Barriers to Foreign Direct Investment Under Political Instability

Upload

independentCategory

view

0download

0

1

A

DISSERTATION

ON

STUDY OF TRENDS OF FOREIGN INSTITUTIONAL

INVESTMENTS IN INDIA

SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIRMENT

FOR THE AWARD OF THE DEGREE OF

MASTER OF ARTS (ECONOMICS)

(2011-2013)

Under the Supervision of Submitted By:

Prof. M.P SINGH MOHAMMAD SABIR

M.A - 4th

Semester

Roll No.-46

FACULTY OF SOCIAL SCIENCES

BANARAS HINDU UNIVERSITY

VARANASI

2

DECLARATION

I hereby declare that the information presented here is correct to the

best of my knowledge and the analysis as per the norms and guidelines

provided for the report. I have utilized the requisite concepts and applied the

required methodologies to analyze the objective collected to reach the

conclusion present in the report.

I claim the report to be my indigenous work and have not been

presented anywhere for any purpose what so ever.

Mohammad Sabir

M.A - 4th

Semester

Roll No.-46

3

ACKNOWLEDGMENT

A project cannot be completed alone .it requires the effort of many individuals’

take the opportunity to thank all those people who helped me to complete this

report.

It is indeed a moment of immense gratitude for me to express my deepest thank to the faculty of Commerce for providing me with any opportunity to carry out this research and help me create research report on trends of foreign institutional investments in India. I am immensely grateful to Prof. V. S. Singh for providing me opportunity to prove my skills and shoulder the responsibilities through this research report. I would also like to convey my sincere gratitude to my project guide Prof. K.K. Jaiswal for his valuable guidance and suggestions while pursuing the project and for taking pains to give his valuable inputs to structure the report. Without his help and valuable inputs and guidelines, the completion of this project would not have been possible. I am also thankful to our faculty and classmates for their suggestion and support to undertake this work and also during the course of study.

Mohammad Sabir

M.A - 4th

Semester

Roll No.-46

4

BANARAS HIND UNIVESITY FACULTY OF Social Sciences MASTER OF ARTS (ECONOMICS)

VARANASI-221005 (U.P.)

This is to certify that Mr. Mohammad Sabir has completed the

dissertation work for the final year of MASTER OF ARTS (ECONOMICS) under

supervision and guidance for Session 2011-13.

His dissertation entitled foreign institutional investors embodies the result

of his investigation during this Period and he was found sincere and dedicated to

his work.

I wish him success in future.

Prof. M.P. SINGH Faculty of Social Sciences Department of Economics Date:- Banaras Hindu University Varanasi -221005 Place:

5

PREFACE

It is great privilege for me to place this report before the Mentor. This

report is concern with the trends of foreign institutional investments India.

This project is done to know about the institution that come India for

investment. This project has been completed with the help of many people

who guided through thick and thin and provided me every kind of support in

completing my project. At last I want to give my thanks to everybody who has

co-operated me a lot in completing my project.

6

Table of content

7

TABLE OF CONTENT

S.No Topic 1 INTRODUCTION 2 OBJECTIVES 3 RESEARCH METHODOLOGY 4 FINDINGS 5 CONCLUSION 6 RECOMMENDATION & SUGESTION 7 LIMITATIONS 8 BIBLIOGRAPHY

9

Foreign institutional investors

Investment-meaning

Investment is putting money into something with the expectation of profit. More specifically, investment is the commitment of money or capital to the purchase of financial instruments or other assets so as to gain profitable returns in the form of interest, dividends, or appreciation of the value of the instrument (capital gains). It is related to saving or deferring consumption. Investment is involved in many areas of the economy, such as business management and finance whether for households, firms, or governments. An investment involves the choice by an individual or an organization, such as a pension fund, after some analysis or thought, to place or lend money in a vehicle, instrument or asset, such as property, commodity, stock, bond, financial derivatives (e.g. futures or options), or the foreign asset denominated in foreign currency, that has certain level of risk and provides the possibility of generating returns over a period of time.

Investment comes with the risk of the loss of the principal sum. The investment that has not been thoroughly analyzed can be highly risky with respect to the investment owner because the possibility of losing money is not within the owner's control. The difference between speculation and investment can be subtle. It depends on the investment owner's mind whether the purpose is for lending the resource to someone else for economic purpose or not.

In the case of investment, rather than store the good produced or its money equivalent, the investor chooses to use that good either to create a durable consumer or producer good, or to lend the original saved good to another in exchange for either interest or a share of the profits. In the first case, the individual creates durable consumer goods, hoping the services from the good will make his life better. In the second, the individual becomes an entrepreneur using the resource to produce goods and services for others in the hope of a profitable sale. The third case describes a lender, and the fourth describes an investor in a share of the business. In each case, the consumer obtains a durable asset or investment, and accounts for that asset by recording an equivalent liability. As time passes, and both prices and interest rates change, the value of the asset and liability also change.

10

An asset is usually purchased, or equivalently a deposit is made in a bank, in hopes of getting a future return or interest from it. The word originates in the Latin "vestis", meaning garment, and refers to the act of putting things (money or other claims to resources) into others' pockets.[4] The basic meaning of the term being an asset held to have some recurring or capital gains. It is an asset that is expected to give returns without any work on the asset per se. The term "investment" is used differently in economics and in finance. Economists refer to a real investment (such as a machine or a house), while financial economists refer to a financial asset, such as money that is put into a bank or the market, which may then be used to buy a real asset.

In finance

In finance, investment is the commitment of funds by buying securities or other monetary or paper (financial) assets in the money markets or capital markets, or in fairly liquid real assets, such as gold or collectibles. Valuation is the method for assessing whether a potential investment is worth its price. Returns on investments will follow the risk-return spectrum.

Types of financial investments include shares, other equity investment, and bonds (including bonds denominated in foreign currencies). These financial assets are then expected to provide income or positive future cash flows, and may increase or decrease in value yielding the investor capital gains or losses.

Trades in contingent claims or derivative securities do not necessarily have future positive expected cash flows, and so are not considered assets, or strictly speaking, securities or investments. Nevertheless, since their cash flows are closely related to (or derived from) those of specific securities, they are often studied as or treated as investments.

Investments are often made indirectly through intermediaries, such as banks, mutual funds, pension funds, insurance companies, collective investment schemes, and investment clubs. Though their legal and procedural details differ, an intermediary generally makes an investment using money from many individuals, each of whom receives a claim on the intermediary.

Within personal finance, money used to purchase shares, put in a collective investment scheme or used to buy any asset where there is an element of capital risk is deemed an investment. Saving within personal finance refers to money put aside, normally on a regular basis. This distinction is important, as

11

investment risk can cause a capital loss when an investment is sold, unlike saving(s) where the more limited risk is cash devaluing due to inflation.

In many instances the terms saving and investment are used interchangeably, which confuses this distinction. For example many deposit accounts are labeled as investment accounts by banks for marketing purposes. Whether an asset is a saving(s) or an investment depends on where the money is invested: if it is cash then it is savings, if its value can fluctuate then it is investment.

Types of investment: 1. Foreign direct investment

2. Foreign institutional investment

Foreign direct investment (FDI) or foreign investment refers to the net inflows of investment to acquire a lasting management interest (10 percent or more of voting stock) in an enterprise operating in an economy other than that of the investor. It is the sum of equity capital, reinvestment of earnings, other long-term capital, and short-term capital as shown in the balance of payments. It usually involves participation in management, joint-venture, transfer of technology and expertise. There are two types of FDI: inward foreign direct investment and outward foreign direct investment, resulting in a net FDI inflow (positive or negative) and "stock of foreign direct investment", which is the cumulative number for a given period. Direct investment excludes investment through purchase of shares. FDI is one example of international factor movements.

Types

A foreign direct investor may be classified in any sector of the economy and could be any one of the following:]

an individual; a group of related individuals; an incorporated or unincorporated entity; a public company or private company; a group of related enterprises; a government body; an estate (law), trust or other social institution; or Any combination of the above.

12

Foreign institutional investors

Meaning-

An institution that is a legal entity established or incorporated outside

India proposing to make investments in India only in securities.

The term is used most commonly in India to refer to outside companies

investing in the financial markets of India. International institutional

investors must register with the Securities and Exchange Board of India

to participate in the market. One of the major market regulations

pertaining to FIIs involves placing limits on FII ownership in

Indian companies.

Foreign Institutional investors are organizations which pool large sums of money and invest those sums in securities, real property and other investment assets. They can also include operating companies which decide to invest its profits to some degree in these types of assets.

Types of typical investors include banks, insurance companies, retirement or pension funds, hedge funds, investment advisors and mutual funds. Their role in the economy is to act as highly specialized investors on behalf of others. For instance, an ordinary person will have a pension from his employer. The employer gives that person's pension contributions to a fund.

The fund will buy shares in a company, or some other financial product. Funds are useful because they will hold a broad portfolio of investments in many companies. This spreads risk, so if one company fails, it will be only a small part of the whole fund's investment.

Institutional investors will have a lot of influence in the management of corporations because they will be entitled to exercise the voting rights in a company. They can actively engage in corporate governance. Furthermore, because institutional investors have the freedom to buy and sell shares, they can play a large part in which companies stay solvent, and which go under. Influencing the conduct of listed companies, and providing them with capital are all part of the job of investment management.

13

Foreign Institutional Investors (FII) includes the following foreign based

categories:

Mutual Funds

Investment Trust

Insurance or reinsurance companies

Investment Trusts

Banks

Endowments

University Funds

Foundations

Charitable Trusts or Charitable Societies

Pension fund

FII AND FDI Foreign investment refers to investments made by the residents of a country in the financial assets and production processes of another country. The effect of foreign investment, however, varies from country to country. It can affect the factor productivity of the recipient country and can also affect the balance of payments. Foreign investment provides a channel through which countries can gain access to foreign capital. It can come in two forms: FDI and foreign institutional investment (FII). Foreign direct investment involves in direct production activities and is also of a medium- to long-term nature. But foreign institutional investment is a short-term investment, mostly in the financial markets. FII, given its short-term nature, can have bidirectional causation with the returns of other domestic financial markets such as money markets, stock markets, and foreign exchange markets. Hence, understanding the determinants of FII is very important for any emerging economy as FII exerts a larger impact on the domestic financial markets in the short run and a real impact in the long run. India, being a capital scarce country, has taken many measures to attract foreign investment since the beginning of reforms in 1991. India is the second largest country in the world, with a population of over 1 billion people. As a developing country, India’s economy is characterized by wage rates that are significantly lower than those in most developed countries. These two traits combine to make India a natural destination for FDI and foreign institutional investment (FII). Until recently, however,

14

India has attracted only a small share of global FDI and FII primarily due to government restrictions on foreign involvement in the economy. But beginning in 1991 and accelerating rapidly since 2000, India has liberalized its investment regulations and actively encouraged new foreign investment, a sharp reversal from decades of discouraging economic integration with the global economy. The world is increasingly becoming interdependent. Goods and services followed by the financial transaction are moving across the borders. In fact, the world has become a borderless world. With the globalization of the various markets, international financial flows have so far been in excess for the goods and services among the trading countries of the world. Of the different types of financial inflows, the FDI and foreign institutional investment (FII)) has played an important role in the process of development of many economies. Further many developing countries consider FDI and FII as an important element in their development strategy among the various forms of foreign assistance. The FDI and FII flows are usually preferred over the other form of external finance, because they are not debt creating, nonvolatile in nature and their returns depend upon the projects financed by the investor. The FDI and FII would also facilitate international trade and transfer of knowledge, skills and technology. The FDI and FII is the process by which the resident of one country (the source country) acquire the ownership of assets for the purpose of controlling the production, distribution and other productive activities of a firm in another country(the host country). According to the international monetary fund (IMF), FDI and FII is defined as “an investment that is made to acquire a lasting interest in an enterprise operating in an economy other than that of investor”. The government of India (GOI) has also recognized the key role of the FDI and FII in its process of economic development, not only as an addition to its own domestic capital but also as an important source of technology and other global trade practices. In order to attract the required amount of FDI and FII it has bought about a number of changes in its economic policies and has put in its practice a liberal and more transparent FDI and FII policy with a view to attract more FDI and FII inflows into its economy. These changes have heralded the liberalization era of the FDI and FII policy regime into India and have brought about a structural breakthrough in the volume of FDI and FII inflows in the economy. In this context,

15

this report is going to analyze the trends and patterns of FDI and FII flows into India during the post liberalization period that is 2006 to 2009 year.

Reasons India attract FII’S

Robust domestic growth story

Second fastest growing

Increasing number of skilled labours

Cost competitiveness

Due to the global recession, sensex plunged to 8,160.4 (as of March 2009) but

within a few months, it surged to 17,198 (as of November 2009). The reason it is

not due to the strong fundamentals or because India is a developing country. In

recent times foreigners are investing huge amounts on Indian stocks. There are

some reasons which greatly attract foreign institutional investors (FIIs), as

discussed below.

Capital gain tax (CGT) A tax charged on capital gains or the profit realized on the sale of a non-inventory

asset that was purchased at a lower price is called as Capital Gains Tax

(abbreviated as CGT). Typically, capital gains are realized from the sale of stocks,

bonds, property and precious metals. Not all countries implement a capital gains

tax and most have different taxation rates for individuals and corporations.

In India, equities are considered as long term capital if the holding period is one

year or more. Long term capital gains from equities are not taxed (ZERO TAX) if

shares are sold through recognized stock exchange. However short term capital

gains from equities held for less than one year, is taxed at 15% (Increased from

10% to 15% after Budget 2008-09) plus surcharge and education cuss. This is

applicable only for transactions that attract Securities Transaction Tax (STT).

The capital gain tax is paid only when an asset is sold, taxpayers can legally avoid

the payment by holding on to their assets, a phenomenon known as the “lock-in

effect”. This means Foreign Institutional Investors (FIIs) can pump in money and

make thousands of cores in profits without paying any income taxes by selling the

shares after one year, making India almost a ‘tax haven’.

Low interest rates in foreign banks The interest rates in the banks in the developed countries like USA and European

countries are very low, now about less than one percent per year. If they invest in

their banks, they get very meager returns.

16

The returns from Indian stock market are attractive. Hence many foreign

institutional investors are investing a small part of their portfolio in the Indian

stock market. Since many of these FII’s have investment portfolios in billions,

even a small 2% investment into India is a big amount for our markets. Typically,

they tend to buy only into the bigger companies in India (which they may consider

mid sized by American and US standards). This means they are buying mostly in

BSE Sensex and BSE 100 type companies. This makes the indices to skyrocket.

Well, they are not interested in investing in the smaller companies – the ticket size

is too small. The big company based indices continue to rise, while good

companies in India which are smaller continue to deal with paucity of funds to

grow.

As each month passes, more foreigners discover the world’s best kept open secret

i.e. the legal tax haven called Indian stock market. As this happens more new FII’s

join the fray the indices continue to skyrocket.

Foreign Institutional Investment Since 1990-91, the Government of India embarked on liberalization and economic reforms with a view of bringing about rapid and substantial economic growth and move towards globalization of the economy. As a part of the reforms process, the Government under its New Industrial Policy revamped its foreign investment policy recognizing the growing importance of foreign direct investment as an instrument of technology transfer, augmentation of foreign exchange reserves and globalization of the Indian economy. Simultaneously, the Government, for the first time, permitted portfolio investments from abroad by foreign institutional investors in the Indian capital market. The entry of FIIs seems to be a follow up of the recommendation of the Norseman Committee Report on Financial System. While recommending their entry, the Committee, however did not elaborate on the objectives of the suggested policy. The committee only suggested that the capital market should be gradually opened up to foreign portfolio investments. From September 14, 1992 with suitable restrictions, FIIs were permitted to invest in all the securities traded on the primary and secondary markets, including shares, debentures and warrants issued by companies which were listed or were to be listed on the Stock Exchanges in India. While presenting the Budget for 1992-93, the then Finance Minister Dr. Man Mohan Singh had announced a proposal to allow reputed foreign investors, such as Pension

17

Funds etc., to invest in Indian capital market. To operationalize this policy announcement, it had become necessary to evolve guidelines for such investments by Foreign Institutional Investors (FIIs). The policy framework for permitting FII investment was provided under the Government of India guidelines vide Press Note date September 14, 1992. The guidelines formulated in this regard were as follows:

1. Foreign Institutional Investors (FIIs) including institutions such as Pension Funds, Mutual Funds, Investment Trusts, Asset Management Companies, Nominee Companies and Incorporated/Institutional Portfolio Managers or their power of attorney holders (providing discretionary and non-discretionary portfolio management services) would be welcome to make investments under these guidelines.

2. FIIs would be welcome to invest in all the securities traded on the Primary and Secondary markets, including the equity and other securities/instruments of companies which are listed/to be listed on the Stock Exchanges in India including the OTC Exchange of India. These would include shares, debentures, warrants, and the schemes floated by domestic Mutual Funds. Government would even like to add further categories of securities later from time to time.

3. FIIs would be required to obtain an initial registration with Securities

and Exchange Board of India (SEBI), the nodal regulatory agency for securities markets, before any investment is made by them in the Securities of companies listed on the Stock Exchanges in India, in accordance with these guidelines. Nominee companies, affiliates and subsidiary companies of a FII would be treated as separate FIIs for registration, and may seek separate registration with SEBI.

4. Since there were foreign exchange controls in force, for various permissions under exchange control, along with their application for initial registration, FIIs were also supposed to file with SEBI another application addressed to RBI for seeking various permissions under FERA, in a format that would be specified by RBI for the purpose. RBI's general permission would be obtained by SEBI before granting

18

initial registration and RBI's FERA permission together by SEBI, under a single window approach.

5. For granting registration to the FII, SEBI should take into account the track record of the FII, its professional competence, financial soundness, experience and such other criteria that maybe considered by SEBI to be relevant. Besides, FII seeking initial registration with SEBI were be required to hold a registration from the Securities Commission, or the regulatory organization for the stock market in the country of domicile/incorporation of the FII.

6. SEBI's initial registration would be valid for five years. RBI's general permission under FERA to the FII would also hold good for five years. Both would be renewable for similar five year periods later on.

7. RBI's general permission under FERA would enable the registered FII

to buy, sell and realize capital gains on investments made through initial corpus remitted to India, subscribe/renounce rights offerings of shares, invest on all recognized stock exchanges through a designated bank branch, and to appoint a domestic Custodian for custody of investments held.

8. This General Permission from RBI would also enable the FII to:

a. Open foreign currency denominated accounts in a designated bank. (There could even be more than one account in the same bank branch each designated in different foreign currencies, if it is so required by FII for its operational purposes);

b. Open a special non-resident rupee account to which could be credited all receipts from the capital inflows, sale proceeds of shares, dividends and interests;

c. Transfer sums from the foreign currency accounts to the rupee account and vice versa, at the market rate of exchange;

d. Make investments in the securities in India out of the balances in the rupee account;

e. Transfer repairable (after tax) proceeds from the rupee account to the foreign currency account(s);

f. Repatriate the capital, capital gains, dividends, incomes received by way of interest, etc. and any compensation received towards sale/renouncement of rights offerings of shares subject to the designated branch of a bank/the custodian being authorized to

19

deduct withholding tax on capital gains and arranging to pay such tax and remitting the net proceeds at market rates of exchange;

g. Register FII's holdings without any further clearance under FERA.

9. There would be no restriction on the volume of investment minimum or maximum-for the purpose of entry of FIIs, in the primary/secondary market. Also, there would be no lock-in period prescribed for the purposes of such investments made by FIIs. It was expected that the differential in the rates of taxation of the long term capital gains and short term capital gains would automatically induce the FIIs to retain their investments as long term investments.

10. Portfolio investments in primary or secondary markets were subject to a ceiling of 30% of issued share capital for the total holdings of all registered FIIs, in any one company. The ceiling was made applicable to all holdings taking into account the conversions out of the full yand partly convertible debentures issued by the company. The holding of a single FII in any company would also be subject to a ceiling of 10% of total issued capital. For this purpose, the holdings of an FII group would be counted as holdings of a single FII.

11. The maximum holdings of 24% for all non-resident portfolio

investments, including those of the registered FIIs, were to include NRI corporate and non-corporate investments, but did not include the following:

a. Foreign investments under financial collaborations (direct

foreign investments), which are permitted up to 51% in all priority areas.

b. Investments by FIIs through the following alternative routes:

I. Offshore single/regional funds; II. Global Depository Receipts;

III. Euro convertibles.

12. Disinvestment would be allowed only through stock exchange in India, including the OTC Exchange. In exceptional cases, SEBI may permit sales other than through stock exchanges, provided the sale

20

price is not significantly different from the stock market quotations, where available.

13. All secondary market operations would be only through the recognized intermediaries on the Indian Stock Exchange, including OTC Exchange of India. A registered FII would be expected not to engage in any short selling in securities and to take delivery of purchased and give delivery of sold securities.

14. A registered FII can appoint as Custodian an agency approved by

SEBI to act as custodian of Securities and for confirmation of transactions in Securities, settlement of purchase and sale, and for information reporting. Such custodian should establish separate accounts for detailing on a daily basis the investment capital utilization and securities held by each FII for which it is acting as custodian. The custodian was supposing to report to the RBI and SEBI semi-annually as part of its disclosure and reporting guidelines.

15. The RBI should make available to the designated bank branches a

list of companies where no investment will be allowed on the basis of the upper prescribed ceiling of 30% having been reached under the portfolio investment scheme.

16. Reserve Bank of India may at any time request by an order a registered FII to submit information regarding the records of utilization of the inward remittances of investment capital and the statement of securities transactions. Reserve Bank of India and/or SEBI may also at any time conduct a direct inspection of the records and accounting books of a registered FII.

17. FIIs investing under this scheme will benefit from a concessional

tax regime of a flat rate tax of 20% on dividend and interest income and a tax rate of 10% on long term (one year or more)capital gains.

These guidelines were suitably incorporated under the SEBI (FIIs) Regulations, 1995. These regulations continue to maintain the link with the government guidelines through an inserted clause that the investment by FIIs should also be subject to Government guidelines. This linkage has allowed the Government to indicate various investment limits including in specific sectors.

21

Foreign Institutional Investors in India Evolution of policy framework Until the 1980s, India’s development strategy was focused on self-reliance and import-substitution. Current account deficits were financed largely through debt flows and official development assistance. There was a general disinclination towards foreign investment or private commercial flows. Since the initiation of the reform process in the early 1990s, however, India’s policy stance has changed substantially, with a focus on harnessing the growing global foreign direct investment (FDI) and portfolio flows. The broad approach to reform in the external sector after the Gulf crisis was delineated in the Report of the High Level Committee on Balance of Payments (Chairman: C. Rangarajan). It recommended, interlaid, a compositional shift in capital flows away from debt to non-debt creating flows; strict regulation of external commercial borrowings, especially short-term debt; discouraging volatile elements of flows from non-resident Indians (NRIs); gradual liberalisation of outflows; and dis-intermediation of Government in the flow of external assistance. After the launch of the reforms in the early 1990s, there was a gradual shift towards capital account convertibility. From September 14, 1992, with suitable restrictions, FIIs and Overseas Corporate Bodies (OCBs) were permitted to invest in financial instruments.2 The policy framework for permitting FII investment was provided under the Government of India Guidelines vide Press Note dated September 14, 1992, which enjoined upon FIIs to obtain an initial registration with SEBI and also RBI’s general permission under FERA. Both SEBI’s registration and RBI’s general permissions under FERA were to hold good for five years and were to be renewed after that period. RBI’s general permission under FERA could enable the registered FII to buy, sell and realize capital gains on investments made through initial corpus remitted to India, to invest on all recognized stock exchanges through a designated bank branch, and to appoint domestic custodians for custody of investments held. The Government guidelines of 1992 also provided for eligibility conditions for registration, such as track record, professional competence, financial soundness and other relevant criteria, including registration with a regulatory organization in the home country. The guidelines were suitably incorporated under the SEBI (FIIs)

22

Regulations, 1995. These regulations continue to maintain the link with the government guidelines by inserting a clause to indicate that the investment by FIIs should also be subject to Government guidelines. This linkage has allowed the Government to indicate various investment limits including in specific c sectors. With coming into force of the Foreign Exchange Management Act, (FEMA), 1999 in 2000, the Foreign Exchange Management (Transfer or issue of Security by a Person Resident Outside India) Regulations, 2000 were issued to provide the foreign exchange control context where foreign exchange related transactions of FIIs were permitted by RBI. A philosophy of preference for institutional funds, and prohibition on portfolio investments by foreign natural persons has been followed, except in the case of Non-resident Indians, where direct participation by individuals takes place. Right 1 Source: Report of Expert Group on Encouraging FII Flows and Checking the Vulnerability of Capital Markets to Speculative flows, November, 2005 2 An OCB is a company, partnership fi rm, society and other corporate body owned directly or indirectly to the extent of at least sixty percent by NRIs and includes overseas trust in which not less than sixty per cent beneficial interest is held by NRIs directly or indirectly but irrevocably. From 1992, FIIs have been allowed to invest in all securities traded on the primary and secondary markets, including shares, debentures and warrants issued by companies which were listed or were to be listed on the Stock Exchanges in India and in schemes floated by domestic mutual funds. Historical evolution of FII Policy is summarized below: Date Policy change September 1992 FIIs allowed to invest by the Government Guidelines in all securities in both primary and secondary markets and schemes floated by mutual funds. Single FIIs to invest 5 per cent and all FIIs allowed to invest 24 per cent of a company’s issued capital. Broad based funds to have 50 investors with no one holding more than 5 per cent. The objective was to have reputed foreign investors, such as, pension funds, mutual fund or investment trusts and other broad based institutional investors in the capital market. November 1996 100 per cent debt FIIs were permitted to give operational flexibility to FIIs.

23

April 1997 Aggregated limit for all FIIs increased to 30 per cent subject to special procedure and resolution. The objective was to increase the participation by FIIs. April 1998 FIIs permitted to invest in dated Government securities subject to a ceiling. Consistent with the Government policy to limit the short-term debt, a ceiling of USD 1 billion was assigned which was increased to USD 1.75 billion in 2004. June 1998 Aggregate portfolio investment limit of FIIs and NRIs/PIOs/OCBs enhanced from 5 per cent to 10 per cent and the ceilings made mutually exclusive. Common ceilings would have negated the permission to FIIs. Therefore, separate ceilings were prescribed. June 1998 Forward cover allowed in equity. FIIs permitted to invest in equity derivatives. The objective was to make hedging instruments Available. February 2000 Foreign firms and high net-worth individuals permitted to invest as sub-accounts of FIIs. Domestic portfolio manager allowed to be registered as FIIs to manage the funds of sub-accounts. The objective was to allow operational flexibility and also give access to domestic asset management capability. March 2001 FII ceiling under special procedure enhanced to 49 per cent. The objective was to increase FII participation September 2001 FII ceiling under special procedure raised to sectoral cap. December 2003 FII dual approval process of SEBI and RBI changed to single approval process of SEBI. The objective was to streamline the registration process and reduce the time taken for registration. November 2004 Outstanding corporate debt limit of USD 0.5 billion prescribed. The objective was to limit short term debt flows. April 2006 Outstanding corporate debt limit increased to USD 1.5 billion prescribed. The limit on investment in Government securities was enhanced to USD 2 bn. This was an announcement in the Budget of 2006-07 November, 2006 FII investment up to 23% permitted in infrastructure companies in the securities markets, viz. stock exchanges, depositories and clearing corporations. This is a decision taken by Government following the mandating of demutualization and corporatization of stock exchanges. January and October, 2007 FIIs allowed to invest USD 3.2 billion in Government Securities (limits were raised from USD 2 billion in two phases of USD 0.6 billion each in January and October.

24

June, 2008 While reviewing the External Commercial Borrowing policy, the Government increased the cumulative debt investment limits from US $3.2 billion to US $5 billion and US $1.5 billion to US $3 billion for FII investments in Government Securities and Corporate Debt, respectively. As is evident from the above, the evolution of FII policy in India has displayed a steady and cautious approach to liberalization of a system of quantitative restrictions (QRs). The policy liberalization has taken the form of (i) relaxation of investment limits for FIIs; (ii) Relaxation of eligibility conditions; and (iii) Liberalization of investment instruments accessible for FIIs. Policy Developments I. Permission for Short selling of Equity Shares by SEBI registered FIIs SEBI registered FIIs / subaccounts of FIIs were permitted to buy / sell equity shares / debentures of Indian companies. However, they were not allowed to engage in short selling and were required to take delivery of securities purchased and give delivery of securities sold. After a due consultation process, it was decided to permit FIIs registered with SEBI and sub-accounts of FIIs to short sell, lend and borrow equity shares of Indian companies, subject to such conditions as may be prescribed in that behalf by the Reserve Bank and the SEBI / other regulatory agencies from time to time. Accordingly, RBI, through a circular dated 31st December, 2007, permitted the above subject to the following conditions: (i) The FII participation in short selling as well as borrowing / lending of equity shares will be subject to the current FDI policy and short selling of equity shares by FIIs would not be permitted for equity shares which are in the ban list and / or caution list of Reserve Bank. (ii) Borrowing of equity shares by FIIs would only be for the purpose of delivery into short sale. (iii) The margin / collateral would be maintained by FIIs only in the form of cash. No interest would be paid to the FII on such margin/collateral. RBI further provided that the designated custodian banks should separately report all transactions pertaining to short selling of equity shares and lending

25

and borrowing of equity shares by FIIs in their daily reporting with a suitable remark (short sold / lent / borrowed equity shares) for the purpose of monitoring by the Reserve Bank. SEBI also issued an amendment to the FII Regulations permitting FIIs to short sell and lend and borrow securities. II. FII investments in Debt Securities SEBI vide its circular dated January 19, 2007 announced the increase in the cumulative debt investment limit available for investment by FIIs/ Sub Accounts in Government Securities/ T-Bills from US $2 billion to US $2.6 billion. This limits was further enhanced to US $3.2 billion vide SEBI circular dated January 31, 2008. It was noticed that there was no uniformity among custodians with respect to considering investments by FIIs in debt oriented mutual fund units either as debt or equity. In consultation wit RBI, SEBI decided that investments by FIIs/ Sub Accounts in debt oriented mutual fund units (including units of money market and liquid funds) should henceforth be considered as corporate debt investments and reckoned within the stipulated limit of US $1.5 billion, earmarked for FII Sub Account investments in corporate debt. In view of the above, the following was made applicable with immediate effect: 1. Henceforth, there would be no demarcation between 100% debt and normal 70:30 FIIs/ Sub Accounts for the purposes of allocation of debt investment limits. The individual limits allocated to the 100% debt FIIs/ Sub Accounts stand cancelled. 2. The allocation of unutilized/ unallocated limits for investments in Government Securities/ T-Bills would be on first come- first-serve basis. The allocation would be valid for a period of 15 days from the date of the allocation letter, on the expiry of which the unutilized limits would lapse. 3. As mentioned above, the investments by FIIs/ Sub Accounts in debt oriented mutual fund schemes should now be Reckoned as investments in corporate debt. On re-calculating the investment fi gores for investments by FIIs/ Sub Accounts in corporate debt, by including their investments in units of debt oriented mutual funds, it is seen that the corporate debt investments exceed the permissible limit of US $1.5 billion. Thus, in order to conform to the stated limit, there should be no further investment, or rollover, of existing position in corporate debt, by both 100% debt and normal 70:30 FIIs, till the holdings fall within the stipulated limit of US $1.5 billion.

26

III. Foreign investment in Commodity Exchanges Government of India decided to allow foreign investment in Commodity Exchanges subject to the following conditions: i) There would be a composite ceiling of 49% Foreign Investment, with a FDI limit of 26% and an FII limit of 23%. ii) FDI will be allowed with specific approval of the Government. iii) The FII purchases in equity of Commodity Exchanges will be restricted only to the secondary markets. iv) Foreign Investment in Commodity Exchanges would also be subject to compliance with the regulations issued, in this regard, by the Forward Market Commission. Accordingly, a necessary circular was issued by RBI on 28th April, 2008. IV. Foreign investment in Credit Information Companies The Government decided to allow foreign investment in Credit Information Companies in compliance with the Credit Information Companies (Regulations) Act 2005 and subject to the following: i) The aggregate Foreign Investment in Credit Information Companies would be 49%. ii) Foreign Investment upto 49% would be allowed only with the prior approval of FIPB and regulatory clearance from RBI. iii) Investment by SEBI Registered FIIs would be permitted only through purchases in the secondary market to an extent of 24%. iv) Investment by SEBI Registered FIIs would be within the overall limit of 49% for Foreign Investment. Accordingly, a necessary circular was issued by RBI on 28th April, 2008. V. FII investments in Debt Securities The Government reviewed the External Commercial Borrowing policy and increased the cumulative debt investment limits from US $3.2 billion to US $5 billion and US $1.5 billion to US $3 billion for FII investments in Government Securities and Corporate Debt, respectively. Accordingly, SEBI issued a necessary circular giving effect to this decision on June 6, 2008. It was further provided that the enhanced limits should be allocated among the FIIs on a ‘first come first served’ basis in terms of SEBI’s earlier circular dated January 31, 2008, subject to a ceiling of US $200 million per registered entity.

27

Entities eligible to invest under FII route: As FII: (i) an institution established or incorporated outside India as a pension fund, mutual fund, investment trust, insurance company or reinsurance company; (ii) an International or Multilateral Organization or an agency thereof or a Foreign Governmental Agency, Sovereign Wealth Fund or a Foreign Central Bank; (iii) an asset management company, investment manager or advisor, bank or institutional portfolio manager, established or incorporated outside India and proposing to make investments in India on behalf of broad based funds and its proprietary funds, if any; (iv) a Trustee of a trust established outside India, and proposing to make investments in India on behalf of broad based funds and its proprietary funds, if any (iv) university fund, endowments, foundations or charitable trusts or charitable societies ‘broad based fund” means a fund established or incorporated outside India, which has at least twenty investor with no single individual investor holding more hat fort-nine percent of the shares or units of the fund As Sub-accounts: The sub account is generally the underlying fund on whose behalf the FII invests. The eligibility conditions for sub-accounts include: (i) The applicant may be an institution or fund or portfolio established or incorporated outside India and proposes to make investment in India; (ii) The applicant may be a broad based fund or proprietary fund or a foreign institutional investor or a foreign corporate or foreign individual; (iii) the Foreign Institutional Investor through whom the application for registration is made to the Board holds a certificate of registration as Foreign Institutional Investor. A non-resident Indian or an overseas corporate body registered with Reserve Bank of India should not be eligible to invest as sub-account or as foreign institutional investor.

Agencies regulating FII in India: RBI:the apex bank FIPB:reviews all foreign investments proposals SEBI: which regulate India’s capital market

28

RBI:

The Reserve Bank of India monitors the ceilings on FII/NRI/PIO investments in Indian companies on a daily basis. For effective monitoring of foreign investment ceiling limits, the Reserve Bank has fixed cut-off points that are two percentage points lower than the actual ceilings. The cut-off point, for instance, is fixed at 8 per cent for companies in which NRIs/ PIOs can invest up to 10 per cent of the company's paid up capital. The cut-off limit for companies with 24 per cent ceiling is 22 per cent and for companies with 30 per cent ceiling, is 28 per cent and so on. Similarly, the cut-off limit for public sector banks (including State Bank of India) is 18 per cent.

Once the aggregate net purchases of equity shares of the company by FIIs/NRIs/PIOs reach the cut-off point, which is 2% below the overall limit, the Reserve Bank cautions all designated bank branches so as not to purchase any more equity shares of the respective company on behalf of FIIs/NRIs/PIOs without prior approval of the Reserve Bank. The link offices are then required to intimate the Reserve Bank about the total number and value of equity shares/convertible debentures of the company they propose to buy on behalf of FIIs/NRIs/PIOs. On receipt of such proposals, the Reserve Bank gives clearances on a first-come-first served basis till such investments in companies reach 10 / 24 / 30 / 40/ 49 per cent limit or the sectoral caps/statutory ceilings as applicable. On reaching the aggregate ceiling limit, the Reserve Bank advises all designated bank branches to stop purchases on behalf of their FIIs/NRIs/PIOs clients. The Reserve Bank also informs the general public about the `caution’ and the `stop purchase’ in these companies through a press release.

FIPB: REVIEWS ALL FOREIGN INVESTMENT PROPOSALS:

The government is likely to exempt foreign institutional investors (FIIs) from seeking its approval each time they decide to pick up stakes in any Indian company, provided the composite foreign investment cap is not breached. This would effectively mean differential treatment to FDI and FII investments in sectors where the approval of the Foreign Investment Promotion Board (FIPB) is required.

The development comes with the finance ministry objecting to the DIPP’s current policy of clubbing FII and FDI investments as it feels this would restrict FII inflows into the country.

29

Once the FII investment is de-linked from FDI, it would work like this: Currently the FDI cap in the telecom sector is 74%. Foreign investments up to 49% are allowed via the automatic route but beyond this, an FIPB approval is required. Once the new norms come into effect, FDI would continue to require prior approval while FII investments would not.

SEBI:which regulates India’s capital market?

As per Regulation 6 of SEBI (FII) Regulations,1995, Foreign Institutional Investors are required to fulfill the following conditions to qualify for grant of registration:

Applicant should have track record, professional competence, financial soundness, experience, general reputation of fairness and integrity;

The applicant should be regulated by an appropriate foreign regulatory authority in the same capacity/category where registration is sought from SEBI. Registration with authorities, which are responsible for incorporation, is not adequate to qualify as Foreign Institutional Investor.

The applicant is required to have the permission under the provisions of the Foreign Exchange Management Act, 1999 from the Reserve Bank of India.

Applicant must be legally permitted to invest in securities outside the country or its in-corporation / establishment.

The applicant must be a "fit and proper" person. The applicant has to appoint a local custodian and enter into an

agreement with the custodian. Besides it also has to appoint a designated bank to route its transactions.

Payment of registration fee of US $ 5,000.00

Market design in India for foreign institutional investors Foreign Institutional Investors means an institution established or incorporated outside India which proposes to make investment in India in securities. A Working Group for Streamlining of the Procedures relating to FIIs, constituted in April, 2003, inter alia, recommended streamlining of

30

SEBI registration procedure, and suggested that dual approval process of SEBI and RBI be changed to a single approval process of SEBI. This recommendation was implemented in December 2003. Currently, entities eligible to invest under the FII route are as follows:

i. As FII: Overseas pension funds, mutual funds, investment trust, asset management company, nominee company, bank, institutional portfolio manager, university funds, endowments, foundations, charitable trusts, charitable societies, a trustee or power of attorney holder incorporated or established outside India proposing to make proprietary investments or with no single investor holding more than 10 per cent of the shares or units of the fund).

ii. As Sub-accounts: The sub account is generally the underlying fund on whose behalf the FII invests. The following entities are eligible to be registered as sub-accounts, viz. partnership firms, private company, public company, pension fund, investment trust, and individuals.

The Government guidelines for FII of 1992 allowed, inter-alia, entities such as asset management companies, nominee companies and incorporated/institutional portfolio managers or their power of attorney holders (providing discretionary and non-discretionary portfolio management services) to be registered as FIIs. While the guidelines did not have a specific provision regarding clients, in the application form the details of clients on whose behalf investments were being made were sought. While granting registration to the FII, permission was also granted for making investments in the names of such clients. Asset management companies/portfolio managers are basically in the business of managing funds and investing them on behalf of their funds/clients. Hence, the intention of the guidelines was to allow these categories of investors to invest funds in India on behalf of their' clients'. These 'clients' later came to be known as sub-accounts. The broad strategy consisted of having a wide variety of clients, including individuals, intermediated through institutional investors, who would be registered as FIIs in India. FIIs are eligible to purchase shares and convertible debentures issued by Indian companies under the Portfolio Investment Scheme.

31

Advantages: Unavailability of corporate debt Increases forex reserves Increases domestic saving and investments Large availability of capital

Disadvantages: Problems of inflation Reduces flexibility of policymakers Hot money False representation on economy Cannot be utilized for long term Problem for small investors

Increasing trends of foreign institutional investments in India.

Portfolio investments in India include investments in American Depository Receipts (ADRs)/ Global Depository Receipts (GDRs), Foreign Institutional Investments and investments in offshore funds. Before 1992, only Non-Resident Indians (NRIs) and Overseas Corporate Bodies were allowed to undertake portfolio investments in India. Thereafter, the Indian stock markets were opened up for direct participation by FIIs. They were allowed to invest in all the securities traded on the primary and the secondary market including the equity and other securities/instruments of companies listed/to be listed on stock exchanges in India. It can be observed from the table below that India is one of the preferred investment destinations for FIIs over the years.

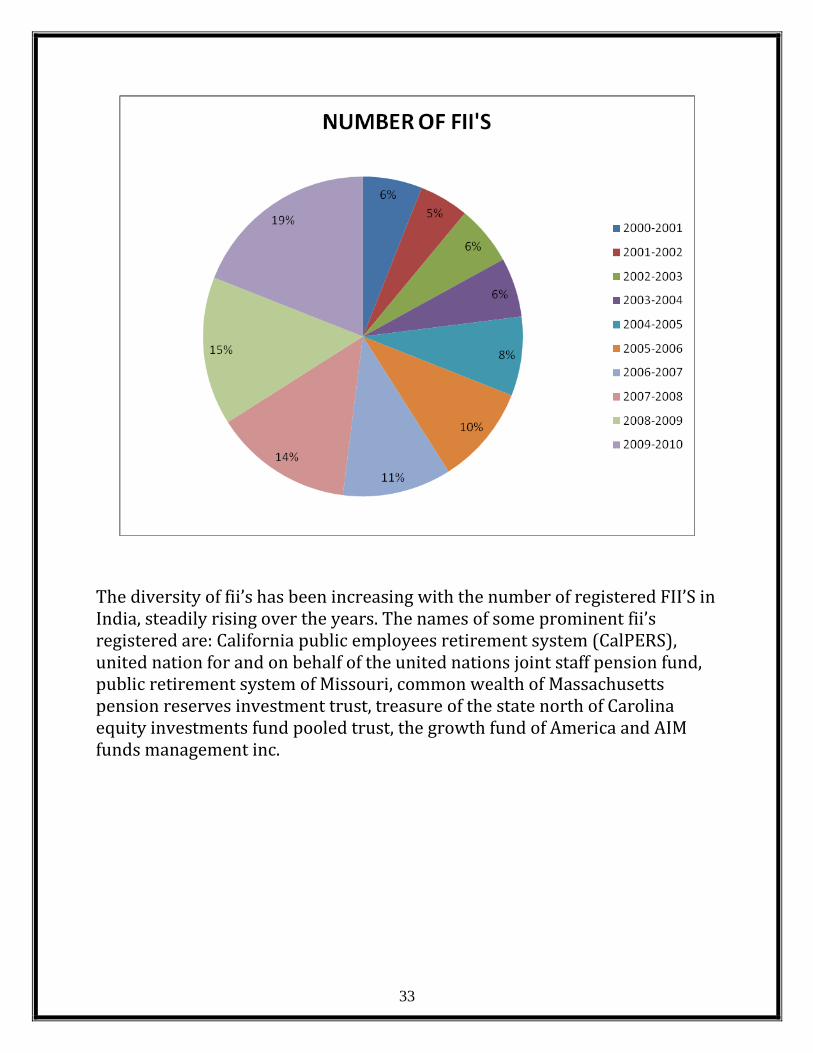

32

year No. of fii’s 2000-01 527

2001-2002 490 2002-2003 502 2003-2004 540 2004-2005 685 2005-2006 882 2006-2007 996 2007-2008 1219 2008-2009 2009-2010

1334 1729

PiECHART REPREsENTATioN of REGisTERED fii’s

33

The diversity of fii’s has been increasing with the number of registered FII’S in India, steadily rising over the years. The names of some prominent fii’s registered are: California public employees retirement system (CalPERS), united nation for and on behalf of the united nations joint staff pension fund, public retirement system of Missouri, common wealth of Massachusetts pension reserves investment trust, treasure of the state north of Carolina equity investments fund pooled trust, the growth fund of America and AIM funds management inc.

34

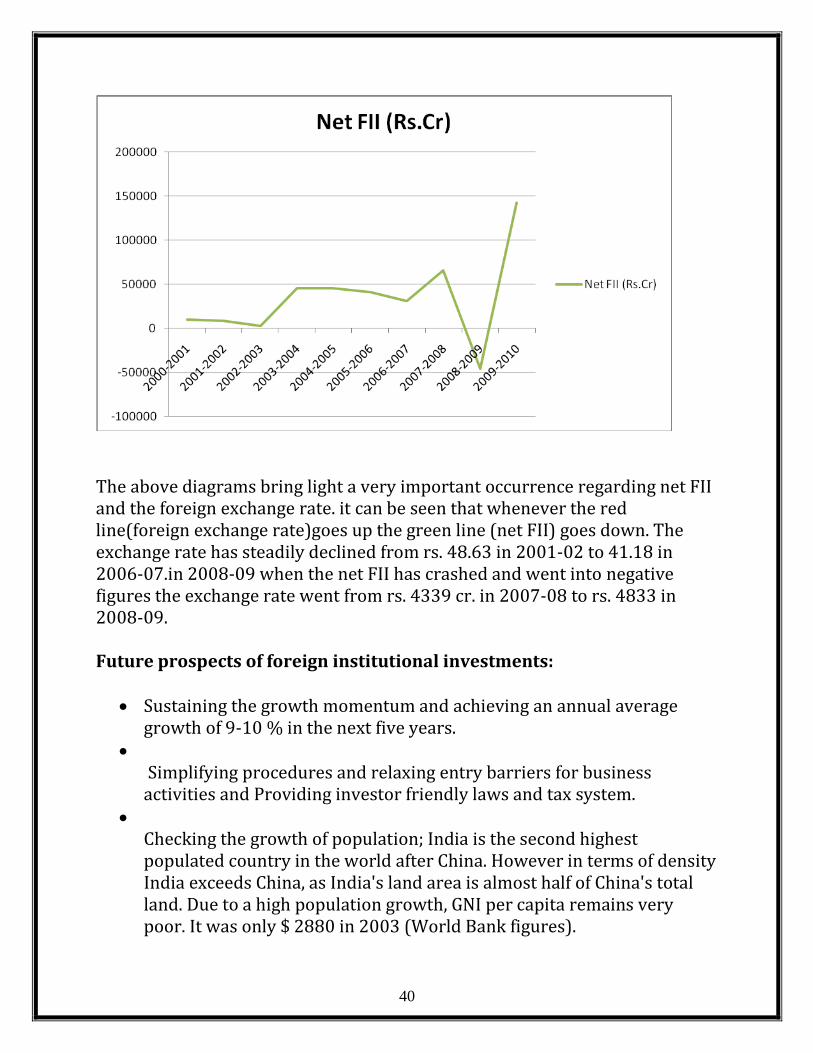

Net foreign institutional investments (fii’s) iN THE lAsT ten years year Net FII ( rs in crore) 2000-2001 9933 2001-2002 8763 2002-2003 2689 2003-2004 45764 2004-2005 45880 2005-2006 41467 2006-2007 30841 2007-2008 66179 2008-2009 -45811 2009-2010 142658 After the liberalization of economy the investment made by the foreign investors started thronging the Indian markets via the portfolio investment route. as Indian industries grow with more and more firms have used the capital markets to raise their finances. Now due to strong demand in the domestic market these companies have been doing well pushing our economy to high levels of GDP growth rate during huge foreign investment in the secondary capital market as the foreign fund managers saw this as a great opening for getting high return on their funds at a pretty low risk. This boom in the Indian industry coupled with easy entry requirements has given an impetus to the FII’S that saw an increasing trend. It was only in 2008 when the global recession broke out that the net investment decline sharply due to heavy selling pressure from the FII’S that is they pulled out virtually all the money invested in the stock market thus causing a crash in the bench mark indices of the country.

35

Net investment shown graphically:

COMPARISION BETWEEN THE NET FII AND THE SENSEX:- Year Sensex Close Net FII (Rs. Cr) 2000-2001 3262 9933 2001-2002 3377 8763 2002-2003 5839 2689 2003-2004 6603 45764 2004-2005 9398 45880 2005-2006 13787 41467 2006-2007 20287 30841 2007-2008 9647 66179 2008-2009 17465 -45811 2009-2010 20509 142658

36

The sensex has increased by 10525 points between 2000-2001 and 2005-2006, an increase of more than 32%. In the corresponding period net fii has increased by more than 31.5%. From 2005-2006 to 2009-10 the sensex gained 6722 points an increase of 49% and in the corresponding period of net fii went up by 24.4%. The sensex fell down by 10640 points in early 2008 i.e. by 52% due to heavy selling by the fii’s who pulled out their money from the stock market due to the sub-prime crisis, credit crunch, bankruptcy, speculation etc. this turned the FIIs into net sellers and hence during 2008-09 the net FII figure is in negative.

Diagram showing comparison between net FII & Sensex:-

37

The blue line denoting the net FII can be called a volatile line from the chart as there are sudden sharp drops and sharp rises. It has fixed pattern. The net FII started declining from 2007-08 till the middle of 2008-09 which caused a sharp fall in sensex also which went below the 1000 level in 2007-08 falling by almost 52% as compared to the previous year. But the FIIs started pouring in again from the end of 2009 after the government s abroad started providing bail-out packages, and various other incentives to the sailing companies. The sensex also rises sharply from 2008-09 after the FIIs turned into net buyers and hence a similar pattern can be found between these two. A COMPARISION BETWEEN THE GDP & NET FII IN LAST TEN YEARS:- Year GDP(at factor cost) Net FII(Rs. Cr) 2000-2001 4.4 9933 2001-2002 5.8 8763 2002-2003 3.8 2689 2003-2004 8.5 45764 2004-2005 7.5 45880 2005-2006 9.5 41467 2006-2007 9.7 30841 2007-2008 9.2 66179 2008-2009 6.7 -45811 2009-2010 7.4 142658

38

The FII curve(blue line) is one with many sharp fluctuations and presents first an increasing trend from 2000-01 to 2003-04 and then becomes stable but has a very gradual declining slope from 2003-04 to 2006-07 going down from Rs. 45764 crs,to Es. 30841 crs, a decrease of 33% whereas in the corresponding the GDP increases from 8.5% to 9.7%. Both the net FII and GDP

39

showed sharp declines in the year 2008-09 owing to various factors like the global recession, sluggish manufacturing industries, inflection, low demand for Indian goods abroad hurting exports, rising interest retested in 2009-2010 the FII shows again a very sharp rise reaching the Rs. 1 lakh crore marks. Similarly the GDP has also recovered but gradually from 6.7% to 7.4%. FOREIGN EXCHANGE RATE & NET FII IN LAST TEN YEARS:- Year USD in terms of Indian

rupee Net FII (Rs. Cr)

2000-2001 47.22 9933 2001-2002 48.63 8763 2002-2003 46.59 2689 2003-2004 45.26 45764 2004-2005 44.00 45880 2005-2006 45.19 41467 2006-2007 41.18 30841 2007-2008 43.39 66179 2008-2009 48.33 -45811 2009-2010 45.65 142658

40

The above diagrams bring light a very important occurrence regarding net FII and the foreign exchange rate. it can be seen that whenever the red line(foreign exchange rate)goes up the green line (net FII) goes down. The exchange rate has steadily declined from rs. 48.63 in 2001-02 to 41.18 in 2006-07.in 2008-09 when the net FII has crashed and went into negative figures the exchange rate went from rs. 4339 cr. in 2007-08 to rs. 4833 in 2008-09. Future prospects of foreign institutional investments:

Sustaining the growth momentum and achieving an annual average growth of 9-10 % in the next five years.

Simplifying procedures and relaxing entry barriers for business activities and Providing investor friendly laws and tax system.

Checking the growth of population; India is the second highest populated country in the world after China. However in terms of density India exceeds China, as India's land area is almost half of China's total land. Due to a high population growth, GNI per capita remains very poor. It was only $ 2880 in 2003 (World Bank figures).

41

Boosting agricultural growth through diversification and development

of agro processing.

Expanding industry fast, by at least 10% per year to integrate not only the surplus labour in agriculture but also the unprecedented number of women and teenagers joining the labour force every year.

Developing world-class infrastructure for sustaining growth in all the sectors of the economy

Allowing foreign investment in more areas.

Effecting fiscal consolidation and eliminating the revenue deficit

through revenue enhancement and expenditure management.

Global corporations are responsible for global warming, the depletion of natural resources, and the production of harmful chemicals and the destruction of organic agriculture.

The government should reduce its budget deficit through proper pricing mechanisms and better direction of subsidies. It should develop infrastructure with what Finance Minister P Chidambaram International Research Journal of Finance and Economics - Issue 5 (2006) 171 of India called “ruthless efficiency” and reduce bureaucracy by streamlining government procedures to make them more transparent and effective.

Empowering the population through universal education and health care, India must maximize the benefits of its youthful demographics and turn itself into the knowledge hub of the world through the application of information and communications technology (ICT) in all aspects of Indian life although, the government is committed to furthering economic reforms and developing basic infrastructure to improve lives of the rural poor and boost economic performance. Government had reduced its controls on foreign trade and investment in some areas and has indicated more liberalization in civil aviation, telecom and insurance sector in the future.

42

Objectives

43

Objectives

• To study the scope and trading mechanism of Foreign Instititutional

investors in India.

To study the trend of FII

To study the activities by the FIIs in the recent past.

To study the growth of registered number of FII in India

To Know The Future Prospects if FII In India

To know the impact of FII on the economy of India.

44

Research methodology

45

RESEARCH METHODOLOGY

Data collection: Secondary Data:

Internet, Books, newspapers, journals and books, other reports and

projects, literatures.

46

Findings

47

Findings 1. As per Regulation 6 of SEBI (FII) Regulations,1995, Foreign Institutional

Investors are required to fulfill the following conditions to qualify for

grant of registration:

• Applicant should have track record, professional competence, financial

soundness, experience, general reputation of fairness and integrity.

• The applicant should be regulated by an appropriate foreign

regulatory authority in the same capacity/category where registration

is sought from SEBI. Registration with authorities, which are

responsible for incorporation, is not adequate to qualify as Foreign

Institutional Investor.

• The applicant is required to have the permission under the provisions

of the Foreign Exchange Management Act, 1999 from the Reserve Bank

of India.

• Applicant must be legally permitted to invest in securities outside the

country or its in-corporation / establishment.

• The applicant must be a "fit and proper" person.

• The applicant has to appoint a local custodian and enter into an

agreement with the custodian. Besides it also has to appoint a

48

designated bank to route its transactions.

• Payment of registration fee of US $ 5,000.00

2. In bearish trend of 2008 the volatility in Indian Stock indices due to FIIs

is more than in bullish trend of 2007. No doubt FII inflow is more in

2007. The domestic investors were also playing an important role in

2007 but in 2008 FIIs are influencing market more as domestic

investors are not in the market.

3. Impact of FIIs on Sensex: In 2007, the correlation coefficient is more

than in 2008 which interprets that the relationship between these two

variables is more in the period when there is bearish trend. But in both

the years FIIs were not much positively correlated, so a less significant

impact of FIIs is seen. The error is very high in both the years which

doesn’t mean that relation is false but we can say that the error in linear

relation is high.

49

Trend of FIIs with the help of economic figures:

• In 2004, FII investments crossed $9 billion, the highest in the history of

Indian capital markets.

• The total net investment for the year up to December 29 stood at US$9,072

million while foreign investors pumped in about US$2,113 million in

December.

• Korea and Taiwan have always been the biggest recipients of FII money. It

was only in 2004 that India managed to receive the second highest FII inflow

at over $8.5bn.

• In 2005 FIIs invested more in Indian equities than in Korean or Taiwanese

equities.

• On 9th March 2009, India's exceptional growth story and its booming

economy have made the country a favorite destination with foreign

institutional investors (FIIs). It has continued to attract investment despite

the Satyam non-governance issue and the global economic contagion impact

on Indian markets.

• According to Mr Gautam Chand, CEO of Instanex, said FIIs are the largest

institutional investors in India with holdings valued at over US$ 751.14 billion

as on December 31, 2008.

• They are also the most successful portfolio investors in India with 102 per

cent appreciation since September 30, 2003.

• As per SEBI, number of registered FIIs stood at 1626 and number of

registered sub-accounts stood at 4972 as on March 17, 2009.

50

Conclusion

51

Conclusion

In developing countries like India foreign capital helps in increasing the

Productivity of labour and to build up foreign exchange reserves to meet the

current account deficit. Foreign Investment provides a channel through which

country can have access to foreign capital.

According to Data analysis and findings, it can be concluded that FII do have

any significant impact on the Indian Stock Market but there are other factors

like government policies, budgets, bullion market, inflation, economical and

political condition, etc. do also have an impact on the Indian stock market.

There is a positive correlation between stock indices and FIIs but FIIs didn’t

have any significant impact on Indian Stock Market.

52

Recommendation and suggestion

53

RECOMMENDATION & SUGGESTION

1) Simplifying procedures and relaxing entry barriers for business activities and providing investor friendly laws and tax system for foreign investors. 2) Allowing foreign investment in more areas. In different industries indices the FIIs should be encouraged through different patterns like futures, options, etc. 3) Somewhere, a restriction related to the track record of Sub- Accounts is also to be made on the investors who withdraw money out of the Indian stock market who have invested with the help of participatory notes. 4) We have to modernize and also have to save our culture. Similarly the laws should be such that it protects domestic investors and also promote trade in country through FIIs. 5) Encourage industries to grow to make FIIs an attractive junction to invest. 6) If the FII’s investments could concentrate in a large number of companies the market value will raise.

7) FII must be increased in India.

54

Limitations

55

LIMITATIONS

Limitations are conditions that restrict the scope of study period or may affect results of the research. it cannot be controlled by the researchers and can even affect the analysis of research adversely.

All the data have been collected from secondary sources .information collected first hand from professionals and scholars through interview would have given the report a larger perspective.

56

Bibliography

57

Bibliography

1. Internet sites : a) www.rbi.org.in/home.aspx b) www.google.com c) www.nseindia.com d) www.sebi.gov.in e) www.economictimes.com f) www.indiatimes.com 2. Books: a) Foreign institutional investors by G Gopal Krishna Murthy.

Copyright © 2022 FDOKUMEN