In this issue - HSBC HK

44

April-June 2012 In this issue Global economy Domestic economy and equity markets Debt markets Union budget 2012-13 Investment and portfolio strategy Funds in focus GLOBAL ECONOMY INVESTMENT AND PORTFOLIO STRATEGY

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of In this issue - HSBC HK

April-June 2012

In this issueGlobal economy

Domestic economy and equity markets

Debt markets

Union budget 2012-13

Investment andportfolio strategy

Funds in focus

�GLOBAL ECONOMY �INVESTMENT AND PORTFOLIO STRATEGY

2 Wealth Strategies - April -June 2012

Disclaimer:

© The Hongkong and Shanghai Banking Corporation Limited, India 2005

52/60 Mahatma Gandhi Road, Mumbai 400 001

For private circulation only. This publication has been issued by The Hongkong and Shanghai Banking Corporation Limited in India (HSBC), incorporated in Hong Kong SAR with limited liability, for the information of its customers who are resident in India. This publication should not be distributed to any other persons and in particular should not be distributed to customers nationals/residents of the United States of America, Canada, Australia and New Zealand. It cannot be reproduced or further disseminated.

This publication does not constitute investment advice or an offer to sell, or a solicitation of an offer to purchase or subscribe for any investment. The information herein is derived from publicly available sources that HSBC considers reliable but which has not been independently verified. Whilst every care has been taken in compiling the information, HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Some of the information in this document is derived from third party sources as specified at the relevant places where such information is set out. The Bank believes such information to be reliable but it has not independently verified the same. Expressions of opinion are those of HSBC only and are subject to change without notice. Opinions expressed herein do not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this publication. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies that may have been discussed in this publication and should understand that the views regarding future prospects may or may not be realised. This document is for circulation in India. The Bank makes no representations that the products or services mentioned in this document are available to persons of any other country or are necessarily suitable for any particular person or appropriate in accordance with their local law. Among other things, this means that the disclosures set forth in this document may not conform to rules of the regulatory bodies of any other country and investment in the products discussed will not afford the protection offered by the local regulatory regime in any other country. The information contained herein is confidential to the recipients thereof and may not be reproduced or otherwise disseminated. The Bank or its affiliates or their officers, directors and employees may have investments in any of the products mentioned in this publication (or in any related products) and may from time to time, add to or dispose of any such investment.

Investment involves risk, value of investment may increase or decrease and may become valueless. Past performance figures shown are not indicative of future performance. The relevant product offering documents should be read for further details.

3 Wealth Strategies - April -June 2012

GLOBAL ECONOMY 05

DOMESTIC ECONOMY AND EQUITY MARKETS 09

DEBT MARKETS 14

UNION BUDGET 2012-13 17

INVESTMENT AND PORTFOLIO STRATEGY 18

Investment Strategy 19

Investing in domestic consumption growth 19

Portfolio positioning in volatile markets 20

Hedge against agri-based inflation 21

Diversification 22

Tactical investment opportunities 22

FUNDS IN FOCUS 23

4 Wealth Strategies - April -June 2012

5 Wealth Strategies - April -June 2012

Direction of crude prices to guide the pace and quantum of global economic recovery.

Global liquidity infusion in the recent months supports global economic recovery.

Green shoots of recovery visible in developed economies.

Global Economy

� Global economic growth, particularly in large developed countries, saw a subdued growth trend in 2011 due to sustained global headwinds like the sovereign debt crisis in southern Europe and the geo-political tensions in the Middle East.

� While there appears to be nascent signs of recovery in the recent months as reflected by stabilisation of global equity and fixed income markets and positive economic data flow in the United States (strengthening consumer demand and improved labour market) downside risks continue to remain on account of structural factors such as high debt and unemployment levels in developed countries.

Developed Nations GDP slowdown in 2011

Source: Bloomberg

-3

-2

-1

0

1

2

3

4

5

Developed Countries GDP

US EU UK Japan Germany

6 Wealth Strategies - April -June 2012

� The fast paced growth of the BRIIC economies has been adversely impacted by a slowdown in the developed economies leading to fall in consumer and discretionary spending within the local nations. Key headwinds which may affect the recovery of the economies might be crude prices, geo-political developments and inflation.

BRIIC refers to Brazil, Russia, India, Indonesia and China.

� Global industrial growth moderated at the 50-mark (reading below 50 indicating a contraction). The Purchasing Managers Index (PMI) for developed markets has increased over the past quarters after sustained efforts of monetary infusion by central banks of large developed countries.

Emerging Nations GDP

Source: Bloomberg

5

6

7

8

9

10

11

12

0123456789

10

Mar-10

Apr-10

May-10

Jun-1

0

Jun-1

1Ju

l-10

Jul-1

1

Aug-10

Aug-11

Sep-10

Sep-11

Oct-10

Oct-11

Nov-10

Nov-11

Dec-11

Dec-10

Jan-1

1

Feb-11

Mar-11

Apr-11

May-11

BRIIC GDPBrazil Indonesia Russia China-RHS India-RHS

World PMI

Source: Bloomberg

World PMI

US UK EU GER China

4547495153555759616365

Jan-1

1

Feb-11

Mar-11

Apr-11

May-11

Jun-1

1Ju

l-11

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-1

2

Feb-12

� Global economic slowdown and a softening of commodity prices have seen an overall moderation in inflationary pressure across economies. The sustained increase in energy prices however may once again raise inflation concerns across economies over the coming quarters.

� Within the BRIIC nations, inflation has seen a marked downward trajectory mainly due to an economic slowdown, softening of hard commodities and stabilising food prices. This has also prompted most central banks to reduce interest rates, though the main headwind faced by these nations continues to be high energy costs.

Developed Market Inflation

Source: Bloomberg

Developed Market Inflation

US UK EU GERMANY

-0.5

1.5

3.5

5.5

Jan-1

1

Feb-11

Mar-11

Apr-11

May-11

Jun-1

1Ju

l-11

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-1

2

Feb-12

Emerging Market Inflation

Source: Bloomberg

BRIIC Inflation

China Indonesia Brazil Russia - RHS India - RHS

3456789

10

012345678

Jan-1

1

Feb-11

Mar-11

Apr-11

May-11

Jun-1

1Ju

l-11

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-1

2

Feb-12

7 Wealth Strategies - April -June 2012

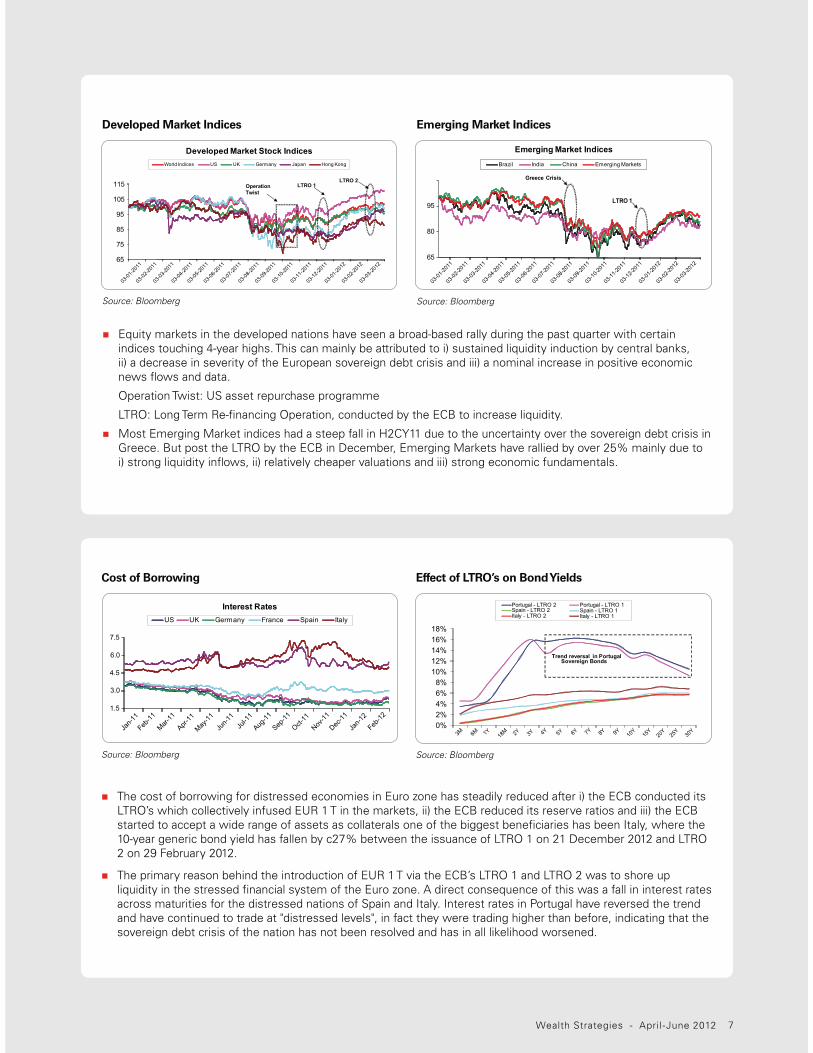

� Equity markets in the developed nations have seen a broad-based rally during the past quarter with certain indices touching 4-year highs. This can mainly be attributed to i) sustained liquidity induction by central banks, ii) a decrease in severity of the European sovereign debt crisis and iii) a nominal increase in positive economic news flows and data.

Operation Twist: US asset repurchase programme

LTRO: Long Term Re-financing Operation, conducted by the ECB to increase liquidity.

� Most Emerging Market indices had a steep fall in H2CY11 due to the uncertainty over the sovereign debt crisis in Greece. But post the LTRO by the ECB in December, Emerging Markets have rallied by over 25% mainly due to i) strong liquidity inflows, ii) relatively cheaper valuations and iii) strong economic fundamentals.

Developed Market Indices

Source: Bloomberg

Developed Market Stock IndicesWorld Indices US UK Germany Japan Hong Kong

65

75

85

95

105

115 LTRO 1 LTRO 2

Operation Twist

03-01

-2011

03-02

-2011

03-03

-2011

03-04

-2011

03-05

-2011

03-06

-2011

03-07

-2011

03-08

-2011

03-09

-2011

03-10

-2011

03-11

-2011

03-12

-2011

03-01

-2012

03-02

-2012

03-03

-2012

Emerging Market Indices

Source: Bloomberg

Emerging Market IndicesBrazil India China Emerging Markets

65

80

95

Greece Crisis

LTRO 1

03-01

-2011

03-02

-2011

03-03

-2011

03-04

-2011

03-05

-2011

03-06

-2011

03-07

-2011

03-08

-2011

03-09

-2011

03-10

-2011

03-11

-2011

03-12

-2011

03-01

-2012

03-02

-2012

03-03

-2012

� The cost of borrowing for distressed economies in Euro zone has steadily reduced after i) the ECB conducted its LTRO’s which collectively infused EUR 1 T in the markets, ii) the ECB reduced its reserve ratios and iii) the ECB started to accept a wide range of assets as collaterals one of the biggest beneficiaries has been Italy, where the 10-year generic bond yield has fallen by c27% between the issuance of LTRO 1 on 21 December 2012 and LTRO 2 on 29 February 2012.

� The primary reason behind the introduction of EUR 1 T via the ECB’s LTRO 1 and LTRO 2 was to shore up liquidity in the stressed financial system of the Euro zone. A direct consequence of this was a fall in interest rates across maturities for the distressed nations of Spain and Italy. Interest rates in Portugal have reversed the trend and have continued to trade at "distressed levels", in fact they were trading higher than before, indicating that the sovereign debt crisis of the nation has not been resolved and has in all likelihood worsened.

Cost of Borrowing

Source: Bloomberg

Interest RatesUS UK Germany France Spain Italy

1.5

4.5

6.0

3.0

7.5

Jan-1

1

Feb-11

Mar-11

Apr-11

May-11

Jun-1

1Ju

l-11

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-1

2

Feb-12

Effect of LTRO’s on Bond Yields

Source: Bloomberg

Portugal - LTRO 2 Spain - LTRO 2Italy - LTRO 2

Portugal - LTRO 1 Spain - LTRO 1 Italy - LTRO 1

0%2%4%6%8%

10%12%14%16%18%

Trend reversal in PortugalSovereign Bonds

3M 6M 1Y 18M 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10

Y15

Y20

Y25

Y30

Y

8 Wealth Strategies - April -June 2012

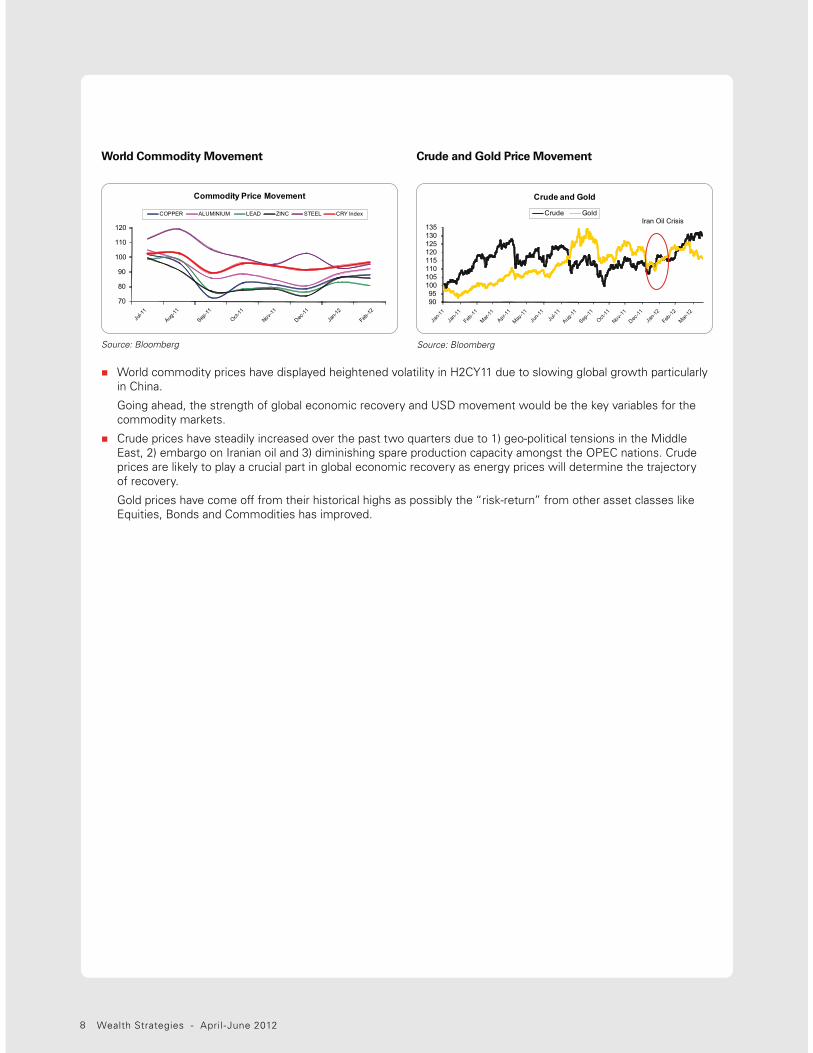

� World commodity prices have displayed heightened volatility in H2CY11 due to slowing global growth particularly in China.

Going ahead, the strength of global economic recovery and USD movement would be the key variables for the commodity markets.

� Crude prices have steadily increased over the past two quarters due to 1) geo-political tensions in the Middle East, 2) embargo on Iranian oil and 3) diminishing spare production capacity amongst the OPEC nations. Crude prices are likely to play a crucial part in global economic recovery as energy prices will determine the trajectory of recovery.

Gold prices have come off from their historical highs as possibly the “risk-return” from other asset classes like Equities, Bonds and Commodities has improved.

World Commodity Movement Crude and Gold Price Movement

Source: Bloomberg Source: Bloomberg

70

80

90

100

110

120

Commodity Price Movement

COPPER ALUMINIUM LEAD ZINC STEEL CRY Index

Crude and Gold

Crude Gold

9095

100105110115120125130135

Iran Oil Crisis

9 Wealth Strategies - April -June 2012

Domestic Economy and Equity Markets

Inflation risks yet to dissipate in the backdrop of high oil prices and volatile INR.

Indian equities regain lost ground backed by strong foreign fund flow in CY12; second best performing market amongst BRIC nation

Union Budget set fiscal deficit target of 5.1% of GDP for FY13; lower on account of expected increase in revenue receipts.

GDP growth moderated during the second half of the year 2011 led by fall in investment growth.

� India’s GDP growth eased further to 6.1% yoy during the Q3FY12 v/s 6.9% yoy in Q2FY12. Services sector registered strong growth of c8% followed by agricultural growth of c2%. Services continue to remain upbeat and shore up the GDP growth rate over the last three quarters while industrial growth was hit by under performance by mining and manufacturing that registered growth of c3% and c0.4% respectively.

� Components of GDP for Q2FY12 saw sharp downward reversion during the quarter. Consumption demand rose from revised growth of 2.92% yoy in Q2FY12 to c6.24% in Q3FY12. Government expenditure and investments too remained muted during the quarter. Going ahead, investment growth is likely to gain momentum as the government rolled out supportive measures such as tax concessions and funding options for infrastructure development in the Union Budget 2012. Government estimates GDP to grow by 6.9% in FY12.

Source: Bloomberg

Growth drops further… Industry growth slumps

14.00

12.00

10.00

8.00

6.00

4.00

2.00

0.00

-2.00

-4.00

Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11

Agriculture Industry Services GDP

Consumption recovers but government spending remains timid…

Source: Bloomberg

8.00%

6.00%

4.00%

2.00%

0.00%

-2.00%

-4.00%

-6.00%

Consumption Govt Expenditure Investments

(%yo

y)

Q2-FY12 Q3-FY12

10 Wealth Strategies - April -June 2012

� A slowdown in economy was mirrored in consumption demand coming off over the last few months. Key economic lead indicators like total car sales and cement dispatches showcased a declining trend on monthly basis, as high interest rate and input cost acted as headwinds.

� Industrial growth continued to remain volatile during the quarter. IIP for January 2012 moved up to 6.8% yoy against revised 2.5% in December 2011. Manufacturing production led the overall recovery, though mining continued to feel the heat on the backdrop of prevailing uncertainty in the mining industry. On the contrary, HSBC PMI eased in March 2012 to 54.7 compared to 56.6 in February 2012 on account of likely moderation in sequential output growth. January 2011 PMI reading was the highest in the last 8 months.

Source: Bloomberg

Industrial output continues to remain volatile…

42

44

46

48

50

52

54

56

58

60

-40

-30

-20

-10

0

10

20

30

40

50

60

Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12

% g

rowt

h (y

-o-y

)

Basic goods Capital goods Intermediate goodsConsumer goods IIP Manufacturing PMI

Source: Bloomberg

Key indicators remain sluggish…

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12

Cement Dispatches (MOM) Car Sales (MOM)

� After holding above the 9% mark since April, WPI Inflation eased to 7.7% (yoy) in December further easing to 6.95% (yoy) in February responding to RBI’s monetary tightening. The slowdown in the pace of inflation was also supported by a favourable base effect of last year when inflation rose by an average of 9.5% and favourable monsoons during CY11 aided in limiting food inflation.

� Upward risks to inflation have however resurfaced in CY12 on increase in global crude oil prices that have shot up to cUSD 127 per barrel (Brent) on geopolitical concerns. The recent depreciation of the INR against the USD has also increased the risks of imported inflation. Moreover, slowing trend in the primary articles index of inflation is showing signs of reversal indicating risks of spillover into food prices.

� In the near term, risks to inflation have increased following the increase in the indirect taxes (excise and custom duties) announced in the Union Budget but will be supported by the high base of last year. However, with the fiscal deficit expected to reduce in FY13, inflation pressures in the medium to long term are expected to ease although it will take cues from factors such as crude oil prices and currency impact.

Crude Oil and Currency may impact the future inflation trajectory

Source: Bloomberg

40

42

44

46

48

50

52

54

80

85

90

95

100

105

110

115

120

125

130

Jan-10

Feb-10

Mar-10

Apr-10

May-10

Jun-10

Jul-10

Aug-10

Sep-10

Oct-10

Nov-10

Dec-10

Jan-11

Feb-11

Mar-11

Apr-11

May-11

Jun-11

Jul-11

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-12

Feb-12

Mar-12

Crude Oil (Brent) INR/ USD (RHS)

Led by favourable base effect, Inflation slowed in recent months

Source: Bloomberg

Repo Rate % WPI Infla�on (yoy %)

4

5

6

7

8

9

10

11

29-01-1019-03-10

20-04-1002-07-10

27-07-1016-09-10

02-11-1003-12-10

16-12-1025-01-11

17-03-1103-05-11

16-06-1126-07-11

16-09-1125-10-11

16-12-1131-12-11

31-01-1229-02-12

Infla�on slowing

pause in monetary �ghtening

11 Wealth Strategies - April -June 2012

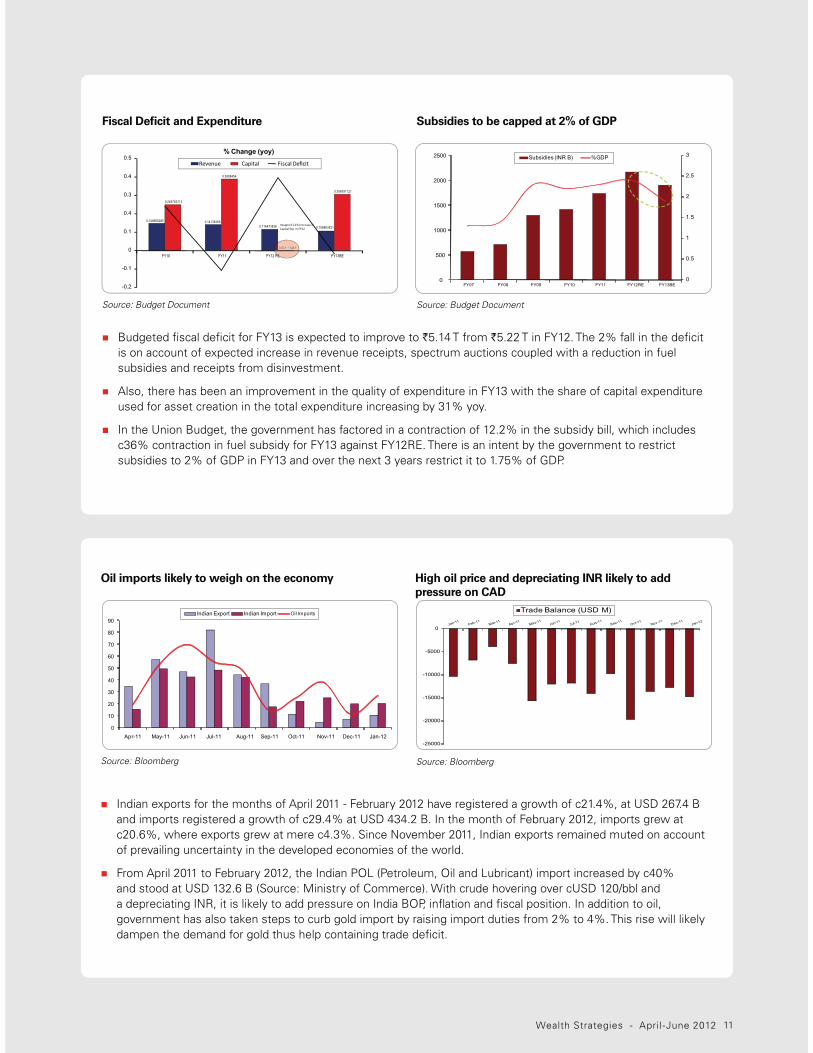

� Budgeted fiscal deficit for FY13 is expected to improve to `5.14 T from `5.22 T in FY12. The 2% fall in the deficit is on account of expected increase in revenue receipts, spectrum auctions coupled with a reduction in fuel subsidies and receipts from disinvestment.

� Also, there has been an improvement in the quality of expenditure in FY13 with the share of capital expenditure used for asset creation in the total expenditure increasing by 31% yoy.

� In the Union Budget, the government has factored in a contraction of 12.2% in the subsidy bill, which includes c36% contraction in fuel subsidy for FY13 against FY12RE. There is an intent by the government to restrict subsidies to 2% of GDP in FY13 and over the next 3 years restrict it to 1.75% of GDP.

Fiscal Deficit and Expenditure

Source: Budget Document

0.148666285 0.141382680.116473836 0.106863521

0.249783713

0.3898454

0.001117461

0.306391121

-0.2

-0.1

0

0.1

0.4

0.3

0.4

0.5

FY10 FY12 RE FY13BEFY11

% Change (yoy) Revenue Capital Fiscal Deficit

0.001117461

RE

meagre 0.11% increase in Capital Exp in FY12

Subsidies to be capped at 2% of GDP

Source: Budget Document

0

0.5

1

1.5

2

2.5

3

0

500

1000

1500

2000

2500

FY07 FY08 FY09 FY10 FY11 FY12RE FY13BE

Subsidies (INR B) %GDP

� Indian exports for the months of April 2011 - February 2012 have registered a growth of c21.4%, at USD 267.4 B and imports registered a growth of c29.4% at USD 434.2 B. In the month of February 2012, imports grew at c20.6%, where exports grew at mere c4.3%. Since November 2011, Indian exports remained muted on account of prevailing uncertainty in the developed economies of the world.

� From April 2011 to February 2012, the Indian POL (Petroleum, Oil and Lubricant) import increased by c40% and stood at USD 132.6 B (Source: Ministry of Commerce). With crude hovering over cUSD 120/bbl and a depreciating INR, it is likely to add pressure on India BOP, inflation and fiscal position. In addition to oil, government has also taken steps to curb gold import by raising import duties from 2% to 4%. This rise will likely dampen the demand for gold thus help containing trade deficit.

Oil imports likely to weigh on the economy

Source: Bloomberg

0

10

20

30

40

50

60

70

80

90

Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

Indian Export Indian Import Oil Imports

High oil price and depreciating INR likely to add pressure on CAD

Source: Bloomberg

-25000

-20000

-15000

-10000

-5000

0

Trade Balance (USD M)

12 Wealth Strategies - April -June 2012

Primary market activity remains muted

Source: SEBI Bulletin February 2012

� Primary market trends during FY12 remained sluggish compared to FY11 as most corporate houses deferred their capital raising activity on account of unsupportive market conditions that prevailed during most part of FY12. Total amount raised till January 2012 stands at `323 B.

Items

Jan-12 Dec-11 2011-12$ 2010-11$

No. of Issues

Amount (` crore)

No. of Issues

Amount (` crore)

No. of Issues

Amount (` crore)

No. of Issues

Amount (` crore)

Public Issues 1 6,300.0 3 10,759.3 42 32,375.8 56 50,046.9

Public Issue (Equity) of which

0 0.0 0 0.0 30 9,559.0 52 47,801.9

IPOs 0 0.0 0 0.0 29 4,980.8 47 34,706.9

FPOs 0 0.0 0 0.0 1 4,578.2 5 13,095.1

� Indian equities regained momentum in the new year backed by strong foreign fund flow and mean reversion sentiments. Indian markets were the second best performing amongst the BRIC nations, gaining c14% as on 30 March 2012. Markets moved in conjunction with global peers as macro sentiments showed signs of improvement. Key domestic events such as state elections, Union Budget and monetary policy review were watched closely by market participants during the quarter.

� Liquidity induction by global Central Banks probably resulted in strong foreign fund flows into Indian equities during the quarter. FII’s were net buyers of cUSD 9 B worth of equities during the first three months of 2012.

BRIC refers to Brazil, Russia, India and China

Indian Equities Overview

Foreign fund flows remained positive in CY12

Source: Bloomberg

0

5000

10000

15000

20000

25000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

6000

Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12

Global Liquidity infusion by Central banks supported FII inflows into equi�es

15

FII (USD M) Sensex

Indian equities gained during the quarter; second best among BRIC nations

Source: Bloomberg

30.00%

20.00%

10.00%

0.00%

-10.00%

-20.00%

-30.00%

Russia India EM Brazil World China

YTD 1 year 6 months

13 Wealth Strategies - April -June 2012

Sensex valuation continues to remain in line with historical average

Industrials and consumption sectors outperform…

Source: BloombergSource: Bloomberg

� On the sectoral front, banking was amongst the top two sectors during the quarter. It gained c23% on account of likely rate cut expectation by the Central Bank. Industrial sectors such as capital goods, metals and power too gained momentum on likely mean reversion sentiments.

� Sensex at 17000 continues to trade in line with historical averages making it a fairly priced market. Going ahead, markets are likely to take cues from global developments such as geopolitical tensions over Iran, Euro sovereign debt crisis, slowdown in China and resurgence of US economy. Key domestic events which are likely to keep markets interested in near term include policy action by the Central Bank, inflation and reform actions by the government. Inflation concerns are likely to continue in near term with rising crude price translating in broad based price rise.

-10.00%-5.00%0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%

Rea

lty

Ban

k

Cap

ital G

oods

Met

al

Con

sum

er D

urab

le

Pow

er

Hea

lth C

are

FMC

G

Oil&

Gas IT

3 months 6 months

Jan-01

Sep-01

Jun-02

Mar-03

Dec-03

Sep-04

Jun-05

Mar-06

Dec-06

Sep-07

Jun-08

Mar-09

Dec-09

Sep-10

Jun-11

Mar-12

30

25

20

15

10

5

0

Historic P/E

14 Wealth Strategies - April -June 2012

Money Market instrument 30-Mar-12 30-Dec-11 Change in bps

CP 1M 11.56 10.05 151

CP 3M 11.27 9.83 144

CP 6M 11.20 9.95 125

CP 12M 10.93 10.10 83

CD 1M 11.45 9.60 185

CD 3M 10.70 9.43 127

CD 6M 10.50 9.69 81

CD 12M 10.15 9.75 40

Debt MarketsFiscal deficit lower than last year but largely financed by market borrowings

Pace and quantum of rate cuts to be determined by evolving growth-inflation dynamics

Shorter maturity bonds underperform, corporate bonds lead the fall

� G-sec yield curve, barring few maturities, moved higher during the quarter in the range of 5 to 40 bps. Corporate bond yields too moved up displaying a similar trend in curve movement. G-sec curve outperformed the corporate bond curve at the shorter end but lagged corporate bonds in the medium to longer end. Meanwhile, money market instruments were the worst hit, rising between 40 to 185 bps on tight liquidity conditions.

� Bond yields were mostly impacted by 1) concerns of fiscal deficit slippages, 2) higher crude oil prices triggering fresh concerns of inflation, 3) delay in monetary easing, 4) tight liquidity conditions impacting demand and 5) high market borrowings planned for FY13.

� Markets were however supported by 1) Open Market Operations (OMOs) conducted by RBI, INR 880 B infused during Q1CY12, 2) infusion of liquidity through a 125 bps cut in Cash Reserve Ratio (CRR), INR 800 B added to the banking system, 3) FII inflows into debt markets, USD 4 B received during the quarter, Qualified Foreign Investors (QFIs) permitted to access corporate bond markets in the Union Budget and 4) easing inflation pressures, WPI inflation rose by c7% each in Jan and Feb.

Bond yields rise during the quarter;

shorter end of the curve underperforms

the longer end

Source: Bloomberg

Corporate Bond Yield Curve

Source: Bloomberg

Money Market instrument yields remain elevated on liquidity tightness

Source: Bloomberg

G-sec and Corporate bond yields move higher during the quarter: G-Sec Yield Curve

Change in bps (RHS) 30-Mar-12 30-Dec-11

9.0%

8.8%

8.6%

8.4%

8.2%

8.0%

7.8%

50

40

30

20

10

-

(10)

91 d

ay

182

day

1 yr

2 yr

4 yr

5 yr

6 yr

7 yr

8 yr

9 yr

10 yr

11 yr

15 yr

30 yr

-40

-20

0

20

40

60

80

9.0%

9.2%

9.4%

9.6%

9.8%

10.0%

10.2%

10.4%

3MO 6MO 1YR 2YR 3YR 4YR 5YR 6YR 7YR 8YR 9YR 10YR 15YR

Change in bps (RHS) 30-Mar-12 30-Dec-11

15 Wealth Strategies - April -June 2012

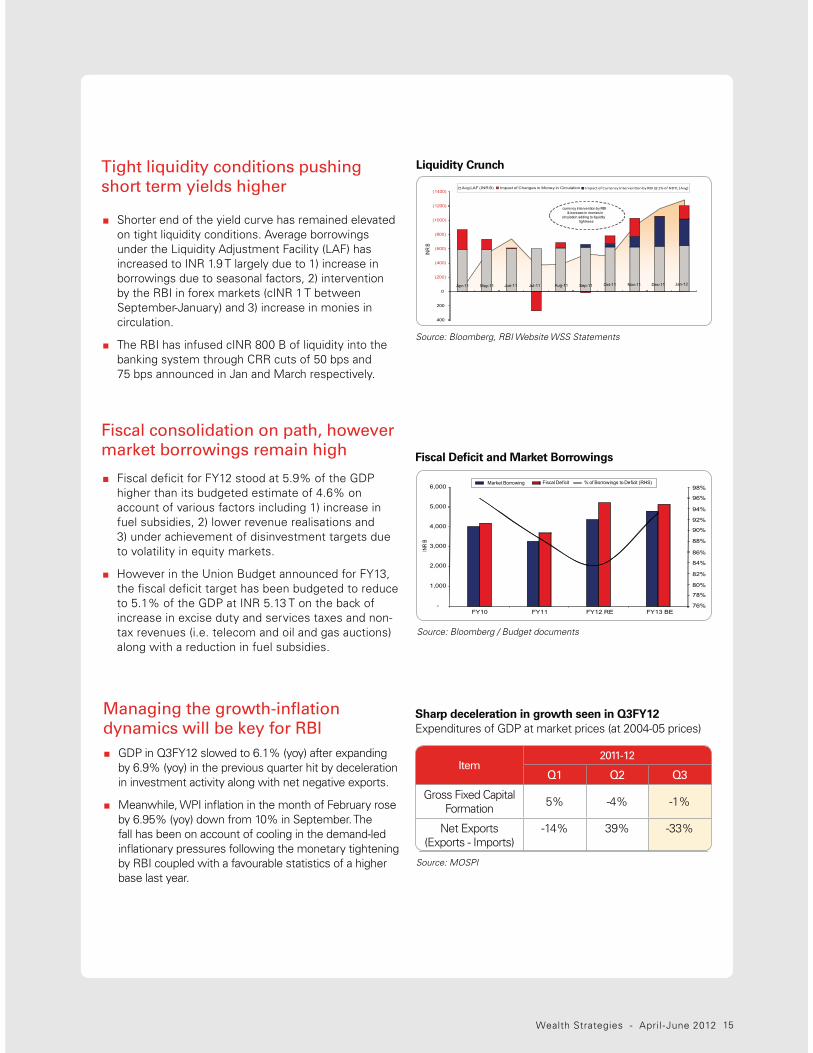

Tight liquidity conditions pushing

short term yields higher

� Shorter end of the yield curve has remained elevated on tight liquidity conditions. Average borrowings under the Liquidity Adjustment Facility (LAF) has increased to INR 1.9 T largely due to 1) increase in borrowings due to seasonal factors, 2) intervention by the RBI in forex markets (cINR 1 T between September-January) and 3) increase in monies in circulation.

� The RBI has infused cINR 800 B of liquidity into the banking system through CRR cuts of 50 bps and 75 bps announced in Jan and March respectively.

Liquidity Crunch

Source: Bloomberg, RBI Website WSS Statements

� Fiscal deficit for FY12 stood at 5.9% of the GDP higher than its budgeted estimate of 4.6% on account of various factors including 1) increase in fuel subsidies, 2) lower revenue realisations and 3) under achievement of disinvestment targets due to volatility in equity markets.

� However in the Union Budget announced for FY13, the fiscal deficit target has been budgeted to reduce to 5.1% of the GDP at INR 5.13 T on the back of increase in excise duty and services taxes and non-tax revenues (i.e. telecom and oil and gas auctions) along with a reduction in fuel subsidies.

Fiscal consolidation on path, however

market borrowings remain high Fiscal Deficit and Market Borrowings

Source: Bloomberg / Budget documents

Managing the growth-inflation

dynamics will be key for RBI

� GDP in Q3FY12 slowed to 6.1% (yoy) after expanding by 6.9% (yoy) in the previous quarter hit by deceleration in investment activity along with net negative exports.

� Meanwhile, WPI inflation in the month of February rose by 6.95% (yoy) down from 10% in September. The fall has been on account of cooling in the demand-led inflationary pressures following the monetary tightening by RBI coupled with a favourable statistics of a higher base last year.

Sharp deceleration in growth seen in Q3FY12Expenditures of GDP at market prices (at 2004-05 prices)

Source: MOSPI

Item2011-12

Q1 Q2 Q3

Gross Fixed Capital Formation 5% -4% -1%

Net Exports (Exports - Imports)

-14% 39% -33%

(1400)

(1200)

(1000)

(800)

(600)

(400)

(200)

0

200

400

Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

INR

B

Avg LAF (INR B) Impact of Changes in Money in Circulation Impact of Currency Interven�on by RBI 1% of NDTL (Avg)

currency intervention by RBI & increase in monies in

circulation adding to liquidity tightness

Market Borrowing Fiscal Deficit % of Borrowings to Deficit (RHS)

-

4,000

3,000

2,000

1,000

5,000

6,000 98%

96%

94%

92%

90%

88%

86%

84%

82%

80%

78%

76%FY10

INR

B

FY11 FY12 RE FY13 BE

16 Wealth Strategies - April -June 2012

Debt Market Outlook

� Going forward, the bond yield curve will likely take cues from:

i. Sustainability in the pace of growth in the coming months. RBI has projected a growth of 7% for FY12.

ii. The inflation trajectory going forward impacted by developments on global crude oil prices, INR levels against the USD, underlying components of inflation including food and non-food, developments on the onset of normal monsoon. Inflation pressures will impact the pace of monetary easing.

iii. Movement of INR against the USD taking cues from foreign inflows, crude oil prices and global developments.

iv. Liquidity conditions easing from these levels will benefit the bond markets especially the shorter end of the curve.

v. Global developments impacting risk aversion diverting flows into riskier assets.

Increase in upward risks to inflation

Source: Bloomberg

� However, the recent surge in crude oil prices on various geopolitical concerns coupled with strengthening of the USD against the INR have increased upwards risks to inflationary pressures. Also, food prices have been showing an upward trend after declining for the past few months.

�� While the Central Bank has stated that further actions will be towards lowering rate, the timing and quantum of rate cuts will be determined by pace of growth and inflationary pressures.

Crude/Currency Impact (RHS)Oil Prices (USD per bbI) RHSFuel & PowerMfgPrimary Articles

18.0

12.2

8.0 8.18.9

8.2

3.6

7.6

2.3

6.5 6.3 5.8

12.814.0

11.0

14.8 15.5 15.014.2

Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

0.0

140

120

100

80

60

40

20

0

nascent fuel

primaryarticles

inflation rising

inflation pressures

4.22

17 Wealth Strategies - April -June 2012

Union Budget 2012-13OverviewThe Budget was presented in the backdrop of moderating growth and deteriorating fiscal balances and private investments. The economy after clocking a yoy growth of above 8% in FY10 and FY11, decelerated in FY12 (expected to grow by 7%) impacted by the global economic slowdown and Euro-region debt concerns, higher crude oil prices and tighter domestic monetary policy. The focus in this Budget has been therefore to strengthen domestic growth drivers including fiscal consolidation, boosting infrastructure expenditure, private investment, develop agriculture sector, improving inclusion and strengthening corporate governance in the backdrop in recovery in macroeconomic environment.

Government FinancesWhile the government’s total budgeted expenditure growth for FY13 has been largely unchanged at c13% yoy, the share of capital expenditure used for asset creation in the total expenditure has increased by 31% yoy (as against a meagre 0.11% growth last year) in FY13, thereby improving the quality of expenditure.

The government has budgeted for a 13% increase in total receipts with the revenue receipts estimated to increase by 22% during FY13, targeting higher revenues to lower its deficit. The jump in revenue receipts is largely expected to come through increases in excise duty and service taxes and spectrum auctions. The increase in indirect taxes could be inflationary in nature in the near term though in the longer term will aid the fiscal consolidation process.

Fiscal ConsolidationThe budgeted fiscal deficit for FY13 therefore stands reduced at 5.1% of the GDP at INR 5.13 T lower by 1.6% over last year’s figure. The government has been able to limit the target fiscal deficit for FY13 on account of expected increase in revenue receipts, spectrum auctions coupled with a reduction in fuel subsidies and receipts from disinvestment. Target for fuel subsidies is estimated at sub-2% of the GDP as against 2.4% of last year. On the flip side though, in FY13, c93% of the fiscal deficit is slated to be financed through market borrowings, raising upward risks to inflation and G-sec supply pressure is therefore expected to remain in FY13.

Revised Estimates

2011 - 2012

Budget Estimates

2012 - 2013

Revenue Deficit 4.4 3.4

Fiscal Deficit 5.9 5.1

(Source: Budget documents)

Infrastructure and investment growth measuresDuring the current year, the growth rate of investment in the economy registered a considerable slowdown as reflected by growth in manufacturing sector. According to Central Statistical Organisation (CSO), the growth in gross capital formulation is estimated to decelerate to 5.8% in the current fiscal year from an average 11% in the previous two years. While the government has announced several measures including external commercial borrowings for various sectors, extending viability gap funding by bringing in more sectors under infrastructure, doubling the amount that can be raised under tax-free bonds, supporting the subsidy payments through the AADHAR platform, there were no announcements on the reforms front (i.e. FDI in the aviation sector, GST). However, the reforms announcement need not be restricted to the Union Budget and may come through in the later part of the year.

SummaryTo summarise, the Budget displays the government’s approach to bring the deficit down to more sustainable levels and at the same time re-orienting expenditure strategy towards priority sectors like health, education, irrigation, infrastructure and investment-related activities. The fiscal policy of 2012-13 has been designed by the government with the assumption that the growth would be bottomed out during 2011-12 at 6.9%. For 2012-13, the government has estimated a real GDP growth of 7.6% with a deviation of 0.25 bps on either side. As with all announcements, the risks to the budgeted projections critically hinge upon policy implementations (including the subsidy reduction) and realisations of the growth forecasts.

18 Wealth Strategies - April -June 2012

Investment and

Portfolio StrategyInvestment Strategy 19

Investing in domestic consumption growth 19

Portfolio positioning in volatile markets 20

Hedge against agri-based inflation 21

Diversification 22

Tactical investment opportunities 22

The above should be read in conjunction with all the disclaimers appearing in the publication.

19 Wealth Strategies - April -June 2012

Global equity markets have recovered from the lows of Q4 2011 primarily led by i) large liquidity infusion by global Central Banks, ii) better than expected growth indicators in the US and Europe and iii) abatement of risk of financial crises. While the recovery in Indian equities have been swift during the quarter, the road ahead for equity markets are likely to be volatile on account of factors such as i) high crude oil prices and its economic impact on currency, interest rates and inflation and ii) recovery in global markets continues to remain subdued due to structural factors such as high unemployment and debt de-leveraging.

On the fixed income space, the current high interest rates will look ahead for policy actions by the Reserve Bank of India (RBI), both on the liquidity front and cost of borrowing, before it heads lower during the course of the year. Besides crude prices, the conduct of large government borrowing by the RBI would be an important variable for longer-term tenure bond yields during the year.

Given the market scenario, investors may consider adopting an asset allocation in line with their risk profile and use a systematic investment and transfer approach to investing. The investor may consider aligning their portfolios towards actively managed products that vary their asset allocation on pre-defined valuation levels, large cap oriented equity funds, and products that invest into high dividend yielding companies. Diversification towards international funds would seek to reduce India-specific risk factors in the portfolio. In the debt space, on a risk-return basis, we remain favourable at the shorter end of the curve.

Investment Strategy

Investing in domestic consumption growth

Product Category

�� Products predominantly maintaining a sizeable exposure to large caps vis-à-vis mid and small cap stocks.

� Products that adopt a bottom-up style of portfolio management focussing on individual stock valuations and not driven by near term market momentum.

� Products that are diversified in nature, avoiding sizeable exposure to a particular sector.

� Products adopting a bottom-up nimble approach to investing capitalising on opportunities presented by sharp market movements.

� Products predominantly investing into dividend yield stocks.

Even as the GDP during Q3FY12 slowed to c6%, India’s economy is expected to grow by 7% in FY12, improving to 7.6% in FY13 led by growth in services and industry sectors. This recovery in growth will also reflect in the broad equity markets. Also while, the recent sell-off in the market has been broad-based, select stocks spread across sectors have displayed strong resilience in the midst of volatility and offer growth opportunities for investors. �� Large Cap oriented funds – Large cap stocks are typically better positioned to tide through market volatility

when compared to mid and small cap stocks on account of deeper and greater participation, comprehensive coverage and higher liquidity.

�� Funds adopting a nimble approach – This style of investing focusses on capitalising on opportunities from steep market movements while being nimble in their approach to investing.

�� Dividend yield funds – These funds invest a considerable part of their portfolio into high dividend yield companies offering stability in returns in the form of dividends.

20 Wealth Strategies - April -June 2012

Markets are expected to remain volatile on developments in the Euro region debt situation, domestic newsflows on inflation, corporate earnings results, pace of economic growth, etc. Also with the increase in global liquidity following stimulus measures adopted by various governments (i.e. Euro and US region) to support their economies, degree of risk aversion will determine the allocations to markets adding to volatility. � Dynamic funds – Adopting an active management style that seeks to play out market trends and developments

across a host of sectors and themes while dynamically changing its asset allocation may help check the portfolio volatility.

�� Asset – Allocation funds – Funds that do not get carried away by market movement and instead focus on disciplined asset allocation aiding in times of market volatility. Asset allocation also enables profit booking during times of optimism while ensuring capital infusion during times of pessimism.

Portfolio positioning in volatile markets

Product Category

�� Products that are dynamically managed generating alpha through adjusting asset allocation based on volatility.

�� Products that adopt a pre-determined approach towards asset allocation regardless of market movement, removing the element of emotion while investing. (e.g. PE-based products)

Risks�� Global developments especially development on the sovereign debt situation in the Euro region and efforts by the

US to revive growth, resulting in change in risk appetite and capital flows in the markets.

�� Domestic factors / developments on corporate result season, policy uncertainties, inflation etc may impact investor sentiment.

�� Products adopting a nimble approach to investing could add to the portfolio turnover adding to the volatility in returns.

�� Products investing into dividend yielding stocks usually defensive in nature and this approach could result in relative underperformance in bullish markets.

21 Wealth Strategies - April -June 2012

� Rising food prices – Rising population globally is putting enormous pressures on the global food supply which is further adversely impacted by environmental pressures and increasing urbanisation leading to inflationary pressures.

Hedge against agri-based inflation

Product Category

�� Products that offer investment opportunity to capture value at various points along the “food chain” investing across the spectrum from agricultural commodities to consumer products.

Risks�� Climatic / environmental changes could lead to volatility in prices.

� Such theme-based funds have higher concentration risks as compared to funds that are well diversified.

� Such products are exposed to region specific risks.

� Products that invest into companies across the world are exposed to currency risks.

Risks�� Global developments especially development on the sovereign debt situation in the Euro region and efforts by

the US to revive growth, resulting in change in risk appetite and capital flows in the markets.

� Domestic factors / developments on corporate result season, policy uncertainties, inflation etc may impact investor sentiment.

� Products adopting a pre-determined asset allocation approach towards investing typically tend to underperform during a surge in an asset class as these products will have limited exposure to it.

� During periods of prolonged volatility, periodic rebalancing would lead to higher expenses.

22 Wealth Strategies - April -June 2012

� Short term opportunities – Yields at shorter end of the yield curve are expected to fall on easing liquidity and expectations of a pause in further interest rates tightening offering opportunities of capital appreciation. Longer term yields while benefiting from a falling yield curve will be volatile on concerns of fiscal consolidations and supply pressure.

Tactical investment opportunities

Product Category

�� Products are positioned to capitalise on opportunities available at the shorter end of the yield curve.

Risks�� Tightness in systemic liquidity.

� Slowdown in the pace of inflation’s downward trajectory.

� Slippages in the fiscal consolidation.

� Regions – Indian equity markets have remained largely range-bound over the past 2 years facing significant resistance primarily on account of valuation concerns, underlying inflation and very recently, high commodity prices. The current investment proposition of investing into companies participating into other growth regions can complement the customers’ portfolio and provide diversification benefits while retaining the high growth orientation.

� Gold – Historically, gold has been considered a hedge against global uncertainties and during times of economic instability, gold acts as an effective hedge against other investments acting as a store of value.

Diversification

Product Category

�� Products investing into companies listed in other growth regions offering opportunities of diversification.

� Products that maintain exposure to gold through ETFs.

Risks�� Many emerging market countries are still in the early stages of modern development and are subject to abrupt and

unexpected changes.

� Product is exposed to region specific risks.

� Such products that invest into companies across the world are exposed to currency risks.

� Financial / speculative interest in gold / related instruments may add to volatility in gold prices.

23 Wealth Strategies - April -June 2012

FT India Dynamic PE Ratio Fund of Funds 24

ICICI Prudential Dynamic Plan 25

Franklin India Bluechip Fund 26

ICICI Prudential Focused Bluechip Equity Fund 27

DSP BlackRock Equity Fund 28

HSBC India Opportunities Fund 29

Birla Sun Life Dividend Yield Plus 30

UTI Dividend Yield Fund 31

DWS Global Agribusiness Offshore Fund 32

HSBC Brazil Fund 33

Reliance Gold Savings Fund 34

FT India Monthly Income Plan 35

HDFC MF Monthly Income Plan - Long Term Plan 36

HSBC MIP - Savings Plan 37

Reliance Monthly Income Plan 38

DSP BlackRock Short Term Fund 39

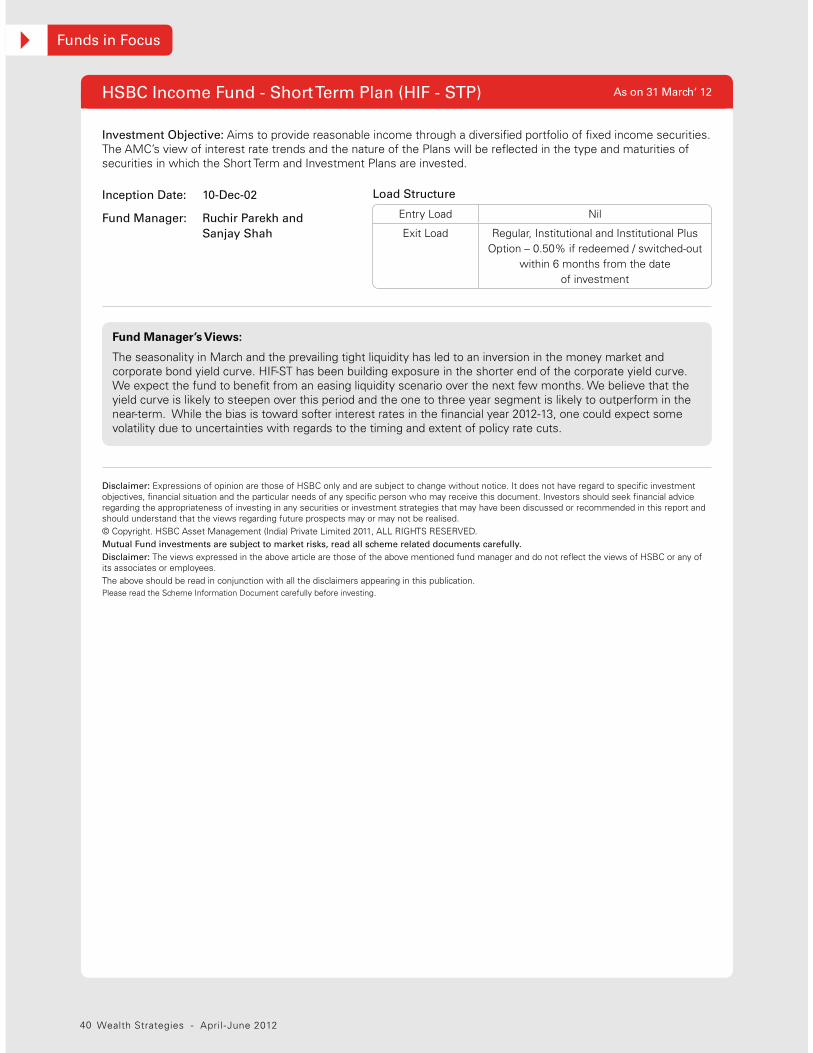

HSBC Income Fund - Short Term Plan 40

ICICI Prudential Short Term Plan 41

IDFC Super Saver Income Fund - Short Term Plan 42

Funds in Focus

Disclaimer:

The funds mentioned in the following pages have been included after considering various quantitative and qualitative factors, including past performance and observed investment style and is based on data which HSBC believes to be accurate but have not been independently verified. Inclusion in the “Funds in Focus” neither suggests that funds is suitable for you, nor that it will continue to perform as it has in the past. “Funds in Focus” should not be considered as buy or sell recommendations. Investors should carefully consider whether any/all of these funds are appropriate for them in view of their investment experience, objectives, financial resources and relevant circumstances. For further risk disclosures, please refer to the disclaimer on the first page of this publication.

Mutual funds and the underlying investments are subject to market risks and there is no guarantee, implied or otherwise, that the general objectives of the fund or any other specific performance targets will be achieved. In particular, investment returns, repayment of capital and the distribution of dividends or income are not guaranteed and the Sponsor of the fund is not responsible or liable for any loss or shortfall resulting from the operations of the fund. Please read the scheme information document carefully before investing.

24

Funds in Focus

Wealth Strategies - April -June 2012

Inception Date: 31-Oct-03

Fund Manager: Anand Radhakrishnan

Investment Objective: An open-end Fund of Funds Scheme with an objective to provide long-term capital appreciation with relatively lower volatility through a dynamically balanced portfolio of equity and income funds.

Load Structure

(Exit loads mentioned are from the date of allotment)

Entry Load Not applicable

Exit Load <= 1 year: 1%> 1 year: Nil

Fund Manager’s Views:

FTDPEF, India’s first fund of fund, is designed to have a smoother ride through volatile markets. The fund helps investors take advantage of India’s long term growth story through a tactical approach to equities and achieve stability from the increased allocation to debt at times of over valuation. It has a unique in-built buy-sell system, which determines tactical allocation between equity and debt based on PE multiples of Nifty which helps in minimising volatility. This discipline takes sentiment away from decision-making and is an ideal product for all long term investors, irrespective of risk profile. The fund currently has an allocation of 60% to Bluechip Fund and 40% to Templeton India Income Fund considering the Nifty's weighted average PE level of 19.09 (As of 29 February 2012).

Risk Factors: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. The NAVs of the schemes may go up or down depending upon the factors and forces affecting the securities market including the fluctuations in the interest rates and there can be no assurance that the schemes’ investment objectives will be achieved. The past performance of the mutual funds managed by the Franklin Templeton Group and its affiliates is not necessarily indicative of future performance of the schemes. The names of the schemes do not in any manner indicate the quality of the schemes, their future prospects or returns. The Mutual Fund is not guaranteeing or assuring any dividend under any of the schemes and the same is subject to the availability and adequacy of distributable surplus and the investment performance of the schemes. The investments made by the schemes are subject to external risks.Disclaimer: The expenses of the scheme will be over and above the expenses charged by the underlying schemes. At the peak of a bull market, a portfolio balanced on PE ratios may not outperform a fully invested portfolio. The existence, accuracy and performance of the S&P CNX Nifty Index will directly affect the scheme's performance.Disclaimer: The views expressed in the above article are those of the above mentioned fund manager and do not reflect the views of HSBC or any of its associates or employees. The above should be read in conjunction with all the disclaimers appearing in this publication.Please read the Scheme Information Document carefully before investing.

FT India Dynamic PE Ratio Fund of Funds (FTDPEF) As on 31 March‘ 12

25

Funds in Focus

Wealth Strategies - April -June 2012

Investment Objective: ICICI Prudential Dynamic Plan is an open-ended equity scheme seeking to generate capital appreciation by actively investing in equity and equity related securities. For defensive considerations, the scheme may invest in debt, money market instruments and derivatives. The investment manager will have the discretion to take aggressive asset calls i.e. by staying 100% invested in equity market/equity related instruments at a given point of time and 0% at another, in which case, the fund may be invested in debt related instruments at its discretion. The AMC may choose to churn the portfolio of the scheme in order to achieve the investment objective. The scheme is suitable for investors seeking high returns and for those who are willing to take commensurate risks. Given the dynamic nature of the investment objective of this scheme and factors such as market volatility and macroeconomic factors, which may at times be unpredictable, there is no assurance that the investment objectives of the scheme will be met.

Risk Factors: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Nothing contained in this document shall be construed to be an investment advise or an assurance of the benefits of investing in any of the schemes of ICICI Prudential Mutual Fund. Recipient alone shall be fully responsible for any decision taken on the basis of this document.Disclaimer: In the preparation of the material contained in this document, the AMC has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the AMC and/or its affiliates and which may have been made available to the AMC and/or to its affiliates. Information gathered and material used in this document is believed to be from reliable sources. The AMC however does not warrant the accuracy, reasonableness and/or completeness of any information. We have included statements / opinions / recommendations in this document, which contain words, or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or variations of such expressions, that are “forward looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and/or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices etc. The AMC (including its affiliates), the Mutual Fund, the trust and any of its officers, directors, personnel and employees, shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. Disclaimer: The views expressed in the above article are those of the above mentioned fund manager and do not reflect the views of HSBC or any of its associates or employees. The above should be read in conjunction with all the disclaimers appearing in this publication.Please read the Scheme Information Document carefully before investing.

Inception Date: 31-Oct-02

Fund Manager: Sankaran Naren and Mittul Kalawadia

Load Structure

(Exit loads mentioned are from the date of allotment)

Entry Load Not applicable

Exit Load <= 1 year: 1%> 1 year: Nil

Fund Manager’s Views:

Directionally markets are expected to remain volatile and thereby provide investment opportunity. We believe that returns can be made due to volatility and there is long term value in the market as there are many stocks with attractive valuations at this point of time. The market will require the government to take the fiscal consolidation roadmap ahead with possible increase in diesel and petrol prices which will be crucial to providing Reserve Bank of India (RBI) headroom for significant rate action. Until then, we continue to look for positive triggers like Brent Crude prices correcting and global growth stabilising to increase allocation to equity. We believe the RBI will continue to watch inflation numbers closely to enable it to take further rate action. RBI is expected to continue the tight-rope walk between short term liquidity management and currency depreciation in the near-term. The portfolio strategy will suit investors who intend to play on volatility theme since this equity-oriented fund aims at generating risk-controlled equity linked returns using a judicious asset allocation approach and help investors to benefit from risk adjusted return potential.

ICICI Prudential Dynamic Plan (Open Ended Diversified Equity Fund) As on 31 March‘ 12

26

Funds in Focus

Wealth Strategies - April -June 2012

Investment Objective: An open-end growth scheme with an objective primarily to provide medium to long-term capital appreciation.

Risk Factors: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. The NAVs of the schemes may go up or down depending upon the factors and forces affecting the securities market including the fluctuations in the interest rates and there can be no assurance that the schemes’ investment objectives will be achieved. The past performance of the mutual funds managed by the Franklin Templeton Group and its affiliates is not necessarily indicative of future performance of the schemes. The names of the schemes do not in any manner indicate the quality of the schemes, their future prospects or returns. The Mutual Fund is not guaranteeing or assuring any dividend under any of the schemes and the same is subject to the availability and adequacy of distributable surplus and the investment performance of the schemes. The investments made by the schemes are subject to external risks.Disclaimer: The views expressed in the above article are those of the above mentioned fund manager and do not reflect the views of HSBC or any of its associates or employees. The above should be read in conjunction with all the disclaimers appearing in this publication.Please read the Scheme Information Document carefully before investing.

Inception Date: 01-Dec-93

Fund Manager: Anand Radhakrishnan and

Anand Vasudevan

Load Structure

(Exit loads mentioned are from the date of allotment)

Entry Load Not applicable

Exit Load <= 1 year: 1%> 1 year: Nil

Fund Manager’s Views:

FIBCF is an open-end diversified equity fund that seeks to achieve capital appreciation through investments in large-cap companies. Launched in 1993, it is one of the oldest equity funds in the country and has consistently out-performed its benchmark BSE SENSEX across time horizons.

The fund follows a bottom-up approach to stock selection with a medium to long term perspective and ignores momentum stocks. The companies that the fund seeks to invest in (a) are well managed; (b) generate high ROCE and (c) demonstrate the ability to deliver sustainable growth in earnings. Our strategy remains focussed on the medium to long term opportunities based on investment and consumption themes.

Franklin India Bluechip Fund (FIBCF) As on 31 March‘ 12

27

Funds in Focus

Wealth Strategies - April -June 2012

Inception Date: 23-May-08

Fund Manager: Manish Gunwani

Investment Objective: ICICI Prudential Focused Bluechip Equity Fund is an open-ended equity scheme that seeks to generate long-term capital appreciation and income distribution to unitholders from a portfolio that is invested in equity and equity related securities of about 20 to 25 companies selected from the Top 200 stocks in terms of market capitalisation on the NSE. If the total assets under management under this scheme goes above `1000 crores, the Fund Manager reserves the right to increase the number of companies to more than 20.

Load Structure

(Exit loads mentioned are from the date of allotment)

Entry Load Not applicable

Exit Load <= 1 year: 1%> 1 year: Nil

Risk Factors: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Nothing contained in this document shall be construed to be an investment advise or an assurance of the benefits of investing in any of the schemes of ICICI Prudential Mutual Fund. Recipient alone shall be fully responsible for any decision taken on the basis of this document.Disclaimer: In the preparation of the material contained in this document, the AMC has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the AMC and/or its affiliates and which may have been made available to the AMC and/or to its affiliates. Information gathered and material used in this document is believed to be from reliable sources. The AMC however does not warrant the accuracy, reasonableness and/or completeness of any information. We have included statements / opinions / recommendations in this document, which contain words, or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or variations of such expressions, that are “forward looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and/or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices etc. The AMC (including its affiliates), the Mutual Fund, the trust and any of its officers, directors, personnel and employees, shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. Disclaimer: The views expressed in the above article are those of the above mentioned fund manager and do not reflect the views of HSBC or any of its associates or employees. The above should be read in conjunction with all the disclaimers appearing in this publication. Please read the Scheme Information Document carefully before investing.

Fund Manager’s Views:

Directionally markets are expected to remain volatile and thereby provide investment opportunity. We believe that returns can be made due to volatility and there is long term value in the market as there are many stocks with attractive valuations at this point of time. The market will require the government to take the fiscal consolidation roadmap ahead with possible increase in diesel and petrol prices which will be crucial to providing Reserve Bank of India (RBI) headroom for significant rate action. Until then, we continue to look for positive triggers like Brent Crude prices correcting and global growth stabilising to increase allocation to equity. We believe the RBI will continue to watch inflation numbers closely to enable it to take further rate action. RBI is expected to continue the tight-rope walk between short term liquidity management and currency depreciation in the near-term. The fund suits investors who seek capital appreciation in the long term though optimal diversification as against excessive diversification. The fund invests in high conviction 20-25 blue-chip stocks of large cap companies having potential to generate alpha over the long term.

ICICI Prudential Focused Bluechip Equity Fund (IPFBF)

(an open-ended equity fund)

As on 31 March‘ 12

28

Funds in Focus

Wealth Strategies - April -June 2012

As on 31 March‘ 12

Investment Objective: DSPBR Equity is an open-ended growth scheme, seeking to generate long term capital appreciation, from a portfolio that is substantially constituted of equity securities and equity related securities of issuers domiciled in India.

Disclaimer and Risk Factors:

Statutory Details: DSP BlackRock Mutual Fund was set up as a Trust and the settlors/sponsors are DSP ADIKO Holdings Pvt. Ltd. and DSP HMK Holdings Pvt. Ltd. (collectively) and BlackRock Inc. (Combined liability restricted to `1 lakh). Trustee: DSP BlackRock Trustee Company Pvt. Ltd. Investment Manager: DSP BlackRock Investment Managers Pvt. Ltd.Risk Factors: Mutual funds like securities investments, are subject to market and other risks and there can be no assurance that the schemes’

objectives will be achieved. As with any investment in securities, the NAV of Units issued under the schemes can go up or down depending on

the factors and forces affecting capital markets. Past performance of the sponsor/AMC/mutual fund does not indicate the future performance of the schemes. Investors in the schemes are not being offered a guaranteed or assured rate of return. Each Scheme/Plan is required to have (i) minimum 20 investors and (ii) no single investor holding >25% of corpus. If the aforesaid point (i) is not fulfilled within the prescribed time, the Scheme/Plan concerned will be wound up and in case of breach of the aforesaid point (ii) at the end of the prescribed period, the investor’s holding in excess of 25% of the corpus will be redeemed as per SEBI guidelines. The names of the schemes do not in any manner indicate the quality of the

schemes, their future prospects or returns. For scheme specific risk factors, please refer the SID. For more details, please refer the Key Information Memorandum cum Application Forms, which are available on the website, www.dspblackrock.com, and at the ISCs/Distributors. Please read the

Scheme Information Document and Statement of Additional Information carefully before investing.Disclaimer: The views expressed in the above article are those of the above mentioned fund manager and do not reflect the views of HSBC or any of its associates or employees.The above should be read in conjunction with all the disclaimers appearing in this publication.Please read the Scheme Information Document carefully before investing.

Allotment Date: 29-Apr-97

Fund Manager: Apoorva Shah

Load Structure

(Exit loads applicable from the date of allotment of units to unitholder)

Entry Load Nil

Exit Load <12 months: 1%>=12 months: Nil

Fund Manager’s Views:

On a sector level, the fund is overweight on Consumer Discretionary (includes Autos) and Industrials. We have increased weight to rate sensitive’s and cyclical sectors as we believe RBI will start cutting key policy rates in the next few weeks owing to moderation in inflation and the GDP slowdown for two consecutive quarters (Q3 GDP came at 6.1%). We have also increased our weight to the Automobiles sector which will benefit if the RBI starts cutting key policy rates in the next few weeks. Financials will benefit with the fall in interest rates, though credit offtake will be the key driver for performance. The fund has been successful in moving across sectors which has helped the funds performance in an environment where the mid caps have outperformed the large caps. Overall the fund is positioned to benefit from an economic recovery which we believe will happen over the next few months.

DSP BlackRock Equity Fund (DSPBR Equity)

29

Funds in Focus

Wealth Strategies - April -June 2012

As on 31 March‘ 12

Investment Objective: Seeks long term capital growth through investments across all market capitalisations, including small, mid and large cap stocks. It aims to be predominantly invested in equity and equity related securities. However, it could move a significant portion of its assets towards fixed income securities, if the fund manager becomes negative on equity markets.

Disclaimer: Expressions of opinion are those of HSBC only and are subject to change without notice. It does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies that may have been discussed or recommended in this report and should understand that the views regarding future prospects may or may not be realised. © Copyright. HSBC Asset Management (India) Private Limited 2011, ALL RIGHTS RESERVED. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Disclaimer: The views expressed in the above article are those of the above mentioned fund manager and do not reflect the views of HSBC or any of its associates or employees.The above should be read in conjunction with all the disclaimers appearing in this publication.Please read the Scheme Information Document carefully before investing.

Inception Date: 24-Feb-04

Fund Manager: Tushar Pradhan

Load Structure

Entry Load Nil

Exit Load 1%, if redeemed/switched out within 1 year from the date of

investments.

Fund Manager’s Views:

The global outlook remains challenging and the focus remains on visible cash flow generators in the portfolio. We have a cautious approach on the Indian economy as signs of slowing Industrial Production indicate softening of manufacturing demand. Our investment philosophy continues to be driven by our globally adopted PB-ROE model, which will help our stock selection to remain focussed on quality and in turn, help achieve our endeavour to deliver long term performance. "A best of both worlds approach" – In a cricketing lingo, a look at the portfolio will highlight that the top order will share commonality with large cap portfolios with the bottom order aiming for alpha creation through a rich sprinkling of mid-caps. These bring in a healthy combination of stability (large caps tend to have lower volatility) and better growth prospects (mid caps tend to have higher growth) to the portfolio.

HSBC India Opportunities Fund (HIOF)

30

Funds in Focus

Wealth Strategies - April -June 2012

Inception Date: 26-Feb-03

Fund Manager: Nishit Dholakia

Investment Objective: The objective of the scheme is to provide capital growth and income by investing primarily in a well-diversified portfolio of dividend paying companies that have a relatively high dividend yield.

Statutory Details: Constitution: Birla Sun Life Mutual Fund has been set up as a Trust under the Indian Trust Act, 1882. Sponsors: Aditya Birla Financial Services Private Limited and Sun Life (India) AMC Investments Inc (liability restricted to seed corpus of `1 lakh). Trustee: Birla Sun Life Trustee Company Pvt. Ltd. Risk Factors: Mutual Funds and securities investments are subject to market risks and there can be no assurance or guarantee that the

objective of the scheme will be achieved. As with any investment in securities, the NAV of the Units issued under the scheme may go up or

down depending on the various factors and forces affecting capital markets and money markets. Past performance of the Sponsor / Investment Manager / Mutual Fund does not indicate the future performance of the scheme and may not necessarily provide a basis of comparison with other investments. The name of the scheme does not, in any manner, indicate either the quality of the scheme or its future prospects or returns.

Unitholders in the scheme are not being offered any guaranteed/assured returns. Investors should read the Scheme Information Document/

Statement of Additional Information/Key Information Memorandum available at Investor Service Centres and with Distributors carefully before

investing.

Disclaimer: The views expressed in the above article are those of the above mentioned fund manager and do not reflect the views of HSBC or any of its associates or employees.The above should be read in conjunction with all the disclaimers appearing in this publication.Please read the Scheme Information Document carefully before investing.

Load Structure

(Exit loads mentioned are from the date of allotment)

Entry Load Not applicable

Exit Load <= 1 year: 1%> 1 year: Nil

Fund Manager’s Views:

Birla Sunlife Dividend Yield Plus invests in stocks having dividend yield twice that of Sensex at the time of making the investment. The objective is to identify business with steady growth prospects and strong management available at reasonable valuation and offering higher risk adjusted returns. After above mentioned filters are met, fund manager identifies and invests in businesses having steady growth in earnings and dividend, strong return ratios on invested capital, strong free cash flow generation, healthy balance sheet and consistency of dividend payments. During market exuberance, the fund may not be able to fully participate in the sharp up move but during extreme market corrections it provides downside cushion to reasonable extent. The scheme typically exhibits lower volatility and over a market cycle would tend to outperform the broader market thereby delivering superior risk adjusted returns. The fund maintains a well diversified equity portfolio. The portfolio dividend yield as of end of March 31, 2012 was 2.7% against 1.5% dividend yield of sensex stocks. The key sectoral exposure in the fund are Banking and Financial Services, Consumer Non Durables and Oil, Gas and Petroleum products and Auto. The fund has around 37% of the portfolio of the fund invested in large cap stocks while balance portfolio is invested in midcap and smallcap stocks. The cash level in the fund is around 5%.

Birla Sun Life Dividend Yield Plus (BDYP) As on 31 March‘ 12

31

Funds in Focus

Wealth Strategies - April -June 2012

As on 31 March‘ 12

Investment Objective: UTI Dividend Yield Fund is an open-ended equity oriented scheme. The investment objective of the scheme is to provide medium to long term capital gains and/or dividend distribution by investing predominantly in equity and equity related instruments, which offer high dividend yield. There can be no assurance that the investment objectives of the scheme will be realised.