ITC BUY - IIFL Capital

58

CMP Rs272 Target 12m Rs350 (29%) Market cap (US$ m) 50,821 Enterprise value (US$ m) 49,466 Bloomberg ITC IN Sector FMCG 09 May 2017 52Wk High/Low (Rs) 293/209 Shares o/s (m) 12147 Daily volume (US$ m) 48 Dividend yield FY17ii (%) 1.7 Free float (%) 100.0 Shareholding pattern (%) Promoter 0.0 FII 20.0 DII 35.7 Others 44.2 Price performance (%) 1M 3M 1Y ITC (0.4) (2.2) 26.1 Absolute (US$) (1.0) 1.9 35.1 Rel. to Sensex (1.2) (7.9) 9.6 CAGR (%) 3 yrs 5 yrs EPS 8.7 13.8 Stock movement Percy Panthaki [email protected] 91 22 4646 4662 Avi Mehta [email protected] 91 22 4646 4650 Sameer Gupta [email protected] 91 22 4646 4672 www.iiflcap.com 0 100 200 300 400 0 20,000 40,000 60,000 80,000 100,000 May‐15 Jul ‐15 Sep‐15 Nov‐15 Jan‐16 Mar‐16 May‐16 Jul ‐16 Sep‐16 Nov‐16 Jan‐17 Mar‐17 May‐17 Vol('000, LHS) Price (Rs., RHS) ITC BUY 1 Growth, re-ignited Detailed report Financial summary (Rs bn) Y/e 31 Mar, Consolidated FY15A FY16A FY17ii FY18ii FY19ii Revenues (Rs bn) 384 391 413 463 519 Ebitda margins (%) 37.0 38.5 37.7 38.2 38.6 Pre‐exceptional PAT (Rs bn) 97 99 104 118 134 Reported PAT (Rs bn) 97 99 104 118 134 Pre‐exceptional EPS (Rs) 8.0 8.2 8.6 9.8 11.1 Growth (%) 8.2 2.3 5.2 13.4 13.2 IIFL vs consensus (%) (1.6) (2.1) (1.5) PER (x) 33.9 33.2 31.5 27.8 24.6 ROE (%) 32.8 30.2 29.0 29.5 29.9 Net debt/equity (x) (0.2) (0.2) (0.1) (0.1) 0.0 EV/Ebitda (x) 22.3 21.3 20.6 18.3 16.2 Price/book (x) 10.2 9.6 8.6 7.7 6.9 Source: Company, IIFL Research. Price as at close of business on 09 May 2017. Institutional Equities We expect growth to revive for ITC (FY17-19 EPS Cagr of 13% vs. 5% for FY14-17) as tax regime turns more rational, non-tax issues are in the base and consumption revives. India has one of the most favourable industry structures (virtual monopoly, FDI ban), which reduces volatility in earnings delivery. Moreover, ITC’s capital allocation has improved, with FCF conversion of ~80%. In light of these factors ITC’s 35% discount to HUL currently (vs. 12% prior to FY13) is set to contract, driving 29% upside to our price target of Rs.350. A change in incidence or structure of tax under GST regime is the main risk to our BUY rating. Growth is set to revive: In the past two budgets, average increase in excise duty has been 8% vs. 18% for the four years prior to that, possibly as the government realizes that a higher tax rate does not increase tax collections but encourages illegal trade. Non tax regulations such as pictorial warnings and ban on public smoking are already in place and others such as banning loose cigarettes are hard to implement. Moreover, revival in consumption would benefit ITC just as it would benefit other FMCG companies. Best industry structure: ITC is a virtual monopoly accounting for 86% of cigarette industry sales and 96% of profits. Moreover, FDI in cigarette manufacture is banned. Due to these factors ITC has high Ebit margins of 66% in the cigarette division vs. global average of 33%. Absence of competition gives ITC pricing power and reduces the risk of market share loss or margin erosion. Moreover, government officials have stated that GST is likely to be tax neutral – thus GST is unlikely to materially alter the industry structure. Reasonable valuation in the light of improved capital allocation: ITC generates 75-80% of its net profit as FCF, vs. an average of 55% over FY03-15. Moreover, ITC trades at a discount of 35% to HUL (with similar expected growth for FY17-19) vs. an average of 12% prior to FY13 when ITC’s EPS growth faltered due to an adverse tax regime. With growth reviving, we believe that this discount would shrink, resulting in an attractive 29% return to our TP. Our extended DCF (terminal FY39) suggests an even higher upside of 46%.

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of ITC BUY - IIFL Capital

CMP Rs272

Target 12m Rs350 (29%)

Market cap (US$ m) 50,821

Enterprise value (US$ m) 49,466

Bloomberg ITC IN

Sector FMCG

09 May 2017

52Wk High/Low (Rs) 293/209

Shares o/s (m) 12147 Daily volume (US$ m) 48

Dividend yield FY17ii (%) 1.7 Free float (%) 100.0

Shareholding pattern (%) Promoter 0.0

FII 20.0

DII 35.7

Others 44.2

Price performance (%)

1M 3M 1Y

ITC (0.4) (2.2) 26.1

Absolute (US$) (1.0) 1.9 35.1

Rel. to Sensex (1.2) (7.9) 9.6

CAGR (%) 3 yrs 5 yrs

EPS 8.7 13.8

Stock movement

Percy Panthaki [email protected] 91 22 4646 4662 Avi Mehta [email protected] 91 22 4646 4650 Sameer Gupta [email protected] 91 22 4646 4672

www.iiflcap.com

0

100

200

300

400

0

20,000

40,000

60,000

80,000

100,000

May‐1

5Ju

l‐1

5Se

p‐1

5N

ov‐

15

Jan‐1

6M

ar‐1

6M

ay‐1

6Ju

l‐1

6Se

p‐1

6N

ov‐

16

Jan‐1

7M

ar‐1

7M

ay‐1

7

Vol('000, LHS) Price (Rs., RHS)

ITC BUY

1

Growth, re-ignited

Detailed report

Financial summary (Rs bn)

Y/e 31 Mar, Consolidated FY15A FY16A FY17ii FY18ii FY19ii

Revenues (Rs bn) 384 391 413 463 519 Ebitda margins (%) 37.0 38.5 37.7 38.2 38.6 Pre‐exceptional PAT (Rs bn) 97 99 104 118 134 Reported PAT (Rs bn) 97 99 104 118 134 Pre‐exceptional EPS (Rs) 8.0 8.2 8.6 9.8 11.1 Growth (%) 8.2 2.3 5.2 13.4 13.2 IIFL vs consensus (%) (1.6) (2.1) (1.5) PER (x) 33.9 33.2 31.5 27.8 24.6 ROE (%) 32.8 30.2 29.0 29.5 29.9 Net debt/equity (x) (0.2) (0.2) (0.1) (0.1) 0.0 EV/Ebitda (x) 22.3 21.3 20.6 18.3 16.2 Price/book (x) 10.2 9.6 8.6 7.7 6.9 Source: Company, IIFL Research. Price as at close of business on 09 May 2017.

Institutional Equities

We expect growth to revive for ITC (FY17-19 EPS Cagr of 13% vs. 5% for FY14-17) as tax regime turns more rational, non-tax issues are in the base and consumption revives. India has one of the most favourable industry structures (virtual monopoly, FDI ban), which reduces volatility in earnings delivery. Moreover, ITC’s capital allocation has improved, with FCF conversion of ~80%. In light of these factors ITC’s 35% discount to HUL currently (vs. 12% prior to FY13) is set to contract, driving 29% upside to our price target of Rs.350. A change in incidence or structure of tax under GST regime is the main risk to our BUY rating.

Growth is set to revive: In the past two budgets, average increase in excise duty has been 8% vs. 18% for the four years prior to that, possibly as the government realizes that a higher tax rate does not increase tax collections but encourages illegal trade. Non tax regulations such as pictorial warnings and ban on public smoking are already in place and others such as banning loose cigarettes are hard to implement. Moreover, revival in consumption would benefit ITC just as it would benefit other FMCG companies.

Best industry structure: ITC is a virtual monopoly accounting for 86% of cigarette industry sales and 96% of profits. Moreover, FDI in cigarette manufacture is banned. Due to these factors ITC has high Ebit margins of 66% in the cigarette division vs. global average of 33%. Absence of competition gives ITC pricing power and reduces the risk of market share loss or margin erosion. Moreover, government officials have stated that GST is likely to be tax neutral – thus GST is unlikely to materially alter the industry structure.

Reasonable valuation in the light of improved capital allocation: ITC generates 75-80% of its net profit as FCF, vs. an average of 55% over FY03-15. Moreover, ITC trades at a discount of 35% to HUL (with similar expected growth for FY17-19) vs. an average of 12% prior to FY13 when ITC’s EPS growth faltered due to an adverse tax regime. With growth reviving, we believe that this discount would shrink, resulting in an attractive 29% return to our TP. Our extended DCF (terminal FY39) suggests an even higher upside of 46%.

ITC – BUY

2 percy.panthaki@iif lcap.com

Institutional Equities

Contents:

Growth is set to revive ..................................................................................... 3

Background ..................................................................................................... 3

Tax increases likely to be reasonable ................................................................... 3

Non-tax issues already in the base ...................................................................... 9

Revival in consumption ..................................................................................... 11

Price elasticity ................................................................................................. 13

Best industry structure .................................................................................. 15

Near monopoly business ................................................................................... 15

Ban on FDI in tobacco ...................................................................................... 16

GST likely to be tax neutral ............................................................................... 19

Capital allocation and valuation ..................................................................... 24

Capital allocation has improved ......................................................................... 24

Healthcare foray not a significant risk ................................................................. 27

Reasonable valuation ....................................................................................... 28

Annexure 1 – Analysis by cigarette length ..................................................... 33

Annexure 2 – FMCG business ......................................................................... 36

Annexure 3 – Hotel business ......................................................................... 40

Annexure 4 – Paperboards business .............................................................. 43

Annexure 5 - Agri business ............................................................................ 46

3

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Growth is set to revive

Background As shown in figure 1, prior to FY15, ITC was on a high growth path (FY02-14 EPS growth 18%). However during FY14-17, continuous steep tax increases took a toll and EPS growth fell to 5%. We now believe that FY17-19 will post a healthy revival with an EPS Cagr of 13%. In this section we discuss in detail the reasons why we believe growth will revive. Figure 1: EPS growth expected to revive in a rational tax regime

Source: Company, IIFL Research

Tax increases likely to be reasonable We believe tax increases will be reasonable in the medium term. As we explain in this note, the sweet spot for tax increases is 8-10% per annum, since at this rate of increase the government is able to optimise the holy trinity of keeping cigarette volume growth close to zero, increasing government revenues at a handsome rate and limit proliferation of illegal cigarettes. 1. Tax rate does not impact tax collections Over FY12-16, excise duties increased aggressively. Tax rates increased at 18% Cagr over this four year period (excluding mix change impact). The decade prior to that i.e. the period of FY03-13 witnessed excise duties increase of 5.7% p.a. The recent past has therefore seen a clear steepening of the tax curve vs. history. However, higher tax rates have not necessarily translated into higher government collections; indeed in some cases steep tax increases have hurt growth in tax collections due to a combination of volume decline and down-trading to shorter cigarette lengths which have a lower excise duty per stick.

0%

5%

10%

15%

20%

25%

30%

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7ii

FY1

8ii

FY1

9ii

ED rates YoY growth EPS growth

High EPS CAGR of 18%

Low EPS CAGR of 5%

Steady EPS CAGR of 13%

EPS growth has fallen to 5% p.a. for the past three years due to a continuous

tax increases; we believe it will revive to 13% p.a. over

the next two years

Excise payment by ITC FY12-16 grew 11% p.a.

despite a higher tax rate growth of 18% p.a.

ITC – BUY

4 percy.panthaki@iif lcap.com

Institutional Equities

Figure 2: Tax collections have dipped despite increase in duty rates

Source: Company, IIFL Research

During the period FY03-12, ITC’s excise payment has increased at a Cagr of 8% vs. a tax rate Cagr of 4%. However, for the period FY12-16 while the tax rate grew at a much sharper Cagr of 18%, the actual tax paid increased at a lower Cagr of 11% due to volume decline and down-trading. 2. High taxation results in proliferation of duty evaded cigarettes and non cigarette tobacco consumption A high tax burden provides arbitrage opportunities for duty-evaded cigarettes to thrive, especially in developing countries where implementation of law is lax. In India, illegal cigarettes account for 20.2% of all cigarettes sold in India in CY15. This has increased from 15.7% in CY10. Most of these cigarettes are available at less than half the price of similar cigarettes (since tax accounts for ~55% of the retail price of a cigarette) and therefore offer significant price competition to legal cigarettes. Figure 3: Illegal cigarette volumes have more than doubled since CY04

Source: Tobacco institute of India, IIFL Research

Moreover, as cigarettes are taxed much higher than bidis or other forms of consumption, an increase in cigarette taxation results in consumption shifting from cigarette to other forms.

‐5%

0%

5%

10%

15%

20%

25%

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

ED paid yoy growth ED per stick YoY growth ED rates yoy growth

11.112.5

13.514.6

16.717.5

18.319.5

20.821.8

22.8 23.9

5

7

9

11

13

15

17

19

21

23

25

CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15

(bn sticks)

Illegal cigarettes contribution to industry

volumes went up from 15.7% in CY10 to 20.2% in

CY16

5

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Figure 4: Comparison of taxes paid by cigarettes and other forms

Figure 5: Contribution from legal cigarettes to overall tobacco consumption

Source: Tobacco institute of India, IIFL Research Source: Tobacco institute of India, IIFL Research

Legal cigarettes account for only 11% of tobacco consumed in India and this share has been declining over the years. Despite this, legal cigarettes account for 87% of taxation on tobacco. Figure 6: Cigarettes are a small part of tobacco consumption but a large part of tobacco taxes

Source: Tobacco institute of India, IIFL Research The problem is accentuated by the fact that the tax on bidis is low, and it does not grow as fast as the tax on cigarettes. Figure 7: Taxation on cigarettes vs. bidis

Source: IIFL Research

33 52

953

2,773

0

500

1,000

1,500

2,000

2,500

3,000

FY06 FY15

Other forms Cigarettes

Excise duty per kg of tobacco used

(Rs)

86 62

320

500

0

100

200

300

400

500

600

FY82 FY16

Legal cigarettes Other tobacco forms(mn kgs)

11%

87%85%

13%

0%

20%

40%

60%

80%

100%

Share of tobacco consumption Share of tax revenues

Legal cigarretes Other tobacco products

1,349 1,584 1,768 2,095 2,238

577 769 930

1,157 1,207

‐

5

10

15

20

25

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY13 FY14 FY15 FY16 FY17

VAT per stick paid by ITC (LHS)Excise duty per stick paid by ITC (LHS)Excise duty per stick on bidi (hand made) (RHS)

ED per 1000sticks (Rs)

ED per 1000sticks (Rs)

Excise duty on cigarettes 100x that of bidis on a per

stick basis

ITC – BUY

6 percy.panthaki@iif lcap.com

Institutional Equities

Illegal cigarettes — case study of a few countries: Malaysia Malaysia has one of the highest illicit cigarette markets in the world in terms of composition of the overall market. Illegal cigarettes comprise ~57% of industry volumes. This is because Malaysia has a tax incidence much higher than neighbouring countries such as Indonesia, resulting in an arbitrage opportunity for duty evaded imports. At USD 3.29 per pack of 20 for the most sold brand, the price of cigarettes in Malaysia is higher than in Indonesia (USD 1.48 per pack), Thailand (USD 1.13), and Vietnam (USD 0.80) in 2015

Figure 8: Malaysia – split of cigarette consumption in 2015 Figure 9: Malaysia – share of illicit cigarettes over the years

Source: IIFL Research, Oxford economics Source: IIFL Research, Oxford economics, *denotes exit 2016 share as

per BAT Malaysia annual report

As per BAT Malaysia annual report (which quoted Nielsen), contribution of illegal cigarettes exit 2016 has gone up to 57%, as the government has increased taxation by ~40%. Experts expect the illegal share to cross 60% in the next few months. In 2016 BAT announced that it would shut its factory at Petaling citing “falling sales due to the presence of illicit cigarettes in the market and high duties imposed by the government”. Pakistan While the illegal cigarettes in Malaysia are mainly imported, in Pakistan these are of domestic origin. An increase in taxes by the Pakistan government has made manufacture of duty evaded cigarettes more attractive. This has led to the share of illegal cigarettes increasing from 25.3% in 2012 to 31.3% in 2015.

Domestic ‐legal,

61.7%

Non domestic ‐legal, 1.7%

Illicit, 36.7%

34.5%35.6%

33.7%

36.7%

57.10%

30%

35%

40%

45%

50%

55%

60%

2012 2013 2014 2015 2016*

Illegal cigarettes in Malaysia outnumber legal cigarettes now as a result

of steep tax hikes

7

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Figure 10: Pakistan –excise duty per stick for most sold brand Figure 11: Pakistan – share of legal and illicit cigarettes

Source: IIFL Research, Oxford economics Source: IIFL Research, Oxford economics

As per annual report of Pakistan Tobacco Company for CY16, illegal cigarettes touched 40% of industry volumes exit 2016. The share has increased every month, starting at 31.9% in January 2016 and ending with 40.6% in December 2016. In the previous year, taxes in Pakistan went up 15-20%. 3. Tax in India is already high and consumption is low Tax as a percentage of MRP in India is ~55%. This is low compared with several other countries Figure 12: Tax as % of MRP in India is lower than many other countries

Source: IIFL Research, WHO

However, this is mainly due to ITC’s virtual monopoly, (Ebit margin is nearly 70% of net sales for ITC’s cigarette division) allowing it to increase prices as required. Therefore, while tax increases have been steep, price has increased correspondingly leading to no significant change in the tax to retail price ratio. If India were a market with enough competition, then the tax to retail price ratio would definitely be higher as the retail price would have been competed down to lower levels. This is not necessarily desirable; the objective of a tax regime is to make cigarettes unaffordable and that is unlikely to be achieved by increasing competition and bringing down the price table, thereby having a higher tax to retail price ratio.

0%

10%

20%

30%

40%

0

200

400

600

800

1,000

1,200

2008 2009 2010 2011 2012 2013 2014 2015

Excise duty per 1000 sticks (LHS)

% growth (RHS)

(Pakistanrupee)

(%)

74.4% 77.1% 74.6%68.6%

21.9% 18.6% 21.1%24.2%

3.5% 4.2% 4.2% 7.1%

50%

70%

90%

2012 2013 2014 2015

Domestic ‐ legal Domestic ‐ illicitNon domestic ‐ illicit

25%

45%

65%

85%

Vie

tnam USA

Ch

ina

Sou

th A

fric

a

Ind

on

esi

a

Mal

aysi

a

Au

stra

lia

Ind

ia

Pak

ista

n

Bra

zil

Me

ixco

Arg

en

tin

a

Ge

rman

y

Thai

lan

d

Egyp

t

Sri L

anka

Ph

ilip

pin

es

Po

rtu

gal

Ban

glad

esh

Spai

n

Turk

ey

UK

Tax as % of MRP on most sold brand

Illegal cigarettes contributed 40% to

industry volumes in Dec 2016, up sharply from 31%

in CY15

Tax as a percentage of MRPin India is lower than

several countries, but that is only due to ITC’s virtual

monopoly giving it significant pricing power

ITC – BUY

8 percy.panthaki@iif lcap.com

Institutional Equities

What is relevant is the retail price or the tax in relation to per capita income of the consumer. On both these parameters we observe that cigarettes in the Indian market are highly unaffordable.

Figure 13: Tax per 100 packs on most sold brand as a percentage of GDP per capita

Figure 14: MRP of 100 packs of most sold brand as a percentage of GDP per capita

Source: IIFL Research, WHO Source: IIFL Research, WHO

India is already quite low in terms of per capita consumption of cigarettes as well as tobacco.

Figure 15: Per capita consumption of cigarettes per adult Figure 16: Per capita tobacco consumption

Source: IIFL Research, World Library Source: IIFL Research

Percentage of adults who consume tobacco in India is not very high. Here are some facts • 34.6% of adults, 47.9% of males and 20.3% of females consume

any form of tobacco • 14% of adults smoke tobacco (24.3% makes and 2.9% females)

o 5.7% of adult smoke cigarettes (10.3% males and 0.3% females)

o 9.2% of adults smoke bidis (16% males and 1.9% females) • 25.9% of adults consume smokeless tobacco (32.9% males and

18.4% females)

0%

2%

4%

6%

8%

10%

12%

USA

Ch

ina

Arg

en

tin

aG

erm

any

Au

stra

liaB

razi

lP

hili

pp

ine

sSp

ain

Vie

tnam

Mal

aysi

aP

ort

uga

lM

eix

coP

akis

tan

Sou

th A

fric

aU

KEg

ypt

Ind

on

esi

aTh

aila

nd

Turk

ey

Ban

glad

esh

Ind

iaSr

i Lan

ka0%

2%

4%

6%

8%

10%

12%

14%

16%

USA

Arg

en

tin

aG

erm

any

Ph

ilip

pin

es

Ch

ina

Spai

nB

razi

lA

ust

ralia

Po

rtu

gal

UK

Me

ixco

Egyp

tM

alay

sia

Turk

ey

Thai

lan

dP

akis

tan

Vie

tnam

Ind

on

esi

aSo

uth A

fric

aB

angl

ade

shIn

dia

Sri L

anka

0

400

800

1,200

1,600

2,000

Ind

iaB

angl

ade

shSr

i Lan

kaM

eix

coSo

uth A

fric

aP

akis

tan

Bra

zil

Mal

aysi

aTh

aila

nd

UK

Ph

ilip

pin

es

Vie

tnam USA

Au

stra

liaA

rge

nti

na

Ge

rman

yIn

do

ne

sia

Egyp

tP

ort

uga

lTu

rke

yC

hin

aSp

ain

No. of cigarettes per year

438 461 468

743

1,1451,256

0

200

400

600

800

1,000

1,200

1,400

Pakistan Nepal India World China USA

(gms per year)

Taxation and retail price of cigarettes in conjunction

with per capita income reveals India as one of the

highest taxed countries

India has one of the lowestper capita consumption of cigarettes at 96 p.a.; only

5.7% of Indian adults smoke cigarettes

Key data related to tobacco consumption

Country GDP per capita (USD)

Tobacco consumption

Sticks per adult per year

Cigarette MRP USD (20’s pack)

MRP as % of GDP per capita (%)

Tax as % of MRP (%)

Tax as % of GDP per capita (%)

Advertisement restrictions Smoking restrictions Pictorial warnings

India 1,627 96 1.76 10.8% 60.4% 6.5% All forms of advertisements including surrogate, are banned

Prohibited in public places including auditoriums, cinemas, hospitals, pub-lic transport, restaurants, hotels, bars, educational institutes and parks

Pictorial and text health warnings to cover 85% of pack

Pakistan 1,287 468 0.48 3.7% 60.7% 2.3% Advertisements banned in print and electronic media, some promotional activities allowed in PoS

Banned in public places Pictorial and text health warnings to cover 40% of pack, new regulations to increase this to 85% have been delayed

Sri Lanka 6,844 195 9.24 13.5% 73.8% 10.0% Restrictions on advertising and promo-tions, but product displays at PoS are allowed

Banned in enclosed public places Pictorial and text health warnings to cover 80% of pack

Bangladesh 2,520 154 1.93 7.7% 76.0% 5.8% Advertising prohibited in all print and electronic media, including PoS

Banned in indoor public places GHW to cover atleast 50% of main display areas of the pack

Thailand 5,546 560 2.03 3.7% 73.1% 2.7% Most forms of tobacco advertising banned.

Banned in indoor public places, indoor workplaces and public transport

GHW to cover 85% of principal dis-play areas of the pack

Malaysia 11,059 539 3.76 3.4% 55.4% 1.9% All forms of tobaco advertisement and promotion, prohibited

Banned in public transport, specified public places and workplaces

Combined GHW and text warnings to occupy 50% of front and 60% of back of the pack

Indonesia 3,398 1085 1.58 4.7% 53.4% 2.5% Tobacco advertising and promotions are allowed with certain restrictions

Prohibited in public transport and designated public places

Pictorial health warnings are required to cover 40% of main display areas of the pack

China 7,570 1711 1.62 2.1% 44.4% 1.0% Tobacco advertising prohibited in mass media, public places, means of public transport and outdoors

Banned in at least 28 indoor public places including medical facilities, restaurants, and bars

Required warnings are text only, and cover at most 35% of the pack

Vietnam 2,071 1001 0.88 4.3% 41.6% 1.8% Tobacco advertising and promotions are prohibited, PoS displays are however allowed

Banned in select public places such as health and educational facitlities

Combined picture and text warnings to cover 50% of the pack

Philippines 2,938 838 0.62 2.1% 74.3% 1.6% Tobacco advertising and promotions are prohibited, PoS displays and free distri-bution of tobacco products are however allowed

Banned in select places, transport facilities and restrictions on access to minors

Combined picture and text warnings to cover 50% of the pack

UK 44,216 750 12.69 2.9% 82.2% 2.4% Tobacco advertising and promtions are prohibited with few exceptions such as retailer incentive programmes

Banned in all closed places and public places. Smoking also prohibited in private cars carrying a child

Standardised packaging for all packs

Institutional Equities

Key data related to tobacco consumption

Country GDP per capita (USD)

Tobacco consumption

Sticks per adult per

year

Cigarette MRP USD (20’s pack)

MRP as % of GDP per capita (%)

Tax as % of MRP

(%)

Tax as % of

GDP per capita (%)

Advertisement restrictions Smoking restrictions Pictorial warnings

Germany 41,613 1045 6.45 1.6% 72.9% 1.1% Tobacco advertising prohibited in TV, radio and print. Advertising at PoS and print advertising such as posters, are allowed

Prohibited in indoor workplaces and public places

One of the two authorized text warning to occupy 30% of front of the pack, and one of 14 authorized text warning to occupy 40% of the back of the pack

Spain 31,000 1757 6.82 2.2% 78.1% 1.7% Tobacco advertising prohibited, PoS ad-vertising being the exception

Prohibited in indoor public places, work-places and public transport

One of the two authorized text warning to occupy 30% of front of the pack, and one of 14 authorized text warning to occupy 40% of the back of the pack

Portugal 21,733 1114 6.02 2.8% 74.5% 2.1% Total sponsorship and advertising ban, including PoS advertising. Electronic ciga-rettes and herbal smoking products also included

Prohibited in all enclosed public places, work places and public transport

Warnings to cover 65% of most relevant area of the pack

Turkey 10,523 1399 3.82 3.6% 82.1% 3.0% Tobacco advertising prohibited, PoS ad-vertising is also regulated

Prohibited in indoor workplaces and public places

Warnings to cover 65% of the pack

South Africa 6,360 459 2.97 4.7% 48.8% 2.3% Tobacco advertising prohibited, PoS ad-vertising is also regulated

Partially banned in indoor public areas, 25% of indoor public areas are allowed for smoking

Pictorial and text health warnings to cover 15% of the front of the pack, and 25% of the back of the pack

Egypt 3,343 1104 1.12 3.4% 73.1% 2.4% Tobacco advertising and promotions prohibited, but law does not cover spon-sorship or financial contributions by the tobacco industry

Banned in specified public places Warnings to cover 50% of of the pack

Brazil 11,092 504 2.54 2.3% 64.9% 1.5% Tobacco advertising prohibited, PoS ad-vertising is the only exception

Prohibited in all enclosed public and workplaces

GHW to cover 30% of front side of the pack, 100% of back and one side of the pack

Argentina 12,734 1042 1.77 1.4% 69.8% 1.0% Most forms of tobacco advertising banned.

Prohibited in indoor work and public places and public transport

Warnings to cover 50% of of the pack

Mexico 10,849 371 3.45 3.2% 65.9% 2.1% Most forms of tobacco advertising banned, but directed advertising to adults such as adult magazines, are al-lowed

Banned in designated public places, isolated areas in other public and work-places are allowed

Warnings to cover 30% of front, 100% of back and 100% of one side of the pack

Australia 62,846 1034 15.9 2.5% 56.8% 1.4% Most forms of tobacco advertising banned, restrictions on PoS advertising

Banned in indoor work and public places and public transport

GHW and text warnings to cover 75% of front and 90% of back. Additionally, an informational mes-sage to be included on one full side

USA 54,649 1028 6.23 1.1% 42.5% 0.5% NA NA NA

Institutional Equities

9

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Figure 17: Adults smoking tobacco is relatively low in India, and smoking cigaretteseven lower

Source: WHO, IIFL Research. *The proportion of cigarette smokers is even lower at 5.7%

4. Tax increases have been benign in recent times The past two budgets have been relatively benign in terms of increase in excise duties. The budget in Feb 2016 increased excise duties by 10% and the one in Feb 2017 increased duties by 6% only. Moreover, several government officials have mentioned that GST would be tax neutral for tobacco. These developments lead us to believe that the government stance on tobacco has become less aggressive since it has realised that steep tax increases do not lead to additional revenue but they make production and sale of duty evaded cigarettes more attractive. Non-tax issues already in the base Tobacco control consists of tax as well as non-tax measures. In the previous section we argued why tax measures are likely to be manageable in the medium term. In this section we look at the possible risks on the non-tax front. We argue that most of the non-tax measures have already been implemented in India over the past several years, and that there are very few areas on which India is not already compliant. Therefore, the pressure due to non-tax regulations coming into force will be lower in the future vs. what it was in the past. The only possible issues that could come up are a ban on loose cigarettes and increasing the minimum age of a customer to whom cigarettes can be sold. Both these measures are so difficult to implement as to have no material impact. FCTC (Framework Convention for Tobacco Control) stipulates several non-tax measures to control consumption. India is compliant with most of the main measures: • Ban on public smoking – India announced a nationwide ban on

public smoking in October 2008. Places where smoking was restricted included auditoriums, cinemas, hospitals, public transport, restaurants, hotels, bars, educational institutes and parks among others, with offenders being charged a fine of Rs200.

• Pictorial warnings – In India, pictorial warnings increased from 40% to 85% of the pack in April 2016

0%

10%

20%

30%

40%

50%

Ke

nya

Me

xico

Pak

ista

n

Egyp

t

Ph

ilip

pin

es

Thai

lan

d

Ind

ia*

Ind

on

esi

a

Ru

ssia

Ban

glad

esh

Tobacco users Tobacco smokers Smokeless tobacco users

% of adults

Excise hikes in the past twobudgets have averaged 8%vs. 18% in the four budgets

before that

Most of the FCTC non tax recommendations such as

ban on public smoking, ban on advertisement and pictorial warnings are

already in place

ITC – BUY

10 percy.panthaki@iif lcap.com

Institutional Equities

Figure 18: Pictorial warnings now make up ~85% of the pack area

Source: IIFL Research

• Ban on advertising – There is almost a complete ban on

advertising of tobacco products. Even surrogate advertising is not allowed. The only form of advertisement allowed is billboards on retail shops

There are only a few areas where there could be regulatory pressure, but we believe that these are difficult to implement Ban on loose cigarettes About 70% of cigarettes in India are bought loose and therefore a ban on public smoking could theoretically affect the industry adversely. Under Section 18 of the Legal Metrology Act, “No person shall manufacture, pack, sell, import, distribute, deliver, offer, expose or possess for sale any pre-packaged commodity unless such package is in such standard quantities or number and bears thereon such declarations and particulars in such manner as may be prescribed.” Tobacco products were included in May 2015 and they came in effect from January 2016 within the purview of this section. Under section 7 of COTPA (Cigarettes and other tobacco products Act) loose cigarettes cannot be sold as the section deals with health warnings. The sale of cigarettes without pictorial and other warnings is not allowed and therefore the interpretation could be that loose cigarette sales cannot be allowed as the consumer does not get to see the pictorial warning. There is a bill to amend the COTPA to give it more teeth and make the ban on loose cigarettes more explicit. Despite these laws, there is no dearth of availability of loose cigarettes in India. Some states have enacted their own laws or issued notification based on existing laws to prevent sale of loose cigarettes. However, this has not impacted the availability of loose cigarettes. Cigarette retail is largely unorganised in India with 7.5mn retail points most of which are small mom and pop retail kiosks. Therefore it is very difficult to implement a ban on loose cigarettes. Even the ban on public smoking, which is already in place since the past eight years, has not resulted in any significant number of people being

Ban on loose cigarettes are difficult to implement; we

expect no significant impact on availability and pricing

11

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

fined for violating this law. While it is imposed in metros and big cities, our experience is that implementation elsewhere of the ban on public smoking is very lax. Implementation of ban on loose cigarettes is almost non-existent even in large cities such as Mumbai. We believe that even if the states and centre turn more serious on this ban, loose cigarettes will continue to be available freely, but retailers may charge a premium of about Rs.1 per stick to offset any fines or bribes they may have to pay as a result of strict implementation. Hence, in the worst case, it seems that a ban on loose cigarettes will be equivalent to a one time price increase of 5-10%. Increase in the minimum age There is a proposal to increase the minimum age of consumers to whom cigarettes can be sold from 18 years to 21 years and gradually to 25 years. We believe this provision is likely to be completely ignored in terms of implementation. Given the millions of retail points for cigarettes it is very difficult to check the age of the person buying a cigarette. Revival in consumption Slowdown in FMCG sales Over the past 3-4 years, performance of ITC’s cigarette division has deteriorated both in terms of growth in consumer spending on its products, as well as volume growth. The deceleration has coincided with the period when tax rates increased steeply. Figure 19: Sales growth has suffered in the past few years for ITC

Source: Company, IIFL Research

This has led to the belief that the deceleration in ITC’s performance has been solely due to the continuous steep tax increases. Although the tax increase certainly has had an important role to play in the deceleration, the fact is that overall FMCG spending slowed down and that is likely to have hurt cigarette consumption as well.

‐10%

‐5%

0%

5%

10%

15%

20%

25%

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Volume Excise duty per stick Gross sales (including VAT)

% growth

Increase in minimum age of consumers to whom

cigarettes can be sold is even more difficult to

implement than banning loose cigarettes

Slowdown in ITC’s sales is often blamed solely on

steep tax increases as bothhave happened at the same

time; however, overall slowdown in FMCG is also a

factor which is often overlooked

ITC – BUY

12 percy.panthaki@iif lcap.com

Institutional Equities

Figure 20: Consumer slowdown has also affected ITC’s cigarettes division

Source: Company, IIFL Research

We (and indeed most analysts as well as investors) are building in an increase in sales growth for the FMCG sector, denoting a recovery for the sector. Consequently, there should be a recovery in cigarettes as well. Figure 21: Expect a recovery in FMCG as well as cigarettes going forward

Source: Company, IIFL Research

Cigarettes gross sales linked at least partially to macro indicators We plot gross sales growth for ITC’s cigarette division for the past 20 years and compare it to nominal GDP growth and rural agri wage growth

0%

5%

10%

15%

20%

25%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Growth in FMCG excl ITC Growth in ITC's gross cigarette sales

6.2%

7.7%

11.2%10.1%

0%

2%

4%

6%

8%

10%

12%

FMCG excl ITC sales growth ITC's gross cigarette sales growth

FY14‐17 FY17‐19ii

We expect cigarette sales growth to be higher in the

future compared to the past, and this is no different

from our estimates for FMCG in general

13

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Figure 22: Gross sales growth has been in‐line with macro indicators

Source: Company, IIFL Research

As with other FMCG products, cigarette sales growth too has moved in line with macro indicators. Even as tax increases have hampered ITC’s sales growth in recent times, on a broad basis, ITC’s cigarettes division has registered a sales growth (gross of VAT and excise), in-line with other macro indicators such as nominal GDP growth and rural agri-wage growth. Thus, an improvement in these macro factors should also lead to revival of the growth in ITC’s cigarettes division (on a gross basis). Price elasticity We have data for ITC’s price growth (including mix changes) and volume from FY95 onwards. There is a clear negative correlation (R=-0.71) over the period FY95-FY17.

Figure 23: Volume and pricing growth trends for ITC cigarettes Figure 24: Price elasticity for cigarettes

Source: IIFL Research Source: IIFL Research

The slope of the curve over this period is -0.74 i.e. for a 100 bps increase in price, the volume drops by 74 bps. However, the slope of the curve for the past 10 years (FY08-17) is lower at -0.54. If we consider the past three years as the period of decelerating growth and exclude these from our analysis and look at the slope of the curve for the 10 year period FY05-14, it is not significantly different at -0.56.

‐5%

0%

5%

10%

15%

20%

25%

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

ITC's gross cigarette sales growth Nominal GDP growth

Rural agri wage growth

‐10%

‐5%

0%

5%

10%

15%

20%

25%

FY9

5FY

96

FY9

7FY

98

FY9

9FY

00

FY0

1FY

02

FY0

3FY

04

FY0

5FY

06

FY0

7FY

08

FY0

9FY

10

FY1

1FY

12

FY1

3FY

14

FY1

5FY

16

FY1

7

Volume growth Price growthy = ‐0.7351x + 0.0988

‐10%

‐5%

0%

5%

10%

15%

20%

25%

0% 5% 10% 15% 20% 25%

Vo

lum

e g

row

th

Price growth

ITC’s sales are at least partially impacted by macro

indicators such as GDP growth and rural agri wage

growth; the current slowdown in sales coincides

with a slowdown in these indicators

ITC – BUY

14 percy.panthaki@iif lcap.com

Institutional Equities

Alternate view of elasticity - Actual vs. projected volume Using the data of FY95-17 the regression equation is Y = -0.74X + .099. We plug this equation into all the years and project volume growth as per the equation. We ascertain the difference between the actual volume growth and the projected volume growth and plot it as below Figure 25: Actual growth tends to fall below projected growth during periods whereconsumption is weak

Source: IIFL Research

We notice that in the past three years the actual volume growth is indeed below the projected volume growth by 4-6%, implying an adverse impact on the price elasticity. This may be construed as a breakdown in price elasticity due to continuous steep increases in tax. And surely, that is certainly an important reason for the lower–than-projected volume growth. However, we notice that the other period where volume growth fell below projected levels was the period of the early 2000s. Anyone who has been tracking Indian FMCG for long enough will know that this period is well known for the collapse of FMCG growth dragged by slow rural growth and indeed lower overall GDP growth. The fact that the volume growth falls below projected only in periods when FMCG consumption is under stress seems to suggest that the consumption climate is an important factor affecting volume growth and that volume growth is not (as the popular opinion seems to be) solely a function of price elasticity having broken down or changed due to steep tax increases.

‐10%

‐5%

0%

5%

10%

15%

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

The years where projected volume (using past data

regression) has fallen below actual volume have

been years of general FMCGslowdown; the tax impact in the overall slowdown is

therefore overstated

15

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Best industry structure Near monopoly business Dominant player ITC is a dominant player in the Indian tobacco business due to legacy reasons. The three listed players via ITC, GPI and VST account for ~95% of the market volumes. Taking these three as the universe, ITC accounts for 86% of net sales and 96% of profits.

Figure 26: Revenue share as on FY16 (on net sales) Figure 27: Profit share as on FY16 (on Ebit)

Source: Company, IIFL Research Source: Company, IIFL Research

High profit margins Due to its dominant market position, ITC is able to make healthy margins, which are above global peers as well as Indian competitors. The Indian competitors have been forced to compete purely on price and in the lower priced 64mm segment as ITC has superior distribution strength as well as better brand recall. Figure 28: ITC’s EBIT margin is one of the highest among Asian and global peers

Source: Company, IIFL Research

Sri Lanka has a monopoly on cigarette manufacture, and the margins of Ceylon tobacco are therefore similar to ITC.

ITC, 86%

VST, 4%

GPI, 9%ITC, 96%

VST, 2%

GPI, 2%

13% 14% 15% 16%23% 24% 26% 27%

34% 36% 38%45% 47%

66% 67%

0%

20%

40%

60%

80%

Go

dfr

ey

Ph

ilip

s

Gu

dan

g ga

ram

Ph

ilip M

orr

is

HM S

amp

oe

rna

VST In

du

stri

es

Pak to

bac

co

Swe

dis

h M

atch

BA

T M

alay

sia

Bri

tish A

me

rica

n T

ob

acco

Re

yno

lds

Am

eri

ca

Jap

an T

ob

acco

Inc

Alt

ria

Imp

eri

al B

ran

ds

ITC

Ce

ylo

n T

ob

acco

Co P

LC

Ebit margin

ITC accounts for 86% of industry sales and 96% of

industry profit

ITC has one of the highest cigarette Ebit margins

amongst peers

ITC – BUY

16 percy.panthaki@iif lcap.com

Institutional Equities

Ban on FDI in tobacco In April 2010, the government of India banned FDI in cigarette manufacturing, following pressure from the Health ministry on the grounds that being a signatory of the Framework Convention on Tobacco control, it was the government’s responsibility to reduce consumption. The new DIPB notification stated “FDI is prohibited in manufacturing of cigars, cheroots, cigarillos and cigarettes, of tobacco or of tobacco substitutes”. The earlier policy permitted FDI up to 100% with prior permission from the Foreign Investment Promotion Board (FIPB), and subject to the company obtaining an industrial license. However, this was as good as defunct as no new industrial license was issued since 1999. Further, the cabinet in November 2016 proposed to ban FDI in cigarettes in any form, including licensing for franchise, trademark, brand name and management contracts. Over the years, FDI policies have become more stringent and access to foreign capital has become increasingly difficult. The case studies of Japan Tobacco Inc and Godfrey Philips India illustrate this point. Case study - JTI (Japan Tobacco Inc) Figure 29: JTI India – timeline of events

Year Event

1993 Japan Tobacco Inc enters India through a 50:50 JV with Mumbai based Thakkar family

2008 With the JV facing losses, JTI seeks permission of FIPB to infuse equity and increase stake from 50% to 74%

2010 While the proposal stays in abeyance with FIPB, the government bans any new FDI in cigarette manufacturing

2010 JTI India issues shares to JTI at a premium while also issuing equal number of shares to Thakkar family, thus investing Rs2.9bn in the company without altering the equity structure

2010 The transaction comes under the scrutiny of the Finance ministry

2011 Unable to infuse equity, JTI exits the JV

Source: IIFL Research

JTI based its decision of exiting the JV on “accumulation of investment and an unsustainable business model in an operating environment where readymade cigarette demand has not evolved, with several foreign investment, regulatory, duty and tax related uncertainties”.

FDI ban on tobacco manufacturing builds a

strong moat for ITC

JTI exited India due to unfavourable regulatory

environment

17

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Case study - GPI (Godfrey Philips India) Figure 30: Phillip Morris in India – timeline of events

Year Event

1936 Godfrey Philips India (GPI) is promoted by Godfrey Philips, London

1968 Philip Morris acquires Godfrey Philips, London

1979 Philip Morris reduces stake in GPI and K.K. Modi group enters the business

2003 Philip Morris launches its greatest selling brand "Marlboro", through an arrangement with a local distributor ‐ Barkat Foods and Tobacco, sidelining GPI. This resulted in strained relations between Philip Morris and the Modi group

2009 Both parties reconcile, resulting in GPI getting the rights of manufacturing, distribution and sales of Marlboro

2010 GPI launches a 69mm cigarette under the Marlboro brand – “Marlboro Gold Advance Compact” in Mumbai and Pune. However ITC countered it with launch of “Players Gold Leaf” at a 14% discount, after which the product failed to gain any traction

Source: IIFL Research

Phillip Morris despite being present in India in some form or the other has not been able to make any significant inroads. In October 2010, Marlboro was launched in the 69mm segment which accounted for ~80% of industry volumes at that time. Prior to this Marlboro was present only in the 84mm segment. With this new variant, it was expected that Marlboro’s market share would increase, but due to the strong competitive positioning of ITC, and the inability of Phillip Morris to compete aggressively due to stifling regulation, Marlboro was not able to garner significant market share in India. As per a Euromonitor report, Marlboro’s volume market share in India in 2015 was just 1%. In recent times, there have been talks to split the business of GPI into two entities with Philip Morris Inc controlling the marketing and distribution of brands, and the Modi group controlling manufacturing. However, such an arrangement would not be possible if the proposed ban on FDI in any form (i.e. not just on manufacturing but even on selling and distribution) goes through. Licenses required for manufacturing One might argue that since only manufacturing is banned, any foreign company could have set up a 100% subsidiary, got the manufacturing outsourced to a local party and handled the sales, distribution and marketing. However, putting up a new factory or increasing capacity requires government licensing, and therefore in practice this route does not work well. Moreover, foreign companies are not comfortable sinking in large investments in a structure where they do not have control over the whole operation. This is the reason why foreign companies have largely stayed away from the Indian market. Now with the cabinet proposal to ban FDI in tobacco in a more comprehensive manner, companies will be even more wary to enter into India given the risk that they may be asked to shut shop at any time. Advantages of FDI ban The FDI ban is therefore, a substantial competitive moat for ITC. It ensures that

Marlboro volume market share is 1% despite being present in India for over a

decade

Due to license requirementsit is difficult for foreign

companies to operate in India even via third party

manufacturing

ITC – BUY

18 percy.panthaki@iif lcap.com

Institutional Equities

• There is no risk of market share loss; market shares have been largely stable over the past few years.

Figure 31: ITC is able to maintain market shares at a high level for a long period

Source: Company, IIFL Research

In markets such as Indonesia, with 3-4 strong players, market shares tend to fluctuate. Figure 32: Fluctuations in market shares are larger in more competitive countries like Indonesia

Source: IIFL Research

• There is minimal risk of margin erosion; over the past several

years, cigarette Ebit for ITC has continuously increased as ITC can take the price increases it deems necessary without worrying about competition undercutting and taking away market share

86% 86% 85% 85% 85% 84% 85% 85% 85% 86%

5% 4% 4% 4% 4% 4% 4% 4% 4% 4%10% 10% 11% 11% 11% 11% 11% 11% 11% 9%

0%

20%

40%

60%

80%

100%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

ITC VST GPI

20%

21%

21%

22%

22%

23%

23%

27%

29%

31%

33%

35%

37%

CY10 CY11 CY12 CY13 CY14 CY15 CY16

HM Sampoerna (LHS) Gudang garam (RHS)

Indonesia ‐ Market shares of top two players

19

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Figure 33: Margins for ITC’s cigarette business have improved continuously over theyears

Source: Company, IIFL Research

Other companies have seen substantial gyration in margins over the years – ITC’s margins in contrast have been much more stable and moving up continuously. Figure 34: ITC’s margins have been gradually increasing vs. high volatility among other global peers

Source: Company, IIFL Research, Bloomberg

GST likely to be tax neutral India is on the cusp of implementing GST. There is uncertainty as to how this will impact ITC, but there have been multiple statements from government officials stating that GST will be tax neutral for tobacco. Initially we did not give much importance to these statements because GST implementation was far away. But now, with the government having come out with cess caps, and implementation just a few weeks away these statements have been re-iterated. The fact that these statements are being made when we are at an advanced stage of implementation give them a higher credence than the same statements made six months ago, in our view.

53% 53%55%

53%54%

55%

59%

64%66% 66%

40%

45%

50%

55%

60%

65%

70%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

ITC's Ebit margin in cigarettes

30%

40%

50%

60%

70%

0%

10%

20%

30%

40%

50%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Imperial Brands (LHS) Japan Tobacco Inc (LHS) ITC (RHS)

Ebit Margin

As per government officials,GST is unlikely to change

tax incidence for ITC

ITC – BUY

20 percy.panthaki@iif lcap.com

Institutional Equities

Figure 35: Statements made by government personnel on tobacco taxation over time

Date Person Designation Excerpt of Statement

12/7/2015 Arvind Subramanian Chief Economic Advisor "Our recommendations on the demerit rate are very much based on what happens currently. De facto, some of these goods are taxed at close to what we are recommending. So, we are not changing anything,"

11/3/2016 Arvind Subramanian Chief Economic Advisor “…in all those things (i.e. goods on which cess is applicable) the current incidence will be maintained broadly and there will be no increase in incidence on that. So, that is the decision.”

3/16/2017 Krishna Byre Gowda GST Council member, Minister for agriculture, Karnataka

“Compared to the current tax structure, the GST along with the cess will only alter the composition of the taxes on tobacco products, there will be no increase in tax rates for tobacco due to GST”. Although, he added that there may be a variation in the taxation of tobacco from state to state

Source: IIFL Research

Cess caps announced: The cess cap for cigarettes is announced at Rs.4170 per thousand sticks or 290% or a combination of both. We believe that the ad valorem rate will not apply to cigarettes as the specific rate tallies exactly with the rate of excise on the Kings segment just before the budget on 1st Feb 2017. While government officials have stated that GST will be tax neutral for tobacco, the exact modus operandi is unclear. We believe that the modus operandi could be the following

• Excise duty could be made zero (although government will have the right to increase this in the future).

• Cess could be introduced at pre budget rates (i.e. at the maximum cap announced). This will result in excise duty reducing ~6% from the current level, as the increase in the budget this year was 6%.

• GST would be levied at 28% while VAT which is currently 25% (weighted average of different states) will cease to exist. Thus, there will be a 300 bps increase in the ad valorem taxes.

• The 300 bps increase in ad valorem tax is roughly equal to the 600 bps decline in specific duty, and therefore GST as an event will be tax neutral. Or in other words, FY18 will witness an increase of ~600 bps of excise duty vs. FY17 – the same that was announced in the budget in Feb 2017 – and no change in ad valorem tax.

There is a reason to believe that cess will replace excise under the GST regime. By law, cess does not have to be shared with the states and it accrues only to the centre. Excise duty has to be shared with the states and therefore depletes the central kitty. We believe that the government will want to increase its cess collections as they could help pay the states in case there is any deficit in collection. Higher ad valorem component a risk if ad valorem rate increases in future Although GST is likely to be tax neutral, the exact tax structure is not known. Therefore, it is possible that it may not pan out the way we believe as outlined above. It is possible that while the total tax paid is the same, a higher element of it is ad valorem. There is a belief that higher ad valorem taxes are less desirable than specific duties. As the company takes a price increase, the ad

Higher ad valorem component by itself is not aproblem; if it is higher and

increases from over the years, that is an issue

21

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

valorem tax rises automatically even without a change in the rate, unlike a specific per stick tax which does not change with price increase and therefore a higher part of the price increase may be retained at the net sales level if taxes are specific rather than ad valorem. While there is an element of truth in this, we believe that in the current environment, and the current expectations, a higher ad valorem component is not necessarily negative, unless the higher ad valorem rate once established moves up in future. If the ad valorem component is higher, or even if 100% of the tax collected is ad valorem in nature, there is no problem unless the rate goes up. The current expectation is a stable low double digit medium-long term Cagr in the cigarette Ebit. This is very different from the period of FY05-14 where cigarette Ebit grew at ~18%. Also, it would be imprudent to believe that even in the absence of GST, excise duty hikes would average mid single digits in future. A more reasonable estimate is at ~8-10% increase in excise duty with approximately flat volume growth. If we plug in these estimates, we get approximately the same net sales growth in scenario A (current i.e. pre GST duty structure) and scenario B (assuming all taxes are ad valorem). Figure 36: Net sales growth remains similar under both scenarios

Rs.per stick Scenario A Scenario B

FY17 FY18 YoY change

FY17 FY18 YoY change

Retail price 6.51 7.16 10% 6.51 7.16 10%

Trade margin 0.65 0.71 10% 0.65 0.71 10%

Gross sales 5.86 6.45 10% 5.86 6.45 10%

VAT / GST 1.17 1.29 10% 3.36 3.70 10%

Gross sales reported 4.69 5.16 10% 2.50 2.75 10%

Excise duty 2.19 2.41 10% 0.00 0.00 ‐

Net sales 2.50 2.75 10% 2.50 2.75 10%

Source: IIFL Research

As per Figure 36, in scenario A, the excise duty and VAT are separate, as is currently the case. In scenario B, excise (i.e. calculated per stick) duty is made zero and is replaced by an ad valorem regime. The total tax under both these situations remains the same in the base year i.e. FY17. Now assuming that the government wants to follow an objective tax policy, i.e. a policy that would meet the following objectives

• Limit the volume growth of the industry – i.e. volumes should not increase

• Limit growth of the illicit industry – as it is much more difficult to regulate and a shift from legal to illegal not only leads to revenue loss, but is also futile from a health point of view – an illegal cigarette is at least as harmful if not more harmful as a legal one.

• Keeping the above two objectives in mind, maximising revenue growth.

Net sales growth under scenario A (current i.e. pre

GST duty structure) and scenario B (assuming all

taxes are ad valorem) would be the same.

ITC – BUY

22 percy.panthaki@iif lcap.com

Institutional Equities

Scenario A: We believe that in the current macroeconomic environment, where GDP growth (nominal) is ~10%, it is reasonable to expect that the growth in consumer spending on the category will also be ~10%. If volume growth is to be maintained at zero, it would mean that price growth would contribute 10%. This would mean that the optimum growth in tax revenues would also be 10%, given that the company would want to maintain net sales growth at 10% in order to achieve a low double digit Ebit growth (some benefit from operating leverage). If the government decides that tax revenues need to grow at higher than optimum rate i.e. say 15%, it would result in ITC increasing price by more than 10%, resulting in volume decline. A large part of this decline would be picked up by the illegal trade; a sub-optimal outcome. So what the government will do is increase excise duty by 10%, assuming a flat ad valorem rate. The company will increase prices by 10%, resulting in zero volume growth, 10% increase in VAT revenue automatically and net sales growth of 10%. Scenario B In this scenario, we assume no specific tax, only ad valorem, but the same quantum in FY17 as scenario A. Therefore, the total tax in FY17 in both scenarios is assumed at Rs.3.36 per stick. Now assuming that the macro economic scenario remains the same, the total tax rate increase possible is 10% as demonstrated above. To achieve that 10% growth, government can keep rates unchanged. With a 10% price increase, tax revenues will automatically increase 10%, volumes will remain flat and net sales will grow 10% - which is the same outcome as scenario A. There are two reasons why things may not pan out as expected above 1. Ad valorem rate is kept unchanged by the government but ITC

decides to increase price by only 5% hoping to increase volumes by 5%, giving 10% gross sales, net sales and increase in government revenues. However, the objective of not letting volume grow is not met here.

2. The government increases its ad valorem rate itself. As per our forecasts, if ad valorem rate is increased from 134% of net sales to 140% of net sales, then with a 10% price increase, net sales will increase by 7.5% in scenario B vs. 10% in scenario A. It is very difficult to bridge this gap – if the company takes a higher price increase, volume dips and therefore total sales and total profit is adversely impacted due to lower volume. However, we believe that a scenario where all taxes will be made ad valorem is highly unlikely.

Also, note that if the overall tax remains unchanged, a higher ad valorem component by itself is not negative. It is negative only if that higher proportion is then increased again. The scenario of 100% of taxes being ad valorem however, is unrealistic in our view. It is possible that the ad valorem component goes up due to GST, but certainly the government would want to maintain a specific tax as well, to maintain a minimum price for a cigarette. With a 100% ad valorem tax, ITC would be able to slash

23

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

prices for certain brands way low and make them affordable to drive volume growth. GST rate may not change, but tax may go up The central government has guaranteed a 14% Cagr in tax revenues to the states for the next five years and any shortfall to this figure will be reimbursed by the centre to the states. Therefore, states are unlikely to have any incentive to have the GST rate on tobacco increased, like they do in the current VAT regime. What is likely to happen in the second year and onwards is that the central government will increase the excise duty (which we believe will be zero in year one).

ITC – BUY

24 percy.panthaki@iif lcap.com

Institutional Equities

Capital allocation and valuation Capital allocation has improved Capital employed vs. Ebit One of the main issues with ITC has been that the other businesses use up a lot of the free cash flow generated by the cigarettes business.

Figure 37: Split of capital employed across segments (FY16) Figure 38: Split of Ebit across segments (FY16)

Source: Company, IIFL Research

Source: Company, IIFL Research Note – total Ebit taken excluding unallocated cost, and segment contributions calculated on this denominator

Cigarettes account for 80% of ITC’s Ebit, but only 17% of ITC’s capital employed. On the other hand, businesses such as FMCG and hotels barely achieve breakeven but account for 15% each of the capital employed in the company. Consequently, pre tax returns on capital employed (Ebit divided by segment capital employed) is significantly different for different segments. Cigarette division, due to low fixed and working capital intensity, generates 205% pre tax ROCE, whereas FMCG and Hotels, due to depressed margins, generate only 1% ROCE. However, it must be noted that the agri business generates a decent return of 41% and paperboards too is not too bad at 17%. Figure 39: Pre tax ROCE is highest for cigarettes business, followed by agri

Source: Company, IIFL Research

Cigarettes, 16.7%

FMCG, 14.6%

Hotels, 15.2%

Agri, 7.2%

Paper, 16.1%

Unallocated/Others,

30.2%

Cigarettes, 79.7%

FMCG, 0.4% Hotels,

0.4%

Agri, 6.0%

Paper, 5.9%

Unallocated/Others,

7.6%

205%

1% 1%

41%

17%

47%

0%

50%

100%

150%

200%

250%

Cigarettes FMCG Hotels Agri Paper Overall

Segment wise ROCE ‐ FY16

Cigarette business accountsfor 80% of segmental Ebit

but only 17% of capital employed

25

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Capex flat lining Over the past several years, ITC has been keeping incremental capital employed in check. Moreover, despite EPS growing 14% over the past five years (FY11-16), capex has remained flat and has even come down in FY16.

Figure 40: Incremental capital employed over the years Figure 41: Segment wise capex over the years

Source: IIFL Research Source: IIFL Research

We believe that capex will not increase materially in the future vs. the past few years’ average and will remain around Rs.24bn • Cigarette volume growth is likely to remain flat, requiring low

capex. However some capex will be required for modernisation etc

• Hotels division has seen an average of Rs.6.5bn capex in the past five years. Unlike other hotel players who have been severely impacted by the slowdown and therefore have gone slow on investments, ITC with its cigarette cash flow has been able to invest steadily in the business.

• Paperboards is to an extent linked to cigarette demand which is likely to remain flat, and FMCG demand overall is in line or below historic averages

Figure 42: Capex levels likely to remain moderate in medium term

Source: Company, IIFL Research

Working capital for the business fluctuates depending on the inventory on balance sheet date of leaf tobacco and other agri commodities. However, in the past few years, it has averaged 17%

(10)

‐

10

20

30

40

50

FY12 FY13 FY14 FY15 FY16

(Rs bn)

Unallocated/Others PaperAgri HotelsFMCG CigarettesTotal

Incremental capital employed

0

5

10

15

20

25

30

FY12 FY13 FY14 FY15 FY16

Others Paper Agri

Hotels FMCG Cigarettes

(Rs bn)

Capex

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

5

10

15

20

25

30

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17ii FY18ii FY19ii

Overall capex (LHS) change YoY (RHS)(Rs bn) (%)

Capex unlikely to grow materially from current

levels

ITC – BUY

26 percy.panthaki@iif lcap.com

Institutional Equities

of sales, in line with the number seen in FY16. We believe that it should continue around this number in the future. Figure 43: Working capital levels likely to remain near current levels

Source: Company, IIFL Research

FCF generation at 75-80% Free cash flow to net profit has improved and is likely to remain at 75-80%. Over the past five years FY11-16, EPS has increased at a Cagr of 14% whereas capex has been flat to negative. This has resulted in significant improvement in the free cash flow conversion of the company. Figure 44: FCF generation likely to remain in the 75‐80% band

Source: Company, IIFL Research

FCF generation for ITC compares well to other companies in our coverage universe

10%

12%

14%

16%

18%

20%

22%

20

30

40

50

60

70

80

90

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17ii FY18ii FY19ii

Working capital (LHS) As % of sales (RHS)(Rs bn) (%)

40%

50%

60%

70%

80%

90%

20

40

60

80

100

120

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17ii FY18ii FY19ii

FCF (LHS) FCF to net profit (RHS)(Rs bn) (%)

FCF to net profit ratio of 75-80% quite similar to other

FMCG companies

27

ITC – BUY

percy.panthaki@iif lcap.com

Institutional Equities

Figure 45: FCF generation for ITC compares well with peers

Source: Company, IIFL Research

Healthcare foray not a significant risk ITC has received shareholder approval to enter the healthcare vertical, possibly opening up multi-specialty hospitals across the country. According to the company, such an initiative would leverage the company's repertoire of knowledge and experience in the hospitality and tourism sector and can be used for medical tourism for the country using the multi-specialty world class facilities. This has caused concern among some analysts and investors in terms of capital allocation. Our view is that it is preferable that ITC does not go into a new vertical, but the fact that it has decided to do so is not a significant negative. We look at the financials of other listed hospital plays. Apollo, the largest hospital chain in India trades at a PE of over 43x on FY18 consensus estimates. Moreover, the EV/IC of most hospital chains is >1, implying that for every rupee invested in the business, the enterprise value attributed is higher – thus the business is value accretive for investors

Figure 46: FY18 P/E for major healthcare services players Figure 47: EV/IC for major healthcare services players

Source: IIFL Research Source: IIFL Research

In our SOTP valuation, hospitals would be valued at higher than the invested capital in the business. Any investment in hospitals does not worry us much. Moreover, the investments in this business even

0%

50%

100%

150%

200%

GC

PL

Bri

tan

nia

Co

lgat

e

Emam

i

Dab

ur

ITC

HU

L

Baj

aj C

orp

GSK

C

on

sum

…

Mar

ico

Jyo

thy

Lab

s

Ne

stle

FY16 FY18‐19ii average

FCF to Net profit

19 20

44 54 58

95

0

20

40

60

80

100

120

Ko

vai M

ed

ical

Ind

rap

rast

ha

Me

dic

al

Ap

ollo

Ho

spit

als

Nar

ayan

a H

rud

ayal

aya

Fort

is H

eal

thca

re

HC

G

PE on FY18 EPS

2.3 2.3 3.2

3.5

5.1 5.8

0

1

2

3

4

5

6

7

Fort

is

He

alth

care

Ind

rap

rast

ha

Me

dic

al HC

G

Ap

ollo

Ho

spit

als

Ko

vai M

ed

ical

Nar

ayan

a H

rud

ayal

aya

EV/IC (FY16)

Enterprise value of listed hospitals much higher than

invested capital; potential investments by ITC in this area therefore unlikely to

be value destructive

ITC – BUY

28 percy.panthaki@iif lcap.com

Institutional Equities

over a 10 year period are unlikely to be material from the point of view of ITC’s market cap. For example, if we assume that ITC invests Rs.5bn each year into this business, and the entire investment is a write-off, Rs.50bn attrition from ITC’s market cap would result in ITC’s stock price falling just 1.5%. Reasonable valuation We value ITC on an SOTP business, taking a separate value for each business vertical. Before providing details of the SOTP valuation, we would like to calculate DCF value of the business just for reference. DCF valuation We believe that ITC can clock 10-12% Ebit Cagr in cigarettes business for a long time even with a 0-2% volume decline p.a. The assumptions to arrive at this are as follows • Industry size (at retail price) in value terms grows at 9-10%, in

line or marginally below nominal GDP growth. Cigarette industry at MRP is Rs.60bn – as a percentage of GDP this works out to 0.5%. At such a nascent level, we believe that there is limited downside to this number. We believe that despite tax increases, Indians will continue to spend at least 0.5% of their GDP on cigarettes.

• Tax hikes by the government average 10% - as explained earlier in the report, we believe that a 10% hike is optimal in terms of maximizing government revenue, minimising volume growth of legal players and halting the growth of the illegal trade.

• This will result in 9-10% increase in net sales for the cigarettes division.

• With some operating leverage, cigarettes Ebit can grow ~100-200 bps higher than sales growth i.e. 10-12%

We believe that this kind of situation can continue for 20 years before we can give a terminal growth. This would mean that at the end of 20 years, the per capita consumption of cigarettes would drop by a third, from 96 currently to 62 by FY39 (1% volume decline Cagr and 1.2% population increase Cagr). Despite this cigarettes bottom-line can grow at 11% as explained above. Based on a 10% discounting rate, 11% earnings growth FY19-39 and a 5% terminal growth rate, and a free cash flow to net profit of 78%, we arrive at a price target of Rs.397 per share (including Rs.19 per share of cash and financial investments; our FCF does not include non operating income). Figure 48: Sensitivity analysis of ITC’s DCF

Semi explicit growth rate

Discounting

rate

9% 10% 11% 12% 13%

9.0% 393 451 518 597 690

9.5% 345 393 450 517 594

10.0% 307 348 397 453 519

10.5% 276 312 354 402 459

11.0% 250 282 318 360 409

Source: Company, IIFL Research

Assuming 78% FCF to net profit, 11% EPS growth

FY19-39, 5% terminal and 10% WACC, we get a 12

month fair value of Rs.397

29

ITC – BUY

percy.panthaki@iif lcap.com

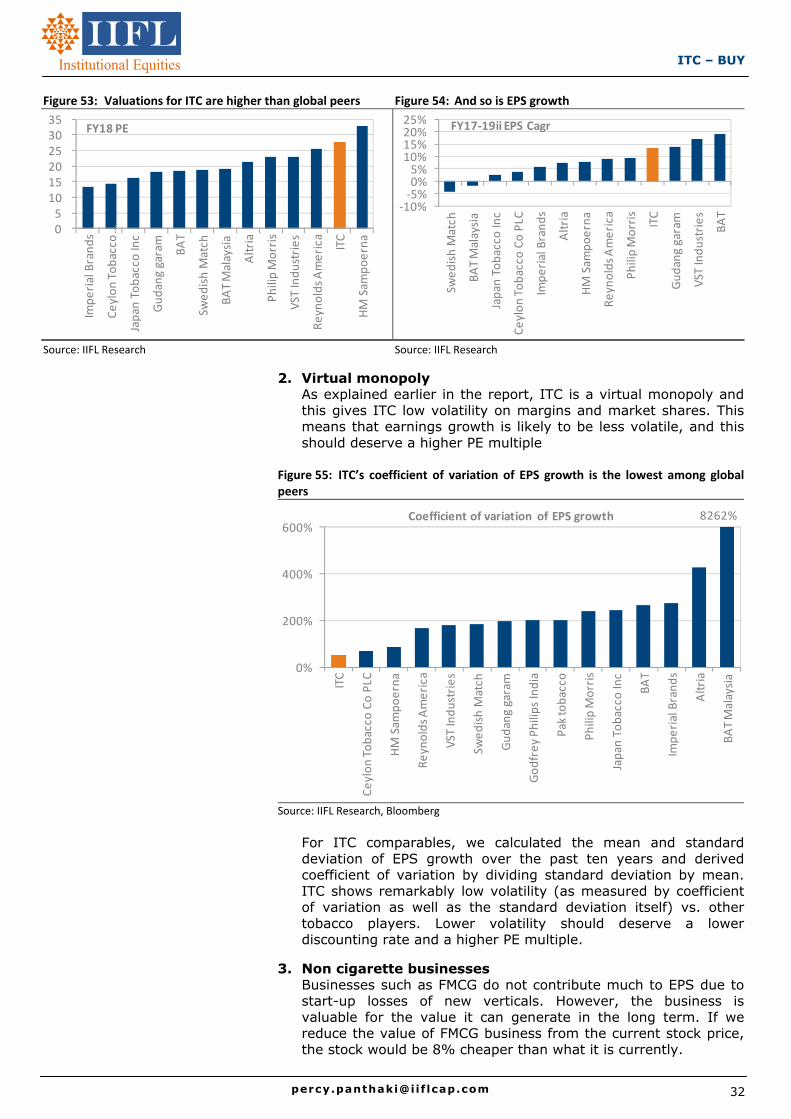

Institutional Equities