Islamic financing as a strategy for the reduction of SMEs failure

42

ISLAMIC FINANCING AS A STRATEGY FOR THE REDUCTION OF SMEs FAILURES I N NIGERIA NAME: NURUDEEN Y.Z BUSINESS DEPARTMENT OF BUSINESS ADMINISTRATION FACULTY OF MANAGEMENT SCIENCES KOGI STATE UNIVERSITY, ANYIGBA. ABSTRACT The roles and opportunities of Small and Medium- scale Enterprises (SMEs) in National Growth and Development in all Economies is well documented. In Nigeria, these opportunities are not exploited effectively. as a result of high rate of SME failures. SMEs in Nigeria represent 97% of all enterprise in the economy (NBS, 1999) of these, more than 85% failed in t heir first five years of operation. High failures, low progress and low intensification of SMEs are due to commercial bank practices prevailing in high interest rates, high burden of collateral guarantees and provision of funds to large firms on the assumption that SMEs 1

Transcript of Islamic financing as a strategy for the reduction of SMEs failure

ISLAMIC FINANCING AS A STRATEGY FOR THE REDUCTION

OF SMEs FAILURES I N NIGERIA

NAME: NURUDEEN Y.ZBUSINESS DEPARTMENT OF BUSINESS ADMINISTRATION

FACULTY OF MANAGEMENT SCIENCES

KOGI STATE UNIVERSITY, ANYIGBA.

ABSTRACT

The roles and opportunities of Small and Medium-

scale Enterprises (SMEs) in National Growth and

Development in all Economies is well documented. In

Nigeria, these opportunities are not exploited

effectively. as a result of high rate of SME

failures. SMEs in Nigeria represent 97% of all

enterprise in the economy (NBS, 1999) of these,

more than 85% failed in t heir first five years of

operation. High failures, low progress and low

intensification of SMEs are due to commercial bank

practices prevailing in high interest rates, high

burden of collateral guarantees and provision of

funds to large firms on the assumption that SMEs

1

involves high risk investment. The paper identifies

basic Islamic Financing Strategy that could be

adopted for reducing and sustaining SMEs risk and

failures, and Entrepreneurial development in

Nigeria. This paper revealed (Riba) interest rate

as a major cause of the problem. The paper

recommends the adoption of Islamic mode of

financing as a tool in reducing high rate of SMEs

failures, thereby increasing entrepreneurial

development in the economy.

ISLAMIC FINANCING AS A STRATEGY FOR THE REDUCTION

OF SMEs FAILURE IN NIGERIA

The health of Small and Medium Scale

Enterprises (SMEs) sector is very important for the

over all economic growth and development of all

nations especially in the developing countries. The

SMEs sector is a principal driving forces for

economic growth and employment. In most of these

countries including Nigeria, SMEs represents over

90% of business contribution to over 50% of GDP and

account for about 65% of employment. (NBS, 1999)

2

Thus, the significance of this sector in expanding

enterprises for economic development and employment

generation has attracted the attention of

researcher’s and academic policy makers in many

countries (Bernice and Meradith, 1997).

The existence of a healthy SMEs sector is necessary

for the growth of an economy not only in employment

generation but also in the increment of number of

products or services offered to the society.

Therefore, it improves the level of societal

welfare. SMEs make more efficient use of inputs

(raw materials, capital and labour than big

companies. They can be places of learning and

training for people of all levels and functions

(directors, managers, and workers), a capacity that

could be used in other sectors of the economy. They

facilitate the creation and use of other-wise non

existent or unused saving (Lassort and Clavies

(1989) in Onuoha, 2011).

Furthermore, SMEs helps in the diversification of

the economy, and more importantly, stimulation of

indigenous entrepreneurships (Onuoha, 2011). In

some cases, Inventions that were rejected by major

3

big firms were later brought to market by small

start up enterprise (Almaida, 1999).

In theory, these assertions holds, but in reality

especially in developing countries such as Nigeria,

the performance of SMEs falls below expectation, as

the number of failed SMEs keep increasing; the rate

of business failure is as high as 90% in the first

year of operation when failure was defined as

bankruptcy, 65% of the survived failed in their

second year and 55% of those that survived in their

second year failed in their third year of their

operation (Dun and bradstreet, 1963). Specifically,

the root causes of SMEs failures are likely to

differ from country to country depending on the

nature of the SMEs, its business cycle and

differences in the level of economic growth and

development of each country. As such, major factors

of SMEs failure for one economy might not be for

another. In Nigeria, the major factors inhibiting

the growth and development of SMEs sector are

corruption and financial factor hinging basically

on collateral and interest rate.

4

Therefore, the study attempt to point out the root

factors, that contributes to SME failures in

Nigeria. Additionally, effort is made in the study

to develop a strategy for the success of SMEs

basically using Islamic mode of Business financing.

The other sections are;

- Summary of SMEs sector in Nigeria and

government efforts towards its growth and

development.

- Interest rate and SMEs growth

- Summary, conclusion and policy recommendation

are offered in section five.

The SMEs sector constitutes the largest proportion

of the entire business in Nigeria. The Federal

office of Statistics (2009) reveals that about 97%

of the entire enterprises in the country are SMEs

and employ an average of 50% of the working

population as well as, contributing up to 50% to

the industrial outputs. It is suggested that SMEs

in Nigeria are the catalyst of economic growth and

development.

SUMMARY OF SMES SECTOR IN NIGERIA

5

Recognizing the importance’s of SMEs in the

economy, the federal government has been taken

various initiatives including fiscal, monetary and

industrial policies that could promote the growth

and development of SMEs in Nigeria. The federal

government also established specialized financial

institutions such as; Small Scale Industry, Credit

Schemes (SSICSs), Nigerian Bank of Industries (BOI)

with the aim of providing long-term credit

facilities to SMEs.

The government also helped in facilitating and

guaranteeing external finance from World Bank and

other international financial institutions. The

government also established National Directorate of

Employment (NDE) to help the unemployed to acquire

skills necessary for self employment in 1990. The

National Economic Reconstruction Fund (NERFUND) was

also set up top provide medium to long term local

and foreign loans for small and medium scale

businesses. The industrial development centre and

Small and Medium Industry Equity Investment Scheme

(SMIEIS) were set up (Olorunshola, 2003). SMIEIS is

a scheme set up by the Banker’s Committee requiring

6

all banks operating in Nigeria to contribute 10%

percent of their profit before taxation (PBT) for

equity investment and promotion of small and medium

industries and the transformation of Nigerian

Agricultural and Cooperative Bank (NACB) to Micro

Finance bank (MB).

Analyzing these SMEs developmental initiatives, one

would ask if SMEs in Nigeria are performing despite

government efforts to promote them. Not much

progress has been achieved judging by SMEs failure

rates.

The performance of SMEs falls below expectation

(Arinative, 2006) irrespective of all these

initiatives, SMEs in Nigeria still face many

obstacles including corruption, unfavorable macro

economic environment, debilitating infrastructures

and administrative challenges.

Gross under capitalization strained by difficulty

in accessing credits from banks and other financial

institutions are the most significant impediments

to creation, survival and growth of SMEs in

Nigeria. The chance of SMEs accessing loan from

conventional bank is low and difficult. Small

7

enterprises have no collateral that would create

opportunities for accessing loan. This will result

in limited recourses that are needed for innovation

and diversification of risk. Also, the exchange

parity rates, is not favorable, making importation

of raw materials too expensive and SMEs products

uncompetitive relative to foreign products.

Due to these financial disadvantages, there is a

tendency that most of the SMEs will fail in their

first five years of operation. Survived SMEs,

which could access credit in one way or the other,

do so, at high interest rates. Thus, the profit

generated will be reduced as the same percentage of

interest and proportionally as increasing the cost

of production.

This high interest rates dilemma leaves SMEs as a

high risks profile investment.

SMEs risk is observed, are basically intensified as

a result of high interest rates as a way of’; firms

profit reduction and increment in the firms cost of

production.

The consequence of profit reduction decreases the

firm financial resources thereby obstructing firm’s

8

expansion that could have generated economies of

scale.

Moreover, the high cost of production affects

firm’s competitive standing in a liberalized and

perfectly competitive market. In Nigeria, high

interest rates decrease firms` profit and increase

firms` cost of production while in the long run

lead to SME failure. Therefore, the most factors

leading to small business failure in Nigeria is

high interest rate (Altab and Rahim, 1989;

Expengong, 1983; Akamokor, 1983). High rate of

inflation; increasing cost of capital and

collateral has are basically an impediment to SMEs

growth; as its effects erode the profits of SMEs.

INTEREST

RATES

Financial institutions play an important role in

the growth and development of SMEs in all

capitalist economies. Interest rate is a key

variable in the financial system; it is capable of

affecting aggregate demand for money, and

consequently investment opportunities.

9

One common characteristic of conventional banks is

the charging of interest rates. Interest from

Islamic perspective means “RIBA”. Arabic words that

means an inverse, expansion or growth. It is

defined by Sharia as a “premium” that must be paid

by the borrower to the lender including the

principal as a condition for the loan (Nurudeed and

Ameh, 2011). Interest rate is the amount charged on

loan. It is usually expressed as the percentage of

the amount borrowed. Interest rates according to

Jighan (1999) are classified into; deposit rate,

lending rate, treasury bills rate, exchange rate

and inter bank rate. All these rates affect SMEs in

different proportions.

Going by the Keynesian investment theory; low

interest rate as a component of cost administered,

is detrimental to increase in saving and hence

investment demand. It was further argued that, high

interest rates will have positive effects on saving

which can be utilized in investment; as those with

excess liquidity are motivated to save.

The excess liquidity generated from high interest

rate on saving is serving as loanable funds. The

10

determination of investment from interest rate can

only stand the test of time in the short-run. In

the long-run, high interest rate tend to choke off

investment ( Khat and Balhia, 1993). Interest rate

as an addition to the principal borrowed and hence

discourages investment. For SMEs operating with

small profit margins, increase in the cost of

borrowing not only reduce the profit but also

increase the level of inflation in an economy.

The effects of high interest rates on SMEs

profitability, is too significant. Normal profit

helps SMEs to transform from small to big. This

increase in size creates an ability to employ

skillful managers, workers and to acquire more

efficient technology and facilities needed for

growth (Nijewardena and Cooray, 1995; and Riding,

Scolf and Orser, 2000). The imposition of high

interest rates and collateral as a necessary

condition left SMEs trapped in a vicious cycle;

they can not get access to finance unless they

offer sufficient collaterals. They can not posses’

tangible collateral unless they build a strong

productive base, they cannot improve their

11

productive base unless they get access to finance.

They lack access to finance basically because of

high interest rate and collaterals (Argenti, 1976;

Dun and Braodstreet, 1969; Whichmann, 1983). it is

typical of Nigerian entrepreneurs to be lacking

collateral to meet the existing critical conditions

of risk averse bank (World Bank ,2000).

Specifically, exchange rate has served as the

lethal variables killing most of the SMEs in

Nigeria especially the textile industries. The

floating of Naira as a result of economic

liberalization policy has significantly led to the

devaluation of Naira; thus creating unfavorable

competitive environment for Nigerian SMEs relative

to their foreign rivals. As noted, with an exchange

rate of 1$ to about N150, this economic index will

definitely affect the performance of SMEs in

Nigeria. More importantly, higher interest rates

enhance investment in non real sector because; the

rate of return is more than the real sector. This

movement in interest rate retards the growth and

development of SMEs. The effects of interest rates

on economic growth and development are becoming so

12

pervasive, that businesses all over the world are

failing towards recession and depression.

By its effects on profitability, high interest

rates creates possibility of default i.e. SMEs

failing to repay some or even all of a loan and

interest. This possibility of defaulting May

therefore creates a recession or slow down in

economic activities that could further depress the

profitability of SMEs, expiring its ability to

repay its loan.

All notable depression right from 1929 depression

down to the current global economic meltdown is

attributed to high interest rates. Confirming this,

World Bank Report (2009) categorically stated

“where there is room, Central Bank should explore

in cutting down interest rates further and keep

them low until a durable recovery is underway. To

lend credence to the world trade report, IMF (2009)

says financial condition has improved more than

expected, mainly due to public intervention in

interest rates reduction.

Confirming the effects of interest rates on

inflation, compitiveness and profitability of SMEs

13

in Nigeria, the table below and its explanatory

analysis are results of a survey of Nigerian Small

and Medium Sized Enterprises Development under

Trade Liberalization (Oboko, 2008)

Analysis of the Aggregate of 25 SMEs Partly Finance

by Owners Funds and Loans

The ROI for this group was also computed using the

aggregate assets and aggregate profits posted for

each year by the 25 manufacturing SMEs that their

operations are partly financed by owners’ funds and

loans. The difference between the ROI and the

interest rates for each year gave the MOS. From the

table, it was observed that except for 1997, 1999,

2000 and 2006 years of operation, the computed MOS

for this group of SMEs were all negative. The worst

years of the MOS were 1995, 2002 and 2004 when the

interest rates ranged from 19.46% to 20.48%. Apart

from inflation and the naira depreciation, the

factor that affected these SMEs most is the

interest rates. Since they were partly financed by

14

loans or credit facilities which attracted monthly

or annually as the case may be, the cost of

operation increased by the financial cost or the

cost of borrowing which is the interest rate on the

loan facility. This was unlike the first group that

were most affected by the inflation rate and

depreciation of the naira. In other words, this

group of SMEs that financed their operation with

owners’ funds and loans were worse hit by the

deregulation of interest rates and the depreciate

ion of the naira.

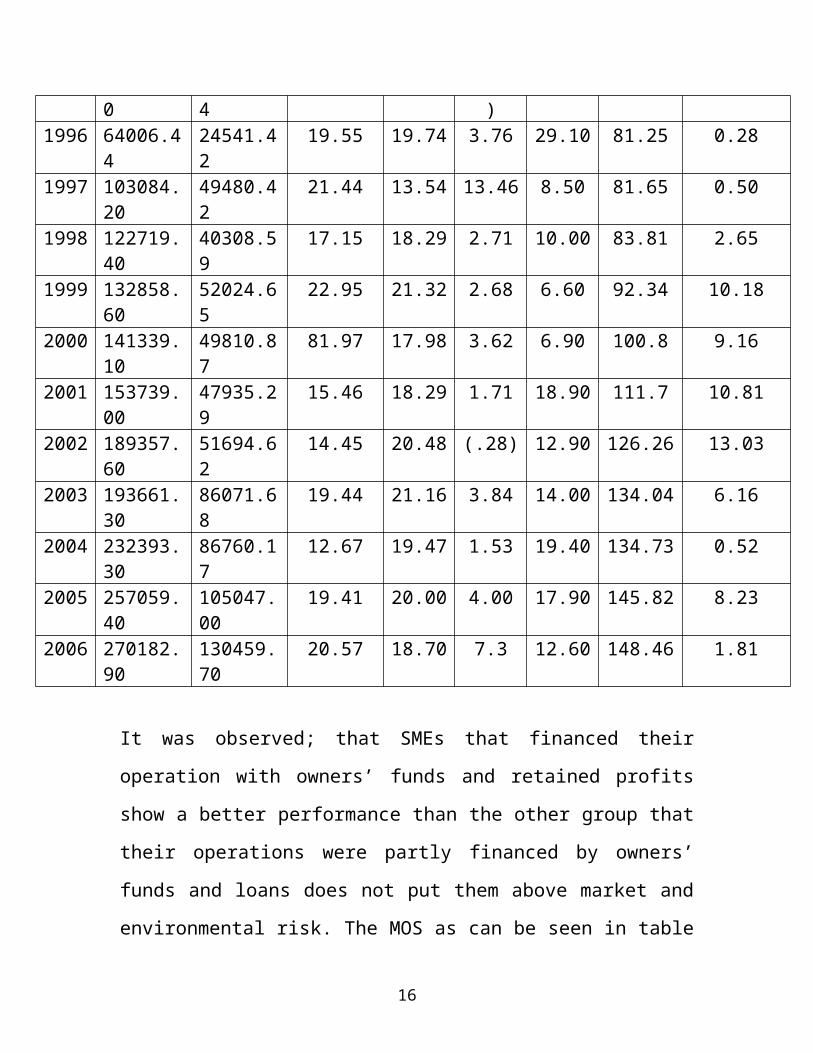

Table 3: Showing Aggregate Asset, Profits, Computed ROI of25 Sampled SMEs, Interest Rates, Inflation Rates, NairaExchange Rate to One US$ and the Rate of Naira Depreciationto One US$

Year Asset in Naira(N’ 000)

Profit in Naira (N’ 000)

Return onInvestment (ROI)(in %)

Interest Rate(COC)

(ROI)-(COC)=MOS(in %)

Inflation Rate

Naira Exchange Rate toOne US$

Rate of Naira Depreciation to OneUS$

1994 Nil Nil Nil 21.00 Nil 57.00 21.87 (0.82)1995 44916.8 13475.0 15 20.18 (0.18 73.10 81.02 270.46

15

0 4 )1996 64006.4

424541.42

19.55 19.74 3.76 29.10 81.25 0.28

1997 103084.20

49480.42

21.44 13.54 13.46 8.50 81.65 0.50

1998 122719.40

40308.59

17.15 18.29 2.71 10.00 83.81 2.65

1999 132858.60

52024.65

22.95 21.32 2.68 6.60 92.34 10.18

2000 141339.10

49810.87

81.97 17.98 3.62 6.90 100.8 9.16

2001 153739.00

47935.29

15.46 18.29 1.71 18.90 111.7 10.81

2002 189357.60

51694.62

14.45 20.48 (.28) 12.90 126.26 13.03

2003 193661.30

86071.68

19.44 21.16 3.84 14.00 134.04 6.16

2004 232393.30

86760.17

12.67 19.47 1.53 19.40 134.73 0.52

2005 257059.40

105047.00

19.41 20.00 4.00 17.90 145.82 8.23

2006 270182.90

130459.70

20.57 18.70 7.3 12.60 148.46 1.81

It was observed; that SMEs that financed their

operation with owners’ funds and retained profits

show a better performance than the other group that

their operations were partly financed by owners’

funds and loans does not put them above market and

environmental risk. The MOS as can be seen in table

16

2 are still too small to cater for dividend

assuming these businesses were to pay dividends to

shareholders.

Looking at SMEs from these perspectives, and

thinking about how loan should perform its function

effectively and efficiently in the financing of

SMEs, then interest rates must be reviewed

ISLAMIC FINANCIAL SYSTEM

AND SMEs

The basic frame work for an Islamic financial

system is a set of principles, rules and laws,

collectively referred as Shariah governing

economic, social, political and cultural aspects of

Islamic societies. By Shariah, we mean the

applications, practices and explanations that are

based on Quran and Sunnah.

Islamic finance therefore means that aspect of

finance that is based on Sharia. the basic

principles and practice of Islamic mode of

financing can be summarized as follows;

- Interest Free Mode of Finance: Under this

principle, the basic emphasis is on profit

17

and it is shared on an agreed term. In case

of loss; of the lost that was incurred does

not emanate from the entrepreneurs, then the

total loss will be born by the financier

which is the bank.

- It is based on social justice, equality and

property right regarding the societal

resources.

- More importantly, Islamic finance not only

provides free interest rate but also as one

of its practices, it is enterprise risk

management. Relating this, the cooperation

between potential entrepreneurs and

commercial lending financial institutions is

usually held back on the following reasons;

To protect their investment and ensuring

the safety of the loan, banks require

substantial collaterals. In some cases,

the value of the collateral is more than

the cost of the loan. In Islamic finance,

collateral comes from the concept of joint

liability. In this concept SMEs and Bank

involved in the operation.

18

More importantly, the conditions set by

the commercial banks are extremely not

feasible for most of the entrepreneurs.

Given these reason, securing finance for SMEs are

extremely difficult leaving SMEs seeking for

another financing alternative.

An Islamic financial system can play vital roles in

the growth and development of SMEs in Nigeria. This

is possible through the mobilization of dormant

saving that are been intentionally kept out of

interest based financial channel and by

facilitating the development of capital market at

the same time. The development of this system would

enable savers and borrowers to choose financial

instruments compatible with their business needs,

social values and religious belief. Under Islamic

mode of financing, borrowers and lenders share

rewards as well as loss in an equitable

distribution. Thus, the process of resource

allocation and distribution in the economy can now

be fair and representative of true productivity. As

interest is free, suppliers of funds become

inventors, t he provider of financial capital and

19

entrepreneur share risk in return for profit

sharing. Moreover, borrowing-lending process with

charging interest as practiced in today’s financing

are leading SMEs to failure. This is because the

creditor is not encouraged to take or make

financial assessment. As a result, the volume of

unhealthy credits will substantially increase and

lead to excessive leverage, and to an unsustainable

rise in asset prices, living beyond means, and

speculative investment. (Chapra, 2008)

All these are possible through the adoption of

Islamic modes of financing.

ISLAMIC MODES OF

FINANCING SMEs

There are various modes of Islamic financing that

are available for any particular SMEs. The most

effective of these are;

Murabaha (Cost–Plus Financing): The

Murabaha is a method of asset acquisition

finance. It involves a contract between

the bank and its client for the sale of

goods at a price that includes an agreed

profit margin, their percentage of the

20

purchase price or a lump sum. The bank

will purchase the goods as requested by

its client and will sell them to the

client with a mark-up. The profit mark-up

is fixed before the deal closes and cannot

be increasd, even if the client does not

take the goods within the time stipulated

in the contract. Some Islamic banks use an

agency arrangement, where the client takes

delivery of goods from the seller as an

agent of the bank. Payment will usually be

over time by installment.

Mudaraba (Profit Sharing): The Mudaraba is

a profit sharing contract, with one party

providing 100 percent of the capital and

the other party (the Mudarib) providing

its expertise to invest the capital,

manage the investment project and, if

appropriate, provide labour. Profit

generated is distributed according to a

predetermined ratio, but like the capital

itself, cannot be guaranteed. Losses

accrued are therefore borne by the

21

provider of the capital, who has no

control over the management of the

project. Mudaraba structures are often

used for investment funds, with investors

providing money to the Islamic bank, which

it invests as Mudarib, taking a management

fee.

Musharaka) Partnership Financing): The

Musharaka involves a partnership between

two parties who both provide capital

towards the financing of new established

projects. Both parties share the profits

on a pre-agreed ration. Allowing

managerial skills to be remunerated, with

losses being shared on the basis of equity

participation. One or both parties can

undertake management of the project. As

both parties take on project risk, it is

relatively rare for banks to participate

in Musharaka transactions.

Ijara (Leasing): The Ijara is a contract

where the bank buys and leases out

equipment required by the client for a

22

rental fee. The duration of the lease and

rental fees are agreed in advance.

Ownership of the equipment remains with

the lessor bank, which will seek to

recover the capital cost of the equipment

plus a profit margin out of the rentals

payable. There are two types of Ijara:

operating leases and lease purchase. In a

lease purchase, the obligation to purchase

the equipment at the end of the lease and

the price at which the assets will be

bought is pre-agreed. Rental fees already

paid constitute part of the final

purchasing price. Where an asset is

financed through floating rate funds, the

owner will usually pass the risk of rate

of fluctuations down to the lessee through

the rentals payable by the lessee. This

creates a problem under Islamic finance

principles as lease rentals cannot be

expressed by reference to interest rates.

This difficulty is partly surmountable. In

leasing transactions the lessor is

23

providing an asset, not funds, so t he

return is in the form of rent, rather than

principal and interest. In an Ijara lease,

t he amount and timing of the lease

payments should be agreed in advance,

though the amount of those payments may be

subject to adjustment on a predetermined

basis. Way in which the problem has been

overcome therefore include: referring to

the rent payable under the lease at the

date of signing but subject to adjustments

by reference to provisions in other

documents; or adjusting the rent be cross-

referenced to LIOBOR or to a fluctuating

rent payable under a non-Islamic lease

singed at ..

Istisna’a (Commissioned Manufacture):

Islamic principle of Gharar prevents one

from selling something that one dose not

own. The technique of Istisna’a has been

developed as an exception to this. As

defined by the Islamic Development Bank.

Istisna’a is a contract whereby a party

24

undertakes to produce a specific thing

that is possible to be made according to

certain agreed specifications at a

determined price and for a fixed of

delivery’. Accordingly, the technique is

particularly useful in providing an

Islamic element in the construction phase

of a project, as it is akin to a fixed

price turnkey contract. As the Istisna’a

contract is one of procurement and sale of

an asset, it also lends itself to non-

recourses financing. In an Istisna’a

transaction, a financier may undertake to

manufacture an asset and sell it one

receipt of monetary installments. As banks

do not normally carry out manufacturing, a

parallel contract structure will typically

be used. T he ultimate buyer of the asset

will commission it from the bank, which

will institute a parallel contract under

which the bank commissions the asset from

the manufacturer. The bank charges t he

buyer the price it pays the manufacturer

25

plus a reasonable profit. The bank t her

fore takes the risk of manufacture of the

asset.

SUKUK: The significant importance of Islamic

financing is the development of SPV (Special

Purpose Vehicle) known as Sukuk. This vehicle helps

SMEs through capital market to generate funds from

the public.The issuance of Sukuk, while helping

SMEs to benefit from both debt and equity financing

from the Islamic Financial Institution. Under this

mode, Assets and inventory are financed on debt

terms. While other aspects that require financing

can be on an equity (revenue sharing) basis as

mention above. More importantly, Sukuk helps in

spreading SMEs risk between Islamic Financial

Institution and the public through the capital

market.

CONCLUSION

As observed, access to capital is an impediment to

the growth of SMEs in developing countries and in

particular Nigeria. SMEs are considered to have

high risk investment profile, as such, the

26

conventional bank attached a stringent stiff

conditions: High interest rates and collateral in

other to safeguard the loan going to SMEs. These

conditions further increased the chance of SMEs to

fail. High interest rates extremely reduce the

profit that could have been used for innovation

needed for expansion and growth.

Assessing SME failure from these; high interest

rate and collateral, the best alternative for

financing SMEs in developing countries should be

Islamic financing; as its principles and practice

depend neither on interest rate nor collateral but

on profit sharing and risk mitigation.

RECOMMENDATION

The introduction of Islamic mode of financing in

Nigeria is a step forward. It is an opportunity not

only for free interest rate and collateral for

loaning credits to SMEs, but also an opportunity in

exploiting new market that will attracts Foreign

Direct Investment (FDI) from most of the Arab

economies with their significance funds of Islamic

investor seeking for Shari’ah compliant investment.

27

Therefore, it is recommended that, entrepreneurs

should tap into these pools of opportunities to

explore the nascent market either by creating a

global partnership with the Arab investors that

need interest free investments or partnering with

available Islamic financial institutions such as

JAIZ.

For this to be an effective SMEs financing

strategies, the global human resources must be

developed to acquire the necessary techniques and

applications that are necessary for an effective

operation of Islamic mode of financing.

An effective legal regulatory framework must be

clearly laid by government as support guidance.

More importantly; business professional, academic

practitioners and the entire public

should be motivated to promote the

significances of Islamic modes of financing

through seminars, conference and more

importantly, the introduction of Islamic

financial courses in our higher institution is a

priority.

28

REFERENCES

A Primer for Selecting New Enterprises for your

Farm

Abdallahi, A. (1999), Partnership (Musharakah): A

New Option for Financing Small

Enterprises. Arab Quarterly Journal.

Abdallhi A. (1999); Partnership (Musharaka): A New

Option for Financing Small Enterprises:

Arab Quarterly Journal Publication.

29

Abdul-Raham, Yahia (2006), “Islamic Instrument for

Managing Liquidity.International Journal

of Islamic Financial services Vol. 1 No.

1.

Aecher,S. and Abdullkarim, R.A. (2002), Islamic

Finance; Innovation and Growth, Euro

Money.

Aftab K and E. Rahim 1998 Barriers to the growth of

Informal Sector Firm, a Case Study:

Journal of Development Studies 25(4).

Akamiokor, G.A (1983) “Financing Small-Scale

Enterprises”. Central Bank of Nigeria.

Ayub. M. (2007), “Understanding Islamic Finance,”

John Wiley and Sons Ltd, England.

Bernice K. and Meredith G. (1997), Relationship

among Owner/Manager Personal Values,

Business Strategies, and Enterprise

30

Performance Journal of Small Business

Management, 35:2.

Balunywa Waswa, What are Small Scale Enterprises?

Entrepreneurship,and Small Business

Enterprise. Makerere University Business

School Accessed December

2010 at http://evancarmicheal.com/Africa Ac

count/1639/40What is Small scale

Enterprises-Entrepreneurship-and-Small-

Business-Enterprises-Growth-i

Beckley Peter (1988): Foreign Direct Investment by

Small and Medium Sized Enterprises: The

Theoretical Background. Bradford, United

Kingdom. University of Bradford Management

Centre.

Chapra, Umar (2008), “The Global Financial Crises:

Can Islamic Finance Help? Paper of Ibn

31

Khaldun Lecture Series, Institute of

Islamic Banking, and Insurance London.

Chapra Segrado (2005):“Islamic Micro Finance and

Socially Responsible Investments Media

Project, University of Torino.

Chiara Segrado (2005): Islamic Micro and Socially

Responsible Investment Media Project

University of Toronto

Chima Omoha B. (2011), Strategies fro Successful

Entrepreneurship in the Third World.

Journal of Public Administration `Vol. 1No

1. Kogi State University, Anyigba

Dnbsmall Business. Com. au/News/business-failures

Ju

Ekpenyong, D.B (2002); Performance of Small Scale

Enterprises in Nigeria during the

Structural Adjustment Programmes

32

Implantation; Survey Findings’, Journal of

Financial Management Analysis Vol. 15 No

1.

Ekpenyong, D.B and M.O. Nyong, (1992): “Small and

Medium Scale Enterprises Development in

Nigeria. Their Characteristic, Problems

and Sources of Finance. A Draft Report

Presented at a Seminar on Economic Policy

Research for Policy Design and Management

in Nigeria”. Ibadan.

Epics and Biggs

European Commission (2007) Enterprises and

Industry: SME Definition. Accessed at

http://europa.eu.int/comm/enterprise/enter

prisepolicy/smedefinition/indexen.htm

Farming Alternatives: A Case to Evaluating the

Feasibility of New Farm Based Enterprises

33

Federal Office of Statistics (1999): Poverty and

Welfare in Nigeria Lagos.

National Bureau of Statistic 1999 Report

Federal Republic of Nigeria .Second National

Development Plan 1970-1974.

Henderson, J. (2002): Building the Rural Economy

with high growth Entrepreneurs, Economic

Review.

Henderson, J. (2002); Building the Rural Economy

with High- Growth Entrepreneurs, Economic

Review

http://agelbb.missiour.edu/mac

http://www.oznet.ksu.edu/lirary/agecz/mf2184.pdf

James Robertson (1990), Future Wealth: A New

Economics for 21st Century, Cassel

Publication.

34

Joshua Mindle (2008): Small and Medium Scale

Business as Instrument of Economic Growth

in Nigeria. Lagos. Kingston Publishers.

Jhingan, M.L (1999), Macro Economic Theory, 10th

Revised ed., India, Stosiusn Inc.

Kibera and Kibera (1997), As Cited in Balunywa

Waswa .What are Small Scale Enterprises?

Entrepreneurship and Small Business

Enterprise. Makerere University Business

School Accessed December 2010 at

http//evancarmicheal.com/Africa-Account/16

39/40What are Small Scale Enterprises-

Entrepreneurship- and-small-business-

enterprises-growth-I.

Macqueen D. (2006) Governance towards Responsible

Forest Business. Guidance on Different

Types of Forest Business and the Ethics to

35

which they gravitate. International

Institute for Environment and Development

(IIED) London, United Kingdom.

Nurudeen.Y.Z. and Ameh. A.A (2011), Islamic

Financing as a Strategy for Poverty

Reduction in Nigeria Journal of Public

Administration Vol. I No. 1.Kogi State

University Anyigba.

Balunywa Waswa(1999),What are Small Scale

Enterprises? Entrepreneurship and Small

Business Enterprise. Makerere University

Business Schoool Accessed December 2010 at

http://envancarmicheal.com/africa-

Account/1639/40What are Small Scale

Enterprises-Entrepreneurship-and- Small-

Business-Enterprises-Growth-i

36

Njoju (2002), As Cited in www.valuefronteraonline/

publication.jsp?

typeaponeindustrialeconomics-smes

Obokoh, L.O (2008), “Small and Medium Sized

Enterprises Development under Trade

Liberalization: A Survey of Nigerian

Experiences” International Journal of

Business and Management. Vol. 3, No 12.

Odedokun M.O (1998); Effectiveness of selective

Credit Policies Alternative Framework of

Evaluation and World Development Vol. 16

Pp. 120-122.

Olarewaju (2001), As Cited in

www.valuefronteronline/publication.jsp?

typeaponeindustrialeconomics-smes

Ogechukwu Ayozie (2006), The Role of Small Scale

Industry in National Development in

37

Nigeria. Texas Corpus Christi, Texas,

United State. November 1-3 2006.

Ogujuiba K.K. Ohuche F.K and Adenuga A.O (2004);

Credit Availability to Small and Medium

Scale Enterprises in Nigeria. The

Importance of New Capital Base for

Banks.Background and Issues. Working Paper

Accessed in December 2010 in

www.valuefronteraonline.com/publication.js

p?type=aponeindustrialeconomics-smes.

Omotola Derinola(2008), Small Scale Enterprises,

Economic Reform and National Development

in Nigeria. Lagos, Adejo Publishing.

Onugu Basil (2005): Small and Medium Enterprise in

Nigeria (SMEs) Problem and Prospect. Being

a Dissertation Submitted to St. Clement

University in Partial Fulfillment of the

38

Award of the Degree of Doctor of

Philosophy in Management.

Olurunshola, J.A (2003): Problems and Prospects of

Small and Medium Scale Industries in

Nigeria Being a Paper at CBN Seminar on

Small and Medium Industries Scheme.

Online Library.wiley.com/doi/10/.1111/j.1365-2648

Patricia Schaefer (2006): “Why Small Business Font”

Alfred Communications, Inc.

Rehman, F. (2002), “Interest Free Micro Credit

Program (IMCP). Designed for Urban Areas

of Pakistan,” Emerald Group Publishing

Limited. Vol. 26 No 1.

World Bank, “Review on Small Business Activities”.

39

World Bank, 2001 World Development Report.

Washington. Oxford University Press for

the W Report, orld Bank.

World Bank, Study on “Small and Medium Scale

Enterprises”. 1989.

Salami, IT (2003): Guidelines and Stake Holder

Responsibilities. SMIES in Seminar on

Small and Medium Industries Equity

Investment Schemes (SMIEIS), Central Bank

of Nigeria CBN Training Centre.

The Holy Quran, Usuf Ali, A. (2007), Lushana Books

The Holy Quran, Yusuf Ali, a (2007) Lusiana Books

Ugwushi Bellema Ihua (2009), SMEs Key Failures

Factors: A Comparison between the United

Kingdom and Nigeria. Kent Business School.

40

Unleashing Entrepreneurships: Report by the

Commission on the Private Sector and

Development of the United Nations, 2004.

Unleashing Entrepreneurships: Report by the

Commission on the Private Sector and

Development of the United Nations 2004.

Usasbe.org/../USASBE 1997A Proceeding P. 125 Wije

Wardena. PDF

Watson, J. (2003), Failure Rates for Fewole

Controlled Biz: Are Italy any different?

Journal of Small Biz Mgt Vol. 41 No 3

World Bank (2000), “Nigeria at a Glance”. The World

Bank Washington D.C

World Bank and Central Bank of Nigeria (1995);

“Nigeria; a Diagnostic Renew of the Small

and Medium Scale Enterprises, “Lagos: CBN

Press.

41

World Bank and IMF “Financial Sector Assessment

Hard Book 2005”

World Bank and IMFs “Financial Sector Assessment

Hand Book 2005

World Bank Group (2010): Doing Business in Nigeria.

42