Internship report on General Banking Activities & Customer ...

Upload

khangminh22Category

view

1download

0

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 1 of 46

GENERAL BANKING

FOREIGN ACCOUNT TAX COMPLIANCE ACT (FATCA): HO CIRCULAR 65/2017:

FATCA is a tax reporting system under which all financial institutions including our bank, mutual funds, private equity funds, etc. to report information to CBDT (Central Board of Direct Taxes) about U.S.

reportable persons (for e.g. our NRI account holders resident in USA) and certain entities in which U.S.

persons hold a substantial ownership interest, in India. Such information, in turn, will be passed on by

CBDT to the Tax Authorities of USA.

At branches, we will be furnishing certain basic and vital information regarding our NRI customers, who

are residents of USA, through CBDT to IRS (Internal Revenue Service) – the USA equivalent of our Income Tax Department.

This information is to be given to CBDT for all new NR accounts opened on or after 1.11.2015.

COMMON REPORTING STANDARD (CRS)

As the FATCA reporting pertains to USA, CRS remediation relates to countries other than USA.

Example: If any German citizen is having an account in a Bank in India, under CRS the account information will be shared by the Bank, to the German tax authority through CBDT irrespective of the

balance in the account at the Customer-id level if it is a new account i.e. account opened on or after

01.01.2016.

WHY WE HAVE TO DO THIS?

Because, India has signed two global agreements:

a. IGA - Inter Global Agreement on 9.7.2015 with the Govt of USA to implement FATCA

b. Multilateral Competent Authority Agreement (MCAA) on 3.6.15 to implement CRS

for automatic exchange of tax information and reciprocal basis. i.e. Our country will also be getting

similar information from USA and other countries.

HO CIRCULAR 61/2017:

Latest list of KYC documents in case of opening of PROPRIETORSHIP ACCOUNTS:

(Any two of the documents alongwith KYC documents of Proprietor)

For Proprietary concerns, in addition to the Officially Valid Documents applicable to

theindividual (proprietor), any two of the following documents in the name of the proprietary

concern should be submitted:

a) Registration Certificate (in the case of a registered concern).

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 2 of 46

b) Certificate / licence issued by the Municipal authorities under Shop & Establishment Act.

c) Sales and income tax returns.

d) CST / VAT certificate.

e) Certificate / registration document issued by Sales Tax / Service Tax / Professional Tax

authorities.

f) Licence / certificate of practice issued in the name of the proprietary concern by any

professional body incorporated under a statute. (like ICAI etc.)

g) The complete Income Tax return (not just the acknowledgement) in the name of the sole

Proprietor where the firm’s income is reflected, duly authenticated/acknowledged by the Income

Tax Authorities.

h) Utility bills such as electricity, water and landline telephone bills.

i) IEC (Importer Exporter Code) issued to the proprietary concern by the office of DGFT /

Licence/certificate of practice issued in the name of the proprietary concern by any professional

body incorporated under a statute.

In cases where it is not possible to furnish two such documents, we can accept only one of those

documents as activity proof. In such cases,we have to verify and satisfy ourselves that the

business activity is actually conducted from theaddress of the Proprietory concern.

Documents to be obtained from Government or its Departments, Societies, Universities and

Local Bodies like Village Panchayats:

For opening of accounts of juridical persons , such as Government or itsDepartments, Societies,

Universities and Local Bodies like Village Panchayats, a certifiedcopy of the following

documents shall be obtained:

i. Document showing name of the person authorised to act on behalf of the entity;

ii. Officially Valid Documents for proof of identity and address in respect of the personholding a

power of attorney to transact on its behalf and

iii. Such documents as may be required by the Bank to establish the legal existence of

such an entity/juridical person.

HO CIRCULAR 62/2017

COMPREHENSIVE RBI GUIDELINES ON KYC :

RESPONSIBILITIES OF CUSTOMERS UNDER KYC COMPLIANCE:

(i) Required to submit an Officially Valid Document (OVD) for proof of identity and proof of

address and a recent photograph, while opening a normal bank account. In addition to this, the e-

KYC service of Unique Identification Authority of India (UIDAI) is also accepted as a valid

process for KYC verification.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 3 of 46

(ii) Customer also has to provide information to the bank about the nature of business activity

undertaken by him, location of customer and his clients, mode of payments, volume of turnover,

social and financial status etc. to enable bank to decide risk profile.

(iii) When a customer does not possess any of the OVDs including those prescribed under

‘simplified procedure’, banks are allowed to open ‘small accounts’ for such customers by taking

the customer’s signature/thumb impression in the presence of a bank official and a self-attested

photograph. Customer has to remain physically present in the bank branch for opening “Small

account.”

(iv) Customers have to note that Small accounts, however, would be subject to certain limitations

the aggregate credits (not more than Rupees one lakh in a year), aggregate withdrawals (not more

than Rupees ten thousand in a month) and balance in the accounts (not more than Rupees fifty

thousand at any point in time). These small accounts would be valid normally for a period of

twelve months. Thereafter, such accounts would be allowed to continue for a further period of

twelve more months, if the account holder provides a document showing that she/he has applied

for any of the OVDs, within twelve months of opening the small account.

(v) If any of the OVDs submitted does not have the address details (either current or permanent)

of the customer, then another OVD for proof of address has to be submitted.

(vi) If an existing KYC compliant customer of a bank desires to open another account in the

same bank, there should be no need for submission of fresh proof of identity and/or proof of

address for the purpose.

(vii) KYC once done by a branch of the bank is valid while transferring the account to any other

branch of the same bank without restrictions and on the basis of declaration of his/her local

address for communication.

(viii) In case a customer categorised as low risk is unable to submit the KYC documents due to

genuine reasons, she/he may submit the documents to the bank within a period of six months

from the date of opening account

(ix) If the address of the customer mentioned as per ‘proof of address’ undergoes a change, fresh

proof of address may be submitted to the branch within a period of six months.

(x) OVD with the current address is not necessary if the customer submits an OVD with

permanent address. In such cases, however, the customer has to submit a declaration about his

current address which the banks have to verify independently.

(xi) KYC verification of all the members of Self Help Groups (SHGs) is not required while

opening the savings bank account of the SHG and KYC verification of only the officials of the

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 4 of 46

SHGs would suffice. No separate KYC verification is needed at the time of credit linking the

SHG.

(xii) Foreign students have been allowed a time of one month for furnishing the proof of local

address.

(xiii) Existing customers have to submit KYC documents and photograph, if they had not

submitted documents at the time of opening account, as rules applicable at that time did not

provide for document based KYC.

(xiv) Existing customers are required to submit KYC documents for periodic updation of KYC.

The periodicity of KYC updation is 2/8/10 years for high/medium/low risk customers.

(xv) Banks need not seek fresh proofs of identity and address at the time of periodic updation,

from those customers who are categorized as ‘low risk’, in case of no change in status with

respect to their Identities and addresses. A self-certification by the customer to that effect should

suffice in such cases. In case of change of address of such ‘low risk’ customers, they could

merely forward a certified copy of the document (proof of address) by mail/post, etc. Banks may

not insist on physical presence of such low risk customer at the time of periodicupdation.

(xvi) Banks may impose partial freezing in a phased manner and after giving due notice for non-

compliance of KYC.

RESPONSIBILITIES OF BANKS UNDER KYC COMPLIANCE:

Banks have thefollowing responsibilities also as per KYC/AML/CFT requirements:

(i) To ensure that no account is opened in anonymous or fictitious/benami name.

(ii) Identify the beneficial owners of customer accounts, wherever required.

(iii) Rating the customers as per the risk perception into low, medium and high risk.

(iv) Regular monitoring of accounts to check whether there is any unusual/abnormal/suspicious

transactions.

(v) File Cash Transaction Reports (CTR) and Suspicious Transaction Reports (STRs) with FIU-

IND.

(vi) To nominate a Designated Director and appoint Principal Officer as required in terms of

PML Act and Rules.

(vii) Freezing and if required, closing of KYC non-compliant accounts.

(viii) Take into account the list of individuals and entities notified under UNSC Resolutions so

that no new accounts are opened in their names and existing accounts in such names are reported

to the Government.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 5 of 46

II. CHECK LISTS - for KYC processes to be followed by different customers and for

different activities, based on customer profiling.

A. Individuals

OVDs (Officially Valid Documents)notified by the Government are

(1) the passport

(2) the driving licence

(3) the Permanent Account Number (PAN) Card

(4) the Voter’s Identity Card issued by Election Commission of India

(5) job card issued by NREGA duly signed by an officer of the State

Government

(6) the letter issued by the Unique Identification Authority

of India containing details of name, address and Aadhaar number.

Alternatively, biometric e-KYC process through Aadhaar may be used.

(ii) A recent photograph of the customer

(iii) If a customer is rated as ‘low risk’ by the bank and if he/she does not have an OVD for proof

of identity, then under simplified procedure, for proof of identity, the bank can accept one of the

following two documents as OVD:

(1) identity card with applicant's Photograph issued by Central/State Government Departments,

Statutory/Regulatory Authorities, Public Sector Undertakings, Scheduled Commercial Banks,

and Public Financial Institutions;

(2) letter issued by a gazettedofficer,with a duly attested photograph of the person;

(iv) If customer does not have any of the above mentioned documents, and is happy with the

account with restrictions on transactions/balance etc., open a small account.

B. Proprietory concerns

i. OVDs as a proof of identity and proof of address in respect of the sole proprietor.

ii. Apart from these documents, seek any two documents as mentioned below as a proof of

business activity, in the name of the firm.

iii. Proof of the name, address and activity of the concern, like registration certificate (in the case

of a registered concern), certificate/licenceissued by the Municipal authorities under Shop &

Establishment Act, sales and income tax returns, CST/VAT certificate,certificate/registration

document issued by Sales Tax/Service Tax/Professional Tax authorities,

Licence issued by the Registeringauthority like Certificate of Practice issued by Institute of

Chartered Accountants of India, Institute of Cost Accountants of India, Institute of Company

Secretaries of India, Indian Medical Council, Food and Drug Control Authorities,

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 6 of 46

registration/licensing document issued in the name of the proprietary concern by the Central

Government or State Government Authority/Department.

(Importer Exporter Code) issued to the proprietary concern by the office of DGFT, the complete

Income Tax Return (not just theacknowledgement) in the name of the sole proprietor where the

firm'sincome is reflected, duly authenticated/acknowledged by the IncomeTax authorities, utility

bills such as electricity, water, and landline telephone bills in the name of the proprietary concern

as required documents for opening of bank accounts of proprietary concerns.

iv. If bank is satisfied that it is not possible to furnish two such documents, they would have the

discretion to accept only one of those documents as activity proof. In such cases, the banks,

however, would have to undertake contact point verification, collect such information as would

be required to establish the existence of such firm, confirm, clarify and satisfy themselves that

the business activity has been verified from the address of the proprietary concern.

C. Partnership firms

Obtain the following documents:

i. In case of registered partnership firms

a. Registration certificate for registered partnership firms;

b. Partnership deed; and

c. An officially valid document in respect of the person holding an attorney to transact on its

behalf.

ii. In case of non-registered partnership firms

a. Partnership deed;

b. An officially valid document in respect of the person holding an attorney to transact on its

behalf; and

c. Such information as may be required by the bank to collectively establish the legal existence

of such firm.

iii. Identify beneficial owner

a. the natural person(s), who, has ownership of/entitlement to more than fifteen percent of capital

or profits of the partnership;

b. or the relevant natural person who holds the position of senior managing official.

D. Companies

i. Obtain the following documents:

a. Certificate of incorporation;

b. Memorandum and Articles of Association;

c. A resolution from the Board of Directors and power of attorney granted to its managers,

officers or employees to transact on its behalf; and

d. An officially valid document in respect of managers, officers or

employees holding an attorney to transact on its behalf.

ii. Identify beneficial owner

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 7 of 46

a. the beneficial owner is the natural person(s), who, has a controlling ownership interest means

ownership of or entitlement to more than twenty-five percent of shares or capital or profits of the

company;or who exercises control through other means.

b. or the relevant natural person who holds the position of senior managing official.

c. In case of listed companies, identification of beneficial owner is not necessary.

E. Trusts

i. Obtain the following documents:

a. Registration certificate;

b. Trust deed; and

c. An officially valid document in respect of the person holding a power of attorney to transact

on its behalf.

ii. Identify beneficial owner

a. identification of the author of the trust, the trustee, the beneficiaries with fifteen per cent or

more interest in the trust and

b. any other natural person exercising ultimate effective control over the trust through a chain of

control or ownership.

F. Unincorporated bodies

i. Obtain the following documents:

a. Resolution of the managing body of such association or body of individuals;

b. Power of attorney granted to him to transact on its behalf;

c. An officially valid document in respect of the person holding an attorney to transact on its

behalf; and

d. Such information as may be required by the bank to collectively establish the legal existence

of such an association or body of individuals.

ii. Identify beneficial owner

a. the natural person(s), who, has ownership of or entitlement to more than fifteen percent of the

property or capital or profits of such association or body of individuals; or

b. the relevant natural person who holds the position of senior managing official.

G. Walk-in-Customers

a. Verify customer's identity and address if the amount of transaction is equal to or exceeds

rupees fifty thousand, or if transaction is a single transaction or several transactions that appear

to be connected, or if a bank has reason to believe that a customer is intentionally structuring a

transaction into a series of transactions below the threshold of Rs.50,000/-.

b. Consider filing a suspicious transaction report (STR) to FIU-IND.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 8 of 46

H. Remittances

a. Banks should ensure that any remittance of funds by way of demand draft, mail/telegraphic

transfer or any other mode and issue of travellers’ cheques for value of Rupees fifty thousand

and above is effected by debit to the customer’s account.

b. Foreign remittance exceeding USD 1000 is not allowed into the accounts of foreign students,

within the period of first thirty days, when local address is not verified.

c. Foreign remittances are not allowed to be credited in the small accounts.

.

J. Introduction of new technologies/products

Banks should ensure full compliance with all KYC/AML/CFT guidelines issued from time to

time, in respect of internet banking service and debit/credit/gift card holders including add-on/

supplementary cardholders also.

HO CIR 69/2017

A FEW ITEMS OF DOCUMENTS/RECORDS TO BE PRESERVED PERMANENTLY

Records to be preserved permanently -

(H.O., C.O., Branch and all other Offices, as the case may be)

01. Safe Deposit Locker Agreements.

02. specimen Signature cards.

03. Claims Files / Death Claims Register / Nomination Register.

04. Sundry Assets Files

05. Office Order Book

06. ATM/Debit Card issue – Registers/Applications.

07. Acknowledgement for receipt of PIN/ Password/User ID.

08. Register for recording Deposit of Title Deeds

09. Jewel Appraiser’s File.

10. Bonus Paid Register /File.

11. Matters relating to Branch Licence, Branch shifting/timings, policy matters advised to

Branches

SOME IMPORTANT RATES: (AS ON 24.2.2017)

Bank Rate 6.75 %

Cash Reserve Ratio 4.00 %

Statutory Liquidity Ratio 20.50 %

Repo Rate 6.25 % (rate at which RBI injects money )

Reverse Repo Rate 5.75 % (rate at which RBI sucks money)

SB Rate 4 % wef

OUR BANK MCLR RATES: (WEF 7.1.2017)

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 9 of 46

OverNight 8.20 %

One Month 8.25 %

Three Month 8.30 %

Six Month 8.40 %

One Year 8.45 %

CUSTOMER RISK CLASSIFICATION:

All customer profiles/accounts of:

HIGH RISK CUSTOMERS:

NRIs, HNIs, PEP(Politically exposed persons), NGOs, Trusts, Cooperative Societies, HUF,

Exporters, Importers and Accounts having Beneficial Owners;

Customers against whom complaints from Police/Legal enforcement authorities or reports of

fraud are received;

Blocked accounts and Unclaimed deposits;

Accounts of dealers in Jewellery,gold/silver/billions,diamonds and other

precious metals/stones.

Newly opened CASA accounts which have notcompleted 6 months ( except Staff,

exstaff,Pensioners ,Small accounts, financial inclusion and Basic savings bank accounts ).

Address proof / ID proof updation to be done:

Low risk Once in 10 years

Medium risk Once in 8 years

High risk Once in 2 years

Updation of risk profile : Twice a year - 15 May and 15 Nov.

Options : CIM 50 CH021 BO REPORT : 170070A

BO report for KYC non compliant account is 170113I

Parameters for defining High Net worth Individuals:

Average balance of Rs.2.00 lakh and above in SB/NRE SB.

Balance of Rs.10.00 lakh and above in Term deposit, Domestic/NR.

Balance of Rs.5.00 lakh and above in CA.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 10 of 46

Enjoying Fund based limits/term loans exceeding Rs.30.00 lakh.

Salary credit of Rs.25000/- and above in a Super saving salary A/c.

Business contribution/opinion makers /VIPs such as head of village/Town/City, Top

Executives of Companies etc.

Withdrawals in Employees Accounts- Authorisation

Upto Rs.5000/- by supervisor

Upto Rs.10,000/- by officer

Above Rs.10,000/- by Manager/Sr.Manager

In extension counters, official in charge can authorize above Rs.5000/-

Use of Ultraviolet Lamps(Cir. 315/2008)

Cash cheques/DD Rs.1000/- and above, transfer items above Rs.5000/- are to be

screened under Ultraviolet lamp.

Payment of Cheque after Business Hours

Managers/Senior Managers are empowered

After business hours but within office hours

Maximum Rs.10,000/- per party – with in the available balance , no TOD.

Employees not eligible.

Dishonour of inward cheques/ ECS (Cir. 134/2010, 181/2015,205/16):

Cheques which have not been drawn as per apparent tenor or without adequate balance shall be

dishonored. Apart from charging appropriate penal charges and interest, Bank reserves the right

to close the account. In such cases, account should be closed after giving 14-day notice to the

account holder.

Dishonour of cheques of value less than Rs.1 crore, on six occasions during the financial year

will attract stoppage of cheque book facility and closure of account

If cheque is returned for 5th time, send caution notice to customer and inform that if cheque is

returned for 6th time during a financial year, account will be closed.

Bank will be constrained to close the account, if ECS mandates are dishonored for the reason

insufficient funds on four occasions during the financial year. Serve notice to party after

returning ECS for third time.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 11 of 46

Bank has the discretion to waive the above condition, on case to case basis

In the event of dishonor of cheques valuing more than Rs.1 Crore and above and cheque

favouring stock exchange irrespective of amount on 4 occasions during a financial year for want

of funds, NO fresh cheque book should be issued and Bank may consider closure of such

account.

Closure of such accounts (including OD / OCC A/c) may be considered at Discretion

Atal Pension Yojana(216/2015,518/2015, 546/2015,587/2015)

GoI has launched scheme to provide social security to unorganized sector workers w.e.f.01.06.15

Scheme is administred by PFRDA and NSDL act as Central Recored keeping Agency

Eligibility : All Bank account holders aged between 18-40 years, who are not the member of any

statutory social scheme. Swavablamban subscribers would be automatically migrated to APY.

Pension payment commences at the age of 60 years. Minimum contribution is for 20 years.

Delayed contribution attract penaly. Contribution can be monthly, quarterly and half yearly.

If there is inadequate balance in SB a/c of subscriber till last date of the month /last date of the

first month in quarter / last day of the first month in a half year , it will be treated as a default and

contribution will have to be paid in the subsequent month along with overdue interest for delayed

payment.

Overdue interest for delayed contribution: Rs. 1 per month per Rs. 100 or part thereof, for each

delayed monthly payment. Overdue interest amount collected will remain as part of the pension

corpus of the subscriber (587/15)

Fixed pension ranges between Rs. 1000-Rs. 5000 ( depend upon age and contribution)

Central Government co-contributes 50% of subscriber‘s contribution (Maximum Rs. 1000 for 5

years till 2019-20). For co-contribution subscriber should join NPS before 31st March 2016

For co-conribution subscriber‘s should not be a tax payer. Upon death after 60 years of age,

spouse would get monthly pension.Corpus would be paid to nominee on death of subscriber and

spouse both.

Trinity Circle ,Bangalore branch is focal point.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 12 of 46

For New APY accounts mobilized by BCs ,incentive of Rs. 50/- is permitted on receipt of

commission by Bank Eligible APY accounts mobilized & also for conversion of existing

Swavalamban Accounts into APY by our Staff Members on designated APY log-in days and

APY log-in Weeks, incentives are payable, as one time measure. To be eligible to these

minimum 5 accounts should be mobilized. New APY account mobilized :Upto 25 account @ Rs.

30 per account ,upto 50 account @ Rs. 40 per accounts and above 50 mobilized account Rs. 50

per account incentive is provided by sharing commission Conversion of existingSwavalamban

accounts : Rs. 30 per converted accounts (546/2015)

The existing swavalambanscbscriber whose age is above 40 years and subscribers aged between

18-40 in unwilling to migrate to Atal pension Yojana can continue in existing swavalamban

scheme.(327/15)

List of existing SB account holders in the age group of 18-40 years is published branch wise in

Business Objects Report 170192.

If the APY account is closed due to terminal illness or death of the subscriber, the accumulated

corpus (subscriber contribution, Government co-contribution and the returns thereon) in the

subscriber account will be returned to the subscriber or the nominee as the case may be.(341/16)

In case a subscriber, who has availed of Government co-contribution under APY, chooses to

voluntarily exit APY before attaining the age of 60 years, he/she shall be refunded the

contributions made by him/her to APY along with the net accrued income earned on his/ her

contributions after deducting the account maintenance, investment management, etc. charges.

The Government co-contribution and the accrued income earned on the Government co-

contribution shall not be given to such subscribers. (341/16)

APY accounts which are closed within a period of 12 months from their opening or which have

NIL balances, no incentive will be admissible to Banks from the Government for such

accounts.(341/2016)

Pradhan Mantri Suraksha BimaYojana

(PMSBY)(215/2015,276/2015 ,352/2015)

Bank has entered MoU with UIICL for offering PMSBY to SB customers

All SB customer aged between 18-70 years are eligible to take cover under PMSBY

Accidential death and disability coverof Rs. 2 Lacs at annual premium of Rs. 12 +

ST is available

The policy under PMSBY has to be renewed every year for continuation of protection

cover. Cover shall be from 1st June to 31st May every year.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 13 of 46

In case of multiple SB accounts held by an individual in one or different Banks, the

person would be eligible to join the scheme through one SB account only.

All enrolments done on or after 01/06/2016 would get coverage from the date of debit of

premium.

Aadhhar would be primary KYC for the Bank account.

Coverage of Rs. 2 Lacs is available for total and irrecoverable loss of both eyes or loss of

use of both hands or feet or loss of sight of one eye and loss of use of hand or foot

Coverage of Rs. 1 lac for total and irrecoverable loss of sight of one eye or loss of use of

one hand or foot.

The premium will be deducted from SB account through ‗auto debit facility in one

installment on or before 1st June of each annual coverage period under the scheme. In

case where auto debit takes place after 1st June, the cover shall commence from the first

day of the month following the auto debit.

All enrolments should be captured and authorized in the 3S package on day to day basis

to facilitate auto debit of premium and submission of premium and MIS to UIICL

Status query : Customer can send SMS ―SSSQ<Space> last four digits of a/c number‖ to

92666-23333 through his registered mobile number. The status will be sent to customer‘s

mobile by a return SMS.

For claim, notice within 30 days from the date of accident/loss to be given to

Bank Branch.All papers should be submitted to insurer within 60 days from date of

accident/loss.The accidental injury resulting into death/disablement within a period from

the death of accident only becomes admissible under the policy.

UIICL process the claim and disburse the money within 30 days from the receipt of the

claim from Bancassurance section ,HO.

Insurance cover is restricted to only one SB account of the member and the premium paid

in more than one account shall be liable to be forefeited.

If the insurance cover is ceased due to any technical reasons such as insufficient

balance on due date or due to any administrative issues, the same can be reinstated

on receipt of full annual premium .

Appropriation of premium:

Insurance company : Rs. 10/- per annuam per member

BC/Bank : Rs. 1/- per annum per member

Bank : Rs. 1/- per annum per member

Pradhan Mantri Jeevan Jyoti Bima Yojana( PMJJBY)(214/2015)

The Govt of India, as a part of its Social Security Measures, has announced PMJJBY

offering Life Insurance Cover of Rs. 2 lacs( payable on death ) at annual premium of

Rs. 330/- + ST as applicable to all SB account holdersaged between 18 and 50 years.

Bank has entered into MoU with LIC of India to offer PMJJBY cover to all eligible SB

customers.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 14 of 46

In case of multiple SB accounts held by an individual in one or different Banks ,the

person would be eligible to join the scheme through one savings bank account only.

The scheme will be a one year cover ,renewable from year to year. Cover will start from

1st June every year.Customer has to opt to join/pay by auto debit from SB account , by

31st May every year .

Individuals who exit the scheme at any point may re-join the scheme in future years by

submitting a declaration of good health.New entrants may also join ,subject to submission

of self certificate of good health.

Aadhar would be the primary KYC for the Bank account

Termination :

On attaining age 55 Years ( age neared birth day) subject to annual renewal up to that

date ( No entry beyond the age of 50 years)

Closure of account/ Insufficiency of balance

In case a member is covered under PMJJBY with LIC/other company through more than

one account and premium is received by LIC/other company, insurance cover will be

restricted to Rs. 2 lacs and the premium shall be liable to be forfeited.

If the insurance cover is ceased due to any technical reasons such as insufficient balance ,

the same may be reinstated on receipt of full annual premium and a satisfactory statement

of good health.

Bank remit the premium to insurance companies in case of regular enrolment on or

before 30th of june every year and in other cases in the same month when received.

Appropriation of premium

Insurance premium to LIC ; Rs. 289/- per annum per member

BC/Bank : Rs. 30/- per annum per member

Bank: Rs. 11/- per annum per member

Coverage under Scheme is in addition to cover under any other insurance scheme .

All enrolments done on or after 01.06.2016 will have a 45 days lien clause whereby

claims for death which occur during the first 45 days from the date of enrolment will not

be paid. The 45 days lien clause will be applicable only to PMJJBY enrolment not

renewed on or before 30.06.2016 and PMJJBY fresh enrolments done on or after

01.06.2016

All PMJJBY enrolments done on or before 31.05.2016 can be renewed upto 30.06.2016

without any break in Insurance Cover.

Death due to accident is exempted from lien clause.

Sovereign Gold Bond Scheme(527/2015, 530/2015,387/16,575/16)

GoI has developed this financial asset (Sovereign Gold Bond) as an alternative to

purchasing metal Gold. It would be sold by RBI on behalf of GoI to resident Indian

entities, including individuals, HUFs, Trusts, Universities, Charitable Institutions.

The bond will be issued in tranches. Bond are eligible for conversion into demat form.

Bond can be used as collateral for loans.

Size: Denominated in multiples of grams of Gold with a basic unit of 1 Gram

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 15 of 46

.Minimum permissible investment will be 1 gram. Max 500 grams per

person per fiscal year. In case of Joint holding investment limit will apply to first

applicant only.

Tenor: 8 Years. Exit option from 5th year to be exercised on the interest payment dates

Price: Issue and redemption price fixed in INR on the basis of previous week‘s (Monday-

Friday) simple average of closing price of gold of 999 purity published by Indian Bullion

and Jewelers Association Ltd ( IBJA)

Interest Rate: 2.75% p.a. payable semi-annually on the initial value of investment.

Interest will be taxable and capital gain tax will remain same as in case of physical Gold.

Bond will be eligible for SLR.

The bonds can be traded now in BSE/NSE Stock Exchanges.

Commission: for distribution shall be paid at the rate of 1 % of the subscription amount.

Government Link Cell, Nagpur, would act as a Link Branch for the Scheme.

The Subscription Amount may be placed in the SB Account of the Subscriber with the

Designated Branch. Interest will be paid at SB rate from the date of realization of

payment to the settlement date, i.e. the period for which they are out of funds.

Tenure of any Loan (including moratorium period) under Bank‘s respective scheme will

be subject to Maximum of 8 years or residual period of maturity of SGB, whichever is

lower.

SGB bonds for accepted as Primary / Collateral Security should be dematerialized

format; however shall not be accepted as margin for BG /LC

The Joint holder of Bond should be taken either as Co-applicant or Guarantor for the loan

No Loan shall be granted for purchase of Sovereign Gold Bond.

Scheme for Providing Furniture / Fixtures To The Officers.(Cir 303/2013, 609/2013,

467/2014)

Eligibility: The scheme will be applicable to the Officers residing in Bank‘s accommodation/

leased residence / residence owned by the Officers and / or residence taken by the Officers on

rent.

a) All confirmed Officers in Scale-I to Scale-VII are eligible.

b) Promotee Scale-I Officers on probation are eligible to avail the scheme.

c) Direct Recruit Probationary Officers (including Specialist Officers) who are posted to

a Branch/Office on regular posting during probation are eligible to avail the facility under

the scheme, subject to execution of the BOND for the total cost of the furniture items

purchased. Whereas, Direct Recruit Probationary Officers posted to different Branches /

Offices for on the Job training periodically are not eligible to avail the facility till their

confirmation.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 16 of 46

d) Officers on contract are not entitled to avail the facility under the scheme. Monetary

ceiling/limit fixed (including taxes)for purchase of furniture / fixtures in respect of

various scales of officers are as under :

JMGS I : Rs. 1 lac , MMGS II & III : Rs. 1.75 Lacs, SMGS IV : Rs.2.25 Lacs , SMGS V: Rs.

3.00 Lacs , TEGS VI : Rs. 4.25 Lacs, TEGS VII : Rs. 4.50 Lacs

Staff Meeting: (Cir no.224/04, 75/2005, 217/2007,136/2012 ,183/2014 )

It aims at ‗Open Culture‘, ‗Family Feeling‘, ‗Group Synergy‘ and‗Talent

Recognition‘ .

Agenda can reflect variety, topicality of issues and branch specific priorities.

Conducting staff meeting on third Friday of every month is mandatory. It may be

conducted during office hours and may stretch beyond office hours at time

Once in a month with agenda decided well in advance.

Expenditure: Rs. 20/- per person, per month/meeting.

The minutes of staff meeting are to be sent to the concerned HRM/Staff Administration

Sections / respective Wing CGMs‘/GMs‘ Secretariats. Circle Offices/Secretariats should

submit a consolidated report on Staff Meeting to HR&OD Section on or before 5th of the

succeeding month.

Job Rotation(Cir.75/2005, 217/2007):Compulsory both at branches and also at

administrative units upto II Line Managers.

The Job Rotation should be normally effected once in every six months. However, the

branch-in-charge, depending on the size of the branch and departments handled, can have

some flexibility regarding the period. But, the same should not be more than 12 months.

This is to ensure smooth change over without affecting the customer service.

Employees Suggestion Scheme:(Cir no.14/2004, 233/2010)

To put in place system, procedures & reduce risk to inculcate team spirit.

All employees of the Bank are eligible to participate.

Employees in O&M Section, Management Audit System, Inspection Wing and their

overseeing executives are not eligible.

Group of employees: Minimum 3 and Maximum 5.

Suggestion through e mail to: [email protected]

Accepted Suggestions will be rewarded as follows:

Appreciation letters signed by DGM of the Circle/GM Personnel Wing

It will be noted in personal records

Cash awards Rs.3,000/- & Rs.5,000/- for individual and team respectively.

Names with photographs of the prize winners will be published annually in Shreyas.

Memo will be issued.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 17 of 46

Annual Awards: 6 Best Suggestions : I – Rs.10,000/- II – Rs.7,500/- & III – Rs.5,000/-

and 3 consolation prizes : Rs.3000/- each.

Special Award :adhoc by CMD for reduction in expenditure or in preventing frauds.

Marketing officers‘ suggestion scheme(166/16):

Scheme cover suggestions pertaining to marketing of bank‘s products/services

Cash rewards of Rs. 3000 to all accepted suggestions and top four suggestion received

during the financial year shall be rewarded with annual awards.

Cash prize for top four annual awards is Rs. 10000, Rs. 7500,Rs. 5000 &Rs. 3000/-

Marketing Officers‘ can send suggestions directly to MCRM section, Marketing & RR

wing HO without routing through Marketing Executives.

Whistle blowing:

It means reporting of irregular practices in any operational areasincluding frauds and alpractices

by an employee to higher authorities.

Whistleblowing to be done to any of the following: Vigilance department, HO/ Executives in

Charge of HRM in CO; Executives @ ZI // AGM @ Personnel wing, HO.

Brain Storming:Periodicity is quarterly. A corporate topic is debated at all levels by involving a

cross section of employees and valuable feedback gathered will help HO to introduce new

systems/ bringing changes in existing systems and procedures/schemes, etc. Report should be

sent to controlling office.

Talent Bank Scheme(16/2016)

Talent Bank Scheme is to give an opportunity to all employees to self-assess their

talent/skill and core competitive area. Bank call for an option from all willing employees

to identify their core area and submit their willingness to be groomed for such

challenging assignments/responsibilities

Coverage : Scale I/II / III/IV employees with maximum age limit 40/48/48/52 Years

Areas are: Credit , Risk Management , Information Technology , Alternate Banking

Technology & E- Transaction/Payments ,Forex and Treasury operations, Marketing &

Sales, Recovery Management & HRM

Study Circle:

Under this forum of Study Circle, important topics can be discussed like Time

Management, Stress Management, Yoga and Meditation, Taxation, Blood Donation,

Basel II norms, Quiz Program, etc. However, care to be taken to see that the topic chosen

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 18 of 46

is interesting one and kindle desire in the minds of employees and active their thinking

process.

Periodicity of conducting study Circle meeting is once in 3 months in case of branch and

bi-monthly in CO.

Topics of banking/non-banking will be discussed by inviting a guest speaker who is well

versed with the topics.

Honorarium of Rs.200 can be paid in case of branch having staff strength of less than 50

and Rs.500 in case of CO/Branch having more than 50 staff strength.

Presentation of Milestone Awards:(Cir 130/2000, 247/2011)

Wef February 1990. After completion of 25 years of meritorious service

The award will be in the form of any one article, like wrist watch, silver, salver or any

other article of the officer‘s choice.

The cost of the award should not exceed Rs.5000/-

Debit to: General Charges-Staff Welfare Account and the bills will be lodged with the

(third copy) of the GC slip at the branch itself.

The award will be presented in the monthly staff meeting.

Award may be presented during the staff meeting of April / October – Every Year

Incentive Scheme for capacity building for officer and clerical employees:

(165/2016)

The existing Incentive Scheme ( 311/06,256/11,271/11 & 23/12) for Officers and Clerical

employees for taking up Post Graduate/Certificate/ Diploma Courses has been

revised/modified and rechristened as ―Incentive Scheme for Capacity Building for

Officers and Clerical Employees

Cash incentive : Group –I course → Rs. 6000 , Group II course → Rs. 10000

Fee reimbursement : Actual ( Maximum Rs. 50000)

Under Group II ,employee will be eligible for fee reimbursement and cash incentive both

,only upon securing 60% or more marks

Employee may pursue only one course in either group at a time.

Employee can avail benefits for any number of courses for Group I course and benefits

for only two courses under group II

Life insurance and general insurance certification :Rs. 3000 and fee Reimbursement

Disclosure policy 2008-09 of the Bank(cir 217/08)–Authorised Spokespersons:

(Cir.290/2010)

Information regarding the Bank shall be disclosed externally to media, investors&

analysts only by the Authorized Spokespersons in accordance with the relevant internal

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 19 of 46

policies. Only the C & MD and the Executive Director/s shall speak on the Bank‘s behalf

on financial matters, with the media, investors and analysts.

They may from time to time designate others to speak on behalf of the Bank or respond

to specific enquiries from the investment community or media.

No other officer or employee of the Bank shall speak to analysts, institutional

shareholders or journalists regarding the Bank‘s financial matters.

Incentive Scheme To Honor Alert Staff - Fraud Prevention(Cir 255/07, 324/2009)

Upto Rs.10000/- : Cash Award Rs.500/- + Appreciation letter – CO Head

10001/- to Rs.1 Lac – Cash Award upto Maximum of Rs.2000/- + Appreciation letter by

CO Head

100001 to Rs.5 lac - Rs.7000/- + App. Letter by ED

Rs.500001 and above - Rs.10,000/- + App. Letter by CMD

Same above for culprits caught in the branch

Frauds under advances - detection of kite flying, hypothecation of spurious stocks,

impersonation to be detected within 3 months,

Branches have to report all cases of actual/suspected frauds immediately on detection –

within 24 hours to Review & Reporting Section – Technology Risk and Fraud Prevention

(TR & FP) Wing (Earlier with Inspection Wing), Ho with copy to CO. Observations of

the concurrent auditor/inspecting officials are to be furnished in the fraud report.

Police complaint has to be lodged immediately including attempted frauds without fail

after obtaining permission from R & L, CO. No discretion to waive lodging of police

complaint. Reports should be signed by branch in charge.

Cash Matters:

Currency of below Rs.50/- and coins to be kept in Single Lock

Single lock key to be kept by the staff handling cash

Cash received on account of recovery/deposits on NPBW days may be accepted and

treated as late cash

Rs.2000/- denomination notes should be counted by an officer Special Assistants to count

uptoRs. 500 denomination notes.

Where the shortage is Rs.10000/- and above, investigation has to be conducted by an

officer appointed by the concerned DGM/GM and appropriate action to be taken.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 20 of 46

Where the shortage is Rs.2500/- and above but less than Rs.10000/-, discretion to DGM

for conducting investigation

Cash shortage is more than Rs.25000/- and is permitted to be recovered in installments,

the employee may not be allowed to work in cash department for a year or so long as the

amount of shortage is not fully paid whichever is later

All cases of cash shortages involving more than Rs.5000/- detected by Managers and

Inspectors(which was not informed by cashier), shortage of Rs.10,000/- though informed

by cashier have to be reported as cases of frauds to R & R section, Vigilance Wing, HO

with a copy to R&L Section of Circle Office

Excess cash – claim by remitter –can be paid by Manager upto Rs.500/-. Above that, the

claim should be passed by referring to HRM, CO.

For claim above Rs.5000/- stamped indemnity ( fornon customers)

At the end of the financial year, excess cash to be transferred to commission account

Remittance by insured post - maximum Rs.10000/-

Status of legal tender for Rs. 500/- and Rs. 1000 /- withdrawn w.e.f. expiry of 8th

November 2016.

Transmission of cash

Sub-staff – upto Rs.5000/

Upto Rs.25000/- by a person not below the rank of clerk.

Above Rs.25000/- by a person not below the rank of clerk and at least one more

employee to accompany him. For remittance upto Rs.20 lakhs – no armed guard.

Above Rs.20 lakhs upto Rs.50 lakhs should be accompanied by one armed guard

Above Rs.50 lakhs ,atleast two armed guards

Insurance Cover for Money and securities in transit – Rs.5 crores

Insurance cover for ATM cash: Rs.20 lakhs

Insurance cover for unauthorized withdrawal from ATM : Rs.50,000/-

Insurance for loss or damage to ATM : Rs.25 lakhs

Mutilated note – cut into 2 or more pieces

Standard Cash limit is fixed by CO

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 21 of 46

Detection, Impounding, reporting of fake Notes and filing of FIRs (HO Cir 396/2014,

452/2015)

Each banknote, which, on examination of various security features /parameters, is determined as

a counterfeit one, shall be branded with a stamp‖ COUNTERFEIT BANK NOTE‖. For this

purpose, a stamp with a uniform size of 5 cm x 5 cm may be used.

These Counterfeit Notes at branches (returned by police after investigation) should be subjected

to verification on a half yearly basis (on 31st March and 30th September) by the Officer-in-

Charge of the branch concerned. These Counterfeit Notes should be preserved for a period of

three years from the date of receipt from the police authorities.

Counterfeit Currency Reports(396/2014):Branches and Currency Chests are required to submit

Counterfeit Currency Reports (CCRs) within 7 days from the date of detection of counterfeit

currency note/s. Counterfeit currency detected in the soiled notes is also to be reported in the

CCR.

Filing of FIR on detection of Forged / Counterfeit Notes above 4 pieces in a single transactions is

mandatory. Liberalized definition of Cut Notes & Soiled Notes (Cir.298/2010, 237/2011)

Single numbered notes – Rs.1/-, Rs.2/- & Rs.5/-: Note presented should not be in more than two

pieces. No essential feature of the note should be missing and complete number should be

available in an undivided area on one of the pieces. Both the pieces should be of the same note.

II.Double numbered notes–Rs.10/-,Rs.20/-,Rs.50/-,Rs.100/-,Rs.500/-& Rs.1000/-: The note

presented should not be in more than two pieces. No essential feature of the note should be

missing. Both the pieces should be of the same note. The above types of notes will be treated as

soiled notes and be kept along with soiled notes.

Mutilated Notes – Presentation and Passing: (Cir.298/2010, 237/2011): A mutilated note is a

note of which a portion is missing or which is composed of more than two pieces. Mutilated

notes may be presented either at designated bank branches of commercial banks. Mutilated

notes so presented may be passed as per the Rules framed under Reserve Bank of India (Note

Refund) Rules2009.

All Currency Chests/branches should provide exchange facility of soiled notes/ mutilated/

defective on all working days and report under DN2 statement.Without justification, submission

of ‗NIL‘ statement from Currency Chests will be construed as not extending the facility.(58/16)

Currency Chests to submit the monthly statement on adjudicated notes to the Regional Offices of

RBI.(58/16)

Notes which have turned extremely brittle or badly burnt, charred or inseparably stuck up

together and, therefore, cannot withstand normal handling, shall not be accepted by the branches

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 22 of 46

for exchange. Instead, the holders may be advised to tender these notes to the concerned Issue

Office where they will be adjudicated under a Special Procedure.

Notes bearing ―PAY‖/‖PAID‖―REJECT‖ stamps should be rejected under Rule 6(2) of Reserve

Bank of India (Note Refund) Rules, 2009 and the tenderer should be advised that the value of

such (defective) note/s cannot be paid since the same has already been paid.

Notes bearing slogans / political messages: it ceases to be a legal tender and the claim on such a

note will be rejected.

Deliberately Cut note: should be rejected under Rule 6(3)ii of Reserve Bank of India (Note

Refund) Rules, 2009.

―Star Series‖ Banknote:

RBI has adopted the ―STAR series‖ numbering system for replacement of defectively printed

banknotes, at the printing presses. To begin with, this will be for banknotes of Rs.10, Rs.20 and

Rs.50, Rs.100 denomination. The Star series banknotes are exactly like the existing Mahatma

Gandhi Series banknotes, but have an additional character viz., a *(star) in the number panel in

the space between the prefix and the number. The packets containing these banknotes will not,

therefore, have sequential serial numbers, but contain 100 banknotes, as usual. To facilitate easy

identification, the bands on such packets clearly indicate the presence of these banknotes in the

packet.

Exchange of soiled notes:

Where the number of notes presented by a person is up to 20 pieces with a maximum value of

Rs. 5000 per day, banks should exchange them over the counter, free of charge.

Where the number of notes presented by a person exceeds 20 pieces or Rs. 5000 in value per

day, banks may accept them, against receipt, for value to be credited later. Banks may levy

service charges

Exchange of mutilated and imperfect notes:

Where the number of notes presented by a person is up to 5 pieces, non-chest branches should

normally adjudicate the notes and pay the exchange value over the counter. If the non-chest

branches are not able to adjudicate the mutilated notes, the notes may be received against a

receipt and sent to the linked currency chest branch for adjudication. The probable date of

payment should be informed to the tenderers on the receipt itself and the same should not exceed

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 23 of 46

30 days. Bank account details should be obtained from the tenderers for crediting the exchange

value by electronic means.

Where the number of notes presented by a person is more than 5 pieces not exceeding Rs..5000

in value, should be advised to send such notes to nearby currency chest branch by insured post

giving his / her bank account details (a/c no, branch name, IFSC, etc.) or get them exchanged

thereat in person. All other persons tendering mutilated notes whose value exceeds Rs..5000

should

be advised to approach nearby currency chest branch. Currency chest branches receiving

mutilated notes through insured post should credit the exchange value to the account of sender

by electronic means within 30 days of receipt of notes.

Commission In Respect Of Government Business(Cir 212/2012)

For Physical Receipts Rs.50 per challan / transaction

For e mode Receipts Rs.12 per challan / transaction

For Pension payments Rs.65 per transaction

For other payments 5.5 paise per Rs.100/- turnover

Death Claim Settlement – Delegation of Powers, without nomination:

Managers/Senior Managers heading the branches : Rs.2.00 lakhs

Executives in Scale IV in CO/Branches : Rs.3.00 lakhs

Executives in Scale V in CO/Branches : Rs.5.00 lakh

Wherever Scale IV or V heading branches, are on leave, Absence beyond 7 days, powers to

Managers/Sr.Mgr: Rs.2.00 lakhs

DGM heading branches/Circle : FULLPOWERS

Safe Deposit Lockers and Safe Custody Articles, irrespective Of amount: DGM of CO

The delegated power that are available to Scale VI of Circle for settlement of death claim are

provided to Scale V heading Circle also.(Cir 365/2010)

Simple claim settlement procedure upto Rs.10000/-.

Wherever Nomination is there, branch in charge can settle the claim irrespective of amount /

Locker.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 24 of 46

Banking Codes And Standards Board Of India (BCSBI):(Cir no.230/2007)

BCSBI is a registered society and our bank is a member of it - Formed on the recommendations

of committee on Procedures and Performance Audit on Public Services TaraporeCommittee).

Voluntary Code

Instant Credit: Upto Rs.15,000/- for parties having satisfactory dealings for 6 months. OSCs

without request of party and Clearing cheques with request of party

In case of cheque return (ICDB) interest chargeable is from the date of RETURN of such cheque

till recovery. ROI : Applicable to customer‘s other limits for ROI applicable upto Rs.2 lacsie

Base Rate

Delay upto 14 days, SB rate of interest, beyond 14 days – term deposit rate and beyond 90 days –

2% over TD rate of interest(253/2009)

OSC lost in transit, interest payable for 15 days at SB rate

ICDB cheques credited to OD/OCC, returned unpaid – Rate of interest : 2% above applicable

rate of OD/OCC from date of credit, till reversal.

Branch manager will be responsible for the resolution of the complaints/grievances in respect of

customer‘s service by branch

Customers‘ Day : 15th of every month. Branch in charge should present between 3pm and 5 pm.

7 days time for grievance of complaint in case of Branch/CO/HO each

Redressal of complaints – Adopted by our Bank : General complaints -21 days,

RBI,MPs,VVIPs – 15 days, PMS office – 7 days

If any cheque paid after stop payment instruction, bank has to reverse the entry within 2 working

days

Normally customers have to be contacted between 07-00 hrs and 19-00 hrs. Retail Customers at

residence and Business/Residence in case of others

Cir 176/08: Compensation Policy – If customer is suffered due to deficiency of services : In case

of fraud by staff, bank has to pay just the claim of customer. In case branch is at fault, branch to

compensate the customer without any demur. In case where neither the branch nor the customer

is at fault, but the fault lies elsewhere in the system, the branch should compensate the

customerupto Rs.5,000/- or actual loss whichever is lower and the same will be on merits of the

case.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 25 of 46

The Governing Council of BCSBI has decided to rate the member banks based on the level of

awareness and implementation of these Codes among Employees. These ratings of Banks

awarded by the BCSBI will be in the public domain.

Safe Deposit Lockers(Cir no.253/07)

Relationship - Lessor (bank) and Lessee (customer)

In case of new parties, 3 years rent + charges for break open of locker in case of

eventuality : to be collected in advance is kept in FDR

If no operations of lockers continuously for 3 years or more in case of Medium Risk

category and One year in case of High Risk Category customers - Branches should send

notice and break open the locker.

No nomination facility for Safe Custody Articles held by more than one person

In case of Locker hired by Jointly with Joint Operations and nomination, if any hirer dies,

access will be given Jointly to survivor and nominee.

Loss of locker key : Charges: Rs.200/- (in addition to actual break open charges)

Locker Operations : 12 operations free p.a.,

Rs.100/- per operation beyond 12 plus applicable Sertax.

Charges for delayed remittance of rentals is as per period of delay as per

following chart

Upto and incl of 1 Qtr – 10% of applicable annual rental

Upto and incl of 2 Qtr – 25% of applicable annual rental

Upto and incl of 3 Qtr – 40% of applicable annual rental

Upto and incl of 4 Qtr – 50% of applicable annual rental

1 Yr and above- 100% of applicable annual rental

This is governed by Transfer of Property Act.

Straight Through Processing (STP) system between SAFE and CBS-FCR for collection

of locker rent is in place. (HO Cir 210/2014, 114/2015)

Biometric authentication for Locker access in SAFE module is enabled (HO Cir.325/

2014)

RTGS Service Charges( 119/2016) w.e.f. 01.04.2016

Transaction above Rs. 2 Lacs & upto Rs.5 Lacs:

1. 0800 to 1100 a.m. : Nil ,

2.1100 to 1300 p.m. : Rs.27

3 1300 to 1630 p.m. : Rs.30

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 26 of 46

Transaction above Rs.5 Lacs

1.0800 to 1100 a.m. : Nil

2.1100 to 1300 p.m. : Rs.52

3.1300 to 1630 p.m. : Rs.55

NEFT Service Charges(Cir 693/2016) after 30.12.2016

For Fund transfer upto Rs.100000 : Nil

For Fund transfer above Rs.1 to 2 lakh : Rs.15.00 per transaction

For Fund transfer above Rs.2 Lakh : Rs.25.00 per transaction

General Charges:Cir 177/2008, 309/2010, 318/2010, 21/2011,216/16)

Revenue Powers Delegated To Various Authorities Other Than Premises,

Computers, Printing & Stationery (Cir.216/2016)

1.Scale I officers heading branches, second line manager ( Scale II/III) ,faculty of STC/RSTCs:

Rs. 1000

2.Managers/Sr Managers heading branches and administration units : Rs. 1500

3.Sr Manager in VLBs/ELBs/FDs/PCBs/Premier Branches: Rs. 2200

4.Manager/Sr Manager in administration units other than premises/ general section at

RO/CO/HO: Rs. 5000

5. Manager/Sr Manager of premises/ general section at RO/CO/HO: Rs. 10000

6.DM CO/RO and CM : Rs. 20000

7.AGM ( Branches ) : Rs. 35000

8.DGM/AGM-GA wing/AGM-CO/DGM-Branches: Rs. 50000

9.DGM/AGM heading RO : Rs. 200000

10.DGM heading circle and DGM ( in GM headed circles) :Rs. 7.5 Lakhs

11. GM heading circle, GM/DGM GA wing : Rs. 15 lakhs

12. ED : Rs. 30 lakhs

13. MD &CEO : Rs. 50 Lakhs

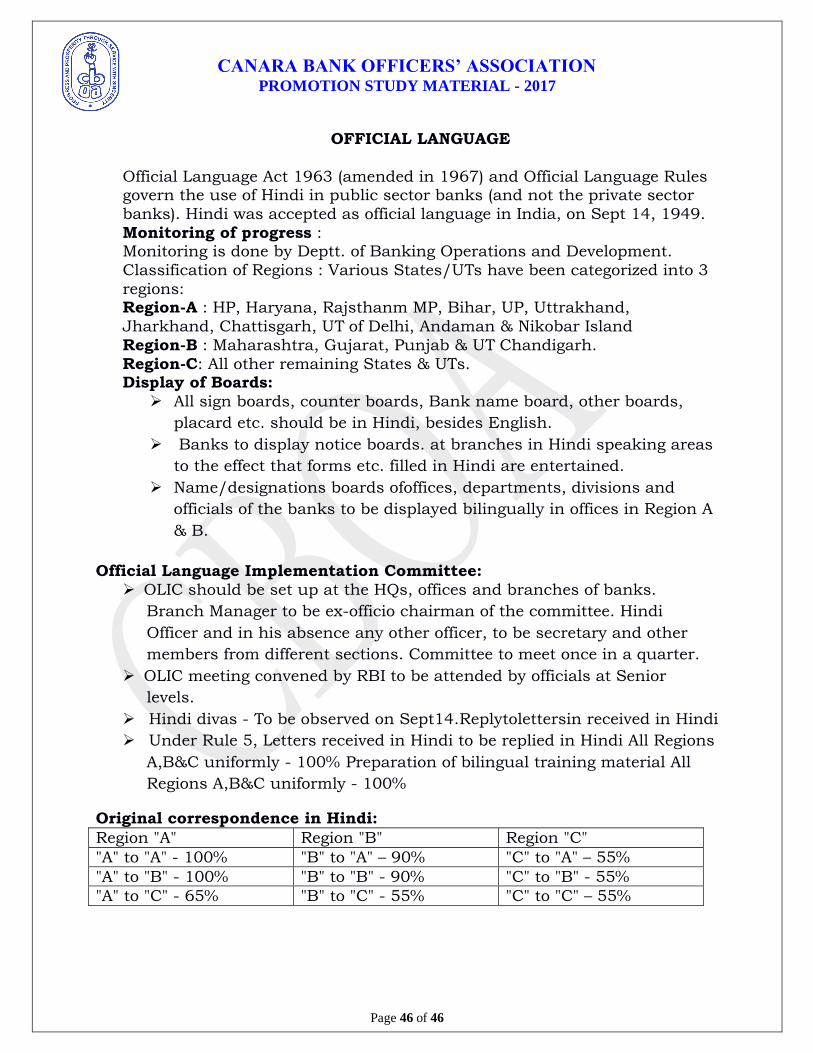

(Hindi was declared as Official Language of Union on14.09.1949. Therefore every year Hindi

Day is celebrated on 14 September).

TheOfficial Language Policy came in force with effect from 26.1.1950. The Act was passed in

the year 1963.) Official Language Rules were framed in 1976

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 27 of 46

Banking Ombudsman

Established under Scheme 1995 by RBI in exercise of powers vested in it under Section 35A of

the BR Act. Applies to J & K.

Complaints alleging deficiency in banking service.Non payment /inordinate delay in payment or

collection of collection of cheques, bills drafts etc.

Non acceptance of small denominations

Non issuance of DDs, non adherence to working hours, failure to honour guarantee, claims

regarding fraudulent withdrawal of amounts, NRI remittances etc. Non opening of accounts

without valid reasons for refusal.

Loans: Non observance of RBI directives regarding interest rates, delay in sanctions etc.

Party has to first complain to Bank. Wait for 1 month for response. If no settlement or no

response is there, it is cause of action and the party can file within 1 year from cause of action,

his complaint with Ombudsman. (Total period available to customer for complaining to Banking

Ombudsman is 13 months)

After receiving complaint, Ombudsman calls for views of bank and waits for 1 month to settle

the issue by concerned bank. If not settled in the above period, ombudsman shall announce

award. Maximum award up to Rs.10 lakhs only.

After receiving ombudsman‘s award, the customer has to furnish letter of acceptance within 30

days from the date of receipt of copy of award. If acceptance is not given within 30 days, the

award shall not be binding on the bank.

Compliance of bank with in 1 month of receipt of acceptance from customer.

If bank is aggrieved on the award, it can make application for review to appellate authority

(Deputy Governor, RBI) within 30 days of the date of receipt of award.

For appeal, bank has to take permission from CMD or ED.

BO as an arbitrator: dispute between bank and customer or between bank and another bank, of

both parties agree, if such claim is not exceeding Rs.10 lakh.(But upto Rs.1.00 lacs only for

credit card matters)

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 28 of 46

LOANS & ADVANCES AND STAFF MATTERS

Clean loan facility

Eligibility: Three years of confirmed service

Quantum: ` One and half months gross salary for every completed year of

service with a maximum of 15 months gross salary or the following

amount whichever is less:

o (a) Officers - `5.00 lacs

o (b) Workmen`3.00 lacs

o (c) Sub-staff / PTE - `1.75 lacs.

NTH 40%

Repayment : 120 months

Rate of interest 9% p.a. compounded monthly

Car Loan to Officer ( 4 Wheeler)

Eligibility: Officers confirmed service

Quantum:

o a)Brand new vehicles : 90% of the cost of car which includes

insurance, registration and taxes subject to a maximum of `

10,00,000/-.

o b)For purchase of used car: The maximum quantum of loan

amount for used cars shall be 80% of the value as per approved

valuation by the approved qualified automobile engineer or actual

purchase consideration/price or original price whichever is least,

subject to a maximum ceiling of ` 6,00,000/-.

NTH : 35% (Min ` 10000).

Margin: 10% for new vehicle and 20% of old vehicle

Repayment : 180 monthly instalments (120 months towards principal

liability @ ` 834 per lakh & 60 months towards interest @ ` 714 per lakh.

Rate of interest: 8.5% Simple

Car Loan to workmen employees ( 4 Wheeler)

Eligibility: Five years of confirmed service

Quantum:

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 29 of 46

o a)Brand new vehicles : 90% of the cost of car which includes

insurance,registration and taxes subject to a maximum of `

5,00,000/-.

o b)For purchase of used car: The maximum quantum of loan

amount for used cars shall be 80% of the value as per approved

valuation by the approved qualified automobile engineer or actual

purchase consideration/price or original price whichever is least,

subject to a maximum ceiling of ` 3,50,000/-.

NTH : 35% (Min ` 10000).

Margin: 10% for new vehicle and 20% of old vehicle

Repayment : 180 monthly instalments (120 months towards principal

liability @ ` 834 per lakh & 60 months towards interest @ ` 798 per lakh.

Rate of interest: 9.5% Simple

LHV (Two wheelers) for Staff

Eligibility: All officers confirmed officers and workmen in the services

Quantum:

o New 2-wheeler: ` 1,00,000/- or 90% of the cost of the vehicle

whichever is less.

o Used 2-Wheeler: ` 50,000/- or 80% of the cost of the vehicle

whichever is less

NTH : 25%

Margin: 10% for new vehicle and 20% of old vehicle

Repayment : 84 monthly instalments (66 months towards principal

liability & 18 months towards interest) or before the employee ceases to

be in the services of the Bank, whichever is earlier

Rate of interest:

o Upto ` 40,000/- 7.5% p.a. simple

o Above ` 40,000/- upto ` 1,00,000/- 8.5% p.a. simple

Special Vehicle Loan

Eligibility: For purchase of brand new two-wheeler by employees of the

bank during the probationary period

Quantum: ` 1 lakh or 90% of the cost of the vehicle whichever is less

Repayment : 84 months

Rate of interest On going Base rate

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 30 of 46

Employees' Housing Loan Scheme

Eligibility: All confirmed officer employees and (b) all confirmed workmen

employees who have completed 2 years of continuous service are eligible

to avail the loan

Margin : 10% of the project cost

Repayment: 360 Months

Rate of Interest : 8% p.a.simple

NTH : 25%

Quantum:

Cadre EHL

Executives Sc-VI & VII ` 75.00 Lacs

Executives Sc-IV & V ` 60.00 Lacs

Officers I to III ` 50.00 Lacs

Clerical Staff ` 30.00 Lacs

Sub-ordinate Staff ` 20.00 Lacs

Loan amount for repairs/ maintenance/ renovation/ enlargement of

existing dwelling unit in case the employee has not availed loan under

EHL: Loan Amount (` in lacs) 10.00, 7.00 & 4.00 for Officers, Clerical

staff & Sub-staff respectively

Housing Loan scheme to Retired Employees of the Bank

Eligibility: All retired employees who have not availed EHL or Housing

Loan from our Bank / or any other bank during their active service and

do not own a house but retired on superannuation. Employees who

ceased to be in the services of the Bank due to Voluntary Retirement,

CRS, termination, resignation etc., are not eligible

Margin : 10% of the project cost

Repayment: 15 years or till the borrower attains age of 75 years,

whichever is earlier

Rate of Interest : 8.5% p.a.simple

NTH : 25% or ` 5,000/-, whichever is higher

Quantum :

o Officers (Scale–I and above) : ` 30 Lacs ,

o Cerical staff – ` 18 Lacs,

o Sub Staff –` 12 Lacs

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 31 of 46

IBA Medical Insurance Scheme

The coverage under the insurance scheme is as under

CADRE INSURANCE COVER

Officers ` 4.00 lakhs

Clerical ` 3.00 lakhs

Sub-ordinate ` 3.00 lakhs

The scheme covers employee + spouse + dependent children + any two of

the dependent parents/ parents-in-law.

Hospitalisation would mean admission in a hospital / nursing home for a

minimum period of 24 consecutive hours of inpatient care except for

specified procedures/ treatments Medical expenses incurred immediately

30 days before the insured person is hospitalized and relevant medical

expenses incurred immediately 90 days after the insured person is

discharged from the hospital are covered provided that such medical

expenses are incurred for the same condition for which the insured

person‘s hospitalization was required.

Domiciliary treatment expenses reimbursement is covered

o upto `.30, 000/- for workman retirees and spouses of such

deceased employees/ retirees with overall Sum Insured of `.

3,00,000/-.

o Similarly, for retired officers/ spouses of deceased officers / retired

officers domiciliary treatment expenses reimbursement is covered

upto `. 40,000/- with overall Sum Insured of `. 4,00,000/-.

Domiciliary treatment reimbursement is optional and subject to payment

of additional premium to avail such domiciliary reimbursement facility.

Mother‘s maternity expenses upto ` 50,000/- for normal delivery and `

75,000/- for caesarean section

Ambulance charges are payable upto `.2500/- per trip to hospital.

Taxi and auto expenses in actual maximum upto ` 750/- per trip will

also be reimbursable

Staff Accountability in Credit Proposals

Following four circumstances may emerge in any credit proposal: a. Deficiencies have been pointed out and the proposal has been

recommended by the recommending authority with justifications.

b. Deficiencies have been pointed out and the proposal has been

recommended by the recommending authority without justifications. c. Deficiencies have been pointed out and the proposal has NOT been

recommended by the recommending authority.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 32 of 46

d. Deficiencies have NOT been pointed out and the proposal has been

recommended by the recommending authority.

In the circumstances described in (a) & (c), generally no accountability shall fall on the concerned officials who had appraised

processed/prepared/recommended the proposal. However in the

circumstances described in (b) & (d) above, accountability shall also be fixed on the concerned officials who had appraised/processed/ prepared/recommended

the proposal.

Generally the accountability shall not be fixed in respect of decision

taken by the Credit Approval Committee or any other committee duly

constituted by the Competent Authority, except under the following cases

like:

o frauds committed with the involvement/ connivance of the

members of committee;

o decision influenced by personal/ vested interest;

o decision based on extraneous factors not relevant to the business

interest of the bank;

o decision tainted with ulterior motive;

o decision which are not bonafide; and

o decision taken under influence/ pressure from outsiders, though

such decision is not in the interest of the bank and in violation/

deviation of the critical mandatory norms which seriously affects

the bank's interest.

In the cases like above the members of such committee shall be

accountable collectively as well as individually.

REPORTING OF FRAUDS

Reporting of Frauds to Reserve Bank of India:

RBI‘s framework for dealing with loan fraud shall be implemented by

Credit Administration & Monitoring wing for loan frauds above ` 500

million

Reporting : RR section ,TR & FP Division, RL & FP wing shall report all fraud detected by Bank to RBI as under

1. FMR1: Fraud involving ` 0.1 million and above

2. Flash report : For Fraud involving ` 50 million and above

3. FMR2:Quarterly report on fraud outstanding 4. FMR3:Case wise quarterly progress report on frauds involving ` 0.1

million and above

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 33 of 46

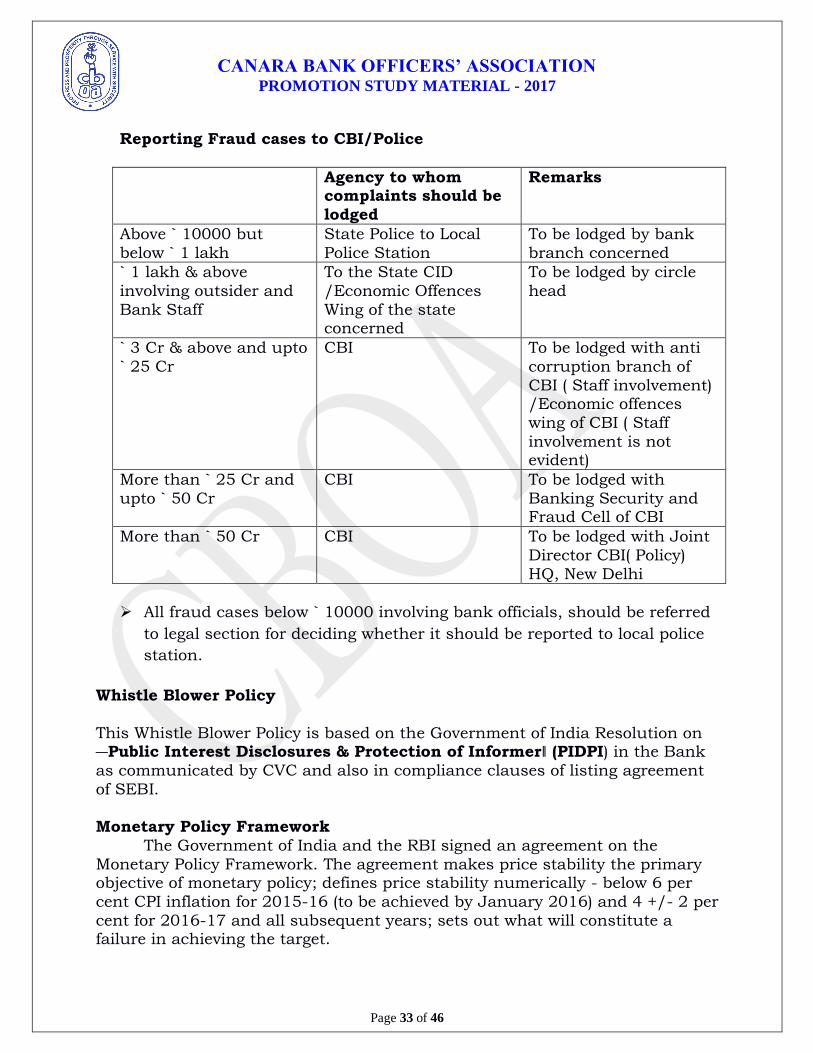

Reporting Fraud cases to CBI/Police

Agency to whom complaints should be

lodged

Remarks

Above ` 10000 but

below ` 1 lakh

State Police to Local

Police Station

To be lodged by bank

branch concerned

` 1 lakh & above

involving outsider and

Bank Staff

To the State CID

/Economic Offences

Wing of the state concerned

To be lodged by circle

head

` 3 Cr & above and upto

` 25 Cr

CBI To be lodged with anti

corruption branch of

CBI ( Staff involvement) /Economic offences

wing of CBI ( Staff

involvement is not evident)

More than ` 25 Cr and

upto ` 50 Cr

CBI To be lodged with

Banking Security and Fraud Cell of CBI

More than ` 50 Cr CBI To be lodged with Joint

Director CBI( Policy)

HQ, New Delhi

All fraud cases below ` 10000 involving bank officials, should be referred

to legal section for deciding whether it should be reported to local police

station.

Whistle Blower Policy

This Whistle Blower Policy is based on the Government of India Resolution on ―Public Interest Disclosures & Protection of Informer‖ (PIDPI) in the Bank

as communicated by CVC and also in compliance clauses of listing agreement

of SEBI.

Monetary Policy Framework

The Government of India and the RBI signed an agreement on the

Monetary Policy Framework. The agreement makes price stability the primary objective of monetary policy; defines price stability numerically - below 6 per

cent CPI inflation for 2015-16 (to be achieved by January 2016) and 4 +/- 2 per

cent for 2016-17 and all subsequent years; sets out what will constitute a failure in achieving the target.

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 34 of 46

The framework specifies that the Reserve Bank in the event of failure will

report to the government on:

a) Reasons for deviation of inflation from the target over three

consecutive quarters;

b) Remedial measures

c) An estimated time frame over which inflation will be brought back to

the target.

CURRENT RATES

BANK RATE 6.75 % w.e.f .(04.10.2016

MSF 6.75 % w.e.f. (04.10.2016)

CASH RESERVE RATIO 4.00 %

STATUTORY LIQUIDITY RATIO 20.50 % w.e.f.(01.01.2017

REPO RATE 6.25 % w.e.f. (04.10.2016)

REVERSE REPO RATE 5.75 % w.e.f . (04.10.2016)

BASE RATE OF OUR BANK 9.50 % wef 07.01.2016 (Cir 11/2017

ECNOS One Year MCLR+ 525 Basis Point

(Cir 200/16) Base Rate+5 %

FOREIGN CURRENCY ECNOS 12m LIBOR + 6.5% (IO/19/2010)

BPLR 14.45 % w.e.f 01.01.2014

CLEAN RATE Base Rate + 7=16.50 %

SB RATE 4 % w.e.f 03.05.2011

OVER NIGHT MCLR 8.20 % ( w.e.f.07.01.2017)

ONE MONTH MCLR 8.25 % ( w.e.f. 07.01.2017)

THREE MONTH MCLR 8.30 % ( w.e.f. 07.01.2017)

SIX MONTHS MCLR 8.40 % ( w.e.f. 07.01.2017)

ONE YEAR MCLR 8.45 % ( w.e.f. 07.01.2017)

FIVE SCSS 2004 8.50 % (w.e.f.01.01.17 to 31.03.17)

PPF SCHEME 2016 8.00 % (w.e.f. 01.01.17 to 31.03.17)

KISAN VIKAS PATRA 7.70 % (w.e.f. 01.01.17 to 31.03.17)

SUKANYA SAMRIDDHI ACCOUNT

SCHEME

8.50 % (w.e.f. 01.01.17 to 31.03.17)

Banking Codes And Standards Board Of India (BCSBI):(Cir no.230/2007)

BCSBI is a registered society and our bank is a member of it - Formed on

the recommendations of committee on Procedures and Performance Audit on Public Services (Tarapore Committee).

Instant Credit: Upto `15,000/- for parties having satisfactory dealings for 6

months. OSCs without request of party and Clearing cheques with request of party

CANARA BANK OFFICERS’ ASSOCIATION PROMOTION STUDY MATERIAL - 2017

Page 35 of 46

In case of cheque return (ICDB) interest chargeable is from the date of

RETURN of such cheque till recovery. ROI : Applicable to customer‘s other

limits for ROI applicable upto `2 lacsie Base Rate Delay upto 14 days, SB rate of interest, beyond 14 days – term deposit rate

and beyond 90 days – 2% over TD rate of interest(253/2009)

OSC lost in transit, interest payable for 15 days at SB rate ICDB cheques credited to OD/OCC, returned unpaid – Rate of interest :

2% above applicable rate of OD/OCC from date of credit, till reversal.