Empirical Stylized Facts Modelling and Forecast Evaluations for Energy and Stock Markets

39

This article was downloaded by: [Kim Leng Tan] On: 20 March 2015, At: 19:32 Publisher: Taylor & Francis Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Click for updates Journal of Statistics and Management Systems Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/tsms20 Empirical Stylized Facts Modelling and Forecast Evaluations for Energy and Stock Markets Kim Leng Tan a , Wen Cheong Chin b & Siow Hooi Tan a a Faculty of Management Multimedia University 63100 Cyberjaya, Selangor Malaysia. E-mail: b Faculty of Computing and Informatics Multimedia University 63100 Cyberjaya, Selangor Malaysia Published online: 13 Nov 2014. To cite this article: Kim Leng Tan, Wen Cheong Chin & Siow Hooi Tan (2014) Empirical Stylized Facts Modelling and Forecast Evaluations for Energy and Stock Markets, Journal of Statistics and Management Systems, 17:4, 311-347, DOI: 10.1080/09720510.2014.914296 To link to this article: http://dx.doi.org/10.1080/09720510.2014.914296 PLEASE SCROLL DOWN FOR ARTICLE Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) contained in the publications on our platform. However, Taylor & Francis, our agents, and our licensors make no representations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of the Content. Any opinions and views expressed in this publication are the opinions and views of the authors, and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon and should be independently verified with primary sources of information. Taylor and Francis shall not be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use of the Content. This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &

-

Upload

harmfulalgae -

Category

Documents

-

view

2 -

download

0

Transcript of Empirical Stylized Facts Modelling and Forecast Evaluations for Energy and Stock Markets

This article was downloaded by: [Kim Leng Tan]On: 20 March 2015, At: 19:32Publisher: Taylor & FrancisInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Click for updates

Journal of Statistics and ManagementSystemsPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/tsms20

Empirical Stylized Facts Modelling andForecast Evaluations for Energy andStock MarketsKim Leng Tana, Wen Cheong Chinb & Siow Hooi Tana

a Faculty of Management Multimedia University 63100 Cyberjaya,Selangor Malaysia. E-mail:b Faculty of Computing and Informatics Multimedia University 63100Cyberjaya, Selangor MalaysiaPublished online: 13 Nov 2014.

To cite this article: Kim Leng Tan, Wen Cheong Chin & Siow Hooi Tan (2014) Empirical StylizedFacts Modelling and Forecast Evaluations for Energy and Stock Markets, Journal of Statistics andManagement Systems, 17:4, 311-347, DOI: 10.1080/09720510.2014.914296

To link to this article: http://dx.doi.org/10.1080/09720510.2014.914296

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoever orhowsoever caused arising directly or indirectly in connection with, in relation to or arisingout of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &

Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

*E-mail: [email protected]

Empirical Stylized Facts Modelling and Forecast Evaluations for Energy and Stock Markets

Kim Leng Tan 1,*

Wen Cheong Chin 2

Siow Hooi Tan 1

1 Faculty of ManagementMultimedia University63100 Cyberjaya, SelangorMalaysia2 Faculty of Computing and InformaticsMultimedia University63100 Cyberjaya, SelangorMalaysia

AbstractThis paper applies autoregressive heteroscedasticity (ARCH) family models for the

purpose of comparing stylized facts such as volatility clustering, leverage eff ect, long mem-

ory volatility and risk-return tradeoff for energy and stock markets. Empirical results have

found that the presences of volatility clustering in both markets and the impact of volatility

shocks to the conditional volatility display hyperbolic rather than exponential rate of decay.

Meanwhile, only stock markets denote the leverage eff ect, which implies that ‘bad’ news

has a greater impact on volatility than ‘good’ news at the same magnitude. Additionally,

empirical results also highlighted that Kerosene and Brent crude oil are the only energy

commodities exhibit risk-return tradeoff . For forecast evaluations, the FIAPARCH model in-

dicates superior out of sample forecasts over short and long time horizon for stock markets.

Nevertheless, FIAPARCH model suits better over long term as compared to short term for

energy markets. Finally, the Superior Predictive Ability (SPA) tests suggested that overall

asymmetric long memory GARCH models display higher forecasting accuracy than the stan-

dard GARCH models.

Keywords: Stylized facts, Energy markets, Stock markets, Comparison, ARCH.

Journal of Statistics & Management SystemsVol. 17 (2014), No. 4, pp. 311–347

©

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

312 K. L. TAN, W. C. CHIN AND S. H. TAN

1. Introduction

In recent years, interests of researchers regarding stylized facts have

been constantly growing especially in energy markets and stock markets.

Empirical stylized facts refer to observations that are consistent and have

been made in many contexts (e.g., across a wide range of instruments,

markets and time periods). They are accepted as truths, to which theories

must fi t (Cont 2001; 2008, Mukherjee et al. 2011). The common empirical

stylized facts include fat-tail asset returns, volatility clustering, long mem-

ory volatility and leverage eff ect in global fi nancial markets. Theoretically,

stylized facts are obtained via applying a common denominator among

the properties observed in studies of diff erent markets and instruments.

However, stylized facts exhibit ineff iciency especially in distinguishing

among the various types of parametric models. In this study, we are focus-

ing on some common stylized facts such as volatility clustering, leverage

eff ects, long memory volatility and risk-return tradeoff for both the energy

and stock markets.

One of the empirical stylized facts is clustering volatility. Persistence

of volatility is a well established stylized fact and remains the salient

feature of many models (Chen and Ghysels, 2010). Volatility clustering

simply refers to the property that there are periods of high and low (con-

ditional or unconditional) variance. As noted by Mandelbrot (1963), “large

changes tend to be followed by large changes, of either sign, and small

changes tend to be followed by small changes”. Therefore, it is crucial in

predicting the price volatility while deeply understanding and managing

the risk associated with price volatility in order to allow better targeted

policy (Regnier, 2007). Commonly, volatility clustering and leptokurtosis

are observed in the fi nancial time series and magnitude for the response

of future volatility diff ers depending on whether past news are positive or

negative (Li, Hamill and Opong 2010; Black 1976 and Pagan 1996).

The relation between price movement and volatility is also an inter-

esting stylized facts that had been widely studied in fi nancial research.

Empirical research found that information arrival is positively correlated

with volatility according to Aguilar and Ringgenberg (2011). Information

may aff ect prices which are unknowable in the present and appears ran-

domly in the future (Lee and Lee, 2009; Kaufmann and Laskowski, 2005).

Hence, with only historical data for prices and returns, future prices are

best predicted using current prices. While for the return (or changes in

price), it tends to be zero and thus unpredictable. This is the essence of

weak-form Eff icient Market Hypothesis (EMH) which well related to ran-

dom walk.

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

EMPIRICAL STYLIZED FACTS MODELLING 313

Negative asymmetric volatility or leverage eff ect is another stylized

facts commonly found in market returns in response to fl owing of new

information. In general, it is believed that positive or negative shocks tend

to aff ect the volatility of market returns. Specifi cally, volatility tends to

respond more to negative shocks or ‘bad’ news rather than the positive

shocks or ‘good’ news under the same magnitude. According to Paytakhti

and Shamsavari (2011), asymmetric is tentatively important in fi nancial

decision making especially in selecting portfolio, managing risk, hedging

and pricing the fi nancial derivatives. In term of volatility modeling, the

existence of leverage eff ects suggest that investor’s response to shocks is

not symmetric, which is contrary with the assumptions behind autore-

gressive conditional heteroscedasticity (ARCH) model and the gener-

alized autoregressive conditional heteroscedasticity (GARCH) model

(Ismail 2011). Hence, asymmetric ARCH models such as TGARCH model

and GJR GARCH model served this purpose better than the symmetric

GARCH model.

Long memory volatility is one of the interesting stylized facts in

fi nance. In an informationally ineff iciency market, long memory has

become one of the important considerations in the modeling specifi ca-

tion. It describes the correlation structure of a series at long lags whereby

such series normally characterized by distinct but non-periodic cyclical

patterns. According to Butler, Gerken and Okada (2011), long memory is

characterized by slow hyperbolic decay in the autocovariances of squared

returns or transformations of squared returns in the conditional volatility

of a univariate fi nancial time series.

Another well-known stylized fact is known as risk-return tradeoff

or risk premium which represents a factor including in the estimation of

shareholders equity, cost of debt (by adding the credit risk spread) used

in corporate fi nance and in the valuation of the fi nancial assets. Risk pre-

mium in fi nance is defi ned as the returns over and above risk free rate of

return that an investor expects in exchange for each additional unit of risk.

Markowitz portfolio theory indicates that rational investors only accept

additional risk if they expect a greater return and hence refers this greater

return as risk-return tradeoff . Literally, it is acceptable in general that ex-

pected returns of the market is positively and proportionally related to

the conditional volatility. In other words, risk-averse investors normally

require a higher expected return (higher risk premium) as the compensa-

tion of higher expected risks.

The above discussed stylized facts are the most common identifi ed

stylized facts. However, there are other stylized facts such as heavy tails,

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

314 K. L. TAN, W. C. CHIN AND S. H. TAN

intermittency, aggregational Gaussianity and asymmetry in time scales

that are not discussed in this study. Empirical evidence showed that

there has an existence of fundamentally diff erent ubiquitous properties

called “stylized facts”, such as fat-tailed distribution, volatility clustering,

and scaling / multiscaling in fi nancial time series (He and Zheng, 2008).

Specifi cally the recent research on the similarities and diff erences between

the energy and stock market are such as Dellate and Lopez (2012) who

modeled the dependence between commodity and stock markets from

January 1990 to February 2012. They found that the dependence was time-

varying, symmetric and occurred most of the time. Besides that, Creti, Marc

and Valerie. (2012) studied the volatility together with the link between

stock and commodity markets and shown that correlations between com-

modity and stock markets was time-varying and highly volatile. However,

Gorton and Rouwenhorst (2005), Chong and Miff re (2010) and also Hong

and Yogo (2009) reached similar conclusions over the more recent studies.

These studies concluded that equity and commodity future contracts had

the same average returns along with a negative correlation for bonds and

equities and thus presented less volatile returns. On the other hand, study

of Chong and Miff re (2010) showed that there was weakness correlation

between commodity and conventional stock and bond returns which did

not happened in the study of Silvennoinen and Thorp (2010). Nevertheless,

Gorton and Rouwenhorst (2005) indicated also risk premium on commod-

ity futures was essentially same as equities. However, there is still lack of

consensus in the empirical papers investigating and comparing the simi-

larities and diff erences of stylized facts between energy and stock markets.

This paper attempts to model and compare some common stylized

facts between energy and stock markets using the ARCH family models.

After that, a series of forecast evaluation measurements are conducted

to select the most appropriate models which suit both the fi nancial mar-

kets. The rest of the paper is organized as follows. Part 2 literally reviews

the previous related studies and Part 3 explains the data involved and

methods used in this study. Meanwhile, Part 4 presents and discusses the

empirical results and at last but not least, Part 5 of this paper provides

conclusions and suggestions for future expansion.

2. Methodology

2.1. Data Source

The study period starts from January 1999 to December 2007 whereby

the data for last year, (i.e., January 2007 to December 2007) is reserved for

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

EMPIRICAL STYLIZED FACTS MODELLING 315

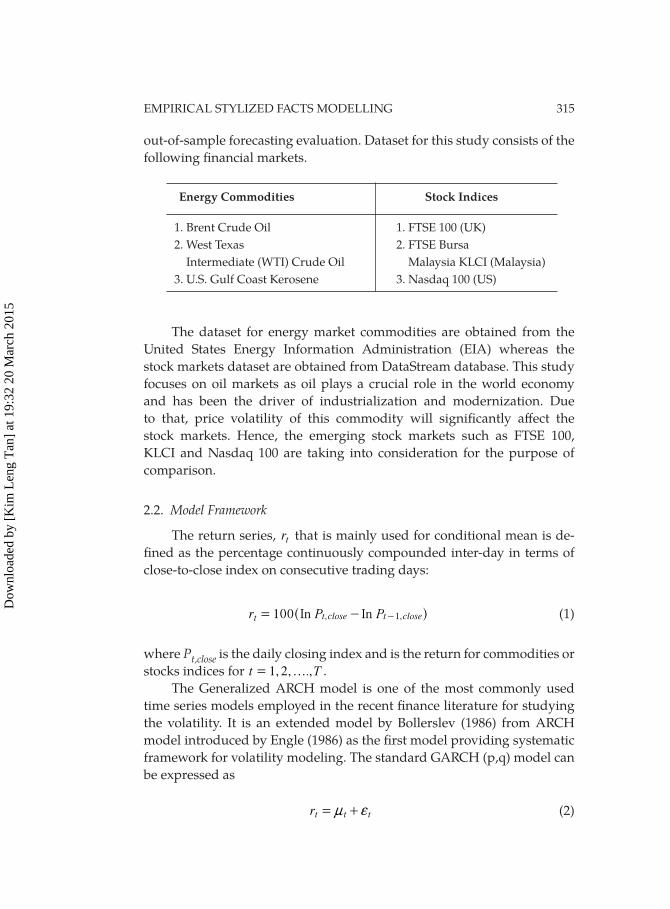

out-of-sample forecasting evaluation. Dataset for this study consists of the

following fi nancial markets.

Energy Commodities Stock Indices

1. Brent Crude Oil 1. FTSE 100 (UK)

2. West Texas 2. FTSE Bursa

Intermediate (WTI) Crude Oil Malaysia KLCI (Malaysia)

3. U.S. Gulf Coast Kerosene 3. Nasdaq 100 (US)

The dataset for energy market commodities are obtained from the

United States Energy Information Administration (EIA) whereas the

stock markets dataset are obtained from DataStream database. This study

focuses on oil markets as oil plays a crucial role in the world economy

and has been the driver of industrialization and modernization. Due

to that, price volatility of this commodity will signifi cantly aff ect the

stock markets. Hence, the emerging stock markets such as FTSE 100,

KLCI and Nasdaq 100 are taking into consideration for the purpose of

comparison.

2.2. Model Framework

The return series, tr that is mainly used for conditional mean is de-

fi ned as the percentage continuously compounded inter-day in terms of

close-to-close index on consecutive trading days:

In Inr P P100 , ,t close t close1= - -t ^ h (1)

where Pt,close is the daily closing index and is the return for commodities or

stocks indices for 1,2, .,…t T= .

The Generalized ARCH model is one of the most commonly used

time series models employed in the recent fi nance literature for studying

the volatility. It is an extended model by Bollerslev (1986) from ARCH

model introduced by Engle (1986) as the fi rst model providing systematic

framework for volatility modeling. The standard GARCH (p,q) model can

be expressed as

r n f= +t tt (2)

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

316 K. L. TAN, W. C. CHIN AND S. H. TAN

where nt denotes the conditional mean and zf v=t t t with ( , )z NID 0 1+t

or ( , )z GED 0 1+t for our study. Meanwhile, conditional variance, 2vt is

given by

2 2 2v ~ af bv= + +t t t1 1- - , (3)

with the restrictions of , ,0 0 02 2 2~ a b and .11a b+

The standard GARCH model only focuses on short-term volatility

specifi cations and forecasting. In order to include the long memory styl-

ized fact in the modeling, fractionally integrated generalized ARCH (FI-

GARCH) model has been introduced by Baillie, et al. (1996). The standard

FIGARCH (1,d,1) model is given by

( ) ( ) ( )L L L1 1 1 1 d2 2 1 2v ~ bv b { f= + + - - - --t t T1- 6 @ (4)

where , ,0 1 12 1 1~ { b and .d0 1# # L represents the lag operation

and d is the parameter for fractional integration which allows autocorre-

lations to decay at a slow hyperbolic rate, and therefore characterize the

long memory property in volatility. When 0,d 2 the main characteristic

of this model is non-stationary. The non-integer value of d can be written

in a binomial expansion as follow:

( 1) ( 1)

( )L

d kkd

L11d

k 0x x

x-

+ - +=

+3

=

k^ h /

( ) ( ) ( )dL d d L d d d L121 1 1 1 2

6f= - - - - - -2 3

k ( )c d Lk

=3

=1

k/ (5)

Fractionally Integrated Asymmetric Power ARCH (FIAPARCH)

model was developed by Tse (1998) in order to allow news impact and

long memory volatility. Specifi cations for FIAPARCH (1,d,1) model can be

represented by

( ) ( )

( )L

k d kd

L11 1

1d

k 0

vx x

x- =

+ - ++3

d

=t

k^ h / (6)

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

EMPIRICAL STYLIZED FACTS MODELLING 317

with the restriction of , , , ,0 1 0 1 1 12 1 2 1 1 1~ { d b c- and

.d0 1# # When 0c = and 2c = , the FIAPARCH process will be reduced

to FIGARCH. Another advantage of this specifi cation is the volatility can

be expressed by power factor of standard deviation. Hence, the volatility

representation is not restricted to variance and standard deviation.

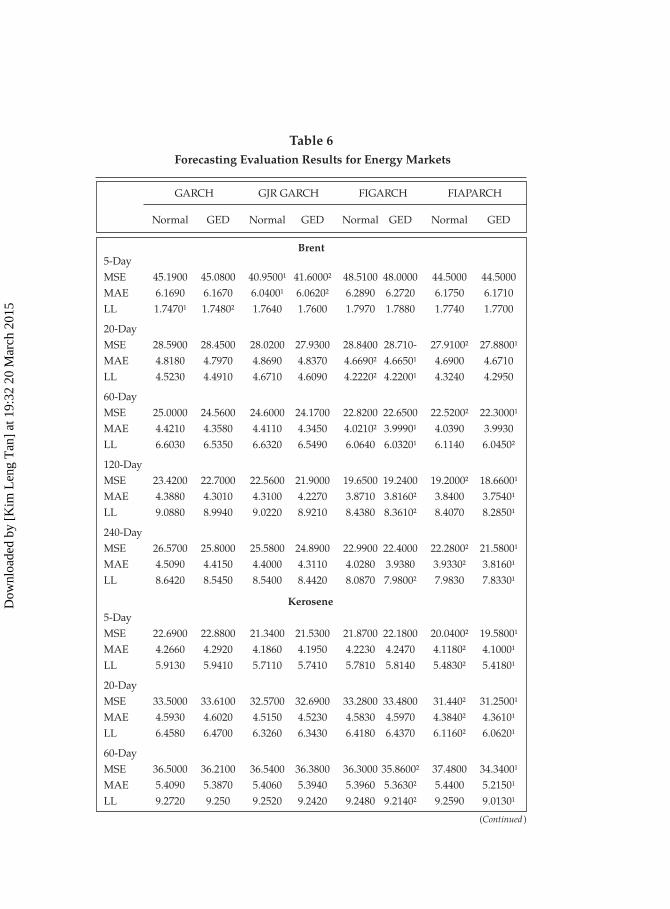

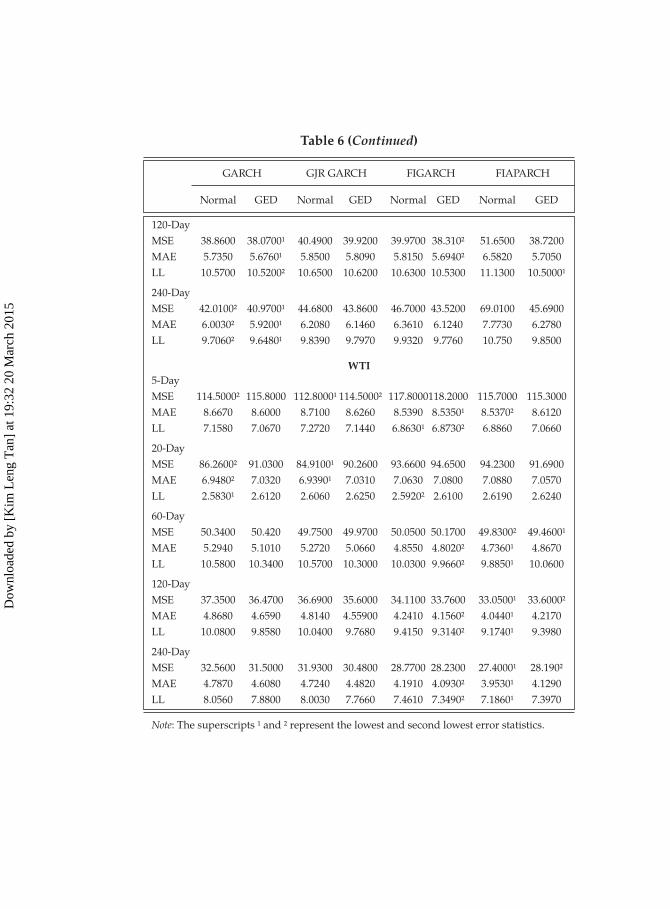

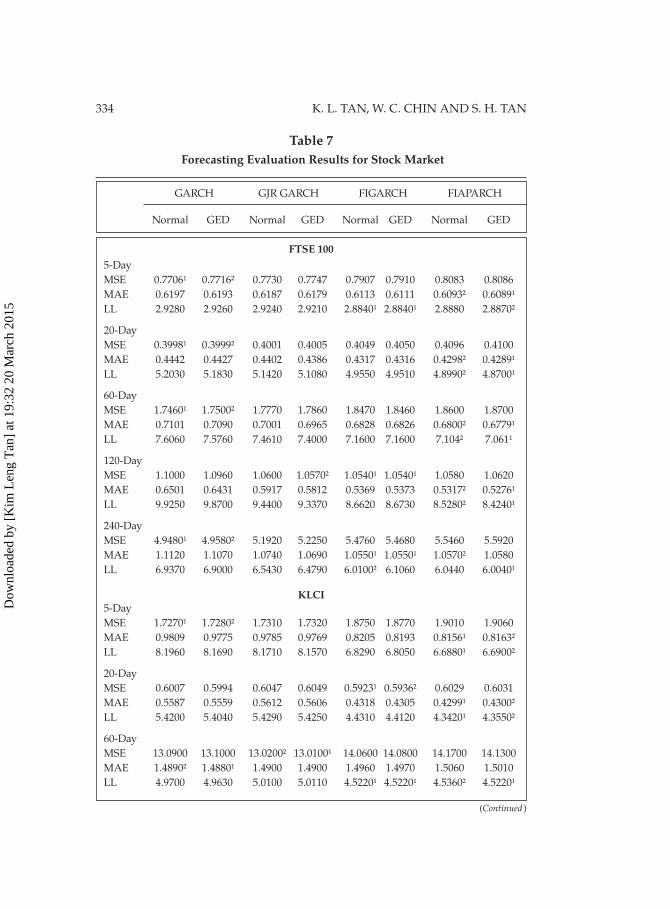

2.3. Forecasting Evaluations

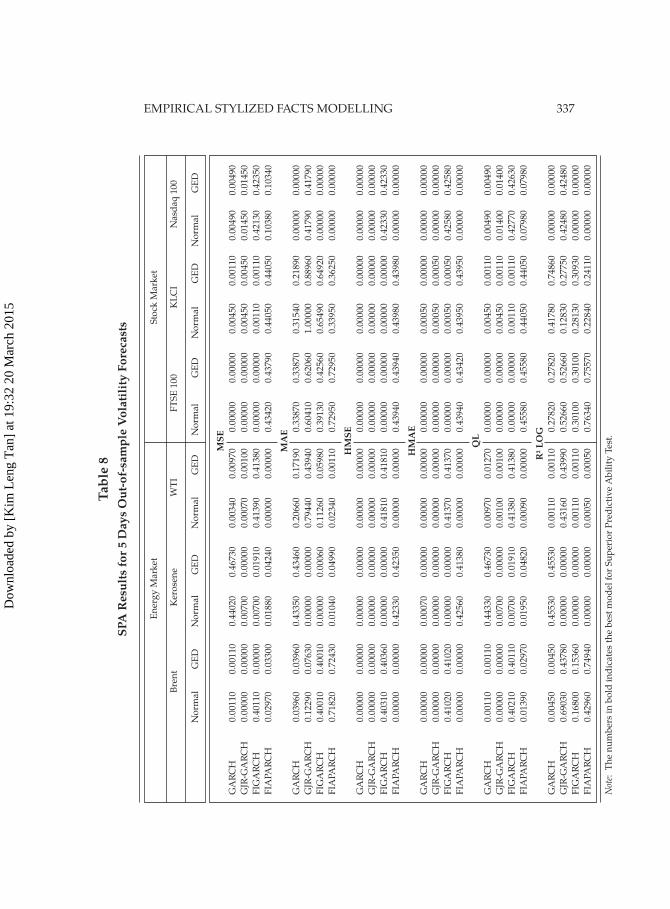

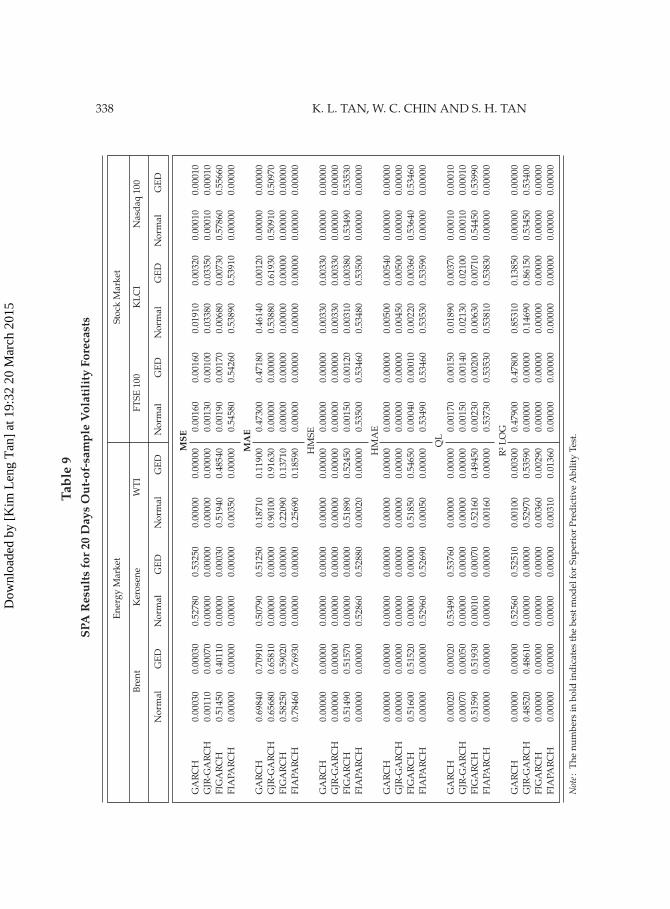

The performance of forecasts are normally based on the out-of-sam-

ple forecast evaluations whether the volatility model is able to control the

over fi tting or parameterization problems. Various forecasting criteria or

loss functions can be considered to assess the predictive accuracy of vola-

tility models. For this purpose, daily actual volatility (variance) is assessed

using the daily square returns, r2t and indicated as whereas the estimated

volatility forecast is denoted by 2vtt . Six diff erent accurate loss functions

are used to evaluate the forecast performance of the respected individual

time series :

MSE nt

n1 2 2

1

2v v= --

=t t

t^ h/ (7)

MSE nt

n1 2 2

1

2v v= --

=t t

t^ h/ (8)

/HMSE n 1t

n1 2 2 2

1

v v= --

=t t

t^ h/ (9)

/HMSE n 1t

n1 2 2 2

1

v v= --

=t t

t^ h/ (10)

In( ) /QLIKE nt

n1 2 2 2

1

v v v= -

=t t tt t^ h/ (11)

In /R LOG nt

n2 1 2 2

1

v v= -

=t t

2t6 @/ (12)

where

n – Number of forecasting data;

MSE – Mean Square Error;

MAE – Mean Absolute Error;

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

318 K. L. TAN, W. C. CHIN AND S. H. TAN

HMSE – Hetoroscedasticity Mean Square Error;

HMAE – Hetoroscedasticity Mean Absolute Error;

QLIKE – Quasi Likelihood; and

R2LOG – Return Square Logarithm

The Superior Predictive Ability (SPA) test can be implemented to

compare the performances of two or more forecasting models. This test

is extended from White (2000) by Hansen (2005). Besides that, SPA test

can also be applied to economic theory that places restrictions on the pre-

dictability of certain variables, such as eff icient market hypothesis (EMH)

(Sullivan, Timmermann, and White, 1999; Hansen, 2005). According to

Wei, Wang and Huang (2010), this test has been proven to be more ro-

bust and have good power properties than other approaches. Hence, it has

been applied by Koopman, Jungbacker and Hol (2005) and Hansen and

Lunde (2005) in their research.

In SPA test, a pre-specifi ed loss function is used to evaluate the fore-

casts, and model that produces the smallest expected loss is the ‘best’ fore-

cast model. The loss function relative to the benchmark model at time t,

can be expressed as:

, , 1, .., 1, ,, … ……d L Y Y Y Y m t nL k= =- =, ,k t t t k t,t0t t^ ^h h (13)

where ( , )L Y Y ,t t0t is the value of the loss function at time t for a benchmark

model and k( , )L Y Y ,t tt is the value of loss function at time t for another com-

petitive model, k. The issue here is whether any of the models, 1, ..,…k m= are outperform as compared to benchmark model. In order to analyze this

issue, testable hypothesis that the benchmark model is the best forecasting

model can be formulated as

: 0 Or : [ ] 0 for all 1, ..,…maxH H E d k m0 # #n =,k t0k (14)

One way to test this hypothesis according to Hansen (2005) is to con-

sider the test statistic of

k

T n d/k

1 2

~=n

k

maxSPA

t (15)

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

EMPIRICAL STYLIZED FACTS MODELLING 319

where kd n d1

t

n

1

==

,k t/ and kvar n d/2 1 2~ =kt t ^ h is a consistent estimator of the

asymptotic variance klim v r n da /2 1 2~ =k n "3 ^ h. Under the regularity condi-

tion, it holds that

k k

n T d/ k p1 2

~ ~n

=-n

k kmax max kSPA

t (16)

which is greater than zero if and only if 0>nk for some k. Therefore, we

can test H0 using the test statistics TnSPA .

3. Results and Discussions

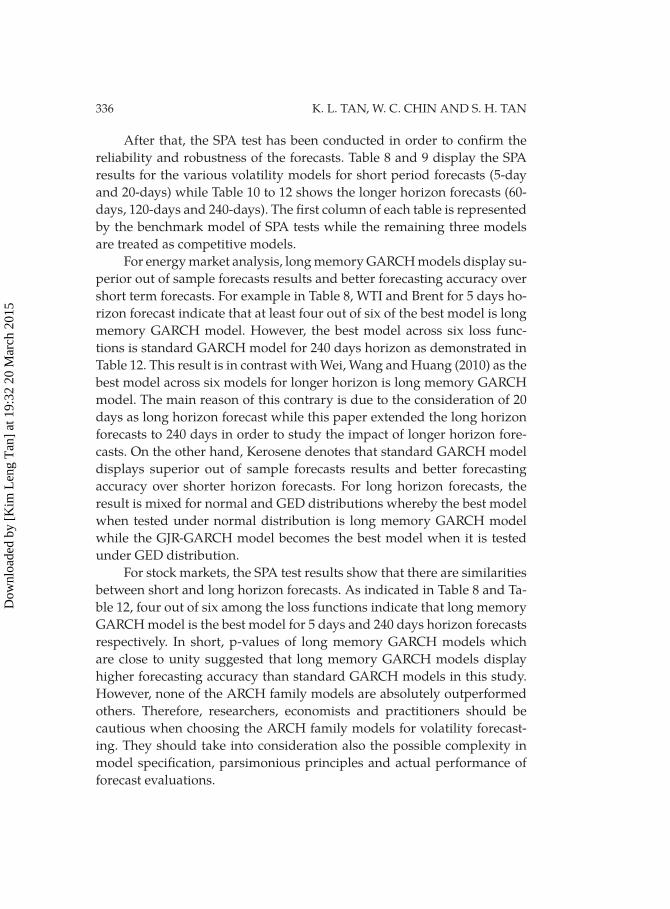

3.1. Descriptive Statistics

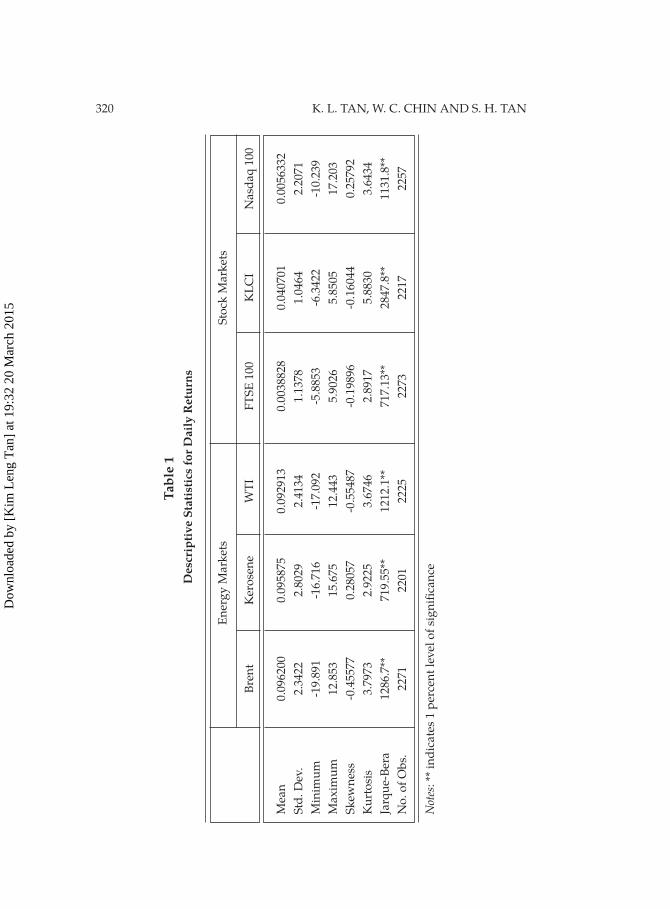

Table 1 represents the descriptive statistics for daily returns of en-

ergy markets and stock markets. Sample mean of the return series for

both markets are positive with the values close to zero. As a comparison,

sample mean of stock markets is relatively smaller than energy markets.

Meanwhile, standard deviation of energy markets is slightly higher as

compared to stock markets which implied that energy markets are more

volatile than stock markets for the selected studies period. Overall, energy

markets indicate higher kurtosis and heavier tails as compared to stock

markets. Finally, Jarque-Bera statistics indicate that the null hypothesis of

normality is rejected at one percent signifi cance level.

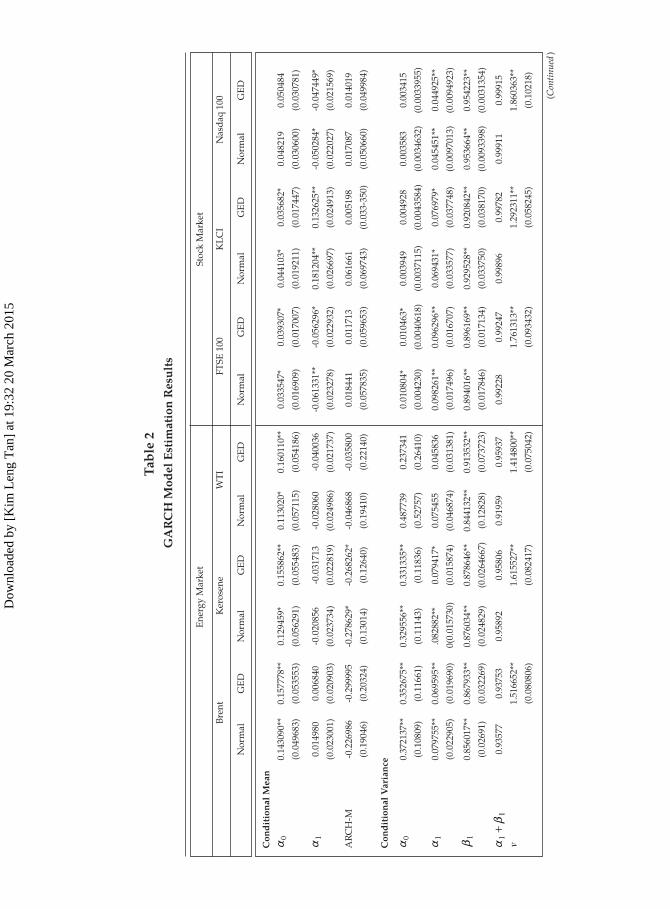

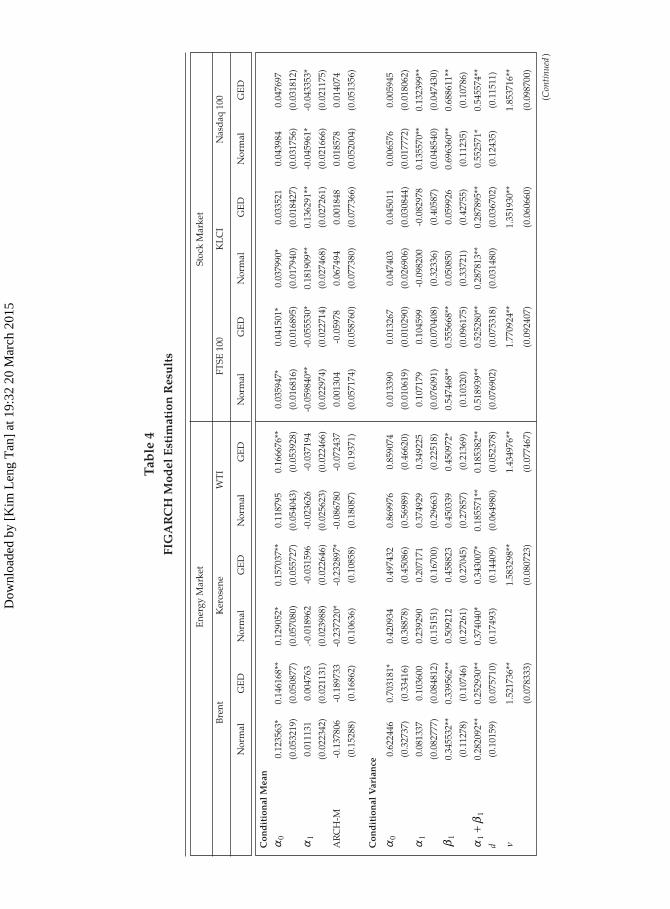

3.2. Estimation Results

Table 2 to Table 5 display the estimation results for both the markets

using normal and generalized error (GED) distributions of GARCH, GJR

GARCH, FIGARCH and FIAPARCH models. The fi rst-order autocorrela-

tion AR (1) indicates a mixture of positive and negative parameters in both

energy and stock markets. For energy markets, all the fi rst lag of returns is

insignifi cant at 5 percent level under normal and GED distribution. On the

other hand, stock markets denote signifi cance of joint estimated AR (1) co-

eff icient at 1 percent or 5 percent signifi cant level under both normal and

GED distributions. However, Nasdaq 100 displays insignifi cant coeff icient

for FIAPARCH model under normal and GED distributions.

For tail distribution analysis, GED distributions of GARCH, GJR

GARCH, FIGARCH and FIAGRACH models exhibit heavy-tails which

could be highlighted by degrees of freedom (v). All energy commodities

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

320 K. L. TAN, W. C. CHIN AND S. H. TAN

Tabl

e 1

Des

crip

tive

Stat

istic

s fo

r Dai

ly R

etur

ns

E

ner

gy

Mark

ets

Sto

ck M

ark

ets

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

Mea

n

0.0

96200

0.0

95875

0.0

92913

0.0

038828

0.0

40701

0.0

056332

Std

. D

ev.

2.3

422

2.8

029

2.4

134

1.1

378

1.0

464

2.2

071

Min

imu

m

-19.8

91

-16.7

16

-17.0

92

-5.8

853

-6.3

422

-10.2

39

Max

imu

m

12.8

53

15.6

75

12.4

43

5.9

026

5.8

505

17.2

03

Sk

ewn

ess

-0.4

5577

0.2

8057

-0.5

5487

-0.1

9896

-0.1

6044

0.2

5792

Ku

rto

sis

3.7

973

2.9

225

3.6

746

2.8

917

5.8

830

3.6

434

Jarq

ue-

Ber

a

1286.7

**

719.5

5**

1212.1

**

717.1

3**

2847.8

**

1131.8

**

No

. o

f O

bs.

2271

2201

2225

2273

2217

2257

Not

es: **

in

dic

ate

s 1 p

erce

nt

lev

el o

f si

gn

ifi c

an

ce

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

Tabl

e 2

GA

RC

H M

odel

Est

imat

ion

Res

ults

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Con

ditio

nal M

ean

0a

0.1

43090**

0.1

57778**

0.1

29459*

0.1

55862**

0.1

13020*

0.1

60110**

0.0

33547*

0.0

39307*

0.0

44103*

0.0

35682*

0.0

48219

0.0

50484

(0

.049683)

(0.0

53553)

(0.0

56291)

(0.0

55483)

(0.0

57115)

(0.0

54186)

(0.0

16909)

(0.0

17007)

(0.0

19211)

(0.0

17447)

(0.0

30600)

(0.0

30781)

a1

0.0

14980

0.0

06840

-0.0

20856

-0.0

31713

-0.0

28060

-0.0

40036

-0.0

61331**

-0

.056296*

0.1

81204**

0.1

32625**

-0

.050284*

-0.0

47449*

(0

.023001)

(0.0

20903)

(0.0

23734)

(0.0

22819)

(0.0

24986)

(0.0

21737)

(0.0

23278)

(0.0

22932)

(0.0

26697)

(0.0

24913)

(0.0

22027)

(0.0

21569)

AR

CH

-M

-0.2

26986

-0.2

99995

-0.2

78629*

-0.2

68262*

-0.0

46868

-0.0

35800

0.0

18441

0.0

11713

0.0

61661

0.0

05198

0.0

17087

0.0

14019

(0

.19046)

(0.2

0324)

(0.1

3014)

(0.1

2640)

(0.1

9410)

(0.2

2140)

(0.0

57835)

(0.0

59653)

(0.0

69743)

(0.0

33-3

50)

(0.0

50660)

(0.0

49984)

Con

ditio

nal V

aria

nce

0a

0.3

72137**

0.3

52675**

0.3

29556**

0.3

31335**

0.4

87739

0.2

37341

0.0

10804*

0.0

10463*

0.0

03949

0.0

04928

0.0

03583

0.0

03415

(0

.10809)

(0.1

1661)

(0.1

1143)

(0.1

1836)

(0.5

2757)

(0.2

6410)

(0.0

04230)

(0.0

040618)

(0.0

037115)

(0.0

043584)

(0.0

034632)

(0.0

033

955)

a1

0.0

79755**

0.0

69595**

.0

82882**

0.0

79417*

0.0

75455

0.0

45836

0.0

98261**

0.0

96296**

0.0

69431*

0.0

76979*

0.0

45451**

0.0

44925**

(0

.022

905)

(0.0

19690)

0(0

.015730)

(0.0

15874)

(0.0

46874)

(0.0

31381)

(0.0

17496)

(0.0

16707)

(0.0

33577)

(0.0

37748)

(0.0

097013)

(0.0

094923)

b1

0.8

56017**

0.8

67933**

0.8

76034**

0.8

78646**

0.8

44132**

0.9

13532**

0.8

94016**

0.8

96169**

0.9

29528**

0

.920842**

0.9

53664**

0.9

54223**

(0

.02691)

(0.0

32269)

(0.0

24829)

(0.0

264667)

(0.1

2828)

(0.0

73723)

(0.0

17846)

(0.0

17134)

(0.0

33750)

(0.0

38170)

(0.0

093398)

(0.0

031354)

ab

+1

1

0.9

3577

0.9

3753

0.9

5892

0.9

5806

0.9

1959

0.9

5937

0.9

9228

0.9

9247

0.9

9896

0.9

9782

0.9

9911

0.9

9915

v

1.5

16652**

1.6

15527**

1.4

14800**

1.7

61313**

1.2

92311**

1.8

60363**

(0.0

80806)

(0

.082417)

(0

.075042)

(0

.093432)

(0

.058245)

(0

.10218)

(Con

tinue

d )

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

Mod

el S

elec

tion

Lo

g (

L)

-4589.5

19

-4565.9

53

-4718.6

26

-4707.1

64

-4534.2

15

-4495.5

80

-2771.2

84

-2767.4

85

-2491.4

68

-2432.9

03

-4025.1

02

-4024.0

12

AIC

4.

537796

4.5

15509

4.8

44744

4.8

34014

4.5

94347

4.5

56256

2.7

48796

2.7

46025

2.5

35773

2.4

77302

4.0

18048

4.0

17958

SIC

4.5

51656

4.5

32142

4.8

59040

4.8

51170

4.6

08489

4.5

73226

2.7

62684

2.7

62691

2.5

49956

2.4

94321

4.0

32016

4.0

34720

Dia

gn

ost

ic

Q(1

0)

6.4

0047

6.7

1329

4.3

3626

4.8

4011]

6.3

3255

6.9

5763.

58268

3.3

0949

14.7

272

24.0

471**

9.4

5223

9.3

8792

[0

.6992639]

[0.6

669418]

[0.8

879207]

[0.8

480176

[0.7

062293

[0.6

415311]

[0.9

366752]

[0.9

507513]

[0.0

987082]

[0.0

042274]

[0.3

9661

87]

[0.4

022630]

Q2(

10)

15.4

262

17.0

140*

3.3

8038

3.4

5297

5.6

5645

10.2

139

15.1

265

15.3

595

23.3

488**

18.9

363*

16.4

769*

16.5

579*

[0

.0513684]

[0.0

299634]

[0.9

082723]

[0.9

028089]

[0.6

856514]

[0.2

503310]

[0.0

567325]

[0.0

525211]

[0.0

029442]

[0.0

152042]

[0.0

36

0414]

[0.0

50568]

AR

CH

(10)

1.4

791

1.6

339

0.3

3841

0.3

4398

0.5

2777

0.9

5327

1.4

930

1.4

730

2.2

326*

1.8

176

1.6

222

1.6

330

[0

.1408]

[0.0

912]

[0.9

708]

[0.9

302]

[0.8

716]

[0.4

827]

[0.1

432]

[0.1

356]

[0.0

139]

[0.0

528]

[0.0

944]

[0.0

915]

Not

es: *a

nd

**

den

ote

5%

an

d 1

% s

ign

ifi c

ian

t le

vel

res

pec

tiv

aly

. Ja

rqu

e-B

era s

tati

stic

s te

st f

or

the

nu

ll h

yp

oth

esis

of

no

rmali

ty i

n t

he

sam

pel

ret

urn

dis

trib

uti

on

. T

he

nu

mb

er i

np

are

nth

eses

are

erro

r o

f th

e es

tim

ati

on

Lo

g (

L)i

s th

e lo

gari

tham

max

imu

m l

ick

lih

oo

d f

un

ctio

n v

alu

e. A

IC i

s th

e av

erag

e A

kaik

e in

form

ati

on

cri

teri

on

an

d S

IC i

s th

e av

erag

e S

chw

arz

in

form

ati

on

cri

teri

on

.

Q(1

0)

an

d Q

2 (

10)

are

th

e L

jun

g-B

ox

Q-s

tati

stic

s o

f o

rder

10 c

om

pu

ted

on

th

e st

an

dard

ized

res

idu

als

an

d s

qu

red

sta

nd

rad

ized

res

idu

als

res

pec

tiv

ely

AR

CH

(10)

is t

he

no

n -

het

ero

sces

dast

icit

y

stati

stic

of

ord

er 1

0 P

-valu

es o

f th

e st

ati

stic

are

rep

ort

ed i

n s

qu

are

bra

cket

s. T

he

AR

CH

-in

Mea

n c

oeff

ici

ent

is e

xclu

ded

fro

m t

he

esti

mati

on

mo

del

s.

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Tabl

e 2

(Con

tinu

ed)

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

Tabl

e 3

GJR

-GA

RC

H M

odel

Est

imat

ion

Res

ults

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Con

ditio

nal M

ean

0

a

0.1

10970**

0.1

39370**

0.1

53594**

0.1

73140**

0.0

97487

0.1

51366**

0.0

06590

0.0

13137

0.0

32519

0.0

28979

0.0

22619

0.0

26517

(0

.051681)

(0.0

49630)

(0.0

57961)

(0.0

57132)

(0.0

53057)

(0.0

54309)

(0.0

16843)

(0.0

17244)

(0.0

19177)

(0.0

17136)

(0.0

29813)

(0.0

30308)

a1

0.0

16

342

0.0

07532

-0.0

22373

-0.0

32968

-0.0

32624

-0.0

42445

-0.0

64726**

-0

.059776**

0.1

85002**

0

.135093**

-0

.051741*

-0.0

48796*

(0

.023

097)

(0.0

20997)

(0.0

23634)

(0.0

22523)

(0.0

24485)

(0.0

22862)

(0.0

23536)

(0.0

22931)

(0.0

26264)

(0.0

13515)

(0.0

22109)

(0.0

21560)

AR

CH

-M

-0.2

99292

-0.3

48755

-0.3

03561*

-0.2

95049*

0.0

08290

-0.0

04208

-0.0

01824

0.0

00465

0.0

43187

-0.0

02268

-0.0

05148

-0.0

06760

(0

.18282)

(0.1

9117)

(0.1

3524)

(0.1

3260)

(0.2

0792)

(0.0

47946)

(0.0

59715)

(0.0

60400)

(0.0

66846)

(0.0

67246)

(0.0

47285)

(0.0

47098)

Con

ditio

nal V

aria

nce

0a

0.5

220

85**

0.4

72385**

0.3

05784**

0.5

96861

0.2

62579

0.0

12116**

0.0

11647**

0.0

04892

0.0

059570

.005006

0.0

04749

0.3

04337**

(0

.18

944)

(0.1

9300)

(0.1

0465)

(0.1

1069)

(0.7

6285)

(0.3

6061))

(0

.0039528)

(0.0

037548)

(0.0

040523)

(0.0

046490)

(0.0

039725)

(0.0

038976)

a1

0.0

25

081

0.0

27091

0.1

04529**

0.1

00526**

0.0

53981

0.0

25790

0.0

07595

0.0

04351

0.0

54482*

0.0

64381*

0.0

18829*

0.0

17944*

(0

.017

777)

(0.0

16364)

(0.0

23581)

(0.0

22834)

(0.0

35465)

(0.0

27923)

(0.0

15020)

(0.0

13127)

(0.0

21988)

(0.0

26245)

(0.0

093910)

(0.0

090365)

b1

0.8

28795**

0.8

44345**

0.8

79621**

0.8

82243**

0.8

22430**

0.9

10957**

0.9

19679**

0.9

21113**

0.9

21972**

0.9

12386**

0.9

53929**

0.9

54364**

(0

.045588)

(0.0

47538)

(0.0

23746)

(0.0

25236)

(0.1

7639)

(0.0

96346)

(0.0

14849)

(0.0

14384)

(0.0

32668)

(0.0

36480)

(0.0

085716)

(0.0

083990)

c

0.1

05354*

0.0

83619

-0.0

41126

-0.0

39546

0.0

46717

0.0

32740

0.1

17280**

0.1

20783**

0.0

45784

0.0

43017

0.0

51827**

0.0

52767**

(0

.051653)

(0.0

43007)

(0.0

25171)

(0.0

23828)

(0.0

65263)

(0.0

33196)

(0.0

26385)

(0.0

24719)

(0.0

30327)

(0.0

28707)

(0.0

16872)

(0.0

16507

v

1.5

43084**

1.6

21099**

1.4

15141**

1.7

99136**

1.3

01592**

1.8

85177**

(0.0

78735)

(0

.081370)

(0

.074339)

(0

.11151)

(0

.057871)

(0

.10510)

(Con

tinue

d )

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Tabl

e 3

(Con

tinu

ed)

Mod

el S

elec

tion

Lo

g (

L)

-4580.6

97

-4560.9

65

-4716.5

84

-4705.5

80

-4532.6

46

-4494.3

55

-2749.6

49

-2746.8

81

-2486.2

01

-2430.1

06

-4014.6

03

-4013.8

71

AIC

4.5

30071

4.5

11570

4.8

43676

4.8

33415

4.5

93771

4.5

56027

2.7

28366

2.7

26614

2.5

31438

2.4

75476

4.0

08577

4.0

08845

SIC

4.5

46703

4.5

30974

4.8

60832

4.8

53430

4.6

10741

4.5

75826

2.7

45031

2.7

46058

2.5

48458

2.4

95332

4.0

25339

4.0

28399

Dia

gnos

tic

Q(1

0)

6.6

7097

6.6

0776

4.5

1500

5.0

6105

6.0

5973

6.6

3592

3.2

0185

2.9

6727

15.3

269

24.8

722**

8.3

6791

8.2

8251

[0

.6713323]

[0.6

778826]

[0.8

743756]

[0.8

289544]

[0.7

339256]

[0.6

749656]

[0.9

557514]

[0.9

655784]

[0.0

823400]

[0.0

031158]

[0.4

97

5369]

[0.5

059462]

Q2(

10)

14.9

621

16.0

488

2.8

5882

2.8

7003

5.2

7124

9.0

5208

12.4

721

12.3

612

17.0

493*

14.4

452

18.1

232*

18.3

033*

[0

.0598861]

[0.0

416875]

[0.9

429024]

[0.9

422468]

[0.7

282316]

[0.3

379215]

[0.1

313503]

[0.1

358028]

[0.0

296002]

[0.0

708745]

[0.0

20

3216]

[0.0

190639]

AR

CH

(10)

1.4

302

1.5

322

0.2

8396

0.2

8283

0.4

8535

0.8

4177

1.1

965

1.1

856

1.6

424

1.3

892

1.8

089

1.8

324

[0

.1606]

[0.1

217]

[0.9

849]

[0.9

851]

[0.9

005]

[0.5

882]

[0.2

882][

0.2

956]

[0.0

890]

[0.1

790]

[0.0

542]

[0.0

505]

Not

es :

* an

d *

* d

eno

te 5

% a

nd

1%

sig

nifi

can

ce l

evel

res

pec

tiv

ely.

Jarq

ue-

Ber

a s

tati

stic

s te

sts

for

the

nu

ll h

yp

oth

esis

of

no

rmali

ty i

n t

he

sam

ple

ret

urn

dis

trib

uti

on

.T

he

nu

mb

ers

in p

are

nth

eses

are

sta

nd

ard

err

or

of

the

esti

mati

on

. L

og

(L)

is t

he

log

ari

thm

max

imu

m l

ikel

iho

od

fu

nct

ion

valu

e. A

IC i

s th

e av

erag

e A

kaik

e in

form

ati

on

cri

teri

on

an

d S

IC i

s th

e av

erag

e S

chw

arz

in

form

ati

on

crit

erio

n. Q

(10)

an

d Q

2 (1

0)

are

th

e L

jun

g-

Bo

x Q

-sta

tist

ics

of

ord

er 1

0 c

om

pu

ted

on

th

e st

an

dard

ized

res

idu

als

an

d s

qu

are

d s

tan

dard

ized

res

idu

als

res

pec

tiv

ely.

AR

CH

(10)

is t

he

no

n-

het

ero

sces

dast

icit

y s

tati

stic

of

ord

er 1

0. P

-valu

es o

f th

e st

ati

stic

s are

rep

ort

ed i

n s

qu

are

bra

cket

s. T

he

AR

CH

-in

Mea

n c

oeff

ici

ent

is e

xclu

ded

fro

m t

he

esti

mati

on

mo

del

s.

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

Tabl

e 4

FIG

AR

CH

Mod

el E

stim

atio

n R

esul

ts

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Con

ditio

nal M

ean

0a

0.1

23563*

0.1

46168**

0.1

29052*

0.1

57

037**

0.1

18795

0.1

66676**

0.0

35947*

0.0

41501*

0.0

37990*

0.0

33521

0.0

43984

0.0

47697

(0

.053

219)

(0.0

50877)

(0.0

57080)

(0.0

55727)

(0.0

54043)

(0.0

53928)

(0.0

16816)

(0.0

16895)

(0.0

17940)

(0.0

18427)

(0.0

31756)

(0.0

31812)

a1

0.0

11131

0.0

04763

.-0.0

18962

-0.0

31596

-0.0

23626

-0.0

37194

-0.0

59840**

-0

.055530*

0.1

81909**

0

.136291**

-0

.045961*

-0.0

43353*

(0

.022

342)

(0.0

21131)

(0.0

23988)

(0.0

22646)

(0.0

25623)

(0.0

22466)

(0.0

22974)

(0.0

22714)

(0.0

27468)

(0.0

27261)

(0.0

21666)

(0.0

21175)

AR

CH

-M

-0.1

37806

-0.1

89733

-0.2

37220*

-0.2

32897*

-0.0

86780

-0.0

72437

0.0

01304

-0.0

5978

0.0

67494

0.0

01848

0.0

18578

0.0

14074

(0

.15288)

(0.1

6862)

(0.1

0636)

(0.1

0858)

(0.1

8087)

(0.1

9371)

(0.0

57174)

(0.0

58760)

(0.0

77380)

(0.0

77366)

(0.0

52004)

(0.0

51356)

Con

ditio

nal V

aria

nce

0a

0.6

22

446

0.7

03181*

0.4

20934

0.4

97432

0.8

69976

0.8

59074

0.0

13390

0.0

13267

0.0

47403

0.0

45011

0.0

06576

0.0

05945

(0

.32

737)

(0.3

3416)

(0.3

8878)

(0.4

5086)

(0.5

6989)

(0.4

6620)

(0.0

10619)

(0.0

10290)

(0.0

26906)

(0.0

30844)

(0.0

17772)

(0.0

18062)

a1

0.0

81337

0.1

03600

0.2

39290

0.2

07171

0.3

74929

0.3

49225

0.1

07179

0.1

04599

-0.0

98200

-0.0

82978

0.1

35570**

0.1

32399**

(0

.082

777)

(0.0

84812)

(0.1

5151)

(0.1

6700)

(0.2

9663)

(0.2

2518)

(0.0

76091)

(0.0

70408)

(0.3

2336)

(0.4

0587)

(0.0

48540)

(0.0

47430)

b1

0.3

45532**

0.3

39562**

0.5

09212

0.4

58823

0.4

50339

0.4

50972*

0.5

47468**

0.5

55668**

0.0

50850

0.0

59926

0.6

96360**

0.6

88611**

(0

.11278)

(0.1

0746)

(0.2

7261)

(0.2

7045)

(0.2

7857)

(0.2

1369)

(0.1

0320)

(0.0

96175)

(0.3

3721)

(0.4

2755)

(0.1

1235)

(0.1

0786)

ab

+1

1

0.2

820

92**

0.2

52930**

0.3

74040*

0.3

43007*

0.1

85571**

0.1

85382**

0.5

18939**

0.5

25280**

0.2

87813**

0.2

87895**

0.5

52571*

0.5

45574**

d (0

.10159)

(0.0

75710)

(0.1

7493)

(0.1

4409)

(0.0

64980)

(0.0

52378)

(0.0

76902)

(0.0

75318)

(0.0

31480)

(0.0

36702)

(0.1

2435)

(0.1

1511)

v

1.5

21736**

1.5

83298**

1.4

34976**

1.7

70924**

1.3

51930**

1.8

53716**

(0.0

78333)

(0

.080723)

(0

.077467)

(0

.092407)

(0

.060660)

(0

.098700)

(Con

tinue

d )

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Tabl

e 4

(Con

tinu

ed)

Mod

el S

elec

tion

Lo

g (

L)

-4584.8

65

-4562.4

07

-4726.7

95

-4713.1

90

-4528.1

90

-4493.2

11

-2766.2

30

-2762.8

41

-2463.9

13

-2415.1

17

-4022.9

67

-4021.7

65

AIC

4.5

34188

4.5

12995

4.8

54149

4.8

41220

4.5

89261

4.5

54869

2.7

44782

2.7

42417

2.5

08800

2.4

60250

4.0

16916

4.0

16714

SIC

4.5

50820

4.5

32399

4.8

71304

4.8

61235

4.6

06231

4.5

74668

2.7

61448

2.7

61861

2.5

25819

2.4

80107

4.0

33677

4.0

36269

Dia

gnos

tic

Q(1

0)

7.0

1565

7.3

5293

4.1

6894

4.7

6615

5.9

8324

6.6

6511

3.9

1710

30.7

1023

3.7

10273

9.5

133*

10.1

370

10.0

565

[0

.6354895]

[0.6

004256]

[0.8

999453]

[0.8

541986]

[0.7

415944]

[0.6

719404]

[0.9

167836]

[0.9

294294]

[0.1

654627]

[0.0

211652]

[0.3

39

5116]

[0.3

459279]

Q2(

10)

12.8

788

14.6

534

3.1

4120

3.0

4444

4.8

5688

5.4

9848

11.2

527

17.0

207

4.5

0056

4.5

0056

10.9

917

10.7

674

[0

.1160900]

[0.0

662458]

[0.9

251866]

[0.9

315376]

[0.7

727574]

[0.7

032080]

[0.1

877875]

[0.5

216832]

[0.8

086767]

[0.8

093771]

[0.2

02

1671]

[0.2

152277]

AR

CH

(10)

1.2

946

1.4

616

0.3

1503

0.3

0060

0.4

6636

0.5

2223

1.1

459

1.1

511

0.4

4263

0.4

4789

1.0

883

1.0

655

[0

.2276]

[0.1

477]

[0.9

776]

[0.9

812]

[0.9

123]

[0.8

756]

[0.3

236]

[0.3

199]

[0.9

258]

[0.9

229]

[0.3

673]

[0.3

856]

Not

es : *

an

d *

* d

eno

te 5

% a

nd

1%

sig

nifi

can

ce l

evel

res

pec

tiv

ely.

Jarq

ue-

Ber

a s

tati

stic

s te

sts

for

the

nu

ll h

yp

oth

esis

of

no

rmali

ty i

n t

he

sam

ple

ret

urn

dis

trib

uti

on

.T

he

nu

mb

ers

in p

are

nth

eses

are

sta

nd

ard

err

or

of

the

esti

mati

on

. L

og

(L)

is t

he

log

ari

thm

max

imu

m l

ikel

iho

od

fu

nct

ion

valu

e. A

IC i

s th

e av

erag

e A

kaik

e in

form

ati

on

cri

teri

on

an

d S

IC i

s th

e av

erag

e S

chw

arz

in

form

ati

on

crit

erio

n. Q

(10)

an

d Q

2 (1

0)

are

th

e L

jun

g-B

ox

Q-s

tati

stic

s o

f o

rder

10 c

om

pu

ted

on

th

e st

an

dard

ized

res

idu

als

an

d s

qu

are

d s

tan

dard

ized

res

idu

als

res

pec

tiv

ely.

AR

CH

(10)

is t

he

no

n-

het

ero

sces

dast

icit

y s

tati

stic

of

ord

er 1

0. P

-valu

es o

f th

e st

ati

stic

s are

rep

ort

ed i

n s

qu

are

bra

cket

s. T

he

AR

CH

-in

Mea

n c

oeff

ici

ent

is e

xclu

ded

fro

m t

he

esti

mati

on

mo

del

s.

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

Tabl

e 5

FIA

PAR

CH

Mod

el E

stim

atio

n R

esul

ts

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Con

ditio

nal M

ean

0a

0.0

95552

0.1

29335**

0.1

60610**

0.1

82187**

0.0

96871

0.1

50089**

0.0

04688

0.0

10265

0.0

29156

0.0

28127

0.0

17879

0.0

22581

(0

.051460)

[0.0

49804]

(0.0

59387)

(0.0

57429)

(0.0

50891)

(0.0

53416)

(0.0

16754)

(0.0

16655

)(0.0

18803)

(0.0

17433)

(0.0

30788)

(0.0

31326)

a1

0.0

12787

0.0

06026

-0.0

30157

-0.0

39128

-0.0

32113

-0.0

41596

-0.0

55740*

-0.0

52412*

0.1

83791**

0.1

38235**

-0

.042786

-0.0

40266

(0

.022608)

(0.0

21073)

(0.0

24646)

(0.0

22376)

(0.0

24708)

(0.0

23104)

(0.0

23919)

(0.0

21970)

(0.0

25862)

(0.0

18392)

(0.0

22166)

(0.0

21471)

AR

CH

-M

-0.3

07552*

-0.3

24834*

-0.1

87688

-0.2

36957*

-0.0

78619

-0.0

69242

-0.0

71416

-0.0

65029

0.0

19353)

-0.0

19470

-0.0

05721

-0.0

08139

(0

.12722)

(0.1

2811)

(0.1

1468)

(0.1

1507)

(0.1

4681)

(0.1

6369)

(0.0

72877)

(0.0

69922)

(0.0

70624

(0.0

53566)

(0.0

51034)

(0.0

50440)

Con

ditio

nal V

aria

nce

0a

0.7

98144*

0.8

36679*

0.0

86491

0.2

50967

0.2

11353

1.0

02495

0.0

35380

0.0

34380

0.0

10474

0.0

14566

0.0

10725

0.0

07207

(0

.38340)

(0.3

6367)

(0.0

45102)

(0.3

4851)

(0.1

4078)

(0.9

0210)

(0.0

19504)

(0.0

18852)

(0.0

27176)

(0.0

27292)

(0.0

36838)

(0.0

36928)

a1

0.1

00753

0.1

19302

-0.0

15887

0.1

34005

0.8

08363**

0.1

89941

0.2

18021**

0.2

20033**

-0

.286172

-0.3

12920

0.1

37738

0.1

34315

(0

.10018)

(0.0

97372)

(0.1

3633)

(0.1

7278)

(0.0

82996)

(0.5

0317)

(0.0

50947)

(0.0

49600)

(0.2

4296)

(0.3

3197)

(0.0

78108)

(0.0

77428)

b1

0.2

55362**

0.2

66506**

0.8

95822**

0.7

09322*

0.8

50106**

0.2

69911

0.5

63604**

0.5

67868**

-0

.178917

-0.2

11612

0.5

17672**

0.5

13778**

(0

.096730)

(0.1

0031)

(0.0

55828)

(0.3

5658)

(0.0

71852)

(0.5

3264)

(0.0

81655)

(0.0

77896)

(0.2

5707)

(0.3

5578)

(0.1

5590)

(0.1

5342)

c

0.3

77546

0.3

57260

-0.1

50743

-0.1

66482

0.2

76093

0.3

80641

0.6

48098**

0.6

72313**

0.1

33471*

0.1

26123*

0.2

97065*

0.3

00837*

(0

.22571)

(0.2

1291)

(0.0

86694)

(0.0

85928)

(0.1

6679)

(0.2

8824)

(0.2

0463)

(0.1

9497)

(0.0

64076)

(0.0

60093)

(0.1

3125)

(0.1

3030)

d

1.8

46652**

1.8

49915**

1.3

06489**

1.3

64452**

2.0

27061**

1.5

24998**

1.4

27385**

1.4

06893**

2.2

75997**

2.2

50136**

1.8

76705**

1.8

78107**

(0

.25633)

(0.2

6748)

(0.2

2024)

(0.3

7789)

(0.3

2667)

(0.4

8282)

(0.1

8957)

(0.1

7409)

(0.1

5697)

(0.1

5214)

(0.1

3340)

(0.1

3320)

d 0.1

95027

0.1

83568*

0.9

95968**

0.6

45854

0.1

74405**

0.1

64713*

0.4

05104**

0.4

06932**

0.2

33097**

0.2

36462**

0.3

93974**

0.3

91947**

(0

.10468)

(0.0

86835)

(0.1

3633)

(0.5

1533)

(0.0

61285)

(0.0

81144)

(0.0

70082)

(0.0

69250)

(0.0

44531)

(0.0

46555)

(0.0

98749)

(0.0

9666

3)

v

1.5

43080**

1.6

03356**

1.4

40074**

1.8

25344*

1.3

50898**

(0.0

96663

(0.0

79771)

(0

.077434)

(0

.076243)*

(0.1

1472)

(0

.060305)

1.8

82829**

d =

1

3.3

02977

3.1

77490

1.3

91614

0.9

64439

3.1

44032

1.0

87358

2.2

54497

2.3

37257

8.1

28923

8.2

18483

6.5

7200

6.5

92395

d =

2

-0.5

98244

-0.5

61107

-3.1

48888

-1.6

81833

-0.0

82839

-0.9

83808

-3.0

20599

-3.4

06899

1.7

58279

1.6

45590

-0.9

24250

-0.9

15113

(Con

tinue

d )

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

E

ner

gy

Mark

et

Sto

ck M

ark

et

B

ren

t K

ero

sen

e W

TI

FT

SE

100

KL

CI

Nasd

aq

100

N

orm

al

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

No

rmal

GE

D

Tabl

e 5

(Con

tinu

ed)

Mod

el S

elec

tion

Lo

g (

L)

-4577.8

89

-4558.0

12

-4719.6

67

-4708.6

25

-4523.3

66

-4489.9

51

-2743.7

98

-2741.8

11

-2456.4

59

-2410.6

75

-4013.8

40

-4013.0

78

AIC

4.5

29273

4.5

10629

4.8

48890

4.8

38590

4.5

86402

4.5

53594

2.7

24553

2.7

23575

2.5

03260

2.4

57770

4.0

09811

4.0

10048

SIC

4.5

51449

4.5

35578

4.8

71764

4.8

64323

4.6

09029

4.5

79049

2.7

46774

2.7

48574

2.5

25953

2.4

83300

4.0

32159

4.0

35190

Dia

gnos

tic

Q(1

0)

7.0

6318

7.1

2535

4.8

7439]

5.1

7838

5.4

9338

6.2

6573

3.1

8132

3.1

7688

13.3

508

19.4

627*

8.8

0815

8.7

9923

[0

.6305417]

[0.6

240708]

[0.8

451174

[0.8

184898]

[0.7

893554]

[0.7

130564]

[0.9

566702]

[0.9

568672]

[0.1

473634]

[0.0

215340]

[0.4

551

690][

0.4

560102]

Q2(

10)

13.8

679

14.8

395

4.6

1440

5.6

0394

6.6

6737

5.2

9262

11.4

487

11.3

946

3.4

0134

3.4

3883

8.1

4139

8.0

5227

[0

.0852751]

[0.0

623432]

[0.7

978816]

[0.6

914994]

[0.5

729081]

[0.7

258911]

[0.1

775490]

[0.1

803253]

[0.9

067100]

[0.9

038846]

[0.4

19

7822]

[0.4

283810]

AR

CH

(10)

1.3

442

1.4

395

0.4

5644

0.5

2717

0.6

5417

0.4

8406

1.2

071

1.2

039

0.3

3791

0.3

4429

0.8

1910

0.8

0991

[0

.2009]

[0.1

567]

[0.9

181]

[0.8

720]

[0.7

677]

[0.9

013]

[0.2

811]

[0.2

833]

[0.9

709]

[0.9

689]

[0.6

102]

[0.6

192]

Not

es : *

an

d *

* d

eno

te 5

% a

nd

1%

sig

nifi

can

ce l

evel

res

pec

tiv

ely.

Jarq

ue-

Ber

a s

tati

stic

s te

sts

for

the

nu

ll h

yp

oth

esis

of

no

rmali

ty i

n t

he

sam

ple

ret

urn

dis

trib

uti

on

.T

he

nu

mb

ers

in p

are

nth

eses

are

sta

nd

ard

err

or

of

the

esti

mati

on

. L

og

(L)

is t

he

log

ari

thm

max

imu

m l

ikel

iho

od

fu

nct

ion

valu

e. A

IC i

s th

e av

erag

e A

kaik

e in

form

ati

on

cri

teri

on

an

d S

IC i

s th

e av

erag

e S

chw

arz

in

form

ati

on

crit

erio

n. Q

(10)

an

d Q

2 (1

0)

are

th

e L

jun

g -

Bo

x Q

-sta

tist

ics

of

ord

er 1

0 c

om

pu

ted

on

th

e st

an

dard

ized

res

idu

als

an

d s

qu

are

d s

tan

dard

ized

res

idu

als

res

pec

tiv

ely.

AR

CH

(10)

is t

he

no

n-

het

ero

sces

dast

icit

y s

tati

stic

of

ord

er 1

0. P

-valu

es o

f th

e st

ati

stic

s are

rep

ort

ed i

n s

qu

are

bra

cket

s. T

he

AR

CH

-in

Mea

n c

oeff

ici

ent

is e

xclu

ded

fro

m t

he

esti

mati

on

mo

del

s.

Dow

nloa

ded

by [

Kim

Len

g T

an]

at 1

9:32

20

Mar

ch 2

015

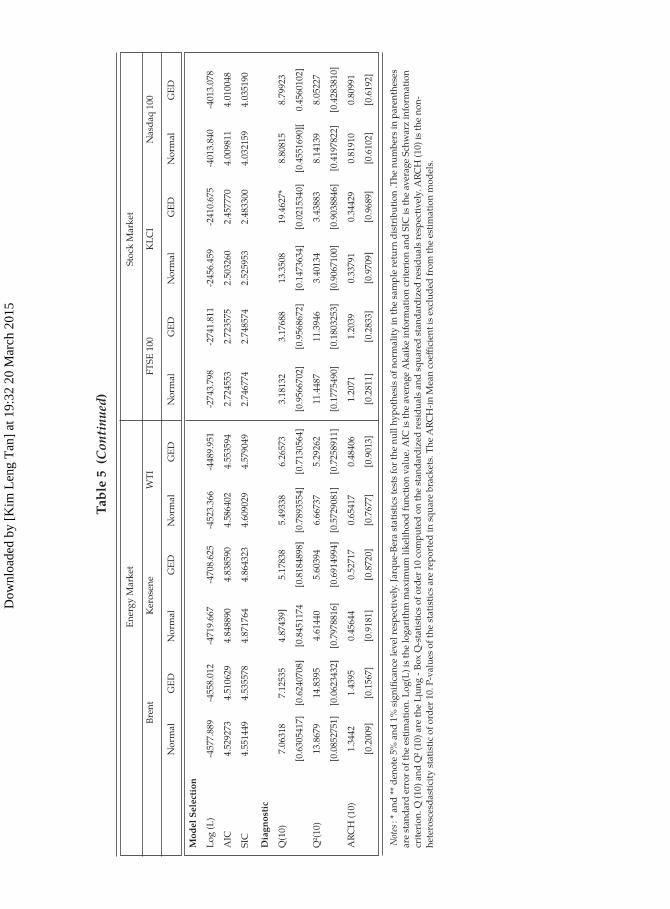

EMPIRICAL STYLIZED FACTS MODELLING 329

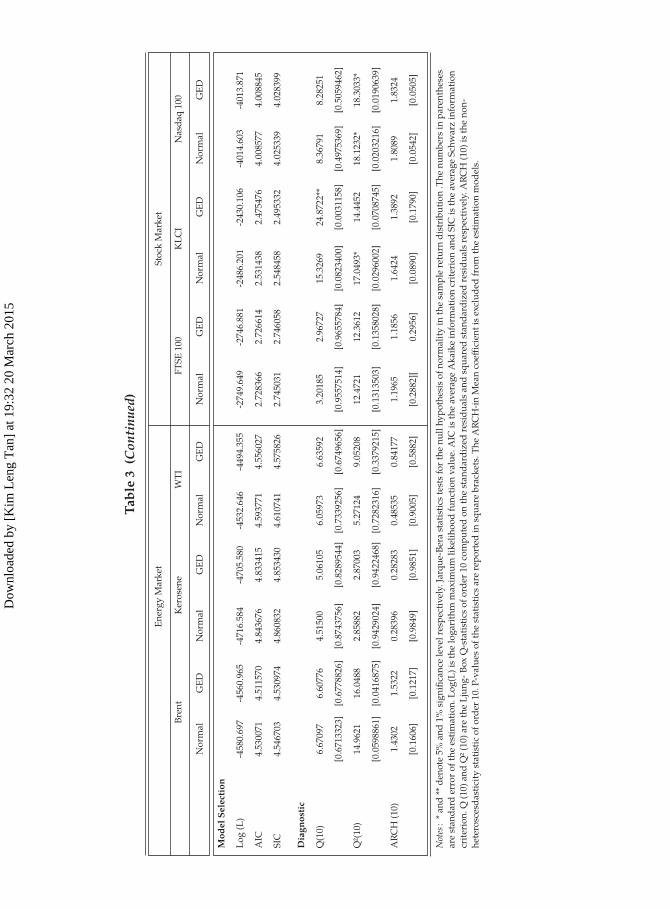

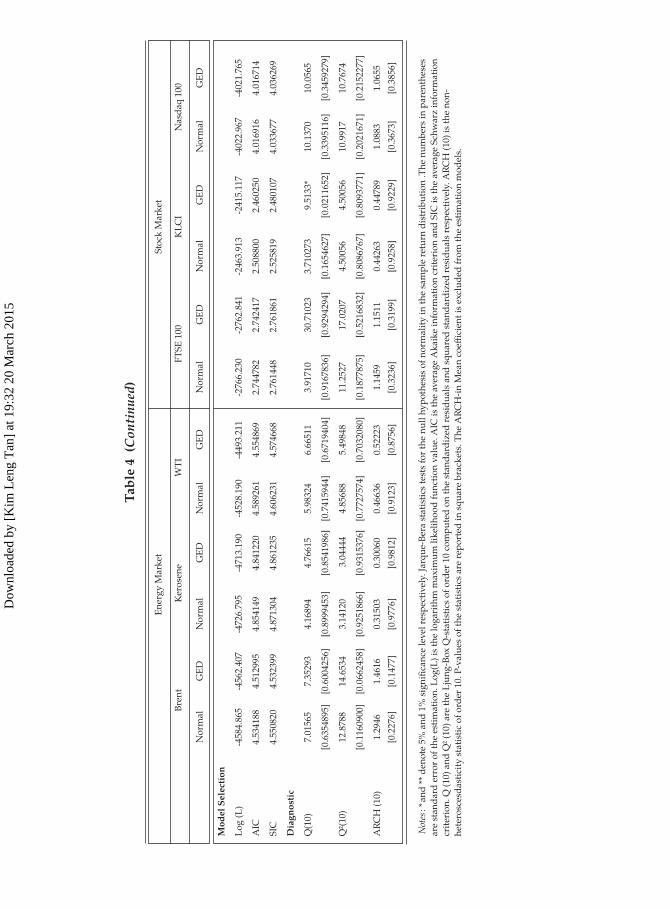

and stock indices show a positive degrees of freedom at 1 percent level of

signifi cant that vary from 1.414800 to 1.621099 and 1.292311 to 1.885177

for energy markets and stock markets respectively. Anyhow, as according

to Chin (2009) and Giot and Sebastian (2003), common energy markets

often exhibit heavy tails around three to six degrees of freedom. There-

fore, a normal distribution assumption will fi ts well for higher degrees of

freedom.

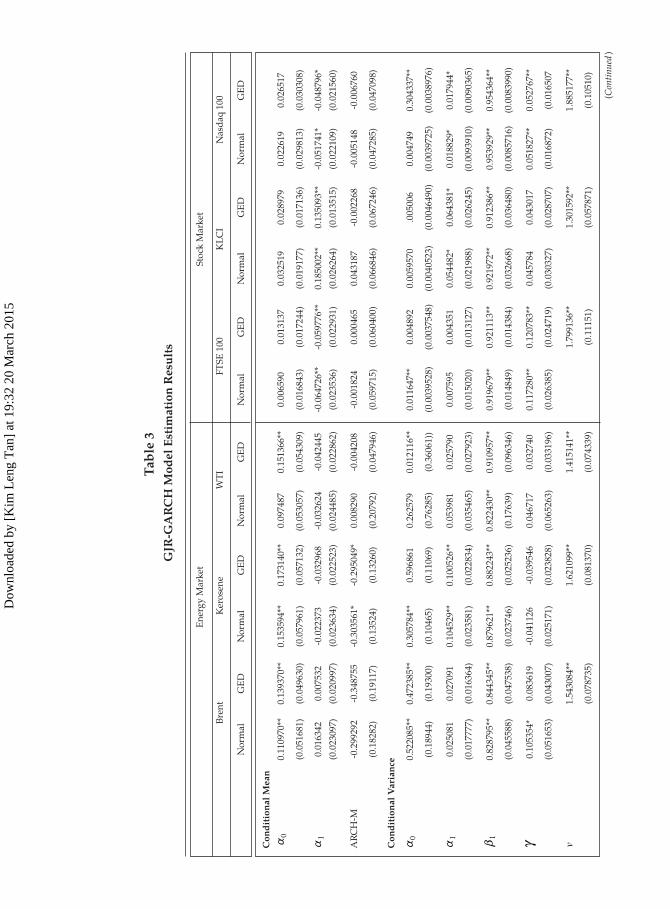

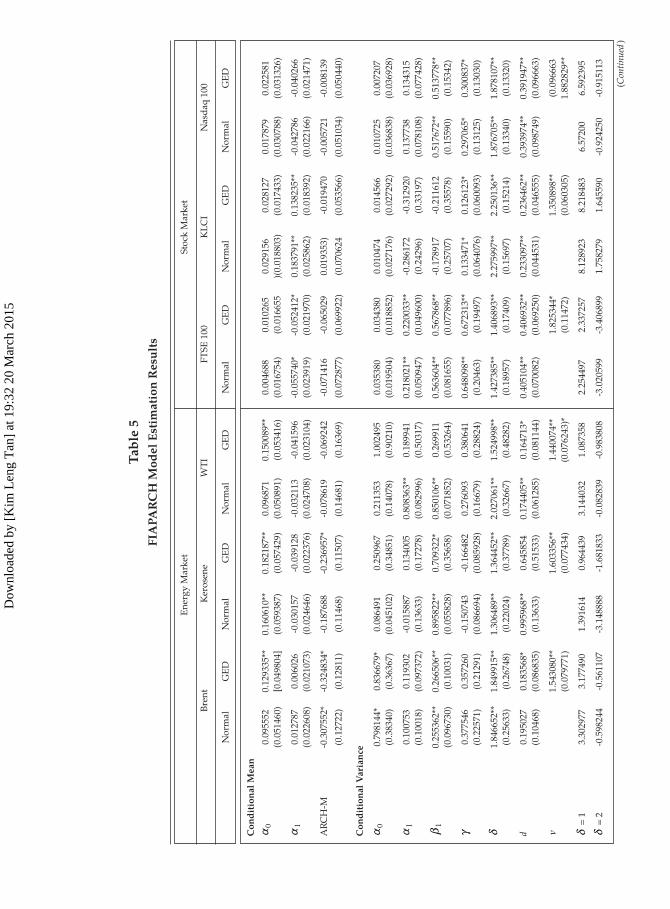

Reponses of market volatility to price movements are examined

by the asymmetric news impact coeff icient, γ where only GJR and FI-

APARCH are capable to capture this feature. According to Table-3 and

Table 5, energy markets show no response on ‘good’ or ‘bad’ news ex-

cept for Brent crude oil which presents a signifi cant positive coeff icient

for γ under normal distribution of GJR GARCH model. Meanwhile, stock

markets display a signifi cant positive of γ under normal and GED distri-

bution of GJR GARCH and FIAPARCH model. However, KLCI denotes

an insignifi cant positive coeff icient for both normal and GED distribution

under GJR GARCH model. Since γ is positive and signifi cant for stock

markets, this implies that there are leverage eff ects in stock market, where

negative innovation (news) has a greater impact on volatility than a posi-

tive innovation (news). From the economics perspective, the above results

are expected as events like the Asian fi nancial crisis, Sub-prime mortgage

crisis and gain tax rates will cause the stock or commodity prices to drop

and subsequently increase the volatility. However, not all events will have

similar impacts on both energy and stock markets. For example, crude

oil crisis might have a direct impact on energy markets rather than stock

markets.

Phenomenon of volatility clustering has attracted the attention from

researchers and inspired numerous debates as to whether there is mem-

ory in volatility. This phenomenon is often attributed to traders’ switch-

ing between chartist and fundamentalist strategies (Kirchler and Huber,

2007). According to Cont (2005), although returns are uncorrelated, abso-

lute returns or their squares often display positive, signifi cant and slowly

decaying autocorrelation functions. The persistence of absolute returns

autocorrelation is a sign for volatility clustering. Both energy and stock

markets show persistence, positive, signifi cant and slowly decaying to

zero over long lags for the autocorrelation function of absolute returns

and their squares. Meanwhile, the estimated fractional diff erence param-

eter, d, as show in Table 4 and Table 5 are all statistically signifi cant dif-

ferent from zero. However, Brent crude oil under normal distribution and

Kerosene under GED distribution of FIAPARCH model are insignifi cant

Dow

nloa

ded

by [

Kim