DEMAND POLICIES FOR LONG-RUN GROWTH: BEING KEYNESIAN BOTH IN THE SHORT AND IN THE LONG RUN?

21

DEMAND POLICIES FOR LONG-RUN GROWTH: BEING KEYNESIAN BOTH IN THE SHORT AND IN THE LONG RUN? Marco Missaglia* University of Pavia (October 2004; revised April 2005) ABSTRACT The idea of demand-led growth is defended by neo-Kaleckians and neo-Keynesians using very spe- cific assumptions. In their models the paradox of costs is always valid in the long run. The central message of this paper is that these specific and strong assumptions are not needed to defend the Kaleckian perspective of a demand-driven long-run growth. What is needed is simply a less demand- ing theory of flexible mark-ups in an open economy. The formal model developed in this paper shows that long-run growth may be demand driven even when the paradox of costs does not hold in the long run. 1. THE PARADOX OF COSTS AND THE LONG-RUN DETERMINATION OF THE RATE OF CAPACITY UTILIZATION The two most important results of the Kaleckian models of distribution and growth are the paradox of thrift (an increase in the propensity to save decreases the rate of accumulation even in the long run) and the paradox of costs (higher real wages may be associated with higher rates of accumulation even in the long run). Hence, higher rates of accumulation may be accom- panied by higher real wages even without technical progress. For this Kaleck- ian result to be possible, the rate of capacity utilization must be endogenous in the long run. To see why, just start from the national accounts of a closed economy, where the value of aggregate output is equal to the sum of wage costs and realized profits on capital: * I am indebted to professors Renata Targetti, Amit Bhaduri and Gianni Vaggi, whose com- ments have significantly improved previous versions of the paper. I received extremely useful suggestions from two anonymous referees. Of course, I am responsible for any remaining errors. Metroeconomica 58:1 (2007) 74–94 © 2007 The Author Journal compilation © 2007 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford, OX4 2DQ, UK and 350 Main St, Malden, MA 02148, USA

Transcript of DEMAND POLICIES FOR LONG-RUN GROWTH: BEING KEYNESIAN BOTH IN THE SHORT AND IN THE LONG RUN?

DEMAND POLICIES FOR LONG-RUN GROWTH: BEINGKEYNESIAN BOTH IN THE SHORT AND IN THE LONG RUN?

Marco Missaglia*University of Pavia

(October 2004; revised April 2005)

ABSTRACT

The idea of demand-led growth is defended by neo-Kaleckians and neo-Keynesians using very spe-cific assumptions. In their models the paradox of costs is always valid in the long run. The centralmessage of this paper is that these specific and strong assumptions are not needed to defend theKaleckian perspective of a demand-driven long-run growth. What is needed is simply a less demand-ing theory of flexible mark-ups in an open economy. The formal model developed in this paper showsthat long-run growth may be demand driven even when the paradox of costs does not hold in thelong run.

1. THE PARADOX OF COSTS AND THE LONG-RUN DETERMINATIONOF THE RATE OF CAPACITY UTILIZATION

The two most important results of the Kaleckian models of distribution andgrowth are the paradox of thrift (an increase in the propensity to savedecreases the rate of accumulation even in the long run) and the paradox ofcosts (higher real wages may be associated with higher rates of accumulationeven in the long run). Hence, higher rates of accumulation may be accom-panied by higher real wages even without technical progress. For this Kaleck-ian result to be possible, the rate of capacity utilization must be endogenousin the long run. To see why, just start from the national accounts of a closedeconomy, where the value of aggregate output is equal to the sum of wagecosts and realized profits on capital:

* I am indebted to professors Renata Targetti, Amit Bhaduri and Gianni Vaggi, whose com-ments have significantly improved previous versions of the paper. I received extremely usefulsuggestions from two anonymous referees. Of course, I am responsible for any remainingerrors.

Metroeconomica 58:1 (2007) 74–94

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford, OX42DQ, UK and 350 Main St, Malden, MA 02148, USA

PY wL rPK= +

where P is the price of the only good produced by the economy, w is themoney wage, r is the rate of return on capital (the rate of profit), L and K are,respectively, the amount of labour and capital employed in the economy. Letb = L/Y the input–output labour coefficient (the inverse of labour productiv-ity) and u = Y/K a proxy for the rate of capacity utilization. The nationalaccounts’ cost decomposition may be thus rewritten as

r u w P b= − ( )[ ]1 (1)

It is easy to see from equation (1) that when the rate of capacity utilization isconsidered to be exogenous in the long run and there is no technical change,a higher rate of profit requires a lower real wage. If a plausible, positiverelation between the rate of capital accumulation and the rate of profit isadded, it follows that the paradox of cost can never hold. How can the rateof capacity utilization be made endogenous in the long run? After all, severalneo-Ricardian and Sraffian (Vianello, 1985; Garegnani, 1992; Kurz, 1996;Park, 1997; Garegnani and Palumbo, 1998; Ciampalini and Vianello, 2000)as well as Marxist (Auerbach and Skott, 1988; Duménil and Lévy, 1999)authors have claimed that in the long run the realized rate of profit and therealized rate of capacity utilization must be equal to their ‘normal’ values;otherwise a model lacks logical consistency in that the steady state of theeconomy is not a final, fully adjusted position where no economic mecha-nisms are at work to change such a long-run configuration. This argumentmay be sketched following Lavoie (2002), whose contribution is an extremelyclear illustration of how the post-Keynesians and the neo-Kaleckians inter-pret and criticize the Sraffian/neo-Ricardian/Marxist view we have just men-tioned. Consider a modern, industrial economy where the product market isnot perfectly competitive and prices are fixed by firms according to the usualmark-up rule:

P m wb= +( )1

where m is the mark-up rate over variable costs. According to this formula,total profits are equal to mwbY. Imagine now that firms have some target rateof return, or ‘normal’ (standard) rate of profit in their minds and let us call itrs. The target profit bill is therefore equal to rsPK. Assuming, for the sake ofthe argument, that firms have also a normal (standard) rate of capacity

Demand Policies for Long-run Growth 75

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

utilization in their minds, us, the target profit bill may be rewritten as rsPY/us.By solving mwbY = rsPY/us we get the mark-up rate consistent with thenormal rates of profit and capacity utilization and may rewrite the pricingformula as

P u u r wb= −( )[ ]s s s (2)

Combining equations (1) and (2)1 we get the relation among realized andstandard rates of profits and capacity utilization:

r r u u= ( )s s (3)

from which it is clear that when the realized rate of capacity utilization isequal to its normal value, the actual rate of profit is then equal to the target,standard rate of profit. In other (and to our purpose more important) words,if firms are able, or powerful enough at least in the long run, to fix prices soas to realize their target rate of return (r = rs), then the rate of capacityutilization will be in the end equal to its predetermined, normal or standardvalue and no room will be left for the paradox of costs to hold. The pointmade by Sraffian/neo-Ricardian/Marxist authors is precisely that in the longrun there are major economic forces guaranteeing the convergence of r to rs.For instance, when the realized rate of profit is higher than the target rate ofreturn (r > rs), firms will revise upward their target, i.e. they will increase themark-up rate incorporated in the pricing formula (2). Under plausible con-ditions, this will depress aggregate demand and reduce the realized rate ofprofit. This process will go on until the equality r = rs is restored and a fullyadjusted position is reached. But are firms powerful enough to fix prices so asto realize their target rate of return?

2. THE NEO-KALECKIAN THEORY OF INFLATION AND THERESURGENCE OF THE PARADOX OF COSTS

Neo-Kaleckian authors have tried different routes to face the Sraffian/neo-Ricardian/Marxist critique and preserve the basic insights of the Kaleckian

1 Of course, a meaningful model requires that us > rs, which must always be true since thisinequality simply says that there must be some worker employed in the production process (thewage share must be positive).

76 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

macro model of growth and distribution. Chick and Caserta (1997) arguethat the very notion of ‘long run’ is irrelevant to the understanding of realeconomies and show that the Kaleckian results hold in the ‘medium’ run,which according to them is the relevant time frame to be considered. Butthis is a way of avoiding rather than solving the problem posed by theSraffian/neo-Ricardian/Marxist critique. Dutt (1997) describes an economicsystem with heterogeneous firms, each of them with two different levels of‘normal’ capacity utilization (high and low). But this is a someway ad hocassumption and the (Kaleckian) results of the model do not rest on a solid,general and less naive ground. Lavoie (1992, 1995, 1996, 2002, 2003) triesa couple of solutions. On the one hand, he makes endogenous the normaldegree of capacity utilization and shows this is a way of preserving themain results of the Kaleckian macro model. But, as observed by Commen-datore (2004), he does so at the price of a conspicuous loss of the Keyne-sian nature of the model, since accumulation decisions are determined by agiven set of initial conditions. On the other hand, Lavoie suggests Kaleck-ian results may be salvaged by putting into the picture the inter-class, dis-tributive conflict between capitalists and workers, i.e. the structuralisttheory of inflation based on social conflict.2 This is a point to be exploredmore in-depth, since it will open the way to the core message of this paper,i.e. a new, different answer to the Sraffian/neo-Ricardian/Marxist critique.According to Lavoie, the rate of return that firms actually incorporate intothe pricing rule may be different from the rate of return they desire becauseof workers’ strength. Workers and firms have conflicting claims on thedomestic social product and the rate of return actually incorporated intothe pricing rule comes out of a bargaining process. Firms are capable ofincorporating their desired rate of return into the pricing rule if and only ifthe workers lack any bargaining power, which is not the case in a moderncapitalist economy. So, a theory of conflict inflation is the device used byneo-Kaleckian authors to re-establish the possibility for the paradox of costto hold in a long-run equilibrium. In order to ease later discussion, let ussummarize (and someway simplify) this neo-Kaleckian argument3 throughthe help of a straightforward formalization:

g sr= (4)

g g g u g r= + +0 1 2 (5)

2 Cassetti (2002) seeks a similar integration of Kaleckian growth theory and conflict inflationtheory.3 For a complete analysis see Lavoie (2002).

Demand Policies for Long-run Growth 77

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

r r u u= ( )s s (6)

where g is the rate of capital accumulation (the rate of growth of the capitalstock) and s the (fixed) propensity of the capitalists to save out of theirincome. Equation (4) simply says that in this closed economy with no gov-ernment there is no saving out of wage income. Equation (5) is the traditionalstructuralist investment function:4 the intercept term is a proxy for the stateof business confidence (‘animal spirits’); g1 and g2 are positive coefficientsattached to the rate of capacity utilization (firms want to maintain a desiredlevel of excess capacity) and to the rate of profit. The last term makes sensein that financial markets are imperfect and therefore higher profits enhanceinvestment by both increasing corporate savings and reducing borrowers’and lenders’ risk and thereby permitting easier access to external finance. Thesystem (4)–(6) can be easily solved in its three unknowns, g, r and u. Thesolutions are

u g u r s g g u

r g r r s g g u

g sg r r s g g u

= −( ) −[ ]= −( ) −[ ]= −( ) −

0 1

0 2 1

0 2 1

s 2 s

s s

s ss[ ](7)

where the usual condition for a positive and stable solution:

r s g g us s−( ) − >2 1 0 (C1)

is assumed to be met. This is not the end of the story. The neo-Kaleckianarguments goes on by adding to solutions (7) a theory of how rs is deter-mined. According to this theory—the theory of conflict inflation––rs, which isnow to be interpreted as the rate of return actually incorporated into thepricing formula, is not exogenous, but depends on two elements: the targetrate of return desired by firms, rsf, and the target rate of return desired byworkers or unions, rsw. The conflicting claims of capitalists and workerstranslate into a wage–price spiral that may push the economy onto an infla-tionary path. In general, it can be written rs = f(rsf, rsw), since the rate of return

4 The arguments of the investment function have been a subject of contention in the Keynesian/Kaleckian debate, especially after the seminal work of Marglin and Bhaduri (1990). However,this is not the focus of this paper and, despite every possible investment function can be defendedonly up to a point, a function such as (5) helps make later discussion clearer.

78 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

actually incorporated into the pricing formula will come out of a bargainingprocess whose final outcome depends on the relative strength of workers andcapitalists. If one combines this theory of conflict inflation––rs = f(rsf, rsw),where frsf > 0 and frsw

––with solutions (7), then a new solution is found for theunknowns of the system:

u g u f r r s g g u

r g f r r f r r s g

= ( ) −( ) −[ ]= ( ) ( ) −(

0 2 1

0 2

s sf sw s

sf sw sf sw

,

,, )) −[ ]= ( ) ( ) −( ) −[ ]

g u

g sg f r r f r r s g g u1

0 2 1

s

sf sw sf sw s, ,(7 bis)

Nothing guarantees that r = rsf. If this equality does not hold, the solution athand cannot be labelled as a ‘fully adjusted’ position, since the discrepancybetween the actual rate of return and the firms’ target rate of return willinduce firms to adjust the latter. Lavoie (2002) suggests the following adjust-ment rule:

�r r rsf sf= −( )ϕ (8)

where j > 0 is the speed of adjustment and a dot over a variable indicatesas usual its time derivative. Now, the point to be stressed is that the adjust-ment process underlying equation (8) involves the firms’ target rate ofreturn rather than the rate of return actually incorporated into their pricingstrategy, simply because the latter is not autonomously decided by thefirms, but determined by the conflicting interaction between firms andworkers. Equation (8) describes a stable adjustment process: each time thatr > rsf, rsf goes up; then rs (= f(rsf, rsw)) will do the same and the realized rateof profit, r, will diminish without ambiguity since, as can be seen using (7)or (7 bis),

d d s s s sr r g g u r s g g u= − −( ) −[ ] <0 1 2 12 0 (9)

At the end of this process, therefore, we will have r = rsf; in general, however,it will be r � rs. In other words, at the end of the adjustment process theeconomy is in a long-run, steady-state position since there is no more reasonfor the firms to revise their target rate of return, but in this steady-stateposition r � rs and therefore, according to (6), u � us: in this long-run posi-tion the rate of capacity utilization is endogenous, the paradox of costs might

Demand Policies for Long-run Growth 79

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

hold even in the long run and, reversing the Duménil and Lévy (1999)suggestion, being Keynesian both in the short and in the long term becomespossible.

This neo-Kaleckian argument is interesting and powerful. True, it implic-itly assumes a fully accomodatory central bank, but the introduction ofa more active central bank would not change the main conclusion ofLavoie’s model.5 However, a significant limitation of Lavoie’s argument isthat it necessarily implies the validity of the paradox of cost in the long run.To prove this point, first note from (2) that the real wage can be expressedas

w P u r bu u f r r bu= −( ) = − ( )[ ]s s s s sf sw s,

and its derivative with respect to us is always positive. Therefore, we canincrease us to see what are the long-run consequences of a higher real wage.Note, again, that (7 bis) implies that in the steady state (where r = rsf) thefollowing relation must hold:

r f r r s g g u g f r rsf sf sw s sf sw, ,( ) −( ) −[ ] − ( ) =2 1 0 0

By totally differentiating this expression we can get what we are interested in,i.e. the long-run reaction of the profit rate (r = rsf) to an increase in the realwage:

d d ,sf s sf sf sw s sfsfr u g r f r r g u f r s g gr= ( ) −[ ] + −( ) −[ ]{ }1 1 2 0

The numerator is positive and the first term in the denominator is alsopositive because of the required short-run stability of the model. Given thatf > 0, it follows that we can say that the paradox of cost holds in the long runif rsf(s - g2) - g0 > 0. But this condition is always true. To see why, assume it

5 Indeed, a scenario can be envisaged where money supply is endogenous (created by loans); thecentral bank actively pursues its objectives by manoeuvring its policy tools (reserve require-ments, open market interventions, discounting rate applied to commercial banks and moralsuasion); these central bank policy choices, through the influence they exert on the level ofeconomic activity, affect either the firms’ and workers’ desired rate of return (rsf and rsw) or therelative bargaining power of the two social groups (the shape of the function f ) or both. Theactive central bank behaviour will ultimately affect rs, but this does not change Lavoie’s con-clusion in any significant respect.

80 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

is not: rsf(s - g2) - g0 < 0. This would imply (remember that in the steady stater = rsf) g0 + g2r > sr. In turn this inequality, combined with the investmentfunction (5), which of course must hold both in the short and in the long haul,implies g1u < 0. This is clearly absurd, since we cannot observe a steady statewith a negative degree of capacity utilization. It follows that drsf/dus is posi-tive and the paradox of cost always applies in the long run. In this paper wewill try to understand whether the main insight of the Kaleckian model ofgrowth and distribution—the long-run endogeneity of the degree of capacityutilization—may be preserved in a more general framework where theparadox of cost may or may not apply in the long run. A story of conflict,again, but this time the conflict we want to stress is not the conflict betweencapitalists and workers over the shares of domestic social product, but theconflict among domestic and foreign firms over the shares of nationalmarket. According to this view, domestic firms are unable to incorporatetheir desired rate of return into the pricing formula because of foreigncompetition.

3. FLEXIBLE MARK-UP IN AN OPEN ECONOMY

According to Kalecki the puzzle of ‘economic imperialism’ could be solvedby noting that:

The capitalists of a country which manages to capture foreign markets from othercountries are able to increase their profits at the expense of the capitalists of theother countries. (Kalecki [1954], 1991, p. 245)

However simplistic,6 this view paves the way to a different theory on how therate of return actually implemented into firms’ pricing strategy, rs, is deter-mined. Indeed, as clearly pointed out by Blecker (1999), Kalecki’s theory ofmark-up pricing can be extended to an economy exposed to internationalcompetition. Basically, international competition affects the rate of returnactually implemented by firms in two ways. First, a greater exposure tointernational competition reduces the degree of concentration of a givenindustry (an ‘industry’ being now defined on a larger scale) and therefore islikely to reduce rsf, the firms’ own target. Second, international competition

6 According to this view a trade surplus is always expansionary, which of course may not be thecase (think of a trade surplus due to a fall in import demand during a recession).

Demand Policies for Long-run Growth 81

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

changes the way firms react to an increase of the wage rate (or a reduction inlabour productivity), preventing them from passing through the entire wageincrease (productivity reduction) into a higher price. Formally, we wouldneed a theory according to which rs = f(rsf, z), where z is an index of competi-tiveness defined as follows:

z eP wb= f (10)

where e is the nominal exchange rate, Pf is the foreign price and w and b havealready been defined. The meaning of z is self-evident: any increase in z meansa higher degree of competitiveness of the domestic economy, while anyreduction provokes a loss of competitiveness. The theory we are looking forhas been developed by Blecker (1999) and used by this author to discussshort-run issues (indeed, as we are going to see, this theory is not expressed interms of target pricing and standard rates of capacity utilization and profit).In contrast, we are discussing a long-run, steady-state issue and this is whyBlecker’s argument will be slightly modified and then complemented in orderto adapt it to our purposes. Let us first have a look at Blecker’s argument.The aforementioned two ways in which international competition affectsmark-ups and distributive shares may be captured by a price adjustmentequation (for the sake of convenience it is expressed in natural logarithmsand, as usual, a ‘hat’ over a variable indicates its growth rate) such as thefollowing:

ˆ ln ln lnP f= −( ) +α ω ω θ ρ (11)

In this equation, w represents the wage share in total income; w f is the wageshare targeted by firms (a target in terms of wage share is equivalent to atarget in terms of mark-up rate); r is the real exchange rate, defined as theratio between the domestic currency price of imports and the price of domes-tic production (ePf/P); finally, a and q are positive parameters representingspeeds of adjustment. Equation (11) postulates that: (1) firms decide toincrease their price when the actual wage share exceeds their target (whichmeans that the actual profit share falls short of their target), which is a veryreasonable assumption, and (2) firms react positively to variations in the realexchange rate: a currency devaluation or an increase of the price decided bytheir foreign competitors induces domestic firms to adjust their own price.Now, it is definitionally true that the real exchange rate equals the productbetween the index of competitiveness and the wage share, i.e. r = zw. Equa-tion (11) can be therefore rewritten as

82 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

ˆ ln ln ln lnfP z= −( ) + +( )α ω ω θ ω (12)

In a steady state without labour productivity growth (and, when imports ofnon-competitive intermediates are taken into account, without variations inthe relevant technical coefficients), the distributive shares and the realexchange rate must be constant. Hence, assuming that Pf is given, in thesteady state it must be P = w = e. In order to concentrate on the issue ofinternational competitiveness and infra-capitalist conflict over market shares(rather than inter-class conflict over product shares), let us assume that w (thewage rate) is fixed and then its growth rate is nil. As a consequence, priceinflation must be nil as well in the steady state. At this point it is easy to solve(12) to get the (logarithm of the) steady-state value of the wage share:

lnln lnω α ω θ

α θ= −

+

f z

from which we can express the steady-state wage share as a function of thewage share targeted by firms and the index of competitiveness:

ω ω ω ω ω ω= ( ) >f f, and z < 0z ∂ ∂ ∂ ∂0 (13)

This is the kind of theory we were looking for, a theory such that rs = f(rsf, z).To see why, just note, going back to equation (2),7 that

ω = −( )u r us s s

from which it follows that, given a standard (normal, target) rate of capacityutilization, (a) a steady state of the wage share is equivalent to a steady stateof the rate of return actually incorporated into the firms’ pricing strategy (rs)and (b) a firms’ target expressed in terms of the wage share (wf) is equivalentto a firms’ objective expressed in terms of targeted rate of return (rsf). Hence,we can write

r f r z r r r zs sf s sf s, with and= ( ) > >∂ ∂ ∂ ∂0 0 (14)

7 Nothing relevant would change by putting into the picture imported raw materials. Hence,they will be assumed away for the sake of simplicity.

Demand Policies for Long-run Growth 83

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

In words, the steady-state value of the actual rate of return implemented intofirms’ pricing strategy varies positively with both the desired target rate ofreturn and the index of competitiveness. Imagine for instance that a negativeproductivity shock occurs (b increases and consequently z falls): this willsqueeze the actual target rate of return since domestic firms will not passthrough the entire labour productivity reduction into higher prices to avoida contraction of their market shares.

4. STEADY STATES AND FULLY ADJUSTED POSITIONS INAN OPEN ECONOMY

In order to discuss the issue of the possibly endogenous determination of thedegree of capacity utilization in the long run, the theory expressed by equa-tion (14) must be now inserted into the broader framework of a fully deter-mined open economy model of growth and distribution. The long-runequilibrium of such an economy can be described by the following system ofsix equations:

g sr t u= + ( )ρ, (15)

g g g u g r= + +0 1 2 (16)

r r u u= ( )s s (17)

r r zs sf= ⋅ + ⋅α β (18)

z u u r= ⋅ −( )ρ s s s (19)

t uρ,( ) = 0 (20)

Equations (15)–(17) are nothing but the open economy version of equations(4)–(6). Of course, as can be seen from (15), saving supply must now includethe current account deficit per unit of capital (expressed in domestic cur-rency), t. In the long run, however, the current account deficit must be zero,

84 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

as stated by equation (20). As usual, the current account deficit is supposedto be a positive function of the degree of capacity utilization (tu > 0) and anegative function of the real exchange rate8 (tr < 0). Equation (18) is thelinear version of (14), our theory of the endogenous determination of rs. Ofcourse, it must be a > 0 and b > 0. Equation (14) has been made linear for thesake of simplicity: none of the conclusions of this paper are affected by thissimplifying assumption and, as the reader can easily check, the linear formu-lation (18) guarantees that the elasticities of rs with respect to both rsf and zare positive and less than one, as one should expect them to be. Finally,equation (19) comes from (2) and the definitions of the real exchange rate andthe index of competitiveness:

ρ = =

−⋅

= − ⋅ePP

ePu

u rwb

u ru

zf f

s

s s

s s

s

It is interesting to look at equations (18) and (19) together. Equation (18)establishes that the pricing strategy adopted by domestic firms is affected bythe international competitiveness of the economy; equation (19) says thatobviously the opposite must be true as well: the international competitivenessof the economy depends on the pricing strategy of domestic firms. As we shallsee, this loop introduces a non-linearity into the system (15)–(20) withoutcompromising, however, the possibility of getting a single, determinedsolution.

The system describes a long-run equilibrium for the economy at hand inthat equations (15)–(20) must hold in the long run and not necessarily inthe short; in particular, the current account is balanced in the long run andthe rate of return actually implemented into firms’ pricing strategy takes thevalue given by equation (18) only in the long run, when the process

8 The Marshall–Lerner condition is assumed to be met. The reader should also be made awarethat treating the index of competitiveness as an endogenous variable, as we do, implies that theratio (e/w) must also be considered endogenous (foreign prices and labour productivity are takenas given). Either the nominal exchange rate or the nominal wage (or both) must therefore bedetermined endogenously by the system, which is likely to be the case in this long-run model ofgrowth and distribution. In other words, we know from our analysis in section 3 that once theeconomy is in the steady state the rate of growth of money wages must be the same as the rateof growth of the nominal exchange rate, but this does not prevent these two variables fromgrowing at different rates in the traverse from one steady state to the other.

Demand Policies for Long-run Growth 85

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

described in section 3 has fully deployed its effects. However, such an equi-librium is not necessarily either a steady state or a fully adjusted position.Indeed, in general, in the equilibrium of the system (15)–(20) it will ber* � rsf � rs, having denoted with r the realized rate of profit. We canfollow Lavoie (2002) and assume that when there is a discrepancy betweenthe realized rate of return, r, and the target rate of return desired by firms,rsf, the latter adjust their target according to the same rule illustrated before(see (8)):

�r r rsf sf*= −( )ϕ (21)

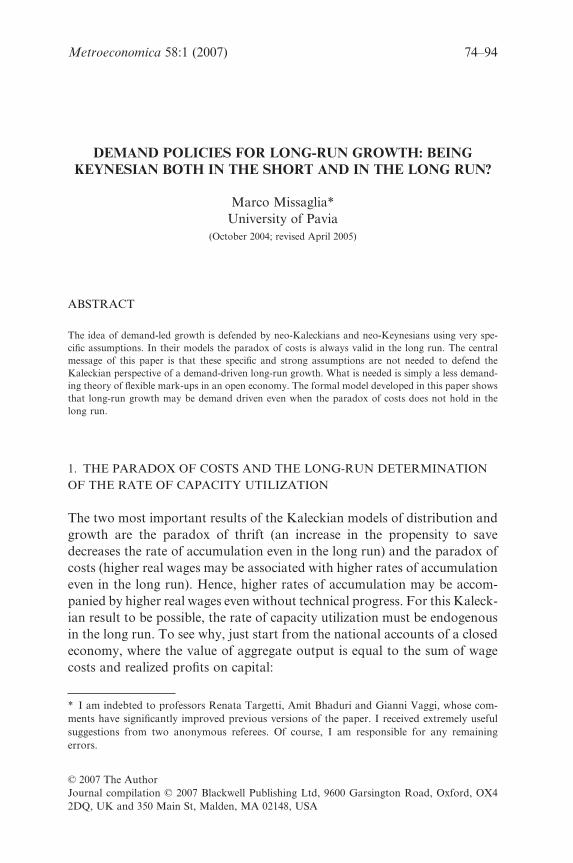

In words, when firms see they are realizing higher (lower) profits thanexpected (better: than targeted), they revise their target upward (down-ward). Here the interesting point is to see whether the adjustment rule (21)implies the convergence between r and rsf and a steady state such as the oneillustrated in figure 1 may actually materialize. If it does, then it will bepossible to conclude that we do not need a theory of conflict inflation toreject the idea of a normal or standard rate of capacity utilization that aneconomy must necessarily reach in a ‘fully adjusted’ position. An arguably

ARR

CO

45°

45°

z

RER

u

r

r

PC

E

CB

ED

E

E

E

rs=rsf*

rs arsf

u*us

Figure 1. The steady state of the economy.

86 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

more general theory of flexible mark-ups in an open economy may do thesame job. Before coming to this stability issue, however, let us representdiagrammatically the equilibrium of the system (15)–(20). Indeed, sucha system is completely simultaneous and its solution can hardly be foundout explicitly. A graphical representation may illustrate the points at stakemuch more clearly.

In the North/East (NE) quadrant the subsystem (15)–(17) is represented,with the profit–cost (PC) curve representing equation (17) and the effectivedemand curve (ED) representing the subsystem (15)–(16). The PC curve issteeper than the ED curve since (C1) is assumed to be met. In the South/East(SE) quadrant the current balance (CB) curve represents all the combinations(r, u) such that the current account is balanced, i.e. equation (20). Of course,an increase in the degree of capacity utilization, which stimulates imports,must be compensated by a real devaluation to maintain the external balance.In the South/West (SW) quadrant the 45-degree curve is used to move theequilibrium value of the real exchange rate from the SE to the North/West(NW) quadrant. The real exchange rate (RER) curve represents the relationbetween the real exchange rate and the index of competitiveness as estab-lished by equation (19). Finally, in the NW quadrant the competitivenesscurve (CO) relates the index of competitiveness and the rate of return (therate actually incorporated into firms’ pricing strategy) according to equation(19), whereas equation (18) is represented by the actual rate of return (ARR)curve. Of course, for a long-run equilibrium of this open economy to exist,the ARR and CO curves must intersect. The condition for such an intersec-tion to occur is

u r us s s− ⋅( ) − ⋅ ⋅ ≥α ρ β2 4 0 (C2)

(C1) and (C2) constitute the set of restrictions that have to be met in orderto guarantee the existence of the equilibrium. Figure 1 must be read asfollows: the intersection between the ARR and CO curves at point E deter-mines the equilibrium value of z and rs; once rs is known, the slope of thePC curve can be established and the PC–ED intersection at point E in theNE quadrant determines the equilibrium values of r, the realized rate ofprofit, and u, the degree of capacity utilization. The equilibrium value of umust then be associated with an equilibrium value for the real exchangerate on the CB curve in the SE quadrant. Finally, the equilibrium value forthe real exchange rate and the RER curve in the SW quadrant determinean equilibrium value for the index of competitiveness, z, that must be

Demand Policies for Long-run Growth 87

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

coherent with the value determined by the ARR–CO intersection in theNW quadrant.9

In the equilibrium illustrated in figure 1, it is rsf � r* � rs. In other words,that equilibrium is a steady state, a long-run position from which there is noincentive to move. Still, the rate of capacity utilization is endogenous andmay thus be affected even in the long run by some kind of demand policy(shifts of the ED curve). So, let us try to understand at which conditions asteady state such as the one illustrated in figure 1 is (locally) stable.

The adjustment rule (21) implies that a sufficient (but not necessary) con-dition for stability is

∂∂

rr*

sf

< 0

Through very tedious but simple manipulations, we get an expression for therelevant derivative (see the Appendix, equation (A1), for the details):

∂∂

rr

g aut u r

t u r z s g r g u s g*

sf

s s

s s s s

=− −( )

−( ) −[ ] −( ) −[ ] − −( )1

2 1 2

ρ

ρ β ββut uu s[ ](22)

Given our assumptions, the numerator of this expression is always positive(remember that the current account deficit responds negatively to a realdevaluation); hence, a sufficient condition for the stability of the steadystate is

u r zs s−( ) > β (C3)

To understand the meaning of this sufficient condition note that

d d d d d dsf s s sfr r r r r r= ( )( )

and since the first derivative on the right-hand side is always negative10 (seeequation (9)), the sign of (∂r/∂rsf) will only depend on the sign of (∂rs/∂rsf). The

9 The reader may easily check that there is no problem of multiple equilibria in this model, sincea point such as F in figure 1 does not constitute an equilibrium. If it did, it would be associatedwith an equilibrium value of the real exchange rate different from the intercept of the CO curve,which is a contradiction.10 The fact that dr/drs < 0 implies that this model is ‘stagnationist’ (Marglin and Bhaduri, 1990).A higher rs, i.e. a higher price level, reduces the real wage, which in turn depresses consumption

88 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

latter, as the reader may easily check using the same technique exposed in theAppendix, is positive if and only if (C3) is met. So, imagine that the economyis in an equilibrium out of the steady state where, for instance, r > rsf. Weknow from the adjustment rule (21) that rsf will rise. But, on top of thismechanics, what will happen to the price level? What are the consequences ofincreasing rsf? Will the actual mark-up increase or decrease? The rise of rsf

puts a direct upward pressure on rs (look at equation (18)) and the price level;but the associated loss of competitiveness exerts an indirect downward pres-sure on rs and the price level. The sufficient condition for the stability of thesteady state says that the direct and upward pressure dominates: there will bean increase in the price level and, due to lower real wages, a reduction in theaggregate demand will result (see footnote 10). Hence, according to thetraditional Kaleckian/Keynesian argument, the realized rate of profit will godown and the equality between r and rsf will be finally restored. It may beinteresting to note that one reason why (C3) could not be met is a lowsensitivity of imports to the activity level and/or a strong sensitivity ofexports to the real exchange rate. In this case, the direct and positive pressureon the price level induced by the rising rsf would prompt a serious deteriora-tion of the current account, the competitiveness effect would dominate and atthe end of the story rs and the price level would shrink. Having clarified theissue of the stability of the steady state, we can now try to understandwhether in this open economy Kaleckian framework the paradox of costsmay still hold. In other words, starting from a given steady state, is it possibleby increasing the real wage to get a new steady state characterized by a highergrowth rate? To answer this question, note from equation (2) that the realwage may be written as

w P u r bu= −( )s s s

from which it is clear that

d d iff d ds s s s sw P u r u r u( ) > <0 (23)

Since this condition is always met (see the Appendix, equation (A2)), we canincrease us to study the long-run impact of an increase in the real wage. The

demand (since the propensity to consume of the workers is higher than that of the capitalists).The reduction in consumption demand, given the form chosen for the investment function, isgreater than the increase in investment demand. Hence, the fall of aggregate demand and theassociated reduction of the realized rate of profit. We will see that this stagnationist feature doesnot imply that the paradox of costs necessarily holds.

Demand Policies for Long-run Growth 89

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

first step to evaluate such an impact consists in the assessment of the varia-tion of the realized rate of profit induced by a higher real wage (see theAppendix, equation (A3)):

∂∂

rr

t g ur u u r u r z

u u r t u r*

sf

s s s s s s

s s s s s

=− + −( ) −( ) −[ ]{ }

−( ) −ρ

ρ

1 βρ β(( ) −[ ] − −( ) +[ ] + −( )[ ]β βz s g r g u s g ut u2 1 2s s u s

(24)

Using (19) it can be immediately checked that the numerator of this expres-sion is always positive. Hence, the relevant condition for (24) to be positive is

β βz u r

uu t s gt g u r s g

− −( ) < −( )− −( )[ ]s s

s u

s s

2

1 2ρ(25)

which is exactly (C3), the sufficient condition for the stability of the steadystate. So, when condition (25) is met, the steady state of the system is stableand an increase in the real wage will make the realized rate of profit grow.The degree of capacity utilization and the growth rate of the economy will behigher as well (just look at equation (A1) in the Appendix and the investmentfunction (16)). This new equilibrium is not yet a new steady state. Indeed, thehigher rate of profit will be such that r > rsf and, as we know, firms will reviseupward their target rate of return, rsf. But, given that (25) holds, the systemis stable and (∂r/∂rsf) < 0, the realized rate of profit will go down and theequality between r and rsf will be finally restored at a higher level than inthe original steady state. So, in the new steady state the realized rate of profit,the rate of capacity utilization and the rate of growth of the capital stock willall be higher than before. The paradox of costs may well hold in this openeconomy Kaleckian framework. Does this mean that in such a framework theparadox of costs always holds? If it did, this would impoverish the model alot, since a hopefully general model should leave room for a more standard,negative long-run relation between the real wage and the growth rate.Suppose that the sufficient condition for the stability of the steady state isviolated and instead

β βz u r

uu t s gt g u r s g

− −( ) < −( )− −( )[ ]s s

s u

s s

2

1 2ρ(26)

holds. We know that in such a circumstance (∂r/∂us) < 0 and a lower real wageincreases the realized rate of profit, the rate of capacity utilization and the

90 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

rate of growth. However, this is not enough to say that the standard, negativelong-run relation between real wages and growth may actually materialize inthis economy. To this purpose we have to show that, although (25) does nothold and (∂r/∂rsf) > 0, the model is still stable. This will force us to look at thenecessary condition for the stability of the steady state, i.e. (∂r/∂rsf) < 1. From(22), this condition amounts to

ββ α

z u ruu t s g t g u u r

t g u r s g− −( ) >

−( ) − −( )− −( )[ ]s s

s u s s

s s

2 1

1 2

ρ

ρ(27)

which is not necessarily implied by (26). However, it is straightforward to seethat (26) and (27) may well coexist and in this case the model has a stablesteady state where the paradox of costs does not hold. We can thereforeconclude that under some parametric conditions and starting from someequilibria, the model is stable and the paradox of costs does not apply;instead, under other parametric conditions and starting from other equilib-ria, the model is stable but the paradox of costs holds. Briefly, this post-Keynesian model is sufficiently general, it does not necessarily imply thevalidity of the paradox of costs and therefore its essential conclusion—thepreservation of the main result of the Kaleckian model, i.e. the endogenousdetermination of the degree of capacity utilization in the long run—may betaken seriously.

5. CONCLUSION

In this paper I have tried to argue that the preservation of the key charac-teristic of the Kaleckian model––the endogenous determination in the longrun of the degree of capacity utilization—does not require either very specificassumptions concerning the notions of ‘long-run’ and ‘normal’ degree ofcapacity utilization or a model where the paradox of costs is necessarily validin the long run. A less demanding theory of flexible mark-ups in an openeconomy may do the job. This theory, compared with previous contributionsin this same direction, has some degree of generality, since the open economyKaleckian model that has been proposed does not imply as a necessary resultthe validity of the paradox of costs, which is just a possibility. Shifting theemphasis from the conflict between workers and capitalists over productshares to the infra-capitalistic conflict between domestic and foreign firmsover market shares preserves the Kaleckian vision of the long run––i.e. a

Demand Policies for Long-run Growth 91

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

theory of demand-led growth––while at the same time providing a moreconvincing description of modern, globalized and oligopolistic economies.

APPENDIX

To study the stability of the steady-state equilibrium for the system (14)–(19),we have to calculate the derivative of r, the realized rate of profit, with respectto rsf, the rate of return targeted by firms. To this purpose, just totallydifferentiate the system (14)–(19):

s g r g u−( ) − =2 1 0d d (A1)

d d ds

s ssu

ur

rur

r= − (A2)

d d ds sfr r z= +α β (A3)

d d + ds

s s s ssz

uu r

zu r

r=− −

ρ (A4)

t t uρd diρ + = 0 (A5)

Using (A5), (A4) can be rewritten as

d d ds s

su s

s s

zz

u rr

t ut u r

u=−

−−( )ρ

(A6)

Now insert (A6) into (A3) to get

d d dss s

s ssf

u s

s s

ru r

u r zr

t ut u r z

u= −( )−( ) −

−−( ) −[ ]

αβ

ββρ

(A7)

Then insert (A7) into (A2):

92 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

d ds s s

s s s u s

s s

s

uu t u r z

rt u r ut ur

ut u r

rt u=

−( ) −[ ]−( ) −[ ]

−−( )ρ

ρ

ρ

ρ

ββ

αss s u s

sfd−( ) −[ ]r ut u

rβ (A8)

Finally, by putting (A8) into (A1), one gets expression (24) of the text.

REFERENCES

Auerbach, P., Skott, P. (1988): ‘Concentration, competition and distribution’, InternationalReview of Applied Economics, 2, pp. 42–61.

Blecker, R. (1999): ‘Kaleckian macro models for open economies’, in Deprez, J., Harvey, J. T.(eds): Foundations of International Economics. Post Keynesian Perspectives, Routledge,London and New York.

Cassetti, M. (2002): ‘Conflict, inflation, distribution and terms of trade in the Kaleckian model’,in Setterfield, M. (ed.): The Economics of Demand-led Growth. Challenging the Supply-sideVision of the Long Run, Edward Elgar, Cheltenham, UK & Northampton, MA, USA.

Chick, V., Caserta, M. (1997): ‘Provisional equilibrium and macroeconomic theory’, in Arestis,P., Palma, G., Sawyer, M. (eds): Markets, Unemployment and Economic Policy: Essays inHonour of Geoff Harcourt, vol. 2, Routledge, London and New York.

Ciampalini, A., Vianello, F. (2000): ‘Concorrenza, accumulazione del capitale e saggio delprofitto’, in Pivetti, M. (ed.): Piero Sraffa, Carocci, Rome.

Commendatore, P. (2004): ‘Are Kaleckian models of growth and distribution relevant in thelong run?’, Paper presented at the conference ‘Economic Growth and Distribution: on theNature and Causes of the Wealth of Nations’, Lucca, Italy, June 16–18, 2004.

Duménil, G., Lévy, D. (1999): ‘Being Keynesian in the short term and classical in the long term:the traverse to classical long term equilibrium’, Manchester School of Economics and SocialStudies, 67, pp. 684–716.

Dutt, A. K. (1997): ‘Equilibrium, path dependence and hysteresis in post-Keynesian models’, inArestis, P., Palma, G., Sawyer, M. (eds): Markets, Unemployment and Economic Policy:Essays in Honour of Geoff Harcourt, vol. 2, Routledge, London and New York.

Garegnani, P. (1992): ‘Some notes for an analysis of accumulation’, in Halevi, J., Laibman, D.,Nell, E. (eds): Beyond the Steady State: a Revival of Growth Theory, MacMillan, London.

Garegnani, P., Palumbo, A. (1998): ‘Accumulation of capital’, in Kurz, H. D., Salvadori, N.(eds): The Elgar Companion to Classical Economics, Edward Elgar, Cheltenham.

Kalecki, M. (1991): Collected Works of Michal Kalecki, vol. II, Capitalism: Economic Dynamics(ed. Osiatynski, J.; trans. Kisiel, C. A.), Oxford University Press, Oxford.

Kurz, H. D. (1996): ‘Normal positions and capital utilisation’, Political Economy, 2 (1),pp. 37–54.

Lavoie, M. (1992): Foundations of Post-Keynesian Economic Analysis, Edward Elgar,Cheltenham, UK & Northampton, MA, USA.

Lavoie, M. (1995): ‘The Kaleckian model of growth and distribution and its neo-Ricardian andneo-Marxian critique’, Cambridge Journal of Economics, 19 (6), pp. 789–818.

Lavoie, M. (1996): ‘Traverse, hysteresis, and normal rates of capacity utilization in Kaleckianmodels of growth and distribution’, Review of Radical Political Economics, 28 (4), pp.113–47.

Lavoie, M. (2002): ‘The Kaleckian growth model with target return pricing and conflict infla-tion’, in Setterfield, M. (ed.): The Economics of Demand-led Growth. Challenging theSupply-side Vision of the Long Run, Edward Elgar, Cheltenham, UK & Northampton, MA,USA.

Lavoie, M. (2003): ‘Kaleckian effective demand and Sraffian normal prices: towards a recon-ciliation’, Review of Political Economy, 15 (1), pp. 53–74.

Demand Policies for Long-run Growth 93

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd

Marglin, S., Bhaduri, A. (1990): ‘Unemployment and the real wage: the economic basis forcontesting political ideologies’, Cambridge Journal of Economics, 14, pp. 375–93.

Park, M. S. (1997): ‘Normal values and average values’, Metroeconomica, 48, pp. 188–99.Vianello, F. (1985): ‘The pace of accumulation’, Political Economy Studies in the Surplus

Approach, 1, pp. 69–87.

Marco MissagliaUniversity of PaviaDepartment of Public EconomicsC.so Strada Nuova 6527100 PaviaItalyE-mail: [email protected]

94 Marco Missaglia

© 2007 The AuthorJournal compilation © 2007 Blackwell Publishing Ltd