Gateshead & Newcastle upon Tyne

225

Opinion Research Services | The Strand • Swansea • SA1 1AF | 01792 535300 | www.ors.org.uk | [email protected] Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 Report of Findings August 2017

-

Upload

khangminh22 -

Category

Documents

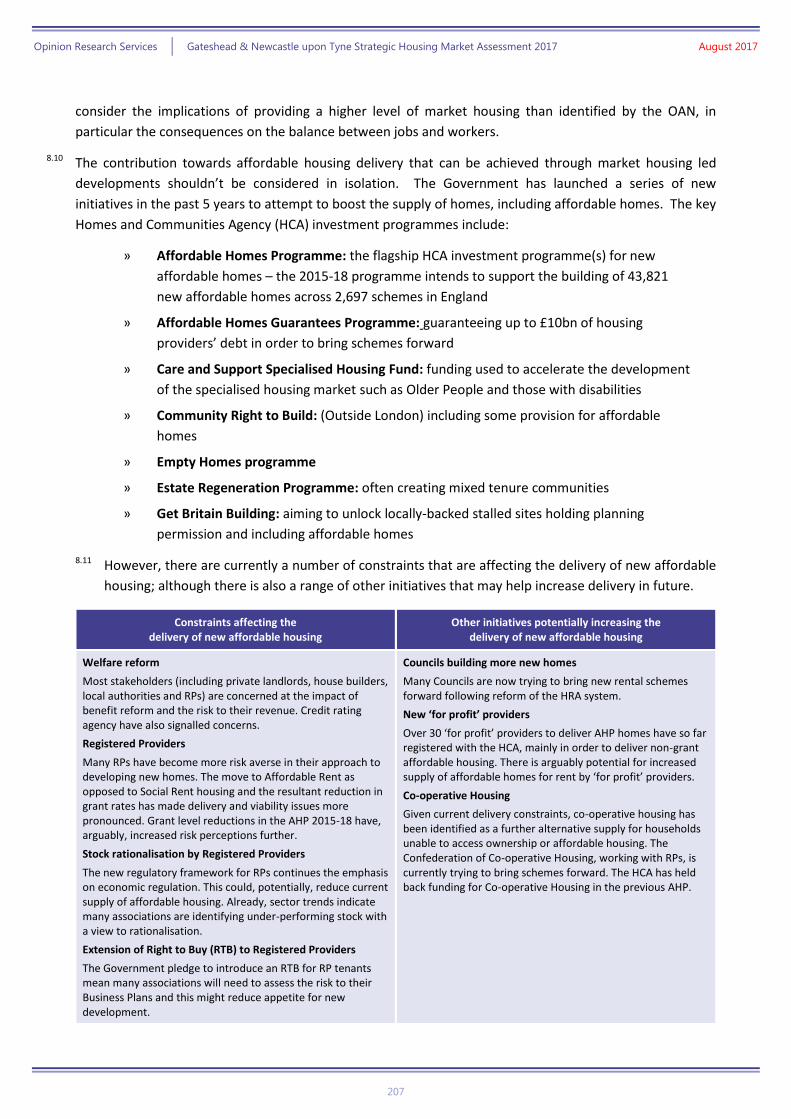

-

view

0 -

download

0

Transcript of Gateshead & Newcastle upon Tyne

Opinion Research Services | The Strand • Swansea • SA1 1AF | 01792 535300 | www.ors.org.uk | [email protected]

Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017

Report of Findings August 2017

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

2

Opinion Research Services | The Strand, Swansea SA1 1AF

Jonathan Lee | Nigel Moore | Karen Lee | Trevor Baker | Scott Lawrence

enquiries: 01792 535300 · [email protected] · www.ors.org.uk

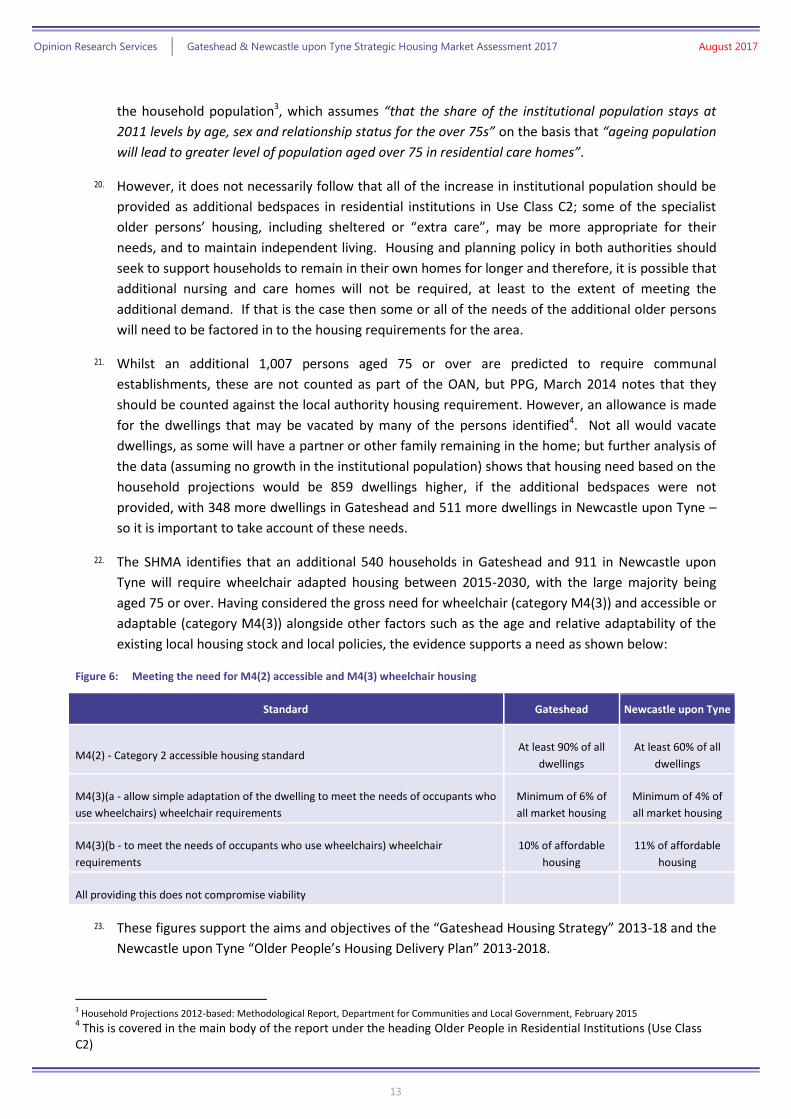

© Copyright August 2017

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

3

Contents Executive Summary ............................................................................................ 7

Summary of Key Findings and Conclusions 7

Introduction ................................................................................................................................................. 7

Calculating Objectively Assessed Needs ..................................................................................................... 8

Household Projections ................................................................................................................................ 9

Affordable Housing Need .......................................................................................................................... 11

Need for Older Person Housing ................................................................................................................. 12

Market Signals ........................................................................................................................................... 14

Conclusions ................................................................................................................................................ 15

Nationally Described Space Standards ...................................................................................................... 17

1. Introducing the Study .................................................................................. 19

Background to the project and wider policy context 19

Government Policy .................................................................................................................................... 19

Duty to Co-operate .................................................................................................................................... 21

Gateshead and Newcastle upon Tyne Joint Core Strategy 2010-2030 ............................................... 21

Housing White Paper .......................................................................................................................... 22

2. Defining the Housing Market Area .............................................................. 23

An evidence base to identify functional housing markets 23

Functional Housing Market Areas ............................................................................................................. 23

Planning Practice Guidance ................................................................................................................. 23

Geography of Housing Market Areas (NHPAU/CURDS) ...................................................................... 24

ONS Travel to Work Areas ................................................................................................................... 25

House Prices ........................................................................................................................................ 26

Valuation Office Agency Broad Rental Market Areas ......................................................................... 27

Administrative Boundaries and Housing Market Areas ............................................................................ 28

Key Statistics for Gateshead and Newcastle upon Tyne HMA .................................................................. 31

Migration within the UK to and from Gateshead and Newcastle upon Tyne ..................................... 31

Travel to Work Patterns ...................................................................................................................... 33

Containment within the Combined Area ............................................................................................ 34

Conclusions ................................................................................................................................................ 34

3. Demographic Projections ............................................................................ 38

The starting point for Objectively Assessed Need 38

Process for Establishing Objectively Assessed Need ................................................................................. 38

Gateshead and Newcastle upon Tyne Joint Core Strategy 2010-30 ................................................... 39

Official Population and Household Projections .................................................................................. 39

Official Population Projections ............................................................................................................ 40

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

4

Population and Household Projections based on Local Circumstances ............................................. 42

Reviewing the Official Population Estimates - Gateshead ........................................................................ 44

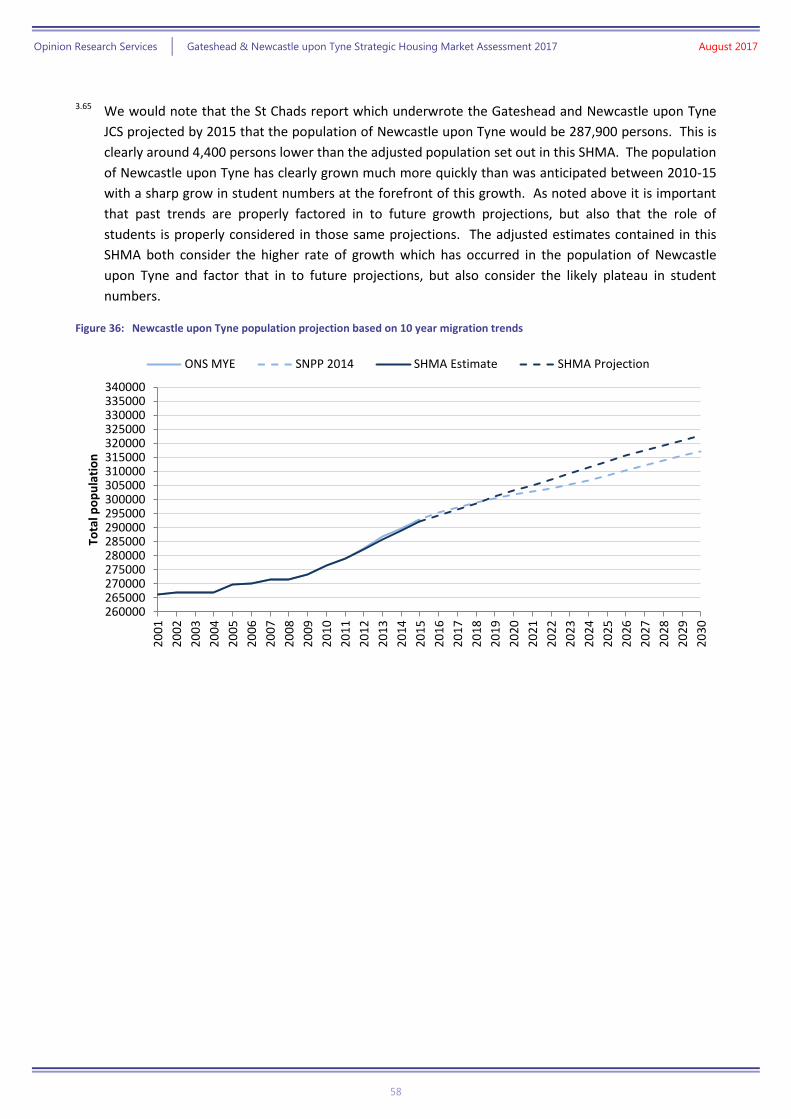

Components of Population Change .................................................................................................... 45

Estimating Population Change with Other Data ................................................................................. 48

Reviewing the Official Population Estimates – Newcastle upon Tyne ...................................................... 49

Components of Population Change .................................................................................................... 50

Estimating Population Change with Other Data ................................................................................. 53

Student Housing and the OAN .................................................................................................................. 54

Summary of Population Projection Adjustments ...................................................................................... 56

Establishing Population Projections .................................................................................................... 56

Economic Activity Projections ................................................................................................................... 59

Labour Market Participation Projections ............................................................................................ 61

Older People ........................................................................................................................................ 61

Female Participation ........................................................................................................................... 63

Young People ....................................................................................................................................... 64

Projecting Future Economic Activity for Gateshead ........................................................................... 65

Projecting Future Economic Activity for Newcastle upon Tyne .......................................................... 66

Household Population and Institutional Population ........................................................................... 67

Household Representative Rates ........................................................................................................ 69

Household Projections ........................................................................................................................ 71

Conclusions ................................................................................................................................................ 72

4. Affordable Housing Need ............................................................................ 73

Identifying households who cannot afford market housing 73

Introduction ............................................................................................................................................... 73

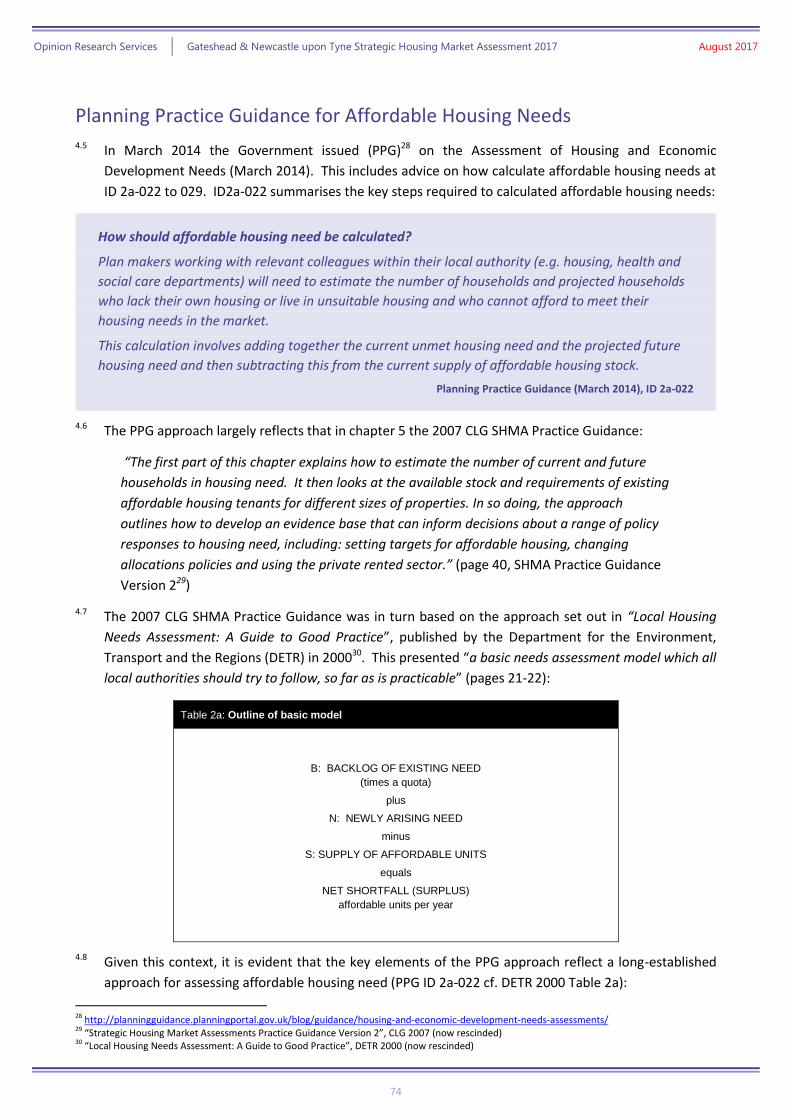

Planning Practice Guidance for Affordable Housing Needs ...................................................................... 74

Assessing Affordable Housing Needs ........................................................................................................ 75

Modelling Affordable Needs ..................................................................................................................... 76

Backlog of Affordable Housing Needs for Gateshead and Newcastle upon Tyne .................................... 78

Past Trends and Current Estimates of the Need for Affordable Housing ................................................. 79

Local Authority Data: Homeless Households and Temporary Accommodation ................................. 79

Census Data: Concealed Households and Overcrowding ................................................................... 80

English Housing Survey Data ............................................................................................................... 84

Housing Register Data ......................................................................................................................... 88

Households Unable to Afford their Housing Costs ............................................................................. 91

Establishing Affordable Housing Need ...................................................................................................... 93

Current Unmet Need for Affordable Housing ..................................................................................... 94

Projected Future Affordable Housing Need ........................................................................................ 98

Assessing the Overall Need for Affordable Housing ......................................................................... 104

Conclusions .............................................................................................................................................. 107

5. Objectively Assessed Need ........................................................................ 109

Analysing the evidence to establish overall housing need 109

National Context for England .................................................................................................................. 110

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

5

Household Growth ............................................................................................................................ 110

International Migration ..................................................................................................................... 110

Market Signals ................................................................................................................................... 111

Converting to Dwellings .................................................................................................................... 111

Establishing Objectively Assessed Need for Gateshead & Newcastle upon Tyne .................................. 112

CLG Household Projections ............................................................................................................... 112

Adjustments for Local Demography and Long-term Migration ........................................................ 113

Affordable Housing Need .................................................................................................................. 113

Need for Older Person Housing ............................................................................................................... 114

Employment Trends ................................................................................................................................ 114

Market Signals ................................................................................................................................... 117

House Prices ...................................................................................................................................... 118

Affordability ...................................................................................................................................... 121

Private Rent ....................................................................................................................................... 123

Housing Development ....................................................................................................................... 125

Overcrowding .................................................................................................................................... 127

Summary of Market Signals .............................................................................................................. 128

Housing Backlog ...................................................................................................................................... 130

Conclusions .............................................................................................................................................. 130

6. Housing needs of different groups ............................................................ 133

Considering the need for all types of housing 133

Projected Population Age Profile ............................................................................................................ 134

Household Projections ............................................................................................................................ 136

Housing Mix: Size and Tenure ................................................................................................................. 139

The Private Rented Sector ....................................................................................................................... 148

Black and Minority Ethnic Population ..................................................................................................... 154

Service Families ....................................................................................................................................... 157

People Wishing to Build their Own Homes ............................................................................................. 158

Housing for Older People ........................................................................................................................ 160

Households with Specific Needs ............................................................................................................. 165

Assessing the level of need for accessible and wheelchair housing ....................................................... 165

Current Planning Policy Context ....................................................................................................... 168

Population and health demographics ............................................................................................... 169

Wheelchair accessible homes ........................................................................................................... 176

Meeting the need for M4(2) accessible and M4(3) wheelchair user housing ........................................ 178

Older people – local context ................................................................................................................... 184

Gateshead ......................................................................................................................................... 184

Newcastle upon Tyne ........................................................................................................................ 186

Cost benefits of providing accessible and adaptable housing ................................................................ 188

7. Space Standards ........................................................................................ 192

Compliance with the 2015 Nationally Described Space Standards (NDSS) for Gross Internal Area

(GIA) 192

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

6

Background .............................................................................................................................................. 192

Compliance with the 2015 NDSS for GIA 192

Background: Summary ............................................................................................................................ 193

Gateshead ............................................................................................................................................... 194

Newcastle ................................................................................................................................................ 194

8. Housing Requirements .............................................................................. 205

Considering the policy response to identified housing need 205

Affordable Housing Need ........................................................................................................................ 206

Older People in Residential Institutions (Use Class C2) .......................................................................... 209

Student Housing ...................................................................................................................................... 210

Gypsies and Travellers ............................................................................................................................. 212

Appendix 1: Stakeholder Engagement with the BME Community ................. 214

Stakeholder Engagement with the BME Community .............................................................................. 214

Stakeholder Fieldwork Consultation in Gateshead and Newcastle ........................................................ 215

Table of Figures .............................................................................................. 220

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

7

Executive Summary Summary of Key Findings and Conclusions

Introduction

1. Opinion Research Services (ORS) was commissioned by Gateshead Council and Newcastle upon Tyne

City Council to undertake a Strategic Housing Market Assessment to establish the Objectively

Assessed Need for housing and review housing and planning policies ahead of their new Local Plans.

2. The National Planning Policy Framework (NPPF)1 requires Local Planning Authorities to “ensure that

their Local Plan meets the full, objectively assessed needs for market and affordable housing in the

housing market area” and “identify the scale and mix of housing and the range of tenures that the

local population is likely to need over the plan period which meets household and population

projections, taking account of migration and demographic change” (paragraphs 47 and 159).

3. The Gateshead and Newcastle upon Tyne Joint Core Strategy was adopted in March 2015 and this

SHMA represents a review and update of the evidence base which underwrote this document.

Figure 1: Gateshead and Newcastle upon Tyne Joint Core Strategy

Gateshead and Newcastle upon Tyne Joint Core Strategy 2010-30

Adopted 2015 following examination in 2014

Sets a joint target for 30,000 homes and 22,000 across the 2 authorities

Viability in both authorities is quite low so the affordable housing target was set at 15%

North Tyneside Local Plan has been examined separately and sets a target of 790 dwellings per annum.

4. The Joint Core Strategy includes a provision for 30,000 more homes, 22,000 more jobs and also a

need for 15% of all new homes to be affordable housing on qualifying sites.

5. However, these figures were not evenly distributed across the 20 year period. Figure 2 shows the

estimated distribution of the housing target across the 15 year period starting in 2015. This shows

an annual need for Gateshead over the period 2015-30 of 535 dwellings per annum and 1,040

dwellings per annum for Newcastle upon Tyne for the same period.

1 https://www.gov.uk/government/publications/national-planning-policy-framework--2

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

8

Figure 2: Gatesheand and Newcastle upon Tyne Existing Housing Targets (Source: Gatershead and Newcastle upon Tyne Joint

Core Strategy)

2015-2020 2020-2025 2025-2030 Total 2015-30

Gateshead 2,420 4,020 1,580 8,020

Newcastle upon Tyne 4,800 5,400 5,400 15,600

Total 7,220 9,420 6,980 23,620

6. In March 2014, the government produced new guidance on conducting housing needs assessments

in the form of ‘Guidance for Housing and Economic Development Needs Assessments’. Paragraphs

2-21 of this new guidance cover overall housing needs and paragraphs 22-29 cover affordable

housing needs. The new guidance includes a number of significant changes since the 2007 SHMA

Practice Guidance which underwrote much of the work leading to the Joint Core Strategy.

7. Alongside past changes to housing and planning policy, the Housing White Paper, “Fixing our broken

housing market’ was published in February 2017. One change flagged in the White Paper is a

change in definition for affordable housing to include Starter Homes at 20% discounts of market

prices. The inclusion of Starter Homes in a wider definition of affordable housing will require a

fundamental revision of who is considered to be in affordable housing need because the current

definition is based upon who can afford market housing, not owner occupied housing. Therefore, if

the Government proceed to include Starter Homes in the definition of affordable housing products,

they will also need to count many more households as being in affordable housing need than is

currently the case because all non-owning households who wish to purchase Starter Homes will

need to be included. Therefore, the affordable housing needs assessed in this study may require a

revision if and when the government applies this new definition.

Calculating Objectively Assessed Needs

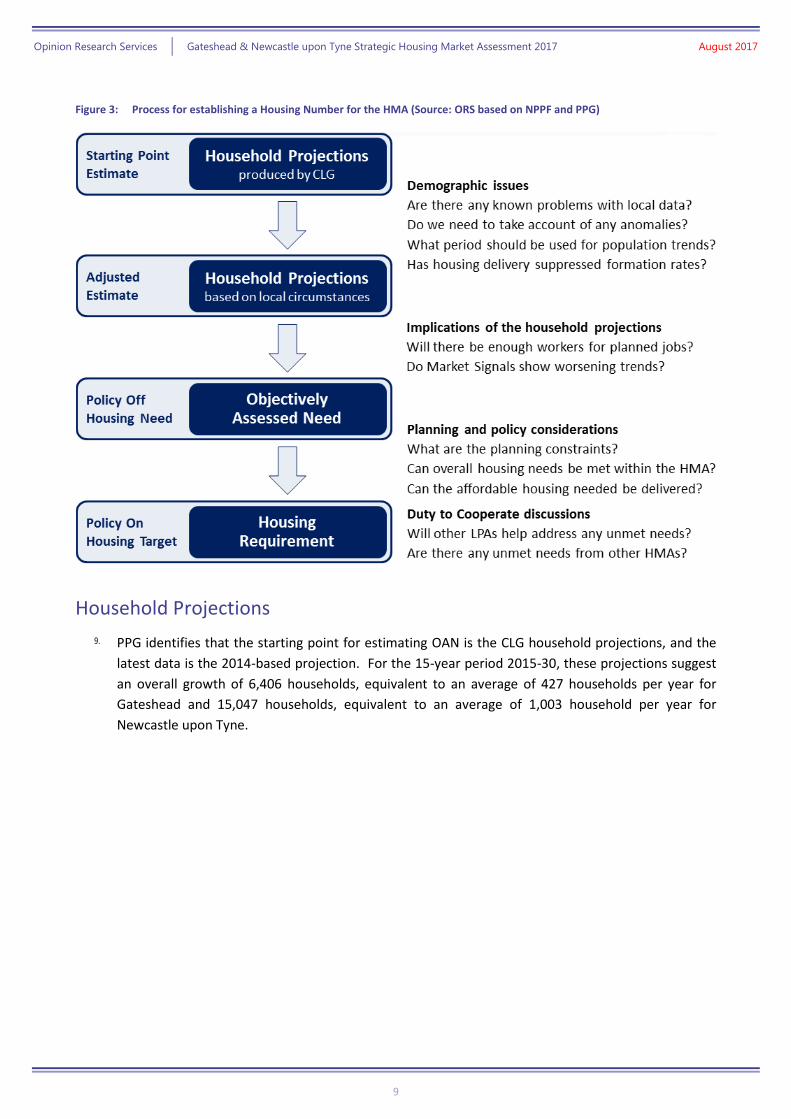

8. Figure 3 sets out the process for establishing Objectively Assessed Need (OAN). Planning Policy

Guidance (PPG)2 identifies that “household projections published by the Department for

Communities and Local Government should provide the starting point estimate of overall housing

need” (ID 2a-015) which should be adjusted to take account of local circumstances. External market

and macro-economic constraints are then applied (‘Market Signals’) in order to embed the need in

the real world. It is important to recognise that the OAN does not take account of any possible

constraints to future housing supply. Such factors will be subsequently considered by the Councils

before establishing the final Housing Requirement.

2 http://planningguidance.planningportal.gov.uk/blog/guidance/housing-and-economic-development-needs-assessments/

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

9

Figure 3: Process for establishing a Housing Number for the HMA (Source: ORS based on NPPF and PPG)

Household Projections

9. PPG identifies that the starting point for estimating OAN is the CLG household projections, and the

latest data is the 2014-based projection. For the 15-year period 2015-30, these projections suggest

an overall growth of 6,406 households, equivalent to an average of 427 households per year for

Gateshead and 15,047 households, equivalent to an average of 1,003 household per year for

Newcastle upon Tyne.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

10

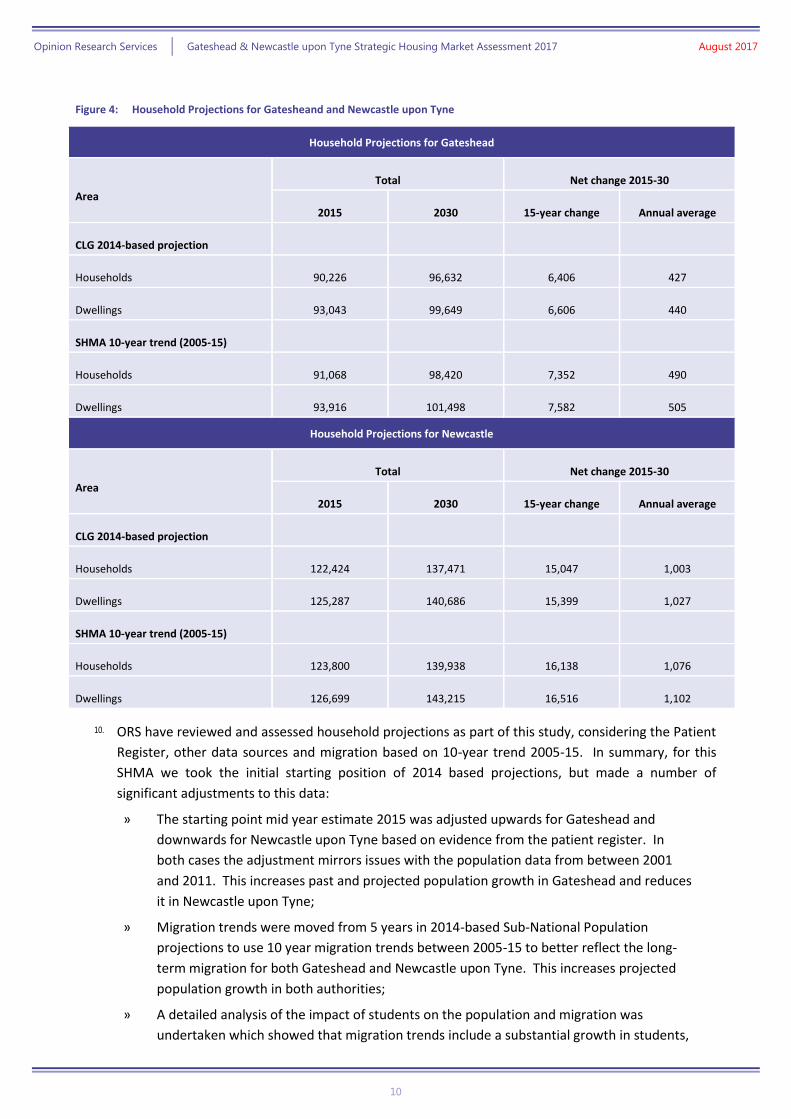

Figure 4: Household Projections for Gatesheand and Newcastle upon Tyne

Household Projections for Gateshead

Area

Total Net change 2015-30

2015 2030 15-year change Annual average

CLG 2014-based projection

Households 90,226 96,632 6,406 427

Dwellings 93,043 99,649 6,606 440

SHMA 10-year trend (2005-15)

Households 91,068 98,420 7,352 490

Dwellings 93,916 101,498 7,582 505

Household Projections for Newcastle

Area

Total Net change 2015-30

2015 2030 15-year change Annual average

CLG 2014-based projection

Households 122,424 137,471 15,047 1,003

Dwellings 125,287 140,686 15,399 1,027

SHMA 10-year trend (2005-15)

Households 123,800 139,938 16,138 1,076

Dwellings 126,699 143,215 16,516 1,102

10. ORS have reviewed and assessed household projections as part of this study, considering the Patient

Register, other data sources and migration based on 10-year trend 2005-15. In summary, for this

SHMA we took the initial starting position of 2014 based projections, but made a number of

significant adjustments to this data:

» The starting point mid year estimate 2015 was adjusted upwards for Gateshead and

downwards for Newcastle upon Tyne based on evidence from the patient register. In

both cases the adjustment mirrors issues with the population data from between 2001

and 2011. This increases past and projected population growth in Gateshead and reduces

it in Newcastle upon Tyne;

» Migration trends were moved from 5 years in 2014-based Sub-National Population

projections to use 10 year migration trends between 2005-15 to better reflect the long-

term migration for both Gateshead and Newcastle upon Tyne. This increases projected

population growth in both authorities;

» A detailed analysis of the impact of students on the population and migration was

undertaken which showed that migration trends include a substantial growth in students,

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

11

but there is no expectation that this will continue in to the future. Therefore the net

impact of students has been removed from the migration data. This reduces population

growth in both authorities; and

» Net migration from Newcastle upon Tyne to Gateshead grew from 2001 to 2011, for the

purposes of this study, and forecast trends, it has been assumed that the growth of

students in Newcastle led to an increase in out migration from Newcastle to Gateshead.

As previous student growth trends are expected to no longer continue it is also likely that

out migration to Gateshead will reduce. This assumption can be monitored over time.

11. On this basis, the data shows household numbers across the study area would increase over the 15-

year Plan period 2015-30 by an average of 490 per year in Gateshead and 1,076 per year in

Newcastle upon Tyne. These figures provide the most appropriate demographic projection on

which to base the Objectively Assessed Need (OAN) for housing. This difference is mainly due to a

higher projected increase in population in the SHMA projections. The figures represent an increase

on the starting point for Gateshead of 15% and for Newcastle upon Tyne of 7%. The figures for

Gateshead are slightly lower than those in the Joint Core Strategy for 2015-30, while the figures for

Newcastle upon Tyne are slightly higher. However, both figures are very close to the existing policy

positions in each authority with a rise across the two authorities of 2.1%.

Affordable Housing Need

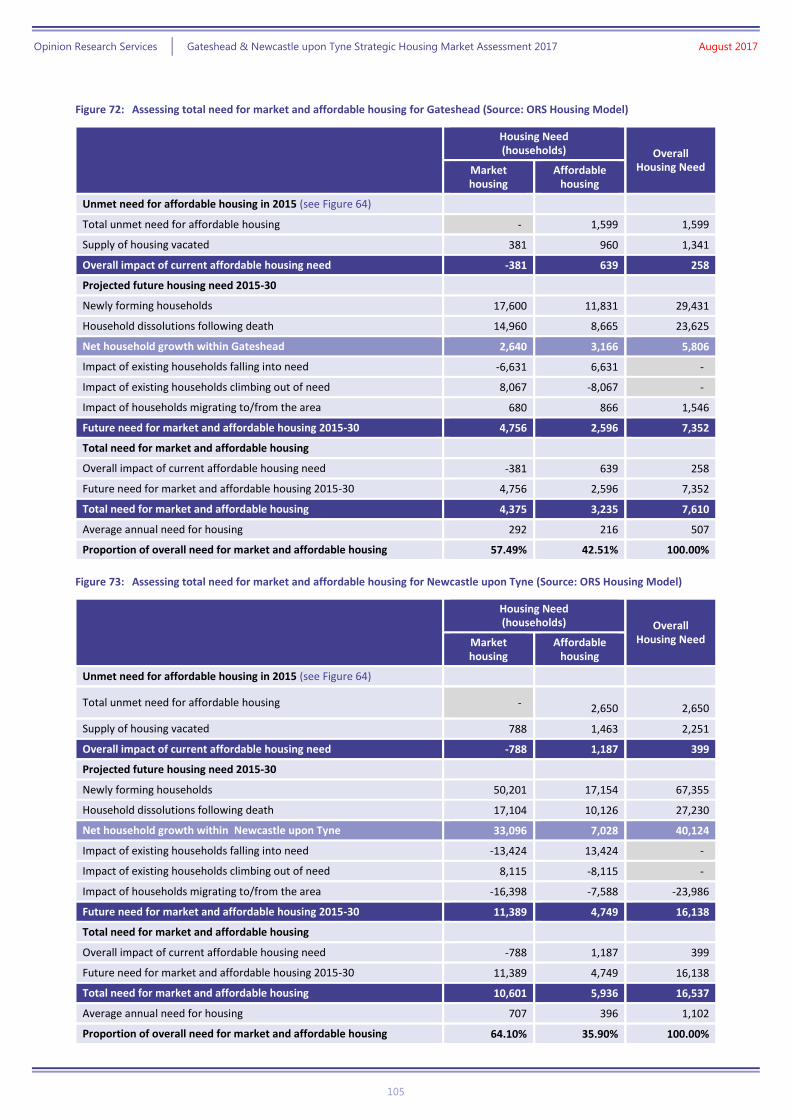

12. The SHMA has undertaken a comprehensive analysis of the existing unmet need for affordable

housing. This analysis identified that the overall housing need by 258 households in Gateshead and

399 households in Newcastle upon Tyne to take account of concealed families and homeless

households that would not be captured by the household projections. When the unmet needs from

existing households living in unsuitable housing were also included, the analysis established there

to be 1,599 households in need of affordable housing in 2015 in Gateshead there to be 2,650

households in need of affordable housing in Newcastle upon Tyne.

13. However, as 960 of these already occupied an affordable home but need to move for reasons such

as overcrowding in Gateshead and 1,463 in Newcastle upon Tyne, therefore there is a net need from

639 households in Gateshead (1,599 less 960= 639) and 1,187 households in Newcastle upon Tyne

(2,650 less 1,463 = 1,187) who need affordable housing and do not currently occupy affordable

housing in 2015.

14. Based on the household projections, the SHMA has established the balance between the future

need for market housing and affordable housing. The analysis identifies that the number of

households in need of affordable housing will increase by 2,596 households in Gateshead and

4,749 households in Newcastle upon Tyne over the period 2015-30, alongside an increase of 4,756

households in Gateshead and 11,389 in Newcastle upon Tyne able to afford market housing.

15. Overall, there will be a need to provide additional affordable housing for 3,235 (2,596 + 639 =

3,235) households (3,277 dwellings) over the period 2015-30 in Gateshead (42.5% of the projected

household growth) and 5,936 (4,749+1,187 = 5,936) households (6,014 dwellings) in Newcastle

upon Tyne (35.9% of the projected household growth). This is equivalent to an average of 216

households per year in Gateshead and 396 households per year in Newcastle upon Tyne. Both of

these figures are the identified need for those who cannot afford market housing in each area.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

12

However, planning practice guidance and case law are both clear that while all affordable housing

needs should be identified, they may not necessarily have to be provided because delivery may be

constrained by viability and the ability of market housing to support the delivery of affordable

housing. Therefore, the amount of affordable delivered may be different from the identified need.

16. These figures are significantly higher than those set out in the Gateshead and Newcastle upon Tyne

SHMA 2013, but that featured a different definition of affordable housing need and also used a

different model to assess households who require affordable housing.

17. Any losses from the current affordable stock (such as demolition or clearance, or sales through Right

to Buy) would increase the number of affordable dwellings needed by an equivalent amount.

Meanwhile any vacant affordable dwellings returned to use would count as part of the supply

necessary to meet the need for affordable housing. Both of these scenarios are important in

Gateshead and Newcastle upon Tyne with both areas having seen recent demolitions to facilitate

renewals, but also both areas having a number of hard to let properties which are currently vacant.

If these hard to let properties could be brought back in to use, then they can be counted as the

equivalent of new housing delivery in the area.

Need for Older Person Housing

18. The population aged 65 or over is projected to increase by 9,750 persons in Gateshead and 14,200 in

Newcastle upon Tyne between 2015 and 2030.

Figure 5: Population Projections for Gatesheand and Newcastle upon Tyne 2015-30 by 5-year age cohort based SHMA

population projections

Gateshead

2015 2030 Change 2015-2030

Age 65+ 38,548 48,294 9,745

Age 75+ 17,947 24,101 6,153

Age 85+ 4,744 7,110 2,366

Total – all ages 203,098 212,652 9,554

Newcastle upon Tyne

2015 2030 Change 2015-2030

Age 65+ 41,783 55,977 14,194

Age 75+ 19,777 27,572 7,796

Age 85+ 5,880 8,369 2,489

Total – all ages 292,281 322,963 30,682

19. The SHMA has identified that between 2015 and 2030, groups in institutional population is likely to

increase by 414 persons aged 75 years or over in Gateshead and 593 persons in Newcastle upon

Tyne. This increase in institutional population is a consequence of the CLG approach to establishing

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

13

the household population3, which assumes “that the share of the institutional population stays at

2011 levels by age, sex and relationship status for the over 75s” on the basis that “ageing population

will lead to greater level of population aged over 75 in residential care homes”.

20. However, it does not necessarily follow that all of the increase in institutional population should be

provided as additional bedspaces in residential institutions in Use Class C2; some of the specialist

older persons’ housing, including sheltered or “extra care”, may be more appropriate for their

needs, and to maintain independent living. Housing and planning policy in both authorities should

seek to support households to remain in their own homes for longer and therefore, it is possible that

additional nursing and care homes will not be required, at least to the extent of meeting the

additional demand. If that is the case then some or all of the needs of the additional older persons

will need to be factored in to the housing requirements for the area.

21. Whilst an additional 1,007 persons aged 75 or over are predicted to require communal

establishments, these are not counted as part of the OAN, but PPG, March 2014 notes that they

should be counted against the local authority housing requirement. However, an allowance is made

for the dwellings that may be vacated by many of the persons identified4. Not all would vacate

dwellings, as some will have a partner or other family remaining in the home; but further analysis of

the data (assuming no growth in the institutional population) shows that housing need based on the

household projections would be 859 dwellings higher, if the additional bedspaces were not

provided, with 348 more dwellings in Gateshead and 511 more dwellings in Newcastle upon Tyne –

so it is important to take account of these needs.

22. The SHMA identifies that an additional 540 households in Gateshead and 911 in Newcastle upon

Tyne will require wheelchair adapted housing between 2015-2030, with the large majority being

aged 75 or over. Having considered the gross need for wheelchair (category M4(3)) and accessible or

adaptable (category M4(3)) alongside other factors such as the age and relative adaptability of the

existing local housing stock and local policies, the evidence supports a need as shown below:

Figure 6: Meeting the need for M4(2) accessible and M4(3) wheelchair housing

Standard Gateshead Newcastle upon Tyne

M4(2) - Category 2 accessible housing standard At least 90% of all

dwellings

At least 60% of all

dwellings

M4(3)(a - allow simple adaptation of the dwelling to meet the needs of occupants who

use wheelchairs) wheelchair requirements

Minimum of 6% of

all market housing

Minimum of 4% of

all market housing

M4(3)(b - to meet the needs of occupants who use wheelchairs) wheelchair

requirements

10% of affordable

housing

11% of affordable

housing

All providing this does not compromise viability

23. These figures support the aims and objectives of the “Gateshead Housing Strategy” 2013-18 and the

Newcastle upon Tyne “Older People’s Housing Delivery Plan” 2013-2018.

3 Household Projections 2012-based: Methodological Report, Department for Communities and Local Government, February 2015 4 This is covered in the main body of the report under the heading Older People in Residential Institutions (Use Class

C2)

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

14

Market Signals

24. NPPF sets out that “Plans should take account of market signals…” (paragraph 17) and PPG identifies

that “the housing need number suggested by household projections (the starting point) should be

adjusted to reflect appropriate market signals”.

25. The SHMA has considered the Market Signals for Gateshead and Newcastle upon Tyne and

compared these to other areas which have similar demographic and economic characteristics. On

the basis of this data we can conclude:

House Prices: lower quartile prices are lower than the national average in both Gateshead and

Newcastle upon Tyne, with lower quartile prices of £92,000 and £111,000 respectively

compared to England’s £142,000 (based on 2015-16 prices). The current lower quartile price in

the comparator area Liverpool and Knowsley is lower again at £76,800; the prices in

comparator areas Sheffield and Manchester and Salford are £102,000 and £103,600

respectively; and lower quartile prices in Leeds are higher than both Gateshead and Newcastle

upon Tyne at £115,000. Prices in Gateshead and Newcastle upon Tyne have risen at a similar

rate to most of the comparator areas and the national rate over the past 5 years; however

there was a higher rate of increase in Manchester and Salford (20%) and a small reduction in

lower quartile prices in Liverpool and Knowsley (-2%);

Rents: for average private sector rents in 2015-16, both Gateshead and Newcastle upon Tyne

are lower than the national average, they are however broadly in line with private sector rents

in comparator areas. When we look at the growth in rent over the past 5 years, Newcastle

upon Tyne has a higher rate of growth than the national average (30% compared to growth of

18% in England as a whole) whereas the rate of growth in private sector rents in Gateshead was

less than 1%;

Affordability ratio (in terms of the ratio between lower quartile house prices and lower quartile

earnings) is much lower in both Gateshead and Newcastle upon Tyne than across England as a

whole (5.0 and 5.8 respectively cf. 7.0). This means for example in Gateshead that lower

quartile house prices are 5 times higher than the salary of a full-time workers whose earnings

are at the lower quartile. Affordability ratios have got marginally “worse” since 2010, with the

ratio in Gateshead increasing from 4.9 to 5.0 and the ratio in Newcastle upon Tyne increasing

from 5.5 to 5.8. This is in line with the equivalent rate for England, where the ratio increased

from 6.7 to 7.0, a change of 5%;

Rate of development (in terms of increase in dwelling stock over the last 10 years) shows that

rate of development in Gateshead has been lower than England (5.7% cf. 8.3%). The rate of

development in Newcastle upon Tyne was lower again at 3.5%. Rates of development were

higher in most of the comparator areas than both Gateshead and Newcastle upon Tyne with

the rate of change in Manchester and Salford reaching 13.6% over the last 10 years;

Overcrowding (in terms of 2011 Census occupancy rates) 6.2% of households in Gateshead are

assumed to be overcrowded based on an objective measure, which is lower than England

(8.7%). The proportion of overcrowded households in Newcastle upon Tyne was slightly higher

than England (9.1%). The proportion of overcrowded households in Newcastle upon Tyne has

increased over the last 10 years but at a lower rate than England (17% cf. 23%). Overcrowding

has also increased in Gateshead but only marginally (1%). The proportion of overcrowded

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

15

households and rate of increase over the last 10 years was much worse in comparator areas

Manchester and Salford and Sheffield.

26. Given this context, it is apparent that the indicators generally indicate that housing market pressures

in Gateshead and Newcastle upon Tyne are generally comparable to those in similar areas, with

some indicators being a little better and some a little worse. Overall, (and given that many of these

areas show lesser pressures than the national average - in particular the market signals relating to

price), conditions across Gateshead and Newcastle upon Tyne suggest that the level of Objectively

Assessed Need should not be higher than suggested by household projections.

Conclusions

27. We have calculated Objectively Assessed Need based on demographic projections and assessed

these against Market Signals to determine if a higher rate of housing delivery is necessary to address

housing market problems. This takes account of household growth based on CLG 2014-based

projections (the starting point); adjusts for long-term migration trends; responds to suppressed

household formation (through providing for the growth of concealed families between 2001 and

2011); and takes account of vacant and second homes.

28. Figure 7 summarises each of the stages for establishing the Full Objectively Assessed Need for

Housing.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

16

Figure 7: Full Objectively Assessed Need for Housing for Gateshead and Newcastle upon Tyne 2015-30

Gateshead Newcastle upon

Tyne Total

Demographic starting point: CLG household

projections 2015-30 6,406 15,047 21,453

Baseline household projections taking account of local

circumstances 7,352 16,138 23,490

Allowance for transactional vacancies and second

homes: based on dwellings without a usually resident

household

230 378 608

Dwellings 7,582 16,516 24,098

Adjustment for suppressed household formation

rates: concealed family growth 2001-11 and homeless

households

258 + 8 = 266 399 + 9 = 408 657 + 17 = 674

Baseline housing need based on demographic

projections 7,848 16,924 24,772

Further adjustments

needed…

In response to balancing

jobs and workers: 0 0 0

In response to market signals

0 0 0

Combined impact of the identified adjustments 0 0 0

Full Objectively Assessed Need for Housing 2015-30 7,848 16,924 24,772

29. Across the two authorities CLG Household Projections suggest a growth of 21,453 households over

the 15-year period 2015-30; however, this is based on short-term migration trends. Demographic

projections based on 10-year migration trends provide a more reliable and appropriate basis for

establishing future housing need. The SHMA has identified an increase of 23,490 households over

the 15-year period 2015-30.

30. The baseline household projections should be increased by 657 households to take account of

concealed families and homeless households that would otherwise not be captured due to

suppressed household formation rates. This adjustment responds to identified un-met need for

affordable housing, and addresses suppressed household formation rates. Any new C2 provision

(residential institutions) does not count as a contribution towards the housing requirement as

population living in this type of provision is outside the OAN assessment.

31. Providing for this increase in households yields a baseline housing need of 24,772 dwellings; with

7,848 in Gateshead and 16,924 in Newcastle upon Tyne. .

32. The evidence from planned jobs and workers identifies that there will be sufficient extra workers for

the forecast increase in jobs, so there is no need to increase housing delivery to provide any

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

17

additional workers. On the basis of the Market Signals evidence, we would not propose an overall

uplift of the housing need identified based on the household projections.

33. Of course, it is important to remember that “establishing future need for housing is not an exact

science” (PPG ID 2a-014). Whilst the OAN must be underwritten by robust evidence that is based on

detailed analysis and informed by reasonable assumptions, the final conclusions should reflect the

overall scale of the housing needed in the housing market area without seeking to be spuriously

precise.

34. The SHMA therefore identifies the Full Objective Assessed Need for Housing in Gateshead to be

7,848 dwellings over the 15-year period 2015-30, equivalent to an average of 523 dwellings per

year. This includes the Objectively Assessed Need of Affordable Housing for 3,277 dwellings over

the same period, equivalent to an average of 218 per year.

35. The SHMA also identifies the Full Objective Assessed Need for Housing in Newcastle upon Tyne to

be 16,924 dwellings over the 15-year period 2015-30, equivalent to an average of 1,128 dwellings

per year. This includes the Objectively Assessed Need of Affordable Housing for 5,936 dwellings

over the same period, equivalent to an average of 396 per year.

36. Importantly, these OAN figures are extremely close to those set out in the Joint Core Strategy for the

period 2015-30 which show an annual need for Gateshead over the period 2015-30 of 535 dwellings

per annum and 1,040 dwellings per annum for Newcastle upon Tyne for the same period. Therefore,

it would seem to be appropriate to continue with the Joint Core Strategy housing target figures.

37. We would note that paragraph 29 of PPG proposes that:

‘An increase in the total housing figures included in the local plan should be considered

where it could help deliver the required number of affordable homes.’

38. While the guidance is clear that an uplift should be considered, it is also clear that this is not

necessarily required. In areas such as Gateshead and Newcastle upon Tyne the relatively low level of

viability for affordable housing implies that an uplift is unlikely to deliver significant additional,

amounts of affordable housing. It should also be remembered that the Housing White Paper, “Fixing

our broken housing market’ published in February 2017 indicates that up to 10% of all larger sites

should be affordable home ownership dwellings. This implies that an increase in total dwelling

delivery would first deliver more affordable home to buy, rather than those to rent which are

required to meet the identified need.

39. We would also note that the Housing White Paper proposed that there would be a future

consultation on a new standardised methodology for undertaking OAN calculations. This is

scheduled for consultation in September 2017 and to be in place by April 2018. The impact of this

methodology for Gateshead and Newcastle upon Tyne is currently unknown, and the government

have indicated that there will be flexibility in its application.

Nationally Described Space Standards

40. This report includes an assessment of the compliance with the Nationally Described Space Standards

(NDSS) in Gateshead and Newcastle. A summary is shown below:

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

18

Figure 8: Compliance with the 2015 Nationally Described Space Standards (NDSS) for Gross Internal Area (GIA)

Compliance with the 2015 Nationally Described Space Standards (NDSS) for Gross Internal Area (GIA)

Evidence

Gateshead An Analysis of Space Standards in Gateshead in January 2016

Newcastle upon Tyne Analysis of completions over previous two years August 2017

Conclusions

The two studies support each other in general conclusions: Evidence behind the conclusions:

A third of house types assessed failed to meet the space

standards

36% of house types in the Gateshead study failed to meet the NDSS,

the majority (64%) of 2, 3 and 4- bedroom properties in the

Newcastle upon Tyne analysis failed to meet the standard

There is some evidence that mid-sized house types, notably 3-

bedrooms are more likely to fail to meet space standards than

1 bedroom or larger house types

27% of 3-bedroom properties failed to meet the standard in the

Newcastle upon Tyne analysis compared to 56% of 1-bedroom

properties and 47% of 4-bedroom properties

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

19

1. Introducing the Study Background to the project and wider policy context

1.1 Opinion Research Services (ORS) was commissioned by Gateshead Council and Newcastle upon Tyne

City Council to undertake a Strategic Housing Market Assessment to establish the Objectively Assessed

Need for housing.

1.2 The National Planning Policy Framework (NPPF) sets out government's planning policies for England

and how these are expected to be applied. The Framework acts as guidance for local planning

authorities and decision-takers, both in drawing up plans and making decisions about planning

applications.

1.3 Planning Practice Guidance (PPG) on the assessment of housing and economic development needs was

published in March 2014. Previous SHMA Guidance (2007) and related documents were rescinded at

that time, so the approach taken in preparation of this report is focused on meeting the requirements

of the NPPF and PPG and therefore, many aspects of the previous SHMA required replacing.

1.4 The study methodology was also mindful of Planning Inspector Decisions and High Court Judgements,

as well as emerging good practice including the technical advice note about Objectively Assessed Need

(OAN) and Housing Targets Second Edition published by the Planning Advisory Service (PAS) in July

20155.

Government Policy 1.5 The NPPF has at its heart a presumption in favour of sustainable development, and states that Local

Plans should meet the full, objectively assessed needs for market and affordable housing in the

housing market area. Given that Regional Spatial Strategies are now revoked, the responsibility for

establishing the level of future housing provision required rests with the local planning authority.

“At the heart of the National Planning Policy Framework is a presumption in favour of sustainable

development, which should be seen as a golden thread running through both plan-making and

decision-taking.

Local planning authorities should positively seek opportunities to meet the development needs of

their area.

Local Plans should meet objectively assessed needs, with sufficient flexibility to adapt to rapid

change, unless any adverse impacts of doing so would significantly and demonstrably outweigh the

benefits, when assessed against the policies in this Framework taken as a whole.”

National Planning Policy Framework (NPPF), paragraph 14

5 Objectively Assessed Need and Housing Targets Second Version (PAS, July 2015)

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

20

“To boost significantly the supply of housing, local planning authorities should use their evidence

base to ensure that their Local Plan meets the full, objectively assessed needs for market and

affordable housing in the housing market area.”

National Planning Policy Framework (NPPF), paragraph 47

1.6 Given this context, the key objective is to provide the robust and strategic evidence base required to

establish the Objectively Assessed Need (OAN) for housing in the Housing Market Area (HMA) and

provide information on the appropriate mix of housing and range of tenures needed.

“Local planning authorities should have a clear understanding of housing needs in their area.

They should prepare a Strategic Housing Market Assessment to assess their full housing needs,

working with neighbouring authorities where housing market areas cross administrative boundaries.

The Strategic Housing Market Assessment should identify the scale and mix of housing and the

range of tenures that the local population is likely to need over the plan period which:

» meets household and population projections, taking account of migration and demographic

change;

» addresses the need for all types of housing, including affordable housing and the needs of

different groups in the community (such as, but not limited to, families with children, older

people, people with disabilities, service families and people wishing to build their own homes);

and

» caters for housing demand and the scale of housing supply necessary to meet this demand;”

National Planning Policy Framework (NPPF), paragraph 159

1.7 Modelling future housing need requires a consideration of the housing market from a high-level,

strategic perspective; in this way an understanding of how key drivers and long-term trends impact on

the structure of households and population over the full planning period can be delivered.

1.8 The objective of this study was to establish the OAN for housing (both market and affordable),

ensuring that this was fully compliant with the requirements of the NPPF and PPG. Using secondary

data, this study sought to:

» Identify the housing market area covering Gateshead and Newcastle upon Tyne;

» Provide evidence of the need and demand for housing based on demographic projections;

» Consider market signals about the balance between demand for and supply of dwellings;

» Establish the Objectively Assessed Need for housing;

» Identify the appropriate balance between market and affordable housing; and

» Address the needs for a range of specific household types.

1.9 It is important to recognise that the information from this document should not be considered in

isolation, but forms part of a wider evidence base to inform the development of housing and planning

policies. This document does not seek to determine rigid policy conclusions, but instead provides a

key component of the evidence base required to develop and support a sound policy framework.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

21

Duty to Co-operate 1.10 The Duty to Co-operate was introduced in the 2011 Localism Act and is a legal obligation.

1.11 The NPPF sets out an expectation that public bodies will co-operate with others on issues with any

cross-boundary impact, in particular in relation to strategic priorities such as “the homes and jobs

needed in the area”.

“Public bodies have a duty to cooperate on planning issues that cross administrative boundaries,

particularly those which relate to the strategic priorities set out in paragraph 156. The Government

expects joint working on areas of common interest to be diligently undertaken for the mutual

benefit of neighbouring authorities.

Local planning authorities should work collaboratively with other bodies to ensure that strategic

priorities across local boundaries are properly coordinated and clearly reflected in individual Local

Plans. Joint working should enable local planning authorities to work together to meet development

requirements which cannot wholly be met within their own areas – for instance, because of a lack of

physical capacity or because to do so would cause significant harm to the principles and policies of

this Framework. As part of this process, they should consider producing joint planning policies on

strategic matters and informal strategies such as joint infrastructure and investment plans.”

National Planning Policy Framework (NPPF), paragraphs 178-179

1.12 How councils have complied with their legal requirements under the Duty to Co-operate will be

considered when plans are submitted for examination. One key issue is how any unmet development

and infrastructure requirements can be provided by co-operating with adjoining authorities (subject to

tests of reasonableness and sustainability). The NPPF sets out that co-operation should be “a

continuous process of engagement” from “thinking through to implementation”.

“Local planning authorities will be expected to demonstrate evidence of having effectively

cooperated to plan for issues with cross-boundary impacts when their Local Plans are submitted for

examination. This could be by way of plans or policies prepared as part of a joint committee, a

memorandum of understanding or a jointly prepared strategy which is presented as evidence of an

agreed position. Cooperation should be a continuous process of engagement from initial thinking

through to implementation, resulting in a final position where plans are in place to provide the land

and infrastructure necessary to support current and projected future levels of development.”

National Planning Policy Framework (NPPF), paragraph 181

Gateshead and Newcastle upon Tyne Joint Core Strategy 2010-2030 1.13 The Gateshead and Newcastle upon Tyne Joint Core Strategy was adopted in March 2015 and this

SHMA can be seen as a review and update of the evidence base which underwrote this document. The

Joint Core Strategy includes a provision for 30,000 more homes, 22,000 more jobs and also a need for

15% of all new homes to be affordable housing on qualifying sites.

1.14 The Joint Core Strategy was based upon evidence produced in 2013 or earlier, although relevant

evidence and guidance that was made available by or during the examination of the Core Strategy in

2014 was considered. In March 2014, the government produced new guidance on conducting housing

needs assessments in the form of ‘Guidance for Housing and Economic Development Needs

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

22

Assessments’. Paragraphs 2-21 of this new guidance cover overall housing needs and paragraph 22-29

covers affordable housing needs. The new guidance includes a number of significant changes since the

2007 SHMA Practice Guidance which underwrote much of the work leading to the Joint Core Strategy.

1.15 This study should also be seen in the context of the wider situation in the North East of England. At

the time of writing, North Tyneside Council have adopted their Local Plan. Northumberland County

Council has withdrawn their local Plan from examination, while Sunderland City Council has published

their Core Strategy. Durham County Council and South Tyneside Council are developing their Local

Plans for publication.

Housing White Paper 1.16 We would also note that the Housing White Paper, “Fixing our broken housing market’ was published

in February 2017. One change flagged in the White Paper is a change in definition for affordable

housing to include Starter Homes at 20% discounts of market prices and also Build to Rent with rents

to remain at 20% below market prices. Build to rent does not affect the need for affordable homes

because the rents would be similar to Affordable Rents, just on the private sector not with a registered

provider

1.17 However, the inclusion of Starter Homes in a wider definition of affordable housing will require a

fundamental revision of who is considered to be in affordable housing need because the current

definition is based upon who can afford market housing including private rent as well as owner

occupied housing. Therefore, if the Government proceed to include Starter Homes in the definition of

affordable housing products, they will also need to count many more households as being in

affordable housing need than is currently the case because all non-owning households who wish to

purchase Starter Homes will need to be included.

1.18 On this basis, this study should be seen as sitting between two points in time in terms of the modelling

of affordable housing need. Past studies, including the Gateshead and Newcastle upon Tyne SHMA

2013 have applied very strict affordability test to assess who requires affordable housing, while this

study applies the much looser definition currently in force. However, it is likely that by April 2018

many more households which are not currently counted as being in affordable housing need will be

added to the figures because of the move to include Starter Homers in the definition of affordable

housing products.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

23

2. Defining the Housing Market Area

An evidence base to identify functional housing markets

2.1 The National Planning Policy Framework (NPPF) refers to Local Plans meeting the “full objectively

assessed needs for market and affordable housing in the housing market area” (paragraph 47,

emphasis added). The identification of the Housing Market Area (HMA) is therefore the first relevant

building block in the evidence for identifying objectively assessed needs for the study.

2.2 This Chapter considers the historic and current evidence about housing market areas relating to

Gateshead and Newcastle upon Tyne.

Functional Housing Market Areas 2.3 The definition of a functional housing market area is well-established as being “...the geographical area

in which a substantial majority of the employed population both live and work and where those

moving house without changing employment choose to stay” (Maclennan et al, 1998)6.

Planning Practice Guidance 2.4 Planning Practice Guidance (PPG) on the Assessment of Housing and Economic Development Needs

(March 2014) reflects this existing concept, confirming that the underlying principles for defining

housing markets are concerned with the functional areas in which people both live and work:

What is a housing market area?

A housing market area is a geographical area defined by household demand and preferences for all

types of housing, reflecting the key functional linkages between places where people live and work.

It might be the case the housing market areas overlap. The extent of the housing market areas

identified will vary, and many will in practice cut across various local planning authority

administrative boundaries. Local planning authorities should work with all the other constituent

authorities under the duty to cooperate.

Planning Practice Guidance (March 2014), ID 2a-010

2.5 Therefore, PPG requires an understanding of the housing market area and says this can be defined

using three different sources of information:

» House prices and rates of change in house prices

» Household migration and search patterns

» Contextual data (e.g. travel to work area boundaries, retail and school catchment areas)

6 Local Housing Systems Analysis: Best Practice Guide. Edinburgh: Scottish Homes

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

24

2.6 These sources are well-established, being consistent with those previously identified in the CLG advice

note “Identifying sub-regional housing market areas” published in 20077. We would note that retail

catchment area is predominately used for economic market area, rather than housing market areas,

while school catchment areas are used to consider more localised housing markets. Therefore they

are not included in this study.

Geography of Housing Market Areas (NHPAU/CURDS) 2.7 CLG also published a report on the ‘Geography of Housing Market Areas’ in 20108 which was

commissioned by the former National Housing and Planning Advice Unit (NHPAU) and undertaken by

the Centre for Urban and Regional Development Studies (CURDS) at Newcastle upon Tyne University.

This study explored a range of potential methods for calculating housing market areas for England and

applied these methods to the whole country to show the range of housing markets which would be

generated. The report also proposed three overlapping tiers of geography for housing markets:

» Tier 1: framework housing market areas defined by long distance commuting flows and the

long-term spatial framework within which housing markets operate;

» Tier 2: local housing market areas defined by migration patterns that determine the limits of

short term spatial house price arbitrage: i.e. households moving without changing jobs;

» Tier 3: sub-markets defined in terms of neighbourhoods or house type price premiums.

2.8 The report recognised that migration patterns and commuting flows were the most relevant

information sources for identifying the upper tier housing market areas, with house prices only

becoming relevant at a more local level and when establishing housing sub-markets. The report also

outlined that no one single approach (nor one single data source) will provide a definitive solution to

identifying local housing markets; but by using a range of available data, judgements on appropriate

geography can be made.

2.9 Advice published in the Planning Advisory Service (PAS) technical advice note about Objectively

Assessed Need (OAN) and Housing Targets (originally published in June 2014, with a second edition9 in

July 2015) also suggests that the main indicators will be migration and commuting (second edition,

paragraph 5.4).

“The PPG provides a long list of possible indicators, comprising house prices, migration and

search patterns and contextual data including travel-to-work areas, retail and school

catchments. In practice, the main indicators used are migration and commuting.”

The PAS OAN technical advice note also suggests that analysis reported in the CLG report

“Geography of Housing Market Areas” (CLG, November 2010) should provide a starting point

for drawing HMAs (Figure 9).

2.10 Figure 9 shows the local authority boundary (in black) with Gateshead and Newcastle upon Tyne

shaded blue. It compares these with the CURDS study (in green) to consider their alignment. It is

apparent that the CURDS study concluded that Gateshead and Newcastle upon Tyne are part of a

larger HMA which also covers North Tyneside and South Tyneside to the east, along with

7 Identifying sub-regional housing market areas (CLG, March 2007); paragraph 1.6 8 Geography of Housing Market Areas (CLG, November 2010) 9 http://www.pas.gov.uk/documents/332612/6549918/OANupdatedadvicenote/f1bfb748-11fc-4d93-834c-a32c0d2c984d

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

25

Northumberland to the north and west, and part of County Durham to the south. A separate

Sunderland HMA lies adjacent to the south east which includes the eastern part of County Durham.

Figure 9: NHPAU Study – PAS OAN technical advice note ‘Starting Point’ (Source: NHPAU/CURDS 2010)

ONS Travel to Work Areas 2.11 PPG defines housing market areas on the basis that they will reflect “the key functional linkages

between places where people live and work” (ID 2a-010). Furthermore, PPG identifies Office for

National Statistics Travel to Work Areas (TTWAs) as one of the identified data sources that should be

considered when establishing housing market areas.

Travel to work areas can provide information about commuting flows and the spatial structure of

the labour market, which will influence household price and location. They can also provide

information about the areas within which people move without changing other aspects of their lives

(e.g. work or service use).

Planning Practice Guidance (March 2014), ID 2a-011

2.12 The Office for National Statistics (ONS) defines official Travel to Work Areas for those involved in

labour market analysis and planning. These areas are also based on analysis of Census commuting

flow data, and TTWAs based on data from the 2011 Census were published in August 2015. A total of

228 TTWAs were defined for the whole of the UK based on 2011 data, a reduction from the 243

TTWAs that were previously defined based on 2001 Census data.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

26

2.13 Figure 10 shows the defined TTWAs (2015), in blue, and these are based on the commuting flow data

from the 2011 Census.

Figure 10: ONS Travel To Work Areas (Source: ONS 2015)

2.14 Though smaller than the NHPAU Study HMA, once again, the TTWA including Gateshead and

Newcastle upon Tyne extends to the east to include North Tyneside and part of South Tyneside, along

with parts of Northumberland to the north and west, and part of County Durham to the south. The

remainder of South Tyneside is in a separate TTWA to the south east with Sunderland and the eastern

part of County Durham.

House Prices 2.15 As noted earlier, PPG also suggests that house prices should be considered in identifying the HMA for

an area. However, PAS OAN Technical Note suggests that migration and commuting should be

considered as being more important.

2.16 Figure 11 shows house prices across the study area and its neighbouring local authorities in quintiles,

so 20% of all properties sold fall in to each colour band. Areas in dark green have the lowest house

price and those in bright red have the highest prices.

2.17 For an area to be considered to be a HMA there would typically be a range of property types and

values across the area to allow all types of households with different levels of affordability to be able

to live in the area. The map shows large variations in house prices within each of the local authorities.

Therefore, an analysis of house prices does not help to simplify the process of identifying HMAs across

the wider North East.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

27

Figure 11: House Prices 2016-17 (Source: Land Registry)

Valuation Office Agency Broad Rental Market Areas 2.18 The Broad Rental Market Area (BRMA) is the geographical area used by the Valuation Office Agency

(VOA) to determine the Local Housing Allowance rate (LHA), the allowance paid to Housing Benefit

applicants. The BRMA area is based on an area where a person could reasonably be expected to live

taking into account access to facilities and services for the purposes of health, education, recreation,

personal banking and shopping.

2.19 When determining BRMAs the Rent Officer takes account of the distance of travel, by public and

private transport, to and from these facilities and services. The boundaries of a BRMA do not have to

match the boundaries of a local authority and BRMAs will often fall across more than one local

authority area. Therefore BRMAs are areas within which it would be reasonable to expect a household

needing local housing allowance support to move to another settlement within the area in order to

find suitable housing.

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

28

The BRMA areas for Gateshead and Newcastle upon Tyne, and surrounding areas are shown, in red, in

Figure 12. It is evident that they again fall into one BRMA with North Tyneside, part of South Tyneside

and a large rural area in Northumberland to the west and north west. Again, the south part of South

Tyneside is in a separate BRMA with Sunderland and the eastern part of County Durham. The

remainder of County Durham is in a separate BRMA to the south, centred around Durham and Bishop

Auckland.

Figure 12: VOA Broad Rental Market Area Boundaries

Administrative Boundaries and Housing Market Areas 2.20 The NPPF recognises that housing market areas may cross administrative boundaries, and PPG

emphasises that housing market areas reflect functional linkages between places where people live

and work. The previous 2007 CLG advice note10 also established that functional housing market areas

should not be constrained by administrative boundaries, nevertheless it suggested the need for a

“best fit” approximation to local authority areas for developing evidence and policy (paragraph 9):

“The extent of sub-regional functional housing market areas identified will vary and many

will in practice cut across local authority administrative boundaries. For these reasons,

regions and local authorities will want to consider, for the purposes of developing evidence

bases and policy, using a pragmatic approach that groups local authority administrative

areas together as an approximation for functional sub-regional housing market areas.”

2.21 This “best fit” approximation has also been suggested by the PAS OAN technical advice note, which

suggests (second edition, paragraph 5.9):

10

Identifying sub-regional housing market areas (CLG, March 2007)

Opinion Research Services | Gateshead & Newcastle upon Tyne Strategic Housing Market Assessment 2017 August 2017

29

“boundaries that straddle local authority areas are usually impractical, given that planning

policy is mostly made at the local authority level, and many kinds of data are unavailable for

smaller areas.”

2.22 This means there is a need for balance in methodological approach:

» On the one hand, it is important that the process of analysis and identification of the functional

housing market areas should not be constrained by local authority boundaries. This allows the

full extent of each functional housing market to be properly understood and ensures that all of the

constituent local planning authorities can work together under the duty to cooperate, as set out in

Guidance (PPG, ID 2a-010).

On the other hand, and as suggested by the PAS OAN technical advice note (and the previous

CLG advice note), it is also necessary to identify a “best fit” for each functional housing

market area that is based on local planning authority boundaries. This “best fit” area

provides an appropriate basis for analysing evidence and drafting policy, and would normally

represent the group of authorities that would take responsibility for undertaking a Strategic

Housing Market Assessment.

2.23 In summary, therefore, the approach to defining housing market areas needs to balance robust

analysis with pragmatic administrative requirements.

2.24 Based on the range of analysis that we have considered, it is evident that the geography of housing

market areas around Gateshead and Newcastle upon Tyne is complex. There are important functional

relationships with North Tyneside, South Tyneside, Northumberland and County Durham, so it is

relevant to note that PPG recognises that “it might be the case that housing market areas overlap”

(paragraph 10). The three national mapped sources (NHPAU/CURDS Study, VOA BRMAs), used in

defining HMAs, all indicate Gateshead and Newcastle upon Tyne to be in a HMA with North Tyneside.

The NHPAU Study HMA indicates Gateshead and Newcastle upon Tyne to be in a HMA with South

Tyneside and Northumberland. The ONS Travel to Work Areas indicate Gateshead and Newcastle upon

Tyne to be in a HMA with parts of South Tyneside, Northumberland and County Durham, while the

VOA BRMAs indicate Gateshead and Newcastle upon Tyne to be in a HMA with parts of South Tyneside

and Northumberland.

2.25 Given the evidence from the three national mapped sources, it is necessary to assess whether