PLASTIC MONEY AND CUSTOMER SATISFACTION: TWO CASE ...

116

PLASTIC MONEY AND CUSTOMER SATISFACTION: TWO CASE STUDIES FROM PAKISTANI BANKING SECTOR A Dissertation submitted in partial fulfillment of the requirements for the Degree of Master of Business Administration by Sanish Kalhoro Department Of Management Science Faculty of Computer & Management Sciences Isra University, Hyderabad April 2010

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of PLASTIC MONEY AND CUSTOMER SATISFACTION: TWO CASE ...

PLASTIC MONEY AND CUSTOMER SATISFACTION: TWO CASE STUDIES FROM

PAKISTANI BANKING SECTOR

A Dissertation submitted in partial fulfillment of the requirements for the Degree of Master of Business Administration

by

Sanish Kalhoro

Department Of Management Science Faculty of Computer & Management Sciences

Isra University, Hyderabad

April 2010

PLASTIC MONEY AND CUSTOMER SATISFACTION: TWO CASE STUDIES FROM

PAKISTANI BANKING SECTOR

by

Sanish Kalhoro

Examination Committee

Shabina Shaikh(Supervisor) Assistant Professor of Management Science

Prof.Dr. Arshad Haroon(Co-Supervisor)

Professor of Management Science

Qamaruddin Mahar (Co-Supervisor) Assistant Professor of Management Science

ACKNOWLEDGEMENTS

First of all, I reverently thank Almighty Allah who made me skillful

enough so that I can make some contributions to the huge understanding of

the world and who also awarded me the capability to complete the MBA

dissertation fruitfully which otherwise would have been unfeasible for me to

complete.

I am tremendously thankful to my supervisor Assistant Professor Ms.

Shabina Shaikh, Department of Management Sciences, Isra University

Hyderabad for her faithful attention, continuous suggestions, and

encouragement in compiling my research work. Her creativity and logical

judgment helped a lot during the whole writing of this dissertation.

I would like to convey the extraordinary and great thankfulness to

Assistant Professor Dr. Arshad, Department of Management Sciences, Isra

University, for his wholehearted effort and concern. With his precious advice,

help and encouragement, I was able to comply with this dissertation.

I would like to expand my gratitude to Assistant Professor Mr. Qamar-

udin-Mahar for his great support during the dissertation work.

I am grateful to Professor Dr. Gulham Hussain Siddiqui Director

Research, Extension and Advisory Services, as well as Professor Iqbal Bhatti

Dean Faculty of Computer and Management Sciences ,Isra University for

providing me their supervision and support ,and helping me in carrying out

the dissertation on time.

ABSTRACT This research is about customer satisfaction and awareness of plastic

money. Plastic money is another name of credit cards and debit cards. The

research is focused on credit card. Increasing usage of plastic money day by

day has given confusion in customers about choosing the most suitable bank

for using plastic money. Plastic Money business is definitely going big time

here in Pakistan. In a country where 10 years back people have hardly heard

the word plastic money or credit card, more than 7000 merchants are

accepting above 140,000 cards. Pakistan’s banking infrastructure consists of

two major sectors, offering plastic money one is domestic and another one is

foreign. Customers of two banks, domestic bank that is UBL and foreign bank

that is Bank Alfalah, are selected to find satisfaction level regarding plastic

money which they use. The research is to explore the transparency of plastic

money handled by banks, finding customer awareness, and customer

satisfaction in both concern banks. Research data is gathered through

primary and secondary sources. Questionnaire is used to get the view of

customers regarding awareness and satisfaction. Result shows the customer

satisfaction and awareness of plastic money of Alfalah (Foreign Bank) is

higher than UBL (Domestic Bank).

ABBREVIATIONS Abbreviations Term

ATM-------------------------------------------------------------Automated Teller Machine

BAL---------------------------------------------------------------------Bank Alfalah Limited

SBP------------------------------------------------------------------State Bank of Pakistan

UBL----------------------------------------------------------------------United Bank Limited

TABLE OF CONTENTS

Page

ACKNOWLEDGEMENTS -----------------------------------------------------ABSTRACT -----------------------------------------------------------------------ABBREVIATIONS--------------------------------------------------------------- TABLE OF CONTENTS ------------------------------------------------------- LIST OF TABLES --------------------------------------------------------------- LIST OF FIGURES -------------------------------------------------------------

iii iv v vi ix x

CHAPTER I – INTRODUCTION --------------------------------------------- 01 1. General -------------------------------------------------------------------------2. Research Problems --------------------------------------------------------- 3. Research Questions -------------------------------------------------------- 4. Research Purposes --------------------------------------------------------- 5. Research Objectives --------------------------------------------------------6. Hypotheses --------------------------------------------------------------------7. Scope of Research ---------------------------------------------------------- 8. Research Design and Methodology ------------------------------------

01 01 01 02 02 02 02 03

CHAPTER II – LITERATURE REVIEW ---------------------------------- 04 1. Plastic Money and its types ----------------------------------------------- 1.1 Origin of Credit card--------------------------------------------------- 1.2 Plastic Money in Pakistan ------------------------------------------- 1.3 Market Scenario------------------------------------------------------- 2. Importance of Customer Satisfaction ----------------------------------- 3. Types of Plastic Money Offered by UBL and BAL ------------------ 3.1 Types of Plastic Money Offered by BAL-------------------------- 3.1.1 Platinum card---------------------------------------------------- 3.1.2 Titanium card---------------------------------------------------- 3.1.3 Professional card------------------------------------------------ 3.1.4 Supplementary Card------------------------------------------- 3.2 Fringe and Benefits of plastic money offered by Bank

Alfalah Limited--------------------------------------------------------------- 3.2.1 No Joining Fee Step By Step Plan------------------------- 3.2.2 Balance Transfer Facility-------------------------------------- 3.2.3 Global Acceptability-------------------------------------------- 3.2.4 Cash Advance Facility 50% Of Credit Limit-------------- 3.2.5 Revolving Credit------------------------------------------------- 3.2.6 Supplementary Cards------------------------------------------ 3.2.7 Card Expiry period---------------------------------------------- 3.2.8 24-Hours Phone Banking Service-------------------------- 3.2.9 Zero Loss Liability----------------------------------------------- 3.2.10 All Billing in Pak Rupees------------------------------------- 3.2.11 Comprehensive Travel Protection------------------------- 3.2.12 Credit Limit indicating----------------------------------------- 3.2.13 Payment Due Date-------------------------------------------- 3.2.14 Current Balance-----------------------------------------------

04 05 06 06 10 12 12 12 12 13 13 13 15 15 16 16 16 16 17 17 17 18 18 18 18 19

3.2.15 Fortunes-------------------------------------------------------- 3.2.16 Acceptance at 1LINK ATMs-------------------------------- 3.2.17 Instant SBS Monthly Installment Plan-------------------- 3.2.18 Utility Bill Payments------------------------------------------ 3.2.19 Call and Pay Facility------------------------------------------ 3.2.20 Prepaid Mobiles Top ups------------------------------------ 3.2.21 Alfalah Credit on Phone------------------------------------- 3.3 Types of Plastic Money offered by United Bank Limited------ 3.3.1 Chip Credit Card------------------------------------------------ 3.3.2 Galleria-Picture Card------------------------------------------- 3.3.3 Auto Credit Card------------------------------------------------- 3.4 Features and Benefits of Plastic Money offered by United

Bank Limited----------------------------------------------------------------- 3.4.1 Low Balance Transfer Rate---------------------------------- 3.4.2 24-Hour Customer Service----------------------------------- 3.4.3 Cash Advance--------------------------------------------------- 3.4.4 4 free supplementary Cards---------------------------------- 3.4.5 Free Road miles or Classic Reward points--------------- 3.4.6 Buy Today ,Pay Later ----------------------------------------- 3.4.7 Credit Guardian------------------------------------------------- 3.4.8 Free Travel Accident Insurance----------------------------- 3.4.9 Zero Loss Liability----------------------------------------------- 3.4.10 Free CIP Lounge Access----------------------------------- 3.4.11 Cash at Counter-----------------------------------------------

19 19 19 20 20 20 20 21 21 22 23 24 25 25 25 26 26 26 27 27 27 28 28

CHAPTER III – RESEARCH DESIGN AND METHODOLOGY ------ 29 1. Introduction --------------------------------------------------------------------2. Research Design ------------------------------------------------------------ 3. Data Collection Methods and Techniques ---------------------------- 3.1 Questionnaire instrument --------------------------------------------- 3.2 Internet Sources -------------------------------------------------------- 3.3 Interviews------------------------------------------------------------------4. Sample Size -------------------------------------------------------------------5. Measures ----------------------------------------------------------------------

29 29 32 32 34 35 35 35

CHAPTER IV – DATA ANALYSIS AND RESULTS -------------------- 36

1. Introduction --------------------------------------------------------------------2. Findings about Objectives ------------------------------------------------- 2.1 Findings about Credit Card Awareness --------------------------- 2.1.1 Findings about Credit card Awareness of bank Alfalah

limited --------------------------------------------------------------------- 2.1.2 Findings about Credit card Awareness of United bank

limited --------------------------------------------------------------------- 2.2 Findings about comparison of result of Awareness level ----- 2.3 Finding the Customer Satisfaction level in concerning banks 2.3.1 Findings about Customer Satisfaction level of BAL----- 2.3.2 Findings about Customer Satisfaction level of UBL----- 2.4 Findings comparison of result of customer satisfaction level-3. Hypotheses Testing --------------------------------------------------------- 3.1 Hypothesis 1 ------------------------------------------------------------ 3.2 Hypothesis 2 ------------------------------------------------------------ CHAPTER V – CONCLUSIONS AND DISCUSSION------------------ 1. Conclusions-------------------------------------------------------------------- 1.1 Conclusion about findings--------------------------------------------- 1.2 Conclusion about Hypotheses--------------------------------------- 1.2.1 Hypothesis 1----------------------------------------------------- 1.2.2 Hypothesis 2------------------------------------------------------2. Discussion--------------------------------------------------------------------- CHAPTER VI – RECOMMENDATIONS----------------------------------- 1. Recommendations for further Research--------------------------------2. Recommendations for concern banks---------------------------------- REFERENCES------------------------------------------------------------------- APPENDEX-----------------------------------------------------------------------

36 37 37 37 48 59 61 61 74 88 90 90 93 97 97 97 98 98 99 99 100 100 100 103 104

LIST OF TABLES

Table Page

III – 1 Measures Related Awareness------------------------------------------ 33

III – 2 Measures Related to Customer Satisfaction------------------------ 34

IV – 1 Measures related to Credit card awareness along with mean values of BAL--------------------------------------------------------------

47

IV – 2 Measures related to Credit card awareness along with mean values of UBL--------------------------------------------------------------

58

IV– 3 Measures related to Customer satisfaction along with mean values of BAL--------------------------------------------------------------

73

IV – 4 Measures related to Customer satisfaction along with mean values of UBL--------------------------------------------------------------

87

IV – 5 Descriptive statistics of hypothesis 1--------------------------------- 91

IV – 6 T-Test of hypothesis 1---------------------------------------------------- 92

IV – 7 Descriptive statistics of hypothesis 2--------------------------------- 94

IV –8 T-Test of hypothesis 2---------------------------------------------------- 95

LIST OF FIGURES

Figure Page III – 1 Research Design------------------------------------------------------- 31 IV – 1 Variables used for Case Studies----------------------------------- 36 IV – 2 Responses related to Supplementary cards ------------------- 37 IV – 3 Responses related to Zero loss liability-------------------------- 38 IV – 4 Responses related to Credit guardian---------------------------- 39 IV – 5 Responses related to CIP lounge--------------------------------- 40 IV – 6 Responses related to Balance transfer-------------------------- 41 IV – 7 Responses related to Expiry date -------------------------------- 42 IV – 8 Responses related to Travel insurance-------------------------- 43 IV – 9 Responses related to Deduction charges----------------------- 44 IV – 10 Responses related to Cash advance facility------------------- 45 IV – 11 Responses related to Cancellation of card--------------------- 46 IV – 12 Responses related to Supplementary cards------------------- 48 IV – 13 Responses related to Zero loss liability------------------------- 49 IV – 14 Responses related to Credit guardian--------------------------- 50 IV – 15 Responses related to CIP lounge--------------------------------- 51 IV – 16 Responses related to Balance transfer-------------------------- 52 IV – 17 Responses related to Expiry date-------------------------------- 53 IV – 18 Responses related to Travel insurance------------------------- 54 IV – 19 Responses related to Deduction charges---------------------- 55 IV – 20 Responses related to Cash advance facility------------------- 56 IV – 21 Responses related to Cancellation of card--------------------- 57 IV – 22 comparison of result of awareness level------------------------ 59 IV – 23 Responses related to 24-hour banking service--------------- 61 IV– 24 Responses related to Step by step installment payment--- 62 IV – 25 Responses related to Paying of outstanding balance------- 63 IV – 26 Responses related to Drop box----------------------------------- 64 IV – 27 Responses related to Credit card limit--------------------------- 65

IV – 28 Responses related to Reward programs------------------------ 66 IV – 29 Responses related to Service charges-------------------------- 67 IV – 30 Responses related to Monthly transactions-------------------- 68 IV – 31 Responses related to Guide lines-------------------------------- 69 IV – 32 Responses related to Issuance of card------------------------- 70 IV – 33 Responses related to Interest rate------------------------------- 71 IV – 34 Responses related to Like to become customer of another

bank---------------------------------------------------------------------- 72

IV – 35 Responses related to 24-hour banking service--------------- 75 IV – 36 Responses related to Step by step installment payment--- 76 IV – 37 Responses related to Paying of outstanding balance------- 77 IV – 38 Responses related to Drop box----------------------------------- 78 IV – 39 Responses related to Credit card limit--------------------------- 79 IV – 40 Responses related to Reward programs------------------------ 80 IV – 41 Responses related to Service charges-------------------------- 81 IV – 42 Responses related to Monthly transactions-------------------- 82 IV – 43 Responses related to Guide lines-------------------------------- 83 IV – 44 Responses related to Issuance of card------------------------- 84 IV – 45 Responses related to Interest rate------------------------------- 85 IV – 46 Responses related to Like to become customer of another

bank---------------------------------------------------------------------- 86

IV – 47 Comparison of Customer Satisfaction--------------------------- 88

CHAPTER I

INTRODUCTION

1. General

Plastic money is the alternative to the cash or the standard 'money'.

Plastic money is used to refer to the credit cards or the debit cards that we

use to make purchases in our everyday life. Plastic money is much more

convenient to carry around as you do not have to carry a huge some of

money with you. It is also much safer to carry it along or to travel with it as if it

is stolen you can consult the bank whose service you are using and get it

blocked hence saving your money from getting stolen or even lost. Generic

term for all types of bank cards, credit cards, debit cards, smart cards, etc.

2. Research Problem

Increasing usage of plastic money day by day has resulted the

confusion in customers about choosing the most suitable bank for using

plastic money.

3. Research Questions

Research question of my study are:

• Which bank is more stronger in offering plastic money?

• Which bank’s customers are more satisfied?

4. Research purpose Purposes behind the research are:

1. To discover the transparency of plastic money handled by both

banks.

2. To find out their weak points.

3. To over come the flaws, customer awareness.

5. Research Objective

1. To get the awareness level of plastic money of both comprising banks.

2. To discover the comparison of result of awareness level.

3. To acquire the customer satisfaction level in concerning banks.

4. To obtain the comparison of result of customer satisfaction level.

6. Hypotheses

• Customers of BAL have high awareness of using credit card than

customers of UBL.

• Customer satisfaction level is same in customers of BAL and UBL.

7. Scope of Research

• Scope of research is limited in the boundaries of Hyderabad and two

banks are taken one is domestic that is United Bank Limited (UBL)

and another one is foreign bank which is Bank Alfalah Limited.

• Data is collected on randomly basis from customers of both banks.

8. Research Design and Methodology

There are diverse data collection sources however; Research is designed on

the basis of the primary sources of data (structured questionnaires, likert

scale and interviews) and secondary sources of data such as:

Articles

Internet

Books

Newspapers

Bank’s annual reports

CHAPTER II LITERATURE REVIEW

1. Plastic money and its types

Plastic money is the generic term for all types of bank cards, credit

cards, debit cards, smart cards, etc. They are the alternative to the cash or

the standard 'money'. The usage of plastic money(Cards) has increased in

the mode of payment of huge amount and time by time there are lots of

different types of plastic money has introduced which enhanced the features

of plastic money like we can use it to anywhere in the world and etc. Now the

world is becoming globalize so every card is accepted everywhere with the

power of VISA which interconnect the different countries. As we have the

different type of card as listed below:

1. Credit Card

2. Debit Card

3. Charge Card

4. Amex Card

5. MasterCard & Visa

6. Smart Card

7. Dinners Club Card

8. Photo Card

9. Global Card

10. Co-branded Card

11. Affinity Card

12. Add-on Card.

These cards are performing the function of money with different ways.

These cards are accepted worldwide, in which you can utilize your own

money and also bank’s money. The card through which you spend your own

money is known as debit card. The card through which you spend the

amount of bank as loan is called credit card.

Why has plastic money? “Charge it!” has become like a fashion

statement and it is commonly heard in various service establishments like

malls, multiplexes and hyper markets. People buying food or shopping for

clothes using their credit cards has now become a trend. A credit card is

supposed to be used for necessities and not as a luxury.

1.1 Origin of credit card

The origin of the credit card can be traced back to 1914, when

American company Western Union began issuing metal plates to customers

who would buy on credit. The transactions would be recorded on these

plates. However, the credit card as we know it took other 40-odd years to

evolve. In 1950 the Diners Chub in New York pioneered a charge card for

meals, heralding the arrival of "plastic money," a credit account that the user

paid off, with interest, at the end of each month. Eight years later American

Express Company developed a card used for goods and services at member

establishments across the country, again with the provision that the borrower

pay the total balance monthly.

The Bank of America pioneered the first true domestic "revolving" credit

card used nationally when it introduced the Bank America card in 1959.

1.2 Plastic Money In Pakistan

Plastic Money business is definitely going big time here in

Pakistan. In a country where 10 years back people have hardly heard the

word plastic money or credit card, more than 7000 merchants are accepting

above 140,000 cards.

It has been estimated that there are likely to be around half

million potential card users in the near future. This forecasting derive

credibility from the fact that more and more local and international financial

institutions are exhibiting enthusiasm in this direction. This in turn reflects

prospects in Pakistan market in accommodating numerous credit card

competitors operating on the circuit, ensuring healthy and competitive card

business deals.

1.3 Market Scenario

Although credit card was introduced in Pakistan decades ago

when Habib Bank, the largest bank in Pakistan, launched its gold card, but

people had hardly know about this card because of its very limited issuance.

Allied Bank of Pakistan had launched its Master Card. Than after two years

Citibank had launched its VISA Card and that was the turning point in the

history of Plastic Money in Pakistan.

Citibank had done a tremendous job to educate people of

Pakistan, as well as, financial industry about credit cards and its significance

in today's world. Because of very aggressive marketing and heavy

investment in technology, Citibank is well deserve to be called the industry

leader of Pakistan's credit card business.

After successful launch of Citibank card, Muslim Commercial

Bank, Bank of America, and National Bank of Pakistan had launched their

credit cards.

The expansion of market occurred once after deregulation

regime introduction in financial sector. There on, numerous banks set on

enlisting credit card on top of financial solutions. Barring Islamic banks, now

almost every commercial banks in Pakistan offer credit card. Credit card in all

over the world is recognized for its giving immediate monetary solution to its

holder. In developed countries, people like to have associations with banks to

meet their pecuniary needs through consumer loans because they are sure

of prowess of financial laws. In Pakistan, the situation is quite reversed firstly

since per capita income of the country fellows suffices barely to fulfill basic

needs, leaving no vacuum for saving to waste on principal plus high interest

against loans. Secondly, illiteracy rate in the country is drastically low, and

since bank-consumer relationship, based on complicated legal epithets,

requires education and literate consumers, parity in it is difficult to maintain.

Basically, two different kinds of people suffer into banking

disputes associated with the consumer loans; people with out awareness,

and people with having intention to exploit consumer loans, Recently, credit

card conflicts appeared in public, some times representing kindred sprits of

later set of people those who even without befitting source of monthly income

indulged in out of pockets credits.

Besides, prudential regulation of State Bank bound all banks (foreign

or local) to have separate consumer complaint center and redress consumer

grievances with 45 days of conversance. After the deregulation of banking

and financial system in Pakistan, numbers of banking consumers is rising

day by day, and so do the counts in complaints. As consumer financing is

expanding more rapidly than any other financial services, it has become

more prone to fall to financial aberration owing to being passed through,

perhaps, an evolutionary stage.

Basically, the use of a credit card involves three parties, as

under:

i) The card holder. ii) The retailer or the supplier of goods or services. iii)

The credit card company.

The Cardholder:

The main benefit to a cardholder is less need to carry cash

when shopping. This ensures increased security much desired in the law and

order situation obtaining in Pakistan.

Benefits may be:

(i) Saving on excise duty as a large number of scattered purchases

(ii) Availability of free credit for 25 to 28 days

(iii) Rolling credit facility if the cardholder chooses to pay in installments

(iv) Cash can be obtained on holidays and during off hours without the

need to carry a cheque book.

But, the question is, and it is indeed a crucial question, that how

many Pakistanis are capable to avail of these facilities by making use of

credit cards. A reply to this question alone shall determine whether or not we

are adequately equipped to switch over to such sophisticated techniques of

transfer of funds

Use of credit card, on the one hand, creates indebtedness on

account of the cardholders, which may not be commensurate with their

repaying capacity. On the other hand, in the form of additional credit utilized

by the cardholders, it adds to the "money supply" in the country's money

market, and raises the inflation level proportionately. However, it also tends

to increase the demand for goods and services which, in turn, should

increase production and reduce unemployment.

The Supplier or Retailer:

The benefits to the suppliers of goods and services may be as

follows:

i) Greater sales, as customers are attracted towards the establishments

accepting their credit cards.

ii) Less cash handling, and therefore increased security.

iii) Credit vouchers which a retailer pays into his account are treated as

cash; thus increased liquidity. It also cuts on the time usually taken in

collecting of cheques.

The only disadvantage to a retailer is that he is required to pay

to the credit card company a percentage of his sale income from card

transactions.

The Credit Card Companies:

According to a conservative estimate, more than 50% of the

cardholders tend to pay their bills in full within the prescribed time limit to

avail of the free card facility.

The customers who do not withhold payment beyond the specified

date are called "free riders" in card business.

2. Importance of customer satisfaction

There are number of credit cards varieties that are offered by the

companies. The main thing is the selection of the best credit card that suits

you well. One-size cards are not suitable for all. There is a good type of cards

for the selection that are offered by the companies. Some are provided for

the special groups and others credit cards are provided for those who want

not only the standard card but also more.

Standard cards are issued simply for your use. These cards will not

provide you any great deal but you can easily transfer your balances to this

card. Standard card is the very common sort of plastic currency in your

pockets, these cards provide you with that interest rate which is far beyond

your imagination and it is so because it does not provided you any kind of

special option or features. What all you need is just some amount of credit on

your name, and than this card is ready for you

There are many types of credit cards available in the market but one

among those is a specialty credit card. The term itself shows the distinction of

this card, the word “specialty” indicates to the particular group of customers.

Under this type you can also get cards such as, student credit cards that are

meant particularly for students. The student credit cards are good for

students as they have less interest rate as well as there is no need to pay

immediately. This facility given by this card is very attractive for the students.

Another kind of credit card is the card, which is used for business

purposes and is very useful for a businessman is business credit card. These

cards are issued to the employees through their trade, and business cards

have long credit limits as well as these cards have additional perks, which

come all along with the card. These cards are ideal selection done by the

people who are in to business. Business plastic normally has various

features.

Credit cards are an extremely useful way of paying for products and

services. They are often more convenient than cash or checks, and they are

almost universally accepted (including over the phone). Additionally, they are

a great way for you to establish your creditworthiness. And some cards offer

additional benefits But credit cards are a mixed blessing. They can

encourage excessive spending.

3. Types of plastic money offered by Bank Alfalah

Limited and United Bank Limited.

3.1. Types of plastic money offered by Bank Alfalah

Limited

Bank Alfalah Limited is a private bank in Pakistan owned by the Abu

Dhabi Group. Bank Alfalah was incorporated on June 21, 1992 as a public

limited company under the Companies Ordinance 1984. Its banking

operations commenced from November 1, 1992. Launched in Hyderabad city

in March, 2003.

3.1.1 Platinum Card

It is accepted at nearly 29 million locations in more than 150

countries around the globe and at over 27,000 establishments in Pakistan.

3.1.2 Titanium card

Titanium MasterCard is your partner everywhere and is globally

accepted and welcomed at locations displaying the MasterCard logo.

3.1.3 Professional card

A perfect card combination for all segments of salaried &

professional individuals.

3.1.4 Supplementary Cards

All Bank Alfalah basic credit card members can apply for

supplementary cards for their sons, daughters (Children who are above 13

years of age), house staff or anyone you like thus giving you complete

freedom of choice.

3.2. Fringe and Benefits of plastic money offered by Bank

Alfalah Limited:

No Joining Fee

No Annual/Renewal Fee

Balance Transfer Facility

Global Acceptability

Cash Advance Facility

Revolving Credit

Supplementary Cards

Card Expiry Period

24-Hours Phone Banking Service

Zero Loss Liability

All Billing in Pak Rupees

Comprehensive Travel Protection

Statement of Account

Fortunes

Acceptance at 1Link ATMs

Instant SBS Monthly Installment Plan

Utility bill Payments

Call and Pay Facility

Prepaid Mobiles Top ups

Alfalah Credit on Phone

Credit Card bill Payment through Hilal Card

Special Offer on Warid post paid connection

Step By Step Plan

Non Alfalah Card members

3.2.1 No Joining Fee Step By Step Plan

Join Alfalah VISA without paying any joining fee. Start enjoying your

free card from the moment you get hold of it.

3.2.2 Balance Transfer Facility

Bank Alfalah offers balance transfer facility to all its Cardmembers -

the easy and convenient way to settle unsettled credit card payments on all

existing credit cards in Pakistan. As an Alfalah VISA Cardmember you can

avail balance transfer facility at a low rate of only 2% (24% APR) per month

(for initial six months), which is the lowest in Pakistan. The balance transfer

facility can only be availed if the total outstanding balance does not exceed

beyond the credit limit assigned by Bank Alfalah for Alfalah VISA card.

Avail balance transfer facility by filling out our Balance Transfer Facility

Form. Print the form, fill out all the fields, sign it and send it to us through

courier.

OR

Drop it in at any of Bank Alfalah drop boxes available in all Bank

Alfalah Branches.

3.2.3 Global Acceptability

Your Bank Alfalah VISA card is your partner everywhere and is

globally accepted and welcomed at locations displaying the VISA logo. It is

accepted at nearly 29 million locations in more than 150 countries around the

globe and at over 27,000 establishments in Pakistan.

3.2.4 Cash Advance Facility 50% Of Credit Limit

Now you can avail Cash Advance Facility up to 50% of your available

credit limit. Enjoy the benefits of this exclusive offer on your Bank Alfalah

Credit Cards. You can get cash from Alfalah ATMs or cash counters of Bank

Alfalah branches and other VISA member banks in Pakistan.

3.2.5 Revolving Credit

With Alfalah VISA you have the option of paying only 5% of your

outstanding balance by the payment due date. Service charges will be levied

on the balance unpaid spending and carried forward. These charges are

calculated on a daily basis from the transaction date for all cash and retail

transactions. The following month you have the option of either the full

amount payment or if you wish, pay only the minimum amount due and

revolve again.

3.2.6 Supplementary Cards

Gift your family members with exclusive Alfalah VISA supplementary

cards and let them also enjoy the privileges of Alfalah VISA. Only Alfalah

VISA gives you the unique feature of having up to six free supplementary

cards for anyone you care for. All supplementary Cardmembers share your

credit limit. All charges incurred on the supplementary cards will be reported

on your monthly statement.

3.2.7 Card Expiry Period

Effective 7 June 2005, all VISA credit cards being issued by our Card

Division will have an expiry of 3 years on them.

3.2.8 24-Hours Phone Banking Service

Our well-trained and qualified phone banking team Is available to help

you 24 hours a day. Just dial 111-225-111 for:

Activating your card

Answering your queries

Registering and resolving your complaints

Reporting a lost/stolen card

3.2.9 Zero Loss Liability

If you ever lose your card, Bank Alfalah ensures that you never have

to worry about it. You are covered for all fraudulent charges made on your

card as soon as it has been reported lost to us. Just make sure that you

report the lost card immediately upon discovery. You are completely secure

against loss/theft after the card loss has been reported to us.

3.2.10 All Billing in Pak Rupees

Whether you make transactions in Dollars or any other currency, for

your convenience, all your billing will be in PAK Rupees.

3.2.11 Comprehensive Travel Protection

Alfalah VISA offers a comprehensive cover up to Rs. 3.5 Million on

Alfalah VISA Gold Card in case of an accident, while traveling on any

common carrier. It is applicable only if the tickets are charged through Alfalah

VISA card.

3.2.12 Credit Limit indicating:

The total credit limit assigned to you for all your card accounts

(principal and supplementary).

3.2.13 Payment Due Date

Indicating the date by which your payment should reach Bank Alfalah

to avoid any late payment charges.

3.2.14 Current Balance

Indicating the total outstanding amount on your card account on the

statement date.

Payment coupon: To be used for making payments.

3.2.15 Fortunes

For every Rs. 50 you spend on your Alfalah VISA card, you will earn

one fortune point. Your accumulated fortune points can be exchanged for a

whole range of items displayed in our Fortunes Catalogue.. It offers a wide

range of lifestyle categories always catering to you and your family's taste.

Once you have accumulated enough points to redeem the gift of your

choice, fill out a simple form available at all Bank Alfalah branches or call our

24 hour phone banking service and order the item of your choice. The fortune

items will be delivered at your doorstep.

3.2.16 Acceptance at 1LINK ATMs

Avail Cash Advance upto 50% of your credit limit at over 2200 1Link

ATMs in Pakistan in addition to over 1.2 million ATMs worldwide.

3.2.17 Instant SBS Monthly Installment Plan

Bank Alfalah cardholders can convert any transaction of Rs. 3,000 or

above into easy installments of 3,6,12,18,24,30 and 36 months’ tenures at

the time of transaction.

3.2.18 Utility bill Payments

Now Utility bill payments* can be made through Alfalah VISA credit

cards either by calling Call Centre or through Direct Debit instructions.

*Available on FESCO, LESCO, SSGC, SNGPL ,IESCO, HESCO, GEPCO,

KESCO, PTCL & WARID. Other companies will be added soon.

3.2.19 Call and Pay Facility

Cardholders now have the convenience of using their cards to make

payments even on locations where credit cards are not accepted by calling

our 24 hours Call Center and getting pay orders issued to any third party

through debit to Alfalah Visa Credit Card.

3.2.20 Prepaid Mobiles Top ups

Alfalah cardholders are also being provided the facility to get their prepaid

mobile connections of any company topped up by just one call to 24 hours

Call Center. Alfalah credit cardholders can also use their reward points to get

the prepaid mobile top ups.

3.2.21 Alfalah Credit on Phone

Alfalah cardholders can call the Call Center and get credit upto 75% of

their available credit limit assigned by Bank Alfalah or available credit limit

whichever is lower at just 2.0% per month (24% APR). Payment of credit

amount can be made to them through a cheque at the doorstep or directly

into the account in Bank Alfalah.

3.3 Types of Plastic Money offered by United Bank Limited

UBL is domestic bank of Pakistan has assets of over Rs. 550 billion and

a solid track record of fifty years - in addition to the convenience of over 1112

branches serving you throughout the country and also at several overseas

locations. Established in November 7, 1959.

3.3.1 Chip Credit Card

Pakistan’s 1st Chip Credit Card that guarantees you both enjoyment and

high value. It assures you global acceptability in more than 22 million

establishments worldwide in 130 countries and in more than 12, 000 outlets

within Pakistan.

CHIP based credit cards have globally proven to be the most secure way of

conducting credit card transactions. This unique high tech CHIP guarantees

your financial security while conducting transactions on credit cards, both

within Pakistan and around the world.

3.3.2 Galleria - Picture Card

Design your Credit Card your way!Your choices say a lot about your

personality. Shouldn't your Credit Card!.

Being different was never so easy! Now UBL Credit Card gives you the

flexibility to make a statement by letting you design your credit card in almost

any manner you want. Galleria, by UBL Cards is Pakistan’s first picture credit

card that gives you freedom of choice and expression as you can now

customize it with your favorite image and make your credit card as unique as

you are.

Express your individuality. Add a personal touch. Keep a loved one close

to your heart. Or simply make a statement.

Personalize your card with a picture of your choice on it. Choose

whatever you think defines you or represents your personality, your passions,

your style or your likes. Perhaps you could put up pictures of yourself, your

loved ones or anything you please. It’s entirely up to you. For the first time

ever in Pakistan, a card that lets you express your true self.

3.3.3 Auto Credit Card

Pakistan’s First Auto Credit Card!!

The UBL Credit Cards team now brings Pakistan’s 1st Auto Credit Card -

UBL PSO Auto Credit Card. Keeping in mind the success story of our

standard UBL Card, with annual fee wavier and free liters of fuel as reward

against spend, we are introducing a complete auto card solution with PSO

with high value incentives and discounts on fuel and other automobile related

products.This card is clearly aimed at offering a value-for-money proposition,

with a touch of both incentive and functional appeal as well as a clear

objective of making UBL PSO Auto Credit Card, a truly preferred card in the

market. Positioned as Pakistan’s First Auto Credit Card, it will offer 5% Free

Fuel on PSO stations* and 1% on non PSO outlets. Card members can also

avail various exciting discounts and benefits given below

Free Accidental Insurance.

Discount on Avis Rent-a-Car services.

Discount on PSO lubricants (DEO and Carient).

Discount on tracking devices from C-Track.

Special offers at authorized 3S dealers of Honda, Suzuki and Toyota.

Discounted rates on car insurance from TDI.

Discount on installation of CNG Kit.

Discounted Rent-A-Car traveling.

Discounted car accessories.

Discounts on tyres and stereo systems

3.4. Features and Benefits of Plastic Money offered by United

Bank Limited

Low Balance Transfer Rate

24 Hour Customer Service

Cash Advance

4 Free Supplementary Cards

Free Roadmiles or Classic Reward points

Buy Today, Pay Later

Credit Guardian

Free Travel Accident Insurance

Zero Loss Liability

Free CIP Lounge Access

Cash at Counter

3.4.1 Low Balance Transfer Rate

Now you can really save big time with your UBL Credit Card Balance

Transfer Facility! You have the opportunity to pay off balances you owe to

other banks through your UBL Credit Card on a low balance transfer rate.

3.4.2 24 Hour Customer Service

By simply calling our 24 hour ‘UBL Contact Center’ at 111-825-888 or

logging onto our website www.ubl.com.pk, you can avail the following

facilities on your UBL Credit Card, 24 hours a day, 7 days a week.

3.4.3 Cash Advance

You can now withdraw cash through your UBL Credit Card’s instant cash

advance facility from any designated UBL Card Payment Branches

nationwide and more than 780,000 ATMs and financial institutions worldwide

displaying VISA/PLUS logo.

The service charges for cash advance will be applied from the day of the

transaction. A cash advance fee will also apply for each cash withdrawal.

3.4.4 4 Free Supplementary Cards

To share the value, excitement and benefits of your UBL Credit Card with

your loved ones, your UBL Credit Card offers you up to 4 free supplementary

cards.

3.4.5 Free Roadmiles or Classic Reward points

The more spending there is on your supplementary cards, the more Free

Roadmiles or Classic Reward points are earned on your account. Also, the

supplementary card holder benefits by earning instant and exciting UBL Chip

Rewards on his/her own card.

3.4.6 Buy Today, Pay Later

Your UBL Credit Card gives you the financial flexibility to buy today and

pay after a month at no extra charge. You have the option of paying a

minimum 5% of the outstanding balance or any other amount of your choice

up to your total account balance.

A service charge of only 3.25% per month will apply to whatever

remaining unpaid balance that is carried forward.

3.4.7 Credit Guardian

UBL takes care of its Credit Cardmembers payments in time when they

cannot. Our Cardmembers can now get total peace of mind and insure

themselves against unforeseen emergencies. In the event of any temporary

disability where UBL Cardmember is unable to pay his/her monthly dues,

Credit Guardian will allow payment of the outstanding monthly amount.

Moreover, in the unfortunate event of permanent disability or death, the entire

outstanding amount will be waived off. Credit Guardian Facility is available

for a minimal fee, charged automatically on the card balance every month.

3.4.8 Free Travel Accident Insurance

Each time our Cardmembers use their UBL Credit Card to purchase

airline, train or bus tickets, they are automatically covered against any sort of

accident that might befall them while traveling:

3.4.9 Zero Loss Liability

Isn’t it comforting to know that if you lose your card, you have nothing to

worry about! You are covered for all fraudulent charges made on your card

as soon as it has been reported lost to us.

3.4.10 Free CIP Lounge Access

Take advantage of the special CIP Lounge at Karachi International

Airport with free secretarial services, free buffet, internet connection, reading

material and 24 - Hour porter facilities.

3.4.11 Cash at Counter

You can make cash payment at all designated UBL Card Payment

Branches nationwide during banking hours (see designated Card Payment

branches list at the back of the Card Payment envelope).

CHAPTER III RESEARCH DESIGN AND METHODOLOGY

1. Introduction

Research is a diligent and systematic inquiry or investigation into a

subject in order to discover or revise facts, theories, applications, etc.

Methodology is the system of methods followed by particular discipline.

This chapter presents and justifies the suitable research design and

methodology to answer the research questions. It begins with research

design, discusses on data collection methods and techniques and provides

sample size and measures.

2. Research Design

Research design is the blueprint for achieving objectives and

answering questions. Choosing a design can be complicated because there

are many varieties of methods, techniques, procedures, protocols, and

sampling plans available.

Choosing the suitable case study design is a critical matter on the

quality of research findings and it is often influenced by the nature of the

research (Yin 1994; 2003). Four types of case study designs were proposed

by Yin (1994; 2003): (a) single case (holistic), (b) single case (embedded), (c)

multiple cases (holistic) and (d) multiple cases (embedded).

The single case study design is appropriate when: (1) the case

provides an essential test for established theory, (2) embodies an exceptional

or a unique event, (3) is a distinguishing or typical case, or (4) provides a

longitudinal or revelatory aim (Yin 1994; 2003).

On the other hand, using multiple cases design is used where each

case study is regarded as single experiment or investigation (Yin 1994;

2003). Therefore, there is no doubt that the multiple case study design is the

most appropriate design for the current research because it is not aiming to

test theory or to understand a unique and typical phenomenon as in the

single case design.

In short, the multiple cases design is preferred over the single case

design because it provides strong and exact grounds for good quality

research (Yin 1994; 2003)

As specified by Yin (1994; 2003) the case study design represents the

research plan that guides the process of data collection, analysis and

interpretation. Accordingly, the main steps involved in the process of

designing the current research are shown in Figure III – 1.

Define Research Questions

Design Case Questionnaire

Cross Analysis of

Study Customers Satisfaction of Bank Alafalah limited

Select Case Studies

Study Customers Satisfaction of United Bank Limited

Findings about Research

Review

Figure III – 1 Research Design

Source: Developed for current research by author

3. Data Collection Methods and Techniques

Case study research can include both qualitative and quantitative data

and recent methodologists have identified several techniques of data

collection of case study based-research but it is not necessary to utilize all of

these methods (Yin 1994; 2003). These techniques include (1) interviews, (2)

questionnaire, (3) archival records, (4) direct observation, (5) participant

observation, (6) documentation and (7) physical artifacts.

3.1 Questionnaire Instrument

The questionnaire [Appendix] is prepared and designed to measure

the level of customer satisfaction and awareness regarding plastic money.

For measuring the level of credit card awareness 10 questions are

extracted from questionnaire, those questions carry measures which focus

on credit card awareness (Table III - 1)

Table III – 1 Measures Related Awareness

Question

s

Measures

Q.1 Supplementary cards.

Q.2 Zero loss liability.

Q.3 Credit guardian.

Q.4 CIP lounge.

Q.5 Balance transfer.

Q.6 Expiry date.

Q.7 Travel insurance.

Q.8 Deduction charges.

Q.9 Cash advance facility.

Q.10 Cancellation of card.

For measuring the level of customer satisfaction 12 questions are

extracted from questionnaire [Appendix], those questions carry measures

which focus on customer satisfaction (Table III - 2)

Table III – 2 Measures Related to Customer Satisfaction

Question

s

Measures

Q.1 24-hour banking service.

Q.2 Step by step installment payment.

Q.3 Paying of outstanding balance.

Q.4 Drop box.

Q.5 Credit card limit.

Q.6 Reward programs.

Q.7 Service charges.

Q.8 Monthly transactions.

Q.9 Guide lines.

Q.10 Issuance of card.

Q.11 Interest rate.

Q.12 Like to become customer of another bank.

3.2 Internet Sources

The selected cases have internet websites which contains some

information about the organization products, credit card policies,fringe and

benefits and operations. This information is used as a secondary source of

data to acquire additional information about the organisations.

3.3 Interviews

Interviews are also taken from the credit card department of both banks.

This information is primary source of data used to find out that how they

inform about their credit card and its benefits and other legal information to

customer. Simply how they aware their customers about their credit card.

4. Sample Size

The study is aims to measure customer satisfaction and usage. which

is done through the survey of two banks that is United Bank Limited(UBL)

and Bank Alfalah Limited. 50 customers of each bank are selected on

random basis.

5. Measures

One of many methods for the analysis is questionnaire.

Questionnaires are frequently used in socio-economic and business

research, using mainly 5-point (Waldman et al., 2001) or 7-point (Papadakis

et al., 1998) Likert scale type questionnaires. In this thesis a 5-point Likert of

interval measures is adopted.

CHAPTER IV DATA ANALYSIS AND RESULTS

1. Introduction This chapter discusses about findings from two case studies in light of

research questions. The main motive with this study is to investigate

customer awareness and customer satisfaction regarding credit card of both

banks. The findings of two variables are compared with each other and in the

end hypotheses are tested. Figure IV – 1 represents variables which are

used for the case studies.

Fig. IV – 1: Variables used for Case Studies

Case Studies

Case 1: UBL Case 2: BAL

Credit Card Awareness

Customer Satisfaction

Credit Card Awareness

Customer Satisfaction

2. Findings about objectives.

2.1 Findings about Credit Card Awareness.

2.1.1 Findings about credit card awareness of Bank Alfalah Limited.

For measuring the level of Credit card awareness 10 questions are

extracted from [Appendix].

Fig. IV – 2 Responses related to Supplementary cards

In question 1 regarding awareness, 30 customers are strongly

agree that their card gives option of more than 5 supplementary cards

and 20 are agree.

Supplementary cards

0

5

10

15

20

25

30

35

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Supplementary cards

Fig. IV – 3 Responses related to Zero loss liability

In question 2,20 customers are strongly agree that their card

has zero loss liability while 15 are agree ,10 are neither agree nor

disagree and 5 are disagree.

Zero loss liability

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Zero loss liability

Fig. IV – 4 Responses related to Credit guardian

In question 3, the measure is credit guardian.10 customers are

strongly agree that their card has option of credit guardian and 20 are

agree ,20 are neither disagree nor agree.

Credit guardian

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Credit guardian

Fig. IV – 5 Responses related to CIP lounge

In question 4, 20 customers are strongly disagreeing that their

card has not the option of CIP lounge, 15 are disagree and 15 are

neither agree nor disagree.

CIP lounge

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagree nor

Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

CIP lounge

Balance transfer

15

20

25

ust

om

ers

Fig. IV – 6 Responses related to Balance transfer

In question 5,15 customers are strongly agree that their card

has option of balance transfer ,10 are agree ,20 are neither agree nor

disagree and 5 are disagree.

Expiry date

15

20

25

30

of

Cu

sto

mer

s

E i d t

Fig. IV – 7 Responses related to Expiry date

In question 6,25 customers are strongly agree ,10 are agree ,7

are neither disagree nor agree and 8 are disagree with measure that

their card has expiry date till 3 years.

Travel insurance

6

8

10

12

14

16

ces

of

Cu

sto

mer

s

Travel insurance

Fig. IV – 8 Responses related to Travel insurance

In question 7 ,12 are strongly agree,15 are agree ,15 are

neither agree nor disagree and 8 are disagree that their credit card

has travel insurance.

Deduction charges

8

10

12

14

16

of

Cu

sto

mer

s

Deduction charges

Fig. IV – 9 Responses related to Deduction charges

In question 8,12 are strongly agree,8 are agree ,15 are neither

agree nor disagree and 15 are disagree that deduction charges are

same as mentioned in charges schedule.

Cash advance facility

8101214161820

s o

f C

ust

om

ers

Cash advance facility

Fig. IV – 10 Responses related to Cash advance facility

In question 9 ,the responses came from customers are 18 are

strongly agree,11 are agree,12 are neither agree nor disagree ,5 are

disagree and 4 are strongly disagree.

Cancellation of card

6

8

10

12

14

16

es o

f C

ust

om

ers

Cancellation of card

Fig. IV – 11 Responses related to Cancellation of card

In question 10 the responses collected from customers was 12

customer were strongly agree that their card has facility of easily

cancelation while 8 are agree ,15 are neither agree nor disagree ,7 are

disagree 8 are strongly disagree.

Table IV – 1 present’s measures related to questions along with their

mean values related to credit card awareness.

Table IV – 1: Measures related to Credit card awareness along with

mean values of BAL

Questions Measures Mean

Q.1 Supplementary cards 4.60

Q.2 Zero loss liability 4.0000

Q.3 Credit guardian 3.7800

Q.4 CIP lounge 1.9000

Q.5 Balance transfer 3.7000

Q.6 Expiry date 4.0400

Q.7 Travel insurance 3.6200

Q.8 Deduction charges 3.3000

Q.9 Cash advance facility 3.6800

Q.10 Cancellation of card.

3.1800

The scale of measurement is from 1 – 5, 1 represents strongly

disagree and 5 represents strongly agree to the question. The mean

value of question 1 from the customers of ABL is 4.60 which mean

most of the customers of ABL are agreed with statement that their

bank is giving the option of more than 5 supplementary cards. For

question 2 most of customers are agreed with zero loss liability which

we came to know from the mean value 4.00. The mean value 3.78 of

question 3 says that credit guardian is available in their card. Most of

customers of ABL disagreed that they don’t have awareness of CIP

lounge which is calculated from the mean value 1.9 of question 4.

From question 5 having mean 3.70.in question 6 the mean value is 4.4

which represents that their card has expiry date till 3 years. we came

to know that much of customers are aware of balance transfer for

question, 7, 8, 9 mean values are in between 3-4, it mean customers

are sure whether theirs cards expiry date is till 3 years or not, travel

insurance is available or not, deduction charges are same as

mentioned in charges schedule or not, and can avail cash advance

facility up to 50% of available credit limit or not respectively. We came

to know that more customers are aware of cancellation of card of

question 10 having mean 3.1.

2.1.2 Findings about Credit Card Awareness of bank UBL.

For measuring the level of Credit card awareness 10 questions

are extracted from questionnaire [Appendix].

Fig. IV – 12 Responses related to Supplementary cards

In question 1,27 are strongly disagree that their has more than

5 supplementary cards ,13 are disagree and 10 are neither agree nor

disagree.

Supplementary cards

0

5

10

15

20

25

30

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Supplementary cards

Fig. IV – 13 Responses related to Zero loss liability

In question 2, 15 are strongly disagreeing that their card has

zero loss liability, 15 are disagree, 10 are neither disagree nor agree

and 10 are agree.

Zero loss liability

0

2

4

6

8

10

12

14

16

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Zero loss liability

Credit guardian

15

20

25

Cu

sto

mer

s

Fig. IV – 14 Responses related to Credit guardian

In question 3, 5 are strongly disagree ,5 are disagree ,20 are

neither disagree nor agree 10 are agree and 10 are strongly agree

that their card option of credit guardian.

CIP lounge

30

40

50

60

s o

f C

ust

om

ers

CIP lounge

Fig. IV – 15 Responses related to CIP lounge

In question 4,18 are strongly agree, 10 are agree, 10 are

neither agree nor disagree ,10 are disagree and 7 are strongly

disagree that their card has CIP lounge regarding question 4.

Balance transfer

15

20

25

30

of

Cu

sto

mer

s

Balance transfer

Fig. IV – 16 Responses related to Balance transfer

In question 5,25 are strongly disagree ,15 are disagree ,10 are

neither agree nor disagree that their card has balance transfer facility.

Expiry date

10

15

20

25

s o

f C

ust

om

ers

Expiry date

Fig. IV – 17 Responses related to Expiry date

In question 6, 20 customers are strongly disagree ,13 are

disagree ,15 are neither agree nor disagree and 2 are agree that their

card has expiry date till 3 years.

Travel insurance

68

101214161820

ces

of

Cu

sto

mer

s

Travel insurance

Fig. IV – 18 Responses related to Travel insurance

In question 7,14 are strongly disagree ,3 are agree ,18 are

neither agree nor disagree,15 are agree that their card has travel

insurance.

Deduction charges

25

30

35

sto

mer

s

Fig. IV – 19 Responses related to Deduction charges

In question 8, 15 are strongly disagree ,5 are agree ,30 are

neither agree nor disagree that deduction charges are same as

mentioned in charges schedule.

Cash advance facility

15

20

25

of

Cu

sto

mer

s

Cash advance facility

Fig. IV – 20 Responses related to Cash advance facility

In question 9,18 are strongly disagree ,20 are agree ,12 are

neither agree nor disagree that their card has facility of availing 50% of

available credit limit.

Cancellation of card

25

30

sto

mer

s

Fig. IV – 21 Responses related to Cancellation of card

In question 10 the measure used is facility of easily cancellation

of card the 5 customers are strongly disagree,7 are disagree ,25 are

neither agree nor disagree ,13 are agree.

Table IV – 2: Measures related to Credit card awareness along with

mean values of UBL

Questions Measures Mean

Q.1 Supplementary cards 1.6600

Q.2 Zero loss liability 2.3000

Q.3 Credit guardian 3.3000

Q.4 CIP lounge 3.6000

Q.5 Balance transfer 1.7200

Q.6 Expiry date 1.9800

Q.7 Travel insurance 2.6800

Q.8 Deduction charges 2.3200

Q.9 Cash advance facility 1.8800

Q.10 Cancellation of card.

2.9200

The scale of measurement is from 1 – 5, 1 represents strongly

disagree and 5 represents strongly agree to the question. The mean

value of question 1 from the customers of UBL is 1.66 which means

most of the customers of UBL are not agreed with statement that their

bank is giving the option of more than 5 supplementary cards. For

question 2 most of customers are agreed with zero loss liability which

we came to know from the mean value 2.3. The mean value 3.30 of

question 3 says that credit guardian is available in their card. Most of

customers of UBL agreed that they do have awareness of CIP lounge

which is calculated from the mean value 3.60 of question 4. from

question 5 having mean 1.7 we came to know that not much of

customers are aware of balance transfer .for question 6,7,8,9 mean

values are in between 1.8-2.8, it mean customers are not sure

whether theirs cards expiry date is till 3 years or not, travel insurance

is available or not, deduction charges are same as mentioned in

charges schedule or not, and can avail cash advance facility up to

50% of available credit limit or not respectively. We came to know that

more customers are not aware of cancellation of card of question 10

having mean 2.9.

2.2. Findings about comparison of result of awareness level

Fig. IV – 22 comparison of result of awareness level

By comparing mean result of awareness level of both banks we

came to know that in question 1,customers of BAL are more aware

0

1

2

3

4

5

Mea

n

Number of Questions

Comparision of Awareness

BAL 4.6 4 3.8 1.9 3.7 4 3.6 3.3 3.7 3.2

UBL 1.7 2.3 3.3 3.6 1.7 2 2.7 2.3 1.9 2.9

1 2 3 4 5 6 7 8 9 10

that their card has more than 5 supplementary cards by getting the

mean of 4.6 than the customers of UBL having the mean of 1.7.in

question 2,many customers are aware that their card has zero loss

liability of BAL having mean 4 than the UBL which has mean value 2.3

.in question 3 ,having mean 3.8 this means that BAL customer’s are

aware of credit guardian and they know that their card has facility of

credit guardian while in UBL 3.3 mean value shows that their

customers are also aware about about credit guardian but less than

BAL customers. In question 5 mean value 1.9 shows that customers of

BAL are aware of CIP lounge than the customers of UBL, having

mean value of 3.6 which shows the UBL’s customers are more aware

of CIP lounge. in question 5,3.7 mean shows that customers of BAL

are aware that their card has facility of balance transfer option while

1.7 mean of UBL shows that customers are not aware with it.

In question 6,mean value 4 shows that much customers are aware

that expiry date of their card is till 3 years while 2 mean value of UBL

show that customers are not agree. In question 7, mean value 3.6

shows that customers of BAL are agree that their card has travel

insurance while 2.7mean of UBL shows that customers are not highly

disagree nor agree. in question8,mean value of 3.3 of BAL show that

customers are more customers knows that the deduction charges are

same as mentioned in charges schedule while 2.3 mean of UBL

shows that customers are a little aware about this. in question 9 ,the

measure used is cash advance facility up to 50% of available credit

limit got the mean value 3.7 of BAL shows that customers are agree

while 1.9 mean value of UBL shows that customers are not much

aware. in question 10 the mean value 3.2 of BAL shows that

customers are aware of facility of easily cancellation of card while 2.9

mean value of UBL shows that they are aware but less than BAL.

2.3 Finding the customer satisfaction level in concerning banks.

2.3.1 Findings about Customer satisfaction level of bank BAL

For measuring the level of Customer satisfaction 12 questions

are extracted from [Appendix].

Fig. IV – 23 Responses related to 24-hour banking service

In question 1,the measure used is supplementary card.20

customers are strongly agree, 20 customers are just agree, 10

customers are neither agree nor disagree.

24-hour banking service

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

24-hour banking service

Fig. IV – 24 Responses related to Step by step installment payment

In question 2,10 customers are strongly agree, 10 customers

are just agree, 20 customers are neither agree nor disagree, 10

customers are disagree that their card has the option of step by step

installment payment.

Step by step installment payment

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Step by step installmentpayment

Fig. IV – 25 Responses related to Paying of outstanding balance

In question 3,15 customers are strongly agree, 18 customers

are just agree, 10 customers are neither agree nor disagree, 7

customers are disagree related to paying of outstanding balance.

Paying of outstanding balance

02468

101214161820

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Paying of outstandingbalance

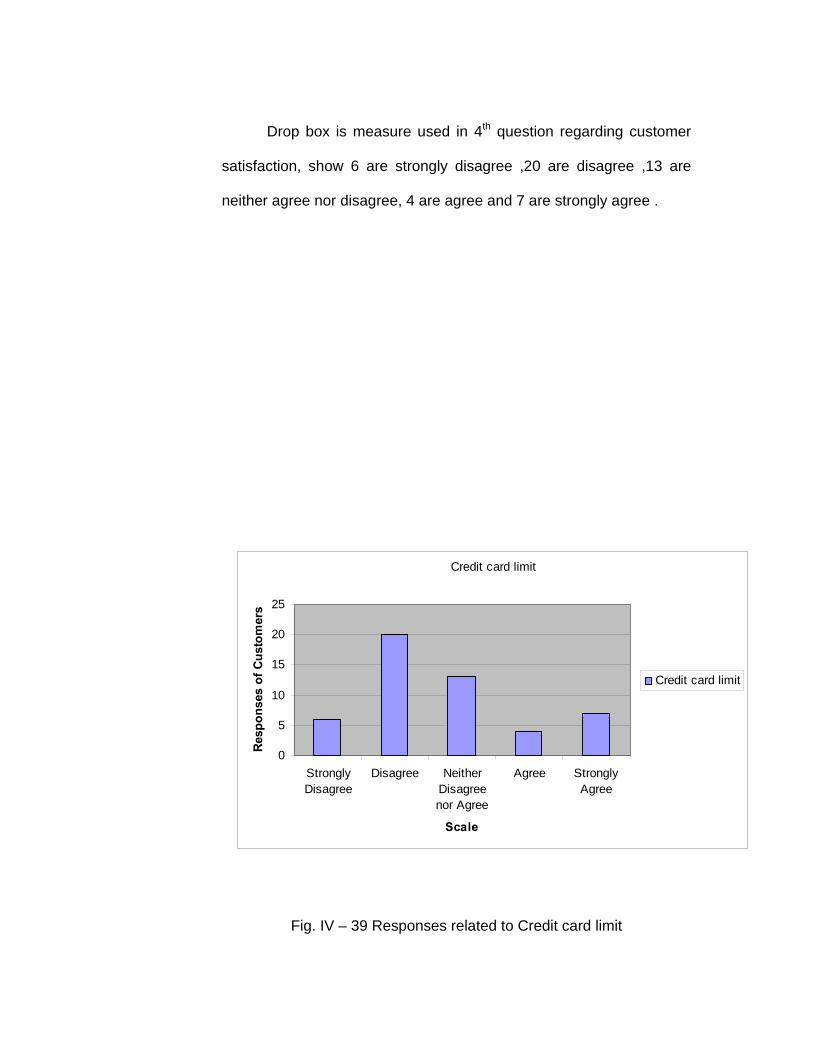

Fig. IV – 26 Responses related to Drop box

In question 4, 25 customers are strongly agree, 20 customers

are just agree, 5 customers are neither agree nor disagree regarding

to the usage of drop box.

Drop box

0

5

10

15

20

25

30

StronglyDisagree

Disagree NeitherDisagree nor

Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Drop box

Fig. IV – 27 Responses related to Credit card limit

In question 5,10 customers are strongly agree, 18 customers

are just agree, 8 customers are neither agree nor disagree, 14

customers are disagree related to limit of the credit card.

Credit card limit

02468

101214161820

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Credit card limit

Fig. IV – 28 Responses related to Reward programs

In question 6,15 customers are strongly agree, 25 customers

are just agree, 10 customers are neither agree nor disagree that they

are happy with the reward program of the card.

Reward programs

0

5

10

15

20

25

30

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Reward programs

Fig. IV – 29 Responses related to Service charges

In question 7,25 customers are strongly agree, 15 customers

are just agree, 10 customers are neither agree nor disagree related to

service charges.

Service charges

0

5

10

15

20

25

30

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Service charges

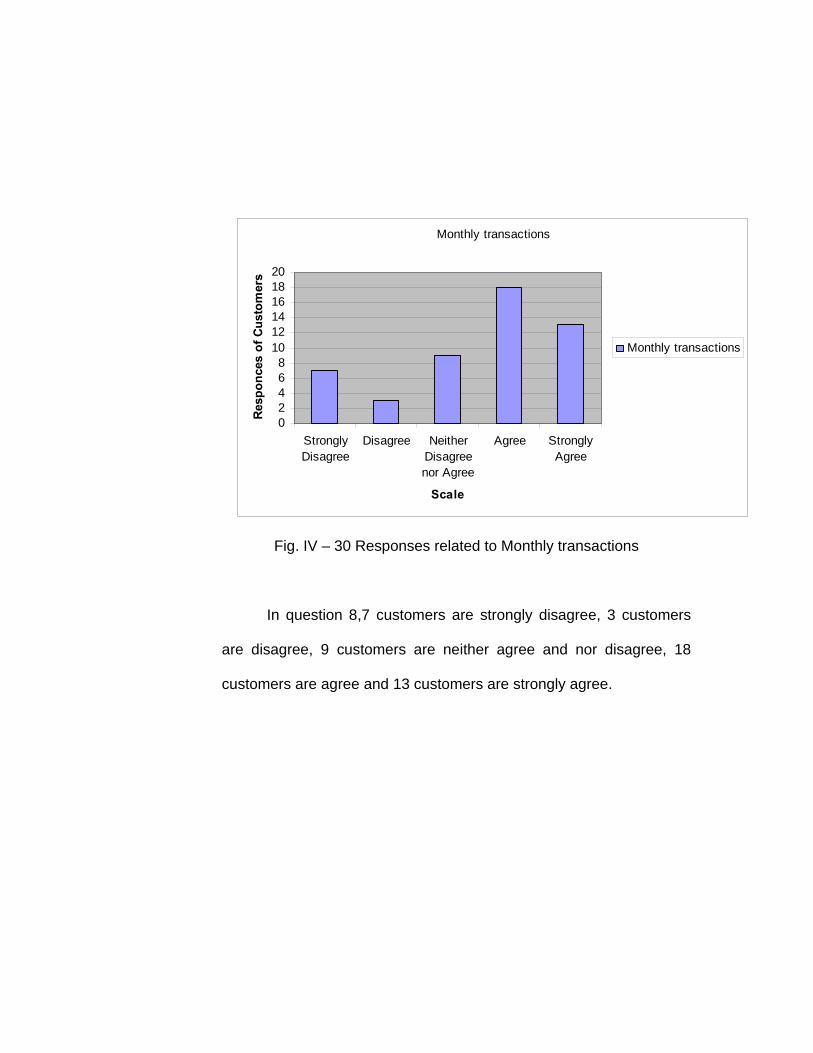

Fig. IV – 30 Responses related to Monthly transactions

In question 8,7 customers are strongly disagree, 3 customers

are disagree, 9 customers are neither agree and nor disagree, 18

customers are agree and 13 customers are strongly agree.

Monthly transactions

02468

101214161820

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Monthly transactions

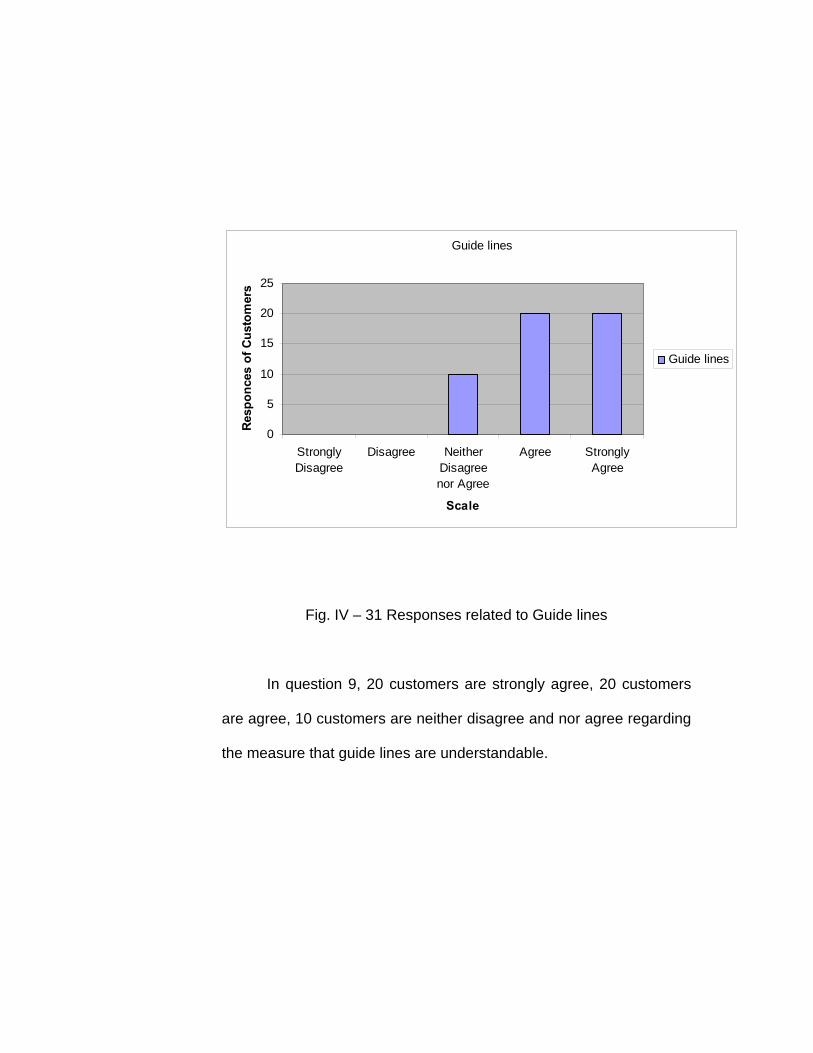

Fig. IV – 31 Responses related to Guide lines

In question 9, 20 customers are strongly agree, 20 customers

are agree, 10 customers are neither disagree and nor agree regarding

the measure that guide lines are understandable.

Guide lines

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Guide lines

Fig. IV – 32 Responses related to Issuance of card

In question 10, 22 customers are strongly agree, 16 customers

are agree, 12 customers are neither agree and nor disagree that

issuance of card is easy.

Issuance of card

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Issuance of card

Fig. IV – 33 Responses related to Interest rate

7 customers are strongly disagree,8 are disagree,15 are neither

agree nor disagree,12 are agree,8 are strongly agree related to

Interest rate.

Interest rate

0

2

4

6

8

10

12

14

16

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Interest rate

Fig. IV – 34 Responses related to like to become customer of another

bank

10 customer are strongly disagree,15 are agree,19 are neither

agree nor disagree,5 are agree and 1 is disagree.

like to become customer of another bank

02468

101214161820

Str

ongl

yD

isag

ree

Nei

ther

Dis

agre

eno

rA

gree

Str

ongl

yA

gree

Scale

Res

po

nce

s o

f C

ust

om

ers

like to become customer ofanother bank

Table IV – 3 Presents measures related to questions along with their

mean values related to Customer satisfaction.

Table IV – 3 Measures related to Customer satisfaction along with

mean values of BAL

Questions Measures Mean

Q.1 24-hour banking service 4.2000

Q.2 Step by step installment

payment

3.4000

Q.3 Paying of outstanding

balance

4.0400

Q.4 Drop box 4.4000

Q.5 Credit card limit 3.4800

Q.6 Reward programs 4.1000

Q.7 Service charges 4.3200

Q.8 Monthly transactions 4.2000

Q.9 Guide lines 3.9000

Q.10 Issuance of card 4.2000

Q.11 Interest rate 3.1200

Q.12 Like to become customer of

another bank

3.5800

Mean value 4.2 shows that customers are strongly agree with

measure 24-hour banking.3.4 mean value of measure step by step

payment shows that customer are agree with this.4.0 mean value of

3rd measure shows that customers are more than agree.4.4 mean

value of measure drop box again shows that customers are more than

agree. Mean value 3.48 shows that customers are below agree with

credit card limit. Customers are happy with reward program, service

charges and monthly transactions, showed by mean value 4.1,4.3,4.2

respectively. Customers are nearly agreed with measure that

guidelines are easily understandable. 4.2 mean value of question 10

shows that customers are satisfied that issuance of card is easy.

interest rate are satisfactory came by the mean value of question 11

which is 3.1200.question 12 has mean value of 3.5 shows that

average customers like to become customer of any other bank.

2.3.2 Findings about Customer satisfaction level of UBL

For measuring the level of Customer satisfaction 12 questions

are extracted from [Appendix].

Fig. IV – 35 Responses related to 24-hour banking service

Responses of customers regarding question 1”24-hour banking

services” of UBL,20 are strongly agree,10 are agree, around 15 are

neither agree nor disagree and 5 are disagree .

24-hour banking service

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

24-hour banking service

Fig. IV – 36 Responses related to Step by step installment payment

Step by step installment payment

0

5

10

15

20

25

StronglyDisagree

Disagree NeitherDisagreenor Agree

Agree StronglyAgree

Scale

Res

po

nce

s o

f C

ust

om

ers

Step by step installmentpayment