Makhado - Municipal Money

15

+ - Leaflet | Map data © OpenStreetMap contributors, CC-BY-SA

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Makhado - Municipal Money

Makhado

in Vhembe, LimpopoB4 local municipality

Population: 401 444 Size: 7 623.6 km² Density: 52.7 / km²

+

-

Leaflet | Map data © OpenStreetMap contributors, CC-BY-SA

Contacts Last updated October 2020

Civic Center

Erasmus/Krough Str

Louis Trichardt

0950

Secretary of Mayor/Executive Mayor

Mayor/Executive Mayor

Mr N.S Munyai

015 519 3002

Ms T.R Phaweni

015 519 3002

Secretary of Municipal Manager

Municipal Manager

Mr KM Nemaname(Acting Municipal Manager)

015 519 3210

Ms S Nefolovhodwe

015 519 3003

Secretary of Deputy Mayor/Executive Mayor

Deputy Mayor/Executive Mayor

Secretary of Financial Manager

Chief Financial O�cer

Mr N.G Raliphada( Acting Chief Financial Of

015 519 3056

Ms HC Mokoena

015 519 3214

015 519 3000

Email municipality

http://www.makhado.gov.za

Financial Performance

Audit Outcomes

Cash Balance 2014-2015

Cash balance at the end of the �nancial year.

2011-2012 2012-2013 2013-2014 2014-2015

R 0

R10m

R20m

R30m

R40m

R50m

Show average for similar municipalities or

2014-2015

Quali�ed

Read report

2013-2014

Unquali�ed - Emphasis of

Matter items

Read report

2012-2013

Quali�ed

Read report

2011-2012

Disclaimer of opinion

Read report

What do di�erent audit outcomes mean?

Unquali�ed Opinion

No Findings

Same as an Unquali�ed Opinion with no �ndings, but the

Auditor-General wants to bring something particular to the

attention of the reader.

Unquali�ed Opinion

Emphasis of Matter Items

Same as an Unquali�ed Opinion with no �ndings, but the

Auditor-General wants to bring something particular to the

attention of the reader.

Quali�ed Opinion

The Auditor-General expresses reservations about the fair

presentation of the �nancial statements. There is some

departure from the Generally Recognised Accounting Practices

(GRAP) but is not su�ciently serious as to warrant an adverse

opinion or disclaimer of opinion.

Adverse Opinion

This is expressed when the auditor concludes that the annual

�nancial statements do not present the municipality’s �nancial

position, results of operations and cash �ows in line with

Generally Recognised Accounting Practices (GRAP).

Disclaimer of Opinion

The Auditor-General does not have all of the underlying

documentation needed to determine an opinion. For example,

the lack of underlying documentation and the amounts in

question may be so great so that it is impossible to give any

opinion on all.

An Outstanding Opinion

Means that the Auditor General raised queries with the

municipality and therefore has not submitted another opinion.

R47 449 950

A municipality's cash balance refers to the money

it has in the bank that it can access easily. If a

municipality's bank account is in overdraft it has a

negative cash balance. Negative cash balances

are a sign of serious �nancial management

problems. A municipality should have enough cash

on hand from month to month so that it can pay

salaries, suppliers and so on.

About this indicator

in Limpopo nationally

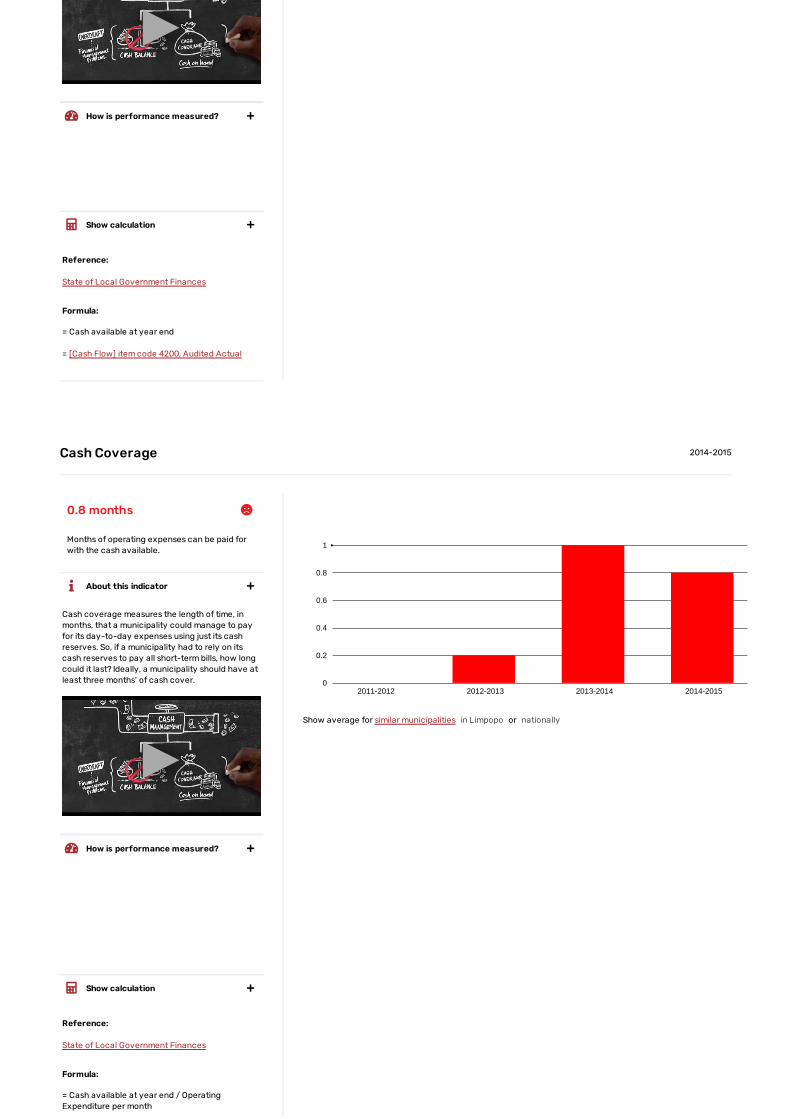

Cash Coverage 2014-2015

Months of operating expenses can be paid for

with the cash available.

2011-2012 2012-2013 2013-2014 2014-20150

0.2

0.4

0.6

0.8

1

Show average for similar municipalities or

▶▶

How is performance measured?

Good Positive balance

Bad Negative balance

Reference:

State of Local Government Finances

Formula:

= Cash available at year end

= [Cash Flow] item code 4200, Audited Actual

Show calculation

0.8 months

Cash coverage measures the length of time, in

months, that a municipality could manage to pay

for its day-to-day expenses using just its cash

reserves. So, if a municipality had to rely on its

cash reserves to pay all short-term bills, how long

could it last? Ideally, a municipality should have at

least three months' of cash cover.

▶▶

About this indicator

How is performance measured?

Good > 3 months

Average 1-3 months

Bad < 1 month

Reference:

State of Local Government Finances

Formula:

= Cash available at year end / Operating

Expenditure per month

Show calculation

in Limpopo nationally

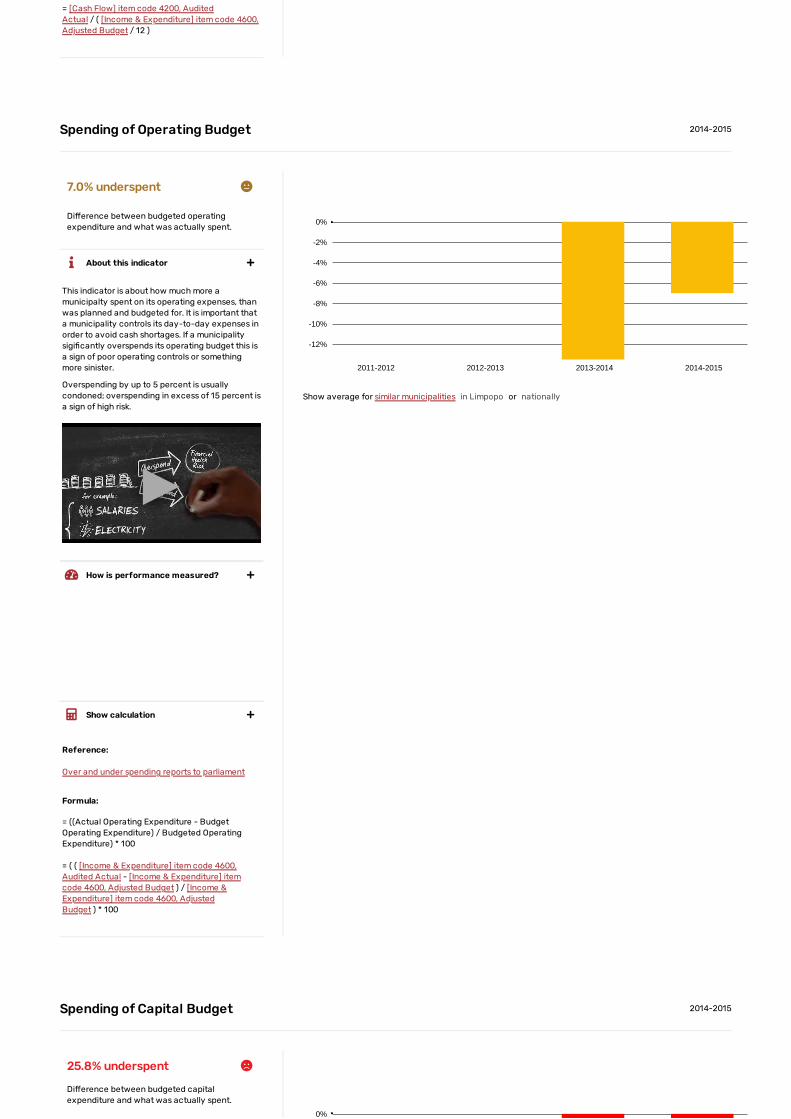

Spending of Operating Budget 2014-2015

Di�erence between budgeted operating

expenditure and what was actually spent.

2011-2012 2012-2013 2013-2014 2014-2015

-12%

-10%

-8%

-6%

-4%

-2%

0%

Show average for similar municipalities or

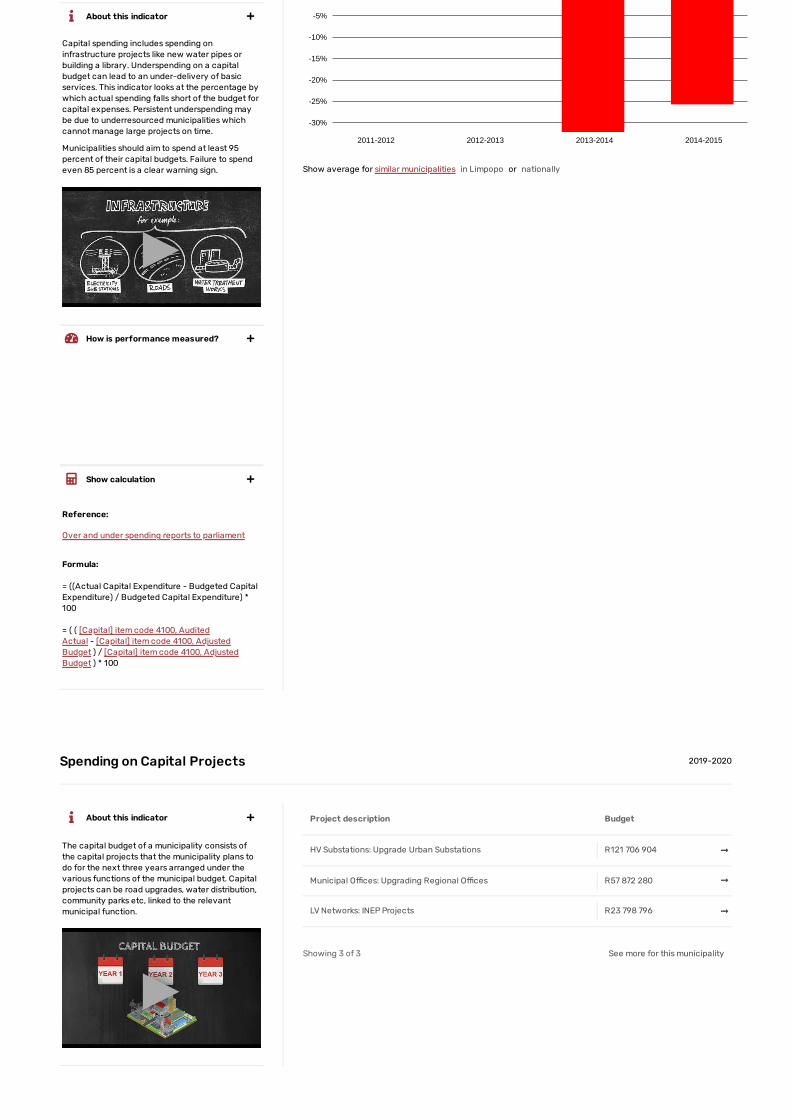

Spending of Capital Budget 2014-2015

Di�erence between budgeted capital

expenditure and what was actually spent.

0%

= [Cash Flow] item code 4200, Audited

Actual / ( [Income & Expenditure] item code 4600,

Adjusted Budget / 12 )

7.0% underspent

This indicator is about how much more a

municipalty spent on its operating expenses, than

was planned and budgeted for. It is important that

a municipality controls its day-to-day expenses in

order to avoid cash shortages. If a municipality

sigi�cantly overspends its operating budget this is

a sign of poor operating controls or something

more sinister.

Overspending by up to 5 percent is usually

condoned; overspending in excess of 15 percent is

a sign of high risk.

▶▶

About this indicator

How is performance measured?

Good 0% - 5%

Average 5% - 15%

Bad > 15%

Reference:

Over and under spending reports to parliament

Formula:

= ((Actual Operating Expenditure - Budget

Operating Expenditure) / Budgeted Operating

Expenditure) * 100

= ( ( [Income & Expenditure] item code 4600,

Audited Actual - [Income & Expenditure] item

code 4600, Adjusted Budget ) / [Income &

Expenditure] item code 4600, Adjusted

Budget ) * 100

Show calculation

in Limpopo nationally

25.8% underspent

2011-2012 2012-2013 2013-2014 2014-2015

-30%

-25%

-20%

-15%

-10%

-5%

Show average for similar municipalities or

Spending on Capital Projects 2019-2020

Capital spending includes spending on

infrastructure projects like new water pipes or

building a library. Underspending on a capital

budget can lead to an under-delivery of basic

services. This indicator looks at the percentage by

which actual spending falls short of the budget for

capital expenses. Persistent underspending may

be due to underresourced municipalities which

cannot manage large projects on time.

Municipalities should aim to spend at least 95

percent of their capital budgets. Failure to spend

even 85 percent is a clear warning sign.

▶▶

About this indicator

How is performance measured?

Good 0% - 5%

Average 5% - 15%

Bad > 15%

Reference:

Over and under spending reports to parliament

Formula:

= ((Actual Capital Expenditure - Budgeted Capital

Expenditure) / Budgeted Capital Expenditure) *

100

= ( ( [Capital] item code 4100, Audited

Actual - [Capital] item code 4100, Adjusted

Budget ) / [Capital] item code 4100, Adjusted

Budget ) * 100

Show calculation

in Limpopo nationally

The capital budget of a municipality consists of

the capital projects that the municipality plans to

do for the next three years arranged under the

various functions of the municipal budget. Capital

projects can be road upgrades, water distribution,

community parks etc, linked to the relevant

municipal function.

▶▶

About this indicator Project description Budget

HV Substations: Upgrade Urban Substations R121 706 904

Municipal O�ces: Upgrading Regional O�ces R57 872 280

LV Networks: INEP Projects R23 798 796

Showing 3 of 3 See more for this municipality

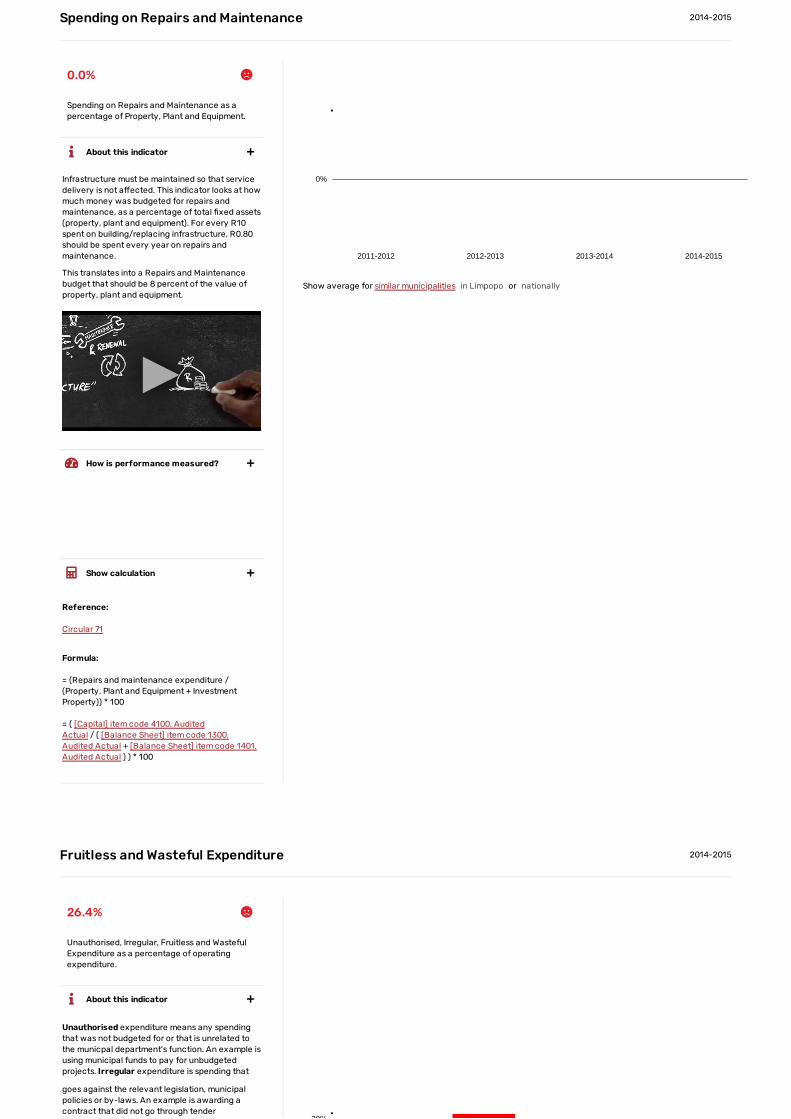

Spending on Repairs and Maintenance 2014-2015

Spending on Repairs and Maintenance as a

percentage of Property, Plant and Equipment.

2011-2012 2012-2013 2013-2014 2014-2015

0%

Show average for similar municipalities or

Fruitless and Wasteful Expenditure 2014-2015

Unauthorised, Irregular, Fruitless and Wasteful

Expenditure as a percentage of operating

expenditure.

30%

0.0%

Infrastructure must be maintained so that service

delivery is not a�ected. This indicator looks at how

much money was budgeted for repairs and

maintenance, as a percentage of total �xed assets

(property, plant and equipment). For every R10

spent on building/replacing infrastructure, R0.80

should be spent every year on repairs and

maintenance.

This translates into a Repairs and Maintenance

budget that should be 8 percent of the value of

property, plant and equipment.

▶▶

About this indicator

How is performance measured?

Good > 8%

Bad < 8%

Reference:

Circular 71

Formula:

= (Repairs and maintenance expenditure /

(Property, Plant and Equipment + Investment

Property)) * 100

= ( [Capital] item code 4100, Audited

Actual / ( [Balance Sheet] item code 1300,

Audited Actual + [Balance Sheet] item code 1401,

Audited Actual ) ) * 100

Show calculation

in Limpopo nationally

26.4%

Unauthorised expenditure means any spending

that was not budgeted for or that is unrelated to

the municpal department's function. An example is

using municipal funds to pay for unbudgeted

projects. Irregular expenditure is spending that

goes against the relevant legislation, municipal

policies or by-laws. An example is awarding a

contract that did not go through tender

About this indicator

2011-2012 2012-2013 2013-2014 2014-20150%

5%

10%

15%

20%

25%

30%

Show average for similar municipalities or

Current Ratio 2014-2015

The value of a municipality's short-term assets

as a multiple of its short-term liabilities.

2011-2012 2012-2013 2013-2014 2014-20150

0.5

1

1.5

2

2.5

Show average for similar municipalities or

procedures. Fruitless and wasteful expenditure

concerns spending which was made in vain and

would have been avoided had reasonable care

been exercised. An example of such expenditure

would include paying a deposit for a venue and

not using it and losing the deposit.

▶▶

How is performance measured?

Good 0%

Bad > 0%

Reference:

Circular 71

Formula:

= (Unauthorised, Irregular, Fruitless and Wasteful

Expenditure / Actual Operating Expenditure) * 100

= ( [unde�ned] item code

irregular,fruitless,unauthorised / [Income &

Expenditure] item code 4600, Audited

Actual ) * 100

Show calculation

in Limpopo nationally

1.90

The current ratio compares the value of a

municipality's short-term assets (cash, bank

deposits, etc) compared with its short-term

liabilities (creditors, loans due and so on). The

higher the ratio, the better. The normal range of

the current ratio is 1.5 to 2 (the municipality has

assets more than 1.5 to 2 times its current debts).

Anything less than that and the municipality may

struggle to keep up with its payments.

▶▶

About this indicator

How is performance measured?

Good > 1.5

Average 1 - 1.5

in Limpopo nationally

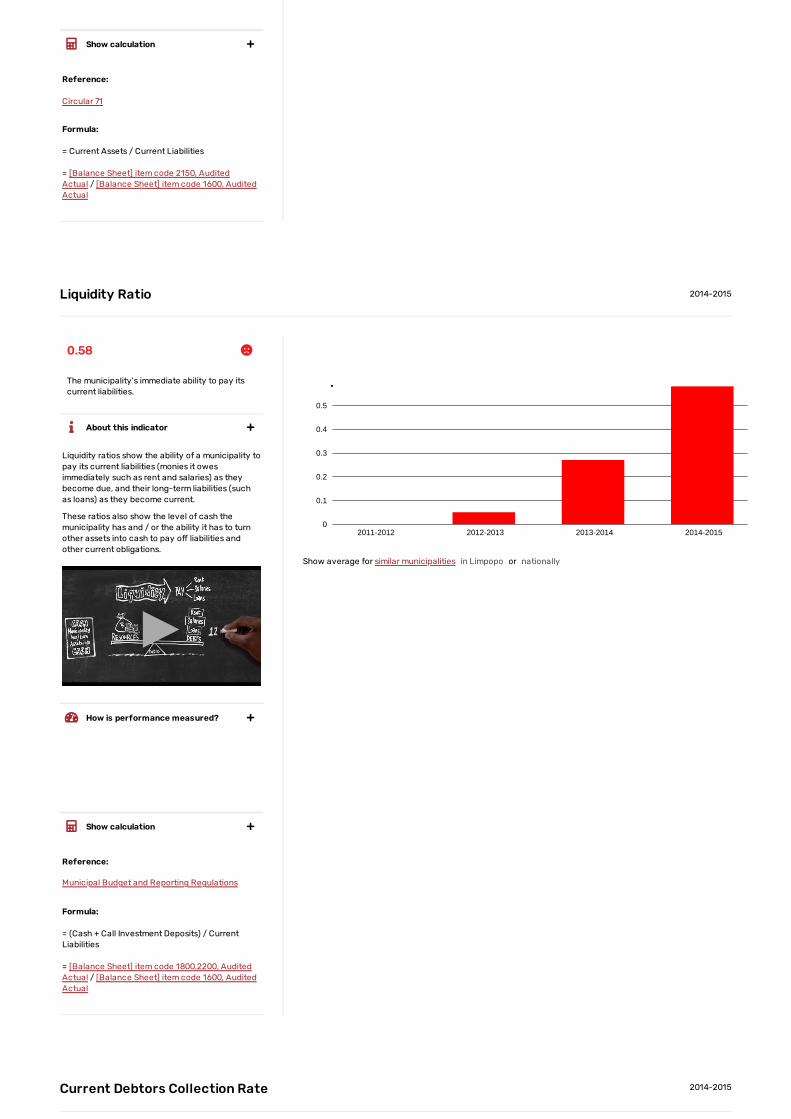

Liquidity Ratio 2014-2015

The municipality's immediate ability to pay its

current liabilities.

2011-2012 2012-2013 2013-2014 2014-20150

0.1

0.2

0.3

0.4

0.5

Show average for similar municipalities or

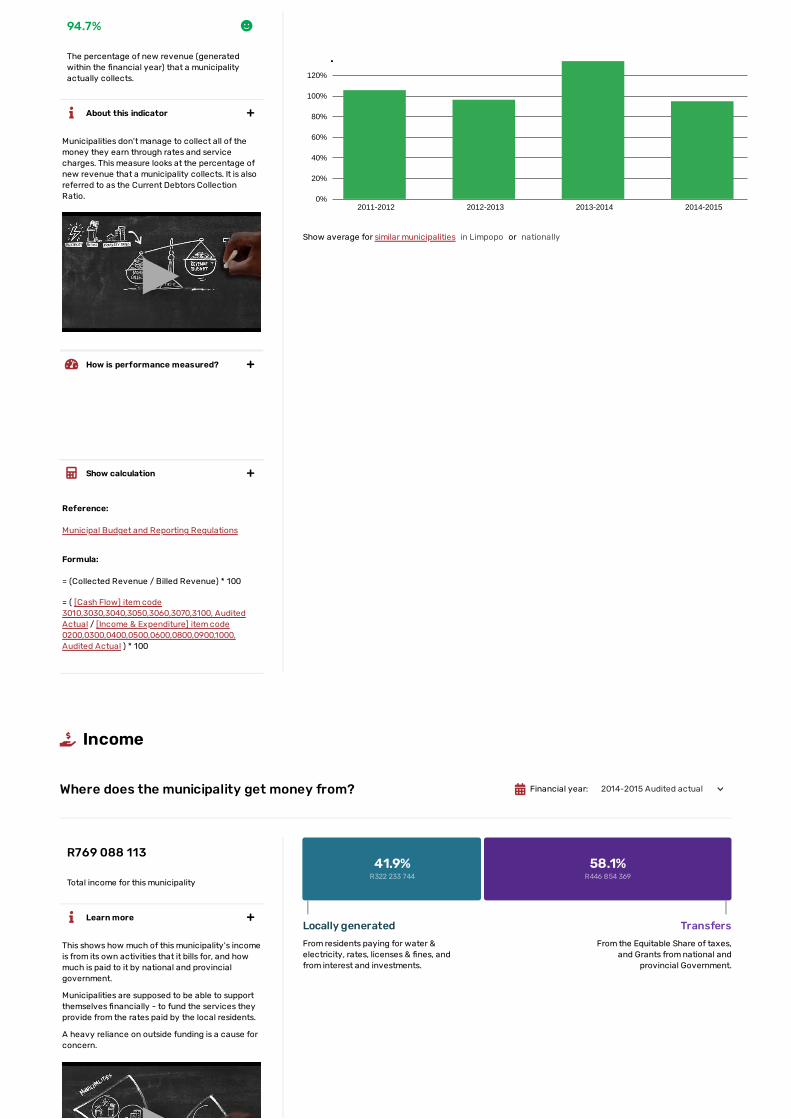

Current Debtors Collection Rate 2014-2015

Bad < 1

Reference:

Circular 71

Formula:

= Current Assets / Current Liabilities

= [Balance Sheet] item code 2150, Audited

Actual / [Balance Sheet] item code 1600, Audited

Actual

Show calculation

0.58

Liquidity ratios show the ability of a municipality to

pay its current liabilities (monies it owes

immediately such as rent and salaries) as they

become due, and their long-term liabilities (such

as loans) as they become current.

These ratios also show the level of cash the

municipality has and / or the ability it has to turn

other assets into cash to pay o� liabilities and

other current obligations.

▶▶

About this indicator

How is performance measured?

Good > 1

Bad < 1

Reference:

Municipal Budget and Reporting Regulations

Formula:

= (Cash + Call Investment Deposits) / Current

Liabilities

= [Balance Sheet] item code 1800,2200, Audited

Actual / [Balance Sheet] item code 1600, Audited

Actual

Show calculation

in Limpopo nationally

The percentage of new revenue (generated

within the �nancial year) that a municipality

actually collects.

2011-2012 2012-2013 2013-2014 2014-20150%

20%

40%

60%

80%

100%

120%

Show average for similar municipalities or

94.7%

Municipalities don't manage to collect all of the

money they earn through rates and service

charges. This measure looks at the percentage of

new revenue that a municipality collects. It is also

referred to as the Current Debtors Collection

Ratio.

▶▶

About this indicator

How is performance measured?

Good > 95%

Bad < 95%

Reference:

Municipal Budget and Reporting Regulations

Formula:

= (Collected Revenue / Billed Revenue) * 100

= ( [Cash Flow] item code

3010,3030,3040,3050,3060,3070,3100, Audited

Actual / [Income & Expenditure] item code

0200,0300,0400,0500,0600,0800,0900,1000,

Audited Actual ) * 100

Show calculation

in Limpopo nationally

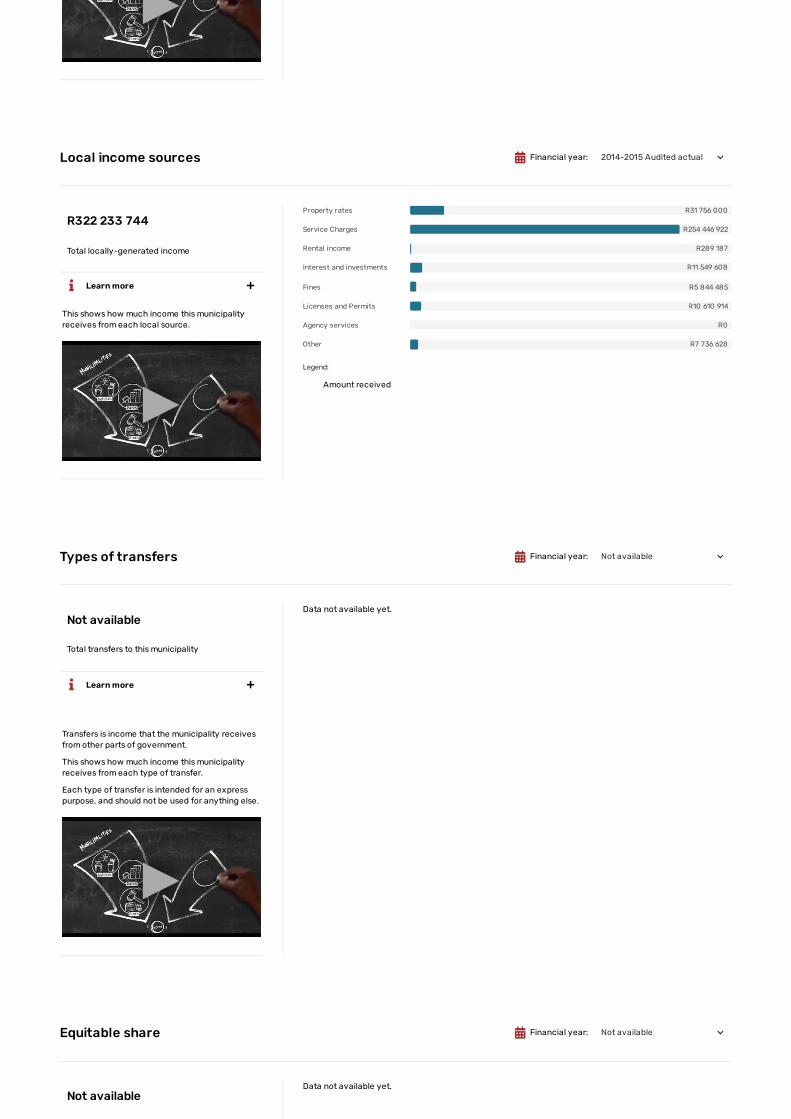

Income

Where does the municipality get money from?

Total income for this municipality

R769 088 113

This shows how much of this municipality's income

is from its own activities that it bills for, and how

much is paid to it by national and provincial

government.

Municipalities are supposed to be able to support

themselves �nancially - to fund the services they

provide from the rates paid by the local residents.

A heavy reliance on outside funding is a cause for

concern.

▶▶

Learn more

41.9%R322 233 744

58.1%R446 854 369

Locally generated

From residents paying for water &

electricity, rates, licenses & �nes, and

from interest and investments.

Transfers

From the Equitable Share of taxes,

and Grants from national and

provincial Government.

Financial year: 2014-2015 Audited actual

Local income sources

Total locally-generated income

R31 756 000

R254 446 922

R289 187

R11 549 608

R5 844 485

R10 610 914

R0

R7 736 628

Legend:

Types of transfers

Total transfers to this municipality

Data not available yet.

Equitable share

Data not available yet.

▶▶

R322 233 744

This shows how much income this municipality

receives from each local source.

▶▶

Learn more

Property rates

Service Charges

Rental income

Interest and investments

Fines

Licenses and Permits

Agency services

Other

Amount received

Not available

Transfers is income that the municipality receives

from other parts of government.

This shows how much income this municipality

receives from each type of transfer.

Each type of transfer is intended for an express

purpose, and should not be used for anything else.

▶▶

Learn more

Not available

Financial year:

Financial year:

Financial year:

2014-2015 Audited actual

Not available

Not available

Total equitable share allocated to this

municipality

National conditional grants

Total income from conditional grants from

national departments for this municipality.

R5 000 000

R1 600 000

R38 717 000

R17 000 000

R172 264 000

R930 000

R1 335 000

Legend:

Provincial transfers

Total transfers from provincial government to

this municipality.

Data not available yet.

Legend:

This shows how much income this municipality

receives as their equitable share.

Equitable share comes from the taxes paid to

national government, and is intended to ensure

that no one in South Africa shall go without their

basic needs being met.

Provincial and national government also receive

equitable share to fund the services that are

provided by those spheres of government.

▶▶

Learn more

R236 846 000

Conditional grants are money paid to

municipalities and provinces to achieve speci�c

outcomes.

This might be to ensure money is available for

building infrastructure, or ensuring sta� at the

municipality receive the training needed to

perform their job.

This shows how much money has been allocated

to the municipality for each grant that they are

receiving, how much has been paid to the

municipality so far, and how much they have

spent.

▶▶

Learn more

Energy E�ciency and Deman…

Local Government Financial …

Integrated National Electri�…

Integrated National Electri�…

Municipal Infrastructure Gra…

Municipal Systems Improve…

Expanded Public Works Prog…

Allocations Amount transferred up to 2016 Q4 Amount spent up to 2016 Q4

Not available

Provincial transfers are income from the

Learn more

Amount budgeted

Financial year:

Financial year:

2015-2016 Allocations

Not available

Planned and actual income over time

How much income is planned for, and how

much is actually received?

2011-2012 2012-2013 2013-2014 2014-2015 2015-2016 2016-2017 2017-2018

R0

R200.0m

R400.0m

R600.0m

R800.0m

R1.0bn

Legend:

Where did the di�erences in planned income occur? 2014-2015

Which sources provided more or less income

than planned?

Legend:

government of the province where this

municipality is located.

This income could be for services that are

provided by the municipality under an agreement

with the province, when it is actually the

provincial government's responsibility. This can

happen when the municipality is better-placed to

provide that service.

It could also be for conditional grants paid by the

province for disaster relief or other purposes.

This shows how much income the municipality

receives from each provincial department.

▶▶

Municipalities must plan for the income they can

realistically receive.

Unrealistic plans result in disappointing service

delivery.

On the time series we can see whether the

municipality regularly over- or under-estimates

how much money it will receive.

▶▶

Learn more

Original budget Adjusted budget Audited actual Forecast budget

By looking at where the di�erences in planned

and actual income occurred, we can start seeing

whether it was bad planning on unforeseeable

circumstances.

▶▶

Learn more

Original Budget

Original to adjusted budget Original budget to audited outcome

Fines

Government Transfers

Interest and investments

Licenses and Permits

Other

Property rates

Rental income

Service Charges

−R1.6m -49.78%

R2.7m 87.44%

−R114.1m -28.14%

R41.5m 10.23%

−R7.6m -34.27%

−R10.6m -47.91%

−R3.2m -23.2%

−R3.4m -24.13%

−R6.1m -23.64%

−R18.2m -70.18%

R6.4m 18%

−R3.6m -10.07%

R171.0k 66.28%R31187

12.09%

R2.6m 0.99%

−R9.7m -3.67%

Change within category%

Spending

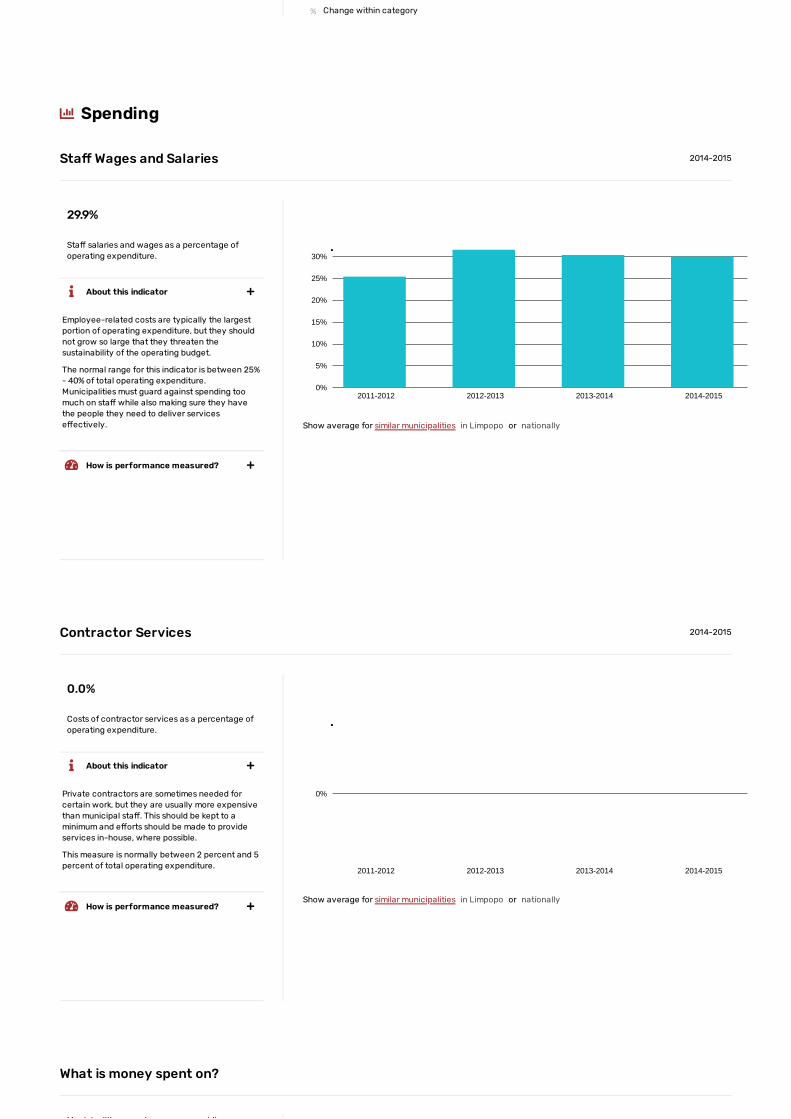

Sta� Wages and Salaries 2014-2015

Sta� salaries and wages as a percentage of

operating expenditure.

2011-2012 2012-2013 2013-2014 2014-20150%

5%

10%

15%

20%

25%

30%

Show average for similar municipalities or

Contractor Services 2014-2015

Costs of contractor services as a percentage of

operating expenditure.

2011-2012 2012-2013 2013-2014 2014-2015

0%

Show average for similar municipalities or

What is money spent on?

M i i liti d idi

29.9%

Employee-related costs are typically the largest

portion of operating expenditure, but they should

not grow so large that they threaten the

sustainability of the operating budget.

The normal range for this indicator is between 25%

- 40% of total operating expenditure.

Municipalities must guard against spending too

much on sta� while also making sure they have

the people they need to deliver services

e�ectively.

About this indicator

How is performance measured?

Good 25% - 40%

Bad < 25% or > 40%

in Limpopo nationally

0.0%

Private contractors are sometimes needed for

certain work, but they are usually more expensive

than municipal sta�. This should be kept to a

minimum and e�orts should be made to provide

services in-house, where possible.

This measure is normally between 2 percent and 5

percent of total operating expenditure.

About this indicator

How is performance measured?

Good 0% - 5%

Bad > 5%

in Limpopo nationally

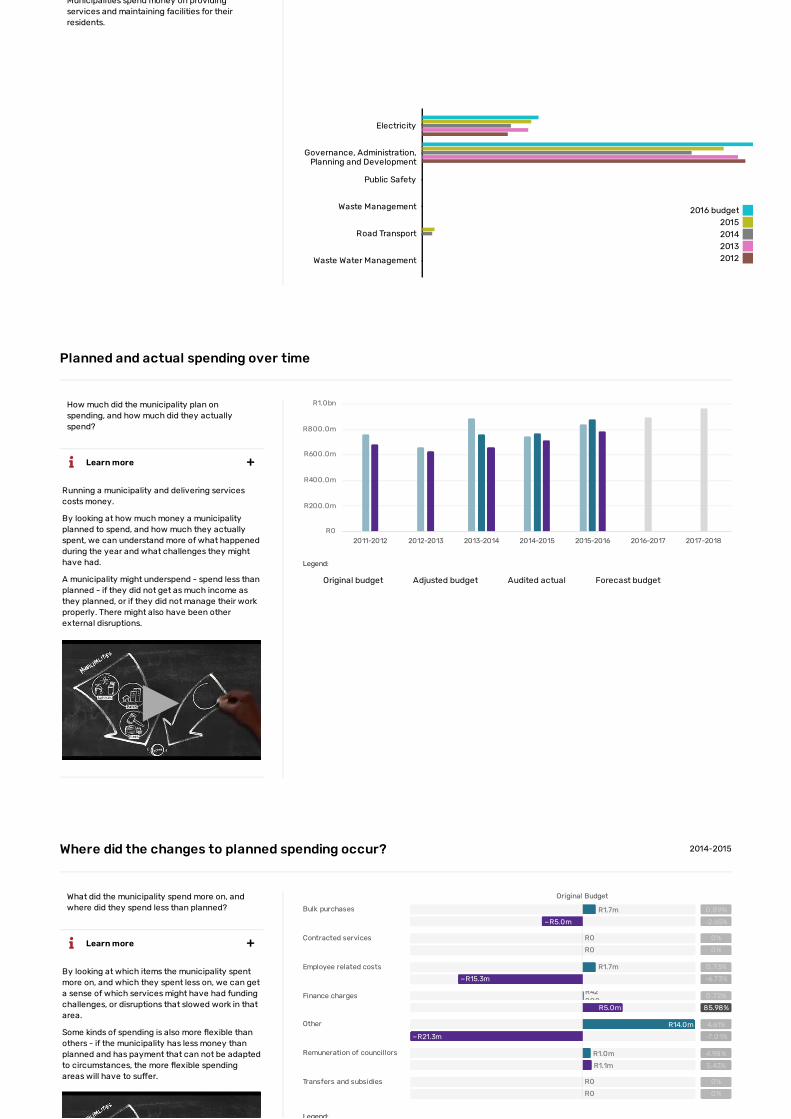

Municipalities spend money on providing

services and maintaining facilities for their

residents.

Electricity

Governance, Administration,Planning and Development

Public Safety

Waste Management

Road Transport

Waste Water Management

2016 budget

2015

2014

2013

2012

Planned and actual spending over time

How much did the municipality plan on

spending, and how much did they actually

spend?

2011-2012 2012-2013 2013-2014 2014-2015 2015-2016 2016-2017 2017-2018

R0

R200.0m

R400.0m

R600.0m

R800.0m

R1.0bn

Legend:

Where did the changes to planned spending occur? 2014-2015

What did the municipality spend more on, and

where did they spend less than planned?

Legend:

Running a municipality and delivering services

costs money.

By looking at how much money a municipality

planned to spend, and how much they actually

spent, we can understand more of what happened

during the year and what challenges they might

have had.

A municipality might underspend - spend less than

planned - if they did not get as much income as

they planned, or if they did not manage their work

properly. There might also have been other

external disruptions.

▶▶

Learn more

Original budget Adjusted budget Audited actual Forecast budget

By looking at which items the municipality spent

more on, and which they spent less on, we can get

a sense of which services might have had funding

challenges, or disruptions that slowed work in that

area.

Some kinds of spending is also more �exible than

others - if the municipality has less money than

planned and has payment that can not be adapted

to circumstances, the more �exible spending

areas will have to su�er.

Learn more

Original Budget

Bulk purchases

Contracted services

Employee related costs

Finance charges

Other

Remuneration of councillors

Transfers and subsidies

R1.7m 0.89%

−R5.0m -2.65%

R0 0%

R0 0%

R1.7m 0.73%

−R15.3m -6.73%

R42000

0.72%

R5.0m 85.98%

R14.0m 4.61%

−R21.3m -7.01%

R1.0m 4.98%

R1.1m 5.43%

R0 0%

R0 0%

Municipal Money is an initiative of the National

Treasury, which has collected extensive

municipal �nancial data over several years

and would like to share this information with

the public.

Learn more

Jump to a metro

Bu�alo City

City of Cape Town

Ekurhuleni Municipality

City of eThekwini

City of Johannesburg

Mangaung Municipality

Nelson Mandela Bay Municipality

City of Tshwane

Useful links

Help center

Municipal Money API

Terms of use

Feedback

Github

A project by National Treasury, created under The MIT License (MIT). In partnership with:

Legend:

▶▶Original to adjusted budget Original budget to audited outcome

Change within category%

Household Bills

Household bills data not available for this municipality.

Resources

Understanding MunicipalFinance

Treasury's Municipal Finance website is �lled

with resources on municipal �nance.

Circular 71 explains many of the �nancial norms

and indicators used to gauge the �nancial

performance of Municipalities.

MFMA Return Forms submitted by

Municipalities to National Treasury.

Understanding these forms can help you

understand the information on Municipal

Money.

A Million Bags of a Million Rand - a video by the

Auditor General's o�ce which simpli�es audit

outcomes.

Understanding the Standard Chart of Accounts

- a video by the National Treasury on mSCOA.

Understanding the Public Finance Management

Act & Municipal Finance Management Act - a

video by the National Treasury on irregular

expenditure and material irregularity.

Financial reportsRead more about Local Government Finances and

learn about how your money is spent.

Annual Financial Statements of municipalities

since 2002-2003. These include the Notes to

the Annual Financial Statements where you

can �nd explanations of speci�c accounting

practises and calculations used by the

municipality in its �nancial reporting and some

decision making.

State of Local Government Finances reports

are published every year by National Treasury

and describe in detail how Municipalities are

performing.

In-year Management, Monitoring and

Evaluation of Municipal Finances . Annual and

quarterly PDF and Excel reports on Municipal

�nances since 2007.

Further readingResources from the South African and international

community.

Local Government in South Africa – Part 5,

Finances, 19 March 2014 by Corruption Watch

Engaging with Government Budgets. An

Activist’s Guide to South African Government

Budgets at Local, Provincial and National Level

produced in 2012 by Ndifuna Ukwazi and the

Social Justice Coalition

Infographic: South Africa: Public Participation

Mechanisms in Fiscal Matters, 01 July 2015 by

Global Initiative for Fiscal Transparency (GIFT)

Infographic: High Level Principles on Fiscal

Transparency, 04 July 2015 by Global Initiative

for Fiscal Transparency (GIFT)

A Guide to Conducting Social Audits in South

Africa, November 2015 by International Budget

Partnership (IBP)

Infographic: Open Budget Survey 2015 by

International Budget Partnership (IBP)

Open Budget Survey 2015 by International

Budget Partnership (IBP)