Decision Making in Marketing and Finance

206

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Decision Making in Marketing and Finance

Decision Making in Marketing and Finance

This page intentionally left blank

Decision Making in Marketing and Finance

An Interdisciplinary Approach to Solving Complex

Organizational Problems

Paul Sergius Koku

decision making in marketing and finance

Copyright © Paul Sergius Koku, 2014.

All rights reserved.

First published in 2014 byPALGRAVE MACMILLAN®in the United States— a division of St. Martin’s Press LLC,175 Fifth Avenue, New York, NY 10010.

Where this book is distributed in the UK, Europe and the rest of the world, this is by Palgrave Macmillan, a division of Macmillan Publishers Limited, registered in England, company number 785998, of Houndmills, Basingstoke, Hampshire RG21 6XS.

Palgrave Macmillan is the global academic imprint of the above companies and has companies and representatives throughout the world.

Palgrave® and Macmillan® are registered trademarks in the United States, the United Kingdom, Europe and other countries.

ISBN 978-1-349-47882-8

Library of Congress Cataloging-in-Publication Data

Koku, Paul Sergius, 1955– Decision making in marketing and finance : an interdisciplinary

approach to solving complex organizational problems / Paul Sergius Koku.

pages cm Includes bibliographical references and index.

1. Decision making. 2. Marketing. 3. Budget in business. I. Title.

HD30.23.K645 2014658.800199—dc23 2014006312

A catalogue record of the book is available from the British Library.

Design by Newgen Knowledge Works (P) Ltd., Chennai, India.

First edition: August 2014

10 9 8 7 6 5 4 3 2 1

Softcover reprint of the hardcover 1st edition 2014 978-1-137-37947-4

ISBN 978-1-137-44477-6 (eBook)DOI 10.1057/9781137444776

Dedicated to Aurelia, Ruth Violet, and Emma

This page intentionally left blank

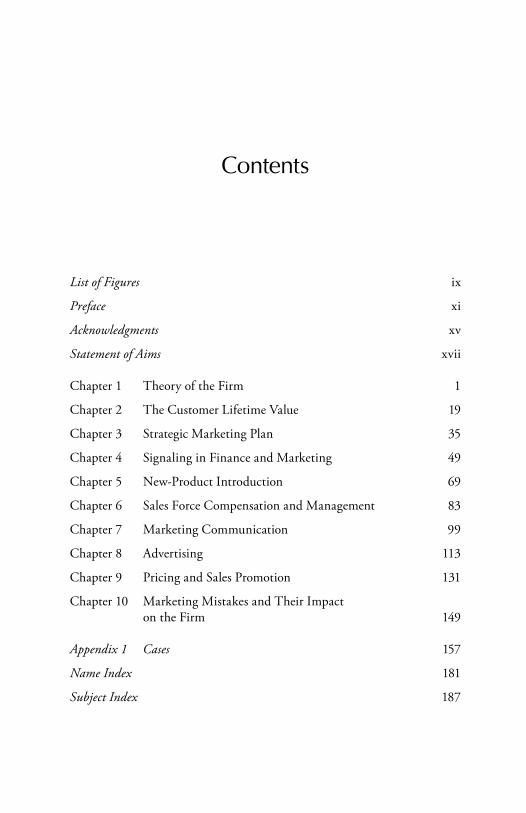

Contents

List of Figures ix

Preface xi

Acknowledgments xv

Statement of Aims xvii

Chapter 1 Theory of the Firm 1

Chapter 2 The Customer Lifetime Value 19

Chapter 3 Strategic Marketing Plan 35

Chapter 4 Signaling in Finance and Marketing 49

Chapter 5 New-Product Introduction 69

Chapter 6 Sales Force Compensation and Management 83

Chapter 7 Marketing Communication 99

Chapter 8 Advertising 113

Chapter 9 Pricing and Sales Promotion 131

Chapter 10 Marketing Mistakes and Their Impact on the Firm 149

Appendix 1 Cases 157

Name Index 181

Subject Index 187

This page intentionally left blank

Figures

3.1 The customer-centered four-legged stool 373.2 The dual distribution approach 448.1 A simplified communication process 1158.2 The AIDA model 1189.1 Full-cost and variable-cost pricing strategies 132

This page intentionally left blank

Preface

Decision making in business does not take on the color or tenor of any one particular functional area; in fact, busi-ness decisions generally cut across disciplines. Yet, with the

exception of a few progressive schools, we continue to teach courses in business schools as though decisions are made in functional silos. Part of the problem, we think, is due to the fact that most of the text-books we use today are written that way. A textbook in finance hardly discusses anything related to marketing and vice-versa, this approach is far removed from reality where solving a marketing problem may require expertise in finance or operations management. This book is, however, different from other textbooks in the sense that we take an approach that is reality based. We take an interfunctional and cross-disciplinary approach, hence the title—Decision Making in Marketing and Finance.

We believe that turf protection and the so-called silo mentality are due to the fact that many people fail to see the company as an entity that works best when “all hands are on deck” or where people realize that everyone’s success or failure impacts everyone else. No one would be left behind, not even the best department, when a company fails and closes its doors. For that reason alone, if for none other, all the departments must work together for the good of each other.

This book stresses the interdisciplinary approach of decision making in organizations, and thus can be used as a textbook or reference book. It is written primarily as a strategy book, however, because it seeks to appeal to a broad audience; every care has been taken to express the con-cepts it discusses in everyday English without jargons and mathematics.

xii l Preface

Unlike many other textbooks, this book reviews both the classic and contemporary literature on the subjects discussed and relates them to the business decision being made or the business problem being solved. In this respect, it is suitable for use in both undergraduate and MBA courses.

Overview of the Book

Much has been said during the past three decades about the need for interdisciplinary approach to teaching business courses, yet very few text-books have been written for that purpose. This book is based on the belief that to teach across disciplines requires that we write books across disciplines.

This first edition of Decision Making in Marketing and Finance con-sists of ten chapters and an appendix with ten cases. All the cases have been created from scratch and only serve as platforms for further dis-cussing the concepts covered in the chapters. Chapter 1 discusses the firm as a composite of different departments, each of them necessary but incapable of steering the firm to success by itself, hence the need for interfunctional cooperation. The chapter draws on Coase’s 1937 seminal article on the theory of the firm and other popular and well-regarded articles on principal-agent relationships to motivate the discussions.

Chapter 2 discusses the Customer Life Time Value concept and uses it to make a case for relationship marketing and cross-selling.

Chapter 3 discusses usage of the 4Ps (product, price, place, and pro-motion) in strategic marketing planning; however, unlike the traditional textbooks, it takes an interdisciplinary approach and shows how each of the functional areas can and should make viable contributions to the plan.

Chapter 4 discusses signaling theory and its application in marketing. It reviews signaling theory from evolutionary biology through econom-ics and marketing by drawing on Michael Spence’s 1973 seminal paper on labor marketing signaling. This chapter also discusses the source of information asymmetry in marketing and how marketing variables such as advertising, new product introduction, warranties, and so on could be used as marketing variables.

Chapter 5 discusses new-product introduction. It relates new-prod-uct introduction to the product life cycle and signaling theory. It also

Preface l xiii

uses the new-product introduction as a topic to call for interfunctional cooperation.

Chapter 6 talks about sales force compensation and management. It nicely ties in agency problems that have been minimally discussed in marketing strategy textbooks. It also discusses the decision on whether a company should hire its own sales force or contract the selling activities to an independent agent.

Chapter 7 discusses the quintessential integrated marketing com-munication (IMC) strategy minus advertising, which is discussed in chapter 8. It ties the IMC to signaling and discusses the decision regard-ing which element of the communication mix to emphasize and when.

Chapter 8 focuses on advertising as a part of the communication mix. Because of the major role that advertising plays in the communication strategy of many companies and amount of money that is being spent on it, the chapter discusses seminal papers on the effectiveness of adver-tising campaigns and whether to view advertising as an expense or an investment. Again, an interdisciplinary approach is taken in discussing the issues.

Chapter 9 discusses the ever so important issue of pricing and sales promotion. It discusses the different forms of pricing techniques—from full-cost pricing approach to activity-based pricing approach. It also dis-cusses pricing as a signaling variable and the use of high price as an indicator of high quality.

Chapter 10 talks about marketing mistakes of all kinds, from product names to decisions regarding not recalling defective products from the market. The chapter uses the mistakes to highlight the need for cross-functional cooperation.

This page intentionally left blank

Acknowledgments

This book could not have been written without the help of sev-eral individuals. My past and present students have contributed indirectly to this book because I was able to “try” my ideas on

them. My colleagues, particularly Dr. Allen Smith, freely gave of their time. Allen often stayed to work in his office at school up to 2:00 or 3:00 a.m. so that I would know that there was someone else on the “floor” while I was “putting in my long hours.” Besides his time and intellectual contributions, he gave me unlimited access to his well-cataloged collec-tion of journal articles. Dr. Eric Shaw was also generous in lending me books from his vast collection of “out of circulation” books. I know few in the world who can match his collection. Ms. Selen Savas, my research assistant, was invaluable in her assistance. She was always there when I needed her.

The seed for the book was planted in December 1999 when I designed and taught a graduate course on Finance and Marketing Interface at Monash University, Melbourne, Australia. At that time, there was no suitable textbook on the market that I could use, so I cobbled together a collection of articles and cases. I started thinking then that I would write an interdisciplinary book that fills the void I perceived, but the idea simply remained just that—an idea. I wrote and rewrote this book in my head for over 14 years, but never wrote down a word on paper!

There are also many others who have directly or indirectly contributed to this book. Some people have contributed by challenging my thinking on certain issues—my nephew Dan an intellectual historian, with whom

xvi l Acknowledgments

I have had many long and vigorous discussions whenever I visited, is one of those. Some individuals have contributed by giving me uninterrupted time and space, and others by encouraging me—I wish to thank them all. While I view this book as a product of collective effort, I alone bear the full responsibility for all the mistakes of omission or commission.

Paul Sergius Koku

Statement of Aims

This book has three main objectives. First, the book shows how value could be created for shareholders and other stakeholders if managers or internal decision makers of a firm design solutions

with an interfunctional mind-set. Thus, the book approaches decision making within the firm using the critical links between finance and marketing. Second, by linking marketing and finance decisions, the book illustrates what many marketers have long argued, but seldom clearly demonstrated, that is, how marketing decisions directly affect the firm’s financial position. Third, the book intends to provide a much-needed teaching material for interdisciplinary approach for case analysis.

The continued use of cases to teach in business schools, especially the MBA programs, shows recognition of the superior outcomes of an interdisciplinary approach to solving business problems. However, functional departmental silos still exist mainly because of inertia and turf protection, and can only be eliminated through educa-tion on several fronts. Education of future internal decisions makers (business students at all levels) that shows not only the suboptimal solutions achieved in many instances through the “functional silo” method, but also the superior solutions that can be achieved, in many instances, through the cross-functional approach. This education to change a long-held mind-set should not be limited to only future decision makers (students), but current decision makers could also be persuaded through continuing education and the executive MBA programs.

xviii l Statement of Aims

For these reasons, this book is written for a very broad audience and does not make any assumption on possession of prior knowledge. In addition to being used as a teaching material, this book can also be read by the practitioners for background theoretical knowledge. It is also our hope that this book provides yet one more persuasive reason to break down functional silos.

CHAPTER 1

Theory of the Firm

There is a fable in many cultures of what an elephant looks like to six blind men. The first of the six men who felt the elephant’s tail with his fingers described the elephant to be as thin as a rope or a

snake. The second man who felt the elephant’s leg described the elephant like a huge pillar. The third man who felt the elephant’s tusk said the elephant was like a pipe. To the fourth man who felt the animal’s belly, the elephant was like a wall. To the fifth who felt the elephant’s ear, it was like a hand fan, and to the sixth man who felt the elephant’s trunk, the animal was like a tree branch.

While the origin of this story cannot be determined, it reminds us of the various definitions of the firm. It also, in a very practical way, demonstrates the imports of the bounded rationality theory. Our under-standing and knowledge of a phenomenon at any time, say t2, could be completely different and perhaps even superior to the one at time t1 because of availability of new and perhaps superior information at a later time (t2); and so is our understanding of the firm. A note of caution, while the “firm,” a “corporation,” and an “organization” could have dif-ferent meanings, in this chapter, we use the terms interchangeably in a generic sense to mean the same thing—the firm.

Corporations occupy a very special place in every modern economy regardless of whether the economy is characterized as an advanced, a newly developed, or a developing economy. Indeed, the contemporary firm can be referred to as the nucleus of a country’s economic engine and therefore deserving of special attention. The concept of the firm

P.S. Koku, Decision Making in Marketing and Finance© Paul Sergius Koku 2014

2 l Decision Making in Marketing and Finance

is not new even though it has, over the years, undergone several refine-ments. The fact that very few post-1937 academic discussions on the firm are held without any reference to Coase’s (1937) work on the nature of the firm is a testament to his insightful contribution to the theory. As alluded to by Coase, many macroeconomic analyses unintentionally but erroneously begin with an “industry” as the starting point because the concept of the firm, though not new, had not been clearly defined by economists. So what is the firm?

The importance of the firm as well as the brilliance in its “invention” can be appreciated when observed through the chain of changes that it has brought to the marketplace. First is the logic of specialization of labor. With specialization of labor, individuals get to work at or “pro-duce” what they can do best. So an individual A who is good at putting together automobiles may become a mechanic while individual B who is good at tilling land and tending to animals may become a farmer of some sort. Similarly, some individuals may choose to become accountants or lawyers while others may become doctors or marketing specialists.

Besides the intrinsic satisfaction that goes with doing what one enjoys best, specialization of labor also implicates several other issues. For example, with specialization comes cost advantage and high effi-ciency. Consumers enjoy lower costs when specialization occurs because there is less wastage in terms of material and time during production. However, if everyone specializes in what they do best, then how can one get the other things that one needs but cannot produce? To answer this question, we must introduce the concept of exchange or trade. So, one can argue that specialization necessitates exchange, which also comes with its own problems. For example, how much of product C should one exchange for product D? Economists refer to this problem as a problem of finding a unit of account or a numeraire, which for the sake of sim-plicity we will refer to here as the problem of “value.” So, in other words, how is C valued against D? However, there is another problem besides that of value.

Imagine the number of exchanges one has to make in order to get through the day. The mechanic may not just need to find a farmer who is willing to exchange food for his services, but also a carpenter, and perhaps teachers for his children and a doctor for his wife. The nature of the problem becomes easily evident. These bilateral exchanges come with enormous costs; for example, finding someone to exchange

Theory of the Firm l 3

products/services with. If the mechanic spends all day looking for indi-viduals to exchange services with, he will not have the time to work as a mechanic, and then, of course, he will have nothing to exchange.

The invention of money solved a major part of the problem; however, unresolved issues remained. For example, how does the farmer know how much to produce so that his produce does not go waste, and how does he ensure that he gets the best price for his produce? Most econo-mists before Coase (1937) assigned this problem and others like it to the market forces in a free market economy. However, as pointed out by Coase, the price mechanism or market forces do not always clear the market at the lowest cost. In other words, there are costs associated with the price mechanism’s clearance of the market. Coase referred to these costs as “transaction costs.” It can therefore be argued that the firm is an additional mechanism that facilitates clearance of the market in a more efficient manner. But how does the firm accomplish this? We will dis-cuss this later when we discuss features of the firm. In the meantime, we should discuss a few other noteworthy definitions of the firm.

Other Definitions and Objectives of the Firm

Coase (1937) was not alone in grappling with a realistic definition for the firm. It is noteworthy that in trying to come to a realistic defi-nition of the firm, Coase reverted to the two canons established by Professor Robinson (1932) in making assumptions. According to Professor Robinson, first, assumptions must be tractable; second, they must be realistic. Using these assumptions, Coase’s discussion on the firm intended, as he put it, to “bridge what appears to be a gap in eco-nomic theory between the assumption (made for some other purposes) that resources are allocated by means of the price mechanism and the assumption (made for other purposes) that this allocation is dependent on the entrepreneur- coordinator” (p. 389).

Behavioral Theory

Consistent with the canons used by Coase (1937), that is, making assumptions tractable and realistic, several other scholars including Simon, March, and Cyert (Simon, 1955, 1964; March and Simon, 1958; Cyert and March, 1963) proposed new definitions of the firm that draw

4 l Decision Making in Marketing and Finance

on the theories of human behavior and are different from those of neo-classical economists. According to these scholars, firms have not been created solely by the “entrepreneur-coordinator,” but instead emerge from coalitions and subcoalitions of individuals and groups such as managers, employees, shareholders, and lawmakers. This definition sets the groundwork for one of the most debated points between neoclassical economists and organizational theorists on the role of the firm.

It should come as no surprise (using Cyert and March’s (1963) defini-tion of the firm) that all the different coalitions and subcoalitions of the firm have different objectives that may be in conflict and impose dif-ferent constraints on the firm. According to this school of thought, the firm’s realistic objective therefore cannot be the maximization of share-holders’ profit since shareholders are only a part of the larger coalition or subcoalition. Furthermore, according to Simon (1964), because of com-putational limitations and the lack of perfect information, managers can only “satisfice” instead of maximize firm objectives.

To put things in context, it must be understood that up to this point in time, the neoclassical viewpoint of the firm—that the primary objec-tive of the firm was to maximize its profits—still prevailed. This view was clearly articulated by Friedman (1962) as follows:

The view has been gaining widespread acceptance that corporate offi-cials and labor leaders have a “social responsibility” that goes beyond serving the interest of their stockholders or their members. This view shows a fundamental misconception of the character and nature of a free economy. In such an economy, there is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition, without deception or fraud. (p. 133)

Friedman’s more poignant indictment of corporate social responsibility, which was cited by Carroll (1999, p. 277), states, “Few trends could so thoroughly undermine the very foundations of free society as the accep-tance by corporate officials of a social responsibility other than to make as much money for their stockholders as possible” (see also Friedman, 1970). It would appear that in Friedman’s world the managerial discre-tions that lead to expenditures on corporate social responsibility activities

Theory of the Firm l 5

are simply the result of agency problems (Lee, 2007), which will be dis-cussed in detail later in this book.

Pfeffer and Salancik’s (1978) definition of the firm contains elements similar to that of Cyert and March (1963). As in Cyert and March, Pfeffer and Salancik define the firm as a “coalition of interests.” These interests can be divided into two main factions, the internal and the external. The “internal” faction comprises union, managers, and the like, while the “external” faction consists of suppliers, regulators, legislators, environ-mentalists, and a pool of potential talents (potential employees). Because every firm generally intends to exist forever (an assumption that argu-ably formed the basis for accrual accounting, i.e., accounts receivable and accounts payable), the ability of the firm to draw resources as well as support from the external environment is important.

Thus, firms negotiate with their external environments to ensure and facilitate their survival. Part of “negotiating” with the external environ-ments involves taking steps to win the support of the community in which the firm exists. Some of these activities include donating in cash or kind to the community food bank to feed the homeless, buying sport-ing uniforms for the local little league, and the like. Activities such as these, of course, make many scholars question the objective of corporate social responsibility activities. Some wonder if the practice is not merely a public relations ploy designed to facilitate the attainment of resources for the firm and ensure its survival or a genuine recognition on the part of the firm that it needs to “legitimize” its existence by being a “citizen” of a community.

Modern Finance Theory

The usage of modern finance theory has also dramatically changed the definition of the firm. Differing from the neoclassical theory of the firm as a value maximizing entity, Fama and Miller (1972) have argued that firms exist over several periods, if not in perpetuity, instead of a single period. Furthermore, as a part of ensuring that they remain profitable and/or exist in perpetuity, firms frequently take on new projects and eliminate nonprofitable ones. Engaging in this process changes their risk levels; thus, it is not quite accurate to assume that the objective of firms is to maximize their value. Rather, the more accurate description of the objective of the firm under the modern theory of the firm, according to

6 l Decision Making in Marketing and Finance

Fama and Miller, is to maximize the firm’s present value. This objective/definition of the firm is different from the previous in two ways. First, it integrates into the definition of the firm the concept of present value of the firm’s shares. This step is an implicit recognition that owners of the firm do hold ownership of the firm by holding shares. Second, the definition also integrates the methods of estimating riskiness of projects, which not only make up the firm, but also determine its value.

Jensen and Meckling (1976) provide a new definition of the firm that focuses on the ownership structure of firms. The authors reechoed Coase’s (1937) observation that economists have failed to clearly define the firm; instead, what economists generally refer to as the theory of the firm is actually “a theory of markets in which firms are important actors.” Jensen and Meckling reviewed the definitions of the firm pro-vided by previous authors and concluded,

Organizations are simply legal fictions which serve as a nexus for a set of contracting relationships among individuals. This includes firms, non-profit institutions such as universities, hospitals and foundations, mutual organizations such as savings banks and insur-ance companies and co-operatives, some private clubs, and even government bodies such as cities, states and Federal governments, government enterprises such as TVA, the Post Office, transit sys-tems, etc. (p. 310)

Jensen and Meckling (1976) arrived at a new theory of the firm by inte-grating the three main theories: the theory of property rights, which was implicit in Coase’s view of the firm as a network of contracts; agency theory, which was also referred to by Coase when he discussed the conditions that could arise when the “entrepreneur-coordinator” hires someone else to manage the firm; and the theory of finance.

Because of agency problems, previous commentators on the “firm” including Adam Smith (1776) have attributed certain amount of inef-ficiencies to the arrangements that involve separation of owners from managers. In the words of Adam Smith (The Wealth of Nations, p. 700) cited by Jensen and Meckling (1976),

The directors of such [joint-stock] companies, however, being the managers rather of other people’s money than of their own, it

Theory of the Firm l 7

cannot well be expected, that they should watch over it with same anxious vigilance with which the partners in a private copartnery frequently watch over their own. Like the stewards of a rich man, they are apt to consider attention to small matters as not for their master’s honour, and very easily give themselves a dispensation from having it. Negligence and profusion, therefore, must always prevail, more or less, in the management of the affairs of such a company. (p. 305)

However, Jensen and Meckling (1976) characterized some of the problems with previous definitions of the firm as “special cases” of the theory of agency relationships and identified the components of agency costs as (a) monitoring costs incurred by the principal, (b) the bonding costs incurred by the agent, and (c) the residual loss. Assuming that a firm can issue only stocks and bonds, Jensen and Meckling examined how the principal and agent could arrive at an equilibrium contractual form given each party’s incentive to maximize his utility.

On property rights, the authors observed that the finer issues of the specification of individual rights are aspects of property rights that are critical for the definition of the firm. Such is the case, they argued, because individual rights determine the nature of contracts between individuals and organizations. They also determine the costs and rewards among people within organizations. Because firms are made up of a network of contracts with individuals that at times have conflicting objectives, firms often behave like markets in bringing the conflicting demands into equilibrium; thus, it would be misleading to personal-ize the firm in references such as its “objective functions” or its “social responsibility.”

Notwithstanding the above insights, Fama (1980) in explaining the nature of the firm suggests that the firm in which ownership is separated from management, despite the agency problems, functions much better than acknowledged by several commentators. He suggests that concerns over the seriousness of agency problems and the managerial propensity to shirk might be misplaced. In arriving at this conclusion, Fama also acknowledges the fact that to survive and thrive organizations need different expertise and different resources. The firm therefore acquires these resources in order to pursue the purpose for which it has been put together. Using the theory of property rights, Fama also argues along the

8 l Decision Making in Marketing and Finance

lines of other economists such as Coase (1937), Alchian and Demsetz (1972), and Jensen and Meckling (1976) that ownership of the skills and resources that make up organizations reside in those who possess them by ownership rights.

Reiterating the definition of the firm a la Coase (1937), Fama (1980) too suggests that the firm is a network of contracts between individu-als who have property rights to certain skills, expertise, or resources. However, unlike previous definitions of the firm as in Coase (1937) and Jensen and Meckling (1976), Fama argues that managers who are sepa-rate from owners might not necessarily shirk at the expense of owners because they are disciplined by competition from other firms and mana-gerial markets.

Competition from rival firms forces every firm to try to be effi-cient otherwise their cost of production will be unsustainably high and they will go out of business. Because shirking by managers is an inef-ficient use of resources, it will raise the cost of production, and because it is in the interest of every party in contract with the firm to see the firm remains in business, they will monitor the behavior of managers. Furthermore, a manager whose firm goes out of business will also have to look for employment elsewhere, and because the managerial market will not favorably view a manager whose firm goes out of business, it is in the managers own interest to be efficient or in other words cut down on shirking.

It is clear from most of the discussions above that most of the different conceptualizations of the firm revolve around the concept of separation of ownership from control that creates agency costs. The presence of agency costs in modern corporations with widely dispersed sharehold-ers was emphasized by Berle and Means (1932) in their seminal work. This point was revisited by several other authors including Coase (1937), Jensen and Meckling (1976), and Fama (1980). Demsetz (1983), how-ever, took a different approach to defining the firm. He argues that Berle and Means’s approach to defining the firm looks at the firm from two viewpoints that are completely different. The first viewpoint considers the firm during the pre-nineteenth-century era, as it existed before the corporate forms. The firm as it existed during that period approximated economists’ viewpoint of the firm that considers the firm as a device that allows profit maximization to take place and where managers do not consume perquisites on the job at the owners’ expense. The second

Theory of the Firm l 9

viewpoint, however, looks at the firm not as an efficient device to maxi-mize profit, but rather as an institution controlled by management that is interested in satisfying its own utility (which could be in the form of income and perquisites), and making only a minimum profit that will satisfy shareholders.

Demsetz (1983) cautioned, “It is a mistake to confuse the firm of economic theory with its real-world namesake.” In other words, there is a real gap in how economists see the firm and the firm as it exists in a layperson’s view. To Demsetz, the firm is not solely concerned with production for others because some level of consumption also does take place within the firm. This view is quite practical because it rec-ognizes managerial consumption of perquisites. Similarly, he does not view households to be concerned primarily with consumption because some level of production also takes place even within households. He gives an interesting example of a homeowner renting a room in his house to a boarder as a kind of production that could take place within households.

Looking at the firm and households this way, Demsetz (1983) pro-ceeds to address the preoccupation of previous economists with agency problems, specifically the problems associated with the separation of firm owners from managers. It is important to be aware that agency prob-lems can arise in other situations also, for example, a situation involving cooperative efforts involving two or more persons even though there is no clear principal-agent relationship involved (Jensen and Meckling, 1976).

Demsetz (1983) observes that it is unreasonable to assume that the diffused ownership of firms represented by stock ownership will militate against profit maximization motive of the firm, and that self-interest of owners will work in such a way that managers will have checks and bal-ances on their behavior. Furthermore, managers will not risk the many years they have invested in their training (“human capital”) and their reputation by shirking, since shirking could possibly make their opera-tions inefficient and put the firm in danger either of bankruptcy or of becoming a likely takeover target.

Citing empirical evidence, Demsetz (1983) argues that managers’ compensation not only in salaries and bonuses but also in stock own-erships correlates with stock performance. Furthermore, since signifi-cant number of managers do have ownership stocks, the said separation

10 l Decision Making in Marketing and Finance

between ownership and control is not “so separate as is often supposed.” The author concludes with an interesting observation,

The picture painted by management shareholdings, the importance of stock-based managerial income, and the size of minority share-holdings is that of a strong linkage between management and owner interests . . .

How could it be otherwise? In a world in which self-interest plays a significant role in economic behavior, it is foolish to believe that own-ers of valuable resources systematically relinquish control to managers who are not guided to serve their interests. (p. 390)

Features of the Firm

Having gone through the above discussions and the different viewpoints of the firm, we should now discuss features of the firm. Because these features, to a large extent, make the firm what it is, we revert to the ques-tion we posed at the beginning of this chapter for guidance: What is the firm?

There are legally many corporate forms that can be referred to as a firm, however, a simple generic view of the firm will suffice in answer-ing the question posed above. Examining features of the firm will help in understanding how it helps in clearing the market more efficiently in the world of Ronald Coase (1937). First, many economists including Salter cited by Plant (1932) and Hayek (1933) have argued that the “price mechanism” is the driving force that allocates resources in a free mar-ket. This price mechanism eventually clears the market, thus there is no need for a central planning authority that will coordinate resources. This argument is at the heart of the classical economic theory and consistent with Adam Smith’s (1776) invisible hands thesis. However, as argued by Coase, the firm, regardless of its size, unlike the market, by its very nature must have a coordinator. This coordinator is referred to as the entrepreneur in some contexts if he is also the founder of the firm, and by varying other titles such as the chief executive officer (CEO), the manag-ing director (MD), and so on, if he is hired to coordinate the resources in a large organization.

The main responsibility of the coordinator, quite naturally, is to organize the resources of the firm in an efficient manner to pursue the

Theory of the Firm l 11

goals of the organization. Hence, the coordination function of a central authority is key to the firm. Because coordination is vital to pursuing the organization’s mission, Marshall (1890) refers to it as the fourth factor of production, of course, the first three factors of production being land, labor, and capital. One of the objectives of the firm that is often glossed over in the discussions of the firm is to be as efficient as possible in pur-suing its goals. This has to be the case because firm AF will be driven out of business by firm BF in a free market system if firm BF can offer what firm AF is offering at a lower price, which can be achieved by producing what firm AF produces more efficiently or at a lower cost, given the same level of quality.

The coordination function of the CEO in the firm takes several forms and can be complex or simple depending on several factors including, but not limited to, what the organization “makes” and its size. One of the primary coordinating functions is decision making; thus, the CEO in course of coordinating the network of contracts makes several deci-sions on almost continual basis. Notice that in a market system the price mechanism drives how resources are allocated. Therefore, if resource E is in short supply in the market, it will in the short run command a higher price and consequently more resources will be converted into E until equilibrium is reestablished.

Take, for instance, the case of supply shortage of computer program-mers in the market. In the short run, the salaries of programmers will go up, as there is more demand for them (of course, that is why there is a shortage to begin with). This higher salary will attract more people who will switch from whatever they are doing or intend to do to computer programming so long as they have the aptitude for it. This movement will exert downward pressure on the salary for computer programmers until the supply is equal to demand. At that point, the higher salary will disappear. This process (the autonomous movement of resources from an area of low demand to that of high demand), however, does not occur within firms. The CEO dictates or controls this movement as a part of his coordinating responsibilities. This point was made by Coase in his seminal paper on the nature of the firm. However, as observed later by Jensen and Meckling (1976), Alchian and Demsetz (1972) disagreed with Coase’s (1937) point that the manager of the firm wields a coordi-nating authority over resources within the firm, and instead suggested that through property rights, contracts with resource owners serve as a

12 l Decision Making in Marketing and Finance

mechanism for “voluntary exchange.” Of course, the idea here is that the manager, in a free market, does not serve as a benevolent dictator.

The argument that the organization has to concern itself with the interests of other interested parties (the stakeholders in general), rather than only those of its shareholders, represents a significant development in the theory of the firm, which will be discussed later. However, it is well established that the CEO’s coordinating functions do not stop within the boundaries of his organization. Indeed, they extend beyond the boundaries of the firm as the organization also deals with its suppli-ers, forms alliances with other competitors, and deals with the immedi-ate community as well as the general society in which it exists.

Resource Allocation

As established earlier, because specialization leads to efficiency and one of the objectives of the firm is to be efficient, it makes sense after some point, for example, after having attained a certain size, to organize the firm into departments or specialized units. The economic and structural justification for the so-called functional departments has thus emerged. The four traditional functional departments within the firm are pro-duction, marketing, finance, and accounting. However, the functional departments of any firm in the contemporary business environment depend on the nature of industry in which it exists.

To have a purpose and direction, every good organization creates a mission statement. These mission statements are broken down into aspi-rational statements and measurable goals, some of which are couched in the units of certain departments. For example, a firm can create a measurable goal that states its goal as increasing the organization’s mar-ket share, using marketing terms, or attaining an X percent return on investment (ROI), using finance terms. Or yet still, an organization can express its goal in production terms such as attaining a certain capac-ity utilization rate by a certain date. All these efforts have led to some departments taking more prominence than others as organizations pur-sue strategic planning.

Managing the organization to attain its goals often calls for devising rules to allocate its resources, which are often limited, among its depart-ments. The departments that are prominent often get the lion’s share of the resources. This process, though logical, results in unintended

Theory of the Firm l 13

negative consequences. The various departments start competing with each other for scarce resources. To justify getting more resources, each department starts putting its interest above that of the organization and engages in processes inimical to the objectives of efficient use of resources. For example, in order to justify getting a budget similar or larger than what was allocated to them in the previous year, many departments go on wasteful spending of funds so that no budgeted funds would be left when the current fiscal year comes to its end.

The natural evolution of strategic importance of functional areas and the practice of allocating more resources to departments based on the departments “making a case for it” has led to the so-called silo mental-ity. The more pernicious part of the silo mentality is not so much as the departments working in isolation, but rather “working” indirectly against the attainment of the organizational objective. For example, if the marketing department fails to share all the relevant information that the accounting department needs in order to make a more realistic accounts receivable forecast then the firm as a whole is going to suffer. Similarly, if the marketing department fails to interface well with the finance department in order to derive a competitive pricing strategy for a product and make a realistic cash flow projection that could sup-port the company’s debt position, then entire firm is going to pay the price for the failure of the two departments. Can you think of a similar breakdown as a result of a failure of the marketing department to com-municate with the production department? The result is rather obvious and disastrous—for example, failure to accommodate demand, quality defects, and the like.

So, What Is the Firm?

We will close this chapter with a metaphoric illustration of the firm. One could argue that a firm is a team, pretty much like a soccer team operating in a league—a league of the marketplace. A soccer team is managed by the head coach, the equivalent of the CEO in a firm, and the head coach works with other coaches with a common objective, which is to make the team win. Similarly, the CEO of a firm should work with other managers and department heads to make the firm a success. Every player on a soccer team is skilled at playing a specific position. The goal of a team is to allow (1) each player to play to the best

14 l Decision Making in Marketing and Finance

of his ability, and (2) yet play with other team members so well that the team outwits the opposing team. By executing these two tasks, the team is positioned to win. No individual player out of the 11 wins a game. It is the team that wins.

In much the same way, no department of the firm can be successful individually. It is the firm that can be a success or failure. No one depart-ment can exist by itself when a firm files for bankruptcy. Thus, every department needs to coordinate with each other.

Current Trends

Many contemporary researchers of business strategy who have also examined the nature of the firm have either commented directly on the counterproductiveness of the silo mentality with which many modern corporations operate or have made a case for interfunctional cooperation as a better approach for “maximizing” the present value of the firm. We use the term “maximizing” as opposed to “optimizing” or “satisficing” because it is still the term used in finance journals and textbooks and defended by scholars of finance (Jensen and Meckling, 1976). Similarly, many commentators have argued against pedagogy in business schools that is conducted along the lines of “functional silos” under the guise of discipline-based department curricula. According to Behrman and Levin (1984 cited by Crittenden and Wilson, 2006), problems in the real world of business “do not yield to a single-discipline solution”; they are better attacked by multidisciplinary solutions. Thus, cross-disciplinary teaching is a must in business schools.

Business research during the past four decades is increasingly show-ing cross-disciplinary approach. For example, Anderson (1982) in lucid exposition explains (1) why it is better for all the functional areas of the firm to be involved in setting the goals of the firm, (2) reviews evolution in the development of theory of the firm, and (3) proposes a new theory of the firm that specifies the role of marketing and other functional areas in the “goal setting and strategic planning process.”

Anderson (1982) cited Hayes and Abernathy (1980) to support the proposition that short-term consideration of top management that led to dominance of financial and legal specialists in the management rungs in large US corporations led to the unfortunate “slighting of technologi-cal considerations in product development.” Against this background,

Theory of the Firm l 15

he argues that marketing department must form coalition with other functional areas that involve customer support to ensure the long-term survival of the firm:

For example, the long run investment perspective implicit in the marketing concept can be made more comprehensive if it is couched in the familiar terms of capital budgeting analysis. (p. 24)

Other interdisciplinary studies specifically involving marketing and finance include the works of Koku, Jagpal, and Viswanath (1997), which showed that new-product introduction decisions are both mar-keting and finance decisions as they involve not only cash flow implica-tions, but risk implications for the firm as well. Others such as Lovett and MacDonald (2005) reiterate similar views and show through dynamic modeling techniques that marketing activities do affect stock market measures. They showed through linkages that marketing activi-ties impact the consumption markets, which in turn affect the financial markets, and when these markets work in unison, they lead to long-run superior performance of firms.

Conclusion

The discussions above have not only illustrated the original thoughts that went into formulating the theory of the firm, but they also touched on some of the contemporary extensions to the original thoughts. While several lessons could be learned from this chapter, the arching theme that should come through is that as a network of contracts everyone is responsible for everyone else in the firm. In other words, the firm func-tions best as a true network and not in functional silos; for that reason, interdisciplinary collaboration is a must and not an option.

Knowledge Application Exercise for Chapter 1

Having now completed reading chapter 1, it is recommended that you test your understanding of the materials covered in the chapter by analyzing/discussing case 1, appendix 1, titled “Jack Gordon, CPA.”

16 l Decision Making in Marketing and Finance

References

Anderson, P. F. (1982). “Marketing, Strategic Planning and the Theory of the Firm,” Journal of Marketing 44:15–26.

Alchian, A. A., and Demsetz, H. (1972). “Production, Information Costs, and Economic Organization,” American Economic Review 62 (5): 777–795.

Behrman, J. N., and Levin, R. I. (1984). “Are Business Schools Doing Their Job?” Harvard Business Review 62 (January/February): 140–147.

Berle, A. A., and Means, G. C. (1932). The Modern Corporation and Private Property. New York: Macmillan Company.

Carroll, A. (1999). “Corporate Social Responsibility: Evolution of a Definitional Construct,” Business and Society 38 (3): 268–295.

Coase, R. (1937). “The Nature of the Firm,” Economica 4 (16): 386–405.Crittenden, V. L., and Wilson, E. J. (2006). “An Exploratory Study of Cross-

Functional Education in the Undergraduate Marketing Curriculum,” Journal of Marketing Education 28 (April): 81–86.

Cyert, R. M., and March, J. G. (1963). A Behavioral Theory of the Firm. Englewood Cliffs, NJ: Prentice Hall.

Demsetz, H. (1983). “The Structure of Ownership and the Theory of the Firm,” Journal of Law & Economics 26:375–390.

Fama, E. (1980). “Agency Problems and the Theory of the Firm” Journal of Political Economics 88 (2): 288–307.

Fama, E., and Miller, M. H. (1972). The Theory of Finance. Hinsdale, IL: Dryden Press.

Friedman, M. (1962). Capitalism and Freedom. Chicago: University of Chicago Press.

Friedman, M. (1970). “The Social Responsibility of Business Is to Increase Its Profits,” New York Times, September 13, 122–126.

Hayek, F. A. (1933). “The Trend of Economic Thinking,” Economica 40 (May): 121–137.

Hayes, R. H., and Abernathy, W. J. (1980). “Managing Our Way to Economic Decline,” Harvard Business Review 38 (July–August): 67–77.

Jensen, M. C., and Meckling, W. H. (1976). “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure,” Journal of Financial Economics 3 (October): 305–360.

Koku, P. S., Jagpal, S., and Viswanath, P. V. (1997). “The Effect of New Product Announcements and Preannouncements on Stock Price,” Journal of Market-Focused Management 2 (2): 183–199.

Lee, M-D, P. (2007). “A Review of the Theories of Corporate Social Responsibility: Its Evolutionary Path and the Road Ahead,” International Journal of Management Reviews 10 (1): 53–73.

Lovett, M. J., and MacDonald, J. B. (2005). “How Does Financial Performance Affect Marketing? Studying the Marketing-Finance Relationship from

Theory of the Firm l 17

a Dynamic Perspective,” Academy of Marketing Science Journal 33 (4): 476–485.

March, J. G., and Simon, H. A. (1958). Organizations. New York: John Wiley & Sons.

Marshall, A. (1890). The Principles of Economics. London: MacMillan Company.

Pfeffer, J., and Salancik, G. R. (1978). The External Control of Organizations. New York: Harper and Row.

Plant, A. (1932). “Trends in Business Administration,” Economica 35 (February): 45–62.

Robinson, J. (1932). Economics Is a Serious Subject: The Apologia of an Economist to the Mathematician, the Scientist and the Plain Man. Cambridge, UK: W. Heffer & Sons.

Simon, H. A. (1955). “A Behavioral Model of Rational Choice,” Quarterly Journal of Economics 69 (February): 99–118.

Simon, H. A. (1964). “On the Concept of Organizational Goal,” Administrative Science Quarterly 9 (June): 1–22.

Smith, A. (1776). An Inquiry in to the Nature and Cause of the Wealth of Nations, 1st ed. London: W. Strahan.

CHAPTER 2

The Customer Lifetime Value

How much is a customer worth to my firm, and is the cus-tomer worth retaining? Calculating as these may sound, they are issues that today’s managers often have to wrestle with.

Common as the questions are, the answers are not simple, and the fact that such questions are now the norm suggests the following:

1. There are costs associated with getting and retaining a customer.2. Not every customer is desirable.3. There is a connection between having a customer and profits.

Commenting on the importance of customer loyalty, Reichheld states, “Experience has shown us that disloyalty at current rates stunts corporate performance by 25 to 50 percent, sometimes more. By contrast, busi-nesses that concentrate on finding and keeping good customers, produc-tive employees, and supportive investors continue to generate superior results. Loyalty is by no means dead. It remains one of the great engines of business success” (1996, p. 1).

It is not difficult to see the connection between customers and a com-pany’s profit; however, the connection between customers and cost to the company requires a little more probing. This chapter is therefore divided into three sections. The first two sections deal with how the company cultivates or wins over customers, the strategies used, and the associated costs. The third section deals with computations involving the customer lifetime value (CLV).

P.S. Koku, Decision Making in Marketing and Finance© Paul Sergius Koku 2014

20 l Decision Making in Marketing and Finance

To get and retain a customer, many firms use a combination of ele-ments of the marketing mix (product, place, promotion, and price) and the communication mix (personal communication, advertising, sales promotion, publicity/public relations, instructional materials, and cor-porate design). It is clear from the list of elements (variables) that the marketing and communication mix are not mutually exclusive. Some elements, or variables as they are also called, are common to both the marketing and the communication mix. Below are some explanations on how these variables are used.

Marketing Mix Elements

Product

Many companies put significant efforts into designing their products/services so that they can appeal to the intended target market. The auto-mobile companies are well known for designing vehicles to appeal to certain demographic segments. However, automobile companies are not alone in trying to appeal to consumers through product design. Have you ever wondered why the shape of the Yoplait yogurt is unique? In addition to product design, many companies use free product samples to encourage consumers to try a new product. Samples are often smaller packages or versions of the actual product. In using samples, manu-facturers realize that many consumers suffer from inertia, which is the reluctance to change or try something new. With free product samples, companies try to nudge the consumer to, at no out-of-pocket cost, try the new offering.

Place

While the use of the “place variable” in getting the consumer to try the offering (product/service) is not always visible, it is nonetheless used. The objective is to make the initial offering (a sample or whatever) easily available to the consumer. Again, in designing its marketing strategy, the company realizes that not only are customers likely to suffer from inertia when it comes to trying new offerings, but they are also not likely to go out of their way to look for new offerings. Faced with this problem, the company tries to make the initial offering easily accessible to the potential target market. This is done through mailing the sample to the targets’ homes, freestanding-trial aisle displays, and the like.

The Customer Lifetime Value l 21

Promotion

Massive advertisements that stress the uniqueness of the new offering and attractive package designs and labeling are used to promote the offer-ing at the initial stage to “entice” consumers to try the new offering.

Price

Oftentimes companies subsidize consumers’ purchase price at the initial stages of product adoption. This is done by selling at a significant dis-count. The psychology of heavy price discounts at the initial stage is to try to overcome consumers’ unwillingness to purchase a product they might not like. However, with a heavily discounted price, customers feel that they would not lose a lot of money if the offering turns out to be something they do not like.

In addition to heavily subsidized prices, it is not uncommon, for example, in the services industry for the initial service fee to be waived to entice current or new consumers to try a new offering. Such exam-ples abound in the physical fitness industry where gym memberships are waived during the first month for new members. Similarly, it is not uncommon for credit card companies or financial institutions to waive the first year’s membership fee for new members in an effort to entice them with a new credit card.

The Communication Mix

Personal Communication

Personal communication as distinguished from impersonal communica-tion has been defined as “messages that move in both directions between two parties” (Lovelock and Wright, 2002, p. 199). As you may have already guessed, impersonal communication moves in only one direc-tion. Generally, it is from the company and directed to a large group of customers or potential customers. They can be identified by the “generic” tone, particularly in the salutation. They often begin this way—“Dear Customer,” “Account holder,” or “Sent from: XYZ, To: UVW.” Personal communication, in contrast, actually tries to address the specific needs of the recipient and the salutation is often individual specific. For example, they can begin as “Dear David” if David is the name of the customer or potential customer.

22 l Decision Making in Marketing and Finance

Clearly, it is cheaper for a company to use impersonal communication as a means to reach its customers or potential customers. However, tech-nology and availability of large databases have now made it inexpensive for firms to try to create the appearance of using personal communica-tion to reach their current and potential customers. The major issue now is for the firm to undertake a rigorous cost-benefit analysis in order to decide which approach to use.

Advertising

Advertising has been defined variedly by different people. Kotler and Keller (2009) define it as “any paid form of non-personal, presenta-tion and promotion of ideas, goods or services by an identified spon-sor” (p. 472). However, Mooradian, Matzler, and Ring (2012) suggest that “advertising entails communicating messages via paid-for, imper-sonal media (television, radio, newspaper, etc.) in which the sponsor is identified or known” (p. 300), while Ghewal and Levy (2006) define advertising as “a paid form of communicating from an identifiable source, delivered through a communication channel and designed to persuade the receiver to take some action, now or in the future” (p. 470).

It is evident from all the various definitions that advertising is a form of communication directed at an audience. Ghewal and Levy’s defini-tion goes a little beyond the other two definitions and tells us what we all know too well about advertising, that is, it is intended to get the tar-get consumers to take some action now or in the future. Several actions could be required from existing consumers. For example, they could be encouraged to consume more, refer others to try the product/service, or they themselves could avail its upgraded version. To potential consum-ers, the primary message is to overcome the inertia and try the product/service.

Sales Promotion

This is a short-term activity or incentive that is geared at stimulating pur-chase of the product/service. The objective of sales promotion is to get the current or potential customers to accelerate their purchase decisions. Thus, sales promotions are undertaken for only a specified, and generally

The Customer Lifetime Value l 23

limited, time. They involve the use of samples, coupons, competitive events, and door prizes. It is evident from the discussions that sales pro-motions involve definite costs on the part of companies.

Publicity/Public Relations

These involve efforts designed to create positive image or favorable press/media coverage for the company. They are usually undertaken by a third party on behalf of the company and involve activities such as club spon-sorships, special events, adoption of highways, and visual displays of the company’s logo, symbol(s), or colors.

Instructional Materials

Though not necessarily used to win new customers, instructional mate-rials teach customers how to use new equipment and give information on new offerings.

Corporate Design

As a part of the communication mix, corporate design includes colors that are associated with the company, lettering, symbols, and logos. These are used to distinguish the company from competitors and to cre-ate a connection with the current and potential consumers.

CLV

CLV computations are actually the present-value calculations that are made based on projections of a customer’s lifetime expenditure. The pro-jected expenditure is treated as a stream of future cash flows from the customer, and therefore it becomes a lump sum in today’s dollar value. In simple mathematical terms, if i is the ith customer, t is the t th time, r is the discount rate, and n is the forecasting horizon, that is, the length of time that the customer remains with the company, the equation can be formulated as follows:

CLVi tt

n

r=

+=∑ ( )

( )Future gross profits Future costsit it-

11

The CLV gives managers a sense of how much a customer is worth to them in terms of dollars, and is thus helpful in the decisions on whether to undertake a certain level of expenditure to entice a potential customer

24 l Decision Making in Marketing and Finance

or how much the firm should be willing to spend to keep an existing customer.

While such calculations were not exactly welcomed in the past, they have now become a common tool in the tool kits of the practitioners as well as a common topic of research for academics. Several reasons have contributed to this change. First, accounting practices have undergone significant changes partly due to integration of technology that now allows them to do things quickly with spreadsheet calculations. Second, the use of spreadsheets has made it easier for managers to see a truer picture of a customer’s value to the firm. Furthermore, some scholars posit that relatively newer practices such as activity-based accounting also allow managers to evaluate the true value of a customer’s relation (Berger et al., 2006).

There are three important components to the CLV formulation accord-ing to many who have studied the CLV (Kerin and Peterson, 2013). The first step is to derive the per-period cash margin of the customer, which we will call here $X (X dollars). The per-period cash margin is the antici-pated revenue (purchases) from the customer, less all the expenses asso-ciated with the sale (discussed above, e.g., promotions, discounts, etc.) during a period. A period is a nonspecific term that could be specified by the manager. It could be a month, a quarter, or even a year. The next term is the retention rate; we shall call this term r, which captures the likelihood of retaining the customer. The third term, i, is the interest rate to be used in discounting the future stream of income. With these definitions CLV is algebraically specified as follows:

CLV X=+ −

$1

1 i r (2)

Equation 2 is a simplification of a slightly more complex formulation. It has been shown by Gupta and Lehmann (2003) that the more complex formulation reduces to equation 1 when the margin and retention rates are constant over time with an infinite time horizon.

Given equation 1 as it is, what does it mean in terms of numbers? Consider a popular mass merchandiser whose annual margin on a cus-tomer is $3,000.00. Note that we have chosen an annual margin to make the computations simple and straightforward. We could have very well chosen a monthly or quarterly margin, which we would need to

The Customer Lifetime Value l 25

annualize, however, having chosen an annual margin at the outset we do not need to annualize the margin again. Let r, the retention rate, be 75% while, i, the interest rate, is 10%. Applying the formula with these values for the variables, we can compute the CLV as:

CLV 3000=+ −

$. .1

1 0 10 0 75

Sophisticated firms measure the rate of growth in the customer’s margin and can use that to estimate the customer’s CLV.

CLV = $3000 × 2.857

= $8,571.40

Can you think of how a firm could improve its CLV? A close exami-nation of the formula suggests a number of possibilities. What about increasing the margin? This could be done through a number of ways:

1. It can be done by decreasing costs associated with enticing or retaining the customer.

2. It can be done by holding down the cost of retaining or enticing the customer while the customer is encouraged to increase his/her spending.

3. It can also be done by increasing r. An argument can be made that the CLV can be increased by changing i also, but we must note that i is not within the control of the firm, hence in terms of strategic decisions, the company will take i as given.

4. A simultaneous increase in the margin and retention rate would also increase the CLV to the firm.

It is important to note that other factors such as competitive activity and the industry structure directly affect a firm’s margin. A consequence of monopolistic competition in an industry, that is, an industry in which there are many sellers and buyers and all the sellers sell the same things that are slightly different, all other things being equal, is a lower price level that will naturally affect a firm’s margin. Take for instance gas stations; because there are many gas stations as well as buyers in many towns, the margin on a gallon of gas is small. The opposite is theoretically true for

26 l Decision Making in Marketing and Finance

a monopoly except for the fact that they are generally regulated by the government, the utility companies being an example. Having duly noted what has just been discussed let us examine the effect of a change in the margin on the CLV as below.

If $X increases from $3,000.00 to $4,000.00 per year, then CLV becomes

CLV =+ −

$. .

40001

1 0 10 0 75

= $4000 × 2.857= $11,428.00 (an increase of about 33%)

What if the margin remains the same but the retention rate is improved, and therefore rises from 75% to 85%? In this case, the new CLV becomes,

=+ −

$. .

30001

1 0 10 0 85

= $3000 × 4= $12,000.00

Thus, it can be seen that by increasing the retention rate by approxi-mately 10%, that is, from 75% to 85%, the CLV increases by 40%. This suggests that increasing the retention rate is preferable to increasing the customer’s margin as far as enhancing the CLV is concerned.

Sophisticated firms measure the rate of growth in the customer’s mar-gin and can use that to estimate the customer’s CLV. Here let us assume that margin rate increases at a constant rate of j per year. In this case,

CLV X=+ − −

$

11 i r j

If we take j to be 5% per year with the variable values of r as 75% and i as 10%, as in the first case above, then

CLV 3000.10

=+ − −

$. .

11 0 0 75 0 05

= $3000 × 3.333= $10,000.00

The Customer Lifetime Value l 27

As evidenced by this computation, a 5% constant annual growth rate in the firm’s margin rate leads to an increase of 16.66% or $1,428.60 in a CLV—a change from $8571.40 to $10,000.00.

In addition to the contributions from the accounting profession, for the past two decades the CLV has attracted the attention of aca-demics who have, through their research, shed more light on how the model works and how it could be enhanced. For example, it has helped to connect the dots between CLV and customer relationship marketing.

Relationship marketing has been variedly defined by several researchers. Kotler and Keller instead of providing a direct definition chose to describe it in terms of its objectives: “It aims to build mutu-ally satisfying long-term relationship with key constituents in order to earn and retain their business.” Baran, Galka, and Strunk (2008) also described it as “a focus on the relationship between the firm and its customers based on cooperation and collaboration. The ongoing process of engaging in cooperative and collaborative activities and pro-grams with immediate and end-user customers to create or enhance mutual economic value at a reduced cost” (p. 499), while Ryals and Knox (2005), citing Berry (1983), said it is “attracting, maintaining, and enhancing customer relationship.” We can conclude from these definitions that relationship marketing extols the virtues of a continu-ing mutually beneficial relationship in which the needs of both par-ties, the customer and seller, are satisfied. Ryals and Knox tied the CLV concept to relationship marketing and cited previous studies such as Reichheld and Sasser (1990) and Reichheld (1996), which showed, from the businesses they studied, that a 5% improvement in customer retention from 85% to 90% could lead to a significant improvement, from 35% to 95%, in the net present value.

We must, however, note that studies such as Carrol (1991) have criti-cized the CLV estimations of Reichheld and Sasser (1990) on method-ological grounds; nonetheless, the fact that improvement in customer retention rates leads to improvement in a firm’s profitability is not in dispute even by Carrol. However, notwithstanding the evidence from studies and the fact that even many practitioners seem to accept the customer relationship concept, Riyals and Knox cite studies such as Christopher, Payne, and Ballantyne (2003) that have shown that 80% of the 200 firms studied in the United Kingdom still overinvest in

28 l Decision Making in Marketing and Finance

customer acquisition and only 10% of the firms studied overinvest in customer retention.

Ryals and Knox (2005) argue that while single-period value cus-tomer profitability or forecasted CLV computations are commonly used attempts to capture the value of a customer and to give a dashboard view to the firm, they may not be the most appropriate metric for measur-ing the value of customer relationships or for managing the relation-ship marketing. They tend to overestimate the customers’ value to the firm because the values derived are not adjusted for the risks inherent in developing the relationships. The authors argued further that if the objective of the CLV is to measure marketing’s contribution to share-holder value, then the CLV should be measured for value instead of profit. This means that the CLV should be risk-adjusted; otherwise an activity such as investment in customer relationship could appear to be profitable, while it in fact provides minimal or even negative returns to shareholders.

How might this problem be solved? Ryals and Knox (2005) suggest that the problem could be solved through proper assessment of customer risk that takes into consideration risks in generating revenue streams, particularly from customers in whom the firm has made significant investments. The researchers call the combination of CLV with future customer risk the economic value (EV) and empirically show that it is a better metric of customers’ value to shareholders.

Reporting the outcome of the “Thought Leadership Conference” on CLV, which consisted of both academics and practitioners, Gupta and his coauthors listed three reasons why an increasing number of corpo-rations are adopting the CLV (Gupta et al., 2006). The authors made a number of arguments. First, they posit that the increasing pressure on marketing departments to show returns on marketing investments has caused many of them to look beyond the traditional metrics of brand awareness, attitudes, sales volume, and market share. Second, financial metrics, such as the stock price, are of limited use in holding marketing accountable because they reflect aggregated data and do not show customers that are not profitable, which a company should get rid of. Third, they argue that improvements in information technology have made large data collection on customers and subsequent analyses easier.

The Customer Lifetime Value l 29

The authors further discussed the link between customer equity (CE), that is, the CLV of the current and future customers and its linkage to the stock price and then dwelt on the different mathematical models for com-puting the CLV and their associated econometric problems. They noted that the literature on customer relationship management (CRM) takes the firm’s perspective in modeling CLV and therefore uses terms such as “customer acquisition,” “retention,” and “expansion.” The literature on choice modeling, however, takes customers’ perspective and therefore uses terms such as “when,” “what,” and “where” the product can be purchased and “for how much.” It is clear that the two approaches come from differ-ent ends of the transaction spectrum; nonetheless, there are overlaps.

Berger et al. (2006), for example, proposed, what they termed, the “chain of framework” in which the CLV serves as a link, among other things, between the firm’s actions and shareholders’ value. In enhancing the CLV, they introduced the notion of “prescient” value of the CLV, which they called CLV-P.

The authors argue that a firm’s customer behavior includes other things such as customer acquisition, retention or defection, and devel-opment and their associated costs. Furthermore, they assert that like products, customers also go through a sequential product-life-cycle type of life stages with a firm. Even though not every customer necessarily goes through every stage, they begin from the acquisition stage through retention, and then go through either development or defection. The authors explained that customer behavior is guided by the customer’s mind-set toward a firm’s offerings (products/services) as well as those of its competitors and channels, and that the customer’s mind-set plays a role in how they perceive a product’s value and therefore in how brand equity is developed.

What might be the other components of a customer’s mind-set? According to Berger et al. (2006), other components of the mind-set are (i) awareness, (ii) association, (iii) attitude, (iv) attachment, and (v) advo-cacy. The authors explained awareness as the extent to which custom-ers can recall or recognize a firm’s offerings, association as the strength of benefits and “positives” attributed to the firm’s offerings, attitude as overall evaluation of the firm’s quality, attachment as the extent of the customer’s loyalty, and advocacy as the likelihood of the customer rec-ommending the offering to others.

30 l Decision Making in Marketing and Finance

Berger et al. (2006) have made several important points to improve the value of CLV as used and have provided the theoretical framework for doing so. First, they observed that even though an aggregate CLV is sufficient to estimate the link between the CLV and shareholders’ value, for strategic purposes, it is important to calculate the CLV on an individual basis. Second, to link the CLV to the sharehold-ers’ value, a 3-step process that uses “recency, frequency and mon-etary value data and various profits and cost measures” must be used. Third, the CLV must be related to marketing programs and strate-gies. In doing this, it is essential that the CLV is forward looking. What does a forward-looking CLV mean, and how is it estimated? According to Berger and his colleagues, a CLV could be estimated in the following two ways: (1) through the traditional maximization of expected CLV means, and (2) through the risk-adjusted measure. The latter requires an incorporation of “real options” valuation methods often used in finance and require probabilistic distributions of val-ues implied in marketing programs such as the benefits that would accrue to the firm in the future if it changes its business model or abandons unprofitable customers.

Tying everything together, the forward-looking CLV discussed above is referred to by the authors as CLV-P or the prescient value. The CLV-P is the highest value a firm is able to receive from a cus-tomer or a “complete real option value.” While the concept of the CLV-P sounds good in theory, it is not without econometric problems in practice; thus, the authors suggest some methods in overcoming these problems.

In a real-world example of how firms use CLV, Kumar and his col-leagues reported on how IBM used CLV to determine the level of mar-keting efforts to allocate to an account, given its CLV. The marketing contacts that were available to be used for each customer consisted of direct mail, telesales, email, and catalogs (Kumar et al., 2008). The study involved 35,000 accounts on which IBM implemented the CLV-driven resource allocation instead of allocating marketing resources based on past spending history. Fourteen percent of the accounts saw a reallocation in their marketing contacts with the implementation of CLV-driven allocation. This effort resulted in an increase in revenue of approximately $20 million (a tenfold increase) without any changes in the level of marketing investment. The increase in revenue realized

The Customer Lifetime Value l 31

by IBM by changing the allocation of marketing resources alone is a clear evidence that CLV could be a useful tool in improving corporate profit, but like everything else in marketing and management, if used properly.

The phenomenal success enjoyed by IBM in using CLV to allocate marketing resources suggests that firms segment and profile their customers. Customers are segmented on factors such as CLV and size of wallet, and business customers on market share and firmograph-ics, which includes employee size, revenue size, industry, number of customers, and the like. IBM’s success also suggests that firms understand customer migration, that is, how customers move from higher to lower segments over time or vice versa in order to enhance retention.