INVESTMENT IN PUBLIC ENTERPRISES

113

Investment in Public Enterprises 51 5 Section I Analysis, Sources, Growth and Pattern INVESTMENT IN PUBLIC ENTERPRISES pending allotment and long term loans. Investment herein includes the paid up value of shares issued as bonus shares by capitalizing free reserves and excludes amount of paid up capital and long term loan written off due to restructuring or otherwise. The investment in central public sector enterprises from 2000-01, without making any adjustment on account of share capital invested by holding companies in their subsidiaries and/or long-term loans given by holding companies to their subsidiaries or vice-versa, is given below: Table 5.1 (Rs. in crore) Year ending No. of Paid up Share Long term Investment enterprises capital application loans (3+4+5) money 1 2 3 4 5 6 As on 31.3.2001 250 86215 3225 184758 274198 As on 31.3.2002 240 101247 2933 218635 322815 As on 31.3.2003 240 109306 2933 223408 335647 As on 31.3.2004 242 111874 7087 231033 349994 As on 31.3.2005 237 117787 6494 233568 357849 Sources of Investment 5.1.2 The Central Government has contributed a major share of investment in public enterprises. In addition to Central Government, some State Governments, holding companies which are themselves public sector enterprises, financial institutions, banks and private parties (both Indian and foreign) have also contributed to the investment of these enterprise.The details of investment by different parties for the last five years are given below— 5.1 Public Sector today covers a wide spectrum of industrial activities starting from core and strategic industries to consumer goods, trading and marketing activities, transportation activities, contract and consultancy services, tourist services, financial services, development of small industries, etc. Analysis of Investment 5.1.1 Investment is the aggregate of paid- up share capital, share application money

-

Upload

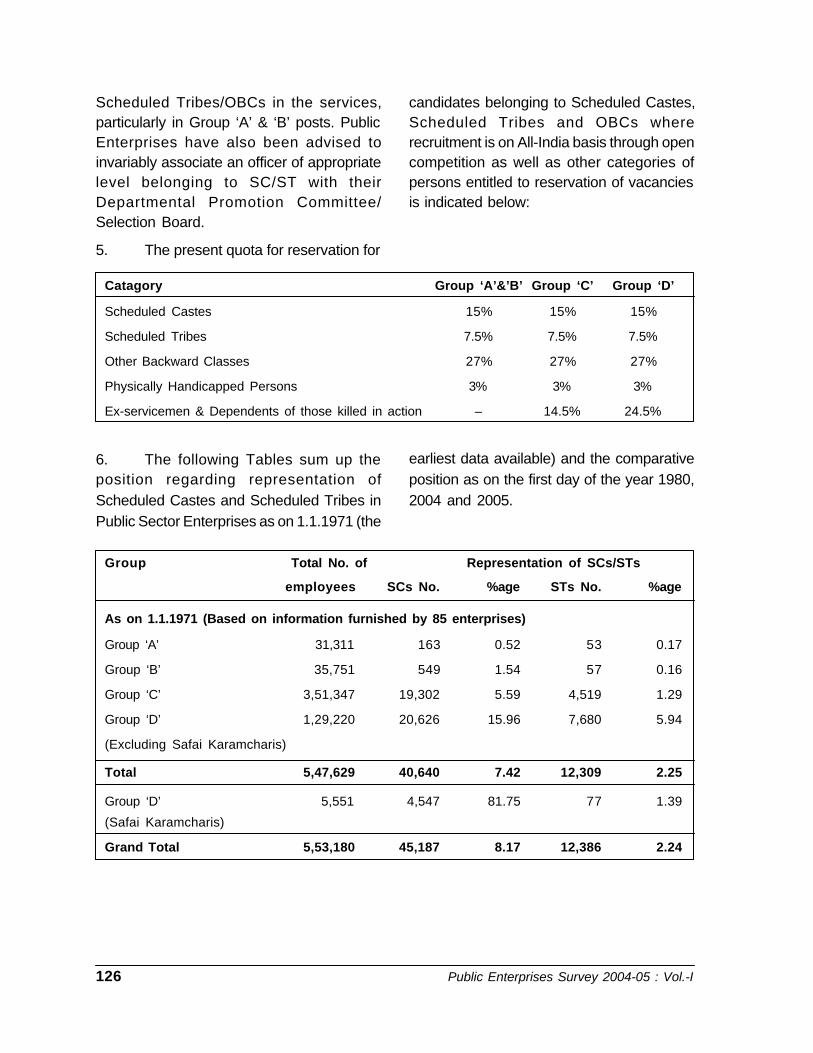

khangminh22 -

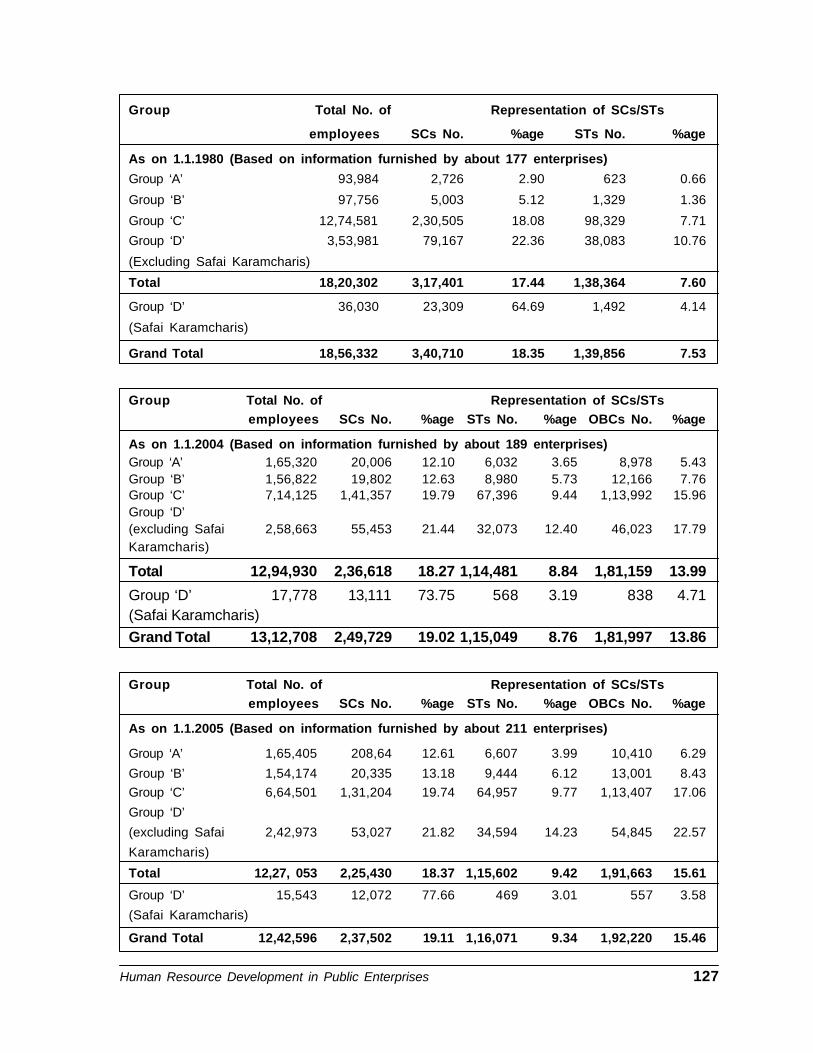

Category

Documents

-

view

0 -

download

0

Transcript of INVESTMENT IN PUBLIC ENTERPRISES

Investment in Public Enterprises 51

5Section I

Analysis, Sources, Growth and Pattern

INVESTMENT IN PUBLIC ENTERPRISES

pending allotment and long term loans.Investment herein includes the paid up valueof shares issued as bonus shares bycapitalizing free reserves and excludesamount of paid up capital and long term loanwritten off due to restructuring or otherwise.The investment in central public sectorenterprises from 2000-01, without makingany adjustment on account of share capitalinvested by holding companies in theirsubsidiaries and/or long-term loans given byholding companies to their subsidiaries orvice-versa, is given below:

Table 5.1(Rs. in crore)

Year ending No. of Paid up Share Long term Investmententerprises capital application loans (3+4+5)

money

1 2 3 4 5 6

As on 31.3.2001 250 86215 3225 184758 274198

As on 31.3.2002 240 101247 2933 218635 322815

As on 31.3.2003 240 109306 2933 223408 335647

As on 31.3.2004 242 111874 7087 231033 349994

As on 31.3.2005 237 117787 6494 233568 357849

Sources of Investment

5.1.2 The Central Government hascontributed a major share of investment in

public enterprises. In addition to Central

Government, some State Governments,holding companies which are themselves

public sector enterprises, financial

institutions, banks and private parties (both

Indian and foreign) have also contributed tothe investment of these enterprise.The

details of investment by different parties for

the last five years are given below—

5.1 Public Sector today covers a widespectrum of industrial activities starting fromcore and strategic industries to consumergoods, trading and marketing activities,transportation activities, contract andconsultancy services, tourist services,financial services, development of smallindustries, etc.

Analysis of Investment

5.1.1 Investment is the aggregate of paid-up share capital, share application money

52 Public Enterprises Survey 2004-05 : Vol.-I

Table 5.2

SOURCES OF INVESTMENT(Rs. in crore)

Particulars Central State Holding Foreign FI/Banks Total Share TotalGovt. Govt. Company Parties & Others Application Investment

moneypending

allotment

(1) (2) (3) (4) (5) (6) (7) (8) (9)(2 to 6) (7+8)

As on 31.3.2001

Equity 71771 1368 9866 756 2454 86215

Loan 49068 21 13183 4657 117829 184758

Total 120839 1389 23049 5413 120283 270973 3225 274198

As on 31.3.2002

Equity 86444 1468 10329 575 2431 101247

Loan 56710 26 16018 33261 112620 218635

Total 143154 1494 26347 33836 115051 319882 4732 324614

As on 31.3.2003

Equity 91368 2542 11453 545 3398 109306

Loan 56699 10 21808 29835 115056 223408

Total 148067 2552 33261 30380 118454 332714 2933 335647

As on 31.3.2004

Equity 93415 3200 11154 767 3338 111874

Loan 50864 262 23675 27394 128838 231033

Total 144279 3462 34829 28161 132176 342907 7087 349994

As on 31.3.2005

Equity 98313 3113 11391 1421 3549 117787

Loan 36453 266 28722 28550 139577 233568

Total 134766 3379 40113 29971 143126 351355 6494 357849

Growth of Investment

5.1.3 The investment in public sectorenterprises has grown from Rs. 29 crore ason 1.4.1951 to Rs. 357849 crore as on

31.3.2005. The growth of investment in publicsector enterprises, including enterprisesunder construction, over the years is givenbelow—

Investment in Public Enterprises 53

Table 5.3

Growth in Investment

Particulars Total EnterprisesInvestment (Numbers)(Rs. crore)

At the commencement of the 1st Five Year Plan (1.4.1951) 29 5

At the commencement of the 2nd Five Year Plan (1.4.1956) 81 21

At the commencement of the 3rd Five Year Plan (1.4.1961) 948 47

At the end of 3rd Five Year Plan (31.3.1966) 2410 73

At the commencement of the 4th Five Year Plan (1.4.1969) 3897 84

At the commencement of the 5th Five Year Plan (1.4.1974) 6237 122

At the end of 5th Five Year Plan (31.3.1979) 15534 169

At the commencement of the 6th Five Year Plan (1.4.1980) 18150 179

At the commencement of the 7th Five Year Plan (1.4.1985) 42673 215

At the end of 7th Five Year Plan (31.3.1990) 99329 244

At the commencement of the 8th Five Year Plan (1.4.1992) 135445 246

At the end of 8th Five Year Plan (31.3.1997) 213610 242

At the end of 9th Five Year Plan (31.3.2002) 324614 240

As on 31.3.2003 335647 240

As on 31.3.2004 349994 242

As on 31.3.2005 357849 237

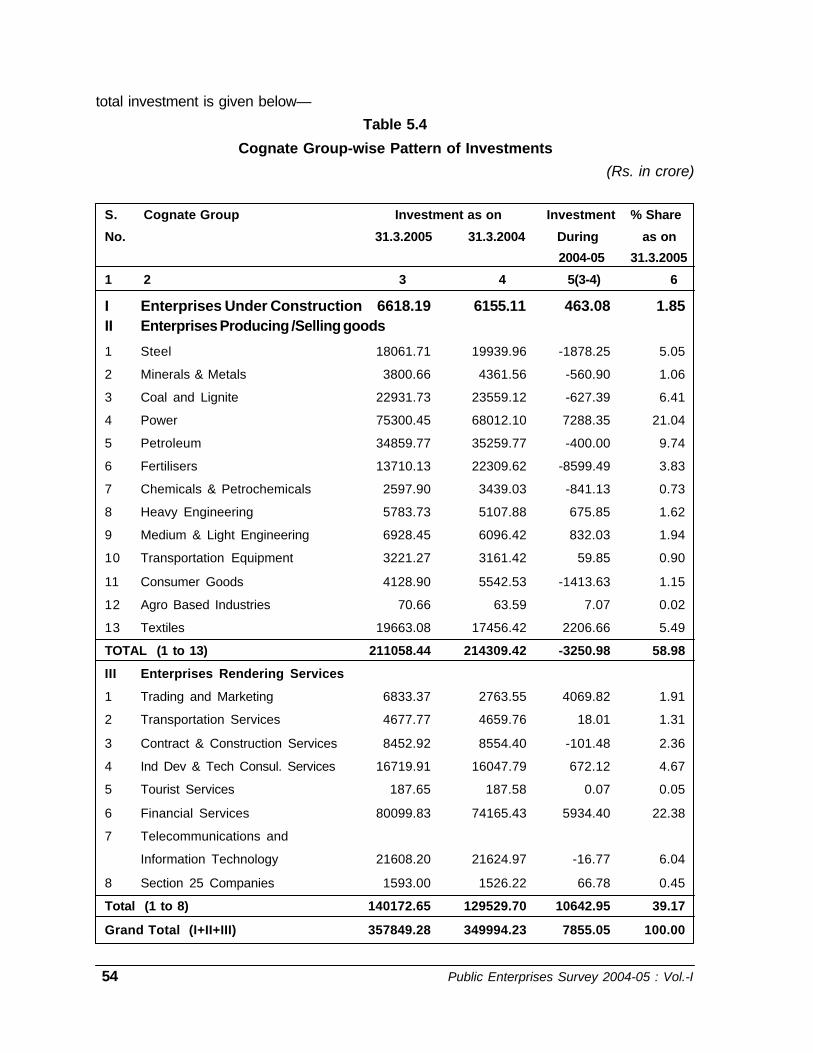

Pattern of Investment

5.1.4 The statement showing the totalinvestment for the last two years in various

cognate groups, changes in investmentduring the year and percentange share ofinvestment in each cognate group to the

54 Public Enterprises Survey 2004-05 : Vol.-I

total investment is given below—

Table 5.4

Cognate Group-wise Pattern of Investments

(Rs. in crore)

S. Cognate Group Investment as on Investment % Share

No. 31.3.2005 31.3.2004 During as on

2004-05 31.3.2005

1 2 3 4 5(3-4) 6

I Enterprises Under Construction 6618.19 6155.11 463.08 1.85II Enterprises Producing /Selling goods

1 Steel 18061.71 19939.96 -1878.25 5.05

2 Minerals & Metals 3800.66 4361.56 -560.90 1.06

3 Coal and Lignite 22931.73 23559.12 -627.39 6.41

4 Power 75300.45 68012.10 7288.35 21.04

5 Petroleum 34859.77 35259.77 -400.00 9.74

6 Fertilisers 13710.13 22309.62 -8599.49 3.83

7 Chemicals & Petrochemicals 2597.90 3439.03 -841.13 0.73

8 Heavy Engineering 5783.73 5107.88 675.85 1.62

9 Medium & Light Engineering 6928.45 6096.42 832.03 1.94

10 Transportation Equipment 3221.27 3161.42 59.85 0.90

11 Consumer Goods 4128.90 5542.53 -1413.63 1.15

12 Agro Based Industries 70.66 63.59 7.07 0.02

13 Textiles 19663.08 17456.42 2206.66 5.49

TOTAL (1 to 13) 211058.44 214309.42 -3250.98 58.98

III Enterprises Rendering Services

1 Trading and Marketing 6833.37 2763.55 4069.82 1.91

2 Transportation Services 4677.77 4659.76 18.01 1.31

3 Contract & Construction Services 8452.92 8554.40 -101.48 2.36

4 Ind Dev & Tech Consul. Services 16719.91 16047.79 672.12 4.67

5 Tourist Services 187.65 187.58 0.07 0.05

6 Financial Services 80099.83 74165.43 5934.40 22.38

7 Telecommunications and

Information Technology 21608.20 21624.97 -16.77 6.04

8 Section 25 Companies 1593.00 1526.22 66.78 0.45

Total (1 to 8) 140172.65 129529.70 10642.95 39.17

Grand Total (I+II+III) 357849.28 349994.23 7855.05 100.00

Investment in Public Enterprises 55

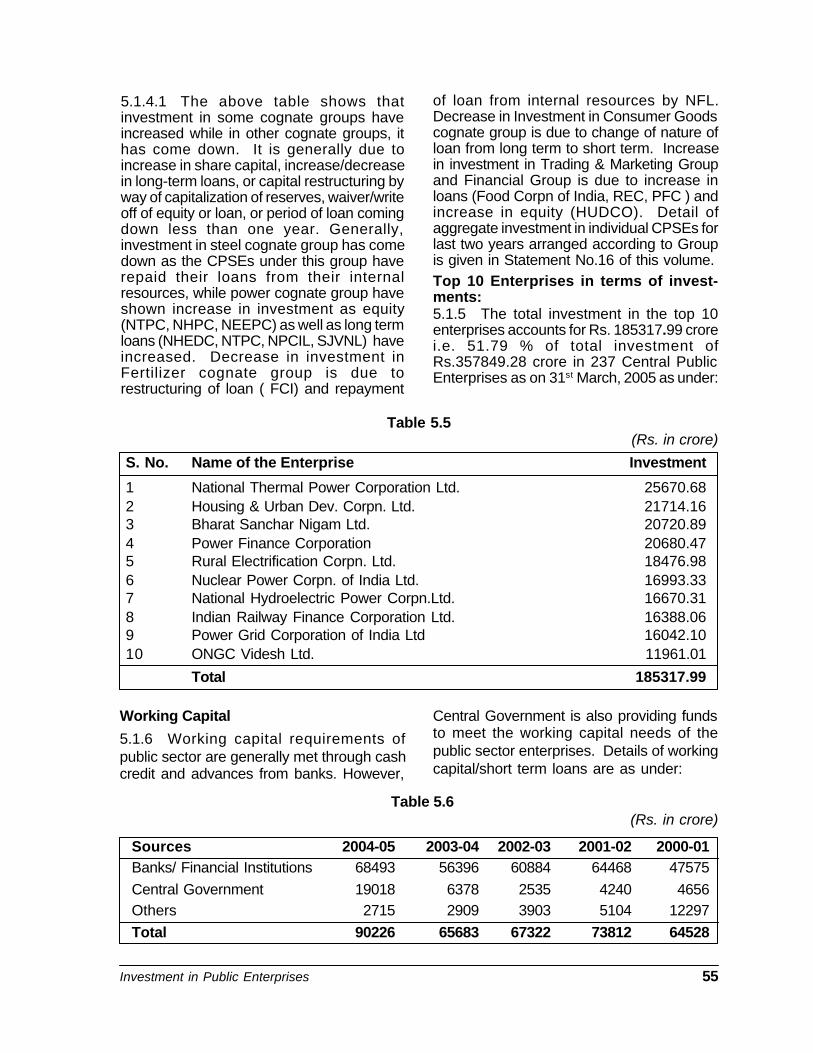

Table 5.5(Rs. in crore)

S. No. Name of the Enterprise Investment

1 National Thermal Power Corporation Ltd. 25670.682 Housing & Urban Dev. Corpn. Ltd. 21714.163 Bharat Sanchar Nigam Ltd. 20720.894 Power Finance Corporation 20680.475 Rural Electrification Corpn. Ltd. 18476.986 Nuclear Power Corpn. of India Ltd. 16993.337 National Hydroelectric Power Corpn.Ltd. 16670.318 Indian Railway Finance Corporation Ltd. 16388.069 Power Grid Corporation of India Ltd 16042.1010 ONGC Videsh Ltd. 11961.01

Total 185317.99

5.1.4.1 The above table shows thatinvestment in some cognate groups haveincreased while in other cognate groups, ithas come down. It is generally due toincrease in share capital, increase/decreasein long-term loans, or capital restructuring byway of capitalization of reserves, waiver/writeoff of equity or loan, or period of loan comingdown less than one year. Generally,investment in steel cognate group has comedown as the CPSEs under this group haverepaid their loans from their internalresources, while power cognate group haveshown increase in investment as equity(NTPC, NHPC, NEEPC) as well as long termloans (NHEDC, NTPC, NPCIL, SJVNL) haveincreased. Decrease in investment inFertilizer cognate group is due torestructuring of loan ( FCI) and repayment

of loan from internal resources by NFL.Decrease in Investment in Consumer Goodscognate group is due to change of nature ofloan from long term to short term. Increasein investment in Trading & Marketing Groupand Financial Group is due to increase inloans (Food Corpn of India, REC, PFC ) andincrease in equity (HUDCO). Detail ofaggregate investment in individual CPSEs forlast two years arranged according to Groupis given in Statement No.16 of this volume.Top 10 Enterprises in terms of invest-ments:5.1.5 The total investment in the top 10enterprises accounts for Rs. 185317.99 crorei.e. 51.79 % of total investment ofRs.357849.28 crore in 237 Central PublicEnterprises as on 31st March, 2005 as under:

Table 5.6(Rs. in crore)

Sources 2004-05 2003-04 2002-03 2001-02 2000-01Banks/ Financial Institutions 68493 56396 60884 64468 47575Central Government 19018 6378 2535 4240 4656Others 2715 2909 3903 5104 12297Total 90226 65683 67322 73812 64528

Working Capital

5.1.6 Working capital requirements ofpublic sector are generally met through cashcredit and advances from banks. However,

Central Government is also providing fundsto meet the working capital needs of thepublic sector enterprises. Details of workingcapital/short term loans are as under:

56 Public Enterprises Survey 2004-05 : Vol.-I

5.2 Under the Articles of Association, theBoard of Directors of PSEs enjoy certainamount of financial powers and autonomy inrespect of recruitment, promotion and otherservice conditions of below Board levelemployees. The Board of Directors of a PSEexercises the delegated powers subject tobroad policy guidelines issued byGovernment from time to time. TheGovernment have granted enhanced powersto the Boards of profit making enterprisesunder various schemes like Navratna andMiniratna.

5.2.1 Keeping in view the pledge made inthe National Common Minimum Programme(NCMP) that full managerial and commercialautonomy will be devolved to successful profitmaking companies operating in a competitiveenvironment, the Government have reviewedthe powers delegated to the Board ofDirectors of Navratna, Miniratna and otherprofit making PSEs and have decided inAugust, 2005 to enhance the powers.

Navratna scheme

5.2.2 Under this scheme, the Governmenthas delegated higher powers to PSEs havingcomparative advantage and the potential tobecome global players. The Navratna PSEsare:

(i) Bharat Heavy Electricals Ltd.

(ii) Bharat Petroleum Corporation Ltd.

(iii) GAIL (India) Ltd.

(iv) Hindustan Petroleum CorporationLtd.

(v) Indian Oil Corporation Ltd.

(vi) Mahanagar Telephone Nigam Ltd.

(vii) National Thermal Power CorporationLtd.

(viii) Oil & Natural Gas Corporation Ltd.

(ix) Steel Authority of India Ltd.

5.2.2.1 The powers presently delegated tothe Boards of Navratna PSEs are as under: -

(a) To incur capital expenditure on purchaseof new items or for replacement, withoutany monetary ceiling.

(b) To enter into technology joint ventures orstrategic alliances.

(c) To obtain by purchase or otherarrangements, technology and know-how.

(d) To effect organisational restructuringincluding establishment of profit centres,opening of offices in India and abroad,creating new activity centres, etc.

(e) Creation and winding up of all postsincluding and upto those of non-Boardlevel Directors, i.e., Functional Directorswho may have the same pay-scales asthat of Board level Directors, but whowould not be members of the Board. Allappointments upto this level would alsobe in the powers of the Boards andwould include the power to effect internaltransfers and re-designation of posts.

(f) The Board of Directors of these PSEshave the power to further delegate thepowers relating to Human ResourceManagement (appointments, transfer,posting, etc.) of below Board levelexecutives to sub-committees of theBoard or to executives of the PSE, asmay be decided by the Board of thePSE.

(g) To raise debt from the domestic capitalmarkets and for borrowings frominternational market, which would besubject to the approval of RBI/Department of Economic Affairs as maybe required and should be obtainedthrough the administrative Ministry.

(h) To establish financial joint ventures andwholly owned subsidiaries in India or

Section-II

DELEGATION OF ENHANCED FINANCIAL POWERS TO CPSEs

Investment in Public Enterprises 57

abroad with the stipulation that the equityinvestment of the PSE should be limitedto the following: -

i. Rs. 1000 crore in any one project,

ii. 15% of the networth of the PSEin one project,

iii. 30% of the networth of the PSEin all joint ventures/ subsidiariesput together.

(i) Mergers and acquisitions, subject to theconditions that (i) it should be as per thegrowth plan and in the core area offunctioning of the PSE, (ii) conditions/limits would be as in the case ofestablishing joint ventures/subsidiaries,and (iii) the Cabinet Committee onEconomic Affairs would be keptinformed in case of investments abroad.

(j) To approve business tours abroad offunctional directors up to 5 days’duration (other than study tours,seminars, etc.) in emergency, by theChief Executive of the PSE underintimation to the Secretary of theadministrative Ministry. In all other casesincluding those of Chief Executive, toursabroad would continue to require theprior approval of the Minister of theAdministrative Ministry/ Department

5.2.2.2 The above mentioned delegation issubject to the following conditions andguidelines:-

a) The proposals must be presented to theBoard of Directors in writing andreasonably well in advance, with ananalysis of relevant factors andquantification of the anticipated resultsand benefits. Risk factors, if any, mustbe clearly brought out.

b) The Government Directors, the FinancialDirectors and the concerned FunctionalDirector(s) must be present when majordecisions are taken, especially whenthey pertain to investments, expenditureor organizational/ capital restructuring.

c) The decisions on such proposals shouldpreferably be unanimous.

d) In the event of any decision on importantmatters not being unanimous, a majoritydecision may be taken, but at least twothirds of the Directors should be present,including those mentioned above, whensuch a decision is taken. The objections,dissents, the reasons for over-rulingthem and those for taking the decisionshould be recorded in writing andminuted.

e) No financial support or contingent liabilityon the part of the Government shouldbe involved.

f) These PSEs will establish transparentand effective systems of internalmonitoring, including the establishmentof an Audit Committee of the Board withmembership of non-official Directors.

g) All the proposals, where they pertain tocapital expenditure, investment or othermatters involving substantial financial ormanagerial commitments or where theywould have a long term impact on thestructure and functioning of the PSE,should be prepared by or with theassistance of professionals and expertsand should be appraised, in suitablecases, by financial institutions or reputedprofessional organizations withexpertise in the areas. The financialappraisal should also preferably bebacked by an involvement of theappraising institutions through loans orequity participation.

h) The exercise of authority to enter intotechnology joint ventures and strategicalliances shall be in accordance with theGovernment guidelines as may beissued from time to time.

i) The Boards of these PSEs should berestructured by inducting at least fournon-official Directors as the first stepbefore the exercise of the enhanceddelegation of authority.

j) These public sector enterprises shall not

58 Public Enterprises Survey 2004-05 : Vol.-I

depend upon budgetary support orGovernment guarantees. The resourcesfor implementing their programmesshould come from their internalresources or through other sources,including the capital markets.

Miniratna scheme

5.2.3 In October 1997, the Governmenthad also decided to grant enhancedautonomy and delegation of financial powersto some other profit making companiessubject to certain eligibility conditions andguidelines to make them efficient andcompetitive. These companies, calledMiniratnas, are in two categories, namely,Category- I and Category-II. The eligibilityconditions and criteria are:

(i) Category-I PSEs should have madeprofit in the last three years continuously,the pre-tax profit should have beenRs.30 crores or more in at least one ofthe three years and should have apositive net worth.

(ii) Category-II PSEs should have madeprofit for the last three yearscontinuously and should have a positivenet worth.

(iii) These PSEs shall be eligible for theenhanced delegated powers providedthey have not defaulted in therepayment of loans/interest payment onany loans due to the Government.

(iv) These public sector enterprises shall notdepend upon budgetary support orGovernment guarantees.

(v) The Boards of these PSEs should berestructured by inducting at least threenon-official Directors as the first stepbefore the exercise of enhanceddelegation of authority.

(vi) The administrative Ministry concernedshall decide whether a Public SectorEnterprise fulfilled the requirements ofa Category-I/Category-II companybefore the exercise of enhancedpowers.

5.2. 3.1 Presently there are 44 MiniratnaPSEs. Their names are as under:

Category-I

1. Bharat Dynamics Ltd.

2. Bharat Electronics Ltd.

3. Bongaigaon Refinery & PetrochemicalsLtd.

4. Central Warehousing Corporation

5. Chennai Petroleum Corporation Ltd.

6. Container Corporation of India Ltd.

7. Dredging Corporation of India Ltd.

8. Engineers India Ltd.

9. Hindustan Aeronautics Ltd.

10. Hindustan Newsprint Ltd.

11. Housing & Urban DevelopmentCorporation Ltd.

12. India Tourism Development CorporationLtd.

13. IRCON (International) Ltd.

14. Kochi Refineries Ltd.

15. Kudremukh Iron Ore Company Ltd.

16. M M T C Ltd.

17. National Aluminium Company Ltd.

18. National Fertilizers Ltd.

19. National Mineral DevelopmentCorporation Ltd.

20. Neyveli Lignite Corporation Ltd.

21. Numaligarh Refinery Ltd.

22. Oil India Ltd.

23. Power Finance Corporation Ltd.

24. Power Grid Corporation Ltd.

25. Rashtriya Chemicals & Fertilizers Ltd.

26. Rural Electrification Corporation Ltd.

27. Shipping Corporation of India Ltd.

28. State Trading Corporation of India Ltd.

29. Telecommunications Consultants (India)Ltd.

Investment in Public Enterprises 59

Category-II1. Balmer Lawrie & Co. Ltd.

2. Educational Consultants (India) Ltd.3. Ferro Scrap Nigam Ltd.

4. HMT (International) Ltd.5. Hospital Services Consultancy

Corporation (I) Ltd.6. India Trade Promotion Organisation.7. Indian Medicines Pharmaceuticals

Corporation Ltd.8. M S T C Ltd.

9. Manganese Ore India Ltd.10. M E C O N Ltd.

11. National Film Development CorporationLtd.

12. P E C Ltd.13. Rajasthan Electronics & Instruments Ltd.14. R I T E S Ltd.

15. Water & Power Consultancy Services(India) Ltd.

5.2.3.2 The delegation of decision-makingauthority available at present to the Boardsof these PSEs is as follows:

(i) Capital Expenditure

(a) For PSEs in category I: The powerto incur capital expenditure on newprojects, modernization, purchaseof equipment, etc., withoutGovernment approval upto Rs. 500crore or equal to net worth,whichever is less.

(b) For PSEs in category II: The powerto incur capital expenditure on newprojects, modernization, purchaseof equipment, etc., withoutGovernment approval upto Rs. 250crore or equal to 50% of the Networth, whichever is less.

(ii) Joint ventures and subsidiaries:

(a) Category I PSEs: To establish jointventures and subsidiaries in Indiawith the stipulation that the equity

investment of the PSE in any oneproject should be limited to 15% ofthe networth of the PSE or Rs. 500crore, whichever is less. The overallceiling on such investment in allprojects put together is 30% of thenetworth of the PSE.

(b) Category II PSEs: To establish jointventures and subsidiaries in Indiawith the stipulation that the equityinvestment of the PSE in any oneproject should be 15% of thenetworth of the PSE or Rs. 250crore, whichever is less. The overallceiling on such investment in allprojects put together is 30% of thenetworth of the PSE.

(iii) Mergers and acquisitions

The Board of Directors of these PSEshave the powers for mergers andacquisitions, subject to the conditionsthat (i) it should be as per the growthplan and in the core area of functioningof the PSE, (ii) conditions/limits wouldbe as in the case of establishing jointventures/subsidiaries, and (iii) theCabinet Committee on Economic Affairswould be kept informed in case ofinvestments abroad.

(iv) Scheme for HRD

To structure and implement schemesrelating to personnel and humanresource management, training,voluntary or compulsory retirementschemes, etc. The Board of Directors ofthese PSEs have the power to furtherdelegate the powers relating to HumanResource Management (appointments,transfer, posting, etc.) of below Boardlevel executives to sub-committees ofthe Board or to executives of the PSE,as may be decided by the Board of thePSE.

(v) Tour abroad of functional Directors

The Chief Executive of the PSE havethe power to approve business tours

60 Public Enterprises Survey 2004-05 : Vol.-I

abroad of functional directors up to 5days’ duration (other than study tours,seminars, etc.) in emergency, underintimation to the Secretary of theadministrative Ministry. In all other casesincluding those of Chief Executive, toursabroad would continue to require theprior approval of the Minister of theAdministrative Ministry/ Department.

(vi) Technology Joint Ventures andStrategic Alliances

To enter into technology jointventures, strategic alliances and to obtaintechnology and know-how by purchase orother arrangements, subject to Governmentguidelines as may be issued from time totime.

5.2.3.3 The above delegation of powers issubject to similar conditions as are applicableto Navratna PSEs.

Other profit making PSEs

5.2.4 Those PSEs which have shown aprofit in each of the 3 preceding accountingyears and have a positive net worth arecategorized as ‘other profit making PSEs’ andhave been delegated enhanced powers asunder:-

(i) The power to incur capital expenditurewithout Government approval standsrevised to Rs. 150 crore or equal to 50%of the Net worth, whichever is less.

(ii) The Chief Executive of the PSE shallhave the power to approve businesstours abroad of functional directors upto 5 days’ duration (other than studytours, seminars, etc.) in emergency,under intimation to the Secretary of theadministrative Ministry. In all other casesincluding those of Chief Executive, toursabroad would continue to require theprior approval of the Minister of theAdministrative Ministry/ Department.

5.2.4.1 The delegation is subject to thefollowing conditions:

(a) inclusion of the project in theapproved Five Year and AnnualPlans and outlays provided for.

(b) The required funds can be foundfrom the internal resources of thecompany and extra budgetaryresources (EIBR) and theexpenditure is incurred on schemesincluded in the capital budgetapproved by the Government.

Disinvestment 61

DISINVESTMENT66.1 The policy of the Government onDisinvestment has evolved over a period oftime.The National Common MinimumProgramme (NCMP) outlines the presentpolicy of the Government with respect to thePublic Sector, including disinvestment ofGovernment's equity in Central Public SectorEnterprises (CPSEs). The salient features ofthe policy as laid down in NCMP are asfollows:-

• “The Government is committed to astrong and effective public sectorwhose social objectives are met by itscommercial functioning.

• The Government is pledged to devolvefull managerial and commercialautonomy to successful, profit-makingcompanies operating in a competitiveenvironment.

• Generally profit making companies willnot be privatised.

• All privatisations will be considered ona transparent and consultative case-by-case basis.

• The Government will retain existing“navaratna” companines in the publicsector while these companies raiseresources from the capital market.

• While every effort will be made tomodernize and restructure sick publicsector comapnies and revive sickindustry, chronically loss-makingcompanies will either be sold-off, orclosed, after all workers have got theirlegitimate dues and compensation.

• The Government will induct privateindustry to turn around companies thathave potential for revival.

• The Governement believes thatprivatisation should increasecompetition, not decrease it. It will notsupport the emergence of anymonopoly that only restrictscompetition. It also believes that theremust be a direct link betweenprivatisation and social needs—like, forexample, the use of privatisationrevenues for designated socialschemes. Public sector companies andnationalised banks will be encouragedto enter the capital market to raiseresources and offer new investmentavenues to retail investors.”

6.2 The chronology of evolution of policyon disinvestment since 1991-1992 is givenin Annexure-I. Disinvestment ofGovernment equity in Public Sector beganin 1991-92.Till 1999-2000, it was primarilythrough sale of minority shares in small lots.From 1999-2000 till 2003-2004, theemphasis of disinvestment changed infavour of Strategic Sale. At present, theemphasis is to list, large, profitable CPSEson domestic stock exchanges and toselectively sell small portions of equity inlisted, profitable CPSEs (other than thenavratnas).

6.3 The proceeds from disinvestmentfrom April, 1991 to November, 2005amounted to Rs.47,671.62 crore. Details ofthe annual realisation and themethodologies adopted are given inAnnexure-II.

62 Public Enterprises Survey 2004-05 : Vol.-I

6.4 The Ministry of Industry (Department

of Public Enterprises) vide a resolution dated23rd August,1996, constituted a Public

Sector Disinvestment Commission for a

period of three years. The term was furtherextended till 30th November,1999. The

Commission submitted its reports on 58

PSEs. The Commission was reconstituted inJuly, 2001 for a period of two years. The

term of this Commission was subsequently

extended till October,2004. Thereconstituted Commission submitted its

Reports on 41 PSEs, including review cases

of earlier Commission’s recommendationson 4 PSEs. The term of the Commission

expired on 31st October, 2004 and it has

been wound up.

Disinvestment 63

Annexure-1

Chronology of the evolution of the policy on disinvestment since 1991-92

Date Event

1991-92 Interim Budget Government announced its intention to divest upto 20%of Government equity in slected PSEs in favour of publicsector institutional investos.

Industrial Policy Statement In the case of selected enterprises, part of Governmentdated 24.7.1991 holdings in the equity share capital of the enterprises

will be disinvested in order to provide further marketdiscipline to the performance of public enterprises.

Rangarajan Committee-April,1993 It emphasized the need for substantial disinvestmentand stated that while the percentage of equity to bedivested should be not more than 49% for industiresexplicity reserved for the public sector, it should beeither 74% or 100% for others.

Budget speech-1998-1999 “Government have also decided that in the generalityof cases, the Government shareholding in public sectorenterprises will be brought down to 26 per cent. In casesof public sector enterprises involving strategicconsiderations, Government will continue to retainmajority holding. The interest of workers shall beprotected in all cases.”

Budget speech-1999-2000 “Government strategy towards public sector enterpriseswill continue to encompass a judicious mix ofstrengthening strategic units, privatising non-strategicones through gradual disinvestment of strategic saleand devising viable rehabilitation strategies for weakunits.”

Cabinet decision dated 16.3.1999 Public Sector Enterprises (PSEs) have been classifiedinto strategic and non-strategic areas for the purposeof disinvestment.

Strategic PSEs would be those in the areas of:

(a) Arms and ammunitions and the allied items ofdefence equipment, defence air-crafts and warships;

(b) Atomic engery (except in the areas related to theoperation of nuclear power and applications of radiationand radio-isotopes to agriculture medicine and non-strategic industries);

64 Public Enterprises Survey 2004-05 : Vol.-I

(c) Railway transport

All other PSEs were to be considered as non-strategic.For the non-strategic PSEs, it was decided that thereduction of Government stake to 26% would not beautomatic.

Decision in regard to the percentage of disinvestmenti.e., Goverment’s stake going down to less than 51%or to 26% would be taken on the followingconsiderations :

a) Whether the industrial sector requires the presenceof the public sector as a countervailing force to preventconcentration of power in private hands; and

b) Whether the industrial sector requires a properregulatory mechanism to protect the cosumer interestbefore Public Sector Enterprises are privatised.

Budget speech 2000-2001 Government announced its decision to reduce its stakein the non-strategic PSEs even below 26%, ifnecessary. There would be increasing emphasis onstrategic sale and the entire proceeds fromdisinvestment/privatisation would be deployed in socialsector, restructuring of PSEs and retirement of publicdebts.

Decision dated 23.6.2000 In order to secure the presence of the public sector asa Countervailing force, the Government took thedecision of not going for disinvestment of GAIL, IOC andONGC, and retaining them as flagship companies.

Decision dated 7.9.2002 Central Public Sector Enterprises (PSEs), CentralGovernment owned Cooperative Societies (whereGovernment’s ownership is 51% or more) should not bepermitted to participate in the disinvestment of otherPSEs as bidder. If in some specific cases any deviationfrom these restrictions is considered desirable in publicinterest. the Ministry/Department may bring anappropriate proposal for consideration of the CoreGroup of Secretaries on Disinvestment.

Budget Speech 2003-04 Details about the already announced DisinvestmentFund and Asset Management company, to hold residualshares post disinvestment, shall be finalised early in2003-04.

Disinvestment 65

Budget Speech 2004-05 The Disinvestment and privatization are useful(July 2004) economic tools. Government will selectively employ

these tools, consistent with the declared policy.Government will establish a Board for Reconstructionof Public Sector Enterprises (BRPSE). The Board willadvise the Government on the measures to be takento restructure PSEs, including cases wheredisinvestment or closure or sale is justified. Thedisinvestment revenues will be part of the ConsolidatedFund of India. While presenting the Budget for 2005-06, the manner in which the said revenues have beenor will be applied for specified social sector schemeswill be reported to the House.

Decision dated 27.01.2005 (i) Government decided, in principle, to list large,profitable Public Sector Enterprises (PSEs) on domesticstock exchanges and to selectively sell a minority stakein listed, profitable PSEs while retaining atleast 51% ofthe shares alongwith full management control so as notto disturb the Public Sector character of the companies.

(ii) Government has also decided to constitute a"National Investment Fund" into which the realisationfrom sale of minority shareholding of the Governmentin profitable PSEs would be channelised. The Fundwould be maintained outside the Consolidated Fund ofIndia. The income from the Fund would be used for thefollowing broad investment objectives:-

(a) Investment in social sector projects whichpromote education, health care andemployment;

(b) Capital investment in selected profitable andrevivable Public Sector Enterprises that yieldadequate returns in order to enlarge their capitalbase to finance expansion/ diversification.

66 Public Enterprises Survey 2004-05 : Vol.-I

Annexure-IISummary of disinvestment target and realisation since 1991-92 and the methodologies adopted

Year No. of Budgeted Receipts Receipts Receipts Total Main transactionstransa- receipt through sale through sale through receiptsctions (Rs. crore) of residual/ of shares Strategic (Rs.

minority shares to CPSEs sale crore)(Rs. crore) (Rs. crore) (Rs. crore)

1991-92 47 2500 3037.74 0.00 0.00 3037.74 Minority shares sold in Dec 1991 andFeb 1992 by auction method in bundlesof “very good”, “good” and “average”companies

1992-93 29 2500 1912.42 0.00 0.00 1912.42 Shares sold separately for eachcompany by auction method.

1993-94 - 3500 0.00 0.00 0.00 0.00 Equity of 6 companies sold by openauction but proceeds received in 94-95.

1994-95 17 4000 4843.10 0.00 0.00 4843.10 Shares sold by auction method.1995-96 4 7000 168.48 0.00 0.00 168.48 Shares sold by auction method.1996-97 1 5000 379.67 0.00 0.00 379.67 GDR -VSNL in international market.1997-98 1 4800 910.00 0.00 0.00 910.00 GDR -MTNL in international market.1998-99 5 5000 5371.11 0.00 0.00 5371.11 GDR-VSNL; Domestic offerings of

CONCOR and GAIL; Cross purchase by3 Oil sector companies i.e. GAIL, ONGCand IOC.

1999-00 5 10000 1479.27 0.00 380.87 1860.14 GDR-GAIL; Domestic offering of VSNL;capital restructuring of BALCO; Strategicsale of MFIL.

2000-01 5 10000 0.00 1317.23 554.03 1871.26 Strategic sale of BALCO and LJMC;Sale of KRL, CPCL and BRPL toCPSEs.

2001-02 8 12,000 0.00 0.00 5657.44 5657.44 Strategic sale of CMC, HTL, VSNL, IBP,PPL and sale of hotel properties of ITDC& HCI; Special dividend from STC andMMTC; sale of shares to VSNLemployees.

2002-03 8 12,000 0.00 0.00 3347.98 3347.98 Strategic sale of HZL, IPCL, and sale ofhotel properties of HCI & ITDC; Controlpremium from renunciation of rightsissue from MUL; Put Option of MFIL;sale of shares to employees of HZL andCMC.

2003-04 2 14,500 15205.35 0.00 342.06 15547.41 Strategic sale of JCL; Call Option of HZL;IPO / Offer for Sale of MUL, IBP IPCL,CMC, DCI, GAIL and ONGC; Sale ofshares of ICI Ltd.

2004-05 3 4,000 2700.06 0.00 64.81 2764.87 Offer for Sale of NTPC; sale of sharesto IPCL employees etc.

Total 96800 36007.20 1317.23 10347.19 47671.62

Generation of Internal Resources by Public Enterprises 67

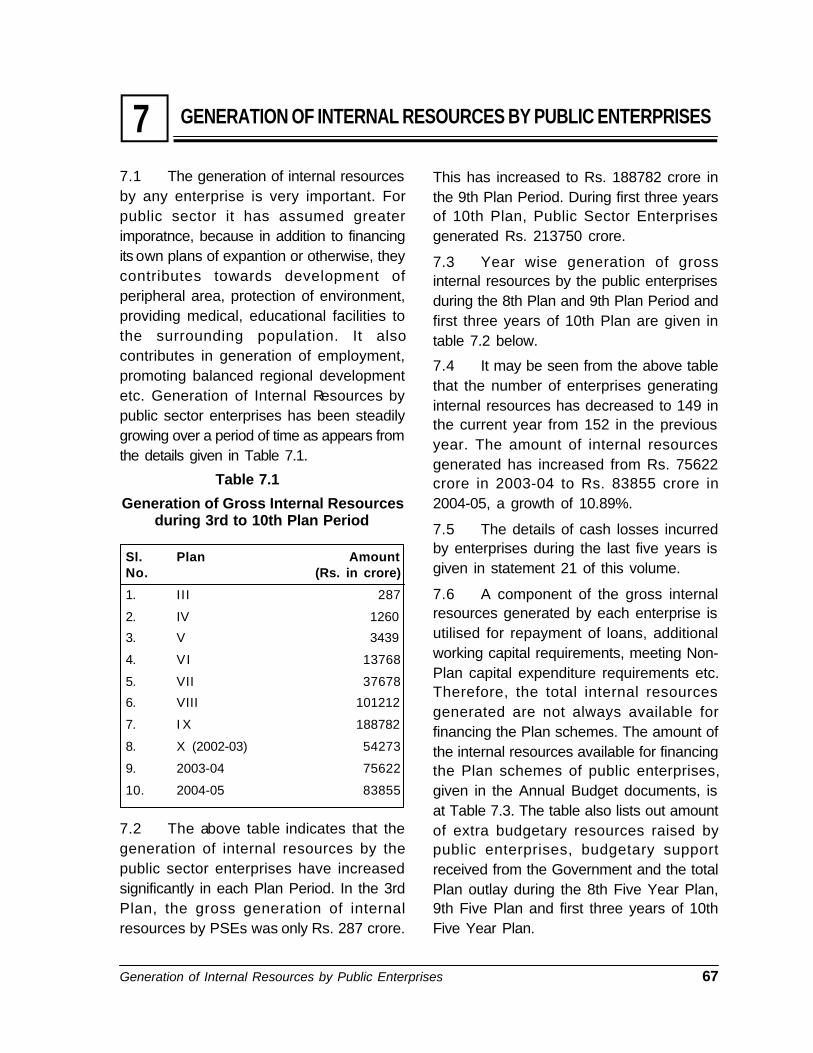

GENERATION OF INTERNAL RESOURCES BY PUBLIC ENTERPRISES77.1 The generation of internal resourcesby any enterprise is very important. Forpublic sector it has assumed greaterimporatnce, because in addition to financingits own plans of expantion or otherwise, theycontributes towards development ofperipheral area, protection of environment,providing medical, educational facilities tothe surrounding population. It alsocontributes in generation of employment,promoting balanced regional developmentetc. Generation of Internal Resources bypublic sector enterprises has been steadilygrowing over a period of time as appears fromthe details given in Table 7.1.

Table 7.1

Generation of Gross Internal Resourcesduring 3rd to 10th Plan Period

Sl. Plan AmountNo. (Rs. in crore)

1. III 287

2. IV 1260

3. V 3439

4. VI 13768

5. VII 37678

6. VIII 101212

7. I X 188782

8. X (2002-03) 54273

9. 2003-04 75622

10. 2004-05 83855

7.2 The above table indicates that thegeneration of internal resources by thepublic sector enterprises have increasedsignificantly in each Plan Period. In the 3rdPlan, the gross generation of internalresources by PSEs was only Rs. 287 crore.

This has increased to Rs. 188782 crore inthe 9th Plan Period. During first three yearsof 10th Plan, Public Sector Enterprisesgenerated Rs. 213750 crore.

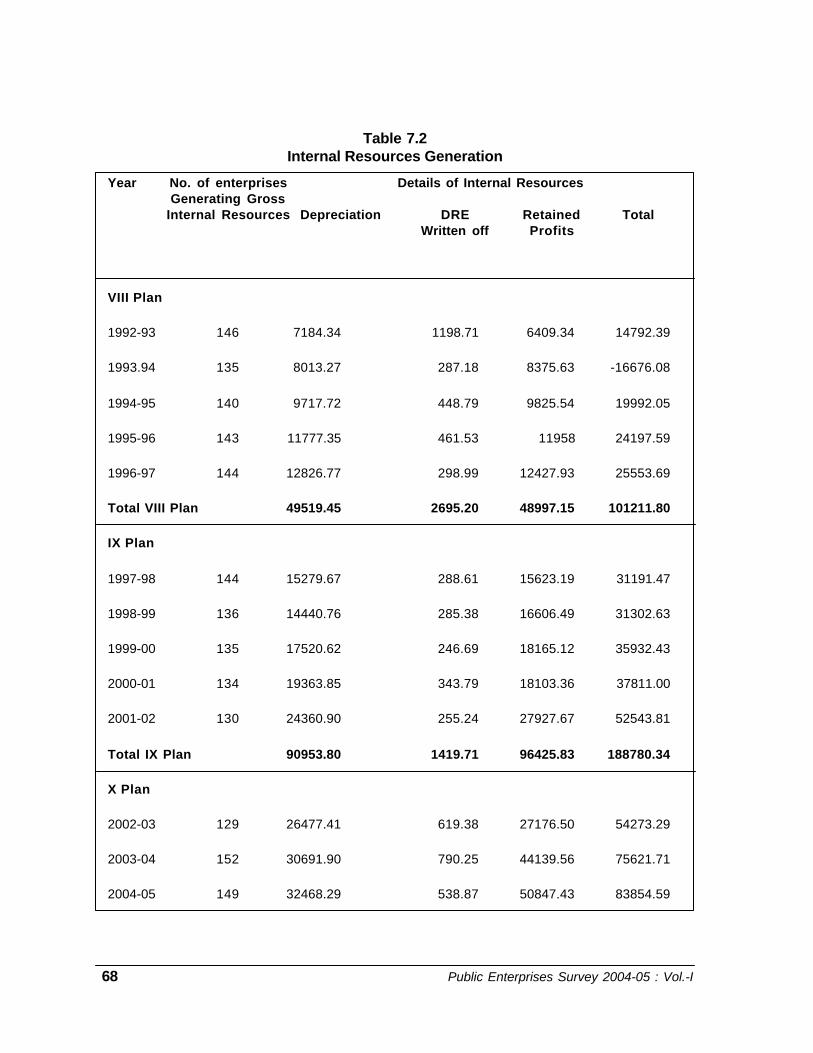

7.3 Year wise generation of grossinternal resources by the public enterprisesduring the 8th Plan and 9th Plan Period andfirst three years of 10th Plan are given intable 7.2 below.

7.4 It may be seen from the above tablethat the number of enterprises generatinginternal resources has decreased to 149 inthe current year from 152 in the previousyear. The amount of internal resourcesgenerated has increased from Rs. 75622crore in 2003-04 to Rs. 83855 crore in2004-05, a growth of 10.89%.

7.5 The details of cash losses incurredby enterprises during the last five years isgiven in statement 21 of this volume.

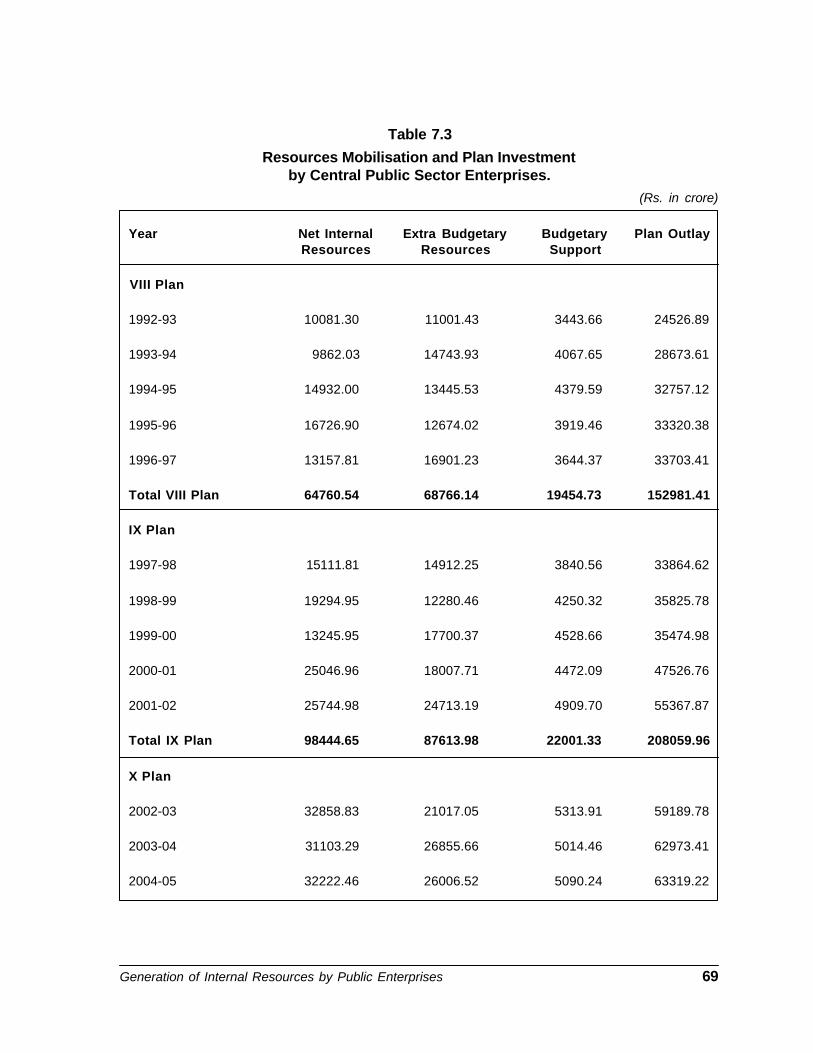

7.6 A component of the gross internalresources generated by each enterprise isutilised for repayment of loans, additionalworking capital requirements, meeting Non-Plan capital expenditure requirements etc.Therefore, the total internal resourcesgenerated are not always available forfinancing the Plan schemes. The amount ofthe internal resources available for financingthe Plan schemes of public enterprises,given in the Annual Budget documents, isat Table 7.3. The table also lists out amountof extra budgetary resources raised bypublic enterprises, budgetary supportreceived from the Government and the totalPlan outlay during the 8th Five Year Plan,9th Five Plan and first three years of 10thFive Year Plan.

68 Public Enterprises Survey 2004-05 : Vol.-I

Table 7.2Internal Resources Generation

Year No. of enterprises Details of Internal ResourcesGenerating Gross

Internal Resources Depreciation DRE Retained TotalWritten off Profits

VIII Plan

1992-93 146 7184.34 1198.71 6409.34 14792.39

1993.94 135 8013.27 287.18 8375.63 -16676.08

1994-95 140 9717.72 448.79 9825.54 19992.05

1995-96 143 11777.35 461.53 11958 24197.59

1996-97 144 12826.77 298.99 12427.93 25553.69

Total VIII Plan 49519.45 2695.20 48997.15 101211.80

IX Plan

1997-98 144 15279.67 288.61 15623.19 31191.47

1998-99 136 14440.76 285.38 16606.49 31302.63

1999-00 135 17520.62 246.69 18165.12 35932.43

2000-01 134 19363.85 343.79 18103.36 37811.00

2001-02 130 24360.90 255.24 27927.67 52543.81

Total IX Plan 90953.80 1419.71 96425.83 188780.34

X Plan

2002-03 129 26477.41 619.38 27176.50 54273.29

2003-04 152 30691.90 790.25 44139.56 75621.71

2004-05 149 32468.29 538.87 50847.43 83854.59

Generation of Internal Resources by Public Enterprises 69

Table 7.3

Resources Mobilisation and Plan Investmentby Central Public Sector Enterprises.

(Rs. in crore)

Year Net Internal Extra Budgetary Budgetary Plan OutlayResources Resources Support

VIII Plan

1992-93 10081.30 11001.43 3443.66 24526.89

1993-94 9862.03 14743.93 4067.65 28673.61

1994-95 14932.00 13445.53 4379.59 32757.12

1995-96 16726.90 12674.02 3919.46 33320.38

1996-97 13157.81 16901.23 3644.37 33703.41

Total VIII Plan 64760.54 68766.14 19454.73 152981.41

IX Plan

1997-98 15111.81 14912.25 3840.56 33864.62

1998-99 19294.95 12280.46 4250.32 35825.78

1999-00 13245.95 17700.37 4528.66 35474.98

2000-01 25046.96 18007.71 4472.09 47526.76

2001-02 25744.98 24713.19 4909.70 55367.87

Total IX Plan 98444.65 87613.98 22001.33 208059.96

X Plan

2002-03 32858.83 21017.05 5313.91 59189.78

2003-04 31103.29 26855.66 5014.46 62973.41

2004-05 32222.46 26006.52 5090.24 63319.22

70 Public Enterprises Survey 2004-05 : Vol.-I

PRICING POLICY IN PUBLIC ENERPRISES8A. PRICING POLICY

8.1 The investment policy of theGovernment aims at channelising publicinvestment in basic and infrastructural sectorand for continuing with the provisions ofessential commodities. The pricing policiesin the Central Public Sector Enterprises(CPSEs) are therefore, interlinked with theinvestment policies. Another dimension ofthe pricing policy is to create a balancebetween the social obectives of theseenterprises and their commercial viabilityand also the overall economic policies of theGovernment.

8.2. It has been accepted principle thatprices of products produced and servicesrendered by public enterprises should be sodetermined that at a satisfactory level ofcapacity utilization these enterprises not onlycover their costs of production, but alsogenerate a reasonable amount of surplus.This will assist in capital formation andenable redeployment of the capital forfurther strengthening of economic and socialinfrastructure. In this sense, product makingin public enterprises is not quite inconsistentwith the public purpose. It is theGovernment’s expectation that with themassive investment in the public sectorenterprises, these enterprises do not at anystage erode the resources base, butstrengthen it. It is therefore, recognized thatsubect to the total overall impact of certainproduct prices on the economy, theproducers in the public sector shouldgenerally have proper control in determiningthe prices of their commodities.

8.3. However with the dismantling ofadministered price mechanism, opening up

various sectors for private partipation andglobalisation of Indian economy, prices ofproducts and service in public sector alsoare generally determined by market forcesThe CPSEs have to compete with othercompanies in India as well as abroad.Indiviual CPSE, are generally fix price fortheir products & services on their ownexcept for certain sectors details of whichare given in subsequent para's.

8.4 Govt. of India has evolved pricingpolicies in respect of certain sectors. Thesepolicies are applicable to public sector aswell as private sector and are discussedbelow:

(i) AGRICULTURE

8.4.1 Agriculutural products comprise bothfood grains and industrial raw materials. Thestress is on adoption of a pricing policywhich will provide a minimum fair return tothe producers, reduce fluctuations in pricesand achieve an equitable distribution ofessential consumer goods. An efficientpublic distribution system is an essentialingredient to ensure that this pricing strategyworks equitably. Under this policy, Govt. ofIndia fixes Minimum Support Prices (MSP)in respect of major food grains and industrialraw materials on the recommendation of theCommission on Agricultural Costs Prices(CACP). At the same time, Governmentensures supply of major food grains toweaker sections of society at reasonablerates through public distribuition system.Food Corporation of India implementprocurement and public distributution policyfor food grains while jute Corporation ofIndia and Cotton Corporation Indiaimplement MSP policy for jute and cottonrespectively.

Socio-Economic and Welfare Measures 71

ii) COAL

8.4.2 The pricing of coal has beencompletely deregulated after Colliery ControlOrder, 1945. Under the Colliery ControlOrder, 2000, the Central Government has nopower to fix the prices of coal and the coalcompanies themselves are competent to fixgrade-wise prices for coal produced by thembased on marketing economics.

(iii) FERTILIZERS

8.4.3 At present, only urea, which is themain nitrogenous fertilizer constituting about60% of the total fertilizer consumption in thecountry, is under statutory price and partialdistribution control. Urea is sold/madeavailable to the farmers at statutory notifiedsale price. All other varieties of fertilizerswere removed from price and distributioncontrol between August '92 and June '94.However, Government of India still indicatesthe MRP in respect of major phosphatic andcomplex fertilizers, namely Di-AmmoniumPhosphate (DAP), Muriate of Potash (MOP)and Complex Fertilizers. The MRP for SingleSupper Phosphates (SSP) are indicated bythe respective State Government. Thestatutorily notified sale price and indicativeMRP is generally kept less than the cost ofproduction of the respective manufacturingunit. The difference between the cost ofproduction and the selling price/MRP is paidas subsidy/concession to manufacturers. Asthe consumer prices of both indigenous andimported fertilizers are fixed uniformly,financial support is also given on importedurea and decontrolled phosphatic andpotassic fertilizers.

(iv) STEEL

8.4.4 Prices of steel products have beenfully decontrolled and the Central PublicSector Enterprises (CPSEs) are free to8determine prices of their products/servicesbased on free interplay to market forces.

However, the Government, through its policyinnitiatives attempts to ensure adequateavailability of Steel in the domestic marketand a stable price regime.

(v) PETROLEUM PRODUCTS

8.4.5 Effective from 1/4/02, pricing ofpetroleum products except for PDSKerosene and domestic LPG, has becomemarket determined. As per the decisiontaken at the time of announcement of APMdismantling, post APM Governmentsubsidies on PDS Kerosene and DomesticLPG were to be on flat rates basis to beprovided from the fiscal budget and afterproviding for this subsidy, the retail priceswere to vary as per changes in theinternational prices. These subsidies were tobe phased out in three to five years effectivefrom 1/4/2002. The subsidies from fiscalbudget were based on international pricesof Kerosene and LPG prevailing in Arab Gulfmarket during the month of March, 2002, i.e.$23.65 per barrel and $194 per MTrespectively. At present subsidy is beingallowed at the rate of Rs. 22.58 per cylinderand Rs. 0.82 per litre in respect of LPG(Domestic) and SKO(PDS) respectively.

8.4.5.1 The financial year 2004-05 witnessedsharp and spiraling increase in internationalprices of Crude Oil and petroleum products.There was a severe escalation in prices ofCrude Oil and Petroleum products during2004-05 vis-a-vis March, 2002.

8.4.5.2 The impact of such phenomenal priceincrease in the international market is boundto have major impact on Oil Industry whichis heavily dependent on imports for crudeprocurement. However, if Import ParityPricing (IPP) mechanism had been allowedfull play that would have caused severehardship to the end consumers. To insulatethe end consumers it was decided that theshare of burden has been divided between

72 Public Enterprises Survey 2004-05 : Vol.-I

various stakeholders i.e. Government, Oilcompanies and consumers. Hence, series ofduty structuring and some price revisionswere carried out to distribute the burden ofprice hike in an equitable manner.

8.4.5.3 Moderate imcreases to the extent ofRs.2 per litre on petrol, Re.1 per litre on dieseland Rs.20 per LPG Cyllinder were effectedon 16-6-2004, coupled with excise dutyreductions of 4% on Petrol, 3% on diesel andand 8% on LPG (Domestic).

8.4.5.4 In order to mitigate the hardships ofoil companies, Government had worked outa new methodology with effect from 1s t

August, 2004 allowing OMCs limited freedomto revise the prices of MS/HSD within a priceband. The concept of price band is basedon the principles of rolling average prices ofthese products in the international markets.Accordingly, oil companies are permitted dtocarry out autonomous adjustments in priceswithin a band of +/- 10% of the mean of rollingaverage C&F prices of last 12 months andlast quarter, i.e. three months.

8.4.5.5 In case of breach of this band, theOMCs have to approach the Ministry ofFinance through MOP&NG to modulate theexcise duty rates so that the spiraling pricesprevailing in the international markets do notcause undue hardships to the consumers.Further on 19/08/2004 the Governmentreduced Customs duty by 5% in respect ofPetrol, Diesel. SKO (PDS) and LPG(Domestic) and Excise Duty by 3% on Petroland Diesel and by 4% in respect of SKO(PDS).

8.4.5.6 However, the international prices wentup further during the month of October, 2004.With the under-recoveries on petrol and dieselmounting, further increases were announcedeffective 5-11-2004. Retail selling price of

petrol was fixed in line with the import parityprice. The retail price of petrol was furtherrevised downwards in line with internationalprices effective 16-11-04. However, theincrease in the diesel retail price was peggedat 50% of the level of increase required onthe basis of import parity and no furtherincrease wsa made in the diesel price on 16-11-2004.

8.4.5.7 The retai selling price of LPG (PackedDomestic) was revised again by the oilmarketing companies effective 5 th November,2004 by Rs.20 per cylinder in view of theabnormally high prices of crude oil andpetroleum products in the international market.However, there was no hike in retail sellingprice of PDS Kerosene which has remainedunchanged (except minor correction indealers’ commission / VAT by StateGovernment since March, 2002.

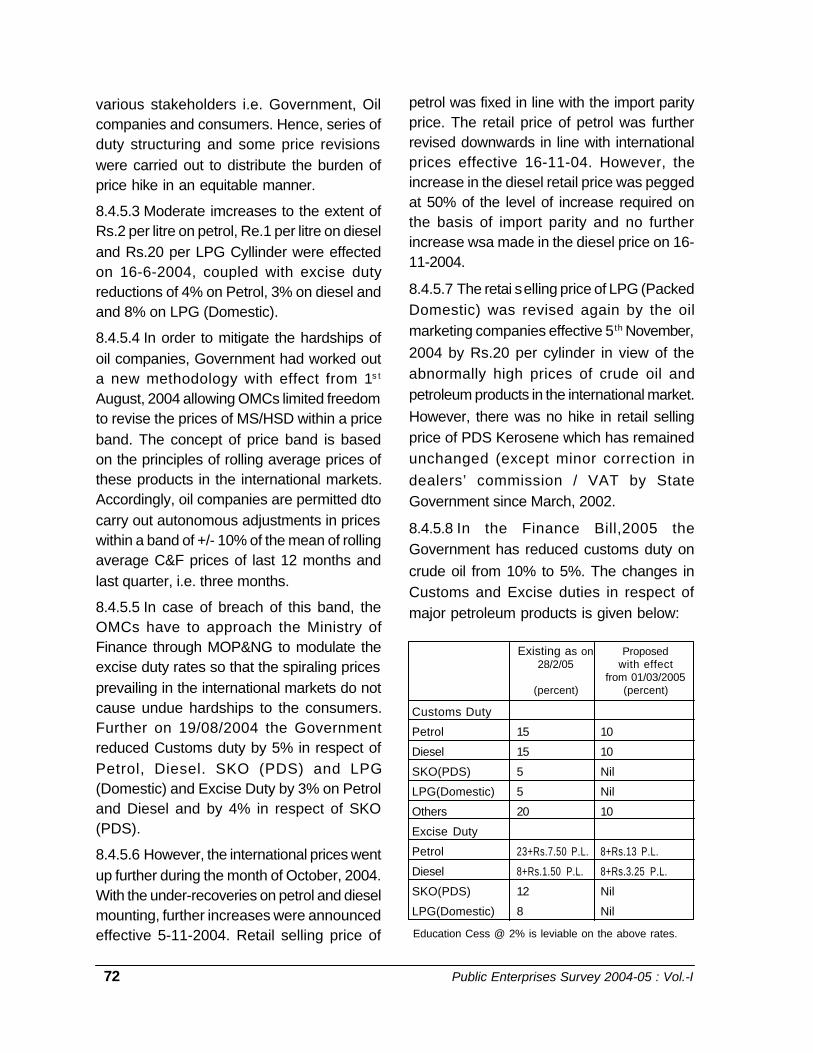

8.4.5.8 In the Finance Bill,2005 theGovernment has reduced customs duty oncrude oil from 10% to 5%. The changes inCustoms and Excise duties in respect ofmajor petroleum products is given below:

Existing as on Proposed28/2/05 with effect

from 01/03/2005(percent) (percent)

Customs Duty

Petrol 15 10

Diesel 15 10

SKO(PDS) 5 Nil

LPG(Domestic) 5 Nil

Others 20 10

Excise Duty

Petrol 23+Rs.7.50 P.L. 8+Rs.13 P.L.

Diesel 8+Rs.1.50 P.L. 8+Rs.3.25 P.L.

SKO(PDS) 12 Nil

LPG(Domestic) 8 Nil

Education Cess @ 2% is leviable on the above rates.

Socio-Economic and Welfare Measures 73

(vi) POWER

8.4.6 The power tariff for the sale of powerby the generation company to thedistribution company and to other personsis determined/regulated as per the termsand conditions notified by the Governmentof India vide its notification dated 30th March,1992 and subsequent amendments madetherein from time to time.

8.4.6.1 In 1998, the Electricity RegulatoryCommission Act was enacted for creation ofRegulatory Commissions at the Centre andin the States with powers inter-alia toregulate/determine traiff. Under theprovisions of the Act, the CentralGovernment created Central ElectricityRegulatory Commission (CERC) whichregulate/determine traiff of the CentralGovernment owned companies engaged ingeneration and inter-state transmission.CERC also issued order on availabilityBased Tariff for ensuring grid discipline.

8.4.6.2 The power sector reforms effected inrecent years necessitated the enactment ofthe Electricity Act, 2003 and repeal of theERC Act, 1998. The provisions of theElectricity Act, 2003 serve to consolidate thelaws relating to generation, transmission,distribution, trading and use of electricity.The Act is aimed at taking measuresconducive to development of electricityindustry, promoting competition therein,protecting interest of the consumers andsupply of electricity to all areas,rationalization of electricity tariff, ensuringtransparent policies regarding subsidies,promotion of efficient and environmentallybenign policies, constitution of CentralElectricity Authority, RegulatoryCommissions and establishment ofAppellate Tribunal and for matters

connected therewith or incidental thereto.However, at present the CERC constitutedunder the ERC Act, 1998 as also its powersin terms of regulation/ determination of Statetariff of the Central Government ownedcompanies involved in generation and inter-transmission have been retained.

8.4.6.3 As per the Electricity Act, 2003, theRegulatory Commission shall be guided byElectricity Tariff Policy to be notified by theCentral Government in near future.

(vii) PHARMACEUTICALS

8.4.7 For fixations of prices ofpharmaceutical products in Central PublicSector Enterprises (CPSEs), the Drugs PriceControl Order (DPCO), 1995 is followed. Asper DPCO, the pharmaceutical products arecategorized as Scheduled and Non-Scheduled formulations. The prices ofScheduled products are fixed by theNational Pharmaceutical Pricing Authority(NPPA) under the provisions of DPCO. TheMaximum Retail Prices (MRP) of Scheduledformulations are fixed and revised as perannouncement/notification by theGovernment of India.

8.4.7.1 In case of Non-scheduledformulations the prices are fixed by theCPSEs on cost plus basis.

B. PURCHASE PREFRENCE POLICY

8.5 The policy of purchase preference forproducts and services of Central PublicSector Enterprises (CPSEs) by GovernmentDepartments/Organisations and otherCPSEs was introduced in 1992 by replacingthe earlier policy of both price and purchasepreference operating since 1971. Theunderlying objective of this policy is to enableCPSEs to adjust to the new environment ofcompetitiveness and market mechanism in

74 Public Enterprises Survey 2004-05 : Vol.-I

the wake of liberalization/globalization and toassist these enterprises in improving theirprofitability by better utilization of theirinstalled capacities.

8.5.1 The purchase preference policy (PPP)was initially made applicable for a period ofthree years. However, over the period of timeit has been reviewed and extended from timeto time with or with out certain modifications.The policy was last reviewed by theGovernment in June, 2005 and extended videO.M. dated 18.07.2005 it with certainmodifications for a period of three yearsbeyond 31.3.2005 with clear stipulation thatthe policy will be terminated with effect from31.3.2008.

8.5.2 As per PPP if the price quoted by aCPSE/subsidiary company is within 10% ofthe evaluated valid price bid (L 1), purchasepreference will be granted to the enterpriseconcerned at L 1 price. Joint ventures withprivate partners are not eligible for availingof purchase preference.Provisions forpurchase preference will be made in tendersincluding civil works and turnkey contractsof Rs. 5 crore and above but not exceedingRs. 100 crore. A minimum value addition of20% will be ensured by the CPSEs foravailing of purchase preference.

8.5.3 PSEs should be subject to the samequalification process as any other bidder. Ifthe PSE does not meet the minimumqualifications, it should be subject todisqualification. However, in suitable cases,the purchasers / clients may relax thecondition of “net worth” from the list ofminimum qualifications. If the PSE, which hashad the benefit of the Purchase Preference

Policy, fails to perform, it should also besubject to payment of liquidated damages orany other penalty included in the contract.

8.5.4 Each Ministry shall make a list ofCPSEs that would require PPP support andif there is no possibility of making a positivelist, they may attempt a negative list of CPSEswhich may not require PPP support.

8.5.5 Ministry of Power will be grantedexemption from the PPP, subject to thecondition that they will place certain ordersupon BHEL on a negotiated basis pricebenchmarked through competitively bidprojects every year. Ministry of Power andDepartment of Heavy Industry will work out,at the beginning of the year, the number andvalue of the orders to be placed upon BHELduring the financial year.

8.5.6 All Ministries /Departments/ CPSEs /Autonomous Bodies except Ministry of Powerwill continue to grant purchase preferenceto CPSEs/subsidiary companies. RespectiveMinistries /Departments / CPSEs /Autonomous Bodies will be responsible forimplementing the Purchase PreferencePolicy in letter and in spirit. For any deviationincluding exclusion of the purchasepreference clause from NIT, it will beobligatory on the concerned Ministry/Department / CPSE / Autonomous Body toobtain prior exemption from the Cabinet inconsultation with the Department of PublicEnterprises.

8.5.7 The cases which were underconsideration from 1.4.2005 till the date ofissue of the order extending the policy wouldstand covered under the policy except thosewhich have already been decided otherwise.

Productivity in Public Enterprises 75

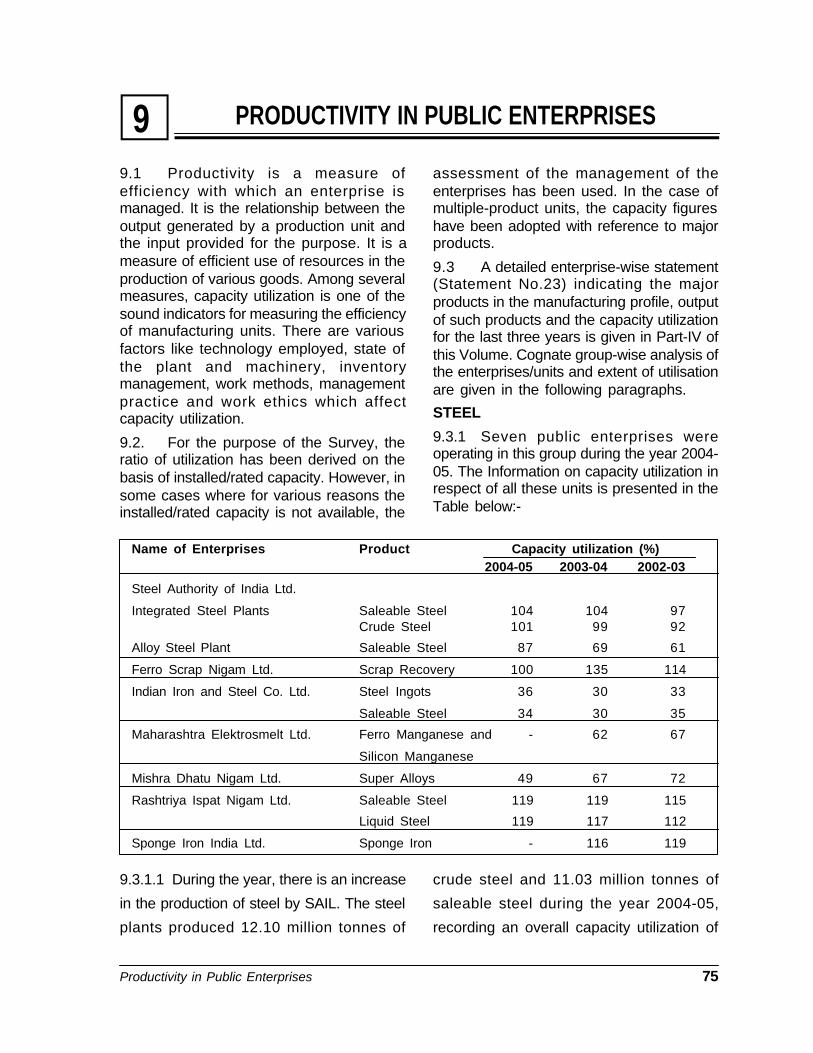

PRODUCTIVITY IN PUBLIC ENTERPRISES99.1 Productivity is a measure ofefficiency with which an enterprise ismanaged. It is the relationship between theoutput generated by a production unit andthe input provided for the purpose. It is ameasure of efficient use of resources in theproduction of various goods. Among severalmeasures, capacity utilization is one of thesound indicators for measuring the efficiencyof manufacturing units. There are variousfactors like technology employed, state ofthe plant and machinery, inventorymanagement, work methods, managementpractice and work ethics which affectcapacity utilization.

9.2. For the purpose of the Survey, theratio of utilization has been derived on thebasis of installed/rated capacity. However, insome cases where for various reasons theinstalled/rated capacity is not available, the

assessment of the management of theenterprises has been used. In the case ofmultiple-product units, the capacity figureshave been adopted with reference to majorproducts.

9.3 A detailed enterprise-wise statement(Statement No.23) indicating the majorproducts in the manufacturing profile, outputof such products and the capacity utilizationfor the last three years is given in Part-IV ofthis Volume. Cognate group-wise analysis ofthe enterprises/units and extent of utilisationare given in the following paragraphs.

STEEL

9.3.1 Seven public enterprises wereoperating in this group during the year 2004-05. The Information on capacity utilization inrespect of all these units is presented in theTable below:-

Name of Enterprises Product Capacity utilization (%)2004-05 2003-04 2002-03

Steel Authority of India Ltd.

Integrated Steel Plants Saleable Steel 104 104 97Crude Steel 101 99 92

Alloy Steel Plant Saleable Steel 87 69 61

Ferro Scrap Nigam Ltd. Scrap Recovery 100 135 114

Indian Iron and Steel Co. Ltd. Steel Ingots 36 30 33

Saleable Steel 34 30 35

Maharashtra Elektrosmelt Ltd. Ferro Manganese and - 62 67

Silicon Manganese

Mishra Dhatu Nigam Ltd. Super Alloys 49 67 72

Rashtriya Ispat Nigam Ltd. Saleable Steel 119 119 115

Liquid Steel 119 117 112

Sponge Iron India Ltd. Sponge Iron - 116 119

9.3.1.1 During the year, there is an increase

in the production of steel by SAIL. The steel

plants produced 12.10 million tonnes of

crude steel and 11.03 million tonnes of

saleable steel during the year 2004-05,

recording an overall capacity utilization of

76 Public Enterprises Survey 2004-05 : Vol.-I

101% and 104% respectively. The

corresponding figures for the previous year

were 11.83 million tonnes of crude steel and

11.026 million tonnes of saleable steel with

capacity utilization of 99% and 104%

respectively.

9.3.2 The Alloy Steel plant at Durgapur

and the Salem Steel Plant together

produced 3.79 lakh tonnes of saleable steel

as compared to the previous year's

production of 2.98 lakh tonnes.

9.3.3 The Indian Iron and Steel Co. Ltd.

produced 3.57 lakh tonnes of crude steel

and 2.74 lakh tonnes of saleable steel

during 2004-05 as compared to 3.01 lakh

tonnes of crude steel and 2.58 lakh tonnes

of saleable steel during the previous year.

9.3.1.4 The Mishra Dhatu Nigam Ltd.

produced 1337 MT of alloys during 2004-05

with 49 per cent utilization of the capacity

as against a production of 1819 MT in the

previous year at 67 percent of the capacity.

9.3.1.5 The Rashtriya Ispat Nigam Ltd.

produced 3.56 lakh tonnes of liquid steel

and 3.17 lakh tonnes of saleable steel

during 2004-05 as against a production of

3.51 lakh tonnes of liquid steel and 3.17 lakh

tonnes of saleable steel during the previous

year.

Minerals and Metals

9.4.1 Nine public enterprises were operating

in the Minerals and Metals group during the

year 2004-05. The information in respect of

two are not available and the information in

respect of the remaining seven enterprises is

presented in the Table below: -

Name of Enterprise Product Capacity utilization (%)2004-05 2003-04 2002-03

Bharat Refractories Ltd. Bricks and Masses 48 39 26

Hindustan Copper Ltd. KCC-Cathodes 51 64 77

Wire Rod 46 47 51

Indian Rare Earths Ltd. Limenite 90 89 74

Rutile 68 66 56

Zircon 102 103 98

Kudremukh Iron Ore Ltd. Iron Ore Concen. 65 76 83

Iron Ore Pellets 95 92 86

Manganese Ore (India) Ltd. Manganese Ore 100 118 106

Elect. Mon Diox 112 97 93

Ferro Manganese 103 109 60

National Aluminium Co. Ltd. Bauxite 101 100 100

Calcined Alumina 100 98 94

Aluminium Metal 98 104 8

Power (Net) 101 105 88

National Mineral Dev. Iron Ore 110 103 109

Corporation Ltd. Diamonds 93 85 100

Productivity in Public Enterprises 77

9.4.1.1 National Aluminium Company Ltd.produced 3.385 lakh tonnes of aluminiummetal during the year 2004-05 as against2.982 lakh tonnes during the previous year.The production of calcined alumina andbauxite was 15.667 lakh tonnes and 48.52lakh tonnes with capacity utilization at 100%and 101% respectively.

9.4.1.2 The National Mineral DevelopmentCorporation Ltd. produced 207.43 lakh MTof iron ore during the year 2004-05 ascompared to 179.59 lakh MT in the previousyear. The production of diamonds at Pannaunit was 78217 carats as against 71163carats of previous year.

9.4.1.3 The Hindustan Copper Ltd.produced 24186 tonnes of cathode and27423 tonnes of wire rod during 2004-05 ascompared to 30598 tonnes of cathode and28003 tonnes of wire rod during the previousyear respectively.

9.4.1.4 The Manganese Ore India Ltd.produced 9.43 lakh tonnes of manganese

Name of Enterprise Product Capacity utilization (%)2004-05 2003-03 2002-03

Bharat Coking Coal Ltd. Raw Coal 64 64 74

Central Coalfields Ltd. Raw Coal 74 99 90

Eastern Coalfields Ltd. Raw Coal 82 85 83

Mahanadi Coalfields Ltd. Coal 100 102 101

Northern Coalfields Ltd. Coal - 112 106

South Eastern Coalfields Ltd. Coal 115 105 97

Western Coalfields Ltd. Coal 113 105 104

Coal India Ltd. (Total) Coal - 90 89

Neyveli Lignite Corpn. Ltd. Lignite 90 86 78

ore during 2004-05 against the productionof 7.99 lakh tonnes during the previous year.The production of bricks and masses by theBharat Refractories Ltd. during the year2004-05 was 65485 MT with capacityutilization of 48% as compared to 53116 MTwith capacity utilization of 39% during theprevious year. There is an improvement inthe capacity utilization as compared to theprevious year.

9.4.1.5 The Indian Rare Earths Ltd.produced 417275 MT ilmenite, 16317 MTrutile and 23376 MT zircon during the year2004-05. The corresponding figures for theprevious year were 414631, 15753 and23634 MT respectively.

Coal and Lignite

9.5.1 Nine public enterprises wereoperating in the Coal and Lignite groupduring the year 2004-05. The information oncapacity utilization in respect of all theseunits is presented in the Table below:-

9.5.1.1 The total production of raw coal byCoal India Ltd. including its seven coalproducing subsidiaries during the year 2004-05 was 323.58 million tonnes as comparedto 306 million tonnes in the previous year.

9.5.1.2 The Neyveli Lignite Corporation Ltd.produced 21.57 MT of lignite during 2004-

05 as compared to 20.56 MT during theprevious year.

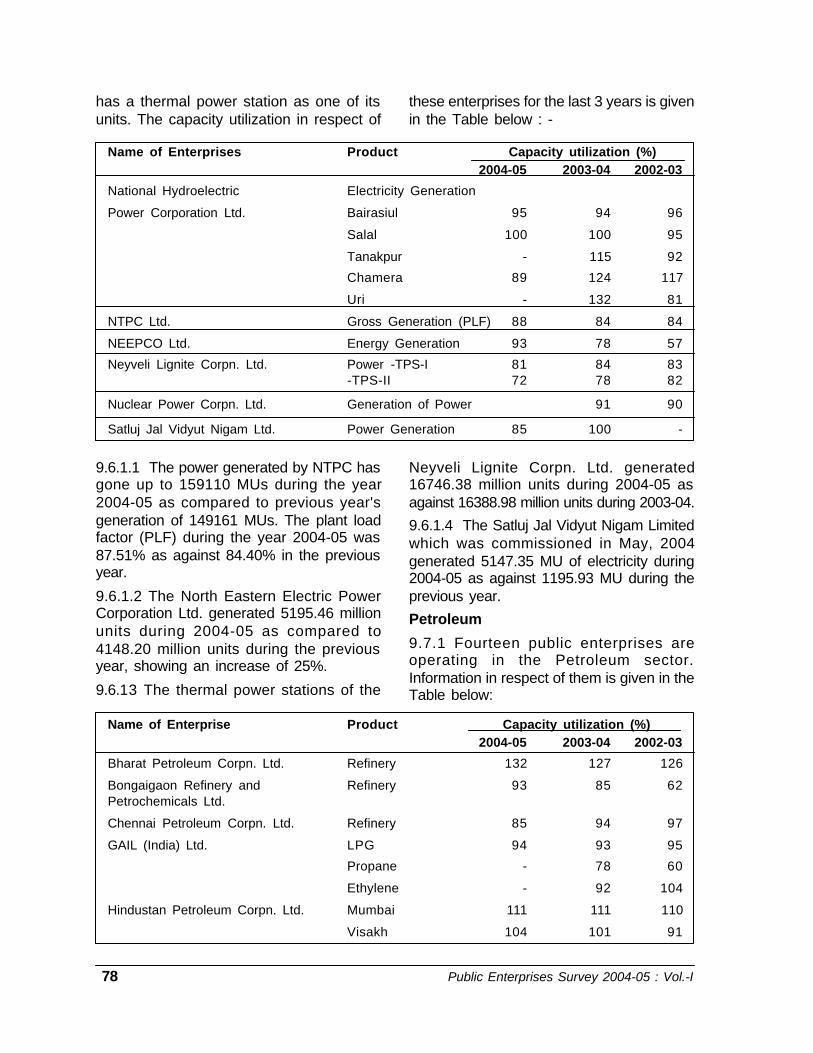

Power

9.6.1 Six public enterprises are engaged inthe generation of power. The information inrespect of one of them is not received. Inaddition, the Neyveli Lignite Corporation Ltd.

78 Public Enterprises Survey 2004-05 : Vol.-I

has a thermal power station as one of itsunits. The capacity utilization in respect of

these enterprises for the last 3 years is givenin the Table below : -

Name of Enterprises Product Capacity utilization (%)2004-05 2003-04 2002-03

National Hydroelectric Electricity Generation

Power Corporation Ltd. Bairasiul 95 94 96

Salal 100 100 95

Tanakpur - 115 92

Chamera 89 124 117

Uri - 132 81

NTPC Ltd. Gross Generation (PLF) 88 84 84

NEEPCO Ltd. Energy Generation 93 78 57

Neyveli Lignite Corpn. Ltd. Power -TPS-I 81 84 83-TPS-II 72 78 82

Nuclear Power Corpn. Ltd. Generation of Power 91 90

Satluj Jal Vidyut Nigam Ltd. Power Generation 85 100 -

Name of Enterprise Product Capacity utilization (%)2004-05 2003-04 2002-03

Bharat Petroleum Corpn. Ltd. Refinery 132 127 126

Bongaigaon Refinery and Refinery 93 85 62Petrochemicals Ltd.

Chennai Petroleum Corpn. Ltd. Refinery 85 94 97

GAIL (India) Ltd. LPG 94 93 95

Propane - 78 60

Ethylene - 92 104

Hindustan Petroleum Corpn. Ltd. Mumbai 111 111 110

Visakh 104 101 91

9.6.1.1 The power generated by NTPC hasgone up to 159110 MUs during the year2004-05 as compared to previous year'sgeneration of 149161 MUs. The plant loadfactor (PLF) during the year 2004-05 was87.51% as against 84.40% in the previousyear.

9.6.1.2 The North Eastern Electric PowerCorporation Ltd. generated 5195.46 millionunits during 2004-05 as compared to4148.20 million units during the previousyear, showing an increase of 25%.

9.6.13 The thermal power stations of the

Neyveli Lignite Corpn. Ltd. generated16746.38 million units during 2004-05 asagainst 16388.98 million units during 2003-04.

9.6.1.4 The Satluj Jal Vidyut Nigam Limitedwhich was commissioned in May, 2004generated 5147.35 MU of electricity during2004-05 as against 1195.93 MU during theprevious year.

Petroleum

9.7.1 Fourteen public enterprises areoperating in the Petroleum sector.Information in respect of them is given in theTable below:

Productivity in Public Enterprises 79

Name of Enterprise Product Capacity utilization (%)2004-05 2003-04 2002-03

Indian Oil Blending Ltd. Lubricating Oil 88 94 98

Greases 93 90 87Indian Oil Corpn. Ltd. Barauni 85 72 71

Gujarat 85 93 91Guwahati 100 89 46Haldia 90 75 98

Mathura 80 103 103Panipat 106 106 102

Digboi 100 92 89IBP Co. Ltd. Explosives 43 61 65

Cryo-containers 63 45 64

Kochi Refineries Ltd. Refinery 106 105 101MRPL Refinery 122 104 75

Numaligarh Refinery Ltd. Refinery 68 73 63Oil and Natural Gas Corpn. Crude Oil NA NA NA

Natural Gas NA NA NA

VAP 99 104 108Oil India Ltd. Crude Oil 94 88 86

LPG 99 101 106Natural Gas 124 117 107

9.7.1.1 The Bharat Petroleum CorporationLtd. processed 9.14 million tonnes of crudeduring 2004-05 as aganist 8.76 milliontonnes during 2003-04.

9.7.1.2 The crude throughput for theBongaigaon Refinery and PetrochemicalsLtd. during 2004-05 was 2.18 million MT asagainst 2.00 million MT during the previousyear.

9.7.1.3 The Chennai Petroleum Corpn. Ltd.processed 8.923 million MT crude during theyear 2004-05 as against 7.039 million MTprocessed during the previous year.

9.7.1.4 The GAIL (India) Ltd. produced10.94 lakh MT of LPG during 2004-05 asagainst a production of 10.89 lakh MT duringthe previous year.

9.7.1.5 The Mumbai refinery of HindustanPetroleum Corporation Ltd. processed 6.12MMT of crude oil during the year 2004-05and Visakh refinery processed 7.82 MMT as

compared to 6.11 MMT and 7.59 MMTrespectively during the previous year

9.7.1.6 The IBP Co. Ltd. produced 51204MT of industrial explosives and 10381cryocontainers during 2004-05 as comparedto 52266 MT of industrial explosives and7496 cryocontainers during the previousyear.

9.7.1.7 The Indian Oil Blending Ltd.produced 1.98 lakh KL lubricating oil during2004-05 at 88% capacity utilization asagainst a production of 2.11 lakh KL during2003-04 a capacity utilization of 94%. Theproduction of greases was 12959 MT during2004-05 as compared to 12607 MT in theprevious year.

9.7.1.8 The combined throughput by theseven refineries of the Indian Oil CorporationLtd. during the year 2004-05 was 36.63million tonnes as against the previous year'sthroughput of 37.66 million tonnes. The

80 Public Enterprises Survey 2004-05 : Vol.-I

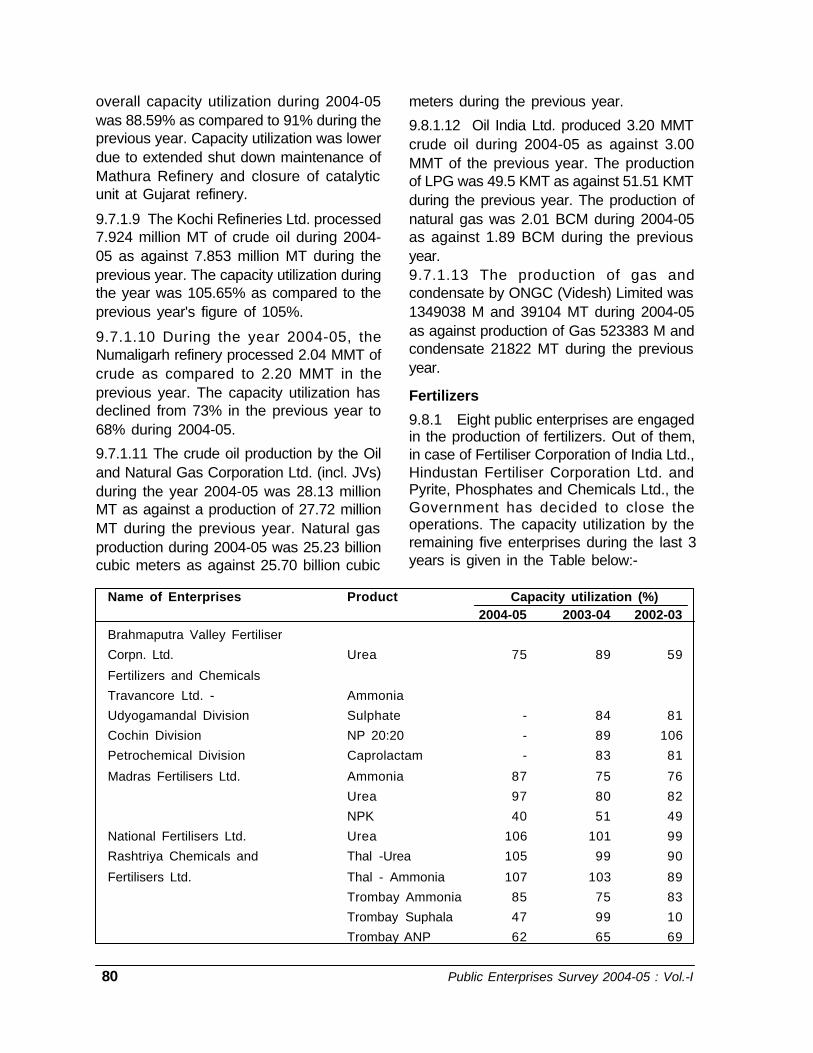

overall capacity utilization during 2004-05was 88.59% as compared to 91% during theprevious year. Capacity utilization was lowerdue to extended shut down maintenance ofMathura Refinery and closure of catalyticunit at Gujarat refinery.

9.7.1.9 The Kochi Refineries Ltd. processed7.924 million MT of crude oil during 2004-05 as against 7.853 million MT during theprevious year. The capacity utilization duringthe year was 105.65% as compared to theprevious year's figure of 105%.

9.7.1.10 During the year 2004-05, theNumaligarh refinery processed 2.04 MMT ofcrude as compared to 2.20 MMT in theprevious year. The capacity utilization hasdeclined from 73% in the previous year to68% during 2004-05.

9.7.1.11 The crude oil production by the Oiland Natural Gas Corporation Ltd. (incl. JVs)during the year 2004-05 was 28.13 millionMT as against a production of 27.72 millionMT during the previous year. Natural gasproduction during 2004-05 was 25.23 billioncubic meters as against 25.70 billion cubic

meters during the previous year.

9.8.1.12 Oil India Ltd. produced 3.20 MMTcrude oil during 2004-05 as against 3.00MMT of the previous year. The productionof LPG was 49.5 KMT as against 51.51 KMTduring the previous year. The production ofnatural gas was 2.01 BCM during 2004-05as against 1.89 BCM during the previousyear.9.7.1.13 The production of gas andcondensate by ONGC (Videsh) Limited was1349038 M and 39104 MT during 2004-05as against production of Gas 523383 M andcondensate 21822 MT during the previousyear.

Fertilizers

9.8.1 Eight public enterprises are engagedin the production of fertilizers. Out of them,in case of Fertiliser Corporation of India Ltd.,Hindustan Fertiliser Corporation Ltd. andPyrite, Phosphates and Chemicals Ltd., theGovernment has decided to close theoperations. The capacity utilization by theremaining five enterprises during the last 3years is given in the Table below:-

Name of Enterprises Product Capacity utilization (%)2004-05 2003-04 2002-03

Brahmaputra Valley Fertiliser

Corpn. Ltd. Urea 75 89 59

Fertilizers and Chemicals

Travancore Ltd. - Ammonia

Udyogamandal Division Sulphate - 84 81

Cochin Division NP 20:20 - 89 106

Petrochemical Division Caprolactam - 83 81

Madras Fertilisers Ltd. Ammonia 87 75 76

Urea 97 80 82

NPK 40 51 49

National Fertilisers Ltd. Urea 106 101 99

Rashtriya Chemicals and Thal -Urea 105 99 90

Fertilisers Ltd. Thal - Ammonia 107 103 89

Trombay Ammonia 85 75 83

Trombay Suphala 47 99 10

Trombay ANP 62 65 69

Productivity in Public Enterprises 81

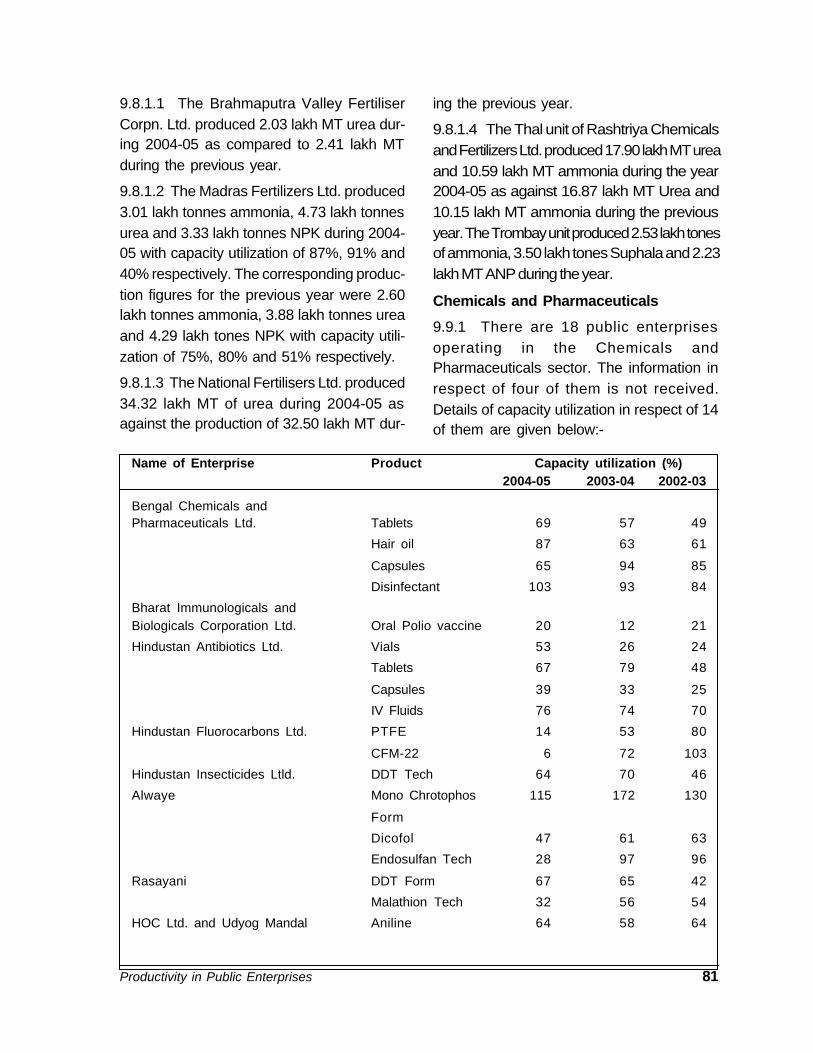

9.8.1.1 The Brahmaputra Valley FertiliserCorpn. Ltd. produced 2.03 lakh MT urea dur-ing 2004-05 as compared to 2.41 lakh MTduring the previous year.

9.8.1.2 The Madras Fertilizers Ltd. produced3.01 lakh tonnes ammonia, 4.73 lakh tonnesurea and 3.33 lakh tonnes NPK during 2004-05 with capacity utilization of 87%, 91% and40% respectively. The corresponding produc-tion figures for the previous year were 2.60lakh tonnes ammonia, 3.88 lakh tonnes ureaand 4.29 lakh tones NPK with capacity utili-zation of 75%, 80% and 51% respectively.

9.8.1.3 The National Fertilisers Ltd. produced34.32 lakh MT of urea during 2004-05 asagainst the production of 32.50 lakh MT dur-

ing the previous year.

9.8.1.4 The Thal unit of Rashtriya Chemicalsand Fertilizers Ltd. produced 17.90 lakh MT ureaand 10.59 lakh MT ammonia during the year2004-05 as against 16.87 lakh MT Urea and10.15 lakh MT ammonia during the previousyear. The Trombay unit produced 2.53 lakh tonesof ammonia, 3.50 lakh tones Suphala and 2.23lakh MT ANP during the year.

Chemicals and Pharmaceuticals

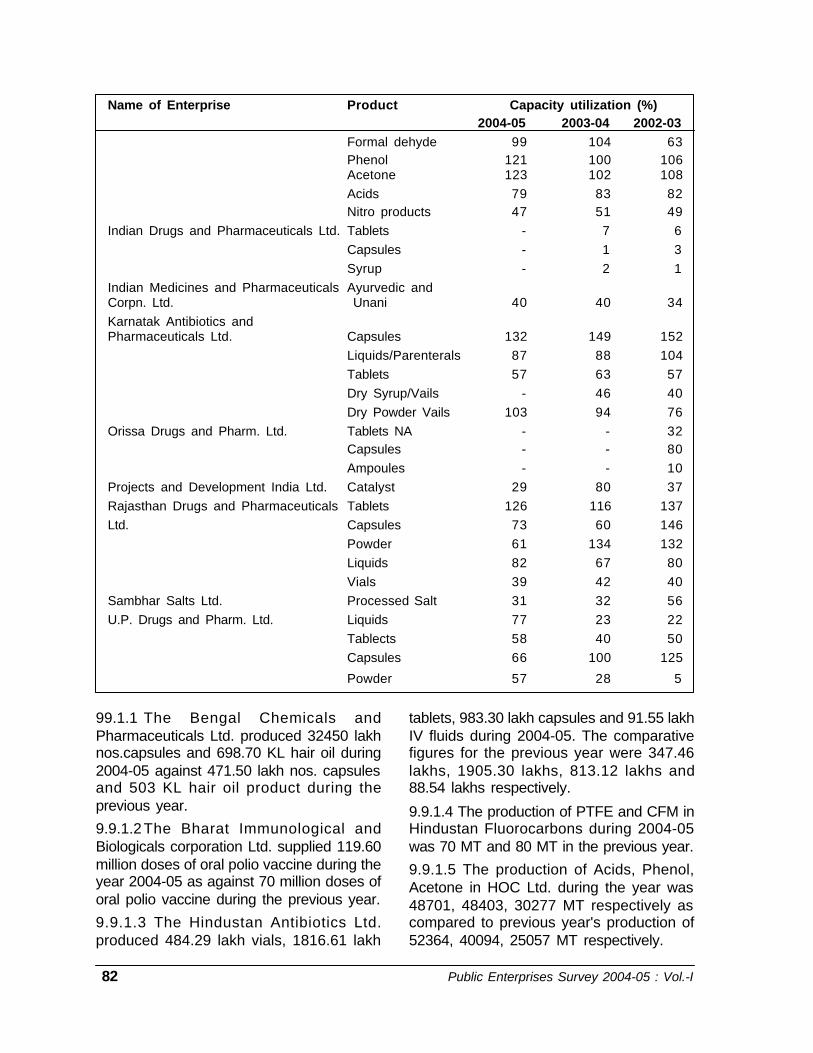

9.9.1 There are 18 public enterprisesoperating in the Chemicals andPharmaceuticals sector. The information inrespect of four of them is not received.Details of capacity utilization in respect of 14of them are given below:-

Name of Enterprise Product Capacity utilization (%)2004-05 2003-04 2002-03

Bengal Chemicals andPharmaceuticals Ltd. Tablets 69 57 49

Hair oil 87 63 61

Capsules 65 94 85

Disinfectant 103 93 84

Bharat Immunologicals andBiologicals Corporation Ltd. Oral Polio vaccine 20 12 21

Hindustan Antibiotics Ltd. Vials 53 26 24

Tablets 67 79 48

Capsules 39 33 25

IV Fluids 76 74 70

Hindustan Fluorocarbons Ltd. PTFE 14 53 80

CFM-22 6 72 103

Hindustan Insecticides Ltld. DDT Tech 64 70 46

Alwaye Mono Chrotophos 115 172 130

Form

Dicofol 47 61 63

Endosulfan Tech 28 97 96

Rasayani DDT Form 67 65 42

Malathion Tech 32 56 54

HOC Ltd. and Udyog Mandal Aniline 64 58 64

82 Public Enterprises Survey 2004-05 : Vol.-I

Name of Enterprise Product Capacity utilization (%)2004-05 2003-04 2002-03

Formal dehyde 99 104 63Phenol 121 100 106Acetone 123 102 108Acids 79 83 82Nitro products 47 51 49

Indian Drugs and Pharmaceuticals Ltd. Tablets - 7 6Capsules - 1 3Syrup - 2 1

Indian Medicines and Pharmaceuticals Ayurvedic andCorpn. Ltd. Unani 40 40 34Karnatak Antibiotics andPharmaceuticals Ltd. Capsules 132 149 152

Liquids/Parenterals 87 88 104Tablets 57 63 57Dry Syrup/Vails - 46 40Dry Powder Vails 103 94 76

Orissa Drugs and Pharm. Ltd. Tablets NA - - 32Capsules - - 80Ampoules - - 10

Projects and Development India Ltd. Catalyst 29 80 37Rajasthan Drugs and Pharmaceuticals Tablets 126 116 137Ltd. Capsules 73 60 146

Powder 61 134 132Liquids 82 67 80Vials 39 42 40

Sambhar Salts Ltd. Processed Salt 31 32 56U.P. Drugs and Pharm. Ltd. Liquids 77 23 22

Tablects 58 40 50Capsules 66 100 125

Powder 57 28 5

99.1.1 The Bengal Chemicals andPharmaceuticals Ltd. produced 32450 lakhnos.capsules and 698.70 KL hair oil during2004-05 against 471.50 lakh nos. capsulesand 503 KL hair oil product during theprevious year.

9.9.1.2The Bharat Immunological andBiologicals corporation Ltd. supplied 119.60million doses of oral polio vaccine during theyear 2004-05 as against 70 million doses oforal polio vaccine during the previous year.

9.9.1.3 The Hindustan Antibiotics Ltd.produced 484.29 lakh vials, 1816.61 lakh

tablets, 983.30 lakh capsules and 91.55 lakhIV fluids during 2004-05. The comparativefigures for the previous year were 347.46lakhs, 1905.30 lakhs, 813.12 lakhs and88.54 lakhs respectively.

9.9.1.4 The production of PTFE and CFM inHindustan Fluorocarbons during 2004-05was 70 MT and 80 MT in the previous year.

9.9.1.5 The production of Acids, Phenol,Acetone in HOC Ltd. during the year was48701, 48403, 30277 MT respectively ascompared to previous year's production of52364, 40094, 25057 MT respectively.

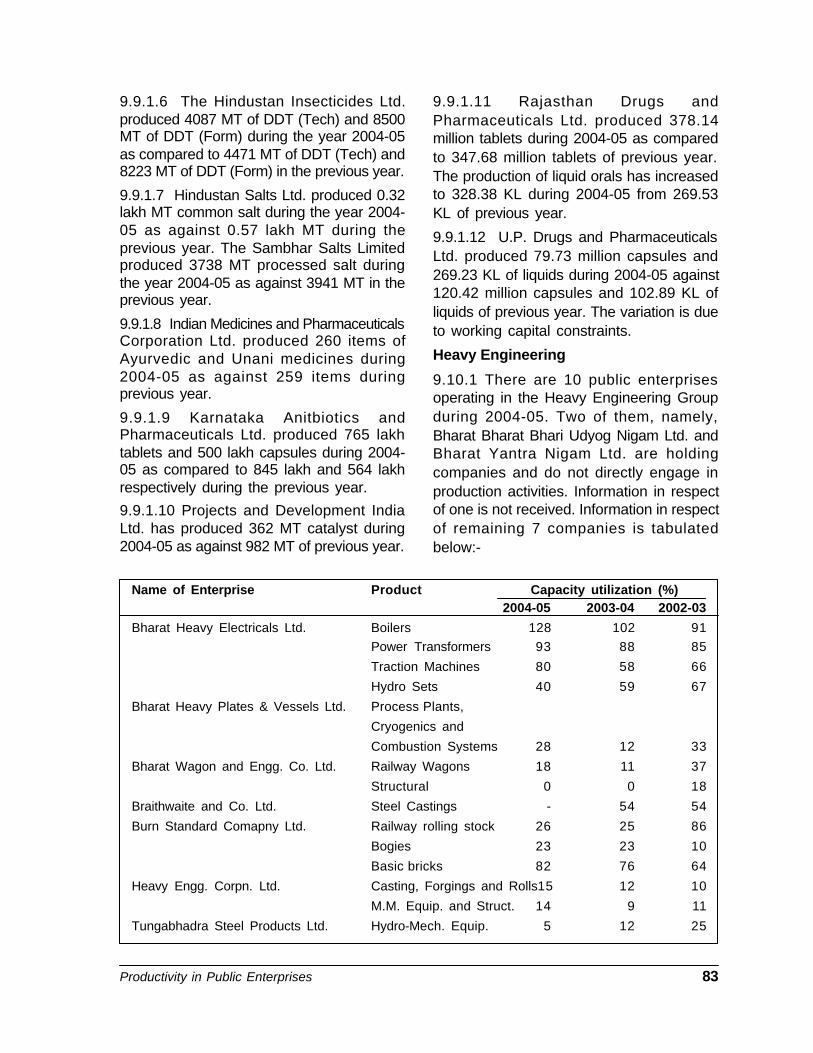

Productivity in Public Enterprises 83

9.9.1.6 The Hindustan Insecticides Ltd.produced 4087 MT of DDT (Tech) and 8500MT of DDT (Form) during the year 2004-05as compared to 4471 MT of DDT (Tech) and8223 MT of DDT (Form) in the previous year.

9.9.1.7 Hindustan Salts Ltd. produced 0.32lakh MT common salt during the year 2004-05 as against 0.57 lakh MT during theprevious year. The Sambhar Salts Limitedproduced 3738 MT processed salt duringthe year 2004-05 as against 3941 MT in theprevious year.

9.9.1.8 Indian Medicines and PharmaceuticalsCorporation Ltd. produced 260 items ofAyurvedic and Unani medicines during2004-05 as against 259 items duringprevious year.

9.9.1.9 Karnataka Anitbiotics andPharmaceuticals Ltd. produced 765 lakhtablets and 500 lakh capsules during 2004-05 as compared to 845 lakh and 564 lakhrespectively during the previous year.

9.9.1.10 Projects and Development IndiaLtd. has produced 362 MT catalyst during2004-05 as against 982 MT of previous year.

9.9.1.11 Rajasthan Drugs andPharmaceuticals Ltd. produced 378.14million tablets during 2004-05 as comparedto 347.68 million tablets of previous year.The production of liquid orals has increasedto 328.38 KL during 2004-05 from 269.53KL of previous year.

9.9.1.12 U.P. Drugs and PharmaceuticalsLtd. produced 79.73 million capsules and269.23 KL of liquids during 2004-05 against120.42 million capsules and 102.89 KL ofliquids of previous year. The variation is dueto working capital constraints.

Heavy Engineering

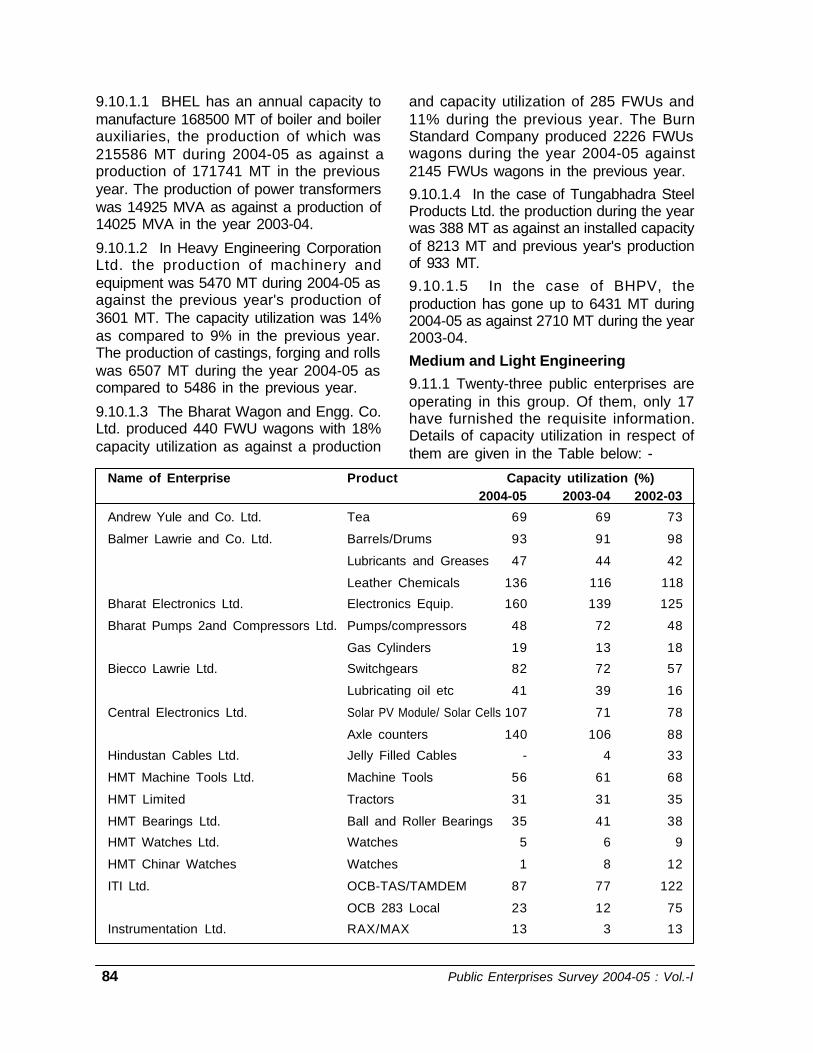

9.10.1 There are 10 public enterprisesoperating in the Heavy Engineering Groupduring 2004-05. Two of them, namely,Bharat Bharat Bhari Udyog Nigam Ltd. andBharat Yantra Nigam Ltd. are holdingcompanies and do not directly engage inproduction activities. Information in respectof one is not received. Information in respectof remaining 7 companies is tabulatedbelow:-

Name of Enterprise Product Capacity utilization (%)2004-05 2003-04 2002-03

Bharat Heavy Electricals Ltd. Boilers 128 102 91Power Transformers 93 88 85

Traction Machines 80 58 66

Hydro Sets 40 59 67

Bharat Heavy Plates & Vessels Ltd. Process Plants,

Cryogenics and

Combustion Systems 28 12 33