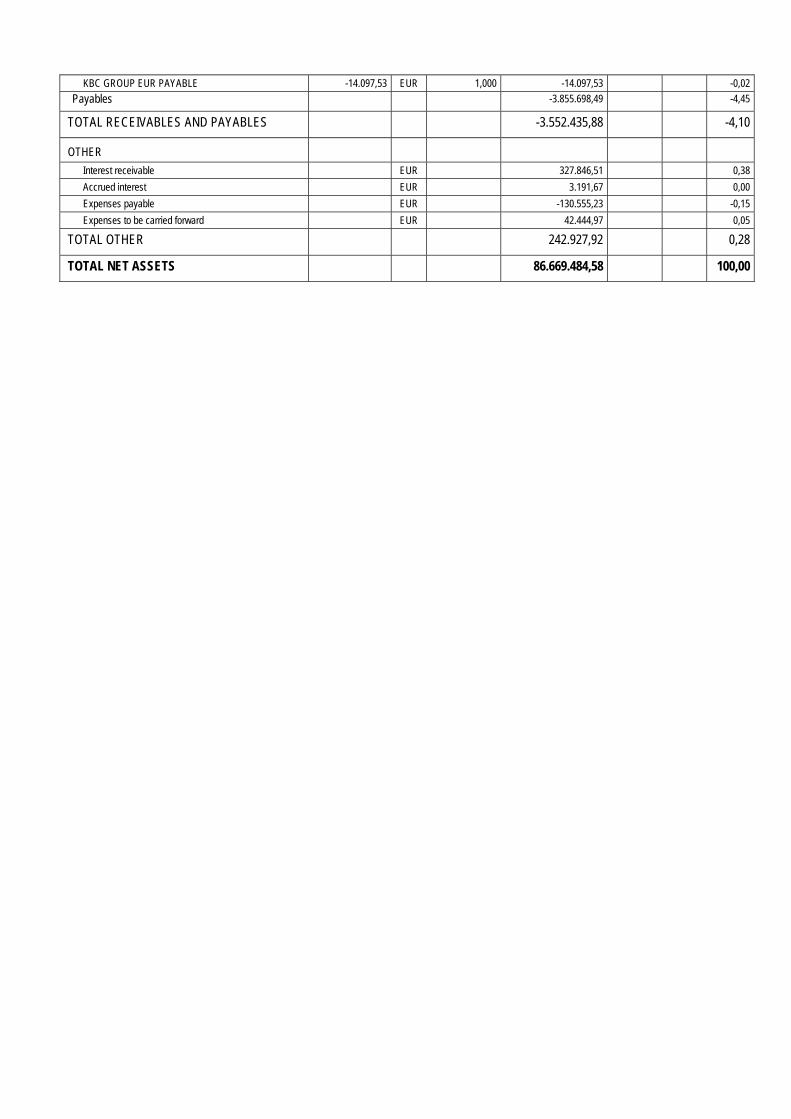

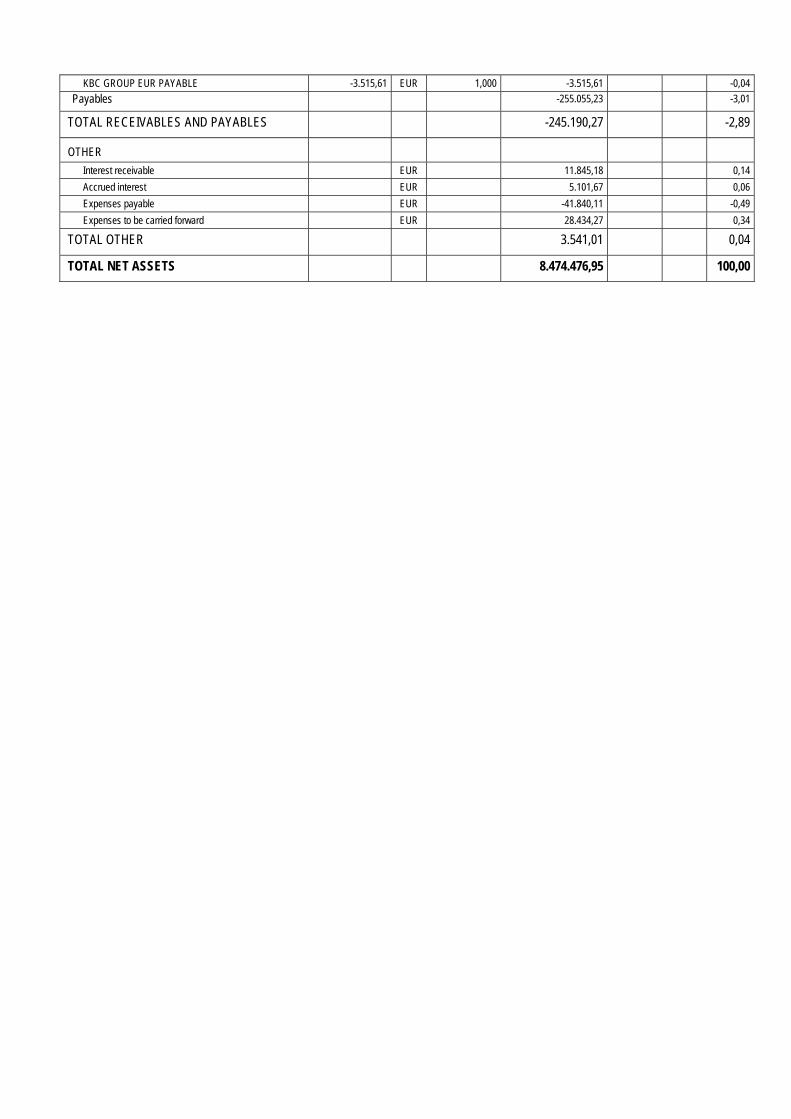

OTHER

Interest receivable CZK 977.805,70 0,25

Accrued interest CZK 35.162,63 0,01

Expenses payable CZK -250.439,02 -0,07

Expenses to be carried forward CZK 77.235,33 0,02

TOTAL OTHER 839.764,64 0,22

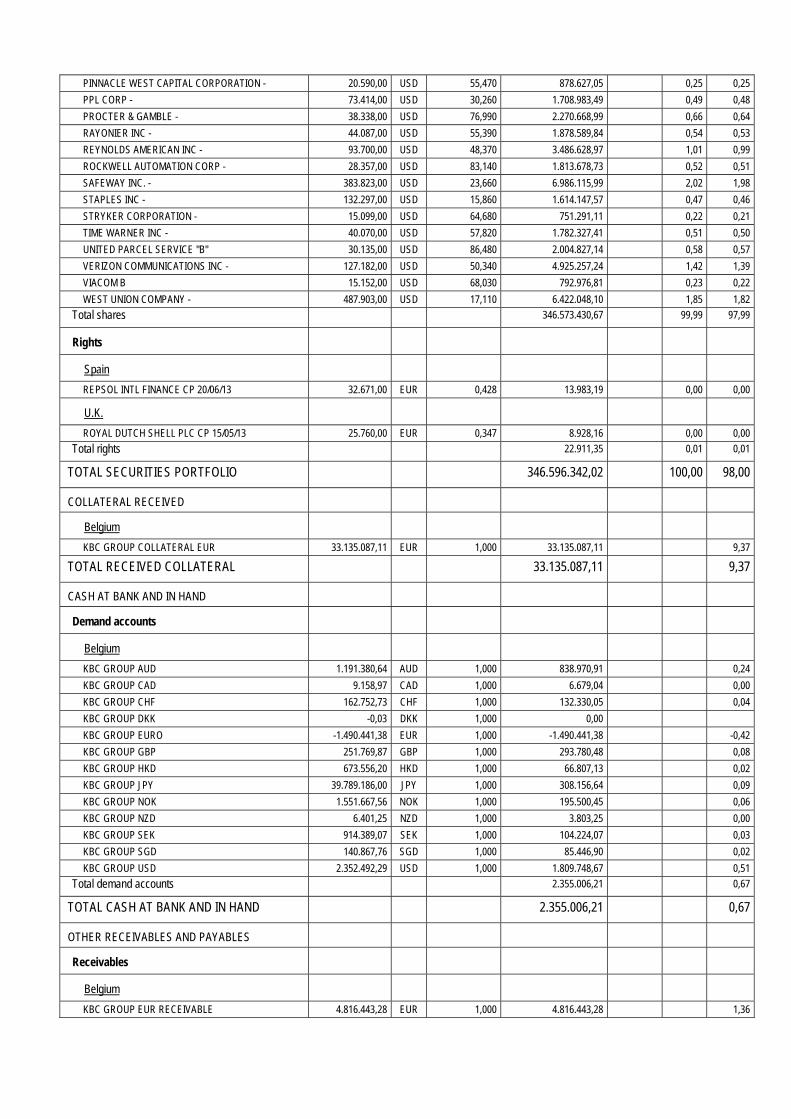

TOTAL NET ASSETS 387.198.928,66 100,00

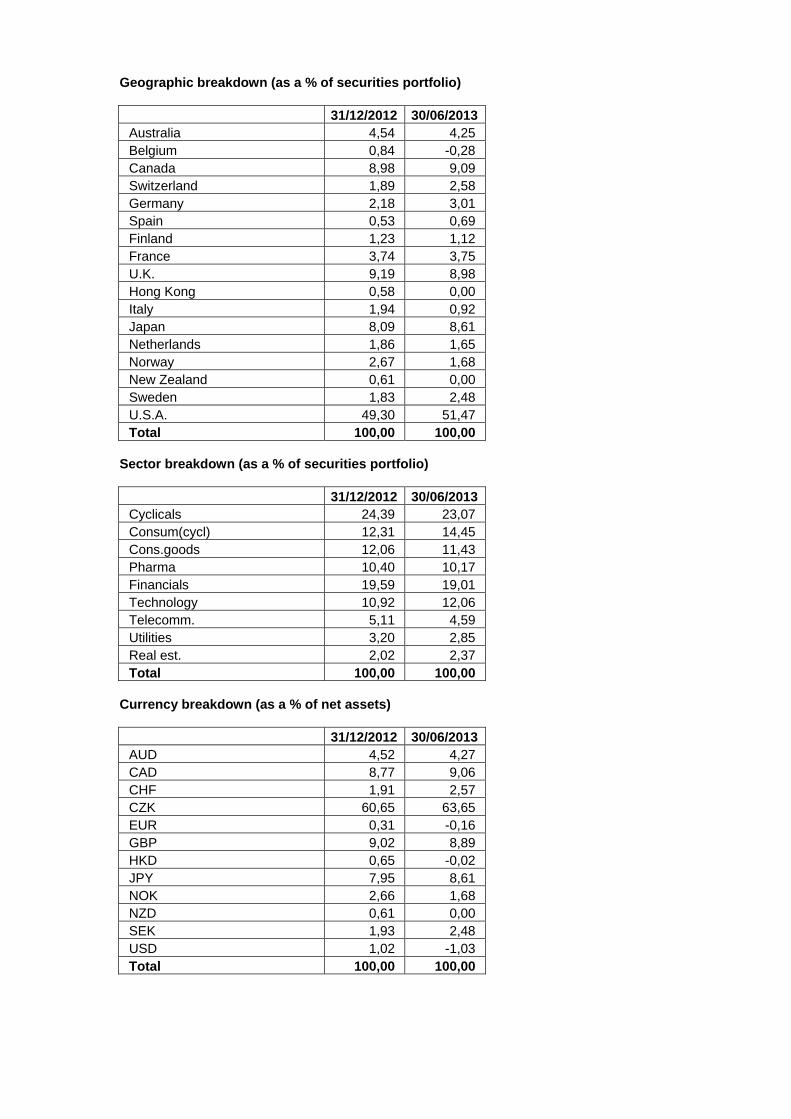

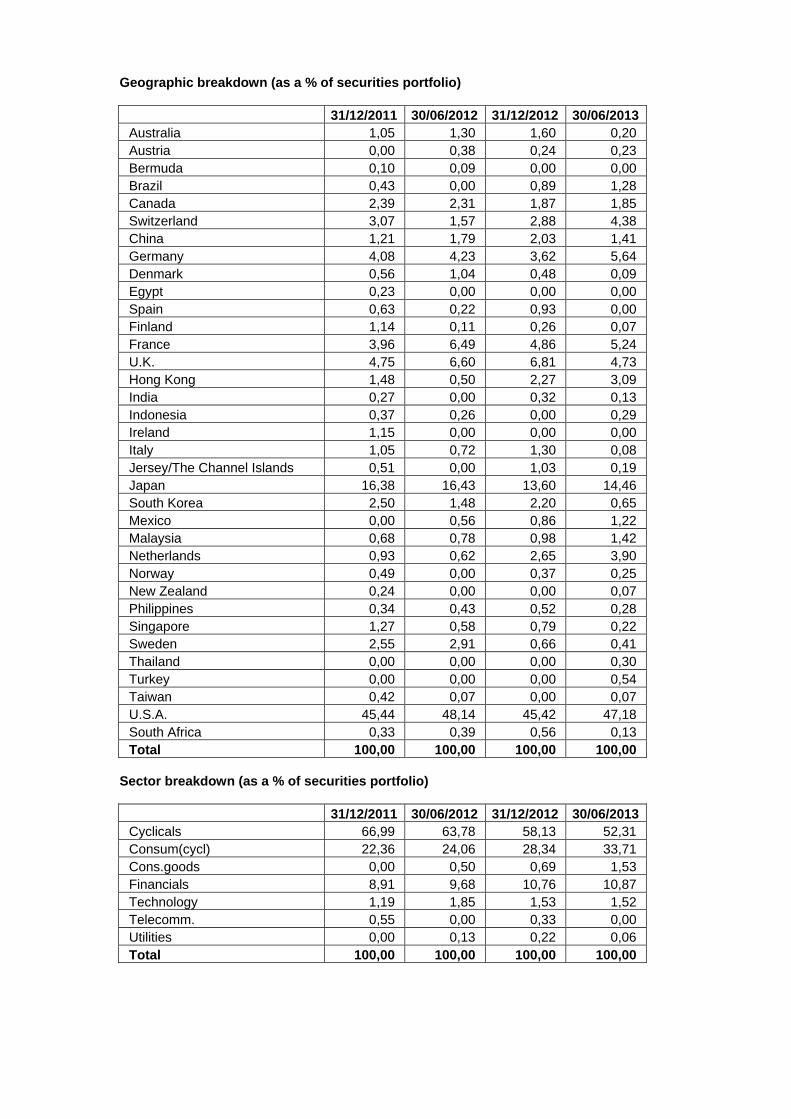

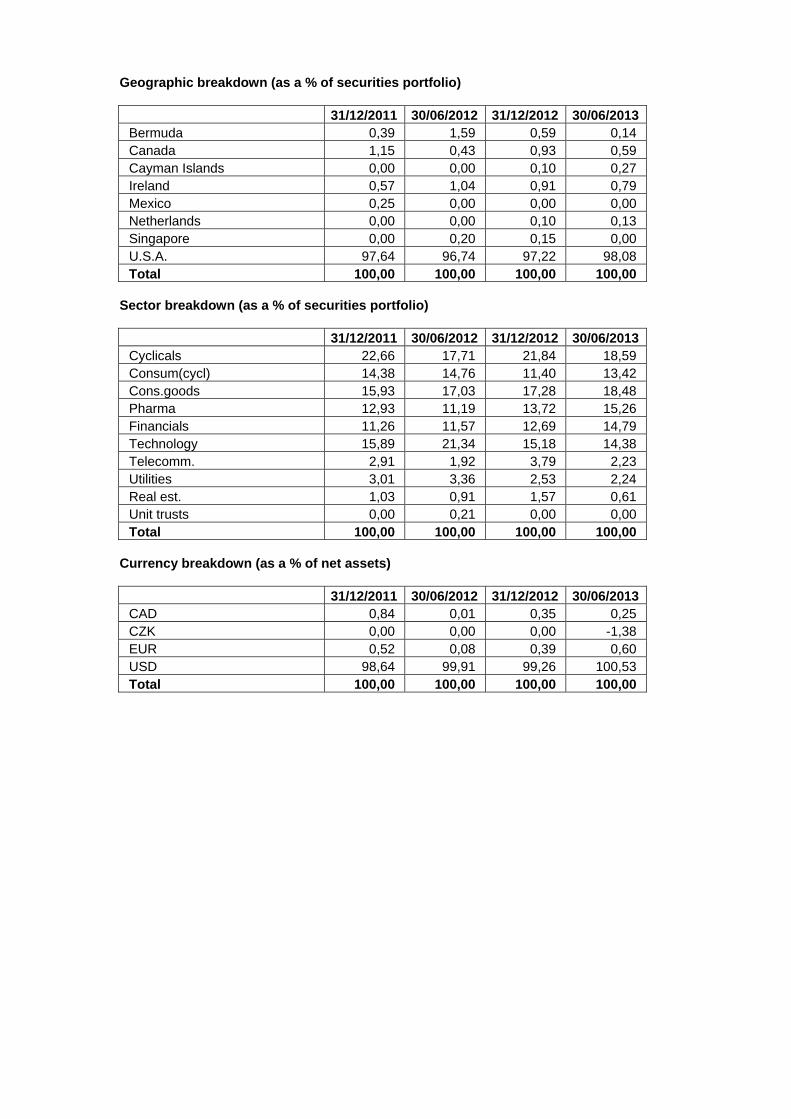

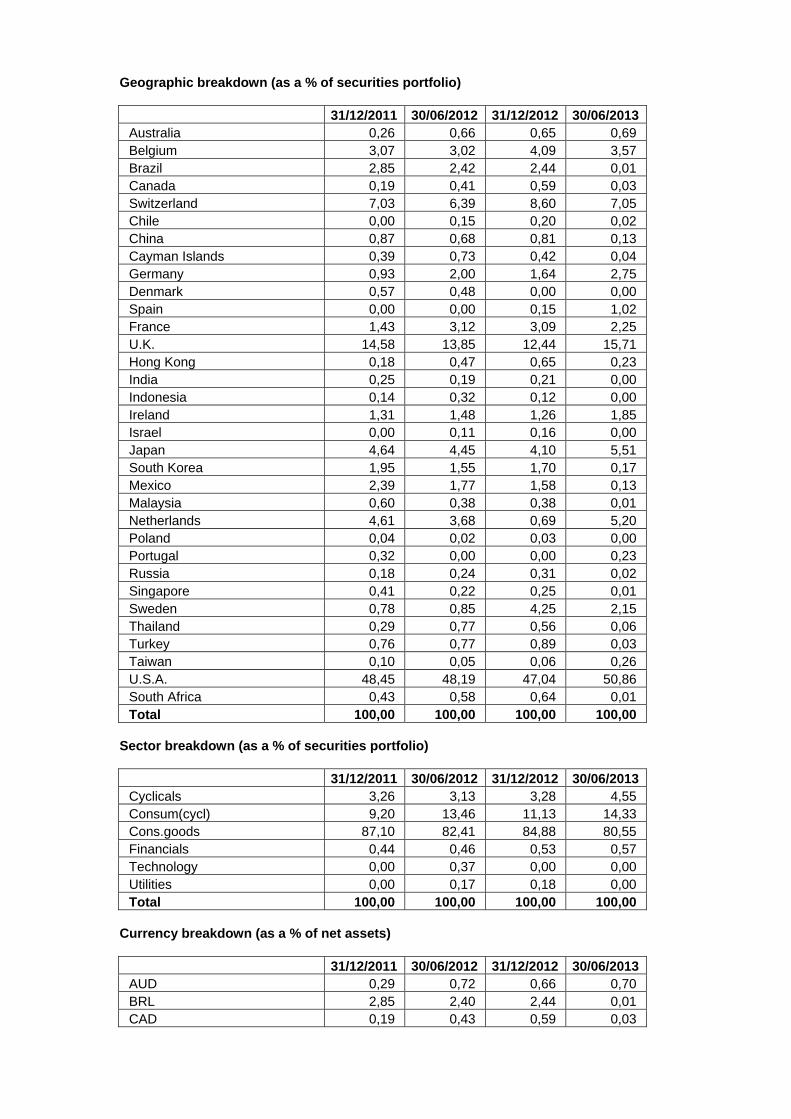

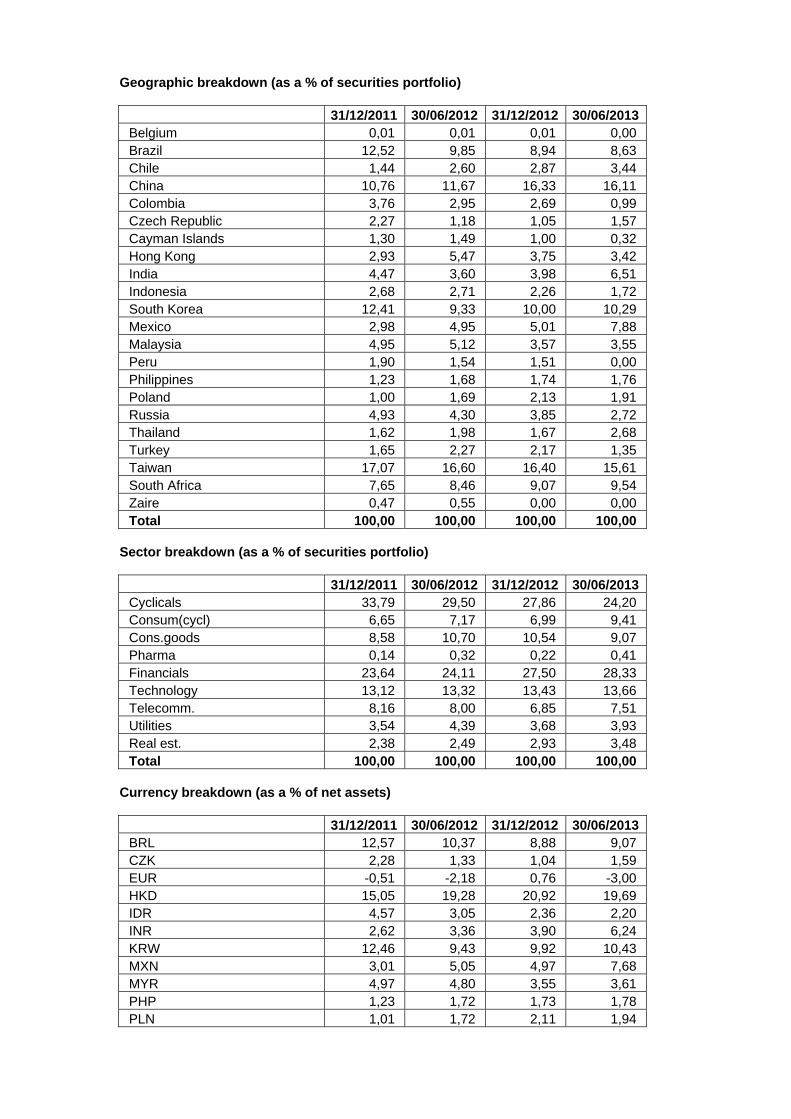

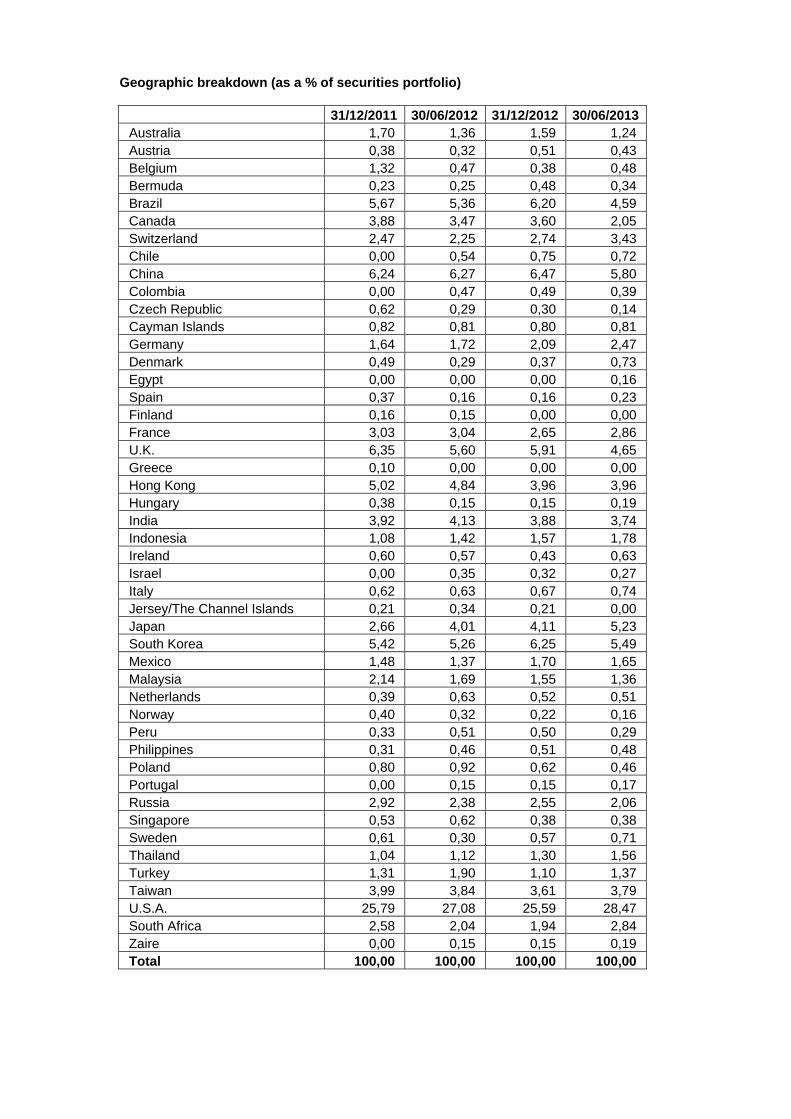

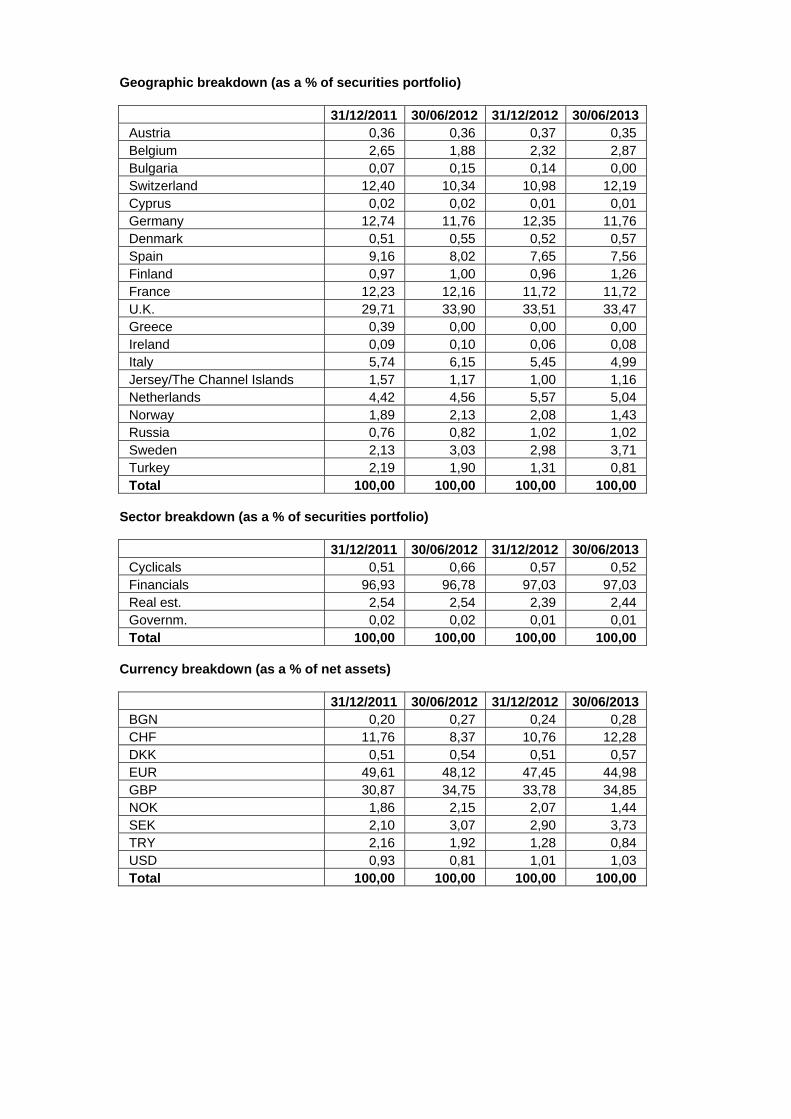

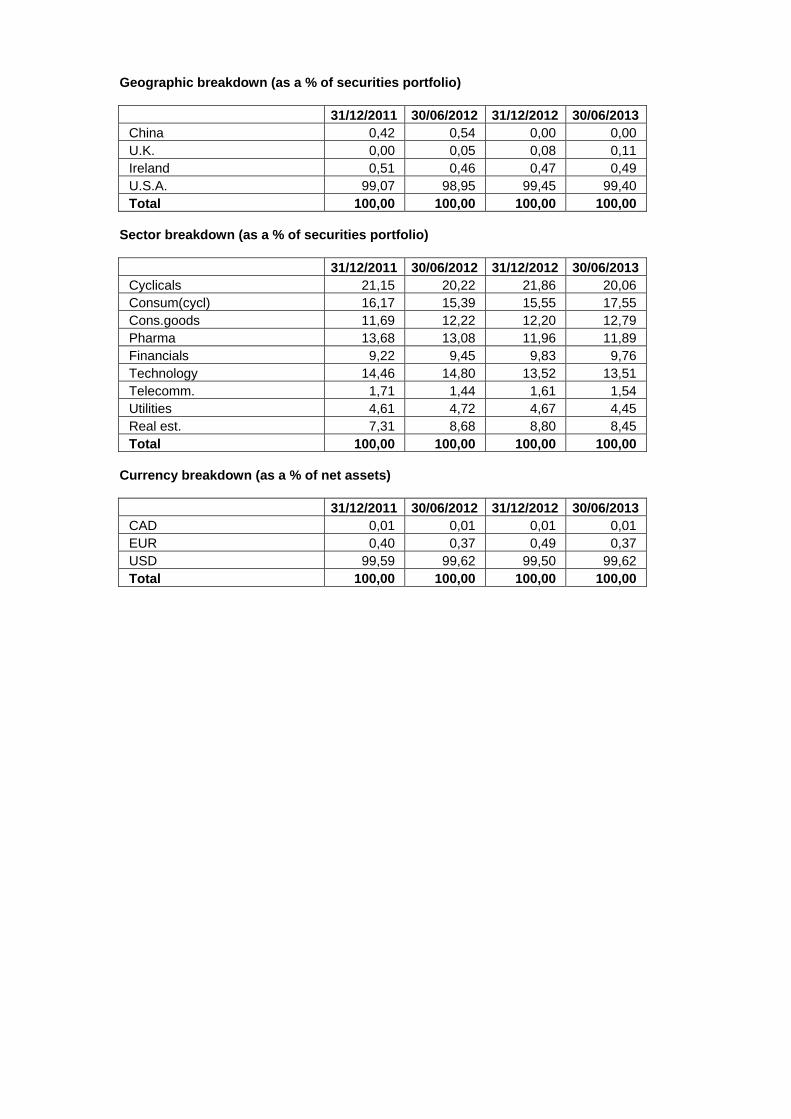

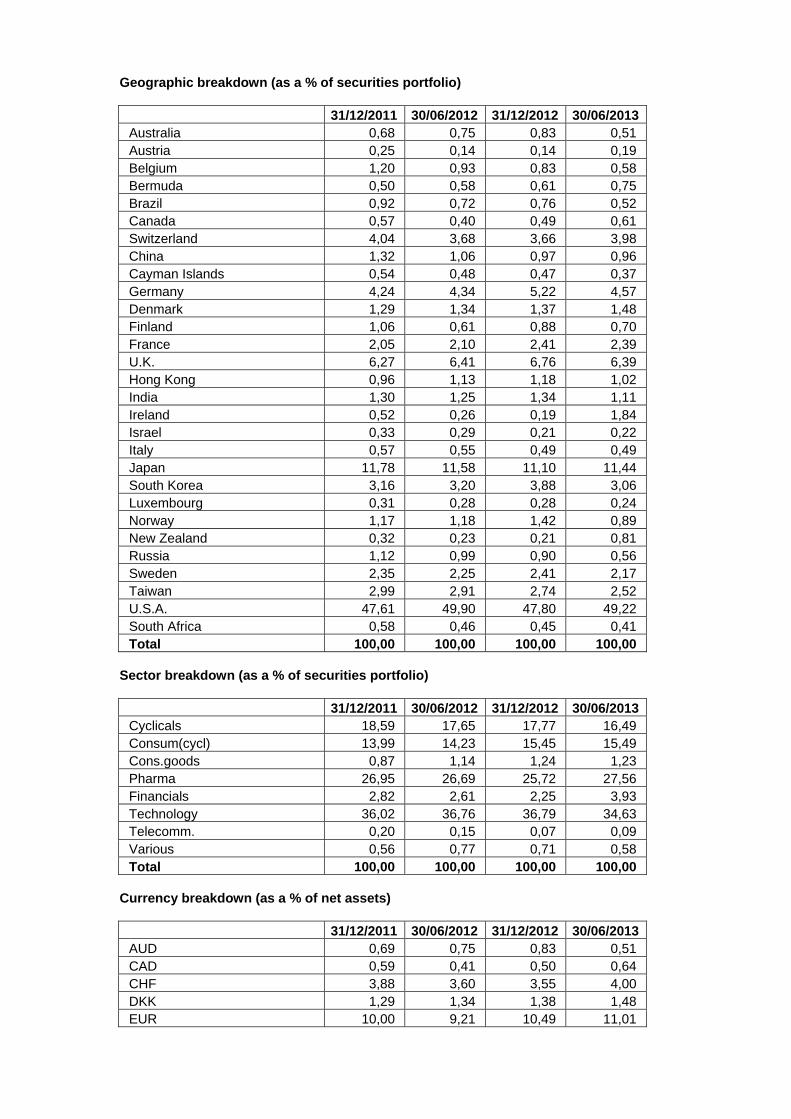

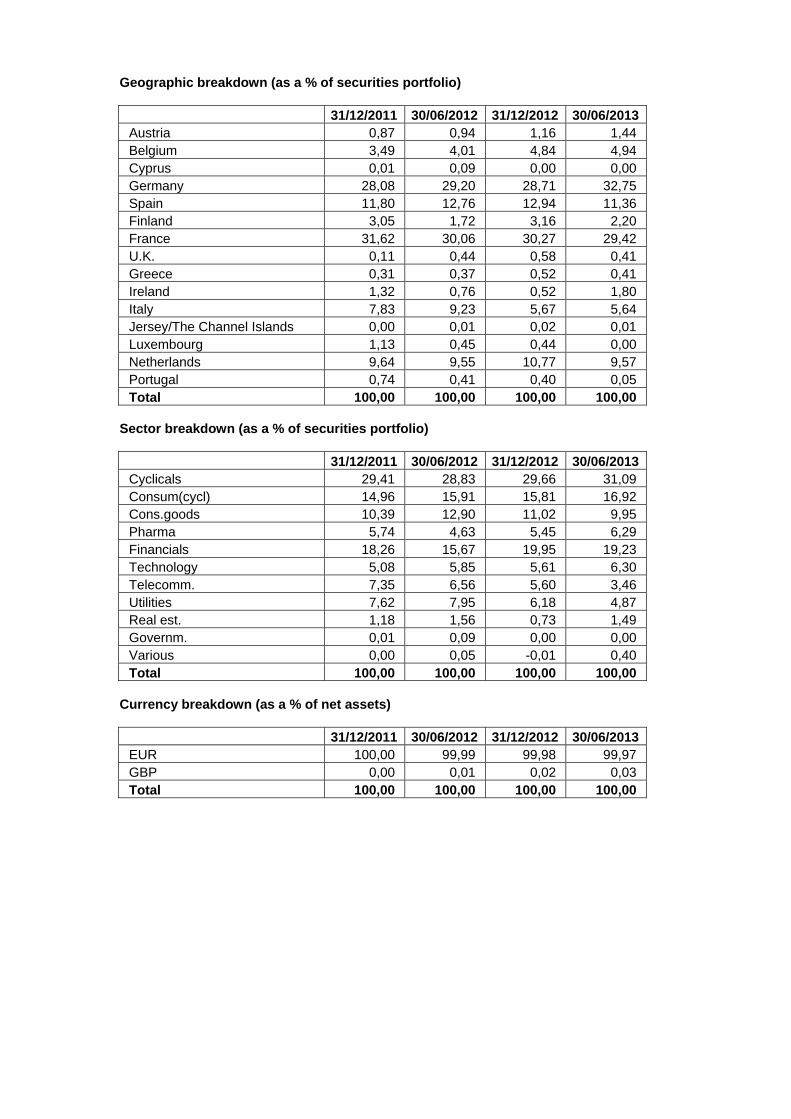

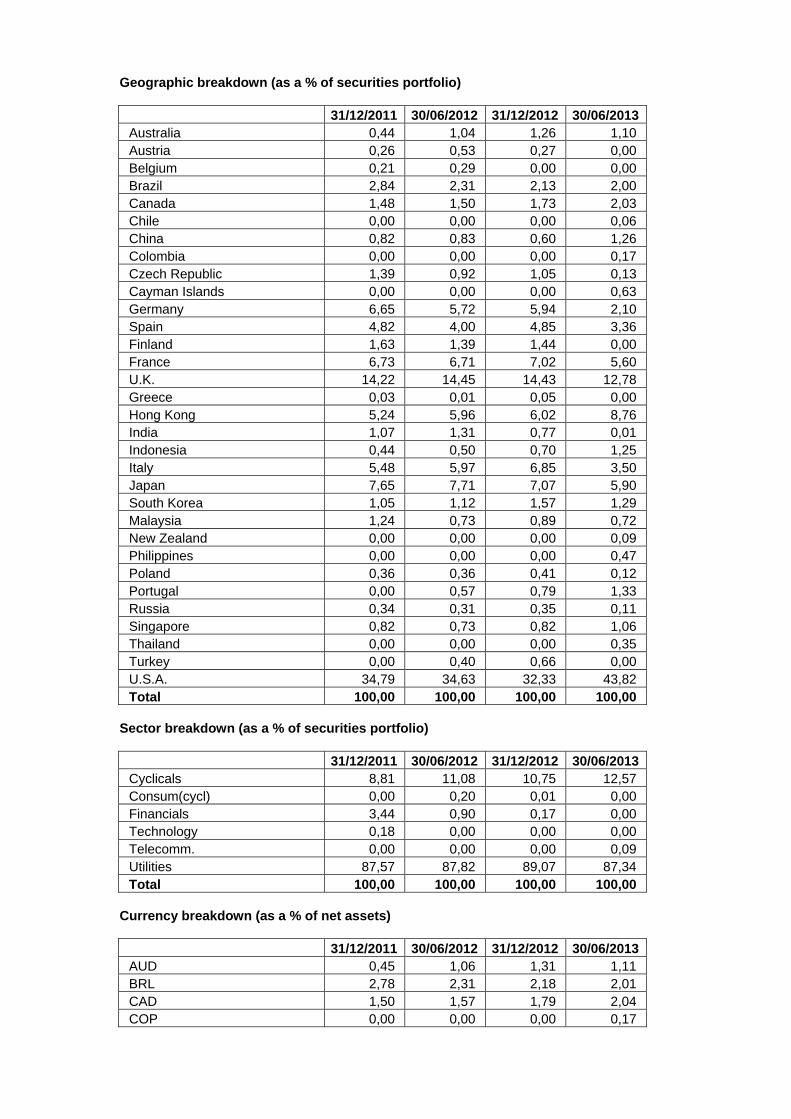

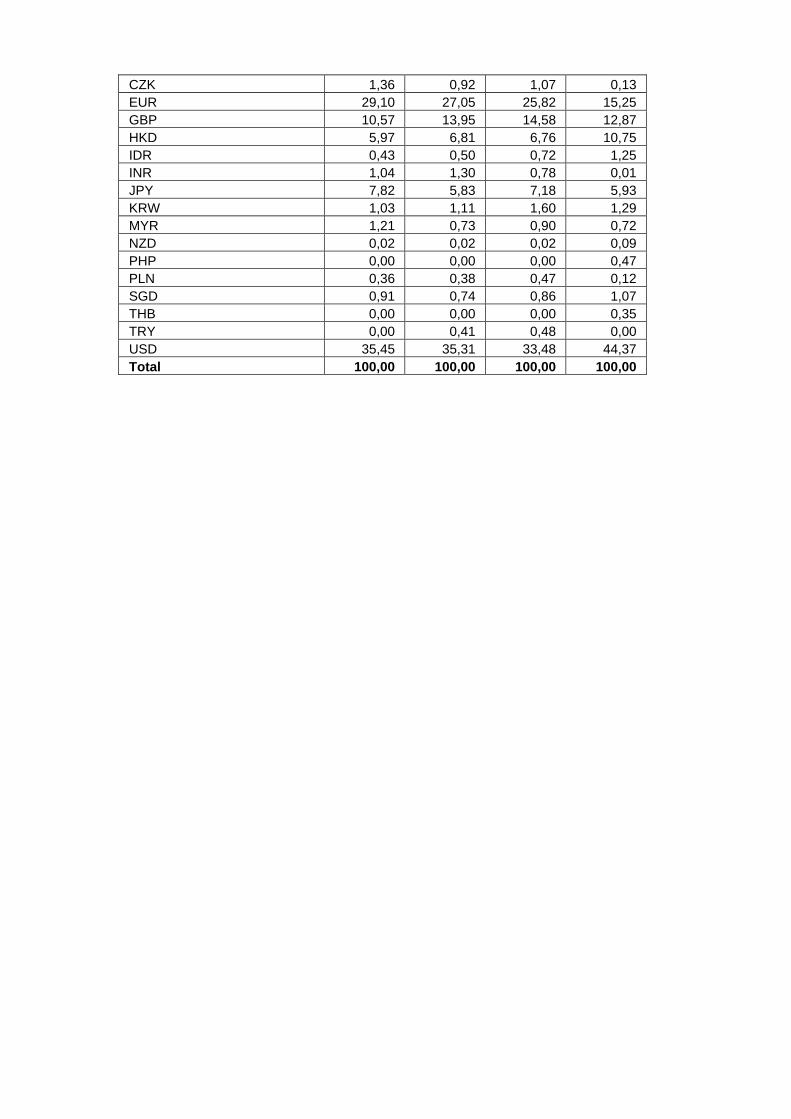

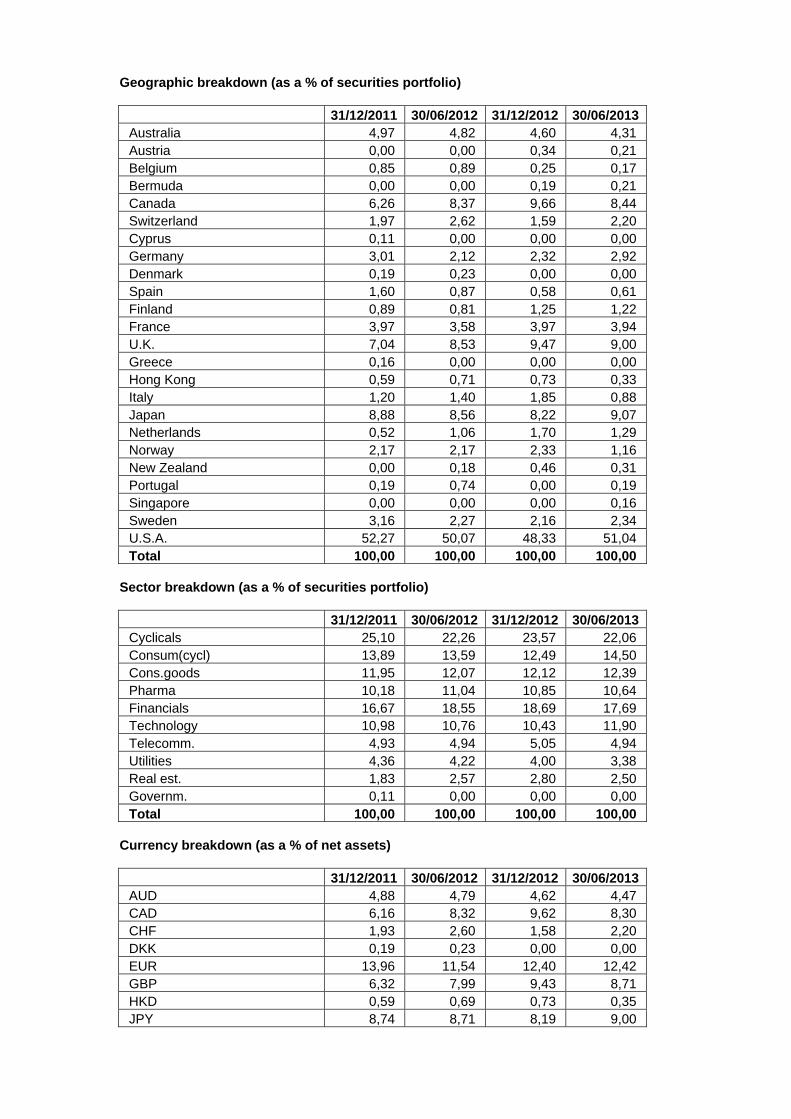

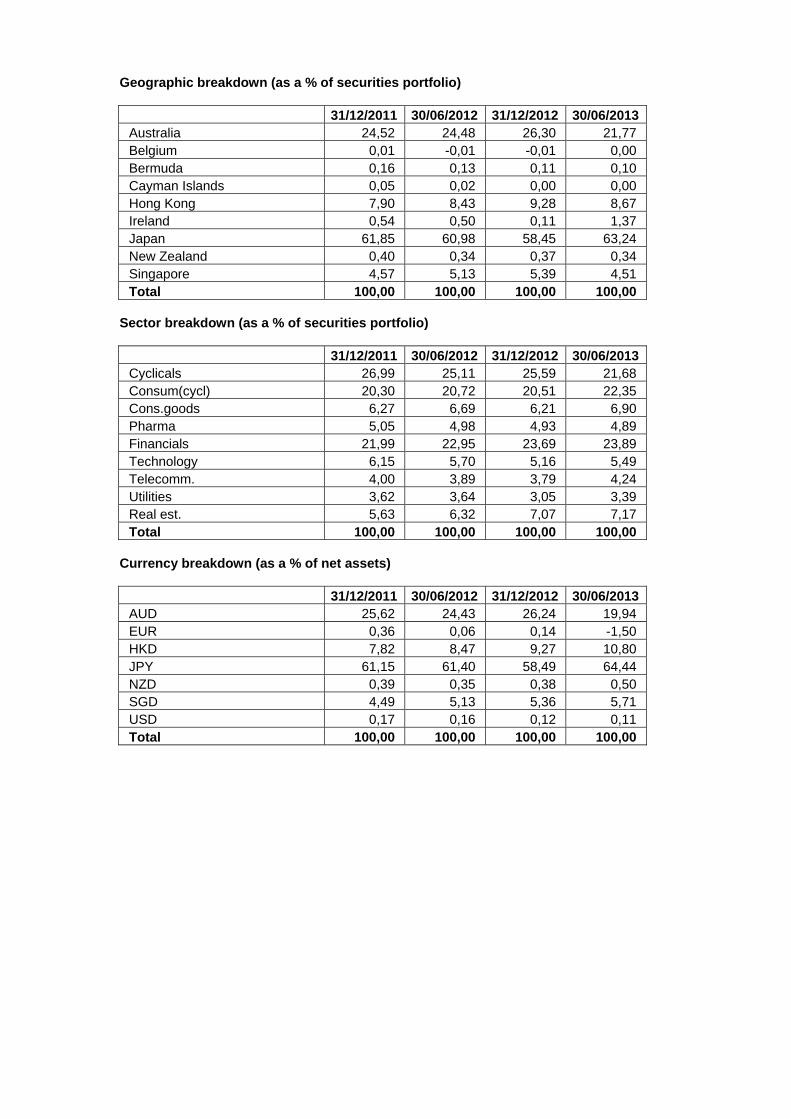

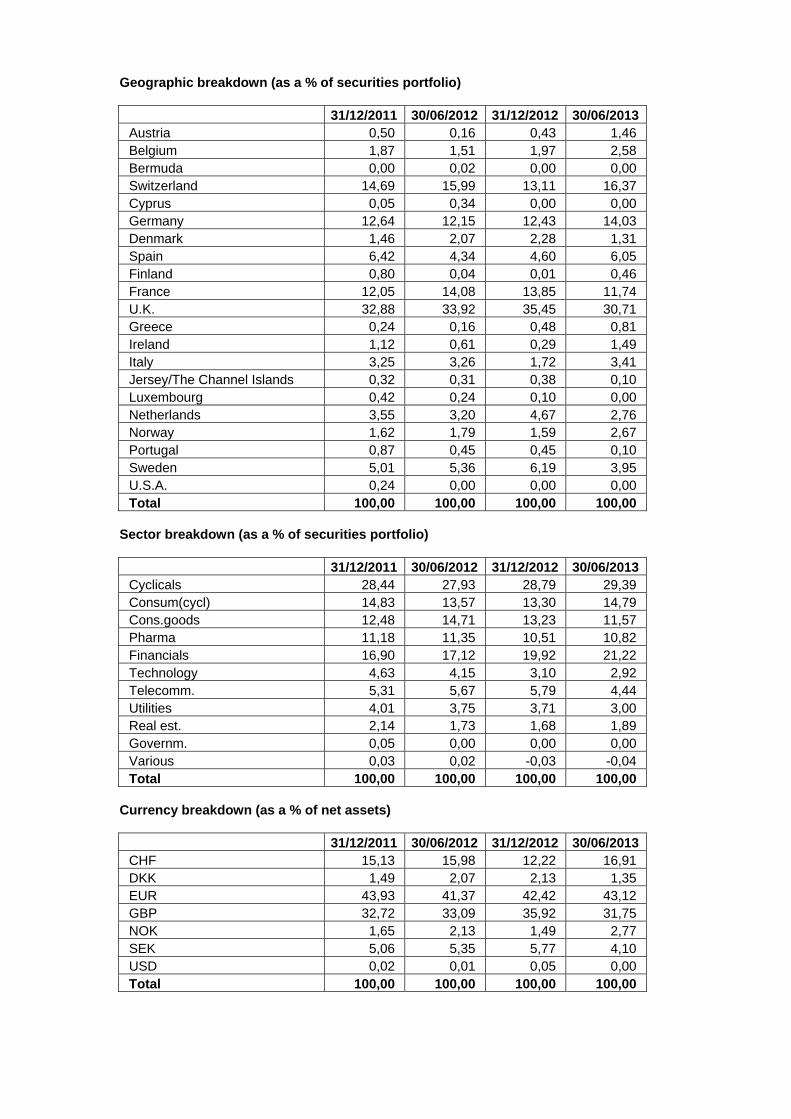

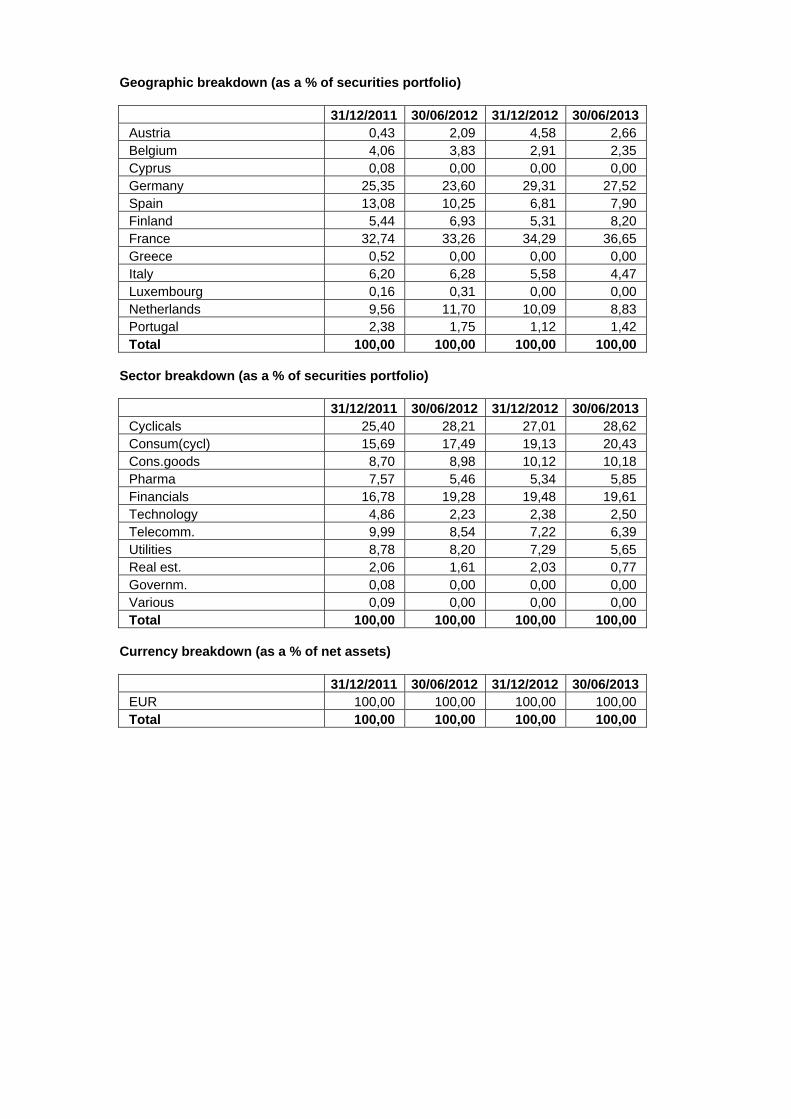

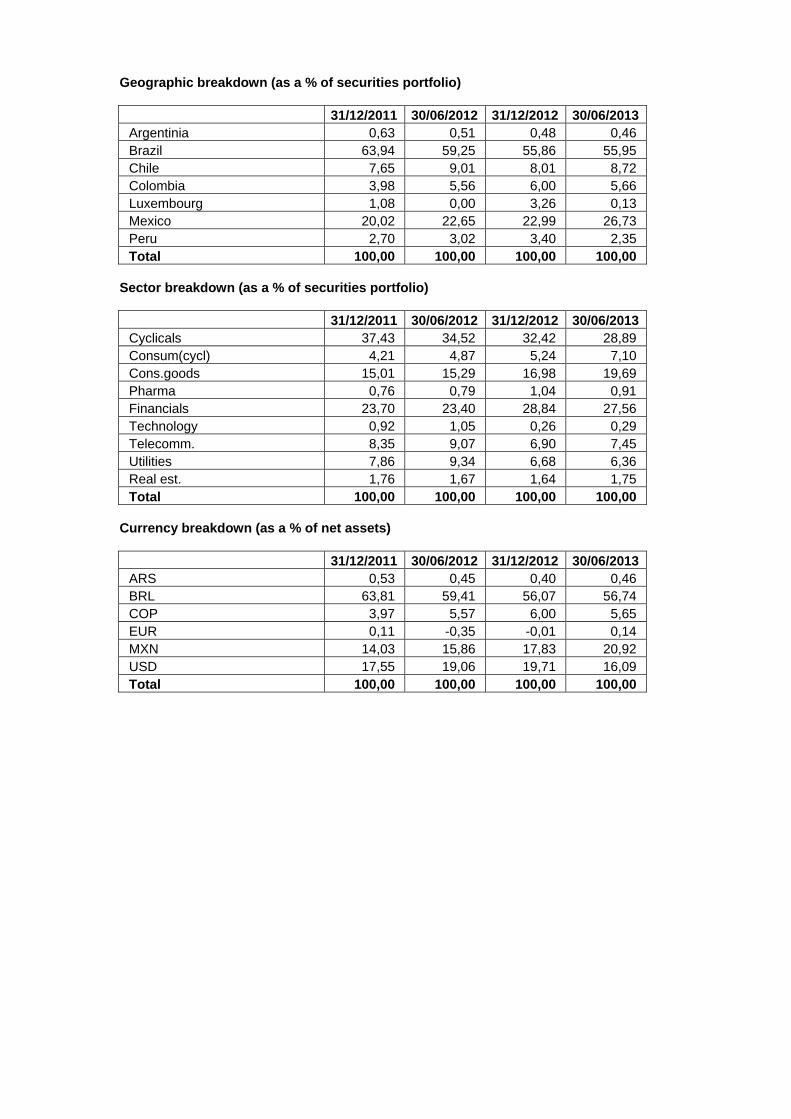

Geographic breakdown (as a % of securities portfolio)

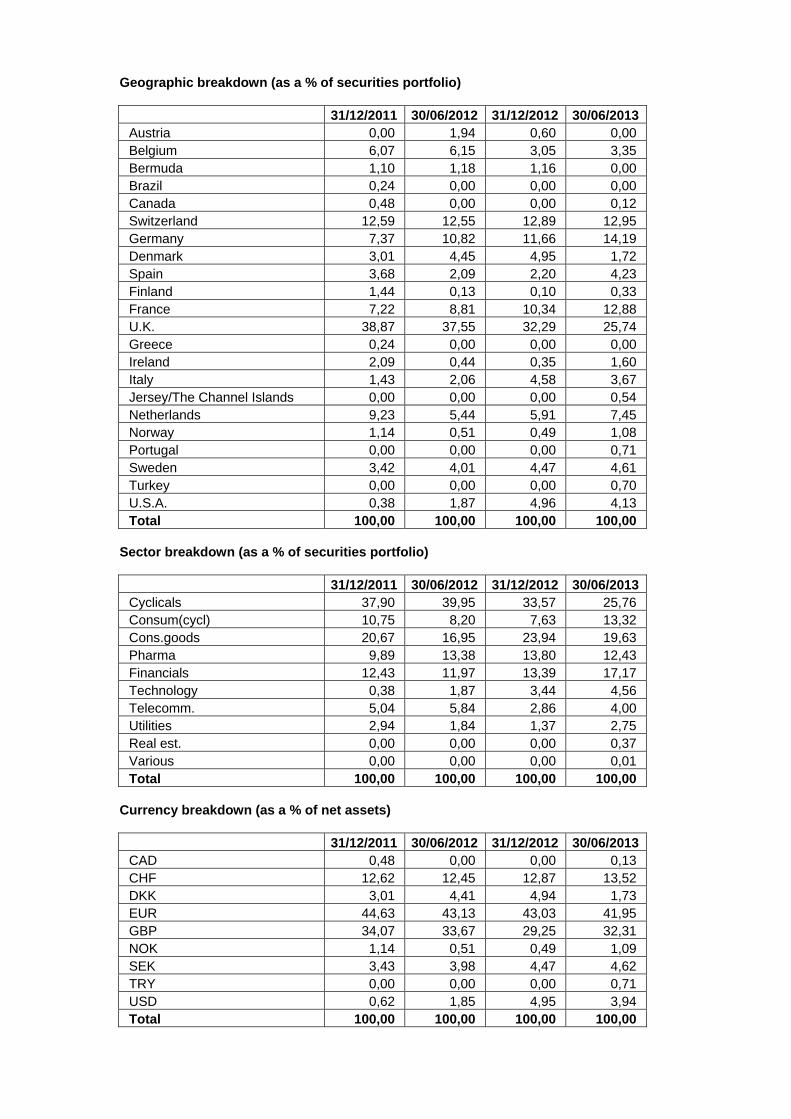

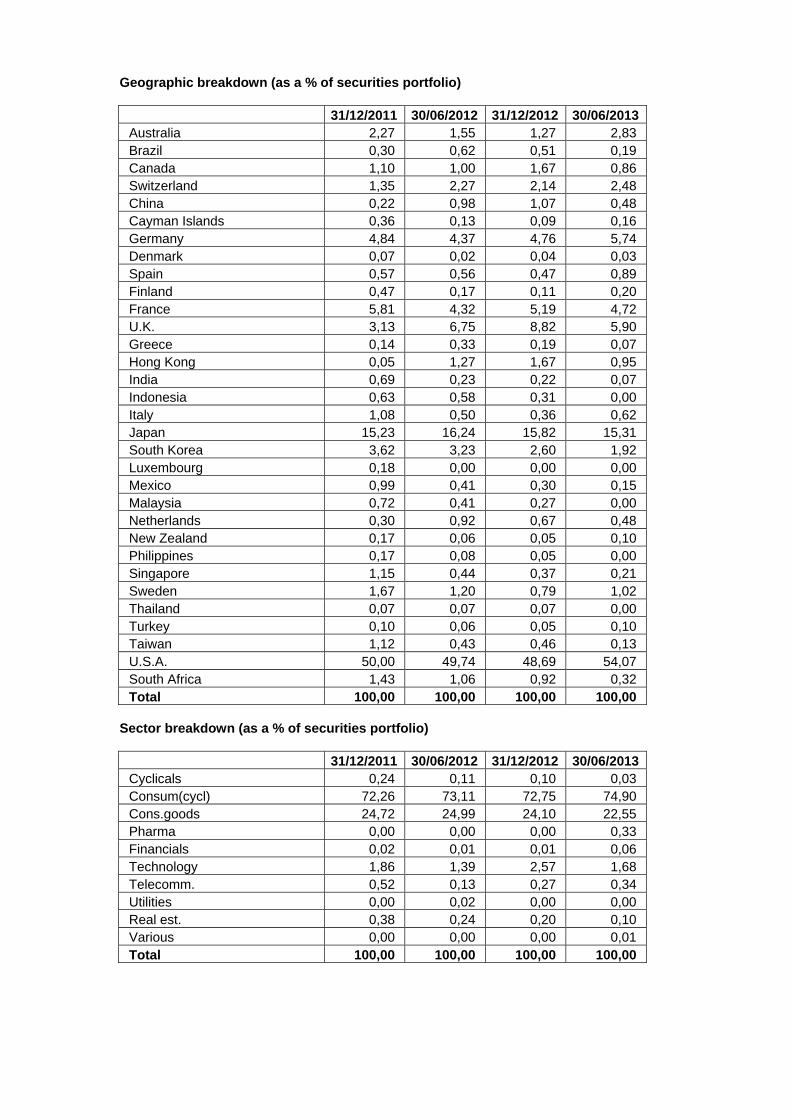

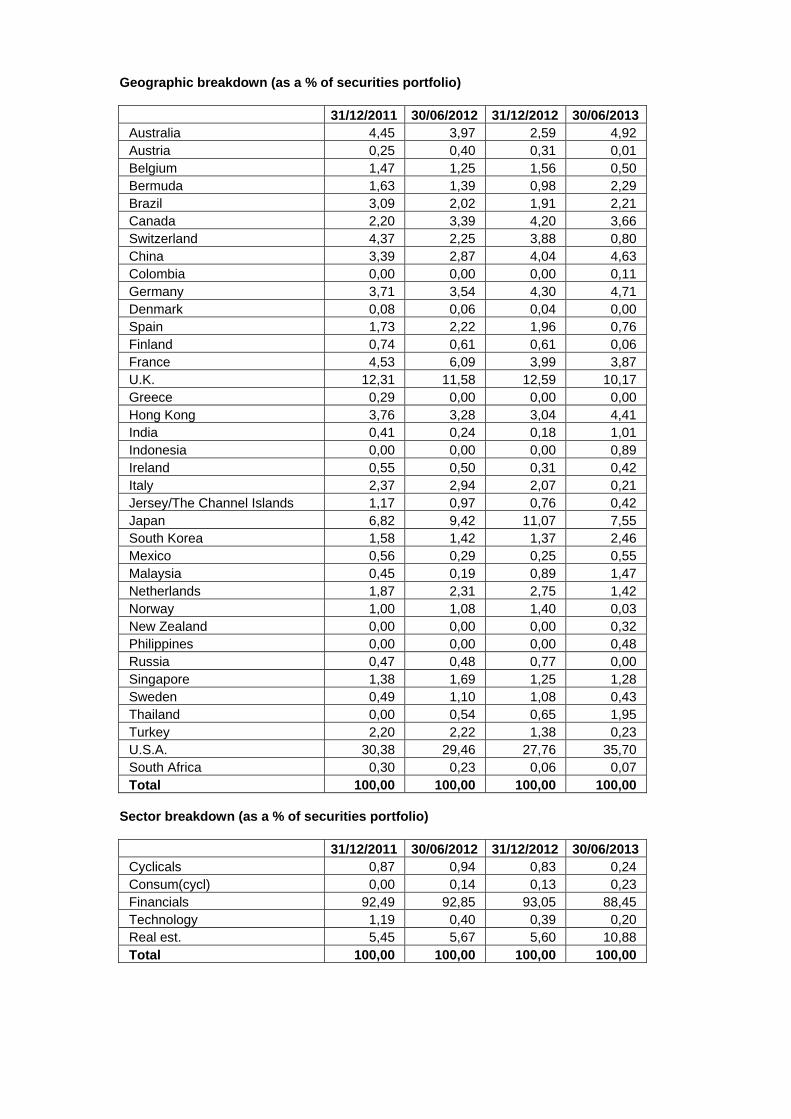

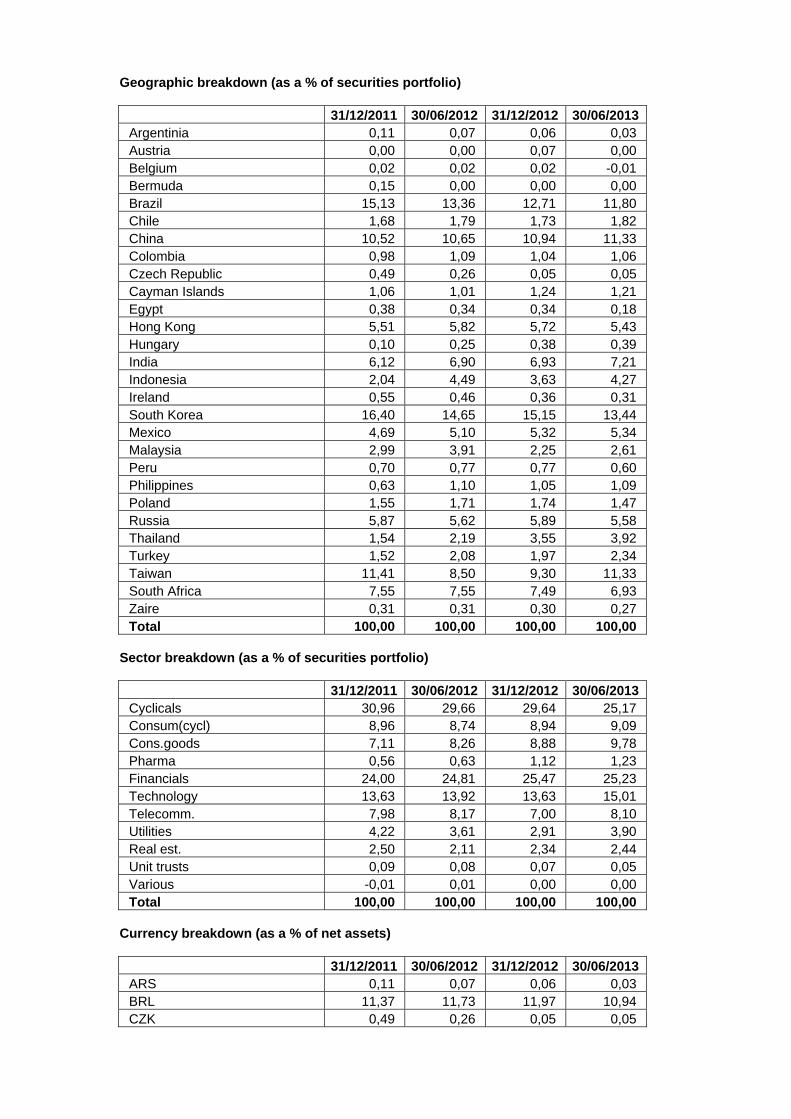

31/12/2012 30/06/2013Australia 4,54 4,25 Belgium 0,84 -0,28 Canada 8,98 9,09 Switzerland 1,89 2,58 Germany 2,18 3,01 Spain 0,53 0,69 Finland 1,23 1,12 France 3,74 3,75 U.K. 9,19 8,98 Hong Kong 0,58 0,00 Italy 1,94 0,92 Japan 8,09 8,61 Netherlands 1,86 1,65 Norway 2,67 1,68 New Zealand 0,61 0,00 Sweden 1,83 2,48 U.S.A. 49,30 51,47 Total 100,00 100,00

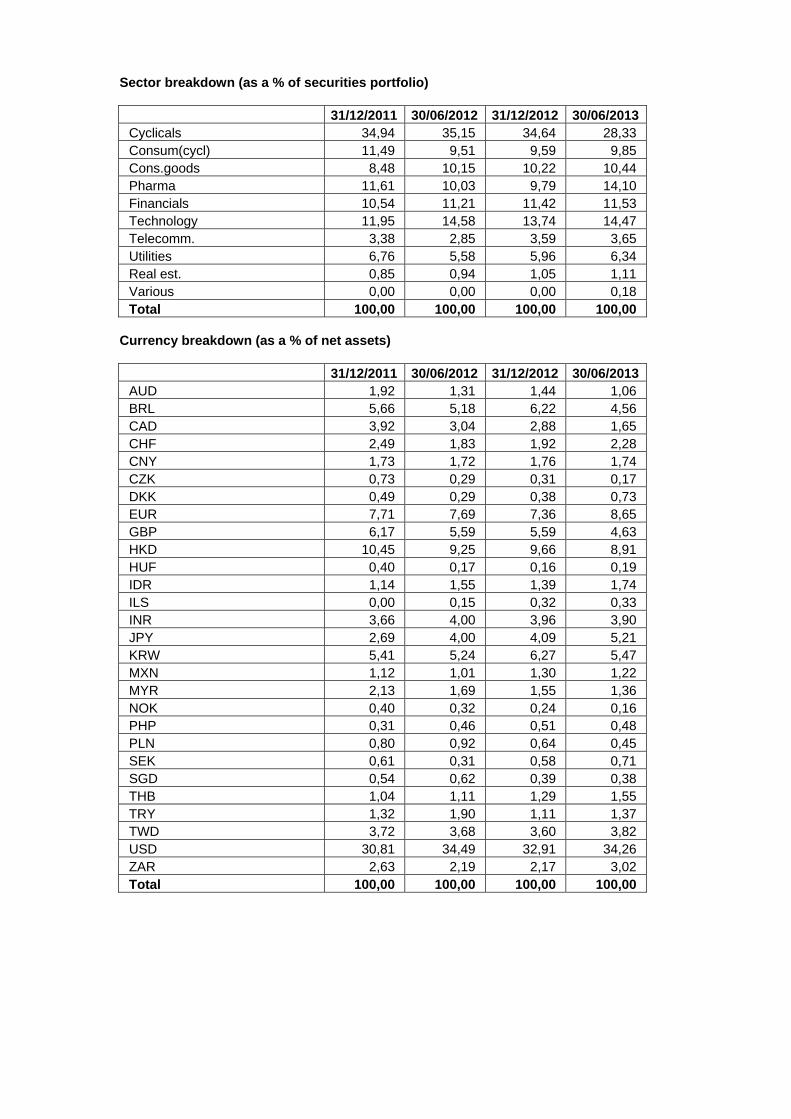

Sector breakdown (as a % of securities portfolio)

31/12/2012 30/06/2013Cyclicals 24,39 23,07 Consum(cycl) 12,31 14,45 Cons.goods 12,06 11,43 Pharma 10,40 10,17 Financials 19,59 19,01 Technology 10,92 12,06 Telecomm. 5,11 4,59 Utilities 3,20 2,85 Real est. 2,02 2,37 Total 100,00 100,00

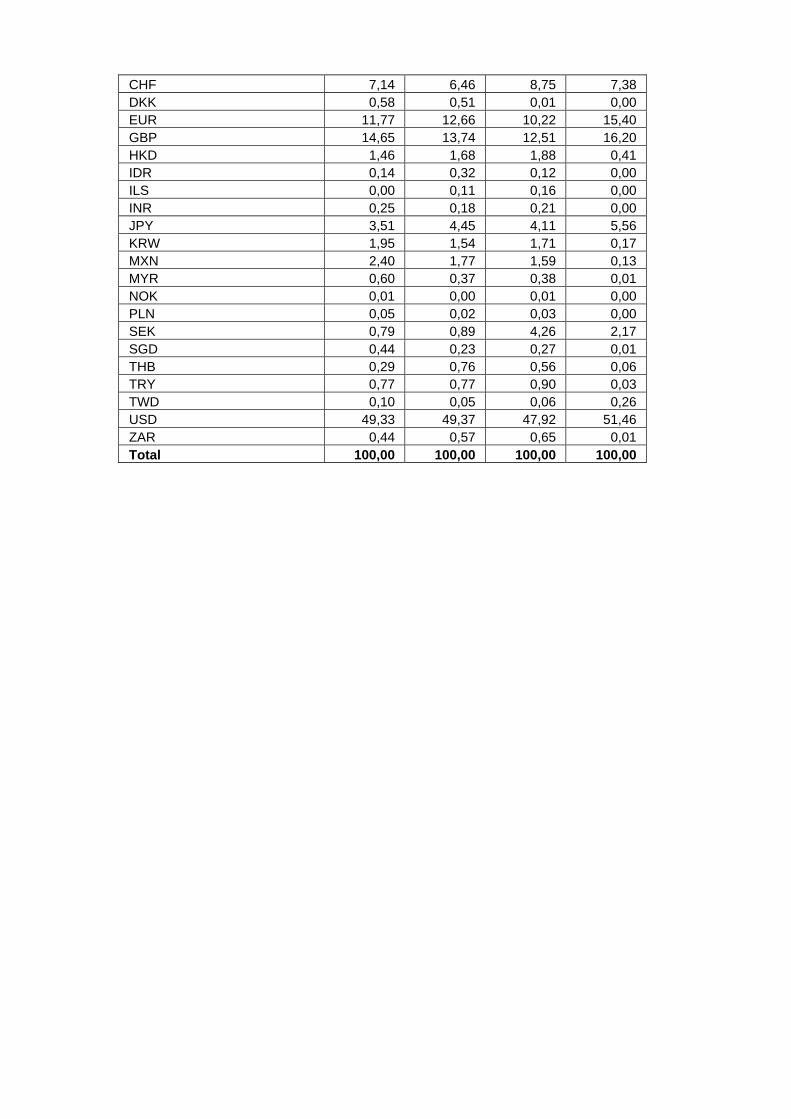

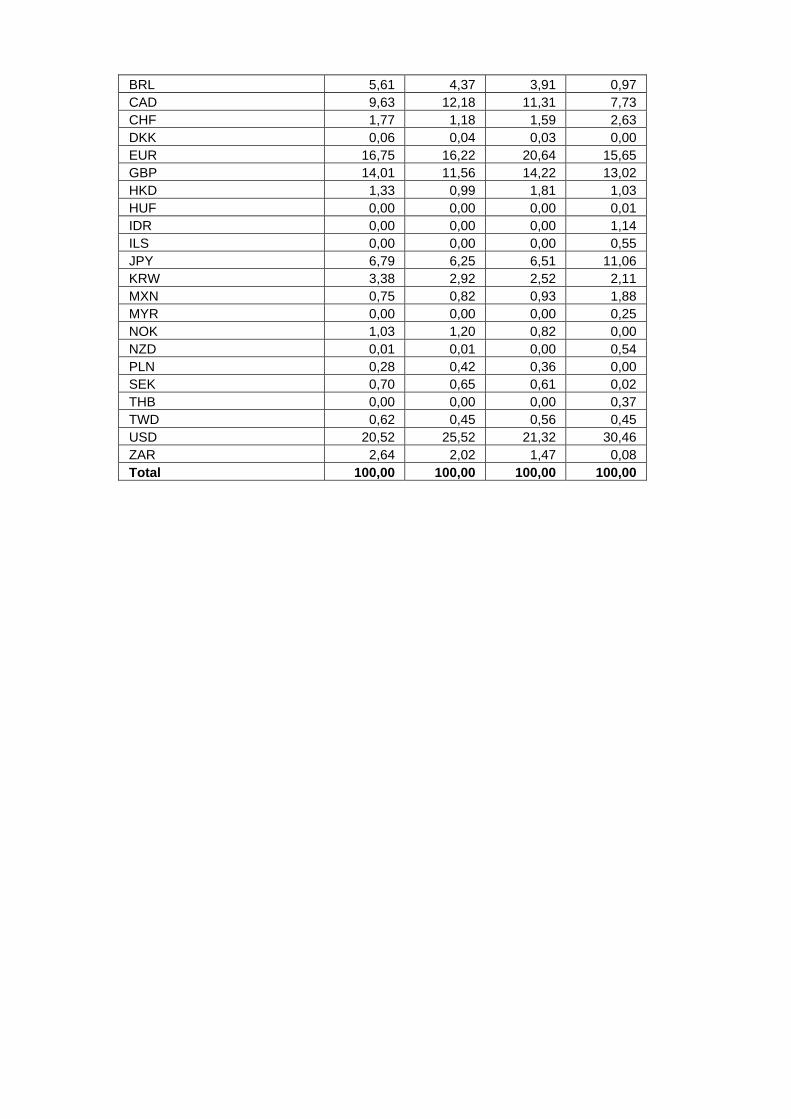

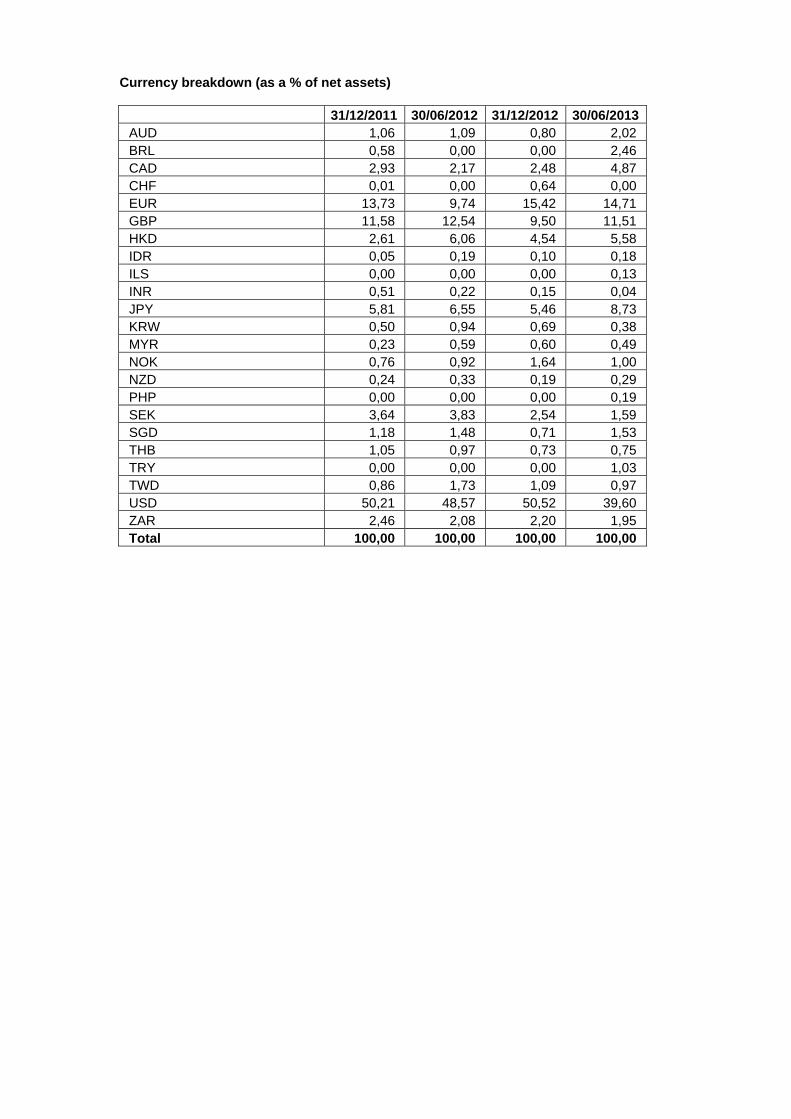

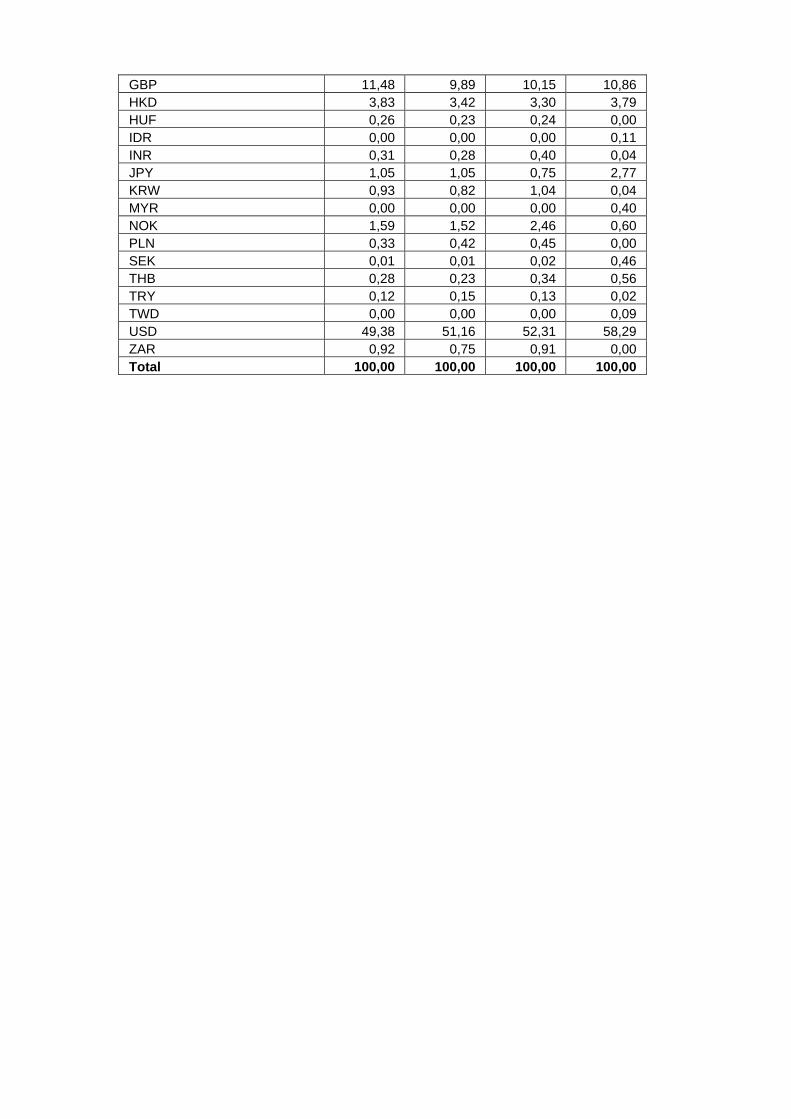

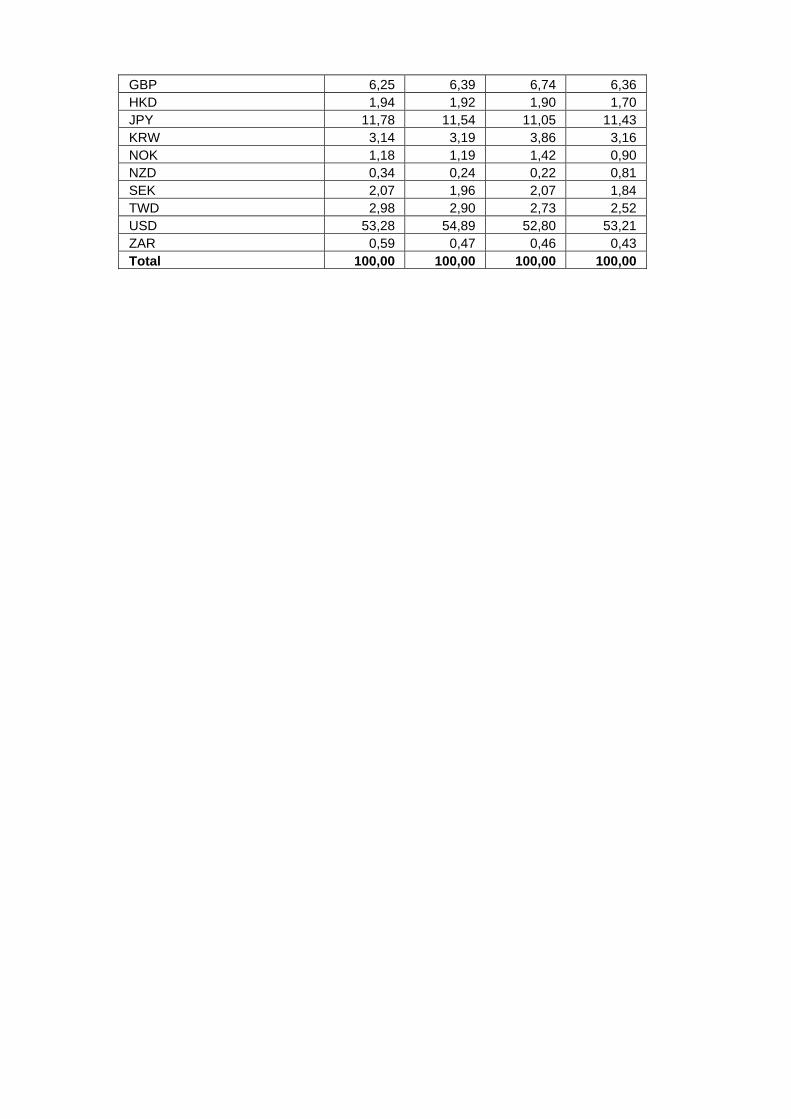

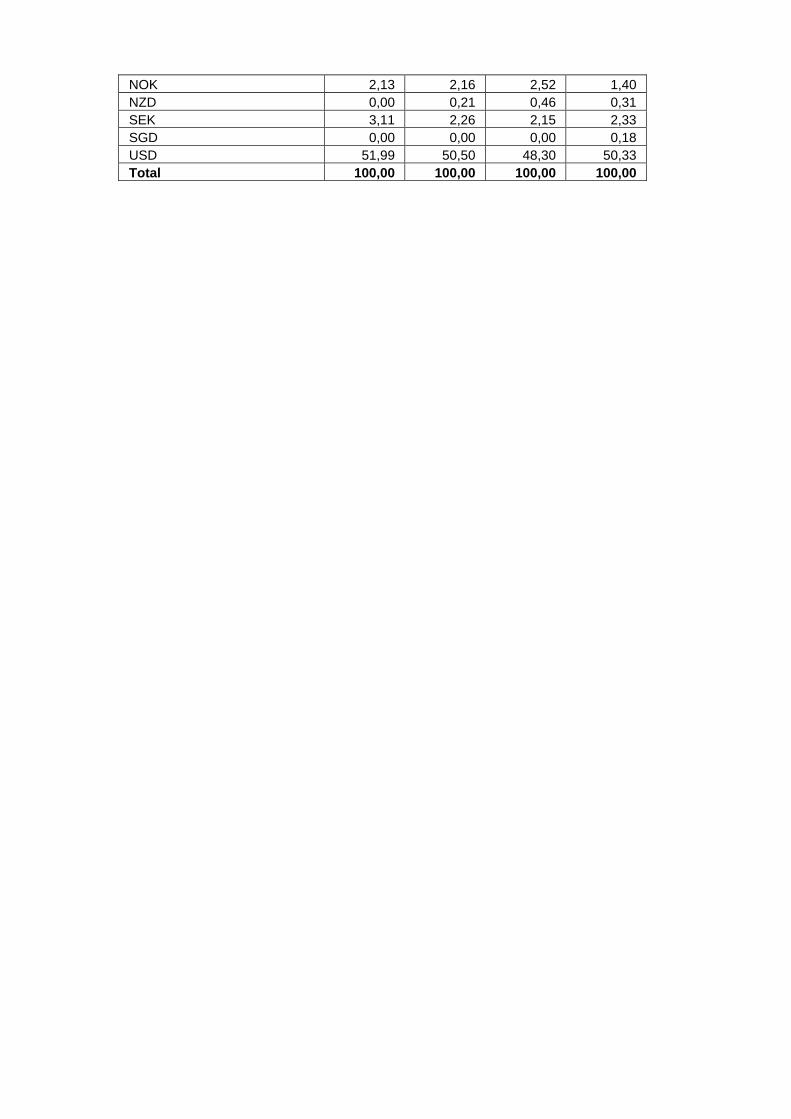

Currency breakdown (as a % of net assets)

31/12/2012 30/06/2013AUD 4,52 4,27 CAD 8,77 9,06 CHF 1,91 2,57 CZK 60,65 63,65 EUR 0,31 -0,16 GBP 9,02 8,89 HKD 0,65 -0,02 JPY 7,95 8,61 NOK 2,66 1,68 NZD 0,61 0,00 SEK 1,93 2,48 USD 1,02 -1,03 Total 100,00 100,00

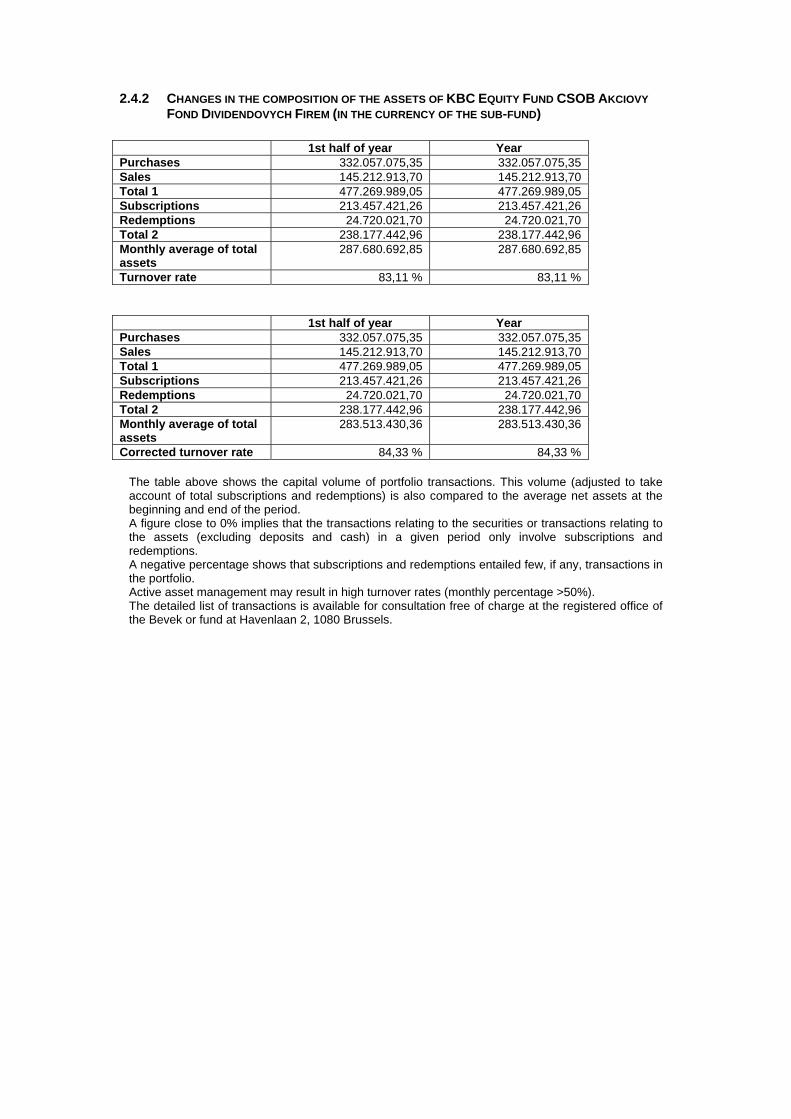

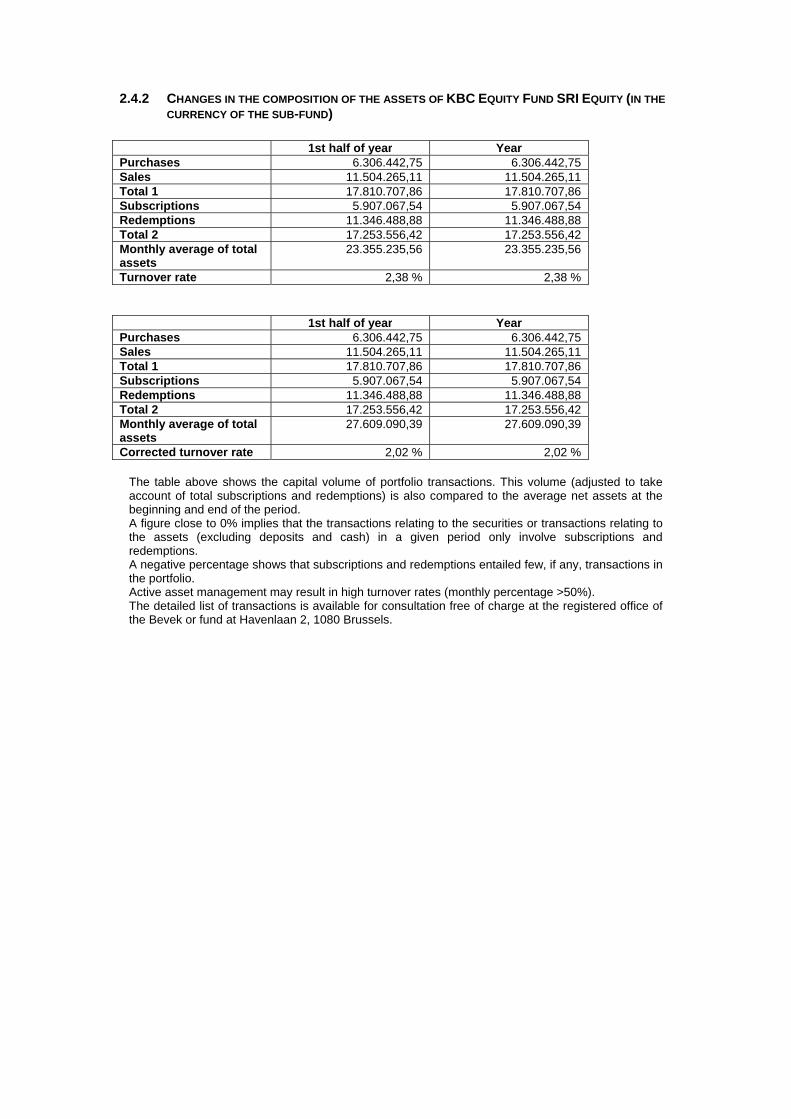

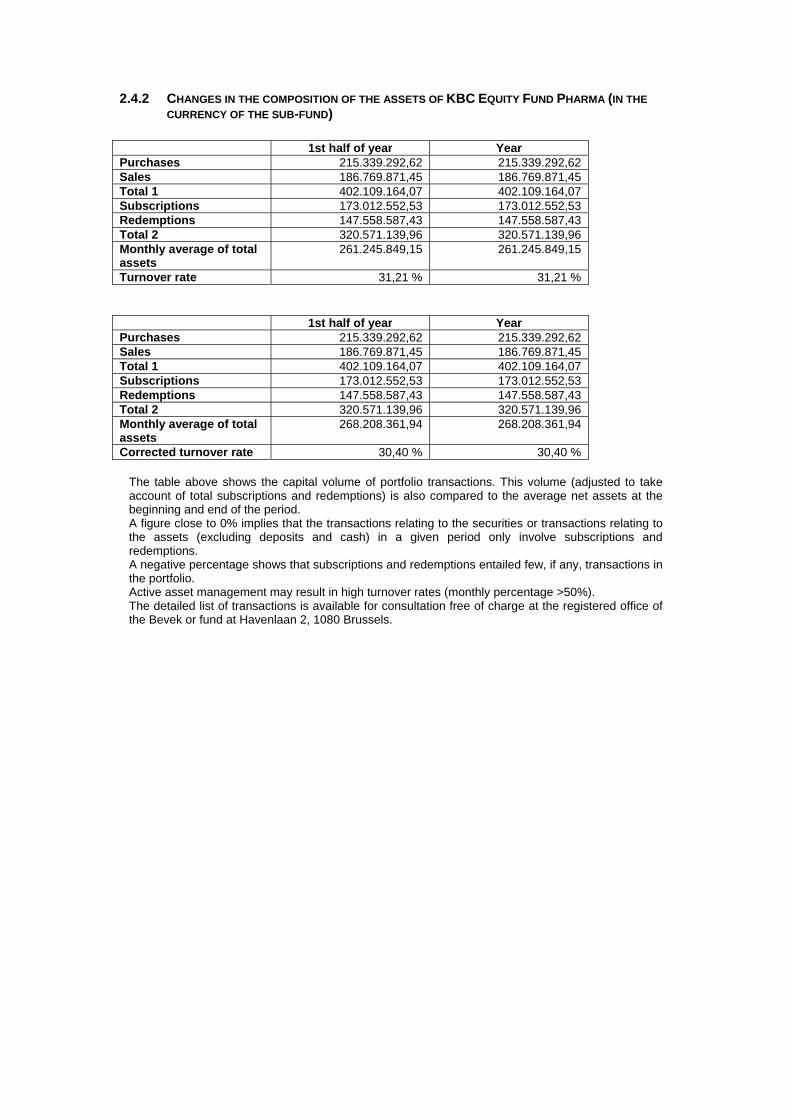

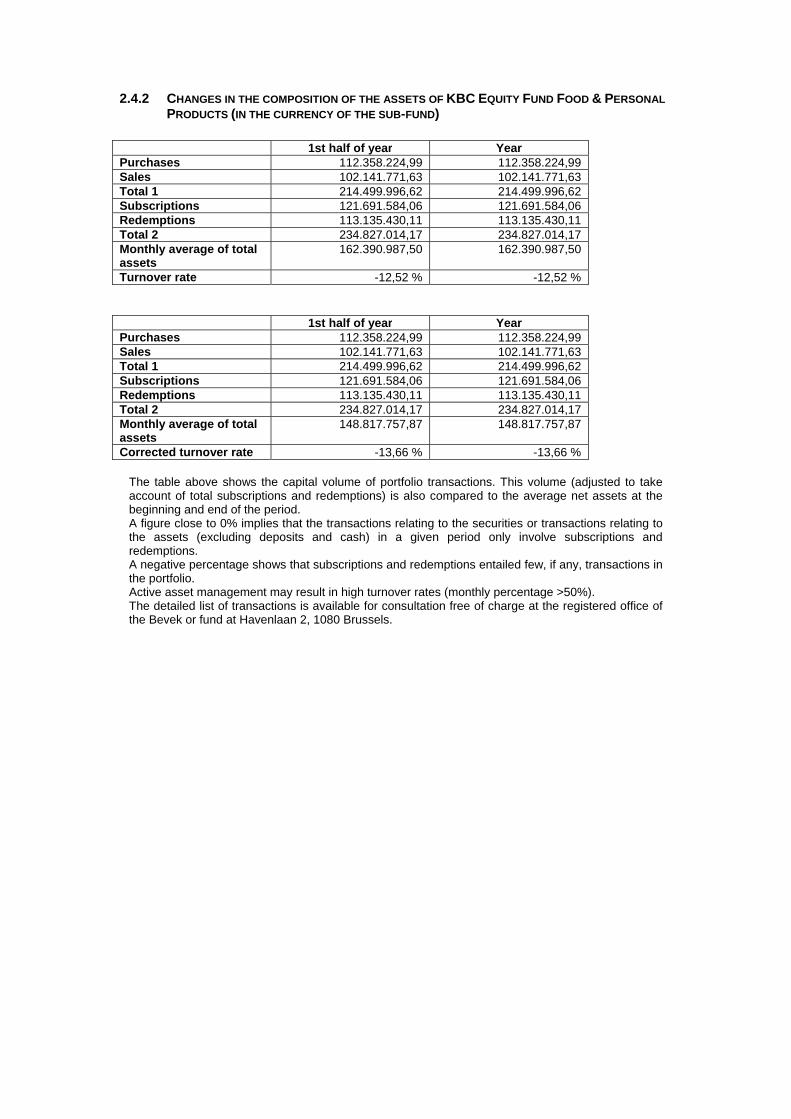

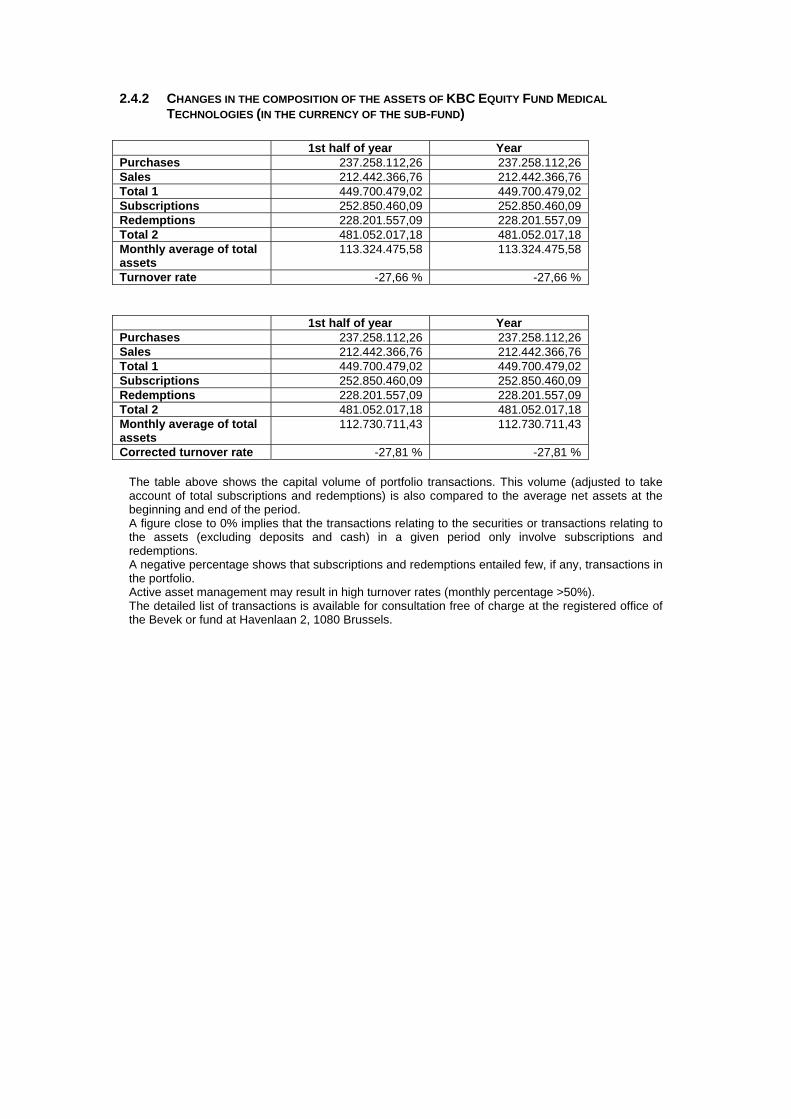

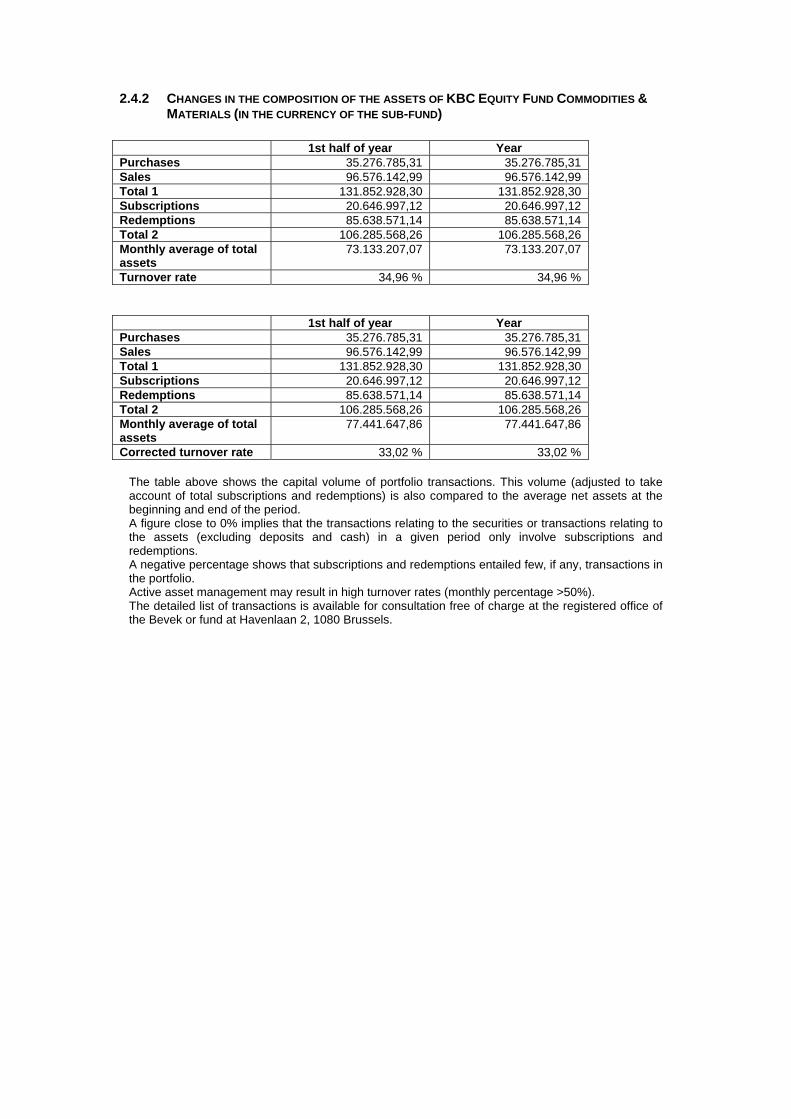

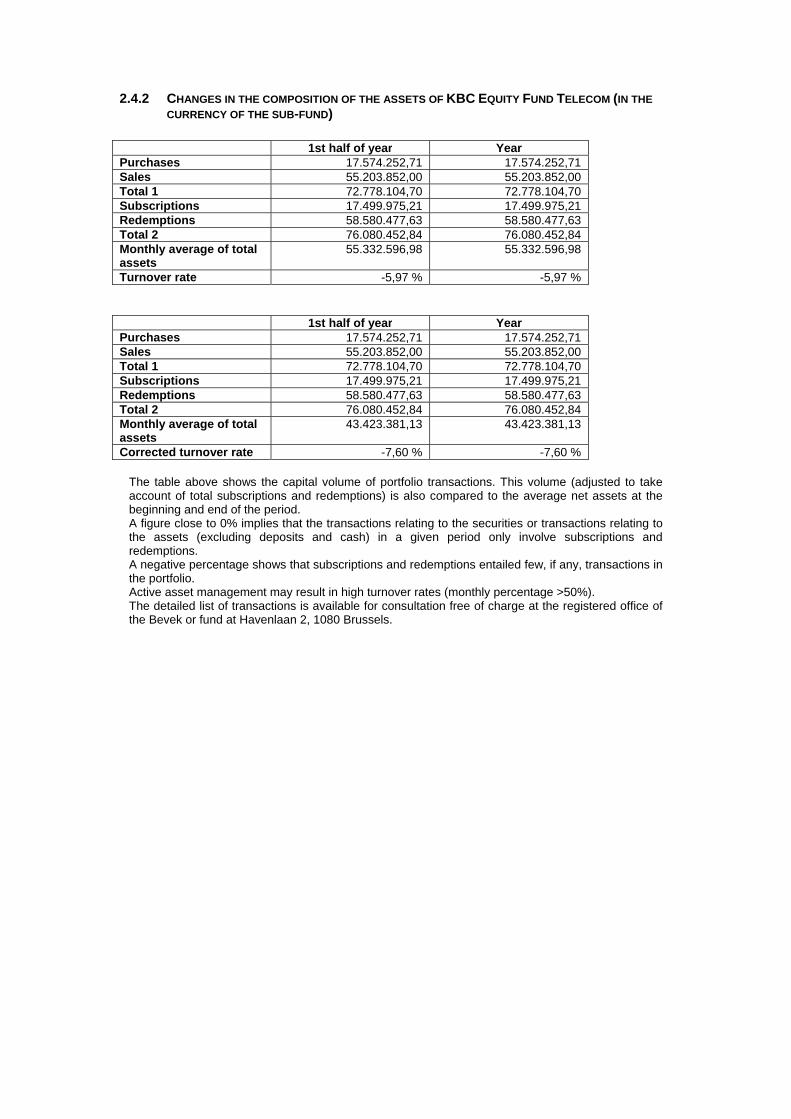

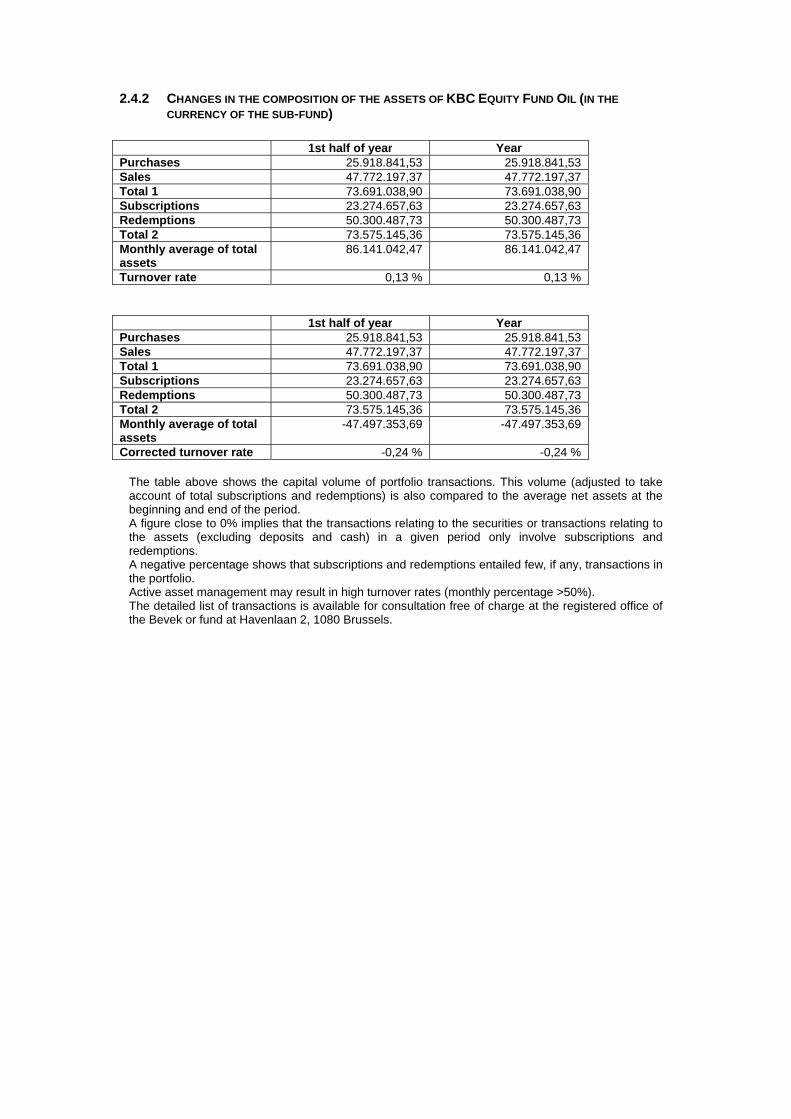

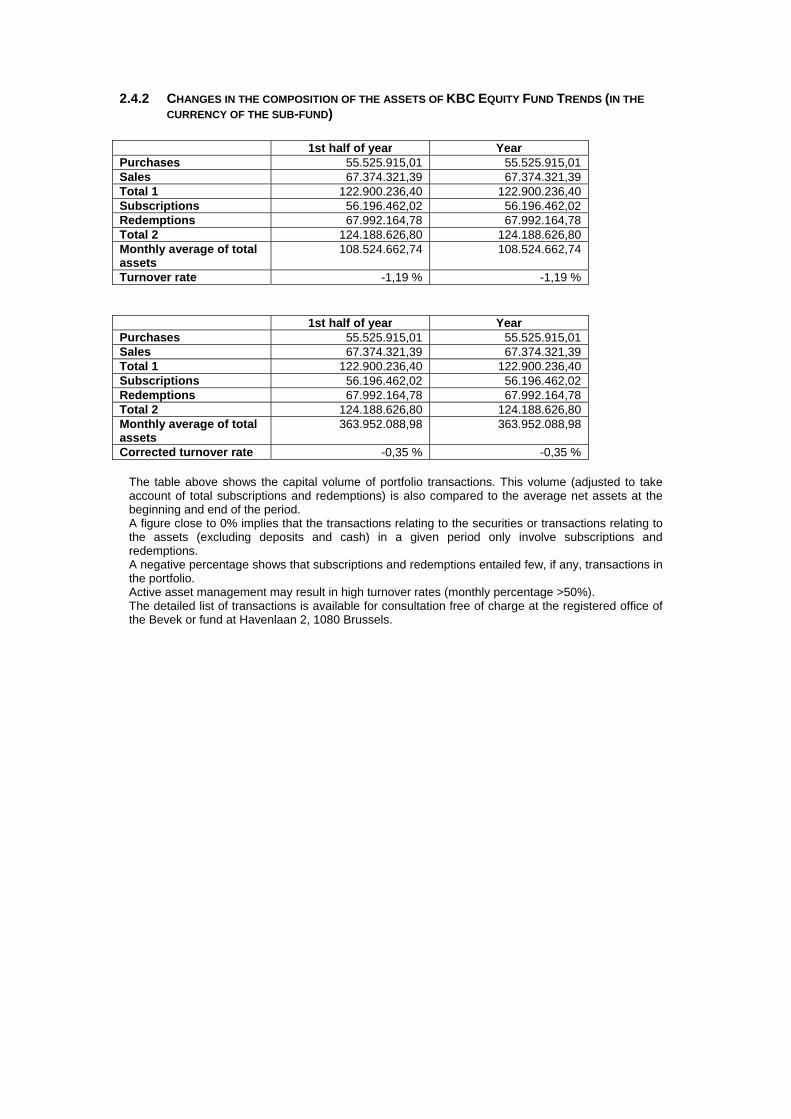

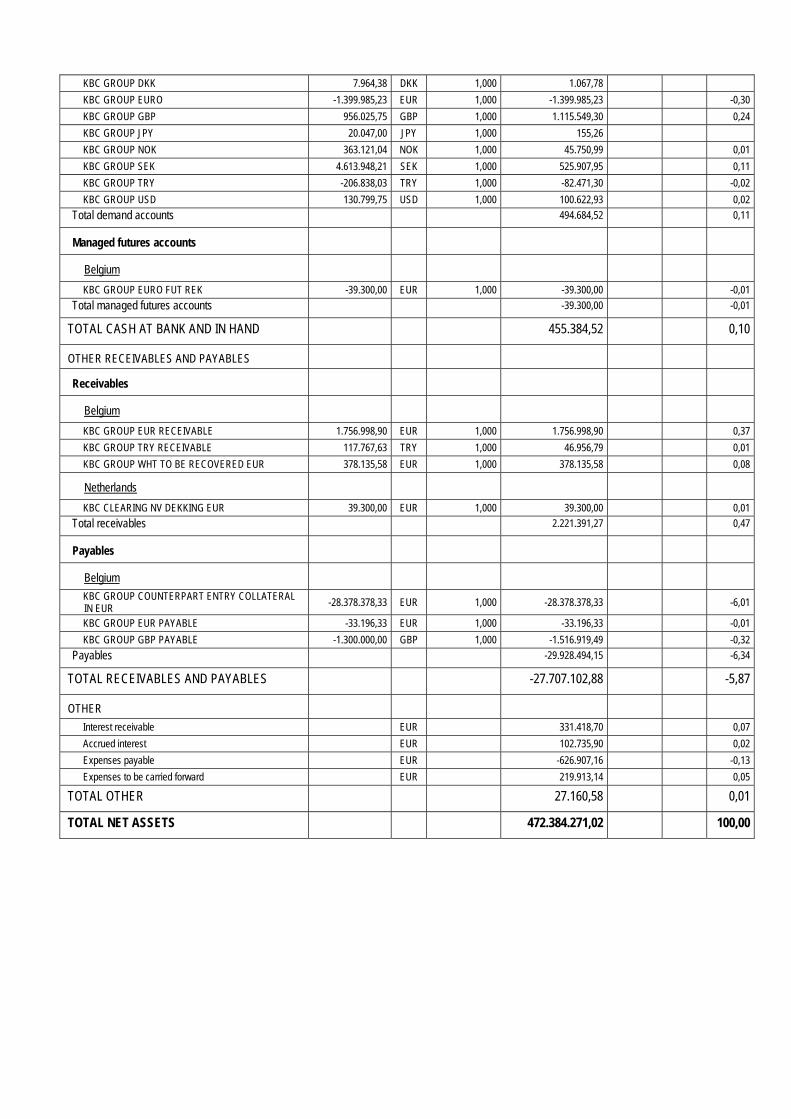

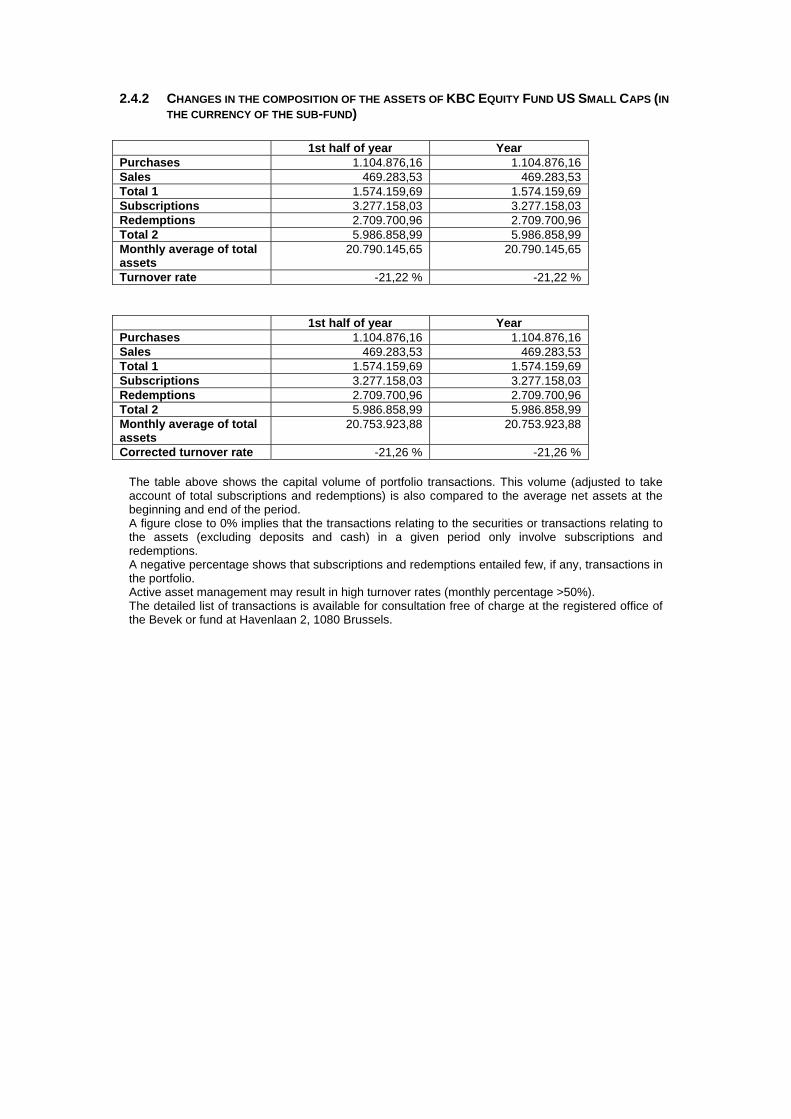

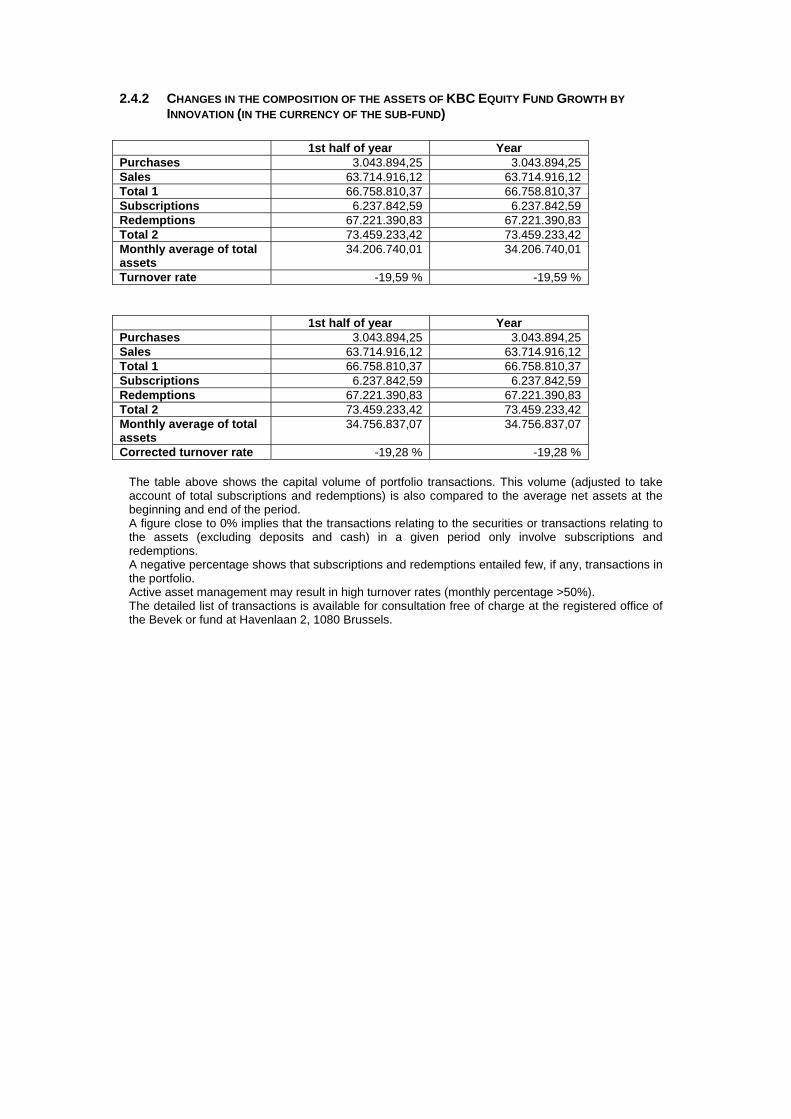

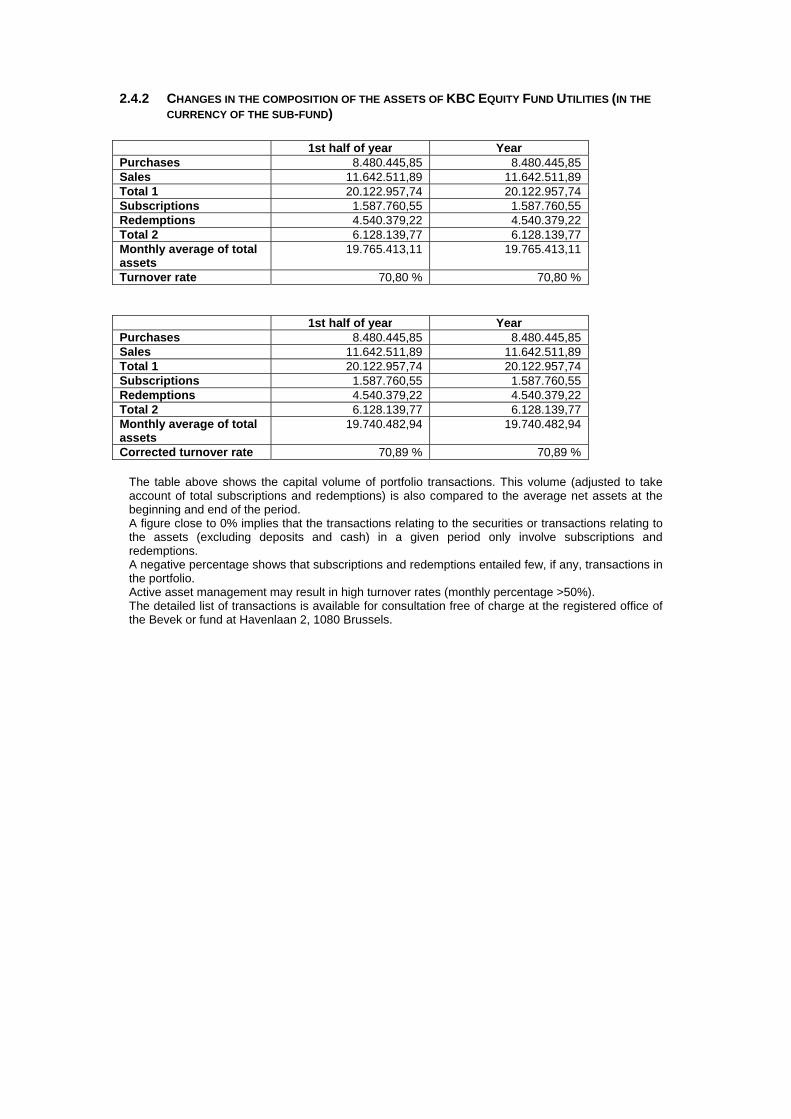

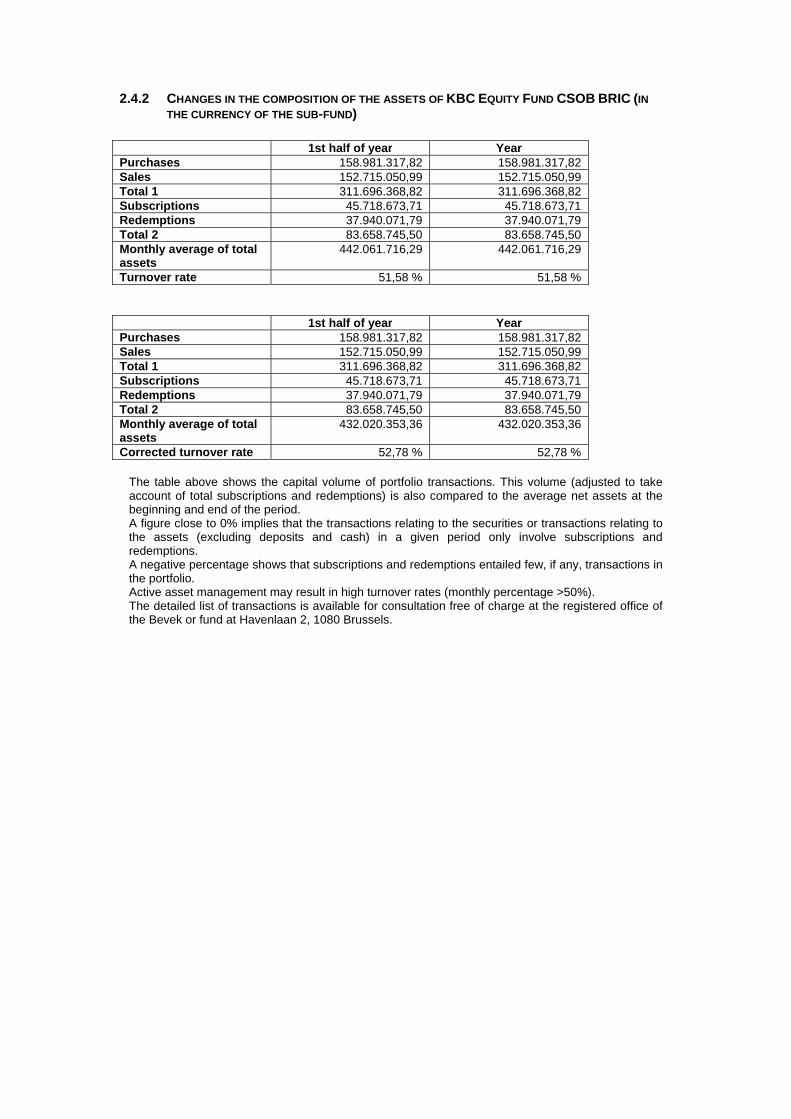

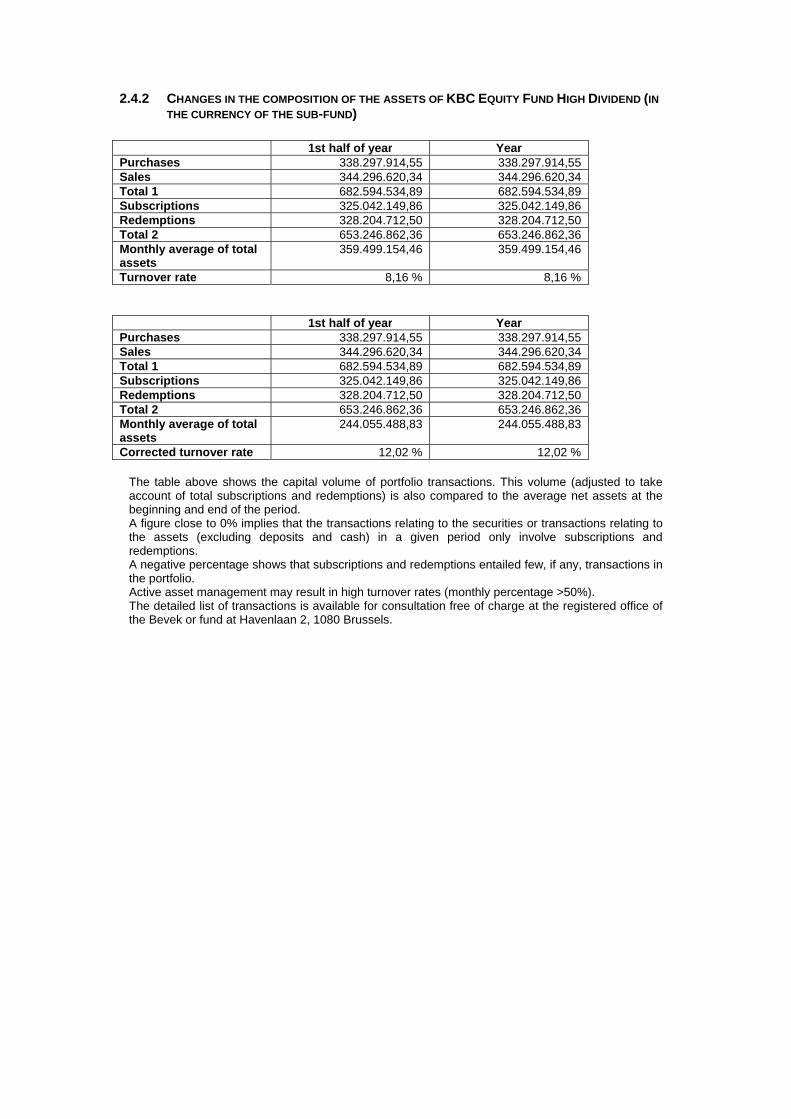

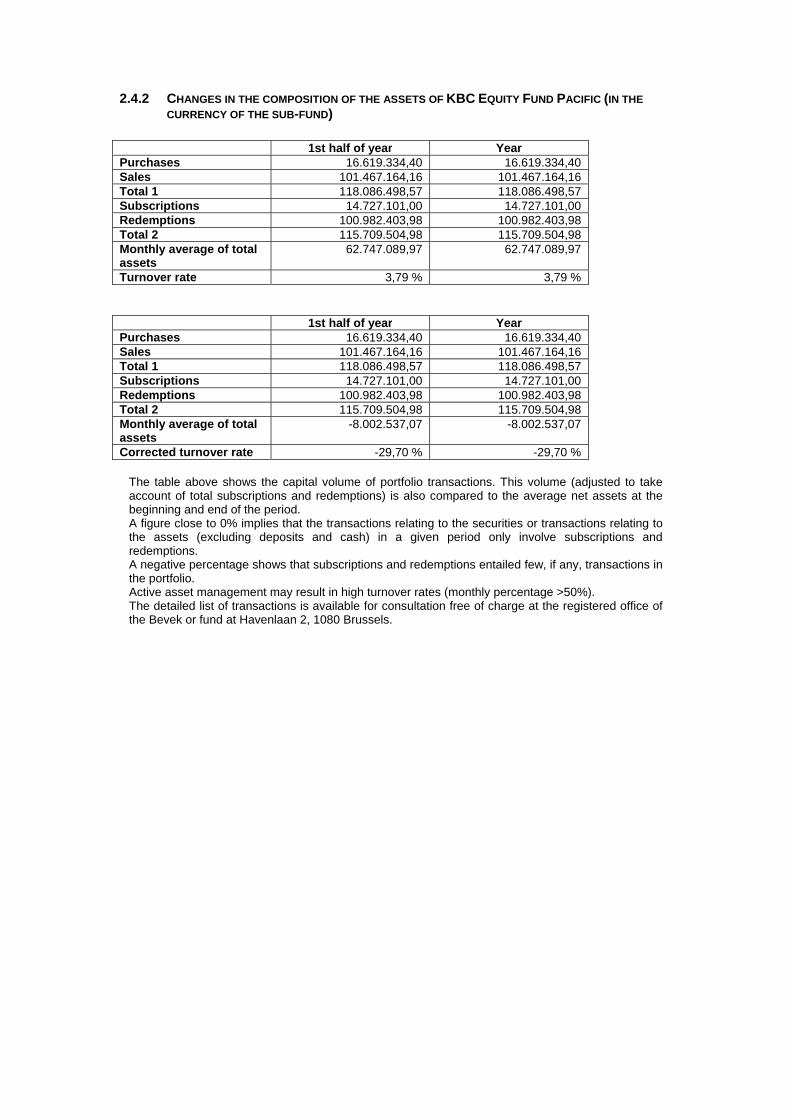

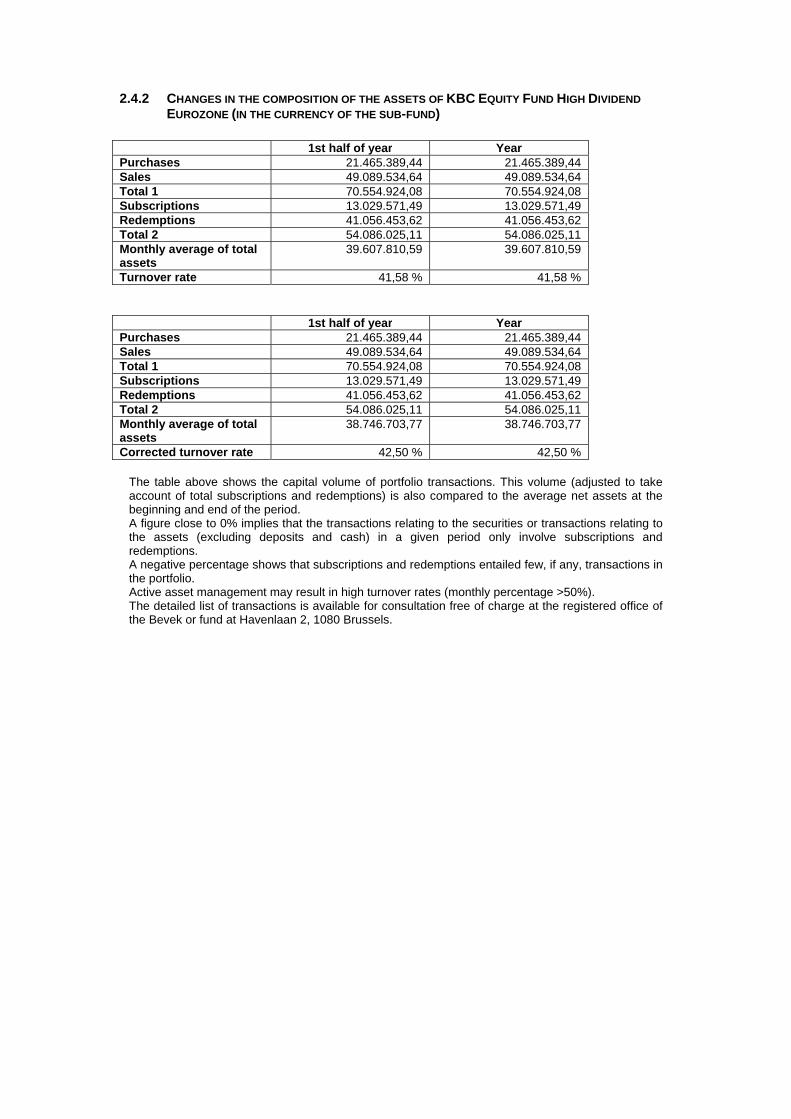

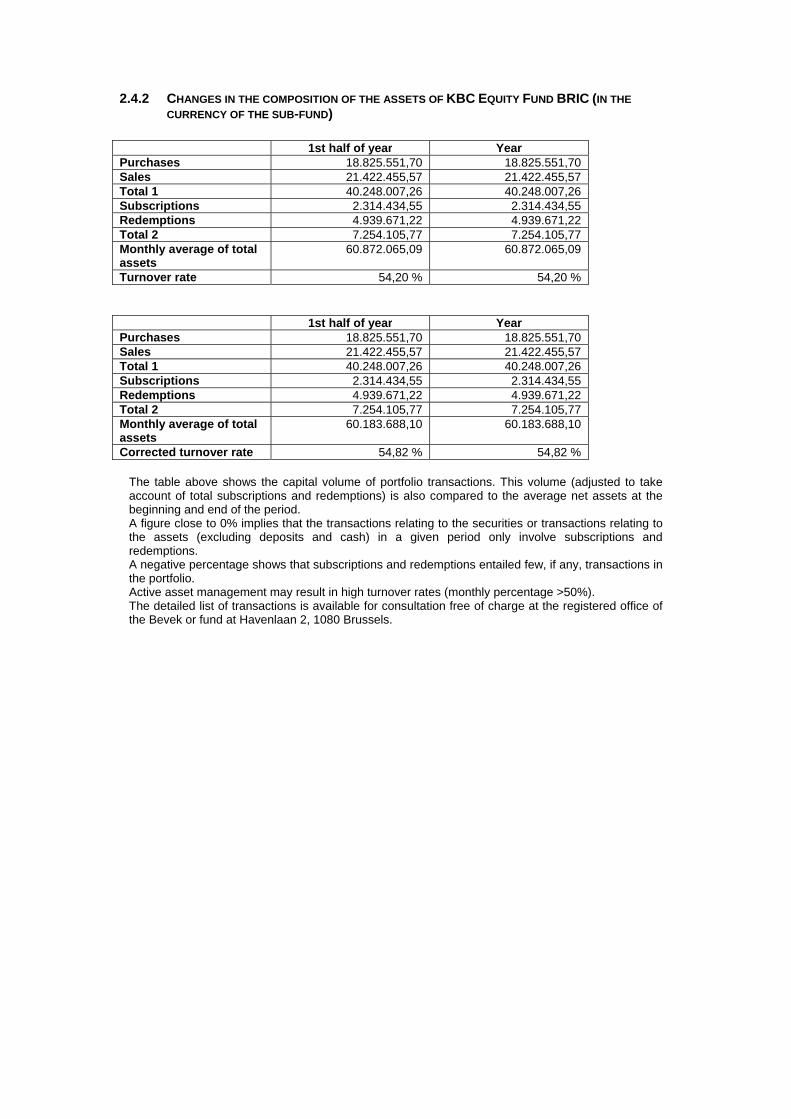

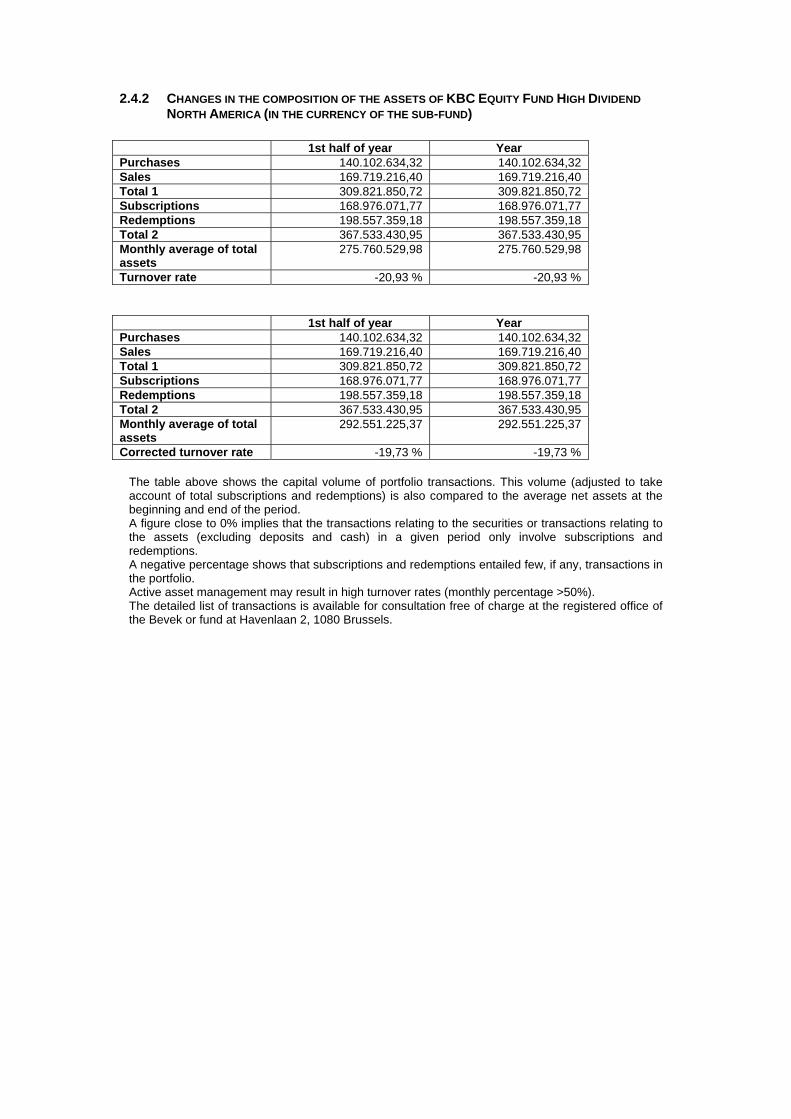

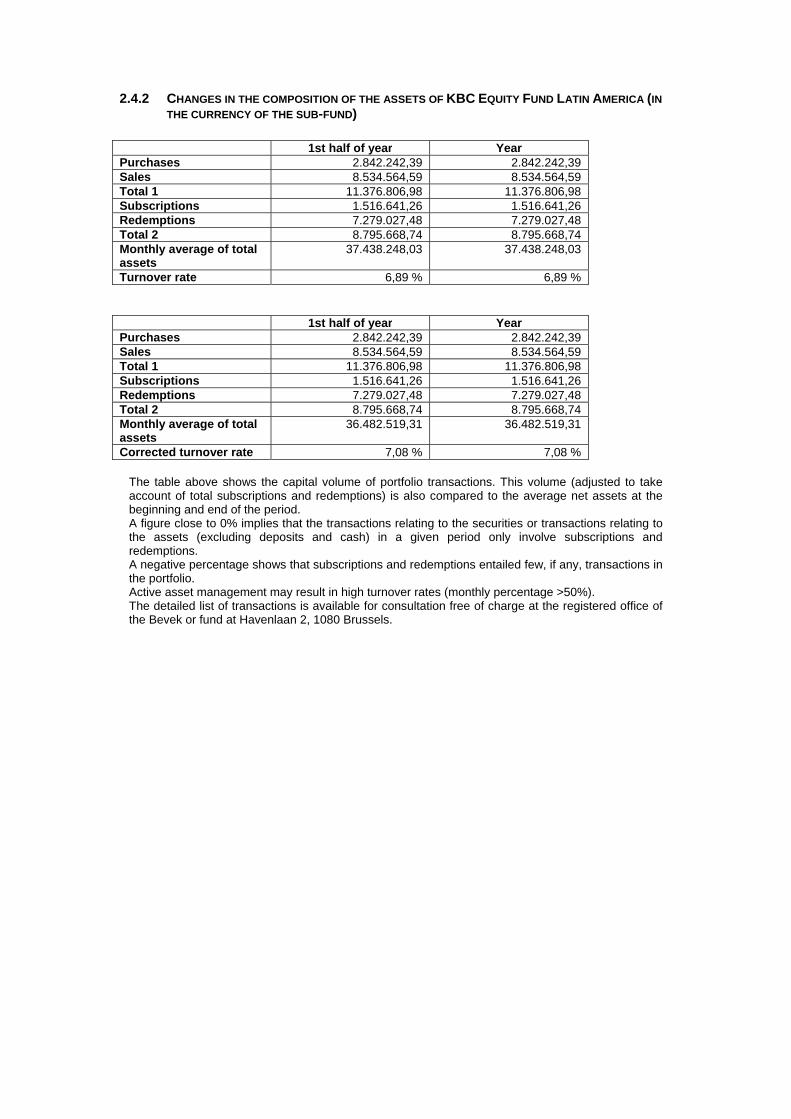

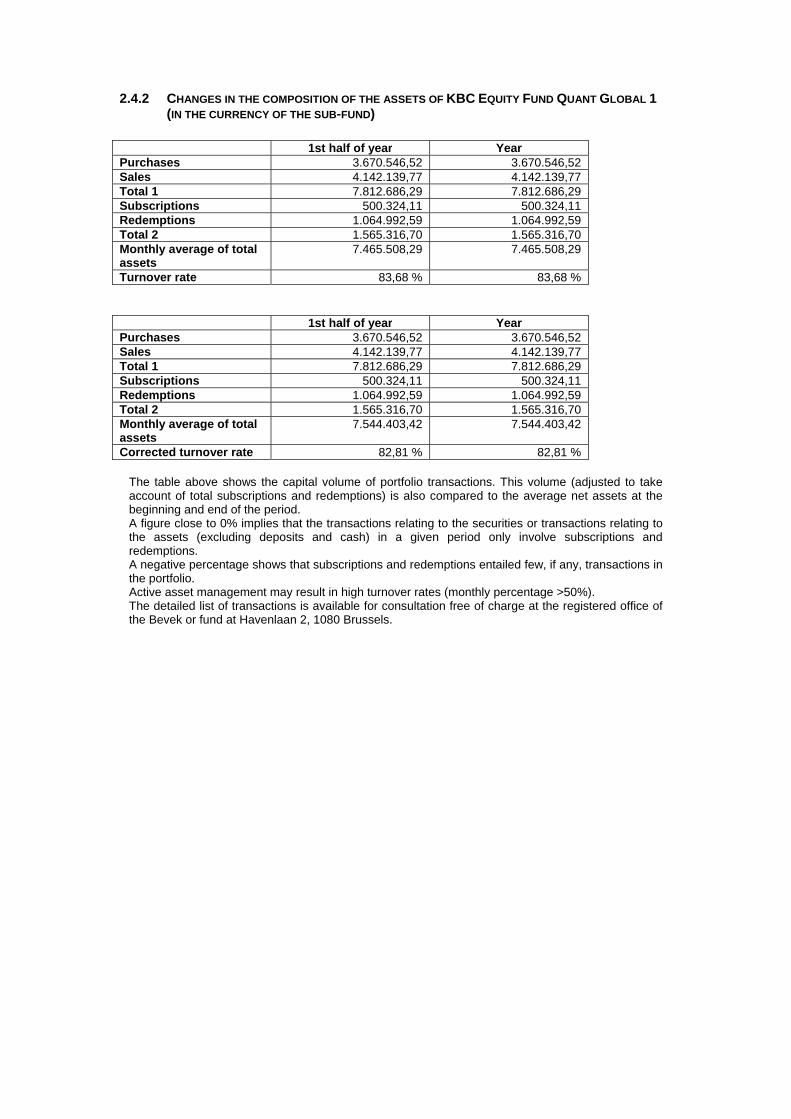

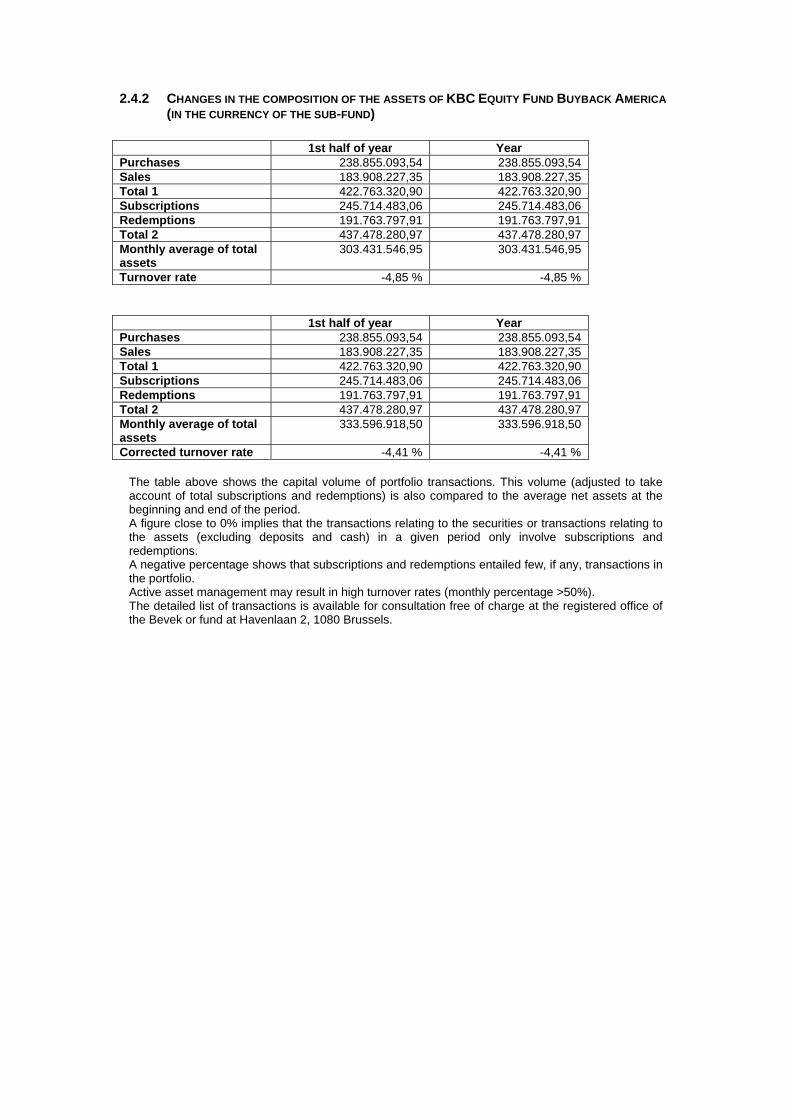

2.4.2 CHANGES IN THE COMPOSITION OF THE ASSETS OF KBC EQUITY FUND CSOB AKCIOVY

FOND DIVIDENDOVYCH FIREM (IN THE CURRENCY OF THE SUB-FUND)

1st half of year YearPurchases 332.057.075,35 332.057.075,35 Sales 145.212.913,70 145.212.913,70 Total 1 477.269.989,05 477.269.989,05 Subscriptions 213.457.421,26 213.457.421,26 Redemptions 24.720.021,70 24.720.021,70 Total 2 238.177.442,96 238.177.442,96 Monthly average of total assets

287.680.692,85 287.680.692,85

Turnover rate 83,11 % 83,11 %

1st half of year YearPurchases 332.057.075,35 332.057.075,35 Sales 145.212.913,70 145.212.913,70 Total 1 477.269.989,05 477.269.989,05 Subscriptions 213.457.421,26 213.457.421,26 Redemptions 24.720.021,70 24.720.021,70 Total 2 238.177.442,96 238.177.442,96 Monthly average of total assets

283.513.430,36 283.513.430,36

Corrected turnover rate 84,33 % 84,33 %