Money and Banking

158

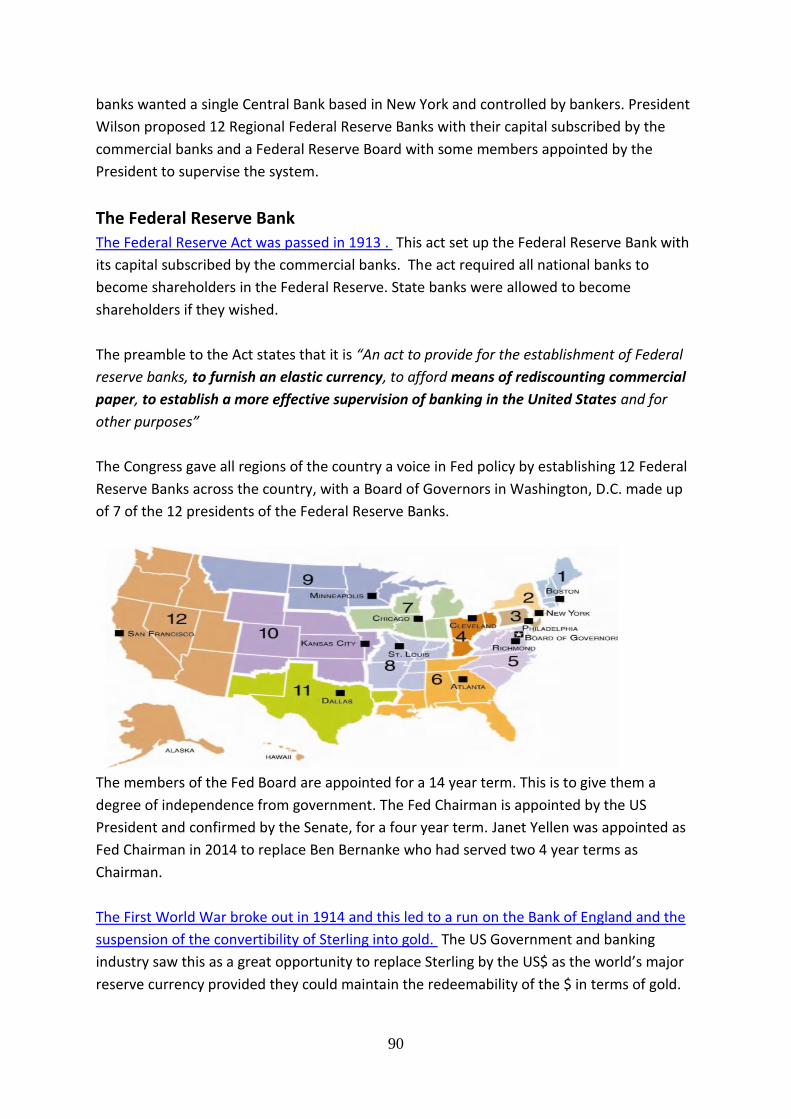

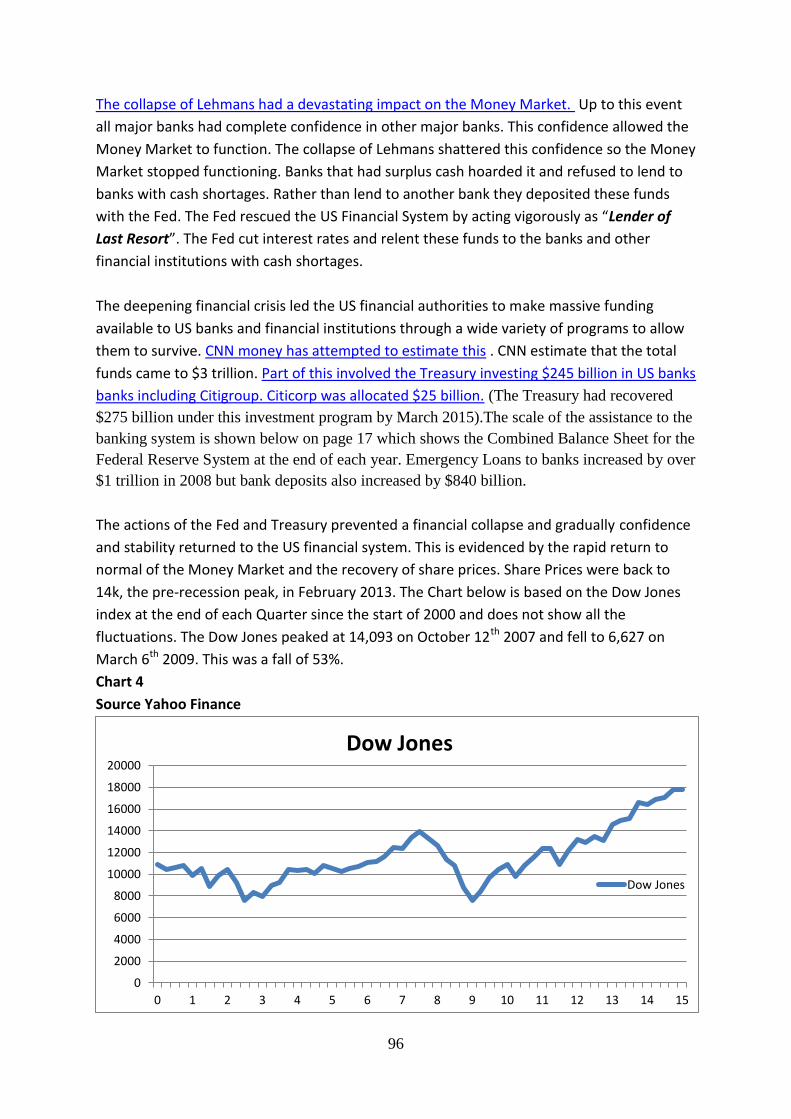

1 Money and Banking Notes for the Money and Banking students, Course BSB 6301, in Bahrain Polytechnic Section Title Page 1 Bahrain Economy and Financial System 2 2 Money and the Financial System 14 3 Commodity Markets 42 4 Macro-Economics 59 5 The British Financial System 75 6 The US Financial System 88 7 The Eurozone and its currency 108 8 Asset Valuation 126 9 Bills, Bonds and Interests Rates 139 10 International Finance 150

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Money and Banking

1

Money and Banking

Notes for the Money and Banking students, Course BSB 6301, in Bahrain Polytechnic

Section Title Page

1 Bahrain Economy and Financial System 2

2 Money and the Financial System 14

3 Commodity Markets 42

4 Macro-Economics 59

5 The British Financial System 75

6 The US Financial System 88

7 The Eurozone and its currency 108

8 Asset Valuation 126

9 Bills, Bonds and Interests Rates 139

10 International Finance 150

2

Bahrain Economy and Financial System

Introduction

This section covers Bahrain’s population and employment, resources, economy, government

budget, currency and exchange rate, financial institutions, “Vision 2030” and the

International Competitiveness Survey.

Bahrain covers an area of 750 square kilometers but has a sea area of 7,500 square

kilometers. Bahrain only has a very small amount of agricultural land and is therefore highly

dependent on food imports. Bahrain has a rapidly depleting oil and gas resource which

underpinned the economy in the past. Bahrain therefore urgently requires economic

diversification. A very good source of information on all countries including Bahrain is CIA

Bahrain.

Bahrain Population and Employment

Table 1

The Population of Bahrain in 2011 was:

Bahrainis 584,688

Non-Bahrainis 610,322

Total 1,195,020

Table 2, below, shows the rapid growth in the population of the country since the first

census was taken in 1941.

Table 2

Year Bahrainis Non-Bahrainis Total

1941 74k 15k 89k

1971 178k 38k 216k

1981 238k 112k 351k

1991 323k 185k 508k

2001 406k 245k 650k

2011 585k 610k 1,195k

Source for Tables 1 and 2, Central Informatics organization

The Bahraini part of the population is growing steadily at about 2.0% pa. In 2013 there were

15k births and only 2k deaths among the Bahraini section of the population.

The Non-Bahraini part has grown very rapidly but the rate of growth is very unstable, eg -

the number fell by over 7% between 2010 and 2011, and varies with the state of the

economy.

3

Bahrain is highly dependent on a Non-Bahraini workforce as they make up 77% of the

workers in the Country. The Table below shows the workforce in different sectors.

Table 3

Employment in Sectors Total Bahrainis Non-Bahrainis

Manufacturing 81k 15k 65k

Construction 131k 11k 120k

Trade 127k 24k 103k

Finance 14k 9k 5k

Government 58k 53k 5k

Domestic 95k 0k 95k

Other 142k 36k 107k

Total 648k 148k 500k

Source, Bahrain Economic Development Board

The Employment Participation Rate in Bahrain is low by international standards. The

standard method of measuring Employment Participation Rates is to calculate the

percentage of the population aged between 24 and 65 who are working. The table below

gives Employment Participation rates for Bahrain and the 27 countries of the European

Union. The Participation Rates for Bahraini Females is very low by international standards.

Table 4

Bahrain EU 27

Male 82% 74%

Female 40% 62%

Total 61% 68%

Sources, Bahrain CIO and Eurostat

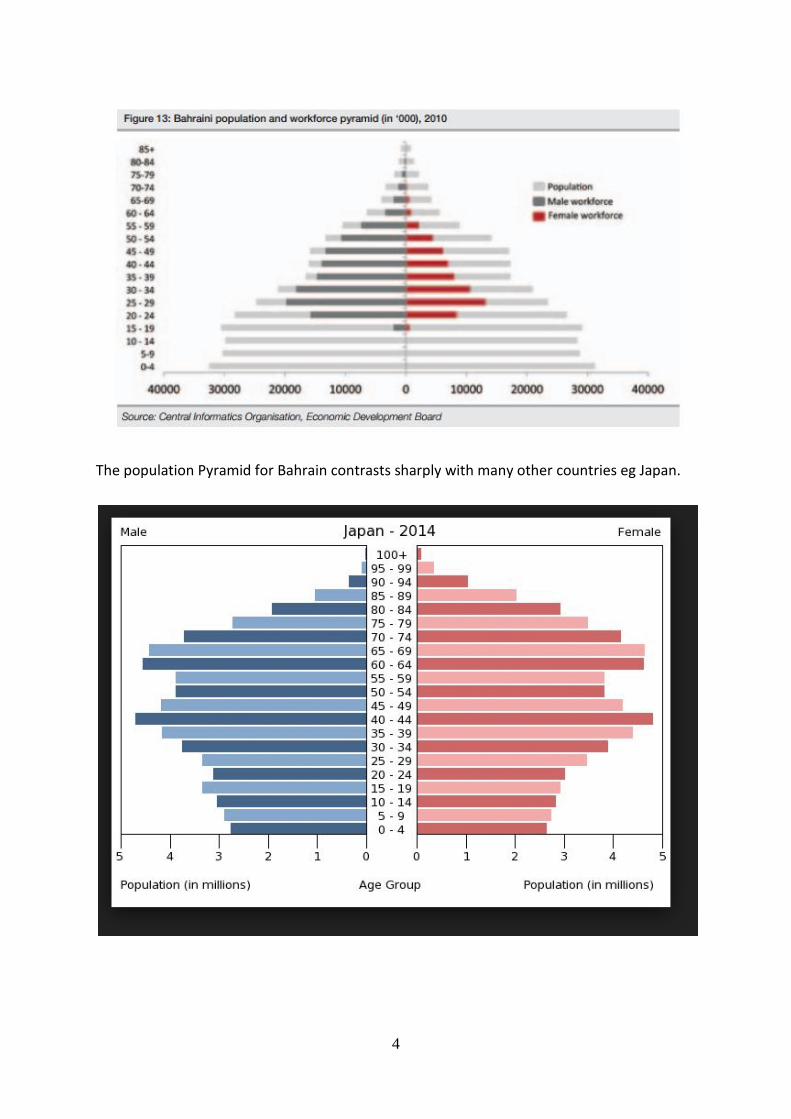

The Bahrain Population and workforce can be represented as a pyramid. This diagram is

copied for the 2013 Annual Report of the Bahrain Economic Development Board. The shape

of the population pyramid reflects the rapid population growth and youn age structure of

the population.

4

The population Pyramid for Bahrain contrasts sharply with many other countries eg Japan.

5

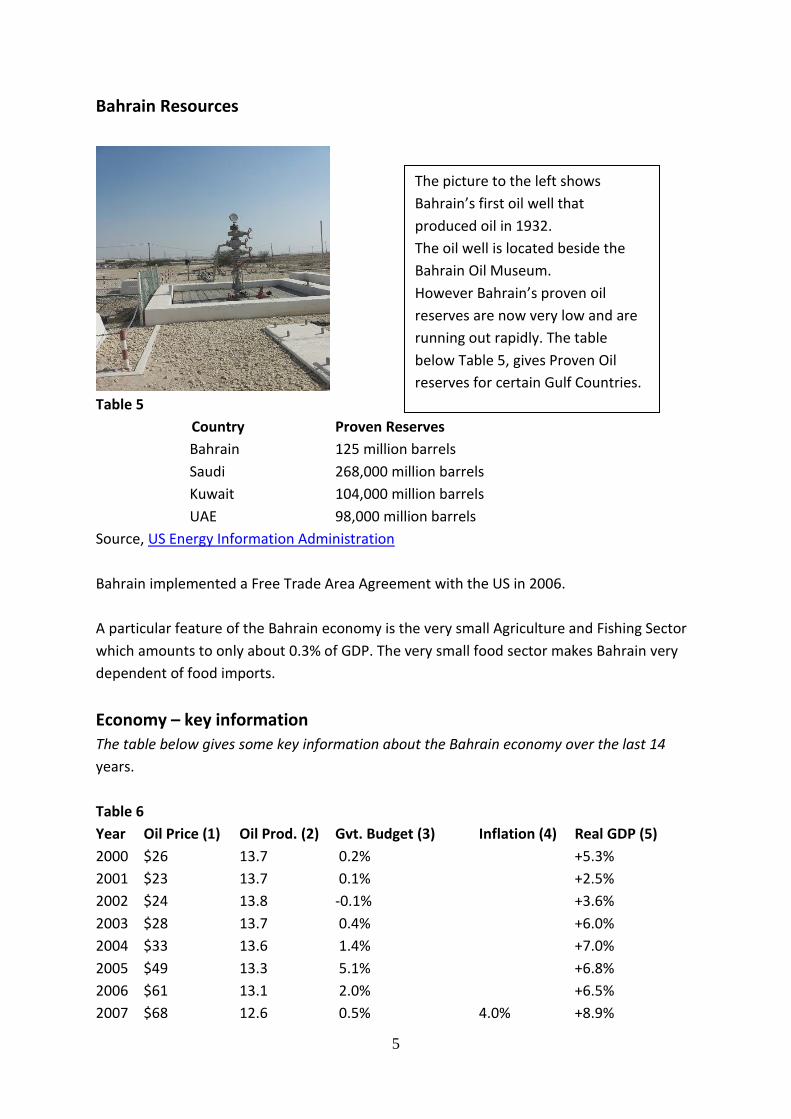

Bahrain Resources

Table 5

Country Proven Reserves

Bahrain 125 million barrels

Saudi 268,000 million barrels

Kuwait 104,000 million barrels

UAE 98,000 million barrels

Source, US Energy Information Administration

Bahrain implemented a Free Trade Area Agreement with the US in 2006.

A particular feature of the Bahrain economy is the very small Agriculture and Fishing Sector

which amounts to only about 0.3% of GDP. The very small food sector makes Bahrain very

dependent of food imports.

Economy – key information

The table below gives some key information about the Bahrain economy over the last 14

years.

Table 6

Year Oil Price (1) Oil Prod. (2) Gvt. Budget (3) Inflation (4) Real GDP (5)

2000 $26 13.7 0.2% +5.3%

2001 $23 13.7 0.1% +2.5%

2002 $24 13.8 -0.1% +3.6%

2003 $28 13.7 0.4% +6.0%

2004 $33 13.6 1.4% +7.0%

2005 $49 13.3 5.1% +6.8%

2006 $61 13.1 2.0% +6.5%

2007 $68 12.6 0.5% 4.0% +8.9%

The picture to the left shows

Bahrain’s first oil well that

produced oil in 1932.

The oil well is located beside the

Bahrain Oil Museum.

However Bahrain’s proven oil

reserves are now very low and are

running out rapidly. The table

below Table 5, gives Proven Oil

reserves for certain Gulf Countries.

6

2008 $94 12.0 3.9% 0.5%* +3.1%

2009 $62 11.8 -8.4% 1.6% +2.7%

2010 $78 11.1 -8.0% 1.0% +4.4%

2011 $106 15.5 -3.0% 0.2% +1.9%

2012 $110 16.6 -2.0% 2.6% +3.4%

2013 $105 -5.3% 4.0% +5.3%

2014 $96 +4.5%

(1) $ per barrel. Source, World Bank, Dubai Price Series

(2) Crude Oil produced in Bahrain in millions of barrels pa. Source, BEDB, Economic

Development Board

(3) Budget Surplus/Deficit as % of GDP. Source, Ministry of Finance,

https://www.mof.gov.bh/

(4) Consumer price Index, Source, Central Informatics Organization, * November 2008

(5) GDP Growth adjusted for inflation, Source, BEDB

Government Budget

The Bahrain Government Budgets for 2013 and 2014 are as follows:

Table 7

Revenue in millions of BD 2013(O) 2014(F) 2014(O) 2015(F)

Oil and Gas Revenue 2,600 2,404 2,662 1,824

Taxation and Fees 224 199 203

Gvt. Goods and Services 53 54 54

Investments and Gvt. Property 18 76 82

Grants 0 38 28

Sale of Capital Assets 0 0 1

Fines, Penalties and Miscellaneous 49 22 59

Total Revenue 2,944 2,793 3,089 2097

Recurrent Expenditure

Manpower 1,300 1,393 1,379

Services 211 193 223

Consumables 131 144 148

Assets 31 34 36

Maintenance 67 68 69

Transfers 695 800 729

Grants and Loan Interest 442 520 511

Total Recurrent Expenditure 2,877 3,153 3,096 3,136

Projects 477 826 448 435

Total Expenditure 3,354 3,978 3,544 3,570

Surplus (Deficit) in Budget (410) (1185) (455) (1,474)

7

Notes, (O) = Outturn, (F) = Forecast

Sources Ministry of Finance, Consolidated Final Accounts

Ministry of Finance, Projections for 2015 and 2016

The dependence of Bahrain on Oil and Gas Revenue, which are both subject to commodity

price fluctuations, makes budgeting very difficult.

The Next table shows the Overall Budget Outturn for the Bahrain Government for the last

14 years:

Table 8

Year Revenue Expenditure Balance

2005 1,671 1,289 382

2006 1,840 1,558 281

2007 2,037 1,818 219

2008 2,678 2,173 547

2009 1,708 2,154 -446

1020 2,176 2,635 -460

2011 2,821 2853 -31

2012 3,034 3,261 -226

2013 2,944 3,354 -410

2014 3,098 3,544 -455

Sources, Ministry of Finance,

The Budget Deficits of recent years are leading to an increase in Bahrain’s National Debt.

The Table below gives the Bahrain’s Public Debts Instruments as a % of GDP for some recent

years.

Table 9

Year Public Debt Instruments as % of GDP

2009 18.3%

2010 29.0%

2011 29.0%

2012 33.9%

2014 41.4%

Source CBB, Economic Indicators

Bahrain Government Bonds have a BBB rating with Standard and Poor and the rates of

interest on Bahrain Government Bills and Bonds are given below on page 10 below.

8

Currency and Exchange Rate

The major currency in use in Bahrain up to 1959 was the Indian Rupee issued by Reserve

Bank of India. The Rupee was pegged to the £ Sterling at 13.33 = £. Rupees circulating in

the Gulf were used to circumvent Indian restrictions on the purchase of gold. In 1959 the

Reserve Bank of India issued a new “Gulf Rupee” which had the same value as the “Indian

Rupee” but which had restriction on its use for purchasing gold.

The Gulf Rupee was the dominant currency in Bahrain from 1959 to 1965. In 1965 Bahrain

set up the Bahrain Currency Board and introduced the Bahrain Dinar (BD). The value of the

BD was set at 1.86621 grams of gold and 10 Gulf Rupees. (The BD has strengthened relative

to the Rupee and is now, December 2014, worth 164 Rupees) The notes were printed by De

La Rue in London. The BD became the Legal Tender in Bahrain and the Gulf Rupees were

exchanged for BDs.

After independence in 1971 Bahrain set up the Bahrain Monetary Agency to act as a Central

Bank for Bahrain. The Bahrain currency was rocked by counterfeiting of BD 20 notes in 1998

but this was overcome by printing a new set of BD 20 notes.

In 2006 the Central Bank of Bahrain (CBB) was set up and it took over the duties of the

Bahrain Monetary Agency. The CBB is responsible for Monetary Policy and Bank Regulation.

http://www.cbb.gov.bh/

Bahrain has a long history of pursuing a fixed exchange rate policy. The Economist Magazine

reported on August 1st 1964 that one of the reasons that Bahrain was going to introduce its

own currency was “to avoid being pulled into a forced devaluation by India”. The Dinar was

pegged to the $ in 1980. In 2001, the fixed exchange rate with the USD was made official.

Bahrain is committed to an exchange rate peg at BHD 0.376 per US Dollar, corresponding to

approximately BHD 1 = USD 2.65957.

The exchange rate peg aims at protecting the currency’s external value while ensuring

internal price stability. Within this framework, the Central Bank has flexibility to alter

domestic monetary conditions by changing policy interest rates, introducing prudential

guidelines on bank lending and adjusting reserve requirements to achieve the required

balance between price stability and growth.

Since Bahrain is a small and open economy with foreign trade accounting for more than

110% of nominal GDP, the exchange rate represents a logical anchor for monetary policy. It

reduces transaction costs and exchange rate uncertainty, and thereby stimulates trade.

Given the role of the US Dollar as the leading global reserve currency as well as its central

role in international trade and finance, pegging the Bahrain Dinar to the Dollar enhances the

credibility of monetary policy and contributes to financial stability.

9

The Central Bank of Bahrain (CBB) defines its role as “the main authority responsible for

maintaining monetary and financial stability, and having the instruments and operational

independence in pursuing its policy objectives. It is also the single integrated regulator of

Bahrain’s financial industry “.

The CBB utilizes three main monetary policy instruments to influence liquidity conditions in

the banking sector:

Exchange rate facility: CBB offers to buy/sell Bahraini Dinars against the US

Dollar at rates very close to the official exchange rate. CBB provides this

facility to all commercial banks located in the Kingdom of Bahrain.

Standing facilities: A set of lending and deposit facilities designed to influence

overnight liquidity, overnight interest rates and steering the short-term

money market to the key policy rate determined by the CBB. The lending

facilities are Overnight Secured Loans and One week Repo Loans. The rate of

interest on these loans was 2.25% in June 2014. The rate of interest on

deposits was 0.5% in June 2014.

Reserve Requirements: All commercial banks operating in the Kingdom of

Bahrain are required to maintain reserves deposited at the CBB amounting to

5% of the value of non-bank deposits denominated in Bahraini dinars. The

reserves are not remunerated.

The Bahrain Central Bank is responsible for Financial Stability in Bahrain. The central bank

licences and regulates the banks in Bahrain and if any bank gets into trouble the CBB will

intervene to protect depositors or other creditors. In July 2009 Bahrain's central bank took

control of Awal Bank because there was a substantial shortfall in their assets relative to

their liabilities. This decision was appealed in court by persns linked to Awal bank but the

court found that CBB had acted legally

Financial Institutions

Bahrain has a very large financial services industry relative to the size of the economy. In

2012 the country had 405 firms involved in financial services.

Table 10

Category Number of Firms

Conventional Banks 77

Islamic Banks 26

Insurance Companies 152

Investment Firms 49

Specialized Financial Firms 79

Capital Markets Firms 22

Total 405

10

Source CIO

The Money Supply in Bahrain at the end of April 2014 was as follows:

Table 11

Category BD in Millions

Currency outside the banking system 486

Private Demand Deposits 2,468

M1, Narrow Money Supply 2,953

Term and Savings Deposits 6,650

M2, Medium Money Supply 9,603

Government Deposits 1,821

M3, Broad Money Supply 11,425

Source CBB, Page 3

The table below gives some aggregated information about the Assets of the Bahrain banking

System:

Table 12

Category BD billions

Total Assets of Banking System 193

Retail Bank Assets 78

Wholesale Bank Assets 115

Islamic Banks 24

Domestic Assets 50

Source, CBB

The Lending by the Banking System was broken down as follows by Sector for end of 2012.

Table 13

Business Sector Total Lending

Personal 2,368

Government 198

Transport 249

Trading 960

Construction 1,642

Agriculture and Fishing 12

Mining and Quarrying 9

Manufacturing 538

Others 874

Total 6,849

Source CBB, Page 9

11

An interesting feature of Bahrain bank lending was the rapid growth in Bank Lending to

Construction between the end of 2005 and the end of 2008. During this period the total

lending by Bahrain banks to the construction Industry increased from BD302 million to BD

1540 million. This massive growth in bank lending followed the pattern in many parts of the

world including the US where bank lending fuelled a property bubble.

The Interest rates on various Financial Assets was as follows for April 2014:

Table 14

Financial Asset Interest Rate

Personal Loans 6.24%

Business Loans 4.73%

Interest on Deposits 1.05%

Money market rates, 3 Months 0.24%

Money market rates, 6 Months 0.34%

Treasury Bills, 3 Months 0.87%

Treasury Bills, 6 Months 1.08%

Treasury Bills, 12 Months 1.25%

Source, CBB

The CBB issues Government Bonds on behalf of the Government. An example is as follows,

GDEV. BND 19 which was issued on 08/11/2012 and will mature on 08/11/2019. This was

issued in BD1,000 units and has an interest rate of 4.3%. The average rate of interest on

Bahrain Government Bonds was 2.62% in April 2014

The rates of interest on the Bahrain Money market over the last 9 years are shown in the

next diagram which is taken from the BEDB 2013 Annual Report.

12

Vision 2030

Vision 2030 is a comprehensive long-term economic and social vision for the development

of Bahrain. Vision 2030 was adopted in 2008 after wide consultation. Bahrain Vision 2030 is

a vision for Bahrain as it addresses the issues linked to a decline in oil revenues and a rapidly

growing population. Oil revenues played a vital role in the economy of the country for the

last 80 years. The population of Bahrain is growing rapidly with the population growing by

over 13 times between 1941 and 2011.

The following extracts from the document highlight some of the challenges facing Bahrain:

“We aspire to shift from an economy built on oil wealth to a productive, globally

competitive economy, shaped by the government and driven by a pioneering private sector

– an economy that raises a broad middle class of Bahrainis who enjoy good living standards

through increased productivity and high wage jobs.”

“Our society and government will embrace the principles of sustainability and fairness to

ensure that every Bahraini has the means to live a secure and fulfilling life and reach their

full potential”.

“Bahrain is facing a shortage of both quality employment and appropriate skills.”

“4,000 Bahrainis a year are entering the job market with at least a college degree. The

private sector is creating on average only 1,100 jobs per annum with a monthly salary of at

least BHD 500 for Bahrainis and about 2,700 for non-Bahrainis.”

“Bahrainis are not the preferred choice for employers in the private sector since the

education system does not provide the young people with the skills and knowledge needed

to succeed in our labour market.”

“For many years Bahrain has been able to address these issues by redistributing oil revenues

and offering citizens jobs in the public sector. This has left us with an oversized public sector

– a situation that will be unsustainable in the future considering the gradual decline of oil

revenues.”

“The sustainability of government finances is strengthened by reducing dependence on oil

revenues to fund current expenditure”

“The most sustainable way of resolving the imbalance and raising the quality of employment

is a transformation to an economy driven by a thriving private sector – where productive

enterprises, engaged in high value added activities offer attractive career opportunities to

suitably skilled Bahrainis.”

13

“On a Global scale, Bahraini innovation is currently negligible.”

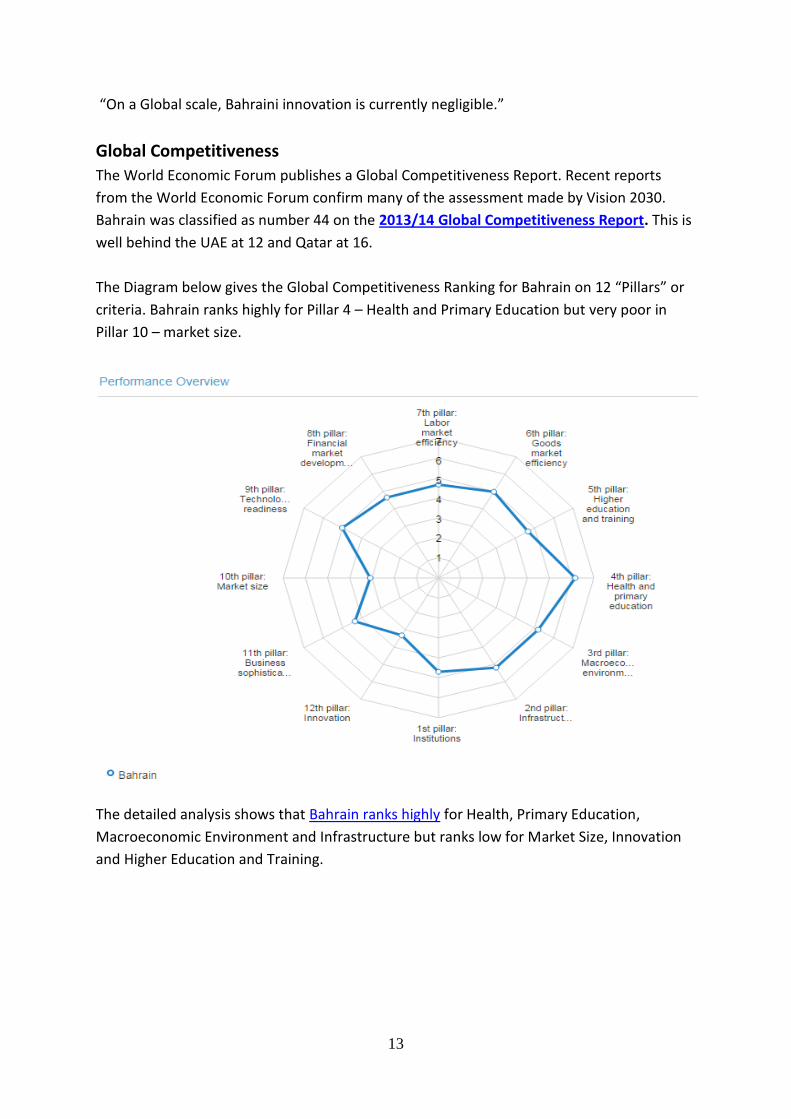

Global Competitiveness

The World Economic Forum publishes a Global Competitiveness Report. Recent reports

from the World Economic Forum confirm many of the assessment made by Vision 2030.

Bahrain was classified as number 44 on the 2013/14 Global Competitiveness Report. This is

well behind the UAE at 12 and Qatar at 16.

The Diagram below gives the Global Competitiveness Ranking for Bahrain on 12 “Pillars” or

criteria. Bahrain ranks highly for Pillar 4 – Health and Primary Education but very poor in

Pillar 10 – market size.

The detailed analysis shows that Bahrain ranks highly for Health, Primary Education,

Macroeconomic Environment and Infrastructure but ranks low for Market Size, Innovation

and Higher Education and Training.

14

Money and the Financial System

Introduction

Money and the financial system play a complex and central role in the functioning of the

modern economy. This note on money and the financial system will cover the definition of

money, the role of money, how money affects the real economy, the evolution of

commercial banks, the Bank of England, bank licensing and regulation, money creation by

banks, the 2007/08 financial crisis, the Gold Standard, British Inflation during the 20th

century, inflationary spirals and hyperinflation, deflation, Fisher’s Equation, the role of a

central bank, financial stability, Systemically Important Banks, Monetary Policy,

“Unconventional Monetary Policy” and inflation targets. This section ends with a Glossary of

Banking Terminology from the Central Bank of Bahrain Rulebook.

Definition of Money

Money is a highly complex social convention for the recording of debts and obligations

arising out of exchange transactions. A social convention gives meaning to something that is

accepted by most members of a community and therefore influences the actions of persons

within that community. Language is a social convention in that members of the language

community accept the meaning of words and use these words in accordance with rules that

give these words meaning. Money is a social convention in that members of that economic

community accept it as a form of payment for goods and services on the understanding that

it can be used to buy the equivalent value of goods and services at some point in the future.

Language evolved in human communities because communication was vital for human

survival. Money evolved as a social convention because it allows exchange to operate much

more efficiently especially in large and complex communities. Efficient exchange was

needed to allow communities take advantage of the benefits of specialization in production

Money is enormously difficult to define. The Collins Reference Dictionary of Economics, for

example, defines money as “An asset that is generally acceptable as a medium of

exchange”. In a historical sense this definition is correct in that money originated with the

use of real assets such as gold in exchange. Modern forms of money including coins, paper

money and bank deposits are not “real assets”. These forms of money are claims on a share

of the real resources (assets, goods and services) that are traded within a community. The

claim is guaranteed by the organization, or the community which the organization

represents, issuing the money. So a better definition of money is “A claim to a share of the

real resources that are traded in a community that is issued and guaranteed by an

organization which has the credibility to have its guarantees accepted”. The person who has

a Bahrain Dinar has a note which allows him/her to claim one BD’s worth of resources that

15

are traded in Bahrain and the Central Bank of Bahrain has the credibility to have its

guarantee accepted.

Money is totally different when seen from the perspective of any individual or

group/organisation in a community or the perspective of that community as a whole.

Economics looks at the functioning of the economy from the perspective of the overall

community so economics usually looks at money from that perspective.

Business looks at money from the perspective of an individual or group/organisation within

the community. Money, looked on from this perspective, is an asset and the more money

the individual or group/organization has then the richer they are. From the perspective of

the overall community, however, money is not an asset and an increase in the amount of

money in circulation will not make the community richer. From the point of view of the

overall community money is merely a way of keeping the economy functioning. Adam

Smith, the Scottish Economist, described money as a “great wheel of circulation” in his book

The Wealth of Nations , p 235, which was published in 1776 (Pennsylvania University

eCopy).

The definition of money by central banks as M1, M2 or M3 depends on how easily the

money can be spent. M1, the simplest definition of money, involves money in a form that

can be spent immediately. MI involves cash and demand deposits held by the public

(individuals and all non-bank organisations).

Role of Money

In any well-functioning economy money fulfills the following roles, Medium of Exchange

Measure of Value

Store of Value

By medium of exchange is meant that goods and services are not exchanged directly for

each other as in barter but that money is used as an intermediary. In a modern economy the

exchange value or price of goods and services is measured in money. Wealth can be saved in

money whether it is cash or bank deposits.

Money and the "Real Economy”

When an act of exchange takes place in a money-based economy then goods/services or

resources and money of equal value are exchanged.

Real Flows ++++> +++++++Resources +++++++>

<+++++++Income +++++++++

Money Flows ****>

******> Spending *******>

<+++ Goods and Services <++

Households

Business

16

When looking at an economy you can focus on the money flows (****) or focus on the

goods/services and resources (++++) which are being exchanged for the money. If you are

focusing on the goods and services which are being produced and exchanged, instead of on

the money flows, you are said to be dealing with the “Real Economy”.

In the US this distinction is often put as “Wall Street” and “Main Street”. When the financial

system came under stress in 2007/2008, policy makers were concerned to ensure that the

problems of the financial system did not push the economy into a deep recession. This was

described as preventing “Wall Street” from affecting “Main Street”.

The Financial System is so important to the modern economy that the maintenance of an

efficient financial system is a key priority of most governments. This was shown by the

global reaction to the financial crisis of 2008 where there was an orchestrated global

reduction of central bank interest rates and coordinated refinancing of banks in the EU,

Britain, Japan, China and the US.

History of Money

The money systems which we use evolved over many years from the bartering of goods and

services directly for each other.

Barter economy

Use of items of intrinsic value as money

Use of coins made from precious metal

Receipts for gold as Paper Money

Paper Money

Bank Deposits

The simplest exchange system is that of barter where goods and services are exchanged

directly for each other. Barter, however, is a very cumbersome method of exchange. Barter

remained important in parts of Europe into the 19th century. When farmers were selling

their grain in the public markets of Europe they often had to give a 1/32nd part to the owner

of the market.

In traditional societies there was only limited use of money. People exchanged goods and

services among each other within the local community based on well understood rights and

obligations without the use of money. These rights and obligations were based on custom

and law. In Europe the social system known as Feudalism was based on the ordinary people

who were known as Serfs having the right to work land that was allocated to them and to

receive protection from the Lord in exchange for labour, goods and service.

17

Up to the 1950s farmers in the West of Ireland often exchanged “days”. Farmer A would

help farmer B for a number of days and B would end up “owing” A that number of days and

would pay back these days at some future time. Farmers who exchanged days would often

be linked by blood or friendship connections. Occasionally one day owed might be

transferred to a third farmer. If B owed A one day and if A owed C one day then the debts

could be settled by B giving C one day.

The exchange of goods and services without the use of money and the consequent debts

and obligations, can only work on a small scale and at a local level so precious metals were

used in different societies as ways of recording these debts or claims and obligations when

exchanges spread beyond the local level. There are however significant difficulties with

using precious metals to record debts. These difficulties are linked to the weighing of metals

and assessing the purity of metals.

Coins were minted and stamped with a state seal to guarantee their weight and purity. The

first gold coins were minted by Croesus, King of Lydia, (modern-day Turkey), in the period

560 to 546 BC. Minted coins became the accepted money in all countries. The original

English silver penny contained 1/240 of a pound of pure silver and so the English pound

Sterling, being worth 240 pennies, was equivalent to a pound (lb Troy measure) of pure

silver. (The Troy pound is about 37% of a Kilogram).

Bank notes, which were, in effect, receipts for silver or gold, started to circulate at the end

of the 17th century. The first bank notes in Britain were those circulated in London by the

“Goldsmith Bankers”. These were receipts for gold. Bank deposits, whose ownership can be

transferred by cheques or EFT (Electronic Funds Transfer), are now the major form of

money. The Money Supply now consists of cash held by the public and bank deposits. There

are different technical definitions of the Money Supply chiefly depending on whether or not

Time Accounts are included. M1, which is the money supply narrowly defined, just includes

cash held by the public and demand deposits of the private sector.

Central Bank of Bahrain Financial Statistics show that M1 for Bahrain was BD2,943 million in

April 2014. M2 includes cash and all private sector bank deposits. M2 for Bahrain was

BD9,603 million. M3, which is the money supply broadly defined, also includes all bank

deposit, both private and public sector. M3 for Bahrain in April 2014 was BD11,425 million.

Evolution of Commercial Banks

Commercial Banks in Europe gradually evolved from the business of Goldsmiths and

Moneylenders who provided a safe storage facility to merchants and stored their gold and

silver coins.

18

The first modern bank is believed to have been set up in Venice in Italy in 1157. Venice was

then a great trading city and port. The oldest surviving bank in the world is the Monte dei

Paschi di Siena Bank (MPS), of Siena in Italy, which was founded in 1472. MPS made losses

of €7 billion in 2011 and failed the ECB stress testing in 2014. This created a situation where

MPS was required to increase its capital by €2 billion.

Accounting was invented by Italian Bankers and was widely practiced in Italy after 1300.

(The first book on accounting by Luca Pacioli, explaining double entry, was only published in

1494 in Venice).

Italian goldsmiths and moneylenders started to arrive in Britain at the end of the 13th the

century from Florence, Venice and Genoa. Edward II, King of England gave a grant of land in

the City of London to a group of these goldsmiths, money-lenders and bankers from

northern Italy in 1318. They were called Lombards and the street is called Lombard Street.

They brought with them knowledge of banking and accounting (double entry). The Italian

money lenders also brought the notation for English money £sd, or Lira, Soldi and Denarii.

The development of Banking can be shown by looking at the evolution of the balance sheet

of a representative goldsmith/moneylender/banker in London such as Francis Child.

These businessmen, known as “Goldsmith Bankers”, started storing gold for merchants and

other wealthy persons in London. As London developed into a major trading centre the

need for safe storage of wealth grew. These Goldsmith Bankers developed both their money

storage activities, especially around the time of the English Civil Wars from 1642 to 1651,

and their lending activities and their businesses evolved into banks.

Stage 1 Merchant needed a safe place to store their gold. Francis Child stored gold for a

Merchant for a fee.

Assets Liabilities

Gold in Vault 100 oz Gold from Merchants 100 oz

-------- --------

100 oz 100 oz

(FC was making profits made from storing Gold for Merchants)

Stage 2 Francis Child found that he could lend some of the gold that he was being paid to

store.

Gold in Vault 40 oz Gold from Merchants 100 oz

Loans 60 oz

------- -------

100 oz 100 oz

(FC started making large profits from storing gold and lending the gold stored by him)

19

Stage 3 Francis Child could give loans by issuing Gold Receipts to the borrower.

As the scale of their business expanded Goldsmiths needed to keep better records and

started issuing “Warehouse Receipts” to those who deposited gold with them. These

“Warehouse Receipt” started to circulate among the public as payment for goods and

services. About 1680 Francis Child started issuing these “Warehouse Receipts” in standard

denominations. These are regarded as the first true banknotes in the Western World.

Gold in Vault 40 oz Gold from Merchants 100 oz

Loans by Warehouse Receipts 300 oz Receipts for Gold 240 oz

-------- -------

340 oz 340 oz

(FC started making increased profits from a massively expanded level of Lending)

Stage 4 The balance sheet of a modern bank looks as follows

Assets Liabilities

Cash 2% Capital 10%

Deposits with Central Bank 5% Bonds 10%

Bills and Bonds 18% Money Market 10%

Loans and Investments 73% Current Deposits 20%

Premises and Other Assets 2% Savings Deposits 50%

----- -----

100% 100%

(Profit from Lending and Banking Services)

The Bank of England

In 1694 a group of London businessmen offered the government of William of Orange, who

had recently deposed his father-in law as King of England and was involved in a war with

France, a loan of £1.2 million, at an interest rate of 8% per annum. These businessmen also

got a Royal Charter for a bank, with important privileges, to be known as the Bank of

England.

The Bank of England Notes, in the BoE’s own word’s “became a widely accepted currency as

people seldom doubted that the “promise to pay” which referred to gold coin of the realm

would be honored”. The BoE always redeemed their banknotes with gold coins at the rate of

one gold coin for a pound. (The gold coins which the bank used to redeem one Pound held

0.25 ounces of gold)

From its foundation the BoE acted as the government bank in Britain and managed the

national debt. The bank became the dominant bank in England and Wales. The banks notes

were made legal tender in 1833. The BoE, as the government’s bank, was used by the British

government to manage financial crises and so evolved into what is now called a Central

20

Bank. A Central Bank is a bank that manages the financial system of a country. The BoE was

a private bank from 1694 until it was nationalized in 1946.

Bank Types

There are now a wide variety of bank types or bank categories. These types or categories

vary from country to country so it is impossible to classify banks internationally other than

by the banking services they provide.

The simplest form of banking is deposit taking, personal lending and money transfer. Most

small banks provide these services and these banks are often referred to as “Retail Banks”.

Some banks specialize in providing banking services to business and these are often referred

to as “Commercial Banks”. Some banks, such as Coutts in London, specialize in providing

banking services to high net-worth individuals and these are referred to as “Private Banks”.

Banks, such as Goldman Sachs, that provide a range of advisory and funding services, such

as IPOs and Bond Sales, to large businesses are referred to as “Investment banks”. Goldman

Sachs has been involved in IPOs since they handled the launch of Sears Roebuck on the NYSE

in 1906. Investment Banks are also usually involved in proprietary trading and investment.

Up until 2008 US Investment banks did not hold banking licenses. Banking licenses in the US

restricted banks from engaging in high risk and high profit activities such as proprietary

trading and investment so the investment banks chose to operate without a banking license

to avoid regulation as banks. This however meant that they could not accept deposits or

access emergency funding from the Federal Reserve Bank. During the financial crisis this

form of unregulated US banking disappeared.

Banks in Britain and Europe were much less restricted, by banking legislation, in their

activities so most large British banks such as Barclays and Deutsche Bank provide a full

range of banking services including Retail, Commercial, Private and Investment Banking.

Barclays website says that “Our banking services cover everything from credit cards to

corporate banking, across the globe”.

In Bahrain there are 4 categories of banks. These are Conventional Banks, divided between

Retail and Wholesale, and Islamic Banks, divided into Retail and Wholesale. Conventional

Retail Banks provide the full range of banking services required by ordinary customers such

as deposit accounts, loans, credit card and foreign exchange. The Wholesale banks are

restricted by the scale of deposits as the minimum deposit in a wholesale bank is BD 7

million.

Islamic banks provide a variety of products, including Murabaha, Ijara, Mudaraba,

Musharaka, Al Salam and Istitsna'a, restricted and unrestricted investment accounts,

syndications and other structures used in conventional finance, which have been

21

appropriately modified to comply with Shari’a principles. An example of this is BisB which

provides Retail and Commercial Banking Services in Bahrain.

The CBB has a Register of Banks .There were 78 banks in Bahrain holding “Conventional

Licenses” in May 2015. These involve 22 Conventional Retail Banks and 56 Conventional

Wholesale banks. There were 24 banks in Bahrain holding “Islamic Licenses” in May 2015.

These involve 6 Islamic Retail and 18 Islamic Wholesale Banks.

Bank Licensing and Regulation

Banks are so important in the functioning of a modern economy that they are subject to

much stricter licensing and regulation than ordinary businesses. The systems for Bank

licensing vary from country to country and these systems evolve in response to political and

financial events.

In the US banks can apply for either State Banking Licenses or National Banking Licenses.

Each state has its own Licensing Authority. Holders of state banking licenses can only

operate in the state where they hold a license. In New York the state banks are licensed by

the Department of Financial Services of the State of New York. Banks that are allowed to

operate all over the US are called National Banks and are licensed by the Office of the

Controller of the Currency (Agency within the US Treasury set up in 1863 by President

Lincoln). Federal Savings Banks are licensed by the Office of Thrift Supervision (Agency

within the US Treasury)

In the UK bank licensing in now the responsibility of the Financial Conduct Authority but was

previously the responsibility of the Financial Services Authority . The financial crisis in Britain

in 2008 led to the splitting up of the Financial Services Authority and is role was divided

between the Financial Conduct Authority and the Prudential Regulation Authority , which is

an agency within the Bank of England.

In Bahrain bank licensing is the responsibility of the Central Bank of Bahrain . No person or

company can carry on banking activities in Bahrain without holding a banking license from

the CBB.

A summary of the bank licensing process in Bahrain can be found in the CBB Guide to

Licensing. Complete details of the CBB licensing process and requirements are prescribed in

the CBB Rulebook. Each Volume of the Rulebook contains a Module setting out the CBB's

licensing requirements, with respect to the sector covered by the Volume in question,

including a full description of the relevant Regulated Services. Volume 1 covers

“Conventional Banking and Volume 2 covers Islamic Banking.

Bank Regulation regimes vary significantly from country to country with major differences

between regulation in the US, Britain and Bahrain.

22

US banking regulation is highly complex with banks being subject to regulation by multiple

agencies. The Federal Reserve Bank , the Federal Deposit Insurance Commission , the Office

of the Controller of the Currency , Office of Thrift Supervision and the state bank regulator

are all involved in aspects of bank regulation.

All banks that are members of the Federal Reserve System are regulated by the Federal

Reserve. All banks that accept deposits must be covered by deposit insurance and are

subject to regulation by the Federal Deposit Insurance Corporation. State banks that are not

members of the Federal Reserve System are regulated by the Office of the Controller of the

Currency. Federal Savings banks are regulated by the Office of Thrift Supervision.

In Britain banks are regulated by the Financial Conduct Authority and by the Prudential

Regulation Authority.

Bahrain has a single regulator, the Central Bank of Bahrain. The Central Bank of Bahrain

(CBB), in its capacity as the regulatory and supervisory authority for all financial institutions

in Bahrain, issues regulatory instruments that licensees and other specified persons are

legally obliged to comply with. These regulatory instruments are contained in the CBB

Rulebook. The Regulated Banking Services are:

(a) Deposit-taking (b) Providing Credit (c) Accepting Sharia money placements/deposits (d) Managing Sharia profit/loss sharing investment accounts (e) Offering Sharia Financing Contracts (f) Dealing in financial instruments as principal (g) Dealing in financial instruments as agent (h) Managing financial instruments (i) Safeguarding financial instruments (j) Operating a Collective Investment Undertaking (k) Arranging deals in financial instruments (l) Advising on financial instruments (m) Providing money exchange/remittance services; or (n) Issuing/administering means of payment

Volume 1 covers Conventional Bank Licensees. It contains prudential requirements (such as

rules on minimum capital and risk management). Collectively, these requirements are aimed

at ensuring the safety and soundness of CBB-licensed conventional banks and providing an

appropriate level of protection to the clients of such banks

Volume 2 covers Islamic Bank Licensees. It contains prudential requirements (such as rules

on minimum capital and risk management). Collectively, these requirements are aimed at

ensuring the safety and soundness of CBB-licensed Islamic banks and providing an

appropriate level of protection to the clients of such banks

23

The website version of the Rulebook acts at all times as the definitive version of the

Rulebook.

The CBB Rulebook has a Glossary of Financial terms which may be useful. Some of these

financial terms are explained at the end of this section.

Money Creation by Banks

Bank lending is closely linked to money creation. Bank loans are not counted as money but

bank deposits are included in the money supply. When a person gets a loan from a bank

what normally happens is that the bank opens a loan account and transfers the amount of

the loan from the loan account into the person’s current account. The amount in the current

account is money since it is available for spending. When the borrower spends the money,

for example in the purchase of a house, ownership of the deposits is transferred within the

banking system.

This short video from the Bank of England shows how Money is created when a loan is given

by a bank. It is traditional to see the giving of the loan as the creation of money and the

bank as the creator. However when a loan is given there are two parties involved. The

borrower commits himself/herself to repay the bank so looked at from this perspective the

borrower is involved in creating money by committing herself to repay the bank. The money

is therefore created by the bank risking the loan and the borrower committing her future to

the deal.

Confidence is crucial in bank lending. The person borrowing must be confident that s/he can

repay out of future cash flow and the bank must be confident that it will get its money back.

When a loan is repaid to a bank what normally happens is that money is taken from deposits

to repay the loan. This reduces deposits and therefore reduces the money supply. So the

change in the total amount of lending by banks, how new loans compare with the

repayment of existing loans, is what affects the money supply.

In the examples above the banks took a certain amount of cash and created a much larger

amount of money based on this small cash holding. The power of a single bank in any

country to create money is limited. When any bank gives a loan it will almost certainly

create a deposit at the same time but once the deposit is spent the money will migrate to

another bank so its ability to create deposits is limited. However if all banks are increasing

their lending then the money supply can grow as all are generating deposits and these

deposits will be spread throughout the banks.

24

Banking Crises

The nature of banking is that the lending is usually for long period but the deposits, or

Money Market Funding, can be withdrawn at short notice. This creates the potential for

instability and there have been banking crisis since the invention of banking. If there is a loss

of confidence in a bank then there will be a “run on the bank” where savers withdraw all

deposits from the bank and other banks refuse to lend to that bank on the Money Market.

A recent example of a banking crisis was in Bulgaria in June 2014 where two of the largest

banks in the country were affected by massive withdrawal of deposits. (Confidence is

therefore crucial to both bank lending and bank deposits).

A run on the Northern Rock Bank started in England in September 2008. It is believed that

the run on the Northern Bank in England was triggered by the announcement by the Bank of

England that they had given an emergency loan to Northern. The legislation under which the

BoE then operated required it, in the interest of transparency, to make public information

about emergency lending. This was the first run on a bank in living memory in Britain. The

Chancellor of the Exchequer in Britain announced on 17/9/2007 that the UK Government

would guarantee all deposits in Northern Rock and the Bank of England lent £23bn to

Northern. These measures restored confidence and ended the run on the bank.

The UK government attempted to bring in private investors to take over the Northern but

these attempts failed and the Government announced that they were nationalizing the

Northern on 18/2/2008. In October 2008 the UK reacted to the continuing bank crisis by

guaranteeing all deposits held by UK banks and investing directly in a number of banks

including the Royal Bank of Scotland, Lloyds TSB and Halifax Bank of Scotland.

Bank Failures

Bank failures, such as that of Northern Rock in the UK in 2008 whose failure is described in

The Economist Magazine , are linked to a range of risk factors including:

Dependence on Money Market,

Asset Growth Rate,

Excessive Concentration on one industry,

Excessive Concentration on a small number of Companies/Individuals,

Structure of Employee Bonuses.

Banks, such as Northern Rock, which want to grow very fast, often depend heavily on the

Money Market. Money Market loans are very short-term and have to be replaced

continuously by other loans from the Money Market. This type of funding is not nearly as

secure as deposits and Money Market loans dry up if there is even a hint of the bank getting

into difficulty.

25

Banks which want to grow rapidly usually take higher risks including purchasing other banks.

The Royal Bank of Scotland grew rapidly, under the leadership of Fred Goodwin - Chief

Executive, until it was the largest company in the world in terms of assets at £1,900 billion in

2008. This rapid growth was largely driven by acquisitions. In 2008 RBS paid €71 billion for

the Dutch/French bank ABN/Amro. ABN/Amro was heavily exposed to the US Sub-Prime

Mortgage business where it made massive losses. The RBS had to be rescued by the UK

Government in 2008.

Many banks lent excessively to the property market in the period 2000 to 2007 and ended

up being too heavily exposed to a single industry. The collapse of property prices in 2008

led to the collapse of many bank debtors and the value of the property that was used as

collateral for loans also collapsed. Some of banks also lent far too heavily to a small number

of companies and individuals. Many of these companies and individuals were involved in

property and the collapse in the property market bankrupted them.

During the period 2001 to 2007 banks all over the world were trying to grow rapidly and

they created attractive bonus structures for lending officers and executives based on the

amount of loans. This bonus structure encouraged lending officers and executives to take

excessive risks in lending. One of the post-2008 bank reforms has been the reform of the

bank bonus structure in banks such as Barclays .

The Gold Standard

During the 19th century all Currencies were redeemable at a legally determined value in

terms of gold. The exchange rate between currencies was determined by their gold value.

The £ was worth 113 grains of gold (originally 120 grains) and the $ was worth just below

23.22 grains of gold giving an exchange rate of £ = $4.87 (which is based on 113/23.22 =

4.86). There are 480 grains of gold in an ounce “Troy” measure. This system was known as

the Gold Standard. Britain went off the Gold Standard in 1914 in order to prevent a run on

the Bank of England.

The US did not go off the Gold Standard in 1914 and this is one of the reasons why the $

replaced the £ as the main international reserve currency.

Under the Gold Standard banks could only issue paper money if they had sufficient Gold

Reserves to back the money they were issuing. This meant that the amount of money was

controlled by the amount of gold being mined. At present annual production of gold is about

2.5k tons per year. This adds very little to the total world supply of about 155k tons of which

about 31k tons are held by central banks.

The link between Sterling and gold meant that the level of prices in Britain remained very

stable (no inflation) over the entire 19th century. Since the ending of the Gold Standard

26

system in 1914 the money supply in any country is not linked to gold. This has led to a

massive increase in the amount of money in circulation and a loss in the value of, for

example, the £ measured in gold. In 1914 1oz of gold was worth £4.24 but 1oz of gold is

now (June 2014) worth £736 this means that the £ is now only worth about 0.5% of what it

was worth in 1914 or you would need 170 times as much money to buy an equivalent

amount of gold. Prices on average in Britain have risen about 100 times since 1914. This

means that the purchasing power of gold has risen over this period. Average prices over the

period 1914 to 2014 have fallen by about 40% when measured in terms of gold.

British Inflation

Inflation means a rise in the average level of prices and so means a reduction in the

purchasing power of money Inflation. Inflation is usually measured by the Consumer Price

Index (CPI). The CPI is a statistical estimate constructed using the prices of a weighted

sample of representative items whose prices are collected periodically. Britain has

experienced inflation over most of the century from 1914 to 2014. But over that century the

inflation rate varied significantly with periods of rapid inflation, periods of low inflation and

even periods of deflation or falling prices.

Period Inflation Rate over this Period

1900 - 1914 Low inflation, prices rose by 6% over this period.

1914 - 1920 Rapid Inflation caused by WW1, Prices doubled over this period.

1920 - 1935 Deflation. Over this period, 1920 to 1935, average prices fell by 20%.

1935 - 1970 Low Inflation but prices rose by 4.5 times in total over this period.

1970 - 1985 Rapid Inflation. In some years over this period, prices rose by 15%.

1985 – 2008 Low Inflation.

2009 Deflation. Prices fell slightly in the Spring of 2009.

2010 – 2014 Low Inflation.

Inflationary Spirals and Hyperinflation

An Inflationary Spiral is a situation where the following sequence of events takes place,

Rising Prices -> Wage Increases -> Cost Increases -> Further Price Rises and further Wage

Increases.

Stable Governments are always afraid of allowing an Inflationary Spiral to develop because

it is very hard to stop inflation once it gets going. If inflation gets out of control there is

always the possibility of Hyper-inflation as in Germany in 1923 and in Russia after the fall of

Communism. Hyper-inflation involves prices rising at least 100% per annum. Hyperinflation

creates massive problems for the financial system in any country.

The Hyperinflation in the German Weimar Republic in 1923 is well known . The German

government in 1922 was unable to meet the “reparations” (repayments) demanded under

27

the Versailles Treaty. (The Versailles Treaty was concluded after the end of the First World

War from 1914 to 1918. Germany had been defeated in the war and the victors, US, Britain

and France, imposed very harsh penalties including these “reparations” on Germany). The

French and Belgian armies occupied the Ruhr, Germany’s key industrial area. The German

government ordered the workers in the Ruhr to go on a general strike. The revenue of the

government collapsed and it financed its expenditure by printing money. This triggered a

hyperinflationary spiral. Prices rose at about 40% per day in October 1923. One loaf of bread

which had cost 163 marks in 1922 cost 200 billion marks by November 1923. In September

1923 Germany got a new Chancellor, Gustav Streseman who put together a rescue plan. The

workers in the Ruhr were ordered back to work, a loan was negotiated from the US and a

new currency called the Rentenmark was introduced. This stabilized the economy which

then recovered rapidly over the period 1924 to 1929.

Russia experienced Hyper-Inflation after the collapse of Communism in 1991. The

purchasing power of the Ruble fell rapidly as prices in Russia increased and this is indicated

by the exchange rate between the Ruble and the $ over the period 1991 to 2005. (In looking

at the exchange rates you have to take into account that in 1998 the old Ruble was replaced

by a new Ruble at the rate of 1000 old to 1 new)

Year Rubles $US

1975 0.75 Old Rubles = $1

1991 42 Old Rubles = $1

2005 28,000 Old Rubles or 28 (New) Rubles = $1

The hyperinflation in Russia, like in South America, led to a massive hoarding of dollars. It is

estimated that Russians had a hoard of $40bn to $50bn in cash in the early 2000s.

The new Ruble, the high oil price and the political stability brought about by President Putin

stabilized the Russian Ruble from 2005 to 2013 although developments linked to the

Ukraine reduced the value of the Ruble in 2014.

An example of a country that experienced Hyper-Inflation in recent times is Zimbabwe. The

official inflation rate for Zimbabwe the period 2004 to 2007 was as follows:

Year Official Inflation rate

2004 133%

2005 585%

2006 1,033%

2007 12,500%

Zimbabwe experienced an outbreak of cholera at the end of 2008 as the country’s water

and sewage systems collapsed. In January 2009 the Zimbabwe Government acknowledged

the final collapse of the Zimbabwe Currency by allowing the use of other currencies as legal

28

tender. In June 2015 the Zimbabwe Central Bank announced that they would exchange

Zimbabwe Dollars for US at the rate of Z$35Quadrillion for 1$US.

Hyper-Inflation usually results from a Government having a budget deficit and financing its

budget deficit by printing paper or borrowing from the banking system while the banking

system expands credit. This is referred to as increasing the money supply.

Hyper-Inflation always causes economic catastrophe, the wiping out of savings, the

impoverishment of all those on fixed incomes, a hoarding of foreign currency and exchange-

able goods, a complete collapse in banking and investment, a tendency to return to a barter

economy and a collapse in Government tax revenue.

Deflation

The term deflation refers to a situation where prices are falling and overall demand in the

economy is too low to maintain the level of economic activity. Prices fell in many countries

including the US, Britain and Bahrain during 2009 as the World economy experienced its first

period of deflation for over 50 years. The massive fall in oil prices in 2014 has caused overall

prices to fall in many countries including the US and UK.

Fisher’s Equation

The connection between the money supply and the level of prices was formulated in 1911

by Irving Fisher. For every money-based exchange the quantity of money paid is equal to the

value of the goods or services sold. This means that the total amount of money paid in

transactions in an economy over a year has to be equal to the total value of the goods and

services sold.

The total of money payments = Money Stock * Velocity of Circulation. Velocity of Circulation

means the number of times money is used in transactions over a defined period. The total

value of goods and services sold = Price level * number of Transaction.

This means that MV = PT.

M is the money stock, V is the velocity of circulation, P is the price level and T is the number

of transaction. If V and T remain constant all changes in M must be reflected in changes in P.

Example of Fishers equation in an economy where the only thing that is traded is bags of

rice.

Total Annual Sales of Rice = 1,000 bags

Price per bag = BD2

Total value of Sales = PT = BD 2,000

Money Supply = 200 BD coins

Velocity of Circulation = 10 times per annum

Total Purchases = MV = BD 2,000

29

There are massive difficulties in practice with attempting to use Fishers Equation. The

amount of money in an economy depends on confidence. Bank Credit is not money but Bank

Deposits are and the amount of Bank Deposits is closely linked to Bank Credit. Also in a

confident time in business most companies will be relaxed about credit terms. This facilitates

economic activity. The velocity of circulation is not constant with a higher V where there is

inflation for example.

The Role of a Central Bank

The leading central banks in the World are the Federal Reserve Bank of the US, The

European Central Bank (ECB) of the Eurozone, the Bank of Japan, the Peoples Bank of China

and the Bank of England of the UK.

The Bank of England was founded in 1694 as a private Joint Stock Bank. The BoE was the

Government's Bank and was much stronger financially than the other banks. During the

19th century the BoE became increasingly the agent of the Government in controlling the

banking system and was finally nationalized in 1946. The BoE evolved into a central bank

and became a role model for central banks all over the world.

The central bank in any country will normally play the following roles

Currency Role, Issue and Manage the Currency

Government Bank Manage the Government Account and the National Debt

Financial Stability Regulate the activities of the commercial banks

(Banker’s Bank) Act as Lender of Last Resort to commercial banks

Monetary Policy Manage the Exchange Rate and the Rate of Interest

In most countries it is the role of the central bank to issue the currency. The Federal Reserve

Bank does this in the US and the Central Bank of Bahrain does this for Bahrain. In the UK

some notes are issued by regional banks in Scotland and Northern Ireland although most

Sterling is issued by the Bank of England.

In most countries the government finances are managed by the central bank of the country.

This is the case in the US, Britain and Bahrain.

Financial Stability

Definition of Financial Stability

Central banks in all countries are responsible for ensuring financial stability in their country.

It is however extremely difficult to define Financial Stability although it is easy to recognize

Financial Instability in practice. The entire basis for the financial system in a country is

confidence in the currency and the institutions which are involved in financial transactions.

A good working definition is “Financial Stability is a situation where there is a high level of

30

confidence in all the key institutions within the financial system so that the normal financial

activities necessary for the operation of the economy can take place smoothly.” The Central

Bank of Bahrain has issued a paper on the Definition of Financial Stability.

During the twenty years leading up to the 2007/08 financial crisis there was overconfidence

in the financial system and financial stability was taken for granted. This led to a relaxation

in financial regulation by central banks. In the US strict regulations under the Glass-Seagal

Act, which were introduced during the Great Depression in the 1930s, were relaxed.

In Britain the Bank of England’s role as financial regulator was transferred to a new agency

called the Financial Services Authority in 2001. Ireland followed the British example and set

up an Independent Financial Services Authority (Independent of the Central bank) with

disastrous results. Luckily Bahrain kept the CBB as the financial regulator.

The Bank for International Settlements

The Bank for International Settlements (BIS) was established in 1930 in Basel, Switzerland.

The mission of the BIS is to “serve central banks in their pursuit of monetary and financial

stability, to foster international cooperation in those areas and to act as a bank for central

banks”.

The breakdown of the Bretton Woods fixed exchange rates system, over the period 1971 to

1973, led to turmoil on foreign exchange markets and created significant problems for

central bankers. In 1974 the governors of the G10 (10 Largest economies in the World)

Central Banks set up a Committee on Banking Supervision as a forum for cooperation on

bank supervision. The membership of the Committee on Banking Supervision has expanded

and now includes representatives of 28 leading economies. Guidelines issued by the

Committee have no legal force but are used by central banks and commercial banks to guide

their activities.

Basel Guidelines on Banking Capital The Committee on Banking Supervision issued guidelines on banking capital in 1988 and

these are known as Basel 1. These guidelines were revised in 1999 and these guidelines

were known as Basel 2.

The financial crisis of 2008 led to new guidelines known as Basel 3. The Basel 3 Guidelines

were issued in 2010 to try and prevent a recurrence of the financial instability that occurred

in 2008.

Basel 1 recommended that banks have Total Capital of 8% of Risk Weighted Assets. (Risk

Weighting is designed to force banks that have a large amount of risky assets to hold more

capital). This Capital includes Tier 1 and Tier 2. Tier 1 Capital includes Equity and Reserves.

31

Tier 2 involves Unsecured Subordinated Bonds. Unsecured Subordinated Bonds are bonds

that are not secured on any assets and are subordinated to depositors and ordinary

creditors in the event of a bank “resolution”. (Bank resolution means the sorting out of a

bank that is in danger of failing).

The Basel 3 guidelines cover Capital Adequacy and Liquidity

The Basel 3 Capital Adequacy Guidelines, summarized in Annex 1 on page 64, recommended

a Minimum Capital Ratio of 8% from 2013 rising to Minimum Capital Ratio of 10.5% in 2019.

In the run-up to 2019 banks must have at least 8% and then there is what is called a

“Conservation Buffer” of 2.5% where banks are restricted in terms of payouts to

shareholder.

The Minimum Capital Ratio under Basel 3 also includes a Counter-cyclical Buffer of 0 – 2.5%.

“The countercyclical buffer aims to ensure that banking sector capital requirements take

account of the macro-financial environment in which banks operate. It will be deployed by

national jurisdictions when excess aggregate credit growth is judged to be associated with a

build-up of system-wide risk to ensure the banking system has a buffer of capital to protect

it against future potential losses”.

This means that the Total Minimum Capital Ratio for a bank in a booming economy after

2019 could be as high as 13%.

Davis Polk have an online tool to calculate the risk weighting of assets of US banks. Some

assets, such as cash and deposits with the central bank, which have no risk, have a 0%

weighting and payments due to the bank which are delayed beyond 46 days have a 1,250%

weighting. This means that two banks with the same amount of assets can end up with

significantly different Risk-Weighted Assets. The table below gives an outline of Risk

Weighting for Basel 3 for US banks and is based on the Davis Polk Risk Weighting Tool.

Assets Class US Risk Weighting

Cash and Deposits with the Central Bank 0%

Residential Mortgages, 50%

Publically-traded Equities 300%

High risk Equities 600%

Payments due delayed beyond 46 days 1,250%

The Central Bank of Bahrain issued a plan for the Implementation of Basel 3 in Bahrain in

June 2013. This plan directed that all banks in Bahrain were required to have a Capital

Adequacy Ratio of 12.5% by 2015.

32

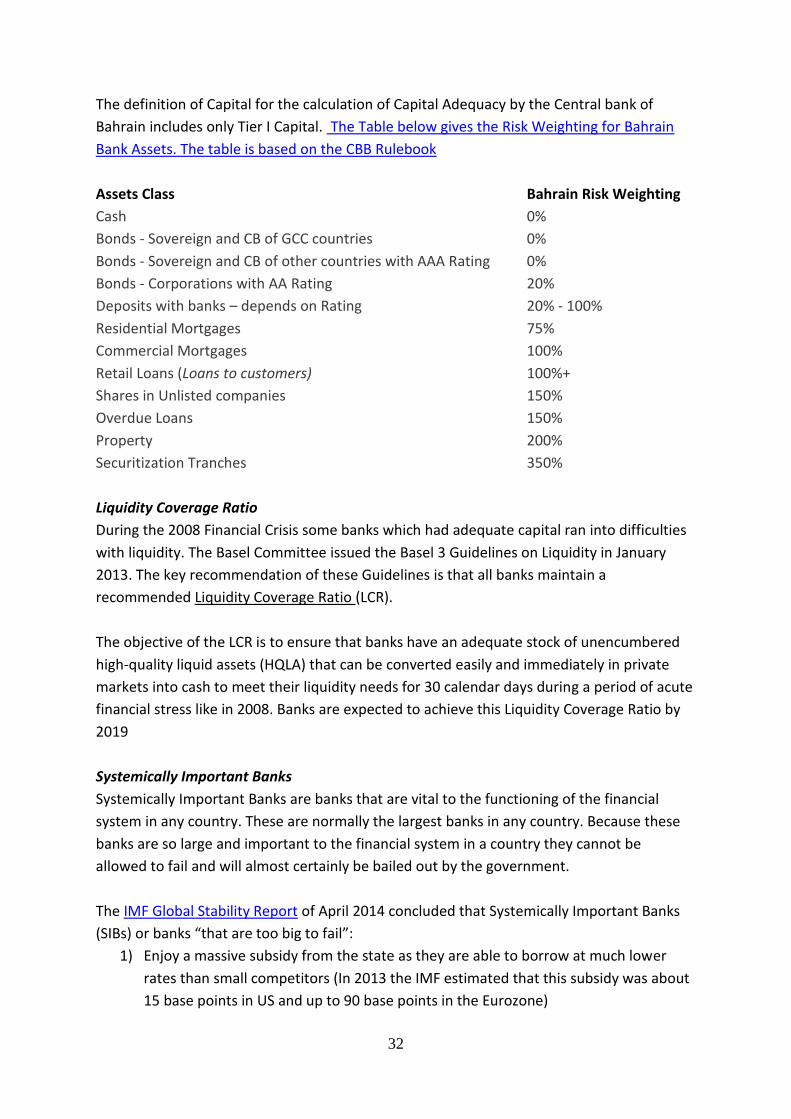

The definition of Capital for the calculation of Capital Adequacy by the Central bank of

Bahrain includes only Tier I Capital. The Table below gives the Risk Weighting for Bahrain

Bank Assets. The table is based on the CBB Rulebook

Assets Class Bahrain Risk Weighting

Cash 0%

Bonds - Sovereign and CB of GCC countries 0%

Bonds - Sovereign and CB of other countries with AAA Rating 0%

Bonds - Corporations with AA Rating 20%

Deposits with banks – depends on Rating 20% - 100%

Residential Mortgages 75%

Commercial Mortgages 100%

Retail Loans (Loans to customers) 100%+

Shares in Unlisted companies 150%

Overdue Loans 150%

Property 200%

Securitization Tranches 350%

Liquidity Coverage Ratio

During the 2008 Financial Crisis some banks which had adequate capital ran into difficulties

with liquidity. The Basel Committee issued the Basel 3 Guidelines on Liquidity in January

2013. The key recommendation of these Guidelines is that all banks maintain a

recommended Liquidity Coverage Ratio (LCR).

The objective of the LCR is to ensure that banks have an adequate stock of unencumbered

high-quality liquid assets (HQLA) that can be converted easily and immediately in private

markets into cash to meet their liquidity needs for 30 calendar days during a period of acute

financial stress like in 2008. Banks are expected to achieve this Liquidity Coverage Ratio by

2019

Systemically Important Banks

Systemically Important Banks are banks that are vital to the functioning of the financial

system in any country. These are normally the largest banks in any country. Because these

banks are so large and important to the financial system in a country they cannot be

allowed to fail and will almost certainly be bailed out by the government.

The IMF Global Stability Report of April 2014 concluded that Systemically Important Banks

(SIBs) or banks “that are too big to fail”:

1) Enjoy a massive subsidy from the state as they are able to borrow at much lower

rates than small competitors (In 2013 the IMF estimated that this subsidy was about

15 base points in US and up to 90 base points in the Eurozone)

33

2) May take excessive risks, as they are confident that they will be bailed out by the

state and these excessive risks may endanger the stability of the entire financial

system

3) Have become even more important as the Financial Crisis of 2008 led to industry

consolidation. Many countries have over 50% of bank assets controlled by three

banks.

The Global Financial Crisis of 2008 led to increased concern about SIBs and particularly G-

SIBs or Global-Systemically Important Banks. The G20, the club of the leading economies in

the world, set up the Financial Stability Board (FSB) in 2009.

The FSB and the Basel Committee on Bank Supervision have coordinated the global

response to SIBs. They have recommended:

1) Higher Capital Ratios for all SIBs

2) More Intense Supervision of all SIBs

The Basel 3 recommendations involve significantly higher Capital and Liquidity Ratios for

SIBs and many countries have even prescribed ratios even higher than Basel 3. Many Central

Banks, including the BoE and the ECB, have adopted new supervisory regimes with more

intense supervision of SIBs.

The Financial Stability Board has identified 30 large banks such as Goldman Sachs and HSBC

which are Global Systemically Important Banks. The FSB recommended in November 2014

that these Global SIBs be required to have Total Capital (Equity and Bonds) equal to 16% –

20% of Risk Weighted Assets.

Monetary Policy

Monetary policy, now often referred to a “Conventional Monetary Policy”, means the

control of interest rates and the value of a currency on the foreign exchange. In dealing with

Interest Rates it is useful to distinguish between the level of Interest Rates and the spread of

Interest Rates. These two topics are discussed below.

It is normally through the “Money Market” that the level of Interest Rates is established.

The “Money Market” is the market for unsecured short-term loans operated by the major

financial institutions. The interaction of Demand and Supply on the Money Market

determines the R of I for Short-Term Funds. The interest rate in the London Money Market

is called the Libor (London Interbank Offered Rate), the US rate is the Fed Funds Rate and

the Eurozone rate is the Euribor Rate. In normal times all other interest rates move in line

with Money Market rates although long-term rates tend to move less than short-term rates.

34

At any time Money Market Rates depend on the policy of the central bank and the level of

confidence in the currency. Central Banks have significant power to influence the R of I in

their economy. Central Banks try to control Money Market Rates through controlling the

amount of cash within the banking system and the rate of interest at which they lend for

short periods to the commercial banks and accept deposits.

The Central Bank of Bahrain, as of June 2014, was willing to lend to commercial banks at

2.25% and pays a rate of interest on 0.5% on deposits. This means that the Bahrain Money

Market rate cannot go above 2.25% or below 0.5%. If money market rates go above 2.25%

the commercial banks will borrow from the CBB and if money market rates go below 0.5%

the commercial banks will put their excess cash on deposit with the CBB.

Normally banks are able to borrow directly from each other for short periods through the

money market however the collapse of Lehman’s Bank in New York in 2008, the largest

bankruptcy in US history, led to a crisis of confidence in banking and a reluctance of banks to

lend to each other. What started to happen was that this money flooded into Central Banks

and short-term Government Bonds. Central Banks then lent the money to banks. This was

often referred to as “Emergency Liquidity Support”. The US Federal Reserve Bank, the Bank

of England and the ECB engaged in “Emergency Liquidity Support” in 2008 and 2009. In June

2009, for example, the ECB lent over €400 billion to Eurozone banks as part of this program.

The Federal Reserve System in the US was founded by Congress in 1913 “to provide the

nation with a safer, more flexible, and more stable monetary and financial system”.

Traditionally the US Federal Reserve Bank has attempted to control the Business Cycle in the

US Economy using the rate of interest.

The Fed controls the Money Market rate through its “Fed Rate” which is the Rate of Interest

on Reserves held by Commercial Banks with the Federal Reserve. Commercial banks borrow

and lend these Reserves between each other and the rate at which this money is traded is

the “Fed Rate”. The Fed sets a target for the “Fed Rate”.

The European Central Bank, which has been in control of interest rates in the Eurozone since

1999, has as its only/main target to keep inflation around 2%. The main rate of interest used

by the ECB to influence bank interest rates within the Eurozone is its Refinancing Rate or

“Refi Rate”. As the Great Recession developed the ECB gradually cut its Refi Rate to 0.25% in

2013 and then to 0.05% in 2014.

The level of confidence in a currency will influence Money Market rates. Confidence in a

currency is linked to the likelihood of devaluation. If there is a perception that a currency is

likely to be devalued, on the foreign exchanges, then any person who is able will try and

35

exchange the weak currency for other currencies and this will create a financial crisis and

drive up Money Market Rates.

The level of confidence in a currency is also linked to the level of inflation. If there is high

inflation the rate of interest will have to reflect this. The close link between inflation and

interest rates can be shown by international comparisons. High inflation countries have high

rates of interest and low inflation countries have low rates.

“Unconventional Monetary Policy”

The Financial Crisis in 2007/08 had such an impact on economies all over the World that

many central banks got involved in what is now called “Unconventional Monetary Policy”.

“Conventional Monetary Policy” involves adjusting short-term interest rates down to

manage overall demand in the economy. The difficulty with this policy is that it is very

difficult to push short-term interest rates much zero and the situation in 2007/08 warranted

negative short-term interest rates. This led central banks to start using “Unconventional

Monetary Policy”. Unconventional Monetary Policy involved using two new monetary policy

tools called “Quantitative Easing” and “Forward Guidance”.

The US Federal Reserve started a program of purchasing government bonds and asset-

backed securities at the end of 2008 when the US economy was plunging into deep

recession. “Quantitative Easing”, as it involves the central bank buying bonds and other

forms of securities, means that the amount of cash held by the banking system and the

public increases. (The term “Monetary Base” is used to describe the amount of cash held by

the public and the banks and the bank’s reserves with the central bank). Central banks

therefore make it easy for banks to increase their lending by Quantitative Easing (QE). QE

also increases the balance sheet of a central bank as it has paid out cash which is a liability

of the central bank and received in exchange a bond which is an asset.

Other central banks have also carried out large-scale asset purchase programs. The Bank of

Japan began a large-scale asset purchase program in 2009. In its most recent program,

launched in 2010, it has bought roughly $1.1 trillion in Japanese government bonds and

other assets. In March 2009, the Bank of England announced a “Large Scale Asset Purchase”

program and purchased $600 billion of assets (mostly of British government bonds).

The ECB did not use Quantitative Easing until Autumn 2014 because of German objections.

The Germans argued that increasing the money supply through Quantitative Easing would

lead to inflation.

The other “Unconventional Monetary Policy” tool is “Forward Guidance”. Central banks