CSC Steel Holdings (CSCS MK) - Maybank Kim Eng

38

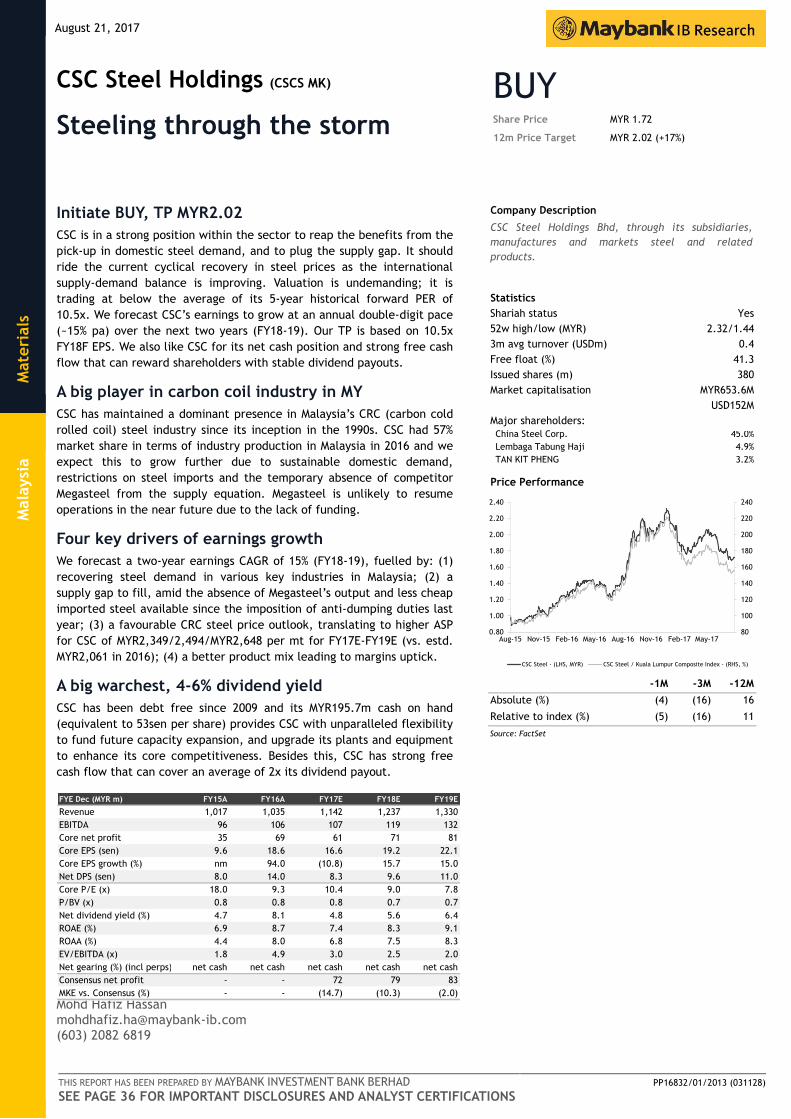

August 21, 2017 Materials Malaysia THIS REPORT HAS BEEN PREPARED BY MAYBANK INVESTMENT BANK BERHAD SEE PAGE 36 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS PP16832/01/2013 (031128) Mohd Hafiz Hassan [email protected] (603) 2082 6819 CSC Steel Holdings (CSCS MK) Steeling through the storm Initiate BUY, TP MYR2.02 CSC is in a strong position within the sector to reap the benefits from the pick-up in domestic steel demand, and to plug the supply gap. It should ride the current cyclical recovery in steel prices as the international supply-demand balance is improving. Valuation is undemanding; it is trading at below the average of its 5-year historical forward PER of 10.5x. We forecast CSC’s earnings to grow at an annual double-digit pace (~15% pa) over the next two years (FY18-19). Our TP is based on 10.5x FY18F EPS. We also like CSC for its net cash position and strong free cash flow that can reward shareholders with stable dividend payouts. A big player in carbon coil industry in MY CSC has maintained a dominant presence in Malaysia’s CRC (carbon cold rolled coil) steel industry since its inception in the 1990s. CSC had 57% market share in terms of industry production in Malaysia in 2016 and we expect this to grow further due to sustainable domestic demand, restrictions on steel imports and the temporary absence of competitor Megasteel from the supply equation. Megasteel is unlikely to resume operations in the near future due to the lack of funding. Four key drivers of earnings growth We forecast a two-year earnings CAGR of 15% (FY18-19), fuelled by: (1) recovering steel demand in various key industries in Malaysia; (2) a supply gap to fill, amid the absence of Megasteel’s output and less cheap imported steel available since the imposition of anti-dumping duties last year; (3) a favourable CRC steel price outlook, translating to higher ASP for CSC of MYR2,349/2,494/MYR2,648 per mt for FY17E-FY19E (vs. estd. MYR2,061 in 2016); (4) a better product mix leading to margins uptick. A big warchest, 4-6% dividend yield CSC has been debt free since 2009 and its MYR195.7m cash on hand (equivalent to 53sen per share) provides CSC with unparalleled flexibility to fund future capacity expansion, and upgrade its plants and equipment to enhance its core competitiveness. Besides this, CSC has strong free cash flow that can cover an average of 2x its dividend payout. Share Price MYR 1.72 12m Price Target MYR 2.02 (+17%) BUY Company Description Statistics Shariah status 52w high/low (MYR) 3m avg turnover (USDm) Free float (%) Issued shares (m) Market capitalisation Major shareholders: 45.0% 4.9% 3.2% 380 0.4 CSC Steel Holdings Bhd, through its subsidiaries, manufactures and markets steel and related products. Yes China Steel Corp. Lembaga Tabung Haji TAN KIT PHENG 2.32/1.44 41.3 MYR653.6M USD152M Price Performance 80 100 120 140 160 180 200 220 240 0.80 1.00 1.20 1.40 1.60 1.80 2.00 2.20 2.40 Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17 CSC Steel - (LHS, MYR) CSC Steel / Kuala Lumpur Composite Index - (RHS, %) -1M -3M -12M Absolute (%) (4) (16) 16 Relative to index (%) (5) (16) 11 Source: FactSet FYE Dec (MYR m) FY15A FY16A FY17E FY18E FY19E Revenue 1,017 1,035 1,142 1,237 1,330 EBITDA 96 106 107 119 132 Core net profit 35 69 61 71 81 Core EPS (sen) 9.6 18.6 16.6 19.2 22.1 Core EPS growth (%) nm 94.0 (10.8) 15.7 15.0 Net DPS (sen) 8.0 14.0 8.3 9.6 11.0 Core P/E (x) 18.0 9.3 10.4 9.0 7.8 P/BV (x) 0.8 0.8 0.8 0.7 0.7 Net dividend yield (%) 4.7 8.1 4.8 5.6 6.4 ROAE (%) 6.9 8.7 7.4 8.3 9.1 ROAA (%) 4.4 8.0 6.8 7.5 8.3 EV/EBITDA (x) 1.8 4.9 3.0 2.5 2.0 Net gearing (%) (incl perps) net cash net cash net cash net cash net cash Consensus net profit - - 72 79 83 MKE vs. Consensus (%) - - (14.7) (10.3) (2.0)

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of CSC Steel Holdings (CSCS MK) - Maybank Kim Eng

August 21, 2017

Mate

rials

M

ala

ysi

a

THIS REPORT HAS BEEN PREPARED BY MAYBANK INVESTMENT BANK BERHAD

SEE PAGE 36 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

PP16832/01/2013 (031128)

Mohd Hafiz Hassan [email protected] (603) 2082 6819

CSC Steel Holdings (CSCS MK)

Steeling through the storm

Initiate BUY, TP MYR2.02

CSC is in a strong position within the sector to reap the benefits from the

pick-up in domestic steel demand, and to plug the supply gap. It should

ride the current cyclical recovery in steel prices as the international

supply-demand balance is improving. Valuation is undemanding; it is

trading at below the average of its 5-year historical forward PER of

10.5x. We forecast CSC’s earnings to grow at an annual double-digit pace

(~15% pa) over the next two years (FY18-19). Our TP is based on 10.5x

FY18F EPS. We also like CSC for its net cash position and strong free cash

flow that can reward shareholders with stable dividend payouts.

A big player in carbon coil industry in MY

CSC has maintained a dominant presence in Malaysia’s CRC (carbon cold

rolled coil) steel industry since its inception in the 1990s. CSC had 57%

market share in terms of industry production in Malaysia in 2016 and we

expect this to grow further due to sustainable domestic demand,

restrictions on steel imports and the temporary absence of competitor

Megasteel from the supply equation. Megasteel is unlikely to resume

operations in the near future due to the lack of funding.

Four key drivers of earnings growth

We forecast a two-year earnings CAGR of 15% (FY18-19), fuelled by: (1)

recovering steel demand in various key industries in Malaysia; (2) a

supply gap to fill, amid the absence of Megasteel’s output and less cheap

imported steel available since the imposition of anti-dumping duties last

year; (3) a favourable CRC steel price outlook, translating to higher ASP

for CSC of MYR2,349/2,494/MYR2,648 per mt for FY17E-FY19E (vs. estd.

MYR2,061 in 2016); (4) a better product mix leading to margins uptick.

A big warchest, 4-6% dividend yield

CSC has been debt free since 2009 and its MYR195.7m cash on hand

(equivalent to 53sen per share) provides CSC with unparalleled flexibility

to fund future capacity expansion, and upgrade its plants and equipment

to enhance its core competitiveness. Besides this, CSC has strong free

cash flow that can cover an average of 2x its dividend payout.

Share Price MYR 1.72

12m Price Target MYR 2.02 (+17%)

BUY

Company Description

Statistics

Shariah status

52w high/low (MYR)

3m avg turnover (USDm)

Free float (%)

Issued shares (m)

Market capitalisation

Major shareholders:

45.0%

4.9%

3.2%

380

0.4

CSC Steel Holdings Bhd, through its subsidiaries,

manufactures and markets steel and related

products.

Yes

China Steel Corp.

Lembaga Tabung Haji

TAN KIT PHENG

2.32/1.44

41.3

MYR653.6M

USD152M

Price Performance

80

100

120

140

160

180

200

220

240

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17

CSC Steel - (LHS, MYR) CSC Steel / Kuala Lumpur Composite Index - (RHS, %)

-1M -3M -12M

Absolute (%) (4) (16) 16

Relative to index (%) (5) (16) 11

Source: FactSet

FYE Dec (MYR m) FY15A FY16A FY17E FY18E FY19E

Revenue 1,017 1,035 1,142 1,237 1,330

EBITDA 96 106 107 119 132

Core net profit 35 69 61 71 81

Core EPS (sen) 9.6 18.6 16.6 19.2 22.1

Core EPS growth (%) nm 94.0 (10.8) 15.7 15.0

Net DPS (sen) 8.0 14.0 8.3 9.6 11.0

Core P/E (x) 18.0 9.3 10.4 9.0 7.8

P/BV (x) 0.8 0.8 0.8 0.7 0.7

Net dividend yield (%) 4.7 8.1 4.8 5.6 6.4

ROAE (%) 6.9 8.7 7.4 8.3 9.1

ROAA (%) 4.4 8.0 6.8 7.5 8.3

EV/EBITDA (x) 1.8 4.9 3.0 2.5 2.0

Net gearing (%) (incl perps) net cash net cash net cash net cash net cash

Consensus net profit - - 72 79 83

MKE vs. Consensus (%) - - (14.7) (10.3) (2.0)

August 21, 2017 2

CSC Steel Holdings

6.7%

7.6%7.2%

8.0%

8.9%

7.3%

8.3%7.9%

8.8%

9.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

FY15 FY16 FY17E FY18E FY19E

Return on assets Return on equity

0%

2%

4%

6%

8%

10%

12%

0

10

20

30

40

50

60

70

80

90

FY15 FY16 FY17E FY18E FY19E

MYR'm FCF (LHS) Div payout (LHS) Div yield (RHS) FCF yield

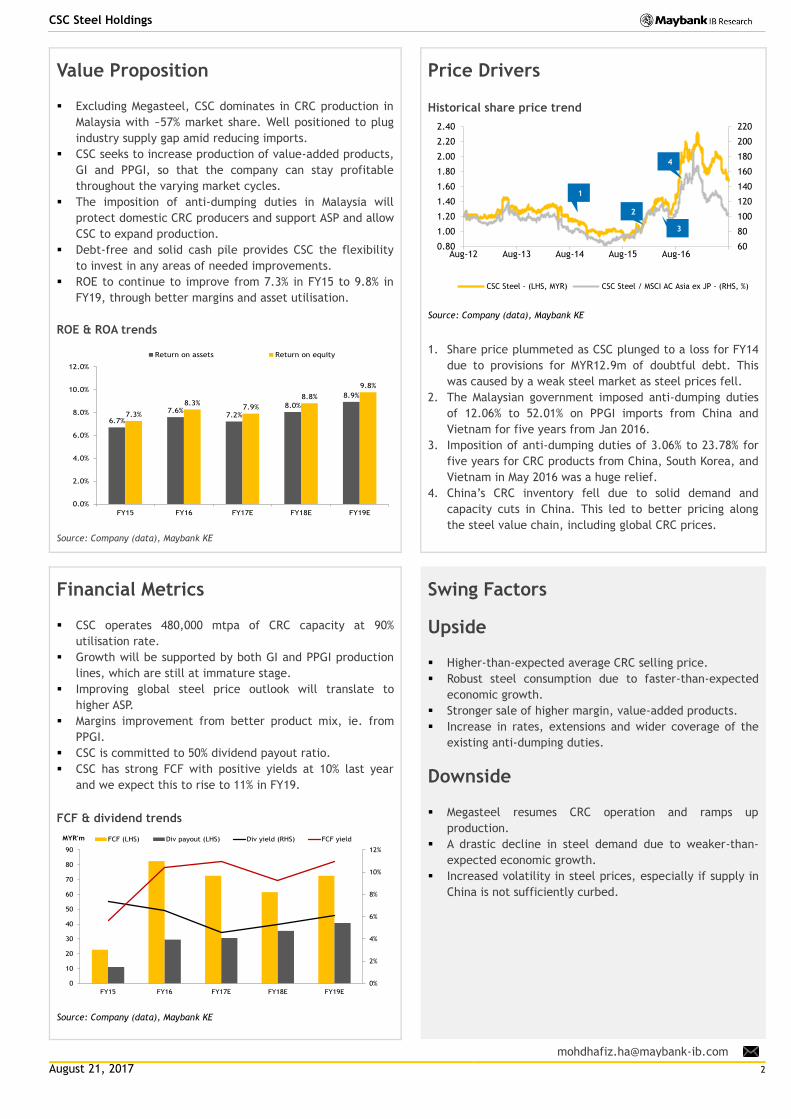

Value Proposition

Excluding Megasteel, CSC dominates in CRC production in

Malaysia with ~57% market share. Well positioned to plug

industry supply gap amid reducing imports.

CSC seeks to increase production of value-added products,

GI and PPGI, so that the company can stay profitable

throughout the varying market cycles.

The imposition of anti-dumping duties in Malaysia will

protect domestic CRC producers and support ASP and allow

CSC to expand production.

Debt-free and solid cash pile provides CSC the flexibility

to invest in any areas of needed improvements.

ROE to continue to improve from 7.3% in FY15 to 9.8% in

FY19, through better margins and asset utilisation.

ROE & ROA trends

Source: Company (data), Maybank KE

Price Drivers

Historical share price trend

Source: Company (data), Maybank KE

1. Share price plummeted as CSC plunged to a loss for FY14

due to provisions for MYR12.9m of doubtful debt. This

was caused by a weak steel market as steel prices fell.

2. The Malaysian government imposed anti-dumping duties

of 12.06% to 52.01% on PPGI imports from China and

Vietnam for five years from Jan 2016.

3. Imposition of anti-dumping duties of 3.06% to 23.78% for

five years for CRC products from China, South Korea, and

Vietnam in May 2016 was a huge relief.

4. China’s CRC inventory fell due to solid demand and

capacity cuts in China. This led to better pricing along

the steel value chain, including global CRC prices.

Financial Metrics

CSC operates 480,000 mtpa of CRC capacity at 90%

utilisation rate.

Growth will be supported by both GI and PPGI production

lines, which are still at immature stage.

Improving global steel price outlook will translate to

higher ASP.

Margins improvement from better product mix, ie. from

PPGI.

CSC is committed to 50% dividend payout ratio.

CSC has strong FCF with positive yields at 10% last year

and we expect this to rise to 11% in FY19.

FCF & dividend trends

Source: Company (data), Maybank KE

Swing Factors

Upside

Higher-than-expected average CRC selling price.

Robust steel consumption due to faster-than-expected

economic growth.

Stronger sale of higher margin, value-added products.

Increase in rates, extensions and wider coverage of the

existing anti-dumping duties.

Downside

Megasteel resumes CRC operation and ramps up

production.

A drastic decline in steel demand due to weaker-than-

expected economic growth.

Increased volatility in steel prices, especially if supply in

China is not sufficiently curbed.

60

80

100

120

140

160

180

200

220

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

CSC Steel - (LHS, MYR) CSC Steel / MSCI AC Asia ex JP - (RHS, %)

1

1

2

3

4

August 21, 2017 3

CSC Steel Holdings

Table of Contents

1. Investment thesis .................................................................................................................... 4

2. Focus Charts .......................................................................................................................... 6

3. Corporate Information .............................................................................................................. 7

4. Moving up the value chain .......................................................................................................... 10

5. Plugging the growth and supply gaps ............................................................................................. 10

6. Better pricing will improve bottomline .......................................................................................... 15

7. Protection from the Malaysian government ..................................................................................... 18

8. Financial analysis .................................................................................................................... 19

9. Valuations ............................................................................................................................. 23

10. Risks .................................................................................................................................... 27

11. Appendix ............................................................................................................................... 28

August 21, 2017 4

CSC Steel Holdings

Investment thesis

In a strong position for higher production

CSC has maintained a dominant presence in Malaysia’s CRC (carbon cold rolled

coil) industry. It has 45% share of the country’s 1.06m mtpa of active installed

production capacity. If including Megasteel’s 1.45m mtpa capacity, which ceased

operations in 2016, CSC would have 19.1% share of Malaysia’s total installed

capacity. In terms of production, CSC’s share is bigger, at 57% (Fig 1). With plant

capacity of 480,000 mtpa, CSC has made inroads into the CRC market over the

past three years. This was despite a lacklustre domestic steel market and

increase in CRC imports. All the while, competitors’ output was relatively

stagnant. CSC is in a strong position to capture a greater share of production and

to plug the supply gap as the market had been reliant on imported CRC. Imports

of CRC peaked at 1.10m mt in 2015 to fill the supply gap between net production

(excluding exports) of 502,000 mtpa and domestic consumption of 1.6m mtpa.

Moving up the value chain

CSC is moving up the value chain into galvanized iron (GI) and pre-painted

galvanized iron (PPGI) products to diversify its revenue sources and to improve

margins. There is ample room for CSC’s GI and PPGI production to grow as

utilisation rates are still low at 68% and 58% respectively. These products are

priced at a premium to conventional CRC products. This will help CSC to boost

margins. CSC’s revenue has been relatively stable in recent years despite the

decline in (hot rolled coil) HRC and CRC prices in China. Even more surprising,

CSC’s core net profit margin expanded from a low of 1.7% in FY11 to 2.4% in FY15

during turbulent times for steel prices.

Sustainability of domestic demand

The latest reading of Malaysia’s index of leading economic indicators shows a

positive trend after the better-than-expected 1Q17 GDP, signalling sustainable

momentum in economic activities. This should bode well for steel consumption,

and we believe CSC’s CRC will be mostly supplied to domestic industries. We

expect CSC to benefit from sustained/increasing orders from downstream

manufacturers in various steel-consuming sectors. Taking the improved outlook

into consideration, we expect CSC to increase CRC production to approximately

434,000/442,000/451,000 mtpa at capacity utilisation rates of 91%/92%/94% in

FY17E/FY18E/FY19E from 432,000 mt in FY16. Growth rates of CRC production

are approximately 1.8-2% pa.

Better pricing will improve bottomline

A silver lining for the sector has been the recovery in the ASP of CRC, led by a

broad-base upturn in China steel prices, which serve as the benchmark for

international steel prices. This ASP recovery has been due to the improvement in

China’s macro data recently and the government’s effort to curb steel

overcapacity. All these point to stronger CRC demand and ASP outlook. The price

of CRC globally was under stress in recent years due to supply imbalances caused

by dumping by China, which in turn led to oversupply in the international steel

market. We expect further improvement in the steel supply-demand balance in

the international market will help to stimulate CRC prices globally. We forecast

CSC’s CRC ASP to be MYR2,349/MYR2,494/MYR2,648 per mt for FY17E-FY19E, vs

an estimated average of MYR2,061 per mt in FY16.

Excluding Megasteel, CSC’s market share by installed capacity

Source: Companies, MISIF

45%

25%

19%

11%

CSC Steel Bhd

Mycron Steel Bhd

YKGI Bhd

Eonmetall Group

August 21, 2017 5

CSC Steel Holdings

Protection from the Malaysian government

The Malaysian government too has played its part by imposing trade protection

measures against CRC imports from China, South Korea and Vietnam. In May 2016,

the government introduced anti-dumping duties ranging from 3.06% to 23.78%.

This measure will last for five years. Domestic steel producers previously had to

contend with the dumping of China’s excess steel production into the Malaysian

market. The anti-dumping duties should therefore offer some relief to CRC

producers in Malaysia, who have endured years of low selling prices and margins.

We understand that this action has helped to stabilise the domestic price of CRC.

CSC’s FY16 core net profit margin, after stripping out forex effect, increased

substantially to 5.5% from 2.4% in FY15. This was also helped by the recovery in

steel prices. The full positive impact of the duties would be felt from this year

and the next three years.

Initiate BUY, TP MYR2.02

CSC is in a strong position within the sector to reap the benefits from the pick-up

in domestic steel demand, and to plug the supply gap. CSC should ride well on

the current cyclical recovery in steel prices as the international supply-demand

balance is improving. Having seen its share price losing its fizz of late, valuation

is now undemanding. It’s trading at below the average of its 5-year historical

forward PER of 10.5x. We forecast CSC’s earnings to grow at a double-digit pace

(~15% pa) over the next two years (FY18-19). Initiate BUY with a TP of MYR2.02,

based on 10.5x FY18F EPS. We also like CSC for its net cash position and strong

free cash flow that can reward shareholders with stable dividend payouts.

August 21, 2017 6

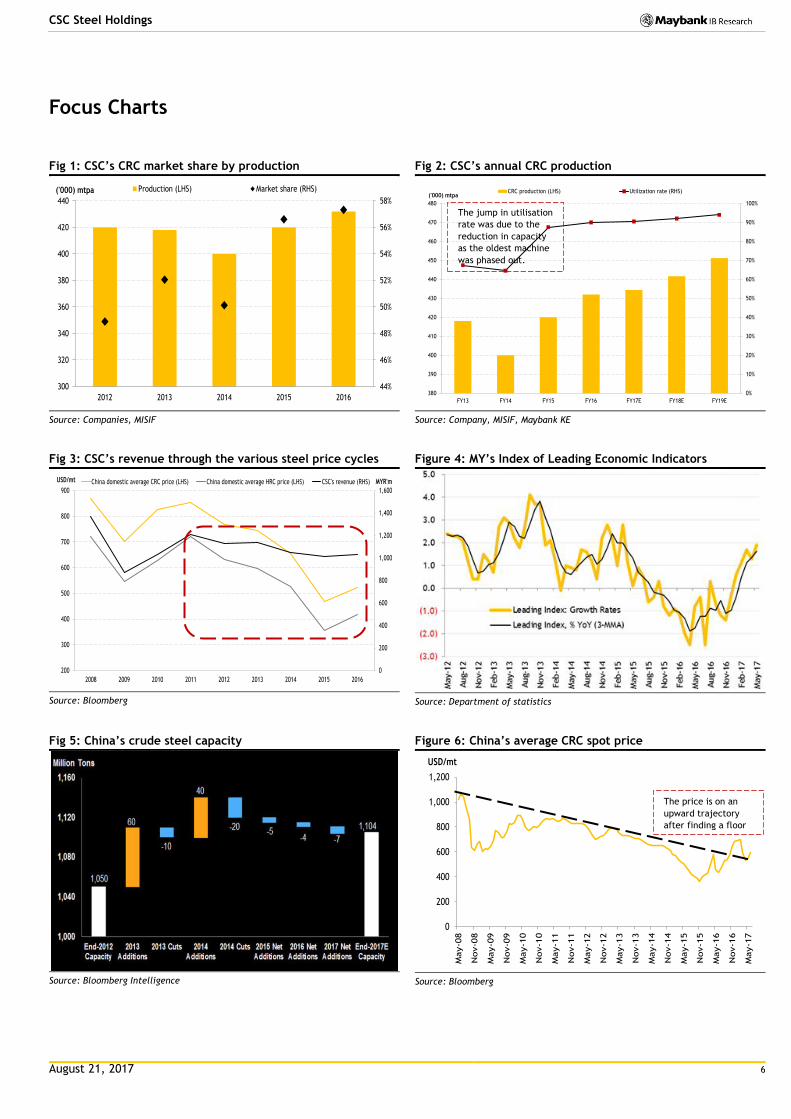

CSC Steel Holdings

Focus Charts

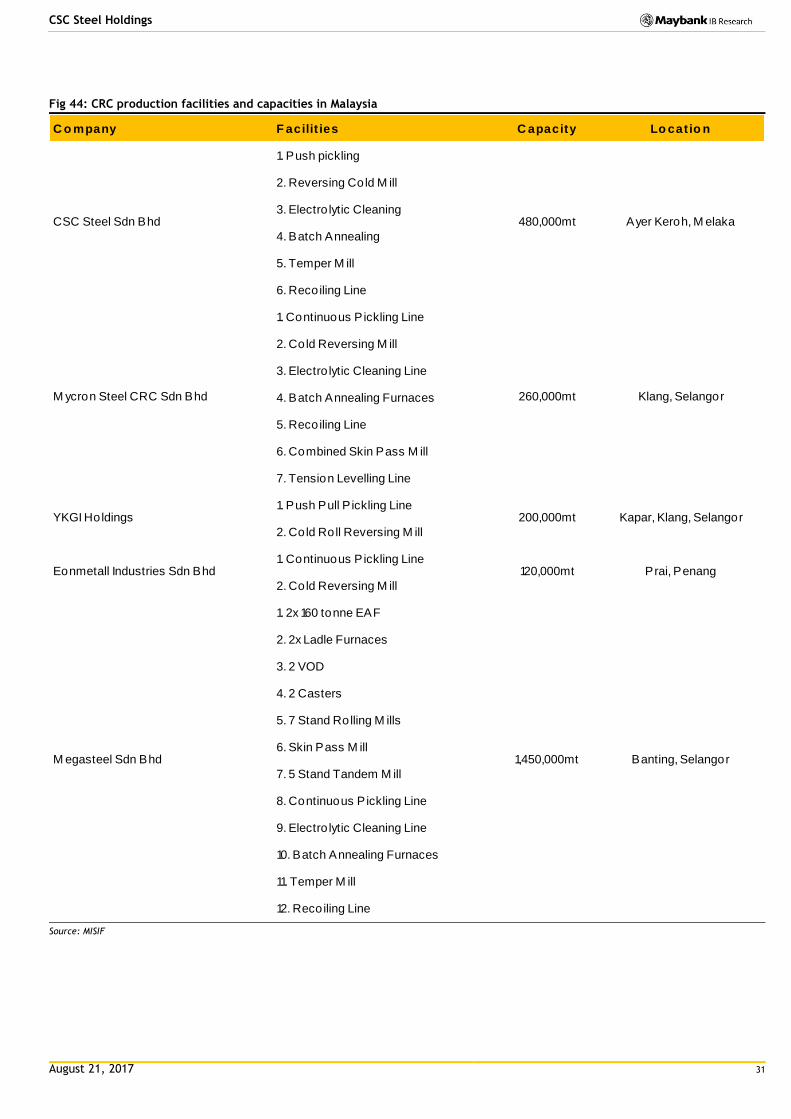

Fig 1: CSC’s CRC market share by production

Source: Companies, MISIF

Fig 2: CSC’s annual CRC production

Source: Company, MISIF, Maybank KE

Fig 3: CSC’s revenue through the various steel price cycles

Source: Bloomberg

Figure 4: MY’s Index of Leading Economic Indicators

Source: Department of statistics

Fig 5: China’s crude steel capacity

Source: Bloomberg Intelligence

Figure 6: China’s average CRC spot price

Source: Bloomberg

44%

46%

48%

50%

52%

54%

56%

58%

300

320

340

360

380

400

420

440

2012 2013 2014 2015 2016

('000) mtpa Production (LHS) Market share (RHS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

380

390

400

410

420

430

440

450

460

470

480

FY13 FY14 FY15 FY16 FY17E FY18E FY19E

('000) mtpaCRC production (LHS) Utilization rate (RHS)

0

200

400

600

800

1,000

1,200

1,400

1,600

200

300

400

500

600

700

800

900

2008 2009 2010 2011 2012 2013 2014 2015 2016

MYR'mUSD/mt China domestic average CRC price (LHS) China domestic average HRC price (LHS) CSC's revenue (RHS)

0

200

400

600

800

1,000

1,200

May-0

8

Nov-0

8

May-0

9

Nov-0

9

May-1

0

Nov-1

0

May-1

1

Nov-1

1

May-1

2

Nov-1

2

May-1

3

Nov-1

3

May-1

4

Nov-1

4

May-1

5

Nov-1

5

May-1

6

Nov-1

6

May-1

7

USD/mt

The jump in utilisation

rate was due to the

reduction in capacity

as the oldest machine

was phased out.

The price is on an

upward trajectory

after finding a floor

August 21, 2017 7

CSC Steel Holdings

Corporate Information

The market leader

CSC Steel Holdings Bhd, previously known as Ornasteel Holdings Bhd, was listed

on the main board of Bursa Malaysia on 30 Dec 2004. CSC is a mid-stream player

in the steel value chain. CSC has the capacity to produce 480,000 mt of CRC steel

pa (inclusive of 40,000 mtpa of pickled and oiled steel). CSC also has the

capacity to produce 240,000 mt of GI and 120,000 mt of PPGI steel annually.

If we exclude Megasteel, CSC is the largest manufacturer of CRC in Malaysia by

installed capacity with 45% market share. In terms of production, CSC has 57%

market share.

Megasteel’s flat steel products plant in Selangor was shut down in 2016 due to its

dire financial condition as it had accumulated losses of MYR2.4b as at FY15 and it

defaulted on a banker’s acceptance payment. The situation was exacerbated by

the fact that no fresh orders were coming in. We believe Megasteel will not be

able to resume production in the near future due to the lack of capital.

Room for further market share gains

CSC’s CRC production dropped to a low of 303,000 mt in 2009 (after peaking at

508,000 mt in 2008) due to the decline in steel prices following the global

financial crisis. Since then, however, CSC’s production has gradually rebounded

and it hit a recent high of 432,000 mt in 2016 (at 90% utilisation rate).

CSC has been on a roll (modest growth of 3-5% pa in production) since

Megasteel’s last output of 50,000mt in 2014 by taking advantage of the

opportunity to fill the supply gap in the industry (Fig 7).

We believe resumption of production by Megasteel in the future (if any) would

not be a threat to CSC’s market share as the former lacks the technical know-

how. In fact, Megasteel had experienced falling output and over the past five

years to 2014, production was less than 5% of its huge capacity.

Fig 7: Production of CRC in Malaysia

Source: Company, MISIF

60

50

25

25

25

110

105

120

110

110

204

180

203

187

187

420

418

400

420

432

65

50

50

0

0

0 100 200 300 400 500 600 700 800 900 1,000

2012

2013

2014

2015

2016

('000) mt/y

Eonmetall Group Bhd YKGI Bhd Mycron Steel Bhd CSC Steel Bhd Megasteel Sdn Bhd

August 21, 2017 8

CSC Steel Holdings

CSC’s position has also strengthened over the past three years despite the

lacklustre domestic steel market and increase in CRC imports while its

competitors’ output has been relatively constant. Therefore, we think CSC is in a

strong position to capture a bigger share of production to plug the supply gap as

the market had been reliant on imported CRC.

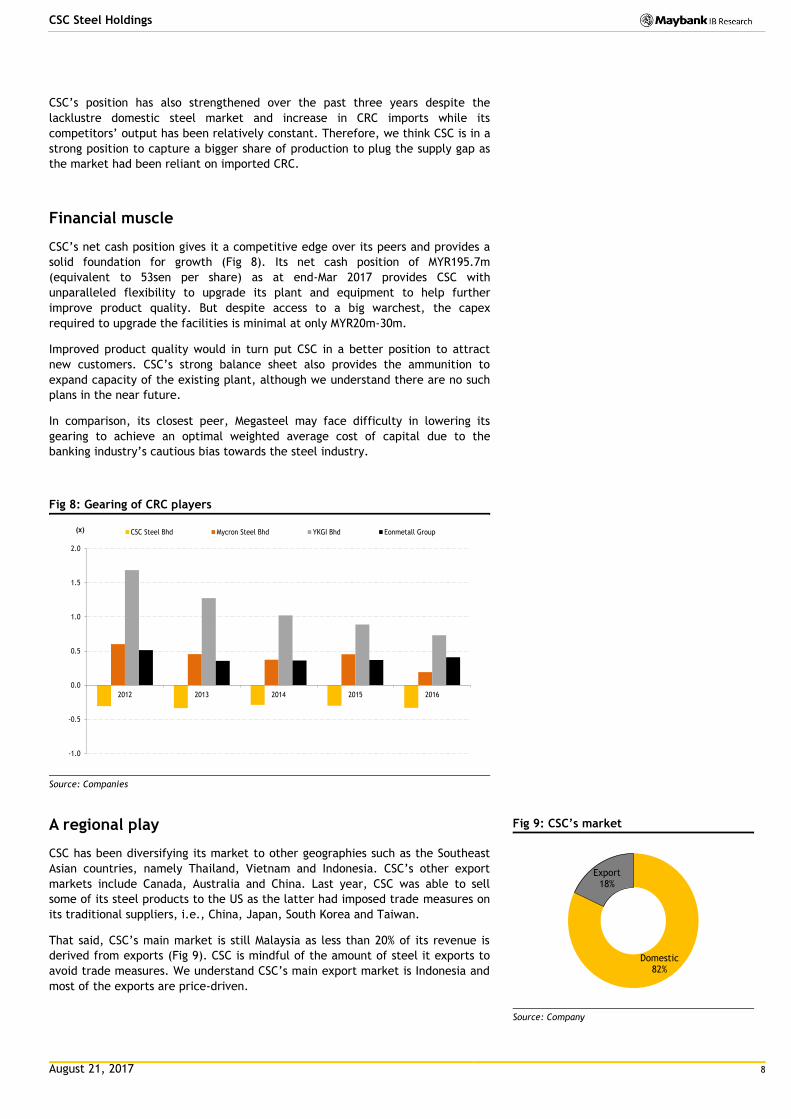

Financial muscle

CSC’s net cash position gives it a competitive edge over its peers and provides a

solid foundation for growth (Fig 8). Its net cash position of MYR195.7m

(equivalent to 53sen per share) as at end-Mar 2017 provides CSC with

unparalleled flexibility to upgrade its plant and equipment to help further

improve product quality. But despite access to a big warchest, the capex

required to upgrade the facilities is minimal at only MYR20m-30m.

Improved product quality would in turn put CSC in a better position to attract

new customers. CSC’s strong balance sheet also provides the ammunition to

expand capacity of the existing plant, although we understand there are no such

plans in the near future.

In comparison, its closest peer, Megasteel may face difficulty in lowering its

gearing to achieve an optimal weighted average cost of capital due to the

banking industry’s cautious bias towards the steel industry.

Fig 8: Gearing of CRC players

Source: Companies

A regional play

CSC has been diversifying its market to other geographies such as the Southeast

Asian countries, namely Thailand, Vietnam and Indonesia. CSC’s other export

markets include Canada, Australia and China. Last year, CSC was able to sell

some of its steel products to the US as the latter had imposed trade measures on

its traditional suppliers, i.e., China, Japan, South Korea and Taiwan.

That said, CSC’s main market is still Malaysia as less than 20% of its revenue is

derived from exports (Fig 9). CSC is mindful of the amount of steel it exports to

avoid trade measures. We understand CSC’s main export market is Indonesia and

most of the exports are price-driven.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2012 2013 2014 2015 2016

(x) CSC Steel Bhd Mycron Steel Bhd YKGI Bhd Eonmetall Group

Fig 9: CSC’s market

Source: Company

Domestic82%

Export18%

August 21, 2017 9

CSC Steel Holdings

Reliable raw material source is imperative

About 84% of CSC’s cost of goods sold comprises of raw materials, of which 80-

95% is hot rolled coil (HRC), zinc and paint, which are denominated in USD. HRC

is mainly supplied by its parent company, CSC of Taiwan, and a related company,

CSGT Metals Vietnam Joint Stock Company (CSMV) in Vietnam (a joint

venture of six shareholders, inclusive CSC of Taiwan and CSC of Malaysia) .

We understand that there is no transfer pricing by them.

Having support from its parent and a related company has major advantages,

such as: (i) an uninterrupted source of raw material supply; and (ii) cost savings

on logistics through bulk procurement from Vietnam. That said, the savings might

not be significant as the cost makes up less than 10% of total cost of goods sold.

Megasteel was previously the only HRC producer in Malaysia. But as Megasteel

has suspended production of HRC, Malaysian CRC producers will struggle to find a

reliable supplier, hence affecting output. Based on our channel checks, however,

CSC does not have a price advantage over the other CRC producers in terms of

HRC supply after taking into account the logistics costs and forex impact.

In terms of net forex impact, CSC’s net profit is exposed to 55-60% in the

movement of the USD. Based on our sensitivity analysis, every 3% appreciation in

the USD vs MYR would reduce our net profit estimate by 1.3-2% for FY17E-FY19E.

August 21, 2017 10

CSC Steel Holdings

Moving up the value chain

Value-added product mix through the cycle

Much of CSC’s focus has been centred on increasing contributions from GI and

PPGI steel products as these have higher margins. It has been a gradual and

flexible process subject to the market situation. Almost two-thirds of CSC’s

revenue last year comprised of valued-added steel products, namely GI and PPGI

(Fig 10).

As CSC produces CRC, this gives it the flexibility to rapidly change its product mix

as CRC is the feedstock for GI and PPGI. In addition, CSC has ample room to

increase GI and PPGI output as it’s operating at only 68% and 58% utilisation rate,

respectively.

Figure 10: CSC’s revenue breakdown

Source: Source: Company, Maybank KE

Fig 11: Revenue through the various steel price cycles

Source: Company, Bloomberg

As steel producers’ revenues are naturally vulnerable to fluctuations in steel

prices, CSC’s strategy has been to move up the value chain to diversify its

revenue sources and to improve profit margins.

These products are priced at a premium to the conventional CRC products as

they provide better corrosion protection. This strategy has been successful in

maintaining revenue stability for CSC throughout the various steel price cycles,

and even during the difficult pricing environment in 2011-2014.

CSC’s revenue has been relatively stable in recent years despite the decline in

HRC and CRC prices in China (Fig 11). This may be partly due to the higher ASP of

its GI and PPGI steel, even though production volume is relatively small

compared to its CRC output. Its core net profit margin also expanded from a low

of 1.7% in FY11 to 2.4% in FY15 during market turbulence when steel prices faced

downward pressure.

For every 3% decline in CSC’s PPGI steel ASP from our base-case price, assuming

other things remain constant, this would reduce our core net profit estimates by

8-9% for FY17E-FY19E.

468.2 474.3435.4 422.5 430.0

470.7 493.8530.6

401.8 407.0

373.4362.4 369.0

421.0

469.6

506.4

257.1 260.4

239.0232.0 236.1

250.7

273.3

293.0

0

200

400

600

800

1,000

1,200

1,400

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

MYR'm Cold rolled coil (CRC) Hot-dipped galvanized (GI) Pre-painted galvanized (PPGI)

0

200

400

600

800

1,000

1,200

1,400

1,600

200

300

400

500

600

700

800

900

2008 2009 2010 2011 2012 2013 2014 2015 2016

MYR'mUSD/mt China domestic average CRC price (LHS) China domestic average HRC price (LHS) CSC's revenue (RHS)

August 21, 2017 11

CSC Steel Holdings

Plugging the growth and supply gaps

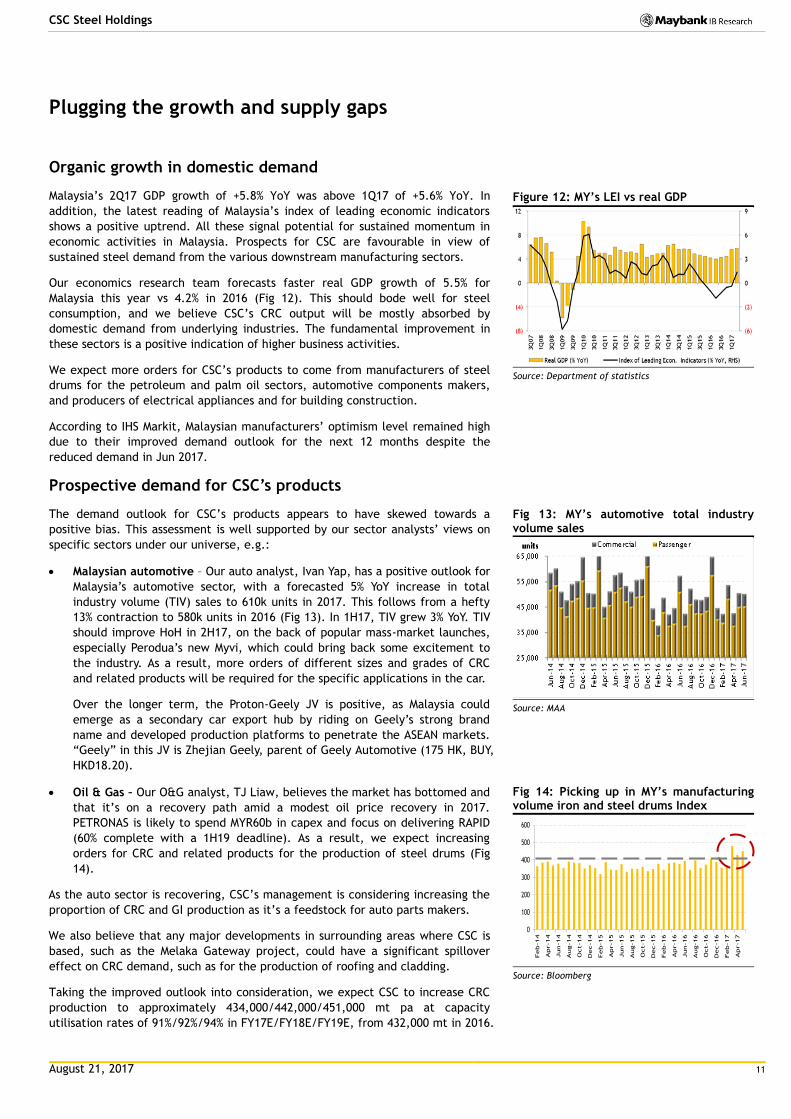

Organic growth in domestic demand

Malaysia’s 2Q17 GDP growth of +5.8% YoY was above 1Q17 of +5.6% YoY. In

addition, the latest reading of Malaysia’s index of leading economic indicators

shows a positive uptrend. All these signal potential for sustained momentum in

economic activities in Malaysia. Prospects for CSC are favourable in view of

sustained steel demand from the various downstream manufacturing sectors.

Our economics research team forecasts faster real GDP growth of 5.5% for

Malaysia this year vs 4.2% in 2016 (Fig 12). This should bode well for steel

consumption, and we believe CSC’s CRC output will be mostly absorbed by

domestic demand from underlying industries. The fundamental improvement in

these sectors is a positive indication of higher business activities.

We expect more orders for CSC’s products to come from manufacturers of steel

drums for the petroleum and palm oil sectors, automotive components makers,

and producers of electrical appliances and for building construction.

According to IHS Markit, Malaysian manufacturers’ optimism level remained high

due to their improved demand outlook for the next 12 months despite the

reduced demand in Jun 2017.

Prospective demand for CSC’s products

The demand outlook for CSC’s products appears to have skewed towards a

positive bias. This assessment is well supported by our sector analysts’ views on

specific sectors under our universe, e.g.:

Malaysian automotive – Our auto analyst, Ivan Yap, has a positive outlook for

Malaysia’s automotive sector, with a forecasted 5% YoY increase in total

industry volume (TIV) sales to 610k units in 2017. This follows from a hefty

13% contraction to 580k units in 2016 (Fig 13). In 1H17, TIV grew 3% YoY. TIV

should improve HoH in 2H17, on the back of popular mass-market launches,

especially Perodua’s new Myvi, which could bring back some excitement to

the industry. As a result, more orders of different sizes and grades of CRC

and related products will be required for the specific applications in the car.

Over the longer term, the Proton-Geely JV is positive, as Malaysia could

emerge as a secondary car export hub by riding on Geely’s strong brand

name and developed production platforms to penetrate the ASEAN markets.

“Geely” in this JV is Zhejian Geely, parent of Geely Automotive (175 HK, BUY,

HKD18.20).

Oil & Gas – Our O&G analyst, TJ Liaw, believes the market has bottomed and

that it’s on a recovery path amid a modest oil price recovery in 2017.

PETRONAS is likely to spend MYR60b in capex and focus on delivering RAPID

(60% complete with a 1H19 deadline). As a result, we expect increasing

orders for CRC and related products for the production of steel drums (Fig

14).

As the auto sector is recovering, CSC’s management is considering increasing the

proportion of CRC and GI production as it’s a feedstock for auto parts makers.

We also believe that any major developments in surrounding areas where CSC is

based, such as the Melaka Gateway project, could have a significant spillover

effect on CRC demand, such as for the production of roofing and cladding.

Taking the improved outlook into consideration, we expect CSC to increase CRC

production to approximately 434,000/442,000/451,000 mt pa at capacity

utilisation rates of 91%/92%/94% in FY17E/FY18E/FY19E, from 432,000 mt in 2016.

Figure 12: MY’s LEI vs real GDP

Source: Department of statistics

Fig 13: MY’s automotive total industry volume sales

Source: MAA

Fig 14: Picking up in MY’s manufacturing volume iron and steel drums Index

Source: Bloomberg

0

100

200

300

400

500

600

Feb-14

Apr-14

Jun-14

Aug-14

Oct-14

Dec-14

Feb-15

Apr-15

Jun-15

Aug-15

Oct-15

Dec-15

Feb-16

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

August 21, 2017 12

CSC Steel Holdings

Growth rates of CSC’s CRC production are approximately 1.8-2% pa. Although

room for growth in CRC output is limited as capacity maxes out at near 100%,

CSC’s revenue growth will be supported by the increase in GI and PPGI

production. CSC has considerable upside in GI and PPGI output as it’s still

operating at only 60-70% capacity utilisation given CSC is still exploring these two

product areas. Revenue contributions from CRC should gradually decline (Fig 15).

CSC’s principal markets

CSC sells its products to downstream manufacturers and service centres. As such,

demand is dependent on the growth of the manufacturing industries (Fig 16),

which are directly linked to the health of both the domestic and global economy.

CSC’s products are mainly sold to the following principle domestic markets:

Fig 16: Principal markets for CSC’s products

Product Principle market Application

CRC

Service centres Cutting, slitting, pressing and shaping of CRC for manufacturers of household products and industrial items

Drum makers Mainly for the manufacturing of drums for storage of palm oil, chemicals and petroleum products

Manufacturers Manufacturing of furniture, electronic and/or electrical home appliances and automobile parts

Pipe and tube makers Most of the pipe tube makers manufacture furniture for the export market

GI and PPGI Manufacturers Manufacturing of roofing sheets, steel truss, steel trunks and air ducts

Source: Company

Major customers will continue to support demand

The group has many long-established customers, with relationships dating back

over 15 years. These customers have contributed significantly to the group over

the years and some of them are public listed companies on Bursa Malaysia. We

understand that the group’s top 10 customers contribute not less than 30% of

group revenue.

Low capacity utilisation – supply availability

Like most other steel products in Malaysia, CSC’s CRC is meant primarily for

domestic consumption with only small quantities exported. There are only five

local producers of CRC sheets, namely CSC, Mycron Steel, YKGI Holdings,

Eonmetall Group and Megasteel, which have a combined capacity of 2.75m mtpa.

The production of CRC in Malaysia was reasonably steady at above 800,000 mt

before declining substantially to 742,000 mt in 2015, with utilisation rate of only

29.6% (Fig 17). This was primarily due to the suspension of output from Megasteel

as it had received no fresh orders for two years.

Based on our channel checks, CRC production in 2016 grew slightly to 754,000mt

with capacity utilisation of 30% (including Megasteel’s capacity) owing to higher

production by CSC. If we exclude Megasteel from the statistics due to the

temporary suspension of its operation last year, the industry’s capacity

utilisation was still low at only 71.1%.

Fig 15: Products’ contribution to revenue

Source: Company, Maybank KE

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY15 FY16 FY17E FY18E FY19E

CRC GI PPGI

August 21, 2017 13

CSC Steel Holdings

Fig 17: CRC production in Malaysia

Source: MISIF

Despite Malaysia’s large installed capacity of CRC, it still needs to import other

grades and qualities of CRC that are not readily available locally. As CSC and a

few other producers have been continuously upgrading their plants, we expect

their production quality to move towards higher grades to meet the local demand.

We understand the domestic market has also been overwhelmed by the influx of

cheaper imports of “boron-added” steel products. These imported products are

of a lower quality and they are used by downstream manufacturers mostly in the

steel tube and furniture sectors.

Imports of CRC peaked at 1.10m mt in 2015 to fill the supply gap between net

production (excluding exports) of 502,000 mtpa and domestic consumption of

1.6m mtpa (Fig 18). The imposition of anti-dumping duties for CRC in mid-2016

should reduce the inflow of these low-priced steel materials into the market and

help to improve the utilisation rate of domestic players.

Fig 18: Production vs consumption, exports vs imports of CRC

Source: MISIF

28%

29%

29%

30%

30%

31%

31%

32%

32%

680

700

720

740

760

780

800

820

840

860

880

2011 2012 2013 2014 2015

('000) mt CRC production (LHS) Capacity utilisation (RHS)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2011 2012 2013 2014 2015

('000) mt Production Import Export Consumption

Supply and demand gap

August 21, 2017 14

CSC Steel Holdings

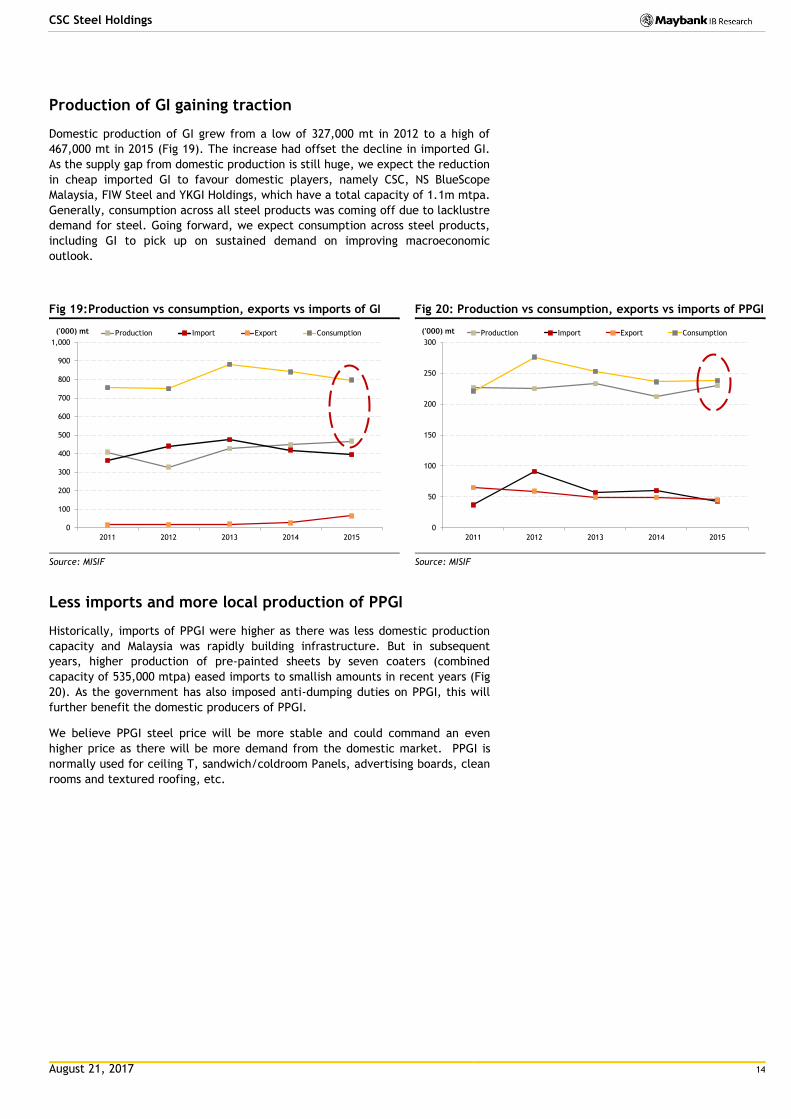

Production of GI gaining traction

Domestic production of GI grew from a low of 327,000 mt in 2012 to a high of

467,000 mt in 2015 (Fig 19). The increase had offset the decline in imported GI.

As the supply gap from domestic production is still huge, we expect the reduction

in cheap imported GI to favour domestic players, namely CSC, NS BlueScope

Malaysia, FIW Steel and YKGI Holdings, which have a total capacity of 1.1m mtpa.

Generally, consumption across all steel products was coming off due to lacklustre

demand for steel. Going forward, we expect consumption across steel products,

including GI to pick up on sustained demand on improving macroeconomic

outlook.

Fig 19: Production vs consumption, exports vs imports of GI

Source: MISIF

Fig 20: Production vs consumption, exports vs imports of PPGI

Source: MISIF

Less imports and more local production of PPGI

Historically, imports of PPGI were higher as there was less domestic production

capacity and Malaysia was rapidly building infrastructure. But in subsequent

years, higher production of pre-painted sheets by seven coaters (combined

capacity of 535,000 mtpa) eased imports to smallish amounts in recent years (Fig

20). As the government has also imposed anti-dumping duties on PPGI, this will

further benefit the domestic producers of PPGI.

We believe PPGI steel price will be more stable and could command an even

higher price as there will be more demand from the domestic market. PPGI is

normally used for ceiling T, sandwich/coldroom Panels, advertising boards, clean

rooms and textured roofing, etc.

0

100

200

300

400

500

600

700

800

900

1,000

2011 2012 2013 2014 2015

('000) mt Production Import Export Consumption

0

50

100

150

200

250

300

2011 2012 2013 2014 2015

('000) mt Production Import Export Consumption

August 21, 2017 15

CSC Steel Holdings

Better pricing will improve bottomline

Bright CRC price outlook but road to recovery is gradual

A silver lining for the sector has been recovery in the ASP of CRC, led by an

upturn across the board in steel prices in China, including China’s domestic CRC

spot price last year (Fig 21). Steel prices in China set the benchmark for

international prices, as China is the world’s largest steel exporter.

CRC prices were under stress in recent years around the world due to pricing

imbalances in the steel value chain (upstream-midstream-downstream), caused

by dumping by China, which in turn led to oversupply in the international steel

market. CRC products dumped by China are offered at prices below those in its

own domestic market.

Fig 21: Average CRC spot price in China

*As of end-June 2017

Source: Bloomberg

China’s average CRC spot price fell to a 10-year low of USD362/mt (equivalent to

MYR1,559) in Nov 2015 but recovered thereafter due to the country’s rosier

macro data, which indicated stronger domestic demand. The Caixin

Manufacturing PMI in China – a gauge to track steel demand outlook - rose to 51.7

in February, beating market expectations. As a result, the average CRC spot

price reached a high of USD702/mt in Feb 2017, but softened to USD535/mt in

Apr 2017 due to moderation in demand for steel and insufficient cuts in crude

steel supply.

While the price rally appears to have stalled, we believe this is likely to be only

temporary. June is traditionally a low season in China, and this would have led

traders to cut prices to reduce large inventories (Fig 22 & 23; Steelhome China

CRC – an indicator for China’s steel stockpile activities) that they had actively

stockpiled at higher prices in 1Q17.

0

200

400

600

800

1,000

1,200

May-0

8

Nov-0

8

May-0

9

Nov-0

9

May-1

0

Nov-1

0

May-1

1

Nov-1

1

May-1

2

Nov-1

2

May-1

3

Nov-1

3

May-1

4

Nov-1

4

May-1

5

Nov-1

5

May-1

6

Nov-1

6

May-1

7

USD/mt

The price is on an uptrend after finding a floor as the price outlook hinges on the level of manufacturing activities and the government’s success in cracking down on overcapacity in China.

August 21, 2017 16

CSC Steel Holdings

Fig 22: Steelhome China CRC total inventory

*As of end-June 2017

Source: Bloomberg

Fig 23: Steelhome China HRC total inventory

*As of end-June 2017

Source: Bloomberg

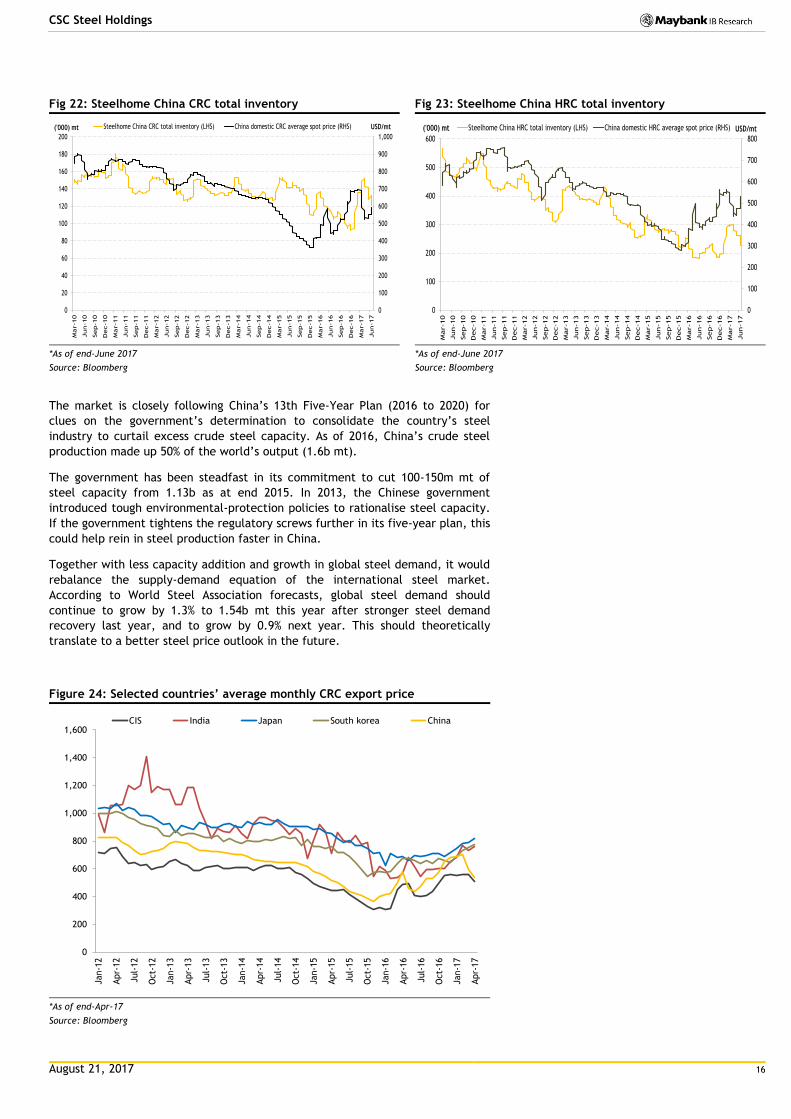

The market is closely following China’s 13th Five-Year Plan (2016 to 2020) for

clues on the government’s determination to consolidate the country’s steel

industry to curtail excess crude steel capacity. As of 2016, China’s crude steel

production made up 50% of the world’s output (1.6b mt).

The government has been steadfast in its commitment to cut 100-150m mt of

steel capacity from 1.13b as at end 2015. In 2013, the Chinese government

introduced tough environmental-protection policies to rationalise steel capacity.

If the government tightens the regulatory screws further in its five-year plan, this

could help rein in steel production faster in China.

Together with less capacity addition and growth in global steel demand, it would

rebalance the supply-demand equation of the international steel market.

According to World Steel Association forecasts, global steel demand should

continue to grow by 1.3% to 1.54b mt this year after stronger steel demand

recovery last year, and to grow by 0.9% next year. This should theoretically

translate to a better steel price outlook in the future.

Figure 24: Selected countries’ average monthly CRC export price

*As of end-Apr-17

Source: Bloomberg

0

100

200

300

400

500

600

700

800

900

1,000

0

20

40

60

80

100

120

140

160

180

200

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

Jun-15

Sep-15

Dec-15

Mar-16

Jun-16

Sep-16

Dec-16

Mar-17

Jun-17

USD/mt('000) mt Steelhome China CRC total inventory (LHS) China domestic CRC average spot price (RHS)

0

100

200

300

400

500

600

700

800

0

100

200

300

400

500

600

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

Jun-15

Sep-15

Dec-15

Mar-16

Jun-16

Sep-16

Dec-16

Mar-17

Jun-17

('000) mt USD/mtSteelhome China HRC total inventory (LHS) China domestic HRC average spot price (RHS)

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

Jan-1

5

Apr-

15

Jul-

15

Oct-

15

Jan-1

6

Apr-

16

Jul-

16

Oct-

16

Jan-1

7

Apr-

17

CIS India Japan South korea China

August 21, 2017 17

CSC Steel Holdings

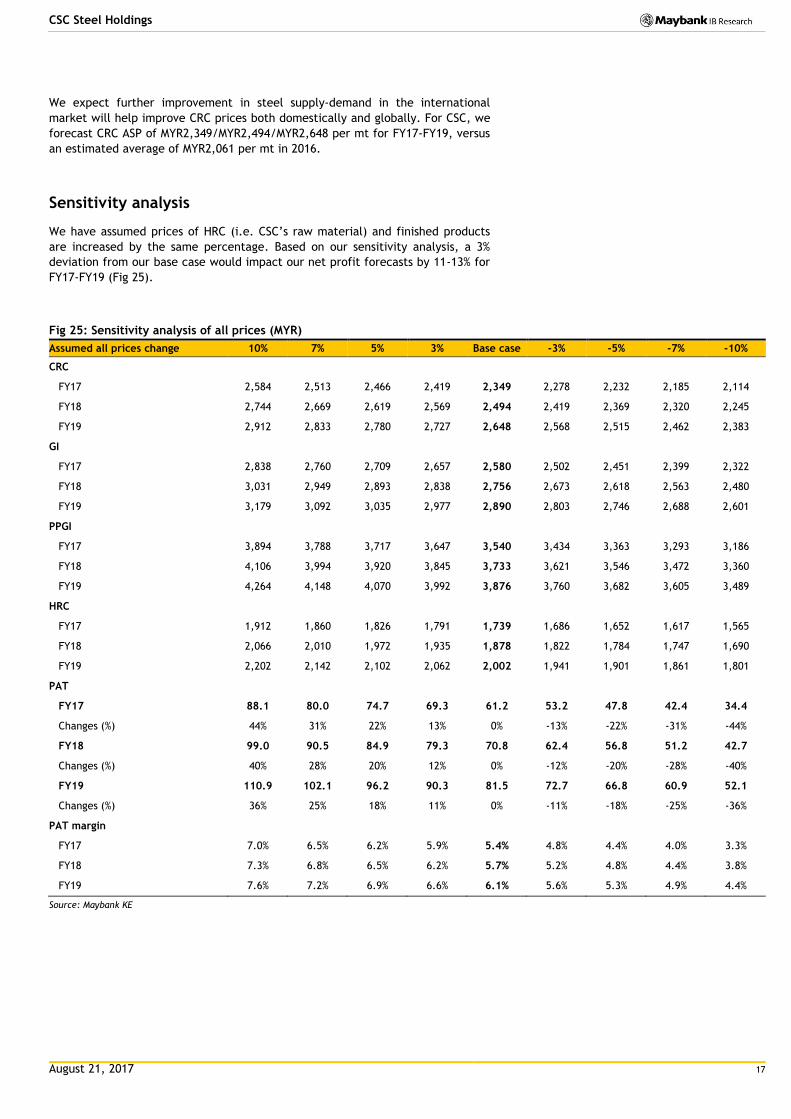

We expect further improvement in steel supply-demand in the international

market will help improve CRC prices both domestically and globally. For CSC, we

forecast CRC ASP of MYR2,349/MYR2,494/MYR2,648 per mt for FY17-FY19, versus

an estimated average of MYR2,061 per mt in 2016.

Sensitivity analysis

We have assumed prices of HRC (i.e. CSC’s raw material) and finished products

are increased by the same percentage. Based on our sensitivity analysis, a 3%

deviation from our base case would impact our net profit forecasts by 11-13% for

FY17-FY19 (Fig 25).

Fig 25: Sensitivity analysis of all prices (MYR)

Assumed all prices change 10% 7% 5% 3% Base case -3% -5% -7% -10%

CRC

FY17 2,584 2,513 2,466 2,419 2,349 2,278 2,232 2,185 2,114

FY18 2,744 2,669 2,619 2,569 2,494 2,419 2,369 2,320 2,245

FY19 2,912 2,833 2,780 2,727 2,648 2,568 2,515 2,462 2,383

GI

FY17 2,838 2,760 2,709 2,657 2,580 2,502 2,451 2,399 2,322

FY18 3,031 2,949 2,893 2,838 2,756 2,673 2,618 2,563 2,480

FY19 3,179 3,092 3,035 2,977 2,890 2,803 2,746 2,688 2,601

PPGI

FY17 3,894 3,788 3,717 3,647 3,540 3,434 3,363 3,293 3,186

FY18 4,106 3,994 3,920 3,845 3,733 3,621 3,546 3,472 3,360

FY19 4,264 4,148 4,070 3,992 3,876 3,760 3,682 3,605 3,489

HRC

FY17 1,912 1,860 1,826 1,791 1,739 1,686 1,652 1,617 1,565

FY18 2,066 2,010 1,972 1,935 1,878 1,822 1,784 1,747 1,690

FY19 2,202 2,142 2,102 2,062 2,002 1,941 1,901 1,861 1,801

PAT

FY17 88.1 80.0 74.7 69.3 61.2 53.2 47.8 42.4 34.4

Changes (%) 44% 31% 22% 13% 0% -13% -22% -31% -44%

FY18 99.0 90.5 84.9 79.3 70.8 62.4 56.8 51.2 42.7

Changes (%) 40% 28% 20% 12% 0% -12% -20% -28% -40%

FY19 110.9 102.1 96.2 90.3 81.5 72.7 66.8 60.9 52.1

Changes (%) 36% 25% 18% 11% 0% -11% -18% -25% -36%

PAT margin

FY17 7.0% 6.5% 6.2% 5.9% 5.4% 4.8% 4.4% 4.0% 3.3%

FY18 7.3% 6.8% 6.5% 6.2% 5.7% 5.2% 4.8% 4.4% 3.8%

FY19 7.6% 7.2% 6.9% 6.6% 6.1% 5.6% 5.3% 4.9% 4.4%

Source: Maybank KE

August 21, 2017 18

CSC Steel Holdings

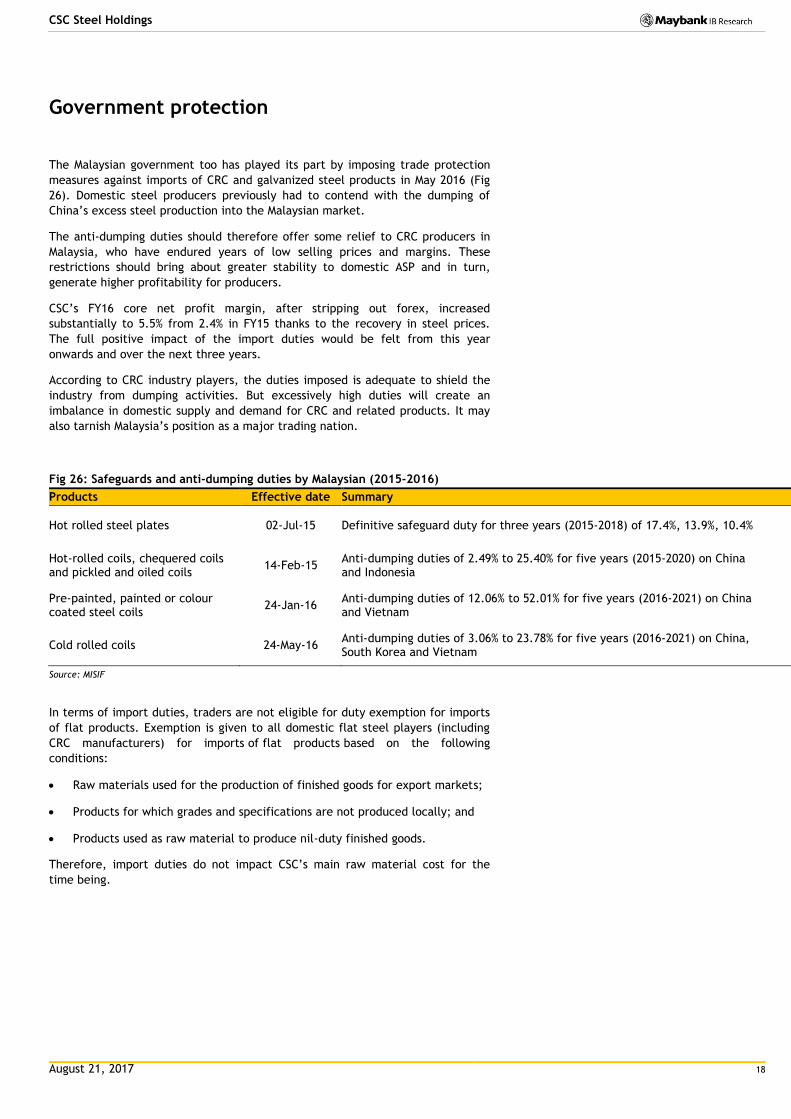

Government protection

The Malaysian government too has played its part by imposing trade protection

measures against imports of CRC and galvanized steel products in May 2016 (Fig

26). Domestic steel producers previously had to contend with the dumping of

China’s excess steel production into the Malaysian market.

The anti-dumping duties should therefore offer some relief to CRC producers in

Malaysia, who have endured years of low selling prices and margins. These

restrictions should bring about greater stability to domestic ASP and in turn,

generate higher profitability for producers.

CSC’s FY16 core net profit margin, after stripping out forex, increased

substantially to 5.5% from 2.4% in FY15 thanks to the recovery in steel prices.

The full positive impact of the import duties would be felt from this year

onwards and over the next three years.

According to CRC industry players, the duties imposed is adequate to shield the

industry from dumping activities. But excessively high duties will create an

imbalance in domestic supply and demand for CRC and related products. It may

also tarnish Malaysia’s position as a major trading nation.

Fig 26: Safeguards and anti-dumping duties by Malaysian (2015-2016)

Products Effective date Summary

Hot rolled steel plates 02-Jul-15 Definitive safeguard duty for three years (2015-2018) of 17.4%, 13.9%, 10.4%

Hot-rolled coils, chequered coils and pickled and oiled coils

14-Feb-15 Anti-dumping duties of 2.49% to 25.40% for five years (2015-2020) on China and Indonesia

Pre-painted, painted or colour coated steel coils

24-Jan-16 Anti-dumping duties of 12.06% to 52.01% for five years (2016-2021) on China and Vietnam

Cold rolled coils 24-May-16 Anti-dumping duties of 3.06% to 23.78% for five years (2016-2021) on China, South Korea and Vietnam

Source: MISIF

In terms of import duties, traders are not eligible for duty exemption for imports

of flat products. Exemption is given to all domestic flat steel players (including

CRC manufacturers) for imports of flat products based on the following

conditions:

Raw materials used for the production of finished goods for export markets;

Products for which grades and specifications are not produced locally; and

Products used as raw material to produce nil-duty finished goods.

Therefore, import duties do not impact CSC’s main raw material cost for the

time being.

August 21, 2017 19

CSC Steel Holdings

Financial analysis

Figure 27: Condensed financial statements

Source: Company, Maybank KE

P&L (Dec yr-end) 2015 2016 2017E 2018E 2019E C/F (Dec yr-end) 2015 2016 2017E 2018E 2019E

Revenue 1,017 1,035 1,142 1,237 1,330 PBT 67 82 81 93 107

CRC 423 430 471 494 531 Depreciation & amortisation 35 33 33 35 36

GI 362 369 421 470 506 Working capital -30 9 -1 -22 -23

PPGI 232 236 251 273 293 Net interest expense -7 -9 0 0 0

COGS -940 -932 -1,027 -1,107 -1,187 Tax paid -9 -18 -19 -22 -26

Gross profit 78 103 115 130 143 Others 1 13 1 1 1

SG&A -39 -45 -47 -50 -51 Operating cash flow 56 109 94 84 95

Other expenses -3 -2 -2 -2 -2 Capex -40 -26 -22 -23 -23

Other income 26 17 7 6 6 Investments 0 -22 0 0 0

EBITDA 96 106 107 119 132 Others 19 6 0 0 0

Depreciation & amortisation -34 -32 -33 -34 -35 Investing cash flow -21 -42 -22 -23 -23

EBIT 62 74 74 85 96 Free cash flow 16 82 73 62 73

Net interest income 7 9 8 10 12 Dividend paid -11 -29 -31 -35 -41

Associates income -2 -1 -1 -1 -1 Net borrowings 0 0 0 0 0

PBT 67 82 81 93 107 Others -3 0 1 0 0

Income tax -15 -13 -19 -22 -26 Financing cash flow -14 -30 -29 -35 -41

PAT 52 69 61 71 81 Net cash flow 21 37 43 26 32

Minority interest 0 0 0 0 0 Beginning 210 231 270 313 339

Core NPAT 35 69 61 71 81 FX 0 1 0 0 0

Ending cash 231 270 313 339 371

B/S (Dec yr-end) 2015 2016 2017E 2018E 2019E

Cash & cash equivalents 231 270 313 339 371 PER SHARE 2015 2016 2017E 2018E 2019E

Receivables 91 89 94 101 109 No.of shares 370 369 369 369 369

Inventories 213 231 231 249 267 EPS 0.10 0.19 0.17 0.19 0.22

Other current assets 40 6 6 6 6 BPS 2.09 2.19 2.28 2.38 2.49

Current assets 576 596 644 696 753 DPS 0.08 0.14 0.08 0.10 0.11

PP&E 227 221 209 197 184 FCF 0.04 0.22 0.20 0.17 0.20

LT investments 9 51 50 49 49

Deferred taxes 0 0 0 0 0 VALUATION 2015 2016 2017E 2018E 2019E

Other assets 18 18 18 17 17 PER (x) 7.8 11.5 10.9 9.4 8.2

Non-current assets 255 290 277 264 250 P / BV (x) 0.5 1.0 0.8 0.8 0.7

Total assets 830 886 921 960 1,003 Dividend yield (%) 7.3 6.5 4.6 5.3 6.1

ST borrowings 0 0 0 0 0 -Payout ratio (%) 83.5% 75.3% 50.0% 50.0% 50.0%

Payables 39 35 38 42 45 P / FCF (x) 17.7 9.6 9.1 10.8 9.1

Other current liabilities 1 22 22 22 22 EV / sales (x) 0.2 0.5 0.3 0.3 0.2

Current liabilities 40 57 60 64 67 EV / EBIT (x) 4.3 7.1 4.8 3.9 3.1

LT borrowings 0 0 0 0 0 EV / EBITDA (x) 2.3 4.9 3.3 2.7 2.2

Deferred taxes 20 20 20 20 20

Non-current liabilities 20 20 20 20 20 BALANCE SHEET 2015 2016 2017E 2018E 2019E

Shareholders' funds 769 809 841 876 917 Receivable days 27 27 27 27 27

Minorities 0 0 0 0 0 Inventory days 85 87 82 82 82

Total stockholders' equity 769 809 841 876 917 Payable days 3 2 2 2 2

Total equity & liabilities 830 886 921 960 1,003 Cash conversion cycle 110 113 107 107 107

Net gearing / (net cash) (%) -30.1% -33.3% -37.2% -38.7% -40.5%

KEY METRICS (Dec yr-end) 2015 2016 2017E 2018E 2019E

Growth (% YoY): DuPont 2015 2016 2017E 2018E 2019E

Revenue -2.9% 1.8% 10.4% 8.3% 7.5% Three-stage

Gross profit 645.8% 32.8% 12.0% 12.7% 10.1% - Net profit margin 5.1% 6.6% 5.4% 5.7% 6.1%

EBIT 91.1% 19.9% -0.5% 14.7% 14.1% - Asset turnover 1.3 1.2 1.3 1.3 1.4

EBITDA 9437.3% 10.5% 0.4% 11.2% 11.0% - Equity multiplier 1.1 1.1 1.1 1.1 1.1

PBT 152.2% 22.9% -1.9% 15.7% 15.0% Five-stage

NPAT 294.4% 93.3% -10.7% 15.7% 15.0% - Tax burden 88.5% 88.5% 88.5% 88.5% 88.5%

EPS 296.2% 94.0% -10.8% 15.7% 15.0% - Interest burden 0 0 0 0 0

- Operating margin 6.0% 7.1% 6.4% 6.8% 7.2%

Margin (%): - Asset turnover 1.3 1.2 1.3 1.3 1.4

Gross 7.6% 10.0% 10.1% 10.5% 10.8% - Equity multiplier 1.1 1.1 1.1 1.1 1.1

EBIT 6.0% 7.1% 6.4% 6.8% 7.2% Return on equity 7.3% 8.3% 7.9% 8.8% 9.8%

EBITDA 9.5% 10.3% 9.3% 9.6% 9.9%

PBT 6.6% 7.9% 7.1% 7.5% 8.1%

NPAT 3.5% 6.6% 5.4% 5.7% 6.1%

August 21, 2017 20

CSC Steel Holdings

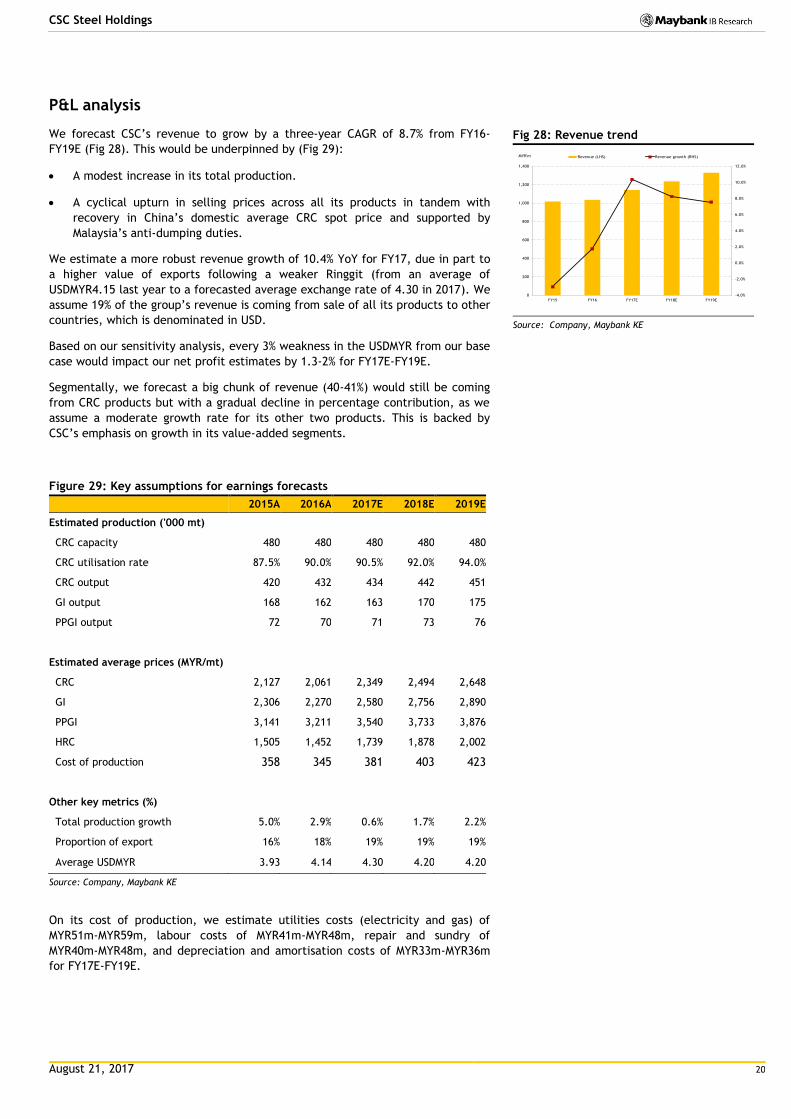

P&L analysis

We forecast CSC’s revenue to grow by a three-year CAGR of 8.7% from FY16-

FY19E (Fig 28). This would be underpinned by (Fig 29):

A modest increase in its total production.

A cyclical upturn in selling prices across all its products in tandem with

recovery in China’s domestic average CRC spot price and supported by

Malaysia’s anti-dumping duties.

We estimate a more robust revenue growth of 10.4% YoY for FY17, due in part to

a higher value of exports following a weaker Ringgit (from an average of

USDMYR4.15 last year to a forecasted average exchange rate of 4.30 in 2017). We

assume 19% of the group’s revenue is coming from sale of all its products to other

countries, which is denominated in USD.

Based on our sensitivity analysis, every 3% weakness in the USDMYR from our base

case would impact our net profit estimates by 1.3-2% for FY17E-FY19E.

Segmentally, we forecast a big chunk of revenue (40-41%) would still be coming

from CRC products but with a gradual decline in percentage contribution, as we

assume a moderate growth rate for its other two products. This is backed by

CSC’s emphasis on growth in its value-added segments.

Figure 29: Key assumptions for earnings forecasts

2015A 2016A 2017E 2018E 2019E

Estimated production ('000 mt)

CRC capacity 480 480 480 480 480

CRC utilisation rate 87.5% 90.0% 90.5% 92.0% 94.0%

CRC output 420 432 434 442 451

GI output 168 162 163 170 175

PPGI output 72 70 71 73 76

Estimated average prices (MYR/mt)

CRC 2,127 2,061 2,349 2,494 2,648

GI 2,306 2,270 2,580 2,756 2,890

PPGI 3,141 3,211 3,540 3,733 3,876

HRC 1,505 1,452 1,739 1,878 2,002

Cost of production 358 345 381 403 423

Other key metrics (%)

Total production growth 5.0% 2.9% 0.6% 1.7% 2.2%

Proportion of export 16% 18% 19% 19% 19%

Average USDMYR 3.93 4.14 4.30 4.20 4.20

Source: Company, Maybank KE

On its cost of production, we estimate utilities costs (electricity and gas) of

MYR51m-MYR59m, labour costs of MYR41m-MYR48m, repair and sundry of

MYR40m-MYR48m, and depreciation and amortisation costs of MYR33m-MYR36m

for FY17E-FY19E.

Fig 28: Revenue trend

Source: Company, Maybank KE

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

200

400

600

800

1,000

1,200

1,400

FY15 FY16 FY17E FY18E FY19E

MYR'm Revenue (LHS) Revenue growth (RHS)

August 21, 2017 21

CSC Steel Holdings

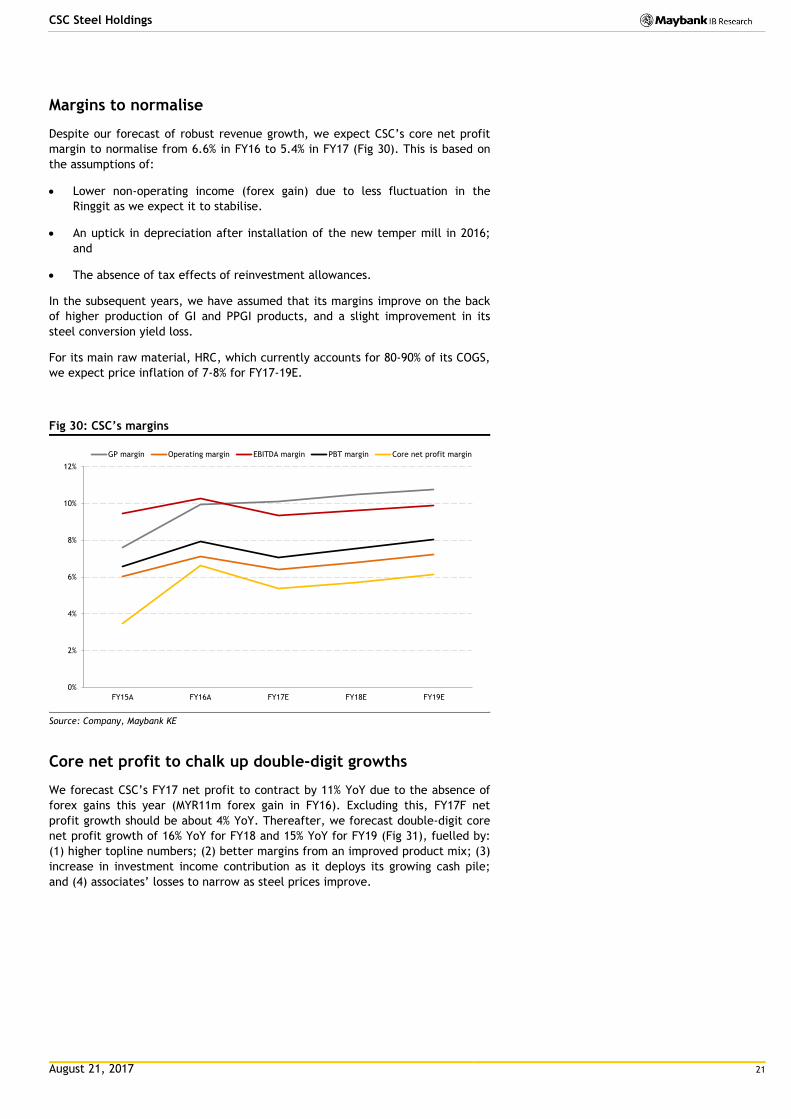

Margins to normalise

Despite our forecast of robust revenue growth, we expect CSC’s core net profit

margin to normalise from 6.6% in FY16 to 5.4% in FY17 (Fig 30). This is based on

the assumptions of:

Lower non-operating income (forex gain) due to less fluctuation in the

Ringgit as we expect it to stabilise.

An uptick in depreciation after installation of the new temper mill in 2016;

and

The absence of tax effects of reinvestment allowances.

In the subsequent years, we have assumed that its margins improve on the back

of higher production of GI and PPGI products, and a slight improvement in its

steel conversion yield loss.

For its main raw material, HRC, which currently accounts for 80-90% of its COGS,

we expect price inflation of 7-8% for FY17-19E.

Fig 30: CSC’s margins

Source: Company, Maybank KE

Core net profit to chalk up double-digit growths

We forecast CSC’s FY17 net profit to contract by 11% YoY due to the absence of

forex gains this year (MYR11m forex gain in FY16). Excluding this, FY17F net

profit growth should be about 4% YoY. Thereafter, we forecast double-digit core

net profit growth of 16% YoY for FY18 and 15% YoY for FY19 (Fig 31), fuelled by:

(1) higher topline numbers; (2) better margins from an improved product mix; (3)

increase in investment income contribution as it deploys its growing cash pile;

and (4) associates’ losses to narrow as steel prices improve.

0%

2%

4%

6%

8%

10%

12%

FY15A FY16A FY17E FY18E FY19E

GP margin Operating margin EBITDA margin PBT margin Core net profit margin

August 21, 2017 22

CSC Steel Holdings

Fig 31: Core net profit trend

Source: Company, Maybank KE

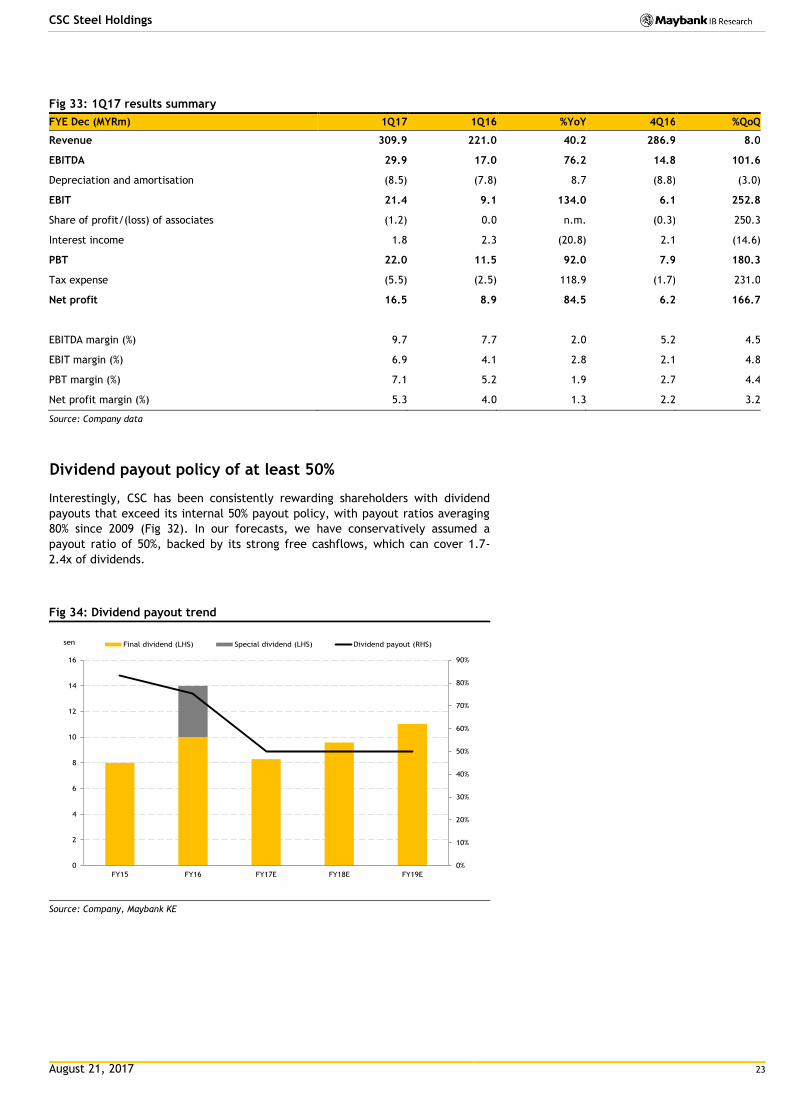

1Q17 results

1Q17 results were encouraging as revenue grew 40% YoY due to higher selling

prices across all steel products and as production volumes rose. This was despite

an increase in production cost. As a result, EBIT margin expanded 2.8%-pts YoY to

6.9% and net profit surged 85% YoY (Fig 35 & 36).

On a QoQ basis, net profit surged 167% despite only 8% QoQ revenue growth as

CSC was able to pass on the higher raw material cost to downstream customers.

We expect revenue growth to moderate in the coming quarters as China steel

prices have eased. All in all, however, we expect CSC to record double-digit FY17

revenue growth of 10.4% to MYR1.14b on improving domestic demand, backed by

a positive outlook for the aforementioned sectors.

Fig 32: Quarterly financial trend

Source: Company data

-50%

0%

50%

100%

150%

200%

250%

300%

350%

0

10

20

30

40

50

60

70

80

90

FY15 FY16 FY17E FY18E FY19E

MYR'm Core profit excl realised forex (LHS) Realised forex (LHS) Core profit excl realised forex growth (RHS) Core profit growth (RHS)

0%

2%

4%

6%

8%

10%

12%

14%

0

50

100

150

200

250

300

350

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

MYR'm Revenue (LHS) Net profit (RHS) Net profit margin

August 21, 2017 23

CSC Steel Holdings

Fig 33: 1Q17 results summary

FYE Dec (MYRm) 1Q17 1Q16 %YoY 4Q16 %QoQ

Revenue 309.9 221.0 40.2 286.9 8.0

EBITDA 29.9 17.0 76.2 14.8 101.6

Depreciation and amortisation (8.5) (7.8) 8.7 (8.8) (3.0)

EBIT 21.4 9.1 134.0 6.1 252.8

Share of profit/(loss) of associates (1.2) 0.0 n.m. (0.3) 250.3

Interest income 1.8 2.3 (20.8) 2.1 (14.6)

PBT 22.0 11.5 92.0 7.9 180.3

Tax expense (5.5) (2.5) 118.9 (1.7) 231.0

Net profit 16.5 8.9 84.5 6.2 166.7

EBITDA margin (%) 9.7 7.7 2.0 5.2 4.5

EBIT margin (%) 6.9 4.1 2.8 2.1 4.8

PBT margin (%) 7.1 5.2 1.9 2.7 4.4

Net profit margin (%) 5.3 4.0 1.3 2.2 3.2

Source: Company data

Dividend payout policy of at least 50%

Interestingly, CSC has been consistently rewarding shareholders with dividend

payouts that exceed its internal 50% payout policy, with payout ratios averaging

80% since 2009 (Fig 32). In our forecasts, we have conservatively assumed a

payout ratio of 50%, backed by its strong free cashflows, which can cover 1.7-

2.4x of dividends.

Fig 34: Dividend payout trend

Source: Company, Maybank KE

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

2

4

6

8

10

12

14

16

FY15 FY16 FY17E FY18E FY19E

sen Final dividend (LHS) Special dividend (LHS) Dividend payout (RHS)

August 21, 2017 24

CSC Steel Holdings

Balance sheet and cash flow analysis

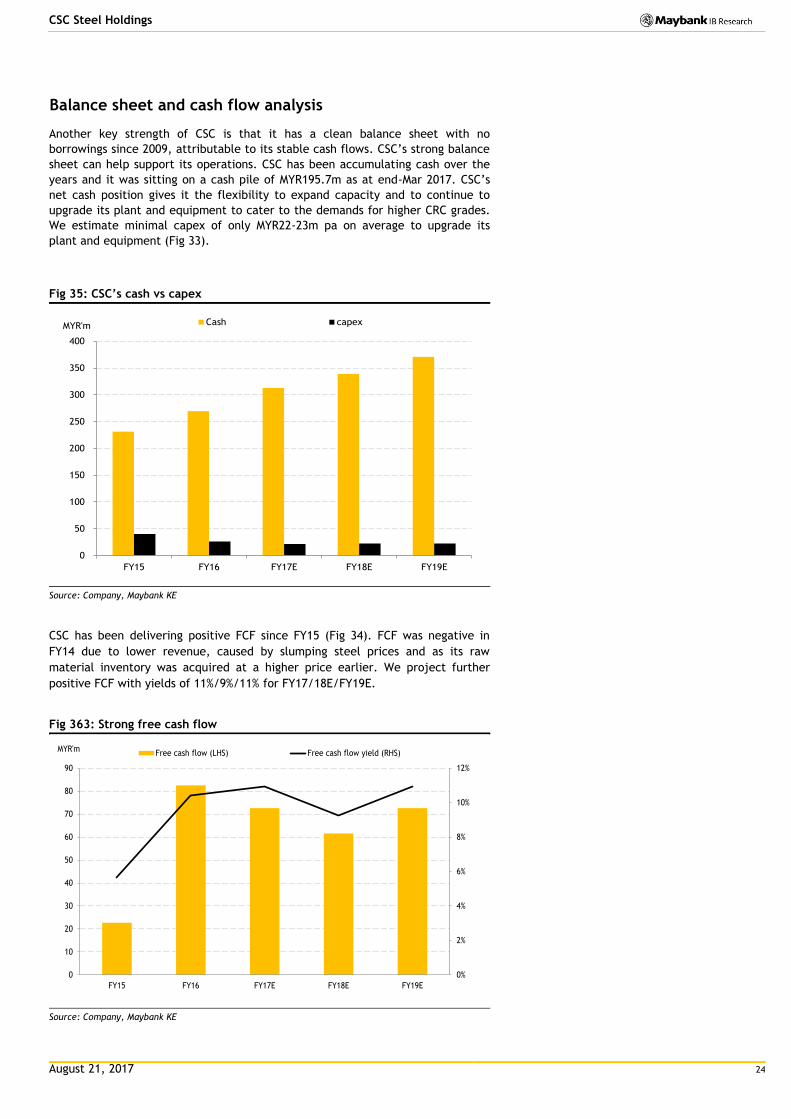

Another key strength of CSC is that it has a clean balance sheet with no

borrowings since 2009, attributable to its stable cash flows. CSC’s strong balance

sheet can help support its operations. CSC has been accumulating cash over the

years and it was sitting on a cash pile of MYR195.7m as at end-Mar 2017. CSC’s

net cash position gives it the flexibility to expand capacity and to continue to

upgrade its plant and equipment to cater to the demands for higher CRC grades.

We estimate minimal capex of only MYR22-23m pa on average to upgrade its

plant and equipment (Fig 33).

Fig 35: CSC’s cash vs capex

Source: Company, Maybank KE

CSC has been delivering positive FCF since FY15 (Fig 34). FCF was negative in

FY14 due to lower revenue, caused by slumping steel prices and as its raw

material inventory was acquired at a higher price earlier. We project further

positive FCF with yields of 11%/9%/11% for FY17/18E/FY19E.

Fig 363: Strong free cash flow

Source: Company, Maybank KE

0

50

100

150

200

250

300

350

400

FY15 FY16 FY17E FY18E FY19E

MYR'm Cash capex

0%

2%

4%

6%

8%

10%

12%

0

10

20

30

40

50

60

70

80

90

FY15 FY16 FY17E FY18E FY19E

MYR'mFree cash flow (LHS) Free cash flow yield (RHS)

August 21, 2017 25

CSC Steel Holdings

Valuations

Initiate BUY and MYR2.02 TP

We initiate coverage on CSC with a BUY and MYR2.02 TP, based on 10.5x FY18F

EPS of 19.2sen. We believe our target PER of 10.5x (the average of its five-year

historical forward PER) is justified given CSC’s market leadership in the domestic

industry (Fig 37). We note that competitor Eonmetall Group’s ROE is higher than

CSC‘s but this is because Eonmetall also manufactures industrial process

machinery, and equipment for the palm oil industry, metalwork machinery and

equipment, and racking systems.

CSC has a healthy balance sheet with net cash per share of 53sen, which implies

an FY18 ex-cash PER of just 7.8x at our TP of MYR2.02. It also translates to a

reasonable 0.85x FY18 P/BV and a decent FY18 dividend yield of 4.7%.

Fig 37: Valuations of Malaysian peers

Stock Rec Share price*

Mkt cap PE (x) PB (x) ROE (%) Div Yield (%) EPS CAGR (%)

16A 17F 16A 17F 16A 17F 16A 17F 15-CY17

(MYR) (MYR'm) (x) (x) (x) (x) % % % % %

Mycron Steel NR 0.82 233 6.5 NA 0.7 NA 10.5 NA 0.0 NA NA

Eonmetall Group NR 0.76 128 10.5 7.9 0.8 0.8 8.0 9.9 3.2 3.2 64.0

YKGI Holdings NR 0.23 80 (6.6) NA 0.4 NA (5.9) NA 0.0 NA NA

Simple average

8.5 7.9 0.6 0.8 9.2 9.9 3.2 3.2 64.0

CSC Steel Holdings BUY 1.70 628 9.1 10.2 0.8 0.8 8.7 7.4 7.8 4.6 31.4

*As of 14th Aug-17

Source: Companies, Bloomberg

A slight premium valuation for multi-usage

Our 10.5x target PER for CSC represents a slight premium to the average for the

long steel sector (upstream production) of 10x (according to our steel analyst,

Yen Ling). We believe this slight premium is fair as CSC’s products are for

downstream manufacturing in various key end markets while long-steel products

are used primarily in the construction sector. Therefore, we can expect CSC’s

earnings to be more stable than long-steel players given CSC’s better product mix.

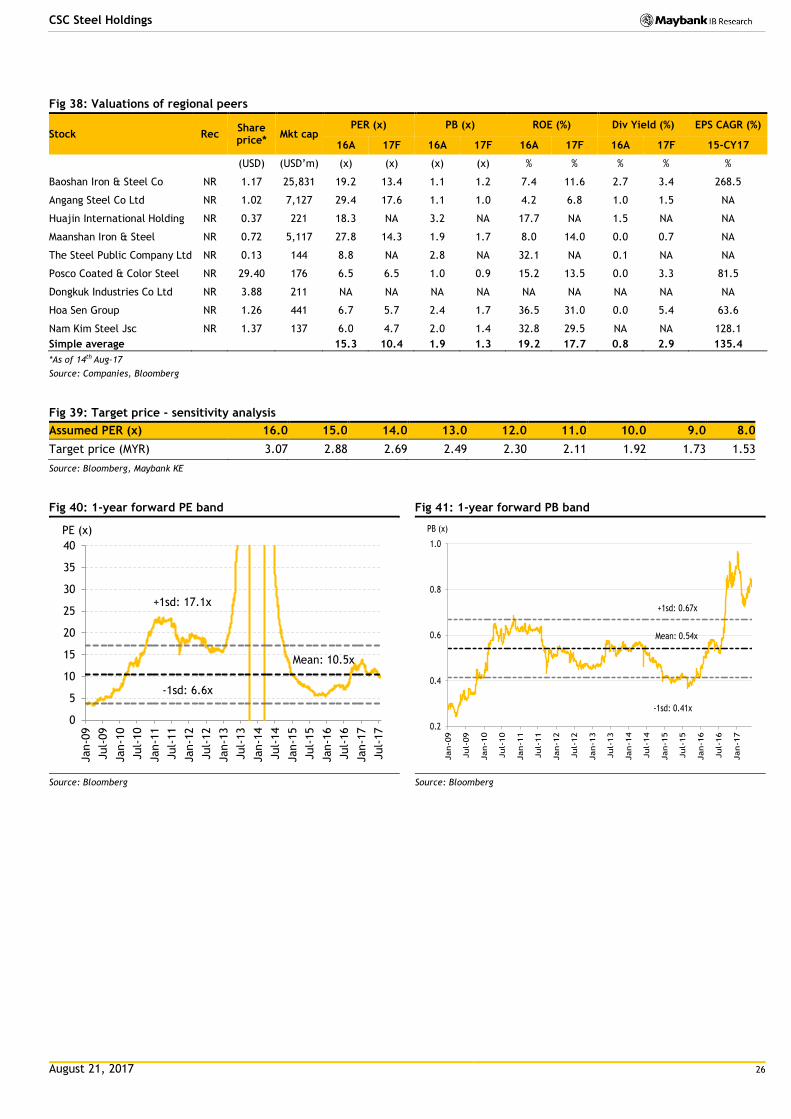

Against regional peers

We note that most of CSC’s regional peers (Fig 38) are involved in the complete

steel production chain. This is versus CSC’s focus on just the mid-stream value

chain. Therefore, we believe our target PER of 10.5x for CSC is reasonable as its

earnings would be less prone to the fluctuation in steel prices. In addition, CSC’s

earnings prospects will benefit from better pricing in the domestic market

following the reduction of cheaper steel imports due to the anti-dumping duties.

August 21, 2017 26

CSC Steel Holdings

Fig 38: Valuations of regional peers

Stock Rec Share price*

Mkt cap PER (x) PB (x) ROE (%) Div Yield (%) EPS CAGR (%)

16A 17F 16A 17F 16A 17F 16A 17F 15-CY17

(USD) (USD’m) (x) (x) (x) (x) % % % % %

Baoshan Iron & Steel Co NR 1.17 25,831 19.2 13.4 1.1 1.2 7.4 11.6 2.7 3.4 268.5

Angang Steel Co Ltd NR 1.02 7,127 29.4 17.6 1.1 1.0 4.2 6.8 1.0 1.5 NA

Huajin International Holding NR 0.37 221 18.3 NA 3.2 NA 17.7 NA 1.5 NA NA

Maanshan Iron & Steel NR 0.72 5,117 27.8 14.3 1.9 1.7 8.0 14.0 0.0 0.7 NA

The Steel Public Company Ltd NR 0.13 144 8.8 NA 2.8 NA 32.1 NA 0.1 NA NA

Posco Coated & Color Steel NR 29.40 176 6.5 6.5 1.0 0.9 15.2 13.5 0.0 3.3 81.5

Dongkuk Industries Co Ltd NR 3.88 211 NA NA NA NA NA NA NA NA NA

Hoa Sen Group NR 1.26 441 6.7 5.7 2.4 1.7 36.5 31.0 0.0 5.4 63.6

Nam Kim Steel Jsc NR 1.37 137 6.0 4.7 2.0 1.4 32.8 29.5 NA NA 128.1

Simple average

15.3 10.4 1.9 1.3 19.2 17.7 0.8 2.9 135.4

*As of 14th Aug-17

Source: Companies, Bloomberg

Fig 39: Target price - sensitivity analysis

Assumed PER (x) 16.0 15.0 14.0 13.0 12.0 11.0 10.0 9.0 8.0

Target price (MYR) 3.07 2.88 2.69 2.49 2.30 2.11 1.92 1.73 1.53

Source: Bloomberg, Maybank KE

Fig 40: 1-year forward PE band

Source: Bloomberg

Fig 41: 1-year forward PB band

Source: Bloomberg

0

5

10

15

20

25

30

35

40

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

Jul-

14

Jan-1

5

Jul-

15

Jan-1

6

Jul-

16

Jan-1

7

Jul-

17

PE (x)

+1sd: 17.1x

Mean: 10.5x

-1sd: 6.6x

0.2

0.4

0.6

0.8

1.0

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

Jul-

14

Jan-1

5

Jul-

15

Jan-1

6

Jul-

16

Jan-1

7

+1sd: 0.67x

Mean: 0.54x

-1sd: 0.41x

PB (x)

August 21, 2017 27

CSC Steel Holdings

Risks

Macro risks

Steel prices are highly cyclical as they’re affected by the strength of the

economy in general and the level of domestic activities. Therefore, a slowdown

in the domestic market would affect the consumption of CSC’s steel products.

Fluctuation in steel prices

Steel prices in China have become the benchmark for international steel prices as

China is the world’s largest steel exporter and as it produces cheaper steel

products. The Chinese government’s failure to curb overcapacity in crude steel in

China would harm prices along the steel value chain, including the primary

sources for HRC production, i.e., iron ore and coking coal.

Dumping activities

Although the Malaysian government has imposed anti-dumping duties on HRC and

CRC from the largest exporting country China and a few other countries, there

are still concerns over the influx of cheap and lower grade steel from other

countries such as India in the guise of boron-added steel products. Such products

fall under the alloy tariff codes, which require no duties and are brought in by

traders or stockists.

Dependence on parent company for HRC supply

CSC is dependent on its parent company in Taiwan for HRC supply for its

production. There could be risk of supply disruptions and discounts on bulk

purchases from its parent are not guaranteed. As such, CSC’s earnings could be

significantly affected if HRC supply from its parent is disrupted.

Regulatory risks

For now, CSC’s imported raw materials are still exempted from import duties

/tariffs under permits granted by the Ministry of International Trade and Industry

as CSC is a major producer in Malaysia. However, there are no assurances that

the Ministry of International Trade and Industry will continue to grant CSC with

such permits and/or exemptions. If the permits are not renewed, CSC would have

to source raw materials from local producers, who might take the opportunity to

increase prices due to higher demand.

Foreign-exchange risks

CSC’s raw material purchases (including HRC, zinc and various chemical

substances) are denominated in USD. Its export products are also denominated in

USD. Therefore, fluctuations in the MYR vs USD will have a material effect on

CSC’s earnings. Based on our sensitivity analysis, every 3% weakness in the MYR

vs USD from our base case would impact our net profit estimates by 1.3%/2%/2%

for FY17E/FY18E/FY19E, respectively.

August 21, 2017 28

CSC Steel Holdings

Appendix

1. CSC’s background

Through its subsidiary, CSC Steel Sdn Bhd, the group’s primary activity is in the

mid-stream segment of the steel value chain, which is the manufacture and

marketing of: (i) pickled and oiled steel coils; (ii) cold rolled steel coils; (iii) hot

dipped galvanized steel coils; and (iv) pre-painted galvanized steel coils.

Fig 42: Group structure

Source: Company

Production capacity

CSC Steel’s factory in Ayer Keroh Industrial Estate, Melaka, started producing and

marketing steel pipes in Jul 1993, followed by CRC in Aug 1994, with a total

capacity of 72,000 mt and 350,000 mt pa respectively at that point in time.

Meanwhile, CSC Steel’s galvanized steel and pre-painted steel plants, with

production capacity of approximately 240,000 mtpa and 120,000 mtpa

respectively, commenced commercial production in 1998.

In 2007, CSC Steel’s new 4-feet reversing cold rolling mill (RCM) started

commercial production. It expanded its CRC production capacity to 620,000mtpa

before the oldest RCM was phased out in 2015 as it was fully depreciated.

Vertical-integration strategy

In 2012, the group acquired 20% of Tatt Giap Group Berhad’s wholly-owned

subsidiary, Tatt Giap Steel Centre Sdn. Bhd, one of its customers. Tatt Giap Steel

provides downstream services and specializes in the slitting and sheering of steel

coils and sheets, thus complementing the overall services offered by CSC.

CSC Steel Holdings Bhd

CSC Steel Sdn Bhd

100%

Constant Mode Sdn Bhd

100%

Group Steel Corporation (M) Sdn Bhd

100%

Tatt Giap Steel Centre Sdn Bhd

20%

August 21, 2017 29

CSC Steel Holdings

Man of steel

CSC is a major subsidiary of Taiwan-based China Steel Corporation CSC of Taiwan.

CSC in Malaysia is headed by Mr Chen Huo-Kun (Fig 43) who has been with CSC of

Taiwan in Taiwan since 1983. Mr Chen was appointed CSC Malaysia’s Group

Managing Director in Aug 2016. He is assisted by executive director Mr Tan Chin

Teng and an experienced senior management team that comprises several people

from the parent company who are experts in their own areas.

Fig 43: CSC’s management team

Name Position Details

Chen, Huo-Kun Group Managing Director

Appointed as Group MD on 4 Aug 16

Graduated from National Sun Yat-Sen University, Taiwan with Doctor in Business Management

More than 30 years of experience in the steel manufacturing industry

Has been employed by China Steel Corporation, Taiwan ("CSC") since 1983, was Production VP at CSC Steel S/B, a subsidiary of CHB, prior to appointment to the Board of CHB

Tan Chin Teng Executive Director (VP

Finance Division)

Appointed as ED on 5 Oct 14

Graduated from Cambridge Management Institute, UK with a MBA

More than 30 years of accounting and finance experience,

More than 25 years of managerial experience overseeing financial matters

Hsu, Tse-Wei VP, Production Division

Date of appointment: 1 Aug 16

Graduated from National Sun Yat-Sen University, Taiwan with Executive MBA

More than 30 years of experience in steel manufacturing

Ten Ling Piew VP, Commercial Division

Date of appointment: 1 July 12

Graduated from National Chung Hsing University, Taiwan with Degree in Business Administration

More than 20 years of experience in marketing

Koh Kang Guan AVP, Production Division

Date of appointment: 1 Jan 07

Graduated from National Taiwan University, Taiwan with Degree in Mechanical Engineering

More than 20 years of experience in the steel manufacturing industry

Juang, Der-Feng AVP, Finance Division

Date of appointment: 1 Aug 16

Graduated from National Sun Yat-sen, Taiwan with Degree in Executive MBA

30 years of experience in finance and accounting

Source: Company

China Steel Corporation of Taiwan

Located in Kaohsiung, Taiwan, CSC of Taiwan was founded in Dec 1971. With

annual production of around 10m tonnes of crude steel, CSC is the largest steel

company in Taiwan, with more than 50% market share.

CSC produces a range of products, including plates, bars, wire rods, hot and cold