Toll Road Financing - PPIAF

26

Session: Finance Topic 2.5. Toll Roads & Road Funds 1 The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent. Return to Grid of Topics Cross-Border Infrastructure: A Toolkit Toll Road Financing Session on Finance Sidharth Sinha Indian Institute of Management, Ahmedabad Cross-Border Infrastructure: A Toolkit Forms of Government Support for Road Concessions • Land acquisition Expropriation of right of way for toll road construction. Cost of land acquired maybe borne either by the government or the concessionaire. • Provision of development rights and third-party revenue This measure involves the transfer of right of commercial development along the toll road to supplement project economics. The advantage is that this enhances project economics but excessive dependence on this measure may reduce incentive to make the road a success.

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Toll Road Financing - PPIAF

Session: FinanceTopic 2.5. Toll Roads & Road Funds

1

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

itToll Road Financing

Session on Finance

Sidharth SinhaIndian Institute of Management, Ahmedabad

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Forms of Government Support for Road Concessions

• Land acquisition Expropriation of right of way for toll road construction. Cost of land acquired maybe borne either by the government or the concessionaire.

• Provision of development rights and third-party revenue This measure involves the transfer of right of commercial development along the toll road to supplement project economics. The advantage is that this enhances project economics but excessive dependence on this measure may reduce incentive to make the road a success.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

2

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

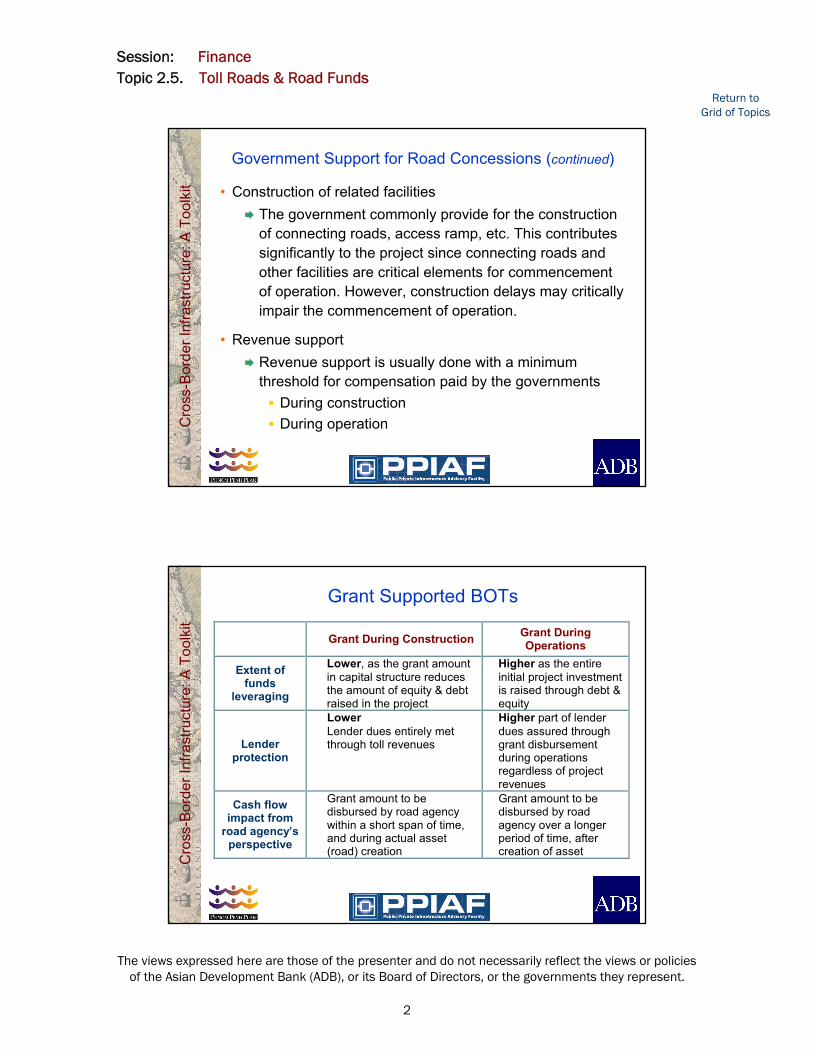

Government Support for Road Concessions (continued)

• Construction of related facilities The government commonly provide for the construction of connecting roads, access ramp, etc. This contributes significantly to the project since connecting roads and other facilities are critical elements for commencement of operation. However, construction delays may critically impair the commencement of operation.

• Revenue support Revenue support is usually done with a minimum threshold for compensation paid by the governments

During constructionDuring operation

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Grant Supported BOTs

Grant During Construction Grant During Operations

Extent of funds

leveraging

Lower, as the grant amount in capital structure reduces the amount of equity & debt raised in the project

Higher as the entire initial project investment is raised through debt & equity

Lender protection

Lower Lender dues entirely met through toll revenues

Higher part of lender dues assured through grant disbursement during operations regardless of project revenues

Cash flow impact from

road agency’s perspective

Grant amount to be disbursed by road agency within a short span of time, and during actual asset (road) creation

Grant amount to be disbursed by road agency over a longer period of time, after creation of asset

Session: FinanceTopic 2.5. Toll Roads & Road Funds

3

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Government Support for Road Concessions (continued)

• Revenue sharing with existing facilities Concession agreements which combine the construction of new stretches with the rehabilitation and upgrading of an existing stretch This would address the problem that the new stretches have low traffic densities making them commercially not viable. Existing stretches could generate enough toll revenue to improve the cash flows of the concessionaire, especially during the construction stage.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Government Support for Road Concessions (continued)

• Shadow toll

Government pays toll to the concessionaires according to the vehicle - kilometers of the traffic counted automatically. This provides for a means of introducing private financing without stimulating resistance to tolling.

Possible financial burden/ fiscal inflexibility in later years may hinder transition to real tolling.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

4

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Government Support for Road Concessions (continued)

• Shadow toll (continued)

A modification to the conventional shadow toll model is suggested, through payment of shadow tolls to the Concessionaire by the road agency in two tiers:

A base payment which is assured regardless of actual traffic on the road;

An additional payment per vehicle that actually uses the road

This provides the concessionaire incentive to improve the road condition and usage.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Fixed IRR or Assured Return

• Guaranteed level of net return on equity/project, taking the time value of money into account.

If the actual traffic is lower than the projected level, the concession period will get extended Although this results in improved project economics, its effect on current cash flow is negligible.

• Since the fixed IRR model guarantees a return over and above the costs of the toll road operator, there is less incentive for cost efficiencies.

Standard problem with rate of return regulation

Session: FinanceTopic 2.5. Toll Roads & Road Funds

5

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Least Present Value of Revenue (LPVR) Based Bidding

• The bidding variable is the present value of revenue throughout the life of the concession that firms are willing to accept to undertake the project.

• The duration of the concession is then flexible and depends on the effective traffic levels encountered.

• Encourages operating and capital cost efficiencies as opposed to fixed IRR mode

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Implications of LPVR

• Tolls can be adjusted without negotiation with the concessionaire

• They transfer political and demand-related risks to the user in the form of an endogenous concession period

• Calculation of compensation payments on concession termination is straightforward at any point in time during the concession period.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

6

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

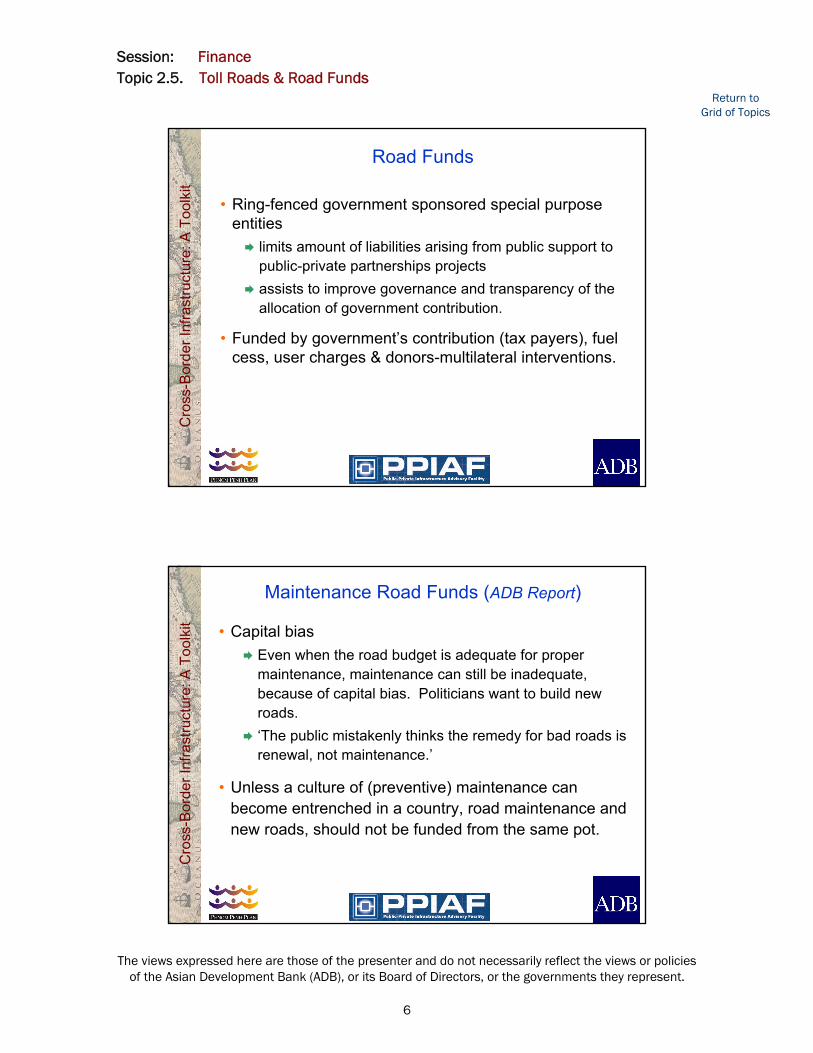

Road Funds

• Ring-fenced government sponsored special purpose entities

limits amount of liabilities arising from public support to public-private partnerships projects assists to improve governance and transparency of the allocation of government contribution.

• Funded by government’s contribution (tax payers), fuel cess, user charges & donors-multilateral interventions.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Maintenance Road Funds (ADB Report)

• Capital biasEven when the road budget is adequate for proper maintenance, maintenance can still be inadequate, because of capital bias. Politicians want to build new roads. ‘The public mistakenly thinks the remedy for bad roads is renewal, not maintenance.’

• Unless a culture of (preventive) maintenance can become entrenched in a country, road maintenance and new roads, should not be funded from the same pot.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

7

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Second Generation Road Funds

• The concept of the second generation road fund and board is that of an autonomous agency

controlling the funding of road maintenance, directed predominantly by road users, having power to raise revenue and control funding allocations, having a strong incentive to insist on commercially

and professionally efficient management.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Evaluation of Road FundsRoad Funds Revisited:

A Preliminary Appraisal of the Effectiveness of the “Second Generation” Road Funds, World Bank, 2002

• The paper is based on detailed reviews of experience in seven African countries in which the World Bank has had some involvement in the establishment of second generation road funds

Most countries are still not able to fully fund their desired levels of road maintenance because of residual controls of the Ministry of Finance over the level of the fuel tax levyMany countries are unable to disburse even those funds that are allocated because of the low absorptive capacity of the maintenance contracting sector.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

8

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Evaluation of Road Funds (continued)

Despite this limitation on overall funding, there is already evidence of increased efficiency in implementation associated with greater security of funding and extended private sector contracting.

There is no strong and systematic link between the form of the fund (user majority on boards, private sector chair, etc) and their performance (reduction in costs, improvement in road condition). Even continued reliance on the budget for a substantial part of funding has not been a particular impediment.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Evaluation of Road Funds (continued)

• “The elements which link and reconcile these conclusions in our sample of countries is a commitment of government to

facilitate a more businesslike approach to road maintenance, and ensure that road maintenance receive high priority in budget allocation.”

• The importance of the creation of the funds has been as much an indicator of the willingness of the country and a focus for change of process as an essential mechanism for efficient maintenance policy.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

9

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Toll Roads - Case Study:Noida Toll Bridge Company Limited (NTBCL)

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Background

• The river Yamuna that runs north-south forms a natural barrier that restrains expansion of Delhi to the east.

• The New Okhla Industrial Development Authority (NOIDA) in the neighbouring state of Uttar Pradesh established a new integrated industrial township in close proximity to Delhi.

• Noida located east of Yamuna is a township that is under development since 1976. Today it has become one of the satellite towns of Delhi.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

10

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Background (continued)

• The traffic that is generated by this satellite town is substantial and the interaction with Delhi is also substantial.

• The traffic between the east of river Yamuna including Noida and Delhi was of the order of 3,70,000 PCUsdaily in 2002 and was serviced by three existing toll free bridges.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Project Alignment

Session: FinanceTopic 2.5. Toll Roads & Road Funds

11

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Background (continued)

• 30% of Delhi’s population lives across the river Yamuna

• NOIDA is inhabited by 700,000 people - 50% of whom commute to Delhi for work

• Population of Noida/Greater Noida will increase manifold over next few years

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Project Development

• Infrastructure leasing and financial services (IL&FS), NOIDA & the Delhi Administration (DA) reached an in-principle agreement for the implementation of a fourth bridge across the Yamuna, the Delhi Noida Toll Bridge, on build, own, operate & transfer (BOOT) basis.

• A tripartite memorandum of understanding (MoU) was signed between IL&FS, NOIDA, & DA on April 7, 1992 for establishing the new bridge and defining the scope and mutual obligation of the various partners.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

12

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Formation of Project Company

• A steering committee consisting of representatives ofGovernment of Uttar Pradesh (GoUP), Delhi Government (DG), Ministry of Urban Affairs and Employment, Government of India, Delhi Development Authority (DDA), NOIDA and IL&FS

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Formation of Project Company (continued)

• Noida Toll Bridge Company limited (NTBCL) was incorporated on April 8, 1996.

• NTBCL, is a special purpose company promoted by Infrastructure Leasing & Financial Services Ltd (IL&FS) for the purpose of development, construction, operation and maintenance of a bridge across the river Yamunaconnecting Delhi and Noida on a build-own-operate-transfer (BOOT) basis.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

13

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

The Project

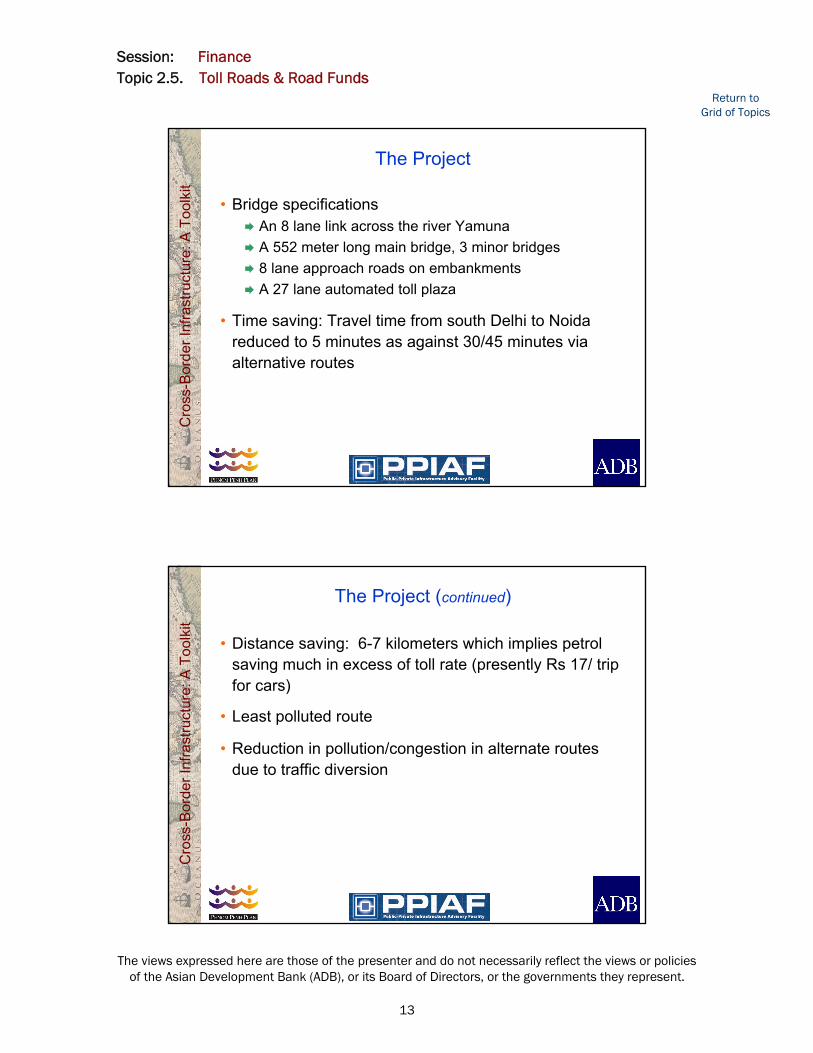

• Bridge specificationsAn 8 lane link across the river YamunaA 552 meter long main bridge, 3 minor bridges8 lane approach roads on embankmentsA 27 lane automated toll plaza

• Time saving: Travel time from south Delhi to Noidareduced to 5 minutes as against 30/45 minutes via alternative routes

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

The Project (continued)

• Distance saving: 6-7 kilometers which implies petrol saving much in excess of toll rate (presently Rs 17/ trip for cars)

• Least polluted route

• Reduction in pollution/congestion in alternate routes due to traffic diversion

Session: FinanceTopic 2.5. Toll Roads & Road Funds

14

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Stakeholders

• Government of India• Governments of Uttar Pradesh (UP) and NCT Delhi

(entered into a support agreement to the concession agreement)

• NOIDA - concession grantor• IL&FS - sponsor• The World Bank - line of credit to IL&FS• Kampsax International, Denmark - project consultants• Mitsui Marubeni Corporation, Japan - EPC contractor• Intertoll, South Africa - O&M operator• Users of the bridge

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Govt. of NCT of Delhi

Govt. of Uttar Pradesh

NOIDA

NTBCL

Support Agreement

Concession Agreement

Banks/FIs

Mitsui Marubeni Corp. Japan

Intertoll South Africa

Investors

Indpt. EngineerIndpt. Auditor

Loan Agreement

Shareholders Agreement

EPC Contract O&M Contract

Session: FinanceTopic 2.5. Toll Roads & Road Funds

15

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Milestones

• Apr 1992: Signing of MOU

• Jun 1993: Appointment of Kampsax

• Jan 1996: World Bank review & approval

• Dec 1996: Delhi Development Authority Technical Committee approval

• Nov 1997: Concession agreement signed

• Nov 1997: Delhi Urban Arts Commission approval

• Jan 1998: Support agreement

• Jan 1998: EPC contract awarded to MMC

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Milestones (continued)

• May 1998: Land acquisition completed

• Aug 1998: Regulation authorising toll collection

• Dec 1998: Appointment of O&M contractor

• Dec 1998: Financial close

• Dec 1998: Commencement of construction

• Feb 2001: Commencement of commercial operations

• Oct 2001: Completion of connecting flyover

Session: FinanceTopic 2.5. Toll Roads & Road Funds

16

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

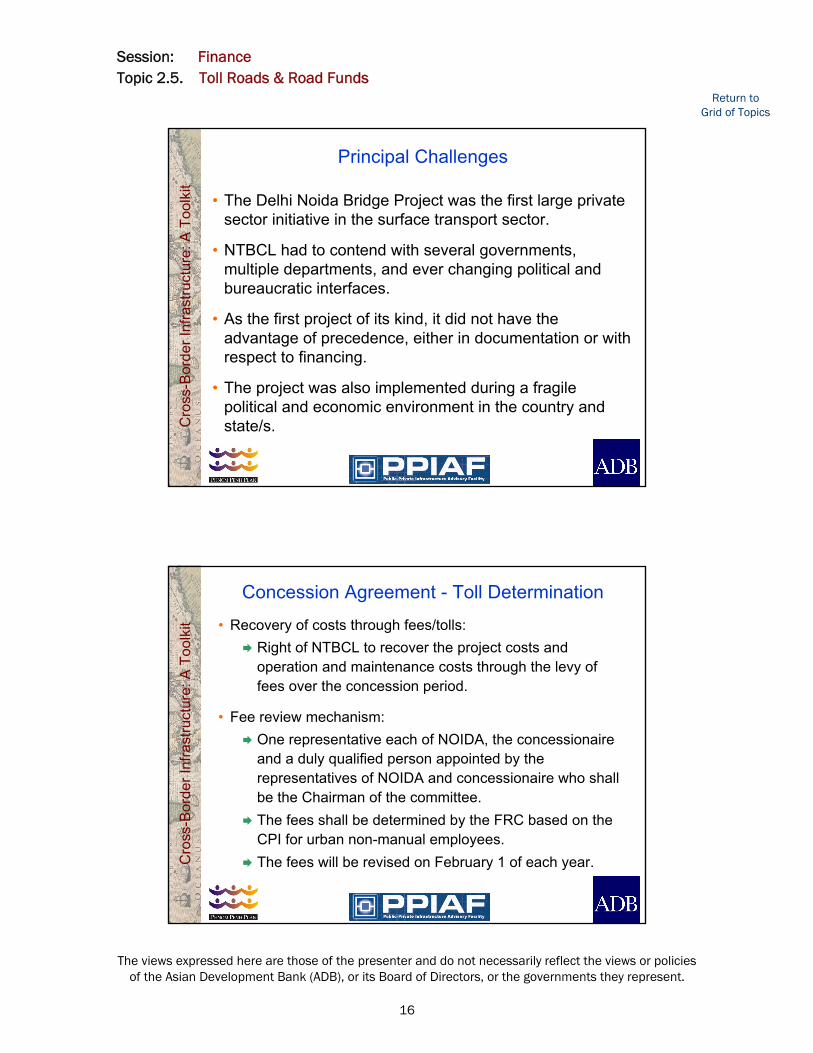

Principal Challenges

• The Delhi Noida Bridge Project was the first large private sector initiative in the surface transport sector.

• NTBCL had to contend with several governments, multiple departments, and ever changing political and bureaucratic interfaces.

• As the first project of its kind, it did not have the advantage of precedence, either in documentation or with respect to financing.

• The project was also implemented during a fragile political and economic environment in the country and state/s.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Concession Agreement - Toll Determination

• Recovery of costs through fees/tolls: Right of NTBCL to recover the project costs and operation and maintenance costs through the levy of fees over the concession period.

• Fee review mechanism:One representative each of NOIDA, the concessionaire and a duly qualified person appointed by the representatives of NOIDA and concessionaire who shall be the Chairman of the committee. The fees shall be determined by the FRC based on the CPI for urban non-manual employees.The fees will be revised on February 1 of each year.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

17

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

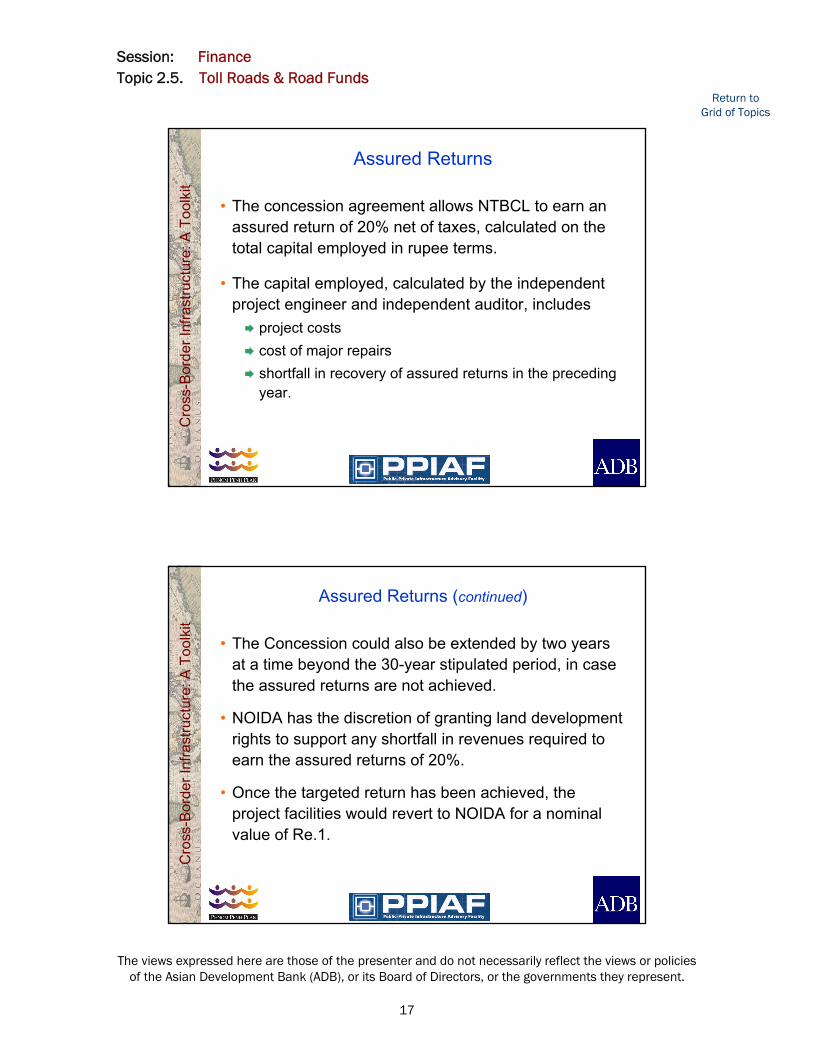

Assured Returns

• The concession agreement allows NTBCL to earn an assured return of 20% net of taxes, calculated on the total capital employed in rupee terms.

• The capital employed, calculated by the independent project engineer and independent auditor, includes

project costs cost of major repairs shortfall in recovery of assured returns in the preceding year.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Assured Returns (continued)

• The Concession could also be extended by two years at a time beyond the 30-year stipulated period, in case the assured returns are not achieved.

• NOIDA has the discretion of granting land development rights to support any shortfall in revenues required to earn the assured returns of 20%.

• Once the targeted return has been achieved, the project facilities would revert to NOIDA for a nominal value of Re.1.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

18

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Current Toll Rates (valid till 31 Jan 2007)

The toll rates were arrived at using:

• willingness to pay surveys• user benefits & VOC

savings • user acceptability• achievement of contracted

returns over concession period

40 to 75Buses/Trucks

35LCVs

17Cars/3-Wheelers

82 Wheelers

Toll Rate (Rs./Trip)

Vehicle categoryC

ross

-Bor

der I

nfra

stru

ctur

e: A

Too

lkit

Support Agreement

• “Support agreement” was signed between the Government of Uttar Pradesh (GoUP) and the Government of NCT Delhi (DG) on 14 January 1998. The salient features of the Support Agreement are:

Leasing of the lands pertaining to the project site and adjacent areas.

Obtain all necessary clearances from the Municipal Corporation of Delhi.

Session: FinanceTopic 2.5. Toll Roads & Road Funds

19

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Support Agreement (continued)

Not to allow construction of any other passage across the Yamuna which is toll free or charges lower toll than the Noida Bridge within a radius of 5 kms from the Delhi Noida Bridge site for a period of 10 years or till the Noida Bridge achieves full rated capacity, whichever is later, without the written consent of NTBCL.

• In the event of any breach of the support agreement GoUP and/or DG shall compensate NTBCL and/or NOIDA for any costs incurred by them and the lenders pertaining to the project.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

O&M Agreement

• O&M contract awarded to M/s Intertoll, South Africa on the basis of competitive bidding. Key contract features:

US$ 2.3 million equity participationUS$ 2.2 million performance guarantee Intertoll shares traffic risk with NTBCL – the O&M fee for first 10 year is directly related to the revenue generationRevenue leakage capped at 0.1% with strong penalties

• After 10 years the O&M fee will comprise of :Variable fee @ Rs 0.725 (US$ 0.015) per vehicle Fixed fee @ Rs 31.9 million (US$ 750,000) per annum

Session: FinanceTopic 2.5. Toll Roads & Road Funds

20

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

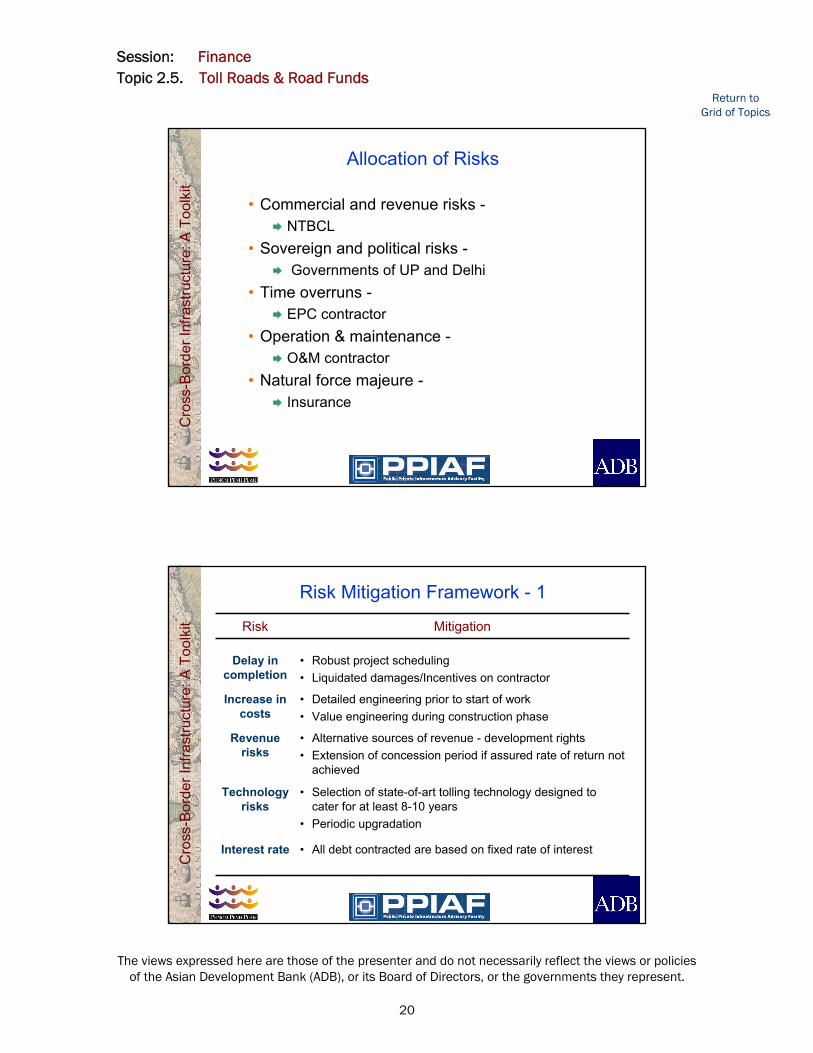

Allocation of Risks

• Commercial and revenue risks -NTBCL

• Sovereign and political risks -Governments of UP and Delhi

• Time overruns -EPC contractor

• Operation & maintenance -O&M contractor

• Natural force majeure -Insurance

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Risk Mitigation Framework - 1

• All debt contracted are based on fixed rate of interestInterest rate

• Selection of state-of-art tolling technology designed to cater for at least 8-10 years

• Periodic upgradation

Technology risks

• Alternative sources of revenue - development rights• Extension of concession period if assured rate of return not

achieved

Revenue risks

• Detailed engineering prior to start of work• Value engineering during construction phase

Increase in costs

• Robust project scheduling • Liquidated damages/Incentives on contractor

Delay in completion

MitigationRisk

Session: FinanceTopic 2.5. Toll Roads & Road Funds

21

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Risk Mitigation Framework - 2

• Insurance policyNatural force majuere risks

• Pre-determined formula for revision in tolls• Independent fee review committee• Revisions do not require approval of NOIDA/Gov’t.

Regulatory risk (delay in toll revision)

• Internationally reputed toll management company• Self auditable toll management system with automatic

vehicle classification (AVC)• Revenue of operator linked to toll collection• Operator to make good any loss of revenue

Revenue leakage

MitigationRiskC

ross

-Bor

der I

nfra

stru

ctur

e: A

Too

lkit

Risk Mitigation Framework - 3

• Toll rates linked to consumer price indexInflation

• Delhi Government has undertaken not to build an toll free facility until project achieves full capacity for a continuous period of 6 months

Competing routes

• Concession agreement provides compensation formula for various types of direct and indirect political risks

• NOIDA to pay lender’s dues as well as cumulative equity returns in case of termination due to political risks

Political risks

MitigationRisk

Session: FinanceTopic 2.5. Toll Roads & Road Funds

22

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it Equity Amount (Rs Million)IL&FS 360.0NOIDA 100.0IFCI 50.0FCD Issue 207.8International Funds 400.0Intertoll (O&M Operator) 106.2

Total Equity 1224.0DebtDeep Discount Bond issue 500.0IL&FS (World Bank L/C) 600.0RTL from FIs/Banks 1758.0

Total Debt 2858.0

Financing PlanC

ross

-Bor

der I

nfra

stru

ctur

e: A

Too

lkit

Public Issue

• First green-field infrastructure project to raise equity and debt from capital markets through

Secured deep discount bonds (DDBs) aggregating Rs. 500 millionSecured fully convertible debentures (FCDs) aggregating to Rs. 207.8 million

• This was also the first initial public offering with take out financing arrangement

Session: FinanceTopic 2.5. Toll Roads & Road Funds

23

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

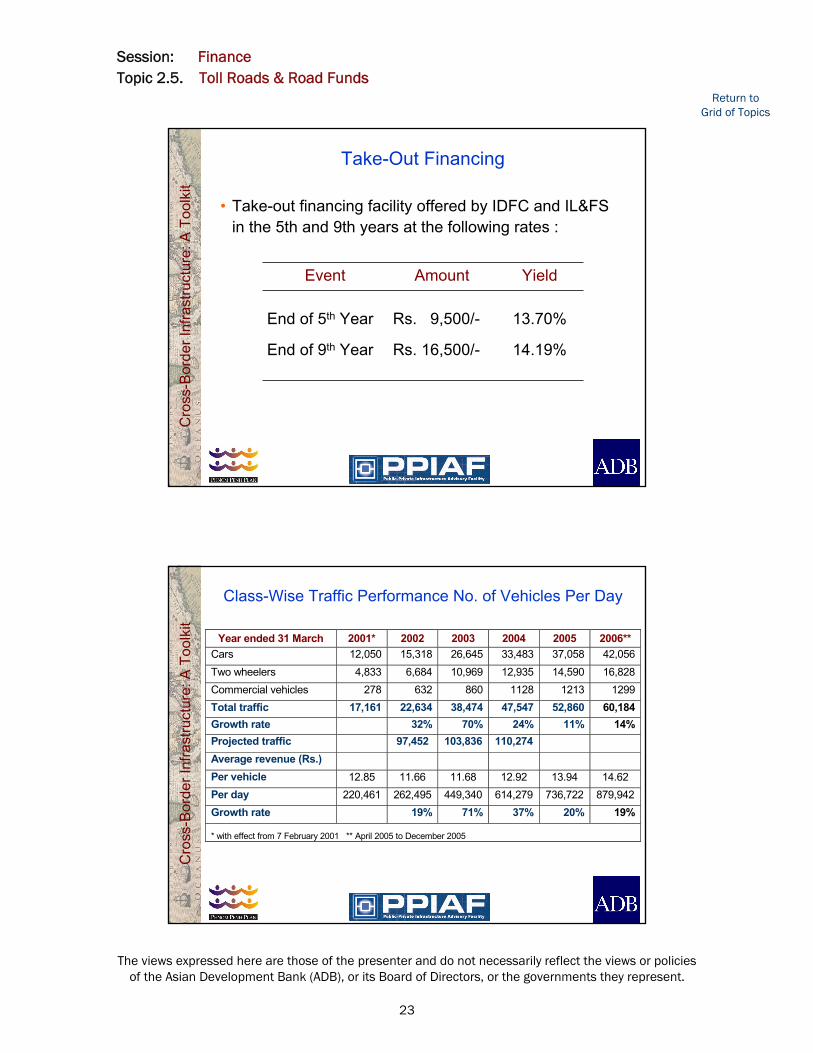

Take-Out Financing

• Take-out financing facility offered by IDFC and IL&FS in the 5th and 9th years at the following rates :

14.19%Rs. 16,500/-End of 9th Year

13.70%Rs. 9,500/-End of 5th Year

YieldAmountEvent

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Class-Wise Traffic Performance No. of Vehicles Per Day

Year ended 31 March 2001* 2002 2003 2004 2005 2006** Cars 12,050 15,318 26,645 33,483 37,058 42,056 Two wheelers 4,833 6,684 10,969 12,935 14,590 16,828 Commercial vehicles 278 632 860 1128 1213 1299 Total traffic 17,161 22,634 38,474 47,547 52,860 60,184 Growth rate 32% 70% 24% 11% 14% Projected traffic 97,452 103,836 110,274 Average revenue (Rs.) Per vehicle 12.85 11.66 11.68 12.92 13.94 14.62 Per day 220,461 262,495 449,340 614,279 736,722 879,942 Growth rate 19% 71% 37% 20% 19%

* with effect from 7 February 2001 ** April 2005 to December 2005

Session: FinanceTopic 2.5. Toll Roads & Road Funds

24

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Financial Performance

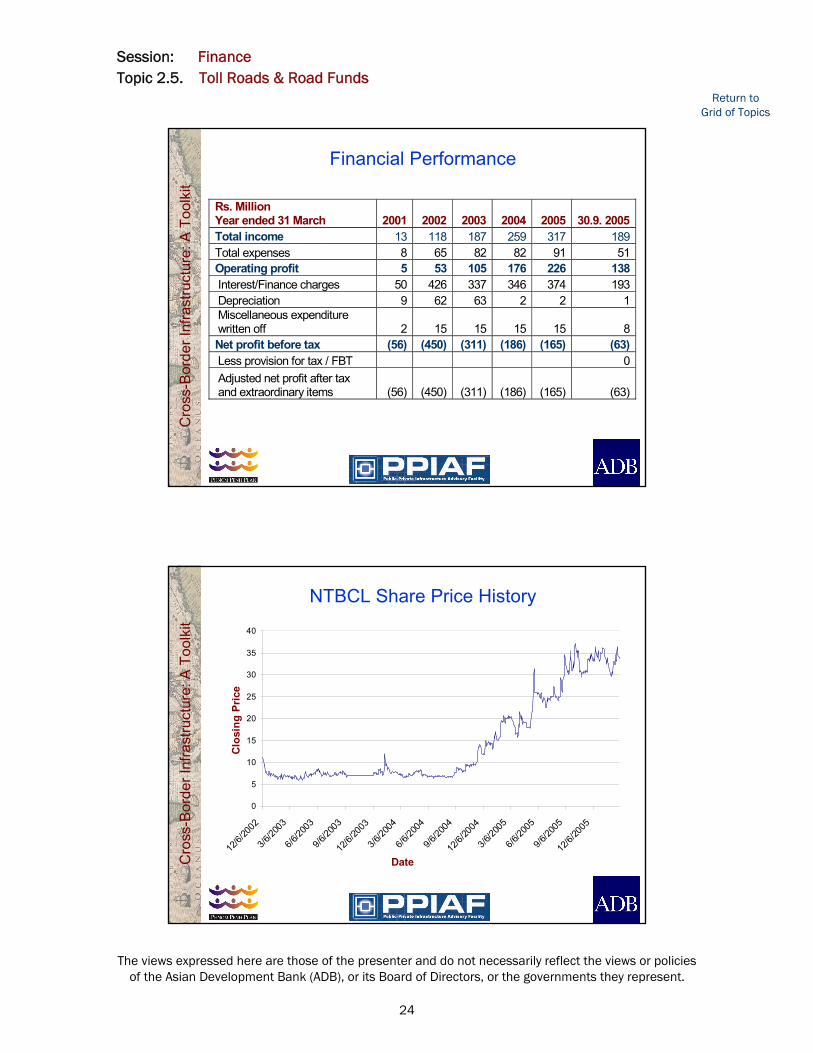

Rs. Million Year ended 31 March 2001 2002 2003 2004 2005 30.9. 2005 Total income 13 118 187 259 317 189 Total expenses 8 65 82 82 91 51 Operating profit 5 53 105 176 226 138 Interest/Finance charges 50 426 337 346 374 193 Depreciation 9 62 63 2 2 1 Miscellaneous expenditure written off 2 15 15 15 15 8 Net profit before tax (56) (450) (311) (186) (165) (63) Less provision for tax / FBT 0 Adjusted net profit after tax and extraordinary items (56) (450) (311) (186) (165) (63)

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

NTBCL Share Price History

0

5

10

15

20

25

30

35

40

12/6/

2002

3/6/20

03

6/6/20

03

9/6/20

03

12/6/

2003

3/6/20

04

6/6/20

04

9/6/20

04

12/6/

2004

3/6/20

05

6/6/20

05

9/6/20

05

12/6/

2005

Date

Clo

sing

Pric

e

Session: FinanceTopic 2.5. Toll Roads & Road Funds

25

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Debt Restructuring

• Original project debt was contracted at an average cost of 15% pa.

• In view of the downward interest rate trends and revised cash flow projections, the effective cost of term loans was reduced to 8.5% pa.

• DDBs were restructured w.e.f. Nov 2004 with revised interest yield of 8.5% pa and are proposed be refinanced in the current financial year.

• The debt restructuring exercise has been fully completed and the current carrying cost of debt is 8.5% pa with complete repayment by 2017.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Valuation of Company

• Market capitalization=Rs. 35*122.4 million= Rs.4,284 million

• Debt book value = Rs.3,700 million

• Approximate enterprise value Rs.8,000 million

• Discounted cash flow value15 year cash flows Rs.7,000 millionTerminal value Rs.9,426 million

Session: FinanceTopic 2.5. Toll Roads & Road Funds

26

The views expressed here are those of the presenter and do not necessarily reflect the views or policies of the Asian Development Bank (ADB), or its Board of Directors, or the governments they represent.

Return to Grid of Topics

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Learnings

• Problem of long-term funding to realize value.

• The back-ended revenue profile coupled with high interest rates lead to restructuring of NTBCL’s debts.

• The concession extension approach assumes that investors are indifferent about the time period over which they earn their return.

Cro

ss-B

orde

r Inf

rast

ruct

ure:

A T

oolk

it

Learnings (continued)

• Financial markets may not offer funds with uncertain debt service and maturity. In that case, sponsors may be unwilling to participate in a concession in which the concession term is uncertain because they would be unable finance the project.

• This approach is akin to a rate of return regulation and does not provide incentives for cost minimization.