Retail Guiden Sweden 2019_2020 - Malmö.pdf - Invest in Skåne

Upload

khangminh22Category

view

2download

0

JUNE 2013 INVEST IN RUSSIASPECIAL ISSUE

Russia offers high investment opportunities, thanks to its good internal market, which will ensure higher demands for any kind of projects

High return investments

EX

PE

RT

.

SP

EC

IAL

IS

SU

E

VECTOR — 70 BILLION IN FOREIGN INVESTMENTS 4This year, Russia hopes to attract foreign invest-ments amounting to 55 billion dollars. In the near future, the Russian government plans to raise the annual volume of attracted foreign capital to 70 billion dollars or more. Sergei Belyakov, Deputy Minister of Economic Development of the Russian Federation talks about this in an interview with the magazine Invest in Russia

STANDARDIZING OUR COUNTRY 8The Investment Standard will be introduced in all the regions of Russia as of this year. It is aimed at significantly improving the business environment in our country and bringing the positions of authori-ties and entrepreneurs closer on a large number of issues related to the development of regional economies

A BIG COUNTRY FOR PROFITABLE INVESTMENTS 12Against the background of ongoing difficulties in the global economy and an investor confidence crisis, Russia, with its growing economy, is looking more and more attractive, a fact that is reflected in the steadily increasing volume of foreign investments

IMPROVING WHAT’S GOOD 16In the past few years, the Khanty-Mansiysk Autono-mous District — Ugra has been actively improving its investment climate. Today, the modernization of investment conditions is required in order to imple-ment new socio-economic goals, outlined in Ugra’s Development Strategy up to 2030

USING YOUR HEAD TO BREAK THROUGH THE WALL! 20Against the background of a stagnating Europe, the growing Russian market and unsatisfied demands for housing are increasingly attracting foreign players despite the complexity of agreements and corrup-tion in this sector

A REGION WORTH 500 BILLION ROUBLES! 24This is the amount of investments that the Kam-chatka Territory aims to attract in the coming years in order to implement projects that should create a new economy in the region

INTERNET FOR ACCELERATED DEVELOPMENT 26Eastern Siberia and the Far East will be one of the most powerful drivers of economic development in

Russia. Reliable communication channels, which are currently being developed in the region, constitute the most important element of success in the state programme for the economic recovery of the east-ern regions of our country

FINDING THE MISSING PIECE 30Our agency announced that 59 private investment projects amounting to $15.6 billion were launched in Russia from August to October, 2012. It seems that this rapid growth in investments has very much to do with the end of a turbulent election period. Foreign capital investments intensified significantly, which seems that, in the long run, it will form the basis for medium-sized industrial business companies

NEW INDUSTRIAL PARKS 36Today, industrial parks in Russia are developing thanks to local initiatives. Private business compa-nies have realized that parks can offer a large scope for investments, whereas regional authorities see them as a means to attract foreign investments

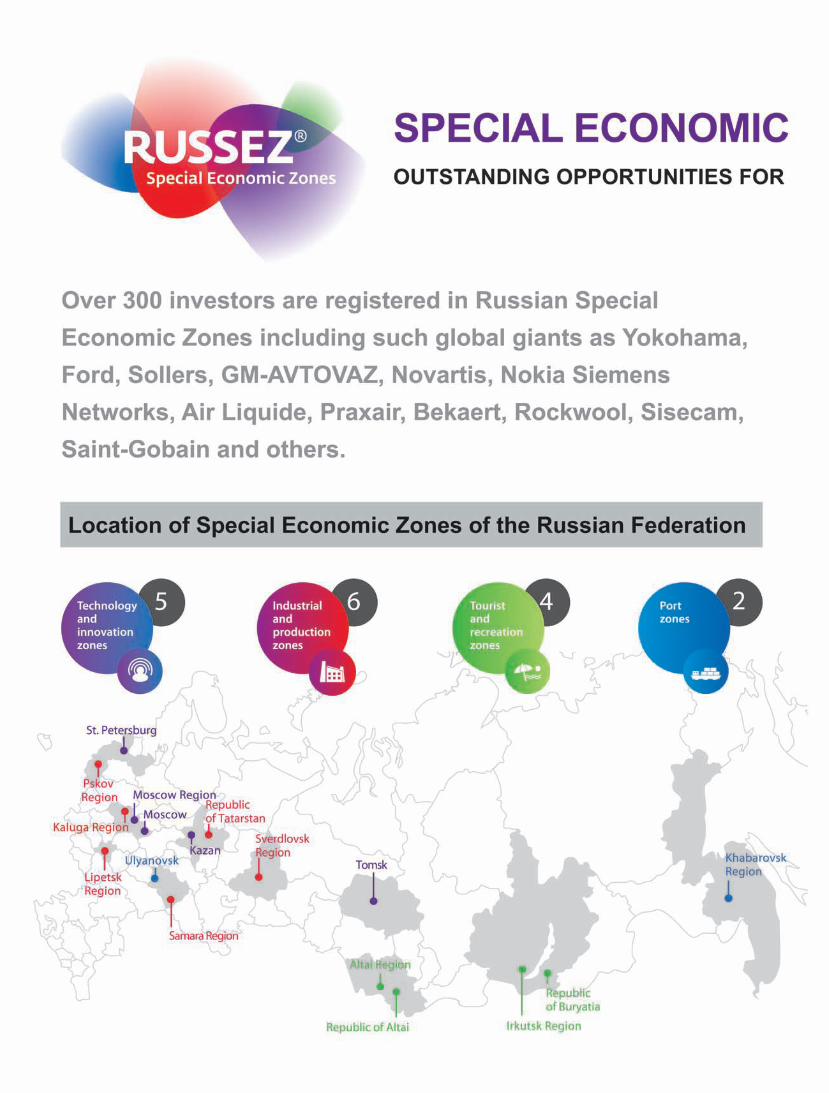

OUR SOURCE OF PRIDE:A NEW ECONOMY 44More than USD 2.5 trillion has been invested in the Russian economy during the post-Soviet pe-riod. One can dispute the efficiency ratio of these investments, but it is definitely not equal to zero. Without getting into discussions about moderniza-tion, several sectors have already been updated and new sectors have been formed.

WHAT WE ARE PROUD OF:OUR LEADERS 50

WHAT WE WILL BE PROUD OF: BREAKTHROUGH AREAS 51Growth potential has been built up in several sec-tors. However, the most serious challenges, prima-rily domestic ones, have yet to be met in order to achieve these targets

STRATEGIES OF STATE-OWNED COMPANIES:NO PARTICULAR AMBITIONS 56The planning horizon at large state-owned com-panies has been extended to 10-20 years. No particular achievements have been planned over this period

IMPORTANT BUSINESS TRENDS: CUSTOMER AND INVESTOR UNIONS 57A new wave of consumer demands and active mod-ernization of fixed assets propelled the manufac-

turing industry to the top of the leadership list in developing dynamics

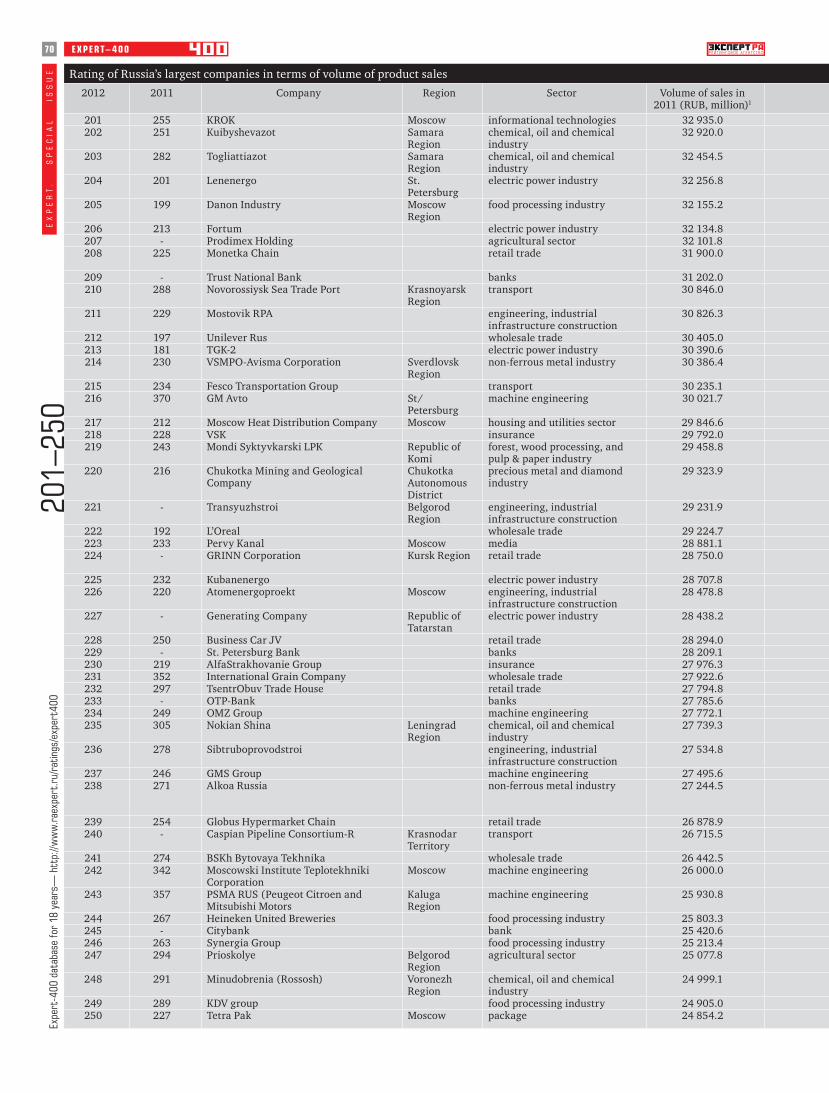

RATING OF RUSSIA’S LARGEST COMPANIES IN TERMS OF VOLUME OF PRODUCT SALES 62

THE APPROACHING THIRD WAVE 78Attention to the social sphere and fiscal discipline, as well as good communication with federal bod-ies — that is the recipe for minimizing investment risks in the post-crisis period. The new wave of investment attractiveness growth will be gener-ated by former peripheral regions with moderate levels of wages

Content

EX

PE

RT

.

SP

EC

IAL

IS

SU

EGeneral Director: Alexandr PrivalovFinance Director: Andrei BoldinInvestment Director: Viktor SuvorovCommercial Director: Tatiana KopitsaDeputy General Director for Sales and Distribution: Yuri MukhtarovSubscription Director: Olga KuleshovaDirector of Retail Distribution: Alexandr TsyganovRegional Development Director: Pavel MarkarianProduction Director: Boris KaganIT Director: Evgeniy Maltsev

Commercial Department:Director for Customer Relations: Irina VaravinaDirector for Advertising Agencies: Tatiana DunyushkinaConsolidated Sales Service:Tel.: (495) 510 56 45, [email protected]: Evgenia Chernysheva, Elena Samokhina,Alexandra Voloshina, Violetta Kreshchuk, Anna Astafurova, Oksana Khromova,Victoria Panik, Olga Kiseleva, Anna Timoshenkova, Irina Sapozhnikova, AnnaRyzhovaHead of Creative Department: Oleg GolovnevHead of Design Team: Elena Drugush

Coordinator of Regional Advertising Group: Anastasia Kosareva

Regional and International Applications:Chief Editor: Alexandr Sychev

Regional, Industrial, and International Project Group:Tel.: (495) 637 94 72, [email protected]: Sergei MaslovSenior Manager: Antonina KorushenkovaSenior Manager: Yulia GnezdilovaManager: Marina Kiryukha

Chief Editor: Valery Fadeev

First Deputy Editor: Tatiana Gurova

Deputy Editors: Pavel Bykov, Alexandr Ivanter, Dan Medovnikov

Scientific Editors: Dmitry Grishankov, Alexandr Privalov

Copy Editor: Helena Saet

Art Director: Sergey Zheglo

Executive Secretary: Asya Arakelian

Creative Director: Kirill Rubtsov /

Designer: Alexandr Kozlov / Infographics:

Liudmila Kadilova /

Artists: Konstantin Batynkov, Sergei Kalinin / Photo Department Director:

Alexandr Sidorov /

Photo Editor: Nika Ziangirova / Photoreporter: Oleg Serdechnikov /

Production and Publishing Department: Vladimir Kotov (Head), Andrei Korobko;

Larisa Son, Mikhail Streltsov /

Scanning: Sergei Biryukov, Konstantin Kudryavtsev /

Layout: Natalia Starodubova, Piotr Kuzmin (designer) /

Literary Editing: Inna Sretenskaya, Anna Shafran /

Proofreading: Olga Ventskovskaya, Miroslava Kurenkova, Liubov Fedetskaya /

Assistant Executive Secretary: Elena Platonova /

Material from following agencies was used to publish blocks of news: AK&M, Interfax, MFD-InfoCenter, Prime-TASS, RosBusinessConsulting, Finmarket, Associated Press. Circulation certified by the

National Circulation Service /

Telephone of Advertising Department of Expert Journal: (495) 510 5645 / Advertising in regional editions of Expert: (495) 789 4465 / Advertising on website: (495) 755 8396 / Group for Work with

Industrial Companies: (495) 637 9472, Fax: (495) 637 9473 / Editorial address: 24 Pravdy St., 6th floor (NGK), 125866, Moscow / Mailing address: POB 33, 127137 Moscow. E-mail: ask@expert.

ru / Website: www.expert.ru / Editorial Board Secretariat – (495) 789 4465, Fax (495) 228 0078; Editor-in-chief, General Manager, Art Director, Deputy Editors, Scientific Editor.

Editorial Departments: Economics, Politics, International, Companies and Management,

Economic Activities, Innovation, Culture and Society, Information Service, Industry, Editorial Office of Regional Operations, Layout, Rewriting, Typing Pool, Photo Archives, Artists, Printing – (495) 789

4465. Administrative Departments: Marketing, Human Resources, Legal – (495) 789 4465. Information Technology – (495) 228 0080, Accounting - (495) 609 6625 / Subscriptions – 8800200 80 10

(toll free for residents of the Russian Federation) or (495) 789 4465, ext. 1393. E-mail: [email protected]; Please call toll-free number at 8800200 8010 in case your subscription is not accepted,

Expert Journal is not available for sales, terms of delivery are not respected, and any other shortcomings in our work.

We take no responsibility for the accuracy of the information published in advertisements and news reports from information agencies. The Editorial Office does not provide reference information. Reprints

from the Expert Journal are allowed only upon agreement with the publisher. Subscription index in the catalogue of the Rospechat Agency 72550. Founder – MediaHolding Expert CJSC. Registered by

Federal Service for Supervision in the Sphere of Telecom, Information Technologies and Mass Communications (ROSKOMNADZOR) under PI No. ФС77-53054 from March 4, 2013.

Published by Expert Group CJSC. ISSN: 1812-1896.

Printed by OJSC «Pushkinskaya ploshchad» (Pushkin Square) Publishing House, 4D Shosseynaya Str., 105948, Moscow. Circulation: 3 000 copies.

Open price. © Expert Group CJSC, 2013.

V IEWPOINT4E

XP

ER

T.

S

PE

CIA

L

ISS

UE

ergei Yurevich, what is your overall assessment of the Russian economy? Which economic indicators are important for foreign investors?

— The Russian economy is developing rapidly. In general, we can make a positive evaluation for GDP growth, the unemployment rate, the government debt

level, and the amount of gold reserves. Let me remind you that our economy grew by 3.4% in 2012. This is lower than in 2011, when growth stood at 4.3%, but higher than the growth rate of world economy, which, I remind you, increased by 2.5%. We can say that unemployment is at the lowest and quite favourable level — 5.5%. Inflation has dropped by almost half since 2008 — from 13% to 6.6%. It was 6.1% in 2011 — a record low. As of January 1, 2013, the volume of gold reserves amounted to over 530 billion dollars. This is 77% more than in 2007. I can say with certainty that all these posi-tive indicators are the result of the government’s economic policy. Even though, in many ways, the Russian economy isn’t growing as fast as we would like.

— Let’s talk about foreign investments: What factors consti-tute the appeal and, inversely, risks of the Russian economy for foreign capital?

— It’s common knowledge that investments in Russia mean a high rate of return. High investment opportunities in Russia are dependent on a good domestic market, which is capable of provid-ing demands for any kind of project. Our domestic market has a population of 140 million, and if you include the Customs Union with Kazakhstan and Belarus, that makes 169 million people. In such a case, the purchasing power of people in Russia is growing, and that’s very important because household incomes haven’t de-clined as in some countries, but on the contrary, average incomes have increased. Don’t forget about the geopolitical position of Rus-sia, which is located at the junction of Europe and Asia, and our country’s highly educated population. On the other hand, these attractive points can be equated with risks that are traditionally associated with Russia.

— What are these risks?— The main risks are connected to our economy’s dependence

on the price of traditional Russian exports — oil and gas. Another risk, which is very real, is corruption. Unfortunately, there is a dis-crepancy between the law on paper and how it is applied in practice. However, it should be noted that this negative image, which doesn’t always correspond to reality, doesn’t play in favour Russia. We can’t say that everything’s rosy in the garden. But, our image is worse than what is really true. And, do you know who’s saying that? The companies that already have experience implementing projects in Russia. If you look at foreign companies that already have projects in Russia, more than 70% say that they’re satisfied with their decision to invest, and believe that their investments are successful. Well, those companies that don’t have experience working in Russia focus on external sources, which often distort reality. We’re not trying to make it look better than it really is, but we want the information about our country to be objective. We understand that it’s necessary to fill that information gap, which leads to distorted information. So, we’re now actively working in this direction.

— What should the state do in order to improve the investment climate in our country?

— The government has focused on eliminating obstacles, which foreign companies in Russia are talking about. By the way, these are very specific targets. They include procedures that an investor must go through before launching his business in Russia, and especially the time and costs involved. In addition to putting a company into operation, we’re talking about the cost of doing business and the degree of state control. The experience of different regions suggests that under current federal legislation and with no drastic changes, it’s quite possible to create favourable conditions for investors. The main lesson that we’ve learnt is that what matters is the motivation of regional and local authorities. If they want to attract investments, and this, by the way, refers not only to foreign investments, if they want to develop the business industry, then all the tools they need are already there… they just have to want to use them.

— In your opinion, what areas of investment into the Russian economy are particularly attractive to foreign companies?

— I think that we can’t single out any particular areas. It’s where the investor sees himself, where he wants to go, and that’s where we can help. I happened to mention the word “help”. As long as institutions supporting investments haven’t been formed, such manual support is sometimes essential. Especially in cases when the investor, before launching his project, is informed about spe-cific conditions, then it turns out that this information doesn’t correspond to reality. In such cases, “manual” support is actually required. Therefore, all investments are important to us, but of course, “long-term” projects are more appreciated. We’re ready to support any kind of production or service that companies may want to locate in Russia. At the same time, if you remember, five so-called presidential priorities were designated in 2008. These were power engineering and energy efficiency, telecommunica-tions and aerospace technology, nuclear technology, medicine and pharmaceuticals, and computer technology and software. Having announcing these priority sectors, we proceeded from where we actually needed new technologies and new competency. Therefore, the development potential of these industries is reasonably high. We have human resources capable of absorbing these investments and implementing projects in these areas.

— What might be some ways to encourage federal and local authorities to attract foreign investment?

— We have to admit that profile ministries sometimes behave irresponsibly towards investors. If you feel that a foreign company is intruding into a territory with too much attention from the gov-ernment, then you should say at once that you don’t welcome that company’s investments. That will be fair, and such an answer is sometimes possible. However, the most irresponsible and harmful policy possible, which we have unfortunately witnessed, is when interest in foreign investments is shown at the very beginning. And then, when company arrives, it runs into various bureaucratic dif-ficulties, when authorities are too embarrassed to say directly that they’re just not interested in these investments, and start setting up the nine circles of hell. That’s totally unacceptable. If the federal and regional ministries think that they’ll always have a long queue

Alexei Grammatchikov

Vector — 70 billion in foreign investmentsThis year, Russia hopes to attract foreign investments amounting to 55 billion dollars. In the near future, the Russian government plans to raise the annual volume of attracted foreign capital to 70 billion dollars or more. Sergei Belyakov, Deputy Minister of Economic Development of the Russian Federation talks about this in an interview with the magazine Invest in Russia

–S

5

of investors at their door, then they’re sadly mistaken. In order to break this cycle, we’ve developed a system of key performance indicators for heads of federal ministries and heads of constituent subjects of the Russia Federation, where the important indicator will be the volume of attracted investments. Because there’s noth-ing that destroys Russia’s image more than examples of unsuc-cessful investments. The worst scenario for investors is when real actions don’t correspond to earlier statements. This undermines their confidence.

— How does the state of the global economy influence the process of attracting investment into Russia?

— Unfortunately, the growth rate of global economy has slowed down. The volume of investment resources that exists in world mar-kets isn’t growing either. According to various estimates, it’s now about one and a half trillion dollars. Private funds and investors are now quite careful in choosing investment options; they prefer to save rather than invest. These conditions impose even greater

V IEWPOINT

EX

PE

RT

.

SP

EC

IAL

IS

SU

E

Sergei Belyakov, Deputy Minister of Economic Development of the Russian Federation

OLE

G S

ERD

ECH

NIK

OV

V IEWPOINTE

XP

ER

T.

S

PE

CIA

L

ISS

UE

6

demands on our country. Creating comfortable conditions for doing business, we must do something to prevent investments from fleeing to other countries, and encourage them to come here. I repeat, we have tremendous opportunities for investments, but we don’t use these opportunities to the full extent.

— Can Russia become a “safe haven” for global investment funds?

— We’re still a very long way from becoming a “safe haven”. Of course, we’d love to be just that, but you need to be very effective in questions related to business reforms. So far, we’ve announced our priority, but when this priority is expressed not only in words but also in daily work operations performed by specific officials, then Russia can, and will, at last, become a “safe haven” for invest-ments. Foreign investors find it impossible to even get through to some of our colleagues. After several months, they can’t even reach and just talk to administration officials of any ministry. Moreover, representatives of some ministries don’t even bother to meet and establish some sort of dialogue.

— What examples of successful foreign investments could you name?

— We have examples in various fields. For example, in the high-tech field, when foreign companies created R & D centres here. We can recall investment projects in the automobile industry, wood processing, pharmaceuticals, and many other areas. Unfortunately, there aren’t as many projects as there could be; once again, this is partly due to the unfavourable environment, in part because of the cautious attitude towards investments prevailing throughout the whole world. Incidentally, even in China, the growth rate of foreign investment has slowed down.

— What are some examples of unsuccessful foreign investments?

— These are infrastructure projects with enormously inflated budgets. Moreover, they concern government, and not foreign investments. And that’s depressing. It means that we could use our investment resources more prudently. As to purely foreign projects, well, there aren’t any clearly unsuccessful examples because for-eign companies take them very seriously at the early decision-making stage. However, as failures, I could mention the projects that could have been initiated, but failed to take off because of red tape and the demotivating behaviour of regional and federal officials; after meeting and talking with these officials, investors decided not to invest. There are examples when it was difficult to defend completed investments, bearing in mind the position of

regional authorities and heads of municipalities. This is typical, for example, in regions such as the Krasnodar Territory, where investors are informed first about some investment conditions, and then there’s a completely different approach in practice. Generally speaking, this generates a strong distrust of the government, and it contributes to the unfavourable image of Russia that we have to fight against. To call a spade a spade — in such cases, officials often act in their own selfish interests. That explains why they lobby in favour of companies connected to themselves in some way or another and allocate contracts with inflated costs. We need to get rid of these practices.

— In your opinion, how will the global economy develop in the near future, and how will that affect investments in Russia?

— I’d really like to be optimistic and say that we’re on the thresh-old of economic growth. Unfortunately, I can’t say this for the time being. The examples of the European Union show us that when economically wealthy countries have to support economically weak countries, they’re forced to spend their own resources on them. On the other hand, we’re also seeing the crisis of the so-called welfare state. When the state, which provides quite a high quality standard of living, has to rethink its policy in this time of economic crisis, that is, how and what to spend its money on. The question arises — is the pace of economic growth compatible to the obligations which the state itself is responsible for? What is the source of these com-mitments? It’s still possible to maintain this balance in Russia.

We can definitely say that Russia isn’t interested in seeing the global economic crisis get worse. Today, the world’s economy has become so globalized that it’s better for Russia if the global economy grows and not drops. But, Russia’s economy has reserves of stability thanks to the fact that today, Russian economy is largely depend-ent on government actions. Although we’re open to the outside world, although we’ve joined the WTO, we’re still more focused on ourselves. 2008 showed us that we can readjust quickly enough. By the way, the actions of the Russian government were greatly appreciated by the international community at that time.

— And how do you feel about the problem related to the out-flow of capital from Russia?

— This is definitely a problem. If we talk about it, we must un-derstand that it’s not all about capital flight. These figures show transactions made by foreign companies abroad and the acquisition of foreign assets. That’s what it really is — normal economic activ-ity, which is linked to moving and shifting capital assets abroad. Of course, we’d rather see investors buying something here, and not abroad. The outflow, which we register, often turns around and comes back as influx through offshore companies. This means that offshore companies are used as a kind of insurance against legislative risks that exist in our country. Nevertheless, this money comes back because investment yield is high in Russia. This year, we’re planning to attract foreign investments amounting to 55 bil-lion dollars. That’s roughly the same as in 2012. In general, we’re seeking to attract 70 billion dollars per year.

— What are the special features of today’s Saint Petersburg Forum?

— This year’s forum is being held under the slogan — “Global Economic Prospects: Time for Decisive Actions”. In the first place, forum participants will be invited to discuss economic and social impacts of the global crisis, the unstable nature of global economic recovery, changes in the balance of powers existent in the world, and new technological opportunities. In addition, this year is the year of bilateral cooperation between Russia and Germany, and Russia and the Netherlands. In this regard, Angela Merkel, Chan-cellor of Germany will attend the Forum, and the visit of the prime minister of the Netherlands has also been planned. We hope that many interesting discussions will be held and solutions to today’s complex economic problems will be found at the Saint Petersburg Forum. ■

High investment opportu-n i t i es i n Russ i a a re dependent on a good domestic market, which is capable of providing demands for any kind of project

he Agency for Strategic Initiatives (ASI), created on the initiative of Vladimir Putin, President of Russia, in the spring of 2011, has now become an important institution to accelerate social and economic devel-opment in the country. The Agency facilitates the implementation of the most promising projects in

different social and economic sectors. In addition, it formulates strategic goals in order to improve the investment climate in our country, simplify administrative procedures, eliminate bureaucratic barriers for business and promote appropriate programmes worked out with its participation. Andrei Nikitin, the General Director of the Agency talked about its work and operations.

— Last May, in fact, your agency celebrated its second birth-

day. What have you managed to achieve in this period of time?— The Agency was created to promote the most promising

projects initiated by private business. We should select promising proposals, promote them, and help them obtain financing and overcome administrative barriers. These projects must be socially relevant, innovative, supply imported products to our country, or be competitive in foreign markets. To date, entrepreneurs have submitted nearly 4,000 projects to the Agency — 205 are being as-sessed and 59 have been approved by the Supervisory Board, which is headed by Vladimir Putin, the President of Russia.

But, our tasks are not limited to this work. We must work towards radically improving our country’s investment climate. After all, the motive to establish ASI stemmed from unsatisfactory evalua-tions related to investments and doing business in Russia, which were outlined by the business community. At the time the Agency was launched, Russia was at the bottom of almost all the rating scales, which are regularly compiled by international research organizations.

— These rating scales are often very biased…— That’s right. Moreover, some are even very biased, and it’s

certain that all of them get something wrong. Even the World Bank’s rating scale — Doing Business — in which Russia took 124th place at the time that ASI was launched and which we’ve decided to focus on in order to understand in which direction the country is developing, isn’t quite accurate, although this organization’s assessment method is the most transparent and clear. In particular, the World Bank bases its rankings on surveys of business companies. Business owners fill out questionnaires based on some of their own ideas about what it once was like, and their poor awareness of the current situation. Our entrepreneurs are often not very well informed about the positive activities of our government in one direction or another, and so, they unwittingly tend to distort the observations made by the World Bank.

However, it’s not the fault of business, but rather a mistake made by the authorities themselves, which aren’t active enough in communicating the essence of their actions to the general public. In general, information awareness in all segments of society and coordination among different government agencies have become extremely acute problems in Russia. We don’t know how to communicate our achievements to a broad audience; we don’t know

how to conduct a dialogue with the business sector; we aren’t able to show what’s being done and what’s being planned. Among other things, all this generates just another confidence issue.

— Does the Agency help to solve this problem? Is it an active member of this much talked-about dialogue between business and the government or is it just a formal observer?

— It’s important to get live feedback from the business community in order to efficiently and objectively assess the efforts of the authorities to engage business companies in the management process for improving the business climate. A positive experience of dialogue between business and government can be seen in the project — The National Business Initiative to improve the investment climate in the Russian Federation (NBI). The project includes action plans proposed by entrepreneurs to simplify, accelerate and reduce the cost of procedures associated with running a business, and currently functioning in territories of the Russian Federation. This initiative is being implemented by the Agency pursuant to instructions issued by V.V. Putin, President of the Government of the Russian Federation on December 21, 2011.

V IEWPOINT8E

XP

ER

T.

S

PE

CIA

L

ISS

UE

Alexander Sychev

Standardizing our countryThe Investment Standard will be introduced in all the regions of Russia as of this year. It is aimed at significantly improving the business environment in our country and bringing the positions of authorities and entrepreneurs closer on a large number of issues related to the development of regional economies

T

The work format is very important. Work areas were proposed by the business community itself. We’ve established cooperation with professional and entrepreneurial business associations. First of all, these include associations such as Klub Liderov (Leaders Club), the CCI, Opora Rossiyi (Support of Russia), Delovaya Rossiya (Russian Business), and the RUIE. Together with other business organizations specializing in different fields, the Agency forms working groups that include entrepreneurs, experts and officials. Together, they develop a “roadmap” that includes specific actions, timeframes for their realization, and agencies responsible for implementing them. In fact, these maps are a compromise between the entrepreneur and authorities.

After the “roadmaps” of the NBI have been worked out and approved (first, by the Supervisory Board of the ASI, then by a Government order), the Agency monitors their implementation. An important feature of monitoring the implementation of these “roadmaps”, which is conducted by the ASI, is that it’s carried out by the entrepreneurs themselves.

Eight “roadmaps” have already been approved and implemented; they deal with problems related to exports, obtaining building

permits, power supply connections, customs clearance, registration of property and companies, promoting competition and improving antimonopoly legislation, and procurement of state monopolies.

Work on a number of maps, in particular, the simplification of tax administration and appraisal activities, has almost been completed. These documents may be submitted at the next meeting of the Supervisory Board of the ASI.

— Are you certain that these roadmaps will be implemented in practice?

— We believe that publicity, both during the development of roadmaps and the monitoring phase, will be the most important guarantee of quality implementation in practice.

This is why in May we launched a public discussion portal — “Investment Climate RF” — concerning the implementation of roadmaps. This portal will allow entrepreneurs from any region of the Russian Federation to take part in projects to improve the investment climate, and assess changes in the country. It’s important to get feedback from entrepreneurs in order to understand how the implementation of certain points can simplify, accelerate and reduce

9V IEWPOINT

EX

PE

RT

.

SP

EC

IAL

IS

SU

E

Andrei Nikitin, the General Director of the Agency for Strategic Initiatives

10

costs of procedures for doing business in the country, which is very important for further decisions.

— Attracting investments isn’t just a question of activities provided by experts and business, but also a question of effective information. According to Ernst & Young, 85% of foreign entrepreneurs have a very distorted view of Russia; some of them go so far as to believe that bears can be seen wandering around the Red Square; some are afraid of the incredible crime rate, others believe that we have a terrible investment climate and therefore don’t plan to do business in Russia...

— ...At the same time, 64% of foreign companies, already operating in Russia, plan to expand their work operations in our

country! They believe that we do have some problems, but they aren’t catastrophic, that it’s quite possible to work here and make a very decent profit.

Where do such split opinions come from? The problem is in the correct positioning of our country’s investment potential in global markets. The fact that we haven’t created an information space that would allow foreign investors to obtain comprehensive information about our country, regions, projects and opportunities so that they may compare and immediately see and assess possible risks. In general, the availability of advanced information space isn’t so important to investors who are interested in our large consumer market. They’ll come here in any case, if only there is a financially sound demand. However, for investors bringing in new technologies, it’s extremely important to see the complete picture.

Even we, at the Agency, didn’t have the complete picture when we started working. It was obvious that some regions were more successful than others, but it wasn’t clear what they had done in order to become successful. So, we tried to collect data and analyze the reasons for the achievements of the regions, whose economic growth rate was higher than the national average. However, these regions are very different from each other with regard to resources, geographical location, and workforce potential.

It turned out that rapidly growing regions had a well-established system for attracting investments and working with the business community. For example, last year, direct foreign investments in Tatarstan increased six-fold — from 99 million dollars to 577 million dollars. Thanks to what? The Republic founded its own agency to attract foreign investments, improved its legal frame-

work, developed a system for benefits and preferences, and is trying to establish a dialogue between business and the authorities. The same scenario can be observed in the Kaluga, Ulyanovsk, Sverdlovsk and Lipetsk Regions.

At the same time, we saw that some regions are, at times, actu-ally trying to reinvent the wheel or striving to copy someone else’s experience, although not always so skillfully. So, a strategic objec-tive arose — to instill a common denominator in existent regional management practices.

— Do you mean the Standard for executive authorities, which was introduced in our country last year?

— Last year, it was introduced in eleven pilot regions; two more

regions began to carry out the project independently. At the end of last year, at a meeting of the State Council, the implementation of this Standard was considered successful; it was decided to extend it to all the regions.

So, we tried to identify the best practices and formulate a certain standard that would be available to everyone. However, I want to emphasize that the 15 points laid out in the Standard do not at all impose limits on other possibilities or wishes. This is only a man-datory minimum, creating a single temporary base; the regions should be guided by it, but they should continue moving forwards. It’s like the services of a large bank or, for example, the Russian Post — they can be used anywhere, they have specific standard everywhere. Investors should receive a simple set of services, which are laid out in the Standard, in all the regions. Each region should provide a clearly defined and accessible investment strategy, a plan for infrastructure construction, the Investor Protection Act, the Council for improving investment climate, a specialized organiza-tion to attract investments, and a unified regulation for investment support according to the “single window” principle. I think that it’s not necessary to enumerate all the points. They’re just as specific as those that I’ve mentioned. Beyond that, each region should set its priorities and start working as hard as possible on their own competitive advantages.

— You once said that the secret to the success of leading regions fundamentally lies in three factors that differentiate them from all the other constituent subjects of the Federation — the determination and will of regional heads, an effective and coordinated management team, and a truly equal dialogue with the business community…

V IEWPOINTE

XP

ER

T.

S

PE

CIA

L

ISS

UE

Rapidly growing regions had a well-

established system for attracting

investments and working with the business

community

11

— These are extremely important components for success, but, of course, the list is far from exhaustive. Determination alone isn’t enough. For example, in business, executives are retrained at least every two years. Representatives from the authorities should also be retrained. They should have the opportunity to learn about best practices completely and methodically, and not accidentally stumble upon them in the course of their work. Let me give you an example. Maintaining and developing a complex diversified economy requires coordinating strategies to attract investments with strategies for developing higher and secondary vocational education. Such coordination has been established in Tatarstan. There, university and college administrations know where their graduates will go, and what competence they will need. Investors have remarked this factor as one of the major advantages of the republic. I think it should be so in every region if it doesn’t want to be the private domain of a single plant or a single industry.

— Is it possible to involve entrepreneurs in creating a more favourable investment climate and a general business environment in the regions? As far as can be judged, business distrust of official authorities is strong, and moreover, so is the reluctance of authorities to burden themselves with the different views of entrepreneurs.

— That’s why the mechanism for implementing the Standard, developed by the Agency, is based on enforcing dialogue. Distrust can be overcome only through communication and collaboration. Moreover, the results of implementing the Standard in administrative work practice are submitted to entrepreneurs selected in the expert group by the Agency. It’s a pool of experts, which, in addition to regional entrepreneurs, also includes professional consultants, representatives of the academic community, and federal business communities.

The control system is very effective. There was one case that involved one of the requirements of the Standard, namely, that a plan for developing infrastructure sites in the region should be worked out for investors. In addition to such a plan being available, it should also be comprehensible. Anyway, in Kaluga, employees of the Ministry of Economy submitted for approval a business plan for infrastructure development to the expert group, but the members of the group refused to approve it; the proposed plan was very difficult to put into operation. The office had to do some more work on it, and three months later, they introduced an interactive map, whereby any untrained person could choose the type of infrastructure and see when and where these sites of interest would be built. This means that any investor can now quickly and easily identify possible sites for locating his business.

Such a control system isn’t limited to the implementation process. Even now, expert groups in pilot regions, where the Standard was introduced in 2012, have started the monitoring process. The institutions that were created or reformed within the framework of the Standard should act, and not just exist. Their functionality will also be evaluated by the business community in the future.

Once again, dialogue between the parties is crucial. It was during the discussion on “roadmaps” according to the National System of competences and qualifications that I was able to overcome my own doubts about the need to improve the investment climate in our country. It turned out to be extremely interesting for business. The plan should create conditions for re-training specialists and supplying the economy with highly qualified personnel.

At the May conference — “National system of competence and qualifications: from personnel disasters to a long-term policy” — Andrei Belousov, the Minister of Economic Development cited the following data — in real economy, Russia employs 67 million people, of whom 31 million work in large and medium-sized businesses, 15 million are employed in small business companies and individual enterprises, and 4 million are temporarily unemployed. What do

the other 17 million Russians do, and what qualifications do they have? The new ASI programme should create a national system for competence and qualifications. Currently, the share of highly skilled workers employed in the economic field reaches 16%. It should be at least 33% by 2020.

Now, we should clearly indicate questions related to motivating people to improve their skills, better assess necessary investments in vocational education, and carefully think out a system for validating qualifications. This “roadmap” was prepared by academic scholars, experts, and business representatives — a total of 3,200 people from more than 100 organizations. As a result of this programme, the economic sector should welcome 4.5 million graduates from a modern system of vocational education, whose knowledge level will almost equate a bachelor’s degree, and about 20 million people will be retrained.

— The experience in implementing the Standard for executive authorities in pilot regions was considered successful. In your opinion, when can statistically set changes be expected?

— The first results will hopefully be marked in statistics by the end of 2013. The implementation of the Standard is already noticeable; the situation has changed in pilot regions; systemic shifts in the relationship between business and government have become apparent. The Standard can make a serious contribution to the rising popularity of Russia and its regions as an investment platform. Moreover, constituent subjects of the Russian Federation will cease to be “blank spots” on the world map for foreign investors. Having seen that the basic rules of the game are the same everywhere, even regional entrepreneurs, who are used to operating within their own administrations, will become bolder and enter the federal level or move towards neighbouring regions.

We hope that statistical data will confirm our speculations and allow us to evaluate business efficiency, understand how clear rules for attracting investments affect GDP growth rate, and improve the economic structure of the regions and the country as a whole. On this basis, it’ll be possible to determine the next steps in the formation of a coherent system for attracting investments into our economy.

By the way, last year, Russia rose to the 112th place in the Doing Business rating scale. Of course, this isn’t because of the Standard, but the result of steps taken at the federal level within the framework of implementing “roadmaps” of the National Business Initiative. However, I’m sure that standardized regional efforts to attract investments and create a favourable business climate will firmly propel Russia closer to global leaders.

For reference:The first roadmaps, approved by the Supervisory Board of the Agency: “Supporting access to foreign markets and export promotion”, “Improving Customs administration”, “Improving access to energy infrastructure”, and “Improving the business climate in the construction sector” were ratified by the Government of the Russian Federation on June 29, 2012, June 30, 2012, and August 16, 2012.

In addition, in December 2012, the following roadmaps were approved: “Improving the quality of public services in cadastral registration of immovable property and state registration of rights to and transactions in immovable property”, and “Developing com-petition and improving antimonopoly policies” under orders of the Government of the Russian Federation dated December 1, 2012 and December 28, 2012.

Under the order of the Government of the Russian Federation dated March 7, 2013, the roadmap — “Optimizing procedures for the registration of legal entities and individual entrepreneurs” was approved in March, 2013.

The deadline for implementing 126 points as part of seven road-maps was set for the period from July 2012 to April 2013. ■

V IEWPOINT

EX

PE

RT

.

SP

EC

IAL

IS

SU

E

V IEWPOINT12E

XP

ER

T.

S

PE

CIA

L

ISS

UE

he Russian Direct Investment Fund, the capitalization of which is estimated at $10 billion US, was created for investments in the most promising and rapidly growing sectors of the economy. Kirill Dmitriev, Gen-eral Director, talked about the fund’s activities and operations.

— This year, the Russian Direct Investment Fund (RDIF) will be two years old. What has it achieved? How many projects have been implemented with the participation of the RDIF, and in which sectors?

— We’re already seeing good payoffs – both for specific projects and for general trends. During the first year of the fund’s existence, the number of long-term investors, who are will-ing to step up their investments in Russia, has doubled— from 25% to 48%. This isn’t just an inner feeling, but objective data.In the first quarter of 2013, Russia received $60.4 billion US in foreign investments. This is 65.4% more than in the first three months of 2012. Direct foreign investments in the Russian economy amounted to $6.3 billion US in January— March, 63.2% more than in the same period last year.

Our fund has attracted dozens of major partners over two years. I’m talking about leading companies. Their investments into our country were a signal for other investors to start working with Russia. Since it was launched, the RDIF has attracted a total of $2.3 billion US, $500 million US of which are the fund’s own assets. The RDIF has also attracted $3.2 billion US of foreign capital into the Russian economy, building a number of long-term strategic partner-ships. We continue to work actively with strategic investors, the re-sults of which will be announced at the Saint Petersburg Forum.

In the very near future, we’ll also tell you about new investments in such sectors as IT, agricultural equipment, manufacturing, and oth-ers. We try to cover the most popular and most promising industries.An example of such significant transactions would be investments in the Moscow Stock Exchange, and then, our programme to support pre-IPO. We have attracted an entire consortium with the partici-pation of the BlackRock and Templeton Funds, and, according to co-investment procedures, we also support Russian companies that are prepared to invest on the Moscow Stock Exchange.

We’d like to draw your attention to the geography of our partners. In a literal sense, they are all major regions, from where we might expect major investments. We launched an automatic co-investment mechanism with the Kuwait Investment Fund. Along with AGC Equity Partners, we attracted the largest investment in history from the Middle East into OJSC Enel OGK-5— $175 million US for a total of $600 million US in transactions. In Europe, we’re working closely with the Caisse des Dépôts and the Eastern Committee of German Economy. By the way, today Germany is one of the largest and most successful investors in the Russian economy.

Another priority region— APEC countries. An investment con-sortium was created together with the State Bank of India— up to a billion dollars in bilateral projects. The Russian-Chinese Invest-ment Fund was founded on an equal footing with the CIC – we’re planning to invest up to two billion dollars in projects, and attract

the same amount from outside sources. Our countries have com-mon needs and rapidly growing markets. So, we’re talking about both good investment revenues and the development of our mutual economies. A similar scheme was launched in Japan: within the framework of the Investment Platform, we plan to invest in priority regions, above all in the Far East.

— The fund was established as a classic capitalist enterprise; its main purpose is to make a profit. However, when the fund was established, the initiators still referred to the “five indus-tries for modernization and five sectors for innovation”, that is, they were worried about priority areas in our country. Was this all just wishful thinking or have you taken them into account somehow? What are the Fund’s investment priorities? How are work operations in these areas coming along?

— I’ll remind you that the capital of the fund is very substantial— up to $10 billion US, while, in fact, we’re not limited to making a special selection of industries. But, our priorities remain the same as at the beginning: these are areas that should make our economy more efficient and more competitive. On the one hand, the state is interested in their development; on the other hand, they are in great demand, they are needed by both the population and the business community. By selecting these projects, we’re giving investors an opportunity to make large profits, especially by today’s standards, and modernizing the economy at the same time.

Take transportation and logistics – these are basic sectors for mod-ernization among other priorities of the RDIF. Shortcomings in infra-structure and technology are very significant in these fields. If enough tools are provided, investments in these areas will be very extensive and profitable. Vnesheconombank has considerable experience in in-frastructure projects, and we’re actively working with the Chairman of Vnesheconombank, Vladimir Dmitriev, on different joint projects.We’re talking about long-term investments, that is, a market where funds and companies tend to act quite carefully. I’m sure that as soon as global investors see a payoff, we can attract them into more complex industries. For example, into the aerospace industry, which, again, is listed as a priority.

— How far do investment realities differ from the original wishes of the initiators of the Fund?

— Most of the industries designated when the fund was launched proved to be truly interesting for investors. In fact, we even had to think more broadly. During the selection process, we saw that many other spheres corresponded to our interests, had a high profitability rate and promoted modernization. So, we invested in a network of high-tech medical centres in the Russian regions, and we attracted the world’s largest investment fund – BlackRock – as a partner.

Investors have great expectations with regard to the consumer sector and infrastructure. We have repeatedly pointed out that the Russian middle class has grown three times over the past five years, and this is a guarantee for product and service demands, which can be provided by respective companies. Therefore, the fund has focused on healthcare, an efficient urban environment and other consumer segments.

During the IPO, the RDIF, together with BlackRock, Russia Part-ners and other qualified investors bought shares in the MD Medical

Alexander Sychev

A big country for profitable investmentsAgainst the background of ongoing difficulties in the global economy and an investor confidence crisis, Russia, with its growing economy, is looking more and more attractive, a fact that is reflected in the steadily increasing volume of foreign investments

T

13

Group, which manages the largest network of private prenatal clin-ics in Russia. Another good example is the purchase of a controlling stake in Karo Film, carried out jointly with Baring Vostok Capital Partners and UFG.

If we talk about the difference between wishes and reality, of course, we need to expand the list of investment instruments to infrastructure and other needed areas. We need to issue infrastruc-ture bonds, attract pension funds, and work out special incentives for specific industries, such as green energy.

— Currently, the state is trying to launch new developments in the eastern territories. As an investment company, are you interested in the distant border regions of our country? What prospects do you see for your Fund and your partners in Eastern Siberia and the Far East?

— In our opinion, these regions present many advantages. No one disputes the fact that APEC countries represent a new source of growth, and one of the very few existing today. The eastern territories mean convenient locations and resource bases, that is, there are great conditions here for deep processing projects, and many others as well.

As I said before, we have several major partners who are know-ingly interested in the Far East and Eastern Siberia. We’ve agreed to work actively in these regions along with the CIC and the Russian-Chinese Investment Fund, as well as with our new partners – the Ja-pan Bank for International Cooperation. We associate the main per-spectives with transport, logistics and other infrastructure projects to create high added value and alternative energy solutions. It’s

worth noting that there are already positive results— at the begin-ning of the year, the RDIF announced the first investment made by the Russian-Chinese Investment Fund into Russia Forest Products, the second largest timber processing company in Russia.

— How do you go about looking for investment projects or selecting co-investors?

— When we built a fund management team, we tried to in-clude competent industry executives. They’re highly competent people, and they’re familiar with practical work, and not theo-ries, and as a rule, they’re also familiar with several sectors. Our task is to choose the most effective and promising of all avail-able projects and bring them to the stage of actual transactions.As for the selection of co-investors, the RDIF is trying to attract the largest and most competent partners so that the others should try to catch up to them. However, we introduce funds and companies to Russian possibilities in a clear and strong manner and explain the benefits. Many potential investors have started showing interest on their own, and then they join the list of our partners.

What are the guidelines for the Fund with the Russian regions? Only rapidly growing regions can rely on reciprocity and show decent profitability, that is, those who don’t have it so bad in terms of direct investments?

— The participation of authorities, with an interested approach on their part, in the true sense of the word, eliminates many risks for investment projects. If a regional administration focuses on at-tracting investments, it can be considered, as a rule, as an already rapidly growing region. These constituent subjects usually have

V IEWPOINT

EX

PE

RT

.

SP

EC

IAL

IS

SU

E

Kirill Dmitriev

V IEWPOINT14E

XP

ER

T.

S

PE

CIA

L

ISS

UE

good experience in raising private funds by the time the RDIF arrives.

Investment projects are successful, especially where invest-ments are welcome. We don’t have strict restrictions with regard to economic indicators of the regions, with which we should work. It’s clear that if you rely on large investments, you need to take a proactive stance. The main thing for us is good potential and a high interest in investments, and in principle, that can be said of most Russian regions. We have a few RDIF agreements with constituent subjects of the Russian Federation, in particular, with the Krasnoyarsk Territory, Saratov and Leningrad Regions, the Republic of Bashkortostan and Tatarstan. Our documents contain secured agreements on the establishment of a favourable invest-ment climate and the development of future projects. Governments, which sign such memorandums, inform the fund of potentially attractive projects. Moreover, such transactions always mean new technologies and industries, and new jobs for the constituent sub-jects themselves.

— Direct Investment Fund acts not only as co-investor with other companies, but it also creates joint investment funds with similar organizations, and even other countries. What form is preferable? How do they differ from each other, and what ad-vantages do they present?

— Our fund functions in various formats; first and foremost, they differ in their objectives. We do have a few, I would say, strategic partners with whom we expect to work long and effectively. Bilat-eral joint funds have been established with China; we’ve launched the total investment platform with Japan, and a cooperation agree-ment with India. The largest state-owned financial institutions of partner countries are involved in such transactions. In this format, we have the opportunity to invest in an entire package of industries and projects that lie in the field of economic interests of our respec-tive states. If we’re talking about an individual perspective project, then we’ll use a standard mechanism of co-investments and attract profile companies and funds.

— How does the ongoing global economic crisis influence the Fund’s work operations? There are fewer investments and profits are declining…?

— In a sense, the global crisis has played into the hands of invest-ments into Russia. We’re seeing a growing deficit and an investor confidence crisis in the financial world. Against this background, Russia is starting to look much more attractive than many other countries. According to IMF forecasts, Russian economy will grow from two to three trillion dollars in the next five years. In addition, investors tend to trust countries with low levels of external debt, which is true of the Russian Federation.

— It’s estimated that today some 30 trillion dollars can be called free assets that are ready to be invested through-

out the world. There are very many contenders for this money. What advantages does Russia have so that we can hope to acquire a significant portion of these funds?— Returning to the subject of growth, I’d say that it’s namely growth and development that constitute the main advantage for Russia and the main prerequisite for investment interest. Many developed econo-mies are close to stagnation, while the relatively slow rate of GDP, even low by our own standards, makes our country appealing to investors.Russian GDP has also increased and even when calculated per capita. Therefore, spheres focusing on the end user of-fer very promising opportunities to multiply investments.In Davos, the RDIF launched a new initiative called “Russia means growth!” Within the framework of this programme, we tell interna-tional investment communities about real economic performance indicators of the Russian Federation, whose dynamics are actually much greater than those mentioned by western statistics.

— By the way, in April, the U.S. representative trade office in Moscow (incidentally, America isn’t our biggest investor) sud-denly publicly declared that the investment climate in Russia was unfavourable. What is your partners’ opinion?

— Our partners continue to invest in Russia, in-creasing their f inancial placements. I think that suf-f ic ient ly character izes their posit ion on this issue.Of course, the economic community has much to complain about in relation to Russian realities. The Russian Federation has yet to eliminate many administrative barriers for investors and what is also very important, dispel many stereotypes.

T he economic situation is not always represented as it real-ly is in Russia. With the participation of Ernst & Young and the Moscow State University Centre of National Intellectual Re-serve, we recently conducted a study on the outflow of capital. It turned out that the indicators announced for 2011 were in-flated by at least two times. In fact, given the nature of trans-actions, the situation with capital outflow from Russia is com-parable to such economies as Kuwait, Norway and Japan.In this case, judging by new research studies – “The confidence barometer for direct investment funds”— such structures have maintained their interest in the Russian market. Early last year, only 11% of the foreign investors believed Russia to be one of the most attractive places for investment. This figure rose to 19% in nine months. Potential and existing partners primarily focus on the large volume of the Russian domestic market, a cost-balanced and high-quality labour force, potential growth of productivity and advanced telecommunications.

— The idea of establishing the Fund was f irst an-nounced at the Saint Petersburg Investment Forum. You have, so to speak, “a family bond” with it. What importance does the forum represent for the f und?— For the RDIF, the Saint Petersburg Forum is, above all, a platform where we can work with the international investment community. Wherever major funds and companies gather, we can see the op-portunity to attract new and effective partners to our projects. This year, the Petersburg Forum will have a special meaning for us.As you know, Russia is chairing the “Group of Twenty”, and in our opinion, as many benefits as possible must be gained from this situation. In this regard, our fund has been an active participant in the working group – “Investments and Infrastructure”, within the framework of “Business Twenty”. Several meetings have al-ready been held, at which business representatives developed preliminary recommendations on restoring economic growth, primarily by improving the investment climate and expanding joint infrastructure investments. Officially, we’ll present these recommendations at the Saint Petersburg Forum, during which the B20 summit will take place. Then our proposal and those of other working groups will be discussed by the leaders at the “Group of Twenty” in September. ■

Our fund has attracted dozens of major

partners over two years. I’m talking about

leading companies. Their investments

into our country were a signal for other

investors to start working with Russia

IN FOCUS16E

XP

ER

T.

S

PE

CIA

L

ISS

UE

o prepare the operational Development Strategy of the Khanty-Mansiysk Autonomous District — Ugra up to 2030, a Territorial Information System (TIS) was created, various data on all industrial sectors was collected, and public hearings were held, dur-ing which the inhabitants of the region could talk

about their vision for Ugra’s future and put forth suggestions for regional development. TIS will keep track of real changes in regional development parameters: it will collect, store, process information and make it available to the general public through official government portals of the autonomous district on the basis of information exchange agreements.

In addition, a Community Council was formed to implement the Strategy — 2030 — a permanent body, the composition of which will be updated annually. Members of the Council will provide public and expert support for the execution of the Strategy. “The Strategy is aimed at ensuring sustainable development, enhancing Ugra’s current and future potential, improving living standards, and guaranteeing long-term regional development.” stated Na-talia Komarova, Governor of the Khanty-Mansiysk Autonomous District — Ugra. “However, the Strategy is not just a picture of the future, but a roadmap which will help us to move forward from the very first day of adoption of the document. The Strategy update system will incite action — we are introducing a new approach to Russian strategic planning, involving periodic updating of the base document along with complex scientific and expert support of such work on an ongoing basis.”

A Solid Base as Before, but not Only OneThe Khanty-Mansiysk Autonomous District — Ugra is a very spe-cial region of Russia. In 2012, Ugra took first place in oil extrac-tion, including gas condensate (50.3%) and power electricity production (8%), and second place in gas production (4.9%), industrial production (7.6%) and amount of tax revenues paid into the budget of the Russian Federation, and third place in terms of investments in fixed assets.

Oil is still the main asset of the region, ensuring our country’s energy security. More than half of Russia’s global share of oil production is extracted here. For more than half a century, Ugra oil has been a major source of revenue for the federal budget and the cornerstone of Ugra’s economic power, contributing more than 63% GRP of the district.

However, regional oil production has recently gone through hard times; the region entered a period of natural decline in oil production. The record 360 million tons produced in 1985 has become a page in history. This record volume will not be repeated. 278.4 million tons of oil were extracted in 2007; production volume dropped to 259.9 million tons in 2012. There are several reasons for this slide: the instability of global prices for hydrocarbons may threaten the price of Russian oil, making it drop to a $40 US per barrel and forcing mining companies to save on investments, the after-effects of perestroika, reduced exploitation drilling, insuffi-cient geological exploration of new deposits and slow development of surveyed fields. Finally, the old deposit fields have been depleted

Alexander Sychev

Improving What’s GoodIn the past few years, the Khanty-Mansiysk Autonomous District — Ugra has been actively improving its investment climate. Today, the modernization of investment conditions is required in order to implement new socio-economic goals, outlined in Ugra’s Development Strategy up to 2030

T

Natalia Komarova, Governor of the Khanty-Mansiysk Autonomous District — Ugra

17

— a total of more than 10 billion tons of oil has been produced in Ugra. The Governor of the district cites these reasons amongst many others: “In the last decade, most of the oil companies operat-ing in the district have not implemented their projects in terms of drilling new wells or improving the effectiveness of existing ones. Geological surveys were made in 2002, but they ensured only half of the standard growth of hydrocarbon reserves. The state is no longer able to take care of preparations for new reserves.”

The current period of turmoil in the world economy has clearly demonstrated the vulnerability of a resource-based economy. Al-though oil still represents a fairly long-term base for the regional economy, it has become quite obvious that it would be unreason-able to continue building society around this unique resource only. Therefore, two fundamental goals are defined in the new Strategy. First of all, as oil will remain the foundation of Ugra’s economy in the foreseeable future, oil companies should be encouraged to extend and recover the mineral and resource base: exploration of new deposit fields, introduction of advanced technology to enhance the output in old beds, and development of geologically complex deposit fields. According to experts and oil companies, at least another 20 billion tons of oil can be recovered from Ugra’s deep reserves, that is, twice as much as was produced in previous years. “All participants should have a clear understanding of their responsibilities for the recovery of the mineral and resource base.” said the Governor. However, this sense of responsibility cannot arise in a complete vacuum. Therefore, in order to stimulate in-vestments in fixed assets, and increase the volume of geological surveys, two laws were adopted in Ugra. Companies engaged in investment activities in the fuel and energy sector and in geo-logical prospecting will be exempt from profits tax and corporate property taxes. This will come to a total of roughly 19.7 billion rubles. “These measures will help stabilize oil production and increase the volume of geological exploration carried out in Ugra by different companies.” said Natalia Komarova confidently.

In fact, Gazprom Neft’s implementation of shale oil extraction technology is in line with the region’s strategy on innovative de-velopment of the oil-producing industry. Projects to develop and introduce new technologies in extracting reserves in the Bazhenov Suite and other hard-to-recover reserves will be implemented as innovative projects. Ugra’s hydrocarbon deposits are mostly found in multi-layer beds, requiring new production techniques.

In addition, the value and economic importance of small- and medium-sized oil-producing companies and service companies using innovative methods to enhance oil recovery will increase substantially in Ugra in the coming years. This will be facilitated by a set of support measures drawn up by Ugra authorities.

Current efforts are already yielding positive results — almost 260 million tons of oil were produced in 2012; the production decline rate decreased from 2.5% in 2009 to 1.2% in the past year. Eight new fields were put into operation, 3,888 new exploitation wells were drilled, while the volume of exploitation drilling ex-ceeded 13.6 million meters.

In the period from 2013 to 2020, it is expected that the fol-lowing fields will be put into operation: Priobskiy, Prirazlomny, Malobalykskiy (OJSC Rosneft NK), the southern sections of the Priobskiy deposit (OJSC Gazprom Neft), as well as the Samot-lorskiy (OJSC TNK-BP Holding) and Fedorovskiy sections (OJSC Surgutneftegaz). In total, it is planned to invest more than 15 trillion rubles in the oil-producing industry up to 2030. Neverthe-less, by the end of the current Development Strategy, the share of mining operations, including oil drilling, will drop to 40% in Gross Regional Product. Based on unique regional advantages, the Strategy will kick off a new phase of economic diversification, development of culture, education and healthcare, and create a more comfortable lifestyle. That constitutes the second important objective of the Strategy.

Diversification through ClustersThe current protracted global economic crisis has enabled experts to identify a number of Ugra’s economic sectors that have resisted external negative influences. In the medium term, the electric power sector is projected to have the highest growth rate. Today, Ugra’s electric power engineering is redundant. Regional power plants produce more than 75 billion kilowatt/hour of electricity per year, whereas just over 60 billion kW are consumed. Taking into account the implementation of all the investment projects and the prospects for exploiting resources in the Polar Ural Region, electricity consumption will very quickly exceed available surplus and inevitably, there will be a very serious obstacle to the develop-ment of Ugra’s economy, which many regions of our country must face today — lack of energy. Therefore, the number of investment projects related to electric power engineering is second to Ugra’s petrochemical cluster (see Table). Currently, Surgut State District Power Stations 1 and 2 and the Nizhnevartovsk State Power Sta-tion are being rehabilitated, while the Nyagan State District Power Station is being built.

In addition, new low capacity power plants are under construc-tion. Oil-producing companies are mainly engaged in this field. The fact is that in the early 2000s the federal government decided to stop ineffective flaring of valuable hydrocarbons — associated petroleum gas (APG) — and imposed a penalty factor.

Since January of this year, the ratio in the formula for calculat-ing payments for inappropriate use of APG (in fact — penalties) in-creased from 4.5 to 12, and will reach 25 as of next year. “In 2011, fines exceeded 350 million rubles, and the amount has increased significantly in the past year. These fines are distributed between three levels of the budget: 20% go to the federal budget, 40% — to the regional and local budgets respectively. Seeing that the decree of the Government of the Russian Federation, increasing penalties for non-normative amounts of gas flaring, has come into force, our fines will be very high this year.” confirmed the Governor.

Thanks to the motivating effect of this decree, the Ministry of Natural Resources and Environment of Russia believes that roughly 44.4 billion rubles will be invested in APG utilization projects, and that the gas utilization indicator will reach 95% by 2014. In the Khanty-Mansiysk Autonomous District — Ugra, the level of 89% was attained last year against 85.3% in 2011.

Utilization of APG for the production of heat and electricity is the simplest way to avoid a penalty, but gas processing projects for a broad fraction of light hydrocarbons (NGLs) used for the produc-tion of polymers are still a priority for the autonomous district. Next year, two processing plants will be launched in Ugra. One will be built by RN-Yuganskneftegaz. Projected power capacity of this plant will reach 1.2 billion cubic meters per year. The other plant, with similar power capacity, will be constructed by RussNeft.

Forestry has also recently become a highly efficient industry in Ugra. The region is rich for all kinds of forestry industries: wood-cutting areas total up to 24.7 million cubic meters. Only 7.5% of this wood is currently used. A target programme was approved to develop the forest industry. Nine projects have been planned for timber processing and production of particle boards, plank timber, fuel pellets, and other products. Companies are investing their own and borrowed funds — roughly 10 billion rubles. The district budget will contribute about 307 million rubles. Ugra will use these funds mainly as subsidies allocated to investors to offset part of the cost of interest payments on loans. In addition, forest management work has been financed by funds from the district treasury. Budget funds were not assigned to directly finance cer-tain projects, but to encourage private investments in the timber industry. As a result, the volume of processed wood will increase by 17% in the district.

In general, all the industries that form the new “skeletal struc-ture” of Ugra’s economy can be grouped into four geographically-

IN FOCUS

EX

PE

RT

.

SP

EC

IAL

IS

SU

E

18

industrial clusters. In addition to the petrochemical and forestry sectors, mining and innovation and technology clusters should also be mentioned. Each of them shows enormous potential.

Huge reserves of various minerals, especially numerous in the Polar Urals, will form the base for the mining cluster. Today, deposits of coal and silica, peat and building materials have been well explored. There is also a rock crystal sub-province in Ugra, where several deposits and occurrences of raw quartz have been discovered. Here, the Polar Quartz Company is building a mod-ern complex for the production of high-purity quartz concentrate and powder for nano-electronic, optical, lighting technology and chemical industries. The project will be completed in 2015.

The High-tech Technopark has become the base for the innova-tion and technology cluster. Since it was launched in 2009, the Technopark has registered 74 innovative companies, whose pro-duction output totaled more than 600 million rubles in 2012.

The Technopark was designed with constantly improving tech-nological infrastructures to encourage successful innovative ac-tivities. In particular, it is home to the Certification and Analysis Centre and the Network Centre for collective use of unique scien-tific equipment. A Prototyping Centre was launched here in 2011; its equipment produces 3D-model products ordered by innovative enterprises. The Technopark will open branches in major cities of the region. Such a Technopark network and government support will provide an effective innovation environment in the region. Ugra’s innovative companies receive subsidies and grants from the Department of Economic Development of the autonomous district, and grants from the Entrepreneurship Support Fund. In total, more than 55 million rubles and counting private investments — about 400 million rubles — have been invested in scientific and technical spheres from different sources.

The next challenge is to promote and develop Ugra’s infra-structure. It is planned to create a Ugra Technopolis and build industrial parks and technology platforms in the large cities of the autonomous district. In this way, an important number of re-search and science and innovation potentials will be concentrated in one large area in view of generating new ideas, creating new products, technologies, and promoting fundamental and applied research.

In addition, an educational system has been included in the district’s innovation process. Coherent programmes for gen-eral, vocational and further education have been implemented in Ugra; they take into account specific features of regional economy and the socio-cultural development of concrete ter-ritories. “We will improve the effectiveness and targeting of investments in human capital, relying on the development of modern education and science, high-tech healthcare, improving the quality of social services, and facilitating access to culture and sport. The purpose of such investments is to create the best conditions allowing for the comprehensive development and maximum self-fulfillment of Ugra’s inhabitants. Ugra is rich in talent and we should create a fertile environment that will en-able them to materialize, create innovative ideas in the region, and work towards maintaining our competitiveness and the district’s sustainable development.” announced the Governor of Ugra, Natalia Komarova.