FINNOVA BANKING SOFTWARE

72

FINNOVA BANKING SOFTWARE END-TO-END, EFFICIENT, OPEN, INNOVATIVE

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of FINNOVA BANKING SOFTWARE

FINNOVA BANKING SOFTWAREEND-TO-END, EFFICIENT, OPEN, INNOVATIVE

FINNOVA BANKING SOFTWARE IN FIGURES

Swiss banks trusts in the Finnova Banking Software

product suites

partners

customer banks

employees

users at banks and operating partners

e-banking clients

Swiss francs balance sheet total of the Finnova banks application possibilities of our software through an individual parameterisation and thanks to the choice of different operating models

1 in 3

5

70

100

400

10 000

400 000

300 000 000 000

∞

4

Smarter Banking 5

Finnova Banking Software at a glance 13

Finnova Channel Suite 27

Finnova Front Suite 33

Finnova Management Suite 39

Finnova Expert Suite 43

Finnova Solution Suite 57

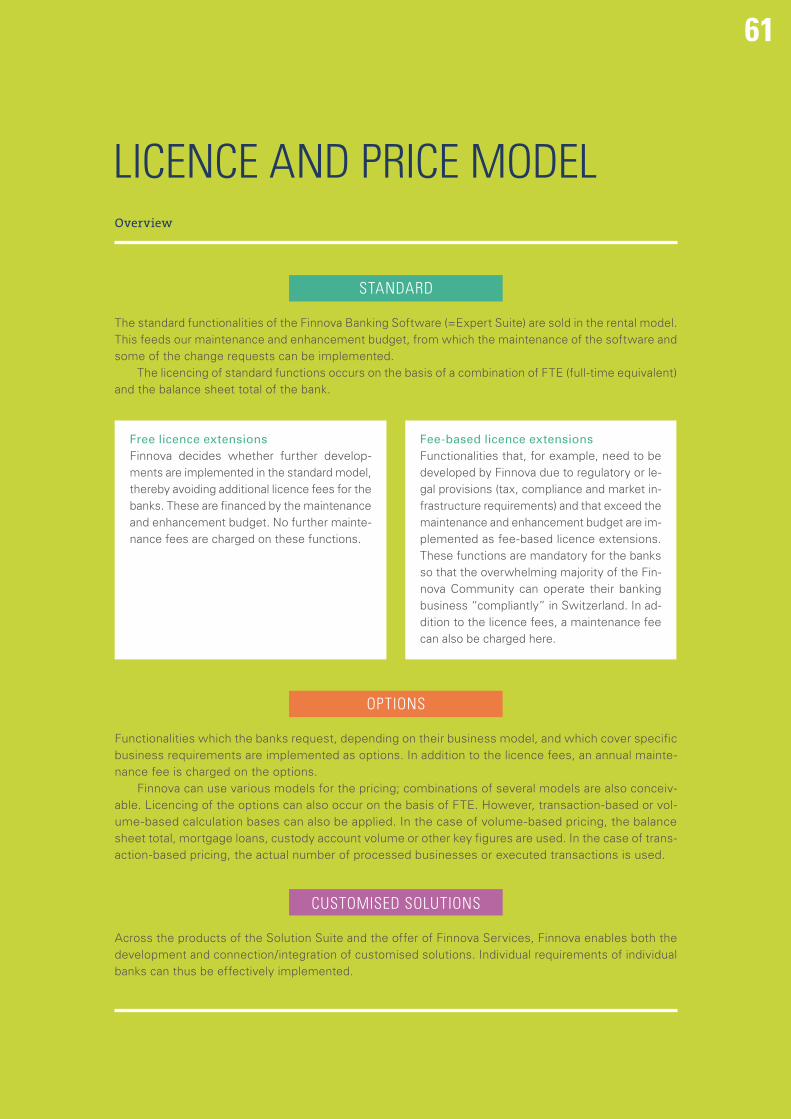

Licence and price model 61

Table of contents

Lenzburg, January 2017

5

SMARTER BANKINGIn the future, successful business models in banking will be determined more than ever by the intelligent use of technology. Growing cost pressure resulting from the erosion of margins, increasing compliance requirements and the digitalisation of banking are driving forces here. In this interplay, we offer our customers efficient and innovative IT solutions, enabling “smarter banking”.

Number of articles in Swiss media in the Dow Jones/Factiva database that address the topic in relation to banks

6

Banking in a time of change In the last ten years, the banking environment in Switzer-land has fundamentally changed, marking the beginning of a new era for many. The change is driven in particular by three far-reaching trends: erosion of margins, regulation and digi-talisation.

Erosion of marginsThe international credit crunch from 2007 to 2009 substan-tially changed the market environment for Swiss banks. In many countries, the generally fragile global economic situa-tion, combined with deflationary trends, led to an expansive monetary policy of historic proportions. This is particularly evident in Switzerland as the Swiss National Bank is fighting the upward pressure on the Swiss franc with negative inter-est. For Swiss banks, this results in eroding interest margins, which they particularly need to offset on the cost side in view of restricted earnings potential. Since 2008, employment at Swiss banks has decreased by over 5 %, while the number of banks has dropped by 17 %.

Banks can now only achieve substantial cost reductions by thoroughly optimising their value-added chain. Industrial- isation of the banking business, along with standardisation and automation of processes and outsourcing of sub-processes, is becoming increasingly important. New technologies and growing digitalisation help the banks structure their business in a more process-oriented way and focus on their own added value contribution. On the one hand, the banks’ IT itself is the subject of optimisation and on the other hand, new technolo-gies enable the implementation of more efficient end-to-end business processes.

2006

500

2007 2008 2009 2010 2011 2012 2013

450

400

350

300

250

200

150

100

50

02014 2015 2016

Erosion of margins in the Swiss media

2006

200

2007 2008 2009 2010 2011 2012 2013

180

160

140

120

100

80

60

40

20

02014 2015 2016

Industrialisation in the Swiss media

Source: Finnova

7

RegulationIn response to the international credit crunch, regulators worldwide have tightened their standards in the last few years. In particular, they focus on measures to in-crease system stability, consumer protection and international financial transpar-ency. The wave of regulation primarily affects banks with a focus on cross-border private client business. Bank-internal processes need to take into account not only increased local regulatory requirements, but also an increasing number of extrater-ritorial provisions. This results in an enormous segmentation of business cases and exponentially increases complexity.

All regulatory requirements need to be implemented in the banks’ IT as effi-ciently as possible while ensuring compliance with rules at all times. This task is becoming a real competitive factor. In order to optimise their models and processes and thus gain a competitive advantage, banks need to use intelligent client profiling models, take into account dynamic client and market behaviour, use all structured and unstructured data available to them, and automate processes.

2006 2007 2008 2009 2010 2011 2012 2013

3500

2014 2015 2016

Regulation in the Swiss media

3000

2500

2000

1500

1000

500

0

Source: Finnova

“In the years to come, we will invest heavily in the expansion of our product and services

portfolio and intensify our cooperation with partner companies. This will allow us to support our

customer banks with innovative solutions in this time of radical change in the banking sector.”

Charlie Matter, Chief Executive Officer

Number of articles in Swiss media in the Dow Jones/Factiva database that address the topic in relation to banks

9

50

20

25

30

35

40

45

0

5

10

0 2

SHORT FUSE, BIG BANG

LONG FUSE,BIG BANG

LONG FUSE,SMALL BANG

SHORT FUSE, SMALL BANG

3 4 5

Banking

Insurance

Professional Services

Retail

ICT & Media

Timing (years)

Impact (% of change in business)

Education Manufacturin

Transportation

Healthcare

Utilities

Mining, Oil, Gas, Chemicals

Agriculture

Government

Real Estate

Food Services

Leisure

Construction

1

DigitalisationThe digitalisation of society is now well advanced. For a long time, its impact on the banking sector played a rather subordinate role. Lately, however, it has become clearer in which areas and to what extent digitalisation has the potential to transform the banking sector. Here, contact points with clients are frequently of primary importance. However, the basically disruptive potential of digitalisation goes beyond that. Major technological driving forces, such as cloud computing, big data & analytics, mobility, social media or the internet of things, enable new business models and fundamen-tally change some of the existing models. In addition to innovations in the front office, they allow for an increased standardisation and automation of processes. An analysis performed by Deloitte Digital and Heads (“Survival through Digital Leadership”, 2015) shows that, in comparison with other sectors, digitalisation in banking is expected to have an above-average impact on the existing business in the next few years.

In addition to the established players, fintech companies are increasingly coming to the fore. With their innovative solutions, they are the catalysts of the digital trans-formation. An international study by Citigroup (Citi GPS, 2016) shows that private investment in fintech companies worldwide has increased tenfold in the last five years, reaching USD 19 billion in 2015. This means that, in the coming years, up until 2020, up to 10% of the expected revenues in retail banking will be in jeopardy.

Source: “Survival through Digital Leadership”, 2015, Deloitte Digital and Heads

Impact of digitalisation on the business model of selected sectors

10

50

20

25

30

35

40

45

0

5

10

0 2

SHORT FUSE, BIG BANG

LONG FUSE,BIG BANG

LONG FUSE,SMALL BANG

SHORT FUSE, SMALL BANG

3 4 5

Banking

Insurance

Professional Services

Retail

ICT & Media

Timing (years)

Impact (% of change in business)

Education Manufacturin

Transportation

Healthcare

Utilities

Mining, Oil, Gas, Chemicals

Agriculture

Government

Real Estate

Food Services

Leisure

Construction

1

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Digitalisation in the Swiss media1200

1000

800

600

400

200

0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fintech in the Swiss media

600

500

400

300

200

100

0

Source: Finnova

Relevance of selected digitalisation topics

Mobile Payment 55 % 860

Cryptocurrencies 12 % 251

Big Data & Analytics 63 % 226

Mobile Banking 66 % 197

Online Banking 80 % 135

Blockchain 8 % 117

Social Media 39 % 101

Crowdfunding 12 % 90

Omnichannel Banking 46 % 74

Online Mortgages 42 % 68

Robo Advisory 27 % 63

PFM 59 % 47

P2P Marketplaces 27 % 42

Social Trading 16 % 17

In this situation, it is important for banks to pursue their own strategy to deal with digitalisation. Where are their strengths and weaknesses, opportunities and threats? Which projects offer the greatest potential: differentiation in the market or process automation? Which implementation strategy is the most promising: in-house, with established partners or with fintech start-ups? There is a wide range of digitalisation top-ics and it is easy to be tempted by trends.

Media response **Impact on the business model *

* Expected impact of selected fintech developments on the business model in the next five years; source: IFZ Retail Banking Study 2015, Lucerne Univer-sity of Applied Sciences and Arts

** Number of articles in the Swiss media in the Dow Jones/Factiva data-base in the last two years that address the listed topics in relation to banks; source: Finnova

Number of articles in Swiss media in the Dow Jones/Factiva database that address the topic in relation to banks

11

FINNOVA ECOSYSTEM & DELIVERY

Solution SuiteChannel Suite Management Suite Expert Suite

SYSTEMS OF ENGAGEMENT

FINNOVA AS ABUSINESS ENABLER

FINNOVA AS ABUSINESS DRIVER

SYSTEMS OF INSIGHT

SYSTEMS OF RECORDS

Front Suite

Ecosystem for innovative and efficient end-to-end bankingFinnova’s strategyIt is our ambition for the future to be the leading reference for end-to-end banking in Switzerland. We want to enable banks, operating partners and selected intermediaries, together with third-party providers, to cope with the dynamics and chal-lenges of eroding margins, regulation and digitalisation. We focus our efforts on our roughly 100 existing customers – they are the ones we want to grow with first and foremost. We will invest heavily in our product and services portfolios so that we can launch innovative solutions faster, be it in the form of Finnova developments or together with partners.

Finnova Banking Software as an open ecosystemWe are expanding the Finnova Banking Software into an open ecosystem. The Systems of Records stand for structured and increasingly unstructured data storage, and this with sharply rising volumes, great speed and increasing process orienta-tion. The Finnova Expert Suite covers these functions and thus forms the actual core element of the Finnova Banking Software.

The data is provided to the Systems of Engagement (Finnova Channel Suite and Front Suite) and the Systems of Insight (Finnova Management Suite). The Systems of Engage-ment address customer experience, mobility and context-ori-ented services and information – with the aim of reinforcing the ties of clients to the bank and its services. Last but not least, the Systems of Insight provide analyses concerning cli-ents, products and markets as well as in-house procedures – with the aim of continually introducing improvements and innovations and having risks under control at all times.

The Finnova Solution Suite enables the opening up of the Finnova Banking Software, not only externally for third-party system, development and service partners, but also internally to ensure the integration of our own applications and suites. This helps create an open ecosystem in which Finnova plays the role of business driver for the Systems of Records, while for the Systems of Engagement and the Systems of Insight, it plays the role of business enabler.

13

FINNOVA BANKING SOFTWARE AT A GLANCEThe Finnova Banking Software is a comprehensive front-to-back software platform for retail, universal and private banks. A consistent process orientation and a modular architecture enable flexible adaptation and integration of the business functionalities required by banks, their clients and BPO providers today.

Payments

Financing

Investments

Bank Management

Compliance

Business Process Management

CHAN

NEL

SUI

TE

FRON

T SU

ITE

MAN

AGEM

ENT

SUIT

E

EXPE

RT S

UITE

SOLU

TION

SUI

TE

Value Creation Processes

Management Processes

“Our existing customers and partners take centre stage for us. We wish to grow together with

them, with new products and services related to the major banking sector trends: digitalisation,

industrialisation and compliance.”

Hendrik Lang, Chief Customer Officer

14

Value Creation ProcessesIn times of increasing market transparency in terms of market performance, banks are required to focus on the market ser-vices that create a genuine added value for their clients and for which the clients are therefore willing to pay an appropriate price. The banks can thus optimise their profitability via the added value generated. The turnover of the banks is primarily composed of the three following value creation processes.

>> PaymentsDigitalisation has significantly simplified the basic func-tion ‘Payment Transactions’. Nowadays, payments are in-creasingly made from mobile devices, around the clock. Thanks to a consistent optimisation of front-to-back bank-ing processes, it is possible to design almost trivial touch-points for the client as a way to create a unique client experience. In order for this to happen, straight through processing and a performant processing engine are also necessary.

>> FinancingWhile financing needs were previously addressed mainly at a regional level, digitalisation has eliminated geograph-ical restrictions to a large extent. Banks across Switzer-land now compete against each other, and as a result of digitalisation, the competition may soon spread to Europe. The importance of fast, cost-efficient and effective front-to-back processing in the lending business is growing, with due consideration of regulatory requirements – from client acquisition to an overall view from a management perspective.

>> InvestmentsThe complexity of processes in the investment business is continuously increasing as well. This places higher de-mands on all those involved, from the client to the client advisor, through to compliance and back-office staff – es-pecially as not only national regulatory authorities and do-mestic and foreign tax authorities, but also special bilateral solutions play a part in this. New and innovative technol-ogy-based business models challenge conventional ad-visory methods. In this context, it is important to create added value for the bank clients that can be offset. Simple implementation and costs play an important role for the bank. This places considerable demands on the flexibility of multiple systems such as tracking, valuation, alert, ex-ception handling and reporting, to name but a few.

Management ProcessesThe effective control of a bank and fulfilment of compliance requirements front to back require clearly defined processes along the value added chain of a bank, as well as consistent data storage and aggregation.

>> Bank managementControlling a bank in a dynamic environment with an ev-er-increasing number of competitors and in an increas-ingly regulated market challenges many banks and their managers. Management decisions need to be taken on the basis of verifiable facts and profound analyses, which requires a comprehensive, coherent and consistent data and information base.

>> ComplianceIncreasing compliance requirements on the part of regu-lators and authorities also present new challenges for the client-bank relationship. These challenges can be met by consistently focusing our software development on the cli-ent and thus on the banking needs. Therefore, compliance is becoming an integral part of the interaction between the client and the bank.

>> Business process managementBy consistently aligning bank transactions to the clients’ needs, banks are able to create a genuine added value for their clients. User-centred, effective and flexible pro-cess management is growing in importance – and with it, technical software support in the form of integrated front-to-back core banking solutions like the Finnova Banking Software.

15

The Finnova Banking Software is divided into five user-oriented product suites, which themselves are divided into product groups. Many product groups are al-ready available, notably in the Expert Suite and the Channel Suite, while the other suites are still being developed. The options available today in addition to the stand-ard product are presented in this brochure in the associated suite and in the appen-dix. We inform our customers and partners about the further development of the Finnova Banking Software in the quarterly Finnova Product Update.

Five suites for Smarter BankingThe Finnova Banking Software is divided into five suites addressing the five differ-ent stakeholder groups. The Expert Suite is the real backbone of the Finnova Bank-ing Software for achieving high-performance industrialisation and digitalisation and ensuring 24/7 operation in straight through processing (STP) and real time. All other suites tie in with the Expert Suite, for example the client-oriented Channel Suite and Front Suite. While the Channel Suite provides a self-service area for bank clients,from mobile banking and e-banking through to ATM self-service features, the Front Suite actively supports the client advisors’ work processes. As its name suggests, the Management Suite constitutes the information and management centre for the bank management. The Solution Suite represents the link between customised and third-party solutions and the individual suites.

SERVICES Consulting & Academy Data & Analytics Application Management Support & Quality Assurance

Payments

Financing

Investments

Bank Management

Compliance

Business Process Mgmt.

E-Banking

Digitalisation Data, Analytics & Compliance Industrialisation, Standardisation Ecosystem

Mobile Banking

Independent Investment Advisory

Financial Accounting

Finnova Control

Regulatory Reporting

Advisory Apps

Advisor Workbench

Risk & Compliance

Payments

InvestmentOperations

Investment Management

Certified Runtime Environment

CRM Quality Assurance Framework

Development Framework

Solution Integration

CHANNEL SUITE FRONT SUITE MANAGEMENT SUITE

STRATEGIC FOCUS

EXPERT SUITE SOLUTION SUITE

Branch & ATM

Business Banking

Financing

Tax

Clients & Products

Bank Clients Client Advisors Bank Managers Selected Third PartiesMiddle Office, Back Office & BPO Experts

FINNOVA BANKING SOFTWAREFinnova Banking Software

16

>> Finnova Channel SuiteWith the Finnova Channel Suite, we directly focus on the channels to the end clients of the banks. The Channel Suite primarily deals with the self-service of banking services. A consistent user experience across the various channels is paramount for this. The Finnova Channel Suite is being expanded on an ongoing basis. We take into account the continuously increasing demands of end clients in mobile banking and electronic banking, and support innovations in the area of ATMs. In the areas of external asset man-agement and in the repositioning of our customer banks in the branch business, we also offer attractive solutions which enable banks to differentiate themselves on the market with modern information and communication tech-nologies.

>> Finnova Front SuiteThe Finnova Front Suite has been developed for advisors and supports them in their overall daily sales activities. With the modular, role-based and process-controlled Ad-visor Workbench, advisors maintain an overview of their portfolio and all important information about their clients, can initiate advisory processes and perform these effi-ciently while being supported by the system. The Finnova Front Suite is both the starting point and focus of all im-portant advisory and distribution processes – from part-ner and client management (client onboarding) to prod-uct management, as well as entire advisory processes for investments, financing, pension provision etc. The Front Suite supports the latest desktop and tablet UI technolo-gies and thus enables unique user experiences in the in-teractive advisory discussions.

>> Finnova Management SuiteThe Finnova Management Suite addresses needs in the areas of integrated bank management, risk, distribution, financing and controlling, as well as compliance. The Man-agement Suite is thus the comprehensive instrument for bank and risk management. It bundles analyses, reports and the control channels for the bank. Furthermore, its functionality covers the ever-increasing compliance re-quirements in the banking sector.

>> Finnova Expert SuiteThe Finnova Expert Suite is the workplace above all for the middle and back office as well as for our BPO partners. It is and remains the backbone of the Finnova Banking Soft-ware and comprises the known expert modules.

The modular structure of the Finnova Expert Suite covers all modules, from payment transactions, financ-ing, investment and portfolio management to client and advisory modules. The parameterisable process manage-ment guarantees the banks an efficient and individual in-tegration. The focal point of the Finnova Expert Suite lies in the quick and comprehensive processing of all business cases and the unrestricted, role-based access to all data.

.>> Finnova Solution Suite

The Finnova Solution Suite makes the Finnova ecosys-tem more accessible to customers, partners and third-party providers. It embodies the openness of the Finnova Banking Software and its solutions. In times of ever faster change, innovation and agility are sought-after qualities. In order to be able to better satisfy these needs, the Finnova Solution Suite is being designed and further developed on an ongoing basis in close cooperation with key players in the Finnova ecosystem. Digitalised and industrialised banking will be possible in the future if solutions are built and operated to be compatible with XaaS. The five Solu-tion Suite product groups target our different stakeholders, who all have specific needs and requirements – from indi-vidual developments via Solution Integration and Business Process Integration to quality assurance and high-perfor-mance, cost-effective operation.

17

>> New Development from Licencing Business >> Architecture Reconstruction>> Maintenance

Services

Solution Suite

Expert Suite

Management Suite

Front Suite

Channel Suite

Existing Business

>> DWH Analytics>> Quality Assurance>> Consulting

>> Development Framework>> Solution & Business Integration>> Quality Assurance Framework>> Certified Runtime Environment

>> Compliance & Tax>> Harmonisation of Payment Transactions>> Loan Processing>> Industrialisation>> UX Renewal

>> Finnova Control>> MIS Analytics>> Data Store/DWH>> Compliance & Risk Control

>> Advisor Workbench>> Managed Investment Advisory Processes >> Customer Relationship Management

>> New Generation of E-Banking>> Personal Finance Management >> Mobile Payments/P2P>> Advisory Portal >> (Customer Experience)

Investment focuses for the product and services portfolio until 2020

Focal points in product developmentThe five suites with their product groups point the way along which we further develop the Finnova Banking Software. Many product groups are already available, notably in the Ex-pert Suite and the Channel Suite, while the other suites are still being developed. Between 2016 and 2020, we will in-vest a total of around 200 million Swiss francs to provide our customers with efficient and innovative functionalities that allow them to optimally position themselves in the market. The further development of the Channel Suite and the Front Suite offer new possibilities for a distinctive client experience, for interaction with the bank client, but also for process auto-mation. The expansion of the Management Suite allows the banks to efficiently implement new compliance requirements and facilitates integrated bank management. In the Expert Suite, we continue to work on process optimisation and au-tomation. The Solution Suite provides flexibility for fast, cus-tomised solutions.

In the further development of the Finnova Banking Software, we are guided by the following objectives:

>> Our product is the leading stable, flexible and easy-to-model banking software with the best total cost of own-ership compared with competitors.

>> The Finnova Banking Software is an integrated standard product which is open for the integration of third-party systems and the development of customised solutions (custom development) via defined Integration & Business Services. We thereby ensure end-to-end banking and re-main flexible so that we can play an active role in the dy-namic developments of digitalisation and industrialisation.

>> Our product offers customers and business process out-sourcing providers measurable quantitative and qualitative added value. This is maximised through a carefully selected and actively maintained partner ecosystem.

>> The Finnova Banking Software uses state-of-the-art tech-nology. It supports new, evolving operating models of the banks and BPO providers and optimally covers the require-ments of mobility and contemporary user experience.

“Within the Finnova Community, we work in close cooperation with our customers

and partners to systematically drive innovation forward. Setting stringent priorities is

crucial to bringing promising solutions to market in a timely manner.”

Jörg Steinemann, Chief Corporate Development & Finance

FINNOVA SERVICES

19

Consulting & AcademyThe Finnova Consulting, Account System Engineering (ASE) and Academy teams combine know-how and practical expe-rience concerning the Finnova Banking Software. If effective-ness and efficiency are important to you, no doubt you will draw on our network of pooled resources.

Optimised use of software to the advantage of the customersThanks to their close cooperation with the Development depart-ment, frequent contact with financial institutions and profound knowledge of the Finnova Banking Software and the operation of the required hardware and middleware, our specialists are able to ensure an optimal software implementation for the cus-tomers, meeting their requirements without compromise. The professionals in our teams have expert knowledge of the bank-ing environment and the technical basics. They quickly grasp the problems, work out the best solutions possible and offer support in the following five areas, either as part of an individ-ual mandate or as a general contractor: analyses, studies, con-sulting, implementations and training.

Data & Analytics Consistent databases through effective data management guarantee the smooth operation of the systems – this is where our core competence lies. We make a measurable contribution to cost and project efficiency. On top of that, we support our customers in guaranteeing and opti-mising the operation of the software throughout its entire life cycle, for example in acquisitions or sales, mergers, reorganisations or platform changes.

Valuable analyses for managers and expertsWe support decision makers in the company with meaningful analyses from a consistent data-base. Together with customers, we implement an efficient, multitenant-capable solution that provides added value for a wide range of banking business models. Thanks to jointly developed analytical solutions, we ensure that the bank’s needs are the focus of our services and our ac-tions. Our top priority is to use existing data and generate faster results, with the most attractive conditions possible and with a standardised solution. Individual requests can be implemented thanks to the use of standard technology and thanks to the chosen software architecture. The autonomy of the solution is ensured at all times. We provide support for individual analyses of customer-specific needs and the conversion to effective and performant DWH or big-data solu-tions. We map reports and data views from different perspectives, depending on where the focus lies: sales opportunities, further product developments, cost optimisation potentials or management/department reporting.

ServicesKnow-how and experience are key factors for successful IT projects. Offering a wide range of services, Finnova enables banks, BPO providers and implementation partners to tap into the internal know-how and decades of experience in project planning, project realisation, implementation and operation of the Finnova Banking Software. This saves time and minimises project risks.

FINNOVA SERVICES

20

Support & Quality Assurance Our commitment towards our customers continues after they have purchased our software. We aim to support our customers throughout the entire life cycle of the software. Various meas-ures, such as automated testing, redefinition of processes and intensification of quality checks, are continually being pushed forward.

Practical training courses enable a tailored operation of the software geared towards the various requirements of front of-fice and application management staff. Our comprehensive mul-tilingual documentation offers answers should any questions arise. If Finnova users require further support, our three-level support process is set into action. In case the first two support levels cannot solve the problem or provide the necessary assis-tance, our customers can count on the third level support pro-vided by Finnova Customer Support.

Furthermore, we offer attractive QA service packages. These focus in particular on automated testing, with which re-peatable test cases can be defined and performed, including a system evaluation of the results achieved. Thanks to the test case scenarios that have been verified by us, our customers can reduce their quality assurance costs.

Application ManagementAt our customers’ request, Finnova Services also ensures application management. Our ba-sic service package covers all maintenance efforts across the board. With this, the ongoing operation of the Finnova platform and second level support are ensured. It also includes the testing and installation of monthly software updates in the productive environment, as well as a specific quota of advisory and support services for ad hoc orders.

We regard application management as a central knowledge and experience base that we consistently integrate into our software development. We also make this know-how available to our partners that operate the Finnova Banking Software for other banks. The services pro-vided by application management enable efficient use and the highest possible performance of the Finnova platform, whether it is operated by Finnova or by one of its experienced partners.

Moreover, we provide advice and assistance to our customers when it comes to creating implementation concepts for the efficient introduction of options, or if they need to purchase additional software components.

“With its development-related know-how of the Finnova Banking Software,

Finnova Services creates added value for the customers. We consider ourselves

a competent partner for innovations in business.”

Daniel Bernasconi, Chief Services Officer

21

22

Value proposition for our customersAs a leading provider of banking software in the Swiss financial centre, we support banks and outsourcing providers in achieving growth in banking even in challenging times. A wide spec-trum of customer segments, both in Switzerland and abroad, can benefit from our Finnova Banking Software. These are notably universal, retail, private and transaction banks, and BPO/BSP providers, but also fintech and development companies.

>> Universal and retail banksThe focus of universal and retail banks is on increased efficiency and comprehensive func-tionalities. We support them with our highly automated software, high STP rates and effi-cient processes. The Finnova Banking Software standard solution already contains a very broad functionality for universal and retail banks that can be individually extended, notably through our open partner ecosystem.

>> Private banksThe change in private banking with growing compliance requirements, margin pressure and changed client needs results in new business models. We support the private banks with our efficient and future-oriented solutions.

>> Transaction banksA most efficient processing possible of payments, securities, foreign exchange and loans for other banks is the core competence of transaction banks. The Finnova Banking Soft-ware helps them achieve this with maximum scalability, high STP rates and maximum automation.

>> BPO providersEfficiency in banking is achieved today by breaking down the value chain and outsourcing standard processes to BPO providers. The Finnova Banking Software is ideally suited as a backbone for the industrialisation of banking processes. In addition, it offers a user plat-form especially designed for BPO providers with which processes for several banks can be handled simultaneously.

>> Fintech and development companiesDesigned to focus on the interplay of the different actors, the Finnova Solution Suite is primarily aimed at development companies, fintech companies, banks’ own development departments and BPO partners. It helps to increase agility in the provision of functionali-ties and to meet the challenges resulting from the breakdown of the value chain and the technological change in banking more quickly.

Operating modelsIn times of eroding margins and increased cost pressure, a low total cost of ownership is impor-tant for the competitiveness of banks. For this, the selection of the right and suitable operating model of its IT solution plays a central role for the bank.

The Finnova model is based on an open partner approach. Our customers can choose be-tween different partners and operating models.

In practice, different operating models and integrations of third-party solutions have become established – from individual installations to multi-tenant towers with a parallel operation of 50 banks, from cost-effective standard solutions to the implementation of complex special require-ments with third-party solutions, for example in the private banking sector.

GKB SÄNTIS SWISSCOMFULL -SERVICEBANK

43 x

SOFTWARE PROVIDER

FINNOVALICENCE

SWISSCOMRESELLER

5 x

SOFTWARE PROVIDER

FINNOVALICENCE

2 x

SOFTWARE PROVIDER

FINNOVALICENCE

AMINVENTX

BPOGKB

ITOINVENTX

5 x

ITOECONIS

BPOFOR EACH OTHER

AMFINNOVA

SOBACO INCORE BANK9 x

SOFTWARE PROVIDER

FINNOVALICENCE

5 x

SOFTWARE PROVIDER

FINNOVALICENCE

AMSOBACO

BPOFINANZ-LOGISTIK

ITOSOBACO

5 x

ITOINVENTX

BPOINCORE BANK

AMINVENTX

AMSWISSCOM

BPOSWISSCOM

ITOSWISSCOM

ESPRIT19 x

SOFTWARE PROVIDER

FINNOVALICENCE

5 x

ITOSWISSCOM

BPOFINANZ-LOGISTIK

AMSWISSCOM

Existing multi-tenant towers

24

GKB SÄNTIS SWISSCOMFULL -SERVICEBANK

43 x

SOFTWARE PROVIDER

FINNOVALICENCE

SWISSCOMRESELLER

5 x

SOFTWARE PROVIDER

FINNOVALICENCE

2 x

SOFTWARE PROVIDER

FINNOVALICENCE

AMINVENTX

BPOGKB

ITOINVENTX

5 x

ITOECONIS

BPOFOR EACH OTHER

AMFINNOVA

SOBACO INCORE BANK9 x

SOFTWARE PROVIDER

FINNOVALICENCE

5 x

SOFTWARE PROVIDER

FINNOVALICENCE

AMSOBACO

BPOFINANZ-LOGISTIK

ITOSOBACO

5 x

ITOINVENTX

BPOINCORE BANK

AMINVENTX

AMSWISSCOM

BPOSWISSCOM

ITOSWISSCOM

ESPRIT19 x

SOFTWARE PROVIDER

FINNOVALICENCE

5 x

ITOSWISSCOM

BPOFINANZ-LOGISTIK

AMSWISSCOM

TechnologyWe support banks in implementing digital business models in the front office by expanding the Finnova Banking Software, especially in the suites close to the front end, and by opening up the software with the Solution Suite. Modern, digital cli-ent experiences present new requirements for design, mobil-ity and intuitive operation. At the same time, the integration with the Finnova core and a secure and consistent data flow need to be guaranteed.

Finnova addresses these challenges by applying new tech-nological concepts for new developments such as the Front Suite. A new technology stack that uses current technological possibilities and concepts has been developed for these ap-plications. It also allows for the implementation of innovative and efficient operating models. With the Finnova Integration Layer, new architectural and technological concepts are also used for modular integration in the Finnova Core.

New architectural and technological conceptsThe Finnova Core is based on an established technology stack that, especially in the Expert Suite, provides for consistent data storage, efficient transaction processing, individualis-ation through parameterisation and high scalability thanks to multi-tenant capability. We continue to rely on our standard software with a tower concept and single-source approach.

In the area of front-office applications, greater flexibility and individualisation are necessary. A technology and architec-ture stack that facilitates this in an efficient way has been developed. The standardisation of interface technologies, the consistent use of recognised open-source products and new operating models guarantee a low TCO.

Central features of the new technology, such as failover, scaling, isolation of data storage, software distribution etc., reduce the complexity of operating, developing and even in-tegrating customised products, which leads to lower operat-ing and project costs. Thanks to the open and independent development platform, topics like excellent user experience or data analytics can be addressed more easily.

New operating modelsAdditional operating models are needed in order to implement in-dividual solutions that differ considerably from a single-source ap-proach, especially in the area of front-office applications. Through the use of modern cluster solutions (Docker Swarm), a model for the operation of new applications is introduced that allows Finnova and the operators to run an individual solution for each customer – a dedicated infrastructure is not necessary.

These new operating models are also based on open-source components like Linux or Docker Swarm, i.e. no proprietary hard-ware and software need to be acquired. Despite a high degree of individualisation, the TCO thus remains low thanks to the use of mainstream hardware and license-free operating systems. With the resulting relief of the transaction-related systems in the Finnova Core, the operating costs can potentially be further reduced in the future.

27

FINNOVA CHANNEL SUITEWith the Finnova Channel Suite, we directly focus on the channels to the end clients of the banks. The Channel Suite primarily deals with the self-service of banking ser-vices. A consistent user experience across the various channels is paramount for this.

The Finnova Channel Suite is being expanded on an ongoing basis. We take into account the continuously increasing de-mands of end clients in mobile banking and electronic bank-ing, and support innovations in the area of ATMs. In the areas of external asset management and in the repositioning of our customer banks in the branch business, we also offer attrac-tive solutions which enable banks to differentiate themselves on the market with modern information and communication technologies.

E-BankingWith the Finnova E-Banking application, private and business clients are provided with a modern and high-performance solu-tion that is optimised for desktop and tablet display.

In the Finnova E-Banking application, account, balance and posting queries are made, and payments are entered and pro-cessed. Thanks to options for analysing expenditure, house-hold budgets or future account transactions, clients have an up-to-date and clear presentation of their financial situation at all times. The financial circumstances can be broken down according to currencies, countries or securities types. The as-set overviews here correspond to those of the client advisor in the Portfolio Management System.

Furthermore, stock exchange orders can be entered, ex-ecuted, queried and processed by means of straight through processing (STP) in the E-Banking application. PayNet, Elec-tronic Archive and Secure Mail are further modules for secure communication with the bank. Whether from the Payment Transactions or Stock Exchange application, Finnova accepts the orders and further processes them in real time. The numer-ous partnerships enable a flexible choice of authentication and transaction signing procedures such as text message/mTAN, Crontosign, Smartcard, Kobil AST or MobileID.

All information and processing jobs in the E-Banking ap-plication occur in real time, and all data is directly stored in the central database. This results in advantages in terms of data consistency and lower operation costs.

E-Banking

Mobile Banking

Branch & ATM

Independent Investment Advisory

CHANNEL SUITE

Business Banking

Option 7: Internet Banking

Option 85: E-Banking Campaign Management

28

The new generation of Finnova E-BankingThe distinguishing feature of the new Finnova E-Banking solution is its modern, user-oriented interface, which has shorter navigation paths and an attractive design. It provides bank clients with extensive functionalities, from the latest payment transaction entry methods to the top-ics of investments, financing and cards, as well as self-service and product openings, and specific functions for business clients, investment clients and external asset managers.

The progressive digitalisation of society means that e-banking channels are becoming increasingly important. The excellent user ex-perience of the new Finnova e-banking solution is optimised for modern tablets and desktop de-vices. Native smartphone apps (Finnova Mobile Banking) are also available in iOS and Android for small screens.

Shorter navigation paths, user-friendly de-sign and a wide selection of functionalities make this the leading e-banking solution on the mar-ket for bank clients. Thought-out responsiveness for tablets and desktop computers is more than just a technically adjusted display on the corre-sponding screen. Real responsiveness means that bank clients can see context-dependent, relevant data at a glance at any time. A wide selection of authentication mechanisms provides bank cli-ents with secure access to their data in real time at all times.

Contovista’s fully-integrated personal financial assistant analyses expenditure and credit card transactions across all accounts and enables an overview of the current household budget in real time. It can also be used to comfortably man-age other budgets, for example for paying taxes or achieving savings goals. Stock exchange and market information from third-party provid-ers can be seamlessly integrated. News, mar-ket information, virtual portfolios and lists are thereby available to clients.

Implementation of E-Banking

The general contractor offer of Finnova Services for the implementation of the new e-banking

solution at a fixed price with guaranteed milestones and deadlines means a ready-to-use imple-

mentation from one source. Whether the E-Banking application with or without Mobile Banking

and the PFM solution, we take care of the project planning, the detailed conceptual work includ-

ing documentation, tests and training, according to the requirements and wishes of the customer.

Ex ternal asset managers

(EAM)

100%

Business clie

nts

Investment clients

Reta

il clie

nts

FINNOVAE-BANKING

CLIENTS

29

30

Option S2: Finnova Mobile Banking

Option S10 & S11: Personal Finance Management (PFM Mobile & PFM Web)

Implementation of Contovista’s

Personal Finance Management

(PFM)

In addition to the purchase of our

newest generation e-banking ver-

sion and our Mobile Banking app,

Contovista’s Personal Finance

Management can also be acquired

in the same general contractor

mandate from Finnova Services.

We guarantee a streamlined

implementation project at a fixed

price, with fixed milestones and

deadlines – a threefold digital

competitive advantage.

Implementation of Mobile

Banking

The implementation of the Mobile

Banking app can be obtained as

a general contractor mandate

from Finnova Services. Provided

that the customer already has our

e-banking solution or is consider-

ing acquiring it, it is also possible

to acquire the Mobile Banking

functionality ready to use. In the

general contractor mandate, we

guarantee an implementation

project from one source at a fixed

price and with binding deadlines –

simply “smarter banking”.

Mobile BankingThe Finnova Mobile Banking app has been designed for all bank clients who wish to access their bank and asset information (account, custody account, portfolio) independently and at any time. Complete payment transaction and stock exchange functionalities are available. The app ena-bles the ordering of documents and ensures direct connection to a client advisor via Secure Mail. As a matter of course, a comfortable document scanner for inpayment slips is available. Additionally, functionalities of the personal finance assistant (PFM) are integrated for analysing the in-come and expenditure of mobile banking end users. The Mobile Banking app is available as a native app on Android and iOS.

31

Branch & ATMTellerThe Finnova Teller application enables banks to efficiently serve their cli-ents in the branch. Various client needs are covered here: Deposits and disbursements to/from an account in Swiss francs or foreign currencies, cash exchange in foreign currencies, precious metals, coins, collection of cheques, coupons, securities and cash deposit for subscribed medi-um-term notes.

Finnova enables the creation of client and bank documents including the barcode on a laser printer for the ultimate fully-automated archiving of documents via document scanning. Furthermore, different types of automated teller safes can be controlled.

The Teller application also contains auxiliary functions which enable control activities in the operation. In order to guarantee a maximum level of security, the most important business cases are also available in crit-ical situations thanks to the integrated offline operating mode.

ATMThe ATM application enables the operation of ATMs with the Finnova application. Processes carried out at the ATM run completely in the Fin-nova Banking Software – with the exception of the PIN check and the authorisation of third-party bank withdrawals. The application processes services for cards issued by the bank and third-party cards, like with-drawals, deposits and account transfers. At the same time, it is possible to query and monitor the ATMs. The cashing-up is also performed with the management functions. The application supports the withdrawal of foreign currencies and the management of so-called multi-accounts. In the process, a multitude of accounts can be assigned to a card and indi-vidual authorisations can be defined per account.

Independent Investment AdvisoryExternal asset managers work with Finnova directly or via the E-Banking application. For this purpose, they have various additional functions tai-lored to their needs at their disposal. The functionalities include, for ex-ample, the entry of aggregated stock exchange orders or the search for all managed clients who hold a certain security in their custody account.

Business BankingThe Finnova ZV application puts banks in a position to offer their de-manding business clients competitive payment transactions and cash management. The support of this important client segment is gaining in significance, in particular also in international competition. This includes the processing of electronically submitted payment files, client cash re-porting in line with market requirements, as well as the support of cli-ents with several bank accounts (multi-banking). The offer is completed by requirements-based business connectivity solutions for providing the electronic channels and interfaces to the bank. This comprises the connection of third-party ERP and business software solutions, as well as the support of current formats and standards, e.g. EBICS.

Option 25: CSV Interface for Files from Abacus

Option 72: Cash Exchange Machine

Option 105: Multi-Banking

Option 124: Submission of Payment Files in XML Format (CH)

Option 125: Client Cash Reporting in XML Format (CH)

Option 127: Cut-Off Times in Pay-ment Transactions

32

33

FINNOVA FRONT SUITEThe Finnova Front Suite has been developed for advisors and supports them in their overall daily sales activities.

With the role-based and process-controlled Advisor Work-bench, advisors maintain an overview of their portfolio and all information about their clients, can initiate advisory processes and perform these efficiently while being supported by the sys-tem. The basic Front Suite modules will be available in 2017 and will gradually be extended.

Depending on the banks’ requirements, the Finnova Front Suite can be extended as both the starting point and the focus of all important advisory and distribution processes – from part-ner and client management (client onboarding) to product man-agement, as well as entire advisory processes for investments, financing, pension provision, etc. The Front Suite supports the latest desktop UI technologies and thus enables unique user experiences in the interactive advisory discussions.

With the modularly structured Front Suite, the highly variable requirements of the banks for an advisory solution can be met efficiently. Via the Solution Suite, and with a corresponding ser-vice offer, Finnova additionally offers customised solutions for banks that would like to connect advisory and investment solu-tions popular on the market or supplement or replace managed processes of third-party providers.

34

Advisor WorkbenchAdvisors start their daily activity here. Depending on their role, all necessary information about clients, products and pending tasks is available to them at a glance. The respective advisory processes can be launched from the Advisor Workbench.

The Finnova Front Suite supports the advisor with effici-ently managed processes. The advisor can use these during client onboarding, when opening and modifying bank products, as well as when entering and changing payments and stock exchange orders.

Implementation of the Advisor

Workbench module in the general

contractor mandate

The Workplace module of the

Finnova Front Suite can be imple-

mented in the general contractor

mandate from one source with

Finnova Services. Advisory

solutions can then be additionally

integrated to adapt them to the

individual needs. On request,

Finnova Services takes over the

project planning, conception,

installation and configuration, as

well as testing and transition into

operation.

Advisory Apps

Advisor Workbench

CRM

FRONT SUITE

Finnova Front Suite on the starting block The development of the first Front Suite modules as part of the pilot project is progressing well. General availability is planned for autumn 2017. The Finnova Front Suite Basic Plus consists of a central Advisor Workbench with a 360° client perspective, a pending task dashboard as well as client and product opening processes for natural persons with nationality and domicile ‘Switzer-land’ (according to CDB16). The scope of the Front Suite is gradually being expanded further with additional functions and processes such as order processing (Payment Transactions and Stock Ex-change applications).

As part of the pilot project, the Finnova Front Suite is being extended with Swisscom’s eVoja advisory modules together with swissQuant’s ImpaQt plus for professional investment advisory. Complete connection via Business Services is planned in the medium term to bring about a well integrated, comprehensive advisory solution.

35

Implementation of advisory

solutions in the general contractor

mandate

Finnova Services offers the

integration of advisory solutions

like Swisscom’s eVoja in the Front

Suite in the general contractor

mandate. This minimises the com-

plexity and risk for the customer.

Depending on the customer’s

wishes, requirements analyses,

the realisation of individual

adjustments, conception, imple-

mentation, testing and project

management can be combined as

a service on an individual basis.

Advisory appsThrough the connection of partner solutions, such as Swiss-com’s eVoja advisory modules together with swissQuant’s Im-paQt plus for professional investment advisory or comparable third-party products, the Front Suite innovatively supports direct client advisory discussions through process management and illustration on the tablet. This gives rise to a special client expe-rience in investment, financing or pension provision advisory.

CRMWith the Customer Relationship Management (CRM) mod-ule, the Finnova Banking Software currently offers detailed information and structured evaluations in the Expert Suite. In future, some of these and further functionalities will also be directly available in the Advisor Workbench.

36

3737

38

39

The Management Suite is thus the complete instrument for bank and risk man-agement. It pools analyses and reports and in addition, its functionality covers the ever-increasing compliance requirements in the banking sector.

FINNOVA MANAGEMENT SUITEThe Finnova Management Suite addresses needs in the area of integrated bank management such as financing, risk management, compliance and legal reporting.

40

Implementation of net cash flow, profitability and overhead costs

Finnova Services offers support in the implementation of Finnova Control. Our specialists assist

customers during the implementation and organise the available large amounts of data in our

DWH framework according to their needs. Big data key figures are not empty marketing shells for

us, but rather specific tools to enable customers to make their business even more successful.

Financial Accounting

Finnova Control

Regulatory Reporting

Risk & Compliance

MANAGEMENT SUITE

Option 74: Finnova Control – Net Cash Flow

Financial AccountingThe balance sheet and profit and loss account are available daily online. For the balance sheet and profit and loss account, various evaluations can be created periodically (daily, monthly). Thanks to a daily cut-off concept, various balance sheet month-ends can be kept open in parallel. Using recurring events, the evaluations for the balance sheet and profit and loss account can be “subscribed” for the time of the definitive balance sheet month-end. In addition to the balance sheet and profit and loss account, a turnover balance sheet and an average balance sheet are available. The balance sheet and profit and loss account can be corrected manually. These changes are documented to make them auditable. Several balance sheet structures can be entered in parallel with accounts/items, some of which are contained only in one structure or in all balance sheet structures with the corresponding profit determination per balance sheet/profit and loss account structure.

Finnova ControlFinnova Control consists of the modules Net Cash Flow, Over-head Costs and Profitability.

The ‘Finnova Control – Net Cash Flow’ option calculates the liquidity-relevant inflows and outflows of business volume, client assets, client receivables and off-balance sheet items of a bank over a defined period. It provides information about whether the business volume has increased or decreased on both the assets and liabilities side of the balance sheet and where exactly the inflows and outflows occurred. It not only supports the bank in the fulfilment of regulatory requirements, but also delivers important key figures for strategic manage-ment to the bank management. The calculated figures can also be used for targeted personnel management.

As part of a pilot project, Finnova Services is currently de-veloping solutions for the consistent determination of over-head costs and profitability. On this basis, we offer interested banks customised services solutions for effective bank man-agement.

The Overhead Costs module maps the costs of a bank pro-portionally. The functionality provides information about where real costs have been incurred and who is responsible for the costs. By means of detailed postings from main and subsidi-ary ledgers, internal cost allocations and cost apportionment of overhead costs, the bank can distribute the incurred costs over the various organisational units and cost centres. The end result is cost transparency for the bank in the form of a cost distribution sheet and cost type/cost centre accounting.

Risk & ComplianceThe extensive risk management and simulation include the el-ements of Asset & Liability Management (ALM), own secu-rities management and liquidity management, as well as the loan portfolio for an entire bank.

Regarding risk control, Finnova currently draws on various third-party solutions via interfaces.

The compliance managers are informed promptly, and in consolidated and compressed form, about critical processes within the bank and have the possibility to observe progress in the detection and dissolving of processes that do not conform with compliance, as well as the effectiveness of the elimina-tion and prevention measures taken.

By comparing client relationships with entries in embargo, sanction and PEP lists, as well as by means of risk-based pro-filing, and peer group and link analyses, suspicious financial transactions and client behaviour are analysed and detected, and undesired and high-risk client relationships and money laundering activities are identified and prevented in time.

The Profitability module determines the key figures of the contribution margin accounting required for the statement of a bank’s profit or loss at client, product and organisational unit level. On the income side, both income from interest-bearing transactions (including interest margin calculation) and fees and commissions are taken into account. On the expenditure side, the corresponding interest and commission expenditure as well as the incurred costs are taken into account. This mod-ule is the basis of a multi-level contribution margin account-ing. Thanks to a high variability in the organisation of key fig-ures while taking into account the individuality of the bank, it can be optimally served with a tailor-made solution. With this module, the bank obtains the result of both a calculation of client and product profitability and a profit centre accounting.

.

Finnova Compliance Framework

The ‘Finnova Compliance Framework’ service package of Finnova Services shows where prob-

lems lie. Together with the customer, a tailor-made concept for the implementation of cleanup

jobs within the customer’s own client master data is developed and possible enrichment and

migration scenarios are checked. Using a detailed plan of measures, the identified optimisation

plans can be implemented transparently.

Compliance control also covers the detection and prevention of internal and external misuse and fraud by continuously ana-lysing relevant indicia for their compliance conformity and pre-senting them in compressed form.

The highest possible transparency, traceability and accu-racy of the investigations and reports through optimised detec-tion rates and minimised wrong detections are paramount here in order to guarantee smooth compliance processes within the bank. Consolidated and detailed reporting enables the man-agers responsible to get comprehensive information and to make optimised decisions in real time.

Regulatory ReportingThe Capital Adequacy Ordinance obliges the banks to provide regular reports on equity capital and risk diversification. Fin-nova offers the FINMA Reporting II application, also known under the short designation ERIKA II (from German ‘Eigenmit-tel-, Risiko- und Klumpen-Applikation’ = Equity, Risk and Con-centrations Application), for the automatic creation of these reports for the Swiss Financial Market Supervisory Authority (FINMA). As a fully integrated application, it offers the habitual user interface and makes optimum use of the technical infra-structure of the Finnova Banking Software. The output occurs on internal lists and on prescribed reporting forms.

Finnova draws on various solutions of third-party provid-ers via interfaces for the creation of statistics for the SNB and liquidity reporting for FINMA.

43

FINNOVA EXPERT SUITEThe Finnova Expert Suite is the workplace for the middle and back office as well as for our BPO partners. It is and remains the backbone of the Finnova Banking Software and comprises the known expert modules.

The modular structure of the Finnova Expert Suite covers all modules, from payment transactions, financing, investment and portfolio management to client and advisory modules. Accord-ingly, the master data storage is located in this central suite of the Finnova Banking Software.

Option 5: Extended client work-flow, PEP check and whitelist

Option 22: Extended Card Functions

Option 31: Fee Functions

44

Payments

Investment Management

Investment Operations

EXPERT SUITE

Financing

Tax

Clients & Products

ISO Payments

ISO 20022 is changing the world

of payment transactions. All

market players are affected. As

a leading provider of software

for financial institutions, Finnova

provides comprehensive support

to its customers with a set of

service packages, be it in the role

of financial institution when man-

aging the complexity along the

three dimensions system, bank

and client, or during the technical

implementation in its position as

application service provider for

financial institutions.

ZV Quality Check

With the ZV Quality Check of

Finnova Services, our consultants

screen the parameterisation of

the Finnova Banking Software

in the Payment Transactions

module. We conduct interviews

with the users in order to gain an

insight into their work process-

es. We create a comprehensive

report from these findings, which

assesses the quality of the param-

eterisation and contains optimi-

sation proposals to facilitate the

day-to-day work.

Finnova Services offering for ISO payments

PaymentsThe Finnova Payment Transactions (ZV) module is designed for efficiency and automation. It supports standards and procedures established in Switzerland and internationally (including SEPA), and the structured and efficient entry and processing of payment orders. As a matter of course, client and interbank payments are supported in the current XML format according to ISO 20022.

As a result of the optimal integration of electronic channels into the Finnova Payment Transactions module, optimal processing of client pay-ment orders can take place and electronic account statement information can be provided quickly and as needed.

Innovative market developments such as peer-to-peer payments or person-to-merchant payments (e.g. Paymit, Twint or WIR Pay) are seam-lessly integrated into the Finnova ZV application via the Finnova Payment Solution Adapter, and offer private or business clients a broad spectrum of payment options.

The payment channels for outgoing payments in interbank payment transactions are predefined on the basis of previous transactions and are reusable, i.e. it is a “learning” system. Thus, the Finnova ZV application allows banks to process their bulk business very efficiently.

If back office employees are required to intervene in the processing, they are supported by smart processes (automatic triggering or process-ing of returns, inquiries or SWIFT cancellation requests).

The banks’ requirements of scalable and cost-effective processing of payment transactions are paramount. Depending on the bank›s oper-ating model, the payment transactions application can either be an in-tegral part of the Finnova Banking Software or it supports the modular connection to a BPO provider.

Client

Bank

System

Technical development

Client

Application

Basis

Stocktaking ofmarket measures Business

Client processing

Ban

k/Cl

ient

Inte

rban

k

45

Processes can be adapted to bank-specific requirements. The predefined workflows guarantee the highest level of security and reproducibility.

In addition to the manual entry of payment orders, various ZV scanning systems are supported. Orders from the E-Bank-ing application enter directly into the Payment Transactions application without redundant storage. Standing orders are directly entered and managed in the Finnova ZV application. Both the bank and the client can edit standing orders in the E-Banking application.

In order to support banks in the fight against fraud, cus-tomers can check the originator profile before the execution of payment orders. In the case of incoming payments, the bank can choose from a broad set of criteria whether the credit en-try should be made immediately or not.

The future of payment transactionsThe Finnova Payment Transactions application supports banks in meeting the current requirements for efficiency and automation in the back office and the future challenges for the business model, which is constantly changing as a result of innovative market developments such as peer-to-peer payments. Pay-ment transactions of the future have an impact on both the business and op-erating models of banks.

Payment transactions – trends and innovationIn particular, the new mobile payments are worth mentioning here. Bank cli-ents do not have a problem with paying in principle, but rather are looking for added value. Clients will only change their payment habits and use their smartphones instead of cash at the checkout if a solution is simple, transpar-ent and secure. At the same time, competition is growing in this area as also non-banks and non-payment transaction providers – including smartphone hardware manufacturers, mobile operators and online stores – are part of the value-added chain.

Payment transactions – technologyNew technology means new solutions for which bank infrastructure is no longer necessary, or only partially necessary. Emerging technologies such as blockchain have the potential to completely redefine operating models. This means that regulatory frameworks will first need to be defined and adapted.

Payment transactions – automationOngoing standardisation of processes, harmonisation of formats, and digital-isation mean banks can focus on the parts of the value-added chain that set them apart from competitors. In future, it will be easier to outsource non-dif-ferentiating areas. This development is supported by emerging BPO providers.Rather than focusing only on traditional revenue criteria, banks are now also investing in payment transactions in order to set themselves apart from com-petitors and to retain clients.

With beneficiary matching, which can be extended to phonetic equality, the greatest possible security in the allocation and at the same time a high degree of automation are achieved. Naturally, it is possible to perform a check with regard to po-litically exposed persons and embargoed countries.

Processed payment orders are immediately posted, the notifications are created for the clients and the documents are stored in the electronic archive.

46

47

FinancingThe loan system is characterised by a high degree of flexibil-ity when mapping various loan constellations that can be fully processed, from the loan advisory and the opening of the loan order to the posting of capital and interest.

The Loans module enables the entry of all loan products such as loans, overdraft facility, Libor mortgage, Lombard loan, cash loan, leasing or surety bond. In addition, it assigns collateral, determines amortisations and allocates execution accounts as well as client-specific conditions (debit interest, credit commissions). Loan transactions are supported by pro-cedural organisation stages and by the periodic processing of interest, amortisations, fixed annuities (of loans, cash loans and leasing) and collateral.

The loan system contains the master data management of individual loans and credit lines as well as collateral in Swiss francs and foreign currencies. The application manages ac-count balances, custody accounts, portfolio collateral, guar-antees, insurances and all other collateral. Mortgage collateral is generated and updated from the Real Estate application.

All loan-relevant data is displayed in an overview image with drill-down functionality. The module allows the portfolio status with all loan-relevant data to be printed. The screens for the management of client information (income, assets, li-abilities, balance sheet ratios, taxes, debt enforcements, ex-cerpts from the commercial register) as well as the client contacts and pending tasks can be directly called. The entire credit management process is supported by the workflow.

The Finnova Banking Software offers the possibility of man-aging and administering different limits such as counterparty, nostro, credit or card limits. Changes are updated online and have a direct impact on the calculation of the available balance. Limits can be directly entered and automatically updated via the Loans application. The Limits module enables the defini-tion of simple and complex limits, for example if several ac-counts show an amount as the initial value. All Finnova ap-plications that provide current balances, like for the account query, take into account the fixed limits in the calculation of the available balance.

The regulation of competences within the bank is gov-erned via the Competences module: This module deter-mines for all other modules which employees are allowed to deal with and/or authorise which business cases up to what amount. With the definition of the competences, it is con-trolled who receives, further processes or concludes which pending tasks in the workflow.

The Collateral module manages all securities as collateral in the Finnova application, from real estate liens to portfolio, account and custody account balances through to securities. In addition, this module also comprises insurances, guaran-tees and other collateral.

In addition to comprehensive and detailed master data for real estate and mortgage notes, the Real Estate module al-lows the connection of digital images. With the Finnova Bank-ing Software, even complex ownership structures can be re-corded and all data for the detailed appraisal of a property is provided. Hedonic pricing models are also integrated. The module creates a variety of documents, like appraisal reports for the land register office. These and other documents to be created frequently, such as registration and deregistration in the register of mortgage holders, can be printed by means of a simple mouse click.

Option 1: Loan Advisory 2 and Extended Credit Control

Option 73: eGRIS Connection

Option 100: Credit Line

Option 132: Central Mortgage Bond Institution

48

Investment ManagementThe Portfolio Management System (PMS) module integrated into the Expert Suite optimally supports activities in discre-tionary asset management and advisory. In the PMS, alloca-tion structures (trees) adapted to bank-specific client strate-gies, which serve as a basis for the various strategies, tactics, benchmarks and model portfolios, can be determined in any desired depth. Customised investment proposals in advisory and efficient bulk processing in asset management are also offered.

The ‘Global Order’ functionality enables the periodic restructuring of mandates in a practical and efficient manner. Both dynamic and static investment models can be imple-mented. A global restructuring can take place, dependently or independently of model portfolios, for all investments in the portfolio, for individual segments or also only for individ-ual securities. Using the ‘Cash Management’ function, cash holdings for mandates can be managed separately from global restructuring processes. A seamless transition of the gener-ated stock exchange and foreign exchange orders for execu-tion into the downstream modules is guaranteed.

Bank- and client-specific investment guidelines and pref-erences can be easily maintained via the ‘Investment restric-tions’ function and monitored in the pre-trade restriction check for an individual investment proposal, or within a bulk restruc-turing in asset management. The periodic post-trade check of investment restrictions in investment controlling is efficiently supported by checklists. Violations are directly reported to the mailbox of the user responsible for further processing.

Option 61: Global Order

Option 66a: PMSplus Basis (without GIPS)

Option 66b: MSplus Basis (with GIPS) “Full version”

Option 70: Securities Compliance Functions

Option 104: PMS Reporting

Option 119: Cash Management

Option 141: Funds Breakdown in the PMS

In addition to self-occupied property (single family house, multi-family residence, condominium ownership), the appli-cation also enables the management of other properties such as industrial and commercial properties, hotels, restaurants, sports facilities, etc. Thanks to the versatile connection pos-sibilities, even complex residential developments can be fully mapped, for example, multi-family residences with condomin-ium ownership and co-ownership of the underground car park. The module enables individual levels of detailing: the more precise the data, the more comprehensive the appraisal re-port. Mortgage notes that have been entered into the system are handled as collateral in the Loans application.

As an interface, the Mortgage Bond Bank module ena-bles the digital reporting of pledged properties such as real estate or real estate compounds to the mortgage bond bank. A mortgage bond property is only transmitted if all required fields are filled in completely. The corresponding information can be parameterised by the bank according to its needs. The individual data has to be entered in the master applications Real Estate, Loans and Client Master and are transferred into the Mortgage Bond Bank module using the ‘Update’ function. Data that cannot be maintained in the master applications is updated in the Mortgage Bond Bank module.

49

50

Comprehensive configurable ad hoc analyses for asset allo-cation, asset development, performance calculation (TWR, MWR, before/after taxes/fees, etc.) and performance attri-bution facilitate the day-to-day business of client advisors, asset managers and portfolio controlling. A variety of key fig-ures (Sharpe ratio, Treynor ratio, Jensen’s alpha, information ratio, VaR, volatility, PRC, etc.) are available for risk monitoring.

The modular structure of the reporting enables the com-pilation and preparation of a targeted investment reporting, which allows not only the inclusion of ex-custody portfolios, but also a consolidation across all clients.

Furthermore, the PMS includes the configuration, man-agement and calculation of composites according to the spec-ifications of the Global Investment Performance Standards (GIPS). The periodic certification check is supported with de-tailed control reports.

FXLinX: Automation of foreign exchange tradingIn order to offer the Finnova banks even more flexibility and efficiency in for-eign exchange trading, Finnova is implementing a direct connection to the trad-ing partner via the FX FIX interface. This way, the Finnova bank can individu-ally control its risk tolerance and the degree of automation. Costs and manual effort can be reduced and potential sources of error can be eliminated as a result of the automation. Thanks to the FIX interface, the bank also benefits from an attractive quotation as no third-party providers (e.g. FX brokers) are involved.

In the case of explicit spot and forward foreign exchange transactions, as well as in the case of implicit transactions from Stock Exchange, Payment Transactions, E-Banking or Corporate Actions, trading can be controlled accord-ing to individual logic.