Characteristics of Socio-Technical Systems 1 Introduction to the Concept of Socio-Technical Systems

Upload

independentCategory

view

5download

0

1

CHAPTER-1

INTRODUCTION

1.1 INTRODUCTION TO THE CONCEPT OF STUDY

Inventory management is the process of efficiently

overseeing the constant flow of units into and out of an

existing inventory. This process usually involves controlling

the transfer in of units in order to prevent the inventory

from becoming too high, or dwindling to levels that could put

the operation of the company into jeopardy. Competent

inventory management also seeks to control the costs

associated with the inventory, both from the perspective of

the total value of the goods included and the tax burden

generated by the cumulative value of the inventory.

Balancing the various tasks of inventory management means

paying attention to three key aspects of any inventory. The

first aspect has to do with time. In terms of materials

acquired for inclusion in the total inventory, this means

understanding how long it takes for a supplier to process an

order and execute a delivery. Inventory management also

demands that a solid understanding of how long it will take

for those materials to transfer out of the inventory be

established. Knowing these two important lead times makes it

possible to know when to place an order and how many units

must be ordered to keep production running smoothly.

2

Calculating what is known as buffer stock is also key to

effective inventory management. Essentially, buffer stock is

additional units above and beyond the minimum number required

to maintain production levels. For example, the manager may

determine that it would be a good idea to keep one or two

extra units of a given machine part on hand, just in case an

emergency situation arises or one of the units proves to be

defective once installed. Creating this cushion or buffer

helps to minimize the chance for production to be interrupted

due to a lack of essential parts in the operation supply

inventory.

Inventory management is not limited to documenting the

delivery of raw materials and the movement of those materials

into operational process. The movement of those materials as

they go through the various stages of the operation is also

important. Typically known as a goods or work in progress

inventory, tracking materials as they are used to create

finished goods also helps to identify the need to adjust

ordering amounts before the raw materials inventory gets

dangerously low or is inflated to an unfavourable level.

Finally, inventory management has to do with keeping

accurate records of finished goods that are ready for

shipment. This often means posting the production of newly

completed goods to the inventory totals as well as subtracting

the most recent shipments of finished goods to buyers. When

the company has a return policy in place, there is usually a

sub-category contained in the finished goods inventory to

3

account for any returned goods that are reclassified as

refurbished or second grade quality. Accurately maintaining

figures on the finished goods inventory makes it possible to

quickly convey information to sales personnel as to what is

available and ready for shipment at any given time.

In addition to maintaining control of the volume and

movement of various inventories, inventory management also

makes it possible to prepare accurate records that are used

for accessing any taxes due on each inventory type. Without

precise data regarding unit volumes within each phase of the

overall operation, the company cannot accurately calculate the

tax amounts. This could lead to underpaying the taxes due and

possibly incurring stiff penalties in the event of an

independent audit.

1.2 THEORETICAL BACKGROUND

A manufacturing inventory consists of three different parts:

raw materials, work in process and finished goods. Using a

leather crafting business as my sample craft company, here are

definitions and examples of the three:

RAW MATERIALS

This type of inventory includes any goods used in the

manufacturing process, such as components used to assemble a

finished product. Raw materials may also include partially

finished goods or materials. For example, for an orange juice

company, oranges, sugar and preservatives are raw materials;

4

while for a computer manufacturer, chips, circuit boards and

diodes are raw materials. Inventory items may be classified as

raw materials if the organization has purchased them from an

outside company, or if they are used to make components.

WORK-IN-PROCESS

Work-in-process inventory items are those materials and parts

that are waiting to be made into something else. These may

include partially assembled items that are waiting to be

completed. Work-in-process inventory items may include

finished goods that have not yet been packaged and inspected,

as well as raw materials that have moved from storage to a

preassembly area. For example, in an orange juice company, the

oranges may come in to a storage area, where they are raw

goods, but once they have been moved out of the storage area

and onto the assembly line for juicing, they become work-in-

process inventory. In a small company, work-in-process goods

may be stored in the same area as raw materials and finished

goods.

FINISHED GOODS

Finished goods are any products that are ready to be shipped

out or sold directly to customers, including to wholesalers

and retailers. Finished goods may be waiting in a storage area

or on a shop floor. If the amount of inventory of finished

goods increases faster that the amount of raw goods and work-

in-process goods, then production may need to slow down until

more finished goods are sold. In some businesses, goods are

5

not included in the finished goods inventory until they are

sold. For example, in companies where goods are made to order.

1. To meet anticipated demand.

2. To smooth production requirements.

3. To decouple operations.

4. To protect against stock-outs.

5. To take advantage of quantity discounts.

6. To permit operations.

7. To help hedge against price increases.

8. To take advantage of order cycles.

VARIOUS COSTS ON INVENTORY

Inventory procurement, storage and management is

associated with huge costs associated with each these

functions.

INVENTORY COSTS ARE BASICALLY CATEGORIZED INTO THREE

HEADINGS:

1. Ordering Cost

2. Carrying Cost

3. Shortage or stock out Cost & Cost of Replenishment

a. Cost of Loss, pilferage, shrinkage and

6

obsolescence etc.

b. Cost of Logistics

c. Sales Discounts, Volume discounts and other

related costs.

ORDERING COST

Cost of procurement and inbound logistics costs form a part of

Ordering Cost. Ordering Cost is dependant and varies based on

two factors - The cost of ordering excess and the Cost of

ordering too less.

Both these factors move in opposite directions to each other.

Ordering excess quantity will result in carrying cost of

inventory. Whereas ordering less will result in increase of

replenishment cost and ordering costs.

These two above costs together are called Total Stocking Cost.

If you plot the order quantity vs. the TSC, you will see the

graph declining gradually until a certain point after which

with every increase in quantity the TSC will proportionately

show an increase.

This functional analysis and cost implications form the basis

of determining the Inventory Procurement decision by answering

the two basic fundamental questions - How Much to Order and

When to Order. How much to order is determined by arriving at

the Economic Order Quantity or EOQ.

7

CARRYING COST

Inventory storage and maintenance involves various types

of costs namely:

Inventory Storage Cost

Cost of Capital

Inventory carrying involves Inventory storage and management

either using in house facilities or external warehouses owned

and managed by third party vendors. In both cases, inventory

management and process involves extensive use of Building,

Material Handling Equipments, IT Software applications and

Hardware Equipments coupled managed by Operations and

Management Staff resources.

INVENTORY STORAGE COST

Inventory storage costs typically include Cost of Building

Rental and facility maintenance and related costs. Cost of

Material Handling Equipments, IT Hardware and applications,

including cost of purchase, depreciation or rental or lease as

the case may be. Further costs include operational costs,

consumables, communication costs and utilities, besides the

cost of human resources employed in operations as well as

management.

COST OF CAPITAL

Includes the costs of investments, interest on working

capital, taxes on inventory paid, insurance costs and other

costs associate with legal liabilities.

8

The inventory storage costs as well as cost of capital are

dependent upon and vary with the decision of the management to

manage inventory in house or through outsourced vendors and

third party service providers.

Current times, the trend is increasingly in favor of

outsourcing the inventory management to third party service

provides. For one thing the organizations find that managing

inventory operations requires certain core competencies, which

may not be in line with their business competencies.

Secondly in case of large-scale warehouse operations, the

scale of investments may be too huge in terms of cost of

building and material handling equipments etc. Besides the

project may span over a longer period of several years, thus

blocking capital of the company, which can be utilized into

more important areas such as R & D, Expansion etc. than by

staying invested into the project.

1.3 REVIEW OF LITERATURE

Praveen, Singh (2008)1 on his paper “Inventory and working

capital management: an empirical analysis” tries to evaluate

the effect of the size of inventory and the impact on working

capital through inventory ratios, working capital ratios,

trend analyses. Finally, the study found that the size of

inventory directly affects working capital and its management.

F.Samiloglu and K.Demirgunes, (2008)2 on his paper “The effect

of working capital management on firm profitability: Evidence

from Turkey” aim of the study is to analyze the effects of

9

working capital management on firm profitability. Empirical

findings of the study show that accounts receivables period,

inventory period and leverage effect firm profitability

negatively; while growth (in sales) affects the firm

profitability. Results suggest that firm profitability can be

increased by shortening accounts receivables and inventory

periods.

AcaDemon Kanyanyuz(2005)3 in his paper “Fixed Asset Inventory

System” with the objective to design and develop a database

that will maintain the asset registers. The project emphasis

was mainly put on tracking the assets of the organisation

hence development of a register that will be used by the

auditors who come to audit the organization. The main the

objective was tracking assets of the organisation whereas this

project is looking at the managing of stocks meant to be sold.

______________________________________________________________

_____________

1.Praveen Singh, “Inventory and working capital management: an

empirical analysis”, the ICFAI Journal of accounting research,

apparel 2008, vol.7, No.2.pp.53-73.

2.Samiloglu and K.Demirgues, “The effect of working capital

management on firm profitability: Evidence from Turkey”, the

international journal of applied economics and France, 2008,

vol.no.2 (1), pp.44-50.

10

3.AcaDemon,(2005) Inventory Control Systems-Inventory control

systems as related to overall Production for a company.

[Online] http://www.academon.com/lib/paper/57872.html 15th

September 2005

B.J. Grablowsky, (2005)4 on his paper “Financial management of

inventory” surveyed small business inventory management

practices and compared with techniques commonly employed by

large corporations. It appears that smaller firms rely on

simple controls. Of those small firms which did not use

quantitative methods for determining inventory order and stock

levels, the most common qualitative methods were "past

experience" and "executive judgment".

Bwire (2004)5 on his paper “Stores Management Information

System” determines the stock levels by computing the received

and distributed commodities. The aim of the study was to

provide an Automated Computerised System for securing, quick

evaluation and manipulation of records of goods received and

distributed at the store. The paper mainly deals with stores

looking at the aspect of goods whereby the control of services

is not tackled. Ronald .H.Ballou, (2000)6 on his paper “Evaluating inventory

management performance using a turnover curve” examines the

inventory turnover ratio. Turnover curve is used to estimate

the impact of changing the inventory control procedures or to

set new targets of inventory levels. It is simple yet powerful

11

tool for evaluating inventory managerial performance can be

developed from readily available company data.

4.B.J. Grablowsky, 2005 “Financial Management of Inventory”

International Journal of Production Economics, Volumes 93-94,

Pages 239-25.

5.Bwire (2004), Project report entitled Stores Management

Information System.

6.Ronald H. Ballot.”Evaluating inventory management

performance using a turnover curve” international journal of

physical distribution & logistics management, 2000, vol. 30.

Kibera (1996)7 in his paper “Introduction to Business” examines

Inventory in most organisations is the largest single

investment. Its therefore sensible that the management

understands what it is and also effectively controls it.

Automation of inventory will effectively maintain a sufficient

buffer stock for the smooth running of the organization.

LalithGoonatilake (1990)8 On his paper “Inventory management

in the manufacturing sector in developing countries” examines

that the industrialization policies adopted by developing

12

countries and assesses its impact on inventory management

factors influencing inventory demand are identifies and the

interaction between production planning and inventory control

is considered as a key parameter. A reversal of inventory

management objectives in the developing country environment is

brought to light where the efficiency objective is given more

significance then the cost objective.

______________________________________________________________

_____________

7.Kibera.N. (1996), “Introduction to Business”, a Kenya

Perspective. Kenya Literature Bureau.

13

8.Lalithgoonatilale. (1990). “Inventory management in the

manufacturing sector in developing countries” Engineering

costs and production economics, 19(1-3), pp19 -24

1.4 STATEMENT OF THE PROBLEM

Control of inventory, which typically represents 45% to

90% of all expenses for business, is needed to ensure that the

business has the right goods on hand to avoid stock-outs, to

prevent shrinkage (spoilage/theft), and to provide proper

accounting. Many businesses have too much of their limited

resource, capital, tied up in their major asset, inventory.

Inventory Management ties up capital, requires handling, uses

storage space, deteriorates, sometimes becomes obsolete,

requires insurance, incurs taxes, can be stolen or gets lost.

Inventory must be considered at each of the planning levels

with production planning concerned with overall inventory,

master planning with end items and materials requirements

planning with components parts and raw material. The primary

function of inventory is buffering and decoupling. It serves

as a shock absorber between customer demand and the

manufacturer’s production capability, between input materials

required for an operation and the output of the preceding

operation, between the manufacturing process and the supplier

of raw materials.

1.5 OBJECTIVE

14

To categorise the inventory and highlight the most valued

items for manufacturing process.

The determine the effectiveness of existing inventory

management system.

1.6 SCOPE OF THE STUDY

The scope of the study is to analyse the inventory model

for Pricol Limited with the past 3 year’s reports (2010-2012).

Effectiveness of the present inventory system is also studied

with the help of information collected by questionnaire from

the employees who are in charge on each module in the

organisation.

1.7 METHODOLOGY

1.7.1 TYPE OF STUDY

The study carried out is descriptive research study. To

find the effectiveness of the existing inventory system and to

suggest the techniques which are helpful for further effective

control.

1.7.2 TOOLS FOR DATA COLLECTION

15

Secondary method of data collection is done through

websites, books, journals and annual records of the

organisation.

Primary data using questionnaire.

1.7.3 TOOLS OF ANALYSIS

Ratio Analysis

Percentage analysis

1.8 LIMITATIONS

The study depends more on the secondary data.

There might be personal bias.

1.9 CHAPTER SCHEME

INTRODUCTION

16

The chapter provides an introduction to the concept of

study, explains the theoretical background of the study, the

various review of literature, statement of problem, list of

objectives of study, explain various sources of research and

sample design, statistical and financial tools used in study,

scope of study and limitations.

ORGANISATIONAL PROFILE

This chapter provides details about the organisation

which includes history, management details, organisational

structure and board of directors, product profile and market

potential, information about competitive strength of company,

future plans and overall description of various functional

areas.

MICRO MACRO ECONOMIC ANALYSIS

This chapter briefly discuss about the prevailing

economic scenario with respect to the organisation

ANALYSIS AND INTERPRETATION

This chapter shows the implementation of various

statistical and financial tools for analysis of inventory and

financial performance and interpretation of results.

CONCLUSION

This chapter organises the various results and analysis

discussions and provide recommendations suggested to the users

of research findings.

17

CHAPTER-2

ORGANIZATION PROFILE

2.1 HISTORY OF THE ORGANISATION

Premier Instruments & Controls Limited is primarily an

Automobile Ancillary Unit with diversification in the recent

years into Electronic Control Instruments, Precision Machine

Tools, Panel and Sensor Instruments for Defence and Industrial

Gauges. Its main line of business is manufacture of auto

instruments and allied accessories.

The Company was established in 1972 and commenced

commercial production in the year 1975 with an initial

capacity of 4 lakh Nos. of Dashboard Instruments per annum at

its factory at Coimbatore.

The Company registered consistent growth in the turnover

over the years due to its dedicated personnel and commitment

to quality and service. Continuous Research & Development work

and multi disciplinary Engineering Base has strengthened its

capacity to cater to the changing needs of the end users

within a reasonable time. The Company has set up an assembling

18

unit at Gorgon, Haryana, with an annual installed capacity of

5 laky Nos. of dashboard instruments at better service to OME

customers. The production at assembling units.

The Company increased its installed capacity from 4

lakhs Nos.34.50 lakhs Nos. of Dashboard Instruments per annum

over the period and has emerged as the market leader having a

market share of more than 50% of OEM's requirements in the

domestic market, catering to the needs of almost all the

vehicle manufacturers in the country, besides meeting more

than 40% of the replacement market demand through the

countrywide dealers network.

The turnover of the company increased from RS.10lakh

during the year 1975 the year of commencement of commercial

production to RS.5419 in the previous year ending March 2013.

The Company has made a small beginning in Export of its

products with a turnover of Rs. 2.88 lakhs in 1985. The Export

turnover achieved during the last financial year ending 31st

March 2013- Rs.1752 lakhs. The Company is the first among the

few and only one in the automotive instrumentation field to

obtain the coveted ISO 9001 Certificate in this country.

During the year 1985, the Company has entered into

technical collaboration with M/s. NS International Ltd., U.SA.

(A subsidiary of M/s. Nippon Seiko Co. Ltd., Japan) for

upgradation of existing technology in the manufacture of

Dashboard Instruments for two wheelers.

19

During the year 1991-92, the Company has entered into

technical collaboration with M/s. Nippondenso Co. Ltd. Japan

for upgradation of technology in the manufacture of four

wheeler Instruments thereby improving upon its quality levels

and manufacturing methods to keep pace with the international

technological government in the instrumentation field.

The products manufactured by the company caters to the

needs of the established vehicle manufacturers like Maruti,

TELCO, Eicher, DCM, Kinetic Honda, Hero Honda, Escorts, TVS

Suzuki, Ashok Leyland, Mahindra and Mahindra, Bajaj Auto,

Bajaj Tempo, Tafe, Premier Automobiles, Hindustan Motors, etc.

Some milestones are,

1974- Established as premier instrument CBE limited (Plant 1)

1981- Renamed as premier instrument & control united.

1988- Established plant 2 at Gurgoan New Delhi.

1989- Started to manufacture defence products.

1997- Collaborated with Denso Corporation, Japan, to chalk out

the future growth plans of the company. Denso is the World’s

second largest auto ancillary company and has acquired 12.5%

of the equity capital of Pricol.

2004- Renamed as Pricol limited to leverage the brand name

“Pricol”. In the same year, the company established plant 5 in

Pune and PT Pricol surya in Indonesia to fulfil the

requirement of our OME customers in western India and

Indonesia respectively.

20

2007- Set up plant 6 in Bajaj Auto’s manufacturing park at

Pant Nagar, Uttarakhand.

2008- Commenced plant 7 in Tata motor’s Manufacturing Park at

pant Nagar, Uttarakhand; also established a new plant at

Malumichampatti, near Coimbatore in the same year.

2.1.1 CORPORATE VISION

Strive to attain leadership in all the products and

services that we provide, through socially and environmentally

acceptable means.

2.1.2 CORPORATE MISSION

Achieve leadership through constant innovation and continuous

improvement in every sphere of our activity. Enhance value to

our customers, employees, suppliers, shareholders and also

care for the society and environment around us.

2.1.3 CORPORATE CORE VALUES

Passion- Whatever we do, we do it from the

bottom of our heart

Respect- We respect those who add value to

our livesIntegri

ty- We never compromise on our values.

Collabo

rate

- We believe in working towards a

unified goalOwnersh

ip

- We are responsible for all our

actions

21

Listen- We listen to both the spoken and

unspoken before we act

2.1.4 QUALITY POLICY

Pricol will provide value and satisfaction to customers on

products and services. This will be achieved through:

Systematic training and motivation of employees

Complying with customer requirements and applicable

statutory/regulatory requirements

Continually improving the efficiency and effectiveness of the

Quality Management Systems

2.1.5 ENVIRONMENTAL AND OCCUPATIONAL HEALTH & SAFETY POLICY

Pricol is committed in carrying out occupational health,

safety and environmental friendly manufacturing and

management practices.

This will be achieved through

1. Established accident free environment.

2. Minimizing wastes to preserve natural resources.

3. Encouraging innovation to prevent environment pollution,

injury and ill- health.

4. Complying with all legislation, regulation & other

requirement agreed upon.

5. Creating environment preservation, occupational health

and safety awareness amongst interested parties and

2.1.6 TPM POLICY

22

Establish an excellent Total Productive Manufacturing system

with total involvement of all employees to achieve utilization

of all resources.

2.1.7 MANUFACTURING LOCATION AND THE ACTIVITIES UNDERTAKEN:

Plant 1- periyanaikan palayam, Coimbatore

Plant 1 is the mother plant of pricol and it located at

periyanaickan palayam 22kms from Coimbatore, Tamilnadu, India,

manufactures and services automotive instrument & accessories,

Marine instruments and electronic products.

Plant 2 – Gurgaon, Haryana – manufacturing of all products in

Pricol range for OEM customers in North India, namely, Hero

Honda, Maruthi Suzuki and Yamaha.

Plant 3- Chinnamathampalayam, Coimbatore.

Manufacture of pumps group products (mechanical parts ),namely

,oil pumps for two wheelers and stationary engines, Speedo

drive components for two wheelers, auto fuel cocks,valves,

gears and chain tensioners.

Plant 4-karanadai, Coimbatore.

This plant focuses on the electronic group products namely

fleet management solution (FMS), vehicle security systems and

counters& controls for textile machinery. Plant 4 also

manufactures PCBs(Printed Circuit Boards) to support

instruments product group.

Plant 5- Pune, Maharashtra

23

Manufacture of all products in pricol range for OEM customers

in Western India, namely, Tata motors, Mahindra &Mahindra,

Bajaj Auto and John Deere.

Plant 6&7-Pant Nagar, Uttarakhand

This plant is located inside Bajaj Auto’s manufacturing park

and manufactured instrument and pumps group products for Bajaj

Auto. Plant 7 is located inside Tata motor’s manufacturing

park and pumps group products for Tata motors and Hero Honda.

2.2 MANAGEMENT

2.2.1 BOARD OF DIRECTORS

The board of directors consist of 9 directors. The

company is being managed & controlled by the board of

directors. More than 50% of the board is comprised of

independent directors. The members of the board are well-

experienced professionals & industrialists. The day-to-day

management affairs is managed by the chairman & managing

director subject to the supervision ,control & subject to the

supervision , control & direction of the board of directors

and is assisted by the executive Directors and the President &

chief operating officer.

The board of directors:

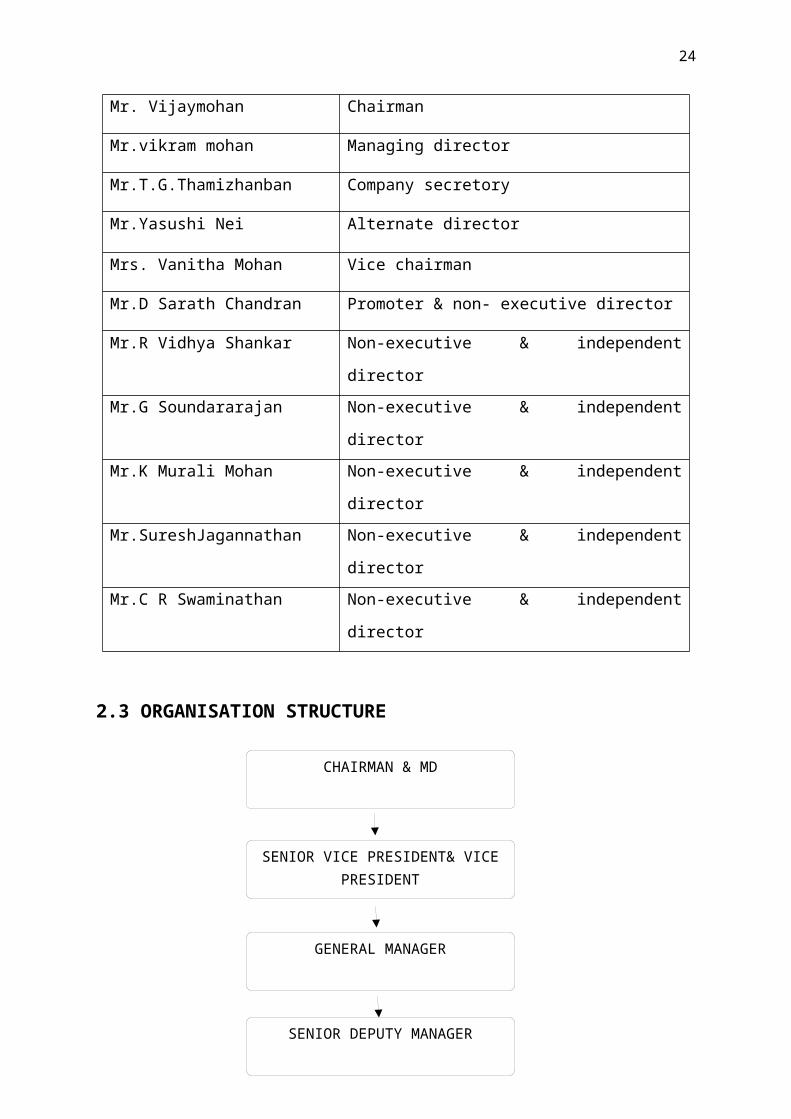

24

Mr. Vijaymohan Chairman

Mr.vikram mohan Managing director

Mr.T.G.Thamizhanban Company secretory

Mr.Yasushi Nei Alternate director

Mrs. Vanitha Mohan Vice chairman

Mr.D Sarath Chandran Promoter & non- executive director

Mr.R Vidhya Shankar Non-executive & independent

directorMr.G Soundararajan Non-executive & independent

directorMr.K Murali Mohan Non-executive & independent

directorMr.SureshJagannathan Non-executive & independent

directorMr.C R Swaminathan Non-executive & independent

director

2.3 ORGANISATION STRUCTURE

SENIOR VICE PRESIDENT& VICEPRESIDENT

GENERAL MANAGER

SENIOR DEPUTY MANAGER

CHAIRMAN & MD

25

2.4 PRODUCT PROFILE & MARKET POTENTIAL

Pricol products are approved and used by most of the

original equipment manufacturers (OMEs) in the Indian

automobile industry. Pricol products are also exported to OEMs

and after – market customers in North America, UK, Australia,

DEPUTY MANAGER

ASSISTANT MANAGER

SENIOR ENGINEER/OFFICER

JUNIOR ENGINEER/OFFICER

ASSISTANT/TECHNICAL ASSISTANT

26

and Turkey. Brazil, China and other European & Asian

countries. The company has developed full- fledged

infrastructure to manufacture and test products to meet

national and international standards. The products are

designed to meet the specific requirement of each customer and

market conditions in the country of use.

The grouping products is as follows

2.4.1 INSTRUMENT PRODUCT GROUPS

Instrument cluster and round instruments, sensors and

switches, gauges, flexible cables, cigarette lighters, heater

ventilation air control panel etc.

2.4.2 ELECTRONICS PRODUCTS GROUP

Fleet management solution (FMS products), vehicle

security systems (VSS) electronic counters & controllers for

textile machinery, auto /taxi fare meters etc.

Electronic product group also includes the printed circuit

boards (PCBs) manufactured to drive electronic instruments

clusters/gauges.

2.5 COMPETITION

STRENGTH

Market leader in Automotive Instrument Industry in India

Established Brand Image

Sole supplier of idle speed control valve (ISCV) to Denso

Haryana Which in turn supplies them to Maruthi Dog Ltd.

27

Pricol Ltd gets technical support from Denso Corporation,

Japan, Which Is one of the largest automotive component

manufacturers.

Strong research and development.

Low cost, Skilled Workforce.

Learning from exports.

2.6 FUTURE PLAN

The vision of Pricol emerged in the form of “VISION 2020

– To achieve sales of Rs.10 billion by 2020 with 50%

contribution from International Business”.

To gain more Market Share & Profit in Exports.

Principle Strategic Challenges of the future

Think long term – but deliver today

Achieve global scale – But be responsive locally

Collaborate – simultaneously compete

Innovative – efficient

Team work – yet have individual accountability

Become flexible – yet standardise

Physical environment depleted – re-create by conservation

& tapping it exercise this year with the help of

Consultants. CIT also coordinates the activities of the

current BPR consultants.

ARCHITECTURE OF THE FUTURE

Strategy – aligned as per aspiration & choice of people &

team.

28

Organisation – Have only permeable boundaries

Processes - Have only minimal critical rules

Resources - Flexible

The future is only based on two factors – People and the

Brand.

2.7 DESCRIPTION OF VARIOUS FUNCTIONAL AREAS

2.7.1 BUSINESS DEVELOPMENT

Business Development (BD) is the front end department

of Pricol that interacts with customers.

Pricol’s businesses can be classified into 3 categories namely

Products for Original Equipment Manufacturers (OEMs)

Fleet Management Solutions (FMS) and

Products for Replacement Markets (Direct market products)

The OEM business contributes to the major portion of Pricol’s

total revenues and hence forms the largest team in BD.

BACKGROUND TO THE FORMATION OF CIT

Quality movement in Pricol commenced with the

implementation of TPM (Total Productive Manufacturing) systems

and practices way back. TPM was launched in several phases

since 1999 and by 2003 we successfully completed over 500

projects.

Pricol also initiated several advanced continuous

improvement approaches in the later years. Six Sigma, a

29

systematic methodology for achieving defect free production

system was launched in 2004 with the guidance of Satyam

Consultants and recently we established the Balanced Score

Card approach to monitor and control our business process.

Besides continuous improvement activities. Pricol

also underwent a Business Process Reengineering (BPR) exercise

way back in 1999 with the support of Renoir Consultants

Limited (UK) and is now undertaken a second BPR.

2.7.2 HUMAN RESOURCE DEPARTMENT

The HR department is primarily divided in to personnel

function, human resource development function

PERSONNEL FUNCTION

Time office, industrial Relations, Employee

welfare, discharging government apprenticeship (ITI) scheme,

HR activities at special vendor units & operationalising

Corporate Social Responsibility through Pricol Rural

Development Project (PRDP), cultural activities through

Kalakshetra & event management are the main key performance

areas of the function.

HUMAN RESOURCE FUNCTION

Competency mapping, assessment &

development, recruitment & new employee orientation, training

& development performance management, career development,

staff salary revision, leadership development, employee

satisfaction survey & aligning HR system with business

30

management system of Pricol are some of the initiatives of

this function.

DEVELOPMENT FUNCTION

Recruitment, training, performance

management, remuneration, performance appraisal, career &

succession planning & integrated human resource management

system.

2.7.3 FINANCE

Finance department is the management of sources &

applications of funds. It is important part of the company &

its function is accounting and reporting.

2.7.4 MACHINE SHOP (I)

The Machine Shop is the one of the main component

manufacturing units of Pricol. It is one of the oldest

departments in Pricol and manufactures back.

2.7.5 MATERIALS DEPARTMENT

Formerly known as Strategic Sourcing (SMS)

division, the Materials Department is bifurcated into

different terms based on the following core activities

Suppliers Quality Assurance (SQA) and Suppliers

Development (SD)

New Product Development (NPD)

Supplier Performance Management (SPM)

Procurement

31

2.7.6 MANUFACTURING ENGINEERING (ME)

The Manufacturing Engineering Department (ME) is the

facility creator for all the production modules of Pricol.

Since most of the products of Pricol are Original Equipment

(OE) products, which require exclusive assembly lines

involving Special Purpose Machines (SPMs), The Need an

engineering department that can develop these facilities in

inevitable.

2.7.7 PRODUCT DEVELOPMENT ENGINEERING-ELECTRONICS

PDEE is the counterpart of PDEI which focuses on the

design and development of electronic parts, mainly PCBs

(Printed Circuit Boards) for the new projects undertaken by

Pricol.

The PCB design and development processes include hardware

design, PCB design, software design, assembling, design

verification and validation etc. The PCB developed by PDEE is

supplied to the S&PM lab during sample assembly stage. Based

on Customers Evaluation of the sample, necessary modifications

are incorporated to the PCB, before freezing the design for

mass production.

2.7.8 PRODUCT DEVELOPMENT ENGINEERING-INSTRUMENTS

Product Development Engineering is the R&D

backbone of Pricol. PDEI (instruments) is one of the biggest

departments in Pricol. It undertakes the R&D activities for

the products belonging to the instruments group (i.e.,

Instrument clusters, round instruments & gauges, switches &

32

sensors etc). The major business divisions in PDEI are 2W

clusters, 4W clusters, off road vehicle clusters, accessories

& exports. Commercial vehicles are clubbed under 4W.

Accessories include switches, sensors, RSL, valves etc.

2.7.9 PLANT MAINTENANCE DEPARTMENT

PMD is the department responsible for carrying out

all the maintenance activities in Pricol. PMD Performs

Preventive and Breakdown Maintenance of all machineries and

utilities installed in Pricol and also undertake minor civil

works relating to renovation of existing facilities, shifting

of machineries, minor construction works etc. The Health,

Safety & Environment (HSE) cell is also attached to PMD.

2.7.10 PRINTING

The Printing department manufactures the dials for

instrument clusters as well as round instruments. The dials

manufactured in Pricol are printed on either Poly Carbonate

sheet or aluminium sheets.

2.7.11 INFORMATION SYSTEMS

To add value to the business process and render

faster and efficient service to the customers, Pricol has

installed IT systems like SAP R3 – ERP (Enterprise Resource

Planning) and Wind-chill (Collaborative Product Commerce)

Pricol Employs IBM Lotus Notes for Intra organization

communication and recently introduced the Sting Software for

facilitating Balanced Scorecard approach.

33

2.7.12 QUALITY ENGINEERING (QE)

Quality engineering is the department responsible for

ensuring quality at all stages of Pricol’s business process.

That is, from procurement stage to production and from

production to delivery of finished goods to customer, QE has

developed systems for quality check in order to ensure that

the final product supplied to customers is free of any defect.

2.7.13 STORES

The stores department in Pricol receives , inspects,

preserves and issues materials to all the internal buyers

(user departments). It handles nearly 60000inventory items.

The department has a centralized management structure but

decentralized operating units. It operates from several

locations near the buyer. However the activities and

procedures practices in all the store locations are the same.

34

CHAPTER -3

MICRO MACRO ECONOMIC ANALYSIS

3.1 MICRO MACRO ECONOMIC FACTOR

The global auto component industry experienced moderate

growth over the last five years and is expected to continue

its growth momentum reaching approximately $730.8 billion in

2017 with a CAGR of 3.2% over next five years (2012-2017).

APAC is anticipated to emerge as the leading growth market

over the forecast period due to high demand and low-cost

manufacturing practices in the region. Lucintel, a leading

global management consulting and market research firm, has

analyzed the global auto component industry and presents its

findings in “Global Auto Component Industry 2012-2017 Trend,

Profit, and Forecast Analysis.” The global auto component

industry is a highly diversified sector that involves engine

35

and auto component manufacturers, including aftermarket parts

manufacturers, suppliers, dealers, and retailers. The

manufacturing of auto components is gradually shifting toward

Asian countries such as China, India, and others because of

higher market potential and the low-cost manufacturing options

available. In China and India, OEMs are focused on helping the

suppliers improve and grow their businesses. Strong growth in

the industry has attracted a pool of companies, including

major foreign companies, to operate in China’s auto component

market. The growing importance of electronics and functional

integration of green components and sustainable products will

drive growth in the industry. Lucintel’s research indicates

that the industry witnessed strong growth during 2010-2011, as

there was an increase in automobile sales and production

coupled with demand for hybrid vehicles. Industry players

rapidly added capacity to meet growing demand from automobile

manufacturers. The industry is transforming and the boost in

demand is expected to give rise to several new players in the

industry. As per the study, searching qualified employees,

managing rising costs while staying competitive on price, and

expanding product portfolios are the biggest challenges for

the industry. Substantial investment in capacity expansion,

increasing after-market demand, and sales and revival in

global auto production with strong recovery in vehicle sales

are anticipated to expand the industry’s footprint. The report

tracks one market segment for four regions; thus, it tracks

four segments of the global auto component industry. This

comprehensive guide from Lucintel provides readers with

36

valuable information and the tools needed to successfully

drive critical business decisions with a thorough

understanding of the market’s potential. This report will save

Lucintel clients hundreds of hours in personal research time

on a global market and it offers significant benefits in

expanding business opportunities throughout the global auto

component industry. In a fast-paced ever-changing world,

business leaders need every advantage available to them in a

timely manner to drive change in the market and to stay ahead

of their competition. This report provides business leaders

with a keen advantage in this regard by making them aware of

emerging trends and demand requirements on an annual basis.

FIGURRE 3.1.1 ANNUAL PRODUCTION OF VEHICLES

The Indian auto component industry has been navigating

through a period of rapid changes with great élan. Driven by

global competition and the recent shift in focus of global

automobile manufacturers, business rules are changing and

37

liberalisation has had sweeping ramifications for the

industry. The global auto components industry is estimated at

US$1.2 trillion. The Indian auto component sector has been

growing at 20% per annum since 2000 and is projected to

maintain the high-growth phase of 15-20% till 2015.

The Indian auto component industry is one of the few

sectors in the economy that has a distinct global competitive

advantage in terms of cost and quality. The value in sourcing

auto components from India includes low labour cost, raw

material availability, technically skilled manpower and

quality assurance. An average cost reduction of nearly 25-30%

has attracted several global automobile manufacturers to set

base since 1991. India’s process-engineering skills, applied

to re-designing of production processes, have enabled

reduction in manufacturing costs of components. Today, India

has become the outsourcing hub for several global automobile

manufacturers.

Innovation and cost pruning hold the key to meeting the global

challenge of rising demand from developed countries and

competition from other emerging economies. Several large

Indian auto component manufacturers are already gearing to

this new reality and are in the process of substantially

investing in capacity expansion, establishing partnerships in

India and abroad, acquiring companies overseas and setting up

greenfield ventures, R&D facilities and design capabilities.

Some leading manufacturers of auto components in India include

Motor Industries Company of India, Bharat Forge, Sundaram

38

Fasteners, Wheels India, Amtek Auto, Motherson Sumi, Rico Auto

and Subros. The India’s Top 500 Companies, published by Dun &

Bradstreet in 2006, listed 22 auto component manufacturers as

top companies in India with a total turnover of US$ 3 bn.

These companies are in the process of making a mark on the

global arena, and some have already acquired assets abroad.

3.2 INDUSTRY STRUCTURE

The total turnover of the Indian auto component industry is

estimated at US$9 bn in 2006. The industry has the resources

to manufacture the entire range of auto products required for

vehicle manufacturing, approximately 20,000 components. The

entry of global manufacturers into India during the 1990s

enabled induction of new technologies, new products, improved

quality and better efficiencies in operations. This in turn

effectively acted as a catalyst to the local development of

the component industry.

The Indian auto component industry is extensive and highly

fragmented. Estimates by the Department of Heavy Industries,

Government of India, indicate there are over 400 large firms

who are part of the organised sector and cater largely to the

Original Equipment Manufacturers (OEMs). Another 10,000 firms

exist in the unorganised sector that operates in a tier-

format. The firms in this segment operate in low technology

products and cater to Tier I and Tier II suppliers and also

serve the replacement market

Around 4% of the companies operating in the auto component

39

segment cater to 80% of the demand emanating from OEMs. Within

the unorganised segment, apart from supplying in the

aftermarket, a number of players are also involved in job work

and contract manufacturing.

FIGURE 3.2.2 CHART OF AUTO COMPONENTS PRODUCT

The range of products manufactured, with each broad product

segment having a different market structure and technology,

has negated any possible concentration of the market in a few

hands. The market is so large and diverse that a large number

of players can be absorbed to accommodate buyer needs.

However, there are a select few large companies that have

integrated their operations across the value chain. The key to

competing in this industry is through specialisation by

product-type, and integrating operations across the related

area of specialisation.

40

An interesting insight provided by a study conducted by the

National Council of Applied Economic Research revealed that

the market segments for auto components included OEMs

constituting 33%, local components having 25% with the balance

42% comprising of spurious market including re-conditioned

parts. A large part of the spurious or grey market companies

are in the unorganised sector.

The regional base of auto component manufacturers is mostly

concentrated in the West, North and South of India. This

regional concentration of auto component manufacturers has

been dictated by the emergence of automobile manufacturers in

these regions. The set up of Tata Motors, Bajaj, Mahindra &

Mahindra and TVS in the 1950s and 1960s laid the foundation

for auto component manufacturers in the West and South, whilst

the entry of Maruti during the 1980s created the base in the

North.

3.3 INDUSTRY GROWTH

Production of auto ancillaries was estimated at US$10 bn in

2005-06 and has been growing at a robust 20% per annum since

2000. Exports of auto components have been strong growing at

24% per annum since 2000. This growth in exports if sustained

for another five years will see India’s auto components

exports will touch US$ 5 bn by 2011 from the US$ 2 bn at

present.

Till the 1990s, the auto component industry was solely

dependent on the domestic automobile industry to drive the

41

demand for ancillary products. This composition of the market

however is undergoing radical changes with global outsourcing

gaining momentum. In recent times, exports has emerged as a

significant driver of growth, and the demand emanating from

global OEMs and Tier I manufacturers has opened new

opportunities for the auto component industry in India. At the

same time, a bright outlook for the domestic automobile

industry also offers significant growth potential, given the

fast rising income levels with a rapidly growing middle and

high income consumers.

Share of exports in total production has risen from 10% in

1997 to 18% in 2006. The composition of exports in terms of

the proportion of OEM and aftermarket has also undergone a

sweeping change since the past decade. The ratio of OEM to

aftermarket has changed from 35:65 in the 1990s to 75:25 in

2006. While exports have been booming, there has been a sharp

rise in imports of auto components as well, especially in the

last three years. From an import of US$ 250 mn in FY03, they

have gone up to US$750 mn in FY06. This is a healthy trend,

indicative of rising domestic demand.

42

3.4 INVESTMENTS

Since 2000, the auto component industry has recorded an

investment level of Rs 18 bn and has attracted US$ 530 mn in

terms of foreign direct investment. Investments in the sector

have been growing at 14% per year. In 2005-06, investments

touched US$ 4.4 bn, and are expected to grow significantly in

future.

The Investment Commission has set a target of attracting

foreign investment worth US$ 5 bn for the next five years to

increase India’s share in the global auto components market

from the present 0.4% to 3-4%. This is a sizeable target

considering the meagre amount of FDI currently coming into the

industry. The changing perception of global auto makers is

however fast altering this scenario.

With less than 1% share in the global market, India has

tremendous potential to emerge as a supply base. Several

global giants like Ford and Toyota have already set up base in

India to source auto components. Outsourcing is fast catching

up with domestic OEMs as well, with most Indian OEMs today

sourcing nearly 70-80% of their component requirements from

vendors.

This changing business scenario is leading to an inevitable

outcome of consolidation within the industry. The takeover of

Kar Mobiles by Rane Engine and of Gero Auto by Uma Precision

is few instances. However, such mergers and takeovers will be

few and far in between in the auto component industry, unlike

43

the churn out anticipated in other emerging industries – the

principal factor being the vastness of the market and the

range of products that need to be delivered.

Rather than domestic consolidation, the general trend at

present is for the large auto component manufacturers to

establish a global presence. Top auto component manufacturers

have already set up base in the global markets, especially in

Europe. Overall, there have already been 16 acquisitions, with

six made in 2005. The industry is the third highest among the

Indian industries after IT and Pharma, in acquiring overseas

assets. These acquisitions have largely been in Europe and the

USA. This trend has been possible as the auto ancillary

industry in these countries have been collapsing, thus making

it affordable to acquire these companies. Nevertheless, this

will provide a base for Indian companies to access the

European and American markets.

Indian auto component companies are also setting up bases in

other emerging economies, who are potential competitors, for

instance, Sundaram Fasteners’ greenfield facility in Zhejiang

and Bharat Forge’s joint venture with the Chinese automotive

major FAW Corporation. Another auto component manufacturer

with plans to enter China is PMP Components, which intends to

set up a sourcing base to establish itself as a low cost

supplier.

These trends are indicative of the changing business

environment in the country. Top auto component manufacturers

are gearing to take big risks. Their cross-border vision has

44

established them as global companies. Though the going-global

phenomenon is limited to a handful of companies, the smaller

companies are also indirectly gearing to this trend by

entering into formal manufacturing contracts and

specialisation.

Prospects

Looking forward, the industry displays tremendous potential in

generating employment and boosting entrepreneurship in the

country. The spate of new investment plans announced by global

and domestic automobile manufacturers promises the emergence

of India as a global hub for auto components.

The industry is transforming, and the boost in demand will see

the emergence of several new players in the industry. The vast

market for auto components, and the diverse products and

technology involved ensures a place and role for many. At the

same time, the entry of several global automobile

manufacturers will bring in more regulation into the industry

and see a pruning of the spurious market. Among the smaller

players in the unorganised segment, this implies moving away

from being standalone companies, to entering into either

contract manufacturing or being ancillary units. The newly

defined rules are specialisation, development and delivery

that hold the key to success in the auto component industry.

45

CHAPTER -4

DATA ANALYSIS AND INTERPRETATION

This chapter deals with analysis and data interpretation

of data collected through secondary analysis and

questionnaire.

INVENTORY MANAGEMENT TECHNIQUES

4.1 ABC ANALYSIS

In supply chain, ABC analysis is an inventory

categorization method which consists in dividing items into

three categories, A, B and C: A being the most valuable items,

C being the least valuable ones. This method aims to draw

managers’ attention on the critical few (A-items) and not on

the trivial many (C-items).

Prioritization of the management attention

Inventory optimization is critical in order to keep

costs under control within the supply chain. Yet, in order to

get the most from management efforts, it is efficient to focus

on items that cost most to the business. The Pareto principle

states that 80% of the overall consumption value is based on

only 20% of total items. In other words, demand is not evenly

distributed between items: top sellers vastly outperform the

rest.

46

The ABC approach states that, when reviewing inventory, a

company should rate items from A to C, basing its ratings on

the following rules:

A-items are goods which annual consumption value is the

highest. The top 70-80% of the annual consumption value of the

company typically accounts for only 10-20% of total inventory

items.

C-items are, on the contrary, items with the lowest

consumption value. The lower 5% of the annual consumption

value typically accounts for 50% of total inventory items.

B-items are the interclass items, with a medium consumption

value. Those 15-25% of annual consumption value typically

accounts for 30% of total inventory items.

TABLE 4.1.1 ABC ANALYSIS

Category Percentage Value

A 69.95

26,73,

7,1670.4B 20.03 7,65,65,922.8

C 10.01

3,82,72,306.0

9

Total 100.00

38,22,09,899.

3

FIGURE 4.1.1 ABC ANALYSIS

47

A B C0.0010.0020.0030.0040.0050.0060.0070.00

ABC analysis

Percentage

4.2 FSN ANALYSIS

By doing FSN analysis materials can be classified based

on their movement from inventory for a specified period. Items

are classified based on consumption and average stay in the

inventory. Higher the stay of item in the inventory, the

slower would be the movement of the material

F – Fast Moving

S- Slow Moving

N- Non moving

This type of classification helps to establish and organize

proper warehouse layout by locating all the fast moving items

near the dispensing window to reduce the handling efforts.

Also, attention of the management is focused on the Non-Moving

items to enable decision as to whether they are in needs in

the future or they can be salvaged or disposed. This will help

to improve organization’s capital utilization and cash flow.

48

TABLE 4.2.1 FSN ANALYSIS

Category Percentage ValueMoving 69.07 18,46,63,901NM-3M 11.35 3,03,49,589.29SM-3M 19.58 5,23,58,180.09Total 100.00 267371670.4

FIGURE 4.2.1 FSN ANALYSIS

Moving NM-3M SM-3M

69.07

11.3519.58

FSN ANALYSISPercentage

4.3 PERCENTAGE OF INVENTORY ON WORKING CAPITAL

TABLE 4.3.1 PERCENTAGE OF INVENTORY ON WORKING CAPITAL

YEAR 2013 2012 2010

49

CURRENT ASSETS 346.93 455.14 409.85CURRENT LIABILITIES 262.27 354.72 218.25WORKING CAPITAL 84.66 100.42 191.6INVENTORIES 67.77 91.23 185.01% OF INVENTORIES IN WORKING

CAPITAL 80.05 90.85 96.56

FIGURE .4.3.1 PERCENTAGE OF INVENTORY ON WORKING CAPITAL

80.0590.85 96.56

INVENTORY ON WORKING CAPITAL

PERCENTAGE

The chart shows the percentage of inventory on working

capital. It keeps increasing year after year i.e. from 2010

(80%) to 2012 (96.56%).

4.4 TREND ANALYSIS

TABLE 4.4.1 TREND ANALYSIS

Month May’

13

Jun’

13

July

’13

Aug’

13

Sep’

13

Oct’

13

Nov’

13

Dec’

13

Jan’

13Invent 408 426 429 439 439 439 439 439 439

50

ory

FIGURE 4.4.1 TREND ANALYSIS

may'13

jun'13

jul'13

aug'13

sep'13

sep'13

oct'13

nov'13

dec'13

jan'14

390400410420430440450

Inventory Trend

inventory

The increasing trend shows the production for thecoming months is been predicted high from 408 units in may

2013 to 439 units in july 2013.

EFFECTIVENESS OF THE PRESENT INVENTORY SYSTEM IS ALSO STUDIED

WITH THE HELP OF INFORMATION COLLECTED BY QUESTIONNAIRE

4.5 AGE OF THE RESPONDENTS

TABLE 4.5.1 AGE OF THE RESPONDENTS

AGE(IN YRS) No. OF. RESPONDENT PERCENTAGE

BELOW 25 5 2025-35 9 5535-45 5 20ABOVE 45 1 5TOTAL 20 100

51

Among the respondents (55%) are between the age of 25-35yrs

and (20%) are below 25yrs and another (20%) from the age of

35-45yrs.

4.6 GENDER OF THE RESPONDENTS

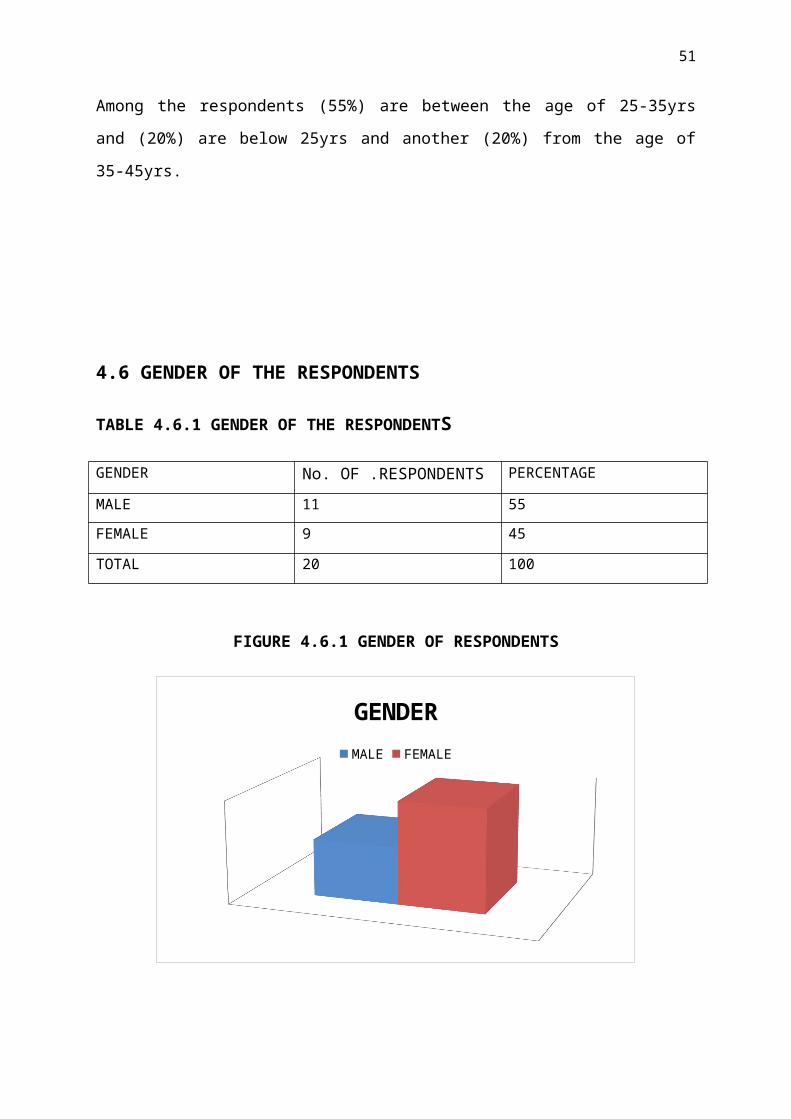

TABLE 4.6.1 GENDER OF THE RESPONDENTS

GENDER No. OF .RESPONDENTS PERCENTAGE

MALE 11 55FEMALE 9 45

TOTAL 20 100

FIGURE 4.6.1 GENDER OF RESPONDENTS

GENDERMALE FEMALE

52

Among the respondents (55%) are male and remaining (45%) are

female employees.

4.7 EDUCATIONAL QUALIFICATION OF THE RESPONDENTS

TABLE 4.7.1 EDUCATIONAL QUALIFICATION OF THE

RESPONDENTS

EDUCATIONAL QUALIFICATION No.

OF .RESPONDENTS

PERCENTAGE

HIGHER SECONDARY 4 20UG 9 50PG 7 30OTHERS - -TOTAL 20 100

Among the respondents (50%) are under graduates and (30%) are

post graduates and remaining (20%) are higher secondary.

4.8 FREQUENCY OF RECEIVING MATERIAL

TABLE 4.8.1 FREQUENCY OF RECEIVING MATERIAL

53

FREQUENCY No.OF RESPONDENTS PERCENTAGEONCE IN 3 Hrs 3 15ONCE IN A DAY 10 55ONCE IN 3 DAYS 5 20ONCE IN A WEEK 2 10TOTAL 20 100

Among the respondents (55%) gets material once in a day and

(20%) gets once in 3 days.

4.9 NUMBER OF INVENTORY

TABLE 4.9.1 NUMBER OF ITEMS IN THE MODULE

NO OF ITEMS No.OF .RESPONDENTS PERCENTAGE

10-20 Nos 2 1020-30 Nos 6 3030-40 Nos 10 5040-50 Nos 2 10TOTAL 20 100

Among the modules (50%) of modules consists of 30-40

inventory items and (30%) with 20-30 inventory items.

54

4.10 TYPE OF COMPONENT PRODUCED

TABLE 4.10.1 TYPE OF COMPONENT PRODUCED

COMPONENT TYPE No.OF .RESPONDENTS PERCENTAGE2 WHEELER METERS 2 104 WHEELER METER 7 35TRUCKS AND LORRY

METERS

4 20

OTHERS 7 35TOTAL 20 100

Among the modules (35%) are producing 4 wheeler meters and

(35%) other type of products.

4.11SYSTEMATIC OPERATING PROCESS FOR INVENTORY

MANAGEMENT SYSTEM

TABLE4.11.1 SYSTEMATIC OPERATING PROCESS FOR INVENTORY

MANAGEMENT SYSTEM

FACTOR No. OF RESPONDENTS PERCENTAGEYES 20 100NO - -

55

TOTAL 20 100

All the respondents feel that their module is operating with

the systematic operating process of inventory management

system.

4.12 COMMUNICATIONS TO THE RESPONSIBLE STAFFS

TABLE 4.12.1 COMMUNICATIONS TO THE RESPONSIBLE STAFFS

FACTOR No. OF RESPONDENTS PERCENTAGEYES 18 90NO 2 10TOTAL 20 100

Among the respondents (90%) expressed that they receive

communication from the management regarding their modules and

only (10%) expressed that they do not receive get proper

communication.

TABLE 4.13 VARIETIES OF INVENTORY IN MODULE

TABLE 4.13.1 VARIETIES OF INVENTORY INMODULE

FACTOR No. OF RESPONDENTS PERCENTAGEYES 14 70NO 6 30TOTAL 20 100

56

Among the respondents (70%) expressed that their module has

variety of inventory and only (30%) expressed that there is no

variety of inventory in their modules.

4.14 MANAGEMENT REVIEWS OF REPORTS

TABLE 4.14.1 REVIEWS OF REPORTS BY MANAGEMENT

FACTOR No. OF RESPONDENTS PERCENTAGEYES 20 100NO - -TOTAL 20 100

All the respondents expressed that the management review the

reports regularly about the inventory of each module.

4.15 LAYOUT OF STORAGE FACILITY

TABLE 4.15.1 LAYOUT OF STORAGE FACILITY

FACTOR No. OF RESPONDENTS PERCENTAGEYES 16 80NO 4 20TOATAL 20 100

Among the respondents (80%) expressed that there is proper

store layout in the modules and only (20%) expressed that

there is no proper layout.

4.16 AREAS FOR RECEIVING AND DISTRIBUTING INVENTORY

TABLE 4.16.1 AREAS FOR RECEIVING AND DISTRIBUTING INVENTORY

57

FACTOR No. OF RESPONDENTS PERCENTAGEYES 12 60NO 8 40TOATAL 20 100

Among the respondents (60%) expressed that there is separate

area for receiving and distributing the inventory and other

(20%) expressed there in so such area for receiving and

distributing inventory.

4.17 TAGS INDICATING SHIPMENT

TABLE 4.17.1 TAGS INDICATING SHIPMENT

FACTOR No. OF RESPONDENTS PERCENTAGEYES 11 55NO 9 45TOATAL 20 100

Among the respondents (55%) expressed that tags are put up

properly indicating the shipment and (45%) expressed there is

no proper tags put up.

4.18 PROCESS AND DOCUMENTS INVOLVED IN DISTRIBUTION

OF GOODS

TABLE 4.18.1 PROCESS AND DOCUMENTS INVOLVED IN DISTRIBUTION OF

GOODS

FACTOR No. OF RESPONDENTS PERCENTAGEYES 10 50

58

NO 10 50TOATAL 20 100

Regarding the process and documents involved in distribution

of goods (50%) expressed that there is proper procedure and

remaining (50%) expressed that there is no such procedure.

4.19 CONTROL WITH REGARD TO INVOICE

TABLE 4.19.1 CONTROL WITH REGARD TO INVOICE

FACTOR No. OF RESPONDENTS PERCENTAGEYES 8 40NO 12 60TOATAL 20 100

FIGURE 4.19.1 CONTROL WITH REGARD TO INVOICE

5

9

CONTROL ON INVOICEYES NO

59

Among the respondents (55%) were given the control of invoice

preparation and remaining (45%) were not given such control

and that is been done centrally.

4.20 DOCUMENTED PROCEDURE FOR STOCK TAKING

TABLE 4.20.1DOCUMENTED PROCEDURE FOR STOCK TAKING

FACTOR No. OF RESPONDENTS PERCENTAGEYES 11 55NO 9 45TOATAL 20 100

Among the respondents (55%) expressed that there is proper

documented procedure for stock taking and (45%) says that

there is no such procedure in taking stock from the store.

4.21MANAGEMENT CONTROL ON FREQUENCY OF STOCK TAKING

TABLE 4.21.1 MANAGEMENT CONTROL ON FREQUENCY OF STOCK TAKING

FACTOR No. OF RESPONDENTS PERCENTAGEYES 10 50NO 10 50TOATAL 20 100

60

Among the (50%) feels that the frequency of taking stock is

been suggested by the management and other (50%) expressed

that it is not been controlled by the management.

4.22 POSSIBILITY OF ADJUSTMENT AFTER COUNTING PROCESS

TABLE .4.22.1 POSSIBILITY OF ADJUSTMENT AFTER COUNTING PROCESS

FACTOR No. OF RESPONDENTS PERCENTAGEYES - -NO 20 100TOATAL 20 100

FIGURE 4.22.1 ADJUSTMENT AFTER COUNTING PROCESS

61

5

9

ADJUSTMENT AFTER COUNTING PROCESS

YES NO

All the respondents (100%) express that there is no

possibility of adjusting the inventory once the initial

counting gets over.

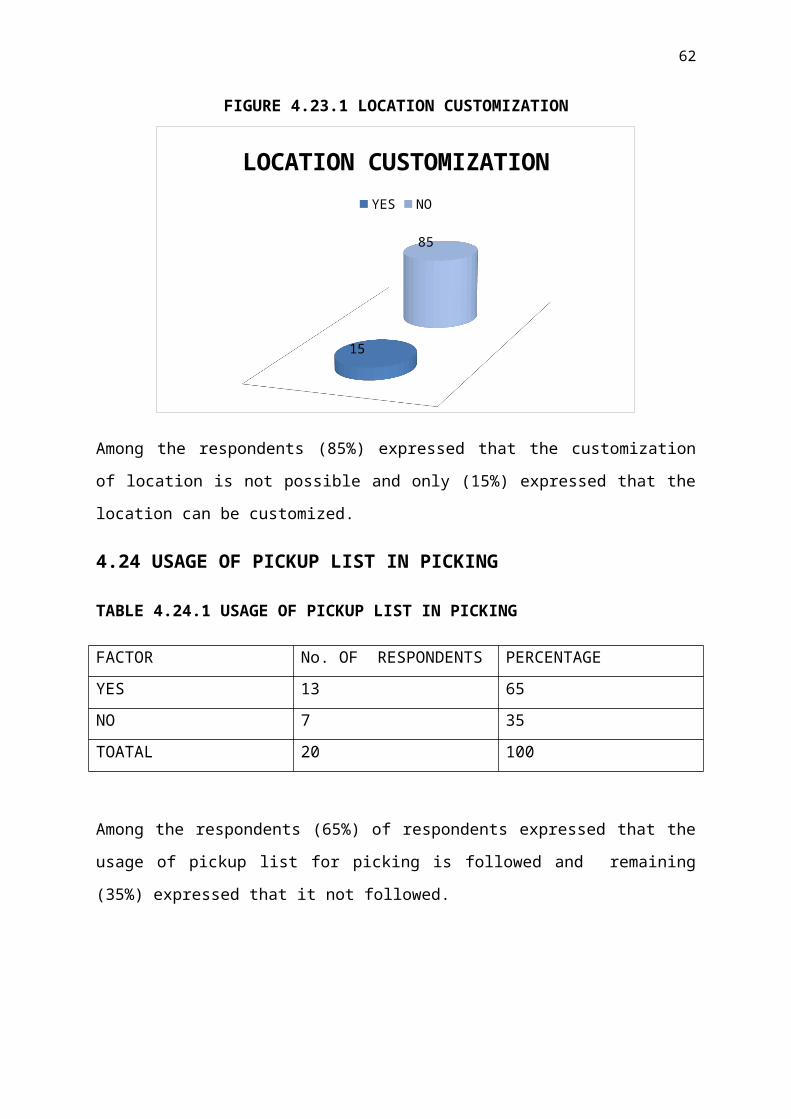

4.23 INVENTORY LOCATION CUSTOMIZABLE

TABLE 4.23.1 INVENTORY LOCATION CUSTOMIZABLE

FACTOR No. OF RESPONDENTS PERCENTAGEYES 3 15NO 17 85TOATAL 20 100

62

FIGURE 4.23.1 LOCATION CUSTOMIZATION

15

85

LOCATION CUSTOMIZATIONYES NO

Among the respondents (85%) expressed that the customization

of location is not possible and only (15%) expressed that the

location can be customized.

4.24 USAGE OF PICKUP LIST IN PICKING

TABLE 4.24.1 USAGE OF PICKUP LIST IN PICKING

FACTOR No. OF RESPONDENTS PERCENTAGEYES 13 65NO 7 35TOATAL 20 100

Among the respondents (65%) of respondents expressed that the

usage of pickup list for picking is followed and remaining

(35%) expressed that it not followed.

63

4.25 PROVISION FOR OBSOLENCE AND INACTIVE ITEM

TABLE 4.25.1.PROVISION FOR OBSOLENCE AND INACTIVE ITEM

FACTOR No. OF RESPONDENTS PERCENTAGEYES 11 55NO 9 45TOATAL 20 100

Among the respondents (55%) expressed that there is provision

for obsolesce and inactive items and remaining (45%) expressed

that there is no such provision.

4.26 UPDATING OF PERPECTUAL INVENTORY

TABLE.4.26.1 UPDATING OF PERPECTUAL INVENTORY

FACTOR No. OF RESPONDENTS PERCENTAGEYES 17 85NO 3 15TOATAL 20 100

Among the respondents (85%) expressed that modules are

updating the perceptual inventory promptly and remaining

(15%) expressed that it is not promptly updated.

64

4.27 DISCREPANCIES BETWEEN PHYSISCAL AND ACTUAL

INVENTORY RECORDED

TABLE.4.27.1DISCREPANCIES BETWEEN PHYSISCAL AND ACTUAL

INVENTORY RECORDED

FACTOR No. OF RESPONDENTS PERCENTAGEYES 14 70NO 6 30TOATAL 20 100

Among the respondents (70%) expressed that the discrepancies

between perpetual and physical inventory are resolved properly

and remaining (30%) expressed that it is not been resolved.

4.28 INTERNAL CONTROL OF MANAGEMENT IN INVENTORY

TABLE.4.28.1INTERNAL CONTROL OF MANAGEMENT IN INVENTORY

FACTOR No. OF RESPONDENTS PERCENTAGEYES 14 70

65

NO 6 30TOATAL 20 100

Among the respondents (70%) expressed that the of modules

that there is internal control of management in inventory

control and remaining (30%) expressed that there is no such

internal control.

4.29 TRAINING FOR INVENTORY MANAGEMENT PERSONNAL

4.29.1 TRAINING FOR INVENTORY MANAGEMENT PERSONNAL

FACTOR No. OF RESPONDENTS PERCENTAGEYES 15 75NO 5 25TOATAL 20 100

Among the respondents (75%) expressed that there is proper

training given to employees who are dealing with inventory

and another (25%) expressed that proper training is not

given.

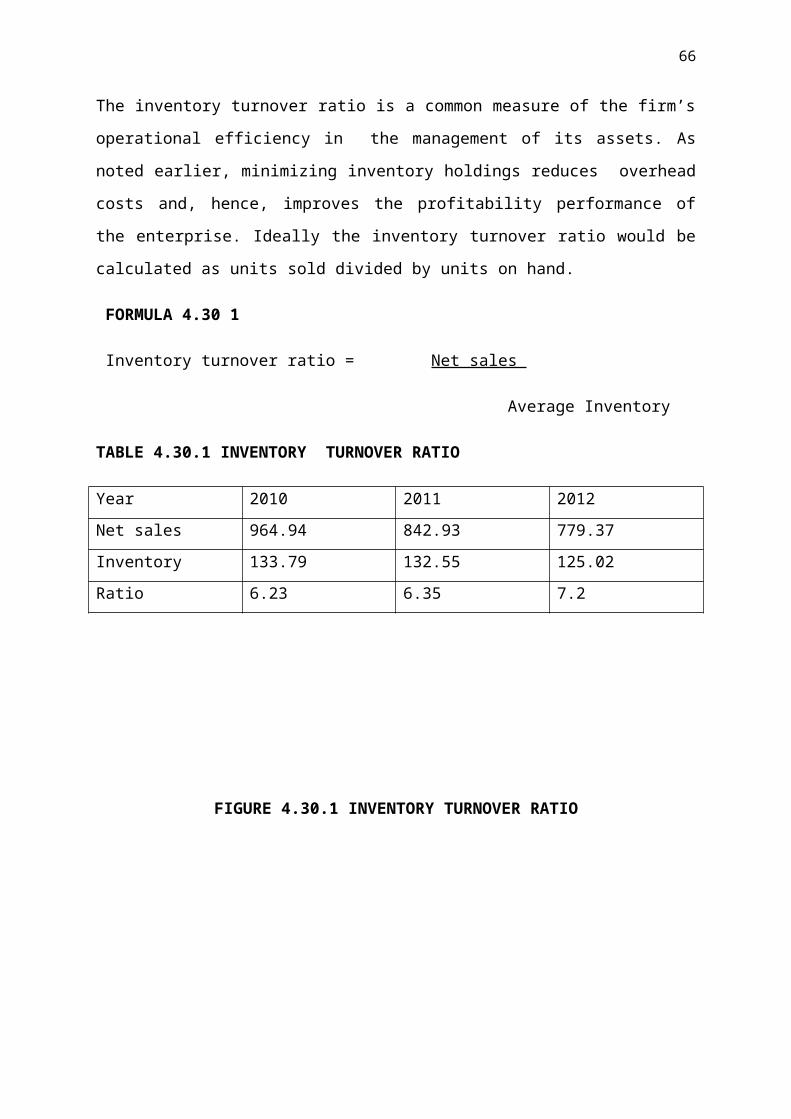

4.30 INVENTORY TURNOVER RATIO

66

The inventory turnover ratio is a common measure of the firm’s

operational efficiency in the management of its assets. As

noted earlier, minimizing inventory holdings reduces overhead

costs and, hence, improves the profitability performance of

the enterprise. Ideally the inventory turnover ratio would be

calculated as units sold divided by units on hand.

FORMULA 4.30 1

Inventory turnover ratio = Net sales

Average Inventory

TABLE 4.30.1 INVENTORY TURNOVER RATIO

Year 2010 2011 2012Net sales 964.94 842.93 779.37Inventory 133.79 132.55 125.02Ratio 6.23 6.35 7.2

FIGURE 4.30.1 INVENTORY TURNOVER RATIO

67

6.23 6.35

7.2

INVENTORY TURNOVER RATIOratio

The inventory is increasing every year from (6.23%)

2010 to (7.2%) 2012 which is reducing inventory stocked idle

before production.

68

CHAPTER -5

CONCLUSION

This chapter deals with the discussions on the

findings and the suggested recommendations based on the

findings.

5.1 RESULT AND DISCUSSIONS

The chart shows the percentage of inventory on working

capital. It keeps increasing year after year i.e. from

2010 (80%) to 2012 (96.56%).

The increasing trend shows the production for the coming

months is been predicted high from 408 units in may 2013

to 439 units in july 2013.

Among the respondents (55%) are between the age of 25-

35yrs and (20%) are below 25yrs and another (20%) from

the age of 35-45yrs.

Among the respondents (55%) are male and remaining (45%)

are female employees.

Among the respondents (50%) are under graduates and (30%)

are post graduates and remaining (20%) are higher

secondary.

Among the respondents (55%) gets material once in a day

and (20%) gets once in 3 days.

Among the modules (50%) of modules consists of 30-40

inventory items and (30%) with 20-30 inventory items.

69

Among the modules (35%) are producing 4 wheeler meters

and (35%) other type of products.

All the respondents feel that their module is operating

with the systematic operating process of inventory

management system.

Among the respondents (90%) expressed that they receive

communication from the management regarding their modules

and only (10%) expressed that they do not receive get

proper communication.

Among the respondents (70%) expressed that their module

has variety of inventory and only (30%) expressed that

there is no variety of inventory in their modules.

All the respondents expressed that the management review

the reports regularly about the inventory of each module.

Among the respondents (80%) expressed that there is

proper store layout in the modules and only (20%)

expressed that there is no proper layout.

Among the respondents (60%) expressed that there is

separate area for receiving and distributing the

inventory and other (20%) expressed there in so such area

for receiving and distributing inventory.

Among the respondents (55%) expressed that tags are put

up properly indicating the shipment and (45%) expressed

there is no proper tags put up.

Regarding the process and documents involved in

distribution of goods (50%) expressed that there is

proper procedure and remaining (50%) expressed that there

is no such procedure.

70

Among the respondents (55%) were given the control of

invoice preparation and remaining (45%) were not given

such control and that is been done centrally.

Among the respondents (55%) expressed that there is

proper documented procedure for stock taking and (45%)

says that there is no such procedure in taking stock from

the store.

Among the (50%) feels that the frequency of taking stock

is been suggested by the management and other (50%)

expressed that it is not been controlled by the

management.

All the respondents (100%) express that there is no

possibility of adjusting the inventory once the initial

counting gets over.

Among the respondents (85%) expressed that the

customization of location is not possible and only (15%)

expressed that the location can be customized.

Among the respondents (65%) of respondents expressed that

the usage of pickup list for picking is followed and

remaining (35%) expressed that it not followed.

Among the respondents (55%) expressed that there is

provision for obsolesce and inactive items and remaining

(45%) expressed that there is no such provision.

Among the respondents (85%) expressed that modules are

updating the perceptual inventory promptly and

remaining (15%) expressed that it is not promptly

updated.

71

Among the respondents (70%) expressed that the

discrepancies between perpetual and physical inventory

are resolved properly and remaining (30%) expressed that

it is not been resolved.

Among the respondents (70%) expressed that the of modules

that there is internal control of management in inventory

control and remaining (30%) expressed that there is no

such internal control.

Among the respondents (75%) expressed that there is

proper training given to employees who are dealing with

inventory and another (25%) expressed that proper

training is not given.

The inventory is increasing every year from (6.23%) 2010

to (7.2%) 2012 which is reducing inventory stocked idle

before production.

5.2 RECCOMENDATION

Since many of the respondents feels that there is no

customization of inventory location the researcher

suggests that the inventory location can be made

customized for the effective usage by the store keepers.

There is no possibility of making adjustment in the

system after counting gets over. Thus the systematic

method of modifying the inventory when the store -keeper

found its been left out while counting can be brought.

There is no proper documentation in distribution of goods

to the modules from the inventory. Thus the process of

72

documentation procedure should be brought in all the

modules.

Copyright © 2022 FDOKUMEN