'CRITICAL SUCCESS FACTORS' FOR IMPLEMENTATION OF THEORY OF CONSTRAINTS IN SMALL & MID-SIZE...

125

[MSC Dissertation] 2012/201 3 ‘CRITICAL SUCCESS FACTORS’ FOR IMPLEMENTATION OF THEORY OF CONSTRAINTS IN SMALL & MID-SIZE ENTERPRISES IN INDIA BY SURENDRA PATIL A DISSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE AWARD OF A MASTERS DEGREE IN ENGINEERING BUSINESS MANAGEMENT SCHOOL OF ENGINEERING UNIVERSITY OF WARWICK OCTOBER 2012

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of 'CRITICAL SUCCESS FACTORS' FOR IMPLEMENTATION OF THEORY OF CONSTRAINTS IN SMALL & MID-SIZE...

[MSC Dissertation]

2012/2013

‘CRITICAL SUCCESS FACTORS’ FOR IMPLEMENTATION OF THEORY OF CONSTRAINTS

IN SMALL & MID-SIZE ENTERPRISES IN INDIA

BY

SURENDRA PATIL

A DISSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE

REQUIREMENTS FOR THE AWARD OF A MASTERS DEGREE IN

ENGINEERING BUSINESS MANAGEMENT

SCHOOL OF ENGINEERING

UNIVERSITY OF WARWICK

OCTOBER 2012

[MSC Dissertation] 2012/2013

Project Submission Pro -Forma

(to be bound in front of the submitted Dissertation) NAME :SURENDRA P. PATIL Student ID :0938536301 I wish the dissertation to be considered for (tick one only)

MSc in Cyber security & Management o

MSc in e-Business Management o

MSc in Engineering Business Management þ

MSc in Engineering Business Management for Defence & Security o

MSc in Enterprise Integration Management o

MSc in Innovation & Entrepreneurship o

MSc in International Technology Management o

MSc in Management for Business Excellence o

MSc in Manufacturing Systems Engineering o

MSc in Process Business Management o

MSc in Programme & Project Management o

MSc in Supply Chain & Logistics Management o

I have checked that my modules meet the requirements of the above award þ I confirm that I have included in my dissertation: An abstract of the work completed þ

A declaration of my contribution to the work and its suitability for the degree þ

A table of contents þ

A list of figures & tables (if applicable) þ

A glossary of terms (where appropriate) þ

A clear statement of my project objectives þ

A full reference list þ

I am willing for my marked dissertation to be used for staff training purposes

Signed: ……………………………………………. Date: 04/11/2012

[MSC Dissertation]

2012/2013

I N D E X

1. Declaration …………………………………………… i

2. Acknowledgement ……………………………………. ii

3. Abstract ……………………………………………….. iii

4. Table of Content ……………………………………… v

5. List of Tables………………………………………….. vii

6. List of Figures…………………………………………. viii

7. List of Annexures……………………………………... ix

8. Chapter – 1 : Introduction…..…………………………. 1

9. Chapter – 2: Literature Review ………………………. 3

10. Chapter – 3: Research Methodologies..………………. 44

11. Chapter – 4: Result Of Survey..………………………. 60

12. Chapter – 5: Discussion & Analysis.…………………. 65

13. Chapter – 6: Conclusions & Recommendations………. 93

14. Works Cited…………………………………………….. 96

15. Annexure – 1 : Cross case summary ..……..…………… 110

[MSC Dissertation] 2012/2013

Declaration

“I have read and understood the rules on cheating, plagiarism and appropriate referencing as outlined in my handbook and I declare that the work contained in this assignment is my own, unless otherwise acknowledged. No substantial part of the work submitted here has also been submitted by me in other assessments for my degree course, and I acknowledge that if this has been done an appropriate reduction in the mark I might otherwise have received will be made”. Surendra Patil

[MSC Dissertation]

ii

2012/2013

Acknowledgement

All my gratitude goes to the following people those who had helped me directly or indirectly for this project work;

My philosopher and role model, Mr. Utpat K D, who induced the interest towards TOC in overall and gave his unstinting support for selection of various organizations;

All consultants and respondents, those who are heading the organizations, and in spite of their busy schedule, gave me their valuable time to talk to me their valuable insights;

My supervisor, Dr. Sharad Varde for his understanding and guidance;

My amazing friends, P R Kulkarni, Jayant, Suresh Athani, Laxmikant Virpe for their help and support;

Last but not least I thank my wife Swati and daughter Pranoti. Without their support I would have not completed this task.

[MSC Dissertation]

iii

2012/2013

Abstract

Purpose of the research: -

Theory of Constraints is the invention of Israeli Physicist, Dr. Eliyahu Goldratt. This is a business philosophy, which helps the organizations (profit or non profit) to achieve global objective or goal of the organization, through systematic approach of understanding the cause and effect relationship and variation in the system in question.

Though in the western countries (especially Europe and US), TOC is well known and acknowledged in various industries, in India it comparatively has limited use, being alien to industrial culture. Recently many of organizations have started using TOC as a methodology for improving organizational performance in large and SME sector as well. Thus providing situational advantage to the researcher in selecting research subject at proper time.

The purpose of this study is to understand the issues pertaining to pre and post implementation and analyze the enablers as well inhibitors while implementing the Theory Of Constraint in Small and Medium size enterprises particularly Indian contest.

Research Methodology: -

To enrich understanding of research question, a relevant literature survey was carried out. The topics covered mainly consist of Indian SMEs characteristics, TOC philosophy, recent advances in the tools and techniques and issues in the change management. Based on literature survey, initial research model was developed for identifying key factors, which will leads to successful implementation of TOC.

As the population of the SMEs those who are exposed to TOC, being limited, researcher opted for interviewing the respondent personally and not administer the question are impersonally to avoid the limitation of survey based research through mailed questionnaire. With the help of TOC consultants, 20 organizations from four different states of India were shortlisted after getting their concurrence. Semi structured questionnaire for interview and structured questionnaire for collecting the data for survey was formulated. And with extensive travel, researcher personally visited to all organizations to meet the respondent and collect the data. Thus providing the researcher advantage of meeting the respondent personally to get the first hand unbiased perception, with which it has significantly enhanced the quality, reliability and credibility

[MSC Dissertation]

iv

2012/2013

of study. After pilot study of three organizations, it was felt necessary to extend the research model further to include the scope of study for the inhibitors for the sustenance of TOC, along with earlier model which was included only enables.

Data collected was analyzed with the help of statistical (SPSS) software and hypothesis testing was done.

Finding: -

• Relation of strategic and tactical factors with organizational performance was found positive while as operational factors does not found relation with organizational performance

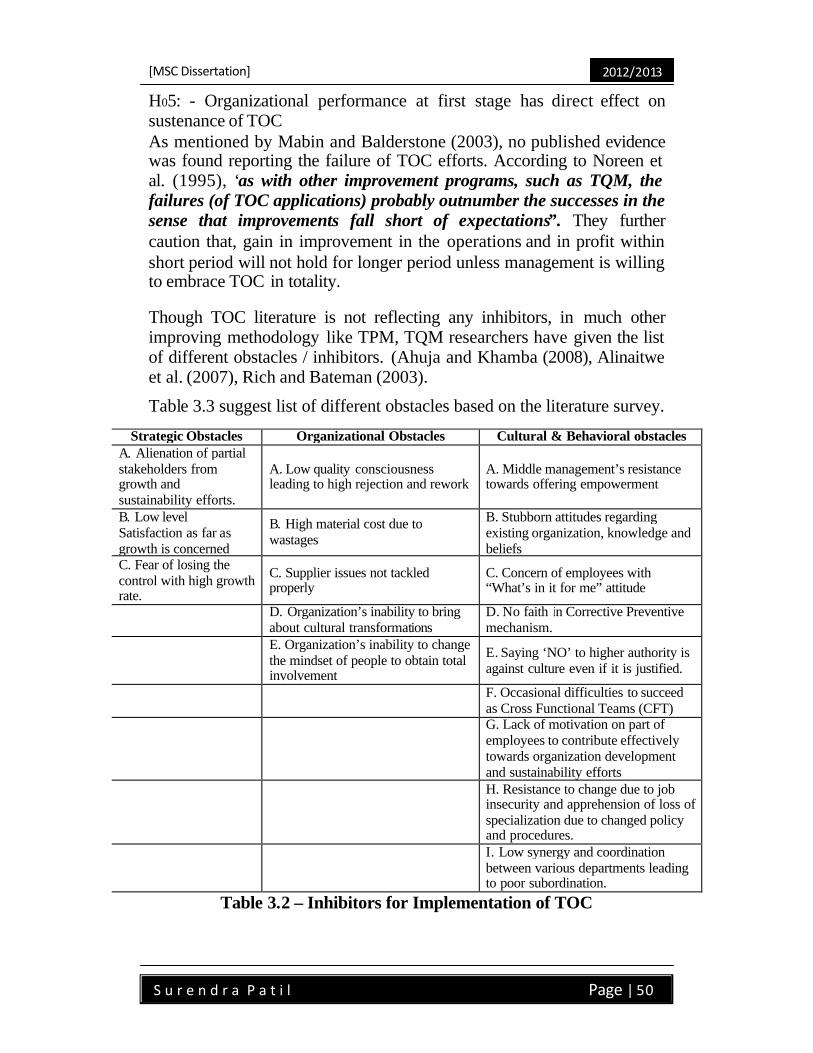

• A strategic and behavioral obstacle was found having positive relation with sustenance of TOC while as; an Organizational obstacle doesn’t show any relation.

• Alignment of operations with TOC principles found positive relation with sustenance of TOC.

• Results at first stage do not have any relation with sustenance.

Implication: -

This research will help SME in shaping their growth strategies and enrich their implementation plan with giving due consideration to CFs and inhibitors while implementing TOC. It will also help them to know the factors, which go against sustenance of TOC

[MSC Dissertation]

v

2012/2013

T a b l e o f C o n t e n t

No. Of Contente

Contentes Page No.

Chapter 1 – Introduction 01 – 02 1.0 Research Background 01

1.1 Research Question 01 1.2 Research Aim & Objective 01 1.3 Research structure 02

Chapter 2 – Literature Review 03 – 43 2.0 Overview of Small and Medium Enterprises in India 03

2.1 Definition of SME 03 2.2 Today’s scenario of SME in India 04 2.3 Current performance of SMEs 08 2.4 Improvement in organizational performance 10

2.4.1 Need for improvement (Why change?) 10 2.4.2 Different Tools & techniques for organizational improvement 11

2.5 Historical background and basic concepts of TOC 15 2.5.1 Various components of TOC 17 2.5.2 Five focusing steps 18 2.5.3 Drum Buffer Rope (DBR) 19 2.5.4 Measurement System & Throughput accounting 19 2.5.5 Thinking Process tools (TP) 22

2.6 Implementation of TOC 26 2.6.1 TOC Implementation Roadmap 26 2.6.2 TOC Five question framework 27 2.6.3 U Shape template for TOC implementation 29 2.6.4 Viable vision 30 2.6.5 Strategy And Tactic tree 30

2.7 Change management 31 2.7.1 Basic Concept 31 2.7.2 Success factors for change management 33

2.8 Change management & TOC 34 2.9 TOC Implementation Results 37

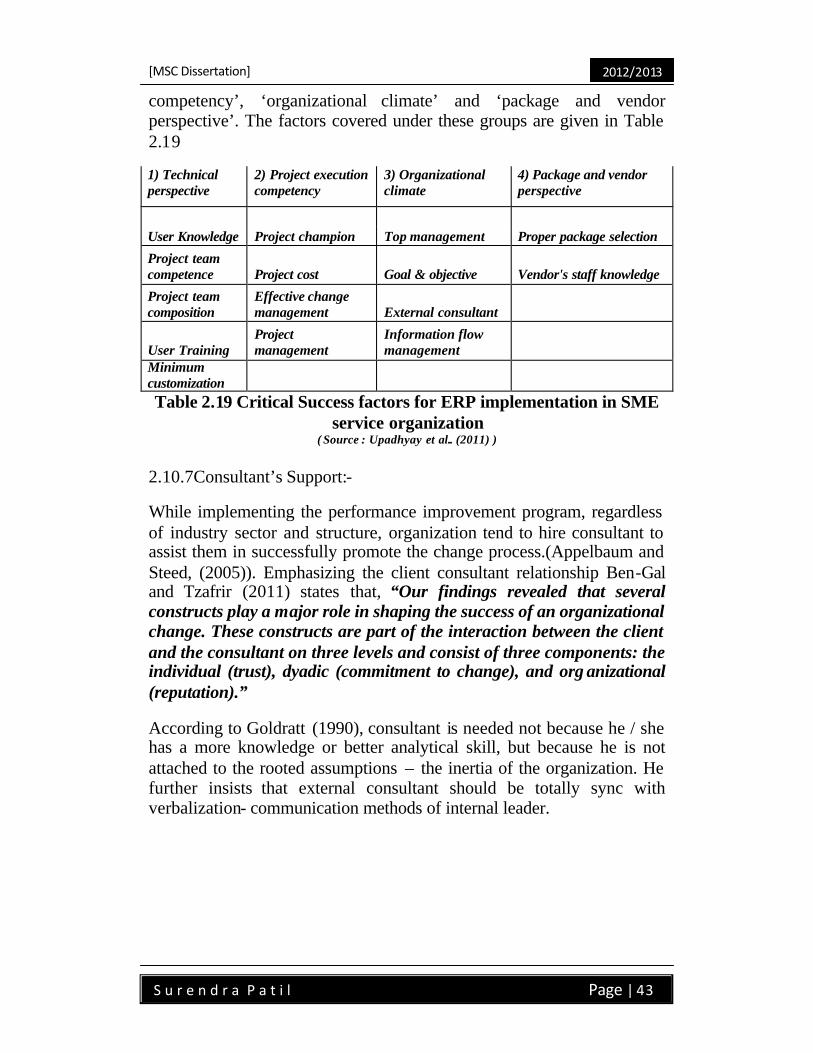

2.10 Critical Success Factors for Improvement project 40 2.10.1 CSF for TMP 41 2.10.2 CSF for TQM 41 2.10.3 CSF for Lean 42 2.10.4 CSF for Six Sigma 42 2.10.5 CSF for ISO-9000 42 2.10.6 CSF for ERP implementation 42 2.10.7 Consultant’s Support 43

[MSC Dissertation]

vi

2012/2013

No. Of Contente

Contentes Page No.

Chapter 3 – Research Methodology 44 – 59 3.0 Research Methodology 44

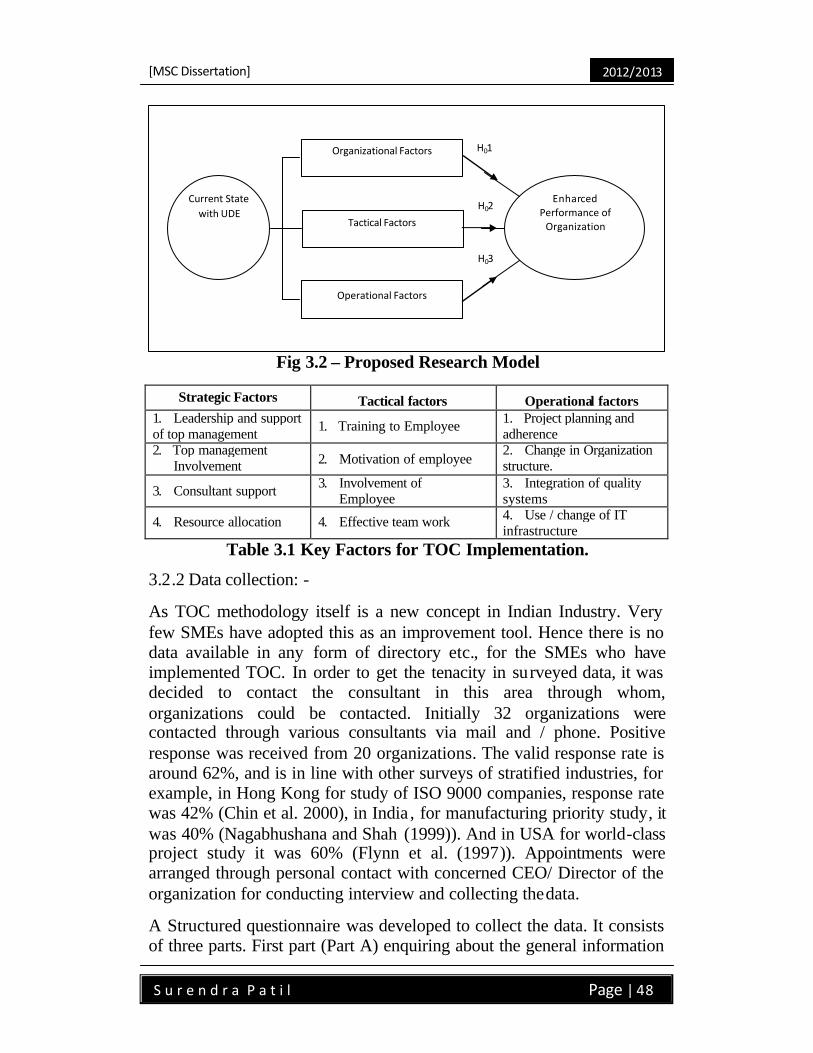

3.1 Selection of Methodology 45 3.2 Research Design 45

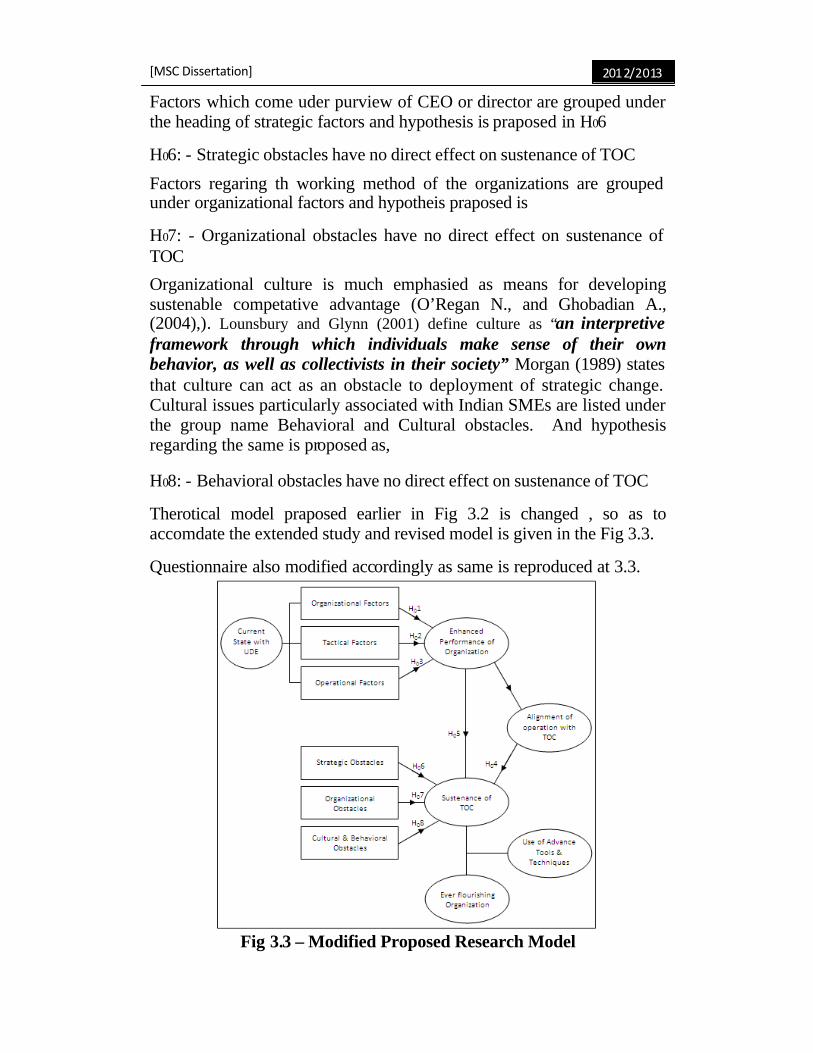

3.2.1 Development of research model and hypothesis 45 3.2.2 Data Collection 48 3.2.3 Pilot study and modification in research frame work 49 3.2.4 Modification in research model 49

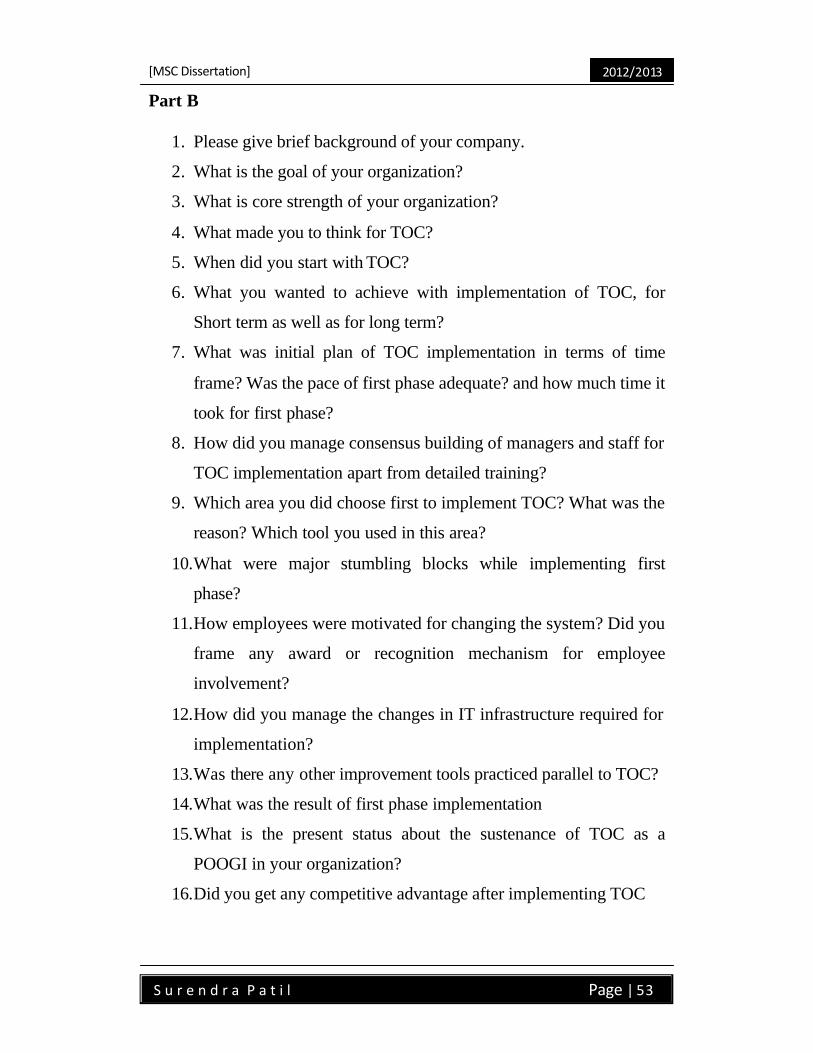

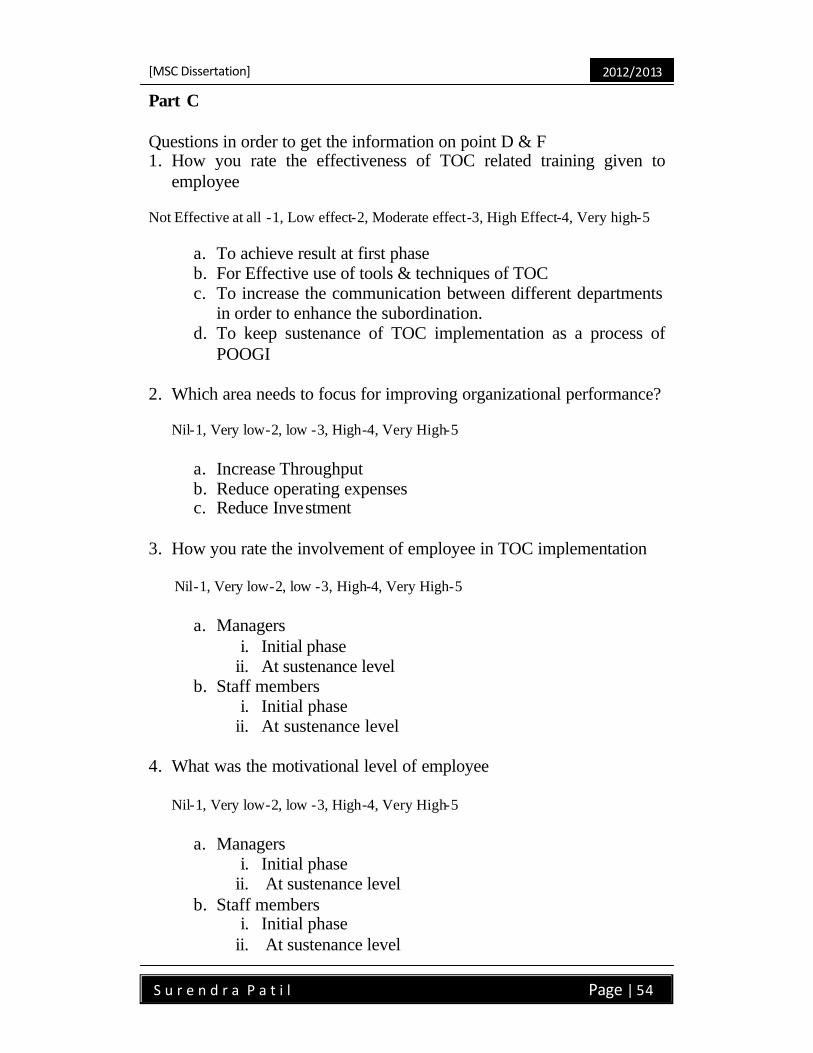

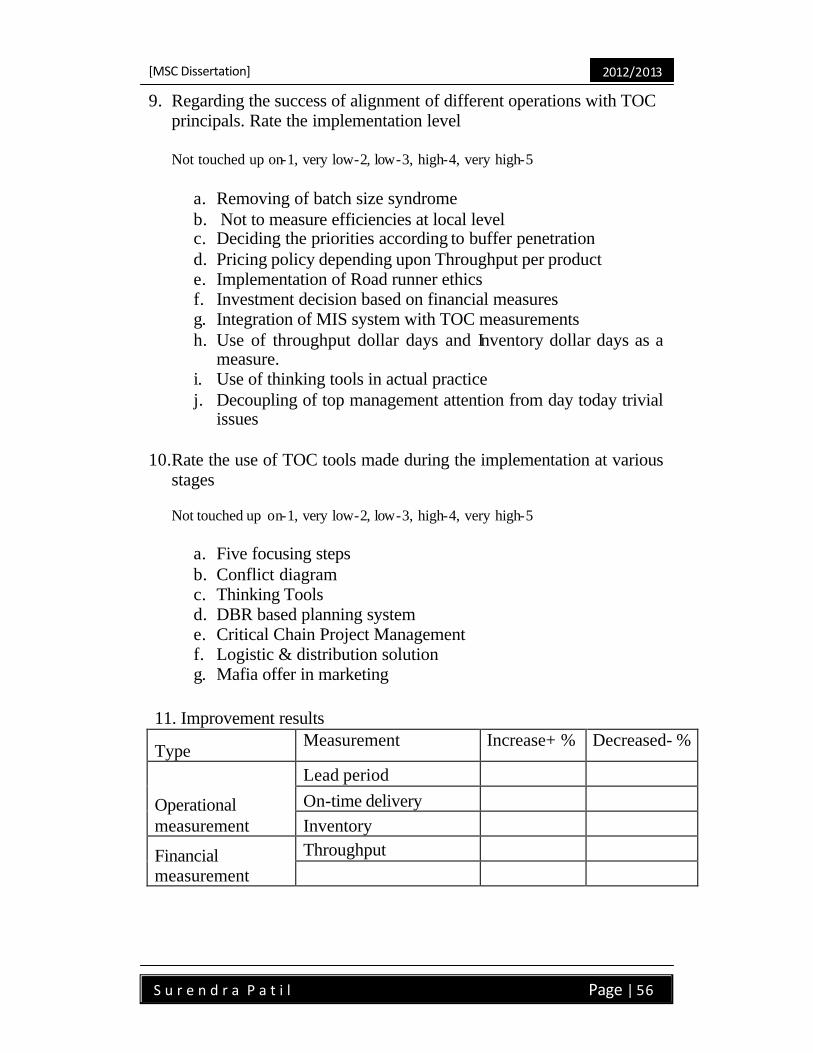

3.3 Questionnaire 51 3.4 Data Analysis 59

Chapter 4 – Result Summary 60 – 64 4.0 Research Results 60 Chapter 5 – Discussion & Analysis 65 – 92 5.0 Analysis and discussion 66

5.1 Demographic analysis 67 5.2 TOC implementation 68

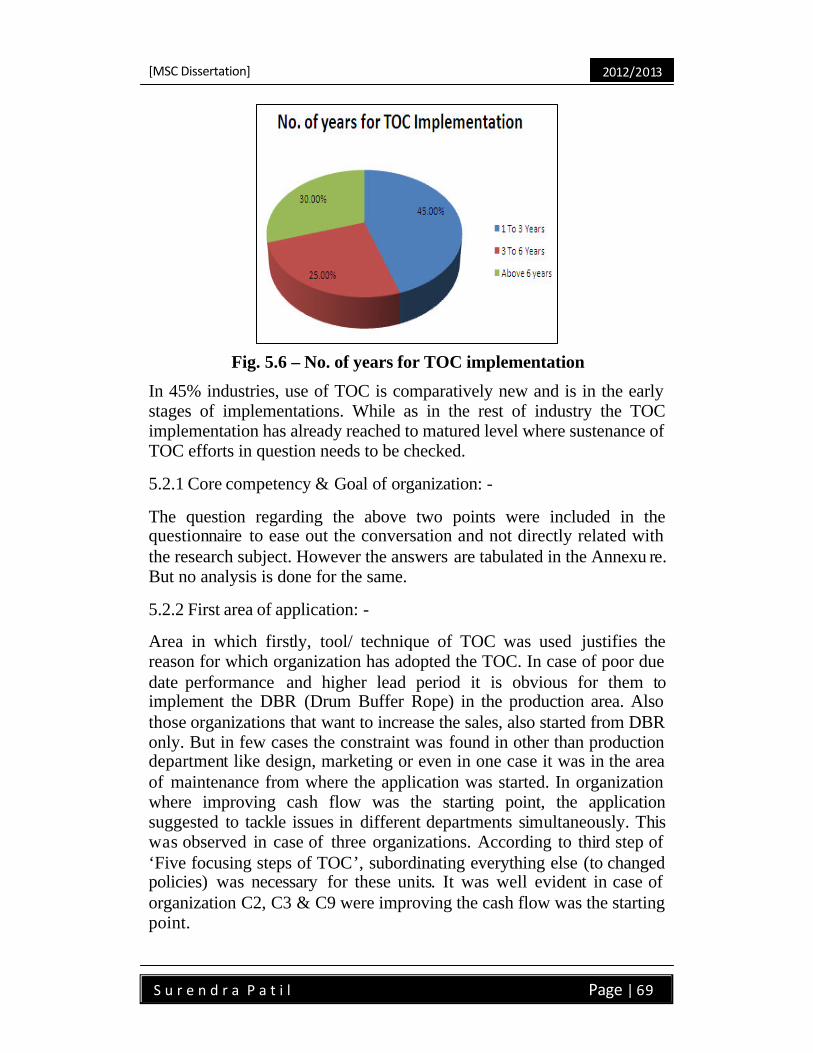

5.2.1 Core competency & Goal of organization 69 5.2.2 First area of application 69 5.2.3 Consensus building & Buy in 70 5.2.4 Major stumbling blocks 70 5.2.5 Employee motivation 70 5.2.6 Use of other tools & technique in support 70 5.2.7 Use of IT infrastructure 71 5.2.8 Competitive advantage 71 5.2.9 Sustenance 71

5.3 Understanding the process of change management 72 5.3.1 Effectiveness of training 72 5.3.2 Motivation, Involvement and resistance offered by employee 72 5.3.3 Top management involvement and support 72 5.3.4 Alignment with TOC thinking& TOC tools 72 5.3.5 Consultant’s support 73 5.3.6 Implementation results 73

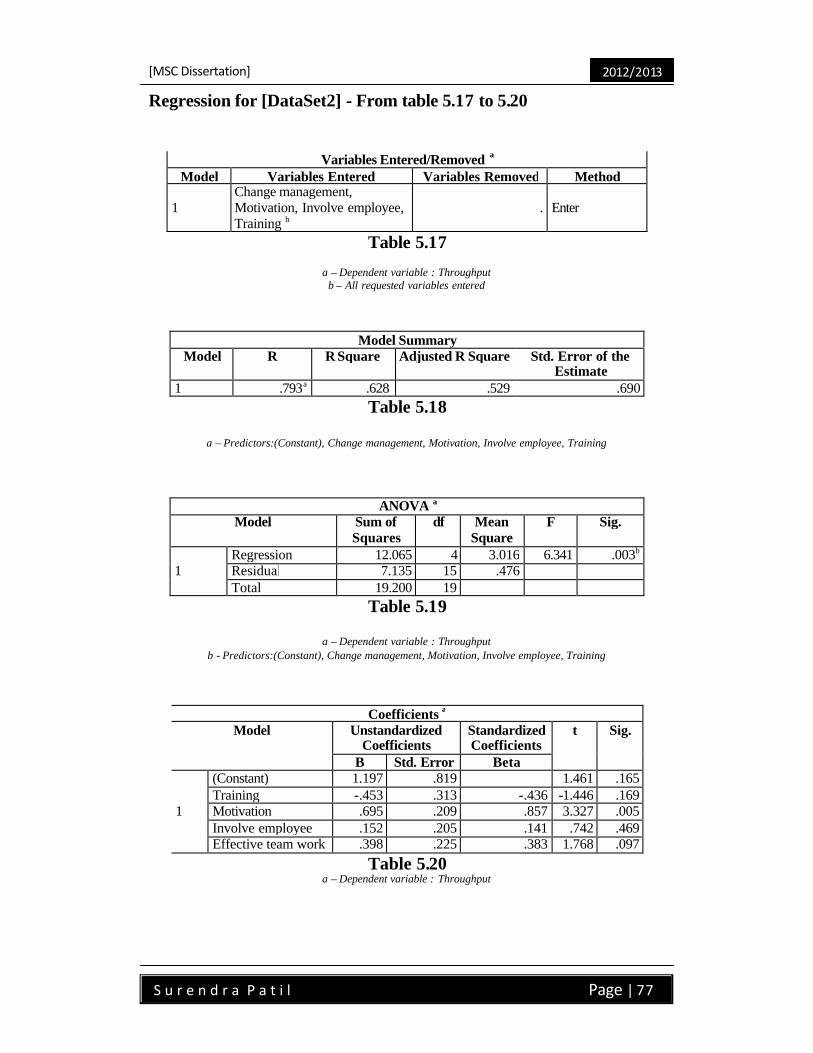

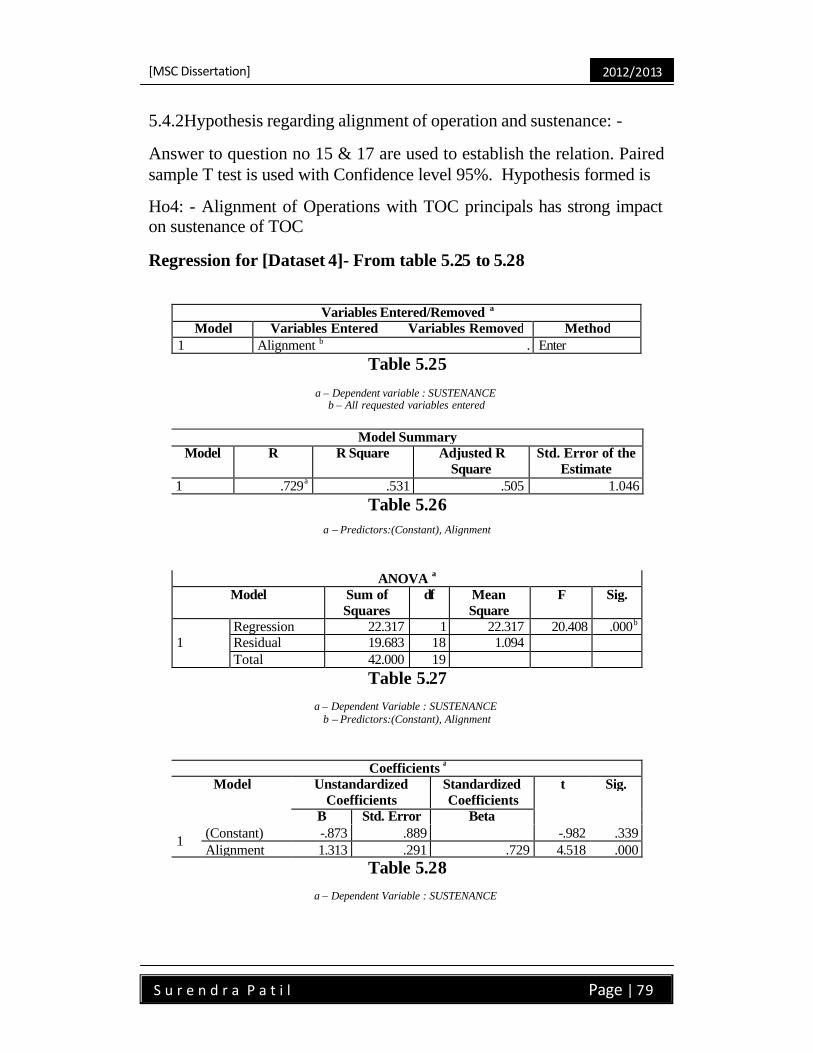

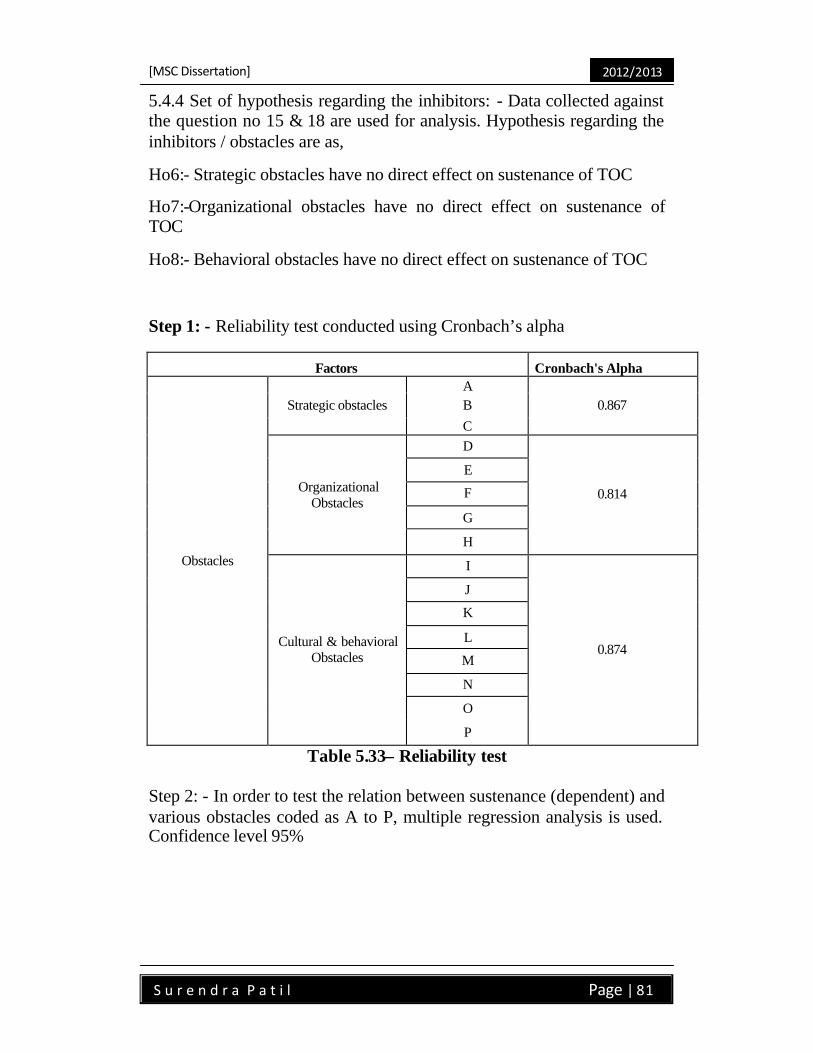

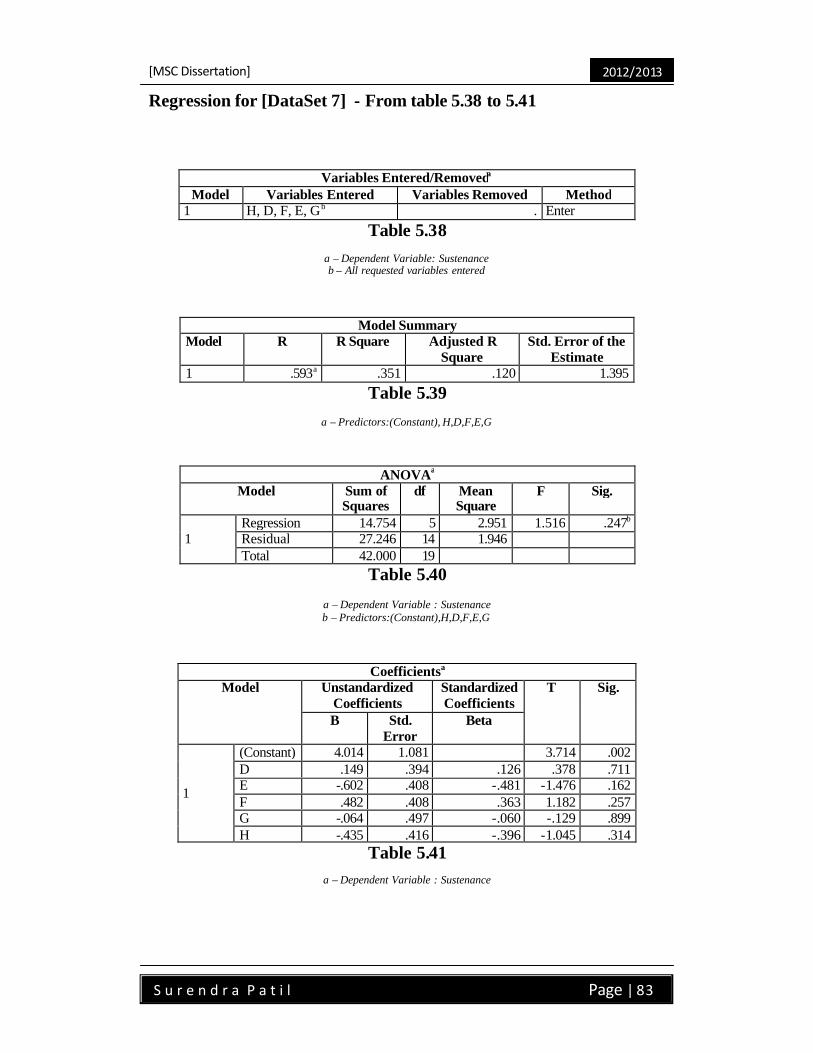

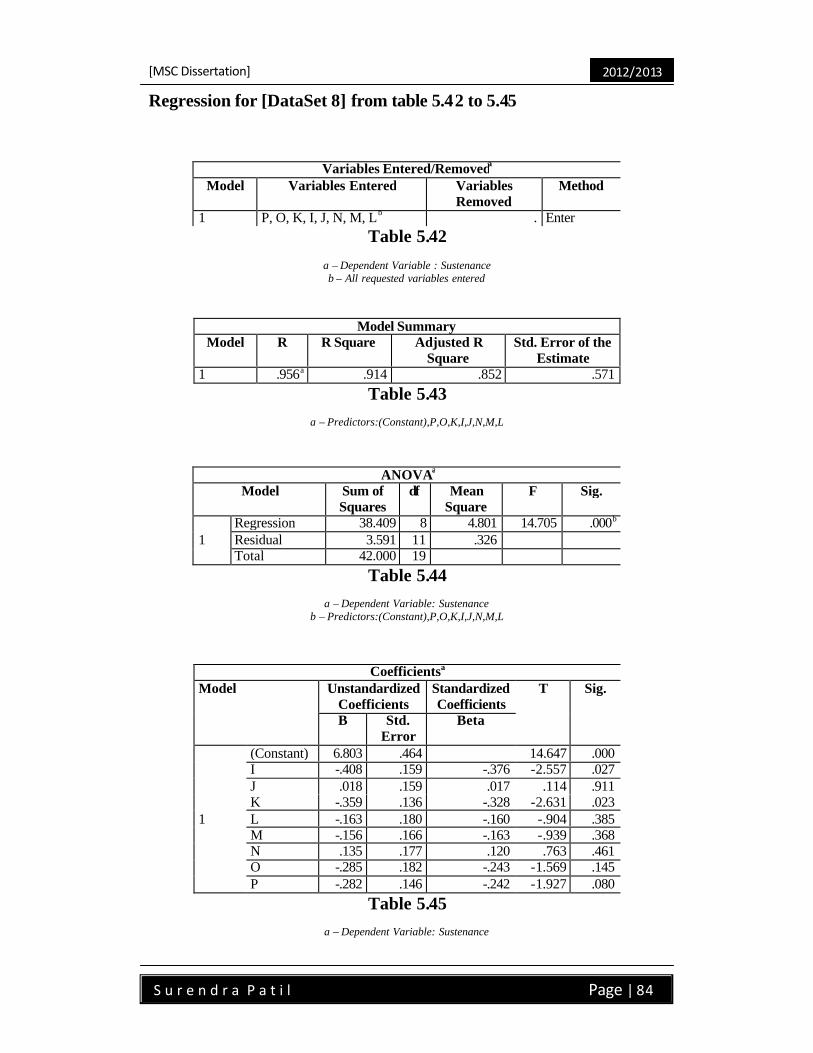

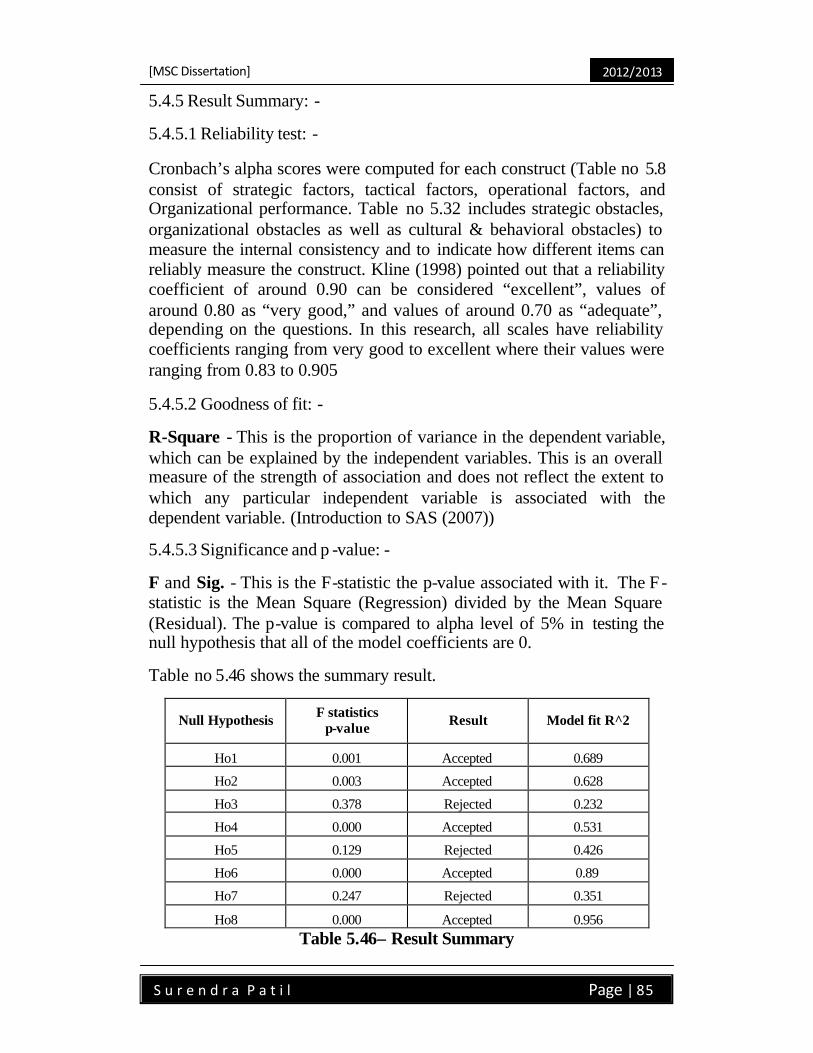

5.4 Rational in hypothesis testing 74 5.4.1 Set of hypothesis regarding key factors 74 5.4.2 Hypothesis regarding alignment of operation and sustenance 79 5.4.3 Hypothesis regarding performance results and sustenance 80 5.4.4 Set of hypothesis regarding the inhibitors 81 5.4.5 Result Summary 85

5.4.5.1 Reliability test 85 5.4.5.2 Goodness of fit 85 5.4.5.3 Significance and p-value 85

5.5 Discussion 86

[MSC Dissertation]

vii

2012/2013

No. Of

Contente Contentes Page No.

5.5.1 Part 1 86 5.5.2 Part 2 89

Chapter 6 – Conclusions & Recommendations 93 – 95 6.0 Conclusion & suggestion for further work 93

6.1 Conclusion 93 6.2 Suggestion for further work 95

Works Cited 96 – 109

List of Tables, Figures & Annexure

[A] List of Tables : Sr. Table No. Title of Table Page No. 1 2.1 MSMEs Performance: Units, Employment, Investments,

Production & Exports. 04

2 2.2 Comparative Data on Growth Rates of MSE Sector 07 3 2.3 Contribution of MSEs in GDP 07 4 2.4 Distribution of unites according to its activities 08 5 2.5 Distribution of unites according to its type 08 6 2.6 Cyclical process improvement methods and their primary

effect 11

2 2.7 High Failure Rate for Various Change Initiatives and IT Projects

14

3 2.8 Net Profit and Return on Investment 23 4 2.9 Application of TOC Thinking Process 23 5 2.10 How the logic trees relate to four management questions

about change 24

6 2.11 Definitions of selected Thinking Processes and concepts 25 7 2.12 TOC Implementation Phases 27 8 2.13 Simplified Generic Continuous Improvement Process Using

TOC’s TP 29

9 2.14 Resistance to change factors and TOC tools to help utilize them

35

10 2.15 Layers of resistance and their relationship to buy- in 36 11 2.16 Change sequence, tools and managerial utility relationships 37 12 2.17 TOC Elements 39 13 2.18 Critical Success factors for TPM implementation in SME 41 14 2.19 Critical Success factors for ERP implementation in SME

service organization 43

17 3.1 Key Factors for TOC Implementation 48 18 3.2 Inhibitor for Implementation of TOC 50

[MSC Dissertation]

viii

2012/2013

Sr. Table No. Title of Table Page No. 19 4.1 Organization Information 60 20 4.2 Effectiveness of Training 61 21 4.3 Mindset Of Organization 61 22 4.4 Involvement, Motivation & resistance offered 62 23 4.5 Top Management Commitment 62 24 4.6 Contribution made by consultant 62 25 4.7 Alignment of operations with TOC principals 63 26 4.8 TOC Tools 63 27 4.9 Improvement Results after TOC implementation 64 28 4.10 Employee Retention 64

5.1 Area of different states and it’s population 65 29 5.2 Organization age wise distribution 65 30 5.3 Employees wise distribution 66 31 5.4 Turnover wise distribution 66 32 5.5 Present investment wise distribution 67 33 5.6 Reasons for Adopting TOC Methodology 68 34 5.7 No. of years for TOC implementation 68 35 5.8 Implementation Results 74 36 5.9 Reliability Test 74 37 5.10–5.12 Factor Analysis 75 40 5.13–5.16 Regression – [Dataset 1] 76 44 5.17–5.20 Regression – [Dataset 2] 77 48 5.21–5.24 Regression – [Dataset 3] 78 52 5.25–5.28 Regression – [Dataset 4] 79 56 5.29–5.32 Regression – [Dataset 5] 80 60 5.33 Reliability test 81 61 5.34–5.37 Regression – [Dataset 6] 82 65 5.38–5.41 Regression – [Dataset 7] 83 69 5.42–5.45 Regression – [Dataset 8] 84 70 5.46 Result Summary 85

[B] List of Figures :

Sr. Fig. No. Title of Figure Page No. 1 2.1 Total MSMEs Vs total employment 05 2 2.2 Comparing the growth rate of MSMEs with IIP &GDP(%) 06 3 2.3 Fixed investment Vs employment in MSMEs 06 4 2.4 TOC Branches 17 5 2.5 Basic TOC tools & It’s use in specific environment 18 6 2.6 An Integrated TOC framework 20 7 2.7 Limits to T, I, and OE 22 8 2.8 Management Priorities 22 9 2.9 The six logical tools as an integrated thinking process 24

[MSC Dissertation]

ix

2012/2013

Sr. Fig. No. Title of Figure Page No. 10 2.10 TOC Implementation Roadmap 26 11 2.11 5-Step roadmap for implementation & monitoring of TOC

project 28

12 2.12 U-S hape & The Question For Improving System 29 13 2.13 Strategy and Tactic tree 31 14 2.14 Eight Stage Model 32 15 2.15 Three dimensions of throughput orientations 40 16 3.1 A systematic approach for empirical research 44 17 3.2 Proposed Research Model 48 18 3.3 Modified Proposed Research Model 51 19 5.1 Organization age wise distribution 66 20 5.2 Employee wise distribution 67 21 5.3 Turnover wise distribution 67 22 5.4 Present investment wise distribution 67 23 5.5 Reasons for adopting TOC methodology 68 24 5.6 No. of years for TOC implementation 69

[C] List of Annexures :

Sr. Annex. No.

Title of Annexure Page No.

1 1 Annexure 1 110

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 1

Chapter 1:Introduction

1.0 Research Background:-Since after adoption of open economy, Indian SMEs are going through crucial phase. Global competition, fast economic growths, increased quality requirements, are some of the challenges faced by SME. To cope up this fast speed of changes in every field SME has adopted some or the other improvement techniques like Lean manufacturing, Six sigma, TQM, TPM etc. TOC is one between recently introduced in India and also increasingly used tool.

Theory of Constraints (TOC) is an overall management philosophy introduced by Dr. Eliyahu M. Goldratt in his 1984 book titled “The Goal” that is geared to help organizations continually achieve their goal. The title comes from the contention that any manageable system is limited in achieving more of its goal by a very small number of constraints, and that there is always at least one constraint. TOC is a large body of knowledge with a strong guiding philosophy of growth. Dr. Eliyahu M. Goldratt, who was the main driving force behind the development and practice of TOC. There is a network of individuals and small companies loosely coupled as practitioners around the world. In Indian SME, in spite of its popularity, use of TOC is limited because of many reasons.

TOC challenges the present way of managing the organization; in turn it fictitiously appears to challenging the ability of existing leader, hurting badly with personal ego at first instance. Because of which it seems to be difficult to buy the acceptance from the current management team at first instance. The success of TOC depends on the actions initiated holistically across the organization and not in one department in isolation. Hence there is big challenge lie in managing the change including the change in the mindset of the people in the organization. Though the tools and techniques are available in ‘Theory’ to manage this change, it would be helpful to check the relevance in case of the Indian and that’s to small and mid size organization. This study will help to guide the rapid progression in adoption of TOC in SME sector.

1.1 Research Question: - “What are the critical factors leading to successful implementation of Theory Of Constraints in Indian, small & mid-sized enterprises”

1.2 Research Aim & Objective: - This research aims to investigate the process through which TOC can be effectively implemented in Indian SME.

The following are the objectives

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 2

1. Understanding the critical steps in implementation of TOC 2. Understanding the dynamics of Indian SMEs in respect of

TOC implementation 3. Compare & identify the commonalities the challenges faced

by various units before, while and after implementation 4. Compare & identify the commonalities in process of

implementation. 5. Hypothesis the key factors of success.

Secondary objectives

1. Evaluate theoretical & empirical development in the area of TOC implementation

2. Address unresolved major issues 3. Introduce the most recent development in the field.

1.3 Research structure: - This work consists of different chapters laid down as below Chapter headings

1. Introduction • This chapter describe the background of research question,

giving overview to reader about the research area 2. Literature review

• Briefly containing the spectrum on which theory is based, current status of knowledge of application tools and broad base to enter in to research area.

3. Research methodologies • Procedure & Methods used to carry out the research in order

to satisfy the academic prerequisites & compliance 4. Result of survey

• Summary of finding of research 5. Discussion & analysis

• Finding of research are analyzed against the literature review and implications of results are discussed for its shortcomings

6. Conclusions & Recommendations • Summarizing whole research against its objective with

outcome of the research.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 3

Chapter 2:Literature Review

2.0 Overview of Small and Medium Enterprises in India: -The small and medium enterprise plays an important role in the industrial development of any country. Its importance is well acknowledged due to its significant contribution to employment generation, building the internal strength through export and satisfying needs of various socio-economic objectives of country.

2.1 Definition of SME: - Defining a Small & Medium Enterprise is itself a challenging task, as every country have their own definition for a SME. In India the Small and Medium Enterprise are broadly classified depending on the investment in plant and machinery, however comparing that to EU where it is based on the parameters of employment, turnover and asset size, and OECD on employment. At the same time the sales turnover has totally different criteria for establishment. According to “Micro, Small and Medium Enterprises Development Act2006” [1] the definitions are as below, Small enterprise

“An enterprise where the investment in plant and machinery [original cost excluding land and building and the items specified by the Ministry of Small Scale Industries vide its notification No. S.O. 1722(E) dated October 5, 2006] is more than Rs.2.5 Million but does not exceed Rs.50 Million” Medium enterprise “A medium enterprise is an enterprise where the investment in plant and machinery (original cost excluding land and building and the items specified by the Ministry of Small Scale Industries vide its notification No. S.O. 1722(E) dated October 5, 2006) is more than Rs.50Million but does not exceed Rs.100 Million.”

Enterprise

“The term enterprise in the manufacturing context stands for an industrial undertaking or a business concern involved in the production, processing or preservation of goods for the list of eligible industries in the First Schedule to the Industries (Development and Regulation Act), 1951”

2.2 Today’s scenario of SME in India: - Small and Medium Enterprises (SME’s) in India constitute an important segment of Indian economy. Before 1990, liberalization in economic ---------------------------------------------------------------------------------------------- [1] Ministry of Micro, Small & Medium Enterprises, Government Of India.http://www.msme.gov.in

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 4

policies, SME was not in the lime light. However in 1991 policies announced by Indian government were changed the scenario for SME. Few concessions of liberalization like, ‘No need for license to run the industry,’ ‘equity participation, no/fewer restriction on import of capital goods’ etc. has given boost to SME sector. This sector, which played important role in overall economy of the country, started playing pivotal role.

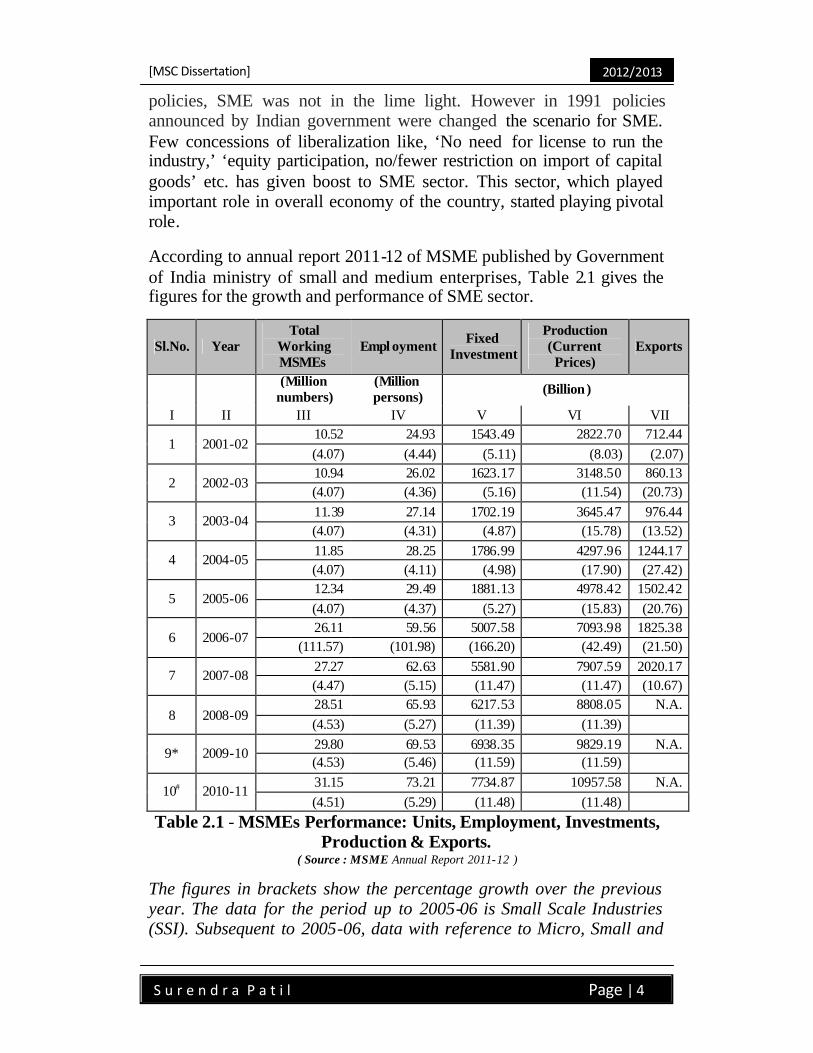

According to annual report 2011-12 of MSME published by Government of India ministry of small and medium enterprises, Table 2.1 gives the figures for the growth and performance of SME sector.

Sl.No. Year Total

Working MSMEs

Empl oyment Fixed Investment

Production (Current Prices)

Exports

(Million numbers)

(Million persons) (Billion)

I II III IV V VI VII

1 2001-02 10.52 24.93 1543.49 2822.70 712.44 (4.07) (4.44) (5.11) (8.03) (2.07)

2 2002-03 10.94 26.02 1623.17 3148.50 860.13 (4.07) (4.36) (5.16) (11.54) (20.73)

3 2003-04 11.39 27.14 1702.19 3645.47 976.44 (4.07) (4.31) (4.87) (15.78) (13.52)

4 2004-05 11.85 28.25 1786.99 4297.96 1244.17 (4.07) (4.11) (4.98) (17.90) (27.42)

5 2005-06 12.34 29.49 1881.13 4978.42 1502.42 (4.07) (4.37) (5.27) (15.83) (20.76)

6 2006-07 26.11 59.56 5007.58 7093.98 1825.38

(111.57) (101.98) (166.20) (42.49) (21.50)

7 2007-08 27.27 62.63 5581.90 7907.59 2020.17 (4.47) (5.15) (11.47) (11.47) (10.67)

8 2008-09 28.51 65.93 6217.53 8808.05 N.A. (4.53) (5.27) (11.39) (11.39)

9* 2009-10 29.80 69.53 6938.35 9829.19 N.A. (4.53) (5.46) (11.59) (11.59)

10# 2010-11 31.15 73.21 7734.87 10957.58 N.A. (4.51) (5.29) (11.48) (11.48)

Table 2.1 - MSMEs Performance: Units, Employment, Investments, Production & Exports.

( Source : MSME Annual Report 2011-12 )

The figures in brackets show the percentage growth over the previous year. The data for the period up to 2005-06 is Small Scale Industries (SSI). Subsequent to 2005-06, data with reference to Micro, Small and

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 5

Medium Enterprises are being compiled. The growth for the year 2010-11 is based on the average growth rate for the previous three years. * : Provisional, # : Projected, N.A. : Not Available

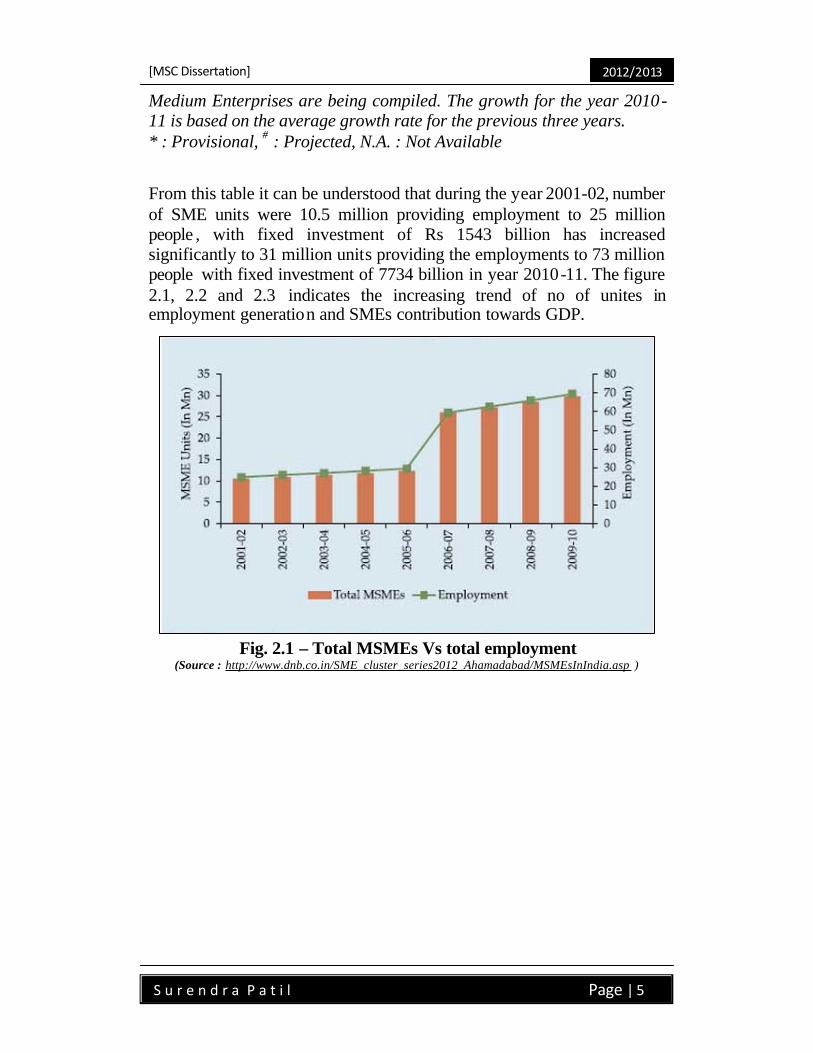

From this table it can be understood that during the year 2001-02, number of SME units were 10.5 million providing employment to 25 million people , with fixed investment of Rs 1543 billion has increased significantly to 31 million units providing the employments to 73 million people with fixed investment of 7734 billion in year 2010-11. The figure 2.1, 2.2 and 2.3 indicates the increasing trend of no of unites in employment generation and SMEs contribution towards GDP.

Fig. 2.1 – Total MSMEs Vs total employment (Source : http://www.dnb.co.in/SME_cluster_series2012_Ahamadabad/MSMEsInIndia.asp )

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 6

Fig. 2.2 – Comparing the growth rate of MSMEs with IIP &GDP(%) ( Source : http://www.dnb.co.in/SME_cluster_series2012_Ahamadabad/MSMEsInIndia.asp)

Fig. 2.3 – Fixed investment Vs employment in MSMEs ( Source : http://www.dnb.co.in/SME_cluster_series2012_Ahamadabad/MSMEsInIndia.asp)

SME sector has maintained a higher rate of growth as compared to overall industrial sector. Table 2 .2 gives the comparative figures for both the sectors. It indicates that growth of SME sectors was always ahead of overall industrial sector.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 7

Year Growth rate of SSI sector [2001-02 base IIP(%age)]

Over all Industrial sector Growth rates

(%age)#

2004-2005 10.88 8.40 2005-2006 12.32 8.00 2006-2007 12.60 11.90 2007-2008 13.00* 8.70 2008-2009 ** 3.20 2009-2010 ** 10.50 2010-2011 ** 7.80

Table 2.2 - Comparative Data on Growth Rates of MSE Sector ( Source : MSME Annual Report 2011-12 )

* : Projected, IIP – Index of Industrial Production # : Source – M/o Statistics and PI website – http://www.mospi.nic.in ** : Due to revised definition of MSMEs Sector, methodological revisions are under progress.

SME sector has been contributing considerably to India’s Gross Domestic production (GDP). The table 2.3 shows that SMEs contribution toward total industrial production was increased from 38 to 45 % from the year 2004-05 to 2008-09. And increase in the GDP was from 5.84% to 8.72%. K Jayakumar, (2011) Joint Secretary, Department of Scientific and Industrial Research, DST, recently said, that, ‘Contribution of small and medium enterprises to the country's gross domestic product (GDP) is expected to increase to 22% by 2020, from the present 17%.’

Year Contribution of MSEs(%) at 1999-2000 prices in

Total industrial Production Gross Domestic Product

(GDP) 2004-2005 38.62 5.84 2005-2006 38.56 5.83 2006-2007 45.62 7.20 2007-2008 45.24 8.00 2008-2009 44.86 8.72

Table 2.3–Contribution of MSEs in GDP ( Source : MSME Annual Report 2011-12 )

The data for the period upto 2005-2006 is for Small Scale Industries(SSI)

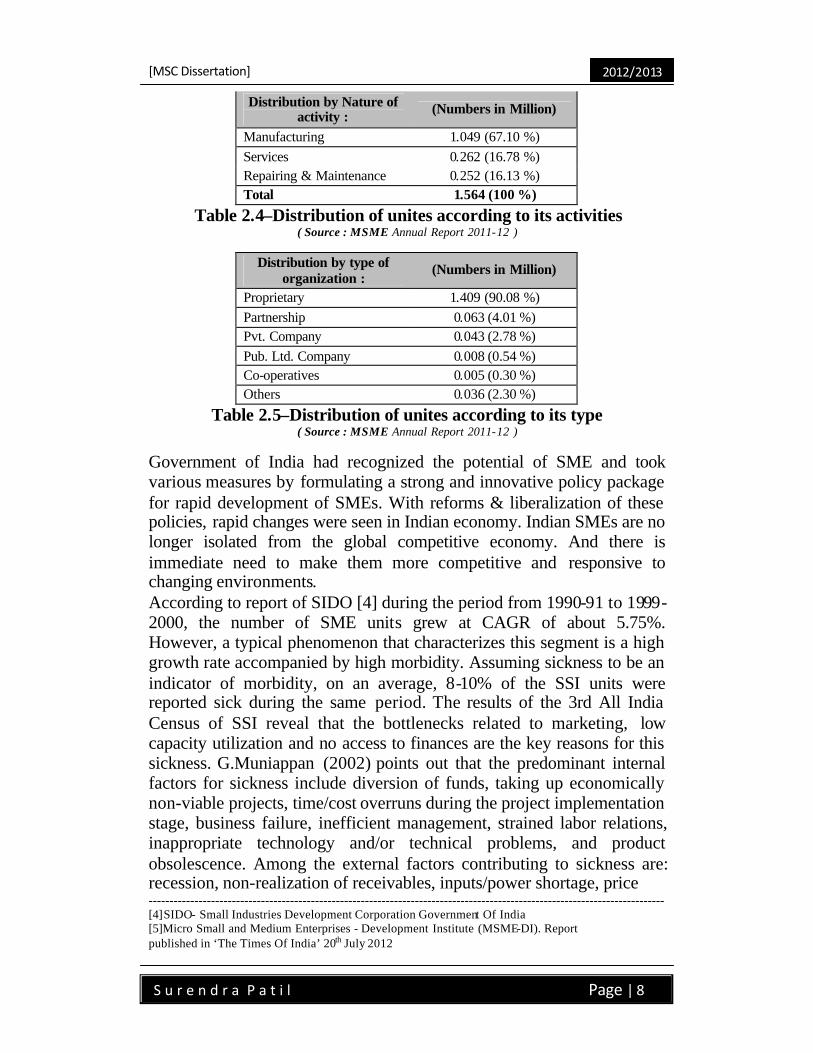

Table 2.4 & 2.5 gives the distribution of units according to its activities and type of organization. Majority of SMEs (67%) are engaged in manufacturing activities and rest engaged in servicing (16.78%) and repairing (16%). The proprietary organization (almost 90.8%) structure is dominant one in SME sector.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 8

Distribution by Nature of activity : (Numbers in Million)

Manufacturing 1.049 (67.10 %) Services 0.262 (16.78 %) Repairing & Maintenance 0.252 (16.13 %) Total 1.564 (100 %)

Table 2.4–Distribution of unites according to its activities ( Source : MSME Annual Report 2011-12 )

Distribution by type of organization :

(Numbers in Million)

Proprietary 1.409 (90.08 %) Partnership 0.063 (4.01 %) Pvt. Company 0.043 (2.78 %) Pub. Ltd. Company 0.008 (0.54 %) Co-operatives 0.005 (0.30 %) Others 0.036 (2.30 %)

Table 2.5–Distribution of unites according to its type ( Source : MSME Annual Report 2011-12 )

Government of India had recognized the potential of SME and took various measures by formulating a strong and innovative policy package for rapid development of SMEs. With reforms & liberalization of these policies, rapid changes were seen in Indian economy. Indian SMEs are no longer isolated from the global competitive economy. And there is immediate need to make them more competitive and responsive to changing environments. According to report of SIDO [4] during the period from 1990-91 to 1999-2000, the number of SME units grew at CAGR of about 5.75%. However, a typical phenomenon that characterizes this segment is a high growth rate accompanied by high morbidity. Assuming sickness to be an indicator of morbidity, on an average, 8-10% of the SSI units were reported sick during the same period. The results of the 3rd All India Census of SSI reveal that the bottlenecks related to marketing, low capacity utilization and no access to finances are the key reasons for this sickness. G.Muniappan (2002) points out that the predominant internal factors for sickness include diversion of funds, taking up economically non-viable projects, time/cost overruns during the project implementation stage, business failure, inefficient management, strained labor relations, inappropriate technology and/or technical problems, and product obsolescence. Among the external factors contributing to sickness are: recession, non-realization of receivables, inputs/power shortage, price ---------------------------------------------------------------------------------------------------------------------------- [4]SIDO- Small Industries Development Corporation Government Of India [5]Micro Small and Medium Enterprises - Development Institute (MSME-DI). Report published in ‘The Times Of India’ 20th July 2012

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 9

escalation, accidents and natural calamities. While mentioning the constraint for growth of SME in India Duke Ghosh (2007), states about weakness in terms of bargaining power vis-à-vis its customer. Many unites are catering to large companies and hence are fairly small in capacity and size with respect to such a customer. He also mention about inadequate and untimely finance made available to SME sector as one of constraint. As a result most players in this sector cannot undertake activities pertaining to product/process development and R&D, which could have improved the situation.

2.3 Current performance of SMEs: -

In order to be competitive one has to utilize its resources to its fullest extent. According to Balasubramaniya (2005), the ability of SMEs to compete in the global market place depends on their access to certain critical resources, the most important of which are finance, technology and managerial skills.

Evolving with changes is highly important to be competitive for SMEs, was stated by Rajiv Bajaj, (2011) He advised MSMEs to concentrate on their core strengths and avoid multi- tasking so that they are able to make the optimum use of their resources.

According to data compiled by the MSME-DI (2012), In India, 79 small business units are turning financially unviable every day. This translates to three units falling sick every hour. Report further states that, out of the total 13.3 Million SME units in the country, more than 0.2 Million are sick now. Around 29,000 units are being added to the sick list every year."Lack of enterprise management skills is the biggest reason, “said S Sivagnanam, director of MSME-DI.

Addressing the issue Pillani (2012) states that, though the government has been attempting various policy measures, however the efforts seemed to be inadequate. The tough competition in the both domestic and international market is very stiff. So there is an urgent need to strengthen the SSI sector in India by improving their organizational performance through various tools and techniques availa ble.

In concluding remark P Bharath (2010) mention that, “With the increasing competition, globalization and the uncertainty due to the global downturn, SMEs will have to continuously incorporate the latest technology into their production processes as well as in their marketing and management functions, to cut costs, gain efficiency and consistency. This will help them become successful, and contribute to the Indian

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 10

economy in the long run.”

While emphasizing to take separate view for SME, Nicholas & Abby (2004) state that,’ It is important to understand that SMEs are not smaller versions of larger firms. Their needs and often their decision-making processes differ significantly from those of larger firms (Shrader et al., 1989). Other distinct differences include limited resources, lack of specialist expertise (Carson, 1985), reliance on a few key customers (Venkatraman et al., 1990), and unable to influence, to any significant degree, the threats of the external environment (Cromie, 1990).’

Ahire (1996) characterized SMEs by a myopic view of management. Lack of planning, systematic decision-making and strategic thinking makes them vulnerable to competitive environment. M Gupta (2010) describe, lack of trained workers, Lack of financial strength and management deficiency, as a critical factors for growth of SME and emphasize the need to configure & manage their operations to support their business and establish themselves.

2.4 Improvement in organizational performance 2.4.1 Need for improvement (Why change?): - Since from the adoption of liberal economy in 1991, SME in India are experiencing unprecedented degree of change, which involves the change in market condition, customer expectation and suppliers attitude. Management forced to adopt the change in overall business approach. As Kumar et al. (2006), states that,’ The contemporary business environment has become considerably complex and challenging, and as a result variety of factors influence the manufacturing organization’s ability to compete effectively. Organizations today compete on several factors such as time, price, technology, innovation, quality, reliability, and information management’.

According to Ahuja & Khamba (2008), dynamic environment has become highly challenging and the manufacturing organizations are finding it extremely difficult to manage competit ion and consumer expectations. The global marketplace has witnessed an increased pressure from customers and competitors for greater value from their purchaser. Quality, faster delivery, and lower cost in manufacturing have become the implied needs for sustainable business growth. Each organization is struggling with the same question, how one can add the value to our customer by keeping cost as low as possible , and delivery within the acceptable time. Organization found answer by using various tools & techniques developed over years.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 11

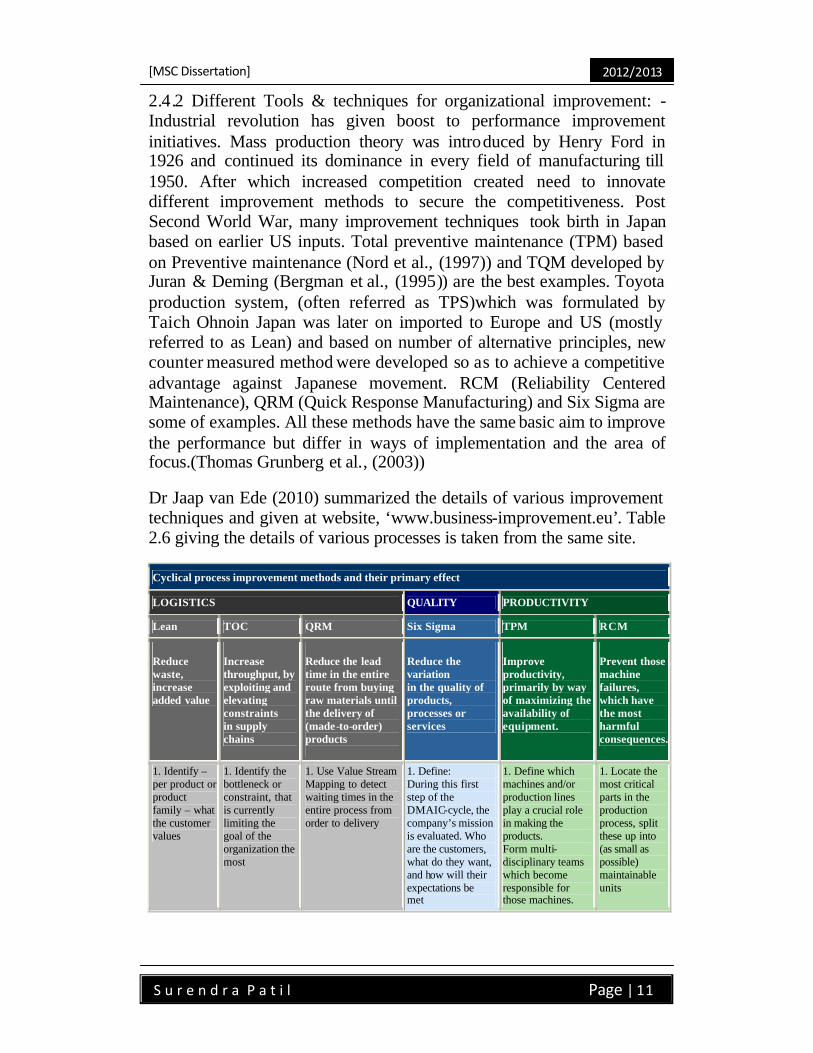

2.4.2 Different Tools & techniques for organizational improvement: - Industrial revolution has given boost to performance improvement initiatives. Mass production theory was introduced by Henry Ford in 1926 and continued its dominance in every field of manufacturing till 1950. After which increased competition created need to innovate different improvement methods to secure the competitiveness. Post Second World War, many improvement techniques took birth in Japan based on earlier US inputs. Total preventive maintenance (TPM) based on Preventive maintenance (Nord et al., (1997)) and TQM developed by Juran & Deming (Bergman et al., (1995)) are the best examples. Toyota production system, (often referred as TPS)which was formulated by Taich Ohnoin Japan was later on imported to Europe and US (mostly referred to as Lean) and based on number of alternative principles, new counter measured method were developed so as to achieve a competitive advantage against Japanese movement. RCM (Reliability Centered Maintenance), QRM (Quick Response Manufacturing) and Six Sigma are some of examples. All these methods have the same basic aim to improve the performance but differ in ways of implementation and the area of focus.(Thomas Grunberg et al., (2003))

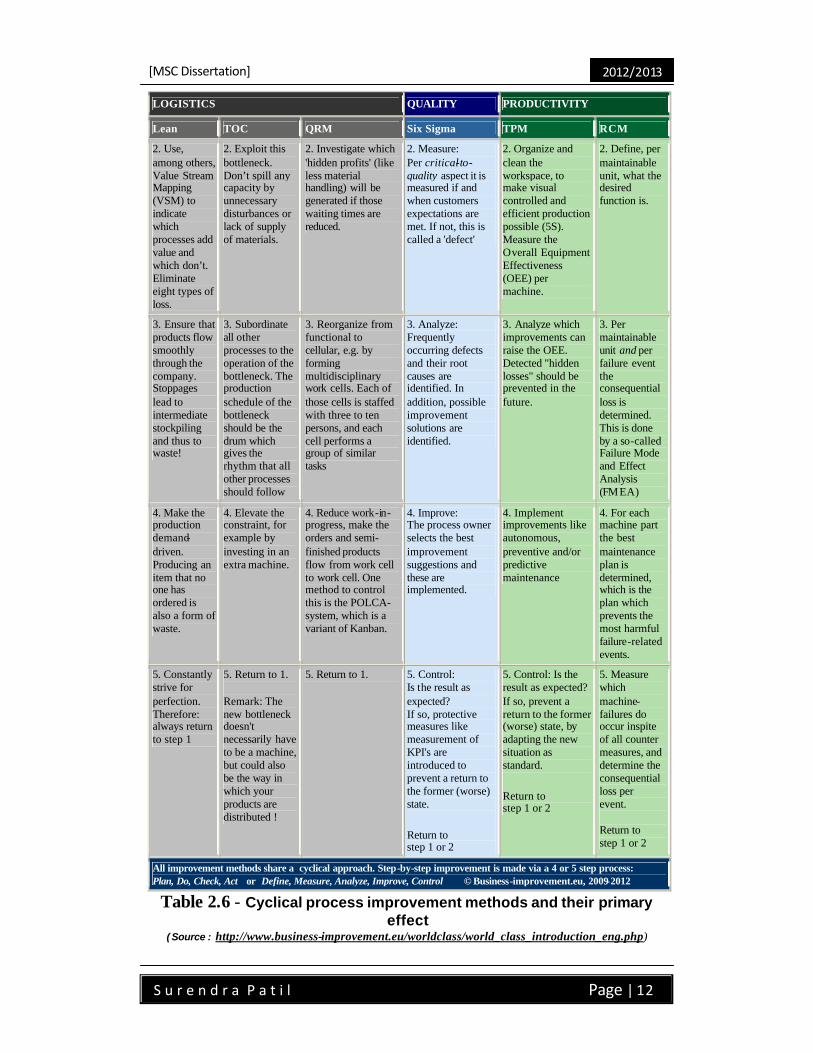

Dr Jaap van Ede (2010) summarized the details of various improvement techniques and given at website, ‘www.business-improvement.eu’. Table 2.6 giving the details of various processes is taken from the same site.

Cyclical process improvement methods and their primary effect

LOGISTICS QUALITY PRODUCTIVITY

Lean TOC QRM Six Sigma TPM RCM

Reduce waste, increase added value

Increase throughput, by exploiting and elevating constraints in supply chains

Reduce the lead time in the entire route from buying raw materials until the delivery of (made-to-order) products

Reduce the variation in the quality of products, processes or services

Improve productivity, primarily by way of maximizing the availability of equipment.

Prevent those machine failures, which have the most harmful consequences.

1. Identify – per product or product family – what the customer values

1. Identify the bottleneck or constraint, that is currently limiting the goal of the organization the most

1. Use Value Stream Mapping to detect waiting times in the entire process from order to delivery

1. Define: During this first step of the DMAIC-cycle, the company’s mission is evaluated. Who are the customers, what do they want, and how will their expectations be met

1. Define which machines and/or production lines play a crucial role in making the products. Form multi-disciplinary teams which become responsible for those machines.

1. Locate the most critical parts in the production process, split these up into (as small as possible) maintainable units

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 12

LOGISTICS QUALITY PRODUCTIVITY

Lean TOC QRM Six Sigma TPM RCM

2. Use, among others, Value Stream Mapping (VSM) to indicate which processes add value and which don’t. Eliminate eight types of loss.

2. Exploit this bottleneck. Don’t spill any capacity by unnecessary disturbances or lack of supply of materials.

2. Investigate which 'hidden profits' (like less material handling) will be generated if those waiting times are reduced.

2. Measure: Per critical-to-quality aspect it is measured if and when customers expectations are met. If not, this is called a 'defect'

2. Organize and clean the workspace, to make visual controlled and efficient production possible (5S). Measure the Overall Equipment Effectiveness (OEE) per machine.

2. Define, per maintainable unit, what the desired function is.

3. Ensure that products flow smoothly through the company. Stoppages lead to intermediate stockpiling and thus to waste!

3. Subordinate all other processes to the operation of the bottleneck. The production schedule of the bottleneck should be the drum which gives the rhythm that all other processes should follow

3. Reorganize from functional to cellular, e.g. by forming multidisciplinary work cells. Each of those cells is staffed with three to ten persons, and each cell performs a group of similar tasks

3. Analyze: Frequently occurring defects and their root causes are identified. In addition, possible improvement solutions are identified.

3. Analyze which improvements can raise the OEE. Detected "hidden losses" should be prevented in the future.

3. Per maintainable unit and per failure event the consequential loss is determined. This is done by a so-called Failure Mode and Effect Analysis (FMEA)

4. Make the production demand-driven. Producing an item that no one has ordered is also a form of waste.

4. Elevate the constraint, for example by investing in an extra machine.

4. Reduce work-in-progress, make the orders and semi- finished products flow from work cell to work cell. One method to control this is the POLCA-system, which is a variant of Kanban.

4. Improve: The process owner selects the best improvement suggestions and these are implemented.

4. Implement improvements like autonomous, preventive and/or predictive maintenance

4. For each machine part the best maintenance plan is determined, which is the plan which prevents the most harmful failure-related events.

5. Constantly strive for perfection. Therefore: always return to step 1

5. Return to 1. Remark: The new bottleneck doesn't necessarily have to be a machine, but could also be the way in which your products are distributed !

5. Return to 1. 5. Control: Is the result as expected? If so, protective measures like measurement of KPI's are introduced to prevent a return to the former (worse) state.

Return to step 1 or 2

5. Control: Is the result as expected? If so, prevent a return to the former (worse) state, by adapting the new situation as standard.

Return to step 1 or 2

5. Measure which machine-failures do occur inspite of all counter measures, and determine the consequential loss per event. Return to step 1 or 2

All improvement methods share a cyclical approach. Step-by-step improvement is made via a 4 or 5 step process: Plan, Do, Check, Act or Define, Measure, Analyze, Improve, Control © Business-improvement.eu, 2009-2012

Table 2.6 - Cyclical process improvement methods and their primary effect

( Source : http://www.business-improvement.eu/worldclass/world_class_introduction_eng.php)

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 13

Many researchers have made the immense contribution to all these tools & techniques & its use in different environment.

Most off SMEs, in order to be competitive, profitable and sustainable in business, pursue the tools based on logistic management perspective. The application of lean thinking has made a significant impact both in academia and industry over the last decade (Peter Hines (2004)). Lean has proven to be a vital tool to successfully achieve growth and sustainability in business.

Goldratt (2008) summarizes the basic concepts used in the tools, which are based on logistic approach as, “both Ford and Ohno followed four concepts

1. Improving flow (or equivalently lead time) is a primary objective of operations.

2. This primary objective should be translated into a practical mechanism that guides the operation when not to produce (prevents overproduction). Ford used space; Ohno used inventory.

3. Local efficiencies must be abolished.

4. A focusing process to balance flow must be in place. Ford used direct observation. Ohno used the gradual reduction of the number of containers and then gradual reduction of parts per container.

He also further states that, Ohnos approach in developing lean demonstrate the difference between the basic concept and its application. The fundamental concepts behind the improvement tool are generic but the application is translation of concept to specific environment. He also emphasizes on verbalizing the assumption behind the specific environment while applying specific tool. To prove his point he states the example of TPS. Most demanding assumption while implementing TPS is stability in the manufacturing environment.

While sharing experiences Ron Moor (2007) mentioned that, “Various tools or methods are touted as a means for a major step forward but never seem to quite deliver the expected results. For example, Bob Williamson, an industry expert in TPM, estimates that some 60% of TPM programs fail after three years of effort; Jeffrey Liker, an industry expert in Lean Manufacturing, estimates that less than1% of U.S. companies are truly effectively applying lean principles. Neil Bloom, an industry expert in reliability-centered maintenance (RCM)

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 14

estimates that over 60% of all RCM programs initiated are never successfully implemented, with many of the rest only done in a superficial way.”

Giving the reasons for such a failure Womack (2007) point out the shortcoming of efforts for tying of various individual tools (available in TPS) together in to system. As results many managers are drowned in techniques while implementing the bites of lean in isolation without understanding the whole system.

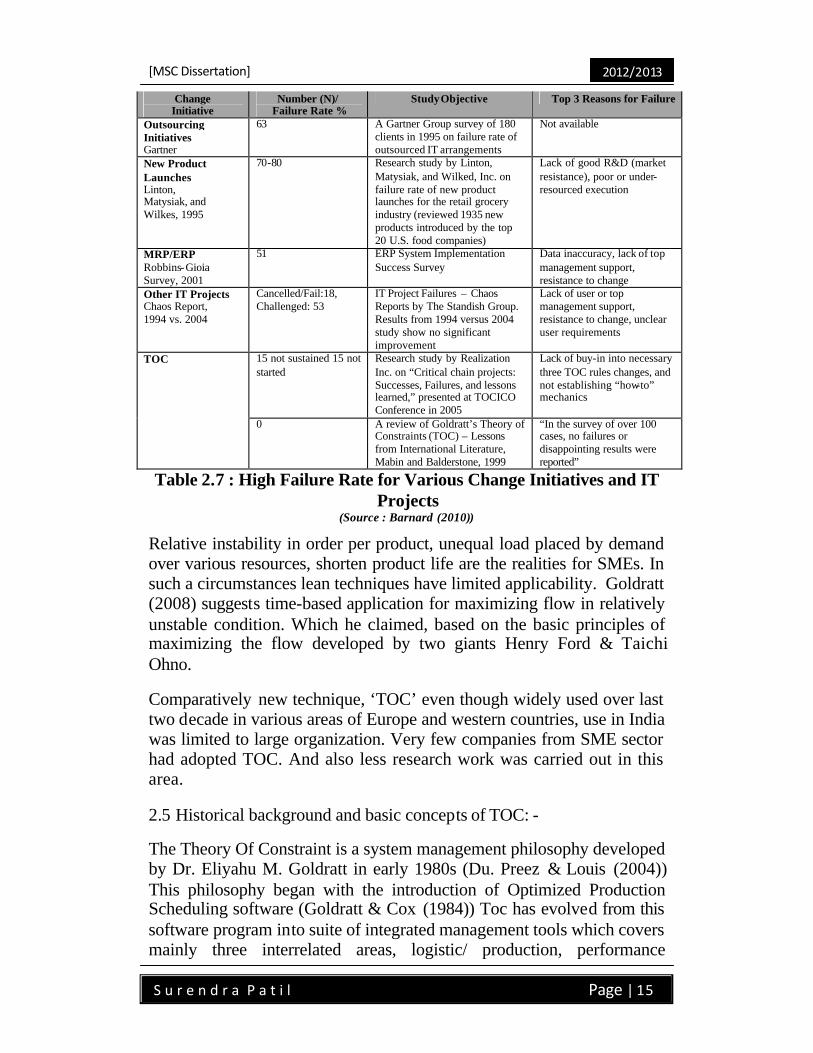

Oakland (2001) importantly pointed out as, understanding the environment of organization in which performance improvement tools are being used needs to be scanned thoroughly and needs translation of basic principals in to guiding mechanism. Barnard (2010) summarizes the various research studies and surveys as shown in Table 2.7. It shows that, 50 to 80 % improvement initiatives fail to meet their original objectives. These initiatives either stopped before completion or sometimes it caused decay in the organization’s performance. Only in case of TOC, study conducted by Mabin & Balderstone shown no failure.

Change Initiative

Number (N)/ Failure Rate %

Study Objective Top 3 Reasons for Failure

TQM A. D. Little, 1992

64(ADL) – 80 (ATK)

Survey of 500 companies by Arthur D. Little, survey by A. T. Kearney of 100 UK companies

Lack of top management support, resistance to change

Six Sigma Angel & Pritchard,2008 R.Farrelly,2008

60 “What went wrong with Six Sigma? A look into Six Sigma’s 60 percent failure rate,” July

Resistance to change and lack of top management support

>50 The top reasons Six Sigma Projects fail: Results from a survey of Six Sigma Projects in 114 companies, Ross Farrelly, AOQ Six Sigma Conference, Melbourne, August 2008

Partial implementation, Project not linked to ROI, poor management support

Lean R. G. Kallage, 2006

Well over 50 “Lean implementation failures: Why they happen, and how to avoid them,” Richard G. Kallage, July 11, 2006

Lack of top management support/poor business case, resistance to change, and poor deployment

Balanced Score Card G. DeBusk, 2006

70 “Does the balanced scorecard improve performance?” Study published in Management Accounting Quarterly, Fall 2006, Gerald K. DeBusk

Not available

Business Process Reengineering Dr. Malhotra, 1998

55-70 “Business process redesign: An overview,” BRINT Institute

Resistance to change (associated with downsizing)

Organizational Transformation J. Kotter, 2009

70 “Leading change: Why transformation efforts fail, survey of 100 company’s transformation efforts,” John P. Kotter, HBR, March 2009

Resistance to change, lack of urgency, lack of support from top management

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 15

Change Initiative

Number (N)/ Failure Rate %

Study Objective Top 3 Reasons for Failure

Outsourcing Initiatives Gartner

63 A Gartner Group survey of 180 clients in 1995 on failure rate of outsourced IT arrangements

Not available

New Product Launches Linton, Matysiak, and Wilkes, 1995

70-80 Research study by Linton, Matysiak, and Wilked, Inc. on failure rate of new product launches for the retail grocery industry (reviewed 1935 new products introduced by the top 20 U.S. food companies)

Lack of good R&D (market resistance), poor or under-resourced execution

MRP/ERP Robbins-Gioia Survey, 2001

51 ERP System Implementation Success Survey

Data inaccuracy, lack of top management support, resistance to change

Other IT Projects Chaos Report, 1994 vs. 2004

Cancelled/Fail:18, Challenged: 53

IT Project Failures – Chaos Reports by The Standish Group. Results from 1994 versus 2004 study show no significant improvement

Lack of user or top management support, resistance to change, unclear user requirements

TOC 15 not sustained 15 not started

Research study by Realization Inc. on “Critical chain projects: Successes, Failures, and lessons learned,” presented at TOCICO Conference in 2005

Lack of buy-in into necessary three TOC rules changes, and not establishing “how-to” mechanics

0 A review of Goldratt’s Theory of Constraints (TOC) – Lessons from International Literature, Mabin and Balderstone, 1999

“In the survey of over 100 cases, no failures or disappointing results were reported”

Table 2.7 : High Failure Rate for Various Change Initiatives and IT Projects

(Source : Barnard (2010))

Relative instability in order per product, unequal load placed by demand over various resources, shorten product life are the realities for SMEs. In such a circumstances lean techniques have limited applicability. Goldratt (2008) suggests time-based application for maximizing flow in relatively unstable condition. Which he claimed, based on the basic principles of maximizing the flow developed by two giants Henry Ford & Taichi Ohno.

Comparatively new technique, ‘TOC’ even though widely used over last two decade in various areas of Europe and western countries, use in India was limited to large organization. Very few companies from SME sector had adopted TOC. And also less research work was carried out in this area.

2.5 Historical background and basic concepts of TOC: -

The Theory Of Constraint is a system management philosophy developed by Dr. Eliyahu M. Goldratt in early 1980s (Du. Preez & Louis (2004)) This philosophy began with the introduction of Optimized Production Scheduling software (Goldratt & Cox (1984)) Toc has evolved from this software program into suite of integrated management tools which covers mainly three interrelated areas, logistic/ production, performance

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 16

measurement, and problem solving/thinking tools (Spencer & Cox (1995)). The Theory of Constraints essential premise is that all firms have at least one critical constraint that limits performance towards achieving its goal. A constraint is any element whatsoever that occurs in a system and that prevents it from achieving optimal performance. (Goldratt (1990)) TOC Philosophy is based on two assumptions, one is system thinking and second one is constraint management (Breen et al. (2002))

Hamilton Pozo (et al.) (2009), writes in article, “TOC claims that a real-world system with more than three constraints is extremely unlikely. This claim is based on linear programming models, which are capable of solving optimization problems for systems with many hundreds of constraints. Researchers found that all but a few such solutions were so unstable that they would be completely impractical amid the noise of a real-world system. Stability had a strong correlation to the number of constraints -- the more constraints, the less stability. TOC practitioners claim that in practice three constraints is the realistic maximum.” Hence it become easy and simple to manage complex system or organization, with focusing on few specific areas in order to increase the performance of the system.

Schragenheim & Dettmer (2001) referred TOC as composition of principles, a set of generic tools and specific application of those tools. The principles explain the systems interaction and guide management for action. While as, tools are specific methods and procedures, for applying principles in particular situation.

Mabin & Balderstone (2000) describe TOC as mainly more than set of tools & technique, fundamentally a paradigm shift in the way we think about our problem, our goal, objectives and as well as our policies, procedures and measures we put in place.

The body of knowledge of TOC was well explained in various books/ novels by Dr. Eliyahu Goldratt and other authors. Fundamental principle of TOC, used in production environment called Drum Buffer Rope was described in ‘The Goal’ (1984) and its application was in second book named ‘The Race’ (1986) Application in project environment was given in book, ‘ Critical chain’ (1997). Constraint handling in marketing was explained in, ‘It’s not Luck’ (1992), while as application of logistic & distribution was discussed in’ Isn’t it Obvious’ (2009)

Large number of articles were published in various journals. Goldratt (1980), Fry et al. (1992), Gardiner et al. (1994) covered the history of

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 17

OPT and TOC. While as, Ronen and Starr (1990) Spencer and Cox (1995) covered the basic concepts of TOC. The application area in project management described by Leach (1999) Umble and Umble (2000), process improvement by Schragenheim and Ronen (1991), supply chain management by Rahman (2002), Watson and and Poilto (2003)

Rigorous academic testing has validated the finding that manufacturing system employing TOC techniques produces greater level of output while reducing inventory and manufacturing lead-time resulting the substantial increase in the bottom line (Mabin and Balderstone(2000))

Though in the initial phase, the TOC was evolved from OPT and widely used in production environment, Thinking process (TPs) developed in later stage have been used for problem identification and problem solving by both large as well as small organization. Additionally the tools also have been used in engineering, finance, marketing and sales, strategy and other business function. (Cox et al. (2005))

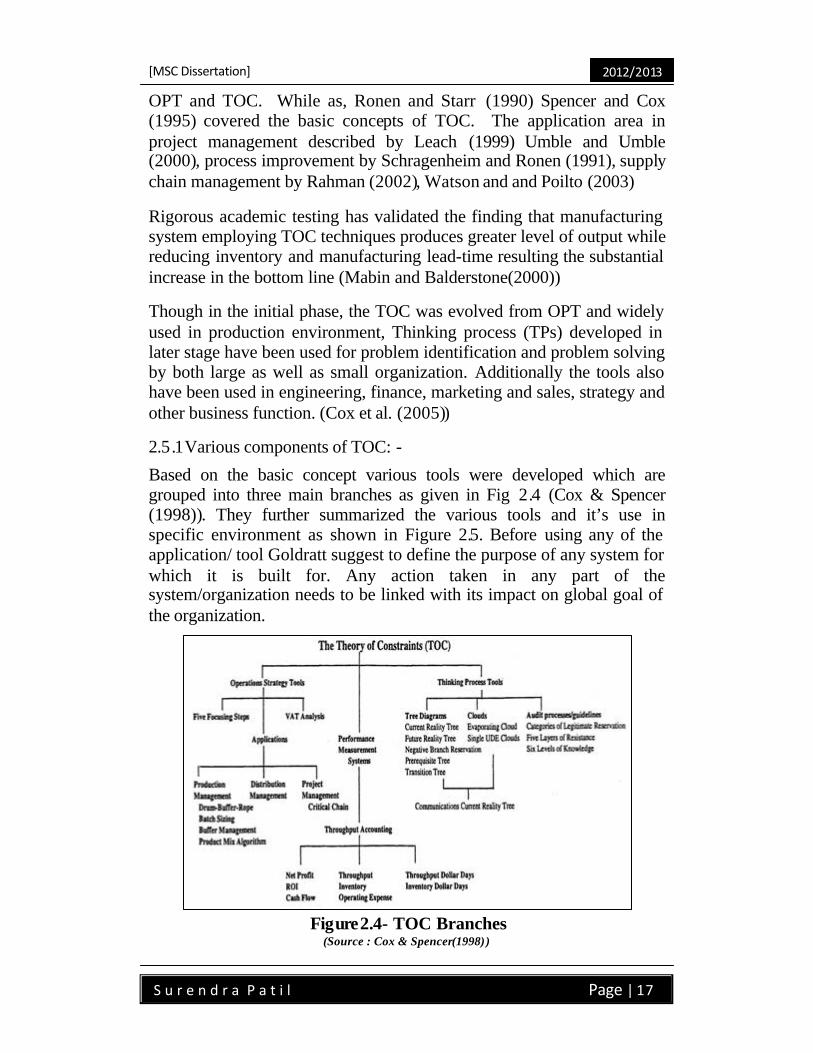

2.5.1Various components of TOC: -

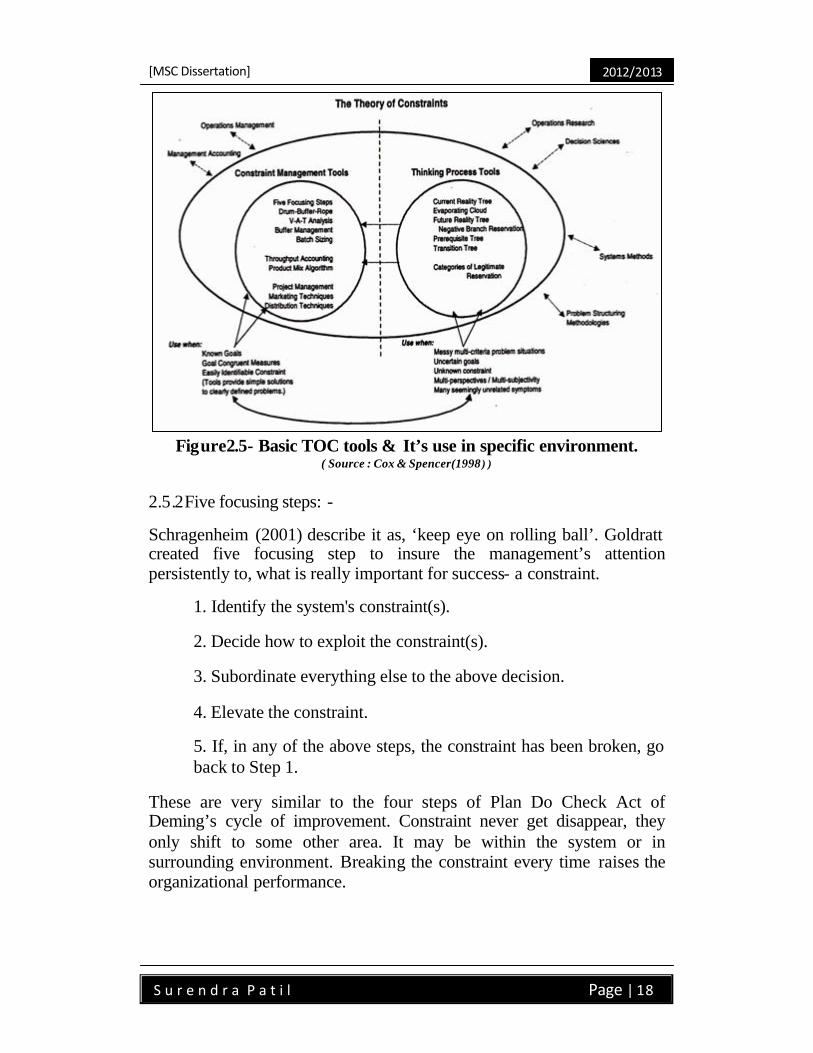

Based on the basic concept various tools were developed which are grouped into three main branches as given in Fig 2.4 (Cox & Spencer (1998)). They further summarized the various tools and it’s use in specific environment as shown in Figure 2.5. Before using any of the application/ tool Goldratt suggest to define the purpose of any system for which it is built for. Any action taken in any part of the system/organization needs to be linked with its impact on global goal of the organization.

Figure2.4- TOC Branches (Source : Cox & Spencer(1998))

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 18

Figure2.5- Basic TOC tools & It’s use in specific environment.

( Source : Cox & Spencer(1998 ) )

2.5.2Five focusing steps: -

Schragenheim (2001) describe it as, ‘keep eye on rolling ball’. Goldratt created five focusing step to insure the management’s attention persistently to, what is really important for success- a constraint.

1. Identify the system's constraint(s).

2. Decide how to exploit the constraint(s).

3. Subordinate everything else to the above decision.

4. Elevate the constraint.

5. If, in any of the above steps, the constraint has been broken, go back to Step 1.

These are very similar to the four steps of Plan Do Check Act of Deming’s cycle of improvement. Constraint never get disappear, they only shift to some other area. It may be within the system or in surrounding environment. Breaking the constraint every time raises the organizational performance.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 19

2.5.3 Drum Buffer Rope (DBR): -

To convert the five focusing steps in production or service environment, a mechanism was developed by Goldratt called DBR. The definition given by Blackstone (2010) as, ‘the slowest station (or the market) that sets the pace for the shop is called drum, the buffer is material (represented as time) upstream of the drum making sure that it is never starved for work. The rope is a signaling mechanism from a buffer to the gateway station pulling the material in to the shop at the rate the drum completes the material.’

Goldratt & Fox (1986) gives the nine OPT rules on which the DBR is based as,

1. Balance the flow not capacity 2. The level of utilization of non bottleneck is not determined by

its own potential but by some other constraint in the system 3. Utilization and activation of resources are not synonomous

[sic]. 4. An hour lost at bottleneck is an hour lost for the total system 5. An hour saved at non-bottleneck is just a mirage 6. Bottleneck govern both throughput and inventory 7. The transfer batch may not and many time should not be

equal to process batch 8. Process batch should be variable and not fixed 9. Schedule should be established by looking at all of the

constraint simultaneously. Lead times are the result of a schedule and cannot be predetermined.

These are very useful rules to be used on shop floor for changing paradigm of people while implementing DBR.

2.5.4 Measurement System& Throughput accounting: -

TOC’s philosophy stated by Srikant and Robertson (1995) focuses on changes at three level (the 3Ms), the Mindset of the organization, the Measurement that drive the organization and the Method employed within the organization.

Scheinkopf (1999) insist that before putting any measurement system, one should understand the very purpose of the system. It is expressed as,

1. Define the system. 2. Define the goal of the system. 3. Define the necessary conditions. 4. Define the fundamental measurements

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 20

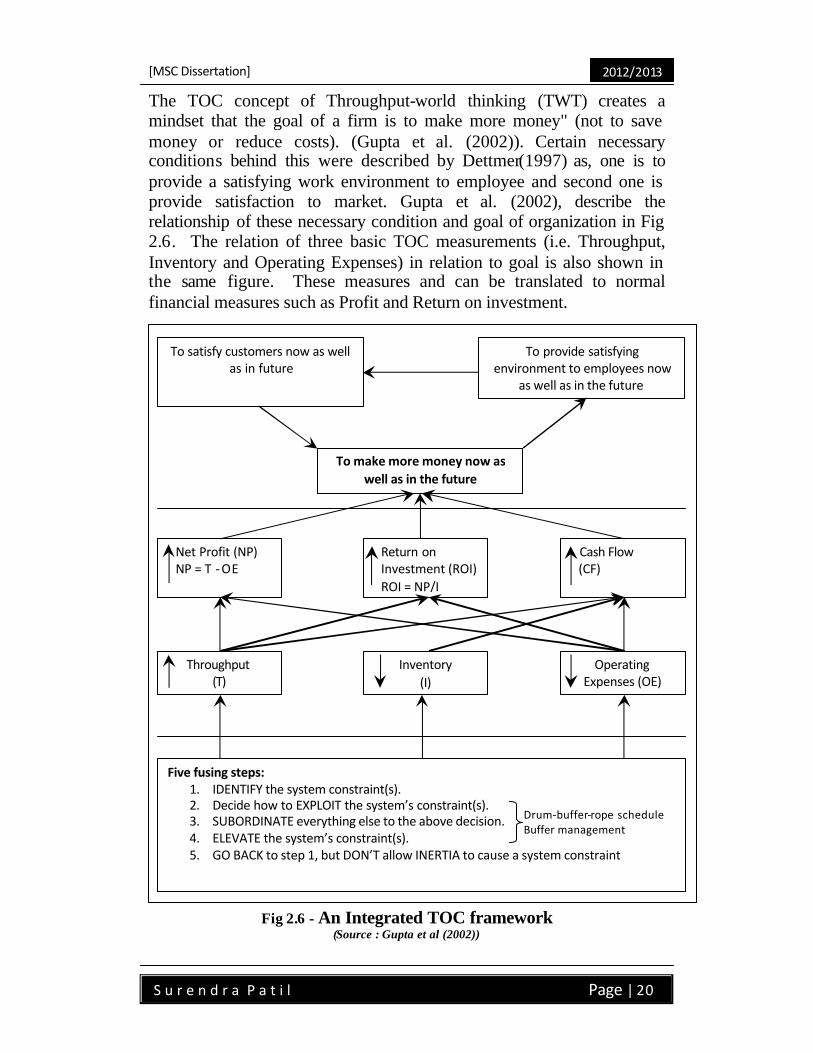

The TOC concept of Throughput-world thinking (TWT) creates a mindset that the goal of a firm is to make more money" (not to save money or reduce costs). (Gupta et al. (2002)). Certain necessary conditions behind this were described by Dettmer(1997) as, one is to provide a satisfying work environment to employee and second one is provide satisfaction to market. Gupta et al. (2002), describe the relationship of these necessary condition and goal of organization in Fig 2.6. The relation of three basic TOC measurements (i.e. Throughput, Inventory and Operating Expenses) in relation to goal is also shown in the same figure. These measures and can be translated to normal financial measures such as Profit and Return on investment.

Fig 2.6 - An Integrated TOC framework

(Source : Gupta et al (2002))

To satisfy customers now as well as in future

To provide satisfying environment to employees now

as well as in the future

To make more money now as well as in the future

Net Profit (NP) NP = T - OE

Return on Investment (ROI) ROI = NP/I

Cash Flow (CF)

Throughput (T)

Inventory (I)

Operating Expenses (OE)

Five fusing steps: 1. IDENTIFY the system constraint(s). 2. Decide how to EXPLOIT the system’s constraint(s). 3. SUBORDINATE everything else to the above decision. 4. ELEVATE the system’s constraint(s). 5. GO BACK to step 1, but DON’T allow INERTIA to cause a system constraint

Drum-buffer-rope schedule Buffer management

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 21

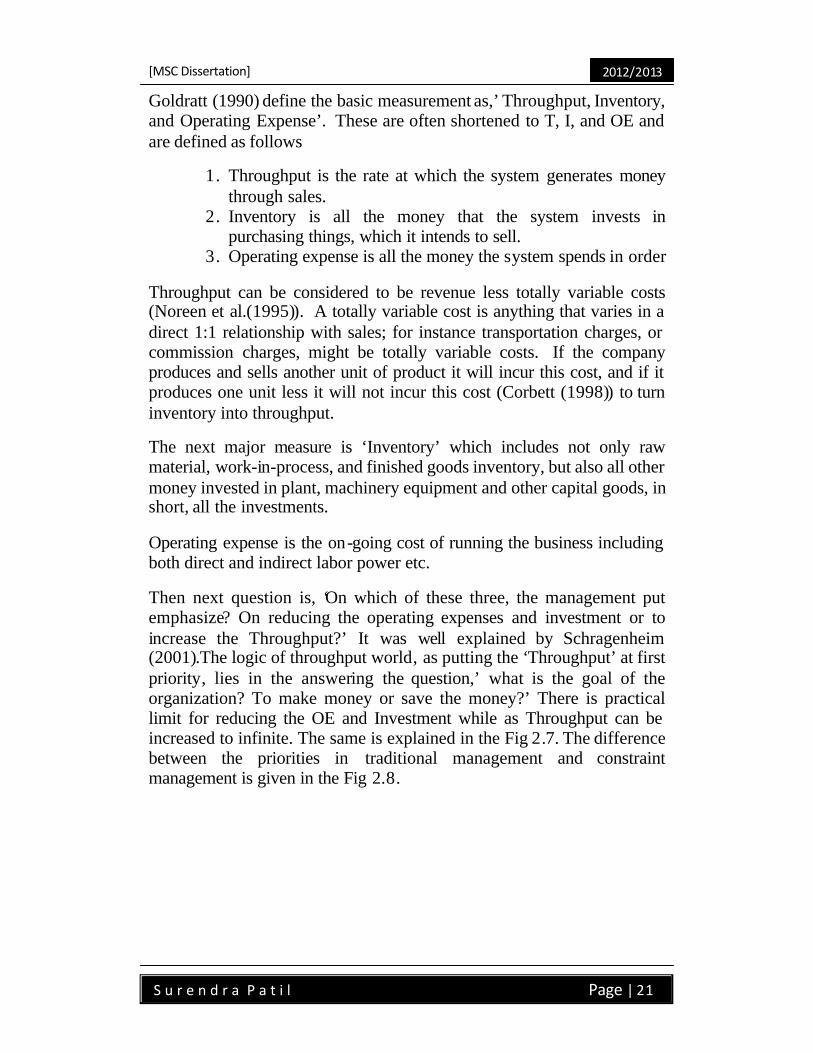

Goldratt (1990) define the basic measurement as,’ Throughput, Inventory, and Operating Expense’. These are often shortened to T, I, and OE and are defined as follows

1. Throughput is the rate at which the system generates money through sales.

2. Inventory is all the money that the system invests in purchasing things, which it intends to sell.

3. Operating expense is all the money the system spends in order

Throughput can be considered to be revenue less totally variable costs (Noreen et al.(1995)). A totally variable cost is anything that varies in a direct 1:1 relationship with sales; for instance transportation charges, or commission charges, might be totally variable costs. If the company produces and sells another unit of product it will incur this cost, and if it produces one unit less it will not incur this cost (Corbett (1998)) to turn inventory into throughput.

The next major measure is ‘Inventory’ which includes not only raw material, work-in-process, and finished goods inventory, but also all other money invested in plant, machinery equipment and other capital goods, in short, all the investments.

Operating expense is the on-going cost of running the business including both direct and indirect labor power etc.

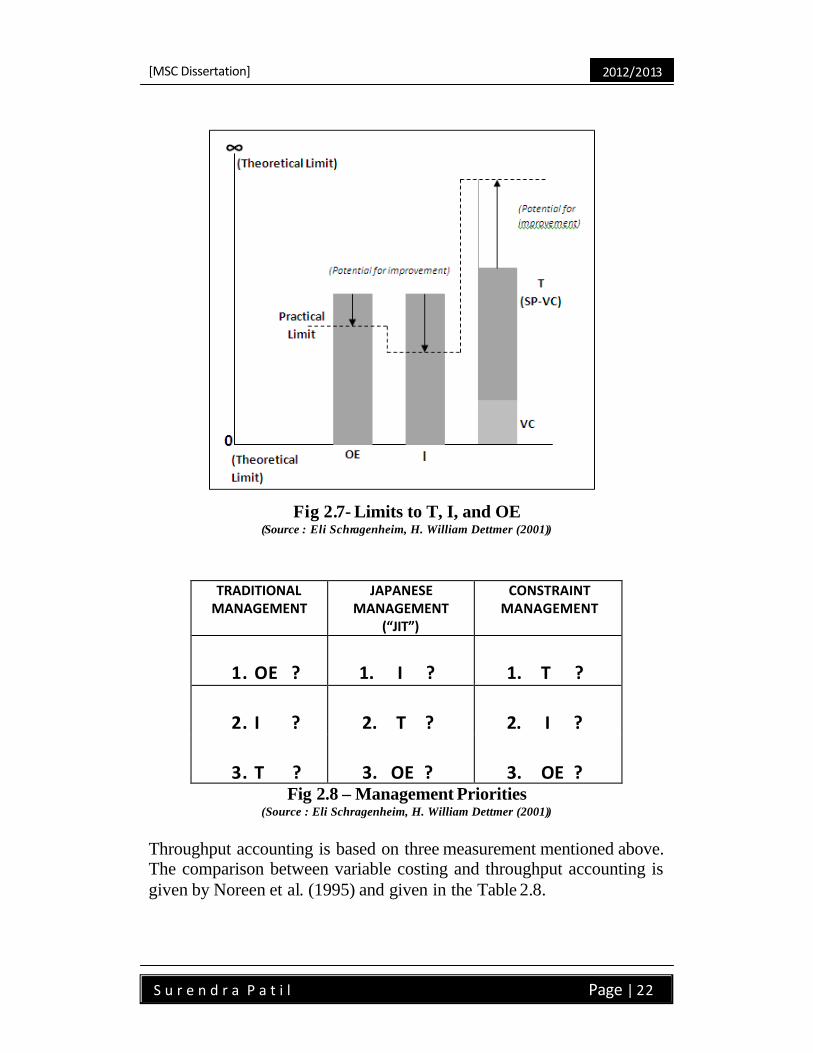

Then next question is, ‘On which of these three, the management put emphasize? On reducing the operating expenses and investment or to increase the Throughput?’ It was well explained by Schragenheim (2001).The logic of throughput world, as putting the ‘Throughput’ at first priority, lies in the answering the question,’ what is the goal of the organization? To make money or save the money?’ There is practical limit for reducing the OE and Investment while as Throughput can be increased to infinite. The same is explained in the Fig 2.7. The difference between the priorities in traditional management and constraint management is given in the Fig 2.8.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 22

Fig 2.7- Limits to T, I, and OE (Source : Eli Schragenheim, H. William Dettmer (2001))

TRADITIONAL MANAGEMENT

JAPANESE MANAGEMENT

(“JIT”)

CONSTRAINT MANAGEMENT

1. OE ?

1. I ?

1. T ?

2. I ?

2. T ?

2. I ?

3. T ?

3. OE ?

3. OE ?

Fig 2.8 – Management Priorities (Source : Eli Schragenheim, H. William Dettmer (2001))

Throughput accounting is based on three measurement mentioned above. The comparison between variable costing and throughput accounting is given by Noreen et al. (1995) and given in the Table 2.8.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 23

Table2.8 : Net Profit and Return on Investment

(Source : Noreen et al (1995) )

2.5.5 Thinking Process tools (TP): -

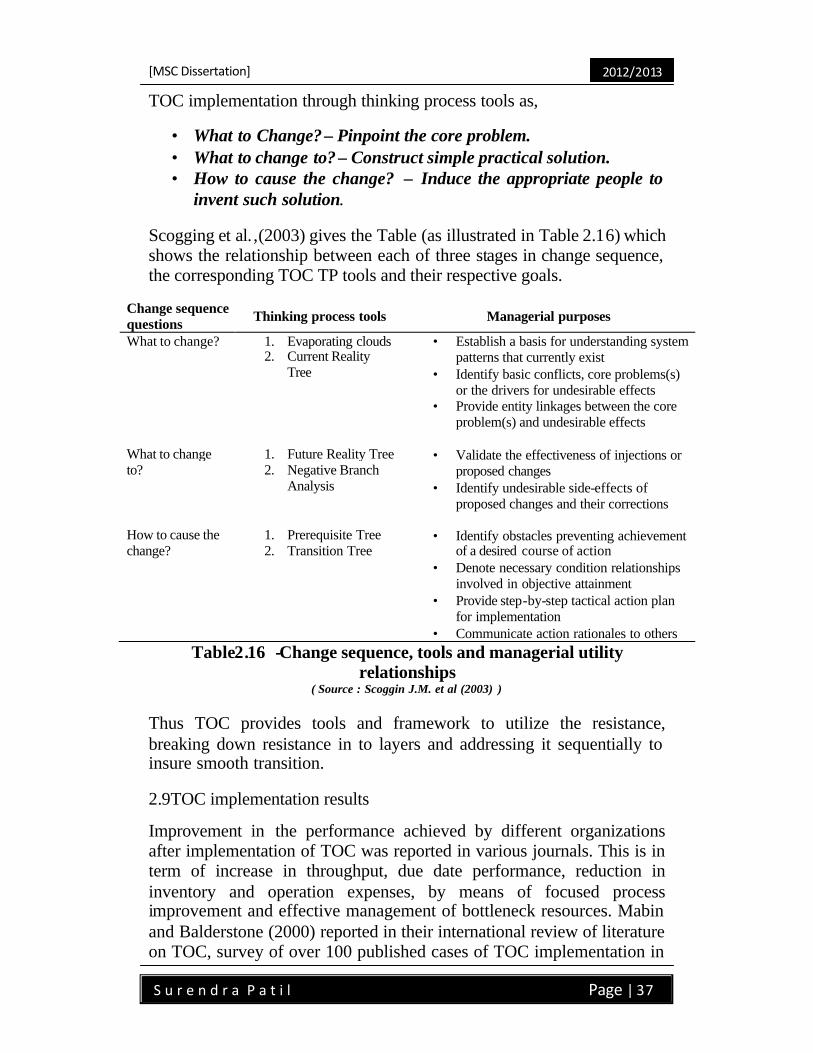

Thinking processes used by Goldratt in the initial stages, for solving the common problematic situations. Goldratt and colleagues then formalized these thinking processes into a suite of TP tools in early 1990s (Goldratt (1990)). The Socratic method described in ‘It’s Not Luck’ by Goldratt, gives the roadmap for discovering novel solution to complex un-structured problem (Mabin & Davis (2010)). The TP provides rigorous and systematic mean to address identification and resolution of un-structured business problem related to management policies (Schragenheim & Dettmer(2001)).

According to Scheinkopf (1999), there are only two TOC Thinking process, one is sufficient cause and second one Necessary condition. There are five applications of these two thinking processes as given in Table 2.9 below

The Sufficient Cause Application Tools The Necessary Condition Application Tools

• Current Reality Tree • Evaporating Cloud • Future Reality Tree • Prerequisite Tree • Transition Tree

Table 2.9 : Application of TOC Thinking Process (Source : Scheinkopf (1999) )

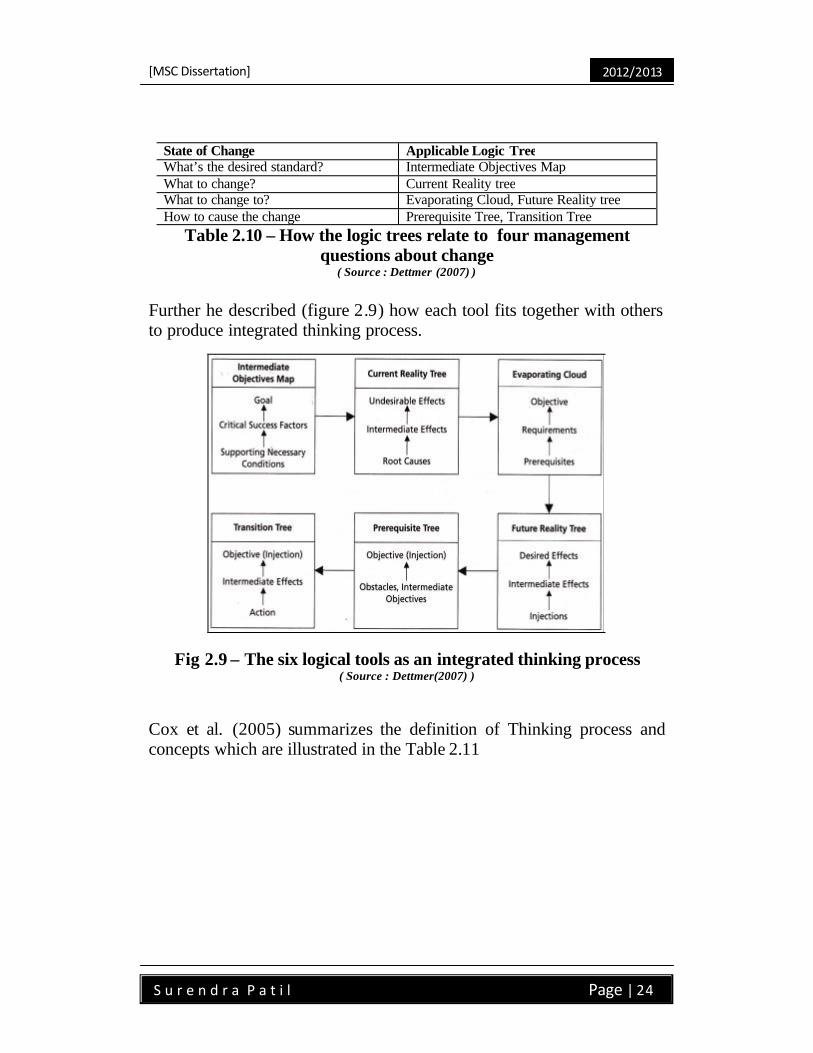

Sixth tool ‘Intermediate Objective’ added afterward by Goldratt, though Goldratt did not pursue it, Dettmer (2007) stressed the importance of it. He suggested the use of these tools in different phases of change management while implementing improvement initiatives, in order to answer the four basic questions as shown in the Table 2.10.

Net Profit= T– OE

Return on Investment

T – OE I

=

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 24

State of Change Applicable Logic Tree What’s the desired standard? Intermediate Objectives Map What to change? Current Reality tree What to change to? Evaporating Cloud, Future Reality tree How to cause the change Prerequisite Tree, Transition Tree

Table 2.10 – How the logic trees relate to four management questions about change

( Source : Dettmer (2007) )

Further he described (figure 2.9) how each tool fits together with others to produce integrated thinking process.

Fig 2.9 – The six logical tools as an integrated thinking process ( Source : Dettmer(2007) )

Cox et al. (2005) summarizes the definition of Thinking process and concepts which are illustrated in the Table 2.11

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 25

Current Reality Branch (CRB)**

A logic-based tool for using cause-and-effect relationships to determine the causal linkages from actions or policies to their effects in the current situation. It provides the starting point for the Negative Branch Reservation and the Current Reality Tree.

Evaporating Cloud (EC)*

A logic-based tool for surfacing assumptions related to a conflict or problem. Once the assumptions are surfaced, actions to break an assumption and hence solve (evaporate) the problem can be determined.

Future Reality Branch (FRB)**

A logic-based tool for examining potential solutions before implementation. It is similar to the FRT except it is used to test and solve problems related to a specific action or evaporating cloud dilemma.

Negative Branch Reservation (NBR)**

An iterative process used to develop the causal logic from the current situation and a proposed action to the negative effects created by that action. Additional actions are proposed and tested to determine their effects until a satisfactory solution (desirable effects) is determined. The product of the NBR process is a future reality branch.

Categories of Legitimate Reservations (CLR)

A set of rules similar to grammatical rules that is used to structure logical arguments.

Undesirable Effect (UDE)*

Most problems are described as an undesirable effect. This terminology is used to distinguish it from the underlying problem that creates the UDE.

Necessity or Necessary Condition Logic

The validity of a relationship where in order for A to occur B must exist or happen. Both the Evaporating Cloud and the P rerequisite Tree use necessary condition logic.

Sufficiency or Sufficient Condition Logic

The validity of a relationship where the cause is sufficient to create the effect – if A then B. B may be created by other causes as well. The Current Reality Tree, Current Reality Branch, Future Reality Tree, Future Reality Branch, Negative Branch Reservation process, and Transition Tree use sufficiency.

Assumption

A condition believed to exist in reality that causes the relationship to exist between the cause and effect. The arrow represents the causal relationship and has an underlying assumption(s). Depending on the TP tool, each arrow in a diagram represents either sufficiency or necessity logic.

Injection

An action that if taken causes the resulting effects. An injection usually breaks an underlying assumption in a causal or necessity relationship and changes or reinforces the effect.

Table 2.11 -Definitions of selected Thinking Processes and concepts ( Source : Cox et al(2005) )

Though there are other components of TOC that exist, like Critical Project management, Distribution solution etc. the same are not covered because the study is limited to the manufacturing environment.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 26

2.6 Implementation of TOC: -

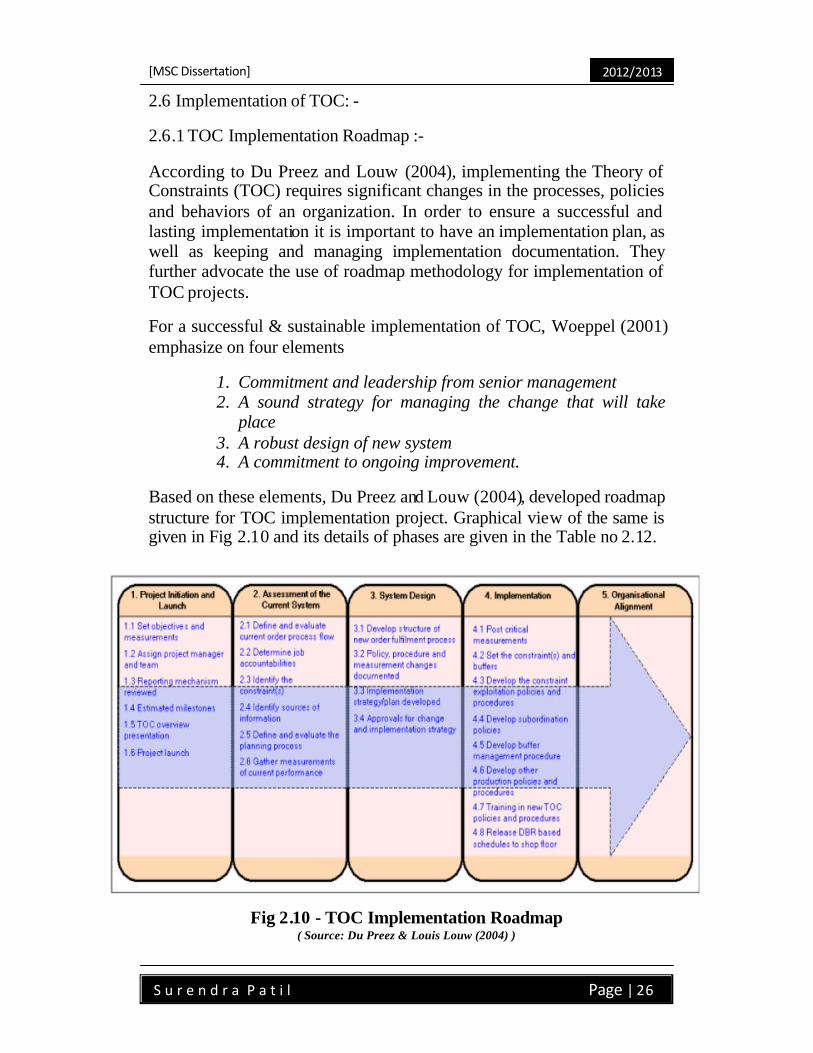

2.6.1 TOC Implementation Roadmap :-

According to Du Preez and Louw (2004), implementing the Theory of Constraints (TOC) requires significant changes in the processes, policies and behaviors of an organization. In order to ensure a successful and lasting implementation it is important to have an implementation plan, as well as keeping and managing implementation documentation. They further advocate the use of roadmap methodology for implementation of TOC projects.

For a successful & sustainable implementation of TOC, Woeppel (2001) emphasize on four elements

1. Commitment and leadership from senior management 2. A sound strategy for managing the change that will take

place 3. A robust design of new system 4. A commitment to ongoing improvement.

Based on these elements, Du Preez and Louw (2004), developed roadmap structure for TOC implementation project. Graphical view of the same is given in Fig 2.10 and its details of phases are given in the Table no 2.12.

Fig 2.10 - TOC Implementation Roadmap ( Source: Du Preez & Louis Louw (2004) )

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 27

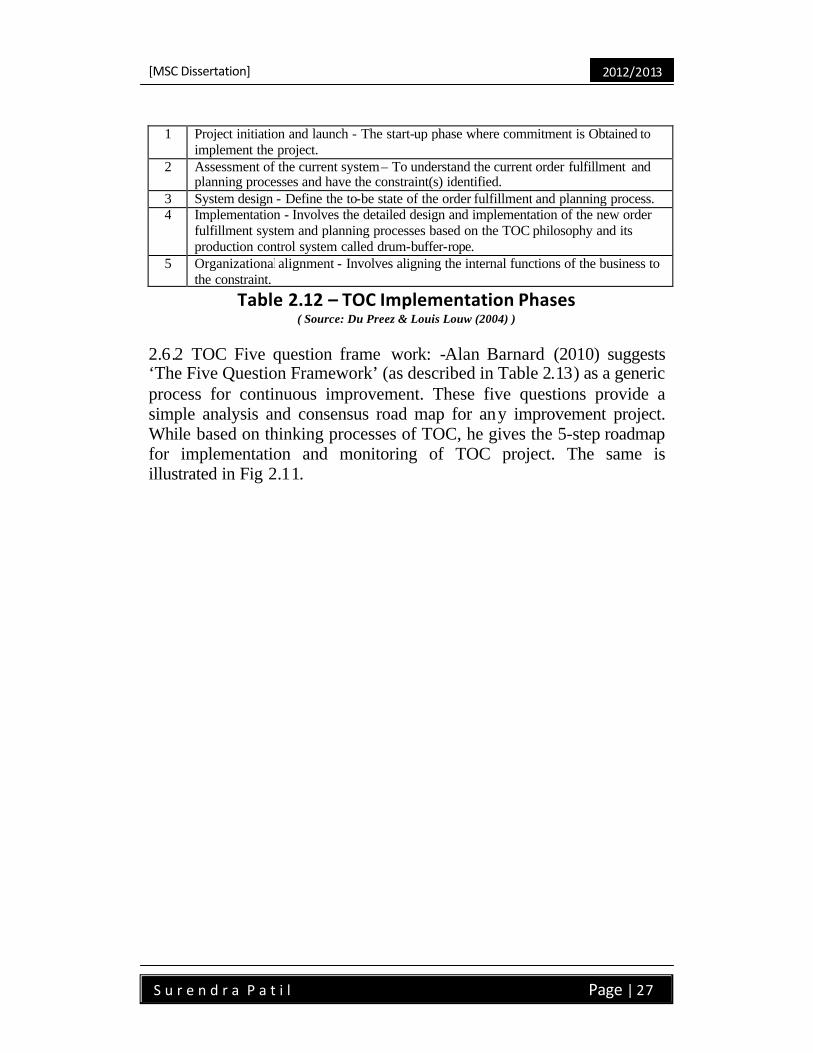

1 Project initiation and launch - The start-up phase where commitment is Obtained to implement the project.

2 Assessment of the current system – To understand the current order fulfillment and planning processes and have the constraint(s) identified.

3 System design - Define the to-be state of the order fulfillment and planning process. 4 Implementation - Involves the detailed design and implementation of the new order

fulfillment system and planning processes based on the TOC philosophy and its production control system called drum-buffer-rope.

5 Organizational alignment - Involves aligning the internal functions of the business to the constraint.

Table 2.12 – TOC Implementation Phases ( Source: Du Preez & Louis Louw (2004) )

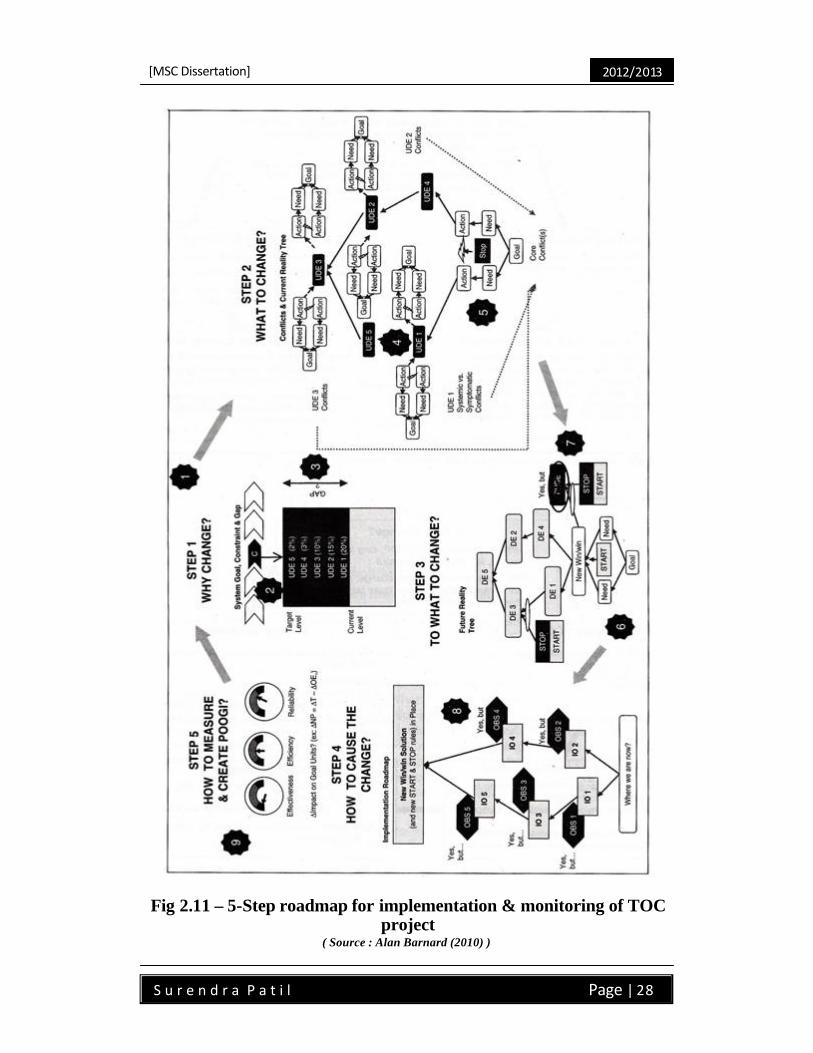

2.6.2 TOC Five question frame work: -Alan Barnard (2010) suggests ‘The Five Question Framework’ (as described in Table 2.13) as a generic process for continuous improvement. These five questions provide a simple analysis and consensus road map for any improvement project. While based on thinking processes of TOC, he gives the 5-step roadmap for implementation and monitoring of TOC project. The same is illustrated in Fig 2.11.

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 28

Fig 2.11 – 5-Step roadmap for implementation & monitoring of TOC project

( Source : Alan Barnard (2010) )

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 29

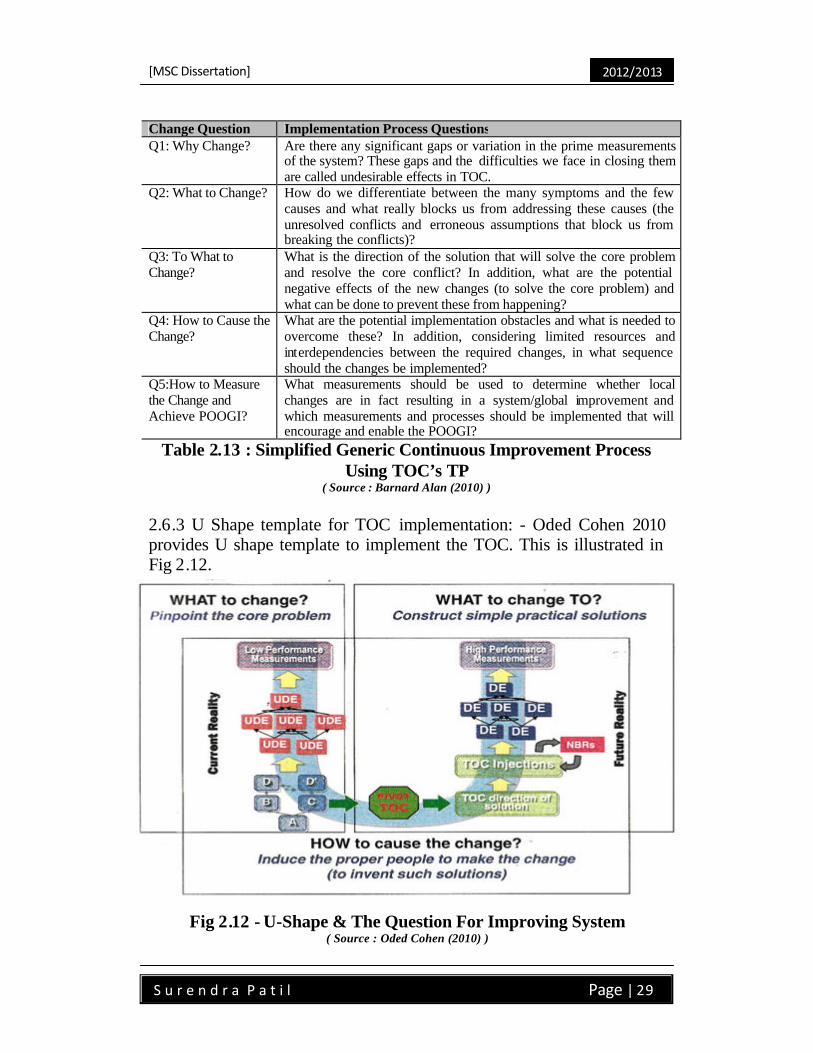

Change Question Implementation Process Questions Q1: Why Change? Are there any significant gaps or variation in the prime measurements

of the system? These gaps and the difficulties we face in closing them are called undesirable effects in TOC.

Q2: What to Change? How do we differentiate between the many symptoms and the few causes and what really blocks us from addressing these causes (the unresolved conflicts and erroneous assumptions that block us from breaking the conflicts)?

Q3: To What to Change?

What is the direction of the solution that will solve the core problem and resolve the core conflict? In addition, what are the potential negative effects of the new changes (to solve the core problem) and what can be done to prevent these from happening?

Q4: How to Cause the Change?

What are the potential implementation obstacles and what is needed to overcome these? In addition, considering limited resources and interdependencies between the required changes, in what sequence should the changes be implemented?

Q5:How to Measure the Change and Achieve POOGI?

What measurements should be used to determine whether local changes are in fact resulting in a system/global improvement and which measurements and processes should be implemented that will encourage and enable the POOGI?

Table 2.13 : Simplified Generic Continuous Improvement Process Using TOC’s TP

( Source : Barnard Alan (2010) )

2.6.3 U Shape template for TOC implementation: - Oded Cohen 2010 provides U shape template to implement the TOC. This is illustrated in Fig 2.12.

Fig 2.12 - U-Shape & The Question For Improving System ( Source : Oded Cohen (2010) )

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 30

U shape connects the problem to solution through pivot-the paradigm shift from the current way of managing to TOC way. He states that the U shape is based on three basic assumptions, which one can say the uniqueness of TOC.

1. Basic assumption 1- Convergence-reality, human based systems are governed by cause-and-effect relationship. Hence it is always possible to find out root cause that affects the system. This is presented in the left side of U shape.

2. Basic Assumption 2- No conflicts between local and global exist. As the conflicts are caused by the people’s perception or by system and there must be solution for every conflict. The implication of this assumption is that there should be win-win solution for every conflict. The win-win solution comprises of the injection on the right side of the U shape

3. Basic assumption 3 - Handle people with respect the entire U shape represent this basic assumption.

2.6.4 Viable vision: - Viable vision is a project to transform any

organization in to ever flourishing state. Exposing the concept of “ever flourishing” company – enjoying both rapid, continuous growth and remarkable stability regardless of external market conditions (Goldratt (2008)). Viable Vision is Goldratt’s offer to suitable businesses to transform current total sales into net profits within 4 years (Kendall (2005)). Organization that decide to move forward in to this challenge need to work out close the ga p bet TOC theory and practice. Whole team need to understand and acquire knowledge of TOC, in order to use in their specific supply chain environment (Heinert et al. (2012)) Embarking on Viable vision project Goldratt (2008) suggest following steps

a. Have supporter b. Determine your Blue Ocean- the decisive competitive

edge/s. c. Remove the engines of disharmony d. One step at a time implementation – prudently

implement S&T tree. e. Cause and effect auditing- educating management in

rigorous & analytical thinking.

2.6.5 Strategy And Tactic tree: - For implementing Viable Vision project Strategy & Tactic trees are the best guiding tools. (This is the tool used in viable vision that improves the communication and synchronization

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 31

dramatically. It provides template for converting strategy to bottom most action. Overall structure of S&T is given in Fig 2.13.

Fig 2.13 - Strategy and Tactic tree

( Source : http://www.goldrattconsulting.com/?categoryId=77828 )

The tree will represent all of the complete elements of Strategy & Tactics as a route map, and through its sound logic, establishes the connection to the desired objective of Viable Vision, to transform into an Ever Flourishing organization. Different S&T are used for different environment with customizing of generic S&T tree

2.7 Change management

2.7.1 Basic Concept

Change management has been defined as ‘the process of continually renewing an organization’s direction, structure, and capabilities to serve the ever-changing needs of external and internal customers’ (Moran and Brightman, 2001: 111)

In today’s ever-changing business environment, it is clear that an organization’s ability to innovate and implement planned change is a requisite for success, if not survival (Hamel, 2002 (2002)). Different management concepts have been developed to meet the challenges evoked by such a rapid change in business environment. Any project

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 32

aiming to improvement in organization’s performance, lead to change in the current working environment.

Theories about organizational change implic itly or explicitly include assumptions about what an organization is and its relationship to its environment.(Haveman (2000)).Change management practices include a variety of organizational interventions that, when executed properly and in consistency with internal and external organizational events, facilitate the enactment of organizational change processes.(Raineri (2011))

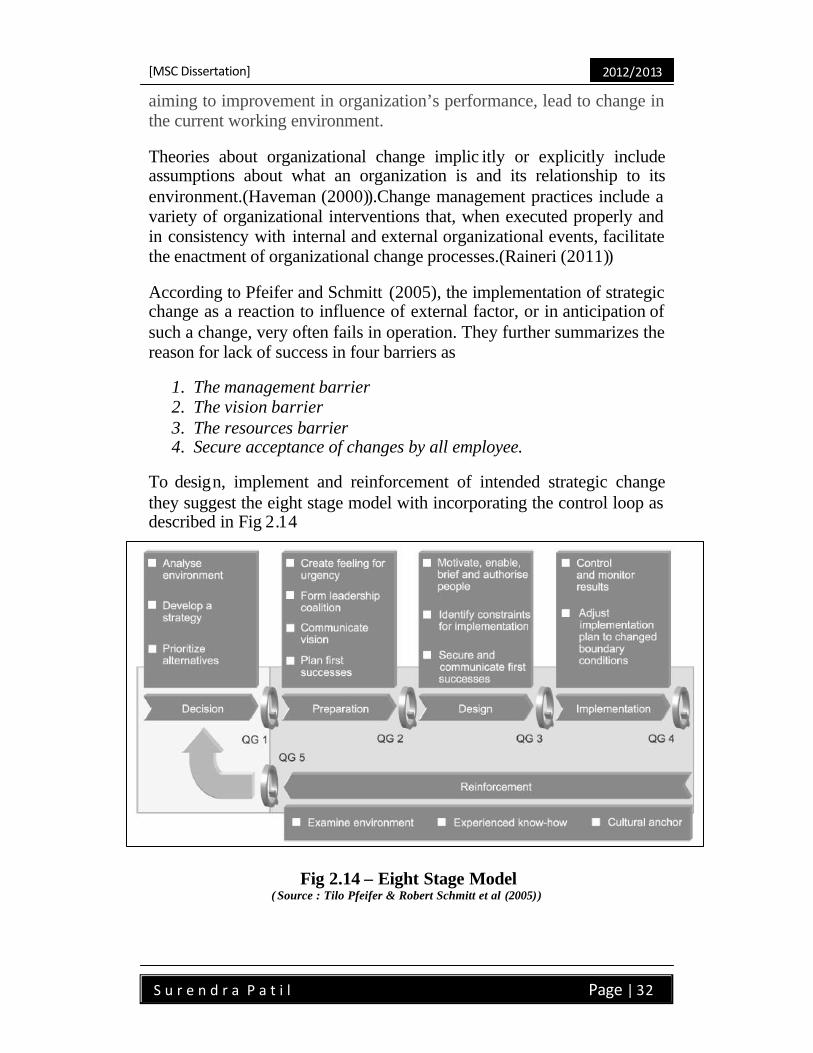

According to Pfeifer and Schmitt (2005), the implementation of strategic change as a reaction to influence of external factor, or in anticipation of such a change, very often fails in operation. They further summarizes the reason for lack of success in four barriers as

1. The management barrier 2. The vision barrier 3. The resources barrier 4. Secure acceptance of changes by all employee.

To design, implement and reinforcement of intended strategic change they suggest the eight stage model with incorporating the control loop as described in Fig 2.14

Fig 2.14 – Eight Stage Model

( Source : Tilo Pfeifer & Robert Schmitt et al (2005))

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 33

Lewin’s (1951) suggest three-step model for change based on the principal of force field analysis. The model recognizes the need to increase the driving force and reduce the restraining force in order to achieve new equilibrium.

• First step consists of Unfreezing the status quo • Second step involves, moving towards desired set of behavior • Third step is refreezing, seeks to stabilize the new quasi-stationary

equilibrium to prevent return to previous behavior

Sangamitra [75] summarizes other change management approaches as,

1. Action research: change process based on systematic collection of data and then selection of a change action based on what analyzed data indicate.

2. Organizational development: change process built on humanistic- democratic values, to improve organizational effectiveness and employee well being.

3. Sensitivity training: training groups to change behavior through unstructured group interaction

4. Survey feedback: use of questionnaires to identify discrepancies among member perceptions

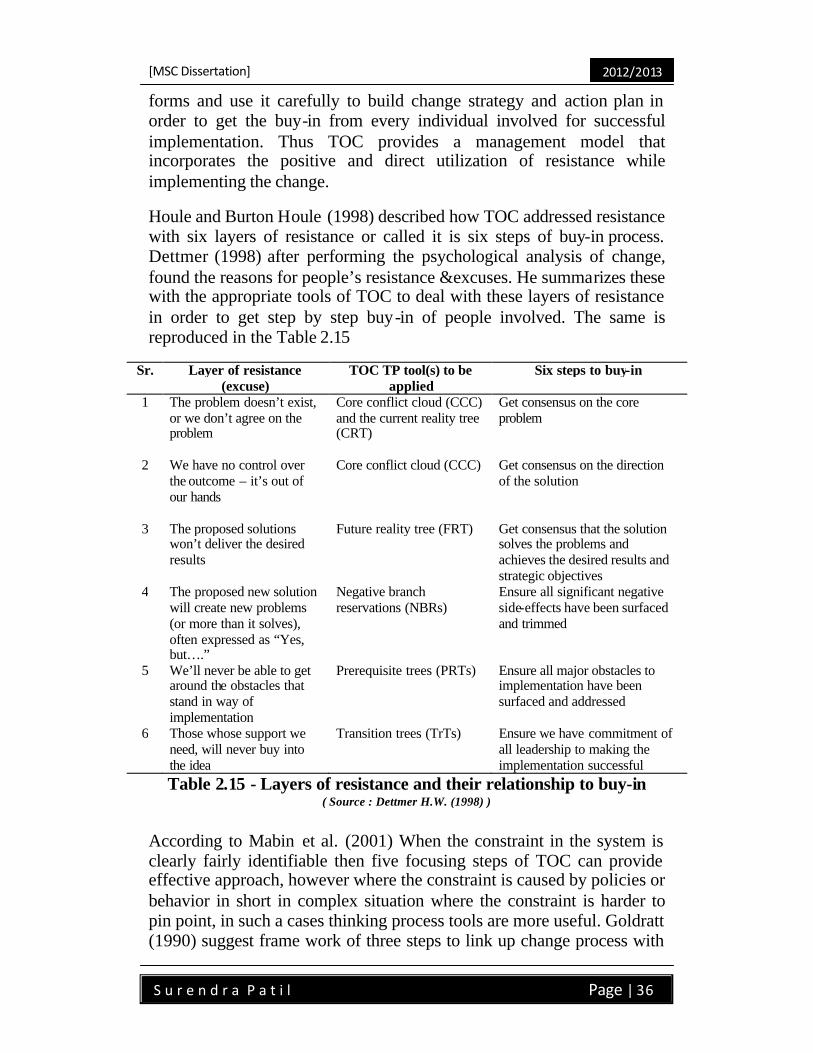

5. Process consultation: a consultant helps client understand process events and identify processes for improvement

2.7.2 Success factors for change management

Page and Pearson (2004) suggest, successful change management requires effective leadership at the top and sensitization of top-level executives. While as Garg and Singh (2005) emphasize the institutionalizing and internalizing. Institutionalization means making change a permanent part of an organization & internalization of change means stabilization of change. Dooley (1995) suggested an approach to surfacing and altering hidden aspects of culture, especially systemic patterns of values, thought, and actions. Some authors suggest, need to develop detailed plan of how change will be implemented, including ambitious but realistic objectives, stages to be achieved, and the timing necessary to coordinate the change project (Nguyen Huy, 2001; (2001) Whelan-Berry et al., 2003 (2003)). Addressing of needs of individual as

[MSC Dissertation]

2012/2013

S u r e n d r a P a t i l Page | 34