evaluation of the capital value, investments and capital - Data ...

203

1 EVALUATION OF THE CAPITAL VALUE, INVESTMENTS AND CAPITAL COSTS IN THE FISHERIES SECTOR No FISH/2005/03 FINAL REPORT by IREPA Onlus In co-operation with IFREMER, France FOI, Denmark SEAFISH, United Kingdom LEI BV, Netherlands FRAMIAN BV, Netherlands October 2006

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of evaluation of the capital value, investments and capital - Data ...

1

EVALUATION OF THE CAPITAL VALUE, INVESTMENTS AND CAPITAL COSTS IN THE FISHERIES SECTOR

No FISH/2005/03

FINAL REPORT

by

IREPA Onlus

In co-operation with

IFREMER, France FOI, Denmark

SEAFISH, United Kingdom LEI BV, Netherlands

FRAMIAN BV, Netherlands

October 2006

2

CONTENTS SUMMARY.................................................................................................................................................................12 1.INTRODUCTION................................................................................................................................................13 2.PROPOSED METHOD ......................................................................................................................................18 2.1 PIM proposed by OECD...................................................................................................................................18 2.2 Application of PIM to fishing fleets .................................................................................................................19 2.3 Calculation of capital costs.................................................................................................................................26 2.4 Valuation model...................................................................................................................................................28 2.5 Valuation of intangible assets ............................................................................................................................34 2.6 Valuation of ‘other assets ...................................................................................................................................36 3.THEORETICAL CONSIDERATIONS...........................................................................................................38 3.1 The conceptual framework ................................................................................................................................38 3.2 Overview of measurement methods.................................................................................................................52 REFERENCES..........................................................................................................................................................56 APPENDIX A: Denmark ........................................................................................................................................58 Introduction: Data sources .......................................................................................................................................58 1. General national situation.....................................................................................................................................58 1.1 Investments in new vessels ................................................................................................................................58 1.2 Investments in fishing rights..............................................................................................................................59 1.3 Investments in 2nd hand vessels.......................................................................................................................60 1.4 Investments in shore facilities............................................................................................................................60 1.5 Approach to calculation of capital value in agriculture .................................................................................61 2. National fleet ..........................................................................................................................................................62 2.1 Description of the case study fleet....................................................................................................................62 2.2 Data and estimation of price per capacity unit ...............................................................................................62 2.3 Capital value and capital costs ...........................................................................................................................66 2.4 Evaluation .............................................................................................................................................................68 3. Fleet under 12 meters............................................................................................................................................69 3.1 Description of the case study fleet < 12m.......................................................................................................69 3.2 Data and estimation of price per capacity unit ...............................................................................................70 3.3 Capital value and capital costs ...........................................................................................................................71 4. Fleet 12 meters and over.......................................................................................................................................72 4.1 Description of the case study fleet >12m........................................................................................................72 4.2 Data and estimation of price per capacity unit ...............................................................................................73 4.3 Capital value and capital costs ...........................................................................................................................73 Appendix A.1 Account Statistics for Fisheries - Denmark .................................................................................75 APPENDIX B: France .............................................................................................................................................78 Introduction: Data sources .......................................................................................................................................78 1. General national situation – national markets for fishery assets ....................................................................79 1.1 Investments in new vessels ................................................................................................................................79 1.2 Investments in fishing rights..............................................................................................................................80 1.3 Investments in 2nd hand vessels.......................................................................................................................81 1.4 Investments in shore facilities............................................................................................................................82 1.5 Approach for the calculation of capital value in agriculture and/or by statistical office .........................83 2. Estimation of value per capacity unit .................................................................................................................83 2.1 Data and estimation of price per capacity unit ...............................................................................................83 2.2 Capital value and capital costs ...........................................................................................................................87 3 Total fleet (under 30meters, NSCA coast).........................................................................................................92 3.1 Description of the case study total fleet...........................................................................................................92

3

3.2 Data and estimation of price per capacity unit ...............................................................................................93 3.3 Capital value and capital costs ...........................................................................................................................93 4. Fleet under 12 meters (NSCA coast) ..................................................................................................................95 4.1 Description of the case study fleet <12m........................................................................................................95 4.2 Data and estimation of price per capacity unit ...............................................................................................96 4.3 Capital value and capital costs ...........................................................................................................................96 5. Fleet 12 - 30 meters (NSCA coast) .....................................................................................................................98 5.1 Description of the case study fleet 12 - 30 m..................................................................................................98 5.2 Data and estimation of price per capacity unit ............................................................................................ 100 5.3 Capital value and capital costs ........................................................................................................................ 100 6. Trawlers 16-24 meters........................................................................................................................................ 102 6.1 Description of the case study Trawlers 16-24 m. ........................................................................................ 102 6.2 Data and estimation of price per capacity unit ............................................................................................ 103 6.3 Capital value and capital costs ........................................................................................................................ 103 7. Passive gears less than 12 meters...................................................................................................................... 105 7.1 Description of the case study Passive gears <12m. .................................................................................... 105 7.2 Data and estimation of price per capacity unit ............................................................................................ 106 7.3 Capital value and capital costs ........................................................................................................................ 106 8. Evaluation ............................................................................................................................................................ 108 References ................................................................................................................................................................ 114 Appendix B.1 : Historical vessel price model ..................................................................................................... 115 APPENDIX C: Italy............................................................................................................................................... 116 Introduction: Data sources .................................................................................................................................... 116 1. General national situation – national markets for fishery assets ................................................................. 116 1.1 Investments in new vessels ............................................................................................................................. 116 1.2 Investments in fishing rights........................................................................................................................... 117 1.3 Investments in 2nd hand vessels.................................................................................................................... 119 1.4 Investments in shore facilities......................................................................................................................... 121 1.5 Approach to calculation of capital value by statistical office..................................................................... 121 2. National fleet ....................................................................................................................................................... 123 2.1 Description of the case study fleet................................................................................................................. 123 2.2 Data and estimation of price per capacity unit ............................................................................................ 123 2.3 Capital value and capital costs ........................................................................................................................ 129 2.4 Evaluation .......................................................................................................................................................... 131 3. Fleet under 12meters .......................................................................................................................................... 132 3.1. Description of the case study fleet <12m.................................................................................................... 132 3.2 Data and estimation of price per capacity unit ............................................................................................ 134 3.3 Capital value and capital costs ........................................................................................................................ 135 3.4 Evaluation .......................................................................................................................................................... 137 4. Fleet 12 meters and over.................................................................................................................................... 137 4.1 Description of the case study fleet >12m..................................................................................................... 137 4.2 Data and estimation of price per capacity unit ............................................................................................ 138 4.3 Capital value and capital costs ........................................................................................................................ 139 4.4 Evaluation .......................................................................................................................................................... 141 5. Passive gears ........................................................................................................................................................ 141 5.1. Description of the case study Passive gears ................................................................................................ 141 5.2 Data and estimation of price per capacity unit ............................................................................................ 143 5.3 Capital value and capital costs ........................................................................................................................ 143 5.4 Evaluation .......................................................................................................................................................... 145 6. Demersal Trawl Fleet ......................................................................................................................................... 146 6.1 Description of the case study Demersal Trawl Fleet .................................................................................. 146 6.2 Data and estimation of price per capacity unit ............................................................................................ 146 6.3 Capital value and capital costs ........................................................................................................................ 147

4

6.4. Evaluation ......................................................................................................................................................... 149 References ................................................................................................................................................................ 150 APPENDIX D: Netherlands ................................................................................................................................ 151 Introduction: Data sources .................................................................................................................................... 151 1.1 Investments in new vessels ............................................................................................................................. 151 1.2 Investments in fishing rights........................................................................................................................... 151 1.3 Investments in 2nd hand vessels.................................................................................................................... 154 1.4 Investments in shore facilities......................................................................................................................... 154 1.5 Approach to calculation of capital value in agriculture .............................................................................. 155 2. Estimation of value per capacity unit .............................................................................................................. 155 2.1 Data and estimation of price per capacity unit ............................................................................................ 155 2.1.1 Replacement value LEI method.................................................................................................................. 156 2.1.2 Insurance value .............................................................................................................................................. 159 2.2 Data, prices and estimation value of intangible capital............................................................................... 166 2.2.1 Licenses ........................................................................................................................................................... 166 2.2.2 Shrimp licenses, list I and list II licenses.................................................................................................... 166 2.2.3 Fish quota ....................................................................................................................................................... 167 3. Total cutter fleet the Netherlands .................................................................................................................... 168 3.1 Description of the case study total cutter fleet (all vessels >12 m.) ......................................................... 168 3.2 Data and estimation of price per capacity unit ............................................................................................ 169 3.3.1 Tangible capital .............................................................................................................................................. 170 3.3.2 Intangible capital............................................................................................................................................ 172 4. Vessels 261-300 hp (beam trawlers over 24 meters) ..................................................................................... 172 4.1 Description of the case study vessels 261-300 hp (beam trawlers <24 m.) ............................................ 172 4.2 Data and estimation of price per capacity unit ............................................................................................ 172 4.3 Capital value and capital costs ........................................................................................................................ 173 4.3.1 Tangible capital .............................................................................................................................................. 173 4.3.2 Intangible capital............................................................................................................................................ 174 5. Vessels >1.501 hp (beam trawlers >24 m.) .................................................................................................... 175 5.1 Description of the case study vessels >1.501 hp (beam trawlers >24m.) ............................................... 175 5.2 Data and estimation of price per capacity unit ............................................................................................ 175 5.3 Capital value and capital costs vessels ........................................................................................................... 176 5.3.1Tangible capital ............................................................................................................................................... 176 6. Evaluation ............................................................................................................................................................ 178 APPENDIX E: United Kingdom........................................................................................................................ 179 Introduction: Data sources .................................................................................................................................... 179 1. General national situation – national markets for fishery assets ................................................................. 179 1.1 Investments in new vessels ............................................................................................................................. 179 1.2 Investments in fishing rights........................................................................................................................... 180 1.3 Investments in 2nd hand vessels.................................................................................................................... 182 1.4 Investments in shore facilities......................................................................................................................... 182 1.5 Approach to calculation of capital value in agriculture and/or by statistical office............................... 182 2. Total fleet ............................................................................................................................................................. 183 2.1 Description of the case study fleet................................................................................................................. 183 2.2 Data and estimation of price per capacity unit ............................................................................................ 184 2.3 Capital value and capital costs ........................................................................................................................ 188 2.4 Evaluation .......................................................................................................................................................... 190 3. Fleet under 12 meters......................................................................................................................................... 191 3.1 Description of the case study fleet................................................................................................................. 191 3.2 Data and estimation of price per capacity unit ............................................................................................ 192 3.3 Capital value and capital costs ........................................................................................................................ 193 4. Fleet 12 meters and over.................................................................................................................................... 195

5

4.1 Description of the case study.......................................................................................................................... 195 4.2 Data and estimation of price per capacity unit ............................................................................................ 195 4.3 Capital value and capital costs ........................................................................................................................ 196 5. Over 40m Pelagic Fleet...................................................................................................................................... 198 5.2 Data and estimation of price per capacity unit ............................................................................................ 198 5.3 Capital value and capital costs ........................................................................................................................ 199 5.4 Evaluation .......................................................................................................................................................... 200 6. Over 24 meters Demersal Trawl Fleet ............................................................................................................ 201 6.1 Description of the case study.......................................................................................................................... 201 6.2 Data and estimation of price per capacity unit ............................................................................................ 201 6.3 Capital value and capital costs ........................................................................................................................ 202

6

TABLES Table 1. Depreciation period of hull, engine and electronics applied in AER by country, 2002..................41 Table 2. Average service lives in Fishing (OECD, 1992) ....................................................................................42 Table 3 Classification of fixed assets.......................................................................................................................47 Table A.1.1 Value of land-based assets owned by commercial Danish fishing vessels ..................................60 Table A.2.1 Distribution of recently build vessels with total fleet structure (%).............................................62 Table A.2 2 Average replacement values for total fleet in 2004 (Euro) ............................................................63 Table A.2.3 Distribution of asset value for the Danish commercial fishing vessels (%)................................63 Table A.2.4 Correlation coefficients between selected physical characteristics ...............................................65 Table A.2.5 Weights used to calculate price indices .............................................................................................65 Table A.2.6 Overview of assumptions made in the Danish case studies (%) ..................................................66 Table A.2.7 Capital value and capital costs and their consequences on profit (mln Euro)............................67 Table A.2 8 Summary of the capital values – comparison of approaches (mln Euro) ...................................67 Table A.2 9 Relative composition of capital (%) .................................................................................................67 Table A.3.1 Average replacement values for vessels below 12 meters in 2004 (Euro)...................................70 Table A.3.2 Capital value and capital costs and their consequences on profit for vessels below 12 meters (mln Euro)...................................................................................................................................................................71 Table A.3.3 Summary of the capital values – comparison of approaches for vessels below 12 meters (mln Euro) ............................................................................................................................................................................71 Table A.3.4 Relative composition of capital (%) for vessels below 12 meters.................................................72 Table A.4.1 Average replacement values for vessels above 12 meters in 2004 (Euro)...................................73 Table A.4.2 Capital value and capital costs and their consequences on profit for vessels above 12 meters (mln Euro)...................................................................................................................................................................74 Table A.4.3 Summary of the capital values - comparison of approaches for vessels above 12 meters (mln Euro) ............................................................................................................................................................................74 Table A.4.4 Relative composition of capital for vessels above 12 meters (%).................................................74 Table B.2.1 Reducing balance rate in the French fiscal regulatory basis...........................................................89 Table B.2. 2 Overview of assumptions made in the French case studies .........................................................90 Table B.3.1Composition of the total fleet < 30m. by main DCR sub-segment ..............................................92 Table B.3.2 Price per capacity unit – Model estimates – Total fleet (NSCA, less than 30.) ..........................93 Table B.3.3 Summary of the capital values – NSCA Fleet <30m. .....................................................................93 Table B.4.1Composition of the fleet < 12m. by main DCR sub-segment .......................................................95 Table B.4.2 Price per capacity unit – Model estimates – Total fleet (NSCA, less than 12 meters) ..............96 Table B.4.3 Summary of the capital values – Fleet < 12m..................................................................................97 Table B.5.1 Composition of the total fleet 12-30 m. by main DCR sub-segment ..........................................99 Table B.5.2 Price per capacity unit – Model estimates – Total fleet (NSCA, 12-30m. ) ............................. 100 Table B.5.3 Summary of the capital values - 12– 30 m. NSCA fleet ............................................................. 100 Table B.6.1 Composition of Trawlers 16-24 m. by main DCR sub-segment ............................................... 102 Table B.6.2 Price per capacity unit – Model estimates –Trawlers, 16-24 m.................................................. 103 Table B.6.3 Summary of the capital values – Trawlers 16-24 m. NSCA coast ............................................. 103 Table B.7.1 Composition of Passive gears <12 m. by main DCR sub-segment .......................................... 105 Table B.7.2 Price per capacity unit – Model estimates –Passive gears <12m. .............................................. 106 Table B.7.3 Summary of the capital values – Passive gears < 12m. ............................................................... 106 Table B.8.1 Results from a sub sample of Trawlers 16 -24 m. (45 vessels)................................................... 108 Table B.8.2 Results from a sub sample of Passive gears <12m. (109 vessels) .............................................. 110 Table C.1.2 II hand market prices per capacity units, 2004 ............................................................................. 119 Table C.1.3 Scales of assistance relating to fishing fleets (Euro)..................................................................... 120 Table C.1.4 Hedonic values ................................................................................................................................... 120 Table C.1.5 Classification of Sectors and Standard Average Service Lives (years)....................................... 122

7

Table C.2.1 Composition of the total fleet by main DCR sub-segment ........................................................ 123 Table C.2.2 RINA indexes: Price per GRT unit, 1992 (Euro)......................................................................... 124 Table C.2.3 Percentage composition of investments by main sub-segment and group of assets.............. 125 Table C.2.4 Depreciation rates by groups of assets........................................................................................... 125 Table C.2.5 Fiscal rates by groups of assets........................................................................................................ 126 Table C.2.6 Prices (€) per capacity units in 1992 and 2004 .............................................................................. 128 Table C.2.7 Qualitative description of the relevant fishing rights................................................................... 128 Table C.2.8 Valuation of the relevant fishing rights .......................................................................................... 129 Table C.2.9 Background for calculation of depreciation and interest for the total fleet ............................. 129 Table C.2.10 Capital value and capital costs and their consequences on profit for the total fleet............. 129 Table C.2.11 Summary of the capital values - comparison of approaches for the total fleet ..................... 130 Table C.2.12 Background for calculation of depreciation and interest .......................................................... 131 Table C.3.1 Composition of the fleet <12m. by main DCR sub-segment .................................................... 133 Table C.3.2 Prices (€) per capacity units of the fleet <12m. in 1992 and 2004 ............................................ 134 Table C.3.3 Valuation of the relevant fishing rights .......................................................................................... 135 Table C.3.4 Background for calculation of depreciation and interest of fleet < 12m. ................................ 135 Table C.3.5 Capital value and capital costs and their consequences on profit of fleet < 12m................... 135 Table C.3.6 Summary of the capital values - comparison of approaches of fleet < 12m. .......................... 136 Table C.4.1 Composition of the 12m. and over fleet by main DCR sub-segment ...................................... 138 Table C.4.2 Prices (€) per capacity units in 1992 and 2004 of the 12m. and over fleet............................... 138 Table C.4.3 Valuation of the relevant fishing rights of the 12m. and over fleet........................................... 139 Table C.4.4 Background for calculation of depreciation and interest of the 12m and over fleet .............. 139 Table C.4.5 Capital value and capital costs and their consequences on profit of the 12m. and over fleet139 Table C.4.6 Summary of the capital values - comparison of approaches of the 12m. and over fleet ....... 140 Table C.5.1 Prices (€) per capacity units in 1992 and 2004 of Passive gears................................................. 143 Table C.5.2 Valuation of the relevant fishing rights of Passive gears............................................................. 143 Table C.5.3 Background for calculation of depreciation and interest of Passive gears ............................... 143 Table C.5.4 Capital value and capital costs and their consequences on profit of Passive gears................. 144 Table C.5.5 Summary of the capital values - comparison of approaches of Passive gears ......................... 144 Table C.6.1 Prices (€) per capacity units in 1992 and 2004 of Demersal Trawl Fleet.................................. 146 Table C.6.2 Valuation of the relevant fishing rights of Demersal Trawl Fleet ............................................. 147 Table C.6.3 Background for calculation of depreciation and interest of Demersal Trawl Fleet................ 147 Table C.6.4 Capital value and capital costs and their consequences on profit of Demersal Trawl Fleet . 147 Table C.6.5 Summary of the capital values - comparison of approaches of Demersal Trawl Fleet.......... 148 Table D.1.1 Average scrapping premiums for capacity Dutch fleet 2005 ..................................................... 154 Table D.2.1 Estimated replacement value vessel and engine grouped by hp-class ...................................... 157 Table D.2.2 Estimated replacement value vessel and engine grouped by fleet segment............................. 157 Table D.2.3 Estimated book value vessel and engine grouped by hp-class................................................... 158 Table D.2.4 Estimated book value vessel and engine grouped by fleet segment ......................................... 158 Table D.2.5 Mean values technical variables ...................................................................................................... 159 Table D.2.6 Results regression.............................................................................................................................. 161 Table D.2.7 Mean values technical variables by hp-class.................................................................................. 162 Table D.2.8 Mean values technical variables per capacity unit by fleet segment.......................................... 162 Table D.2.9 Estimated insurance value grouped by hp-class........................................................................... 163 Table D.2.10 Estimated insurance value grouped per capacity unit by fleet segment................................. 163 Table D.2.11 Estimated average insurance value per capacity unit by hp-class............................................ 164 Table D.2.12 Estimated average insurance value per capacity unit by fleet segment .................................. 164 Table D.2.13 Number of vessels with a license to fish for shrimp by hp-class (2004)................................ 166 Table D.2.14 Number of vessels with a license to fish for shrimp by fleet segment (2004) ...................... 166 Table D.2.15 Total quota for sole, plaice, cod and whiting sorted by hp-class (2004)................................ 167 Table D.2.16 Total quota for sole, plaice, cod and whiting by fleet segment (2004)................................... 167 Table D.2.17 Average quota for sole, plaice, cod and whiting by hp-class (2004) ....................................... 167 Table D.2.18 Average quota per vessel for sole, plaice, cod and whiting by fleet segment (2004) ........... 167

8

Table D.2.19 Estimated values of quota sole and plaice active vessels in the Netherlands........................ 168 Table D.2.20 Estimated value intangible capital active cutter fleet................................................................. 168 Table D.3.1 Technical variables by hp-class ....................................................................................................... 169 Table D.3.2 Estimated average insurance value per capacity unit................................................................... 169 Table D.3.3 Background for calculation of depreciation and interest entire Cutter fleet ........................... 170 Table D.3.4 Capital value and capital costs and their consequences on profit for entire cutter fleet ....... 170 Table D.3.5 Summary of the capital values - comparison of approaches entire cutter fleet ..................... 171 Table D.3.6 Relative composition ........................................................................................................................ 171 Table D.3.7 Level of depreciation ........................................................................................................................ 171 Table D.4.1 Average values for vessels 261-300 hp (12-24m. ) in 2004 (Euro) ........................................... 172 Table D.4.2 Background for calculation of depreciation and interest............................................................ 173 Table D.4.3 Capital value and capital costs and their consequences on profit (sensitivity analysis) ......... 173 Table D.4.4 Summary of the capital values - comparison of approaches...................................................... 174 Table D.4.5 Relative composition ........................................................................................................................ 174 Table D.4.6 Level of depreciation ........................................................................................................................ 174 Table D.4.7 Estimated value intangible capital vessels 261-300 hp................................................................ 175 Table D.5.1 Average values for vessels >1.501 hp in 2004 (Euro)................................................................. 176 Table D.5.2 Background for calculation of depreciation and interest >1.501 hp ........................................ 176 Table D.5.3 Capital value and capital costs and their consequences on profit >1.501 hp.......................... 176 Table D.5.4 Summary of the capital values - comparison of approaches >1.501 hp .................................. 177 Table D.5.5 Relative composition ........................................................................................................................ 177 Table D.5.6 Level of depreciation ........................................................................................................................ 177 Table E.1.2 Depreciation rates for different time periods for agricultural plant and machinery............... 183 Table E.2.1 Registered and active vessels in the UK fleet as at 1 January 2005, split by DCR segment.. 184 Table E.2.2 Characteristics of population and sample vessels for the whole UK fleet case study............ 185 Table E.2.3 Estimated average historic price (insured value indexed to 2004) per capacity unit and estimated replacement value (insured value in money of the day) per capacity unit for the whole UK fleet.................................................................................................................................................................................... 186 Table E.2.4 Correlation coefficients between insured value (adjusted to 2004 equivalent) and selected physical characteristics, based on sample of whole UK fleet........................................................................... 186 Table E.2.5 Assumed depreciation rates applied in the UK calculations....................................................... 188 Table E.2.6 Capital value and capital costs and their consequences on profit (sensitivity analysis)......... 188 Table E.2.7 Summary of the capital values (€ mln) - comparison of approaches ........................................ 189 Table E.2.8 Relative composition of capital ....................................................................................................... 189 Table E.3.1 Characteristics of population and sample vessels for the under 12m. ...................................... 192 Table E.3.2 Estimated average historic price (insured value indexed to 2004) per capacity unit and estimated replacement value (insured value in money of the day) per capacity unit for the under 12m. UK fleet. ........................................................................................................................................................................... 192 Table E.3.3 Correlation coefficients between insured value (adjusted to 2004 equivalent) and selected physical characteristics, based on sample of under 12m. vessels in the UK fleet......................................... 192 Table E.3.4 Capital value and capital costs and their consequences on profit (sensitivity analysis).......... 193 Table E.3.5 Summary of the capital values (€ mln) - comparison of approaches ........................................ 193 Table E.3.6 Relative composition of capital (%)................................................................................................ 194 Table E.4.1 Characteristics of population and sample vessels for the 12m. and over vessel case study .. 195 Table E.4.2 Estimated average historic price (insured value indexed to 2004) per capacity unit and estimated replacement value (insured value in money of the day) per capacity unit for the 12m. and over UK fleet .................................................................................................................................................................... 196 Table E.4.3 Correlation coefficients between insured value (adjusted to 2004 equivalent) and selected physical characteristics, based on sample of over 12m. vessels in the UK fleet ........................................... 196 Table E.4.4 Capital value and capital costs and their consequences on profit (sensitivity analysis).......... 196 Table E.4.5 Summary of the capital values (€ mln) - comparison of approaches ........................................ 197 Table E.4.6 Relative composition of capital (%)................................................................................................ 197

9

Table E.5.1 Characteristics of population and sample vessels for the >40m. pelagic UK fleet case study.................................................................................................................................................................................... 198 Table E.5.2 Estimated average historic price (insured value indexed to 2004) per capacity unit and estimated replacement value (insured value in money of the day) per capacity unit for the >40m. pelagic UK fleet .................................................................................................................................................................... 199 Table E.5.3 Correlation coefficients between purchase price (adjusted to 2004 equivalent) and selected physical characteristics, based on sample of pelagic vessels in the UK fleet................................................. 199 Table E.5.4 Capital value and capital costs and their consequences on profit (sensitivity analysis).......... 199 Table E.5.5 Summary of the capital values (€ mln) - comparison of approaches ........................................ 200 Table E.5.6 Relative composition of capital (%)................................................................................................ 200 Table E.6.1 Characteristics of population and sample vessels for the over 24m. demersal segment case study .......................................................................................................................................................................... 201 Table E.6.2 Estimated average historic price (insured value indexed to 2004) per capacity unit and estimated replacement value (insured value in money of the day) per capacity unit the UK over 24m. demersal trawl fleet ................................................................................................................................................. 202 Table E.6.3 Correlation coefficients between purchase price (adjusted to 2004 equivalent) and selected physical characteristics, based on sample of over 24m. demersal trawl vessels in the UK fleet ................ 202 Table E.6.4 Capital value and capital costs and their consequences on profit (sensitivity analysis).......... 202 Table E.6.5 Summary of the capital values (€ mln) - comparison of approaches ........................................ 203 Table E.6.6 Relative composition of capital (%)................................................................................................ 203

10

FIGURES Figure 1 Application of the PIM in practice by OECD ......................................................................................19 Figure 2 PIM application to fishing fleets.............................................................................................................20 Figure 3 Presentation of the composition of a fleet.............................................................................................23 Figure 4 Procedure for interpretation and estimation of prices per capacity unit...........................................24 Figure 5 Micro / macro calculation of depreciation and interest costs in the year t, tangible assets only (vessel and equipment) ..............................................................................................................................................27 Figure 6 Valuation model..........................................................................................................................................30 Figure 7 Spreadsheet for macro calculation of replacement value, depreciation and interest costs.............31 Figure 8 Spreadsheet for micro calculation of historic value, depreciation and interest costs ......................32 Figure 9 Comparison of macro and micro approach and sensitivity analysis ..................................................33 Figure 10 Accounting for intangible assets ............................................................................................................36 Figure 11. Typical mortality and survival functions .............................................................................................44 Figure A.1.1 Age composition of the Danish commercial fleet per 1/1-2005 (% of total)...........................59 Figure A.2.1 Accounting for tangible assets – decision tree –Denmark...........................................................64 Figure A.3.1 Age distribution of vessels <12 m....................................................................................................70 Figure A.4.1 Age distribution of vessels >= 12m.................................................................................................73 Figure B.1.1 Age composition of the French total fleet at 1rst January 2005..................................................79 Figure B.1.2 Evolution of the transaction rate on the second-hand Market (Atlantic Area) ........................81 Figure B.1.3 Evolution of average price per meter in constant kEuros on the second-hand Market (Atlantic Area).............................................................................................................................................................81 Figure B.1.4 Evolution of theoretical premium to scrap vessel (Atlantic Area) ..............................................82 Figure B.2.1 Accounting for tangible assets – decision tree – France...............................................................86 Figure B.3.1 Age composition of French NSCA fleet .........................................................................................92 Figure B.4.1 Age composition of Fleet < 12m......................................................................................................95 Figure B.5.1 Age composition of fleet 12-30 m....................................................................................................99 Figure B.6.1 Age composition of Trawlers 16-24m. ......................................................................................... 102 Figure B.7.1 Age composition of Passive gears < 12m. ................................................................................... 105 Figure C.1.1 Age composition of the total Italian fleet..................................................................................... 116 Figure C.1.2 Trend in second hand vessels’ prices ............................................................................................ 119 Figure C.2.1 Age composition of the total Italian fleet, 1935 - 2004.............................................................. 123 Figure C.2.2 Production Price Heavy Machinery index (base = 1992) .......................................................... 124 Figure C.2. 3Accounting for tangible assets – decision tree – for each vintage – Italy ............................... 127 Figure C.2.4 Capital values 2004 -Comparison between the general and the Italian assumptions............ 132 Figure C.3.1 Percentage incidence by length classes of the Italian fleet......................................................... 133 Figure C.3.2 Age composition of the fleet <12m.............................................................................................. 134 Figure C.3.3 Capital values 2004 - Comparison between the general and the Italian assumptions for fleet < 12m........................................................................................................................................................................ 137 Figure C.4.1 Age composition of the 12m. and over fleet ............................................................................... 138 Figure C.4.2 Capital values 2004 -Comparison between the general and the Italian assumptions for the 12m. and over fleet ................................................................................................................................................. 141 Figure C.5.1 Percentage incidence by main sub-segment................................................................................. 142 Figure C.5.2 Age composition of Passive gears ................................................................................................. 142 Figure C.5.3 Capital values 2004 - Comparison between the general and the Italian assumptions for Passive gears............................................................................................................................................................. 145 Figure C.6.1 Age composition of Demersal Trawl Fleet .................................................................................. 146 Figure C.6.2 Capital values 2004 - Comparison between the general and the Italian assumptions for the Demersal Trawl Fleet ............................................................................................................................................. 149 Figure D.1.1 Age composition of the active fishing fleet of the Netherlands .............................................. 151

11

Figure D.2.1 Correlation between hp, length of a vessel and the insurance value ....................................... 160 Figure D.2.2 Accounting for tangible assets- decision tree- Netherlands...................................................... 165 Figure D.3.1 Age distribution of vessels entire cutter fleet .............................................................................. 169 Figure D.4.1 Age distribution of vessels 261-300 hp (12-24m.) in 2004 ....................................................... 172 Figure D.5.1 Age distribution of vessels >1.501 hp (beam trawlers >24m.) ................................................ 175 Figure E.1.1 Age composition as percent of total for vessels in the UK 2005 fleet register........................179 Figure E.2.1 Age composition of the total UK fleet..........................................................................................184 Figure E.2.2 Accounting for tangible assets – decision tree – for each vintage – United Kingdom...........187 Figure E.3.1 Age composition of the under 12m. UK fleet...............................................................................191 Figure E.4.1 Age composition of the 12m. and over UK fleet .........................................................................195 Figure E.5.1 Age composition of the UK pelagic fleet.......................................................................................198 Figure E.6.1 Age composition of the UK over 24m. demersal trawl fleet ......................................................201 ABBREVIATIONS AER Annual Economic Report EAA/EAF 97 Economic Accounts for Agriculture and Forestry ESA 95 European Systems of Accounts FADN Farm Accounting Data Network in agriculture GCS Gross Capital Stock GFCF Gross Fixed Capital Formation IASCF International Accounting Standard Committee Foundation IFRS International Financial Reporting Standard MSY Maximum Sustainable Yield PIM Perpetual Inventory Method

12

SUMMARY This study has been carried to improve the quality of assessment of economic performance of the European fishing fleets. The objectives of the study can be summarized as follows: 1. To provide exhaustive definitions of concepts related to capital value and costs 2. To outline an overview of methods to estimate capital value and capital costs 3. To propose a method to be used 4. To demonstrate the applicability of the proposed method in a representative number of case

studies. The project team has reviewed approaches to capital valuation proposed by OECD and used by the national statistical offices and the Farm Accounting Data Network in agriculture. The review shows unambiguously that Perpetual Inventory Method (PIM) has become the most important international standard for valuation of tangible capital goods. This method has been exhaustively described by OECD and therefore the present report reflects only the main issues of relevance. PIM proposes to determine the aggregate value of the tangible capital goods used in the current year by aggregation of the value of all vintages (year classes). Such aggregation can be based either on historical, current or constant prices. Once the value of the capital goods in a given benchmark year has been determined, the capital value of each subsequent year is calculated by adding investments of that year (gross capital formation), revaluing the existing stock and subtracting value of capital goods taken out of operation. The capital costs (depreciation and interest) are than calculated, using agreed depreciation schedule and interest rate. It is important to stress that there is no one unique single definition of capital value and capital costs. The definition to be used depends on the analytical purpose. Two fundamentally different types of analysis are distinguished: - Macro (economic) approach, which values capital at replacement (current) prices and accounts for opportunity costs. - Micro (fiscal) approach, which is close to fiscal accounting, values capital at historical prices and accounts only for interest costs paid. Different schedules of depreciation can be applied in both approaches, although the linear depreciation seems most popular. The proposed method distinguishes among for components of tangible capital: vessel, engine, electronics and other equipment. These four components are valued and depreciated separately. Valuation of intangible assets has been also evaluated. It is proposed to apply the approach established by FADN, i.e. tradable intangibles should be valued at current market price (or a multi year average), independently of the question whether they have or have not been acquired or whether they are or are not linked to specific tangible (e.g. vessel). However, price information on intangibles is scarce and estimations of their value when linked to tangibles are far from simple. Further research n valuation of intangible will be essential, as their value probably exceeds the value of tangible assets in many fisheries.

13

The report points out that other types of capital have traditionally not received any attention, in particular land based assets (cars, buildings, etc.) and liquidity (working capital and reserves).

1. INTRODUCTION

Background The EU legislation regarding collection of data on economic performance of fishing fleets1 obliges the Member States to compile and process data on capital values, investments and capital costs. However, the definitions of the data to be collected have not been sufficiently precise to assure one common approach and analytical interpretation across the EU. Reliable and unified approach to valuation of capital and determination of capital costs is required for the following reasons: - calculation of net profit; - estimation of profitability of invested capital; - assessment of the dynamics of the sector in terms of level of investments (renovation of capital stock) and an evaluation of the ability of the sector maintain its capital value and continue operating in the future.

Objectives

The main goals of the study, as specified in the ToR of this study, are the following: a) To provide an exhaustive definition of the following economic terms in the fishery sector: - Capital value - Investments - Depreciation cost - Opportunity cost

The study has to define all the tangible and intangible assets that compose the capital and the investments by element. It also needs to define criteria in order to classify assets, in terms of age life and share of total capital. A thorough research has to be made as to which components of the fixed capital should be included in the calculation of depreciation.

b) To outline an overview of the existing methods for the estimates of: - capital evaluation (historical value, replacement value, insurance value, book value and the question of fishing rights)

1 - Council Regulation N°1543/2000 of 29 June 2000 establishing a Community framework for the collection and

management of the data, the general principles and the procedures for the content of National Programmes needed to conduct the Common Fisheries Policy (CFP).

- Commission Regulation N° 1639/2001 of 17 August 2001 establishing the minimum and extended Community programmes for the collection of data in the fisheries sector and laying down detailed rules for the application of Council reg. N° 1543/2000.

- Commission Regulation N°1581/2004 of 27 August 2004 amending Regulation (EC) N°1639/2001 establishing the minimum and extended Community programmes for the collection of data in the fisheries sector.

14

- depreciation calculation (perpetual inventory method, “straight line” method) - opportunity cost calculation.

c) To propose the best methods for the evaluation of capital value, investments, calculation of depreciation and opportunity costs, from a theoretical point of view, and to list the problems connected with their implementation. The method must produce results that are comparable between and across European fishing fleets.

Terms of Reference The ToR of the study formulates further the following requirements: The results of the study must be applicable to all the European fishing fleet segments as defined in appendix III of the EU regulation 1581/04. Definitions and methods must be in line with the European System of Accounts and have regard to existing regulations concerning the definition of characteristics for structural business statistics, as well as the OECD report on measuring capital.

Structure of the report The structure of the report is tailored to the needs of the main users i.e. STECF/SGECA and EC in their work on the review of the data collection regulation, which should be introduced in 2008. In the following sections of the introduction several main issues of importance are discussed: - OECD approach and definitions (also accepted by statistical offices) of capital,

investments and capital costs; - applications of Micro and Macro approach with brief definitions; - choice of the basic statistical unit: vessel and/or company. Chapter two presents the proposed method for capital valuation, which is largely based on the Perpetual Inventory Method (PIM) as proposed by OECD. This method has been accepted by many national statistical offices. On certain aspects, e.g. valuation of intangibles, reference is made to FADN and IFRS. This section can be read by those readers who are primarily interested in what needs to be done and how and not so in theoretical considerations, conceptual background or alternative options. Chapter three presents the conceptual background to the proposed method. It elaborates the advantages and disadvantage of alternative approaches and it explains why certain choices have been made. It also makes some further theoretical propositions which could be of relevance in the future (e.g. relation of rent to capital value or inclusion of considerations of risk interest rate). Chapter four compares the main results of the various case studies from five countries (Denmark, France, Italy, Netherlands and United Kingdom), which are presented in detail in appendices. Its primary relevance is to show that the proposed method can be applied in different countries, where data is collected in quite different ways.

15

Finally, appendices contain the case studies of the five countries participating in this study. Capital values have been estimated for the total national fleet, fleet less than 12 meters, fleet 12 meters and over and in some cases also for specific segments, mostly based on DCR definitions.

Structure of the capital Capital value is in principle the sum of all assets (or liabilities) presented on the annual balance sheet. The capital value of the fishing firms is in principle composed of the following components: - Fixed tangible assets – sea-based = vessel, engine, electronics, other equipment on board. - Fixed tangible assets – shore based = buildings, cars and other facilities on shore. - Intangible assets = licences, quota, permits, etc. - Working capital = liquidity (money) required to pay regularly on-going operational

expenses. - Reserves, participations, shares, etc. = resources (money) ‘invested’ in assets not directly

related to the fishing operations, but for example maintained to assure pension payments to the owner.

Until present, capital valuation in fisheries focused primarily on the vessel and its equipment. This report demonstrates that this partial approach falls short of the realities of the fishing sector and the analytical needs of fisheries managers. In particular value of intangible assets plays an important role in operational decision of fishing companies. Other components of capital should be born in mind, but are quantitatively much less important. Capital goods can be valued on the basis of different principles. The two most important principles are: - Historical value, which is the value (or price) paid at the time of the acquisition of that

good. Prices of used vessels (2nd hand market) are also historical values. - Replacement value is the value which would have to be paid for identical capital good now.

Replacement value is also called value at current prices, i.e. prices of the most recent year. Historical values can be in principle observed and recorded. Replacement value has to be estimated. The main problem with estimating replacement values is that technology progresses and in 2006 it is not possible to build a vessel with the same characteristics as a vessel built 20-30 years earlier. In the end it must be assumed that this problem does not really exist. Valuing capital goods, it is necessary to distinguish between gross and net values. - Gross value is the total historical value paid (or replacement value calculated). - Net value is the cross value minus depreciation. Various approaches to depreciation can be

followed. The details are elaborated in chapters 2 and 3. Although not practiced in fisheries, in other sectors capital goods are commonly leased or rented. The value of leased fixed assets should be included in the total value of capital of the firm. The costs are either the lease costs or calculated depreciation plus opportunity costs.

16

OECD approach and definitions

The accepted standard in relation to capital valuation is the OECD Manual ‘Measuring capital – measurement of capital stocks, consumption of fixed capital and capital services’. The main definitions used in the manual are presented below (quotation from Annex 1 of the Manual): - Gross capital stock is the value of all fixed assets still in use when a balance sheet is drawn up, at the actual

or estimated current purchasers’ prices for new assets of the same type, irrespective of the age of the assets. - Gross fixed capital formation (net investment) is measured by the total value of a producer’s acquisitions, less

disposals, of fixed assets during the accounting period plus certain additions to the value of non-produced assets (such as land or subsoil assets) realised by the productive activity of institutional units.

- Gross capital formation is measured by the total value of the gross fixed capital formation, changes in inventories and acquisitions less disposals of valuables for a unit or sector.

- Consumption of fixed capital (depreciation) represents the reduction in the value of the fixed assets used in production during the accounting period resulting from physical deterioration, normal obsolescence or normal accidental damage.

- Net capital stock is the sum of the written-down values of all the fixed assets still in use when a balance sheet is drawn up.

- Net fixed capital formation consists of gross fixed capital formation less consumption of fixed capital. - The net (or written-down) value of a fixed asset is equal to the actual or estimated current purchaser’s price of

a new asset of the same type less the cumulative value of the consumption of fixed capital accrued up to that point in time.

- Tangible fixed assets are non-financial produced assets that consist of dwellings; other buildings and structures; machinery and equipment and cultivated assets.

- Intangible fixed assets are non-financial produced fixed assets that consist of mineral exploration, computer software, entertainment, literary or artistic originals and other intangible fixed assets intended to be used for more than one year.

OECD Manual uses three definitions of prices: - Constant prices - A stock of assets is expressed at constant prices when all members of the stock are valued at

the prices of a single base period. - Current prices - A stock of assets is expressed at current prices when all members of the stock are valued at

the prices of the year in question. - Historic prices - The historic price is the price that was actually paid for an asset when it was first acquired by

a resident user. It is a synonym for “acquisition price”. In the present document the concept of ‘constant prices’ is not considered relevant for the required application and consequently not used. The term current prices refers to the most recent year and is used interchangeably with ‘replacement price’. The term historic prices is used in the above meaning of ‘acquisition value’.

Micro / Macro approach with brief definitions Various approaches to capital valuation and use of different indicators are relevant depending on specific analytical needs. From the perspective of assessment of performance of fishing vessels,

17

two main approaches should be distinguished – micro and macro. Their relevance is characterized in the table below. Micro approach Macro approach Scope Individual firm level Sector and macro / society

level Type of analysis / application Fiscal accounting Economic valuation Time horizon Economic life time of the

capital good or firm Indefinite

Value used Historical value

Replacement value (current prices)

Micro / macro approach are further elaborated in chapters 2 and 3.

Vessel or company as a basic statistical unit The above overview of the structure of capital shows that in some cases data can be collected using vessel as the basic statistical unit, but in other cases it must be the total firm. The latter case refers to shore based capital, reserves, etc. Until present fisheries statistics used fundamentally the vessel as a basic unit. This applied not only to economics, but also to biologic research or to logbook data. There are various arguments for using vessel as the basic unit also in the future: - vessel and its equipment compose the most significant part of the capital, - intangibles are often related to vessel and not to firm, - in most cases, one firm owns only one vessel, so that the link between vessel and firm related

capital components is straightforward2. Consequently, capital costs of a firm which are not directly related to a specific vessel, need to be divided among the vessels belonging to that firm using some division key or assumptions. It must be stressed that this is a very common ‘problem’ in cost accounting and economics3. The only solution is to make the required assumption as realistic or acceptable as possible. In the coming years this may remain a largely artificial problem in fisheries for reasons specified above (one-man-one boat firms, vessel plus intangibles represent most of the capital value). However, should a significant concentration trend occur in the future, than the established vessel-firm accounting may have to be reconsidered.

A unique value of a vessel does not exist It is important to stress that valuation of capital (and consequently calculation of depreciation, interest or opportunity costs) is fundamentally different from keeping accounting records of operational expenses like fuel or maintenance. Capital goods can be valued in different ways, which are appropriate (or not) according to the question asked. A vessel represents a so called

2 However, in some countries (e.g. UK and NL) a significant minority of vessels is owned by fleet operators. 3 See e.g. Robert Kaplan and W. Bruns, Accounting and Management: A Field Study Perspective (Harvard Business School Press 1987 ISBN 0-87584-186-4).

18

sunk investment (i.e. money involved cannot be used for anything else). Its value can be viewed in different ways (overview is not exhaustive): - Net present value of a successfully continued operation – will depend on expectations about

future performance (revenues and costs) and assumed interest rate. - 2nd hand market price – depends on local and international supply of and demand for

comparable vessels. It may be affected by expected decommissioning schemes, which would set a bottom price.

- Book value – historical price less depreciation - Economic value 1, which would also take into account potential benefits and costs of

shifting to a new and more productive technology. - Economic value 2 – from the perspective of the society it could be even desirable to include

the environmental impact.

2. PROPOSED METHOD

2.1 PIM proposed by OECD On the basis of the theoretical considerations and current practices in many countries, it was decided to focus the common method to be developed on the Perpetual Inventory Method (PIM). This method is recommended by OECD as well as by various national statistical offices. Application of PIM is presented in the following figure 1 from OECD (2001a). OECD describes the Perpetual Inventory Method (PIM) as follows: The Perpetual Inventory Method (PIM) generates an estimate of the capital stock by accumulating past purchases of assets over their estimated service lives. The standard, or traditional, procedure is to use the PIM to estimate the gross capital stock, to apply a depreciation function to calculate consumption of fixed capital and to obtain the net capital stock by subtracting accumulated capital consumption from the gross capital stock. The traditional application of the PIM requires the direct estimation of depreciation from which the net capital stock is obtained indirectly. The basic requirements to apply the PIM to estimate the Gross Capital Stock are: - An initial benchmark estimate of the capital stock. - Statistics on gross fixed capital formation extending back to the bench-mark, or, if no bench-mark is

available, back over the life of the longest-lived asset. - Asset price indices. - Information on the average service lives of different assets. - Information on how assets are retired around the average service life (mortality functions). Provided the capital stock series go back as many years as the longest-lived asset, it is possible to estimate the capital stock without having an initial benchmark estimate. However, as the longest lived assets, usually structures, may have service lives in excess of 100 years, most countries need to start their PIM estimates with a bench-mark estimate, at least for assets with long lives. Possible sources for benchmark estimates include: - Population censuses. - Fire insurance records.

19

- Company accounts. - Administrative property records. - Share valuations. None of these sources will give an accurate estimate of precisely what is required – namely the “as new” values of assets in place at a point in time. Once the initial bench-mark of the stock has been estimated, the capital value of each following year can be updated by adding new investments (gross fixed capital formation) and subtracting depreciation and retirements. This is illustrated in figure 1.

Figure 1 Application of the PIM in practice by OECD

Source: OECD Manual, p.59

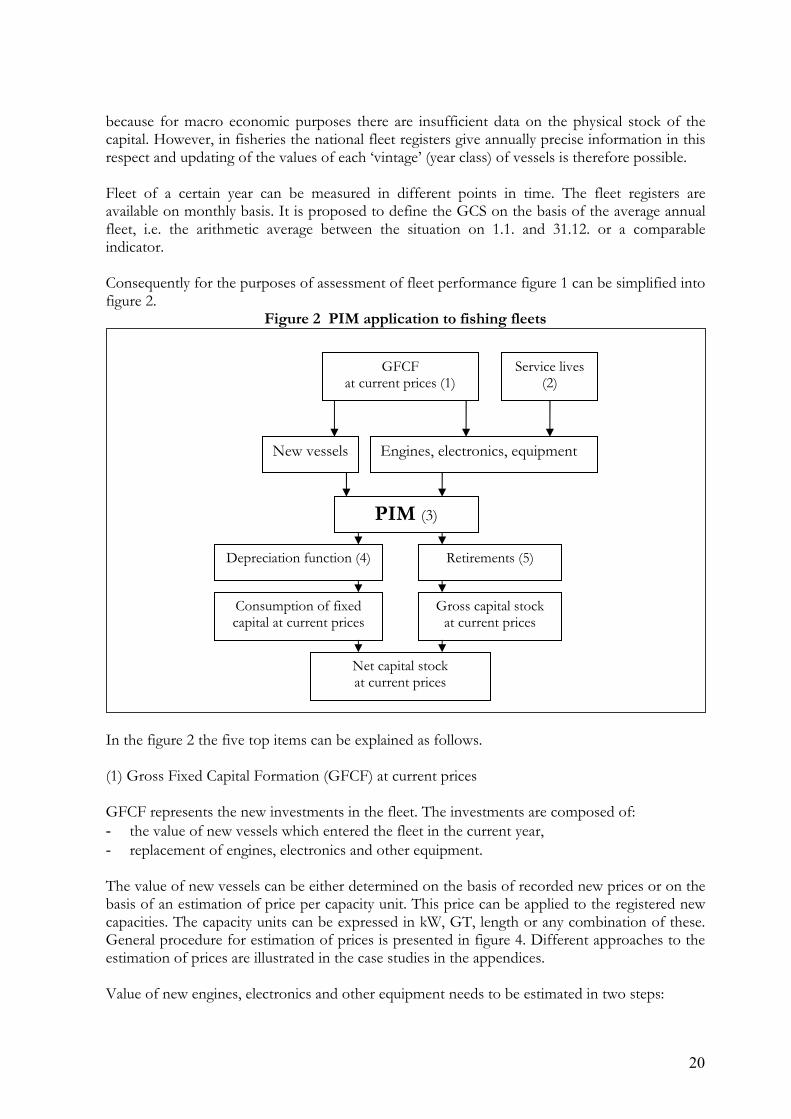

2.2 Application of PIM to fishing fleets For the application to fisheries figure 1 can be slightly reformulated and simplified. Figure 1 assumes that the value of the GCS is expressed in price level of another than the current year. Therefore it is necessary to recalculate the GFCF of the current year to the base year to obtain constant prices. In the proposed application to fisheries the entire GCS is revaluated each year to the current value, because that is analytically relevant. When data on earnings and costs refer to 2005 it does not make sense to insert capital costs referring to another year. OECD proposes specific values for service lives (average life time of an asset) and mortality functions (retirement of the asset around the service life). These functions are introduced

20

because for macro economic purposes there are insufficient data on the physical stock of the capital. However, in fisheries the national fleet registers give annually precise information in this respect and updating of the values of each ‘vintage’ (year class) of vessels is therefore possible. Fleet of a certain year can be measured in different points in time. The fleet registers are available on monthly basis. It is proposed to define the GCS on the basis of the average annual fleet, i.e. the arithmetic average between the situation on 1.1. and 31.12. or a comparable indicator. Consequently for the purposes of assessment of fleet performance figure 1 can be simplified into figure 2.

Figure 2 PIM application to fishing fleets