Corporate social responsibility reporting practices in banking companies in Bangladesh: Impact of...

28

Journal of Financial Reporting and Accounting Corporate social responsibility reporting practices in banking companies in Bangladesh: Impact of regulatory change Md. Hafij Ullah Mohammad Afjalur Rahman Article information: To cite this document: Md. Hafij Ullah Mohammad Afjalur Rahman , (2015),"Corporate social responsibility reporting practices in banking companies in Bangladesh", Journal of Financial Reporting and Accounting, Vol. 13 Iss 2 pp. 200 - 225 Permanent link to this document: http://dx.doi.org/10.1108/JFRA-05-2013-0038 Downloaded on: 18 September 2015, At: 15:29 (PT) References: this document contains references to 75 other documents. To copy this document: [email protected] The fulltext of this document has been downloaded 37 times since 2015* Users who downloaded this article also downloaded: Pauric McGowan, Mark G. Durkin, Lynsey Allen, Colette Dougan, Sheena Nixon, (2001),"Developing competencies in the entrepreneurial small firm for use of the Internet in the management of customer relationships", Journal of European Industrial Training, Vol. 25 Iss 2/3/4 pp. 126-136 http:// dx.doi.org/10.1108/EUM0000000005443 Briga Hynes, Yvonne Costin, Naomi Birdthistle, (2010),"Practice-based learning in entrepreneurship education: A means of connecting knowledge producers and users", Higher Education, Skills and Work-Based Learning, Vol. 1 Iss 1 pp. 16-28 http://dx.doi.org/10.1108/20423891111085366 H. Semih Yildirim, George C. Philippatos, (2007),"Competition and contestability in Central and Eastern European banking markets", Managerial Finance, Vol. 33 Iss 3 pp. 195-209 http:// dx.doi.org/10.1108/03074350710718275 Access to this document was granted through an Emerald subscription provided by emerald- srm:191537 [] For Authors If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service information about how to choose which publication to write for and submission guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information. About Emerald www.emeraldinsight.com Emerald is a global publisher linking research and practice to the benefit of society. The company manages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as well as providing an extensive range of online products and additional customer resources and services. Downloaded by Macquarie University, MD. HAFIJ ULLAH At 15:29 18 September 2015 (PT)

Transcript of Corporate social responsibility reporting practices in banking companies in Bangladesh: Impact of...

Journal of Financial Reporting and AccountingCorporate social responsibility reporting practices in banking companies inBangladesh: Impact of regulatory changeMd. Hafij Ullah Mohammad Afjalur Rahman

Article information:To cite this document:Md. Hafij Ullah Mohammad Afjalur Rahman , (2015),"Corporate social responsibility reportingpractices in banking companies in Bangladesh", Journal of Financial Reporting and Accounting, Vol.13 Iss 2 pp. 200 - 225Permanent link to this document:http://dx.doi.org/10.1108/JFRA-05-2013-0038

Downloaded on: 18 September 2015, At: 15:29 (PT)References: this document contains references to 75 other documents.To copy this document: [email protected] fulltext of this document has been downloaded 37 times since 2015*

Users who downloaded this article also downloaded:Pauric McGowan, Mark G. Durkin, Lynsey Allen, Colette Dougan, Sheena Nixon, (2001),"Developingcompetencies in the entrepreneurial small firm for use of the Internet in the management ofcustomer relationships", Journal of European Industrial Training, Vol. 25 Iss 2/3/4 pp. 126-136 http://dx.doi.org/10.1108/EUM0000000005443Briga Hynes, Yvonne Costin, Naomi Birdthistle, (2010),"Practice-based learning in entrepreneurshipeducation: A means of connecting knowledge producers and users", Higher Education, Skills andWork-Based Learning, Vol. 1 Iss 1 pp. 16-28 http://dx.doi.org/10.1108/20423891111085366H. Semih Yildirim, George C. Philippatos, (2007),"Competition and contestability in Centraland Eastern European banking markets", Managerial Finance, Vol. 33 Iss 3 pp. 195-209 http://dx.doi.org/10.1108/03074350710718275

Access to this document was granted through an Emerald subscription provided by emerald-srm:191537 []

For AuthorsIf you would like to write for this, or any other Emerald publication, then please use our Emeraldfor Authors service information about how to choose which publication to write for and submissionguidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comEmerald is a global publisher linking research and practice to the benefit of society. The companymanages a portfolio of more than 290 journals and over 2,350 books and book series volumes, aswell as providing an extensive range of online products and additional customer resources andservices.

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of theCommittee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative fordigital archive preservation.

*Related content and download information correct at time ofdownload.

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Corporate social responsibilityreporting practices in banking

companies in BangladeshImpact of regulatory change

Md. Hafij UllahDepartment of Business Administration, International Islamic UniversityChittagong, Chittagong, Bangladesh, and Department of Accounting and

Corporate Governance Macquarie University, Sydney, Australia, and

Mohammad Afjalur RahmanDepartment of Business Administration,

International Islamic University Chittagong, Chittagong, Bangladesh

AbstractPurpose – This paper aims to provide a deeper understanding of the nature and extent of corporatesocial responsibility (CSR) reporting in the annual report by banking companies in Bangladesh, identifythe impact of regulatory change on CSR reporting and examine whether there is any relationshipbetween the extent of CSR reporting and bank characteristics. CSR movement and CSR reportingpractices by financial sector have gathered great momentum in recent years. Banking sector is in theleading position in discharging CSR reporting.Design/methodology/approach – The sample composed of all the 30 banking companies enlisted inDhaka Stock Exchange (DSE), and the study used content analysis approach for systematiccategorization and analysis of the contents reported in the annual report. A total of 97 CSR itemsclassified into seven classes were selected through a relevant literature review, as the expected itemsand average, standard deviation, coefficient of variation, percentage and correlation, etc. were used asthe tools of analysis. SPSS software version 19.0 was used to analyze the data. An ordinary least square(OLS) regression model is fitted to the data for assessing the effect of independent variables on total CSRreporting score.Findings – The study found that the extent of CSR reporting in banking companies in Bangladeshvaries from 27.84 to 65.98 per cent, and on an average, they report 47.39 per cent of the expected CSRitems in annual report. It is also observed that banking companies in Bangladesh emphasized onlinguistic or written form than charts, graphs or pictures in reporting CSR activities to theirstakeholders, and the study found no significant influence of the selected bank characteristics on theextent of CSR reporting. Moreover, the study observed significant impact of regulatory change onnature and extent of CSR reporting.Research limitations/implications – The study considered all the listed commercial bankingcompanies in Bangladesh, and the annual report of 2011 was taken as the main source of data.Social implications – Among others, the implications of the study include the following. Bankingcompanies are expected to get a real scenario of CSR reporting of the banking sector in Bangladesh andbanking companies with poor CSR contribution expected to be motivated for contributing more in CSRactivities. Government and other regulatory bodies can also get detailed information regarding CSRreporting practices for formulating guidelines in this regard.Originality/value – This empirical study on the determinants of extent of CSR reporting using alarger number of expected CSR items contributes toward a better understanding of the CSR reporting

The current issue and full text archive of this journal is available on Emerald Insight at:www.emeraldinsight.com/1985-2517.htm

JFRA13,2

200

Received 28 May 2013Revised 13 November 2014Accepted 8 July 2015

Journal of Financial Reporting andAccountingVol. 13 No. 2, 2015pp. 200-225© Emerald Group Publishing Limited1985-2517DOI 10.1108/JFRA-05-2013-0038

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

practices of the banking companies in Bangladesh. The study used a new independent variable “CSRExpenditure” in justifying its influence on CSR reporting and identified the impact of regulatory changeon CSR reporting. The study expects contributing in the enactment of more regulatory requirements forbringing the CSR reporting into a certain framework and encouraging in more CSR reporting inBangladesh.

Keywords Bangladesh, CSR, Bank, Content analysis, Reporting, Annual report

Paper type Research paper

1. IntroductionCorporate social responsibility (CSR) reporting has been getting a good form of priorityover the recent two decades, which is a true breakthrough for the betterment of bankingfraternity. CSR comprises wide areas of issues ranging from business ethics, corporateethics, corporate governance and socially responsible investing to environmentalsustainability and development of community (Das, 2012). CSR is also known as“corporate citizenship” that forms the self-regulation of a firm toward the integration ofbusiness culture, and studies show that enterprise strikes a balance between economicand social goals (Masud, 2011). Businesses not only create wealth and job opportunitiesfor the society, at the same time, they also pollute the environment, which would bringdevastating effect on human health and biodiversity worldwide (Alimullah, 2006). CSRrefers to a company’s voluntary contribution to sustainable development which goesbeyond legal requirements, and emerging trends to practice CSR are concerned toaddress the social problems of the not only stockholder but also stakeholders(Gamerschlag et al., 2011; Masud, 2011). CSR goes beyond philanthropy and complianceand addresses how companies communicate the social and environmental effects oforganizations’ economic actions, as well as their relationships in all key spheres ofinfluence: the marketplace, the supply chain, the community and the public policy realm(Gray et al., 1987).

The banking sector of Bangladesh has a long history of involvement inbenevolent activities like donations to different charitable organizations, poorpeople and religious institutions; city beautification; and patronizing art andculture. Recent trends of these engagements indicate that banks are graduallyorganizing these involvements in more structured CSR initiative format, in line withBangladesh Bank Guidance in Department of Off-site Supervision circular number1 of 2008. Bangladesh Bank Governor Dr Atiur Rahman opined that the spending onCSR by the commercial banks operating in the country increased by 5.5 times tomore than BDT 3 billion in 2012 from BDT 554 million in 2009 (Dhaka Tribune,2013). He added that “Over the past few years, direct and indirect expenditure ofbanks on CSR initiatives have increased manifold”. Total CSR expenditure ofbanking sector in 2011 was BDT 2,188.33 million, in 2012 BDT 3,046.69 million andin 2013 BDT 4,471.49 million. During 2013, CSR expenditures of banks aspercentage of their after-tax profit range from 0.14 to 57.12 per cent (Millat, 2014).

Bangladesh Bank has been working for the sustainable development of the countryfrom its inception in 1972, but the banking practices for social protection started in1990s. But the regulatory framework in banking practices for CSR witnessed atremendous growth in the past half a decade. In June 2008, Bangladesh Bank issued acomprehensive circular titled “mainstreaming corporate social responsibility (CSR) inbanks and financial institutions in Bangladesh” (Millat, 2014).

201

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

The Government of Bangladesh, under the SRO No. 270-Ain/2010, issued on July 1,2010, has specified 22 areas of CSR activities for enjoying 10 per cent tax rebate. InDecember 2010, Bangladesh Bank instructed the banks to establish separate CSR deskto pay special attention on this issue. Simultaneously, Bangladesh Bank startedpublishing annual CSR review report on banking since 2010. National Board of Revenue(NBR) of Bangladesh issued Statutory Regulatory Order (SRO) by providing taxexemption on the expenditure made by corporates for CSR activities in 2011.Immediately after these steps, CSR initiatives in Bangladesh reached at historic highincrease in 2010. Total CSR expenditure of banking sector in 2008 was BDT 410.70million only, but this figure increased to five times in 2010. As it is observed that thereare significant impacts of government regulations in instigating CSR activities ofbanking sector in Bangladesh, the study aims at evaluating the extent of changes in CSRreporting practices of the banking sector due to these regulatory changes. This studyinvestigates the CSR reporting performance against Bangladesh Bank’s regulation forCSR practices and other factors that have been suggested by researchers in their worksregarding CSR reports in Bangladesh and abroad.

The remaining parts of the paper are presented as follows. The next section reviewsthe relevant literature including the results of relevant empirical studies. Section 3delineates the objectives of the study. Section 4 provides details of the research methods,followed by Section 5 dealing with findings and analysis of the study. The last sectionsprovide the implications of the study, direction to future research, limitations andconclusion of the study.

2. Literature reviewCSR reporting has become an important issue in the business world (Waller and Lanis,2009). South Asian countries like India, Pakistan and Bangladesh have a smallernumber of companies that report corporate environmental and social information(Jamali and Mishak, 2007). Although CSR reporting practices have gained a hugemomentum, its practices are apparently a new issue for financial institutions inBangladesh (Khan et al., 2009). Although developing countries are lagging behind thedeveloped countries in CSR practices, a number of studies on CSR have been conducted,including Imam (2000); Belal (2001); Belal and Owen (2007); Sobhani and Azlan (2009);Boje and Farzad (2009); Kang (2010); Rahul (2010); Achda (2006) and Kolk and Lenfant(2010). CSR or sustainability reporting has been increased over the past two decades inthe developed and developing countries (KPMG, 2013; GRI, 2010).

Moneva and Liena (2000) stated that, although there has been a significant increase inquantitative and qualitative reporting by the sample companies, the environmentalreporting has a fundamentally narrative character. The study of Savage (1994) on 115South African companies found that approximately 50 per cent of companies madesocial disclosures with human resource (89 per cent) as the main theme, communityinvolvement (72 per cent) and environmental disclosures (63 per cent). Tsang (1998)conducted a longitudinal study of CSR in Singapore over a 10-year period from 1986 to1995 covering 33 listed companies and found that 17 (52 per cent) companies made socialdisclosures. Recent survey of KPMG (2013) reported that corporate responsibility (CR)reporting is now undeniably a mainstream business practice worldwide, undertaken byalmost three quarters (71 per cent) of the 4,100 companies surveyed in 2013. There hasbeen a dramatic increase in CR reporting rates in Asia-Pacific over the past two years.

JFRA13,2

202

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Almost three quarters (71 per cent) of companies based in Asia-Pacific now publish CRreports – an increase of 22 percentage points since 2011 when less than half (49 per cent)did so (KPMG, 2013).

Compared to developing countries, the disclosure made by the listed companies intheir annual reports in Bangladesh is very disappointing (Hossain et al., 2006) andsignificantly low (Khan et al., 2009; Belal, 2000). Azim et al. (2009), in their study of CSRdisclosures by listed public companies in Bangladesh, revealed that only around 16 percent companies made such voluntary disclosures. The study of Imam (2000) reportedthat disclosure level of human resource, community, consumer and environmentalinformation were very poor and inadequate. Khan (2010) observed that overall CSRreporting by Bangladeshi private commercial bank (PCB) is rather moderate; however,the varieties of CSR items are impressive. Hossain et al. (2006) witnessed that on anaverage, 8.33 per cent of Bangladeshi companies discloses social and environmentalinformation in their corporate annual report. In another study, Belal (1999) observed that90 per cent of the companies studied made some environmental disclosures, 97 per centmade employee disclosures and 77 per cent made ethical disclosures. Imam (2000) foundthat only 25 per cent of sample companies made disclosure regarding community and22.50 per cent environmental disclosure by 40 companies listed in DSE in the years1996-1997.

Common CSR practices in Bangladesh by different banks are centered on mainlypoverty alleviation, health care, education, charity activities, cultural enrichment, youthdevelopment, women empowerment, patronizing sports, etc. (Alam et al., 2010). CSRreporting practice is still an evolving concept that enables corporate executives to createand apply self-determined policies to best meet the needs and demands of itsstakeholders (Alam et al., 2010). Belal (2001) expressed that the nature of the CSRreporting is mainly descriptive in nature and mostly reporting positive news (Imam,2000). Prior studies on CSR disclosures in Bangladesh suggest that pressures frompowerful stakeholders, rather than efficiency incentives, are the drivers for suchdisclosures (Belal and Owen, 2007; Islam and Deegan, 2008). According to Muttakin andKhan (2014), CSR disclosure has positive and significant relationships withexport-oriented sector, firm size and types of industries and a negative relationshipbetween CSR disclosure and family ownership. Company size and strategic motivationcan have a positive impact on CSR because large companies tend to have large CSRexpenditure (Cowen et al., 1987). It has been argued that company age has a positiverelationship with CSR (Delaney and Huselid, 1996). CSR activities also differ in betweenthe types of industries (Kolk, 2003).

3. Objectives of the studyThe main objective of the study is to evaluate the CSR reporting practices in the annualreports of the listed banking companies in Bangladesh. However, the specific objectivesof this study include the following:

• to know the CSR reporting practices in the annual report of the listed bankingcompanies in Bangladesh;

• to know the impact of regulatory changes on volume of CSR information reportedin the annual report of listed banking companies in Bangladesh; and

203

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

• to examine whether there is any relationship between extent of CSR reporting andbank characteristics.

4. Methodology of the studyAs it is a descriptive study, the main source of information is the secondary dataavailable in the annual report of the sample companies. To measure the extent of CSRreporting in annual report of the listed banking companies of Bangladesh, 30 annualreports of all the listed banking companies have been evaluated because annual report isa common and popular means of communication to stakeholders (Guthrie and Parker,1990; Singh and Ahuja, 1983; Adams, 2002; Rahman, 2006). As suggested by Beattie andJones (1992, 1994), CSR reporting is measured in terms of number of words, sentences,pictures, graphs and charts. The methodology followed in this paper is almost similar toUllah (2013) and Ullah and Yakub (2013). The techniques used for analyzing datainclude average, standard deviation, coefficient of variation, percentage and correlationanalysis, etc. SPSS software version 19 was used to analyze the data.

4.1 Selection of the samplesAs the study was conducted on the listed banking companies in Bangladesh, all thelisted banking companies (100 per cent of the population) enlisted in Dhaka StockExchange (DSE) was considered for the study. The list of the banking companiesconsidered for the study has been provided in Appendix 1. Annual reports have beencollected from different branches of the banks, Chittagong Stock Exchange, DSEregional office in Chittagong and the Web sites of the companies. The main reason ofselecting banking companies as the sample is due to the directives of Bangladesh Bankin promoting CSR activities in 2008 and because the banking companies is in the leadingposition in discharging CSR (Chowdhury, 2014) and CSR activities by the banks havebecome an integral part of their business in recent years. Beside this, the listed bankingcompanies usually put importance in publishing quality report for investor orientationas well as statutory obligation.

4.2 Choice of the periodThe Government of Bangladesh, under the SRO No. 270-Ain/2010, issued on July 1, 2010,has specified 22 areas of CSR activities for enjoying 10 per cent tax rebate. In December2010, Bangladesh Bank instructed the banks to establish separate CSR desk to payspecial attention on this issue. Simultaneously, Bangladesh Bank started publishingannual CSR review report on banking since 2010. NBR of Bangladesh issued SRO byproviding tax exemption on the expenditure made by corporates for CSR activities in2011. Immediately after these steps, CSR initiatives in Bangladesh reached at historichigh increase in 2010. Hence, the annual report of 2011 has been chosen to examine thechanges in CSR reporting practices in the annual reports of the banking companies inBangladesh.

4.3 Content analysis and CSR reporting indexThe study used content analysis for systematic categorization and analysis of thecontents reported in the annual report. The quantity and nature of social reporting havebeen measured using content analysis (Holsti, 1969; Krippendorf, 1980). Hossain et al.(1994); Ahmed and Nicholls (1994) and Hossain (2000 and 2001) suggested adichotomous procedure in which an item scores “1” if reported and “0” if not reported.

JFRA13,2

204

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Past experience shows that the use of weighted and un-weighted scores for the itemsreported in the corporate annual reports and calculation can make little or no differenceto the findings (Coomba and Tayib, 1998). Thus, the study used this un-weightedreporting index methodology. So, the un-weighted reporting method measures the totaldisclosure (TD) score of a selected company (suggested by Cooke, 1992) as follows:

TD � �i�1

n

di

Where,d � 1 if the item di is reported;d � 0 if the item is not reported; andn � number of items.

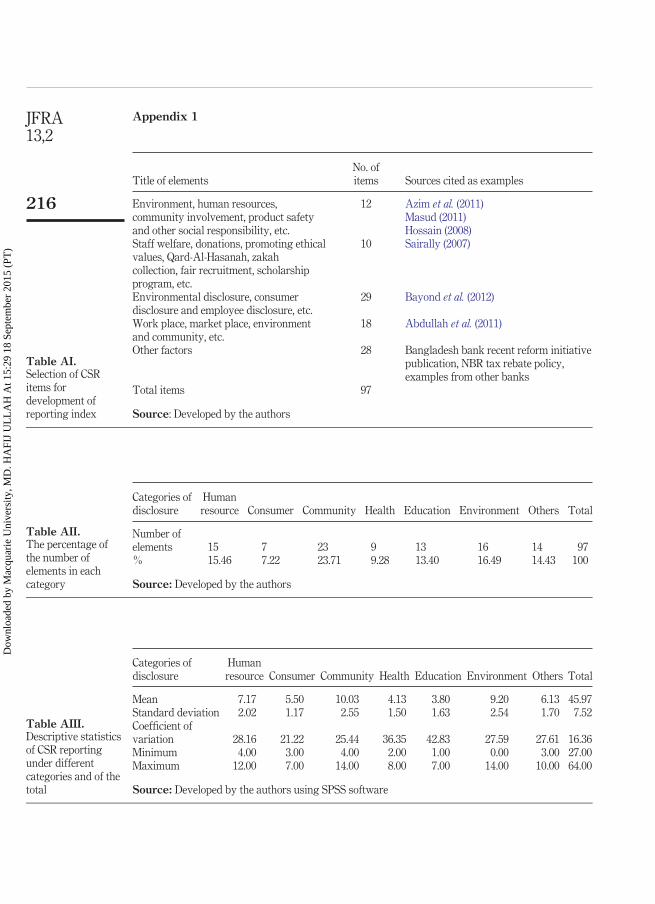

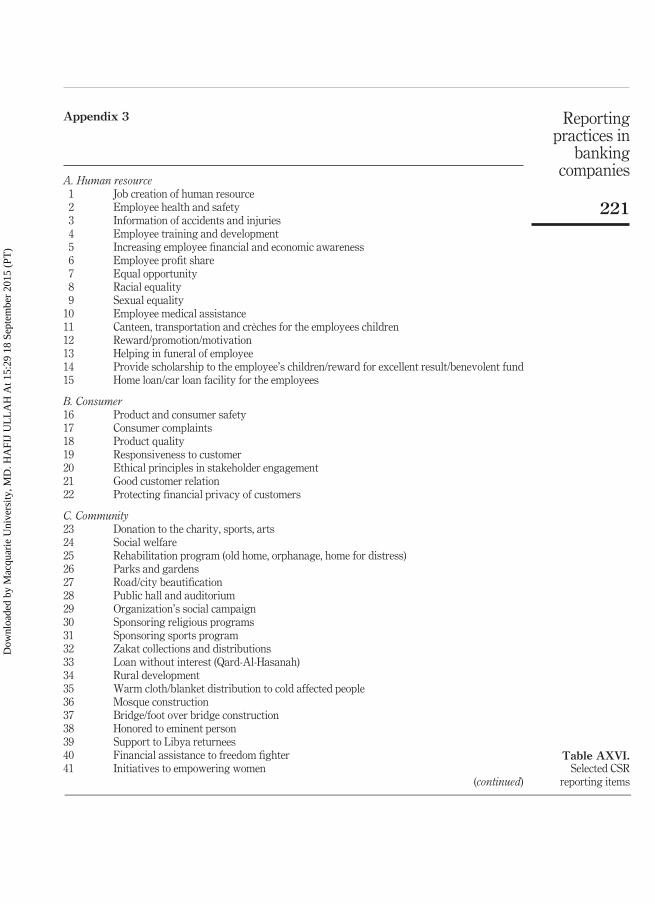

4.4 Selection of CSR items in the reporting indexThe present study developed a reporting index to evaluate the CSR reportingperformance of the banking sector in Bangladesh. For the development of a reportingindex, a list of expected CSR reporting items consisting of 97 elements (list of elementsprovided in Appendix 2) has been developed through reviewing the literature works ofAzim et al. (2011); Masud (2011); Hossain (2008); Sairally (2007); Bayond et al. (2012);Abdullah et al. (2011) and others. The selected CSR reporting items were classified intothe following seven categories for the purpose of better presentation and analysis:

(1) human resource;(2) consumer;(3) community;(4) health;(5) education;(6) environment; and(7) others.

Number of items and their percentages under each category are provided in Table AII.

4.5 Model developmentThe ordinary least square (OLS) regression model is fitted to the data for assessing theeffect of independent variables on total CSR reporting score. The regression model fittedfor the study is as follows:

UDI � � � �1Log_TA � �2Log_TR � �3NOB � �4AGE � �5ROA � �6EPS

� �7Log_CSR_Exp � �8CAR � ei

Where,

UDI � total CSR reporting score received for each bank;� � intercept of the function;� � coefficient (slope of the regression line);SIZE � total assets, total revenue and number of branches;

205

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

AGE � years of operation as a listed public limited company in DSE;PT � profitability is measured by return on assets (ROA) and earnings per

share (EPS);CSR_Exp � corporate social responsibility expenditure;CAR � capital adequacy ratio, measured by the total capital to risk weighted

assets; andei � standard sample error.

4.6 Development of hypothesesThe following hypotheses were developed to examine the relationship between theextent of CSR reporting in annual report and a number of bank characteristics.

4.6.1 Size of the bank. Many disclosure studies (Cooke, 1991; Ahmed and Nicholls,1994) suggest that there is a significant relationship between firm size and the extent ofvoluntary disclosure. Ullah (2013); Hossain (2010); Silva and Christensen (2004); Spiegeland Yamori (2004) and Ismail (2002) found a positive relationship between size and thelevel of information disclosed, whereas McNally et al. (1982) concluded that size is adominant corporate characteristic in establishing the leaders in voluntary reportingpractice. Several measures can be taken as the measure of size of the firms. In the presentstudy, total assets (TA), total revenue (TR) and number of branches (NOB) were used asthe measure of size of the firms. The hypothesis taken here is given as follows:

H1. There is no significant relationship between the size of the bank (measured bytotal assets [TA], total revenue [TR] and number of branches [NOB]) and theextent of CSR reporting.

4.6.2 Age. The extent of a company’s CSR reporting may be influenced by its age (Singhand Ahuja, 1983; Owusu-Ansah, 1998; Akhtaruddin, 2005; Ullah, 2013). Bank with longyears of operation may report more information than newly established banks. The ageis counted from the date of enlistment of the banks in DSE. The hypothesis taken here isgiven as follows:

H2. There is no significant relationship between the age of the bank and the extentof CSR reporting.

4.6.3 Profitability. Banks with higher profit tends to report more information than lowerprofit earning banks. Many researchers have found a positive relationship betweenprofitability and the extent of reporting (Singh and Ahuja, 1983; Hossain, 1998, 2000;Raffournier, 1995; Wallace and Naser, 1995; Inchausti, 1997; Owusu-Ansah, 1998).Profitability here is measured by ROA and EPS. The hypothesis taken here is given asfollows:

H3. There is no significant relationship between the profitability of the bank(measured by ROA and EPS) and the extent of CSR reporting.

4.6.4 CSR expenditure. CSR reporting is also expected to influence by the amount of CSRexpenditure incurred by the banks because more expenditure on CSR is supposed torequire more information about the CSR activities entertained by the banks. It isexpected that the banks will try to uphold their image with more information on CSRactivities if the banks spend more on CSR areas. The hypothesis taken here is given asfollows:

JFRA13,2

206

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

H4. There is no significant relationship between the CSR expenditure (CSR_Exp) ofthe bank and the extent of CSR reporting.

4.6.5 Capital adequacy ratio. Capital adequacy ratio is a measure of overall financialstrength of a bank, which is expressed as a percentage of bank’s risk-weighted creditexposure. Banking companies having high capital adequacy ratio (CAR) may reportmore information in their annual reports than the banks with low capital adequacy ratio(CAR). If the ratio is poor, then the management may try to report less information tohide their lower performance, and if it is high, then they may try to report moreinformation to highlight their performance to the users of the reports (Ahmed, 2009;Ullah, 2013). The hypothesis taken here is given as follows:

H5. There is no significant relationship between the capital adequacy ratio (CAR) ofthe bank and the extent of CSR reporting.

5. Findings and analysis5.1 Total CSR disclosure levelTotal CSR reporting practices of the sample banks were analyzed, classifying the CSRitems into seven different categories. Table AIII shows that of the 97 items of selectedCSR information, on an average, 45.97 (47.39 per cent) items were reported by the samplebanks in their annual reports where the minimum reporting items was 27 (27.84 per cent)and maximum was 64 (65.98 per cent). Under the category of human resource, maximum12 (80 per cent) and minimum 4 (26.67 per cent) items of information were reported inannual report. Under the heading of consumer, maximum seven (100 per cent) items andminimum three (42.86 per cent) items were reported. In community category, maximum14 (60.87 per cent) and minimum number 4 (17.39 per cent) items were reported.Maximum eight (88.89 per cent) items and minimum two (22.22 per cent) items werereported under the category of health. In case of education, maximum seven (53.85 percent) and minimum one (7.69 per cent) items were reported in the annual reports. Underthe category of environment, maximum 14 (87.50 per cent) and minimum 0 items werereported. Finally, in the category of other items, maximum ten (71.43 per cent) andminimum three (21.43 per cent) items were reported by the banks. The bankingcompanies in Bangladesh reported maximum information under the category ofcommunity and minimum in case of environment. Maximum variation (SD � 2.55) isfound in case of community, and minimum variation (SD � 1.17) is in case of consumer.

Table AIV shows the comparative performance of the sample banks in which we seethat Jamuna Bank Limited achieved the highest position by reporting maximum 64items, and by reporting only 27 items, Pubali Bank Limited secured the last position.Detailed score of each bank is shown in Appendix 3.

5.2 Analysis of ways of CSR reportingExamination of the annual reports reveals that banking companies in Bangladesh usedwords, sentences, charts, graphs and pictures in CSR reporting during the study period.Table AVI represents the descriptive statistics of the number of words, sentences,charts, graphs and pictures used in CSR reporting. Appendix 4 provides the detailedways of CSR reporting information by the banking companies in Bangladesh.

As per Table AVI, banking companies in Bangladesh used maximum 9,952 wordsand minimum 433 words in reporting CSR information in their annual report.

207

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Table AVII shows that maximum 21(70 per cent) banks used less than 1,000-200 words,7 (23.33 per cent) banks used 2,000-4,000 words and only 2 banks used more than 6,000words for the CSR reporting in the annual report.

On the basis of Table AVI, it is observed that to report CSR, banking companies inBangladesh used maximum 611 sentences and minimum 31 sentences, and the averageis 128.20. Table AVIII shows that maximum 27 (90 per cent) banks used less than100-200 sentences, and only 2 banks used more than 500 sentences in reporting CSR inthe annual report.

Again, Table AVI shows that sample banks used maximum ten charts in reportingCSR information in their annual report. Table AIX shows that maximum 15 (50 per cent)banks used no chart, and 3 (10 per cent) banks used 7-10 charts relating to CSR activities.Maximum ten charts were used by Islami Bank Bangladesh Limited (Appendix 4).

It is also found that banking companies in Bangladesh used maximum 11 graphs inreporting CSR information in their annual report (Table AVI). Table AX shows thatmaximum 22 (73.33 per cent) banks used no graphs in reporting CSR information inannual report, 5 banks used only 1 graph and 1 bank, namely, Dutch-Bangla BankLimited, used maximum 11 graphs in this regard (Appendix 4).

From Table AVI, it is observed that banking companies in Bangladesh usedmaximum 75 pictures in reporting CSR in the annual report. Table AXI shows that 27(90 per cent) banks used less than 5-20, 2 (6.66 per cent) banks used 21-60 and only 1bank, namely, Dutch-Bangla Bank, used maximum 75 pictures in case of reporting CSRinformation (Appendix 4). Therefore, it is observed that banking companies inBangladesh emphasized on linguistic or written form than through charts, graphs orpictures in reporting CSR activities to their stakeholders.

5.3 Location of CSR reporting in annual reportThe locations of the CSR reporting are presented in Table AXII, which shows that 90 percent of the sample banks report CSR activities in a separate chapter, namely, CSRchapter, in the annual report, indicating that banking companies in Bangladesh aregiving importance to CSR reporting. It may be for two following reasons:

(1) getting tax rebate from government; and(2) increasing the image of the bank to the stakeholders.

On the other hand, only 10 per cent of the banks reported CSR information in the Boardof Director’s report, which is also an important part of the annual report. BangladeshBank observed that out of the listed banks, two state-owned commercial banks (SCBs),one specialized development bank (SDB) and 21 PCBs have reported the CSR activitiesin separate chapters of their annual reports in 2011. Moreover, BRAC Bank Limitedissued a separate report of their CSR activities, and HSBC issued a separate report oftheir CSR activities in Bangladesh in 2011. But, importantly, none of the banks operatingin Bangladesh have followed global reporting initiative (GRI) format of CSR reporting(Bangladesh Bank, 2012).

5.4 Changes in CSR reportingPresent study observed that the CSR regulatory changes can instigate the extent of CSRreporting. Comparative CSR reporting performance of the banking companies inBangladesh are depicted in Table AV. It is found that only two banks reported more

JFRA13,2

208

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

than 60 per cent items and only one bank found to report below 30 per cent items.Maximum 15 (50 per cent) banking companies in Bangladesh reported only 40-50 percent and 10 (33.33 per cent) banking companies reported 50-60 per cent items of theselected CSR items in their annual report. Compared to other studies (Belal, 1999; Azimet al., 2011), overall CSR reporting performance is not satisfactory in banking companiesin Bangladesh. The studies of Singh and Ahuja (1983), Savage (1994) and Tsang (1998)also found similar results, and the findings of the present study shows improvement ofCSR reporting if the results are compared with the findings of Imam (2000), Hossain et al.(2006), Khan et al. (2009) and Khan (2010). Similarly, Bangladesh Bank explained in theirCSR review report of 2011 that all four SCBs, one out of the four SDBs and all 30 PCBshave reported their CSR initiatives as supplements to usual annual financial reports. Outof these, two SCBs, one SDB and 21 PCBs have reported the CSR activities in separatechapters of their annual reports (Bangladesh Bank, 2012). Two SCBs, one SDB and 16PCBs have included plans in these chapters on CSR activities. Most of them haveprovided details of their programs including expenditure outlays in these reports. Oneprivate bank named BRAC Bank Limited issued a separate report of their CSR activities,and HSBC issued a separate report of their CSR activities in Bangladesh in 2011(Bangladesh Bank, 2012). But, importantly, none of the banks operating in Bangladeshhave thus far issued separate reports of their CSR programs and activities incomprehensive standard formats such as the GRI. The survey findings of KPMG (2013)also proved that CSR reporting have been gradually increasing in the Asia-Pacificregion. They opined that there has been a dramatic increase in CR reporting rates inAsia-Pacific over the past two years. Almost three quarters (71 per cent) of companiesbased in Asia-Pacific now publish CR reports – an increase of 22 percentage points since2011 when less than half (49 per cent) did so (KPMG, 2013).

5.5 Correlation and regression analysisTo examine the relationship between bank characteristics and extent of CSR reportingin annual report, size of the bank (measured by total asset, total revenue and number ofbranches), age of the bank, profitability (measured by ROA and EPS), amount of CSRexpenditure and capital adequacy ratio were taken as independent variables. From theTable AXIII, it is evident that, although there is a significant relationship of CSRexpenditure with total asset and EPS at 1 and 5 per cent, respectively, there is nosignificant relationship between the extent of CSR reporting and the selected bankcharacteristics; that is, all the null hypotheses are accepted.

Although different studies including Muttakin and Khan (2014); Belal and Owen(2007); Islam and Deegan (2008); Kolk (2003); Delaney and Huselid (1996) and Cowenet al. (1987) observed significant influence of different factors on CSR disclosure, thisstudy did not. Some reasons of having no relationship between extent of CSR reportingand selected bank characteristics include CSR reporting are voluntary disclosure for thebanking companies in Bangladesh, there is no specific format required for CSRreporting and banking companies do not follow GRI format in CSR reporting.Table AXIV reveals that these independent variables, that is, selected bankscharacteristics explained only 15.80 per cent (R2 � 0.158) of the extent of CSR reporting,and remaining 84.20 per cent of the extent of CSR reporting is influenced by some otherindependent variables which are not considered in this study. As the value of Durbin–Watson test is almost 2, there is no autocorrelation in the regression model.

209

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

6. Summary and conclusionThe study aimed to provide a real scenario of CSR reporting by the listed commercialbanks in Bangladesh. Discussions in the previous sections materialized this objective.The study observed a satisfactory level of CSR reporting by all listed commercial banksin Bangladesh, although there are no mandatory requirements from the legislativebodies regarding reporting of CSR. The study also aimed at evaluating the impact ofregulatory changes during 2008-2010 on CSR reporting in banking companies inBangladesh and found that volume and nature of CSR reporting have significantlyimpacted because of these regulatory changes. The study tried to identify whether thereis any association between the extent of CSR reporting and bank attributes but observedno significant relationship because of voluntary disclosure for the banking companies inBangladesh and because there is no specific format required for CSR reporting andbanking companies do not follow GRI format in CSR reporting (Bangladesh Bank, 2012).The study recommends regulatory bodies in formulating a common reportingframework for CSR reporting.

However, it has some limitations that should be borne in mind while using thefindings of the study. First, the study focuses on CSR reporting in annual report only inbanking companies in Bangladesh. Second, it covers only a single year (2011) and onlythe listed banking companies. Furthermore, the number of reporting items considered inevaluating CSR reporting performance is limited to 97 items. The study has someimplications too. Banking companies are expected to get a real scenario of CSR reportingof the banking sector in Bangladesh, and banking companies with poor CSR activitiesmay be motivated for contributing more in CSR activities. Banking companies ofBangladesh will be able to articulate social reporting and incorporating CSR activities intheir strategic decisions (Khan, 2010). More CSR information disclosure and structuredreporting will create a positive impression among the stakeholders, which, in turn,expect to sustain the banking business in Bangladesh by creating new legislation forthis sector and retaining the efficient employees (Tietenberg, 1998). Government andother regulatory bodies can get detailed information regarding CSR reporting practicesfor formulating guidelines in this regard because information disclosures may influencethe behavior of regulators as well (Stephan, 2002). The parties which need CSRcontribution may get information regarding CSR activities of different banks and cantake appropriate steps in getting CSR contribution. On the other hand, unexpected andinaccurate CSR information may signal devaluation of shares, reduction of profitmargins, increment in liabilities and ineffective management (Stephan, 2002).

The study recommends further researches on CSR reporting by banking companieswith a longitudinal analysis which may provide more insights into reporting,comparative CSR reporting practices between different industries in Bangladesh.Further research is also required to observe comparative CSR reporting practices ofbanking companies of different countries and CSR reporting practices of multinationaland local companies operating in Bangladesh.

The study observes that without any regulation, voluntary reporting like CSRreporting is unlikely to result in either high quality of reporting or sufficient level ofreporting. CSR initiative in the banking companies has been increasing day by day, andthe amount of expenditure varies from bank to bank. Recent CSR initiatives of centralbank pose the banks to develop and implement policies and practices to CSR issues likeenvironment, social, legal and economic theme, as Bangladesh Bank encourage CSR

JFRA13,2

210

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

engagement of the banks and, for the first time, imposed the newly proposed banks tospend 10 per cent of its previous year’s net income to CSR activities. As CSR reportingpractices differ among the banking companies in Bangladesh, legislative requirementsor guidelines from the regulatory bodies are required to bring the CSR reportingpractices into a certain framework and encourage more CSR reporting in Bangladesh.

ReferencesAbdullah, S.N., Mohamad, N.R. and Mokhtar, M.Z. (2011), “Board independence, ownership and

CSR of Malaysian large firms”, Corporate Ownership & Control, Vol. 8 No. 3, pp. 417-431.Achda, B.T. (2006), “The sociological context of corporate social responsibility development and

implementation in Indonesia”, Corporate Social Responsibility and EnvironmentalManagement, Vol. 13 No. 5, pp. 300-305.

Adams, C.A. (2002), “Internal organizational factors influencing corporate social and ethicalreporting: beyond current theorizing”, Accounting, Auditing and Accountability Journal,Vol. 15 No. 2, pp. 223-250.

Ahmed, A.A.A. (2009), “Compliance of financial disclosure in corporate annual reports of bankingsector in Bangladesh”, Unpublished PhD thesis, University of Rajshahi, Rajshahi.

Ahmed, K. and Nicholls, D. (1994), “The impact of non-financial company characteristics onmandatory compliance in developing countries: the case of Bangladesh”, The InternationalJournal of Accounting, Vol. 29 No. 1, pp. 60-77.

Akhtaruddin, M. (2005), “Corporate mandatory disclosure practices in Bangladesh”, InternationalJournal of Accounting, Vol. 40 No. 4, pp. 399-422.

Alam, S.M.S., Hoque, S.M.S. and Hosen, M.Z. (2010), “Corporate social responsibility ofmultinational corporations in Bangladesh: a case study on grameenphone”, Journal ofPatuakhali Science and Technology University, Vol. 2 No. 1, pp. 51-61.

Alimullah, M.M. (2006), “Dynamics of corporate social responsibility – Bangladesh context”,Journal of AIUB Bangladesh, Vol. 3 No. 1, pp. 13-32.

Azim, M.I., Ahmed, E. and D’Netto, B. (2011), “Corporate social disclosure in Bangladesh: a studyof the financial sector”, International Review of Business Research Papers, Vol. 7 No. 2,pp. 37-55.

Azim, M.I., Ahmed, S. and Islam, M.S. (2009), “Corporate social reporting practice: evidence fromlisted companies in Bangladesh”, Journal of Asia-Pacific Business, Vol. 10 No. 2, pp. 130-145.

Bangladesh Bank (2012), “Review of csr initiatives of banks-2011”, Agricultural Credit &Financial Inclusion Department, Bangladesh Bank, available at: www.bangladesh-bank.org/recentupcoming/news/oct022012newse.pdf (accessed 10 November, 2014).

Bayond, N.S., Kavanagh, M. and Slaughter, G. (2012), “Factors influencing levels of corporatesocial responsibility disclosure by Libyan firms: a mixed study”, International Journals ofEconomics and Finance, Vol. 4 No. 4, pp. 13-29.

Beattie, V. and Jones, M.J. (1992), “The use and abuse of graphs in annual reports: a theoreticalframework and empirical study”, Accounting and Business Research, Vol. 22 No. 88,pp. 291-303.

Beattie, V. and Jones, M.J. (1994), “An empirical study of graphical format choices in charityannual reports”, Financial Accountability and Management, Vol. 10 No. 3, pp. 215-236.

Belal, A.R. (1999), “Corporate social reporting in Bangladesh”, Social and EnvironmentalAccounting, Vol. 19 No. 1, pp. 8-12.

Belal, A.R. (2000), “Environmental reporting in developing countries: empirical evidence fromBangladesh”, Eco Management and Auditing, Vol. 7 No. 3, pp. 114-121.

211

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Belal, A.R. (2001), “A study of corporate social disclosures in Bangladesh”, Managerial AuditingJournal, Vol. 16 No. 5, pp. 274-289.

Belal, A.R. and Owen, D.L. (2007), “The view of corporate managers on the current state of, andfuture prospects for, social reporting in Bangladesh: an engagement-based study”,Accounting, Auditing and Accountability Journal, Vol. 20 No. 3, pp. 472-494.

Boje, D.M. and Farzad, R.K. (2009), “Story branding by empire entrepreneurs: Nike, child labor,and Pakistan’s soccer ball industry”, Journal Small Business & Entrepreneurship, Vol. 22No. 1, pp. 9-24.

Chowdhury, S.K.S. (2014), “Policy support to CSR in the context of tax exemption for the bankingsector”, paper presented as Keynote at BIBM Banking Conference, Bangladesh Institute ofBank Management, Mirpur, Dhaka, 26 April, available at: www.bb.org.bd/governor/speech/apr272014gse512.pdf (accessed 11 November, 2014).

Cooke, T.E. (1991), “An assessment of voluntary disclosure in the annual reports of Japanesecorporations”, The International Journal of Accounting, Vol. 26, pp. 174-189.

Cooke, T.E. (1992), “The impact of size, stock market listing and industry type on disclosure in theannual reports of Japanese listed corporations”, Accounting and Business Research, Vol. 22No. 87, pp. 229-237.

Coomba, H.M. and Tayib, M. (1998), “Developing a disclosure index of local authority publishedaccounts: a comparative study of local authority financial reports between the UK andMalaysia”, paper presented at the Asian Pacific Interdisciplinary Research in AccountingConference, Osaka.

Cowen, S.S., Ferreri, L.B. and Parkert, L.D. (1987), “The impact of corporate characteristics onsocial responsibility disclosure: a typology and frequency-based analysis”, Accounting,Organizations and Society, Vol. 12 No. 2, pp. 111-122.

Das, S.K. (2012), “CSR practices and CSR reporting in Indian financial sector”, InternationalJournal of Business and Management Tomorrow, Vol. 2 No. 9, pp. 1-5.

Delaney, J.T. and Huselid, M.A. (1996), “The impact of human resource management practices onperceptions of organizational performance”, Academy of Management Journal, Vol. 39No. 4, pp. 949-969.

Dhaka Tribune (2013), “Banks’ CSR spending soars 5 times in four years”, available at: www.dhakatribune.com/banks/2013/jun/02/banks%E2%80%99-csr-spending-soars-5-times-four-years, June 2, 2013, (accessed 11 November 2014).

Gamerschlag, R., Moller, K. and Verbeeten, F. (2011), “Determinants of voluntary CSR disclosure:empirical evidence from Germany”, Review of Managerial Science, Vol. 5 Nos 2/3,pp. 233-262.

Gray, R.H., Owen, D. and Maunders, K. (1987), Corporate Social Reporting: Accounting andAccountability, Prentice-Hall International, London.

GRI (2010), “GRI sustainability reporting statistics: publishing year 2010”, Global reportingInitiatives TM, available at: www.globalreporting.org/resourcelibrary/GRI-Reporting-Stats-2010.pdf (accessed 12 January 2013).

Guthrie, J. and Parker, L.D. (1990), “Corporate social disclosure practice: a comparativeinternational analysis”, Advances in Public Interest Accounting, Vol. 3, pp. 159-175.

Holsti, O.R. (1969), Content Analysis for the Social Sciences, Addison Wesley, London.

Hossain, M. (2001), “The disclosure of information in the annual reports of financial companies indeveloping countries: the case of Bangladesh”, Unpublished MPhil thesis, The Universityof Manchester, Manchester.

JFRA13,2

212

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Hossain, M.A. (1998), “Disclosure of financial information in developing countries: a comparativestudy of non-financial companies in India, Pakistan and Bangladesh”, PhD dissertation,School of Accounting and Finance, Victoria University of Manchester, Manchester.

Hossain, M.A. (2000), “Disclosure of financial information in developing countries: a comparativestudy of non-financial companies in India, Pakistan and Bangladesh”, Unpublished PhDdissertation, The University of Manchester, Manchester.

Hossain, M. (2008), “The extent of disclosure in annual reports of banking companies: the case ofIndia”, European Journal of Scientific Research, Vol. 23 No. 4, pp. 569-580.

Hossain, M.S. (2010), “Financial reporting practices of listed pharmaceuticals companied inBangladesh”, Unpublished PhD dissertation, National University.

Hossain, M., Tan, L. and Adams, M. (1994), “Voluntary disclosure in an emerging capital market:some empirical evidence from companies listed on the Kuala Lumpur stock exchange”,International Journal of Accounting, Vol. 29 No. 4, pp. 334-351.

Hossain, M., Islam, K. and Andrew, J. (2006), “Corporate social and environmental disclosure indeveloping countries: evidence from Bangladesh”, working paper, Faculty of Commerce,University of Wollongong.

Imam, S. (2000), “Corporate social performance reporting in Bangladesh”, Managerial AuditingJournal, Vol. 15 No. 3, pp. 133-142.

Inchausti, B.G. (1997), “The influence of company characteristics and accounting regulations oninformation disclosed by Spanish firms”, The European Accounting Review, Vol. 1 No. 1,pp. 45-68.

Islam, M.A. and Deegan, C. (2008), “Motivations for an organisation within a developing countryto report social responsibility information: evidence from Bangladesh”, Accounting,Auditing & Accountability Journal, Vol. 21 No. 6, pp. 850-874.

Ismail, T.H. (2002), “An empirical investigation of factors influencing voluntary disclosure offinancial information on the internet in the GCC countries”, Working Paper Series, SocialSciences Research Network, July.

Jamali, D. and Mishak, R. (2007), “Corporate social responsibility (CSR): theory and practice in adeveloping country context”, Journal of Business Ethics, Vol. 72 No. 3, pp. 243-262.

Kang, L.S. (2010), “Personal characteristics and executive compensation: a study of executivedirectors in India”, IUP Journal of Corporate Governance, Vol. 9 No. 3, pp. 28-37.

Khan, M.H.Z. (2010), “The effect of corporate governance elements on corporate socialresponsibility (CSR) reporting: empirical evidence from private commercial banks ofBangladesh”, International Journal of Law and Management, Vol. 52 No. 2, pp. 82-109.

Khan, M.H.Z., Halabi, A. and Samy, M. (2009), “CSR reporting practice: a study of selectedbanking companies in Bangladesh”, Social Responsibility Journal, Vol. 5 No. 3,pp. 344-357.

Kolk, A. (2003), “Trends in sustainability reporting by the fortune global 250”, Business Strategyand the Environment, Vol. 12 No. 5, pp. 279-291.

Kolk, A. and Lenfant, F. (2010), “MNC reporting on CSR and conflict in Central Africa”, Journal ofBusiness Ethics, Vol. 93 No. 6, pp. 241-255.

KPMG (2013), “The KPMG survey of corporate responsibility reporting 2013”, available at: www.kpmg.com/au/en/issuesandinsights/articlespublications/pages/corporate-responsibility-reporting-survey-2013.aspx (accessed 10 November 2014).

Krippendorf, K. (1980), Content Analysis: An Introduction to Its Methodology, Sage, New York,NY.

213

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

McNally, G.M., Eng, L.H. and Hasseldine, R. (1982), “Corporate financial reporting in NewZealand: an analysis of users preferences, corporate characteristics and disclosure practicesfor discretionary information”, Accounting and Business Research, Vol. 13 No. 49, pp. 11-20.

Masud, A.K. (2011), “CSR practices of private commercial bank’s in Bangladesh: a comparativestudy”, MPRA, Paper No. 35496, 24 December.

Millat, K.M. (2014), “Monitoring, evaluation and incentive mechanisms in support of sustainablebanking regulatory frameworks”, available at: http://firstforsustainability.org/media/Millat-BangladeshBank-SBN2014.pdf, (accessed 10 November 2014).

Moneva, J.M. and Liena, F. (2000), “Environmental disclosures in the annual reports of largecompanies in Spain”, European Accounting Review, Vol. 9 No. 1, pp. 7-29.

Muttakin, M.B. and Khan, A. (2014), Determinants of corporate social disclosure: empiricalevidence from Bangladesh, Advances in Accounting, Incorporating Advances inInternational Accounting, Vol. 30, pp. 168-175.

Owusu-Ansah, S. (1998), “The impact of corporate attributes on the extent of mandatorydisclosure and reporting by listed companies in Zimbabwe”, The International Journal ofAccounting, Vol. 33 No. 5, pp. 605-631.

Raffournier, B. (1995), “The determinants of voluntary financial disclosure by Swiss listedcompanies”, The European Accounting Review, Vol. 4 No. 2, pp. 261-280.

Rahman, S.R. (2006), “Corporate social reporting in India-A view from the top”, Global BusinessReview, Vol. 7 No. 2, pp. 313-324.

Rahul, H. (2010), “Corporate social responsibility-an Indian perspective”, Advances inManagement, Vol. 3 No. 6, pp. 42-44.

Sairally, S. (2007), “Community development financial institutions: lessons in social banking forthe Islamic financial industry”, Kyoto Bulletin of Islamic Area Studies, Vol. 1 No. 2,pp. 19-37.

Savage, A.A. (1994), “Environmental reporting: stakeholders’ perspective”, Working paper 94,University of Port Elizabeth, Port Elizabeth.

Silva, W.M. and Christensen, T.E. (2004), “Determinants of voluntary disclosure of financialinformation on the internet by Brazilian firms”, available at: papers.ssrn.com/so13/papers.cfm?abstract_id�638082

Singh, D.R. and Ahuja, J.M. (1983), “Corporate social reporting in India”, International Journal ofAccounting Education and Research, Vol. 18 No. 2, pp. 151-169.

Sobhani, F.A. and Azlan, A. (2009), “Revisiting the practices of corporate social and environmentaldisclosure in Bangladesh”, Corporate Social Responsibility & Environmental Management,Vol. 16 No. 3, pp. 167-183.

Spiegel, M.M. and Yamori, N. (2004), “Determinants of voluntary bank disclosure: evidence fromJapanese Shinkin banks”, CESifo Working Paper No. 1135, Category 6: Monetary Policyand International Finance, February, paper presented at Venice Summer Institute,Workshop on Economic Stagnation in Japan, July.

Stephan, M. (2002), “Environmental information disclosure programs: they work, but why?”,Social Science Quarterly, Vol. 83 No. 1, pp. 190-205.

Tietenberg, T. (1998), “Disclosure strategies for pollution control”, Environmental and ResourceEconomics, Vol. 11 Nos 3/4, pp. 587-602.

Tsang, E.W.K. (1998), “A longitudinal study of corporate social reporting in Singapore: the case ofthe banking, food and beverages and hotel industries”, Accounting Auditing andAccountability Journal, Vol. 11 No. 3, pp. 624-635.

JFRA13,2

214

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Ullah, M.H. (2013), “Accounting and reporting practices of Islamic banks in Bangladesh”,Unpublished MPhil thesis, University of Chittagong, Chittagong.

Ullah, M.H. and Yakub, K.M. (2013), “Environmental reporting practices in annual report ofselected listed companies in Bangladesh”, Research Journal of Finance and Accounting,Vol. 4 No. 7, pp. 45-58.

Wallace, R.S.O. and Naser, K. (1995), “Firm specific determinants of the comprehensiveness ofmandatory disclosure in the corporate annual reports of firms listed on the stock exchangeof Hong Kong”, Journal of Accounting and Public Policy, Vol. 14 No. 4, pp. 311-368.

Waller, D.S. and Lanis, R. (2009), “Corporate social responsibility (CSR) disclosure of advertisingagencies: an exploratory analysis of six holding companies’ annual reports”, Journal ofAdvertising, Vol. 38 No. 1, pp. 109-122.

Further readingGray, R., Kouhy, R. and Lavers, S. (1995), “Corporate social and environmental reporting –A

review of the literature and a longitudinal study of UK disclosure”, Accounting, Auditingand Accountability Journal, Vol. 8 No. 2, pp. 47-77.

Kreuze, J.G., Newell, G.E. and Newell, S.J. (1996), “Environmental disclosures: what companies arereporting?”, Management Accounting, Vol. 78 No. 1, pp. 37-46.

215

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Appendix 1

Table AI.Selection of CSRitems fordevelopment ofreporting index

Title of elementsNo. ofitems Sources cited as examples

Environment, human resources,community involvement, product safetyand other social responsibility, etc.

12 Azim et al. (2011)Masud (2011)Hossain (2008)

Staff welfare, donations, promoting ethicalvalues, Qard-Al-Hasanah, zakahcollection, fair recruitment, scholarshipprogram, etc.

10 Sairally (2007)

Environmental disclosure, consumerdisclosure and employee disclosure, etc.

29 Bayond et al. (2012)

Work place, market place, environmentand community, etc.

18 Abdullah et al. (2011)

Other factors 28 Bangladesh bank recent reform initiativepublication, NBR tax rebate policy,examples from other banks

Total items 97

Source: Developed by the authors

Table AII.The percentage ofthe number ofelements in eachcategory

Categories ofdisclosure

Humanresource Consumer Community Health Education Environment Others Total

Number ofelements 15 7 23 9 13 16 14 97% 15.46 7.22 23.71 9.28 13.40 16.49 14.43 100

Source: Developed by the authors

Table AIII.Descriptive statisticsof CSR reportingunder differentcategories and of thetotal

Categories ofdisclosure

Humanresource Consumer Community Health Education Environment Others Total

Mean 7.17 5.50 10.03 4.13 3.80 9.20 6.13 45.97Standard deviation 2.02 1.17 2.55 1.50 1.63 2.54 1.70 7.52Coefficient ofvariation 28.16 21.22 25.44 36.35 42.83 27.59 27.61 16.36Minimum 4.00 3.00 4.00 2.00 1.00 0.00 3.00 27.00Maximum 12.00 7.00 14.00 8.00 7.00 14.00 10.00 64.00

Source: Developed by the authors using SPSS software

JFRA13,2

216

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Table AIV.The ranking of

sample banks basedon total CSR

reporting score

RankBankname

Totaldisclosure (%) Rank

Bankname

Totaldisclosure (%) Rank Bank name

Totaldisclosure (%)

1 JBL 64 65.97 5 EXIM 50 51.54 11 PREMIER 42 43.292 IBBL 62 63.91 5 NBL 50 51.54 11 RBL 42 43.293 DBBL 54 55.67 6 MBL 48 49.48 12 OBL 41 42.264 FSIBL 51 52.57 7 NCC 46 47.42 12 UBL 41 42.264 BRAC 51 52.57 7 MTBL 46 47.42 13 TBL 40 41.234 PRIME 51 52.57 8 AAIBL 45 46.39 14 SIBL 39 40.204 SEBL 51 52.57 8 UCBL 45 46.39 14 ABBL 39 40.204 BAL 51 52.57 9 EBL 44 45.36 15 IFIC 38 39.174 DBL 51 52.57 10 CBL 43 44.32 16 ICBIBL 35 36.085 SJIBL 50 51.54 11 SBL 42 43.29 17 PUBALI 27 27.83

Source: Developed by the authors on the basis of total CSR reporting score

Table AV.Comparative CSRreporting analysis

Score rangeNo. of banks % in the sample% of the total number of items in CSR reporting index

Less than 30% 1 3.3330-40% 2 6.6740-50% 15 50.0050-60% 10 33.3360% and above 2 6.67Total 30 100.00

Source: Developed by the authors

Table AVI.Descriptive statisticsof number of words,

sentences, charts,graphs and pictures

Ways of disclosure Word Sentence Chart Graph Picture

Mean 2,001.40 128.20 1.83 0.83 12.37Standard deviation 2,216.66 131.09 2.70 2.25 15.68Coefficient of variation 110.76 102.25 147.54 271.09 126.76Minimum 433.00 31.00 0.00 0.00 0.00Maximum 9,952.00 611.00 10.00 11.00 75.00

Source: Developed by the authors using SPSS software

217

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Table AVII.Number of wordsused for CSRreporting

Range of words No. of banks (%)

0-1,000 11 36.671,000-2,000 10 33.332,000-3,000 6 20.003,000-4,000 1 3.334,000-5,000 0 05,000-6,000 0 06,000 and above 2 6.67Total 30 100

Table AVIII.Number of sentencesdevoted to CSRreporting

Range of sentences No. of banks (%)

0-100 16 53.34100-200 11 36.67200-300 1 3.33300-400 0 0400-500 0 0500-600 1 3.33600 and above 1 3.33Total 30 100

Table AIX.Number of chartsdevoted to CSRreporting

Range of charts No. of banks (%)

0 15 50.001-2 7 23.333-4 3 10.005-6 2 6.677 and above 3 10.00

Source: Developed by the authors

Table AX.Number of graphsused for CSRreporting

No. of graphs No. of banks (%)

0 22 73.331 5 16.674 1 3.335 1 3.3311 1 3.33

Source: Developed by the authors

JFRA13,2

218

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Table AXI.Number of pictures

used for CSRdisclosure

Range of pictures No. of banks (%)

0-5 13 43.336-10 5 16.6711-20 9 30.0021-40 1 3.3341-60 1 3.3361-75 1 3.33

Source: Developed by the authors

Table AXII.Location of CSR

reporting in annualreport

Locations No. of banks (%)

Chairman’s statement 0 0Managing Director’s statement 0 0Board of Director’s report 3 10.00Separate CSR chapter 27 90.00Total 30 100.00

Source: Developed by the authors

Table AXIII.The correlation

between CSRdisclosure and bank

attributes

Variables Total_disclosure Log_TA Log_TR NOB Age ROA EPS Log_CSR_Exp CAR

Total_disclosure 1Log_TA 0.225 1Log_TR 0.171 0.708** 1NOB 0.108 0.443* 0.217 1Age �0.045 0.394* 0.163 0.556** 1ROA 0.185 0.310 0.793** 0.117 �0.087 1EPS 0.103 0.380* 0.575** 0.450* 0.245 0.586** 1Log_CSR_Exp 0.230 0.681** 0.341 0.218 0.061 0.080 0.379* 1CAR 0.242 0.336 0.797** 0.155 �0.123 0.952** 0.520** 0.094 1

Notes: ** Correlation is significant at the 0.01 level (two-tailed); * correlation is significant at the 0.05 level (two-tailed)Source: Developed by the authors using SPSS software

219

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Appendix 2

Table AXIV.The model summaryof the studya

Model R R2

Standard errorof the

estimate

Change statisticsDurbin –Watson

R2

changeF

change df1 df2Significance

F change

1 0.397b 0.158 8.11478 0.158 0.492 8 21 0.848 1.960

Notes: a Dependent variable: Total_Disclosure; b predictors: (constant), CAR, Log_CSR_Exp, Age,NOB, EPS, Log_TA, Log_TR, ROASource: Developed by the authors using SPSS software

Table AXV.List of banks understudy

Serial no. Banks Serial no. Banks

1 AB Bank Limited 16 Mutual Trust Bank Limited2 Al-Arafah Islami Bank Limited 17 National Bank Limited3 Bank Asia Limited 18 NCC Bank Limited4 BRAC Bank Limited 19 One Bank Limited5 City Bank Limited 20 Premier Bank Limited6 Dhaka Bank Limited 21 Prime Bank Limited7 Dutch-Bangla Bank Limited 22 Pubali Bank Limited8 Eastern Bank Limited 23 Rupali Bank Limited9 EXIM Bank Limited 24 Shahjalal Islami Bank Limited

10 First Security Islami Bank Limited 25 Social Islami Bank Limited11 ICB Islami Bank Limited 26 Southeast Bank Limited12 IFIC Bank Limited 27 Standard Bank Limited13 Islami Bank Bangladesh Limited 28 Trust Bank Limited14 Jamuna Bank Limited 29 United Commercial Bank Limited15 Mercantile Bank Limited 30 Uttra Bank Limited

JFRA13,2

220

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Appendix 3

Table AXVI.Selected CSR

reporting items

A. Human resource1 Job creation of human resource2 Employee health and safety3 Information of accidents and injuries4 Employee training and development5 Increasing employee financial and economic awareness6 Employee profit share7 Equal opportunity8 Racial equality9 Sexual equality

10 Employee medical assistance11 Canteen, transportation and crèches for the employees children12 Reward/promotion/motivation13 Helping in funeral of employee14 Provide scholarship to the employee’s children/reward for excellent result/benevolent fund15 Home loan/car loan facility for the employees

B. Consumer16 Product and consumer safety17 Consumer complaints18 Product quality19 Responsiveness to customer20 Ethical principles in stakeholder engagement21 Good customer relation22 Protecting financial privacy of customers

C. Community23 Donation to the charity, sports, arts24 Social welfare25 Rehabilitation program (old home, orphanage, home for distress)26 Parks and gardens27 Road/city beautification28 Public hall and auditorium29 Organization’s social campaign30 Sponsoring religious programs31 Sponsoring sports program32 Zakat collections and distributions33 Loan without interest (Qard-Al-Hasanah)34 Rural development35 Warm cloth/blanket distribution to cold affected people36 Mosque construction37 Bridge/foot over bridge construction38 Honored to eminent person39 Support to Libya returnees40 Financial assistance to freedom fighter41 Initiatives to empowering women

(continued)

221

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Table AXVI.

42 Disclosure regarding opening of company’s facilities to the public43 Supporting the development of local industries or community programs and activities44 Schemes for taking on and helping young unemployed45 Financial assistance to small and medium enterprise

D. Health46 Medical college and hospital establishment47 Health campaign48 Medical assistance to distressed people49 Financial assistance to the poor people for treatment50 Sponsoring in medical research51 Sponsoring seminar on health issue52 Financial grants for autism53 Funding in equipment/medicine/ambulance purchase of hospital54 Financial assistance to medical college/hospitals/clinic

E. Education55 Establishment educational institutions (schools, college, madrasha, libraries)56 Sponsoring science fair, math olympiad, quiz competition, art exhibition, etc.57 Funding scholarship program58 Vocational training59 Part-time employment of students or disabled60 Sponsoring science/research project61 Book distribution to school students62 Financial assistance to educational institutions63 Monthly scholarship/stipend to students64 Internship opportunity65 CSR initiative/gift kit for primary school students66 Salary to teachers67 Vehicle gift to educational institutions

F. Environment68 Environmental policy or company concern for the environment69 Energy usage, savings and conservation70 Environmental education71 Tree plantation72 Exemption on environment friendly project/loan73 Sponsoring seminar and conference on environment74 Tourism development75 Agricultural development76 Pure drinking water and sanitation77 Investment in environment friendly project78 Green banking79 Solar panel distribution to the poor people80 Reducing pollution from product use81 Providing online information to reduce pollution82 Use of solar panel in office83 Climate change risk fund

(continued)

JFRA13,2

222

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Table AXVI.

G. Others84 Program for the disabled85 Donations to the non-governmental organizations86 Voluntary blood donation programs87 Food donations88 Disaster relief program89 Donation to PM fund90 Pilkhana BDR Carnage91 Financial contribution in Nimtoli tragedy92 Financial assistance for Sidr affected93 Financial assistance for the family of Mirsarai road accident94 Heritage preservation95 Employment and advancement of minorities96 Employment and advancement of women97 Special care for non-resident Bangladeshis

223

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

Appendix 4

Table AXVII.Total disclosurescore of the banks

BanksHumanresource Consumer Community Health Education Environment. Other Total

IBBL 12 7 13 5 5 13 7 62SJIBL 11 7 9 3 3 11 6 50AAIBL 5 4 13 4 3 10 6 45FSIBL 8 6 14 4 3 9 7 51ICBIBL 4 4 6 3 7 8 3 35EXIM 8 5 11 7 5 10 4 50SIBL 8 3 10 3 3 6 6 39ABBL 6 6 9 3 2 8 5 39BRAC 7 6 12 3 6 10 7 51IFIC 7 3 9 3 5 8 3 38NBL 10 6 12 3 4 9 6 50NCC 4 6 11 5 3 9 8 46TBL 4 7 8 4 5 8 4 40OBL 7 6 9 3 3 9 4 41PRIME 8 6 12 4 7 10 4 51SEBL 7 6 12 5 6 8 7 51SBL 7 6 8 3 3 9 6 42BAL 8 5 8 5 5 14 6 51MBL 8 6 11 4 4 8 7 48PREMIER 5 7 11 2 2 9 6 42JBL 8 5 14 7 6 14 10 64CBL 8 6 9 2 2 8 8 43PUBALI 5 4 4 5 3 0 6 27UBL 7 6 9 4 1 8 6 41DBL 9 6 7 5 4 12 8 51DBBL 5 5 14 8 5 11 6 54MTBL 10 6 6 4 2 10 8 46EBL 5 6 8 6 2 9 8 44UCBL 7 6 10 5 3 10 4 45RBL 7 3 12 2 2 8 8 42

JFRA13,2

224

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)

About the authorsMd. Hafij Ullah has completed his BBA, MBA and M. Phil. and is currently a PhD fellow at theMacquarie University, Sydney, Australia. Hafij is an Associate Professor, Department of BusinessAdministration, International Islamic University Chittagong, Bangladesh. He has more than nineyears of teaching experience at undergraduate and post-graduate levels. Hafij has 16 researchpublications published in national and international journals. His research interests includeEnvironmental accounting and accountability, conventional and Islamic disclosures, Islamicaccounting, Islamic banking, Shari‘ah compliance, etc. Md. Hafij Ullah is the correspondingauthor and can be contacted at: [email protected]

Mohammad Afjalur Rahman has completed his BBA, MBA from International IslamicUniversity Chittagong and currently he is a PhD fellow in the Department of BusinessAdministration at Ataturk University, Turkey. Afjalur is an Adjunct Faculty, Department ofBusiness Administration, International Islamic University Chittagong, Bangladesh. Afjalur hassix research publications published in national and international journals.

For instructions on how to order reprints of this article, please visit our website:www.emeraldgrouppublishing.com/licensing/reprints.htmOr contact us for further details: [email protected]

225

Reportingpractices in

bankingcompanies

Dow

nloa

ded

by M

acqu

arie

Uni

vers

ity, M

D. H

AFI

J U

LL

AH

At 1

5:29

18

Sept

embe

r 20

15 (

PT)