ISLAMIC FINANCING FACILITIES ISLAMIC FINANCING FACILITIES FINANCIAL SECTOR TALENT ENRICHMENT...

43

1 ISLAMIC FINANCING FACILITIES ISLAMIC FINANCING FACILITIES FINANCIAL SECTOR TALENT ENRICHMENT PROGRAMME

Transcript of ISLAMIC FINANCING FACILITIES ISLAMIC FINANCING FACILITIES FINANCIAL SECTOR TALENT ENRICHMENT...

1

ISLAMIC FINANCING FACILITIESISLAMIC FINANCING FACILITIES

FINANCIAL SECTOR TALENT ENRICHMENT PROGRAMME

2

PERSONAL FINANCING-i

3

Term Description 1. Eligibility • Capacity to contract

• Repayment capacity• Integrity• Purpose

2. Margin of financing

• Eligibility of applicant • Bank’s policy

3. Profit rate • Determined from time to time• Flat rate (SOD)

PERSONAL FINANCING-i - TERMS & CONDITIONS

4

Term Description

4. Financing period

2 to 5 years

5. Security** • Savings/Investment a/c – LIEN• Guarantee

**depends on bank’s policy( may be waived )

PERSONAL FINANCING-i - TERMS & CONDITIONS

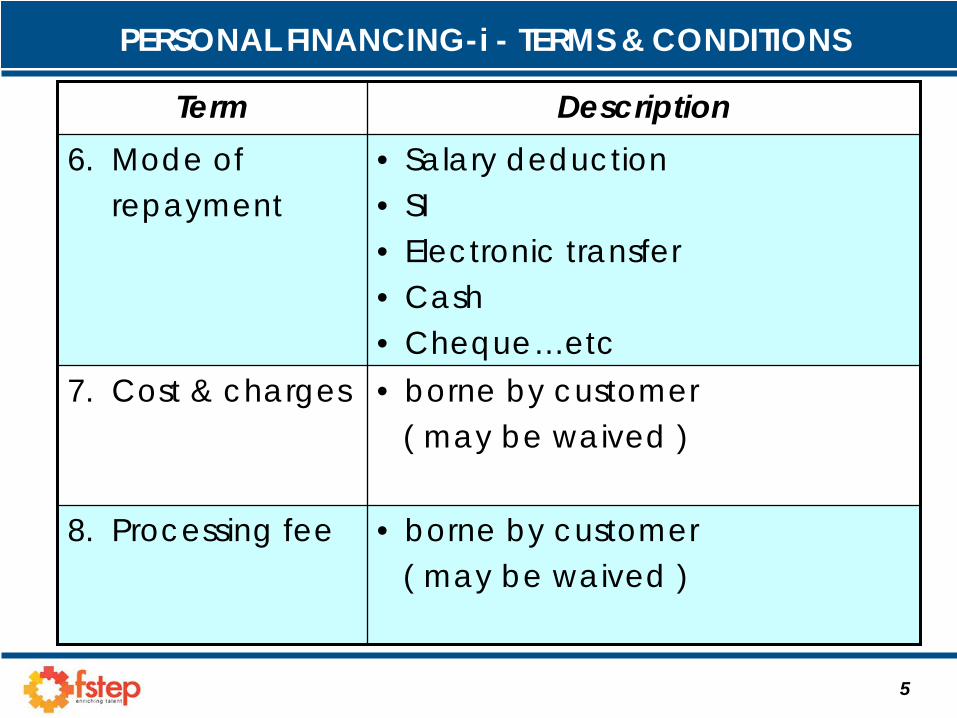

5

Term Description6. Mode of

repayment• Salary deduction• SI• Electronic transfer• Cash• Cheque…etc

7. Cost & charges • borne by customer( may be waived )

8. Processing fee • borne by customer( may be waived )

PERSONAL FINANCING-i - TERMS & CONDITIONS

6

Term Description9. Ibra’ At bank’s discretion …given for

prepayment/full redemption.

10. Guarantor May be waived

11. Contract • Inah• Qard Hasan & Bai…etc

PERSONAL FINANCING-i - TERMS & CONDITIONS

7

MODUS OPERANDI

8

(I) PERSONAL FINANCING (BAI’ ’INAH)

(1) BANK SELLS AN ASSET** FOR RM15,600

(2.2) Bank pays the customer RM10,000(Cash basis)

(1.1) Customer pays RM15,600 by 60 equal monthly installment of RM260

(2) BANK BUYS THE ASSET** FOR RM10,000

**ASSET/MERCHANDISE ?

9

SP = FA + (FA * r * n )

PR = SP / ( n * 12 )

Note: FA … Financing amountr … profit raten … period of financing ( year )

PR … periodical payment

FORMULA : SP BASED ON SOD (RULE 78)

10

Eg.…Based on profit rate of 7%

• FA : RM10,000• r : 8% (flat rate)• n : 5 (years)

• SP = FA + ( FA * r * n )= 10,000 + ( 10,000 * 8% * 5 ) = RM14,000

• PR = 14,000/60 = RM233.34 ( month 1 to 59 )= RM232.94 ( month 60 )

• Profit amount = RM(56,800 - 40,000) = RM16,800

CALCULATION of SP, INSTALLMENT & PROFIT AMOUNT

11

(II) PERSONAL FINANCING (QARD & BAI’)

(1) BANK LENDS RM14,000 (CASH NOTE)

(1.1) Customer pays RM14,000 by 60 monthly installment of RM233.34

(2) CUSTOMER BUYS BANK’S ASSET**(SAR14,000) FOR

RM14,000 using the CASH NOTE

**ASSET- eg. Foreign Currency (SAR)

(3) CUSTOMER SELL THE SAR FOR RM10,000

(4) BANK PAYS RM10,000 (CASH BASIS)

12

STEP DOCUMENTATION

1) Bank lends RM14,000 Qard Agreement(Primary instrument)

2) Customer purchase bank’s SAR

Property Sale Agreement

3) Customer sells back SAR Property Purchase Agreement

DOCUMENTATION – CASH NOTE

13

CREDIT CARD-i

14

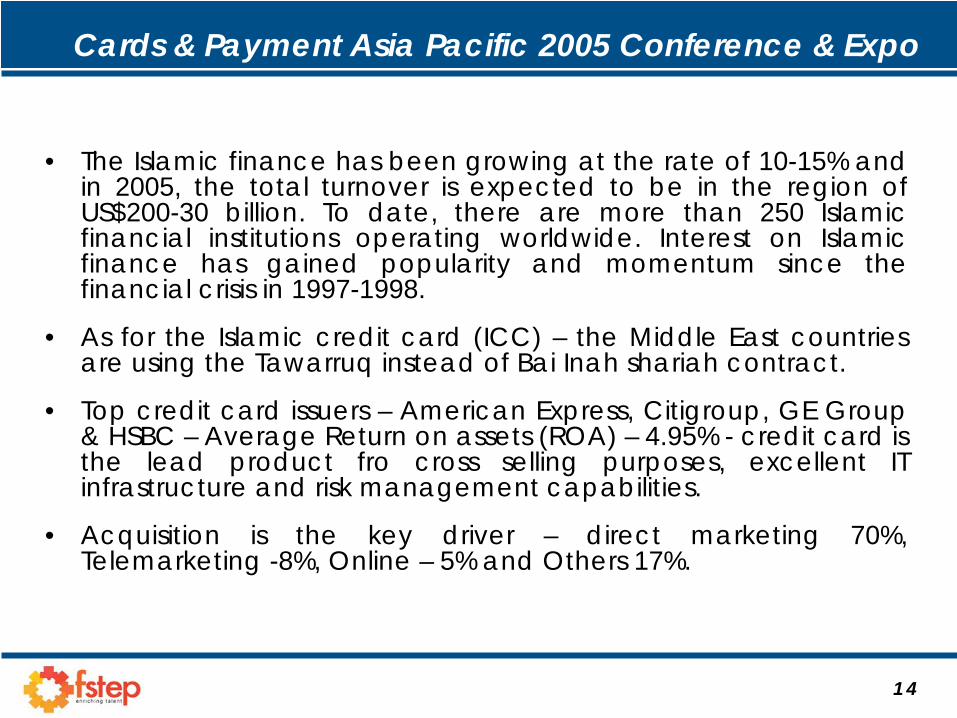

Cards & Payment Asia Pacific 2005 Conference & Expo

• The Islamic finance has been growing at the rate of 10-15% and in 2005, the total turnover is expected to be in the region of US$200-30 billion. To date, there are more than 250 Islamic financial institutions operating worldwide. Interest on Islamic finance has gained popularity and momentum since the financial crisis in 1997-1998.

• As for the Islamic credit card (ICC) – the Middle East countries are using the Tawarruq instead of Bai Inah shariah contract.

• Top credit card issuers – American Express, Citigroup, GE Group & HSBC – Average Return on assets (ROA) – 4.95% - credit card is the lead product fro cross selling purposes, excellent IT infrastructure and risk management capabilities.

• Acquisition is the key driver – direct marketing 70%, Telemarketing -8%, Online – 5% and Others 17%.

15

Shariah Contracts

• Bai Inah

• At Tawarruq

16

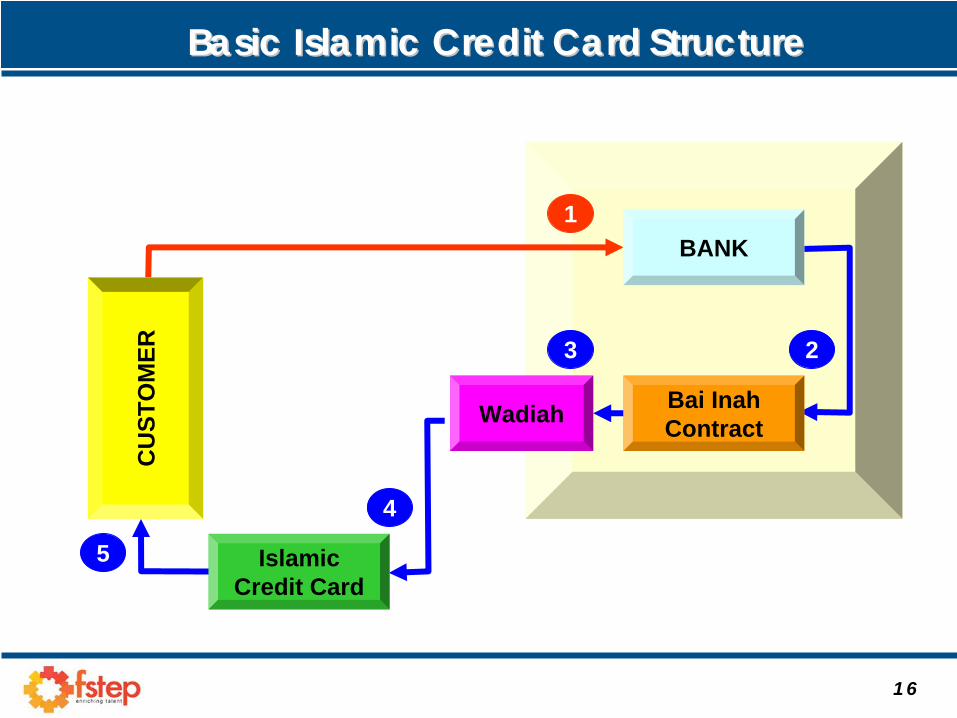

Basic Basic Islamic Credit CardIslamic Credit Card StructureStructure

CU

STO

MER

Wadiah

Islamic Credit Card

BANK

Bai Inah Contract

1

23

4

5

17

Resells the land to BANK for cash at the principal price= RM10,000

Sells a piece of land on deferred payment basis (profit 18 % p.a. eg RM10,000 + RM1800= RM11,800)

Disburse RM10,000 to customer’s ICC Wadiah account

Customer

Bank

Wadiah / Safekeeping

1

2

3

(BAI INAH) / Sell and buy back transaction

Allow customer to use more than available balance in ICC Wadiah account

4

(QARDHUL HASSAN)/ Benevolent Loan

BaiBai InahInah ContractContract

18

Islamic Credit Card (ICC) Account StructureIslamic Credit Card (ICC) Account Structure

Bai’ InahSales/Purchasee.g RM 11,800

Wadiah ICC Purchase Proceeds

e.g RM 10,000

Other Charges

Qardhul Hasan

RetailUsage Limit -100%

of RM 10,000

Ceiling Profit e.g RM 1,800

CashUsage Limit - 50%

of RM 10,000

19

• Free from “riba” and “gharar”.• Term of contract is 3 years.• Fixed ceiling profit – at 18% per annum. • No compounding interest factor• Takaful coverage on outstanding

Islamic Credit Card and its features:Islamic Credit Card and its features:

20

•

National Shariah Advisory Council for Islamic Banking and Takaful BNM.

•

Bank’s Shariah Supervisory Council.

Approved by Shariah Councils

21

• Shafie

& Zahiri: Permissible as a contract

agreed between seller and buyer. •

Hanafi: Permissible only if involve mediator between seller and buyer.

• Maliki: Unacceptable and consider it as a way to legitimize usury (Riba).

• Hanbali: Unacceptable because it could lead to the practice of usury.

Past Islamic Jurists’ views on Bai’ Inah:-

22

• Prohibited by Islamic Financial Services Board (IFSB):

• Para 67 (a) of IFSB Capital Adequacy Standard –

“The asset is intended to be

used by the buyer/lessee for activities or businesses permissible by Sharī`ah; if the asset is leased back to its owner in the first lease period, it should not lead to contract of ‘inah, by varying the rent or the duration.”

Past Islamic Jurists’ views on Bai’ Inah:-

23

• At-Tawarruq

• Derived from al-wariq means silver. The intention of the buyer is for the sake of dirhams, not the subject matter of sale.

• Customer buys an asset from the bank on deferred credit, then immediately resells it for cash to the 3rd party.

• Bai’

Murabahah

(Cost plus) + Bai’

Naqdan

(Cash

Sale).

Alternative for Bai’ Inah Contract:-

24

Buy

Ass

etSe

ll A

sset

Sell Asset (Murabahah + BBA)

Sale

Pro

ceed

s

Get consent from Customer to buy asset

Appoint Bank as Sales Agent to the market

Cash deposited to Customer Wadiah account

Customer

Bank

Broker 1

Broker 2

1

2

3

4

4

5

6

AtAt--TawarruqTawarruq

Wadiah / Safekeeping

25

TREASURYOPERATION

Sell Commodity To Market In Bulk

Buy Commodity In Bulk

*INTERVAL

Send Back To Coordinator

CONTRACT NOTES

ICC 1

ICC 2

ICC 3

ICC4

ICC apps.

Broker 1 Broker 2

BROKER CONTRACT NOTES

1. Internal Contract Notes2. Jobbing/ Chopping/ Distribute

Into Small Pieces/ Multiple Contract Notes

3. Buy & Sell Contract4. Buy Contract - Commodity,

Quantity, Price5. Sell Contract - Commodity,

Quantity, Price

* Interval – Shariah Is Not Very Particular On The Interval Time / Can Be Transacted As Short As One Seconds

1. Application Form2. Letter Of Appointment –

Bank As Agent To Buy And Sell Commodity

3. Financing Processing4. Approval

The Total Amount Of Financing To Be Disbursed With Details

1 2

3

67

4

58

Modus OperandiModus Operandi

26

Modus Operandi - Credit Card-i Calculation ExampleCredit Card - I

Purchase Price (RM) = 5,000.00Selling Price (RM) = 7,700.00Total Profit = 2,700.00Tenor (years) = 3Profit Rate (%) = 18Monthly Instalment (RM) = Minimum 5% or RM50, whichever is higher

Compensation Rate - In Tenor (%) = 1 (on Monthly Installment Due)Compensation Rate - Out-of-Tenor (%) = 6.15

Transaction detail Debit (RM)

Credit (RM)

Activation of card

Retail transaction 200.00

Annual fee 75.00

Statement (RM275.00@ due date 2/1)

Cash advance 500.00

Cash advance fee 50.00

Payment 275.00

Retail transaction 200.00

Profit due

(RM550.00 x 18% x 21/365) 5.70

Statement (RM755.70@ due date 2/2)

Retail transaction 150.00

Payment 100.00

13/2/2007 Profit due

(RM200.00 x 18% x 21/365 = RM2.07)

(RM455.70 x 18% x 31/365 = RM6.97)

* Set off priority for payment of RM100.00 on 28/1/20007 1) Profit due = RM5.70 2) Charges (cash advance fee) = RM50.00 3) Principal = RM44.30 (from RM500 Cash Advance made on 24/12/2007)

9.04

Date

13/1/2007

13/1/2007

15/1/2007

28/1/2007

24/12/2006

24/12/2006

28/12/2006

2/1/2007

8/11/2006

20/11/2006

13/12/2006

13/12/2006

27

Comparison with Conventional Products

Features Islamic ConventionalExistence of Moral and Ethical Standards

Yes No

Control on Transactions Yes No

Type of Transaction Debt arising from trading activities

Interest-based debtor/creditor relationship

Compensation Charges and Profit/Interest Compounding

No Yes

Compensation Charges In-tenor = 1% or RM5Out-of-tenor = IIMM%

In-tenor = Min. 1% or RM10 and max. of RM100Out-of-tenor = 18%

Ceiling or Maximum Charges Yes No

Legal Documents Additional Sales and Purchase agreements plus standard documents

Standard documents

28

ISLAMIC COMMERCIAL FINANCING PRODUCTS

29

CASH LINE FACILITYCASH LINE FACILITY-- ii

30

WORK FLOW : CASH LINE FACILITY WORK FLOW : CASH LINE FACILITY -- ii

Start Customer

Bank

Bank Sell Bank’asset and allow

a deferredpayment terms

ASSET SALE AGGREMENT

Bank Buy Backthe

asset oncash basis

ASSET PURCHASE AGGREMENT

Bank credit“the cash”

as limit in the Facility

Customer utilizeThe limit according

To his need

Customer madepayment

According toAmount utilized

Upon maturitydate, Customer

madefull settlement

After Ibra’

Monthly statement provided by the bank

End

Issuing cheques

or payment and/or remittances instruction

31

INTRODUCTIONINTRODUCTION

Underlying Contract : Bai Inah

A sale in order to get cash not property/good/merchandise or a sale in which a commodity is sold for a deferred payment (thaman mu’ ajjal ) and then it is resold to the seller on cash sale (which is cheaper to deferred payment price). The owner of the commodity will get back the commodity plus the payment which is deferred while the customer will get ‘cash’ but to settle the payment obligation on installment basis.

32

MODUS OPERANDIMODUS OPERANDI1st Contract : Bank sells certain asset to a customer on deferred term.

BANK CUSTOMER

SELLS ASSET @ RM 70,000*

PAYS ON DEFERRED TERM*RM 70,000 = Financing amount + profit margin = Bank' selling price

BANK CUSTOMER

PURCHASES ASSET @ RM 50,000**

PAYS RM 50,000 BY CASH

2nd Contract : Bank immediately purchases back the asset from the customer on cash basis.

**RM 50,000 = Financing amount = amount of cash needed by the customer= Bank's purchase price

33

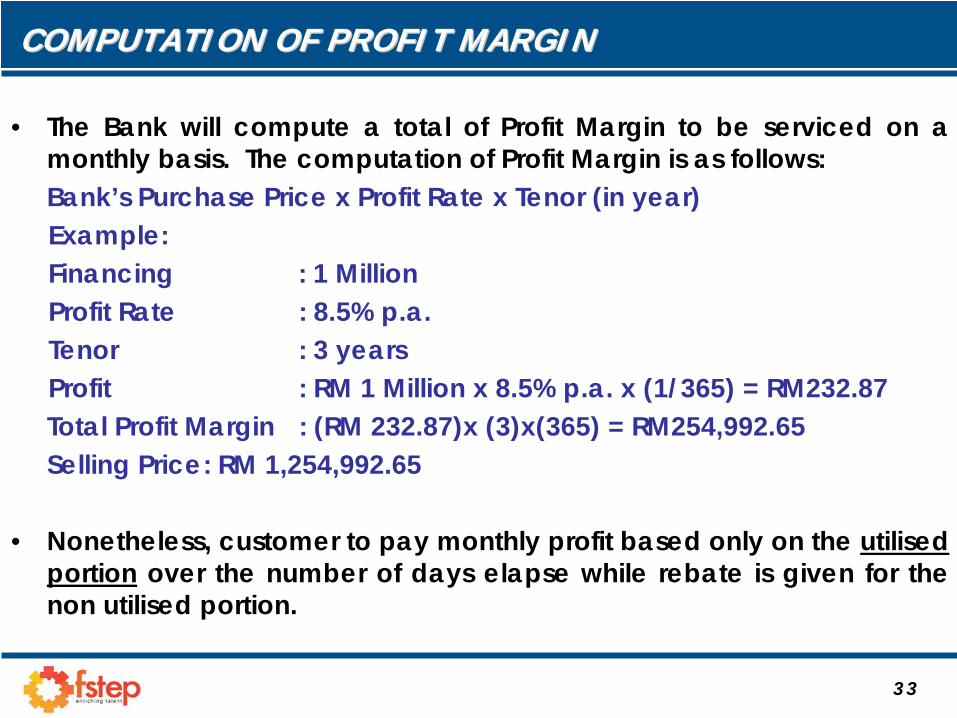

COMPUTATION OF PROFIT MARGINCOMPUTATION OF PROFIT MARGIN

• The Bank will compute a total of Profit Margin to be serviced on a monthly basis. The computation of Profit Margin is as follows:Bank’s Purchase Price x Profit Rate x Tenor (in year)Example:Financing : 1 MillionProfit Rate : 8.5% p.a.Tenor : 3 years Profit : RM 1 Million x 8.5% p.a. x (1/365) = RM232.87Total Profit Margin : (RM 232.87)x (3)x(365) = RM254,992.65Selling Price: RM 1,254,992.65

• Nonetheless, customer to pay monthly profit based only on the utilised portion over the number of days elapse while rebate is given for the non utilised portion.

34

COMPUTATION OF BANKCOMPUTATION OF BANK’’S SELLING PRICES SELLING PRICE

• Bank’s Selling Price is not subjected to any interest rate fluctuations once contract is signed.

• The BSP is equivalent to the Bank’s Purchase Price plus the Profit Margin.

• The computation is as follows: Bank’s Selling Price : Bank’s Purchase Price + Profit MarginExampleBank’s Purchase Price : RM 1,000,000.00Profit Margin : RM 254,992.65Bank’s Selling Price : RM 1,254,992.65

35

COMPUTATION OF MONTHLY PROFIT PAYMENT

0 1 2 3

Maturity

Daily ComputationDay 1- Utilisation of RM 150Ka.RM 1,000,000*8.5%*1/365 :232.87 - Based on full utilisationb.RM 150,000*8.5%*1/365 : 34.93 - Current Profit

:197.94 - Ibra’ (a-b)Day 2-Utilisation of RM 100Ka.RM 1,000,000*8.5%*1/365 :232.87 - Based on full utilisationb.RM 250,000*8.5%*1/365 : 58.21 - Current Profit

:174.66 - Ibra’ (a-b)

No of days

Utilisation of RM 150K

Utilisation of RM 100K

Current Profit amount will be accumulated on a monthly basis and payable on the first of the following month

36

• OD-i facilitates more options to increase our customers base

• OD-i can be offered as a single facility or as a combination together with other Islamic Banking financing products or commercial loans products

• OD-i facilitates BNM compliance in meeting the Islamic Banking Scheme target ( 9.5% of Bank’s total loan and advances by June 2003)

• Increases Business CA-i - assist compliance in Islamic Banking deposit target

WHY OFFER WHY OFFER ODOD--ii ARRAARRANNGEMENT ?GEMENT ?

37

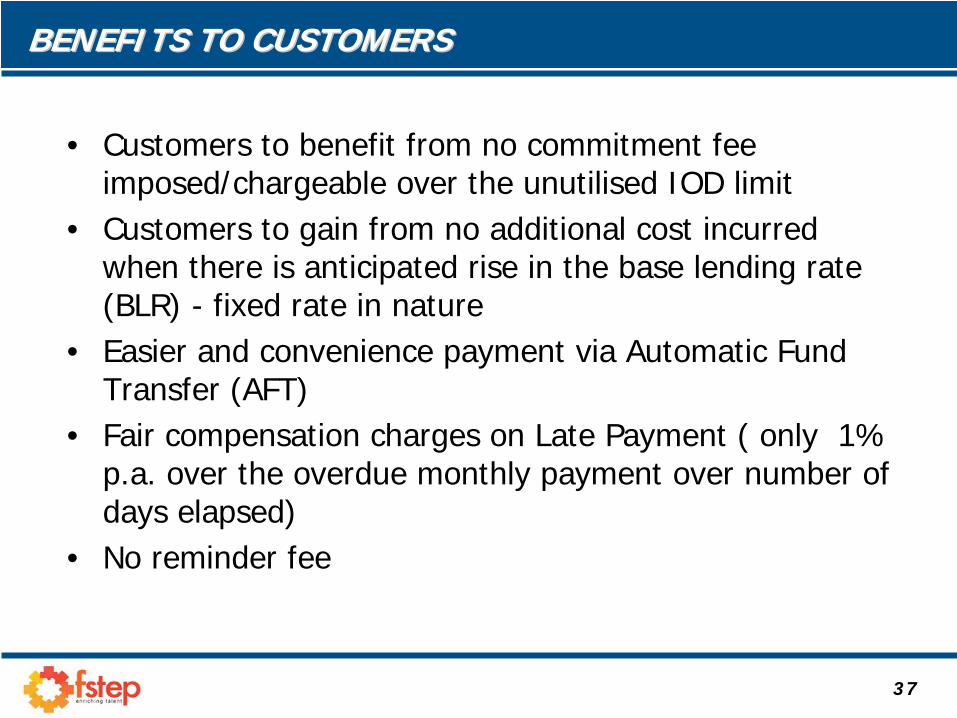

• Customers to benefit from no commitment fee imposed/chargeable over the unutilised IOD limit

• Customers to gain from no additional cost incurred when there is anticipated rise in the base lending rate (BLR) - fixed rate in nature

• Easier and convenience payment via Automatic Fund Transfer (AFT)

• Fair compensation charges on Late Payment ( only 1% p.a. over the overdue monthly payment over number of days elapsed)

• No reminder fee

BENEFITS TO CUSTOMERSBENEFITS TO CUSTOMERS

38

ESSENTIAL ELEMENTSESSENTIAL ELEMENTS

• Buyer• Seller• Object of Contract / Merchandise• Price• Contract (Offer and Acceptance)

39

NECESSARY CONDITIONSNECESSARY CONDITIONS

1. Capable of accepting responsibilities

2. Not restricted from dealing in business transactions

3. Not forced to enter into a contract

40

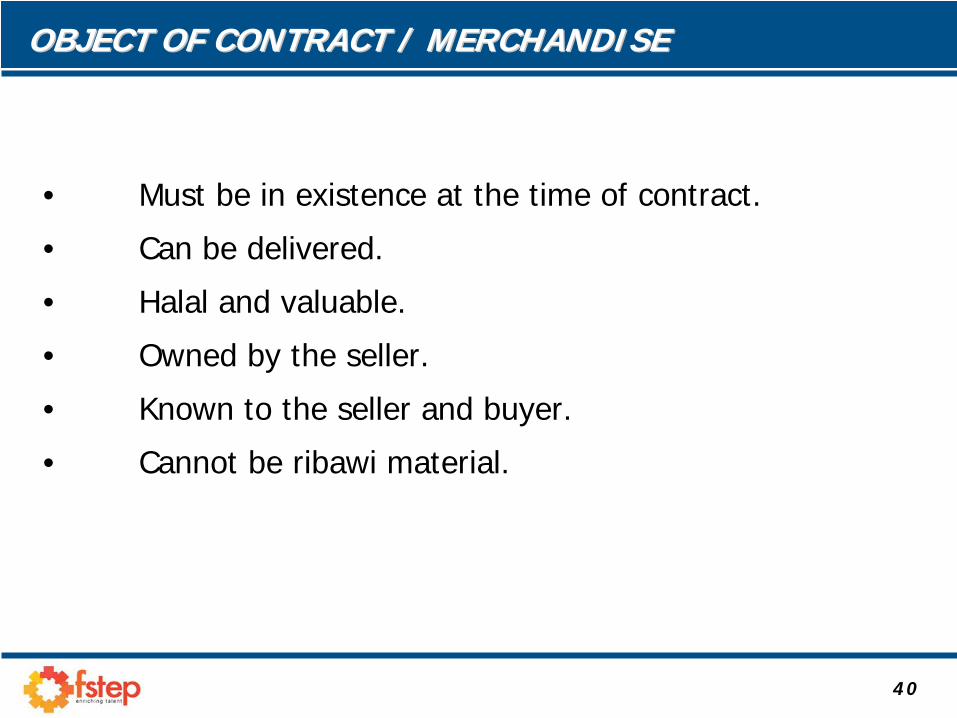

OBJECT OF CONTRACT / MERCHANDISEOBJECT OF CONTRACT / MERCHANDISE

• Must be in existence at the time of contract.

• Can be delivered.

• Halal and valuable.

• Owned by the seller.

• Known to the seller and buyer.

• Cannot be ribawi material.

41

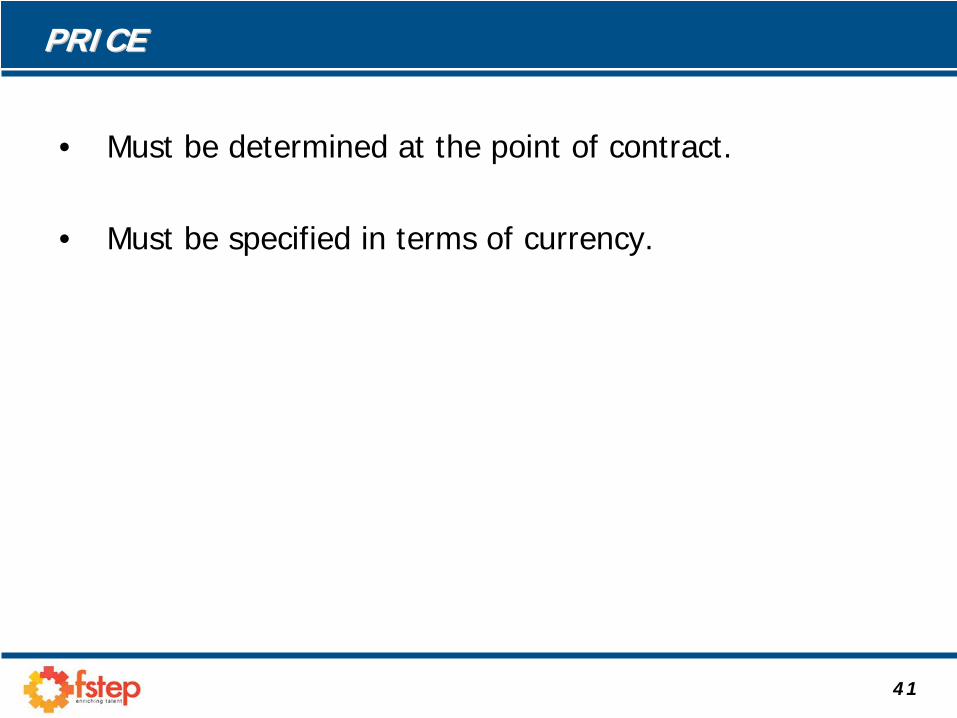

PRICEPRICE

• Must be determined at the point of contract.

• Must be specified in terms of currency.

42

CONTRACT (OFFER & ACCEPTANCE)CONTRACT (OFFER & ACCEPTANCE)

• Must be done in a definite and decisive language.

• Acceptance must be in consistence with the offer made by the seller.

• The contract is done in a contract meeting.

43

Thank you

FINANCIAL SECTOR TALENT ENRICHMENT PROGRAMME