Electronic Customer Relationship Management in banking sector of Pakistan: A challenge from the...

18

www.IndianJournals.com Members Copy, Not for Commercial Sale Downloaded From IP - 212.57.210.1 on dated 8-Oct-2013 Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323 AJRBF Journal of Asian Research Consortium 31 http://www.aijsh.org A Peer Reviewed International Journal of Asian Research Consortium AJRBF: ASIAN JOURNAL OF RESEARCH IN BANKING AND FINANCE ELECTRONIC CUSTOMER RELATIONSHIP MANAGEMENT IN BANKING SECTOR OF PAKISTAN; A CHALLENGE FROM THE EMERGING TECHNOLOGY SHAFI ULLAH*; MANZOOR AHMED**; SYED MUHAMMAD HASAN HASHMI*** *Department of Marketing, College of Business Administration. **Department of Marketing, College of Business Administration, King Saud University, Riyadh, Saudi Arabia. ***Department of Management, College of Business Administration. ABSTRACT PURPOSE Despite the growing debate about Customer Relationship Management has gained a lot of importance in the 21 st century because of globalization and new technology advancement there is little research on role of CRM in banking sector of Pakistan. The banks in developed countries like Sweden are offering their customer relationship management in a quite different way that is through electronic customer relationship management eCRM that helps banks to improve relationships with their customers through electronic communication tools i.e., email, online banking, phone banking, SMS banking, ATM etc. Due to some demographic and economic-political factors banks in Pakistan are using still the old bookkeeping and post-mail methods to interact with their clients. There is a need for an electronic reform in order to uplift the services of this important sector. DESIGN/METHODOLOGY/APPROACH A qualitative secondary data was collected from different sources including web portals and annual reports of several banks in Pakistan including State Bank of

Transcript of Electronic Customer Relationship Management in banking sector of Pakistan: A challenge from the...

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 31

http://w

ww.aijsh.org

A P e e r R e v i e w e d I n t e r n a t i o n a l J o u r n a l o f A s i a n R e s e a r c h C o n s o r t i u m

AJRBF:

A S I A N J O U R N A L O F R E S E A R C H I N B A N K I N G

A N D F I N A N C E

ELECTRONIC CUSTOMER RELATIONSHIP MANAGEMENT IN BANKING SECTOR OF PAKISTAN; A CHALLENGE FROM THE

EMERGING TECHNOLOGY SHAFI ULLAH*; MANZOOR AHMED**; SYED MUHAMMAD HASAN HASHMI***

*Department of Marketing,

College of Business Administration. **Department of Marketing,

College of Business Administration, King Saud University, Riyadh, Saudi Arabia.

***Department of Management, College of Business Administration.

ABSTRACT PURPOSE Despite the growing debate about Customer Relationship Management has gained a lot of importance in the 21st century because of globalization and new technology advancement there is little research on role of CRM in banking sector of Pakistan. The banks in developed countries like Sweden are offering their customer relationship management in a quite different way that is through electronic customer relationship management eCRM that helps banks to improve relationships with their customers through electronic communication tools i.e., email, online banking, phone banking, SMS banking, ATM etc. Due to some demographic and economic-political factors banks in Pakistan are using still the old bookkeeping and post-mail methods to interact with their clients. There is a need for an electronic reform in order to uplift the services of this important sector. DESIGN/METHODOLOGY/APPROACH A qualitative secondary data was collected from different sources including web portals and annual reports of several banks in Pakistan including State Bank of

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 32

http://w

ww.aijsh.org

Pakistan’s annual reports data was analyzed and benchmarked in relevance to our two-basic factors i.e., orthodox banking system and electronic banking system, The aim of this process was to assemble or reconstruct the data in a meaningful or comprehensible fashion.The CRM functioning models of different banks were benchmarked and a fairly new and suitable CRM model was designed. This model provides all the needed ingredients and their performance attribute towards customers and the organizations. FINDINGS The findings show several differences in the levels of CRM activities in banking sectors of Pakistan. And every level has different customers. Banks need to identify these levels and then design the policies accordingly. If the banks firmly classify and properly manage the levels of customers then it is not difficult provide the right services they need. Due to low literacy rate in Pakistan the limitations towards use of CRM is very high and there is a strong interference towards new usage of new technology from banking customers in Pakistan as will. The use of electronic tools of communication will play a vital role in speeding the banking services and winning a proper support from the customers as good awareness program does not mean good retention as well. It means orthodox customers are getting less each day does not mean that IT based facilities cannot be designed for them. The feedback management can provide amazing results through query solve. ORIGINALITY/VALUE The results offer needed empirical support and cross-cultural stability tothe much theorized construct of CRM by exploring its effects within banks of Pakistan. Additionally, it unifies and complements the previous work by integrating the theory of customer relationship management and the need for IT reforms in banking sectors. Thus providing a comprehensive theoretical framework for the future study on the topic and this this study requires empirical evidence from the banking sector in Pakistan. KEYWORDS: Customer Relationship Management, eCRM, Banking sector, Pakistan, CRM Model.

___________________________________________________________________________

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 33

http://w

ww.aijsh.org

INTRODUCTION

Due to globalization and new technology advancement Customer Relationship Management (CRM) has gained a lot of reputation in the current millennium because of; due to this organizations are faced with strong competition also Organizations are now more focused on increasing revenues through customer satisfaction; this can be effectively done by focusing on customer relationship. Concept of marketing has now totally transformed from buying, selling to establishing long term relationships with customers. Research has proven that current customer are easy to retain and less expensive as compared to the old customers. Customer satisfaction is the best way of retaining old and new customers which has a positive impact on brand loyalty as well. By increasing the brand loyalty enhances chances for repeat purchases and sales ultimately increase in profitability and customer retention.

Services related to the financial sector has given more significance to the customer relationship management because a long lasting strong relationship in banking sector with potential customers cannot be easily replaced by the upcoming and the existing competitors because that relationship with the customer act as a competitive edge for banks. Banks profit is directly related to the total customer relationship, the more the relationship with customers there will be increase in profits as well (Godin, S., 1999). Keeping in view the importance of customer relationship management the organizations such as banks and other financial institutions have focused there most of the strategies on developing the long lasting relationship with customers.

There are two main determinants of which CRM is based that is trust and value apart from this there are also other factors which are to be considered that is identifying the need and wants of the customer, fulfilling the requirement of the customer, post sales services after doing all this identify weather the customer is honest and willing to establish long term relationships. Hence all these factors have to be taken into consideration when establishing a relationship with customer. According to Sheth and Parvatiyar (1995) Marketing model has achieved a paradigm shift from product to customer –centered approach because of immense competition faced by organizations. With the change in technology banks have changed their operations as well and they have become more modernized and sophisticated. A revolutionary changed has occurred due to technology and the competition, as due to automated teller machines (ATM) the access to the remote areas have increased (Santos and Peffers, 1995), the branch banking operations have been replaced by the call centers and internet has replaced the mail with fast and speedy services which are free of cost and ultimately one to one interaction will be replaced by interactive television which will one or the other way of maintaining effective customer relationship.

Customer relationship management in banks is handled in a different way that is information about the customer is extracted through data mining from the data ware house and also through customer meetings the information includes in what type of business customer is involved is he financially sound, the contract that he is signing and how much amount, after extracting and analyzing this information the strategy is formulated for the current and new customers in order to retain them. That is why the services of banks varies from customer to customer, for corporate customers the services are entirely different from the regular one. Branch plays a vital role in

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 34

http://w

ww.aijsh.org

offering these services as they are more close to customers than the head office, branches have more understanding of needs and wants of wants of customer they are trained how to retain them and establish long term strategic relationship with them . (Hiebeler, et al, 1998), Different channels of communication are used in maintaining and establishing these relationships these are email, telephones, fax, direct mail etc. these all different channels are used depending upon the business setup of the customer and these channels help in collecting all the customers under a single platform of bank through eCRM (Johnson et al., 2004).

Keeping in view the benefits of the customer relationship management, organizations especially banks and other financial institutions are finding new ways to retain their customers and establish relationship with them and huge cost is incurred by banks to train its employees on new and innovative ways of CRM activities.

LITERATURE REVIEW

INTERNATIONAL SCENE

Customer relationship management has been applied by different organizations all over the world. The customer relationship management has benefited some of the organizations whereas in some countries such as in the context of India there is no strong association between deployments of customer relationship management best practices which are scheduled in the commercial banks (Camp, 1989). According to research there are 29 different customer relationships management practices that are that are useful for the organization in achieving customer relationship deployment. Its extents were examined in all the three different types of banks which are available in India and surprisingly there is no perfect bank which has deployed all the 29 practices of customer relationship management to the full extent.

The impact of customer relationship management has positively affected the performance of the organization that is to say on customer retention in Iranian electronic banking. Different resources of the customer relationship management have positive effect on the customer relationship management processes. From the research it is evident that banks should focus more on the customer services which will lead to high rate of customer retention and ultimately customer relationship management have a positive impact (Keshvari, 2012).

In the banking sector of Saudi Arabia customer relationship management mainly focusing on some of the critical success factors and among them the most important one is the customer retention has a positive impact. These success factors play a vital role in implementing any strategy in an effective manner (Anshari et al. 2009). Customer oriented strategy which is followed by the Saudi Arabian banks plays an important role in the success of the customer relationship management. From the research it is evident that there exists a positive relationship between the critical success factors and the customer relationship management in the context of Saudi Arabia. Critical success factors play a vital role in the successful implementation of the customer relationship management and provide all the benefits that were being promised. Along with the critical success factor it is important to have adequate resources along with top management support for positive customer relationship strategy.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 35

http://w

ww.aijsh.org

The banks in Sweden are offering their customer relationship management in a quite different way that is through electronic customer relationship management which helps them in maintaining a good relationship with customer by using emails which is used as a communication tool to remain intact with their customers and provide all the knowledge about different product and services being offered (Ahmed, 2009). Electronic customer relationship has been successful in providing the customized services to its customers this has increased the effectiveness and the efficiency of services that are provided to the customers, but these customized services are offered to the customer only on its request. With the advancement in the technology websites usage has increased and it is one of the effective mean to provide all the knowledge about the product and services which can be found easily. The usage of email for the business purpose of the bank is less as compared to the customer because of some security issues (Anu, 2001). Other factors can also be beneficial at establishing better relationship with customers those are how friendly the staff is the bank is, and what is the location of the bank, how speedy the services are these determinant have direct relation in maintaining and establishing relationship with customers.

Turkish banks apply the customer relationship management to increase the volume of potential customers in banks; campaign management in banks has been very successful in identifying the potential customers and then establishing long term relationship with them in order to increase their account relationship for long term also [Beckett-Camarata et al. 1998]. Many banks and financial institutions in Turkey keep track of the life stages of customers and then according to their age market the right opportunity or them such as mortgages, educational loans, marriage loans etc .electronics means of banking have been transformed into the strategic lines and its horizon as very broad as compared to the older system as it is successful in catering the needs of multinational corporate customers [Mike et al. 2004]. Data ware house and the data mining are the two main tools that are widely used for customer relationship management. After extracting the valuable information about the customers that is (demographics, product services usage, relationship with banks, ownership of the banks product, global variances etc) marketing campaign is applied according to target market in order to attract and retain more and more people [Cabena et.al. 1999]. Hence this relationship marketing has helped the banks in achieving positive and long term relationship with customers.

NATIONAL SCENE

Customer relationship management helps to establish and maintain long term relationship with their potential customer. In the scenario of Pakistan its application is most prominent in banking sector and helped in achieving increased revenues and profits of the banks. The importance of the customer relationship management is recognized in the banking sector but all of them have not been successful in implementing the complete concept of the customer relationship management as most of them are at the initial stage of it. Only few banks in Pakistan are customer centric due to increase in competition and privatization.(Hussain et. al, 2012). It is important for banks to identify the needs and wants of their customer and then formulates strategy according to their need as they will feel satisfied and more valued customer. Several factors should be kept in consideration for success of the customer relationship management that is diversity issues should be learned and deal in effective way as each customer is different from

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 36

http://w

ww.aijsh.org

other so their needs also vary accordingly. Banks need to seek help from newspaper, media, and magazine in order to create awareness among the customer about the services that are being offered this will increase in the level of trust in them. To build confidence in consumer’s banks should sponsor different cultural and social activities. Banks should hire the expert professional from the local communities as the customer will understand them much better and will develop a sense of belongingness as well(Smith, 2001) . All these ways will helps banking sector in Pakistan in achieving better customer relationship. Providing superior customer services is the only way in differentiating one bank from the other.

In order to increase the retention rate of customer banking sector in Pakistan is more focused on building relationship with customer this can be successfully achieved by offering more products to the customer such as insurances, credit cards, saving, loans and ultimately retention rate of customer will have a positive impact.Well, there are a number of issues that constitute key success factors. One of these is the information problem (Neilson and Chadha, 2008) .The organization has very keen and dedicated staff in the front or branch office, which really do understands customer needs and go out of their way to treat them as special customers. But if the back office processes are incapable of supporting the front office, these people end up over-promising and the result is under-delivery. Lack of integration of the customer facing part of the organization with the back office is one of the biggest problems of CRM implementations. Hence the front deck operation needs to be in line with the back office processes in order to establish positive customer relationship.

Several vendors are available for the small and medium enterprise that provide customer relationship management solution. SAP and Oracles Siebel is most famous customer relationship solution provider now a days and they are capable of providing the right access to right people at the right time. Most banks in Pakistan have implemented the customer relationship management packages through these vendors (Baird, 2008). The major problem is that the banks which are located in the rural areas of Pakistan face a lot of problem because the people have lack of awareness about the new technologies such as automated teller machines (ATM), internet banking hence in such areas there is no concept of customer relationship. Most of the people in the rural areas hesitate to go in banks also because they feel that banks are not made for them they are for the rich people. These differences should be realized by the banks and they should provide some new and innovative ways to attract the rural target market also and should communicate to them in their local language to the will develop a sense of ownership in them. Comparison should be carried out between the banks of Pakistan and the foreign banks in order to fill the gaps and improve performances. Comparative analysis should be done with the banks of United Kingdom as their operations are the most advance.

Research has proved that there are several drawbacks which are causing hindrance in the success of the customer relationship management these issues are Currently, each branch services its own customers with no centralized customer service or telephone-based automated services. Therefore, customer data cannot be tracked and the concept of customer relationship management is virtually impossible.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 37

http://w

ww.aijsh.org

Customers have to restate their information whenever they interact with their bank, and the members of staff are unaware of the previous transactions and have no quick access to records. The Information technology personnel at some of the banks are not fully trained to handle customer’s information packages including customer relationship management [Peppers and Rogers 1995]. The websites are overloaded with graphic data but are not clear, concise and informative. Most of the banks have this drawback that they are not having up-to date website to inform their customers about their latest products and services. In case of any changes in customer’s account such as interest rate etc., some of the banks are not sending any letters or information packs through email or even ‘slow snail mail’ to update information for their customers. Major bank services such as: internet banking and phone banking are not available in more remote banks .In most of the banks, only a cash card is offered through which customers can only withdraw cash from selected cash machines. Without having credit or debit cards, customers are having problems to shop online. Call centers are less efficient and have limited opening hours. In order to have successful implementation of customer relationship management these all issues have to resolve.

The most commonly used customer relationship management practices that are frequently used by the banking sector of Pakistan are the services which are available even after the banking hour through call centers, facility of making the pay order through phone call, having friendly attitude with customers. But the multinational banks are emphasizing on CRM through virtual means e.g. they create pay orders on phone call, customers can either ask about account situation any time, specific banks deals with specific customers .CRM provides online banking facility with transactions; utility bill payments E-statements internet banking for credit cards and many more. Multinational banks have separate managers for VIP marked customers and have special preferences for them. Their relationship officers are highly trained in customer services and account dealing. Separate Help desk is maintained in every branch for Loan, Credit Card and Deposit Account Customers (Payne, Holt and Frow 2001). The multinational banks offer some distinct services such as the preferred customers there are separate Relationship Managers, multinational Preferred Lounges. The staff in the branches treats the customers well by providing quality services to build a strong customers relationship that helps to increase the customer loyalty and customer fleet. Multinational banks which are available in banks increase their market share by following different strategies and among them the most applicable and successful is the offensive one. The difference between the local and the international operations of the banks in Pakistan is that the local banks emphasis more on the number of branches as they feel that more branches will facilitate them achieving the customer relationship role whereas the multinational national banks have totally different opinion as they do not focus on the number of branches but pay great attention in valuing their customers, treat them with respect dignity and also take care of their emotions send them greeting cards on especial occasions’, wish them on their birthdays etc. These things are very minor but play and everlasting role and create a strong bond between the customer and organizations. There is a difference between the facility of automated teller machine and E-banking in both the local and the multinational banks in Pakistan. The local banks have poor performance in providing the ATM and the E-banking services whereas the multinational banks are very active in this segment (Roh et al. 2005). Having all these operations the multinational banks are not as competitive as they should be as

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 38

http://w

ww.aijsh.org

they have the origin the developing countries and need to update most of the systems and technologies in order to compete with the outside world.

By analyzing all factors it is concluded that multinational banks are leader in customer relationship management practices in urban cities of Pakistan which are their prime business area. They are able to achieve customer’s satisfaction in each and every aspect of banking practices. Local banks are also benefiting with the ingress of new technology and a cultural difference is coming to their behavior and working.

METHODOLOGY

Qualitative data contains statements and words not the figures and digits. It cannot offer you numerical evaluations and statistical calculations. It requires lots of creativity, systematic approach and discipline to design the method of interpretation and understanding of this verbal or written data (Crane, 2010)the researcher sorts and sifts them, searching for types, classes, sequences, processes, patterns or wholes. The aim of this process is to assemble or reconstruct the data in a meaningful or comprehensible fashion (Jorgensen, 1989).

Qualitative data analysis has three main steps that is noticing, collecting and again noticing. But the most important thing which must be there in between all these steps is thinking. Think what exactly we want to achieve, what are the basic ingredients of that target issue, how can we identify those ingredients from lots of stuff. The real thinking process guides you to notice the right items of information and news from the research material. Then the collection and again sorting and thinking and noticing about the research question and the process.

In this research paper we collected many research items around the globe and analyze their relevance, reference and importance according to our topic. Then we collected the research model of different organizations and their CRM functions. These models and materials guide us to design a fairly new and suitable CRM model for our research area. This model provides all the needed ingredients and their performance attribute towards customers and the organizations.

In this research paper we will proposed a model of CRM design after a lot of studies and observations from different Pakistani banks. Then we analyze the model scientifically that how well it can work. It will give great learning experience for both students and professionals that how can we design a new framework of a peculiar function and check its performance.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 39

http://w

ww.aijsh.org

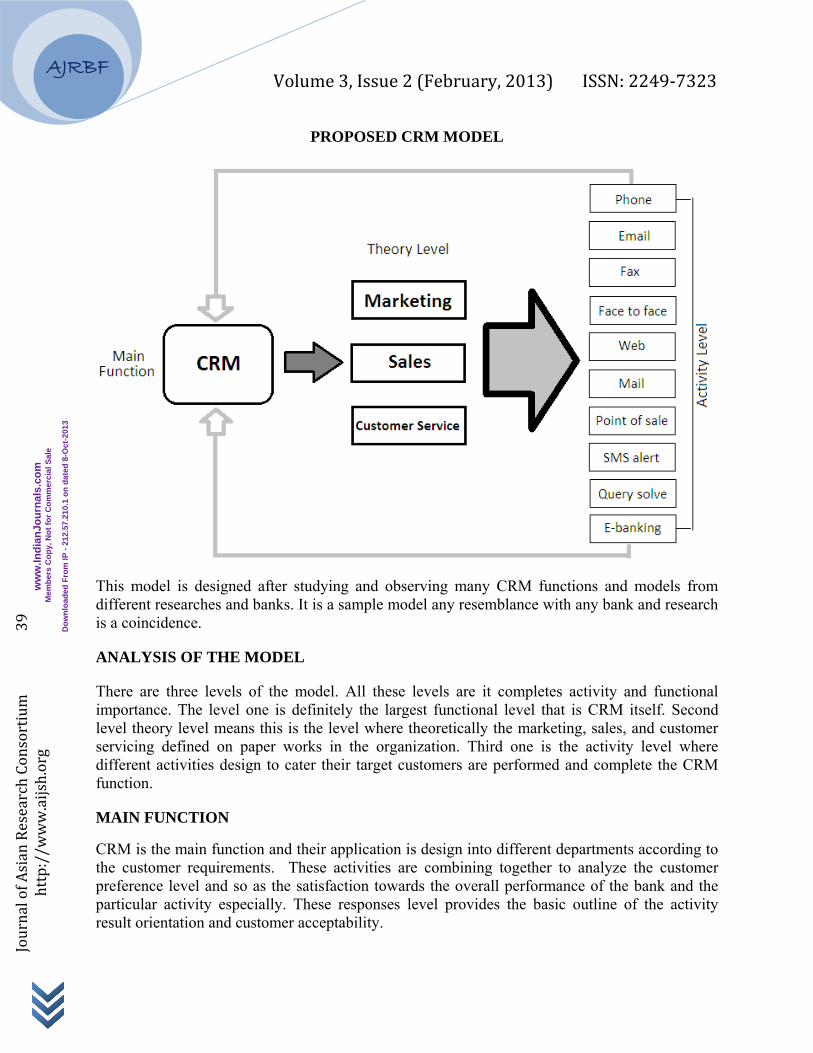

PROPOSED CRM MODEL

This model is designed after studying and observing many CRM functions and models from different researches and banks. It is a sample model any resemblance with any bank and research is a coincidence.

ANALYSIS OF THE MODEL

There are three levels of the model. All these levels are it completes activity and functional importance. The level one is definitely the largest functional level that is CRM itself. Second level theory level means this is the level where theoretically the marketing, sales, and customer servicing defined on paper works in the organization. Third one is the activity level where different activities design to cater their target customers are performed and complete the CRM function.

MAIN FUNCTION

CRM is the main function and their application is design into different departments according to the customer requirements. These activities are combining together to analyze the customer preference level and so as the satisfaction towards the overall performance of the bank and the particular activity especially. These responses level provides the basic outline of the activity result orientation and customer acceptability.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 40

http://w

ww.aijsh.org

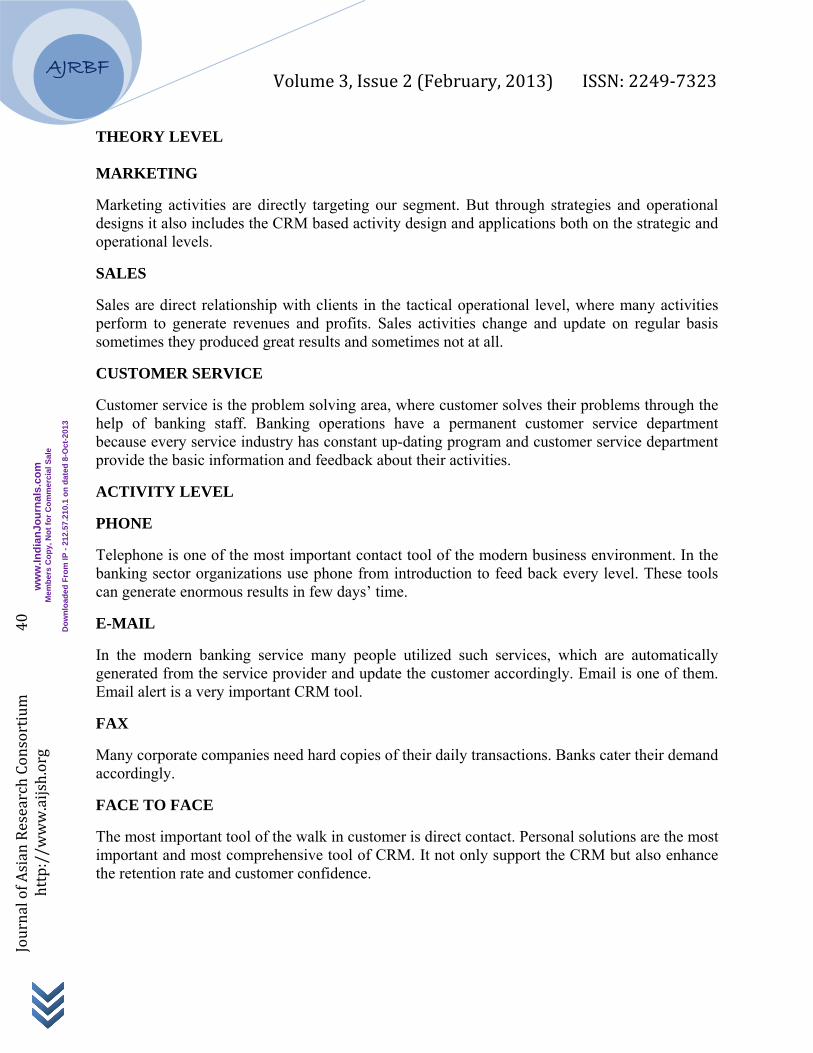

THEORY LEVEL MARKETING

Marketing activities are directly targeting our segment. But through strategies and operational designs it also includes the CRM based activity design and applications both on the strategic and operational levels.

SALES

Sales are direct relationship with clients in the tactical operational level, where many activities perform to generate revenues and profits. Sales activities change and update on regular basis sometimes they produced great results and sometimes not at all.

CUSTOMER SERVICE

Customer service is the problem solving area, where customer solves their problems through the help of banking staff. Banking operations have a permanent customer service department because every service industry has constant up-dating program and customer service department provide the basic information and feedback about their activities.

ACTIVITY LEVEL

PHONE

Telephone is one of the most important contact tool of the modern business environment. In the banking sector organizations use phone from introduction to feed back every level. These tools can generate enormous results in few days’ time.

In the modern banking service many people utilized such services, which are automatically generated from the service provider and update the customer accordingly. Email is one of them. Email alert is a very important CRM tool.

FAX

Many corporate companies need hard copies of their daily transactions. Banks cater their demand accordingly.

FACE TO FACE

The most important tool of the walk in customer is direct contact. Personal solutions are the most important and most comprehensive tool of CRM. It not only support the CRM but also enhance the retention rate and customer confidence.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 41

http://w

ww.aijsh.org

WEB

These days without web portal provide a platform where both customers and senior executives are on the same discussion board. Not a small company can survive without their official web portals. Banks also provides usage services to their customers where they can use their accounts and contacts with the right guy and approach to the senior managers directly for their guidance.

There are many orthodox minded customers who still believe that bank should maintain monthly, quarterly and annual mail system for their up-dation of records. These mails provide them their official records and scrutiny of their personal accounts.

POINT OF SALE

The direct contact or customer sales points are another very important area where service companies must be very strong. Because after the promotional and awareness program the second level and first direct contact is point of sale. If spot selling must not be trained and well defined then it is very easy to create new clientele.

SMS ALERT

Cellular phone is another very important tool of communication. It enhances the horizon of direct contact due to almost 24 hour availability of the phone. It also provides the SMS message service. Many banks offer these services to provide the customer 24 hour updating services.

QUERY SOLVE

This is another new and very important phenomenon. This is after effects or feedback of query solve. In such services the companies provide a dedicated manager who directly touch the problem customer and make sure that his problem is duly solved. This manager does not have any link with customer service department or operation rooms. He personally works under CRM operations systems.

E-BANKING

The most important feature of modern banking system is E-banking which provides the part control of information in the hands of customers about his accounts. There are many banks who are offering even the control of complete system of their accounts management in their online banking system.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

AJR

Journal of Asian Research Consortium 42

http://w

ww.aijsh.org

RBF

CRM AN

THE GR

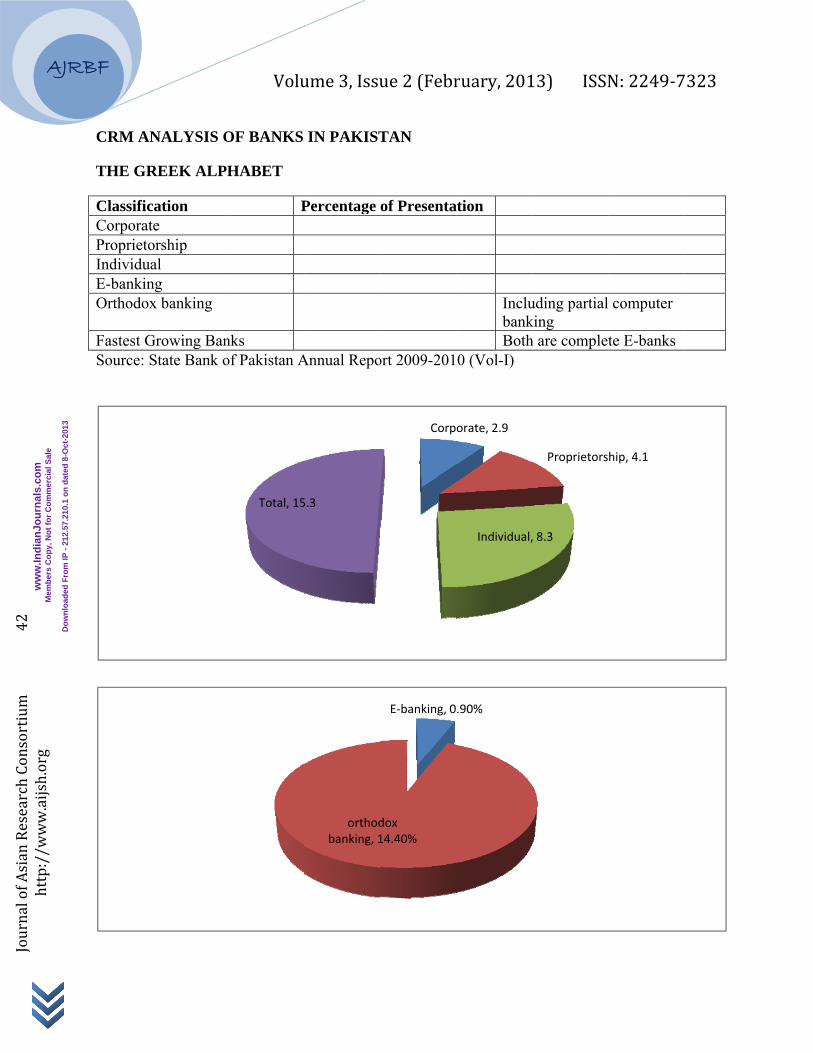

ClassificCorporatProprietoIndividuaE-bankinOrthodox

Fastest GSource: S

NALYSIS O

REEK ALPH

cation te orship al ng x banking

Growing BanState Bank o

Volu

Total, 15

OF BANKS

HABET

P

nks of Pakistan A

ume 3, Issu

5.3

orthodbanking, 1

IN PAKIST

Percentage

Annual Repo

ue 2 (Febr

Corp

E‐banking, 0

dox 14.40%

TAN

of Presenta

ort 2009-201

ruary, 201

orate, 2.9

Individual,

.90%

ation InclubankBoth

0 (Vol-I)

13) ISSN

Proprietors

, 8.3

uding partialking h are complet

N: 2249‐7

hip, 4.1

computer

te E-banks

7323

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 43

http://w

ww.aijsh.org

Above table clearly indicates that there are only 15.3% of total population have bank accounts. Out of them 0.9% is enjoying the E-banking facilities, rest of 14.4% are still having the same orthodox banking. However the computerization is underway in most of the banking. But the growth of e-banking encourages many new users of the banking facilities.

SCIENTIFIC ANALYSIS OF PROPOSED MODEL

Now we will analysis in a scientific manner that how the modern day companies analyze simple form based information with telephone and other sources and combine them with scientific evaluation technique of Gantt chart to produce the desired results.

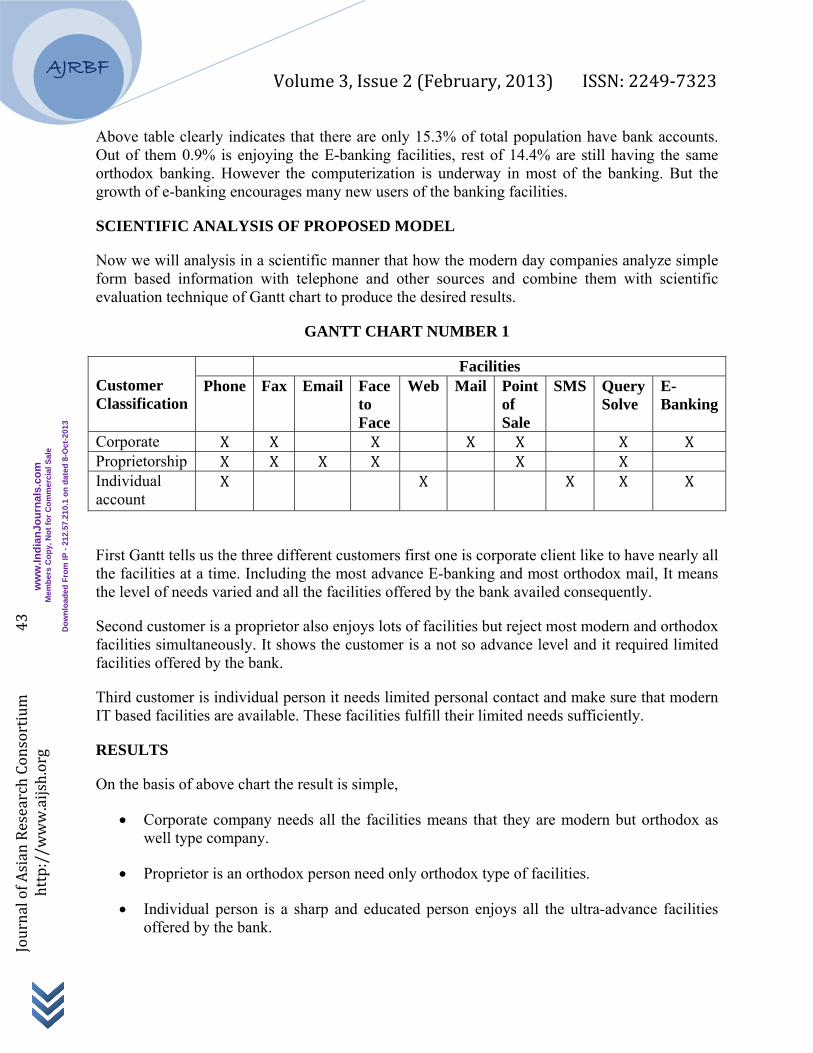

GANTT CHART NUMBER 1

Customer Classification

Facilities Phone Fax Email Face

to Face

Web Mail Point of Sale

SMS Query Solve

E-Banking

Corporate X X X X X X X Proprietorship X X X X X X Individual account

X X X X X

First Gantt tells us the three different customers first one is corporate client like to have nearly all the facilities at a time. Including the most advance E-banking and most orthodox mail, It means the level of needs varied and all the facilities offered by the bank availed consequently.

Second customer is a proprietor also enjoys lots of facilities but reject most modern and orthodox facilities simultaneously. It shows the customer is a not so advance level and it required limited facilities offered by the bank.

Third customer is individual person it needs limited personal contact and make sure that modern IT based facilities are available. These facilities fulfill their limited needs sufficiently.

RESULTS

On the basis of above chart the result is simple,

• Corporate company needs all the facilities means that they are modern but orthodox as well type company.

• Proprietor is an orthodox person need only orthodox type of facilities.

• Individual person is a sharp and educated person enjoys all the ultra-advance facilities offered by the bank.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

AJR

Journal of Asian Research Consortium 44

http://w

ww.aijsh.org

RBF

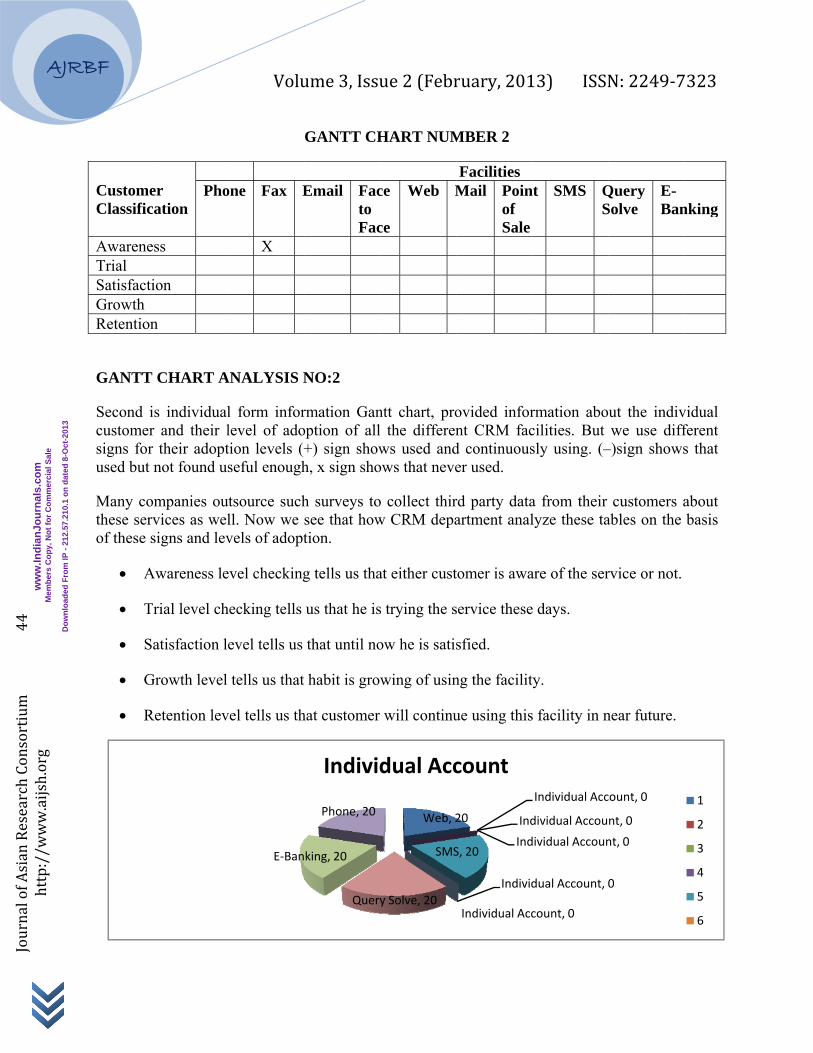

CustomeClassific

AwareneTrial SatisfactiGrowth Retention

GANTT

Second icustomersigns forused but

Many cothese serof these s

• A

• T

• S

• G

• R

er cation

Pho

ess

ion

n

CHART A

is individualr and their lr their adoptnot found us

ompanies ourvices as welsigns and lev

Awareness le

Trial level ch

atisfaction le

Growth level

Retention lev

Volu

E‐Ban

one Fax E

X

ANALYSIS N

l form inforlevel of adotion levels (+seful enough

utsource suchll. Now we vels of adopt

evel checking

hecking tells

evel tells us

tells us that

vel tells us th

ume 3, Issu

Query

king, 20

Phone, 20

Individ

GANTT CH

Email Facto Fac

NO:2

rmation Ganoption of all+) sign showh, x sign sho

h surveys tosee that howtion.

g tells us tha

us that he is

that until no

habit is grow

hat customer

ue 2 (Febr

Web, 2

SMS

y Solve, 20

dual Acc

HART NUM

ce

ce

Web M

ntt chart, prol the differenws used and

ows that neve

o collect thirw CRM depa

at either cust

s trying the s

ow he is satis

wing of usin

will continu

ruary, 201

20 Ind

IndS, 20

Individ

Individual Acc

count

MBER 2

Facilities Mail Poin

of Sale

ovided infornt CRM facd continuouser used.

rd party dataartment anal

tomer is awa

service these

sfied.

ng the facilit

ue using this

13) ISSN

Individual Acc

dividual Accou

dividual Accoun

dual Account, 0

count, 0

nt SMS QS

rmation abocilities. But sly using. (–

a from their lyze these ta

are of the ser

e days.

ty.

s facility in n

N: 2249‐7

count, 0

nt, 0

nt, 0

0

Query Solve

E-Ban

ut the indivwe use diff

–)sign shows

customers aables on the

rvice or not.

near future.

7323

1

2

3

4

5

6

nking

vidual ferent s that

about basis

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

AJR

Journal of Asian Research Consortium 45

http://w

ww.aijsh.org

RBF

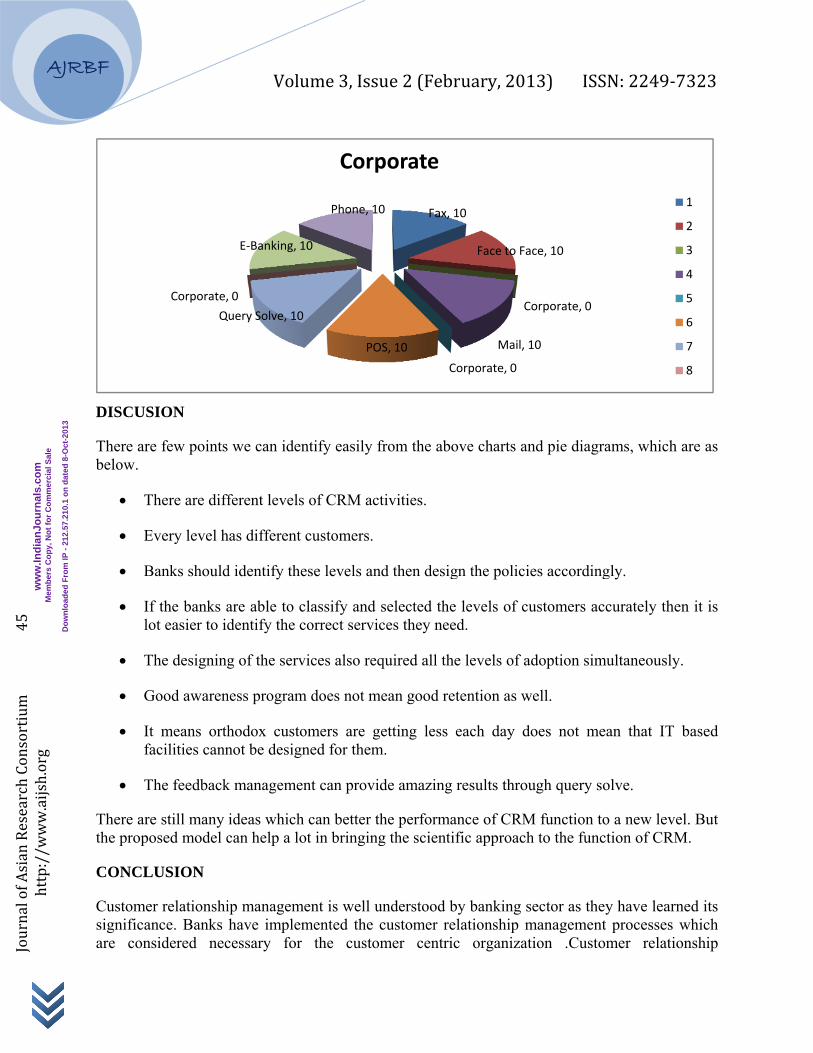

DISCUS

There arebelow.

• T

• E

• B

• Iflo

• T

• G

• Itfa

• T

There arethe propo

CONCL

Customesignificanare cons

Q

Corporate,

SION

e few points

There are diff

Every level h

Banks should

f the banks aot easier to id

The designing

Good awaren

t means orthacilities cann

The feedback

e still many osed model c

LUSION

r relationshince. Banks sidered nec

Volu

uery Solve, 10

0

E‐Banking, 1

we can iden

ferent levels

has different

d identify the

are able to cdentify the c

g of the serv

ness program

hodox custonot be design

k managemen

ideas which can help a lo

ip managemhave implem

cessary for

ume 3, Issu

PO

10

Phone, 10

Corp

ntify easily f

of CRM act

customers.

ese levels an

classify and correct servic

vices also req

m does not m

omers are gned for them

nt can provid

can better thot in bringing

ent is well umented the c

the custom

ue 2 (Febr

Fax, 1

C

OS, 10

0

porate

from the abo

tivities.

nd then desig

selected theces they nee

quired all the

mean good ret

etting less em.

de amazing

he performag the scientif

understood bcustomer remer centric

ruary, 201

10

Face to Fac

Co

Mail, 1

orporate, 0

ove charts an

gn the policie

levels of cud.

e levels of ad

tention as w

each day do

results throu

ance of CRMfic approach

by banking slationship mc organizati

13) ISSN

ce, 10

orporate, 0

10

nd pie diagra

es according

ustomers acc

doption simu

ell.

oes not mea

ugh query so

M function toh to the funct

ector as theymanagement ion .Custom

N: 2249‐7

ams, which a

gly.

curately then

ultaneously.

an that IT b

olve.

o a new leveltion of CRM

y have learneprocesses w

mer relation

7323

1

2

3

4

5

6

7

8

are as

n it is

based

l. But M.

ed its which nship

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

AJR

Journal of Asian Research Consortium 46

http://w

ww.aijsh.org

RBF

managemrelationshbut it’s aunique wrelationshsuccessfucompletecompleteproblem organizatof the cueveryone

REFERE

KeshvariGeneratinResearch

Sheth, J.Business

Santos, Dtechnolog241–259

Godin, Scustomer

Q

Corporate

ment is a comhip managema huge concways to get hip with theul implemene and update informatio

and rectifytion should w

ustomer relate across orga

ENCES

i, S., R. 201ng Competit

h, 5 (4) : 34-5

. N., &Parv Review, 4 (

D., L., B agy applicatio.

S. (1999), Prs, New York

Volu

uery Solve, 10

e, 0

SMS

mplete philoment is not jcept that can

a real custem. Completntation of e informatio

on of its cusy them. Hework as a sintionship mananization in o

12. The Imptive Advant54

vatiyar, A. ((4): 397–418

and Peffers,ons: first mo

Permission k: Simon &

ume 3, Issu

POS

Phone, 10

Prop

osophy whichjust confinedn be implemtomer centrte organizaticustomer reon about itsstomer it wence post sngle unit andnagement anorder to incr

pact of E-CRtages in Iran

(1995). The 8.

K. 1995.overs and ea

marketing: Schuster.

ue 2 (Febr

Fax, 10

Co

S, 10

rietorsh

h needs to bd to one segmented on vric services ional changeelationship s customers

will be impoervices in d have compnd the goalsrease the effe

RM on Custonian Financi

evolution o

. Rewards tarly follower

Turning st

ruary, 201

Email, 10

C

Face to F

orporate, 0

ip

be learned bygment of the various segmin its real

e is requiredmanagemenbecause if

ossible to unorganizationplete coordins and objectiectiveness an

omers Attitual B2B Con

of relationsh

to investorsrs in ATMs.

trangers into

13) ISSN

0

orporate, 0

Face, 10

y the organisales ,servic

ments of thesense to es

d from top tnt. Banks s

the banks nderstand cun play a vination aboutives should nd efficiency

ude and Its Antext. Interna

hip marketin

s in innovat. Organizatio

o friends a

N: 2249‐7

zation. Custces, or marke organizatiostablish life to bottom foshould havedo not hav

ustomer busital role. Wt all the procbe made cley.

Association ational Busi

ng. Internati

tive informaon Science 6

and friends

7323

1

2

3

4

5

6

7

8

tomer keting on in long

or the e the e the

siness Whole cesses ear to

with iness

ional

ation 6(3):

into

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 47

http://w

ww.aijsh.org

Hiebeler, R., Anderson, A., Kelly, T. B., and Ketteman, C. (1998), “Best practices: Building your business with customer-focused solutions”, New Delhi: Simon & Schuster.

Johnson, D., M., and Selnes, F. 2004. “Customer Portfolio Management: Toward A Dynamic Theory of Exchange Relationships,” Journal of Marketing, 68 (2): 1–17.

Camp, R. C. (1989), Benchmarking: The search for industry best practices that lead to superior performance, Milwaukee, WI: ASQC Quality Press.

Anshari M.; Al-Mudimigh A. and Aksoy M. (2009) ―CRM Initiatives of Banking Sector in Saudi Arabia , International Conference on IT to Celebrate S. Charmonman's 72nd Birthday, Bangkok Metro, Thailand March 30. www.Charm09.com www.Charm72.com

Ahmed, T. (2009). Electronic customer relationship management in online banking. Master Thesis. Luleå University Sweden.

Beckett-Camarata, E.J., Camarata, M.R., Barker, R.T., 1998, Integrating Internal and External Customer Relationships Through Relationship Management: A Strategic Response to a Changing Global Environment, Journal of Business Research, 41 (1):71-81.

Anu H. Bask, (2001) "Relationships among TPL providers and members of supply chains –a strategic perspective", Journal of Business & Industrial Marketing. 16 (6):470 - 486

Mike, C., Rick, F. and Richard, C., (2004). Loyalty trends for the 21st century. Journal of Targeting, Measurement and Analysis for Marketing. 12(3) : 199-212

Cabena, P., Choi H.H., Kim I.S., Otsuka S., Reinschmidt J. &Saarenvirta G., 1999. Intelligent Miner for Data Applications Guide. IBM Redbooks, SG24-5252-00.

Don Peppers, Martha Rogers, (1995) "A new marketing paradigm: Share of customer, not market share", Strategy & Leadership, 23(2): 14–18.

Payne, A., Holt, S. and Frow, P. 2001. “Relationship Value Management: Exploring the Integration of Employee, Customer and Shareholder Value and Enterprise Performance Models,” Journal of Marketing Management. 17(7-8): 785-817.

Roh , T . H . , Ahn , C . K .and Han , I . 2005. “The priority factor model for customer relationship management system success”, Expert Systems with Applications. 28(4) :641 – 654 .

Hussian, S. W., Ullah, A., Saeed, M., &Rafiq, M. (2012). Banking Industry-Post Privatization Performance in Pakistan. Journal of Money, Investment and Banking 5 (1): 39-48.

Smith, E. A. (2001). The role of tacit and explicit knowledge in the workplace. Journal of knowledge Management. 5(4): 311-321.

ww

w.In

dia

nJo

urn

als.

com

Mem

ber

s C

op

y, N

ot

for

Co

mm

erci

al S

ale

Do

wn

load

ed F

rom

IP -

212

.57.

210.

1 o

n d

ated

8-O

ct-2

013

Volume 3, Issue 2 (February, 2013) ISSN: 2249‐7323

AJRBF

Journal of Asian Research Consortium 48

http://w

ww.aijsh.org

Neilson, L. C., &Chadha, M. (2008). International marketing strategy in the retail banking industry: The case of ICICI Bank in Canada. Journal of Financial Services Marketing. 13(3):204-220.

Baird, L. (2008). Siebel Crm 100 Success Secrets-100 Most Asked Questions on Siebel Customer Relationship Management Applications Covering Oracle Enterprise Crm, on Demand Software and Business Intelligence. Lulu. com.

Crane, K. K. (2010). Analyzing qualitative data. ASTD Handbook for Measuring and Evaluating Training, 165.

Jorgensen, D. L. (1989). Participant observation: A methodology for human studies (Vol. 15). Sage Publications, Incorporated.

State Bank of Pakistan Annual Report, 2009-2010 (Vol-I), accessed 02/09/2012

http://www.sbp.org.pk/reports/annual/arFY10/Anul-index-eng-10.htm