Financial Statements

24

Financial statements Edwin C. Mbwambo

Transcript of Financial Statements

Financial statements

Edwin C. Mbwambo

Financial statements coverage and objectives

Accounting equationFormats of financial statement as per IAS 1Prepare statement of financial positionCompute missing elements of in a B/S Prepare income statement and statement of comprehensive income

Calculate revenue, cost of sales, gross and net profit

Prepare statement of change in equityUnderstand the interrelationships among financial statements

IntroductionFinancial statements - FormatsStatement of financial position – B/sheet

Income statementStatement of comprehensive incomeStatement of change in equityStatement of cash flow.

Financial position ABC Group - Statement of financial position as at

30th June 20132013 2012

Assets

Non-current Assets

Property, plant and equipment (PPE) -Building, land, machine&equipment etc

350,700 360,020

Goodwill 80,800 91,200Other intangible assets 227,470 227,470Investments in associates 100,150 110,770Available-for-sale financial assets 142,500 156,000

901,620 945,460Current Assets

Inventories 135,230 132,500Trade receivables 91,600 110,800Other current assets 25,650 12,540Cash and cash equivalents 312,400

322,900564,880

578,740Total Assets 1,466,500 1,524,200

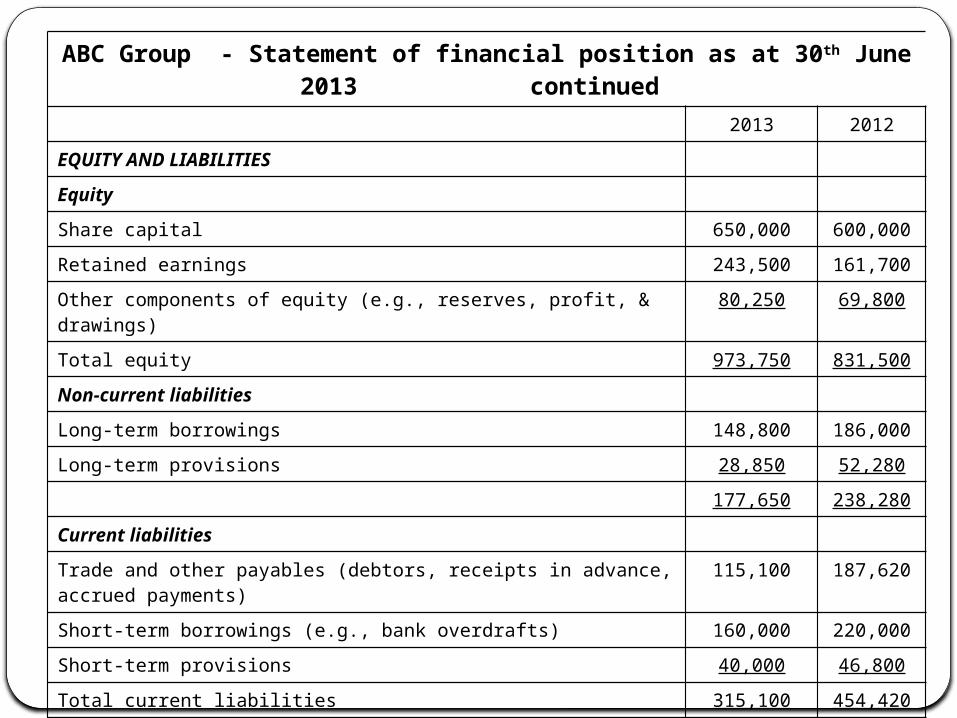

ABC Group - Statement of financial position as at 30th June 2013 continued

2013 2012EQUITY AND LIABILITIES

Equity

Share capital 650,000 600,000Retained earnings 243,500 161,700Other components of equity (e.g., reserves, profit, & drawings)

80,250 69,800

Total equity 973,750 831,500Non-current liabilities

Long-term borrowings 148,800 186,000Long-term provisions 28,850 52,280

177,650 238,280Current liabilities

Trade and other payables (debtors, receipts in advance, accrued payments)

115,100 187,620

Short-term borrowings (e.g., bank overdrafts) 160,000 220,000Short-term provisions 40,000 46,800Total current liabilities 315,100 454,420Total liabilities 492,750 692,700

Total equity and liabilities 1,466,500 1,524,200

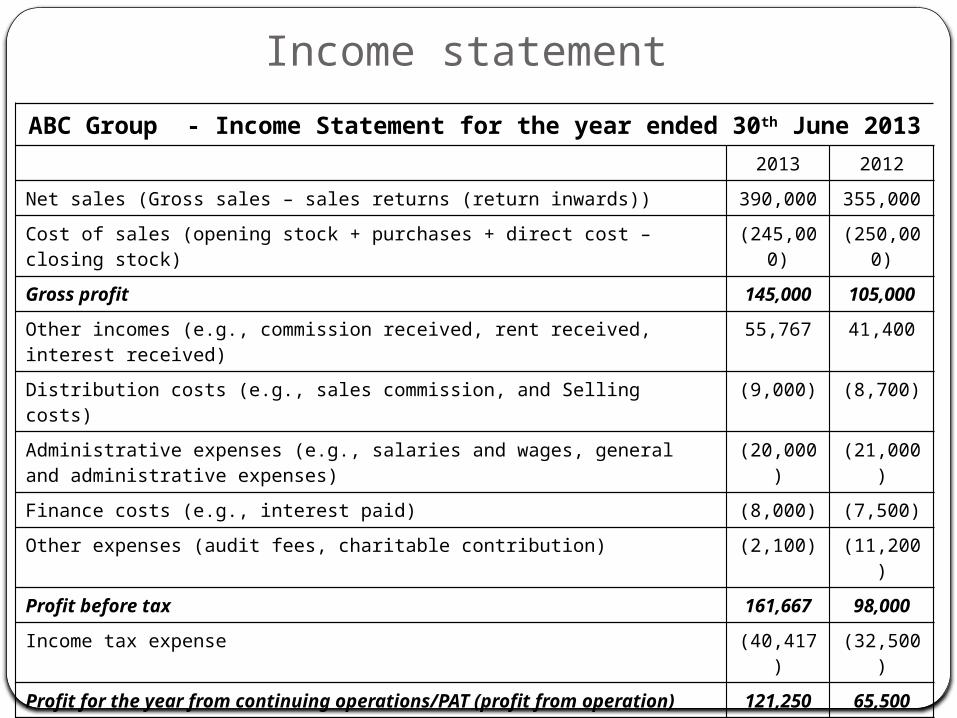

Income statement ABC Group - Income Statement for the year ended 30th June 2013

2013 2012Net sales (Gross sales – sales returns (return inwards)) 390,000 355,000Cost of sales (opening stock + purchases + direct cost – closing stock)

(245,000)

(250,000)

Gross profit 145,000 105,000

Other incomes (e.g., commission received, rent received, interest received)

55,767 41,400

Distribution costs (e.g., sales commission, and Selling costs)

(9,000) (8,700)

Administrative expenses (e.g., salaries and wages, general and administrative expenses)

(20,000)

(21,000)

Finance costs (e.g., interest paid) (8,000) (7,500)Other expenses (audit fees, charitable contribution) (2,100) (11,200

)Profit before tax 161,667 98,000

Income tax expense (40,417)

(32,500)

Profit for the year from continuing operations/PAT (profit from operation) 121,250 65,500

Statement of comprehensive incomeABC Group - Statement of comprehensive income for the year

ended 30th June 20132013 2012

Operating profit 121,250 65,500Exchange differences on translating foreign operations 8,000 10,667Available-for-sale financial assets (24,000

)10,667

Cash flow hedges 1,067 3,300Gains on property revaluation 933 3,366Other comprehensive income for the year, net of tax (14,000

)28,000

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 107,250

93,500

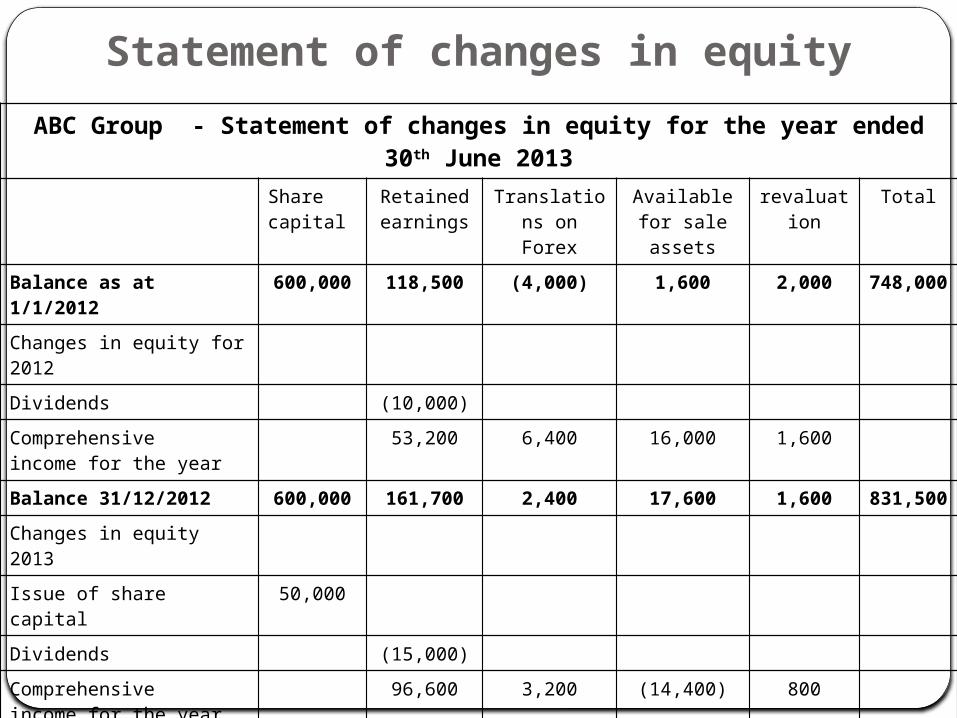

Statement of changes in equityABC Group - Statement of changes in equity for the year ended

30th June 2013Sharecapital

Retained earnings

Translations on Forex

Available for sale assets

revaluation

Total

Balance as at 1/1/2012

600,000 118,500 (4,000) 1,600 2,000 748,000

Changes in equity for 2012Dividends (10,000)Comprehensiveincome for the year

53,200 6,400 16,000 1,600

Balance 31/12/2012 600,000 161,700 2,400 17,600 1,600 831,500Changes in equity 2013Issue of share capital

50,000

Dividends (15,000)Comprehensiveincome for the year

96,600 3,200 (14,400) 800

Transfer to retainedearnings

200 200

Balance 31/12/2013 650,000 243,500 5,600 3,200 2,200 973,750

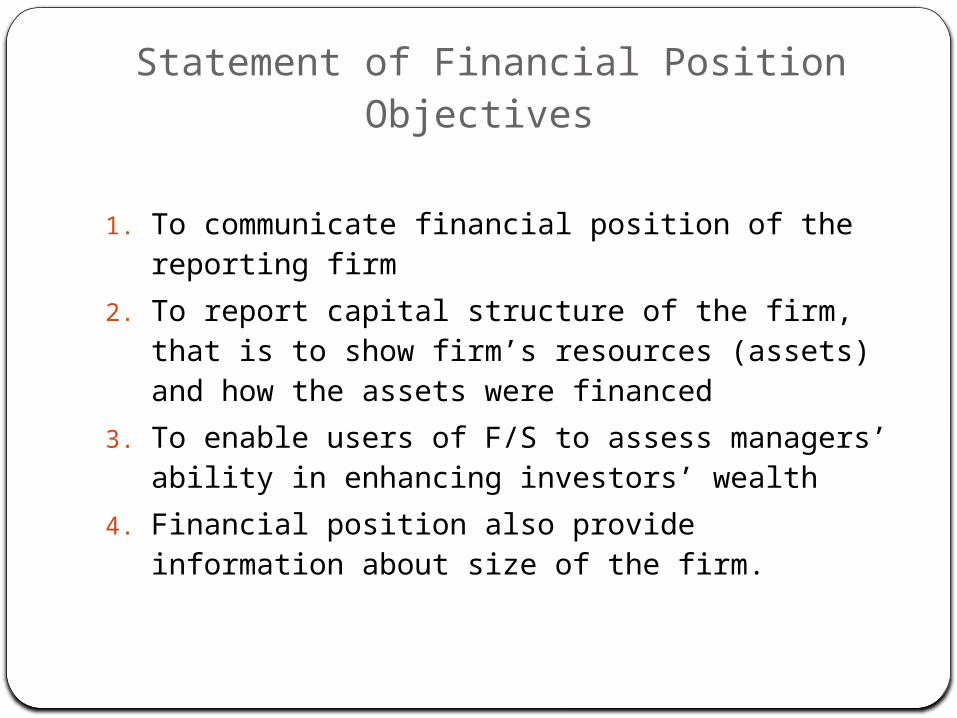

Statement of Financial Position Objectives

1. To communicate financial position of the reporting firm

2. To report capital structure of the firm, that is to show firm’s resources (assets) and how the assets were financed

3. To enable users of F/S to assess managers’ ability in enhancing investors’ wealth

4. Financial position also provide information about size of the firm.

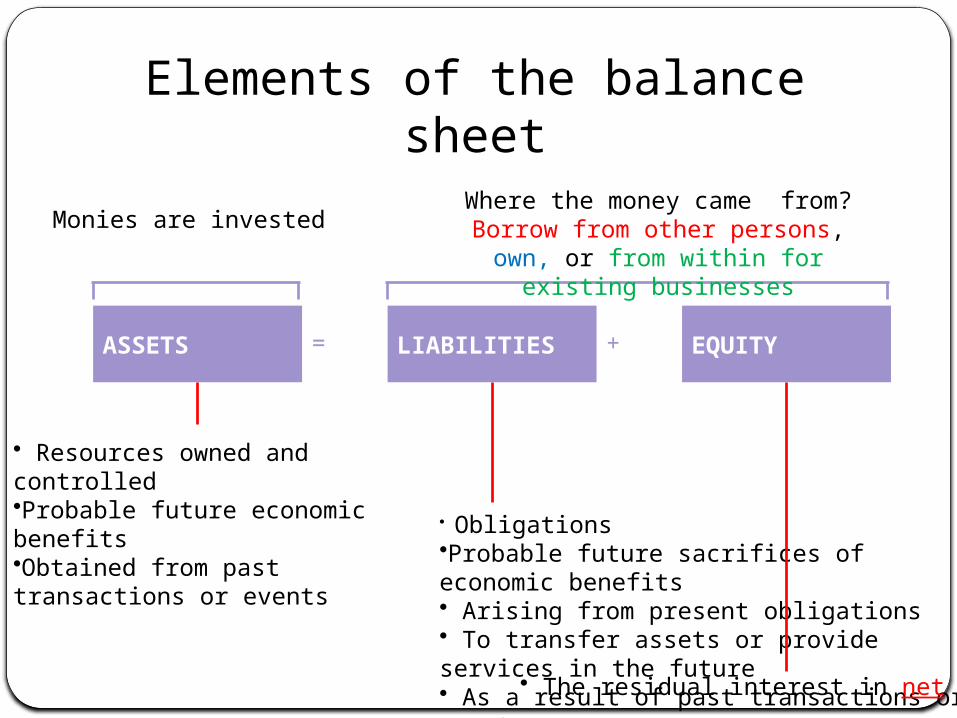

• Resources owned and controlled •Probable future economic benefits•Obtained from past transactions or events

• Obligations•Probable future sacrifices of economic benefits• Arising from present obligations• To transfer assets or provide services in the future• As a result of past transactions or events

• The residual interest in net assets.

ASSETS LIABILITIES EQUITY= +

Monies are invested Where the money came from? Borrow from other persons, own, or from within for

existing businesses

Elements of the balance sheet

LIABILITIES+EQUITY

ASSETS

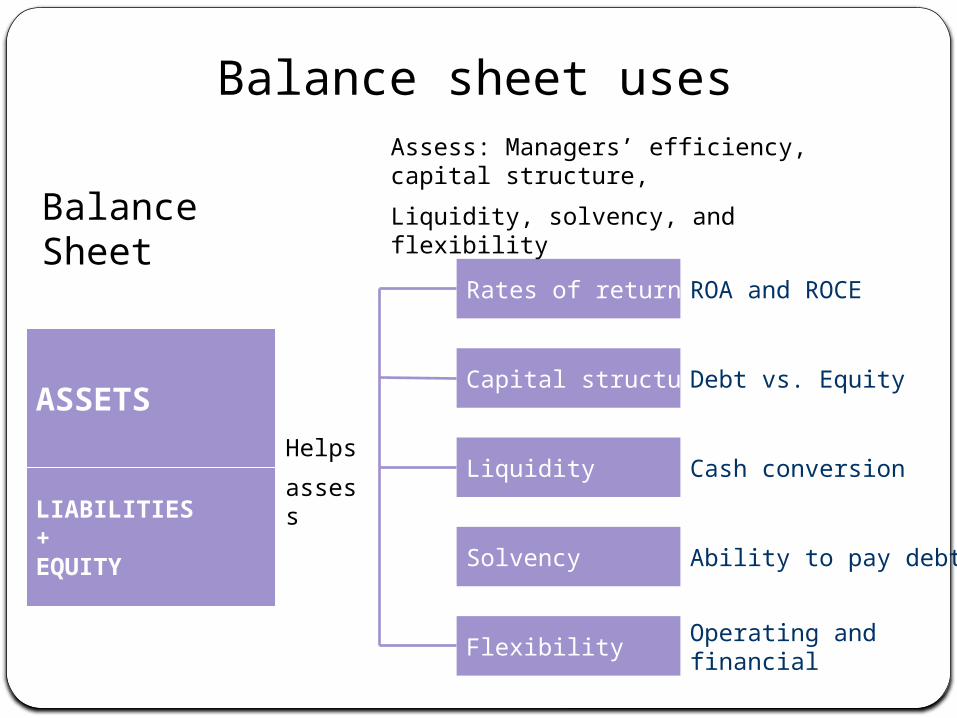

Rates of return

Capital structure

Liquidity

Solvency

Flexibility

ROA and ROCE

Debt vs. Equity

Cash conversion

Ability to pay debt

Operating and financial

Helpsassess

Balance sheet uses

Balance Sheet

Assess: Managers’ efficiency, capital structure,Liquidity, solvency, and flexibility

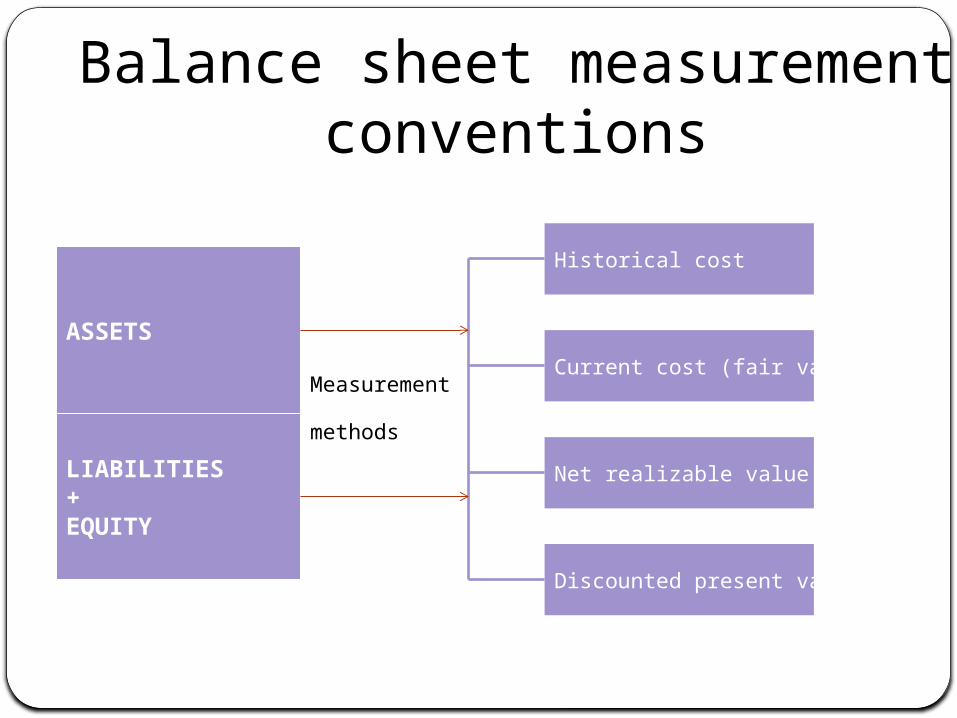

LIABILITIES+EQUITY

ASSETS

Historical cost

Current cost (fair value)

Net realizable value

Discounted present value

Measurement

methods

Balance sheet measurement conventions

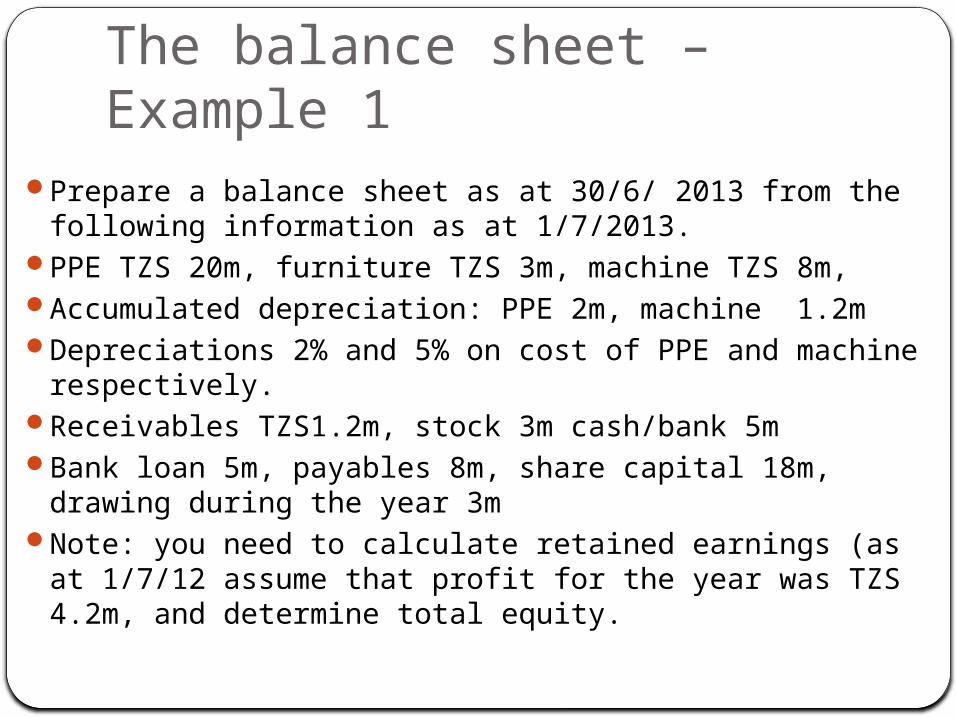

The balance sheet – Example 1

Prepare a balance sheet as at 30/6/ 2013 from the following information as at 1/7/2013.

PPE TZS 20m, furniture TZS 3m, machine TZS 8m,Accumulated depreciation: PPE 2m, machine 1.2mDepreciations 2% and 5% on cost of PPE and machine respectively.

Receivables TZS1.2m, stock 3m cash/bank 5mBank loan 5m, payables 8m, share capital 18m, drawing during the year 3m

Note: you need to calculate retained earnings (as at 1/7/12 assume that profit for the year was TZS 4.2m, and determine total equity.

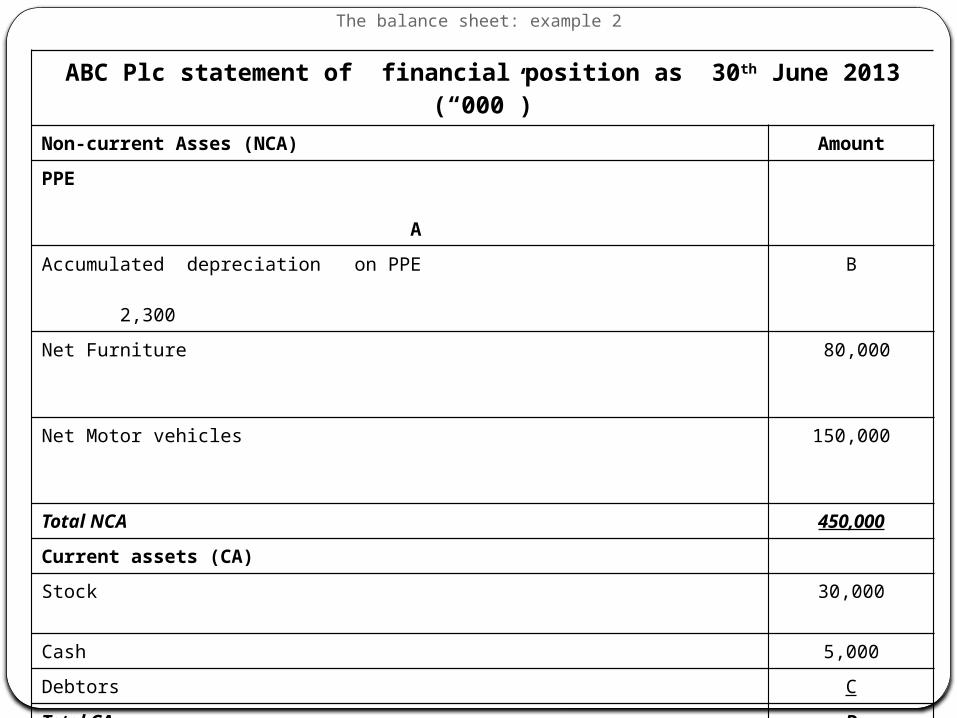

The balance sheet: example 2

ABC Plc statement of financial position as 30th June 2013 (“000”)

Non-current Asses (NCA) AmountPPE AAccumulated depreciation on PPE 2,300

B

Net Furniture

80,000

Net Motor vehicles

150,000

Total NCA 450,000

Current assets (CA)Stock

30,000

Cash 5,000Debtors CTotal CA D

TOTAL ASSESTS E

EQUITY 180,000Long-term liabilities (LTL)Bank Loans 170,000Current liabilities (CL)Creditors 15,000Other payables FTotal equity and liabilities 500,000

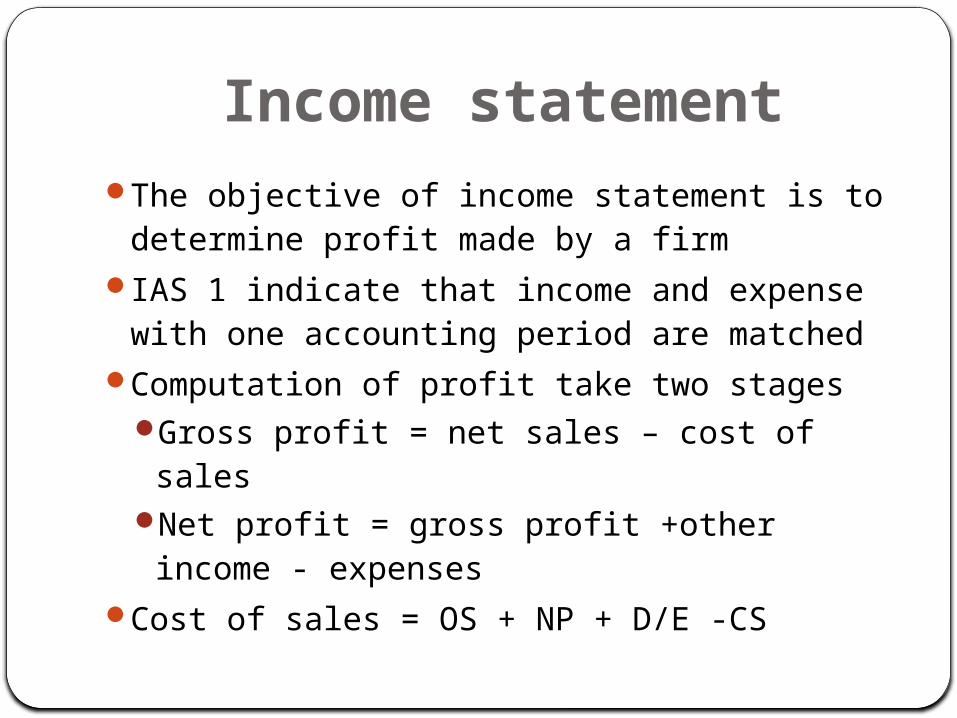

Income statementThe objective of income statement is to determine profit made by a firm

IAS 1 indicate that income and expense with one accounting period are matched

Computation of profit take two stagesGross profit = net sales – cost of sales

Net profit = gross profit +other income - expenses

Cost of sales = OS + NP + D/E -CS

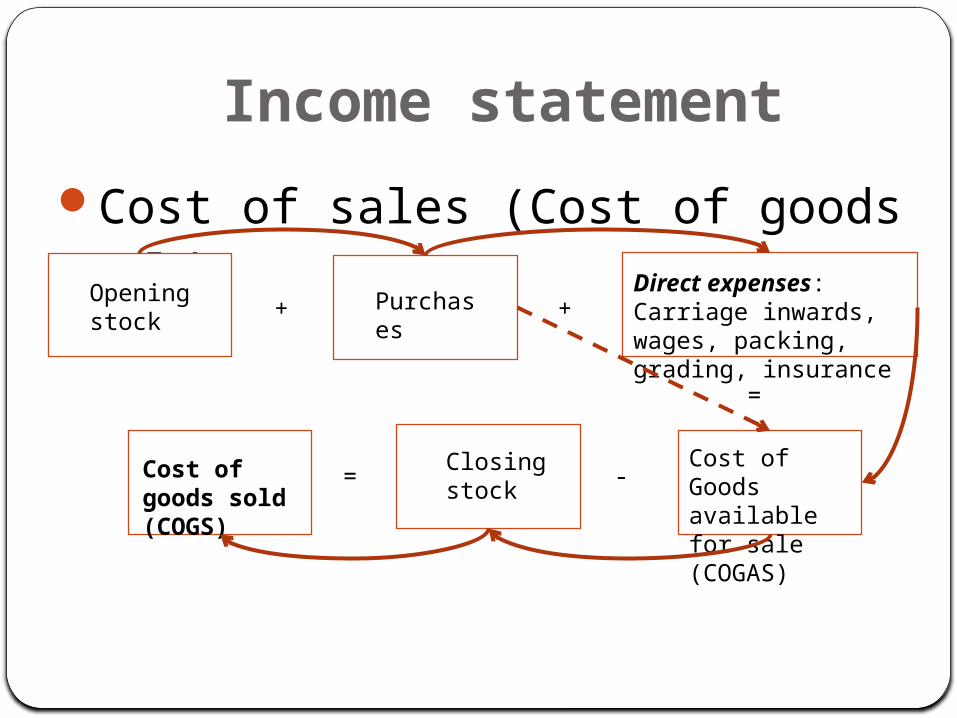

Income statementCost of sales (Cost of goods sold)Opening stock

Cost of Goods available for sale (COGAS)

Purchases

Cost of goods sold (COGS)

Direct expenses: Carriage inwards, wages, packing, grading, insurance

Closing stock

+ +

=

-=

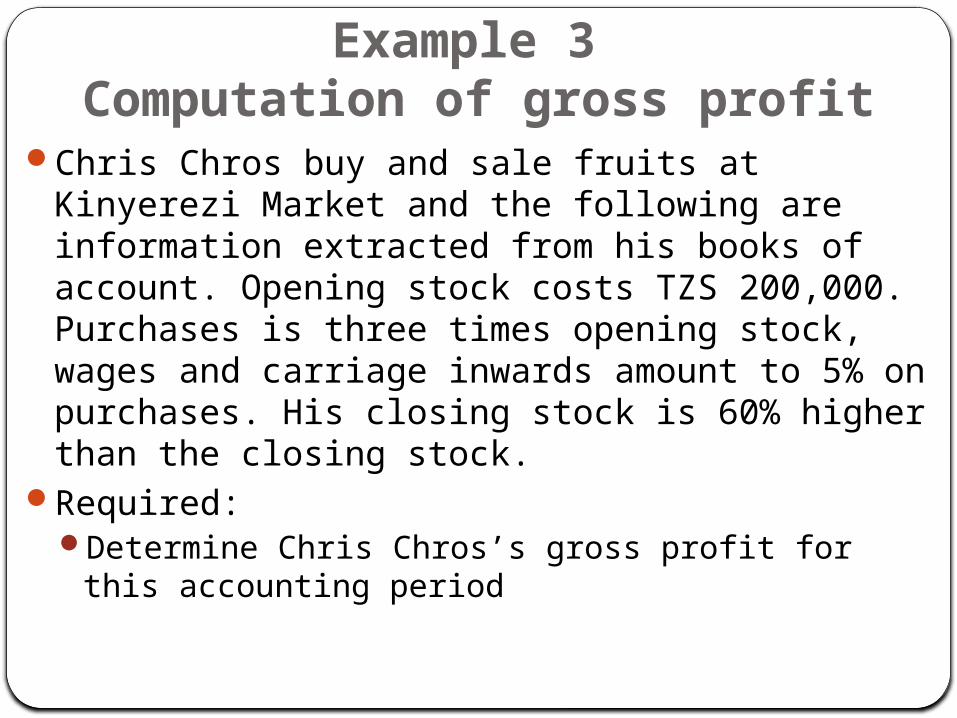

Example 3 Computation of gross profit

Chris Chros buy and sale fruits at Kinyerezi Market and the following are information extracted from his books of account. Opening stock costs TZS 200,000. Purchases is three times opening stock, wages and carriage inwards amount to 5% on purchases. His closing stock is 60% higher than the closing stock.

Required: Determine Chris Chros’s gross profit for this accounting period

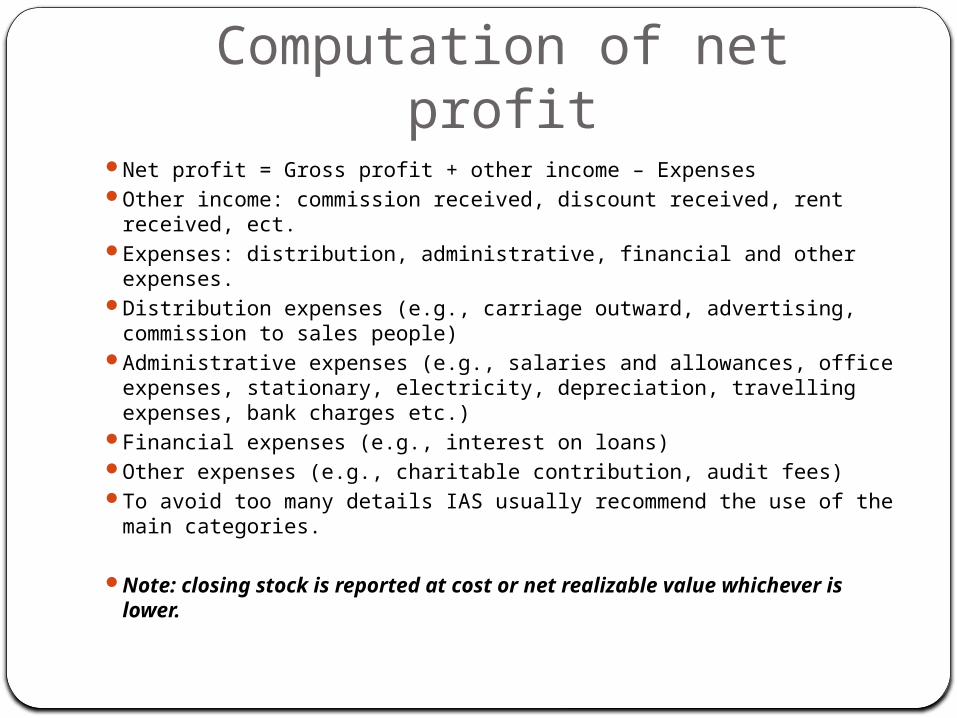

Computation of net profit

Net profit = Gross profit + other income – ExpensesOther income: commission received, discount received, rent received, ect.

Expenses: distribution, administrative, financial and other expenses.

Distribution expenses (e.g., carriage outward, advertising, commission to sales people)

Administrative expenses (e.g., salaries and allowances, office expenses, stationary, electricity, depreciation, travelling expenses, bank charges etc.)

Financial expenses (e.g., interest on loans)Other expenses (e.g., charitable contribution, audit fees)To avoid too many details IAS usually recommend the use of the main categories.

Note: closing stock is reported at cost or net realizable value whichever is lower.

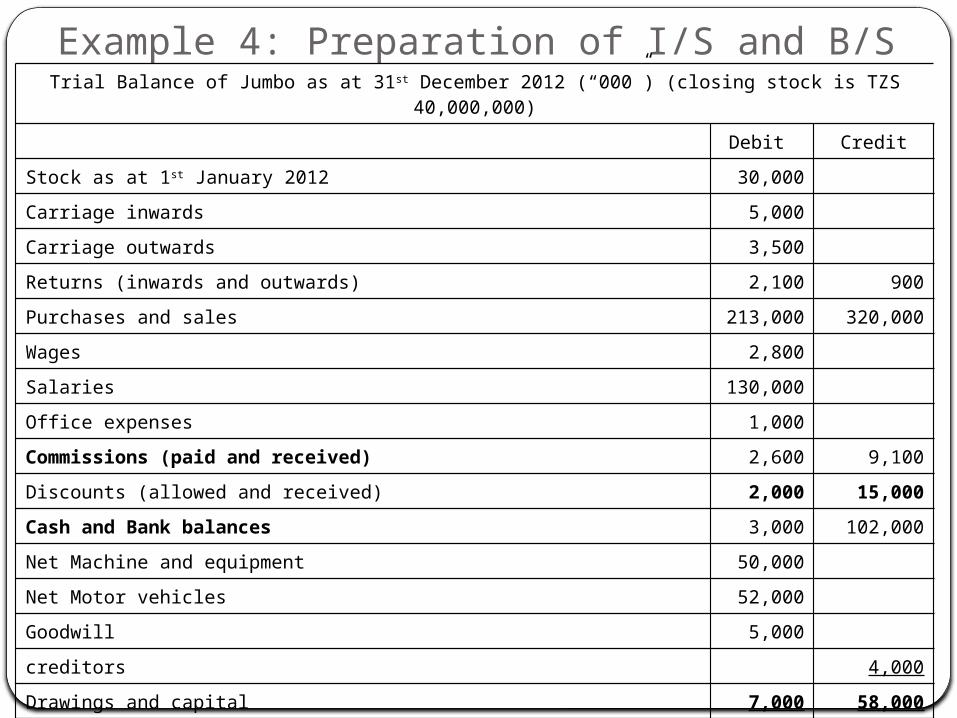

Example 4: Preparation of I/S and B/STrial Balance of Jumbo as at 31st December 2012 (“000”) (closing stock is TZS

40,000,000)Debit Credit

Stock as at 1st January 2012 30,000Carriage inwards 5,000Carriage outwards 3,500Returns (inwards and outwards) 2,100 900Purchases and sales 213,000 320,000Wages 2,800Salaries 130,000Office expenses 1,000Commissions (paid and received) 2,600 9,100Discounts (allowed and received) 2,000 15,000Cash and Bank balances 3,000 102,000Net Machine and equipment 50,000Net Motor vehicles 52,000Goodwill 5,000creditors 4,000Drawings and capital 7,000 58,000Total 509,000 509,000

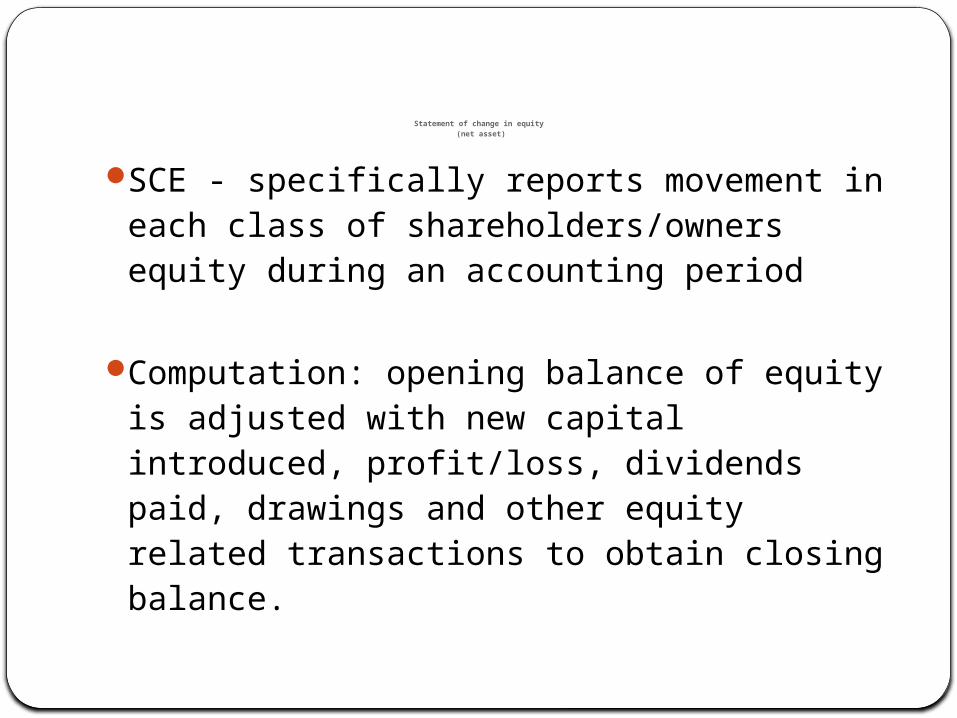

Statement of change in equity (net asset)

SCE - specifically reports movement in each class of shareholders/owners equity during an accounting period

Computation: opening balance of equity is adjusted with new capital introduced, profit/loss, dividends paid, drawings and other equity related transactions to obtain closing balance.

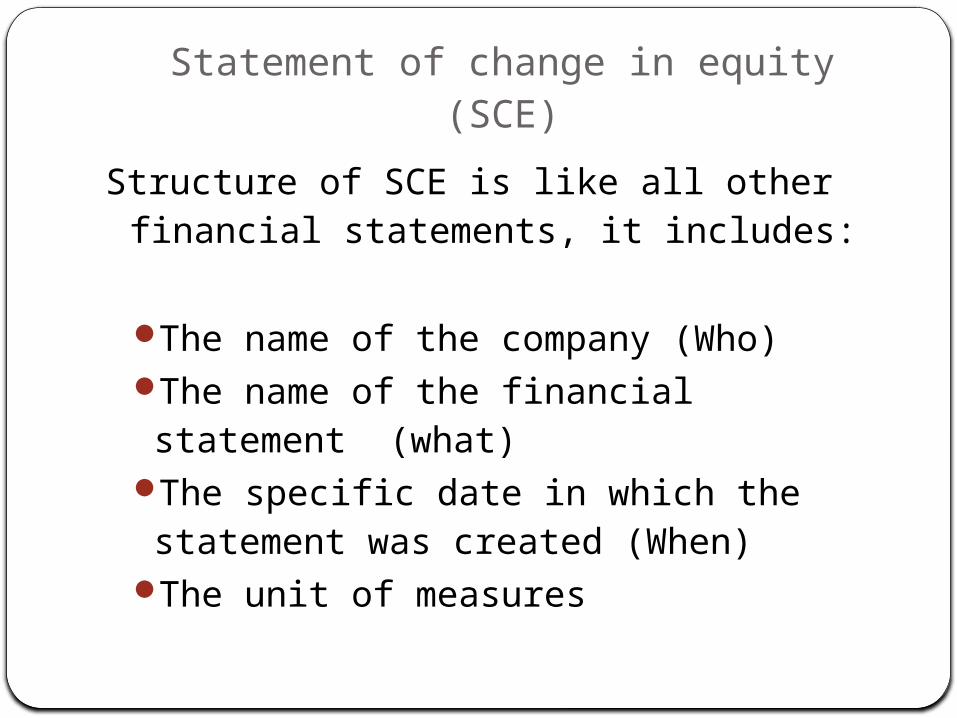

Statement of change in equity (SCE)

Structure of SCE is like all other financial statements, it includes:

The name of the company (Who)The name of the financial statement (what)

The specific date in which the statement was created (When)

The unit of measures

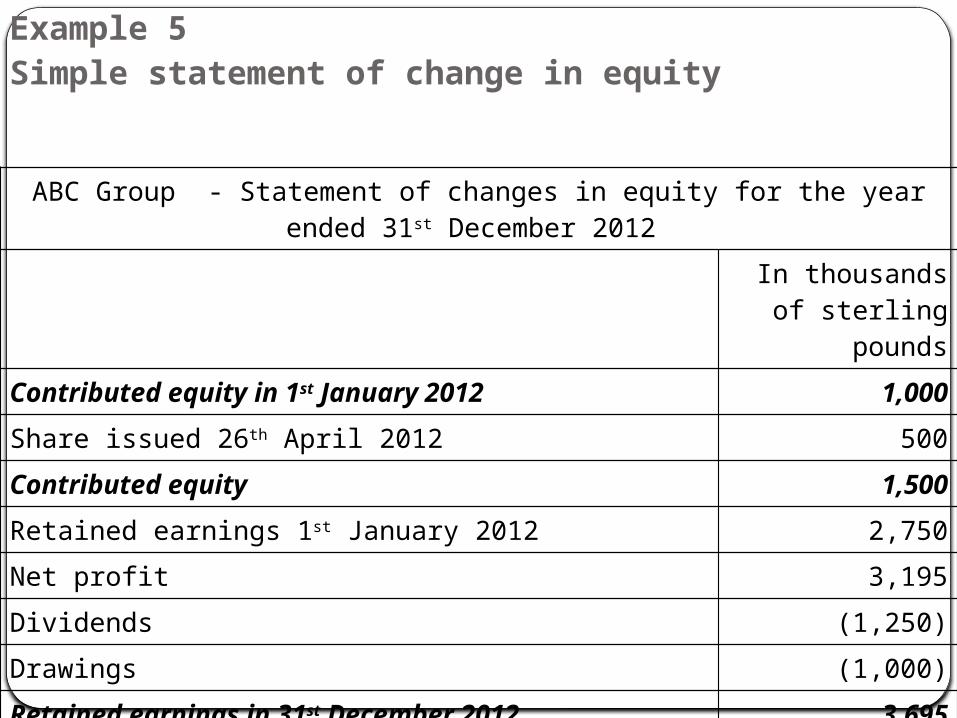

Example 5 Simple statement of change in equity

ABC Group - Statement of changes in equity for the year ended 31st December 2012

In thousands of sterling

poundsContributed equity in 1st January 2012 1,000Share issued 26th April 2012 500Contributed equity 1,500Retained earnings 1st January 2012 2,750Net profit 3,195Dividends (1,250)Drawings (1,000)Retained earnings in 31st December 2012 3,695Total equity in 31st December 2012 5,195

Relationships among financial statements

The income statement reports a company's financial performance while the balance sheet reports its financial health. One proceeds from the other. A company's financial performance regulates its financial health. Performance and health are linked through the net income account on the income statement and the equity account on the balance sheet

The bottom line of I/S represents profit or loss. The company can either distribute the profit directly to the owner as dividend, or it can reinvest the profit in the business. In either case, the profit is reflected in the owner's equity section of the balance sheet. The expanded accounting equation is an affirmation of the interrelationship between the income statement and the balance sheet

The expanded accounting equation incorporates income statement accounts into the basic accounting equation as follows: Assets = Liabilities + [Owner’s Equity + Revenues – Expenses (profit) – Drawings]. The expanded accounting equation is implicit in all financial statements

THANK YOUYou are advised to read IAS

1 for detail about this topic