INTRODUCTION AND DISCOUNTED CASH FLOW VALUATION

66

INTRODUCTION AND DISCOUNTED CASH FLOW V ALUATION Ming Liu International University of Japan

Transcript of INTRODUCTION AND DISCOUNTED CASH FLOW VALUATION

INTRODUCTION AND DISCOUNTED CASH FLOW VALUATION

Ming Liu

International University of Japan

Finance and Financial System • What is Finance?

– Webster's New World dictionary defines it as • money resources, income, etc. • the science of managing money • to supply or get money for a project

– The exchange (allocation) of monetary resources across times and states

– Finance is used by individuals (personal finance), by

governments (public finance), by businesses (corporate finance) and by a wide variety of other organizations, including schools and non-profit organizations.

2

Financial Markets (System) • By channeling funds from surplus to deficit

units, financial markets promote economic efficiency(i.e., makes everyone better off)

Deficit unit benefits because it gets to:

Invest funds to generate greater output and wealth (e.g., a business with investment opportunity) OR

Consume (e.g., use borrowed funds to buy a house)

Surplus unit benefits because it earns a return on funds, otherwise surplus unit earns nothing

3

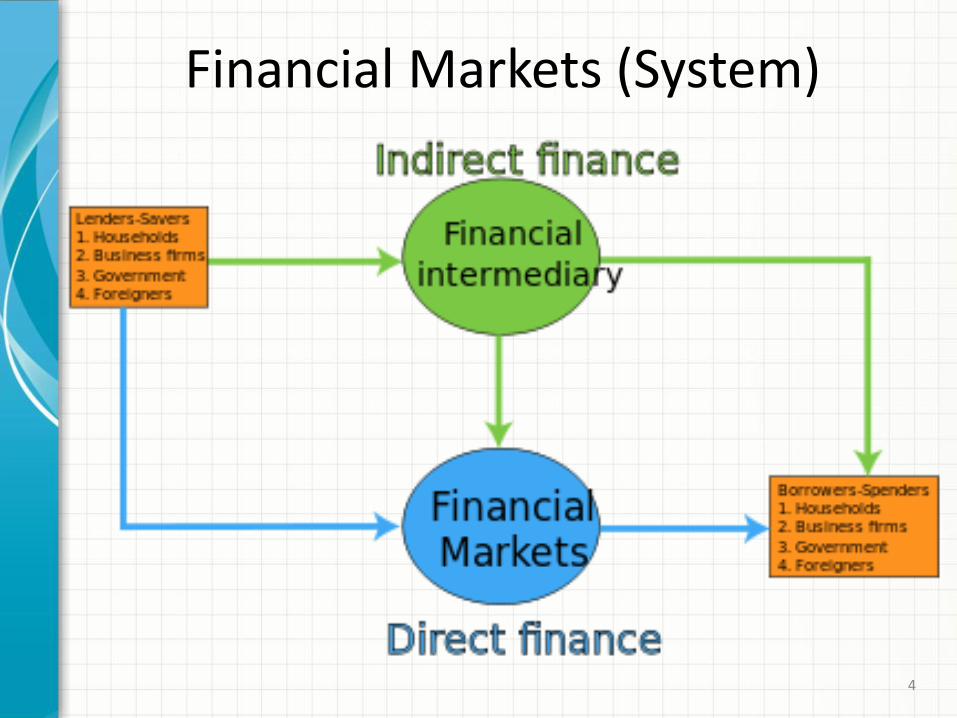

Financial Markets (System)

4

Real and Financial Asset • Real asset:

– An asset used to produce goods and services and thereby generate cash flow.

– Examples: factories, equipment, land/real estate, commodities buildings, knowledge.

• Financial asset:

– A claim on future income (cash flow) generated by a real asset.

– Stock, bond, commercial paper etc. – Also called financial security, financial instrument,

asset, or security.

5

Financialization • Financialization refers to the increasing

importance of financial markets, financial motives, financial institutions, and financial elites in the operation of the economy and its governing institutions, both at the national and international level.

Source: Radical Economic Perspectives on Globalisation, Gerald A. Epstein, 2009

6

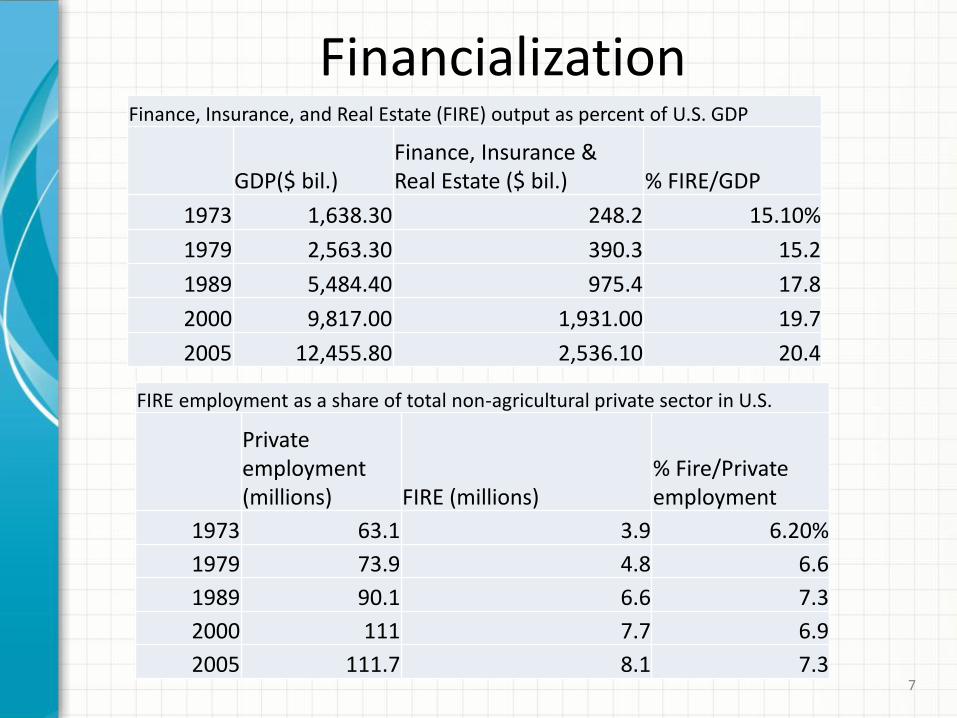

Financialization

Finance, Insurance, and Real Estate (FIRE) output as percent of U.S. GDP

GDP($ bil.) Finance, Insurance & Real Estate ($ bil.) % FIRE/GDP

1973 1,638.30 248.2 15.10%

1979 2,563.30 390.3 15.2

1989 5,484.40 975.4 17.8

2000 9,817.00 1,931.00 19.7

2005 12,455.80 2,536.10 20.4

FIRE employment as a share of total non-agricultural private sector in U.S.

Private employment (millions) FIRE (millions)

% Fire/Private employment

1973 63.1 3.9 6.20%

1979 73.9 4.8 6.6

1989 90.1 6.6 7.3

2000 111 7.7 6.9

2005 111.7 8.1 7.3 7

Financialization • Important questions:

– What are its implications for economic stability and growth? For income distribution? For political power and economic policy?

– What can be done to mitigate the negative impacts of financialization?

Source: Financialization and the World Economy, Gerald A. Epstein, 2006

8

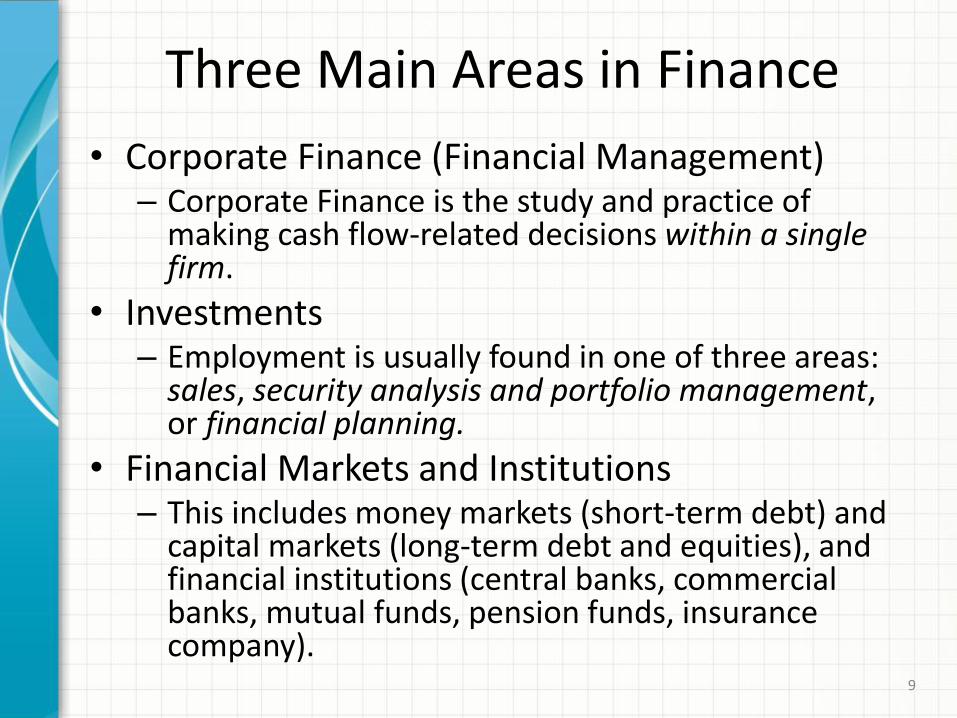

Three Main Areas in Finance

• Corporate Finance (Financial Management) – Corporate Finance is the study and practice of

making cash flow-related decisions within a single firm.

• Investments – Employment is usually found in one of three areas:

sales, security analysis and portfolio management, or financial planning.

• Financial Markets and Institutions – This includes money markets (short-term debt) and

capital markets (long-term debt and equities), and financial institutions (central banks, commercial banks, mutual funds, pension funds, insurance company).

9

Chapter 1 Introduction to Corporate Finance

10

Corporate Finance

• Studies how businesses make decisions regarding: – What long-term investments should the firm take on? – Where will we get the long-term financing to pay for

the investment? • Capital structure • Payout policy

– How will we manage the everyday financial activities of the firm?

• These three areas form financial management function

• Chief Financial Officer (CFO) responsible for financial management

11

Financial Management Decisions

• Capital budgeting – What long-term investments or projects should

the business take on?

• Capital structure & payout policy – Should we use debt or equity to finance the

projects?

– Should we pay dividend or repurchase stocks

• Working capital management – How do we manage the day-to-day finances of

the firm?

12

Financial Management Decisions

• In a survey conducted by Prof. Servaes and Prof. Tufano in 2006, 334 CFOs from public and private businesses were asked a question: what fraction of your company’s value would you attribute to the finance function?

– The average answer is ______.

13

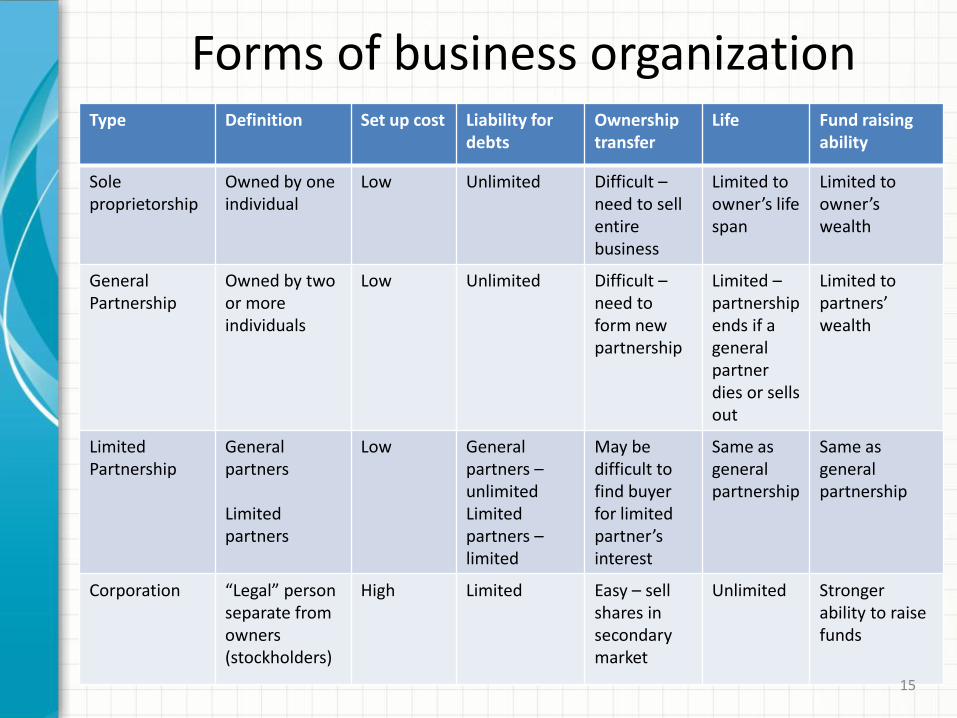

Forms of Business Organization

• Sole proprietorship

– Unincorporated business owned by one individual

• Partnership

– Unincorporated business owned by two or more individuals • General partnership

• Limited partnership

• Corporation

– A business created as a distinct legal entity (legal “person”) • Shareholders

• Directors

• Top management

– Limited liability: debt and equity investors’ liability is limited to the amount they invest

14

Forms of business organization Type Definition Set up cost Liability for

debts Ownership transfer

Life Fund raising ability

Sole proprietorship

Owned by one individual

Low Unlimited Difficult – need to sell entire business

Limited to owner’s life span

Limited to owner’s wealth

General Partnership

Owned by two or more individuals

Low Unlimited Difficult – need to form new partnership

Limited – partnership ends if a general partner dies or sells out

Limited to partners’ wealth

Limited Partnership

General partners Limited partners

Low General partners – unlimited Limited partners – limited

May be difficult to find buyer for limited partner’s interest

Same as general partnership

Same as general partnership

Corporation “Legal” person separate from owners (stockholders)

High Limited Easy – sell shares in secondary market

Unlimited Stronger ability to raise funds

15

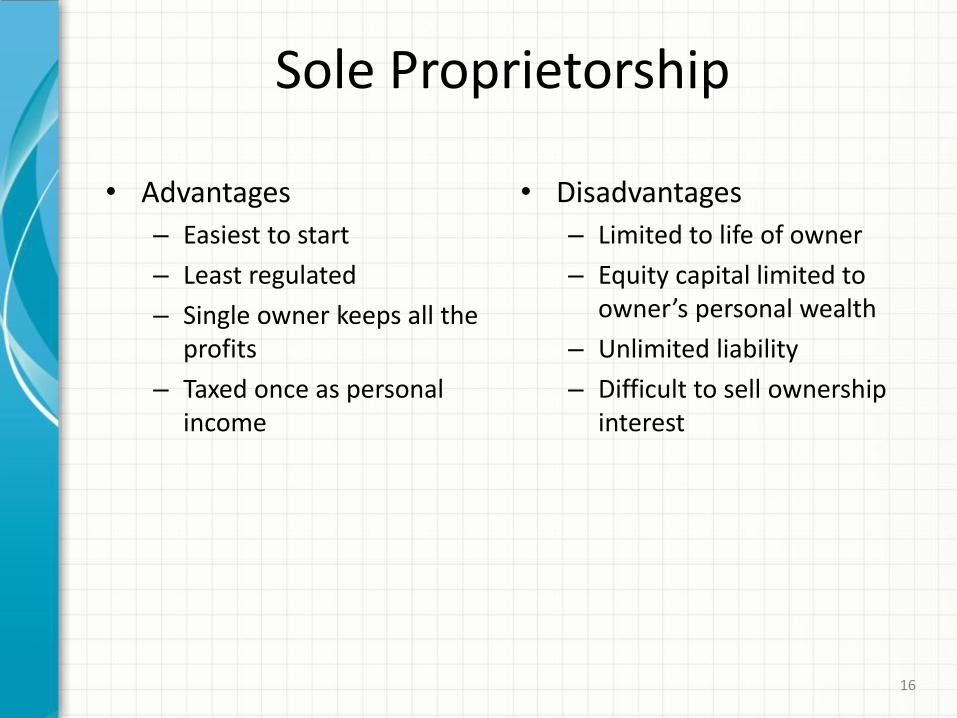

Sole Proprietorship

• Advantages

– Easiest to start

– Least regulated

– Single owner keeps all the profits

– Taxed once as personal income

• Disadvantages

– Limited to life of owner

– Equity capital limited to owner’s personal wealth

– Unlimited liability

– Difficult to sell ownership interest

16

Partnership

• Advantages

– Two or more owners

– More capital available

– Relatively easy to start

– Income taxed once as personal income

• Disadvantages

– Unlimited liability

• General partnership

• Limited partnership

– Partnership dissolves when one partner dies or wishes to sell

– Difficult to transfer ownership

17

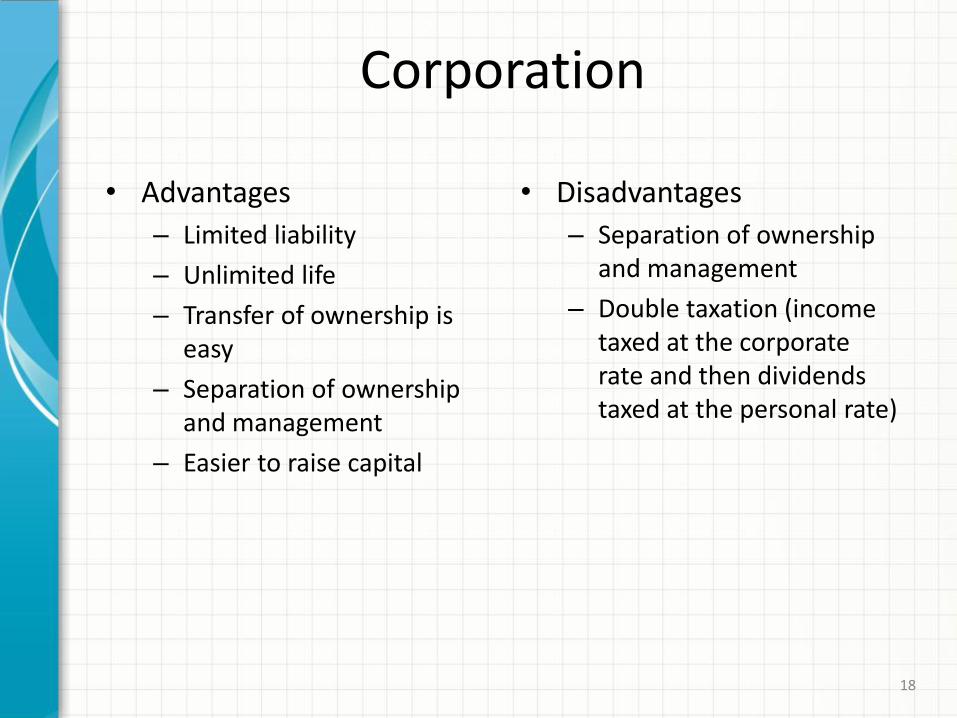

Corporation

• Advantages

– Limited liability

– Unlimited life

– Transfer of ownership is easy

– Separation of ownership and management

– Easier to raise capital

• Disadvantages

– Separation of ownership and management

– Double taxation (income taxed at the corporate rate and then dividends taxed at the personal rate)

18

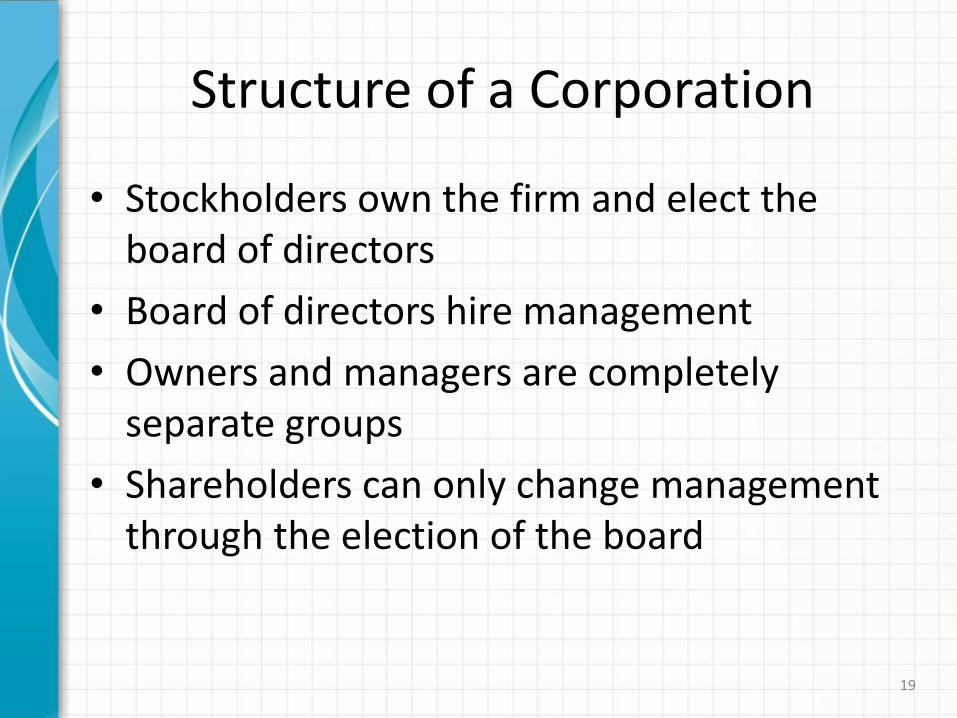

Structure of a Corporation

• Stockholders own the firm and elect the board of directors

• Board of directors hire management

• Owners and managers are completely separate groups

• Shareholders can only change management through the election of the board

19

Goal of Financial Management

• What should be the goal of a corporation?

– Maximize profit?

– Minimize costs?

– Maximize market share?

– Maximize the current value of the company’s stock?

1-20 20

Conflicts of Interest

• Shareholders – Shareholders invest in the firm and share in the

profits • Capital gains &/or dividends

– Vote on major decisions • Directors, mergers, takeovers, etc.

• Managers – Run the firm on a day to day basis

– Want job security, high salaries, fame, perquisites

21

Agency problem in corporations

• Agency relationship – One party (principal) hires another party (agent) to

represent his/her interest – In corporations, stockholders (principals) hire managers

(agents) to maximize shareholder wealth

• Agency (principal-agent) problem – Separation of ownership by stockholders from control by

managers – Managers act in their own interest (e.g., huge salary, big

office, private jet) rather than in shareholders’ interest – Conflict of interest between shareholders and managers

22

Agency problem: Cause and Consequences

• Cause – Information asymmetry: shareholders do not have

complete information about what managers are doing

• Consequences – Perquisite consumption - e.g., private jet – Monitoring cost – hiring auditors to check financial

statements – Poor investment decisions – e.g., overpaying to buy

another company purely for the sake of increasing size of company

– Forgoing profitable but risky investment

23

Dealing with agency problem • Corporate governance: Deal with the ways in

which suppliers of finance to corporations assure themselves of getting a return on their investment – Managerial compensation

• Link manager’s pay to firm performance (e.g., share price) • E.g., give stock options to manager as part of compensation

package

– Career incentives • Promotion opportunities, higher salaries

– Dismissal • Shareholders can fire poorly performing managers • Threat of dismissal acts as deterrent

24

Alternative goals of corporations

• Should the corporations do anything and everything to maximize owners’ wealth?

– Stakeholder

• Employees, customers, suppliers, government

– Corporate social responsibility (CSR)

• Business ethics

– Multinational firms

25

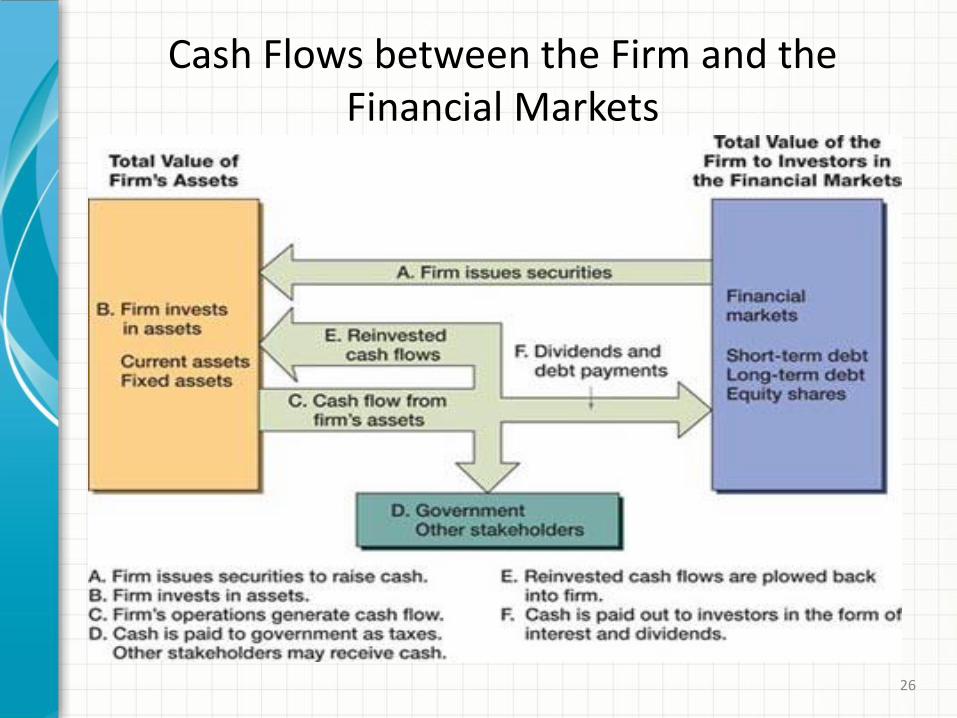

Cash Flows between the Firm and the Financial Markets

26

Chapter 4 Discounted Cash Flow Valuation

27

Scenarios • 1) On March 28, 2012 Toyota Motor Credit

Corporation (TMCC), a subsidiary of Toyota Motor, sold 30-year zero-coupon bonds. Each bond was sold for $24,099 and has a face value of $100,000. If TMCC pays off the bonds when they mature, what is the annual rate of return for a buy-and-hold investor?

• 2) Wal-Mart’s 2007 sales were $374 billion. Suppose sales are projected to increase at a rate of 15% per year. What will Wal-Mart’s sales be in the year 2012?

28

• 3) It will cost $214,690 to send your daughter to a 4-year private college. An insurance company is offering a 12-year college savings plan that promises an 8% return each year. How much must you invest in the plan today to fund your daughter’s college education?

• 4) Suppose you have $100,000. Your bank’s savings account promises 5% interest per year. If you invest your money in the savings account (and assuming your bank won’t be closed down by FDIC) how long will it take for your initial investment to grow to $1 million?

29

Learning Objectives (1) – Time Value of Money

• Calculate the future value of an investment made today

• Calculate the present value of cash to be received at a future date

• Calculate the return on an investment

• Calculate the time it takes for an investment to reach a desired value

• Use the financial calculator or Spreadsheet to solve time value of money problems

30

Future value, FV

• The amount an investment is worth after one or more periods

FV = PV x ( 1 + r )t • PV = present value, i.e., value of investment

today • r = interest rate/ discount rate/ rate of return • t = number of periods, 1

31

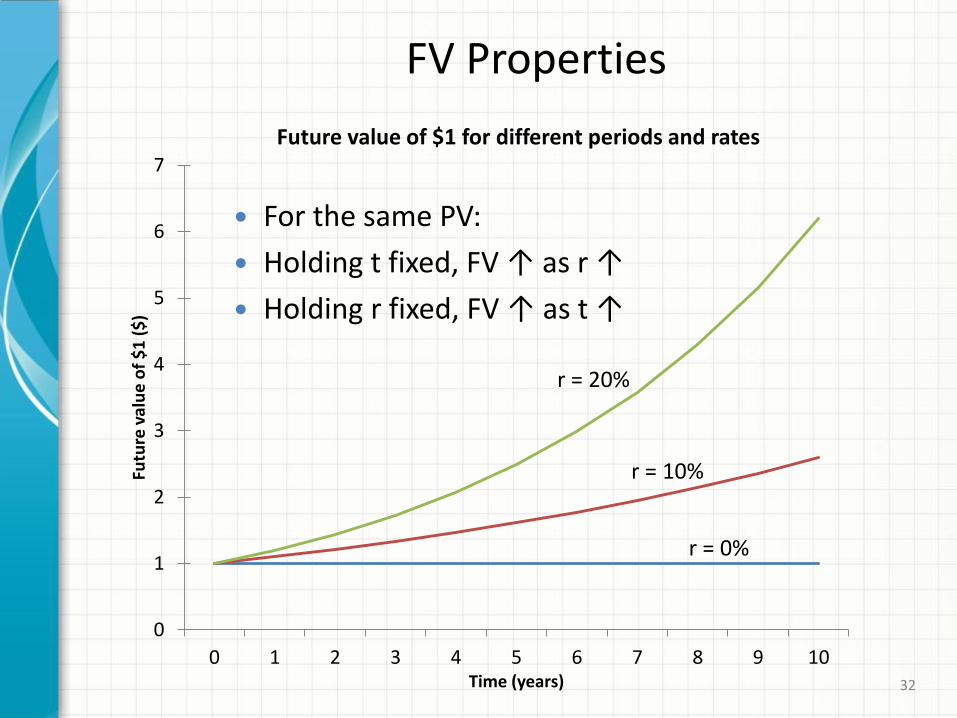

FV Properties

0

1

2

3

4

5

6

7

0 1 2 3 4 5 6 7 8 9 10

Futu

re v

alu

e o

f $

1 (

$)

Time (years)

Future value of $1 for different periods and rates

r = 0%

r = 10%

r = 20%

For the same PV:

Holding t fixed, FV ↑ as r ↑

Holding r fixed, FV ↑ as t ↑

32

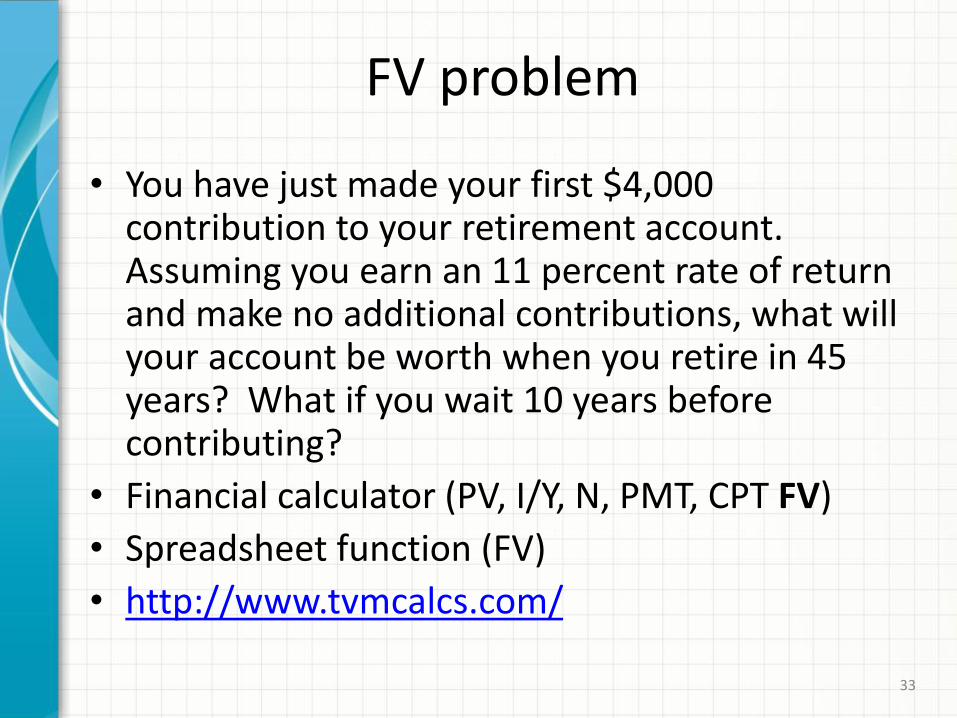

FV problem

• You have just made your first $4,000 contribution to your retirement account. Assuming you earn an 11 percent rate of return and make no additional contributions, what will your account be worth when you retire in 45 years? What if you wait 10 years before contributing?

• Financial calculator (PV, I/Y, N, PMT, CPT FV)

• Spreadsheet function (FV)

• http://www.tvmcalcs.com/

33

Present value, PV

• Suppose we want to solve for PV instead.

• Re-arranging the FV formula gives the formula for PV

PV = FV/( 1 + r )t

34

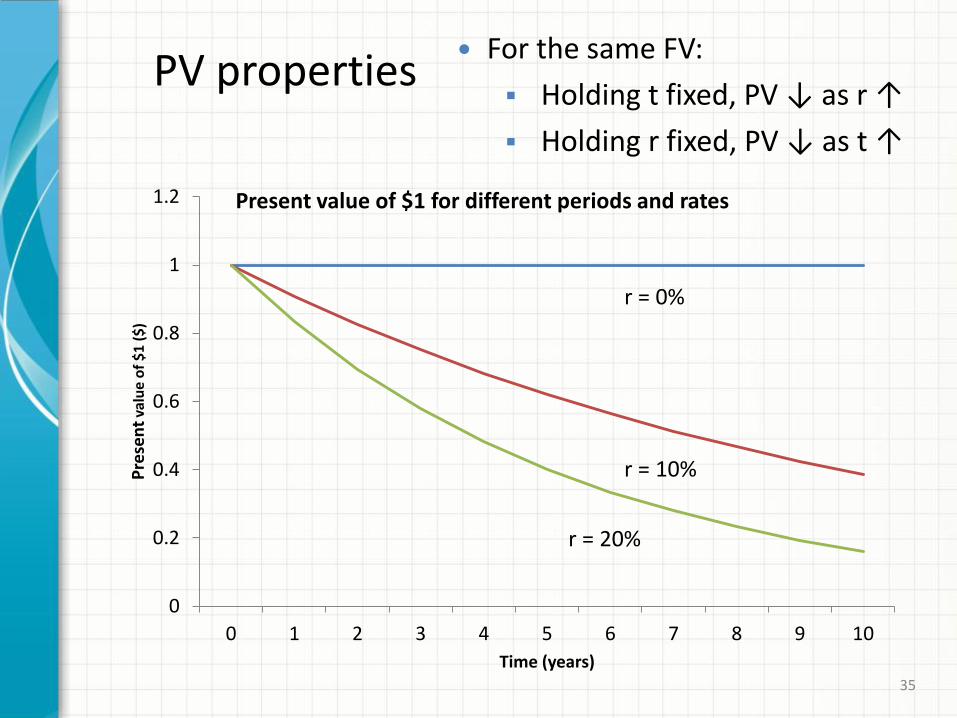

PV properties

0

0.2

0.4

0.6

0.8

1

1.2

0 1 2 3 4 5 6 7 8 9 10

Pre

sen

t va

lue

of

$1

($

)

Time (years)

Present value of $1 for different periods and rates

r = 0%

r = 10%

r = 20%

For the same FV:

Holding t fixed, PV ↓ as r ↑

Holding r fixed, PV ↓ as t ↑

35

PV problem

• You have just received notification that you have won the $1 million first prize in the Centennial Lottery. However, the prize will be awarded on your 100th birthday (assuming you’re around to collect), 80 years from now. What is the present value of your windfall if the appropriate discount rate is 10 percent?

• Financial calculator (FV, I/Y, N, PMT, CPT PV)

• Spreadsheet function (PV)

36

Discount rate, r

• Re-arranging the FV formula yields the formula for the discount rate

r = (FV/PV)1/t - 1

37

Discount rate problem

• Referring to the TMCC security at the start of the class:

1. Suppose that, on March 28, 2020, this security’s price is $38,260. If an investor had purchased it for $24,099 at the offering and sold it on this day, what annual rate of return would she have earned?

2. If an investor had purchased the security at market on March 28, 2020, and held it until it matured, what annual rate of return would she have earned?

• Financial calculator (PV, FV, N, PMT, CPT I/Y)

• Spreadsheet function (RATE)

38

Number of periods, t

• Re-arranging the FV formula yields the formula for the discount rate:

t = Ln(FV/PV)

Ln (1+r) • Ln = natural log function

• You can also solve for t using the financial calculator

39

# of periods problem

• You expect to receive $10,000 at graduation in two years. You plan on investing it at 11 percent until you have $75,000. How long will you wait from now?

40

Learning Objectives (2) – Multiperiod Cash Flows

• Solve TVM problems involving multiple periods and multiple cash flows

• Understand the difference between an ordinary annuity and an annuity due

• Solve TVM problems involving an annuity due

• Understand the difference between effective annual rate and quoted interest rate

41

TVM problems with multiple cash flows

• Two broad categories:

– A) Cash flows are of different amounts

– B) Cash flows are all same

• Tip 1: Draw a time line to help you visualize and understand the problem

• Tip 2: Unless otherwise stated, assume cash flows occur at the end of each period

42

Cash flows are of different amounts

• Future value:

– Compound the accumulated balance forward

one year at a time OR

– Calculate FV of each cash flow first and then add them up

• Use whichever method is most convenient and error-free for you

43

• Present value:

– Discount future cash flows back one period at

a time OR

– Calculate PV of each cash flow first and then add them up

• Again, use whichever method is most convenient and error-free for you

44

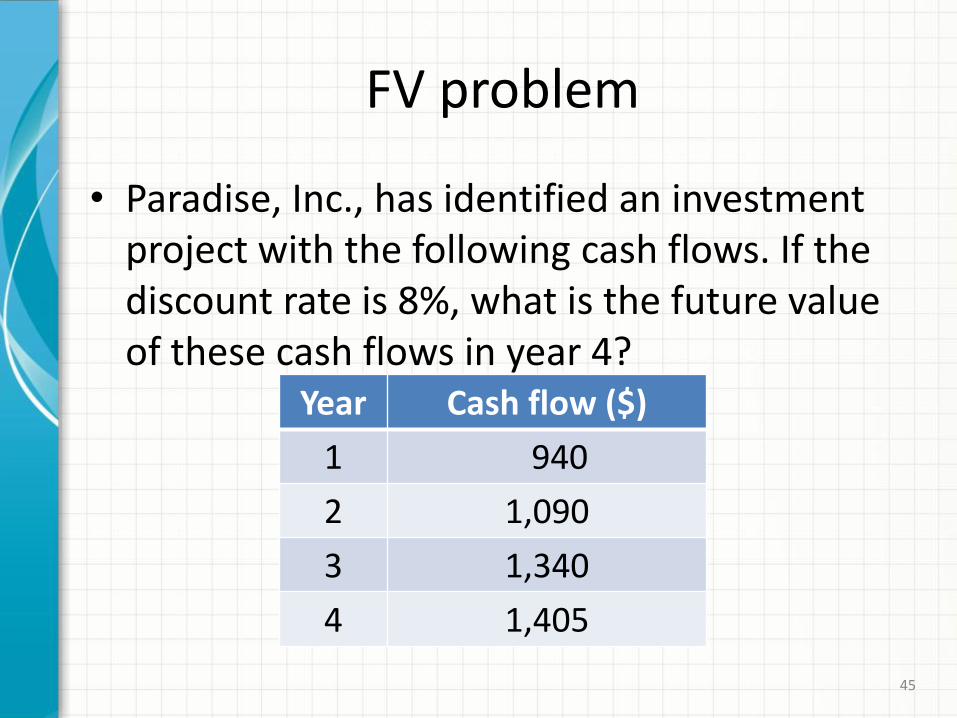

FV problem

• Paradise, Inc., has identified an investment project with the following cash flows. If the discount rate is 8%, what is the future value of these cash flows in year 4?

Year Cash flow ($)

1 940

2 1,090

3 1,340

4 1,405

45

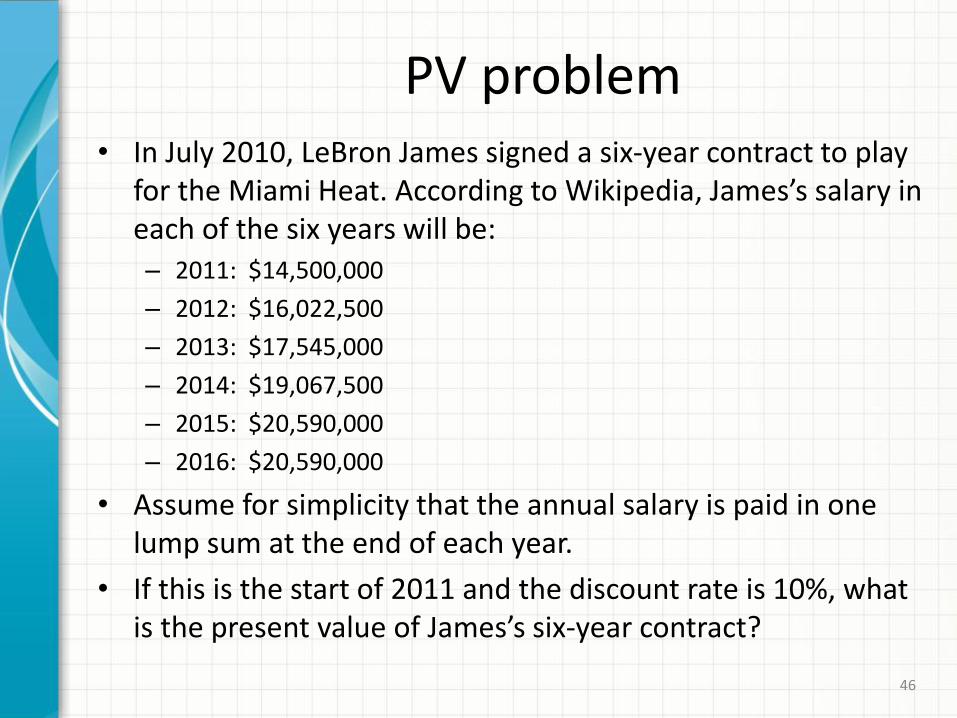

PV problem • In July 2010, LeBron James signed a six-year contract to play

for the Miami Heat. According to Wikipedia, James’s salary in each of the six years will be: – 2011: $14,500,000

– 2012: $16,022,500

– 2013: $17,545,000

– 2014: $19,067,500

– 2015: $20,590,000

– 2016: $20,590,000

• Assume for simplicity that the annual salary is paid in one lump sum at the end of each year.

• If this is the start of 2011 and the discount rate is 10%, what is the present value of James’s six-year contract?

46

Cash flows are all same

• In this category, TVM problems can be analyzed using:

• Annuity OR

• Perpetuity

47

Annuity / Ordinary annuity

• A cash flow stream where a fixed amount is received at the end of every period for a fixed number of periods.

• Example: Monthly installment payments on a car loan.

• In many TVM problems, the cash flow stream is – An annuity combined with a single cash flow

(often at the beginning or the end)

– A combination of two or more annuities

48

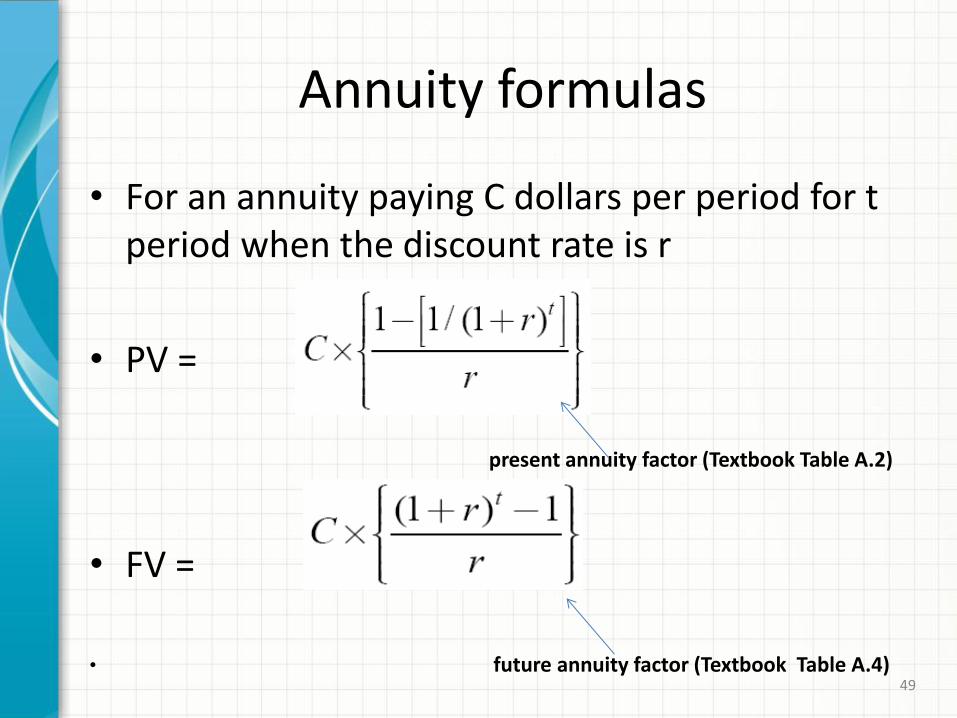

Annuity formulas

• For an annuity paying C dollars per period for t period when the discount rate is r

• PV =

present annuity factor (Textbook Table A.2)

• FV =

• future annuity factor (Textbook Table A.4)

49

Annuity, find PV

• Your company will generate $73,000 in annual revenue each year for the next eight years from a new information database. If the appropriate interest rate is 8%, what is the present value of the savings?

50

Annuity, find FV

• If you deposit $4,000 at the end of each of the next 20 years into an account paying 10 percent interest, how much money will you have in the account in 20 years?

51

Annuity, find C

• You want to have $90,000 in your savings account 10 years from now, and you’re prepared to make equal annual deposits into the account at the end of each year. If the account pays 6% interest, what amount must you deposit each year?

52

Annuity, find r

• You borrow $50,000 today from your bank to start a business selling used textbooks. The loan requires annual payments of $14,000 for the next six years. What is the interest rate on your loan?

53

Annuity, find t

• Your Christmas ski vacation was great, but it unfortunately ran a bit over budget. All is not lost: You just received an offer in the mail to transfer your $10,000 balance from your current credit card, which charges 1% interest per month, to a new credit card charging 0.7% per month. How much faster could you pay the loan off by making your planned monthly payments of $200 with the new card?

54

Annuity due

• An annuity for which the cash flows occur at the beginning of the period.

• Example: rental payments for an apartment

• PV of annuity due = (PV of ordinary annuity) x (1 + r) • FV of annuity due = (FV of ordinary annuity) x (1 + r)

55

Annuity due problem

• You have a rental property that you want to rent for 10 years. Prospective tenant A promises to pay you rent of $12,000 per year with the payments made at the end of each year. Prospective tenant B promises to pay $12,000 per year with payments made at the beginning of each year. Which is a better deal for you if the appropriate discount rate is 10 percent?

56

Perpetuity

• An annuity in which the cash flows continue forever

• Examples:

– UK government consols

– Perpetual preferred stock

• PV of perpetuity = C / r

57

Perpetuity problem

• The Maybe Pay Life Insurance Co. is trying to sell you an investment policy that will pay you and your heirs $25,000 per year forever. If the required return on this investment is 7.2%, how much will you pay for the policy?

• Suppose a sales associate told you the policy costs $375,000. At what interest rate would this be a fair deal?

58

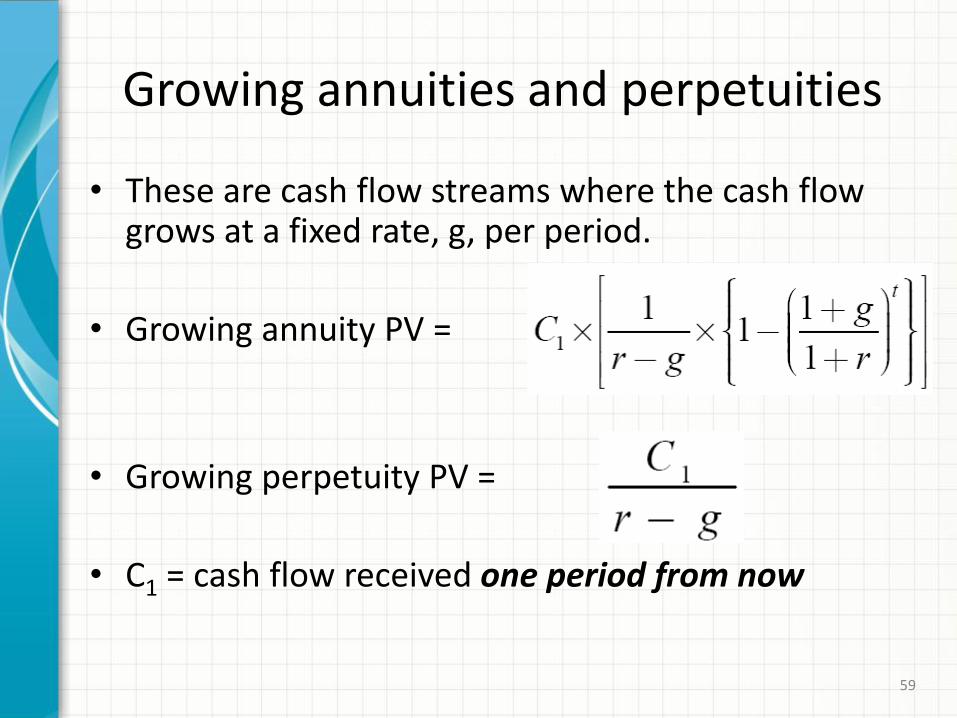

Growing annuities and perpetuities

• These are cash flow streams where the cash flow grows at a fixed rate, g, per period.

• Growing annuity PV =

• Growing perpetuity PV =

• C1 = cash flow received one period from now

59

Growing annuity problem

• Your job pays you only once a year for all the work you did over the previous 12 months. Today, Dec 31, you just received your salary of $50,000 and you plan to spend all of it. However, you want to start saving for retirement beginning next year. You have decided that one year from today you will begin depositing 5% of your annual salary in an account that will earn 11% per year. Your salary will increase at 4% per year throughout your career.

• How much money will you have on the date of your retirement 40 years from today?

60

Effective vs. Quoted interest rate

• Quoted interest rate – Interest rate expressed in terms of the interest

payment made each period

– Also known as stated interest rate

– Examples: annual percentage rate (APR) on a loan, coupon interest on a bond

• Effective interest rate (EAR) – The interest rate expressed as if it were

compounded once per year

61

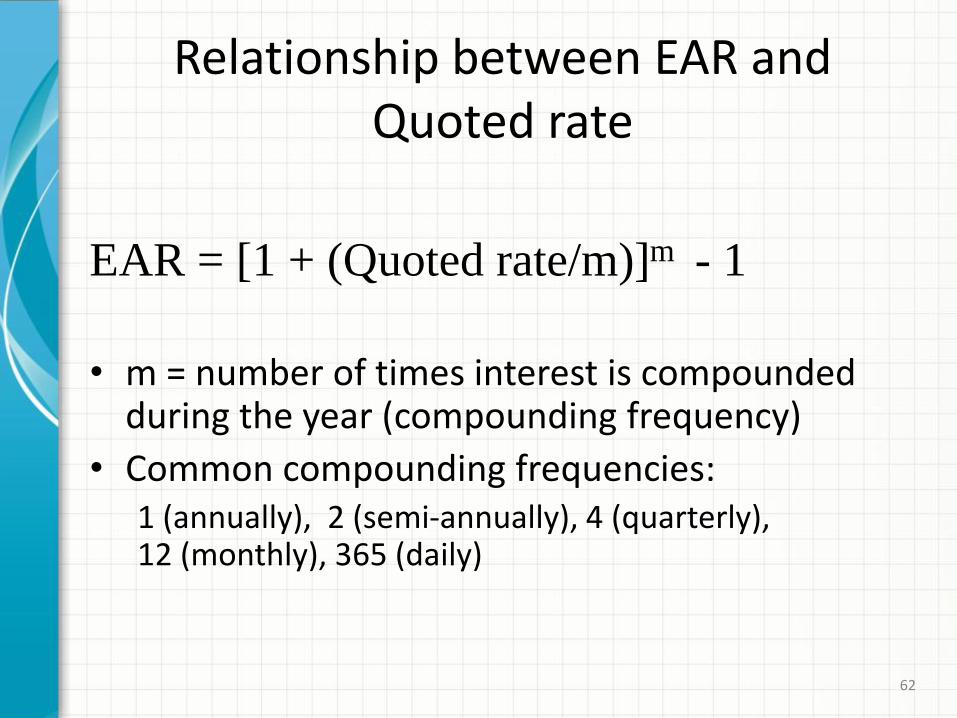

Relationship between EAR and Quoted rate

EAR = [1 + (Quoted rate/m)]m - 1

• m = number of times interest is compounded

during the year (compounding frequency)

• Common compounding frequencies: 1 (annually), 2 (semi-annually), 4 (quarterly), 12 (monthly), 365 (daily)

62

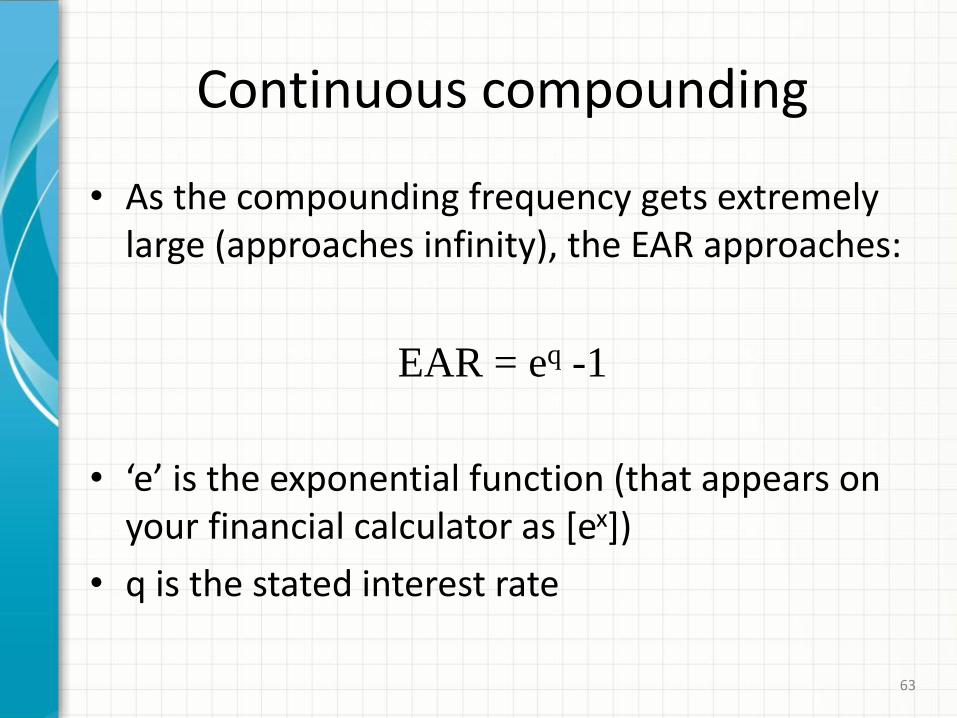

Continuous compounding

• As the compounding frequency gets extremely large (approaches infinity), the EAR approaches:

EAR = eq -1

• ‘e’ is the exponential function (that appears on your financial calculator as [ex])

• q is the stated interest rate

63

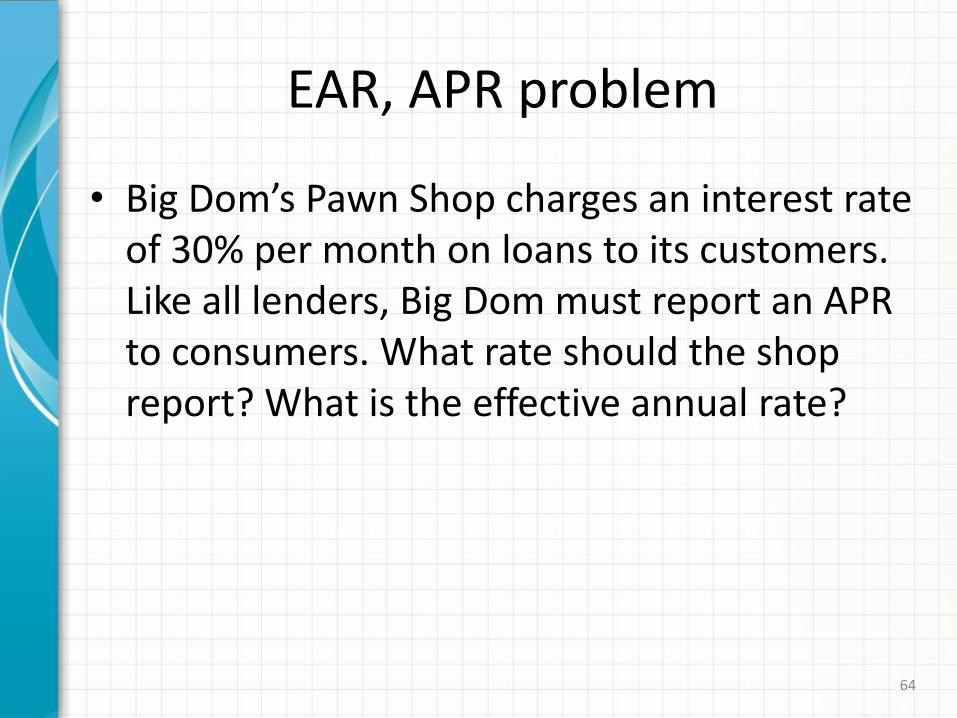

EAR, APR problem

• Big Dom’s Pawn Shop charges an interest rate of 30% per month on loans to its customers. Like all lenders, Big Dom must report an APR to consumers. What rate should the shop report? What is the effective annual rate?

64

Multiple periods of compounding in a year

• Your are planning to save for retirement over the next 30 years. To do this, you will invest $700 a month in a stock account and $300 a month in a bond account. The return of the stock account is expected to be 11% p.a., and the bond account will pay 6% p.a. When you retire, you will combine your money into an account with a 9% p.a. return. How much can you withdraw each month from your account assuming a 25-year withdrawal period?

• (Assume all cash flows are paid or received at the end of each month)

65

For Next Week

• Recommended exercises for Ch.4: 2,3,4,5,6,9,11,13,14,16,17,21,28,33,41,58

• Read Ch.8

66