GENERAL AGREEMENT ON /flugu" 1986 - WTO Documents ...

198

RESTRICTED GENERAL AGREEMENT ON / f l u g u " 1986 TARIFFS AND TRADE Special Distribution PROBLEMS OF INTERNATIONAL TRADE IN FORESTRY PRODUCTS Background Note by the Secretariat Revision Problems of International Trade in Forestry Products was first circulated under the document symbol Spec(84)13. That document was considered by the Working Party on Trade in Certain Natural Resource Products and is herewith re-issued, revised, in follow-up of the Working Party's report (MDF/23), adopted by the CONTRACTING PARTIES on 26 November 1985 (L/5933). 86-1290

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of GENERAL AGREEMENT ON /flugu" 1986 - WTO Documents ...

RESTRICTED

GENERAL AGREEMENT ON / f lugu" 1986 TARIFFS A N D T R A D E Special Distribution

PROBLEMS OF INTERNATIONAL TRADE IN

FORESTRY PRODUCTS

Background Note by the Secretariat

Revision

Problems of International Trade in Forestry Products was first circulated under the document symbol Spec(84)13. That document was considered by the Working Party on Trade in Certain Natural Resource Products and is herewith re-issued, revised, in follow-up of the Working Party's report (MDF/23), adopted by the CONTRACTING PARTIES on 26 November 1985 (L/5933).

86-1290

MDF/W/52 Page 2

Foreword

(i) The present note is a revised and partly up-dated version of document Spec(84)13 and Add.l, both of March 1984, and of Corr.l and Corr.1/Suppl.1 thereto. These documents were considered by the Working Party on Trade in Certain Natural Resource Products and comments and suggestions made by the Group, as well as corrections submitted in writing, are taken up and reflected in the present document. To the extent possible, the note also reflects some recent trade and trade-policy developments of relevance to international trade in forestry products.

(ii) For procedural and practical reasons, the product coverage of the secretariat's note had to be limited, in essence, to the products classifiable in CCCN Chapters 44, 45 and 47, e.g. wood and cork and manufactures thereof (other than furniture) and wood-pulp and cellulose. The limited product coverage notwithstanding, the secretariat did bear in mind the interest manifested by a number of contracting parties in studying also problems of trade for products covered by CCCN Chapter 48, e.g. paper, paperboard and products thereof. One of the countries interested in identifying problems of international trade in that product area did present several position papers dealing, in part or wholly (MDF/W/1, MDF/W/3 and Add.l and MDF/W/49), with forestry products' trade-related issues, including also paper and paper products.

(iii) In relation to forestry products trade problems, the Working Party, under its Chairman Mr. M. Cartland (Hong Kong), met formally in June and September 1984 and again in September 1985. In addition, the mainly interested delegations met informally, in bilateral or plurilateral consultations, with the Group's Chairman, on a number of occasions in the spring and autumn of 1985. Notes on the proceedings of the formal meetings are contained in documents MDF/W/2, MDF/W/16 and MDF/W/53. A summary of the Group's main findings, together with suggestions on possible follow-up, is contained in documents MDF/3 and MDF/23, the Chairman's reports submitted to the GATT Council of Representatives. The report contained in document MDF/23 was forwarded by the Council to the Forty-First Session of the CONTRACTING PARTIES (C/M/194). As noted in document L/5933 and in the Summary Record SR.41/2, page 15, CONTRACTING PARTIES adopted the report on 26 November 1985.

(iv) In the revision of Spec(84)13 - Problems of International Trade in Forestry Products - the originally used paragraph numbers have been kept throughout, if for no better reason than to facilitate reference to comments made by delegations in relation to specific paragraphs. Some wider ranging comments and certain additional information that has come to the fore since Spec(84)13 was issued are accommodated in footnotes.

For views expressed on dealing with problems of international trade in natural resource products attention is invited to the record of discussions in the Senior Official Group in November 1985, notably documents SR.SOG/2 (page 9), SR.SOG/8 (pages 2 and 3) and SR.SOG/11 (page 17) and also to PREP.COM(86)SR/3, pages 35-42 and SR/6 - pages 34 to 37.

MDF/W/52 Page 3

(v) It is realized that a virtually world-wide survey of forestry industry related activities and of trade and trade problems, as has been attempted in this note, can never be more than a sketch or overview, and can never be fully up-to-date. Nevertheless, it is hoped that the data elaborated and presented in this document will be of some use to contracting parties, as discussion background material, for their further work. Suggestions by contracting parties for corrections or amendments that may be required would be appreciated.

MDF/W/52 Page 4

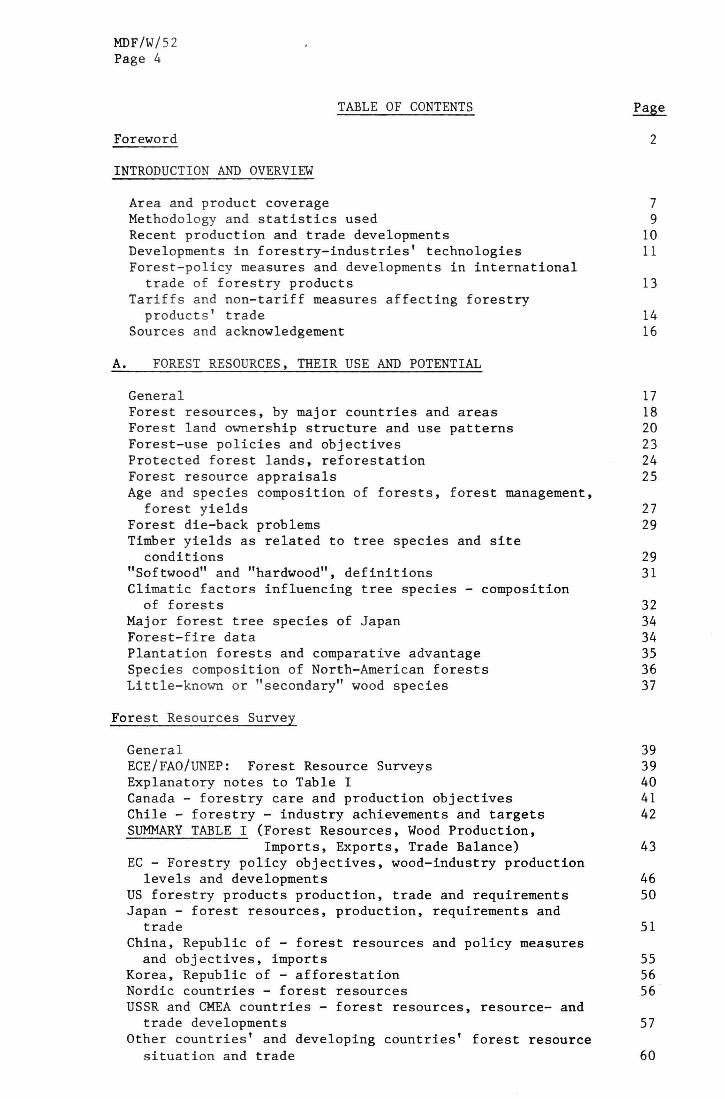

TABLE OF CONTENTS Page

Foreword 2

INTRODUCTION AND OVERVIEW

Area and product coverage 7 Methodology and statistics used 9 Recent production and trade developments 10 Developments in forestry-industries' technologies 11 Forest-policy measures and developments in international trade of forestry products 13

Tariffs and non-tariff measures affecting forestry products' trade 14

Sources and acknowledgement 16

A. FOREST RESOURCES, THEIR USE AND POTENTIAL

General 17 Forest resources, by major countries and areas 18 Forest land ownership structure and use patterns 20 Forest-use policies and objectives 23 Protected forest lands, reforestation 24 Forest resource appraisals 25 Age and species composition of forests, forest management, forest yields 27

Forest die-back problems 29 Timber yields as related to tree species and site conditions 29

"Softwood" and "hardwood", definitions 31 Climatic factors influencing tree species - composition of forests 32

Major forest tree species of Japan 34 Forest-fire data 34 Plantation forests and comparative advantage 35 Species composition of North-American forests 36 Little-known or "secondary" wood species 37

Forest Resources Survey

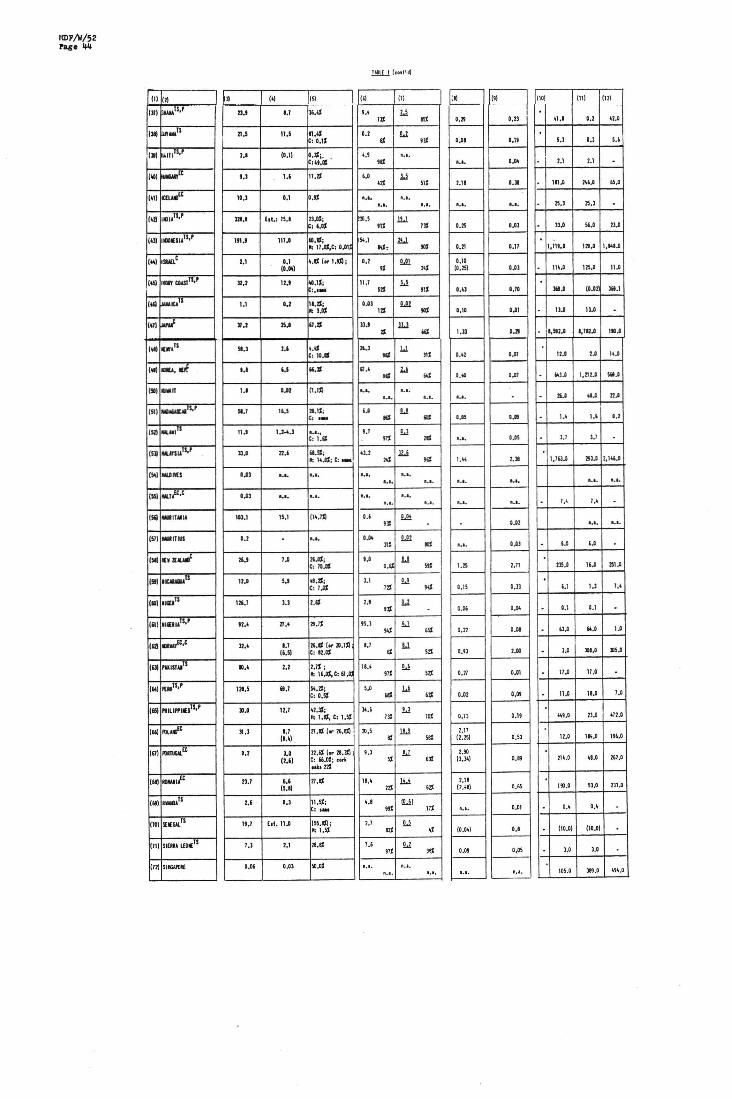

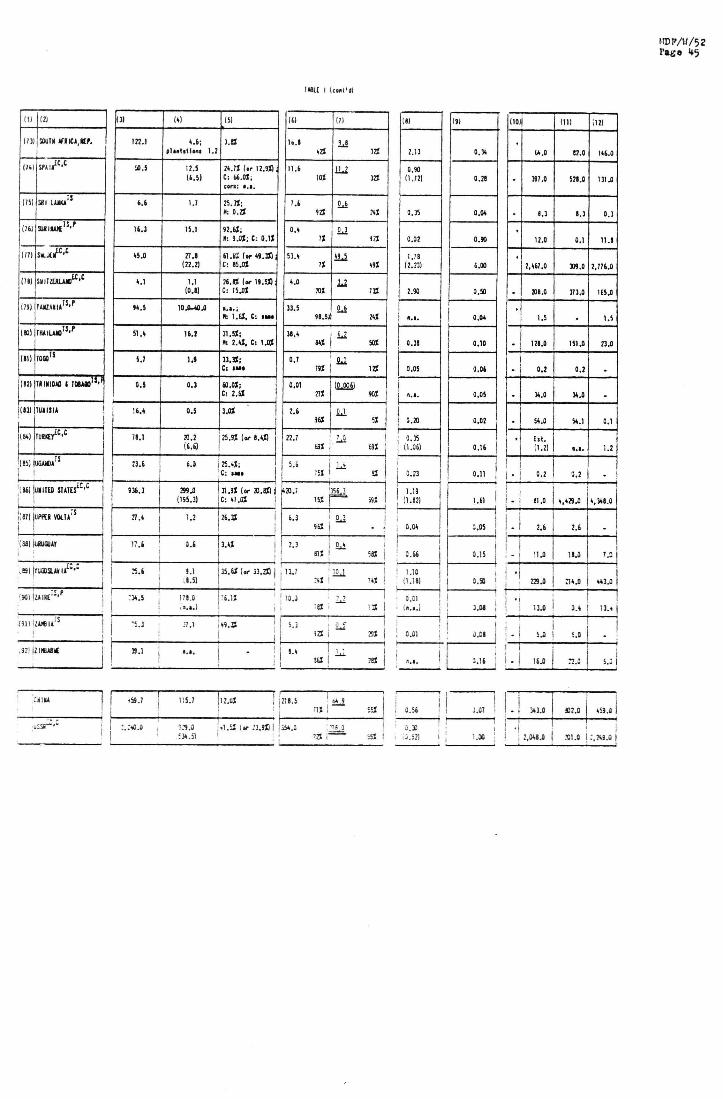

General 39 ECE/FAO/UNEP: Forest Resource Surveys 39 Explanatory notes to Table I 40 Canada - forestry care and production objectives 41 Chile - forestry - industry achievements and targets 42 SUMMARY TABLE I (Forest Resources, Wood Production,

Imports, Exports, Trade Balance) 43 EC - Forestry policy objectives, wood-industry production levels and developments 46

US forestry products production, trade and requirements 50 Japan - forest resources, production, requirements and trade 51

China, Republic of - forest resources and policy measures and objectives, imports 55

Korea, Republic of - afforestation 56 Nordic countries - forest resources 56 USSR and CMEA countries - forest resources, resource- and trade developments 57

Other countries' and developing countries' forest resource situation and trade 60

MDF/W/52 Page 5

TABLE OF CONTENTS (cont'd) Page

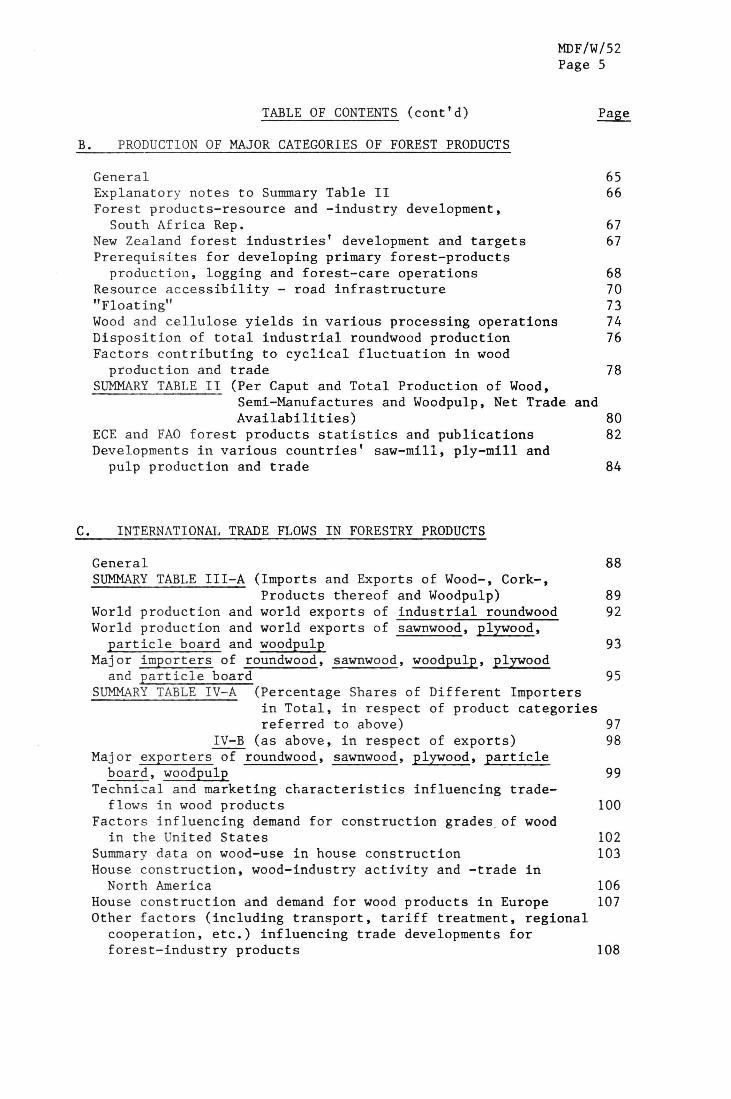

PRODUCTION OF MAJOR CATEGORIES OF FOREST PRODUCTS

General 65 Explanatory notes to Summary Table II 66 Forest products-resource and -industry development, South Africa Rep. 67

New Zealand forest industries' development and targets 67 Prerequisites for developing primary forest-products production, logging and forest-care operations 68

Resource accessibility - road infrastructure 70 "Floating" 73 Wood and cellulose yields in various processing operations 74 Disposition of total industrial roundwood production 76 Factors contributing to cyclical fluctuation in wood production and trade 78

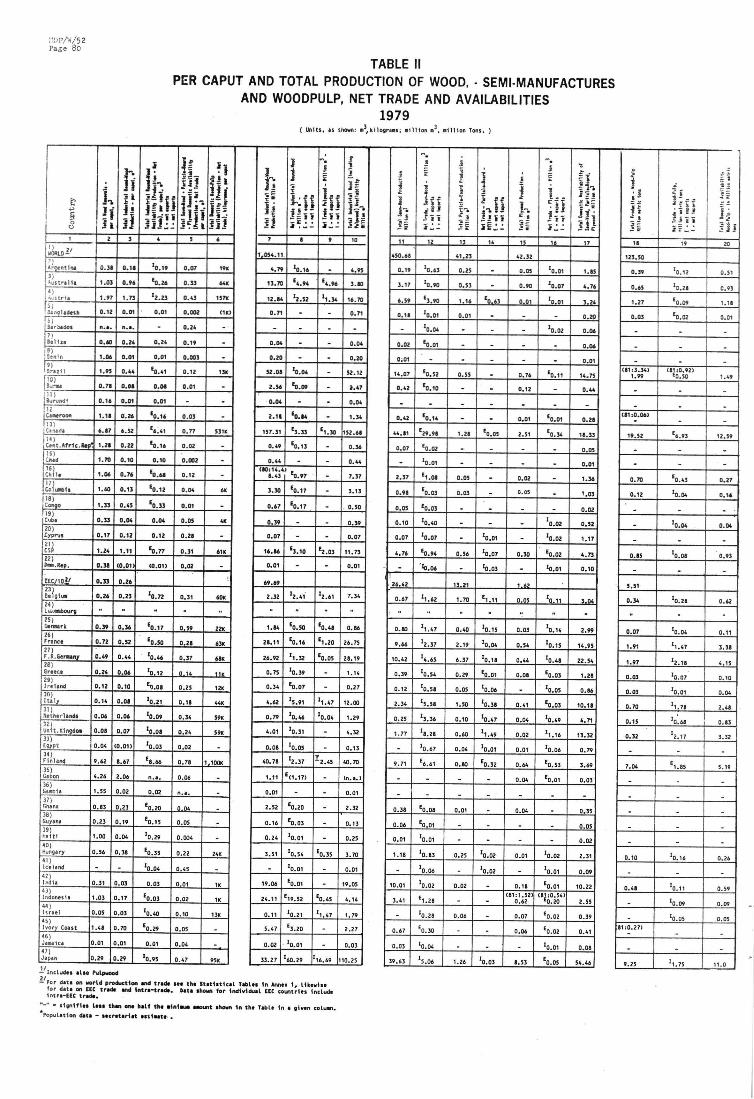

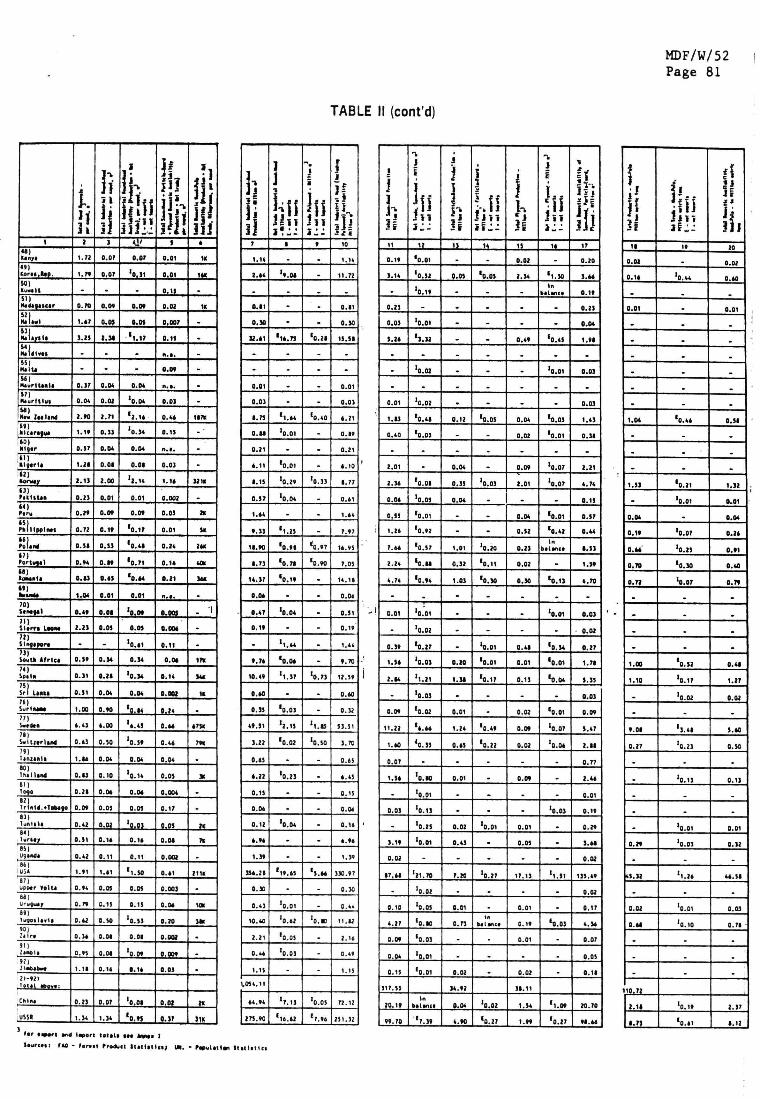

SUMMARY TABLE II (Per Caput and Total Production of Wood, Semi-Manufactures and Woodpulp, Net Trade and Availabilities) 80

ECE and FAO forest products statistics and publications 82 Developments in various countries' saw-mill, ply-mill and pulp production and trade 84

C. INTERNATIONAL TRADE FLOWS IN FORESTRY PRODUCTS

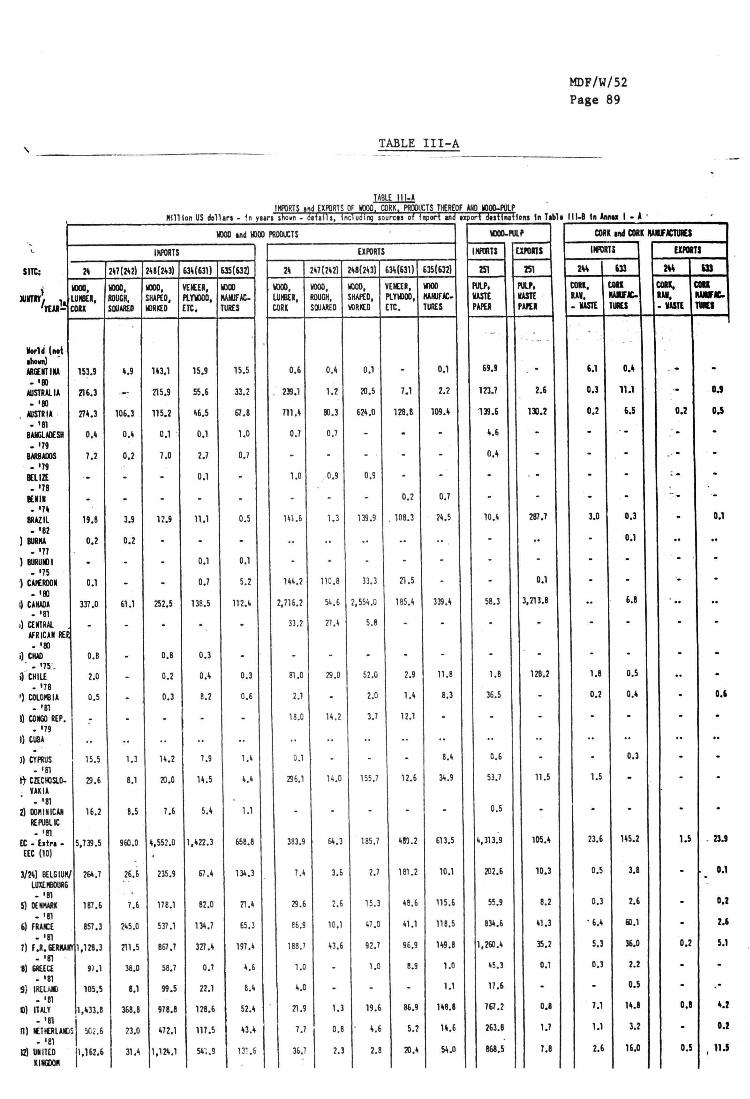

General 88 SUMMARY TABLE III-A (Imports and Exports of Wood-, Cork-,

Products thereof and Woodpulp) 89 World production and world exports of industrial roundwood 92 World production and world exports of sawnwood, plywood, particle board and woodpulp 93

Major importers of roundwood, sawnwood, woodpulp, plywood and particle board 95

SUMMARY TABLE IV-A (Percentage Shares of Different Importers in Total, in respect of product categories referred to above) 97

IV-B (as above, in respect of exports) 98 Major exporters of roundwood, sawnwood, plywood, particle board, woodpulp 99

Technical and marketing characteristics influencing trade-flows in wood products 100

Factors influencing demand for construction grades of wood in the United States 102

Summary data on wood-use in house construction 103 House construction, wood-industry activity and -trade in North America 106

House construction and demand for wood products in Europe 107 Other factors (including transport, tariff treatment, regional cooperation, etc.) influencing trade developments for forest-industry products 108

MDF/W/52 Page 6

TABLE OF CONTENTS (cont'd) Page

D. TARIFFS AND NON-TARIFF MEASURES AFFECTING TRADE

General 111 Private and public ownership patterns 111 Pre-Tokyo Round import tariff treatment for various forestry products 112 Average duty rates, pre- and post-Tokyo Round, by broad product categories 114

SUMMARY TABLE V-A (Pre- and post-Tokyo Round Tariff Rates, at the 4-digit CCCN position level) 118

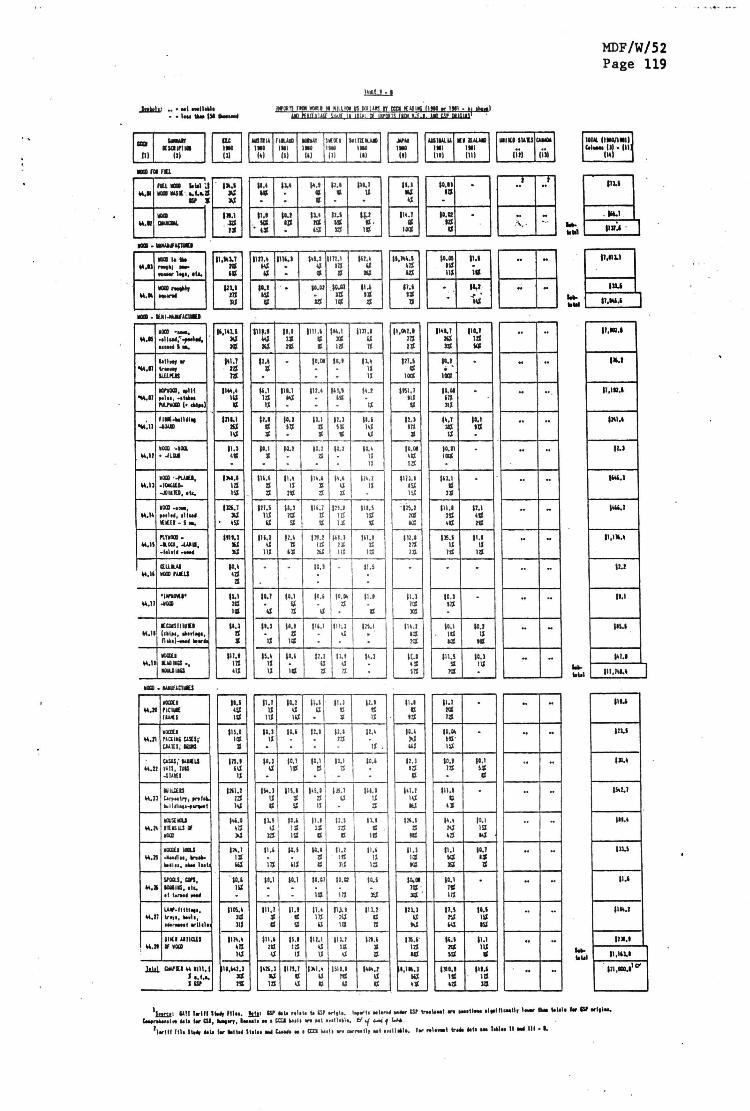

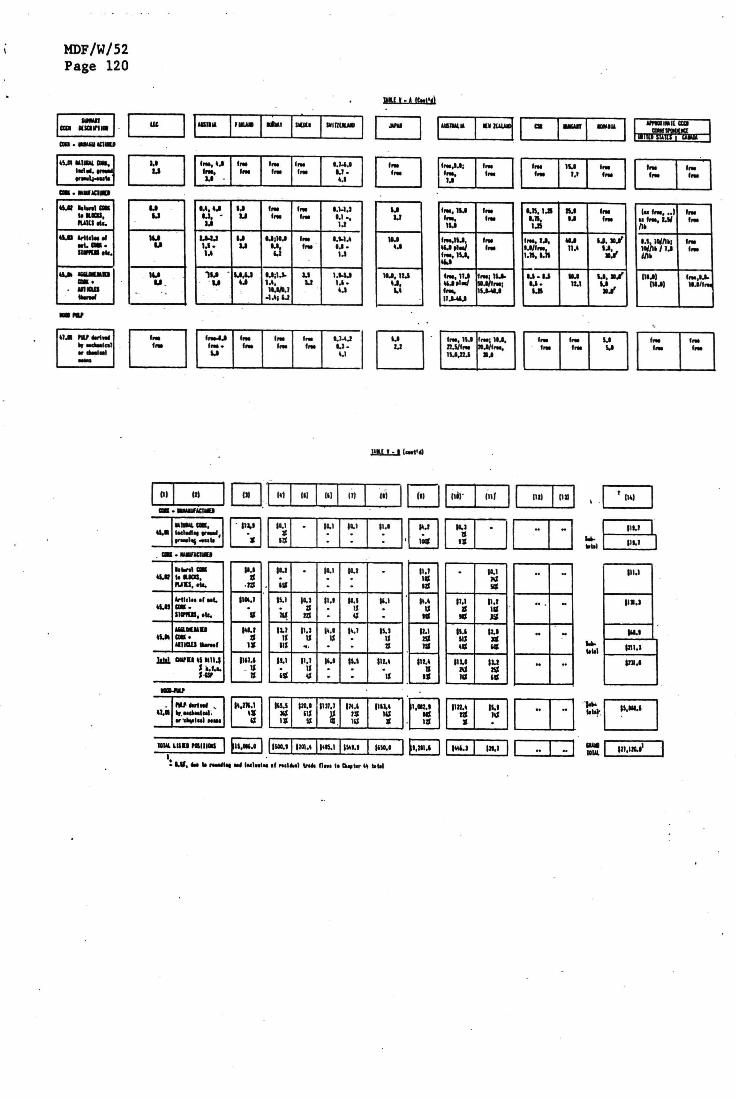

V-B (Value of Imports from World, at the same level of detail, and m.f.n. and GSP origin shares in imports) 119

Notes on data in the preceding Tables 121 Import and/or export duties on forestry products in developing country areas 122

Nominal and effective rates of protection 124 Tariff escalation 125 Classification criteria 127 Distinctions made in tariff schedules for different wood products 128 Technical standards, building codes and traditions 131 Drawing up technical specifications for little-known woods 133 Phyto-sanitary regulations 134 Import licensing, controls, restraints, prohibitions 135 Other policy measures and action affecting production, prices and trade 135

E. ADDITIONAL NOTES RELATING TO CORK

General * 137

ANNEX I-A

SUMMARY TABLE III-B (Imports and Exports of individual GATT member countries of wood, cork and products thereof, and of woodpulp, by origins and destinations) 139

- abbreviations used in Table III-B 164

ANNEX I-B

Volume of Production, Exports and Imports of GATT member countries in

1963, 1973, 1979 and 1981 of: 165

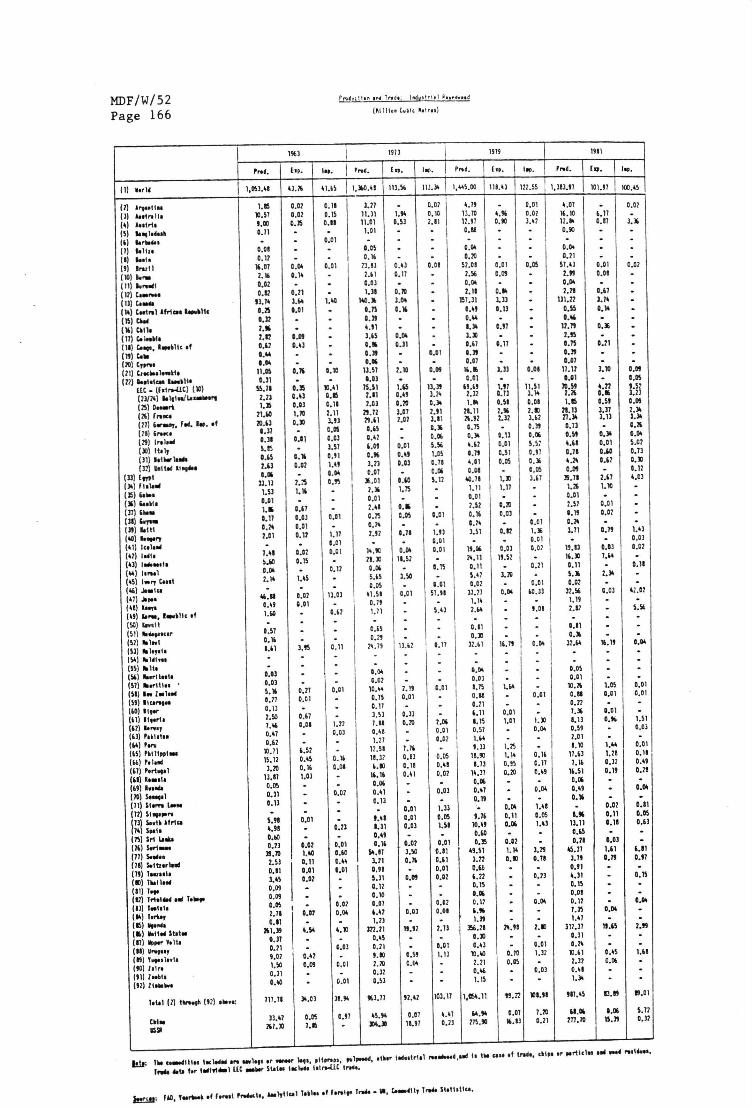

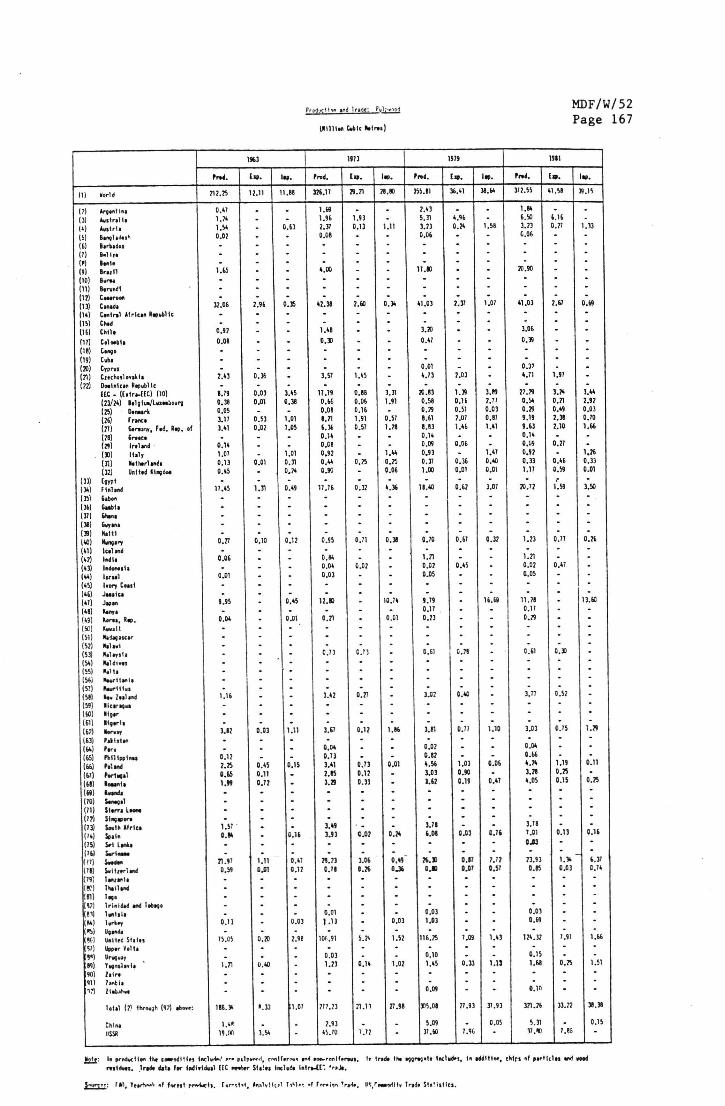

Industrial roundwood 166 - Pulpwood 167

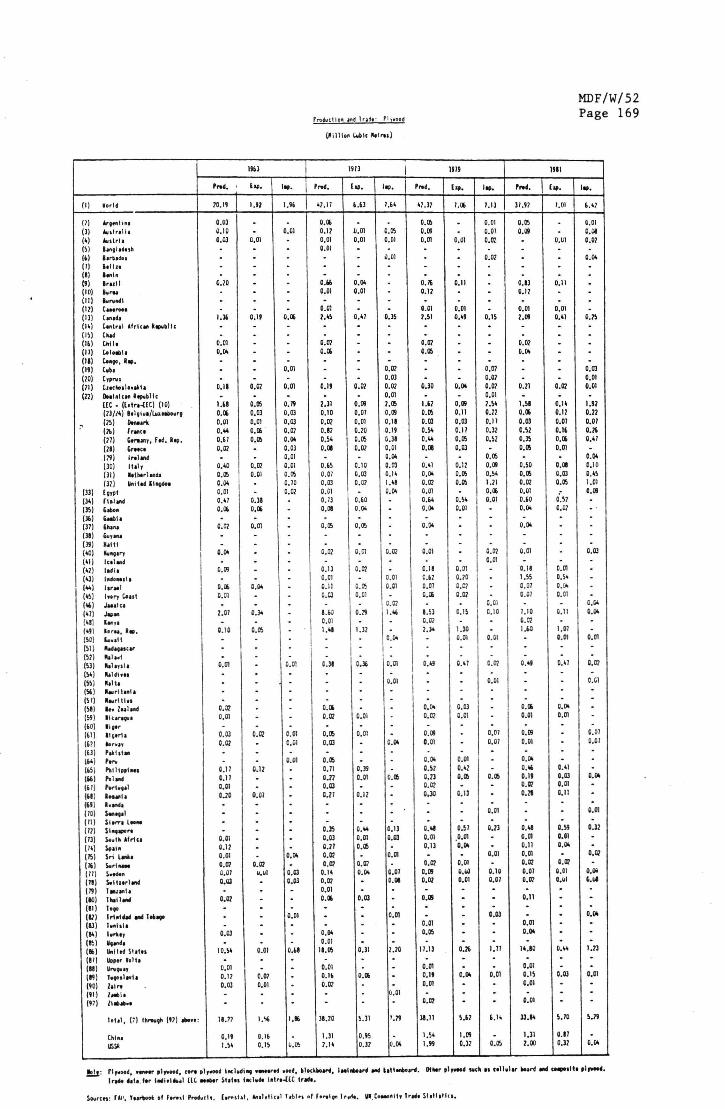

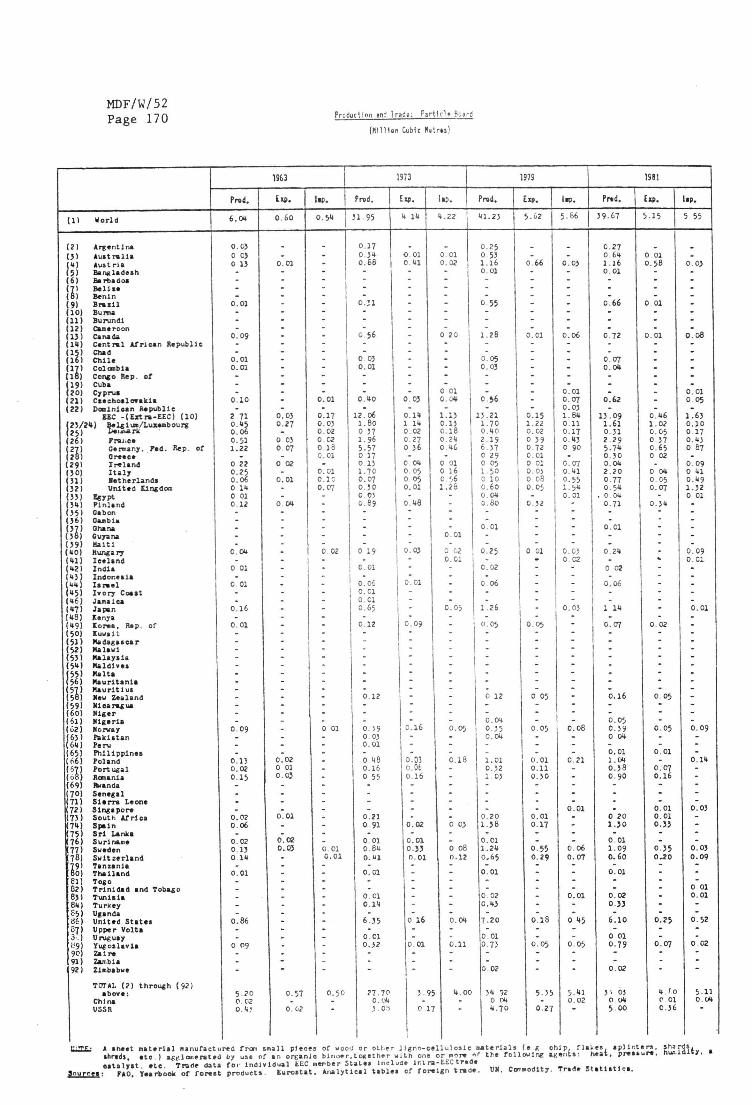

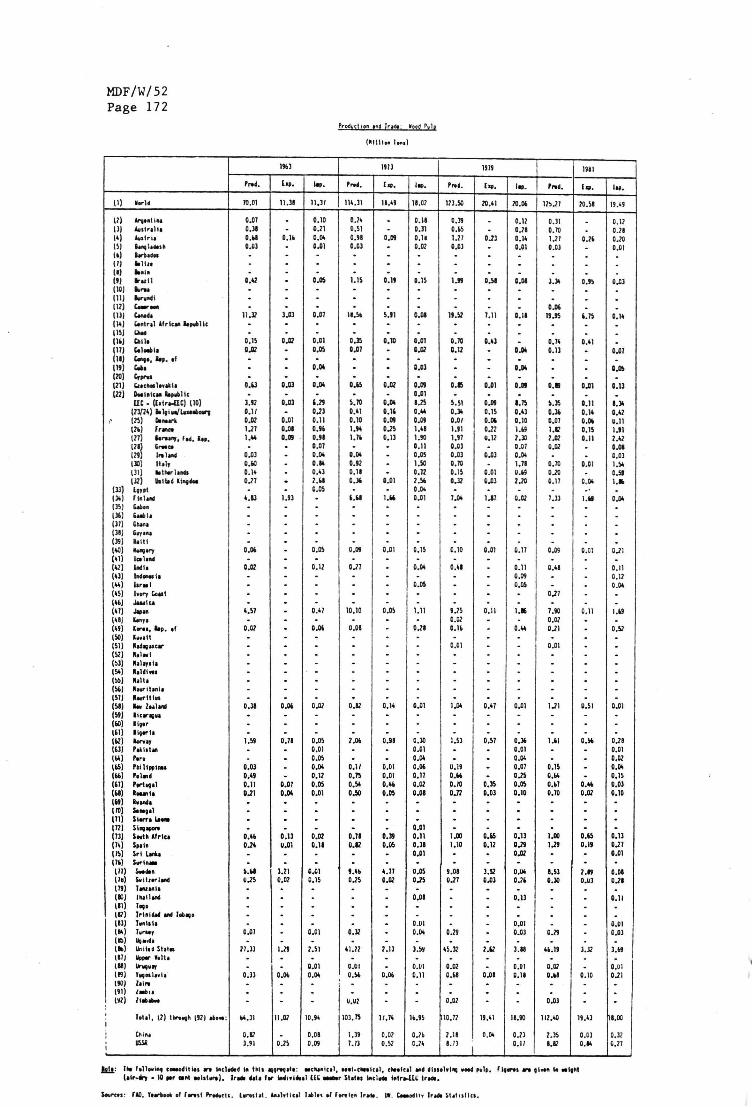

Sawnwood 168 Plywood 169 Particle-board 170 Fibre-board 171 Woodpulp 172

ANNEX II

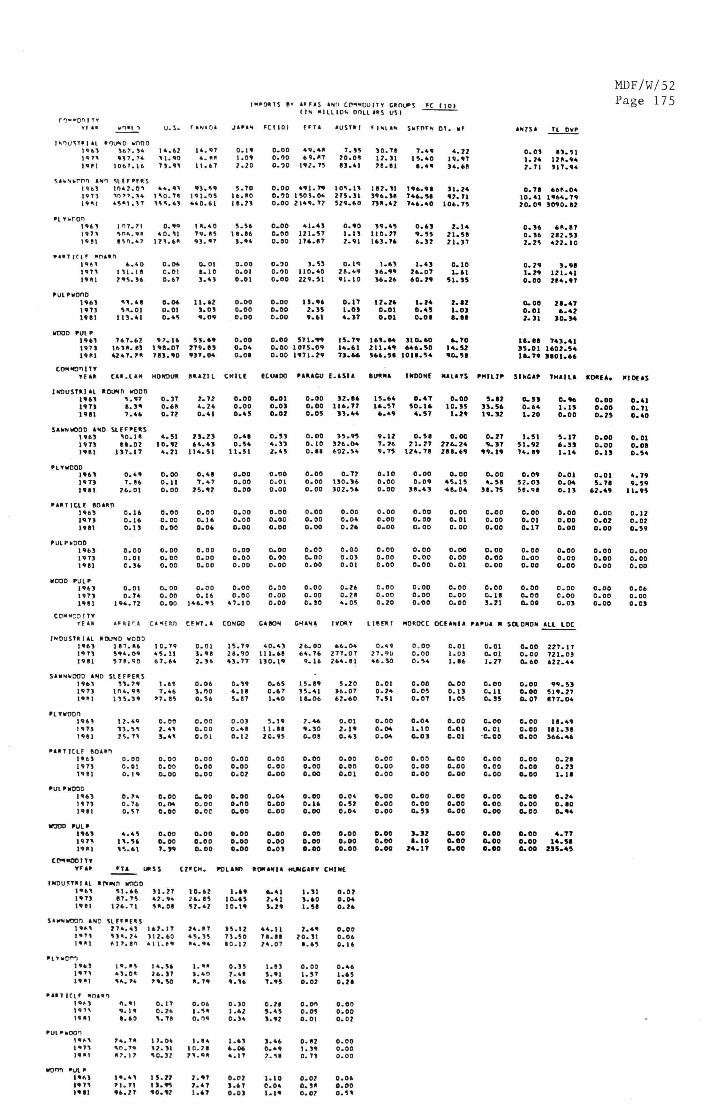

Trade Matrix for Imports of Wood and Wood Semi-Manufactures and Woodpulp for Major Import Markets - 1963, 1973, 1981 - 173

- Reproduction of headnote texts for several of the text summary tables 196

MDF/W/52 Page 7

Introduction and Overview

1. The present information note is one of several background papers the secretariat was requested to prepare, in follow-up of the November 1982 GATT Ministerial Meeting, with a view to addressing problems in international trade in various natural resource products, in their primary form and as semi-manufactures and manufactured products.

2. Natural and/or managed forests of differing size and tree-species composition are found around the globe and are absent only from the climatically most inhospitable regions. An attempt is being made in this note to provide some relevant data for all GATT contracting parties. Summary data relating to resources, production and trade in forestry products are, to the extent possible, also provided in respect of the Republic of China and the USSR.

3. Forests, both the virgin natural forests and forests planted and managed in various ways by man, are a planetary resource of great importance in maintaining and equilibrating the atmospheric-, terrestrial- and oceanic-carbon cycle, as a source of atmospheric oxygen, as wildlife habitat, floristic gene-bank, for watershed protection, for recreational purposes and as a source of construction-and fuel-wood, and of various herbs, medicinal plants, - gums, resins and of several tree fruits and oils, of fibres and of various dyeing-, tanning materials and certain other products for specific industrial uses. Forests are also of importance, in some cases essential, in operating certain agro-forestry activities and, if propery managed, can provide specialized pasture for game-farming operations.

4. Given the many uses to which forest products can be put, the subject is potentially a vast one. For practical and procedural reasons , the present note concentrates on the subject of international trade issues as they relate to wood and cork, and to manufactures thereof, and to one of the main wood derivatives - pulp. More specifically, the products covered in this note are those classified

There are a number of other countries in Latin America, Africa, Asia and Oceania which are significant producers and exporters of forestry products (including, in the latter region, Papua and New Guinea), and there are certain other countries, though not among major producers, for which forestry exports are actually or potentially of importance, but for which, for lack of space, data could not be provided in the Summary Tabulations. Statistics on forestry-production and -trade for these countries are, however, generally available from the relevant FAO forestry statistics and are, to some extent, also provided in footnotes to text-passages and in Annex II.

2 There are 20 four-digit headings in CCCN Chapters 1-24 allocated

exclusively or predominantly to various tree-fruits. 3cf: MDF/23, MDF/3; MDF/W/2, 16, 53; C/W/467 and Add.l, MDF/W/49

and Corr.l; C/M/183, 187, 188, 190, 191 and 192.

MDF/W/52 Page 8

in the Customs Cooperation Council Nomenclature (CCCN) in Chapter 44 (wood and wood products), in Chapter 45 (cork and cork products) and in CCCN Chapter 47 (woodpulp). Details of the product coverage in relation to specific tariff headings and positions in these three CCCN Chapters are shown in Table V.

5. Slightly more than 30 per cent of the earth's land surface is covered by forests or woodlands. Man has exploited forests wherever forest resources were easily accessible, and where uses and markets for forest products could be found, and has changed, in the process, the natural vegetation cover. In the more densely populated areas, forests compete not only with agriculture but also with land-use for urban settlements, industrial establishments and road networks. In other areas of the world forests have been thinned out by use for fuelwood, for pasture, and expanding agriculture, shifting cultivation, in some cases to the point of virtual destruction. In many parts of arid and semi-arid Africa, Asia, South America and certain insular locations the destruction of forests is of crisis proportions.

6. Given the great diversity of forests in the different areas of the world, and the way local populations experience their respective forest, there exists no really adequate way of conveying verbally, in a few succinct paragraphs, a picture of the world's forest-cover and -characteristics. In the circumstances, it was thought that, for purposes of this note, a tabular presentation of some quantitative data would, perhaps, best convey the extent of possible forest resources. This approach does have some limitations as regards possibilities for exact inter-country comparisons and attention is therefore invited to the many caveats in the text preceding Table I in Section A.

7. One of the difficulties in dealing with the subject of international trade in wood and wood semi-manufacturers is the profusion of commercially used names for given species of wood and the large number of tree species. In the 'Sixties it was considered (Elseviers) that there existed more than 2,500 botanical tree species, and hence species of wood. Recent reference books list even more species. For many of the main species there may exist several sub-species and also local variants of names and designations. Considerable time and effort

CCCN Chapter 46 covers plaiting materials and products made thereof. These materials and products are not covered in this note, nor are bamboo poles or rattan, both of which are classifiable in Chapter 14. To the extent that bamboo or rattan has been processed into a product covered in Chapter 44, the tariff information provided in Section D might be relevant.

2 For a development of the question of forest classification and

nomenclature see "Tropical Forests Ecosystem - a state of knowledge report", prepared by UNESCO/UNEP/FAO, 1978. For a short survey of the world's major forest regions, in terms of wood resources, with a summary description of forest characteristics, see "Wood Resources and Their Use as Raw Material", UNIDO/1S.399, Aug. 83 (based on FAO's comprehensive forest documentation) and, for a short descriptive commentary, a special issue of the publication "Co-Evolution", No. 15 (83/84).

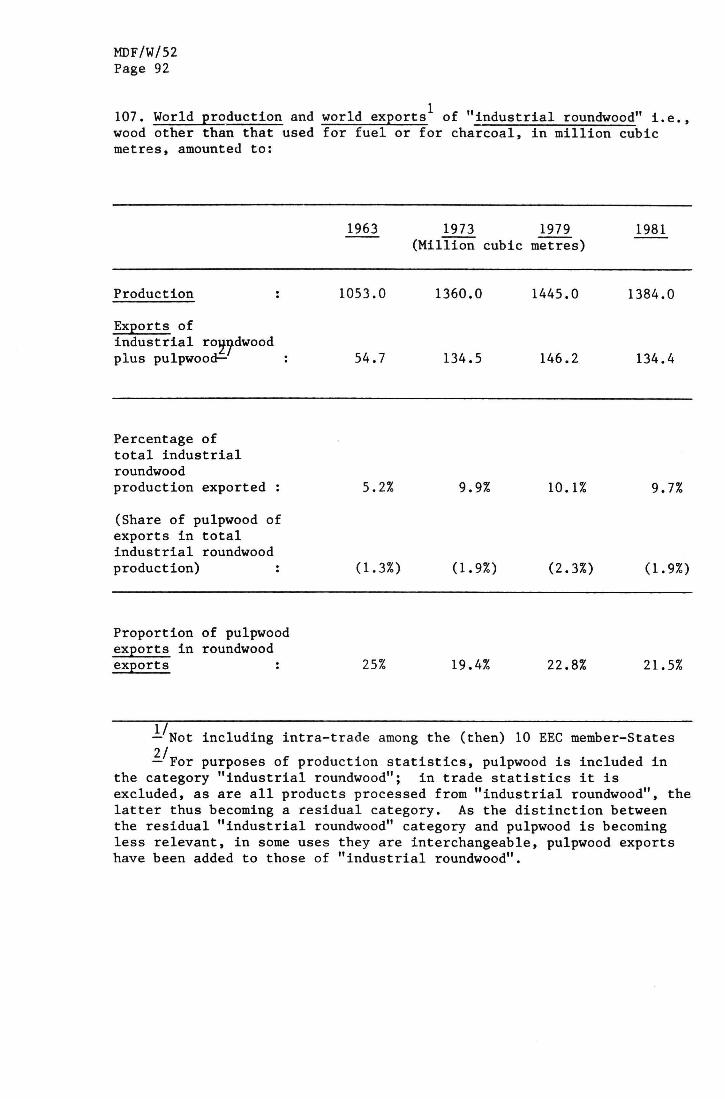

MDF/W/52 Page 9

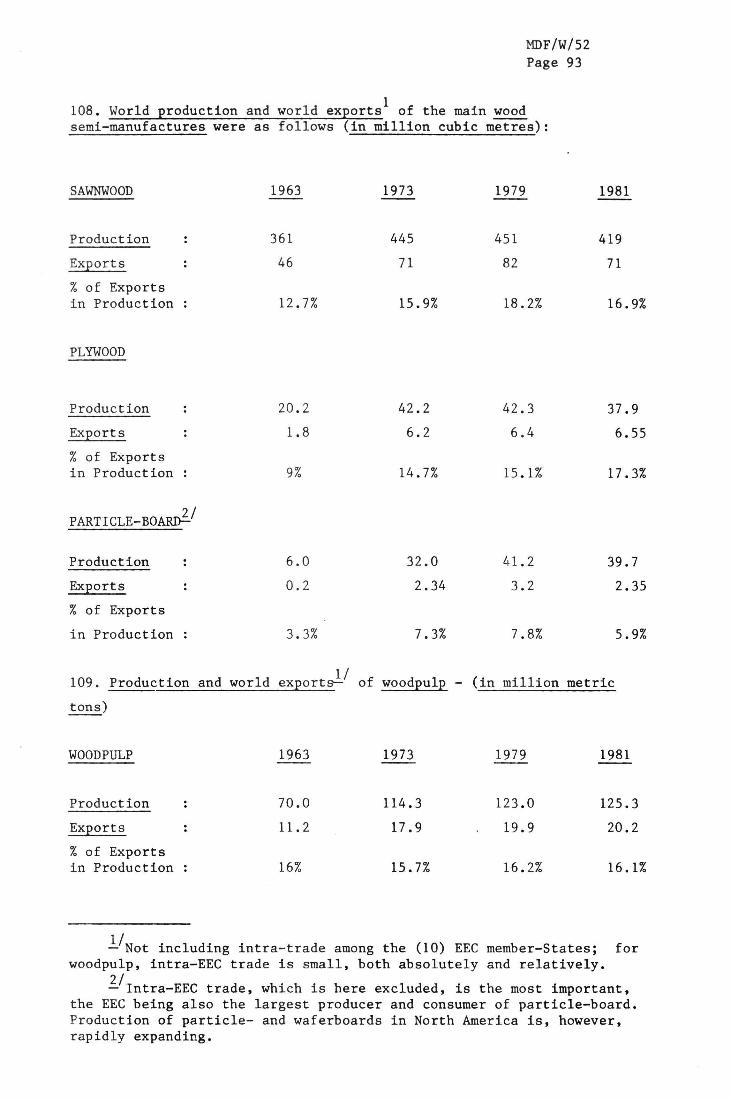

has been invested by many individuals, research institutions and committees in arriving at a uniform international nomenclature for the identification of the main species used and traded. Even so, there remain today at least some five hundred different wood species-varieties which are of actual or potential significance in international trade. It is clearly beyond the possibilities of a note like this one to deal in any detail with all the possible variants. The approach adopted was therefore, to examine, first, the existing import tariff schedules of GATT member countries and, then, to note the kind of distinctions made, by species or otherwise, and, finally, to examine these distinctions and the effect they may have on trade. On the basis of this examination, it can be said that the species-distinctions in the tariff schedules of GATT member countries are, on the whole, quite limited. Nevertheless, such species-distinctions as do exist in the tariff schedules could, in some cases, be a source of uncertainty as to what tariff treatment is applicable to a given wood variety, or to the products made thereof.

8. As regards statistical tabulations, two approaches have been adopted. One, as in Table I - Section A, attempts to provide a "snapshot", as it were, of the situation at a given moment, bringing together various elements which, it is hoped, will permit an overall impression to be gained of forest resources, current forestry production and use and the interaction of resources and needs on trade flows. Similarly, in Table II - Section B, it is attempted to provide follow-through data on timber availabilities, the primary manufacturing stages which the available timber undergoes in given countries (taking account also of net imports or exports) and, finally, an account of the type and approximate volume of wood semi-manufactures and of woodpulp available for further processing. The juxtaposition of the various data is not without risk and in order to avoid, to the extent possible, misleading conclusions to be drawn from these summary tabulations, relating to one year only, attention is invited to the various qualifying remarks in the text of this note. The second approach is of the more customary nature, setting out statistical data on trends in production and trade by means of time-series tabulations; these are shown in Annex I-B and Annex II.

9. Given the vast amount of forestry data which are compiled worldwide and the practical difficulties not only in presenting these, but also in reading tightly packed statistical tables, this note opts for selectivity, limiting the data presented for forest resources and production in the summary tabulations to 1979. For import and export data in Table III (which also gives origins of import and export destinations) and in Table IV, the data shown were the latest available (up to 1982) when Spec(84)13 was issued. Data in Section D (Table V) are, again, the latest available or, for MTN trade concessions, the final MTN tariff rates (i.e. those applied as of 1.1.1986, or 1.1.1987). As regards Annex I-B, production and trada data are shown for 1963, 1973, 1979 and 1981. Data covered in the trade matrix in

Among these, dealing with a wide range of forestry-research related topics, the International Union of Forestry Research Organizations (IUFRO), founded in 1891-92, might be cited. Today, IUFRO has a membership of about ten thousand scientists, and 500 institutes from 85 countries - united in promoting international co-operation in forestry research activities.

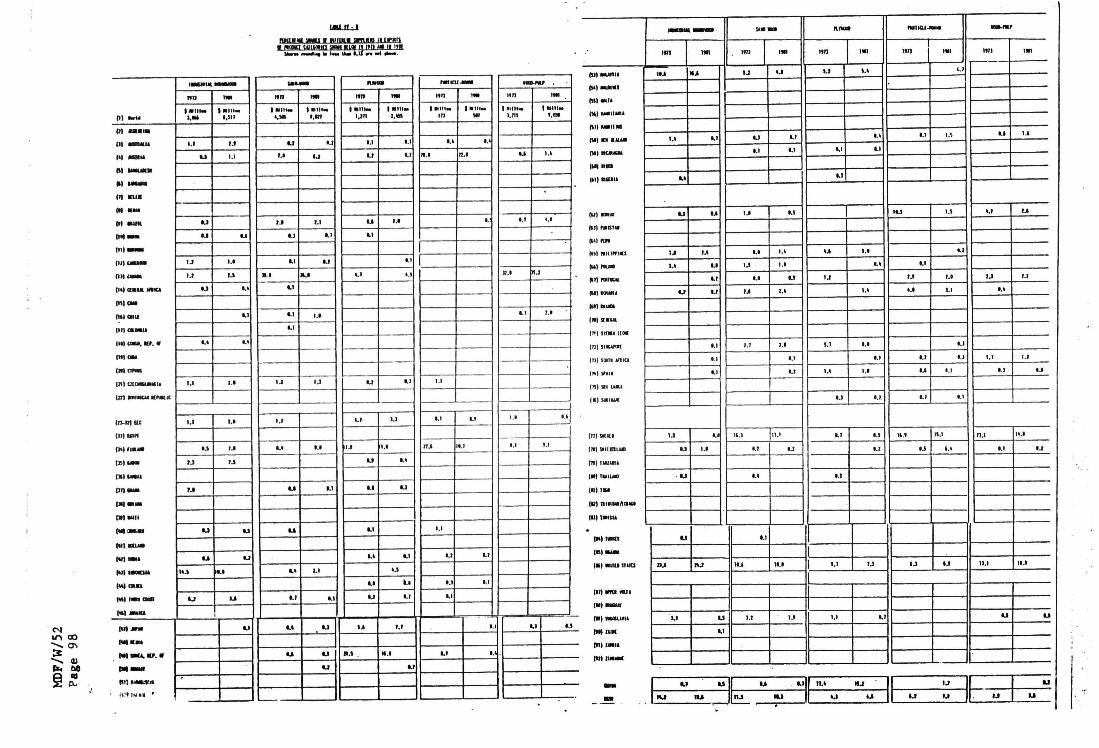

2 An indication is also provided of import duty reductions to be

phased in by Japan over the period 1986 to 1988.

MDF/W/52 Page 10

Annex II cover 1963, 1973 and 1981, unless otherwise indicated. The year 1963 was chosen as a point of departure, because UN statistics available for that year are more readily comparable with statistics for subsequent years than the pre-1963 data. 1973 seemed a logical interval, was a year of high-level wood industry activity in North America, but is also the year in which the post-war housing construction boom in Europe came to an end; 1979 was chosen because much of the resource/cum/production statistics available from different sources could be related to 1979/80 and, finally, 1981 was chosen as the year for which data for a considerable number of countries were available at the time of writing. Several of the developed countries in 1984 and 1985, saw a recovery in forestry industry production and trade, often falling short, however, of the peak levels reached in the mid 1970's, or in 1979. Nevertheless, the data for these earlier years do provide an indication of most countries'forestry related activities and interests. Certain recent trade developments are, to the extent possible, identified separately in later parts of this note.

10. While only a relatively small part of the world's total forestry products production moves into international trade (say, around 10 per cent, in terms of the volume of industrial roundwood production equivalent) exports of wood-, cork- and semi-manufactures thereof and of

The trade situation, which, for practical purposes, in Spec(84)13 had to be frozen in 1981/82, has, of course, further evolved. While the period 1981 through the first half of 1983 can, in general, be characterized as recessionary, for both production and trade in forestry products, an improvement in trade opportunities and in the actual volume of trade flows, particularly those destined to the United States, can be noted as from the second half of 1983, when - in some cases - the high points reached in the 1970s were again attained, or even surpassed, with some exceptions, notably a stagnation or even decline in the volume of shipments of tropical wood semi-manufactures from Africa to Europe, a reflection of the recession in housebuilding and construction activity in Europe (Imports of tropical sawnwood into Europe peaked in 1979). The upturn in demand for forestry products in certain markets over the last two years notwithstanding, the profitability record of the forest product industries was rather mixed, depending not only on past and present management results of the enterprises concerned, but dependent also on the structure of firms, with those firms that could benefit from the earlier and more significant upturn in demand for such downstream products as pulp, paper and paper products experiencing generally better returns than firms dependent on wood products only. Like prices for many other commodities, export prices for logs and lumber in international markets in the mid-Eighties were, on the whole, below those of earlier years (but are now expected to firm). Early 1986 returns point to a slowdown of export growth for several major forestry products exports and possibly a weakening of export prices for woodpulp. It should, however, also be recalled in this context, that, since the trade data for 1979, 1981 and 1982 were recorded, the world's major trading currencies have undergone repeated - and sometimes major -adjustments which have, of course, not been without repercussion on trading opportunities and the direction of trade-flows. Recent changes in petroleum prices will also not be without repercussions on production and trade-flow possibilities.

MDF/W/52 Page 11

woodpulp, from all sources, are important in international trade, amounting to somewhat more than 31 thousand million US dollars annually, on average, in 1979 and 1980 (not including certain finished wood manufactures or furniture), or about 1.7 per cent of world exports of all commodities.

11. It is important to bear in mind that the wood-processing industries have undergone major technical and structural changes since international trading opportunities opened up again, in a significant way, in the mid-1950s, when the combined effect of the ravages of war and, as a result thereof, currency restrictions, had started to be overcome in many countries, and when efforts and institutional arrangements for regional and global co-operation, including those arising from the early GATT multilateral trade negotiation rounds, started to take effect.

12. On the technical side there have been remarkable changes in forest cultivation, -harvesting and -logging practices and facilities. Silviculture, as a science, and in actual practice, has made great progress. At the level of the wood-processing industries, machine-shaping and -joinery has become increasingly widespread, while, unfortunately, artisanal skills have been on the decline, at least relatively so. Increasing reliance on machine processing has favoured the use of uniform, homogeneous inputs. This, in turn, favoured increasing use of the technically more homogeneous coniferous woods (in terms of processing characteristics), then increased use of blockboard, plywood and fibre- and particle-board, of varying characteristics and specifications, and of certain varieties of tropical woods.

13. The increasing availability of these items and particularly so the, by now, widespread use of particle-board and fibre-board (at least in the developed areas), has considerably enlarged the raw material base of the industry. "Wood-waste" (both processing-waste and waste-wood, i.e. wood from species previously considered unfit for joinery, panel-boards, and pulping) has become a very relative term, indeed. New wood-laminating, wood-preservation and wood-colouring techniques have still further enlarged the resource-base for the industry by opening up use-possibilities for less durable and less decorative woods (of which one demand-enhancing variant is a partly transparent overprint process for otherwise non-decorative veneers). As regards pulpwood requirements, the recycling of paper, increased use-possibilities for short-fibre hardwood pulps and of wood chips, including those from rubber trees and mangrove tree varieties, have still further enlarged the raw material base. Moreover, pulping processes which produce larger usable quantities of pulp for a given quantity of wood input, as compared with conventional, chemical, pulp-manufacturing processes, are coming more widely into use. Nor are developments at their end. Great strides are being made in developing production and markets for greater

More than 2.0 per cent if paper were also be included. The 1.7 per cent figure also does not cover the not inconsiderable value of wooden crates and packings, used in exports of non- wood products.

MDF/W/52 Page 12

strength "oriented-flakeboard". The increasing availability and use of medium-density fibreboard - more recently also in Europe - increases competition for natural wood in furniture making. Greater use of exterior-grade flakeboard for construction will increase competitive pressure on construction-grade plywood. Fighting back, the plywood industry has now under development processes and center-less veneer lathes for producing technically acceptable peeled plywood veneer from small-diameter logs. The particle-board industry's response is a further speed-up in panel-forming and pressing processes. Computer control of sorting, sawing and milling operations is starting to spread for producing sawn and milled wood products. Milling machines with microchip-sensors and precise, motor- or hydraulically-controlled, operations, and even high pressure water-jet cutting and laser controlled finishing and cutting techniques are starting to make their appearance. Certain production processes, such as door manufacture (sometimes wafer-thin veneers over a honeycomb cardboard core) and even the fabrication of wall-size panels for pre-fabricated houses (in particular„European modular prefabs), are starting to be fully automated.

14. The whole of the forest products trade has been impacted in a major way by the rapid development of the export trade in tropical timber, estimated by FAO to have grown, in log equivalents, from about 7 million cubic metres in the 1950's to approximately 70 million cubic metres in a recent year. While in the early 1950s only a few dozen tropical wood species were of some significance in international trade, the number of

This is primarily a North American development and is only now starting to spread to Europe where it is also known as structureboard, or waferboard ("Stirlingboard", in the UK). Outer - and inner - layers of thin woodflakes are put down in different directions, rather than at random. This orientation gives more strength (two- or three-fold increase in bending strength). (Because of their matted appearance such boards require veneer or plastic overlays, if intended for furniture surface materials.) As regards medium density fibre (MDF) board it is probably correct to say that (once it becomes more widely available) it could have a wider range of uses than any other manufactured board material. MDF board has high strength, smooth surfaces, excellent machining characteristics (like good, solid wood) good edge quality and good finishing properties.

2 An interesting summary description of modern manufacturing

processes in the wood processing industry and the characteristics and uses of many types of wood semi-manufactures was recently published in "A Review of Technology and Technological Development in the Wood and Wood Processing Industry and its Implications for Developing Countries", document: UNIDO/IS. 413, of Nov. 1983. For somewhat broader aspects of wood industry production and trade developments, with particular emphasis on tropical wood varieties, attention is invited to (FAO) UNIDO document "Wood Resources and their Use as Raw Material", UNIDO/IS. 339, and "First World-Wide Study of the Wood and Wood-Processing Industries", UNIDO/IS. 398. Another, recent, study to be mentioned is "Mechanical Processing of Tropical Hardwood in Developing Countries: Issues and Prospects for the Plywood Industry's Development in the Asia - Pacific Region" in: Case Studies on Industrial Processing of Primary Products, Commonwealth Secretariat and IBRD.

MDF/W/52 Page 13

tropical species traded now is figured in hundreds. Originally, exports from tropical suppliers consisted mainly of logs. Many of these countries now restrict or prohibit, or otherwise discourage, log exports, while encouraging exports of sawnwood and plywood, exports of both of which have expanded manifold, as have exports of other products made of tropical wood varieties.

15. Problems of log restrictions have, in some cases, been overcome through joint ventures for forest-resource exploitation, accompanied by the establishment of transformation industries and international marketing support measures. Many of the forestry enterprises which have sprung up over the last two decades have been geared expressly to supplying export markets and most of these ventures have been quite successful in this respect. Joint ventures and transnational investment have not been limited to developed and developing country co-operation, but are also a feature of developed-cum-developed and developing-cum-developing country co-operation. As joint ventures spread, trade flows were affected, and so were production developments in various locations.

16. Large-scale increases in exports of semi-finished wood products to distant markets have been made possible by standardizing grading, performance specifications, shipping documentation, contract conditions, transport and also improved customs clearance facilities, assisted, inter alia, by the work of international standardizing bodies. Container transport is becoming increasingly important for shipments of wood semi-manufactures and is also widely used for shipping waste paper to be recycled into paper and paperboard manufactures. After the spread of shipping bundled lots, sometimes palletized, the development of specialized ocean transport and of special port terminal-facilities have been key elements in the development of that trade. Part of the trade in woodpulp is conducted on the basis of long-term supply contracts; for transport to Japan some 70 special purpose wood-chip bulk transporters ply the Seas. In some cases the interested industries -particularly in respect of pulp and products made thereof - have diversified both their sources of raw material supplies and their market outlets through international investment in the form of new foreign investment, by acquisitions, or joint ventures, all spurred by increasing demand for wood, pulp and paper, in the face of expanding consumer markets and explosive growth in the needs of the print -, publishing and communications-media, for data-processing uses (so far the paperless office is a myth, but work on many fronts (including by ECE) for standardizing intra- and inter-industry and transport-documentation electronic data interchanges (EDI), aiming at an increasingly paperless office-environment) is accelerating, and in uses for sanitary purposes and by the packaging industries.

For a recent bibliographical listing of ISO standards for wood, wood semi-manufactures, cork and for paper pulp, see ISO document "1 Bibliography", 4th edition, Geneva, March 1984. Among international bodies involved in wood-industry products' standardization work, the UN/ECE should be mentioned. For ECE-recommended standards for construction sawn-wood, cf. Timber Bulletin, Volume XXXIV, supplement 16, November 1982. Work on shipping policies, standardization of freight tariff rules, multi-modal (door to door) container traffic, etc., has been, and continues to be, undertaken by UNCTAD and OECD.

MDF/W/52 Page 14

17. Certain forest resources, hitherto largely inaccessible, are seen as becoming exploitable, for instance additional timber and wood-chips from the USSR could become available for export in the wake of ongoing exploration and development of resources in Siberia and the expansion and improvement of the USSR's transport system. In the Amazon Basin, considerable progress has been made for operating, on a sustained-yield basis, several large woodpulp complexes, the output of which is destined predominantly for export, and, overall, the accessibility of the Amazon region's forest resources is improving, as transport infrastructure-development (including rail) proceeds. In other regions of the world (for instance in New Zealand, South Africa, in several EEC countries and in parts of the United States) output from timber and pulpwood plantations, established in earlier decades, is starting to become available for harvesting and is already a factor in the market. Pulpwood plantations are also being created in several locations in Africa, in Asia and in Oceania. Reforestation efforts are being intensified almost everywhere.

18. While it will be seen from Section A that different regions and countries are differently endowed with forest resources, either in terms of forest per total land-area, or forest resources per caput, and while forestry policy objectives are, by necessity, accorded different levels of importance within different countries' socio-economic policy objectives, it can be said, generally, that the governments of all of the countries covered by this note are keenly aware of the need to protect forest resources and all of them have on their statute books policies for maintaining forests at desirable levels and, whenever possible, to manage this resource so as to obtain sustained yields and to balance short-, medium- and long-term interests. This is true regardless of whether forest-ownership is public, provincial, communal or private. There exists considerable concern and international support for the adoption of appropriate forest management policies and some international financial and technical assistance has been directed to finance efforts for halting desertification and for promoting reforestation, including schemes financed by the EEC, by individual governments and by the IBRD and by regional development-banks and development-associations.

19. As regards trade, it will be noted that, as a result of various regional-integration schemes and -preferential arrangements, the successive Lomé-Conventions and the GSP, a large part of international trade in wood and wood products has been moving free of import duties for some time, at least as far as imports into many developed market-economy countries are concerned. Undoubtedly, the different regional arrangements are of considerable importance in promoting regional economic development and trade expansion. This is the very purpose of these arrangements. Yet, for the group of products covered by this note, an examination of the data in Table III-B, on import-sourcing and export-destinations, shows (North America, perhaps, excepted) that resource- and trade-complementarity is often more important between different regions than within a given region or preference-area.

20. Trade liberalization and duty-reduction or elimination in various contexts notwithstanding, some wood products and wood-derivative products are considered "sensitive" in several developed countries and continue to be (or are now [temporarily]) subject to positive m.f.n. import duties, which may be relatively high, in some instances. M.f.n. import duties on wood and wood products in many of the developing countries are very often high, though, perhaps, not higher than import duties for many other classes of goods.

MDF/W/52 Page 15

21. Since virtually all countries have some forests or woodlands and, associated therewith, some wood production and -processing, imports of wood and wood products are quite often considered as being not among essential import needs and are thus likely to be among restricted items when balance-of-payments import restrictions, currently widespread in the developing areas, are imposed.

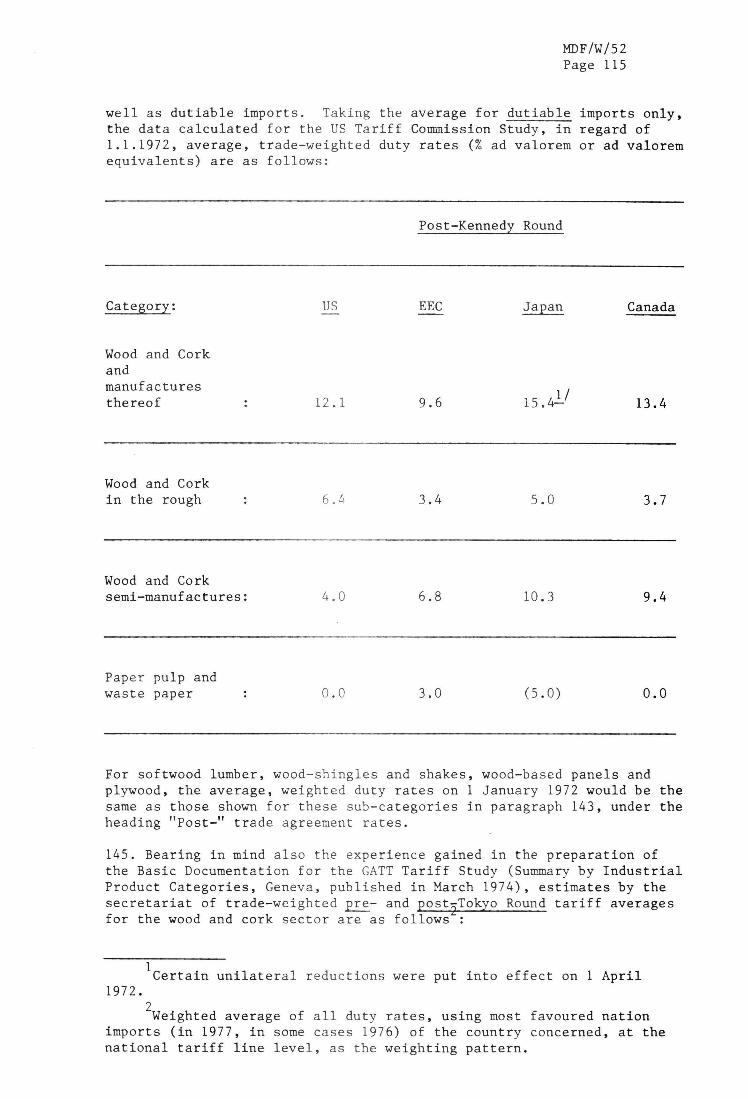

22. Less favourable tariff treatment for wood and wood products, depending on origin, is a matter of serious concern to a number of countries, including some of the major forestry products producers and exporters. In past discussions, these countries have pointed out that for many types of forestry products the market is highly competitive and price sensitive, with the result that even relatively low nominal rates of duty can have disproportionate effects on export marketing possibilities, particularly when tariff protection's on top of such natural protection as significant transport costs. Another area of concern as regards wood products is the existence of differentiation in tariff treatment for given products having the same use, but made from different woods. Another question that arises is the level of effective tariff protection, as compared with nominal tariff levels.

23. From such documentation on non-tariff measures as has been examined for this note, it is evident that certain non-tariff measure obstacles to trade in forestry products exist. Some of these measures are intended to deal with temporary problems (mitigating storm damage, or measures for protecting the balance-of-payments) or with measures designed to protect the flora, or health (formaldehyde emissions, etc.). Other measures may be designed to serve forest-resource maintenance or -development, or social policy objectives. The picture of the many possible and varied government support activities, actual or only perceived, gets blurred, and sometimes very complicated, by the fact that the State is, in many instances, the owner of part, perhaps even the major part, of the forest resource. Forest resource disposition- or development-measures thus become merged with general economic objectives and policies.

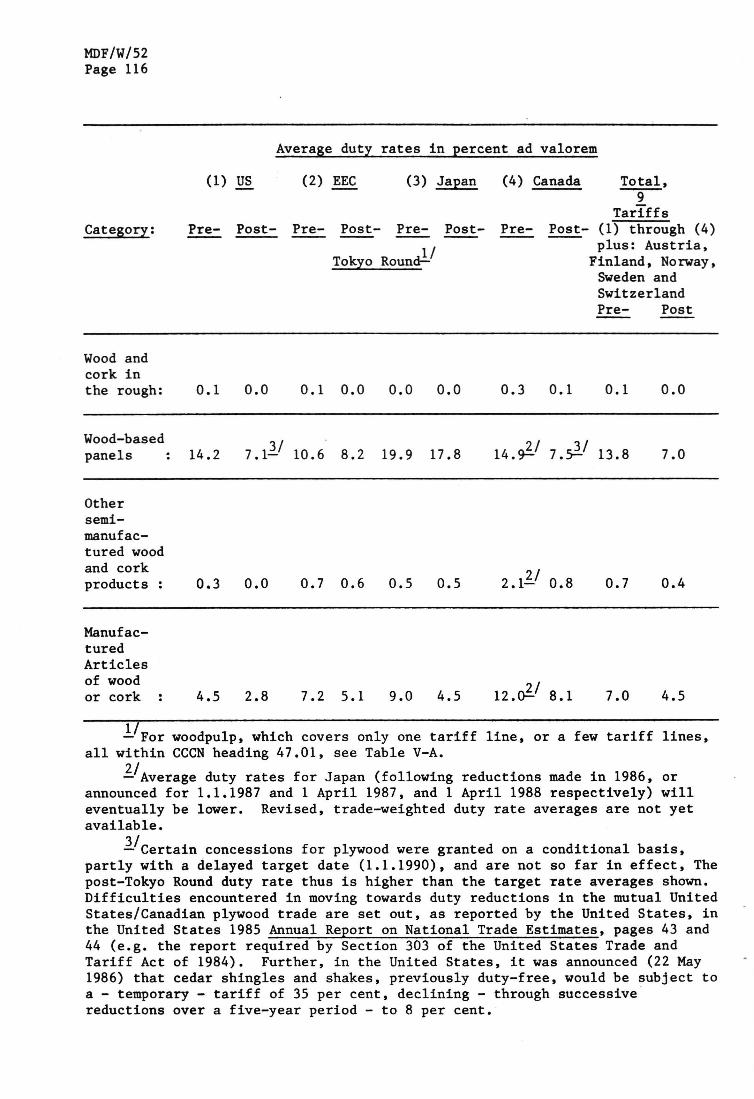

24. Like other sectors of trade, international trade in wood and wood-products is affected by numerous technical standards and regulations. A reading of the relevant documentation suggests that some of the existing technical barriers to trade are, perhaps, due to insufficient familiarity of importers, exporters and administrations with the technical characteristics of wood and wood-products available from, and being offered for export by, suppliers in other countries. There is some indication that problems in this area, notwithstanding the fact that standards are sometimes set and enforced by national- or regional professional or industry associations, can often be, and have in the past been, resolved through bilateral consultations between interested countries.

If recently published data on international transportation cost for US imports in 1981 are generally representative, the freight factor (ratio of international transportation cost to the free-alongside value of the product being shipped) for lumber (and even more so for paper and paperboard) is particularly high, when compared with freight factors for 18 other broad import categories. Ref: H. McFarland "Transportation Cost for US Imports from Developed and Developing Countries" in The Journal of Development Studies, London, Vol. 21, No. 4, July 1985.

MDF/W/52 Page 16

25. Special thanks are due to the Geneva-based Timber Section of the ECE/FAO Agriculture and Timber Division for the generous access provided to their reference library facilities. Without this facility the preparation of the overview note (within a relatively short span of time, when Spec(84)13 was first presented) would not have been possible. The findings arrived at in this note are, of course, the sole responsibility of the author. Suggestions for any corrections or amendments that might be required will be appreciated.

Since Spec(84)13 was circulated, 1985 having been designated "international Year of the Forest", much further research by many individuals and institutes has gone into the investigation of the world's varied forest resources, their protection, and their proper use for social and economic development. Some of the research results, findings and conclusions, for instance those published in connection with the IX World Forestry Congress (Mexico, July 1985) and considered to be relevant for this note, have - to the extent possible - been reflected in this revision and partial up-date. Last, but not least, it should be mentionned that ECE/FAO in September/October 1985 published an up-dated and much expanded survey of "The forest resources of the ECE region (Europe, the USSR, North America)". The wealth of information provided by that survey (some 200 pages, including notes on methodology) goes well beyond the summary information, based to some extent on earlier ECE/FAO survey data, attempted in this note. Other material, such as papers prepared for UNIDO's recent "First World-Wide Study of the Wood and Wood Processing Industries" did become available in time to be reflected, as appropriate, in this note and account has also been taken of some of the major conclusions of the first meeting of ILO's, recently established, Forestry and Wood Industries Committee (cf. ILO, document IC/FWl/1/17 - 1986).

MDF/W/52 Page 17

A. FOREST RESOURCES, THEIR USE AND POTENTIAL

26. The main thrust of this overview note is aimed at trade-related topics. However, as primary production and, thereafter, exports of wood (and some of the products derived therefrom) depend on the existence of an adequate natural resource base, namely forests of various types and species-composition, it seems relevant to consider briefly that resource base, first globally, then by regions and, in tabular form, by countries.

27. On a global basis, were it not for the competition in land-use by agriculture, pasture, fuelwood collection, timber offtake, urban settlement, road networks, and, in some regions, an expanding desert, more than 60 per cent of the world's land surface might be, and presumably once was, covered by forests, nature's way of providing a protective cover for the soil. As it is, the original natural forests have been much thinned out, in some areas to the point of virtual disappearance. Overall, only slightly more than 30 per cent of the earth's land surface, or 4,100 million ha. , is now covered with closed forests or other wooded land, wherein the latter designation, standardizing efforts for common definitions notwithstanding, allows a considerable range of interpretations as to the nature and density of tree-stands. It is estimated that about three-fourths of the world's forest/woodland area would qualify for the designation "closed forests".

28. As regards types of natural forests, one finds pine, spruce, birch, aspens, alders and larch in the boreal forests in the North, then, proceeding southward, vast stretches of increasingly more varied stands of conifers, mixed conifer-broadleaved forests in the temperate regions, sparse tree coverage in most of the Mediterranean regions, some scrubs and woodland in the savanna, then, increasingly dense, humid forests and the wet, evergreen tropical forests of Latin America, Africa and South and South-East Asia and parts of Oceania. Tree coverage decreases again as one moves still farther south, except where a maritime, humid climate favours forest growth, such as in parts of southern Chile. In all regions, elevation above sea level makes a considerable difference as to the type of forests one finds, with, as a rule, coniferous tree-stands on the flanks of the great mountain ranges. Australia and such insular locations as Madagascar are different again as regards flora and forest characteristics. More than one half of all tropical shores are fringed with mangroves and the great river systems on earth have their own characteristic forests. Different tree species have, over the ages, found the particular ecological niche most suited to their needs, or one to which they could adapt. This has led to a bewildering variety of tree species, most of all in the tropical forests.

One hectar (ha.)„= 100 x lOOmetres = 10,000 square metres = 2.47 acres; 100 ha. = 1 km ; 1 million ha. = 10,000 km , cf. also footnote 2 on page 13.

2 "Closed forest" is a forest which has a closed tree canopy.

"Other wooded land" designates, in general, areas where trees predominate, but without constituting a full tree canopy. (Closed

./.

MDF/W/52 Page 18

Footnote (cont'd)

forests - as defined by FAO - are those which, by their different strata and their undergrowth, cover a large part of, or all, the ground and which, in general, do not have a continuous herbaceus stratum (except in certain coniferous forests.) Other wooded land - also "open tree formations" - are those in which the canopy is generally less closed. These are essentially mixed broadleaved forest-grassland formations, such as the South-Amercian "cerrado" and "chaco", the African woodlands and wooded and tree savannas. - FAO Forestry Paper 37). About 1,600 million ha. of closed forests are in the temperate zone and about 1,200 million ha. in the tropical regions. The volume of standing timber per hectar in the closed forest averages 80 to 100 cubic metres in the temperate regions and 100 to more than 200 cubic metres (on account of the more active bioclimatic conditions) in the tropics. The estimated total volume of growing stock of closed forests is 145,000 million in the temperate regions and about 185,000 million in the tropical forest. About 75 per cent of the forest area in the temperate and northern regions is covered with coniferous stands. Coniferous forests account for 2.5 per cent of total forest area in the tropical regions. The term "other wooded land" applies to about 400 million ha. in the temperate zone and 750 million ha. in the tropical area. Total growing stock in these "other" woodlands is estimated at 20,000 million cubic metres, two-thirds of which is in the tropical regions (as defined by FAO, the area occuring between the Tropics of Cancer and Capricorn). Less than one-half of the forest area is considered "operable" - the remainder is not operational for a variety of reasons, such as physical or economic inaccessability, or legal constraints designed to preserve the forest for its protection potential. The operable volume of growing stock in the developed areas is estimated at 96,000 million cubic metres (of which 72,500 million coniferous). The figures for total (figures for coniferous in parentheses) volume of operable growing stock, in 1000 million cubic metres, are: North America - 36.4 (26.6); Europe -14.1 (8.8); USSR - 40.0 (33.2) - other developed - 5.5 (3.9). The estimated volume of total growing stock in the developing areas (much of it not operable, however) is of the order, in 1000 million cubic metres, of close to 80.0 for South, -Central America and Caricom, 38.8 for Africa and 43 for Asia (including insular). Ref: "Wood Resources and Their Use as Raw Material"; op.cit.

MDF/W/52 Page 19

29. Broadly speaking, the USSR accounts for about 22 per cent of the world's forest area (about 29 per cent of world closed forest area). Of the world's coniferous forests, the share of the USSR, in terms of area, is about 60 per cent. Total growing stock (in 1975) was estimated at 74,700 million cubic metres. Growing stock of "operable" forests (i.e. physically accessible and with logging plans) is of the order of close to 50,000 million cubic metres (including stands newly accessible via the BAM railroad and feeder lines). Coniferous species represent more than four-fifths of the USSR's operable forest stock. The corresponding percentages for other regions, as regards total forest area (and closed forests respectively), are: about 19 per cent (7 per cent) for the African continent; about 19 per cent (22.5 per cent) for South- and Central-America; 15.4 per cent (17.6 per cent) for North America; about 13 per cent (15 per cent) for Asia; 4.6 per cent (3 per cent) for the Oceania Pacific region; 4.1 per cent (5.2 per cent) for the European region. For the world as a whole, somewhat more than one half of the forest and woodland area is located in developing countries. Forest resources in terms of ha. of closed forest/per caput (plus ha. of open forest/per caput) in the early 1970s were estimated to be of the following orders of magnitude: North America 2.0 (0.7); Central America 0.5 (0.02); South America 2.4 (0.7); Africa 0.4 (1.3); Europe 0.3 (0.1); USSR 3.0 (0.4); Asia 0.2 (0.3); Oceania and Pacific regions 3.6 (4.8). World average: 0.7 (0.3).

30. In terms of total area under forests, it can be said that in most of the developed countries the forest area is either stable, or increasing slowly. In the developed countries most lumber companies and State forest administrations act on the principle that they are not in the tree-cutting business but in the tree-growing business; the objective is not only to preserve the area under forests but also to make each hectar of forest produce annually more timber than is cut (until final harvest and/or replanting at a given site). In most of the developing countries, despite recent attention and ongoing efforts for reforestation, or afforestation, the total area under forests is still decreasing. As population growth in most developing countries is high (absolutely, or in relative terms), average per caput availabilities of forest land in the developing countries have probably declined since the above estimates were published.

31. Not only is the forest-resource endowment different from region to region, but there are also great differences in the way this resource is used. In the developed countries the overwhelming part of the forest resource, if harvested, is nowadays, it was not always so, destined for the market. In order to be profitable, it is marketed largely for industrial uses. In most of the developing countries,- however, conditions are such that most of the wood removals are for firewood, for cooking and heating.

North America's coniferous forests account for more than one fourth of the world total.

2 Data based on, and adapted from, "The Global 2000 Report to the

President" - US Council on Environmental Quality and US Dept. of State, Washington D.C., 1980. Summary data on land suitable as arable/cum/ cropland and of forest land potential in different regions of the world are given in the GAIA Atlas of Planet Management, Pan Books Ltd, London 1985, pages 24-32. Data on total forest and woodland areas of GATT countries are given in Table I of this note.

MDF/W/52 Page 20

32. While in Latin America, except for unexplored and unsettled areas (such as the vast 'terras devolutas' in Brazil, which are owned by the Federal Government), much of the land, including the forest, is privately owned, in Africa and Asia, and partly in developing Oceania, the forests are administered and exploited on the basis of communal-, rather than individual- or State-ownership, although the State often holds ownership-title. The communal rights and uses include the gathering of forest-fruits and -fibres, the collection of wooden poles etc. for construction, and of firewood, as well as certain grazing and hunting rights. This system works well as long as sufficient forest-space in relation to population and its needs is available. Once population increases significantly, strains on the system develop rapidly, starting normally either from the fuelwood- or the food-shortage end. Once food starts to be in short supply, pressure arises for bringing additional land under cultivation. As easily cultivable land is normally already being exploited, this means recourse to nearby forest land. The forest is cleared, often by burning, and food crops are then planted. Within two to three years, tree-undergrowth and weeds (which are difficult to eliminate from the imperfectly cleared ex-forest plot) take over again, making agricultural pursuits toilsome and unproductive. This provides an incentive to repeat the clearing/cum planting operation on a new plot - i.e. shifting9cultivation, which leaves behind a degraded forest and is at present , probably, the main source of overall forest destruction in the developing areas. In the forests of some of the developed countries, wildlife populations (both small and big game) are rising rapidly, the result both of recent restrictive regulations and reduced forest-care operations. There is some reason to fear long-term degradation and damage to the rejuvenation of existing natural forests

(a matter which is particularly serious in respect of protective mountain forests), due to excessive forest resource use (including for sports and leisure), or destruction by wildlife or, in some cases, feral animals.

33. Collection of wood for fuel needs places a heavy toll on the forest. First, deadwood is collected. When deadwood is gone, branches are chopped off. Finally, the trees go. With fuelwood lacking, agricultural waste materials and dried animal dung are used for fuel. With less natural fertilizer thus available, soil fertility and food production-capacity declines. This produces pressure for more land to be brought under cultivation, which manifests itself in increased pressure on remaining forest lands. When combined pressure for fuelwood and cultivable land leads to increased hillside-farming and fuelwood collection, soil erosion makes rapid headway, followed by silting of water-courses and flooding, creating new and additional problems over wider and wider areas. In the arid and semi-arid zones of the world, wind, rather than water, is the main agent of erosion. Once the protective cover of trees and shrubs is removed, most often for firewood and animal fodder, the destructive force of the wind is unrestrained. The fine fertile soil particles are swept away, leaving the heavier, sandy ones behind. The soil becomes progressively less fertile and less productive. Once wind erosion has started, the moving soil particles add to the process, in sand-blasting fashion, scouring everything in their path.

The question of forest ownership - very relevant in the context of assessing resource potential - is a very complex one. Some of these complexities, starting with the very definition of what constitutes a

./•

MDF/W/52 Page 21

Footnote (cont'd)

forest (with considerable differences between different countries), are highlighted in a "unasylva" review article (in Vol. 37, No. 148 (85/2)) of "Forêt et environnement en droit comparé et international", M. Prieur éd., Presses universitaires de France, 1983.

2 J. Westoby, in a book review article, published in "unasylva",

Vol. 37, No. 148/85-2, makes the point that it is a misconception to assume that tropical deforestation is necessarily the result of overpopulation, recalling that vast areas of tropical forest were destroyed in centuries past, in places and at times "when there was little if any population; indeed, populations - slaves and later indented labour - had to be brought in to accomplish the deforestation ... Brazil's northeast, and most of the Caribbean were deforested in the sixteenth and seventeenth centuries ... in all three tropical regions deforestation accelerated in the nineteenth century ... Throughout the tropics it was export-oriented agriculture that pushed the forest back". Even now, the problem is seen as being caused by shifted cultivators (their lands having been absorbed by other users and, perhaps, uses) rather than by shifting cultivation, which, as previously practised, in accordance with tribal traditions, was ecologically sustainable. All this argues for appropriate reforms in many of the areas where tropical forests are now under assault. More generally it can be said that the term "shifting cultivation" is variously used by different authors, and the practice of shifting cultivation may produce widely differing results. An interesting summary of work conducted by FAO on alternatives to shifting cultivation (in collaboration with research institutes in the UK, Netherlands, France, Tanzania and Ghana) is given in an article by J.P. Lauly, in "unasylva", Vol. 37, No. 147 (85/1).

3Cf. FAO, WFD/1/1985.

MDF/W/52 Page 22

34. In the tropical forests, where fuelwood is not generally in short supply, forest clearing for agricultural uses also has its problems; an estimated 11 million ha. of tropical forest and woodland (of which 7.5 million ha. in the "closed forest" category) are "cleared", or degraded each year. Tropical forest soils are generally poor in nutrients, so much so that no single tree species can establish itself as truly predominant. The great species variety of the tropical forest is a reflection of the poor soil nutrient levels. The bulk of the nutrients is in the living phytomass, e.g. the trees, shrubs and the underbrush. Leaves are shed and new leaf growth occurs round the year, and, apart from a shallow layer of surface soil, there is consequently little humus formation, as everything is recycled very rapidly, especially so as most tropical trees - once fallen or felled - are not very rot-resistant, in the hot and humid environment. When the trees are removed, only few nutrients remain in the soil. The shallow surface layer, even if enriched by ashes - as in slash burning - is quickly destroyed by weathering and leaching. The forest-to-atmosphere, and back again, water-cycle (forests create their own micro-climate) is interrupted, the soils dry out, get parched and become unproductive, as nutrient elements needed for plant growth (nitrogen, phosphorus, potassium, calcium, magnesium) are often in short supply - while levels of aluminium and iron, in a way toxic for plants, are frequently high. Thus, after one or two relatively satisfactory harvests, there is an incentive to shift cultivation to other plots of virgin forest lands, with all the longer-term problems this entails.

35. These are not imagined scenarios. Even though some of the underlying statistics on fuelwood-use and -needs, and on the extent of shifting cultivation, are only estimates, the problems cited are real and widespread. Fortunately, policies and measures for halting the destruction or degradation of forest resources are being adopted almost everywhere. Among measures being introduced are the establishment of fuelwood-plantations, promotion of better coppice practices, the

The fact that most tropical tree varieties (unlike the temperate zone forest-tree varieties, which are mainly fertilized by wind-borne pollens) depend on very specific pollinators (a specific insect variety or a specific animal) for effective pollination, is another reason.

2 A concise summary of the status of the world's rain forests, their

use and protective measures, country-by-country, is contained in "Rain Forests", National Geographic Magazine, Vol. 163, No. 1, January 1983.

3 According to recent FAO estimates, 100 million people in

developing countries already have insufficient fuelwood for cooking and heating. Another 1,000 million people can only meet these needs by depleting fuelwood resources. Asia experiences the most acute fuelwood shortages. Almost all of India and Pakistan are affected by fuelwood shortages, as are the more heavily populated plains and islands of South East Asia. The Himalayas are particularly badly stricken. In Africa the most severe shortages are in East Africa and Madagascar, but all of the arid zones are in danger. In Latin America, the Andean plateau and the Eastern plains of Brazil are the most critical areas. Ref. FAO, document WFD/1/1985. A detailed map of the fuelwood situation in the developing areas, country-by-country, was published in 1981 by FAO, as a "unasylva" supplement.

MDF/W/52 Page 23

introduction of cooking stoves, stricter land-use regulations and improved agro-silviculture practices and, to halt desertification, the planting of windbreaks , hopefully to be complemented by better (holistic!) range-management. With few exceptions, progress in all these endeavours is slow, however.

36. Reduced, and perhaps declining, as the earth's forest coverage may be, the world's forests continue to be so large as to be defined and appraised only with great difficulty. What is even more difficult is an assessment of the way it can be seen as a resource, since forest-policy objectives and -uses overlap with many other sectoral and general policy objectives, to which different importance is attributed in different socio-political contexts, depending also on changing environmental objectives. In some areas of the world, where forest coverage is now much reduced, because of intensive agricultural uses, the increased agricultural land-use option was probably mainly prompted by economic considerations. For many governments, forest-policy considerations carry less importance than agricultural policy objectives. Forests that are being converted to agriculture provide food already in the short term, while the forest itself is seen more as a capital asset, often a not very productive one, or productive only in the longer term. It is, of course, realized that forestry activities, including reforestation work, do provide employment opportunities, an aspect accorded very high importance in some developing and developed countries. It is also recognized that income generated by forestry related employment is fed back into the overall economy. Yet, wherever agricultural land is scarce in relation to food needs, the forests normally lose out to agriculture.

37. While in terms of purely economic returns forestry use objectives may now be determined mainly by medium-term considerations, long-term policy objectives are not absent. Contrary to a widely-held belief, the importance of protecting the environment and preserving, or re-establishing, a proper balance between forestry and other land-uses is not something that has been recognized only recently. In fact, governments of most countries, and earlier on some colonial administrations, have since long attached great importance to proper forest management and the maintenance of a balanced ecosystem generally. In some countries forestry legislation goes back well over a hundred years (in some instances to the late Middle Ages) and in other instances

Partly under bilateral aid schemes, as in Senegal, where - with Canadian assistance - a 300 km. eucalyptus belt has been built to halt the advance of the desert. Other large-scale windbreak plantations, benefiting from international technical and financial' assistance measures, include a project on the high plateaus of Ethiopia, a project in Niger, started some time ago with assistance from the US and certain EC sponsored initiatives in some African countries, etc.; Algeria, on its part, has also made great efforts in combating desertification.

2 Acceptance of wood-burning stoves, or hearths, which permit

10-15 per cent wood-fuel thermal energy content to be recovered (instead of 2-5 per cent in the typical, three-stone, open-pit fire which is, moreover, through high pollutant emissions, very detrimental to the health of users) by local populations is often difficult to achieve. FAO, among others, is doing considerable work for the adoption in developing countries of better technologies for the conversion of wood energy into heat energy and/or mechanical energy. This is only a small part of a much wider, integrated, FAO "Tropical Forestry Action Plan", outlined in FAO document M-30 ('85/'86), bearing that title.

MDF/W/52 Page 24

at least to the beginning of this century. In some cases (for instance, Switzerland, India) forest-policy objectives and prescriptions are written into the Constitution. In many cases forest use and forestry objectives are regulated by national or federal and provincial laws. While the policy objectives are not always the same, virtually all provide for maintaining a balance between silvicultural and agricultural uses, and many of the implementing regulations insist on, and provide for, measures of, at least limited, reforestation. In the case of professionally managed private forest lands reforestation measures are undertaken as a matter of course, even in the absence of State regulations. This is so also in the main tropical wood-producing and -exporting countries, notably those of South and South-East Asia and in West Africa. As a result of these policies and measures, and, of course, also the availability of substitute fuels and industrial raw materials other than wood (formerly based on wood, wood ash, etc.), and the emergence of new sources of wood supplies through trade development, the area under forest in Western Europe and in the United States has been growing, slowly but steadily, with some war-time exceptions, through most of this century. The provisions made for preserving forests for watershed protection purposes, for recreation, and as wildlife and botanical sanctuaries, are also of some significance. In the United States, national parks and federal forest lands, the former fully protected and the latter protected in various ways, were established as from the turn of the century, comprising a very large area, indeed, and total forest area in the US is now larger than at the beginning of the century. Canada, with a total of some 340 million ha.

The Côte d'Ivoire, for instance, is currently intensifying reforestation efforts under a programme envisaging outlays equivalent to close to US$60 million, somewhat more than one-half to be derived from IBRD financing. More generally, in an IBRD, UNDP and World Resources Institute (the latter a private, Washington-based research institute) study it is proposed to spend US$8 billion over a five-year period (beginning in 1987) to begin reversing the trend of tropical deforestation. Many tropical countries are to be covered in this proposed project, with $1.2 billion earmarked for India and $785 million for Brazil. Several countries, including France and FR Germany (FF500 million and DM150 million, respectively, over five years), announced at the February 1986 Silva Conference in Paris large-scale financial assistance for protecting and building up again Africa's forest resources.

2 The federal US Government owns about one third (= 290 million

hectares) of all US land; 100 million hectares have been set aside as national parks, wilderness and primitive areas and other similar reserves. No logging is permitted in these areas, so they are not considered commercial forests. Consequently, a large part of trees in these reserves are over-aged, and thus vulnerable to insect attack and damage (currently a major problem, also for adjoining private timber lands in Texas and Louisiana). Total commercial forest area, including private and other publicly owned forest land, is of the order of 200 million ha., of which about 120 million ha. is owned by private individuals, and about 21 million ha. by forest industry companies. The remaining forests are publicly held in national and state forests, of which 37 million ha. national forests, in which controlled logging is permitted, but sometimes contested (even violently, nail-spiking, "ecotage") by environmentalists.

MDF/W/52 Page 25

of forests, has set aside 9 million ha. as protected parks. In the Brazilian Amazon Basin about 17 million ha. is protected forest and forest reserves in other parts of the country have also been, or are being, created. Some of the countries in East Africa have very large protected areas of savanna woodland. Protected natural parks are also of importance in most of the countries of Western Europe, certain other developed countries, and are also found in a number of developing countries. This has to be taken into account in respect of data on, total forest areas, recorded in Table I for the different countries.

38. Any attempt to appraise the economic value of a given forest area must evidently take into account such factors as forest composition by tree species, -age, growing stock, growth potential, cost of harvesting, transport, nearness to markets, market demand for the wood and other forest products concerned, value and importance attached to other than economic considerations, and, last but not least, alternatives and preferences for either present or future resource use. In other words, the appraisal must take into account, inter alia, both current and future revenue and capital appreciation potential. Options available, and exercised, will depend not only on current market conditions for forest products, and on expectations as to future supply/demand relationships and prices for forestry products, but also on the general economic and fiscal policies prevailing,in countries concerned and on the ownership structure of the forests. That this is not idle

While the latter figure may seem small in relation to the overall level of the resource, the park area nevertheless covers an area larger than the total area under forests in F.R. Germany, the three Benelux countries and Denmark combined. The Canadian forest resource proper, namely "stocked, productive, non-reserved forest land" is of the order of 190 million hectares, of which 36 per cent is mature forest, 3 per cent is over-mature, 45 per cent is immature forest and 8 per cent consists of regenerating areas. The degree of private ownership varies somewhat across Canada, but about 80 per cent of total forest lands are owned and administered by provincial governments and about 11 per cent by the federal government. Private holdings account for over 90 per cent of Prince Edward Islands' (the smallest province) 225,000 hectares of forest land and almost 75 per cent of Nova Scotia's 4.4 million hectares. Public agencies own about 90 per cent of the 120 million hectares located in Ontario and Quebec and over 95 per cent of the 116.5 million hectares found in British Columbia, Alberta, Saskatchewan and Manitoba. Source: Government of Canada - Forestry Service, "Canada's Forests ... Fibre for the World".

2 In Indonesia steps are being taken to require each of the

country's 27 provinces to convert 10 per cent of the land to forest preserves. Once these measures are implemented, the country will have forest preserves totalling about 18 million hectares.

3 For details in respect of ECE countries, see "The forest resources

of the ECE etc.", 1985, op.cit.

That there may be differences of view as to the true value of timberland and other forest industry corporate assets has recently been demonstrated in the context of a number of contested take-over initiatives of some major forest product companies headquartered in North America.

MDF/W/52 Page 26

speculation is demonstrated by the considerable difficulties which wood-processing industries have in some countries, though possessing large forest resources, in persuading private owners to offer timber to the market for industry or for pulping. The disposition to do so, as well as to engage in forest-care activities, will depend, inter alia, on the extent to which forest owners are dependent on forest-resource income, on the marginal tax rate to which such income may be subject (which under a system of progressive income taxes would be different from case to case and, perhaps, year to year), special forestry- and land-tax provisions, inheritance taxes, etc. State aids to forest management and/or forest harvesting, as in the case of some assistance currently provided in the fight against forest die-back, could also make a difference in the way forests are cared for and the level of stocks that are removed and which then come to market.

39. One other important element in regard to forestry resource uses is the fact that, apart from import duties, and from natural protection provided by transport costs (abstracting for the time being from non-tariff measures which could affect supplies and hence market prices), timber prices in many markets are closely related to price developments in the international market. While, in principle, this should be considered desirable, certain problems may arise for proper forest management and -use where such integration into the world market of the forestry resource, and as a consequence fluctuating and often low prices for timber, coincides with forestry activity being carried out jointly with agricultural activities which, through import protection, are less integrated into the international economy, the forest owners being also farmers. In such cases, agriculture, benefiting perhaps from a variety of support measures, while forestry does not, or much less so, proper forest management may become a problem, with forestry activities

With the possible exception of Switzerland (mainly windbreak damage removals so far) and of some of the countries in Eastern Europe, there was no evidence, at the end of 1985, of significant additional quantities of industrial roundwood coming to market as a consequence of forest die-back problems in certain areas of Europe. This may, of course, not hold in the future, but an attempt is being made by the industry to accommodate die-back sanitation fellings (not yet a problem in most areas) through reduced fellings of healthy trees. It should also be pointed out that, apart from some temporary pre-processing storage problems, wood from die-back trees is normally just as strong and useful as that from the, presumably, healthy trees. In the United States South and South-East exceptionally large sanitation fellings in 1985, to combat insect infections, have, however, led to a large imbalance in supply and demand of roundwood, with offer prices falling in some geographic areas to about one-fourth of the national average. (Cf. also footnote 2 on page 24). Developments in European and North-American forest die-back sanitation fellings, which may have an effect on the market, are to be monitored by ECE under a project decided upon in the autumn of 1985.

MDF/W/52 Page 27

being neglected, as compared to agriculture. While, in terms of regulatory policies and -measures for purposes of environmental protection most governments, have, by now, fairly wide authority and intervention possibilities (regardless of the type of forest ownership), possibilities for directing the use of forest resources in the non-State sector are much more limited. Another important element to consider is the degree of vertical integration, namely common ownership of the forest resources and of the downstream forest products industries. In most of the EEC countries, and certain other European countries, there exists very little of such integration, while in the United States, and to some extent in Canada, and also in one or two countries in northern Europe and in countries such as Brazil, vertical integration, in terms of privately-controlled forest-resources and forest product-processing industries, is fairly common. (The integration is not necessarily one of ownership of the primary resources, but may take the form of long-term leases or use-contracts in respect of forest land.) Evidently, vertical integration does provide an additional degree of freedom to management, as far as planning of resource-use and -disposition is concerned.