Bank Competition and Credit Risk in Euro Area Banking - MDPI

Upload

independentCategory

view

4download

0

Hermawan Kartajaya Taufik • Jacky Mussry • Iwan Setiawan • Farid

Subkhan • Melati Astri Maharani • Achmad Yunianto • Reyhan S. Munir.

BANKING COMPETITION IN 2013IN THE TIME OF REGULATORY TRANSITION

ABOUT MARKPLUS, INC.MarkPlus is the premiere and highly-focused

marketing strategy consulting firm in Indonesia. It was established 22 years ago by Hermawan

Kartajaya, co-author of five international marketing books with Prof. Philip Kotler, the Father of Modern

Marketing at the Kellogg School, Northwestern University. Just as early as 2001, an industry

publication had ranked MarkPlus first among national consulting firms.

MarkPlus is able to provide a comprehensive service to its clients without the need to engage

third-party vendors. MarkPlus consist of three main divisions of MarkPlus Consulting, MarkPlus

Insight, and MarkPlus Institute of Marketing, which aim to provide clients with Solution, Insight and

Knowledge respectively. MarkPlus operates in 17 major cities in Indonesia. Since 2004, MarkPlus has established ASEAN operations in Kuala Lumpur and

Singapore. Headquartered in Jakarta, Indonesia, MarkPlus is strategically positioned to provide South East Asian companies with marketing expertise and

breakthrough insights.

4

PERKEMBANGAN DAN PERSAINGAN PASAR PERBANKAN INDONESIADengan nilai pertumbuhan aset sebesar 15.5%, sektor perbankan masih menjadi industri yang menarik bagi para pemain. Para pemain semakin gencar menarik dana pihak ketiga dari nasabah, terutama dalam menyalurkan kredit. Tidak hanya bank-bank umum, Bank Pembangunan Daerah dan Bank Syariah pun semakin menunjukkan eksistensinya dalam persaingan perbankan nasional.

Meski perkembangan perbankan saat ini masih sangat pesat, para pelaku perlu mewaspadai tantangan baru dalam pengumpulan dana pihak ketiga. Saat ini, Lembaga Penjaminan Simpanan menetapkan batasan suku bunga yang relatif rendah dibanding alternatif investasi lain, yaitu 5.5% untuk bank umum dan 8% untuk BPD . Dengan suku bunga yang relatif rendah tersebut, bank perlu lebih kreatif dalam mengumpulkan dana pihak ketiga dari nasabah.

Tidak hanya dari pertumbuhan aset saja, Return on Asset (ROA) perbankan Indonesia pun masih sangat menarik. Dibandingkan dengan sektor perbankan di negara lain, perbankan Indonesia mencatat ROA yang tergolong sangat tinggi. Namun, tetap saja perbankan Indonesia masih

MARKET GROWTH AND COMPETITION

Having recorded a growth of 15.5% in asset value, the banking sector still becomes a promising industry for the players in Indonesia. They have been vigorously competing in optimizing third-party funds from customers, particularly in distributing credit. Not only public banks, but also both regional development banks (BPD) and sharia banks have been seriously attempting to establish their existence among the national competition.

Although the national banking still shows a rapid growth these days, the players still need to wary of a new challenge in collecting the third-party funds. The Indonesia Deposit Insurance Corporation (Lembaga Penjaminan Simpanan) already defines the interest rate limit that is relatively lower than other investment alternatives, namely 5.5% for public bank and 8% for BPD . As a result, such low interest rate will drive the national banks to be more creative in collecting third-party funds from customers.

In addition to the positive growth on asset, Indonesia banking also accomplishes a high Return on Assets (ROA). Compared to other countries, ROA of our national banking can be classified as very high. However, such circumstance occurs in the mid of the domination of only four

1Bank Indonesia, Indonesian Banking Statistics, Oktober 20122Bank Indonesia, Laporan Keuangan Publikasi Bank, September 2012

OVERVIEW:INDONESIAN BANKING INDUSTRY

5

3Suku bunga 15 Desember 2012 – 14 Januari 2013. Source: Lembaga Penjaminan Simpanan, Press Release No.: Press-015/LPS/XII/20124Source: PT Bank Rakyat Indonesia, Tbk, Q3-2012 Financial Update Presentation; PT Bank Mandiri Tbk, Q3-2012 Result Presentation; PT Bank Central Asia Tbk, Corporate Presentation, Jan-Sep 2012 Results; PT Bank Negara Indonesia, Q3-2012 Corporate Presentation

dikuasai oleh empat besar bank. Bahkan, tiga dari empat bank utama tersebut memiliki ROA di atas rata-rata industri.

Masing-masing bank tersebut bisa memiliki ROA yang tinggi karena berhasil membangun posisi yang kuat di segmen yang spesifik. Misalnya saja, Bank Mandiri cukup kuat di segmen kredit korporat dan komersial, dan BRI kuat di kredit usaha kecil dan mikro. Sedangkan BCA dan BNI masih memiliki portfolio kredit yang merata.

Persaingan bank di sektor kredit ini semakin lama semakin sulit. Nasabah saat ini cenderung semakin tidak loyal terhadap bank. Terutama di sektor kredit konsumer, penawaran terbaik dinilai berdasarkan nilai bunga kredit yang diberikan bank. Hal ini menyebabkan bank harus berlomba-lomba untuk menurunkan tingkat bunga kreditnya. Perang harga yang terjadi antar bank ini justru membuat nasabah semakin tidak loyal.

Bukan tidak mungkin, tantangan yang sama juga akan dihadapi oleh bank di kredit korporasi dan komersial. Di era di mana nasabah semakin tidak loyal, bank akan semakin sulit untuk mempertahankan wallet share nasabah. Bank, mau tidak mau, harus merubah cara dalam menarik dan membangun loyalitas nasabah agar mampu

top banks. Three of them even record a higher level of ROA than the industry average.

The accomplishment of recording such high ROA is much driven by their success in establishing a strong position in specific segments. For instance, Bank Mandiri is fairly strong in two segments, corporate credit and commercial credit, while BRI already has a firm position in the SME credit segment. Meanwhile, BCA and BNI have even capability in the credit portfolio.

The competition in the credit sector gets increasingly tougher. Nowadays, customers are inclined to be disloyal toward banks. In the consumer credit sector particularly, the best offering is valued based on the credit interest rate provided by banks. Consequently, banks should race against each other to lower their credit interest rate. However, the price war among players, in fact, makes customers even more disloyal.There will be always a possibility that such challenge will also occur in the corporate credit and commercial credit. In the present time, in which more customers tend to be disloyal anymore, it will be more difficult for banks to maintain customers’ wallet share. Willy-nilly, banks should change their way in attracting customers

6

memperoleh tingkat profit yang lebih sehat, terutama bagi nasabah korporat dan komersial.

TRANSISI REGULATOR DARI BANK INDONESIA KE OTORITAS JASA KEUANGANTantangan lain yang dihadapi pelaku perbankan adalah adanya transisi fungsi regulator perbankan dari Bank Indonesia (BI) ke Otoritas Jasa Keuangan (OJK). Industri perbankan mungkin tidak akan segera dapat merasakan manfaat dari transisi ini karena masa transisi itu sendiri masih menjadi tahapan yang kritis, baik bagi OJK sebagai regulator maupun bank sebagai pemain industri.

Meskipun demikian, keberadaan OJK jelas akan memungkinkan adanya suatu proses pengawasan terhadap lembaga keuangan yang lebih komprehensif. Agar dapat beroperasi secara efektif, OJK sendiri memerlukan waktu transisi selama tiga tahun. Selama masa transisi tersebut, para pelaku perbankan memiliki kesempatan untuk terus mencermati perubahan-perubahan yang terjadi yang mungkin dapat mempengaruhi pelayanan mereka kepada nasabah.

NASABAH BANK SEMAKIN RASIONAL

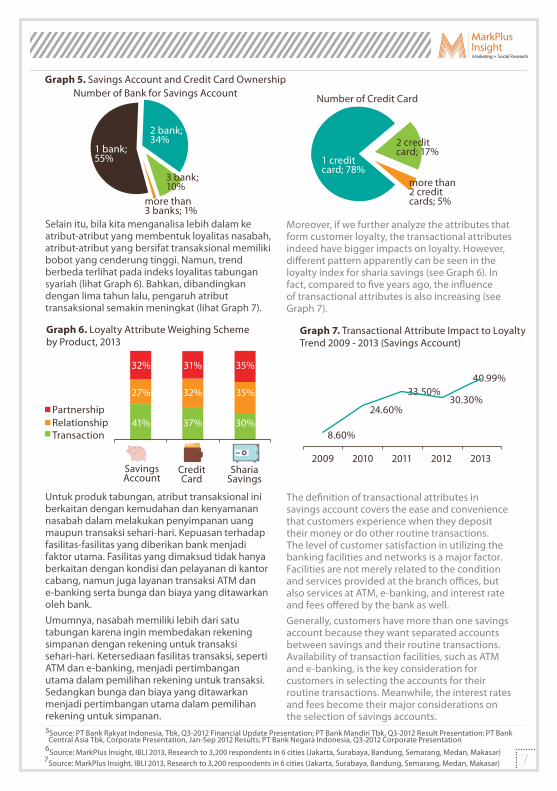

Salah satu trend yang mulai terlihat beberapa tahun terakhir ini adalah kecenderungan nasabah untuk memiliki lebih dari satu rekening tabungan, bahkan juga lebih dari satu rekening kartu kredit, yang aktif (Lihat Graph 5). Fenomena ini menjadi indikasi bahwa nasabah cenderung tidak loyal dan tidak mau terikat dengan salah satu bank. Pemilihan tabungan dan kartu kredit yang digunakan didasarkan pada penawaran yang diberikan oleh bank.

and building a more solid level of customer loyalty in order to gain higher profit, especially for corporates and commercial customers.

TRANSITION OF REGULATOR FUNCTION FROM BANK INDONESIA (BI) TO OTORITAS JASA KEUANGAN (OJK)Another challenge faced by players in the national banking sector is the transition of regulator function from Bank Indonesia (BI) to Otoritas Jasa Keuangan (OJK). The banking industry will not directly feel the benefits of this process because the transition period itself is critical, either for OJK as the regulator and banks as the key players in the banking industry.

The existence of OJK enables a more comprehensive monitoring process toward financial institutions. However, OJK as an institution still needs more time, around three years, for the transition in order to operate effectively. During that transition period, the players in the banking sector need to pay attention toward changes occurring at the present time that will potentially affect their services to customers.

BANK CUSTOMERS ARE BECOMING MORE RATIONALThe tendency of having more than one active savings account, or even credit card, has become a common trend among customers in the last couple of years (see Graph 5). This phenomenon itself is a strong indication that customers nowadays tend to be disloyal and no longer want to be dependent on one bank only. No wonder, banks’ offerings on savings account and credit card become the important factor for customers in selecting a particular bank.

RESEARCH:TRENDS IN CONSUMER LOYALTY

7

Selain itu, bila kita menganalisa lebih dalam ke atribut-atribut yang membentuk loyalitas nasabah, atribut-atribut yang bersifat transaksional memiliki bobot yang cenderung tinggi. Namun, trend berbeda terlihat pada indeks loyalitas tabungan syariah (lihat Graph 6). Bahkan, dibandingkan dengan lima tahun lalu, pengaruh atribut transaksional semakin meningkat (lihat Graph 7).

Untuk produk tabungan, atribut transaksional ini berkaitan dengan kemudahan dan kenyamanan nasabah dalam melakukan penyimpanan uang maupun transaksi sehari-hari. Kepuasan terhadap fasilitas-fasilitas yang diberikan bank menjadi faktor utama. Fasilitas yang dimaksud tidak hanya berkaitan dengan kondisi dan pelayanan di kantor cabang, namun juga layanan transaksi ATM dan e-banking serta bunga dan biaya yang ditawarkan oleh bank.Umumnya, nasabah memiliki lebih dari satu tabungan karena ingin membedakan rekening simpanan dengan rekening untuk transaksi sehari-hari. Ketersediaan fasilitas transaksi, seperti ATM dan e-banking, menjadi pertimbangan utama dalam pemilihan rekening untuk transaksi. Sedangkan bunga dan biaya yang ditawarkan menjadi pertimbangan utama dalam pemilihan rekening untuk simpanan.

6Source: MarkPlus Insight, IBLI 2013, Research to 3,200 respondents in 6 cities (Jakarta, Surabaya, Bandung, Semarang, Medan, Makasar)7Source: MarkPlus Insight, IBLI 2013, Research to 3,200 respondents in 6 cities (Jakarta, Surabaya, Bandung, Semarang, Medan, Makasar)

Moreover, if we further analyze the attributes that form customer loyalty, the transactional attributes indeed have bigger impacts on loyalty. However, different pattern apparently can be seen in the loyalty index for sharia savings (see Graph 6). In fact, compared to five years ago, the influence of transactional attributes is also increasing (see Graph 7).

The definition of transactional attributes in savings account covers the ease and convenience that customers experience when they deposit their money or do other routine transactions. The level of customer satisfaction in utilizing the banking facilities and networks is a major factor. Facilities are not merely related to the condition and services provided at the branch offices, but also services at ATM, e-banking, and interest rate and fees offered by the bank as well. Generally, customers have more than one savings account because they want separated accounts between savings and their routine transactions. Availability of transaction facilities, such as ATM and e-banking, is the key consideration for customers in selecting the accounts for their routine transactions. Meanwhile, the interest rates and fees become their major considerations on the selection of savings accounts.

5Source: PT Bank Rakyat Indonesia, Tbk, Q3-2012 Financial Update Presentation; PT Bank Mandiri Tbk, Q3-2012 Result Presentation; PT Bank Central Asia Tbk, Corporate Presentation, Jan-Sep 2012 Results; PT Bank Negara Indonesia, Q3-2012 Corporate Presentation

8

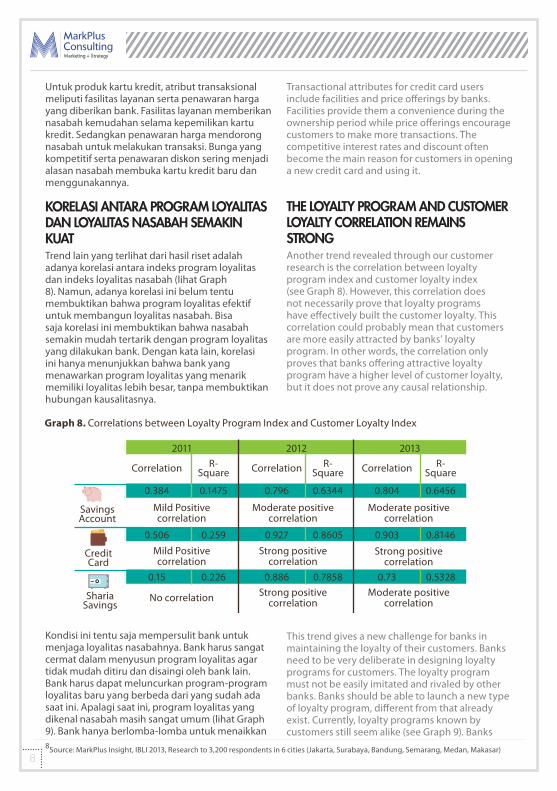

Untuk produk kartu kredit, atribut transaksional meliputi fasilitas layanan serta penawaran harga yang diberikan bank. Fasilitas layanan memberikan nasabah kemudahan selama kepemilikan kartu kredit. Sedangkan penawaran harga mendorong nasabah untuk melakukan transaksi. Bunga yang kompetitif serta penawaran diskon sering menjadi alasan nasabah membuka kartu kredit baru dan menggunakannya.

KORELASI ANTARA PROGRAM LOYALITAS DAN LOYALITAS NASABAH SEMAKIN KUATTrend lain yang terlihat dari hasil riset adalah adanya korelasi antara indeks program loyalitas dan indeks loyalitas nasabah (lihat Graph 8). Namun, adanya korelasi ini belum tentu membuktikan bahwa program loyalitas efektif untuk membangun loyalitas nasabah. Bisa saja korelasi ini membuktikan bahwa nasabah semakin mudah tertarik dengan program loyalitas yang dilakukan bank. Dengan kata lain, korelasi ini hanya menunjukkan bahwa bank yang menawarkan program loyalitas yang menarik memiliki loyalitas lebih besar, tanpa membuktikan hubungan kausalitasnya.

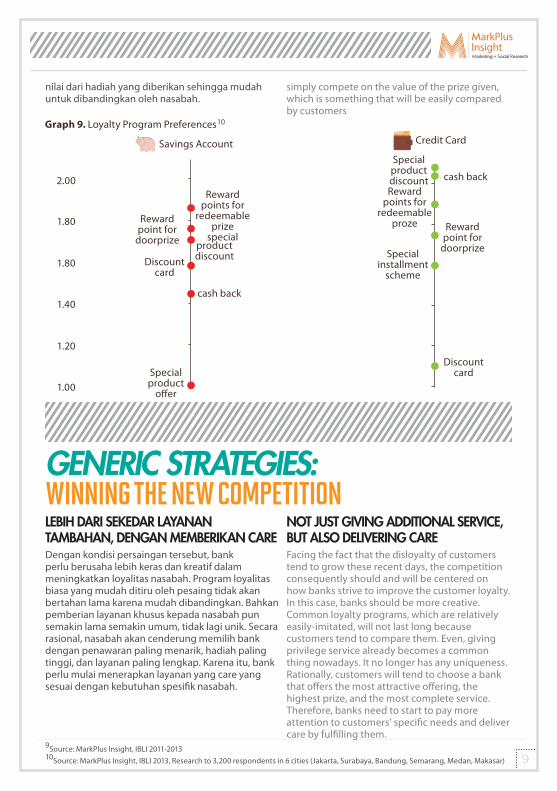

Kondisi ini tentu saja mempersulit bank untuk menjaga loyalitas nasabahnya. Bank harus sangat cermat dalam menyusun program loyalitas agar tidak mudah ditiru dan disaingi oleh bank lain. Bank harus dapat meluncurkan program-program loyalitas baru yang berbeda dari yang sudah ada saat ini. Apalagi saat ini, program loyalitas yang dikenal nasabah masih sangat umum (lihat Graph 9). Bank hanya berlomba-lomba untuk menaikkan 8Source: MarkPlus Insight, IBLI 2013, Research to 3,200 respondents in 6 cities (Jakarta, Surabaya, Bandung, Semarang, Medan, Makasar)

Transactional attributes for credit card users include facilities and price offerings by banks. Facilities provide them a convenience during the ownership period while price offerings encourage customers to make more transactions. The competitive interest rates and discount often become the main reason for customers in opening a new credit card and using it.

THE LOYALTY PROGRAM AND CUSTOMER LOYALTY CORRELATION REMAINS STRONGAnother trend revealed through our customer research is the correlation between loyalty program index and customer loyalty index (see Graph 8). However, this correlation does not necessarily prove that loyalty programs have effectively built the customer loyalty. This correlation could probably mean that customers are more easily attracted by banks’ loyalty program. In other words, the correlation only proves that banks offering attractive loyalty program have a higher level of customer loyalty, but it does not prove any causal relationship.

This trend gives a new challenge for banks in maintaining the loyalty of their customers. Banks need to be very deliberate in designing loyalty programs for customers. The loyalty program must not be easily imitated and rivaled by other banks. Banks should be able to launch a new type of loyalty program, different from that already exist. Currently, loyalty programs known by customers still seem alike (see Graph 9). Banks

9

nilai dari hadiah yang diberikan sehingga mudah untuk dibandingkan oleh nasabah.

simply compete on the value of the prize given, which is something that will be easily compared by customers

LEBIH DARI SEKEDAR LAYANAN TAMBAHAN, DENGAN MEMBERIKAN CAREDengan kondisi persaingan tersebut, bank perlu berusaha lebih keras dan kreatif dalam meningkatkan loyalitas nasabah. Program loyalitas biasa yang mudah ditiru oleh pesaing tidak akan bertahan lama karena mudah dibandingkan. Bahkan pemberian layanan khusus kepada nasabah pun semakin lama semakin umum, tidak lagi unik. Secara rasional, nasabah akan cenderung memilih bank dengan penawaran paling menarik, hadiah paling tinggi, dan layanan paling lengkap. Karena itu, bank perlu mulai menerapkan layanan yang care yang sesuai dengan kebutuhan spesifik nasabah.

9Source: MarkPlus Insight, IBLI 2011-201310Source: MarkPlus Insight, IBLI 2013, Research to 3,200 respondents in 6 cities (Jakarta, Surabaya, Bandung, Semarang, Medan, Makasar)

NOT JUST GIVING ADDITIONAL SERVICE, BUT ALSO DELIVERING CARE Facing the fact that the disloyalty of customers tend to grow these recent days, the competition consequently should and will be centered on how banks strive to improve the customer loyalty. In this case, banks should be more creative. Common loyalty programs, which are relatively easily-imitated, will not last long because customers tend to compare them. Even, giving privilege service already becomes a common thing nowadays. It no longer has any uniqueness. Rationally, customers will tend to choose a bank that offers the most attractive offering, the highest prize, and the most complete service. Therefore, banks need to start to pay more attention to customers’ specific needs and deliver care by fulfilling them.

GENERIC STRATEGIES:WINNING THE NEW COMPETITION

10

10

Banyak persepsi bahwa care adalah layanan khusus dan membutuhkan biaya yang lebih besar, sehingga hanya diberikan kepada nasabah prioritas. Padahal layanan yang bagus tidak selalu berarti lebih mahal, yang penting tepat. Dengan layanan yang tepat dalam menjawab kebutuhan spesifik nasabah, persepsi care dapat muncul di benak nasabah. Bank hanya perlu mengoptimalkan fasilitas layanan yang sudah ada dan memberikannya kepada nasabah yang memang membutuhkan. Layanan yang biasa saja bisa terasa unik dan menyentuh bila diberikan pada saat yang tepat.

Misalnya saja fasilitas pemesanan nomor kursi atau check-in melalui website yang dimiliki maskapai penerbangan akan sangat berguna bagi keluarga yang bepergian dengan anak kecil. Front liner maskapai penerbangan bisa menginformasikan dan menawarkan kepada calon penumpang yang membutuhkan. Atau, adanya fasilitas Wi-fi di ruang tunggu, front liner bisa lebih aktif menginformasikan terutama kepada konsumen yang membutuhkan. Jadi, front liner harus bisa berperan lebih aktif dalam memberikan pelayanan untuk memberikan layanan yang peduli kepada kebutuhan nasabah.

PELAYANAN YANG TERINTEGRASI UNTUK MEMBERIKAN PENGALAMAN YANG SAMA DI SEMUA PRODUKSelain itu, bank juga perlu mengintegrasi layanan untuk semua produknya. Layanan yang terintegrasi ini tidak hanya bertujuan untuk memaksimalkan wallet share nasabah di bank, tapi juga untuk memberikan pengalaman yang sama bagi nasabah di setiap lini produk. Kenyamanan yang dirasakan oleh nasabah saat bertransaksi untuk produk tabungan harus pula dirasakan saat ia bertransaksi kartu kredit.Aplikasi-aplikasi customer relationship management terbukti sangat bermanfaat dalam proses integrasi layanan ini. Namun, tantangan baru muncul dengan adanya pihak lain. Misalnya merchant, yang terlibat dalam proses layanan bank ke nasabah, juga dapat mempengaruhi pengalaman nasabah. Sehingga, bank perlu memetakan seluruh tahapan pengalaman nasabah dalam penggunaan produk dan menentukan pengalaman apa yang ingin diberikan.

It has become a common perception that delivering care means giving privilege services which require greater cost, so it is commonly given to priority customers only. Whereas, providing better level of service does not always mean spending greater cost, but how and when it is delivered is much more important. Giving service that meets customers’ specific needs will automatically create the positive perception of care in the customers’ mind. Thus banks just need to optimize their existing service facilities to fulfill customers’ specific needs on time. Services that are usually perceived as ordinary service can be considered unique and touching when they are delivered at the right time.The airline industry can become the example. The seat-booking and check-in facility through website can be very helpful for the passengers traveling with children, or Wi-Fi service provided in the waiting rooms, children playgrounds, and nursery rooms is also important for those who need internet connection wherever they are. Such facilities should be actively informed, and front liners hold an important role in this case. In delivering care, front liners should be actively engaged in providing right services that meet customers’ needs.

INTEGRATED SERVICE THAT ENABLES EQUAL EXPERIENCE FOR ALL PRODUCTS

In addition to implementing care, banks also need to integrate all of their products. Through integrated service, not only banks can optimize customers’ wallet share but also they can provide the same experience for customers in every product line. Customers must get the same perception of comfort when using their credit card as when they are using their savings account.Customer relationship management applications have been proven to be very useful in the process of integrating services for customers. However, banks will face new challenges when they must deal with the third parties. Merchants, who are directly involved in the customers’ transaction, can also give impact on customers’ experience significantly. Thus, banks need to map all stages of the customer experience and define how to develop a consistent experience and perception.

ABOUT THE AUTHOR• Hermawan Kartajaya is the Managing Partner of MarkPlus Consulting.

He has over 21 years of consulting experience. Hermawan was dubbed as “One of the 50 Gurus Who Have Shaped the Future of Marketing” by Chartered Institute of Marketing, United Kingdom

• Taufik is a Partner at MarkPlus Consulting. He has over 16 years of consulting experience. Taufik has an MBA from the Nanyang Fellows Programme (Nanyang Technological University and MIT Sloan School of Management).

• Jacky Mussry is a Partner at MarkPlus Consulting. He has over 16 years of consulting experience. Jacky has a doctorate degree in Strategic Management from University of Indonesia.

• Iwan Setiawan is a Principal at MarkPlus Consulting. He has over 7 years of consulting experience. Iwan has an MBA from the Kellogg School of Management.

• Farid Subkhan is a Co-Chief Operations of MarkPlus Insight. He has over 10 years of research and consulting experience. Farid has a master’s degree in Management of Development from the University of Turin, Italy.

• Melati Astri Maharani is a Manager at MarkPlus Consulting with over 4 years of consulting experience

• Achmad Yunianto is a Research Manager at MarkPlus Insight with over 10 years of research experience.

• Reyhan S Munir is a Business Analyst at MarkPlus Consulting.

For Inquiries, Please Contact:Iwan Setiawan ([email protected])

Farid Subkhan ([email protected])PT MarkPlus Indonesia Segitiga Emas Business Park CBD B01/01 Jl. Prof. Dr. Satrio Kav. 6 Jakarta Selatan 12940 - Indonesia Phone: +62-21-5790 2338 / Fax: +62-21-5709 712

Copyright© MarkPlus Consulting 2012 All rights reserved

General Disclaimer: This paper has been prepared for general on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this paper

Copyright © 2022 FDOKUMEN