HSBC Private Banking

13

Word count: 3104 ABP 4094 INVESTMENT & PRIVATE BANKING

Transcript of HSBC Private Banking

Word count: 3104

ABP 4094

INVESTMENT & PRIVATE BANKING

1

INDUSTRY CHALLENGES

AND DEVELOPMENTS

MAIN FEATURES OF THE MARKET

Private banking as one of the most profitable sections in financial services industry has been attractive over

decades. That is due to the fact that private banks have solid asset and profitability growth opportunities with

sufficient liquidity as well as relatively low capital requirements. However, since 2008, the crises have triggered a

sequence of challenges due to the upsurge of correlation of volatility in capital markets, low interest rates as well

as the increasing scope of regulation in the US, Europe and other regions. These changes imply the great

difficulties for most private banks worldwide to gain sustainable profitability (McKinsey&Co, 2013). In 2012, a

fourth consecutive year after the financial crisis, private banks all over the world with different business models

have come across substantial challenges. The industry is further constrained by decline in the amount of

transactions made during the year and a rise in cash holding as well as squeezes on margins.

Although positive market movements have been attracting growth in total assets, the industry’s top line revenue

continued being restrained (McKinsey&Co, 2013). However, investors have learnt lessons from the crises and are

becoming more realistic and cautious about risks and leverage. Trust issue in financial services industry is

becoming increasingly concerning. At the meanwhile, clients’ needs have become more complex related to the

more unpredictable markets as well as the growing expectations of transparency. This has caused the rapidly

increased cost of obtaining business. In the meantime, the increase is driven by regulatory compliance with

continually rising personnel costs.

Furthermore, the dynamic distribution of onshore and offshore wealth promotes the complexity of developing

franchises (A.T. Kearney&Newtone Associates, 2012). An increasing number of governments are setting up

regulations to control transfer of funds between countries despite of some legitimate activities. The changes in

regulations put even more pressures on the private banking business operating in those countries, but there are

still some evident exceptions for those big global private banks such as HSBC, UBS and Credit Suisse. However,

their sources of capital have been suffering negative impacts.

However, the recent developments in the marketplace including business structure and scope, breadth and

quality of products and specialists’ ability to service the needs from clients, coupled with political stability and

increasing numbers of HNWIs, are gradually loosening these constraints from economy and regulatory, providing

banks with fresh opportunities catering to clients worldwide and seeking new avenues of growth.

2

RELEVANT DEVELOPMENT IN PRIVATE BANKING

Regardless of where the operations are around the world, private banks still face similar needs emanating from a

certain number of client but in an increasingly complicated operating environment. According to McKinsey’s report

(2013), there are numerous recent developments reshaping the private banking industry’s future.

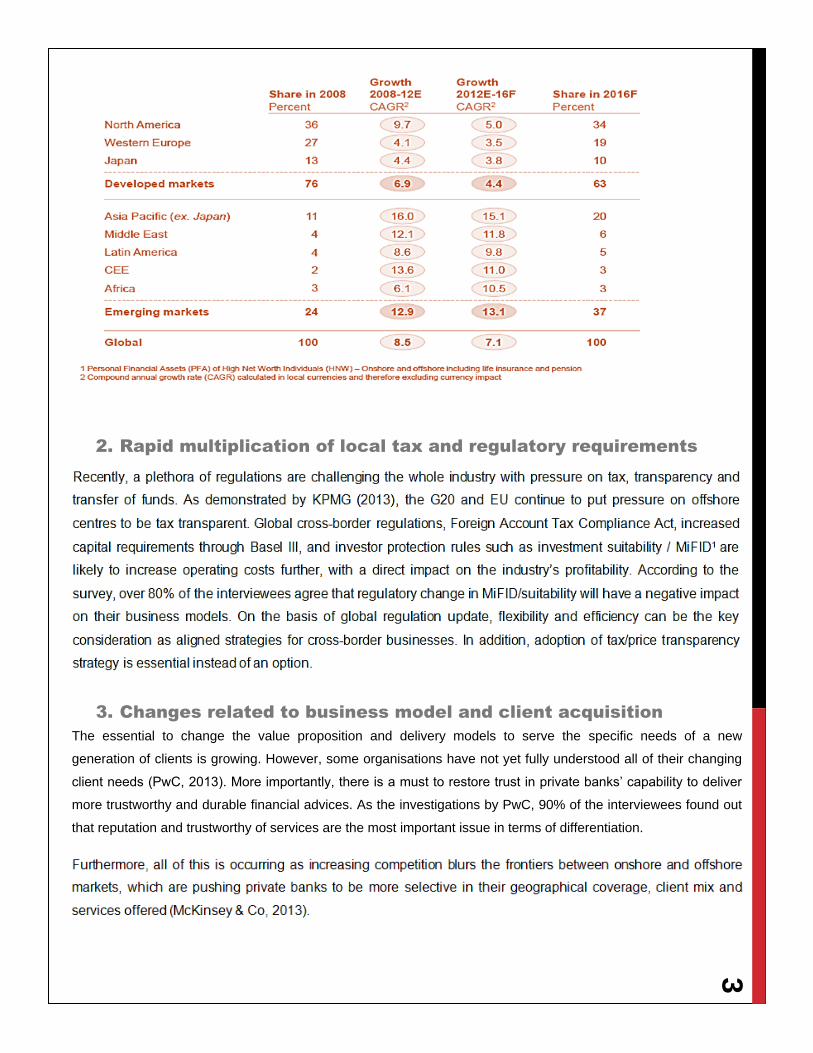

1. Millionaires prosper & growth shift of global profit pools

It is forecasted that total global private banking profit will have a 10% annual growth over next four years, and

expects to exceed $70billion by 2016 (McKinsey&Co, 2013). The vital factor of this growth is identified as the

rapid increase in HNWIs’ assets. Despite slower global economic growth, this driver of the profit growth will

continue as the world millionaire wealth is cumulatively growing – the richer are getting richer. The global

population of millionaire grew by 9.2% reaching 12 million in 2012, and expanded by 2 million in 2013, and on

aggregate HNWIs’ assets increased by almost 14% to reach $52.62 trillion in 2013, reported by Capgemini/RBC

World Wealth Report. According to McKinsey survey (2013), the number of HNWI is expected to rise 30% by

2016 in charge of $80trillion in personal financial assets. In addition, Knight Frank Research (2014) forecasts that

the re w i l l be 28% inc rease in the to ta l number o f UHNWIs a round the wor ld by 2023 .

Another important factor is that the growth of millionaire wealth is gradually shifting from developed to emerging

markets. HNWI assets in emerging markets is expected to grow at about 13% annually while the number is only

around 4.5% in the developed markets. McKinsey (2013) forecasts that by 2016 emerging markets could occupy

around 37% of millionaire wealth globally (as shown in Figure 1). By then, Asia will dominate the increase in

UHNWI by 43% from next decade till 2023 (Knight Frank Research, 2014).

These statistics present a trend of being global to attract the largest amount of net new assets, especially wealth

distribution and fast development in Asian countries such as China and Vietnam. However, the diversification or

the access to net new money is not the only reason for globalisation. By the development of economics as well as

technologies, HNWIs represent increasing demands for products/services in multiple geographies. Their private

financial assets, businesses, properties and next generation education are spanning across the globe. Nowadays,

as the economies among different regions are becoming increasingly divergent over time, HNWIs are leaning to

obtain a global presence for investment opportunities and asset management (Euromoney, 2013).

Figure 1: World Wealth Distribution

3

2. Rapid multiplication of local tax and regulatory requirements

3. Changes related to business model and client acquisition

The essential to change the value proposition and delivery models to serve the specific needs of a new

generation of clients is growing. However, some organisations have not yet fully understood all of their changing

client needs (PwC, 2013). More importantly, there is a must to restore trust in private banks’ capability to deliver

more trustworthy and durable financial advices. As the investigations by PwC, 90% of the interviewees found out

that reputation and trustworthy of services are the most important issue in terms of differentiation.

4

PRODUCTS & SERVICES

FROM HSBC PRIVATE

BANK

In order to fulfil the requirements of the clients in private banking which are more complicated, diversified and

personalized than those in the retail banking, HSBC private bank manages to provide the customers one-to-one

service from a manager. In this way, risk exposure and the costs of special financial services can be controlled

and limited to certain levels as the situation changes. Behind customer managers, there are a large number of

specialists in HSBC Group, the largest capitalised banking groups in the world, connecting the clients to what the

broader market has to offer.

Those highly skilled product managers are capable to help the clients identify and secure their financial objectives

by designing and providing specified products or a set of completely tailored investment and financing solutions

according to individual needs. In a nutshell, HSBC private bank services can be roughly classified into three

categories: banking, investment and wealth planning.

BANKING SERVICES

Including deposit accounts, tailored lending, foreign exchange services, guarantees of payments, Margin trading

facilities and online banking services. The traditional banking service is not the mainstream of the private banking

business. However, due to long history and the amount of customers, credit is still the main source of income for

HSBC private bank (UK) co. LTD.

INVESTING SERVICES

Various investment services and solutions are tailored to meet the needs of wealthy individuals and their families

mainly from four aspects- liquidity needs, portfolio management, lifestyle consideration and multigenerational

issues. The services include:

Discretionary investment management. The clients can delegate the management of their

investment portfolios to investment specialists, provided expert guidance, personalised services with access to

experienced investment managers across the globe. The investment managers will create customised, integrated

5

and diversified solutions across all asset classes, according to customers’ risk appetites, asset allocation

preferences, investment durations and targets.

Advisory Services. HSBC's financial advisers can provide specialist advice and comprehensive

supports instead of making decisions on behalf of clients when they choose to take active roles in their investment

activities. HSBC gives accesses to a range of tools to assist clients with tailored strategies and guidelines. The

financial advisers can research the global/local economic and market dynamics to gain insights into clients’

investment decisions, give commentaries on asset classes and various sectors for local markets across the globe

or present tactical trade ideas for short-term market opportunities. With the comprehensive, consultative

approach, HSBC private bank develops an awareness of clients’ financial circumstances and tailored approaches

to fit their demands.

Alternative investments services. HSBC’s Alternative Investment Group (AIG) is responsible

for creating hedge fund, real estate and private equity solutions for both private and institutional clients. AIG

manages or advises on &27.8billion (at 31st Dec 2013) of client assets. AIG offers a variety of investment service

selections including commingled funds, customised segregated mandates, club deals and co-investment

opportunities.

Services for self-directed investors. HSBC also offers a broad range of tools and solutions

to investors managing their own investment portfolios. For example, they provide researches that give insights

into the global/local dynamics affecting investment decisions, exclusive explanation and professional views for

different asset classes/sectors of various markets worldwide, and a platform supporting the execution of a range

of investments across global markets.

WEALTH PLANNING

One of the primary services is wealth structuring, i.e. to create wealth-structuring solutions that meet particular

demands and ambitions. HSBC private bank can help customer to administer trusts, companies and other

structures, build up private funds to simplify complex financial arrangements and consolidate wealth, as well as

succession planning and estate administration. Apart from wealth structuring, there are services such as family

governance, educating next generation and insurances. In addition, HSBC also arranges philanthropy services for

charity trust and foundations to help wealthy individuals’ and families’ pursuit of important social causes.

6

FINANCIAL

PERFORMANCE

According to Annual Report of HSBC Holdings (2013), the main financial features are summarised as followed:

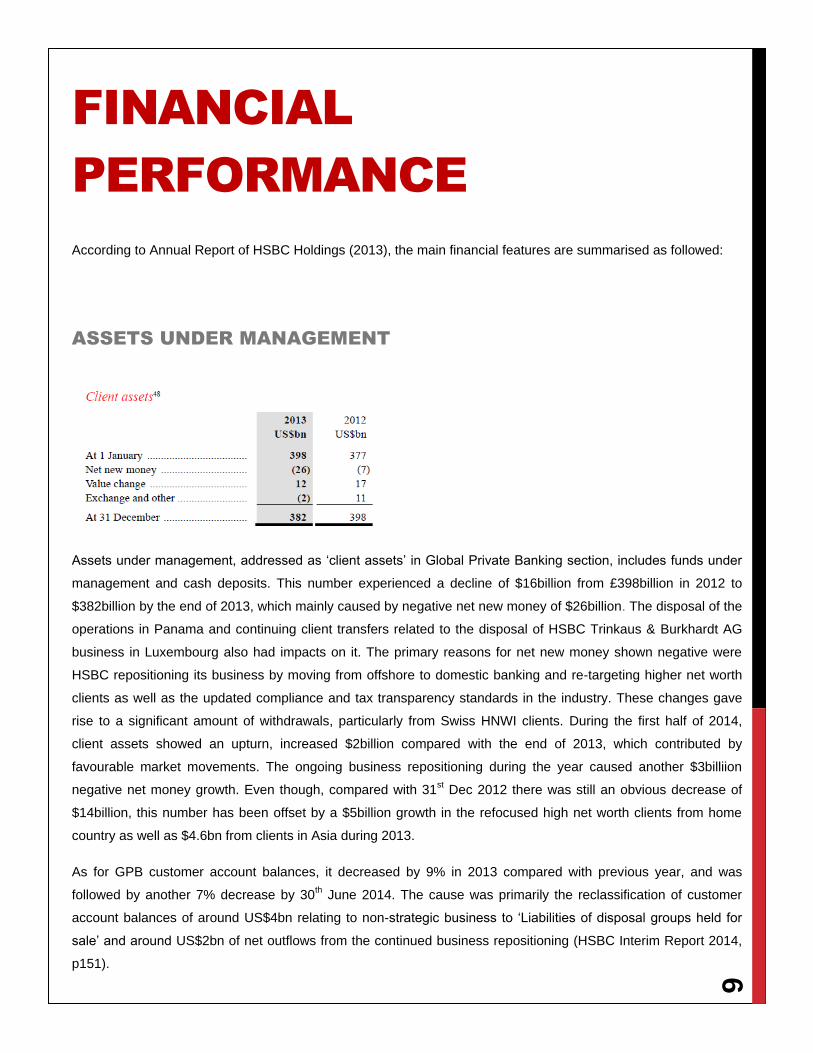

ASSETS UNDER MANAGEMENT

Assets under management, addressed as ‘client assets’ in Global Private Banking section, includes funds under

management and cash deposits. This number experienced a decline of $16billion from £398billion in 2012 to

$382billion by the end of 2013, which mainly caused by negative net new money of $26billion. The disposal of the

operations in Panama and continuing client transfers related to the disposal of HSBC Trinkaus & Burkhardt AG

business in Luxembourg also had impacts on it. The primary reasons for net new money shown negative were

HSBC repositioning its business by moving from offshore to domestic banking and re-targeting higher net worth

clients as well as the updated compliance and tax transparency standards in the industry. These changes gave

rise to a significant amount of withdrawals, particularly from Swiss HNWI clients. During the first half of 2014,

client assets showed an upturn, increased $2billion compared with the end of 2013, which contributed by

favourable market movements. The ongoing business repositioning during the year caused another $3billiion

negative net money growth. Even though, compared with 31st Dec 2012 there was still an obvious decrease of

$14billion, this number has been offset by a $5billion growth in the refocused high net worth clients from home

country as well as $4.6bn from clients in Asia during 2013.

As for GPB customer account balances, it decreased by 9% in 2013 compared with previous year, and was

followed by another 7% decrease by 30th June 2014. The cause was primarily the reclassification of customer

account balances of around US$4bn relating to non-strategic business to ‘Liabilities of disposal groups held for

sale’ and around US$2bn of net outflows from the continued business repositioning (HSBC Interim Report 2014,

p151).

7

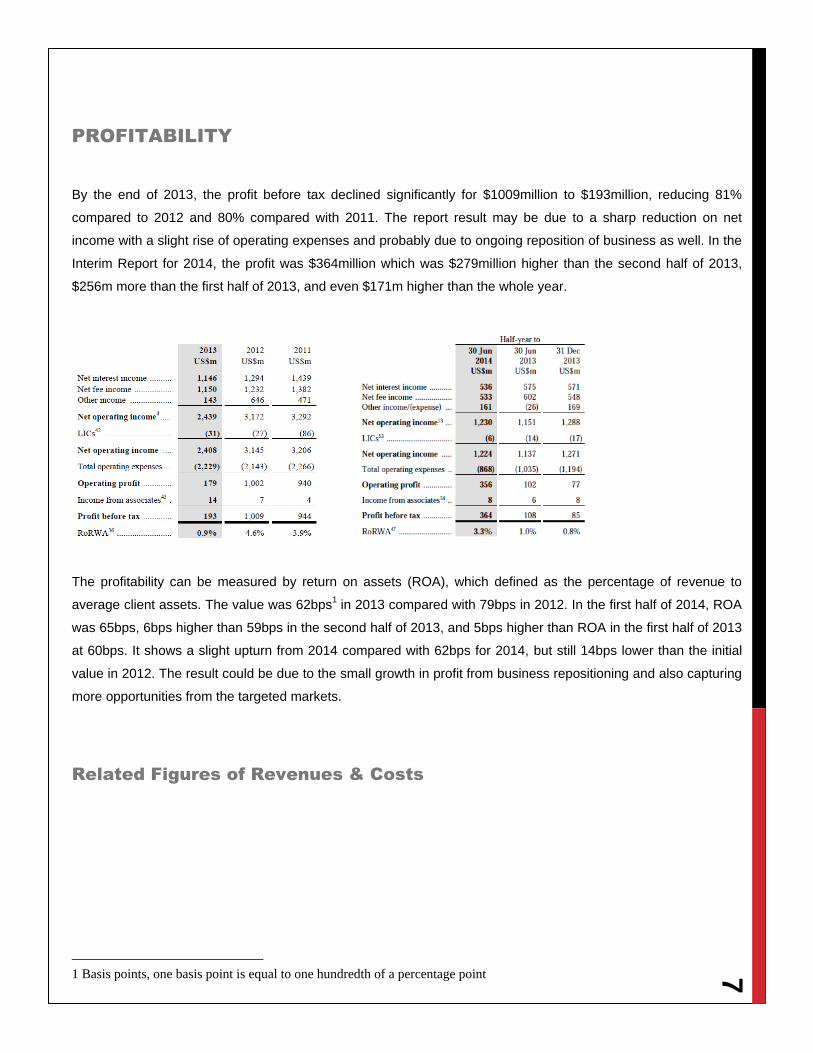

PROFITABILITY

By the end of 2013, the profit before tax declined significantly for $1009million to $193million, reducing 81%

compared to 2012 and 80% compared with 2011. The report result may be due to a sharp reduction on net

income with a slight rise of operating expenses and probably due to ongoing reposition of business as well. In the

Interim Report for 2014, the profit was $364million which was $279million higher than the second half of 2013,

$256m more than the first half of 2013, and even $171m higher than the whole year.

The profitability can be measured by return on assets (ROA), which defined as the percentage of revenue to

average client assets. The value was 62bps1 in 2013 compared with 79bps in 2012. In the first half of 2014, ROA

was 65bps, 6bps higher than 59bps in the second half of 2013, and 5bps higher than ROA in the first half of 2013

at 60bps. It shows a slight upturn from 2014 compared with 62bps for 2014, but still 14bps lower than the initial

value in 2012. The result could be due to the small growth in profit from business repositioning and also capturing

more opportunities from the targeted markets.

Related Figures of Revenues & Costs

1 Basis points, one basis point is equal to one hundredth of a percentage point

8

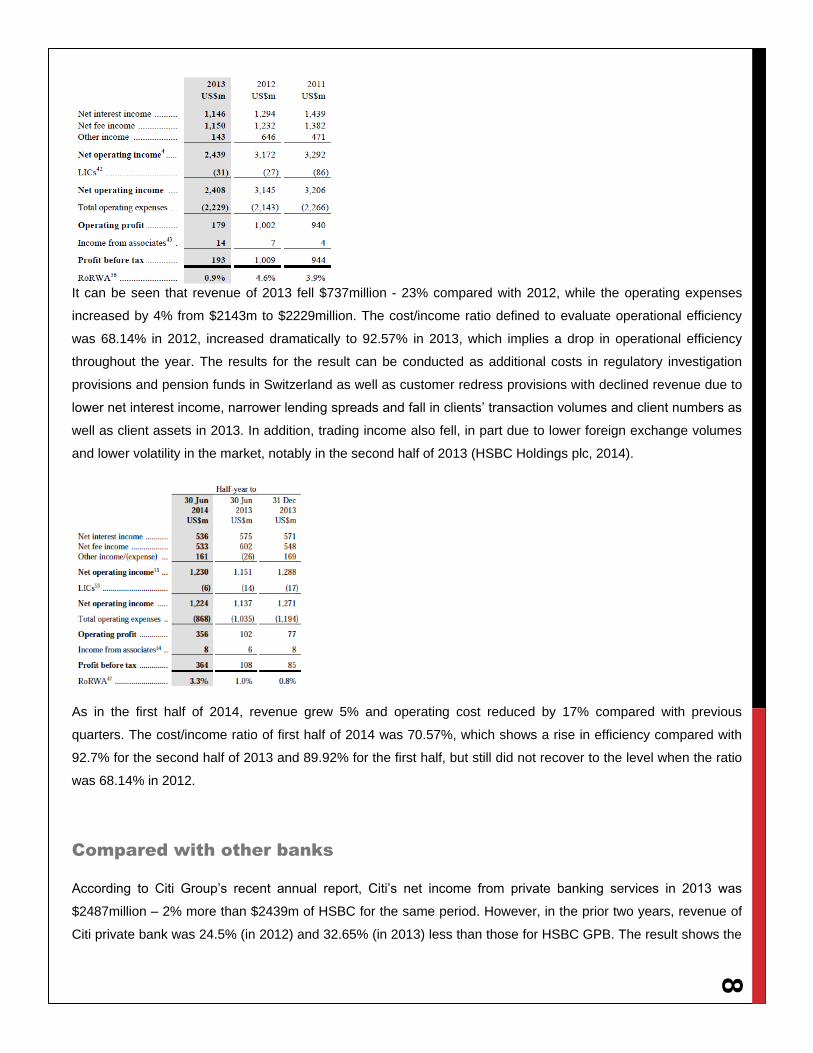

It can be seen that revenue of 2013 fell $737million - 23% compared with 2012, while the operating expenses

increased by 4% from $2143m to $2229million. The cost/income ratio defined to evaluate operational efficiency

was 68.14% in 2012, increased dramatically to 92.57% in 2013, which implies a drop in operational efficiency

throughout the year. The results for the result can be conducted as additional costs in regulatory investigation

provisions and pension funds in Switzerland as well as customer redress provisions with declined revenue due to

lower net interest income, narrower lending spreads and fall in clients’ transaction volumes and client numbers as

well as client assets in 2013. In addition, trading income also fell, in part due to lower foreign exchange volumes

and lower volatility in the market, notably in the second half of 2013 (HSBC Holdings plc, 2014).

As in the first half of 2014, revenue grew 5% and operating cost reduced by 17% compared with previous

quarters. The cost/income ratio of first half of 2014 was 70.57%, which shows a rise in efficiency compared with

92.7% for the second half of 2013 and 89.92% for the first half, but still did not recover to the level when the ratio

was 68.14% in 2012.

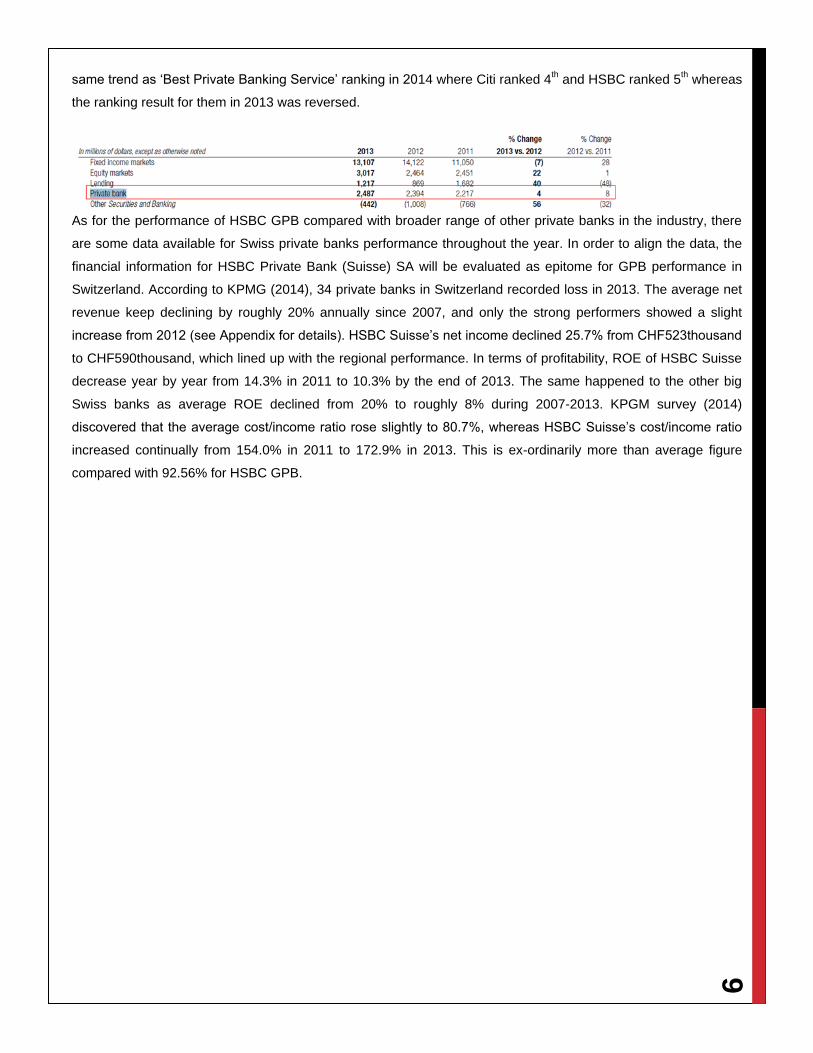

Compared with other banks

According to Citi Group’s recent annual report, Citi’s net income from private banking services in 2013 was

$2487million – 2% more than $2439m of HSBC for the same period. However, in the prior two years, revenue of

Citi private bank was 24.5% (in 2012) and 32.65% (in 2013) less than those for HSBC GPB. The result shows the

9

same trend as ‘Best Private Banking Service’ ranking in 2014 where Citi ranked 4th and HSBC ranked 5

th whereas

the ranking result for them in 2013 was reversed.

As for the performance of HSBC GPB compared with broader range of other private banks in the industry, there

are some data available for Swiss private banks performance throughout the year. In order to align the data, the

financial information for HSBC Private Bank (Suisse) SA will be evaluated as epitome for GPB performance in

Switzerland. According to KPMG (2014), 34 private banks in Switzerland recorded loss in 2013. The average net

revenue keep declining by roughly 20% annually since 2007, and only the strong performers showed a slight

increase from 2012 (see Appendix for details). HSBC Suisse’s net income declined 25.7% from CHF523thousand

to CHF590thousand, which lined up with the regional performance. In terms of profitability, ROE of HSBC Suisse

decrease year by year from 14.3% in 2011 to 10.3% by the end of 2013. The same happened to the other big

Swiss banks as average ROE declined from 20% to roughly 8% during 2007-2013. KPGM survey (2014)

discovered that the average cost/income ratio rose slightly to 80.7%, whereas HSBC Suisse’s cost/income ratio

increased continually from 154.0% in 2011 to 172.9% in 2013. This is ex-ordinarily more than average figure

compared with 92.56% for HSBC GPB.

10

PAST AND FUTURE

STRATEGIES

A clear vision over client and service development is central to sustained success. Banks that seek to differentiate

themselves – through products and services, client advisory or technology, among other factors – and have a

targeted, market-oriented strategy will be best positioned to compete in this demanding market (KPMG, 2013).

HSBC has been approaching towards business repositioning, operational efficiency and development of

digitalisation during recent years and is planning further down to business model transformation, global business

acquisition and online PB platform in 2014.

MAIN STRATEGICAL ACTIVITIES IN THE PAST

Repositioning the business

To align with the strategy focusing on targeted clients with wider social and global connections with in the

domestic and priority markets as well as reducing the amount of clients in non-priority markets, HSBC GPB

agreed to sell a collection of clients’ private banking assets in non-priority markets booked with LGT Bank

(Switzerland) Ltd. The portfolio contained $12.5billion of client assets at 31st Dec 2013, accounting for about 15%

of client assets in Switzerland. Following this, the associated balances held for sale were re-classified at 30th Jun

2014, and will be transacted in the second half of 2014.

11

Growth opportunities capturing and collaboration of revenue

They enhanced their product offering to clients for more investment opportunities through three strengthened

Alternatives products during 2013 and 2014 comprising five private equity funds (three in 2013 and two in 2014),

three real estate portfolio (two in 2013; one in 2014) and a fund of hedge funds. Moreover, the investment group

was improved via the implementation of Global Product Lines, which allows them to offer a consistent global

proposition for key products and utilise more efficiently GB&M and Global Asset Management Services and

products.

Since the second half of 2013, Global Priority Clients (GPC) initiative has been formalised and implemented.

GPC was defined as a cooperative venture between GPB, CMB and GB&M (Global Banking and Markets) for the

Group’s most significant dual banked clients. The initiative could help to ensure the private and corporate needs

of the most significant and complex clients via an enhanced coverage model, so that HSBC could gather

significant incremental revenue opportunities by benefiting these clients and deepening the relationships with

them. The collaboration created $5billion of net new money in 2013 and continued to drive momentum in the first

half of 2014 and over 60 important relationships were identified for further revenue opportunities.

12

BIBLIOGRAPHY

A.T. Kearney & Newtone Associates, 2012. Private Banking in the New Era, s.l.: s.n.

Euromoney, 2013. The 2013 Guide to Private Banking and Wealth Management, s.l.: Euromoney

Research Guide.

HSBC Bank plc, 2013. Annual Report and Accounts, London: Global Publishing Services, HSBC Bank

plc.

HSBC Holdings plc, 2013. Annual Report and Accounts, London: Group Finance, HSBC Holdings plc.

HSBC Holdings plc, 2014. Interim Report, s.l.: s.n.

Knight Frank Research, 2014. The Wealth Report 2014, s.l.: Knight Frank LLP.

KPMG, A., 2013. Performance through focus - Seizing the global private banking opportunity,

Switzerland: KPMG Holding AG/SA.

McKinsey&Co, 2013. Global Private Banking Survey 2013 - Capturing the new generation of clients,

www.mckinsey.com: McKinsey Banking Practice.

PwC, 2013. Global Private Banking and Wealth Management Survey 2013 - Navigating to tomorrow:

serving clients and creating value, www.pwc.com/wealth: Forest Stewardship Council.