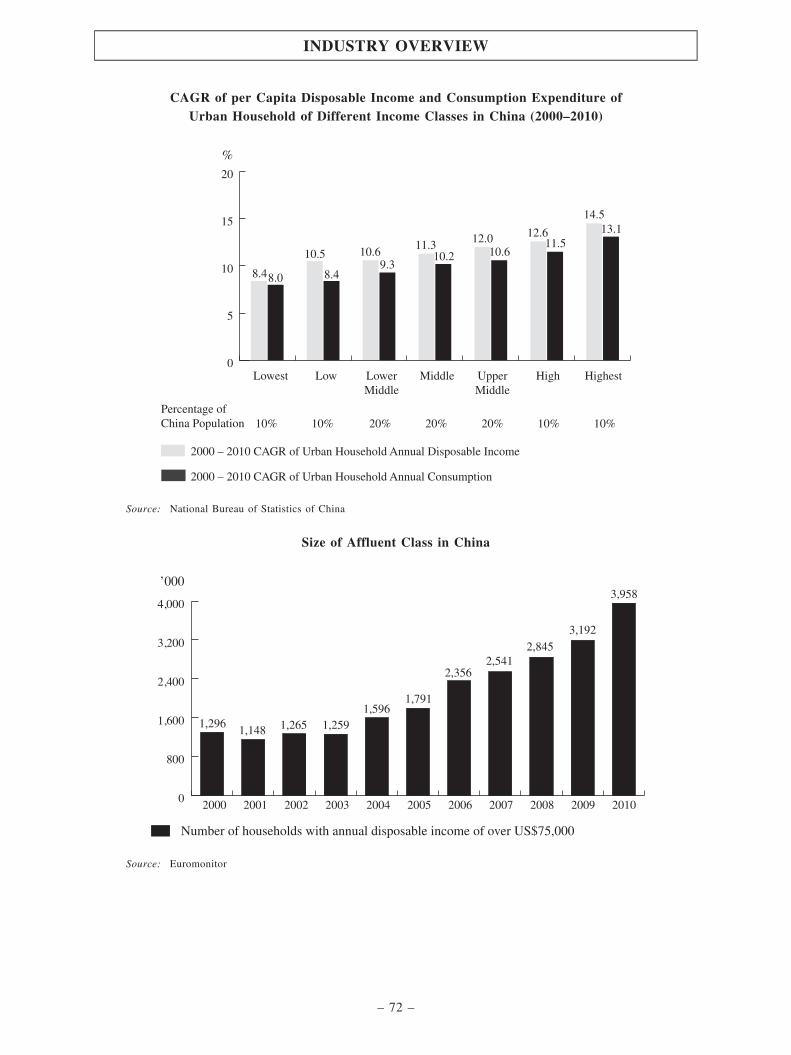

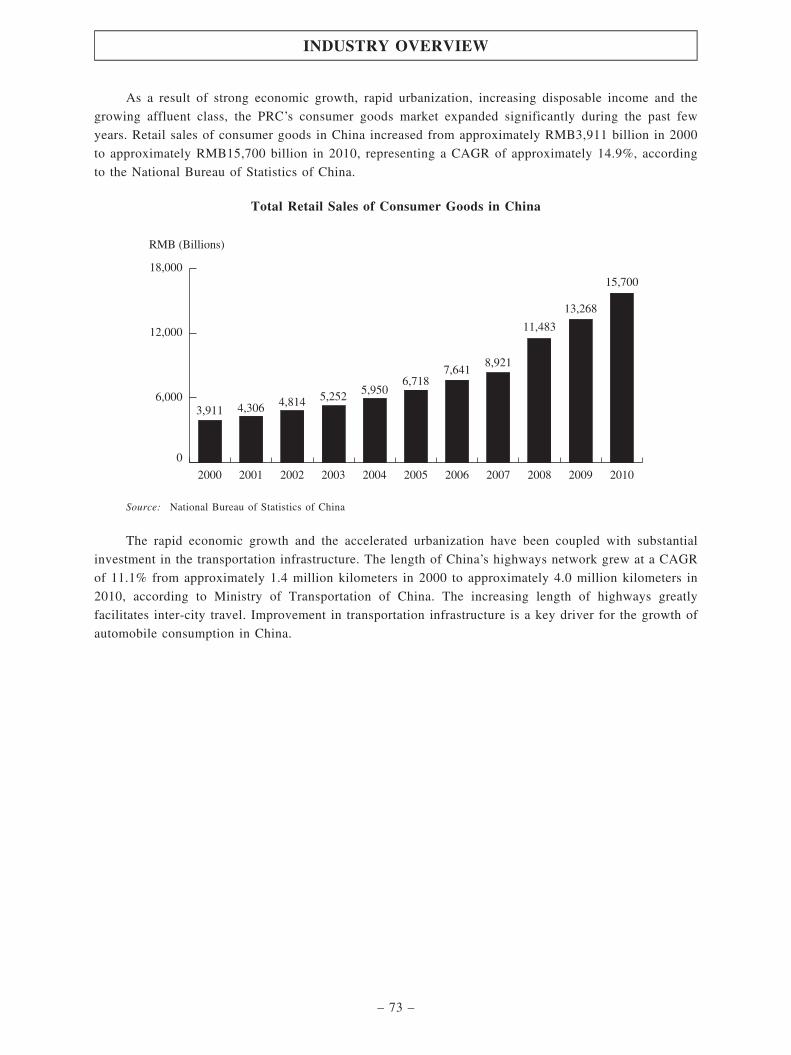

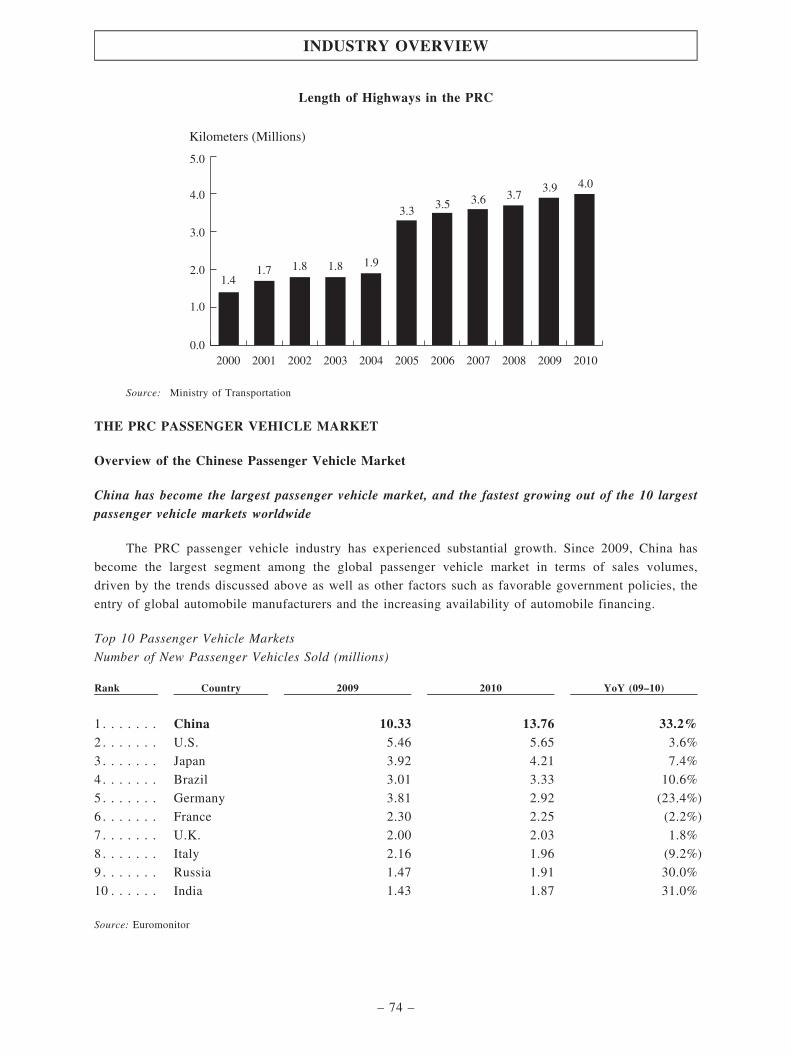

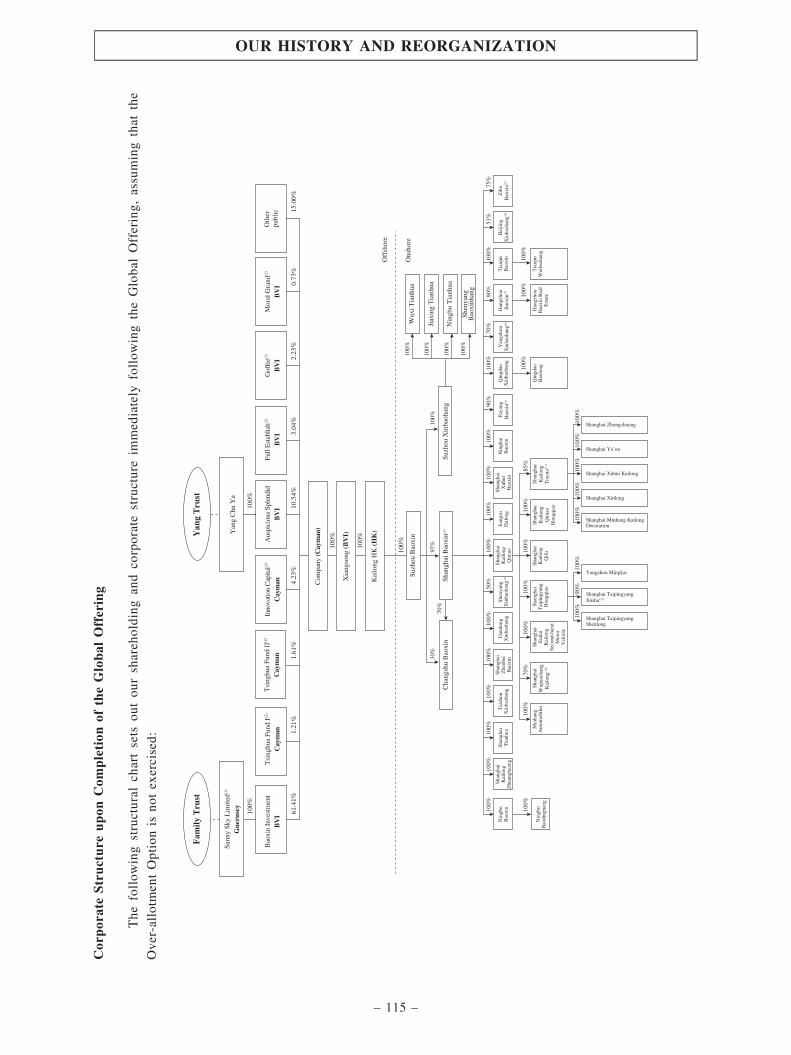

OFFERING - HKEXnews

395

Stock code: 1293 GLOBAL OFFERING (Incorporated in the Cayman Islands with limited liability) BAOXIN AUTO GROUP LIMITED 寶信汽車集團有限公司 Joint Bookrunners and Joint Lead Managers Joint Sponsors Sole Global Coordinator For identification purposes only

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of OFFERING - HKEXnews

Stock code: 1293

GLOBAL OFFERING

(Incorporated in the Cayman Islands with limited liability)

BAOXIN AUTO GROUP LIMITEDBAOXIN AUTO GROUP LIMITED 寶信汽車集團有限公司寶信汽車集團有限公司

BAO

XIN AU

TO G

ROU

P LIMITED

寶信汽車集團有限公司

Joint Bookrunners and Joint Lead Managers

Joint Sponsors

Sole Global Coordinator

For identification purposes only

BaoXin_Final_2b.indd 1 11年11月29日 上午10:58

IMPORTANT: If you are in any doubt about the contents of this prospectus, you should seek independent professional advice.

BAOXIN AUTO GROUP LIMITED寶 信 汽 車 集 團 有 限 公 司*

(Incorporated in the Cayman Islands with limited liability)

GLOBAL OFFERING

Number of Offer Shares under theGlobal Offering

: 379,320,000 Shares (comprising 328,740,000new Shares and 50,580,000 Sale Shares,subject to the Over-allotment Option)

Number of Hong Kong Offer Shares : 37,932,000 Shares (subject to adjustment)Number of International Offer Shares : 341,388,000 Shares (comprising 290,808,000

new Shares and 50,580,000 Sale Shares,subject to adjustment and the Over-allotment Option)

Maximum Offer Price : HK$10.80 per Offer Share plus brokerage of1.0%, SFC transaction levy of 0.003% andHong Kong Stock Exchange trading fee of0.005% (payable in full on application inHong Kong dollars and subject to refund)

Nominal value : HK$0.01 per ShareStock code : 1293

Sole Global Coordinator

Joint Sponsors

Joint Bookrunners and Joint Lead Managers

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contentsof this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance uponthe whole or any part of the contents of this prospectus.

A copy of this prospectus, having attached thereto the documents specified in the section headed ‘‘Documents Delivered to the Registrar of Companies and Available for Inspection’’ inAppendix VII to this prospectus, has been registered by the Registrar of Companies in Hong Kong as required by Section 342C of the Companies Ordinance (Chapter 32 of the Laws ofHong Kong). The Securities and Futures Commission of Hong Kong and the Registrar of Companies in Hong Kong take no responsibility for the contents of this prospectus or any ofthe other documents referred to above.

The Offer Price is expected to be determined by agreement between the Joint Bookrunners (on behalf of the Underwriters), the Selling Shareholder and our Company on or aboutWednesday, December 7, 2011 and, in any event, not later than Thursday, December 8, 2011. The Offer Price will be not more than HK$10.80 per Offer Share and is currentlyexpected to be not less than HK$8.50 per Offer Share, unless otherwise announced. Investors applying for the Hong Kong Offer Shares must pay, on application, the maximum OfferPrice of HK$10.80 per Offer Share, together with brokerage of 1.0%, SFC transaction levy of 0.003% and Hong Kong Stock Exchange trading fee of 0.005%, subject to refund if theOffer Price is less than HK$10.80 per Offer Share.

The Joint Bookrunners (on behalf of the Underwriters), with the consent of our Company and the Selling Shareholder, may reduce the indicative Offer Price range stated in thisprospectus and/or reduce the number of Offer Shares being offered pursuant to the Global Offering at any time on or prior to the morning of the last day for lodging applications underthe Hong Kong Public Offering. In such a case, notices of the reduction of the indicative Offer Price range and/or the number of Offer Shares will be published in the South ChinaMorning Post (in English) and the Hong Kong Economic Times (in Chinese), on the Company’s website at www.klbaoxin.com and the Stock Exchange’s website at www.hkexnews.hknot later than the morning of the last day for lodging applications under the Hong Kong Public Offering. Further details are set out in the sections headed ‘‘Structure of the GlobalOffering’’ and ‘‘How to Apply for the Hong Kong Offer Shares’’ in this prospectus. If, for any reason, the Offer Price is not agreed between our Company, the Selling Shareholder andthe Joint Bookrunners (on behalf of the Underwriters), the Global Offering (including the Hong Kong Public Offering) will not proceed and will lapse. Please also see the sectionheaded ‘‘Underwriting—Underwriting Arrangements and Expenses—The Hong Kong Public Offering—Grounds for Termination’’ in this prospectus.

The Offer Shares have not been and will not be registered under the U.S. Securities Act or any state securities law in the United States and may not be offered or sold within the UnitedStates except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act. Accordingly, the Offer Shares are being offeredand sold within the United States only to ‘‘qualified institutional buyers’’ as defined in Rule 144A. The Offer Shares may be offered, sold or delivered outside the United States inoffshore transactions in accordance with Regulation S.

* For identification purposes only

IMPORTANT

December 2, 2011

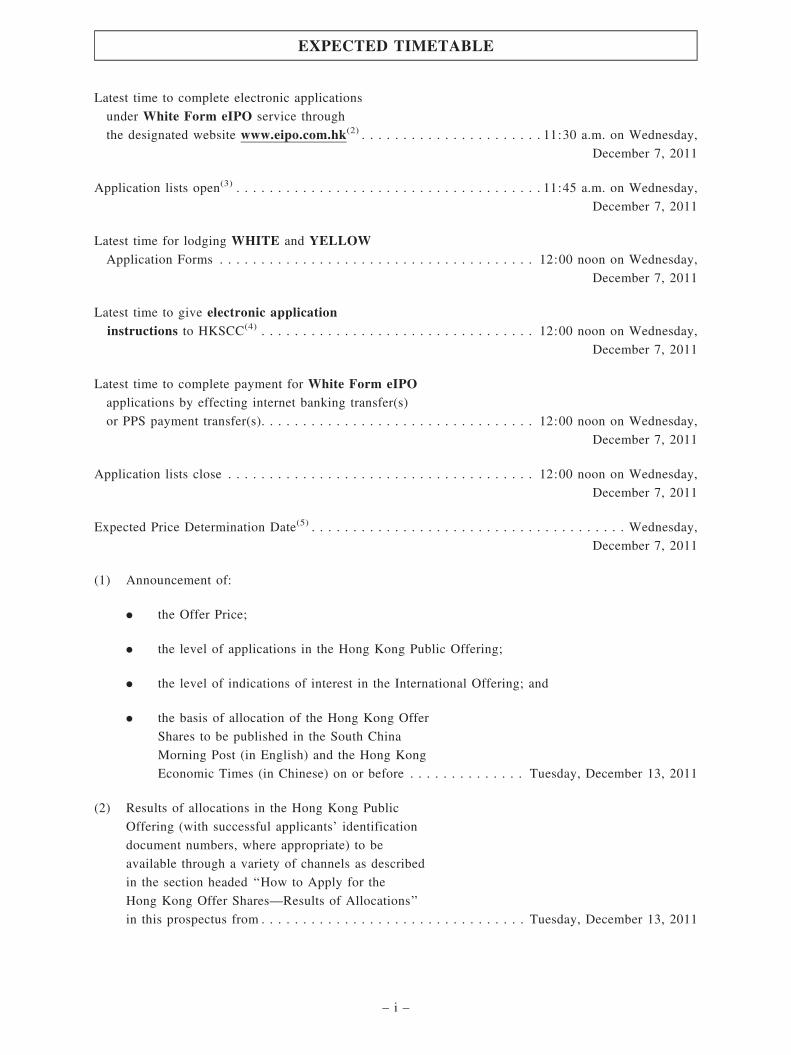

Latest time to complete electronic applications

under White Form eIPO service through

the designated website www.eipo.com.hk(2) . . . . . . . . . . . . . . . . . . . . . . 11:30 a.m. on Wednesday,

December 7, 2011

Application lists open(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11:45 a.m. on Wednesday,

December 7, 2011

Latest time for lodging WHITE and YELLOWApplication Forms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Wednesday,

December 7, 2011

Latest time to give electronic applicationinstructions to HKSCC(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Wednesday,

December 7, 2011

Latest time to complete payment for White Form eIPOapplications by effecting internet banking transfer(s)

or PPS payment transfer(s). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Wednesday,

December 7, 2011

Application lists close . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Wednesday,

December 7, 2011

Expected Price Determination Date(5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Wednesday,

December 7, 2011

(1) Announcement of:

. the Offer Price;

. the level of applications in the Hong Kong Public Offering;

. the level of indications of interest in the International Offering; and

. the basis of allocation of the Hong Kong Offer

Shares to be published in the South China

Morning Post (in English) and the Hong Kong

Economic Times (in Chinese) on or before . . . . . . . . . . . . . . Tuesday, December 13, 2011

(2) Results of allocations in the Hong Kong Public

Offering (with successful applicants’ identification

document numbers, where appropriate) to be

available through a variety of channels as described

in the section headed ‘‘How to Apply for the

Hong Kong Offer Shares—Results of Allocations’’

in this prospectus from . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Tuesday, December 13, 2011

EXPECTED TIMETABLE

– i –

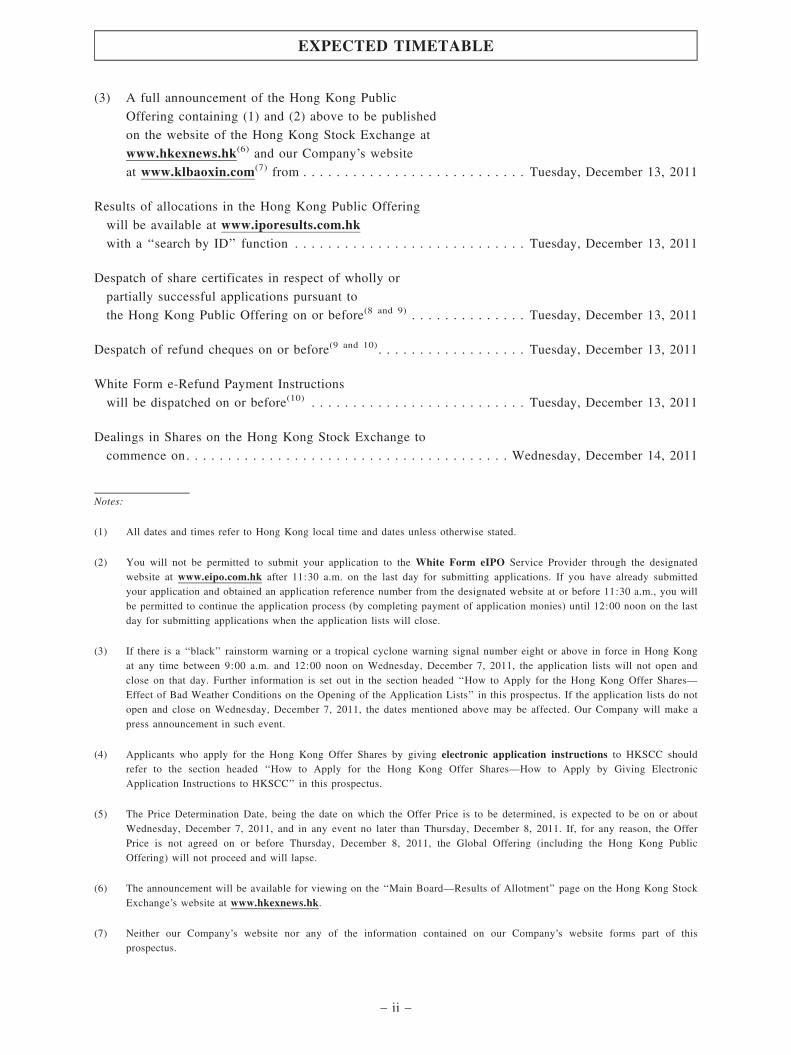

(3) A full announcement of the Hong Kong Public

Offering containing (1) and (2) above to be published

on the website of the Hong Kong Stock Exchange at

www.hkexnews.hk(6) and our Company’s website

at www.klbaoxin.com(7) from . . . . . . . . . . . . . . . . . . . . . . . . . . . Tuesday, December 13, 2011

Results of allocations in the Hong Kong Public Offering

will be available at www.iporesults.com.hkwith a ‘‘search by ID’’ function . . . . . . . . . . . . . . . . . . . . . . . . . . . . Tuesday, December 13, 2011

Despatch of share certificates in respect of wholly or

partially successful applications pursuant to

the Hong Kong Public Offering on or before(8 and 9) . . . . . . . . . . . . . . Tuesday, December 13, 2011

Despatch of refund cheques on or before(9 and 10) . . . . . . . . . . . . . . . . . . Tuesday, December 13, 2011

White Form e-Refund Payment Instructions

will be dispatched on or before(10) . . . . . . . . . . . . . . . . . . . . . . . . . . Tuesday, December 13, 2011

Dealings in Shares on the Hong Kong Stock Exchange to

commence on. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Wednesday, December 14, 2011

Notes:

(1) All dates and times refer to Hong Kong local time and dates unless otherwise stated.

(2) You will not be permitted to submit your application to the White Form eIPO Service Provider through the designatedwebsite at www.eipo.com.hk after 11:30 a.m. on the last day for submitting applications. If you have already submittedyour application and obtained an application reference number from the designated website at or before 11:30 a.m., you willbe permitted to continue the application process (by completing payment of application monies) until 12:00 noon on the last

day for submitting applications when the application lists will close.

(3) If there is a ‘‘black’’ rainstorm warning or a tropical cyclone warning signal number eight or above in force in Hong Kongat any time between 9:00 a.m. and 12:00 noon on Wednesday, December 7, 2011, the application lists will not open and

close on that day. Further information is set out in the section headed ‘‘How to Apply for the Hong Kong Offer Shares—Effect of Bad Weather Conditions on the Opening of the Application Lists’’ in this prospectus. If the application lists do notopen and close on Wednesday, December 7, 2011, the dates mentioned above may be affected. Our Company will make apress announcement in such event.

(4) Applicants who apply for the Hong Kong Offer Shares by giving electronic application instructions to HKSCC shouldrefer to the section headed ‘‘How to Apply for the Hong Kong Offer Shares—How to Apply by Giving ElectronicApplication Instructions to HKSCC’’ in this prospectus.

(5) The Price Determination Date, being the date on which the Offer Price is to be determined, is expected to be on or about

Wednesday, December 7, 2011, and in any event no later than Thursday, December 8, 2011. If, for any reason, the OfferPrice is not agreed on or before Thursday, December 8, 2011, the Global Offering (including the Hong Kong PublicOffering) will not proceed and will lapse.

(6) The announcement will be available for viewing on the ‘‘Main Board—Results of Allotment’’ page on the Hong Kong StockExchange’s website at www.hkexnews.hk.

(7) Neither our Company’s website nor any of the information contained on our Company’s website forms part of thisprospectus.

EXPECTED TIMETABLE

– ii –

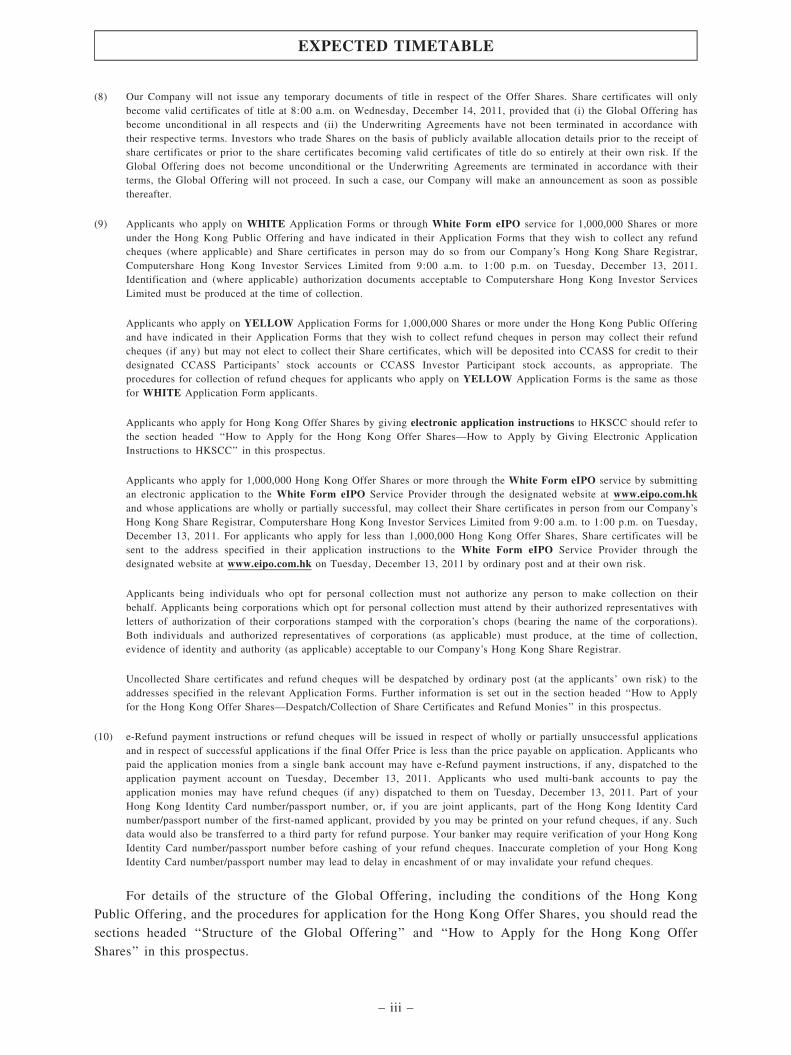

(8) Our Company will not issue any temporary documents of title in respect of the Offer Shares. Share certificates will onlybecome valid certificates of title at 8:00 a.m. on Wednesday, December 14, 2011, provided that (i) the Global Offering hasbecome unconditional in all respects and (ii) the Underwriting Agreements have not been terminated in accordance withtheir respective terms. Investors who trade Shares on the basis of publicly available allocation details prior to the receipt ofshare certificates or prior to the share certificates becoming valid certificates of title do so entirely at their own risk. If theGlobal Offering does not become unconditional or the Underwriting Agreements are terminated in accordance with theirterms, the Global Offering will not proceed. In such a case, our Company will make an announcement as soon as possiblethereafter.

(9) Applicants who apply on WHITE Application Forms or through White Form eIPO service for 1,000,000 Shares or moreunder the Hong Kong Public Offering and have indicated in their Application Forms that they wish to collect any refundcheques (where applicable) and Share certificates in person may do so from our Company’s Hong Kong Share Registrar,Computershare Hong Kong Investor Services Limited from 9:00 a.m. to 1:00 p.m. on Tuesday, December 13, 2011.Identification and (where applicable) authorization documents acceptable to Computershare Hong Kong Investor ServicesLimited must be produced at the time of collection.

Applicants who apply on YELLOW Application Forms for 1,000,000 Shares or more under the Hong Kong Public Offeringand have indicated in their Application Forms that they wish to collect refund cheques in person may collect their refundcheques (if any) but may not elect to collect their Share certificates, which will be deposited into CCASS for credit to theirdesignated CCASS Participants’ stock accounts or CCASS Investor Participant stock accounts, as appropriate. Theprocedures for collection of refund cheques for applicants who apply on YELLOW Application Forms is the same as thosefor WHITE Application Form applicants.

Applicants who apply for Hong Kong Offer Shares by giving electronic application instructions to HKSCC should refer tothe section headed ‘‘How to Apply for the Hong Kong Offer Shares—How to Apply by Giving Electronic ApplicationInstructions to HKSCC’’ in this prospectus.

Applicants who apply for 1,000,000 Hong Kong Offer Shares or more through the White Form eIPO service by submittingan electronic application to the White Form eIPO Service Provider through the designated website at www.eipo.com.hkand whose applications are wholly or partially successful, may collect their Share certificates in person from our Company’sHong Kong Share Registrar, Computershare Hong Kong Investor Services Limited from 9:00 a.m. to 1:00 p.m. on Tuesday,December 13, 2011. For applicants who apply for less than 1,000,000 Hong Kong Offer Shares, Share certificates will besent to the address specified in their application instructions to the White Form eIPO Service Provider through thedesignated website at www.eipo.com.hk on Tuesday, December 13, 2011 by ordinary post and at their own risk.

Applicants being individuals who opt for personal collection must not authorize any person to make collection on theirbehalf. Applicants being corporations which opt for personal collection must attend by their authorized representatives withletters of authorization of their corporations stamped with the corporation’s chops (bearing the name of the corporations).Both individuals and authorized representatives of corporations (as applicable) must produce, at the time of collection,evidence of identity and authority (as applicable) acceptable to our Company’s Hong Kong Share Registrar.

Uncollected Share certificates and refund cheques will be despatched by ordinary post (at the applicants’ own risk) to theaddresses specified in the relevant Application Forms. Further information is set out in the section headed ‘‘How to Applyfor the Hong Kong Offer Shares—Despatch/Collection of Share Certificates and Refund Monies’’ in this prospectus.

(10) e-Refund payment instructions or refund cheques will be issued in respect of wholly or partially unsuccessful applicationsand in respect of successful applications if the final Offer Price is less than the price payable on application. Applicants whopaid the application monies from a single bank account may have e-Refund payment instructions, if any, dispatched to theapplication payment account on Tuesday, December 13, 2011. Applicants who used multi-bank accounts to pay theapplication monies may have refund cheques (if any) dispatched to them on Tuesday, December 13, 2011. Part of yourHong Kong Identity Card number/passport number, or, if you are joint applicants, part of the Hong Kong Identity Cardnumber/passport number of the first-named applicant, provided by you may be printed on your refund cheques, if any. Suchdata would also be transferred to a third party for refund purpose. Your banker may require verification of your Hong KongIdentity Card number/passport number before cashing of your refund cheques. Inaccurate completion of your Hong KongIdentity Card number/passport number may lead to delay in encashment of or may invalidate your refund cheques.

For details of the structure of the Global Offering, including the conditions of the Hong Kong

Public Offering, and the procedures for application for the Hong Kong Offer Shares, you should read the

sections headed ‘‘Structure of the Global Offering’’ and ‘‘How to Apply for the Hong Kong Offer

Shares’’ in this prospectus.

EXPECTED TIMETABLE

– iii –

Page

Expected Timetable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Forward-looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Waivers from Compliance with the Listing Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Information About this Prospectus and the Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Directors and Parties Involved in the Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Corporate Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

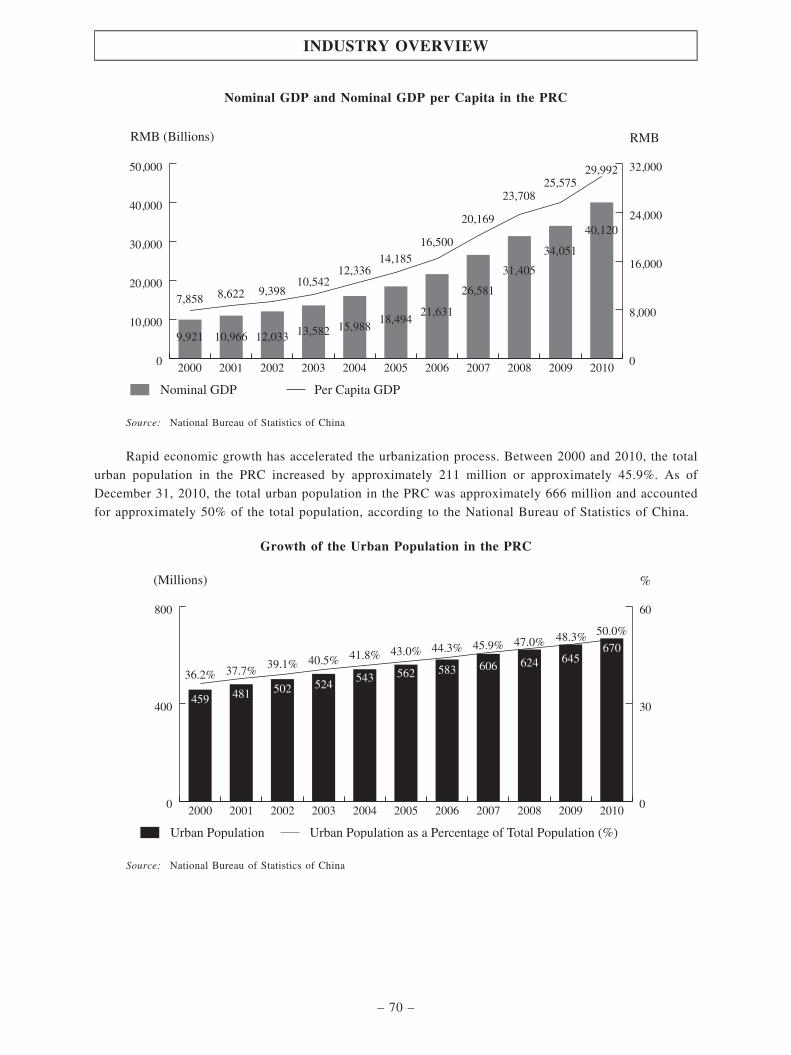

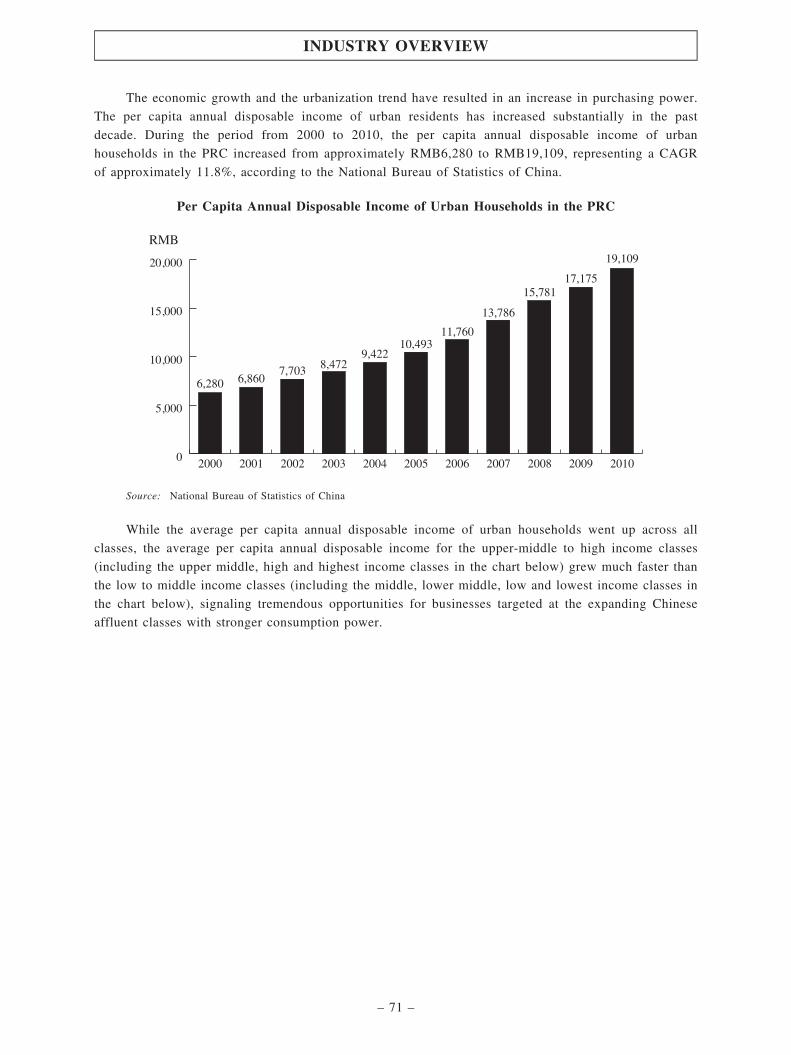

Industry Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Regulatory Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Our History and Reorganization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

Our Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

Relationship with Our Controlling Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

Directors and Senior Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

Substantial Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

Share Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160

Financial Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

Future Plans and Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 205

Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 208

Structure of the Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 217

How to Apply for the Hong Kong Offer Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 226

CONTENTS

– iv –

Page

Appendix I — Accountants’ Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-1

Appendix II — Unaudited Pro Forma Financial Information . . . . . . . . . . . . . . . . . . . . . . . II-1

Appendix III — Profit Forecast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . III-1

Appendix IV — Property Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . IV-1

Appendix V — Summary of the Constitution of Our Company andCayman Companies Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . V-1

Appendix VI — Statutory and General Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VI-1

Appendix VII — Documents Delivered to the Registrar of Companiesand Available for Inspection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VII-1

CONTENTS

– v –

This summary aims to give you an overview of the information contained in this prospectus.As it is a summary, it does not contain all the information that may be important to you. Youshould read the whole document in its entirety before you decide to invest in the Offer Shares.There are risks associated with any investment. Some of the particular risks in investing in theOffer Shares are set out in the section headed ‘‘Risk Factors’’ of this prospectus. You should readthat section carefully before you invest in our Offer Shares.

In this prospectus, a ‘‘4S’’ dealership store refers to an authorized dealership store that offers‘‘sales, spare parts, services and surveys’’, namely, a full range of dealership products and servicesthat include sales of automobiles and spare parts, approved maintenance and repair services andthe conduct of customer and market surveys for automobile manufacturers. Non-4S dealershipstores only offer a portion of the products or services available at 4S dealership stores.

The number of 4S dealership stores referred to in this prospectus includes a jointly-controlledentity whose revenues and sales volume are not included in our combined data. Accordingly, ourfinancial results, including sales revenues, gross profits and gross profit margins, and operatingdata, such as sales volumes, discussed in this prospectus do not include corresponding results ordata of that jointly-controlled entity.

OUR BUSINESS

Overview

According to Euromonitor, we are a leading luxury 4S dealership group in China in terms of sales

volume and number of dealership stores for BMW with a rapidly growing ultra-luxury dealership

business. We have a well-established network comprising 28 4S dealership stores (including a jointly-

controlled entity) as of September 30, 2011, 18 of which were luxury and ultra-luxury brand stores. As

of the Latest Practicable Date, we had received manufacturers’ authorizations, conditional approvals and

non-binding letters of intent to establish another 14 luxury and ultra-luxury brand 4S dealership stores,

showrooms and repair center, including five stores which we expect to commence operations by

December 31, 2011. All of our 4S dealership stores are strategically located in populous and affluent

regions in China with rapidly growing local economies. Our strong brand portfolio includes luxury

brands such as BMW, MINI, Audi, and Cadillac, ultra-luxury brands such as Land Rover & Jaguar, and

other popular mid-to-upper market brands, such as Buick, Toyota, Honda, Nissan, Volkswagen,

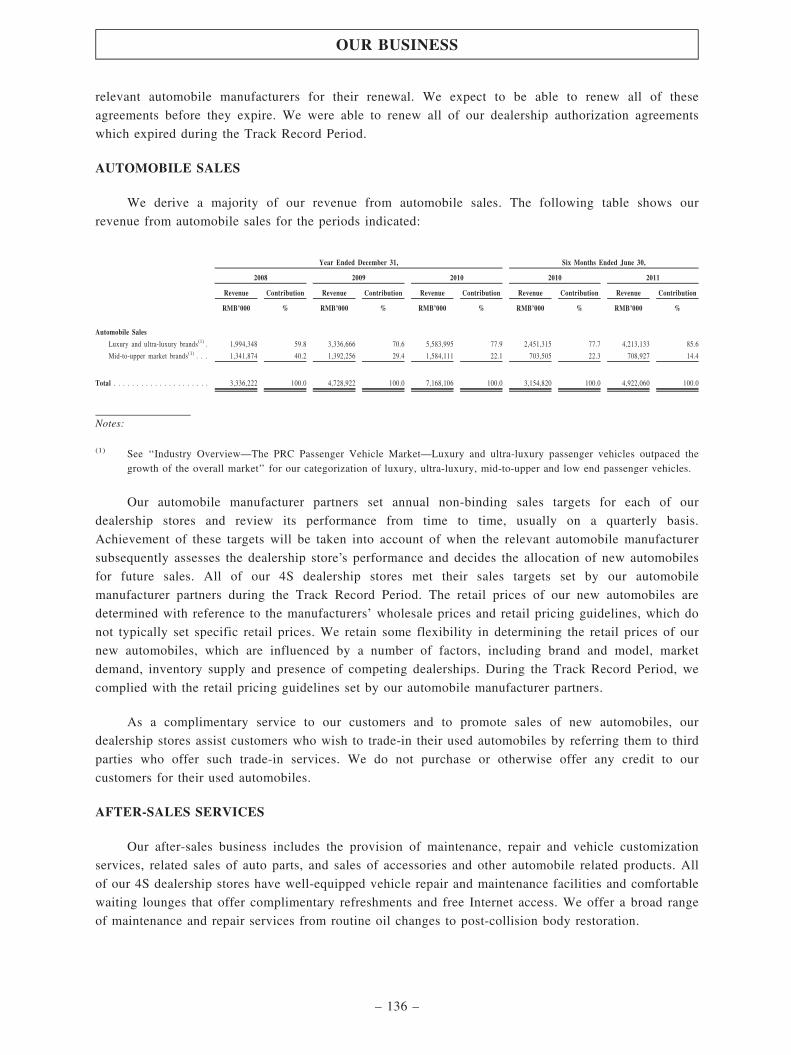

Chevrolet and Hyundai. Sales under our luxury and ultra-luxury brands have contributed to an

increasing percentage of our revenue and gross profit from automobile sales over the Track Record

Period, accounting for 59.8%, 70.6%, 77.9% and 85.6% of our revenue from automobile sales, and

80.4%, 80.9%, 87.8% and 93.8% of our gross profit from automobile sales, in 2008, 2009, 2010 and the

six months ended June 30, 2011, respectively. We believe that our focus on luxury and ultra-luxury

brands has enabled us to achieve rapid revenue and profit growth and increasing profit margins over the

Track Record Period.

SUMMARY

– 1 –

Our Track Record

Since we commenced operation in 1999 and became one of the first authorized dealerships for

Audi in 1999, we have established a proven track record in building successful, high quality 4S

dealership stores. We opened one of the first BMW Brilliance authorized 4S dealership stores in China

in 2004 and have since become one of BMW’s most important and largest dealerships in China in terms

of 2010 sales volume. BMW was one of the best-selling and one of the fastest growing luxury

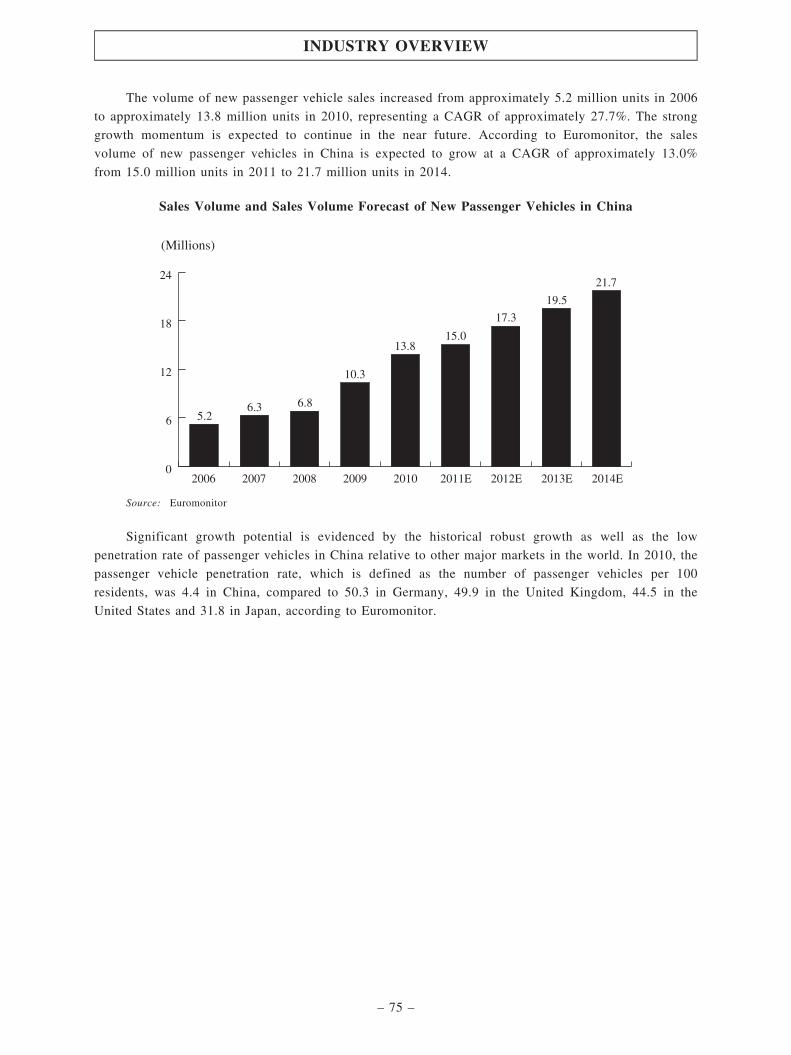

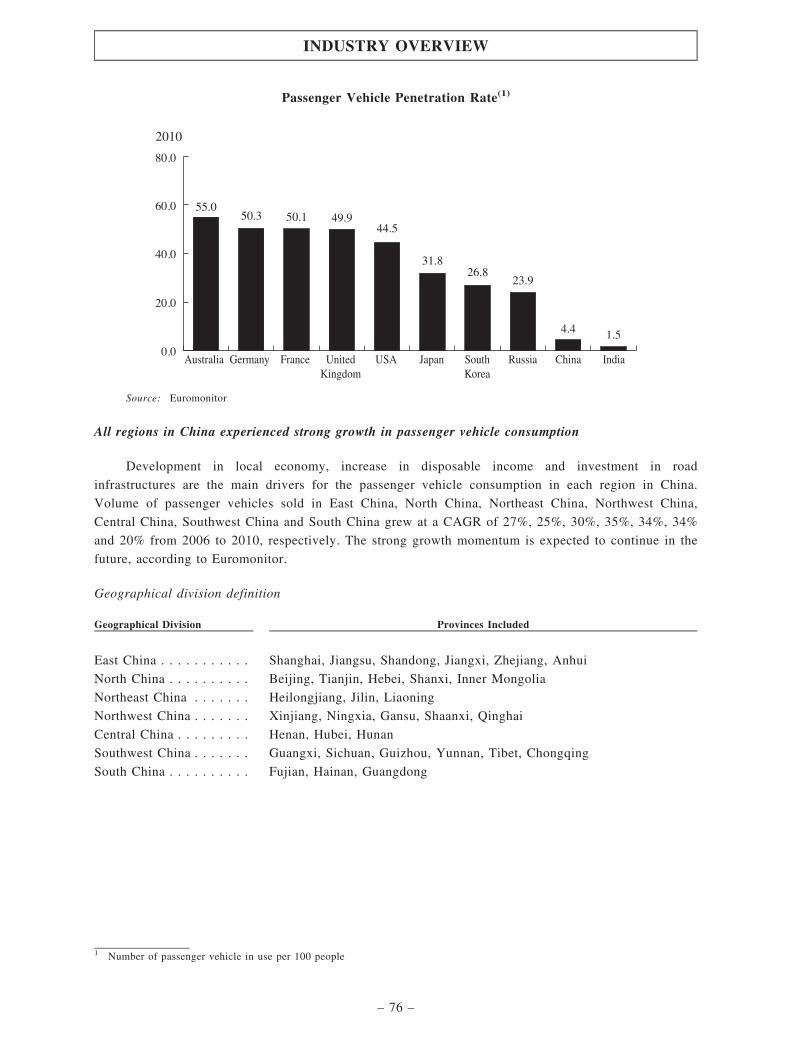

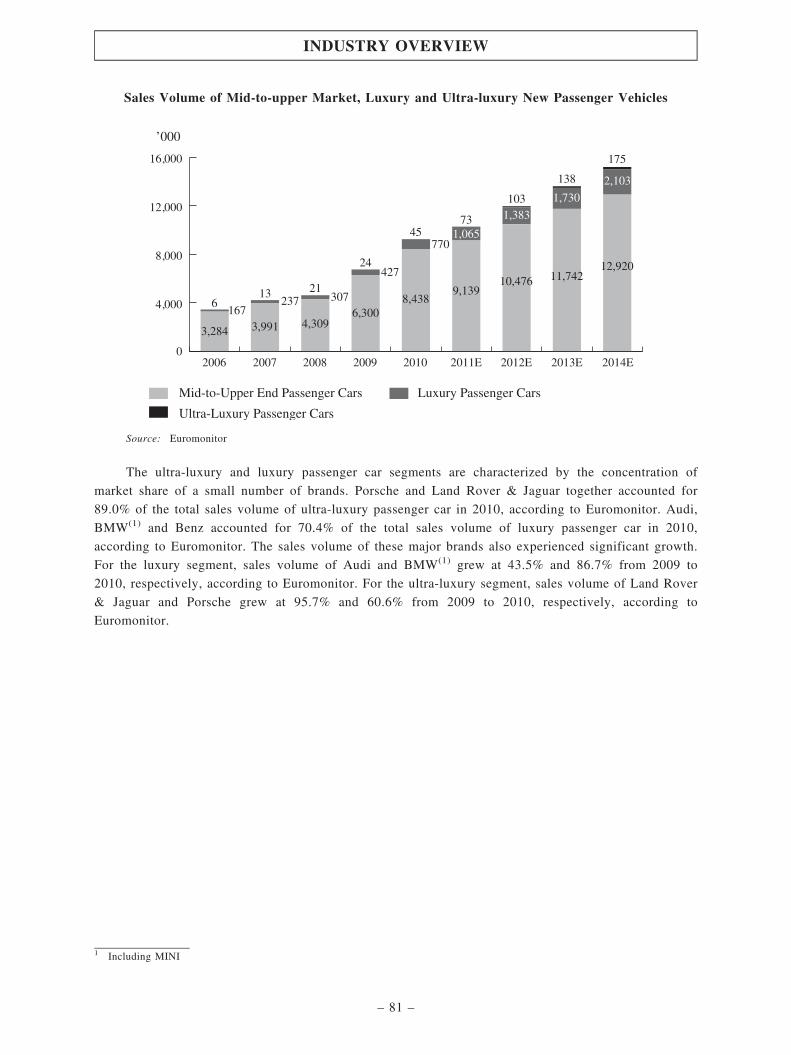

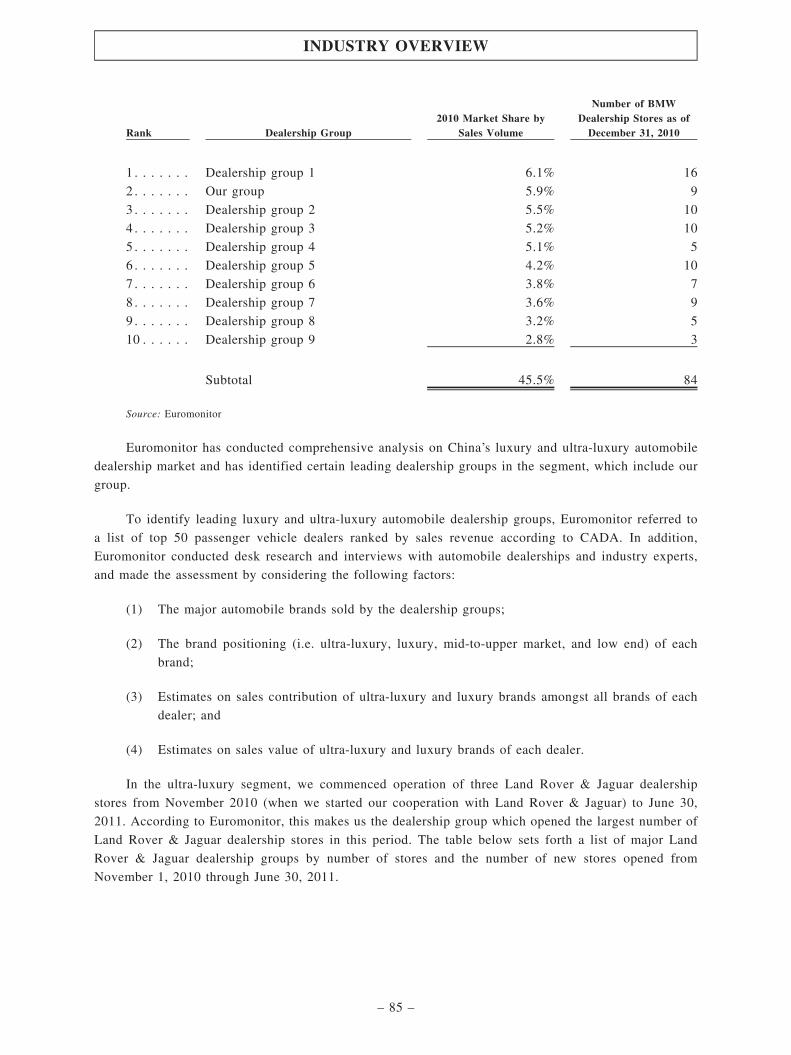

automobile brands in terms of sales volumes in China in 2010, according to Euromonitor. See ‘‘Industry

Overview—The PRC Passenger Vehicle Market—Luxury and ultra-luxury passenger vehicles outpaced

the growth of the overall market’’ for our categorization of luxury, ultra-luxury, mid-to-upper and low

end passenger vehicles. In 2010, China was the third largest market for BMW, and the fastest growing

of its three largest markets worldwide in terms of sales volume according to BMW’s 2010 annual report.

In 2010, three of our BMW 4S dealership stores ranked 2nd, 3rd and 9th, respectively, out of the 10

BMW 4S dealership stores nationwide that won its Best Dealership Quality Award. This ranking takes

into account all operational aspects of a 4S dealership store, including sales performance, customer

service quality and customer satisfaction rates. We were the only dealership group to achieve multiple

placings in this ranking by BMW, which had around 170 authorized 4S dealership stores in China at the

time of the ranking. In addition, in 2010, two of our BMW stores were ranked 1st and 3rd, respectively,

in BMW’s list of its 10 best 4S dealership stores nationwide for after-sales business. We commenced

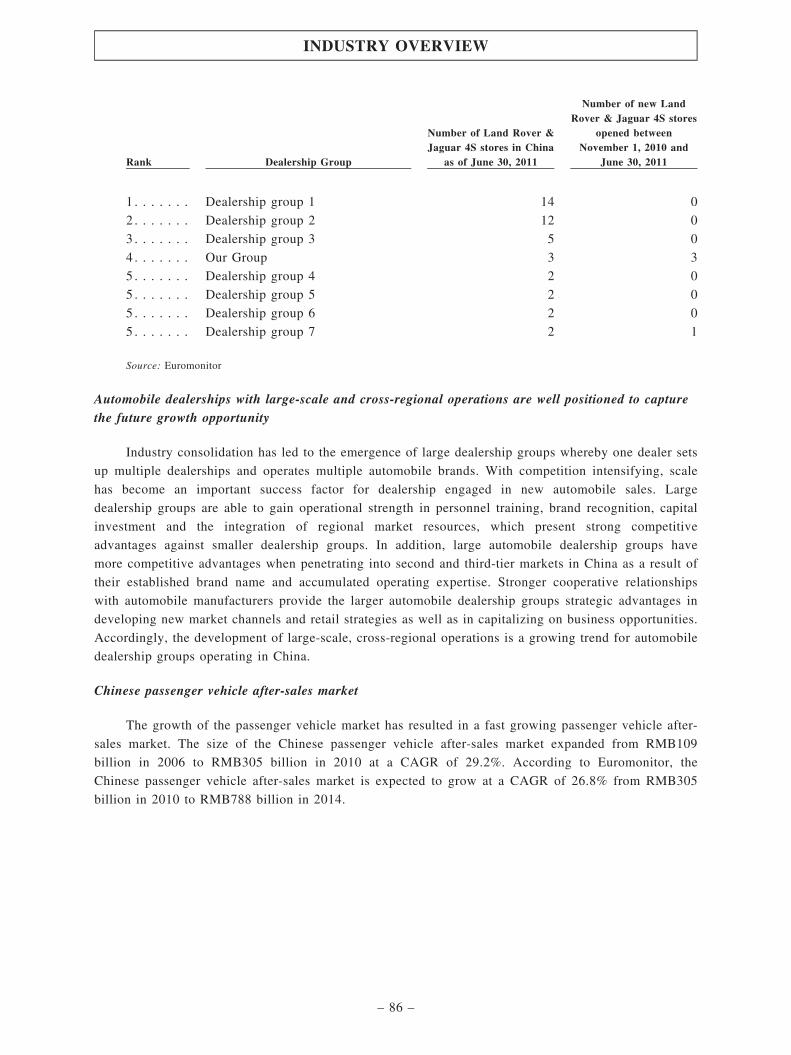

operation of three Land Rover & Jaguar dealership stores from November 2010 (when we started our

cooperation with Land Rover & Jaguar) to June 30, 2011. According to Euromonitor, this makes us the

dealership group which opened the largest number of Land Rover & Jaguar dealership stores in this

period and one of the largest Land Rover & Jaguar dealership groups in eastern China in terms of the

number of stores as of June 30, 2011. We believe that our leading position and superior operational

capabilities and expertise have enabled us to develop long term and stable relationships with leading

automobile manufacturers and placed us in a strong position to win additional authorizations from

existing and new automobile manufacturers in the future for our organic expansion and potential

acquisitions.

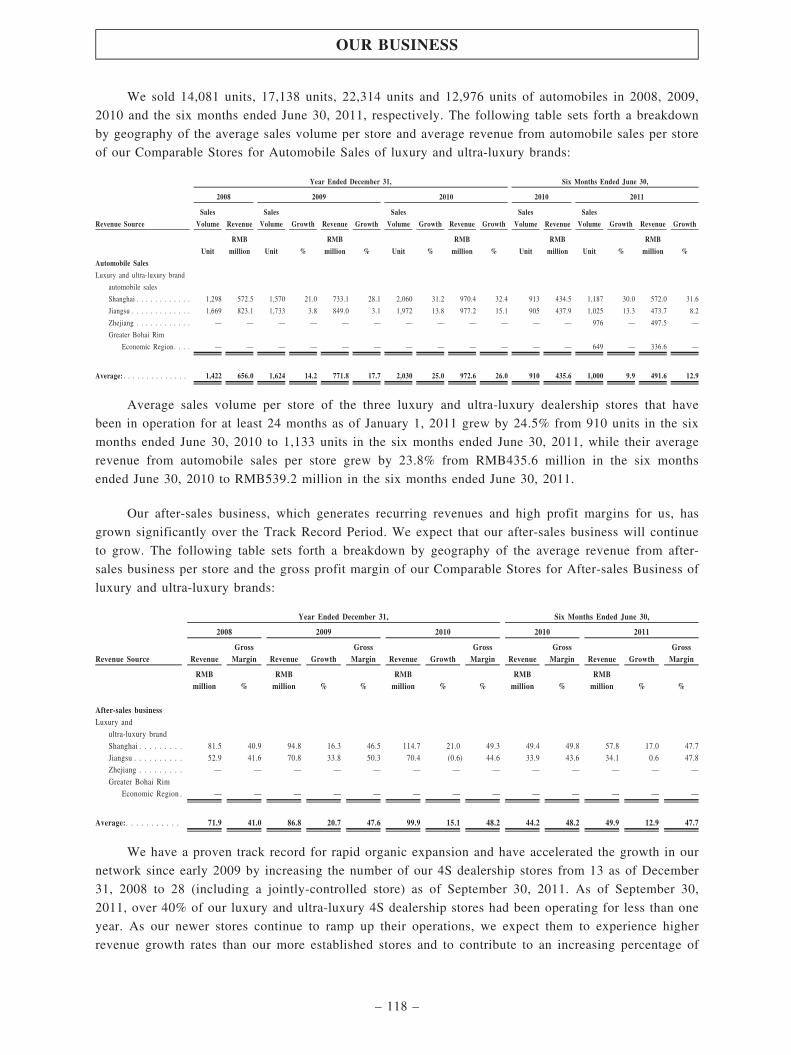

We sold 14,081 units, 17,138 units, 22,314 units and 12,976 units of automobiles in 2008, 2009,

2010 and the six months ended June 30, 2011, respectively. The following table sets forth a breakdown

by geography of the average sales volume per store and average revenue from automobile sales per store

of our Comparable Stores for Automobile Sales of luxury and ultra-luxury brands:

Year Ended December 31, Six Months Ended June 30,

2008 2009 2010 2010 2011

Revenue Source

Sales

Volume Revenue

Sales

Volume Growth Revenue Growth

Sales

Volume Growth Revenue Growth

Sales

Volume Revenue

Sales

Volume Growth Revenue Growth

Unit

RMB

million Unit %

RMB

million % Unit %

RMB

million % Unit

RMB

million Unit %

RMB

million %

Automobile Sales

Luxury and ultra-luxury brand

automobile sales

Shanghai . . . . . . . . . . . . 1,298 572.5 1,570 21.0 733.1 28.1 2,060 31.2 970.4 32.4 913 434.5 1,187 30.0 572.0 31.6

Jiangsu . . . . . . . . . . . . . 1,669 823.1 1,733 3.8 849.0 3.1 1,972 13.8 977.2 15.1 905 437.9 1,025 13.3 473.7 8.2

Zhejiang . . . . . . . . . . . . — — — — — — — — — — — — 976 — 497.5 —

Greater Bohai Rim

Economic Region. . . . — — — — — — — — — — — — 649 — 336.6 —

Average: . . . . . . . . . . . . . . 1,422 656.0 1,624 14.2 771.8 17.7 2,030 25.0 972.6 26.0 910 435.6 1,000 9.9 491.6 12.9

SUMMARY

– 2 –

Average sales volume per store of all of our three luxury dealership stores that have been in

operation for at least 24 months as of January 1, 2011 grew by 24.5% from 910 units in the six months

ended June 30, 2010 to 1,133 units in the six months ended June 30, 2011, while their average revenue

from automobile sales per store grew by 23.8% from RMB435.6 million in the six months ended June

30, 2010 to RMB539.2 million in the six months ended June 30, 2011.

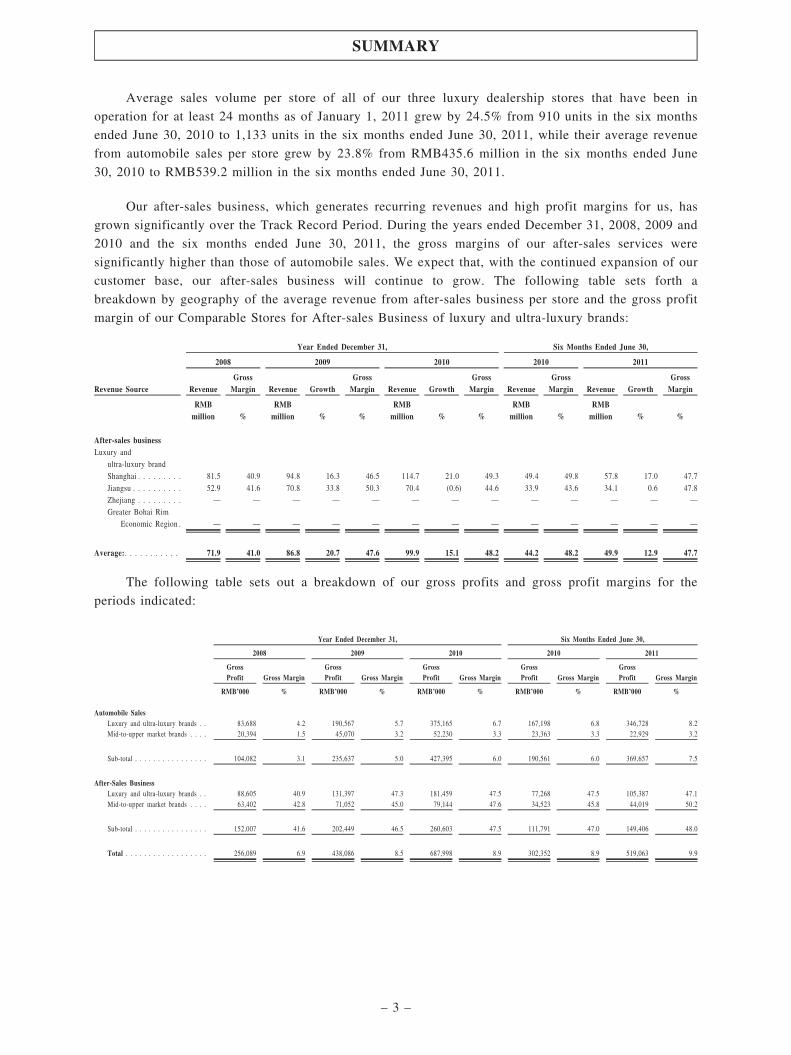

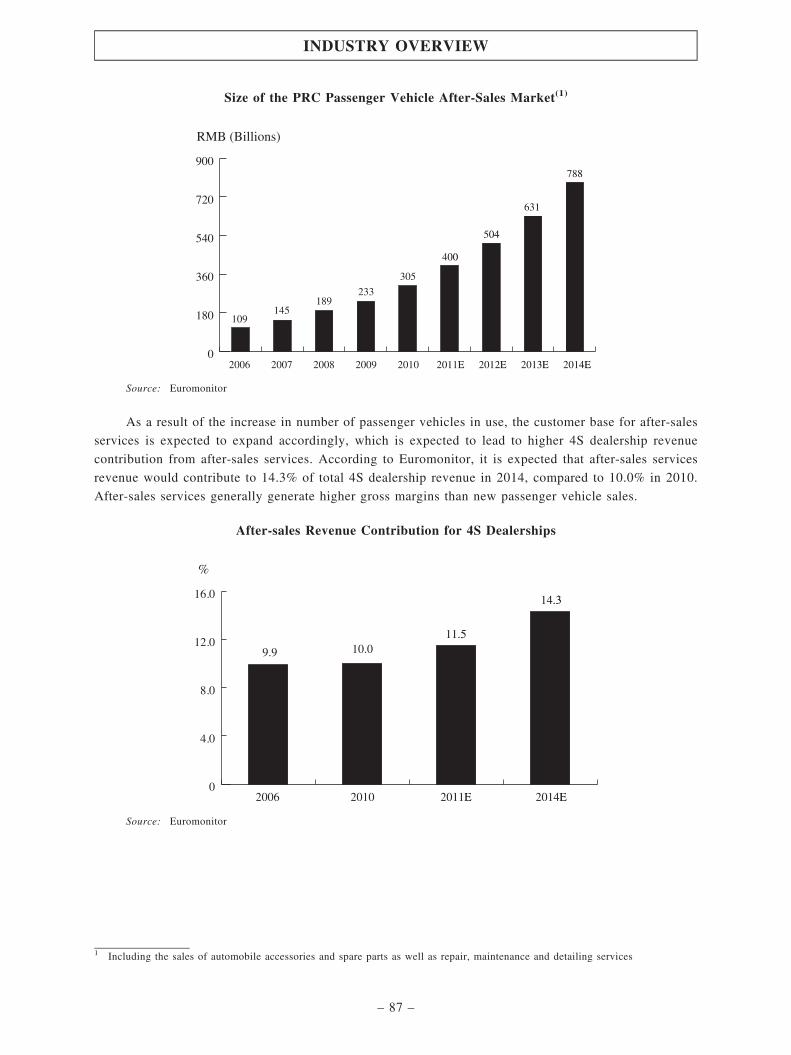

Our after-sales business, which generates recurring revenues and high profit margins for us, has

grown significantly over the Track Record Period. During the years ended December 31, 2008, 2009 and

2010 and the six months ended June 30, 2011, the gross margins of our after-sales services were

significantly higher than those of automobile sales. We expect that, with the continued expansion of our

customer base, our after-sales business will continue to grow. The following table sets forth a

breakdown by geography of the average revenue from after-sales business per store and the gross profit

margin of our Comparable Stores for After-sales Business of luxury and ultra-luxury brands:

Year Ended December 31, Six Months Ended June 30,

2008 2009 2010 2010 2011

Revenue Source RevenueGrossMargin Revenue Growth

GrossMargin Revenue Growth

GrossMargin Revenue

GrossMargin Revenue Growth

GrossMargin

RMBmillion %

RMBmillion % %

RMBmillion % %

RMBmillion %

RMBmillion % %

After-sales businessLuxury and

ultra-luxury brand

Shanghai . . . . . . . . . 81.5 40.9 94.8 16.3 46.5 114.7 21.0 49.3 49.4 49.8 57.8 17.0 47.7

Jiangsu . . . . . . . . . . 52.9 41.6 70.8 33.8 50.3 70.4 (0.6) 44.6 33.9 43.6 34.1 0.6 47.8

Zhejiang . . . . . . . . . — — — — — — — — — — — — —

Greater Bohai Rim

Economic Region . — — — — — — — — — — — — —

Average: . . . . . . . . . . . 71.9 41.0 86.8 20.7 47.6 99.9 15.1 48.2 44.2 48.2 49.9 12.9 47.7

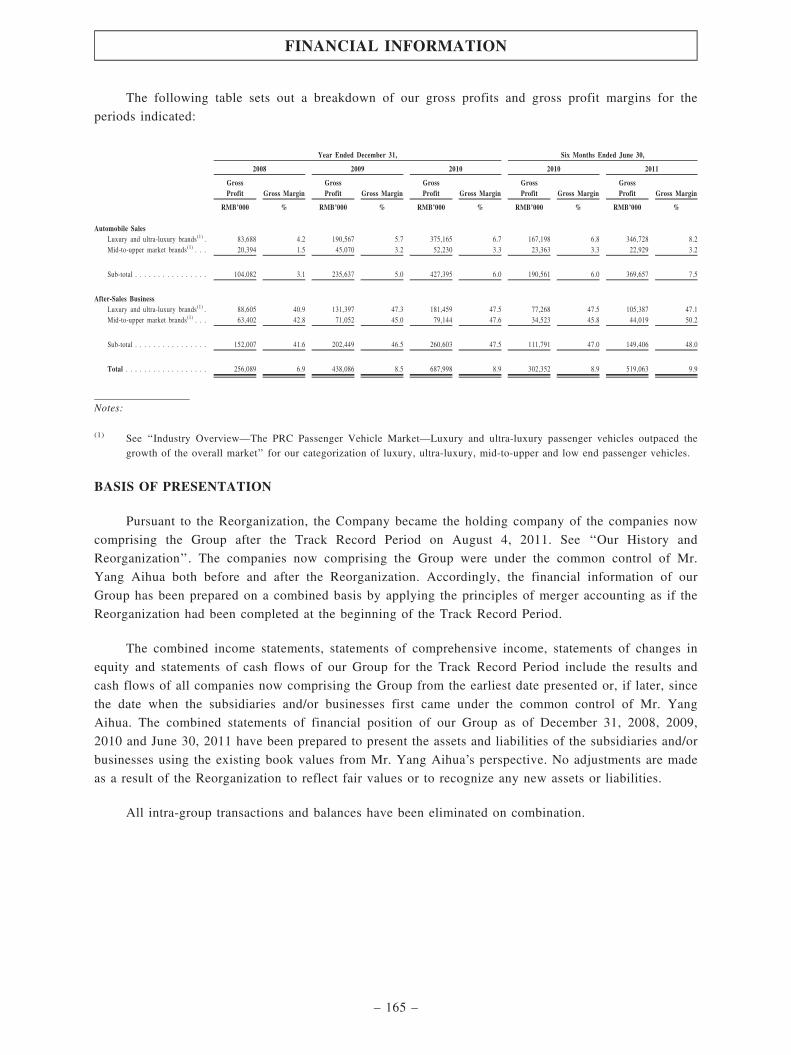

The following table sets out a breakdown of our gross profits and gross profit margins for the

periods indicated:

Year Ended December 31, Six Months Ended June 30,

2008 2009 2010 2010 2011

GrossProfit Gross Margin

GrossProfit Gross Margin

GrossProfit Gross Margin

GrossProfit Gross Margin

GrossProfit Gross Margin

RMB’000 % RMB’000 % RMB’000 % RMB’000 % RMB’000 %

Automobile SalesLuxury and ultra-luxury brands . . 83,688 4.2 190,567 5.7 375,165 6.7 167,198 6.8 346,728 8.2Mid-to-upper market brands . . . . 20,394 1.5 45,070 3.2 52,230 3.3 23,363 3.3 22,929 3.2

Sub-total . . . . . . . . . . . . . . . . 104,082 3.1 235,637 5.0 427,395 6.0 190,561 6.0 369,657 7.5

After-Sales BusinessLuxury and ultra-luxury brands . . 88,605 40.9 131,397 47.3 181,459 47.5 77,268 47.5 105,387 47.1Mid-to-upper market brands . . . . 63,402 42.8 71,052 45.0 79,144 47.6 34,523 45.8 44,019 50.2

Sub-total . . . . . . . . . . . . . . . . 152,007 41.6 202,449 46.5 260,603 47.5 111,791 47.0 149,406 48.0

Total . . . . . . . . . . . . . . . . . . 256,089 6.9 438,086 8.5 687,998 8.9 302,352 8.9 519,063 9.9

SUMMARY

– 3 –

We have recorded significant growth in our revenues and profits during the Track Record Period.

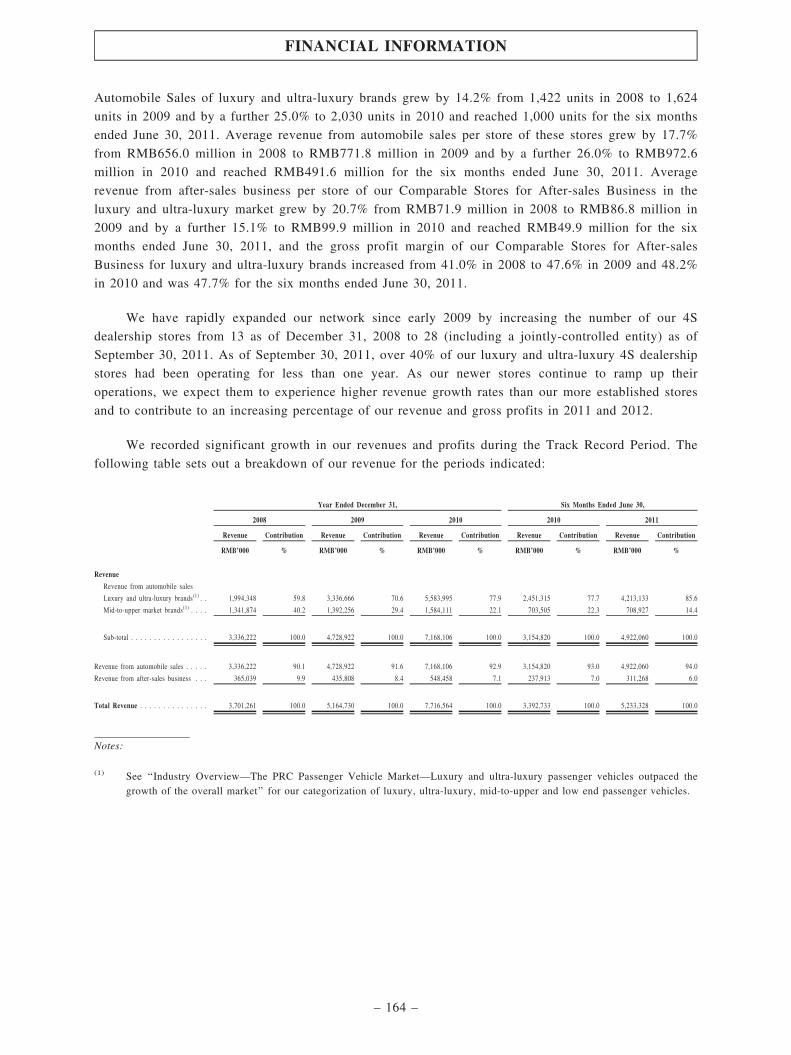

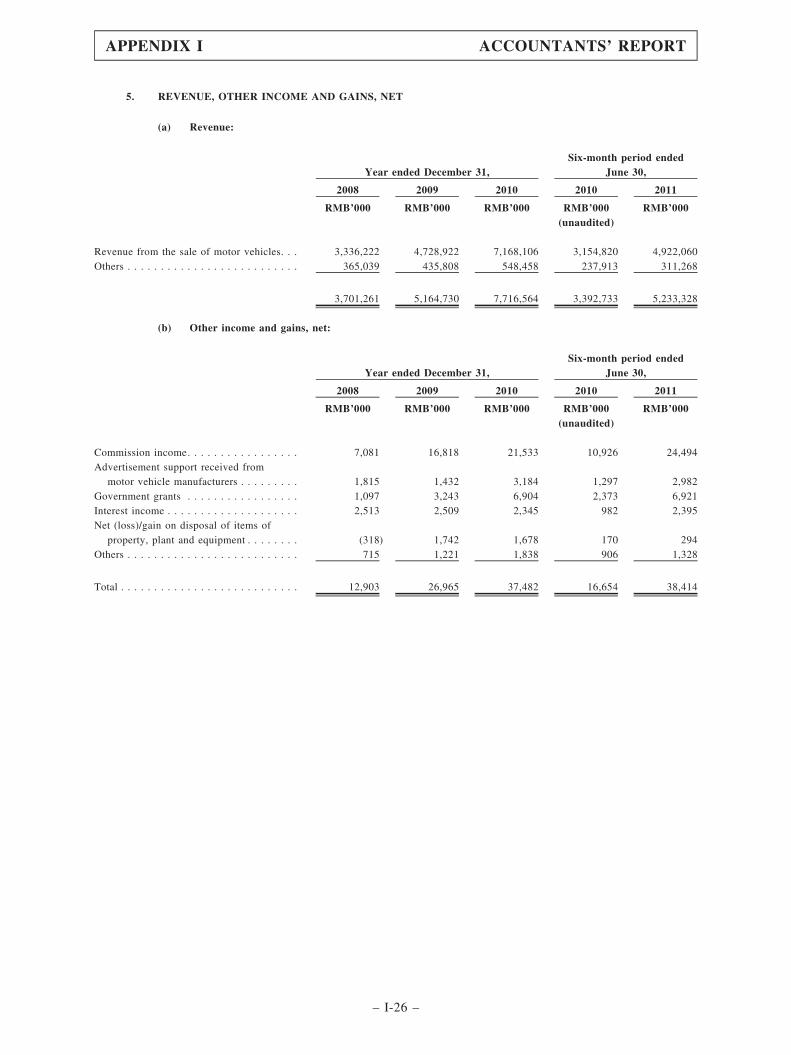

Our revenue increased from RMB3,701.3 million in 2008 to RMB5,164.7 million in 2009 and

RMB7,716.6 million in 2010, representing a CAGR of 44.4%, and grew by 54.3% from RMB3,392.7

million for the six months ended June 30, 2010 to RMB5,233.3 million for the same period of 2011

while our net profits increased from RMB57.5 million in 2008 to RMB175.8 million in 2009 and

RMB307.7 million in 2010, representing a CAGR of 131.3%, and grew by 63.0% from RMB131.2

million for the six months ended June 30, 2010 to RMB213.9 million for the same period of 2011. Our

gross profit margins for automobile sales increased from 3.1% in 2008 to 5.0% in 2009, 6.0% in 2010

and 7.5% for the six months ended June 30, 2011, while our gross profit margins for our after-sales

business increased from 41.6% in 2008 to 46.5% in 2009, 47.5% in 2010 and 48.0% for the six months

ended June 30, 2011.

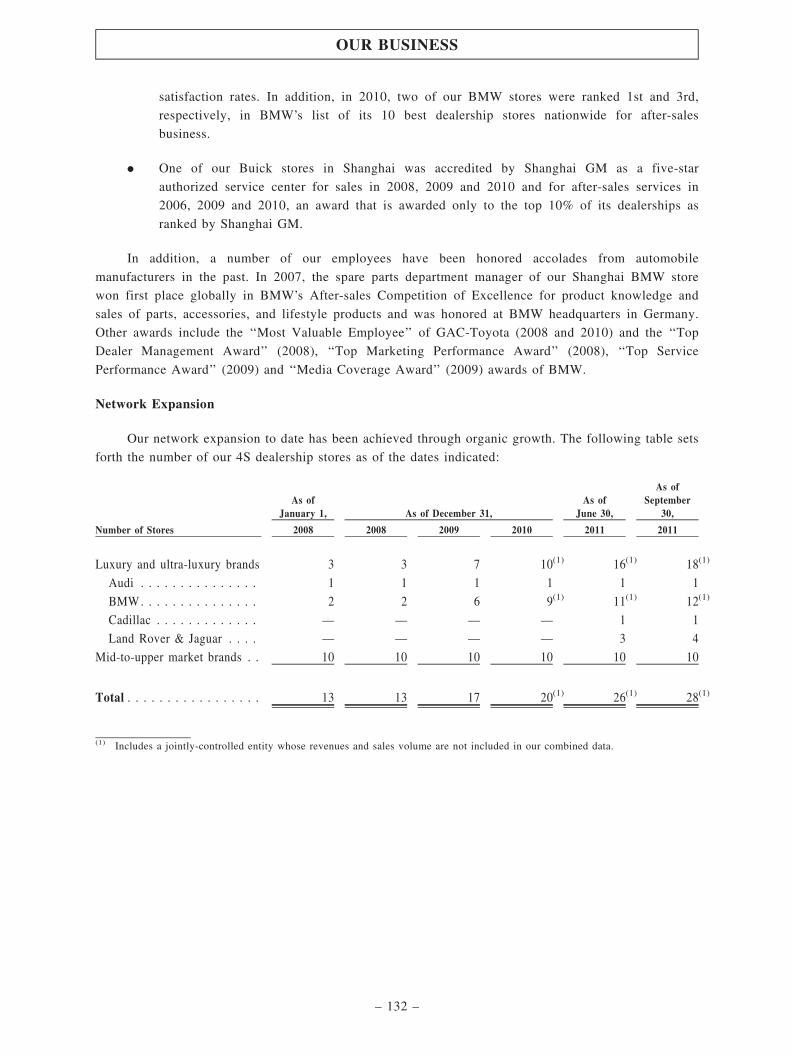

Network Expansion

We have a proven track record for rapid organic expansion and have accelerated the growth in our

network since early 2009 by increasing the number of our 4S dealership stores from 13 as of December

31, 2008 to 28 (including a jointly-controlled store) as of September 30, 2011. As of September 30,

2011, over 40% of our luxury and ultra-luxury 4S dealership stores had been operating for less than one

year. As our newer stores continue to ramp up their operations, we expect them to experience higher

revenue growth rates than our more established stores and to contribute to an increasing percentage of

our revenues and gross profits in 2011 and 2012. We operated two, six, nine and 11 BMW 4S

dealership stores as of December 31, 2008, 2009, 2010 and June 30, 2011, respectively. In addition, we

opened a BMW authorized repair center in 2010. Revenues derived from these BMW dealership stores

and the repair center were RMB1,680.6 million, RMB2,958.2 million, RMB5,075.4 million and

RMB3,403.9 million in 2008, 2009, 2010 and the six months ended June 30, 2011, respectively,

accounting for 45.4%, 57.3%, 65.8% and 65.0% of our total revenue for the relevant period. Since July

1, 2011, we have commenced operation at a new BMW dealership store, and as of the Latest Practicable

Date, we received BMW’s authorizations, conditional approvals and non-binding letters of intent to

establish four additional BMW 4S dealership store and showrooms by the end of 2011 and another six

BMW 4S dealership stores and a repair center in 2012. We will seek opportunities to expand through

further organic expansion and selective acquisitions in existing and new areas and to diversify our

portfolio of luxury and ultra-luxury automobile brands. With our large and strategically located

dealership network, we have been able to achieve synergies that provide significant competitive

advantages in China’s highly fragmented automobile dealership industry. Our operating scale allows us

to better manage our automobiles and spare parts inventory turnover, coordinate and aggregate our

purchases of automobile accessories and other products and implement a systematic approach to train

and promote talented personnel.

Our Dealership Arrangements

Each of our 4S dealership store is subject to a non-exclusive dealership authorization agreement

between us and the PRC affiliate or representative of the relevant automobile manufacturer. The terms

and conditions of these dealership authorization agreements vary according to the policies and practices

of different automobile manufacturers. In general, each agreement specifies the location of the

dealership store and requires the store to sell only the brands and models of the relevant automobile

manufacturer and to observe its recommended retail pricing guidelines from time to time. These

agreements range in duration from one to three years but are subject to early termination in the event of

SUMMARY

– 4 –

default. None of our dealership authorization agreements were subject to early termination or not

renewed upon expiry during the Track Record Period. See ‘‘Our Business—Our Dealership Network—

Dealership Arrangements’’ for further information regarding our dealership agreements.

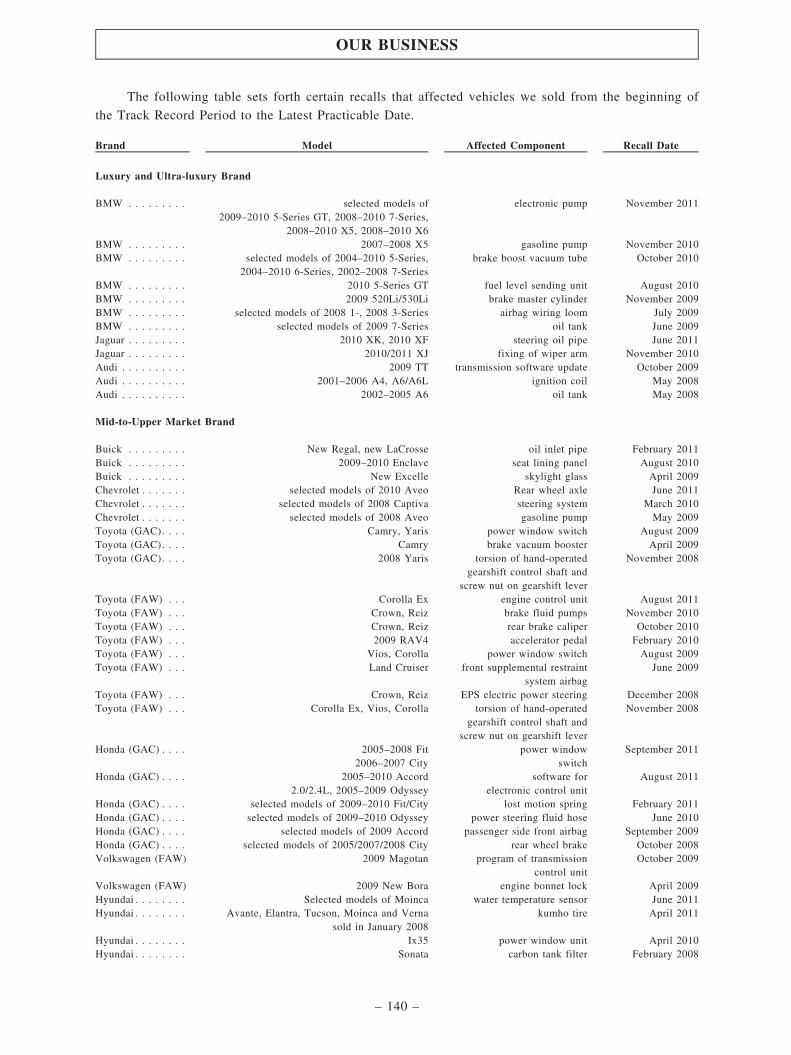

Automobile Recalls

We assist automobile manufacturers to process and handle recalls of their automobiles at their

request. Automobile recalls are usually made as a result of design or production defects in the affected

automobiles and related policies and procedures vary for different automobile manufacturers. We are

compensated by automobile manufacturers for the repair services performed by us in connection with

their automobile recalls and are not liable under PRC law or our dealership authorization agreements for

design or production defects in the automobiles sold through our dealership stores. See ‘‘Our Business—

After-Sales Services—Automobile recalls’’ for additional information.

Regulatory Matters

Under the Catalogue of Industries for Guiding Foreign Investment promulgated by MOFCOM and

NRDC, non-PRC investors are not permitted to own more than 49% of any automobile dealership

groups with more than 30 dealership stores. Upon completion of the Reorganization, all of our PRC

subsidiaries will be wholly- or majority-owned directly or indirectly by our Company, a company

incorporated in the Cayman Islands. We operated 28 4S dealership stores as of September 30, 2011. As

of the Latest Practicable Date, we received automobile manufacturers’ authorizations, conditional

approvals and non-binding letters of intent to establish another 14 luxury and ultra-luxury brand 4S

dealership stores, showrooms and repair center. Eight of these planned stores have been duly established

with the relevant approvals from the relevant local branches of SAIC. We have been advised by our

PRC legal advisors, Jingtian & Gongcheng, that there will be no substantive legal impediment for us to

obtain approval from MOFCOM or its local counterparts for the establishment of the planned new

stores. See ‘‘Risk Factors—Risks Relating to Our Business—Our status as a foreign enterprise could

complicate our efforts to make acquisitions or expand our dealership network in the PRC’’ and

‘‘Regulatory Overview—Regulations Relating to the PRC Automobile Industry—30 Dealership

Limitation’’ for additional information.

There are no current litigation or arbitration proceedings or any pending or threatened litigation or

arbitration proceedings against us or any of our Directors that could have a material adverse effect on

our financial condition or results of operations. In the opinion of our PRC legal advisors, we have

complied with relevant PRC laws, rules and regulations in all material respects, save as disclosed under

‘‘Risk Factors—Risks Relating to Our Business—We have not yet obtained valid titles or rights to use

certain properties or the required permits for construction and development on certain properties

occupied by us’’ and ‘‘Our Business—Legal Proceedings and Regulatory Compliance’’. Our PRC legal

advisors, Jingtian & Gongcheng, have confirmed that we have been in compliance with all relevant PRC

laws, rules and regulations in all material respects during the Track Record Period.

OUR COMPETITIVE STRENGTHS

Our competitive strengths include the following:

. As a leading luxury 4S dealership group in China, we are well positioned to benefit from the

anticipated rapid growth in China;

SUMMARY

– 5 –

. We have a well-established network of stores strategically located in populous and affluentregions with rapidly growing economies;

. Our superior sales, after-sales services and other operational capabilities and expertiseenabled us to form strong partnerships with leading automobile manufacturers;

. We have a proven track record for rapid organic expansion and successfully managing ourstore network across different areas;

. We are led by an experienced senior management team with a proven track record and wehave a large and growing pool of skilled employees to support our expanding network andbusiness; and

. Our large operating scale allows us to enjoy competitive advantages in China’s highlyfragmented automobile dealership industry.

OUR STRATEGIES

We intend to implement the following principal strategies to grow our business:

. Continue to expand our dealership network and brand offerings through organic store growthand selective acquisitions;

. Continue to enhance and expand our after-sales capabilities and capacity;

. Further enhance our operational capabilities and sales and marketing efforts; and

. Continue to attract, train and retain skilled employees to support our future growth andexpansion.

SELLING SHAREHOLDER

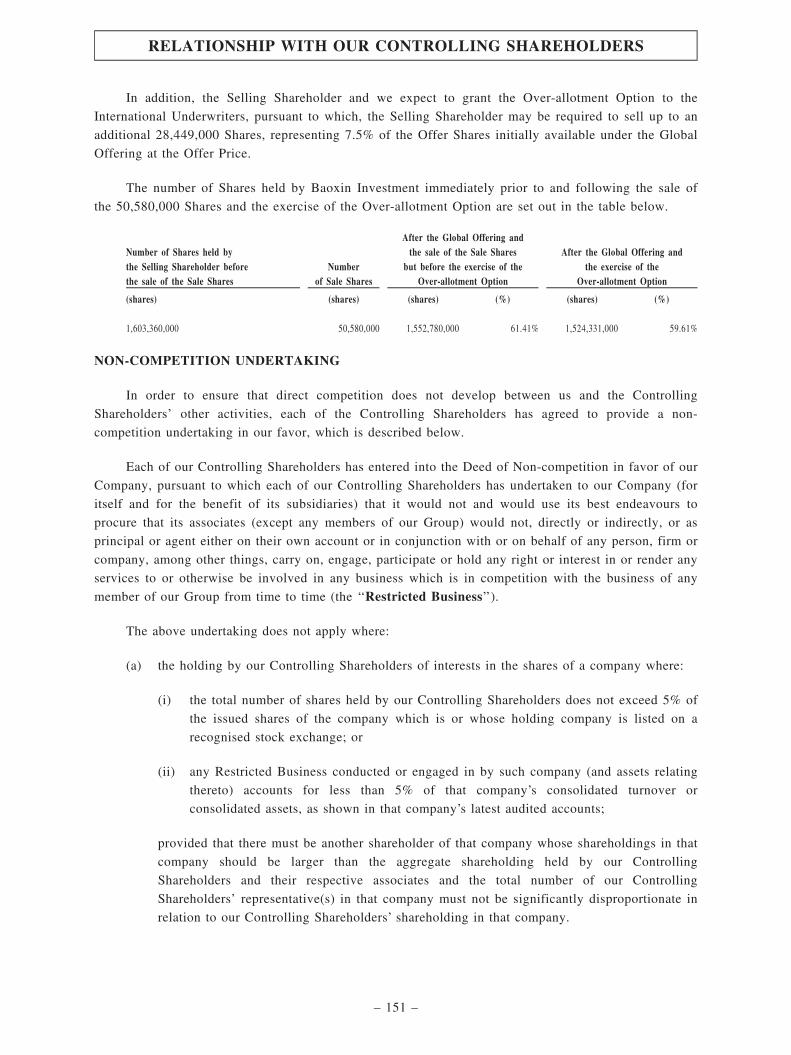

Pursuant to the International Underwriting Agreement, Baoxin Investment will sell 50,580,000Shares, representing approximately 2.00% of the total issued share capital of our Company immediatelyfollowing completion of the Global Offering (assuming that the Over-allotment Option is not exercised).In addition, the Selling Shareholder and we expect to grant the Over-allotment Option to theInternational Underwriters, pursuant to which, the Selling Shareholder may be required to sell up to anadditional 28,449,000 Shares, representing 7.5% of the Offer Shares initially available under the GlobalOffering at the Offer Price.

For more details of the Selling Shareholder, please see the section headed ‘‘Relationship with ourControlling Shareholders—Selling Shareholder’’ in this prospectus.

PRE-IPO INVESTORS

On August 4, 2010, Shanghai Baoxin, amongst others, entered into an investment agreement(supplemented by a supplemental agreement dated December 2, 2010) with Huakong Innovation andHuakong Industry pursuant to which Huakong Innovation and Huakong Industry agreed to subscribe foran aggregate of 11.11% of the equity interests in Shanghai Baoxin for a consideration of RMB500million. As part of the reorganisation of the Group, on June 28, 2011, Suzhou Baoxin entered into anequity transfer agreement with each of the shareholders of Shanghai Baoxin, pursuant to which HuakongInnovation and Huakong Industry transferred 4.866% and 3.244% of the equity interests in ShanghaiBaoxin to Suzhou Baoxin, respectively. On July 8, 2011, Tsinghua Fund I, Tsinghua Fund II, Innovation

SUMMARY

– 6 –

Capital, the Company and others entered into a shareholders’ agreement which contains similar rights asthat of the investment agreement (as supplemented) dated August 4, 2010 between Shanghai Baoxin andothers as a result of which Tsinghua Fund I, Tsinghua Fund II and Innovation Capital subscribed for atotal of 8.11% of the entire issued shares in the Company. The management and the ultimate investorsof Huakong Innovation and Huakong Industry are identical to Innovation Capital and Tsinghua Fund I,Tsinghua Fund II respectively.

ONSHORE ACQUISITION

Following the pre-IPO investment and other transactions described above, Huakong Innovation andHuakong Industry owned 3% in Shanghai Baoxin. With a view to further increasing our shareholdinginterests and consolidating control in Shanghai Baoxin and its subsidiaries and following the investmentof the pre-IPO investors in Shanghai Baoxin and the overseas reorganisation, Suzhou Baoxin enteredinto an equity transfer agreement with Huakong Innovation and Huakong Industry on June 28, 2011,pursuant to which Huakong Innovation and Huakong Industry agreed to sell and Suzhou Baoxin agreedto purchase 3% of the equity interests in Shanghai Baoxin at a consideration of RMB550,000,000 uponcompletion of the Global Offering. The consideration will be financed by the proceeds obtained from theGlobal Offering. The transfer of equity interests is expected to be completed within two weeks after theListing Date. Such transaction was not entered as a condition to the Pre-IPO Investors investment in2010. For details of the transfer please refer to ‘‘Our History and Reorganization—Reorganization—Onshore Acquisition’’.

SUMMARY

– 7 –

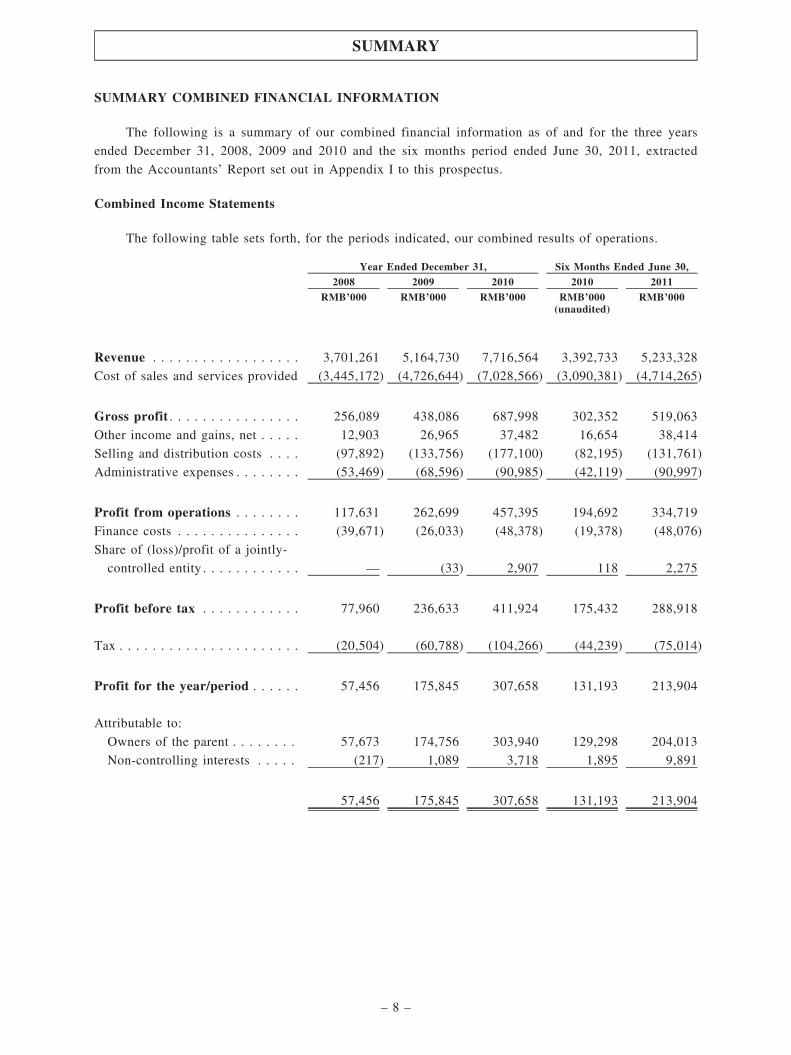

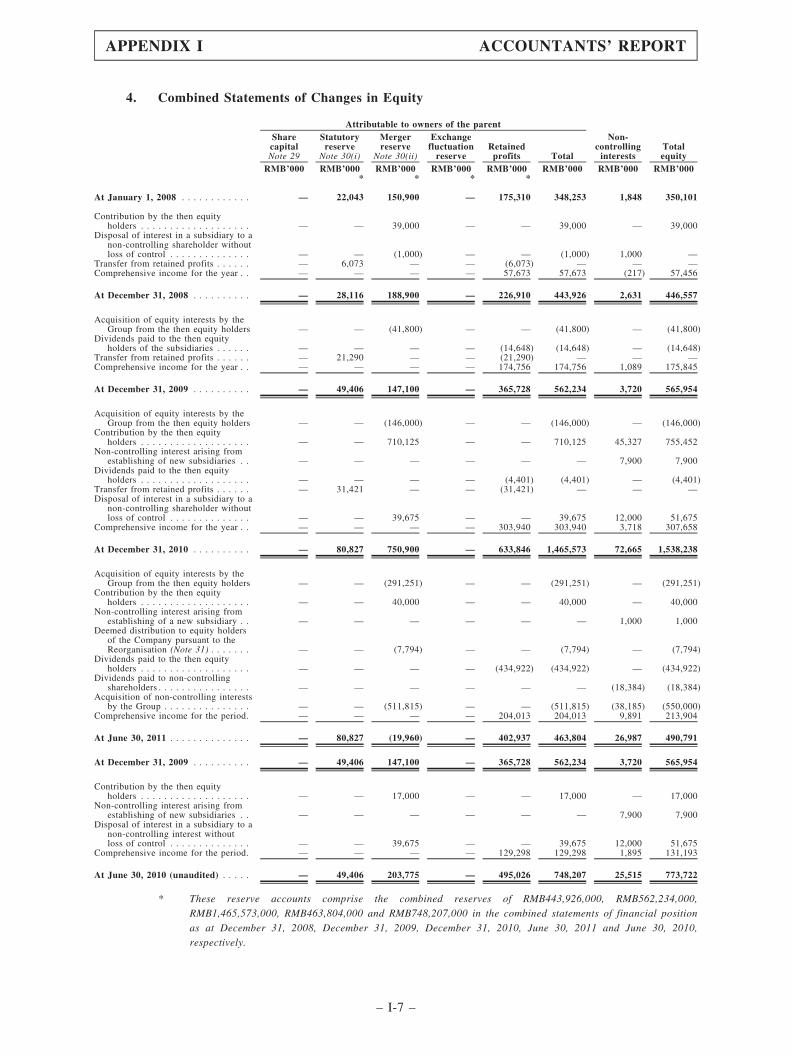

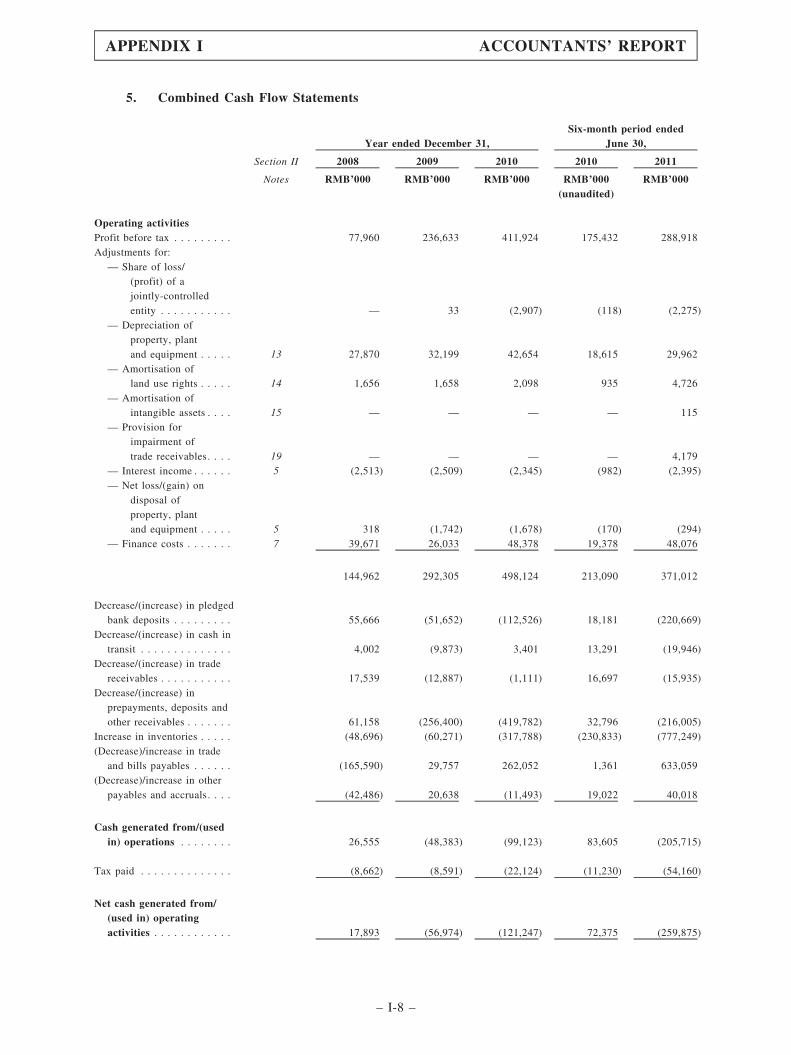

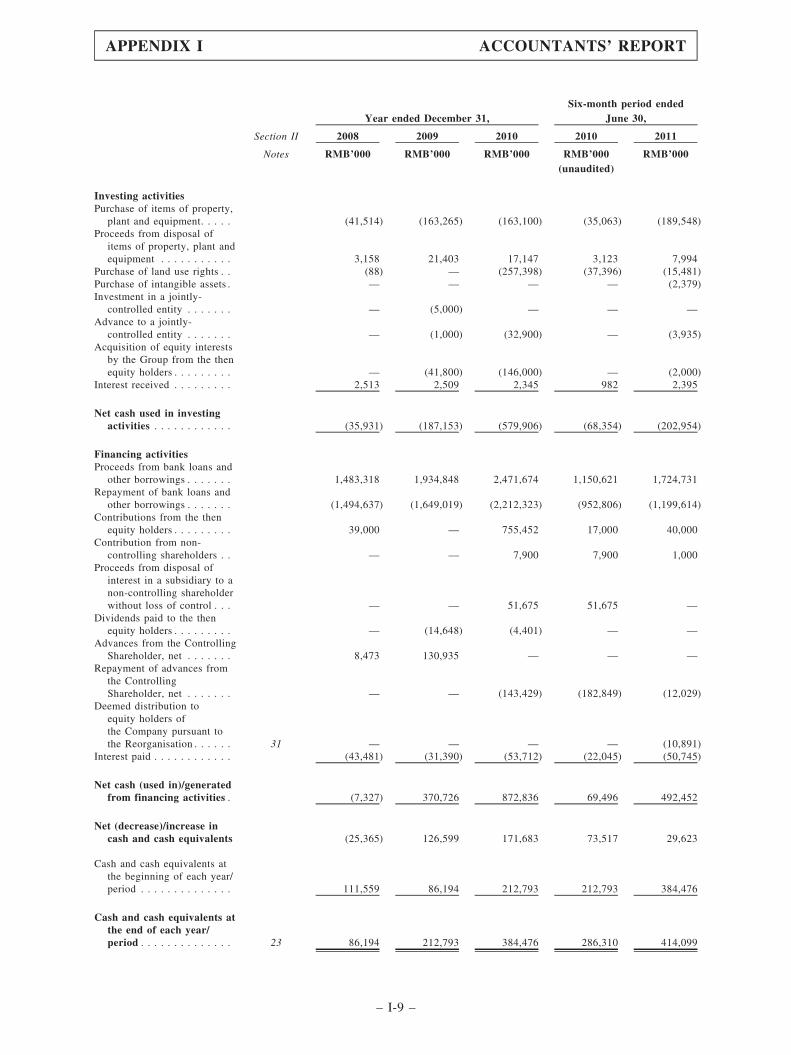

SUMMARY COMBINED FINANCIAL INFORMATION

The following is a summary of our combined financial information as of and for the three years

ended December 31, 2008, 2009 and 2010 and the six months period ended June 30, 2011, extracted

from the Accountants’ Report set out in Appendix I to this prospectus.

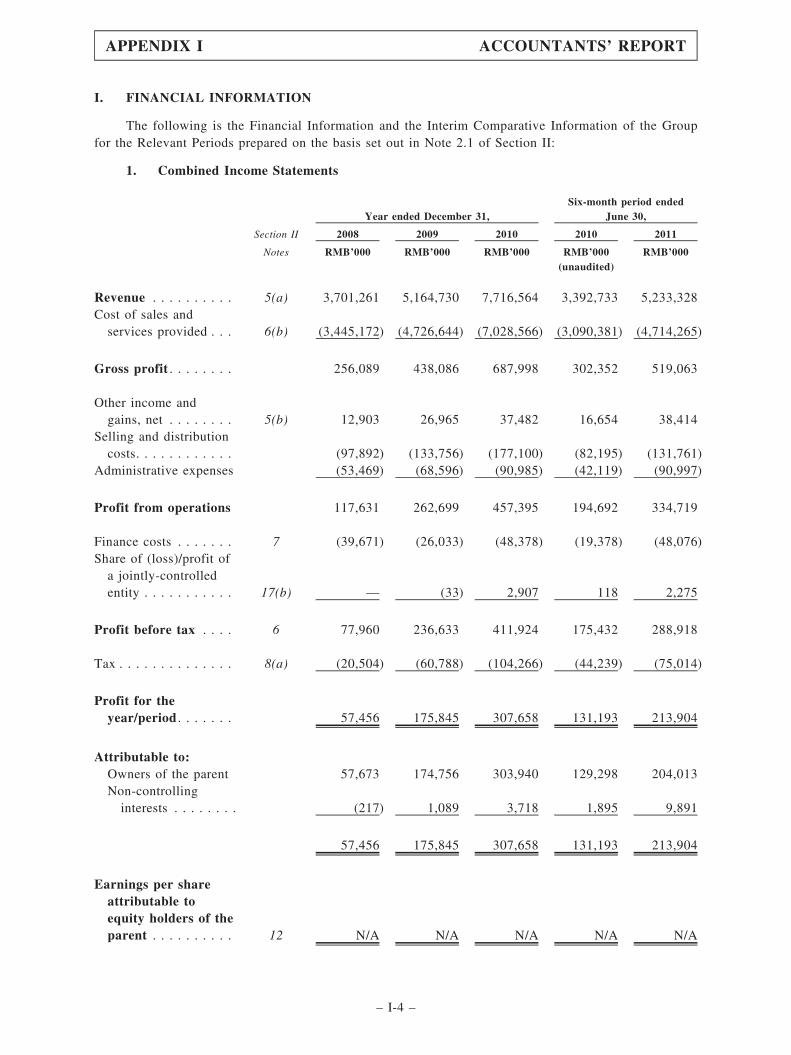

Combined Income Statements

The following table sets forth, for the periods indicated, our combined results of operations.

Year Ended December 31, Six Months Ended June 30,

2008 2009 2010 2010 2011

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(unaudited)

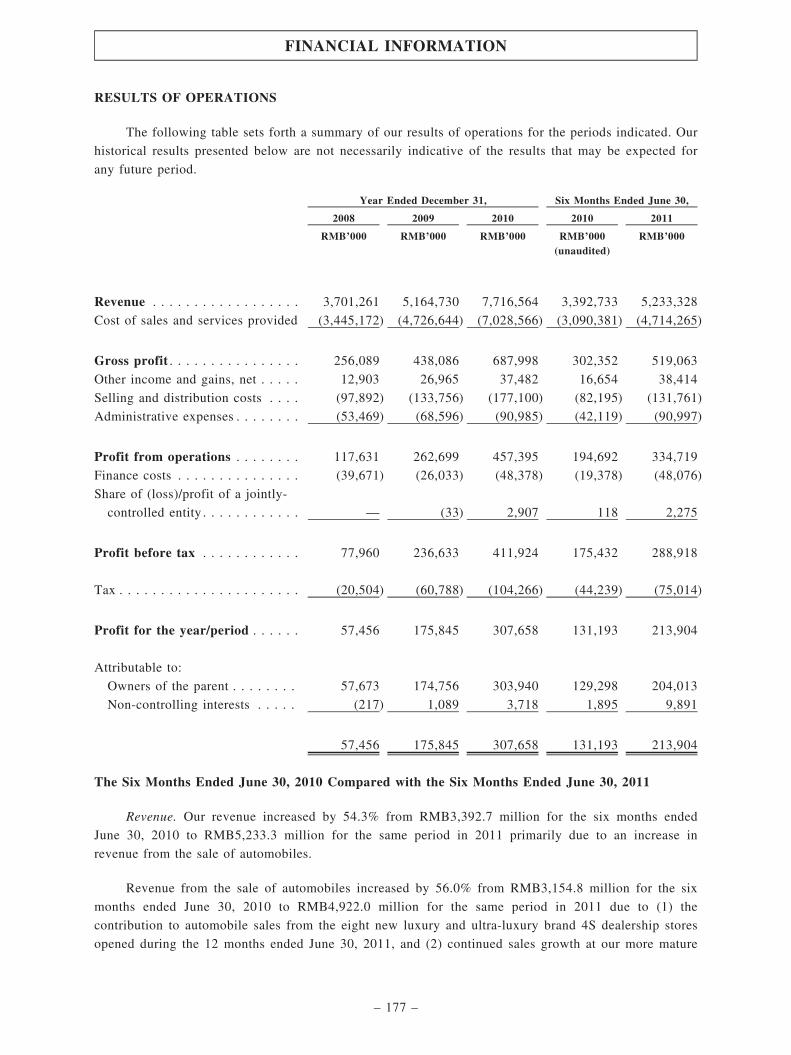

Revenue . . . . . . . . . . . . . . . . . . 3,701,261 5,164,730 7,716,564 3,392,733 5,233,328

Cost of sales and services provided (3,445,172) (4,726,644) (7,028,566) (3,090,381) (4,714,265)

Gross profit . . . . . . . . . . . . . . . . 256,089 438,086 687,998 302,352 519,063

Other income and gains, net . . . . . 12,903 26,965 37,482 16,654 38,414

Selling and distribution costs . . . . (97,892) (133,756) (177,100) (82,195) (131,761)

Administrative expenses . . . . . . . . (53,469) (68,596) (90,985) (42,119) (90,997)

Profit from operations . . . . . . . . 117,631 262,699 457,395 194,692 334,719

Finance costs . . . . . . . . . . . . . . . (39,671) (26,033) (48,378) (19,378) (48,076)

Share of (loss)/profit of a jointly-

controlled entity . . . . . . . . . . . . — (33) 2,907 118 2,275

Profit before tax . . . . . . . . . . . . 77,960 236,633 411,924 175,432 288,918

Tax . . . . . . . . . . . . . . . . . . . . . . (20,504) (60,788) (104,266) (44,239) (75,014)

Profit for the year/period . . . . . . 57,456 175,845 307,658 131,193 213,904

Attributable to:

Owners of the parent . . . . . . . . 57,673 174,756 303,940 129,298 204,013

Non-controlling interests . . . . . (217) 1,089 3,718 1,895 9,891

57,456 175,845 307,658 131,193 213,904

SUMMARY

– 8 –

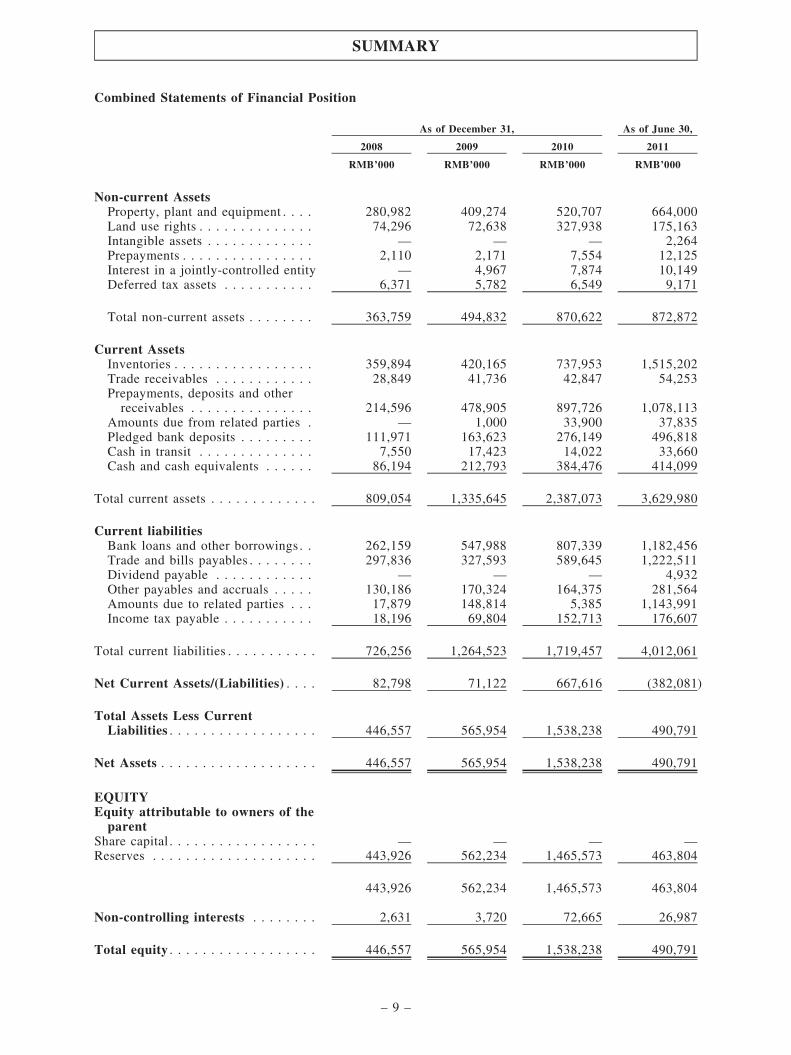

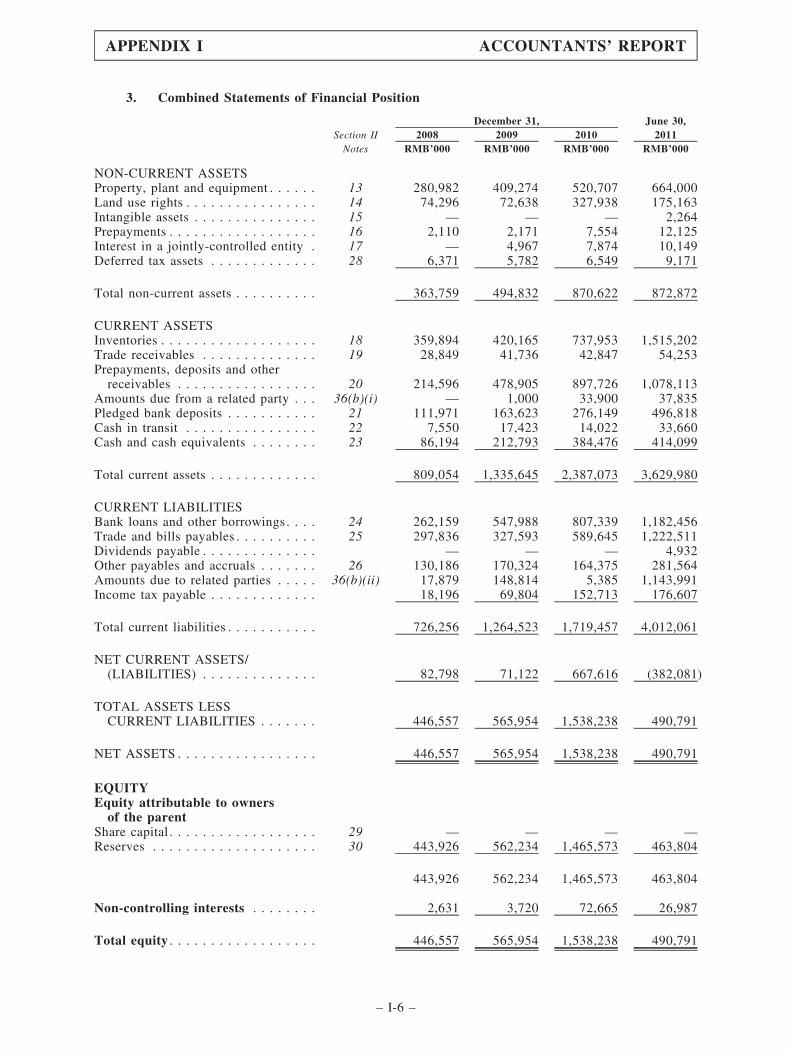

Combined Statements of Financial Position

As of December 31, As of June 30,

2008 2009 2010 2011

RMB’000 RMB’000 RMB’000 RMB’000

Non-current AssetsProperty, plant and equipment . . . . 280,982 409,274 520,707 664,000Land use rights . . . . . . . . . . . . . . 74,296 72,638 327,938 175,163Intangible assets . . . . . . . . . . . . . — — — 2,264Prepayments . . . . . . . . . . . . . . . . 2,110 2,171 7,554 12,125Interest in a jointly-controlled entity — 4,967 7,874 10,149Deferred tax assets . . . . . . . . . . . 6,371 5,782 6,549 9,171

Total non-current assets . . . . . . . . 363,759 494,832 870,622 872,872

Current AssetsInventories . . . . . . . . . . . . . . . . . 359,894 420,165 737,953 1,515,202Trade receivables . . . . . . . . . . . . 28,849 41,736 42,847 54,253Prepayments, deposits and otherreceivables . . . . . . . . . . . . . . . 214,596 478,905 897,726 1,078,113

Amounts due from related parties . — 1,000 33,900 37,835Pledged bank deposits . . . . . . . . . 111,971 163,623 276,149 496,818Cash in transit . . . . . . . . . . . . . . 7,550 17,423 14,022 33,660Cash and cash equivalents . . . . . . 86,194 212,793 384,476 414,099

Total current assets . . . . . . . . . . . . . 809,054 1,335,645 2,387,073 3,629,980

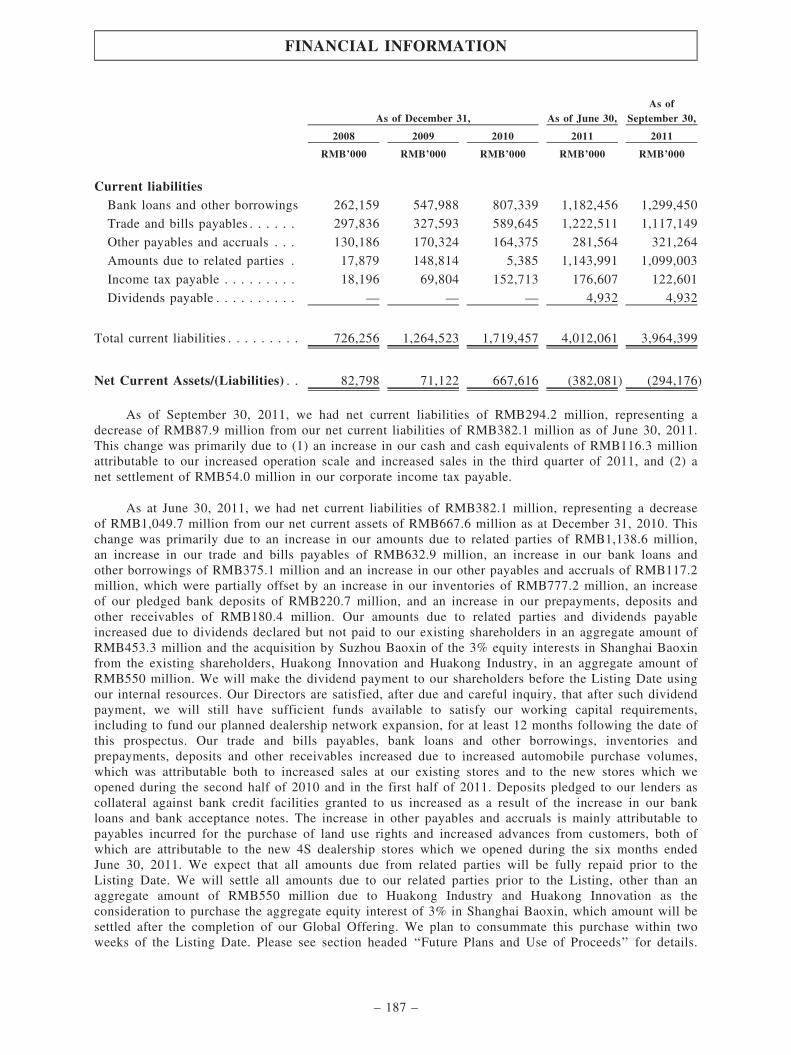

Current liabilitiesBank loans and other borrowings . . 262,159 547,988 807,339 1,182,456Trade and bills payables . . . . . . . . 297,836 327,593 589,645 1,222,511Dividend payable . . . . . . . . . . . . — — — 4,932Other payables and accruals . . . . . 130,186 170,324 164,375 281,564Amounts due to related parties . . . 17,879 148,814 5,385 1,143,991Income tax payable . . . . . . . . . . . 18,196 69,804 152,713 176,607

Total current liabilities . . . . . . . . . . . 726,256 1,264,523 1,719,457 4,012,061

Net Current Assets/(Liabilities) . . . . 82,798 71,122 667,616 (382,081)

Total Assets Less CurrentLiabilities . . . . . . . . . . . . . . . . . . 446,557 565,954 1,538,238 490,791

Net Assets . . . . . . . . . . . . . . . . . . . 446,557 565,954 1,538,238 490,791

EQUITYEquity attributable to owners of the

parentShare capital . . . . . . . . . . . . . . . . . . — — — —

Reserves . . . . . . . . . . . . . . . . . . . . 443,926 562,234 1,465,573 463,804

443,926 562,234 1,465,573 463,804

Non-controlling interests . . . . . . . . 2,631 3,720 72,665 26,987

Total equity . . . . . . . . . . . . . . . . . . 446,557 565,954 1,538,238 490,791

SUMMARY

– 9 –

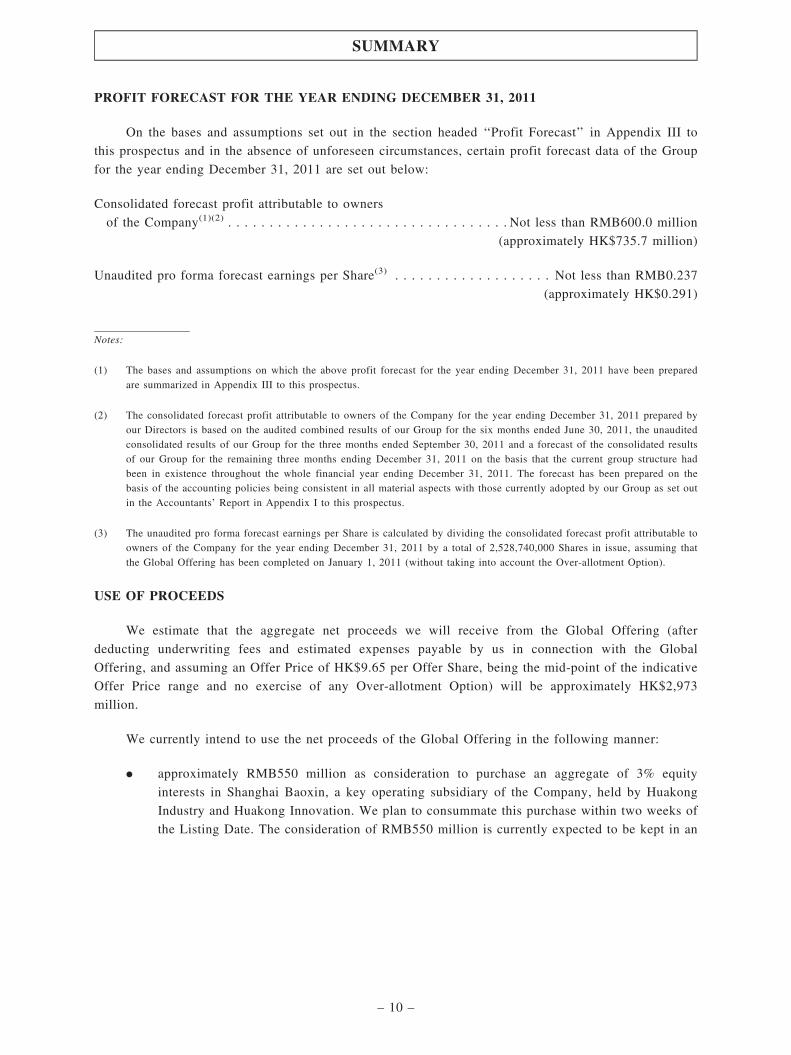

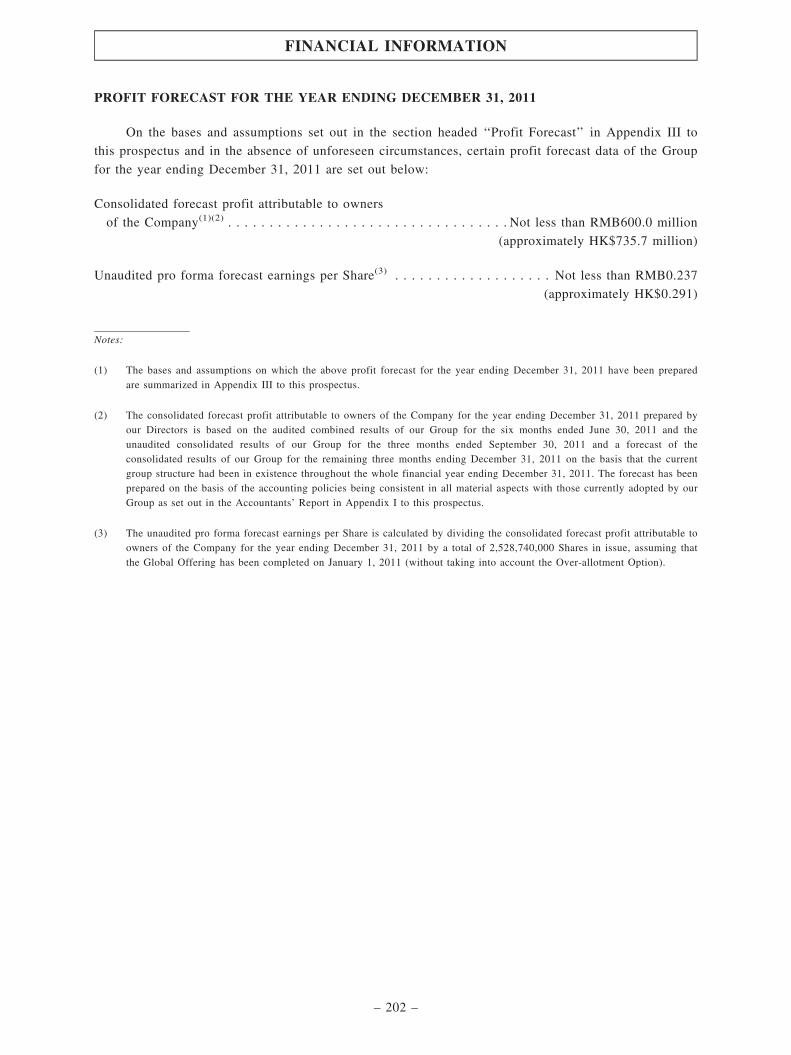

PROFIT FORECAST FOR THE YEAR ENDING DECEMBER 31, 2011

On the bases and assumptions set out in the section headed ‘‘Profit Forecast’’ in Appendix III to

this prospectus and in the absence of unforeseen circumstances, certain profit forecast data of the Group

for the year ending December 31, 2011 are set out below:

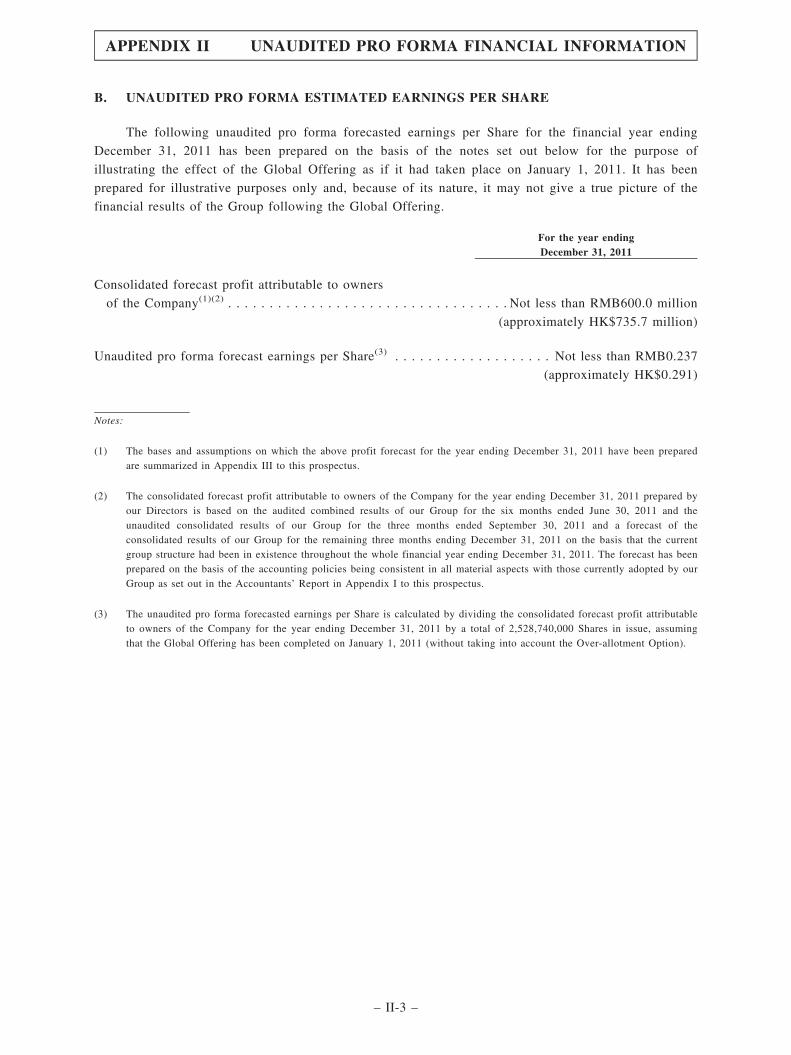

Consolidated forecast profit attributable to owners

of the Company(1)(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Not less than RMB600.0 million

(approximately HK$735.7 million)

Unaudited pro forma forecast earnings per Share(3) . . . . . . . . . . . . . . . . . . . Not less than RMB0.237

(approximately HK$0.291)

Notes:

(1) The bases and assumptions on which the above profit forecast for the year ending December 31, 2011 have been prepared

are summarized in Appendix III to this prospectus.

(2) The consolidated forecast profit attributable to owners of the Company for the year ending December 31, 2011 prepared byour Directors is based on the audited combined results of our Group for the six months ended June 30, 2011, the unaudited

consolidated results of our Group for the three months ended September 30, 2011 and a forecast of the consolidated resultsof our Group for the remaining three months ending December 31, 2011 on the basis that the current group structure hadbeen in existence throughout the whole financial year ending December 31, 2011. The forecast has been prepared on thebasis of the accounting policies being consistent in all material aspects with those currently adopted by our Group as set out

in the Accountants’ Report in Appendix I to this prospectus.

(3) The unaudited pro forma forecast earnings per Share is calculated by dividing the consolidated forecast profit attributable toowners of the Company for the year ending December 31, 2011 by a total of 2,528,740,000 Shares in issue, assuming that

the Global Offering has been completed on January 1, 2011 (without taking into account the Over-allotment Option).

USE OF PROCEEDS

We estimate that the aggregate net proceeds we will receive from the Global Offering (after

deducting underwriting fees and estimated expenses payable by us in connection with the Global

Offering, and assuming an Offer Price of HK$9.65 per Offer Share, being the mid-point of the indicative

Offer Price range and no exercise of any Over-allotment Option) will be approximately HK$2,973

million.

We currently intend to use the net proceeds of the Global Offering in the following manner:

. approximately RMB550 million as consideration to purchase an aggregate of 3% equity

interests in Shanghai Baoxin, a key operating subsidiary of the Company, held by Huakong

Industry and Huakong Innovation. We plan to consummate this purchase within two weeks of

the Listing Date. The consideration of RMB550 million is currently expected to be kept in an

SUMMARY

– 10 –

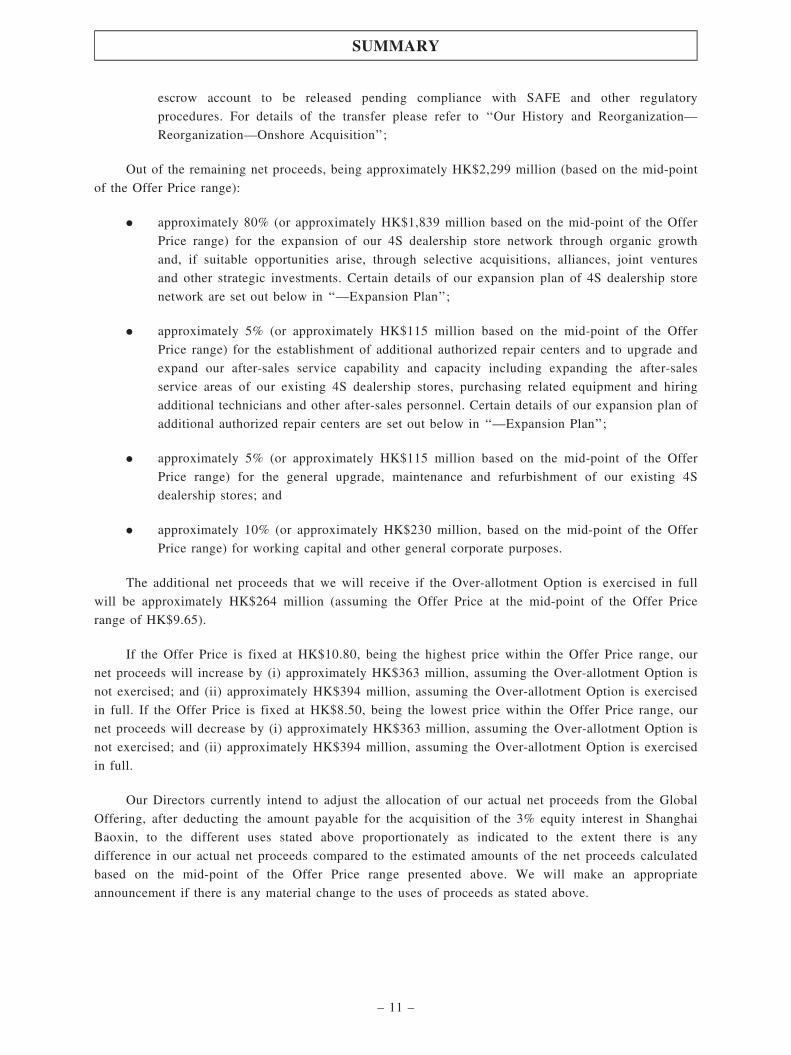

escrow account to be released pending compliance with SAFE and other regulatory

procedures. For details of the transfer please refer to ‘‘Our History and Reorganization—

Reorganization—Onshore Acquisition’’;

Out of the remaining net proceeds, being approximately HK$2,299 million (based on the mid-point

of the Offer Price range):

. approximately 80% (or approximately HK$1,839 million based on the mid-point of the Offer

Price range) for the expansion of our 4S dealership store network through organic growth

and, if suitable opportunities arise, through selective acquisitions, alliances, joint ventures

and other strategic investments. Certain details of our expansion plan of 4S dealership store

network are set out below in ‘‘—Expansion Plan’’;

. approximately 5% (or approximately HK$115 million based on the mid-point of the Offer

Price range) for the establishment of additional authorized repair centers and to upgrade and

expand our after-sales service capability and capacity including expanding the after-sales

service areas of our existing 4S dealership stores, purchasing related equipment and hiring

additional technicians and other after-sales personnel. Certain details of our expansion plan of

additional authorized repair centers are set out below in ‘‘—Expansion Plan’’;

. approximately 5% (or approximately HK$115 million based on the mid-point of the Offer

Price range) for the general upgrade, maintenance and refurbishment of our existing 4S

dealership stores; and

. approximately 10% (or approximately HK$230 million, based on the mid-point of the Offer

Price range) for working capital and other general corporate purposes.

The additional net proceeds that we will receive if the Over-allotment Option is exercised in full

will be approximately HK$264 million (assuming the Offer Price at the mid-point of the Offer Price

range of HK$9.65).

If the Offer Price is fixed at HK$10.80, being the highest price within the Offer Price range, our

net proceeds will increase by (i) approximately HK$363 million, assuming the Over-allotment Option is

not exercised; and (ii) approximately HK$394 million, assuming the Over-allotment Option is exercised

in full. If the Offer Price is fixed at HK$8.50, being the lowest price within the Offer Price range, our

net proceeds will decrease by (i) approximately HK$363 million, assuming the Over-allotment Option is

not exercised; and (ii) approximately HK$394 million, assuming the Over-allotment Option is exercised

in full.

Our Directors currently intend to adjust the allocation of our actual net proceeds from the Global

Offering, after deducting the amount payable for the acquisition of the 3% equity interest in Shanghai

Baoxin, to the different uses stated above proportionately as indicated to the extent there is any

difference in our actual net proceeds compared to the estimated amounts of the net proceeds calculated

based on the mid-point of the Offer Price range presented above. We will make an appropriate

announcement if there is any material change to the uses of proceeds as stated above.

SUMMARY

– 11 –

We estimate that the net proceeds to be received by the Selling Shareholder from the Global

Offering will range from approximately HK$413 million (assuming an Offer Price of HK$8.50 per

Share, being the low end of the proposed Offer Price range) to HK$524 million (assuming an Offer

Price of HK$10.80 per Share, being the high end of the proposed Offer Price range), after deducting any

fees and/or expenses which may be payable by the Selling Shareholder to the Joint Bookrunners in

relation to the Global Offering and assuming the Over-allotment Option is not exercised. The additional

net proceeds that the Selling Shareholder will receive if the Over-allotment Option is exercised in full

will be approximately HK$264 million (assuming the Offer Price at the mid-point of the stated Offer

Price range of HK$9.65). We will not receive any of the net proceeds from the sale of 50,580,000

Shares by the Selling Shareholder in the Global Offering or the offer of the additional 28,449,000

Shares by the Selling Shareholder pursuant to the exercise of the Over-allotment Option.

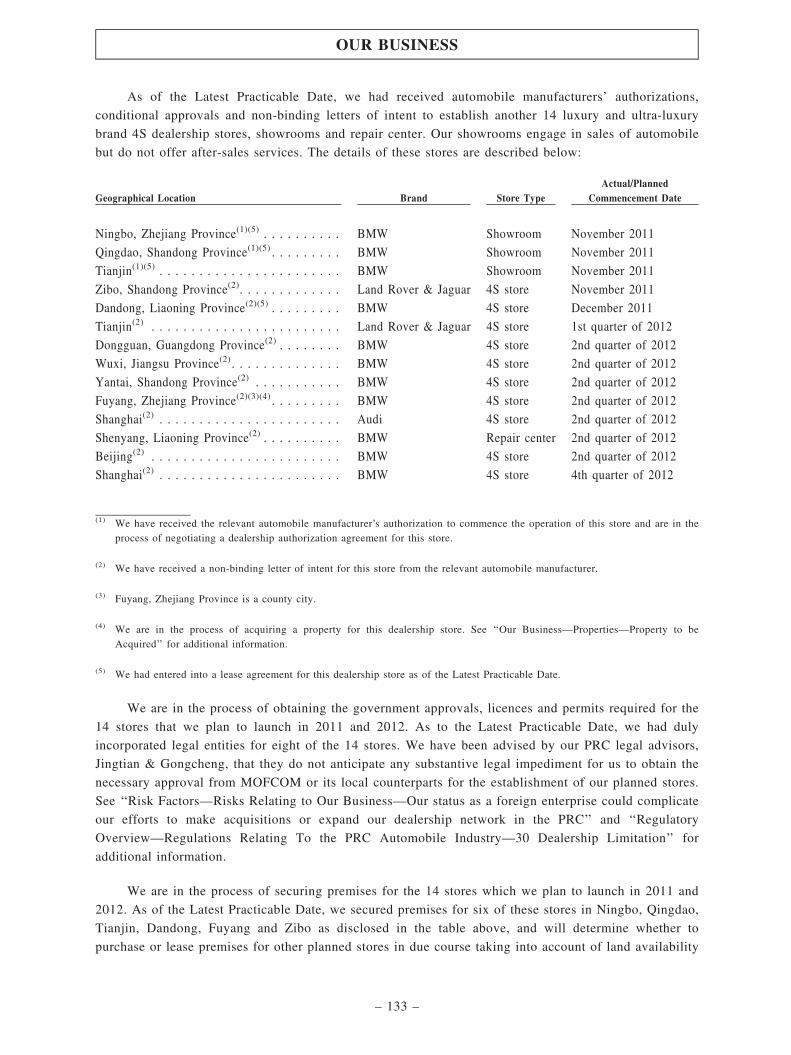

Expansion Plan

As of the Latest Practicable Date, we had received automobile manufacturers’ authorizations,

conditional approvals and non-binding letters of intent to establish another 14 luxury and ultra-luxury

brand 4S dealership stores, showrooms and repair center. Our showrooms engage in sales of automobiles

but do not offer after-sales services. The details of these stores are described below:

Geographical Location Brand Store TypeActual/Planned

Commencement Date

Ningbo, Zhejiang Province . . . . . . . . . . . . . BMW Showroom November 2011

Qingdao, Shandong Province. . . . . . . . . . . . BMW Showroom November 2011

Tianjin . . . . . . . . . . . . . . . . . . . . . . . . . . BMW Showroom November 2011

Zibo, Shandong Province . . . . . . . . . . . . . . Land Rover & Jaguar 4S store November 2011

Dandong, Liaoning Province . . . . . . . . . . . . BMW 4S store December 2011

Tianjin . . . . . . . . . . . . . . . . . . . . . . . . . . Land Rover & Jaguar 4S store 1st quarter of 2012

Dongguan, Guangdong Province . . . . . . . . . BMW 4S store 2nd quarter of 2012

Wuxi, Jiangsu Province . . . . . . . . . . . . . . . BMW 4S store 2nd quarter of 2012

Yantai, Shandong Province . . . . . . . . . . . . . BMW 4S store 2nd quarter of 2012

Fuyang, Zhejiang Province . . . . . . . . . . . . . BMW 4S store 2nd quarter of 2012

Shanghai . . . . . . . . . . . . . . . . . . . . . . . . . Audi 4S store 2nd quarter of 2012

Shenyang, Liaoning Province . . . . . . . . . . . BMW Repair center 2nd quarter of 2012

Beijing . . . . . . . . . . . . . . . . . . . . . . . . . . BMW 4S store 2nd quarter of 2012

Shanghai . . . . . . . . . . . . . . . . . . . . . . . . . BMW 4S store 4th quarter of 2012

Approximately 80% and 5% of the remaining net proceeds from the Global Offering, after

deducting approximately RMB550 million as consideration for purchasing the 3% equity interest in

Shanghai Baoxin, will be used for (i) the expansion of our 4S dealership store network and (ii)

establishing additional authorized repair centers and to upgrade and expand our after-sales service

capabilities, respectively, including to establish and launch the stores described above. Apart from the

remaining net proceeds (if any) from the Global Offering, we expect to fund our capital expenditure for

establishing additional 4S dealership stores, showrooms and repair centers by (i) cash from automobile

sales and after-sales business, (ii) cash from other operating activities, such as automobile insurance

commissions; and (iii) proceeds from bank loans and other borrowings.

SUMMARY

– 12 –

As at the Latest Practicable Date, we do not have any understanding, commitment or agreement,

and we are not engaged in any related negotiations and have not entered into any letter of intent (legallybinding or otherwise), with respect to any acquisitions, alliances, joint ventures or strategic investments.

See ‘‘Our Business—Our Strategies—Continue to expand dealership network and brand offeringsthrough organic store growth and selective acquisitions’’.

To the extent that any net proceeds are not immediately applied to the above purposes and to the

extent permitted by applicable law and regulations, we intend to deposit such amounts into short-termdemand deposit accounts with authorized financial institutions. Our PRC legal advisors, Jingtian &

Gongcheng, have confirmed that no provision for PRC enterprise income tax should be required for anyinterest income arising from the proceeds of the Global Offering as our Group does not intend to deposit

the proceeds of the Global Offering in PRC banks or financial institutions. When we receive the netproceeds from the Global Offering, we will apply for the relevant approvals from the PRC Government

authorities to remit such proceeds to our subsidiaries in the PRC. There is no assurance regardingwhether or when such approvals can be obtained.

OFFER STATISTICS

Based on an OfferPrice per Shareof HK$8.50

Based on an OfferPrice per Shareof HK$10.80

Market capitalisation of our Shares(1) . . . . . . . . . . . . . . . . . . . . HK$21,494

million

HK$27,310

million

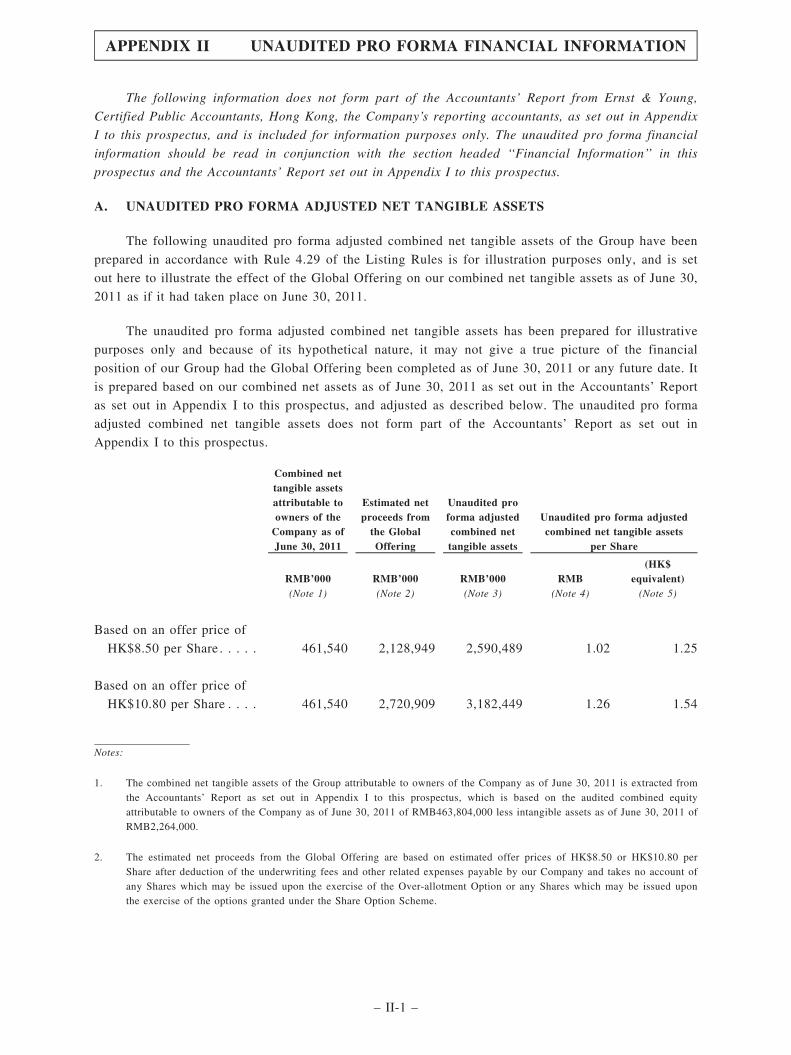

Unaudited pro forma adjusted consolidated net tangible

asset value per Share(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . .

RMB1.02

(HK$1.25)

RMB1.26

(HK$1.54)

(1) The calculation of market capitalisation is based on 2,528,740,000 Shares expected to be in issue immediately following

completion of the Global Offering and the Capitalisation Issue. It does not take into account any Shares which may beissued upon exercise of the Over-allotment Option or the options which may be granted under the Share Option Scheme.

(2) The unaudited pro forma adjusted consolidated net tangible assets attributable to the equity holders of the Company per

Share has been arrived on the basis of a total of 2,528,740,000 Shares in issue immediately following completion of theGlobal Offering and the Capitalisation Issue. It does not take into account any Shares which may be issued upon exercise ofthe Over-allotment Option or the options which may be granted under the Share Option Scheme.

DIVIDEND POLICY

Our Shareholders will be entitled to receive dividends that we declare. The payment and the

amount of any dividends will be at the discretion of our Directors and will depend on our future

operations and earnings, capital requirements and surplus, general financial condition, contractual

restrictions and other factors that our Directors deem relevant. Any declaration and payment as well as

the amount of dividends will be subject to our constitutional documents and the Companies Law,

including the approval of our Shareholders. In addition, our Controlling Shareholders will be able to

influence the approval by our Shareholders in a general meeting for any payment of dividends.

SUMMARY

– 13 –

Subject to the factors above, our shareholders have resolved that an accumulated earnings of

RMB227.6 million generated by our subsidiaries in China during the Track Record Period will be

retained and used by these subsidiaries in China for further business development purposes when

appropriate opportunities arise and will not be distributed in the foreseeable future. In 2008, our

subsidiaries in China did not declare any dividends. In the years ended December 31, 2009, 2010 and

the six months ended June 30, 2011, our subsidiaries in China declared dividends of RMB14.6 million,

RMB4.4 million and RMB453.3 million, respectively. The dividends declared by our subsidiaries in

2009 and 2010, respectively, have been paid to Mr. Yang Aihua. The dividends declared by our

subsidiaries in the six months ended June 30, 2011 will be funded by our internal resources and paid to

our shareholders before the Listing Date. Our Directors are satisfied, after due and careful inquiry, that

after such dividend payment, we will still have sufficient funds available to satisfy our working capital

requirements, including to fund our planned dealership network expansion, for at least 12 months

following the date of this prospectus. We currently intend to pay dividends of no more than 30% of our

profits available for distribution of each accounting year beginning from the year ended December 31,

2011. Going forward, we will re-evaluate our dividend policy in light of our financial position and the

prevailing economic climate. The determination to pay dividends, however, will be made at the

discretion of our Board and will be based upon our earnings, cash flow, financial condition, capital

requirements, statutory fund reserve requirements and any other conditions that our Directors deem

relevant. The payment of dividends may also be limited by legal restrictions and by financing

agreements that we may enter into in the future. The amounts of distribution that we have declared and

made in the past should not be taken as indications of the dividends, if any, that we may pay in the

future.

Future dividend payments will also depend on the availability of dividends received from our

operating subsidiaries in China. PRC laws require that dividends be paid only out of the net profit

calculated according to PRC accounting principles, which differ in many aspects from generally

accepted accounting principles in other jurisdictions, including IFRS. PRC laws also require our

subsidiaries in China to set aside part of their net profit as statutory reserves, which are not available for

distribution as cash dividends. Distributions from our operating subsidiaries may also be restricted if

they incur debt or losses or in accordance with any restrictive covenants in bank credit facilities,

convertible bond instruments or other agreements that we or our subsidiaries may enter into in the

future.

RISK FACTORS

There are certain risks involved in our operations, many of which are beyond our control. These

risks can be categorized into (i) risks relating to our business; (ii) risks relating to our industry; (iii)

risks relating to conducting business in the PRC; and (iv) risks relating to the Global Offering.

Additional risks and uncertainties presently not known to us or not expressed or implied below, or that

we currently deem immaterial could also harm our business, financial condition and operating results.

SUMMARY

– 14 –

Risks Relating to Our Business

. Our business and operations depend on, and are subject to restrictions imposed by, our

dealership authorization agreements with our automobile manufacturer partners. If one or

more of these agreements is terminated or not renewed, or if our business dealings with any

automobile manufacturer are otherwise reduced, our business, results of operations and

prospects could be adversely affected.

. Our business and operations are subject to restrictions imposed by automobile manufacturers,

and we depend on their cooperation in many different aspects of our operations. If our

relationship with any automobile manufacturer were to deteriorate, our business, results of

operations and growth could be negatively affected.

. We depend on our BMW brand dealership stores and our dealership arrangements with our

other major automobile manufacturer partners for a significant portion of our revenues.

. Our status as a foreign enterprise could complicate our efforts to make acquisitions or expand

our dealership network in the PRC.

. A substantial majority of our existing stores are located in Shanghai, Jiangsu and Zhejiang.

. We have experienced significant growth over the Track Record Period and we may not

sustain similar growth rates or financial performance in the future. We have recorded, and

may continue to record, negative operating cashflows due to our rapid expansion.

. We recorded net current liabilities as of June 30, 2011 and we cannot assure you that we will

not have net current liabilities in the future.

. Implementing our expansion plan may expose us to certain risks.

. Our business and financial performance depends on our ability to manage our inventory

effectively.

. We may not be able to obtain adequate financing on commercially reasonable terms on a

timely basis or at all. Any future equity may dilute your interest in our Company, and any

debt financing may contain covenants that restrict our business or operations.

. We depend on key individuals of our senior management team and our ability to attract,

train, motivate and retain an adequate number of skilled personnel.

. We have not yet obtained valid titles or rights to use certain properties or the required

permits for construction and development on certain properties occupied by us.

. Any automobile recall could have a negative impact on our results of operations, financial

condition and growth prospects.

. Our insurance coverage may be inadequate to protect us from certain types of losses.

. We depend on our information technology systems.

SUMMARY

– 15 –

. Our business is subject to seasonal fluctuation.

Risks Relating to Our Industry

. Our performance and growth prospects may be adversely affected by the increasingly

competitive nature of the PRC automobile dealership industry.

. The global economy is facing significant risks from the ongoing economic crisis in various

developed countries, which may adversely affect the PRC economy and our business and

results of operations.

. If there is any further fiscal or credit tightening by the PRC Government, demand for our

automobiles and after-sales services, as well as our access to external financing, may

decrease.

. Higher fuel prices, stricter fuel economy and emission standards and higher fuel-related taxes

on automobile consumption may reduce the demand for automobiles.

. We operate in a highly regulated industry, and any failure by us to comply with applicable

laws, rules or regulations, or to obtain or maintain necessary approvals, licenses and permits,

may adversely affect our business and operations and subject us to fines and other penalties.

. Anti-congestion regulations and ordinances of certain Chinese cities may restrict local

demand for automobiles.

Risks Relating to Conducting Business in the PRC

. Changes in PRC economic, political and social conditions, as well as government policies,

could have a material adverse effect on our business, financial condition, results of operations

and prospects.

. Uncertainties with respect to the PRC legal system could have a material adverse effect on

us.

. There are significant uncertainties under the EIT Law relating to our PRC enterprise income

tax liabilities.

. Under the EIT Law, we may be classified as a ‘‘resident enterprise’’ of the PRC. Such

classification could result in unfavorable tax consequences to us and our non-PRC

shareholders.

. PRC regulation of loans and direct investment by offshore holding companies in PRC entities

may delay or prevent us from using the proceeds we receive from this offering to make loans

or additional capital contributions to our PRC subsidiaries.

. Our ability to pay dividends and utilize cash resources in our subsidiaries is dependent upon

our subsidiaries’ earnings and distributions.

SUMMARY

– 16 –

. Failure by our Shareholders or beneficial owners who are PRC residents to make any

required applications and filings pursuant to regulations relating to offshore investment

activities by PRC residents may prevent us from being able to distribute profits and could

expose us and our PRC resident shareholders to liability under the PRC laws.

. Government control over currency conversion may affect the value of our Shares and limit

our ability to utilize our cash effectively.

. Fluctuation in the exchange rates of the Renminbi may have a material adverse effect on your

investment.

. It may be difficult to effect service of process upon, or to enforce against, us or our Directors

or members of our senior management who reside in the PRC, in connection with judgements

obtained in non-PRC courts.

. The state of the PRC’s political relationships with other countries may affect the performance

of our business.

Risks Relating to the Global Offering

. The interests of the Company’s Controlling Shareholders may conflict with the best interests

of its other shareholders.

. Investors will experience dilution in the pro forma net tangible book value per Share because

the Offer Price is higher than our net tangible book value per Share.

. The trading volume and market price of our Shares following the Global Offering may be

volatile.

. Future sales or perceived sales of substantial amounts of our securities in the public market,

including any future sale of our Shares by those Shareholders that are currently subject to

contractual and/or legal restrictions on share transfers, could have a material adverse effect

on the prevailing market price of our Shares and our ability to raise capital in the future, and

may result in dilution of your shareholding in our Company.

. Due to a gap of up to five business days between pricing and trading of our Shares and given

that our Shares will not commence trading on the Hong Kong Stock Exchange until the

Listing Date, the initial trading price of our Shares could be lower than the Offer Price.

. An active trading market in our Shares may not develop, which could have a material adverse

effect on our Share price and your ability to sell your Shares.

. There are risks associated with forward-looking statements.

. Certain industry statistics contained in this prospectus are derived from various publicly

available government or official sources and may not be accurate or reliable.

SUMMARY

– 17 –

In this prospectus, unless the context otherwise requires, the following terms shall have themeanings set out below.

‘‘Application Form(s)’’ WHITE Application Form(s), YELLOW Application Form(s)

and GREEN Application Form(s) or, where the context so

requires, any of them

‘‘Articles’’ or ‘‘Articles of

Association’’

the articles of association of our Company (as amended from time

to time) adopted on November 22, 2011, a summary of which is

set out in Appendix V to this prospectus

‘‘Auspicious Splendid’’ Auspicious Splendid Global Investments Limited (瑞華環球投資

有限公司), an investment holding company incorporated under

the laws of the BVI on February 11, 2011 and a Controlling

Shareholder

‘‘Baoxin Investment’’ Baoxin Investment Management Ltd., an investment holding

company incorporated under the laws of the BVI on September 6,

2010 and a Controlling Shareholder

‘‘Beijing Hyundai’’ 北京現代汽車有限公司 (Beijing Hyundai Motor Co. Corp.), a

joint venture in the PRC between Beijing Automotive Investment

Co. Ltd., a subsidiary of Beijing Automotive Industry Holding

Co., Ltd., and Hyundai Motor Co., an Independent Third Party

‘‘Beijing Xinbaohang’’ 北京信寶行置業有限公司 (Beijing Xinbaohang Real Estate Co.,

Ltd.), a limited liability company incorporated in the PRC on

June 24, 2010, which is 51% owned by Shanghai Baoxin and

49% owned by 力天集團有限公司 (Liten Group Co., Ltd.), an

Independent Third Party apart from its equity interests herein

‘‘Bentai PRC’’ 上海奔泰投資管理有限公司 (Shanghai Bentai Investment

Management Co., Ltd.), a limited liability company incorporated

in the PRC, a former shareholder of Shanghai Baoxin and an

Independent Third Party

‘‘BMW Brilliance’’ 華晨寶馬汽車有限公司 (BMW Brilliance Automotive Ltd.), a

joint venture in the PRC between BMW Group and Brilliance

China Automotive Holdings Ltd., an Independent Third Party

‘‘BMW China’’ 寶馬(中國)汽車貿易有限公司 (BMW China Automotive Trading

Ltd.), a PRC subsidiary of the BMW Group, an Independent

Third Party

‘‘Board’’ or ‘‘Board of Directors’’ the board of directors of our Company

DEFINITIONS

– 18 –

‘‘business day’’ any day (other than a Saturday, Sunday or public holiday) on

which banks in Hong Kong are generally open for business

‘‘BVI’’ the British Virgin Islands

‘‘CADA’’ China Automobile Dealers’ Association

‘‘CAGR’’ compound annual growth rate

‘‘Capitalization Issue’’ the issue of 2,100,000,000 Shares upon capitalization of certain

sums standing to the credit of the share premium account of our

Company referred to in the section ‘‘A. Further Information

About Our Group—3. Resolutions of Our Shareholders’’ in

Appendix VI to this prospectus

‘‘Cayman Companies Law’’ or

‘‘Companies Law’’

the Companies Law, Cap.22 (Law 3 of 1961, as consolidated and

revised) of the Cayman Islands

‘‘CCASS’’ the Central Clearing and Settlement System established and

operated by HKSCC

‘‘CCASS Clearing Participant’’ a person admitted to participate in CCASS as a direct participant

or a general clearing participant

‘‘CCASS Custodian Participant’’ a person admitted to participate in CCASS as a custodian

participant

‘‘CCASS Investor Participant’’ a person admitted to participate in CCASS as an investor

participant who may be an individual or joint individuals or a

corporation

‘‘CCASS Participant’’ a CCASS Clearing Participant, a CCASS Custodian Participant or

a CCASS Investor Participant

‘‘Changshu Baoxin’’ 常熟寶信汽車銷售服務有限公司 (Changshu Baoxin Automobile

Sales & Services Co., Ltd.), a limited liability company

incorporated in the PRC on August 9, 2006, which is 70% owned

by Shanghai Baoxin and 30% owned by Suzhou Baoxin

‘‘Chiheng PRC’’ 上海馳恒投資管理有限公司 (Shanghai Chiheng Investment

Management Co., Ltd.), a limited liability company incorporated

in the PRC, a former shareholder of Shanghai Baoxin and an

Independent Third Party

‘‘China’’ or ‘‘the PRC’’ the People’s Republic of China excluding, for the purpose of this

prospectus, Hong Kong, Macau Special Administrative Region

and Taiwan

DEFINITIONS

– 19 –

‘‘Companies Ordinance’’ the Companies Ordinance (Chapter 32 of the Laws of Hong

Kong), as amended or supplemented from time to time

‘‘Company’’ or ‘‘our Company’’ Baoxin Auto Group Limited (寶信汽車集團有限公司) (formerly

known as Baoxin Auto Group Ltd.), an exempted company

incorporated in the Cayman Islands on September 6, 2010

‘‘Comparable Stores for After-sales

Business’’

those of our 4S dealership stores that are located in a provincial,

sub-provincial or prefectural city and have been in operation for

at least 24 months as of January 1 of a particular fiscal year and