Does Money Matter in Africa? New Empirics on Long- and Short-run Effects of Monetary Policy on...

40

Indian Growth and Development Review Does money matter in Africa?: New empirics on long- and short-run effects of monetary policy on output and prices Simplice A. Asongu Article information: To cite this document: Simplice A. Asongu , (2014),"Does money matter in Africa?", Indian Growth and Development Review, Vol. 7 Iss 2 pp. 142 - 180 Permanent link to this document: http://dx.doi.org/10.1108/IGDR-12-2012-0048 Downloaded on: 13 November 2014, At: 02:30 (PT) References: this document contains references to 69 other documents. To copy this document: [email protected] The fulltext of this document has been downloaded 21 times since 2014* Users who downloaded this article also downloaded: Philip Kostov, Thankom Arun, Samuel Annim, (2014),"Banking the unbanked: the Mzansi intervention in South Africa", Indian Growth and Development Review, Vol. 7 Iss 2 pp. 118-141 http://dx.doi.org/10.1108/ IGDR-11-2012-0046 Kenneth Backlund, Tomas Sjögren, Jesper Stage, (2014),"Optimal tax and expenditure policy in the presence of emigration: Are credit restrictions important?", Indian Growth and Development Review, Vol. 7 Iss 2 pp. 98-117 http://dx.doi.org/10.1108/IGDR-09-2012-0040 Michael Keen, (2014),"Targeting, cascading and indirect tax design", Indian Growth and Development Review, Vol. 7 Iss 2 pp. 181-201 http://dx.doi.org/10.1108/IGDR-02-2013-0009 Access to this document was granted through an Emerald subscription provided by Token:JournalAuthor:6F95467C-5349-48C0-AAF7-79BB16C495CA: For Authors If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service information about how to choose which publication to write for and submission guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information. About Emerald www.emeraldinsight.com Emerald is a global publisher linking research and practice to the benefit of society. The company manages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as well as providing an extensive range of online products and additional customer resources and services. Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation. *Related content and download information correct at time of download. Downloaded by Mr Asongu Simplice At 02:30 13 November 2014 (PT)

Transcript of Does Money Matter in Africa? New Empirics on Long- and Short-run Effects of Monetary Policy on...

Indian Growth and Development ReviewDoes money matter in Africa?: New empirics on long- and short-run effects of monetarypolicy on output and pricesSimplice A. Asongu

Article information:To cite this document:Simplice A. Asongu , (2014),"Does money matter in Africa?", Indian Growth and Development Review, Vol.7 Iss 2 pp. 142 - 180Permanent link to this document:http://dx.doi.org/10.1108/IGDR-12-2012-0048

Downloaded on: 13 November 2014, At: 02:30 (PT)References: this document contains references to 69 other documents.To copy this document: [email protected] fulltext of this document has been downloaded 21 times since 2014*

Users who downloaded this article also downloaded:Philip Kostov, Thankom Arun, Samuel Annim, (2014),"Banking the unbanked: the Mzansi intervention inSouth Africa", Indian Growth and Development Review, Vol. 7 Iss 2 pp. 118-141 http://dx.doi.org/10.1108/IGDR-11-2012-0046Kenneth Backlund, Tomas Sjögren, Jesper Stage, (2014),"Optimal tax and expenditure policy in thepresence of emigration: Are credit restrictions important?", Indian Growth and Development Review, Vol. 7Iss 2 pp. 98-117 http://dx.doi.org/10.1108/IGDR-09-2012-0040Michael Keen, (2014),"Targeting, cascading and indirect tax design", Indian Growth and DevelopmentReview, Vol. 7 Iss 2 pp. 181-201 http://dx.doi.org/10.1108/IGDR-02-2013-0009

Access to this document was granted through an Emerald subscription provided byToken:JournalAuthor:6F95467C-5349-48C0-AAF7-79BB16C495CA:

For AuthorsIf you would like to write for this, or any other Emerald publication, then please use our Emerald forAuthors service information about how to choose which publication to write for and submission guidelinesare available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comEmerald is a global publisher linking research and practice to the benefit of society. The companymanages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as well asproviding an extensive range of online products and additional customer resources and services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committeeon Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archivepreservation.

*Related content and download information correct at time of download.

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Does money matter in Africa?New empirics on long- and short-run effects

of monetary policy on output and pricesSimplice A. Asongu

African Governance and Development Institute, Yaoundé, Cameroon

AbstractPurpose – The purpose of this paper is to examine the effects of monetary policy on economic activityusing a plethora of hitherto unemployed financial dynamics in inflation-chaotic African countries forthe period of 1987-2010.Although in developed economies, changes in monetary policy affect realeconomic activity in the short-run, but only prices in the long-run, the question of whether thesetendencies apply to developing countries remains open to debate.Design/methodology/approach – Vector autoregresion (VARs) within the frameworks of VectorError Correction Models and simple Granger causality models are used to estimate the long- andshort-run effects, respectively. A battery of robustness checks are also used to ensure consistency in thespecifications and results.Findings – The tested hypotheses are valid under monetary policy independence and dependence,except few exceptions. H1: Monetary policy variables affect prices in the long-run but not in theshort-run. For the first-half (long-run dimension) of the hypothesis, permanent changes in monetarypolicy variables (depth, efficiency, activity and size) affect permanent variations in prices in thelong-term. But in cases of disequilibriums, only financial dynamic fundamentals of depth and sizesignificantly adjust inflation to the cointegration relations. With respect to the second-half (short-runview) of the hypothesis, monetary policy does not overwhelmingly affect prices in the short-term. Hence,but for a thin exception, H1 is valid. H2: Monetary policy variables influence output in the short-termbut not in the long-term. With regard to the short-term dimension of the hypothesis, only financialdynamics of depth and size affect real gross domestic product output in the short-run. As concerns thelong-run dimension, the neutrality of monetary policy has been confirmed. Hence, the hypothesis is alsobroadly valid.Practical implications – A wide range of policy implications are discussed. Inter alia: the long-runneutrality of money and business cycles, credit expansions and inflationary tendencies, inflationtargeting and monetary policy independence implications. Country-/regional-specific implications, themanner in which the findings reconcile the ongoing debate, measures for fighting surplus liquidity andcaveats and future research directions are also discussed.Originality/value – By using a plethora of hitherto unemployed financial dynamics (that broadlyreflect monetary policy), we provide significant contributions to the empirics of money. The conclusionof the analysis is a valuable contribution to the scholarly and policy debate on how money matters as aninstrument of economic activity in developing countries.

Keywords Africa, Banking, Inflation, Monetary policy, VECM, Output effects

Paper type Research paper

1. IntroductionIn large industrial economies, changes in monetary policy affect real economic activityin the short-term but only prices in the long-run. In transitioning and developing

JEL classification – E51, E52, E58, E59, O55The author is highly indebted to the editor and referees for their useful comments.

The current issue and full text archive of this journal is available atwww.emeraldinsight.com/1753-8254.htm

IGDR7,2

142

Indian Growth and DevelopmentReviewVol. 7 No. 2, 2014pp. 142-180© Emerald Group Publishing Limited1753-8254DOI 10.1108/IGDR-12-2012-0048

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

countries, however, the question of whether monetary policy variables affect output inthe short-run is open to debate (Starr, 2005). Conversely, the evidence of real effects in adeveloped economy is supportive of the idea that monetary policy can be used to counteraggregate shocks. Economic theory traditionally suggests that money influencesbusiness cycles, not the long-term potential real output. This suggests monetary policyin neutral in the long-run. The neutrality of money has been substantially documentedin the literature (Olekalns, 1996; Serletis and Koustas, 1998; Bernanke and Mihov, 1998;Bullard, 1999; Bae et al., 2005; Nogueira, 2009). In spite of the theoretical and empiricalconsensus on this neutrality (Lucas, 1980; Gerlach and Svensson, 2003), the role ofmoney as an informational variable for decision-making has remained open to debate(Roffia and Zaghini, 2008; Nogueira, 2009; Bhaduri and Durai, 2012)[1].

The potential for using monetary policy in affecting real prices is also less clear. Incountries that have experienced high inflation or in which labor markets are chronicallyslack, prices and wages are unlikely to be particularly sticky, so that monetary policychanges could pass quickly through prices and have little real effect (Gagnon and Ihrig,2004). Moreover, the globalization of financial markets undercut the potential ofindependent policy by significantly eroding the ability of small-open economies todetermine interest rates independently of world markets (Dornbusch, 2001; Frankelet al., 2004).

In light of the above, three challenges are central in the literature. First, the extent towhich monetary policy affects output in the short-run, and prices in the long-run indeveloping countries remains an open debate. Hence, the need to contribute to thescholarly and policy debates on the manner in which money matters in economicactivity by providing an answer to the open question. Second, but for a few exceptions(Moosa, 1997; Bae and Ratti, 2000; Starr, 2005; Nogueira, 2009), the literature on thelong-run economic significance of money has focused on developed countries for themost part. Evidence provided by these studies may not be relevant for African countriesbecause their financial dynamics of monetary policy have different tendencies. Forexample, financial depth (liabilities) in the perspective of money supply is not asrelevant in African countries because a great chunk of the monetary base does nottransit through the banking sector (Asongu, 2014a). Third, the empirical investigationthat has focused on monetary aggregates has failed to take account of other proxies thatare exogenous to money supply. For instance, other financial dynamics of efficiency (atbanking and financial system levels), activity (from banking and financial systemperspectives) and size (credit of the banking sector in relation to that of the financialsystem) substantially affect the velocity of money and, hence, the effectiveness ofmonetary policy (both in the short- and long-run). Indeed, financial allocation efficiencyis a serious issue in African countries because of surplus liquidity issues (Saxegaard,2006) and, consequently, limited financial activity (credit).

The contribution of this paper to the literature is therefore fivefold. First, it assessesthe effects of monetary policy on output and prices in a continent (Africa) that has notreceived much scholarly attention. Second, there are certain specificities in monetarypolicy variables in developed economies that are not very relevant in Africa. Inter alia:on the one hand, financial depth in the perspective of money supply as applied in thedeveloped world cannot be transported to Africa because a great chunk of the monetarybase in the continent does not transit through the banking system; on the other hand, theeffectiveness of the credit channel of monetary policy is an issue in Africa owing to the

143

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

substantially documented surplus liquidity issues (Saxegaard, 2006; Fouda, 2009).Third, soaring food prices that have recently marked the geopolitical landscape ofAfrica have not been braced with adequate short-run monetary measures to stem therising price tide[2]. Fourth, embryonic African monetary unions like the proposed WestAfrican Monetary Zone (WAMZ) and East African Monetary Zone (EAMZ) need to beinformed on the relevance of money as an instrument of economic activity (growth andprice control). Fifth, the use of a plethora of hitherto unemployed monetary policyvariables complements existing literature by contributing to the empirics of monetarypolicy.

The rest of the paper is organized as follows. Section 2 highlights the debate anddiscusses monetary policy in Africa. The intuition motivating the empirics, the data andthe methodology are discussed in Section 3. Empirical analysis is covered in Section 4.Section 5 concludes.

2. The debate and African monetary policy2.1 The debateFor organizational purposes, we present the debate in two strands:

(1) the traditional discretionary monetary policy strand; and(2) the second strand of nontraditional policy regimes that limit the ability of

monetary authorities to use policy to offset output fluctuations.

In recent years, the rewards of shifting from traditional discretionary monetary policy toarrangements that favor commitments to price stability and international economicintegration (such as inflation targeting, monetary unions, dollarization, etc.) have beendiscussed substantially. An appealing prospect of discretionary policy is that themonetary authority can use policy instruments to offset adverse shocks to output bypursuing expansionary policy when output is below its potential and, contractionarypolicy when output is above its potential. For instance in the former situation, apolicy-controlled interest rate can be lowered in a bid to reduce commercial interest ratesand stimulate aggregate spending. Conversely, a monetary expansion that lowers thereal exchange rate may improve the competitiveness of a country’s products in domesticand world markets and thereby, boost demand for national output (Starr, 2005). As amatter of principle, a flexible countercyclical monetary policy can be practiced withinflation targeting (Ghironi and Rebucci, 2000; Mishkin, 2002; Cavoli and Rajan, 2008;Cristadoro and Veronese, 2011; Levine, 2012).

In the second strand, nontraditional policy regimes limit the ability of the monetaryauthorities to use policy to offset output fluctuations. The degree to which a givencountry can use monetary policy to affect output in the short-term is open to debate.Findings for the USA are consistent with the fact that, a decline in the key interest ratecontrolled by the Federal Reserve tends to boost output over the next two to three years.But the effect dissipates thereafter, so that the long-run effect is limited to prices (Starr,2005). Several studies have assessed whether the short-term effects of monetary policyon output in other countries are similar to those in the USA. Mixed results have beenfound in 17 industrialized countries (Hayo, 1999), and studies on two middle-incomecountries have found no evidence of Granger-causality from money to output,regardless of money used (Agénor et al., 2000). Hafer and Kutan (2002) find that interestrate generally plays a relatively more important role in explaining output in 20

IGDR7,2

144

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Organisation for Economic Co-operation and Development (OECD) countries, whileGanev et al. (2002) find no such evidence in Central and Eastern Europe. TheInternational Monetary Fund (IMF) places great emphasis on monetary policy in itsprograms for developing countries, especially in sub-Saharan Africa (SSA). It viewssuch a policy as crucial in managing inflation and stabilizing the real exchange rate.According to Weeks (2010), such an approach is absurdly inappropriate, as the vastmajority of governments in SSA lack the instruments to make monetary policyeffective[3].

2.2 Monetary policy in AfricaKhan (2011) has looked at the relationship between the growth of gross domesticproduct (GDP) and different monetary aggregates in 20 economies of SSA and foundempirical support for the hypothesis that credit-growth is more closely linked than inmoney-growth to the growth of real GDP. Mangani (2011) has investigated the effects ofmonetary policy on prices in Malawi and established the lack of unequivocal evidence insupport of the conventional channel of monetary policy transmission mechanism. Thefindings suggest that exchange rate was the most important variable in predictingprices. The study recommends that authorities should be more concerned with importedcost-push inflation than with demand-pull inflation[4]. In a slight contradiction,Ngalawa and Viegi (2011) have also investigated the process through which monetarypolicy affects economic activity in Malawi and found that, bank rate is a more effectivemeasure of monetary policy than reserve money.

Some studies have also focused on South Africa, with Gupta et al. (2010a) finding thathouse price inflation was negatively related to money policy shocks; Gupta et al. (2010b)showing that during the period of financial liberalization, interest rate shocks hadrelatively stronger effects on house price inflation irrespective of house sizes; and Ncubeand Ndou (2011) complementing Gupta et al. (2010a2010b)[5] with the suggestion that,the direct effects of high interest rates on consumption appear to be more important intransmitting monetary policy to the economy than through indirect effects. Hence, theinference that monetary policy tightening can marginally weaken inflationarypressures (arising from excessive consumption) operating via house wealth and thecredit channel. To demonstrate that monetary expansions and contractions may havedifferent effects in different regions of the same country, Fielding and Shields (2005)have estimated the size of asymmetries across the nine provinces of South Africa (overthe period 1997-2005) and found substantial differences in the response of prices tomonetary policy.

Consistent with the position of Weeks (2010) on the inherent ineffectiveness ofmonetary policy in African countries discussed above, the insights from the “Blindercredit-rationing model” are useful in solidifying the intuition for African empirics.According to Blinder (1987, p. 2), a rethinking new monetary policy dynamics is neededat times:

The reader should understand that this is merely an expositional device. I would not wish todeny that the interest elasticity and expectational error mechanisms have some validity. Butthe spirit of this paper is that those mechanisms do not seem important enough to explain thedeep recessions that are apparently caused by central bank policy.

145

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

The postulation of Blinder is even more relevant when existing monetary and exchangerate responses have not been effective in addressing the recent food inflation (VonBraun, 2008).

In light of the points presented in the introduction and the section above, thefollowing hypotheses will be tested in the empirical section:

H1. Monetary policy variables affect prices in the long-run but not in the short-run.

H2. Monetary policy variables influence output in the short-term but not in thelong-term.

3. Data and methodology3.1 Intuition for the empiricsAlthough there is vast empirical work on the effects of monetary policy on economicactivity based on aggregate measures of money supply, there is yet (to the best of ourknowledge) no usage of fundamental financial performance dynamics (that reflect thequantity of money supply) in the assessment of the long-run and short-term effects ofmonetary policy on output and prices. With this fact in mind, we are aware of the risksof “doing measurement without past empirical basis” and assert that reporting facts,even in the absence of past supporting studies (in the context of an outstandingtheoretical model), may be a useful scientific activity. Moreover, applied econometricshave other tasks than merely validating or refuting economic theories with existingexpositions and prior analytical frameworks (Asongu, 2014a, 2013e). Hence, the need tounderstand the economic/monetary intuition motivating the employment of a plethoraof financial performance measures in the assessment of the incidence of monetary policyvariables on economic activity.

From a broad standpoint, money supply can be understood in terms of the followingfour points:

(1) Financial intermediary depth could be defined both from an overall economicperspective and a financial system standpoint. This distinction, as will bedetailed in the data section, is worth emphasizing because unlike the developedworld, in developing countries, a great chunk of the monetary base does nottransit through the banking sector (Asongu, 2014b).

(2) Financial activity (observed from banking and financial system perspectives)reflects the ability of banks to grant credit to economic operators.

(3) Financial allocation efficiency (from banking and financial system standpoints)that reflects the fulfillment of the fundamental role of banks (in transformingmobilized deposits into credit for economic operators) could also intuitively beconceived as the ability of banks to increase the velocity of money.

(4) Financial size (deposit bank assets/total assets) mirrors the credit allocated bybanking institutions as a proportion of total assets in the financial system(deposit bank assets plus central bank assets).

Hence, financial intermediary performance dynamics are exogenous to money supplyand corrolarily monetary policy.

The choice of the monetary policy variables is broadly consistent with the empiricalunderpinnings of recent African monetary literature targeting inflation (Asongu, 2013a,

IGDR7,2

146

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

2013b) and real GDP output (Asongu, 2013c). These financial dynamic fundamentals entailall the dimensions identified by the Financial Development and Structure Database (FDSD)of the World Bank (WB). We are not the first to think out of the box when it comes to theempirics of monetary policy. Blinder (1987, p. 2) in assessing the effects of monetary policyon economic activity, completely banished interest rate elasticities:

In order to make credit rationing mechanism stand out in bold relief, most other channels ofmonetary policy (such as interest elasticities and expectational errors) are banished from the model.

3.2 DataWe investigate a panel of 10 African countries with data from African DevelopmentIndicators and the FDSD of the WB. The resulting balanced panel spans from 1987 to2010 due to constraints in data availability and the interest of obtaining results withupdated policy implications. In a bid for robustness, we are poised to control for theperiod of 2007-2009, during which the rise in food prices was very substantial. Hence, asub-panel of the period of 1987-2006 will be used to assess the consistency of findings.

We are limited to only 10 African cross-sections because some countries in the continentinherently do not exhibit a unit root in consumer price inflation. Owing to the problemstatements of the study, it is imperative to have non-stationary (chaotic) consumer priceinflation for consistent long-run modeling. Hence, in accordance with recent Africanlaw-finance literature (Asongu, 2011), African French Colonies (CFA) franc[6] countries ofthe Economic and Monetary Community of Central African States (CEMAC)[7] andEconomic and Monetary Community of West African States (UEMOA)[8] zones have notbeen included[9] in the sample. Beside these justifications for eliminating CFA franccountries, the seminal work of Mundell (1972) has shown that African countries with flexibleexchange rates regimes have more to experience in “money and inflation dynamics” thantheir counterparts with fixed exchange rate regimes[10].

Consistent with the literature, the dependent variables are measured in terms of annualpercentage change in the Consumer Price Index and real GDP output (Bordo and Jeanne,2002; Hendrix et al., 2009; Bae et al., 2005; Kishor and Ssozi, 2010; Moorthy and Kolhar, 2011).For organizational clarity, the independent variables are presented in terms of money(financial depth), credit (financial activity), efficiency and size. First, from a moneyperspective, we are consistent with the FDSD and recent African finance literature (Asongu,2013a, 2013b) in measuring financial depth both from overall-economic and financial systemperspectives with indicators of broad money supply (M2/GDP) and financial systemdeposits (Fdgdp), respectively. Whereas the former denotes the monetary base plus demand,saving and time deposits, the latter represents liquid liabilities of the financial system. It isinteresting to distinguish between these two aggregates of money supply because, as we aredealing exclusively with developing countries, a great chunk of the monetary base does nottransit via the banking sector. Second, credit is appreciated in terms of financialintermediary activity. Thus, the paper seeks to lay emphasis on the ability of banks to grantcredit to economic operators. We proxy for both banking-system-activity andfinancial-system-activity with “private domestic credit by deposit banks: Pcrb” and “privatecredit by deposit banks and other financial institutions: Pcrbof”, respectively. Third,financial size is measured in terms of deposit bank assets as a proportion of total assets(deposit bank assets plus central bank assets). Fourth, financial efficiency[11] measures theability of deposits (money) to be transformed into credit (financial activity). This fourth

147

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

measure appreciates the fundamental role of banks in transforming mobilized deposits intocredit for economic operators. We adopt indicators of banking-system-efficiency andfinancial-system-efficiency (respectively “bank credit on bank deposits: Bcbd” and “financialsystem credit on financial system deposits: Fcfd”).

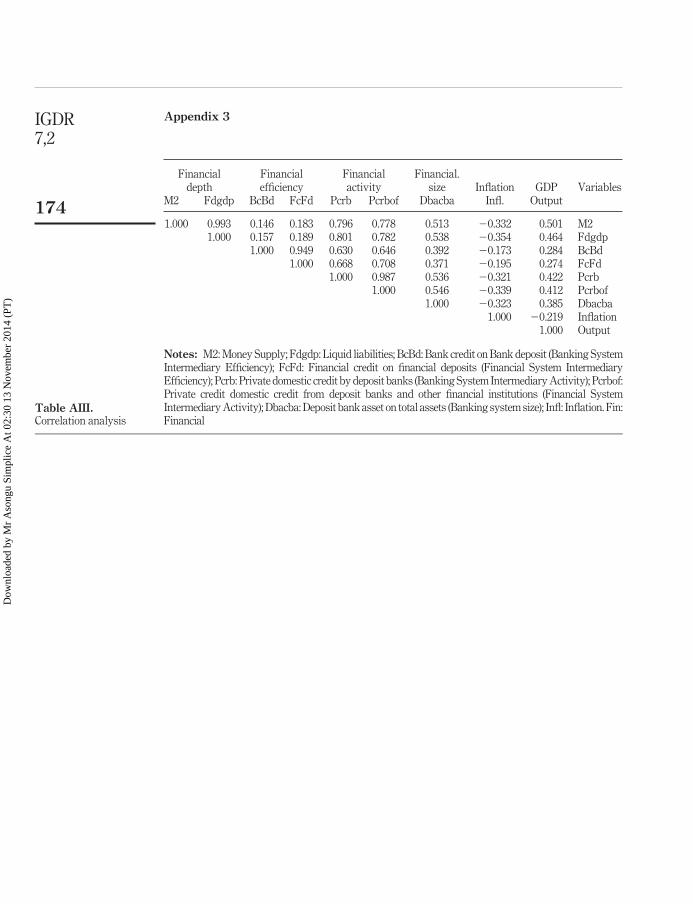

Whereas definitions of the variables and their corresponding sources are presented inAppendix 2, summary statistics (with presentation of countries) and correlationanalysis are detailed in Appendix 1 and Appendix 3, respectively. From a preliminaryassessment of the summary statistics, we are confident that reasonable estimated nexuswould emerge. The correlation analysis provides empirical validity for the theoreticalcategorization of banking and financial system indicators into fundamentals of depth,efficiency, activity and size.

3.3 MethodologyThe estimation technique typically follows mainstream literature on testing the long-runneutrality of monetary policy (Nogueira, 2009) and the short-run effects of monetary policyvariables on output and prices (Starr, 2005). The approach involves unit root andcointegration tests that assess the stationary properties and long-term equilibriums,respectively. In these assessments, the Vector Error Correction Model (VECM) is applied forlong-run effects, while simple Granger causality is used for short-term effects. Whileapplication of the former model requires that variables exhibit unit roots in levels and havea long-run relationship (cointegration), the latter is applied on the condition that variables arestationary (do not exhibit unit roots). Impulse response functions are used to further assessthe tendencies of significant Granger causality results.

4. Empirical analysis4.1 Unit root testsWe investigate evidence of stationarity with first- and second-generation panel unit roottests. When the variables exhibit unit roots in levels, we proceed to test for stationarityin their first difference. Employment of the VECM requires that the variables have a unitroot (non stationary) in levels. Two main types of panel unit root tests have beendocumented: first-generation (that supposes cross-sectional independence) and thesecond-generation (based on cross-sectional dependence). Accordingly, it is convenientto perform several panel unit root tests to infer an overwhelming evidence to verify theorder of integration of a series, as none of these tests is immune from statisticalshortcomings in terms of size and power properties. With regard to the first-generationtests, the Levin et al. (2002) and Im et al.(2003) tests are applied. Whereas the former is ahomogenous-based panel unit root test (common unit roots as null hypothesis), the latteris a heterogeneous-oriented test (individual unit roots as null hypotheses). When theresults are different, Im et al.(2003) takes precedence over Levin et al. (2002) indecision-making because, consistent with Maddala and Wu (1999), the alternativehypothesis of Levin et al. (2002) is too powerful. While Im et al.(2003) controls forcross-sectional dependence to a certain degree, Pesaran (2007) has put forward a testwhich allows for the presence of more general cross-sectional dependence patterns. Thistest can be considered as a second-generation of panel unit root tests. In accordance withLiew (2004), goodness of fit (or optimal lag selection) is ensured by the Hannan-QuinnInformation Criterion (HQC) for the Levin et al. (2002) and the Akaike Information

IGDR7,2

148

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Criterion (AIC) for the Im et al.(2003) and Pesaran (2007) tests. Ultimately, Pesaran (2007)takes precedence over Levin et al. (2002) and Im et al.(2003) in decision-making.

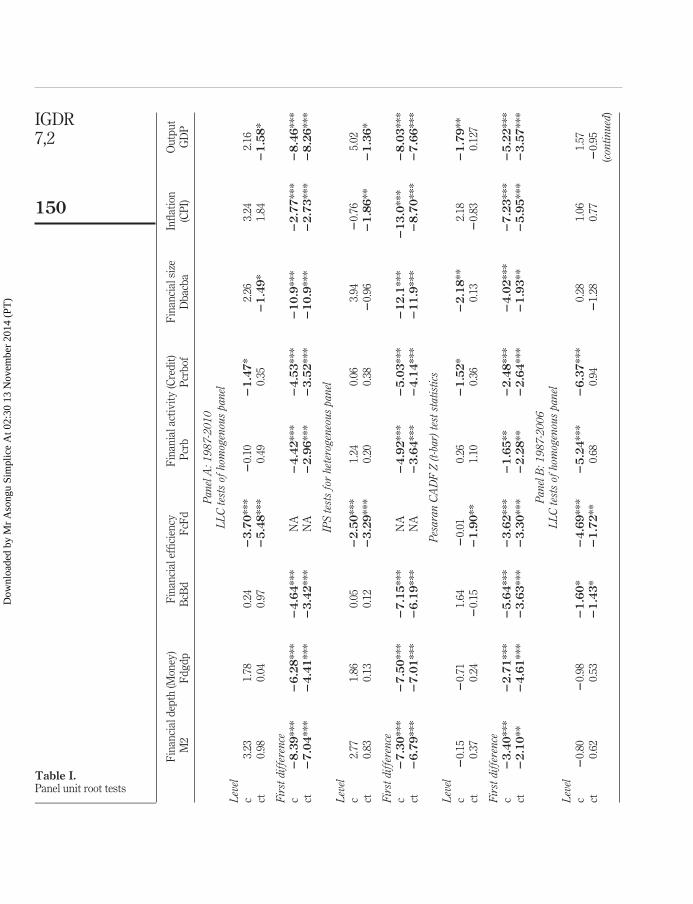

Table I reports the panel unit root tests results. While Panel A presents the findingsfor the period of 1987-2010, Panel B is for the 1987-2006 span. Based on two informationcriteria, “constant and trend” and Pesaran (2007), only financial system efficiency inPanel A is stationary in levels. Hence, the findings indicate the possibility ofcointegration (long-run equilibrium) among the variables; because, in line with theEngel–Granger theorem, two variables that are not stationary may have a linearcombination in the long-run (Engle and Granger, 1987).

4.2 Cointegration testsConsistent with the cointegration theory, two (or more) variables that have a unit root inlevels may have a linear combination (equilibrium) in the long-run. In principle, if twovariables are cointegrated, it implies permanent movements of one variable affectingpermanent movements in the other variable. To assess the potential long-runrelationships, we test for cointegration using the Engle–Granger-based Pedroni test,which is a heterogeneous panel-based test. Whereas we have earlier used bothhomogenous and heterogeneous panel-based unit roots tests in Section 4.1, we disagreewith Camarero and Tamarit (2002) in applying a homogenous Engle–Granger-basedKao panel cointegration test because it has less deterministic components. Accordingly,application of Kao (1999), in comparison to Pedroni (1999), presents substantial issues indeterministic assumptions[12]. The same deterministic trend assumptions used in theIm et al.(2003) unit root tests are used in the Pedroni (1999) heterogeneous cointegrationtest. However, like in panel unit root tests, panel cointegration tests also suffer fromcross-sectional dependence. A second-generation cointegration test such as Westerlund(2007) can control for cross-sectional dependence via bootstrapping. The choice ofbivariate statistics has a twofold advantage (justification): on the one hand, it isconsistent with the problem statements and, on the other hand, it mitigatesmisspecification issues in causality estimations[13].

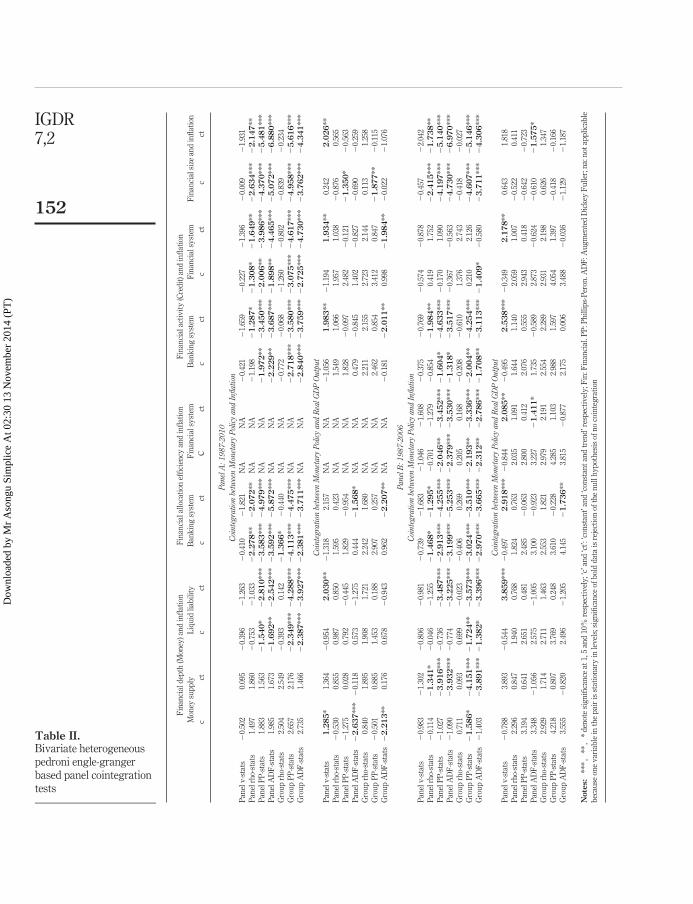

Tables II and III present the Pedroni and Westerlund cointegration results,respectively. Panel A (B) in both tables presents findings for the period 1987-2010(1987-2006). In Table II, based on the information criterion of “constant and trend”, thereis absence of cointegration between money supply (financial system activity) andinflation in Panel A (B). There is overwhelming (scanty) evidence of long-runequilibriums between monetary policy variables and inflation (output). These findingsare broadly consistent with the predictions of economic theory, which indicates thatmonetary policy has no incidence in real output in the long-run, but affects prices in thedistant future. Put in other words, the absence of a long-run relationship betweenmonetary policy variables and output shows the long-term neutrality of money. Itfollows that, permanent changes in financial intermediary dynamics (exogenous tomonetary policy) do not affect permanent changes in real GDP output in the long-run.Hence, the need to assess short-run effects by simple Granger causality (Section 4.4).Conversely, permanent movements in monetary policy variables influence prices in thelong-tem. Hence, the need to examine the short-term adjustments to the correspondingequilibriums with the VECM (Section 4.3).

The inferences above fail to consider the presence of common factors that affectmonetary policy across countries. Table III presents bivariate Westerlund cointegration

149

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Table I.Panel unit root tests

Fina

ncia

ldep

th(M

oney

)Fi

nanc

iale

ffici

ency

Fina

nial

activ

ity(C

redi

t)Fi

nanc

ials

ize

Infla

tion

Out

put

M2

Fdgd

pB

cBd

FcFd

Pcrb

Pcrb

ofD

bacb

a(C

PI)

GD

P

Pane

lA:1

987-

2010

LLC

test

sof

hom

ogen

ous

pane

lLe

vel

c3.

231.

780.

24�

3.7

0**

*�

0.10

�1

.47

*2.

263.

242.

16ct

0.98

0.04

0.97

�5

.48

***

0.49

0.35

�1

.49

*1.

84�

1.5

8*

Firs

tdiff

eren

cec

�8

.39

***

�6

.28

***

�4

.64

***

NA

�4

.42

***

�4

.53

***

�1

0.9

***

�2.7

7**

*�

8.4

6**

*ct

�7

.04

***

�4

.41

***

�3

.42

***

NA

�2

.96

***

�3

.52

***

�1

0.9

***

�2.7

3**

*�

8.2

6**

*

IPS

test

sfo

rhe

tero

gene

ous

pane

lLe

vel

c2.

771.

860.

05�

2.5

0**

*1.

240.

063.

94�

0.76

5.02

ct0.

830.

130.

12�

3.2

9**

*0.

200.

38�

0.96

�1.8

6**

�1.3

6*

Firs

tdiff

eren

cec

�7

.30

***

�7

.50

***

�7

.15

***

NA

�4

.92

***

�5

.03

***

�1

2.1

***

�13.0

***

�8.0

3**

*ct

�6

.79

***

�7

.01

***

�6

.19

***

NA

�3

.64

***

�4

.14

***

�1

1.9

***

�8.7

0**

*�

7.6

6**

*

Pesa

ran

CA

DF

Z(t

-bar

)tes

tsta

tistic

sLe

vel

c�

0.15

�0.

711.

64�

0.01

0.26

�1

.52

*�

2.1

8**

2.18

�1.7

9**

ct0.

370.

24�

0.15

�1

.90

**1.

100.

360.

13�

0.83

0.12

7

Firs

tdiff

eren

cec

�3

.40

***

�2

.71

***

�5

.64

***

�3

.62

***

�1

.65

**�

2.4

8**

*�

4.0

2**

*�

7.2

3**

*�

5.2

2**

*ct

�2

.10

**�

4.6

1**

*�

3.6

3**

*�

3.3

0**

*�

2.2

8**

�2

.64

***

�1

.93

**�

5.9

5**

*�

3.5

7**

*

Pane

lB:1

987-

2006

LLC

test

sof

hom

ogen

ous

pane

lLe

vel

c�

0.80

�0.

98�

1.6

0*

�4

.69

***

�5

.24

***

�6

.37

***

0.28

1.06

1.57

ct0.

620.

53�

1.4

3*

�1

.72

**0.

680.

94�

1.28

0.77

�0.

95(c

ontin

ued)IGDR

7,2

150

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Table I.

Fina

ncia

ldep

th(M

oney

)Fi

nanc

iale

ffici

ency

Fina

nial

activ

ity(C

redi

t)Fi

nanc

ials

ize

Infla

tion

Out

put

M2

Fdgd

pB

cBd

FcFd

Pcrb

Pcrb

ofD

bacb

a(C

PI)

GD

P

Firs

tdiff

eren

cec

�7

.27

***

�5

.69

***

NA

NA

�2

.43

***

�2

.37

***

�6

.43

***

�12.0

***

�5.6

4**

*ct

�6

.21

***

�5

.35

***

NA

NA

�4

.81

***

�5

.03

***

�6

.21

***

�8.2

4**

*�

7.5

1**

*

IPS

test

sfo

rhe

tero

gene

ous

pane

lLe

vel

c�

2.0

7**

�0.

98�

1.9

7**

�3

.71

***

�3

.39

***

�4

.33

***

1.00

�2.1

8**

4.50

ct�

0.40

�0.

82�

1.4

4*

�2

.12

**0.

231.

12�

0.60

�2.5

0**

*�

0.02

Firs

tdiff

eren

cec

�5

.45

***

�5

.68

***

NA

NA

�3

.01

***

�3

.05

***

�7

.27

***

NA

�4.7

9**

*ct

�5

.03

***

�4

.80

***

NA

NA

�4

.81

***

�5

.31

***

�7

.54

***

NA

�6.1

4**

*

Pesa

ran

CA

DF

Z(t

-bar

)tes

tsta

tistic

sLe

vel

c0.

36�

0.06

�0.

72�

1.29

0.00

�0.

77�

2.8

5**

*13

.32

0.21

ct0.

310.

65�

1.06

�0.

632.

041.

90�

0.56

�0.

111.

47

Firs

tdiff

eren

cec

�2

.62

***

�1

.88

**�

4.5

6**

*�

2.1

1**

�2

.79

***

�2

.29

**�

3.2

7**

*�

5.9

5**

*�

3.3

3**

*ct

�1

.50

*�

3.2

7**

*�

3.2

0**

*�

2.2

2**

�1

.77

**�

1.7

0**

�1

.70

**�

3.5

7**

*�

2.6

5**

*

Not

es:

***,

**,

*den

ote

sign

ifica

nce

at1,

5an

d10

%,r

espe

ctiv

ely.

‘c’an

d‘ct

’:‘co

nsta

nt’a

nd‘co

nsta

ntan

dtr

end’

resp

ectiv

ely;

max

imum

lag

is6

and

optim

alla

gsar

ech

osen

via

HQ

Cfo

rLLC

test

and

the

AIC

forI

PSIm

etal

.(20

03)a

ndPe

sara

n(2

007)

test

s;LL

C:Le

vin

etal

.(20

02).

IPS:

Imet

al.(

2003

);M

2:m

oney

supp

ly;

Fdgd

p:liq

uid

liabi

litie

s;B

cBd:

bank

ing

syst

emef

ficie

ncy;

FcFd

:fina

ncia

lsys

tem

effic

ienc

y;Pc

rb:b

anki

ngsy

stem

activ

ity;P

crbo

f:fin

anci

alsy

stem

activ

ity;

Dba

cba:

depo

sitb

ank

asse

tson

tota

lass

ets;

CPI:

cons

umer

pric

einfl

atio

n;G

DP:

gros

sdom

estic

prod

uct;

CAD

F:cr

oss-

augm

ente

ddi

ckey

fulle

r;si

gnifi

canc

eofb

old

data

isre

ject

ion

ofth

eun

itro

otnu

llhy

poth

esis

151

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Table II.Bivariate heterogeneouspedroni engle-grangerbased panel cointegrationtests

Fina

ncia

ldep

th(M

oney

)and

infla

tion

Fina

ncia

lallo

catio

nef

ficie

ncy

and

infla

tion

Fina

ncia

lact

ivity

(Cre

dit)

and

infla

tion

Fina

ncia

lsiz

ean

din

flatio

nM

oney

supp

lyLi

quid

liabi

lity

Ban

king

syst

emFi

nanc

ials

yste

mB

anki

ngsy

stem

Fina

ncia

lsys

tem

cct

cct

cct

Cct

cct

cct

cct

Pane

lA:1

987-

2010

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dIn

flatio

nPa

nelv

-sta

ts�

0.50

20.

095

�0.

396

�1.

263

�0.

410

�1.

821

NA

NA

�0.

421

�1.

659

�0.

227

�1.

396

�0.

009

�1.

931

Pane

lrho

-sta

ts1.

497

1.86

0�

0.75

3�

1.03

3�

2.2

78

**�

2.0

72

**N

AN

A�

1.19

8�

1.2

87

*�

1.3

08

*�

1.6

49

**�

2.6

34

***

�2

.14

7**

Pane

lPP-

stat

s1.

883

1.56

3�

1.5

40

*�

2.8

10

***

�3.5

83

***

�4.9

79

***

NA

NA

�1.9

72

**�

3.4

50

***

�2.0

06

**�

3.9

86

***

�4

.37

0**

*�

5.4

81

***

Pane

lAD

F-st

ats

1.98

51.

673

�1.6

92

**�

2.5

42

***

�3.5

92

***

�5.8

72

***

NA

NA

�2.2

29

**�

3.6

87

***

�1.8

98

**�

4.4

65

***

�5

.07

2**

*�

6.8

80

***

Gro

uprh

o-st

ats

2.50

42.

549

�0.

393

0.14

2�

1.3

66

*�

0.44

0N

AN

A�

0.77

2�

0.06

8�

1.26

0�

0.80

2�

0.83

9�

0.23

4G

roup

PP-s

tats

2.65

72.

176

�2.3

49

***

�4.2

88

***

�4.1

13

***

�4.4

75

***

NA

NA

�2.7

18

***

�3.5

80

***

�3.0

75

***

�4.6

17

***

�4

.95

8**

*�

5.6

16

***

Gro

upA

DF-

stat

s2.

735

1.46

6�

2.3

87

***

�3.9

27

***

�2.3

81

***

�3.7

11

***

NA

NA

�2.8

40

***

�3.7

59

***

�2.7

25

***

�4.7

30

***

�3

.76

2**

*�

4.3

41

***

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dR

ealG

DP

Out

put

Pane

lv-s

tats

1.2

85

*1.

364

�0.

954

2.0

30

**�

1.31

82.

157

NA

NA

�1.

056

1.9

83

**�

1.19

41.9

34

**0.

242

2.0

26

**Pa

nelr

ho-s

tats

�0.

530

0.85

50.

987

0.85

01.

595

0.42

3N

AN

A1.

549

1.06

61.

957

1.03

8�

0.87

60.

565

Pane

lPP-

stat

s�

1.27

50.

028

0.79

2�

0.44

51.

829

�0.

954

NA

NA

1.82

8�

0.09

72.

482

�0.

121

�1

.35

0*

�0.

563

Pane

lAD

F-st

ats

�2.6

37

***

�0.

118

0.57

3�

1.27

50.

444

�1.5

68

*N

AN

A0.

479

�0.

845

1.40

2�

0.82

7�

0.69

0�

0.25

9G

roup

rho-

stat

s0.

840

1.89

51.

908

1.72

12.

242

1.68

0N

AN

A2.

211

2.15

52.

723

2.14

40.

113

1.25

8G

roup

PP-s

tats

�0.

501

0.88

51.

453

0.18

82.

907

0.25

7N

AN

A2.

462

0.85

43.

412

0.84

7�

1.8

77

**�

0.11

5G

roup

AD

F-st

ats

�2.2

13

**0.

176

0.67

8�

0.94

30.

962

�2.2

07

**N

AN

A�

0.18

1�

2.0

11

**0.

998

�1.9

84

**�

0.02

2�

1.07

6

Pane

lB:1

987-

2006

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dIn

flatio

nPa

nelv

-sta

ts�

0.98

3�

1.30

2�

0.80

6�

0.98

1�

0.73

9�

1.68

3�

1.04

6�

1.60

8�

0.37

5�

0.76

9�

0.57

4�

0.87

8�

0.45

7�

2.04

2Pa

nelr

ho-s

tats

�0.

114

�1.3

41

*�

0.04

6�

1.25

5�

1.4

68

*�

1.2

95

*�

0.70

1�

1.27

9�

0.85

4�

1.9

84

**0.

419

1.75

2�

2.4

15

***

�1

.73

8**

Pane

lPP-

stat

s�

1.02

7�

3.9

16

***

�0.

736

�3.4

87

***

�2.9

13

***

�4.2

55

***

�2.0

46

**�

3.4

52

***

�1.6

04

*�

4.6

33

***

�0.

170

1.09

0�

4.1

97

***

�5

.14

0**

*Pa

nelA

DF-

stat

s�

1.09

0�

3.9

32

***

�0.

774

�3.2

25

***

�3.1

99

***

�5.2

53

***

�2.3

79

***

�3.5

30

***

�1.3

18

*�

3.5

17

***

�0.

367

�0.

563

�4

.73

0**

*�

6.9

70

***

Gro

uprh

o-st

ats

0.71

10.

093

0.69

9�

0.02

3�

0.40

60.

269

0.20

50.

168

�0.

208

�0.

610

1.37

62.

743

�0.

418

�0.

027

Gro

upPP

-sta

ts�

1.5

86

*�

4.1

51

***

�1.7

24

**�

3.5

73

***

�3.0

24

***

�3.5

10

***

�2.1

93

**�

3.3

36

***

�2.0

04

**�

4.2

54

***

0.21

02.

126

�4

.60

7**

*�

5.1

46

***

Gro

upA

DF-

stat

s�

1.40

3�

3.8

91

***

�1.3

82

*�

3.3

96

***

�2.9

70

***

�3.6

65

***

�2.3

12

**�

2.7

86

***

�1.7

08

**�

3.1

13

***

�1.4

09

*�

0.58

0�

3.7

11

***

�4

.30

6**

*

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dR

ealG

DP

Out

put

Pane

lv-s

tats

�0.

788

3.89

3�

0.54

43.8

59

***

�0.

497

2.9

18

***

�0.

844

2.0

85

**�

0.49

52.5

38

***

�0.

349

2.1

78

**0.

643

1.81

8Pa

nelr

ho-s

tats

2.29

60.

847

1.94

00.

768

1.82

40.

763

2.03

51.

091

1.64

41.

140

2.05

91.

007

�0.

522

0.41

1Pa

nelP

P-st

ats

3.19

40.

641

2.65

10.

481

2.48

5�

0.06

32.

800

0.41

22.

076

0.55

52.

943

0.41

8�

0.64

2�

0.72

3Pa

nelA

DF-

stat

s3.

348

�1.

056

2.57

5�

1.00

53.

100

�0.

923

3.22

7�

1.4

11

*1.

735

�0.

589

2.87

3�

0.62

4�

0.61

0�

1.5

75

*G

roup

rho-

stat

s2.

929

1.71

42.

711

1.46

32.

553

1.82

12.

979

2.19

12.

554

2.28

92.

931

2.19

80.

626

1.34

7G

roup

PP-s

tats

4.21

80.

807

3.76

90.

248

3.61

0�

0.22

84.

285

1.10

32.

988

1.59

74.

054

1.39

7�

0.41

8�

0.16

6G

roup

AD

F-st

ats

3.55

5�

0.82

02.

496

�1.

205

4.14

5�

1.7

36

**3.

815

�0.

877

2.17

50.

006

3.48

8�

0.03

6�

1.12

9�

1.18

7

Not

es:

***

,**

,*

deno

tesi

gnifi

canc

eat

1,5

and

10%

resp

ectiv

ely;

‘c’a

nd‘c

t’:‘c

onst

ant’

and

‘con

stan

tand

tren

d’re

spec

tivel

y;Fi

n:Fi

nanc

ial.

PP:P

hilli

ps-P

eron

.AD

F:A

ugm

ente

dD

icke

yFu

ller;

na:n

otap

plic

able

beca

use

one

vari

able

inth

epa

iris

stat

iona

ryin

leve

ls;s

igni

fican

ceof

bold

data

isre

ject

ion

ofth

enu

llhy

poth

esis

ofno

coin

tegr

atio

n

IGDR7,2

152

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Table III.Bivariate westerlund

panel cointegration tests

Fina

ncia

ldep

th(M

oney

)and

infla

tion

Fina

ncia

lallo

catio

nef

ficie

ncy

and

infla

tion

Fina

ncia

lact

ivity

(cre

dit)

and

infla

tion

Fina

ncia

lsiz

ean

din

flatio

nM

oney

supp

lyLi

quid

liabi

lity

Ban

king

syst

emFi

nanc

ials

yste

mB

anki

ngsy

stem

Fina

ncia

lsys

tem

Cct

cCt

cct

cct

cct

cct

cct

Pane

lA:1

987-

2010

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dIn

flatio

nG

t(Z-

valu

e)4.

079

2.84

84.

703

3.46

30.

011

�3.2

03

***

NA

NA

2.77

72.

422

2.03

51.

701

3.47

62.

509

Ga

(Z-v

alue

)2.

491

2.95

22.

860

3.18

91.

492

0.0

05

**N

AN

A3.

246

3.95

22.

811

3.46

92.

714

1.98

3Pt

(Z-v

alue

)2.

602

1.70

93.

194

2.58

6�

0.64

2�

3.8

28

***

NA

NA

�1.6

83

*�

0.64

3�

2.7

93

**�

0.94

13.

237

3.09

0Pa

(Z-v

alue

)1.

594

1.07

92.

031

1.42

1�

0.39

8�

1.7

60

**N

AN

A�

0.74

10.

927

�1.4

42

*0.

820

1.99

12.

197

BP

CDT

est(

Chi2 )

272.4

55

***

321.3

10

***

205.6

05

***

200.7

05

***

259.7

41

***

250.1

88

***

28

3.7

60

***

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dR

ealG

DP

Out

put

Gt(

Z-va

lue)

1.83

52.

983

2.58

23.

988

0.07

52.

412

NA

NA

1.57

96.

313

0.78

95.

377

�0.

064

2.43

6G

a(Z

-val

ue)

1.74

82.

861

1.63

13.

166

0.63

23.

148

NA

NA

0.78

04.

064

0.1

88

**3.

736

�0

.01

1*

2.73

9Pt

(Z-v

alue

)�

3.3

62

**0.

802

�3.5

95

**1.

061

0.47

43.

200

NA

NA

�3.5

65

**2.

554

�3.2

21

***

2.31

40.

614

3.37

7Pa

(Z-v

alue

)�

1.9

02

*1.

112

�3.1

51

**0.

864

0.46

92.

668

NA

NA

�4.2

79

**1.

056

�4.1

52

***

1.10

7�

1.25

82.

160

BP

CDT

est(

Chi2 )

203.3

72

***

210.3

10

***

205.1

28

***

181.0

99

***

160.2

62

***

174.2

66

***

16

4.5

90

***

Pane

lB:1

987-

2006

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dIn

flatio

nG

t(Z-

valu

e)1.

352

0.58

31.

339

0.35

8�

2.0

07

**�

1.5

55

*�

5.4

94

***

�3.8

59

***

�3.9

09

***

�2.0

32

**�

4.4

18

***

�2

.35

5*

2.27

60.

236

Ga

(Z-v

alue

)2.

053

2.77

22.

051

2.53

91.

081

2.28

70.4

87

*2.

076

0.95

93.

023

0.74

43.

131

2.65

93.

182

Pt(Z

-val

ue)

�0.

077

�0.

002

�0.

276

�0.

324

�3.9

30

**�

3.1

45

*�

6.3

17

***

�5.2

69

**�

4.5

60

**0.

083

�3.6

68

**�

0.00

32.

761

4.95

3Pa

(Z-v

alue

)�

0.67

10.

889

�0.

485

0.77

1�

0.67

11.

476

�1.5

30

**1.

106

�1.5

03

*1.

587

�1.4

94

**1.

535

1.55

02.

988

BP

CDT

est(

Chi2 )

220.3

03

***

251.1

17

***

170.6

52

***

174.7

23

***

184.0

55

***

206.7

27

***

19

2.4

62

***

Coi

nteg

ratio

nbe

twee

nM

onet

ary

Polic

yan

dR

ealG

DP

Out

put

Gt(

Z-va

lue)

3.09

81.

147

3.55

41.

222

�2.2

84

**0.

047

�4.7

96

***

�2.3

29

**�

1.4

10

*3.

186

�2.3

48

**2.

385

�1

.98

4**

�0.

266

Ga

(Z-v

alue

)3.

365

3.29

03.

263

3.29

30.2

48

*2.

484

0.5

15

*2.

164

1.61

34.

196

0.99

63.

869

0.9

78

*3.

009

Pt(Z

-val

ue)

�0.

728

1.33

8�

0.88

01.

962

�1.

549

�0.

467

�4.8

50

**�

2.17

9�

2.9

66

*0.

694

�1.

164

1.32

4�

1.9

10

*1.

898

Pa(Z

-val

ue)

0.56

92.

090

0.38

72.

254

�0.

282

1.53

0�

0.65

11.

194

0.03

12.

159

�0.

656

1.82

5�

0.61

61.

900

BP

CDT

est(

chi-s

quar

e)222.7

81

***

242.6

43

***

182.5

64

***

176.6

32

***

205.2

88

***

231.8

35

***

13

1.7

66

***

Not

es:

***

,**

,*

deno

tesi

gnifi

canc

eat

1,5

and

10%

,res

pect

ivel

y;‘c

’and

‘ct’:

‘con

stan

t’an

d‘c

onst

anta

ndtr

end’

,res

pect

ivel

y;Fi

n:Fi

nanc

ial;

the

lag

and

lead

leng

ths

are

sett

oon

e;ch

oosi

ngto

om

any

lags

and

lead

sca

nre

sult

ina

dete

rior

atio

nof

the

smal

l-sam

ple

prop

ertie

sof

the

test

;to

cont

rolf

orcr

oss-

sect

iona

ldep

ende

nce,

robu

stcr

itica

lval

ues

isob

tain

edth

roug

h30

0bo

otst

rap

repl

icat

ions

;BP

CDT

est:

Bre

usch

–Pag

anLM

test

ofin

depe

nden

ce;s

igni

fican

ceof

bold

data

isre

ject

ion

ofth

enu

llhy

poth

esis

ofno

coin

tegr

atio

n

153

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

tests that control for cross-sectional dependence[14]. Based on the information criterionof “constant and trend”, while the long-run neutrality of money is still broadlyconfirmed, evidence of cointegration between monetary variables and inflation isscanty.

Modeling with the VECM and simple Granger causality (unrestricted vectorautoregresion (VAR)) will be based on the hypotheses of cross-sectional dependence andindependence in cointegration for the following reasons. First, it eases comparison of thepresent study with prior 2007 Pedroni-based literature. Accordingly, studies before theemergence of the Westerlund (2007) test still constitute useful scientific activity. Second,both assumptions are necessary to fully examine the postulated hypotheses underinvestigation. Third, new comparative insights into monetary policy independence anddependence could emerge. For instance, if no significant differences in results emerge, itcould be established that monetary policy dependence does not really matter. Fourth, asan intuition for independence, African monetary union countries (with the likelihood ofcommon monetary policies) have not been considered in the dataset. Fifth, theassumption of independence matters only for the money–inflation nexus and not for themoney– output linkage because Westerlund (2007) is consistent with Pedroni (1999) onthe long-run neutrality of money. Hence, one of the underlying hypotheses motivatingthe study remains sound. Sixth, the label of “empirics” on the paper’s title means we canmake the assumption without being afraid of “econometrics polices”.

4.3 VECM for monetary policy and inflationLet us consider inflation and money with no lagged differences, such that:

Inflationi,t � �Moneyi,t (1)

The resulting VECMs are the following for equation (1):

�Inflationi,t � �(Inflationi,t�1 � �Moneyi,t�1) � �i,t (2)

�Moneyi,t � (Moneyi,t�1 � kInflationi,t�1) � ei,t (3)

In equations (2) and (3), the right-hand terms are the Error Correction Terms (ECTs). Atequilibrium, the value of the ECT is zero. When the ETC is non-zero, it means thatinflation and money have deviated from the long-run equilibrium; and the ECT helpseach variable to adjust and partially restore the equilibrium relationship. The speed ofthese adjustments are measured by � and for inflation and money, respectively.Therefore, equations (2) and (3) are replicated for all the “finance and inflation” pairs.The same deterministic trend assumptions used in the cointegration tests are used.

Table IV shows results for the VECM. While the findings in the upper-sections ofboth panels are consistent with equation (1), those in the lower-sections correspond toequations (2) and (3). Specifically, the first line in the lower-sections (D[Inflation])corresponds to equation (2), whereas the estimates shaping the diagonal are consistentwith equation (3). The signs of the cointegration relations in the upper-sections of thepanels are in accordance with the predictions of economic theory. This confirms theexisting consensus that in the long-run, money has a positive relationship with inflation.Among the long-run relationships of monetary policy variables, that of financial size isthe most significant. In other words, the ratio of bank assets in proportion of total assets

IGDR7,2

154

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Table IV.Vector error correction

model (cointegration andshort-term adjustment

coefficients)

Pane

lA:1

987-

2010

Est

imat

esof

coin

tegr

atio

nre

latio

nshi

psFi

nanc

iald

epth

(Mon

ey)

Mon

eysu

pply

NA

––

––

––

Liqu

idlia

bilit

ies

–2.

854

––

––

–(0

.126

)

Fina

ncia

lallo

catio

nef

ficie

ncy

Ban

king

syst

em–

–4.

259

––

––

(0.2

45)°

Fina

ncia

lsys

tem

––

–N

A–

––

Fina

ncia

lact

ivity

(Cre

dit)

Ban

king

syst

em–

––

–13

.750

––

(0.5

00)

Fina

ncia

lsys

tem

––

––

–15

.716

–(0

.627

)

Fina

ncia

lsiz

eB

anki

ngsy

stem

––

––

––

29.5

42

**(2

.169)

Est

imat

esof

shor

t-ter

mad

just

men

tcoe

ffici

ents

D[In

flatio

n]N

A�

0.2

04

***

�0

.19

0**

*N

A�

0.2

00

***

�0

.20

2**

*�

0.2

53

***

(�5

.18

2)

(�5

.04

4)°

(�5

.13

6)

(�5

.139)

(�5.4

69)

Fina

ncia

ldep

th(m

oney

)D

[Mon

eysu

pply

]N

A–

––

––

–D

[Liq

uid

liabi

litie

s]–

�0

.00

01

**–

––

––

(�2

.55

2)

Fina

ncia

lallo

catio

nef

ficie

ncy

D[B

anki

ngsy

stem

]–

–�

0.00

03–

––

–(�

1.05

4)°

D[F

inan

cial

syst

em]

––

–N

A–

––

(con

tinue

d)

155

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Table IV.

Fina

ncia

lact

ivity

(cre

dit)

D[B

anki

ngsy

stem

]–

––

–�

0.00

0088

7–

–(�

1.29

2)D

[Fin

anci

alsy

stem

]–

––

––

�0.

0000

960

–(�

1.34

2)

Fina

ncia

lsiz

eD

[Ban

king

syst

em]

––

––

––

�0.0

004

**(�

2.0

95)

Pane

lA:1

987-

2006

Est

imat

esof

coin

tegr

atio

nre

latio

nshi

psFi

nanc

iald

epth

(Mon

ey)

Mon

eysu

pply

9.36

5–

––

––

–(0

.404

)Li

quid

liabi

litie

s–

10.4

45–

––

––

(0.3

70)

Fina

ncia

lallo

catio

nE

ffici

ency

Ban

king

syst

em–

–8.

639

––

––

(0.3

98)°

Fina

ncia

lsys

tem

––

–7.

892

––

–(0

.398

)°Fi

nanc

iala

ctiv

ity(C

redi

t)B

anki

ngsy

stem

––

––

21.6

62–

–(0

.618

)Fi

nanc

ials

yste

m–

––

––

NA

–

Fina

ncia

lsiz

eB

anki

ngsy

stem

––

––

––

58.0

27

***

(4.7

42)

(con

tinue

d)IGDR7,2

156

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

Table IV.

Est

imat

esof

shor

tter

mad

just

men

tcoe

ffici

ents

D[In

flatio

n]�

0.2

03

***

�0

.20

7**

*�

0.1

89

***

�0

.19

0**

*�

0.2

02

***

NA

�0.2

86

***

(�4

.44

8)

(�4

.55

2)

(�4

.39

6)°

(�4

.40

3)°

(�4

.50

9)

(�4.8

40)

Fina

ncia

ldep

th(M

oney

)D

[Mon

eysu

pply

]�

0.0

00

2**

*–

––

––

–(�

3.0

59

)D

[Liq

uid

liabi

litie

s]–

�0

.00

01

**–

––

––

(�2

.45

5)

Fina

ncia

lallo

catio

nef

ficie

ncy

D[B

anki

ngsy

stem

]–

–�

0.00

02–

––

–(�

0.67

9)°

D[F

inan

cial

syst

em]

––

–�

0.00

01–

––

(�0.

582)

°

Fina

ncia

lact

ivity

(Cre

dit)

D[B

anki

ngsy

stem

]–

––

–�

0.00

0076

8–

–(�

1.22

5)D

[Fin

anci

alsy

stem

]–

––

––

NA

–

Fina

ncia

lsiz

eD

[Ban

king

syst

em]

––

––

––

�0.0

007

***

(�3.5

22)

Not

es:

***,

**,

*den

ote

sign

ifica

nce

at1,

5an

d10

%,r

espe

ctiv

ely;

the

dete

rmin

istic

tren

das

sum

ptio

nsan

dla

gse

lect

ion

crite

ria

for

the

VE

CMar

eth

esa

me

asin

the

coin

tegr

atio

nte

sts;

():t

-sta

tistic

s;D

[]:F

irst

diff

eren

ce.°

:val

ues

also

appl

yfo

rth

em

onet

ary

polic

yde

pend

ence

hypo

thes

is.n

a:ab

senc

eof

coin

tegr

atio

nor

stat

iona

ryin

leve

ls;s

igni

fican

ceof

bold

data

isre

ject

ion

ofth

enu

llhy

poth

esis

ofno

coin

tegr

atio

nan

dre

ject

ion

ofth

enu

llhy

poth

esis

nosi

gnifi

cant

erro

rco

rrec

tion

term

s

157

Does moneymatter in Africa?

Dow

nloa

ded

by M

r A

song

u Si

mpl

ice

At 0

2:30

13

Nov

embe

r 20

14 (

PT)

(Deposit bank assets plus Central bank assets) has the most significant positiverelationship with inflation in the long-run.