PROPOSAL PAPER FOR OFFERING A PACKAGE OF ISLAMIC FINANCING FACILITIES TO REPLACE THE EXISTING...

14

INCEIF The Global University of Islamic Finance ASSIGNMENT TOPIC: PROPOSAL PAPER FOR OFFERING A PACKAGE OF ISLAMIC FINANCING FACILITIES TO REPLACE THE EXISTING CONVENTIONAL BANKING LOAN FACILITIES (Case Study: Premier Foods Manufacturing Limited (PFM)) OPTION ONE (1) Facilitator: Zainal Abidin Mohd Tahir Student Name: Abukar Mohamed Jimale Student ID: 1100389 Date submitted: 01 April 2014 JANAURY SEMESTER 2014, CIFP PART II IB2001 STRUCTURING FINANCIAL REQUIREMENTS

-

Upload

stiudarulhikmah -

Category

Documents

-

view

1 -

download

0

Transcript of PROPOSAL PAPER FOR OFFERING A PACKAGE OF ISLAMIC FINANCING FACILITIES TO REPLACE THE EXISTING...

INCEIF The Global University of Islamic Finance

ASSIGNMENT TOPIC:

PROPOSAL PAPER FOR OFFERING A PACKAGE OF ISLAMIC FINANCING FACILITIES TO REPLACE THE EXISTING

CONVENTIONAL BANKING LOAN FACILITIES

(Case Study: Premier Foods Manufacturing Limited (PFM))

OPTION ONE (1)

Facilitator: Zainal Abidin Mohd Tahir

Student Name: Abukar Mohamed Jimale

Student ID: 1100389

Date submitted: 01 April 2014

JANAURY SEMESTER 2014, CIFP PART II

IB2001 STRUCTURING FINANCIAL REQUIREMENTS

1. INTRODUCTION

This paper provides a framework of financing assessment and implementation of

replacing the existing conventional loan/credit facilities with Islamic facilities to cover the

all needs for the new client company namely Premier Foods Manufacturing Limited

(PFM).

1.1. Benefit of financial assessments

The benefit of the financial assessment is to help gather the facts so the company

(PFM) can take an honest look at its finances. This should help the company to gain

more enjoyment from its financing product (Islamic banking facility) and realize its

financial goals.

The primary objective of financing assessment is to persuade the company (PFM) over

all facilities that the bank Wataniah Islami (BWI) offers to its customers is under Islamic

principles, rules and practices.

The main principles followed by the bank Wataniah Islami (BWI) are:

a) Prohibition of interest in all forms of transactions;

b) Undertaking business and trade activities on the basis of legitimate profits; and

c) Giving Zakat.

Where the normal banking practices do not clash with the Islamic principles, the bank

has adopted the current banking practices and procedures to accomplish its banking

activities. In some cases as in some Muslim countries such as Malaysia a Shari’ah

Advisory Committee is constituted to advise the bank on the operations of the banking

business in order to ensure that they do not involve any element which is not approved

by the religion of Islam.

Like conventional banks, the bank provides short, medium and long term funding facility.

Since the Islamic banks are prohibited from making loans with interest to their

customers, all financing operations are either based on profit-loss sharing or based on

fixed charges.

Unlike conventional banks, some Islamic banks are also actively involved in social

activities. The services that are considered as social services include benevolent loans,

collection and distribution of Zakat funds and activities that will enhance Islamic values

and ways of life.

1.2. SERVICES AVAILABLE

a) Deposit facilities

Current Accounts

Saving Accounts

Investment Accounts

The three types of deposit facilities available at Islamic banks can fall within various

grouping of Islamic principles such as profit and loss sharing, free services and ancillary

principles. The most common principles used by the Islamic banks are Mudarabah from

the category of profit and loss sharing, Qard Hassan from the category of free services,

and Wadiah from the category of ancillary principles.

b) Financing facilities

Musharakah

Mudarabah

Murabahah

Ijarah

Qard Hassan.

c) Other facilities

Letters of Credit-i (LC)

Letters of Guarantee-i (LG)

Collection of Bills

Sale and Purchase of foreign Currencies-i

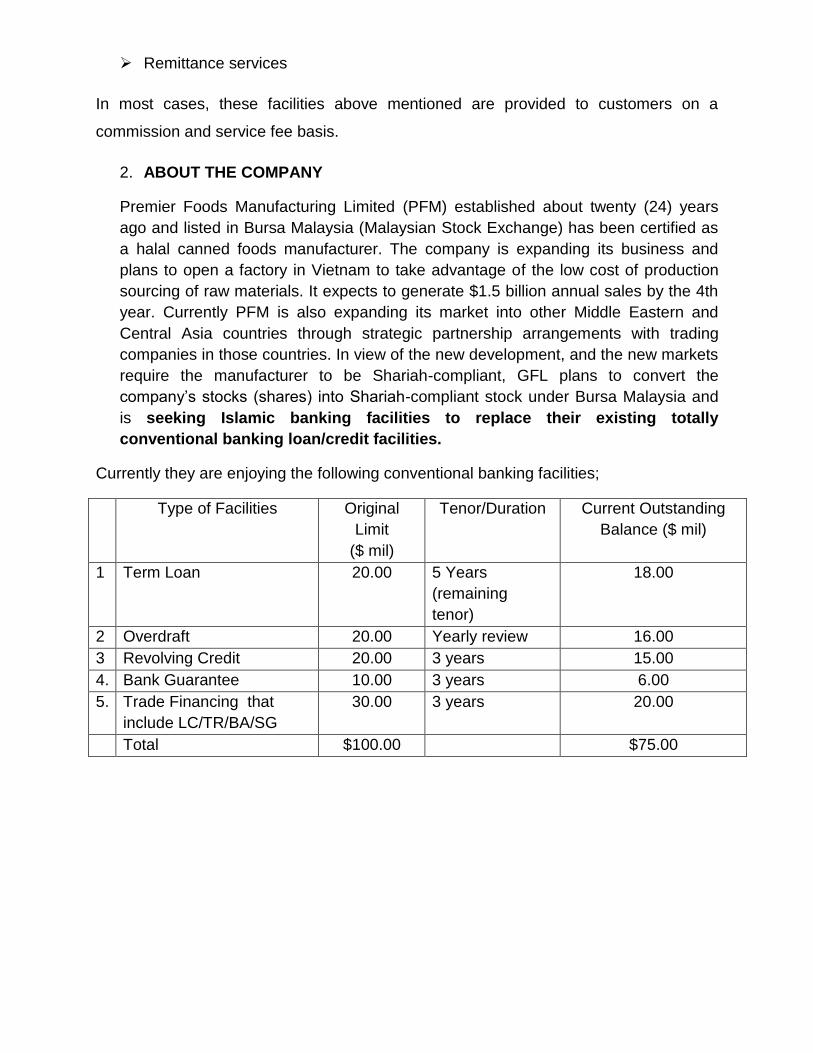

Remittance services

In most cases, these facilities above mentioned are provided to customers on a

commission and service fee basis.

2. ABOUT THE COMPANY

Premier Foods Manufacturing Limited (PFM) established about twenty (24) years

ago and listed in Bursa Malaysia (Malaysian Stock Exchange) has been certified as

a halal canned foods manufacturer. The company is expanding its business and

plans to open a factory in Vietnam to take advantage of the low cost of production

sourcing of raw materials. It expects to generate $1.5 billion annual sales by the 4th

year. Currently PFM is also expanding its market into other Middle Eastern and

Central Asia countries through strategic partnership arrangements with trading

companies in those countries. In view of the new development, and the new markets

require the manufacturer to be Shariah-compliant, GFL plans to convert the

company’s stocks (shares) into Shariah-compliant stock under Bursa Malaysia and

is seeking Islamic banking facilities to replace their existing totally

conventional banking loan/credit facilities.

Currently they are enjoying the following conventional banking facilities;

Type of Facilities Original

Limit

($ mil)

Tenor/Duration Current Outstanding

Balance ($ mil)

1 Term Loan 20.00 5 Years

(remaining

tenor)

18.00

2 Overdraft 20.00 Yearly review 16.00

3 Revolving Credit 20.00 3 years 15.00

4. Bank Guarantee 10.00 3 years 6.00

5. Trade Financing that

include LC/TR/BA/SG

30.00 3 years 20.00

Total $100.00 $75.00

The below table demonstrates the compatible Islamic products/facilities with the existing

conventional banking facilities, that Bank Wataniah Islami (BWI) plans to offer to

Premier Foods Manufacturing Limited (PFM).

. Conventional financing Facilities

(interest based)

Bank Wataniah Islami (BWI) products

(interest free based)

1 Term Loan BBA House financing

2 Overdraft Bai’ Inah

3 Revolving Credit Revolving Credit-i

4. Bank Guarantee (BG) Bank Guarantee – i

5. Letter of Credit (LC) Letter of Credit – i

6. Trust Receipt (TR) Trust Receipt-i (TR-i)

7. Bank Acceptance (BA) Bank Acceptance (BA)

8. Shipping Guarantee (SG) Shipping Guarantee (SG-i)

1. BBA HOUSE FINANCING VS. TERM LOAN

The BBA house financing is an Islamic house financing facility, which is based on the

Shariah concept of Al Bai’ Bithaman Ajil (BBA). It is a contract of deferred payment sale

i.e. the sale of goods on deferred payment basis at an agreed selling price, which

includes a profit margin agreed by both parties. Profit in this context is justified since it is

derived from the buying and selling transaction as opposed to interests accruing from

the principal lent out.

In conventional practice, Term loan is a loan from a bank for a specific amount that has

a specified repayment schedule and a floating interest rate. Term loans almost always

mature between one and 10 years.

1.1 Main Characteristics of BBA house financing

All the components to determine the selling price have to be fixed because the selling

price has to be fixed at the time the contract is made. Hence, the profit rate for the BBA

financing is fixed throughout the period of financing.

1.2 mechanisms of the BBA house financing

Customer identifies the asset to be purchased.

Bank determines the requirements of the customer, in relation to the

financing period and nature of repayment.

Bank purchases the assets concerned.

Bank subsequently sells the relevant asset/property to the customer at an

agreed price, which consist of:

o Actual cost of the asset to the bank i.e. financing amount; bank’s profit

margin.

o Customer is to settle the payment by installment payment throughout

the project financing period.

1.3 BBA house financing vs. An ordinary conventional housing loan

An ordinary conventional housing loan is given on the basis of debtor/creditor

relationship. Whereby, the amount of loan is being charged interest, normally quoted at

a certain percentage above the base lending rate (BLR) over the loan period, repayable

in periodic installment. The BLR will fluctuate up or down and it will affect the total loan

cost. Simultaneously, arrears in conventional loans are normally capitalized.

However, under the Islamic banking scheme, since the BBA concept is being applied, a

seller-buyer relationship will be established and the selling price is fixed upfront. The

sales price is then repaid in periodic installments and the agreed installments will

remain fixed throughout the financing period. As such, a customer’s interest rate risk is

eliminated. Furthermore, arrears will not be capitalized.

The BBA financing scheme is not tagged to the BLR. Thus, the installments will be fixed

according to the rates declared upon agreement. It is possible to compute the selling

price as per the formula:

Selling price = (monthly installment X number of financing months) + grace period profit

(if any).

Monthly installment is computed using the agreed profit rate on a constant rate of return

and monthly rest. The grace period profit is charged when the bank is financing property

under construction. As such, during the construction period, customer will pay the grace

period profit only.

Example:

Financing amount: RM100, 000-00

Profit rate: 8%

Financing period: 20 years

Installment per month: RM837-00

Selling price = (RM837-00 X (20 X 12)) + 0 = RM200, 880-00

1.4 Early settlement under the BBA financing facility

The client is not required to give advance notice to the bank for the early settlement i.e.

financing is settled before the completion of the financing tenor. As such, there is no

early settlement penalty fees/charges imposed on the client.

1.5 If the customer entitled for rebate (Ibra’) in case of early settlement

The customer will be entitled for a rebate on the concept of Ibra’ for the unearned profit

at the bank’s discretion. The rebate is in the form of a reduction in the balance

outstanding. The early settlement amount is the net figure after deducting the rebate.

1.6 The period of financing for the BBA house financing

Normally for house or residential property financing, the maximum repayment period is

30 years or at the age of 65, whichever is earlier. It might differ from one bank to

another. The margin of financing differs from one bank to another as well. Generally, the

margin ranges from 70% to 100% against the sales & purchase value or the current

market value. Again, the customer’s repayment capacity will also affect the margin of

financing that the bank can offer.

1.7 Security/collateral requirement under the BBA house financing

The property financed by the bank will be used as the security/collateral for the

financing facility under the BBA house financing. The property is usually secured by way

of first party charge.

1.8 Legal documents for the BBA house financing

Letter of offer

Property sale agreement

Property purchase agreement

Legal charge or,

Assignment and power of attorney

Or any other Islamic financing documents that are required for the

house financing

1.9 Any restriction in applying for the BBA house financing

Under the BBA house financing scheme, the purpose of financing is important. It must

be clearly stated and revealed to ensure that the bank is not financing a customer

whose income or nature of business income is derived from a forbidden source or

haram income under the requirement of the Shariah. These include but not limited to

the following:

Customers who are selling alcohol, drugs, pork and items relating to them

Customers who are operating gambling business and entertainment outlets

selling liquors

Customers who are involved in immoral business such as prostitution Properties

that are going to be used for haram activities.

1.10 If a non-Muslim can apply for the BBA house financing

The same financing facility is available to the non-Muslim. The financing facility is also

open to a foreigner or non-resident. However, they are subjected to the BNM ECM 6,

which includes property value must be RM250,000and above, the FIC approval is

required and maximum margin of financing is 60%.

1.11 A Mortgage Takaful

Mortgage Takaful is the equivalent of the MRTA, whereby a protection on the financing

amount will be given, in case any unto ward incidents were to befall the customer. Even

though it is not compulsory, most banks are making it a financing condition to

encourage this mortgage takaful protection, which is beneficial to the customers and

their next of kin.

Most banks are providing financing assistance for the takaful premium. Normally, the

mortgage takaful premium will be included in the financing amount and will be subjected

to the agreed margin of financing.

1.12 The advantages of the BBA house financing

The total cost of the property purchased is determined at the time of

contract or aqd.

There is no additional or “hidden” cost that will change the price of the

property purchased.

The transaction is transparent.

There is no element of uncertainties or Gharar.

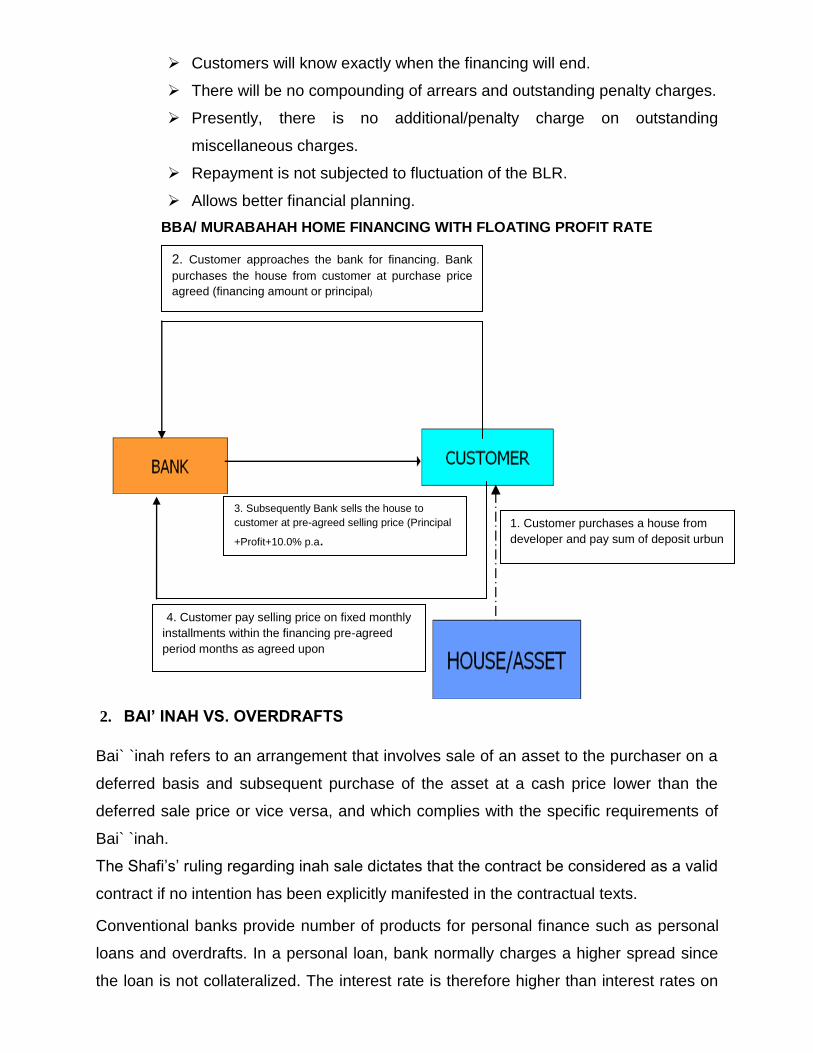

Customers will know exactly when the financing will end.

There will be no compounding of arrears and outstanding penalty charges.

Presently, there is no additional/penalty charge on outstanding

miscellaneous charges.

Repayment is not subjected to fluctuation of the BLR.

Allows better financial planning.

BBA/ MURABAHAH HOME FINANCING WITH FLOATING PROFIT RATE

2. BAI’ INAH VS. OVERDRAFTS

Bai` `inah refers to an arrangement that involves sale of an asset to the purchaser on a

deferred basis and subsequent purchase of the asset at a cash price lower than the

deferred sale price or vice versa, and which complies with the specific requirements of

Bai` `inah.

The Shafi’s’ ruling regarding inah sale dictates that the contract be considered as a valid

contract if no intention has been explicitly manifested in the contractual texts.

Conventional banks provide number of products for personal finance such as personal

loans and overdrafts. In a personal loan, bank normally charges a higher spread since

the loan is not collateralized. The interest rate is therefore higher than interest rates on

2. Customer approaches the bank for financing. Bank

purchases the house from customer at purchase price

agreed (financing amount or principal)

4. Customer pay selling price on fixed monthly

installments within the financing pre-agreed

period months as agreed upon

1. Customer purchases a house from

developer and pay sum of deposit urbun

3. Subsequently Bank sells the house to

customer at pre-agreed selling price (Principal

+Profit+10.0% p.a.

housing and car loans. Normally, consumers apply for a personal loan for the sole

reason that they can spend the money any way they like.

In conventional system, the loan contract guarantees the bank the principle loan and

interest.

As Islam prohibited interest as riba, a customer who is looking for personal loan cannot

utilize the above facilities. But he is willing to pay the necessary charges required by the

bank as long as the contract is free from riba. The bank too wants to generate income

for every dollar it gives away for financing. But the essence of the story is still the fact

that the customer wants a loan and the bank is willing to lend but at a price.

2.1 Bai’ inah in Nature

Each sale contract in a Bai` `inah arrangement is binding in nature. Thus, neither of the

sale contracts shall be terminated unilaterally by any of the contracting parties. The

inherent nature of each sale contract in a Bai` `inah arrangement is the transfer of

ownership of the asset from the seller to the purchaser in two separate and independent

sale contracts.

The Bai` `inah arrangement may occur in the following forms:

a. The owner sells the asset to the purchaser at a deferred price and

subsequently the initial owner buys the asset on a cash basis at a lower

price than the deferred sale price; or

b. The owner sells the asset to the purchaser on a cash basis and

subsequently the initial owner buys the asset at a deferred price which is

higher than the cash sale price.

BASIC TERMS AND CONDITIONS OF BAI INAH OVERDRAFT FACILITY

Shariah Principle Applied Bai Inah/ Tawarruq

Purpose of the financing Providing Cash Line facility to meet business/ customer's requirement

Financing margin

Identified subject to business requirement PFM may require USD 20 million for overdraft facility

Duration Three years subject to yearly review

Profit rate

Capping Rate Selling Price at 10% p.a

Effective Profit Rate - BFR + 1.5% spread subject to changes on floating rate within the selling price Profit is calculated on daily average balance

Disbursement

Cash Line limit will be make available into Wadiah Current Account which is to be opened by customer

Repayment

Monthly payment of profit on utilized amount

Yearly reducing limit or lump-sum payment at the end of facility period

Collateral

Assignment of contract

Director’s Guarantee

Charge on property or other collateral acceptable to the bank

documentation

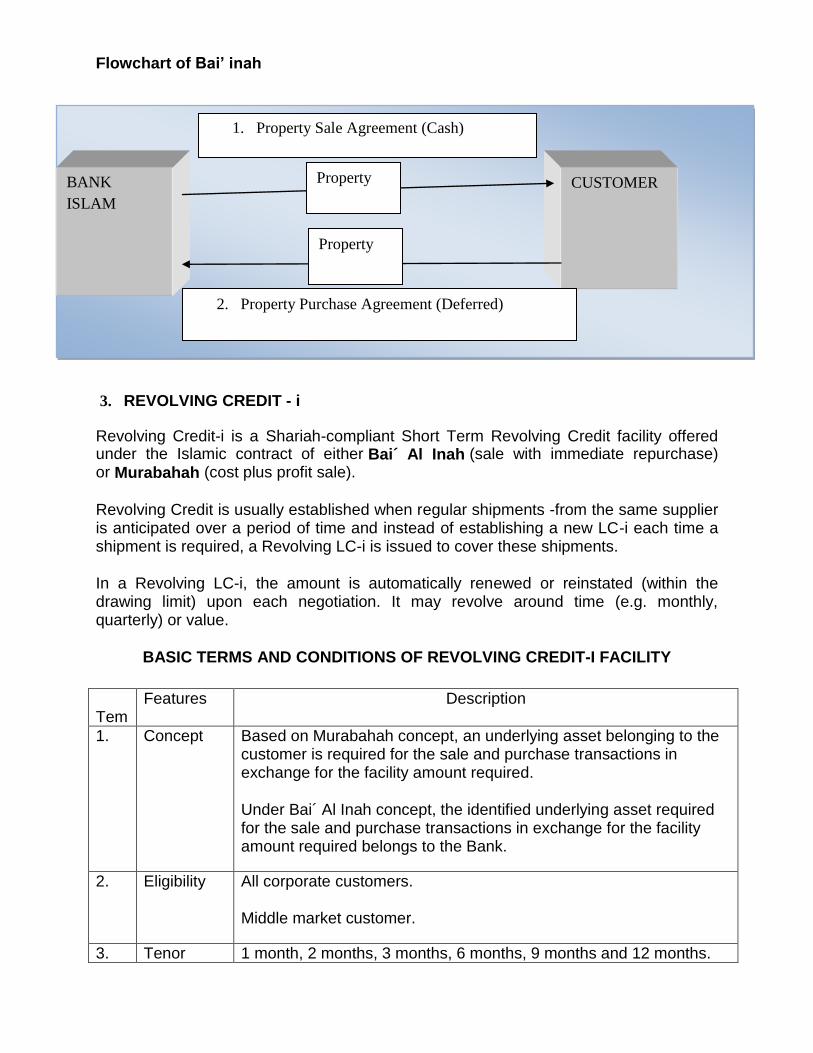

1) Bai Inah CL: - Property Sales Agreement (PSA) and Property Purchase Agreement (PPA).

Bai Inah must meet the following requirements:

1. There must be two separate contracts properly executed. First the contract of

sale by A to B on deferred payment terms. Second the contract of repurchase by

A from B on cash terms, or vice versa.

2. The asset must not be a ribawi material in the medium of exchange category

(gold, silver or currency) because all payments for purchases are made in

money.

3. Each of the two contracts must have the essential elements (arkan) and each of

the essential elements must meet the necessary conditions (shurut).

Flowchart of Bai’ inah

3. REVOLVING CREDIT - i

Revolving Credit-i is a Shariah-compliant Short Term Revolving Credit facility offered under the Islamic contract of either Bai´ Al Inah (sale with immediate repurchase) or Murabahah (cost plus profit sale).

Revolving Credit is usually established when regular shipments -from the same supplier is anticipated over a period of time and instead of establishing a new LC-i each time a shipment is required, a Revolving LC-i is issued to cover these shipments.

In a Revolving LC-i, the amount is automatically renewed or reinstated (within the drawing limit) upon each negotiation. It may revolve around time (e.g. monthly, quarterly) or value.

BASIC TERMS AND CONDITIONS OF REVOLVING CREDIT-I FACILITY

Tem

Features Description

1. Concept Based on Murabahah concept, an underlying asset belonging to the customer is required for the sale and purchase transactions in exchange for the facility amount required.

Under Bai´ Al Inah concept, the identified underlying asset required for the sale and purchase transactions in exchange for the facility amount required belongs to the Bank.

2. Eligibility All corporate customers.

Middle market customer.

3. Tenor 1 month, 2 months, 3 months, 6 months, 9 months and 12 months.

CUSTOMER BANK

ISLAM

Property

Property

2. Property Purchase Agreement (Deferred)

1. Property Sale Agreement (Cash)

4. Rate Variable Rates i.e

Ceiling Rate BFR + 4 or 10% whichever is higher. This rate is used to calculate the Selling Price. Effective Rate To be pegged to the Bank's Cost of Funds (COF) plus a credit spread. COF is made up of KLIBOR plus (liquidity and reserve costs etc) plus margin.

4. KAFALAH BANK GUARANTEE–i

Under Kafalah concept the bank undertakes to pay an agreed sum to the beneficiary in

the event of customer fails to honor his/her obligation in accordance with the terms and

conditions the guarantee/agreement/contract.

Currently the company (PFM) is enjoying bank guarantee amounting USD 10.00 Million,

with tenor of 3 years, having an outstanding balance equal to USD 6.0 Million, so

Islamic bank guarantee can replace its existing conventional facility.

Basic Features:

1.Shariah Principle

Kafalah- Surety given by one party who agrees to discharge

a liability of a third party in case the third party defaults in fulfilling his

obligation.

2.Purpose/type Tender, performance, payment, shipping Guarantee etc.

3.Facility limit As requested by customer and approved by the bank.

4. Duration Depending on requirement.

5. Fee/commission 0.12% p.m or ABM/AIBIM rate.

6.Security/

Guarantee

10% Security Deposit, Assignment of contract, Director's Guarantee,

Charge on property or other collateral acceptable to the bank.

7. Documentation Facility Agreement, Guarantee and charge document.

Flowchart of Bank Guarantee -i

Secured a contract

1. Apply for BG-i

Beneficiary Customer

Bank

3. In the event the customer defaults, beneficiary claims from the bank

2. Issue BG-I favoring beneficiary

5. TRADE FINANCE

The Bank may provide specific facilities and/or financing mostly on short-term basis for

the purpose of facilitating trade or working capital for its customers. This

facilities/financing may be granted in connection with the purchase/import and

sale/export of goods and machinery, and the acquisition and holding of stock and

inventories, spares and replacements, raw materials and semi-finished goods.

Mixture of shariah principles or contracts applied to the products such as Wakalah,

Musyarakah, Murabahah, kafalah, Al-sarf and Bai’ Al-dayn. The facilities/financing

currently provided includes:

Letter of Credit under the principle of Al-Wakalah

Letter of Credit Under The Principle of Al-Musyarakah

Letter of Credit under the Principle of Al-Murabahah

Trust receipt (TR-i) under principle of Murabahah

Shipping Guarantee (SG-i) under Kafalah concept

Conclusion

With increasing maturity of Islamic finance, the differences between Islamic and

Conventional loan products have narrowed significantly.

I f inal ly advocate the company (PFM) to replace its existing conventional

financial facilities with the Shariah compliant financial facilities. This practice will

facilitate the company to generate profit under shari’ah based financing products and

be one of companies which enjoy Shariah Compliant stock instead to be an interest-

based financing products company.