DATA ANALYSIS FOR DECISION MAKING IN HSBC

29

DATA ANALYSIS FOR DECISION MAKING IN HSBC Business Decision Making NGUYEN NGOC MINH – F06B PREPARE FOR: BOARD OF DIRECTOR OF HSBC

Transcript of DATA ANALYSIS FOR DECISION MAKING IN HSBC

DATA ANALYSIS FOR DECISION MAKING IN HSBC

Business Decision Making

NGUYEN NGOC MINH – F06B

PREPARE FOR: BOARD OF DIRECTOR OF HSBC

Executive summary

As the newly appointed Junior Data Research Officer work in

HSBC which branch located in Vietnam, the report show 3 tasks

related to the financial services departments in the banks and provide

the suitable recommendation for the bank to increase the efficiency

and productivity. The bank should use multiplicative model method

for calculating and forecasting the actual sales of bank in the next

year. There are 5 useful software which are recommended for the

bank to help them increase the efficiency and productivity. The report

has create the detail plan for the bank to follow which is reasonable

and have the lowest cost. In the final test, the report have shown the

way to evaluate the project by 2 method NPV and IRR and make the

conclusion for the bank to choose which one is the good project for

the bank in the future.

Contents

Executive summary ......................................................................................................................... 0

Introduction ..................................................................................................................................... 1

Task 1: Forecasting techniques ...................................................................................................... 2

I. Additive model..................................................................................................................... 2

The seasonal variations for 4 years’ sales (‘000) are as follows: ........................................... 2

The estimate of average quarterly variation: .......................................................................... 3

Calculating the forecast of sales for 2013 ............................................................................... 4

The diagram to show the trend-line and forecast sales ........................................................... 5

II. Multiplicative model ........................................................................................................ 6

1. The seasonal variations for 4 years’ sales (‘000) are as follows: ................................. 6

The estimate of average quarterly variation: .......................................................................... 7

Calculating the forecast of sales for 2013 ............................................................................... 7

The diagram to show the trend-line and forecast sales ........................................................... 8

III. Least squares regression model ........................................................................................ 9

1. The regression line – trend line .................................................................................... 9

The diagram of the trend-line ............................................................................................... 10

IV. Conclusion ...................................................................................................................... 11

Task 2: Information processing tools ............................................................................................ 13

Task 3: Project planning ............................................................................................................... 17

I. The activities comprise a project of customer services ..................................................... 17

II. The network diagram for the activity of HSBC bank in financial services ................... 17

III. The grant chart which show the planning of the project ................................................ 18

Task 4: Discount cash flow (DCF) methods ................................................................................. 20

I. The Net Present Value method (NPV)............................................................................... 20

V. The Internal Rate of Return method (IRR) .................................................................... 20

“Papa loves Mommy” investment ........................................................................................ 21

“Family” investment ............................................................................................................. 22

Conclusion .................................................................................................................................... 25

References ..................................................................................................................................... 26

Introduction

As the newly appointed Junior Data Research Officer work in HSBC which branch located

in Vietnam, the report show 3 task related to the financial services departments in the banks. At

the first task is the forecasting technique, which shows various way to calculate the actual sales of

the bank in the future, and then show the formal report for the Board of director. In the next task

in the reports, there is the information processing tools which shows the decision level and

information types in each department and the recommendation for the software for each part of

department. In the third task, the project planning have been show the way to prepare the schedule

of giving gift for customer and the number of employee should have in this project. In the last task,

it is the evaluation of two projects – “PLM” and “Family”. The calculation and recommendation

of the suitable project are provide in the end of the report.

ITP – F06-092

2

BDM A2 - Max

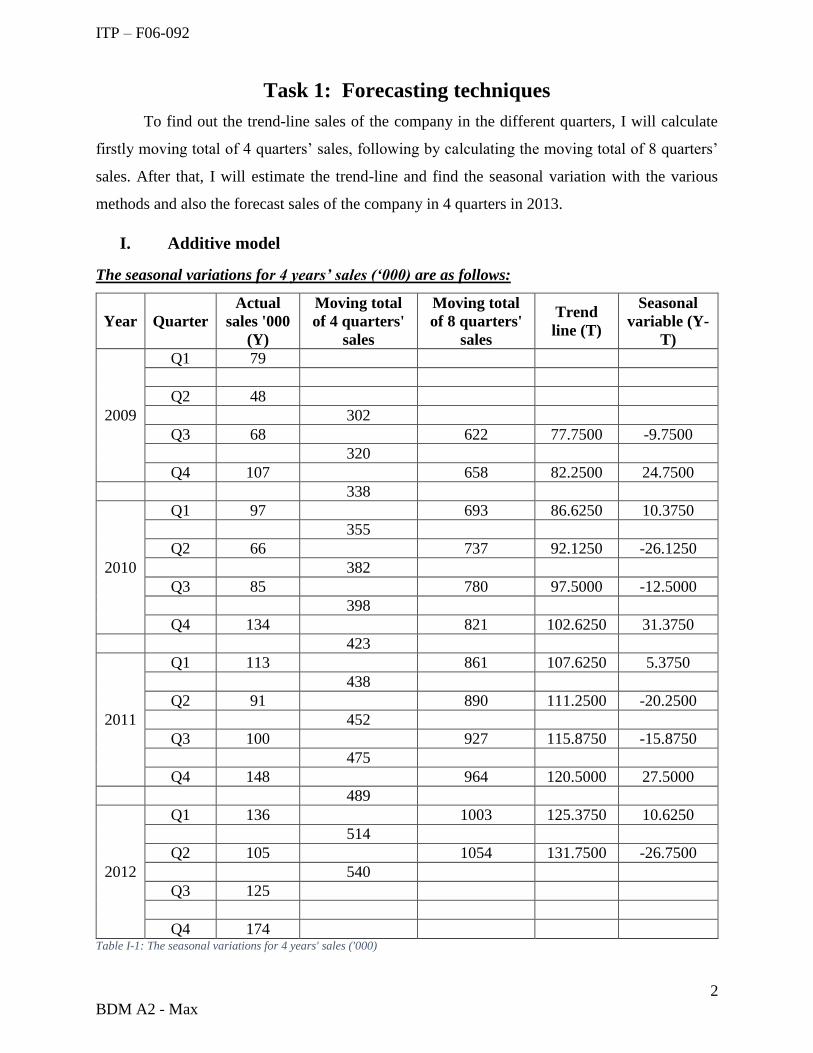

Task 1: Forecasting techniques

To find out the trend-line sales of the company in the different quarters, I will calculate

firstly moving total of 4 quarters’ sales, following by calculating the moving total of 8 quarters’

sales. After that, I will estimate the trend-line and find the seasonal variation with the various

methods and also the forecast sales of the company in 4 quarters in 2013.

I. Additive model

The seasonal variations for 4 years’ sales (‘000) are as follows:

Year Quarter

Actual

sales '000

(Y)

Moving total

of 4 quarters'

sales

Moving total

of 8 quarters'

sales

Trend

line (T)

Seasonal

variable (Y-

T)

2009

Q1 79

Q2 48

302

Q3 68 622 77.7500 -9.7500

320

Q4 107 658 82.2500 24.7500

338

2010

Q1 97 693 86.6250 10.3750

355

Q2 66 737 92.1250 -26.1250

382

Q3 85 780 97.5000 -12.5000

398

Q4 134 821 102.6250 31.3750

423

2011

Q1 113 861 107.6250 5.3750

438

Q2 91 890 111.2500 -20.2500

452

Q3 100 927 115.8750 -15.8750

475

Q4 148 964 120.5000 27.5000

489

2012

Q1 136 1003 125.3750 10.6250

514

Q2 105 1054 131.7500 -26.7500

540

Q3 125

Q4 174 Table I-1: The seasonal variations for 4 years' sales ('000)

ITP – F06-092

3

BDM A2 - Max

Explanation:

o At first, I summed the actual sales of four quarters in 2009 which are 79, 48, 68 and 107

respectively, the result of this calculation (302) was the first “Moving total of 4 quarters’

sales”. The total sales of four quarters from 2nd quarter of 2009 to the 1st quarter of 2010

which are 48, 68, 107 and 97, is the second result of “Moving total of 4 quarters’ sales”.

Keep going like this, I got all the results of “Moving total of 4 quarters’ sales” from 2009

to 2012

o In the next step, I continued to calculate the “Moving total of 8 quarters’ sales”. The result

of this part is the sum of two consecutive numbers of the before part – “Moving total of 4

quarters’ sales”. (302+320=622). Continue calculating like this I got all the result for this

part from 2009 to 2012.

o To calculate the trend-line, in each respective result of “moving total of 8 quarters’ sales”,

I divided this result by 8 which are (622/8=77.75) in 3rd Quarter 2009. After that, I

calculated continuously to get all the approximate results for the “Trend line” from 2009

to 2012.

o In the last column – “seasonal variation”, I calculated them by taking the “actual sales” of

respective quarter minus the “Trend-line” as (68-77.75= -9.75) in the 3rd quarter 2009. And

then, I find out all the result of seasonal variation from 2009 to 2012.

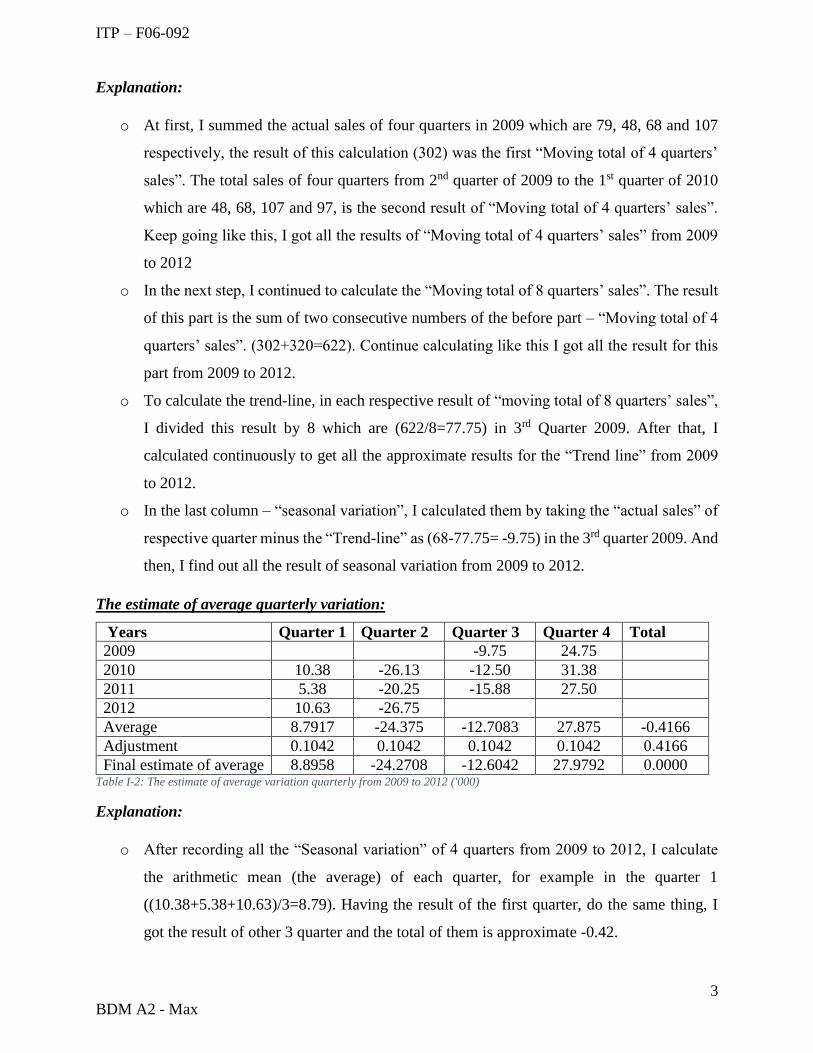

The estimate of average quarterly variation:

Years Quarter 1 Quarter 2 Quarter 3 Quarter 4 Total

2009 -9.75 24.75

2010 10.38 -26.13 -12.50 31.38

2011 5.38 -20.25 -15.88 27.50

2012 10.63 -26.75

Average 8.7917 -24.375 -12.7083 27.875 -0.4166

Adjustment 0.1042 0.1042 0.1042 0.1042 0.4166

Final estimate of average 8.8958 -24.2708 -12.6042 27.9792 0.0000 Table I-2: The estimate of average variation quarterly from 2009 to 2012 ('000)

Explanation:

o After recording all the “Seasonal variation” of 4 quarters from 2009 to 2012, I calculate

the arithmetic mean (the average) of each quarter, for example in the quarter 1

((10.38+5.38+10.63)/3=8.79). Having the result of the first quarter, do the same thing, I

got the result of other 3 quarter and the total of them is approximate -0.42.

ITP – F06-092

4

BDM A2 - Max

o To increase the total variance to 0, I added 0.42 in “Adjustment”, and divided into 4 quarter

by dividing the result by 4. So that, I had approximate 0.104 in each quarter.

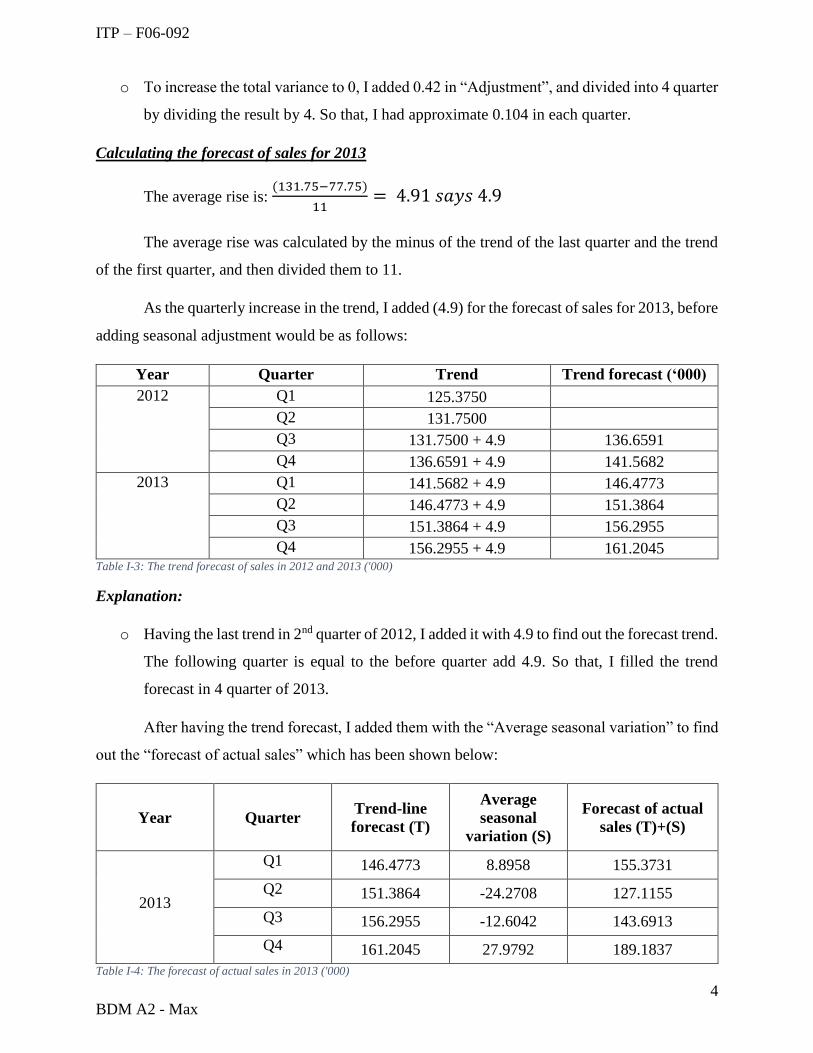

Calculating the forecast of sales for 2013

The average rise is: (131.75−77.75)

11= 4.91 𝑠𝑎𝑦𝑠 4.9

The average rise was calculated by the minus of the trend of the last quarter and the trend

of the first quarter, and then divided them to 11.

As the quarterly increase in the trend, I added (4.9) for the forecast of sales for 2013, before

adding seasonal adjustment would be as follows:

Year Quarter Trend Trend forecast (‘000)

2012 Q1 125.3750

Q2 131.7500

Q3 131.7500 + 4.9 136.6591

Q4 136.6591 + 4.9 141.5682

2013 Q1 141.5682 + 4.9 146.4773

Q2 146.4773 + 4.9 151.3864

Q3 151.3864 + 4.9 156.2955

Q4 156.2955 + 4.9 161.2045 Table I-3: The trend forecast of sales in 2012 and 2013 ('000)

Explanation:

o Having the last trend in 2nd quarter of 2012, I added it with 4.9 to find out the forecast trend.

The following quarter is equal to the before quarter add 4.9. So that, I filled the trend

forecast in 4 quarter of 2013.

After having the trend forecast, I added them with the “Average seasonal variation” to find

out the “forecast of actual sales” which has been shown below:

Year Quarter Trend-line

forecast (T)

Average

seasonal

variation (S)

Forecast of actual

sales (T)+(S)

2013

Q1 146.4773 8.8958 155.3731

Q2 151.3864 -24.2708 127.1155

Q3 156.2955 -12.6042 143.6913

Q4 161.2045 27.9792 189.1837

Table I-4: The forecast of actual sales in 2013 ('000)

ITP – F06-092

5

BDM A2 - Max

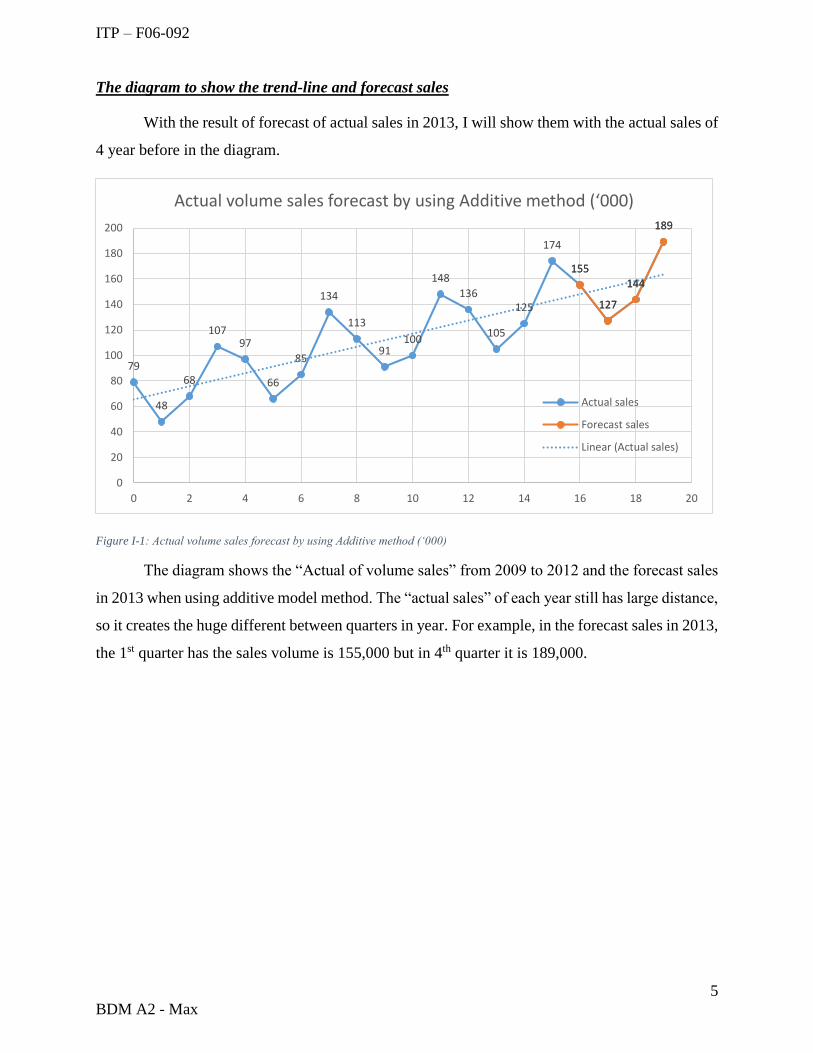

The diagram to show the trend-line and forecast sales

With the result of forecast of actual sales in 2013, I will show them with the actual sales of

4 year before in the diagram.

Figure I-1: Actual volume sales forecast by using Additive method (‘000)

The diagram shows the “Actual of volume sales” from 2009 to 2012 and the forecast sales

in 2013 when using additive model method. The “actual sales” of each year still has large distance,

so it creates the huge different between quarters in year. For example, in the forecast sales in 2013,

the 1st quarter has the sales volume is 155,000 but in 4th quarter it is 189,000.

79

48

68

10797

66

85

134

113

91100

148

136

105

125

174

155

127

144

189

155

127

144

189

0

20

40

60

80

100

120

140

160

180

200

0 2 4 6 8 10 12 14 16 18 20

Actual volume sales forecast by using Additive method (‘000)

Actual sales

Forecast sales

Linear (Actual sales)

ITP – F06-092

6

BDM A2 - Max

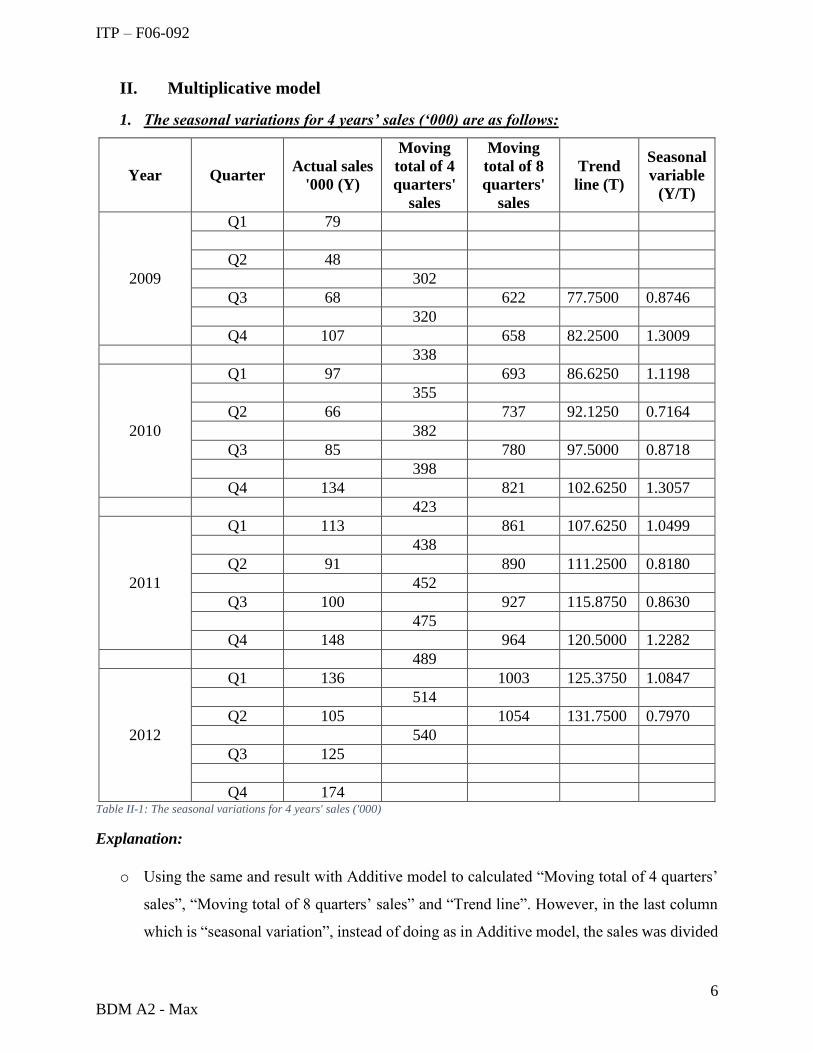

II. Multiplicative model

1. The seasonal variations for 4 years’ sales (‘000) are as follows:

Year Quarter Actual sales

'000 (Y)

Moving

total of 4

quarters'

sales

Moving

total of 8

quarters'

sales

Trend

line (T)

Seasonal

variable

(Y/T)

2009

Q1 79

Q2 48

302

Q3 68 622 77.7500 0.8746

320

Q4 107 658 82.2500 1.3009

338

2010

Q1 97 693 86.6250 1.1198

355

Q2 66 737 92.1250 0.7164

382

Q3 85 780 97.5000 0.8718

398

Q4 134 821 102.6250 1.3057

423

2011

Q1 113 861 107.6250 1.0499

438

Q2 91 890 111.2500 0.8180

452

Q3 100 927 115.8750 0.8630

475

Q4 148 964 120.5000 1.2282

489

2012

Q1 136 1003 125.3750 1.0847

514

Q2 105 1054 131.7500 0.7970

540

Q3 125

Q4 174 Table II-1: The seasonal variations for 4 years' sales ('000)

Explanation:

o Using the same and result with Additive model to calculated “Moving total of 4 quarters’

sales”, “Moving total of 8 quarters’ sales” and “Trend line”. However, in the last column

which is “seasonal variation”, instead of doing as in Additive model, the sales was divided

ITP – F06-092

7

BDM A2 - Max

by the trend line. By that way, I calculated all the results of “Seasonal variation” from 2009

to 2012.

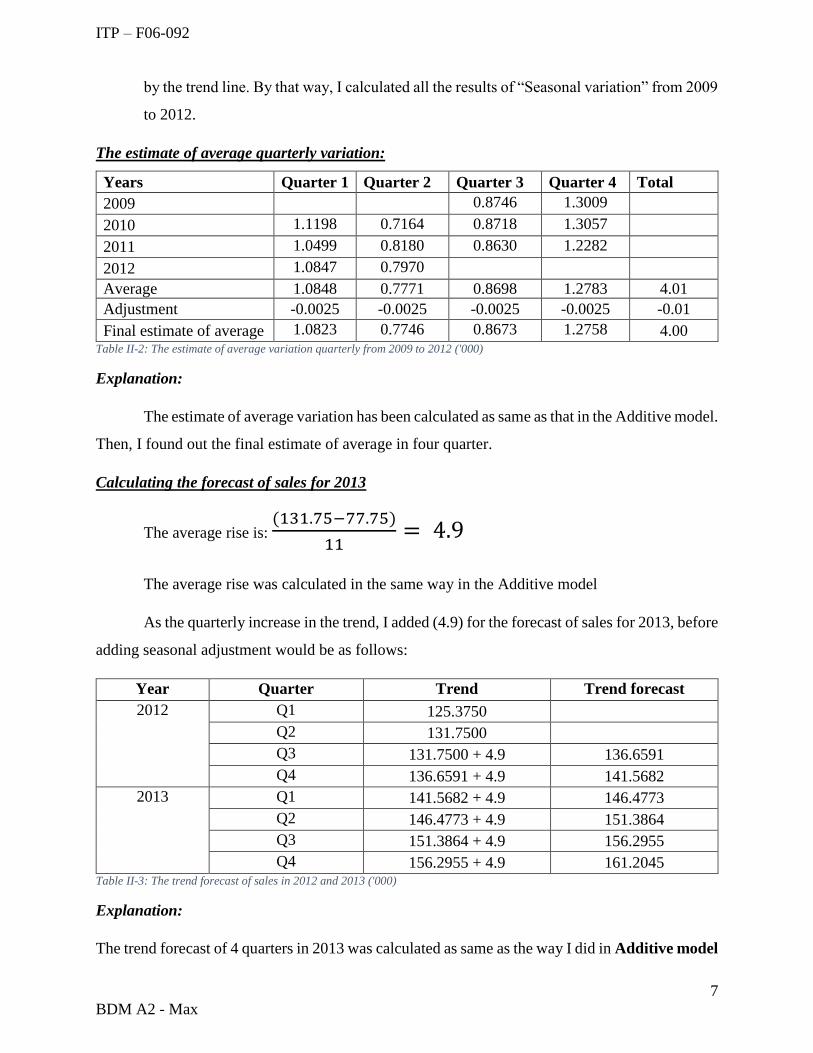

The estimate of average quarterly variation:

Years Quarter 1 Quarter 2 Quarter 3 Quarter 4 Total

2009 0.8746 1.3009

2010 1.1198 0.7164 0.8718 1.3057

2011 1.0499 0.8180 0.8630 1.2282

2012 1.0847 0.7970

Average 1.0848 0.7771 0.8698 1.2783 4.01

Adjustment -0.0025 -0.0025 -0.0025 -0.0025 -0.01

Final estimate of average 1.0823 0.7746 0.8673 1.2758 4.00 Table II-2: The estimate of average variation quarterly from 2009 to 2012 ('000)

Explanation:

The estimate of average variation has been calculated as same as that in the Additive model.

Then, I found out the final estimate of average in four quarter.

Calculating the forecast of sales for 2013

The average rise is: (131.75−77.75)

11= 4.9

The average rise was calculated in the same way in the Additive model

As the quarterly increase in the trend, I added (4.9) for the forecast of sales for 2013, before

adding seasonal adjustment would be as follows:

Year Quarter Trend Trend forecast

2012 Q1 125.3750

Q2 131.7500

Q3 131.7500 + 4.9 136.6591

Q4 136.6591 + 4.9 141.5682

2013 Q1 141.5682 + 4.9 146.4773

Q2 146.4773 + 4.9 151.3864

Q3 151.3864 + 4.9 156.2955

Q4 156.2955 + 4.9 161.2045 Table II-3: The trend forecast of sales in 2012 and 2013 ('000)

Explanation:

The trend forecast of 4 quarters in 2013 was calculated as same as the way I did in Additive model

ITP – F06-092

8

BDM A2 - Max

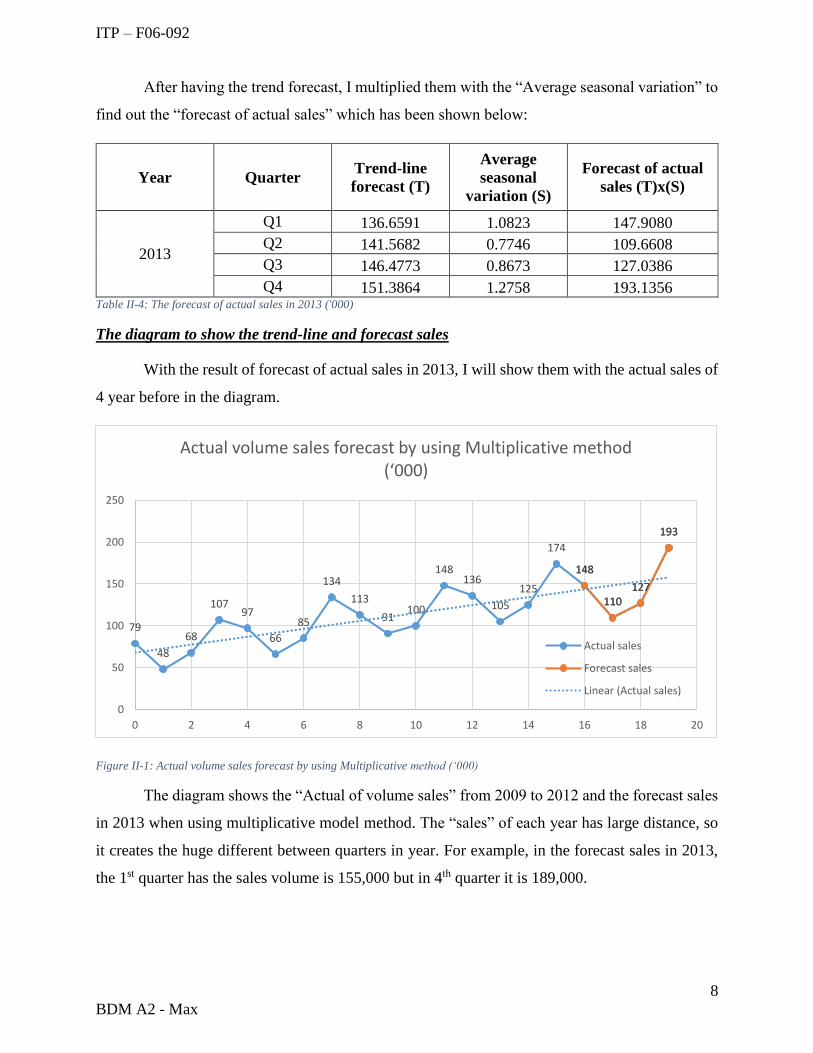

After having the trend forecast, I multiplied them with the “Average seasonal variation” to

find out the “forecast of actual sales” which has been shown below:

Year Quarter Trend-line

forecast (T)

Average

seasonal

variation (S)

Forecast of actual

sales (T)x(S)

2013

Q1 136.6591 1.0823 147.9080

Q2 141.5682 0.7746 109.6608

Q3 146.4773 0.8673 127.0386

Q4 151.3864 1.2758 193.1356 Table II-4: The forecast of actual sales in 2013 ('000)

The diagram to show the trend-line and forecast sales

With the result of forecast of actual sales in 2013, I will show them with the actual sales of

4 year before in the diagram.

Figure II-1: Actual volume sales forecast by using Multiplicative method (‘000)

The diagram shows the “Actual of volume sales” from 2009 to 2012 and the forecast sales

in 2013 when using multiplicative model method. The “sales” of each year has large distance, so

it creates the huge different between quarters in year. For example, in the forecast sales in 2013,

the 1st quarter has the sales volume is 155,000 but in 4th quarter it is 189,000.

79

48

68

10797

66

85

134

113

91100

148136

105

125

174

148

110127

193

148

110127

193

0

50

100

150

200

250

0 2 4 6 8 10 12 14 16 18 20

Actual volume sales forecast by using Multiplicative method (‘000)

Actual sales

Forecast sales

Linear (Actual sales)

ITP – F06-092

9

BDM A2 - Max

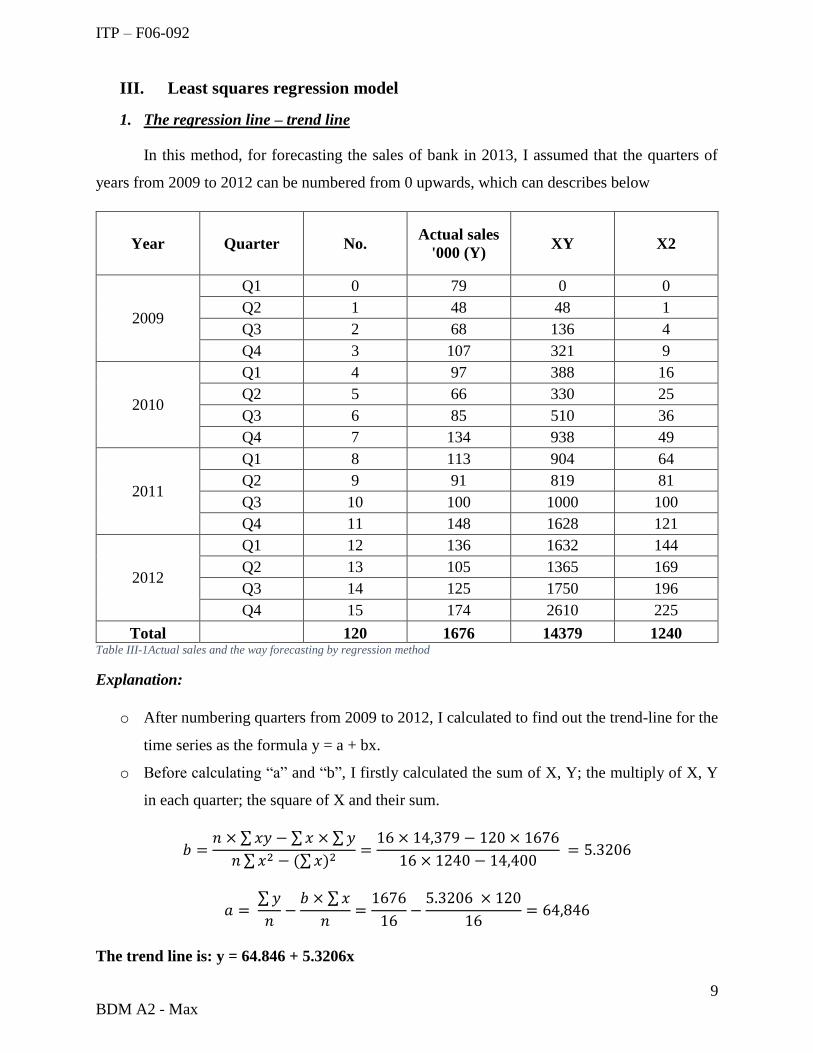

III. Least squares regression model

1. The regression line – trend line

In this method, for forecasting the sales of bank in 2013, I assumed that the quarters of

years from 2009 to 2012 can be numbered from 0 upwards, which can describes below

Year Quarter No. Actual sales

'000 (Y) XY X2

2009

Q1 0 79 0 0

Q2 1 48 48 1

Q3 2 68 136 4

Q4 3 107 321 9

2010

Q1 4 97 388 16

Q2 5 66 330 25

Q3 6 85 510 36

Q4 7 134 938 49

2011

Q1 8 113 904 64

Q2 9 91 819 81

Q3 10 100 1000 100

Q4 11 148 1628 121

2012

Q1 12 136 1632 144

Q2 13 105 1365 169

Q3 14 125 1750 196

Q4 15 174 2610 225

Total 120 1676 14379 1240 Table III-1Actual sales and the way forecasting by regression method

Explanation:

o After numbering quarters from 2009 to 2012, I calculated to find out the trend-line for the

time series as the formula y = a + bx.

o Before calculating “a” and “b”, I firstly calculated the sum of X, Y; the multiply of X, Y

in each quarter; the square of X and their sum.

𝑏 =𝑛 × ∑ 𝑥𝑦 − ∑ 𝑥 × ∑ 𝑦

𝑛 ∑ 𝑥2 − (∑ 𝑥)2=

16 × 14,379 − 120 × 1676

16 × 1240 − 14,400 = 5.3206

𝑎 = ∑ 𝑦

𝑛−

𝑏 × ∑ 𝑥

𝑛=

1676

16−

5.3206 × 120

16= 64,846

The trend line is: y = 64.846 + 5.3206x

ITP – F06-092

10

BDM A2 - Max

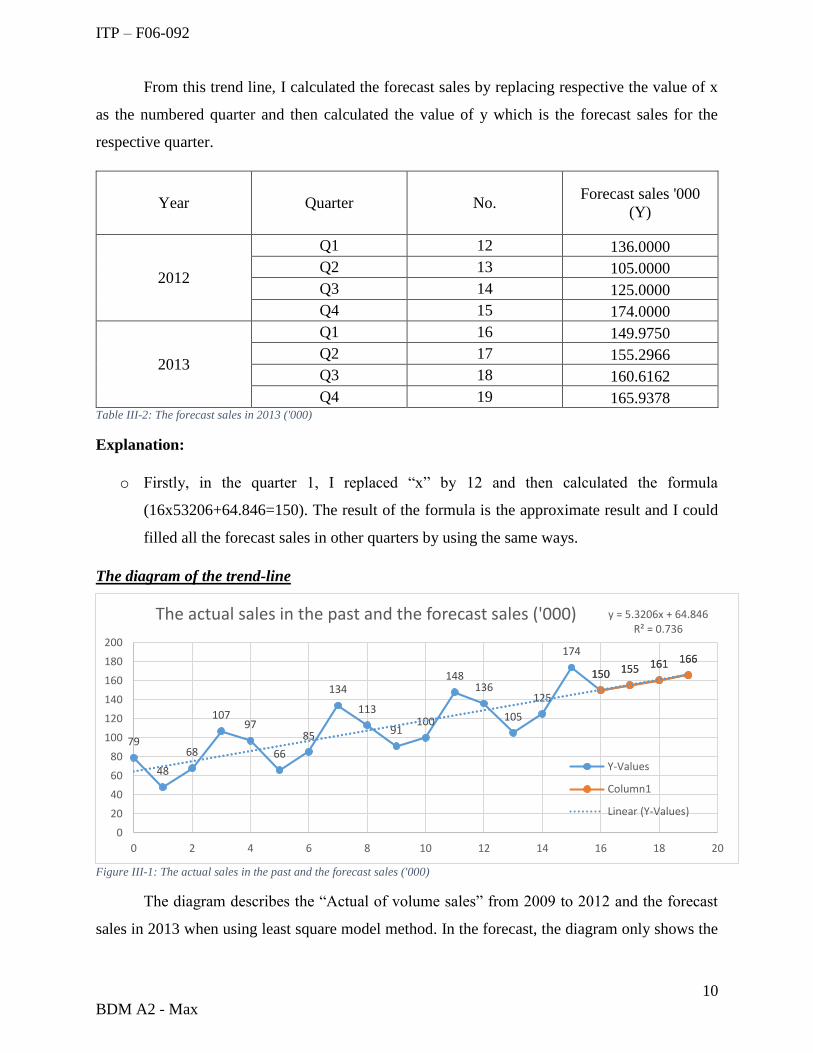

From this trend line, I calculated the forecast sales by replacing respective the value of x

as the numbered quarter and then calculated the value of y which is the forecast sales for the

respective quarter.

Year Quarter No. Forecast sales '000

(Y)

2012

Q1 12 136.0000

Q2 13 105.0000

Q3 14 125.0000

Q4 15 174.0000

2013

Q1 16 149.9750

Q2 17 155.2966

Q3 18 160.6162

Q4 19 165.9378 Table III-2: The forecast sales in 2013 ('000)

Explanation:

o Firstly, in the quarter 1, I replaced “x” by 12 and then calculated the formula

(16x53206+64.846=150). The result of the formula is the approximate result and I could

filled all the forecast sales in other quarters by using the same ways.

The diagram of the trend-line

Figure III-1: The actual sales in the past and the forecast sales ('000)

The diagram describes the “Actual of volume sales” from 2009 to 2012 and the forecast

sales in 2013 when using least square model method. In the forecast, the diagram only shows the

79

48

68

10797

66

85

134

113

91100

148136

105

125

174

150 155 161 166

150 155 161 166

y = 5.3206x + 64.846R² = 0.736

0

20

40

60

80

100

120

140

160

180

200

0 2 4 6 8 10 12 14 16 18 20

The actual sales in the past and the forecast sales ('000)

Y-Values

Column1

Linear (Y-Values)

ITP – F06-092

11

BDM A2 - Max

trends of the sales which is increasing, but does not show the fluctuation as well as the real actual

of volume sales in the future.

IV. Conclusion

There are three different methods in calculating and forecasting the sales of company,

which show three different results.

In additive model method, the seasonal variation over period of time is expected to be

unchanged, but it is not always right. In fact, the trend is decreasing and increasing over time and

the seasonal variation is fluctuate too. Because of the effect of many different reason such as

performance of business or government policy, the sales of the company could be affected directly

or indirectly, which make the seasonal variation hard to be a constant number over time. Thus, it

is hard to find the reliability in this method.

In the multiplicative model method, the problem is seemed to be solve in this method. To

face with the variation of seasonal variation over period, by multiplying trend values by a seasonal

variation factor, this method have what it takes in follow the changing of seasonal variations. It

means that the seasonal variation in this method changes when the trend changes. Thus, this

method give a better forecast than the others. So that, the bank should choose this method to

calculate and forecast the sales result in 2013.

In the least square method, the sales have been forecasted to grow regularly, which show

the incorrectly in this method. In the least square method, the past result in the company is ignore

and it shows the forecast sale with no relationship with the fluctuation of actual sale in the past.

So that, using this method is not a good way, even though it show an amazing steady growth for

the company.

In sum up, forecasting is a significant role in running a bank. Using 3 methods, it is easily

to be seen that, in each method, the bank can have a different result which can effect to the profit

of the bank as well as the plan they have to prepare for the next year. In 3 methods, using the

additive and multiplicative method are more realistic than using the least square regression

method, which make the bank does not know about the fluctuation of the sales in each quarter.

Recommendation

In the recommendation for the bank, the bank should use the multiplicative method for

forecasting the sales in the future, which is not only cannot be affected by the level of sales but

also can expresses each actual figure as a proportion of the trend.

ITP – F06-092

12

BDM A2 - Max

REPORT ON ASSISTING THE FINANCIAL SERVICES DEPARTMENTS OF HSBC

To: Board of Directors, HSBC Ltd

From: Nguyen Ngoc Minh, Data Research Officer

Status: Confidential

Date: 21/5/2014

I. INTRODUCTION AND TERMS OF REFERENCE

This report details the results of producing a sales forecast by the past sales data in three

years ago. We were asked to consider the sales of the company in the past of three years

from 2009 to 2012 and to identify the forecast sales of the company in the next year

(2013)

II. METHOD

The following investigatory procedures were adopted:

1. Collection of the past sales data from 2009 to 2012 of the financial services

departments.

2. Using different method to try and produce a sales forecast for 2013

Additive model

Multiplicative model

Least squares regression model

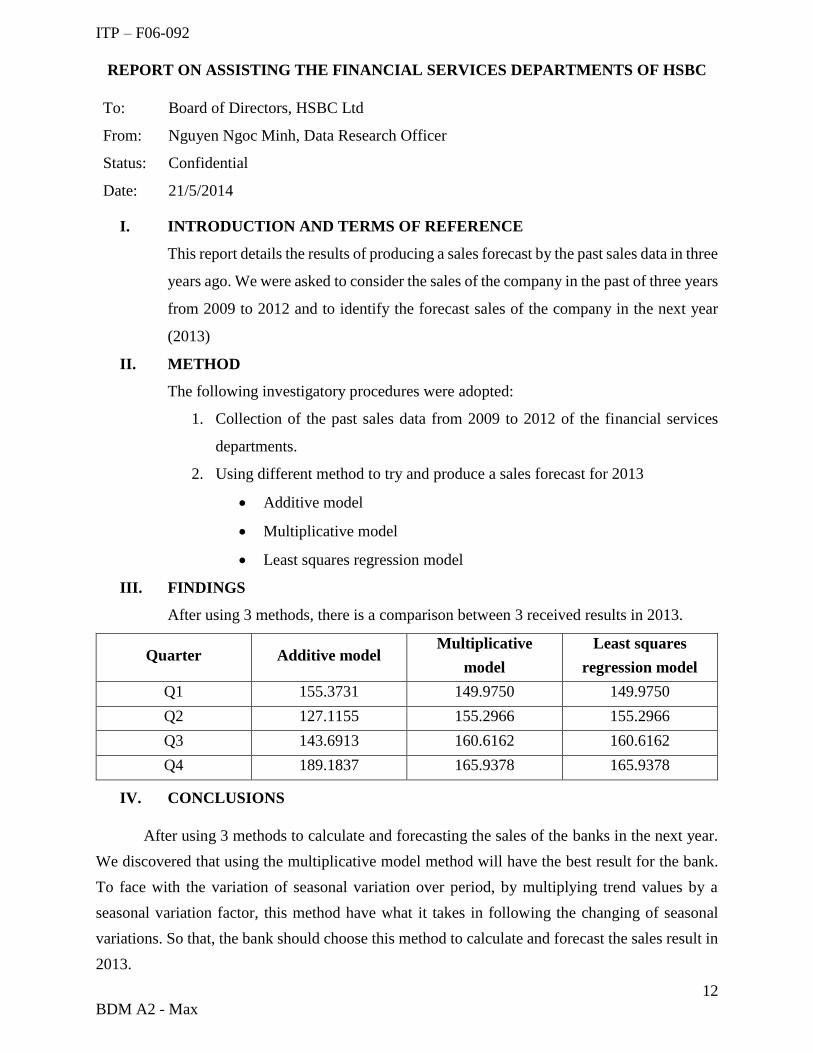

III. FINDINGS

After using 3 methods, there is a comparison between 3 received results in 2013.

Quarter Additive model Multiplicative

model

Least squares

regression model

Q1 155.3731 149.9750 149.9750

Q2 127.1155 155.2966 155.2966

Q3 143.6913 160.6162 160.6162

Q4 189.1837 165.9378 165.9378

IV. CONCLUSIONS

After using 3 methods to calculate and forecasting the sales of the banks in the next year.

We discovered that using the multiplicative model method will have the best result for the bank.

To face with the variation of seasonal variation over period, by multiplying trend values by a

seasonal variation factor, this method have what it takes in following the changing of seasonal

variations. So that, the bank should choose this method to calculate and forecast the sales result in

2013.

ITP – F06-092

13

BDM A2 - Max

Task 2: Information processing tools

Important of Manager Information System (MIS) with HSBC Bank

No Department Decision

level

Information

type Instrument Image Staff

1 Human

Resources

Strategic

level

Executive

Support

Systems (ESS)

Prophix’s

personnel planning

Executive

2 Finance

Department

Management

level

Management

Information

Systems (MIS)

Axiom EPM's

Budgeting and

Forecasting

Finance

manager

3 Marketing

Department

Knowledge

level

Office

Automation

System (OAS)

CorelDRAW

Marketing

online staff

4

Research and

Development

Department

Management

level

Decision

supporting

system (DSS)

Tyler Analytics

R&D

Manager

5 Accounting

Department

Operating

level

Transaction

Processing

system (TPS)

IBM Transaction

processing

Accounting

Staff

Prophix’s personnel planning for Human Resources Department

Belong to the Strategic level, the Executive Support System (ESS) help Human resources

director with long-term planning, to ensure changes in the external environment which are matched

by the company’s capabilities. The ESS pools data from internal and external source and provide

the senior managers with easy access to key internal and external information, which are drawn

from internal MIS and DSS and from external data of competitors, external database… To meet

such needs of senior managers, the large-scale integrated corporate systems known as Enterprise

resource planning, which is essential and depend on the complexity of the undertaking and the

degree of competition.

ITP – F06-092

14

BDM A2 - Max

As one of many software in Enterprise resource planning (ERP), Prophix have its own

function to help the director prepare: (Prophix, n.d.)

Detailed personnel reporting aligned with overall company reporting (internal

resources)

The potential to hold department managers accountable by streamlining the payroll

planning process.

A true depiction of employee costs by department, versus a strictly consolidated view.

Applying in the HBSC bank, the main reason why this software should be used in the bank

is that it is suitable with the purpose of the ESS. It helps the manager have the large vision about

the personnel plan in the bank and help him sync all the information from internal and external

resources such as TPS data, financial data or share prices, Market research.

Axiom EPM's Budgeting and Forecasting for Finance department

In the management-level, the system in this level help the manager monitor and control.

These systems check if things are working well or not. The Management Information System

(MIS) will interact with the same systems as that at operational level. The MIS condenses and

converts TPS data into information. For the manager to prepare annual budget, the instrument

suitable with him is Axiom EPM's Budgeting and Forecasting for the bank, which have various

function: (Axiomepm, 2014)

Test and understand how changing assumptions impact financial results using

drivers such as interest rates, deposit growth rates, number of new accounts, and

other variable income and expense factors

Align business measurement with business planning

Create full annual budget for the bank which have the best-practice

Applying in HSBC bank, because of the various function of this software, the finance

manager can convert directly data from TPS into information, which can help him to create the

budget for the bank each year. With the high-technology and beautiful design, the software suitable

for him to plan a suitable budget for the bank each year.

CorelDraw for Marketing department

The knowledge-level system help knowledge and data workers design products, distribute

information and perform administrative tasks. These systems help the company integrate new and

ITP – F06-092

15

BDM A2 - Max

existing knowledge into the business and to reduce the reliance on paper documents. In this level,

the employee uses Knowledge Work System (KWS) which are information systems that facilitate

the creation and integration of new knowledge into an organization. Such as in the manufacturing

department in the bank, the employee who have responsibility to design the credit card for the

customer have to have a software to improve the quality of result and save time. The designer

software he should use is CorelDRAW which will increase the work productivity.

Its function are (Corel, 2012):

Designing the prototype of banner advertise for each services, event…

Extracting the completed design for manufacturing

Repaid and renew the design of image immediately

Applying in the HSBC bank, using this software for the jobs of designer, the employee

who have responsibility in increase bank’s image, have more tool to draw his idea and perform it

well on the laptop or PC, which easy for him to send for the manager or repaid in the future.

Besides, the software help him to extract the completed design in the right form with high quality

which make easier to post it on the website, newspaper, and banner.

Tyler Analytics for Research and Development department

Also in the management-level system, the type of information called “Decision supporting

system” allow the manager evaluate the alternative in variable situation. For research and

development department, DSS used for evaluating the potential to consider which one is the good

change to invest. In HSBC Bank, the step is quite important to analysis all the information to make

the final decision. Thus, the tools available for types of information is Tyler Analytics software.

Its functions are (T.A.C, 2012):

Bank industry data comparisons

Forecasting

Decision analysis

Ratio Analysis

Prepare a report of full information analysis

Apply to the HSBC bank, this software help the R&D manager to analyses the information

from lower level to have the fully vision. Because of many functions, the software give the

ITP – F06-092

16

BDM A2 - Max

manager the various decision or action for selecting the best and make him more understand and

communicate with the potentials and the risks out-side the bank.

IBM Transaction processing for Accounting department

The software system which is called Transaction Processing Systems (TPS) helps the bank

to keep track of daily activities. In the bank industry, the suggestion for the HSBC bank is the IBM

transaction processing which is useful for the accounting manager and his staff to collect, storage

and control the transaction data (IBM Corperation, 2013). IBM transaction processing have

function of

Provides a flexible entry solution into network computing and e-business, with a

scalable and reliable growth path.

Delivers comprehensive client support for IBM and non-IBM platforms

Applying in the HBSC bank, the accounting staff are supported to keep the daily activities

of bank. With the high connection to the data server, this software help the accounting manager to

see overall the activities of bank in day or month, and have the full vision of the bank to make a

report which provide information to the higher level of system.

ITP – F06-092

17

BDM A2 - Max

Task 3: Project planning

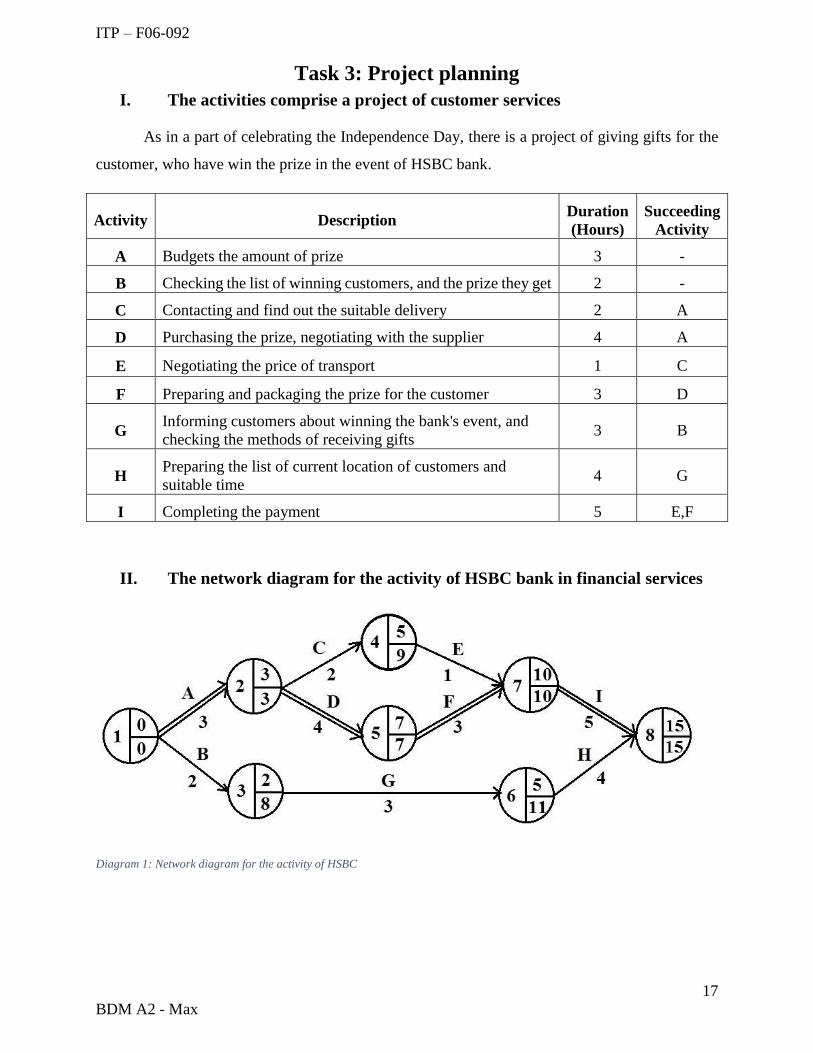

I. The activities comprise a project of customer services

As in a part of celebrating the Independence Day, there is a project of giving gifts for the

customer, who have win the prize in the event of HSBC bank.

Activity Description Duration

(Hours)

Succeeding

Activity

A Budgets the amount of prize 3 -

B Checking the list of winning customers, and the prize they get 2 -

C Contacting and find out the suitable delivery 2 A

D Purchasing the prize, negotiating with the supplier 4 A

E Negotiating the price of transport 1 C

F Preparing and packaging the prize for the customer 3 D

G Informing customers about winning the bank's event, and

checking the methods of receiving gifts 3 B

H Preparing the list of current location of customers and

suitable time 4 G

I Completing the payment 5 E,F

II. The network diagram for the activity of HSBC bank in financial services

Diagram 1: Network diagram for the activity of HSBC

ITP – F06-092

18

BDM A2 - Max

Path Duration (Hours)

A-C-E-I 3+2+1+5 11

A-D-F-I 3+4+3+5 15

B-G-H 2+3+4 9

The critical path is A-D-F-I, with a duration of 15 weeks.

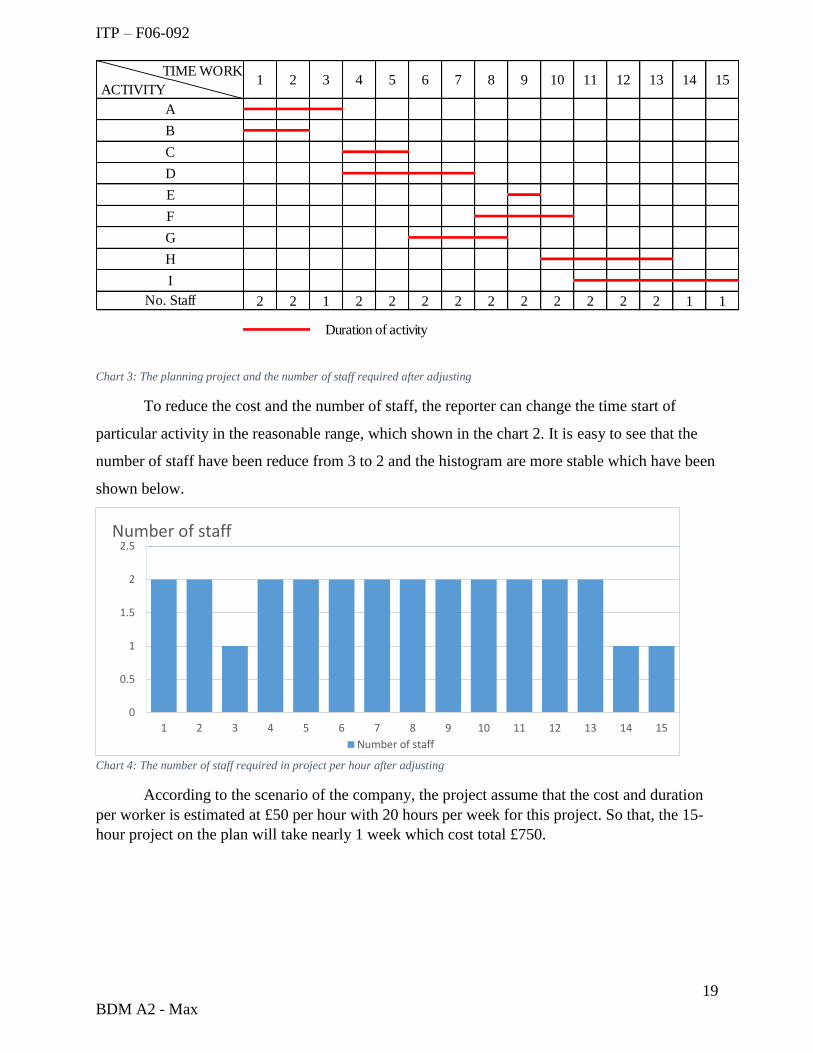

III. The grant chart which show the planning of the project

Chart 1: The planning project and the number of staff required

In the chart 1, activity C and D cannot start until activity A is completed. Therefore, C and

D are drawn as starting at the end of week 3 on the chart. Besides, the activity E which follows C

and activity F which follows D, have the time to start right after activity C and D complete

respectively. From that, we can easy identify the time of each activity. However, the number of

staff required each hour is simply obtained by adding the staff requirements per activity for

relevant hour number, which shows the fluctuate histogram below.

TIME WORKS

ACTIVITY

2 2 1 3 3 3 2 2 2 1 1 1 1 1 1

6

Duration of activity Float time of activity

14 159 10 11 12

A

B

C

7 81 2 3 4 5

No. Staff

D

E

F

G

H

I

13

0

0.5

1

1.5

2

2.5

3

3.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Number of staff

Number of staffChart 2: The number of staff required in the projects per hour

ITP – F06-092

19

BDM A2 - Max

Chart 3: The planning project and the number of staff required after adjusting

To reduce the cost and the number of staff, the reporter can change the time start of

particular activity in the reasonable range, which shown in the chart 2. It is easy to see that the

number of staff have been reduce from 3 to 2 and the histogram are more stable which have been

shown below.

According to the scenario of the company, the project assume that the cost and duration

per worker is estimated at £50 per hour with 20 hours per week for this project. So that, the 15-

hour project on the plan will take nearly 1 week which cost total £750.

TIME WORKS

ACTIVITY

2 2 1 2 2 2 2 2 2 2 2 2 2 1 1

Duration of activity

13 14

G

H

I

1 2 3 4

C

D

E

F

No. Staff

12 15

A

B

6 7 8 9 10 115

0

0.5

1

1.5

2

2.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Number of staff

Number of staff

Chart 4: The number of staff required in project per hour after adjusting

ITP – F06-092

20

BDM A2 - Max

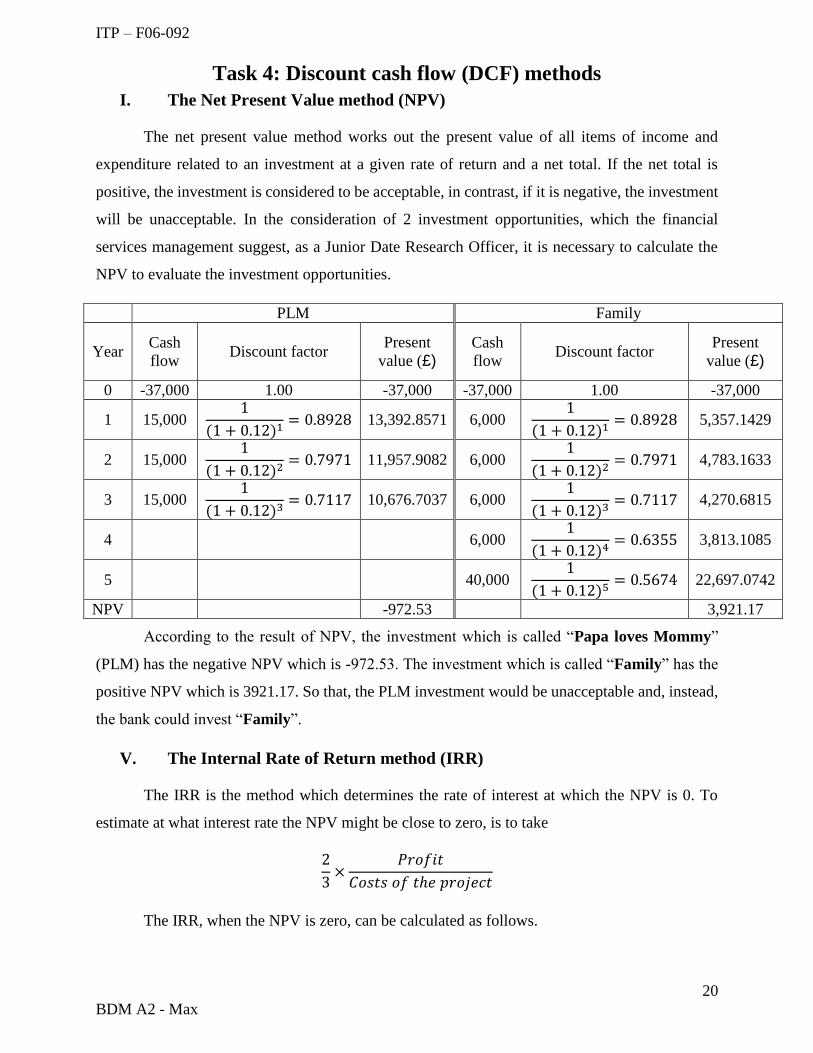

Task 4: Discount cash flow (DCF) methods

I. The Net Present Value method (NPV)

The net present value method works out the present value of all items of income and

expenditure related to an investment at a given rate of return and a net total. If the net total is

positive, the investment is considered to be acceptable, in contrast, if it is negative, the investment

will be unacceptable. In the consideration of 2 investment opportunities, which the financial

services management suggest, as a Junior Date Research Officer, it is necessary to calculate the

NPV to evaluate the investment opportunities.

PLM Family

Year Cash

flow Discount factor

Present

value (£) Cash

flow Discount factor

Present

value (£)

0 -37,000 1.00 -37,000 -37,000 1.00 -37,000

1 15,000 1

(1 + 0.12)1= 0.8928 13,392.8571 6,000

1

(1 + 0.12)1= 0.8928 5,357.1429

2 15,000 1

(1 + 0.12)2= 0.7971 11,957.9082 6,000

1

(1 + 0.12)2= 0.7971 4,783.1633

3 15,000 1

(1 + 0.12)3= 0.7117 10,676.7037 6,000

1

(1 + 0.12)3= 0.7117 4,270.6815

4 6,000 1

(1 + 0.12)4= 0.6355 3,813.1085

5 40,000 1

(1 + 0.12)5= 0.5674 22,697.0742

NPV -972.53 3,921.17

According to the result of NPV, the investment which is called “Papa loves Mommy”

(PLM) has the negative NPV which is -972.53. The investment which is called “Family” has the

positive NPV which is 3921.17. So that, the PLM investment would be unacceptable and, instead,

the bank could invest “Family”.

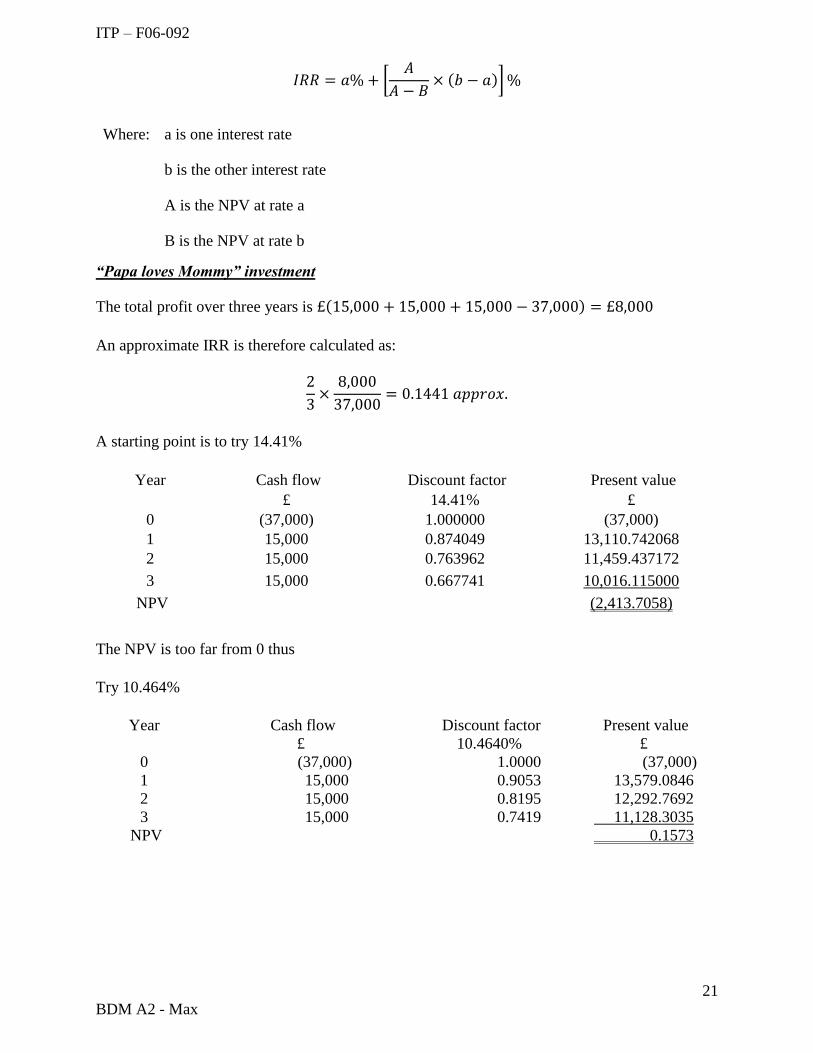

V. The Internal Rate of Return method (IRR)

The IRR is the method which determines the rate of interest at which the NPV is 0. To

estimate at what interest rate the NPV might be close to zero, is to take

2

3×

𝑃𝑟𝑜𝑓𝑖𝑡

𝐶𝑜𝑠𝑡𝑠 𝑜𝑓 𝑡ℎ𝑒 𝑝𝑟𝑜𝑗𝑒𝑐𝑡

The IRR, when the NPV is zero, can be calculated as follows.

ITP – F06-092

21

BDM A2 - Max

𝐼𝑅𝑅 = 𝑎% + [𝐴

𝐴 − 𝐵× (𝑏 − 𝑎)] %

Where: a is one interest rate

b is the other interest rate

A is the NPV at rate a

B is the NPV at rate b

“Papa loves Mommy” investment

The total profit over three years is £(15,000 + 15,000 + 15,000 − 37,000) = £8,000

An approximate IRR is therefore calculated as:

2

3×

8,000

37,000= 0.1441 𝑎𝑝𝑝𝑟𝑜𝑥.

A starting point is to try 14.41%

Year Cash flow Discount factor Present value

£ 14.41% £

0 (37,000) 1.000000 (37,000)

1 15,000 0.874049 13,110.742068

2 15,000 0.763962 11,459.437172

3 15,000 0.667741 10,016.115000

NPV (2,413.7058)

The NPV is too far from 0 thus

Try 10.464%

Year Cash flow Discount factor Present value

£ 10.4640% £

0 (37,000) 1.0000 (37,000)

1 15,000 0.9053 13,579.0846

2 15,000 0.8195 12,292.7692

3 15,000 0.7419 11,128.3035

NPV 0.1573

ITP – F06-092

22

BDM A2 - Max

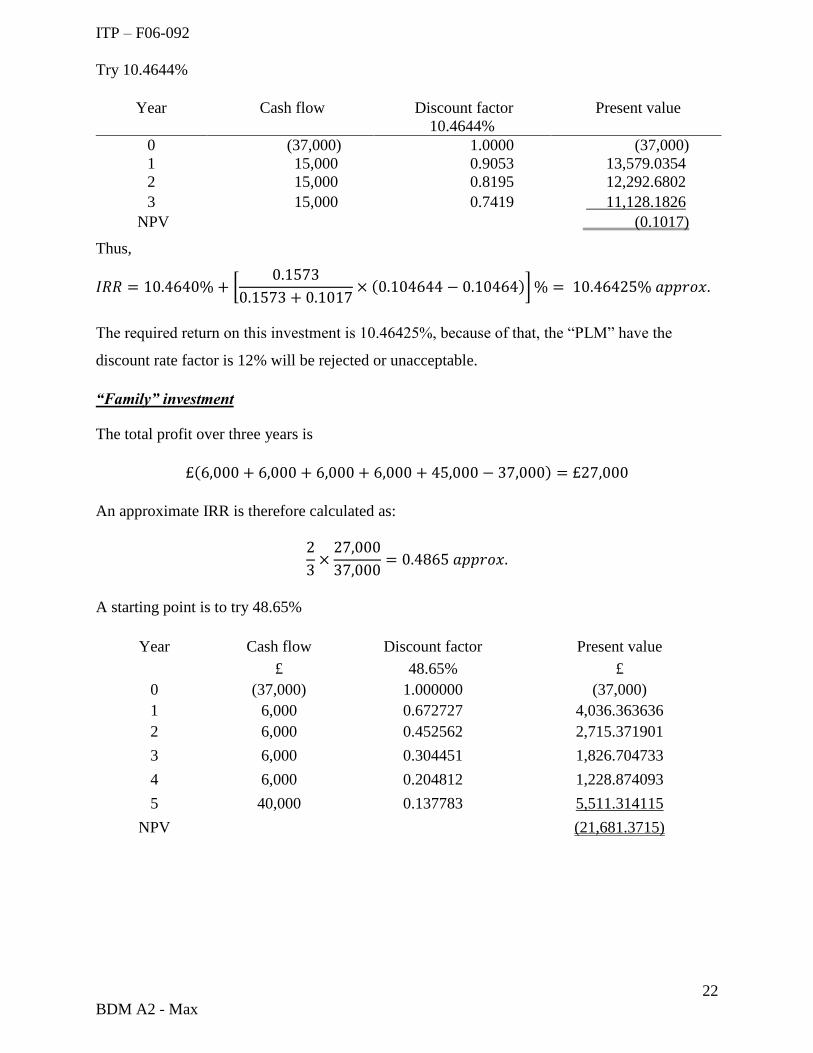

Try 10.4644%

Year Cash flow Discount factor Present value

10.4644%

0 (37,000) 1.0000 (37,000)

1 15,000 0.9053 13,579.0354

2 15,000 0.8195 12,292.6802

3 15,000 0.7419 11,128.1826

NPV (0.1017)

Thus,

𝐼𝑅𝑅 = 10.4640% + [0.1573

0.1573 + 0.1017× (0.104644 − 0.10464)] % = 10.46425% 𝑎𝑝𝑝𝑟𝑜𝑥.

The required return on this investment is 10.46425%, because of that, the “PLM” have the

discount rate factor is 12% will be rejected or unacceptable.

“Family” investment

The total profit over three years is

£(6,000 + 6,000 + 6,000 + 6,000 + 45,000 − 37,000) = £27,000

An approximate IRR is therefore calculated as:

2

3×

27,000

37,000= 0.4865 𝑎𝑝𝑝𝑟𝑜𝑥.

A starting point is to try 48.65%

Year Cash flow Discount factor Present value

£ 48.65% £

0 (37,000) 1.000000 (37,000)

1 6,000 0.672727 4,036.363636

2 6,000 0.452562 2,715.371901

3 6,000 0.304451 1,826.704733

4 6,000 0.204812 1,228.874093

5 40,000 0.137783 5,511.314115

NPV (21,681.3715)

ITP – F06-092

23

BDM A2 - Max

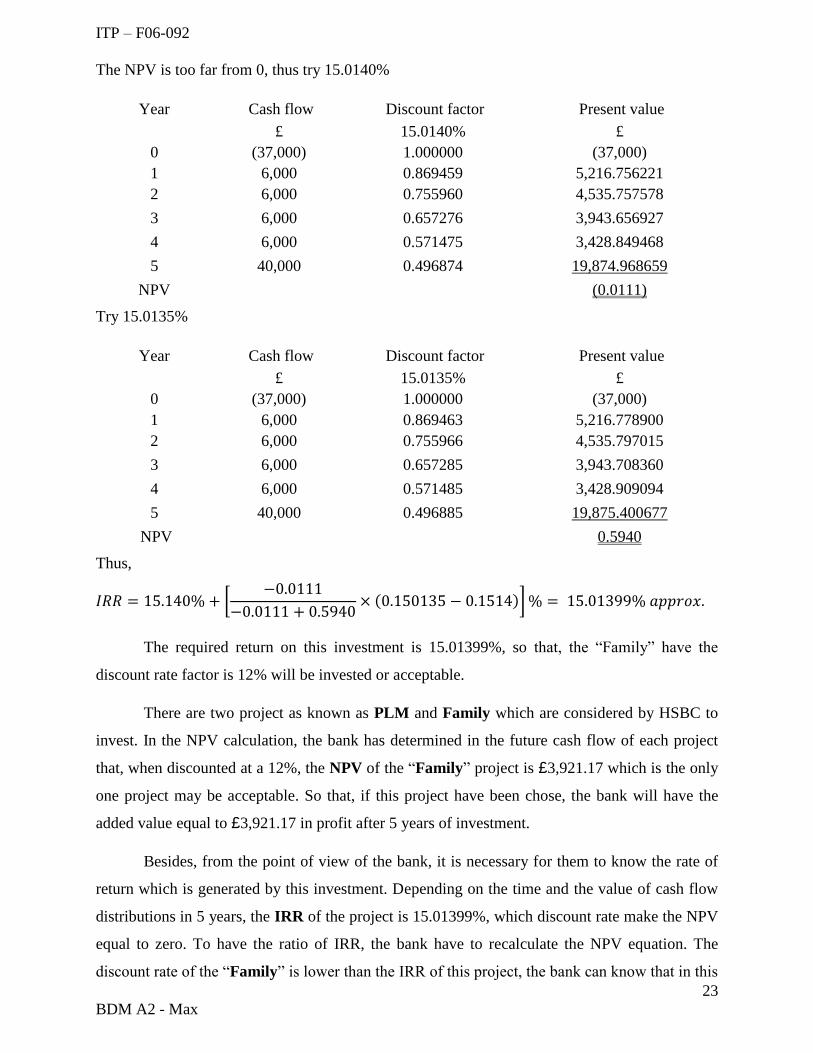

The NPV is too far from 0, thus try 15.0140%

Year Cash flow Discount factor Present value

£ 15.0140% £

0 (37,000) 1.000000 (37,000)

1 6,000 0.869459 5,216.756221

2 6,000 0.755960 4,535.757578

3 6,000 0.657276 3,943.656927

4 6,000 0.571475 3,428.849468

5 40,000 0.496874 19,874.968659

NPV (0.0111)

Try 15.0135%

Year Cash flow Discount factor Present value

£ 15.0135% £

0 (37,000) 1.000000 (37,000)

1 6,000 0.869463 5,216.778900

2 6,000 0.755966 4,535.797015

3 6,000 0.657285 3,943.708360

4 6,000 0.571485 3,428.909094

5 40,000 0.496885 19,875.400677

NPV 0.5940

Thus,

𝐼𝑅𝑅 = 15.140% + [−0.0111

−0.0111 + 0.5940× (0.150135 − 0.1514)] % = 15.01399% 𝑎𝑝𝑝𝑟𝑜𝑥.

The required return on this investment is 15.01399%, so that, the “Family” have the

discount rate factor is 12% will be invested or acceptable.

There are two project as known as PLM and Family which are considered by HSBC to

invest. In the NPV calculation, the bank has determined in the future cash flow of each project

that, when discounted at a 12%, the NPV of the “Family” project is £3,921.17 which is the only

one project may be acceptable. So that, if this project have been chose, the bank will have the

added value equal to £3,921.17 in profit after 5 years of investment.

Besides, from the point of view of the bank, it is necessary for them to know the rate of

return which is generated by this investment. Depending on the time and the value of cash flow

distributions in 5 years, the IRR of the project is 15.01399%, which discount rate make the NPV

equal to zero. To have the ratio of IRR, the bank have to recalculate the NPV equation. The

discount rate of the “Family” is lower than the IRR of this project, the bank can know that in this

ITP – F06-092

24

BDM A2 - Max

project the NPV will be positive with 12% of discount rate. Thus, it is easy to see that the IRR

measurement have ability to show the return of investment opportunities and compare them.

However, NPV is better than IRR in the long time, because of basing on discount rate factor at

present. In the fluctuation of the rate on the time changed, the IRR may be wrong. So that, The

NPV is useful in evaluate the long-time investment, and the IRR is good way for company to

evaluate the short one.

ITP – F06-092

25

BDM A2 - Max

Conclusion

In sum up, the report have been shown detail and correctly the information of the company

in each task and provide the suitable recommendation for the bank to increase the efficiency and

productivity. In task 1, the bank should use multiplicative model method for calculating and

forecasting the actual sales of bank in the next year. In the second task, there are 5 useful software

which are recommended for the bank to help them increase the efficiency and productivity. In the

task 3, the report has create the detail plan for the bank to follow which is reasonable and have the

lowest cost. In the final test, the report have shown the way to evaluate the project by 2 method

NPV and IRR and make the conclusion for the bank to choose which one is the good project for

the bank in the future.

ITP – F06-092

26

BDM A2 - Max

References

Axiomepm, 2014. BUDGETING AND FORECASTING. [Online]

Available at: http://www.axiomepm.com/solutions/industry/banking/budgeting

[Accessed 23 May 2014].

Corel, 2012. http://www.corel.com. [Online]

Available at: http://www.corel.com/corel/product/index.jsp?pid=prod5190074

[Accessed 1 June 2014].

IBM Corperation, 2013. Http://www.IBM.Com. [Online]

Available at: http://www-03.ibm.com/software/products/en/category/transaction-processing

[Accessed 1 June 2014].

Prophix, n.d. prophix.com. [Online]

Available at: http://www.prophix.com/solutions/personnel-planning/

[Accessed 23 May 2014].

T.A.C, 2012. http://www.tyleranalytics.com/. [Online]

Available at: http://www.tyleranalytics.com/products/banking.asp

[Accessed 1 June 2014].