Online & Internet Banking & Its effect on Customer Satisfaction

50

Online & Internet Banking & Its effect on Customer Satisfaction (Focusing on "Online & Internet Banking Users" of Brac Bank Limited.) Supervisor: Mahfuza Khatun Assistant Professor Department of Finance & Banking Jahangirnagar University A Research By: A. B. M. Mehedi Hasan Student ID: 20122070 3rd Batch, EMBA Program Department of Finance & Banking Jahangirnagar University, Savar, Dhaka 1342, Bangladesh Submission Date: January 10, 2015

Transcript of Online & Internet Banking & Its effect on Customer Satisfaction

Online & Internet Banking & Its effect on Customer Satisfaction

(Focusing on "Online & Internet Banking Users" of Brac Bank Limited.)

Supervisor:

Mahfuza Khatun

Assistant Professor

Department of Finance & Banking

Jahangirnagar University

A Research By:

A. B. M. Mehedi Hasan

Student ID: 20122070

3rd Batch,

EMBA Program

Department of Finance & Banking

Jahangirnagar University,

Savar, Dhaka 1342, Bangladesh

Submission Date: January 10, 2015

LETTER OF TRANSMITTAL

January 10, 2015The ChairmanFaculty of Business Studies (EMBA Program)Jahangirnagar UniversitySavar, Dhaka-1342, Bangladesh

Subject: Submission of the Research on Online & Internet Banking & Its effect on Customer

Satisfaction (Focusing on "Online & Internet Banking Users" of Brac Bank Limited.)

Dear Sir,

I am very happy & excited to submit this paper on “Online & Internet Banking & Its effect onCustomer Satisfaction (Focusing on "Online & Internet Banking Users" of Brac Bank Limited.).

This research paper is submitted under supervision of Ms. Mahfuza Khatun, Assistant Professor,Faculty of Business Studies, Jahangirnagar University, as part of the partial fulfillment of theEMBA program.

The purpose of this study is to identify factors which affect the customer satisfaction of theonline & internet banking services in this era of advanced banking.

I am grateful to you for providing me the opportunity to have such an excellent experience.

Sincerely yours,

A. B. M. Mehedi Hasan

ID: 20122070

EMBA Program

Department of Finance & Banking

Faculty of Business Studies

Jahangirnagar University

ACKNOWLEDGEMENT

First of all thanks to almighty ALLAH for for blessing me with strength, aptitude & patience for

successfully completing my master's thesis research. I would like to express the heartfelt

gratitude and indebtedness to Ms. Mahfuza Khatun, Assistant Professor, Department of Finance

& Banking of Jahangirnagar University, Savar, Bangladesh for her helpful guidance, skilled

supervision, continuous encouragement and moral supports to carry out necessary activities

throughout the study period. Her valuable directions and suggestions were the source of my

inspiration.

I am also deeply debited to Dr. Sheikh Abu Taher, Assistant Professor, Department of Finance &

Banking of Jahangirnagar University, Savar for his constructive and valuable advice. I would

like to acknowledge appreciation to other faculty members and staffs of Faculty of Business

Studies, Jahangirnagar University for their co-operation. I sincerely thank to them for their

assistance at different occasions during the course of this thesis.

I would like to thank officers of Brac Bank Limited Ashkona Branch, Uttara Branch and Ms

Sharmin Sultana, Service Officer of Brac Bank Limited, Dakshinkhan Branch, Dhaka city, for

their kind co-operation.

January 10, 2015 Author

A. B. M. Mehedi Hasan

ContentsLETTER OF TRANSMITTAL ....................................................................................................................2

ACKNOWLEDGEMENT ............................................................................................................................3

EXECUTIVE SUMMERY ...........................................................................................................................6

ABSTRACT..................................................................................................................................................7

CHAPTER 1 .................................................................................................................................................8

INTRODUCTION ........................................................................................................................................ 8

1.1 Introduction of the research ...............................................................................................................8

1.2 Background of the research................................................................................................................8

1.3 Organization Preview : A corporate profile Brac Bank Limited at a glance ..................................... 9

1.4 Internet Banking Process of Brac Bank Limited..............................................................................10

1.5 Statement of the Problem .................................................................................................................14

1.6 Purpose of the Study ........................................................................................................................15

1.7 Objective of the study ......................................................................................................................15

1.8 Methodology of the study ................................................................................................................16

1.9 Limitations of the study ...................................................................................................................17

CHAPTER 2 ...............................................................................................................................................18

LITERATURE REVIEW ...........................................................................................................................18

2.1 Literature Review.............................................................................................................................18

2.2 Conceptual Framework ....................................................................................................................23

2.3 Research Questions ..........................................................................................................................23

CHAPTER 3 ...............................................................................................................................................24

RESEARCH METHODOLOGY................................................................................................................24

3.1 Research Design...............................................................................................................................24

3.2 Research Type...................................................................................................................................24

3.3 Data Analysis ....................................................................................................................................24

3.4 Findings.............................................................................................................................................37

3.5 Discussion .........................................................................................................................................37

CHAPTER 4 ...............................................................................................................................................38

CONCLUSION AND RECOMMENDATION ..........................................................................................38

4.1 Conclusion: ......................................................................................................................................38

4.2 Recommendation: .............................................................................................................................40

BIBLIOGRAPHY .......................................................................................................................................42

APPENDIX A .............................................................................................................................................44

APPENDIX B ............................................................................................................................................46

EXECUTIVE SUMMERY

This research paper has been prepared as a partial requirement of the master thesis part of EMBA

program in Jahangirnagar University, Savar, Dhaka, Bangladesh. The following topic has been

tried to be covered - "Online & Internet Banking & Its effect on Customer Satisfaction (Focusing

on "Online & Internet Banking Users" of Brac Bank Limited.)". The Impact of Online & Internet

Banking in Customer Satisfaction in the Context of "Brac Bank Limited" attempts to

evaluate the overall internet banking condition and its impact on the customers of Brac Bank

Limited. It focuses on the necessity, variables and gaps of the Internet Banking process of Brac

Bank Limited in the internal context of its few branches. The report is aiming the influence of

internet banking on the customers and their different opinions toward it. Mainly it is focusing the

impact of internet banking on the customers of Brac Bank Limited, Ashkon, Dakshinkhan &

Uttara branches of Dhaka city. It will also show the analytical sense developed by analyzing the

output processed on the surveys in that branch.

There are four chapters of the report. First chapter is consisting of the Introduction of the whole

research. In the second chapter there is the review of literature and the conceptual frame work of

the study which indicate the research question and hypothesis.

The third chapter of the report is consist of the research methodology. The fourth chapter is

consisting of conclusion and recommendation about the study.

In Conclusion & Recommendations part those problems along with some suggested

recommendations have been given. Being the one of first computerized online banking service

provider, Brac Bank Limited’s general banking activities are the major sources of fund

mobilization. But it definitely depends on the financial strength relating with its efficiency is

engaged with providing regular services to the client on a regular basis and at the end

Bibliography and Appendices have been given as well.

ABSTRACT

This is the era of most advanced & quick banking for the customers. Information Technology has

reduced the cost of banking for customers & also that has enabled different quick services. The

key purpose of this study is to find out the impact of internet banking to satisfy customers in the

context of Brac Bank Limited deposit & financing has been made very easy when customers

need. There are some key factors that have an important impact on customer satisfaction in the

internet banking. The main findings of the study will indicate that the factors, which

are Reliability, Security and Privacy, Service Quality & Assurance have impacts on customer

satisfaction in terms of Internet Banking of Brac Bank Customers.

In this research, the factors are being treated as the Independent variables and Customer

Satisfaction as the Dependent variable. It will be a causal study aimed to measure that, the

existence of or a change in Independent variables causes or leads to a change in the

Dependent variable. This study is based on the primary data to understand the level of

Reliability, Security and Privacy, Service Quality & Assurance and their impact on the

satisfaction of customers in the context of internet banking of Brac Bank Limited. The

information of the research have gathered by a questionnaire survey among the customers of

Brac Bank Limited. I have distributed 125 questionnaires among 125 respondents, who are the

clients of Brac Bank Limited and use their internet banking service. A random sampling

technique was adopted to do the survey. I have collected data from the survey and then analyzed

it. After analysis, I got significant results of both the dependent and independent variables. From

this, now we can get an idea that how internet banking impacts on customer satisfaction.

CHAPTER 1

INTRODUCTION

1.1 Introduction of the research

In general sense we mean "Bank" as a financial institution that deals with money. Now-a day's

banking sector is modernizing and expanding its hand in different financial events every day. At

the same time the banking process is becoming faster, easier and is becoming wider. In order to

survive in the competitive field of the banking sector all organizations are looking for better

service opportunities to provide their fellow clients.

Internet Banking depends on some factors which are very important. Internet access, internet

banking features, internet literacy, internet use. Internet Banking can offer a quicker and

dependable services to the customers for which they may be relatively satisfied than that of

manual system of banking which needs additional time & cost for banking. Internet Banking

system not only helps in transactions, it can get its better dealings with customers. To continue

with the thirteen years of excellence in customer services Brac Bank Limited began Internet

Banking Service. And the research topic is on the "Online & Internet Banking & Its effect on

Customer Satisfaction".

For last few years, internet banking is a very common service that is provided by most of the

commercial banks in Bangladesh. Brac Bank Limited is one of them. Now internet banking is a

very popular form of transaction among peoples. Because by this they can do their various

banking activities (Only which are allowed) without going to the bank and in a very short time.

1.2 Background of the research

In this study a research is conducted on "Online & Internet Banking & Its effect on Customer

Satisfaction (Focusing on "Online & Internet Banking Users" of Brac Bank Limited.)". The main

objective of this research is to identify the key factors that influence the internet banking and

helps to retain customers of the Brac Bank Limited. By this research we shall be able to know

that which factors and how they influence internet banking of Brac Bank Limited to retain

customer with satisfaction. It is also a requirement of my academic course under 'master's thesis'.

1.3 Organization Preview : A corporate profile Brac Bank Limited at a glance

Corporate Profile: 1 BRAC Bank started its journey on 4th July, 2001 as a private commercial

bank focused on Small and Medium Enterprises (SME). In just a decade, the Bank has become a

leading bank in Bangladesh, keeping its core focus in SME yet becoming one of country’s

leading financial hypermarket. Today BRAC Bank holds a dynamic network of 157 branches,

400 SME unit offices, 500 Remittance Delivery Points, nearly 350 ATMs and 14 Financial

Kiosks across the country. The stakeholders of the bank are BRAC, the largest non-government

organization in the world and International Finance Corporation, the private sector arm of The

World Bank.

Achievements and Recognitions:Its success reflects its rapidly expanding global footprint and commitment to delivering high

quality, client-centric integrated wealth management solutions and advice. In 12 years of

operating BRAC Bank has achieved a significant amount of respect, honor and recognition from

home and abroad shows commitment towards quality services as a bank. In these years BRAC

Bank has achieved -

Best managed Bank Award 2013 from Asian Banker

Retail Banker Award 2011 from Asian Banker

Best Retail Banker Award 2011 from Asian Banker

FT-IFC Sustainable Bank of the Year 2010 (Emerging Markets, Asia)

IFC awarded BRAC Bank as the Most Active Global Trade Finance Program (GTFP)

Issuing Bank in South Asia in 2010

Member of Global Alliance for Banking on Values (GABV)

ICAB National Award 2009

1 See, https://www.linkedin.com/company/brac-bank-ltd-

DHL–Daily Star Bangladesh Business Awards 2008

NBR National Award as the Highest VAT payer for the financial year 2007-2008

Subsidiaries:Being pioneer in the financial industry, BRAC Bank also ventures towards its subsidiaries to

explore more and more new areas of businesses considering new requirement from its

consumers. The subsidiaries are -

BRAC EPL Investments Limited

BRAC EPL Stock Brokerage Ltd

bKash (Mobile banking service) Ltd

BRAC Saajan Exchange Limited

BRAC IT Services Limited (BITS)

1.4 Internet Banking Process of Brac Bank Limited

All resident and non-resident customers of BRAC Bank (Retail, Probashi, Proprietorship

Account Holders and Joint Account Holders with either or survivor mode) may apply for Internet

Banking. In terms of joint account holders (operating in either or survivor mode), only one of the

applicants will be entitled for requesting and receiving all Internet Banking associated services. 2

A customer may visit any branch and fill up an Internet Banking application form or download

the Form from the official website of BRAC Bank Limited (BBL);

Customer must:

Fill up the Internet Banking application form with accurate information

Be physically present at the branch to submit his/her Internet Banking application form to

a customer service officer

Customer has the option to select Hardware / Software Token for performing Internet

Banking Transactions or he can also choose none of these, but, in such case customer will

avail “View Option (Non-transactional mode)” only.

2 See, https://ibanking.bracbank.com/bblonline/RegistationPDF/InternetBankingFAQ.pdf

2FA Device is a Two Factor Authentication device, which generates a random OTP (One Time

Password) that acts as a second level of authentication. After registering for BRAC Bank Internet

Banking, customer will require the 2FA Device whenever customers login to their Internet

Banking accounts for secured and successful transactions. In these particular and other

associated documents we are referring 2FA Device as “Hardware Token” or “Software Token”.

2FA is an advanced method of security which requires:

Information that one knows (Customer's PIN & User ID)

One Time Password (OTP3) from the bank (that is the randomly generated by 2FA4

Device)

Software Token: It is a software application which is available for download from Google Play

Store, iPhone App Store, etc. To use Software Token, customer requires a smart phone/device

that runs with any of following operating systems -

Android

Windows Mobile

iOS

BlackBerry

Getting Hardware Token & Software Token:For Existing Customer:Customer will have the request option after login at Internet Banking interface.

For New Customer:Customer can request for 2FA Device by visiting any of the BRAC Bank branches by filling out

Internet Banking Enrolment form.

3 OTP = One Time Password. See, http://en.wikipedia.org/wiki/One-time_password4 2FA = Second Factor Authentication (2FA) is an additional layer of security used by the bank to verify customer'sonline identity. With 2FA, Brac Bank Internet banking customers are required to provide a unique Additional LogonPIN for accessing personal account details and to perform online transactions.

For both types of customers, delivery date for 2FA device will be informed by sending an e-mail.

On the delivery date, customer needs to visit the branch where he has requested for Hardware /

Software Token. On that particular date, he will be provided with a 2FA Device and a PIN

mailer or a PIN mailer only (For Software Token).

2FA device is a PIN protected security device which randomly generates OTP (One Time

Password) to execute Internet Banking Transactions. It provides customer an additional level of

protection for each of the Fund Transfer / Bill Payment / Tuition Fees payment/any other

payment by generating e-signature.

The device (Hardware / Software Token) itself is PIN protected, avoiding misuse /mishandling /

exploitation of the device and applying additional level of protection from a large variety of

online risks

e-Signature is basically a six digit security code randomly generated by 2FA device for re-

authenticating a transaction on Internet Banking. After login to Internet Banking by entering

Login ID, Password and OTP, customers need to generate e Signature for performing the

transactions.

To generate e-Signature customer needs to insert last six digits (Will be displayed by system for

customer convenience) of his beneficiary account number into Hardware / Software Token

screen and thus a six digit e-Signature is generated.

The following services are available from Internet Banking: Account details

Mini Statement

Fund Transfer (Within BRAC Bank and BRAC Bank to other Bank Account)

Credit Card Bill Payment

Utility Bill Payment

Qubee5, and all mobile operators prepaid and postpaid bill payment

5 Qubee is an internet service provider in Bangladesh. See www.qubee.com.bd

ALICO6 Payment

University Tuition Fee Payment (Currently Supports Brac University7 Only)

Password change (Login Password)

Statement of accounts for maximum of one month during any period for last six months.

Applicable for only Current/savings account.

Daily fund transfer limit through internet banking details are given below: Account(s) under same CIF (Within BRAC Bank) : Minimum BDT 100 and Maximum

BDT 5 Lacs

Account(s) Under Different CIF (Within BRAC Bank) : Minimum BDT 100 and

Maximum BDT 3 Lacs

Other Bank Fund Transfer (EFT) : Minimum BDT 100 and Maximum BDT 1 Lac

Daily Credit Card Bill payment : Minimum BDT 1 and Maximum BDT 5 Lacs

For Qubee and Mobile Top up bill payment : Minimum BDT 100 and Maximum BDT

3000

ALICO payment : Minimum BDT 1 and Maximum BDT 5 Lacs

BRAC University Tuition Fee : Total Semester Fee

Per day total IB transaction number count : Maximum 5 transactions

Transferring fund (EFT8) to any other bank’s (outside BRAC BANK) account:Customer can transfer fund to any other bank’s (outside BRAC BANK) account through Brac

Bank Limited's Internet Banking. Customer can daily make maximum one EFT through our

internet banking.

Transfer of funds from BDT account to Foreign Currency (FCY) account or vice versa:At this time fund transfer from BDT account to FCY account or vice versa is not allowed.

6 MetLife Alico Bangladesh. See, www.metlifealico.com.bd7 Brac University. See, www.bracu.ac.bd8 Electronic Funds Transfer (EFT). See, http://en.wikipedia.org/wiki/Electronic_funds_transfer

Paying credit card bill through Internet Banking:The payment becomes updated with the credit card account after 3 hours and customers can see

the reflection on his/her account the next day.

Utility bill payment through Internet Banking:Customers can pay all mobile operators’ prepaid and postpaid bill within the BDT 3000/- limit

per day for each operator in a maximum of 5 transactions daily. (In case top up is unsuccessful,

the money is credited back to customer's account within next 2 hours)

Internet Banking subscription who maintains multiple accounts under multiple CIF9:All multiple accounts under multiple CIF will be automatically linked under a single CIF.

Customers do not need different 2FA device for those different CIFs. By login into the main CIF,

customer can view and make transaction into other linked accounts.

Use of OTP and Master key for transaction:Customer can select either OTP or Master key at a time for successful login.

Without Hardware or Software token:Even if you do not avail a Hardware or Software Token, you can continue Internet Banking with

VIEW ONLY mode. You can view your Account details and can request for Hardware or

Software Token if you want to. You cannot do any Transaction or fund transfer.

1.5 Statement of the Problem

By this study, researchers will investigate the impact of Internet Banking on customer

satisfaction. Brac Bank Limited. is a well-established Bank over the last few years, but due to

rise in customer complaints and customers preferring- banking services of other banks, it has

come to the light that their Internet banking service quality is not one of the best compared to

their other banking services. That's why Brac Bank Limited is threatened to lose their customer.

9 EFT = Customer Information File. See, http://www.investopedia.com/terms/c/customer-information-file.asp

This has enticed them to conduct a survey to find alternative solutions to improve service quality

of their Internet Banking. I was assigned to find the factors (that they need to look at or do

further research) of Internet Banking that can help them to improve service quality and retain

customers.

1.6 Purpose of the Study

The purpose of this study is to find out the factors of internet banking that can impact to retaining

customer in the context of Brac Bank Limited. It will help the researchers to look into the overall

condition of internet banking service of Brac Bank Limited.

1.7 Objective of the study

Broad objective: Prepare the report on "The impact of internet banking on customer retention in

the context of Brac Bank Limited." to complete my Master's Thesis program of EMBA.

• Specific Objectives:

To understand the internet banking system of Brac Bank Limited. To identify the

problems of internet banking system of Brac Bank Limited.

To find out the problem of client to amend in internet banking of Brac Bank Limited.

To identify the problem in operation of internet banking in the banks website.

To know the terms, rules and condition of internet banking given by Brac Bank Limited

to their clients.

To provide suggestions for the improvement of the internet banking system of the Bank.

1.8 Methodology of the study

It includes Research Design, data sources and collection procedures, sampling method, sample

size and data analysis procedures.

HypothesisHo (Null hypothesis): There is a relation between Customer Satisfaction in Internet Banking of

Brac Bank Limited and Reliability, Security and Privacy, Service Quality & Assurance.

Ha (Alternative Hypothesis): There is no relation between Customer Satisfaction in Internet

Banking of Brac Bank Limited and Reliability, Security and Privacy, Service Quality &

Assurance.

Data Sources & Collection ProceduresData have been collected from both – Primary sources and Secondary sources.

Primary Sources: A structured questionnaire was used as the research instrument to collect

primary data from the customer of internet banking from different Branches of Brac Bank

Limited. Starting with Age & Sex, questionnaire comprised to the key questions that determines

overall satisfaction level of customer in using Internet Banking services. A 5 point likert scale

(From 1 strongly disagree to 5 for strongly agree) was used.

Secondary Sources: Secondary data, such as several academic articles and books have been

analyzed to form and clarify the topic of the research, and thus to identify the key variables

related to the response and attribution of the customer. The secondary data sources were journal,

websites, books, annual reports of Brac Bank Limited, Bangladesh Bank etc.

Sampling PlanThe population of the research is formed by the customers of Brac Bank Limited. The sampling

frame for the research will be the official list of customers in the Banks database in selected

branches. So it will be the probability sampling. Which is a subset of a statistical population in

which each member of the subset has an equal probability of being chosen.(Levin & Rubin,

2000). The respondents who are using Internet Banking of Brac Bank Limited are considered as

sample. 125 sample size was taken. The customers were selected by mixed of convenience and

random sampling method.

Data Analyzing Techniques Statistical Software (IBM SPSS, Version 20.0 for Windows 64 Bit Edition)

Microsoft Excel 2007

1.9 Limitations of the study

There were some limitations of doing the study:

I have completed the surveying process within 2 months only. Most probably 15-20

minutes for each person. My target was to survey at least 200 Internet Banking users of

Brac Bank Limited. But it was very hard to find out them as most of people do not use

internet banking. Some of them were not interested to express their opinion.

The Dakshinkhan & Ashkona branch of Brac Bank Limited is not so large. As mentioned

above it was hard to find out Internet Banking customers, for this, the sample size

(population) is limited in terms of its size and composition.

I had to face some limitations to collect some information's about internet banking of

Brac Bank Limited as these were not so available for the general people.

Respondents were too busy to read the questions properly and tick the answer just for the

sake of completing the survey quickly. So there is no guarantee that the data collected is

100% correct and hence while analyzing the researcher has considered level of

significance. At most cases I had to ask them questions in Bengali (Local Language).

CHAPTER 2

LITERATURE REVIEW

2.1 Literature Review

Internet Banking: The rise of Internet Banking is also due to its number of benefits for both the

provider and the customer as well. From the bank's perspective these are mainly related to cost

savings (Sathye, 1999; Robinson, 2000) and Internet Banking remains one of the cheapest and

more efficient delivery channels (see Pikkarainen et al., 2004). Other rationales for the adoption

of such services are also related to competition as Internet Banking strategy has been an

interesting way to retain existing customers and attract new ones (Robinson, 2000). Among the

numerous advantages to banks feature mass customization, more effective marketing and

communication at lower costs amongst others (Tuchila, 2000). Benefits for the end users are

numerous as well and include mainly convenience of the service (time saved and globally

accessible service); lower cost of transaction and more frequent monitoring of accounts among

others (see Pikkarainen et al., 2004). It is noteworthy that there is also a number of push factors

encouraging the adoption of internet banking that have been evoked in the literate In spite of all

these numerous advantages of Internet Banking, many people still prefer to conduct their

banking transactions at the bank, something which they had been doing for years. Thus, apart

from security aspects, there are numerous factors and barriers that making people still prefer the

traditional way for their banking transactions. Internet banking is advantageous to both the banks

and customers.

Service Quality: Service quality has become an issue that businesses have focused up on with e-

services that enable electronic communication; information gathering, transaction processing

and data interchange between online vendors and customers across time and space (Featherman

and Pavlou, 2002). In online environments, service quality is defined as the extent to which a

website facilitates efficient and effective shopping, purchasing, and delivery of product and

services (Zeithaml et al., 2002). Santos (2003) described e-service quality in terms of overall

customer evaluations and judgments regarding the excellence and the quality of e-service

delivery in the virtual marketplace. A study by Parasuraman et al. (2005) on the Internet service

quality of online shopping websites resulted in the development of a service quality scale, the e-

SQ scale, consisting of seven dimensions: efficiency, system availability, fulfillment, privacy,

compensation and contact. It is slightly different from the e-SQ scale developed by Zeithaml et

al. (2001) which has 11 dimensions: reliability, responsibility, access, flexibility, and ease of

navigation, efficiency, assurance, security, price knowledge, site aesthetics and customization I

personalization. Furthermore, a study by Ribbink et al. (2004) in an e-commerce context (online

book and CD stores) the service quality dimensions consisted of: ease of use, escape, and

customization. Cristobal et al. (2007) further developed a service quality scale which consists

of multidimensional constructs of web design, customer service, assurance and order

management.

This dimension is concerned with dealing with the customer's requests, questions and complaints

promptly and attentively. Handling of problems and returns through the site. A Bank is known to

be responsive when it communicates to its customers how long it would take to get answers or

have their problems dealt with. To be successful, companies need to look at from the view point

of the customer rather than the company's perspective (Zeithaml et al., 2006). also captures the

notion of flexibility and ability to customize the service to customers need. Standard for speed

and promptness that's refects the companies view of process requirement may be very different

from the customer requirement. This concerns the willingness or eagerness of employees for

service provision. It involves turnaround time of service actions like timely dispatch of a receipt

or quickly calling back the customer (Zethaml et al., 2002).

Privacy and Security: Trust has been identified as an important factor for those financial related

internet services; moreover, empirical study supports that consumers make many online

decisions almost solely on the basis of trust (Avinandan & Prithwiraj, 2003; Urban, Sultan and

Qualls, 2000). For Internet banking, trust plays an extremely important role for the acceptance

and use, which has been supported by both research and empirical studies, especially in

developing countries (Benamati and Serva, 2007). Trust building is very important for internet

banking adoption. Privacy and security concern are the two crucial factors for trust building,

which has been pointed out as the top two factors influencing user' adoption. Privacy and

security have been discussed broadly both in academia and practice. Privacy is defined as the

ability to control and manage information about oneself (Belanger, Hiller and Smith, 2002).

Security is defined as the ability to protect against potential threats.

From consumers' standpoint, security is the ability to protect consumers' information from

information fraud and theft in the online banking business. Customers have doubts about the

trust ability of the e-bank's privacy policies (Gerrard and Cunningham, 2003). Trust has striking

influence on user's willingness to engage in online exchanges of money and personal sensitive

information (Friedman et al, 2000; Wang et al, 2003). Privacy is an important dimension that

may affect users' intention to adopt e-based transaction systems. Encryption technology is the

most common feature at all bank sites to secure information privacy, supplemented by a

combination of different unique identifiers, for instance, a password, mother's maiden name, a

memorable date, or a few minutes of inactivity automatically logs users off the account. Besides,

the Secure Socket Layer, a widely-used protocol use for online credit card payment, is designed

to provide a private and reliable channel between two communicating entities; the use of Java

Applet that runs within the user's browser; the use of a Personal Identification Number, as well

as an integrated digital signature and digital certificate associated with a smart card system

(Hutchinson and Warren, 2003). Thus, a combination of smart card and biometric recognition

using fingerprints offers a more secure and easier access control for computers than the password

method. Zeithaml et al (2000) developed e-SERVQUAL for measuring e-service quality,

identifying 11 dimensions: access; ease of navigation; efficiency; flexibility; reliability;

personalization; security; privacy; assurance trust; site aesthetics and price knowledge. Hence,

it is hypothesized that privacy has a positive effect on customer satisfaction.

Assurance: Assurance refers to the ability the internet banking convey trust and confidence to

their consumers. Madu and Madu argued that the online banking must ensure that their

employees are knowledgeable about their operation, and courteous in their responses to the

customers. Schneider and Perry suggested some web features that help promote the assurance to

consumers. For instances, providing detailed banks information (e.g. background, mission

statement, announcement, banks handling private data, a direct relationship might be

established among the three concepts. Assurance is defined as "the employees' knowledge and

courtesy and the service provider's ability to inspire trust and confidence" (Zeithaml et al., 2006).

According to Andaleeb and Conway (2006), assurance may not be so important relative to other

industries where the risk is higher and the outcome of using the service is uncertain. The trust

and confidence may be represented in the personnel who link the customer to the organization

(Zeithaml et al., 2006. Assurance is a set of courtesy and knowledge of employees along their

ability to instill confidence. The assurance dimension is taken from an integrated Assurance is a

set of courtesy and knowledge of employees along their ability to instill confidence. The

assurance dimension is taken from an integrated.

Reliability: Reliability means the quality of being dependable or reliable on something (Lin and

Chin 2007). Reliability is defined as "the ability to perform the promised service

dependably and accurately" or "delivering on its promises" (Zeithaml et al, 2006, p. 117).

Regarding to service quality dimension of reliability the internet has big affect on it. Madu2002.

Santos 2002 defines reliability as the ability to perform the promise service accurately and

frequently updating the website. Since most of the online customers are really concerned about

the reliability of virtual service providers. (Yant and fand 2004).( Gilly 2002) sate reliability as

the product that came was represent accurately by the website, you get what you ordered from

the site the product was delivered in time promise by the bank. Based on the theoretical review in

this study it is found that reliability is one of the most highly frequently mention dimension in e

service quality. (Parasyraman 1985, Johnston 1988). Reliability is found as important in banking

perspective however it's different from customer perspective. For internet banking reliability is

mostly based on physical bank. It is important for the bank to conduct business both online and

offline. It is also suggest that technical function and accurate record provided by internet should

be focused on by banking service provider in on line services. Madu2002. Reliability involves

dependability and uniformity in performance. It means the firm honors the commitments it

makes. Specifically, billing accuracy, proper record maintenance and delivering the service

within acceptable time limit describes the reliability of online services (Saha and Zhao, 2005).

Customer Satisfaction & Retention: Customer retention means the activity that a selling

organization undertakes in order to reduce customer defections. Successful customer retention

starts with the first contact an organization has with a customer and continues throughout the

entire lifetime of a relationship. Previous studies have identified the benefits that customer

retention delivers to an organization. In fact, the longer a customer stays with an organization or

company the more utility than seeking new customers. (Edvardsson et al, 2000). Many factors

consisting of higher initial costs of finding and attracting new customers, increases in both the

value and number of purchases, positive word of mouth promotion and the customer better

understanding of the organization affects the loyalty of customers and the time that customers

stay with the organization. Apart from the benefits that the longevity of customers brings,

research findings also suggest that the costs of customer retention activities are less comparing

the costs of acquiring new customers. For example, (Rust and Zagorsk) declared that the cost of

attracting new customers may be five times of keeping existing customers. However,

maintaining high levels of satisfaction will not, by itself causes customer loyalty. Today,

retaining customers becomes a priority. In spite of importance of customer retaining, some

research shows that longevity does not alone leads to profitability (Andreassen, 1999).

In other research, (Beckett et al, 2000) found interesting conclusions as to why consumers appear

to remain loyal to the same financial provider such as banks, in spite of in many factors they

hold less favorable views toward these service providers. For example, many consumers appear

to perceive little differentiation between banks, because according to their opinion, the change of

banks essentially is useless. Secondly, consumers appear motivated by convenience.

Finally, consumers associate changing banks with high switching costs in terms of the potential

sacrifice and effort involved. Furthermore, it is necessary for bank management to be carefully

considering the factors that might increase customer loyalty and retention rates. There are little

empirical researches that investigate the reasons result in customer loyalty and retention.

Previous surveys focused on identifying factors which causing customer retention. Others

researches have focused on developing measures of customer satisfaction, customer value and

customer loyalty without specifically looking into other potential meaningful factors. Examples

of mentioned factors are competitive advantage.

2.2 Conceptual Framework

2.3 Research Questions

Does Reliability affect Customer Satisfaction in context of Brac Bank Limited?

Does Privacy & Security affect Customer Satisfaction context of Brac Bank Limited?

Does Service Quality affect Customer Satisfaction in context of Brac Bank Limited?

Does Assurance affect Customer Satisfaction in context of Brac Bank Limited?

Reliability

Privacy & Security

Service Quality

Assurance

Customer Satisfaction& Retention

Independent Variable

Dependent Variable

Diagram 1: Conceptual Framework

CHAPTER 3

RESEARCH METHODOLOGY

3.1 Research Design

As shown in the "Diagram 1: Conceptual Framework" of this research there are four

independent variables and one dependent variable. The conceptual framework also shows that

there is a direct relationship between the Independent variables and the dependent variable. It is

very important to explore the type & intensity of this relationship so that the earlier mentioned

purpose of the study can be met. The study will enable the bank to understand the factors of

internet banking which actually helps to improve the Customer satisfaction & retention too. Thus

they can plan for their future plan of action or strategies and try to provide a good internet

banking service to retain more customers.

3.2 Research Type

This research is Descriptive in nature. Under descriptive research it will be a causal study.

Because the type of study that will be carried out to test the hypothesis and to answer the

research questions will be a causal study. This type of study will show a cause and effect

relationship of the independent and dependent variables.

3.3 Data Analysis

Frequency Table:The sample size of the research consists of 6 female & 119 male respondents. 4.8% of female

and 95.2% of male customers participates in this survey which is shown below. Among the

respondents 35 customers age was between 19-25 years, 63 customers age was between 26-30

years, 27 customers age was between 31-42 years.

Sex

Frequency Percent Valid Percent

Cumulative

Percent

Valid Female 6 4.8 4.8 4.8

Male 119 95.2 95.2 100.0

Total 125 100.0 100.0

Statistics

Age

N Valid 125

Missing 0

Age

Frequency Percent Valid Percent

Cumulative

Percent

Valid 19.00 1 .8 .8 .8

21.00 1 .8 .8 1.6

22.00 5 4.0 4.0 5.6

23.00 10 8.0 8.0 13.6

24.00 6 4.8 4.8 18.4

25.00 12 9.6 9.6 28.0

26.00 14 11.2 11.2 39.2

27.00 12 9.6 9.6 48.8

28.00 10 8.0 8.0 56.8

29.00 15 12.0 12.0 68.8

30.00 12 9.6 9.6 78.4

31.00 1 .8 .8 79.2

32.00 11 8.8 8.8 88.0

33.00 6 4.8 4.8 92.8

34.00 3 2.4 2.4 95.2

35.00 1 .8 .8 96.0

36.00 1 .8 .8 96.8

37.00 1 .8 .8 97.6

39.00 1 .8 .8 98.4

41.00 1 .8 .8 99.2

42.00 1 .8 .8 100.0

Total 125 100.0 100.0

Reliability Analysis with Cronbach's Alpha10:

Scale: ALL VARIABLES

Case Processing Summary

N %

Cases Valid 125 100.0

Excludeda 0 .0

Total 125 100.0

a. Listwise deletion based on all variables in the

procedure.

Scale: Reliability & Customer Satisfaction:

Reliability Statistics

Cronbach's Alphaa N of Items

0.274 2

Interpretation: Here the alpha value is 0.274, which is positive. So, the question is clear to theaudience. Here I discarded the Question 4 for some reason.

Scale: Privacy & Security & Customer Satisfaction:

Reliability Statistics

Cronbach's Alphaa N of Items

0.118 3

10 Cronbach's alpha is a measure of internal consistency, that is, how closely related a set of items are as a group. Itis considered to be a measure of scale reliability. A "high" value for alpha does not imply that the measure isunidimensional. See, http://en.wikipedia.org/wiki/Cronbach's_alpha

Interpretation: Here the alpha value is 0.118, which is positive. So, the question is clear to theaudience.

Scale: Service Quality & Customer Satisfaction

Reliability Statistics

Cronbach's Alphaa N of Items

0.207 2

Interpretation: Here the alpha value is 0.207, which is positive. So, the question is clear to theaudience.

Scale: Assurance & Customer Satisfaction

Reliability Statistics

Cronbach's Alphaa N of Items

0.229 2

Interpretation: Here the alpha value is 0.229, which is positive. So, the question is clear to theaudience.

Regression Analysis:

Reliability & Customer Satisfaction:

Variables Entered/Removeda

Model

Variables

Entered

Variables

Removed Method

1 Question7,

Question1b . Enter

a. Dependent Variable: CustomerSatisfaction

b. All requested variables entered.

Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .149a .022 .006 .77069

a. Predictors: (Constant), Question7, Question1

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1 Regression 1.648 2 .824 1.387 .254b

Residual 72.464 122 .594

Total 74.112 124

a. Dependent Variable: CustomerSatisfaction

b. Predictors: (Constant), Question7, Question1

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 1.975 .273 7.237 .000

Question1 -.088 .056 -.144 -1.589 .115

Question7 .051 .068 .068 .752 .454

a. Dependent Variable: CustomerSatisfaction

Interpretation: Here the value of ² is 0.022 means 2.2%. That means the effect of Reliabilityon Customer Satisfaction is 2.2%.

Privacy - Security & Customer Satisfaction:

Variables Entered/Removeda

Model

Variables

Entered

Variables

Removed Method

1 Question8,

Question2,

Question3b

. Enter

a. Dependent Variable: CustomerSatisfaction

b. All requested variables entered.

Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .111a .012 -.012 .77780

a. Predictors: (Constant), Question8, Question2, Question3

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1 Regression .910 3 .303 .501 .682b

Residual 73.202 121 .605

Total 74.112 124

a. Dependent Variable: CustomerSatisfaction

b. Predictors: (Constant), Question8, Question2, Question3

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 1.646 .442 3.726 .000

Question2 -.045 .080 -.052 -.568 .571

Question3 .038 .085 .040 .444 .658

Question8 .066 .065 .092 1.012 .313

a. Dependent Variable: CustomerSatisfaction

Interpretation: Here the value of ² is 0.012 means 1.2%. That means the effect of Privacy &Security on Customer Satisfaction is 1.2%.

Service Quality & Customer Satisfaction:

Variables Entered/Removeda

Model

Variables

Entered

Variables

Removed Method

1 Question6,

Question5b . Enter

a. Dependent Variable: CustomerSatisfaction

b. All requested variables entered.

Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .078a .006 -.010 .77702

a. Predictors: (Constant), Question6, Question5

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1 Regression .453 2 .227 .375 .688b

Residual 73.659 122 .604

Total 74.112 124

a. Dependent Variable: CustomerSatisfaction

b. Predictors: (Constant), Question6, Question5

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 1.707 .326 5.233 .000

Question5 -.022 .065 -.030 -.336 .738

Question6 .066 .079 .076 .833 .407

a. Dependent Variable: CustomerSatisfaction

Interpretation: Here the value of ² is 0.006 means 0.6%. That means the effect of ServiceQuality on Customer Satisfaction is 0.6%.

Assurance & Customer Satisfaction:

Variables Entered/Removeda

Model

Variables

Entered

Variables

Removed Method

1 Question10,

Question9b . Enter

a. Dependent Variable: CustomerSatisfaction

b. All requested variables entered.

Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .178a .032 .016 .76699

a. Predictors: (Constant), Question10, Question9

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1 Regression 2.343 2 1.172 1.991 .141b

Residual 71.769 122 .588

Total 74.112 124

a. Dependent Variable: CustomerSatisfaction

b. Predictors: (Constant), Question10, Question9

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 1.439 .293 4.914 .000

Question9 -.006 .065 -.009 -.096 .923

Question10 .126 .064 .179 1.989 .049

a. Dependent Variable: CustomerSatisfaction

Interpretation: Here the value of ² is 0.032 means 3.2%. That means the effect of ServiceQuality on Customer Satisfaction is 3.2%.

Correlation Analysis:

Relationship between Reliability and Customer Retention:

Correlations

CustomerSatisf

action Question7

CustomerSatisfaction Pearson Correlation 1 .045

Sig. (2-tailed) .619

N 125 125

Question7 Pearson Correlation .045 1

Sig. (2-tailed) .619

N 125 125

Figure: Scatter Diagram of Reliability & Customer Satisfaction

Interpretation: According to the Pearson correlation test & figure there is a positive relationship

between Reliability and Customer Satisfaction but there is a weak relationship between

Reliability & Customer Satisfaction. Here P > 0.05 which is 0.619 so we fail to reject Ho

Hypothesis. Therefore Ha is also rejected. We do not have enough evidence to prove it at this

stage of research.

Correlation Analysis:

Relationship between Reliability and Customer Retention:

Correlations

CustomerSatisf

action Question7

CustomerSatisfaction Pearson Correlation 1 .045

Sig. (2-tailed) .619

N 125 125

Question7 Pearson Correlation .045 1

Sig. (2-tailed) .619

N 125 125

Figure: Scatter Diagram of Reliability & Customer Satisfaction

Interpretation: According to the Pearson correlation test & figure there is a positive relationship

between Reliability and Customer Satisfaction but there is a weak relationship between

Reliability & Customer Satisfaction. Here P > 0.05 which is 0.619 so we fail to reject Ho

Hypothesis. Therefore Ha is also rejected. We do not have enough evidence to prove it at this

stage of research.

Correlation Analysis:

Relationship between Reliability and Customer Retention:

Correlations

CustomerSatisf

action Question7

CustomerSatisfaction Pearson Correlation 1 .045

Sig. (2-tailed) .619

N 125 125

Question7 Pearson Correlation .045 1

Sig. (2-tailed) .619

N 125 125

Figure: Scatter Diagram of Reliability & Customer Satisfaction

Interpretation: According to the Pearson correlation test & figure there is a positive relationship

between Reliability and Customer Satisfaction but there is a weak relationship between

Reliability & Customer Satisfaction. Here P > 0.05 which is 0.619 so we fail to reject Ho

Hypothesis. Therefore Ha is also rejected. We do not have enough evidence to prove it at this

stage of research.

Relationship between Privacy-Security and Customer Retention:

Correlations

CustomerSatisf

action

Privacy &

Security

CustomerSatisfaction Pearson Correlation 1 .092

Sig. (2-tailed) .310

N 125 125

Privacy & Security Pearson Correlation .092 1

Sig. (2-tailed) .310

N 125 125

Figure: Scatter Diagram of Privacy-Security & Customer Satisfaction

Interpretation: According to the Pearson correlation test & figure there is a positive relationship

between Privacy-Security and Customer Satisfaction but there is a weak relationship between

Privacy-Security & Customer Satisfaction. Here P > 0.05 which is 0.310 so we fail to reject Ho

Hypothesis. Therefore Ha is also rejected. We do not have enough evidence to prove it at this

stage of research.

Relationship between Service Quality and Customer Retention:

Correlations

CustomerSatisf

action Service Quality

CustomerSatisfaction Pearson Correlation 1 .072

Sig. (2-tailed) .424

N 125 125

Service Quality Pearson Correlation .072 1

Sig. (2-tailed) .424

N 125 125

Figure: Scatter Diagram of Service Quality & Customer Satisfaction

Interpretation: According to the Pearson correlation test & figure there is a positive relationship

between Service Quality and Customer Satisfaction but there is a weak relationship between

Service Quality & Customer Satisfaction. Here P > 0.05 which is 0.424 so we fail to reject Ho

Hypothesis. Therefore Ha is also rejected. We do not have enough evidence to prove it at this

stage of research.

Relationship between Assurance and Customer Retention:

Correlations

CustomerSatisf

action Assurance

CustomerSatisfaction Pearson Correlation 1 .014

Sig. (2-tailed) .873

N 125 125

Assurance Pearson Correlation .014 1

Sig. (2-tailed) .873

N 125 125

Figure: Scatter Diagram of Assurance & Customer Satisfaction

Interpretation: According to the Pearson correlation test & figure there is a positive relationship

between Assurance and Customer Satisfaction but there is a weak relationship between

Assurance & Customer Satisfaction. Here P > 0.05 which is 0.873 so we fail to reject Ho

Hypothesis. Therefore Ha is also rejected. We do not have enough evidence to prove it at this

stage of research.

3.4 Findings

After analyzing the data I have found that there is positive reliability between the independent

variables and dependent variables. That means the questions are almost clear to the audience. At

this stage, after the regression analysis we can see that the value of the independent variables

have a positive effect on the dependent variable. But the effect of independent variables are low.

There might be other factors lying behind this research. In the correlation analysis there are

moderately positive but weak relationship between the independent variables and the dependent

variable. We failed to reject Ho Hypothesis that why cannot accept Ha Hypothesis for any of 4

independent variables with dependent variable.

3.5 Discussion

Bank must satisfy its customers at any cost. It will bring them a good health of the organization.

Internet Banking can be part of bank's success and finally a par of good financial health. It is

very important for a bank to take care of its customers with satisfaction created as much as

possible, because it is the satisfaction of loyal customers who in turn may bring new customers

for the bank in future. It is much cost effective for the bank to satisfy & finally to retain its

customers than to attract new customers which would require further promotional expense.

Through this research, I have mentioned some factors which are helpful for retaining customers.

But there might be other factor hiding behind this research. At this stage the variables are:

1) Reliability

2) Privacy & Security

3) Service Quality

4) Assurance.

CHAPTER 4

CONCLUSION AND RECOMMENDATION

4.1 Conclusion:

While researching on Internet Banking customers of Brac Bank Limited I have truly enjoyed my

thesis program from the learning and experience viewpoint. I am confident that this time of

experience will definitely help me to encourage my research career in future.

Hopefully this research primarily indicates that internet banking features of Brac Bank Limited

Ltd. might be very important to satisfy customers but we need to account other factors too. I

would like to refine this research and go on developing it with huge amount of data collection. If

the bank plans to expand the customer base of internet banking they should focus more on

service quality, privacy & security, assurance and reliability factors of internet banking. Proper

web hosting is required for this. Customers should also be made aware of unethical practices like

sniffing, spoofing, phishing and other malicious software which can be used by hackers.

Attention should also be given in the encryption of the information which is exchanged between

the users and the bank. More ever the bank should be more aware to make their internet banking

service more quality full for their customers. I think this research will be helpful for Brac Bank

Limited to make their internet banking much better in future. This research will be also

beneficiary for other researcher who wants to do research on this topic in future.

CustomerSatisfaction

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly Disagree 48 38.4 38.4 38.4

Disagree 48 38.4 38.4 76.8

Moderate 29 23.2 23.2 100.0

Total 125 100.0 100.0

The overall satisfaction level of Brac Bank's internet based customer is 1.8480 (out of 5) which

might be important information for Brac Bank Limited. Also the factors or variables are chosen

here all cannot affect the overall satisfaction level. Strong and customer beneficial initiatives can

change the scenario in term of customer satisfaction.

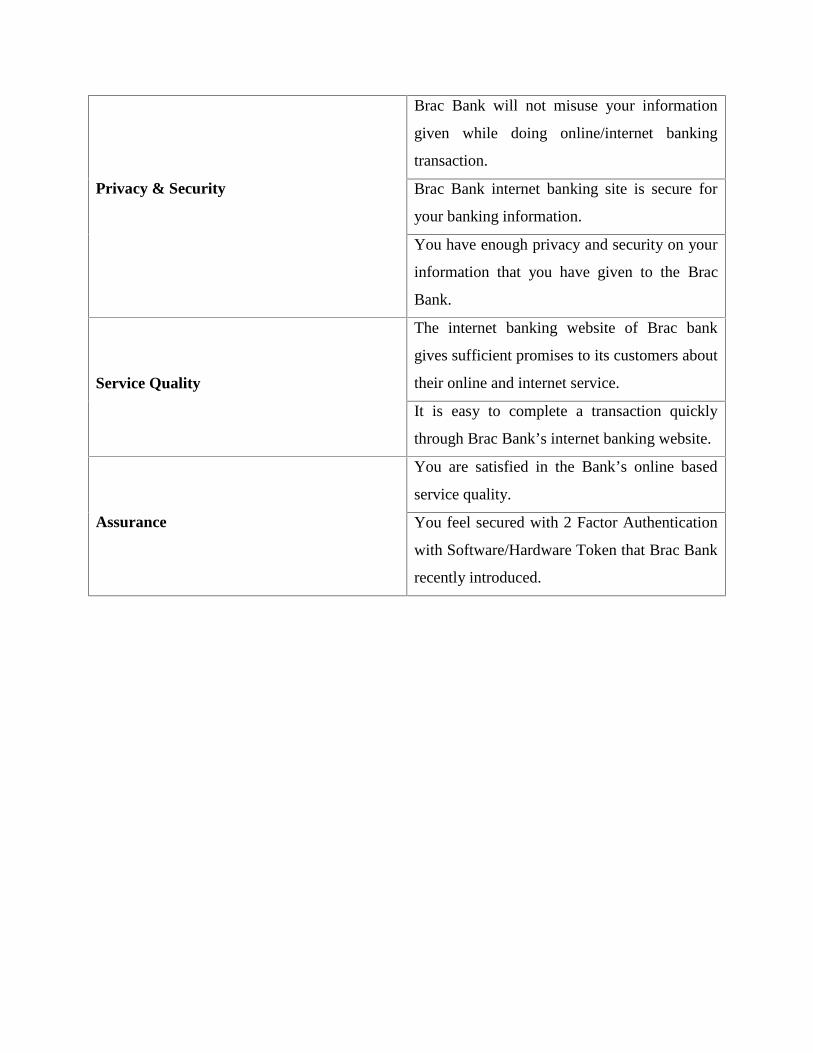

Selected Variables Questions

Reliability

Brac Bank Insures your deposits made through

online banking.

You feel safe in the online transaction with Brac

Bank.

The function of the internet banking transaction is

easy to operate and you rely on it.

Privacy & Security

Brac Bank will not misuse your information given

while doing online/internet banking transaction.

Brac Bank internet banking site is secure for your

banking information.

You have enough privacy and security on your

information that you have given to the Brac Bank.

Service Quality

The internet banking website of Brac bank gives

sufficient promises to its customers about their

online and internet service.

It is easy to complete a transaction quickly through

Brac Bank’s internet banking website.

Assurance

You are satisfied in the Bank’s online based service

quality.

You feel secured with 2 Factor Authentication with

Software/Hardware Token that Brac Bank recently

introduced.

4.2 Recommendation:

I suggest to continue best researches on Internet Banking so the people of Bangladesh can be

habituated on latest & time saving Technology. The Information & Communication Technology

sector of Bangladesh is being developed day by day. We should take the chance to develop

ourselves not only in Banking but also for the possible betterment of the nation. We still dream

to see the internet connectivity at each corner of Bangladesh and its safe use everywhere.

Customer comments & experiences can be a great asset to research further to bring the success in

not only Internet Banking but also different ICT fields.

Working with large population sample may help to get more improved & sophisticated result.

There should be more factors involved in customer satisfaction. If Brac Bank allows to reveal its

real information on customer database & internet user database the research will be better than

this. Brac Bank Limited may create an internet based survey which will be more easier to reach

Internet Banking customers. It can be a mandatory once when they login to their Internet

Banking Interface. All of the major banks that are operating in Bangladesh should take necessary

steps to make Internet Banking more reliable, easily accessible that will definitely reduce the

cost of both parties.

Here are the selected independent variables & questions related to this -

Selected Variables Questions

Reliability

Brac Bank Insures your deposits made through

online banking.

You feel safe in the online transaction with

Brac Bank.

The function of the internet banking

transaction is easy to operate and you rely on

it.

Privacy & Security

Brac Bank will not misuse your information

given while doing online/internet banking

transaction.

Brac Bank internet banking site is secure for

your banking information.

You have enough privacy and security on your

information that you have given to the Brac

Bank.

Service Quality

The internet banking website of Brac bank

gives sufficient promises to its customers about

their online and internet service.

It is easy to complete a transaction quickly

through Brac Bank’s internet banking website.

Assurance

You are satisfied in the Bank’s online based

service quality.

You feel secured with 2 Factor Authentication

with Software/Hardware Token that Brac Bank

recently introduced.

BIBLIOGRAPHY

Annual Report 2010, 2011, 2012, 2013 of Brac Bank Limited

Brac Bank Limited Website

http://www.bracbank.com

Khaled A. G. (2010). Costumers' Satisjaction with Online Banking: A Case Study on HSBC

Egypt

H. Rullis, B. Sloka (2011). Internet Banking Quality: Marketing Possibilities and Customers'

Loyalty. (Research papers).

Nupur, J.M. (2010). E-Banking and Customers' Satisfaction in Bangladesh: An Analysis.

Guangying Hua, (April 2009), “Internet Banking and Commerce”, Journal of internet

banking, vol. 14, no.1

(http://www.arraydev.com/commerce/jibc/2009-04/Online%20Banking_GHua.pdf)

Khalid A. S. (2012). Banking Services and Customer's Satisfaction in Qatar: A Statistical

Analysis.

Shar, P. Zhao, Y. (2005.) Relationship between online Banking Service Quality and Customer

Satisfaction. (Master's Thesis)

Asli Yuksel Mermod, (April 2011), “Internet Banking and Commerce”, Journal of

internet banking, vol. 16, no.1

(http://www.arraydev.com/commerce/jibc/2010-08/1104-Publ_PDFVersion.pdf).

Chun Wang and Zheng Wang, (2006:07), “The Impact of Internet on Service Quality in

the Banking Sector”

(http://epubl.ltu.se/1653-0187/2006/07/LTU-PB-EX-0607-SE.pdf).

Anesh Maniraj Singh, (2004), “Trends in South African Internet Banking”, Aslib

Proceedings, Vol.56, Iss: 3 pp.187-196.

Blanca Hernandez-Ortega, (December 2007), “Internet Banking and Commerce”, Journal

of internet banking, vol. 12, no.3

(http://www.arraydev.com/commerce/jibc/2007-12/Blanca_Final.pdf)

APPENDIX A

Questionnaire

Good Morning / Good Afternoon, I am A B M Mehedi Hasan doing my Master Thesis in

EMBA Program (3rd Batch), under supervision of MS. Mahfuza Khatun, Assitant Professor,

Faculty of Business Studies, Jahangirnagar University. My Registered Student ID is:

20122070

For this reason I am conducting a survey on Brac Bank Limited. customers. I would be glad

and grateful if you help me in the process through answering few simple survey questions.

No personal information will be exposed outside of the research.

Questionnaire Type

This questionnaire is designed focusing on the Internet & Online Banking of Brac BankLimited as well as what customers think of the services they are being delivered/Served.

In this questionnaire you will be asked 10 simple questions where each question will have

following answers with weight (Likert) -

Answers Weight of Answer

Strongly Disagree 1

Disagree 2

Moderate 3

Agree 4

Strongly Agree 5

Please turn over the page...

Age: ___________ Sex: ___________

Questions StronglyDisagree

Disagree Moderate Agree StronglyAgree

1. Brac Bank Insures your depositsmade through online banking.2. You feel safe in the onlinetransaction with Brac Bank.

3. The function of the internet bankingtransaction is easy to operate and yourely on it.4. Brac Bank will not misuse yourinformation given while doingonline/internet banking transaction.5. Brac Bank internet banking site issecure for your banking information.

6. You have enough privacy andsecurity on your information that youhave given to the Brac Bank.

7. The internet banking website ofBrac bank gives sufficient promises toits customers about their online andinternet service.8. It is easy to complete a transactionquickly through Brac Bank’s internetbanking website.

9. You are satisfied in the Bank’sonline based service quality.

10. You feel secured with 2 FactorAuthentication withSoftware/Hardware Token that BracBank recently introduced.

11. What is your overall satisfaction ofInternet Banking of Brac BankLimited?

APPENDIX B

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Age 125 19.00 42.00 28.0000 4.03413

Sex 125 1.00 2.00 1.9520 .21463

Question1 125 2.00 5.00 3.3120 1.25990

Question2 125 2.00 5.00 3.3760 .87680

Question3 125 1.00 5.00 3.5280 .82868

Question4 125 2.00 5.00 3.6000 1.17775

Question5 125 1.00 5.00 3.4080 1.08580

Question6 125 2.00 5.00 3.2720 .89241

Question7 125 1.00 5.00 3.2320 1.02498

Question8 125 1.00 5.00 3.3920 1.07685

Question9 125 1.00 5.00 3.2880 1.06116

Question10 125 2.00 5.00 3.4000 1.09250

CustomerSatisfaction 125 1.00 3.00 1.8480 .77310

Valid N (listwise) 125

Frequency Table

Sex

Frequency Percent Valid Percent

Cumulative

Percent

Valid Female 6 4.8 4.8 4.8

Male 119 95.2 95.2 100.0

Total 125 100.0 100.0

Question1

Frequency Percent Valid Percent

Cumulative

Percent

Valid Disagree 48 38.4 38.4 38.4

Moderate 27 21.6 21.6 60.0

Agree 13 10.4 10.4 70.4

Strongly Agree 37 29.6 29.6 100.0

Total 125 100.0 100.0

Question2

Frequency Percent Valid Percent

Cumulative

Percent

Valid Disagree 21 16.8 16.8 16.8

Moderate 48 38.4 38.4 55.2

Agree 44 35.2 35.2 90.4

Strongly Agree 12 9.6 9.6 100.0

Total 125 100.0 100.0

Question3

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly Disagree 1 .8 .8 .8

Disagree 9 7.2 7.2 8.0

Moderate 53 42.4 42.4 50.4

Agree 47 37.6 37.6 88.0

Strongly Agree 15 12.0 12.0 100.0

Total 125 100.0 100.0

Question4

Frequency Percent Valid Percent

Cumulative

Percent

Valid Disagree 33 26.4 26.4 26.4

Moderate 22 17.6 17.6 44.0

Agree 32 25.6 25.6 69.6

Strongly Agree 38 30.4 30.4 100.0

Total 125 100.0 100.0

Question5

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly Disagree 3 2.4 2.4 2.4

Disagree 25 20.0 20.0 22.4

Moderate 39 31.2 31.2 53.6

Agree 34 27.2 27.2 80.8

Strongly Agree 24 19.2 19.2 100.0

Total 125 100.0 100.0

Question6

Frequency Percent Valid Percent

Cumulative

Percent

Valid Disagree 25 20.0 20.0 20.0

Moderate 53 42.4 42.4 62.4

Agree 35 28.0 28.0 90.4

Strongly Agree 12 9.6 9.6 100.0

Total 125 100.0 100.0

Question7

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly Disagree 1 .8 .8 .8

Disagree 34 27.2 27.2 28.0

Moderate 42 33.6 33.6 61.6

Agree 31 24.8 24.8 86.4

Strongly Agree 17 13.6 13.6 100.0

Total 125 100.0 100.0

Question8

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly Disagree 3 2.4 2.4 2.4

Disagree 25 20.0 20.0 22.4

Moderate 40 32.0 32.0 54.4

Agree 34 27.2 27.2 81.6

Strongly Agree 23 18.4 18.4 100.0

Total 125 100.0 100.0

Question9

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly Disagree 2 1.6 1.6 1.6

Disagree 32 25.6 25.6 27.2

Moderate 38 30.4 30.4 57.6

Agree 34 27.2 27.2 84.8

Strongly Agree 19 15.2 15.2 100.0

Total 125 100.0 100.0

Question10

Frequency Percent Valid Percent

Cumulative

Percent

Valid Disagree 30 24.0 24.0 24.0

Moderate 44 35.2 35.2 59.2

Agree 22 17.6 17.6 76.8

Strongly Agree 29 23.2 23.2 100.0

Total 125 100.0 100.0

CustomerSatisfaction

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly Disagree 48 38.4 38.4 38.4

Disagree 48 38.4 38.4 76.8

Moderate 29 23.2 23.2 100.0

Total 125 100.0 100.0

Age

Frequency Percent Valid Percent

Cumulative

Percent

Valid 19.00 1 .8 .8 .8

21.00 1 .8 .8 1.6

22.00 5 4.0 4.0 5.6

23.00 10 8.0 8.0 13.6

24.00 6 4.8 4.8 18.4

25.00 12 9.6 9.6 28.0

26.00 14 11.2 11.2 39.2

27.00 12 9.6 9.6 48.8

28.00 10 8.0 8.0 56.8

29.00 15 12.0 12.0 68.8

30.00 12 9.6 9.6 78.4

31.00 1 .8 .8 79.2

32.00 11 8.8 8.8 88.0

33.00 6 4.8 4.8 92.8

34.00 3 2.4 2.4 95.2

35.00 1 .8 .8 96.0

36.00 1 .8 .8 96.8

37.00 1 .8 .8 97.6

39.00 1 .8 .8 98.4

41.00 1 .8 .8 99.2

42.00 1 .8 .8 100.0

Total 125 100.0 100.0