Deposits and Financing Operations of Maybank Islamic

24

INTROUCTION The course Deposit Mobilization and Financing Management enables the students to know the importance and various types of deposits and investment products. Therefore, in order to have better understanding on this subject, we are assigned to do an assignment on Deposits and Financing Operations of Islamic Banks. The main objective of this assignment is to have comprehensive idea for deposit and investment products available currently at the Malaysian Islamic Bank. Hence, in this paper, we discussed on all the deposits and investment products available at Maybank Islamic. We have also highlighted on Commodity Murabahah based products in this paper. As we all know there are over 16 Islamic Banks in Malaysia namely AmIslamic Bank, CIMB Islamic Bank, Alliance Islamic Bank, RHB Islamic Bank, Maybank Islamic Bank and so on. However, we chose Maybank Islamic because it is the largest bank in Malaysia. To conduct our assignment, we have visited to the headquarters of Maybank at Menara Maybank, 100, Jalan Tun Perak, 50050 Kuala Lumpur, Wilayah Perseketuan, Kuala Lumpur. Besides, to get further information on their Islamic products, we also visited Maybank Investment Bank at level 10, Tower C, Dataran Maybank, 1, Jalan Maarof, 59000 Kuala Lumpur. Moreover, the details on whom and when we met the higher officers are as follow:

-

Upload

independent -

Category

Documents

-

view

8 -

download

0

Transcript of Deposits and Financing Operations of Maybank Islamic

INTROUCTION

The course Deposit Mobilization and Financing Management enables

the students to know the importance and various types of deposits

and investment products. Therefore, in order to have better

understanding on this subject, we are assigned to do an

assignment on Deposits and Financing Operations of Islamic Banks.

The main objective of this assignment is to have comprehensive

idea for deposit and investment products available currently at

the Malaysian Islamic Bank. Hence, in this paper, we discussed on

all the deposits and investment products available at Maybank

Islamic. We have also highlighted on Commodity Murabahah based

products in this paper.

As we all know there are over 16 Islamic Banks in Malaysia namely

AmIslamic Bank, CIMB Islamic Bank, Alliance Islamic Bank, RHB

Islamic Bank, Maybank Islamic Bank and so on. However, we chose

Maybank Islamic because it is the largest bank in Malaysia.

To conduct our assignment, we have visited to the headquarters of

Maybank at Menara Maybank, 100, Jalan Tun Perak, 50050 Kuala

Lumpur, Wilayah Perseketuan, Kuala Lumpur. Besides, to get

further information on their Islamic products, we also visited

Maybank Investment Bank at level 10, Tower C, Dataran Maybank, 1,

Jalan Maarof, 59000 Kuala Lumpur.

Moreover, the details on whom and when we met the higher officers

are as follow:

Department Person DateGlobal Banking Zatil

Hanani( Business

Relationship

Executive)

14th April 2015

Business Management

Office

Lau Suet

Foong(Business

Management

Executive)

17th April 2015

Retail Equities Prem Kumar( Head of

Business Management

Office)

21st April 2015

COMPANY BACKGROUND

The Malaysia’s largest financial services group, Maybank was

established on 1st May 1960. It is the largest company by market

capitalization on the Bursa Malaysia. Maybank is the number 1

banking group in Malaysia and ranks fourth in Asean in terms of

assets, loans and deposits. They also remain at top 5 players in

the regional market. The diagram of market positioning of Maybank

is as followed:

Aligned with above diagram, Maybank would not have achieved

without their vision and mission.

VISION: To become a regional leader in financial services through

realization of our true potential across key Home Markets and

beyond.

MISSION: To humanize financial services drives us and underpins

our desire to strengthen our relationship with the communities we

serve.

In order to accomplish their mission, on 1st February 2008,

Maybank Islamic Berhad began to operate as a new subsidiary of

Maybank. Now the customer enjoys a better range of Islamic

products and services. Moreover, Maybank offer a range of

products and services that includes commercial banking,

investment banking, Islamic banking, stock broking and so on.

On the other hand, even though the Maybank Islamic is still less

a decade in the financial market, it has been honoured with many

awards and recognitions for the past 7 years. In this section, we

have attached Maybank Islamic latest awards and recognition for

the year 2014.

DEPOSIT

Deposit is money placed into banking institution for safe keeping

for example like saving account, current account and so on. The

account holder has rights to withdraw any deposited funds as they

agreed in the contract.

Maybank Islamic are famous in provide deposit products.

Today we can see Maybank Islamic provide around 17 type of

deposit products by using the contract of wadiah, mudharabah,

musyarakah, and etc. But now Maybank Islamic are more concern on

commodity murabahah products.

There are 4 type of deposit products that they offering

which is on using commodity murabahah contracts such as Foreign

Currency Commodity Murabahah Deposit-i , Islamic Fixed Deposit-

i / Fixed Rate Term Deposit-i and Profit Now! Account-i (PNA-i).

The unique product which Maybank Islamic offered and it is

not offered by other banks is Profit Now! Account-i (PNA-i). This

product is unique because it will give profit to the customer as

we compare with other products. It is Islamic term deposit based

on the shariah contract of murabahah which specific shariah-1 2

compliant commodity as the underlying asset for the sale and

purchase transaction between the customer and bank.

Explanations

• Customer will appoint Maybank Islamic as agent to purchase

the commodity murabahah.

• Then the bank will purchase that from the open market.

Indirect transaction will happen when the bank will send the

commodity to the customer not in the agreement it’s will

show like customer purchase the commodity and send to the

bank.

• Then customer will sell back the commodity to the bank. And

bank will pay as deferred payment to the customer. So as the

result of this product customer can gain the profit.

Benefits of Profit Now! Account-i (PNA-i) product is:

3CUSTOMERMAYBANK ISLAMICMARKET

Benefit of this product is higher profit rate compared to normal

Saving Account-i. This means that the rate of this product is for

tenure 1st month to 12 month is 3.15% to 3.40% and compare to the

Saving Account-i is 0.40% to 1.75% only. From this we can say

that this product can give us profit and gain the good returns as

compare to the Saving Account-i. And as we know that these

products give costumer profit rather than the bank. By purchasing

these products not only give benefit in return but Maybank

Islamic also protect the customer by providing free Personal

Accident Takaful Coverage (PATC) plus medical and funeral

expenses in the case of the accident only. This will help the

costumer to make easy as they no need to find out the Takaful

Insurance personally. Another benefit that we can get from this

product is Maybank Islamic acceptance the collateral to fulfill

these Banking facilities. As we can see that they were exchange

commodity murabahah in the transaction.

FOREIGN CURRENCY

In 2008, Maybank Islamic was launching two treasury products

using Commodity Murabahah principle which is Foreign Currency

Commodity Murabahah Deposit-i (FCMD-i) and Foreign Currency

Commodity Murabahah Placement-i (FCMP-i).

The Foreign Currency Commodity Murabahah Deposit-i (FCMD-i)

is a Shariah-Compliant liquidity management product to facilitate

investors to mobilize their surplus funds into the Islamic

financial market. It is aimed at corporate and businesses with

revenue inflow denominated in foreign currency, the source of

which range from export or trade-related proceeds to all kinds of

receivables. These are the segment of customers with a natural

hedge position, who have commitments and liabilities in foreign

currency to be settled either in the short-term or on short

notice. Maybank Islamic also welcomes high net-worth individuals

to participate in the program. The minimum deposit in foreign

currencies offered is equivalent to RM1 million for a minimum

tenure of 14 days.

The Foreign Currency Commodity Murabahah Placement-i (FCMP-

i) is a Shariah-Compliant liquidity management product which can

be used to facilitate interbank transactions. It is a channel

through which Maybank Islamic makes available foreign currency

denominated funds to the players in the Islamic interbank market.

The common Murabahah (sale on cost-plus basis) contract will

be applicable for both products. However, as the contracts employ

the Islamic principle of Tawarruq, customers will be required to

appoint Maybank Islamic as the agent to make sale and purchase

transactions of commodities with a third party on their behalf.

The commodity traders have been designed in a manner such that

the transaction cost is kept at the minimal.

The launching of the two Shariah-Compliant products is in

line with Maybank Islamic's strategy to grow its business under

the International Currency Business Unit (ICBU). In January 2008,

it became the first bank in the country to launch the Offshore

Foreign Currency Financing, which is a short term trade financing

facility for exporters and importers and the Foreign Currency

Account, a Mudarabah deposit account. Maybank Islamic expects its

ICBU unit to have a comprehensive range of foreign currency

products by the end of the year.

FINANCING

There is a lot of financing products offer by Maybank such as:

But only 4 products are using Commodity Principle such as

Commodity Murabahah Shophouse financing-i, Commodity Murabahah

Term Financing-i, Commodity Murabahah Home Financing-i and ASB

financing-i.

Commodity Murabahah Shophouse financing-i is Financing

purchase of properties based on the concept of Murabahah via

Tawarruq agreement whether completed or under construction units

example like Shop houses, shop offices, commercial lots in

shopping complex, office lots, factories and industrial

buildings. Next, Commodity Murabahah Term Financing-i is a

Shariah based term financing facilities for acquiring completed

or under construction (for CMTF-i only) assets such as landed

properties, plant and machinery, vessels and commercial vehicles.

Moreover, ASB Financing is another form of term financing to

purchase ASB unit trust based on Shariah principles of Murabahah

via Tawarruq arrangement.

The most famous or popular financing product that Maybank

customer purchased is Commodity Murabahah Home Financing-i. The

Bank provides home financing to customer via trading of

identified Shariah-compliant commodities such as Crude Palm Oil

and RBD Palm Olein. Maybank give home financing based on the

concept of Murabahah via Tawarruq or Commodity Murabahah

arrangement. Maybank implement this contract according to

structure below:

Explanations:

1) Maybank Islamic will purchase the commodity form trader 1

for example purchase Crude Palm Oil.

2) Maybank Islamic will sell Crude Palm Oil to Customer at cost

plus profit margin for example RM 27,000 and the customer

will pay instalment basis.

3) Customer wants financing not commodity so customer will

appoint Maybank as agent to sell Crude Palm Oil to Trader 2

behalf of the customer.

TRADER 2

TRADER 1

MAYBANKISLAMIC

CUSTOMER

12

34

4) Maybank will sell the Commodity based on market price for

example RM 20,000 and the payment will be made by the Trader

2 lump sum in cash. Maybank will give money to customer and

customer purchase the house.

Benefit s of Maybank Commodity Murabahah Home Financing-i such

as:-

1) No compounding of profit and other charges

2) Lower monthly instalment with the longer payment period of

up to 35 years or until the age of 70

3) Higher financing margin of up to 100% of the value of the

house (including capitalisation of related expenses such as

MRTT contribution)

4) MRTT coverage, which settles your outstanding mortgage and

transfers the title deed to your family in the event of

death or total and permanent disability

5) Convenient payment options of your instalment via Maybank

and Maybank Islamic branches, ATMs, Kawanku Phone Banking,

and online via Maybank2u.com

INVESTMENT

In this section, we are going to further discuss on investment

product offered my Maybank Islamic. The investment product is

named as H.O.T Broking. It is a wide opportunity for customers to

invest in shares and securities based on Islamic Murabahah

principles. The H.O.T stands for Honest, Open and Transparent.

H.O.T Broking consists of two schemes which are Margin

Financing and Non Margin. Firstly, margin financing is borrowing

money to invest and speculate the stock market by the customer.

The tenure for this scheme would be 5 years and can be renewed

after reviewing the customer’s performance. Margin financing is

also the most preferable scheme among the customers. On the other

hand, non-margin is customer uses their own money to invest.

People tend to choose H.O.T Broking to expand their leverage.

Say, I invest a small amount of RM100,000 and will obtain double

of RM200,000 in future depending on the volatility of my

investment portfolio. Under these two schemes, there is a method

of payment called Transaction Day + 3 (T+3). It is a full payment

where the customer had to pay in three days of time. For example,

if I bought the shares on Monday, then I will have to settle the

payment in full on Thursday. The normal T+3 method is applicable

in non-margin. Whereas, in margin financing, it is slightly vary

from non-margin. In this case, the bank will pay in advance for

the customer and hold the shares as collateral. Below is the flow

of margin financing:

As labeled above, the bank will also monitor the share price.

Let’s say if the share price goes down, then the customer must

top up or force sells the shares. Be it profit or lose, the

customer should bare it. However, in the case of non-margin

financing, if the customer default to make payment after third

day, then the shares should be force sells and the profit or lose

made should be bare by the customer itself.

In addition, both schemes must have collateral. The collateral

for Margin Financing and Non-Margin should be in the features

showed as below:

Scheme

Margin Financing Non-Margin

Trading

Facility

Resident A/C & Non- Resident A/C

Resident A/C &

Non- Resident A/C

Collateral

Margin

Facility

Trading

Facility

TotalTrading

Facility

Collateral

TotalTrading

Facility

Approved Shariah Shares

1.5x 1.0x 2.5x Approved Shariah Shares

2.0x

GIA /FD

2.5x 1.0x 3.5x GIA / FD 3.0x

Cash 1.5x 1.0x 2.5x Cash 3.0x

Based on the table above, it shows that margin financing and non-

margin have its own collateral portion or ratio for the trading

facility. As for fixed deposit, the conventional fixed deposit is

accepted but the interest in the account will not be capitalized.

Next, for property, it must be fully paid and should be a landed

property only.

Moreover, in this section, we are also going to discuss on how

the margin financing works or flows. Let’s take an example of Mr.

Alex who would like to apply for an Islamic Margin Financing

facility of RM100,000 to be paid in 5 years. He “brought” his

asset, say shares which is at currently at market price of

RM100,000 to the bank. The bank agreed to purchase the asset from

Mr. Alex at RM100,000 and both parties signs the Asset Purchase

Agreement (APA). Immediately, the bank will re-sell the asset at

RM150,000 with deferred payment of 5 years. Upon the acceptance

by Mr. Alex on the offer, both parties will sign the Asset Sales

Agreement (ASA). The Margin Financing flow diagram is as follow:

However, the issue arises if the shares been declared as non-

Shariah. Relating to the above example, if RM20,000 worth shares

have been declared as non-Shariah, then automatically these

shares will be zero value. Therefore, these shares have to be

removed from the account immediately. Besides, since the

financing amount given was RM150,000, so the customer had to top

up the balance or has the option to force sells.

The specialty of H.O.T Broking is about investment and not

trading. It is a long term plan for investment. In addition, 88%

of the stocks are Shariah compliant based on Bursa Malaysia.

ISLAMIC INTERBANK MONEY MARKET

Every Islamic Interbank Money Market need to undergo Bank Negara

Malaysia, to proceed their transaction. There is few types of

instrument that currently being practiced in Maybank Islamic

such as Mudharabah Interbank Investment (MII), Wadiah Acceptance,

Government Investment Issues (GII), Bank Negara Monetary Notes-I

(BNMN-I), Cagamas Mudharabah Bond and include Commodity

Murabahah. As a part of Bank Negara Malaysia’s initiative to

support Islamic Finance development in Malaysia, they have

introduced Commodity Murabahah Programme to facilitate liquidity

management and investment purposes. Commodity Murabahah is an

efficient instrument for mobilization of funds between surplus

and deficit units. In addition, Commodity Murabahah Programme is

designed to be the first ever commodity-based transaction that

utilizes the Crude Palm Oil based contracts as the underlying

assets. The structure and mechanism will be as below:

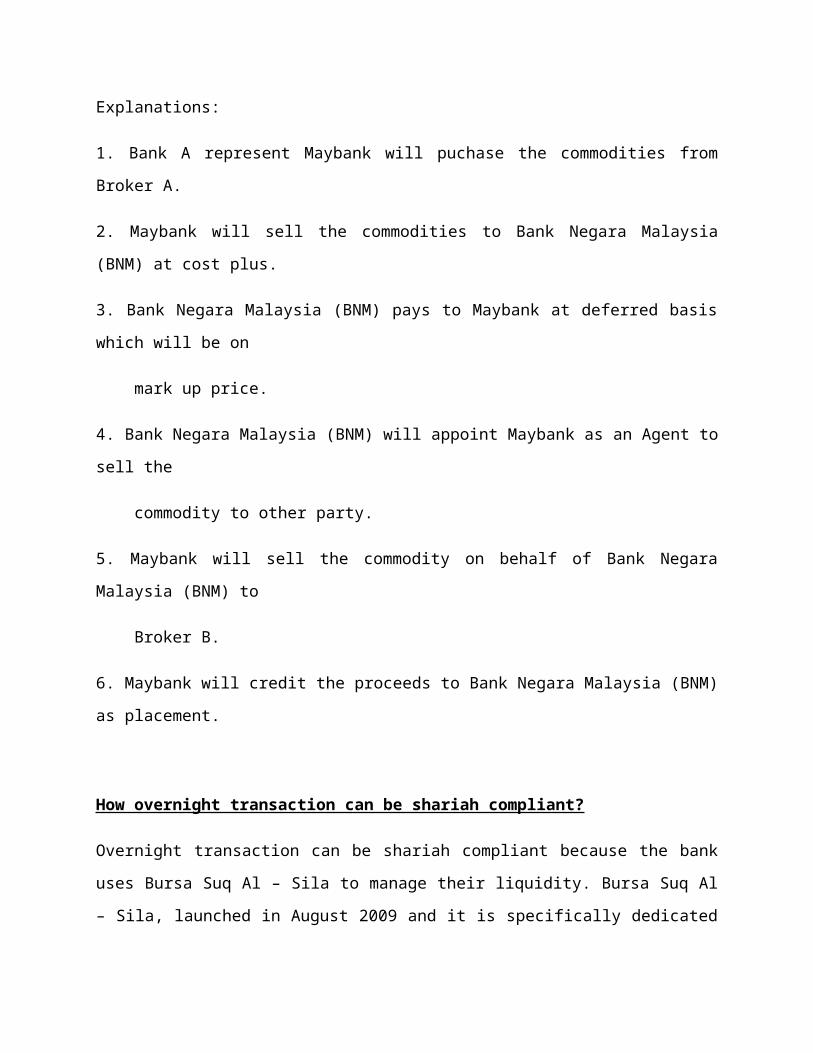

Explanations:

1. Bank A represent Maybank will puchase the commodities from

Broker A.

2. Maybank will sell the commodities to Bank Negara Malaysia

(BNM) at cost plus.

3. Bank Negara Malaysia (BNM) pays to Maybank at deferred basis

which will be on

mark up price.

4. Bank Negara Malaysia (BNM) will appoint Maybank as an Agent to

sell the

commodity to other party.

5. Maybank will sell the commodity on behalf of Bank Negara

Malaysia (BNM) to

Broker B.

6. Maybank will credit the proceeds to Bank Negara Malaysia (BNM)

as placement.

How overnight transaction can be shariah compliant?

Overnight transaction can be shariah compliant because the bank

uses Bursa Suq Al – Sila to manage their liquidity. Bursa Suq Al

– Sila, launched in August 2009 and it is specifically dedicated

to facilitating Islamic liquidity management and financing by

Islamic financial institutions. It is the world’s first end-to-

end Shariah compliant commodity trading platform. Besides that,

this transaction also can be done through online and it is

available for 24 hours and 7 days (24/7).

WHY MUST INVEST IN MAYBANK

Leading financial services group in Malaysia. Maybank Islamic

leading in provider of consumer, SME and wholesale banking

services, as well as insurance and Takaful products. On 31

December 2014, Maybank achieve as largest Islamic Bank by assets

which is about USD 38.7billion. Customer who invest their money

in Maybank Islamic will be secure and have confident that this

bank will not fall in default as Maybank are giving good

services. In case Maybank going to default, they have ability to

overcome that default by bare the losses by own. That why Maybank

Islamic is leading in the market.

Emerging regional financial services leader. Maybank Islamic is

the 3rd best emerging market in the world, behind China and South

Korea. We can see that the Maybank Islamic managed to raise their

profit by 17.6% compare to the both country which is China with

13% and South Korea 8% for this year. And Maybank also can obtain

30% of its profits from overseas business which is home market in

Laos and Cambodia. This was making them become one of the top 5

banks in Asean.

Transformation programme spurring strong performance where

Maybank launched its new ‘House of Maybank’ organisation

structure in July 2010 to support its regional growth. Only three

states are consists of ‘House of Maybank’ which is Malaysia,

Indonesia and Singapore. These three states are performing well

as compare to the other, as we can see in their GDP, System loan

and System deposits. Malaysia in GPD is 5.4%, loan 9.8% and

deposit 9.6%. Singapore GDP is 3.7%, loan 9% and deposit 6%. And

last Indonesia with GDP 5.6%, loan 17% and deposit 12.5%. Compare

to other bank like China where their GDP is 4.7%, loan 9% and

deposit with 5%.

High dividend payout and robust capitalization where Maybank

consistently rewards shareholders with dividends in excess of

policy of 40-60% Dividend Payout Ratio while preserving capital

through the introduction of the Dividend Reinvestment Plan (DRP).

They can excess this dividend because of the costumer

performance. As Maybank gives good rate to the customer and in

the return they can gain the good return from the investing, so

the customer think that they never regret by investing in the

Maybank Islamic.

CONCLUSION

In a nutshell, Maybank Islamic holds the position for uniqueness

in their deposit, financing, investment and Islamic interbank

money market products. This reflects the niche of Maybank to

spark out from other banks in Malaysia and automatically attracts

many customers. In a result of having numerous customers, Maybank

had open up many branches in Malaysia which is 402 branches.

Besides, in this paper, it has given a clear picture on the

deposit, financing, investment, Islamic interbank money market in

real practice compared to the theory we have learnt in class.

This is because in real banking system, they have implemented the

Islamic contract, say like commodity murabahah in many innovative

products. As discussed in this paper, using commodity murabahah

principle itself, Maybank Islamic has introduced products like

Profit Now Account i, Commodity Murabahah Home Financing, Foreign

Currency Commodity Murabahah and H.O.T Broking Investment. Those

products are the boom factor and unique in the Maybank Islamic.

There is a saying goes, every steps to success will be obtained

from the obstacles that we faced. However, same goes to this

assignment, we had to face many challenges in order to complete

this paper. Challenges that we faced was difficulties in meeting

the higher officers due to their busy schedule, limitation of

information on internet and officers with lack of knowledge in

Islamic banking.

Finally, we managed to overcome those challenges and accomplished

this assignment on time. It reflects the saying, no pain, and no

gain. To justify this paper, we would strongly suggest people to

consume or invest in Maybank Islamic.

REFERENCES

Malayan Banking Berhad. (2015, March 13). Annual Reports. Retrieved

April 2, 2015, from Investor Relations>Reports & Events:

http://www.maybank.com/en/investor-relations/reporting-

events/reports/annual-reports.page

Malayan Banking Berhad. (2015, April 30 ). maybank2u.com.

Retrieved April 13, 2015, from Fixed deposit rates:

http://www.maybank2u.com.my/mbb_info/m2u/public/personalDeta

il04.do?channelId=&cntTypeId=0&programId=RTS-

Rates&cntKey=RTS03&chCatId=/mbb/Personal

Rahman., A. A. (2010). E-Imtiyaz. Retrieved April 13, 2014, from

Bursa Malaysia's Suq Al-Sila' (Commodity Murabahah House) as

an Alternative Platform for Tawarruq Transaction:

http://ddms.usim.edu.my/handle/123456789/5388