Banking Laws

40

THE AWESOME NOTES BANKING LAWS FISCAL TAMBASACAN Page of 1 40 I. GENERAL BANKING LAW (RA 8791) A. DEFINITION OF BANKS • entities engaged in the lending of funds obtained in the form of deposits. B. BANKING SERVICES SEC. 53 A bank may perform the ff activities: 1. receive in custody funds, documents and valuable objects; 2. act as a financial agent and buy and sell, by order of and for the account of their customers, shares, evidences of indebtedness and all type of securities; 3. make collection and payments for the accounts of others and perform such, other services for their customers as are not incompatible with banking business 4. upon prior approval of the MB, as managing agent, adviser, consultant or investment management/advisory/ consultancy account; and 5. rent out safety deposit boxes. *** it shall keep the funds, securities and other effects which it receives duly separate from the bank's own assets and liabilities RELATIONSHIP CREATED BETWEEN BANK AND DEPOSITOR SERRANO VS. CA 96 SCRA 96 - creditor and debtor relationship established with the bank as debtor and the depositor as creditor NATURE OF RELATIONSHIP PBCOM VS CA 269 SCRA 695 - fiduciary in nature FIDUCIARY - one assumes to ac as an agent for another and the other repose confidence in him, although there is no written contract or no contract at all. ff the fiduciary nature of relationship; DILIGENCE REQUIRED - highest degree of care is required, not merely DOAGFOAF PROHIBITED SERVICES SEC. 54 PROHIBITED TO ACT AS INSURER - a bank shall not directly engaged in insurance business as the insurer SEC. 55 PROHIBITED SERVICES NO DIRECTOR, OFFICER, EMPLOYEE OR AGENT OF ANY BANK SHALL: • make any false entries in any bank report statement or participate in any fraudulent transaction, thereby affecting the financial interest of,or causing damage to, the bank or any person; • without order of court of competent jurisdiction DISCLOSE to any authorized person any information relative to the funds or properties in the custody of the bank belonging to private individual, corporation or any other entity. PROVIDED that with respect to bank deposits, the provisions of existing laws shall prevail. • accepts gifts, fees, or commissions or any other form of remuneration IN CONNECTION WITH - the approval of lain or other credit accommodation from said bank • overvalue or aid in overvaluing any security FOR THE PURPOSE OF influencing in any way the actions of the bank or any bank • outsource INHERENT banking functions prepared by: ronie ablan

-

Upload

daportfolio -

Category

Documents

-

view

0 -

download

0

Transcript of Banking Laws

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �1 40

I. GENERAL BANKING LAW (RA 8791)

A. DEFINITION OF BANKS • entities engaged in the lending of funds

obtained in the form of deposits. B. BANKING SERVICES SEC. 53 A bank may perform the ff activities: 1. receive in custody funds, documents and

valuable objects; 2. act as a financial agent and buy and sell,

by order of and for the account of their c u s t o m e r s , s h a r e s , e v i d e n c e s o f indebtedness and all type of securities;

3. make collection and payments for the accounts of others and perform such, other services for their customers as are not incompatible with banking business

4. upon prior approval of the MB, as managing agent, adviser, consultant or i nves tmen t management /adv iso ry /consultancy account; and

5. rent out safety deposit boxes. *** it shall keep the funds, securities and other effects which it receives

duly separate from the bank's own assets and liabilities

RELATIONSHIP CREATED BETWEEN BANK AND DEPOSITOR SERRANO VS. CA 96 SCRA 96 - creditor and debtor relationship established with the bank as debtor and the depositor as creditor NATURE OF RELATIONSHIP PBCOM VS CA 269 SCRA 695 - fiduciary in nature

FIDUCIARY - one assumes to ac as an agent for another

a n d t h e o t h e r r e p o s e confidence in him,

although there is no written contract or no contract at all.

f f t h e fi d u c i a r y n a t u r e o f relationship; DILIGENCE REQUIRED - highest degree of care is required, not merely DOAGFOAF

PROHIBITED SERVICES SEC. 54 PROHIBITED TO ACT AS INSURER - a bank shall not directly engaged in insurance business as the insurer SEC. 55 PROHIBITED SERVICES NO DIRECTOR, OFFICER, EMPLOYEE OR AGENT OF ANY BANK SHALL: • make any false entries in any bank report

statement or participate in any fraudulent transaction,

thereby affecting the financial interest of,or causing damage to, the bank or any person;

• without order of court of competent jurisdiction

DISCLOSE to any author ized person any information relative to the funds or properties in the custody of the bank

belonging to private individual, corporation or any other entity.

PROVIDED that with respect to bank deposits, the provisions of existing laws shall prevail.

• accepts gifts, fees, or commissions or any other form of remuneration

IN CONNECTION WITH - the approval of lain or other credit accommodation from said bank

• overvalue or aid in overvaluing any security FOR THE PURPOSE OF

influencing in any way the actions of the bank or any bank

• outsource INHERENT banking functions

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �2 40

NO BORROWER OF A BANK SHALL • FRAUDULENTLY OVERVALUE

property offered as a security for a loan or other credit accommodation from the bank

• F U R N I S H F A L S E , O R M A K MISREPRESENTATION OR SUPPRESSION OF

material facts for the purpose of obtaining, renewing or increasing a loan or other credit accommodation or extend the period thereof.

• ATTEMPT TO DEFRAUD said bank in the event of a court action to recover a loan or other credit accommodation; or

• OFFER any director, officer, agent or employee of a bank

any gift, fee, commission, or a n y o t h e r f o r m o f compensation

in order to influence s u c h p e r s o n i n t o approving a loan or o t h e r c r e d i t a c c o m m o d a t i o n application.

NO - examiner, officer or employee of the BSP; or - any department, bureau, office and or agency of the government

that is assigned to supervise, examine, assist, or render technical assistance to any bank

= SHALL COMMIT any of the ff acts enumerated in this section or aid in the commission of the same. THE MAKING OF FALSE REPORTS OR MISREPRESENTATION OR SUPPRESSION OF MATERIAL FACTS BY: personnel of BSP

shall constitute fraud and shall be subject to the administrative and criminal sanctions provided under the NCBA.

NO BANK - shall employ casual and non-regular personnel or too lengthy probationary personnel

in the conduct of its business involving bank deposits (consistent with Bank Secrecy law)

C. CLASSES OF BANKS SEC. 3 1. universal banks 2. commercial banks 3. thrift banks, composed of (i) savings and

mortgaged banks, (ii) stock savings and loan associat ions, and ( i i i ) pr ivate development banks

4. rural banks 5. cooperative banks 6. islamic banks 7. other classifications of banks as determined

by the MB of BSP

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �3 40

UNIVERSAL

BANKSCOMMERCIAL

BANKS

AS TO THEIR POWERS 1. has a l l the powers granted to commerc ia l banks 2. power of an investment h o u s e a s p r o v i d e d i n existing laws and 3. power to invest in non- allied enterprises CORPORATE POWERS 1. to adopt, alter and use a corporate seal, which shall be judicially noticed 2. to enter into contracts 3. to lease or own real and personal property, and to sell or otherwise dispose the same. 4. to sue and be sued 5. perform any and all things that may be necessary or proper to carry out the purpose

AS TO THEIR POWERS in addition to the general p o w e r s i n c i d e n t t o corporations - all such powers as may be necessary to carry on the business of commercial banking, such as 1. accepting drafts 2. issuing letters of credit 3 . d i s c o u n t i n g a n d negot ia t ing promissory no tes , d ra f t s , b i l l s o f e x c h a n g e a n d o t h e r evidence of debts 4, accepting or creating demand deposits 5. receiving other types of d e p o s i t s a n d d e p o s i t substitute 6. buying and selling foreign exchange and gold and silver bullion 7. acquiring marketable bonds and o the r deb t securities; and 8. extending credit subject to such rules as the MB may promulgate ***such rules may include the determination of bonds and other debt securities eligible for investment, the maturities and the aggregate amount of such investment.

AS TO THEIR EQUITY INVESTMENT I. the total investment in equities, allied and non-allied enterprises - SHALL NOT EXCEED 50% of the net worth of the bank II. the equity investment in any one enterprise, whether allied or non-allied - SHALL NOT EXCEED 25% of the net worth of the bank ***NET WORTH - the total of the unimpaired paid-in capital including the paid-in surplus, retained earnings and undivided profit , net of valuat ion r e s e r v e s a n d o t h e r adjustments as may be required by the BSP. *** the acquisition of such equity/ies - is subject to the approval of the MB which shal l promulgate appropriate guidelines to govern such investment

AS TO THEIR EQUITY INVESTMENT ~ cannot invest in non-allied enterprises ~ can invest only to allied enterprises, financial or non-financial (exe as the MB may otherwise provide) I. the total investment in equities of allied enterprises - SHALL NOT EXCEED 35% of the net worth of the bank II. the total investment in any one enterprise - SHALL NOT EXCEED 25% of the net worth of the bank

I N R E : E Q U I T Y I N V E S T M E N T I N F I N A N C I A L A L L I E D ENTERPRISES I. can own up to 100% of the equity in a - thrift bank - rural bank; or - financial allied enterprises II. a publicly-listed universal or commercial bank may own up to 100% - of the voting stock of only one other UB or CB

I N R E : E Q U I T Y I N V E S T M E N T I N F I N A N C I A L A L L I E D ENTERPRISES I. can own up to 100% of the equity in a - thrift bank - rural bank; or II. if on other financial allied enterprise, including other commercial bank - such investment shall r e m a i n a M I N O R I T Y HOLDING in that enterprise

I N R E : E Q U I T Y INVESTMENT IN NON-F I N A N C I A L A L L I E D ENTERPRISE may own up to 100% - of the equity of NFAE

I N R E : E Q U I T Y INVESTMENT IN NON-F I N A N C I A L A L L I E D ENTERPRISE may own up to 100% - of the equity of NFAE

I N R E : E Q U I T Y INVESTMENT IN NON-ALLIED ENTERPRISE the equity investment of a UB or of i ts wholly or majority owned subsidiaries - in a single non-allied enterprise SHALL NOT EXCEED 35% OF THE - t o t a l e q u i t y i n t h a t enterprise nor - vo t i ng s tock in tha t enterprise

N/A

I N R E : E Q U I T Y INVESTMENT IN QUASI BANK to promote competi t ive cond i t i ons in financ ia l markets, the MB may - further limit to 40% equity investmnt of UB in quasi-banks

same. ***QUASI-BANKS - entities engaged in the 1 . bo r row ing o f funds th rough the i ssuance , endorsement or assignment with recourse; or 2. acceptance of deposit substitutes for the purpose of relending or purchasing of receivables and other obligations ***DEPOSIT SUBSTITUTES - are alternative form of obtaining funds from the public, other than deposits THROUGH the issuance, endorsement, or acceptance of debt i n s t r u m e n t s f o r h e borrower's own account FOR THE PURPOSE OF relending or purchasing of rece i vab les and o the r obligations this may include - banker 's acceptance, p r o m i s s o r y n o t e s , participations, certificates of assignment and similar instruments with recourse and repurchase agreements. ***WITH RECOURSE - term used in indorsing negotiable instruments b y w h i c h t h e i n d o r s e indicates that he remains liable for payment of the instrument.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �4 40

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �5 40

D. ACQUISITION OF REALTY; RULE AND EXE SEC. 51: Ceiling on Investment in Certain Assets any bank may acquire real estate

as shall be necessary for its own use PROVIDED HOWEVER - that the total investment in such real estate and improvements thereof including bank equipments

SHALL NOT EXCEED 50% of combined capital accounts

PROVIDED FURTHER - that the equity investment of bank in another corporation engaged primarily in real estate

SHALL BE CONSIDERED - as part of the bank's total investment in real estate

UNLESS: otherwise provided by the MB.

SEC. 52; Acquisition of real estate by way of satisfaction of claims NOTWITHSTANDING the limitations of the preceding sec A BANK MAY ACQUIRE, HOLD OR CONVEY R E A L P R O P E R T Y U N D E R T H E F F CIRCUMSTANCES 1. such as shall be, mortgaged to it in gf by

way of security for debts 2. such as shall be conveyed to it in

satisfaction of debts previously contracted in the course of its dealings; or

3. such as it shall purchase at sales under judgments, decrees, mortgages, or trust deeds held by it and such as it shall purchase to sure debts due it.

ANY REAL PROPERTY ACQUIRED I N A N Y O F T H E A B O V E ENUMERATED CIRCUMSTANCES - shall be disposed of by the bank

WITHIN A PERIOD OF 5 YEARS O R A S M A Y B E PRESCRIBED BY THE MB

PROVIDED HOWEVER; - that the bank may, after said period, continue to hold the property for it's own use, subject to the limitations of the preceding section. NOTES: meaning, even though 5 years had lapse, the bank may still hold the real estate, provided that that such real

property, included on its total capital account, does not exceed 50%... UNION BANK VS, TIU (SEPT 7, 2011)

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �6 40

E. BSP FUNCTIONS SEC. 4: SUPERVISORY FUNCTIONS SHALL INCLUDE • the issuance of rules of conduct or

the establishment of standards of operation for uniform application to all institutions or functions covered,

taking into consideration the - distinctive character of the operations of institutions; and - the substantive similarities of specific functions to which s u c h r u l e s , m o d e s o r standards are to be applied.

• the conduct of examination to determine - compliance with laws and regulations

if the circumstances s o w a r r a n t a s determined by the MB

• overseeing to ascertain - that the laws and regulations are complied with

• regular investigation which shall not be oftener than - once a year

from the last date of examination

to determine whether an institution is conducting its business on a safe and sound basis. PROVIDED t h a t t h e d e fi c i e n c i e s /irregularities found by or discovered by an audit

shall be immediately addressed

• inquiring into the solvency and liquidity of the institution

• enforcing prompt corrective action

***ENTITIES COVERED - aside from banks, BSP's regulatory and supervisory power extends to the ff entities 1. quasi-banks 2. trust entities 3. other financial institutions which

under special laws are subject to the BSP

SEC. 5: POLICY DIRECTION, R A T I O S , C E I L I N G S A N D LIMITATIONS BSP SHALL PROVIDE POLICY DIRECTIONS - in areas of 1. money 2. banking; and 3. credit

FOR THIS PURPOSE - the MB may prescribe

ratio, ceilings, limitations, or other forms of regulations

ON - different types of accounts and - practices of banks and quasi banks

to the extent feasible, conform to internationally accepted standards, including t h e B a n k I n t e r n a t i o n a l Settlements.

- MB may exempt particular categories of transaction

from such ratio, ceilings and limitations BUT NOT LIMITED TO

1. exceptional cases; or 2. to enable a bank or quasi

bank under rehabilitation du r i ng a merge r o r consolidation

= to continue in business with s a f e t y t o i t s c r e d i t o r s , depositors and general public.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �7 40

F. ORGANIZATION OF BANKS SEC. 8: Requisites for organization of banks and quasi banks 1. that the entity is a stock corporation 2. that its funds are obtained from the public,

which shall mean 20 or more persons 3. that the minimum capital requirements

prescribed by the monetary board for each category of banks are satisfied

PLUS: 1. must be registered with the SEC (SEC14)

REQ: the AOI and By-Laws must be accompanied by - certificate of authority, stating compliance of all the requisites issued by the Mb of the BSO

2. incorporate in the application • bank's ownership structure • directors and senior • management • its operating plan; and • internal control • as well as its projected financial condition

and capital base. S E C . 1 4 : R E Q U I S I T E S F O R REGISTRATION OF AOI OR ANY AMENDMENT THERETO MUST BE ACCOMPANIED BY - certificate of authority issued by the MB, under seal REQ: FOR THE ISSUANCE OF CERTIFICATE OF AUTHORITY after the MB is satisfied from the evidence submitted to it that 1. all requirement of existing laws

and regulations to engage in the business for which the applicant is proposed to be incorporated have been complied with

2. the public interest and economic conditions, both general and local, justify the authorization; and

3. that the amount of capital, the financing organization, direction and administration, as well as the integrity and responsibility of the organizers and administrators reasonably assure the safety of deposits and public interest.

REQ: FOR REGISTRATION OF BY-L AW S O R A N Y A M E N D M E N T THERETO - must be also accompanied by certificate of authority from BSP

SEC. 9: ISSUANCE OF STOCK THE MB MAY PRESCRIBE RULES AND REGULATIONS

1. on the types of stock a bank may issue 2. including the terms thereof; and 3. the rights appurtenant thereto

TO DETERMINE - compliance with laws and regulations governing capital and equity structure of bank PROVIDED: bank shall issue ONLY - par value stock

SEC. 10: TREASURY STOCKS NO BANK SHALL 1. purchase or acquire shares of its own

capital stock; or 2. accept its own shares as a security for a

loan EXE: - when authorized by the MB

PROVIDED: that in every case the stock so purchased or acquired shall

- WITHIN 6 MOS from the time of its purchase or acquisition,

be sold or disposed of at a public or private sale

SEC. 11: FOREIGN STOCK HOLDINGS foreign individuals and non-bank corporations MAY OWN OR CONTROL

UP TO 40% - of the voting stock of a domestic bank

***this rules shall apply to all Filipinos and domestic non-bank corporations THE PERCENTAGE OF FOREIGN-OWNED VOTING STOCK IN A BANK SHALL BE DETERMINED - by the citizenship of the individual stock-holders in that bank

***the citizenship of the corporation which is a SH in a bank - shall ff the citizenship of the controlling SH of the corporation

irrespective of the place of incorporation.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �8 40

SEC. 12: STOCKHOLDINGS IF FAMILY GROUPS OR RELATED INTEREST FAMILY GROUPS OR RELATED INTERESTS - individuals related to each other

WITHIN 4th degree of consanguinity or affinity, legitimate or common-law

T H E S TO C K H O L D I N G S O F FA M I LY GROUPS OR RELATED INTERESTS - must be fully disclosed in all transactions

by such an individual with the bank NOTES: if the family groups or related interests transact with a bank which they belong to --- the law only requires full disclosure of such transaction RELATED INTEREST - two or more corporations owned or controlled by the same family group or same group of persons

SEC. 13: CORPORATE STOCKHOLDINGS --- same sa related interest mentioned above. SEC. 15: BOARD OF DIRECTORS THERE MUST BE - at least 5, but not more than 15 - 2 of whom must be an independent director

***INDEPENDENT DIRECTOR - a person other than an officer or employee of the bank, its subsidiaries or affiliates or related interest

NON-FILIPINO CITIZEN MAY BECOME A MEMBER OF THE BOD - to the extent of he foreign participation in the equity of said bank. MEETINGS OF BOD; MANNER - allowed; through modern technologies, such as; tele-conferencing and video-conferencing.

SEC. 16: FIT AND PROPER RULE RATION: 1. t o m a i n t a i n t h e q u a l i t y o f b a n k

management; and 2. afford better protection to depositors and

the public in general FIT AND PROPER RULE The MB shall prescribe, pass upon and review the 1. qualifications and disqualifications of

individuals elected or appointed bank directors or officers; and

2. disqualify those found unfit SHOULD MB FINDS A DIRECTOR OR OFFICER - commits or omits an act which render him unfit

AFTER DUE NOTICE - MB may disqualify, suspend or remove him

MEASURE: IN DETERMINING WHETHER THE DIRECTOR OR OFFICER IS FIT shall consider the ff: 1. integrity 2. experience 3. education 4. training; and 5. competence.

SEC. 17: DIRECTORS OF MERGED OR CONSOLIDATED BANKS BASTA: the numbers of directors shall NOT EXCEED 20.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �9 40

SEC. 18: COMPENSATION MB MAY REGULATE (to protect the funds of the creditors and depositors) the payment by the bank to its directors and officers of 1. compensation 2. allowance 3. fees 4. bonuses 5. stock options 6. profit sharing; and 7. fringe benefits

BUT ONLY IN EXCEPTIONAL CASES AND WHEN THE CIRCUMSTANCES WARRANTS such as but not limited to the ff: 1. w h e n t h e b a n k i s u n d e r

comptrollership or conservatorship 2. when the bank is found by the MB

to be conducting business in an unsafe or unsound manner; or

3. when a bank is found by the MB to be in an unsatisfactory financial condition.

SEC. 19: PROHIBITION OF PUBLIC OFFICIALS GEN RULE no appointive or elective public officials, whether full-time or part-time,

shall, at the same time serve as officer of any private bank

EXE: 1. when such service is incidental to financial

assistance provided by the government or gocc to the bank; or

2. unless otherwise provided under existing law (Rural Banks RA 7353)

SEC. 20: BANK BRANCHES UB AND CB MAY OPEN BRANCHES OR OTHER OFFICES - within or outside the PHL

REQ: prior approval of the BSP

BRANCHING BY ALL OTHER BANKS - shall be governed by pertinent laws A BANK, subject to prior approval of he MB, USE ANY OR ALLOF ITS BRANCHES AS • outlet for the presentation and/or sale of the

financial product = of its allied undertaking or of its investment house units A BANK AUTHORIZED TO ESTABLISH BRANCHES OR OTHER OFFICE

SHALL BE RESPONSIBLE - for all business conducted in such branches and offices

TO THE SAME EXTENT AND IN THE SAME MANNER - as though such business had all been conducted in the head office

*** a bank and its branches and offices shall be treated - as one unit

SEC. 21: BANKING DAYS AND HOURS GEN RULE all banks including their branches and offices shall transact business • on all working days • for at least 6 hours a day EXE: • may open for business on Sun, Sat, or

Holidays, for at least 3 hrs PROVIDED - shall report to the BSP during which they or heir branches or offices shall transact business;or

• if authorized by the BSP in the interest of the banking public

***WORKING DAYS - mon to friday, unless if such days are holidays.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �10 40

G. LOAN LIMITATIONS; SBL; DOSRI; SECURITY; FORECLOSURE SEC. 35: LIMITS ON LOANS, CREDIT ACCOMMODATIONS AND GUARANTEES SINGLE BORROWER LIMIT GEN RULE: THE LIMIT; loans and credit accommodations and guarantees that may be extended to any persons, partnership, association, corporation or any entity

SHALL NOT EXCEED 25% of the net worth of such bank

EXE: as MB may prescribe for the reasons of national interest

* * * B A S I S I N D E T E R M I N I N G COMPLIANCE WITH SBL - is the total credit commitment of the bank to the borrower. ***NET WORTH the total of the unimpaired paid-in capital including the paid-in surplus, retained earnings and undivided profit, net of valuation reserves and other adjustments as may be required by the BSP.

REQ: WHEN IT MAY BE INCREASED BY ADDITIONAL 10% - as may be prescribed by the MB

PROVIDED: the additional liabilities if any borrower are adequately secured by 1. trust receipts 2. shipping documents 3. warehouse receipts; or 4. o t h e r s i m i l a r d o c u m e n t s

transferring or securing title covering: - readily marketable, non-perishable goods - which must be fully covered by insurance.

THE PRESCRIBE CEILING SHALL INCLUDE 1. direct liability of the - maker or acceptor of paper,

discounted with or sold to such bank; and

- of general indorser, drawer, or guarantor, who obtains the loan or other credit accommodation from, or discounted paper with, or sells paper to such bank

2. in case of an individual who owns or control a majority interest in a corporation, partnership or association or any other entity

the liability of said entity to such bank.

3. in case of corporation, all liabilities to such bank of all subsidiaries in which such corporation owns or controls a majority interest

4. in case of partnership, association or other entity,

the liabilities of the members thereof to such bank. NOTE: even if a parent corp, part, assoc, entity or individual - who owns or control a majority interest in such entities - has no liability to the Bank, THE MB MAY PRESCRIBE THE COMBINATION OF THE LIABILITIES OF SUBSIDIARY CORPORATIONS O R M E M B E R S O F T H E PARTNERSHIPS, ASSOCIATION, ENTITY OR SUCH INDIVIDUAL under certain circumstances, including but not limited to any of the ff situations: 1. parent corp, part, assoc, entity of individual - guarantees the repayment of he liabilities 2. the liabilities were incurred - for accommodation of the parent corp or subsidiary or of a PAEI; or 3. the subsidiaries, through separate entities - operate merely as departments or divisions of a single entity

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �11 40

L O A N S , O T H E R C R E D I T ACCOMMODATIONS AND GUARANTEES SHALL EXCLUDE 1. loans and other credit accommodations

secured by obligations of the BSP or of the Phil Govt

2. loans and other credit accommodations fully guaranteed by the government as to the payment of the principal and interest

3. loans and other credit accommodations covered by assignment of deposits maintained in the lending bank and held in the phil.

4. loans, credi t accommodat ions and acceptances under letters of credit to he extent covered by margin deposits; and

5. other loans or credit accommodations which the MB may from time to time, specify as non-risk items

BUT SHALL INCLUDE (AS TO THE LIMIT) - loans and other credit accommodations, deposits

maintained with and usual guarantees by a bank to any other bank or non-bank entity, whether locally or abroad. NOTE: certain types of contingent accounts of borrower may be included among subject to these prescribed limits - as may be determined by the MB.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �12 40

DOSRI/INSIDER LENDING SEC. 36 : RESTRICT ION ON BANK EXPOSURE TO DIRECTORS, OFFICERS, SH AND THEIR RELATED INTERESTS NO DIRECTOR OR OFFICER OF ANY BANK SHALL DIRECTLY OR INDIRECTLY - for himself or as a representative or agent of others, 1. borrow from such bank 2. become a guarantor, indorser or surety for

loans from such bank to others; or 3. in any manner be an obligor or incur any

contractual liability to the bank EXE: (REQ) 1. with written approval of the majority of all

the directors of said bank 2. written approval shall be entered upon the

record of the bank 3. copy of such entry shall be transmitted

forthwith to the appropriate supervising and examining department of the BSP.

EXE TO EXE: written approval of the majority of the dir shall not be required - w h e n t h e l o a n , c r e d i t accommodations or advances made to the officer

is made pursuant to its fringe benefit plan approved by the BSP.

ADD REQ: AS IDE FROM WRITTEN APPROVAL (IGGY'S BOOK) 1. the dealing if a bank with any of its DOSRI

shall be upon such terms not less favorable to the bank than those offered to others

2. the DOSRI borrower must waive the secrecy of his or her deposits of whatever nature in all banks in the Phil

3. the ceiling/limitations NATURE OF BANK DEALING WITH DOSRI - shall be upon terms

NOT LESS favorable to the bank than those offered to others

CONSEQUENCE OF VIOLATION - the office if any bank director or officer who violates this shall be declared vacant; and - the officer or director shall be subject to he penal provisions of NCBA.

REQ: after due notice to the BOD of the bank

LIMIT OF THE OUTSTANDING LOANS, C R E D I T A C C O M M O D AT I O N S A N D GUARANTEES WHICH A BANK MAY EXTEND TO EACH OF ITS DOSRI shall be limited by the amount equivalent to their respective 1. unencumbered deposits and 2. book value of their paid-in capital

contribution in the bank. BUT SHALL EXLUDE FROM SUCH LIMIT - loans, credit accommodations and guarantees secured by assets considered as non-risk by the MB AND SHALL NOT BE SUBJECT TO INDIVIDUAL LIMIT - if extended to DOSRI in accordance with its Fringe Benefit Plan, duly approved by the MB.

NOTE: LIMIT SHALL NOT APPLY TO - to those extended by cooperative bank to is cooperative shareholders.

GIST: WHEN LIMITS SHALL NOT APPLY 1. secured by assets considered as

non-risk by the MB 2. in the form of fringe benefits

granted in accordance with rules as may be prescribed by the MB;

3. extended by a cooperative bank to its cooperative sh.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �13 40

***RELATED INTERESTS (BSP CIRC NO. 170) 1. spouse or relative within the first degree of

consanguinity or affinity or relative by legal adoption, of a director, officer or sh of the bank

2. partnership of which a DOS or his souse or relative within first degree of consanguinity of affinity, or relative by legal adoption, is general partner

3. co-owner with the DOS or his SRw/1stca/Rla, of the property or interest or right mortgaged, pledged or assigned to secure the loan or credit accommodations, EXE when the mortgage, pledge or assignment covers only said co-owner's undivided interest

4. corporations, associations, or firm of which a DO of the bank or his spouse is also a DO of such corporation, assoc or firm

EXE: a. where the securities of such

corporations, assoc or firm are listed and traded in the big board or commercial and industrial board of domestic stock exchange, less than 50% of the voting stocks thereof is owned by any one person or by persons related to each other within 3rd degree of consanguinity or affinity

b. where the DOS of he lending bank sits as a representative of the b a n k i n t h e B O D o f s u c h corporation. PROVIDED; that the bank representative shall not have any equity interest in the borrower corporation, EXE for the minimum shares required by law,rules and regulations, or by the by-laws of the corporat ion. PROVIDED FURTHER, that the borrowing corporation under (a) or (b) is not among those mentioned in item (5) and (6) hereof

5. Corporations, assoc or firm of which any or group if DOS of the lending bank and/or their SRw/1stca/Rla holds/owns more than 20% of the subscribed capital of such corporation, or of the equity of such assoc or firm 6. corp, assoc, or firm, wholly or majority-owned or controlled b any related entity or a group of related entities mentioned in item (2), (4), and (5) hereof.

SEC. 37: LOANS AND OTHER CREDIT ACCOMMODATIONS AGAINST REAL ESTATE LIMIT SHALL NOT EXCEED

• 75% of the appraised value of the real estate security

• plus; 60% of the appraised value of the insured improvements

AND SUCH LOANS MAY BE MADE TO THE - owner of the real estate; or - to his assignees

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �14 40

SEC. 47: FORECLOSURE OF REAL ESTATE MORTGAGE in the event of foreclosure, - whether judicially or extrajudicially, - of any mortgage on real estate which is securi ty for any loan or other credit accommodation granted THE MORTGAGOR OR DEBTOR SHALL HAVE THE RIGHT TO REDEEM THE PROPERTY

whose real property has been sold for the full or partial payment of his obligation TIMEFRAME - within 1 yr after the sale of the real estate HOW EXERCISED by paying the 1. amount due under the mortgage

deed, 2. with interest thereon, at the rate

specified in the mortgage; and 3. all costs and expenses incurred by

the bank or institution from the sale and custody of said property

LESS: the income derived therefrom

RIGHTS OF THE PURCHASER IN THE AUCTION SALE, whether judicially or extrajudicially 1. to enter upon and take possession of such

property immediately after the date of the confirmation of the auction sale; and

2. administer the same in accordance with law.

NOTE: any petition in court to enjoin the foreclosure proceedings instituted SHALL BE GIVEN DUE COURSE ONLY - upon the filing by the petitioner of a bond - in an amount fixed by the court - conditioned that he will pay all damages which the bank may suffer by the enjoining or the restraint of the foreclosure proceedings

SHOULD THE MORTGAGOR IS A JURIDICAL PERSON (Act. 3135) - whose property is being sold pursuant to an extra-judicial foreclosure

MAY REDEEM THE PROPERTY FORECLOSED TIMEFRAME - not after the registration of the certificate of foreclosure sale with he applicable Register of Deeds - which in no case shall be more than 3 mos after foreclosure, = whichever is earlier

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �15 40

CONSERVATORSHIP RECEIVERSHIP

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �16 40

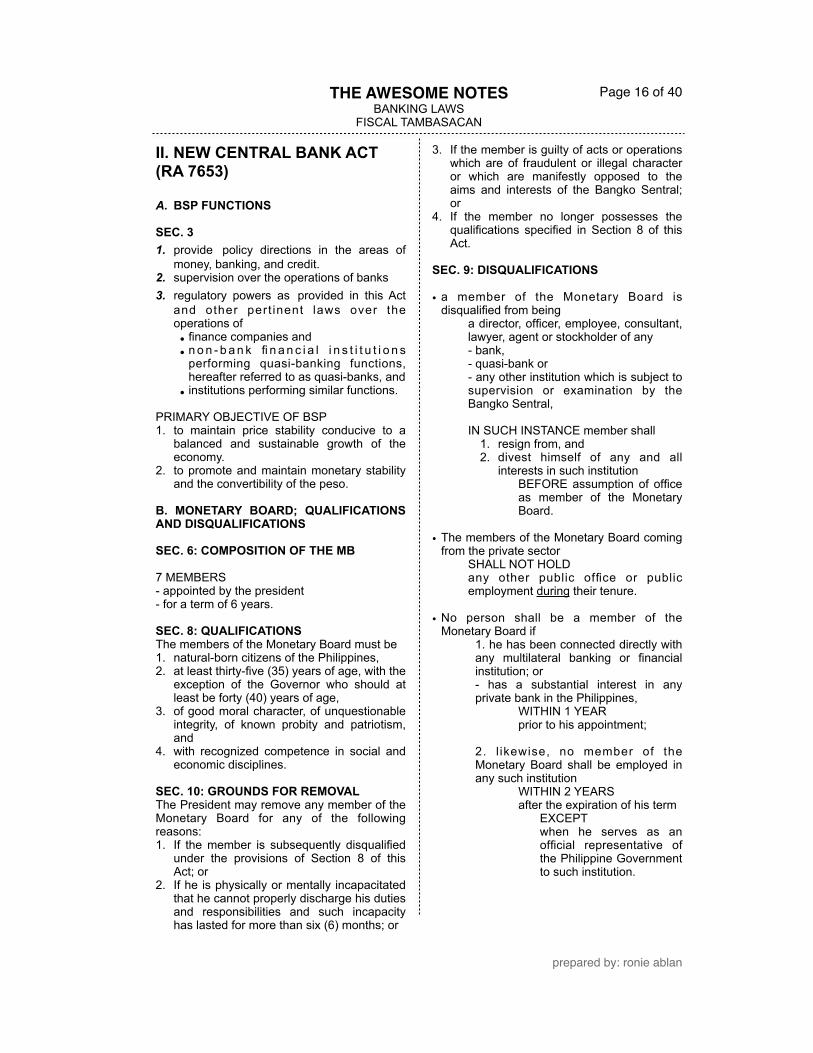

II. NEW CENTRAL BANK ACT (RA 7653) A. BSP FUNCTIONS SEC. 3 1. provide policy directions in the areas of

money, banking, and credit. 2. supervision over the operations of banks 3. regulatory powers as provided in this Act

and other pert inent laws over the operations of • finance companies and • n o n - b a n k fi n a n c i a l i n s t i t u t i o n s

performing quasi-banking functions, hereafter referred to as quasi-banks, and

• institutions performing similar functions. PRIMARY OBJECTIVE OF BSP 1. to maintain price stability conducive to a

balanced and sustainable growth of the economy.

2. to promote and maintain monetary stability and the convertibility of the peso.

B. MONETARY BOARD; QUALIFICATIONS AND DISQUALIFICATIONS SEC. 6: COMPOSITION OF THE MB 7 MEMBERS - appointed by the president - for a term of 6 years. SEC. 8: QUALIFICATIONS The members of the Monetary Board must be 1. natural-born citizens of the Philippines, 2. at least thirty-five (35) years of age, with the

exception of the Governor who should at least be forty (40) years of age,

3. of good moral character, of unquestionable integrity, of known probity and patriotism, and

4. with recognized competence in social and economic disciplines.

SEC. 10: GROUNDS FOR REMOVAL The President may remove any member of the Monetary Board for any of the following reasons: 1. If the member is subsequently disqualified

under the provisions of Section 8 of this Act; or

2. If he is physically or mentally incapacitated that he cannot properly discharge his duties and responsibilities and such incapacity has lasted for more than six (6) months; or

3. If the member is guilty of acts or operations which are of fraudulent or illegal character or which are manifestly opposed to the aims and interests of the Bangko Sentral; or

4. If the member no longer possesses the qualifications specified in Section 8 of this Act.

SEC. 9: DISQUALIFICATIONS • a member of the Monetary Board is

disqualified from being a director, officer, employee, consultant, lawyer, agent or stockholder of any - bank, - quasi-bank or - any other institution which is subject to supervision or examination by the Bangko Sentral, IN SUCH INSTANCE member shall

1. resign from, and 2. divest himself of any and all

interests in such institution BEFORE assumption of office as member of the Monetary Board.

• The members of the Monetary Board coming from the private sector

SHALL NOT HOLD any other public office or public employment during their tenure.

• No person shall be a member of the Monetary Board if

1. he has been connected directly with any multilateral banking or financial institution; or - has a substantial interest in any private bank in the Philippines,

WITHIN 1 YEAR prior to his appointment;

2. l ikewise, no member of the Monetary Board shall be employed in any such institution

WITHIN 2 YEARS after the expiration of his term

EXCEPT when he serves as an official representative of the Philippine Government to such institution.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �17 40

C . C O N S E R V A T O R S H I P A N D RECEIVERSHIP S E C . 2 9 : A P P O I N T M E N T O F CONSERVATOR GROUNDS FOR PLACING BANKS AND QUASI BANKS UNDER CONSERVATORSHIP If after the MB finds, based on the report submitted by the appropriate supervising or examining department

that the bank or quasi bank is in the state of continuing inability or unwillingness to maintain a condition of liquidity,

deemed adequate to protect the interest of the depositors and creditors

POWERS OF CONSERVATOR such powers as the Monetary Board shall deem necessary to 1. take charge of the assets, liabilities, and

the management thereof, 2. reorganize the management, 3. collect all monies and debts due said

institution, and 4. exercise all powers necessary to restore its

viability. 5. to overrule or revoke the actions of the

previous management and board of directors of the bank or quasi-bank.

DUTIES OF THE CONSERVATOR report and be responsible to the Monetary Board QUALIFICATIONS OF THE CONSERVATOR. should be competent and knowledgeable in bank operations and management. TERM OF THE CONSERVATORSHIP shall not exceed one (1) year.

SALARY OF THE CONSERVATOR fixed by the Monetary Board in an amount

NOT TO EXCEED 2/3 of the salary of the president of the institution in one (1) year,

payable in twelve (12) equal monthly payments:

RULE: WHEN CONSERVATORSHIP IS TERMINATED BEFORE 1 YR PERIOD EXPIRES, I. if on the ground that the institution can operate on its own,

the conservator shall receive the balance of the remuneration

which he would have received up to the end of the year;

II. if the conservatorship is terminated on other grounds,

the conservator shall not be ent i t led to such remaining balance.

W H E N N O T E N T I T L E D T O RENUMERATION when the conservator appointed by the MB is connected with the BSP

E X P E N S E S AT T E N D A N T T O T H E CONSERVATORSHIP; shall be borne by: - the bank or quasi-bank concerned. G R O U N D S F O R T E R M I N AT I O N O F CONSERVATORSHIP The Monetary Board shall terminate the conservatorship when it is satisfied that 1. the institution can continue to operate on its

own and the conservatorship is no longer necessary; or

2. on the basis of the report of the conservator or of its own findings, determine that the continuance in business of the institution would involve probable loss to i ts depositors or creditors, in which case the provisions of Section 30 shall apply.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �18 40

SEC. 30: PROCEEDINGS IN RECEIVERSHIP ANDLIQUIDATION GROUNDS FOR PLACING BANKS AND QUASI BANKS UNDER R AND L Whenever, upon report of the head of the supervising or examining department, the Monetary Board finds that a bank or quasi-bank: 1. is unable to pay its liabilities as they

become due in the ordinary course of business: Provided, That this shall not include inabi l i ty to pay caused by extraordinary demands induced by financial panic in the banking community;

2. has insufficient realizable assets, as determined by the Bangko Sentral, to meet its liabilities;

3. cannot continue in business without involving probable losses to its depositors or creditors; or

4. has willfully violated a cease and desist order under Section 37 that has become final, involving acts or transactions which amount to fraud or a dissipation of the assets of the institution;

SHOULD THE GROUNDS ARE PRESENT the Monetary Board may summarily and without need for prior hearing

1. FORBID the institution from doing business in the Philippines and 2. DESIGNATE PDIC as receiver of the banking institution.

FOR QUASI BANKS any person of recognized competence in banking or finance may be designed as receiver.

DUTIES OF THE RECEIVER The receiver shall 1. immediately gather and take charge of all

the assets and liabilities of the institution, 2. administer the same for the benefit of its

creditors, and 3. exercise the general powers of a receiver

under the Revised Rules of Court BUT SHALL NOT pay or commit any act that will involve the transfer or disposition of any asset of the institution: EXE: a. administrative expenditures, b. deposit or place the funds of the

institution in non-speculative investments.

4. determine as soon as possible, but not later than ninety (90) days from take over,

whether the institution • may be rehabilitated or otherwise • placed in such a condition so that it

may be permitted to resume b u s i n e s s w i t h s a f e t y t o i t s depositors and creditors and the general public:

PROVIDED, That any determination for the resumpt ion of business of the institution

shall be subject to prior approval of the MB

S H O U L D T H E R E C E I V E R D E T E R M I N E S T H A T T H E I N S T I T U T I O N C A N N O T B E REHABILITATED OR PERMITTED TO RESUME BUSINESS Monetary Board shall notify in writing the board of directors of its findings and direct the receiver to proceed with the liquidation of the institution.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �19 40

IN HERE: FF DUTIES OF THE RECEIVER • file ex parte with the proper regional trial

court, and without requirement of prior notice or any other action,

a petition for assistance in the liquidation of the institution pursuant to a liquidation plan adopted by the PDIC

for general application to all closed banks.

IN CASE IF QUASI BANKS, the liquidation plan shall be adopted by the MB. THE COURT SHALL THEN Upon acquiring jurisdiction, upon motion by the receiver after due notice,

1. ad j ud i ca te d i spu ted c l a i m s a g a i n s t t h e institution,

2. assist the enforcement of individual liabilities of the stockholders, directors and officers, and

3. decide on other issues as may be ma te r i a l t o implement the liquidation plan adopted.

****The receiver shall pay the cost of the proceedings f r o m t h e a sse t s o f t h e institution.

• convert the assets of the institutions to money,

• dispose of the same to creditors and other parties,

PURPOSE paying the debts of such institution in accordance w i th the ru les on concurrence and preference of credit under the Civil Code of the Philippines and he may, in the name of the institution, and

• with the assistance of counsel as he may retain, institute such actions as may be necessary to collect and recover accounts and assets of, or defend any action against, the institution.

The assets of an institution under receivership or liquidation • shall be deemed in custodia legis in

the hands of the receiver and • from the moment the institution was

placed under such receivership or liquidation,

BE EXEMPT FROM any order of garnishment, levy, attachment, or execution.

NOTE: The actions of the Monetary Board taken under this section or under Section 29 of this Act shall be

1. final and executory, and 2. may not be restrained or set aside by the court

EXCEPT petition for certiorari on the ground - that the action taken was in excess o f jurisdiction or with s u c h G A D a s t o amount to lack or excess of jurisdiction. who can file can only be filed by the SH of record -

• representing the majority of the capital stock

within ten (10) days from receipt by the BOD of the institution of the order d i r e c t i n g receivership, liquidation or conservatorship.

The designation of a conservator under Section 29 of this Act or the appointment of a receiver under this section shall be vested exclusively with the Monetary Board. Fur the rmore , t he des igna t ion o f a conservator is not a precondition to the designation of a receiver.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �20 40

D . C U R R E N C Y; L E G A L T E N D E R ; REPLACEMENT AND RETIREMENT OF CURRENCIES SEC: 49: CURRENCY; DEFINED all Philippine notes and coins issued or circulating in accordance with the provisions of this Act.

IN ACCORDANCE WITH THIS ACT; means: - Phil currency issued by the BSP

SEC. 52: LEGAL TENDER All notes and coins issued by the BSP

• shall be fully guaranteed by the - Government of the Republic of the Philippines

• and shall be legal tender in the Philippines

- for all debts, both public and private: Provided, however, That, unless otherwise fixed by the Monetary Board, coins shall be legal tender in amounts not exceeding Php 50

for denominations of 25 c and above, not exceeding P20.00

for denominations of 10 c or less. SEC. 55: INTERCONVERTABILITY OF CURRENCY BSP SHALL EXCHANGE, ON DEMAND AND WITHOUT CHARGE Philippine currency of any denomination for

Philippine notes and coins of any other denomination requested. If for any reason the Bangko Sentral is temporarily unable to provide notes or coins of the denominations requested, it shall meet its obligations by:

delivering notes and coins of the denominations

w h i c h m o s t n e a r l y a p p r o x i m a t e t h o s e requested.

SEC. 56: REPLACEMENT OF CURRENCY UNIT FOR CIRCULATION ThE BSP shall • withdraw from circulation and • shall demonetize all notes and coins

which for any reason whatsoever are - unfit for circulation

• and shall replace them by adequate notes and coins.

NOTE: Notes and coins in such mutilated conditions shall be - withdrawn from circulation and - demonetized

W I T H O U T compensation to the bearer

PROVIDED HOWEVER, That the BSP SHALL NOT replace notes and coins 1. the identification of which is

impossible, 2. coins which show signs of filing,

clipping or perforation, and 3. notes which have lost more than

two-fifths (2/5) of their surface or all of the signatures inscribed thereon.

. SEC. 57: RETIREMENT OF OLD NOTES AND COINS The BSP may call in for replacement

FOR NOTES those more than 5 years old FOR COINS those which are more than 10 yrs old.

Notes and coins called in for replacement in accordance with this provision SHALL REMAIN A LEGAL TENDER

• for a period of 1 year • from the date of call.

AFTER THIS PERIOD (LAPSE OF 1 YR FROM CALL)

they shall cease to be legal tender BUT DESPITE OF SUCH LAPSE

• during the following year, or • for such longer period as the

Monetary Board may determine, THEY MAY BE EXCHANGED - at par and without charge - in the BSP and by agents duly authorized by the BSP for this purpose.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �21 40

AFTER THE EXPIRATION OF 1 Y R P E R I O F A F T E R T H E EXPIRATION OF 1 YR FROM CALL OF RETIREMENT - and the notes and coins which have not been exchanged shall • cease to be a liability of the

Bangko Sentral and • shall be demonetized. The Bangko Sentral shall also demonetize all notes and coins which have been called in and replaced.

G I S T : T H E F F S H A L L B E DEMONITIZED

• all notes and coins which have been called in and replaced

- those unfit for circulation - those which has been mutilated

• all coins and notes which has not been exchanged after the lapse of 1 year, counted from the expiration of 1 year from the call of retirement by the BSP

SEC. 60: LEGAL CHARACTER CHECKS representing demand deposits

DO NOT HAVE legal tender power and

their acceptance in the payment of debts, both public and private, is at the option of the creditor:

PROVIDED HOWEVER That a check which has been cleared and credited to the account of the creditor

SHALL BE EQUIVALENT TO a delivery to the creditor of cash in an amount equal to the amount credited to his account.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �22 40

E. RESERVES SEC. 65: INTERNATIONAL RESERVES PURPOSE In order to maintain the international stability and convertibility of the Philippine peso.

FOR THIS PURPOSE (Sec. 66) The Monetary Board shall

1. endeavor to hold the foreign exchange resources of the B a n g k o S e n t r a l i n f r e e l y convertible currencies;

2. give particular consideration to the prospects of continued strength and convertibility of the currencies in which the reserve is maintained, as well as to the anticipated demands for such currencies.

3. issue regulations determining the other qualifications which foreign exchange assets must meet in order to be included in the international reserves of the Bangko Sentral

DUTY REPOSED UPON BSP shall maintain international reserves

adequate to meet any foreseeable net demands on the Bangko Sentral for foreign currencies.

GUIDELINES IN JUDGING THE ADEQUACY OF INTERNATIONAL RESERVES 1. the prospective receipts and payments of

foreign exchange by the Philippines. 2. the volume and maturity of the Bangko

Sentral 's own l iabi l i t ies in foreign currencies, to the volume and maturity of the foreign exchange assets and liabilities of other banks operating in the Philippines and,

3. insofar as they are known or can be estimated, the volume and maturity of the foreign exchange assets and liabilities of all o ther persons and ent i t ies in the Philippines.

S E C . 6 6 : C O M P O S I T I O N O F INTERNATIONAL RESERVES The international reserves of the Bangko Sentral may include but shall not be limited to the following assets: 1. gold; and 2. assets in foreign currencies in the form of:

a. d o c u m e n t s a n d i n s t r u m e n t s cus tomar i l y emp loyed f o r t he international transfer of funds;

b. demand and time deposits in central banks, treasuries and commercial banks abroad;

c. foreign government securities; and d. foreign notes and coins.

. NOTE: The Bangko Sentral shall be free to convert any of the assets in its international reserves into other assets as described in 1 and 2.

SEC. 94: RESERVE REQUIREMENTS PURPOSE OF MAKING A RESERVE In order to control the volume of money created by the credit operations of the banking system DUTY IMPOSED UPON 1. all banks operating in the Philippines

shall be required to maintain reserves against their deposit liabilities

2. all banks and/or quasi-banks to maintain reserves

against funds held in trust and liabilities for deposit substitutes.

As the MB my prescribe in its discretion.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �23 40

***DEPOSIT SUBSTITUTE an alternative form of obtaining funds from the public, other than deposits, through the • issuance, • endorsement, or • acceptance of

debt instruments for the borrower's own account,

for the purpose of relending or purchasing of receivables and other obligations.

These instruments may include, but need not be limited to, 1. bankers acceptances, 2. promissory notes, 3. participations, 4. c e r t i fi c a t e s o f

assignment and 5. similar instruments with

r e c o u r s e , a n d repurchase agreements.

THE FF SHALL NOT BE C O N S I D E R E D A S A DEPOSIT SUBSTITUTE The deposit substitutes of commercial, industrial and o t h e r n o n - fi n a n c i a l companies for the limited purpose of 1. financing the i r own

needs or 2. t he needs o f t he i r

agents or 3. dealers

REQUIRED RESERVES BANKS shall be proportional to the volume of its deposit liabilities

FORM ordinarily, deposit to BSP NOTE: Reserve requirements shall be applied to all banks of the same category uniformly and without discrimination.

RESERVES AGAINST DEPOSIT SUBSTITUTE, if imposed, shall be determined in the same manner as provided for reserve requirements against regular bank deposits,

with respect to the imposition, increase, and computation of reserves.

WHEN RESERVE REQUIREMENT IS DISPENSED WITH deposits and deposit substitutes 1. with remaining maturities of 2 yrs or more, 2. as well as interbank borrowings. FOR RESERVE DEPOSITS, BSP IS NOT LIABLE TO PAY FOR INTEREST

RATION Since the requirement to maintain bank reserves is imposed primarily to control the volume of money, EXE: MB decides otherwise as warranted by circumstances.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �24 40

SEC. 102: INTERBANK SETTLEMENT • The BSP shall establish facilities for

interbank clearing under such rules and regulations as the Monetary Board may prescribe:

• The BSP may charge administrative and other fees for the maintenance of such facilities.

The deposit reserves maintained by the banks in the Bangko Sentral in accordance with the provisions of Section 94 of this Act SHALL SERVE AS A BASIS • for the clearing of checks and • the settlement of interbank balances,

subject to such rules and regulations as the MB may issue with respect to such operations:

SHOULD A BANK INCUR OVERDRAWING IN ITS DEPOSIT ACCOUNT WITH BSP shall fully cover said overdraft, including interest thereon

AT A RATE • equivalent to 1/10 of 1% per day or • the prevai l ing ninety-one-day

treasury bill rate PLUS three percentage points,

= whichever is higher, not later than the next clearing day:

***and the overdrawing bank must be officially notified of such overdrawn. THAT SETTLEMENT OF CLEARING BALANCES SHALL NOT BE EFFECTED FOR ANY ACCOUNT which continues to be overdrawn for

5 consecutive banking days UNTIL • such time as the overdrawing is

fully covered or • otherwise converted into an

emergency loan or advance pursuant to the provisions of Section 84 of this Act:

OPTIONS OF THE OVERDRAWING BANK 1. convert the overdraft into an emergency

loan or advance with a plan of payment, or 2. settle such overdrafts, and that,

IN CASE OF AILURE TO COMPLY the BSP shall take such action against the bank as may be warranted under this Act.

S E C . 1 0 3 : E X E M P T I O N F R O M ATTACHMENT AND OTHER Deposits maintained by banks with the Bangko Sentral as part of their reserve requirements

shall be exempt from • attachment, • garnishments, or • any other order or process of any

court, government agency or any other administrative body

issued to satisfy the claim of a party

EXE: for claim of the 1. Government, or 2. its political subdivisions or 3. instrumentalities.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �25 40

III. BANK SECRECY LAW (RA 1405) A. RULE AND EXCEPTIONS WHAT LAW GOVERNS SECRECY OF NAK DEPOSITS RA. 1405 - all deposits of whatever nature including investment with banks

ARE CONSIDERED absolutely confidential in nature; and may not be examined, inquired, or looked into by any person, govt official, bureau or office

DEPOSITS COVERED all deposits of whatever nature including investment with banks

HENCE not only limited to deposits but also investment - as otherwise, the word investment should not have been included in the definition of the word deposit. THIS INCLUDE

TRUST ACCOUNT - included in the phrase "deposits of whatever nature"

BUT DOES NOT INCLUDE/COVER M O N E Y M A R K E T PLACEMENT - as neither it is a deposit or an investment in govt funds ALSO; SBD does not cover inquiry as to the name of the drawer SAFETY DEPOSIT BOX - as not strictly a deposit, but a spec ia l k ind o f depos i t . relationship created between the bank and the lessee of the safety deposit box is bailee-bailor relationship. akin to bailment, being for hire and mutual benefit has been adopted in this jurisdiction.

H O W E V E R ; a n y information regarding the existence of the safety deposit box is still considered secret and confidentiak in view of Sec. 55, 1(b) - any in fo rmat ion relative to FUNDS and P R O P E R T I E S o f clients of a bank are to be kept confidential by such bank and its d i rectors, officers, employees or agents. - such information cannot be disclosed to a n y u n a u t h o r i z e d person without court order. NOTE: bank is liable for the loss of the thing kept in safety deposit box - if it is due to the fraud, negligence, or delay or contravention of the tenor of the agreement.

***DEPOSITS - for SBD purposes; broad application, and not merely limited to account which give rise to a creditor-debtor relationship between the depositor and the bank.

RATION OF THE BROAD APPLICATION

1. to give encouragement to the people to deposit their money in banking institution

2. to discourage private hoarding so that the same may be purely ut i l ized by banks in authorized loan to assist i n t h e e c o n o m i c d e v e l o p m e n t o f y e country

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �26 40

NOTE: any information in violation of the SBD Law, shall not be rendered inadmissible - as nowhere in RA 1405 which provides for such - what the law merely provides is that

any violation of this law will subject the o f f e n d e r u p o n c o n v i c t i o n , t o a n imprisonment if not more than 5 years and a fine of not more than 20k or both, in the discretion of the court.

PERSONS BANNED FROM LOOKING INTO BANK DEPOSITS any person, government official, bureau or office.

DOS NOT COVER; OMBUDSMAN PROVIDED; requisites 1. only in-camera inspection is

allowed 2. there must be a pending case

before a court of competent jurisdiction

3. the account must be clearly identified

4. the inspection is limited to the account subject of the court case

5. the bank personnel and account holder must be notified to be present during the inspection.

there must be a pending case - does th i s cover p re l im ina ry investigation?

PERSONS BANNED FROM DISCLOSING ANY INFORMATION CONCERNING BANK DEPOSITS; any 1. official or employee of a bank, or 2. an independent auditor hired by the bank to

conduct its regular audit. DOES NOT COVER - those person who overheard such information and thereafter disclose it. if such person is not an official or e m p l o y e e o f a b a n k , o r a n independent auditor hired by the bank.

EXCEPTIONS TO THE SBD 1. in case of an examination, general or special, of the MB

after being satisfied that - there is a reasonable ground to believe that a bank fraud or serious irregularity has been or is being committed - and that it is necessary to look into the deposit to establish such fraud or irregularity

2. in case of examination by an independent auditor, hired by the bank

- for audit purposes only - and the result thereof shall be for the exclusive use of the bank

3. written permission of the depositor 4. in case of impeachment. 5. upon order of competent court,

in case of - bribery - dereliction of duty of public officials

***unexplained wealth - akin to dereliction of duty

***plunder cases - akin to bribe

6. in case where the money deposited or invested is the subject matter of litigation 7. in case of inquiry of the BIR of bank accounts of a decedent

for estate tax purposes or in case of tax compromise

8. incidental disclosure of the unclaimed balances

under the Unclaimed Balance Law 9. upon order of competent court

in cases of violation of the AMLA 10. the examination of a bank account based in sec. 10 rule 57 of the rules of court

the examination of a party whose property is attached and person indebted to a defendant or controlling his property. NOTE: IN ANTI-GRAFT CASES - inquiry into illegally acquired property / or property nor legitimately acquired

EXTENDS even to cases where such property is concealed by being held by or recorded in the n a m e o f t h e s p o u s e , ascendants, descendants and re l a t i ves o f t he pe rson investigated, and those in the name of other persons.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �27 40

NOTE: inquiry by the SH on corporate books, supposing SH of a bank, such right must be exercised in GF or for legitimate reasons, otherwise, would amount to violation of the SBD law, supposing what is being inquired into is an specific account if a depositor. S B D D O E S N O T I N C L U D E P R O H I B I T I O N A G A I N S T GARNISHMENT - as there is no real inquiry, and if the deposit is disclosed in the process, such is merely incidental to the execution process.

NOTE: IF THE DEPOSIT IS M E R E L Y A S U B J E C T M A T T E R O F A N ATTACHMENT - it does not make it a subjct matter of litigation - such attachment will not justify its disclosure

EXE TO EXE WHEN A DEPOSIT EVEN THOUGH A SUBJECT MATTER OF LITIGATION, STILL CANNOT BE INQUIRED INTO - FCDA

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �28 40

I V. F O R E I G N C U R R E N C Y DEPOSIT ACT RA. 6426 A. RULE AND EXCEPTIONS FOREIGN CURRENCIES COVERED - all kinds of foreign currency deposits, deposited in Philippine Banks in good standing

HENCE; does not cover - those maintained in foreign banks

INQUIRY ON FOREIGN CURRENCY DEPOSITS

GEN RULE: NOT ALLOWED - foreign currency deposits shall not be allowed to be examined, inquired into by any person, government official, bureau or office,

w h e t h e r j u d i c i a l o r administrative or legislative

or any other entity whether private or public. EXCEPTIONS: 1. upon a written permission of the

depositor 2. upon order of a competent court in

case of violation of AMLA, when it has been established that there is a cause that the deposit involved are in any way related to money laundering offense.

3. Human Security Act 4. Chinabank vs. Ca (Dec 18, 2006)

- pro hac vice lang to ha. F O R E I G N C U R R E N C Y D E P O S I T S , EXEMPTED FROM GARNISHMENT

EXE 1. amla 2. chinabank case

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �29 40

V. TRUTH IN LENDING ACT RA 3765 - is an act to require the disclosure if finance charges in connection with the extension of credit REQUIRES - any creditor is required to furnish each person to whom credit is extended, prior to the consummation of the transaction

clear statement in writing setting forth, to the extent applicable and in accordance with the rules and regulations prescribed by the MB, the ff info: 1. the cash price or the delivered price

- of the property or service to be acquired.

2. the amount, if any - to be credi ted as downpayment and/or trade-in

3. the difference between the amount set forth under 2 and 3 4. the charges

individually itemized, - which are to be paid by s u c h p e r s o n i n connect ion wi th the transaction - but which are not incident to the extension of credit.

5. the total amount to be financed 6. the finance charge

- expressed in terms of pesos and centavos

8. the percentage that the finance charge bears to the total amount to be financed

- expressed as simple a n n u a l r a t e o n t h e o u t s t a n d i n g u n p a i d balance of the obligation

CREDITORS UNDER TLA - any person engaged in the business of extending credit

who requires as an incident to the extension of credit - the payment of the finance charge.

THIS INCLUDE - any person who as a regular business, practices

• loan • sells or rents property or

services = on a time, credit or installment basis,

either as a principal or an agent.

FINANCE CHARGE; include under TLA 1. interest fee 2. service charge 3. discounts; and 4. such other charges incident to he

extension of credit as Board may by regulation prescribed.

IMPLICATION OF NON-COMPLIANCE WITH THE TLA 1. creditor shall pay a fine of 100 or double

the amount of the finance charge, BUT in no case shall exceed 2k

2. in case of willful violation, the fine shall not be less than 1k but not more than 5k, or imprisonment for not less than 6mod, nor more than 1 year or both

H O W E V E R , I T D O E S N O T AFFECT THE ENFORCEABILITY OF THE CONTRACT NOTE: in credit card transaction - the store from which a person used the credit card, need not comply with the TLA

a s t h e t r a n s a c t i o n involved therein is not on installment basis, - it was the credit card company which extends the privilege of payin in installments

NOTE: TLA DOES NOT ADMIT SUBSTANTIAL COMPLIANCE. - dapat; full disclosure in writing of any matter in connection with the extension of credit,

must be made prior to such extension.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �30 40

VI. UNCLAIMED BALANCE LAW ACT 3936 A. COVERAGE SHALL INCLUDE 1. credits 2. deposits of money 3. bullion 4. security; or 5. other evidence of indebtedness

WITH a. banks b. buildings and loan associations;

and c. trust corporations

IN FAVOR OF A PERSON • known to be dead; or • who has not made further deposits or

withdrawals during the preceding 10 yrs or more.

WHAT WILL HAPPEN TO THE UNCLAIMED BALANCE (including the increase and the proceeds thereof) - shall be subjected to escheat proceedings.

SHALL BE DEPOSITED - with the Treasurer of the RP TO THE CREDIT OF - the Gov't of the Phil TO BE USED - as the National Assembly may direct. (Congress)

PUBLICATION REQUIREMENT (DUE PROCESS) 1. notify the owner, by sending a copy of the

notice to the last known address of the depositor

2. publish said notice 3. notice contained in the publication is the

name of the owner and the fact which give rise to the escheat proceedings. note; not the amount.

~absence, everything becomes null and void.

NOTE: the publication here is an exception of SBD

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �31 40

V I I . P H I L I P P I N E D E P O S I T INSURANCE CORPORATION RA 3591 A. C O V E R A G E ; H O W A M O U N T

COMPUTED PURPOSE OF PDIC - to insure deposit of all banks which are entitled to the benefits of insurance RISK INSURED AGAINST - bank closure TYPES OF DEPOSITS COVERED 1. savings account 2. current account 3. time deposits; and 4. deposits in acceptable foreign currencies

pursuant to FCDA QUALIFICATION: - that the deposit must be made in the regular course of business NOTE: DOES NOT COVER Trust funds

NATURE OF LIABILITY OF PDIC - statutory

NOTE: mere s ta tement in the certificate that the same is insured by PDIC - is not binding to the latter. for PDIC be held l iab le, there must be compliance with the requirement of RA 3591.

DEPOSIT; as defined in PDIC Law unpaid balance of money or its equivalent received by a bank in the usual course of business

- for which it has given or is obliged to give credit to • commercial • savings • time; or • thrift account; or - as evidenced by a • passbook • check and/or • certificate of deposit

printed or issued in accordance with BSP rules and regulations and other applicable laws

together with such other obligations of a bank

which is consistent with banking usage and practices,

the Board of the PDIC shall determine and prescribe by regulations to be deposit liabilities of the bank.

NOTE: DEPOSIT DOES NOT COVER Any obligations of a bank which is payable at the office of the bank located outside the Phil.

HOWEVER subject to the approval of the Board of the PDIC - any insured bank which maintains a branch outside the Phil

may elect to include f o r i n s u r a n c e i t s deposit obligations

payable only a t s u c h branch.

INSURED DEPOSIT; defined amount due to any depositor for deposits in an insured bank

net of any obligation of the depositor to the insured bank

as of the date of closure BUT NOT EXCEEDING 500k

NOTE: HOLDER OF A NEGOTIABLE CERTIFICATE OF DEPOSIT

NOT ENTITLED TO THE RIGHT OF AN INSURED DEPOSITOR EXE - his name is registered as owner/holder thereof in the books of the issuing bank.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �32 40

HOW AMOUNT DUE TO DEPOSITOR DETERMINED add together - all deposits in the bank

maintained in the same right and capacity for his benefit

either in his own name or in the name of others.

I. FOR JOINT ACCOUNTS - regardless of the conjunction used; "and," "or," or "and/or"

shall be insured separately from any individually owned deposit account.

RULE ON DIVISION AMONG CO-OWNER 1. equal share 2. if there is a stipulation,

stipulation shall prevail. 3. but if one of the co-owner is

a juridical entity - all the proceeds shall be presumed to belong to the JE. 4. if both are JE, apply 1 or 2.

II. SINGLE DEPOSITOR ACCOUNT - basta, add lahat, kahit na yung depositor has different account. - ie. may checking, savings and time deposit sya, yung aggregate nun yung basis ng computation. III. IN TRUST FOR ACCOUNT ITF ACCOUNT - the depositor merely acts as an agent. - hence, in this instance, the deposit made by such depositor shall not be included in the computation of his individual aggregate deposit with the insured bank IBA ITO SA JOHN DOE BY JUAN DE LA CRUZ - juan dela cruz is the agent here. so in determining the amount of the insured deposit of John Doe, the deposit made by Juan dela cruz shall be included in the computation of his aggregate individual deposits with the insured bank. BASTA: refer to Iggy's book for concrete, blow by blow, examples. :)

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �33 40

VIII. ANTI-MONEY LAUNDERING ACT RA 10167, 10168, 9160, 9194 MONEY LAUNDERING; defined - is a crime, whereby the proceeds of an unlawful activity are transacted,

thereby making them appear to have originated from legitimate sources

A. COVERED INSTITUTIONS I. banks, non-banks, quasi-banks, trust entities, and all other institutions and their subsidiaries and affiliates supervised or regulated by the BSP II. insurance companies and all other institutions supervised or regulated by the Insurance Commission; and III. • securities dealers, brokers, salesmen,

investment houses and other similar entities managing securities or rendering services as investment agent, advisor, or consultant;

• mutual funds, c lose-end investment companies, common trust funds, pre-need companies and other similar entities;

• foreign exchange corporations, money changers, money payment, remittance, and transfer companies and other similar entities; and

• other entities administering or otherwise dealing in currency, commodities or financial derivatives based thereon, valuable objects, cash substitutes and other similar monetary instruments or property supervised or regulated by the SEC.

B. COVERED TRANSACTIONS I. a single, series, or combination of transactions

INVOLVING a total amount in excess of

• Php 4M or • an equivalent amount in foreign

currency b a s e d o n t h e p r e v a i l i n g exchange rate within five (5) consecutive banking days

EXCEPT those between a covered institution and a person who,

at the time of the transaction was a properly identified client

and the amount is commensurate with • the business or financia l

capacity of the client; or • those with an underlying legal

or trade obligation, purpose, origin or economic justification.

II. single, series or combination or pattern of UNUSUALLY LARGE AND COMPLEX TRANSACTION in excess of Php 4M

especially cash deposits and investments

h a v i n g n o c r e d i b l e p u r p o s e o r o r i g i n , underlying trade obligation or contract.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �34 40

C. SUSPICIOUS TRANSACTIONS 1. there is no underlying legal or trade

ob l i ga t i on , pu rpose , o r economic justification

2. the client is not properly identified 3. the amount involved is not commensurate

with the business or financial capacity of the client

4. t a k i n g i n t o a c c o u n t a l l k n o w n circumstances, it may be perceived that the client's transaction is structured in order to avoid being the subject of reporting requirement under the act

5. any c i rcumstances re lat ing to the transaction which is observed to deviate from the profile of the client and/or the client's past transactions with the covered institution

6. the transaction is in any way related to an unlawful activity or any money laundering activity or offense under this Act that is about to be, is being or has been committed.

7. any transaction that is similar, analogous or identical to any of the foregoing.

D. PREDICATE CRIMES TO MONEY LAUNDERING 1. Kidnapping for ransom 2. Sections 3, 4, 5, 7, 8 and 9 of Article Two of

Dangerous Drugs Act 3. Section 3 paragraphs B, C, E, G, H and I of

Republic Act No. 3019, as amended, otherwise known as the Anti-Graft and Corrupt Practices Act

4. Plunder; 5. Robbery and extortion under Articles 294,

295, 296, 299, 300, 301 and 302 of the Revised Penal Code, as amended;

6. Jueteng and Masiao punished as illegal gambling under Presidential Decree No. 1602;

7. Piracy on the high seas under the Revised Penal Code, as amended and Presidential Decree No. 532;

8. Qualified theft under Article 310 of the Revised Penal Code, as amended;

9. Swindling under Article 315 of the Revised Penal Code, as amended;

10.Smuggling under Republic Act Nos. 455 and 1937;

11. Violations under Republic Act No. 8792, otherwise known as the Electronic Commerce Act of 2000;

12.Hijacking and other violations under Republic Act No. 6235; destructive arson and murder, as defined under the Revised Penal Code, as amended, including those

perpetrated by terrorists against non-combatant persons and similar targets;

13.Fraudulent practices and other violations under Republic Act No. 8799, otherwise known as the Securities Regulation Code of 2000;

14.Felonies or offenses of a similar nature that are punishable under the penal laws of other countries.

E. HOW VIOLATION COMMITTED 1. Any person knowing that any monetary instrument or property represents,

involves, or relates to, the proceeds of any unlawful activity,

transacts or attempts to transact said monetary instrument or property.

2. Any person knowing that any monetary instrument or property

involves the proceeds of any unlawful activity,

performs or fails to perform any act as a result of which

he facilitates the offense of money laundering referred to in paragraph (a) above.

3. Any person knowing that any monetary instrument or property

is required under this Act to be • disclosed and • filed with the Anti-Money Laundering

Council (AMLC), fails to do so.

F. SAFE HARBOR PROVISION NO admin i s t ra t i ve , c r im ina l o r c i v i l proceedings, SHALL LIE AGAINST

any person for having made a • covered transaction report; or • a suspicious transaction report

in the regular performance of his duties and in good faith,

whether or not such reporting results in any criminal prosecution under this Act or any other Philippine law.

prepared by: ronie ablan

THE AWESOME NOTES BANKING LAWS

FISCAL TAMBASACAN

Page � of �35 40

G. PROHIBITION AGAINST POLITICAL PERSECUTION THIS ACT SHALL NOT BE USED • for political persecution or harassment or • as an instrument to hamper competition in

trade and commerce. • No case for money laundering may be filed

against and • no assets shall be frozen, attached or

forfeited TO THE PREJUDICE of a candidate for an electoral office during an election period.

H. FREEZE ORDER AND INQUIRY ORDER INQUIRY NOTWITHSTANDING

FCDA, SBD, GBL and other laws THE AMLC MAY INQUIRE AND EXAMINE any particular deposit or investment

with any banking institution or non-bank financial institution UPON order of any competent court

in cases of violation of this Act when it has been established that there is probable cause that the deposits or investments involved

are in any way related to a money laundering offense: