Financial Market Imperfections and Irregular Growth Cycles

13

Scottish Journal of Political Economy, Vol. 43, No 2. May 19% Q Scottish Economic Society 1996. Published by Blackwell Pubhhen Lid. 108 Cowley Road. Oxford OX4 IJF. UK and 238 Main S r m t . Cambndge. MA 02142. USA FINANCIAL MARKET IMPERFECTIONS AND IRREGULAR GROWTH CYCLES Domenico Delli Gatti* and Mauro Galleg&** ABSTRACT In this paper we analyze the generation of endogenous growth and irregular fluctuations in a simple New Keynesian model whose background assumptions are borrowed from a class of asymmetric information models popularized by Greenwald and Stiglitz. We extend the framework put forward by Greenwald and Stiglitz taking explicitly into account technological progress as the engine of growth. We show how irregular endogenous fluctuations can arise around an endogenous trend: the traditional view of fluctuations as ‘short run’ phenomena must be abandoned in favour of models of fluctuating growth. I INTRODUCIION In the last decade, since the Slutsky-Frisch approach has become the standard framework for analyzing the business cycle, a twofold interpretation of trend and cycles has emerged. In particular, Blanchard (1989) and Blanchard-Quah (1989) have resumed the ‘traditional’ interpretation of macroeconomic fluctuations according to which demand shocks, which are characterized as transitory shocks, generate stationary cycles while supply shocks, i.e. permanent shocks, affect the trend. In this paper, we present and discuss a simple non-linear model of macro- economic growth and fluctuations based upon asymmetric information, which can be thought of as an extension and modification of a prototypical New Keynesian model developed by Greenwald and Stiglitz (Greenwald and Stiglitz, 1993a, 1993b; Greenwald, Kohn and Stiglitz, 1990). In our framework, we can still distinguish a transitory and a permanent component of the dynamics generated by the model: the former is responsible for the generation of fluctuations while the latter influences mainly the trend. Instead of transitory and permanent shocks, however, we introduce behavioral equations to model the wage change (a transitory element) and the change in productivity (which is a permanent component of the dynamics). The wage rate and the level of employment are linked by a ‘no shirkmg constraint’ (Shapiro and Stiglitz, 1984). The change in productivity is a function of R&D expenditure as in * Universit? Cattolica, Milano Universit? G. D.’Annunzio, Pescara ** 146

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Financial Market Imperfections and Irregular Growth Cycles

Scottish Journal of Political Economy, Vol. 43, No 2. May 19% Q Scottish Economic Society 1996. Published by Blackwell Pubhhen Lid. 108 Cowley Road. Oxford OX4 IJF. UK and 238 Main Srmt. Cambndge. MA 02142. USA

FINANCIAL MARKET IMPERFECTIONS A N D IRREGULAR GROWTH CYCLES

Domenico Delli Gatti* and Mauro Galleg&**

ABSTRACT

In this paper we analyze the generation of endogenous growth and irregular fluctuations in a simple New Keynesian model whose background assumptions are borrowed from a class of asymmetric information models popularized by Greenwald and Stiglitz. We extend the framework put forward by Greenwald and Stiglitz taking explicitly into account technological progress as the engine of growth. We show how irregular endogenous fluctuations can arise around an endogenous trend: the traditional view of fluctuations as ‘short run’ phenomena must be abandoned in favour of models of fluctuating growth.

I INTRODUCIION

In the last decade, since the Slutsky-Frisch approach has become the standard framework for analyzing the business cycle, a twofold interpretation of trend and cycles has emerged. In particular, Blanchard (1989) and Blanchard-Quah (1989) have resumed the ‘traditional’ interpretation of macroeconomic fluctuations according to which demand shocks, which are characterized as transitory shocks, generate stationary cycles while supply shocks, i.e. permanent shocks, affect the trend.

In this paper, we present and discuss a simple non-linear model of macro- economic growth and fluctuations based upon asymmetric information, which can be thought of as an extension and modification of a prototypical New Keynesian model developed by Greenwald and Stiglitz (Greenwald and Stiglitz, 1993a, 1993b; Greenwald, Kohn and Stiglitz, 1990). In our framework, we can still distinguish a transitory and a permanent component of the dynamics generated by the model: the former is responsible for the generation of fluctuations while the latter influences mainly the trend. Instead of transitory and permanent shocks, however, we introduce behavioral equations to model the wage change (a transitory element) and the change in productivity (which is a permanent component of the dynamics). The wage rate and the level of employment are linked by a ‘no shirkmg constraint’ (Shapiro and Stiglitz, 1984). The change in productivity is a function of R&D expenditure as in

* Universit? Cattolica, Milano Universit? G. D.’Annunzio, Pescara **

146

FINANCIAL MARKET IMPERFECTIONS 147

Greenwald, Kohn and Stiglitz, 1990. By means of this device, we introduce a process of endogenous growth into the system: consequently, short term fluctuations develop around an endogenously determined long term trend.

In such a way, we overcome the main limit of the literature on fluctuating growth (from Goodwin’s model of the 1960’s to the work of Day, 1981, 1993), in which either the growth rate or the cyclical process is exogenous. Anticipating some conclusions, we may say that ‘short term’ components generate fluctuations, while ‘long term’ ones affect both growth and fluctuations.

The growth potential of the economy, which is a function of productivity, is hampered (strengthened) by the tendency of wages to rise (fall) with increases (decreases) in the unemployment rate. The interaction of these two tendencies can generate, depending on the parameters’ configuration, convergence to the steady state, periodic cycles or chaotic dynamics.’

It is worth noting that the generation of endogenous growth and fluctuations in this model does not rely upon the price and wage rigidities (either nominal or real) envisaged in the mainstream of New Keynesian literature.

The paper is organized as follows. In Section 11, we develop a simple model of the dynamics of firms’ ‘equity base’ or ‘net worth’, which is the main determinant of output, on the simplifying assumption of a given and constant productivity of labour. We end up with a logistic map, which can generate chaotic dynamics under appropriate circumstances.

In Section I11 we extend the model in order to take into account the dynamics of productivity. We link the growth of productivity to R&D expenditure, which in turn is determined by the accumulation of internal funds (net worth). We end up with a system of two non-linear difference equations in the equity base and labour productivity, which can generate both growth and (possibly irregular) fluctuations. The mathematical details of the analysis of the dynamical system are confined to the Appendix.

In section IV we draw some conclusions.

I1 A NEW KEYNESIAN ASYMMETRIC INFORMATION MODEL In this section we build a model which can be thought of as an extension of Greenwald and Stiglitz (1993b). We modify their model essentially by talung into account the dynamics of the wage rate. In the next section we will introduce the process of techca l change, which is driven by R&D expenditure.

Following Greenwald and Stiglitz, we assume that in an uncertain environ- ment, in which futures markets do not exist and inputs must be paid before output is sold (there is a one-period time lag between production and sale), any

’ Note that if the R&D coefficient were nil, one would have either convergence toward the steady state or aperiodic cycles, but not growth. This helps to explain a well known stylized fact: namely that while reference cycles are asymmetric, i.e. expansions last longer than contractions, growth cycles are symmetric (Zarnovitz, 1992). According to this model, the asymmetric behavior of the reference cycle can be explained by the presence of the trend component which introduces a biased (toward expansion) factor in the time series.

0 Sconish Efonomic Society 19%

148 DOMENICO DELL1 GA’ITI AND MAURO GALLEGATI

decision to produce is a risky (investment) decision. Since capital markets are characterized by informational imperfections, firms’ ability to raise funds on the Stock markets is restricted (equity rationing). Therefore, firms must rely upon internally generated funds and bank loans to finance production. In this context, they run the risk of bankruptcy. If bankruptcy occurs, firms incur additional costs. The probability of bankruptcy is a decreasing function of the firms’ net worth or equity base. In fact, the higher the volume of internally generated funds, the lower the level of indebtedness and the lower the probability of bankruptcy.

Firms face a real wage w, and, at that wage they can hire as much labour as they want. Firms can also borrow from banks as much as they want at terms which must yield the lender an expected real return of r (in equilibrium, this rate of return is equal to households’ intertemporal preference rate).

In this framework, Greenwald and Stiglitz (19938) derive the following law of motion of the ‘equity base’ in real terms:

where: a = firms’ equity base; 4 =output; p = price level (e stands for ‘expected’); 6 = discount rate in the utility function of the representative consumer

w = real wage; 1 = employment.

(in equilibrium this equals the real rate of interest, r);

Production requires only labour. We assume a constant returns to scale (CRS) technology incorporated in the following production function:

According to equation (2), output is a linear increasing function of labour. @‘/’>O is labour productivity, @ > O will be referred to hereafter as the ‘productivity coefficient’.

Moreover, we assume the aggregate supply function:

q,= ha, h>O (3)

according to which in each period output is determined by the equity base. Equation (3) can be thought of as the solution of an optimization problem in which the representative firm maximizes expected profit taking explicitly into account the cost of bankruptcy.’ This result is a consequence of the hypothesis

*In more general terms, an equity-determined supply function of the form q = q(a ) can be thought of as the solution of the following maximization problem:

m a x E ( n ) - c q F = q - ( l + d ) ( w l ( q ) - o ) - c q F ( o ) where l (q) is labour input (the inverse of the production function), c is the average bankruptcy cost F(o) is the probability of bankruptcy, which is a decreasing function o f the equity base.

0 Scottish Economic Society 1996

FINANCIAL MARKET IMPERFECTIONS 149

of asymmetric information: under this assumption the Modigliani-Miller theorem does not hold true, and a financing hierarchy can be envisaged in which internal funds are cheaper than external finance. As a consequence, aggregate supply is a function of the equity base, which is the integral of internally generated funds.

We introduce, at this point, a 'no shirking constraint (Shapiro and Stiglitz, 1984): the real wage that firms must pay to elicit effort from workers is an increasing function of employment,

w, = bl,. (4)

where b > 0. Substituting equations (2)-(4) into (1) and assuming that expectations are

fulfilled ( p ; + , = p, + I ) r we get the following first-order non-linear difference equation:

where rl = h + 1 + 6; r2 I (1 + 6)(bh2/$) . We can reduce equation ( 5 ) to a logistic map (Iooss, 1979) by means of a

change of variable. Assuming that: r 2 a , = y , . in fact, we can rewrite (5) as follows:

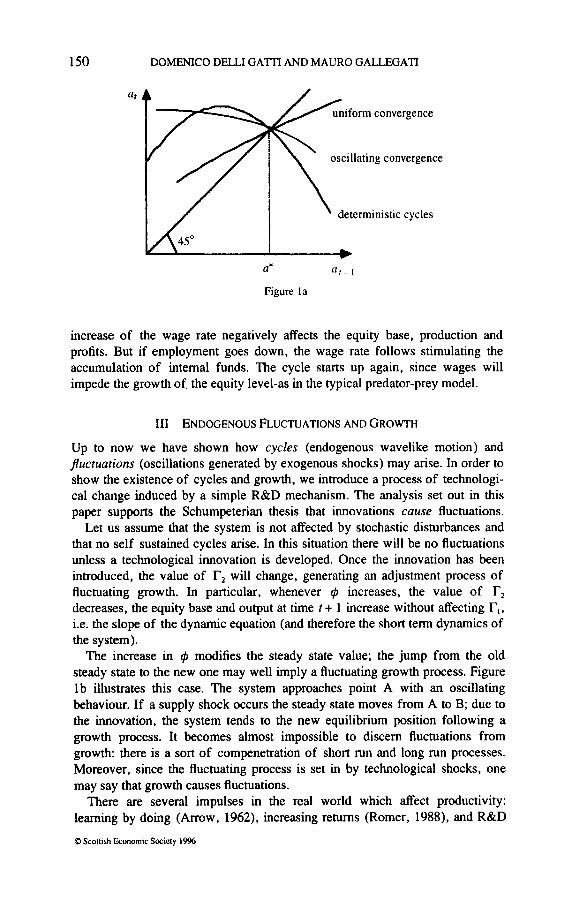

From the analysis of nonlinear maps (Mira. 1987; Brock el al., 1991). we know that a solution exists if 0 c rl G 4. In particular, if rl c 3 there is uniform convergence towards the steady state; if 3 c rl G 4, equation (6) generates periodic orbits. In this case, if rl > 3.57 . . . the dynamics can be characterized as chaotic. In other words, in every period, a deterministic cycle of multiple periodicity occurs if the slope of the curve (6) is negative and the slope is sufficiently high in absolute value when it crosses the 45" line: see Figure la (Grandmont, 1985).

If TI c 3, the Slutsky-Frisch approach to the determination of fluctuations can be applied (as it is by Greenwald and Stiglitz, 1993b). In this case, oscillations would be generated by stochastic recurring disturbances. In our model, however, instead of affecting only the periodicity of the time series generated by a deterministic dynamic model, a stochastic disturbance affects the qualitative behaviour of the system. Within this framework, several dynamic solutions are therefore possible (convergence to a fixed point, limit cycles, and chaotic dynamics), depending on the timing of the shucks.

On the contrary, when rl > 3, a deterministic oscillatory path may emerge. In particular, if 3 c rl s 4, we can detect periodic orbits and if TI > 3.57, because of chaotic dynamics, cycles follow an erratic path, i.e. their periodicity is random (but some regularities can still be identified: Goodwin, 1990). A simple Goodwin-Stiglitz story can be used to interpret the oscillatory pattern of the equity base and income. In a period of increasing activity, wages go up. The 0 Scottish Economic Society 19%

150 DOMENICO DELL1 GA'ITI AND MAURO GALLEGATI

a' ' 1 , - I

Figure la

increase of the wage rate negatively affects the equity base, production and profits. But if employment goes down, the wage rate follows stimulating the accumulation of internal funds. The cycle starts up again, since wages will impede the growth of. the equity level-as in the typical predator-prey model.

111 ENWENOUS FLUCTUATIONS AND GROWTH

Up to now we have shown how cycles (endogenous wavelike motion) and fluctuations (oscillations generated by exogenous shocks) may arise. In order to show the existence of cycles and growth, we introduce a process of technologi- cal change induced by a simple R&D mechanism. The analysis set out in this paper supports the Schumpeterian thesis that innovations muse fluctuations.

Let us assume that the system is not affected by stochastic disturbances and that no self sustained cycles arise. In this situation there will be no fluctuations unless a technological innovation is developed. Once the innovation has been introduced, the value of r2 will change, generating an adjustment process of fluctuating growth. In particular, whenever q5 increases, the value of Tz decreases, the equity base and output at time t + 1 increase without affecting r,. i.e. the slope of the dynamic equation (and therefore the short term dynamics of the system).

The increase in q5 modifies the steady state value; the jump from the old steady state to the new one may well imply a fluctuating growth process. Figure lb illustrates this case. The system approaches point A with an oscillating behaviour. If a supply shock occurs the steady state moves from A to B; due to the innovation, the system tends to the new equilibrium position following a growth process. It becomes almost impossible to discern fluctuations from growth: there is a sort of compenetration of short run and long run processes. Moreover, since the fluctuating process is set in by technological shocks, one may say that growth causes fluctuations.

There are several impulses in the real world which affect productivity: leaming by doing (Arrow, 1962), increasing returns (Romer, 1988), and R&D

Q Scottish Economic Society 1936

FINANCIAL MARKET IMPERFECTIONS 15 1

" t

Figure lb

expenditure (Greenwald et al., 1990) are just a few of the possibilities that have been investigated. We model the change in technological knowledge as

@r+I=@t+V(R&D)r (7)

Greenwald et al., 1990, and several empirical studies, suggest that R&D activity is primarily linked to the equity base, i.e.

(R&D), = {ar. (8) In an asymmetric information setting, external finance is more costly than the

equity base. Risk averse firms finance production and investment by means of a mix of external finance and equity base, while R&D expenditure, whose impact on productivity is uncertain, will be preferably financed by means of equity base alone. In particular, up to a certain level of the equity base, firms will not spend on R&D, prefemng instead to replace depreciated capital stock or to expand production; only if the equity base is large enough will they become involved in a lund of expenditure which is very profitable but whose probability of success is extremely low. Thus, if the equity base is high, R&D expenditure, the rate of technological progress and wage change are also high.3.

Wages can vary between a ceiling (a reservation wage, when unemployment is very high) and a floor (when, in full employment, wages absorb output completely): cereris paribus, an increase in labour productivity decreases the real wage and employment, while it increases profits. Equations (6) and (8) form the nonlinear first order map in a and @ that we examine hereafter.

'If the increase in wages is higher than the increase in productivity, as appears to be the case in the last stage of the expansion, the change of the equity base will be reduced, thus lowering the R&D expenditure and the growth rate. Trend is therefore inevitably segmented in this contest because fast (slow) equity accumulation will produce growth (stagnation).

Q Scottish Economic Society 19%

I52 DOMENICO DELL1 GA’ITI AND MAURO GALLEGATI

Equation (8) can be simplified as follow^:^

af a,+, = aa, - - $

$ 1 + I = 9, + Ya, where Y = qt (9)

In order to calculate the steady state solutions of the system, we divide (8a) by (619

af aa, - - $1

@ , + I $f+Pf

1, + I = /,(a 1 1 ) / ( 1 + Yl , )

-- - a,+,

or, denoting the ratio of a to $ by 1 = a / $ :

(9a)

whose steady state values are 1; = 0, I , = ( a - 1)/( 1 + y) . In the following we interpret the dynamics of the system, referring the reader

interested in the mathematical technicalities to the Appendix. During an upswing, the increase of output leads to a rise of the wage rate

which reduces profits, the equity base and output. Therefore the labour requirement decreases and so does the real wage. These processes restore profitability and the cycle can begin again.

So far, we have applied a ceteris paribus condition, i.e. no increase in productivity has been taken into account, and the cycle is a replica of the Lotka-Volterra predator-prey model discussed in Section 11. When a R&D expenditure function is introduced, the whole situation changes because, whenever output rises, the productivity coefficient will also increase, thus lowering the demand for labour. This means that, in this case, two contrasting tendencies are at work: on the one hand, output will increase because of the R&D process; on the other, it will decrease because of the no shirking constraint. The direction of output will thus depend on which of the two effects predominates, since the former tendency will cause the system to grow, while the latter will produce fluctuations around the trend.

Plotting the dynamics of equations (6) and (8a) on the equity-time axes, we obtain Figures 2a-b, drawn from a computer simulation’ (with a = 3 . 9 , y = 0401. and initial conditions in Figure a-b, respectively, a, = 1, q, = 0.22. and a, = 1, qo = 0.19 (0.21). The system is asymptotically stable and generates fluctuating growth in which changes surrounding troughs are larger than changes surrounding peaks, because of the productivity change element which generates the asymmetric behaviour (see McQueen and Thorley, 1993).

Note that the growth process which has been detected seems to possess a random nature, while fluctuations around the trend maintain a constant variance (no heteroscedasticity problem arises) since they are bounded in a cone (see the

41nordertoobtain ( 8 a ) w e i m p o s e a = l + d + h , (1+6)bhZ=1 . ’The software program which runs the simulation, elaborated by G. Gallo, is in Medio,

*

(1993).

(d Scottish Economic Society 1996

FINANCIAL MARKET IMPERFECTIONS 153

t

Figure 2a t

Figure 2b

Appendix for further details). In more technical terms, the growth process and fluctuations are constrained by critic lines (Mira, 1987). As is usual in non-linear maps with chaotic dynamics, the growth process is sensitive to initial conditions.

Since fluctuations also depend on the parameters of equation (8a), their changes can amplify or reduce the frequency and the amplitude of fluctuations. If economic policy can affect these coefficients, the business cycle will also be affected. Segmented trends can also arise when different R&D rules are adopted. In particular, whenever institutional change or Schumpeterian innovation lato Senm affecting the learning coefficient are taken into account, the model will exhibit a segmented trend.

IV CONCLUSIONS

In this paper we have analyzed the generation of endogenous growth and fluctu- ations in a New Keynesian framework. We have built a simple macrodynamic model which shares some features of a class of asymmetric information models recently popularized by Greenwald and Stiglitz. In our model, however, we extend and modlfy the original framework in order to take into account technological progress as the main determinant of growth, as in the new growth theory’.

Moreover, we show that irregular endogenous fluctuations can develop around an endogenous trend. In a sense, therefore the traditional view of fluctuations as typically short run phenomena has to be abandoned. This is a first modest step towards integrating growth and the cycle, i.e. towards a deeper understanding of the behavior of real time series.

APPENDIX

Chaotic growth

Rewrite equations ( 5 ) and (8) as follows:

a‘ = aa - (a2/@) .I @’ = $J + ya

where a > 1 and y > 0. Q Scottish Economic Society 1996

154 DOMENICO DELL1 GA'ITI AND MAURO GALLEGATI

All the points of the @-axis are fixed points. Since

J ( O . @ ) = ( a 0

all the fixed points are repulsive (as a > 1). The straight line ( T i ) of equation Cp = mia is mapped by T into the straight

line (ri + I ) of equation @ = mi + Iu with mi + I = mi(mi + y ) /am i - 1 (see Figure 3).

The straight line qj = l / a a (with slope m= l / a ) is an antecendent of the y- axis lines of fixed points.

Map T can be decomposed, that is, expressed in a different form, as follows: let

(a;, @,I = Ui(1, m,)

where

then

mi(* + r) ( u ~ + ~ , @ ~ + ~ ) = ai a - - , a , ( m , + y ) = a i a - - ( ( : ) ( :)(I* am-1 ) and we can consider

T : U , + ~ = U , a - - ( b)

The dynamic behaviour of the sequences of the slopes mi is determined from the one-dimensional map

1 m+-

am- 1 a

m(m + Y ) m' = f ( m ) f ( m ) =

fixed points: m = 0 m = m* = - I c y >o. a-1

Map f ( m ) possesses two fixed points: m = 0 (locally stable) and m = m* > 1 / a > 0 (see Figure 4).

0 Scottish Economic Society 1%

FINANCIAL MARKET IMPERFECTIONS 155

X

Figure 3

Figure 4

For the local stability we consider

am2 - 2m - y f (m) = (am - 1)’ ’

So that:

a > 1 f (m* ) c 1, while

3 + Y f ’ (m) 2 1 - a < a* = - 1-Y

In the range of a :

1 < a < a*, m* is locally attractive; at a = a , it is f ’ (m* ) = - 1: flip bifjuraction. *

for a > a*. we have a sequence of flip- and fold-bifurcations, analogous to those that occur in the logistic map.

Recall that the interval I = [c, c , ] ; where c = f ( m + ) critical point of f. and c, = f ( c ) . is absorbing for all m> l / a .

0 Scottish Economic Society 1996

156 DOMENICO DELL1 GATTI AND MAURO GALLEGATI

As regards map T , in the positive quadrant of the (a , @)-plane, this means that the cone r,, bounded by the straight lines r ( c ) and r(cI), ( r ( c ) of equation: @ = ca, r(cI): @ = c la) is an absorbing region; its basin of attraction. D,, is the cone bounded by the straight line @ = ( l / a ) a and its consequent: the @-axis ( r ( c ) and r (c , ) are critical curves of T ) (see Figure 5).

Every point of the cone D,, has a consequent of finite rank inside rl. Let us now look for the dynamics of T inside rl. For 1 < a < a* = 3 + y / 1 - y all the straight lines in rl are convergent to the straight-line r(m*)( @ = m*a). On the line r (m*) , the consequents of a point with abscissa a,, have abscissae given by

and since

1 1 + a y * > 1 (fora > l),

nz l + y

we have that

a,, - +=. n-c-

Hence, it follows that also the generic sequence a, of a point (a,), 4") belonging to r,, is divergent. Numerically, we observe that in a few iterations the consequent of a point p o = (a0, &) E rl is almost on the straight-line r (m*) , and that P , ~ tends towards the point at infinity on r(m*).

For a > a*, when map f(m) has an attractive cycle of period-q then map T has an attractive cycle of straight-lines of period q, say

I d m , ) , r ( m 2 ) , ..., r(m,)l

r(m,) of equation @ = m p ; { m , , ..., nzq] cycle-q of map f ( m ) . Each r(nz,) is a unit straight-line for map T , .

s

Figure 5

8 Scottish Economic Society 1996

FINANCIAL MARKIT IMPERFECTIONS 157

To prove that trajectories are divergent on these lines, let

pI = u l ( l , m , ) E r (mi ) , then

a , = u , a - - a-- ... a - - ( :I)( :J ( so that iff, > 1 it results

All the cycles of map f, attractive of repulsive, are cycle-straight-lines of map T, and we know that increasing a from a* cycles of any period 4 will appear for map f, and chaotic intervals. As regards map T, we can observe, numerically, that the factors f, are greater than 1 for all periods q. When the sequences of m, are chaotic, the sequences of p i are divergent with chaotic transient in the sector I', (absorbing into D,).

ACKNOWLEDGEMENTS

The authors wish to thank R. Day, L. Gardini and J. Stiglitz for very useful comments.

REFERENCES

ARROW, K., (1962). The economic implications of learning by doing. Review of

BLANCHARD, 0. J. (1989). A traditional interpretation of macroeconomic fluctuations.

BLANCHARD, 0. J. and QUAH, D. (1989). The dynamic effects of aggregate demand and

BROCK, W., HSIEH, D. and LEBARON, B. (1991). Nonlinear Dynamics, Chaos and

DAY, R. H. (1981). Irregular growth cycles. American Economic Review, 72, pp.

DAY, R. H. (1993). Complex economic dynamics. In M. H. Pesaran, S. M. Potter, Nonlinear Dynamics Chaos and Econometrics. Wiley, London, pp. 1 - 16.

GOODWIN, R. (1990). Chaotic Economic Dynamics. Clarendon Press, Oxford. GRANDMONT, J. M. (1985). On endogenous competitive business cycles. Econometrica,

GREENWALD, B., KOHN, M. and STIGLITZ, J. E. (1990). Financial market imperfections and productivity growth. Journal of Economic Behavior and Organization, 13, pp.

GREENWALD, B. and STIGLITZ, J. E. (1993a). New and old Keynesians. Journal of Economic Perspectives, 7, pp. 23-44.

GREENWALD, B. and STIGLITZ, J. E. (1993b). Imperfect information, finance constraints and business fluctuations. Quarterly Journal of Economics, 108, pp. 107-44.

IOOSS, G. (1979). Bifurcation of Maps and Applications. North Holland, Amsterdam. MCQUEEN, G. and THORLEY, S. (1993). Asymmetric business cycle turning points.

Journal of Monetary Economics, 31, pp. 341 -62.. MEDIO, A. (1993). Chaotic Dynamics, Cambridge University Press, Cambridge. MIRA, C. (1987). Chaotic Dynamics. World Scientific: New York.

Economic Studies, 29, pp. 155-73.

American Economic Review, 79, 1146-164.

supply disturbances. American Economic Review, 79, pp. 655-73.

Instability. MIT Press, Cambridge.

406- 14.

53, pp. 995-1046.

321-45.

0 Scottish Efonomic Society 19%

158 WMENICO D E L I GA'ITI AND MAURO GALLEGATl

ROMER, P. (1988). Endogenous technological change. Journal of Political Economy, 94, OD. 1002-7. r r ~~ ~

SHAPIRO, C. and STIGLITZ, J. E. (1984). Equilibrium unemployment as a worker discipline device. American Economic Review, 74, pp. 433-44.

Date of receipt of final manuscript: 26 September 1995.

0 Scottish Economic Society I y y 6