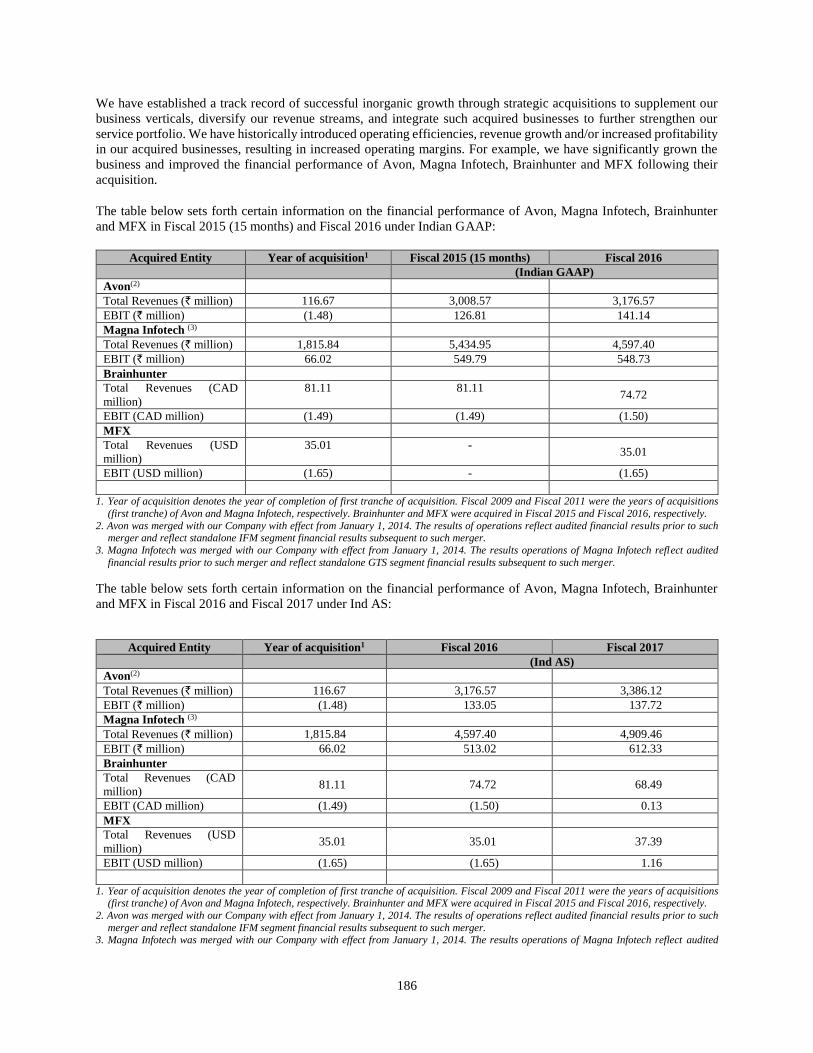

QUESS CORP LIMITED - IIFL Capital

561

Red Herring Prospectus Dated: August 8, 2017 QUESS CORP LIMITED Registered & Corporate Office: 3/3/2, Bellandur Gate, Sarjapur Main Road, Bengaluru 560 103, Karnataka, India Tel: +91 80 6105 6000; Fax: +91 80 6105 6406 Contact Person: Sudershan Pallap, Company Secretary and Compliance Officer Email: [email protected]; Website: www.quesscorp.com (Incorporated on September 19, 2007 in the Republic of India with limited liability with Corporate Identity Number (L74140KA2007PLC043909) under the Companies Act, 1956) Issue of up to [●] equity shares of face value `10 each (the “Equity Shares”) of Quess Corp Limited (the “Company”) at a price of `[●] per Equity Share (the “Issue Price”), aggregating up to `11,500 million (the “Issue”). THIS ISSUE AND THE DISTRIBUTION OF THIS RED HERRING PROSPECTUS (THE “RED HERRING PROSPECTUS”) IS BEING MADE IN RELIANCE ON CHAPTER VIII-A OF THE SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE OF CAPITAL AND DISCLOSURE REQUIREMENTS) REGULATIONS, 2009, AS AMENDED (THE “SEBI REGULATIONS”). THIS RED HERRING PROSPECTUS DOES NOT CONSTITUTE AN OFFER OR INVITATION OR SOLICITATION OF AN OFFER TO ANY PERSON OR CLASS OF INVESTORS OTHER THAN QUALIFIED INSTITUTIONAL BUYERS (“QIBS”) WITHIN OR OUTSIDE INDIA. ISSUE ONLY TO QUALIFIED INSTITUTIONAL BUYERS The Issue is being made through the Institutional Placement Programme, wherein at least 25% of the aggregate number of Equity Shares to be Allotted in the Issue shall be Allocated and Allotted to Mutual Funds (as defined hereinafter) and Insurance Companies (as defined hereinafter), subject to valid ASBA Applications (as defined hereinafter) being received at or above the Issue Price, provided that if this portion or any part thereof to be Allotted to Mutual Funds and Insurance Companies remains unsubscribed, such minimum portion or part thereof may be Allotted to other QIBs. QIBs may participate in this Issue only through an application supported by blocked amount (“ASBA”) providing details about the ASBA Account (as defined hereinafter) which will be blocked by the Self Certified Syndicate Bank. For details, see “Issue Procedure” on page 213. This Red Herring Prospectus has not been reviewed or approved by the Securities and Exchange Board of India (the “SEBI”), the Reserve Bank of India (“RBI”), The National Stock Exchange of India Limited (the “NSE”), the BSE Limited (the “BSE”, together with the NSE the “Stock Exchanges”) and is intended only for use by QIBs. A copy of this Red Herring Prospectus has been delivered to the Stock Exchanges and SEBI and registered with the Registrar of Companies, Bangalore (the “RoC”). Copies of the Prospectus will be filed with the Stock Exchanges, SEBI and the RoC. This Red Herring Prospectus will only be circulated or distributed to QIBs, and will not constitute an offer to any other class of investors in India or any other jurisdiction. The Equity Shares offered in the Issue have not been recommended or approved by SEBI, nor does SEBI guarantee the accuracy or adequacy of this Red Herring Prospectus. The Equity Shares of the Company are listed and traded on the BSE and the NSE. The Equity Shares offered in the Issue are securities of the Company of the same class and in all respects uniform as the Equity Shares listed and traded on the Stock Exchanges. In-principle approvals under Regulation 28 of the SEBI Listing Regulations for listing of the Equity Shares offered in the Issue have been received from the BSE and NSE on August 7, 2017. Applications will be made to the Stock Exchanges for obtaining listing and trading approvals for the Equity Shares offered through this Red Herring Prospectus. The Stock Exchanges assume no responsibility for the correctness of any statements made, opinions expressed or reports contained herein. Admission of the Equity Shares offered in the Issue to trading on the Stock Exchanges should not be taken as an indication of the merits of the business of the Company or such Equity Shares. INVESTMENTS IN EQUITY SHARES INVOLVE A DEGREE OF RISK AND PROSPECTIVE INVESTORS SHOULD NOT INVEST IN THIS ISSUE UNLESS THEY ARE PREPARED TO TAKE THE RISK OF LOSING ALL OR PART OF THEIR INVESTMENT. PROSPECTIVE INVESTORS ARE ADVISED TO CAREFULLY READ “RISK FACTORS” ON PAGE 41 BEFORE MAKING AN INVESTMENT DECISION IN THIS ISSUE. EACH PROSPECTIVE INVESTOR IS ADVISED TO CONSULT ITS OWN ADVISORS ABOUT THE PARTICULAR CONSEQUENCES OF AN INVESTMENT IN THE EQUITY SHARES BEING ISSUED PURSUANT TO THIS RED HERRING PROSPECTUS. Invitations, offers and issuances of Equity Shares offered in the Issue shall only be made pursuant to this Red Herring Prospectus together with the ASBA Applications and Confirmation of Allocation Notes. Please see “Issue Procedure” on page 213. The distribution of this Red Herring Prospectus or the disclosure of its contents without the prior consent of the Company to any person, other than QIBs and persons retained by QIBs to advise them with respect to their subscription of the Equity Shares offered in the Issue is unauthorised and prohibited. Each prospective investor, by accepting delivery of this Red Herring Prospectus, agrees to observe the foregoing restrictions and make no copies of this Red Herring Prospectus or any documents referred to in this Red Herring Prospectus. The information on the website of the Company or any website directly or indirectly linked to the website of the Company, other than this Red Herring Prospectus does not form part of this Red Herring Prospectus and prospective investors should not rely on such information contained in, or available through, any such website. The Equity Shares are being issued under the institutional placement programme and that the offer is being made only to the QIBs. The Equity Shares have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the “U.S. Securities Act”) or any other applicable state securities laws of the United States and, unless so registered, may not be offered or sold within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and applicable state securities laws. The Equity Shares are being offered and sold (a) in the United States only to persons who are reasonably believed to be qualified institutional buyers (as defined in Rule 144A under the U.S. Securities Act (“Rule 144A”)) (“U.S. QIB”) pursuant to Section 4(a)(2) or another available exemption from registration under the U.S. Securities Act; for avoidance of doubt, the term U.S. QIBs does not refer to a category of institutional investors defined under applicable Indian regulations and referred to in this Red Herring Prospectus as “QIBs” and (b) outside the United States in offshore transactions in reliance on Regulation S under the U.S. Securities Act (“Regulation S”) and the applicable laws of the jurisdiction where those offers and sales are made. For further information, see section titled “Selling Restrictions” on page 233 and “Purchaser Representations and Transfer Restrictions” on page 242. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE Axis Capital Limited 1st Floor, Axis House C-2, Wadia International Centre Pandurang Budhkar Marg, Worli Mumbai 400 025 Tel: +91 22 4325 2183 Fax: +91 22 4325 3000 Email: [email protected] Website: www.axiscapital.co.in Contact Person: Lohit Sharma SEBI Registration Number: INM000012029 ICICI Securities Limited ICICI Centre H.T. Parekh Marg Churchgate Mumbai 400 020 Maharashtra, India Tel: +91 22 2288 2460 Fax: +91 22 2282 6580 E-mail: [email protected] Website: www.icicisecurities.com Contact Person: Anurag Byas SEBI Registration Number: INM00001179 IIFL Holdings Limited # 10 th Floor, IIFL Centre Kamala City Senapati Bapat Marg Lower Parel (West) Mumbai 400 013 Maharashtra, India Tel: +91 22 4646 4600 Fax: +91 22 2493 1073 E-mail: [email protected] Website: www.iiflcap.com Contact Person: Sachin Kapoor and Kunur Bavishi SEBI Registration Number: INM000010940 Link Intime India Private Limited C-101,1st Floor, 247Park, L.B.S. Marg Vikhroli (West) Mumbai 400 083 Maharashtra, India Tel: +91 22 4918 6200 Fax: +91 22 4918 6195 Email: [email protected] Website: www.linkintime.co.in Contact Person: Shanti Gopalkrishnan SEBI Registration Number: INR000004058 ISSUE PROGRAMME* BID/ISSUE OPENS ON: [●]* BID/ISSUE CLOSES ON: [●]* * Details of the Issue programme shall be disclosed in the Floor Price / Price Band Announcement to be issued at least one day prior to the Issue Opening Date. Investors should refer to the pre- Issue advertisement and the Floor Price / Price Band Announcement for further details. Investors are advised to read the above mentioned announcements together with this Red Herring Prospectus # Chandran Ratnaswami is a director on the board of our Company and IIFL Holdings Limited, Further, Fairfax Financial Holdings Limited indirectly holds equity shares of IIFL Holdings Limited and our Company. Hence, in compliance with the proviso to Regulation 21A(1) of the SEBI Merchant Bankers Regulations, read with the proviso to Regulation 5(3) of the SEBI Regulations, IIFL Holdings Limited will be involved only in marketing of the Issue The information in this Red Herring Prospectus is not complete and may be changed. The Issue is meant only for QIBs and is not an offer to any other class of investors to purchase or subscribe for the Equity Shares. This Red Herring Prospectus is not soliciting an offer to subscribe to or buy Equity Shares in any jurisdiction where such offer or subscription is not permitted. It is being issued for the sole purpose of information or discussion relating to the Equity Shares that may be Allotted through the Prospectus.

-

Upload

khangminh22 -

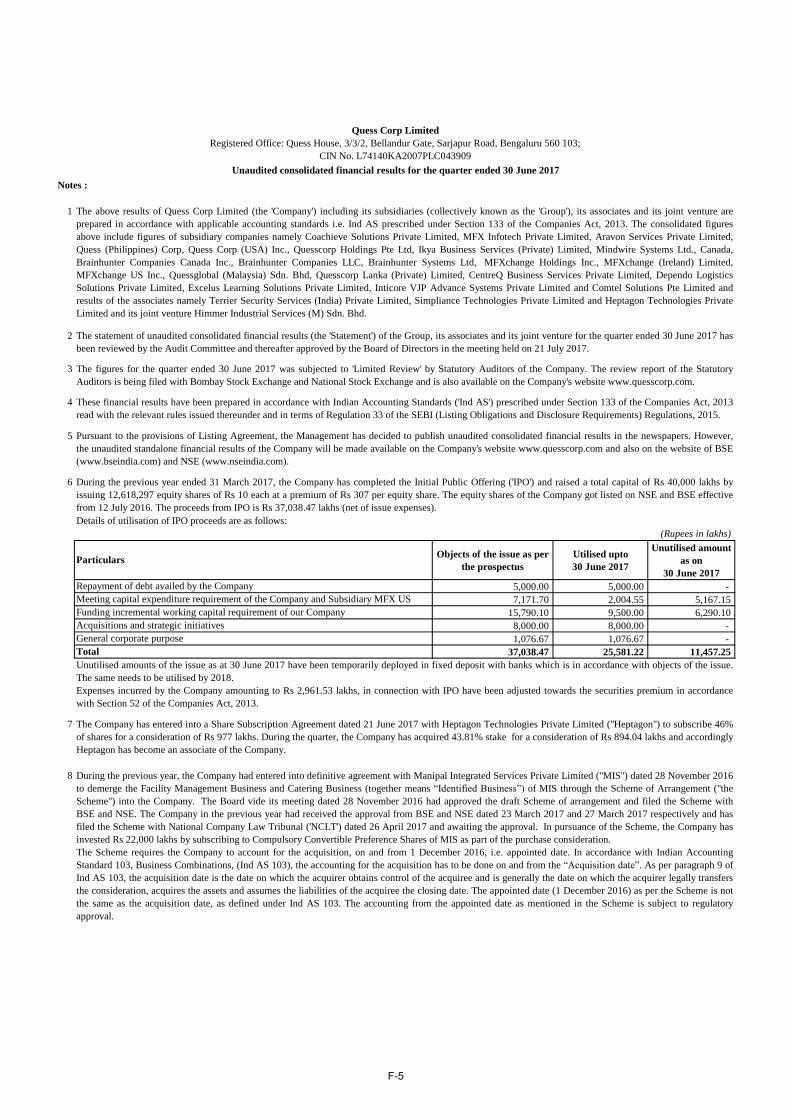

Category

Documents

-

view

0 -

download

0

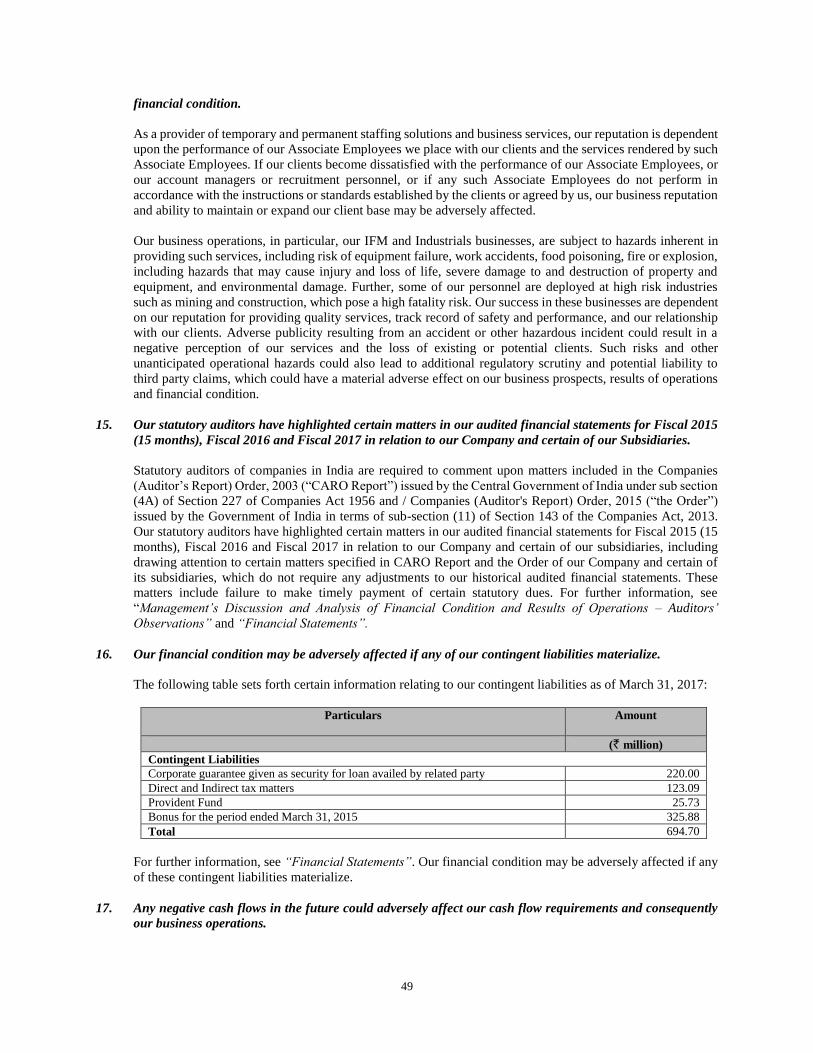

Transcript of QUESS CORP LIMITED - IIFL Capital

Red Herring Prospectus

Dated: August 8, 2017

QUESS CORP LIMITED

Registered & Corporate Office: 3/3/2, Bellandur Gate, Sarjapur Main Road, Bengaluru 560 103, Karnataka, India

Tel: +91 80 6105 6000; Fax: +91 80 6105 6406

Contact Person: Sudershan Pallap, Company Secretary and Compliance Officer

Email: [email protected]; Website: www.quesscorp.com

(Incorporated on September 19, 2007 in the Republic of India with limited liability with Corporate Identity Number (L74140KA2007PLC043909)

under the Companies Act, 1956)

Issue of up to [●] equity shares of face value `10 each (the “Equity Shares”) of Quess Corp Limited (the “Company”) at a price of `[●] per Equity Share (the “Issue Price”), aggregating up to `11,500 million

(the “Issue”).

THIS ISSUE AND THE DISTRIBUTION OF THIS RED HERRING PROSPECTUS (THE “RED HERRING PROSPECTUS”) IS BEING MADE IN RELIANCE ON CHAPTER VIII-A OF THE

SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE OF CAPITAL AND DISCLOSURE REQUIREMENTS) REGULATIONS, 2009, AS AMENDED (THE “SEBI REGULATIONS”). THIS

RED HERRING PROSPECTUS DOES NOT CONSTITUTE AN OFFER OR INVITATION OR SOLICITATION OF AN OFFER TO ANY PERSON OR CLASS OF INVESTORS OTHER THAN

QUALIFIED INSTITUTIONAL BUYERS (“QIBS”) WITHIN OR OUTSIDE INDIA.

ISSUE ONLY TO QUALIFIED INSTITUTIONAL BUYERS

The Issue is being made through the Institutional Placement Programme, wherein at least 25% of the aggregate number of Equity Shares to be Allotted in the Issue shall be Allocated and Allotted to Mutual Funds

(as defined hereinafter) and Insurance Companies (as defined hereinafter), subject to valid ASBA Applications (as defined hereinafter) being received at or above the Issue Price, provided that if this portion or any

part thereof to be Allotted to Mutual Funds and Insurance Companies remains unsubscribed, such minimum portion or part thereof may be Allotted to other QIBs. QIBs may participate in this Issue only through

an application supported by blocked amount (“ASBA”) providing details about the ASBA Account (as defined hereinafter) which will be blocked by the Self Certified Syndicate Bank. For details, see “Issue

Procedure” on page 213.

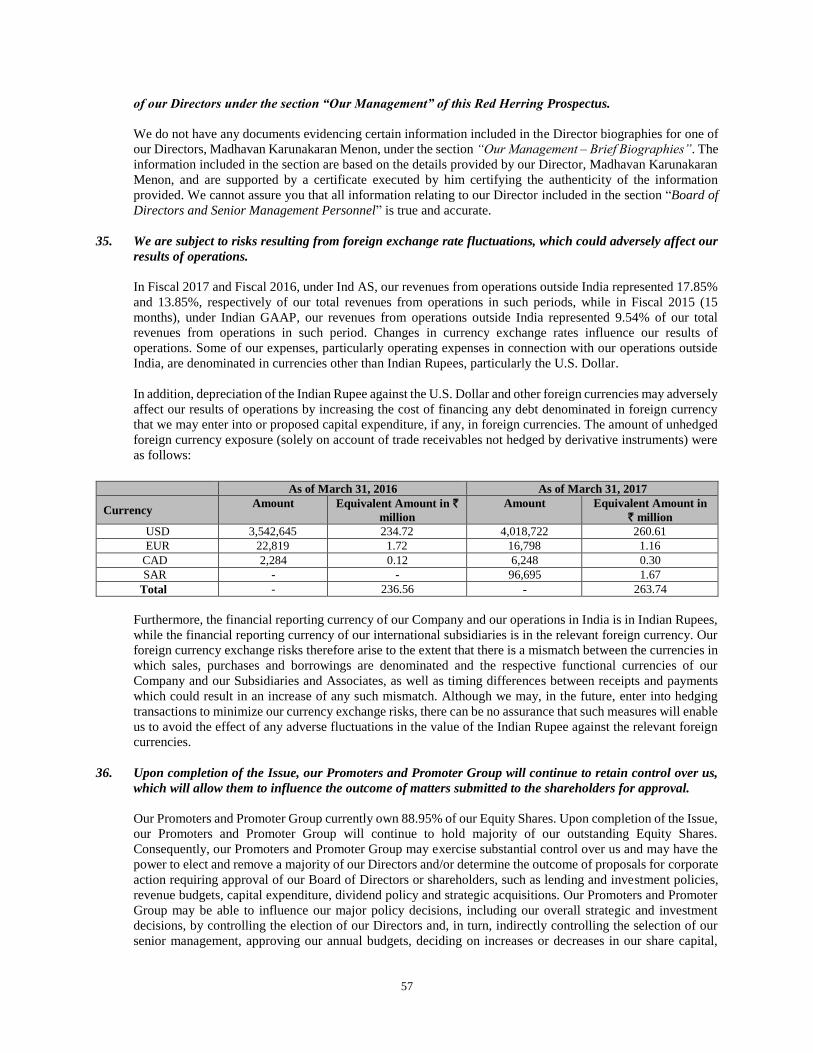

This Red Herring Prospectus has not been reviewed or approved by the Securities and Exchange Board of India (the “SEBI”), the Reserve Bank of India (“RBI”), The National Stock Exchange of India Limited

(the “NSE”), the BSE Limited (the “BSE”, together with the NSE the “Stock Exchanges”) and is intended only for use by QIBs. A copy of this Red Herring Prospectus has been delivered to the Stock Exchanges

and SEBI and registered with the Registrar of Companies, Bangalore (the “RoC”). Copies of the Prospectus will be filed with the Stock Exchanges, SEBI and the RoC. This Red Herring Prospectus will only be

circulated or distributed to QIBs, and will not constitute an offer to any other class of investors in India or any other jurisdiction. The Equity Shares offered in the Issue have not been recommended or approved by

SEBI, nor does SEBI guarantee the accuracy or adequacy of this Red Herring Prospectus.

The Equity Shares of the Company are listed and traded on the BSE and the NSE. The Equity Shares offered in the Issue are securities of the Company of the same class and in all respects uniform as the Equity

Shares listed and traded on the Stock Exchanges. In-principle approvals under Regulation 28 of the SEBI Listing Regulations for listing of the Equity Shares offered in the Issue have been received from the BSE

and NSE on August 7, 2017. Applications will be made to the Stock Exchanges for obtaining listing and trading approvals for the Equity Shares offered through this Red Herring Prospectus. The Stock Exchanges

assume no responsibility for the correctness of any statements made, opinions expressed or reports contained herein. Admission of the Equity Shares offered in the Issue to trading on the Stock Exchanges should

not be taken as an indication of the merits of the business of the Company or such Equity Shares.

INVESTMENTS IN EQUITY SHARES INVOLVE A DEGREE OF RISK AND PROSPECTIVE INVESTORS SHOULD NOT INVEST IN THIS ISSUE UNLESS THEY ARE PREPARED TO TAKE

THE RISK OF LOSING ALL OR PART OF THEIR INVESTMENT. PROSPECTIVE INVESTORS ARE ADVISED TO CAREFULLY READ “RISK FACTORS” ON PAGE 41 BEFORE MAKING

AN INVESTMENT DECISION IN THIS ISSUE. EACH PROSPECTIVE INVESTOR IS ADVISED TO CONSULT ITS OWN ADVISORS ABOUT THE PARTICULAR CONSEQUENCES OF AN

INVESTMENT IN THE EQUITY SHARES BEING ISSUED PURSUANT TO THIS RED HERRING PROSPECTUS.

Invitations, offers and issuances of Equity Shares offered in the Issue shall only be made pursuant to this Red Herring Prospectus together with the ASBA Applications and Confirmation of Allocation Notes. Please

see “Issue Procedure” on page 213. The distribution of this Red Herring Prospectus or the disclosure of its contents without the prior consent of the Company to any person, other than QIBs and persons retained

by QIBs to advise them with respect to their subscription of the Equity Shares offered in the Issue is unauthorised and prohibited. Each prospective investor, by accepting delivery of this Red Herring Prospectus,

agrees to observe the foregoing restrictions and make no copies of this Red Herring Prospectus or any documents referred to in this Red Herring Prospectus.

The information on the website of the Company or any website directly or indirectly linked to the website of the Company, other than this Red Herring Prospectus does not form part of this Red Herring Prospectus

and prospective investors should not rely on such information contained in, or available through, any such website.

The Equity Shares are being issued under the institutional placement programme and that the offer is being made only to the QIBs.

The Equity Shares have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the “U.S. Securities Act”) or any other applicable state securities laws of the United States

and, unless so registered, may not be offered or sold within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities

Act and applicable state securities laws. The Equity Shares are being offered and sold (a) in the United States only to persons who are reasonably believed to be qualified institutional buyers (as defined

in Rule 144A under the U.S. Securities Act (“Rule 144A”)) (“U.S. QIB”) pursuant to Section 4(a)(2) or another available exemption from registration under the U.S. Securities Act; for avoidance of

doubt, the term U.S. QIBs does not refer to a category of institutional investors defined under applicable Indian regulations and referred to in this Red Herring Prospectus as “QIBs” and (b) outside

the United States in offshore transactions in reliance on Regulation S under the U.S. Securities Act (“Regulation S”) and the applicable laws of the jurisdiction where those offers and sales are made.

For further information, see section titled “Selling Restrictions” on page 233 and “Purchaser Representations and Transfer Restrictions” on page 242.

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

Axis Capital Limited

1st Floor, Axis House

C-2, Wadia International Centre

Pandurang Budhkar Marg, Worli

Mumbai 400 025

Tel: +91 22 4325 2183

Fax: +91 22 4325 3000

Email: [email protected]

Website: www.axiscapital.co.in

Contact Person: Lohit Sharma

SEBI Registration Number:

INM000012029

ICICI Securities Limited

ICICI Centre

H.T. Parekh Marg

Churchgate

Mumbai 400 020

Maharashtra, India

Tel: +91 22 2288 2460

Fax: +91 22 2282 6580

E-mail: [email protected]

Website: www.icicisecurities.com

Contact Person: Anurag Byas

SEBI Registration Number: INM00001179

IIFL Holdings Limited#

10th Floor, IIFL Centre

Kamala City

Senapati Bapat Marg

Lower Parel (West)

Mumbai 400 013

Maharashtra, India

Tel: +91 22 4646 4600

Fax: +91 22 2493 1073

E-mail: [email protected]

Website: www.iiflcap.com

Contact Person: Sachin Kapoor and Kunur Bavishi

SEBI Registration Number: INM000010940

Link Intime India Private Limited

C-101,1st Floor,

247Park, L.B.S. Marg

Vikhroli (West)

Mumbai 400 083

Maharashtra, India

Tel: +91 22 4918 6200

Fax: +91 22 4918 6195

Email: [email protected]

Website: www.linkintime.co.in

Contact Person: Shanti Gopalkrishnan

SEBI Registration Number: INR000004058

ISSUE PROGRAMME*

BID/ISSUE OPENS ON: [●]* BID/ISSUE CLOSES ON: [●]*

* Details of the Issue programme shall be disclosed in the Floor Price / Price Band Announcement to be issued at least one day prior to the Issue Opening Date. Investors should refer to the pre-

Issue advertisement and the Floor Price / Price Band Announcement for further details. Investors are advised to read the above mentioned announcements together with this Red Herring

Prospectus # Chandran Ratnaswami is a director on the board of our Company and IIFL Holdings Limited, Further, Fairfax Financial Holdings Limited indirectly holds equity shares of IIFL Holdings

Limited and our Company. Hence, in compliance with the proviso to Regulation 21A(1) of the SEBI Merchant Bankers Regulations, read with the proviso to Regulation 5(3) of the SEBI

Regulations, IIFL Holdings Limited will be involved only in marketing of the Issue

Th

e in

form

atio

n i

n t

his

Red

Her

ring P

rosp

ectu

s is

not

com

ple

te a

nd

may

be

chan

ged

. T

he

Issu

e is

mea

nt

on

ly f

or

QIB

s an

d i

s no

t an

off

er t

o a

ny

oth

er c

lass

of

inves

tors

to p

urc

has

e o

r su

bsc

ribe

for

the

Equit

y S

hare

s. T

his

Red

Her

rin

g P

rosp

ectu

s is

not

soli

citi

ng a

n o

ffer

to s

ubsc

ribe

to o

r bu

y E

qu

ity

Sh

ares

in

an

y j

uri

sdic

tio

n w

her

e su

ch o

ffer

or

sub

scri

pti

on

is

no

t p

erm

itte

d.

It i

s bei

ng i

ssued

for

the

sole

purp

ose

of

info

rmat

ion o

r dis

cuss

ion r

elat

ing t

o t

he

Eq

uit

y S

har

es t

hat

may

be

All

ott

ed t

hro

ugh

the

Pro

spec

tus.

TABLE OF CONTENTS

NOTICE TO INVESTORS ................................................................................................................................................. 1

REPRESENTATIONS BY INVESTORS .......................................................................................................................... 4

OFFSHORE DERIVATIVE INSTRUMENTS ................................................................................................................. 9

PRESENTATION OF FINANCIAL AND OTHER INFORMATION ......................................................................... 10

INDUSTRY AND MARKET DATA ................................................................................................................................ 12

FORWARD-LOOKING STATEMENTS ........................................................................................................................ 14

ENFORCEMENT OF CIVIL LIABILITIES .................................................................................................................. 15

EXCHANGE RATES ........................................................................................................................................................ 16

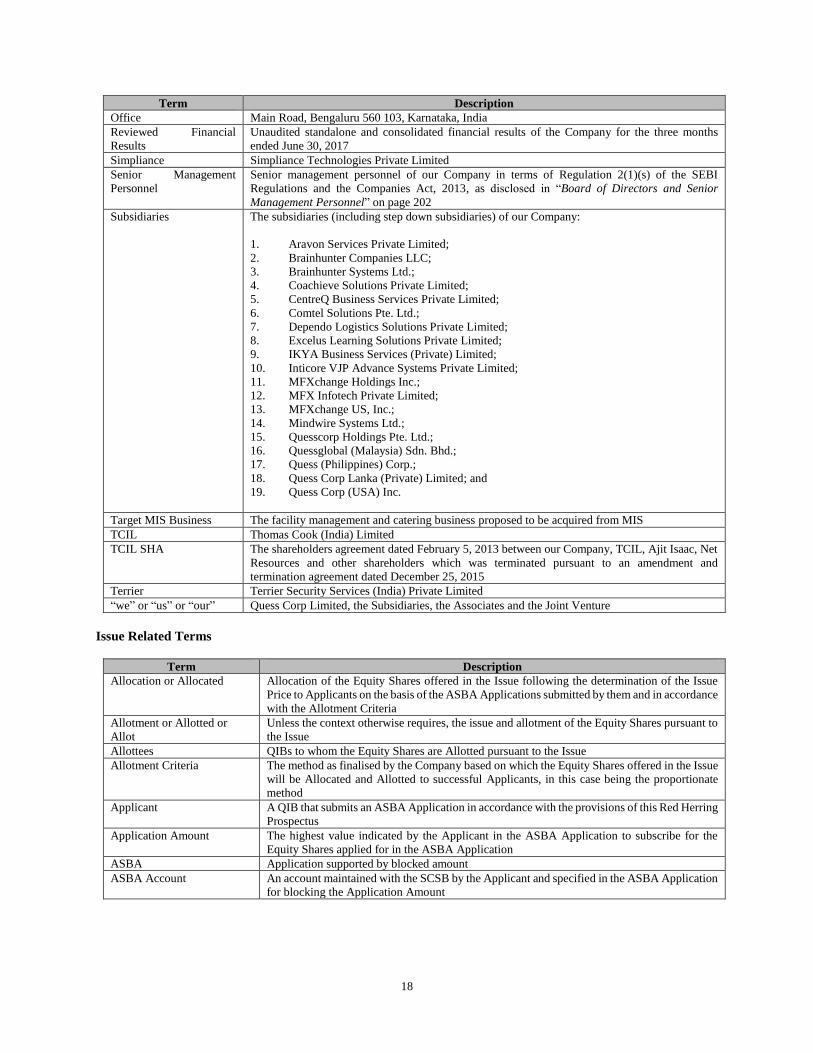

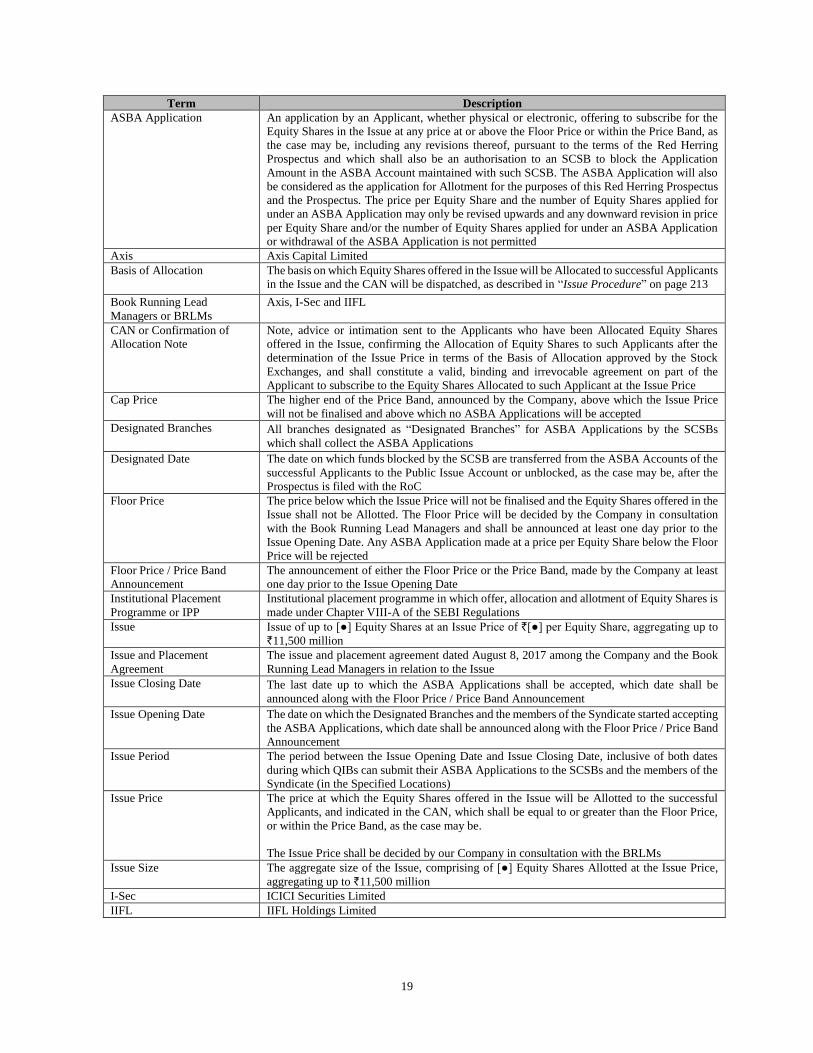

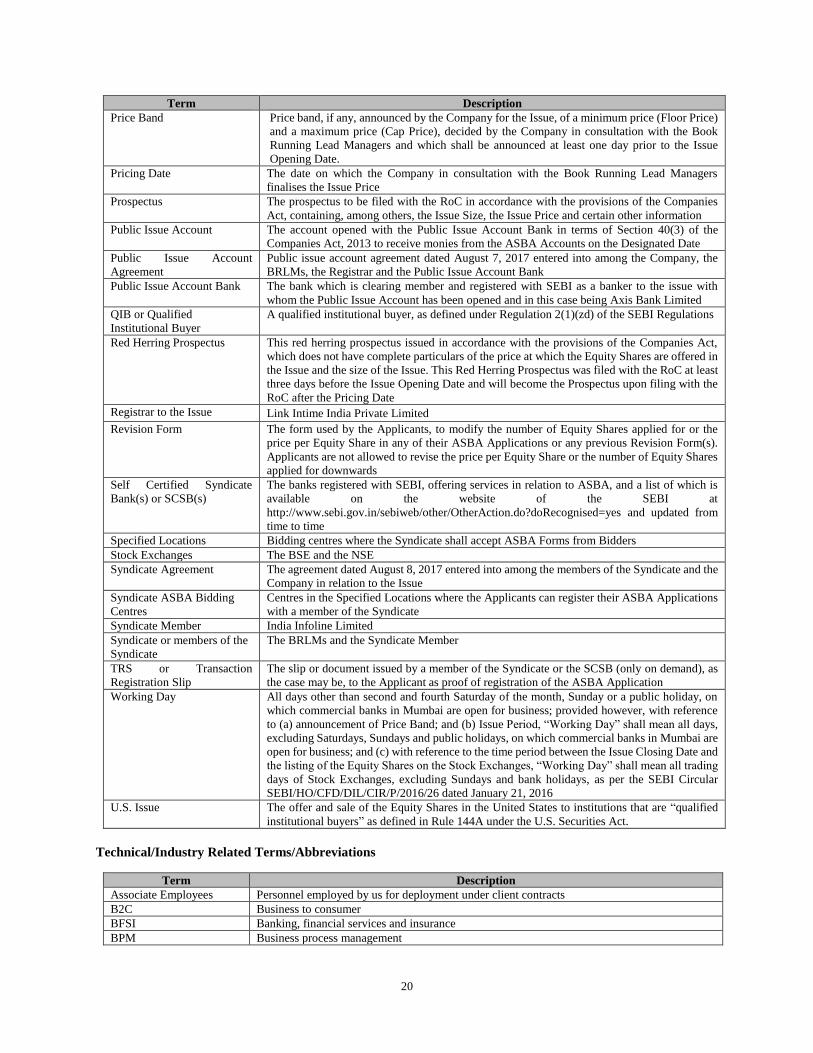

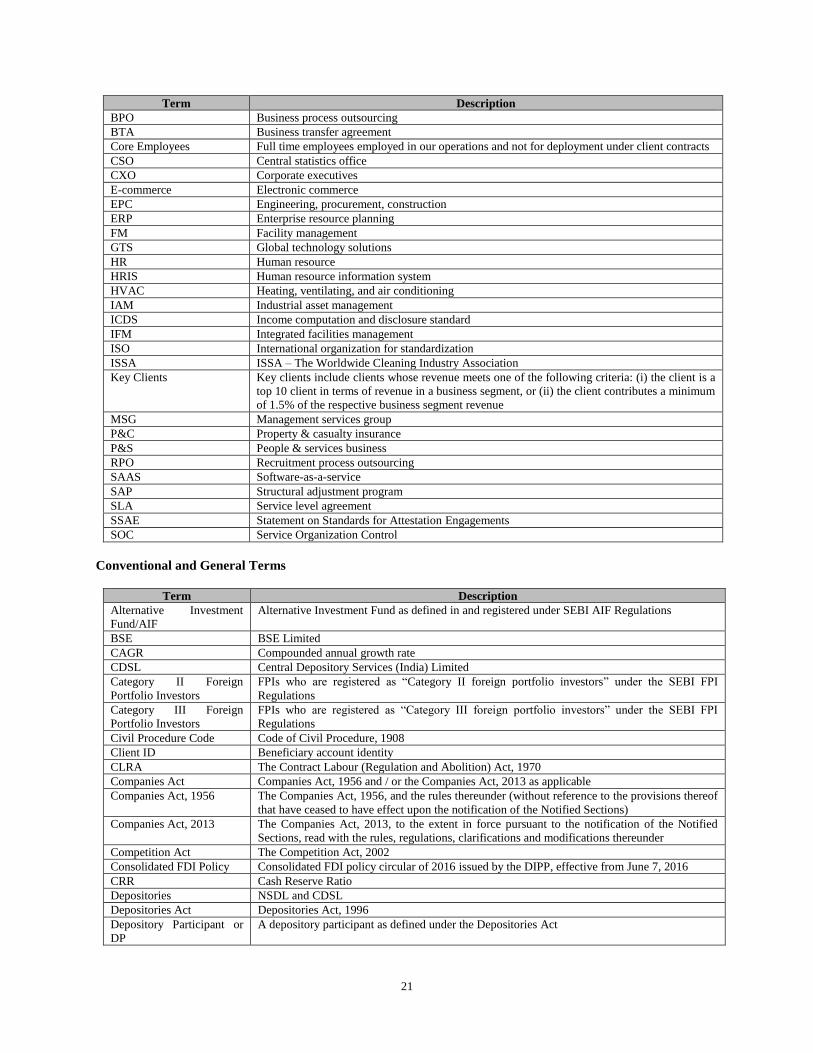

DEFINITIONS AND ABBREVIATIONS ........................................................................................................................ 17

SUMMARY OF THE ISSUE ............................................................................................................................................ 24

SELECTED FINANCIAL INFORMATION................................................................................................................... 26

RISK FACTORS ................................................................................................................................................................ 41

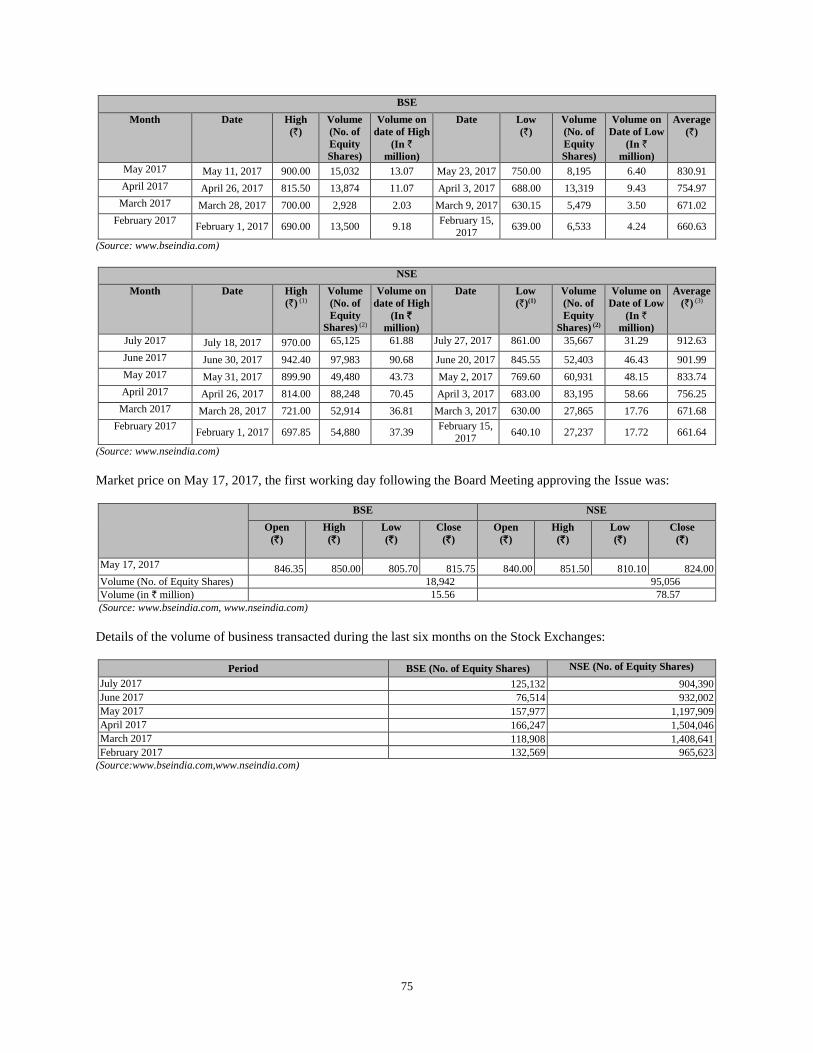

MARKET PRICE INFORMATION ................................................................................................................................ 74

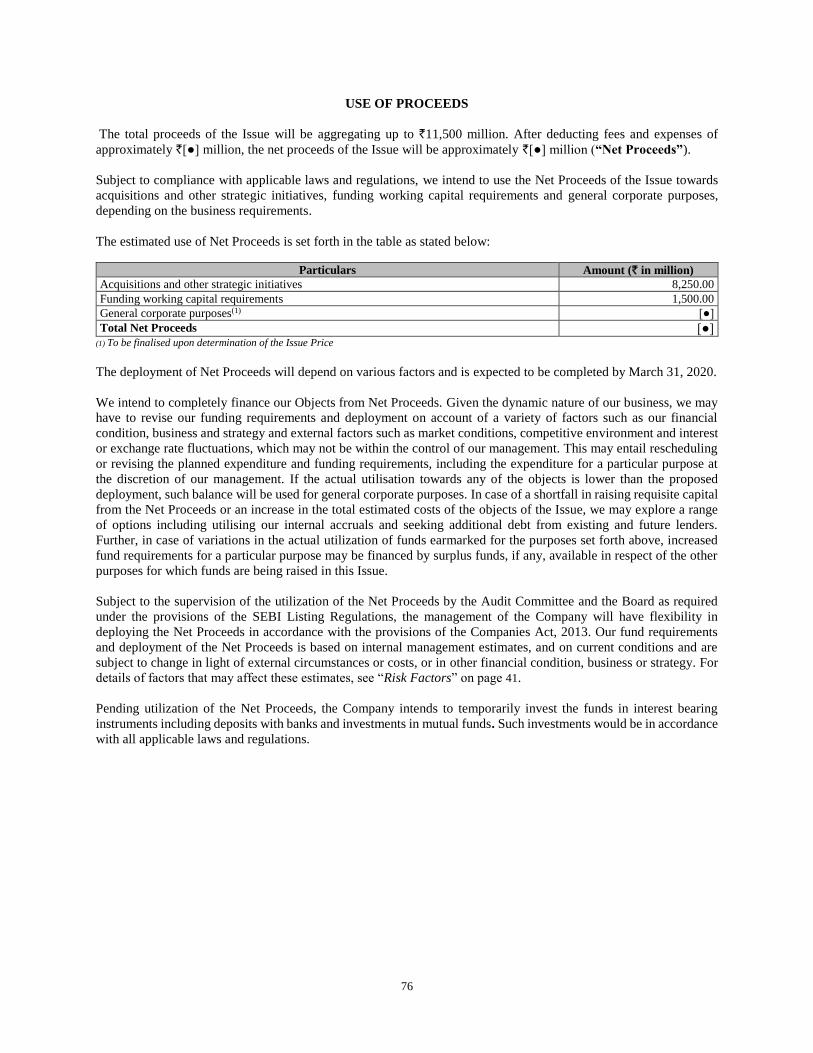

USE OF PROCEEDS ......................................................................................................................................................... 76

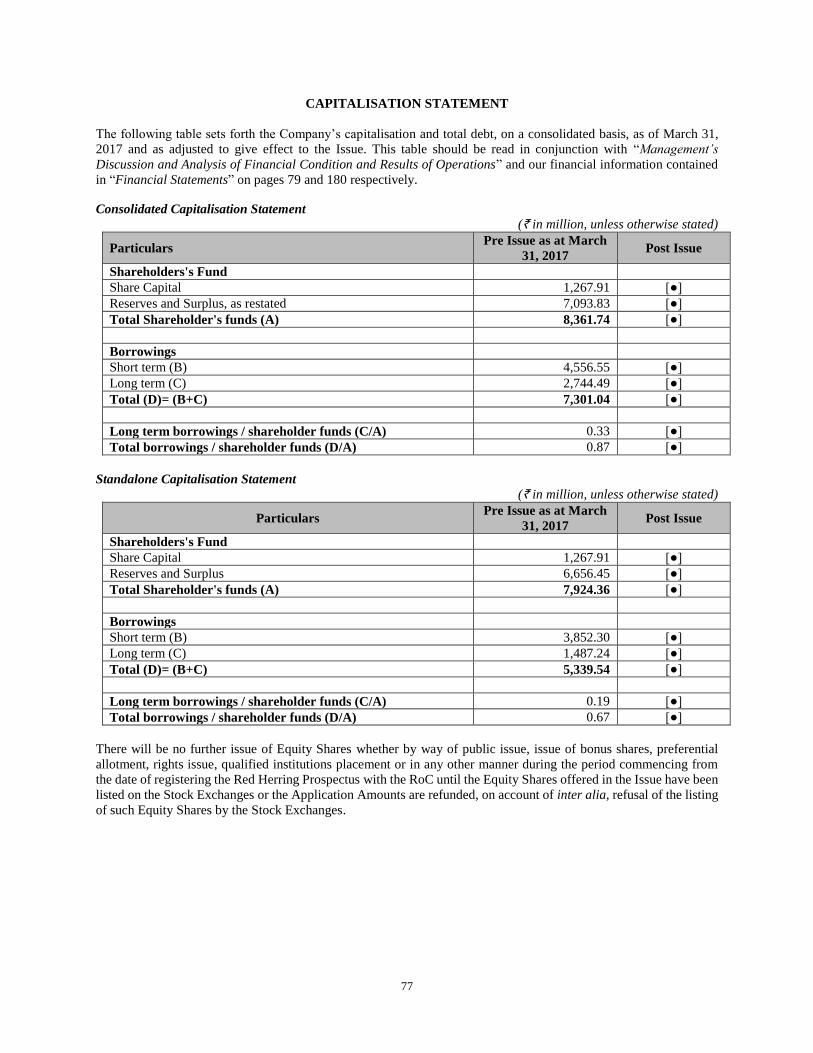

CAPITALISATION STATEMENT ................................................................................................................................. 77

DIVIDENDS ....................................................................................................................................................................... 78

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS ................................................................................................................................................................... 79

INDUSTRY OVERVIEW ............................................................................................................................................... 143

OUR BUSINESS ............................................................................................................................................................... 180

BOARD OF DIRECTORS AND SENIOR MANAGEMENT PERSONNEL ............................................................ 202

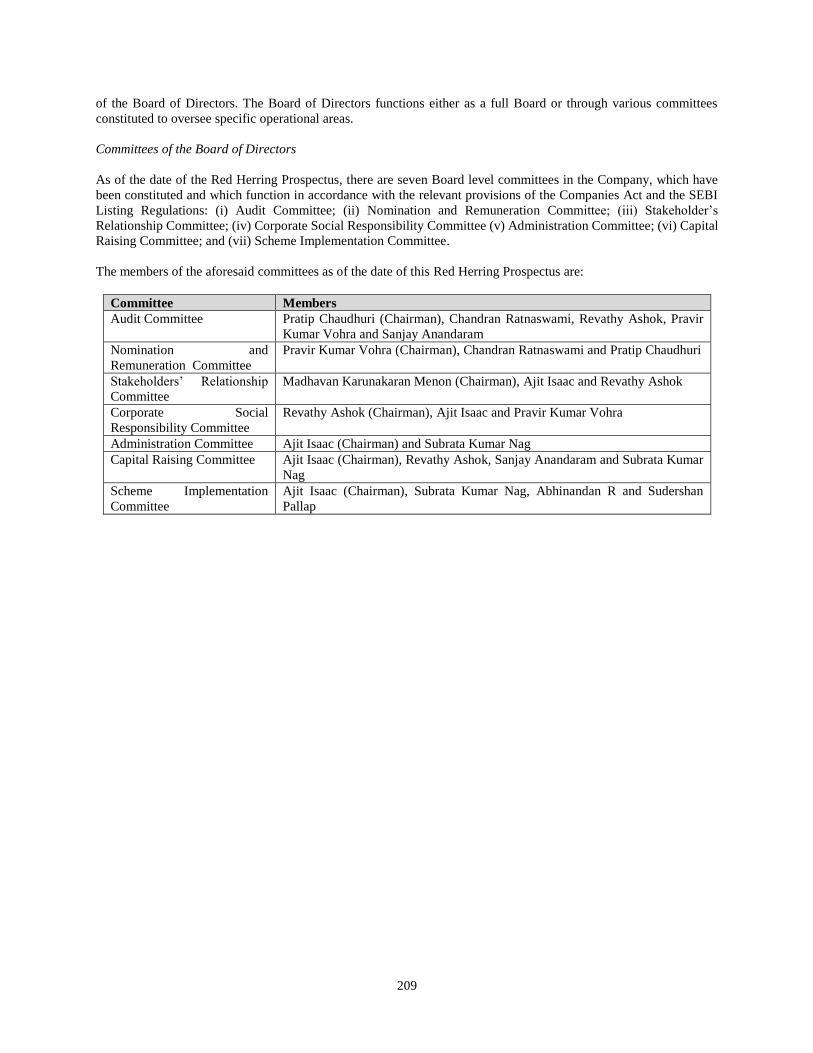

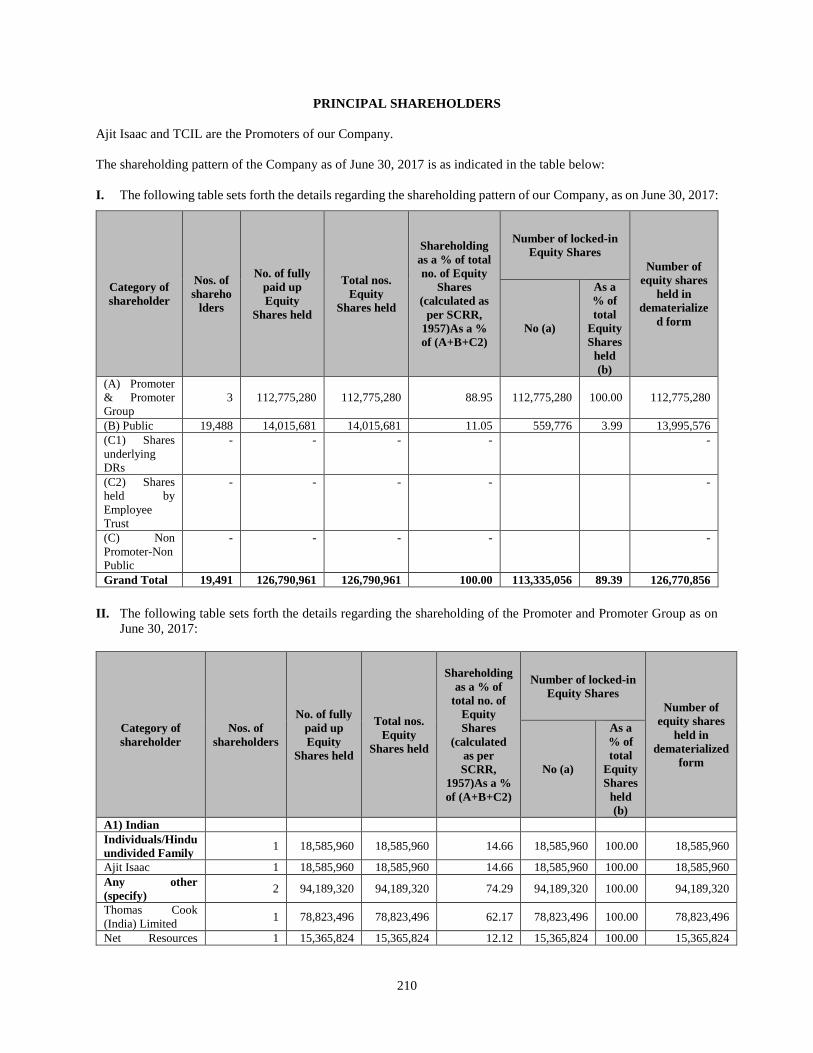

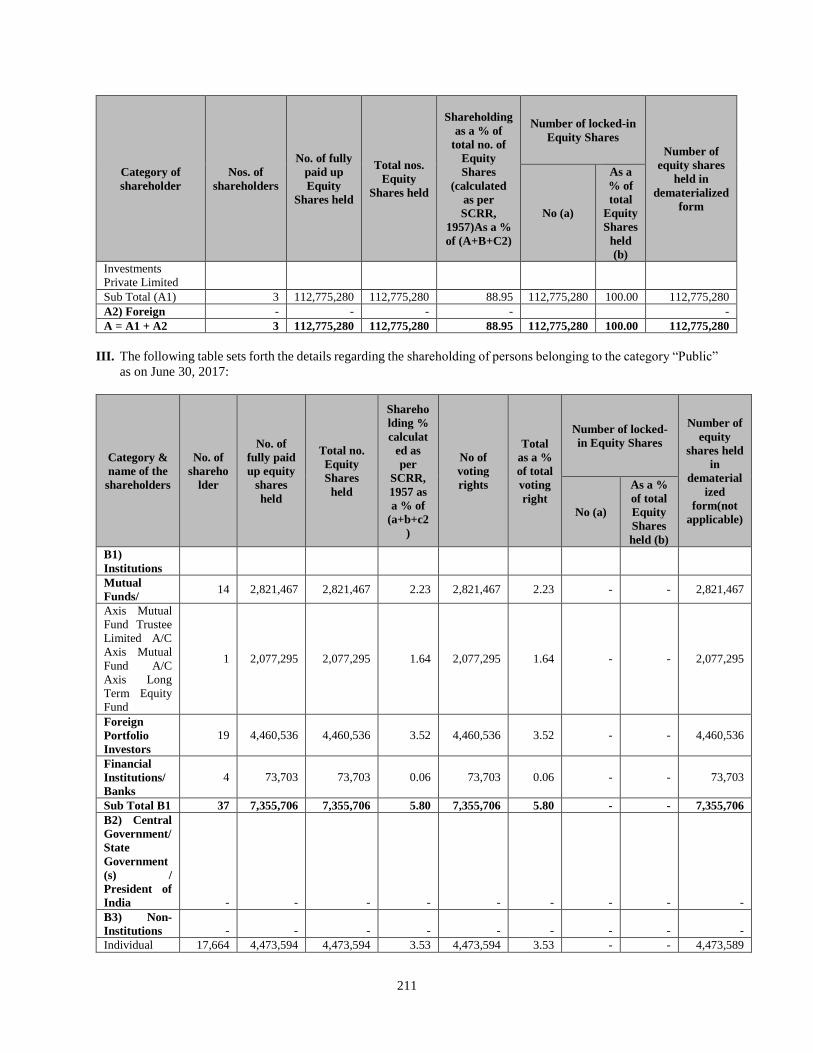

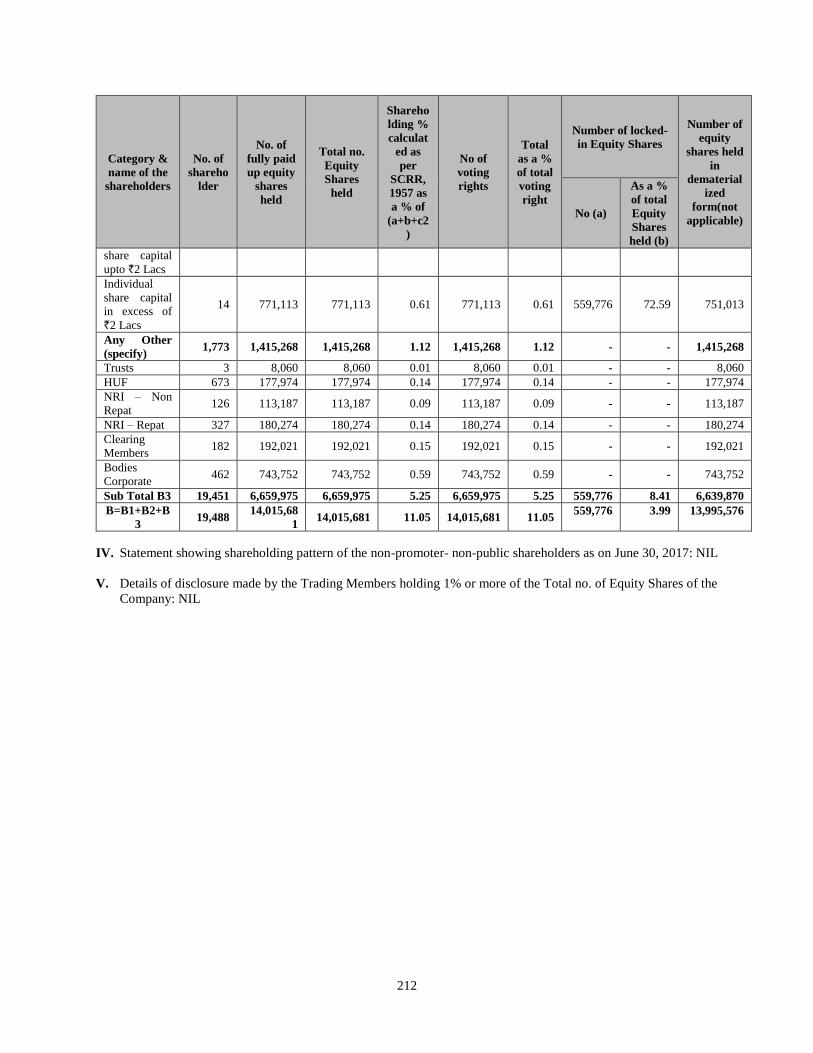

PRINCIPAL SHAREHOLDERS .................................................................................................................................... 210

ISSUE PROCEDURE ...................................................................................................................................................... 213

PLACEMENT .................................................................................................................................................................. 231

SELLING RESTRICTIONS ........................................................................................................................................... 233

PURCHASER REPRESENTATIONS AND TRANSFER RESTRICTIONS ............................................................ 242

THE SECURITIES MARKET OF INDIA .................................................................................................................... 245

DESCRIPTION OF THE EQUITY SHARES ............................................................................................................... 248

TAXATION ...................................................................................................................................................................... 251

LEGAL PROCEEDINGS ................................................................................................................................................ 254

INDEPENDENT ACCOUNTANTS ............................................................................................................................... 258

GENERAL INFORMATION ......................................................................................................................................... 259

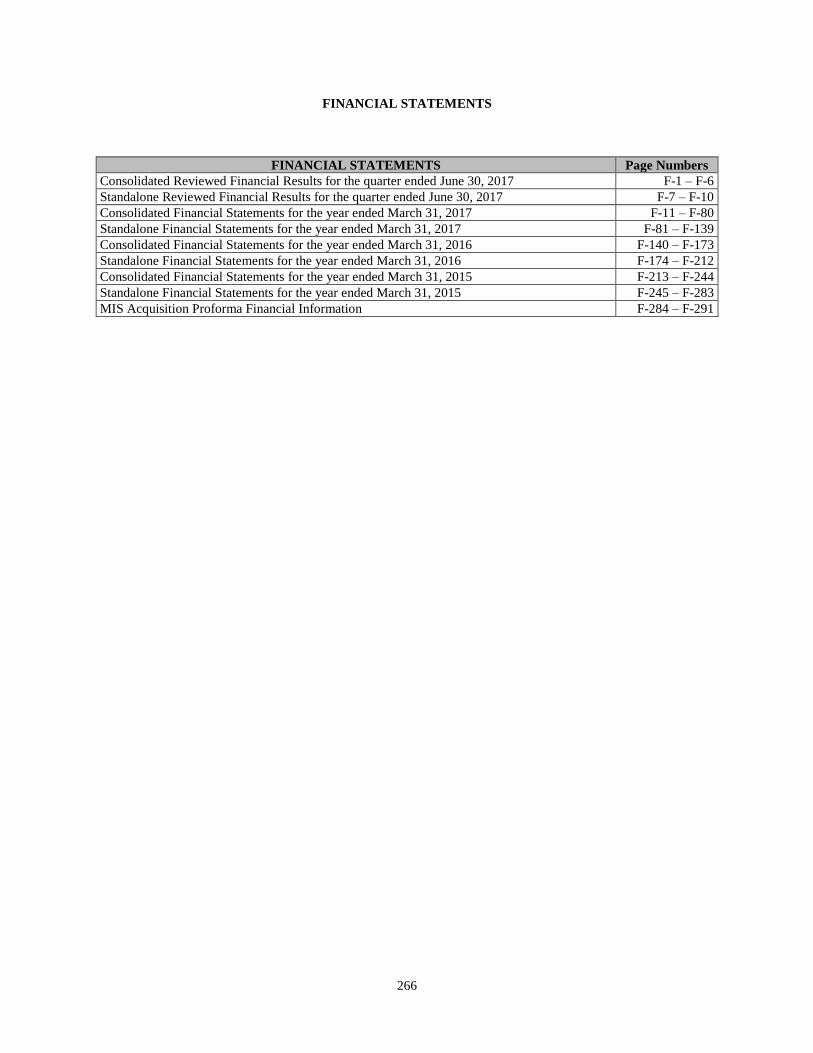

FINANCIAL STATEMENTS ......................................................................................................................................... 266

DECLARATION .............................................................................................................................................................. 267

1

NOTICE TO INVESTORS

The Company has furnished and accepts full responsibility for all of the information contained in this Red Herring

Prospectus and, having made all reasonable enquiries confirms that, this Red Herring Prospectus contains all

information with respect to the Company, the Subsidiaries, the Associates and the Joint Venture and the Equity Shares

offered in the Issue that is material in the context of the Issue. The statements contained in this Red Herring Prospectus

relating to the Company and the Equity Shares are, in every material respect, true and accurate and not misleading.

The opinions and intentions expressed in this Red Herring Prospectus with regard to the Company, the Subsidiaries,

the Associates and the Joint Venture and the Equity Shares are honestly held, have been reached after considering all

relevant circumstances, are based on information presently available to the Company and are based on reasonable

assumptions. There are no other facts in relation to the Company and the Equity Shares, the omission of which would,

in the context of the Issue, make any statement in this Red Herring Prospectus misleading in any material respect.

Further, all reasonable enquiries have been made by the Company to ascertain such facts and to verify the accuracy

of all such information and statements.

No person is authorised to give any information or to make any representation not contained in this Red Herring

Prospectus and any information or representation not so contained must not be relied upon as having been authorised

by or on behalf of the Company or Axis Capital Limited, ICICI Securities Limited and IIFL Holdings Limited (the

“Book Running Lead Managers”) or the Syndicate Member. The delivery of this Red Herring Prospectus at any

time does not imply that the information contained in it is correct as of any time subsequent to its date.

The Equity Shares issued pursuant to the Issue have not been approved, disapproved or recommended by any

regulatory authority in any jurisdiction, including the U.S. Securities and Exchange Commission, any other

federal or state securities authorities in the United States, the securities authorities of any non-U.S. jurisdiction

and any other U.S. or non-U.S. regulatory authority. No authority has passed on or endorsed the merits of this

Issue or the accuracy or adequacy of this Red Herring Prospectus. Any representation to the contrary is a

criminal offence in the United States and may be a criminal offence in other jurisdictions.

The Equity Shares have not been and will not be registered under the U.S. Securities Act or any other applicable state

securities laws of the United States and, unless so registered, may not be offered or sold within the United States

except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S.

Securities Act and applicable state securities laws. The Equity Shares are being offered and sold (a) in the United

States only to persons who are reasonably believed to be U.S. QIBs pursuant to Section 4(a)(2) or another available

exemption from registration under the U.S. Securities Act; for avoidance of doubt, the term U.S. QIBs does not refer

to a category of institutional investors defined under applicable Indian regulations and referred to in this Red Herring

Prospectus as “QIBs” and (b) outside the United States in offshore transactions in reliance on Regulation S under the

U.S. Securities Act (“Regulation S”) and the applicable laws of the jurisdiction where those offers and sales are made.

The distribution of this Red Herring Prospectus and the Issue may be restricted by law in certain countries or

jurisdictions. As such, this Red Herring Prospectus does not constitute, and may not be used for or in connection with,

an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorised, or to any

person to whom it is unlawful to make such offer or solicitation. In particular, no action has been taken by the Company

or the Book Running Lead Managers which would permit an offering of the Equity Shares offered in the Issue or

distribution of this Red Herring Prospectus in any country or jurisdiction, other than India, where action for that

purpose is required. Accordingly, the Equity Shares to be issued pursuant to the Issue may not be offered or sold,

directly or indirectly, and neither this Red Herring Prospectus nor any Issue materials in connection with the Equity

Shares offered in the Issue may be distributed or published in or from any country or jurisdiction except under

circumstances that will result in compliance with any applicable rules and regulations of any such country or

jurisdiction.

This Red Herring Prospectus has been filed with SEBI and the Stock Exchanges and delivered to the RoC for

registration, and has been displayed on the websites of the Stock Exchanges and the Company stating that it is in

connection with the Institutional Placement Programme and that the Issue is being made only to QIBs.

In making an investment decision, investors must rely on their own examination of the Company and the terms of the

Issue, including the merits and risks involved. Investors should not construe the contents of this Red Herring

2

Prospectus as legal, tax, accounting or investment advice. Investors should consult their own counsel and advisors as

to business, legal, tax, accounting and related matters concerning the Issue. In addition, none of the Company, the

Book Running Lead Managers or the Syndicate Member are making any representation to any offeree or subscriber

of the Equity Shares offered in the Issue regarding the legality of an investment in such Equity Shares by such

subscriber or purchaser under applicable laws or regulations.

Each QIB subscribing to the Equity Shares offered in the Issue is deemed to have acknowledged, represented

and agreed that it is eligible to invest in India and in the Company under Indian law, including Chapter VIII-

A of the SEBI Regulations, and is not prohibited by SEBI or any other statutory authority from buying,

subscribing to, selling or dealing in securities.

The information on the Company’s website, except this Red Herring Prospectus, or the website of the Book Running

Lead Managers does not constitute nor form part of this Red Herring Prospectus. Prospective investors should not rely

on the information contained in, or available through such websites, except this Red Herring Prospectus. This Red

Herring Prospectus contains summaries of terms of certain documents, which are qualified in their entirety by the

terms and conditions of such documents.

NOTICE TO INVESTORS IN THE UNITED STATES

The Equity Shares have not been recommended by any U.S. federal or state securities commission or regulatory

authority. Furthermore, the foregoing authorities have not confirmed the accuracy or determined the adequacy of this

Red Herring Prospectus. Any representation to the contrary is a criminal offence in the United States.

The Equity Shares have not been and will not be registered under the U.S. Securities Act or any other applicable state

securities laws of the United States and, unless so registered, may not be offered or sold within the United States

except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S.

Securities Act and applicable state securities laws. The Equity Shares are being offered and sold (a) in the United

States only to persons who are reasonably believed to be U.S. QIBs pursuant to Section 4(a)(2) or another available

exemption from registration under the U.S. Securities Act; for avoidance of doubt, the term U.S. QIBs does not refer

to a category of institutional investors defined under applicable Indian regulations and referred to in this Red Herring

Prospectus as “QIBs” and (b) outside the United States in offshore transactions in reliance on Regulation S under the

U.S. Securities Act (“Regulation S”) and the applicable laws of the jurisdiction where those offers and sales are made.

For further information, see section titled “Selling Restrictions” on page 233 and “Purchaser Representations and

Transfer Restrictions” on page 242. Purchasers in the U.S. Issue will be required to make the various representations

set forth in the ASBA Application, which are also included in this Red Herring Prospectus under the heading

“Purchaser Representations and Transfer Restrictions – U.S. Issue Purchaser Representations and Transfer

Restrictions” on page 242 of this Red Herring Prospectus.

Each purchaser of Equity Shares that is located within the United States will be required to represent and agree, among

other things, that such purchaser (i) is a U.S. QIB; and (ii) will only reoffer, resell, pledge or otherwise transfer the

Equity Shares in an “offshore transaction” in accordance with Rule 903 or Rule 904 of Regulation S or in a transaction

otherwise exempt from the registration requirements of the U.S. Securities Act. Each other purchaser of Equity Shares

will be required to represent and agree, among other things, that such purchaser is acquiring the Equity Shares issued

pursuant to the Issue in an “offshore transaction” in accordance with Regulation S.

This Red Herring Prospectus is being furnished on a confidential basis solely for the purpose of enabling a prospective

investor to consider subscribing for the particular securities described herein. The information contained in this Red

Herring Prospectus has been provided by the Company and other sources identified herein.

Distribution of this Red Herring Prospectus to any person other than the offeree specified by the Book Running Lead

Managers or their representatives, and those persons, if any, retained to advise such offeree with respect thereto, is

unauthorized, and any disclosure of its contents, without prior written consent of the Company, is prohibited.

Any reproduction or distribution of this Red Herring Prospectus in the United States, in whole or in part, and any

disclosure of its contents to any other person is prohibited.

3

CERTAIN UNITED STATES MATTERS

THE EQUITY SHARES OFFERED HEREBY HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER

THE U.S. SECURITIES ACT OR ANY OTHER APPLICABLE STATE SECURITIES LAWS OF THE UNITED

STATES AND, UNLESS SO REGISTERED, MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED

STATES EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO,

THE REGISTRATION REQUIREMENTS OF THE U.S. SECURITIES ACT AND APPLICABLE STATE

SECURITIES LAWS. ACCORDINGLY, THE EQUITY SHARES ARE BEING OFFERED AND SOLD (A) IN

THE UNITED STATES ONLY TO PERSONS WHO ARE QUALIFIED INSTITUTIONAL BUYERS (AS

DEFINED IN RULE 144A UNDER THE U.S. SECURITIES ACT AND REFERRED TO IN THIS RED HERRING

PROSPECTUS AS “U.S. QIBs”) (FOR THE AVOIDANCE OF DOUBT, THE TERM U.S. QIB DOES NOT REFER

TO A CATEGORY OF INSTITUTIONAL INVESTOR DEFINED UNDER APPLICABLE INDIAN

REGULATIONS AND REFERRED TO IN THIS RED HERRING PROSPECTUS AS QIBS OR QUALIFIED

INSTITUTIONAL BUYERS) PURSUANT TO SECTION 4(a)(2) UNDER THE U.S. SECURITIES ACT, AND (B)

OUTSIDE THE UNITED STATES IN OFFSHORE TRANSACTIONS IN RELIANCE ON REGULATION S

UNDER THE U.S. SECURITIES ACT AND THE APPLICABLE LAWS OF THE JURISDICTION WHERE

THOSE OFFERS AND SALES ARE MADE. FOR A DESCRIPTION OF CERTAIN RESTRICTIONS ON

TRANSFER OF THE EQUITY SHARES, SEE “PURCHASER REPRESENTATIONs AND TRANSFER

RESTRICTIONS”.

THE SECURITIES OFFERED HEREBY HAVE NOT BEEN REGISTERED WITH, OR APPROVED OR

DISAPPROVED BY, THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION (THE “SEC”) OR

ANY STATE SECURITIES COMMISSION IN THE UNITED STATES OR ANY OTHER UNITED STATES

REGULATORY AUTHORITY. FURTHERMORE, THE FOREGOING AUTHORITIES HAVE NOT PASSED

ON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THIS RED

HERRING PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE IN

THE UNITED STATES.

NOTICE TO INVESTORS IN CERTAIN OTHER JURISDICTIONS

For information to investors in certain other jurisdictions, see “Selling Restrictions” and “ Purchaser Representations

and Transfer Restrictions”.

4

REPRESENTATIONS BY INVESTORS

By subscribing to any Equity Shares offered in the Issue, you are deemed to have represented, warranted,

acknowledged and agreed to the Company, the Book Running Lead Managers and the Syndicate Member, as follows:

You are a QIB (hereinafter defined), having a valid and existing registration under applicable laws and

regulations of India, and undertake to acquire, hold, manage or dispose of any Equity Shares offered in the

Issue that are Allotted to you in accordance with Chapter VIII-A of the SEBI Regulations;

You are eligible to invest in India under applicable law, including the FEMA Regulations, and any

notifications, circulars or clarifications issued thereunder, and have not been prohibited by SEBI or any other

regulatory authority, from buying, selling or dealing in securities;

If you are not a resident of India, but are a QIB, you are a FPI, having a valid and existing registration with

SEBI under the applicable laws in India and are eligible to invest in India under applicable law, including the

FEMA Regulations, and any notifications, circulars or clarifications issued thereunder, and have not been

prohibited by SEBI or any other regulatory authority, from buying, selling or dealing in securities;

You will make all necessary filings with appropriate regulatory authorities, including RBI, as required

pursuant to applicable laws;

If you are Allotted the Equity Shares pursuant to the Issue, you shall not, for a period of one year from the

date of Allotment, sell such Equity Shares so acquired except on the Stock Exchanges;

You are aware that this Red Herring Prospectus has not been reviewed, verified or affirmed by SEBI, RBI,

the Stock Exchanges or any other regulatory or listing authority, and has only been filed with the RoC

pursuant to the applicable provisions of the Companies Act, and is intended only for use by QIBs;

You are entitled to subscribe for the Equity Shares offered in the Issue under the laws of all relevant

jurisdictions that apply to you and you have necessary capacity, have obtained all necessary consents,

governmental or otherwise, and authorisations and complied with all necessary formalities, to enable you to

commit to participation in the Issue and to perform your obligations in relation thereto (including, without

limitation, in the case of any person on whose behalf you are acting, all necessary consents and authorisations

to agree to the terms set out or referred to in this Red Herring Prospectus), and will honour such obligations;

You confirm that, either: (i) you have not participated in or attended any investor meetings or presentations

by the Company or its agents (the “Company Presentations”) with regard to the Company or the Issue; or

(ii) if you have participated in or attended any Company Presentations: (a) you understand and acknowledge

that the Book Running Lead Managers and the Syndicate Member may not have knowledge of the statements

that the Company or its agents may have made at such Company Presentations and are therefore unable to

determine whether the information provided to you at such Company Presentations may have included any

material misstatements or omissions, and, accordingly you acknowledge that the Book Running Lead

Managers have advised you not to rely in any way on any information that was provided to you at any such

Company Presentations, and (b) you confirm that, to the best of your knowledge, you have not been provided

any material or price sensitive information relating to the Company and the Issue that was not made publicly

available by the Company;

Neither the Company nor the Book Running Lead Managers nor the Syndicate Member nor any of their

respective shareholders, directors, officers, employees, counsel, representatives, agents or affiliates are

making any recommendations to you or advising you regarding the suitability of any transactions it may enter

into in connection with the Issue and your participation in the Issue is on the basis that you are not, and will

not, up to the Allotment of the Equity Shares offered in the Issue, be a client of the Book Running Lead

Managers or the Syndicate Member. Neither the Book Running Lead Managers nor the Syndicate Member

nor any of their shareholders, directors, officers, employees, counsel, representatives, agents or affiliates have

any duties or responsibilities to you for providing the protection afforded to its or their clients or customers

5

or for providing advice in relation to the Issue and are not in any way acting in any fiduciary capacity;

All statements other than statements of historical facts included in this Red Herring Prospectus, including

those regarding the Company’s financial position, business strategy, plans and objectives of management for

future operations (including development plans and objectives relating to the Company’s business), are

forward-looking statements. Such forward-looking statements involve known and unknown risks,

uncertainties and other important factors that could cause actual results to be materially different from future

results, performance or achievements expressed or implied by such forward-looking statements. Such

forward-looking statements are based on numerous assumptions regarding the Company’s present and future

business strategies and environment in which the Company will operate in the future. You should not place

undue reliance on forward-looking statements, which speak only as of the date of this Red Herring

Prospectus;

You are aware of and understand that the Equity Shares to be issued pursuant to the Issue are being offered

only to QIBs and are not being offered to the general public and the Allocation and Allotment shall be in

accordance with the Basis of Allocation, Allotment Criteria and the CAN. See “Issue Procedure” on page

213;

You have made, or been deemed to have made, as applicable, the representations and warranties set forth in

“Purchaser Representations and Transfer Restrictions” and “Selling Restrictions” on pages 242 and 233

respectively;

You have read this Red Herring Prospectus in its entirety, including in particular, “Risk Factors” on page 41;

In making your investment decision, you have (i) relied on your own examination of the Company and the

terms of the Issue, including the merits and risks involved, (ii) made your own assessment of the Company

on a consolidated basis, the Equity Shares offered in the Issue and the terms of the Issue based solely on the

information contained in this Red Herring Prospectus and publicly available information about the Company

and no other disclosure or representation by us or any other party, (iii) consulted your own independent

counsel and advisors or otherwise have satisfied yourself concerning, the effects of local laws, (iv) received

all information that you believe is necessary or appropriate in order to make an investment decision in respect

of the Company and the Equity Shares offered in the Issue, and (v) relied upon your own investigation and

resources in deciding to invest in the Issue;

Neither the Book Running Lead Managers nor the Syndicate Member nor any of their shareholders, directors,

officers, employees, counsel, representatives, agents or affiliates, have provided you with any tax advice or

otherwise made any representations regarding the tax consequences of purchase, ownership and disposal of

the Equity Shares offered in the Issue (including the Issue and the use of proceeds from such Equity Shares).

You will obtain your own independent tax advice and will not rely on the Book Running Lead Managers or

any of their shareholders, directors, officers, employees, counsel, representatives, agents or affiliates, when

evaluating the tax consequences in relation to the Equity Shares offered in the Issue (including, in relation to

the Issue and the use of proceeds from the Equity Shares offered in the Issue). You waive, and agree not to

assert any claim against, any of the Company, the Book Running Lead Managers, the Syndicate Member or

any of their respective shareholders, directors, officers, employees, counsel, representatives, agents or

affiliates, with respect to the tax aspects of the Equity Shares offered in the Issue or as a result of any tax

audits by tax authorities, wherever situated;

You are a sophisticated investor who is seeking to subscribe to the Equity Shares offered in the Issue for your

own investment and not with intent to distribute such Equity Shares and have such knowledge and experience

in financial, business and investments as to be capable of evaluating the merits and risks of the investment in

the Equity Shares offered in the Issue. You and any accounts for which you are subscribing to the Equity

Shares offered in the Issue; (i) are each able to bear the economic risk of the investment in the Equity Shares

to be issued pursuant to the Issue; (ii) are able to sustain a complete loss on the investment in the Equity

Shares to be issued pursuant to the Issue; (iii) have no need for liquidity with respect to the investment in the

Equity Shares offered in the Issue; (iv) have sufficient knowledge, sophistication and experience in financial

6

and business matters so as to be capable of evaluating the merits and risk of subscribing to the Equity Shares

offered in the Issue; and (v) have no reason to anticipate any change in your or their circumstances, financial

or otherwise, which may cause or require any sale or distribution by you or them of all or any part of the

Equity Shares offered in the Issue. You acknowledge that an investment in the Equity Shares offered in the

Issue involves a high degree of risk and that such Equity Shares are, therefore, a speculative investment. You

are seeking to subscribe to the Equity Shares offered in this Issue for your own investment and not with a

view to resale or distribution;

If you are acquiring the Equity Shares offered in the Issue, for one or more managed accounts, you represent

and warrant that you are authorised in writing, by each such managed account to acquire such Equity Shares

for each managed account and make the representations, warranties, acknowledgements and agreements

herein for and on behalf of each such account, reading the reference to ‘you’ to include such accounts;

You are neither a Promoter nor a person related to the Promoter, either directly or indirectly, and your ASBA

Application does not directly or indirectly represent the Promoter or the Promoter Group or persons related

to the Promoter. For the purposes of this representation you will be deemed to be related to the Promoter if

you have any rights under any shareholders’ agreement or voting agreement entered into with the Promoter

or persons related to the Promoter, any veto rights or any right to appoint any nominee director on the Board,

other than the rights, if any, acquired in the capacity of a lender not holding any Equity Shares;

You have no right to withdraw your ASBA Application or revise the price per Equity Share or the number

of Equity Shares mentioned in your ASBA Application downwards;

You are eligible to apply for and hold the Equity Shares offered in the Issue, which are Allotted to you

together with any Equity Shares held by you prior to the Issue. You confirm that your aggregate holding after

the Allotment of the Equity Shares offered in the Issue shall not exceed the level permissible as per any

applicable regulations;

The ASBA Application submitted by you would not result in triggering a tender offer under the Takeover

Regulations;

You, together with other QIBs that belong to the same group as you or are under common control with you,

shall not be Allotted Equity Shares in excess of 25% of the offer size in terms of Regulation 91H of the SEBI

Regulations. For the purposes of this representation:

a. The expression ‘belong to the same group’ shall have the same meaning as ‘companies under the

same group’ as provided in sub-section (11) of Section 372 of the Companies Act, 1956 (hereinafter

defined); and

b. The expression ‘control’ shall have the same meaning as is assigned to it under Regulation 2(1)(e)

of the Takeover Regulations;

For meaning of the terms ‘companies under the same group’ under sub-section (11) of Section 372 of the

Companies Act and ‘control’ under Regulation 2(1)(e) of the Takeover Regulations, see “Issue Procedure”

on page 213.

You shall not undertake any trade in the Equity Shares issued pursuant to the Issue and credited to your

Depository Participant account until such time that the final listing and trading approvals for such Equity

Shares are issued by the Stock Exchanges;

You are aware that (i) applications for in-principle approval, in terms of Regulation 28 of the SEBI Listing

Regulations, for listing and admission of the Equity Shares offered in the Issue and for trading on the Stock

Exchanges, were made and approval has been received from each of the Stock Exchanges; and (ii) the

application for the final listing and trading approval will be made after Allotment of the Equity Shares in the

Issue. There can be no assurance that the final approvals for listing of the Equity Shares issued pursuant to

7

the Issue will be obtained in time, or at all. The Company shall not be responsible for any delay or non-receipt

of such final approvals or any loss arising from such delay or non-receipt;

By participating in the Issue, you confirm that you have neither received nor relied on any other information,

representation, warranty or statement made by, or on behalf of, the Book Running Lead Managers, the

Syndicate Member or the Company or any of their respective affiliates or any other person acting on their

behalf and neither the Book Running Lead Managers, nor the Syndicate Member nor the Company nor any

of their respective affiliates or other person acting on their behalf will be liable for your decision to participate

in the Issue based on any other information, representation, warranty or statement that you may have obtained

or received;

You confirm that the only information you are entitled to rely on, and on which you have relied in committing

yourself to acquire the Equity Shares offered in the Issue is contained in this Red Herring Prospectus, such

information being all that you deem necessary to make an investment decision in respect of the Equity Shares

offered in the Issue and neither the Book Running Lead Managers, nor the Syndicate Member nor the

Company will be liable for your decision to accept an invitation to participate in the Issue based on any other

information, representation, warranty or statement that you may have obtained or received;

The Book Running Lead Managers or the Syndicate Member do not have any obligation to purchase or

acquire all or any part of the Equity Shares subscribed for by you or to support any losses directly or indirectly

sustained or incurred by you for any reason whatsoever in connection with the Issue, including non-

performance by the Company of any of its obligations or any breach of any representations and warranties

by the Company, whether to you or otherwise;

You understand that the Equity Shares offered in the Issue have not been and will not be registered under the

U.S. Securities Act or with any securities regulatory authority of any state of the United States and

accordingly, may not be offered or sold within the United States, except in reliance on an exemption from

the registration requirements of the U.S. Securities Act;

If within the United States, you are a U.S. QIB who is or are acquiring the Equity Shares for your own

account or for the account of an institutional investor who also meets the requirements of a U.S. QIB, for

investment purposes only, and not with a view to, or for resale in connection with, the distribution (within

the meaning of any United States securities laws) thereof, in whole or in part and are not our affiliate or a

person acting on behalf of such an affiliate;

If you are outside the United States, you are purchasing the Equity Shares offered in the Issue in an offshore

transaction in reliance on Regulation S under the U.S. Securities Act, and are not our affiliate or a person

acting on behalf of such affiliate;

You are not acquiring or subscribing for the Equity Shares as a result of any general solicitation or general

advertising (as those terms are defined in Regulation D under the U.S. Securities Act) or directed selling

efforts (as defined in Regulation S) and you understand and agree that offers and sales are being made in

reliance on an exemption to the registration requirements of the U.S. Securities Act provided by Section

4(a)(2) under the U.S. Securities Act or Regulation S or another available exemption from registration under

the U.S. Securities Act and the Equity Shares may not be eligible for resale under Rule 144A thereunder.

You understand and agree that the Equity Shares are transferable only in accordance with the restrictions

described under the sections “Selling Restrictions” and “Purchaser Representations and Transfer

Restrictions”;

You agree that any dispute arising in connection with the Issue will be governed by and construed in

accordance with the laws of Republic of India, and the courts in Mumbai, India shall have exclusive

jurisdiction to settle any disputes which may arise out of or in connection with the Issue, this Red Herring

Prospectus and the Prospectus;

Each of the representations, warranties, acknowledgements and agreements set out above shall continue to

8

be true and accurate at all times up to and including the Allotment, listing and trading of the Equity Shares

issued pursuant to the Issue on the Stock Exchanges;

You agree to indemnify and hold the Company, the Book Running Lead Managers, the Syndicate Member

and their respective affiliates harmless from any and all costs, claims, liabilities and expenses (including legal

fees and expenses) arising out of or in connection with any breach or alleged breach of the foregoing

representations, warranties, acknowledgements and undertakings made by you in this Red Herring

Prospectus. You agree that the indemnity set forth in this paragraph shall survive the resale of the Equity

Shares issued pursuant to the Issue by, or on behalf of, the managed accounts;

You agree to abide by the Basis of Allocation provided in this Red Herring Prospectus, and the Allocation

done in accordance with the Basis of Allocation as overseen by the Stock Exchanges;

You agree to provide additional documents as may be required by the Company, the Book Running Lead

Managers and the Syndicate Member for finalisation of the Basis of Allocation along with the Stock

Exchanges. The Company, the Book Running Lead Managers, the Syndicate Member and their affiliates may

rely on the accuracy of such documents provided by you; and

The Company, the Book Running Lead Managers, the Syndicate Member, their respective affiliates and

others will rely on the truth and accuracy of the foregoing representations, warranties, acknowledgements

and undertakings, which are given to the Book Running Lead Managers and the Syndicate Member on their

own behalf and on behalf of the Company, and are irrevocable.

9

OFFSHORE DERIVATIVE INSTRUMENTS

Subject to compliance with all applicable Indian laws, rules, regulations, guidelines and approvals in terms of

Regulation 22 of the SEBI FPI Regulations, a FPI (other than a Category III foreign portfolio investors and unregulated

broad based funds which are classified as Category II FPI by virtue of their investment manager being appropriately

regulated), including the affiliates of the Book Running Lead Managers or the Syndicate Member, may issue,

subscribe or otherwise deal in offshore derivative instruments as defined under the SEBI FPI Regulations as any

instrument, by whatever name called, which is issued overseas by a FPI against securities held by it that are listed or

proposed to be listed on any recognised stock exchange in India, as its underlying and all such offshore derivative

instruments are referred to herein as “P-Notes” for which they may receive compensation from the purchasers of such

P-Notes. These P-Notes may be issued only in favour of those entities which are regulated by any appropriate foreign

regulatory authorities in the countries of their incorporation or establishment subject to compliance with “know your

client” requirements. An FPI must ensure that the P-Notes are issued in compliance with all applicable laws including

Regulation 4 and Regulation 22 of the SEBI FPI Regulations and circular no. CIR/IMD/FIIC/20/2014 dated November

24, 2014 issued by SEBI. P-Notes have not been and are not being offered or sold pursuant to this Red Herring

Prospectus. This Red Herring Prospectus does not contain any information concerning P-Notes, including, without

limitation, any information regarding any risk factors relating thereto.

Any P-Notes that may be issued are not securities of our Company and do not constitute any obligations of, claim on,

or interests in our Company. Our Company has not participated in any offer of any P-Notes, or in the establishment

of the terms of any P-Notes, or in the preparation of any disclosure related to any P-Notes. Any P-Notes that may be

offered are issued by, and are solely the obligations of, third parties that are unrelated to our Company. Our Company,

the Book Running Lead Managers and the Syndicate Member do not make any recommendation as to any investment

in P-Notes and do not accept any responsibility whatsoever in connection with any P-Notes. Any P-Notes that may be

issued are not securities of the Book Running Lead Managers or the Syndicate Member and do not constitute any

obligations of, or claims on, the Book Running Lead Managers or the Syndicate Member. FPI affiliates (other than

Category III FPIs and unregulated broad based funds which are classified as FPI by virtue of their investment manager

being appropriately regulated) of the Book Running Lead Managers or the Syndicate Member may purchase, to the

extent permissible under law, Equity Shares in the Issue, and may issue P-Notes in respect thereof.

Prospective investors interested in purchasing any P-Notes have the responsibility to obtain adequate disclosure

as to the issuer(s) of such P-Notes and the terms and conditions of any such P-Notes from the issuer(s) of such

P-Notes. Neither SEBI nor any other regulatory authority has reviewed or approved any P-Notes or any

disclosure related thereto. Prospective investors are urged to consult with their own financial, legal, accounting

and tax advisors regarding any contemplated investment in P-Notes, including whether P-Notes are issued in

compliance with applicable laws and regulations.

DISCLAIMER CLAUSE

As required, a copy of this Red Herring Prospectus has been delivered to each of the Stock Exchanges and SEBI and

for registration to the RoC. The Stock Exchanges, SEBI and the RoC do not in any manner:

(1) warrant, certify or endorse the correctness or completeness of the contents of the Red Herring Prospectus;

(2) warrant that the Equity Shares issued pursuant to the Issue will be listed or the Equity Shares will continue

to be listed on the Stock Exchanges; or

(3) take any responsibility for the financial or other soundness of the Company, its Promoter, its management or

any scheme or project of the Company.

It should not for any reason be deemed or construed to mean that the Red Herring Prospectus has been reviewed or

approved by the Stock Exchanges or SEBI. Every person who desires to apply for or otherwise acquire any Equity

Shares offered in the Issue may do so pursuant to an independent inquiry, investigation and analysis and shall not have

any claim against the Stock Exchanges, SEBI and the RoC whatsoever, by reason of any loss which may be suffered

by such person consequent to or in connection with, such subscription/acquisition, whether by reason of anything

stated or omitted to be stated herein, or for any other reason whatsoever.

10

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

In this Red Herring Prospectus, unless the context otherwise indicates or implies, references to ‘you’, ‘your’, ‘offeree’,

‘purchaser’, ‘subscriber’, ‘recipient’, ‘investors’, ‘prospective investors’ and ‘potential investor’ are to the prospective

investors in the Issue, references to ‘the Company’ are to Quess Corp Limited, and references to ‘we’, ‘us’, ‘our’ or

‘our Company’ are to Quess Corp Limited, its Subsidiaries, Associates and Joint Venture on a consolidated basis

unless otherwise specified.

In this Red Herring Prospectus, all references to “Indian Rupees” “`” and “Rs.” are to Indian Rupees and all references

to “U.S. dollars”, “USD” and “U.S.$” are to United States dollars. All references herein to the “U.S.” or the “United

States” are to the United States of America and its territories and possessions and all references to “India” are to the

Republic of India and all references herein to ‘Government’ or GoI or the ‘Central Government’ or the ‘State

Government’ are to the Government of India, Central or State, as the case maybe .

The financial year of the Company commences on April 1 of each calendar year and ends on March 31 of the

succeeding calendar year, so, unless otherwise specified or if the context requires otherwise all references to a

particular financial year or fiscal year are to the twelve month period ended on March 31 of that year.

In this Red Herring Prospectus, certain monetary thresholds disclosed as (` in million) have been subjected to rounding

adjustments; accordingly, figures shown as totals in certain tables may not be an arithmetic aggregation of the figures

which precede them.

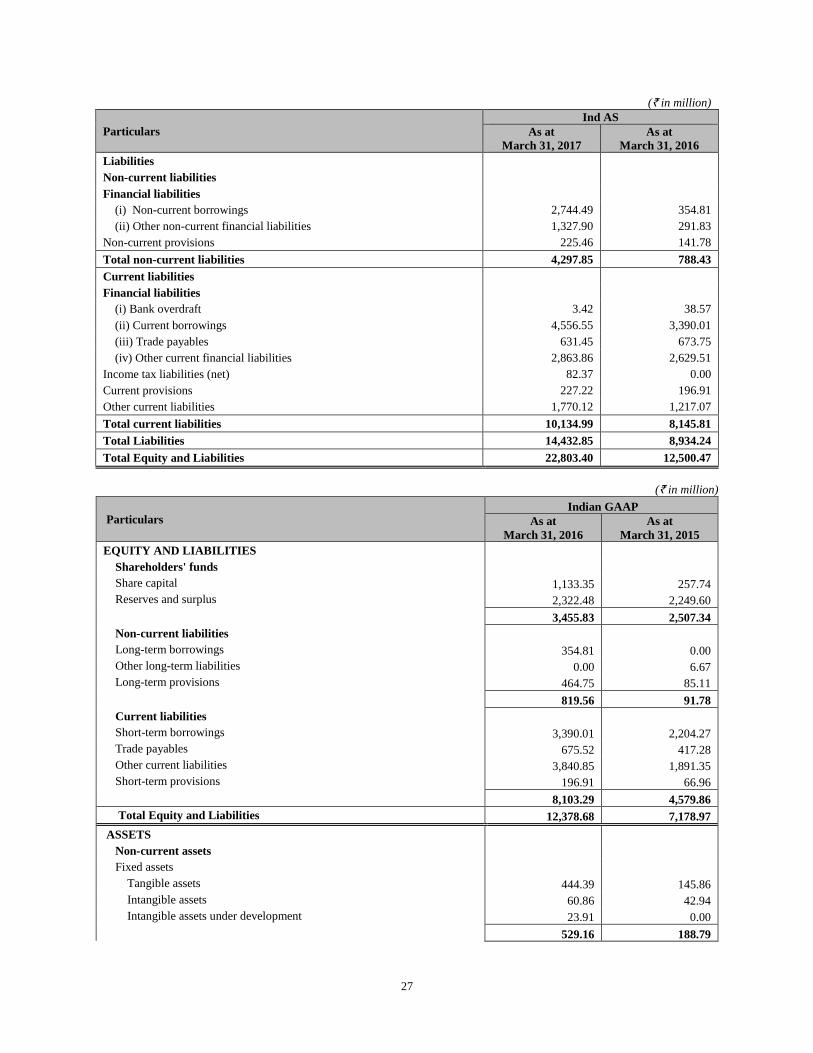

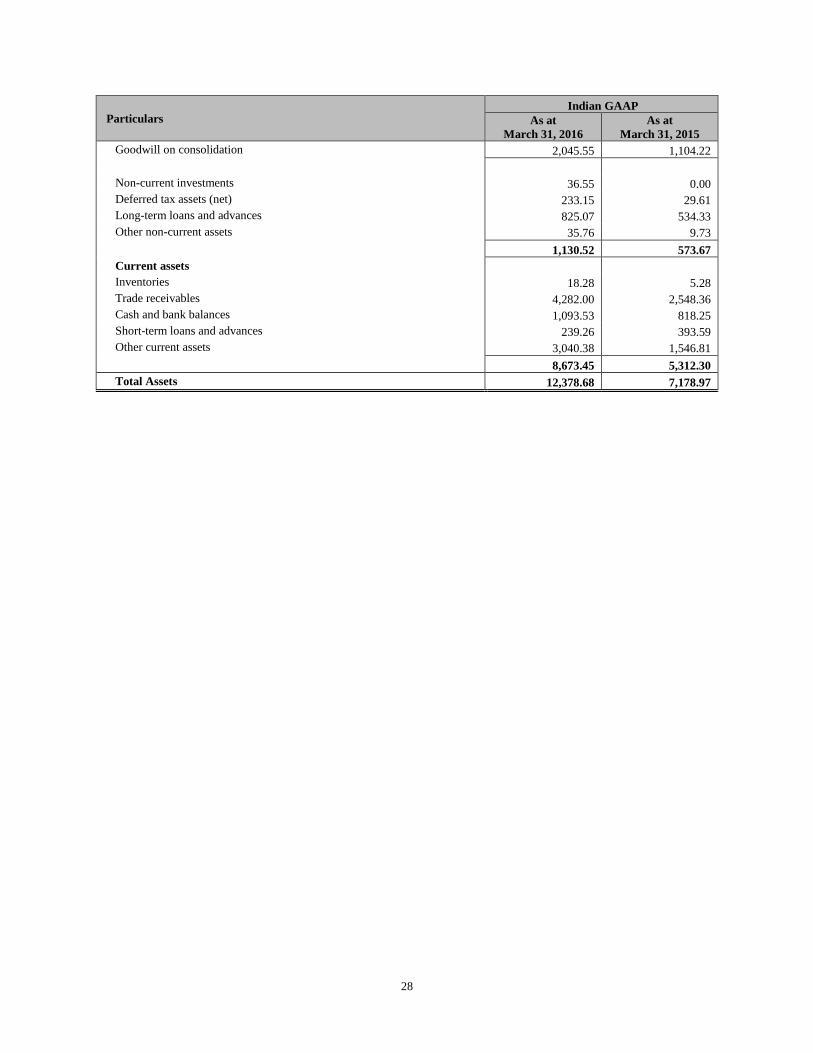

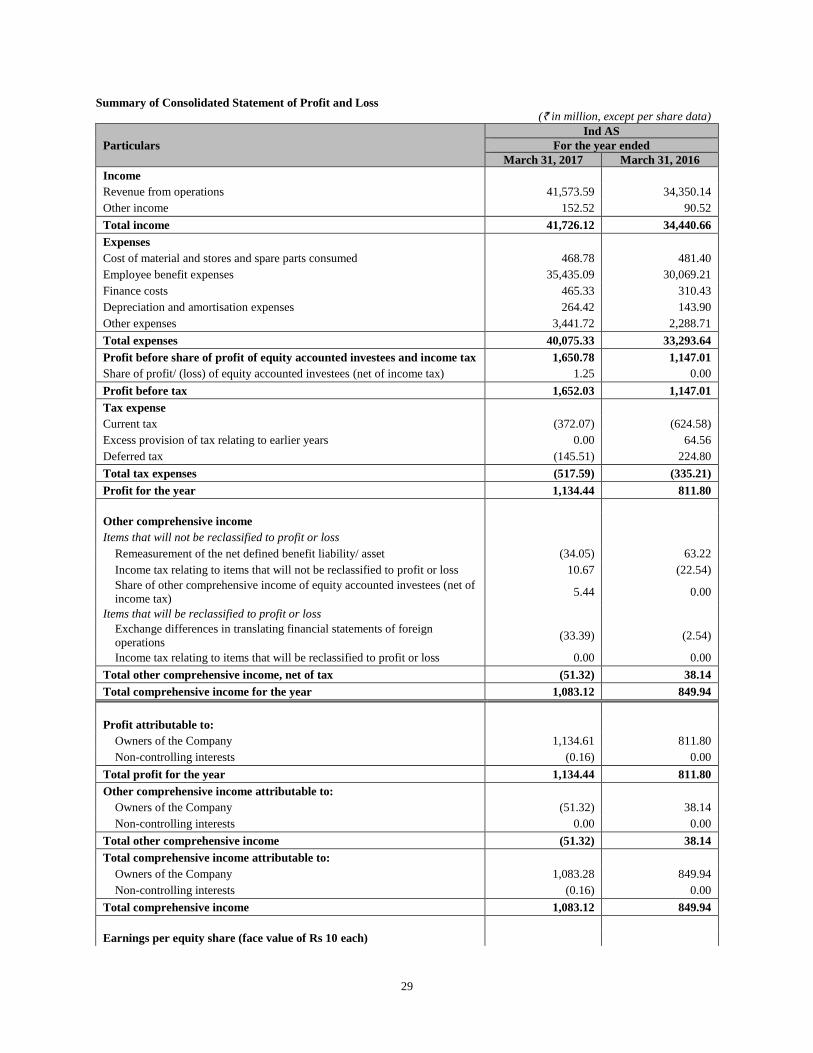

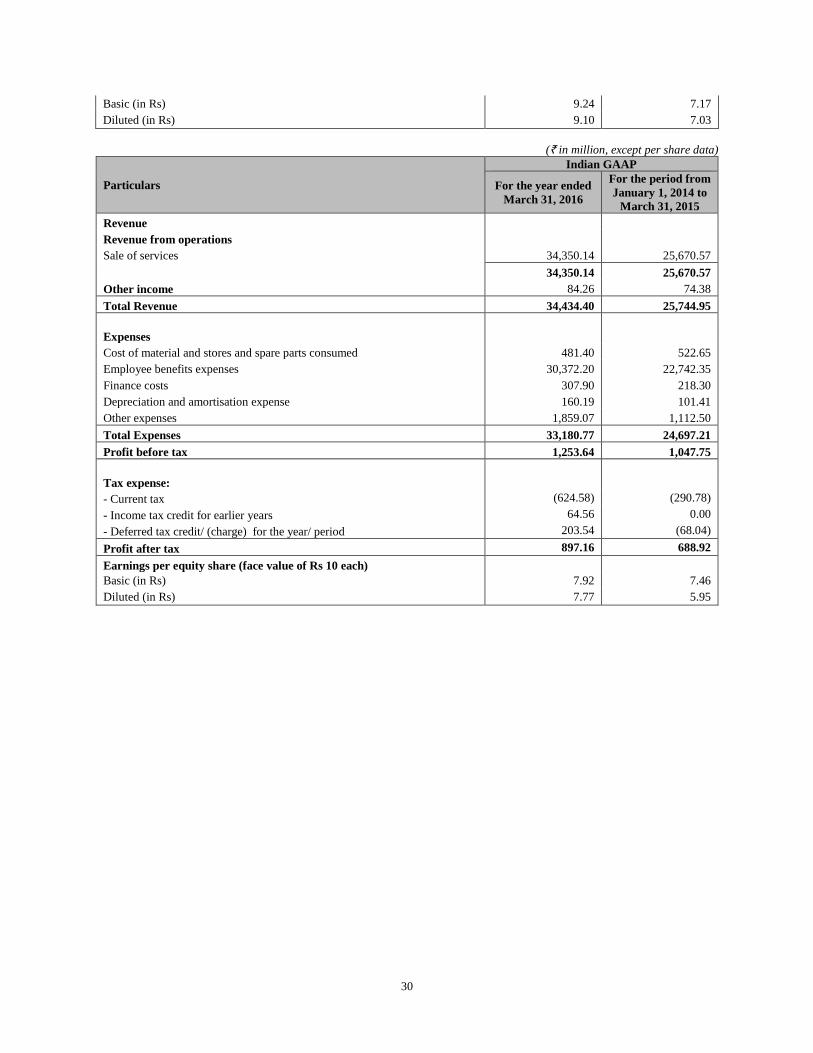

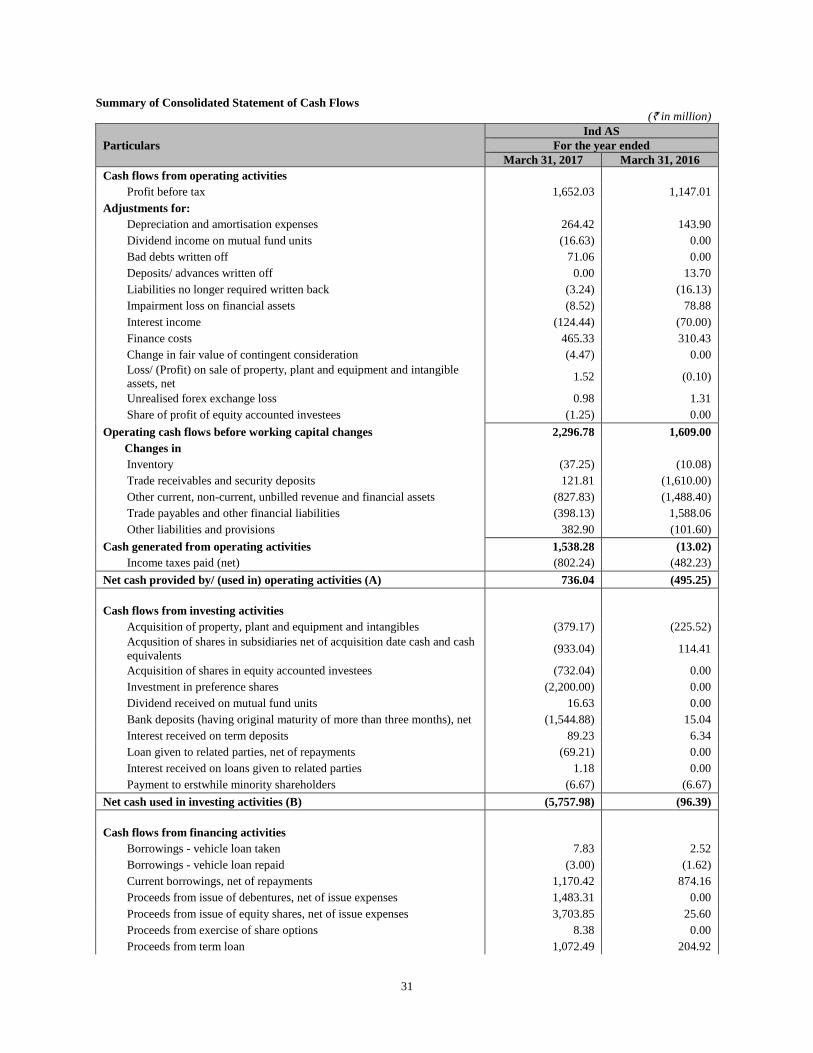

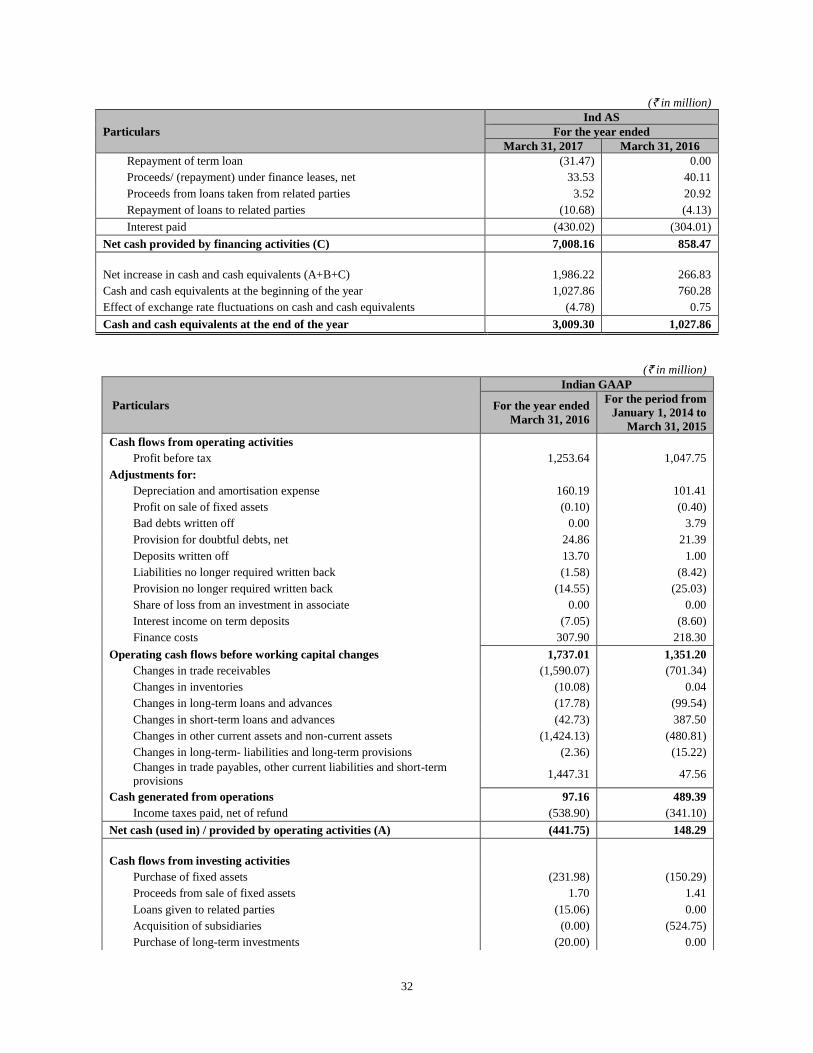

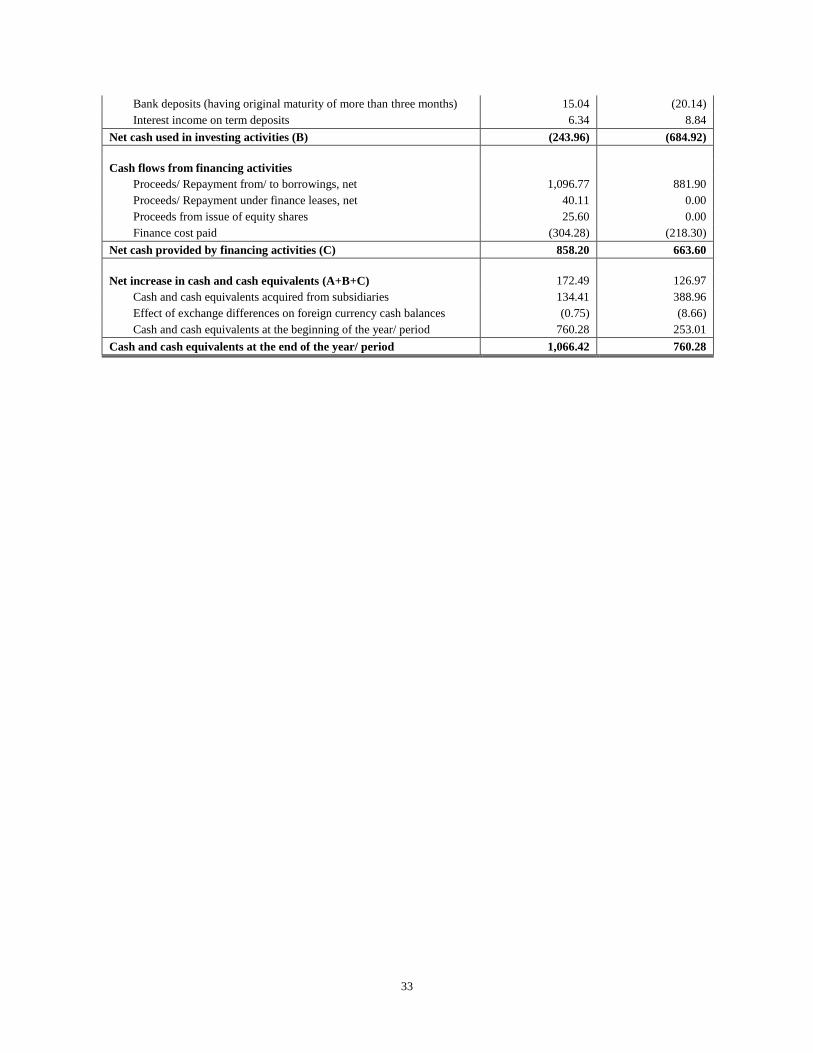

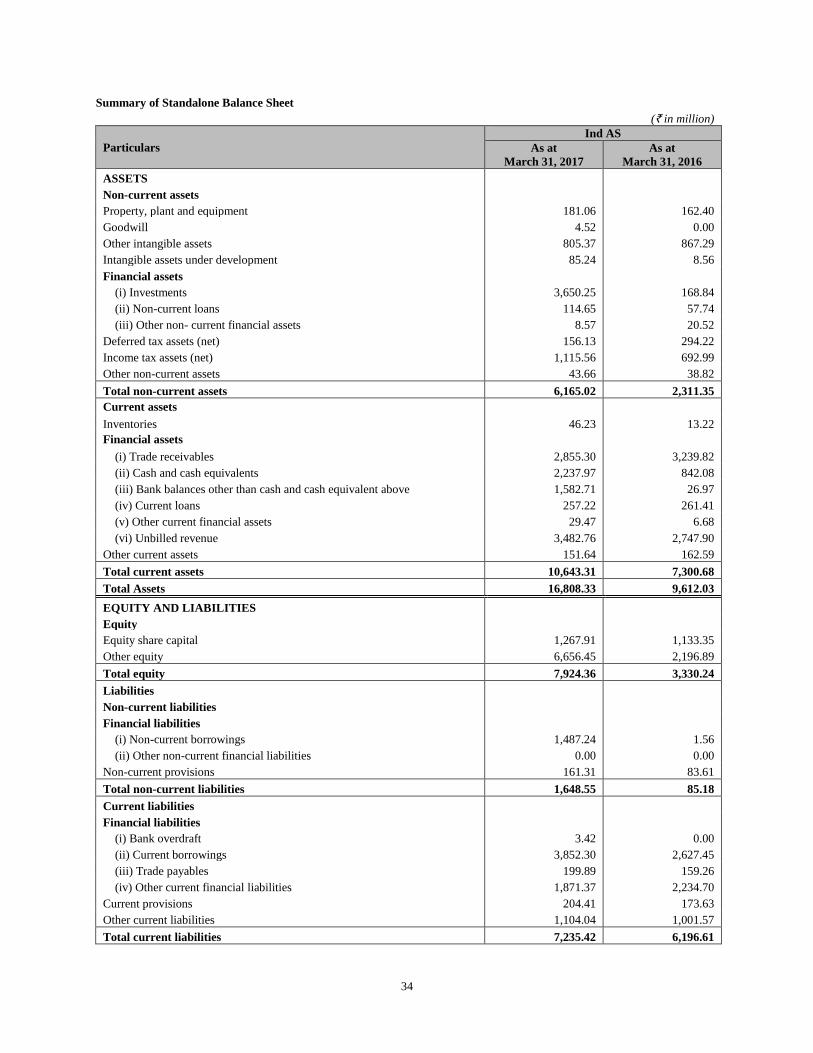

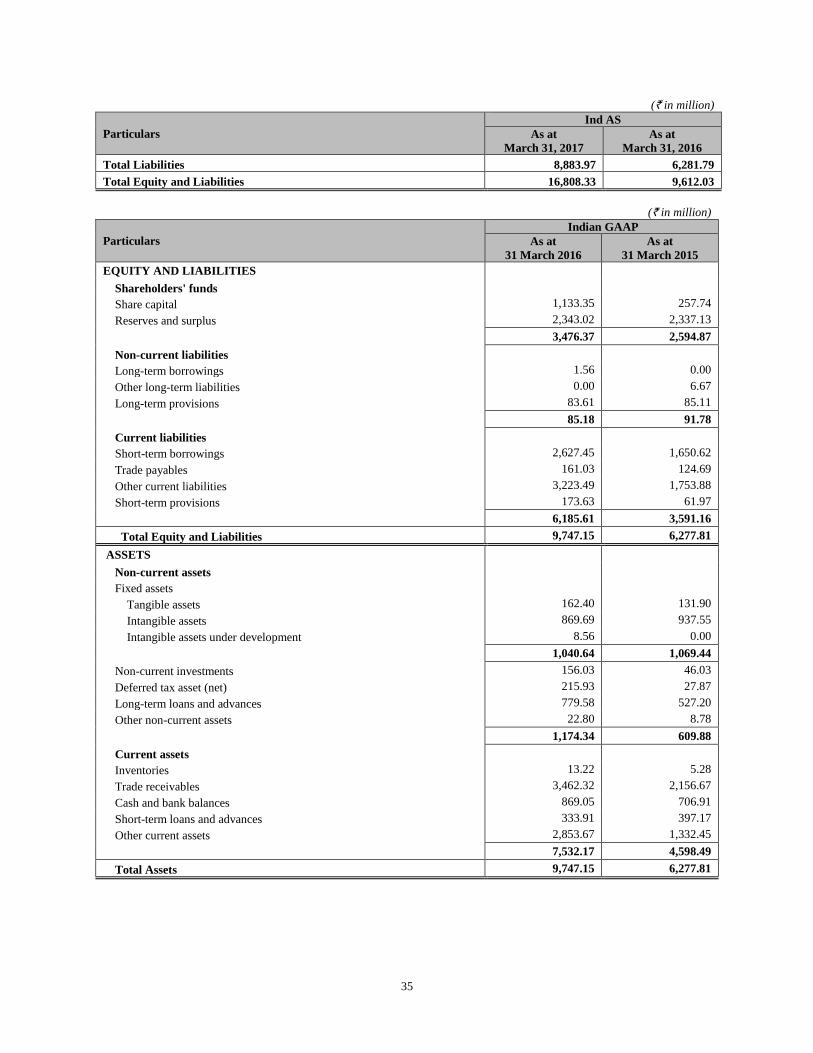

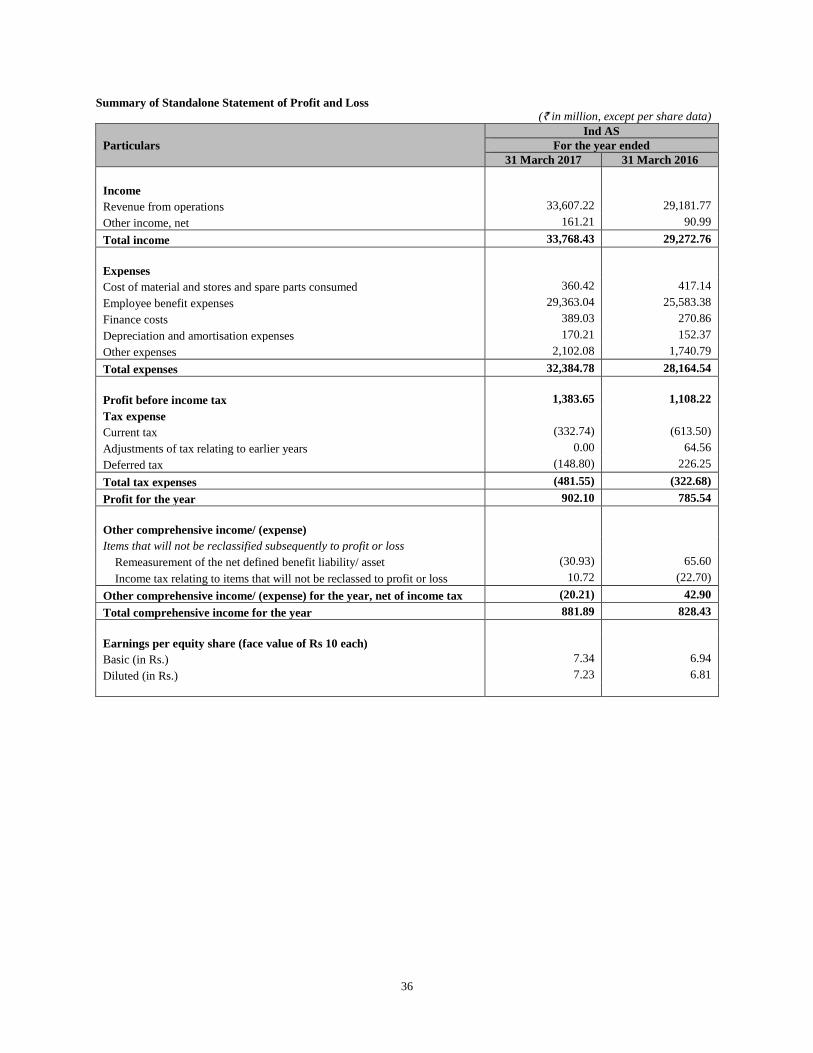

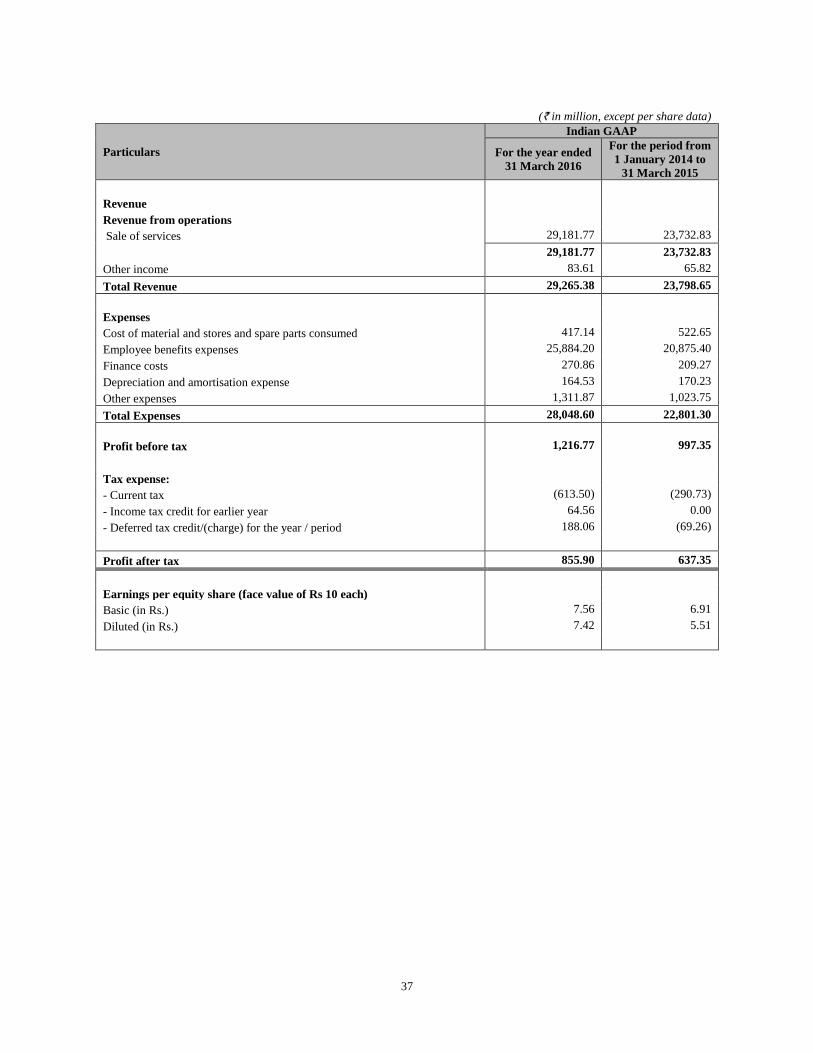

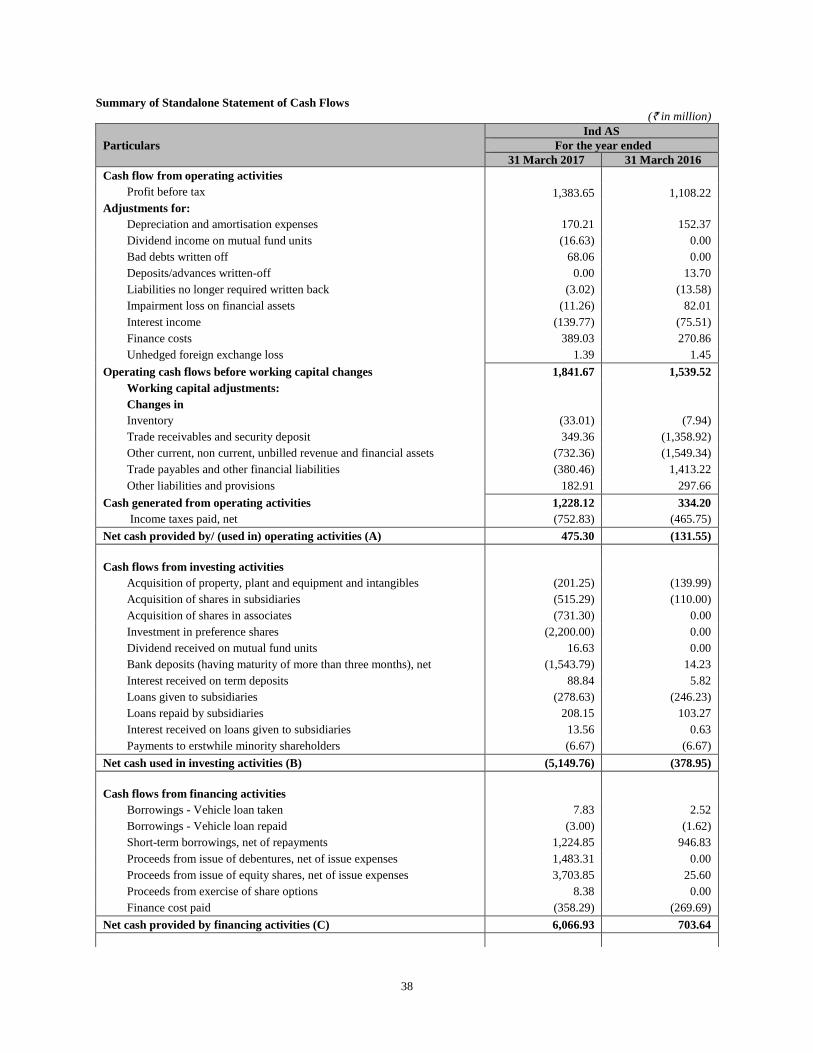

Transition from Indian GAAP to Ind AS Financial Statements

As a subsidiary of our Corporate Promoter, TCIL (which was required to prepare and present its financial statements

in accordance with Ind AS with effect from April 1, 2016), our Company was also required to prepare standalone and

consolidated financial statements in accordance with Ind AS for Fiscal 2017 (together with the corresponding

standalone and consolidated financial statements under Ind AS for Fiscal 2016). Our historical audited standalone and

consolidated financial statements for Fiscal 2015 (15 months) and for Fiscal 2016 were originally prepared in

accordance with Indian GAAP.

Ind AS varies in many respects from Indian GAAP, and accordingly our Ind AS financial statements for Fiscal 2016

and Fiscal 2017 are not comparable with our historical Indian GAAP financial statements for Fiscal 2015 (15 months)

and Fiscal 2016. See “Risk Factors – We were required to prepare and present our financial statements under Ind AS

with effect from April 1, 2016. In this Red Herring Prospectus, we have included our Ind AS Audited Financial

Statements for Fiscal 2016 and Fiscal 2017 which are not comparable with the historical Indian GAAP Audited

Financial Statements for Fiscal 2015 (15 months) and Fiscal 2016 included herein.” on page 43.

In this Red Herring Prospectus we have therefore included (i) the audited consolidated and standalone financial

statements under Indian GAAP for Fiscal 2015 (15 months) and Fiscal 2016 (the “Indian GAAP Audited Financial

Statements”) and (ii) the audited consolidated and standalone financial statements under Ind AS for Fiscal 2016 and

Fiscal 2017 (the “Ind AS Audited Financial Statements”). Note 55 to our consolidated Ind AS Audited Financial

Statements also includes a reconciliation statement of the Fiscal 2016 consolidated Ind AS Audited Financial

Statements with the Fiscal 2016 consolidated Indian GAAP Audited Financial Statements explaining the impact of

transition to Ind AS on the preparation and presentation of our financial statements.

We have therefore included below management’s discussion and analysis of our financial condition, results of

operations and cash flows (i) under Indian GAAP in Fiscal 2016 compared to that in Fiscal 2015 (15 months); and (ii)

under Ind AS in Fiscal 2017 compared to that in Fiscal 2016.

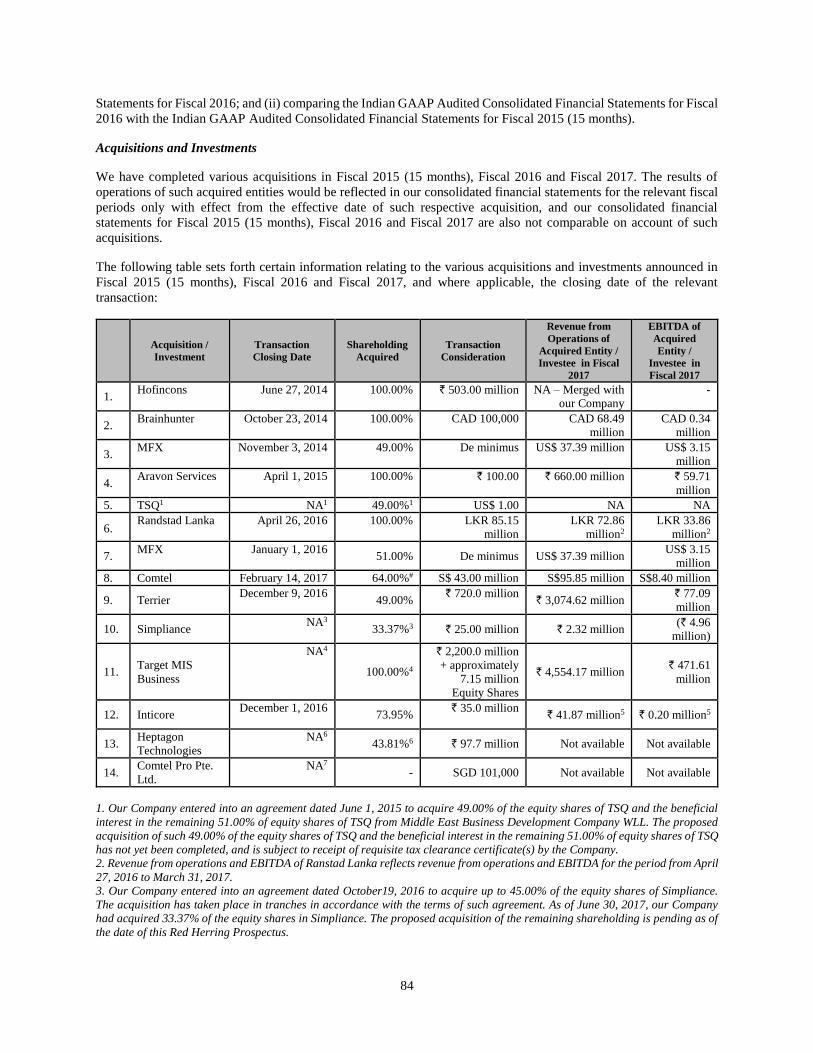

We have completed various acquisitions in Fiscal 2015 (15 months), Fiscal 2016 and Fiscal 2017. The results of

operations of such acquired entities would be reflected in our consolidated financial statements for the relevant fiscal

periods only with effect from the effective date of such respective acquisition, and our consolidated financial

statements for Fiscal 2015 (15 months), Fiscal 2016 and Fiscal 2017 are also not comparable on account of such

acquisitions.

11

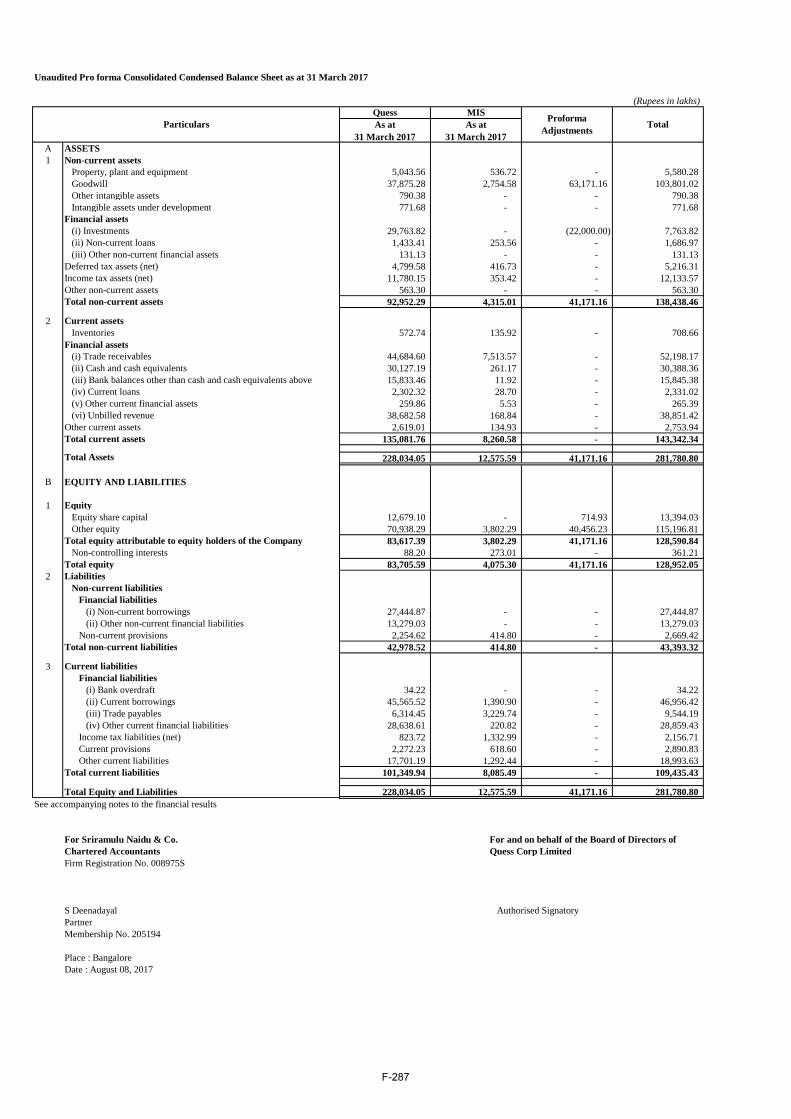

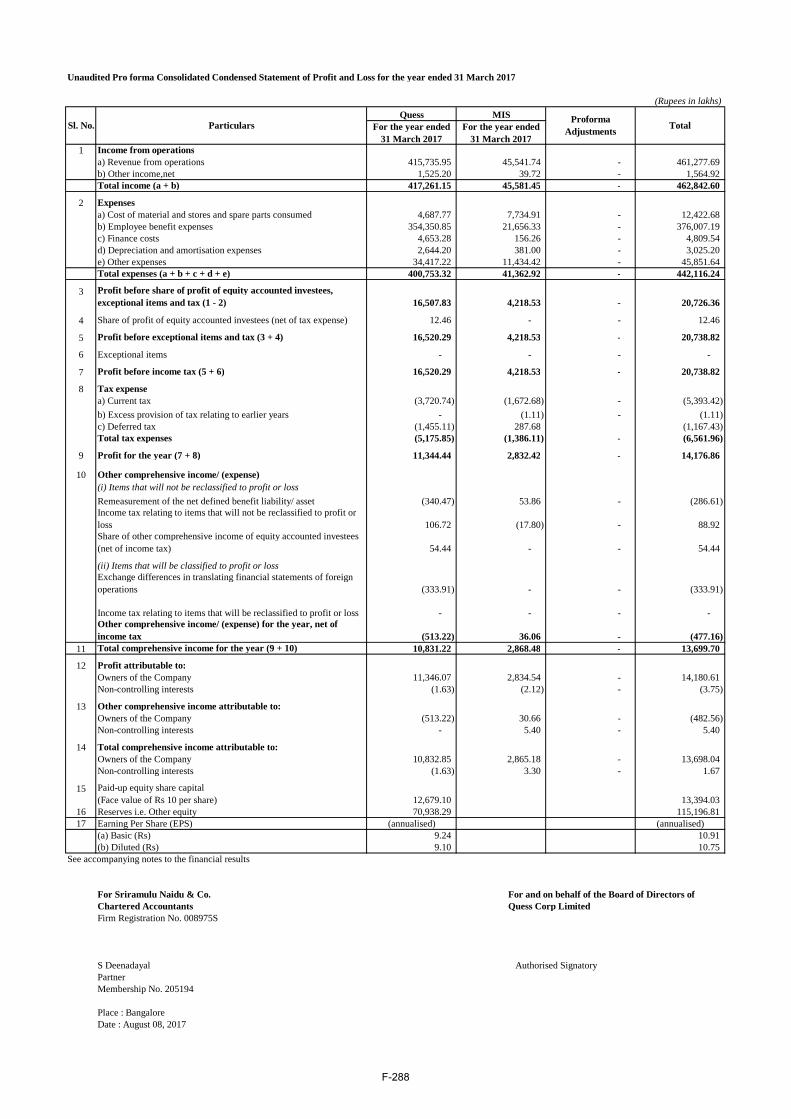

Proforma Financial Information on Proposed MIS Acquisition

On November 28, 2016, we entered into definitive agreements relating to the demerger of the facility management

and catering businesses of Manipal Integrated Services Private Limited (“MIS”) into our Company through a scheme

of arrangement (such proposed acquisition, the “Proposed MIS Acquisition”). The completion of the Proposed MIS

Acquisition is subject to various conditions, including the approval of the shareholders and creditors, the sanction of

the scheme of arrangement by the National Company Law Tribunal as well as other relevant regulatory approvals.

Since the Proposed MIS Acquisition has not been completed, the effect of the Proposed MIS Acquisition is not

currently reflected in our audited consolidated financial statements for Fiscal 2017. In the event that all applicable

regulatory and other approvals are received, the Proposed MIS Acquisition will be deemed to be effective from

December 1, 2016 in accordance with the scheme of arrangement filed with respect to the Proposed MIS Acquisition.

The investment for the Proposed MIS Acquisition is material in the context of our financial condition, and we have

accordingly included in this Red Herring Prospectus certain proforma financial information with respect to the

Proposed MIS Acquisition (such proforma financial information, the “MIS Acquisition Proforma Financial

Information”). The MIS Acquisition Proforma Financial Information seeks to present the impact of the Proposed

MIS Acquisition on our historical audited consolidated financial statements for Fiscal 2017.

The MIS Acquisition Proforma Financial Information involves various assumptions as stated therein, including (i)

assumptions relating to the preparation of historical financial information of the demerged facility management and

catering businesses of MIS (not taking into account the hostels business of MIS that is not proposed to be acquired by

us), including allocation of revenue, costs, assets and liabilities; and (ii) that the Proposed MIS Acquisition had taken

place with effect from April 1, 2016.

The MIS Acquisition Proforma Financial Information has been prepared by the management and reported on by

Sriramulu Naidu & Co, Chartered Accountants, who have been engaged by us for such purposes on account of their

familiarity with the underlying financial statements of MIS. The MIS Acquisition Proforma Financial Information is

based on (i) the financial statements for Fiscal 2017 prepared under Ind AS for the facility management and catering

businesses of MIS that have been subjected to a limited review by Sriramulu Naidu & Co, Chartered Accountants;

and (ii) our audited consolidated financial statements for Fiscal 2017 under Ind AS.

Although we have included the MIS Acquisition Proforma Financial Information with respect to Fiscal 2017, given

that MIS is a private limited company and is not required under applicable laws to prepare quarterly financial

statements for the three months ended June 30, 2017, and given that the acquisition is still not completed, we have

been unable to include any proforma financial information with respect to the Proposed MIS Acquisition with respect

to the quarter ended June 30, 2017.

The MIS Acquisition Proforma Financial Information has been prepared for illustrative purposes only based on

various assumptions stated therein, does not purport to predict our future financial condition, results of operations or

cash flows in the event of completion of the Proposed MIS Acquisition, and potential investors should not place undue

reliance on such information in connection with any investment decision.

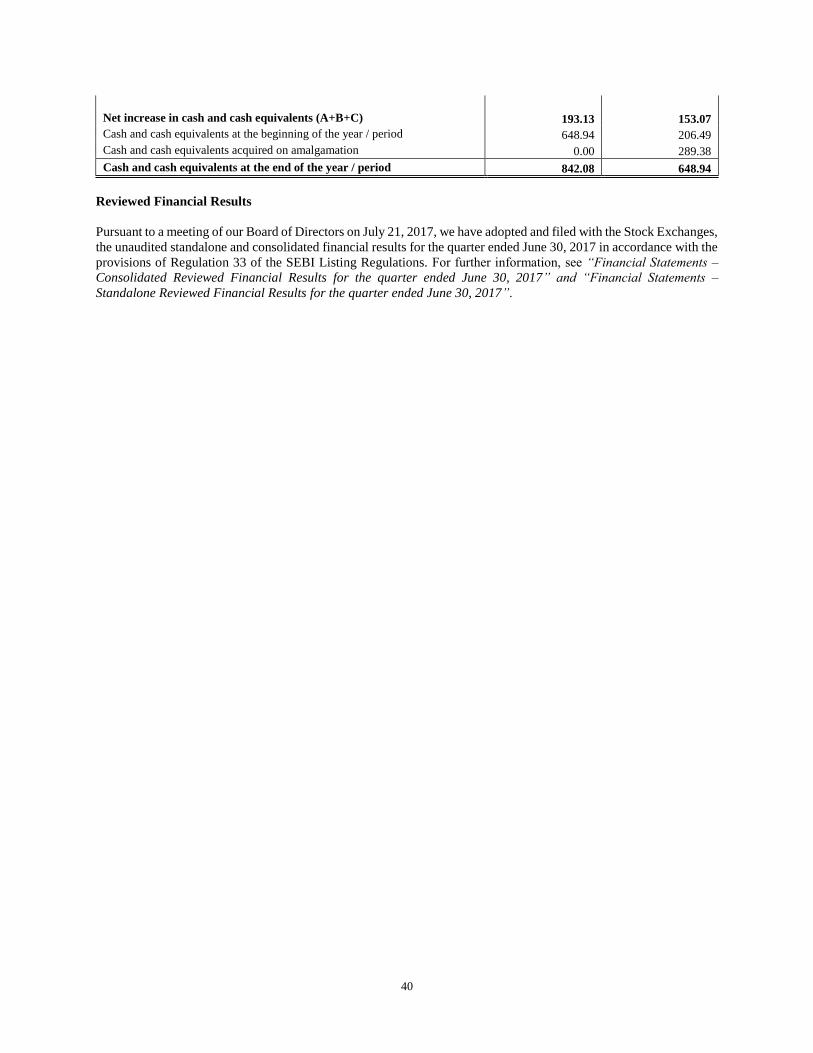

Reviewed Financial Results

Pursuant to a meeting of our Board of Directors on July 21, 2017, we have adopted and filed with the Stock Exchanges,

the unaudited standalone and consolidated financial results for the quarter ended June 30, 2017 in accordance with the

provisions of Regulation 33 of the SEBI Listing Regulations.

Potential investors should carefully take into account the disclosures above and our Indian GAAP Audited Financial

Statements and Ind AS Audited Financial Statements included in this Red Herring Prospectus in evaluating our

business and financial performance and in making any investment decision.

12

INDUSTRY AND MARKET DATA

Unless stated otherwise, industry and market data used in this Red Herring Prospectus have been obtained or derived

from publicly available information as well as industry publications and sources.

Industry publications generally state that the information contained in those publications has been obtained from

sources believed to be reliable but that their accuracy and completeness are not guaranteed and their reliability cannot

be assured. Although we believe that industry and market data used in this Red Herring Prospectus is reliable, it has

not been independently verified by either our Company or the Syndicate or any of their respective affiliates or advisors.

Information has been included in this Red Herring Prospectus from the publications titled “Assessment of Outsourced

Services Market in India, Frost & Sullivan, July, 2017” and “Assessment of IT Staffing Market in Singapore, Frost &

Sullivan, July, 2017” prepared by Frost & Sullivan, which report has been commissioned by the Company for the

purposes of confirming its understanding of the industry in connection with the Issue and which includes the following

disclaimer:

“The market research process for this study has been undertaken through secondary/desktop research as well as

primary research, which involves discussing the status of the market with leading participants and experts. The

research methodology used is the Export Opinion Methodology. Quantitative market information was sourced from

interviews by way of primary research as well as from trusted portals, and therefore, the information is subject to

fluctuations due to possible changes in the business and market climate. Frost & Sullivan’s estimates and assumptions

are based on varying levels of quantitative and qualitative analyses, including industry journals, company reports and

information in the public domain.

Forecasts, estimates, predictions and other forward-looking statements contained in this report are inherently

uncertain because of changes in factors underlying their assumptions, or events or combinations of events that cannot

be reasonably foreseen. Actual results and future events could differ materially from such forecasts, estimates,

predictions or such statements.

This study has been prepared for inclusion in the Issue Materials of “Quess Corp Limited” in relation to rights issue

and/or public issue.

This report and extracts thereof are for use in the Issue Materials issued by the Company and all presentation

materials (including press releases) prepared by or on behalf of the Company (and reviewed by Frost & Sullivan) in

relation to the Issue exercise. The Company is permitted to use the same in internal and external communications as

needed in the context of the Listing exercise. If required by any regulatory authority in relation to the Listing, the

Company is also permitted to make this report open for inspection from the public from the date of registration of the

red herring prospectus with the registrar of companies till the closing of the period of subscription in the IPO.

However, no part of the report may be distributed for any other commercial gain to parties not connected with the

said Listing exercise.

This report has exclusively been prepared for the consumption of Quess Corp Limited, and any unauthorised access

to or usage of this material by others is forbidden and illegal.

Frost & Sullivan has prepared this study in an independent and objective manner, and it has taken adequate care to

ensure its accuracy and completeness. We believe that this study presents a true and fair view of businesses in which

company operates within the limitations of, among others, secondary statistics and primary research, and it does not

purport to be exhaustive. Our research has been conducted with an “overall industry” perspective, and it will not

necessarily reflect the performance of individual companies in the industry. Frost & Sullivan shall not be liable for

any loss suffered because of reliance on the information contained in this study. This study should also not be

considered as a recommendation to buy or not to buy the shares of any company or companies as mentioned in it or

otherwise.”

In addition, information has been included in this Red Herring Prospectus from the publication titled “SMA Research:

2017 IT Spending and Priorities (Extract) dated 13 July, 2017” prepared by Strategy Meets Action (“SMA”), which

includes the following disclaimer:

13

“The material and observations contained in this publication have been developed from sources believed to be

reliable. SMA shall have no liability for omissions or errors and no obligation to revise or update any data or

conclusions should new information become available or future events occur. The opinions expressed in this report

are subject to change without notice.”

The extent to which the market and industry data used in this Red Herring Prospectus is meaningful depends on the