BS Project-Coal Prices in India

23

2013 By: Group-5 Vivek Kumar, Roll No 34 Puninder Singh Bhatia, Roll No 24 Bhawna, Roll No 24 EPGDCFM 12- 14 IIFT, Delhi Coal Prices affecting Electricity Tariff in India

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of BS Project-Coal Prices in India

2013

By:

Group-5

Vivek Kumar, Roll No 34

Puninder Singh Bhatia, Roll No 24

Bhawna, Roll No 24

EPGDCFM 12-14

IIFT, Delhi

Coal Prices affecting Electricity Tariff in India

Coal Prices Affecting Electricity Tariffs in India 2

Abstract Coal has many important uses worldwide. The most significant uses are in electricity generation, steel production, cement manufacturing and as a liquid fuel. Since 2000, global coal consumption has grown faster than any other fuel. The five largest coal users - China, USA, India, Russia and Japan - account for 76% of total global coal use. Different types of coal have different uses. Steam coal - also known as thermal coal - is mainly used in power generation. Coking coal - also known as metallurgical coal - is mainly used in steel production. The biggest market for coal is Asia, which currently accounts for over 67% of global coal consumption; although China is responsible for a significant proportion of this. Independent regulation of the coal sector becomes essential for ensuring that the sector becomes competitive, is able to fix formulae for price revision for long-term fuel supply agreements, and fix trading margins as well as improving exploitation and allocation of available resources. Because of the volatility, it is difficult to compare international coal prices with domestic prices. However, even after the decline in international prices, the price of imported coal is much higher than the price of domestic coal. In order to compare the prices of coal on account of imported coal and increasing rise in the retail tariff of distribution companies due to increase in Average Power Purchase Cost from Central Gencos. We are analyzing the prices of Domestic coal for the past 8 years and its corresponding impact on Energy sector especially on Distribution companies like BSES Rajdhani Power Ltd (BRPL) and BSES Yamuna Power Ltd (BYPL).

Coal Prices Affecting Electricity Tariffs in India 3

Table of Contents

Executive Summary….............................................................................................................4 Coal Sector in India..…………………………………………………………………………………………………5 The Regulatory Framework of Coal …………………………………………………………………………….6 Function of Regulator in Coal …………………………………………………………………………………….7 Prices of Coal Since Decontrol……………………………………………………………………………………8 Electricity Sector in India………………………………………………………………………………………....10 Regulators in Power Sector…………………………………………………..…………………………………..11 Power Distribution Companies in Delhi ……………………………………………………………………...13 Retail Tariff of Domestic consumers of Delhi Discoms……………………………………………….…..13 Net Power Purchase Costs of Delhi Discoms………………………………………………………………..16 Comparison between Retail Tariff and the Net Power Purchase Cost……………………………….18 Comparison between Retail Tariff, Net Power Purchase Cost & Cost of Coal …………………….19 Conclusion……………………………………………………………………………………………………………..21 References……………………………………………………………………………………………………………..22

Coal Prices Affecting Electricity Tariffs in India 4

Executive Summary

Coal provides 30.3% of global primary energy needs and generates 42% of the world's electricity. In 2011 coal was the fastest growing form of energy outside renewables. Its share in global primary energy consumption increased to 30.3% - the highest since 1969. Total Global Coal Production (including hard coal and lignite)

7678Mt (2011) 7201Mt (2010) 4677 (1990)

Top Ten Coal Producers in 2011

PR China 3471Mt Russia 334Mt USA 1004Mt South Africa 253Mt India 585Mt Germany 189Mt Australia 414Mt Poland 139Mt Indonesia 376Mt Kazakhstan 117Mt

Total world coal production reached a record level of 7,678Mt in 2011, increasing by 6.6% over 2010. The average annual growth rate of coal production since 1999 was 4.4%. Total Global Hard Coal Production

6637Mt (2011):967Mt coking coal, 5670Mt steam coal 6217Mt (2010): 900Mt coking coal, 5317Mt steam coal 3493Mt (1990): 598Mt coking coal, 2894Mt steam coal

There are two internationally recognised methods for assessing world coal reserves. The first one is produced by the German Federal Institute for Geosciences and Natural Resources (BGR) and is used by the IEA as the main source of information about coal reserves. The second one is produced by the World Energy Council (WEC) and is used by the BP Statistical Review of World Energy. According to BGR there are 1004 billion tonnes of coal reserves left, equivalent to 130 years of global coal output in 2011. Coal reserves reported by WEC are much lower - 861 billion tonnes, equivalent to 112 years of coal output

Coal Prices Affecting Electricity Tariffs in India 5

Coal Sector in India The Ministry of Coal has the overall responsibility of determining policies and strategies in respect of

exploration and development of coal and lignite reserves, sanctioning of important projects of high

value and for deciding all related issues. These key functions are exercised through its public sector

undertakings, namely, Coal India Limited (CIL) and Neyveli Lignite Corporation (NLC) Limited and

Singareni Collieries Company Limited (SCCL), which is a joint sector undertaking of Government of

Andhra Pradesh and Government of India with equity capital in the ratio of 51:49.

Coal is the mainstay of India’s energy sector and accounts for over 50 per cent of the primary

commercial energy supply. Around 74 per cent of the coal produced in India is consumed in power

generation. Compared to other sources of energy that are available in the country, known coal reserves

are expected to last for over 70 years at the present levels of production.

The growing gap between the demand and domestic supply of coal has made it imperative to augment

domestic production from the public sector as well as from the private sector and expedite the reform

process for realizing efficiency gains through increased competition in the sector during the Eleventh

Plan. The Eleventh Plan envisaged augmenting domestic production with a long-term perspective

keeping in view the sharp increase in demand in the power sector and the long gestation periods of coal

projects. A new feature of the Eleventh Plan was the strategy of augmenting coal production from

captive sources, including captive coal mines in the private sector. An important area of the Plan

concerns revival of loss making companies, restructuring of the coal sector by providing autonomy,

setting up a regulatory authority for ensuring fair competition, and facilitating private sector

participation in commercial coal mining by means of necessary legislative amendments. Coal

production was targeted to grow at 9.56 per cent per annum during the Eleventh Plan against an annual

growth of 5.6 per cent per annum in the Tenth Plan. The estimated growth in the first three years of the

Plan was 7.31 per cent, reaching 7.89 per cent in the total Eleventh Plan period. Although the growth in

production will be lower than the Eleventh Plan target of 9.56 per cent, it will be higher than that in the

Tenth Plan.

Current market price for world thermal coal is around US$ 70 per tonne, a 40 per cent decline from the

peak US$ 121 in 2008 and even below the US$ 62 thermal coal price average in 2007. Because of this

Coal Prices Affecting Electricity Tariffs in India 6

volatility, it is difficult to compare international coal prices with domestic prices. However, even after

the decline in international prices, the price of imported coal is much higher than the price of domestic

coal. The landed cost of imported non-coking coal from Indonesia at Chennai port in August 2009 was

reported to be Rs 3,389 per tone and for coal imported from South Africa it was Rs 4,288 per tonne.

Against this, the price of non-coking coal supplied by the Mahanadi Coalfields Limited (MCL) situated

at Talcher, Chennai is reported to be Rs 1,560 per tonne for Ennore power station and Rs 1,492 at the

North Chennai power plant (based on pre-revised prices). The present Talcher coal cost is Rs 640 per

tonne. In other words, even though the cost of delivered domestic coal is more than 2.42 times the cost

of coal at the pit head but it is still cheaper than imported coal.

The Regulatory Framework of Coal The management of mineral resources in India is the responsibility of both Central Government and

State Governments as per the Constitution of India. The Mines and Minerals (Development and

Regulation) Act, 1957 (‘MMDRA’), and the Mines Act, 1952, together with the rules and regulations

framed under them constitute the basic laws governing the mining sector in India. The Mines and

Minerals (Development and Regulation) Act, 1957, is one of the two overarching pieces of legislation

affecting the coal sector in India. The other is the coal Mines (Nationalisation) Act, 1973, which, unlike

the MMDRA, is specific to the coal sector. The MMDRA classifies minerals into major and minor

categories. Major minerals such as coal, lignite, mineral oils, iron ore, copper, zinc, atomic minerals, etc.

are listed in Schedule A,which is reserved exclusively for the public sector, and minor minerals in

Schedule B, in which the private sector was allowed to participate in mining activities along with the

public sector (NMP). According to MMRD Act 1957, prior approval of the Government of India is

necessary before the grant renewal of mineral concession for minerals specified in Schedule 1 of the

said Act. Presently, 23 minerals are included in Schedule 1. Of these 11 minerals are atomic minerals,

one mineral (coal and lignite) is a fuel mineral are remaining 10 are metallic ores and industrial minerals.

Important supplementary rules in force under the MMDRA are the Mineral Concession Rules, 1960, and

the Mineral Conservation and Development Rules, 1988. The Mineral Concession Rules, 1960 outline

the procedures and conditions for obtaining a Prospecting License or Mining Lease. The Mineral

Conservation and Development Rules, 1988 lays down guidelines for ensuring mining on a scientific

basis, while at the same time, conserving the environment. It is noteworthy, however, that the MCR

and MDCR do not apply to coal, atomic minerals, and minor minerals (RSPAS).

Coal Prices Affecting Electricity Tariffs in India 7

The coal Mines (Nationalisation) Act of 1973 reinforces the spirit of the MMDRA, because by

nationalising the mines, it firmly consigned coal to the purview of the public sector. The Coal Mines

(Nationalisation) Act 1973 categorically states that ‘no person, other than the central government or a

government company or a corporation owned, managed or controlled by the central government shall

carry on coal mining operation in India, in any form’ (Lahiri-Dutt, 2006).

According to the Planning Commision (2006), under the coal Mines (Nationalisation) Act 1973, and

clarifications issued from time to time, the following institutions and agencies are entitles to do coal

mining without the restriction of captive consumption. These are:

Central government or a company owned by the Central or State Government engaged in coal

production.

A government company owned by the state or central government which now takes up coal

mining.

Responsibility for overseeing mines and mineral development (and implementation of legislation) rests

jointly with the central and state governments. Basically the responsibilities are divided amongst the

central and state governments, with the former having exclusive power to make laws with respect to

regulation of mines and major minerals development. The state governments are largely responsible

for implementing the laws, but are constrained to act within the framework laid down by the central

government. The states do, however, have the power to make rules in respect of minor minerals under

section 15 for the Act. They are able to device specific supplementary legislations to promote

investment within the state, and have, over time, started taking initiatives to attract private players

(including foreign investors) to the states.

Function of Regulator in Coal (Prior to 1996)

Office of Coal Controller (earlier Coal Commissioner), established in 1916, is one of the oldest office in

Indian Coal sector. Main aim behind setting up this office was to have Government control to

adequately meet the coal requirement during First World War. Acute scarcity of coal necessitated

promulgation of Colliery Control Order, 1944 for effective control on production, distribution and

Coal Prices Affecting Electricity Tariffs in India 8

pricing of coal. Subsequently, it was revised by a more comprehensive order in 1945.. As a result,

functions of Coal Controller’s Office remained more or less same except for the work of distribution and

allotment of coal.

Functions of Coal Controller’s Organisation are listed as below-

To lay down procedure and standard for sampling of coal

Inspection of collieries so as to ensure the correctness of the class, grade or size of coal.

To issue directives for the purpose of declaration and maintenance of grades of a seam mined in a colliery.

To act as the appellate authority in case of dispute between consumers and owner arising out of declaration of grade and size of coal.

To regulate disposal of stock of coal or the expected output of coal in the colliery.

Quality surveillance with respect to loading of coal in wagons/ trucks according to laid down procedures regarding grades and sizes.

To grant opening /reopening permission of coal mine, seam or a section of seam or to subdivide a mine.

Assessment and collection of excise duty levied on all raw coal raised and dispatched.

Coal Controller has been made the statistical authority with respect to coal and lignite statistics. Entrusted the responsibility of carrying out Annual Coal & Lignite survey.

Submission of monthly coal data to different ministries of central and state Govt., national and international organization.

Collection of Statistics relating to coal washeries.

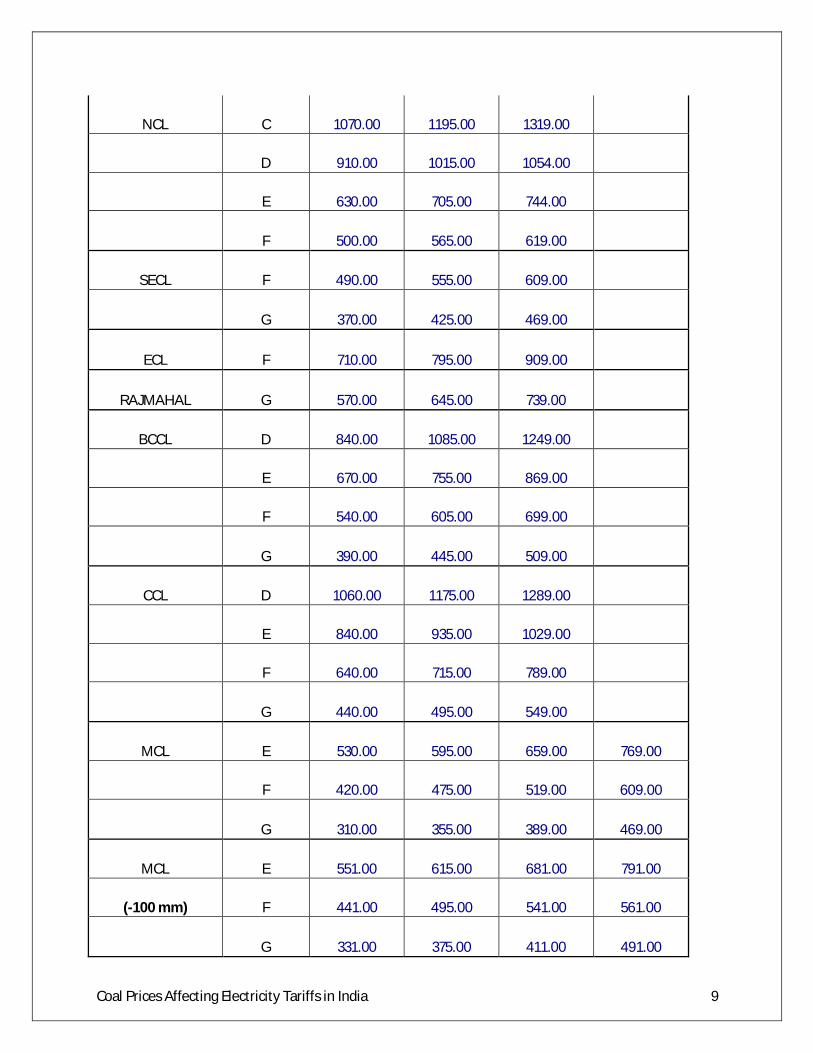

PRICES OF COAL SINCE DECONTROL Later in 1996, distribution and pricing of coal was deregulated. Therefore, Colliery Control Order, 2000 superseded the previous order After deregulating the price, the price of Domestic Coal of Different grades charges by Different companies from the Generating companies since 2004 to 2011 based on the Useful Heat Value (UHV) Is as under with their subsequent revisions as carried out by CIL/ Ministry of Coal.

Price of domestic coal (Rs./Tn.) with effective date

COALFIELD GRADE 15.06.04 13.12.07 16.10.09 27.02.11

Coal Prices Affecting Electricity Tariffs in India 9

NCL C 1070.00 1195.00 1319.00

D 910.00 1015.00 1054.00

E 630.00 705.00 744.00

F 500.00 565.00 619.00

SECL F 490.00 555.00 609.00

G 370.00 425.00 469.00

ECL F 710.00 795.00 909.00

RAJMAHAL G 570.00 645.00 739.00

BCCL D 840.00 1085.00 1249.00

E 670.00 755.00 869.00

F 540.00 605.00 699.00

G 390.00 445.00 509.00

CCL D 1060.00 1175.00 1289.00

E 840.00 935.00 1029.00

F 640.00 715.00 789.00

G 440.00 495.00 549.00

MCL E 530.00 595.00 659.00 769.00

F 420.00 475.00 519.00 609.00

G 310.00 355.00 389.00 469.00

MCL E 551.00 615.00 681.00 791.00

(-100 mm) F 441.00 495.00 541.00 561.00

G 331.00 375.00 411.00 491.00

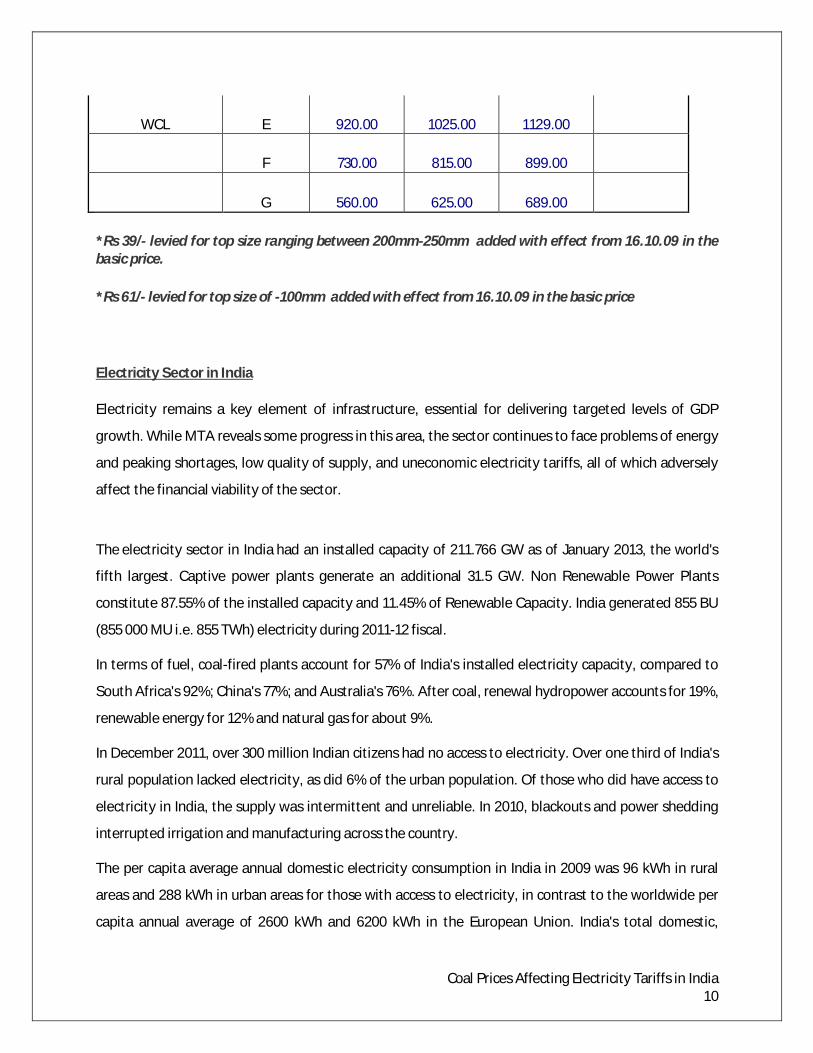

Coal Prices Affecting Electricity Tariffs in India 10

WCL E 920.00 1025.00 1129.00

F 730.00 815.00 899.00

G 560.00 625.00 689.00 *Rs 39/- levied for top size ranging between 200mm-250mm added with effect from 16.10.09 in the basic price. *Rs 61/- levied for top size of -100mm added with effect from 16.10.09 in the basic price Electricity Sector in India Electricity remains a key element of infrastructure, essential for delivering targeted levels of GDP

growth. While MTA reveals some progress in this area, the sector continues to face problems of energy

and peaking shortages, low quality of supply, and uneconomic electricity tariffs, all of which adversely

affect the financial viability of the sector.

The electricity sector in India had an installed capacity of 211.766 GW as of January 2013, the world's

fifth largest. Captive power plants generate an additional 31.5 GW. Non Renewable Power Plants

constitute 87.55% of the installed capacity and 11.45% of Renewable Capacity. India generated 855 BU

(855 000 MU i.e. 855 TWh) electricity during 2011-12 fiscal.

In terms of fuel, coal-fired plants account for 57% of India's installed electricity capacity, compared to

South Africa's 92%; China's 77%; and Australia's 76%. After coal, renewal hydropower accounts for 19%,

renewable energy for 12% and natural gas for about 9%.

In December 2011, over 300 million Indian citizens had no access to electricity. Over one third of India's

rural population lacked electricity, as did 6% of the urban population. Of those who did have access to

electricity in India, the supply was intermittent and unreliable. In 2010, blackouts and power shedding

interrupted irrigation and manufacturing across the country.

The per capita average annual domestic electricity consumption in India in 2009 was 96 kWh in rural

areas and 288 kWh in urban areas for those with access to electricity, in contrast to the worldwide per

capita annual average of 2600 kWh and 6200 kWh in the European Union. India's total domestic,

Coal Prices Affecting Electricity Tariffs in India 11

agricultural and industrial per capita energy consumption estimate vary depending on the source. Two

sources place it between 400 to 700 kWh in 2008–2009. As of January 2012, one report found the per

capita total consumption in India to be 778 kWh.

India currently suffers from a major shortage of electricity generation capacity, even though it is the

world's fourth largest energy consumer after United States, China and Russia. The International Energy

Agency estimates India needs an investment of at least $135 billion to provide universal access of

electricity to its population.

Regulators in Power Sector

Central Regulator

Central Electricity Regulatory Commission (CERC)

As entrusted by the Electricity Act, 2003 the Commission has the responsibility to discharge the following functions:-

Mandatory Functions:-

to regulate the tariff of generating companies owned or controlled by the Central Government;.

to regulate the tariff of generating companies other than those owned or controlled by the

Central Government specified in clause (a), if such generating companies enter into or

otherwise have a composite scheme for generation and sale of electricity in more than one

State;

to regulate the inter-State transmission of electricity ;

to determine tariff for inter-State transmission of electricity;

to issue licences to persons to function as transmission licensee and electricity trader with

respect to their inter-State operations;

Improve access to information for all stakeholders.

to adjudicate upon disputes involving generating companies or transmission licensee in regard

to matters connected with clauses (a) to (d) above and to refer any dispute for arbitration;

to levy fees for the purposes of the Act;

to specify Grid Code having regard to Grid Standards;

to specify and enforce the standards with respect to quality, continuity and reliability of service

by licensees;

to fix the trading margin in the inter-State trading of electricity, if considered, necessary;

Coal Prices Affecting Electricity Tariffs in India 12

to discharge such other functions as may be assigned under the Act.

Advisory Functions:-

formulation of National Electricity Policy and Tariff Policy; promotion of competition, efficiency and economy in the activities of the electricity industry; promotion of investment in electricity industry; any other matter referred to the Central Commission by

State Regulator

State Electricity Regulatory Commission (SERC)

As entrusted by the Electricity Act, 2003, The State Commission shall discharge the following functions, namely: -

(a) determine the tariff for generation, supply, transmission and wheeling of electricity, wholesale, bulk or retail, as the case may be, within the State:

Provided that where open access has been permitted to a category of consumers under section 42, the State Commission shall determine only the wheeling charges and surcharge thereon, if any, for the said category of consumers;

(b) regulate electricity purchase and procurement process of distribution licensees including the price at which electricity shall be procured from the generating companies or licensees or from The Electricity Act, 2003 other sources through agreements for purchase of power for distribution and supply within the State;

(c) facilitate intra-State transmission and wheeling of electricity; (d) issue licences to persons seeking to act as transmission licensees, distribution licensees and electricity traders with respect to their operations within the State;

(e) promote co-generation and generation of electricity from renewable sources of energy by providing suitable measures for connectivity with the grid and sale of electricity to any person, and also specify, for purchase of electricity from such sources, a percentage of the total consumption of electricity in the area of a distribution licensee;

(f) adjudicate upon the disputes between the licensees, and generating companies and to refer any dispute for arbitration;

(g) levy fee for the purposes of this Act; (h) specify State Grid Code consistent with the Grid Code specified under clause (h) of sub-section (1) of section 79;

(i) specify or enforce standards with respect to quality, continuity and reliability of service by licensees;

Coal Prices Affecting Electricity Tariffs in India 13

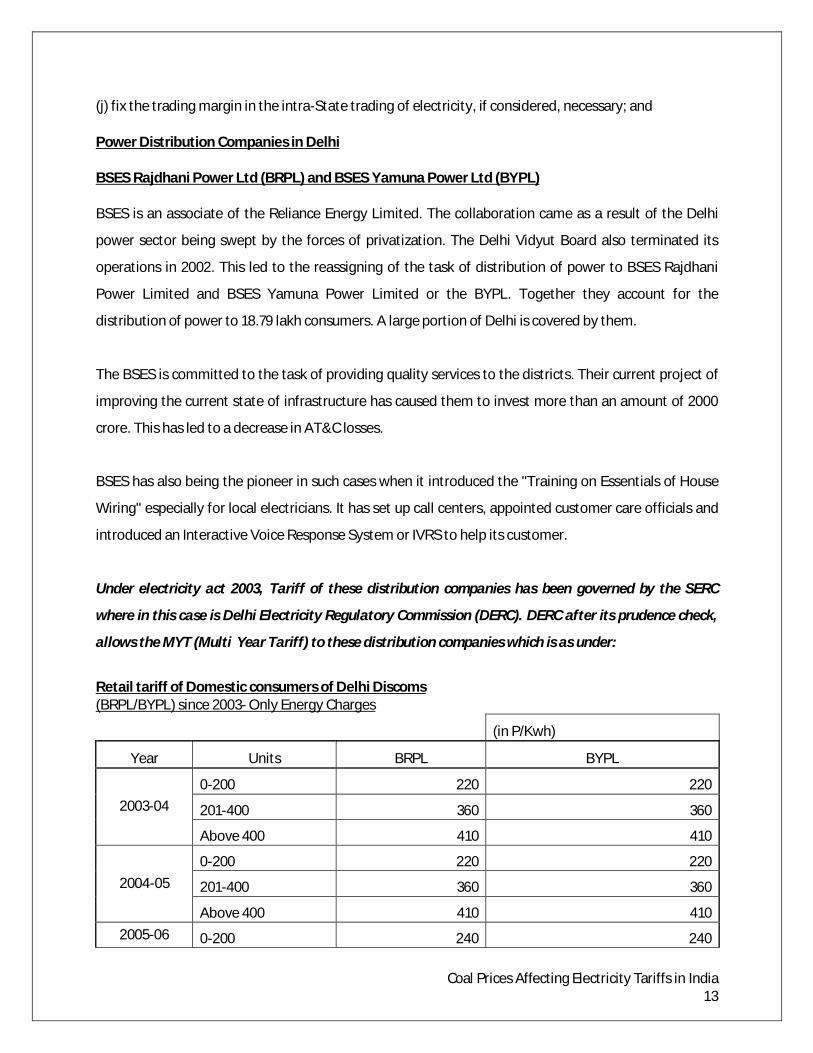

(j) fix the trading margin in the intra-State trading of electricity, if considered, necessary; and

Power Distribution Companies in Delhi BSES Rajdhani Power Ltd (BRPL) and BSES Yamuna Power Ltd (BYPL) BSES is an associate of the Reliance Energy Limited. The collaboration came as a result of the Delhi

power sector being swept by the forces of privatization. The Delhi Vidyut Board also terminated its

operations in 2002. This led to the reassigning of the task of distribution of power to BSES Rajdhani

Power Limited and BSES Yamuna Power Limited or the BYPL. Together they account for the

distribution of power to 18.79 lakh consumers. A large portion of Delhi is covered by them.

The BSES is committed to the task of providing quality services to the districts. Their current project of

improving the current state of infrastructure has caused them to invest more than an amount of 2000

crore. This has led to a decrease in AT&C losses.

BSES has also being the pioneer in such cases when it introduced the "Training on Essentials of House

Wiring" especially for local electricians. It has set up call centers, appointed customer care officials and

introduced an Interactive Voice Response System or IVRS to help its customer.

Under electricity act 2003, Tariff of these distribution companies has been governed by the SERC

where in this case is Delhi Electricity Regulatory Commission (DERC). DERC after its prudence check,

allows the MYT (Multi Year Tariff) to these distribution companies which is as under:

Retail tariff of Domestic consumers of Delhi Discoms (BRPL/BYPL) since 2003- Only Energy Charges

(in P/Kwh)

Year Units BRPL BYPL

0-200 220 220

201-400 360 360 2003-04

Above 400 410 410

0-200 220 220

201-400 360 360 2004-05

Above 400 410 410 2005-06 0-200 240 240

Coal Prices Affecting Electricity Tariffs in India 14

201-400 390 390

Above 400 460 460

0-200 240 240

201-400 390 390 2006-07

Above 400 460 460

0-200 245 245

201-400 395 395 2007-08

Above 400 465 465

0-200 245 245

201-400 395 395 2008-09

Above 400 465 465

0-200 245 245

201-400 395 395 2009-10

Above 400 465 465

0-200 245 245

201-400 395 395 2010-11

Above 400 465 465

0-200 300 300

201-400 480 480 2011-12

Above 400 570 570

* Subject to be truing by Delhi Electricty Regulatory Commission

Based on the above increase in energy charges of distribution companies (BRPL and BYPL), the

graphical representation of the retails tariff to be paid for 0-200 units and 201-400 units of

electricity consume by the consumers to BRPL and BYPL respectively.

Coal Prices Affecting Electricity Tariffs in India 15

Figure 1:- 0-200 units

Figure 2:- 201- 400 units

Coal Prices Affecting Electricity Tariffs in India 16

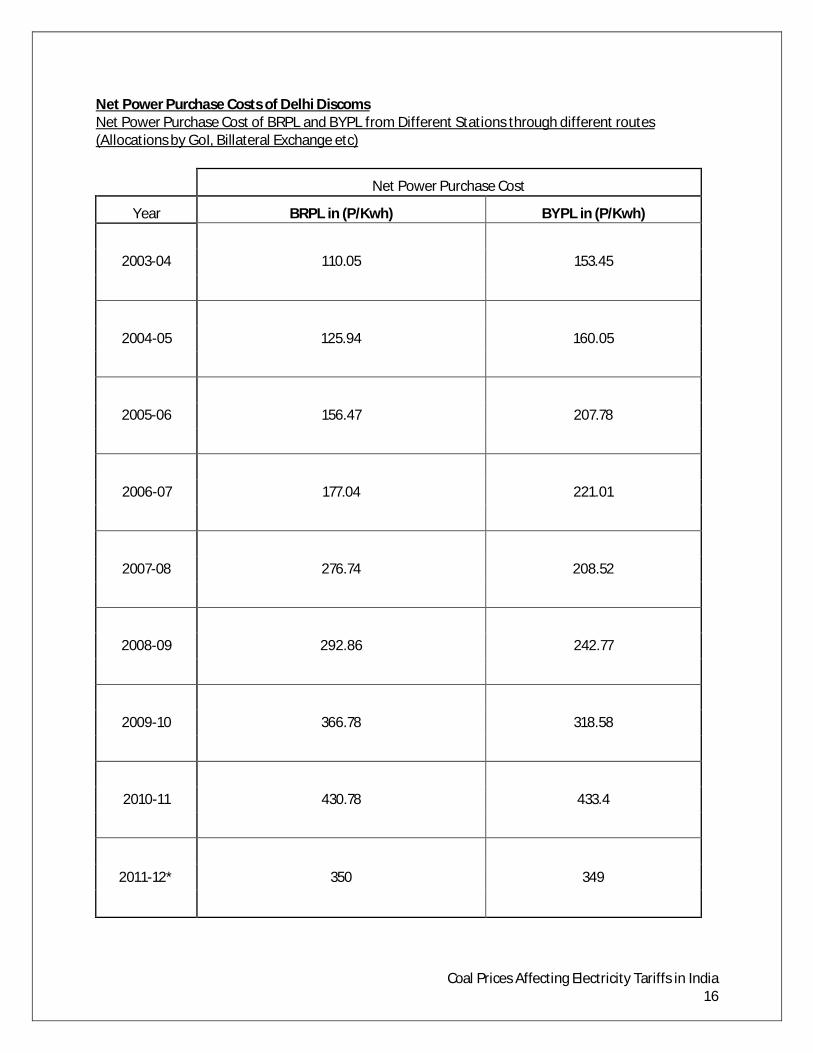

Net Power Purchase Costs of Delhi Discoms Net Power Purchase Cost of BRPL and BYPL from Different Stations through different routes (Allocations by GoI, Billateral Exchange etc)

Net Power Purchase Cost

Year BRPL in (P/Kwh) BYPL in (P/Kwh)

2003-04 110.05 153.45

2004-05 125.94 160.05

2005-06 156.47 207.78

2006-07 177.04 221.01

2007-08 276.74 208.52

2008-09 292.86 242.77

2009-10 366.78 318.58

2010-11 430.78 433.4

2011-12* 350 349

Coal Prices Affecting Electricity Tariffs in India 17

Graphical Representation of Power Purchase Cost of BRPL and BYPL( in P/Kwh):

Figure 3: Net Power Purchase Cost of BRPL in P/Kwh

Coal Prices Affecting Electricity Tariffs in India 18

Figure 4: NET Power Purchase Cost of BYPL in P/Kwh

As it is evident from the figure 3 and 4, the power purchase cost of these distribution companies has

gone up significantly since 2004 i.e. approx 291% for BRPL and 182% for BYPL whereas the average

retail tariff of these distribution companies which was governed by the DERC has allows the increase

in tariff rate of approx 36% since 2004 to 2011.

Comparing the retail tariff of BRPL with the Net Power Purchase Cost (in P/Kwh):

Figure 5: Comparison of Retail Tariff Vs Power Purchase Cost (BRPL)

Comparing the retail tariff of BYPL with the Net Power Purchase Cost (in P/Kwh):

Figure 6: Comparison of Retail Tariff Vs Power Purchase Cost (BYPL)

Coal Prices Affecting Electricity Tariffs in India 19

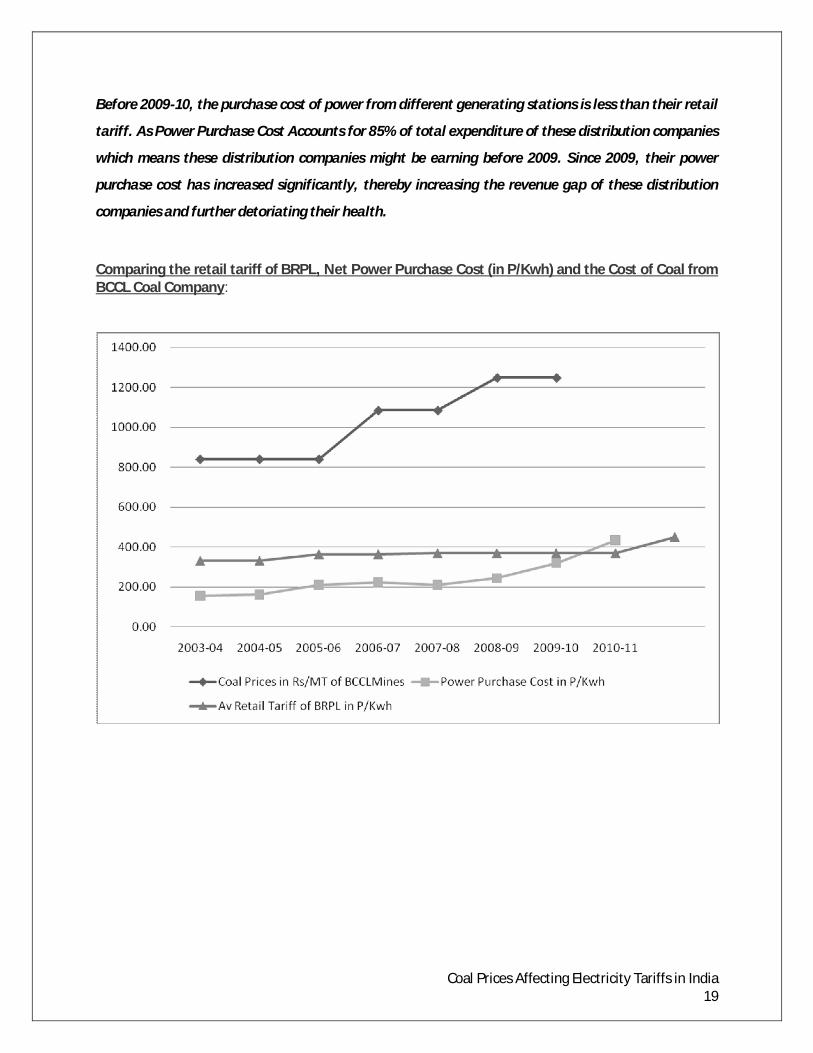

Before 2009-10, the purchase cost of power from different generating stations is less than their retail

tariff. As Power Purchase Cost Accounts for 85% of total expenditure of these distribution companies

which means these distribution companies might be earning before 2009. Since 2009, their power

purchase cost has increased significantly, thereby increasing the revenue gap of these distribution

companies and further detoriating their health.

Comparing the retail tariff of BRPL, Net Power Purchase Cost (in P/Kwh) and the Cost of Coal from BCCL Coal Company:

Coal Prices Affecting Electricity Tariffs in India 20

Domestic Coal prices supplied by Coal India Ltd and its subsidiaries have not increases much since

2004, I.e. increases about 50%. Coal Companies supply the coal to the Interstate Generating

Station as per the Annual Contracted Quantity (ACQ) agreed by both the parties in the Fuel Supply

Agreement (FSA). In the Two part tariff adopted by the CERC i.e. Fixed Charges and Variable

Charges, fixed charges of central generating stations is determined by CERC. It is evident from the

fact the Central Regulator ensuring the profitability of the generators and the end user consumers

decides the fixed charges of the generating stations after prudence check. But as the variable

charges of these generating stations is dependent on the Fuel consumed during the particular tariff

period, increase in fuel prices thereby increases the variable charges of these generating

companies. Since as per CERC Regulations, Variable charges is pass through to the beneficiaries

(Distribution companies), their power purchase cost will rise up automatically with the increase in

price of coal.

Coal Prices Affecting Electricity Tariffs in India 21

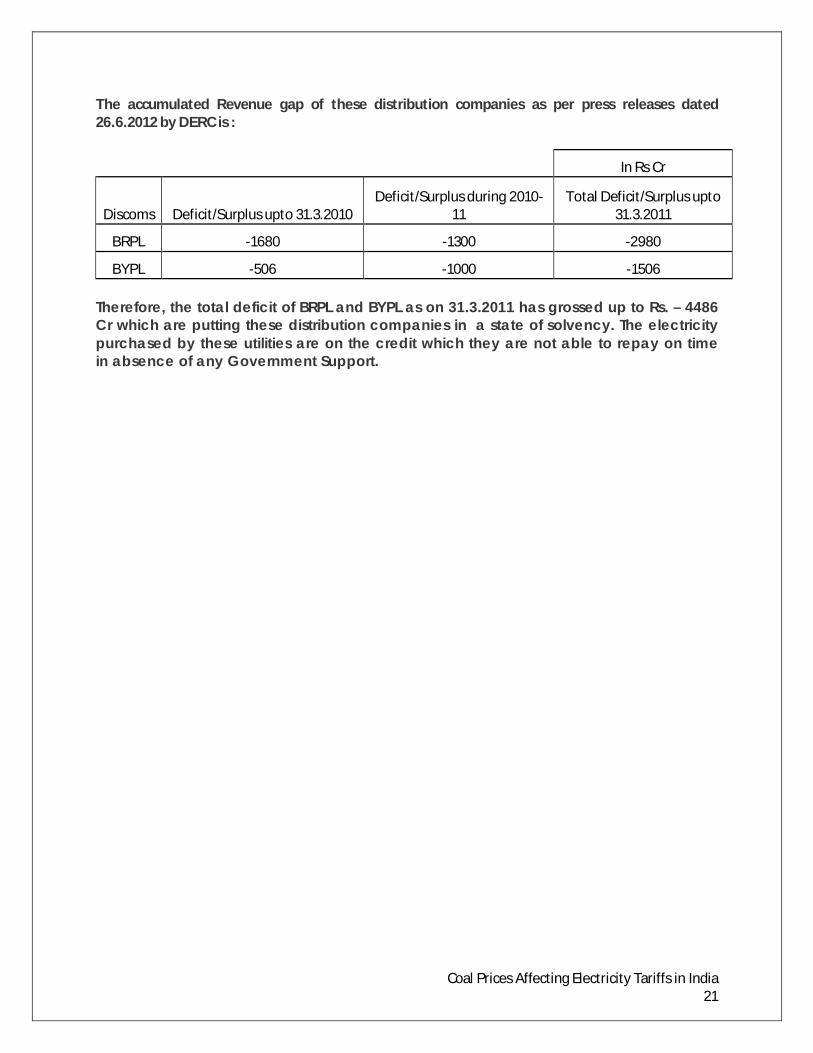

The accumulated Revenue gap of these distribution companies as per press releases dated 26.6.2012 by DERC is :

In Rs Cr

Discoms Deficit/Surplus upto 31.3.2010 Deficit/Surplus during 2010-

11 Total Deficit/Surplus upto

31.3.2011

BRPL -1680 -1300 -2980

BYPL -506 -1000 -1506 Therefore, the total deficit of BRPL and BYPL as on 31.3.2011 has grossed up to Rs. – 4486 Cr which are putting these distribution companies in a state of solvency. The electricity purchased by these utilities are on the credit which they are not able to repay on time in absence of any Government Support.

Coal Prices Affecting Electricity Tariffs in India 22

Conclusion Since 2004, continuous rise in Domestic coal prices in India has adversely affected the power sector. The Regulators are doing their best to bail out both the generators and Distribution companies from this loophole. Even though with increase in the cost of coal, the generators are forced to increase their generation tariff (Variable charges) and subsequently the power purchase cost of the distribution companies will also rise accordingly. Continuous increase in the power procurement cost has put additional burden to these distribution companies as the retail tariff which are governed by the State Regulator are not increasing to cover the increasing revenue gap of these utilities. As evident from the fact, the financials of these discoms clearly shows a dent of Rs. 1300 crores to BRPL and Rs. 1000 crores to BYPL in the FY 2010-11, because of a surge of approx. 25% in power purchase price of BRPL and 31% in power purchase price of BYPL. Therefore, the price rise by these distribution companies in 2012-13 with the corresponding increase in coal prices was justifiable.

Coal Prices Affecting Electricity Tariffs in India 23

References

Electricity Act 2003, as amended in 2007

CERC Regulations 2004 and 2009.

www.cercind.gov.in

www.derc.gov.in

www.powermin.nic.in

www.BSESdelhi.com

www.coalindia.in

www.wikipedia .com