enroll and be successful in college transfer level mathematics.

260

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of enroll and be successful in college transfer level mathematics.

A. Bridging the Gap Initiative Project Goals

• To double the number of students who, upon graduation from high school, will enroll and be successful in college transfer level mathematics.

• To redefine and implement new math pathways (grades 6-16) in a Linked

Learning context.

B. Project Overview Proposed Partnership The Peralta Community College District (PCCD), in partnership with Oakland Unified School District, Berkeley Unified School District, and California State University East Bay, have formed a partnership (a subset of our broader East Bay Career Pathways Consortium and our East Bay Linked Learning Hub of Excellence) to further integrate and expand our policies and practices to create successful student secondary to postsecondary transitions. As part of a commitment to ensure all students in Oakland and Berkeley graduate from college, the Mayors of both cities are currently leading efforts to establish “College Promise” initiatives that will align with and support the proposed pilot project. Background Our proposed pilot project will build on the work our high schools and community colleges have been doing for two years – with the assistance of the California Community College Linked Learning Initiative (CCCLLI) and the Career Pathways Trust (CPT) – to address some of the well known inter-segmental barriers between our systems: mathematics assessment, mathematics placement, early outreach and counseling, early exposure to college level work aligned to a career pathway rooted in rigorous academics, and a meaningful sequence of work-based learning related to a student’s pathway. Additionally, the pilot project will build on extensive work within OUSD and BUSD to upgrade to Common Core State Standards, including new Board Policy in both districts outlining course sequences for secondary mathematics. During the past year, our region has made tremendous strides in each area: Assessment and Placement: This year, PCCD launched an Improved Placement Initiative and is participating in the statewide Multiple Measures Assessment Pilot (MMAP) as part of the Common Assessment Initiative. Last year, Peralta English and math faculty from all four of the Peralta Colleges collaborated and agreed to adopt the MMAP framework for placement based on GPA and transcript data. In addition, PCCD now has student transcript data sharing agreements with our partner K12 Districts enabling the District to provide Peralta Counselors easy access to the recommended placement information.

Early Outreach and Integrated Counseling: The Peralta Colleges are adding Outreach Specialists embedded in their counseling departments and OUSD has added counselors at high schools. Last year, teams from each high school partnered with each of the Peralta Colleges to bring graduating seniors to the campuses, tour CTE and other classrooms, and meet faculty and students. Peralta counselors and Outreach Specialists visited the high schools to conduct information, assessment, and initial placements based on student transcript data. Early College Credit: Also this year, PCCD and Oakland Unified School District negotiated and adopted an 18-month pilot MOU to facilitate and scale the number of opportunities for students to earn early college credit via dual enrollment. This semester, Peralta instructors are teaching more than 15 college courses at Oakland high school campuses. Next semester, we anticipate that number quadrupling. In the next few months, PCCD will be negotiating with all of the K12 Districts in our region to form College and Career Access Pathways (CCAP0 partnership agreements per AB 288) that build off of the pilot with OUSD. Work-based Learning: Our region is building significant capacity to increase the number of employers connected with students and educators in a variety of levels, K-14. Workforce Coordinators at the college campuses, Work-based Learning Specialists at the high schools and ROP’s, Workforce Development Board staff, local Chambers of Commerce, community-based organizations and others are hiring staff so that there is greater capacity for offering work-based learning opportunities. These new personnel will help prepare students for the world of work, collaborate with each other to scale the quantity and quality of employers connecting with both students and faculty, and support our local CTE pathway action teams to refine the sequence of work-based learning in each pathway K-14. The East Bay Hub of Excellence, hosted at the Oakland Metropolitan Chamber of Commerce, is just now hiring staff to help convene and facilitate this broad set of interests and align them on behalf of students. Transition To Common Core State Standards (CCSS): Over the past 4 years, OUSD and BUSD have made significant strides to provide development and learning opportunities for teachers, TK-12, and to upgrade systems to support students to reach and exceed the higher demands of the Common Core Standards. To date, the work has included professional development for teachers, a curriculum overhaul, and new assessments. In addition, the districts have worked on Board Policy outlining the math course sequencing, grades 6-12, to include significant math content increases at the middle grades, and a strategy to align resources to ensure all students have access to the math content tested at the end of 11th grade, through the Smarter Balanced Assessment Consortium (SBAC), to determine readiness for college and career.

New Opportunities

Recent developments at the state level have created new opportunities for our region to further integrate and expand our efforts:

1. The recent announcement by the CSU Office of the Chancellor’s General Education Advisory Committee that CSU “authorizes temporary recognition of statistics pathways curriculum in satisfaction of the Quantitative Reasoning requirement for transfer admission and completion of lower-division coursework in general education.”

2. The passage of AB 288 (Holden) which specifies that regional partnership agreements “shall certify that any remedial course taught by community college faculty at a partnering high school campus shall be offered only to high school students who do not meet their grade level standard in math, English, or both on an interim assessment in grade 10 or 11, as determined by the partnering school district, and shall involve a collaborative effort between high school and community college faculty to deliver an innovative remediation course as an intervention in the student’s junior or senior year to ensure the student is prepared for college-level work upon graduation.”

The CSU announcement opens up an exciting opportunity to bring CSU East Bay into our K-14 Linked Learning pathway work, particularly in the context of the idea that there may be many college and career pathways and, in particular, “many math pathways.” The CSU (and University of California) decision to allow for a “statistics pathway” opens the door for secondary and community college partners to explore differentiated pathways, rather than a singular mathematics progression. AB 288 strengthens our ability to integrate academic content standards, aligned with college and career opportunities, to ensure that all students experience rigorous academics that maximize articulation between high school and postsecondary without the need for remediation. AB 288 offers a unique opportunity to accelerate completion of credentials, certificates, and degrees. Our partnership is proposing to build on both the CSU and AB 288 developments to focus in on rethinking math pathways grades 6-16, with a particular emphasis on the use of the 12th grade to address any need for remediation or acceleration in math in the context of students’ many college and career pathway options. Description of Proposed Pilot Project Our partnership reflected on the Bridging the Gap Framework and spent quite a bit of time on the pros and cons of choosing different “slices” of the Framework on which to focus. In our region, we are fortunate in that we have CCCLLI, CPT, and other resources to support our work across the Framework and the spectrum of student momentum. Our goal was to identify an area for this project that is firmly embedded and which supports all of the other work we are doing to: build robust Linked Learning pathways K-14, accelerate access to college, explore transition curricula and opportunities for early college credit, enhance our Improved Placement Initiative and

provide more student supports during the transition process. We also recognize that extending the partnership and framework to include the 4-year institutions is critical and we look forward to jumping on that opportunity in the context of this project. In the end, our Partnership chose to propose work focused on grade 6-16 math pathways because we feel it will lift up and strengthen all of our other efforts and relationships while pushing us to revise our policies and practices in some key ways that will yield positive impacts across the Framework. Our math-focused project allows for deep learning and informed action in an area that is a particular pain point for our students, as revealed by data cited below. We feel that work done on this “slice” of our inter-segmental work will inform all that is simultaneously happening in various other slices: ELA and ELL, science, civic engagement, career and technical education, work-based learning, etc.). In our experience working in a complex time of major education and system change at every level, the best course is one that builds on and supports efforts that are already underway, while pushing the envelope and furthering the existing efforts in new ways. Our regional partnership proposes to dramatically increase the number of students who, upon graduation from high school, will enroll and be successful in college transfer level mathematics. Today, approximately 62% of students enrolling in the Peralta Colleges need some form of remediation in math. At CSU East Bay, 54% of incoming students require remediation in math. While Peralta’s Improved Placement Initiative will improve the accuracy of math and English placements through the use of transcript data in addition to the use of the Compass Assessment Test, preliminary analysis of that transcript data as applied to the MMAP placement rules suggests that only 25-35% of OUSD high school students enrolling in the Peralta Colleges next year will be eligible to see a positive impact from this Initiative. The remaining students have GPAs or course records that fall below the requirements of the placement rules. Berkeley City College (BCC) and College of Alameda (COA) participated in the California Acceleration Project to re-evaluate how the Colleges can accelerate the math remediation sequence, recognizing that only 17% of students who begin their Peralta experience in remedial math courses ever complete a degree or certificate, let alone transfer to CSU or UC. And only 11% of students who begin a Basic Skills math course successfully complete a transfer level math course. At California State University East Bay (CSUEB), one of the CSU system’s most diverse campuses, 54% of the Fall 2013 entering freshmen required at least one quarter of developmental (remedial) math. Of the 54% of freshmen taking remedial math, roughly one-third require the first course in a three-course sequence covering pre-Algebra, and roughly one-third of these students do not pass the course on the first try in the fall quarter (CSUEB Institutional Data, 2013). The number of first-time freshman students at CSUEB requiring developmental math, as well as developmental English, has significant implications for both first- and second-year students’ persistence and

retention, and for students’ preparation for the workforce. Students who fail to pass the developmental math sequence are subject to removal from the university once opportunities for remediation have been exhausted. To suggest, however, that the “remediation” problem will be solved by improving assessment, placement, and remediation strategy at the college-level alone misses the power and promise of inter-segmental work. This pilot project proposes to understand more deeply the secondary math course sequence context so that K-16 we can take advantage of the true opportunities that linked learning pathways afford. During our planning process, our regional partnership will study and develop strategy to:

1. Build a robust partnership so that high school, community college, and CSU East Bay math faculty and administrators are in dialogue about math pathways, including how our high school preparation and developmental math sequences can and should align and how our math assessments should be understood and embedded in the educational segments sending students to take those assessments.

2. Look at our student-level data more closely to understand together the shortcomings in existing (de facto) math pathways, and the possible math pathway alternatives and their implications for students.

3. Define equity-focused outcomes for our students: figure out what math-related opportunities, experiences and results we are actively trying to change for students, particularly students historically ill-served by our educational system.

4. Evaluate new 12th grade options in math, refine and implement new options, with a goal of offering remedial college credit bearing math courses as one of several options.

5. Seek alignment with Linked Learning pathways, capitalizing on AB 288 and the CSU announcement with respect to statistics pathways to evaluate and offer more contextualized math courses in the 11th and 12th grades.

6. Align our “Language of Math” so that all three of our educational segments are sharing the same math vocabulary. We anticipate learning from a WestEd-led cross-walk analysis of college-readiness assessments: SBAC, ELM, and the community college assessment.

7. Conduct an early pilot between BCC and Berkeley High School to start framing these questions while looking at real-time data. This coming spring, Berkeley City College will offer Math 206 at Berkeley High School and is currently redesigning their intake process to supplement the District’s Improved Placement Initiative: if a high school 12th grader successfully completes Math 206, he or she can automatically enroll in Math 13 (college level math) without having to take the assessment test. As a result, we will be able to review the impact of the modified math pathway on students, their transition to community college, the role of counselors in assisting students both before and after their senior year experience during our planning phase and adjust our implementation phase accordingly.

8. Explore options for students to migrate from one math pathway to another and back again so that students can change their mind about being on a STEM pathway.

9. Explore offering CSU developmental math courses at the community colleges. 10. Build “embedded transitions” such that the community college Common

Assessment and CSU’s Entry Level Math Assessment are embedded in the curriculum and teacher practices at each level. High school students, parents, and teachers will be aware of and exposed to each assessment and the consequences of the assessment on college and career pathways, not just their math pathway.

11. Strengthen student supports in high school and community college by providing clear guidance and professional development for counselors and other support providers in terms of a student’s math choices and their implications for assessments, ability to transition to the next segment, and career options. Build student agency and positive math identity through the course selection process. Reframe issues of “course placement” to be “course options” so that students are the empowered actor rather than the passive subject of improved systems. We need to figure out how the inclusion of student choice in the multiple measures approach will interrupt historic patterns of self-selected tracking of students of color and women out of STEM-related fields.

12. Explore opportunities for creating and even sharing a pool of math teachers. Our partners recognize that most of the remedial math courses at the community colleges are taught by part-time math faculty with little to no training in pedagogy and that all of CSU East Bay’s developmental math courses are taught by graduate students. The secondary institutions also have difficulty finding and retaining teachers that are both highly skilled in high school pedagogy and mathematics. We will strive to find solutions to this problem together and to coordinate recruitment, hiring, and professional development for teachers and faculty across the segments. A related goal is establishing a pipeline of potential math teachers from CSU East Bay to the K12’s and community colleges.

13. Explore possible changes to Peralta’s minimum qualifications for teaching developmental math. Faculty teaching lower level courses may not require a master’s degree in mathematics. This would be discussed with OUSD, BUSD, CSU East Bay as well as our faculty union and shared governance committees.

14. Anticipate programmatic and professional development implications 2-3 years out, as the proposed work begins to shift what students and faculty see as highest need.

Target Population Our target population is those high school students who, given their progression through the 11th grad11e, are at risk of not graduating or graduating without the math preparation necessary to continue in their linked learning pathway through to a certificate, diploma, or transition to a 4-year university or college. Ability to collect and share data

PCCD has data sharing agreements in place with both Oakland and Berkeley Unified School Districts. Our ability to collect and share student data related to our target population is greatly enhanced, as is the community of practice our region has built among institutional research directors across educational segments. Under the auspices of the CPT activities in our region, our IR Directors are in frequent contact and have demonstrated a willingness to work together to solve problems, innovate solutions, and improve practices. Under the auspices of this Initiative, CSU East Bay would be added to the data sharing agreements.

C. Partnership Capacity Lead Organization The Peralta Community College District will lead this effort. Math faculty and administrators from all of the Peralta Colleges, Oakland and Berkeley Unified School Districts, as well as the CSU East Bay Math Department Chair and the Institute for STEM Education, met to shape this proposal and made this decision on the basis of BCC’s and COA’s participation in the California Acceleration Project, their faculty’s development of new pre-stats curriculum, and their field-testing of an accelerated remedial math sequence over the past few years. Berkeley City College and Berkeley High School will be piloting this pre-stats class (Math 206) this spring. Our partnership will be using this pilot to evaluate some of our early thinking about math pathways. The Peralta Colleges have led our regional CCCLLI work in collaboration with OUSD, and, for the past two years, have served as the fiscal agent and lead on the work of the East Bay Career Pathways Consortium. All of the proposed partners, with the exception of CSU East Bay, are active participants in that effort and have made great strides together in terms of creating student momentum in the Bridging the Gap framework. The Peralta Colleges will serve as the fiscal agent and, as such, the employer of record for the Project Director whose assistance will benefit all of the partners by working with each partner as well as across partners.

D. Alignment and Leverage As described in the Project Overview Background section, this proposal will align with, leverage, and build upon many past and present student success initiatives in our region, including the California Career Pathways Trust, The California Community College Linked Learning Initiative, the Linked Learning District Initiative, extensive CCSS mathematics development work at the K-12 level, and recent work at CSU East Bay in rethinking their developmental math sequence. The proposed project explicitly aligns with institutional effectiveness strategies, including:

OUSD Superintendent’s Strategic Plan, Pathways to Excellence, which aims to engage every high school student in a linked learning college and career pathway by 2020, so that all students graduate college, career and community ready. This plan won community investment in the form of a parcel tax, which guarantees focused funding for high school improvement (through the linked learning approach) until 2026. Additionally, OUSD is deeply engaged in improving its various STEM pathways, with tremendous investment and support from both philanthropy and industry (e.g. Atlantic Philanthropy, Bechtel Foundation, Intel Foundation, SAP, CISCO, Chevron), and all of these pathways must have a strong math infrastructure, or students will not be prepared for STEM careers. BUSD and BCC are partners with the City of Berkeley in Berkeley 2020, a workforce and economic development vision and plan for Berkeley residents. In addition, they are both active partners with Mayor Tom Bates in crafting a “Berkeley College Promise.” BCC’s early work sharing counselors with Berkeley High and piloting an ICT pathway program under the auspices of the CCCLLI project with Skyline High School in 2013 led to a grant from SAP and a deepening of that partnership which is leading to tremendous gains for students as they transition from secondary to post-secondary. PCCD recently updated the District’s Strategic Plan which emphasizes and reinforces our implementation of each College’s Students Success Plan, Equity Plan, and so many of our current strategic initiatives which support these: CCCLLI, Career Pathways Trust, AB 104 Adult Education reform, etc. The District recently launched an Office of Student Success and Equity at the District level which will be assisting and integrating efforts at the campuses in establishing Centers for Your Educational Success (CYES) which will integrate and provide additional students supports to students aligned with each campus’ equity goals. The Peralta Colleges are, like many community colleges, launching new efforts to synthesize their development of career pathways with the priorities and initiatives identified in their Equity Plans. One recurring theme in this work is the need for improved student supports in early outreach, improved transitions to college, and a supporting environment through college. As the work we have done on college and career pathways development evolves and as counselors and English and math teachers engage in and see the impact of our Improved Placement Initiative, more attention is being focused on those issues - like those identified in this proposal - where students experience the greatest barriers. East Bay Linked Learning Hub of Excellence The proposed partners, along with our East Bay Career Pathways Consortium colleagues, are members of the East Bay Linked Learning Hub of Excellence and share the vision for that organization (hosted at the Oakland Metropolitan Chamber of Commerce) that it will serve to help scale and improve Linked Learning across the region. Already, OUSD serves as a mentor district to other districts in the

region. Chamber staff and incoming Hub staff have committed to helping the proposed partners disseminate their learning from the proposed pilot. Policies and practices that the proposed partners change as a result of this pilot will be shared across the East Bay region. Cal State East Bay (CSUEB) Adding to the emerging articulation between OUSD, BUSD, and Peralta Community Colleges, CSUEB has invested significant resources in an effort to increase students’ success in developmental math classes. Specifically, faculty from CSUEB’s Math Department have designed and are researching student outcomes associated with a new three-course (one year)sequence in which each course serves as a prerequisite for the next course in the sequence. This program is titled Changing Remedial Math (ChaRM):

• MATH 805 Introduction to Algebra: fractions, signed numbers, percentages, introduction to geometry, simplifying algebraic expressions, solving linear equations, straight lines.

• MATH 806 Elementary Algebra: Operations with integers, exponents, order of operations, solving linear equations, operations with polynomials, operations with rational expressions, complex fractions, slopes and intercepts, solving and graphing inequalities.

• MATH 807 Intermediate Algebra: Operations with algebraic expressions, exponents and radicals; linear and quadratic equations; systems of equations and inequalities; linear and quadratic functions and their graphs; elementary conic sections; word problems.

The entry point for each student is based on his or her Entry Level Math (ELM) Exam score. The grading for the remedial math courses is A, B, C, or no credit. Once students pass Math 807, the remedial math flag is lifted and they are free to take college-level classes for credit.

• The courses differ from those previously offered at CSUEB in the following seven ways: Small Class Size: Course enrollments are limited to 20 students

• Group work: Working in groups is the norm, to allow discussion, exploration, and investigation.

• Learning Progressions: Instructors have developed workbooks that are used in-lieu of traditional textbooks. This has allowed the professors to organize learning material into distinct units that address key math concepts and skills.

• Hands on, Inquiry-Based Teaching and ‘Conceptual Hooks’ for Mathematical Understanding: Instructors use concrete materials, such as two-color chips for integers, algebra tiles for expressions and equations, to introduce topics to students to help students understand and internalize the underlying

math concepts. Then instructors transition to a semi-concrete portrayal of the concrete material by using appropriate diagrams, and finally, move to the abstract. The unfolding of each new concept is handled by having students do explorations, looking for patterns on their own so that a “rule” is something they discover, rather than being told by the teacher.

• Use of Technology to Personalize Instruction: Students’ homework is conducted online during the week. The online program is ALEKS, a web-based adaptive program that uses "artificial intelligence" to learn and adjusts its math questions based on individual student performance. Students must master a skill set before moving on to the next skill set.

• Teaching for Mastery and Assessments: At the outset of the courses, students sign a contract agreeing to work with their classmates to master the course material. There are three exams over the quarter, each one covering approximately two Units. In order to pass the course, students must receive at least 70% on EACH exam. Thus, no content knowledge falls through the cracks.

CSUEB recognizes that the knowledge and background of the instructor and his/her familiarity with the curriculum is a key component of the mathematics program. It also recognizes that Master’s Degree students are often employed as lecturers to teach developmental mathematics. Thus, in addition to redesigning the developmental math courses, CSUEB has developed a one-unit Robust Teaching Associate teacher training course (Math 6005) for ChaRM instructors. The course for ChaRM instructors includes: 1) day-long orientation prior to the start of the course, 2) weekly meetings (70 minutes) to discuss math concepts found in next week’s course material, what was successful and what needs improvement, technical difficulties, and class management issues, 3) creation of a feedback loop to continually improve course materials and structure, and 4) overall support to TAs. Preliminary data suggests that the redesigned math courses have enhanced CSUEB students’ math development. During the planning phase of this proposal, partners will explore this approach as one possibility for coursework that could be offered jointly across institutions. Conclusion Our Partnership is dedicated to the work described in this proposal. We have committed to doing it, regardless of funding. Our concern is that without funding, our efforts might be delayed and more students will have to wait to see the tremendous positive impact of the work we are proposing to do together. We continue to be so grateful for the support and guidance of the James Irvine Foundation, Career Ladders Project, and the many partners supported by the James Irvine Foundation who find a way to meaningfully engage with and support our public systems for the benefit of our students. We hope to be able to work with you and our colleagues around the state on this project.

East Bay Math Pathway Partnership List of key proposed project personnel Peralta Community College District Tram Vo Kumamoto, Vice President of Instruction, Berkeley City College Kelly Pernell, Math Department Chair, Berkeley City College Daniel Najjar, Adjunct Math Faculty, Berkeley City College Vanson Nguyen, Math Department Chair, College of Alameda Kathy Williamson, Math Department Chair, Laney College Tae Soon Park, Math Department Chair, Merritt College Denise Richardson, Dean of Math and Science, Laney College Char Perlas, Dean of Applied Sciences, College of Alameda Karen Engel, Director of Economic & Workforce Development, Educational Services, Peralta Community College District Michael Orkin, Vice Chancellor, Educational Services Oakland Unified School District Phil Tucher, Director of Mathematics Barbara Shreve, Secondary Mathematics Coordinator Preston Thomas, Executive Director, College and Career Readiness Gretchen Livesey, Director, Linked Learning Berkeley Unified School District Erin Schweng, Assistant Principal, Berkeley High School Pat Sadler, Director of Special Projects, Berkeley Unified School District Donald Evans, Superintendent, Berkeley Unified School District California State University, East Bay Julie Glass, Chair, Mathematics Department Stephanie Couch, Interim Associate Vice President of Research and Director, Institute for STEM Education Bruce Simon, Associate Director, Gateways East Bay STEM Network East Bay Linked Learning Hub of Excellence (support to the Partnership) Barbara Leslie, President and CEO, Oakland Metropolitan Chamber of Commerce Rebecca Lacocque, Director, East Bay Career Pathways Consortium Linked Learning Specialist, TBD Each of the proposed partners is an established, public education institution dedicated to providing effective, quality instruction to all students and to working together to overcome institutional barriers to student success.

Regional Hub of Excellence: East Bay Linked Learning Hub of ExcellenceAmount Requested: $150,000

Expense CategoryAmount Requested

from IrvineComplete Project

BudgetSalaries

CSU East Bay Math Department Chair Julie Glass $27,621 $27,621OUSD Director of Mathematics $0 $25,000

OUSD Secondary Mathematics Coordinator $0 $25,000BUSD Assistant Principal, Berkeley High School $0 $6,000

BUSD Special Projects Director $0 $6,000Benefits

Benefits for CSU East Bay employees $518 $518Benefits for Peralta faculty(s) $2,527 $3,370

Benefits for high school faculty $2,356 $5,700Consultant(s)

Project Director (consultant) $42,000 $50,000Meeting/Convening Expenses

Friday night collaborations - food $4,000 $6,000Friday night collaborations - facilities $0 $5,000

Stipends/Release TimeAdditional release time for Peralta math faculty chairs (4x$12K) $48,000 $48,000

Stipends for Peralta additional math faculty $2,000 $10,000Stipends for high school math faculty (10x$1.6K) $10,000 $16,000

Stipends for institutional researchers at partner institutions $0 $10,000Travel/TransportationMileage to cover transportation to meetings (20 meetings x 10 people @0.58/mi x 10 miles) $1,160 $2,000Subtotal $140,182 $246,209Indirect Costs (10%) $9,818 $11,943TOTAL $150,000 $258,152

Peralta Community College District

Board of Trustees

Profiles & Area Descriptions

Bill Withrow– Area 1

Bill Withrow has a B.S. in Business from the University of Colorado and MBA in Finance from Harvard University. He

served for twenty-four years on active duty in the U.S. Navy, retiring with the rank of Captain, Supply Corps he also

worked as a financial professional for the past twenty years, retiring from Wells Fargo and Company. He served as

Mayor of Alameda and Alameda as a Councilmember. As Chair of the Board of Trustees of the Robert Lippert Founda-

tion, he helped to provide college scholarships to Alameda students and Alameda charities. Term began

11/02/2004. Current term ending 11/2016.

Meredith Brown, President— Area 2

Meredith Brown has over 20 years of experience in complex litigation and representing public agencies. She received

her Bachelor of Science from Cornell University and her Juris Doctor Degree from Boston University School of Law. Ms.

Brown served as a clerk for United States Magistrate Joyce London Alexander, First Circuit in Boston, Massachu-

setts. Her community involvement includes service as a delegate to the 2008 Democratic National Convention, and

leadership with the Alameda County Democratic Lawyers Club, Montclair Soccer Club, National Women Political Cau-

cus – Alameda County North, and a volunteer Judge Pro Tem for Alameda County. Term began 12/11/2012. Current

term ending 11/2016.

Linda Handy— Area 3

Linda Handy has a long resume of community service and college administration experience. She has a M.S. in Organi-

zational Development and Analysis from the Weatherhead School of Management at Case Western Reserve University.

She is a Laney College alumna and a former president of the Oakland Coalition of Congregations. She represents part

of the Laurel district as well as the San Antonio, Fruitvale, Brookdale, Fairfax and Maxwell Park districts in Oak-

land. Term began 11/05/2002. Current term ending 11/2018.

Nicky González Yuen— Area 4

Nicky González Yuen earned both a Ph.D. and JD degree from the University of California, Berkeley and a B.A., summa

cum laude, in political science from Carleton College, Northfield, Minn. He has been a teacher at De Anza Community

College for 15 years where he teaches courses in US politics, Grassroots Political Activism and Race and Gender. A

former Congressional Fellow for the late Senator Paul Wellstone (D-MN), Nicky González Yuen also brings to the Peral-

ta Board a long history of organizing for voting rights, educational access, peace, justice and civil rights and environ-

mental sustainability. Term began 11/02/2004. Current term ending 11/2016.

William Riley, Vice President— Area 5

William Riley was first elected to the Board of Trustees in 1998 and represents an area that includes Oakland’s

Rockridge District and the City of Piedmont. He has served as President of the Board twice and also as Vice President.

He is a Merritt College alumnus and has served in public education over 30 years, including the Oakland, East Palo Al-

to/Ravenswood and San Ramon School Districts. He earned an Ed.D., in Educational Policy and a B.A. in Sociology

and Physical Education from the University of San Francisco and an M.A. in Educational Administration from San Fran-

cisco State University. Term began 11/03/1998. Current term ending 11/2018

Cy Gulassa — Area 6

Area 6

A graduate of UC Berkeley with a M.A. in English, Cy Gulassa has taught at institutions such as Frostburg State Univer-

sity in Maryland and the Philadelphia College of Art, as well as teaching English at De Anza College for 30 years. He

served as president of the Foothil-De Anza District Faculty Association for fifteen years and founded the Bay Facul-

ty Association. He lectures on community college reform and governance issues, and has published over 150 articles.

In 1994, he was named Faculty Member of the Year and was honored by State Assembly and Senate resolutions and a

commendation from President Clinton. Term began 11/02/2004. Current term ending 11/2016.

Julina Bonilla — Area 7

Julina Bonilla is a community college graduate and received her B. A. from U. C. Berkeley. She is a former Oakland ele-

mentary teacher and eventually moved into workforce development providing education and job training to young adults

in Northern California. Her community work and active memberships include: Board Vice President of Tradeswomen

Inc., National Women’s Political Caucus-AN, and she served as a member of the Oakland Workforce Investment Board

and co-chair of the Oakland Youth Council. Today, she is the Program Director of the West Oakland Job Resource Cen-

ter. Term began 12/09/2014. Current term ending 11/2018.

Adrien Abuyen, Co-Student Trustee

Adrien Abuyen, co-student trustee, representing students from all four campuses, has been active in the College of Ala-

meda (COA) community. Term began 6/1/2015. Current term ending 5/31/2016.

Justin Hyche, Co-Student Trustee

Justin Hyche, co-student trustee, representing students from all four campuses, has been active in the Berkeley City Col-

lege (BCC) community. Term began 6/1/2015. Current term ending 5/31/2016.

2015-16 2014-15 2014-15

Final Budget Final Adopted Budget

Estimated Actuals 2013-14 Actuals % Change $ Change

Revenue8199 Other Federal Revenue -$ -$ -$ 10,816$ 0.00% -$ Federal Revenue -$ -$ -$ 10,816$ 0.00% -$ 8611 State General 55,320,523$ 50,471,783$ 45,118,320$ 53,065,413$ 9.61% 4,848,740$ 8613 2% Enrollment Fees 140,262$ 151,497$ 295,412$ 277,404$ 0.00% (11,235)$ 8618 Apprenticeship 16,486$ 32,198$ 27,477$ 32,327$ 0.00% (15,712)$ 8619 State Prior Year -$ -$ 766,433$ (812,511)$ 0.00% -$ 8630 Education Protection Acct. 18,940,304$ 13,285,340$ 19,477,070$ 14,425,273$ 42.57% 5,654,964$ 8661 Part-time Parity Pay 408,873$ 408,873$ 408,873$ 408,873$ 0.00% -$ 8672 Homeowners Prop Tax 170,871$ 170,871$ 168,246$ -$ 0.00% -$ 8681 State Lottery Proceeds 2,510,189$ 2,372,580$ 2,673,205$ 2,486,121$ 5.80% 137,609$ 8682 State Mandated Cost 545,993$ 503,771$ 1,293,620$ 510,428$ 8.38% 42,222$ 8699 Other State Revenue 11,179,006$ -$ -$ 4,045$ 0.00% 11,179,006$ State Revenue 89,232,507$ 67,396,913$ 70,228,656$ 70,397,373$ 32.40% 21,835,594$ 8811 Tax Secured Roll 16,954,902$ 16,381,988$ 18,208,197$ 16,573,866$ 3.50% 572,914$ 8812 Tax Supplement Roll 208,317$ 208,317$ 257,701$ 346,945$ 0.00% -$ 8813 Tax Unsecured 1,135,660$ 1,135,660$ 1,099,718$ 1,052,466$ 0.00% -$ 8814 PY Tax Secured Roll -$ -$ (139,077)$ (427,773)$ 0.00% -$ 8815 PY Tax Supplemental Roll -$ -$ (1,072)$ (9,129)$ 0.00% -$ 8816 PY Tax Unsecured RL -$ -$ (346,869)$ 3,440$ 0.00% -$ 8818 ERAF 10,748,806$ 10,748,806$ 14,197,660$ 8,500,437$ 0.00% -$ 8851 Facility & Athletic Field Rentl -$ -$ 978$ 0.00% -$ 8861 Interest/Investment Inc -$ -$ (42,632)$ (38,017)$ 0.00% -$ 8874 Enrollment 6,423,060$ 8,644,557$ 7,430,064$ 6,279,473$ 0.00% (2,221,497)$ 8877 Instruct Matl Fees & Sales -$ -$ 50$ -$ 0.00% -$ 8879 Student Records 65,000$ 65,000$ 95,223$ 97,075$ 0.00% -$ 8880 Tuition Out of St 3,855,542$ 1,800,864$ 3,479,983$ 2,283,175$ 114.09% 2,054,678$ 8881 Parking Servcs -$ -$ -$ 390$ 0.00% -$ 8882 F-1 VisaTuition 4,701,220$ 3,825,323$ 4,852,905$ 4,726,999$ 22.90% 875,897$ 8883 Student Center -$ -$ -$ -$ 0.00% -$ 8884 Student AC Transit 1,021,000$ 1,249,934$ 921,585$ 921,249$ 0.00% (228,934)$ 8886 Application Fee 5,600$ 5,600$ 46,452$ 35,344$ 0.00% -$ 8887 Capital Outlay Fee -$ -$ -$ 92,831$ 0.00% -$ 8893 AC Transit-Student Bus Passes -$ -$ 14,472$ (1,620)$ 0.00% -$ 8895 St Drop Fees 5,000$ 5,300$ 5,270$ 5,680$ 0.00% (300)$ 8896 Student Health Fees 1,055,788$ 1,108,706$ 1,094,348$ 1,112,264$ 0.00% (52,918)$ 8897 Indirect Income -$ 845,569$ 146,906$ 260,030$ 0.00% (845,569)$ 8899 Miscellaneous 431,378$ 656,459$ 140,934$ 640,686$ 0.00% (225,081)$ Local Revenue 46,611,273$ 46,682,083$ 51,462,796$ 42,455,811$ 0.00% (70,810)$ 8982 Interfund Transfers-In 243,785$ -$ -$ -$ 0.00% 243,785$ 8983 Intrafund Transfers-In 12,756,929$ 13,128,094$ 10,915,411$ 11,188,145$ 0.00% (371,165)$ Trans Res Revenue 13,000,714$ 13,128,094$ 10,915,411$ 11,188,145$ 0.00% (127,380)$

Revenue Total 148,844,494$ 127,207,090$ 132,606,863$ 124,052,145$ 17.01% 21,637,404$

Expenses1101 Instructor 24,988,857$ 21,217,148$ 20,254,652$ 18,138,900$ 17.78% 3,771,709$ 1102 Instructor -Subs -$ 136,542$ -$ 113,285$ 0.00% (136,542)$ Full Time Academic 24,988,857$ 21,353,690$ 20,254,652$ 18,252,185$ 17.02% 3,635,167$ 1201 Administrators 5,374,168$ 4,864,416$ 4,803,073$ 4,214,079$ 10.48% 509,752$ Academic Admin 5,374,168$ 4,864,416$ 4,803,073$ 4,214,079$ 10.48% 509,752$ 1202 Department Chair 290,577$ 998,623$ 1,086,645$ 1,091,575$ 0.00% (708,046)$ 1203 Counselors 2,720,000$ 2,599,622$ 2,254,163$ -$ 4.63% 120,378$ 1204 Librarians 1,149,875$ 1,126,596$ 905,241$ -$ 2.07% 23,279$ 1205 Faculty-Reassign 1,339,585$ 787,116$ 1,032,804$ 710,984$ 70.19% 552,469$ 1206 Nurse 252,822$ 167,874$ 118,625$ 106,900$ 50.60% 84,948$ 1209 Counselors/Librarian-Lts -$ -$ -$ -$ 0.00% -$ 1210 Librarians-Lts -$ -$ -$ 55,229$ 0.00% -$ Other Faculty 5,752,859$ 5,679,831$ 5,397,478$ 1,964,688$ 1.29% 73,028$ 1351 Instructor-PTime & Ext-Se 9,103,384$ 6,786,415$ 10,407,276$ 12,237,944$ 34.14% 2,316,969$ 1352 Instructor-Sub-Daily/Sick 750$ -$ 91,189$ 66,521$ 0.00% 750$ 1353 Instructor - Retiree -$ -$ 801,100$ 595,281$ 0.00% -$ 1356 Instructor-Pt-Office Hour -$ -$ 463,770$ 406,830$ 0.00% -$ 1357 Instructor-Parity 408,873$ 408,873$ 317,264$ 507,144$ 0.00% -$ 1452 Department Chairs 20,234$ 17,242$ 67,614$ 48,917$ 17.35% 2,992$ 1453 Counselors 413,237$ 400,434$ 154,397$ 393,087$ 3.20% 12,803$ 1454 Librarians 74,233$ 126,799$ 276,539$ 233,936$ 0.00% (52,566)$ 1455 Coaches 145,724$ 89,576$ 132,865$ 104,835$ 62.68% 56,148$ 1456 Other Non-Teaching 325,815$ 272,756$ 365,678$ 293,372$ 19.45% 53,059$ 1457 Non-Teaching Retirees 4,019$ 4,019$ 131,486$ 65,966$ 0.00% -$ 1458 Partity Pay for Non Teaching Fac -$ -$ 60,325$ 65,002$ 0.00% -$ 1459 Staff Developing Training Fac 110,905$ 120,000$ 1,000$ -$ 0.00% (9,095)$

Final vs. Final Budget

Peralta Community College DistrictUnrestricted General Fund Detail

2015-16 Final Budget

2015-16 2014-15 2014-15

Final Budget Final Adopted Budget

Estimated Actuals 2013-14 Actuals % Change $ Change

Final vs. Final Budget

Peralta Community College DistrictUnrestricted General Fund Detail

2015-16 Final Budget

Part Time Academic 10,607,174$ 8,226,114$ 13,270,503$ 15,018,835$ 28.95% 2,381,060$ 2101 Administrators 4,313,920$ 3,960,810$ 3,901,502$ 3,586,324$ 8.92% 353,110$ 2102 Clerical Tech & Sup Staff 18,369,067$ 17,338,711$ 16,057,812$ 15,150,499$ 5.94% 1,030,356$ 2201 Instructional Aides 1,431,705$ 1,326,582$ 1,212,569$ 1,123,136$ 7.92% 105,123$ 2351 Trustee Members - Board 84,344$ 84,180$ 87,263$ 88,438$ 0.19% 164$ 2352 Cler Tech & Sup Stf 591,652$ 449,365$ 1,304,132$ 900,482$ 31.66% 142,287$ 2353 Student Employee Asst. 319,011$ 345,830$ 449,466$ 469,245$ 0.00% (26,819)$ 2354 Overtime 142,761$ 114,544$ 353,797$ 236,248$ 24.63% 28,217$ 2357 Classified Retirees 31,037$ 8,000$ 117,555$ 163,838$ 287.96% 23,037$ 2359 Inst. Aides - (non-classroom) 7,000$ -$ -$ -$ #DIV/0! 7,000$ 2451 Instructional Aides 466,838$ 413,614$ 345,349$ 480,952$ 12.87% 53,224$ 2452 Inst. Aides - Student 367,847$ 417,733$ 445,249$ 395,800$ 0.00% (49,886)$ 2453 Inst. Aides-O/T/Perm 3,500$ 5,500$ -$ -$ 0.00% (2,000)$ Classified Salary 26,128,682$ 24,464,869$ 24,274,694$ 22,594,962$ 6.80% 1,663,813$ 3110 STRS - Academic 3,626,162$ 2,812,854$ 3,035,306$ 2,660,442$ 28.91% 813,308$ 3140 STRS Cash Balance 369,463$ 260,649$ 242,854$ 286,215$ 41.75% 108,814$ 3220 PERS 2,968,691$ 2,669,954$ 2,767,927$ 2,508,428$ 11.19% 298,737$ 3310 OASDHI (FICA) -$ -$ 526$ -$ 0.00% -$ 3320 OASDHI Classified 1,549,878$ 1,403,960$ 1,508,777$ 1,411,943$ 10.39% 145,918$ 3340 Medicare - Academic 654,084$ 555,860$ 576,993$ 593,230$ 17.67% 98,224$ 3350 Medicare - Classified 363,041$ 331,407$ 377,625$ 328,630$ 9.55% 31,634$ 3411 Medical -Academic 7,385,050$ 6,686,584$ 8,915,956$ 7,735,833$ 10.45% 698,466$ 3412 Dental - Academic 467,821$ 455,669$ 393,438$ 396,542$ 2.67% 12,152$ 3415 Life Ins. -Academic 87,176$ 78,975$ 82,702$ 72,532$ 10.38% 8,201$ 3421 Medical -Classified 6,781,265$ 6,301,365$ 5,681,741$ 5,238,692$ 7.62% 479,900$ 3422 Dental -Classified 468,376$ 479,558$ 404,778$ 462,741$ 0.00% (11,182)$ 3425 Life Insurance-Class 64,283$ 61,427$ 75,543$ 69,303$ 4.65% 2,856$ 3431 Medical reimbursement (120,000)$ (120,000)$ (88,375)$ (93,554)$ 0.00% -$ 3432 Dental reimbursement (2,000)$ (2,000)$ -$ (954)$ 0.00% -$ 3435 Life ins. reimbursement -$ (300)$ (228)$ (105)$ 0.00% 300$ 3510 Unemployment Ins.-Aca 39,619$ 23,386$ 26,108$ 21,700$ 69.41% 16,233$ 3520 Unemployment Ins -Class 17,732$ 12,059$ 16,997$ 11,680$ 47.04% 5,673$ 3610 Work Comp-Academic 679,848$ 535,653$ 564,800$ 535,284$ 26.92% 144,195$ 3620 Work Comp-Classfd 342,170$ 299,480$ 300,881$ 272,384$ 14.25% 42,690$ 3712 OPEB Instructional 3,868,500$ 2,830,530$ 4,076,195$ 3,698,071$ 36.67% 1,037,970$ 3720 Apple Ret. 1,847$ 2,487$ 39,245$ 29,740$ 0.00% (640)$ 3722 OPEB Classified 1,946,305$ 1,783,377$ 2,007,215$ 1,880,726$ 9.14% 162,928$ 3912 Retiree Benefits 8,835,784$ 11,135,146$ 7,560,474$ 8,756,303$ 0.00% (2,299,362)$ Fringe Benefits 40,395,095$ 38,598,080$ 38,567,478$ 36,875,806$ 4.66% 1,797,015$ 4101 Classroom-Books 5,000$ 5,000$ 7,282$ 7,023$ 0.00% -$ 4102 Book for Student Program 8,000$ -$ 998$ -$ 0.00% 8,000$ 4103 Office Professional Refer/ 283$ -$ -$ -$ 0.00% 283$ 4301 Instructional Supplies 83,890$ 87,489$ 90,858$ 38,296$ 0.00% (3,599)$ 4303 Subs Periodicals 18,064$ 34,962$ 19,095$ 16,270$ 0.00% (16,898)$ 4304 Supplies-office 705,939$ 598,307$ 685,770$ 601,024$ 17.99% 107,632$ 4305 Fuel - gasoline/petroleum 16,550$ 16,550$ 16,568$ 14,385$ 0.00% -$ 4306 Computer software/site lic.-cl 34,406$ 39,714$ 56,307$ 11,059$ 0.00% (5,308)$ 4307 Computer software/site lic.-ad 47,500$ 47,000$ 32,273$ 28,053$ 1.06% 500$ 5102 Guest Speakers Lectures-Non 16,510$ 5,320$ 1,525$ 450$ 210.34% 11,190$ 5103 Legal 320,543$ 340,946$ 358,665$ 119,943$ 0.00% (20,403)$ 5104 Audit 147,227$ 142,447$ 181,730$ 173,826$ 3.36% 4,780$ 5105 Independent Contractor/Consult 5,652,966$ 5,007,426$ 6,245,159$ 5,817,322$ 12.89% 645,540$ 5106 Events/Programs-Outside Prod 131,626$ 67,576$ 68,120$ 31,865$ 94.78% 64,050$ 5107 Election Cost 7,500$ 76,758$ 186,908$ -$ 0.00% (69,258)$ 5109 Legal Settlements 30,000$ 5,000$ 75,516$ 53,529$ 500.00% 25,000$ 5110 Instructor Events-Personal Svs 6,000$ 8,880$ 4,994$ 10,142$ 0.00% (2,880)$ 5202 Travel Non-Local 276,344$ 175,680$ 188,652$ 156,513$ 57.30% 100,664$ 5203 Travel Local 65,913$ 35,751$ 19,807$ 10,553$ 84.37% 30,162$ 5204 Student Transportation 2,900$ 3,244$ 3,977$ 1,985$ 0.00% (344)$ 5205 Conference/Seminar Reg 160,260$ 95,897$ 139,975$ 76,376$ 67.12% 64,363$ 5206 Internal Training- Staff Dev 36,550$ 11,550$ 11,679$ 8,653$ 216.45% 25,000$ 5301 Dues and Membership 339,155$ 359,338$ 314,028$ 279,213$ 0.00% (20,183)$ 5407 Student Accident Insurance 215,760$ 114,847$ 125,680$ 106,231$ 87.87% 100,913$ 5501 Garbage and Trash 307,164$ 281,681$ 213,074$ 230,388$ 9.05% 25,483$ 5502 Gas 372,731$ 566,113$ 458,730$ 521,639$ 0.00% (193,382)$ 5503 Light and Power (Electricity) 2,271,958$ 2,006,089$ 2,166,865$ 1,878,415$ 13.25% 265,869$ 5504 Sewer Use 199,376$ 163,050$ 135,976$ 81,939$ 22.28% 36,326$ 5505 Telephone Services 369,147$ 514,466$ 370,752$ 245,098$ 0.00% (145,319)$ 5506 Main Water System 418,805$ 370,306$ 397,944$ 417,525$ 13.10% 48,499$ 5507 Pest Control 42,414$ 43,533$ 39,457$ 39,985$ 0.00% (1,119)$ 5602 Facility/Building Leases - Ann 592,500$ 537,806$ 542,459$ 516,120$ 10.17% 54,694$ 5603 Facility/Building Rentals-Mont 50,650$ 25,494$ 47,360$ 40,040$ 98.67% 25,156$

2015-16 2014-15 2014-15

Final Budget Final Adopted Budget

Estimated Actuals 2013-14 Actuals % Change $ Change

Final vs. Final Budget

Peralta Community College DistrictUnrestricted General Fund Detail

2015-16 Final Budget

5604 Equipment Lease - Annual 125,214$ 128,880$ 92,137$ 107,051$ 0.00% (3,666)$ 5605 Equipment Rentals - Mon-Mon 62,410$ 51,731$ 26,066$ 27,075$ 20.64% 10,679$ 5607 Print & Dup. Equip Leases/Rent 148,000$ 90,419$ 83,062$ 78,174$ 63.68% 57,581$ 5701 Athletics Meals and Lodging 35,466$ 25,456$ 38,413$ 26,760$ 39.32% 10,010$ 5702 Graduation Exprenses 43,000$ 25,196$ 78,101$ 25,824$ 70.66% 17,804$ 5704 Health Services 4,630$ 3,576$ 6,524$ 2,140$ 29.47% 1,054$ 5706 Misc. Student Services -$ -$ 3,106$ -$ 0.00% -$ 5708 Athletic Transportation 48,781$ 37,810$ 29,947$ 29,903$ 29.02% 10,971$ 5864 Instructional Services -$ -$ 10,855$ -$ 0.00% -$ 5865 Publishing/ Doc Publication 175,863$ 185,114$ 83,325$ 117,266$ 0.00% (9,251)$ 5866 Testing License and Material 2,265$ 1,400$ -$ 452$ 61.79% 865$ 5867 Postage 103,763$ 100,181$ 102,499$ 69,643$ 3.58% 3,582$ 5870 Cross Enrollment Waiver 935$ -$ 3,543$ 184$ 0.00% 935$ 5875 Employee Waiver 130,422$ -$ 49,998$ 47,781$ 0.00% 130,422$ 5877 Payment of Fines -OSHA & Misc 1,200$ 1,500$ 1,200$ -$ 0.00% (300)$ 5880 Radio Licensing 500$ -$ -$ -$ 0.00% 500$ 5881 Building Repairs & Services 232,531$ 130,867$ 291,129$ 253,424$ 77.68% 101,664$ 5882 Equip Repairs Maint. & Svc 198,583$ 118,470$ 65,794$ 169,422$ 67.62% 80,113$ 5883 Net Internet Fees and Subs. 47,630$ 33,177$ 23,425$ 82,472$ 43.56% 14,453$ 5884 Laundry Services 8,750$ 7,960$ 7,288$ -$ 9.92% 790$ 5885 Misc. Operational Exp. 7,652,556$ 2,340,013$ 1,810,702$ 1,234,924$ 227.03% 5,312,543$ 5886 Program TV License 18,000$ 18,000$ 18,141$ 19,870$ 0.00% -$ 5887 Advertising/Radio/TV 6,435$ 11,573$ 110,000$ 205,563$ 0.00% (5,138)$ 5888 Advertising Print/ADS 77,430$ 58,795$ 87,931$ 62,705$ 31.69% 18,635$ 5889 Grounds Maintenance 40,600$ -$ -$ -$ 0.00% 40,600$ 5890 Service Contract-Equipment 94,207$ 141,278$ 156,542$ 103,917$ 0.00% (47,071)$ 5891 Service Contract-Software-DP 506,918$ 511,432$ 623,919$ 482,989$ 0.00% (4,514)$ 5892 Service Contract-Hardware-DP 80,000$ 135,414$ 61,532$ 82,151$ 0.00% (55,414)$ 5893 Permits & Fees - Risk Mgmt 5,000$ 12,000$ 5,364$ 12,305$ 0.00% (7,000)$ 5894 Moving/Relocation Expenses -$ -$ 2,905$ -$ 0.00% -$ Books, Supplies, Services 22,804,720$ 15,958,462$ 17,081,631$ 14,775,855$ 42.90% 6,846,258$ 6120 Site Improvement -$ -$ 8,445$ -$ 0.00% -$ 6130 Special Assessments 2,693$ 8,745$ -$ -$ 0.00% (6,052)$ 6206 Building Improvement -$ 2,693$ -$ -$ 0.00% (2,693)$ 6301 College Library Books 26,000$ -$ -$ 12,812$ 0.00% 26,000$ 6303 College Library Periodicals 8,000$ 4,800$ 4,745$ 12,899$ 66.67% 3,200$ 6305 Library Textbooks -$ -$ -$ 3,093$ 0.00% -$ 6306 Library Databases -$ -$ -$ 14,788$ 0.00% -$ 6402 Inst Equipment and Furn 90,880$ 32,913$ 115,077$ 46,880$ 176.12% 57,967$ 6403 Non-Instructional Equip & Furn 138,774$ 91,269$ 140,283$ 100,237$ 52.05% 47,505$ 6404 Telephone System Purchase 2,000$ -$ 398$ -$ 0.00% 2,000$ 6406 Laptop Computers 29,244$ 3,500$ 23,774$ 20,969$ 735.54% 25,744$ 6407 PC,SERV, Other Comput,Peripher 59,103$ 32,656$ 199,029$ 115,474$ 80.99% 26,447$ Equipment Cap Outlay 356,694$ 176,576$ 491,751$ 327,152$ 102.01% 180,118$ 7110 Debt Service - Bonds 2,349,253$ -$ -$ -$ 0.00% 2,349,253$

2015-16 2014-15 2014-15

Final Budget Final Adopted Budget

Estimated Actuals 2013-14 Actuals % Change $ Change

Final vs. Final Budget

Peralta Community College DistrictUnrestricted General Fund Detail

2015-16 Final Budget

7120 Debt Interest - Bonds 5,797,337$ 6,727,397$ 6,727,392$ 5,895,949$ 0.00% (930,060)$ 7301 Interfund Transfers 3,507,655$ 1,157,655$ 1,157,655$ 1,157,665$ 203.00% 2,350,000$ 7302 Special Reserve #1 -$ -$ -$ -$ 0.00% -$ Debt Service Transfer 11,654,245$ 7,885,052$ 7,885,047$ 7,053,614$ 47.80% 3,769,193$ 7530 Tuition Reduction -$ -$ 386$ -$ 0.00% -$ 7535 OPD Payment for Academy 132,000$ -$ 198,280$ -$ 0.00% 132,000$ 7630 Book Vouchers -$ -$ 29,171$ 835$ 0.00% -$ Financial Aid 132,000$ -$ 227,837$ 835$ 0.00% -$ 7901 Reserve 1,000,000$ -$ -$ -$ 0.00% 1,000,000$ 7920 PFT Leave Banking -$ -$ -$ -$ 0.00% -$ Fund Balance 1,000,000$ -$ -$ -$ 0.00% 1,000,000$

Expense Total 149,194,494$ 127,207,090$ 132,254,144$ 121,078,011$ 17.28% 21,987,404$

Beginning Fund Balance 16,150,132$ 15,797,413$ 12,823,279$ Revenues over Expenses (350,000) 352,719 2,974,134 Ending Fund Balance 15,800,132$ 16,150,132$ 15,797,413$

PERALTA COMMUNITYCOLLEGE DISTRICT

ANNUAL FINANCIAL REPORT

JUNE 30, 2014

PERALTA COMMUNITY COLLEGE DISTRICT

TABLE OF CONTENTSJUNE 30, 2014

FINANCIAL SECTIONIndependent Auditor's Report 2Management's Discussion and Analysis 4Basic Financial Statements - Primary Government

Statement of Net Position 15Statement of Revenues, Expenses, and Changes in Net Position 16Statement of Cash Flows 17Fiduciary Funds

Statement of Net Position 19Statement of Changes in Net Position 20

Notes to Financial Statements 21

REQUIRED SUPPLEMENTARY INFORMATIONSchedule of Other Postemployment Benefits (OPEB) Funding Progress 56

SUPPLEMENTARY INFORMATIONDistrict Organization 58Schedule of Expenditures of Federal Awards 59Schedule of Expenditures of State Awards 62Schedule of Workload Measures for State General Apportionment Annual (Actual) Attendance 63Reconciliation of Education Code Section 84362 (50 Percent Law) Calculation 64Reconciliation of Annual Financial and Budget Report (CCFS-311) WithAudited Fund Balance 67Proposition 30 Education Protection Act (EPA) Expenditure Report 68Reconciliation of Governmental Funds to the Statement of Net Position 69Note to Supplementary Information 70

INDEPENDENT AUDITOR'S REPORTSReport on Internal Control Over Financial Reporting and on Compliance and OtherMatters Based on an Audit of Financial Statements Performed in Accordance WithGovernment Auditing Standards 73Report on Compliance for Each Major Program and Report on Internal Control OverCompliance Required by OMB Circular A-133 75Report on State Compliance 78

SCHEDULE OF FINDINGS AND QUESTIONED COSTSSummary of Auditor's Results 81Financial Statement Findings and Recommendations 82Federal Award Findings and Questioned Costs 83State Awards Findings and Questioned Costs 92Summary Schedule of Prior Audit Findings 95

1

FINANCIAL SECTION

2

INDEPENDENT AUDITOR'S REPORT

Board of TrusteesPeralta Community College DistrictOakland, California

Report on the Financial Statements

We have audited the accompanying financial statements of the business-type activities of Peralta CommunityCollege District (the District) as of and for the year ended June 30, 2014, and the related notes to the financialstatements, which collectively comprise the District's basic financial statements as listed in the Table of Contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordancewith accounting principles generally accepted in the United States of America; this includes the design,implementation, and maintenance of internal control relevant to the preparation and fair presentation of financialstatements that are free from material misstatements, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted ouraudit in accordance with auditing standards generally accepted in the United States of America and the standardsapplicable to financial audits contained in Government Auditing Standards issued by the Comptroller General ofthe United States. Those standards require that we plan and perform the audit to obtain reasonable assuranceabout whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in thefinancial statements. The procedures selected depend on the auditor's judgment, including the assessment of therisks of material misstatement of the financial statements, whether due to fraud or error. In making those riskassessments, the auditor considers internal control relevant to the District's preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in the circumstances, but not for thepurpose of expressing an opinion on the effectiveness of the District's internal control. Accordingly, we expressno such opinion. An audit also includes evaluating the appropriateness of accounting policies used and thereasonableness of significant accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

We believe the audit evidence we have obtained is sufficient and appropriate to provide a basis for our auditopinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financialposition of the business-type activities of the District as of June 30, 2014, and the changes in net position and cashflows for the year then ended in accordance with accounting principles generally accepted in the United States ofAmerica.

8270 Aspen Street Rancho Cucamonga, CA 91730 Tel: 909.466.4410 Fax: 909.466.4431 www.vtdcpa.com

Vavrinek, Trine, Day & Co., LLPCertified Public Accountants

VALUE THE D IFFERENCE

FRESN O • L AGUN A H I L LS • PALO ALTO • P LEASANTON • RAN C HO CUC AMON GA • R I v E R S I d E • SACRAMENTO

3

Emphasis of Matter - Change in Accounting Principles

As discussed in Note 17 to the financial statements, the District has elected to change its method of accounting forcost of debt issuance as prescribed by Governmental Accounting Standards Board (GASB) Statement No. 65,Items Previously Reported as Assets and Liabilities. Our opinion is not modified with respect to this matter.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require the Management's Discussionand Analysis on pages 4 through 14 and the Schedule of Other Postemployment Benefits (OPEB) FundingProgress on page 56 be presented to supplement the basic financial statements. Such information, although not apart of the basic financial statements, is required by the Governmental Accounting Standards Board, whoconsiders it to be an essential part of financial reporting for placing the basic financial statements in anappropriate operational, economic, or historical context. We have applied certain limited procedures to therequired supplementary information in accordance with auditing standards generally accepted in the United Statesof America, which consisted of inquiries of management about the methods of preparing the information andcomparing the information for consistency with management's responses to our inquiries, the basic financialstatements, and other knowledge we obtained during our audit of the basic financial statements. We do notexpress an opinion or provide any assurance on the information because the limited procedures do not provide uswith sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the District's basic financial statements. The accompanying supplementary information listed in theTable of Contents, including the Schedule of Expenditures of Federal Awards, as required by U.S. Office ofManagement and Budget (OMB) Circular A-133, Audits of States, Local Governments, and Non-ProfitOrganizations, is presented for purposes of additional analysis and is not a required part of the basic financialstatements.

The accompanying supplementary information, including the Schedule of Expenditures of Federal Awards, is theresponsibility of management and was derived from and relates directly to the underlying accounting and otherrecords used to prepare the basic financial statements. Such information has been subjected to the auditingprocedures applied in the audit of the basic financial statements and certain additional procedures, includingcomparing and reconciling such information directly to the underlying accounting and other records used toprepare the basic financial statements or to the basic financial statements themselves, and other additionalprocedures in accordance with auditing standards generally accepted in the United States of America. In ouropinion, the accompanying supplementary information is fairly stated, in all material respects, in relation to thebasic financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated December 16, 2014, onour consideration of the District's internal control over financial reporting and on our tests of its compliance withcertain provisions of laws, regulations, contracts, grant agreements, and other matters. The purpose of that reportis to describe the scope of our testing of internal control over financial reporting and compliance and the results ofthat testing, and not to provide an opinion on the internal control over financial reporting or on compliance. Thatreport is an integral part of an audit performed in accordance with Government Auditing Standards in consideringthe District's internal control over financial reporting and compliance.

Rancho Cucamonga, CaliforniaDecember 16, 2014

4

Introduction

The following discussion and analysis provides an overview of the financial position and activities ofPeralta Community College District (the District) for the year ended June 30, 2014. The discussion has beenprepared by management and should be read in conjunction with the financial statements and notes which followthis section.

The Peralta Community College District was founded in 1964, and serves six cities in the East Bay Area,including Albany, Alameda, Berkeley, Emeryville, Oakland, and Piedmont. The colleges are Berkeley CityCollege, College of Alameda, Laney College, and Merritt College. The District has a reputation for developingeffective approaches to serving the varied interests and needs of its vibrant community. The District serves over25,000 students a semester, and is one of the top community college districts in California in transferring studentsinto the UC system. Currently, the District has about 750 full-time employees and over 1,535 part-time facultyand staff.

Selected Highlights

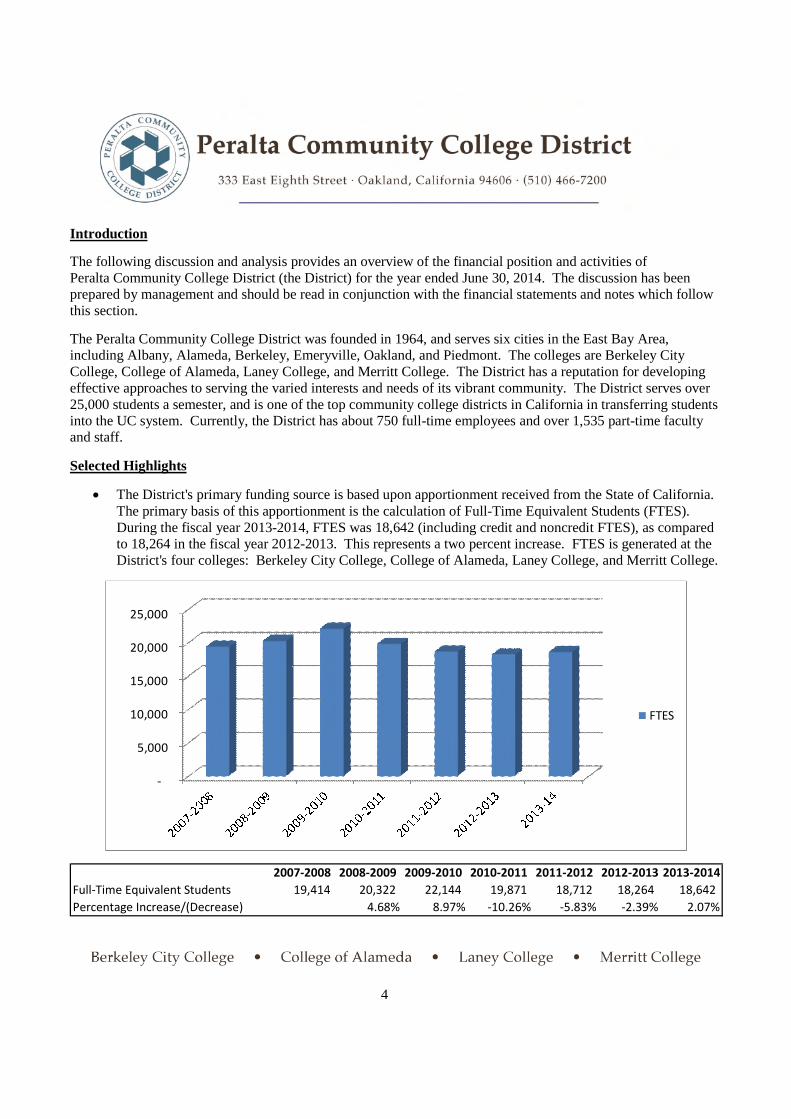

The District's primary funding source is based upon apportionment received from the State of California.The primary basis of this apportionment is the calculation of Full-Time Equivalent Students (FTES).During the fiscal year 2013-2014, FTES was 18,642 (including credit and noncredit FTES), as comparedto 18,264 in the fiscal year 2012-2013. This represents a two percent increase. FTES is generated at theDistrict's four colleges: Berkeley City College, College of Alameda, Laney College, and Merritt College.

-

5,000

10,000

15,000

20,000

25,000

FTES

2007-2008 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013 2013-2014

Full-Time Equivalent Students 19,414 20,322 22,144 19,871 18,712 18,264 18,642

Percentage Increase/(Decrease) 4.68% 8.97% -10.26% -5.83% -2.39% 2.07%

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

5

Unrestricted General fund revenues for the year were $115.7 million, an increase of 5.1 percent fromprior year's revenue of $110.0 million.

Medical benefit rates for both employees and retirees increased for Kaiser 9.8 percent and decreased forthe Self-Insurance plan 2.72 percent over the prior year. The District continues to provide retirees whowere hired prior to July 1, 2004, with lifetime medical benefits. For employees hired after July 1, 2004,medical benefits upon retirement are provided until age 65 or Medicare eligibility. The actuarial accruedliability at a 6.75 percent discount rate for the District as of June 30, 2014, is $174.7 million. InDecember 2005, the District issued $153 million in Other Postemployment Benefits (OPEB) Bonds. Theproceeds of the bonds have been placed in a revocable trust fund, which may be used only to pay orreimburse the District for payment of retiree health benefit costs or related debt service. In January 2006,the bond proceeds were invested in a strategic allocation that mirrors the asset allocation of CalPERS.

The District is using Measures A and E bonds to pay for various capital improvements to our educationalfacilities. They include, but are not limited to, the following:

o Investment in our technology infrastructure District-wide.o Renovate and construct classrooms and facilities to enhance the community outreach capabilities

of the District among the numerous ethnic communities living in and served by the District.o District-wide safety systems including disaster preparedness, campus security, and hazardous and

toxic waste handling.o Technological infrastructure for distance learning.o Renovation of student service buildings and facilities at Laney College, Merritt College, and

College of Alameda.o Landscape improvements at Merritt College.o Improvements in laboratories and power supplies District-wide.o Cabling and power upgrade for technology.o Construction of a six story urban campus for Berkeley City College in Berkeley.

The District is using Measure B, special parcel tax, as approved by the voters in June 2012 in thefollowing manner:

o Restore and maintain core academic programs such as Math, Science, and English.o Train students for careers.o Prepare students to transfer to four-year universities.

Statement of Net Position

The Statement of Net Position presents the assets, liabilities, and net position of the District as of the end of thefiscal year and was prepared using the accrual basis of accounting, which is similar to the accounting basis usedby most private-sector organizations. The Statement of Net Position is a point-of-time financial statement whosepurpose is to present to the reader a fiscal snapshot of the District. The Statement of Net Position presents end-of-year data concerning assets, liabilities, and net position.

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

6

From the data presented, the reader of the Statement of Net Position is able to determine the assets available tocontinue operations of the District. The reader is also able to determine how much the District owes to vendorsand employees. Finally, the Statement of Net Position provides a picture of the assets and their availability forexpenditure by the District.

The difference between total assets and total liabilities is one indicator of the current financial condition of theDistrict; the change in net position is an indicator of whether the overall financial condition has improved orworsened during the year. Assets and liabilities are generally measured using current values. One notableexception is capital assets, which are stated at historical cost, less accumulated depreciation.

The net position is divided into three major categories. The first category, invested in capital assets, provides theequity amount in property, plant, and equipment owned by the District. The second category is expendablerestricted assets; these assets are available for expenditure by the District, but must be spent for purposes asdetermined by external entities and/or donors that have placed time or purpose restrictions on the use of the assets.The final category is unrestricted net position, which is available to the District for any lawful purpose of theDistrict.

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

7

A summary of the Statement of Net Position as of June 30, 2014 and June 30, 2013, is presented below:

NET POSITIONAs of June 30,

(in thousands)Increase Percent

2014 *2013 (Decrease) ChangeASSETSCurrent Assets

Cash and investments 368,087$ 373,198$ (5,111)$ -1.4%Accounts receivable 29,827 35,217 (5,390) -15.3%Other current assets 442 1,100 (658) -59.8%

Total Current Assets 398,356 409,515 (11,159) -76.49%Noncurrent Assets

Capital assets (net of depreciation) 423,489 400,414 23,075 5.8%TOTAL ASSETS 821,845 809,929 23,075 5.8%

DEFERRED OUTFLOWS OF RESERVESDeferred charge on refunding 8,339 7,990 349 4.4%Interest rate SWAP 14,431 11,760 2,671 22.7%

TOTAL DEFERRED OUTFLOWS 22,770 19,750 3,020 27.08%LIABILITIESCurrent Liabilities

Accounts payable and accrued liabilities 19,170 32,663 (13,493) -41.3%Unearned revenue 3,301 3,365 (64) -1.9%Other current liabilities 36,348 31,089 5,259 16.9%Current portion of long-term obligations 14,283 13,467 816 6.1%

Total Current Liabilities 73,102 80,584 (7,482) -20.2%Noncurrent Liabilities

Bonds payable 622,984 629,535 (6,551) -1.0%Other long-term liabilities 38,140 34,130 4,010 11.7%

Long-term obligations 661,124 663,665 (2,541) -0.4%TOTAL LIABILITIES 734,226 744,249 (10,023) -20.6%

DEFERRED INFLOWS OF RESERVESSWAP liability 14,431 11,760 2,671 22.7%Interest rate SWAP 376 1,054 (678) -64.3%

TOTAL DEFERRED INFLOWS 14,807 12,814 1,993 -41.6%NET POSITION

Net investment in capital assets 85,546 72,104 13,442 18.6%Restricted for:

Debt service 15,124 13,973 1,151 8.2%Capital projects 4,969 4,108 861 21.0%Other activities 17,132 13,027 4,105 31.5%

Unrestricted (27,189) (30,596) 3,407 11.1%TOTAL NET POSITION 95,582$ 72,616$ 22,966$ 31.6%

* As restated.

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

8

Invested inCapital Assets,Net of Related

Debt89%

Restricted forDebt Service

16%

Restricted forCapital Projects

5%

Restricted forOther Activities

18%

Unrestricted-28%

NET POSITION - JUNE 30, 2014

Approximately 89 percent of the cash balance is cash deposited in the Alameda County Treasury Pool andapproximately 11 percent is cash deposited in local financial banking institutions. All funds are investedin accordance with Board Policy, which emphasizes prudence, safety, liquidity, and return on investment.The Statement of Cash Flows contained within these financial statements provides greater detailregarding the sources and uses of cash, and the net decrease in cash during fiscal years 2013-2014 and2012-2013.

The majority of the accounts receivable balance is from Federal and State sources for apportionment,grant and entitlement programs, and student receivables. Receivables totaling approximately$14.2 million for the June 2014 apportionment and categorical deferrals, approximately $9.8 million forreimbursements from Federal and State agencies related to grant awards, and $5.8 million for studentreceivables.

Capital assets had a net increase of $23.1 million. The District had additions of $16 million related toconstruction in progress. Depreciation expense of $14.3 million was recognized during 2013-2014. Thecapital asset section of this discussion and analysis provides greater detail.

Accounts payable are amounts due as of the fiscal year end for goods and services received as of June 30,2014. Total accounts payable are $9.8 million; $4.5 million of the balance was accrued in the CapitalProjects fund, Bond fund, and Special Revenue fund related to capital outlay. Five hundred andsixty-nine thousand dollars is for amounts due to or on behalf of employees for wages and benefits.

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

9

The District's noncurrent liabilities primarily consist of bonds payable, related to the issuance ofElection 2000 Series B, C, and D of the District General Obligation Bonds; 2005 Series A and BRefunding of the District General Obligation Bonds; Election 2006 Series A, B, and C of the DistrictGeneral Obligation Bonds; and Election 2009 and Other Postemployment Benefit Bonds. The face valueof these bonds at the time of initial sale totaled $700.1 million, and $637.3 million represents theremaining long-term debt to satisfy these obligations.

Statement of Revenues, Expenses, and Change in Net Position

The Statement of Revenues, Expenses, and Change in Net Position presents the financial results of the District'soperations, as well as its nonoperating activities. The distinction between these two activities involves theconcepts of exchange and nonexchange. Operating activities are those in which a direct payment or exchange ismade for the receipt of specified goods or services. For example, tuition fees paid by the student are consideredan exchange for instructional services. The receipt of State apportionments and property taxes, however, do notinclude this exchange relationship between the payment and receipt of specified goods or services. Theserevenues and related expenses are classified as nonoperating activities. It is because of the methodology used tocategorize between operating and nonoperating, combined with the fact that the primary source of funding thatsupports the District's instructional activities comes from State apportionment and local property taxes, results in anet operating loss for the District's operations.

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

10

The Statement of Revenues, Expenses, and Changes in Net Position for the years ended June 30, 2014 andJune 30, 2013, is summarized below:

Statement of Revenues, Expenses, and Changes in Net Positionfor the Years Ended June 30,

(in thousands)Increase Percent

2014 2013 (Decrease) ChangeOperating Revenues

Tuition and fees 16,198$ 14,557$ 1,641$ 11.3%Other revenues 1,239 1,853 (614) 100%

Total Operating Revenues 17,437 16,410 1,027 6.3%Operating Expenses

Salaries and benefits 128,421 123,037 5,384 4.4%Supplies and maintenance 24,130 25,679 (1,549) -6.0%Student financial aid 41,304 38,326 2,978 7.8%Depreciation 14,304 15,348 (1,044) -6.8%

Total Operating Expenses 208,159 202,390 5,769 2.9%Loss on Operations (190,722) (185,980) (4,742) -2.5%

Nonoperating Revenues and (Expenses)State apportionments 68,496 58,547 9,949 17.0%Grants and contracts 58,292 54,592 3,700 6.8%Property taxes 67,647 73,572 (5,925) -8.1%State revenues 6,045 5,122 923 18.0%Net investment income (671) (2,147) 1,476 -68.7%Other nonoperating revenues and transfers 11,875 10,038 1,837 18.3%

Total Nonoperating Revenues (Expenses) 211,684 199,724 11,960 6.0%Other Revenues

State and local capital income 2,004 1,127 877 77.8%Total Other Revenues 2,004 1,127 877 77.8%Net Increase in Net Position 22,966$ 14,871$ 8,095$ 54.4%

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

11

Tuition and fees6%

Stateapportionments

30%

Grants andcontracts

25%

Property taxes29%

State revenues3%

Net investmentincome

1%

Other operatingand nonoperating

revenue6%

TOTAL REVENUES - JUNE 30, 2014

Salaries andbenefits

61%

Supplies andmaintenance

11%

Student financialaid

20%

Depreciation7%

Interest Expense1%

TOTAL EXPENSES - JUNE 30, 2014

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

12

The primary components of tuition and fees are the $46 per unit enrollment fee that is charged to allstudents registering for classes and the additional $213 per unit fee that is charged to all non-residentstudents.

Personnel costs account for 62 percent of operating expenses in fiscal year 2014 compared to 60 percentin 2013. The balance of operating expenses is for supplies, materials, other operating expenses, financialaid, equipment, maintenance, and depreciation expense.

The principal components of the District's nonoperating revenue are: noncapital Federal and State grants,State apportionment, local property taxes, other State funding, and interest income. With the exception ofinterest income, the majority of this revenue is received to support the District's instructional activities.The amount of State general apportionment received by the District is dependent upon the number ofFTES generated and reported to the State, less amounts received from enrollment fees and local propertytaxes. Increases in either of the latter two revenue-categories lead to a corresponding decrease inapportionment.

A schedule of functional expenses is displayed below:

Supplies,Material,and Other

Salaries Operating Studentand Expenses Financial

Benefits and Services Aid Depreciation TotalInstructional activities 58,155,265$ 1,943,692$ -$ -$ 60,098,957$

Academic support 9,747,032 590,805 - - 10,337,837Student services 19,093,994 4,475,664 - - 23,569,658Plant operations and

maintenance 6,158,386 1,448,660 - - 7,607,046Planning, policymaking,

and coordination 5,429,978 2,751,873 - - 8,181,851Instructional support

services 24,720,029 8,638,261 - - 33,358,290Community services and

economic development 241,046 49,839 - - 290,885Ancillary services and

auxiliary operations 3,685,686 4,231,315 - - 7,917,001Student aid - - 41,303,971 - 41,303,971Physical property and

related acquisitions 1,189,399 - - - 1,189,399

Unallocated expense - - - 14,304,212 14,304,212Total 128,420,815$ 24,130,109$ 41,303,971$ 14,304,212$ 208,159,107$

PERALTA COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2014

13

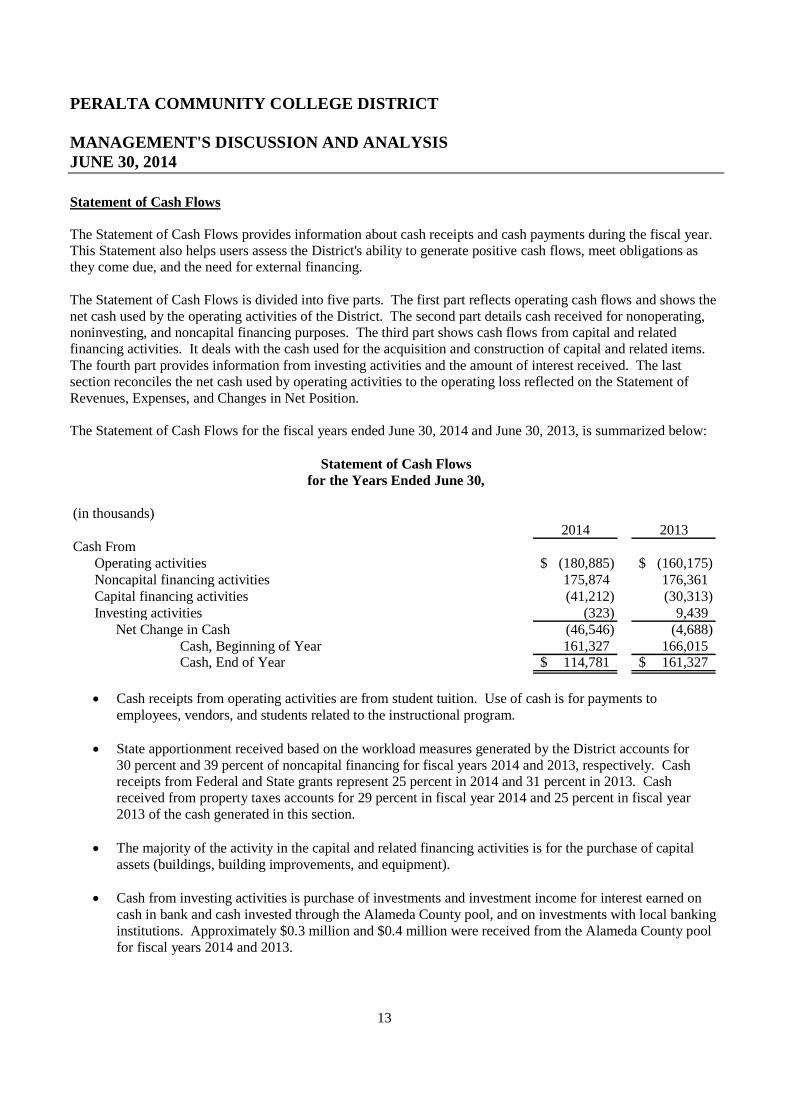

Statement of Cash Flows

The Statement of Cash Flows provides information about cash receipts and cash payments during the fiscal year.This Statement also helps users assess the District's ability to generate positive cash flows, meet obligations asthey come due, and the need for external financing.