Electronic banking dup

32

PREFACE 1 Transmission of Traditional Banking System to Digital Banking System Electronic banking (e-banking), one of the major elements of e-commerce, does not mean only 24/7-hours access to cash through an Automated Teller Machine (ATM) or Direct Deposit of pay checks into checking or savings accounts as many consumers may think Electronic banking (e-banking) involves many different types of transactions. 1 “E-banking” refers to systems that enable bank customers to access accounts and general information on bank products and services through a personal computer (PC) or other intelligent device which exchange electronic signals between financial institution, rather than exchange of cash, cherubs or other negotiable instruments. Its products and services can include wholesale products for corporate customers as well as retail and fiduciary products for consumers. The focuses of this discussion are as follows: Importance e-banking for the banks Prospects of e-banking Technological status of e-banking for the banks Challenges of ebanking Responses of the clients to e-banking services Economic, and social influences to e-banking Environmental influences to e-banking With the expansion of global Information and Communication Technology (ICT) infrastructure and the internet, e-banking is set to play a pivotal role in the national economic development of any country. But appropriate software, technology, infrastructure, skilled manpower and cyber law are crucial for the implementation of e-banking in the country. It reveals that E-banking mostly depends on IT. Now IT is a subject of widespread interest in Bangladesh. The government has declared IT as a thrust sector. 1 24/7 refers to continuous working not from 9 pm to 7 am but all the time.

Transcript of Electronic banking dup

PREFACE

1

Transmission of Traditional Banking System to Digital Banking System

Electronic banking (e-banking), one of the major elements ofe-commerce, does not mean only 24/7-hours access to cashthrough an Automated Teller Machine (ATM) or Direct Deposit ofpay checks into checking or savings accounts as many consumersmay think Electronic banking (e-banking) involves manydifferent types of transactions.1

“E-banking” refers to systems that enable bank customersto access accounts and general information on bank products andservices through a personal computer (PC) or otherintelligent device which exchange electronic signals betweenfinancial institution, rather than exchange of cash, cherubs orother negotiable instruments. Its products and services caninclude wholesale products for corporate customers as well asretail and fiduciary products for consumers. The focuses ofthis discussion are as follows:

Importance e-banking for the banksProspects of e-bankingTechnological status of e-banking for the banksChallenges of ebankingResponses of the clients to e-banking servicesEconomic, and social influences to e-bankingEnvironmental influences to e-banking

With the expansion of global Information and CommunicationTechnology (ICT) infrastructure and the internet, e-banking isset to play a pivotal role in the national economic developmentof any country. But appropriate software, technology,infrastructure, skilled manpower and cyber law are crucial forthe implementation of e-banking in the country. It revealsthat E-banking mostly depends on IT. Now IT is a subject ofwidespread interest in Bangladesh. The government has declaredIT as a thrust sector.

1 24/7 refers to continuous working not from 9 pm to 7 am but all the time.

2

Transmission of Traditional Banking System to Digital Banking System

This report, in addition, reviewed the issues associated withvarious forms of e-bank. It study recommends that acomprehensive E-banking will be possible only when there will be political commitment with better ITinfrastructure, internal network, country domain and, aboveall, a high speed fiber optic link to the informationsuperhighway.

Local and foreign private banks operating in Bangladesh arethe pioneers to introduce the electronic banking facilities inthe country. Among the indigenous banks, the private banks areahead of the public banks. The e-banking services provided bythe banks in Bangladesh could be divided in three groups:

1. ATM Services, 2. Internet Banking (iBanking), and 3. SMS Banking.

CitiDirect®: To gain more control over ones cash positions,one needs easy access to accounts and information in realtime. One will need the convenience of local banking and theglobal solutions of an industry leader. The solution isCitiDirect® EBanking. The motto of CitiDirect® is “Money isn’teverything but it can be everywhere”. The availablefacilities are:

Online Direct Debit Transaction Process Information Reporting Real-time information reporting for more effective

cash managementDelivered with the highest level of security Easy-to-use application

PRESENT STATUS OF EBANKING IN BANGLADESH

3

Transmission of Traditional Banking System to Digital Banking System

World Link through CitiDirect Comprehensive payment transaction solution Flexible, streamlined functionality Reliability, speed and information Payments through CitiDirect A comprehensive payments solution globally and

locally Simplified, secure transaction management Timely, accurate information E-mail and Wireless Banking Alerts by CitiDirect

The following banks especially are plying vital role in termsof promoting embanking in Bangladesh through relevantactivities.

DUTCH-BANGLA BANK LIMITED (DBBL)

Provides mobile banking facilities;Fast Track During the Q1 of 2010, Dutch Bangla Bank Ltd.introduced "Fast Track" in the country. Fast Track isfirst of its kind in the country that is like a minibranch. Along with the generic ATM withdrawal service, itlets the customer deposit small amounts of money to DBBLaccount. The limit is currently 20,000 BDT. Moreover, theFast Track also provides account opening service and loaninformation. As on 10 October 2010, DBBL has installed 50numbers of Fast Tracks in Dhaka, Chittagong and Sylhetcities.Internet Payment On 3 June 2010, Dutch Bangla Bank Ltd.announced to allow internet payments system. Usingtheir Internet Payment Gateway merchants will be able tocharge their customers' Visa, Masters, DBBL Nexus andMaestro cards. This is going to be revolutionizing the[e-commerce] in Bangladesh.

4

Transmission of Traditional Banking System to Digital Banking System

Facilitates Any Visa/MasterCard cardholder (local oroverseas) to use their cards to pay at a number of e-Merchants against their purchase of goods. They can payDESCO electricity bills. Working with airlines, railways, utility companies,educational institutions, and stock exchanges forfacilitating purchase of tickets, payment of bills/feesand IPO subscription through the Internet PaymentGateway. It is also working to make an interface withPayPal.The first bank in Bangladesh to introduce ATM and e-banking in 2003; Has adopted the same exact automation solution used byinternational banking giants.2 Provides Clients with unlimited access to banking fromany DBBL branch, ATM and Point of Sale (POS). Made clients’ ATM access to all DBBL is unlimited andfree of cost. Has the largest ATM network in Bangladesh which gives itsclients full access to 'anytime anywhere' banking Withmore than 900 ATMs nationwide DBBL. Provides facility all international and many local banksto use the ATM network of DBBL for their clients. Primary license holder for both VISA and MasterCard.Has an off-site Data Recovery Site (DRS) which ensuresthat customer records are safe, backed-up, and up to datein the event of a major catastrophe at the Electronic-Banking Division headquarters Has introduced mobile and SMS banking Since 2004Has established drawing arrangement network with bankslocated in the important countries of the world namely inthe United Arab Emirates, State of Kuwait, State ofQatar, State of Bahrain, Italy, Canada and USA.Facilitates Bangladeshi Wage Earners can send and receivemoney quickly from over 225,000 Western Union Agentlocated in 197 countries and territories worldwide only

2 DBBL Annual Report, 2010

5

Transmission of Traditional Banking System to Digital Banking System

by visiting any branches of Dutch-Bangla Bank Limited inBangladeshHas set up a representation agreement with Western UnionFinancial Services Inc, USA, which is a reliableinternational money transfer company. Offers banking facilities through a wide range of mobilephones. Facilitates Customer using HTML browser has access to theinternet banking facilities of DBBL.

PREMIER BANK LTD.

Has set up Wide Area Network using Radio, Fiber-Optics &other communication systems to provide branch banking toits customers.3

Facilitates customer of one branch to deposit andwithdraw money at any of the branches. Includes All Branches in the Wide Area Network. So, noTT/DD or cash carrying is necessary. Has been giving SMS Banking Service since 2006. Provides customers information about banking transactionsand inquiries through SMS Banking. Facilitates customers to check their balance, stop acheque payment, or get statements. provides the customers with real time account informationby using mobile phones and instruction capabilities fromthe mobile phones at ‘anywhere, anytime, anyhow’ throughSMS Banking. Provides service round the clock seven days a week. Provides SMS banking service free for customers.

PRIME BANK LTD.

3 Premier Bank Annual Report, 2010

6

Transmission of Traditional Banking System to Digital Banking System

Provides Internet Banking with a secure connection of theclient’s access to the accounts 24 hours a day, 7 days aweek from any Internet connection.4. Provides the opportunity to verify account balances,transfer funds, and pay loans, every time when thecustomers log on to their on-line account. Facilitates customers to monitor account activity, getreal-time account balance, and transfer funds atconvenience. Requires no special software; it is available through itswebsite. Account access isn't limited to a specific PC withspecial software installed and data stored. Facilitates customers to access to the Internet, accessto their Prime bank accounts anywhere. Provides Internet Banking to the customers to downloadtheir latest on-line account information. Gives opportunity of bill paying for its customersthrough Prime bank's Bill Payer program.

ISLAMI BANK BANGLADESH LIMITED (IBBL)

Provides different services of e-banking to itscustomers.5 Has introduced ATM, SMS banking and Internet banking. ForSMS banking registration is required. Facilitates customers to get different services. SMS andiBanking facilities, however, are applicable only foronline branches. The contract could be terminated byeither side giving 30 days’ prior notice.6

BANK ASIA LTD.

4 Prime Bank Annual Report, 20105 Islami Bank Annual Report, 20106 The Internet Based Banking of IBBL is called iBanking whichhas been introduced since 2009.

7

Transmission of Traditional Banking System to Digital Banking System

Has centralized Database with online ATM, SMS andInternet query service.Has hundreds of ATMs as a member of ETN along witheleven other banks.Maintains its competitiveness by leveraging on itsEBanking Software and modern IT infrastructure Introduce innovative products like SMS banking, and underthe ATM Network the Stellar EBanking software enablesdirect linking of a client’s account, withoutthe requirement for a separate account.

BRAC BANK LTD.

Deployed a layer of security system for itsInternet Banking. These measures extend from dataencryption to firewalls. BRAC Bank uses the mostadvanced commercially available Secure Socket Layer(SSL) encryption technology to ensure that theinformation exchange between the customer’s Computerand BRACBank.com over the internet is secure andcannot be accessed by any third party. SSL has beenuniversally accepted on the World Wide Web forauthenticated and encrypted communication betweencustomers’ computers and servers. bKash Limited, a joint venture between BRAC Bank Ltd.,Bangladesh, and Money in Motion LLC, USA is ensuringaccess to a broader range of financial services for thepeople of Bangladesh is the ultimate objective of bKash. Has a special focus to serve the low income people of thecountry and promote sustainable micro-savings to achievebroader financial inclusion by providing financialservices that are convenient, affordable and reliable. Working both as an extension of BRAC Bank and as a full-scale mobile phone-based payment switch. This will highlybenefit the country as 83% of the population lives under$2 a day and access to finance can help in improving

E- Banking products and services

8

Transmission of Traditional Banking System to Digital Banking System

their economicsituation.

Less than 15% of Bangladeshis are connected to the formalfinancial system whereas 44% of total population ishaving mobile phones. Providing financial services usingthis mean can make the service more accessible and costeffective for the vast population of Bangladesh.Provides 24-hours access to the key financial informationof your account.Facilitates access of account's current information likebalance, last few transactions and a range of otherfinancial information by typing a pre-defined key letter(Like 'A' for Account Balance and 'T' for last fewTransactions).

HSBC LTD.

Enables a person to receive credit of all the cashor cheque deposits along with inward remittanceand make all local payments Provide access to the wide range of services forthe business requirements. With Easy Pay Machines both HSBC and Non-HSBC customerscan make deposits and pay their utility bills, credit cardpayments and etc.

9

Transmission of Traditional Banking System to Digital Banking System

E-Banking products and services can include wholesaleproducts for corporate customers as well as retail and fiduciaryproducts for individual customers. Ultimately, the products and services obtainedthrough internet banking may mirror products and services offered throughother bank delivery channels. A brief description of retail and wholesaleproducts and services is given below:

Debit Card Credit Card EFT (Electronic FundTransfer) Check Truncation Home Banking Retail Automated Clearing House Service Wire Transfer Corporate Automated Clearing House etc. Core BankingCluster Banking

Mobile BankingSMS BankingInternet BankingVarious CardsATM Shared (VISA/MASTER)ATM own (VISA/MASTER)SWIFTPC BankingPOS TerminalBanking KIOSKOffline Branch Computerization

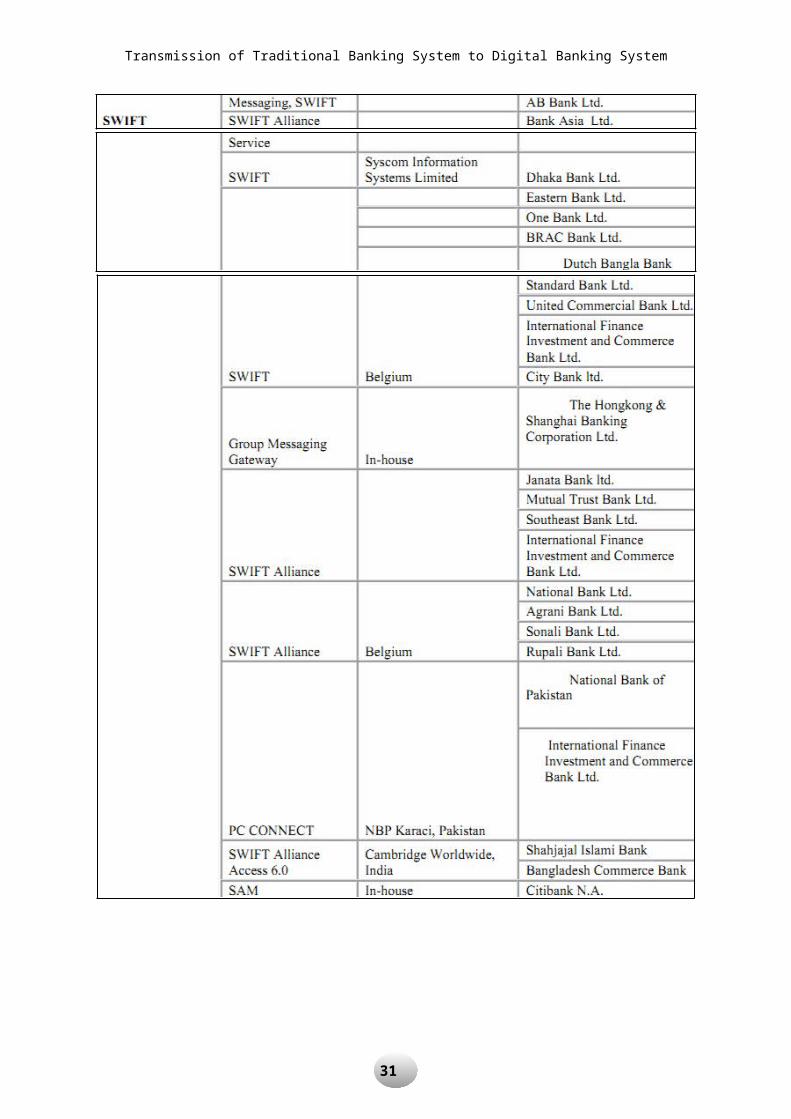

Detail of the field survey regarding software uses’, vendor’sname and services are given in the appendix in Table: A.

Problems & Challenges of

Ebanking

10

Transmission of Traditional Banking System to Digital Banking System

Numerous factors including competitive cost,customer service, and demographic considerations are affecting banks to evaluatetheir technology and assess their electronic commerce and Internet bankingstrategies. Today customers can apply for loan, verify theiraccount information, financial transactions etc. round-the-clock, even on weekends, through the electronic banking.Bangladesh is in the elementary stage of E-banking wherethe developed countries are in the stage of ‘Virtual banks’(No man Banks) that have no physical offices in thetraditional sense. Internet can be seen as a truly globalphenomenon that has made time & distance irrelevant tomany transactions. But Bangladeshi companies, organizationsare facing problem to start full swing ebanking due to

Submarine cable with slow bandwidth Bangladesh has beenconnected to worldwide Internet Super High Way from 2006through an undersea submarine cable. But this single submarinecable frequently faces disruption resulting in slow bandwidth.

High cost: Under the private initiative, Internet wasstarted in 1996 by ISN in Bangladesh. ISN is the first ISPoperator in this country. Still now all the Internet serviceproviders have the server in abroad, for which they are facingcompetitive disadvantage, as cost remains high.

11

Transmission of Traditional Banking System to Digital Banking System

Slow motion in networking: Network is a mode ofcommunications with the computers. And According to a reportpublished in The Daily Star (4th April, 2010) Bangladeshranked 118th in the global Network Readiness Index in 2009-10up from 130th a year ago, showing an upward trend in theinformation and communication technology sector whereas inSouth Asia, India ranked 43rd, Sri Lanka 72nd, Pakistan 87thand Nepal 124th in the 'Global Information Technology Report2009-2010' released by The World Economic Forum (WEF) on 3rdApril, 2010.

Low density in developed services of mobile: Again Telephonedensity is awfully little in Bangladesh. It is far much lessin comparison with other developed nations of the world aswell as neighboring countries. It is depicted that MobilePhones (millions) are 36.4, Fixed Lines (PSTN) (millions) are3.4 Total telecom users (millions) are 47.6, Teledensity (%)is 36.8 in the year.

Centralization problem: Apart from some educationalinstitutes outside Dhaka, observation finds that most of theLAN setups are Dhaka centric.

Unwillingness of the respected parties: BangladeshTelecommunication Regulatory Commission (BTRC) is not playingdue role in the development process of communication sector.

Underdeveloped infrastructure: Outside Dhaka, at present afew computer network infrastructures have been developed sofar. Infrastructural problems are creating less scope tosuccessfully implement e-banking.

Security problem

Lack of digital accessible personnel

12

Transmission of Traditional Banking System to Digital Banking System

Limited time period: At present weekly bank holiday inBangladesh is in Friday and Saturday where as in rest of theworld it is in Sunday. As such Bangladesh has only 4 bankingdays for foreign exchange transactions in preliminary stage e-banking facilities

Banks’ limited ebanking services: At present the banks inBangladesh are using the limited electronic banking services.It is expected that bank can attain more profit and offerbetter services to its customers by, introducing on linebanking facilities. They provide ATM, Debit Card, Credit Card,Home Banking, Internet Banking, Phone Banking, on line bankingetc. services.

Most of the existing banking system in the country outsideDhaka and Chittagong city is manual (paper based) that’s whyis awkward, slow and error-prone. It, in one hand, fails tomeet the customers’ demand and, on the other hand, it causessome significant losses both for the banking authority andtraders.

The lack of communication channel and technological andtechnical infrastructure support may be seen as the secondcrucial challenges of e-banking in Bangladesh. It is notenough that there are enough communication channels, but theymust be efficient, competitive, competent, cost effective andsupportive to the services. In the millennium of ICT everynation has to think global, so worldwide efficient networkingand WAP have to be ensured.

The success of the e-banking depends on the acceptance ofthe services by the clients of banks. So the users of theservice must be made aware of it. First of all the servicesmust cost effective and financially genuinely attractive tothe clients. The technology and the services must be cheap,user-friendliness, easy to navigate, and simple to use.

Initiatives Taken by Government & Other

Bodies

13

Transmission of Traditional Banking System to Digital Banking System

The Government of Bangladesh has taken some importantinitiatives to develop our IT sector. Still we arewaiting to see a fruitful change in our InformationTechnology. However, some remarkable steps of government arehighlighted for information.

Bangladesh Bank (BB) is going to introduce a unique ATMsystem from where customer of any bank can make theirtransactions. For this BB will provide unique cards (debitcard & credit card) to all. Along with these cardsMasterCard, VISA, American express can be used by this ATMsystem. Bangladesh bank is trying to implement automatedclearinghouse (Magnetic Ink Character Recognizer) MICRprocedure. IT has been declared as a thrust sector. Quick implementations of the recommendations of JRC report(a high powered committee for software export).Waiving all taxes and duties from import of computerhardware and software. Hundred percent remittances of profit and capital gainsfor foreign investors without any approval. BTTB's implementation of Digital Data Network (DDN)service. Decision to link Bangladesh to global highway throughsubmarine cable link by next two years. National Information and Communication Technology (ICT)Policy has been approved in 2002. An independent regulatory body, BangladeshTelecommunication Regulatory Commission (BTRC) has beenestablished, functioning since 2002. Recently started the establishment of ICT Park to boostup the country’s ICT activities. The govt. is liberalizing telecom sector in phases, with

Customers’Response

14

Transmission of Traditional Banking System to Digital Banking System

increased participation ofprivate sector.Copyright Act 2000 named Intellectual Property Rights(IPR) Law related to ICT is in the process offinalization and is in the process of enactment bythe Parliament. Identify the operational process and the performance ofE-banking in Bangladesh in comparison to other developed nations.Finally, to identifying the macro level benefits ofelectronic banking operations in Bangladesh.

ITC possesses necessary tools to process transactions forbanks and retailers. It has the largest independent network ofmore than thousands of ATMs in the country.

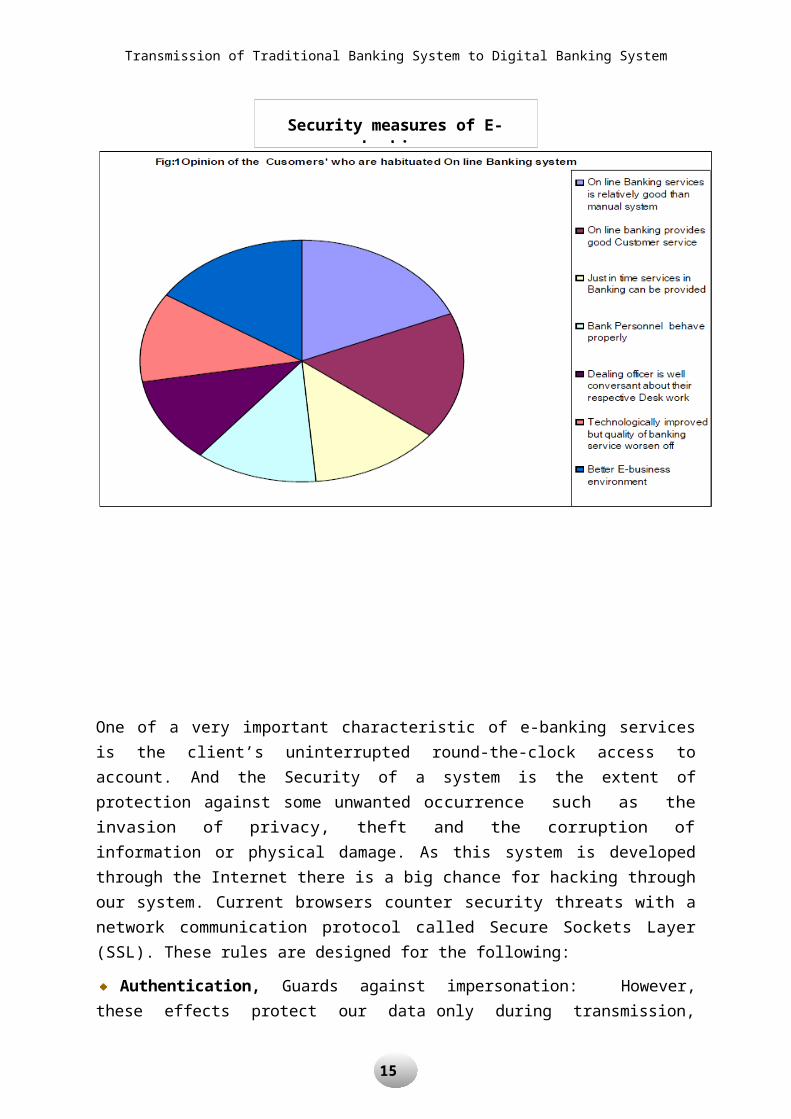

Out of five hundred customers’ who have been using on linebanking system, following results have been gathered from thequestionnaire through using snowball sampling technique.

Table: 1 Customers’ Response who have been using on linebanking system (% of

Respondents who expressed “Yes” comment)

Diagrammatic representation of responses of various services

Security measures of E-banking

15

Transmission of Traditional Banking System to Digital Banking System

One of a very important characteristic of e-banking servicesis the client’s uninterrupted round-the-clock access toaccount. And the Security of a system is the extent ofprotection against some unwanted occurrence such as theinvasion of privacy, theft and the corruption ofinformation or physical damage. As this system is developedthrough the Internet there is a big chance for hacking throughour system. Current browsers counter security threats with anetwork communication protocol called Secure Sockets Layer(SSL). These rules are designed for the following:

Authentication, Guards against impersonation: However,these effects protect our data only during transmission,

16

Transmission of Traditional Banking System to Digital Banking System

That is, network security protocols do not protect ourdata before we send it. Just as we trust merchants not toshare our credit card information, we must trust the recipients of our on-line datanot to mishandle it. In ebanking for the authentication of thecustomers different technologies have been used, which include

Passwords, PIN, Public key infrastructure (PKI) and Physical devices such as cards and biometric

identifications i.e. finger prints. Encryption: Encryption is the scrambling of information for

transmission back and forth between two points. When we sendout a letter to our friend, we communicate in a language thatboth of us understand. Since, our language is understood bythousands of other people also, if someone else gets hold ofour letter, he will not have any problem in understanding itscontents.

Decryption: Encryption refers to the encoding of informationthat a user sends over the Internet. If an unauthorized partytries to read that, it would be impossible for them to readit. Decryption is reverse technique of Encryption. Afterreceiving encrypted data it is converted to original data.

Secure Socket Layer: Secure Socket Layer (SSL) provides

sound privacy protection by encrypting the channel of

communication between server and the customer. Using a

mathematical formula, SSL puts the information into a

complex code. Even if information is intercepted, that would

be extremely difficult to read. So SSL’s only role is to

encrypt or decrypt message. Conclusion

17

Transmission of Traditional Banking System to Digital Banking System

Throughout the discussion on electronic banking in Bangladeshit is shown that, though Bangladesh is a developing countryhaving wide spread poverty and illiteracy, according to theview of the bank officials as in the most developed countriesof the world e-banking is equally important and relevant forBangladesh. Instead of the fact that ICT is one the fastestgrowing and developing sectors, the banks in Bangladeshprovide big weight to the prospect of the e-banking. Thetechnology of e-banking is developing in its mature form. Itis available and transferable in the banking sector of thecountry. Though experts are not very much easy to get andcostly, the banks are convinced that it will not be a majorhindrance for the expansion of the Ebanking in size and depth.Successful introduction of the e-banking will expedite theeconomic and social progress of the country. Governmentshould, therefore, establish or facilitate the establishmentof the required educational institution and favorable legaland environmental framework for the e-banking. In brief thestudy leads to conclude that in view of the technologytransfer, the world could not be divided according to thedevelopment status of developed and developing countries. Juston the contrary, modernization of the economy through transferand adaptation even of the most developed technology helpultimately expediting the economic progress and removing thedevelopment gap between developed and under developedcountries.

WAP is very important for the viable introduction e-banking.So, steps must be undertaken to introduce, develop andextend the WAP.National as well as the international communication must beextended.

Suggestions for Introducing ElectronicBanking in Bangladesh

18

Transmission of Traditional Banking System to Digital Banking System

e-banking technology is mature, dependable, available andviable, so arrangement must be made for the introduction ofthe latest InTechnology.The distribution channels of e-banking must be sufficient,technologically sound and up-to-date.e-banking service must be convenient, uncomplicated, quick,easy available and user-friendly.e-banking experts are available, however with the growingneeds more experts must be there. So, respective educationand training institutes must be established following thegrowing needs of the market.Clients are aware of e-banking services; they do not resistthe introduction of e-banking. However, it would not harm ifcampaign is set to popularize the e-banking.E-banking service must be made cheap.Career path of hardware and software engineers should beproperly designed. Otherwise professionals will be de-motivated and they won’t work with job satisfaction.Market size seems to be important for e-banking. However, itmust not be very big for the success of the e-banking. Itseems to be modern art of banking.Under development is not detrimental to Ebanking. Certainly,speedy economic development would accelerate theintroduction-banking.Unemployment is also very much detrimental toe-banking.Naturally, enhancing literacy rate would create moreenabling environment for Ebanking.Poverty and illiteracy seem to play no detrimental role fore-banking. It hints that technology accepts no limitation.It may be so that just modern technology is essential toovercome the poverty and illiteracy.Piracy and fraudulent are no threat for Ebanking. Governmentand banks must take effective preemptive measures againstpiracy and fraudulent.No rhetoric but effective, sincere and practical effortsfrom the side of the government are expected for successfuland timely introduction of e-banking.

19

Transmission of Traditional Banking System to Digital Banking System

Government should create a congenial environment for thissector, and provide adequate training and technologicalsupport to develop the manpower.Banks should have their own Strategic plans for-banking.There should be career design for the experts in thissector.Banks should have adequate research and technologicalbackground in this regard.Banks should try to promote awareness of the clients aboutthe e-banking.Bank should charge normal profit to enlarge the market sizeof the electronic banking products.Digital Bangladesh may be activated by 2021 to develop theeconomy of Bangladesh. Successful team building with acoherent manner for developing human ware, hardware,software and web ware are required to increase e-bankingprocess in a systematic way. In Bangladesh, on line banking systems are yet at a take offstage. The Clearing House operation in Bangladesh should befully automated system. Banks and business organizationsespecially corporate houses should have adequate research,skilled manpower and technology driven strategies in thisregard.Initiatives to develop integrated e – banking softwarethrough in house built may be taken. Preference should begiven by the bank authority to use local software overforeign software. Common gateway is required so thatinterbank transactions can be feasible. Bank can chargenormal profit to enlarge the market size on the on linebanking products. Banks should have their own strategicplans to implement on line banking system. Creatingawareness and consciousness among the clients of the banksare also required.The country needs to develop e-business with the help of ICTfacilities. ICT application and development of software arevery much dependent on the quality of the workforce, andsupportive infrastructure and environment. Upzilla level may

20

Transmission of Traditional Banking System to Digital Banking System

be considered as the base unit which may be connected withdistrict and then connectivity with the capital of thecountry can be done. However, more stress should be given onwire free connectivity for which priority should be given onWIMAX technology.Public and private participation (PPP) for e-business shouldbe encouraged for economic development. Spread of on linebanking is a very good initiative. But it is not onlysufficient. Business sector as a whole should be focused onusing E-business. E-business should be used both for agricultural sector andindustrial sector. Equal importance should be given so thatdomestic trade and international trade can be effective.Distortion from the market should be driven out andinformation should be passes systematically.E-business can help to improve total quality management.This can also ensure quality assurance of the businesssector. As such business policy formulation and strategiesare required and this should be properly implemented. Quality maintenance of local software should be arranged.Initiatives should be taken to set up hardware industry sothat computer and computer accessories can be prepared inthe country and easily purchasable for the lower and lowermiddle class people. More high-speed fiber optical data communicationinfrastructures should be well established for speedy datacommunication for domestic and global high speedcommunication system. This will help to attain better e-business including on line banking system. BTRC as a regulatory body should work with long term vision,mission and fulfillment of goal oriented strategies. They should work as a facilitator rather not creating hindrance. VOIP should be legalized after examining and finalizing proper rules and regulations in the country

21

Transmission of Traditional Banking System to Digital Banking System

22

Transmission of Traditional Banking System to Digital Banking System

Index of services given by banks

23

Transmission of Traditional Banking System to Digital Banking System

24

Transmission of Traditional Banking System to Digital Banking System

25

Transmission of Traditional Banking System to Digital Banking System

26

Transmission of Traditional Banking System to Digital Banking System

27

Transmission of Traditional Banking System to Digital Banking System

28

Transmission of Traditional Banking System to Digital Banking System

29

Transmission of Traditional Banking System to Digital Banking System

30

Transmission of Traditional Banking System to Digital Banking System

31

Transmission of Traditional Banking System to Digital Banking System

32

Transmission of Traditional Banking System to Digital Banking System