Final fin casebfgjyki piop

82

1. Introduction “The Kalimantan Paper Project” which was introduced by Ibrahim Hanaffi, a prominent Indonesion industrialist. He took this project on hand but the fact was that lack of financial position creates a barrier to fulfil this project. For that, on April 1, 1988, Ibrahim sent a request to three country's prominent bank (such as Deutsche Handelsbank AG of West Germany, the Metropolitan Bank of New York and the Kamakura Bank of Japan) and arranged a discussion session. The main aim of this discussion was within the end of June,each bank should be prepared enough to offer indicative terms for making funds available to the project with loan signing. Ibrahim also got support from the Indonesian Ministry of Finance (MOF) and the bank of Surabaya. Product of the Project Ibrahim Hanaffi wanted to produce high quality paper. 2. Analysis the Economy Economy is determined by country's GDP. So, the most important factor is population of Indonesia. Indonesia is the largest Islamic populated country in the world. It has more than 13000 islands and considered as a wide diversity country in terms of culture. Many ethnic groups are seen including Chinese, Indians, Arabs, Micronesians, Malay and Melanesia. Among those, Malay is the most dominant ethnic 1

Transcript of Final fin casebfgjyki piop

1. Introduction

“The Kalimantan Paper Project” which was introduced byIbrahim Hanaffi, a prominent Indonesion industrialist. Hetook this project on hand but the fact was that lack offinancial position creates a barrier to fulfil this project.For that, on April 1, 1988, Ibrahim sent a request to threecountry's prominent bank (such as Deutsche Handelsbank AG ofWest Germany, the Metropolitan Bank of New York and theKamakura Bank of Japan) and arranged a discussion session.The main aim of this discussion was within the end ofJune,each bank should be prepared enough to offer indicativeterms for making funds available to the project with loansigning. Ibrahim also got support from the IndonesianMinistry of Finance (MOF) and the bank of Surabaya.

Product of the Project

Ibrahim Hanaffi wanted to produce high quality paper.

2. Analysis the Economy

Economy is determined by country's GDP. So, the mostimportant factor is population of Indonesia. Indonesia isthe largest Islamic populated country in the world. It hasmore than 13000 islands and considered as a wide diversitycountry in terms of culture. Many ethnic groups are seenincluding Chinese, Indians, Arabs, Micronesians, Malay andMelanesia. Among those, Malay is the most dominant ethnic

1

group and only it introduced a official language “MalayLanguage”. Over 250 distinct native spoke and use thislanguage. Indonesia got independence in 1945. Afterdefeating the Dutch colonialists in 1949, the economy ofIndonesia was positive. But due to Sukarno (The firstpresident of Indonesia), economy was going downward. For thefirst time, economy faced hyperinflation, closed the economyto outside competition, ruined the plantations, embarked anineffective and costly military confrontation with Malaysia,introduced chronic budget deficits, and nationalized thefinancial sector. For those reason, Indonesia's business didnot raise as much as predict. Foreign investor did not enterinto Indonesia because of high inflation and close economy.Paper industry did not grow up due to ruin forest andplantation. The business relationship between Indonesia andMalaysia was decreasing. All these were liable for overcontrol of economy. But Suharto gives his best and broughtthe economy under control.

In 1970's, Indonesia's economy followed a path ofdevelopment. It tried to protect domestic economy, basicallyan agriculture industry, Indonesia moved from being a grainimporter to self sufficiency. The Government introduced atransmigration program by which poor farmer were givengovernment subsidies to resettle the sparsely populatedregion of East Kalimantan. This program was expensive butsaw it as an economic and cultural expedient. The Indonesiancurrency, the rupiah can be convertible easily to the U.Sdollar. So it creates a big opportunity to expend businessin US market and US investor easily came here for runningbusiness. Due to increase foreign private capital toIndonesia, domestic savings (GDP) was increasing. Economyboost in 1970's due to oil industry. Indonesia's economyturns into good position due to export commodities such as

2

rubber, tropical wood, coffee and spices. Budget surplusesto soak up liquidity that save the country from seriousinflation.

In 1980's, the boom economy of Indonesia was bust in 1980'swhile oil price steeply declined. Suddenly oil exportdecline from US $ 15 billion to US $ 505 billion by 1986.Due to increase import (Trade Balance Deteriorate), debt wasincreasing and international market was decreased by higherdebt service obligation.

Asian Financial Crisis

The Asian Financial Crisis that began to affect Indonesia inmid-1997 became an economic and political crisis.Indonesia's initial response was to float the rupiah, raisekey domestic interest rates, and tighten fiscal policy. InOctober 1997, Indonesia and the International Monetary Fund(IMF) reached agreement on an economic reform program aimedat macroeconomic stabilization and elimination of some ofthe country's most damaging economic policies, such as theNational Car Program and the clove monopoly, both involvingfamily members of President Soeharto. The rupiah remainedweak, however, and President Soeharto was forced to resignin May 1998. In August 1998, Indonesia and the IMF agreed onan Extended Fund Facility (EFF) under President B.J Habibiethat included significant structural reform targets.President Abdurrahman Wahid took office in October 1999, andIndonesia and the IMF signed another EFF in January 2000.The new program also has a range of economic, structuralreform and governance targets.

3

The effects of the financial and economic crisis weresevere. By November 1997, rapid currency depreciation hadseen public debt reach US$60 bn, imposing severe strains onthe government's budget. In 1998, real GDP contracted by13.7%. The economy reached its low point in mid-1999 andreal GDP growth for the year was 0.3%. Inflation reached 77%in 1998 but slowed to 2% in 1999.

The rupiah, which had been in the Rp 2,600/USD1 range at thestart of August 1997 fell to 11,000/USD1 by January 1998,with spot rates around 15,000 for brief periods during thefirst half of 1998. It returned to 8,000/USD1 range at theend of 1998 and has generally traded in the Rp 8,000–10,000/USD1 range ever since, with fluctuations that arerelatively predictable and gradual.

This is a chart of trend of gross domestic product ofIndonesia at market prices by the IMF with figures inmillions of rupiah.

Year GDP

USDexchange(rupiah)

Inflationindex(2007=100)

Nominal PerCapita GDP(as % of USA)

PPP PerCapita GDP(as % ofUSA)

1980

60,143.191 627 10 5.25 5.93

1985

112,969.792 1,111 11 3.47 5.98

1990

233,013.290 1,843 16 3.01 6.63

1995

502,249.558 2,249 24 4.11 8.14

200 1,389,769 8,396 53 2.32 6.92

4

0 .7002005

2,678,664.096 9,705 83 3.10 7.51

2010

6,422,918.230 8,555 121 6.38 9.05

For purchasing power parity comparisons, the US dollar isexchanged at 3,094.57 rupiah only.Mean wages were $2.32 per man-hour in 2009.

InflationIn 2011, Indonesia's inflation rate was 3.79 percent, belowthe government-set target of 5.65 percent.[33] It was thelowest inflation rate since 1998.[

International Economy for Pulp and Paper

The paper industry began a hasty expansion, during the1960s, in response to rapid increases in demand. Consumptionin the two main subdivisions of the industry, bulk papergrades (products used in publishing, container and foodindustries) and value-added grades (stationary and coatedpaper), grew at 5 percent annually. During this timeCanadian interests supplied the United States and EuropeanCommunity with pulp and newsprint grades they could notproduce for themselves; Scandinavian producers supplied theEuropean Community; and any surplus produce of pulp and

5

paper products were exported to Asia, particularly Japan(Waitt 1994a, 1994b).

In the 1970s industry growth shifted and slowed due to tradeliberalization and a fall in demand from 5 percent to 2percent per annum. This decade was characterised by fallingtariff duties, maturing markets (for newspaper and writingpaper grades), and increasing paper prices. As pricesincreased quantity-demanded responded appropriately, asconsumers conserved and substituted for paper by using newforms of media - particularly the electronic medium.It was also during the 1970s that the industry made atransition from predominantly family owned businesses toprofessionally managed transnational corporations via mergeror takeover acquisitions. Acquisitions fulfilled twopurposes, internationalisation of production, and verticalor horizontal integration. Waitt observes that: "formationof large, diversified, pulp and paper conglomerates was thecorporate strategy around the world. The diversificationoccurring within the industry referred to by Waitt wasprimarily geographical, providing a secure access to growthopportunities lacking in local markets; and it waspredominantly North American and Scandinavian companieswhich came to dominate international activity.

From 1983 onwards the industry once again gained momentum asconsumer and corporate markets expanded for high qualitypaper grades, especially in graphic and coated paper.However, as suggested above, the pulp and paper industry isnotorious for its 'boom and bust' cycles. "No sooner hashealth been restored to the industry than managers andinvestors have begun to worry about the timing and severityof their next recession". Continually, during the pastthirty years, any surge in demand has, according to Kerski

6

(1995: 144), resulted in more investment in productioncapacity than is required to meet it. Firms have attemptedto aggressively increase their market share by carelesslyexpanding capacity, hoping to become price setters with theaim of minimizing price-falls when the cycle turned.

The boom which began in 1983 went bust from 1989 to 1993,sending the pulp and paper industry into another severerecession. Pulp prices fell by more than half to a fiftyyear low, industry profit levels fell by nearly 50 percent,and bankruptcies and divestments became common. Therecession was primarily a result of the industry's previousforay into strategies of diversification, expansion andacquisitions which resulted in greatly increased capacityand oversupply. Mergers and acquisitions in the industrycontinued to sharply between 1992 and 1994 (Paper &Packaging Analyst, August, 1994). Many companies also beganto reorganize by concentrating on niche markets and sellingor swapping assets. The oversupply situation was furtherexacerbated by a world recession (Edwards 1995). Ayres(1993) and Chege (1994) further suggest that theintensifying burden of overcapacity, oversupply, anddeclining prices was due, in part, to a rapid increase innew paper plants in Asia whilst demand for paper in Westernmarkets was declining. In the United States and Europe, thedemand for newsprint, which accounts for 13 per cent oftotal paper production worldwide, declined as consumersturned more to the electronic media for entertainment andnews (Chege 1994). Leffler (1994) likened the state of thepulp and paper industry in Europe and North America duringthis period to the steel industry crisis on those continentstwenty years ago.

7

Typically, 1994 registered a rapid turnaround with paperprices skyrocketing and profits rising. The price of pulpclimbed from a low of US$380 per tonne at the end of 1993 toUS$750 per tonne in January 1995 and to US$1000 by June,1995. Furthermore, the price of "everything from liner board- used for the outside of corrugated cardboard - tonewsprint and fine paper were climbing too" (The Economist14 January, 1995: 67). Pulp and paper factories wereoperating at about 90 per cent of capacity on average, andprofits in 1995 increased by 130 percent (Business Week 9January, 1995).

However, Stefan Kay, chairman of the Paper Federation ofGreat Britain, interposed a more gloomy prognosis: "I nowbelieve that the headlong and almost unprecedented increasein world market pulp prices is laying the basis not only forthe next recession but perhaps for the long-term decline ofthe paper industry" (Kay 1995). Kay went on to identifythree long-term consequences: first, non-integrated millswill continue to close as has been the case in the UnitedStates and Europe where a number of less specialised millshave already closed or announced closure, citing aninability to pass on pulp costs as a major factor; second,more printers will close as technological innovation andincreasing capacities leave less room; and third: "grotesqueprofits from pulp will excite new investment (and kick offthe next collapse)".

The advice firms are now receiving from industry journals isto invest in automation technology and information-management systems, and to change the 'just-in-time'production mode. Whether this will exacerbate or alleviatecyclical turns in the industry remains to be seen.

8

3. Analysis of the industry

3.1 PESTEL Analysis

This is used to perform an external environmental analysisby examining the many different external factors affectingan organization.

It never ceases to amaze me why so many businesses fail totake the time to look at the macro and the microenvironments when completing their business plans andstrategies. These external forces will play a big part inshaping the final outcome of the ultimate corporateachievement. Yet, most managers’ focus only on internalfactors and it is fair to say that sales growth and profitsremain high on their agenda.

The macro environment tends to have a long term impact andrequires extensive research. Couple this with the fact thatmany managers are over worked and under resourced and webegin to see why the process is often not completed. There

9

is no published evidence to confirm this hypothesis, justanecdotal hearsay.

The remainder of this article will illustrate an example ofa Macro or PESTLE analysis for the pharmaceutical industry.It is set at a very general level but it can be used as atemplate or adapted to be more specific if required:

The six attributes of PESTLE:

Political (Current and potential influences from

political pressures)

Economic (The local, national and world economy impact)

Sociological (The ways in which a society can affect an

organization)

Technological (The effect of new and emerging

technology)

Legal (The effect of national and world legislation)

Environmental (The local, national and world

environmental issues)

10

The Political and legal factor-

Government has attempted to encourage domestics and foreigninvestors. Government gives different type of facility like-simplification of permission procedure, trade regulations,banking facilities, allocation of land for plantation andreforestation policy. Government trade regulation policy onimport tariff for pulp and paper production has beencontinuously reduced.from25 to 30% in 1994. Government alsoprovide tax exemption for betterment of pulp and paperIndustry.

Regulation for foreign capital investment

The government has paid much attention to foreign capitalinvestment(PMA), as reflected in following provisions-

PMA companies that obtained government’s approvalsunder law no. 1/1967 are given a 30 years’ period ofinvestment from the date of establishment of the legalbusiness.

Pma companies that have committed investment accordingto the government’s approval can apply for a permit toexpand

Pma companies are required to be in the form of jointventures and a minimum of 20% of the company’s sharesis to be national capital at the time of investment andit is to increase to 51 percent within 15 years fromthe commitment of the commercial production.

Pma companies are entitled to the same facilities aspmdn companies if the government owns 51% of theshares, or national private companies , on conditionthat 20% of the total shares are sold through the

11

stock exchange as market as shares on behalf of publicshare.

The pulp and paper industry is now attracted PMAinvestors, as Indonesians’ conditions are consideredcompetitive, particularly for export purpose.

Facilities for investment

Financial facilities provided to PMA/PMDN companiesintroduced in law no. 7 of 1983 regarding valueadded tax for goods and services and sales tax forluxurious goods and law no.13 of 1985 concerningStamp Duties for Fiscal Facilities are as follows:

I. Reduction of / exemption from import duty for machinesand spare parts, except for specified types alreadyproduced locally.

II. Exemption from import duty for raw materials/supporting materials for a two years period ofproduction.

III. Exemption from Chang of Name Duty for the first shipregistration act applied in Indonesia.

IV. Exemption from income tax for importers of capitalgoods and raw materials for a one year period for newcompanies on condition that the company is not underobligation to pay income tax.

In the 1960s, the economy deteriorated drastically as aresult of political instability, a young and inexperiencedgovernment, and economic nationalism, which resulted insevere poverty and hunger. By the time of Soekarno'sdownfall in the mid-1960s, the economy was in chaos with

12

1,000% annual inflation, shrinking export revenues,crumbling infrastructure, factories operating at minimalcapacity, and negligible investment. Following PresidentSoekarno's downfall in the mid-1960s, the New Orderadministration brought a degree of discipline to economicpolicy that quickly brought inflation down, stabilized thecurrency, rescheduled foreign debt, and attracted foreignaid and investment. ( Berkeley Mafia). Indonesia was untilrecently Southeast Asia's only member of OPEC, and the 1970soil price raises provided an export revenue windfall thatcontributed to sustained high economic growth rates,averaging over 7% from 1968 to 1981.High levels ofregulation and a dependence on declining oil prices, growthslowed to an average of 4.3% per annum between 1981 and1988. A range of economic reforms were introduced in thelate 1980s including a managed devaluation of the rupiah toimprove export competitiveness, and de-regulation of thefinancial sector, Foreign investment flowed into Indonesia,particularly into the rapidly developing export-orientedmanufacturing sector, and from 1989 to 1997, the Indonesianeconomy grew by an average of over 7%.

GDP per capita grew 545% from 1970 to 1980 as a result ofthe sudden increase in oil export revenues from 1973 to1979.

Suharto, the 2nd president of Indonesia. Under his New Orderadministration, the country enjoyed the sustained economicdevelopment from 1970s to 1996.

High levels of economic growth from 1987–1997 masked anumber of structural weaknesses in Indonesia's economy.Growth came at a high cost in terms of weak and corruptinstitutions, severe public indebtedness through

13

mismanagement of the financial sector, the rapid depletionof Indonesia’s natural resources, and a culture of favoursand corruption in the business elite. Corruptionparticularly gained momentum in the 1990s, reaching to thehighest levels of the political hierarchy as Suharto becamethe most corrupt leader according to TransparencyInternational's corrupt leaders list. As a result, the legalsystem was very weak, and there was no effective way toenforce contracts, collect debts, or sue for bankruptcy.Banking practices were much unsophisticated, withcollateral-based lending the norm and widespread violationof prudential regulations, including limits on connectedlending. Non-tariff barriers, rent-seeking by state-ownedenterprises, domestic subsidies, barriers to domestic tradeand export restrictions all created economic distortions.

SOCIAL FACTORS AFFECTING THE PULP AND PAPER INDUSTRY

Linked to the economic factors above social changes havesignificantly impacted the pulp and paper industry inrelation to changing demographics in terms of the customersit targets. As such then changes in customer’s needs andpreferences for quality paper products and changingpreference towards the paper rather than fiber or plastichave increased the pace of the demand in terms of meetingthese needs. Increased globalization arguably has led tocustomers demanding faster responses to their needs creatingmuch more competitive business fields attempting to satisfythese desires. The industry is not only about technology butabout pictures illustrating the industry attempt to relateto the lifestyles of consumers. This is because customershave become more environmental sensitive as well astechnique and quality orientated as a result of higher

14

educational levels and income levels creating much morediscerning customers in relation to these.

The sociological context of human resource has been a majorinfluence. Flexibility in terms of labor in Indonesian pulpand paper industry has been mainly achieved by enlarging thescope of tasks and a relaxation of organizational boundarieswithin the business industry. Paper manufacturers areproducing white paper and supply it at a concessional rateto the educational sector and to the governmentaldepartments as well as per regulation given by thegovernment.

TECHNOLOGICAL FACTORS AFFECTING THE PULP AND PAPER INDUSTRY

Currently, governmental as well as sector initiatives focuson overcoming the acute raw material constraints,implementing and adopting better technologies, increasingproduction, productivity and efficiency, expanding toeconomies of scale and decreasing environmental effluents.Various new technologies are entering the Indonesian marketthat supports these movements.

Presently, large pulp and paper mills are more efficient,using better and more modern technologies and appropriatingeconomies of scale. Additionally, they provide chemicalrecovery facilities which reduce both emissions and externalenergy requirements. However, the large paper mills alsoface severe basic problems such as high production costs,raw material constraints and low productivity. Overallperformance has been best in medium size firms with regardsto average profitability

15

Environmental factor:

G eographical location:

Its geographic environment is one of the most complexes andvaried in the world. By one count, it has situated in South-Eastern Asia between the Indian Ocean and thePacific Ocean.It has total 1,904,569 sq km area in that land is 1,811,569sq km and water is93, 000 sq km. basically it is hot andhumid country. At least 669 distinct languages and well over1,100 different dialects are spoken. The nation encompassessome 13,667 islands; the landscape ranges from rain forestsand steaming mangrove swamps to arid plains and snow-cappedmountains. Indonesia is very attractive industry for pulpand paper productions for its natural recourses with lowcost. Geographically plant is matured at least 7 yearswhere, North America and Europe require twenty five to fiftyyears to reach maturity. Time zone: Indonesia is time zone is UTC+7 mean seven hours ahead ofGMT and 16 hours ahead of U.S. Pacific Standard Time. Natural or environmental disaster:

Due to its geographic location, several times Indonesia hasfaced many natural disasters. In the same way, due to its mountainous interior regions ofKalimantan,Sulawesi, and Sumatra, country has faceddeforestation, soil erosion and massive forest fires.In1983, about 3 million hectares of prime tropical forestworth at least US$10 billion weredestroyed in a fire in

16

Kalimantan Timur Province. The disastrous scale of this firewas made possible by the piles of dead wood left behind bythe timber industry. Even discounting the calamitous effectsof the fire, in the mid-1980s Indonesia's deforestation ratewas the highest in Southeast Asia, at 700,000 hectares peryear and possibly as much as 1 million hectares per year.

3.2 Porter’s 5 Factors

17

Rival among existing firm

There is large number of players in pulp and paper industry,which increases rivalry among them. There is an intenserivalry as pulp and paper have high storage cost. There is ahigher level of rivalry as there is a low level of productdifferentiation. Industry growth rate is high and demand ofthe product is also high. So, continuously new firm willcome. In Indonesia cost of wood and raw materials is lowerthan other country and government is not so struck tocontrol the environment. The more firm the moredeforestation but government concern about the economicgrowth.

Bargaining power of suppliers

A producing industry requires raw materials - labour,components, and other supplies. This requirement leads tobuyer-supplier relationships between the industry and the

18

firms that provide it the raw materials used to createproducts. Indonesia has the world's second-largesttropical rain forest, after Brazil, wood prices are halfthose in Taiwan. Most of the Pulp and paper industry arevertically integrated. Industries raw materials like ricestraw, bamboo, bagasse, pulp, waste paper and chemicalsetc are available in Indonesia so this industry is notdominated by supplier. Even Fuel costs are low becauseIndonesia is a major oil producer. Wage costs, whichaccount for 22 percent of the total cost of production,are about one third of those in Thailand and Malaysia andone tenth of Taiwan. They sometimes involves as suppliersbecause this industry is vertically integrated.Government also give the opportunity to use the forestand land to collect and produce plant. Without plant thisindustry is not possible to go ahead because it is themain factor to produce pulp and paper. So most of theinvestor control the supplier.

Bargaining power of buyers

The power of buyers is the impact that customers have on aproducing industry. In paper industry, buyers are powerfulas they purchase a significant proportion of output, andthey possess a credible backward integration threat, theyare weak as they are fragmented.

Entry and Exit barriers

Entry barriers

Government policy

19

Economies of scale

Capital requirement

Special access to distribution

Switching cost

Expected retaliation from present players

Large investments in technology, not capable of alternate uses

Exit barriers

Easy to exit as exit cost is low and it is an independent business. If firm has high debt, it has to repay on this debt so huge cost incur to exit.

Threat from substitutes

In Porter's model, substitute products refer to products inother industries. 6 GB pen drive can hold the same datawhere 6 tons of paper can hold. Substitutes for paper is pendrives, PCs, etc and in case of packaging, glasses, aluminumfoil, plastics, etc.. Threat arises from the price change ofsubstitute product and also their availability which givesmore choice for the customers.

20

4. Analysis of the Company

4.1 Ratio Analysis (Liquidity ratios)

IV.1.1 Current Ratio

21

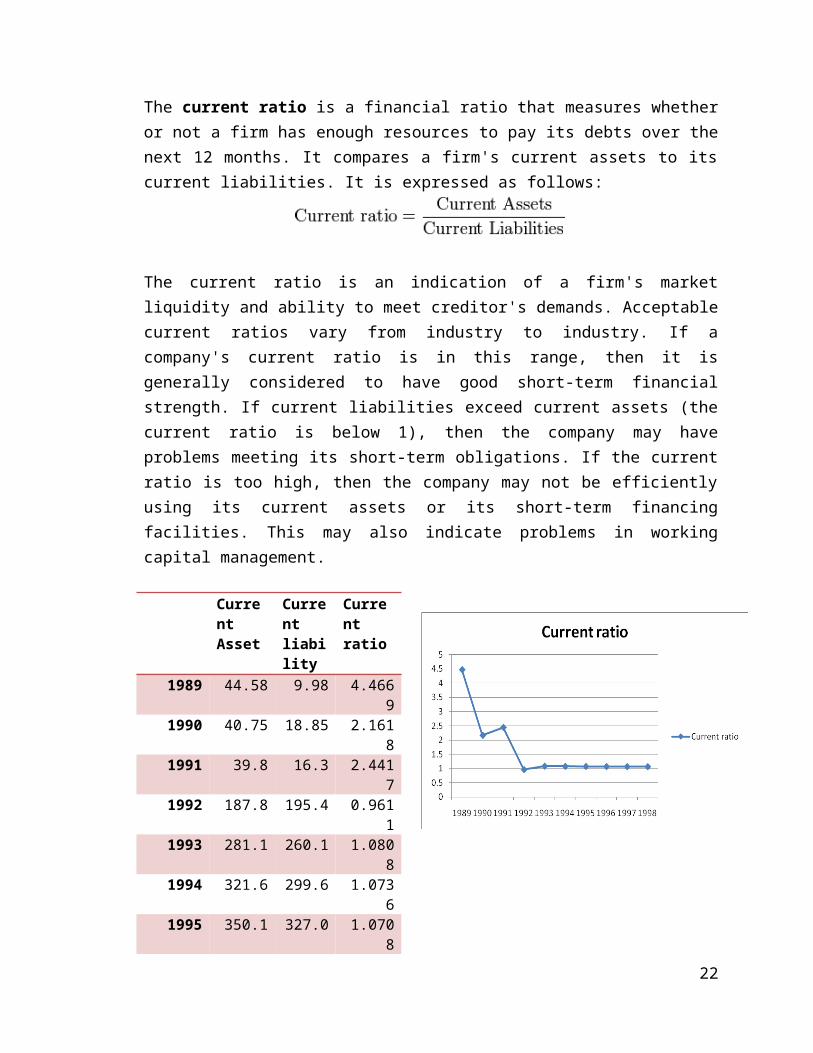

The current ratio is a financial ratio that measures whetheror not a firm has enough resources to pay its debts over thenext 12 months. It compares a firm's current assets to itscurrent liabilities. It is expressed as follows:

The current ratio is an indication of a firm's marketliquidity and ability to meet creditor's demands. Acceptablecurrent ratios vary from industry to industry. If acompany's current ratio is in this range, then it isgenerally considered to have good short-term financialstrength. If current liabilities exceed current assets (thecurrent ratio is below 1), then the company may haveproblems meeting its short-term obligations. If the currentratio is too high, then the company may not be efficientlyusing its current assets or its short-term financingfacilities. This may also indicate problems in workingcapital management.

Current Asset

Current liability

Current ratio

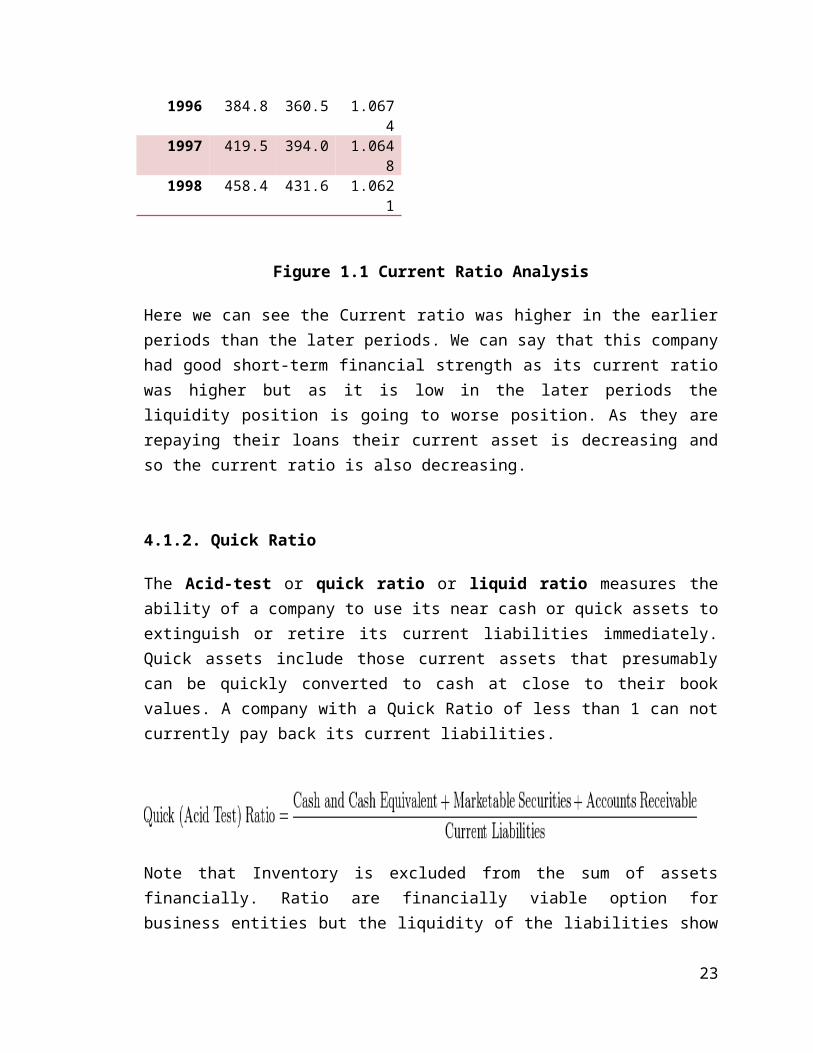

1989 44.58 9.98 4.4669

1990 40.75 18.85 2.1618

1991 39.8 16.3 2.4417

1992 187.8 195.4 0.9611

1993 281.1 260.1 1.0808

1994 321.6 299.6 1.0736

1995 350.1 327.0 1.0708

22

1996 384.8 360.5 1.0674

1997 419.5 394.0 1.0648

1998 458.4 431.6 1.0621

Figure 1.1 Current Ratio Analysis

Here we can see the Current ratio was higher in the earlierperiods than the later periods. We can say that this companyhad good short-term financial strength as its current ratiowas higher but as it is low in the later periods theliquidity position is going to worse position. As they arerepaying their loans their current asset is decreasing andso the current ratio is also decreasing.

4.1.2. Quick Ratio

The Acid-test or quick ratio or liquid ratio measures theability of a company to use its near cash or quick assets toextinguish or retire its current liabilities immediately.Quick assets include those current assets that presumablycan be quickly converted to cash at close to their bookvalues. A company with a Quick Ratio of less than 1 can notcurrently pay back its current liabilities.

Note that Inventory is excluded from the sum of assetsfinancially. Ratio are financially viable option forbusiness entities but the liquidity of the liabilities show

23

financial stability. Generally, the acid test ratio shouldbe 1:1 or higher, however this varies widely by industry. Ingeneral, the higher the ratio, the greater the company'sliquidity (i.e., the better able to meet current obligationsusing liquid assets). We will compare this ratio with ourindustry average

Figure 1.2 Quick ratios Analysis.

Here we can see the quick ratio washigher in the earlier periods than thelater periods. We can say that thiscompany had good short-term financial

strength as its quick ratio was higher but as it is low inthe later periods the liquidity position is going to worseposition. As they are repaying their loans their currentasset is decreasing and so the quick ratio is alsodecreasing.

Asset Management Ratios

4.1.3. Inventory Turnover

24

Quick Ratio

1989 4.40681363

1990 2.02917772

1991 2.19631902

1992 0.81346912

1993 0.81311286

1994 0.77583939

1995 0.75761636

1996 0.73982121

1997 0.72721974

1998 0.7161867

Inventory turnover is the ratio of cost of goods sold toaverage inventory. It is an activity / efficiency ratio andit measures how many times per period, a business sells andreplaces its inventory again.

Inventory Turnover

1989 17.6666667

1990 91991 6.251992 4.824956

671993 3.952586

211994 3.385650

221995 2.985351

561996 2.684165

961997 2.450375

941998 2.265907

57

Figure 1.3: Inventory Turnover ratios analysis.

Based on our calculation we found that inventory turnoverratio was higher in the earlier periods. But in laterperiods it becomes lower. This ratio suggest that thiscompany is holding excess stocks of inventory and excessstocks are, of course, unproductive and represent aninvestment with a low or zero rate of return. So the company

25

also hold excess inventory and they had not enough liquidasset.

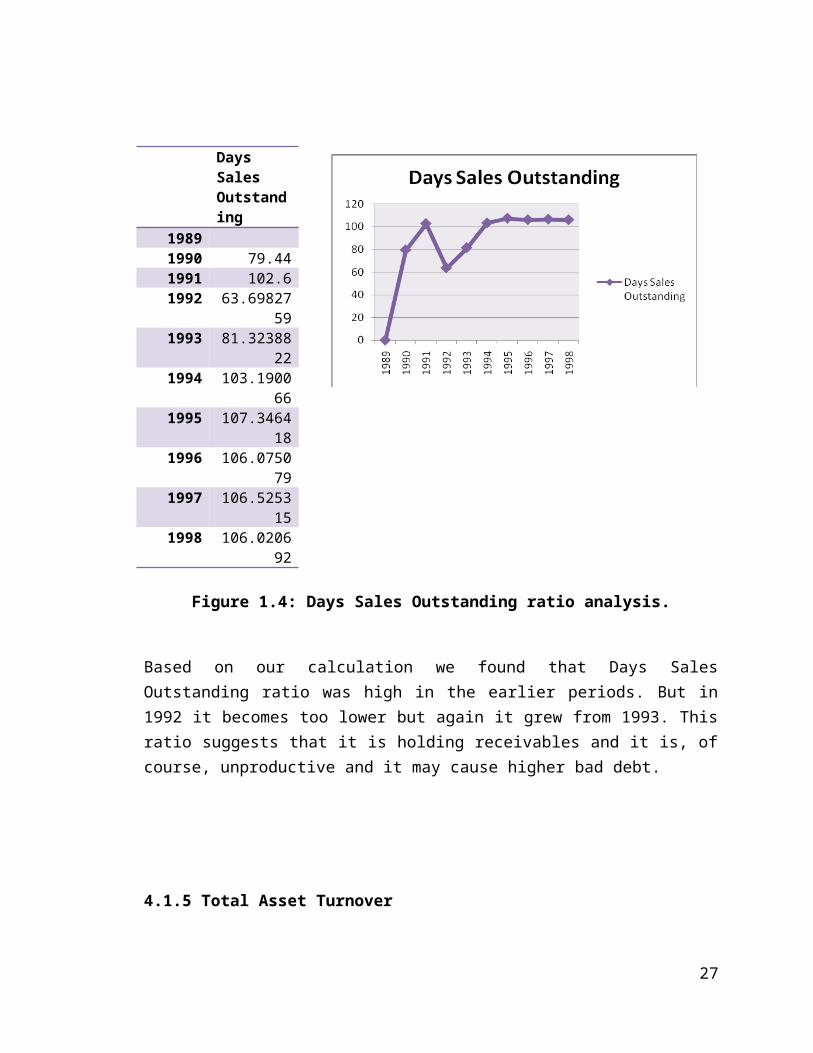

4.1.4. Days Sales Outstanding

DSO is a measure of the average number of days that acompany takes to collect revenue after a sale has beenmade. A low DSO number means that it takes a company fewerdays to collect its accounts receivable. A high DSOnumber shows that a company is selling its product tocustomers’ credit and taking longer to collect money.

Days sales outstanding is calculated as:

Due to the high importance of cash in running a business, itis in a company’s best interest to collect outstandingreceivables as quickly as possible. By quickly turning salesinto cash, a company has the chance to put the cash to useagain – ideally, to reinvest and make more sales. TheDSO can be used to determine whether a company is trying todisguise weak sales, or is generally being ineffective atbringing money in.

26

Days Sales Outstanding

1989 1990 79.441991 102.61992 63.69827

591993 81.32388

221994 103.1900

661995 107.3464

181996 106.0750

791997 106.5253

151998 106.0206

92

Figure 1.4: Days Sales Outstanding ratio analysis.

Based on our calculation we found that Days SalesOutstanding ratio was high in the earlier periods. But in1992 it becomes too lower but again it grew from 1993. Thisratio suggests that it is holding receivables and it is, ofcourse, unproductive and it may cause higher bad debt.

4.1.5 Total Asset Turnover

27

The total asset turnover ratio measures the ability of acompany to use its assets to efficiently generate sales.This ratio considers all assets, current and fixed. Thoseassets include fixed assets, like plant and equipment, aswell as inventory, accounts receivable, as well as any othercurrent assets.

The calculation for the total asset turnover ratio is:

Net Sales/Total Assets

The lower the total asset turnover ratio, as compared tohistorical data for the firm data, the more sluggish thefirm's sales. This may indicate a problem with one or moreof the asset categories composing total assets - inventory,receivables, or fixed assets.

Total Asset turn

1989 0.054476

1990 0.080142

1991 0.11374

1992 0.639089

1993 0.880179

1994 0.851455

1995 0.794373

1996 0.752508

1997 0.711828

671998 0.6784

73

Figure 1.5: Total Asset Turnover ratio analysis.

The total asset turnover ratios indicate that over thehistorical years, the company's efficiency had decreased,but according to their projection it is indicating that thecompany's efficiency was increasing from 1991 to 199 whichmay be because of their very high growth rate of projection.But from 1994 to 1998 it is decreasing.

4.1.6. Fixed Asset Turnover

A financial ratio of net sales to fixed assets. The fixed-asset turnover ratio measures a company's ability togenerate net sales from fixed-asset investments- specifically property, plant and equipment (PP&E) - net ofdepreciation. A higher fixed-asset turnover ratio shows thatthe company has been more effective in using the investmentin fixed assets to generate revenues.

The fixed-asset turnover ratio is calculated as:

29

Fixed Asset turnover

1989 0.074386

1990 0.098684

1991 0.146199

1992 4.884211

1993 9.192982

1994 9.611331995 9.26579

51996 9.15076

11997 8.959691998 8.85770

8

Figure 1.6: Fixed Asset Turnover ratio analysis.

The fixed-asset turnover ratio was lower in the earlierperiods as company's ability to generate net sales fromfixed-asset investments was lower. But in later periods isbecome higher and a higher fixed-asset turnover ratio showsthat the company has been more effective in using theinvestment in fixed assets to generate revenues.

Debt Management Ratios

30

4.1.7. Debt Ratio

Debt ratio is a ratio that indicates what proportion of debta company has relative to its assets. The measure gives anidea to the leverage of the company along with the potentialrisks the company faces in terms of its debt-load.

A debt ratio of greater than 1 indicates that a company hasmore debt than assets, meanwhile, a debt ratio of less than1 indicates that a company has more assets than debt. Usedin conjunction with other measures of financial health, thedebt ratio can help investors determine a company's level ofrisk.

Debt Ratio

1989 0.743036

1990 0.821906

1991 0.77252

1992 11993 0.8320

271994 0.8445

811995 0.8495

931996 0.8557

291997 0.8606

1

31

1998 0.865619

Figure 1.7: Debt ratio analysis.

From 1989 to 1991 the debt ratio was lower for this firm butit grew in 1992 as it took more debt then again it camedown. But still this is a high ratio which indicates higherdebt and for this reason investor will not be attracted asthere is too much risk in this project.

4.1.8. TIE

A metric used to measure a company's ability to meet itsdebt obligations. It is calculated by taking a company'searnings before interest and taxes (EBIT) and dividing it bythe total interest payable on bonds and other contractualdebt. It is usually quoted as a ratio and indicates how manytimes a company can cover its interest charges on a pretaxbasis. Failing to meet these obligations could force acompany into bankruptcy.

Ensuring interest payments to debt holders and preventingbankruptcy depends mainly on a company's ability to sustainearnings. However, a high ratio can indicate that a companyhas an undesirable lack of debt or is paying down too muchdebt with earnings that could be used for other projects.

The rationale is that a company would yield greater returnsby investing its earnings into other projects and borrowing

32

at a lower cost of capital than what it is currently payingto meet its debt obligations.

Figure 1.8: Time interest earned ratio analysis.

From 1989 to 1994 the time interest earned ratio was lowerfor this firm but it grew in 1995 as it took more debt. Butthis is higher from 1987 to 1989 which indicates thiscompany is in better position and it can easily meet itsobligation with its earnings.

4.1.9. EBITDA

A financial metric used to assess a company's profitabilityby comparing its revenue with earnings. More specifically,since EBITDA is derived from revenue, this metricwould indicate the percentage of a company is remainingafter operating expenses.

33

Calculated

Figure 1.9: EBITDA coverage ratio analysis.

34

Profitability Ratios

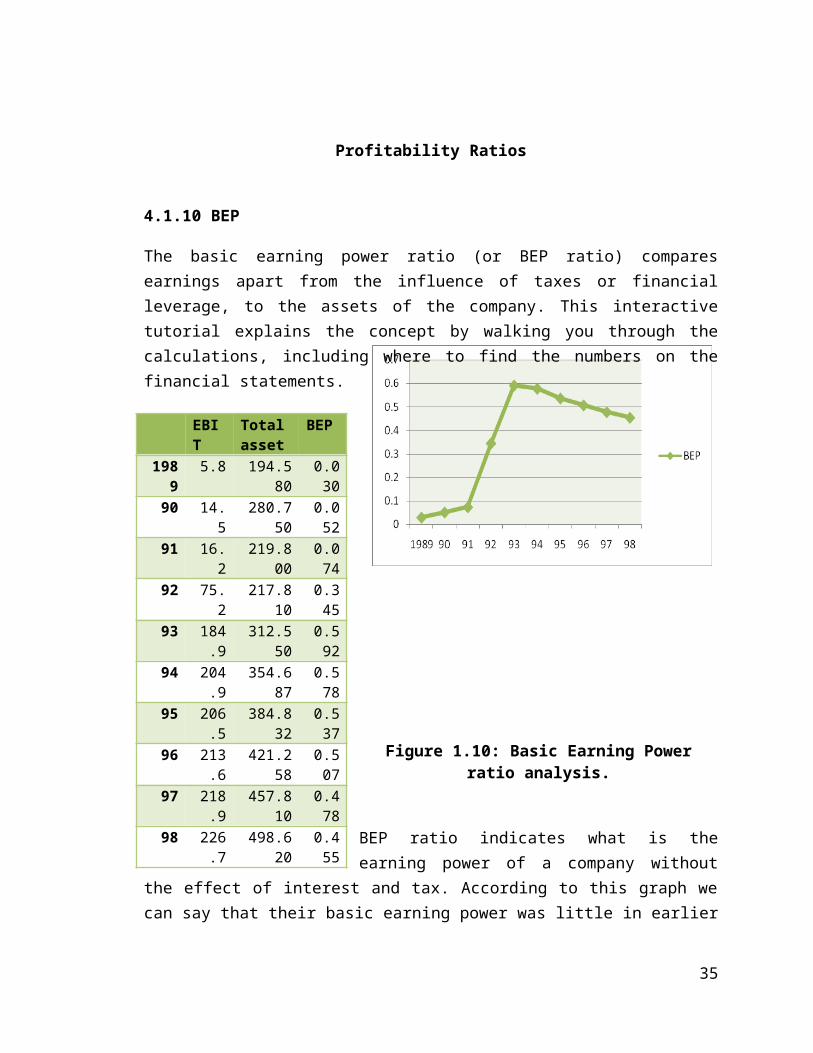

4.1.10 BEP

The basic earning power ratio (or BEP ratio) comparesearnings apart from the influence of taxes or financialleverage, to the assets of the company. This interactivetutorial explains the concept by walking you through thecalculations, including where to find the numbers on thefinancial statements.

Figure 1.10: Basic Earning Powerratio analysis.

BEP ratio indicates what is theearning power of a company without

the effect of interest and tax. According to this graph wecan say that their basic earning power was little in earlier

35

EBIT

Totalasset

BEP

1989

5.8 194.580

0.030

90 14.5

280.750

0.052

91 16.2

219.800

0.074

92 75.2

217.810

0.345

93 184.9

312.550

0.592

94 204.9

354.687

0.578

95 206.5

384.832

0.537

96 213.6

421.258

0.507

97 218.9

457.810

0.478

98 226.7

498.620

0.455

periods but in 1992 and 1993 it grew but after that it wasdecreasing. There is a scope for improvement.

4.1.11 Profit Margin

A ratio of profitability calculated as net income divided byrevenues, or net profits divided by sales. It measureshow much out of every dollar of sales a company actuallykeeps in earnings.

Profit margin is very useful when comparing companies insimilar industries. A higher profit margin indicates a moreprofitable company that has better control over its costscompared to its competitors. Profit margin is displayed as apercentage; a 20\% profit margin, for example, means thecompany has a net income of $0.20 for each dollar of sales. Looking at the earnings of a company often doesn't tell theentire story. Increased earnings are good, but an increasedoes not mean that the profit margin of a company isimproving. For instance, if a company has costs that haveincreased at a greater rate than sales, it leads to a lowerprofit margin. This is an indication that costs need to beunder better control.

Net income

Sales

PM

1989

5.8 10.6 55%

90 14.5 22.5 64%91 16.2 25 65%92 75.2 139.

254%

36

93 144.4 275.1

52%

94 173.9 302 58%95 184.9 305.

760%

96 201.5 317 64%97 216.1 325.

966%

98 223.9 338.3

66%

Figure 1.11: Profit Margin ratio analysis.

As their net income is good so their profit margin is quite good so there is a scope for improvement.

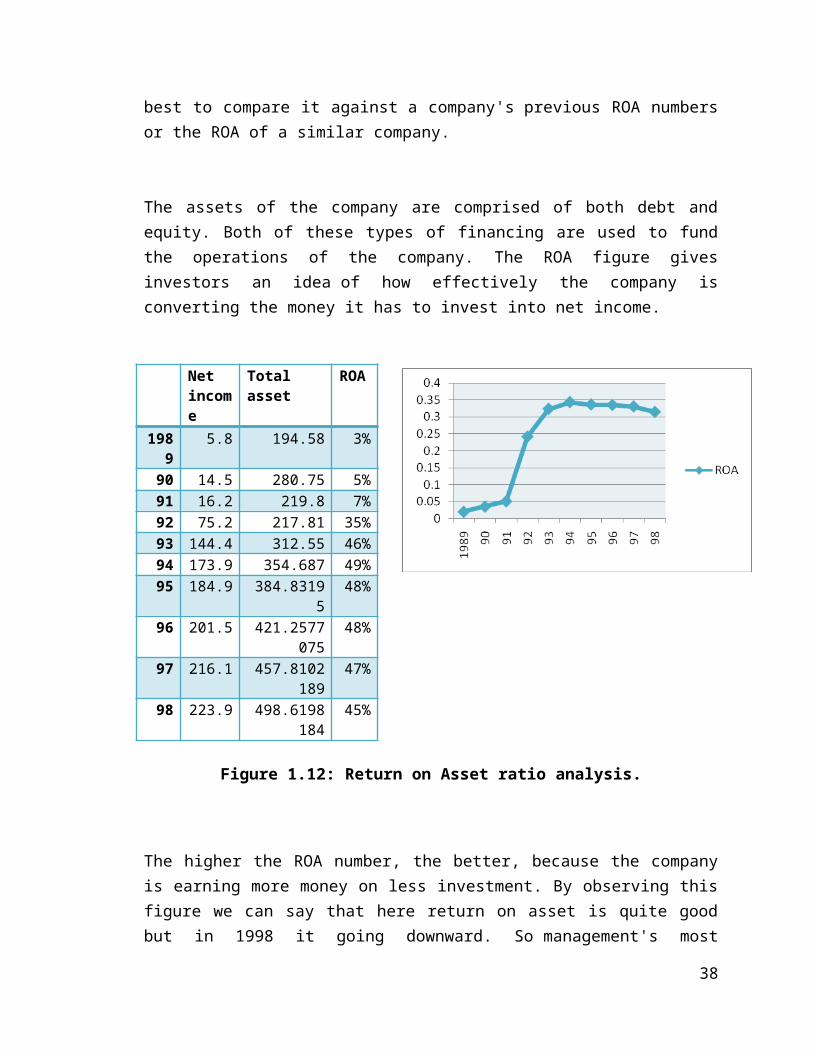

4.1.12 Return on Asset

An indicator of how profitable a company is relative to itstotal assets. ROA gives an idea as to howefficient management is at using its assets to generateearnings. Calculated by dividing a company's annual earningsby its total assets, ROA is displayed as a percentage.Sometimes this is referred to as "return on investment".

The formula for return on assets is:

ROA tells you what earnings were generated from investedcapital (assets). ROA for public companies can varysubstantially and will be highly dependent on the industry.This is why when using ROA as a comparative measure, it is

37

best to compare it against a company's previous ROA numbersor the ROA of a similar company.

The assets of the company are comprised of both debt andequity. Both of these types of financing are used to fundthe operations of the company. The ROA figure givesinvestors an idea of how effectively the company isconverting the money it has to invest into net income.

Net income

Total asset

ROA

1989

5.8 194.58 3%

90 14.5 280.75 5%91 16.2 219.8 7%92 75.2 217.81 35%93 144.4 312.55 46%94 173.9 354.687 49%95 184.9 384.8319

548%

96 201.5 421.2577075

48%

97 216.1 457.8102189

47%

98 223.9 498.6198184

45%

Figure 1.12: Return on Asset ratio analysis.

The higher the ROA number, the better, because the companyis earning more money on less investment. By observing thisfigure we can say that here return on asset is quite goodbut in 1998 it going downward. So management's most

38

important job is to make wise choices in allocating itsresources.

4.1.13 Return on Equity

The amount of net income returned as a percentage ofshareholders equity. Return on equity measures acorporation's profitability by revealing how much profit acompany generates with the money shareholders haveinvested.

ROE is expressed as a percentage and calculated as:

Return on Equity = Net Income/Shareholder's Equity

Net income is for the full fiscal year (before dividendspaid to common stock holders but after dividends topreferred stock.) Shareholder's equity does not includepreferred shares.

Netincome

Commonequity

ROE

1989

5.8 50 12%

90 14.5 50 29%91 16.2 50 32%92 75.2 0 #DIV/

39

0!93 144.4 52.5 275%94 173.9 55.125 315%95 184.9 57.88125 319%96 201.5 60.77531

25332%

97 216.1 63.81407813

339%

98 223.9 67.00478203

334%

Figure 1.13: Return on Equity ratio analysis.

The higher the ROE number, the better, because theshareholders are earning more money on less investment. Byobserving this figure we can say that here return on equityis quite good.

4.1.14 Earnings per Share

40

Figure 1.14: Earning per share ratio analysis.

Here Earning per share ratios are quite good in the laterperiods as their earnings increases but when the earning waslow that time their earning per share was lower.

Figure 1.15: cash flow per share ratio analysis.

Here cash flow per share ratios are quite good in the laterperiods as their earnings increases but when the earning waslow that time their cash flow per share was lower.

41

Figure 1.16: Book value per share ratio analysis.

Here book value per share ratios are higher in the laterperiods as their equity increases but when the equity waslow that time their cash flow per share was lower.

42

4.2 DU PONT

A method of performance measurement that was started by theDuPont Corporation in the 1920s. With this method, assetsare measured at their gross book value rather than at netbook value in order to produce a higher return on equity(ROE). It is also known as "DuPont identity".

DuPont analysis tells us that ROE is affected by threethings:

-Operating efficiency, which is measured by profit margin.

-Asset use efficiency, which is measured by total assetturnover

-Financial leverage, which is measured by the equitymultiplier

ROE = Profit Margin (Profit/Sales) * Total Asset Turnover(Sales/Assets) * Equity Multiplier (Assets/Equity)

It is believed that measuring assets at gross book valueremoves the incentive to avoid investing in new assets. Newasset avoidance can occur as financial accountingdepreciation methods artificially produce lower ROEs in theinitial years that an asset is placed into service. If ROEis unsatisfactory, the DuPont analysis helps locate the partof the business that is underperforming.

43

year PM TATO EquityMultipli

er

DuPont(ROE)

1989 0.54717 0.054476 3.8916 0.11690 0.644444 0.080142 5.615 0.2991 0.648 0.11374 4.396 0.32492 0.54023 0.639089 #DIV/0! #DIV/0!93 0.5249 0.880179 5.953333 2.75047694 0.575828 0.851455 6.434231 3.15464995 0.604841 0.794373 6.648646 3.19447196 0.635647 0.752508 6.931395 3.31549197 0.663087 0.711867 7.174126 3.386498 0.661839 0.678473 7.441556 3.341553

By observing this figure of Du Pont return on equity waslower in the earlier periods but in later periods it hadgrown. Here we can see that profit margin ratio was lower inthe beginning as their cost was high relatively to theirsales. In the later periods though the cost increased theirincome also increased so the profit margin ratio grewupward. From this situation we can say that if they canminimize their cost then the PM ratio will grow more. The total asset turnover was very poor from 1989 to 1991. Inlater periods it grew. Their fixed asset turnover is in goodposition. So we can say that the problem is in the currentassets. Their DSO is in worse position that means they arenot able to collect their receivables early and theirinventory turnover is also in bad position that means thereis access inventory. If they are able to quicken theseratios then their total asset turnover ratio will be in goodposition.

44

Equity multiplier indicates that whether the firm isutilizing more debt or not. More equity multiplier ratio isnot always good. There should be a limit in using debt. Thisproject is financed by more debt and less equity. So theyshould take less debt or up to a certain level of time.

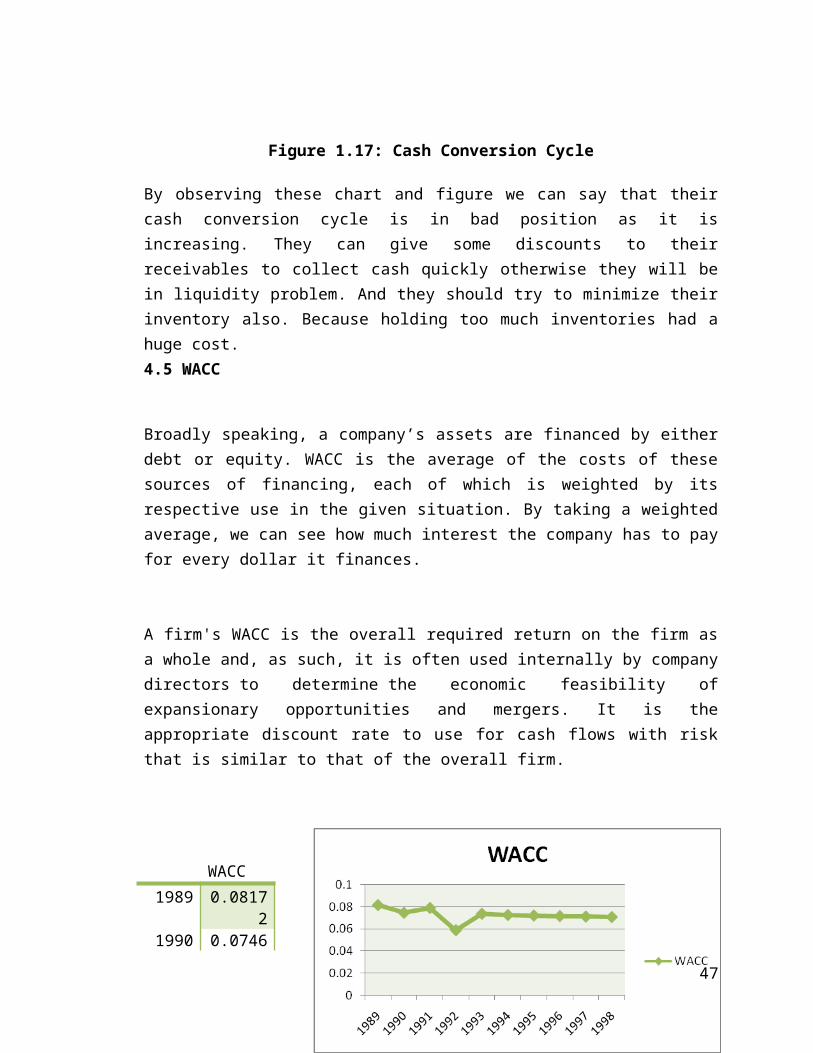

4.3 Cash Conversion Cycle

A metric that expresses the length of time, in days, that ittakes for a company to convert resource inputs into cashflows. The cash conversion cycle attempts to measure theamount of time each net input dollar is tied up in theproduction and sales process before it is converted intocash through sales to customers. This metric looks at theamount of time needed to sell inventory, the amount of timeneeded to collect receivables and the length of time thecompany is afforded to pay its bills without incurringpenalties. Calculated as:

Where:DIO represents days inventory outstandingDSO represents days sales outstandingDPO represents days payable outstanding

Usually a company acquires inventory on credit,which results in accounts payable. A company can also sellproducts on credit, which results in accounts receivable.Cash, therefore, is not involved until the company pays theaccounts payable and collects accounts receivable. So the

45

cash conversion cycle measures the time between outlay ofcash and cash recovery.

This cycle is extremely important for retailers and similarbusinesses. This measure illustrates how quickly a companycan convert its products into cash through sales. Theshorter the cycle, the less time capital is tied up in thebusiness process, and thus the better for the company'sbottom line.

Year Inventoryturnover

Days SalesOutstandin

g

PayableDeferredPeriod

CashConversion

Cycle1990 69.75 79.44 100.8 48.391991 132.9545 102.6 120.2727 115.28181992 92.39063 63.69828 71.6625 84.42641993 196.4634 81.32388 107.7007 170.08661994 294.3769 103.1901 121.5232 276.04381995 347.6613 107.3464 124.6663 330.34141996 383.8491 106.0751 123.441 366.48321997 422.4112 106.5253 123.8804 405.05621998 455.3226 106.0207 123.4032 437.94

46

Figure 1.17: Cash Conversion Cycle

By observing these chart and figure we can say that theircash conversion cycle is in bad position as it isincreasing. They can give some discounts to theirreceivables to collect cash quickly otherwise they will bein liquidity problem. And they should try to minimize theirinventory also. Because holding too much inventories had ahuge cost.4.5 WACC

Broadly speaking, a company’s assets are financed by eitherdebt or equity. WACC is the average of the costs of thesesources of financing, each of which is weighted by itsrespective use in the given situation. By taking a weightedaverage, we can see how much interest the company has to payfor every dollar it finances.

A firm's WACC is the overall required return on the firm asa whole and, as such, it is often used internally by companydirectors to determine the economic feasibility ofexpansionary opportunities and mergers. It is theappropriate discount rate to use for cash flows with riskthat is similar to that of the overall firm.

WACC1989 0.0817

21990 0.0746

47

851991 0.0790

91992 0.0587

981993 0.0737

821994 0.0726

621995 0.0722

151996 0.0716

671997 0.0712

321998 0.0707

85

Figure 1.18: WACC

As they are using more debt so there weighted average costof capital is also higher. If they take less debt then thisweighed average cost of capital will also decrease.

4.6 Strengths and weaknesses

Strengths

48

The liquidity position for this project is

quite good for this time. So there is scope for

improvement.

Their debt management is still quite good as

their TIE ratio is good.

Weaknesses

The asset management of this project is not

good as their inventory turnover, Total asset

turnover are decreasing and Days Sales

Outstanding is increasing.

They are taking too much debt so this project

may become more risky.

Their profitability is decreasing as Profit

Margin ratio; Basic earning power, Return on

asset and return on equity are decreasing.

The cash conversion cycle is in very bad

position as it is increasing beyond the limit

and for this reason they will be soon in

liquidity crisis.

49

4.7 Cash Freed Up

INDUSTRY AVERAGE Days Sales Outstanding

63.6982759

Inv Turnover17.6666

667

Cash freed upfrom DSO

Cash freed upfrom INV

Total Cash Freed upfor 1998

1989 1.87556034

0.6 2.47556

1990 3.98114224

1.273584906

5.254727

1991 4.42349138

1.41509434

5.838586

1992 24.63 7.879245283

32.50925

1993 48.6760991

15.57169811

64.2478

1994 53.4357759

17.09433962

70.53012

1995 54.0904526

17.30377358

71.39423

1996 56.0898707

17.94339623

74.03327

1997 57.66463 18.44716 76.111850

36 9811998 59.85868

5319.14905

6679.00774

Here we can see the amount of cash freed up from reducinginventories and days sales outstanding. With this free cashthis project can take more advantages such as

It can help in expanding the business thenprofitability will increase

It can reduce its debt by paying out the debtthen interest will be low and so net incomewill increase.

4.8 NPV Analysis

51

PV of outflows Total 187.

7248.165

8176.824 71.4424

3684.13

22PV of inflows NPV

187.7

286.6184

239.7571

100.655 814.7306

130.5983

The NPV of these cash flows of the Kalimantan Paper Projectis positive. And for this reason investors can invest inthis project.

Cash FlowsIRR 8%WACC 8.17%

Here we can see that the IRR of this project is 8% which islower than the weighted average cost of capital. . And forthis reason investors can invest in this project.

Investor can recover their invested money within 2.19 years.

52

Discounted Paybackperiod

2.19years

4.9 SWOT Analysis

“The Kalimantan Paper Project” which was introduced byIbrahim Hanaffi, a prominent Indonesian industrialist. Hetook this project on hand but the fact was that lack offinancial position creates a barrier to fulfil this project.Ibrahim Hanaffi wanted to produce high quality paper.

Every corporation has some internal and external factorunder which some factor encourage them and some factordiscourage them. So, “The Kalimantan Paper Project” has somestrengths and weakness which indicate internal factor of“The Kalimantan Paper Project” and also has someopportunities and threats which indicate external factor of“The Kalimantan Paper Project”.

53

Internal factors:

Strength:

The site offered not only suitable terrain for clear-

cutting and subsequent planting of the forest

plantation, but also offered exploitable growing

timber.

Nearby settlements of Javanese migrants promised a

reliable source of production and forestry labor.

The Indonesian government had shifted its policies from

import substitution to export growth, and had

implemented a ban on export of hardwood logs.

The EDC of Canada had committed in a letter of intent

to provide up to $ 115 million in term financing at a

fixed annual rate of interest of 8 % directly to the

54

importer in return for receipt of a guarantee from a

prime international bank or the MOF and various

undisclosed fees to be received from the exporter. The

remaining $125 million of export credit equipment

financing could be secured on terms not significantly

different from those indicated by Hermes and the EDC.

Malaysia can provide high quality pulp wood for paper

Expert in timber trade

Location is sparsely populated, suitable region on the

Celebes Sea coast north of Samarinda in East

Kalimantan.

Deep water bay, where a pier to facilitate

transportation of raw materials and finished goods

could be built. Javanese migrants promised a reliable

source of production and forestry labour.

KND is very strong equipment supplier

Haniffi had joined the investors

KBJ is with this project because they comfortable with

reasonable developing- country project risk.

55

Weakness:

The investors argued that they were taking a high risk

in investing in a facility using plantation technology

untested in Indonesia.

They had to repayment their loan amount in eight

semiannual repayments starting in June 1993 and ending

December 1996. Rupiah principal outstanding at the end

of construction period is left as working capital

facility through life of project.

Equity is highly leveraged nonrecourse financing

Investor would be far in excess of paid in capita

Need financial alternative

External factor:

Opportunities:

The investors were eligible for a five-year corporate

tax holiday following commissioning.

56

The Bank of Surabaya and other local bankers would

provide short term rupiah funds for working capital of

up to $60 million.

The investors remained highly flexible with regard to

the capital structure of the project. They would

consider any serious financing alternative.

Government had shifted policy from import substitution

to export growth.

8% consensus rate

Five years corporate tax holiday and anticipated no

coporate income tax.

Bank of Surabaya and other local bank provide short

term fund as working capital of up to 60 million.

Investor had worked with its leasing subsidiary in

Jakarta.

Threats:

According to the estimation, among the top 50 countries ininstitutional investor’s country risk ratings in 1998; theIndonesia rating is 42 number ranks in both 1988 & 1987. The

57

investors will be unsecured to invest the highly riskcountry project.

Five similar project showed signs of life

Interest volatility is very high

Metro Politian was keen to consider complex arrangement

which could justify higher spreads and fees from the

borrowers and could entice providers of capital-

either debt or external equity- with sufficient

expected return to justify the project risk.

Deutsche Handelsbank want it’s risk return criteria

4.10 Risk Analysis:

Risk is defined as the variation from the expected return.Risk is measured by the standard deviation of return.Business risk and financial risk is total risk of a firm.Two types of risk in a firm,

58

Business RiskFinancial Risk

If the firm does not have debt:

59

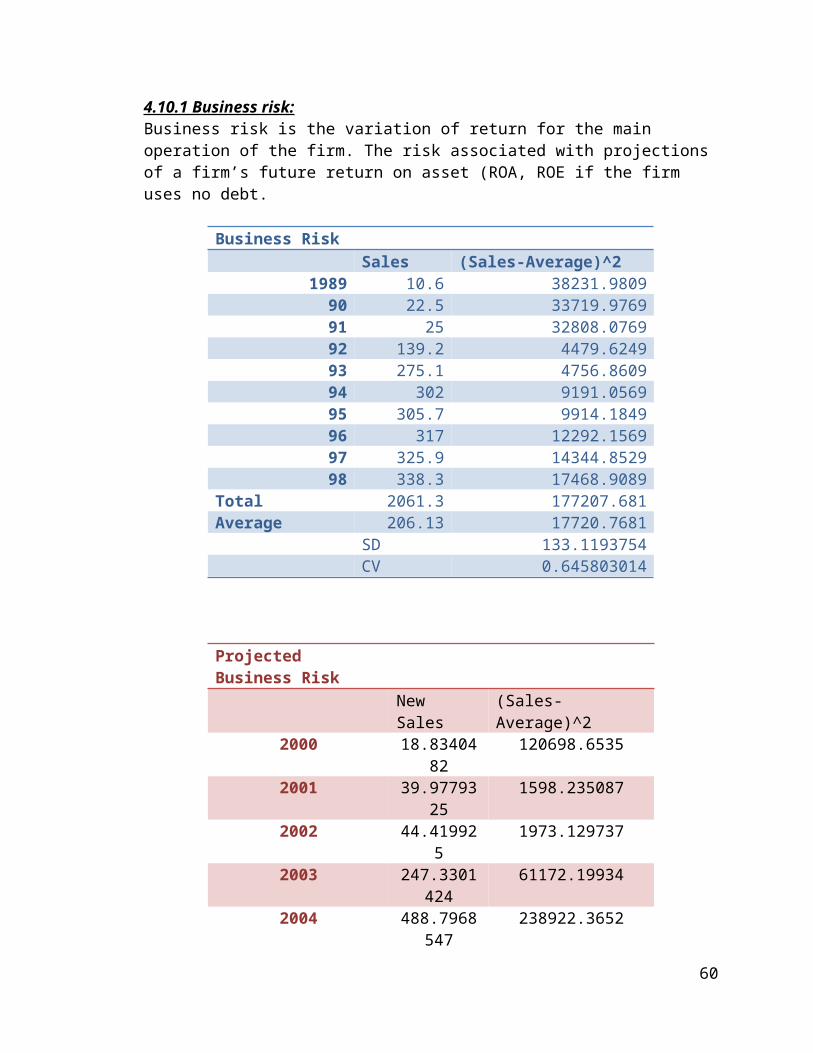

4.10.1 Business risk:Business risk is the variation of return for the main operation of the firm. The risk associated with projections of a firm’s future return on asset (ROA, ROE if the firm uses no debt.

Business Risk Sales (Sales-Average)^2

1989 10.6 38231.980990 22.5 33719.976991 25 32808.076992 139.2 4479.624993 275.1 4756.860994 302 9191.056995 305.7 9914.184996 317 12292.156997 325.9 14344.852998 338.3 17468.9089

Total 2061.3 177207.681Average 206.13 17720.7681 SD 133.1193754 CV 0.645803014

Projected Business Risk

New Sales

(Sales-Average)^2

2000 18.8340482

120698.6535

2001 39.9779325

1598.235087

2002 44.419925

1973.129737

2003 247.3301424

61172.19934

2004 488.7968547

238922.3652

60

2005 536.592694

287931.7193

2006 543.1668429

295030.2192

2007 563.244649

317244.5346

2008 579.0581423

335308.3322

2009 601.0904251

361309.6991

Total 3662.511656

2021189.087

Average 366.2511656

202118.9087

SD 449.58CV 1.23

Here we find, the variability of sales was not high in thehistorical years but according to projections, it mayincrease a little bit.

Degreeof

Operating

Leverage

Sales % Changes insales

EBIT %Changesin EBIT

DOL

1989 10.6 5.8 90 22.5 1.122641509 14.5 1.5 1.33613

491 25 0.111111111 16.2 0.11724

11.05517

292 139.2 4.568 75.2 3.64197

50.79728

93 275.1 0.976293103 184.9 1.458777

1.494199

94 302 0.097782625 204.9 0.108167

1.106194

95 305.7 0.012251656 206.5 0.007809

0.637358

96 317 0.036964344 213.6 0.034383

0.930155

61

97 325.9 0.02807571 218.9 0.024813

0.883779

98 338.3 0.038048481 226.7 0.035633

0.936508

Figure 1.20: DOL

Operating leverage is a measure of how revenue growthtranslates into growth in income. Leverage, and of how risky(volatile) a company's operating income is.

Here we see, the sensitivity of operating profit to changesin sales had found an decreasing trend but after 1996 it hasincreasing trend which is showing that though the businessis not high now it may go to increase in near future.

Business risk depends on:

62

Demand variability:

In Kalimantan paper project, Indonesia’s economy facedrecession when the price of oil steeply declined in 1980. Itwas offset by aid financing of project and raising debt ininternational financing market, which brought with it higherdebt service obligation. As considered the equipment demandvariation is high with the economic condition, the businessrisk is also high for the project.

Sales price variability:

The project components are hardwood log sales, plywoodproduction and pulp & paper production. The components salesprices variation is too high in 1989 to 1998 throughout theproject. The sales price direction is increasing butbusiness risk is high for changes the sales prices.

Input cost variability:

The Kalimantan paper project raw material is timber cost,plywood materials and paper materials which prices alsovariation throughout the project. The business risk is alsohigh.

Ability to adjust output prices for changes in input cost:

The project adjusts the output prices for changes in input out following year. So, business risk is comparatively low.

Foreign risk exposure

63

Indonesian currency, he rupiah, was easily convertible and pegged to the USA dollar. So heir foreign risk exposure is low. So, business risk is comparatively low.

Operating leverage:

Operating leverage is the extent to which cost are fixed. InKalimantan paper project, the fixed cost percentage isalmost 80% or above. Depending on fixed cost in operatingthe project increases the business risk of the project.

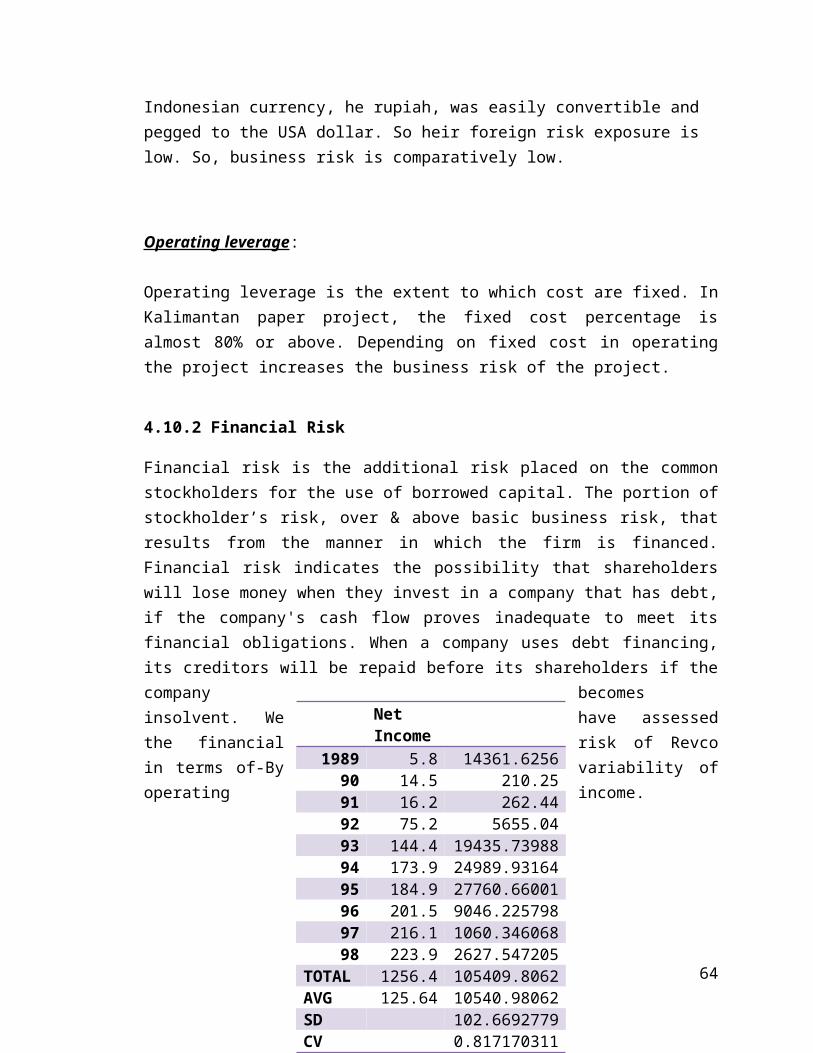

4.10.2 Financial Risk

Financial risk is the additional risk placed on the commonstockholders for the use of borrowed capital. The portion ofstockholder’s risk, over & above basic business risk, thatresults from the manner in which the firm is financed.Financial risk indicates the possibility that shareholderswill lose money when they invest in a company that has debt,if the company's cash flow proves inadequate to meet itsfinancial obligations. When a company uses debt financing,its creditors will be repaid before its shareholders if thecompany becomesinsolvent. We have assessedthe financial risk of Revcoin terms of-By variability ofoperating income.

64

Net Income

1989 5.8 14361.625690 14.5 210.2591 16.2 262.4492 75.2 5655.0493 144.4 19435.7398894 173.9 24989.9316495 184.9 27760.6600196 201.5 9046.22579897 216.1 1060.34606898 223.9 2627.547205

TOTAL 1256.4 105409.8062AVG 125.64 10540.98062SD 102.6692779CV 0.817170311

Projected Income Statement

2000 4.98787758

31986.77

2001 15.8179592

250.21

2002 18.2846945

334.33

2003 106.388351

11318.48

65

2004 248.662955

61833.27

2005 275.159606

75712.81

2006 277.427029

76965.76

2007 288.142532

83026.12

2008 296.11001 87681.142009 307.38231

794483.89

Total 1838.36333

523592.77

Average 183.836333

52359.28

SD 228.821495CV 1.244702236

It indicates that the company's financial risk is lowaccording to the historical performance. But according tothe projection, we see that they are expecting that theirfinancial risk will go to increase in the projected years.

Degree of Financial Leverage Sale

s% Changes in sales

EBIT EBIT-Interest

DFL

1989 10.6 5.8 5.8 190 22.5 1.122641

50914.5 14.5 1

91 25 0.111111111

16.2 16.2 1

92 139.2

4.568 75.2 75.2 1

93 275.1

0.976293103

184.9 144.4 1.280471

94 302 0.097782625

204.9 173.9 1.178263

95 305.7

0.012251656

206.5 184.9 1.11682

66

96 317 0.036964344

213.6 201.5 1.06005

97 325.9

0.02807571

218.9 216.1 1.012957

98 338.3

0.038048481

226.7 223.9 1.012506

Figure 1.21: DFL

If Kalimantan paper project takes long term debt thenfinancial risk will arise. A debt ratio indicates that acompany has more assets, meanwhile, a debt ratio of moreassets than debt which creates asset availability risk. TheKalimantan paper project debt ratio can help investorsdetermine a company’s level of risk which is financial risk.

67

The project’s main sources of financing were to be exportcredit loans (US $ 360 million) which interest rates areassumed to be 8%, a syndicated Eurodollar loan (US$ 100million) at 9% interest rates and with a revolving rupiahdebt on 12% interest rates. The term loan is repaid in eightsemi-annual repayments starting in June 1993 and ending inDecember 1996. As the interest is capitalized duringconstruction.

Total Debt (745-150) =595 US$Total Equity =150 US$

5. Problem Statement

5.1 Immediate problem

In Kalimantan paper project each participants have somethingto gain from the project, as long as it was structured toallow those gains, but each could achieve the desiredproject structure only with the cooperation of otherdecision makers. If all participant thinks about their ownreturn then this project will not be attractive to everyoneso every decision maker had not only to accurately evaluate

68

its own project risk-return tradeoffs, but also those of allproject stakeholders.

5.2 Different Investors Perspectives

MetroPolitan Bank, Management, which would have to approveany loan, was concerned with the risk-return trade-off. Withconsideration project finance experience, Metropolitan waskeen to consider complex arrangements which could justifyhigher spreads and fees from the borrowers and could enticeproviders of capital- either debt or external equity- withsufficient expected return to justify project risk.Metropolitan’s legal department would have to sign off onany documentation and had been particularly concerned thatoffer letters reflect the kinds of detailed specificationsof availability, security, representation, warranties,covenants and events of defaults which would be required inthe final loan agreement negotiation.

A checklist prepare

The bank of Surabaya, having worked with those projections,it was keenly aware of the degree to which the sales volume,cost, price, and timing assumption implied in theprojections affected project viability. It was confidentthat the projections constituted a “best guess” as toproject outcome, but that the actual realization would besubject to considerable variation. The bank of Surabayaconsidered that, with the participation of other domesticbanks, it could arrange for as much working capital andshort-term rupiah financing as the project needed- providedthe credit was appropriately structured. It could serve asdomestic loan agent for project monitoring and would behappy to take the role as collateral agent for loansecurity. Because its valued customer, Hanaffi, was leadingthe project, the bank’s staff members had a strong incentive

69

to do whatever they could within the strictures of prudentbanking to see the project successfully financed.

6. Alternative Courses of Action

6.1 By Introducing New Technology

6.2 Minimizing Cost

6.3 Joint venture

6.4 By Contracting with New Supplier from Brazil

6.4 By Issuing Common Stock

6.5 Paying out loan by freed up cash

7. Analysis of Each Alternative

7.1 By Introducing New Technology

70

The investors argued that they were taking a high risk ininvesting in a facility using plantation technology untestedin Indonesia. Only after 2001 (after the first plantationtrees on the clear-cut land had matured and had beenharvested) would the feasibility of that technology beestablished. Hence, the investors had negotiated with thegovernment considerable discount on the timber tax, whichconstituted the largest part of the annual timber costs.More important, they still had the right to use theKalimantan forest site from which they were permitted toharvest hardwood logs for up to ten years, provided theproject was implemented. The investors planned toconcentrate log harvesting in the early years, which wouldboth meet the clear-cutting needs of the plantation andmaximize early cash flow for debt service. The logs would besold to the investors’ own mills elsewhere in Indonesia, andwere expected to bring profits to those mills of roughly 75%of their purchase price from Kalimantan parer. In addition,contract for the preproduction site, civil works not part ofthe turnkey contract, and marine insurance on equipmentshipments were expected to be awarded to interests under thecontrol of the investors.

If this company introduces new technology then they will beable to generate or produce more qualitiful papers. Thenmore customers will be attracted towards this papers. Thenprofitability will also increase.

They can also use new technology to cut trees more quicklyand process quickly. Then time will not be wasted more andcost will be minimized.

7.2 Minimizing Cost

Kamakura Bank of Japan had flexibly provided low-costfacilities to hanaffi on many occasions, and other membersof the investors had worked with its leasing subsidiary inJakarta. The investors had originally engaged Metropolitan

71

as its financial adviser because of the bank’s project-financing experience and contacts with export creditagencies. They viewed Metropolitan as entitled to itssuccess fee if it earned it by lead-managing the finalfinancing package. Their acquaiance with deutscheHandelsbank was recent but positive. They were keen to usethe export credit loans which Deutsche Handelsbank washelping to arrange and to take advantage of the 8%concessionary U.S. dollar financing. Notwithstanding thecash flow projections and negotiations carried on to date,however, the investors remained highly flexible with regardto the capital structure of the project. This would considerany serious financing alternative.

Especially in bringing new technologies to Indonesia, and asbecause that support would be seen as a signal to theinternational business community of the favourableIndonesian climate. However. The MOF was equally concernedthat it be seen as even-handed, especially in the light ofthe fact that the project involved one of the country’sdepletable natural resources hardwood timber stands.If this company is able to minimize its cost, thenprofitably will increase. 7.3 Joint venture

This project is financed by largely debt amount so it is toorisky project. If this project can merge with anotherproject which has low debt ratio then risk can be minimizedand total debt ratio will be in under control.

7.4 By Contracting with New Supplier from Brazil

Here is an opportunity of buying their raw materials fromBrazil. Because in Brazil there is a forest plantation offastest growing tropical pine and eucalyptus, which maturein 8 to 14 years and this can provide a cheaper source ofhigh quality pulpwood for paper, where it takes 25 to 50

72

years to mature in North America and Europe. Indonesia cantake this opportunity to buy the raw materials from Brazil.If they can bring it in cheaper cost by a contract withBrazil then it can able to minimize its raw material costand which leads a higher return. By this way investors willalso be able to get higher returns.7.4 By Issuing Common StockThis Kalimantan Paper Project is financed by taking moredebt and less equity. When any company or country takes moredebt than equity then power goes to the debt holders. Andmany covenants restricted the management decisions. The sameproblem will arise in this project. So if we issue morecommon stock in the market to raise our capital then debtholder will not be able to get more power.

7.5 Paying out loan by freed up cash

The firm can use the free cash in paying out loans. We knowwhen borrower pays loan effectively and timely then theparty who gives loan they have a faith on the borrowers andso they give loan with lower interest in next time. Thus wayit results in lower weighted average cost of capital. Afterreducing WACC this project’s value will be maximized with acertain amount. On the other hand debt will be reduced andas well as the interest expense will reduce then net incomewill increase. And this will result on higher return onasset, return on equity and profit margin.

73

Effects on WACC

Here are the charts and graphs of previous WACC and afterpayment of debt WACC.

Before WACC

74

After loan repayment

WACC

1989 7.74%1990 6.98%1991 7.48%1992 5.25%1993 7.27%1994 7.10%1995 7.01%1996 6.92%1997 6.85%1998 6.77%

Repayment

1989 8.17%1990 7.47%1991 7.91%1992 5.88%1993 7.38%1994 7.27%1995 7.22%1996 7.17%1997 7.12%1998 7.08%

Figure 1.10: Profit Margin ratio analysis.

75

Effects on Return on Asset

ROA aftercash freed up

1989 4.25%90 7.04%91 10.03%92 49.45%93 66.76%94 68.91%95 66.60%96 65.41%97 63.83%98 60.75%

Figure 1.11: Profit Margin ratio analysis.

76

ROA1989 3.0%

90 5.2%91 7.4%92 34.5%93 46.2%94 49.0%95 48.0%96 47.8%97 47.2%98 44.9%

Effects on Return on equity

77

ROE1989

11.6%

90 29.0%91 32.4%92 #DIV/0!93 275.0%94 315.5%95 319.4%96 331.5%97 338.6%98 334.2%

ROE after cash freed up

1989 16.6%90 39.5%91 44.1%92 #DIV/0!93 397.4%94 443.4%95 442.8%96 453.4%97 457.9%98 452.1%

Figure 1.12: Profit Margin ratio analysis.

Effects on Profit Margin

78

PM after cash freed up

1989 78.1%90 87.8%91 88.2%92 77.4%93 75.8%94 80.9%95 83.8%96 86.9%97 89.7%98 89.5%

PM1989 55%90 64%91 65%92 54%93 52%94 58%95 60%96 64%97 66%98 66%

Figure 1.13: Profit Margin ratio analysis.

8. Recommendation

The asset management of this project is not good as theirinventory turnover, Total asset turnover are decreasing andDays Sales Outstanding is increasing. So they shouldaccelerate the collecting periods from receivables by givingsome financial incentives such as cash discounts.

This project is financed by largely debt amount so it is toorisky project. If this project can merge with anotherproject which has low debt ratio then risk can be minimizedand total debt ratio will be in under control.

79

The Kalimantan paper project can freed up a certain amountof cash from reducing the receivables and inventories. Theyshould use this freed cash in reducing their debt becausethey are using too much debt. Otherwise in future thisproject will be in liquidity crisis by paying too muchinterest.

By taking this project economy can be expanded.

The investors argued that they were taking a high risk ininvesting in a facility using plantation technology untestedin Indonesia. Industrialist Hannafi can test this project assoon as possible in a short way to attract the investors.

The investors were eligible for a five-year corporate taxholiday. Thus way this information can help to attractinvestors.

9. Conclusion

80

Kalimantan paper project was continuing their project worked

with a lot of difficult circumstances. Their largely equity

was financed by external debt, which is highly risky for the

project. The organisers were always tried to run the project

and the investors were also associated to finance the

project in liquidity problem time. The NPV of these cash

flows of the Kalimantan Paper Project is positive. And for

this reason investors can invest in this project. If all

participant thinks about their own return then this project

will not be attractive to everyone so every decision maker

had not only to accurately evaluate its own project risk-

return tradeoffs, but also those of all project

stakeholders. Economy faced hyperinflation, closed the

economy to outside competition, ruined the plantations,

embarked an ineffective and costly military confrontation

with Malaysia, and introduced chronic budget deficits.

Foreign investor did not enter because of high inflation and

close economy.Paper industry did not grow up due to ruin

forest and plantation. In 1970's, Indonesia's economy

followed a path of development. Economy boost in 1970's due

to oil industry. Indonesia's economies turn into good

position due to export commodities.

81

82

![De Apocalipsis, Cristianismo, Juicio Final y Fin de los Tiempos [1a. Pt.]](https://static.fdokumen.com/doc/165x107/630b9a1248b1375a9e0fcad4/de-apocalipsis-cristianismo-juicio-final-y-fin-de-los-tiempos-1a-pt.jpg)