Fixed Asset Depreciation Case

13

H 141 – MALAM Kelompok 1 Case 7-1 Stern Corporation (B) Accounting for Manager Presented by: 1. Irfan Fauzi 2. Joseph Tampubolon 3. Maria Veronika Dede 4. Medisa Aris Ginanjar 5. Reza Meidyawati 6. Nasrul Nabil Sangadji

Transcript of Fixed Asset Depreciation Case

H 141 – MALAM

Kelompok 1

Case 7-1Stern Corporation (B)Accounting for Manager

Presented by:

1. Irfan Fauzi2. Joseph Tampubolon3. Maria Veronika Dede4. Medisa Aris Ginanjar5. Reza Meidyawati6. Nasrul Nabil Sangadji

H 141 – MALAM

Kelompok 1

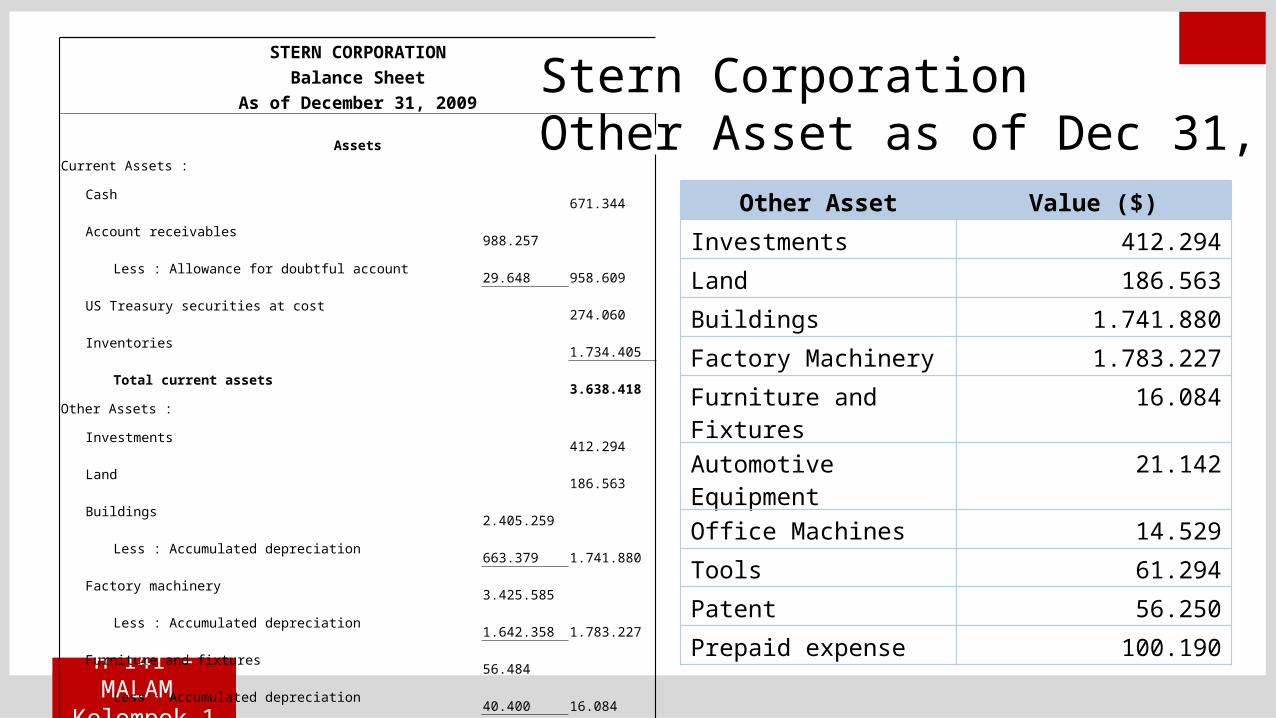

STERN CORPORATIONBalance Sheet

As of December 31, 2009

AssetsCurrent Assets :

Cash 671.344

Account receivables 988.257

Less : Allowance for doubtful account 29.648

958.609

US Treasury securities at cost 274.060

Inventories 1.734.405

Total current assets 3.638.418

Other Assets :

Investments 412.294

Land 186.563

Buildings 2.405.259

Less : Accumulated depreciation 663.379

1.741.880

Factory machinery 3.425.585

Less : Accumulated depreciation 1.642.358

1.783.227

Furniture and fixtures 56.484

Less : Accumulated depreciation 40.400

16.084

Automotive equipment 58.298

Less : Accumulated depreciation 37.156

21.142

Office machines 42.534

Less : Accumulated depreciation 28.005

14.529

Tools 61.294

Patent 56.250

Prepaid expense 100.190

Total assets 8.031.871

Stern Corporation Other Asset as of Dec 31, 2009

Other Asset Value ($)Investments 412.294Land 186.563Buildings 1.741.880Factory Machinery 1.783.227Furniture and Fixtures

16.084

Automotive Equipment

21.142

Office Machines 14.529Tools 61.294Patent 56.250Prepaid expense 100.190

H 141 – MALAM

Kelompok 1

Questions :

1. In a manner of similiar to that used in Stern Corporation (A), analyze the effect of each of these transactions on the property, plant, and equipment accounts, accumulated depreciation, and any other accounts that may be involved. Prepare journal entries for these transactions.

2. Give the correct totals for the property, plant, and equipment, and the amount of accumulated depreciation as of December 31, 2010, after the transaction affecting them had been recorded.

H 141 – MALAM

Kelompok 1

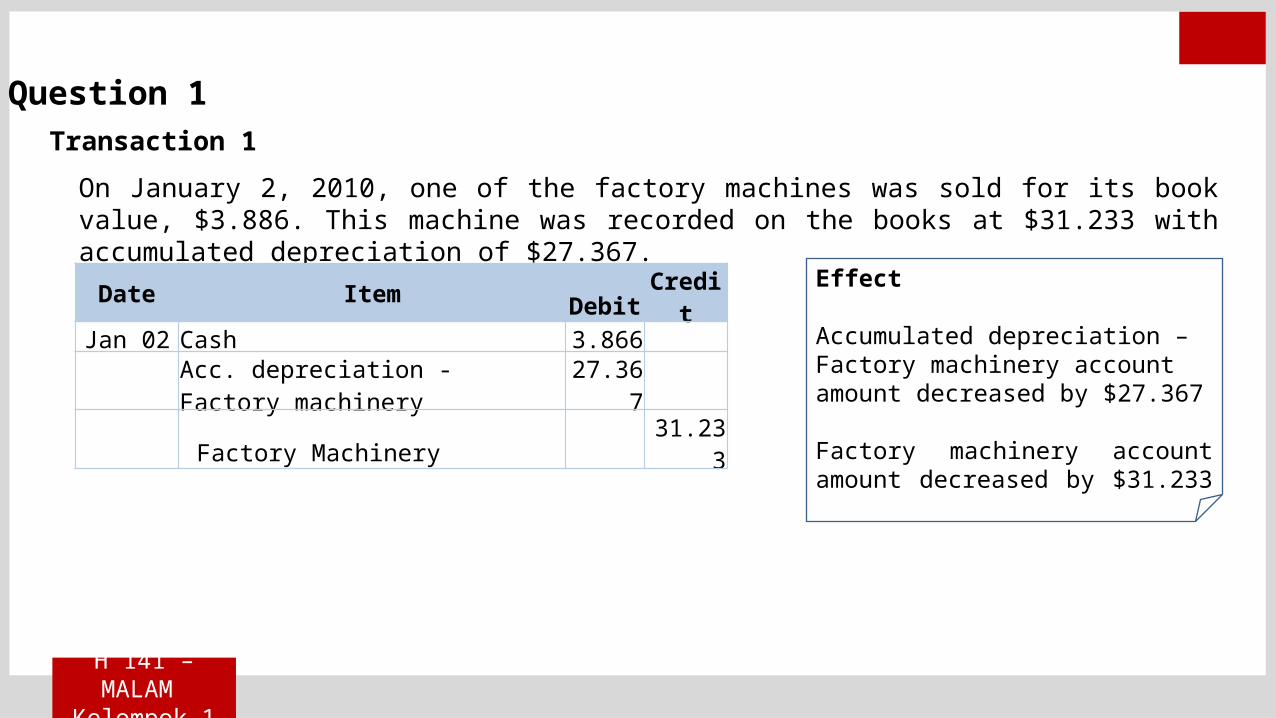

On January 2, 2010, one of the factory machines was sold for its book value, $3.886. This machine was recorded on the books at $31.233 with accumulated depreciation of $27.367.Date Item Debit

Credit

Jan 02 Cash 3.866Acc. depreciation - Factory machinery

27.367

Factory Machinery31.23

3

Effect

Accumulated depreciation – Factory machinery account amount decreased by $27.367

Factory machinery account amount decreased by $31.233

Transaction 1Question 1

H 141 – MALAM

Kelompok 1

Tools were carried on the books at cost, and at the end of each year a physical inventory was taken to determine what tools still remained. The account was written down to the extent of the decrease in tools as ascertained by the year-end inventory. At he end of 2010, it was determined that there had been a decrease in the tool inventory amounting to $7.850. Effect

Tools account amount decreased by $7.850

Date Item Debit Credit

Dec 31Tools expense 7.850Tools 7.850

Transaction 2

H 141 – MALAM

Kelompok 1

On March 1, 2010, The company sold for $2.366 cash of automobile that was recorded on the books at a cost of $8.354 and had an accumulated depreciation of $5.180, giving a net book value of $3.174 as of January 1, 2010. In this and other cases of the sale of long-lived assets during the year, the accumulated depreciation and depreciation expense items were both increased by amount that reflected the depreciation chargeable for the months in 2010 in which the asset was held prior the the sales, as rates listed in item 7 below.Effect

Acc. Depreciation –Automotive equipment account amount decreased by $5.458

Automotive equipment account amount decreased by $8.354

Loss on sale of other assets recognized by $560

Transaction 3

Date Item DebitCredit

March 1 Cash 2.336

Acc. Depreciation - Automotive equipment 5.458Loss on sale of other assets 560Automotive Equipment 8.354

H 141 – MALAM

Kelompok 1

The patent listed on the balance sheet had been purchased by the Stern Corporation. The cost of the patent was written off as an expense over the remainder of its legal life as of December 31, 2009, the patent’s remaining legal life was five years.

Effect

Patent account amount decreased by $11.250

Date Item Debit Credit

Dec 31Patent Amortization Expense 11.250Patent 11.250

Transaction 4

H 141 – MALAM

Kelompok 1

On July 1, 2010, a typewriter that had cost $1.027 and had been fully depreciated on December 31, 2009, was sold for $75.

Effect

Acc. Depreciation –Office machines account amount decreased by $1.027

Office machines account amount decreased by $1.027

Gain on sale of other assets recognized by $75

Date Item Debit CreditJuly 1 Cash 75

Acc. depreciation - Office machines 1.027Gain on sale of other assets 75Office machines 1.027

Transaction 5

H 141 – MALAM

Kelompok 1

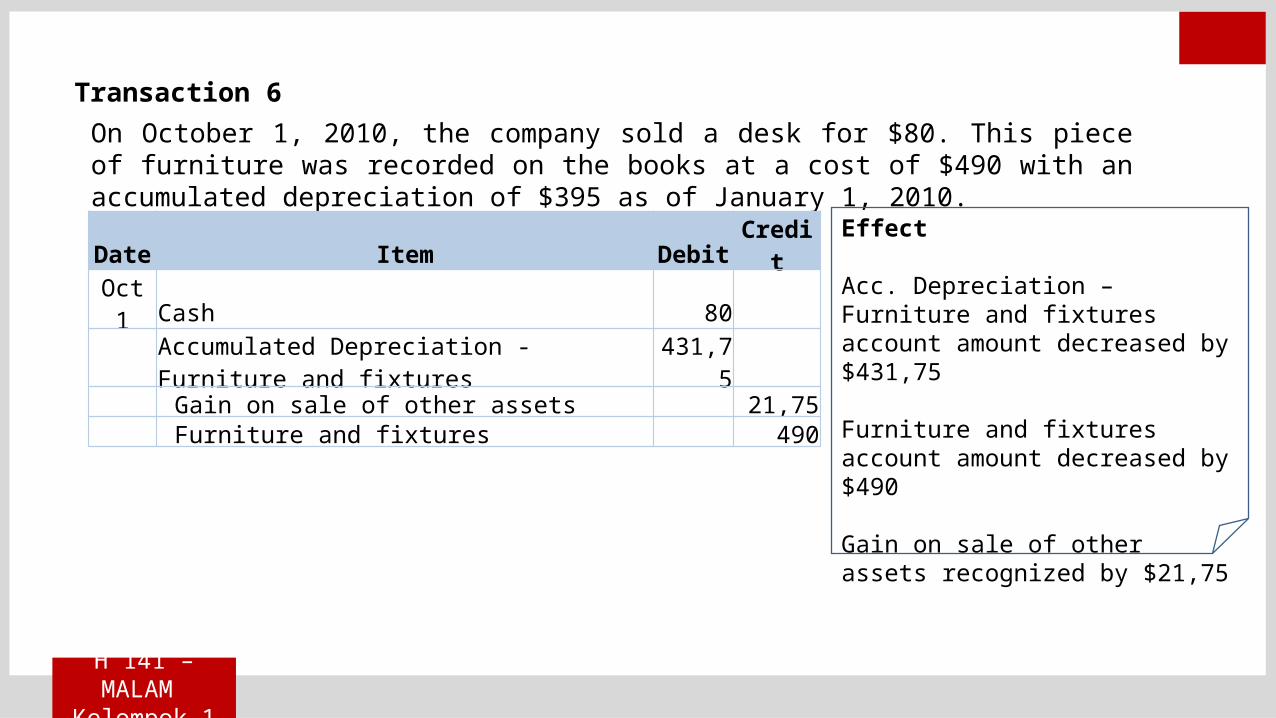

On October 1, 2010, the company sold a desk for $80. This piece of furniture was recorded on the books at a cost of $490 with an accumulated depreciation of $395 as of January 1, 2010.

Effect

Acc. Depreciation – Furniture and fixtures account amount decreased by $431,75

Furniture and fixtures account amount decreased by $490

Gain on sale of other assets recognized by $21,75

Transaction 6

Date Item DebitCredit

Oct 1 Cash 80

Accumulated Depreciation - Furniture and fixtures

431,75

Gain on sale of other assets 21,75Furniture and fixtures 490

H 141 – MALAM

Kelompok 1

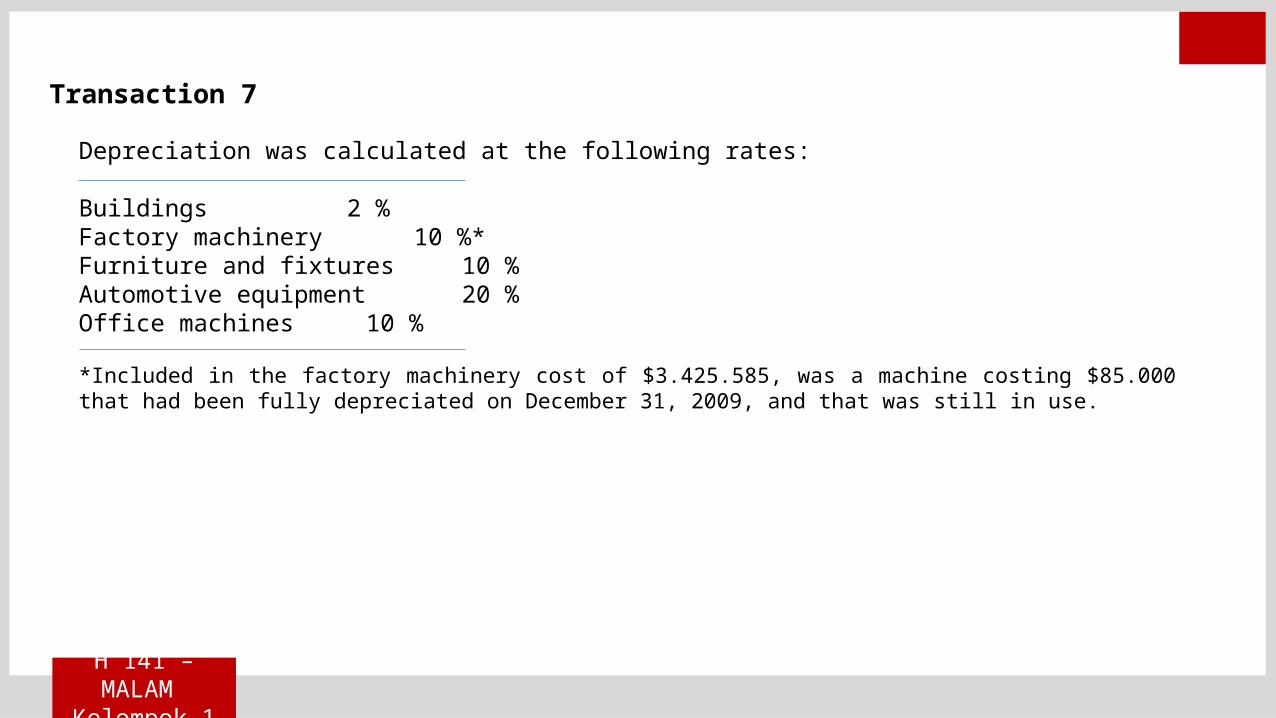

Transaction 7

Depreciation was calculated at the following rates:

Buildings 2 %Factory machinery 10 %* Furniture and fixtures 10 %Automotive equipment 20 %Office machines 10 %

*Included in the factory machinery cost of $3.425.585, was a machine costing $85.000 that had been fully depreciated on December 31, 2009, and that was still in use.

H 141 – MALAM

Kelompok 1

Date Item Debit CreditDec 31Depreciation Expense - Buildings 48.105

Acc. Depreciation - Buildings 48.105($2.405.259 x 2% = $48.105)

Dec 31Depreciation Expense - Factory machinery

330.935

Acc. Depreciation - Factory machinery

330.935

($3.425.585 - $31.233 - $85,000) x 10% = $330.935

Dec 31Depreciation Expense - Furniture and fixtures 5.599Acc. Depreciation - Furniture and fixtures 5.599

($56.484 - $490) x 10% = $5.599

Dec 31Depreciation Expense - Automotive equipment 9.989Acc. Depreciation - Automotive equipment 9.989

($58.298 - $8.354) x 20% = $9.989

Dec 31Depreciation Expense - Office machines 4.151Acc. Depreciation - Office machines 4.151

($42.534 - $1.027) x 10% = $4.151

H 141 – MALAM

Kelompok 1

Other Assets Value ($)

Investments 412.294

Land 186.563

Buildings 2.405.259

Less : Accumulated depreciation 711.484

1.693.775

Factory machinery 3.394.352

Less : Accumulated depreciation 1.945.926

1.448.426

Furniture and fixtures 55.994

Less : Accumulated depreciation 45.604

10.390

Automotive equipment 49.944

Less : Accumulated depreciation 41.965

7.979 Office machines 41.507

Less : Accumulated depreciation 31.129 10.378

Tools 53.444

Patent 45.000

Prepaid expense

100.190

Question 2

H 141 – MALAM

Kelompok 1

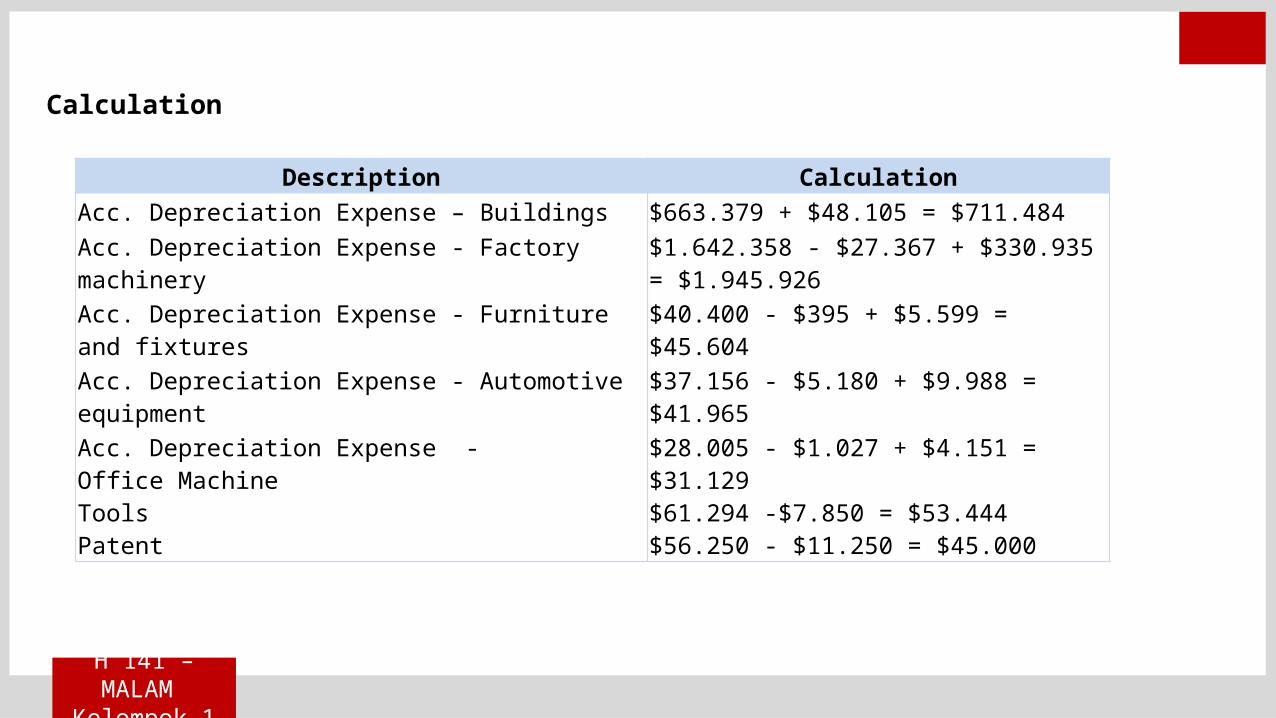

Description CalculationAcc. Depreciation Expense – Buildings $663.379 + $48.105 = $711.484 Acc. Depreciation Expense - Factory machinery

$1.642.358 - $27.367 + $330.935 = $1.945.926

Acc. Depreciation Expense - Furniture and fixtures

$40.400 - $395 + $5.599 = $45.604

Acc. Depreciation Expense - Automotive equipment

$37.156 - $5.180 + $9.988 = $41.965

Acc. Depreciation Expense - Office MachineToolsPatent

$28.005 - $1.027 + $4.151 = $31.129$61.294 -$7.850 = $53.444$56.250 - $11.250 = $45.000

Calculation