Offering Circular - India INX

744

NOTICE THIS OFFERING IS AVAILABLE ONLY TO INVESTORS WHO ARE OUTSIDE THE UNITED STATES IN ACCORDANCE WITH REGULATION S (AS DEFINED BELOW). IMPORTANT: You must read the following before continuing. The following applies to the offering circular (the “Offering Circular”) following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the Offering Circular. In accessing the Offering Circular, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933 (THE “SECURITIES ACT”), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S., EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORISED AND WILL NOT BE ABLE TO PURCHASE ANY OF THE SECURITIES DESCRIBED IN THE OFFERING CIRCULAR. Confirmation of your Representation: The Offering Circular is being sent at your request and by accepting the e-mail and accessing the Offering Circular, you shall be deemed to have represented to us that the electronic mail address that you gave us and to which this e-mail has been delivered is not located in the United States and that you consent to delivery of such Offering Circular by electronic transmission. The attached Offering Circular is being furnished in connection with an offshore transaction as defined in the Securities Act in compliance with Regulation S under the Securities Act (“Regulation S”). You are reminded that the Offering Circular has been delivered to you on the basis that you are a person into whose possession the Offering Circular may be lawfully delivered in accordance with the laws of jurisdiction in which you are located and you may not, nor are you authorised to, deliver the Offering Circular to any other person. The materials relating to any offering of securities described in the Offering Circular do not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensed broker or dealer and the underwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction, the offering shall be deemed to be made by the underwriters or such affiliate on behalf of the relevant Issuer in such jurisdiction.

-

Upload

khangminh22 -

Category

Documents

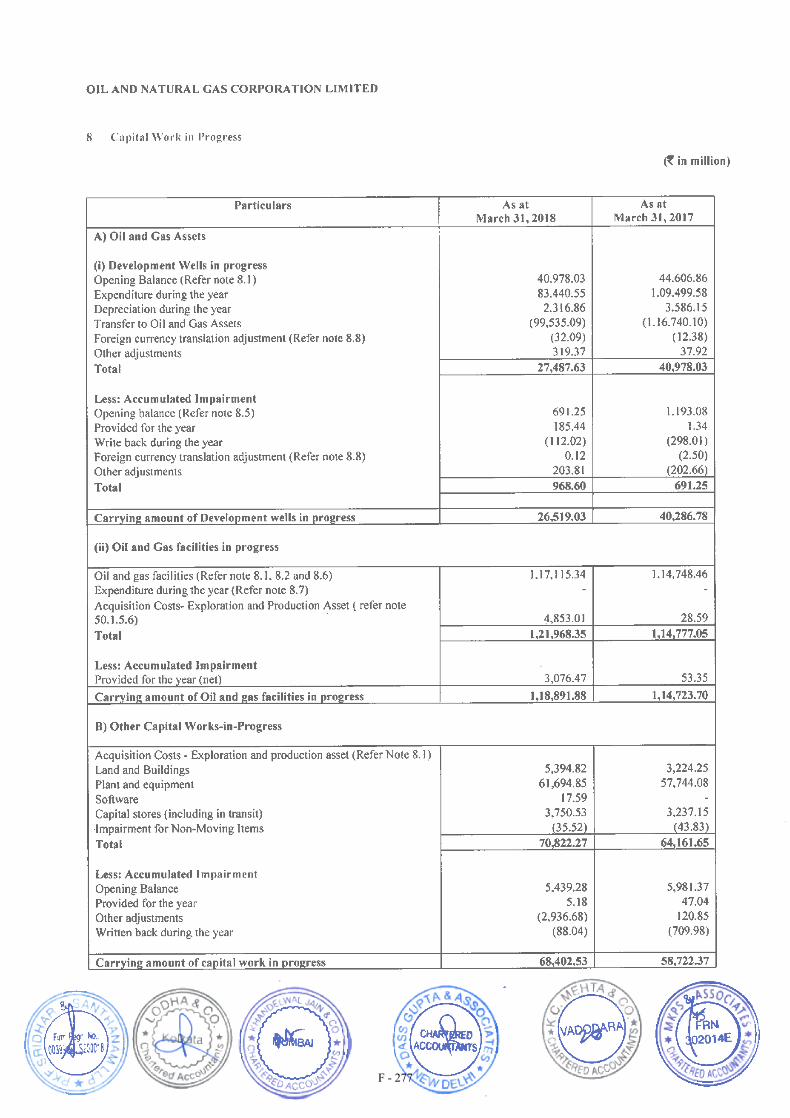

-

view

1 -

download

0

Transcript of Offering Circular - India INX

NOTICE

THIS OFFERING IS AVAILABLE ONLY TO INVESTORS WHO ARE OUTSIDE THE

UNITED STATES IN ACCORDANCE WITH REGULATION S (AS DEFINED BELOW).

IMPORTANT: You must read the following before continuing. The following applies to the offering

circular (the “Offering Circular”) following this page, and you are therefore advised to read this carefully

before reading, accessing or making any other use of the Offering Circular. In accessing the Offering Circular,

you agree to be bound by the following terms and conditions, including any modifications to them any time

you receive any information from us as a result of such access.

NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF

SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT

IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE,

REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933 (THE “SECURITIES ACT”), OR THE

SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE

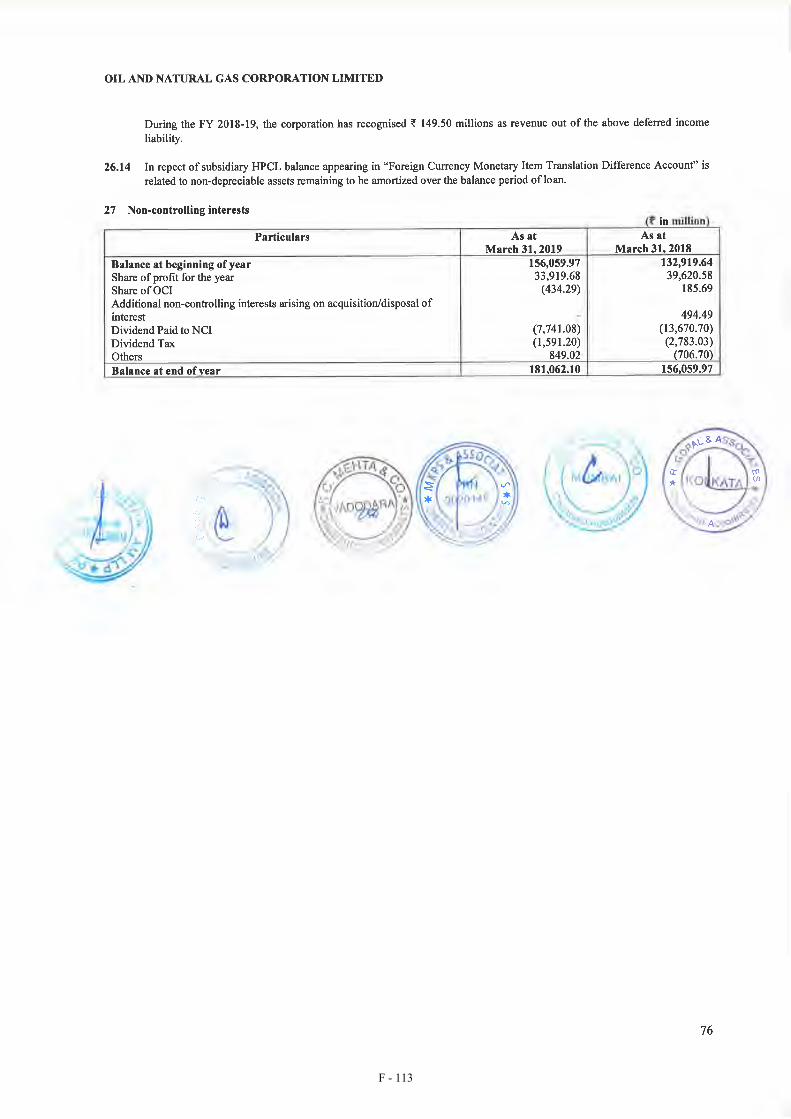

SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S., EXCEPT PURSUANT TO AN

EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION

REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL

SECURITIES LAWS.

THE OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY

OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN

PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. ADDRESS. ANY FORWARDING,

DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS

UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A

VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER

JURISDICTIONS. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO

ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORISED AND WILL NOT BE

ABLE TO PURCHASE ANY OF THE SECURITIES DESCRIBED IN THE OFFERING CIRCULAR.

Confirmation of your Representation: The Offering Circular is being sent at your request and by

accepting the e-mail and accessing the Offering Circular, you shall be deemed to have represented to us that the

electronic mail address that you gave us and to which this e-mail has been delivered is not located in the United

States and that you consent to delivery of such Offering Circular by electronic transmission. The attached

Offering Circular is being furnished in connection with an offshore transaction as defined in the Securities Act

in compliance with Regulation S under the Securities Act (“Regulation S”).

You are reminded that the Offering Circular has been delivered to you on the basis that you are a person

into whose possession the Offering Circular may be lawfully delivered in accordance with the laws of

jurisdiction in which you are located and you may not, nor are you authorised to, deliver the Offering Circular

to any other person.

The materials relating to any offering of securities described in the Offering Circular do not constitute,

and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are

not permitted by law. If a jurisdiction requires that the offering be made by a licensed broker or dealer and the

underwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction, the offering

shall be deemed to be made by the underwriters or such affiliate on behalf of the relevant Issuer in such

jurisdiction.

As per the provisions of applicable Indian regulations, only investors that are compliant with the ECB

Investor Requirements (as defined in the Offering Circular) are eligible to purchase the Indian Issuer Notes (as

defined in the Offering Circular) issued by the relevant Domestic Issuer (as defined in the Offering Circular).

This Offering Circular is being sent at your request and by accepting the e-mail and accessing this Offering

Circular you shall be deemed to have represented to us that you meet the ECB Investor Requirements.

The Offering Circular has not been and will not be registered, produced or made available to all as an

offer document (whether a prospectus in respect of a public offer or an information memorandum or private

placement offer letter or other offering material in respect of any private placement under the Companies Act,

2013 or any other applicable Indian laws) with the Registrar of Companies of India or the Securities and

Exchange Board of India or the Reserve Bank of India or any other statutory or regulatory body of like nature

in India, save and except for any information from any part of this Offering Circular which is mandatorily

required to be disclosed or filed in India under any applicable Indian laws, including, but not limited to, the

Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations 2015, as amended, and

under the listing agreement(s) with any Indian stock exchange pursuant to the Securities and Exchange Board

of India (Listing Obligations and Disclosure Requirements) Regulations 2015, as amended, or pursuant to the

sanction of any regulatory and adjudicatory body in India. The Offering Circular or any other offering document

or material relating to the Notes has not been and will not be circulated or distributed, directly or indirectly, to

any person or the public in India or otherwise generally distributed or circulated in India which would constitute

an advertisement, invitation, offer, sale or solicitation of an offer to subscribe for or purchase any securities in

violation of applicable Indian laws for the time being in force.

The Offering Circular has been sent to you in an electronic form. You are reminded that documents

transmitted via this medium may be altered or changed during the process of electronic transmission and

consequently none of the Issuers (as defined in the Offering Circular), the Guarantor (as defined in the Offering

Circular), Citigroup Global Markets Limited (“Citigroup”), Standard Chartered Bank (Singapore) Limited

(together with Citigroup, the “Arrangers” and the “Dealers”) nor any person who controls each of them nor

any director, officer, employee nor agent of each of them or affiliate of any such person accepts any liability or

responsibility whatsoever in respect of any difference between the Offering Circular distributed to you in

electronic format and the hard copy version available to you on request from the Arrangers and the Dealers.

Actions that you may not take: if you receive this document by e-mail, you should not reply by e-mail

to this notice, and you may not purchase any securities by doing so. Any reply e-mail communications, including

those you generate by using the “Reply” function on your e-mail software, will be ignored or rejected.

You are responsible for protecting against viruses and other destructive items. Your use of this e-

mail is at your own risk and it is your responsibility to take precautions to ensure that it is free from viruses and

other items of a destructive nature.

OFFERING CIRCULAR

OIL AND NATURAL GAS CORPORATION LIMITED(incorporated with limited liability in the Republic of India)

ONGC VIDESH LIMITED(incorporated with limited liability in the Republic of India)

U.S.$2,000,000,000Medium Term Note Programme

Under the U.S.$2,000,000,000 Euro Medium Term Note Programme (the “Programme”), Oil and Natural Gas Corporation Limited (“ONGC”), ONGC Videsh Limited (“ONGC Videsh”) and any New Issuer (as defined in the terms and conditions of the Notes (the “Terms and Conditions of the Notes”)) (the “Issuers”, and each an “Issuer”), subject to compliance with all relevant laws, regulations and directives, may from time to time issue notes (“Notes”) denominated in any currency agreed between the relevant Issuer and the relevant Dealer (as defined below). Notes issued by ONGC Videsh and any New Issuer (each a “Guaranteed Issuer”) will be guaranteed by ONGC (in such capacity, the “Guarantor”), such guarantee (the “Guarantee”) and such Notes (the “Guaranteed Notes”), provided that, at all times, the Guarantee shall, in respect of each Series of Guaranteed Notes, be in respect of an amount not exceeding 109.00 per cent. of the total aggregate nominal amount of such Series of Guaranteed Notes outstanding from time to time (the “Applicable Limit”). The aggregate nominal amount of Notes outstanding will not at any time exceed U.S.$2,000,000,000 (or its equivalent in other currencies calculated as described herein), subject to increase as described herein.

The Programme Agreement, the Trust Deed and the Agency Agreement (each as defined herein) each contain provisions enabling ONGC, from time to time, to nominate any Subsidiary (as defined in the Terms and Conditions of the Notes) of ONGC Videsh to accede as an issuer to issue Notes under the Programme. In such event, ONGC, ONGC Videsh and such New Issuer shall make available a supplemental Offering Circular in relation to such accession. Unless and until a supplemental Offering Circular is published providing details of the accession of such New Issuer, references in this Offering Circular to “the Issuer” or “Issuers” should be taken as references to ONGC and ONGC Videsh, as applicable, only.

The Notes may be issued on a continuing basis to one or more of the Dealers specified under the section entitled “Summary of the Programme” and any further Dealer appointed under the Programme from time to time by the relevant Issuer(s) (each a Dealer and together the Dealers), which appointment may be for a specific issue or on an ongoing basis. References in this Offering Circular to the relevant Dealer shall, in the case of an issue of Notes being (or intended to be) subscribed by more than one Dealer, be to all Dealers agreeing to subscribe to such Notes.

Approval in-principle has been received from the Singapore Exchange Securities Trading Limited (the “SGX-ST”) for the establishment of the Programme and application will be made to the SGX-ST for the permission to deal in, and for the quotation of, any Notes that may be issued pursuant to the Programme and which are agreed at or prior to the time of issue thereof to be so listed on the SGX-ST. Such permission will be granted when such Notes have been admitted to the Official List of the SGX-ST. The SGX-ST assumes no responsibility for the correctness of any of the statements made or opinions expressed or reports contained herein. Admission to the Official List and quotation of any Notes on the SGX-ST are not to be taken as an indication of the merits of the Issuers, the Guarantor, their subsidiaries, their associated companies, the Programme or the Notes. Notice of the aggregate nominal amount of Notes, interest (if any) payable in respect of Notes, the issue price of Notes and any other terms and conditions not contained herein which are applicable to each Tranche (as defined in the Terms and Conditions of the Notes) of Notes will be set out in a pricing supplement (the “Pricing Supplement”) which, with respect to Notes to be listed on the SGX-ST, will be delivered to the SGX-ST on or before the date of issue of the Notes of such Tranche.

The Programme provides that Notes may be listed on such other or further stock exchange(s) as may be agreed between the relevant Issuer, (in the case of Guaranteed Notes) the Guarantor and the relevant Dealer. The Issuers may also issue unlisted Notes.

The Issuers and (in the case of Guaranteed Notes) the Guarantor may agree with any Dealer and Citicorp International Limited as trustee (the “Trustee”) that Notes may be issued in a form not contemplated by the Terms and Conditions of the Notes, in which event (in the case of Notes intended to be listed on the SGX-ST) a supplementary Offering Circular, if appropriate, will be made available which will describe the effect of the agreement reached in relation to such Notes.

Investing in Notes issued under the Programme involves certain risks and may not be suitable for all investors. Prospective investors should have sufficient knowledge and experience in financial and business matters to evaluate the information contained in this Offering Circular and in the relevant Pricing Supplement and the merits and risks of investing in a particular issue of Notes in the context of their financial position and particular circumstances. Prospective investors should have regard, inter alia, to the factors described in the section entitled “Investment Considerations”.

Notes to be listed on the SGX-ST will be accepted for clearance through Euroclear Bank SA/NV (“Euroclear”) and Clearstream Banking S.A. (“Clearstream, Luxembourg”).

The Notes may be issued in bearer form (“Bearer Notes”) or in registered form (“Registered Notes”). Each Tranche of Bearer Notes of each Series (as defined in the section entitled “Form of the Notes”) will initially be represented by either a temporary bearer global note (a “Temporary Bearer Global Note”) or a permanent bearer global note (a “Permanent Bearer Global Note” and, together with a Temporary Bearer Global Note, the “Bearer Global Notes”, and each a “Bearer Global Note”) as indicated in the applicable Pricing Supplement, which, in either case, will be delivered on or prior to the original issue date of the Tranche to a common depositary for Euroclear and Clearstream, Luxembourg. On and after the date (the “Exchange Date”) which, for each Tranche in respect of which a Temporary Bearer Global Note is issued, is 40 days after the Temporary Bearer Global Note is issued, interests in such Temporary Bearer Global Note will be exchangeable (free of charge) upon a request as described therein either for (i) interests in a Permanent Bearer Global Note of the same Series or (ii) definitive Bearer Notes of the same Series.

Registered Notes sold in an “offshore transaction” within the meaning of Regulation S (“Regulation S”) under the U.S. Securities Act of 1933 (the “Securities Act”), which will be sold outside the United States (“U.S.”), will initially be represented by a global note in registered form, without receipts or coupons, (a “Registered Global Note”) deposited with a common depositary for Euroclear and Clearstream, Luxembourg, and registered in the name of a nominee of such common depositary.

The applicable Pricing Supplement will specify that a Permanent Bearer Global Note will be exchangeable for definitive Bearer Notes in certain limited circumstances.

This Offering Circular has not been and will not be registered as a prospectus or a statement in lieu of a prospectus in respect of a public offer, information memorandum or private placement offer letter or any other offering material with the Registrar of Companies of India (the “RoC”) in accordance with the Companies Act, 2013, as amended from time to time (the “Companies Act 2013”), and other applicable Indian laws for the time being in force. This Offering Circular has not been and will not be reviewed or approved by any regulatory or statutory authority in India, including, but not limited to, the Securities and Exchange Board of India, the Reserve Bank of India, any Registrar of Companies or any stock exchange in India. This Offering Circular and the Notes are not and should not be construed as an advertisement, invitation, offer or sale of any securities whether to the public or by way of private placement to any person resident in India. The Notes have not been and will not be, offered or sold to any person resident in India. If you purchase any of the Notes, you will be deemed to have acknowledged, represented and agreed that you are eligible to purchase the Notes under applicable laws and regulations and that you are not prohibited under any applicable law or regulation from acquiring, owning or selling the Notes.

The Notes and the Guarantee have not been and will not be registered under the Securities Act or with any securities regulatory authority of any state or other jurisdiction of the United States, and the Notes may include Bearer Notes that are subject to U.S. tax law requirements and restrictions. Subject to certain exceptions, the Notes may not be offered, sold or in the case of Bearer Notes, delivered within the United States. The Notes are subject to certain restrictions on transfer, for further information see the section entitled “Subscription and Sale”. The Notes are being offered outside the United States in reliance on Regulation S under the Securities Act.

Notes issued under the Programme may be rated or unrated. Where a Tranche of Notes is to be rated, its rating will not necessarily be the same as the rating (if any) applicable to the Programme and (where applicable) such rating will be specified in the applicable Pricing Supplement. A rating is not a recommendation to buy, sell or hold securities and may be subject to suspension, change or withdrawal at any time by the assigning rating agency.

Arrangers and Dealers

Citigroup Standard Chartered Bank

The date of this Offering Circular is 27 August 2019.

A39729228 i

NOTICE TO INVESTORS

Each Issuer and the Company accepts responsibility for the information contained in this Offering

Circular. To the best of the knowledge and belief of each Issuer and the Company (each having taken all

reasonable care to ensure that such is the case) the information contained in this Offering Circular is in

accordance with the facts and does not omit anything that would make the statements therein, in light of the

circumstances under which they were made, misleading. Each Issuer and the Company, having made all

reasonable enquiries, confirms that this Offering Circular contains or incorporates all information which is

material in the context of the Programme and the Notes, that the information contained or incorporated in this

Offering Circular is true and accurate in all material respects and is not misleading, that the opinions and

intentions expressed in this Offering Circular are honestly held and that there are no other facts the omission of

which would make this Offering Circular or any of such information or the expression of any such opinions or

intentions misleading. Each Issuer and the Company accepts responsibility accordingly.

This Offering Circular is to be read in conjunction with all documents which are deemed to be

incorporated herein by reference (for further information, see the section entitled “Documents Incorporated by

Reference”). This Offering Circular shall be read and construed on the basis that such documents are

incorporated and form part of this Offering Circular.

No person is or has been authorised by any of the Issuers or the Company to give any information or to

make any representation other than those contained in this Offering Circular or any other information supplied

in connection with the Programme or the Notes and, if given or made by any other person, such information or

representations must not be relied upon as having been authorised by any Issuer, the Company, any of the

Arrangers or the Dealers, the Trustee or the Agents (as defined in the Terms and Conditions of the Notes) or

any person who controls any of them, or any of their respective officers, employees, advisers or agents, or any

affiliate of any such person. Save as expressly stated in this Offering Circular, nothing contained herein is, or

may be relied upon as, a promise or representation as to the future performance or policies of the Issuers or the

Company.

The Arrangers, the Dealers, the Trustee and the Agents have not separately verified the information

contained in this Offering Circular. None of the Arrangers, the Dealers, the Trustee, the Agents or any person

who controls any of them, or any of their respective officers, employees, advisers or agents, or any affiliate of

any such person, is making any representation or warranty expressed or implied as to the merits of the Notes or

the subscription for, purchase or acquisition thereof, the creditworthiness or financial condition or otherwise of

the Issuer. Further, none of the Arrangers, the Dealers, the Trustee or the Agents or any person who controls any

of them, or any of their respective officers, employees, advisers or agents, or any affiliate of any such person,

makes any representation or warranty as to the Issuers or the Company or as to the accuracy, reliability or

completeness of the information set out herein and the documents which are incorporated by reference in, and

form part of, this Offering Circular.

To the fullest extent permitted by law, none of the Arrangers, the Dealers, the Trustee, the Agents or any

person who controls any of them, or any of their respective officers, employees, advisers or agents, or any

affiliate of any such person, accepts any responsibility for the contents of this Offering Circular or for any other

statement made or purported to be made by the Arrangers, the Dealers, the Trustee or the Agents or on their

behalf in connection with the Issuers, the Company, the Programme or the issue and offering of the Notes. Each

of the Arrangers, each Dealer, the Trustee and each Agent and each person who controls any of them, and each

of their respective officers, employees, advisers and agents, and each affiliate of any such person, accordingly

disclaims all and any liability whether arising in tort or contract or otherwise (save as referred to above) which

it might otherwise have in respect of this Offering Circular or any such statement.

A39729228 ii

Neither the delivery of this Offering Circular (or any part thereof) nor any sale, offering or purchase

made in connection herewith shall, under any circumstances, create any implication that there has been no

change in the prospects, results of operation or general affairs of the Issuers or the Company since the date

hereof or the date upon which this Offering Circular has been most recently amended or supplemented or that

there has been no adverse change in the financial position of the Issuers or the Company since the date hereof

or the date upon which this Offering Circular has been most recently amended or supplemented or that any

other information supplied in connection with the Programme is correct as of any time subsequent to the date

on which it is supplied or, if different, the date indicated in the document containing the same. Investors should

review, inter alia, the most recently published documents incorporated by reference into this Offering Circular

when deciding whether or not to purchase any Notes.

This Offering Circular does not constitute an offer to sell or the solicitation of an offer to buy any Notes

in any jurisdiction to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction.

The distribution of this Offering Circular and the offer or sale of Notes may be restricted by law in certain

jurisdictions. The Issuers, the Company, the Arrangers, the Dealers, the Trustee, the Agents and any person who

controls any of them, and each of their respective officers, employees, advisers and agents, and each affiliate of

any such person, do not represent that this Offering Circular may be lawfully distributed, or that any Notes may

be lawfully offered, in compliance with any applicable registration or other requirements in any such

jurisdiction, or pursuant to an exemption available thereunder, or assume any responsibility for facilitating any

such distribution or offering. In particular, no action has been taken by any of the Issuers, the Company, any of

the Arrangers or the Dealers, the Trustee or the Agents or any person who controls any of them, or any of their

respective officers, employees, advisers or agents, or any affiliate of any such person, which would permit a

public offering of any Notes or distribution of this Offering Circular in any jurisdiction where action for that

purpose is required. Accordingly, no Notes may be offered or sold, directly or indirectly, and neither this

Offering Circular nor any advertisement or other offering material may be distributed or published in any

jurisdiction, except under circumstances that will result in compliance with any applicable laws and regulations.

Persons into whose possession this Offering Circular or any Notes may come must inform themselves about,

and observe, any such restrictions on the distribution of this Offering Circular and the offering and sale of Notes.

In particular, there are restrictions on the distribution of this Offering Circular and the offer or sale of Notes in

the United States, the European Economic Area, the United Kingdom, the Republic of Italy, India, Japan,

Singapore and Hong Kong, for further information, see the section entitled “Subscription and Sale”.

In accordance with applicable provisions of Indian regulations, only investors that meet the ECB

Investor Requirements (as defined in this Offering Circular) are eligible to purchase or subscribe to the Indian

Issuer Notes issued by a Domestic Issuer. By purchasing the Indian Issuer Notes, each investor shall be deemed

to have acknowledged, represented and agreed that such investor is eligible to purchase such Indian Issuer Notes

issued by a Domestic Issuer under applicable laws and regulations and meets the ECB Investor Requirements

and is not otherwise prohibited under any applicable law or regulation from acquiring, owning or selling the

Indian Issuer Notes and that so long as it holds any of the Indian Issuer Notes, it will continue to meet the ECB

Investor Requirements and shall comply with applicable provisions of Indian regulations. For further

information, see the sections entitled “Summary of Relevant Indian Laws and Regulations – Foreign Exchange

Laws” and “Subscription and Sale”.

Neither this Offering Circular nor any other document or information (or any part thereof) delivered and

supplied under or in relation to the Programme or any Notes is intended to provide the basis of any credit or

other evaluation of the Issuer and should not be considered as a recommendation by any of the Issuers, the

Company, the Arrangers, the Dealers, the Trustee, the Agents or any person who controls any of them, or any

of their respective officers, employees, advisers or agents, or any affiliate of any such person, that any recipient

of this Offering Circular or any other financial statements should purchase the Notes. Each potential purchaser

of Notes shall make its own assessment of the foregoing and other relevant matters including the financial

A39729228 iii

condition and affairs and its appraisal of the creditworthiness of the Issuers and the Company and obtain its

own independent legal or other advice thereon, and its investment shall be deemed to be based on its own

independent investigation of the financial condition and affairs and its appraisal of the creditworthiness of the

Issuers and the Company. Accordingly, notwithstanding anything herein, none of the Arrangers, the Dealers,

the Trustee, the Agents or any person who controls any of them, or any of their respective officers, employees,

advisers or agents, or any affiliate of any such person, shall be held responsible for any loss or damage suffered

or incurred by the recipients of this Offering Circular or such other document or information (or such part

thereof) as a result of or arising from anything expressly or implicitly contained in or referred to in this Offering

Circular or such other document or information (or such part thereof and the same shall not constitute a ground

for rescission of any purchase or acquisition of any of the Notes by a recipient of this Offering Circular or such

other document or information (or such part thereof). None of the Arrangers, the Dealers, the Trustee or the

Agents or any person who controls any of them, or any of their respective officers, employees, advisers or

agents, or any affiliate of any such person, undertakes to review the financial condition or affairs of the Issuer

during the life of the arrangements contemplated by this Offering Circular nor to advise any investor or potential

investor in the Notes of any information coming to the attention of any of the Dealers, the Arrangers, the Trustee,

the Agents or any person who controls any of them, or any of their respective officers, employees, advisers or

agents, or any affiliate of any such person.

Any purchase or acquisition of the Notes is in all respects conditional on the satisfaction of certain

conditions set out in the Programme Agreement (as defined herein) and the issue of the Notes by the relevant

Issuer pursuant to the Programme Agreement. Any offer, invitation to offer or agreement made in connection

with the purchase or acquisition of the Notes or pursuant to this Offering Circular shall (without any liability or

responsibility) on the part of the relevant Issuer or any of the Arrangers or Dealers lapse and cease to have any

effect if (for any other reason whatsoever) the Notes are not issued by the relevant Issuer pursuant to the

Programme Agreement.

This Offering Circular does not describe all of the risks and investment considerations (including those

relating to each investor’s particular circumstances) of an investment in Notes of a particular issue. Each

potential purchaser of Notes should refer to and consider carefully the relevant Pricing Supplement for each

particular issue of Notes, which may describe additional risks and investment considerations associated with

such Notes. The risks and investment considerations identified in this Offering Circular and the relevant Pricing

Supplement are provided as general information only.

In making an investment decision, investors must rely on their own examination of the Issuers, the

Company and the terms of the Notes being offered, including the merits and risks involved. Investors should

consult their own financial, tax, accounting and legal advisers as to the risks and investment considerations

arising from an investment in an issue of Notes and should possess the appropriate resources to analyse such

investment and the suitability of such investment in their particular circumstances.

None of the Issuers, the Company, the Arrangers, the Dealers, the Trustee, the Agents or any person who

controls any of them, or any of their respective officers, employees, advisers or agents, or any affiliate of any

such person, makes any representation to any investor in the Notes regarding the legality of its investment under

any applicable laws. Any investor in the Notes should be able to bear the economic risk of an investment in the

Notes for an indefinite period of time.

EEA RETAIL INVESTORS

If the Pricing Supplement in respect of any Notes includes a legend entitled “Prohibition of Sales to EEA

Retail Investors”, the Notes are not intended to be offered, sold or otherwise made available to and should not

be offered, sold or otherwise made available to any retail investor in the European Economic Area (the “EEA”).

For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point

A39729228 iv

(11) of Article 4(1) of Directive 2014/65/EU (as amended, “MiFID II”); (ii) a customer within the meaning of

Directive (EU) 2016/97 (the “Insurance Distribution Directive”), where that customer would not qualify as a

professional client as defined in point (10) of Article 4(1) of MiFID II; or (iii) not a qualified investor as defined

in Regulation (EU) 2017/1129 (the “Prospectus Regulation”). Consequently, no key information document

required by Regulation (EU) No 1286/2014 (as amended, the “PRIIPs Regulation”) for offering or selling the

Notes or otherwise making them available to retail investors in the EEA has been prepared and therefore offering

or selling the Notes or otherwise making them available to any retail investor in the EEA may be unlawful under

the PRIIPs Regulation.

MIFID PRODUCT GOVERNANCE/TARGET MARKET

The Pricing Supplement in respect of any Notes may include a legend entitled “MiFID II Product

Governance” which will outline the target market assessment in respect of the Notes and which channels for

distribution of the Notes are appropriate. Any person subsequently offering, selling or recommending the Notes

(a “distributor”) should take into consideration the target market assessment; however, a distributor subject to

MiFID II is responsible for undertaking its own target market assessment in respect of the Notes (by either

adopting or refining the target market assessment) and determining appropriate distribution channels.

A determination will be made in relation to each issue about whether, for the purpose of the MiFID

Product Governance rules under EU Delegated Directive 2017/593 (the “MiFID Product Governance

Rules”), any Dealer subscribing for any Notes is a manufacturer in respect of such Notes, but otherwise none

of the Arrangers or the Dealers or any of their respective affiliates will be a manufacturer for the purpose of the

MiFID Product Governance Rules.

PRODUCT CLASSIFICATION PURSUANT TO SECTION 309B OF THE SECURITIES

AND FUTURES ACT (CHAPTER 289 OF SINGAPORE)

In connection with Section 309B of the Securities and Futures Act (Chapter 289) of Singapore, as

modified or amended from time to time (the “SFA”) and the Securities and Futures (Capital Markets Products)

Regulations 2018 of Singapore (the “CMP Regulations 2018”), unless otherwise specified before an offer of

Notes, the Issuers have determined, and hereby notifies all relevant persons (as defined in Section 309A(1) of

the SFA), that the Notes are ‘prescribed capital markets products’ (as defined in the CMP Regulations 2018)

and Excluded Investment Products (as defined in MAS Notice SFA 04-N12: Notice on the Sale of Investment

Products and MAS Notice FAA-N16: Notice on Recommendations on Investment Products).

STABILISATION

In connection with the issue of any Tranche of Notes, the Dealer or Dealers (if any) named as the

Stabilising Manager(s) (or persons acting on behalf of any Stabilising Manager(s)) in the applicable Pricing

Supplement may over-allot Notes or effect transactions with a view to supporting the market price of the Notes

of the Series (as defined below) of which such Tranche forms part at a level higher than that which might

otherwise prevail. However, stabilisation may not necessarily occur. Any stabilisation action or over-allotment

may begin on or after the date on which adequate public disclosure of the terms of the offer of the relevant

Tranche of Notes is made and, if begun, may cease at any time, but it must end no later than the earlier of 30

days after the issue date of the relevant Tranche of Notes and 60 days after the date of the allotment of the

relevant Tranche of Notes. Any stabilisation action or overallotment must be conducted by the relevant

Stabilising Manager(s) (or persons acting on behalf of any Stabilising Manager(s)) in accordance with all

applicable laws and rules.

A39729228 v

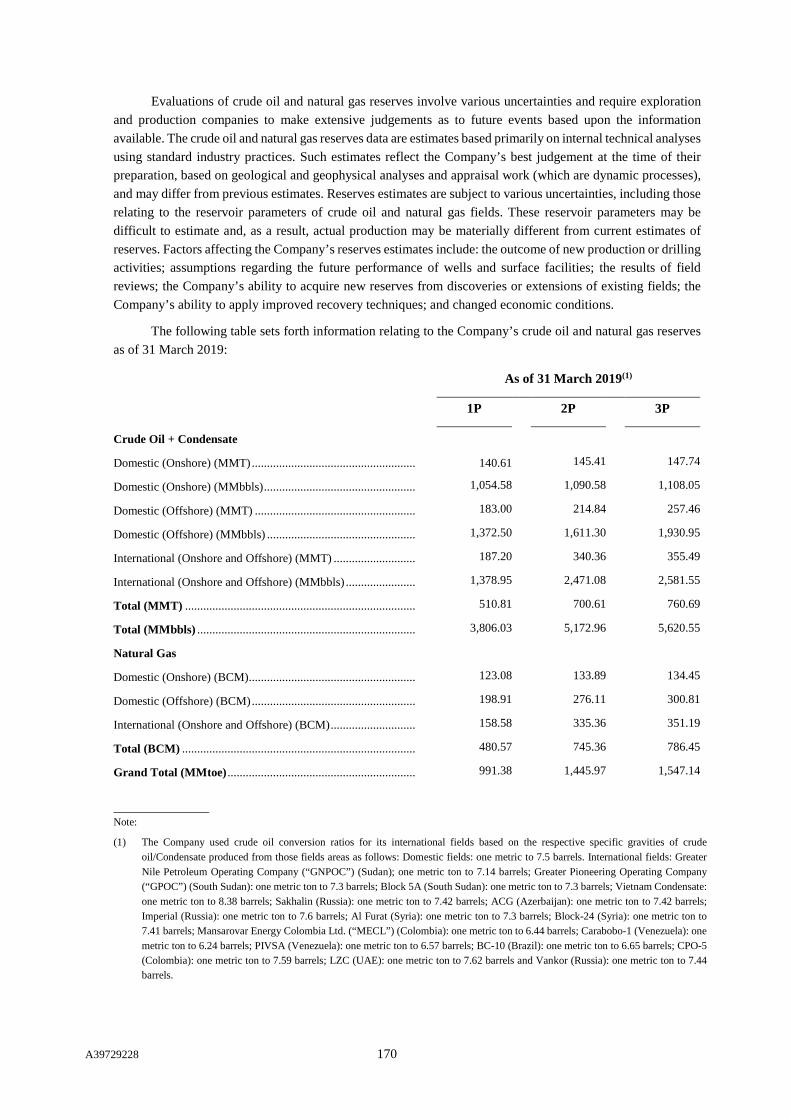

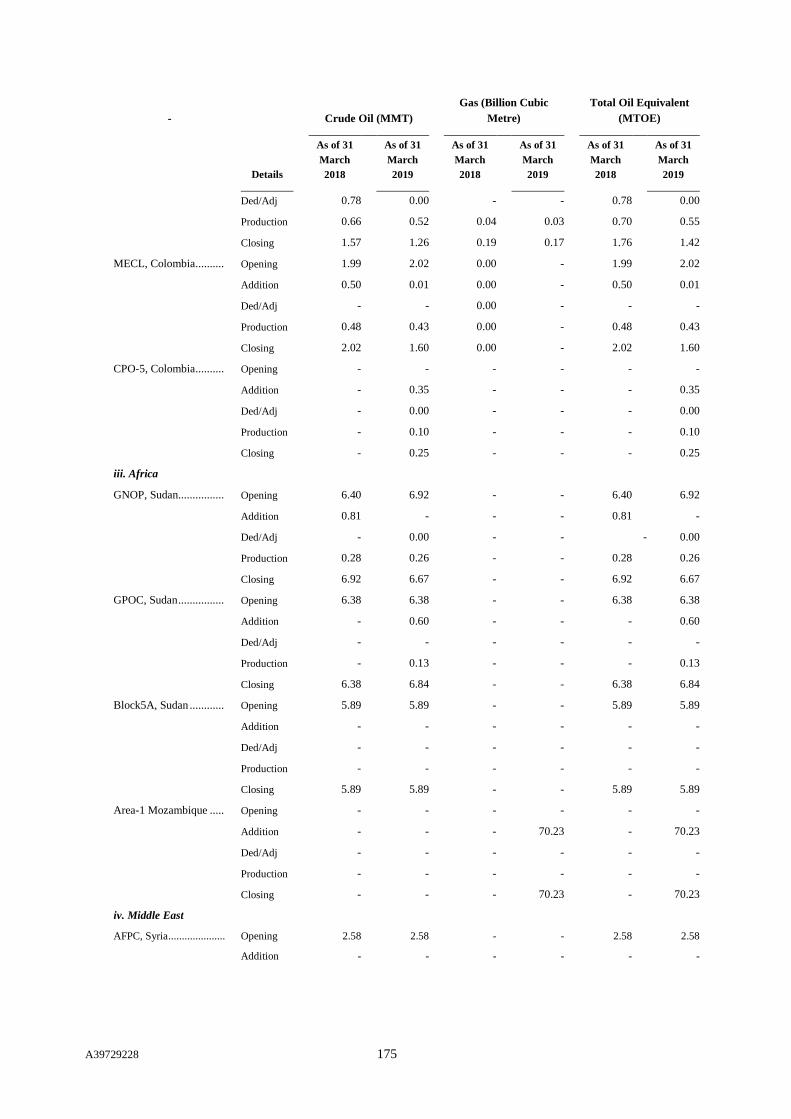

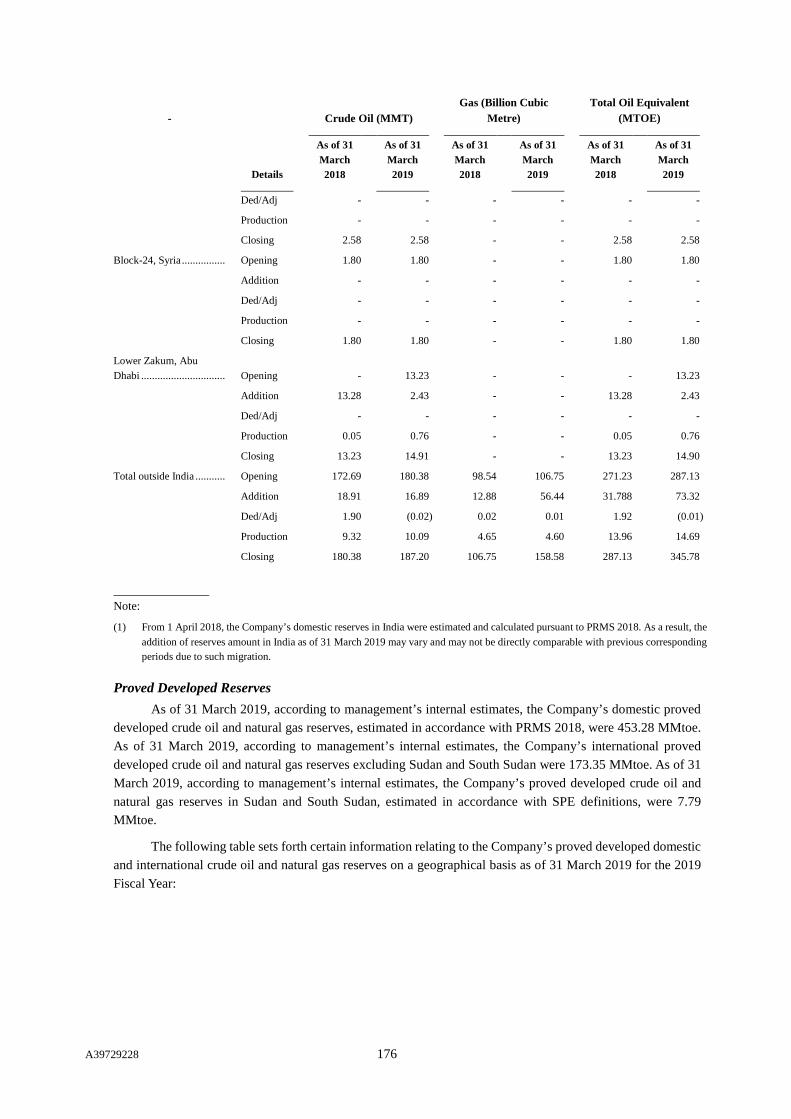

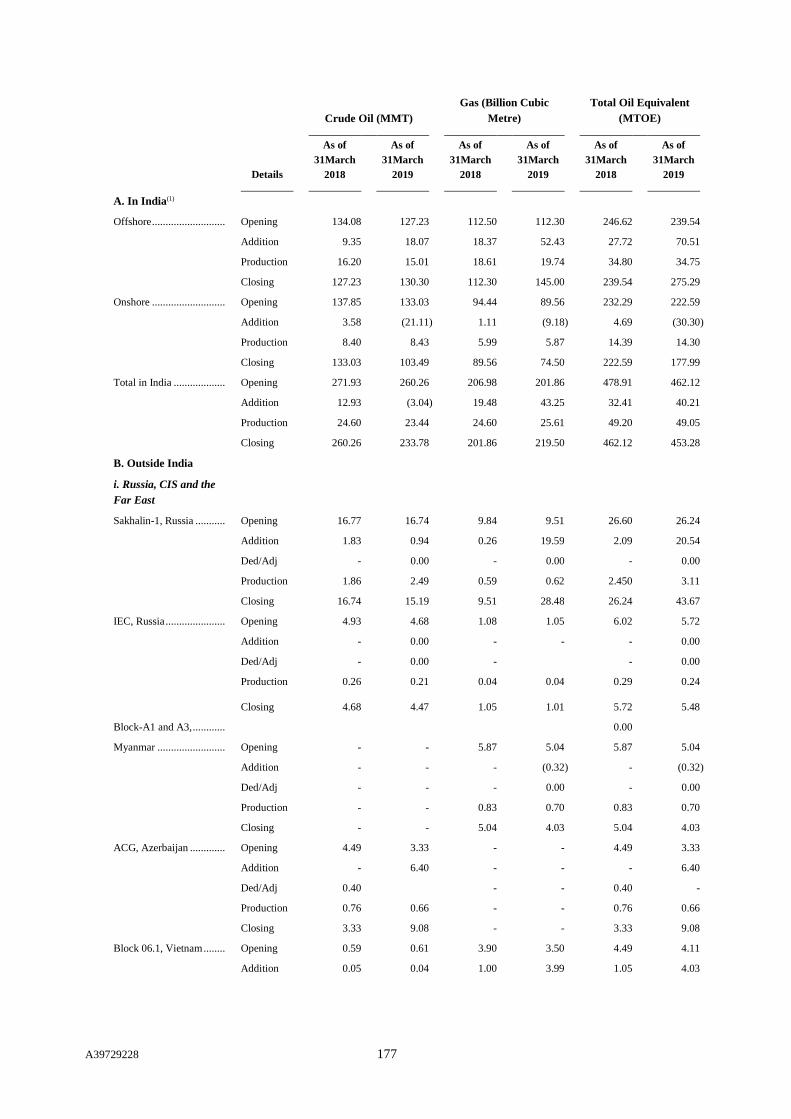

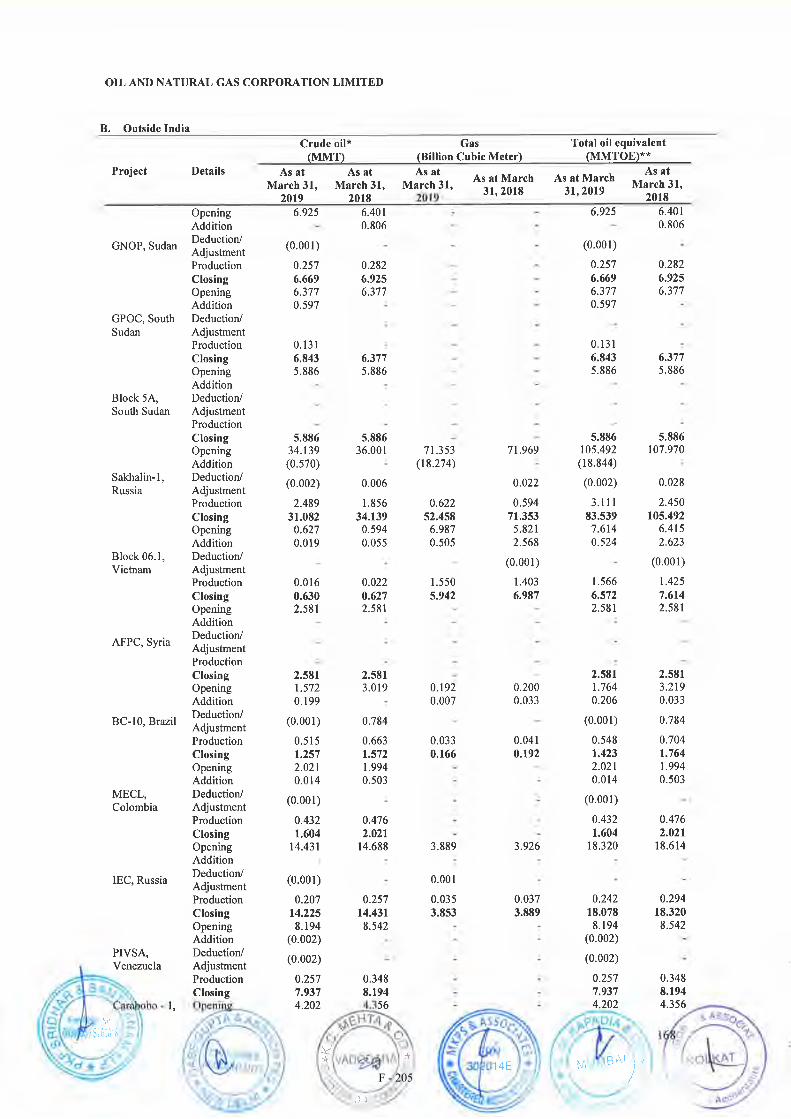

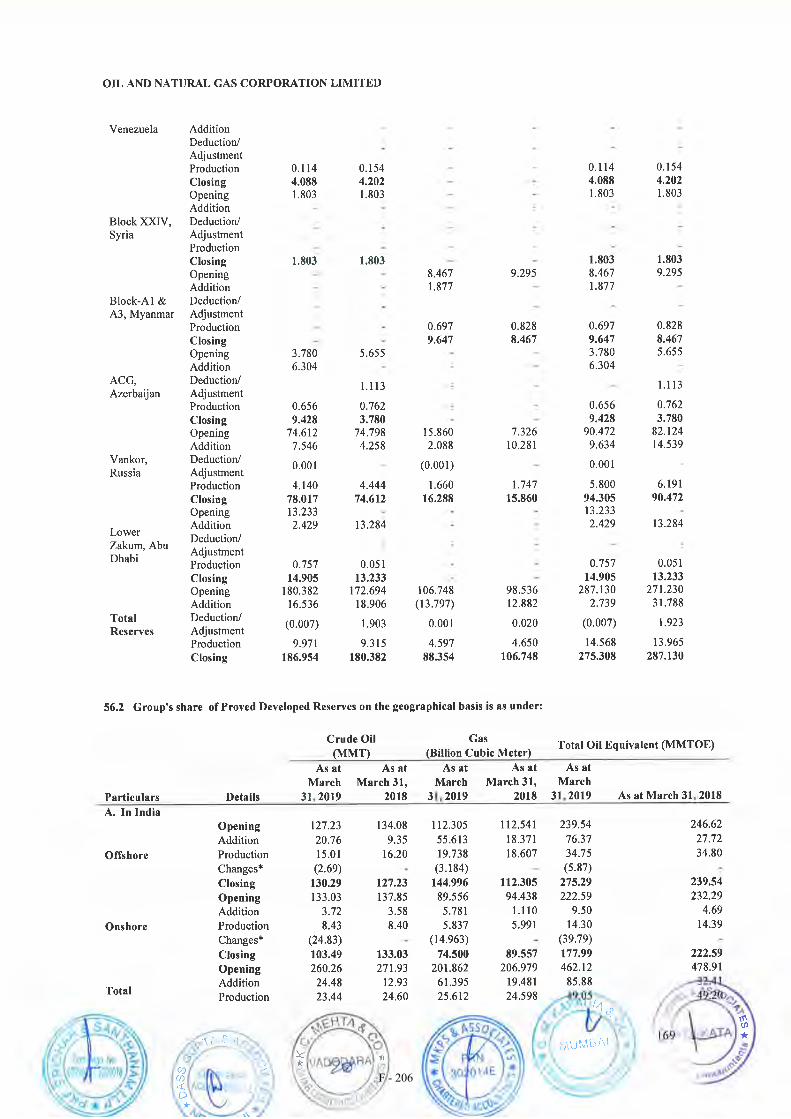

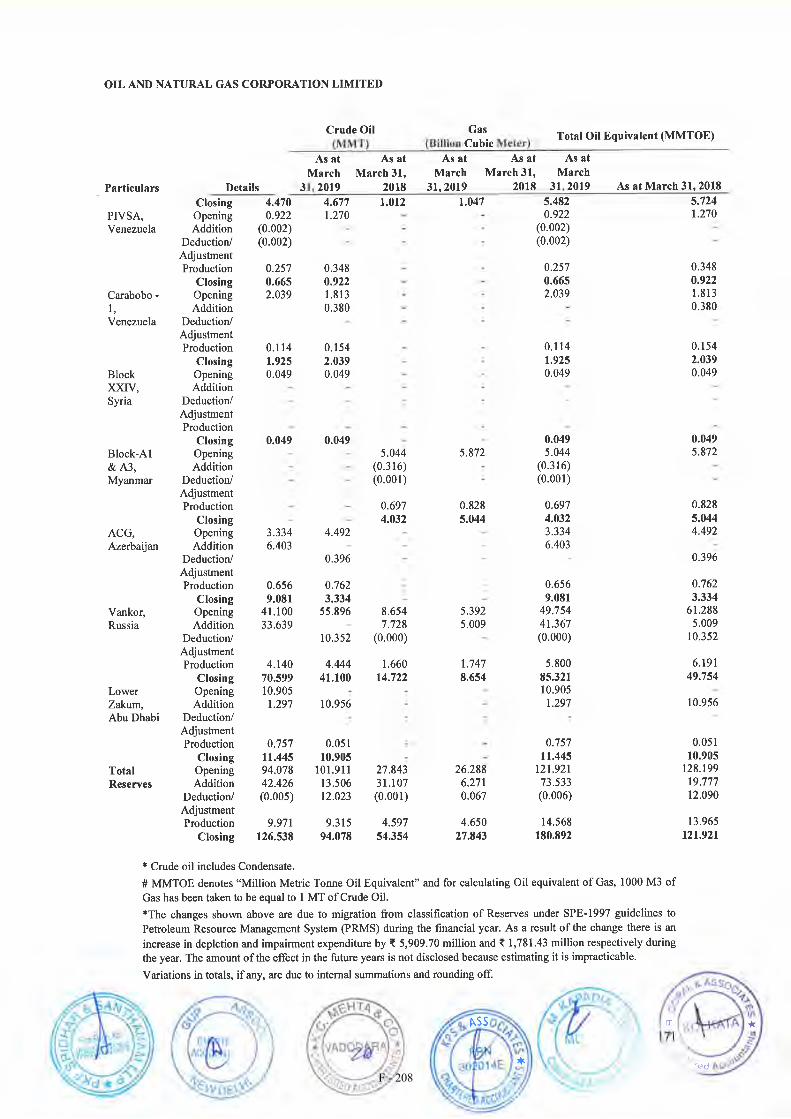

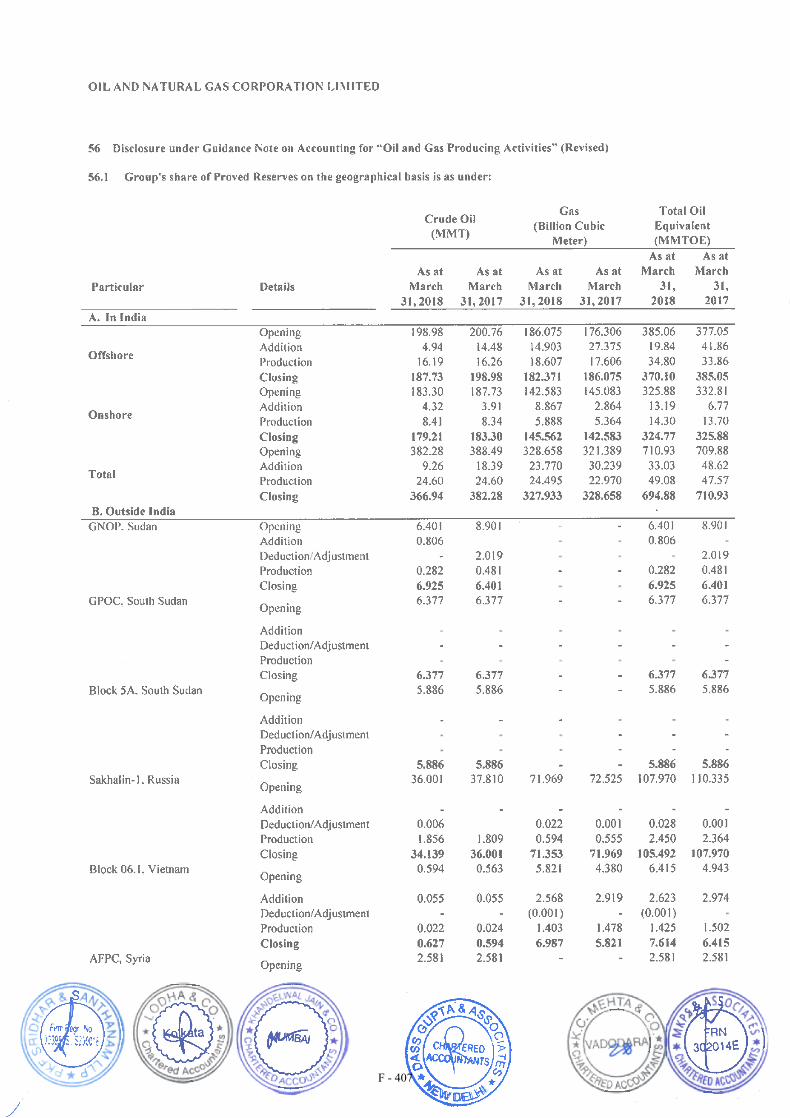

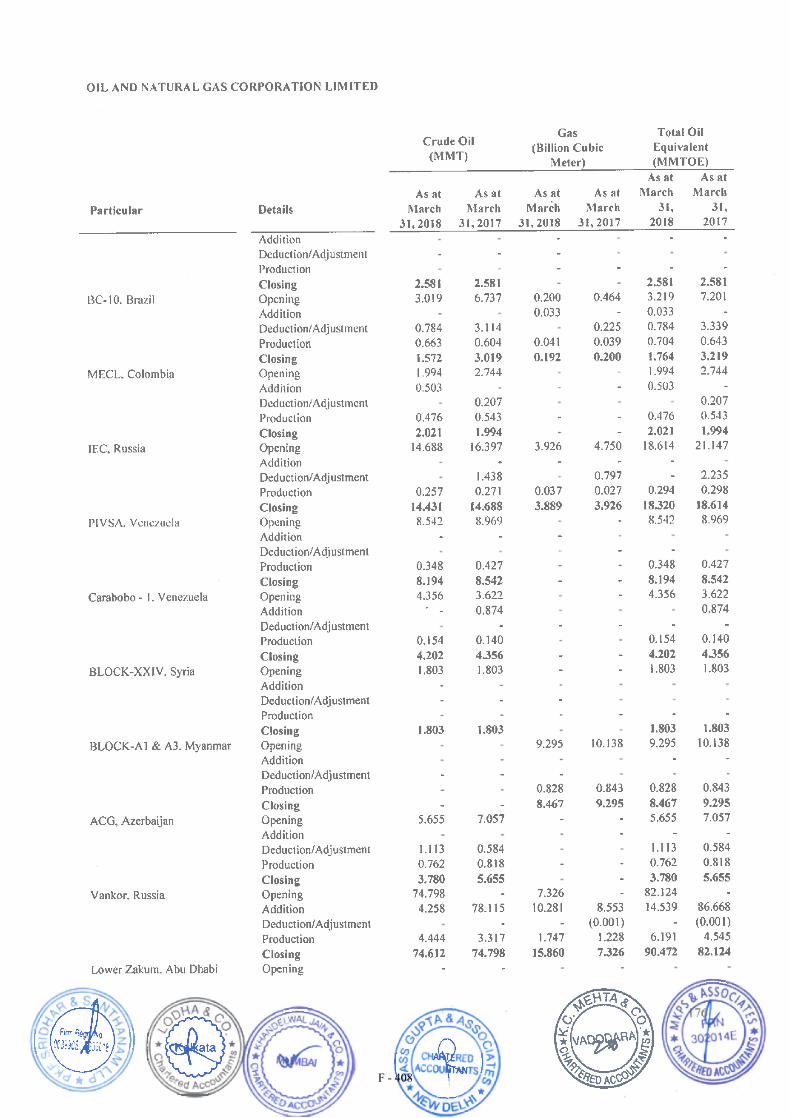

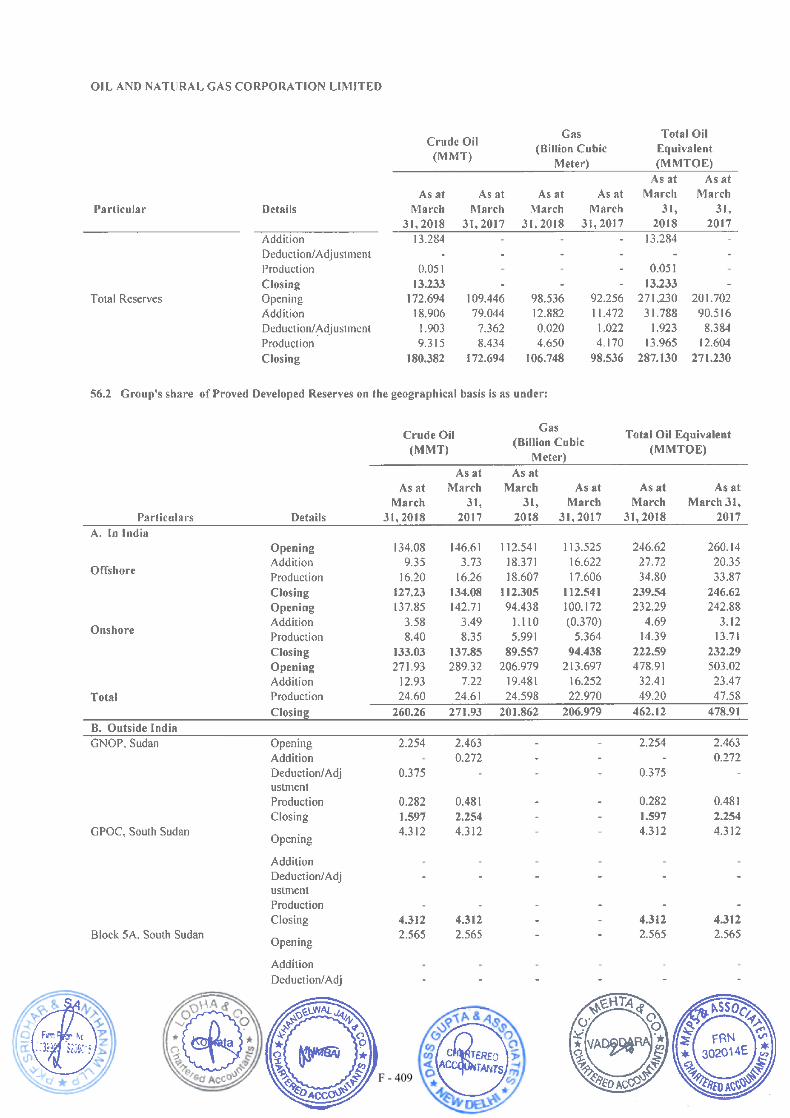

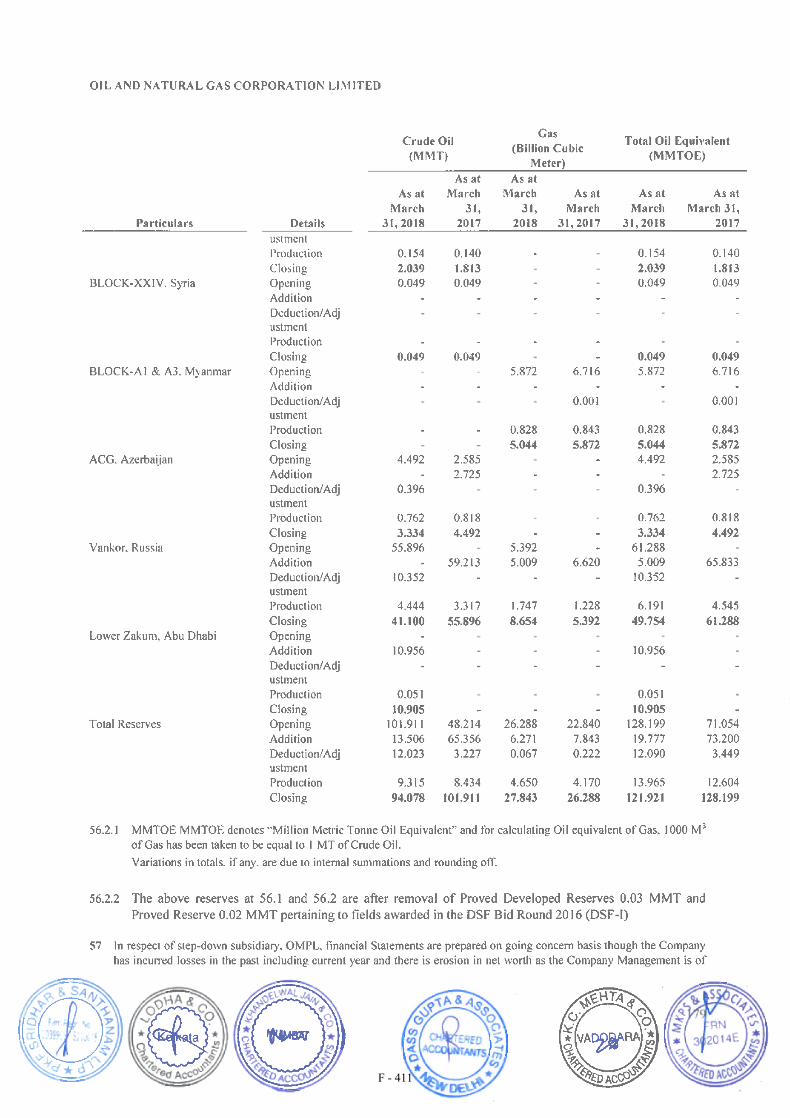

PRESENTATION OF OIL AND GAS RESERVES DATA

The Company has provided certain estimates regarding crude oil and natural gas reserves in this Offering

Circular. These estimates are based solely on volumetric analysis of the Company’s various license areas. In

calculating the Company’s domestic reserves, the Company uses internally-developed definitions that are based

on Petroleum Resources Management System 2018 (“PRMS 2018”). For further information, see the section

entitled “Business – Reserves Classification Standards”. The Company’s internally-developed definitions do

not strictly comply with currently accepted international standards and therefore the Company’s reserves

estimates may not be comparable with other publicly listed companies. For further information, see the sections

entitled “Business — Exploration and Production Business — Presentation of Reserves Estimates” and

“Business — Reserves Classification Standards” for more information. Moreover, the Company’s international

reserves have been calculated based on standards that vary according to the jurisdiction in which the operator

and reserves are located. The Company’s domestic and international management estimates of the reserves are

approved by the Reserve Estimate Committee (the “REC”). The Company’s domestic reserves (other than

domestic reserves held through joint ventures) have historically been audited independently every five years

but there is no assurance that the Company will conduct such audits every five years in the future. Investors

should not place undue reliance on the Company’s management estimates of its reserves. For further

information, see the section entitled “Investment Considerations—Risks Relating to the Company’s Business—

The Company’s crude oil and natural gas reserves estimates involve a degree of uncertainty and may not prove

to be correct over time. Moreover, these estimates may be unaudited or may not be fully audited and may not

accurately reflect actual reserves, or even if accurate, technical limitations may prevent the Company from

producing crude oil or natural gas from these reserves”.

In this Offering Circular, the Company reports 1P, 2P and 3P reserves. “Proved Reserves”, or “1P”,

refers to those quantities of petroleum that, by analysis of geoscience and engineering data, can be estimated

with reasonable certainty to be commercially recoverable from a given date forward from known reservoirs and

under defined economic conditions, operating methods and government regulations. “Proved and Probable

Reserves”, or “2P”, refers to 1P plus those additional Reserves that analysis of geoscience and engineering data

indicates are less likely to be recovered than Proved Reserves but more certain to be recovered than Possible

Reserves. It is equally likely that actual remaining quantities recovered will be greater than or less than the sum

of the estimated Proved and Probable Reserves. In this context, when probabilistic methods are used, there

should be at least a 50 per cent. probability that the actual quantities recovered will equal or exceed the 2P

estimate. “Proved, Probable and Possible Reserves”, or “3P”, refers to 2P plus those additional reserves that

analysis of geoscience and engineering data indicates are less likely to be recoverable than Probable Reserves.

The total quantities ultimately recovered from the project have a low probability to exceed the sum of Proved,

Probable and Possible Reserves, which is equivalent to the high-estimate scenario. When probabilistic methods

are used, there should be at least a 10 per cent. probability (P10) that the actual quantities recovered will equal

or exceed the 3P estimate.

Unless stated otherwise, all of the Company’s 1P, 2P and 3P reserves consist of the Company’s

participating interest in total global reserves, which in turn consists of the Company’s 100.00 per cent. equity

interest in the Company’s independent oil and gas properties and the Company’s participating interest in joint

venture and production-sharing contracts, without reflecting (i) the Company’s share of cash royalties payable

to the Indian central government, Indian state governments and governmental bodies outside of India, (ii) other

contractual payments such as profit petroleum, production-linked payments and bonuses, and (iii)

reimbursement for exploration expenses attributable to the Company’s participating interest. Royalties and

taxes payable to Indian government entities are payable in cash and are not payable in kind. The Company’s

1P, 2P and 3P reserves also do not include an adjustment for taxes or other amounts payable by it.

A39729228 vi

Although the Company generally reports its reserves of crude oil and natural gas in metric tons and cubic

metres, respectively, for purposes of presentation in this Offering Circular, the Company has converted

quantities of domestic crude oil from metric tons to barrels at a rate of one metric ton to 7.5 barrels. The

conversion ratio of one metric ton to 7.5 barrels is based on the weighted average specific gravity of all crude

oil produced from the Company’s domestic fields, including fields operated through joint ventures. The

Company has used crude oil conversion ratios for its international fields based on the respective specific

gravities of crude oil/Condensate produced from those fields areas as follows:

Greater Nile Petroleum Operating Company (“GNPOC”) (Sudan): one metric ton to 7.14 barrels;

Greater Pioneering Operating Company (“GPOC”) (South Sudan): one metric ton to 7.3 barrels;

Block 5A (South Sudan): one metric ton to 6.81 barrels;

Vietnam Condensate: one metric ton to 8.38 barrels;

Sakhalin (Russia): one metric ton to 7.46 barrels;

ACG (Azerbaijan): one metric ton to 7.39 barrels;

Imperial (Russia): one metric ton to 7.58 barrels;

Al Furat (Syria): one metric ton to 7.3 barrels;

Block-24 (Syria): one metric ton to 7.41 barrels;

Mansarovar Energy Colombia Ltd. (“MECL”) (Colombia): one metric ton to 6.62 barrels;

Carabobo-1 (Venezuela): one metric ton to 6.29 barrels;

PIVSA (Venezuela): one metric ton to 6.572 barrels;

BC-10 (Brazil): one metric ton to 6.66 barrels; and

CPO-5 (Colombia): one metric ton to 6.65 barrels.

Where natural gas volumes have been converted into oil equivalent numbers, this has been done using a

factor of 1,000 standard cubic metres of natural gas equalling one metric ton of oil equivalent.

The Company’s reporting policy is not, and is not required to be, derived from, or consistent with oil

and gas reserves reporting requirements for filings with the U.S. Securities and Exchange Commission (“SEC”)

and differs from such requirements in certain material respects. The Company’s reserves would differ from

those described herein if determined in accordance with oil and gas reserves reporting requirements for filings

with the SEC. There are currently no clear regulations governing public disclosure of potential reserves by oil

and gas companies operating in India or their use in securities offering documents.

Information in this Offering Circular is derived or reproduced from the Company’s internal management

estimates. Prospective investors should read the section entitled “Business” for more information on the

Company’s reserves and resources, the assumptions, methods and procedures used in the preparation of the

reserve estimates and the underlying assumptions thereof and the reserves and resources definitions that the

Company uses.

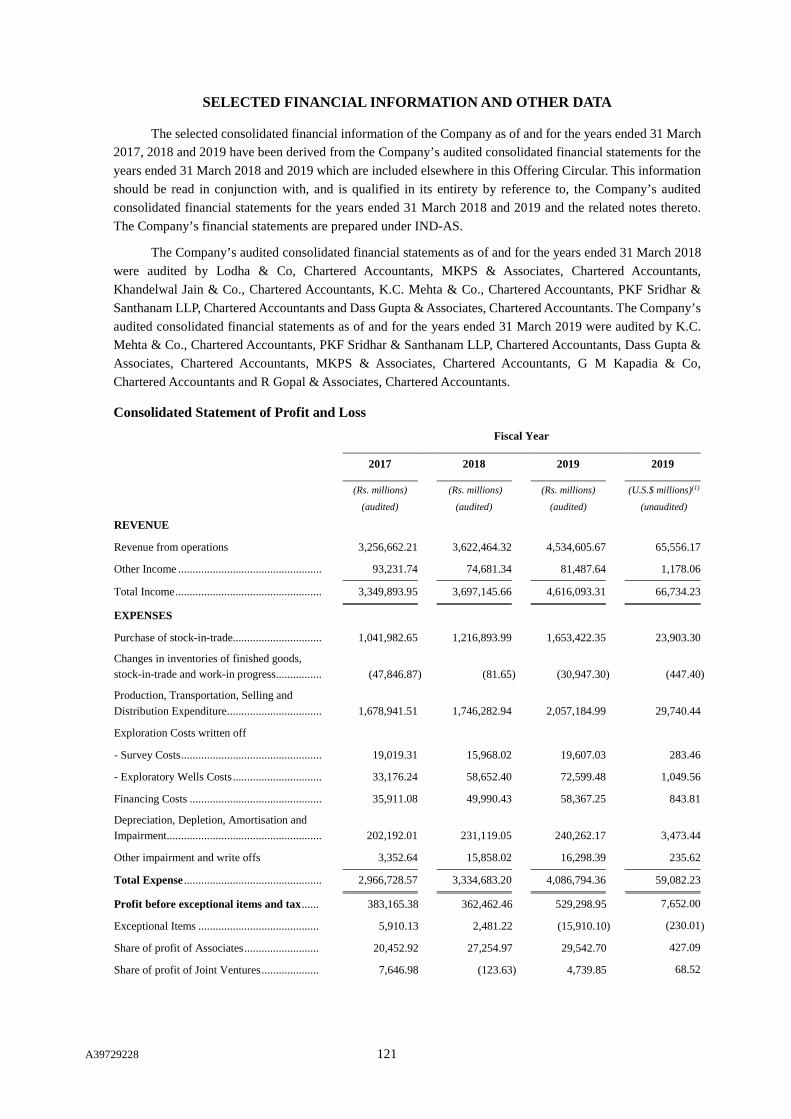

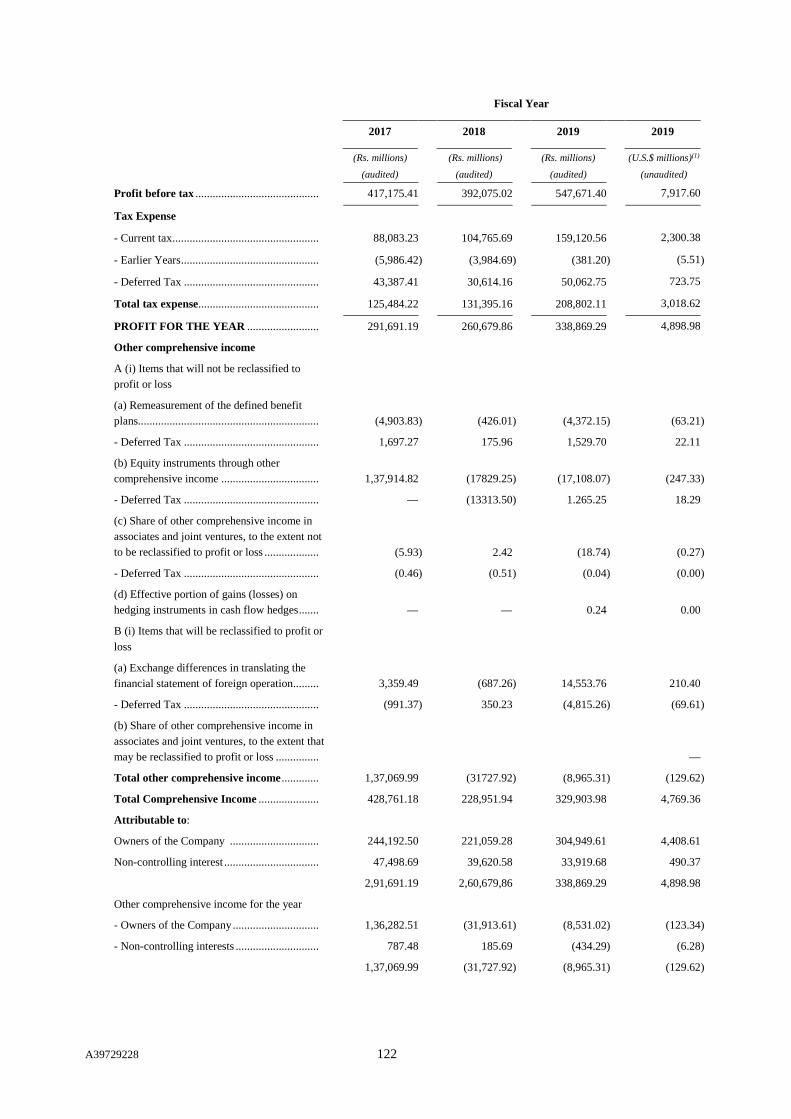

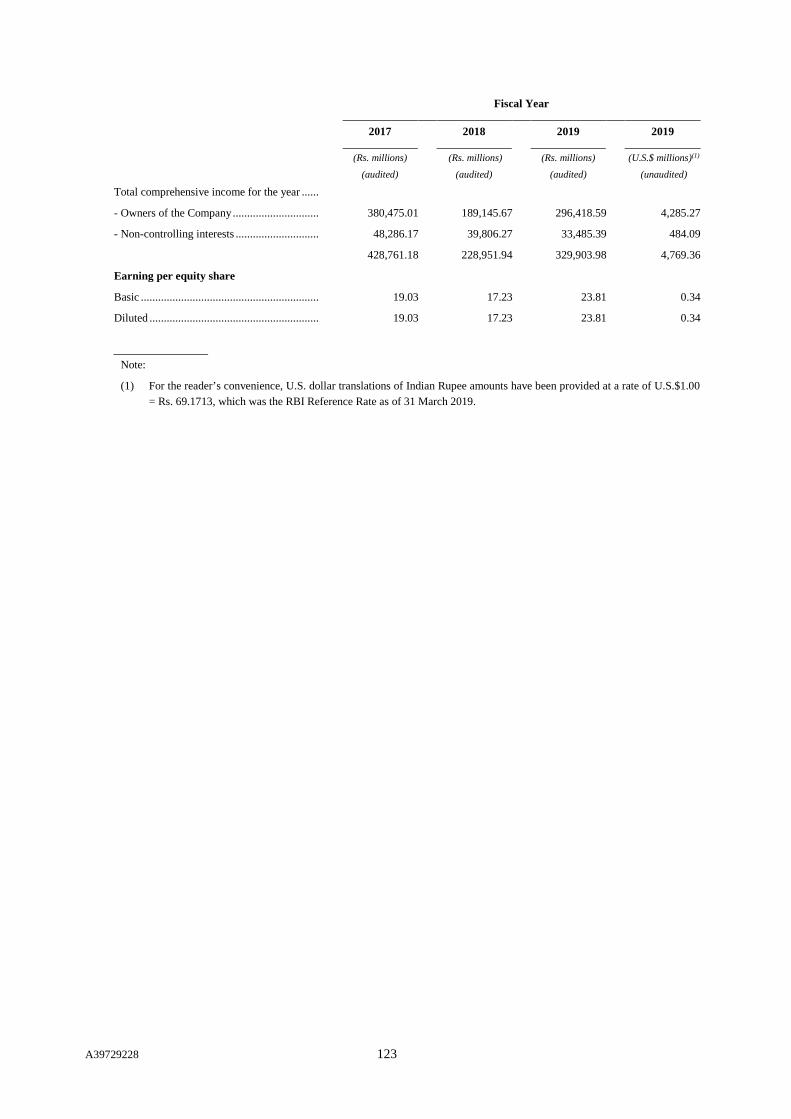

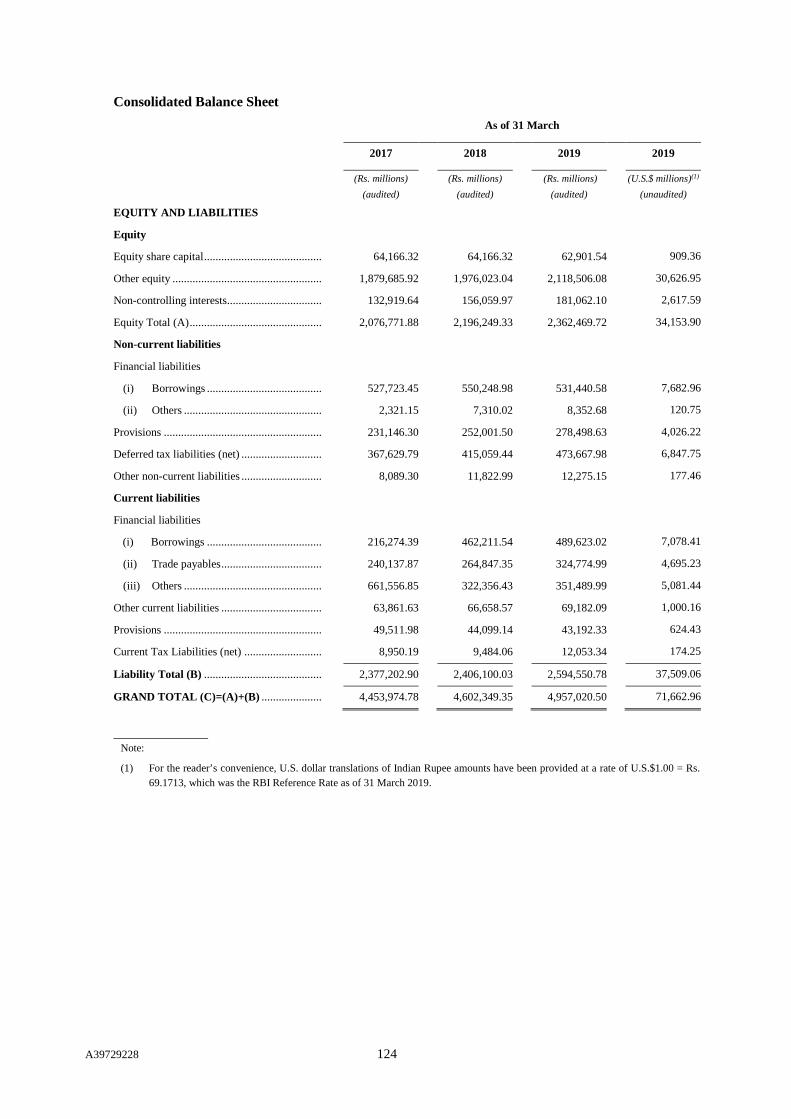

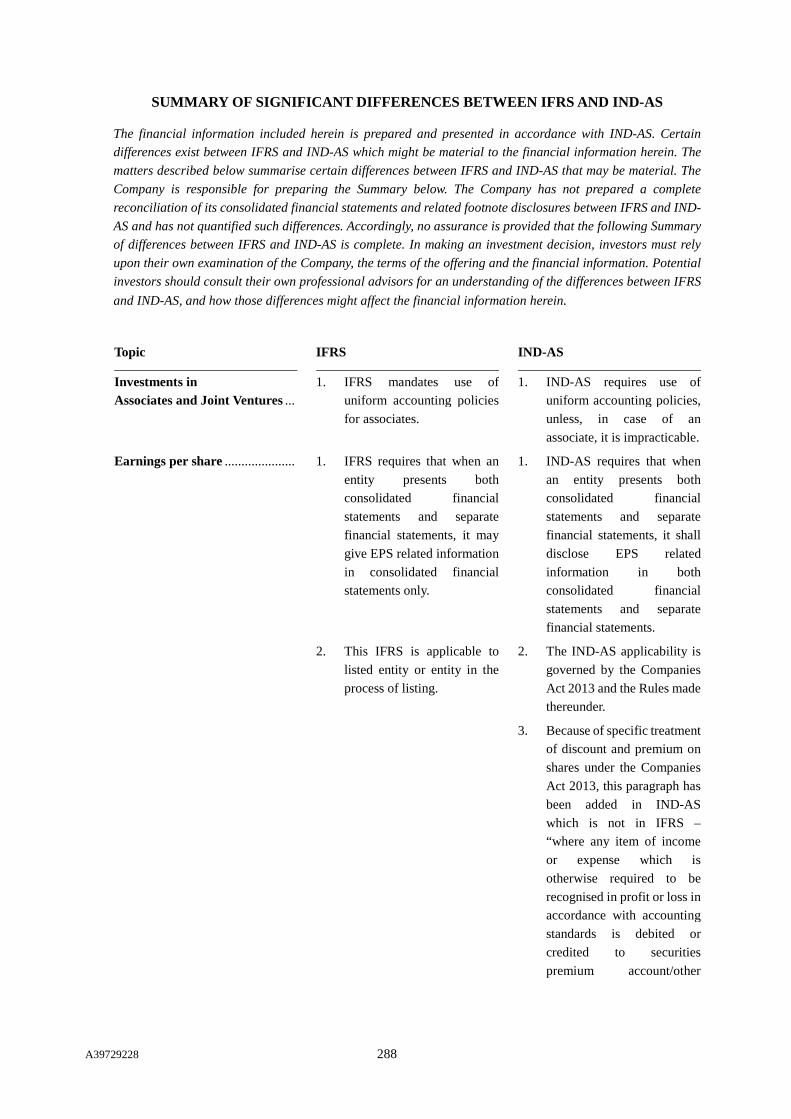

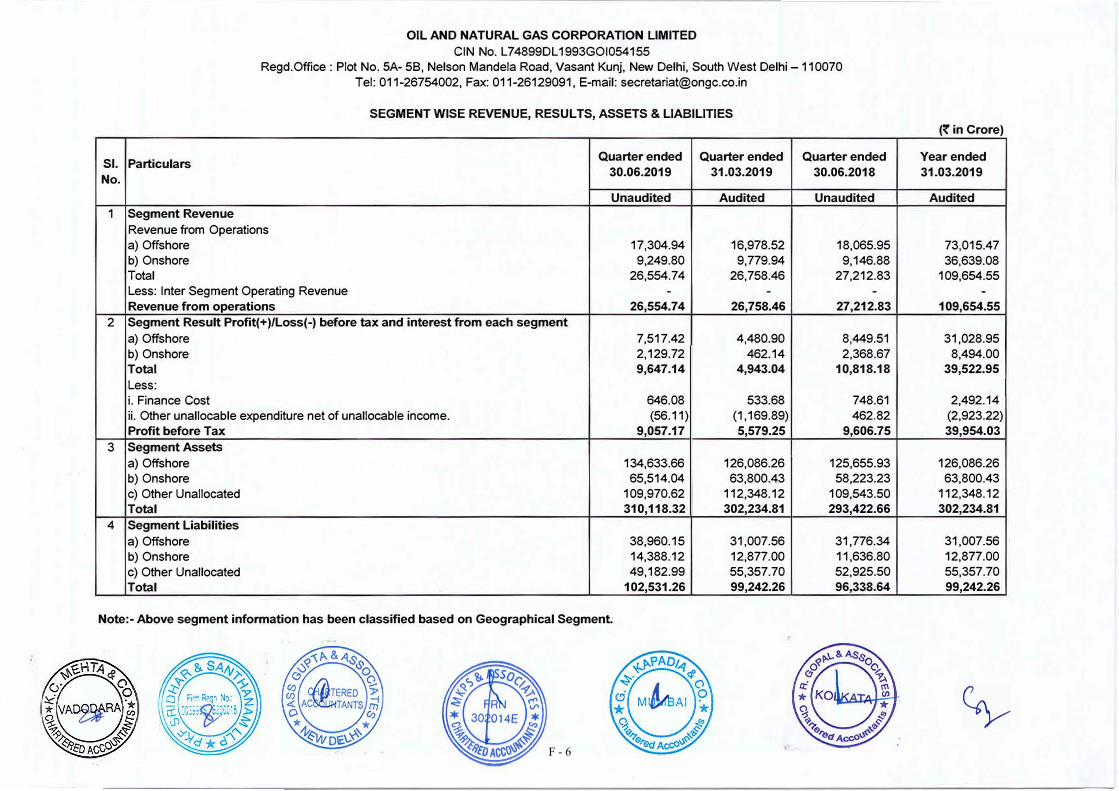

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Since 1 April 2016, the Company has maintained its financial books and records, and prepared its

financial statements, in Rupees, in accordance with the Companies (Indian Accounting Standards) Rules, 2015.

A39729228 vii

The Indian Accounting Standards (“IND-AS”) differ in certain important respects from International Financial

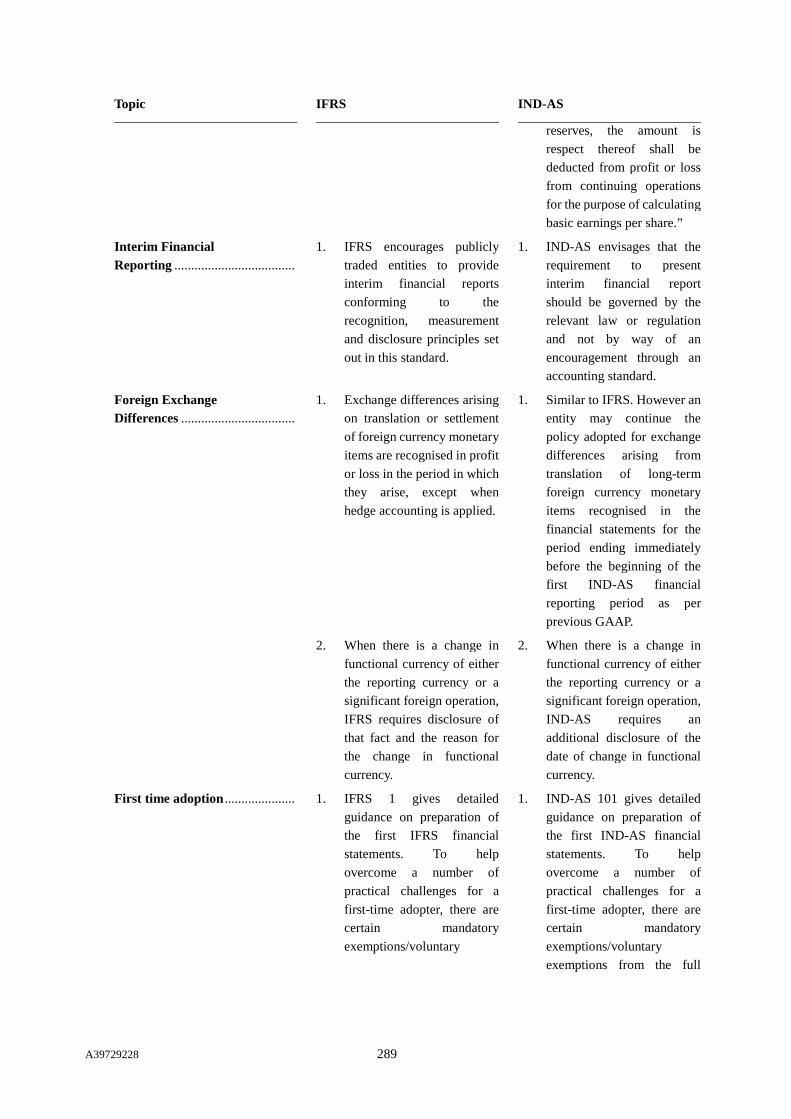

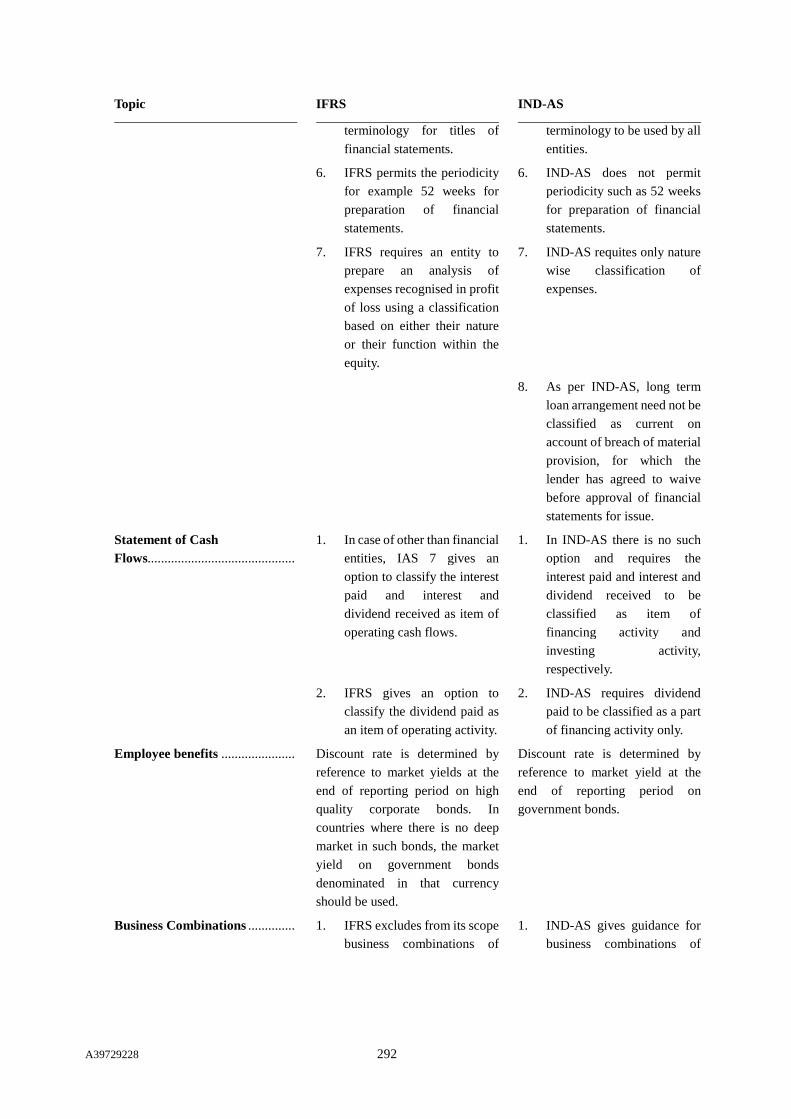

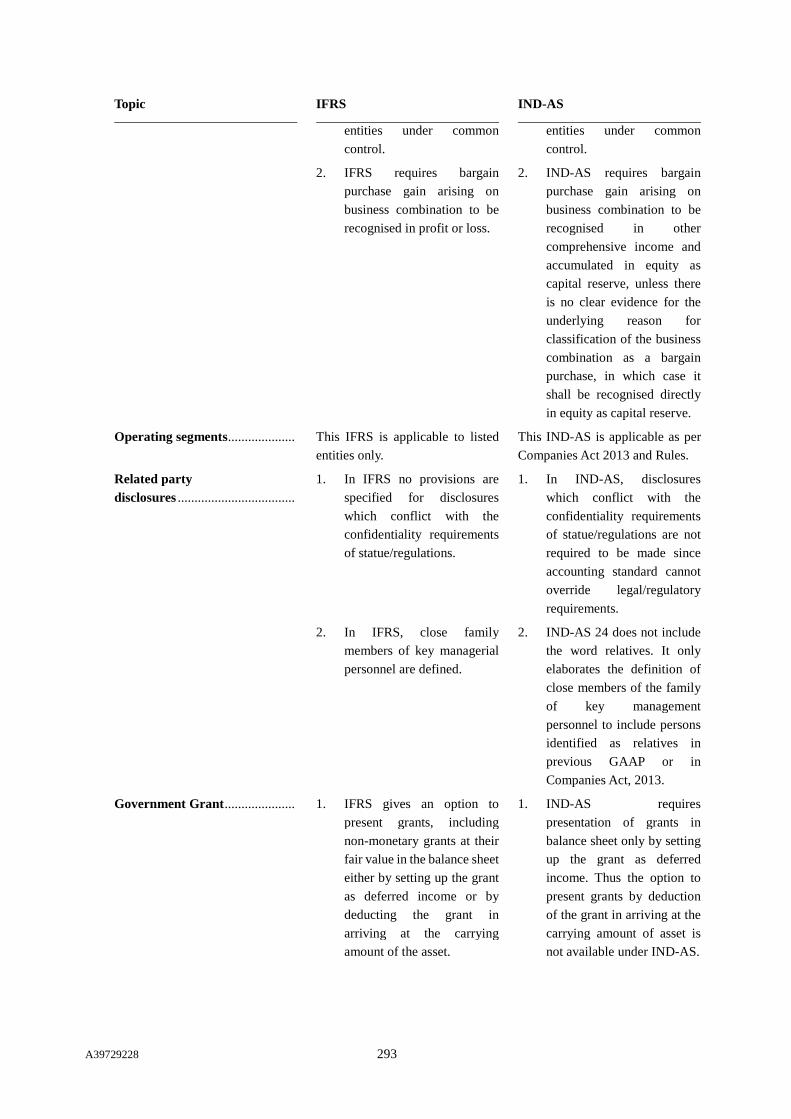

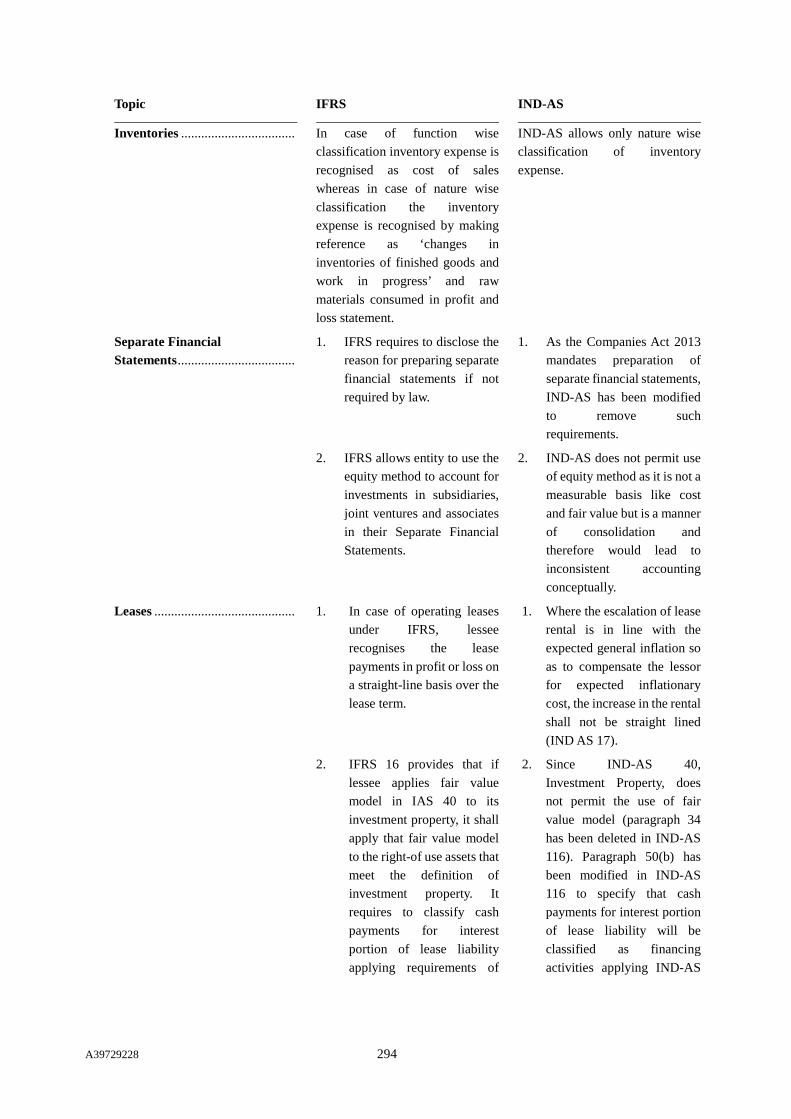

Reporting Standards (“IFRS”). For a discussion of the principal differences between IFRS and IND-AS as they

relate to the Company, see the section entitled “Summary of significant differences between IFRS and IND-AS”.

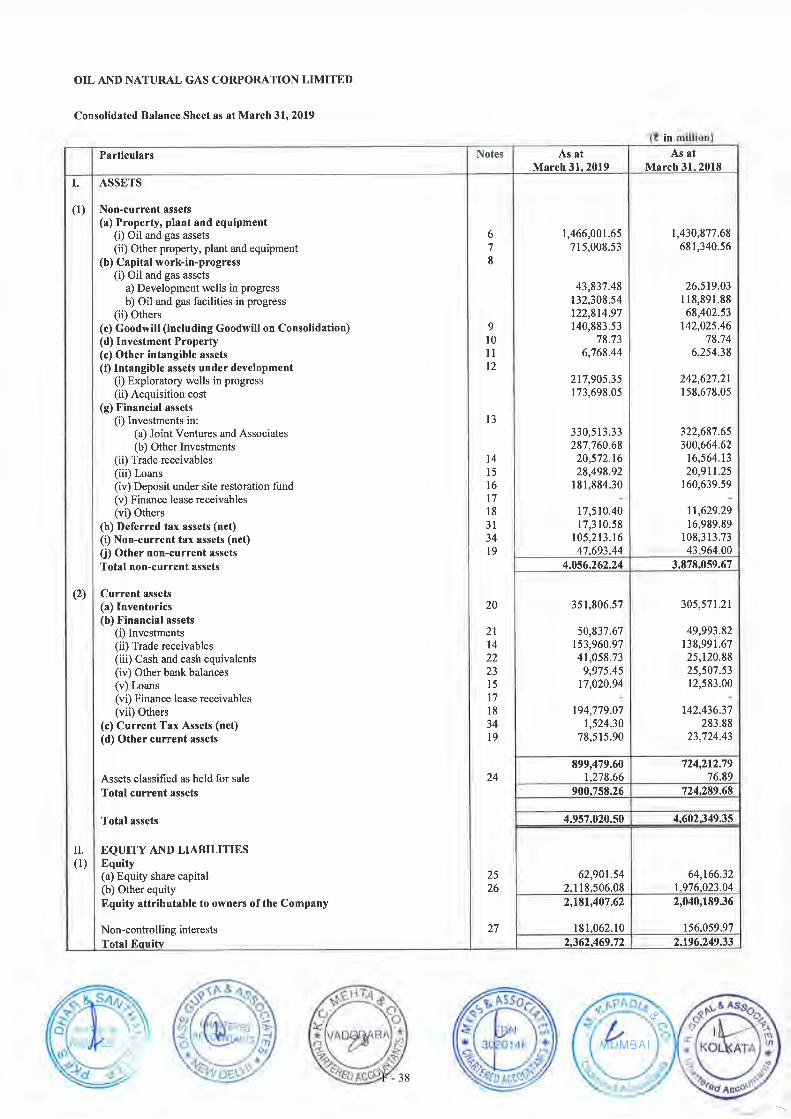

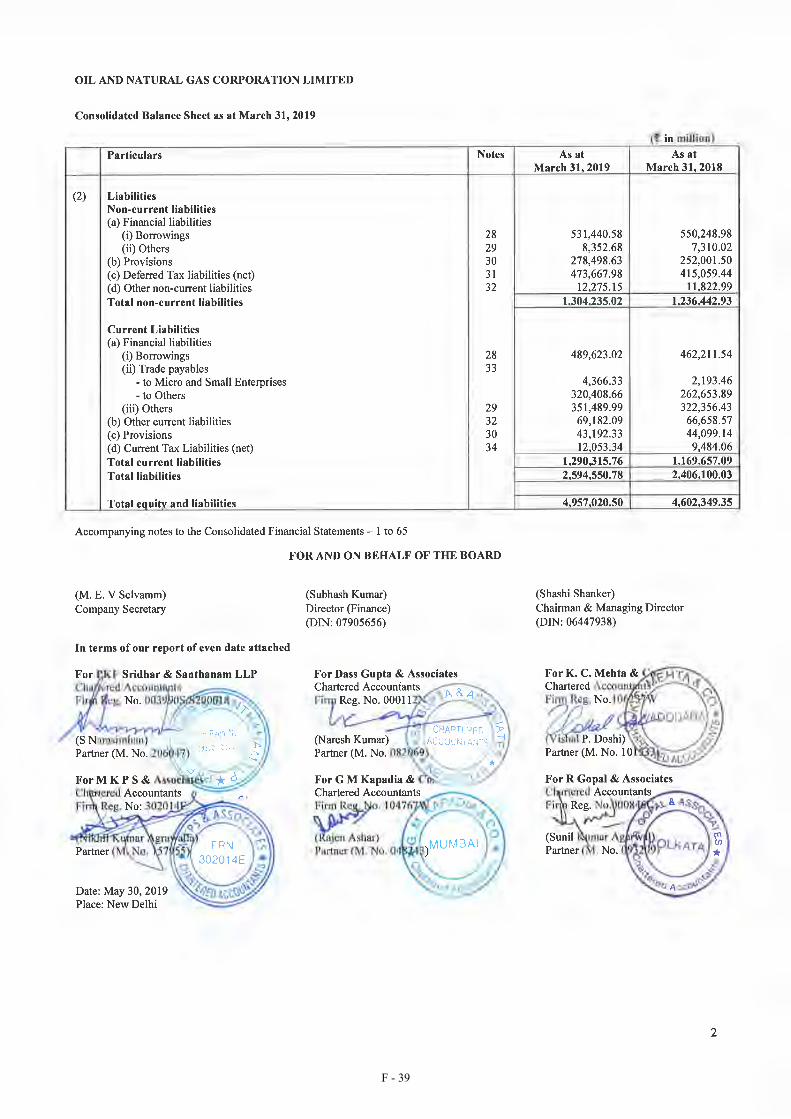

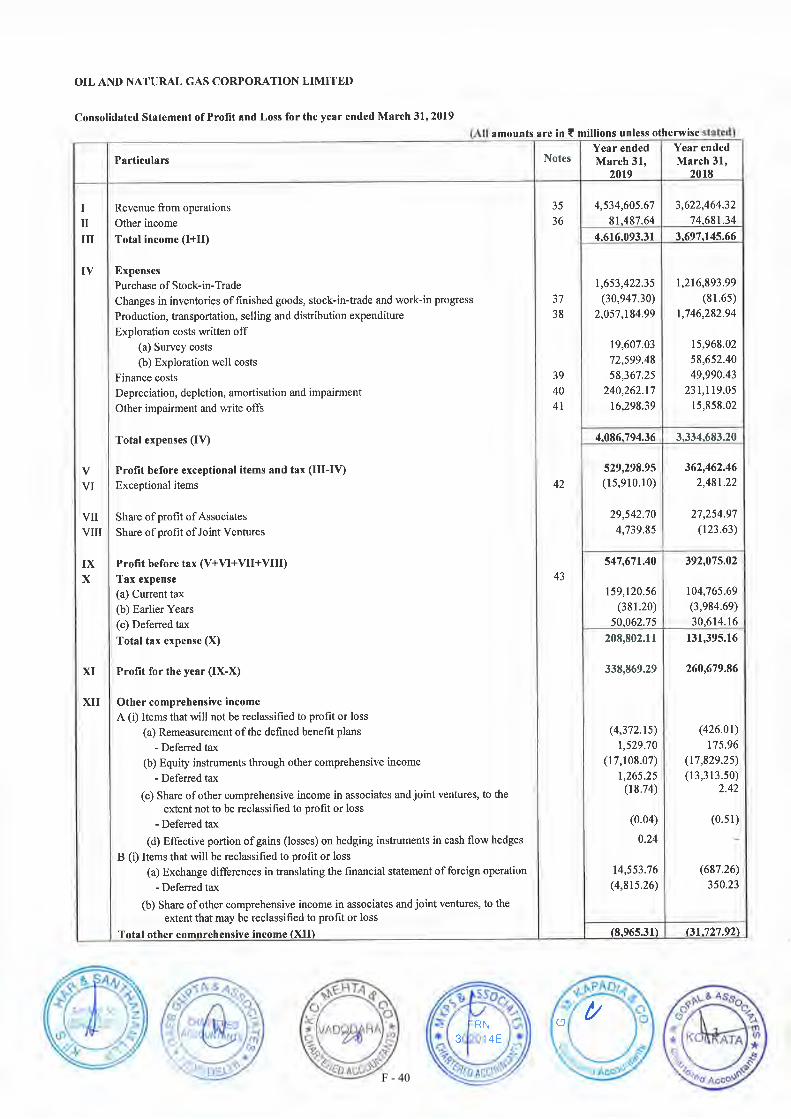

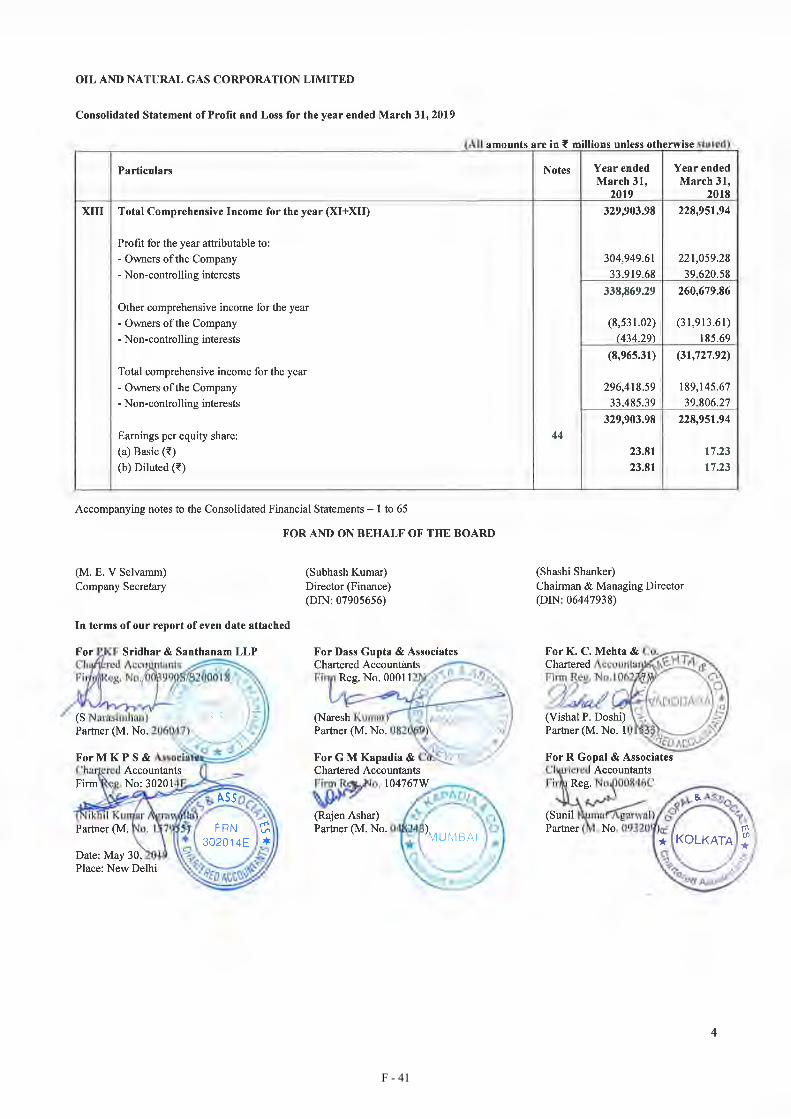

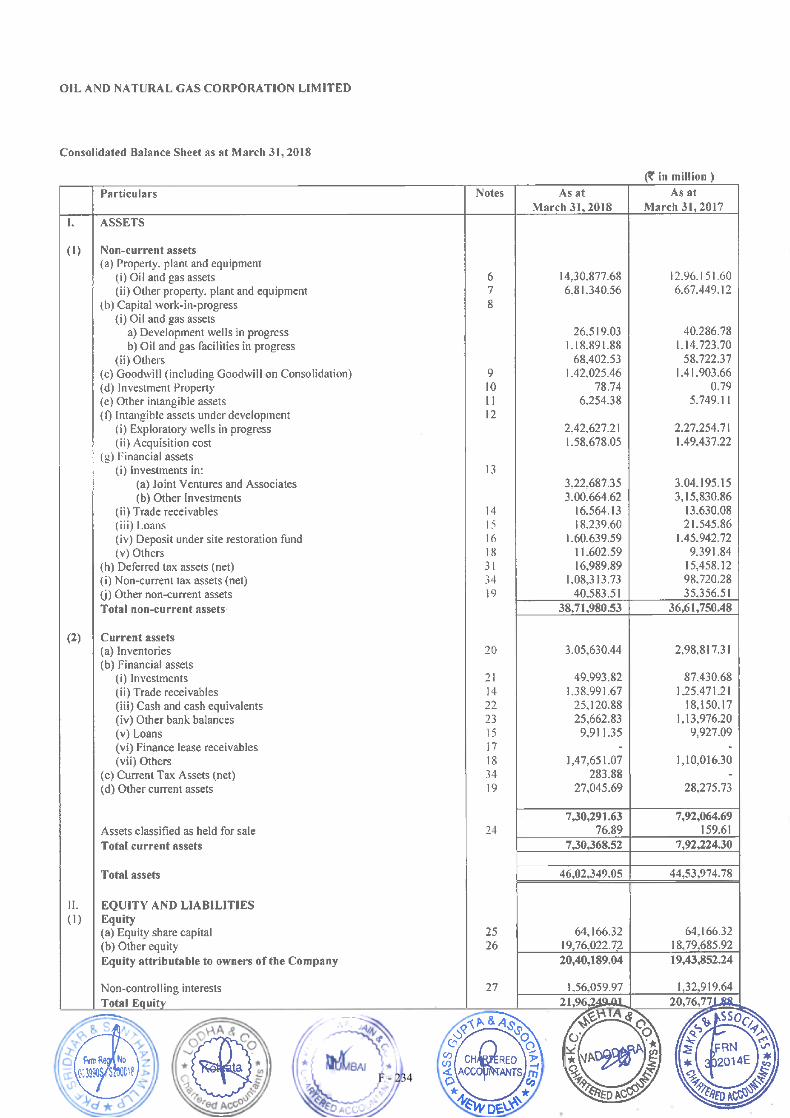

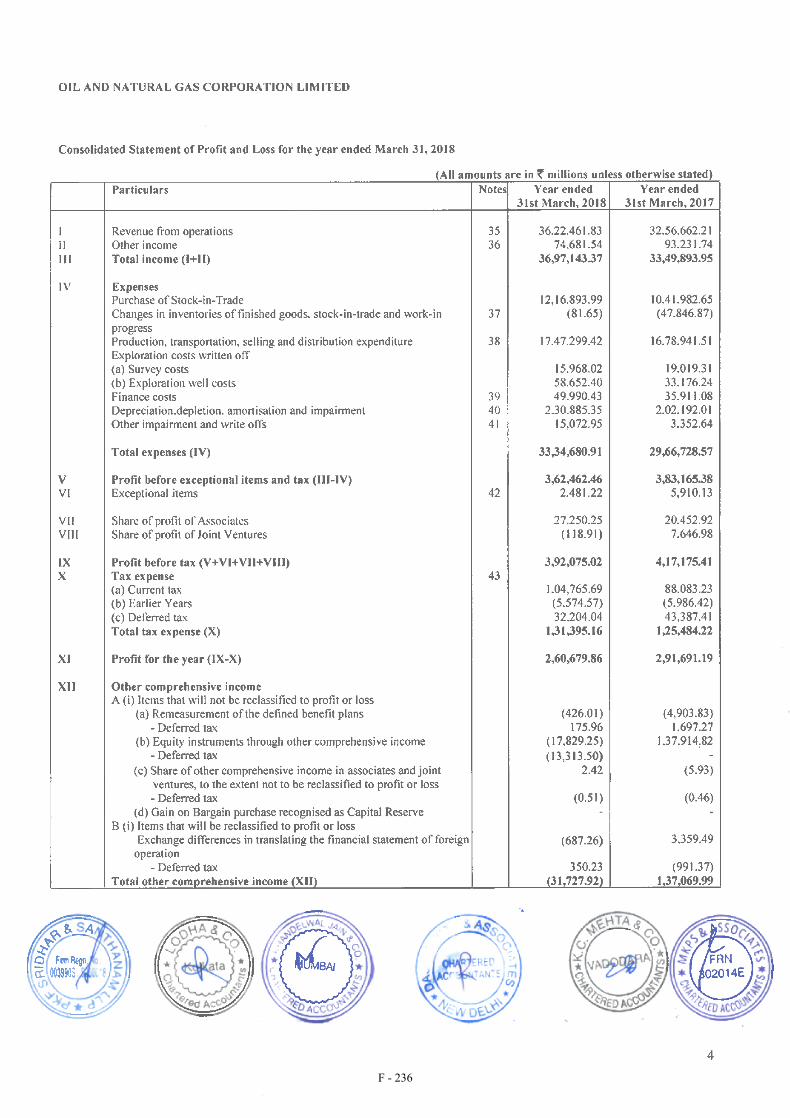

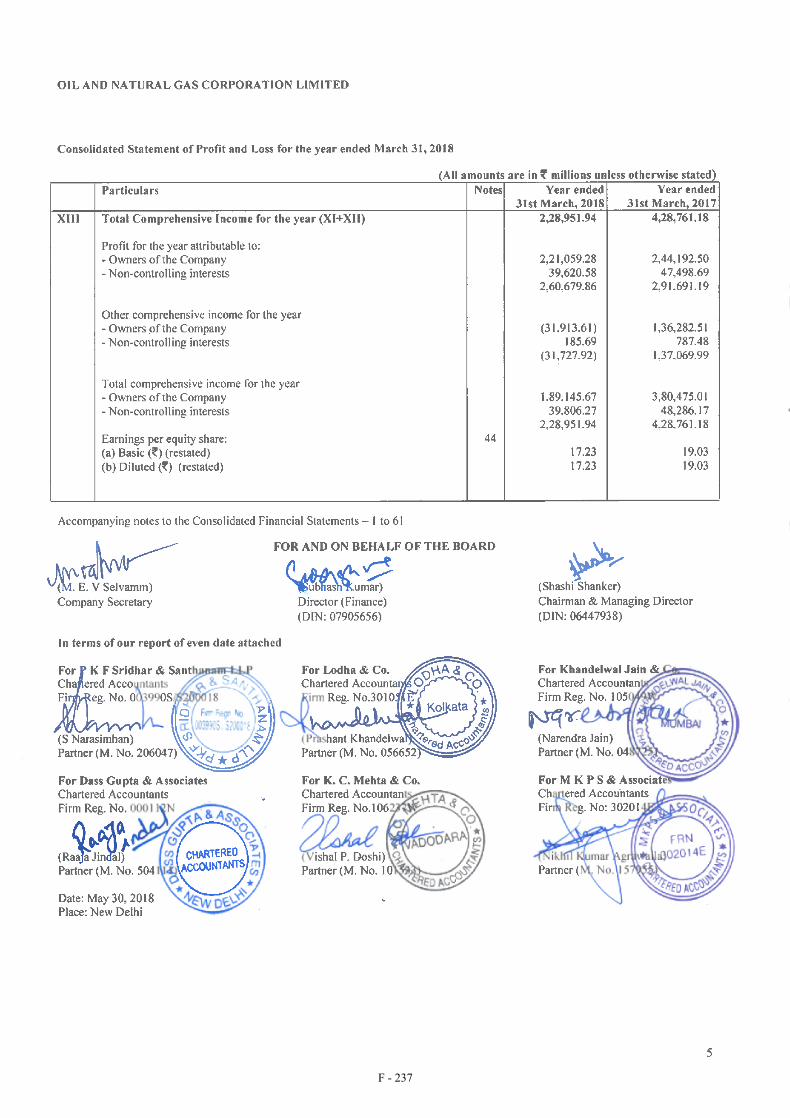

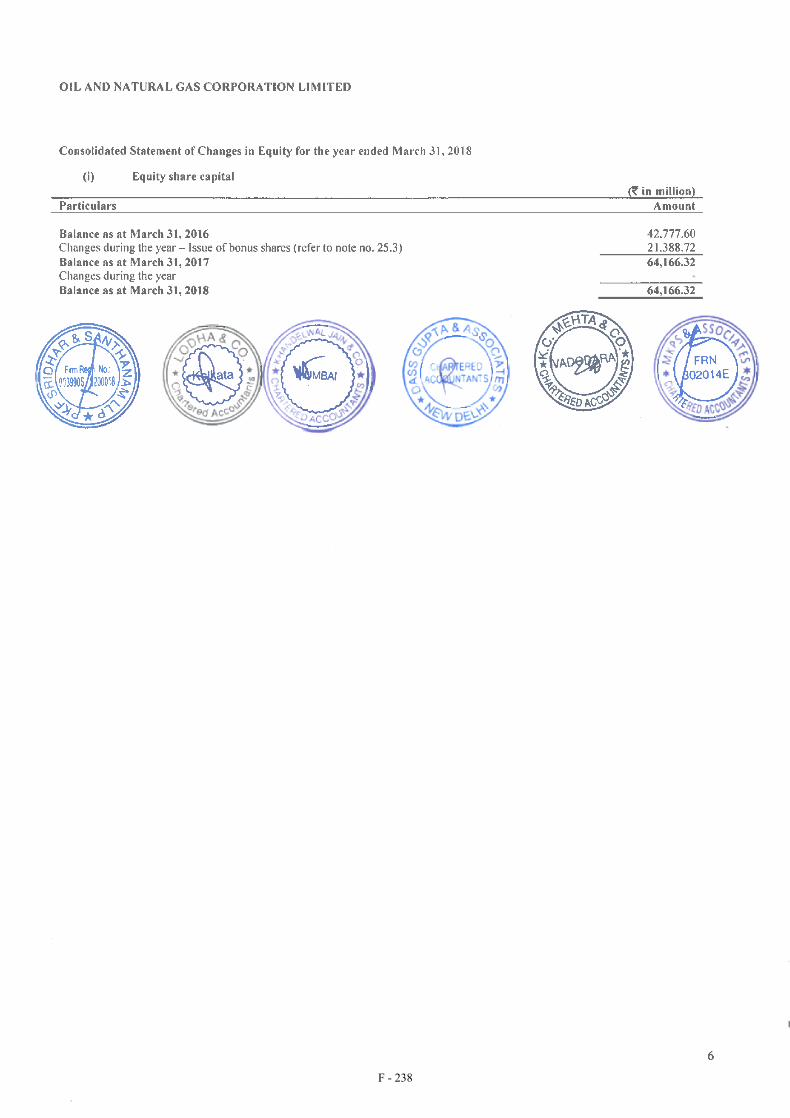

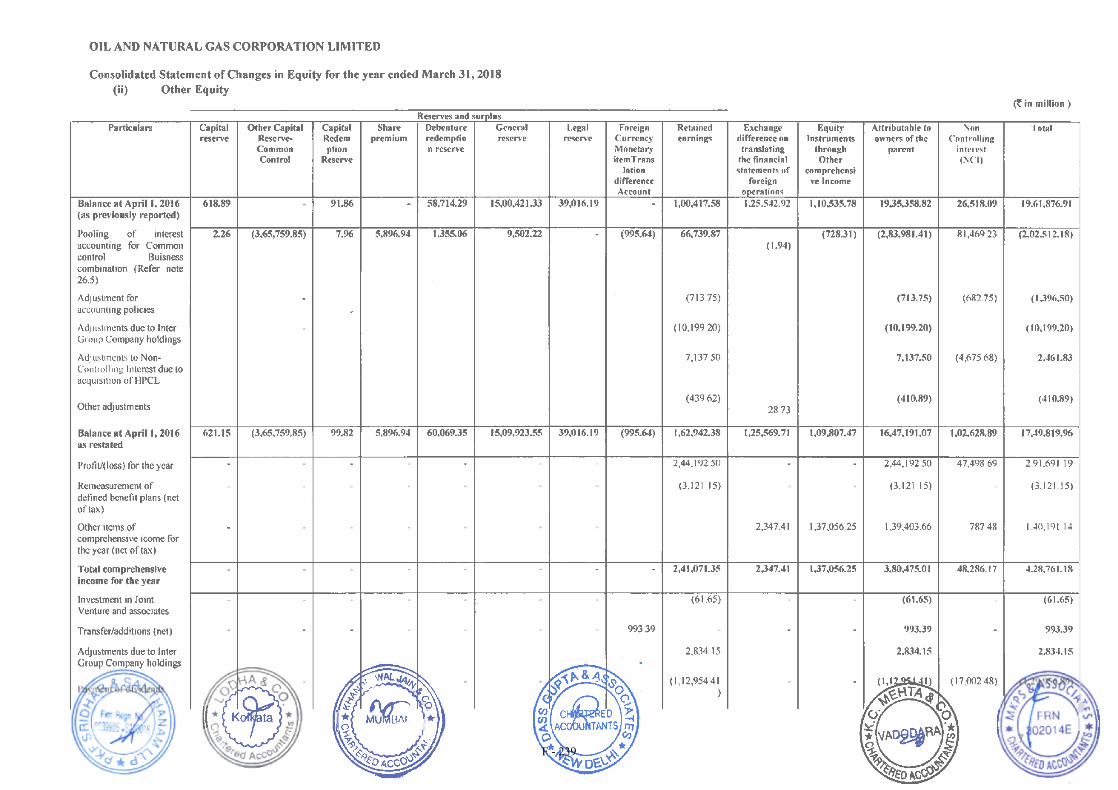

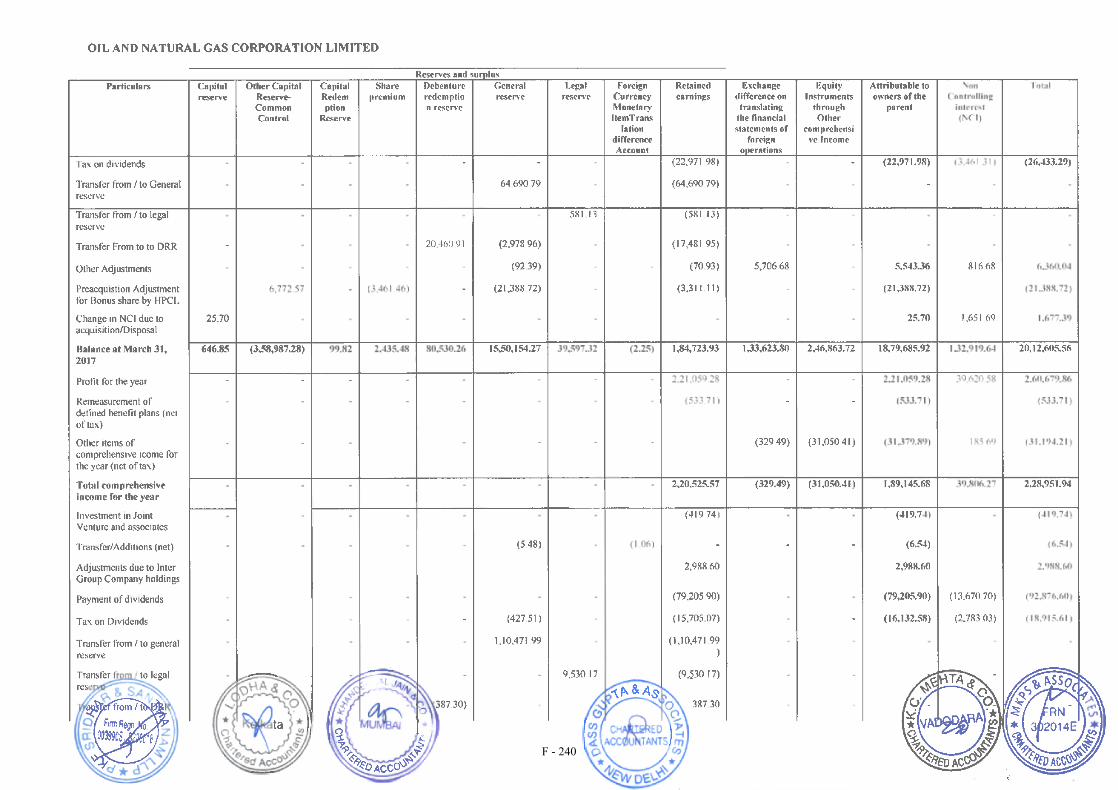

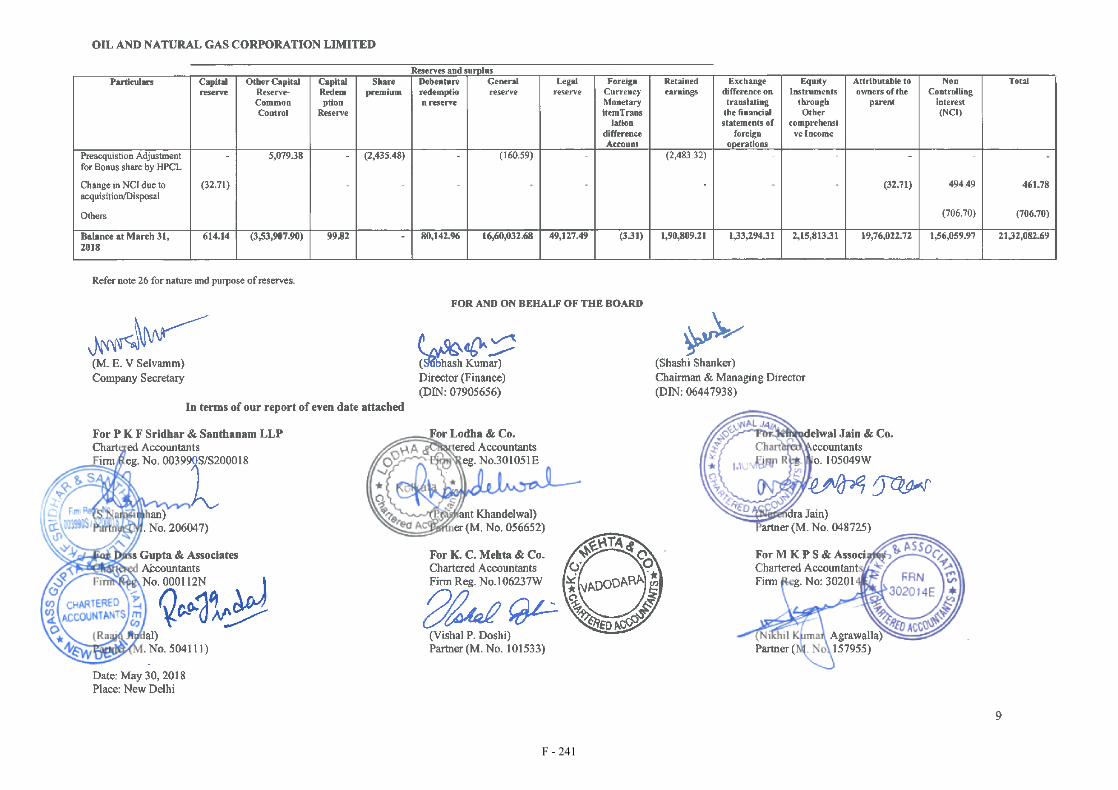

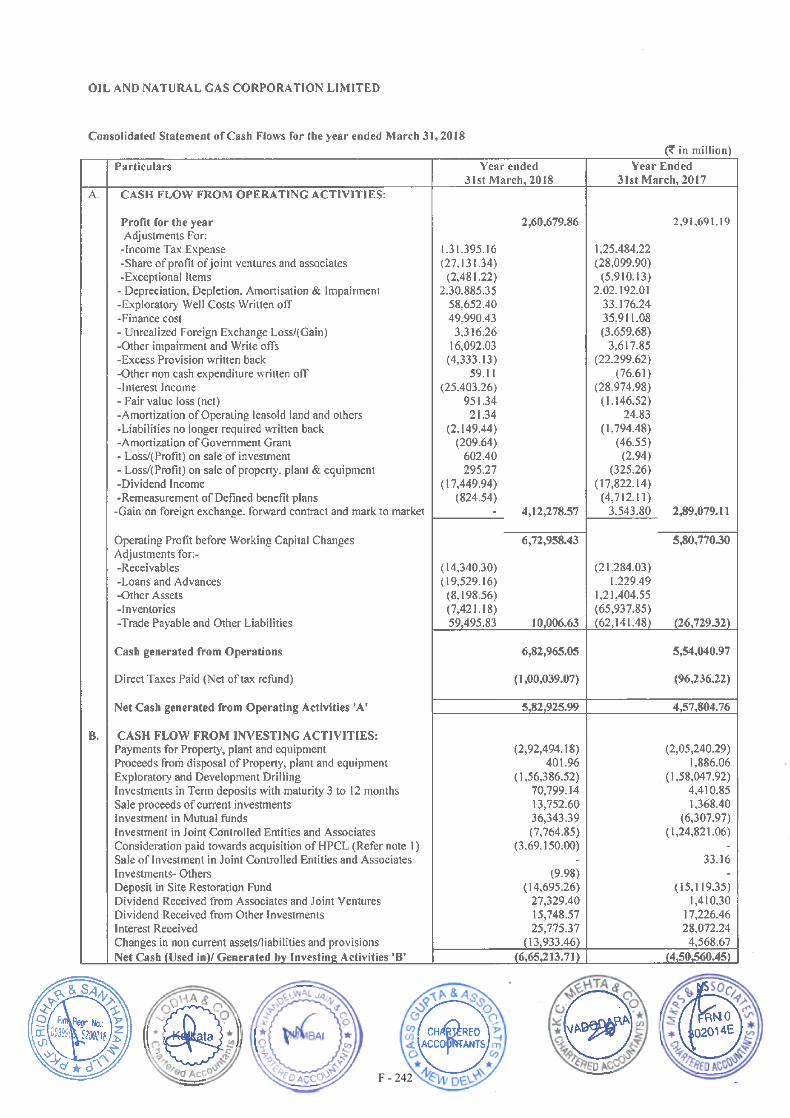

The audited consolidated financial statements of the Company for the years ended 31 March 2018 and

31 March 2019 included in this Offering Circular have been prepared in accordance with IND-AS and have

been audited by the auditors as set out in paragraph 6 of the section entitled “General Information”. The audited

consolidated financial statements of the Company for the years ended 31 March 2018 and 31 March 2019 are

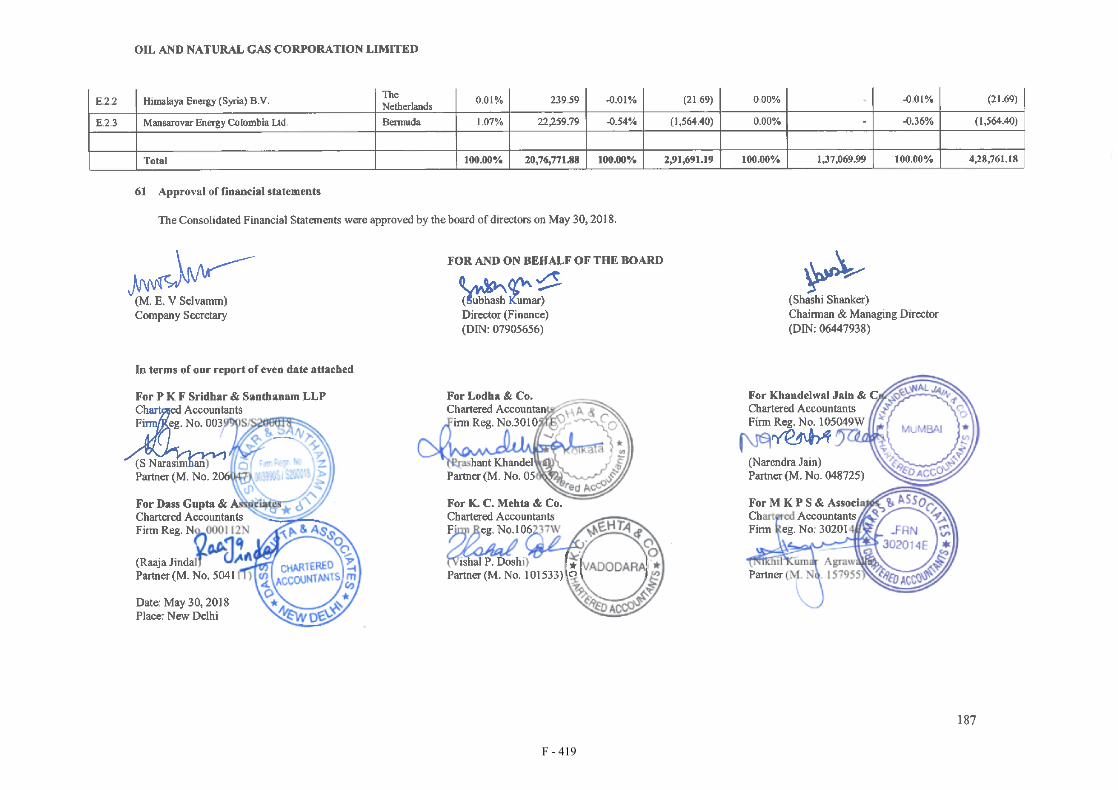

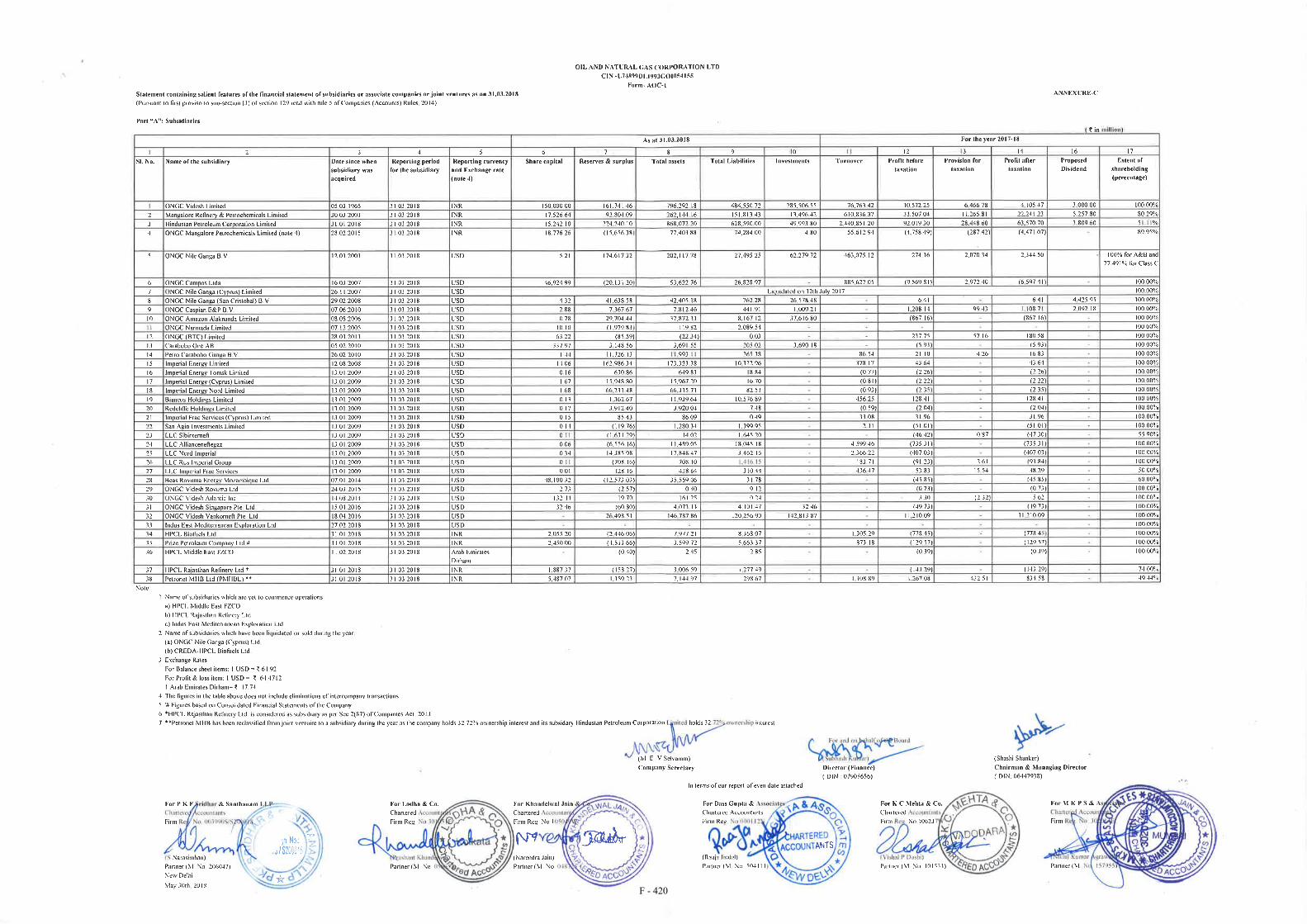

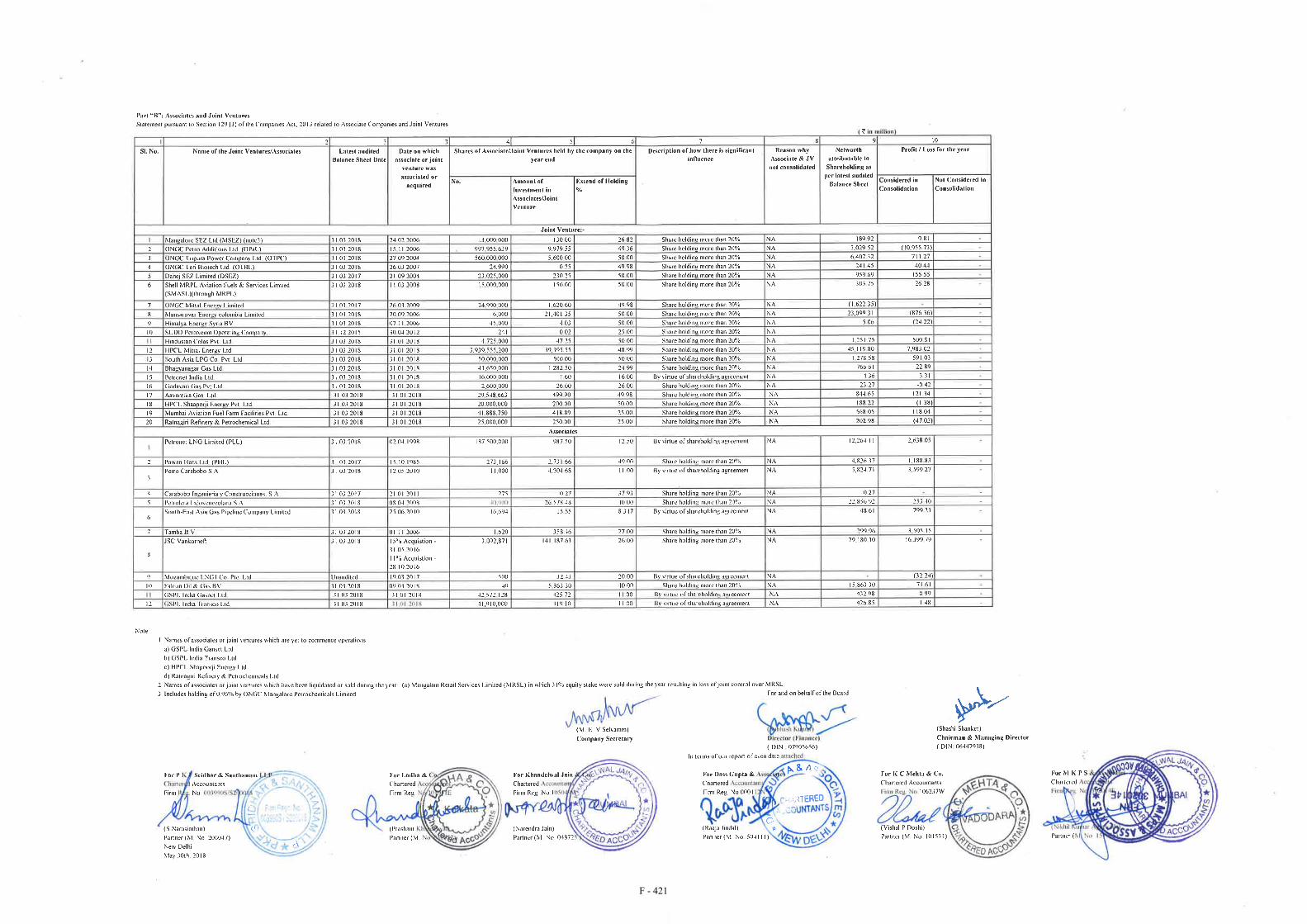

set out on pages F-18 to F-229 and pages F-230 to F-421, respectively, in this Offering Circular. The audited

consolidated financial statements of the Company for the years ended 31 March 2018 and 31 March 2019

should be read in conjunction and in entirety with the related notes thereto.

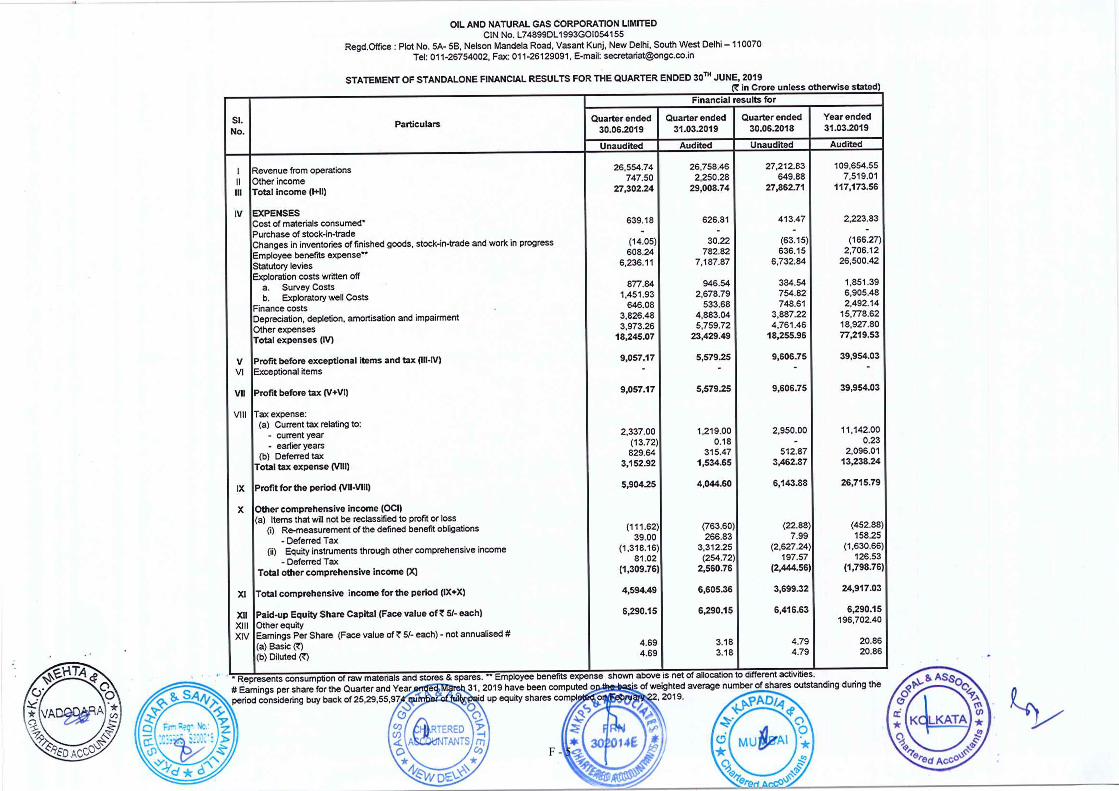

The unaudited and reviewed consolidated financial statements of the Company for the three months

ended 30 June 2019 and the unaudited and reviewed non-consolidated financial statements of the Company for

the three months ended 30 June 2019 included in this Offering Circular have each been prepared in accordance

with IND-AS and have been reviewed by the auditors as set out in paragraph 6 of the section entitled “General

Information”. The unaudited and reviewed consolidated financial statements of the Company for the three

months ended 30 June 2019 and the unaudited and reviewed non-consolidated financial statements of the

Company for the three months ended 30 June 2019 should not be relied upon by investors to provide the same

quality of information associated with information that has been subject to an audit. None of the Arrangers, the

Dealers or any of their respective affiliates, directors or advisers makes any representation or warranty, express

or implied, regarding the sufficiency of such unaudited and reviewed consolidated financial statements of the

Company for the three months ended 30 June 2019 and unaudited and reviewed non-consolidated financial

statements of the Company for the three months ended 30 June 2019, for an assessment of, and potential

investors must exercise caution when using such data to evaluate, the Company’s financial condition, results of

operations and results. The unaudited and reviewed consolidated financial statements of the Company for the

three months ended 30 June 2019 and the unaudited and reviewed non-consolidated financial statements of the

Company for the three months ended 30 June 2019 should not be taken as an indication of the expected financial

condition, results of operations and results of the Company (whether on a consolidated or non-consolidated

basis) for the full financial year ending 31 March 2020. The unaudited and reviewed consolidated financial

statements of the Company for the three months ended 30 June 2019 and the unaudited and reviewed non-

consolidated financial statements of the Company for the three months ended 30 June 2019 are set out on pages

F-2 to F-9 and pages F-10 to F-17, respectively, in this Offering Circular. Each of the unaudited and reviewed

consolidated financial statements of the Company for the three months ended 30 June 2019 and the unaudited

and reviewed non-consolidated financial statements of the Company for the three months ended 30 June 2019

should be read in conjunction and in entirety with their respective related notes thereto.

The Company publishes its financial statements in Indian Rupees. Unless otherwise stated, all

translations from Indian Rupees to United States dollars have been made on the basis of the RBI Reference

Rate as of 31 March 2019 of Rs. 69.1713 = U.S.$1.00. All amounts translated into United States dollars in this

Offering Circular are provided solely for the convenience of the reader, and no representation is made that the

Indian Rupees or United States dollar amounts referred to in this Offering Circular could have been or could be

converted into any other currency, at any particular rate, at the above rates or at all.

CERTAIN DEFINITIONS

In this Offering Circular, references to “India” are to the Republic of India, references to “Indian

Government” or the “Government” are to the Government of India and references to the “RBI” are to the

Reserve Bank of India. References to specific data applicable to particular subsidiaries or other consolidated

entities are made by reference to the name of that particular entity.

A39729228 viii

In this Offering Circular, references to “Fiscal Year” are to the year starting from 1 April and ending on

31 March. For example, “2017 Fiscal Year” is to the 12-month period ended on 31 March 2017, “2018 Fiscal

Year” is to the twelve-month period ended on 31 March 2018 and “2019 Fiscal Year” is to the 12-month period

ended on 31 March 2019.

Unless the context otherwise indicates, all references to the “Company” are to ONGC and its

consolidated subsidiaries, as the context requires, and to “ONGC Videsh” are to ONGC Videsh Limited.

In this Offering Circular, references to “FATF Compliant Country” are to a country that is a member

of the Financial Action Task Force (“FATF”) or a member of a FATF-style regional body and should not be a

country identified in the public statement of the FATF as (a) a jurisdiction having a strategic Anti-Money

Laundering or Combating the Financing of Terrorism deficiencies to which counter measures apply; or (b) a

jurisdiction that has not made sufficient progress in addressing the deficiencies or has not committed to an

action plan developed with the FATF Financial Action Task Force to address the deficiencies, and references to

“IOSCO Compliant Country” are to a country that whose securities market regulator is a signatory to the

International Organisation of Securities Commission's (“IOSCO”) Multilateral Memorandum of

Understanding (Appendix A Signatories) or a signatory to a bilateral Memorandum of Understanding with the

Securities and Exchange Board of India (“SEBI”) for information sharing arrangements.

In this Offering Circular, references to “ECB Guidelines” refers to the Foreign Exchange Management

(Borrowing or Lending) Regulations 2018 and circulars or notifications issued thereunder by the RBI, from

time to time including the Master Direction External Commercial Borrowings, Trade Credits and Structured

Obligations dated 26 March 2019, as amended from time to time and the Master Direction on Reporting under

Foreign Exchange Management Act, 1999, dated 1 January 2016, each as amended from time to time.

All references in this document to “U.S. dollars” and “U.S.$” refer to United States dollars, all

references to “Rupee”, “Rupees”, “INR”, “Rs.” and “₹” refer to Indian Rupees and all references to “S$” and

“SGD” refer to Singapore dollars. In addition, all references to “Sterling”, “GBP” and “£” refer to pounds

sterling and all references to “euro”, “EUR” and “€” refer to the currency introduced at the start of the third

stage of European economic and monetary union pursuant to the Treaty on the Functioning of the European

Community, as amended.

References to “crores” and “lakhs” in the Company’s consolidated financial statements are to the

following:

One lakh ...................................................... 100,000 (one hundred thousand)

One crore .................................................... 10,000,000 (ten million)

Ten crores .................................................... 100,000,000 (one hundred million)

One hundred crores ..................................... 1,000,000,000 (one thousand million or one billion)

In this Offering Circular, where information has been presented in millions or billions of units, amounts may

have been rounded, in the case of information presented in millions, to the nearest ten thousand or one hundred

thousand units or, in the case of information presented in billions, one, ten or one hundred million units.

Accordingly, the totals of columns or rows of numbers in tables may not be equal to the apparent total of the

individual items and actual numbers may differ from those contained herein due to rounding.

INDUSTRY AND OTHER MARKET DATA

While the Company has compiled, extracted, reproduced market or other industry data from external

sources, including third parties, analysts or industry or general publications, the Issuers, the Company, the

Arrangers and the Dealers have not independently verified that data or ascertained the underlying economic

A39729228 ix

assumptions relied upon therein. Reasonable actions have been taken by the Company to ensure that the

information in this Offering Circular that is based on third party sources have been accurately reproduced and,

as far as the Issuers, the Company, the Arrangers and the Dealers are aware and are able to ascertain from

information published by third parties, no facts have been omitted that would render the reproduced information

inaccurate or misleading. Subject to the foregoing, none of the Issuers, the Company, the Arrangers, the Dealers,

the Trustee or the Agents can assure investors of the accuracy and completeness of, or take any responsibility

for, such data. The source of such third-party information is cited whenever such information is used in this

Offering Circular.

FORWARD-LOOKING STATEMENTS

This Offering Circular contains certain “forward-looking statements”. These forward-looking statements

generally can be identified by words or phrases such as “aim”, “anticipate”, “believe”, “estimate”, “expect”,

“intend”, “objective”, “plan”, “project”, “will”, “will continue”, “will pursue” or other words or phrases of

similar import. Similarly, statements that describe the Company’s objectives, strategies, plans or goals are also

forward-looking statements. All forward-looking statements are subject to risks, uncertainties and assumptions

about us that could cause actual results to differ materially from those contemplated by the relevant forward-

looking statement.

Important factors that could cause actual results to differ materially from the Company’s expectations

include, but are not limited to, the following:

the project completion dates, estimated project costs and total value of contracts awarded;

variation in reserves data and estimates relating to contingent and prospective resources, and the Company’s

actual production, revenues and expenditure;

production volumes;

the outcome of exploration and development activity;

the Company’s ability to find, develop or acquire additional reserves;

fluctuations or a substantial or extended decline in international prices for oil and gas;

regulatory changes pertaining to the industries in India or other countries in which the Company has its

businesses and the Company’s ability to respond to them;

claims against the Company due to an environmental disaster, exploration accidents or any other uninsured

event;

the Company’s ability to successfully implement its strategy, growth and expansion;

regulatory changes in the oil and gas sector;

general economic and business conditions in the markets in which the Company operates and in the local,

regional and national economies;

technological changes in the future;

the Company’s exposure to market risks;

general economic and political conditions in India and which have an impact on the Company’s business

activities or investments;

terrorist attacks, civil disturbances, regional conflicts, accidents and natural disasters;

A39729228 x

the monetary and fiscal policies of India, inflation, deflation, unanticipated turbulence in interest rates,

foreign exchange rates, equity prices or other rates or prices;

the performance of the financial markets in India and globally;

changes in domestic laws, regulations and taxes; and

increasing competition in or other factors affecting the industry segments in which the Company operates.

For further discussion of factors that could cause the Company’s actual results to differ, see the section

entitled “Investment Considerations”. By their nature, certain market risk disclosures are only estimates and

could be materially different from what actually occurs in the future. As a result, actual future gains or losses

could materially differ from those that have been estimated. None of the Issuers, the Company, the Arrangers,

the Dealers, the Trustee, the Agents or any person who controls any of them, or any of their respective officers,

employees, advisers or agents, or any affiliate of any such person, have any obligation to update or otherwise

revise any statements reflecting circumstances arising after the date hereof or to reflect the occurrence of

underlying events, even if the underlying assumptions do not come to fruition.

ENFORCEMENT OF FOREIGN JUDGMENTS IN INDIA

Under the Programme, the Notes may be issued by ONGC, ONGC Videsh or any New Issuer (as defined

in the Terms and Conditions of the Notes). ONGC and ONGC Videsh are limited liability public companies

incorporated under the laws of India. A New Issuer may be a company incorporated outside India (an “Offshore

Subsidiary Issuer”) or a company incorporated under the laws of India (a “Domestic Subsidiary Issuer” and

together with the ONGC (in its capacity as an issuer) and ONGC Videsh, the “Domestic Issuers”). ONGC will

be a guarantor in respect of Notes issued by ONGC Videsh or any New Issuer.

All of ONGC Videsh’s directors and executive officers are residents of India and such persons are located

in India. As a result, it may not be possible for investors to effect service of process on ONGC Videsh or such

persons in jurisdictions outside of India, or to enforce against them judgments obtained in courts outside of

India predicated upon civil liabilities of ONGC Videsh or such directors and executive officers under laws other

than Indian law. All of ONGC’s directors and executive officers are residents of India and all or a substantial

portion of the assets of ONGC and such persons are located in India. As a result, it may not be possible for

investors to effect service of process on ONGC or such persons in jurisdictions outside of India, or to enforce

against them judgments obtained in courts outside of India predicated upon civil liabilities of ONGC or such

directors and executive officers under laws other than Indian law. Each Domestic Issuer’s (other than ONGC

Videsh and ONGC) directors and executive officers may be residents of India and all or a substantial portion of

the assets of such Domestic Issuer and such persons may be located in India. As a result, it may not be possible

for investors to effect service of process on such Domestic Issuer or such persons in jurisdictions outside of

India, or to enforce against them judgments obtained in courts outside of India predicated upon civil liabilities

of such Domestic Issuer or such directors and executive officers under laws other than Indian law.

In addition, India is not a party to any international treaty in relation to the recognition or enforcement

of foreign judgments. Recognition and enforcement of foreign judgments is provided for under section 13 and

section 44A of the Indian Code of Civil Procedure, 1908, as amended (the “Civil Code”). Section 44A of the

Civil Code provides that where a foreign judgment has been rendered by a superior court in any country or

territory outside India which the Indian Government has by notification declared to be a reciprocating territory,

it may be enforced in India by proceedings in execution as if the judgment had been rendered by the relevant

court in India. However, section 44A of the Civil Code is applicable only to monetary decrees not being in the

nature of any amounts payable in respect of taxes or other charges of a like nature or in respect of a fine or other

penalty and is not applicable to arbitration awards even if such awards are enforceable as a decree or judgment.

A39729228 xi

The United Kingdom has been declared by the Indian Government to be a reciprocating territory for the

purposes of section 44A of the Civil Code and the High Courts in England as the relevant superior courts.

Accordingly, a judgment of a superior court in the United Kingdom may be enforced by proceedings in

execution and a judgment not of a superior court, by a fresh suit resulting in a judgment or order. A judgment

of a court in a jurisdiction which is not a reciprocating territory may be enforced only by a new suit upon the

judgment and not by proceedings in execution. Section 13 of the Civil Code provides that a foreign judgment

shall be conclusive as to any matter thereby directly adjudicated upon except: (i) where it has not been

pronounced by a court of competent jurisdiction; (ii) where it has not been given on the merits of the case; (iii)

where it appears on the face of the proceedings to be founded on an incorrect view of international law or a

refusal to recognise the law of India in cases where such law is applicable; (iv) where the proceedings in which

the judgment was obtained were opposed to natural justice; (v) where it has been obtained by fraud; or (vi)

where it sustains a claim founded on a breach of any law in force in India. The suit must be brought in India

within three years from the date of the judgment in the same manner as any other suit filed to enforce a civil

liability in India. It is unlikely that a court in India would award damages on the same basis as a foreign court

if an action were brought in India. Furthermore, it is unlikely that an Indian court would enforce a foreign

judgment if it viewed the amount of damages awarded as excessive or inconsistent with Indian practice. A party

seeking to enforce a foreign judgment in India is required to obtain approval from the RBI under the Foreign

Exchange Management Act, 1999, as amended (the “FEMA”) to repatriate outside India any amount recovered

pursuant to execution. Any judgment in a foreign currency would be converted into Indian Rupees on the date

of the judgment and not on the date of the payment. Also, a party may file suit in India against each of the Issuer

and the Guarantor, its directors or its executive directors as an original action.

ENFORCEMENT OF THE GUARANTEE

The primary exchange control legislation in India is FEMA. Pursuant to FEMA, the Indian Government

and the RBI have issued various regulations, rules, circulars and press notes in connection with various aspects

of exchange control. The primary regulations governing overseas direct investments outside India by Indian

residents as well as issuances of guarantees by Indian companies in favour of their overseas subsidiaries are the

Foreign Exchange Management (Guarantees) Regulations, 2000, as amended from time to time, (the “FEMA

Guarantees Regulations”), the Foreign Exchange Management (Transfer or Issue of any Foreign Security)

Regulations, 2004, as amended from time to time (the “Foreign Security Regulations”) and “Master Direction-

Direct Investment by Residents in Joint Venture (JV)/ Wholly Owned Subsidiary (WOS) Abroad” dated 1

January 2016 issued by the RBI, as amended from time to time (the “FEMA ODI Regulations”, together with

the Foreign Security Regulations and FEMA Guarantees Regulations, the “FEMA Guarantee Laws”). The

term “direct investment outside India” has been defined by the FEMA Guarantee Laws to mean investment by

way of contribution to the capital or subscription to the Memorandum of Association (i.e. charter documents)

of a foreign entity or by way of purchase of existing shares of a foreign entity either by market purchase or

private placement or through stock exchange, but does not include portfolio investment.

Indian entities may offer any form of guarantee, corporate or personal (including the personal guarantee

by indirect resident individual promoters of an Indian entity), guarantee by the promoter company, or guarantee

by a group company, sister concern or associate company in India subject to certain conditions.

Pursuant to the FEMA Guarantee Laws, an Indian company is permitted to make direct investments

outside India in its wholly-owned subsidiaries (“WOS”) and joint ventures (“JV”), under the limits of 400 per

cent. of the net worth of the Indian entity in accordance with the last audited balance sheet prescribed by RBI.

Any financial commitment exceeding U.S.$1 billion (or its equivalent) in a financial year requires prior RBI

approval even when the total financial commitment of the Indian entity is within the eligible 400 per cent. net

worth limit under the automatic route. The Indian entity can extend a guarantee to an overseas JV/WOS through

A39729228 xii

(a) an automatic route if it has direct or indirect equity participation in such JV/WOS, or (b) through RBI

approval if it does not have equity contribution in the JV/WOS, in each case provided that such JV/WOS is

located in a FATF Compliant Country. Under the FEMA Guarantee Laws, all financial commitments including

all forms of guarantees should be within the overall ceiling prescribed.

For the purposes of the FEMA Guarantee Laws, “total financial commitment” includes, inter alia, 100

per cent. of the amount of the guarantee (other than any performance guarantee) issued by the Indian entity. The

Indian company (which is making the direct investment outside India) should not be on the RBI’s exporters’

caution list or list of defaulters to the system circulated by specified entities or be under investigation by any

investigation or enforcement agency or regulatory body. However, all such guarantees must specify a maximum

amount and duration of the guarantee upfront, so no guarantee can be open-ended or unlimited. There are

reporting instructions that are applicable in Form ODI which is submitted by the authorised dealer bank of the

Indian entity in India to the RBI.

If a guarantee issued by an Indian company on behalf of its JV/WOS is enforced by a competent court

in a territory other than a “reciprocal territory”, the judgment must be enforced in India by a new suit upon the

judgment and not by proceedings in execution. Such a suit has to be filed in India within three years from the

date of the judgment in the same manner as any other suit filed to enforce a civil liability in India. A party

seeking to enforce a foreign judgment in India is required to obtain RBI approval to repatriate outside India any

amount recovered pursuant to the execution of such a judgment.

The Guarantor is not entitled to immunity on the basis of sovereignty or otherwise from any legal

proceedings in India to enforce the Guarantee or any liability or obligation of the Guarantor arising thereunder.

As the Guarantee is an obligation of a type which Indian courts would usually enforce, the Guarantee

should be enforced against the Guarantor in accordance with its terms by an Indian court, subject to the

following exceptions: (a) enforcement may be limited by general principles of equity, such as injunctions; (b)

the remedy of specific performance may not be available in certain circumstances; and (c) actions may become

barred under the Limitation Act, 1963, or may be or become subject to set-off or counterclaim, and failure to

exercise a right of action within the relevant prescribed limitation period will operate as a bar to the exercise of

such right; (d) any certificate, determination, notification, opinion or the like will not be binding on an Indian

court, which will have to be independently satisfied on the contents thereof for the purpose of enforcement

despite any provisions in the relevant documents to the contrary; and (e) all limitations resulting from the laws

of reorganisation, suretyship or similar laws of general application affecting creditors’ rights.

For details on the requisite filings and the approval granted by the RBI pursuant to which the Guarantee

is issued, see the section entitled “Government Approvals/Filings” below. At all times, the Guarantee by the

Guarantor in respect of each Series of Guaranteed Notes, shall be in respect of an amount not exceeding 109.00

per cent. of the outstanding nominal amount of such Series of Guaranteed Notes. For further information, see

the section entitled “Terms and Conditions of the Notes”.

GOVERNMENT APPROVALS/FILINGS

The relevant Issuer will make all required filings, registrations or reports with the relevant governmental

authorities of its jurisdiction of incorporation from time to time.

The Domestic Issuers will make all required filings, registrations or reports with the relevant governmental

authorities of India from time to time. In respect of any offering of Indian Issuer Notes made by ONGC (in its

capacity as issuer) or ONGC Videsh or by any Domestic Subsidiary Issuer and guaranteed by the Guarantor,

the relevant Domestic Issuer will need to file Form ECB with their authorised dealer bank (the “AD Bank”) to

obtain a loan registration number from the RBI before an issuance of Indian Issuer Notes by such a Domestic

Issuer is effected. A monthly filing in the prescribed form of Form ECB – 2 is also required to be made by the

A39729228 xiii

relevant Domestic Issuer. The maximum amount that can be raised by way of external commercial borrowing

under the automatic route by each Domestic Issuer is U.S.$750 million per financial year or its equivalent. For

any amounts over and above this, a prior RBI approval will be required to be obtained.

For any offering of Notes made by any Offshore Subsidiary Issuer which are guaranteed by the Guarantor,

the guarantee must comply with the FEMA Guarantee Laws if the guarantee is to be provided under the

automatic route and without prior RBI approval. If any of the conditions are not satisfied, then a prior RBI

approval will be required for the guarantee to be provided. The Guarantor will make or procure to make all

required filings or reports with the requisite regulatory or governmental agency or body in India from time to

time, including, but not limited to, the filing of Form ODI prescribed under the FEMA Guarantee Laws of India

in relation to the Guarantee every year on or before 31 December through an authorised dealer of the Indian

entity in India with the RBI.

NOTICE TO POTENTIAL INVESTORS IN NOTES ISSUED BY A DOMESTIC ISSUER

Holders and beneficial owners of Notes to be issued by a Domestic Issuer under this Programme shall be

responsible for compliance with restrictions on the ownership of the Notes imposed from time to time by

applicable laws or by any regulatory authority or otherwise. In this context, holders and beneficial owners of

Notes issued by an Issuer shall be deemed to have acknowledged, represented and agreed that such holders and

beneficial owners are eligible to purchase such Notes under applicable laws and regulations and are not

prohibited under any applicable law or regulation from acquiring, owning or selling such Notes issued by an

Issuer. Potential investors should seek independent advice and verify compliance prior to any purchase of the

Notes.

The holders and beneficial owners of Indian Issuer Notes shall be deemed to confirm that for so long as

they hold any Indian Issuer Notes, they will comply with the ECB Investor Requirements (for further

information, see the section entitled “Summary of Relevant Indian Laws and Regulations – Foreign Exchange

Laws”). Further, all Noteholders (including holders and beneficial owners) represent and agree that the Indian

Issuer Notes issued by a Domestic Issuer will not be transferred or sold or offered on the secondary market to

any person who does not comply with the ECB Investor Requirements or comply with the ECB Guidelines.

To comply with applicable laws and regulations, the relevant Issuer or its duly appointed agent may from

time to time request Euroclear and Clearstream, Luxembourg to provide them with details of the accountholders

within Euroclear and Clearstream, Luxembourg, as may be appropriate, that hold the Notes issued by a

Domestic Issuer and the number of Notes held by each such accountholder.

Euroclear and Clearstream, Luxembourg participants which are holders of the Notes or intermediaries

acting on behalf of such Noteholders would be deemed to have hereby authorised Euroclear and Clearstream,

Luxembourg, as may be appropriate, to disclose such information to the relevant Issuer or its duly appointed

agent.

A39729228 xiv

TABLE OF CONTENTS

Page

DOCUMENTS INCORPORATED BY REFERENCE ...................................................................................... 1

GENERAL DESCRIPTION OF THE PROGRAMME ..................................................................................... 2

SUMMARY OF THE PROGRAMME .............................................................................................................. 3

INVESTMENT CONSIDERATIONS ..............................................................................................................10

FORM OF THE NOTES ...................................................................................................................................67

FORM OF PRICING SUPPLEMENT ..............................................................................................................71

TERMS AND CONDITIONS OF THE NOTES ..............................................................................................82

USE OF PROCEEDS ...................................................................................................................................... 118

CAPITALISATION AND INDEBTEDNESS OF THE COMPANY .............................................................. 119