Essays on Macroeconomics - DiVA

469

Essays on Macroeconomics José Elías Gallegos Dago Institute for International Economic Studies Monograph Series No. 115 Doctoral Thesis in Economics at Stockholm University, Sweden 2022

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Essays on Macroeconomics - DiVA

Essays on Macroeconomics José Elías Gallegos Dago

José Elías Gallegos D

ago Essays on M

acroeconom

ics115

Institute for International Economic StudiesMonograph Series No. 115

Doctoral Thesis in Economics at Stockholm University, Sweden 2022

Department of Economics

ISBN 978-91-7911-882-2ISSN 0346-6892

José Elías Gallegos Dagoholds a M.Sc. in Economics fromUniversidad Carlos III and a B.Sc. inEconomics from UniversidadComplutense.

This thesis consists of four independent and self-contained essays ontopics within monetary policy and macroeconomics. Monetary Policy and Liquidity Constraints: Evidence from the EuroArea quantifies the relationship between the response of output tomonetary policy shocks and the share of liquidity constrainedhouseholds. Reconciling Empirics and Theory: The Behavioral Hybrid NewKeynesian Model develops and estimates a behavioral New Keynesianmodel. HANK beyond FIRE studies the interaction between financial andinformation frictions, and its consequences for the macroeconomy. Inflation Persistence, Noisy Information and the Phillips Curveexplains the fall in inflation persistence and the changes in the Phillipscurve through information frictions.

Essays on MacroeconomicsJosé Elías Gallegos Dago

Academic dissertation for the Degree of Doctor of Philosophy in Economics at StockholmUniversity to be publicly defended on Friday 10 June 2022 at 09.00 in NordenskiöldsalenGeovetenskapens hus, Svante Arrhenius väg 12.

Abstract

Monetary Policy and Liquidity Constraints: Evidence from the Euro AreaWe quantify the relationship between the response of output to monetary policy shocks and the share of liquidity

constrained households. We do so in the context of the euro area, using a Local Projections Instrumental Variablesestimation. We construct an instrument for changes in interest rates from changes in overnight indexed swap rates in anarrow time window around ECB announcements. Monetary policy shocks have heterogeneous effects on output acrosscountries. Using micro data, we show that the elasticity of output to monetary policy shocks is larger in countries that havea larger fraction of households that are liquidity constrained.

Reconciling Empirics and Theory: The Behavioral Hybrid New Keynesian ModelStructural estimates of the standard New Keynesian model are at odds with the microeconomic estimates. To reconcile

these findings, we develop and estimate a behavioral New Keynesian model augmented with backward-looking householdsand firms. We find (i) strong evidence for bounded rationality, with a cognitive discount factor estimate of 0.4 at a quarterlyfrequency; and (ii) that the behavioral setting with backward-looking agents helps us harmonize the New Keynesian theorywith empirical studies. We suggest that both cognitive discounting and anchoring are essential, first, to match the empiricalestimates for certain parameters of interest and, second, to obtain the hump-shaped and initially muted impulse-responsefunctions that we observe in empirical studies.

HANK beyond FIREThe transmission channel of monetary policy in the benchmark New Keynesian (NK) framework relies on the

counterfactual Full–Information Rational–Expectations (FIRE) assumption, both at the partial and general equilibrium(GE) dimensions. We relax the Full-Information assumption and build a Heterogeneous-Agents NK model under dispersedinformation. We find that the amplification multiplier is dampened. This result is explained by the lessened and lagged roleof GE effects in our framework. We then conduct the standard full-fledged NK analysis: we find that the determinacy regionis widened as a result of as if aggregate myopia and show that our framework beyond FIRE does not suffer from the forwardguidance puzzle. Finally, we find that transitory “animal spirits” shocks generate persistent effects in output and inflation.

Inflation Persistence, Noisy Information and the Phillips CurveA vast literature has documented that US inflation persistence has fallen in recent decades. However, this empirical

finding is difficult to explain in monetary models. Using survey data on inflation expectations, I document a positive co-movement between ex-ante average forecast errors and forecast revisions (suggesting forecast sluggishness) from 1968 to1984, but no co-movement afterwards. I extend the New Keynesian (NK) setting with noisy and dispersed informationabout the aggregate state, and show that inflation is more persistent in periods of greater forecast sluggishness. My resultsshow that the change in firm forecasting behavior, documented in survey data, explains around 90% of the fall in inflationpersistence since the mid 1980s. I also find that the disconnect between inflation and the real side of the economy inrecent decades can be explained by the change in information frictions. Contrary to the literature which has emphasizeda flattening of the NK Phillips curve in recent data, I do not find any evidence of the change in the structural slope of thePhillips curve once I control for the change in information frictions.

Keywords: Macroeconomics, Monetary Policy, Inequality, Financial Frictions, Information Frictions, NoisyInformation, Behavioral Frictions, Bounded Rationality.

Stockholm 2022http://urn.kb.se/resolve?urn=urn:nbn:se:su:diva-204070

ISBN 978-91-7911-882-2ISBN 978-91-7911-883-9ISSN 0346-6892

Department of Economics

Stockholm University, 106 91 Stockholm

ESSAYS ON MACROECONOMICS

José Elías Gallegos Dago

Essays on Macroeconomics

José Elías Gallegos Dago

©José Elías Gallegos Dago, Stockholm University 2022 ISBN print 978-91-7911-882-2ISBN PDF 978-91-7911-883-9ISSN 0346-6892 Cover picture: "The Scream, Oil, Tempera and Pastel on Cardboard", Edvard Munch ©Munchmuseet. Back-cover photo by Cecilia López-Diéguez Piñar. Printed in Sweden by Universitetsservice US-AB, Stockholm 2022

To José Elías

Doctoral DissertationDepartment of EconomicsStockholm University

Abstracts

Monetary Policy and Liquidity Constraints: Evidence from theEuro Area We quantify the relationship between the response of out-put to monetary policy shocks and the share of liquidity constrainedhouseholds. We do so in the context of the euro area, using a Local Pro-jections Instrumental Variables estimation. We construct an instrumentfor changes in interest rates from changes in overnight indexed swap ratesin a narrow time window around ECB announcements. Monetary policyshocks have heterogeneous effects on output across countries. Using mi-cro data, we show that the elasticity of output to monetary policy shocksis larger in countries that have a larger fraction of households that areliquidity constrained.

Reconciling Empirics and Theory: The Behavioral HybridNew Keynesian Model Structural estimates of the standard New Key-nesian model are at odds with the microeconomic estimates. To recon-cile these findings, we develop and estimate a behavioral New Keynesianmodel augmented with backward-looking households and firms. We find(i) strong evidence for bounded rationality, with a cognitive discountfactor estimate of 0.4 at a quarterly frequency; and (ii) that the behav-ioral setting with backward-looking agents helps us harmonize the NewKeynesian theory with empirical studies. We suggest that both cognitivediscounting and anchoring are essential, first, to match the empiricalestimates for certain parameters of interest and, second, to obtain thehump-shaped and initially muted impulse-response functions that we ob-serve in empirical studies.

HANK beyond FIRE The transmission channel of monetary pol-icy in the benchmark New Keynesian (NK) framework relies on theFull–Information Rational–Expectations (FIRE) assumption, both at the

partial and general equilibrium (GE) dimensions. We relax the Full–Information assumption and build a Heterogeneous-Agents NK modelunder dispersed information. We find that the amplification multiplieris dampened. This result is explained by the lessened and lagged role ofGE effects in our framework. We then conduct the standard full-fledgedNK analysis: we find that the determinacy region is widened as a resultof as if aggregate myopia and show that our framework beyond FIREdoes not suffer from the forward guidance puzzle. Finally, we find thattransitory “animal spirits” shocks generate persistent effects in outputand inflation.

Inflation Persistence, Noisy Information and the PhillipsCurve A vast literature has documented that US inflation persistencehas fallen in recent decades. However, this empirical finding is difficult toexplain in monetary models. Using survey data on inflation expectations,I document a positive co-movement between ex-ante average forecast er-rors and forecast revisions (suggesting forecast sluggishness) from 1968to 1984, but no co-movement afterwards. I extend the New Keynesian(NK) setting with noisy and dispersed information about the aggregatestate, and show that inflation is more persistent in periods of greaterforecast sluggishness. My results show that the change in firm forecast-ing behavior, documented in survey data, explains around 90% of the fallin inflation persistence since the mid 1980s. I also find that the discon-nect between inflation and the real side of the economy in recent decadescan be explained by the change in information frictions. Contrary to theliterature which has emphasized a flattening of the NK Phillips curve inrecent data, I do not find any evidence of the change in the structuralslope of the Phillips curve once I control for the change in informationfrictions.

Acknowledgments

“This is not the end. It is not even the beginning of the end.But it is, perhaps, the end of the beginning.”

Winston Churchill, 1942.

Dear reader,

This will probably be the most read part of this thesis. I encourageyou to read the introduction, in case you might be interested in theresults and evidence I find, and we can discuss them whenever you want.But I have to be frank with you. Reading the articles in detail is goingto be tedious.

Given these circumstances, I have reserved these lines to tell you, inconfidence and with an open heart, the adventures (and misadventures)that this experience as a doctoral student has brought to me. I couldnot start this section without honestly confessing to you that I considermyself the luckiest person in the world. It is frankly surprising that, everytime I have been exposed to randomness in my life, I have been lucky.Different situations come to mind. Choosing economics without havingfull knowledge of what it entailed, being able to access the bachelor’sdegree with a grade of five out of ten, meeting professors who encouragedme to continue specializing with a master’s degree, and who pushed forme to be admitted to the doctorate in Stockholm, that the IIES selectedme as a doctoral student, and that it gave me the possibility to studyfor a year at Harvard, and finally to find a job at the Banco de España,where I had always dreamed of working. In each of those moments theroad could have been twisted, and all the successes I celebrate todaywould be nothing more than a dream. That is why, I insist on confessingto you, I think I am the luckiest person in the world.

I would like to dedicate a few lines to remember the people who havesupported and helped me the most in these years. First of all, my eternalthanks to my supervisors, Alex and Per. Here comes again the fortune

that I had told you before. First, I sincerely believe that Alex is the mostintrinsically intelligent person at the IIES, and to have his help has beenwonderful. I met Alex through a math course I took at the IIES, andthen I went deeper with a course on imperfect expectations in macroeco-nomics. Although I was passionate about the subject, I found it equallyimpenetrable. However, I continued to be interested in those topics be-cause I saw how fundamentally exciting they were for Alex. Another ofthe qualities that I highlight most about Alex is his closeness. The pa-per thanks to which I got the job at the Banco de España was writtenmainly during the darkest times of the COVID-19 pandemic. Imagine,reader, how insecure I felt working on a subject that was mathematicallycomplex from the home office. However, I had the invaluable support ofAlex, whom I frequently stole time to ask questions and discuss the re-sults I was obtaining. I can say, without a doubt, that this thesis wouldnot have been possible without Alex.

I met Per a little later, when I asked him for a meeting because Iwanted to apply for a PhD student position at the IIES. To put yourselfin a situation: Per is probably the most reputable macroeconomist inSweden, and one of the most reputable in the world. Imagine my surprisewhen I entered his office, and I found a warm person who also spoke tome in Spanish. From Per I have learned what a true academic is. Honestwith the truth, fussy with details, relentless in the face of mediocrity,and a fantastic person outside of work.1 If I have already told you thatmy thesis would not be possible without Alex, I can also tell you thatits level would not have been possible without Per. His deep scientifichonesty has pushed me to my limits on so many occasions that, obviously,it has been reflected in the product. I thank them for the accompanimentduring this journey, especially during the job market in which they werealways available to speak and offer me their help.

I also want to thank the rest of the IIES macroeconomics community.In particular Tobi, who supported me decisively in the labor market. I

1I can also confirm that his football team is not so fantastic.

also remember the hours that Timo, Gustavo, John, Kieran, Kurt, Joshuaand Yimei dedicated to me. I do not know if ever in my life I will everlisten to such intellectually stimulating cateries as the ones we have inthe Macro Group. Outside of macroeconomics, I have enjoyed discussionswith Ingvild, Tessa, Konrad, Jon, Mitch, Arash, Laia, Torsten, Peter,David, Jakob and Anna. A million thanks to them for being interestedin my research topics.

During my year in Boston I was fortunate (again) to meet brilliantscholars from both Harvard and MIT, who were also very generous withtheir time. That is why I thank Xavier, Pol, Iván, Arnaud, Dave, Martín,Emmanuel and Gita for all the comments they made to me and thewarmth with which they made them to me. It was an unforgettableexperience.

Of course, dear reader, I also remember my professors in Spain. AtComplutense I had the incalculable fortune of coinciding with José An-tonio, who transmitted to me the passion for economics. At Carlos III,Luisa was an essential support to get to come to Stockholm to do thedoctorate. Without them, this wonderful journey would not have evenbegun.

I would also like to thank my patient and brilliant co-authors:Mattias, John, Ricardo, Atahan, Richard and Edgar. Certainly, I havelearned more from them than they have been able to learn from me. Iam mainly sticking with Mattias’ logic and economic thinking, thinkingmore outside of the model corset than I do, and how perfectionist andinsightful John is. I would love to look more like them.

Throughout this adventure I have met wonderful people. In my firstyear I spent most of my time with Julian, Francesco and Max. In thesecond year I discovered Luis and Markus. In the third year, my first ofmarriage, Marc, Martin and Miguel Ángel welcomed us with open arms.In the fourth I met Gualti, Stefan and Sebastian, with whom I have hadlunch every day here. In the fifth year I met Juan and Tiago. With allof them I have had wonderful moments.2

2It has been the intense interaction with them that motivated me to explore de-

I have also had wonderful colleagues both on IMDb and outside:Agneta, Iacopo, Dom, Max, Tillmann, Mamarz, Ida, Philipp, Carolina,Evelina, Patrizia, Fredrik, Markus P., Sreyashi, Marijo, Fabian, Xueping,Claire, Binnur, Joakim, Andrew, Domenico, Andrea, Divya, Richard,Markus K., Karin, Kasper, Benni, Has, Serena, Saman, Jaakko, Jonna,Jósef, Sirus, Karl, Mathias, Matilda, Hannes and Erik. From each of themI have learned something, and I have enjoyed very happy moments.

Finally, I would like to thank Christina, Ulrika, Hanna, Tove andKarl. Christina, apart from being the leader of an administrative areathat works fantastically, has been the person who has helped me proof-reading the thesis. I thank her very much for that. Furthermore, I thankUlrika for her help in the printing process in the very last moment.

Outside of academia, I have been fortunate for having started a familyhere. With Uge, Elena, Pepe and Raquel I have learned what is it liketo have a family when ours is far away. They have made this adventuremuch more fun.

In these years in Sweden I have missed my family very much. Theyare the ones who have suffered me when I gave my unsolicited opinions,both on the economy and on other issues. I especially remember Tito,who taught me to program in Mathematica and was a great help for thethesis. Thanks to my grandparents, uncles, cousins, and nephews. I amnot easy to bear.

As for the closest family, dear reader, what am I going to tell yougiven how well you know me. I am a very family-oriented person. WhatI am, I am thanks to them. Thanks to Papá and Mamá not only for theeducation they gave me, but for always giving me their sincere opinioneven though it may contradict what I would like to hear. I know theyhave not agreed with all the steps I have taken in my career, but it makesme very happy to have arrived at a port that makes us all proud. I couldnot have had better parents. As for my siblings, the same. My eternalgratitude to Tití, Paula, Jaime, Jorge and Quique for being as they are

viations from rationality in my research.

with me. Finally, a message: be calm, I found a job. Only took me 30years.

Now that I have gone over people, let me go on to remember a partic-ularly bittersweet moment that keeps repeating itself in my head everyday. On 22 March 2016 I formally received the PhD offer from Jörgen,and just 5 days later I had to send a reply. I knew that it was an offerI could not refuse, but also that the costs were unbearable. I rememberanswering yes between sobs. I knew that leaving my home, my city, andmy life could affect my friendships and my courtship with Cecilia, and Iwas certain that I was saying goodbye to my grandparents, with whomI probably would not have time to say goodbye. And so it was. I hopethey will be able to forgive me for the time together I stole from them.

These years I have had the immense fortune of living in a city likeStockholm. I have lived for the first time in a city with sea, which is alsoa great capital, with a tranquility that I will miss for the rest of my life.Here I have also lived the premieres of Star Wars (on Wednesdays!) andthree Champions League titles for Real Madrid. But what I will alwaysbe grateful to Stockholm for is for giving me the greatest gift I have everreceived: our little suequito. A souvenir for a lifetime. Only the tree isleft.

And what about Cecilia. My life changed when I met her. I still won-der what have I done to make me worthy of her perfectionism, generosityand unconditional love that have shaped me so much.3 She has been theone who has supported the family in the most tense moments. And theone who has put aside her career to join this wonderful adventure thathas taken us to Stockholm, Boston and our first baby. I could not beluckier.

Finally, I wanted to leave the last lines for you, José Elías. If you arehere, receiving compliments and reaping fruits, it is because other JoséElías got up at 5 in the morning or went to bed at 3 in the morningworking. Be aware of it, and fight for your dreams. If they take you to

3From time to time I pinch myself to realize that, for real, I am dating CeciliaLópez-Diéguez, aka the popu.

academia, so it will be. If you are taken to the post of governor, so itwill be. And if they take you into politics, so it will be. Fight intenselyfor each of them, so that the José Elías of the future is as proud of youas I am now of the José Elías of the past.

When I was little I frequently read interviews with footballplayers, my idols. In them, they said they were fulfillinga dream by playing for Real Madrid. I had other dreams,perhaps more mundane, but I knew that dreams are notfulfilled except for a small number of lucky ones. Today, onJune 10, I can say the same thing as my football idols: dreams come true.

An affectionate greeting,

José Elías Gallegos DagoStockholm, Sweden

June 2022

Contents

Introduction i

1 Monetary Policy and Liquidity Constraints: Evidencefrom the Euro Area 11.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . 21.2 Effects of Monetary Policy Shocks on Output . . . . . . . 71.3 Measuring Financial Constraints . . . . . . . . . . . . . . 141.4 Liquidity Constrained Households and Monetary Policy

Effectiveness . . . . . . . . . . . . . . . . . . . . . . . . . . 211.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . 41References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 431.A Income elasticities . . . . . . . . . . . . . . . . . . . . . . 491.B Additional Figures and Tables . . . . . . . . . . . . . . . . 521.C The Global VAR Setting . . . . . . . . . . . . . . . . . . . 571.D Panel LPIV . . . . . . . . . . . . . . . . . . . . . . . . . . 611.E European Overnight Indexed Swap Data . . . . . . . . . . 641.F Obtaining HtM Shares Using Data from the HFCS . . . . 641.G Tenure Status, Mortgages and HtM Status . . . . . . . . . 681.H Local Projections Data . . . . . . . . . . . . . . . . . . . . 71

2 Reconciling Empirics and Theory: The Behavioral Hy-brid New Keynesian Model 752.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . 762.2 The Behavioral Agents and Firms Setting . . . . . . . . . 82

CONTENTS

2.3 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . 922.4 Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . 962.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . 105References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1072.A Model Derivation . . . . . . . . . . . . . . . . . . . . . . . 1142.B Robustness Checks . . . . . . . . . . . . . . . . . . . . . . 1292.C Narrative VAR Identification . . . . . . . . . . . . . . . . 130

3 HANK beyond FIRE 1333.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . 1343.2 The Analytical HANK Model . . . . . . . . . . . . . . . . 1403.3 Information Structure and Equilibrium Dynamics . . . . . 1513.4 Applications and Additional Insights . . . . . . . . . . . . 1563.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . 185References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1873.A Proofs of Propositions in Main Text . . . . . . . . . . . . 1923.B Useful Mathematical Concepts . . . . . . . . . . . . . . . 245

4 Inflation Persistence, Noisy Information and the PhillipsCurve 2494.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . 2504.2 Empirical Challenges . . . . . . . . . . . . . . . . . . . . . 2554.3 Evidence on Information Frictions . . . . . . . . . . . . . 2614.4 Noisy Information . . . . . . . . . . . . . . . . . . . . . . 2664.5 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2804.6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . 289References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2914.A Proofs of Propositions in Main Text . . . . . . . . . . . . 2994.B Robustness on Inflation Persistence and Information Fric-

tions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3294.C Extending Information Frictions to Households . . . . . . 3504.D Persistence in NK Models . . . . . . . . . . . . . . . . . . 3544.E History of Fed’s Gradual Transparency . . . . . . . . . . . 363

CONTENTS

4.F Model Derivation . . . . . . . . . . . . . . . . . . . . . . . 3674.G Extensions to the Benchmark New Keynesian Model . . . 3884.H Useful Mathematical Concepts . . . . . . . . . . . . . . . 413

Sammanfattning (Swedish Summary) 416

CONTENTS

Introduction

This thesis consists of four independent and self-contained essays ontopics within monetary policy and macroeconomics. Although each es-say contributes to a specialized topic, they can be said to have a commondenominator. All essays are, at least in part, an investigation into theimportance of various frictions and their implication for understandingthe behavior of households, firms, and the effect of monetary policy.If individuals face frictions such as borrowing constraints, bounded ra-tionality or dispersed information, monetary shocks and central bankactions have different implications as compared to traditional models,such as representative agent models, in which ex-ante identical individ-uals act as a representative or average agent. In this dissertation I doc-ument, theoretically and empirically, that the aforementioned frictionshave consequences for the overall power of monetary policy, the recon-ciliation between micro and macro parameters, the role of partial andgeneral equilibrium effects, the forward guidance puzzle, the foundationof animal spirits shocks, the fall in the persistence of inflation in recentdecades and the flattening of the Phillips curve.

Having provided the reader with this overall summary, I now proceedto summarize the findings and the contribution of each essay in turn.

Monetary Policy and Borrowing Constraints In this strand of myresearch agenda I am interested in understanding how household wealthheterogeneity affects the transmission of aggregate shocks in the econ-omy. In Monetary Policy and Liquidity Constraints: Evidence from the

i

ii INTRODUCTION

Euro Area (American Economic Journal: Macroeconomics, forthcoming)Mattias Almgren, John Kramer, Ricardo Lima (graduate students at theIIES) and I provide empirical evidence for a mechanism, the amplifica-tion of shocks by financially constrained households, present in modernmonetary models that include household wealth heterogeneity.

Heterogeneous agent models which include constrained agents canhave different policy implications than their representative agent coun-terparts, but empirical evidence on how heterogeneity matters for thetransmission from monetary policy to output is scant. This strand ofthe literature argues that, under household heterogeneity, the partialequilibrium effect (the one arising from households’ consumption-savingoptimal choice) is dampened and the general equilibrium effect (arisingfrom second-order effects on prices, wages and firms’ profits) is enlarged.Whether this framework produces a larger (smaller) effect of monetarypolicy shocks on output will depend on model assumptions.

The theoretical mechanism at play is the following. Consider an econ-omy with financially constrained households and optimizers. A monetaryshock affects consumption through a substitution effect mandated by theoptimizers’ Euler condition, which we denote as the partial equilibrium(PE) effect. Households’ consumption demand is affected, firms adapt tothe new demand schedule and wages (endogenous to labor demand andsupply) in turn change. This income effect through wages affects finan-cially constrained agents, which exhibit large MPCs, and will magnifythe effects of monetary policy. We denote this second round as the gen-eral equilibrium (GE) effect. Under plausible assumptions, constrainedhouseholds amplify the effect of monetary policy.

We quantify the relationship between the response of output to mon-etary policy shocks and the share of liquidity constrained households. Wefocus on the euro area, where member countries have been exposed tothe common monetary policy conducted by the European Central Bank(ECB) since the introduction of their shared currency. However, becauseof long-standing country idiosyncrasies and slow convergence, they stilldiffer along many dimensions, including the share of liquidity constrained

iii

households, as we show. Since we choose this “bird’s eye view”, we canconduct a standard monetary policy analysis, while taking wealth andincome heterogeneity and its influence on output responses into account.

First, we estimate output impulse response functions (IRFs) atmonthly frequencies for each country to the same monetary policyshocks, using Local Projections (LP). Because of endogeneity concernsbetween policy rate changes and output responses, we augment the LPestimation with an instrumental variable (IV) framework. We usehigh-frequency movements in Overnight Indexed Swap (OIS) rates ina 45-minute time window around ECB policy announcements as aninstrument for monetary policy surprises. Because OIS are forwardlooking interest rate derivatives, large rate movements during thewindow imply that ECB’s announcement was not in line with themarket expectations. The identifying assumption is that this measure isuncorrelated with other shocks to output.

In the second part of the paper, we incorporate the income and as-set dimensions by relating the IRFs to the share of liquidity constrainedhouseholds in each country. The idea is that a higher fraction of house-holds less able to smooth the income fluctuations caused by monetarypolicy shocks may lead to a stronger aggregate output response in acountry. While it is not possible to directly measure the fraction, weapproximate it by classifying households in the Household Finance andConsumption Survey (HFCS) as Hand-to-Mouth (HtM) or non-HtM.They show that such a measure is strongly correlated with estimates ofmarginal propensities to consume (MPC). Since the HFCS can only pro-vide data on recent years, we complement it with data from the EuropeanUnion Survey on Income and Living Conditions (EU-SILC), which hasbeen conducted since 2005. In this survey, participating households areasked whether they could finance an unexpected financial expense, fromwhich we infer whether they are financially constrained. Both surveyspoint to a large variation across countries in the share of constrainedconsumers and the pattern is broadly consistent over time.

Our first finding is that, in line with the previous literature, out-

iv INTRODUCTION

put responses to a common European monetary policy surprise are nothomogeneous across countries. There is a significant heterogeneity interms of cumulative impact and peak values. Second, all our measuresof the fraction of liquidity constrained households are significantly cor-related with the strength of the IRFs. On average, countries with higherfractions of liquidity constrained households exhibit stronger cumulativeoutput responses and bigger peak responses to an unexpected interestrate change. We show that the results are driven by the “wealthy HtM”,i.e. households with low levels of liquid wealth, but positive and possiblylarge levels of illiquid wealth. In addition, we calculate aggregate outputIRFs for a constrained and a less-constrained group of countries. Thetwo responses are significantly different at most horizons, with the moreconstrained countries reacting more strongly to the common shock.

The results we present are important for several reasons. First, ourfindings suggest that heterogeneity in the composition of household bal-ance sheets across countries affects the transmission of monetary policyto their economies. The finding that a higher share of low-liquidity house-holds amplifies the output response to an unexpected interest rate changecan guide future theoretical and quantitative work on monetary policy ina Heterogeneous Agent New Keynesian framework. Understanding thereasons for the differences we uncover is crucial in order to calibrate fu-ture policies. Second, we show that LP methods can be used to estimatethe impact of monetary policy for countries within a currency union.Lastly, our results are robust across different specifications of liquidityconstraints.

Importantly, our findings support the notion that research on mon-etary policy needs to account for heterogeneity across the income andwealth distributions. Furthermore, they imply that liquidity is an im-portant factor in how monetary policy shocks affect households and thereal economy. Additional empirical research is needed, however, to un-derstand the mechanism through which this heterogeneity in liquiditydirectly shapes the responses of output to monetary policy shocks. Weconsider this to be a fruitful avenue for future research.

v

Monetary Policy and Bounded Rationality In this strand of myresearch agenda I am interested in reconciling macro-estimated parame-ters with their micro counterpart. In Reconciling Empirics and Theory:The Behavioral Hybrid New Keynesian Model, Atahan Afsar, RichardJaimes, Edgar Silgado and I start from the observation that a set ofmacro-estimated structural estimates of the standard New Keynesianmodel are at odds with the microeconomic estimates. To reconcile thesefindings, we develop and estimate a behavioral New Keynesian modelaugmented with backward-looking households and firms.

An important characteristic of the standard New Keynesian (NK)model is that it can be synthesized in a system of two first-order stochas-tic difference equations that are easy to interpret: the Dynamic IS curveor the demand side, and the Phillips curve or the supply side. Everyslope in these curves is a combination of different parameters in themodel, namely the discount factor, the degree of risk aversion, the Frischelasticity and the Calvo-fairy probability. As a result, by estimating theslopes of the final system of equations, one can retrieve the structuralparameters of the model. However, when the monetary economics liter-ature performed such analyses, the estimated parameters were at oddswith the microeconometric studies.

Our contribution to the literature is threefold. First, we extend thebounded rationality NK setting to allow for household habit persistenceand firm price indexation, inducing anchoring in the model dynamics.Second, we estimate all the structural parameters behind the coefficientsin the behavioral DIS and hybrid NK Phillips curves using Bayesian tech-niques. Thus, we reconcile three key parameters in the theory that wereat odds with the empirical evidence: the subjective discount factor, thedegree of external habits, and the degree of price stickiness. Third, wealso find empirical evidence for considerable bounded rationality behav-ior, supporting the deviation from the standard fully rational behavioralframework. A salient feature of our model is that it can easily be reducedto the benchmark by turning off certain key parameters such as the de-gree of habit persistence, the degree of price indexation, or the bounded

vi INTRODUCTION

rationality parameter. As a result, our model nests those frameworks andallows us to easily compare the estimates.

On the behavioral dimension, we assume an attention coefficient thatthe decision-makers on both sides of the economy assign to a piece ofnewly arriving information, so that the posterior expectation is a convexcombination of the prior mean and the realization value. We follow thisreduced-form approach for two main reasons. First, our core interestis to reconcile the theory with empirical evidence, and this behavioralapproximation of a limited attention model affords us to arrive at thesimple closed-form solutions that are typical of the standard NK modelwhile incorporating the first-order effects of limited inattention. Second,since we estimate this coefficient in our two-sided economy, explicitlymodeling the cost structure and estimating the cost coefficient wouldadd an extra layer without necessarily providing any further insight.

Cognitive discounting is successful in producing myopia but does notproduce anchoring on its own. In fact, when we estimate the forward-looking model, we find an excessively low cognitive discount factor, bi-ased towards zero due to the anchoring that we observe in the data andthat, thus, the model is unable to produce. We find that the cognitive dis-count factor, together with habit persistence and price indexation, is keyfor obtaining macro estimates that align with their micro counterparts,and its estimated coefficient is nearly twice as large as in the benchmarkcase with no backward-looking agents. The cognitive discount factor in-creases the relative weight of the past (anchoring) and reduces the weightof the future (myopia).

For the estimation of the structural parameters, we follow a Bayesianapproach that allows a transparent comparison across models. We es-timate four different models: the standard NK model, the hybrid NKmodel, the behavioral NK model, and the behavioral hybrid NK model.We show that cognitive discounting is successful in producing myopiabut does not produce anchoring on its own. In fact, when we estimatethe behavioral NK model, we find an excessively low bounded rationalityparameter, biased towards zero due to the anchoring that we observe in

vii

the data and that the model is unable to produce. Finally, in order to testthe ability of our set of models to replicate empirical impulse-responsefunctions, we compare them with an estimated monetary policy shock.We find that only our Behavioral NK model with both habit formationand backward-looking firms is able to generate, at the same time, hump-shaped responses and as much output and inflation persistence as weobserve in the data.

We find strong evidence of aggregate myopia, with a cognitive dis-count factor estimate of 0.4 at a quarterly frequency, and we reconcilethree key parameters in the theory that were at odds with the empiricalevidence: the subjective discount factor, the degree of external habits,and the degree of price stickiness.

Monetary Policy and Noisy Information In this strand of my re-search agenda I am interested in understanding how information frictionsaffect the transmission of monetary shocks in the economy.

In HANK beyond FIRE I study the interaction between wealth in-equality and information frictions. There is mounting evidence that in-equality and information frictions are quantitatively relevant and matterfor the transmission of aggregate shocks. The share of financially re-stricted agents is estimated to be 34% in the U.S., in an upward trendsince 2001, and around 31% in Europe with some countries exhibit-ing values greater than 40%. Recent empirical evidence suggests thateconomies with a larger degree of inequality respond more to fiscal andmonetary shocks. On the other hand, surveys of expectations to con-sumers, firms and professional forecasters suggest that agents’ expecta-tions differ significantly from the Full Information Rational Expectations(FIRE) benchmark, thus giving rise to an aggregate underreaction tonews in average forecasts. At the same time, empirical evidence suggeststhat households’ and firms’ aggregate underreaction reduces the effect ofaggregate shocks.

To understand the mechanism of the interaction of these two forces ina clean and transparent manner, I build a tractable heterogeneous agents

viii INTRODUCTION

New Keynesian (HANK) model. Despite its simplicity, this frameworkcaptures the key micro-heterogeneity inputs of the quantitative liter-ature: cyclical inequality, idiosyncratic risk and precautionary savings,which together generate heterogeneous marginal propensities to consume(MPCs). The transmission channel, as discussed under “Monetary Policyand Borrowing Constraints”, relies heavily on the FIRE assumption: notonly are agents (households and firms) perfectly aware that an aggregateshock has occurred, but they are also certain that others have observedit, that others are aware that others have observed it, ad infinitum. Inparticular, the step at which the GE effects kick in, the change in wagesand their income effect, depends deeply on the FIRE assumption. It isat this step when the financially constrained agents magnify the aggre-gate response, since their high MPC interacts with the aggregate wagerate change, giving in turn the well-known amplification result. In thispaper we are interested in exploring whether this result is robust to amicro-consistent deviation from the FIRE assumption.

I couple the HA dimension with a deviation from the benchmarkFIRE assumption. In particular, I assume that agents form rational ex-pectations but have imperfect and dispersed information. In the standardFIRE setting, agents face no uncertainty about the exogenous fundamen-tal, and since the information sets are homogenous across individuals, onothers’ actions. In this paper I accommodate any such doubts. At theindividual level, agents do not only need to forecast the exogenous fun-damental (the monetary policy shock) but also aggregate variables thatare endogenous to individual actions (output and inflation). As a result,an agent needs to predict other agents’ actions.

I find that the magnitude of the amplification multiplier is damp-ened in the dispersed information framework, in which partial equilib-rium (PE) effects initially dominate general equilibrium (GE) effects,compared to the FIRE case. In this private and dispersed informationeconomy, agents need to forecast the exogenous fundamental and aggre-gate inflation and output. While the information friction environmentcomplicates the forecast of the fundamental, it does not give rise to any

ix

higher-order beliefs since the realization does not depend on others’ ac-tions and an agent does not need to predict others’ beliefs about thefundamental. However, forecasting aggregate output and inflation hasthe additional complication of having to deal with higher-order beliefs.In the standard framework, the role of higher-order beliefs is null sincethey coincide with first-order beliefs, whereas in our case higher-orderbeliefs differ from first-order beliefs, and move less than lower-order be-liefs since they are more anchored to the prior. As a product of this, theexpectations of aggregate variables adjust little to the news, and the GEeffect is attenuated.

The main consequence of the different PE vs. GE role is that ag-gregate dynamics will initially be entirely driven by PE effects. Aftersome periods and a sequence of signals, agents will learn that a mon-etary policy shock has occurred, and the aggregate dynamics will relymore and more on GE effects, until the PE vs. GE share converges to thefull information benchmark. Formally, imperfect information reduces thedegree of complementarity of actions across agents, and partially mutesthe amplification multiplier mechanism that critically relies on them. Ifind that (i) the peak response of output is about 1/3 of that in the FIREcase; (ii) impulse responses are hump-shaped, which the standard FIREframework can only produce if there is habit formation, price indexationand lumpy investment; and (iii) when income inequality is countercycli-cal, the response of output after a monetary policy shock is amplified byaround 6%, compared to 10% in the benchmark model. That is, dispersedinformation effectively reduces the amplification multiplier.

I use the theory to shed some light on other questions of first-order im-portance. We find that our framework produces hump-shaped IRFs with-out resorting to ad-hoc micro-inconsistent adjustment costs in habits,pricing or investment decisions. Instead, we microfound aggregate slug-gishness using dispersed information and expectation formation sluggish-ness, for which we provide empirical evidence. This results in a differentPE vs. GE role than in standard FIRE models. We also show that dis-persed information produces “as if” myopia, which extends the equilib-

x INTRODUCTION

rium determinacy region, and is crucial for the solution of the forwardguidance puzzle. Finally, we find that “animal spirits” or belief transitoryshocks produce large and persistent effects in output and inflation.

As in standard noisy information models, individual forecasts of en-dogenous aggregate variables are anchored to agents’ own priors. Becauseexpectations play a key role in determining aggregate variables in modernmacroeconomics, anchoring in expectations effectively translates into ag-gregate anchoring in endogenous aggregate variables and myopia towardsthe future. These two results, taken together, enlarge the determinacyregion of interest rate rules and solve the forward guidance puzzle (FGP).In the NK framework the determinacy result is ultimately linked to theforward-looking behavior of the model equations. The Taylor rule pro-vides an essential stabilization role, and an excessively dovish monetaryauthority ends up creating explosive dynamics in the model equations.Adding information frictions produces aggregate myopia and widens thedeterminacy region. Similarly, the FGP is solved by dispersed informa-tion via the introduction of aggregate myopia.

The last contribution is to study expectation shocks. We considerthe case of public information, and we show that although the non-fundamental shock is only transitory, its effects are persistent. Becauseagents cannot fully disentangle whether the shock to the signal that theyhave observed comes from the fundamental monetary policy rule or thenon-fundamental noise part, the “animal spirits” shock partially inheritsthe properties of the pure monetary shock, which in turn explains itspersistent consequences. In a second extension we consider both publicand private information. We find that monetary policy is more effectiveand closer to the FIRE benchmark, and the effect of belief shocks islessened, as a result of effectively reducing the degree of informationfrictions by including an additional signal.

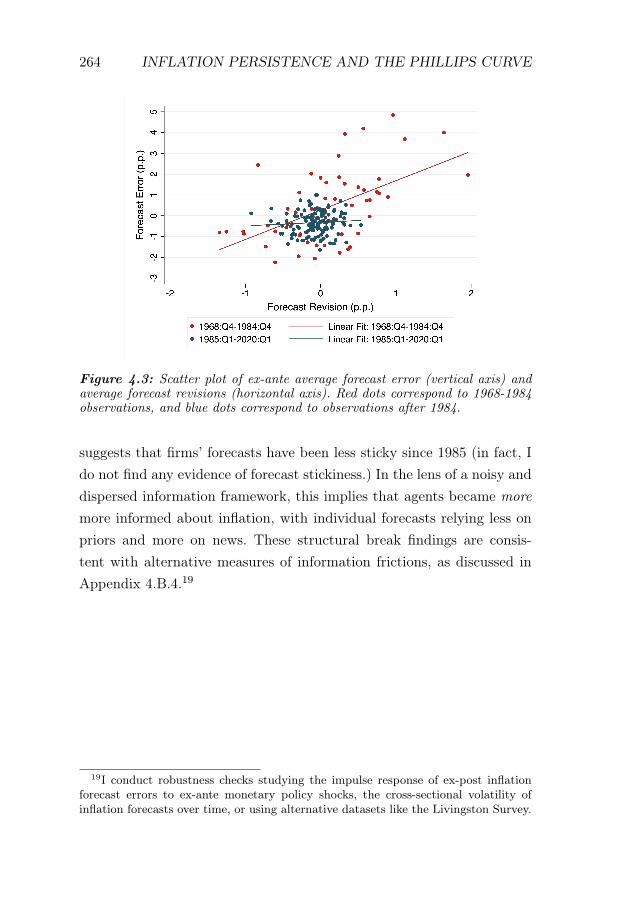

In Inflation Persistence, Noisy Information and the Phillips CurveI show that a change in firm belief formation in the 1980s can help usunderstand two empirical challenges in the literature: the fall in inflationpersistence and the flattening of the Phillips curve. Using survey data on

xi

US firms’ forecasts, I document sluggishness in responses to informationuntil the 1980s, but no evidence of sluggishness afterwards. This breakcoincides with a change in the communication policy of the US FederalReserve, which became more transparent after the 1980s.

Expectations have played a central role in macroeconomics for a longperiod of time. However, most of the work considers a limited theory ofexpectation formation, in which agents are perfectly and homogeneouslyaware of the state of nature and others’ actions. In this paper, I embed atheory of expectation formation that incorporates significant heterogene-ity and sluggishness in agents’ forecasts into an otherwise standard NKmodel by introducing noisy and dispersed information about the centralbank action. I use this framework to interpret two empirical challengesin the literature: the fall in inflation persistence and the flattening of thePhillips curve.

As for the first empirical challenge, inflation exhibits a high degreeof persistence from the 1960s up until the mid 1980s, falling significantlysince then. This fall in inflation persistence is not easily understoodthrough the lens of monetary models, which has resulted in the infla-tion persistence puzzle. This break coincides with a change in the USFederal Reserve’s communication policy, which became more transpar-ent and informative after the mid 1980s.

Using survey data on US Professional Forecasters and Livingston,I document a positive co-movement between ex-ante average forecasterrors and forecast revisions (suggesting forecast sluggishness) until themid 1980s, but no evidence of co-movement afterwards. This positiveco-movement is informative about forecast sluggishness. It implies thatpositive forecast revisions predict positive forecast errors, thus suggestingthat updated forecasts fall short in predicting inflation.

The theoretical framework I build is consistent with this evidence. Iargue that the change in the Fed communication improves firms’ infor-mation and I use my model to show that the reduced stickiness in firms’inflation forecasts explains the fall in inflation persistence. I assume thatfirms do not have complete and perfect information about the aggregate

xii INTRODUCTION

economic conditions. They observe a noisy signal that provides informa-tion on the state of the economy, the monetary policy shock in this case.In terms of the details of my model, I explain the fall in inflation persis-tence through a decrease in the degree of information frictions that firmsface on central bank actions. I show that inflation is more persistent inperiods of greater forecast sluggishness. Noisy information generates anunderreaction to new information because individuals shrink their fore-casts towards prior beliefs when the signals they observe are noisy. Sinceinflation depends on the expectations of future inflation, the change inexpectation formation feeds into inflation dynamics, which endogenouslyreduces the inflation persistence. I find that this change in firm forecast-ing behavior explains around 90% of the fall in inflation persistence sincethe mid 1980s.

The second empirical challenge documents that the Phillips curvehas flattened in recent decades, implying that inflation is less affected byother real variables (the inflation disconnect puzzle). I study the dynam-ics of the Phillips curve over time through the lens of my model. Theprevious literature has documented a fall in the sensitivity of inflationand the real side of the economy. This finding implies that central bankactions, understood as nominal interest rate changes, are less effective inaffecting inflation. In the standard model, the inflation dynamics are re-duced to the Phillips curve, which relates current inflation to the currentoutput gap and expected future inflation. The only possible explanationfor the lack of dependence of inflation on output is a fall in the slope.The literature has focused extensively on this slope, in the hope of doc-umenting that this relation has weakened and that the inflation processis therefore largely independent of any change from the demand side ofthe economy, including changes in the policy rate.

I argue from the perspective of my model that the Phillips curve isenlarged with a backward-looking term on lagged inflation and myopiatowards expected future inflation. Once I correct for the misspecificationin the Phillips curve, there is no evidence of a fall in its slope, but evidenceof a reshuffling from backward-lookingness towards forward-lookingness.

xiii

I also show that, under a general information structure, the Phillipscurve is modified such that current inflation is related to current andfuture output through two different channels: the slope of the Phillipscurve and firms’ expectation formation process. I show that there is noempirical evidence of a change in the slope once I control for a declinein information frictions, using SPF forecasts.

In summary, contrary to the literature which has emphasized a flat-tening of the NK Phillips curve in recent data, I do not find any evidenceof the change in the structural slope once I control for imperfect expec-tations.

xiv INTRODUCTION

Chapter 1

Monetary Policy andLiquidity Constraints:Evidence from the EuroArea∗

∗This chapter has been jointly written with Mattias Almgren, John Kramer and Ri-cardo Lima. We are grateful to Tobias Broer, Per Krusell, Kurt Mitman and KathrinSchlafman for their advice and support. Further, we would like to thank the editorGiorgio Primiceri, four anonymous referees, Adrien Auclert, Martín Beraja, MitchDowney, Xavier Gabaix, Alessandro Galesi, Pierre-Olivier Gourinchas, John Hassler,Greg Kaplan, Peter Karadi, Karin Kinnerud, Kasper Kragh-Sørensen, Jesper Lindé,Benjamin Moll, Haroon Mumtaz, Morten Ravn, Ricardo Reis, Giovanni Ricco, Fed-erica Romei, Maria Sandström, David Schönholtzer, Jósef Sigurdsson, Xueping Sun,Javier Vallés, Has van Vlokhoven, Iván Werning and seminar participants at theIIES, Queen Mary University of London, Stanford University, Stockholm University,Stockholm School of Economics, Università Bocconi and Yale University for usefulfeedback and comments. Björn Hagströmer generously aided us in accessing the swap-rate data. José-Elías Gallegos and John Kramer gratefully acknowledge funding fromthe Tom Hedelius foundation. This paper uses data from the Eurosystem HouseholdFinance and Consumption Survey. The results published and the related observationsand analysis may not correspond to results or analysis of the data producers.

1

2 MONETARY POLICY AND LIQUIDITY CONSTRAINTS

1.1 Introduction

In 2016, 30 percent of households in Germany reported that they couldnot meet an unexpected, immediate financial expense of 985 euros. Atthe same time, 40 percent of Italian households reported that they wereunable to meet an unexpected expense of 800 euros.1 Figures like thesesuggest that a significant portion of households hold little liquid assets,which potentially makes them vulnerable to unexpected shocks to theeconomy. Especially in monetary economics, these households have re-ceived special attention recently.

While theoretical research has shown that heterogeneous agent mod-els which include constrained agents can have different policy implica-tions than their representative agent counterparts, empirical evidence onhow heterogeneity matters for the transmission from monetary policy tooutput is scant.2 In this paper we provide such evidence, showing that ahigher share of liquidity constrained households in a country is associatedwith a stronger output response to a monetary policy surprise.

We focus on the euro area, where member countries have been ex-posed to the common monetary policy conducted by the European Cen-tral Bank (ECB) since the introduction of their shared currency. How-ever, because of long-standing country idiosyncrasies and slow conver-gence, they still differ along many dimensions, including the share of liq-uidity constrained households, as we show. Since we choose this “bird’seye view”, we can conduct standard monetary policy analysis, while tak-ing account of wealth and income heterogeneity and its influence onoutput responses.

First, we estimate output impulse response functions (IRFs) atmonthly frequencies for each country to the same monetary policy

1According to the European Union Survey of Income and Living conditions. Themonetary values represent the country-specific at-risk-of-poverty threshold, definedas 60 % of the national median equivalized disposable income after social transfers.

2See e.g., Bilbiie (2008) for an early theoretical contribution in a two agent settingor Auclert (2019) and Hagedorn et al. (2019) for a setting with fully heterogeneousagents.

INTRODUCTION 3

shocks, relying on the Local Projection (LP) approach pioneered byJordà (2005).3 Because of endogeneity concerns between policy ratechanges and output responses, we augment the LP estimation withan instrumental variable (IV) framework Stock and Watson (2018).4

We use high-frequency movements in Overnight Indexed Swap (OIS)rates in a 45 minute time window around ECB policy announcementsas an instrument for monetary policy surprises. Because OIS areforward looking interest rate derivatives, large rate movements duringthe window imply that the ECB’s announcement was not in line withmarket expectations. The identifying assumption is that this measure isuncorrelated with other shocks to output.

In the second part of the paper, we incorporate the income and as-set dimensions by relating the IRFs to the share of liquidity constrainedhouseholds in each country. The idea is that a higher fraction of house-holds less able to smooth the income fluctuations caused by monetarypolicy shocks may lead to a stronger aggregate output response in acountry. While it is not possible to measure the fraction directly, weapproximate it by classifying households in the Household Finance andConsumption Survey European Central Bank, HFCS as Hand-to-Mouth(HtM) or non-HtM according to a measure proposed by Kaplan et al.(2014). They show that such measure is strongly correlated with esti-mates of marginal propensities to consume (MPC). Since the HFCS canonly provide data on recent years, we complement it with data from theEuropean Union Survey on Income and Living Conditions (EU-SILC),which has been conducted since 2005. In it, participating households

3Mandler et al. (2016) investigate a similar question using a Bayesian VAR for thefour largest economies in the euro area: Germany, Italy, Spain and France. Altavillaet al. (2016) investigate heterogeneous effects of Outright Monetary Transactions(OMT) on the same countries, similarly employing a VAR framework.

4As a robustness check to our main empirical framework, we construct an instru-mented Global VAR (GVAR) based on Georgiadis (2015) and Burriel and Galesi(2018). We build a more structural –and restricted– setting than the LPIV, moresimilar to the widespread VAR estimation in the literature, identifying monetary re-sponses in a GVAR setting using exogenous instruments. To our knowledge, we arethe first to estimate such an instrumented GVAR. We find similar results.

4 MONETARY POLICY AND LIQUIDITY CONSTRAINTS

are asked whether they could finance an unexpected financial expense,from which we infer whether they are financially constrained. Both sur-veys point to large variation across countries in the share of constrainedconsumers and the pattern is broadly consistent over time.

Our first finding is that, in line with previous literature, output re-sponses to a common European monetary policy surprise are not ho-mogeneous across countries. There is significant heterogeneity in termsof cumulative impact and peak values. Secondly, all of our measures ofthe fraction of liquidity constrained households are significantly corre-lated with the strength of the IRFs. On average, countries with higherfractions of liquidity constrained households exhibit stronger cumulativeoutput responses and bigger peak responses to an unexpected interestrate change. For the measure constructed according to Kaplan et al.(2014), we show that the results are driven by the “wealthy HtM”, i.e.households with low levels of liquid wealth, but positive and possiblylarge levels of illiquid wealth. In addition, we calculate aggregate outputIRFs for a constrained and a less-constrained group of countries. Thetwo responses are significantly different at most horizons, with the moreconstrained countries reacting more strongly to the common shock.

The results we present are important for several reasons. First, ourfindings suggest that heterogeneity in the composition of household bal-ance sheets across countries affects the transmission of monetary policyto their economies. The finding that a higher share of low-liquidity house-holds amplifies the output response to an unexpected interest rate changecan guide future theoretical and quantitative work on monetary policy ina Heterogeneous Agent New Keynesian framework. Understanding thereasons for the differences we uncover is crucial in order to calibrate fu-ture policies. Second, we show that LP methods can be used to estimatethe impact of monetary policy for countries within a currency union.Lastly, our results are robust across different specifications of liquidityconstraints, corroborating the measure put forth by Kaplan et al. (2014).

Our research is related to several strands of literature. There is alarge body of research which performs cross-country monetary policy

INTRODUCTION 5

analysis. An early example is Gerlach and Smets (1995) who performa Structural VAR analysis of the G-7 countries and find that responsesto country-specific monetary policy shocks are similar. Mandler et al.(2016), using a large Bayesian VAR, show that output in Spain is lessresponsive to monetary policy, compared to Germany, France and Italy,while prices in Germany respond most within this set or countries. Fewpapers estimate IRFs for multiple countries and try to investigate thetransmission mechanism of monetary policy by relating their findings tocountry characteristics. Two recent examples, both of which use a GlobalVAR (GVAR) method, are Georgiadis (2015) and Burriel and Galesi(2018). Both papers find heterogeneous responses of real GDP acrosscountries and explain some of the variation with wage rigidities and thefragility of the banking sector. Calza et al. (2013) provide evidence thatin countries where the use of flexible mortgage rates is more prevalent,responses to monetary policy shocks are stronger and Corsetti et al.(2021) find that the responses of output and private consumption arelarger in countries where home ownership rates are higher. We try toaccount for previous findings by conducting several robustness checks.

To our knowledge, we are the first to use OIS rates as an instru-ment to identify a cross-country LP estimation in the euro area. Kuttner(2001), Nakamura and Steinsson (2018) and Gertler and Karadi (2015)use high-frequency movements in Federal Funds futures rates in a shortwindow around the Federal Reserve’s policy announcements to identifymonetary policy surprises in the U.S. In the European context, there areno financial instruments equivalent to Fed funds futures which has ledresearchers to employ high-frequency movements in OIS rates instead.Ampudia and van den Heuvel (2019) and Jarociński and Karadi (2020)construct monetary policy shocks from movements in these derivatives.

The empirical results in this paper tie in with the results from theo-retical two-agent New Keynesian (TANK) models such as those in Bilbiie(2008), Galí et al. (2007) and Bilbiie (2020), as well as richer models byGornemann et al. (2016), Werning (2015), Auclert (2019) and Hagedornet al. (2019). As laid out by Bilbiie (2019), a result these models have in

6 MONETARY POLICY AND LIQUIDITY CONSTRAINTS

common is that whether aggregate shocks have bigger or smaller effectson aggregate consumption, compared to the representative agent frame-work, is ambiguous. In a model that combines the tractability of TANKmodels with the most important elements of heterogeneneous agent mod-els, Bilbiie (2019) shows that the output response to shocks is amplifiedif the income elasticity of constrained agents with respect to aggregateincome is larger than one. He refers to this case as cyclical income in-equality; a channel which is strengthened if a larger fraction of agents isconstrained.5 This is in line with our empirical findings, which can guidefuture modeling efforts aimed at understanding the interaction betweenaggregate and distributional outcomes in response to shocks.

Lastly, our findings imply that it is important to separately treatliquid and illiquid assets when describing the wealth distribution of aneconomy. This is in support of the view that wealthy households canhave high marginal propensities to consume, as pointed out by Kaplanet al. (2014), Kaplan and Violante (2014) and Kaplan et al. (2018).6

The paper proceeds as follows. In section 1.2, we describe our identi-fication strategy, how we estimate country-specific local projections andpresent the resulting IRFs. Section 1.3 discusses how we construct theproxies for the fraction of liquidity constrained households across coun-tries. Section 1.4 relates the IRFs to our measures of the fraction ofliquidity constrained households across countries. Section 1.5 concludes.

5In models that focus on the cyclicality of income risk (e.g., Werning, 2015), am-plification of aggregate shocks is caused by an increase in the probability of becomingconstraint for the unconstrained, which leads the latter to save more and consumeless. Our empirical analysis, however, focuses mainly on the level of the HtM shares,as opposed to their changes, and is therefore more closely related to Bilbiie (2019).

6Using data from Norwegian lottery winners, Fagereng et al. (2021) find thathouseholds at the highest liquidity quartile have a significantly lower MPC thanhouseholds at the lowest liquidity quartile.

1.2. EFFECTS OF MONETARY POLICY SHOCKS ON OUTPUT 7

1.2 Effects of Monetary Policy Shocks on Output

1.2.1 Identifying Monetary Policy Shocks

In order to estimate the effects of monetary policy to a variable of interestwe need to identify unexpected deviations from an interest rate rule. Toidentify these in the United States, researchers have used high frequencymovements in Federal Funds futures in a narrow time window aroundannouncements by the Federal Reserve Kuttner (2001), Nakamura andSteinsson (2018). More recently, Ampudia and van den Heuvel (2019)and Jarociński and Karadi (2020) apply the approach to European datausing Overnight Indexed Swap (OIS) rate movements around ECB an-nouncements. These derivatives are traded over-the-counter between twoparties exchanging a fixed interest rate for the floating Eonia overnightinterest rate, both on a notional principal, for a pre-specified amount oftime. Since the principal is not exchanged at any time and the contractsare highly collateralized, there is only minimal counterparty credit risk.When the contract ends, the difference between (i) the fixed interest ac-crued on the principal and (ii) the interest accrued on the principal byinvesting it at the overnight interest rate every day is calculated and thecontract is cash settled.7

We follow the literature and use changes in Eonia OIS during a shorttime window around the ECB’s monetary policy announcement and thesubsequent press conference as our instrument Jarociński and Karadi(2020).8 On days when the Governing Council of the ECB decides thepolicy rate for the euro area, the decision is communicated to the pub-lic via a press statement at 13:45 CET and motivated during a pressconference chaired by the president and vice-president at 14:30 CET.We construct a time series encompassing all such monetary policy an-

7For a detailed discussion of similarities between federal funds futures andovernight indexed swaps, see Lloyd (2020).

8We obtain time series on OIS rates at the minute frequency from Datascope,using the #RIC EUREON3M= and EUREON1Y=. The time format is GMT/UTC.For more information, see Appendix 1.E.

8 MONETARY POLICY AND LIQUIDITY CONSTRAINTS

nouncements by the ECB, starting in December 19999. Figure 1.1 dis-plays the OIS rate on July 5, 2012. The first window starts 15 minutesbefore the press release and ends 30 minutes after. The second windowstarts 15 minutes before the beginning of the press conference and ends30 minutes after. To construct our instrument, on each announcementdate, we calculate the change in the average OIS rates of the pre- andpost-windows for both the press statement and the press conference andthen sum the two.

The OIS can be viewed as an indicator for expectations about futureovernight interest rates in the European interbank market. Hence, a sig-nificant change in the OIS rates shortly after an ECB monetary policyannouncement implies that the content of the announcement was at leastpartly unexpected. The identifying assumption is that there is no otherinformation released during the time window that is systematically re-lated to the policy decision and that the market has access to the sameinformation about economic fundamentals as the ECB. As pointed out byJarociński and Karadi (2020), many of the Bank of England’s announce-ment dates coincide with announcement dates of the ECB, with policystatements released at 13:00 CET and 13:45 CET, respectively. Thismakes the high-frequency approach especially important in our setting.The use of instruments measured at the daily frequency would confoundthe effect of the former and the latter.

We use the 3 month OIS rate obtained from Datascope. To convertthe instrument series obtained in this way to monthly frequency, wefollow Gertler and Karadi (2015). Because the announcement days are atdifferent times during each month, we weigh each observation accordingto when in a month it occurred. Let ad be the cumulative shock series

9To construct monetary shocks starting from January 2000, we start collectingmovements in OIS rates from December 1999, due to the way we construct our in-strument (see below).

EFFECTS OF MONETARY POLICY SHOCKS 9

.12

.14

.16

.18

.2.2

23

Mon

th E

ON

IA O

IS

12:30:00 13:53:20 15:16:40 16:40:00Time

Figure 1.1: Overnight Indexed Swap rates on 05.07.2012.

Note: This figure shows the time series of the 3 month EONIA Overnight IndexedSwap for July 5, 2012. The blue lines represent the borders of our measurementwindows, the red lines indicate the policy events, i.e. the ECB’s press release at 13:45CET and the start of the press conference at 14:30 CET. The first pre-window runsfrom 13:30-13:44 CET and then the first post-window is active between 13:45-14:14CET. Then a second pre-window runs from 14:15-14:29 CET and the second post-window is active between 14:30-14:59 CET.

10 MONETARY POLICY AND LIQUIDITY CONSTRAINTS

at day d in the month, which evolves in the following way

ad =

ad−1 + ∆fd if announcement at day dad−1 otherwise

where ∆fd is the change in the OIS rates calculated as described above.We then weight the series according to

Ft =1Dm

∑d∈m

ad

where Dm is the number of days in month m. Finally, the instrumentfor each month t is

Zt = Ft − Ft−1.

1.2.2 The Effect of Monetary Policy Shocks on Output

We follow Jordà (2005) and Stock and Watson (2018) and estimate theresponse of output to monetary policy shocks using the local projec-tions instrumental variable (LPIV) method, employing the instrumentdiscussed in the previous section. Impulse responses, for each country n,are constructed from the sequence βhnHh=0 from the estimated equations

yn,t+h − yn,t−1 = αhn + βhnit +

p∑j=1

Γhn,jXt−j + un,t+h, h = 0, . . . ,H

(1.1)

where yn is log of output in country n, X is a set of control variablesand i are the fitted values from the first-stage regression10

it = c+ ρZt +

p∑j=1

Dhj Xt−j + et (1.2)

10For a detailed description of the data series used we refer the reader to Appendix1.H.

EFFECTS OF MONETARY POLICY SHOCKS 11

As a benchmark we set the number of lags to p = 3 and the horizon ofthe impulse responses to H = 36.11 In all specifications we include theinterest rate (i), the instrument Z, aggregate euro area output and theprice level in our set of control variables, X.12,13 Notice that Equation(1.2) resembles standard Taylor rule for the ECB: the current interestrate depends on lags of euro area output and inflation, plus lags on theinterest rate itself.14

Our dependent variable, monthly GDP, is measured as the logarithmof real GDP. Given that GDP is only available at quarterly frequencywe follow Chow and Lin (1971) to interpolate real GDP into a monthlyfrequency.15 We use the Euro Overnight Index Average (EONIA) as themonetary policy rate and the logarithm of the deseasonalized Harmo-nized Index of Consumer Prices (HICP) as the measure of the aggregateprice level. We use data from January 2000 to December 2012, capturingthe initial stages of the adoption of the euro and ending during the yearwhen the interest rate hit the zero lower bound.

Figure 1.2 presents impulse responses of real GDP for each countryin our sample to an expansionary shock of one standard deviation inour instrument, following Jarociński and Karadi (2020). The IRFs are

11We also estimate specifications in which the number of lags is allowed to varyacross the countries using the Akaike Information Criteria (AIC). Doing so leaves theresults unaltered and therefore, for simplicity, we choose the same number of lags forall countries.

12As pointed out by Ramey (2016), the construction of the instrument as in Gertlerand Karadi (2015) introduces auto-correlation into the instrument, invalidating ouridentifying assumptions. To alleviate this problem, we include the instrument in ad-dition to the other control variables in X.

13Removing the set of lagged control variables in (1.2), specially the interest rate,leads to very low F-statistics. Since the interest rate is persistent, contemporaneousshocks account for only a small part of its variance. Furthermore, of the contemporaryshocks, the monetary policy shock is only a fraction. Therefore, the explanatory powerof the instrument alone on the interest rate can be expected to be fairly low Stockand Watson (2018). The first state F-statistic in our benchmark specification is 17.42.

14As a robustness check, we conduct the same exercise, including country-specificlags in Equation (1.2), leading to country specific first-stage regressions and countryspecific i s. The results are reported in Figure 1.11 in the Appendix.

15For each euro area country as well as the aggregate euro area we use monthlydata for industrial production, retail trade and unemployment to construct monthlyseries for real GDP.

12 MONETARY POLICY AND LIQUIDITY CONSTRAINTS

represented by the blue lines and, following Stock and Watson (2018),we construct 1 and 2 standard deviation confidence bands that surroundthe point estimates, using Newey-West estimators.16

The estimated impulse response functions reveal that expansionarymonetary policy shocks cause output to increase in most countries. Out-put increases significantly after little less than a year, with the maximumimpact most often occurring later. The response of aggregate euro areaoutput, for example, reaches its peak of 0.23 percentage points after 27months.

There is considerable heterogeneity in the magnitude of theresponses, both in peak and cumulative effect. Moreover, the initialimpacts of monetary policy shocks seem to be on average small andoften not statistically different from zero.

Using the results from Georgiadis (2015) as a proxy for the VARcounterpart of our analysis, we find that the peak values are stronglycorrelated for the subset of countries that overlap with his sample, witha correlation coefficient of approximately 0.84.17 Given that the relativepositions of countries is important for the analysis in the upcoming sec-tion, we consider it to be reassuring that our estimates are in line withthe findings in Georgiadis (2015).

We proceed now by relating the strength of the output responses tothe share of liquidity constrained households in each country.

16The local projection impulse responses for prices are presented in Figure 1.12 inthe Appendix.

17Georgiadis (2015) estimates responses for Austria, Belgium, Finland, France, Ger-many, Greece, Ireland, Italy, Netherlands, Portugal, Slovakia, Slovenia and Spain.

EFFECTS OF MONETARY POLICY SHOCKS 13

0.0

0.5

1.0

0 10 20 30

Out

put (

%)

Austria

0.0

0.5

1.0

0 10 20 30

Belgium

0.0

0.5

1.0

0 10 20 30

Cyprus

0.0

0.5

1.0

0 10 20 30

Estonia

0.0

0.5

1.0

0 10 20 30

Out

put (

%)

Finland

0.0

0.5

1.0

0 10 20 30

France

0.0

0.5

1.0

0 10 20 30

Germany

0.0

0.5

1.0

0 10 20 30

Greece

0.0

0.5

1.0

0 10 20 30

Out

put (

%)

Ireland

0.0

0.5

1.0

0 10 20 30

Italy

0.0

0.5

1.0

0 10 20 30

Latvia

0.0

0.5

1.0

0 10 20 30

Lithuania

0.0

0.5

1.0

0 10 20 30

Out

put (

%)

Luxembourg

0.0

0.5

1.0

0 10 20 30

Malta

0.0

0.5

1.0

0 10 20 30

Netherlands

0.0

0.5

1.0

0 10 20 30

Portugal

0.0

0.5

1.0

0 10 20 30Horizon

Out

put (

%)

Slovakia

0.0

0.5

1.0

0 10 20 30Horizon

Slovenia

0.0

0.5

1.0

0 10 20 30Horizon

Spain

0.0

0.5

1.0

0 10 20 30Horizon

Euro area

Figure 1.2: Impulse responses for output in euro area countries – LPIV.

Note: This figure shows impulse responses of real GDP to an expansionary monetarypolicy shock of one standard deviation. For each euro area country, the response isestimated using LPIV (Equation 1.1). The solid blue lines represent the IRFs producedby our preferred specification (see text for details). The dark and light blue shadedareas represent 1 and 2 standard deviation confidence bands, respectively, constructedusing Newey-West estimators.

14 MONETARY POLICY AND LIQUIDITY CONSTRAINTS

1.3 Measuring Financial Constraints

Bilbiie (2020) describes a TANK economy in which household hetero-geneity is collapsed to being either financially constrained or not. Takingthis idea to the data, our aim is to construct variables that measure thedegree of financial constraints in a given country. To do so, we rely onthe Eurosystem Household Finance and Consumption Survey (HFCS)and the European Union Statistics on Income and Living Conditions(EU–SILC). In the next subsections, we describe these datasets and theconstruction of our measures for financial constraints used in the subse-quent analysis.

1.3.1 The Household Finance and Consumption Survey

The HFCS is conducted by the Household Finance and ConsumptionNetwork (HFCN), tasked by the Governing Council of the ECB. Thesurvey is modeled after the U.S. Survey of Consumer Finances and isharmonized across the euro area, set up to collect micro data on house-hold finances Honkkila and Kavonius (2013). It contains data from in-terviews with over 84,000 households. Three waves have been conducted,with data releases in 2013, 2016 and 2020. In our main analysis, we relyon data from the second wave.

In approximating the share of households who have high MPC, wefollow Kaplan et al. (2014).18 A household is categorized as living HtMif its liquid wealth is smaller than a certain share of monthly income. Intheir set of countries, the share of HtM households is between 20 to 35percent Kaplan et al. (2014).19

Let mi denote liquid assets, ai denote illiquid assets, yi denote in-come and mi be a credit limit for household i.20 We categorize a house-