CORRELATION AMONG INTERNATIONAL EQUITY MARKETS AND INTERNATIONAL DIVERSIFICATION

11

CORRELATION AMONG INTERNATIONAL EQUITY MARKETS AND INTERNATIONAL DIVERSIFICATION Hakan Saritas*, Hakan Aygoren Pamukkale University, The Faculty of Economics and Administrative Sciences, Department of Business Administration *Corresponding author. Hakan Saritas Address: Pamukkale University, I.I.B.F. Kinikli Kampusu 20040 Kinikli / Denizli / Turkey E-mail : [email protected] & [email protected] Tel : +90 258 213 40 30 / 1258 Fax : +90 258 213 40 39 Hakan Aygoren Address: Pamukkale University, I.I.B.F. Kinikli Kampusu 20040 Kinikli / Denizli / Turkey E-mail : [email protected] & [email protected] Tel : +90 258 213 40 30 / 1258 Fax : +90 258 213 40 39

Transcript of CORRELATION AMONG INTERNATIONAL EQUITY MARKETS AND INTERNATIONAL DIVERSIFICATION

CORRELATION AMONG INTERNATIONAL EQUITY MARKETS AND

INTERNATIONAL DIVERSIFICATION

Hakan Saritas*, Hakan Aygoren

Pamukkale University, The Faculty of Economics and Administrative Sciences,

Department of Business Administration

*Corresponding author.

Hakan Saritas

Address: Pamukkale University, I.I.B.F. Kinikli Kampusu 20040

Kinikli / Denizli / Turkey

E-mail : [email protected] & [email protected]

Tel : +90 258 213 40 30 / 1258

Fax : +90 258 213 40 39

Hakan Aygoren

Address: Pamukkale University, I.I.B.F. Kinikli Kampusu 20040

Kinikli / Denizli / Turkey

E-mail : [email protected] & [email protected]

Tel : +90 258 213 40 30 / 1258

Fax : +90 258 213 40 39

CORRELATION AMONG INTERNATIONAL EQUITY MARKETS AND

INTERNATIONAL DIVERSIFICATION

Abstract

The main motivation behind international investing is that global investing offers

investors a larger pool of investment opportunities and tremendous diversification. The

arguments for global portfolio diversification are centered on decreasing portfolio risk or

increasing portfolio expected return relative to a comparable domestic portfolio.

However, the level of correlation among the world’s equity markets has an important

impact on diversification as such that the low correlation among the world’s equity markets

provides the opportunity to enhance risk-adjusted expected return.

This study considers the impact of the level of correlation among the world’s equity

markets on international portfolio diversification. Returns of fifteen international indexes are

regressed against ISE-100 Index (Istanbul Stock Exchange-100 Index) returns using monthly

return data from 1998 through 2002. The results of the study suggest that international

investing may offer domestic investors tremendous diversification opportunities since

international indexes have little correlation to the Turkish market.

Keywords: international investing, international diversification, and correlation.

1. Introduction

International investing provides investors tremendous diversification. A superior rate

of return is one key benefit of international investing. A global focus also offers a larger pool

of investment opportunities. Therefore, international investment is growing rapidly among

private and institutional investors, fueled by the deregulation of national markets and the

relaxation of capital controls.

The trend toward international investments reflects the growing recognition that

international diversification can yield a superior risk-reward trade-off compared to domestic

investments. (Jorion and Roisenberg, 1993). The clear value of moving assets to international

equities is diversification. Plans can reduce their volatility by investing in international

securities. Aiello and Chieffe (1999) suggest that international diversification can reduce

investment risk to about 56% of the level that can be achieved with national diversification.

Although international investing provides tremendous diversification benefits, the

level of correlation among the equity markets around the world has an important impact on

diversification. Speidell and Sappenfield (1992) and Fouse (1992) point out that the low

correlation among the world’s equity markets provides the opportunity to enhance risk-

adjusted expected return.

2. International Investing and Diversification

International investment is growing rapidly among private and institutional investors

mainly because of benefits of global portfolio diversification.

One of the benefits of diversification is that markets tend to move independently, so

their returns balance one another. The arguments for global portfolio diversification are

centered on decreasing portfolio risk or increasing portfolio expected return relative to a

comparable domestic portfolio. The seed of the argument was planted in Markowitz's classic

work on portfolio efficiency. Michaud et al (1996) indicates that globally diversified

portfolios hold out the very real promise of less risk for the same level of expected return, or

more return for the same level of risk, or both, than can be achieved with domestic portfolios.

Markowitz's arguments provide a sound theoretical rationale for the obvious intuitive benefits

of global portfolios: significant expansion of investment opportunities over those of a purely

domestic investor. Global investment vastly widens the number of investment choices,

leading to many opportunities for significantly improving performance.

Michaud et al (1996) indicates that the size and stability over time of correlations

between country indexes impact the likely benefits of international investment. Darbar and

Deb point out that international diversification has been routinely advocated based on low

cross-country correlations. The international capital asset pricing model suggests that the

potential benefits from international diversification for domestic investors are significant if

cross-country covariances are small. However, investors may not be able to diversify away

much domestic risk if the cross-country covariances are large.

Even though global markets have wide differences in historic returns and risk,

correlations among assets may tend to increase because of such factors as that fewer decision-

makers control larger amounts of trading (institutional portfolios represent a larger portion of

trading), that indexing tends to bind stocks together, that increasing integration of the fiscal

and monetary policies of member nations will bind all European equities closer together and

developments of similar unifying trade zones in Asia and the America will make markets

move alike, and that the growth of world trade makes companies in all countries mutually

dependent and the advance of instantaneous communication causes markets respond

simultaneously to global news (Speidell and Sappenfield, 1992).

Akdogan (1996) suggests that higher degrees of segmentation (fraction of a country's

systematic risk compared to a global benchmark portfolio) would offer higher risk-adjusted

returns, and hence make a market more attractive for international investors. Evidence using

this approach suggests that some small to medium-sized European capital markets (Finland,

Denmark, Spain, and Italy) along with most emerging markets exhibit segmentation, and

deserve a closer look by international portfolio managers.

Becker (1999) suggests that European economic, fiscal, and monetary harmonization

will cause fundamental changes in the relative behavior of European capital markets. For

example, over the last decade we have witnessed a gradual movement toward a more

integrated equity market. This evolution implies higher correlations, possibly leading to a

reduction in diversification potential and therefore to higher portfolio risk.

International portfolio diversification opportunities to be exploited are greater in

countries with segmented capital markets than in those with markets (relatively) more

integrated with the rest of the world, typically to a benchmark world market portfolio The

issue of capital market segmentation (or integration) is important for international portfolio

investors because internationally diversified portfolios are likely to exhibit risk-adjusted

returns higher than purely national portfolios. Investors who commit their funds to domestic

markets can diversify away only locally unsystematic risk. More diversification opportunities

are available through foreign markets. In international portfolio investments, domestically

systematic risk or part of it may become idiosyncratic, hence diversifiable. An international

investor can eliminate part of systematic risk that is otherwise undiversifiable in addition to

the local idiosyncratic risk (Akdogan, 1997).

3. Current Study

The main reason that international investing became popular among investors is global

diversification opportunities. By moving assets to international securities, plans can reduce

their volatility exposed in domestic markets.

Darbar and Deb point out that international diversification has been routinely

advocated based on low cross-country correlations. The international capital asset pricing

model suggests that the potential benefits from international diversification for domestic

investors are significant if cross-country covariances are small. However, investors may not

be able to diversify away much domestic risk if the cross-country covariances are large.

In this study, we tried to find out if investors can take advantage of global

diversification benefits from investing in international securities, based on the level of

correlation among markets. We find similar results with Aiello and Chieffe (1999) in that

international investing provides great diversification potential.

4. Research Design

To find out whether investing in international securities may provide domestic

individuals a good diversification opportunity, we have performed both individual and

multiple regressions between the selected international indexes and the domestic index.

We examined the correlation of the international indexes with the ISE-100 Index to

find out if there are diversification benefits to investing in international index funds.

We attempt to answer the following questions: 1) Does a linear relationship exist

between the individual international index returns and the ISE-100 returns?; 2) Does a linear

relationship exist between the returns on the entire portfolio of international indexes and the

returns on the ISE-100?; 3) How much correlation exists between international indexes and

the ISE-100.

In this study, we used monthly return data in USD bases on fifteen international

indexes that are formed, designed and updated by MSCI. The sample period is January 1998

through December 2002. We chose the indexes on such basis that different regions of the

world is covered. The ISE-100 is the benchmark Turkey Index. The three-month Turkish

Treasury bill yield is used as the risk-free rate. We compute excess returns of the indexes in

USD bases from this security.

5. Analysis of Data and Results

Table 1 shows the risk-return data for the fifteen international indexes and the ISE-

100. During the evaluation period, the average monthly return on international indexes is –

0.099 %. The average monthly return on the ISE-100 is 0.401 %. All of the fifteen

international indexes return less than ISE-100. EM Europe & Middle East Index has the

largest monthly returns at 0.206 % and Pacific Index has the smallest at -0.328 %.

The lowest standard deviation is that of EAFE Index at 0.0491. EM Europe & Middle

East Index has the greatest standard deviation at 0.0886. The standard deviation of ISE-100 is

0.2061. The overall average standard deviation for international indexes is 0.0587. The

benchmark index ISE-100 seems to be too risky compared to international indexes.

Table 1. Returns for International Indexes and ISE-100

Index

Average Monthly Return

Standard Deviation

Developed markets INTERNATIONAL INDEXES THE WORLD INDEX -0,126% 0,0504NORTH AMERICA 0,024% 0,0555EAFE -0,260% 0,0491EUROPE -0,179% 0,0530PACIFIC -0,328% 0,0586INTERNATIONAL FREE INDEXES WORLD EX USA -0,236% 0,0495USA 0,013% 0,0553Emerging Markets INTERNATIONAL INDEXES EMF (EMERGING MARKETS FREE) 0,017% 0,0813EM EUROPE & MIDDLE EAST 0,206% 0,0886Combined Markets ALL COUNTRY INDEXES AC EUROPE -0,172% 0,0534EU -0,168% 0,0544ALL COUNTRY FREE INDEXES AC WORLD INDEX FREE EX USA -0,227% 0,0509EAFE + EMF -0,247% 0,0505AC ASIA PACIFIC FREE EX JAPAN 0,184% 0,0740AC AMERICAS FREE 0,012% 0,0559Average International -0,099% 0,0587ISE-100 (IMKB-100) 0,401% 0,2061

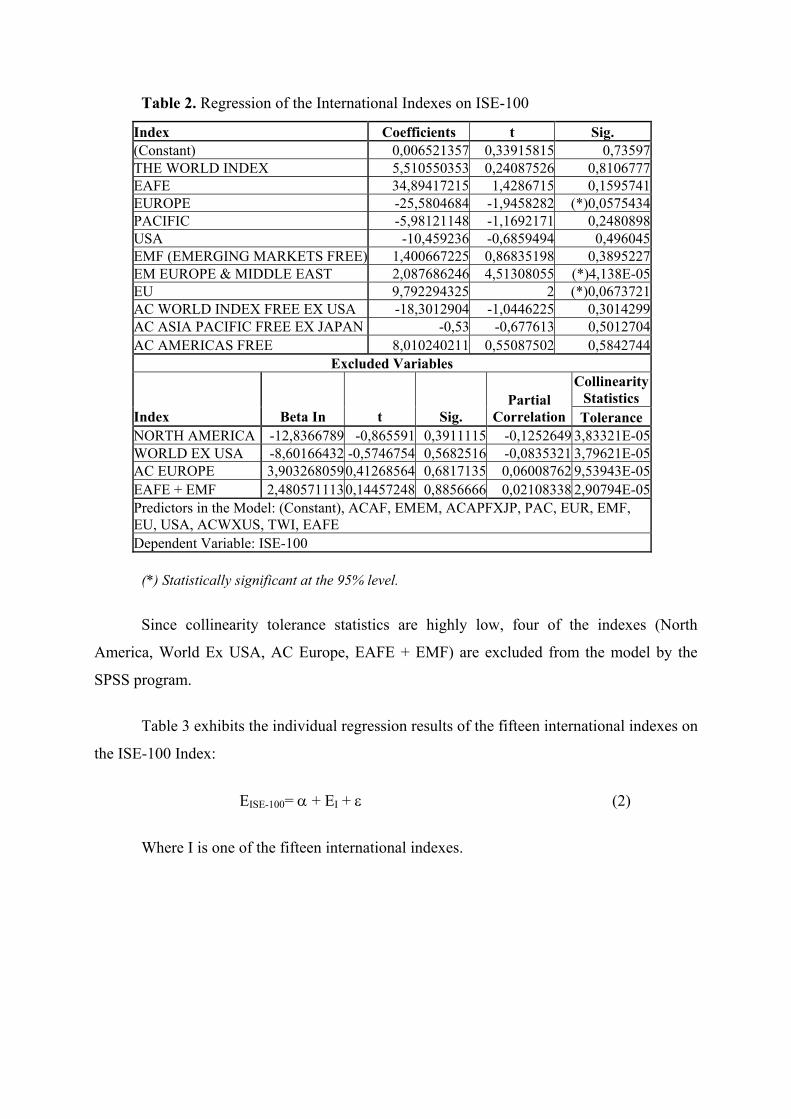

Table 2 shows the results of the regression of the international indexes on the ISE-100

Index:

EISE-100= a + EACAF + EEMEM + EACAPFXJP + EPAC + EEUR +

EEMF + EEU + EUSA + EACWXUS + ETWI + EEAFE + ε (1)

Where E is the excess returns (monthly index return – monthly T-Bill return).

The variation in Europe Index, EM Europe & Middle East Index and EU Index

significantly explains some variation in the ISE-100 Index. While Europe Index is negatively

correlated to the ISE-100 Index, EM Europe & Middle East Index and EU Index are

positively correlated to the ISE-100 Index.

Table 2. Regression of the International Indexes on ISE-100

Index Coefficients t Sig. (Constant) 0,006521357 0,33915815 0,73597 THE WORLD INDEX 5,510550353 0,24087526 0,8106777 EAFE 34,89417215 1,4286715 0,1595741 EUROPE -25,5804684 -1,9458282 (*)0,0575434 PACIFIC -5,98121148 -1,1692171 0,2480898 USA -10,459236 -0,6859494 0,496045 EMF (EMERGING MARKETS FREE) 1,400667225 0,86835198 0,3895227 EM EUROPE & MIDDLE EAST 2,087686246 4,51308055 (*)4,138E-05 EU 9,792294325 2 (*)0,0673721 AC WORLD INDEX FREE EX USA -18,3012904 -1,0446225 0,3014299 AC ASIA PACIFIC FREE EX JAPAN -0,53 -0,677613 0,5012704 AC AMERICAS FREE 8,010240211 0,55087502 0,5842744

Excluded Variables Collinearity

Statistics Index Beta In t Sig.

Partial Correlation Tolerance

NORTH AMERICA -12,8366789 -0,865591 0,3911115 -0,1252649 3,83321E-05 WORLD EX USA -8,60166432 -0,5746754 0,5682516 -0,0835321 3,79621E-05 AC EUROPE 3,9032680590,41268564 0,6817135 0,06008762 9,53943E-05 EAFE + EMF 2,4805711130,14457248 0,8856666 0,02108338 2,90794E-05 Predictors in the Model: (Constant), ACAF, EMEM, ACAPFXJP, PAC, EUR, EMF, EU, USA, ACWXUS, TWI, EAFE Dependent Variable: ISE-100

(*) Statistically significant at the 95% level.

Since collinearity tolerance statistics are highly low, four of the indexes (North

America, World Ex USA, AC Europe, EAFE + EMF) are excluded from the model by the

SPSS program.

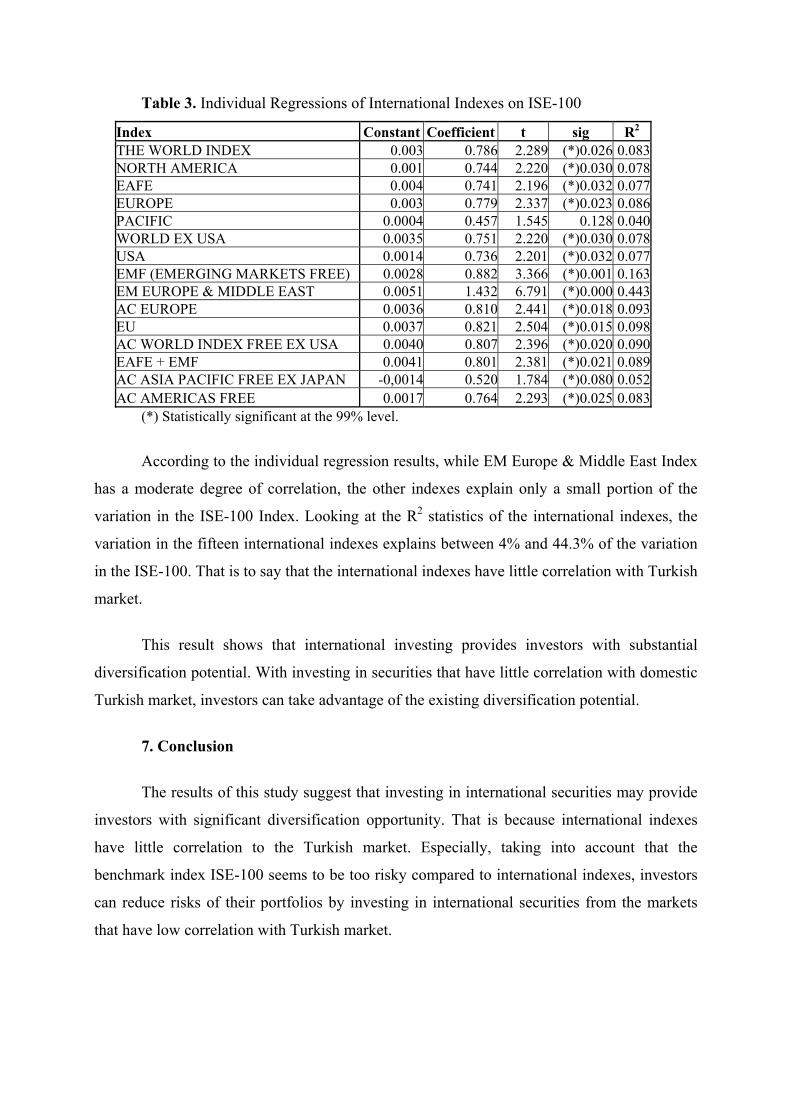

Table 3 exhibits the individual regression results of the fifteen international indexes on

the ISE-100 Index:

EISE-100= α + EI + ε (2)

Where I is one of the fifteen international indexes.

Table 3. Individual Regressions of International Indexes on ISE-100

Index Constant Coefficient t sig R2 THE WORLD INDEX 0.003 0.786 2.289 (*)0.026 0.083NORTH AMERICA 0.001 0.744 2.220 (*)0.030 0.078EAFE 0.004 0.741 2.196 (*)0.032 0.077EUROPE 0.003 0.779 2.337 (*)0.023 0.086PACIFIC 0.0004 0.457 1.545 0.128 0.040WORLD EX USA 0.0035 0.751 2.220 (*)0.030 0.078USA 0.0014 0.736 2.201 (*)0.032 0.077EMF (EMERGING MARKETS FREE) 0.0028 0.882 3.366 (*)0.001 0.163EM EUROPE & MIDDLE EAST 0.0051 1.432 6.791 (*)0.000 0.443AC EUROPE 0.0036 0.810 2.441 (*)0.018 0.093EU 0.0037 0.821 2.504 (*)0.015 0.098AC WORLD INDEX FREE EX USA 0.0040 0.807 2.396 (*)0.020 0.090EAFE + EMF 0.0041 0.801 2.381 (*)0.021 0.089AC ASIA PACIFIC FREE EX JAPAN -0,0014 0.520 1.784 (*)0.080 0.052AC AMERICAS FREE 0.0017 0.764 2.293 (*)0.025 0.083

(*) Statistically significant at the 99% level.

According to the individual regression results, while EM Europe & Middle East Index

has a moderate degree of correlation, the other indexes explain only a small portion of the

variation in the ISE-100 Index. Looking at the R2 statistics of the international indexes, the

variation in the fifteen international indexes explains between 4% and 44.3% of the variation

in the ISE-100. That is to say that the international indexes have little correlation with Turkish

market.

This result shows that international investing provides investors with substantial

diversification potential. With investing in securities that have little correlation with domestic

Turkish market, investors can take advantage of the existing diversification potential.

7. Conclusion

The results of this study suggest that investing in international securities may provide

investors with significant diversification opportunity. That is because international indexes

have little correlation to the Turkish market. Especially, taking into account that the

benchmark index ISE-100 seems to be too risky compared to international indexes, investors

can reduce risks of their portfolios by investing in international securities from the markets

that have low correlation with Turkish market.

References

Aiello, S. and Chieffe, N. (1999). International index funds and the investment

portfolio. Financial Services Review, v8, n1: 27-35.

Akdogan, Haluk. 1996. A suggested approach to country selection in international

portfolio diversification: select countries on the basis of their segmentation scores. Journal of

Portfolio Management, Fall v23 n1: 33-39.

Akdogan, Haluk. 1997. International security selection under segmentation: theory and

application. Journal of Portfolio Management, Fall v24 n1:82-92.

Beckers, Stan. 1999. Investment implications of a single European capital market:

stronger correlations, fewer decision variables, diminished manager opportunities. Journal of

Portfolio Management, Spring v25 i3: 9-17.

Darbar, Salim M.; Deb, Partha. 1997. Co-movements in international equity markets.

Journal of Financial Research, Fall v20 n3: 305-323.

Fouse, W. L. 1992. Allocating assets across country markets. Journal of Portfolio

Management, Wntr v18 n2: 20-27.

Jorion, P. and Roisenberg, L. 1993. Synthetic International Diversification. The

Journal of Portfolio Management, Winter, v19, n2: 65-74.

Michaud, Richard O.;. Bergstrom, Gary L; Frashure, Ronald D.; Wolahan, Brian K.

1996. Twenty years of international equity investing: still a route to higher returns and lower

risks? Journal of Portfolio Management, Fall v23 n1: 9-22.

Speidell, Lawrenece S. and Sappenfield, Ross. 1992. Global diversification in a

shrinking world. Journal of Portfolio Management, Fall v19 n1: 57-68.