India - Auto - IIFL Capital

104

India - Auto 4Q2019 Current headwinds more cyclical, less structural Gearing up for recovery

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of India - Auto - IIFL Capital

India - Auto

4Q2019

Current headwinds more cyclical, less structural

Gearing up for recovery

Joseph [email protected](91 22) 4646 4667

Suraj [email protected] (91 22) 4646 4656

Contents

SectorAuto’s “share of wallet” down sharply ...................................................... 5

Expect auto’s “wallet share” to rebound ................................................. 10

Adverse inventory cycle behind us ........................................................ 12

BS-VI transition: Expect a volatile 1HCY20 ............................................. 16

Scrappage policy: Exaggerated expectations .......................................... 18

PV segment: Least impacted by BS-VI ................................................... 20

2W segment: BS-VI may hurt in near-term ............................................ 24

MHCVs: Expect YoY growth from 2QFY21 .............................................. 28

Margins typically recover with volumes .................................................. 31

Valuations to remain elevated .............................................................. 34

CompaniesMaruti Suzuki (BUY) ............................................................................ 41

Ashok Leyland (BUY)........................................................................... 47

Tata Motors (BUY) .............................................................................. 53

Hero MotoCorp (BUY) .......................................................................... 61

Bajaj Auto (BUY) ................................................................................ 67

Eicher Motors (ADD) ........................................................................... 75

Mahindra & Mahindra (ADD) ................................................................. 83

TVS Motor (SELL) ............................................................................... 91

India - Auto

joseph.george@iif lcap.com

India - Auto

Gearing up for recovery We turn positive on the auto sector with a view that the industry will see a strong up-cycle over the next 2-3 years. In FY20, consumer spend on autos (PV+2W) undershot overall private consumption by 14%. Auto’s “share of wallet” is now almost 20% below its 15-year average. In our assessment, the underlying factors are more cyclical than structural. We expect auto’s "wallet share” to at least revert to mean (if not overshoot) over the next three years. This will result in a total revenue growth of >50% over FY20-23ii, with a magnified impact on earnings. The inventory correction cycle has played out already; when demand improves, we expect re-stocking. 1HCY20 is uncertain, given the weak economy and upcoming emission-norm changes. We believe weakness in stock prices, if any, would provide an opportunity to participate in the medium-term recovery in the sector.

Autos to regain “consumer wallet share”: Auto’s share of wallet is now almost 20% below its 15-year average. The ‘wallet share loss’ happened in FY19-FY20, and coincided with deceleration in the overall economy, NBFC issues (finance availability) and the impending BS-IV to BS-VI transition. As these cyclical factors recede, we expect auto’s "wallet share” to at least revert to mean. We expect this to drive a total revenue growth of >50% over FY20-23ii.

Adverse inventory cycle behind us; expect re-stocking in FY21: We are currently at the end of Stage 3 of the inventory cycle (See figure 16), marked by low wholesales and inventory correction. Inventory level across segments is currently lower compared to last year. We expect retail demand to improve YoY over the course of FY21, after 7-8 quarters of weakness. Reported wholesales may start seeing YoY growth in 2QFY20, as the above-referred Stage 3 enters the YoY comparison base.

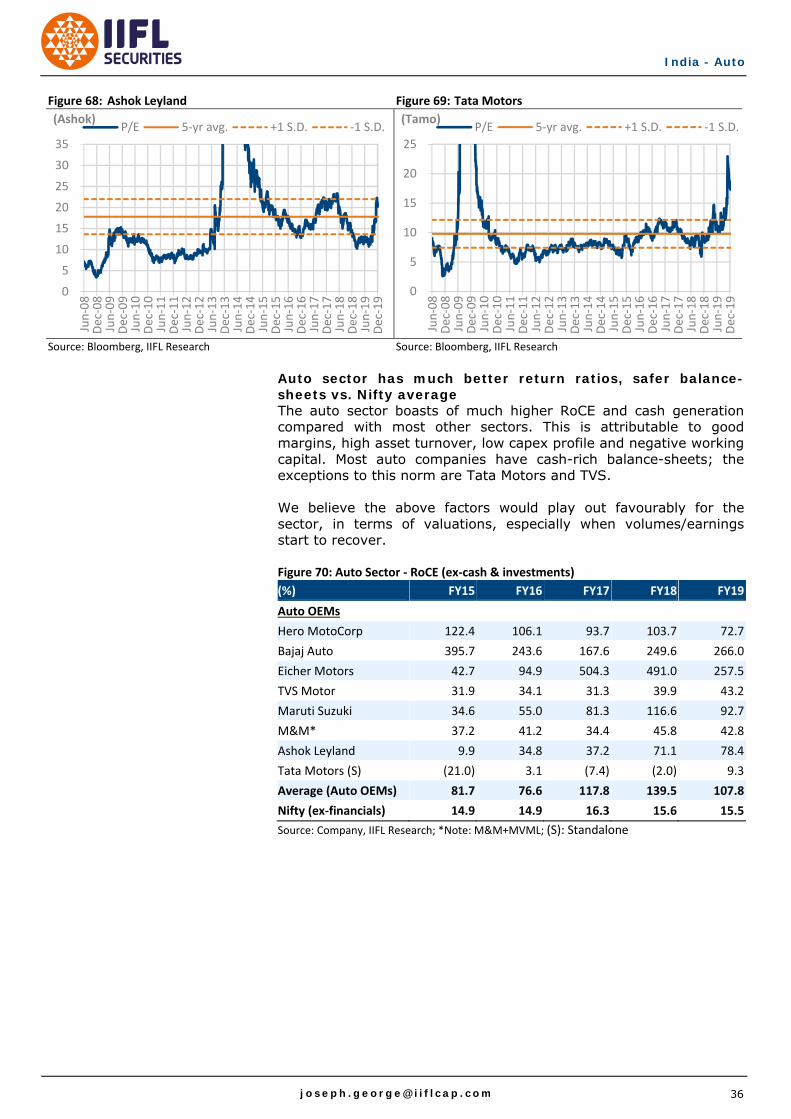

Expect sharp earnings recovery in PV, MHCV: These segments have seen higher adverse impact on earnings in the down-cycle with rise in discounts and negative operating leverage on fixed costs. These factors would reverse in the up-cycle, driving sharp earnings recovery. Sector valuations, which have gone up in the past 3-4 years vs. preceding periods, may remain elevated in the recovery period. The auto sector boasts of higher RoCE, better FCFF generation and cash-rich balance-sheets vs. most other sectors.

Upgrade Ashok Leyland and Eicher: We upgrade Ashok Leyland to BUY with a view that the CV cycle would turn positive starting 2QFY21. We upgrade Eicher Motors to ADD as we believe that the company’s “volumes over margin” approach will improve affordability and volume-growth potential; the structural decline in margins has largely played out. We had recently upgraded Hero MotoCorp to BUY.

Auto OEMs – Valuation summary and key metrics

Company Rating Target

Price (Rs) CMP (Rs)

Mkt Cap (US$ bn)

EPS CAGR (FY20‐22ii)

P/E (x) EV/Ebitda (x) RoE (%)

FY20ii FY21ii FY22ii FY20ii FY21ii FY22ii FY20ii FY21ii FY22iiMaruti Suzuki BUY 9,000 7,242 30.8 23% 36.3 30.6 24.1 21.6 16.4 12.5 13% 14% 16%Ashok Leyland BUY 105 80 3.3 62% 39.6 34.1 15.1 16.7 13.9 7.7 8% 9% 19%Tata Motors BUY 220 175 8.7 138% 44.5 12.8 7.9 3.8 3.5 2.9 2% 8% 12%Hero MotoCorp BUY 3,100 2,312 6.5 12% 14.9 13.9 11.9 9.7 8.8 6.8 23% 23% 24%Bajaj Auto BUY 3,750 3,214 13.1 11% 19.4 17.9 15.9 14.4 12.7 10.7 21% 20% 20%Eicher Motors ADD 24,000 21,736 8.4 13% 27.7 26.4 21.6 18.6 16.5 13.4 22% 19% 20%M&M ADD 590 523 9.1 6% 13.6 13.5 12.2 8.6 8.3 7.3 11% 10% 11%TVS Motor SELL 380 446 3.0 19% 32.5 27.8 22.8 15.2 13.4 11.4 18% 18% 20%

Source: IIFL Research; Priced as on 18 December 2019

1

joseph.george@iif lcap.com

India - Auto

Key charts and tables

Auto’s “share of wallet” in FY20 is almost 20% below the 15‐year average

Source: IIFL Research

Rebound in auto’s “wallet share” to drive recovery; expect volume growth of 22%/16% for PVs/2Ws over FY21ii+FY22ii

PVs 2Ws

FY20ii FY21ii + FY22ii FY20ii FY21ii + FY22ii

Private Final consumption – Nominal Growth (A) 7% 17% 7% 17%

Gain / (Loss) of "share of wallet" (B) ‐13% 16% ‐15% 13%

Total consumer spend on Auto – Growth (C=A+B) ‐6% 33% ‐8% 30%

ASP increase + mix (D) 6% 10% 4% 14%

Volume growth (C‐D) ‐12% 22% ‐12% 16%

Source: IIFL Research

Different stages of the inventory cycle; we are currently at the end of Stage‐3

Source: IIFL Research; *Note: Inv.= Inventory, W= Wholesales, R(x)= Retails (trend)

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

4.50%

4.75%

5.00%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

FY23ii

Spend on autos (PVs+2Ws) as % of pvt. consumption GDP

15‐yr average

0

20

40

60

80

100

120

140

160

180

Apr‐18

May‐18

Jun‐18

Jul‐18

Aug‐18

Sep‐18

Oct‐18

Nov‐18

Dec‐18

Jan‐19

Feb‐19

Mar‐19

Apr‐19

May‐19

Jun‐19

Jul‐19

Aug‐19

Sep‐19

Oct‐19

Nov‐19

Dec‐19

Jan‐20

Feb‐20

Mar‐20

Apr‐20

May‐20

Jun‐20

Jul‐20

Aug‐20

Sep‐20

Oct‐20

Nov‐20

Dec‐20

Retails Wholesales Inventory(Volumes)

Stage‐1 Stage‐2 Stage‐3 Stage‐4 Stage‐5

W > R (weak)Inv. rising

W = R (weak)Inv. stays high

W < R (weak)Inv. correction

W = R (flattish)Inv. stays low

W > R (recovers)Inv. rises to normal

2

joseph.george@iif lcap.com

India - Auto

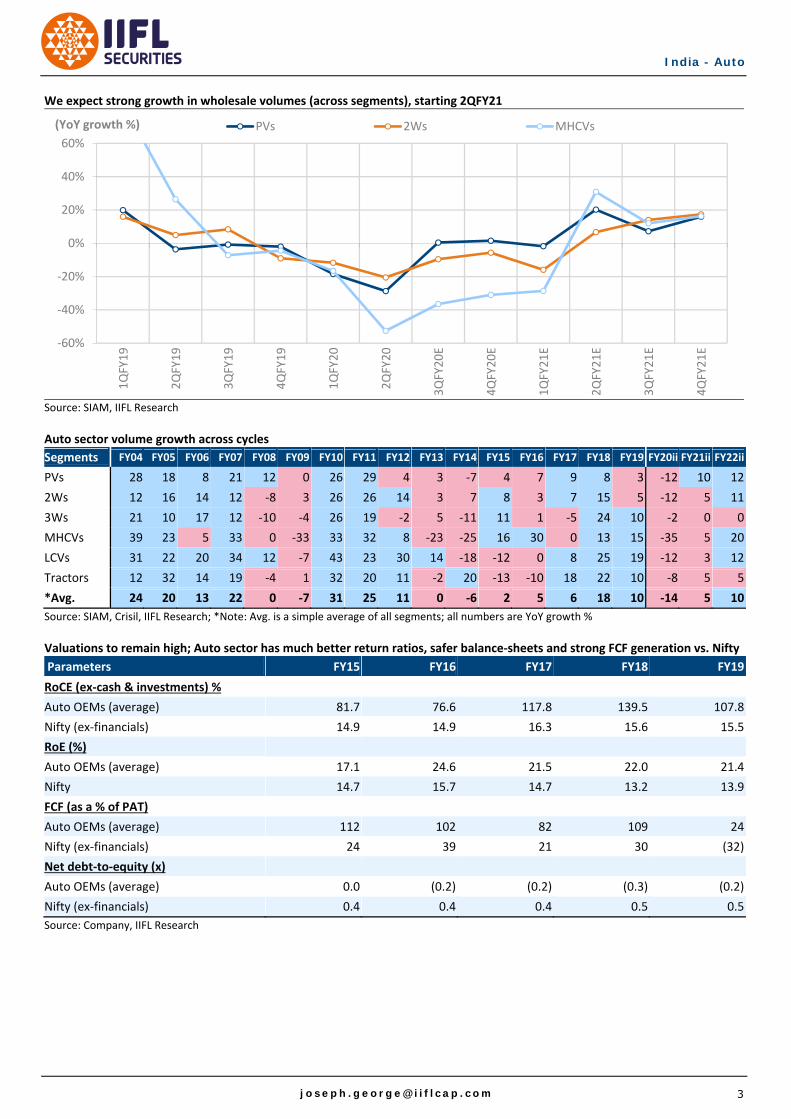

We expect strong growth in wholesale volumes (across segments), starting 2QFY21

Source: SIAM, IIFL Research

Auto sector volume growth across cycles

Segments FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20ii FY21ii FY22ii

PVs 28 18 8 21 12 0 26 29 4 3 ‐7 4 7 9 8 3 ‐12 10 12

2Ws 12 16 14 12 ‐8 3 26 26 14 3 7 8 3 7 15 5 ‐12 5 11

3Ws 21 10 17 12 ‐10 ‐4 26 19 ‐2 5 ‐11 11 1 ‐5 24 10 ‐2 0 0

MHCVs 39 23 5 33 0 ‐33 33 32 8 ‐23 ‐25 16 30 0 13 15 ‐35 5 20

LCVs 31 22 20 34 12 ‐7 43 23 30 14 ‐18 ‐12 0 8 25 19 ‐12 3 12

Tractors 12 32 14 19 ‐4 1 32 20 11 ‐2 20 ‐13 ‐10 18 22 10 ‐8 5 5

*Avg. 24 20 13 22 0 ‐7 31 25 11 0 ‐6 2 5 6 18 10 ‐14 5 10

Source: SIAM, Crisil, IIFL Research; *Note: Avg. is a simple average of all segments; all numbers are YoY growth %

Valuations to remain high; Auto sector has much better return ratios, safer balance‐sheets and strong FCF generation vs. Nifty

Parameters FY15 FY16 FY17 FY18 FY19

RoCE (ex‐cash & investments) %

Auto OEMs (average) 81.7 76.6 117.8 139.5 107.8

Nifty (ex‐financials) 14.9 14.9 16.3 15.6 15.5

RoE (%)

Auto OEMs (average) 17.1 24.6 21.5 22.0 21.4

Nifty 14.7 15.7 14.7 13.2 13.9

FCF (as a % of PAT)

Auto OEMs (average) 112 102 82 109 24

Nifty (ex‐financials) 24 39 21 30 (32)

Net debt‐to‐equity (x)

Auto OEMs (average) 0.0 (0.2) (0.2) (0.3) (0.2)

Nifty (ex‐financials) 0.4 0.4 0.4 0.5 0.5

Source: Company, IIFL Research

‐60%

‐40%

‐20%

0%

20%

40%

60%

1QFY19

2QFY19

3QFY19

4QFY19

1QFY20

2QFY20

3QFY20E

4QFY20E

1QFY21E

2QFY21E

3QFY21E

4QFY21E

PVs 2Ws MHCVs(YoY growth %)

3

joseph.george@iif lcap.com

India - Auto

This page is kept blank intentionally

4

joseph.george@iif lcap.com

India - Auto

Auto’s “share of wallet” down sharply In FY20, consumer spend on autos (new vehicle purchases of PV+2W) undershot private final consumption by around 14%. Compared with the auto sector’s 15-year average “share of wallet”, FY20 was almost 20% below mean. In our assessment, the underlying factors are more cyclical than structural. As GDP growth picks up and cyclical impediments recede, we expect auto’s "share of wallet” to at least revert to mean (if not overshoot). Figure 1: Auto’s FY20 “share of wallet” is almost 20% below the 15‐year average

Source: IIFL Research

A slowdown in the economy and resultant weakness in overall consumption was bound to impact auto sales. However, the impact on the sector was much more magnified than the slowdown in GDP. We attribute this to multiple factors: 1: Weak economic growth India has seen a sharp deceleration in GDP growth, which has been evidently accompanied by a slowdown in private consumption. Our base case of revival in the auto sector is based on pick-up in GDP growth and private consumption in coming years. If overall economic growth continues at the same rate as now, a pick-up in the auto sector would be delayed. Figure 2: GDP growth slowed down substantially in FY20

Source: CEIC, IIFL Research

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

4.50%

4.75%

5.00%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

FY23ii

Spend on autos (PVs+2Ws) as % of pvt. consumption GDP

15‐yr average

0%2%4%6%8%

10%12%14%16%18%20%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

GDP growth ‐ Real Private consumption growth ‐ Nominal

5

joseph.george@iif lcap.com

India - Auto

2: Discretionary nature magnified the impact Needless to say, Autos as a category is discretionary in nature. During times of slowdown, spend on new vehicle purchases can be easily curtailed/postponed. This can be attributed to “prudence in consumer spending” and/or “sentiment”. This is what makes autos cyclical. Auto’s “share of wallet” is impacted by overall economic growth (Figure 3). During times of slowdown, it loses ‘wallet share’ but gains share as the economy picks up. Auto sector revenue is impacted by acceleration/deceleration in overall consumption as well as gain/loss of ‘wallet share’. Figure 3: Discretionary nature has a magnified impact, as GDP growth fluctuates

Source: CEIC, IIFL Research

3: Availability of financing hurt sales; easing now Availability of financing hurt PVs and CVs more than 2Ws. Strict credit assessment of potential vehicle-buyers and lower loan-to-value ratio resulted in loss of sales in the past 12 months. The trigger point for the tightness in financing was the NBFC crisis starting late-2018. While a fall in loan-to-value, from 90% to 80%, does not sound alarming, it effectively doubles the down-payment requirement, which may have been beyond the affordability limit of many potential vehicle-buyers. 4: Confusion over BS-IV to BS-VI transition has led to sales postponement Our dealer checks and interactions with OEMs reveal that some consumers have postponed buying decisions in view of upcoming emission-norm changes. This is because of such consumers preferring to wait for a few months and buying new technology vehicles rather than old-technology ones now. This factor is more valid in case of gasoline cars, where the price difference between BS-IV and BS-VI is not much (1-2%); hence, price is not a major consideration for pre-buying. As regards models where BS-VI upgrades have been launched by OEMs, some customers are waiting for availability of BS-VI fuel instead of risking BS-IV fuel in BS-VI vehicles. Starting April 2020, when BS-VI vehicles and fuel would both be available, these postponements should convert into real sales.

0%2%4%6%8%10%12%14%16%18%20%

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

4.50%

4.75%

5.00%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

Auto's share of wallet (LHS) Private consumption growth (RHS)

6

joseph.george@iif lcap.com

India - Auto

Are there any structural factors that impede growth in autos? Undoubtedly yes. However, in our view, they are not significant enough to bring the sector to a standstill. Structural factors that have been cited as impediments to growth are: i) High levels of penetration (more relevant for 2Ws) ii) Road infrastructure, traffic congestion (more relevant for PVs) iii) Shared mobility (more relevant for PVs) i) High level of penetration The penetration argument is relevant more in the context of 2Ws than cars. Penetration of cars in India is about 2.5% of population and <10% of households. Surely, as income levels grow and so do aspirations, this penetration number is bound to increase. The other connected argument we hear is “everyone who can afford a car, already has a car”. This would largely be the case at any point of time in history. Yet, vehicle sale have grown over the years, as more individuals/households have entered the affordability bracket. In addition, there is the angle of replacement sales. Even a fully penetrated car-market buys a steady number of cars every year. USA, which is a 70-80% penetrated car market, still buys 15-18mn cars every year; this is primarily driven by replacement sales. In India, the first owner of a car typically holds on to the vehicle for 5-7 years; this extends or shortens depending on the state of the economy. The average number of cars that were sold in India 5-7 years ago was 2.6mn. These would come up for replacement in coming years. In comparison, FY20ii PV volume would only be about 3mn. Hence, replacement sales on their own can account for a large part of new-car sales in coming years. Surely, as income level/affordability increases and the above-referred cyclical impediments recede, there would be enough first-time buyers to drive growth in volumes. Figure 4: Replacement by itself would contribute a large chunk of FY21‐22ii sales

Source: SIAM, IIFL Research

Even for 2Ws, a large chunk of sales in FY21-22ii can be contributed by replacement sales. About 16m 2Ws were sold annually in the FY14-16 period; these can come up for replacement soon. In comparison, FY20ii 2W volume would only be about 18.5mn. Here again, replacement sales can account for a large part of new 2W sales in coming years.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

(Domestic PV sales)

Avg sales 2.6mn

7

joseph.george@iif lcap.com

India - Auto

Figure 5: Replacement would contribute a large chunk of FY21‐22ii 2W sales

Source: SIAM, IIFL Research

As regards 2Ws, if we simply compare the 2W population of ~200mn to the ~300mn households in the country, it looks like a fairly penetrated category. However, if we adjust for the fact that there are, on an average, 1.9 2Ws per household, the household-level penetration is only ~40%, with further room for expansion. Figure 6: There are almost two 2Ws in households, which own 2Ws

2001 Census 2011 Census 2019 Est.

Total number of households (mn) 192 247 292

Household penetration of 2Ws 11.7% 21.0% 37.6%

Number of households with 2W (mn) 22 52 109

2W population (mn; 15yr life) 32 88 203

No of 2Ws per household 1.4 1.7 1.9

Source: Census of India, SIAM, IIFL Research

Figure 7: There is room for further expansion in 2W penetration

FY17 FY18 FY19 FY20ii FY21ii FY22ii

2W volumes (mn) 17.6 20.2 21.2 18.6 19.5 21.6

Growth (%) 7% 15% 5% ‐12% 5% 11%

2W population (mn; 15yr life) 159 175 190 203 215 229

Number of households (mn) 276 283 287 292 296 300

Household penetration 58% 62% 66% 70% 73% 76%

No of 2Ws per households 1.8 1.8 1.8 1.9 1.9 1.9

Adj. household penetration 32% 34% 36% 38% 39% 40%

Source: Census of India, SIAM, IIFL Research

Figure 8: No. of middle income & above households to double by 2030 (vs. 2018)

Source: Hero MotoCorp ‐ Corporate presentation (May‐19)

0.0

5.0

10.0

15.0

20.0

25.0

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

(Domestic 2W sales)

Avg sales 16mn

69%

43%

15%

31%

57%

85%

2005 2018 2030E

Mid income & above Low incomeHouseholds (mn)

293 386219

8

joseph.george@iif lcap.com

India - Auto

ii) Road infrastructure, traffic congestion There is no doubt that better road infrastructure would have supported higher growth, especially in PVs. Perhaps, that is why PV growth has trudged along at single-digit Cagr over FY11-19, after logging 27% Cagr for two years (FY09-11). In fact, over this period, 2Ws clocked higher growth vs. PVs. Analysis of state-wise data tells us that states with metro cities have not contributed to volume growth in the past 8 years. Almost the entire growth in the industry came from non-metro states. Figure 9: States with metros have not been contributing to industry growth

Urbanisation

Contribution to sales ‐

FY11

FY11 PV sales

FY19 PV sales

8‐year Cagr

Contribution to growth

Maharashtra 45% 13.8% 346,038 354,480 0%

Delhi 98% 7.5% 189,385 193,922 0%

Tamil Nadu 48% 7.4% 185,309 219,628 2%

West Bengal 32% 3.6% 90,267 104,819 2%

Sum 45% 32.2% 810,999 872,849 1% 7%

Other states 27% 67.8% 1,705,526 2,504,560 5% 93%

Total India 31% 100.0% 2,516,525 3,377,409 4%

Source: SIAM, IIFL Research; Note: Urbanisation is as measured by 2011 Census

Figure 10: Maruti – FY11‐19 growth mainly driven by rural markets

FY11 ‐ Share of volumes FY19 ‐ Share of volumes FY11‐19 Volume Cagr

Urban 80% 61% 2%

Rural 20% 39% 15%

Total 100% 100% 6%

Source: Company, IIFL Research

It is possible that larger cities may not contribute much to growth, even in the future, due to relatively higher level of penetration and infrastructure issues. However, growth may continue outside large cities, especially given the significant under-ownership of PVs. Over time, as the government builds more roads and infrastructure, this would be less of an impediment. iii) Shared mobility The third factor that has been talked about in this context is shared mobility (Uber, Ola). This, again, is a factor that impacts PVs more than 2Ws. Shared mobility accounts for mid-single-digit percentage contribution to PV industry sales. Shared mobility is currently restricted to cities. Outside these cities, shared mobility is not a factor. Even in places where shared mobility is a factor, we believe this would not hurt first-car purchases. The aspiration of owning a car is a huge motivation; this would not be satiated by the ability to hire a car using an App. If at all, this may impact the propensity to buy a second car in the family. As highlighted earlier, with a 2.5% penetration, car sales have a long way to go before “shared mobility” acts as an impediment to first-car purchases.

9

joseph.george@iif lcap.com

India - Auto

Expect auto’s “wallet share” to rebound As mentioned earlier, consumer spend on auto under-shot private final consumption by 14% in FY20ii, thereby losing an equivalent “share of wallet”. We expect the “share of wallet” to rebound over FY21-23ii to its 15-year average, coinciding with a recovery in the overall economy. We build 8% and 9% nominal growth in private final consumption in FY21ii and FY22ii respectively, implying a cumulative growth of 17% over two years. As the economy recovers and other impediments highlighted earlier recede, we expect auto’s “share of wallet” to improve by 15% by FY22ii (back to FY19 levels). Overall, we expect consumer spend of auto to increase by 32% over FY21ii + FY22ii. Of this, we expect about 11% to be lost on account of costs related to emission norm change and mix change, with the remaining 21% translating into volume growth. Figure 11: Rebound in “wallet share” to drive recovery over FY21‐23ii

FY20ii FY21ii + FY22ii

Private Final consumption – Nominal Growth (A) 7% 17%

Gain / (Loss) of "share of wallet" (B) ‐14% 15%

Total consumer spend on Auto – Growth (C=A+B) ‐7% 32%

ASP increase + mix (D) 5% 11%

Volume growth (C‐D) ‐12% 21%

Source: IIFL Research

In case of PVs, we forecast 33% growth in consumer spend over the next two years, driving a 22% volume growth, after adjusting for a 10% ASP increase over FY21ii+FY22ii (mainly BS-VI related). Despite building an 11% Cagr over the next two years, the 5-year PV volume Cagr over FY17-22ii would only be about 4%. Figure 12: PV − We expect 22% volume growth over FY21ii + FY22ii

FY20ii FY21ii + FY22ii

Private Final consumption – Nominal Growth (A) 7% 17%

Gain / (Loss) of "share of wallet" (B) ‐13% 16%

Total consumer spend on Auto – Growth (C=A+B) ‐6% 33%

ASP increase + mix (D) 6% 10%

Volume growth (C‐D) ‐12% 22%

Source: IIFL Research

In case of 2Ws, we forecast 30% growth in consumer spend over the next two years, driving a 16% volume growth, after adjusting for a 14% ASP increase over FY21ii+FY22ii (mainly BS-VI related). Despite building a 16% jump in volumes over two years, absolute 2W volume in FY22ii would only be 2% higher than FY19. Figure 13: 2Ws − We expect 16% volume growth over FY21ii + FY22ii

FY20ii FY21ii + FY22ii

Private Final consumption – Nominal Growth (A) 7% 17%

Gain / (Loss) of "share of wallet" (B) ‐15% 13%

Total consumer spend on Auto – Growth (C=A+B) ‐8% 30%

ASP increase + mix (D) 4% 14%

Volume growth (C‐D) ‐12% 16%

Source: IIFL Research

10

joseph.george@iif lcap.com

India - Auto

How does India stack up vs. USA and China? Indian consumers spend about 2.7% of their wallet on purchasing new cars. In comparison, USA spent about 4.4% and China spent 12.6%. In USA, PV is a matured consumption category with 70-80% car penetration. PV’s share of consumer wallet went up in the first half of 20th century but has been flattening and coming down in recent decades. Figure 14: USA ‐ PV’s share of consumer wallet coming off after peaking

Source: Bloomberg, World Bank, IIFL Research

In China, PV’s share of consumer wallet has gone up 12x since the turn of the century, coinciding with a multi-fold rise in PV volumes. Figure 15: China ‐ PV’s share of wallet significantly higher than in India

Source: Bloomberg, CAAM, World Bank, IIFL Research

0

2

4

6

8

10

12

14

16

18

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%CY76

CY78

CY80

CY82

CY84

CY86

CY88

CY90

CY92

CY94

CY96

CY98

CY00

CY02

CY04

CY06

CY08

CY10

CY12

CY14

CY16

CY18

US PV spend as % of pvt. consumption PV volumes (mn) ‐ RHS

0

6

12

18

24

30

0%

3%

6%

9%

12%

15%

CY99

CY00

CY01

CY02

CY03

CY04

CY05

CY06

CY07

CY08

CY09

CY10

CY11

CY12

CY13

CY14

CY15

CY16

CY17

CY18

China PV spend as % of pvt. consumption PV Volumes (mn) ‐ RHS

11

joseph.george@iif lcap.com

India - Auto

Adverse inventory cycle behind us In the early part of the down-cycle, dealer inventory increases, as wholesales stay high, even as retails weaken. In the late stage of the down-cycle, wholesales are much lower than retails, as inventory gets corrected. This is the worst phase, from a reported volume perspective (wholesales). Different stages of the inventory cycle are depicted in Figure 16. The July-Oct 2019 period was marked by sharp inventory correction across segments (2Ws, PVs and CVs). Commentary from OEMs suggests that dealer inventory levels are currently at the lowest levels in the past two years. Inventory is unlikely to be built up in the next 3-4 months, as most OEMs are focussing on depleting BS-IV inventory ahead of the deadline (March 31, 2020). We believe dealers will enter FY21 with relatively lean levels of inventory. As end-demand (retails) recovers over the course of FY21, we expect wholesales to outpace retails, resulting in an even higher growth in reported volumes. Figure 16: Typical inventory cycle in downturns

Retails Wholesales Dealer inventory

Stage 1 weak > Retails increasing

Stage 2 weak = Retails stays high

Stage 3 weak < Retails reducing

Stage 4 flattish = Retails stays low

Stage 5 recovers > Retails increases to normal

Source: IIFL Research

Figure 17: Different stages of the inventory cycle

Source: IIFL Research

If end-demand holds up over the next 6-7 months, we may see high growth in reported wholesales in the Jul-Sep 2020 period, as companies would stock up before the festive season. The YoY base (Jul-Sep 2019) included inventory correction and no festive stocking-up and would offer a very easy comparable base.

0

20

40

60

80

100

120

140

160

180

Apr‐18

May‐18

Jun‐18

Jul‐18

Aug‐18

Sep‐18

Oct‐18

Nov‐18

Dec‐18

Jan‐19

Feb‐19

Mar‐19

Apr‐19

May‐19

Jun‐19

Jul‐19

Aug‐19

Sep‐19

Oct‐19

Nov‐19

Dec‐19

Jan‐20

Feb‐20

Mar‐20

Apr‐20

May‐20

Jun‐20

Jul‐20

Aug‐20

Sep‐20

Oct‐20

Nov‐20

Dec‐20

Retails Wholesales Inventory(Volumes)

Stage‐1 Stage‐2 Stage‐3 Stage‐4 Stage‐5

12

joseph.george@iif lcap.com

India - Auto

Maruti went through a sharp inventory-correction phase in Jul-Sep 2019, not necessarily in terms of number of units but by way of not filling-in inventory before the festive season (like it does every year). As a result, post the high-volume festive season, Maruti’s dealer inventory was lower compared with that at the end of the 2018 festive season. Figure 18: Maruti’s dealer inventory is lower on a YoY basis

Source: IIFL Research

CV players such as Ashok Leyland and Bharat Benz have reported much lower wholesales than retails in the past few months. As per our estimates, their dealer inventory would now be lower compared with the same time last year. Figure 19: Ashok Leyland’s dealer inventory has come down substantially

Source: IIFL Research

Figure 20: Bharat Benz corrected dealer inventory by a third in 1HFY20

Mar‐18 Jun‐18 Sep‐18 Dec‐18 Mar‐19 Jun‐19 Sep‐19

Bharat Benz Retail 5,759 5,534 4,946 5,270 4,469 4,053 3,548

Bharat Benz Wholesale

6,191 5,796 5,252 5,293 5,549 3,840 2,672

Bharat Benz Retail Growth

28% 70% 8% 9% ‐22% ‐27% ‐28%

Bharat Benz Wholesale Growth

66% 63% 8% 16% ‐10% ‐34% ‐49%

Source: Company, IIFL Research

0

50,000

100,000

150,000

200,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2018 2019(Dealer inventory)

0

4,000

8,000

12,000

16,000

Jun‐19 Jul‐19 Aug‐19 Sep‐19 Oct‐19 Nov‐19

(Dealer inventory)

13

joseph.george@iif lcap.com

India - Auto

Management commentary on inventory-level: Bajaj Auto – Rakesh Sharma (1-Nov-19) “I have not seen such low stock in the channel in the last 18 months.”

Hero MotoCorp – Sanjay Bhan (1-Nov-19) “Thanks to the record retail off-take, our inventory levels are now down to 30 days; this is lowest in the past 24 months”

Tata Motors – Mayank Pareek (1-Nov-19) “In this fiscal, network stock has been reduced by 38%. October end network stock is the lowest in last two years. This will help our network to be prepared for a smooth BS-VI transition.”

Tata Motors – Girish Wagh (25-Oct-19) “I think our stocks are now at a six quarter low and…”

SML Isuzu – Gopal Bansal (4-Dec-19) “The inventory level with the dealers is at the lowest, if you see the last four years data.”

Figure 21: We expect strong growth in wholesales, starting 2QFY21

Source: SIAM, IIFL Research

Seasonally adjusted annual rate (SAAR) shows bottoming out Monthly industry data reveals that SAAR for PVs and MHCVs bottomed out in Sep-2019, coinciding with the highest level of inventory correction. Since then, we have seen SAAR improve. In case of 2Ws, SAAR is still at lows and is yet to show an uptick. We believe 2W SAAR would bottom out sometime in the next six months. Figure 22: PV SAAR bottomed out in Aug‐Sep 2019

Source: IIFL Research

‐60%

‐40%

‐20%

0%

20%

40%

60%

1QFY19

2QFY19

3QFY19

4QFY19

1QFY20

2QFY20

3QFY20E

4QFY20E

1QFY21E

2QFY21E

3QFY21E

4QFY21E

PVs 2Ws MHCVs(YoY growth %)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

Apr‐18

May‐18

Jun‐18

Jul‐18

Aug‐18

Sep‐18

Oct‐18

Nov‐18

Dec‐18

Jan‐19

Feb‐19

Mar‐19

Apr‐19

May‐19

Jun‐19

Jul‐19

Aug‐19

Sep‐19

Oct‐19

Nov‐19

PV SAAR

14

joseph.george@iif lcap.com

India - Auto

Figure 23: MHCV SAAR bottomed out in Sep 2019

Source: IIFL Research

Figure 24: 2W SAAR is still at lows; yet to show up‐tick

Source: IIFL Research

0

100,000

200,000

300,000

400,000

500,000

Apr‐18

May‐18

Jun‐18

Jul‐18

Aug‐18

Sep‐18

Oct‐18

Nov‐18

Dec‐18

Jan‐19

Feb‐19

Mar‐19

Apr‐19

May‐19

Jun‐19

Jul‐19

Aug‐19

Sep‐19

Oct‐19

Nov‐19

MHCV SAAR

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

Apr‐18

May‐18

Jun‐18

Jul‐18

Aug‐18

Sep‐18

Oct‐18

Nov‐18

Dec‐18

Jan‐19

Feb‐19

Mar‐19

Apr‐19

May‐19

Jun‐19

Jul‐19

Aug‐19

Sep‐19

Oct‐19

Nov‐19

2W SAAR

15

joseph.george@iif lcap.com

India - Auto

BS-VI transition: Expect a volatile 1HCY20 We expect vehicle prices to go up by 10-15%, when the industry mandatorily shifts from BS-IV to BS-VI, starting April 2020. The price hikes would be lower for gasoline cars (1-3%) and premium cars/2Ws (5-10%). BS-VI is not applicable to tractors. Figure 25: Major BS‐VI product launches in the market so far

Auto segment Model name Launch date Price hike over BS‐IV

Petrol car Maruti Baleno Apr‐2019 ~2%

Petrol car Maruti Alto 800 Apr‐2019 2‐3%

Petrol car Maruti Swift Jun‐2019 ~2%

Petrol car Maruti Wagon‐R 1.2L Jun‐2019 2‐2.5%

Petrol car Maruti Dzire Jun‐2019 ~2%

Petrol car Maruti Ertiga Aug‐2019 ~1%

Petrol car Maruti Wagon‐R 1.0L Nov‐2019 1.5‐2%

Petrol SUV Mahindra XUV 300 Dec‐2019 ~2%

Executive MC Hero Splendor iSmart Nov‐2019 13%

Premium MC TVS Apache RTR 160 4V Nov‐2019 8%

Premium MC TVS Apache RTR 200 4V Nov‐2019 8%

Scooters Honda Activa 125 Sep‐2019 10‐13%

Scooters TVS Jupiter Classic Nov‐2019 13%

Source: Company, News articles, IIFL Research; Note: price hike % based on ex‐showroom price; MC= Motorcycle

We expect the next six months to see volatility in reported wholesale volumes. OEMs would try to clean up their channel-wide BS-IV inventory over the next 3 months. There is a possibility of ‘pre-buy’ of BS-IV vehicles in 1QCY20, ahead of the BS-VI price hikes. Post the transition, retail volumes may be weak in the first few months due to the price shock and also due to reversal of ‘pre-buy’. During this period, dealers may resist OEMs’ attempt to fill up BS-VI vehicle inventory. We also expect Ebitda margins to be volatile over this period due to i) inability to charge a margin on the BS-VI cost increase or in some cases, inability to fully pass on costs; and ii) negative operating leverage, if volumes are weak. Among segments, for which BS-VI is applicable, gasoline cars would be the most insulated, as this segment would see the lowest price increase. Focusing specifically on Maruti, impact on the gasoline segment would be even lower, as the company has already transitioned majority of its model to BS-VI. Its inventory of BS-IV petrol vehicles is very low and not at all concerning. Maruti may be affected to some extent by its decision to discontinue diesel variants upon transition to BS-VI. If Maruti is not able to switch all its potential diesel customers to gasoline, there may be loss of volumes. This aspect is addressed in the PV section. The % price impact for Eicher (Royal Enfield) would also be comparatively lower, given that it caters to the premium segment. Bajaj would be relatively insulated at the company-level, as 45% of its volumes are exported. That said, we do not expect these companies to charge margins on BS-VI costs, as they are also coming off a weak-demand environment.

16

joseph.george@iif lcap.com

India - Auto

We expect “gross profit per vehicle” to hold In our forecasts for OEMs, we build flattish “gross profit per vehicle” under BS-VI (FY21ii over FY20ii), implying that OEMs are able to pass on the cost increase but not charge a profit margin on the additional cost. In effect, this will bring down gross margin for most OEMs. Ebitda margin for OEMs would be a function of the operating leverage based on volume growth. Maruti would be least impacted, as it has already transitioned most of its gasoline models to BS-VI with limited price increases. An exception to this rule of thumb would be companies that have given out high discounts in FY20. Assuming demand scenario improves in FY21ii over FY20ii, we may see some gross profit benefit as these discounts come off. PV and CV players would benefit on this account. Figure 26: We forecast flattish “gross profit per vehicle” in 2Ws

OEMs FY21 vol.growth

FY21 rev growth

GM/vehicle (Rs) Ebitda margin

FY20ii FY21ii FY19 FY20ii FY21ii FY22ii

Hero 5% 17% 14,078 14,070 14.7% 14.0% 12.7% 13.1%

Bajaj 7% 12% 18,457 18,682 16.5% 15.9% 15.4% 15.7%

Eicher 8% 12% 59,525 59,792 29.6% 25.5% 24.5% 24.9%

TVS 8% 18% 13,047 13,216 7.9% 8.4% 8.0% 8.3%

M&M 2% 8% 190,283 194,392 14.2% 13.6% 13.2% 13.4%

Maruti 8% 9% 139,168 146,315 12.8% 10.3% 11.9% 13.0%

Ashok 6% 19% 421,118 444,254 10.8% 7.1% 7.1% 9.7%

Tata (S) 8% 19% 256,089 265,893 8.3% 5.2% 5.8% 8.4%

Source: IIFL Research

Ashok Leyland and TVS have high EPS sensitivity to margins In the event of OEMs not opting to pass on the full impact of BS-VI cost increases to customers, for fear of losing volumes and/or on account of competitive reasons, industry-level profitability may come off. In this case, companies with low margins would be more impacted. The EPS sensitivity of a 100bps drop in margins is highest for Ashok Leyland and TVS. Figure 27: Auto OEMs – EPS sensitivity to the 100bps change in Ebitda margin

FY21ii Ebitda margin PBT margin EPS Sensitivity

Hero MotoCorp 12.7% 12.6% 7.9%

Bajaj Auto 15.4% 19.5% 5.1%

Eicher Motors 24.5% 26.3% 3.8%

TVS Motor 8.0% 4.9% 20.2%

M&M 13.2% 11.0% 9.1%

Maruti Suzuki 11.9% 10.4% 9.6%

Ashok Leyland 7.1% 4.1% 24.5%

Tata Motors (S) 5.8% ‐2.2% NM

Source: IIFL Research

17

joseph.george@iif lcap.com

India - Auto

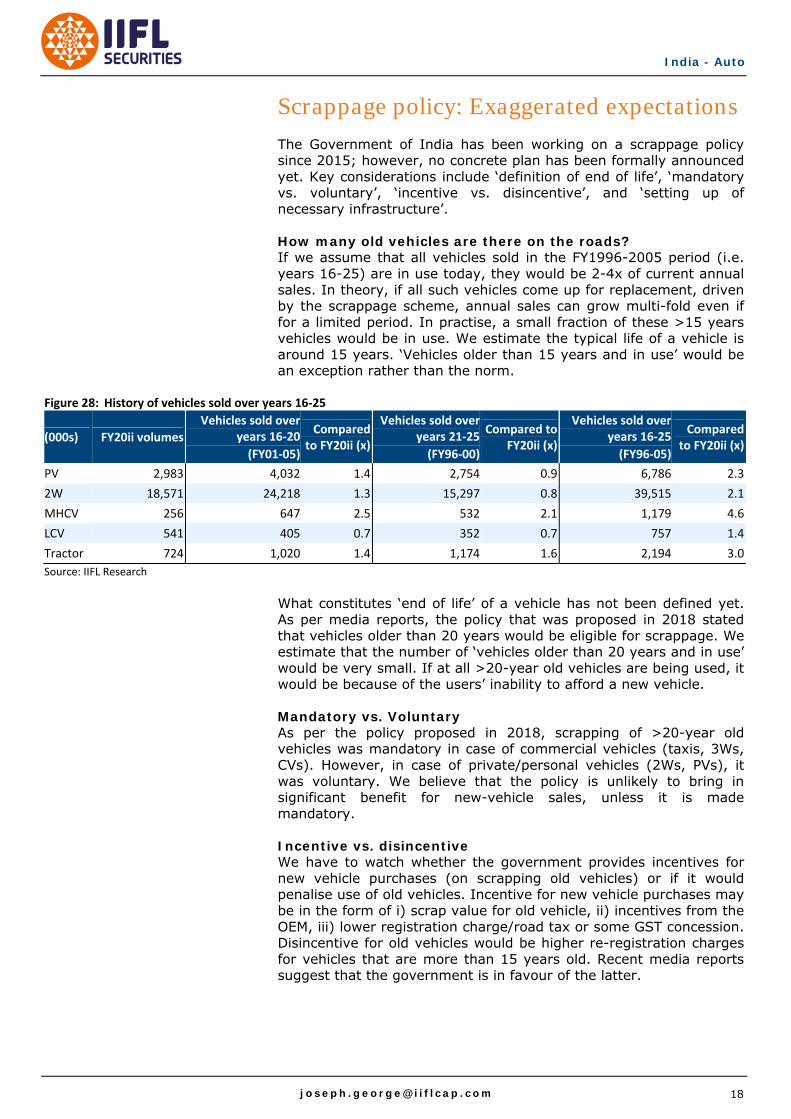

Scrappage policy: Exaggerated expectations The Government of India has been working on a scrappage policy since 2015; however, no concrete plan has been formally announced yet. Key considerations include ‘definition of end of life’, ‘mandatory vs. voluntary’, ‘incentive vs. disincentive’, and ‘setting up of necessary infrastructure’. How many old vehicles are there on the roads? If we assume that all vehicles sold in the FY1996-2005 period (i.e. years 16-25) are in use today, they would be 2-4x of current annual sales. In theory, if all such vehicles come up for replacement, driven by the scrappage scheme, annual sales can grow multi-fold even if for a limited period. In practise, a small fraction of these >15 years vehicles would be in use. We estimate the typical life of a vehicle is around 15 years. ‘Vehicles older than 15 years and in use’ would be an exception rather than the norm.

Figure 28: History of vehicles sold over years 16‐25

(000s) FY20ii volumes

Vehicles sold over years 16‐20

(FY01‐05)

Compared to FY20ii (x)

Vehicles sold over years 21‐25

(FY96‐00)

Compared to FY20ii (x)

Vehicles sold over years 16‐25

(FY96‐05)

Compared to FY20ii (x)

PV 2,983 4,032 1.4 2,754 0.9 6,786 2.3

2W 18,571 24,218 1.3 15,297 0.8 39,515 2.1

MHCV 256 647 2.5 532 2.1 1,179 4.6

LCV 541 405 0.7 352 0.7 757 1.4

Tractor 724 1,020 1.4 1,174 1.6 2,194 3.0

Source: IIFL Research

What constitutes ‘end of life’ of a vehicle has not been defined yet. As per media reports, the policy that was proposed in 2018 stated that vehicles older than 20 years would be eligible for scrappage. We estimate that the number of ‘vehicles older than 20 years and in use’ would be very small. If at all >20-year old vehicles are being used, it would be because of the users’ inability to afford a new vehicle. Mandatory vs. Voluntary As per the policy proposed in 2018, scrapping of >20-year old vehicles was mandatory in case of commercial vehicles (taxis, 3Ws, CVs). However, in case of private/personal vehicles (2Ws, PVs), it was voluntary. We believe that the policy is unlikely to bring in significant benefit for new-vehicle sales, unless it is made mandatory. Incentive vs. disincentive We have to watch whether the government provides incentives for new vehicle purchases (on scrapping old vehicles) or if it would penalise use of old vehicles. Incentive for new vehicle purchases may be in the form of i) scrap value for old vehicle, ii) incentives from the OEM, iii) lower registration charge/road tax or some GST concession. Disincentive for old vehicles would be higher re-registration charges for vehicles that are more than 15 years old. Recent media reports suggest that the government is in favour of the latter.

18

joseph.george@iif lcap.com

India - Auto

Scrappage infrastructure Incentives for scrapping old vehicles and being redeemable against new vehicle purchases would be based on scrappage certificates issued by authorised ‘vehicle scrappage facilities’. Currently, there is only one organised vehicle-scrappage facility. This facility is Cero Recycling, a JV between Mahindra Group and government-owned Metal Scrap Trading Corporation (MSTC) and is based in Greater Noida in the NCR region. Recently, Maruti Suzuki and the Toyota Tsusho Group announced plans to set up a vehicle dismantling & recycling joint venture ‘Maruti Suzuki Toyotsu India’ (MSTI). This unit would be based in Noida and may be commissioned in FY21. Figure 29: Organised vehicle scrappage facilities Entity name Operational from Monthly capacity Annual capacity

Cero Recycling Apr'18 500 vehicles 6,000 vehicles

MSTI FY21 2,000 vehicles 24,000 vehicles

Source: Company, IIFL Research

As is evident (Figure 29), the existing vehicle scrappage capacity is miniscule. In order for scrappage policy to result in even a 10% benefit to new vehicle sales, we need a 15x jump in annual scrappage capacity. There are several small and informal scrappage units in the country. But these are not authorised, nor would they meet the criteria set out by the government for being eligible to issue “scrappage certificates”. The draft scrappage policy put out by the government includes criteria such as “minimum useable treatment area of 4,000sq-mtr for 2Ws/3Ws and 8,000sq-mtr for all other vehicle types (PVs, LCVs, MHCVs, others). Figure 30: Need a 15x jump in ‘vehicle scrappage facilities’ for a 10% volume uplift

Segment Requisite annual scrappage capacity

PV 300,000

MHCV 25,000

LCV 55,000

Tractor 75,000

Total 455,000

Source: IIFL Research

Moreover, Cero recycling (Mahindra JV) and MSTI (Maruti JV) are both based in Noida. For the policy to be effective, a network of scrappage facilities across the country is required. Surely a vehicle based in Mumbai cannot be expected to be driven to Noida for being scrapped. In effect, the probability of the scrappage policy driving replacement demand in FY21 or FY22 is low. The only minor driver, if at all, would be the disincentive of higher re-registration charges on >15-year old vehicles.

19

joseph.george@iif lcap.com

India - Auto

PV segment: Least impacted by BS-VI Consumer spending on PVs (FY20ii) in terms of ‘share of wallet’ is at a 17-year low and 20% below its long-term average. We expect PVs’ wallet share to rebound to the 15-year average over the next three years, as overall GDP growth picks up and other cyclical impediments highlighted earlier recede. Figure 31: We expect PVs’ ‘share of wallet’ to normalise over FY21‐23ii

Source: IIFL Research

As per our estimate, the average on-road ASP would go up by 6% in FY20ii and a further 6% in FY21ii. The ASP increase in FY20ii includes the impact of higher insurance costs, safety norms, BS-VI launches and mix. In FY21ii, it would be driven by BS-VI, partly offset by mix. The price impact would moderate in FY22ii. On a base of 12% volume decline in FY20ii, we forecast an 11% volume Cagr over the next three years. Share of diesel in the industry to come off As price of diesel vehicles would go up significantly (10% or more) vs. that of petrol (1-3%), we expect diesel’s share in the industry to come off substantially. This may not possibly stand true for higher-end cars and large SUVs. Figure 32: We expect share of diesel to fall sharply

Source: IIFL Research

Currently, the difference between on-road prices of comparable diesel and petrol variants is about Rs110,000. Post BS-VI, the price difference would rise to around Rs200,000. Currently, a car-buyer

2.00%

2.25%

2.50%

2.75%

3.00%

3.25%

3.50%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

FY23ii

Spend on PVs as % of pvt. consumption GDP

15‐yr average

0%

10%

20%

30%

40%

50%

60%

70%

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

Diesel share in industry (%)

20

joseph.george@iif lcap.com

India - Auto

would need to drive about 15,000km per annum for fuel savings, to offset the upfront higher cost of diesel cars. This break-even point would rise to about 25,000km under BS-VI. Since personal users of cars do not drive so many kilometres in a year, purchasing diesel cars may not make economic sense. However, taxi/commercial buyers may still find diesel more economical. Figure 33: Break‐even for diesel cars to increase to 25,000km per annum

Source: IIFL Research

Competitive intensity benign; many OEMs losing relevance Over the past few years, many multi-national brands have lost relevance in India. GM and Fiat are not selling cars in India anymore. Ford recently sold a majority stake in its India operations to Mahindra. VW, Skoda and Nissan have been continuously losing share and are now at 1% or lower, in terms of market-share. Mahindra, Tata Motors and Honda are also losing share. The only serious competition for Maruti seems to be from Hyundai and the new entrant Kia. Figure 34: Many OEMs losing relevance; Kia is the only new one to watch

OEM FY15 FY16 FY17 FY18 FY19 FY20YTD

Maruti 45% 47% 47% 50% 51% 50%

Hyundai 16% 17% 17% 16% 16% 18%

Mahindra 9% 8% 8% 8% 8% 7%

Tata Motors 6% 5% 6% 6% 7% 5%

Toyota 5% 5% 5% 4% 4% 4%

Honda 7% 7% 5% 5% 5% 4%

Renault 2% 3% 4% 3% 2% 3%

Ford 3% 3% 3% 3% 3% 3%

Volkswagen 2% 1% 2% 1% 1% 1%

Nissan 2% 1% 2% 2% 1% 1%

Kia 2%

Others 3% 2% 2% 1% 1% 2%

Total 100% 100% 100% 100% 100% 100%

Source: SIAM, IIFL Research

Maruti’s reported market-share may come off slightly We see slight risk to Maruti’s reported market-share due to three reasons: - Decision to exit the <1.3L diesel segment - Growing SUV market, where Maruti has a relatively lesser presence - Cross-badging arrangement with Toyota

0

5,000

10,000

15,000

20,000

25,000

30,000

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

Minimum annual mileage for Diesel car to make economic sense(kms)

21

joseph.george@iif lcap.com

India - Auto

Exit from the <1.3L diesel segment Maruti plans to discontinue diesel vehicles, up to 1.3L engine capacity. This is due to sharp increase in prices of diesel vehicles to make them BS-VI compliant, which may make them unaffordable for prospective buyers. While some of Maruti’s peers have announced a similar decision, others have not. This is where the market-share risk for Maruti emerges. Figure 35: Diesel contributes about 20% to Maruti’s domestic PV volumes

Source: Company, IIFL Research

Diesel currently accounts for about 22% of Maruti’s domestic PV volumes. If Maruti is able to switch all its potential diesel customers to gasoline, there may not be any loss of volumes or market-share. However, there may be some drop-outs: i) Taxi/commercial buyers may still find diesel more economical. ii) Some buyers may prefer driving diesel cars because they enjoy it, even if it does not make economic sense. iii) SUV buyers typically prefer diesel over gasoline. Maruti has not ruled out the possibility of launching BS-VI compliant diesel engines of >1.3L capacity. Media reports suggest that Maruti is planning to launch a BS-VI compliant 1.6L diesel engine in some of its models (Ciaz, S-Cross, Ertiga, XL6). If true, Maruti may be able to offset some of the market-share risk. Growing SUV segment UVs’ contribution to the PV industry has increased, from 28% in FY19 to 34% in FY20 YTD. In the last 3-4 months, it has been as high as 36%. In FY20 YTD, Maruti’s market-share in PV (ex-UV) stood at 63%. This has been rising over the years. However, in the SUV segment, its market-share is relatively lower, at about 25%. There is a risk to Maruti’s UV market-share, due to new launches from competition as well as its decision to exit the diesel segment. On an overall basis, given the sharp rise in UVs’ contribution to the industry, Maruti’s overall market-share may come off a bit.

0%

5%

10%

15%

20%

25%

30%

35%

40%

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

Diesel contribution to Maruti volumes (%)

22

joseph.george@iif lcap.com

India - Auto

Figure 36: Rising UV mix in industry may slightly hurt Maruti’s market share

Source: SIAM, IIFL Research

Cross-badging arrangement with Toyota Maruti is currently supplying the re-badged Baleno to Toyota, as per the agreement announced in March 2018. Toyota sells it under the brand-name Glanza. Maruti would supply the re-badged Vitara Brezza to Toyota under the same agreement as well as the re-badged Ciaz and Ertiga, as per the announcement in March 2019. To the extent that the aforementioned Toyota-branded sales cannibalise Maruti’s sales of the same model, Maruti’s reported market-share (credited to the OEM making final sale) would be lower. That said, these Toyota-badged volumes do form part of Maruti’s P&L and it makes manufacturing margins on sales to Toyota. Figure 37: Maruti Baleno and Toyota Glanza −Monthly sales

Source: SIAM, IIFL Research

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

10%

20%

30%

40%

50%

60%

70%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20ytd

UV industry contribution (RHS) OverallUVs Cars/Vans

(Maruti's mkt share)

0

5,000

10,000

15,000

20,000

25,000

Apr‐18

May‐18

Jun‐18

Jul‐18

Aug‐18

Sep‐18

Oct‐18

Nov‐18

Dec‐18

Jan‐19

Feb‐19

Mar‐19

Apr‐19

May‐19

Jun‐19

Jul‐19

Aug‐19

Sep‐19

Oct‐19

Nov‐19

Maruti Baleno Toyota Glanza(volumes)

23

joseph.george@iif lcap.com

India - Auto

2W segment: BS-VI may hurt in near-term Consumer spending on 2Ws (FY20ii) in terms of ‘share of wallet’ is at a 10-year low and 15% below its long-term average. As in the case of PVs, we expect 2Ws’ wallet share to rebound to the 15-year average over the next three years. Figure 38: We expect 2Ws’ ‘share of wallet’ to normalise over FY21‐23ii

Source: IIFL Research

As per our estimate, the average on-road ASP would go up by 11% in FY21ii, primarily due to the BS-VI transition. The rate of price hikes may be lower in premium 2Ws and higher in low-end segments. This may hurt affordability in the near-term; more so, if there is an element of pre-buy in 4QFY20. We expect retail volumes to stay subdued in 1HFY21. However, wholesales should show YoY growth starting 2QFY21 (inventory correction in 2QFY20). We forecast a 5% volume growth in FY21ii, followed by a sharper 11% growth in FY22ii. Competitive intensity high, but stable The competitive intensity in the industry is high, but largely stable. The four largest players (Hero, Honda, TVS and Bajaj) together hold close to 90% market-share in overall 2Ws. Figure 39: Market‐share movement over FY18‐20ii

2W segments Hero Bajaj HMSI TVS

Scooters ↓ ↔ ↑

Economy motorcycle ↓ ↑ ↔

Executive motorcycle ↑ ↓ ↑ ↓

Premium motorcycle ↓ ↑ ↓ ↑

Overall motorcycle ↔ ↑ ↔ ↔

Overall 2Ws ↓ ↑ ↓ ↔

Source: IIFL Research

Bajaj embarked on a price-led strategy starting early 2018, with price cuts in CT100 and Pulsar. This strategy helped Bajaj gain market-share in the economy segment. Bajaj’s overall motorcycle market-share improved from 15.6% in FY18 to 20% in 2HFY19. Since then, volumes of the CT100 model came off substantially, leading to some moderation in Bajaj’s motorcycle market-share, coming back to about 18% in 1HFY20. Recently, Bajaj launched a 125cc variant of its premium Pulsar model. This has been well

0.80%

0.90%

1.00%

1.10%

1.20%

1.30%

1.40%

1.50%

1.60%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

FY23ii

Spend on 2Ws as % of pvt. consumption GDP

15‐yr average

24

joseph.george@iif lcap.com

India - Auto

received in the market and has helped some market-share revival in recent months. Figure 40: Four players account for almost 90% of the 2W market‐share

Source: SIAM, IIFL Research

In the last two years, the result of the fight for the No.2 position in scooter (behind Honda) is out, with TVS emerging as a clear winner vs. Hero. Figure 41: Scooters − Honda continues to dominate

Source: SIAM, IIFL Research

Bajaj’s price-led strategy has helped it gain share in motorcycles. Figure 42: Overall Motorcycles − Hero steady at ~50%; Bajaj made gains

Source: SIAM, IIFL Research

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY16 FY17 FY18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20E

Hero Bajaj HMSI TVS(Overall 2Ws)

0%

10%

20%

30%

40%

50%

60%

70%

FY16 FY17 FY18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20E

Hero HMSI TVS(Scooters)

0%

10%

20%

30%

40%

50%

60%

FY16 FY17 FY18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20E

Hero Bajaj HMSI TVS RE(Motorcycles)

25

joseph.george@iif lcap.com

India - Auto

Bajaj’s price-led strategy brought temporary market-share gains in economy segment; it has since moderated.

Figure 43: Economy motorcycles − Bajaj’s CT100‐led gain was temporary

Source: IIFL Research

Hero continues to dominate the executive segment, although Honda has made gains in recent quarters.

Figure 44: Executive motorcycles − Hero continues to dominate

Source: IIFL Research

Lower-priced Pulsar variants has helped Bajaj gain share in the premium segment.

Figure 45: Premium motorcycles − Bajaj remains the leader

Source: IIFL Research

0%

10%

20%

30%

40%

50%

60%

70%

FY16 FY17 FY18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20

Hero Bajaj TVS(Economy MC)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

FY16 FY17 FY18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20

Hero Bajaj HMSI TVS(Executive MC)

0%

5%

10%

15%

20%

25%

30%

35%

40%

FY16 FY17 FY18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20

Hero Bajaj HMSI TVS RE(Premium MC)

26

joseph.george@iif lcap.com

India - Auto

FY21: Who gains; Who loses Which OEMs win and which lose will be a function of a few factors: Overall state of the economy and hence, segmental shifts within 2Ws Rural vs. Urban: A sharper recovery in rural markets would benefit motorcycles more than scooters. This would benefit Hero more than others. Income growth: If per-capita income growth is low in FY21, as it was in FY20, we may see down-trading within 2Ws, especially given the sharp increase in vehicle prices. This may benefit Hero and Bajaj more than others, from a volume perspective. Between the two, it would benefit Hero more from an earnings perspective, as Bajaj does not make significant margins on the CT100. Successful adoption of BS-VI technology BS-VI technology adoption would result in material changes to the engine. As of now, we are not in a position to judge whether any OEM would face technological glitches in its BS-VI products. However, this is a factor that we would watch closely. In 2Ws, models competing within a segment are fairly similar to each other. Hence, any product glitches may result in substantial migration to competing products. Type of BS-VI technology – e-Carburetor vs. Electronic Fuel injection (EFI) Our assumption of 11% average ASP increase is based on all OEMs adopting the EFI under BS-VI. We believe that OEMs would stick to EFI for the premium and executive segments. However, at the low end of the spectrum, there is a possibility that OEMs may opt for e-Carburetor over EFI, as the former is much cheaper. Although EFI is more expensive, it boasts of higher fuel efficiency. If OEMs successfully integrate the e-Carburetor option, it may give them a price advantage over competition in the segment. Our market-share projections We have largely maintained our market-share projections for FY21ii and FY22ii at similar levels as FY20ii. As a result, our domestic 2W volume growth projections are largely similar across Hero, Bajaj and TVS. Figure 46: 2W market‐share projections

FY19 FY20ii FY21ii FY22ii

Hero 35.9% 35.1% 35.2% 35.2%

Bajaj 12.0% 12.4% 12.5% 12.5%

TVS 14.8% 14.3% 14.5% 14.5%

Source: SIAM, IIFL Research

27

joseph.george@iif lcap.com

India - Auto

MHCVs: Expect YoY growth from 2QFY21 The MHCV segment continues to see sharp YoY decline in volumes at both the wholesale and retail levels. Wholesales have been underperforming retails in recent months, as OEMs have been in sharp inventory correction mode. We believe that a large part of the inventory correction is behind us. Going forward, wholesales may at least track retails. If demand improves, we may see re-stocking, implying higher growth in wholesales. We expect wholesales to start growing slightly earlier in 2QFY21, as there is a sharp inventory correction in the YoY base (2QFY20). Retails may continue to decline YoY till 2QFY21, especially with the sharp 12-15% price hike scheduled in April 2020 (BS-VI). By the end of 1HFY21, the MHCV segment would have seen almost two years of YoY declines. Post that, we expect retails to also start growing. In the previous two down-cycles, MHCV volumes on a TTM basis had fallen 42% and 44% from the peak, over a period of 15 months and 29 months respectively. This time, we forecast TTM volumes to trough at 235k in June 2020, a 42% decline vs. peak of 407k in Oct 2018. We forecast a 35% decline in overall MHCV volumes in FY20ii, with trucks declining 37% and buses down 9%. In FY21ii, we forecast a 5% volume growth in overall MHCVs. This is split into a 29% decline in 1Q, followed by 19% YoY growth in the last three quarters. We expect the momentum to continue into FY22ii, with a 20% volume growth. We have also seen a sharp fall in tonnage mix. The 37% decline in truck volumes that we are accounting for in FY20ii comes with a 44% decline in tonnage. We believe that when the cycle recovers, the tonnage growth would be much higher than volume growth. This should translate into much higher revenue growth for CV companies. Figure 47: We expect MHCV to start growing YoY in 2QFY21

Source: IIFL Research

There are multiple reasons for the sharp down-cycle in MHCVs: i) Weak GDP/IIP growth ii) Increase in system-wide tonnage post change in axle load norms iii) Availability of financing; lower loan to value ratio

0

100,000

200,000

300,000

400,000

500,000

Mar‐95

Mar‐96

Mar‐97

Mar‐98

Mar‐99

Mar‐00

Mar‐01

Mar‐02

Mar‐03

Mar‐04

Mar‐05

Mar‐06

Mar‐07

Mar‐08

Mar‐09

Mar‐10

Mar‐11

Mar‐12

Mar‐13

Mar‐14

Mar‐15

Mar‐16

Mar‐17

Mar‐18

Mar‐19

Mar‐20

Mar‐21

MHCV volumes(TTM Volumes)

53% fall over 18 months

42% fall over 15 months

44% fall over 29 months

42% fall over 21 months

28

joseph.george@iif lcap.com

India - Auto

Weak GDP/IIP growth MHCV truck sales have a high correlation to IIP growth (Index of Industrial Production). In the past few quarters, we have seen a sharp deceleration in IIP growth, even turning negative during Aug-Sep 2019. Lower industrial production obviously results in lower freight generation in the economy, which in turn impacts demand for trucks, fleet utilisation and profitability. Needless to say, the recovery that we are building in the MHCV cycle is dependent on the Indian economy recovering in FY21. If overall GDP and IIP remain weak, the downturn may continue longer than our expectations. Figure 48: Truck sales vs. IIP growth

Source: SIAM, CEIC, IIFL Research

Change in axle load norms In July 2018, the Ministry of Road Transport and Highways had increased the maximum permissible axle loads and hence truck tonnage by about 15%. Although strict interpretation of the notification applied to new trucks, it was also made applicable to the existing fleet. Figure 49: Change in Maximum Permissible Load per truck

Max load per truck Old tonnage Revised tonnage Change

Rigid 16.2 19.0 17%

Rigid 25.0 28.5 14%

Rigid 31.0 36.0 16%

Semi‐articulated 26.4 30.5 16%

Semi‐articulated 35.2 40.0 14%

Semi‐articulated 40.2 46.0 14%

Semi‐articulated 35.2 40.0 14%

Semi‐articulated 44.0 49.5 13%

Tractor trailer 36.6 42.0 15%

Tractor trailer 44.0 51.5 17%

Tractor trailer 44.0 55.0 25%

Tractor trailer 49.0 55.0 12%

Average increase 15%

Source: Government Notifications, IIFL Research

Our understanding is that ~60% of the truck usage is volume-based (implying nil scope for increasing loads). If we assume that the remaining 40% did not indulge in any over-loading before this

0%

2%

4%

6%

8%

10%

12%

14%

16%

‐60%

‐40%

‐20%

0%

20%

40%

60%

FY86

FY87

FY88

FY89

FY90

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20E

MHCV truck growth (LHS) IIP growth (RHS)(YoY %)

29

joseph.george@iif lcap.com

India - Auto

notification (difficult to believe), a 15% tonnage increase in 40% of the fleet would imply a 6% increase in system wide tonnage. Figure 50: Impact of axle load norm change on fleet

Current truck fleet (%)

Current truck fleet (volume)

Impact of revised norms

Comments

Volume‐based 60% 1,800,000 0 No impact

Weight‐based

(no overloading) 40% 1,200,000 180,000

15% higher tonnage availability

Sum 100% 3,000,000 180,000

Impact on fleet +6%

Source: IIFL Research

On a reported basis, the system-wide tonnage would increase only by about 2% in FY20ii, after growing at 9% in FY19. This is the lowest tonnage growth logged since FY01. If we adjust the growth in system-wide tonnage for the new axle load norms, the growth rates for FY19 and FY20ii would be 12% and 5% respectively. Since the new norms came mid-way in FY19, we estimate a 3% impact each on FY19 and FY20ii annual tonnage growth. Figure 51: System‐wide tonnage growth rate has fallen sharply in FY20ii

Source: IIFL Research

We believe that the additional tonnage generated from the changed norms would surely have been absorbed by the system, by mid-CY20 (almost two years from the date of announcement). Lack of financing Since almost all truck purchases are financed, constraints on finance availability has been a key cause for fall in truck sales. We understand that the financing situation has started easing.

7%

9%10%

14%

10% 10% 10%

9%

2%

12%

5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

FY86

FY87

FY88

FY89

FY90

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20E

Growth in system‐wide tonnage Axle‐norm change impact

30

joseph.george@iif lcap.com

India - Auto

Margins typically recover with volumes In autos, margin typically is a function of volumes/demand. After all, pricing power, promotions, operating leverage are all impacted by demand. The factor that complicates matters is the sharp price increases with adoption of BS-VI. We expect margins to bottom out in the Jun-2020 quarter. As highlighted earlier, gasoline PVs are unlikely to be impacted, as the price increase on account of BS-VI would be low. We forecast lower gross margin for 2W players, as we are not building-in any profit margin on the additional BS-VI cost. In case of PVs, fall in discounts (from FY20 high) would more than offset the gross margin impact due to BS-VI. In case of PVs, gross margin expansion would flow through to the Ebitda margin as well. In case of CVs, lower discounts would partly offset the BS-VI impact. We expect slight Ebitda margin improvement in FY21ii, due to the high fixed cost structure. For 2Ws, we expect gross margin contraction to flow through to the Ebitda margin level as well. Fixed cost as a % of revenue is relatively low for 2Ws. Figure 52: BS‐VI cost increase may hurt reported margins

FY21ii vs. FY20ii Gross margin Ebitda margin

Hero MotoCorp ↓ ↓

Bajaj Auto ↓ ↓

Eicher Motors (S) ↓ ↓

TVS Motor ↓ ↓

Maruti Suzuki ↑ ↑

M&M ↓ ↓

Ashok Leyland ↓ ↔

Tata Motors (S) ↓ ↑

Source: IIFL Research

Commodities: Lower steel prices to aid margins In recent quarters, prices of key inputs such as steel and aluminum have come off from their highs. The benefit of fall in aluminum price (more relevant for 2Ws) is visible in 2Q results. However, benefit of fall in steel price would be visible from 3QFY20. Figure 53: Price of key inputs (Steel, Al) have sizeably come off from the FY19 highs

Source: Bloomberg, IIFL Research

60,000

80,000

100,000

120,000

140,000

160,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

2QFY17

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

4QFY18

1QFY19

2QFY19

3QFY19

4QFY19

1QFY20

2QFY20

Curren

t

Steel (Rs/MT) ‐ LHS Aluminium (Rs/MT) ‐ RHS

31

joseph.george@iif lcap.com

India - Auto

Figure 54: Key commodities and currencies – Quarterly trend

3QFY18 4QFY18 1QFY19 2QFY19 3QFY19 4QFY19 1QFY20 2QFY20 3QFY20* Current

Commodities

Steel (Rs/MT) 39,331 44,250 45,835 45,673 45,507 41,933 41,277 36,400 34,675 35,750

QoQ chg 3.1% 12.5% 3.6% ‐0.4% ‐0.4% ‐7.9% ‐1.6% ‐11.8% ‐4.3% 3.1%

Aluminium (Rs/MT) 136,832 138,195 151,347 144,173 141,118 131,447 124,435 124,027 125,051 126,338

QoQ chg 5.9% 1.0% 9.5% ‐4.7% ‐2.1% ‐6.9% ‐5.3% ‐0.3% 0.8% 1.0%

Rubber (Rs per quintal) 12,926 12,525 12,367 13,072 12,363 12,564 13,827 14,240 12,592 13,200

QoQ chg ‐2.5% ‐3.1% ‐1.3% 5.7% ‐5.4% 1.6% 10.1% 3.0% ‐11.6% 4.8%

Brent crude (USD/bbl) 61.6 67.2 74.9 75.9 68.1 63.8 68.5 62.0 61.5 63.9

QoQ chg 18.2% 9.1% 11.4% 1.4% ‐10.4% ‐6.2% 7.3% ‐9.5% ‐0.7% 3.9%

Lead (Rs/MT) 160,936 162,016 159,556 146,939 141,936 143,657 130,838 142,999 147,741 134,084

QoQ chg 7.5% 0.7% ‐1.5% ‐7.9% ‐3.4% 1.2% ‐8.9% 9.3% 3.3% ‐9.2%

Copper (Rs/MT) 442,076 447,729 460,635 429,471 444,182 438,634 425,254 408,465 415,065 429,987

QoQ chg 8.4% 1.3% 2.9% ‐6.8% 3.4% ‐1.2% ‐3.1% ‐3.9% 1.6% 3.6%

Currencies

USD‐INR 64.72 64.37 66.99 70.14 72.02 70.50 69.56 70.37 71.25 70.84

QoQ chg 0.7% ‐0.5% 4.1% 4.7% 2.7% ‐2.1% ‐1.3% 1.2% 1.3% ‐0.6%

JPY‐INR 0.57 0.59 0.61 0.63 0.64 0.64 0.63 0.66 0.66 0.65

QoQ chg ‐1.1% 3.8% 3.2% 2.5% 1.6% 0.2% ‐1.1% 3.6% 0.1% ‐0.8%

Source: Bloomberg, IIFL Research; *Note: 3QFY20 average based on the quarter‐to‐date data

Currency The impact from currency depends on whether the OEM is a net importer or exporter. Bajaj and TVS being net exporters would benefit in the event of Rupee depreciation. Maruti and Hero have relatively higher import content (including imports by vendors) and hence would be adversely impacted in the event of Rupee depreciation. Figure 55: Currency − Sensitivity of margin and EPS

OEMs Export vol.

share ~Imports (as

% of revs)

Impact of 5% Rupee depreciation*

on Ebitda margin on EPS

Hero MotoCorp 3% 12% (45) bps ‐4%

Bajaj Auto 46% 3% 213 bps 11%

Eicher Motors 6% 4% 8 bps 0%

TVS Motor 25% 10% 77 bps 15%

Maruti Suzuki 7% 20% (67) bps ‐6%

M&M 6% 2% 21 bps 2%

Ashok Leyland 8% 3% 24 bps 6%

Tata Motors (S) 8% 5% 15 bps NM

Source: IIFL Research; * Note: theoretical, assuming no price adjustments

BS-VI costs As highlighted in the BS-VI section, we forecast flattish gross profit per vehicle, assuming that OEMs would not be in a position to charge a profit margin on the incremental costs. Operating leverage Operating leverage from lower volumes/capacity utilisation hurt margins in FY20ii. We expect this to reverse over FY21-22ii. The apparent operating leverage in FY21ii would be higher, as the revenue line would be bloated due to BS-VI price increase.

32

joseph.george@iif lcap.com

India - Auto

Figure 56: Fixed cost (as % of revenue) to come off across OEMs from FY20 highs

OEMs FY15 FY16 FY17 FY18 FY19 FY20ii FY21ii FY22ii

Hero MotoCorp 16.9% 17.4% 18.7% 17.6% 17.8% 20.2% 17.9% 17.8%

Bajaj Auto 13.2% 13.5% 13.9% 13.0% 12.3% 13.6% 13.2% 13.2%

Eicher Motors (S) 17.8% 18.9% 18.2% 18.8% 21.3% 23.5% 23.2% 22.6%

TVS Motor 22.8% 23.0% 22.4% 21.1% 18.3% 20.6% 19.1% 19.0%

Maruti Suzuki 21.5% 22.2% 19.9% 19.4% 20.7% 22.6% 22.3% 21.5%

M&M 20.9% 21.5% 23.3% 22.1% 21.4% 23.8% 23.3% 23.3%

Ashok Leyland 22.0% 21.0% 22.3% 20.7% 20.2% 25.9% 23.5% 22.0%

Tata Motors (S) 35.2% 30.6% 33.1% 27.0% 23.9% 29.5% 26.5% 24.8%

Source: Company, IIFL Research; Note: Fixed costs include depreciation

Figure 57: Recovery in volumes to drive up margins (operating leverage)

Source: IIFL Research

Lower discounts to aid margins in cars, CVs In case of PVs, discount as a % of ASP is currently at 6-7% vs. 3-4% during periods of good demand. In case of MHCVs, discounts are currently at 10-15% of ASP. Lower discounts would provide a margin kicker when the demand scenario improves. Figure 58: Maruti’s discount trend – Currently at a multi‐year high

Source: Company, IIFL Research

2.4%

0.5% 0.8%1.6%

1.0%0.4%

4.0%4.7%

0%

1%

2%

3%

4%

5%

Hero Bajaj Eicher TVS Maruti M&M Ashok Tamo (S)

Ebit margin benefit due to op. leverage over FY20‐22ii

0%

1%

2%

3%

4%

5%

6%

7%

0

5,000

10,000

15,000

20,000

25,000

30,000

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

1QFY20

1QFY20

Discounts per vehicle (Rs) ‐ LHS as % of ASP ‐ RHS

33

joseph.george@iif lcap.com

India - Auto

Valuations to remain elevated The auto sector has seen a significant re-rating in the last five years. Valuation multiples in the past five years has been much higher than the 2010-2011 period, despite the fact that the volume growth in recent years has not been able to match the highs of FY10-11. Maruti, Eicher and TVS have seen a sharp re-rating. Figure 59: Maruti, Eicher and TVS have seen a sharp re‐rating

1‐year forward P/E CY10‐14 avg. CY15‐19 avg. Re‐rating

Hero MotoCorp 12.6 15.5 23%

Bajaj Auto 12.8 16.8 31%

Eicher Motors 17.1 29.8 74%

TVS Motor 10.6 26.2 148%

Maruti Suzuki 14.4 22.7 57%

M&M 14.1 18.0 27%

Source: Bloomberg, IIFL Research

Valuation multiples may expand during period of volume/earnings recovery. After almost two weak years (2HFY19-1QFY21), we expect volume growth to pick over the course of FY21. This should drive a re-rating in cheaper names, while in case of already expensive ones, valuations should, at least, hold.

Figure 60: Auto sector volume growth across cycles

Segments FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20ii FY21ii FY22ii

PVs 28 18 8 21 12 0 26 29 4 3 ‐7 4 7 9 8 3 ‐12 10 12

2Ws 12 16 14 12 ‐8 3 26 26 14 3 7 8 3 7 15 5 ‐12 5 11

3Ws 21 10 17 12 ‐10 ‐4 26 19 ‐2 5 ‐11 11 1 ‐5 24 10 ‐2 0 0

MHCVs 39 23 5 33 0 ‐33 33 32 8 ‐23 ‐25 16 30 0 13 15 ‐35 5 20

LCVs 31 22 20 34 12 ‐7 43 23 30 14 ‐18 ‐12 0 8 25 19 ‐12 3 12

Tractors 12 32 14 19 ‐4 1 32 20 11 ‐2 20 ‐13 ‐10 18 22 10 ‐8 5 5

*Avg. 24 20 13 22 0 ‐7 31 25 11 0 ‐6 2 5 6 18 10 ‐14 5 10

Source: SIAM, Crisil, IIFL Research; *Note: Avg. is a simple average of all segments

Figure 61: We expect sharp improvement in industry Ebitda over FY21‐22ii

Source: IIFL Research

‐40%

‐20%

0%

20%

40%

60%

80%

100%

120%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20ii

FY21ii

FY22ii

Sector aggregate Ebitda ‐ YoY growth

34

joseph.george@iif lcap.com

India - Auto

One-year forward P/E valuation charts

Figure 62: Hero MotoCorp Figure 63: Bajaj Auto

Source: Bloomberg, IIFL Research Source: Bloomberg, IIFL Research

Figure 64: Eicher Motors Figure 65: TVS Motor

Source: Bloomberg, IIFL Research Source: Bloomberg, IIFL Research

Figure 66: Maruti Suzuki Figure 67: M&M

Source: Bloomberg, IIFL Research Source: Bloomberg, IIFL Research

6

8

10

12

14

16

18

20

22

Jun‐08

Dec‐08

Jun‐09

Dec‐09

Jun‐10

Dec‐10

Jun‐11

Dec‐11

Jun‐12

Dec‐12

Jun‐13

Dec‐13

Jun‐14

Dec‐14

Jun‐15

Dec‐15

Jun‐16

Dec‐16

Jun‐17

Dec‐17

Jun‐18

Dec‐18

Jun‐19

Dec‐19

P/E 5‐yr avg. +1 S.D. ‐1 S.D.(Hero)

6

8

10

12

14

16

18

20

22

Jun‐08

Dec‐08

Jun‐09

Dec‐09

Jun‐10

Dec‐10

Jun‐11

Dec‐11

Jun‐12

Dec‐12

Jun‐13

Dec‐13

Jun‐14

Dec‐14

Jun‐15

Dec‐15

Jun‐16

Dec‐16

Jun‐17

Dec‐17

Jun‐18

Dec‐18

Jun‐19

Dec‐19

P/E 5‐yr avg. +1 S.D. ‐1 S.D.(Bajaj)

6111621263136414651

Jun‐08

Dec‐08

Jun‐09

Dec‐09

Jun‐10

Dec‐10

Jun‐11

Dec‐11

Jun‐12

Dec‐12

Jun‐13

Dec‐13

Jun‐14

Dec‐14

Jun‐15

Dec‐15

Jun‐16

Dec‐16

Jun‐17

Dec‐17

Jun‐18

Dec‐18

Jun‐19

Dec‐19

P/E 5‐yr avg. +1 S.D. ‐1 S.D.(Eicher)

051015202530354045

Jun‐08

Dec‐08

Jun‐09

Dec‐09

Jun‐10

Dec‐10

Jun‐11

Dec‐11

Jun‐12

Dec‐12

Jun‐13

Dec‐13

Jun‐14

Dec‐14

Jun‐15

Dec‐15

Jun‐16

Dec‐16

Jun‐17

Dec‐17

Jun‐18

Dec‐18

Jun‐19

Dec‐19

P/E 5‐yr avg. +1 S.D. ‐1 S.D.(TVS)

0

5

10

15

20

25

30

35

Jun‐08

Dec‐08

Jun‐09

Dec‐09

Jun‐10

Dec‐10

Jun‐11

Dec‐11

Jun‐12

Dec‐12

Jun‐13

Dec‐13

Jun‐14

Dec‐14

Jun‐15

Dec‐15

Jun‐16

Dec‐16

Jun‐17

Dec‐17

Jun‐18

Dec‐18

Jun‐19

Dec‐19

P/E 5‐yr avg. +1 S.D. ‐1 S.D.(Maruti)

0

5

10

15

20

25

Jun‐08

Dec‐08

Jun‐09

Dec‐09

Jun‐10

Dec‐10

Jun‐11

Dec‐11

Jun‐12

Dec‐12

Jun‐13

Dec‐13

Jun‐14

Dec‐14

Jun‐15

Dec‐15

Jun‐16

Dec‐16

Jun‐17

Dec‐17

Jun‐18

Dec‐18

Jun‐19

Dec‐19

P/E 5‐yr avg. +1 S.D. ‐1 S.D.(M&M)

35

joseph.george@iif lcap.com

India - Auto

Figure 68: Ashok Leyland Figure 69: Tata Motors

Source: Bloomberg, IIFL Research Source: Bloomberg, IIFL Research