Institutional Investor Monitoring and the Structure of Corporate Boards

67

1 Institutional Investor Monitoring and the Structure of Corporate Boards * David R. Gallagher † Gavin S. Smith ‡ Peter L. Swan § Current Draft: October 2, 2007 School of Banking and Finance, Australian School of Business, The University of New South Wales, Sydney, N.S.W. 2052 Abstract: This study examines the effect of institutional investor influence on the structure of corporate boards. We focus on investor influences with respect to reducing board size and increasing board independence. Measures of institutional influence are negatively related to board size and positively related to board independence. To achieve these aims, institutions remove inside directors. This effect is enhanced when the firm has performed poorly - institutions take corrective action to improve firm performance by punishing those directors deemed responsible for contributing to poor firm performance. Institutional investors do not adjust their monitoring objectives with respect to board size and independence to reflect firm specific characteristics. JEL classification: G23, G32, J33 Keywords: Board of Directors, Monitoring, Institutional Investment Behavior * The authors are grateful to the Australian Research Council (DP0346064) for research funding and to David Yermack for insightful comments. † Email: [email protected] . Phone: 61292369106. ‡ Corresponding author. Email: [email protected] . Phone: 61282473123. § Mail: School of Banking and Finance, The University of New South Wales, UNSW Sydney 2052, Australia. Email: [email protected] . Phone: 61293855871.

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Institutional Investor Monitoring and the Structure of Corporate Boards

1

Institutional Investor Monitoring and the Structure of Corporate Boards*

David R. Gallagher†

Gavin S. Smith‡

Peter L. Swan§

Current Draft: October 2, 2007

School of Banking and Finance, Australian School of Business, The University of New South

Wales, Sydney, N.S.W. 2052

Abstract: This study examines the effect of institutional investor influence on the structure of corporate boards. We focus on investor influences with respect to reducing board size and increasing board independence. Measures of institutional influence are negatively related to board size and positively related to board independence. To achieve these aims, institutions remove inside directors. This effect is enhanced when the firm has performed poorly - institutions take corrective action to improve firm performance by punishing those directors deemed responsible for contributing to poor firm performance. Institutional investors do not adjust their monitoring objectives with respect to board size and independence to reflect firm specific characteristics.

JEL classification: G23, G32, J33

Keywords: Board of Directors, Monitoring, Institutional Investment Behavior

*The authors are grateful to the Australian Research Council (DP0346064) for research funding and to David Yermack for insightful comments. † Email: [email protected]. Phone: 61292369106. ‡ Corresponding author. Email: [email protected]. Phone: 61282473123. § Mail: School of Banking and Finance, The University of New South Wales, UNSW Sydney 2052, Australia. Email: [email protected]. Phone: 61293855871.

2

I. Introduction

Large shareholders, such as institutional investors, possess considerable

influence over firms in which they are shareholders. Because institutional investors

have large investments in firms, they have significant bargaining power and can gain

direct access to the top management of a firm—something atomistic shareholders

cannot achieve. Institutions also have the funds, resources and ability to wage

concerted campaigns to remove or appoint directors—they have the leverage to have

their voice heard. Institutional investors are in principle able to appoint board

members representing their interests. Hence, the effectiveness of corporate

governance typically requires the presence of large institutional investors.

This paper examines the effect of institutional investor influence on the

structure of corporate boards. Institutional investor influence on board structure is an

important issue given the role the board of director’s plays within corporations. The

board of directors is a central organizational mechanism for alleviating agency

problems and to better align management’s interests with those of shareholders. While

the board delegates to management the task of initiating and implementing various

decisions, it is the board that has the control and authority to ratify and monitor major

policy initiatives and to hire, fire and set the compensation of top management (Fama

and Jensen, 1983). By keeping the management and control aspects of the decision-

making process separate, the board is able to reduce agency conflicts. In essence, the

board of directors act as shareholders’ representatives in monitoring management, and

so work to resolve the fundamental agency problem facing firms.

To ensure the board effectively fulfils its role of monitoring management, two

aspects of board structure are scrutinized—board size and board independence. A

3

small board is said to be harder for the CEO to control (Jensen, 1993), allow increased

communication between board members (Lipton and Lorsch, 1992), result in

enhanced shareholder value (e.g., Yermack, 1996; Eisenberg, Sundgren and Wells,

1998; Gertner and Kaplan, 1997) and improved decision making. Similarly, a higher

proportion of boards that consist of non-management affiliated individuals (i.e.,

independent directors), weakens CEO power over the board. Independent directors are

viewed as not being ‘friendly’ to management and are more likely to scrutinize the

behavior of CEOs.

The focus of this study is in determining whether institutional investors

succeed in reducing board size and increasing independence. In understanding

whether institutional influence does result in more effective boards, it is also

important to understand how institutional investors achieve these objectives. Our

study examines director appointments and departures to gain insights into how

institutional investors may potentially alter board size and independence. To isolate

the monitoring objectives of institutions, alternative hypotheses are addressed that

predict optimality of different board structures (e.g. Coles, Daniel and Naveen, 2007;

Boone, Field, Karpoff and Raheja, 2007; Adams and Ferreira, 2007). These

hypotheses predict that firms with certain characteristics may not benefit from a

general prescription of smaller boards and increased independence. Tests are

conducted to determine whether institutional influence varies with firm specific

characteristics.

We find that institutional investor influence is negatively related to board size,

and positively related to board independence using pooled OLS, firm random effects

and firm fixed effects. However, these results do become insignificant using a 2SLS

4

approach which allows us to control for concerns over endogeneity. The low

variability of governance mechanisms makes the determination of causal relations

difficult. This suggests that our instrumental variables approach that orthogonalizes

institutional ownership to board characteristics may be effective; it may also be overly

harsh.

Examining director appointments and departures is potentially a better test of

institutional monitoring as it captures changes in board structure, making the

determination of causal relations more reliable. Institutional investors appear to focus

on removing inside directors as a means of reducing board size and increasing

independence. Institutional influence is also positively related to both the appointment

and departure of inside directors. Since more insiders are being removed than

appointed, this results in an increase in board independence. This relationship is

particularly evident in periods when a firm has performed poorly. Institutions take

corrective action to improve firm performance and punish those directors deemed

responsible for contributing to poor firm performance. This analysis of director

appointments and departures provides support for institutional investors being

effective monitors of corporate boards. We also fail to find consistent support for

claims that institutional investors vary their monitoring objectives away from the

pursuit of smaller boards and increased independence to reflect firm specific

characteristics.

This paper is organized as follows. The next section reviews related literature.

Section III describes the data and measurement of the variables. Section IV presents

our results with respect to the effect of institutional investor influence on board size

and independence. Section V explores the role of institutional investors in influencing

5

the appointment and departure of directors. Section V tests alternative monitoring

hypotheses that suggest the optimality of different board structures, and the final

section concludes.

II. Literature Review

Previous studies have shown that institutions monitor across a number of

dimensions; for example, executive compensation (Smith and Swan, 2007a,b),

earnings management (Chung, Firth and Kim, 2002), anti-takeover charter

amendments (Agrawal and Mandelker, 1990) and forced CEO turnover (Parrino, Sias

and Starks, 2003). Two studies have focused on the effect of institutional investor

influence on board structure. First, Wu (2004) examines the public naming of firms

by a single institution, CalPERS, and finds in the period 1988-1995, median board

size declined from 12 to 11 and the number of inside directors on the board also

declined from three to two. Second, Whidbee (1997) considers the effect of

institutions on 190 publicly traded bank holding companies and finds that board

independence increases when institutional investors own more of the firm. Our study

extends Wu (2004) and Whidbee (1997) by using a more comprehensive sample of

both institutional investors and firms, and also by examining how institutions achieve

their objectives with respect to board structure.

There is also extant literature that provides support for why institutions should

focus on smaller boards and increased board independence. Yermack (1996)

documents, in a sample of large US firms, that board size is inversely related to

Tobin’s Q and also various accounting ratios, such as return on assets. Similarly,

Eisenberg, Sundgren and Wells (1998) examine a sample of small and medium sized

6

Finnish firms that board size is inversely related to industry adjusted return on assets.

In a sample of reverse leverage buyout (LBO) firms Gertner and Kaplan (1997) find

that boards are smaller. This is said to provide evidence from the efficiency of smaller

boards due to the incentives of LBO specialists to structure boards in a way that

maximizes shareholder value. Smaller boards are also associated with improved

decision making. For example, Yermack (1996) finds smaller boards are more likely

to dismiss CEOs for poor performance and increase the sensitivity of CEO salaries

and bonuses to firm performance, while Core, Holthausen and Larcker (1999)

document that larger boards increase the level of CEO compensation.

Disturbingly, given mandated increases in board independence in the U.S. and

more widely1, findings indicating the effect of board composition on firm

performance are mixed. Baysinger and Butler (1985) and Hermalin and Weisbach

(1991) find no significant relationship between board composition and measures of

firm performance. Yermack (1996) and Agrawal and Knoeber (1996) show a

significant negative relation between the proportion of independent directors and

Tobin’s Q. Rosenstein and Wyatt (1990) examine the performance relation from an

event study perspective. They find a positive stock price reaction when a company

appoints an additional outside director. However, Rosenstein and Wyatt find a

stronger price reaction for outside directors who work for financial institutions than

for directors whose principal job is with another unrelated non-financial corporation.2

1 The Sarbanes Oxley Act of 2002 and amended listing requirements have required the appointment of

a higher proportion of outside board members. See, for example, Wintoki (2007). New listing rules in

Australia and elsewhere act in a similar direction. 2 Yet outside directors who work for financial institutions are usually treated as affiliated outside

directors rather than independent directors, because their own firm may be interested in business

dealings with the firm on whose board they sit.

7

Rosenstein and Wyatt (1997) perform an event study of the appointment of

inside directors. A key feature of their findings is that the market reaction to the

appointment of insiders depends on the ownership of the insider. When the insider

owns less than 5% of the firm’s stock, the market reaction is significantly negative.

The market reaction is significantly positive when the ownership is between 5 and

25% and insignificantly different from zero when the ownership exceeds 25%.

Although the performance effects of independent boards are questionable, they

have been shown to provide an episodic monitoring function, by benefiting

shareholders in extraordinary or crisis situations. Increased levels of independent

directors improve the effectiveness of the board when it comes to dismissing poorly

performing CEOs (Weisbach, 1988), selecting new CEOs (Borokhovich, Parrino and

Trapani, 1996) and awarding incentive compensation (Yermack, 1996). Additionally,

independent directors have been found to do a better job negotiating takeovers offers

on behalf of shareholders of target firms (Cotter, Shivdasani and Zenner, 1997), make

better acquisitions (Byrd and Hickman, 1992), produce better value and only adopt

poison pills when they are genuinely in the interests of shareholders (Brickley, Coles

and Terry, 1994). Finally, management led buyouts of firms with outsider boards have

higher abnormal returns than this with insider boards (Lee, Rosenstein, Rangan and

Davidson, 1992).

III. Data

This section discusses the data employed in the study, variable measurement,

descriptive statistics and the methodology. Board of director data is sourced from the

Investor Responsibility Research Center (IRRC). Institutional holdings, used to

8

compute measures of institutional influence, are from the Thomson Financial

CDA/Spectrum database.3 Firm level accounting and stock price data are from S&P’s

Compustat and the Centre for Research in Stock Prices (CRSP), respectively. Data is

collected for the firm fiscal years corresponding to 1996-2002.4 Our sample of firms

is based on the coverage of IRRC. Financial firms are excluded from the sample. Our

matched sample yields a maximum of 9,086 firm years.

A. Board of Director Measures:

Two key characteristic of boards are computed—board size and board

independence. Board size represents the total number of directors on the board. The

natural logarithm of board size is employed throughout the study. Independent

directors are defined as those which have no family relations with directors on the

board, have not worked for the company in the past, are not currently employees, and

also do not have any business relationship with the company. The definition of

independent directors is designed to exclude inside and grey directors that may have

some affiliation with insiders. Insiders are full-time company employees who fulfill

an executive role and are typically on the board. The proportion of independent

directors on the board of directors is then computed as the ratio of independent

directors to the total number of directors on the board.

To better understand how institutional investors shape board size and

independence, various measures of changes in board structure are also computed.

3 This database consists of quarterly 13-F filings of money managers to the U.S Securities and

Exchange Commission (SEC). Institutions with more than $100 million of securities under

management are required to report to the SEC. All positions that are greater than 10,000 shares or

$200,000 must be disclosed (Gompers and Metrick, 2001). 4 If a firm has a fiscal year that does not correspond exactly to a quarter-end, we make an adjustment to

a firm’s fiscal year. The fiscal year is rounded up to the nearest calendar quarter end.

9

First, appointments and departures of directors are observed. The number of

appointments and departures are then scaled by the number of directors up for

election. This measure is used because it provides a better indication of what

institutions can influence contemporaneously. Intuitively, if a firm has a staggered

board, only part of the board is up for election and so institutions are limited in how

they can change the board composition on an annual basis. Indeed, as noted above,

staggered boards are a major contributor to lack of takeover vulnerability. Second, the

departure and appointment of independent and inside directors are computed. Grey

directors are included with insiders. Again, the numbers of independent and inside

directors that have been appointed or departed are scaled by the number of

independent and inside directors nominated for re-election, respectively.

B. Institutional Influence Measures:

To measure institutional influence, ownership-based metrics are employed. 5

Two primary measures of institutional investor influence are utilized. The first

measure is a Herfindahl Index of the ownership of the top5 institutions. This is

defined as the sum of the squared holdings of the top five institutions as a percent of

total shares outstanding, and is designed to capture the concentration of institutional 5 Indirect support for the use of institutional ownership measures comes from several studies that have

found a positive relation between shareholder proposals and institutional ownership. The suggestion

being institutional ownership is an important characteristic in choosing proposal targets. Bizjak and

Marquette (1998), Carleton et al. (1998), Karpoff et al. (1996) and Smith (1996) find that institutional

investor ownership is high. Proposals are high in these firms due to expectation that institutions

cooperate. Moreover, institutional investors, who have far greater incentives to engage in informed

voting compared to individual shareholder because of the size and extent of their holdings, are

hypothesized to vote for proposals enhancing shareholders’ ability to monitor management with greater

frequency. Gordon and Pound (1993) and Gillan and Starks (2000) show that the percentage of votes

cast for shareholder proposals is positively related to institutional ownership.

10

ownership. Concentration is expected to be an important measure of institutional

influence since higher concentrations may decrease the cost of institutional

cooperation, and increase the incentive for institutions to take the lead in activist

efforts (Clay, 2000). The Herfindahl Index of top 5 ownership is winsorized at the 1%

and 99% levels, and also used in log form. This approach is employed to remove the

effect of extreme values in the Herfindahl Index.

The second measure of institutional influence is based on the level of

institutional ownership, computed as the proportion of shares held by the five largest

institutional holders (denoted Top5 Ownership). This measure is meant to capture the

level of ownership of institutions with large holdings. We argue that monitoring costs

decrease with the size of the institutional holding. As long as there is a fixed

component to the cost of gathering and analyzing information on the invested firm,

there will be economies of scale in monitoring technology. The larger the holdings of

an institution, the smaller will be the proportional cost of monitoring. Further, larger

holdings can actually reduce the total costs of monitoring by giving the institution

easier access to management and the board (Chen, Harford, Li, 2007). Carleton,

Nelson and Weisbach (1998) show that institutions with large ownership positions

often have access to board members and senior managers. Institutional investors with

large holdings appear to have greater incentives to monitor since they cannot always

sell shares of underperforming firms. This is not only because trading their larger

holdings could create adverse price shifts and exacerbate losses, but also because

many institutions index a large portion of their holdings. Despite all these advantages

of large monitors acknowledged by Noe (2002), in an incentive-compatible

microstructure trading equilibrium in which monitors have to recover the fixed costs

of monitoring from trading profits, smaller strategic investors will have a higher

11

probability of monitoring than larger incumbents (Noe, 2002). This is because both

monitoring and informed trading have to come as a surprise otherwise spreads rise so

as to choke off profitable trading. Thus to the extent that Top5 ownership is able to

explain board monitoring, as opposed to smaller institutional investors that trade more

actively, the lesser importance must attach for the need for such monitors to recover

costs from informed trading activities. Smith and Swan (2007b) find that smaller

institutional investors trading more intensively, rather than Top5 ownership, is most

associated with higher pay performance sensitivity of option grants and higher

executive pay.

The Top5 Ownership measure of institutional influence is further decomposed

to address issues of institutional investor heterogeneity. One issue that arises in

measuring institutional influence is that not all institutions are willing or able to exert

their influence. Brickley, Lease and Smith (1988) establish that some institutional

investors (e.g., insurance companies and banks through their trust departments) have

either existing or potential business relationships with firms, and, therefore, in order

to protect those relationships they might be less willing to challenge management

decisions. In contrast, institutions such as investment companies, independent

investment advisors and public pension funds do not seek business relationships with

the firms in which they invest (we call these “independent” institutional investors).

Institutions, such as banks and insurance companies, face high costs to monitoring

because they could damage their relationship with firm management and lose existing

or potential business. Thus, independent institutions without potential business ties

face lower costs to monitoring (Chen, Harford and Li, 2007).

Following Almazan, Hartzell and Starks (2005), institutions are categorized

into two groups based on their potential business relations with the firms in which

12

they invest. The first group is defined as Potentially Passive, due to the fact they have

potential business relations with firms and are susceptible to pressure from

management. CDA Spectrum classifications are used; with potentially passive

institutions including banks, insurance companies and institutions that fall into CDA’s

Other category. The second group is defined as Potentially Active, due to the fact

they are not expected to have significant potential business relations with firms and

are therefore not susceptible to pressure from management. These institutions include

investment companies or independent advisers. For each category of institution,

ownership is computed as a proportion of total shares outstanding if the institution is

one of the top 5 holders in the firm.6

For our study we are only interested in measures of institutional influence that

correspond to the fiscal year-end of the firm. If holdings are not reported for the

quarter for which the fiscal year ends, we take the reported holding that is closest to

this date. Moreover, if a stock has a fiscal year that does not correspond exactly to a

quarter-end, we make an adjustment to a firm’s fiscal year. The fiscal year is rounded

up to the nearest calendar quarter-end.

C. Methodology:

This section develops the models used to examine the effect of institutional

investor influence on the structure of corporate boards.

The following general model is estimated to examine the relation between

board attributes (i.e., board size and board independence) and institutional investor

influence:

6 Our measures of institutional heterogeneity are based on the level of ownership, rather than

concentration as used by Almazan et al. (2005) and Hartzell and Starks (2003).

13

( )

( )

( )

( )

( )

( ) 16

15

14

13

12

110

Q sTobin'

Segments Business ofNumber

tionCapitalizaMarket

Dummy CEO New

Dummy Retire

Influence nalInstitutioAttribute Board

−

−

−

−

−

−

+

+

+

+

+

+=

t

t

t

t

t

tt

β

β

β

β

β

ββ

(1)

The following general model is estimated to examine the relation between

board changes (i.e., director appointments and departures) and institutional investor

influence:

( )

( )

( )

( )

( )

( )

( ) 17

16

15

14

13

12

110

tionCapitalizaMarket

Dummy CEO New

Dummy Retire

Segments Business ofNumber in Change

Performace Firm

Dummy ePerformanc FirmPoor Influence nalInstitutio

Influence nalInstitutioChange Board

−

−

−

−

−

−

−

+

+

+

+

+

×+

+=

t

t

t

t

t

t

tt

β

β

β

β

β

β

ββ

(2)

Throughout this study, numerous control variables are used. Market

Capitalization is the multiple of the firm’s stock price and the number of shares

outstanding. The natural logarithm of market capitalization is employed. The number

of business segments is computed as the number of SIC industry segments from

which the firm generates income. Tobin’s Q is defined as the ratio of the market value

of the firm to the replacement value of the firm’s assets (Palia, 2001) but in common

with the way Tobin’s Q is normally calculated, we do not adjust accounting values

from historical to replacement costs. Tobin’s Q is calculated as the ratio of the market

value of equity minus the book value of equity plus the book value of assets to the

book value of assets. Following Hermalin and Weisbach (1991), controls for CEO

14

tenure are also included. A dummy variable equal to one if the CEO has tenure with

the company of less than 4.5 years, and zero otherwise, is referred to as New CEO.

Following Weisbach (1988) controls for retirement are used. A dummy variable equal

to one if the CEO is aged between 62 and 66, and zero otherwise, is referred to as

Retirement Age. Industry and year dummy controls are also included throughout the

study. Market capitalization and Tobin’s Q are log-transformed to mitigate the effect

of variable skewness in estimation. All continuous independent variables are

winsorized at the 1% and 99% levels. Winsorizing is employed to mitigate the effect

of extreme observations.

When estimating equation (1) and (2) several econometric issues are

addressed. In our analysis we run OLS regressions for the pooled sample. A problem

with using a pooled sample is that it is likely that the residuals for each firm will be

correlated across years and residuals may also be correlated across firms within a

single year. Three approached are utilized to overcome this problem: 1) pooled

regressions using year dummies and Rogers’ robust standard errors (Rogers, 1993); 2)

firm random effects with year dummies; and 3) firm fixed effects with year dummies.

The first estimation technique which applies to firm clustering assumes

observations of different firms are independent, but allows for temporal correlation

between observations of the same firm in different years. Year dummies control for

spatial correlation across firms within a year. According to Petersen’s (2004)

simulations, clustered Rogers standard errors are correct in the presence of year

effects (if year dummies are included), with no assumed parametric structure for

within-cluster errors, so that the firm effect can vary both spatially and temporally. If

firm effects vary across time, clustered Rogers standard errors are superior to those

15

from a fixed effects and random effects models, because these model assume time

invariant firm effects.

The second model that is used is a firm random effects with year dummies.

This model allows for errors that are firm-specific and time-invariant. The random

effects model requires that the firm effects be uncorrelated with the independent

variables. The dummies control for spatial correlation or errors across firms within a

given year.

The third model used is firm fixed effects with year dummies. By construction

this model controls for a time-invariant firm effect. The year dummies again control

for spatial correlation across firm. The firm effects model has the advantage over the

random effects model of not requiring that the firm effect be uncorrelated with the

independent variables. It has the disadvantage of using only information from within-

firm variation, while random effects can also use information from between-firm

differences (Black, Kim, Jang and Park, 2005).

It is then necessary to determine which estimation technique is appropriate. A

Breusch-Pagan (1980) Lagrange multiplier is used to compare a simple pooled

regression to firm random effects. Differentiating between firm fixed effects and firm

random effects is necessary because the dummy variable approach of fixed effects is

costly in terms of degrees of freedom lost. However, it does have one virtue in that

there is little justification for treating individual effects as uncorrelated with the other

regressors, as the random effects model assumes. The random effects model, may

suffer from the inconsistency due to this correlation between included variables and

the random effect (Greene, 2003). The Hausman (1978) specification test is used to

test for orthogonality between the random effects and the regressors and thus

determine whether the fixed or random effects model is appropriate.

16

For all combination of board attributes (i.e. board size and board

independence) and institutional influence (i.e., Herfindahl Index, Top5 Ownership,

Potentially Active and Passive Ownership) a Breusch-Pagan (1980) Lagrange

multiplier test rejects a simple pooled regression compared to a firm random effects

model, with p-values of, or close to, zero. This suggests that pooled regression

coefficients may be biased relative to fixed or random effects models. Moreover, a

Hausman test produces p-values of zero meaning we can reject the hypothesis that the

individual effects are uncorrelated with the other regressors in the model. This

suggests that the fixed effects model is appropriate throughout the study.

When estimating the pooled regression using clustered Rogers standard errors

industry and year dummies are included in both equation (2) and (3). The industry

dummy variable takes a value of 1 for the two-digit Standard Industrial Classification

(SIC) in which the firm operates. The year dummy variable takes a value of 1 if the

observation was from the given year.

A second methodological issue is endogeneity. Here the independent variable

may be correlated with the error term and thus produce a biased coefficient. This

correlation can come from two sources: omitted variables bias and reverse causality.

Using a panel data structure helps overcome problems associated with omitted

variable bias. By using either firm fixed effects of firm random effects model, we can

capture unobserved heterogeneity that is firm specific and time invariant. A greater

challenge comes from reverse causality. For example, institutions may self select into

firms based on preferences for existing board structures already in place. An

instrumental variables approach is utilized to address the problem of endogeneity.

This method requires the specification of instrumental variables that are both

correlated with the endogenous variable and uncorrelated with the error term of the

17

original regression. A problem is in identifying an appropriate instrument for

institutional influence. We resort to orthogonalizing institutional influence with

respect to lagged board size, board independence and firm size. We include firm size

in the orthogonalization process to control for size effects in board size. This process

ensures institutional influence is unrelated to lagged board structures.

Using our instruments, a Durbin-Wu-Hausman test for endogeneity is

conducted and two stage least squares regressions are estimated. The Durbin-Wu-

Hausman test procedure is similar to 2SLS. For example, in the first stage we regress

institutional influence on their orthogonalized equivalent and other control variables.

In the second stage we regress the compensation measures on institutional influence,

control variables and the residual from the first stage regression. A significant

coefficient on the first stage residual is evidence of endogeneity. For the Durbin-Wu-

Hausman test and the 2SLS firm fixed effects is employed since the Hausman test

suggests this is the correct model specification.

When estimating model (2) pooled regressions using year dummies and

Rogers’ robust standard errors are used. The fact that model (2) employs board

changes (i.e., director appointments and departures) mitigates problems associated

with reverse causality.

D. Descriptive Statistics:

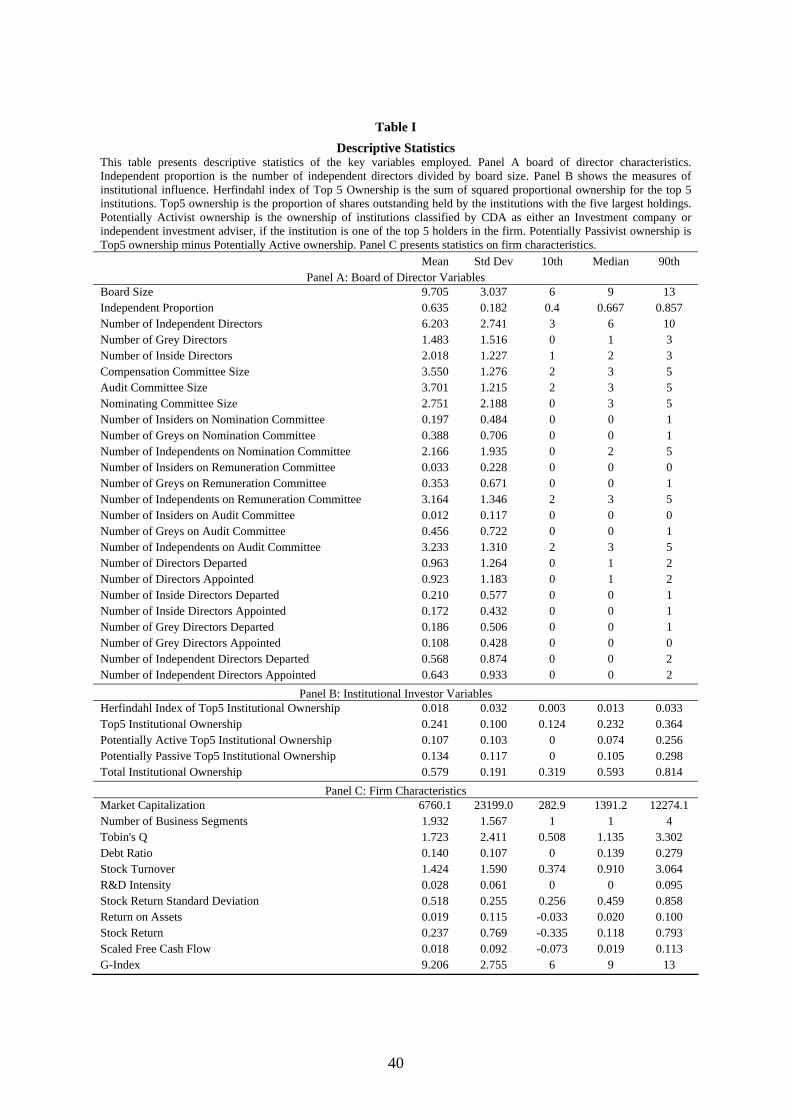

Table I presents descriptive statistics of the key variables. Panel A presents

statistics on the board of directors. Panel B presents statistics on institutional investor

measures of influence and Panel C presents statistics on firm characteristics. In our

sample the average board size is 9.7 with 63.9 percent of the board being composed of

independent directors. The average size of compensation, audit and nominating

18

committees is 3.5, 3.7 and 2.7, respectively. Board size changes very little on an

annual basis, with 0.96 directors departing and 0.92 directors being appointed.

Moreover, inside and grey directors have over time been slowly replaced by

independent directors. On average, 0.21 inside and 0.18 grey directors depart while

only 0.17 inside and 0.10 grey directors are appointed. On the other hand, 0.56

independent directors depart and 0.64 independent directors are appointed. In our

sample, institutions own on average 57.9 percent of the firms in which they invest.

The top five institutions own 24.1 percent of firms, showing that relatively few

institutions can yield considerable influence if they work together. The average

(median) market capitalization of the firm in our sample is $6.7 ($1.3) billion. In

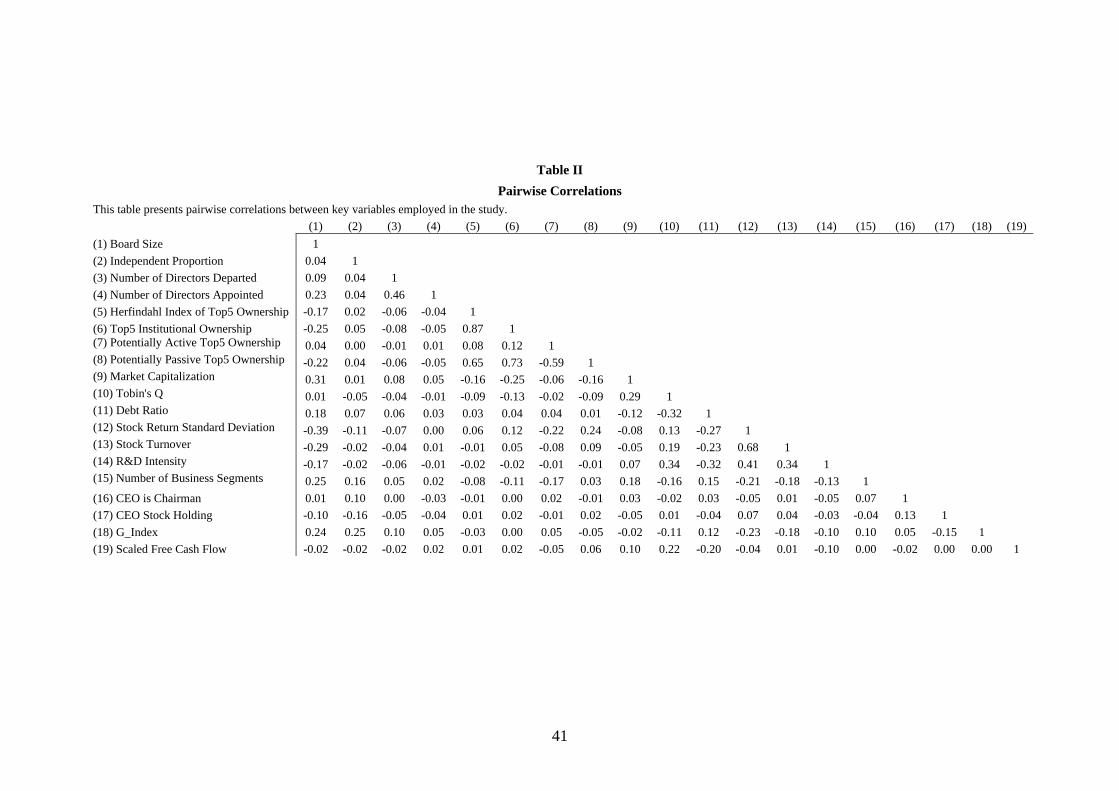

Table II, correlations between the key variables are examined. A negative relation

generally exists between our measures of institutional investor influence and board

size, while a positive relation exists with board independence.

<<INSERT TABLES I AND II>>

IV. Board Size and Independence as a Function of Institutional Investor Influence

In this section the effect of institutional investor influence on board size and

the proportion of independent directors on the board are examined. These board

characteristics are empirically related to improved firm performance and decision-

making by the board. They are also aspects of board structure that activist pension

funds have publicly targeted. For example, TIAA-CREF has stated that it will only

invest in companies that have a majority of outside directors on the board. Similarly,

19

CalPERS recommends that the CEO should be the only inside director on a firm’s

board (Coles, Daniel and Naveen, 2007).

A. Board Size:

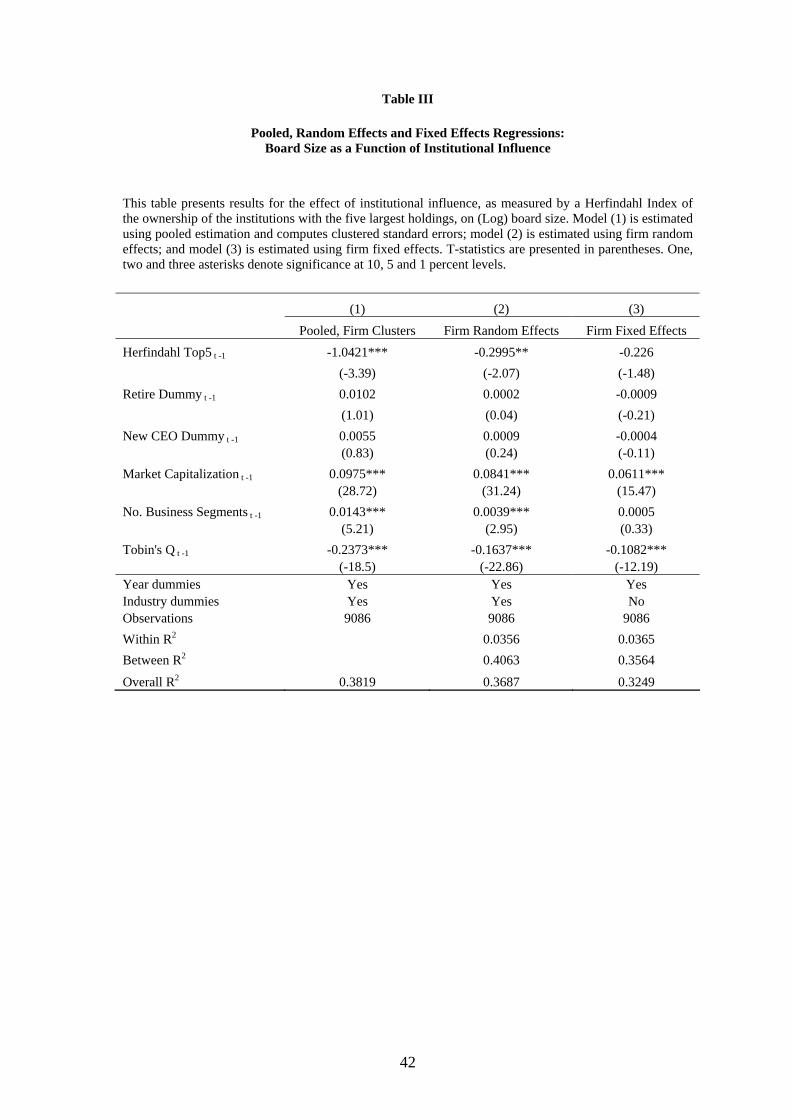

Table III presents the results for the effect of the Herfindahl Index of Top5

Ownership on board size. The Herfindahl Index is negatively related to board size

using pooled OLS with clustered standard errors and also using firm random effects

estimation. However, the lower coefficient in model (2) suggests that the coefficients

from pooled OLS regressions in model (1) are upward biased due to firm-specific and

time-invariant heterogeneity. In model (3) where firm fixed effects is used, the

coefficient for Herfindahl index is insignificant.

<<INSERT TABLE III>>

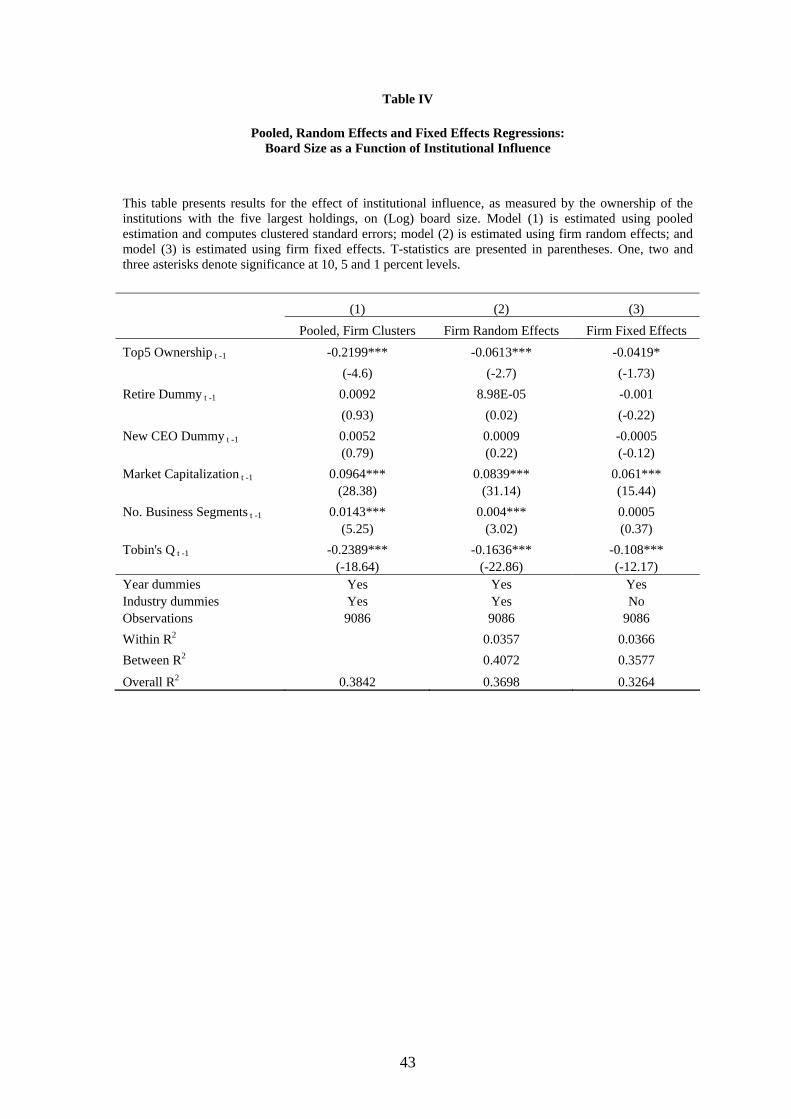

Table IV examines the effect of Top5 institutional ownership on board size.

Top5 Ownership is negatively and significantly related to board size in model (1), (2)

and (3). The results in model (1) imply that a one standard deviation increase in Top5

Ownership will decrease board size by 2.175%, which equates to 0.211 directors for

the average board.7 In model (2) this effect declines, with a similar increase in Top5

Ownership decreasing board size by 0.611% or 0.059 directors.8 In model (3) a one

standard deviation increase in Top5 Ownership will decrease board size by 0.418%,

which equates to 0.041 directors for the average board.9

7 =100*(exp(-0.2199*0.10)-1). 8 =100*(exp(-0.0613*0.10)-1). 9 =100*(exp(-0.0419*0.10)-1).

20

<<INSERT TABLE IV>>

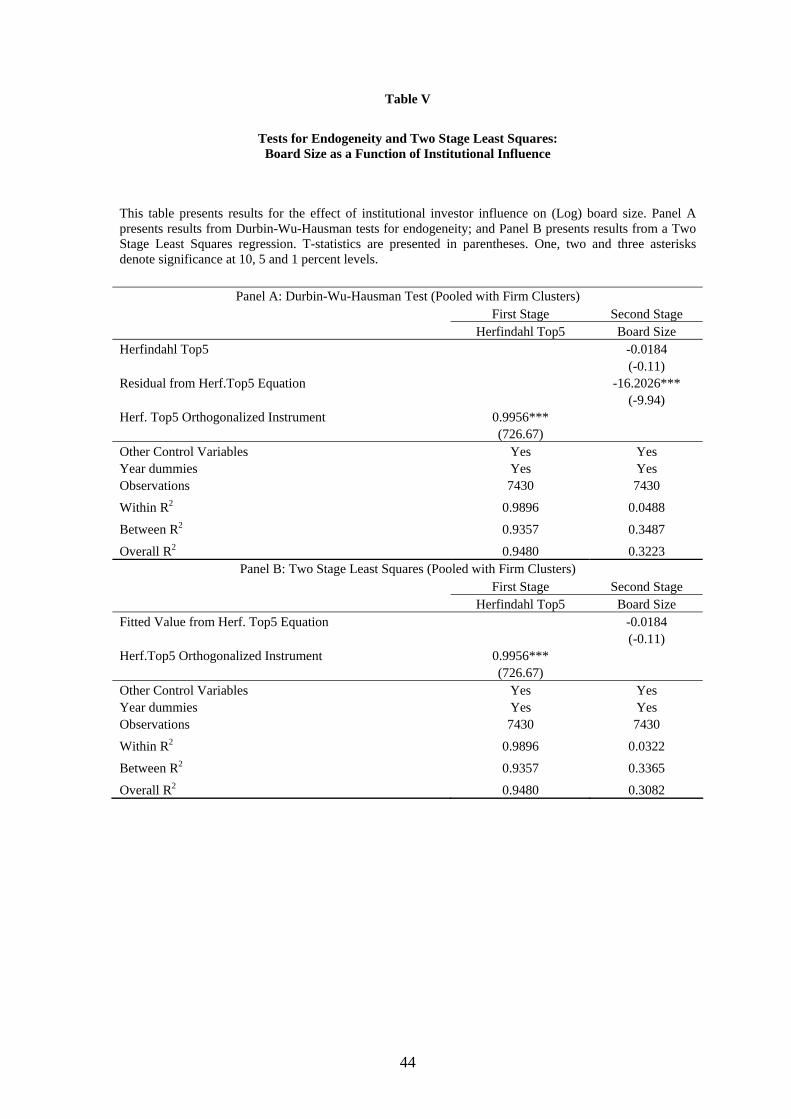

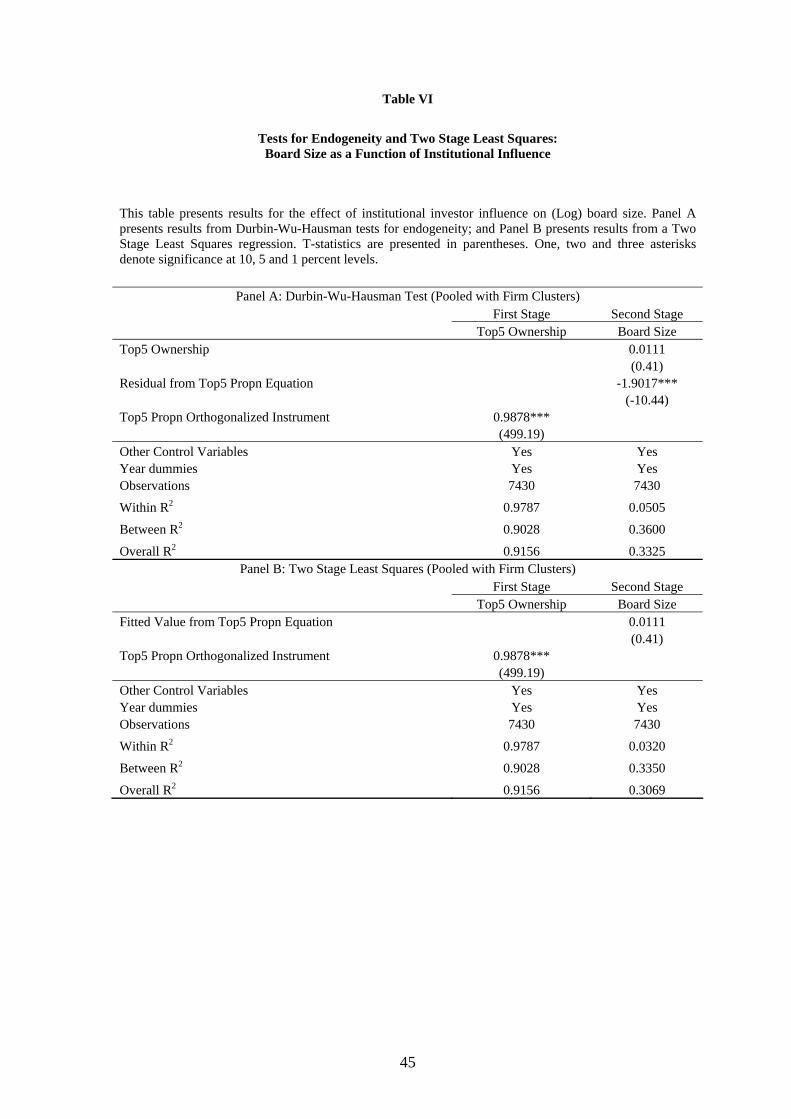

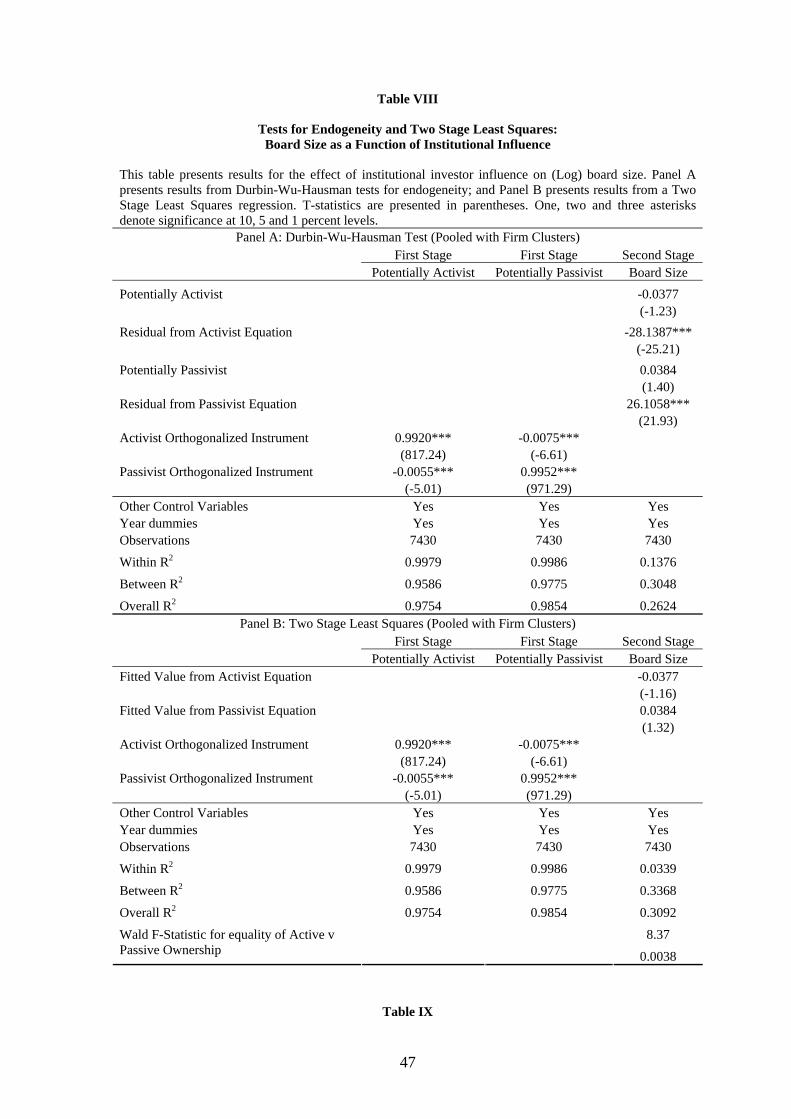

In Table V and IV concerns over endogeneity are addressed. In Panel A of

both Table V and VI results of a Durbin-Wu-Hausman test for endogeneity are

presented. The first stage of the test regresses the respective measure of institutional

influence on an instrument which is the institutional influence measure orthogonalized

with respect to board size and board independence. The residual from this model is

then included as an independent variable in stage two. The significance of this

residual in the second stage of the Durbin-Wu-Hausman test indicates endogeneity of

both Herfindahl Index of Top5 Ownership and also Top5 Ownership. Panel B

presents results for 2SLS, where the in the second stage both Herfindahl Index of

Top5 Ownership and also Top5 Ownership are insignificant. Whereas Top5

Ownership was significant throughout Table IV, most notably using firm fixed

effects, this significance was likely attributable to endogeneity.

<<INSERT TABLE V AND VI>>

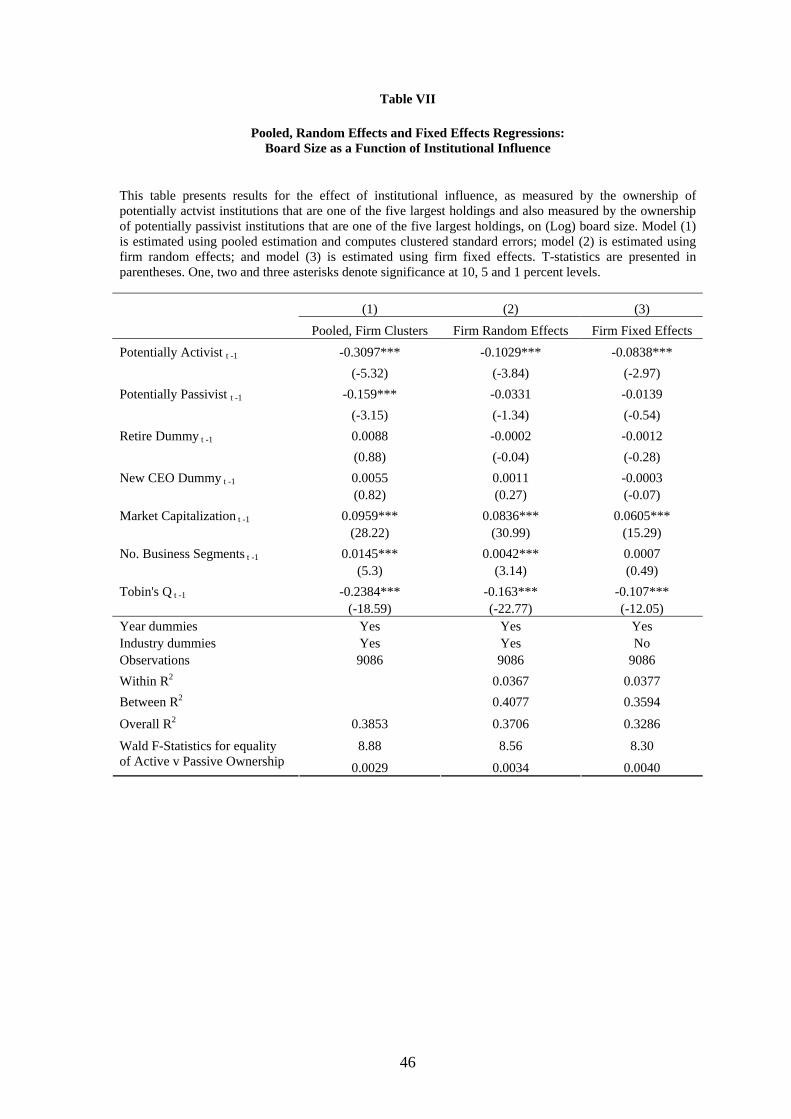

Table VII examines the effect of institutional heterogeneity on board size. The

results indicate that there is a significant difference in the effect of potentially active

and potentially passive institutions on board size. In model (1) both potentially active

and potentially passive institutions have a significant negative effect on board size,

though the coefficient for potentially active institutions is approximately twice that for

potentially passive institutions. A Wald F-test for the difference in coefficients

21

produces a test statistic of 8.88 and a p-value close to zero indicating that the

coefficients are significantly different. To quantify these differences, a one standard

deviation increase in potentially active ownership decreases board size by 3.139% or

0.305 directors for the average board.10 In contrast, a one standard deviation increase

in potentially passive ownership decreases board size by 1.843% or 0.179 directors

for the average board.11 In model (2) and (3) potentially active ownership is

significantly negatively related to board size, whereas potentially passive ownership is

insignificant. The results from model (3) using firm fixed effects imply a one standard

deviation increase in potentially active ownership will decrease board size by 0.859%

which equates to 0.083 directors for the average board.12 A one standard deviation

increase in potentially passive ownership will decrease board size by 0.163% or 0.015

directors for the average board.13 Table VIII examines whether the significance of

potentially active ownership is being inflated by endogeneity. Panel A of Table VIII

indicates that both potentially active ownership and potentially passive ownership are

endogenous. In Panel B where 2SLS results are presented, potentially active

ownership is insignificant. Whilst insignificant, the signs for potentially active and

potentially active institutions are opposed. Potentially active institutions are

negatively related to board size whereas potentially passive institutions are positively

related to board size.

<<INSERT TABLE VII AND VIII>>

10 =100*(exp(-0.3097*0.103)-1). 11 =100*(exp(-0.1590*0.117)-1). 12 =100*(exp(-0.0838*0.103)-1). 13 =100*(exp(-0.0139*0.117-1).

22

B. Board Independence:

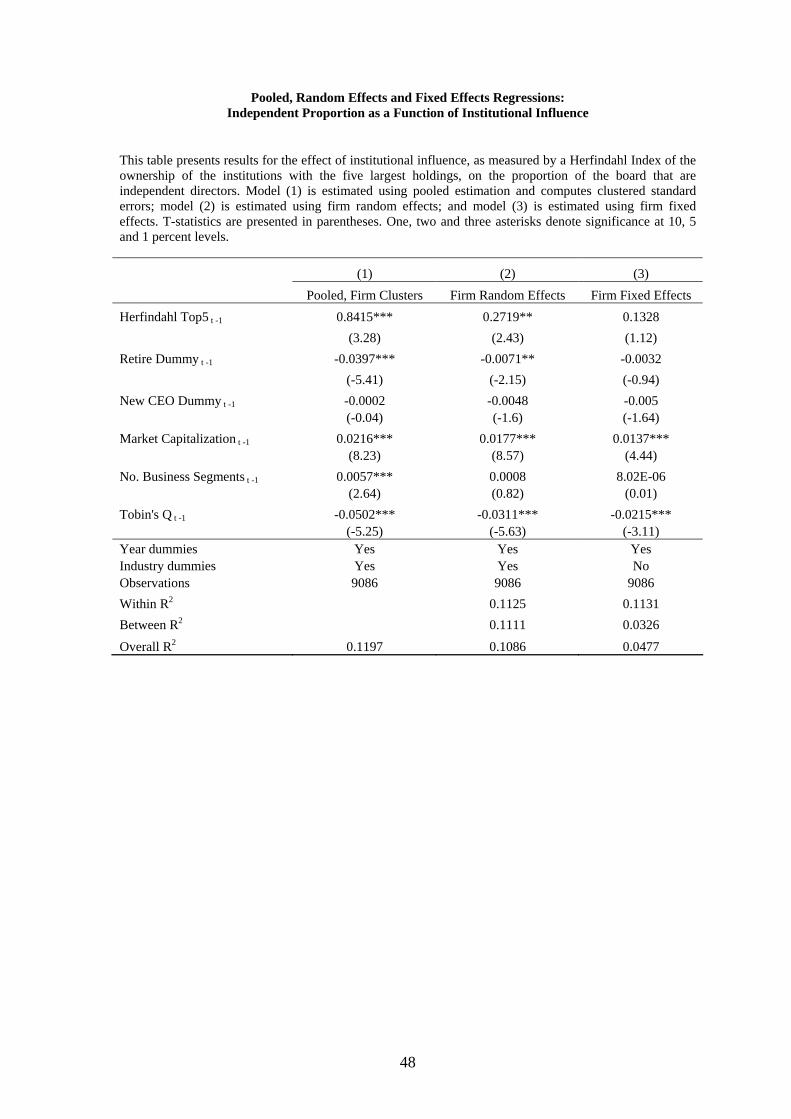

Table IX presents the effect of Herfindahl Index of Top5 Ownership on the

proportion of the board that are independent directors. The Herfindahl Index is

significantly positively related to independent proportion of directors using pooled

OLS and also firm random effects. However, employing firm fixed effects which a

Hausman specification test indicates is the appropriate estimation technique, shows

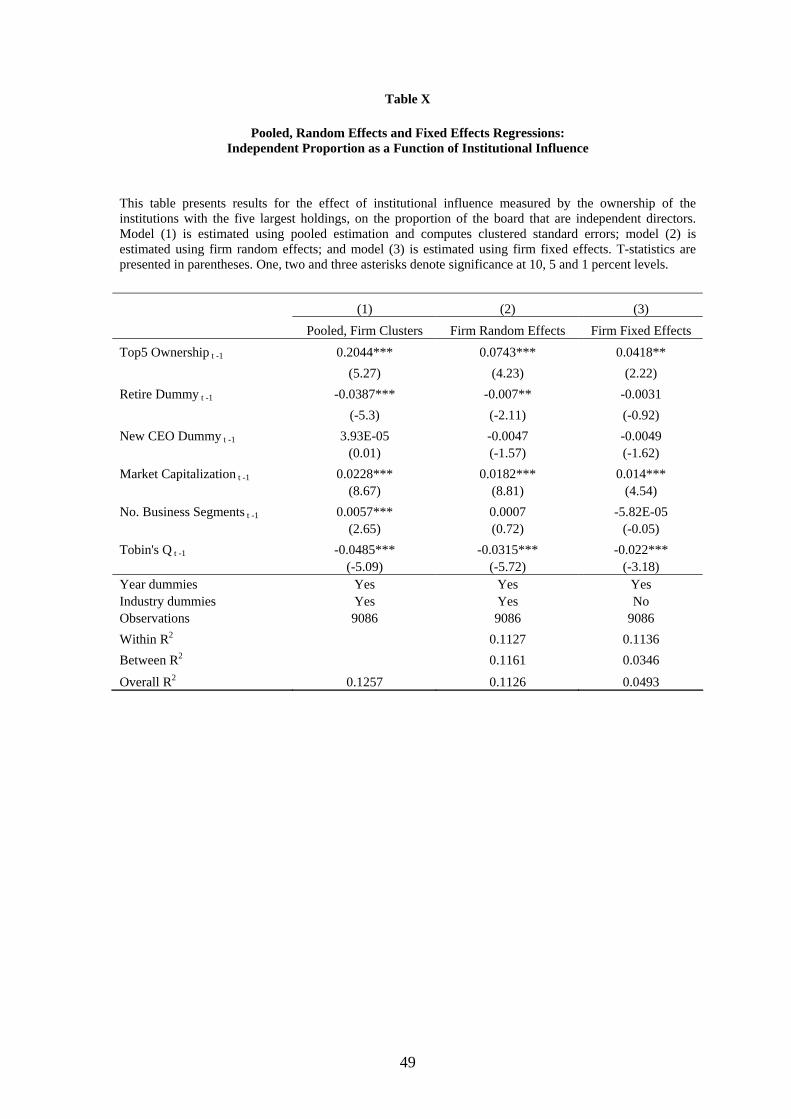

that Herfindahl index is insignificant. In Table X institutional influence is measure

using Top5 Ownership. Top5 Ownership is significantly positively related to

independent proportion of directors using all three model specifications. However, the

lower coefficient in model (2) suggests that the coefficients from pooled OLS

regressions in model (1) are upward biased due to firm-specific and time-invariant

heterogeneity. Model (1) implies that a one standard deviation increase in Top5

Ownership will increase the independent proportion of directors by 0.021, raising the

proportion of independent directors for the average board to 0.6529.14 Model (2) and

(3) imply much smaller changes in the independent proportion of directors. In model

(2) and (3), a one standard deviation increase in Top5 Ownership increases the

independent proportion of directors by 0.007 and 0.004.15

<<INSERT TABLE IX AND X>>

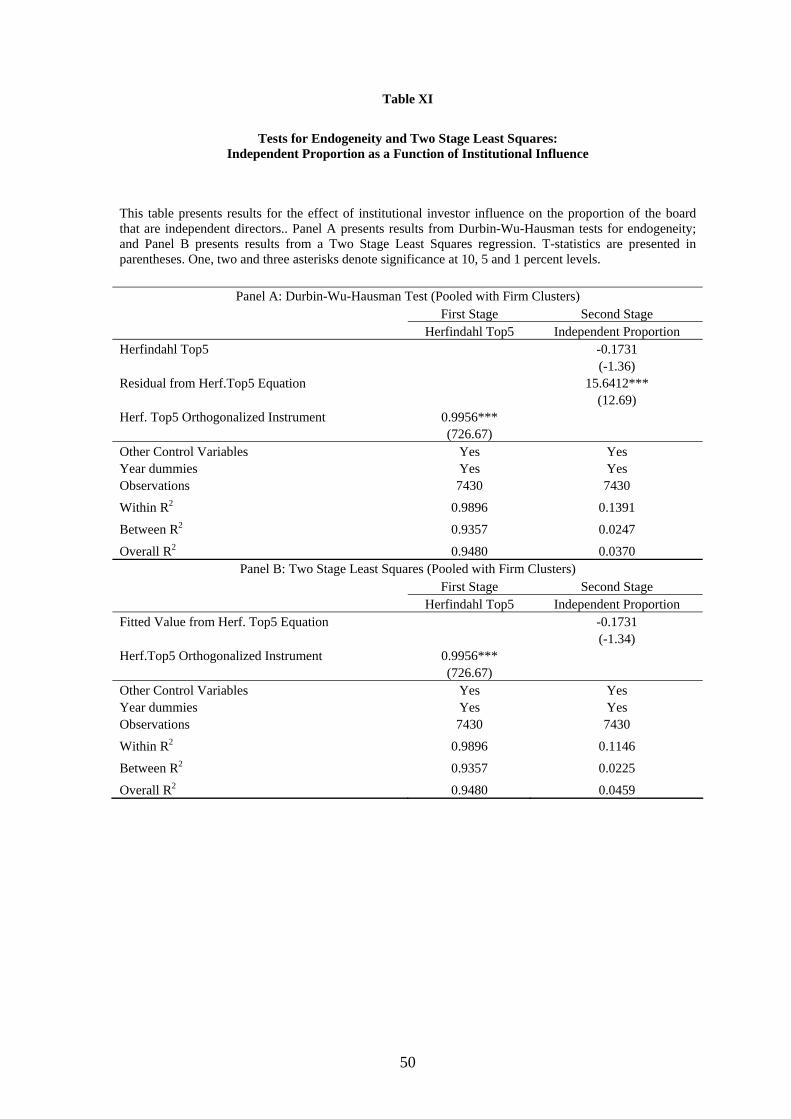

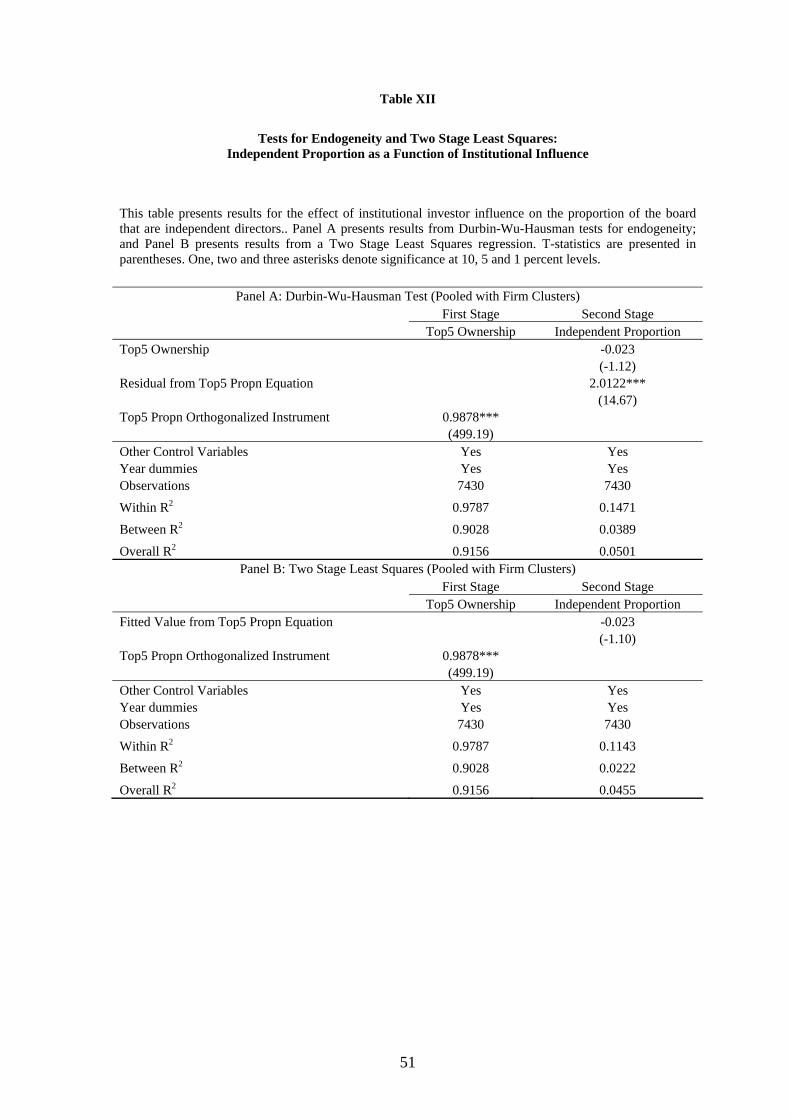

Table XI and XII address the issue of endogeneity. In Panel A of Table XI and

XII, Herfindahl Index and Top5 Ownership are endogenous, as implied by the

significance of the residual in the second stage of the Durbin-Wu-Hausman test. In

14 = 0.2044*0.10. 15 =0.0743*0.10; =0.0418*0.10.

23

Panel B of Table XI and XII, 2SLS indicate that Herfindahl Index and Top5

Ownership are insignificantly related to the independent proportion of directors on the

board.

<<INSERT TABLE XI AND XII>>

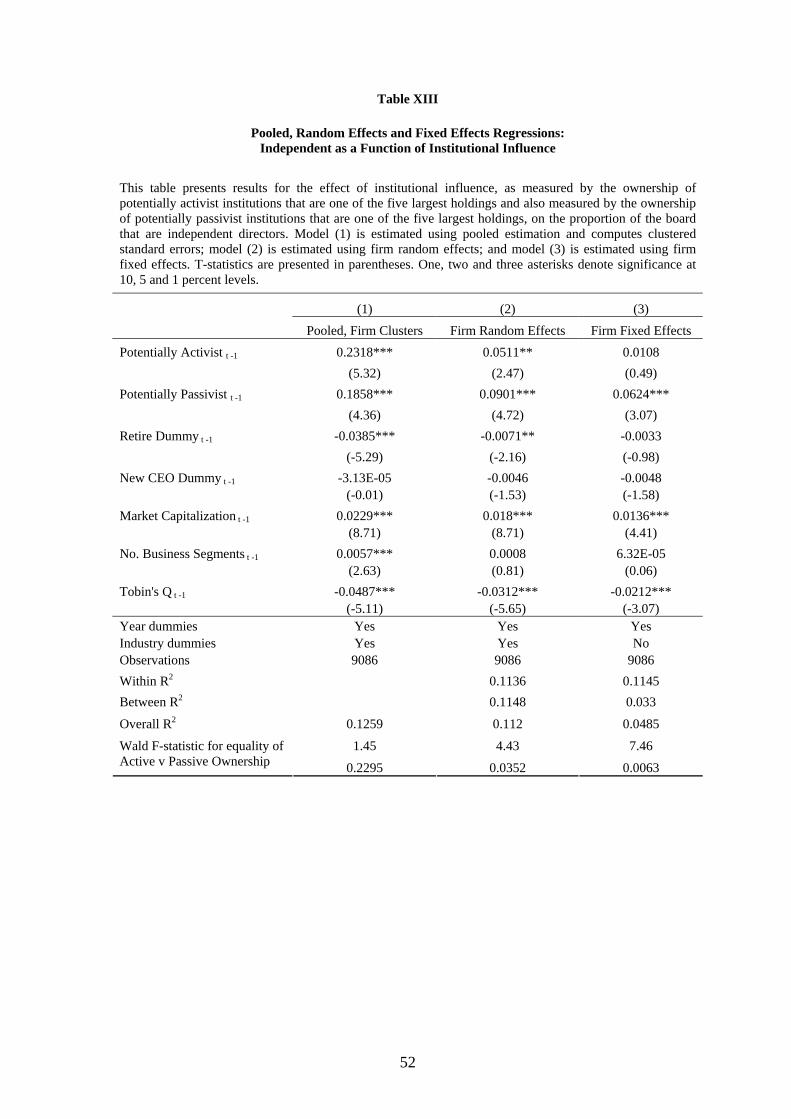

Table XIII examines the effect of institutional heterogeneity on board

independence. Model (1) indicates that potentially active institutions have a

marginally larger effect on board independence then their potentially passive

counterparts. However, a Wald F-test indicates that this difference is not significant

with a test statistic of 1.45 and a p-value of 0.2295. Model (1) implies that a one

standard deviation in potentially active ownership increases the proportion of

independent directors on the board by 0.0238 which produces a new independent

proportion of 0.6563 for the average board.16 Similarly, a one standard deviation in

potentially passive ownership increases the proportion of independent directors on the

board by 0.0217 which produces a new independent proportion of 0.6542 for the

average board.17

<<INSERT TABLE XIII >>

Employing firm random effects and firm fixed effects indicates that potentially

passive institutions have a larger effect on board independence, with a Wald F-test

16 =0.2318*0.103. 17 =0.1858*0.117.

24

indicating that the difference is significant. Using firm fixed effects eliminates any

significant effect of potentially active institutions on board independence. Firm fixed

effects implies a one standard deviation increase in potentially active ownership

increases the proportion of independent directors on the board by 0.001, whereas a

similar increase for potentially passive institutions produces a 0.007 increase.18

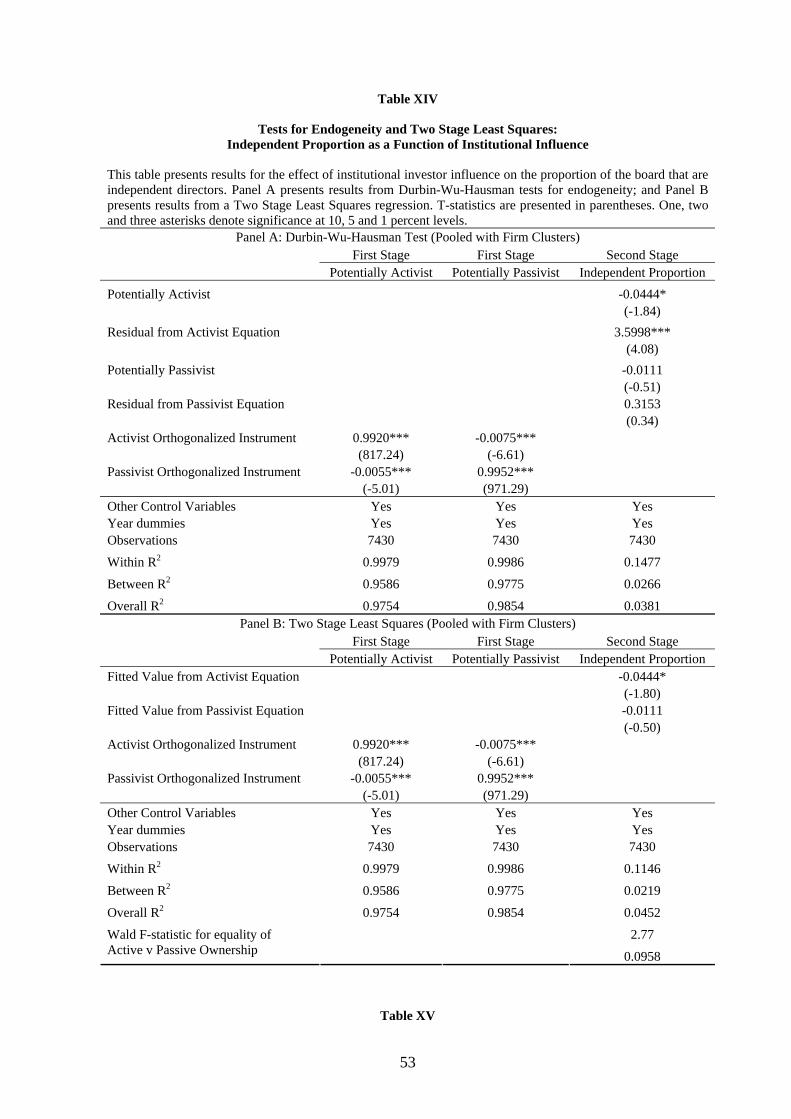

Table XIV addresses any concerns of endogeneity in analyzing institutional

heterogeneity. The second stage results in Panel A indicate that potentially active

ownership is endogenous, though potentially passive ownership is not endogenous. In

Panel B, 2SLS show that potentially active ownership is negatively related to the

independent proportion of directors.

<<INSERT TABLE XIV >>

V. Director Appointments and Departures as a Function of Institutional Investor Influence

The analysis of the effect of institutional influence on board size and board

independence has not provided compelling support for monitoring once correct model

specification and endogeneity issues are taken into account. This may be because

focusing on the levels of the number of directors on the board and the proportion of

independent directors masks real monitoring that institutions perform. This section

focuses on changes in board structure with the emphasis being on the appointment

and departure of director. Moreover, when institutions monitor this may not necessary

18 =0.0108*0.103; =0.0624*0.117

25

result in a continuous exertion of influence. Of particular interest in this section is the

role that firm performance plays in determining institutional investor actions when it

comes to director appointments and departures. Several studies find that firms that

institutional investors target are indeed poor performers (Karpoff, Malatesta and

Walkling, 1996; Strickland, Wiles and Zenner, 1996; Wahal, 1996; Bizjak and

Marquette, 1998; Johnson, Porter and Shackell, 1997, and Opler and Sokobin,

1995).19 When firms are performing poorly, institutional investors are more concerned

with implementing changes that will punish directors deemed responsible, with the

aim of improving firm performance. When the firm is performing well, shareholders

are more willing to leave discretionary authority in the hands of managers.20 Hence,

institutional investor influence is expected to vary due to the relative costs and

benefits of such actions in different states of firm performance. This section examines

the role of institutions in appointing directors and forcing them to depart. An

interactive analysis methodology is employed to test whether performance is an

important factor for institutions when influencing board structure. Institutional

influence measures are interacted with a dummy variable equal to one if the firms’

performance, as measured by return on assets (ROA) or Tobin’s Q respectively, is

below the sample median.

19 Since 1988, the California Public Employees’ Retirement System (CalPERS) has chosen targets

from among the poor performers in its portfolio (Romano, 2001). This is consistent with the CalPERS

approach when their Focus list is compiled. The focus list contains companies that merit public and

market attention due to market performance and corporate governance practices

(http://governance.calpers.org/viewpoint/speeches/carlson5.asp). 20 The comparative advantage of managers is to come up with new ideas to seize profit opportunities,

and that scrutinizing managerial decisions is a time consuming process. Since it is particularly costly to

miss a profit opportunity when the demand for the firm’s product is high, shareholders are more willing

to leave discretionary authority in the hands of managers in good times than in bad times.

26

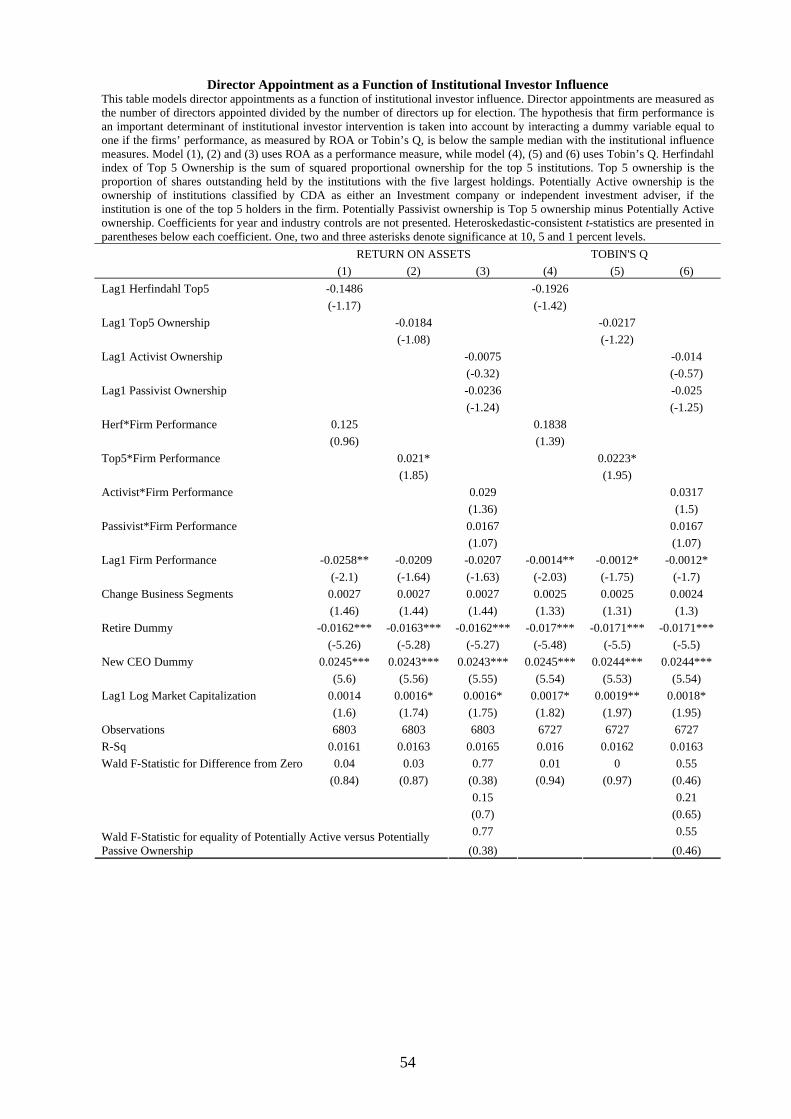

A. Director Appointments:

Table XV shows institutional investors have a negligible impact on director

appointments, even under periods of poor firm performance. The exception is the

Top5 ownership-firm performance interaction variable in models (2) and (5). This

indicates that in periods of poor performance, there is a positive effect on director

appointments. However, the net effect on director appointments, which is the sum of

the coefficient for Top5 Ownership and the Top5*Firm Performance interaction

variable is not different from zero, as indicated by a Wald F-test. The Wald F-test

produces a test statistic of 0.03 and a p-value of 0.87.

A decomposition of director appointments is required to better understand

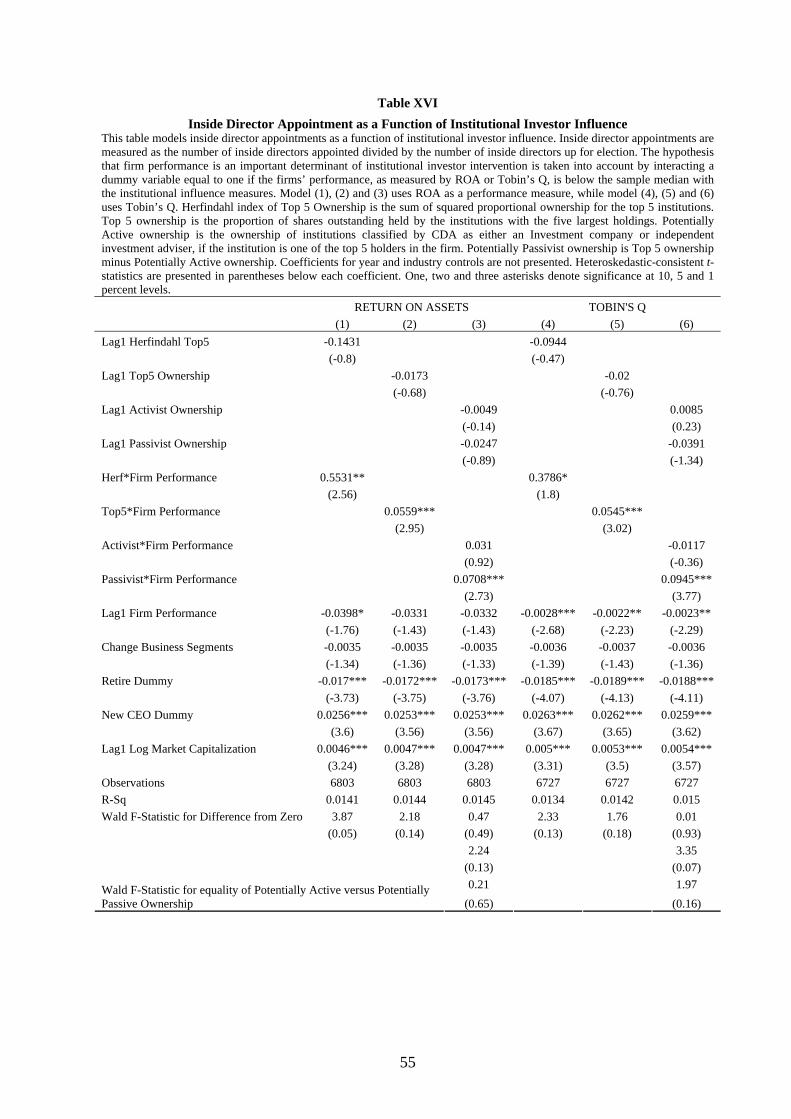

institutional investor influence. Table XVI decomposes the effect of institutional

investors on director appointments and reveals that the Herfindahl Index, Top5

Ownership and ownership of potentially passive institutions increase the likelihood of

inside director appointments when the firm has performed poorly. Though, an F-test

indicates that the net effect on director appointments when the firm has performed

poorly is only statistically different from zero in model (1). This positive adjustment

to institutional influence in periods of poor firm performance can likely be attributable

to the fact that insider directors may be the CEO of the firm, or other high ranking

executives, and they are removed from the firm and consequently depart the firm.

Replacement CEOs, or executives, are then likely to be appointed to the board. In

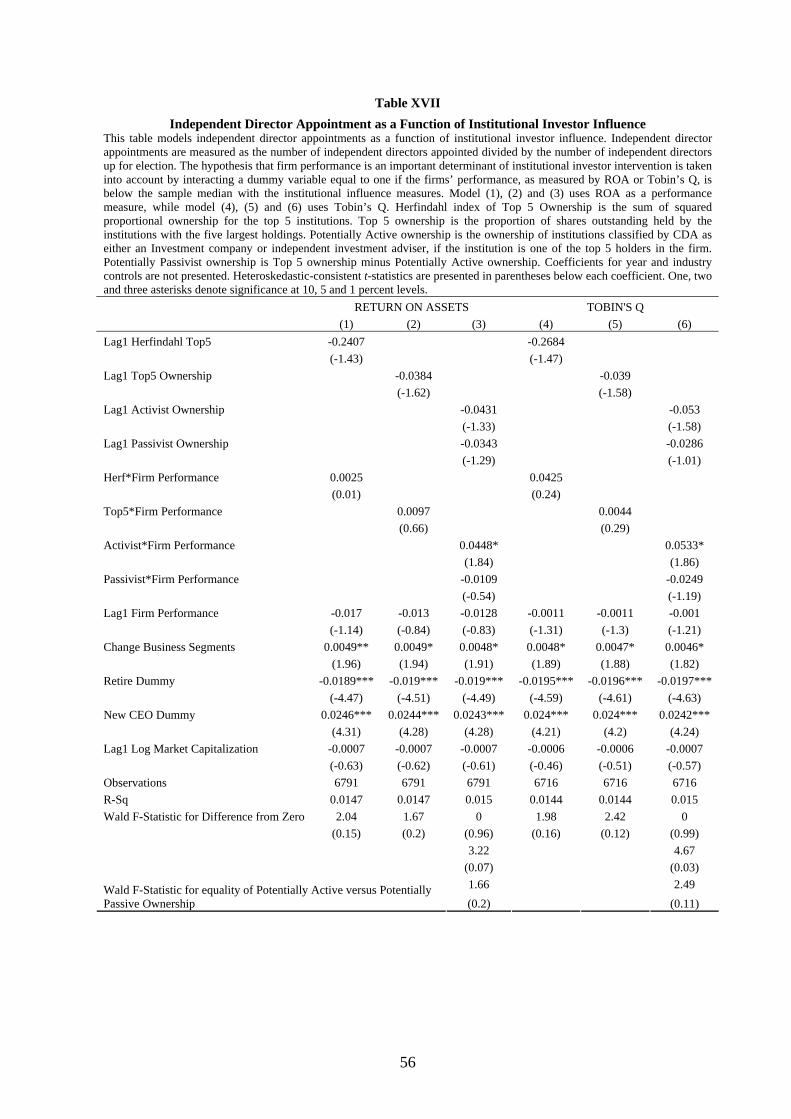

contrast, Table XVII shows that potentially active institutional investors have a

positive effect on independent directors when the firm has performed poorly. The

analysis suggests heterogeneity in the strategies pursued by institutions.

<<INSERT TABLES XV, XVI AND XVII>>

27

B. Director Departures:

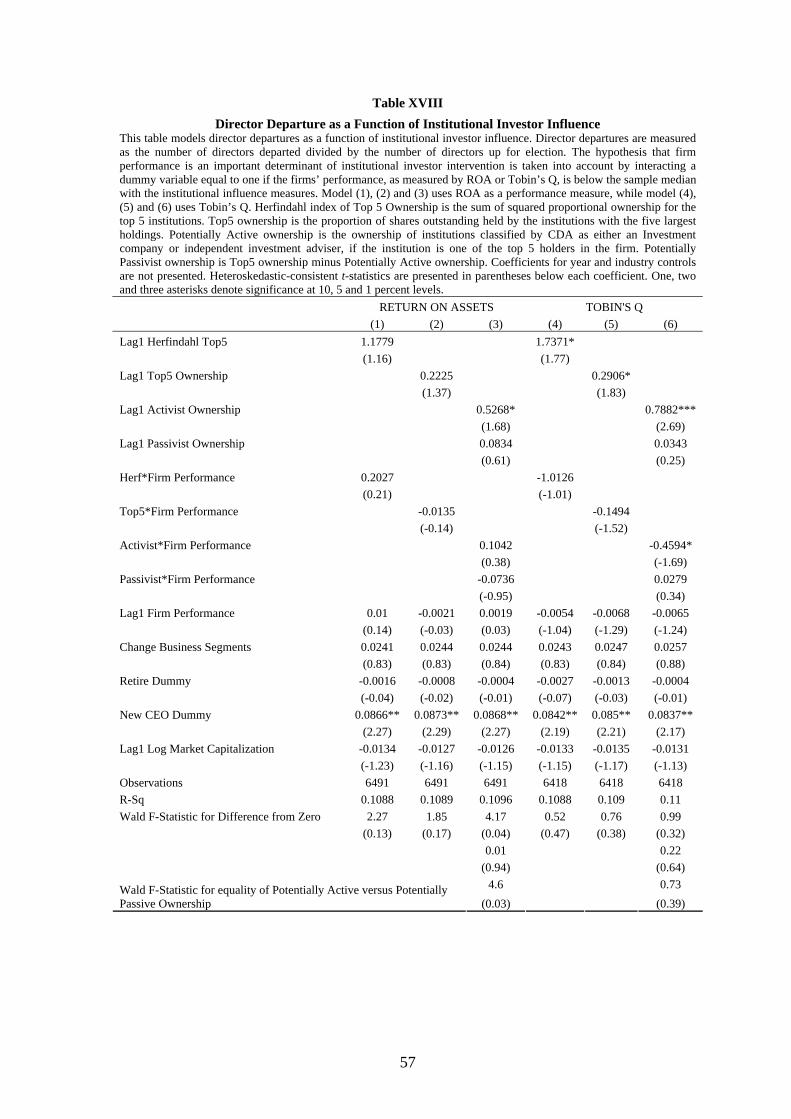

Table XVIII examines the effect of institutions on aggregate director

departures. Model (3) shows that potentially activist institutions have a significant

positive effect on the departure of directors, and this effect does not significantly

change in periods of poor firm performance. In models (4), (5) and (6), using Tobin’s

Q as a performance measure produces different results. The Hefindahl Index, Top5

ownership and potentially activist institutions are positively related to director

departures. However, in model (6), potentially activist institutions significantly lower

the likelihood of director departures in periods of poor performance.

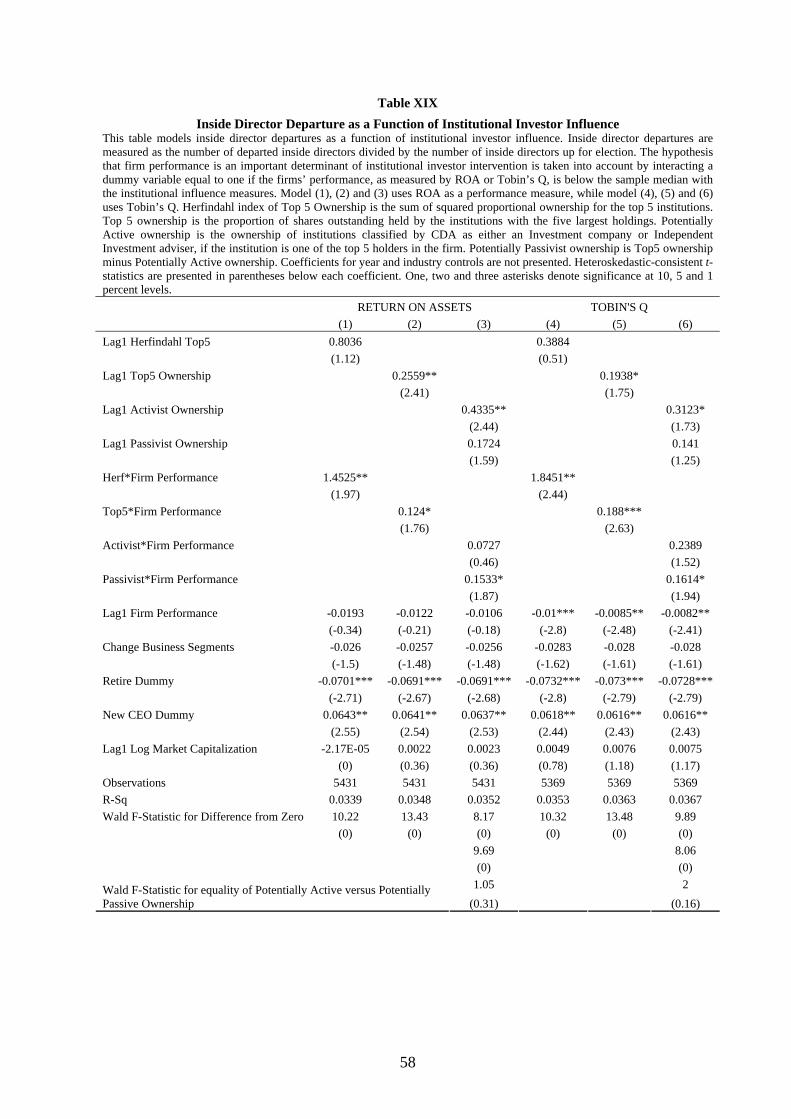

Decomposing director departures helps shed light on the findings in Table

XVIII. Table XIX indicates strong relations between institutional influence and inside

director departures, with firm performance playing an important role. In models (1)

and (4) the Hefindahl Index becomes significant and positively related to inside

director departures only when the firm has performed poorly. In models (2) and (5),

Top5 ownership is significantly related to inside director departures and this effect is

significantly increased in periods of poor firm performance. In models (3) and (6),

potentially activist institutions target inside directors with firm performance playing

an insignificant role in adjusting institutional influence. However, potentially passivist

institutional influence on inside directors is significantly increased when the firm has

performed poorly.

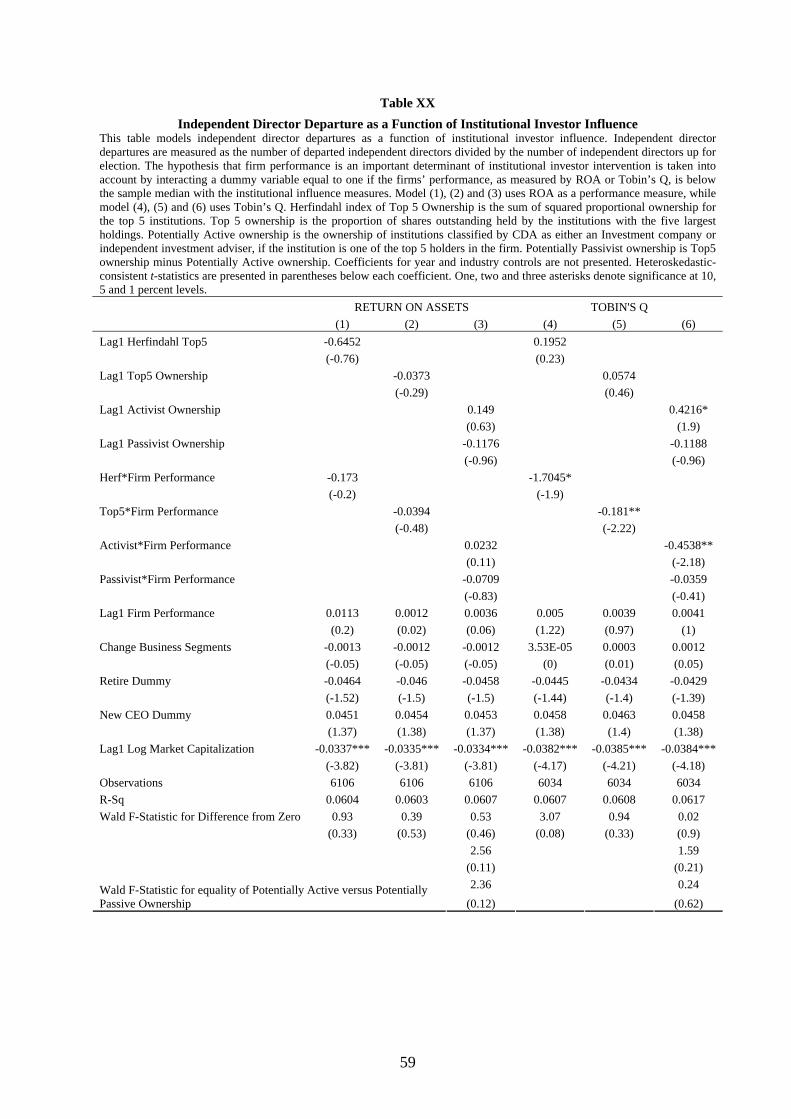

In Table XX, model (6) indicates that potentially activist institutions have a

positive effect on independent director departures, although this effect is tempered in

periods of poor performance. Models (4) and (5) also suggest that institutional

28

investor influence helps to retain independent directors in periods of poor

performance.

<<INSERT TABLE XVIII, XIX AND XX>>

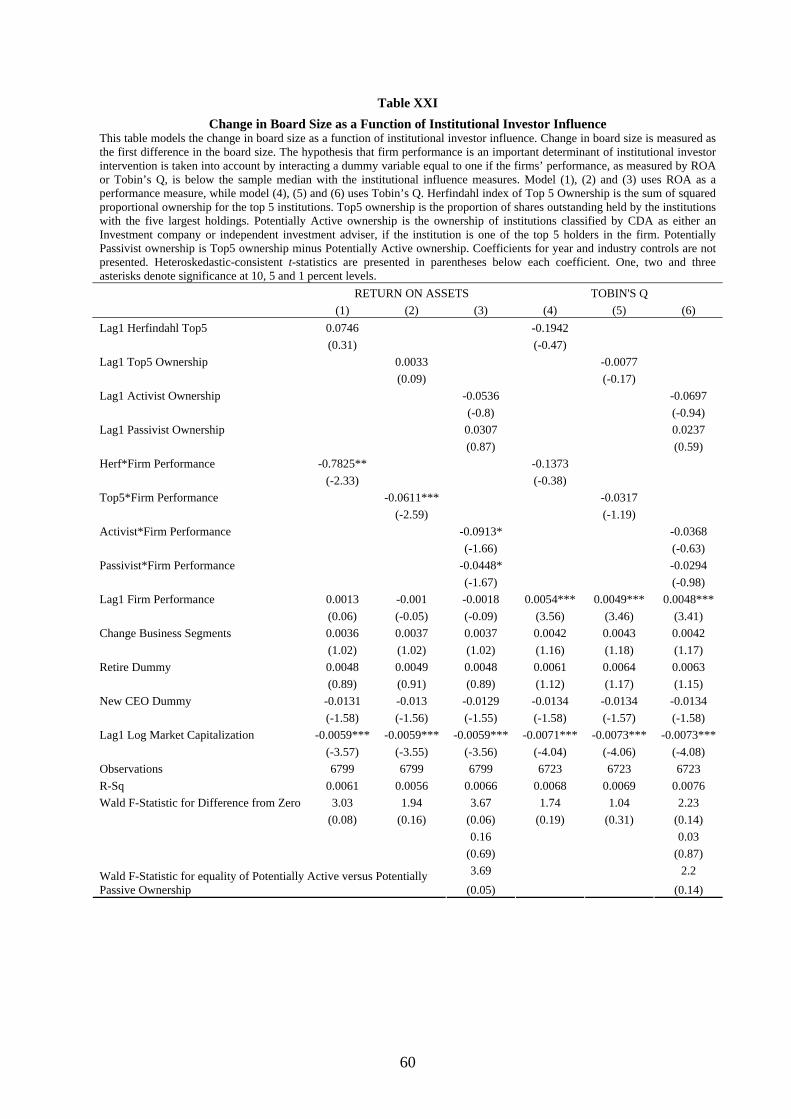

C. Net Change in Board Size and Independence:

The results from the analysis of director appointments and departures indicate

that the concentration and ownership of Top 5 institutions is positively related to

director departures, with insiders departing during periods of poor performance.

Though, independent directors are less likely to depart when the firm has performed

poorly. The concentration and ownership of Top 5 institutions is also positively

related to inside director appointments in periods of poor performance. Moreover, the

likelihood of inside director departures is reduced in periods of poor firm performance

suggesting that some appointments of insiders are simply replacements. Potentially

passive institutions appear to focus on the appointment and departure of inside

directors when the firm has performed poorly. In contrast, potentially activist

institutions exert considerable influence on appointing and retaining independent

directors in periods of poor performance, while exerting pressure on inside directors

to depart irrespective of firm performance. To better understand the net effect of this

influence, the net change in board size and independence is examined.

In Table XXI there is weak evidence of a net decrease in board size.

Institutional influence is negatively related to changes in board size when the firm

performs poorly, but this holds only for models using ROA as a performance control.

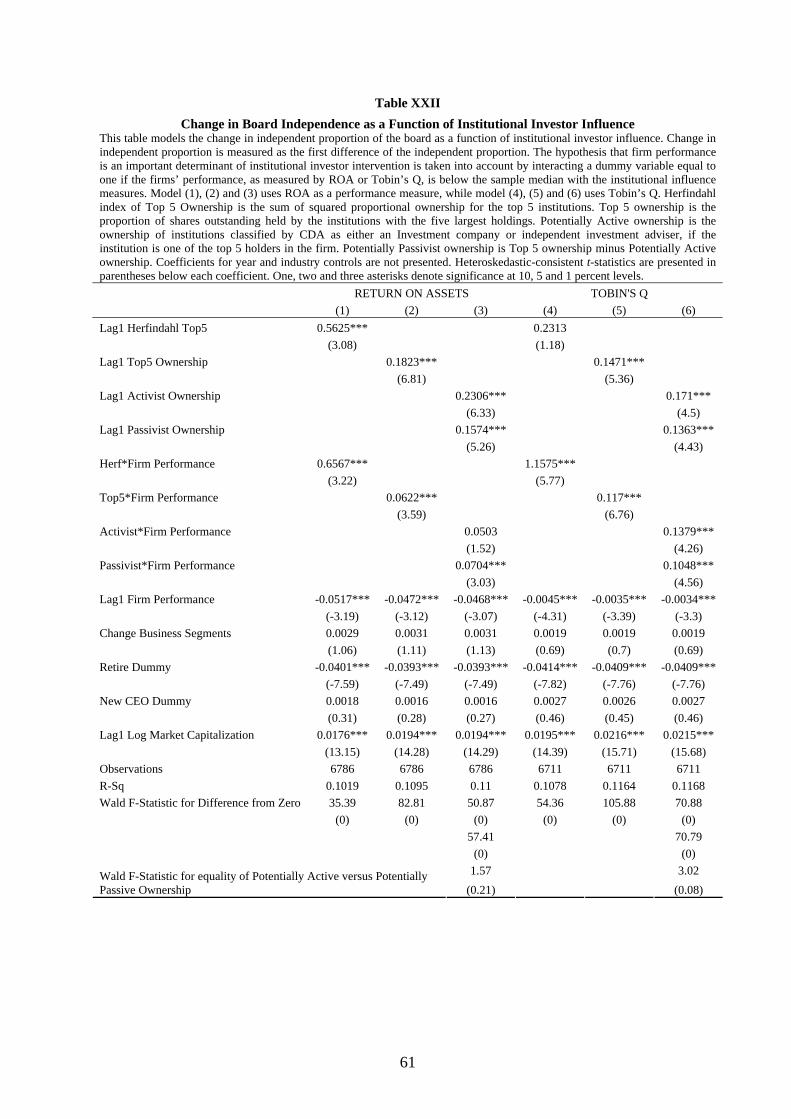

The major effect of institutional influence is realized on board independence. In Table

XXII for both performance controls, institutional investor influence has a significant

29

positive effect on the change in board independence. This suggests that while

institutional influence was positively related to both the appointment and departure of

inside directors, more insiders were being removed than appointed.

<<INSERT TABLE XI AND XII>>

VI. Alternative Monitoring Hypotheses This section re-examines the effect of institutional investor influence on board

size and board independence by accounting for firm specific monitoring requirements.

In this section, alternative monitoring objectives are addressed. Recent theoretical

models have questioned whether all firms should benefit from common prescriptions

with respect to board size and independence. Optimal governance structure depends

on firms’ monitoring needs, and on the costs and benefits of different governance

mechanisms. To the extent that these costs and benefits vary across firms and over

time, optimal governance structure should also vary (Lehn, Patro and Zhao, 2005).

Theoretical models based on such a motivation can be classified according to three

hypotheses—1) Scope of operations hypothesis, 2) Monitoring hypothesis, and 3)

Negotiations hypothesis.

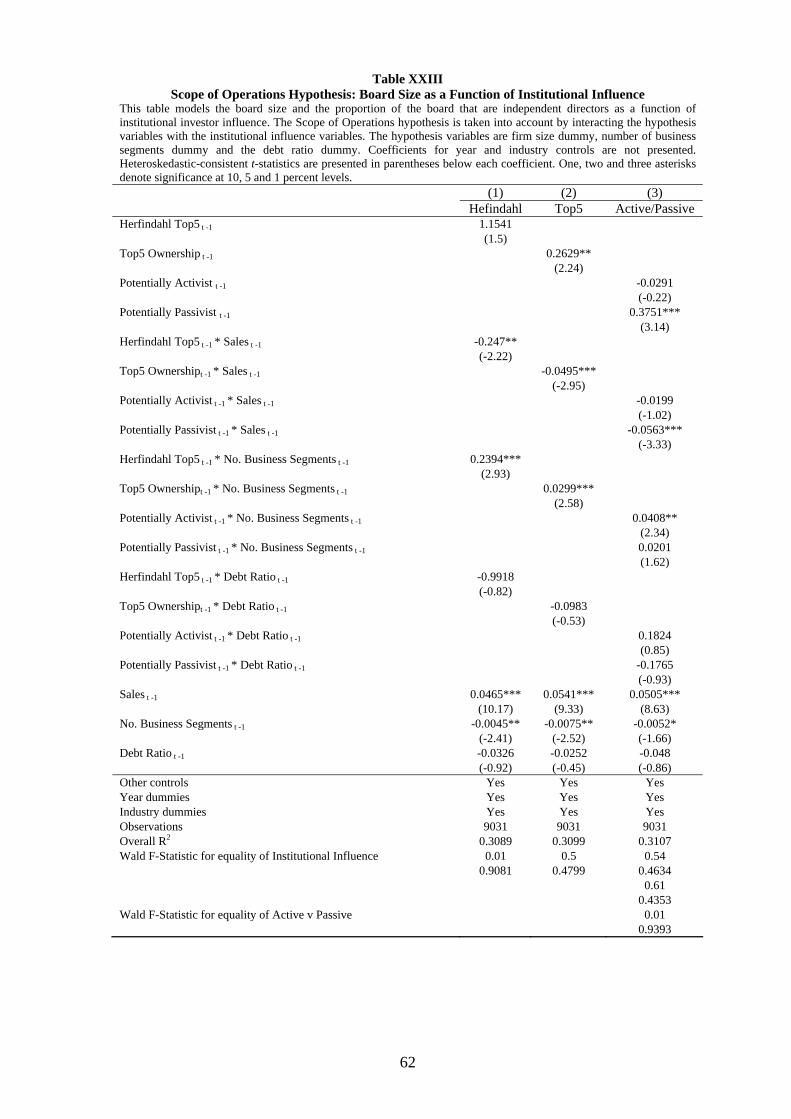

A. Scope of Operations Hypothesis:

The first factor that affects the costs and benefits of different board structures

is the scope of operations which also gives an indication of firms advising needs. The

major advantage of large boards is the collective information possessed by the board.

This information is valuable for both the advisory and monitoring functions of boards.

30

Firms with higher advising needs, such as those operating in diversified industries,

large firms, and those that rely more on debt financing, are all more likely to benefit

from a larger board of directors. In addition, larger firms demand more outside

directors because their size gives rise to more significant agency problems (Boone,

Field, Karpoff and Raheja, 2007). It is tested whether institutional influence is

positively related to board size and independence in complex and diversified firms.

The scope of business operations is measured by sales, number of business operating

segments and leverage (see Coles, Daniel and Naveen, 2007; Boone, Field, Karpoff

and Raheja, 2007). An interactive analysis is employed to test the effect of

institutional influence, where each measure of institutional influence is interacted with

a dummy variable equal to one if the hypothesis variable (e.g. sales) is above the

median, and zero otherwise.

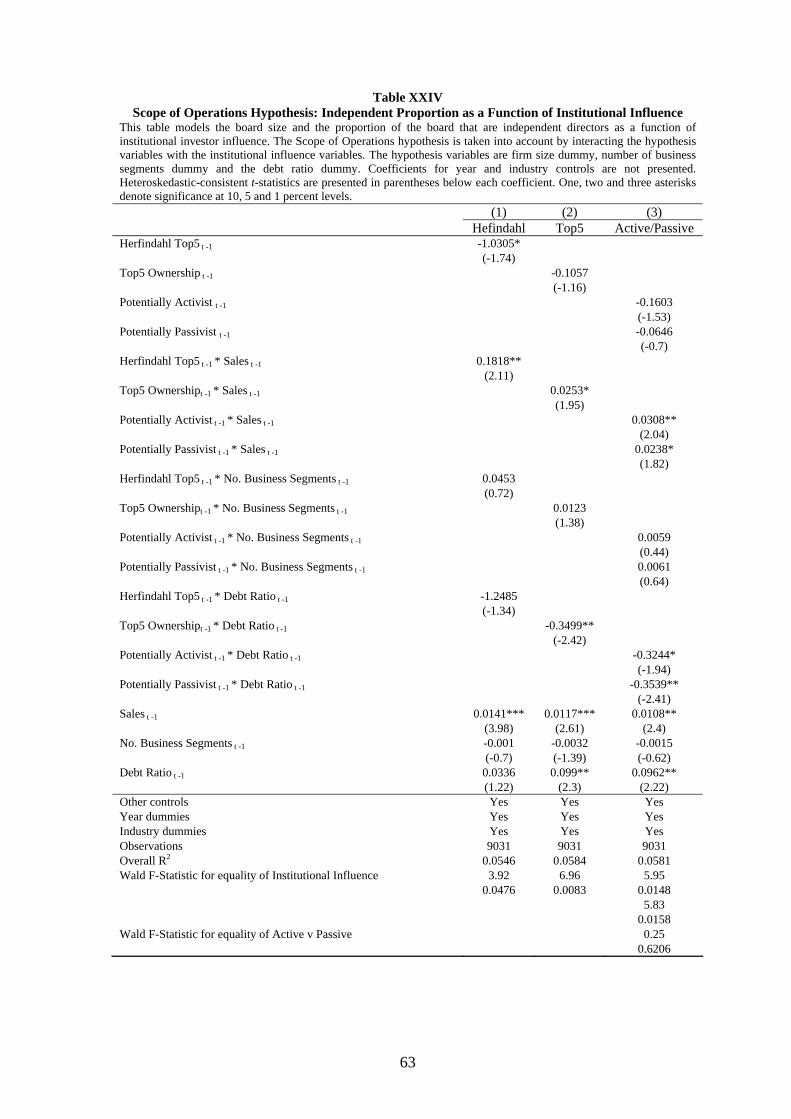

<<INSERT TABLE XXIII AND XXIV>>

Table XXIII examines the effect of institutional influence on board size while

accounting for the scope of a firm’s operations. Institutional influence is negatively

related to board size in large firms, positively related to board size in firms with

numerous operating segments and insignificantly related to board size in firms with

high leverage. Table XXIV examines the effect of institutional influence on board

independence while accounting for the scope of a firm’s operations. Institutional

influence is positively related to board independence in larger firms as measure by

sales. However, institutional influence does not adjust to reflect the diversity of a

firm. In contrast to the scope of operations hypothesis, institutional influence on board

31

independence is lowered in firms with higher levels of leverage. This is surprising

since Booth and Deli (1999) find that commercial bankers serve as directors so that

they can provide bank-debt-market expertise. An alternative and potentially

competing argument is that debt is serving as a monitoring mechanism of

management, thereby reducing the need for independent directors. Overall, there is

weak evidence to support institutional investors adjusting their monitoring objectives

to reflect the scope of a firm’s operations.

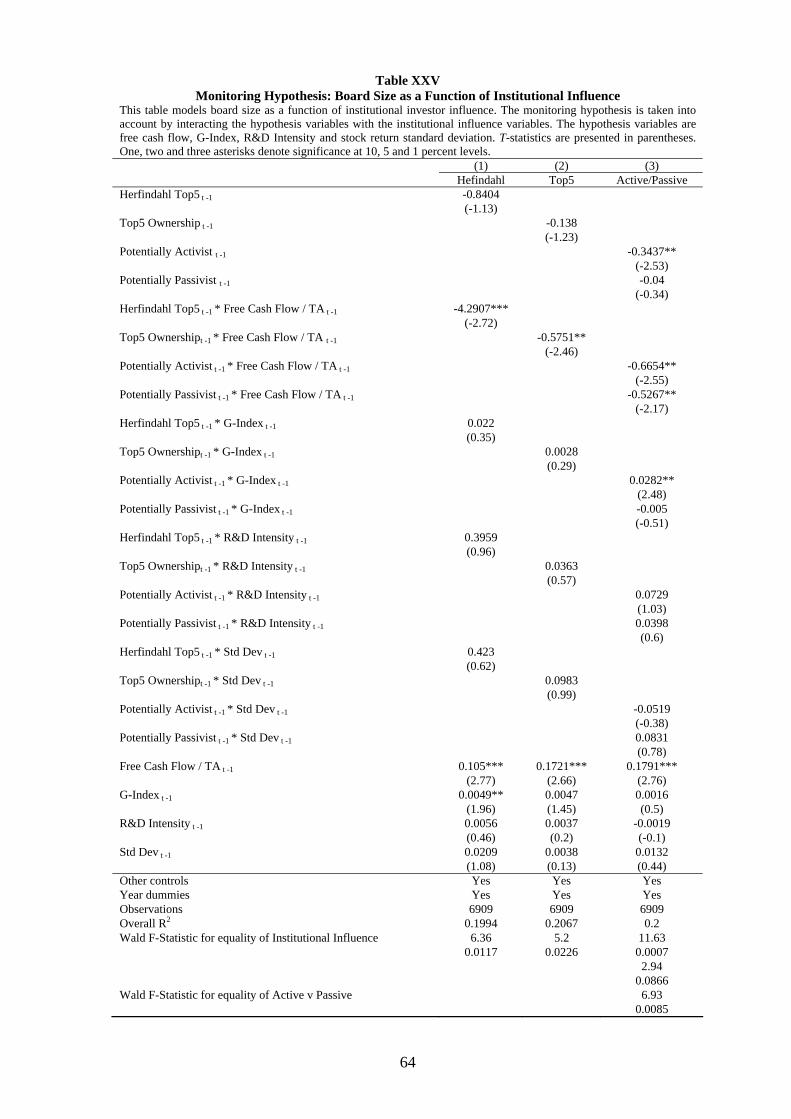

B. Monitoring Hypothesis:

The rationale of the monitoring hypothesis is that the private benefits being

extracted by managers, and also the cost of monitoring the behavior of managers,

needs to be assessed when designing the board. This hypothesis predicts that, as the

opportunity increases for managers to consume private benefits, there should be more

independent directors to monitor management, which thereby results in a bigger

board. The opportunity to consume private benefits is measured by free cash flow and

also the G-Index (Boone, Field, Karpoff and Raheja, 2007). This suggests in firms

exhibiting high potential private benefits for managers, institutional investor influence

should be positively related to the proportion of independent directors and

consequently positively related to board size.

The second part of the monitoring hypothesis predicts that the cost to the

board in monitoring management also affects board structure. Costs associated with

monitoring management are generally accepted to be higher in growth firms due to

the noisiness of their operating environment. In firms where the cost of monitoring

management is high, it is not desirable to have a large board. Lehn, Patro and Zhao

(2005) explain that with larger boards, directors are more inclined to ‘free ride’. That

32

is, when the board is larger, the influence of each board member decreases. As such,

with less influence board members have reduced incentives to actively monitor

managements and bear the costs associated with investing in information needed to

monitor. In order to mitigate the free riding problem and thereby force directors to

have an incentive to accept higher monitoring costs, boards need to be smaller.

Similarly, with respect to board composition, in growth firms there are large

informational asymmetries. This makes it more difficult for independent directors to

monitor management, and means that independent directors have to incur significant

costs to gather information. Therefore, since the firm-specific knowledge of insiders

is relatively more important in growth firms, shareholders are likely to benefit from

greater representation of insiders. The cost of monitoring is measured using research

and development expenses scaled by total assets and also the stock return standard

deviation (see Coles, Daniel and Naveen, 2007; Boone, Field, Karpoff and Raheja,

2007; Gaver and Gaver, 1993). It is expected that the cost of monitoring will increase

with stock return standard deviation. This is because volatility reflects background

uncertainty about the firm’s prospects and performance, and increases the difficulty of

judging managers’ performance (Boone, Field, Karpoff and Raheja, 2007). This

suggests that, in firms with higher costs of monitoring, institutional investor influence

should be negatively related to board size. It should also negatively relate to the

proportion of independent directors.

Table XXV does not support the monitoring hypothesis for board size. For

firms with higher levels of free cash flow, institutions attempt to reduce board size.

Moreover, for other test variables (i.e. G-Index, R&D intensity, Standard Deviation of

stock returns) there is no significant evidence to suggest institution investors adjust

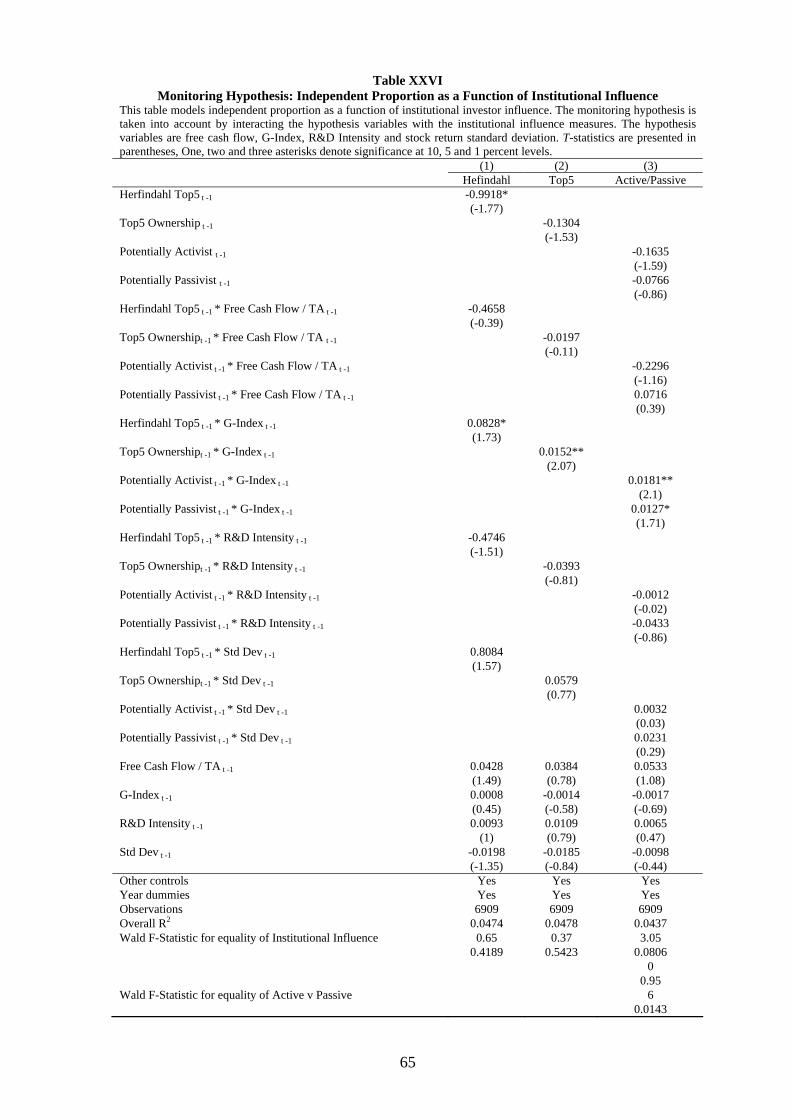

their influence. Table XXVI addresses the monitoring hypothesis with respect to

33

board independence. Institutional influence only adjusts to reflect the extraction of

private benefits, as measure by the G-Index. The general insignificance of the

institutional influence and monitoring hypothesis interaction variables does not

provide support for institutions adjusting their objectives to reflect the private benefits

being extracted by managers, and also the cost of monitoring the behavior of

managers.

<<INSERT TABLE XVI>>

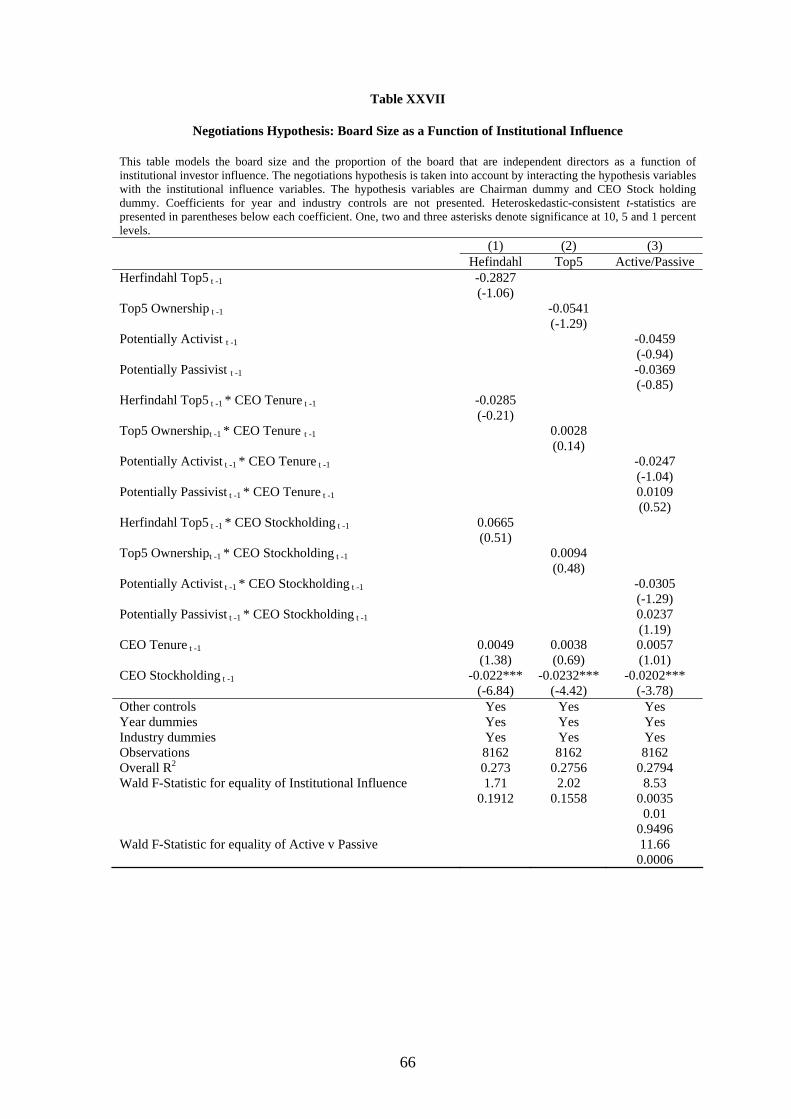

C. Negotiations Hypothesis:

A third factor that affects board structure is the implicit negotiations that occur

between the CEO and outside directors (or institutional investors). Hermalin and

Weisbach (1998) propose that boards reflect the outcome of a negotiation between the

CEO and outside directors. CEOs that generate surpluses for their firms use their

influence to capture some of these surpluses by placing insiders on the board. The

resulting board is not inefficient; rather it is part of the compensation earned by the

CEO. Boone, Field, Karpoff and Raheja (2007) describe this as being the result of

negotiations between the CEO and board.

Adams and Ferreira (2007) develop a similar model whereby ‘management

friendly’ boards may be optimal. The rationale is that the task of the board is to

monitor management, and independent board members are generally accepted as

being better monitors. A manager faces a trade-off in that if the manager shares their

information with the board, they may receive better advice, but they will be monitored

more intensely given the board will be better informed.

34

CEO stock ownership and CEO tenure are used to measure CEO influence and

information asymmetry between the CEO and the firm. We then test whether

institutional investors permit more friendly boards by allowing decreased board

independence and increased board size in situations where the CEO wields

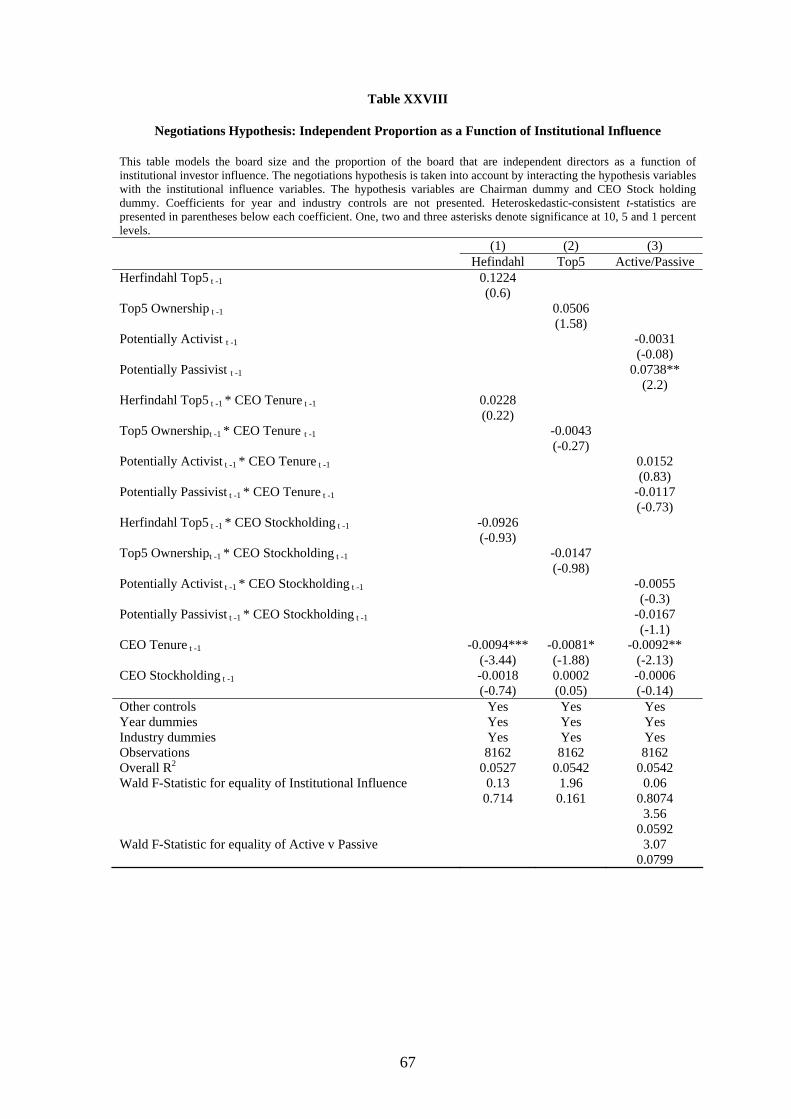

considerable influence and has informational advantages. Table XXVII and XXVIII

do not support the hypothesis that institutional investors structure the board in a

manner that encourages influential or powerful CEOs to reveal their information. All

interaction variables with the negotiations test variables are insignificant.

<<INSERT TABLE XXVII AND XXVIII>>

VII. Conclusion Institutional investors possess considerable influence over firms in which they

have a shareholding. Because institutional investors have significant investments in

firms, they collaboratively enjoy significant bargaining power and can gain direct

access to the top management of a firm—something atomistic shareholders cannot

achieve. They have the funds, resources and ability to wage concerted campaigns to

remove or appoint directors—the leverage to have their voice heard. Institutions can

also use their influence to remove or appoint directors in order to shape the board in a

manner that improves its effectiveness. This paper examines whether institutional

investors use their influence to reduce board size and increase board independence,

two dimensions of board structure shown to have an important impact on the

performance of the firm. The study also examines how institutions achieve their

objectives with respect to board structure.

35

Our study finds that institutional investor influence is negatively related to

board size and positively related to board independence. This is generally consistent

across various estimation techniques, such as pooled OLS with clustered standard

errors, firm random effects and firm fixed effects. However, endogeneity does appear

to be an issue in examining board attributes such as board size and independence.

This is largely due to the low variability of the board attributes. Examining changes in

board structure, such as director appointments and departures, helps alleviate concerns

of endogeneity. Analysis of board changes shows that institutional investors remove

inside directors as a means of reducing board size and increasing independence.

Institutional influence is positively related to both the appointment and departure of

inside directors. More insiders are found to be removed than appointed, resulting in

an increase in board independence. This relationship is particularly evident in periods

when a firm had performed poorly. Institutions appear to take corrective action to

improve firm performance and punish directors deemed responsible for poor

performance. Institutional investors follow the general prescription that smaller

boards and increased independence are better for monitoring managers. They are

successful in achieving their objectives. Moreover, there is not evidence to suggest

institutional investors adapt their influence to reflect firm specific characteristics

which may alter the optimality of smaller boards and increased independence.

Additional research can examine how institutions exert their influence on

board structure – whether it is through private negotiation (Carleton, Nelson and

Weisbach, 1998), public naming (Wu, 2004), proxy voting or a combination.

36

References

Adams, R. and D. Ferreira, 2007, A Theory of Friendly Boards, Journal of Finance 62, 217-250.

Agrawal, A. and G. Mandelker, 1990, Large Shareholders and the Monitoring of Managers: The Case of Antitakeover Charter Amendments, Journal of Financial and Quantitative Analysis 25, 143-161.

Agrawal, A. and C. Knoeber, 1996, Firm Performance and Mechanisms to Control Agency Problems between Managers and Shareholders, Journal of Financial and Quantitative Analysis 31, 377-397.

Almazan, A., J. Hartzell and L. Starks, 2005, Active Institutional Shareholders and Managerial Compensation, Financial Management 34, 5-34.

Baysinger, B. and H. Butler, 1985, Corporate Governance and the Board of Directors: Performance Effects of Changes in Board Composition, Journal of Law, Economics and Organization 1, 101-124.

Bizjak, J. and C. Marquette, 1998, Are Shareholder Proposals All Bark and No Bite? Evidence from Shareholder Resolutions to Rescind Poison Pills, Journal of Financial and Quantitative Analysis 33, 499-521.

Black, B., W. Kim, H. Jang and K. Park, 2005, Does Corporate Governance Predict Firms’ Market Values? Time Series Evidence from Korea, Working Paper University of Texas Law School, KDI School of Public Policy and Management, Korea University Business School.

Boone, A., L. Field, J. Karpoff and C. Raheja, 2007, The Determinants of Corporate Board Size and Composition: An Empirical Analysis, Journal of Financial Economics 85, 65-101.

Booth, J. and D. Deli, 1999, On Executives of Financial Institutions as Outside Directors, Journal of Corporate Finance 5, 227-250.

Borokhovich, K., R. Parrino and T. Trapani, 1996, Outside Directors and CEO Selection, Journal of Financial and Quantitative Analysis 31, 337-355.

Breusch, T. and A. Pagan, 1980, The Lagrange Multiplier Test and Its Implications to Model Specification in Econometrics, Review of Financial Studies 47, 239-253.

Brickley, J., R. Lease and C. Smith, 1988, Ownership Structure and Voting on Antitakeover Amendments, Journal of Financial Economics 20, 267-92.

Brickley, J., J. Coles and R. Terry, 1994, Outside Directors and the Adoption of Poison Pills, Journal of Financial Economics 35, 371-390.

Byrd, J. and K. Hickman, 1992, Do Outside Directors Monitor Managers? Evidence from Tender Offer Bids, Journal of Financial Economics 32, 195-221.

California Public Employees Retirement System, Corporate Governance Core Principles and Guidelines (1998), Available www.calpersgovernance.org/principles/domestic/us/page 01.asp.

Carleton, W., J. Nelson and M. Weisbach, 1998, The Influence of Institutions on Corporate Governance Through Private Negotiations: Evidence from TIAA-CREF, Journal of Finance 53, 1338-40.

37

Chen, X., J. Harford and K. Li, 2007, Monitoring: Which Institutions Matter?, Journal of Financial Economics, Forthcoming.

Chung, R., M. Firth and J. Kim, 2002, Institutional Monitoring and Opportunistic Earnings Management, Journal of Corporate Finance 8, 29-48.

Clay, D., 2000, The Effects of Institutional Investment on CEO Compensation, Working Paper, University of Southern California.

Coles, J., N. Daniel and L. Naveen, 2007, Boards: Does One Size Fit All?, Journal of Financial Economics, Forthcoming.

Core, J., R. Holthausen and D. Larcker, 1999, Corporate Governance, Chief Executive Officer Compensation and Firm Performance, Journal of Financial Economics 51, 371-406.

Cotter, J., A. Shivdasani, M. Zenner, 1997, Do Independent Directors Enhance Target Shareholder Wealth During Tender Offers? Journal of Financial Economics 43, 195-218.

Eisenberg, T., S. Sundgren and M. Wells, 1996, Larger Board Size and Decreasing Firm Value in Small Firms, Journal of Financial Economics 48, 35-54.

Fama, E. and M. Jensen, 1983, Separation of Ownership and Control, Journal of Law and Economics 26, 301-325.

Gaver, J. and K. Gaver, 1993, Additional Evidence on the Association Between the Investment Opportunity Set and Corporate Financing, Dividend, and Compensation Policies, Journal of Accounting and Economics 16, 125-160.

Gertner, R. and S. Kaplan, 1997, The Value-Maximizing Board, Working Paper, University of Chicago.

Gillan, S. and L. Starks, 2000, Corporate Governance Proposals and Shareholder Activism: The Role of Institutional Investors, Journal of Financial Economics 57, 275-305.

Gordon. L. and J. Pound, 1993, Information, Ownership Structure and Shareholder Voting: Evidence from Shareholder-Sponsored Corporate Governance Proposals, Journal of Finance 48, 697-718.

Gompers, P. and A. Metrick, 2001, Institutional Investors and Equity Prices, Quarterly Journal of Economics 116, 229-259.

Greene, W., 2003, Econometric Analysis, Fifth Edition, Prentice Hall.

Hartzell, J. and L. Starks, 2003, Institutional Investors and Executive Compensation, Journal of Finance 58, 2351-2374.

Hausman, J., 1978, Specification Tests in Econometrics, Econometrica 46, 1251-1271.

Hermalin, E. and S. Weisbach, 1991, The Effects of Board Composition and Direct Incentives on Firm Performance, Financial Management 20, 101-112.

Hermalin, B. and M. Weisbach, 1998, Endogenously Chosen Boards of Directors and their Monitoring of the CEO, American Economic Review 88, 96-118.

Jensen, M., 1993, The Modern Industrial Revolution, Exit, and the Failure of Internal Control Systems, Journal of Finance 48, 831-880.

38

Johnson, M., S. Porter and M. Shackell, 1997, Stakeholder Pressure and the Structure of Executive Compensation, Working Paper, University of Michigan and University of Texas at Austin.

Karpoff, J., P. Malatesta and R. Walkling, 1996, Corporate Governance and Shareholder Initiatives: Empirical Evidence, Journal of Financial Economics, 42, 365-395.

Lee, C. S. Rosenstein, N. Rangan and W. Davidson, 1992, Board Composition and Shareholder Wealth: The Case of Management Buyouts, Financial Management 21, 58-72.

Lehn, K., S. Patro and M. Zhao, 2005, Determinants of the Size and Structure of Corporate Boards: 1935-2000, Working Paper, University of Pittsburgh.

Lipton, M. and J. Lorsch, 1992, A Modest Proposal for Improved Corporate Governance, Business Lawyer 48, 59-77.

Noe, Thomas H., 2002, “Investor Activism and Financial Market Structure,” Review of Financial Studies 15, 289-318.

Opler, T. and J. Sokobin, Does Coordinated Institutional Activism Work? An Analysis of the Activities of the Council of Institutional Investors, Working Paper.

Palia, D., 2001, The Endogeneity of Managerial Compensation in Firm Valuation: A Solution, Review of Financial Studies 14, 735-764.

Parrino, R., R. Sias and L. Starks, 2003, Voting With Their Feet: Institutional Ownership Changes around Forced CEO Turnover, Journal of Financial Economics 68, 3-46.

Petersen, M., 2004, Estimating Standard Errors in Financial Panel Data Sets: Comparing Approaches, Working Paper, Northwestern University.

Rogers, W., 1993, Regression Standard Errors in Clustered Samples, Stata Technical Bulletin 13, 357-384.

Romano, R., 2001, Less is More: Making Institutional Investor Activism a Valuable Mechanism of Corporate Governance, Yale Journal on Regulation 18, 174-251.

Rosenstein, S. and J. Wyatt, 1990, Outside Directors, Board Independence, and Shareholder Wealth, Journal of Financial Economics 26, 175-191.

Rosenstein, S. and J. Wyatt, 1997, Inside Directors, Board Effectiveness, and Shareholder Wealth, Journal of Financial Economics 44, 229-250.

Smith, G. and P. L. Swan, 2007a, To Good to be True: Do Institutional Investors Really Reduce Executive Compensation Whilst Raising Incentives?, Working Paper, University of New South Wales.

Smith, G. and P. L. Swan, 2007b, Will the Real Monitors Please Stand Up? Institutional Investors and CEO Compensation, Working Paper, University of New South Wales.

Smith, M., 1996, Shareholder Activism by Institutional Investors: Evidence from CalPERS, Journal of Finance 51, 227-252.

Strickland, D., K. Wiles and M. Zenner, 1996, A Requiem for the USA: Is Small Shareholder Monitoring Effective, Journal of Financial Economics 40, 319-338.

39

Wahal, S., 1996, Pension Fund Activism and Firm Performance, Journal of Financial and Quantitative Analysis 31, 1-23.

Weisbach, S., 1988, Outside Directors and CEO Turnover, Journal of Financial Economics 20, 431-460.

Whidbee, D., 1997, Board Composition and Control of Shareholder Voting Rights in the Banking Industry, Financial Management 26, 27-41.

Wintoki, M. Babajide, 2007, “Corporate Boards and Regulation: The Effect of the Sarbanes-Oxley Act and the Exchange Listing Requirements on Firm Value,” Journal of Corporate Finance, forthcoming.

Wu, Y., 2004, The Impact of Public Opinion on Board Structure Changes, Director Career Progression, and CEO Turnover: Evidence from CalPERS’ Corporate Governance Program, Journal of Corporate Finance 10, 199-227.

Yermack, D., 1996, Higher Market Valuation of Companies with a Small Board of Directors, Journal of Financial Economics 40, 185-212.

40

Table I

Descriptive Statistics This table presents descriptive statistics of the key variables employed. Panel A board of director characteristics. Independent proportion is the number of independent directors divided by board size. Panel B shows the measures of institutional influence. Herfindahl index of Top 5 Ownership is the sum of squared proportional ownership for the top 5 institutions. Top5 ownership is the proportion of shares outstanding held by the institutions with the five largest holdings. Potentially Activist ownership is the ownership of institutions classified by CDA as either an Investment company or independent investment adviser, if the institution is one of the top 5 holders in the firm. Potentially Passivist ownership is Top5 ownership minus Potentially Active ownership. Panel C presents statistics on firm characteristics. Mean Std Dev 10th Median 90th