Commercial Banking-Vs-Islamic Banking

23

Product Differentiation between Islamic Banking and Conventional Banking Submitted by: Name ID Arafat Rauf 2009-2-10-345 A S M Rakib-Ul- Hassan 2009-2-10-190 FIN 380 Section: 2 Group: 10 Fall: 2011 Date of Submission: 23 rd October 2011

Transcript of Commercial Banking-Vs-Islamic Banking

Product Differentiation between Islamic Banking and Conventional Banking

Submitted by:Name ID

Arafat Rauf 2009-2-10-345A S M Rakib-Ul-Hassan

2009-2-10-190

FIN 380Section: 2Group: 10Fall: 2011

Date of Submission: 23rd October 2011

Product Differentiation between Islamic Banking and Conventional Banking

Table of Content

Executive Summary 3

Objective of the Study 3

Limitation of the Study 3

Analysis 4

Bibliography 12

Page 2 of 23

Product Differentiation between Islamic Banking and Conventional Banking

Executive Summary

Islamic banking refers to a system of banking or banking activity

that is consistent with Islamic law (Sharia’h) principles and

guided by Islamic economics. In particular, Islamic law prohibits

usury, the collection and payment of interest, also commonly

called riba. Generally, Islamic law also prohibits trading in

financial risk (which is seen as a form of gambling). In

addition, Islamic law prohibits investing in businesses that are

considered unlawful, or haraam.

Islamic finance has been gaining momentum on a global scale for

the last 30 years.

Conventional banking is based on collateral. In conventional

banks charging interest does not stop unless specific exception

is made to a particular defaulted loan. Interest charged on a

loan can be multiple of the principal, depending on the length of

the loan period. More than half the population of the world is

deprived of the financial services of the conventional banks.

Objective of the StudyPage 3 of 23

Product Differentiation between Islamic Banking and Conventional Banking

Our objective of the study was to know the product

differentiation of Islamic Bank and Conventional bank. In which

way they differ from each other. In our case, we have use

Shajalal Islamic Bank as an Islamic bank and Uttara Bank as a

Conventional bank. We mainly focus on to know the difference of

Islamic bank and conventional bank.

Limitation of the Study

Although we have tried our best to make this term paper perfect

but there were some limitations that obstructed us from doing so.

We have faced some problems while preparing this report. Some of

the limitations encountered while making this report are as

follows:

The topic has so much to cover, so initially we faced some

problem to choose the appropriate field to talk about.

We tried to collect information about Uttara Bank, but as

not much information is available we faced some problem to

make comparison with Shajalal Islamic Bank.

Analysis of the study

Page 4 of 23

Product Differentiation between Islamic Banking and Conventional Banking

ISLAMIC BANKING

Islamic banking refers to a system of banking or banking activity

that is consistent with Islamic law (Sharia’h) principles and

guided by Islamic economics. In particular, Islamic law prohibits

usury, the collection and payment of interest, also commonly

called riba. Generally, Islamic law also prohibits trading in

financial risk (which is seen as a form of gambling). In

addition, Islamic law prohibits investing in businesses that are

considered unlawful, or haraam.

Amongst the governing principles of an Islamic bank are:

* The absence of interest-based (riba) transactions;

* The avoidance of economic activities involving oppression

(zulm)

* The avoidance of economic activities involving speculation

(gharar);

* The introduction of an Islamic tax, zakat;

* The discouragement of the production of goods and services

which contradict the Islamic value (haram)

Islamic law considers a loan to be given or taken, free of

charge, to meet any contingency. Thus in Islamic Banking, the

creditor should not take advantage of the borrower. When money is

lent out on the basis of interest, more often it leads to some

kind of injustice.

Page 5 of 23

Product Differentiation between Islamic Banking and Conventional Banking

(Website of sooperarticles.com)

Conventional Banking

Conventional banking is based on the principle that the more you

have, the more you can get. In other words, if you have little or

nothing, you get nothing. As a result, more than half the

population of the world is deprived of the financial services of

the conventional banks. Conventional banking is based on

collateral. Conventional banks look at what has already been

acquired by a person Conventional banks go into ‘punishment’ mode

when a borrower is taking more time in repaying the loan than it

was agreed upon. They call these borrowers “defaulters”. When a

client gets into difficulty, conventional banks get worried about

their money, and make all efforts to recover the money, including

taking over the collateral. In conventional banks charging

interest does not stop unless specific exception is made to a

particular defaulted loan. Interest charged on a loan can be

multiple of the principal, depending on the length of the loan

period.

(Website of scribd.com)

Uttara bank (UBL)

UBL is one of the largest private banks in Bangladesh. It

operates through 211 fully computerized branches ensuring best

Page 6 of 23

Product Differentiation between Islamic Banking and Conventional Banking

possible and fastest services to its valued clients. The bank

has more than 600 foreign correspondents worldwide. Total

numbers of employees are nearly 3,562. The Board of Directors

consists of 13 members. The bank is headed by the Managing

Director who is the Chief Executive Officer. The Head Office is

located at Bank’s own 18-storied building at Motijheel, the

commercial center of the capital, Dhaka.

Special loan scheme

Consumer credit

Uttaran Consumer-Credit Scheme :

UBL started Uttaran Consumers Credit Scheme from 1996.UBL

offers opportunity of Financial assistance for -

Motor cycle/car- New or re-conditioned.

Refrigerator/ Deep Freeze.

Television/ VCR /VCP/VCD

Radio/ Two-in-one/ Three – in – one

Air-Conditioner/ Water Cooler/ Water Pump

Washing Machine.

Personal Computer/ UPS/ Printer/ Type writer

Sewing Machine.

House hold furniture- Wooden & Steel.

Cellular Telephone.

Fax

Photocopier.

Page 7 of 23

Product Differentiation between Islamic Banking and Conventional Banking

Electric Fan- Ceiling/ Pedestal/ Table.

Bi-Cycle

Dish Antenna.

Baby Taxi, Tempo/Microbus (For self employed persons)

Kitchen articles such as Oven, Micro-oven, Toaster,

Blender, Pressure Cooker etc.Special Features :

No collateral security is required.

Simple rate of interest.

Quick sanction.

Maximum Loan amount Tk.3,00,000/-

5% incentive on total interest charged

Personal Loan :

Personal Loan Scheme for Salaried Officers-

Emergency expenses for own marriage of a service- holder

or his dependents.

Emergency expenses of urgent surgical operation/ medical

treatment.

Emergency educational expenses of the children for

admission/purchase of books, examination fees etc.

Special Features :

Any permanent salaried employee aged between 20 to 55

years is eligible to get loan.

Page 8 of 23

Product Differentiation between Islamic Banking and Conventional Banking

No collateral security is required.

Maximum Amount of loan Tk. 1,00,000.

Maximum period of loan upto 3 years.Deposit scheme:

Saving account

Features :

Minimum amount : Taka 1,000.00

Rate of Interest : 4.50%

Free Cheque-Book facility

Opportunity to apply for - safe deposit locker facility

Collect foreign remittance in both T.C. & Taka draft.

Transfer of fund from one branch to another by

o Demand Draft

o Mail Transfer

o Telegraphic Transfer

Transfer of fund on Standing Instruction Arrangement

Collection of cheques through Clearing House.

Issuance of Payment Order / Call Deposit

1. Special Notice Deposit:

Govt., Semi-Govt., Autonomous organization and an individual

may open SND Account with UBL.

7 days notice required to withdraw.

Page 9 of 23

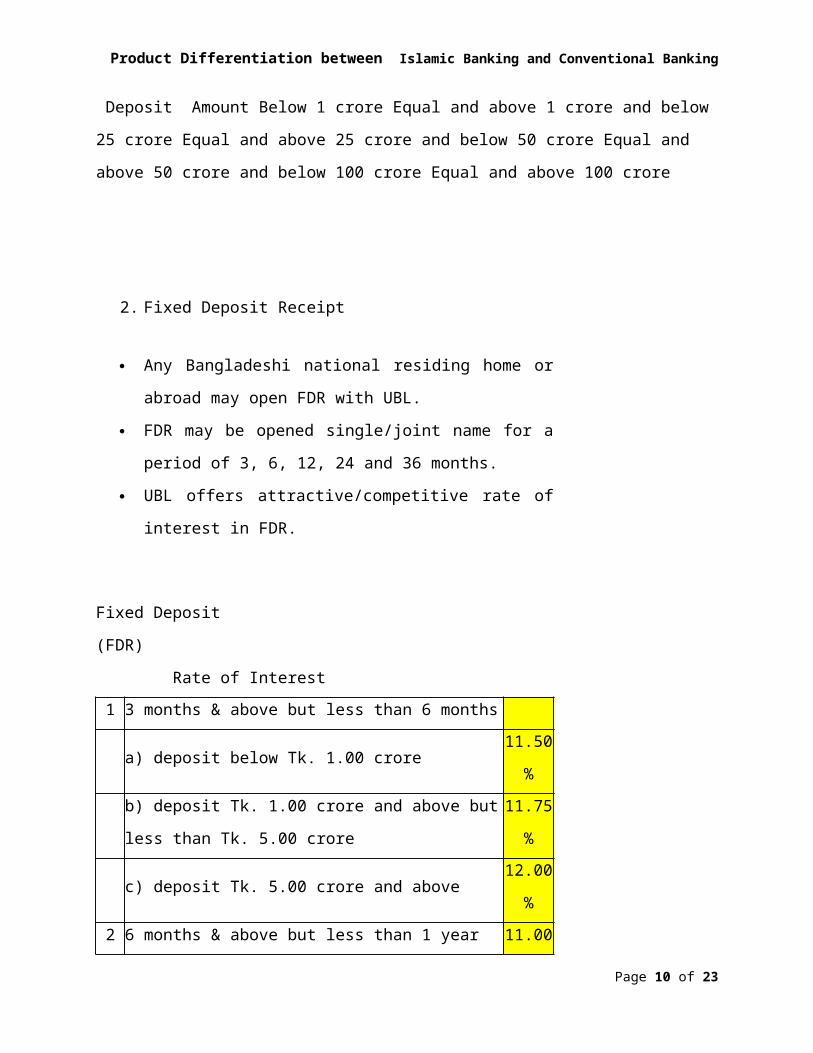

Product Differentiation between Islamic Banking and Conventional Banking

Deposit Amount Below 1 crore Equal and above 1 crore and below

25 crore Equal and above 25 crore and below 50 crore Equal and

above 50 crore and below 100 crore Equal and above 100 crore

2. Fixed Deposit Receipt

Any Bangladeshi national residing home or

abroad may open FDR with UBL.

FDR may be opened single/joint name for a

period of 3, 6, 12, 24 and 36 months.

UBL offers attractive/competitive rate of

interest in FDR.

Fixed Deposit

(FDR)

Rate of Interest1 3 months & above but less than 6 months

a) deposit below Tk. 1.00 crore11.50

%b) deposit Tk. 1.00 crore and above but

less than Tk. 5.00 crore

11.75

%

c) deposit Tk. 5.00 crore and above12.00

%2 6 months & above but less than 1 year 11.00

Page 10 of 23

Product Differentiation between Islamic Banking and Conventional Banking

%

3 1 year & above but less than 2 years11.00

%

42 years & above but not more than 3

years

11.00

%

3. Double Benefit Deposit Scheme

a) Any adult Bangladeshi National will be eligible to open this

account.

b) Minimum Tk.1,00,000/- (Taka One Lac only) and multiples

thereof will be accepted as deposit under this scheme.

c) The period shall be of 8.5 (Eight years Six months) years

term.

d) Deposit may be encashed before its maturity and no interest

will be paid if encashed before 1(one) year of deposit.

e) Interest will be paid at Savings rate if encashed after

1(one) year.

f) Advance will be allowed up to 80% of the deposit after

completion of one year

g) Full amount including interest will be paid on maturity.

h) Govt. tax, Surcharge, Source Tax, Levy, Govt. Excise duty

Page 11 of 23

Product Differentiation between Islamic Banking and Conventional Banking

will be recoveredfrom the depositor’s A/C.

i) Account holder can appoint a nominee against the account.

j) Bank reserves the right to close the account at any time

and make amendment / alteration of the terms & conditions of the

scheme Without assigning any reason.

4. Monthly Deposit Scheme

a) Any adult Bangladeshi National will be eligible to open this

account.

b) The period of the scheme will be 5 (five) years and 10

(ten) years term.

c) Monthly installment will be Tk.500/-, 1000/-, 2000/-,

3000/-, 5000/- & 10000/-

d) Monthly installment to be deposited within 10th day of the

month. After due date a penalty of Tk.50/- will be realized from

the A/C holder. If the A/C holder fails to deposit 3(three) consecutive

monthly Installments, the account will be automatically closed.

e) No cheque book will be issued against the account.

f ) Deposit may be encashed before maturity. But no interest Page 12 of 23

Product Differentiation between Islamic Banking and Conventional Banking

will be paid if encashed before 1(one) year of deposit.

f) Advance will be allowed up to 80% of the deposit after

completion of one year

g) Interest will be paid at Savings rate if encashed after

1(one) year of deposit.

h) Advance will be allowed up to 80% of the deposit after

completion of one year.

i) Full amount including interest will be paid on maturity.

j) Govt. tax, Surcharge, Source Tax, Levy, Govt. Excise duty

will be recovered from the depositor’s A/C.

k) Account holder can appoint a nominee against the account.

l) Bank reserves the right to close the account at any time

and make amendment / alteration of the terms & conditions of the

scheme Without assigning any reason.

(Website of Uttara bank)

Shahjalal Islami Bank Limited (SJIBL)Page 13 of 23

Product Differentiation between Islamic Banking and Conventional Banking

Commenced its commercial operation in accordance with principle

of Islamic Shariah on the 10th May 2001 under the Bank Companies

Act, 1991. During last ten years SJIBL has diversified its

service coverage by opening new branches at different

strategically important locations across the country offering

various service products both investment & deposit. Islamic

Banking, in essence, is not only INTEREST-FREE banking business,

it carries deal wise business product thereby generating real

income and thus boosting GDP of the economy. Management Team is

strong and supportive equipped with excellent professional

knowledge under leadership of a veteran Banker Mr. Md. Abdur

Rahman Sarker.

Their Vision is to be the unique modern Islamic Bank in

Bangladesh and to make significant contribution to the national

economy and enhance customers' trust & wealth, quality

investment, employees' value and rapid growth in shareholders'

equity.

Islamic Mode of Investment

Bai Mechanism:

Bai means purchase and sale of goods in cash or on credit or in

Page 14 of 23

Product Differentiation between Islamic Banking and Conventional Banking

advance at an agreed upon profit, which may or may not be

disclosed to the client. Majority of investments of Islamic banks

are extended through this mechanism. A good number of investment

products have been designed to facilitate mainly working capital

financing which goes as follows:

Bai-Murabaha

Murabaha LC(Sight/Deferred):

Through this mode of indirect facility, the bank facilitates

import of goods of the client at fixed rate of service charge

(LC commission) on invoice value. LC may be opened at 100% cash

or at a different ratio.

Murabaha Post Import TR :

This is a post import finance under the principle of “Bai”,

extended to retire Shipping Documents under LC opened. We buy

the imported goods and sell the same to the importer at a cost

plus an agreed upon profit repayable today or on some date in

the future in lumpsum or by installments. Usually payment is

made by lumpsum from the sale proceeds of the consignment.

Possession of goods remains with the client. Collateral security

is usually obtained to secure the finance.

Murabaha Post Import Pledge :

As like as Murabaha Post Import TR with an exception to

security. Goods remain under the control of the Bank. Collateral

security may or may not be obtained.

Page 15 of 23

Product Differentiation between Islamic Banking and Conventional Banking

Bai-Muajjal

Bai-Muajjal Commercial TR:

It is an agreement between bank and client whereby bank delivers

goods to the client upon deferred payment, i.e. the client shall

pay the price at some future date at a time, by lumpsum or by

installment. Under this mode of investment, bank is not supposed

to disclose cost price and profit separately. Goods are

delivered on trust and Trust Receipt is obtained for legal

implication.

Bai-Muajjal (Real Estate):

Mode of operation and principle of this product are alike Bai-

Mujjal Commercial TR. Difference is with the purpose, i.e. the

facility is only extended against construction or purchase of

building, apartment etc.

Bai-Muajjal (WES Bill):

Investment facility under this Mode is extended to liquidate ABP

liability at maturity, when the client cannot liquidate the

liability as a result of non-repatriation of the related export

proceeds.

Bai-Muajjal (Term):

Under this mode of investment, term facility is given to meet

client’s requirement, which is repaid by a specific repayment

schedule. Purpose is a bit different, such as to meet BG claim,

etc.

Page 16 of 23

Product Differentiation between Islamic Banking and Conventional Banking

Bai-Salam

Bai-Salam (PC):

This is export finance. Bai-Salam is a term used to define a

sale in which the buyer makes advance payment, but the delivery

is delayed until sometime in the future. Usually the seller is

an individual or business and the buyer is the bank.

The Bai-Salam sales serve the interest of both parties:

a. The seller- receives advance payment in exchange for the

obligation to deliver the commodity at some later date. He

benefits from the salam sale buy locking in a price for his

commodity, thereby allowing him to cover his financial

needs whether they are personal expenses, family expenses

or business expenses.

b. The purchaser benefits because he receives delivery of the

commodity when it is needed to fulfill some other

agreement, without incurring storage costs. Second, a Bai-

Salam sale is usually less expensive than a cash sale.

Finally a Bai-Salam agreement allows the purchase to lock

in a price, thus protecting him price fluctuation.

(Website of SJIBL)

Islamic Banking Vs Conventional Banking:

Page 17 of 23

Product Differentiation between Islamic Banking and Conventional Banking

An Islamic bank is distinguishable from its conventional

counterpart by some basic principles, each of which is derived

from the Quran, sunna, or both.

The main difference between Islamic and conventional banking is

that Islamic teaching says that money itself has no intrinsic

value, and forbids people from profiting by lending it, without

accepting a level of risk – in other words, interest (known as

"riba") cannot be charged.

There are two major differences between Islamic Banking and

Conventional Banking:

1. Conventional banking practices are concerned with "elimination

of risk" where as Islamic banks "bear the risk" when involve in

any transaction.

2. When Conventional banks involve in transaction with consumer

they do not take the liability only get the benefit from consumer

in form of interest whereas Islamic banks bear all the liability

when involve in transaction with consumer. Getting out any

benefit without bearing its liability is declared Haram in Islam.

To make money from money is prohibited – wealth can only be

generated through legitimate trade and investment. Any gains

relating to this trading are shared between the person providing

the capital and the person providing the expertise.

Page 18 of 23

Product Differentiation between Islamic Banking and Conventional Banking

(Website of wiki.answers.com)

The unique features of the conventional banking and Islamic

banking are shown in terms of a box diagram as shown below:-

Conventional Banks Islamic Banks

1. The functions and

operating modes of

conventional banks are based

on fully manmade principles.

1. The functions and

operating modes of Islamic

banks are based on the

principles of IslamicShariah.

2. The investor is assured of

a predetermined rate of

interest.

2. In contrast, it promotes

risk sharing between provider

of capital (investor) and the

user of funds (entrepreneur).

3. It aims at maximizing

profit without any

restriction.

3. It also aims at maximizing

profit but subject

to Shariah restrictions.

4. It does not deal

with Zakat.

4. In the modern Islamic

banking system, it has become

one of the service-oriented

functions of the Islamic

banks to be a Zakat Collection

Centre and they also pay out

their Zakat.

Page 19 of 23

Product Differentiation between Islamic Banking and Conventional Banking

5. Lending money and getting

it back with compounding

interest is the fundamental

function of the conventional

banks.

5. Participation in

partnership business is the

fundamental function of the

Islamic banks. So we have to

understand our customer's

business very well.

6. It can charge additional

money (penalty and compounded

interest) in case of

defaulters.

6. The Islamic banks have no

provision to charge any extra

money from the defaulters.

Only small amount of

compensation and these

proceeds is given to charity.

Rebates are give for early

settlement at the Bank's

discretion.

7. Very often it results in

the bank's own interest

becoming prominent. It makes

no effort to ensure growth

with equity.

7. It gives due importance to

the public interest. Its

ultimate aim is to ensure

growth with equity.

8. For interest-based

commercial banks, borrowing

from the money market is

relatively easier.

8. For the Islamic banks, it

must be based on a Shariah

approved underlying

transaction.

9. Since income from the 9. Since it shares profit andPage 20 of 23

Product Differentiation between Islamic Banking and Conventional Banking

advances is fixed, it gives

little importance to

developing expertise in

project appraisal and

evaluations.

loss, the Islamic banks pay

greater attention to

developing project appraisal

and evaluations.

10. The conventional banks

give greater emphasis on

credit-worthiness of the

clients.

10. The Islamic banks, on the

other hand, give greater

emphasis on the viability of

the projects.

11. The status of a

conventional bank, in

relation to its clients, is

that of creditor and debtors.

11. The status of Islamic

bank in relation to its

clients is that of partners,

investors and trader, buyer

and seller.

12. A conventional bank has

to guarantee all its

deposits.

12. Islamic bank can only

guarantee deposits for

deposit account, which is

based on the principle of al-

wadiah, thus the depositors

are guaranteed repayment of

their funds, however if the

account is based on the

mudarabah concept, client

have to share in a loss

position..

Page 21 of 23

Product Differentiation between Islamic Banking and Conventional Banking

(Website of zaharuddin.net)

Bibliography

Here are some web addresses we use in our study:

I. Official website of SJIBL, see

http://www.shahjalalbank.com.bd/default.asp

II. Official website of UBL, see

http://www.uttarabank-bd.com/

III. “Similarities and differences between Islamic banking andconventional banking”, see

http://wiki.answers.com/Q/List_similarities_and_differences_between_Islamic_banking_and_conventional_banking

IV. ‘Islamic Banking”, see

http://www.sooperarticles.com/finance-articles/demystification-islamic-banking-166518.html

V. “Islamic-Banking-vs-Conventional-Banking”, see

http://www.scribd.com/doc/17116904/Islamic-Banking-vs-Conventional-Banking

Page 22 of 23

Product Differentiation between Islamic Banking and Conventional Banking

VI. Rahman Zaharuddin, “Differences between Islamic Bank andConventional Bank” see

http://zaharuddin.net/index.php?option=com_content&task=view&id=297&Itemid=72

(all are accessed in 21st October 2011)

Page 23 of 23